FEDERAL COURT OF AUSTRALIA

Visa International Service Association v Reserve Bank of Australia

[2003] FCA 977

ADMINISTRATIVE LAW – judicial review – credit card schemes – determination by Reserve Bank – access regime – no surcharge standard – interchange fee standard – designation of credit card systems for regulation – alleged uncertainty – alleged failure to take account of relevant considerations – failure to investigate – methodology – Wednesbury unreasonableness – lack of proportionality – wrongful delegation of power

STATUTORY INTERPRETATION – payment system – funds – funds transfer system – circulation of money – standards – access regime – relates to – means and includes – have regard to – competition – efficiency – market – legislative history – extrinsic materials

EVIDENCE – expert economic evidence – admissibility – use – discretion – relevance to judicial review – expert accounting evidence – uncertainty – alleged bias

BANKING – money – funds – transfer of funds – payment systems – Australian payments system – risk – clearing – settlement – payment instruments

Payment Systems (Regulation) Act 1998 (Cth) ss 7, 8, 11, 12, 18

Reserve Bank Act 1959 (Cth) ss 10, 10B, 87

Judiciary Act 1903 (Cth) s 39

Administrative Decisions (Judicial Review) Act 1977 (Cth) s 11

Financial Sector Reform (Amendments and Transitional Provisions) Act 1998 (Cth)

Associated Provincial Picture Houses Ltd v Wednesbury Corporation [1948] 1 KB 223 referred to

Attorney-General (NSW) v Quin (1990) 170 CLR 1 referred to

Corporation of the City of Enfield v Development Assessment Commission (2000) 199 CLR 135 referred to

Minister for Immigration & Multicultural Affairs v Jia Legeng (2001) 205 CLR 507 referred to

Browne v Dunn (1893) 6 R 67 referred to

Libyan Arab Foreign Bank v Bankers Trust Co [1989] 1 QB 728 discussed

A/S Awilco of Oslo v Fulvia SpA Di Navigazione of Cagliari [1981] 1 WLR 314 discussed

National Australia Bank Ltd v KDS Construction Services Pty Ltd (1987) 163 CLR 668 discussed

Re Charge Card Services Ltd [1987] 1 Ch. 150 discussed

Deputy Commissioner of Taxation v Conley (1998) 158 ALR 229 discussed

Zickar v MGH Plastic Industries Pty Ltd (1996) 187 CLR 310 referred to

O’Grady v Northern Queensland Co Ltd (1990) 169 CLR 356 cited

Collector of Customs v Agfa-Gevaert Ltd (1996) 186 CLR 389 cited

Helvering v Gregory (1934) 69 F.2d 809 referred to

Strathfield Municipal Council v Poynting (2001) 116 LGERA 319 referred to

Herald-Sun TV Pty Ltd v Australian Broadcasting Tribunal (1985) 156 CLR 1 discussed

Australian Broadcasting Tribunal v Saatchi & Saatchi Compton (Vic) Pty Ltd (1985) 10 FCR 1 discussed

R v Galvin; Ex parte Metal Trades Employers’ Association (1949) 77 CLR 432 referred to

Re Bolton; Ex parte Beane (1987) 162 CLR 514 discussed

Lowy v The Land and Environment Court of New South Wales (2002) 123 LGERA 179 referred to

Warringah Shire Council v KVM Investments Pty Ltd (1981) 45 LGERA 425 referred to

North Sydney Municipal Council v PD Mayoh Pty Ltd [No 2] (1990) 71 LGRA 222 cited

Conroy v Shire of Springvale and Noble Park [1959] VR 737 discussed

King Gee Clothing Co Pty Ltd v The Commonwealth (1945) 71 CLR 184 discussed

Television Corporation Ltd v The Commonwealth (1963) 109 CLR 59 referred to

Vardon v The Commonwealth (1943) 67 CLR 434 discussed

Bendixen v Coleman, Scott and Croft (1943) 68 CLR 401 discussed

Fraser Henleins Pty Ltd v Cody (1945) 70 CLR 100 referred to

Conley v Commissioner of Taxation (1998) 81 FCR 24 cited

Television Corporation Ltd v The Commonwealth (1963) 109 CLR 59 cited

Federal Commissioner of Taxation v F H Faulding & Co Pty Ltd (1950) 83 CLR 594 referred to

Warringah Shire Council v Pittwater Provisional Council (1992) 26 NSWLR 491 referred to

Dainford Ltd v Smith (1985) 155 CLR 342 referred to

Van Gorkom v Attorney-General (NZ) [1977] 1 NZLR 535 referred to

Racecourse Co-operative Sugar Association Ltd v Attorney-General of the State of Queensland (1979) 142 CLR 460 discussed

Telstra Corporation Ltd v Seven Cable Television Pty Ltd (2000) 102 FCR 517 followed

RG Capital Radio Ltd v Australian Broadcasting Authority (2001) 113 FCR 185 discussed

Buck v Bavone (1976) 135 CLR 110 referred to

Minister for Immigration and Ethnic Affairs v Teo (1995) 57 FCR 194 cited

Minister for Immigration and Ethnic Affairs v Wu Shan Liang (1996) 185 CLR 259 cited

Australian Heritage Commission v Mount Isa Mines Ltd (1997) 187 CLR 297 cited

Minister for Immigration and Multicultural Affairs v Eshetu (1999) 197 CLR 611 referred to

R v Connell; Ex parte Hetton Bellbird Collieries Ltd (1944) 69 CLR 407 applied

Sean Investments Pty Ltd v MacKellar (1981) 38 ALR 363 referred to

Elliott v Southwark London Borough Council [1976] 1 WLR 499 referred to

The Queen v Toohey; Ex parte Meneling Station Pty Ltd (1982) 158 CLR 327 referred to

Minister for Aboriginal Affairs v Peko-Wallsend Ltd (1986) 162 CLR 24 referred to

Turner v Minister for Immigration and Ethnic Affairs (1987) 35 ALR 388 cited

Tobacco Institute of Australia v National Health and Medical Research Council (1996) 71 FCR 265 cited

NIB Health Funds Ltd v Private Health Insurance Administration Council (2002) 115 FCR 561 cited

The Council of the City of Parramatta v Pestell (1972) 128 CLR 305 referred to

Coal Miners’ Industrial Union of Workers of Western Australia v Amalgamated Collieries of Western Australia Ltd (1960) 104 CLR 437 cited

Western Stores Ltd v Orange City Council [1971] 2 NSWLR 36 cited

Minister for Natural Resources v New South Wales Aboriginal Land Council (1987) 9 NSWLR 154 cited

Prasad v Minister for Immigration and Ethnic Affairs (1985) 6 FCR 155 discussed

Tickner v Bropho (1993) 40 FCR 183 cited

Luu v Renevier (1989) 91 ALR 39 cited

Parramatta City Council v Hale (1982) 47 LGRA 319 distinguished

Currey v Sutherland Shire Council (1998) 100 LGERA 365 distinguished

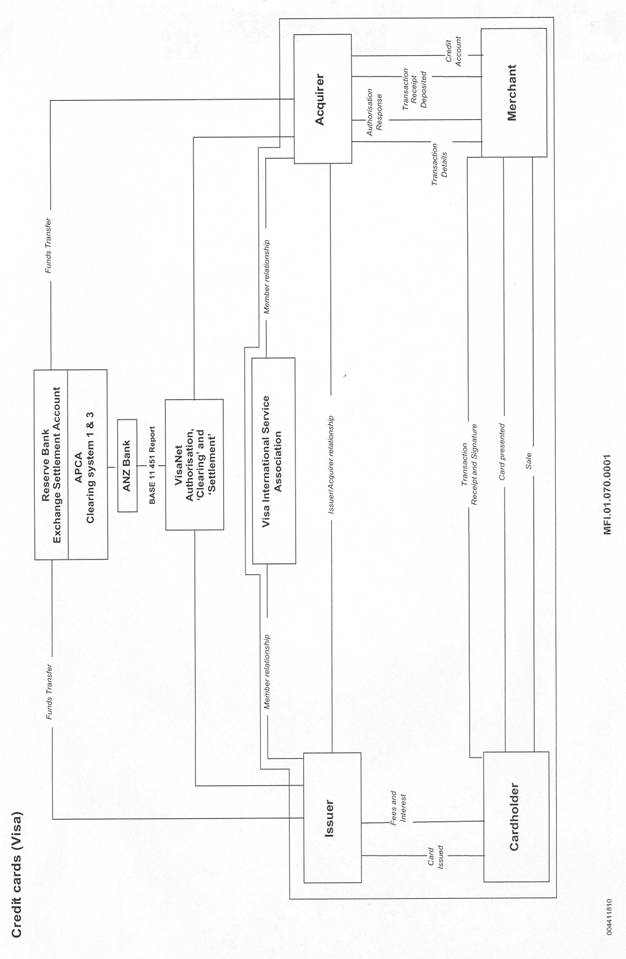

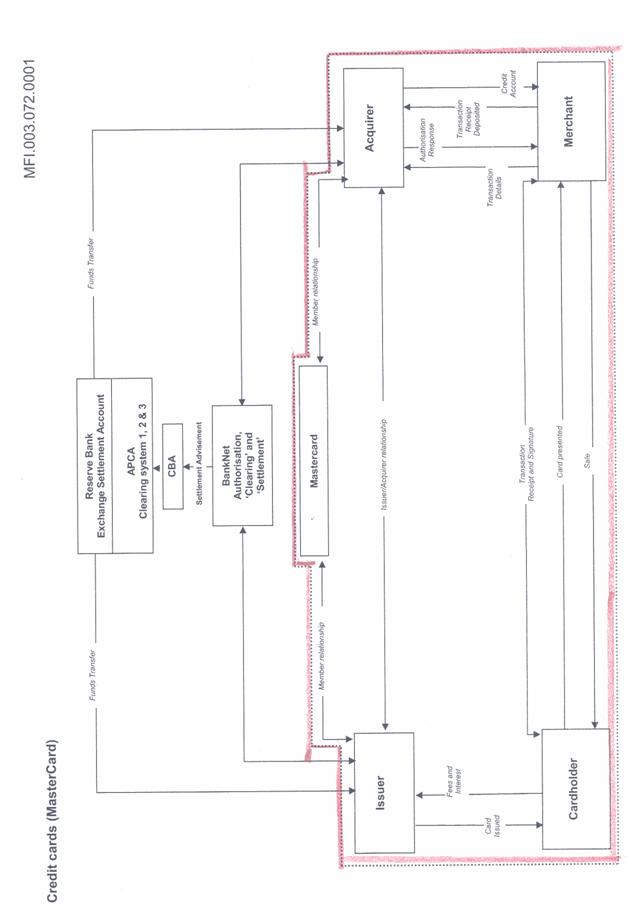

Franklins Ltd v Penrith City Council [1999] NSWCA 134 distinguished

Jones v Dunkel (1959) 101 CLR 298 not applied

Collector of Customs v Agfa-Gevaert Ltd (1996) 186 CLR 389 referred to

Makita (Australia) Pty Ltd v Sprowles (2001) 52 NSWLR 705 cited

Evans Deakin Pty Ltd v Sebel Furniture Ltd [2003] FCA 171 cited

Ancher, Mortlock, Murray & Woolley Pty Ltd v Hooker Homes Pty Ltd [1971] 2 NSWLR 278 referred to

Re Dr Ken Michael AM; Ex parte Epic Energy (WA) Nominees Pty Ltd [2002] WASCA 231 referred to

Allstate Life Insurance Co v Australia and New Zealand Banking Group (No 6) (1996) 64 FCR 79 cited

South Australia v Tanner (1989) 166 CLR 161 referred to

Williams v Melbourne Corporation (1933) 49 CLR 142 referred to

Pearce and Geddes, “Statutory Interpretation in Australia” 5th ed. 2001

Mann, “The Legal Aspects of Money” 5th ed. 1992

Lave, “Benefit-Cost Analysis: Do the Benefits Exceed the Costs? in A. Ogus (ed), Regulation, Economics and the Law

Aaronson and Dyer, “Judicial Review of Administrative Action” 2nded. 2000

VISA INTERNATIONAL SERVICE ASSOCIATION (ARBN 007 507 511)

v RESERVE BANK OF AUSTRALIA

N973 OF 2002

AND

MASTERCARD INTERNATIONAL INCORPORATED

v RESERVE BANK OF AUSTRALIA

N987 OF 2002

TAMBERLIN J

SYDNEY

19 SEPTEMBER 2003

| IN THE FEDERAL COURT OF AUSTRALIA |

|

| NEW SOUTH WALES DISTRICT REGISTRY | N 973 OF 2002 N 987 OF 2002

|

|

|

|

| BETWEEN: | VISA INTERNATIONAL SERVICE ASSOCIATION (ARBN 007 507 511) APPLICANT

|

| AND: | RESERVE BANK OF AUSTRALIA RESPONDENT

|

| BETWEEN: |

MASTERCARD INTERNATIONAL INCORPORATED APPLICANT |

| AND: |

RESERVE BANK OF AUSTRALIA RESPONDENT

|

| TAMBERLIN J | |

| DATE OF ORDER: | 19 SEPTEMBER 2003 |

| WHERE MADE: | SYDNEY |

THE COURT ORDERS THAT:

1. An extension of time is granted to each of the applicants to file applications for review under the Administrative Decisions (Judicial Review) Act 1977 (Cth).

2. The applications for review are dismissed.

3. The question of costs is stood over to a date to be fixed with my associate.

Note: Settlement and entry of orders is dealt with in Order 36 of the Federal Court Rules.

| IN THE FEDERAL COURT OF AUSTRALIA |

|

| NEW SOUTH WALES DISTRICT REGISTRY | N 987 OF 2002 |

| BETWEEN: | VISA INTERNATIONAL SERVICE ASSOCIATION (ARBN 007 507 511) APPLICANT

|

| AND | RESPONDENT

|

| BETWEEN: | MASTERCARD INTERNATIONAL INCORPORATED APPLICANT

|

| AND: | RESERVE BANK OF AUSTRALIA RESPONDENT

|

| JUDGE: | |

| DATE: | 19 SEPTEMBER 2003 |

| PLACE: | SYDNEY |

TABLE OF CONTENTS pars

INTRODUCTION..................................................................................................................................................................... 1

DECISIONS CHALLENGED................................................................................................................................................. 2

JUDICIAL REVIEW................................................................................................................................................................ 8

PARTIES................................................................................................................................................................................. 13

1998 LEGISLATION............................................................................................................................................................ 19

APPLICANTS CASE IN OUTLINE.................................................................................................................................... 34

RBA RESPONSE................................................................................................................................................................... 50

THE HEARING....................................................................................................................................................................... 64

TERMINOLOGY.................................................................................................................................................................... 69

IMPORTANCE OF INTERCHANGE FEES....................................................................................................................... 79

VISA CARD SCHEME PROFILE....................................................................................................................................... 91

MASTERCARD SYSTEM - PROFILE............................................................................................................................ 103

RELATIONSHIPS IN CARD SCHEMES........................................................................................................................ 113

BACKGROUND TO 1998 LEGISLATION.................................................................................................................... 121

EVENTS AFTER 1998 LEGISLATION........................................................................................................................... 154

DESIGNATION DECISION – APRIL 2001................................................................................................................... 191

POST DESIGNATION....................................................................................................................................................... 212

DECISION ON STANDARDS AND ACCESS REGIME IN AUGUST 2002............................................................ 226

FIRST QUESTION: IS EACH OF THE VISA AND MASTERCARD SYSTEMS A PAYMENT SYSTEM?....... 245

INTERPRETATION............................................................................................................................................................ 267

MEANS AND INCLUDES.................................................................................................................................................. 284

RELATES TO....................................................................................................................................................................... 296

LEGISLATIVE HISTORY AND EXTRINSIC MATERIALS....................................................................................... 306

CREDIT CARD SYSTEM RULES AND PROCEDURES............................................................................................. 336

PAYMENT SYSTEM – OTHER CONSIDERATIONS................................................................................................. 352

WAS THE DESIGNATION TOO EXTENSIVE – INTERNATIONAL EFFECT....................................................... 373

WHAT IS A STANDARD? DO THE DECISIONS IMPOSE STANDARDS?........................................................ 374

ARE STANDARDS LIMITED TO TECHNICAL AND OPERATIONAL MATTERS............................................. 394

CAN A PROHIBITION BE A STANDARD.................................................................................................................... 412

ARE THE STANDARDS TOO UNCERTAIN?.............................................................................................................. 423

THE CASE LAW ON UNCERTAINTY............................................................................................................................ 426

THE COST ACCOUNTING EVIDENCE......................................................................................................................... 462

INTERCHANGE - UNAUTHORISED DELEGATION................................................................................................... 506

ACCESS REGIME – INTERPRETATION...................................................................................................................... 523

ACCESS – CONSULTATION.......................................................................................................................................... 548

ACCESS – COMMERCIAL BASIS – FAIR AND REASONABLE TERMS............................................................ 555

RELATIONSHIP BETWEEN PAYMENT SERVICE REGULATION ACT AND THE RESERVE BANK ACT.. 560

INTERPRETATION – RB ACT – S 87........................................................................................................................... 586

RELEVANT ADMINISTRATIVE LAW PRINCIPLES................................................................................................. 588

ADMINISTRATIVE DECISION....................................................................................................................................... 589

REVIEW OF OPINIONS.................................................................................................................................................... 597

THE ROLE OF THE RBA.................................................................................................................................................. 605

ALLEGED ERROR IN APPROACH – DETERMINATION OF INTERCHANGE STANDARD........................... 608

HAVE REGARD TO............................................................................................................................................................ 612

DUTY TO INQUIRE AND INVESTIGATE...................................................................................................................... 622

WHAT WAS CONSIDERED IN THE DECISION MAKING PROCESS.................................................................. 630

HASTY DECISION............................................................................................................................................................. 642

EXPERT EVIDENCE........................................................................................................................................................... 649

THE ECONOMIC EVIDENCE........................................................................................................................................... 670

CONCLUSIONS ON EXPERT ECONOMIC EVIDENCE............................................................................................ 739

DESIGNATION – NO PRIOR OPINION – ALLEGATION OF FOUR FLAWED FINDINGS IN JOINT STUDY748

TRANSPARENCY.............................................................................................................................................................. 777

VISA’S FOUR CENTRAL ISSUES.................................................................................................................................. 788

UNREASONABLENESS AND PROPORTIONALITY................................................................................................ 829

STANDARDS AND ACCESS – FIVE ALLEGED PATENT ERRORS...................................................................... 837

CONCLUSIONS ON CLAIMED PATENT ERRORS................................................................................................... 860

CONCLUSIONS.................................................................................................................................................................. 861

REASONS FOR JUDGMENT

INTRODUCTION

1 The Court has before it applications by Visa International Service Association (“Visa”) and MasterCard International Incorporated (“MasterCard”) for judicial review. Both applications are brought against the Reserve Bank of Australia (“RBA”) to set aside five decisions of the Payment Systems Board (“the PSB”) of the RBA made under the Payment Systems (Regulation) Act 1998 (Cth)(“the PSR Act”). The decisions are part of a regulatory regime imposed by the RBA on what are known as four-party credit card schemes in Australia. The schemes, the subject of the regulations, include issuers (which are financial institutions such as banks that issue credit cards and extend credit to their customers), cardholders (who are purchasers of goods and services from merchants and customers of the issuers), merchants (who accept credit cards and claim on issuers for payment and satisfaction for transactions between merchants and customers, for example, stores, utilities and airlines) and acquirers (financial institutions such as banks that “acquire” merchants’ claims against issuers) which agree to pay the merchant under the credit card schemes.

decisions challenged

2 The first two decisions challenged were taken on 11 April 2001 and gazetted on 12 April. They designated each of the Visa and the MasterCard schemes as “a payment system”. The consequence of these designations was to bring each of the schemes within the reach of the RBA’s powers under the PSR Act as a designated system.

3 The second set of decisions challenged were made on 20 August 2002 and gazetted on 27 August 2002. Those decisions were to determine an “Interchange Standard”, which imposed a limit on “interchange fees”, sometimes described as wholesale fees, which are charged by issuers of four-party credit scheme cards to acquirers participating in the schemes and which are required by the Standard not to exceed a cost-based benchmark to be calculated with reference to eligible costs as defined by the Standard and set in accordance with the methodology prescribed in the Standard.

4 The third set of decisions challenged were also made on 20 August and gazetted on 27 August 2002. They established a “Surcharge Standard”, which permits merchants who use the schemes to impose a charge to customers who use a credit card for their transactions, notwithstanding the rules of the Visa and MasterCard schemes.

5 The fourth set of decisions challenged were also made on 20 August 2002, but had not yet been gazetted and were not operative at the time these two proceedings were heard. These involve the imposition on the applicants of an “Access Regime” which provides for access to the schemes to be available to a greater number of potential participants. These decisions were communicated to the applicants on 27 August 2002. The consequence of this Regime is that scheme operators are required to admit any “authorised deposit-taking institution” (“ADI”) as a participant in the schemes on the same basis as other financial participants. It is designed to prohibit differential treatment by participants in the schemes as between those who wish to become participants only as either issuers or acquirers. In practice participants are both issuers and acquirers.

6 The fifth decision challenged was the RBA’s decision not to revoke the designation of the applicants’ schemes. This challenge has not been pressed and is not an issue in this proceeding.

7 In this case it is particularly important from the outset to keep in mind the function of the Court on a judicial review application. This is because much of the subject matter includes controversial economic issues which, as the evidence demonstrates, are the subject of strong and sharp differences of opinion between economic experts. In such circumstances the danger of sliding into a consideration of the relative merits of economic theories is substantial, especially where, as is the case in these proceedings, claims of Wednesbury unreasonableness are raised: see Associated Provincial Picture Houses Ltd v Wednesbury Corporation [1948] 1 KB 223. It is therefore helpful to refer to those principles at this point.

judicial review

8 The nature of judicial review proceedings before the Court has a bearing on the approach and the matters for consideration by the Court and the limited scope of review. On judicial review the Court does not reconsider the merits of the RBA decisions, but is confined to examining decisions sought to be challenged in order to determine whether the decision-maker complied with the required legal process for decision-making. That is to say that it is not for the Court to perform the function assigned to the RBA by the legislation. The Court on review must not substitute its own conclusion for that of the decision-maker simply because it would have been minded to reach a different conclusion in circumstances where it was reasonably open to the decision-maker to reach that conclusion.

9 The function of the Court on an application for judicial review was described by Brennan J in Attorney-General (NSW) v Quin (1990) 170 CLR 1, at 35-36:

“The duty and jurisdiction of the court to review administrative action do not go beyond the declaration and enforcing of the law which determines the limits and governs the exercise of the repository’s power. If, in so doing, the court avoids administrative injustice or error, so be it; but the court has no jurisdiction simply to cure administrative injustice or error. The merits of administrative action, to the extent that they can be distinguished from legality, are for the repository of the relevant power and, subject to political control, for the repository alone.”

10 The focus by the Court is directed to the legality of the decision-making process taken by the RBA and that must be distinguished from a re-examination of the merits of the decisions made. At 37, his Honour sounded the following caution:

“If it be right to say that the court’s jurisdiction in judicial review goes no further than declaring and enforcing the law prescribing the limits and governing the exercise of power, the next question immediately arises: what is the law? And that question, of course, must be answered by the court itself. In giving its answer, the court needs to remember that the judicature is but one of the three co-ordinate branches of government and that the authority of the judicature is not derived from a superior capacity to balance the interests of the community against the interests of an individual. The repository of administrative power must often balance the interests of the public at large and the interests of minority groups or individuals. The courts are not equipped to evaluate the policy considerations which properly bear on such decisions, nor is the adversary system ideally suited to the doing of administrative justice: interests which are not represented as well as interests which are represented must often be considered. Moreover, if the courts were permitted to review the merits of administrative action whenever interested parties were prepared to risk the costs of litigation, the exercise of administrative power might be skewed in favour of the rich, the powerful, or the simply litigious.”

11 To similar effect are the observations of Gleeson CJ, Gummow, Kirby and Hayne JJ in Corporation of the City of Enfield v Development Assessment Commission (2000) 199 CLR 135, esp. at 152-153, which recently followed and applied the above remarks of Brennan J in Quin.

12 It is not a function of the Court on judicial review to form its own independent opinion in relation to issues on which reasonable minds may differ. That consideration is equally applicable when the ground of unreasonableness is relied on in the application for review, where the Court may be required to examine the decision-maker’s state of satisfaction in evaluating the opinions formed. To similar effect is the decision of the High Court in Minister for Immigration & Multicultural Affairs v Jia Legeng (2001) 205 CLR 507, at 532, where Gleeson CJ and Gummow J described the approach as follows:

“The question then on judicial review is whether the decision‑maker could have attained that satisfaction reasonably, in the sense explained in numerous authorities in this Court. In Foley v Padley, Brennan J emphasised that the question on judicial review is not whether the court would have formed the opinion in question, and that an allegation of unreasonableness in the formation of the opinion by the decision‑maker may prove to be no more than an impermissible attack on the merits of the decision.”

By way of illustration, diametrically opposed views have been expressed by economists as to the advantages and disadvantages of the interchange fee in credit card transactions. It is not the function of the Court in these proceedings to decide which of the two views is correct or preferable. That is a question for the RBA under the legislation.

parties

13 Visa is an incorporated association of members which operates throughout the world. Its business includes the administration and development of credit card services to members. The Visa credit card is one of the activities in Australia. Another is the Visa debit card which is also widely used. There are over 140 Australian members of Visa. Throughout the world there are many thousands. Visa members are issuers who issue Visa cards to cardholders and acquirers who acquire Visa credit card transactions form merchants who accept Visa credit cards. The members of Visa in Australia provide card services to cardholders and to merchants. The network of members that provide those services is administered pursuant to a series of by-laws, regulations and rules. These are referred to later in greater detail.

14 MasterCard is a subsidiary of MasterCard Incorporated and the shares in that company are held by the participants who are issuers and inquirers. It operates a number of payment cards. Its business is managed by a global Board of Directors and regional boards, including one in the Asia-Pacific region. The Australian subsidiary is called MasterCard Australia Limited. It provides administrative services to the scheme’s members. The MasterCard credit card system in Australia has thirteen principal Australian members and thirty-three affiliate members. The principal members are financial institutions which participate directly in card activities. Like Visa, they both issue and acquire. Affiliate members participate indirectly through a principal member under that member’s supervision. MasterCard is governed by a series of by-laws, regulations and rules which are discussed below. The four-party credit card scheme operated by MasterCard in Australia involve the cardholder, the merchant, the issuer and the acquirer. Eight of MasterCard’s principal members are acquirers and all principal members and affiliate members are issuers.

15 The RBA is a body corporate established under the Commonwealth Bank Act 1911 (Cth) and continues in existence under the Reserve Bank Act 1959 (Cth) (“RB Act”). It has two Boards, the Reserve Bank Board (“RBB”) and the Payments System Board (“PSB”). The RBB is responsible for the RBA’s monetary and banking policy and the Bank’s policy on all matters except for its payments system policy. The PSB is responsible for the Bank’s payments system Policy. This division of functions came into existence as a consequence of amendments made to the RB Act in 1998. The Bank is managed by a Governor and there is a Deputy-Governor. Membership of the RBB includes the Secretary of the Department of Treasury and six other members appointed by the Treasurer. The PSB consists of the Governor, one representative of the RBA appointed by the Governor, a representative of the Australian Prudential Regulation Authority (“APRA”) and five other members.

16 More specific powers with respect to payment systems are conferred on the RBA pursuant to the PSR Act which was also enacted at the time the amendments were made to the RB Act. The PSR Act is entitled “an Act to provide for the regulation of payment systems and purchased payment facilities and for related purposes”. These more specific powers provided for by the PSR Act, including those the subject of the present challenge, are conferred on the RBA.

17 Under the RB Act, ss 8A(3) and 10B(1), the PSB is assigned the functions of the RBA in respect of the formulation and implementation of RBA policy concerning the payments system. The payments system is the overall Australian system for the effecting of payments and comprises individual payment systems.

18 It is common ground that decisions of the PSB with respect to the payments system and payment systems are made by the RBA.

1998 legislation

19 Under the RB Act, s 10B, entitled “Functions of Payments System Board” describes the functions of, and empowers, the PSB to determine the RBA’s payments system policy and to take whatever action is necessary to ensure that it gives effect to the policy that it determines. Subsection (3) is of central importance to the present dispute. It provides:

“(3) It is the duty of the Payments System Board to ensure, within the limits of its powers, that:

(a) the Bank’s payments system policy is directed to the greatest advantage of the people of Australia; and

(b) the powers of the Bank under the Payment Systems (Regulation) Act 1998 and the Payment Systems and Netting Act 1998 are exercised in a way that, in the Board’s opinion, will best contribute to:

(i) controlling risk in the financial system; and

(ii) promoting the efficiency of the payments system; and

(iii) promoting competition in the market for payment services,

consistent with the overall stability of the financial system; and

(c) the powers and functions of the Bank under Part 7.3 of the Corporations Act 2001 are exercised in a way that, in the Board’s opinion, will best contribute to the overall stability of the financial system.”

20 Section 5 of the RB Act unhelpfully defines payments system policy in these terms:

“payments system policy means policy for the purposes of the Bank’s functions or powers under:

(a) the Payment Systems (Regulation) Act 1998; and

(b) the Payment Systems and Netting Act 1998; and

(c) Part 7.3 of the Corporations Act 2001”

21 The PSR Act does not define payments system policy, but in s 7, “payment system” is defined as:

“… a funds transfer system that facilitates the circulation of money, and includes any instruments and procedures that relate to the system.”

22 This definition gives rise to a central dispute, namely, whether the Visa and MasterCard credit card systems are payment systems which can be designated in their entirety as the RBA has done.

23 The power of the RBA to designate a payment system is conferred by s 11 of the PSR Act in these terms:

“11. Reserve Bank may designate payment systems

(1) The Reserve Bank may designate a payment system if it considers that designating the system is in the public interest. The designation is to be by notice in writing published in the Gazette.

(2) The designation has effect until it is revoked.

(3) The Reserve Bank may revoke the designation if it no longer considers that it is in the public interest that the system be designated. The revocation is to be by notice in writing published in the Gazette.”

24 The content of the expression public interest is set out in s 8 which provides that:

“8. Meaning of public interest

In determining, for the purposes of this Act, if particular action is or would be in, or contrary to, the public interest, the Reserve Bank is to have regard to the desirability of payment systems:

(a) being (in its opinion):

(i) financially safe for use by participants; and

(ii) efficient; and

(iii) competitive; and

(b) not (in its opinion) materially causing or contributing to increased risk to the financial system.

The Reserve Bank may have regard to other matters that it considers are relevant, but is not required to do so.”

25 The expression “participant” is defined to mean:

“(a) a constitutional corporation that is a participant in the system in accordance with the rules governing the operation of the system; or

(b) a constitutional corporation that is an administrator of the system.”

26 The power to impose an access regime is conferred by s 12 of the PSR Act which provides:

“12. Imposition of access regime

(1) The Reserve Bank may impose an access regime on the participants in a designated payment system.

(2) The access regime imposed must be one that the Reserve Bank considers appropriate, having regard to:

(a) whether imposing the access regime would be in the public interest; and

(b) the interests of the current participants in the system;

(c) the interests of people who, in the future, may want access to the system; and

(d) any other matters the Reserve Bank considers relevant.

(3) The Reserve Bank must not impose the access regime unless it has first consulted in accordance with section 28.

....”

27 Under subs (3) the RBA must not impose the access regime unless it is has first consulted in accordance with s 28. By subs (4) the decision must be in writing and must set out the access regime.

28 The word “access” is defined in s 7 in these terms:

“access, in relation to a payment system, means the entitlement or eligibility of a person to become a participant in the system, as a user of the system, on a commercial basis on terms that are fair and reasonable.”

29 The expression “access regime” in relation to a designated payment system is defined to mean an access regime:

“(a) that has been imposed by the Reserve Bank under section 12; and

(b) that is in force.”

30 This definition is circular, but specifies that it must be a regime that has come into force. Otherwise, the expression is quite open and extends beyond the concept of “access” which is specifically defined.

31 The power to determine “standards” for designated systems is conferred by s 18(1) of the PSR Act which provides that:

“(1) The Reserve Bank may, in writing, determine standards to be complied with by participants in a designated payment system if it considers that determining the standards is in the public interest.”

32 The expression “standard” is unhelpfully defined in s 7 to mean a standard in force under s 18.

33 In these reasons, where necessary, reference will be made to other parts of the legislation but the above provisions are those which are most pertinent for the purpose of the applications before the Court.

applicants case in OUTLINE

34 In broad outline the principal contentions of the applicants are as follows.

35 The applicants submit that each of the decisions made by the RBA is administrative in character and is thus susceptible to judicial review. It is further submitted that even if the RBA’s decisions are not administrative they are still open to challenge. The applications are brought for relief pursuant to s 39B(1A) of the Judiciary Act 1903 (Cth) (“Judiciary Act”) and s 5(1) of the Administrative Decisions (Judicial Review) Act 1977 (Cth)(“ADJR Act”).

36 The applicants first contend that the “designations” on 12 April 2001 were outside the RBA’s power to designate conferred by the PSR Act because their credit card schemes or systems and their governing rules and procedures cannot be described as a payment system, ie, a “funds transfer system that facilitates the circulation of money” or procedures that relate to such a system, within s 7 of the PSR Act. The power to designate is in respect of a “payment system” as defined by that section.

37 It is said that because the designation was not in respect of a payment system it was beyond the power to designate conferred by s 11(1) of the PSR Act, and was therefore invalid because the power provided under the PSR Act was only to designate a payment system and this is a jurisdictional fact.

38 The grounds of challenge to the Interchange and Surcharge Standards are as follows. First, it is said, that under s 18 of the PSR Act, the PSB is exercising the functions of the RBA and can only determine standards which are “technical or operational” in nature. This power does not extend to imposing price controls as the Interchange Standard purports to do. Nor does the power extend to the regulation of commercial relationships between scheme members and merchants as the Surcharge Standard purports to do. Second, there is said to be such a lack of clarity and precision as to the terms and operation of the Interchange Standards imposed that they are not within the description of a standard as provided for under the PSR Act. More specifically, it is said that the Interchange Standard, for example, does not provide any clear and certain measure to fix Interchange fees. It is also said that the power to determine a standard has been delegated to an independent expert. The applicants further submitted that the Standard requires the expert to engage in a vague and uncertain process of assessment and discretionary evaluation, to such a degree that different benchmarks can be determined in the same circumstances according to the approach adopted by the expert charged with that function. The process, so it is said, is inherently uncertain due to the lack of guidance on central matters such as “eligible costs” which are described in the Interchange Standards.

39 The applicants further contend that the proposed Access Regime, which had not yet been gazetted, is invalid because the RBA failed to have regard to preconditions to the exercise of the power under s 12 of the PSR Act. It is said that it failed to consider the interest of current participants in the system and failed to address other relevant considerations.

40 The applicants also submit that other conditions precedent to the decision to impose an access regime were not met, including a failure to consult as required, a failure to consider the impact on the applicants of the proposed Access Regime and a failure to provide sufficient information to participants to enable proper submissions to be made for consideration of such impact. There is a further contention that the terms of the Access Regime traverse the limits of a provision for access, entitlement, or eligibility to participate, by seeking to control conduct after admission as a participant by the imposition of conditions governing later conduct.

41 Additionally, there is a submission that certain paragraphs of the terms of the Access Regime prohibit the rules of participants imposing controls on the issuing and acquiring business of scheme participants. It is said that this goes beyond s 12 of the PSR Act. Further, it is said the broad, unqualified terms and blanket nature of the prohibition on differentiation results in the imposition of terms that are not fair and reasonable commercial conditions. It is submitted that the blanket prohibition does not have regard to the possibility that differences in value or number of a participant’s issuing and acquiring transactions have commercial significance, including the burden cast on other participants who have a higher proportion of issuing transactions. The commercial imperative requiring the avoidance of an imbalance is said to justify the scheme rules requiring participants to maintain a balance in meeting the relative costs as between issuing and acquiring businesses and the imposition of fair and reasonable fees from participants who conduct no issuing business. The latter is said to be necessitated in order to compensate for the additional burden cast on participants as a consequence of being an issuer.

42 A further line of attack is based on the manner in which the decision-making process was implemented and a claimed failure to take into account relevant considerations and acting in a manner that was grossly unreasonable and which breached principles of proportionality.

43 Under this line of attack, it is said that the RBA did not properly consult or consider submissions made to it with an open mind and thereby breached s 28(2) of the PSR Act, which requires consultation prior to the implementation of a proposed action, because the PSB had a fixed position by October 2000 and was not prepared to consider moving from this. This conduct on the part of the RBA is said to invalidate the Standards and the proposed Access Regime.

44 The applicants also contended that the RBA did not have regard to “the public interest” and to the economic concepts of “competition” and “efficiency” as it was bound to do under s 10B of the RB Act and s 8 of the PSR Act.

45 It is also submitted that the RBA did not form the required opinions in relation to the public interest criteria in accordance with the requirements of the PSR Act and the RB Act. Because the formation of such opinions were jurisdictional facts on which the exercise of power was conditioned, the decisions as to the Standards and the Access Regime were invalid.

46 It is submitted that the RBA did not have regard to the criteria in s 8 of the PSR Act and s 10B of the RB Act. Nor did it ask itself the essential preliminary questions required by those provisions in order to form such opinions.

47 Criticism is also levelled at the methodology used by the RBA because the approach adopted was such that it did not form the necessary opinion as to whether the exercise of its powers would best contribute to efficiency and operation where there was a duty to ensure that in the RBA’s opinion the exercise would so operate.

48 Further specific criticisms made are that the RBA:

· did not define and analyse the market for payment services, which was essential to a consideration of the concepts of competition and efficiency;

· did not consider the role which the four-party credit scheme played in the financial system, the payments system and the market for payment services;

· did not consider the impact of its determinations;

· did not form an opinion as to efficiency but was concerned with transaction costs;

· did not form an opinion about whether its actions would promote competition in the market for payment services;

· did not adopt a proper methodology to enable it to consider the promotion of efficiency and competition; and

· did not consider the necessity for action nor the net benefit or detriment of the existing regimes compared with the proposed regimes.

49 The applicants also say that the decisions by the RBA are so unreasonable/or lacking in proportionality that no reasonable regulator could have made them. For these reasons, among others, the applicants say that the determinations were invalid.

RBA response

50 The RBA points to the broad, high level statutory functions with which it is entrusted and in particular, the management of national economic and financial policy, and to the composition and functions of the PSB and the RBA. It also points to the accepted principles relating to the limited nature of judicial review of administrative action, the core of which have been referred to above. It refers to the wide discretionary powers conferred on the RBA and to the extensive consultation process which it engaged in throughout the three year period before making its final decisions relating to standards and access. Furthermore, it refers to the principle that administrative decisions such as those made in this case should not be approached with any predisposition to seek out error, where a fair and reasonable examination would not disclose such error. Particular emphasis is placed on the well-settled principles that the role of the Court in a judicial review application is not to encroach upon the merits of the decision, but to decide purely on the basis of limited administrative review grounds. Furthermore, reference is made to the context of the legislative history and provenance of the 1998 legislative amendments pursuant to which the designations were made, access provided for and standards imposed.

51 As to designation, the RBA states that each of the Visa and MasterCard systems are within the description of “payment system” as defined in s 7 of the PSR Act. This is said to provide for a wide discretion. It submits that the definition of “funds transfer system” must be considered having regard to the whole card system in each case as set out in their governing rules and procedures and that there is no basis to segregate out particular parts of either system and contend that only those parts comprise such a system.

52 The RBA submits that the definition of payment system is and was intended to be broad and includes procedures that relate to the system and those that relate to any instruments and the transfer of funds and that this description is wide enough to include the entire Visa and MasterCard systems.

53 As to the power to make standards, the RBA says that the unqualified language of s 18 of the PSR Act does not confine the RBA power to technical or operational matters. The expression “determine standards” in s 18 in a practical sense is at large and is extensive enough to include a reference to a benchmark which provides for a price to be calculated.

54 With respect to the Access Regime it submits that the Regime provides for access on a commercial basis on terms, which are fair and reasonable. The Regime is within the concept of a standard. The RBA can have regard to the interests of applicants for future access.

55 With respect to the Surcharge Standard, the RBA submits that a “prohibition” can be a “standard” in the ordinary sense of that term and the fixing by an independent expert of an interchange fee ceiling is not an unauthorised delegation of power to the expert because the Standard is made by the RBA and it fixes the criteria and methodology in advance to determine the benchmark with which the participant must comply. The function of the expert is not to determine the Standard, because that is done by the RBA, but rather to apply those fixed specific criteria in order to set the benchmark in a particular case.

56 The criteria set out in the Standards are not uncertain having regard to the authorities. The meaning of the criteria is reasonably precise within current accepted accounting practice and the criteria satisfy that requirement so that the provisions are not invalid for uncertainty. In the present case, the requirement is not to fix a price but to determine a standard. Even if there is any uncertainty in the determination of “eligible costs” in the process, the only uncertainty is in the application of the Standard in a particular context and does not arise as a consequence of uncertainty in the Standard

57 The RBA submits that the power in s 18 has been exercised by the RBA so as to ensure that participants know with certainty the cost-based benchmark they must meet prior to being required to comply with the Standard. The benchmark, it is submitted, must be arrived at prior to any obligation being imposed to calculate the interchange fee.

58 Criteria for calculating the cost-based benchmark do not have to be totally non-subjective. The test to be applied is whether criteria in the Standards are sufficiently certain. It is not necessary that there should be unequivocal precision. The requirement is one of sufficiency namely, that there be sufficient clarity and reasonable precision and this will vary according to legislation and context. It is necessary to adopt a fair and reasonable approach to the construction of the Standard. The wartime decisions relied on by the applicants are based on the fixing of a price which is different from determining a standard. Even in such cases, it is accepted that terms such as substantially or principally can be used without making the process “uncertain” to such a degree that the determination is invalid.

59 In relation to the Access Regime, the RBA says it appreciated its obligations and points to material which was before it, which in its submission, takes account of the interests of current participants. Specifically, it refers to the chapter on Impact Analysis in the Final Reforms and Regulation Impact Statement (“RIS”). It points out that there was ample opportunity on interested parties to make submissions to the RBA. The RBA received more than ninety-five written submissions from October 2000 to August 2002 and held fifty-two meetings, fifteen of which were with the designated card schemes. There is no reason to doubt its statement that it considered the matters raised in these meetings and submissions. In response to the claim that the RBA did not comply with s 28 of the PSR Act because the relevant APRA prudential standards had not been finalised, the RBA says that it complied with s 28(2) by its notice in the Gazette of 14 December 2001. Draft APRA standards had been formulated and had been the subject of consultation. There was no obligation on it to summarise the content of those prudential standards or to have them in final form.

60 The RBA contends that the definition of “access” in s 7 of the PSR Act does not limit the definition of “access regime” in s 12 of that Act. Even if there were such a limitation, there is no basis to import a restriction that an access regime may not deal with matters other than entitlement or eligibility to participate in a scheme. On a proper construction of pars 10-12 of the Access Regime, they are concerned with access because they permit specialist acquirers to participate, they remove burdens on specialist acquirers and they allow merchants to participate as acquirers of their own transactions. The rules of the systems can be regulated to ensure that there is no discrimination after admission in order to prevent evasion of the access rules. The RBA says that the proposed Access Regime provides for access on terms that are fair and reasonable.

61 In relation to the applicants’ attack on its decision-making process, the RBA points to material before it which it says demonstrates that it complied with its obligations under s 10B(3), to have regard to “efficiency” and “competition” and where it considered three available options. The RBA referred specifically to its “mandate” under s 10B throughout various material exhibiting its decision-making process including the Consultation Document, published on 14 December 2001 (“Consultation Document”).

62 As to the RBA’s consideration of the provisions PSR Act, s 8, and the RB Act, s 10B, it is submitted that there is nothing in the legislation which requires the RBA to adopt any particular methodology as to the way in which to form its opinions. The legislation makes it clear in terms that this was solely for the RBA and also that the RBA has complete discretion as to the most appropriate methodology. The RBA says that the approach taken was within a range of reasonably appropriate and available methodologies. The allegations based on manifest unreasonableness and lack of proportionality, it says, are answered by the above submissions.

63 As to the alleged failure to revoke the designations there was no basis shown to warrant revocation on either of the designations. The revocation raises questions of public interest and these are matters for the RBA. It also contemplates that the RBA is to form its own opinion whether the designation is no longer in the public interest.

the hearing

64 The applications brought by Visa and MasterCard were heard together over a period of six weeks. There were three parties represented by thirteen counsel. The proceedings involved discovery and inspection of thousands of documents. Some of these documents exceeded hundreds of pages. There were approximately 1700 pages of transcript and over 1000 pages of written submissions and responses.

65 Much of the evidence focused on the decision-making process undertaken by the RBA over the period August 1998 to August 2002 when the decisions to designate were made and the Standards and Access Regime were determined. Documents in evidence were not limited to those directly relating to the parties to the litigation, but also included correspondence and material concerning submissions and information provided to the RBA by numerous institutions which were not party to the actions brought by Visa and MasterCard. A strict confidentiality regime was implemented by the Court based on agreement reached between the parties to the proceedings, following various consultations with the authors of third party material sought to be tendered.

66 The Court had before it affidavits sworn by bank officers and employees of the applicants. The RBA elected not to call any lay witnesses but tendered three expert reports. Two of the reports, by Professors Katz and Farrell, both eminent experts in their field of economics, provided evidence in relation to the economic theory and application underlying credit card networks. The RBA’s third expert was Associate Professor Briers, who was called to provide the Court with his expert opinion on accounting issues relating to the method of calculation of the interchange fee.

67 Expert reports pertaining to the economic principles underpinning the operation of credit card schemes were also tendered by the applicants. MasterCard called two expert witnesses, Professor von Weizsacker and Dr Veljanovski. Visa called one economic expert, Dr Pleatsikas, an economist with some experience in the field of network and regulatory economics. Two accounting experts were called by the applicants to give evidence in relation to the accounting issues, namely Mr Teer who was retained by MasterCard and Mr Bryant, who was called by Visa.

68 Having regard to the vast amount of material and the complexity of the matter the Court indicated to the parties, and they accepted, that the nature of the proceedings was such that the rule of practice in Browne v Dunn (1893) 6 R 67 would not be applied to require an express challenge to every statement made, provided that there was no unfairness in failing to do so. That approach was followed especially in relation to the expert evidence where a vast array of literature rendered it impracticable for counsel to put to the expert witness every issue that emerged from the literature. Counsel proceeded on that basis in advancing their final submissions to the Court and no Browne v Dunn point was taken.

terminology

69 To appreciate the issues raised on these applications it is necessary to understand the instruments and procedures by which the four-party credit card schemes operate in practice and also the relevant terminology in the context of the provision of payment services.

70 A credit card provides a payment service and a credit facility. The latter will usually provide for an interest-free period before the account needs to be settled by the cardholder and a pre-approved line of credit, often termed a ‘revolving’ line of credit, on which a rate of interest is payable by users. The cardholder pays their credit card account some time after the transaction, according to an established billing cycle. Approximately twenty-five per cent of those who use credit cards pay within the allocated interest-free period and do not incur interest payments. They are known as “transactors”. They derive maximum benefits from the schemes. The remaining portion of credit card users take advantage of the credit facility and as a consequence they incur relatively high interest rates. They are referred to as “revolvers” as users of the revolving line of credit.

71 Visa and MasterCard provide services in what is typically described as a “four-party card scheme” or an “open loop credit card network”because there are four main parties who are involved in the operation of the scheme: the cardholder, their financial institution (the issuer) which issues the card, the recipient of the funds (the merchant) and its financial institution (the acquirer). The cardholder uses the credit card issued by their financial institution to acquire goods and services. They agree to pay fees to the issuer of the credit card together with any interest when they take advantage of the revolving line of credit. In using their credit card, cardholders present their cards to merchants, to whom payment is ultimately made. The merchant’s financial institution, the acquirer, is reimbursed by the issuer for the value of goods or services and the acquirer in turn agrees to pay the issuer an interchange fee. The acquirer will pay to the merchant the full value of an authorised credit card transaction, less any relevant fee charged by the acquirer to the merchant. This amount, payable by the merchant, is known as the merchant service fee. It includes the interchange fee. The expression merchant services includes the acceptance of credit card transactions, collection of the value of transactions from the issuer and reimbursement of the merchant, the provision of electronic terminals, card imprinters, sales vouchers, signage and promotional material and the provision of a call processing centre for authorisation of transactions.

72 Four-party schemes are operated by system administrators. In the present case, Visa and MasterCard administer the credit card network and provide issuers and acquirers, who are members of the scheme, with network administration services, including, for example, the right to use intellectual property. In administering the credit card network, Visa and MasterCard also provide their members with authorisation and settlement services and facilitate the interchange transactions between those members. The payment process involves a flow of information and payment instructions between parties to ensure that payment is made by the cardholder to the merchant. In the case of the Visa scheme, payment processing is completed by using a system known as VisaNet. The MasterCard network uses a similar system knows as BankNet. In some instances in a four-party credit card transaction the issuer and the acquirer are the same entity. These are known as “on us” transactions and there is no interchange fee payable.

73 By contrast, closed loop card networks, which are also known as three-party card schemes, such as those provided by American Express and Diners Club, consist of a network under which a single entity performs all issuing and acquiring functions, in addition to administering the card network. These schemes involve three parties, namely cardholder, merchant and the scheme administrator, which issue cards to cardholders. Cardholders use the card to purchase goods and services, and will usually agree to pay their account in full by the end of the billing cycle if they are issued with a charge card, or interest and fees if they hold a credit card issued by three-party card schemes operators. A charge card does not usually provide for the extension of credit facilities. In a typical three-party card transaction, the merchant receives payment following authorisation of a transaction, with the acquiring function being completed by the same entity which issued the card, namely the scheme administrator, such as American Express or Diners Club. The merchant is bound to pay a service fee in return for the acquiring services provided. However, no interchange fee is paid as part of a three-party card network.

74 In addition to three and four-party schemes, several other card networks exist in Australia, including store cards which are issued by or on behalf of retailers for use by customers within their own store. Store cards, like credit cards, offer an interest-free period and a revolving line of credit. Examples of these include cards issued by large retailers such as Coles Myer and David Jones. The store card issuer issues the card to its customer who is able to use the card to make purchases of goods or services offered by the issuer. The cardholder receives a monthly account from, for example, the retailer, which must be paid in accordance with the billing cycle or incur fees and interest charges. Finance for store cards will either be provided by a third party or, in some instances, a company related to the store card issuer. Thus, GE Capital Finance Australia provides financial services to users of the Coles Myer store card while David Jones Financial Services Limited is the credit provider for store cards issued by David Jones.

75 Other types of payment cards do not extend credit facilities. A debit cardholder for example, has the amounts purchased using the card deducted from his or her designated deposit account by the card issuer on a transaction basis. Unlike credit cards, debit cards usually provide no credit facility to cardholders. Funds to cover debit card transactions are deducted directly from cardholder accounts with little, or no, delay. Debit card transactions that are processed via the Electronic Funds Transfer/Point of Sale (“EFTPOS”) network require the cardholder to verify the transaction by using a keypad to enter a PIN (personal identification number) and result in an interchange fee paid by the card issuer to the merchant’s acquiring institution. These costs are often (at least in part) recovered through transaction fees levied on cardholders.

76 Debit cards are usually combined with Automatic Teller Machine (“ATM”) functions in a single card, so that cardholders can be provided with access to cash and the ability to perform certain banking functions (such as balance inquiries and balance transfers between/among accounts) electronically through ATMs. Under current arrangements, holders of debit cards will typically face a transaction fee for using a debit card (usually after a number of fee-free transactions). As at June 2002, there were more than 16,000 ATMs in Australia as compared with fewer than 9,000 in 1997.

77 A smart card is a plastic payment card fitted with a microchip, as opposed to a magnetic strip, thus allowing for greater security by reducing the prospect of fraudulent use of the card. A smart card can be programmed so that stored monetary value in the form of digital information can be loaded onto the card. Conversely, the ‘electronic value’ can be deducted or transferred onto other cards using the appropriate hardware. The cardholder is then able to use the card to for the purchase of goods or services by the electronic transfer of the digital information from the microchip on the card to a merchant’s microchip. An example of a smart card is a prepaid telephone card.

78 One feature of four-party credit schemes in Australia is the interchange fee payable as part of payment processing by the acquirer to the issuer. In credit card payment networks, interchange fees are set collectively by members and are paid by the acquirer to the cardholder’s financial institution (the issuer). These fees are said to be justified on the basis that they allow the acquirer to recoup costs of the card infrastructure and processing. The interchange fee is passed by the acquirer to the merchant who can then bear it or pass it onto all customers, both cardholders and non-cardholders, by way of a general price increase.

IMPORTANCE OF INTERCHANGE FEES

79 There are currently in excess of ten million credit and charge cards on issue in Australia. According to the RBA, consumers use credit cards to finance thirty-six per cent of their spending. The debt on card transactions exceeded $24 billion as at June 2003. On a global comparison Australia ranks third after the United States and New Zealand in credit card usage. Credit card transactions have increased more than twenty-four per cent per annum over the past five years. In 2001, there were on average forty-three card transactions for every person in Australia.

80 Interchange fees generate substantial income for issuers and acquirers as a consequence of the use of credit cards. The Consultation Document states that:

“…. interchange fees currently generate revenues of around $775 million a year to issuing banks). Revenue from this source accounted for about one-third of total issuing revenues …. The other two-thirds of total issuing revenues is generated by cardholders who make use of the revolving line of credit (‘revolvers’), that is, who do not pay off their accounts by the end of the interest-free period. Preliminary data from the Reserve Bank’s new payments system collection indicate that about three-quarters of credit card outstandings are interest-bearing. Credit cardholders who use the credit card purely as a payment instrument (‘transactors’), that is, who pay off their balance by the end of the interest-free period, make only a very small contribution to total issuing revenues, mainly through annual fees.

The Joint Study found that interchange fees in Australia are not reviewed regularly by credit card scheme members on the basis of any formal methodologies. It also found that the fees are higher than the costs incurred by issuers in providing credit card payment services to merchants and that – because of barriers to entry to the schemes - competition does not seem to be bringing these fees into line with costs. The Joint Study concluded that credit card interchange fee arrangements in Australia are contributing to a structure of incentives that has encouraged the growth of the credit card network at the expense of more economical payment instruments.” (Emphasis added)

81 The RBA estimate is that its proposed reforms to credit card schemes will reduce credit card interchange fee amounts by approximately $350 million annually.

82 Interchange fees have been an integral part of the pricing structure in card schemes. They have a strong influence on (i) the revenue flows associated with card transactions, (ii) the costs ultimately borne by merchants and cardholders, (iii) the incentives to use and accept debit and credit cards and (iv) the terms on which financial institutions and other providers of payment services can gain access to some card networks.

83 Visa by far has the greatest share of the credit card market, which is then followed by MasterCard and Bankcard. The shares of the market by Diners Club and American Express schemes are substantially less than those of Visa and MasterCard.

84 The costs incurred by the issuer are said to be in the order of five times the costs that are incurred by the acquiring bank, in a credit card transaction. If all of the costs incurred by the issuing bank are met by the issuing bank’s customers, then the system may not function properly. This is therefore seen to be a justification for an interchange fee from the acquirer to the issuer in order to provide a balancing mechanism for the efficient operation of a credit card scheme.

85 In a typical credit card transaction, the payment of an interchange fee is acknowledged by the RBA to perform a useful function in meeting the discrepancy in costs as between issuer and acquirer. The problem, in the view of the RBA, resides in the lack of transparency arising from the absence of any specific transparent methodology, data input, or monitoring on a systematic basis, and the fact that the level of interchange fees are determined between close competitors in a tightly controlled market.

86 The remedial measures implemented by the RBA after designation of the card schemes, namely the Access Regime and the two Standards are closely inter-related and must be considered as part of a single regulatory scheme largely centred around monitoring and setting interchange fees. At the heart of the regulatory focus in the present reforms is the setting of the interchange fee by reference to specified costs, data and a methodology using review by an independent expert to arrive at a suitable benchmark, with the objective of introducing transparency to the process. This is said to enable interested parties to make more informed economic choices with respect to selection of payment mechanisms, including the use of credit cards.

87 In Australia interchange fees do not apply when customers make payments by cheque, direct credit or direct debit. In those cases, financial institutions seek to recover their costs directly from their customers. One rationale for interchange fees is that they encourage the growth of payment networks by redistributing revenues between participants to induce them to join. In this way the benefits of the payment network may be maximised. Despite the fact that the networks have reached a high level of maturity, pricing is still based on interchange fees set by financial institutions removed from the cardholders and merchants that ultimately bear these fees. The end users of card services do not have any direct influence on the price setting process. This is perceived by the RBA and its advisers to be a distortion of normal market discipline which has implications for efficiency and equity, both of which need to be weighed against potential network benefits.

88 In Australia over ninety per cent of debit and credit card transactions are processed by a relatively small group of financial institutions. The four major banks account for the processing of over ninety-three per cent of credit card transactions.

89 Total fees payable per annum by merchants to acquirers is in the order of $1.5 billion. The RBA estimates that transactors alone receive a benefit in the order of $90 million per annum, being the amount by which revenues received from transactors fall short of the costs of providing the interest-free period together with loyalty points. However, this estimation of $90 million only relates to transactor benefits and does not take account of the substantial benefits to revolvers which have not been quantified in the material. It appears that these total benefits to cardholders must fall somewhere within the range of between $90 million each year and the $1.5 billion in merchant fees, so that benefits are substantially in excess of the $90 million. Although in relative terms to the total revenue generated by credit card transactions these figures may not be a high proportion, nevertheless they are significant amounts in their own right. It is common ground that approximately only twenty-five percent of the credit card users are transactors and that the seventy-five percent majority of persons using four-party credit card schemes are revolvers who pay the relatively high interests rates attracted to these transactions.

90 The interchange fee is at present collectively set by the members of the schemes. Neither the applicants nor their members have provided any significant detail disclosing current procedures and data input explaining the way in which interchange fees in Australia are set. MasterCard asserts that competition among different payment mechanisms ensures that there cannot be a problem with the setting of interchange fees. Visa states that the setting of interchange fees is a complex matter that requires commercial judgment. It is said that this judgment is shaped by the realities of market place competition, which is then tested in the negotiating process over interchange between members and that this process elicits information about the likely outcomes with alternative fee levels.

visa card scheme PROFILE

91 Visa’s international operation includes a world-wide electronic financial processing authorisation clearing and settlement system or service known as VisaNet. This is comprised of a comprehensive network of computers and telecommunication systems that link Visa processing centres to issuers, acquirers and third party processors. VisaNet enables members of Visa to exchange information, both financial and non-financial, reliably, quickly and efficiently.

92 VisaNet provides services to participants which include the following:

(a) an authorisation service, which permits the issuer of a card to approve or decline a transaction before a transaction is completed (that is, before a sale is completed or cash disbursed). Visa also provides various kinds of authorisation services whereby it makes authorisation decisions on behalf of issuers – these are known as “stand in processing services”;

(b) a clearing service which involves the collection of financial information about a transaction form an acquirer and the delivery of that data to the relevant issuer. The issuer is able to use the information to post the transaction to the cardholder’s account; and

(c) a settlement service which involves the calculation of the net financial position of each member for all transactions that are cleared within a particular time period.

93 VisaNet systems provide services of online and offline transaction processing. One of these systems is know as the BASE I System which supports online authorisation processing for relevant transactions. There is also a BASE II System which clears and settles previously authorised transactions, that is to say, authorisation and subsequent clearing and settlement. BASE II processing occurs by way of “batches”, that is, it is not undertaken online, but data is compiled during a collection period and processed at specific settlement times. This system also calculates fees, charges and settlement totals and produces reports to help with reconciliation.

94 Set out below is a diagrammatic illustration of the Visa credit card procedures.

95 The process, in simplified terms, by which transactions are processed through VisaNet in relation to authorisation is generally as follows:

(a) The cardholder wishing to make a purchase or obtain a service presents the Visa credit or debit card to the merchant.

(b) The merchant swipes the card through a point-of-sale terminal and an authorisation request is sent from the terminal to the acquirer via the electronic link between the merchant and its acquirer.

(c) The acquirer’s processing system reads the Bank Identification Number (“BIN”) of the message sent from the merchant terminal. The BIN is the first six digits of the card number and is unique to the cardholder’s issuing bank. That number also indicates whether the transaction is a Visa card transaction or some other card brand. The acquirer’s processing system separates Visa card transactions from other transactions.

(d) The acquirer’s processing system identifies whether or not the acquirer is also the issuer of the card by comparing the BIN on the card to the acquirer’s BIN. If it is, (this transaction is called an “on-us” transaction) the acquirer’s own processing system determines whether the transaction should be authorised. An authorisation request does not go to the VisaNet service.

(e) If the transaction is not “on-us”, the acquirer’s processing system formulates an authorisation request.

(f) The authorisation request is transmitted to the issuer of the card. The issuer’s processing centre determines by reference to conditions set between the issuer and the cardholder whether authorisation for the transaction should be granted.

(g) A response to the authorisation request is formulated by the issuer’s processing centre and that is communicated via the issuer’s system and routed back to the acquirer.

(h) The acquirer forwards the response to the authorisation request to the merchant who is then able to proceed with or decline the transaction.

(i) The authorisation process occurs almost instantaneously over telecommunication lines. The process is “online”. The process described generally takes about six seconds.

(j) VisaNet sometimes provides “stand in” processing services to a participant on request, whereby VisaNet makes authorisation decisions of behalf of an issuer. This is based on parameters previously supplied to Visa by the relevant issuer.

96 The clearingprocess generally occurs as follows:

(a) At a time that is fixed between the merchant and the acquirer, the merchant delivers all of its Visa card transactions for a particular period to the acquirer. This usually occurs automatically at the end of each business day as part of the closing out procedure for the merchant’s terminal. Visa card transactions are generally delivered along with all transactions using any type of card.

(b) The acquirer pays to the merchant the amount reflected by the Visa transactions in accordance with the agreement between the merchant and the acquirer. Payment is usually made within twenty-four hours within Australia. The merchant service agreement usually provides for payment of a fee known as a “merchant service fee” which is deducted from the amount otherwise payable from the acquirer to the merchant on account of the Visa card transactions.

(c) The acquirer’s processing centre collects all of the information concerning Visa card transactions that have been acquired from each of the acquirer’s merchants (except for “on-us” transactions). That information is used by the acquirer to compile an interchange transaction file.

(d) At a pre-determined time, VisaNet sends a message to each acquirer’s interchange transaction file.