Federal Court of Australia

Qoria Limited, in the matter of Qoria Limited (No 2) [2026] FCA 880

File number: | WAD 66 of 2026 |

Judgment of: | JACKSON J |

Date of judgment: | 7 July 2026 |

Date of publication of reasons: | 8 July 2026 |

Catchwords: | CORPORATIONS – scheme of arrangement – application for approval of scheme under s 411(4)(b) of the Corporations Act 2001 (Cth) – acquisition of 100% of shares in plaintiff in return for CHESS Depository Interests in stock of acquirer – scheme approved by necessary majorities of shareholders – orders made approving scheme |

Legislation: | Corporations Act 2001 (Cth) ss 411, 1322 Securities Act of 1933 (US) s 3(a)(10) |

Cases cited: | Fowler v Lindholm [2009] FCAFC 125; (2009) 178 FCR 563 Re Allkem Limited (No 2) [2023] FCA 1657 Re Amcor Limited (No 2) [2019] FCA 842 Re Asaleo Care Limited (No 2) [2021] FCA 636 Re AWA Mutual Limited (No 2) [2024] FCA 104 Re Essential Metals (No 2) [2023] FCA 1306 Re Qoria Limited [2026] FCA 676 |

Division: | General Division |

Registry: | Western Australia |

National Practice Area: | Commercial and Corporations |

Sub-area: | Corporations and Corporate Insolvency |

Number of paragraphs: | 45 |

Date of hearing: | 7 July 2026 |

Counsel for Plaintiff: | Mr SK Dharmananda SC |

Solicitor for the Plaintiff: | Thomsons |

Counsel for the Interested Party: | Ms C McKay |

Solicitor for the Interested Party: | Herbert Smith Freehills Kramer |

ORDERS

WAD 66 of 2026 | ||

IN THE MATTER OF QORIA LIMITED (ACN 167 509 177) | ||

QORIA LIMITED (ACN 167 509 177) Plaintiff | ||

AURA CONSOLIDATED GROUP, INC. (ARN 695 488 843) Interested Party | ||

order made by: | JACKSON J |

DATE OF ORDER: | 7 JULY 2026 |

the court notes that:

A. The plaintiff and the interested party intend to rely on:

(a) the Court’s approval of the Scheme as set out in the reasons for judgment as the basis of a claim to an exemption pursuant to s 3(a)(10) of the Securities Act of 1933 (US) (as amended), and that the approval of the Scheme by the Court will serve as the basis for reliance on the exemption provided by s 3(a)(10) of the Securities Act, from the registration requirements otherwise imposed by the Securities Act, in connection with the implementation of, and provision of consideration under, the Scheme; and

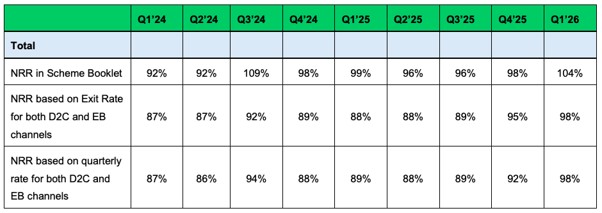

(b) the fact that the Scheme has proceeded under the statutory provisions and procedures of the Corporations Act 2001 (Cth).

the court orders that:

1. Pursuant to s 411(4)(b) of the Corporations Act, the scheme of arrangement (Scheme) between the plaintiff and the holders of fully paid ordinary shares in the plaintiff, in the form set out at pages 980 to 1008 of the second affidavit of Hendrik van Aswegen sworn 26 May 2026, is approved.

2. Pursuant to s 411(12) of the Corporations Act, the plaintiff is exempt from compliance with s 411(11) of the Act in relation to the Scheme.

3. The plaintiff must lodge an office copy of these orders with the Australian Securities and Investments Commission on or before 8 July 2026.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

JACKSON J:

1 On 27 May 2026, I made orders convening a meeting of the shareholders of the plaintiff, Qoria Limited (Scheme Meeting), for the purpose of considering and voting on whether to approve a scheme of arrangement (Scheme): Re Qoria Limited [2026] FCA 676 (Qoria (No 1)).

2 In broad terms, the Scheme provides for the acquisition of 100% of the shares in Qoria by Aura Consolidated Group, Inc. in consideration for interests in common stock of Aura. The legal title to that stock is to be held by CHESS Depository Nominees Pty Ltd under a standard arrangement for the quotation of the securities of foreign companies on the Australian Securities Exchange (ASX). The securities to be quoted will be CHESS depository interests (CDIs), where each Aura CDI will represent one share in the common stock of Aura. By the time of the Scheme Meeting, the ratio for the Scheme consideration was fixed at 1 Aura CDI for approximately every 17.32 shares in Qoria. This had been announced on ASX prior to the start of the meeting.

3 The Scheme Meeting was held on 2 July 2026. Qoria shareholders approved the Scheme by the requisite statutory majorities.

4 On 7 July 2026, the second hearing for approval of the Scheme pursuant to s 411(4)(b) of the Corporations Act 2001 (Cth) was held. No person sought leave to appear to oppose approval. I made orders approving the Scheme on that date. These are the reasons for those orders.

Materials relied on

5 In addition to the evidence adduced at the first hearing, Qoria relied on the following affidavits:

(a) second affidavit of Hedley James Roost, sworn on 2 July 2026;

(b) third affidavit of Stephanie Louise Majteles, affirmed on 2 July 2026;

(c) affidavit of Aura’s Chief Financial Officer, Brian DeCenzo, sworn on 2 July 2026;

(d) affidavit of Mark Harrison Butterfield, one of the independent experts at Grant Thornton, sworn on 3 July 2026;

(e) fourth affidavit of Qoria’s solicitor, Hendrik van Aswegen sworn on 6 July 2026; and

(f) fifth affidavit of Mr van Aswegen sworn on 7 July 2026.

Requirements for approval of a scheme of arrangement

6 Under s 411(4) of the Corporations Act, a scheme of arrangement is binding (relevantly) on shareholders if, and only if, a resolution approving it is passed by the requisite statutory majorities at the Scheme Meeting and it is approved by order of the Court.

7 The principles that guide the Court’s approval in these circumstances are well established. They were summarised in Re Essential Metals (No 2) [2023] FCA 1306 at [6]-[11], which I refer to without repeating here. The Court has a discretion, which will fundamentally be informed by whether the proposal is fair and reasonable. The Court is not a mere rubber stamp, but its jurisdiction is supervisory and will take account of the ability of shareholders to make their own judgements as to what is in their commercial interests. The Court relies heavily on counsel to bring to its attention any features of the scheme that require attention.

8 A number of matters that typically guide the Court’s exercise of the discretion are set out in that passage in Re Essential Metals (No 2) and are addressed below, after consideration of various procedural matters and other prerequisites to the Scheme’s effective implementation.

Procedural matters and other prerequisites

ASIC lodgement

9 Ms Majteles’s third affidavit states that on 27 May 2026 the Scheme Booklet, substantially in the form approved by the Court, was lodged with the Australian Securities and Investments Commission (ASIC) along with the orders convening the Scheme Meeting, and that ASIC then registered the Scheme Booklet and provided a stamped copy of the registered Scheme Booklet. That registration was a mandatory prerequisite to sending the Scheme Booklet to shareholders: s 412(6) of the Corporations Act.

Dispatch of the Scheme materials to shareholders

10 Notice of the Scheme Meeting, the Scheme Booklet and other materials required to be distributed to shareholders by the orders convening the Scheme Meeting were dispatched no later than 2 June 2026 (that being the time required for dispatch by the orders). There were a small number of emails that returned delivery failure notifications (15 in all). Delivery of hard copies to those persons was effected no later than 9 June 2026.

11 Qoria drew my attention to two further matters concerning the dispatch of the Scheme materials to shareholders.

12 The first matter concerned the omission of a document from the hard copy materials sent to the 20 shareholders who had elected to receive meeting documents by post. That document was a letter giving the shareholders the details of how to access the Scheme materials online. The omission was the result of a clerical oversight on the part of Computershare Investor Services Pty Ltd, Qoria’s share registry. The oversight was discovered on 25 June 2026, and the letter was sent to those shareholders by express post on 26 June 2026. However, those shareholders had received a hard copy of the Scheme Booklet by post, effected on 2 June 2026, so it is unlikely that the omission of the letter from that mail out caused any prejudice.

13 The second matter concerned two invalid proxy forms and one proxy form which could not be submitted in time. I reviewed the evidence about this in Ms Majteles’s third affidavit and was satisfied that these were the result of mishaps that were not attributable to fault on the part of Qoria or those acting for it.

14 I was therefore satisfied that these two irregularities did not cause substantial injustice. To the extent that these irregularities might otherwise have invalidated the result of the Scheme Meeting, that outcome is avoided by operation of s 1322 of the Corporations Act: see Re AWA Mutual Limited (No 2) [2024] FCA 104 at [25]-[27] (Anderson J).

Advertising of second court hearing

15 An announcement of the time and date of the second court hearing for the approval of the Scheme was published on the ASX announcements platform on 26 June 2026, in accordance with the Court’s orders of 27 May 2026.

The Scheme Meeting

16 As mentioned above, the Scheme Meeting took place on 2 July 2026. Mr Hedley Roost acted as the chairperson and gave evidence in his second affidavit that the Scheme Meeting was conducted in accordance with the Court’s orders convening the meeting.

17 The resolution was approved by 91.49% of eligible votes cast, with the balance of 8.51% voting against it. The requirement in s 411(4)(a)(ii)(B) of the Corporations Act that a resolution be passed by 75% or more votes was therefore met.

18 In total, 55.67% of the Qoria shares on issue were voted on at the Scheme Meeting, by 4.33% of shareholders by headcount. At less than 10%, that can fairly be described as a low voter turnout: see Re Asaleo Care Limited (No 2) [2021] FCA 636 at [20] (Banks-Smith J). That is not necessarily a reason to refuse to exercise the discretion to approve a scheme, although it may call for inquiry as to whether the low turnout was caused by any deficiency in notice or other matter that may have deterred voters from attending or voting at the Scheme Meeting: see the discussion in Re Essential Metals (No 2) at [33]-[37]. Given what has just been said about the substantial compliance with the orders convening the Scheme Meeting, and the relatively minor extent of the irregularities, there was no reason to suppose that such deficiencies caused the low turnout. Further, on the basis of evidence in Ms Majteles’s third affidavit, the headcount turnout figure for the Scheme Meeting is comparable to (and higher than) the headcount turnout for the last two annual general meetings.

19 For those reasons, I did not consider that the headcount turnout was any reason not to approve the Scheme.

No objection from ASIC

20 Mr van Aswegen’s fourth affidavit annexes a letter in standard form from ASIC, advising that under s 411(17)(b) of the Corporations Act, it has no objection to the Scheme. The prerequisite to Court approval under s 411(17) was therefore satisfied, without any need for the Court to consider under paragraph (a) of that subsection whether the Scheme has been proposed for the purpose of avoiding the operation of the takeovers provisions in Ch 6 of the Act.

Conditions precedent

21 Mr van Aswegen’s fourth affidavit also annexes a certificate verifying that all the conditions precedent that were required to be satisfied by the second hearing for the Scheme to become effective had been satisfied or waived. A number of conditions precedent set out in clause 3.1 of the Merger Implementation Deed between Qoria and Aura are still outstanding, namely: cl 3.1(e) (Court approval); cl 3.1(m) (the conversion of all Aura Preferred Shares to Aura common shares); cl 3.1(q) (exemption from the US Securities Act of 1933); and cl 3.1(s) (amendment of Aura’s Charter).

22 Mr DeCenzo’s affidavit says that he is not aware of any fact or circumstance that would result in any of those conditions precedent not being satisfied prior to the implementation of the Scheme.

The exercise of the discretion

23 I was satisfied that there was no reason not to approve the Scheme. As canvassed in Qoria (No 1), there was no reason to think that the Scheme was proposed other than in good faith and for a legitimate commercial purpose (see [45]), nor was there evidence of any oppression of minority shareholders or differential treatment between shareholders (see [21]-[34]). Nothing has been brought to the Court’s attention to require any change to those assessments.

24 There was also no reason to suggest that the Scheme offended any aspect of public policy.

25 Nor was there any change in opinion by the independent expert, Grant Thornton. No superior proposal had emerged. It will be recalled that the expert considered that the proposed Scheme was not fair but was reasonable and in the best interests of shareholders. The shareholders were suitably informed as to that conclusion at the time when their votes were cast, and the Scheme was such that an intelligent and honest shareholder, properly informed and acting alone, might approve it: see Fowler v Lindholm [2009] FCAFC 125; (2009) 178 FCR 563 at [79] (Emmett, Gordon and Jagot JJ) and Essential Metals (No 2) at [45]-[47]. The shareholders’ approval is prima facie evidence that the Scheme is fair: Re Amcor Limited (No 2) [2019] FCA 842 at [11] (Beach J).

Full and fair disclosure to shareholders

26 In Qoria (No 1), I indicated that I was satisfied that the Scheme Booklet would give Qoria shareholders sufficient disclosure of the advantages and disadvantages of the Scheme to permit them to vote on an informed basis at the Scheme Meeting.

27 Further, summary evidence concerning communications with shareholders contained in Ms Majteles’s third affidavit established that an inbound shareholder communication line was established in accordance with procedures that I was satisfied were appropriate, as outlined in advance of the first hearing. Nothing untoward emerged from the calls that shareholders made to that line.

28 Subject to one matter about to be described, nothing has occurred that would change that state of satisfaction about the adequacy of disclosure to shareholders.

Inconsistency in the presentation of Total Net Revenue Retention in the Scheme Booklet

29 Qoria has brought to the Court’s attention an error in the figures for Net Revenue Retention (NRR) for Aura that were disclosed in the Scheme Booklet. The following is derived from the affidavit of Mr DeCenzo.

30 NRR is a metric that Aura uses to help assess the health of its business. It measures the percentage of recurring revenue retained from a given group of existing customers over a given period. Aura measures this by reference to two ‘core’ business channels: direct to consumer (D2C) and Employee Benefits (EB). As indicated in Qoria (No 1) at [4], a substantial proportion of Aura’s revenue is linked to one particular employee benefits provider in the United States.

31 The NRR for each of Aura’s D2C and EB channels was disclosed in the Scheme Booklet for each quarter of calendar years 2024 and 2025 and the first quarter of 2026. Also disclosed was a blended figure for overall NRR for each of those quarters.

32 The error arose because the basis on which the D2C NRR was measured was different to that for the EB NRR, and no adjustment was made to ensure the figures were truly comparable. The difference relates to the timing of the measurements of NRR. For D2C it was calculated on an ‘exit-month’ basis, meaning that to calculate the NRR, Aura used only the total revenue from the relevant group of customers in the last month of the quarter. For EB it was calculated on quarterly basis, meaning Aura used the entire quarter’s revenue to calculate the NRR.

33 These differences in the method of calculation meant that the figures would need to be adjusted for the blended NRR numbers to have been accurate. That adjustment was not done before the blended NRR was calculated and disclosed in the Scheme Booklet. Mr DeCenzo’s affidavit contains the following table showing the difference the error made.

34 The result of the error was that the Scheme Booklet contained blended NRR figures for various quarters, ranging from 3.2% higher to 18.5% higher than the figures that would have been disclosed, had the D2C and EB NRR figures been combined on a truly comparable basis. (Those low and high percentages come from Q4’25 and Q3’24 respectively).

35 Mr DeCenzo, who has extensive experience in the finance industry and a first hand understanding of Aura’s business, expresses the opinion in his affidavit that this inconsistency in the presentation of the NRR figures is not material. The reasons he gives are (affidavit para 21):

(a) Aura’s “total” NRR for any quarter does not reflect, or impact upon, the actual revenue or revenue growth of Aura’s business disclosed elsewhere in the Scheme Booklet, including in the audited financial information. It merely serves as an indirect predictor of Aura’s future revenue which may be earned from existing customers. Overall revenue growth, which is a key measure of the performance of the business, is impacted by numerous different factors (including growth in new customers) and cannot be predicted using NRR;

(b) the “total” NRR figures (calculated after normalizing for either methodology) remain strong. In most cases, as can be seen from the table above, the difference only reflects a slight reduction from the “total” NRR listed in the table in the Scheme Booklet;

(c) Aura forms only part of the Merged Group, whose financial profile, including ability to generate revenue, will be impacted significantly by the combination of the two businesses. The Scheme Consideration represents an interest in the Merged Group, not the stand-alone Aura business. For this reason, Aura did not include the NRR Information in the Prospectus because it was not considered material for the Merged Group;

(d) The stand-alone NRR figures for each of the D2C and EB channels presented in the ‘Quarterly key performance indicators’ table in the Scheme Booklet are accurate. I believe that sophisticated investors, who may be interested in the NRR figures in the Scheme Booklet, would typically not rely solely on “total” NRR for their own calculations or valuations given that it is an indicative figure only. Instead, they would use the individual revenue, ARR and/or NRR figures included in the Scheme Booklet, which are not affected by discrepancy described above. I believe it unlikely that any retail investors would have regard to the NRR figures in the Scheme Booklet, including the “total” NRR. On that basis, in my view the “total” NRR figures affected by the discrepancy would not be likely to influence any shareholder’s vote or their decision to vote in favour of or against the Scheme; and

(e) Grant Thornton, the independent expert who provided an opinion that the Scheme is not fair but reasonable and in the best interests of Shareholders, has been informed of the inconsistency in the NRR Information and has confirmed that it has not changed its view.

36 The affidavit of the Grant Thornton independent expert, Mr Butterfield, provided a detailed explanation of why, as Mr DeCenzo indicated in the above passage, Grant Thornton did not change the opinions and conclusions in its report after it was told about the error. Essentially, that was because NRR played no part in Grant Thornton’s valuation exercise. Grant Thornton’s report did present figures for Annual Recurring Revenue for both Aura and Qoria, but Mr Butterfield explained that this was calculated differently to and independently from the NRR figures.

37 I had some reservations about Mr DeCenzo’s views about the materiality of the error. As has been noted, the difference in the figures that resulted from the error was in one case as high as 18.5%. I do not think that is a ‘slight’ reduction (and Mr DeCenzo was careful to give that characterisation only to ‘most’ cases). Also, while the NRR figures may not be material to the merged group, their inclusion in the Scheme Booklet means it is possible that Qoria shareholders relied on them in some way. Relatedly, it is not only the behaviour of sophisticated investors that is relevant here. What the Court must assess is the likelihood that Qoria shareholders relied on the inaccurate figures in deciding how to vote at the Scheme meeting, whether those shareholders are fairly described as sophisticated or not.

38 Nevertheless, despite those reservations I did not consider that the error was of such moment as to mean that the Scheme should not be approved. Mr DeCenzo’s affidavit contains evidence to the effect that the discrepancy was the result of human error, that is, inadvertency. I accepted that evidence. It does not lead to any concern about the integrity of the disclosure and verification process for the Scheme Booklet overall. Aura and Qoria took appropriate steps to investigate and disclose the discrepancy, including having it considered by the due diligence committee for the Scheme, which agreed that it was not material.

39 As Mr DeCenzo says, the NRR figures would have been strong even if correctly presented. The larger discrepancies only occurred in a few quarters. If shareholders did pay any attention to the NRR figures, they would have looked at them over the entire period. Further, given that NRR was only one of a number of financial metrics presented for Qoria and Aura in the Scheme Booklet (including conventional ones such as balance sheet net equity and profit and loss), it is unlikely that NRR by itself was important to a significant number of investors.

40 Indeed, senior counsel for Qoria pointed out at the hearing a relevant disclaimer in the Scheme Booklet. It appeared immediately following the tables where the blended NRR figures (and several other metrics) were disclosed. It said that those figures do not have a standardised meaning under certain accepted accounting standards (including the Australian Accounting Standards and US Generally Accepted Accounting Principles), and may not be comparable to similarly titled measures presented by other entities. Thus, the Scheme Booklet said, ‘Qoria Shareholders should not place undue reliance on such measures’. The Scheme Booklet also contained accurate D2C and EB NRR figures and an explanation of NRR which included references to those metrics on bases that were not ‘blended’.

41 I also put weight in this respect on Mr Butterfield’s view that the discrepancy did not change Grant Thornton’s opinion as to the reasonableness of the Scheme proposal.

Exemption under s 3(a)(10) of the Securities Act of 1933 (US)

42 Finally, as foreshadowed in Qoria (No 1), Aura intends to rely on the approval of the Scheme so as to qualify for an exemption from the registration requirements of the US Securities Act of 1933 s 3(a)(10). The exemption would save the issue and exchange of Aura common stock as part of the Scheme consideration from registration and prospectus requirements under that Act.

43 The Court has accepted in the past that these requirements may not need to be met if the scheme of arrangement satisfies the conditions for exemption afforded under s 3(a)(10): see Re Allkem Limited (No 2) [2023] FCA 1657 at [34]-[37] (Banks-Smith J) and the cases cited there. The Court takes a standard approach to describing the relevant effect of its decision to approve a scheme, noting that it is not for the Court to determine whether the requirements for exemption have been satisfied.

44 I will take that approach here. As such, I record the following matters:

(a) the Court was advised before the commencement of the hearing to approve the Scheme that reliance would be placed on the s 3(a)(10) exemption of the Securities Act of 1933 on the basis of the Court’s approval of the Scheme;

(b) the Court has been informed that Aura shares in the form of Aura CDIs are to be offered as scheme consideration, and an independent expert report concluded that the proposal is in the best interests of shareholders of Qoria in the absence of a superior proposal (where none has emerged);

(c) a hearing in open court was held on 7 July 2026 to consider the fairness and reasonableness of the proposed Scheme, and it was open to any member of the public including any member of Qoria to attend;

(d) notice of the date of the approval hearing was included in the Scheme Booklet provided to all shareholders of Qoria prior to consideration of the proposal at the Scheme Meeting, and was advertised on the ASX, so that those to whom the securities are to be issued had the opportunity to oppose or otherwise raise any objection to the Scheme; and

(e) no Qoria shareholder gave notice of any intention to appear at the second court hearing to oppose the approval of the Scheme, and none in fact opposed it.

Scheme approved

45 It was for the reasons above that the orders of 7 July 2026 were made approving the Scheme.

I certify that the preceding forty-five (45) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Jackson. |

Associate:

Dated: 8 July 2026