Federal Court of Australia

Larkspur Tribeca Ltd v iSignthis Ltd [2026] FCA 908

File number(s): | VID 555 of 2019 |

Judgment of: | NESKOVCIN J |

Date of judgment: | 14 July 2026 |

Catchwords: | TRUSTS AND TRUSTEES – Construction of trust deed – principles applicable to construction of trust deeds –requirement for certainty of subject of trust – where assets subject of trust are shares and rights to shares – where rights to shares convert subject to milestones being met – whether trust assets mere expectancy – chose in action as trust asset EQUITY – Participation in the wrongdoing of a trustee – Barnes v Addy – liabilities as a knowing recipient –– liabilities as a knowing assistant – claims not established EQUITY – Rectification – rectification of a deed –whether common intention established – insufficient contemporaneous materials supporting alleged common intention – claim not established CONSUMER LAW – Misleading and deceptive conduct – representation as to a future matter – allegation of misleading and deceptive conduct by “making” an agreement – claim not established EQUITY – Remedies – equitable compensation for breach of trust – where breach involved failure to transfer shares – compensation to be assessed at time of judgment – expert evidence as to price and value of shares |

Legislation: | Australian Consumer Law, being Sch 2 of the Competition and Consumer Act 2010 (Cth) ss 4 and 18 Evidence Act 1995 (Cth) ss 140 and 191 |

Cases cited: | Ancient Order of Foresters in Victoria Friendly Society Ltd v Lifeplan Australia Friendly Society Ltd (2018) 265 CLR 1; [2018] HCA 43 Argo Managing Agency Ltd for and on behalf of the underwriting members of Lloyd’s Syndicate 1200 v Quintis Ltd (subject to deed of company arrangement) [2022] FCAFC 86 Australian Broadcasting Commission v Australasian Performing Right Association Ltd (1973) 129 CLR 99; [1973] HCA 36 Australian Competition and Consumer Commission v TPG Internet Pty Ltd (2020) 278 FCR 450; [2020] FCAFC 130 Australian Securities and Investments Commission v Retail Employees Superannuation Pty Ltd [2024] FCA 1081 Australian Zircon NL v Austpac Resources NL [No 2] [2011] WASC 186 Byrnes v Kendle (2011) 243 CLR 253; [2011] HCA 26 DC Rd DC Pty Ltd v Zhang (Trial Judgment) [2026] FCA 16 Ellison v Sandini Pty Ltd (2018) 263 FCR 460; [2018] FCAFC 44 Equuscorp Pty Ltd v Glengallan Investments Pty Ltd (2004) 218 CLR 471; [2004] HCA 55 Farah Constructions Pty Ltd v Say-Dee Pty Ltd (2007) 230 CLR 89; [2007] HCA 22 Fox v Percy (2003) 214 CLR 118; [2003] HCA 22 Webb v Getswift Limited (No 5) [2019] FCA 1533 Franklins Pty Ltd v Metcash Trading Pty Ltd (2009) 76 NSWLR 603; [2009] NSWCA 407 GM & AM Pearce & Co Pty Ltd v Australian Tallow Producers Pty Ltd [2005] VSCA 113 Grimaldi v Chameleon Mining NL (No 2) (2012) 200 FCR 296; [2012] FCAFC 6 Harstedt Pty Ltd v Tomanek (2018) 55 VR 158; [2018] VSCA 84 Hasler v Singtel Optus Pty Ltd (2014) 87 NSWLR 609; [2014] NSWCA 266 Icon Co (NSW) Pty Ltd v Liberty Mutual Insurance Company Australian Branch trading as Liberty Specialty Markets [2020] FCA 1493 In the matter of the George Hardi Family Trust [2021] NSWSC 1584 KTC v David [2022] FCAFC 60 Lowther Park Pty Ltd as trustee for the Lowther Park Family Trust v Simon Della Marta [2023] NSWSC 1555 Maralinga Pty Ltd v Major Enterprises Pty Ltd (1973) 128 CLR 336; [1973] HCA 23 Mayo v W & K Holdings (NSW) Pty Ltd (in liq) (No 2) [2015] NSWCA 119 Michael Wilson & Partners Ltd v Nicholls (2011) 244 CLR 427; [2011] HCA 48 Nadinic v Drinkwater (2017) 94 NSWLR 518; [2017] NSWCA 114 Norman v Federal Commission of Taxation (1963) 109 CLR 9 North East Equity Pty Ltd v Proud Nominees Pty Ltd (2012) 285 ALR 217; [2012] FCAFC 1 Quintis (subject to deed of company arrangement) v Certain Underwriters at Lloyd's London Subscribing to Policy Number B0507N16FA15350 (2021) 385 ALR 639; [2021] FCA 19 Re Jimmy’s Recipe Pty Ltd (No 2) [2020] NSWSC 632 Re Sirrah Pty Ltd (in prov liq) (2021) 152 ACSR 212; [2021] NSWSC 413 Righi v Kissane Family Pty Ltd [2015] NSWCA 238 Royal Botanic Gardens and Domain Trust v South Sydney City Council (2002) 240 CLR 45; [2002] HCA 5 Ryledar Pty Ltd v Euphoric Pty Ltd (2007) 69 NSWLR 603; [2007] NSWCA 65 Schreuders v Grandiflora Nominees Pty Ltd [2016] VSCA 93 Secure Parking (WA) Pty Ltd v Wilson (2008) 38 WAR 350; [2008] WASCA 268 Self Care IP Holdings Pty Ltd v Allergan Australia Pty Ltd (2023) 277 CLR 186; [2023] HCA 8 Simic v New South Wales Land and Housing Corporation (2016) 260 CLR 85; [2016] HCA 47 St Vincent de Paul Society Qld v Ozcare Ltd [2011] 1 Qd R 4; [2009] QCA 335 The Trust Company (Nominees) Ltd v Banksia Securities Ltd (Receivers and Managers appointed) (in liquidation) [2016] VSCA 324 Trustee for Michael Hayes Family Trust v Commissioner of Taxation [2019] FCA 426 Turner v O’Bryan-Turner (2022) 107 NSWLR 171; [2022] NSWCA 23 Warman International Ltd v Dwyer (1995) 182 CLR 544; [1995] HCA 18 Xiao v BCEG International (Australia) Pty Ltd (2023) 111 NSWLR 132; [2023] NSWCA 48 Youyang Pty Ltd v Minter Ellison Morris Fletcher (2003) 212 CLR 484; [2003] HCA 15 AIB Group (UK) Plc Ltd v Mark Redler [2014] UKSC 58; [2015] AC 1503 Barnes v Addy (1874) LR 9 Ch App 244 Fowler v Fowler (1859) 4 De G & J 250 Gestmin SGPS SA v Credit Suisse (UK) Limited [2013] EWHC 3560 (Comm) Target Holdings Ltd v Redferns [1996] 1 AC 421 Thomas Bates and Son Ltd v Wyndham’s (Lingerie) Ltd [1981] 1 WLR 505 Canson Enterprises Ltd v Boughton & Co [1991] 3 SCR 534 Jacobs' Law of Trusts in Australia, J D Heydon and M J Leeming (8th ed, 2016) The Law of Trusts, G Thomas and A Hudson (2nd ed, 2010) |

Division: | General Division |

Registry: | Victoria |

National Practice Area: | Commercial and Corporations |

Sub-area: | Commercial Contracts, Banking, Finance and Insurance |

Number of paragraphs: | 220 |

Date of hearing: | 30 June – 4 July and 16 September 2025 |

Counsel for the applicants: | A Donald |

Solicitor for the applicants: | Colin Biggers & Paisley |

Counsel for the respondents: | J Mereine and C Lum |

Solicitor for the respondents: | HWL Ebsworth |

ORDERS

VID 555 of 2019 | ||

| ||

BETWEEN: | LARKSPUR TRIBECA LTD (REPUBLIC OF SEYCHELLES, NO. 113890) First Applicant DAVID EDMONDS Second Applicant | |

AND: | ISIGNTHIS LTD (BVI, NO. 667231) First Respondent NICKOLAS JOHN KARANTZIS Second Respondent SELECT ALL ENTERPRISE LIMITED (BVI, NO. 2003943) Third Respondent | |

order made by: | NESKOVCIN J |

DATE OF ORDER: | 14 July 2026 |

THE COURT ORDERS THAT:

1. By 4.00pm on 21 July 2026, the parties are directed to indicate via email to the Chambers of Justice Neskovcin whether or not they wish to be heard further on the issue of equitable compensation.

2. If the parties do not wish to be heard further on that issue, then the parties are directed to confer and seek to agree upon orders to give effect to the reasons in Larkspur Tribeca Ltd v iSignthis Ltd [2026] FCA 908, and submit a minute of proposed orders via email to the Chambers of Justice Neskovcin by 28 July 2026.

3. Liberty to apply.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

NESKOVCIN J:

1 This proceeding involves a dispute as to whether the applicants are entitled to additional fully paid ordinary shares in iSignthis Ltd (ACN 075 419 715) (ASX code: ISX) which were issued on 5 September 2018, after ISX achieved three Performance Milestones (Milestone A, Milestone B and Milestone C) identified in the Prospectus issued on 22 December 2014 (as defined below).

2 The applicants, Larkspur Tribeca Ltd and Mr David Edmonds, allege that pursuant to a trust constituted by an Acknowledgement of Trust dated 15 June 2015 the first respondent, iSignthis Ltd (BVI) (iSignthis BVI), agreed to hold certain “Trust Assets” on trust for the applicants.

3 The applicants brought claims against iSignthis BVI for breach of trust, alternatively, breach of contract. As against the second respondent, Mr John Karantzis, the applicants alleged knowing receipt of property in breach of trust and knowing assistance of iSignthis BVI’s breach of trust, or alternatively its breach of fiduciary duty. As against the third respondent, Select All Enterprise Limited, the applicants alleged knowing receipt by Select of property in breach of trust. Further or alternatively, on the assumption that the breach of trust claim failed, the applicants sought rectification of the Acknowledgement of Trust to record the common intention of the parties. Finally, the applicants further alleged that Mr Karantzis engaged in misleading and deceptive conduct by making a representation which induced the applicants to execute the Acknowledgement of Trust.

4 The respondents denied each of the applicants’ claims. iSignthis BVI’s position was that the fully paid ordinary shares in ISX, which were issued to it on 5 September 2018 after ISX achieved the Performance Milestones, were owned by iSignthis BVI and were never part of the “Trust Assets” or capable of constituting assets held on trust for the applicants.

5 The applicants’ claim for specific performance of the trust was not opened and was taken to have been abandoned. As a result, the principal relief sought by the applicants was a declaration that Select holds the “Performance Shares” referred to in the Acknowledgement of Trust (the Performance Shares) on trust for the applicants or, alternatively, damages or equitable compensation for breach of trust. The applicants did not open a case about tracing any of the “Trust Assets”, other than to say that the effect of the demerger (referred to below at paragraphs 55 – 57) was to convert 10 ISX shares into one share in its subsidiary.

6 For the reasons that follow, I am satisfied that the applicants have established that, by failing to hold the Performance Shares on trust for the applicants and transfer the rights to the Performance Shares to the applicants, iSignthis BVI acted in breach of trust. Furthermore, the applicants are entitled to equitable compensation in respect of iSignthis BVI’s breach of trust. Otherwise, the applicants’ claims against Select and Mr Karantzis, and the balance of the claims against iSignthis BVI, were either not established or were unnecessary to determine.

7 In the reasons, references to the Performance Shares, Consideration Shares and Trust Assets are references to those terms as defined in the Acknowledgement of Trust (also referred to as the “Trust Deed”, see below at paragraph 61) and references to the “Performance Shares” and “Consideration Shares” are references to those terms as defined in the Prospectus, unless stated otherwise.

background

The applicants and associated persons

8 Larkspur is a company incorporated in the Republic of Seychelles which is associated with Mr Ian Tetro. Mr Tetro’s professional background was in marketing and, in 2013 – 2014, he was a marketing executive for Pepsi Co.

9 Mr Edmonds was a director of Bennick Ltd, a company incorporated in the British Virgin Islands. Mr Edmonds previously practised as a solicitor and, in 2013 – 2014, he was based in Singapore providing corporate finance and wealth management services and advice.

10 In 2013 – 2014, Mr Tetro, Mr Edmonds and Mr Benjamin Walmsley were friends, living in Bangkok.

The respondents and associated entities

11 Prior to 2013, Mr Karantzis had invented a payment verification system which he patented and sought to commercialise through iSignthis BVI, with the assistance of Mr Timothy Hart, Mr Todd Richards and Mr Scott Minehane. At that time, iSignthis BVI was a closely held private company, which was incorporated in the British Virgin Islands.

12 ISX was an eMoney, payments and identity technology company listed on the ASX and the Frankfurt Stock Exchange. At the time it was incorporated, ISX was known as Otis Energy Limited (ASX code: OTE). On 15 March 2015, Otis changed its name to ISX as part of the reverse takeover mentioned below.

13 Select is a company incorporated in the British Virgin Islands. Select was incorporated on 8 January 2019 to hold fully paid ordinary shares in the capital of ISX.

14 Mr Karantzis was:

(a) a director of iSignthis BVI from 18 July 2005 to 23 November 2021;

(b) the managing director and Chief Executive Officer of ISX from about 22 December 2014 to 29 December 2021;

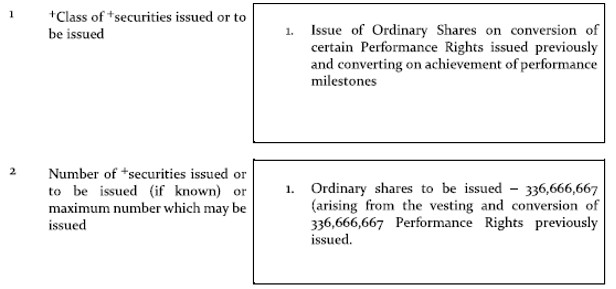

(c) a director of Select from about 17 April 2019 to 23 April 2021 and 13 September 2021 to 23 November 2021; and

(d) the sole shareholder of Select from about 17 April 2019 to 23 March 2021 and 24 June 2021 to 19 October 2021.

Sales and Marketing Agreement

15 In late 2012, Mr Walmsley was introduced to Mr Karantzis as someone with contacts and expertise in Asia. Mr Walmsley introduced Mr Edmonds to Mr Karantzis as a lawyer with experience in assisting start-ups and commercialising ideas.

16 At the time those introductions occurred, iSignthis BVI owned the intellectual property of the ‘iSignthis’ business, comprising a patented system for the authentication of financial instruments used for payment where the owner of the financial instrument is not present.

17 On 8 July 2013, a Sales and Marketing Agreement was executed by iSignthis BVI, Bennick and Ignition Ltd, a Hong Kong company associated with Mr Walmsley. Under the Sales and Marketing Agreement, Bennick and Ignition agreed to pay iSignthis BVI an initial fee of US$500,000 and to establish iSignthis Asia Pte Ltd (Agent), a Singaporean company associated with Mr Edmonds and Mr Walmsley, which was appointed as iSignthis BVI’s agent for the marketing of the iSignthis technology in parts of Asia.

18 By early 2014, a dispute had emerged in relation to the performance of the Agent’s obligations under the Sales and Marketing Agreement. It is unnecessary to mention the nature or reasons for the dispute.

19 On 20 February 2014, the parties to the Sales and Marketing Agreement agreed to resolve the dispute, whereby Mr Walmsley and Mr Edmonds agreed, among other things, to pay an additional US$78,000 (in addition to funds previously paid under the Sales and Marketing Agreement, to make a total capital contribution of US$250,000) for 3% equity in a new holding company (Share Agreement). The commercial intent of the Share Agreement, as stated by Mr Karantzis, both shortly before and after it was signed, was for Mr Walmsley and Mr Edmonds to convert their rights and interests under the Sales and Marketing Agreement into equity in a new holding company.

20 The Share Agreement was later amended to increase the percentage interest to 4% and to include Mr Tetro. Without informing Mr Karantzis, Mr Walmsley and Mr Edmonds arranged for Mr Tetro to pay some of the additional US$78,000 that they had agreed to pay under the Share Agreement. Mr Tetro and Larkspur were not parties to the Share Agreement, and they were not known to Mr Karantzis at the time. After Mr Karantzis became aware of Mr Tetro’s involvement, he spoke with Mr Tetro for the first time in March 2014, and based on that discussion, decided to permit Mr Tetro’s involvement.

21 There was no real dispute that the payments required under the Share Agreement were made.

iSignthis BV

22 In May 2014, iSignthis BV was incorporated in the Netherlands to give effect to Mr Karantzis’ intention of it becoming the entity which would carry on the iSignthis business.

23 The initial plan for iSignthis BV to be the new holding company for the iSignthis business, and for shares in iSignthis BV to be issued to the applicants under the Share Agreement, was overtaken by the idea, which arose in June 2014, of a reverse takeover of Otis.

The reverse takeover

24 The reverse takeover was structured as a sale to Otis of iSignthis BVI’s assets, being shares in iSignthis BV and ISX IP Ltd (by which I infer that the iSignthis business, previously owned by iSignthis BVI, had been or was to be transferred to those entities). iSignthis BVI held all of the issued shares in iSignthis BV, along with all of the shares in ISX IP Ltd, a British Virgin Islands entity, and continued to do so until the reverse takeover was completed.

25 In exchange for the sale of iSignthis BVI’s assets, the “Consideration Shares” in ISX (as defined in the Prospectus, which is mentioned below) were to be transferred to iSignthis BVI. In addition, under the Prospectus, Otis was offering to the public 103,333,333 shares in ISX at an issue price of $0.03, to raise $3,100,000 before expenses.

26 As a result, the new company contemplated by the Share Agreement was not established. However, by September 2014, Mr Karantzis had agreed to the applicants and Mr Walmsley, through Ignition, becoming shareholders in iSignthis BVI (see below at paragraph 35).

27 The reverse takeover, by which shares in Otis were issued to iSignthis BVI in exchange for its assets, was the means by which the founders and shareholders of iSignthis BVI were to profit from their invention and investments and the fundraising under the Prospectus was to fund the business in the early stages.

28 It was not in dispute that the Share Agreement was not a part of the reverse takeover of Otis. Mr Tetro and Mr Edmonds accepted under cross-examination that their investment in the iSignthis business was complete before the reverse takeover of Otis was ever discussed. Further, as the respondents submitted, at the time the idea of the reverse takeover arose, and before it was implemented, neither the applicants nor iSignthis BVI had any interest in or entitlement to the shares in Otis.

Structure and timing of the reverse takeover of Otis by iSignthis BVI

29 In the period from 6 – 31 August 2014, Mr Karantzis, Mr Walmsley, Mr Tetro and Mr Edmonds exchanged correspondence, and on 19 August 2014, attended a meeting on Skype in relation to the reverse takeover of Otis.

30 On 29 August 2014, Mr Karantzis and Mr Richards signed an “Asset Sale Agreement: ASX OTE” (Asset Sale Agreement) purporting to record the proportion and quantity of shares which were to be issued in Otis to iSignthis BVI and available for transfer to the applicants and Ignition (Mr Walmsley’s company) after the mandatory escrow period, which is mentioned below at paragraph 40.

31 On 3 September 2014, Mr Karantzis, Mr Richards, Mr Hart, Mr Minehane, Mr Walmsley and Mr Tetro attended another meeting on Skype in relation to the reverse takeover of Otis.

32 Further correspondence regarding the mechanics of the reverse listing was exchanged between September and November 2014.

Announcement of the reverse takeover

33 On 4 September 2014, Otis announced that it had entered into a “Binding Term Sheet” to acquire 100% of the issued share capital of iSignthis BV and ISX IP Ltd (Acquisition).

34 According to the announcement, in consideration for the Acquisition, Otis was to issue iSignthis BVI:

(a) 298,333,333 fully paid ordinary ISX shares at settlement;

(b) 112,222,222 Class A “Performance Shares” which, on achievement, within three full financial years of Completion, of revenue over a 6 month reporting period equivalent, on an annualised basis, to annual revenue of at least $5,000,000 (Milestone A), would convert on a one for one basis into one ordinary ISX share;

(c) 112,222,222 Class B “Performance Shares” which, on achievement, within three full financial years of Completion, of revenue over a 6 month reporting period equivalent, on an annualised basis, to annual revenue of at least $7,500,000 (Milestone B), would convert on a one for one basis into one ordinary ISX share; and

(d) 112,222,223 Class C “Performance Shares” which, on achievement, within three full financial years of Completion, of revenue over a 6 month reporting period equivalent, on an annualised basis, to annual revenue of at least $10,000,000 (Milestone C), would convert on a one for one basis into one ordinary ISX share.

35 On 15 September 2014, the shareholders of iSignthis BVI passed a resolution to approve the sale of assets to Otis. Mr Walmsley and Mr Tetro were in attendance, and Mr Edmonds gave his proxy to the Chair. I infer that, by this date, Mr Walmsley, Mr Tetro and Mr Edmonds were shareholders of iSignthis BVI.

Share Sale and Purchase Agreement

36 The reverse takeover transaction was documented in a Share Sale and Purchase Agreement dated 21 October 2014 between iSignthis BVI, iSignthis BV, ISX IP Ltd and Otis. That agreement was varied by a letter dated 10 December 2014. The applicants were not parties to the agreement or its variation and they had no direct role in its negotiation.

Prospectus

37 For the purpose of a public offering of shares in Otis, which was part of the reverse takeover, a Prospectus was issued by Otis on 22 December 2014 and a Supplementary Prospectus was issued on 29 January 2015.

38 Under the Prospectus, Otis, which was to be renamed ISX, offered 103,333,333 shares in ISX to the public at an issue price of $0.03, to raise $3,100,000 before expenses (Offer). The Offer was conditional on ISX raising the amount of the Offer and completion of the “Acquisition”, as defined in the Prospectus. The Prospectus stated that, upon completion of the Offer and the “Acquisition”:

(a) 298,333,333 “Consideration Shares” would be issued to iSignthis BVI;

(b) 336,666,667 “Performance Shares” would be issued to iSignthis BVI, on the terms and conditions set out in section 14.2 of the Prospectus, comprising:

(i) 112,222,222 Class A “Performance Shares”;

(ii) 112,222,222 Class B “Performance Shares”; and

(iii) 112,222,223 Class C “Performance Shares”.

39 The Prospectus further stated that:

(a) each class of “Performance Shares” would convert into fully paid ordinary shares in the capital of ISX on a one for one basis upon the achievement of specified Performance Milestones within three full financial years of Completion of the takeover;

(b) the “Performance Shares” were “not transferable”; and

(c) if the Performance Milestone relevant to the “Performance Shares” was not achieved, with the result that conversion into ordinary shares did not occur before the Expiry Date, then the unconverted “Performance Shares” would automatically consolidate into one “Performance Share” and would then convert into a single ordinary ISX share.

40 Under the Prospectus, the “Consideration Shares” to be issued to iSignthis BVI were classified by the ASX as restricted securities and were required to be held in escrow for two years from the date that shares in iSignthis Ltd were reinstated to the ASX.

41 The Supplementary Prospectus was issued to, among other things, provide further information in relation to the sale of the assets to ISX.

The reverse takeover is approved and completed

42 On 22 December 2014, the shareholders of Otis approved the Acquisition.

43 On 5 March 2015, the reverse takeover of Otis was completed and 298,333,333 ordinary ISX shares were issued to iSignthis BVI.

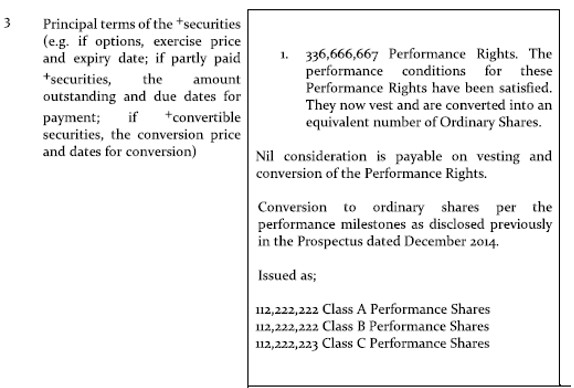

44 On 6 March 2015, ISX made an announcement to the ASX in relation to the completion of the Acquisition.

45 On 16 March 2015, securities in ISX were reinstated to trading on the ASX.

Deed of acknowledgement

46 On 15 June 2015, as already mentioned, the Acknowledgement of Trust was entered into.

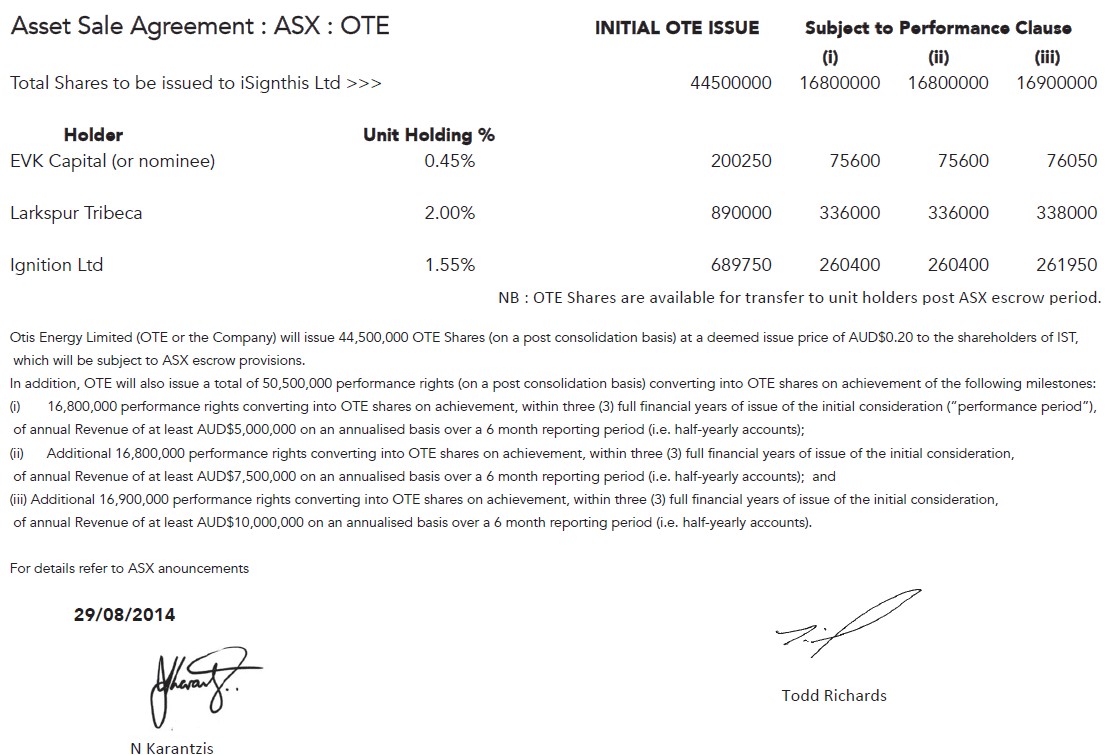

47 Ignition (Mr Walmsley’s company) was not a party to the Acknowledgement of Trust. The reasons why Mr Walmsley did not sign the Acknowledgement of Trust were neither apparent nor relevant to this dispute.

Escrow period under the Prospectus

48 On 16 March 2017, the escrow period under the Prospectus ended. From this date, iSignthis BVI was able to deal with the ordinary ISX shares that had been issued to it under the Share Sale and Purchase Agreement.

49 By 18 May 2017, pursuant to the Acknowledgement of Trust, iSignthis BVI had transferred 2.41% of the Consideration Shares to or at the direction of the applicants. The dispute between the parties did not concern the applicants’ entitlement with respect to the Consideration Shares.

Performance Shares

50 Performance Milestone A, Milestone B and Milestone C were achieved by 30 June 2018.

51 On 29 August 2018, iSignthis Ltd made an announcement to the ASX to the effect that the three Performance Milestones had been achieved and, in the circumstances, 336,666,667 fully paid ordinary shares in the capital of ISX were to be issued.

52 The announcement relevantly stated as follows:

53 On 5 September 2018, following the conversion of the Class A, Class B and Class C “Performance Shares”, ISX issued 149,654,654 fully paid ordinary ISX shares to iSignthis BVI and a total of 187,012,013 fully paid ordinary ISX shares to employees and directors of ISX, or nominees of those persons, other than Mr Karantzis.

54 On 29 April 2019, iSignthis BVI disposed of 446,797,754 ISX shares, with 223,398,878 ISX shares being transferred to Select. As a result, iSignthis BVI was no longer a substantial shareholder of ISX shares.

Demerger

55 On 1 September 2021, ISX announced that it was exploring a proposed demerger of its subsidiary, ISX Financial EU Ltd (ISXFEU), by way of a reduction in the capital of ISX.

56 At a meeting of shareholders of ISX on 12 October 2021, a resolution was passed for the capital of ISX to be reduced by ISX making a pro-rata in specie distribution of approximately 110,079,450 ordinary shares in ISXFEU to all holders of ordinary shares in ISX.

57 The effect of the demerger was that every shareholder of ISX, at the record date, being the date of the general meeting, received 1 ISXFEU share for every 10 ISX shares held on that date.

Delisting of ISX

58 In May 2022, ISX was renamed Southern Cross Payments Ltd and its ASX code was changed to SP1.

59 On 4 November 2022, Southern Cross Payments was delisted from the ASX.

the applicants’ claims

60 The applicants brought the following claims against the respondents.

61 First, the applicants alleged that iSignthis BVI’s conduct in failing and refusing to transfer the Performance Shares to the applicants, disposing of ISX shares (including shares held on trust for the applicants) and giving effect to the demerger resolution, constituted a breach of trust and breach of the “Trust Deed”, constituted by the Acknowledgement of Trust. The document signed by the relevant parties on 15 June 2015, which was entitled “Acknowledgement of Trust”, was executed as a deed and described by the applicants as the “Trust Deed”, which I will adopt from hereon in these reasons.

62 Secondly, and in the alternative to the breach of trust claim, the applicants alleged that iSignthis BVI’s conduct in failing and refusing to transfer the Performance Shares to the applicants was a breach of contract constituted by the Trust Deed.

63 Thirdly, the applicants alleged that the conduct referred to in paragraph 61 was a dishonest, alternatively fraudulent, breach of the fiduciary duties which iSignthis BVI owed to the applicants by reason of the Trust Deed. As against Select and Mr Karantzis, the applicants alleged knowing receipt of property in breach of trust, and they alleged knowing assistance by Mr Karantzis of iSignthis BVI’s breach of trust, alternatively breach of fiduciary duties.

64 Fourthly, and by way of alternative to the above claims, the applicants sought rectification of the Trust Deed to record the common intention of the parties, to the extent that the Trust Deed did not give effect to the applicants’ rights to the Performance Shares.

65 Fifthly, the applicants alleged that, by making the Share Agreement, the composition of which I discuss below at paragraph 157(a), and the Asset Sale Agreement, Mr Karantzis represented to the applicants that they would enjoy rights, including performance rights, if and when issued by Otis and encouraged them to invest in Otis (Representation). The applicants stated that if, as the respondents contended, the trust established under the Trust Deed terminated immediately after seven days following the end of the “Escrow Period” (as defined in the Trust Deed), and the applicants were not entitled to the Performance Shares because, at that time, none had been issued to iSignthis BVI, the Representation was misleading and deceptive or likely to mislead or deceive, and the applicants suffered detriment as a result of their reliance on the Representation, in that they lost their rights in respect of the Trust Assets.

EVIDENCE AND witnesses

66 The parties relied on a Statement of Agreed Facts, setting out facts agreed by the parties for the purpose of s 191 of the Evidence Act 1995 (Cth).

67 The applicants relied on five affidavits, being two affidavits of Mr Tetro, dated 8 March 2023 and 13 March 2025, two affidavits of Mr Edmonds dated 7 March 2023 and 14 March 2025 and one affidavit of Mr Walmsley dated 7 March 2023. They were each required for cross-examination.

68 Mr Tetro gave evidence in relation to the circumstances in which he was brought in, by Mr Walmsley, to be a silent investor in the iSignthis business in Asia, and he agreed to acquire shares in a new holding company. Mr Tetro was a generally good witness. He gave responsive answers to questions in cross-examination. Several propositions were put to him in cross-examination regarding the basis upon which he invested in the iSignthis business and would receive any Performance Shares, which he rejected, without being argumentative or evasive. Mr Tetro had no financial or practical stake in the outcome of the proceeding. Mr Tetro acknowledged that he had agreed to forfeit his interest in the outcome of the proceeding in favour of Mr Walmsley, in return for Mr Walmsley agreeing to hold Mr Tetro harmless in respect of costs.

69 Mr Edmonds gave evidence regarding the resolution of the dispute in relation to the Sales and Marketing Agreement, which led to the relevant parties entering into the Share Agreement and the Trust Deed. Mr Edmonds negotiated and drafted the Trust Deed on behalf of the applicants. Mr Edmonds was also a generally good witness. He had a reasonable recollection of events surrounding his investment and the drafting of the Trust Deed. His answers were direct and responsive. Similarly to Mr Tetro, Mr Edmonds has agreed to forfeit any interest in the outcome of the proceeding in favour of Mr Walmsley on the condition that Mr Walmsley hold him harmless in relation to costs.

70 Mr Walmsley gave evidence in relation to the entry into and dispute concerning the Sales and Marketing Agreement, the resolution of the dispute, discussions regarding the reverse takeover of Otis and emails that were exchanged in relation to the Trust Deed.

71 Mr Walmsley recorded the Skype meetings on 19 August 2014 and 3 September 2014, at which the reverse takeover of Otis was discussed, and later had the recordings transcribed. Although there was an objection to the tender of the transcripts, because Mr Walmsley did not obtain the consent of the participants to record the meetings, the transcript was tendered by agreement on a limited basis under s 136 of the Evidence Act as evidence as to what was said at the meetings, but not as to the truth.

72 Mr Walmsley was not a party to the proceeding and was called to give evidence on behalf of the applicants. Mr Walmsley was, however, funding and conducting the proceeding on behalf of the applicants, who had agreed to forfeit any interest in the outcome of the proceeding to Mr Walmsley, on the condition that he hold them harmless in relation to costs. While Mr Walmsley had less involvement in relevant events than the applicants, it was clear that he had an emotional as well as a financial stake in the proceeding. While this affected his demeanour at times, it is unnecessary to make any findings as to whether this should affect the weight to be given to his evidence for reasons that will follow.

73 The respondents relied on three affidavits, one of Mr Timothy Hart dated 4 April 2025, one of Mr Karantzis dated 6 April 2025 and one of Mr Justin Klintberg dated 7 April 2025. They were each required for cross-examination.

74 Mr Hart was the Executive Chairman of Southern Cross Payments from 29 December 2021 and an independent non-executive Chairman of ISX since March 2015. From 2010 to early 2015, Mr Hart acted as Chairman of the iSignthis business. Mr Hart gave evidence regarding the resolution of the dispute in relation to the Sales and Marketing Agreement, the Share Agreement, discussions and correspondence regarding the reverse takeover of Otis and ISX achieving the Performance Milestones. Mr Hart was a generally good witness who gave forthright answers to questions and made appropriate concessions.

75 Mr Karantzis gave evidence in relation to the entry into the Sales and Marketing Agreement, the resolution of the dispute that emerged, entry into the Share Agreement, the reverse takeover of Otis, the Asset Sale Agreement, the negotiation and entry into the Trust Deed and the issuance of shares to iSignthis BVI after ISX achieved the Performance Milestones. Mr Karantzis was able to recall a significant amount of detail in relation to the relevant events. This, however, contributed to an impression that his evidence and answers to questions in cross-examination were carefully constructed to suit his case. Given his role as a party, Mr Karantzis had an obvious interest in the outcome of the proceeding. Similarly to Mr Walmsley, it is unnecessary to make findings as to whether this should affect the weight to be given to his evidence for reasons that will follow.

76 Mr Klintberg is the founder of a financial services company. Mr Klintberg’s evidence was limited to his involvement, in August 2024, in the acquisition and price of shares in ISXFEU on behalf of a group of buyer entities.

77 The respondents submitted that the Court should disregard the evidence of Mr Walmsley because his stake in the outcome of the proceeding had “tainted” his evidence and because his “vendetta” against Mr Karantzis raised further credibility issues.

78 The applicants made extensive submissions regarding Mr Karantzis’ credit and submitted that Mr Karantzis’ evidence was “recent invention”.

79 The key issue in the proceeding concerns the proper construction of the Trust Deed. Evidence concerning the surrounding circumstances at the time the Trust Deed was entered into was contained in contemporaneous exchanges between the parties. It has been observed that in commercial cases where contemporaneous documents exist, it is often preferable for little if any reliance to be placed on witness testimony, relying on human memory, and for significant weight to be given to evidence contained in contemporaneous documents: Fox v Percy (2003) 214 CLR 118; [2003] HCA 22 at [31] (Gleeson CJ, Gummow and Kirby JJ); Webb v Getswift Limited (No 5) [2019] FCA 1533 at [18] (Lee J), referring to Leggatt J in Gestmin SGPS SA v Credit Suisse (UK) Limited [2013] EWHC 3560 (Comm) at [15 ]– [23]. That observation is apt in the present case. As a result, it is unnecessary to make findings in relation to the credit or credibility of the witnesses, or whose evidence should be accepted where the witnesses’ evidence diverged.

80 Finally, both parties relied on the expert evidence as to quantum. This is dealt with separately below.

Breach of trust

81 The respondents admitted that there was a trust constituted by or under the Trust Deed. They contended, however, that the Trust Assets did not include the Class A, Class B or Class C “Performance Shares” issued under the Prospectus, or any further shares in ISX unless the Performance Milestones were achieved and the Performance Shares had converted into ordinary ISX shares before iSignthis BVI was required to transfer all of the Trust Assets to each beneficiary in their respective proportions. As the former had not occurred before the trust was terminated, the respondents said, they were not obliged to transfer the Performance Shares to the applicants and were free to deal with them, and the corresponding eventual ordinary shares, as they saw fit.

82 The resolution of the breach of trust claim turns on the proper construction of the Trust Deed, which was in dispute between the parties. It is convenient to begin by setting out the relevant terms of the Trust Deed.

The Trust Deed

83 Beginning with the relevant definitions, Trust Assets is defined in clause 1.1 of the Trust Deed, as follows:

Trust Assets means in respect of each Beneficiary and subject to applicable Australian Corporations law, the Australian Securities Exchange rules, and the requirements of the prospectus and supplementary prospectus being met, the Relevant Proportion of:

(a) Consideration shares, representing a total of 298,333,333 ordinary shares of OTE;

(b) Performance Shares, provided that such shares are issued (whether issued before or after the Escrow Period), whereby performance shares shall only be issued upon satisfaction of the Performance Targets nominated in the Prospectus, up to a maximum of three tranches, with each tranche representing 112,222,222 shares that may be issued.

(c) and whilst the Trustee holds on trust the Trust Assets, the proceeds of sale or redemption of any of the property referred to in paragraphs (a) – (d), and

(d) and whilst the Trustee holds on trust the Trust Assets, any rights, dividends, bonus shares or other derivative right of any nature in connection with the property referred to in paragraphs (a) – (e).

84 Consideration Shares and Performance Shares are defined in clause 1.1 to have the meanings given to them in the Prospectus, which are mentioned below.

85 “Escrow Period” is defined in clause 1.1 to mean the period during which the “Trustee”, being iSignthis BVI, is prevented by law from disposing of or otherwise distributing the Trust Assets to the “Subscribers”, being Larkspur and Edmonds.

86 Clause 2, which bears setting out in its entirety as it appears in the Trust Deed, provides as follows:

2. Trust

2.1 Declaration of Trust

The Trustees declare that they hold the Trust Assets on trust for each Beneficiary and the Subscribers in accordance with the terms of this deed. The Trustees may not sell, transfer or dispose of the Trust Assets without the written consent of the Beneficiary.

2.2 Notification regarding Escrow Period

Not later than 21 days before the end of the Escrow Period the Trustees must notify the Subscribers that the Escrow Period will end.

2.3 Transfer of Trust Assets

Not later than seven days after the end of the Escrow Period the Trustees must transfer the Trust Assets to the Beneficiary or otherwise as the each Beneficiary may direct in writing.

2.4 Summary of Trust Assets

The register of interests in below summarises the assets held on trust by the Trustee for each Beneficiary, and includes prospective shares that may be issued subject to the Performance Targets being met. The Beneficiaries have each confirmed in writing their relevant proportions under cover of email dated 17th March 2015

Event/Beneficiary | Larkspur Tribeca | Edmonds |

Consideration shares (post escrow) | 5,966,667 | 1,223,167 |

Performance Tranche 1 (if issued) | 2,244,444 | 460,111 |

Performance Tranche 2 (if issued) | 2,244,444 | 460,111 |

Performance Tranche 3 (if issued) | 2,244,444 | 460,111 |

2.5 No Further Claims

Upon transfer of the Trust Assets by the Trustee, this agreement is in full and final settlement of the Beneficiary’s claims on rights, dividends, bonus shares or other derivative right of any nature in connection with the Trust Assets, jointly or severally.

It is a term of this Agreement that the Beneficiary and/or the Subscribers jointly will not pursue any additional claims relating to the Trust Assets, whether dealt with in this Agreement or not

87 The remaining terms of the Trust Deed dealt with the service of notices and the governing law.

88 Turning to the relevant definitions in the Prospectus, to which the Trust Deed referred, “Consideration Shares” is relevantly defined (in section 13.1(a)), as follows:

The consideration is:

(i) 298,333,333 Shares (on a post consolidation basis);

(ii) 112,222,222 Class A Performance Shares (on a post consolidation basis);

(iii) 112,222,222 Class B Performance Shares (on a post consolidation basis); and

(iv) 112,222,223 Class C Performance Shares (on a post consolidation basis),

(together the Consideration Shares).

The terms and conditions of the Class A Performance Shares, Class B Performance Shares and Class C Performance Shares are set out in Section 14.2

89 “Performance Shares” is defined to mean “the performance shares to be issued on the terms and conditions set out in Section 14.2”.

90 Section 14.2 of the Prospectus relevantly provides:

Class A Performance Shares

1. Conversion of Class A Performance Shares

(a) (Conversion on achievement of Milestone A) On achievement, within three (3) full financial years from Completion, of revenue over a 6 month reporting period (being for a 6 month period ending 30 June or 31 December), on an annualised basis, to annual revenue of at least $5,000,000 (Milestone A), each Class A Performance Share will convert on a one for one basis into a Share.

For the avoidance of doubt, a half year revenue of $2,500,000 will satisfy Milestone A.

(b) (Expiry) Milestone A must be achieved on or before 5.00 pm on the date which is 14 days after the release of the audited financial reports for the third full financial year after Completion being financial year 2017/2018 (Expiry Date).

(c) (Conversion on change of control) If there is a Change of Control Event in relation to the Company prior to the conversion of the Class A Performance Shares, then:

(i) Milestone A will be deemed to have been achieved; and

(ii) each Class A Performance Share will automatically and immediately convert into Shares,

however, if the number of Shares to be issued as a result of the conversion of Class A Performance Shares, together with the number of Shares to be issued as a result of the conversion of the Class B Performance Shares and Class C Performance Shares, due to a Change in Control Event is in excess of 10% of the total fully diluted share capital of the Company at the time of the conversion, then the number of Class A Performance Shares, Class B Performance Shares and Class C Performance Shares to be converted will be prorated so that the aggregate number of Shares issued upon conversion of the Class A Performance Shares, Class B Performance Shares and the Class C Performance Shares is equal to 10% of the entire fully diluted share capital of the Company.

(d) (No conversion) To the extent that Class A Performance Shares have not converted into Shares on or before the Expiry Date, then all such unconverted Class A Performance Shares held by each holder (Class A Holder) will automatically consolidate into one Class A Performance Share and will then convert into one Share.

(e) (Conversion procedure) The Company will issue a Class A Holder with a new holding statement for the Share or Shares as soon as practicable following the conversion of each Class A Performance Share.

(f) (Ranking of shares) Each Share into which the Class A Performance Shares will convert will upon issue:

(i) rank equally in all respects (including, without limitation, rights relating to dividends) with other issued Shares;

(ii) be issued credited as fully paid;

(iii) be duly authorised and issued by all necessary corporate action; and

(iv) be allotted and issued free from all liens, charges and encumbrances whether known about or not including statutory and other pre-emption rights and any transfer restrictions.

91 Section 14.2(2) of the Prospectus dealt with the rights attaching to Class A Performance Shares, and relevantly provides:

(a) (Share capital) Each Class A Performance Share is a share in the capital of the Company.

…

(f) (Not transferable) A Class A Performance Share is not transferable.

92 Section 14.2(3)–(5) contained similar provisions in relation to Class B and Class C Performance Shares, save that the performance milestones were achieved by a higher revenue figure.

Relevant principles

93 It is well established that a share is property that is capable of being held on trust. As Jagot J said in Ellison v Sandini Pty Ltd (2018) 263 FCR 460; [2018] FCAFC 44 at [119 ]–[120]:

A share, it has been said, is “the interest of a shareholder in the company measured by a sum of money for the purpose of liability in the first place and of interest in the second, but also consisting of a series of mutual covenants entered into by all the shareholders” (Archibald at 156). The subsequent abolition of the concept of par value and of authorised capital effected by the Company Law Review Act 1998 (Cth) renders the reference to the measurement by a sum of money in this description inapt (National Mutual Life Association of Australia Ltd v Commissioner of Taxation [2009] FCAFC 96; (2009) 177 FCR 539 at [48] referring to Pilmer v The Duke Group Pty Ltd [2001] HCA 31; (2001) 207 CLR 165 at [19]). In Pilmer at [19] McHugh, Gummow, Hayne and Callinan JJ said:

Once issued, a share comprises "a collection of rights and obligations relating to an interest in a company of an economic and proprietary character, but not constituting a debt" [citing Pennington, "Can shares in companies be defined?", (1989) 10 The Company Lawyer 140 at 144].

For a share to be held on trust there must be “certainty … as to the property bound by the trust” (Herdegen v Federal Commissioner of Taxation [1988] FCA 419; (1988) 84 ALR 271 at [19] citing Federal Commissioner of Taxation v Clarke [1927] HCA 49; (1927) 40 CLR 246 at 283–5; Scott on Trusts, 4th ed, 1987, § 76, 77). In the context of shares which do not need to be numbered and certificated (as permitted by s 1070B(2) of the Corporations Act 2001 (Cth)), as is the case with shares in MIN, the question that arises is the certainty of the subject matter of any trust. This is because shares are considered to be fungible or interchangeable (a concept which, as noted below, itself has attracted criticism).

94 For some time, however, there was uncertainty as to whether a trust could be constituted over a specified number of unidentified shares within a fungible pool. In Ellison v Sandini, after surveying the authorities, Jagot J (with whom Siopis J agreed, at [1]) held that it could. Her Honour said, at [148]:

In terms of principle, the weight of authority is that there can be a valid trust over a fungible pool of assets provided the assets and relevant proportions for the different beneficiaries are identified with sufficient certainty. The better view is that for the requirement of certainty to be satisfied the trust must be over all of the fungible assets in the pool, the beneficial co-ownership proportions reflecting the respective interests of the beneficiaries. In the context of a declaration of trust, there may be a sound basis in principle to uphold the validity of such a trust on the basis that the trustee’s intention must have been to create a valid trust which requires certainty of subject matter.

95 It is also well established that the principles regarding the construction of contracts apply to the construction of trust instruments: Byrnes v Kendle [2011] HCA 26; (2011) 243 CLR 253 at 274-275 [57]-[59] (Gummow and Hayne JJ), 286 [102] (Heydon and Crennan JJ); Trustee for Michael Hayes Family Trust v Commissioner of Taxation [2019] FCA 426 at [55] (Logan J); Schreuders v Grandiflora Nominees Pty Ltd [2016] VSCA 93 at [12]-[15], [21]-[22] (Kyrou, Ferguson and McLeish JJA); The Trust Company (Nominees) Ltd v Banksia Securities Ltd (Receivers and Managers appointed) (in liquidation) [2016] VSCA 324 at [35] (Ashley, Beach and McLeish JJA).

96 The role of the court in interpreting trust instruments is to give effect to the intention of the parties: Banksia Securities at [36]–[37], citing Australian Broadcasting Commission v Australasian Performing Right Association Ltd [1973] HCA 36; (1973) 129 CLR 99 at 109 (Gibbs J, dissenting).

97 As with contracts, the parties’ intentions are to be determined objectively with reference to the instrument they have executed in the context of the surrounding circumstances. As Heydon and Crennan JJ said in Byrnes v Kendle at [98]:

A contract means what a reasonable person having all the background knowledge of the "surrounding circumstances" available to the parties would have understood them to be using the language in the contract to mean. But evidence of pre-contractual negotiations between the parties is inadmissible for the purpose of drawing inferences about what the contract meant unless it demonstrates knowledge of "surrounding circumstances".

[Footnotes omitted]

98 In Schreuders v Grandiflora Nominees, at [21]–[22], the Victorian Court of Appeal said:

… trust instruments are to be given their natural and ordinary meaning unless they have a special or technical meaning. The terms of an instrument must be construed in the context of the entire document and in such a way that renders them ‘all harmonious one with another’.

The parties’ intention must be found in the wording of the trust instrument rather than in what was on their minds when they executed the instrument. Evidence of the actual intention of the parties will not be admissible except in an action for rectification and other limited circumstances. In Byrnes v Kendle, Gummow and Hayne JJ stated:

[T]he expressed intention of the parties is to be found in the answer to the question, ‘What is the meaning of what the parties have said?’, not to the question, ‘What did the parties mean to say?’

[Footnotes omitted]

99 Antecedent correspondence has been considered by the High Court to fall within objective evidence of this kind for the purpose of construing an executed deed: Royal Botanic Gardens and Domain Trust v South Sydney City Council (2002) 240 CLR 45; [2002] HCA 5 at [26] and [30] (Gleeson CJ, Gaudron, McHugh, Gummow and Hayne JJ).

Objective evidence of the surrounding circumstances

100 Although the parties gave evidence about their subjective intentions and understanding regarding the Trust Deed, that evidence must be put to one side. While both parties took the Court to a voluminous amount of correspondence that was exchanged prior to the execution of the Trust Deed, a great deal of that evidence was not relevant or admissible on the question of the proper construction of the Trust Deed. That is because evidence of pre-contractual negotiations between the parties is inadmissible for the purpose of drawing inferences about what the contract meant unless, relevantly here, it demonstrates background knowledge of “surrounding circumstances” available to all parties: Byrnes v Kendle at [98].

101 The Trust Deed was directed at implementing the share issue contemplated by the Asset Sale Agreement, in the context of the mandatory escrow period. In this case, the objective evidence of the surrounding circumstances to which the Court may have regard comprises the Asset Sale Agreement, which purported to record the proportion and quantity of shares which were to be issued in Otis, and the communications referred to below, except where noted. The parties to the Trust Deed had knowledge of the relevant communications referred to below because the communications were either sent or copied to all parties to the Trust Deed or they were public communications, such as prospectuses and ASX announcements, which I infer the parties had knowledge of given their interest in the transaction.

102 The Asset Sale Agreement, which was signed on 29 August 2014 by Mr Karantzis and Mr Richards, stated as follows:

103 On 1 September 2014, Mr Karantzis wrote to Mr Tetro, Mr Walmsley, Mr Edmonds, Mr Richards, Mr Hart and Mr Minehane regarding the Asset Sale Agreement, stating that (emphasis added):

The consideration against the asset sale is for iSignthis [BVI] to be issued 55% of the equity of OTE Ltd, with performance rights to be issued up to ~72.4%.

This is an asset sale agreement with earn-out provisions, with the effect of concluding a reverse takeover of an ASX listed entity, by way of issue of shares as consideration.

[…]

The Shares to be issued as consideration to iSignthis [BVI] for the sale of asset are likely to be held in escrow for 24 months.

At any point following escrow, iSignthis [BVI] is able to transfer the shares off market to individual unit holders.

104 In describing the “key terms”, Mr Karantzis said (emphasis added):

In addition, OTE will also issue a total of 50,500,000 performance rights (on a post consolidation basis) converting into OTE shares on achievement of the following milestones:

(i) 16,800,000 performance rights converting into OTE shares on achievement, within three (3) full financial years of issue of the initial consideration (“performance period”), of annual Revenue of at least AUD$5,000,000 on an annualised basis over a 6 month reporting period (i.e. halfyearly accounts);

(ii) Additional 16,800,000 performance rights converting into OTE shares on achievement, within three (3) full financial years of issue of the initial consideration, of annual Revenue of at least AUD$7,500,000 on an annualised basis over a 6 month reporting period (i.e. half-yearly accounts); and

(iii) Additional 16,900,000 performance rights converting into OTE shares on achievement, within three (3) full financial years of issue of the initial consideration, of annual Revenue of at least AUD$10,000,000 on an annualised basis over a 6 month reporting period (i.e. half-yearly accounts).

[…]

This is consistent with the outline provided during the online meeting held between Tetro/Walmsley/Edmonds + Karantzis/Richards on the 19th August 2015 [sic].

105 On 8 November 2014, Mr Karantzis wrote to Mr Edmonds, Mr Tetro and Mr Walmsley, copying Mr Minehane, Mr Hart and Mr Richards, concerning changes to the mechanics of the agreement with Otis that affected the number of shares to be issued and the issue price. That email contemplated the rights to the Performance Shares to be held by the applicants as something capable of being transferred and sold for value, “off market”, and recorded by iSignthis BVI (bold emphasis added):

Gents,

As you may be aware from the Otis Ltd ASX announcement last Friday, there has been some changes to the mechanics of the agreement with Otis Ltd.

The changes do not affect the sale price of the Intellectual Property etc, which is still valued at $8.95m, nor the market capitalisation at re-list.

It is a change only in the number of shares to be issued, and the issue price.

A change in the ASX listing rules has allowed us to reconstruct the shares at a 10:1 rather than 66.67:1, with a resultant share price of 0.03c rather than 0.20c. Effectively, we are to be issued 6.67 times more shares, but at 6.67 times lower price.

The sale agreement has now moved to unconditional, with the Independent Expert report having concluded that $8.95m is a fair and reasonable price for the acquisition of the IP by Otis Ltd, including technical, patent and commercial due diligence having also been satisfactorily completed by independent parties appointed by Otis.

The attached register of interests has been recalculated based upon the revised Otis shares to be issued as consideration and upon satisfaction of performance requirements.

We are still in discussions with the ASX as to whether (with regards to the re-listed Otis);

1. shares to be allocated to minority interests of the vendor may be released form escrow at any earlier stage

2. If achievement of performance hurdles automatically releases shares from escrow.

We are optimistic as to the second, but consider the first to be unlikely.

Whilst the shares in the newly listed ASX vehicle are likely to remain in escrow, there is no prohibition on any shareholder seeking a buyer for their allocation as noted in the attached register, to be sold off market. The company itself does not facilitate buying or selling of interests or shares, but will record any transaction.

Please do not hesitate to contact myself or Todd with regards to any queries regarding the reconstruction.

Regards

John Karantzis | Executive Director

106 The attached “register of interests” was another version of the Asset Sale Agreement, in which the number of shares to be issued in Otis had changed. The attachment was as follows:

107 On 11 November 2014, in response to a query from Mr Walmsley regarding the shares to be issued as part of the sale transaction, Mr Karantzis sent an email to Mr Walmsley, copying Mr Hart, Mr Minehane and Mr Richards (Mr Tetro was added to the chain subsequently), stating (emphasis added):

iSignthis [BVI] will be issued rights that convert to shares in Otis, per the announcements on the ASX.

Those rights will be held in escrow but notionally by iSignthis [BVI] until the later of;

a) escrow period ending (2 years from re-list), and the rights converting to unencumbered shares or

b) performance hurdles being met, and rights converting to unencumbered shares.

[…]

We have requested the ASX allow us to distribute in specie, but that is not an option the ASX will allow until rights convert to shares, and shares are no longer in the escrow period.

That is, performance rights may convert to shares before the escrow period ends, which means that consideration and converted performance rights would still not be transferable until after escrow.

[…]

Upon issue of the rights (contemporaneous with re-listing), we will issue the individual holding statements, which will bind the directors of isignthis Ltd to transfer the shares (upon conversion of rights) to the holders (or their nominees), after escrow period ends.

108 On 13 November 2014, Mr Karantzis sent to Mr Walmsley an email, copying Mr Edmonds, Mr Tetro, Mr Minehane, Mr Richards and Mr Hart, that included the following (emphasis added):

The position is that we are proceeding with the Otis deal, you (Ignition), and Ian (Lakrspur) and David (Bennick), will be issued documentation to convert your equitable rights into legal rights as soon as reasonably possible following completion with Otis. Your rights will be based mutatis mutandis on the iSignthis Ltd rights with Otis, but will be under escrow for 24 months (like iSignthis).

109 The respondents submitted that the concept of preparing a trust deed arose in early November 2014 in response to Mr Walmsley’s displeasure and that of the applicants about the ASX-imposed escrow period, which prevented iSignthis BVI making an in specie distribution of the shares in ISX that it would receive upon completion of the reverse takeover.

110 On 6 March 2015, ISX made an announcement to the ASX regarding completion of the Acquisition, confirming satisfaction of all conditions precedent and the acquisition by ISX of 100% of the issued share capital of iSignthis BV and ISX IP, which were together referred to as “iSignthis” in the announcement. The announcement also confirmed the issue of the following “Consideration Securities” to the “iSignthis vendors” on 5 March 2015:

Ordinary Shares | Class A Performance Shares | Class B Performance Shares | Class C Performance Shares | |

Consideration Securities | 298,333,333 | 112,222,222 | 112,222,222 | 112,222,222 |

111 In relation to the “Performance Shares”, the announcement further stated that:

Under the terms of the Sale and Purchase Agreement between [Otis] and iSignthis B.V and ISX IP Ltd, the vendors have been issued with Performance Shares as follows:

112,222,222 Class A Performance Shares

112,222,222 Class B Performance Shares

112,222,223 Class C Performance Shares

112 Contrary to the announcement, and as will be explained, “Performance Shares” had not been issued to the “iSignthis vendors” at the date of the announcement. However, 298,333,333 ordinary ISX shares were issued to iSignthis BVI upon completion of the Acquisition.

113 As an aside (because it assists with the chronology but it is not part of the objective surrounding circumstances, as it is unclear whether the below email was passed on to Mr Tetro), Mr Walmsley apparently was confused about the reference in the announcement to the “iSignthis vendors” and, on 8 March 2015, he asked Mr Hart, in his capacity as Chairman of ISX, for details in relation to the “iSignthis vendors” and his “shareholdings in such”. Mr Karantzis replied:

The percentage allocation of the 4% interest in the consideration and performance Shares to be held in Otis to be held in trust on behalf of your parties, has been fixed and agreed between your parties - Tetro/ Edmonds/ Walmsley. We will not revisit that except under signed and written instructions from all parties.

The prospectus (and supp) covers all information that is required to be disclosed.

I am awaiting return comments from David regarding the trust agreement, which I sent approx six weeks ago. I understand that David acts for you in this regard.

To clarify, iSignthis ltd BVI sold its assets to Otis energy ltd. The consideration was shares in Otis, your proportion of which will be held in trust for your parties until end of escrow period.

114 The reference in Mr Karantzis’ email to “the trust agreement” was a reference to a draft of the Acknowledgement of Trust, which Mr Edmonds had prepared. There were five draft versions of the Acknowledgement of Trust provided to the Court, two dated 30 January 2015, one dated 18 March 2015, another dated 20 March 2015, another dated 13 June 2015 and one execution version which was signed on 15 June 2015. Evidence of prior drafts of a deed has been used to assist in establishing the parties’ common understanding or the deed’s context, which is always admissible, as opposed to as a direct aid in construction: see Royal Botanic at [26]–[31] (Gleeson CJ, Gaudron, McHugh, Gummow and Hayne JJ); Righi v Kissane Family Pty Ltd [2015] NSWCA 238 at [46]–[47] (Emmett JA, Ward and Gleeson JJA agreeing at [1] and [99], respectively); Re Jimmy’s Recipe Pty Ltd (No 2) [2020] NSWSC 632 at [54]–[56] (Leeming JA). To the extent that the draft deeds were addressed in closing submissions, the respondents submitted that the “Escrow Period” and clause 2.3 did not change materially after the first draft deed.

115 On 17 March 2015, the percentage split of shares to be allocated to the applicants and Mr Walmsley, totalling an overall 4% in Otis, was confirmed between all the parties as follows:

Ian Tetro (Tribecca [Larkspur]) 2.00%

Benjamin Walmsley (Ignition Limited) 1.59%

David Edmonds (Bennick Ltd) 0.41%

116 On 23 March 2015, Mr Karantzis sent a draft of the Trust Deed to Mr Walmsley’s then solicitor. In the covering email, which was copied to Mr Tetro, Mr Edmonds, Mr Walmsley and Mr Richards, Mr Karantzis described the background to the transaction in the following terms (emphasis added):

Larkspur Tribeca, Ignition and Edmonds jointly subscribed to 4% rights associated with the ‘reverse take over’ by the vendor (iSignthis Ltd (BVI) in the shell Otis Energy Ltd. Each party has a relevant potion [sic] of the 4%, per the attached. The 4% is to be applied to all shares issued to the vendor, as either consideration shares, shortfall shares or subject to meeting performance criteria.

The number of shares to be issued as consideration shares is per the prospectus, and will be held in escrow (and thus trust) by the vendor, on behalf of the subscribers. Shortfall shares have also been issued, per ASX announcement, which will also be held in trust.

Certain performance rights, should performance hurdles be met, will also convert to shares, which shall also be subject to escrow.

The escrow period is 2 years from listing, 16 March 2017.

117 On 15 June 2015, the Trust Deed was signed by Mr Karantzis and Mr Richards, on behalf of iSignthis BVI, Mr Tetro on behalf of Larkspur and Mr Edmonds on his own behalf.

Consideration

118 In my assessment, the Trust Assets comprising the Consideration Shares and the rights to the Performance Shares were identified with sufficient certainty for there to be a valid trust over them, despite the fact that the individual shares or rights were not identifiable by certificates: Ellison v Sandini at [148] (Jagot J). As for the rights to the Performance Shares, the requirement of certainty is satisfied because iSignthis BVI held no other rights to Performance Shares in ISX. Indeed, the parties conducted themselves on the basis that they were bound by the trust in respect of the Consideration Shares, evincing iSignthis BVI’s intention to create a valid trust, over all the Trust Assets, including those referred to in paragraph (b) of the definition of Trust Assets. The matter in dispute concerns whether the applicants had any entitlement to the Performance Shares referred to in paragraph (b) of the definition of Trust Assets.

119 As already mentioned, under the Trust Deed, the Consideration Shares and Performance Shares were defined to have the meaning given to those terms in the Prospectus. In the Prospectus, the “Consideration Shares” incorporated the “Performance Shares” as defined in the Prospectus. However, the incorporation of the “Performance Shares” in the definition of the “Consideration Shares” in the Prospectus did not bring the “Performance Shares” into the trust. It is clear from paragraph (a) of the definition of Trust Assets that, for the purpose of the Trust Deed, the Consideration Shares meant the 298,333,333 ordinary shares in ISX that had been issued to iSignthis BVI upon completion of the Acquisition. That is, they were two separate classes of asset for the purposes of the Trust Deed.

120 Turning then to the meaning of Performance Shares in the Trust Deed, in the Prospectus, the “Performance Shares” was defined to mean the shares to be issued on the terms and conditions set out in Section 14.2. The effect of Section 14.2 was that, if the Performance Milestones, of revenue over a six month reporting period equivalent to annualised revenue between $5,000,000 and $10,000,000, were met before 30 June 2018, the Class A, Class B or Class C “Performance Shares” would convert into ordinary ISX shares on a one for one basis. There were no “Performance Shares” (ie, securities) issued under the Share Sale and Purchase Agreement at the time the Trust Deed was executed. There were, however, rights to be issued “Performance Shares”, on the achievement of the Class A, Class B or Class C Performance Milestones, which would convert into ordinary ISX shares, on a one for one basis. As Mr Karantzis explained, in cross-examination, ‘performance rights’ was a better description, and one that the ASX later adopted, because the “Performance Shares” were not a security per se (T364/26-44).

121 The definition of Trust Assets in the Trust Deed is not simply a list of assets. The additional words in the chapeau of the definition of “Trust Assets”, and alongside the term Performance Shares, shows that the Trust Assets in paragraph (b) of the definition were subject to the requirements in the Prospectus being met.

122 A reasonable person having all the background knowledge of the surrounding circumstances available to the parties set out above, in circumstances where the Performance Milestones had in fact not been met, and the “Performance Shares” therefore had not been issued at the time of the Trust Deed, would have understood paragraph (b) of the definition of Trust Assets to mean the performance rights under the Prospectus, which may convert to “Performance Shares”, “whether issued before or after the Escrow Period”. The performance rights were subject to the proviso in paragraph (b) that such Performance Shares “shall only be issued upon satisfaction of the Performance Targets nominated in the Prospectus, up to a maximum of three tranches, with each tranche representing 112,222,222 shares that may be issued”.

123 It was not in dispute that no “Performance Shares” (ie, securities) were issued until 29 August 2018. At the time the Trust Deed was entered into, the “Performance Shares” could have been issued anywhere between the date of the Trust Deed and up to three years post the date of the Trust Deed. That is, potentially, before or after the end of the “Escrow Period”, which ended on 16 March 2017. This was known by the parties to the Trust Deed at the time the Trust Deed was entered into. If the Performance Milestones had been met before the end of the “Escrow Period”, the Trust Assets, from then on, would include a defined percentage of the Performance Shares issued, otherwise the Trust Assets included the performance rights.

124 Furthermore, clause 2.4 “Summary of Trust Assets”, “summarise[d] the assets held on trust by the Trustee for each Beneficiary” and specifically “include[d] prospective shares that may be issued subject to the Performance Targets being met” (italics added). The Trust Assets also included “the proceeds of sale or redemption of” the Consideration Shares and Performance Shares and, whilst held on trust, any “dividends, bonus shares or other derivative right” in connection with the Consideration Shares and Performance Shares (paragraphs (c) and (d) of the definition).

125 The respondents submitted, and I accept, that the parties’ expressed intention was to end the trust, and for the Trust Assets to be transferred, within seven days of the end of the “Escrow Period”. Contrary to the respondents’ submissions, however, it did not matter for the purpose of clause 2.3 that there were no Performance Shares for iSignthis BVI to transfer “[n]o later than seven days after the end of the Escrow Period”. The applicants’ entitlement was the right to have the Performance Shares issued to them. Such a right was a present chose in action, capable of being held on trust and property subject to a trust: see, although in a particular statutory context, Australian Securities and Investments Commission v Retail Employees Superannuation Pty Ltd [2024] FCA 1081 at [222]–[224], [233], [236], [243] and [249] (Beach J); see, however, for a broader statement of principle Secure Parking (WA) Pty Ltd v Wilson (2008) 38 WAR 350; [2008] WASCA 268 at [100]–[102] (Buss JA); St Vincent de Paul Society Qld v Ozcare Ltd [2011] 1 Qd R 4; [2009] QCA 335 at [56]–[65] (Muir JA, McMurdo P and Chesterman JA agreeing at [2] and [86]); Australian Zircon NL v Austpac Resources NL [No 2] [2011] WASC 186 at [191], [194], [197]–[198] (Corboy J); Jacobs' Law of Trusts in Australia, J D Heydon and M J Leeming (8th ed, 2016) at [1-06]; The Law of Trusts, G Thomas and A Hudson (2nd ed, 2010) at [3.24]–[3.32].

126 The performance rights were valuable rights, and the beneficiaries had a right to call on the Trustee to perform the trust at the end of the Escrow Period. Contrary to the respondents’ submissions, they were not a mere expectancy. The obligation under clause 2.3 could be performed by the Trustee assigning the rights to the “Performance Shares” to the applicants: see, eg, Norman v Federal Commission of Taxation (1963) 109 CLR 9 at 26 (Windeyer J); The Law of Trusts at [5.36]. Indeed, Mr Karantzis contemplated this in his email dated 13 November 2014 to Mr Walmsley, copying Mr Edmonds, Mr Tetro, Mr Minehane, Mr Richards and Mr Hart, that included the following (emphasis added):

… you (Ignition), Ian (Lakrspur) and David (Bennick), will be issued documentation to convert your equitable rights into legal rights as soon as reasonably possible following completion with Otis.

127 It did not matter that the “Performance Shares” were not transferable. The Prospectus prohibited the transfer of the “Performance Shares” themselves, but not the underlying equitable interest. Furthermore, if the Trustee did not perform the obligation under clause 2.3 within the period stipulated, the Trustee was obliged to continue to hold the Trust Assets on trust for the beneficiaries until such time as the trusts under it were performed.

128 The respondents submitted that the applicants were not “entitled” to shares in ISX. Furthermore, that as shareholders of iSignthis BVI, they had no rights or interest in iSignthis BVI’s assets, which in this case were relevantly the shares in ISX. Those submissions selectively overlooked the rights created by the Trust Deed.

129 The respondents further submitted that the trust declared by clause 2.1 of the Trust Deed was a trust in respect of assets that existed at that time, and did not, and could not, include additional shares to be issued by ISX to iSignthis BVI unless, before the trust was dissolved, iSignthis confirmed that the trust applied to those additional ordinary shares. While the respondents were correct that the trust was in respect of assets that existed at that time, this again overlooked that the Trust Assets included existing rights to the Performance Shares, if the Performance Milestones under the Prospectus were met.

130 For completeness, it is necessary to mention a further defence raised by the respondents, to the effect that the applicants were not entitled to “Performance Shares” because they did not perform the obligations in the Sales and Marketing Agreement, or assist ISX to achieve the Performance Milestones in the Prospectus. To say that this defence was poorly pleaded is an understatement. Nevertheless, it was raised in the respondents’ submissions in the terms I have described. There was no substance to this defence. There was nothing in the Prospectus or the contemporaneous documents to support the proposition that the Performance Shares were contingent on the applicants’ performance of the Sales and Marketing Agreement, or their assistance with the Performance Milestones. To the extent that the documents referred to shares being “subject to performance”, or to the need for “us” or “we” to perform, it is clear that the documents were referring to ISX. Furthermore, Mr Karantzis effectively abandoned this defence in cross-examination, in stating that the condition whereby the applicants’ entitlements were contingent on their performance applied to the Share Agreement, which was entered into in 2014, and was not reflected in the Trust Deed (T375/39 – 376/21).

131 For the foregoing reasons, I am satisfied that iSignthis BVI held the rights to Performance Shares on trust for the applicants. At the end of the “Escrow Period”, the applicants were entitled to call on iSignthis BVI to transfer the Trust Assets to them within seven days, pursuant to clause 2.3 of the Trust Deed. At that time, the Performance Milestones had not been met. iSignthis BVI’s obligation to perform the trust meant that it was obliged to assign the rights to the Performance Shares to the applicants, which it failed to do. As a result, iSignthis BVI breached the trust.

132 The remedies that follow from that finding are dealt with below, from paragraph 188.

breach of contract

133 The applicants’ breach of contract claim was to the effect that the Trust Deed was a contract by which the applicants and iSignthis BVI agreed on terms for iSignthis BVI to transfer the Consideration Shares and the Performance Shares to the applicants.

134 The applicants alleged that there were terms of the contract, as follows:

(a) the Consideration Shares would be transferred by iSignthis BVI to the applicants forthwith upon the expiry of the Escrow Period;

(b) the Performance Shares would be transferred by iSignthis BVI to the applicants forthwith upon the issue of the Performance Shares; and

(c) the total number of the Consideration Shares and the Performance Shares to be transferred to the applicants would be the number of shares equating to 2%, in the case of Tribeca, and 0.41%, in the case of Edmonds.

135 In light of those terms, the applicants alleged that the Performance Shares having been issued upon the Performance Milestones being met, iSignthis BVI was obliged to transfer the Performance Shares to the applicants such that the total number of the Consideration Shares and the Performance Shares to be transferred to and held by the applicants was the number of shares equating to, in the case of Larkspur 2% and, in the case of Edmonds 0.41%, of the total number of shares issued by or in ISX. The applicants alleged that, in breach of contract, iSignthis BVI has failed to transfer the Performance Shares to the applicants.

136 In light of the findings that I have reached regarding the applicants’ rights in respect of the Trust Assets under the Trust Deed and the breach of trust claim, it is unnecessary to determine the breach of contract claim.

knowing receipt and knowing assistance

137 The applicants alleged that:

(a) by reason of the Trust Deed, iSignthis BVI owed a fiduciary duty to the applicants in respect of the Trust Assets and it knew, alternatively Mr Karantzis knew or ought to have known, that iSignthis BVI was not permitted to deal with the Trust Assets other than in accordance with the Trust Deed;

(b) after the Performance Milestones were achieved and the Performance Shares were issued on 29 August 2018, iSignthis BVI was obliged to transfer the Performance Shares to the applicants such that the total number of Consideration and Performance Shares issued to them would equate to 2% of the issued shares in ISX in the case of Larkspur and 0.41% in the case of Edmonds;

(c) in April 2019, iSignthis BVI disposed of 446,797,754 ISX shares, 223,398,878 of which were transferred to Select.

138 The applicants alleged that the transfer of shares by iSignthis BVI in April 2019, and the demerger resolution referred to in paragraphs 55–57 above, which has had the effect that every member of ISX thereafter held 1 ISXFEU share for every 10 ISX shares previously held, was:

(a) a breach of trust;

(b) a dishonest, alternatively fraudulent, breach by iSignthis BVI of the fiduciary duties owed to the applicants by reason of the Trust Deed;

(c) the knowing receipt of property in breach of trust by Select and Mr Karantzis; and

(d) the knowing assistance by Mr Karantzis of iSignthis BVI’s breach of trust, alternatively breach of fiduciary duty.