Federal Court of Australia

Commonwealth Director of Public Prosecutions v Fairfull [2026] FCA 748

File number(s): | NSD 2097 of 2025 |

Judgment of: | ABRAHAM J |

Date of judgment: | 19 June 2026 |

Catchwords: | CRIMINAL LAW – sentencing – accused pleaded guilty to making false or misleading statements likely to induce persons to apply for financial products, and dishonest use of his position as a director with the intention of directly gaining an advantage |

Legislation: | Corporations Act 2001 (Cth) ss 184(2), 1041E(1), 1311(1) Crimes Act 1914 (Cth) ss 16A(1), (2), 16BA Treasury Laws Amendment (Strengthening Corporate and Financial Sector Penalties) Act 2019 (Cth) sch 1 item 140 |

Cases cited: | Bugmy v The Queen [1990] HCA 18; (1990) 169 CLR 525 Cahyadi v The Queen [2007] NSWCCA 1; (2007) 168 A Crim R 41 Commonwealth Director of Public Prosecutions v Kirby [2025] FCA 757 Deakin v The Queen [1984] HCA 31; (1984) 58 ALJR 367 Director of Public Prosecutions (Cth) v Gregory [2011] VSCA 145; (2011) 34 VR 1 Director of Public Prosecutions (Cth) v Nippon Yusen Kabushiki Kaisha [2017] FCA 876; (2017) 254 FCR 235 Director of Public Prosecutions (Cth) v Page [2006] VSCA 224 Director of Public Prosecutions (Cth) v Wallenius Wilhelmsen Ocean AS [2021] FCA 52; (2021) 368 ALR 98 Directory of Public Prosecutions (Cth) v De La Rosa [2010] NSWCCA 194; (2010) 79 NSWLR 1 Forrest v Commonwealth Director of Public Prosecutions [2026] FCAFC 69 Hili v The Queen [2010] HCA 45; (2010) 242 CLR 520 Hurt v The King [2024] HCA 8; (2024) 281 CLR 286 Joffe v R; Stromer v R [2012] NSWCCA 277; (2012) 82 NSWLR 510 Markarian v The Queen [2005] HCA 25; (2005) 228 CLR 357 Mill v The Queen [1988] HCA 70; (1988) 166 CLR 59 Muldrock v The Queen [2011] HCA 39; (2011) 244 CLR 120 Postiglione v The Queen [1997] HCA 26; (1997) 189 CLR 295 Power v The Queen [1974] HCA 26; (1974) 131 CLR 623 R v Donald [2013] NSWCCA 238 R v Gajjar [2008] VSCA 268; (2008) 192 A Crim R 67 R v Glynatsis [2013] NSWCCA 131; (2013) 203 A Crim R 99 R v Hatahet [2024] HCA 23; (2024) 282 CLR 392 R v Jones [2004] VSCA 68 R v Moylan [2014] NSWSC 944 R v Olbrich [1999] HCA 54; (1999) 199 CLR 270 R v Pantano (1990) 49 A Crim R 328 R v Pham [2015] HCA 39; (2015) 256 CLR 550 R v Phelan (1993) 66 A Crim R 446 R v Rivkin [2004] NSWCCA 7; (2004) 59 NSWLR 284 R v Silver [2020] QCA 102 R v Smith [2000] NSWCCA 140; (2000) 114 A Crim R 8 R v Verdins [2007] VSCA 102; (2007) 16 VR 269 Regina v Shawn Darrell Richard [2011] NSWSC 866 Sigalla v R [2021] NSWCCA 22 Tran v The Queen [2021] VSCA 292 Attorney-General’s Application under s 37 of the Crimes (Sentencing Procedure) Act 1999 (No 1 of 2022) [2002] NSWCCA 518; (2002) 56 NSWLR 146 Weininger v The Queen [2003] HCA 14; (2003) 212 CLR 629 Wong v The Queen [2001] HCA 64; (2001) 207 CLR 584 |

Division: | General Division |

Registry: | New South Wales |

National Practice Area: | Federal Crime and Related Proceedings |

Number of paragraphs: | 122 |

Date of hearing: | 15 May 2026 |

Counsel for the Prosecutor: | Mr A Chhabra |

Solicitor for the Prosecutor: | Commonwealth Director of Public Prosecutions |

Counsel for the Accused: | Mr W Shukoor |

Solicitor for the Accused: | Sydney Criminal Lawyers |

ORDERS

NSD 2097 of 2025 | ||

BETWEEN: | COMMONWEALTH DIRECTOR OF PUBLIC PROSECUTIONS Prosecutor | |

AND: | DAVID FRAZER EWAN FAIRFULL Accused | |

order made by: | ABRAHAM J |

DATE OF ORDER: | 19 JUNE 2026 |

THE COURT ORDERS THAT:

1. Mr David Frazer Ewan Fairfull is convicted of Count 1 and Count 2.

2. On Count 1, Mr Fairfull is to be sentenced to 7 years and 6 months imprisonment, to commence on 19 June 2026.

3. On Count 2, Mr Fairfull is to be sentenced to 3 years imprisonment, to commence on 18 June 2032.

4. Pursuant to s 19AB(1) of the Crimes Act 1914 (Cth), a single non-parole period of 5 years and 4 months is fixed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

ABRAHAM J:

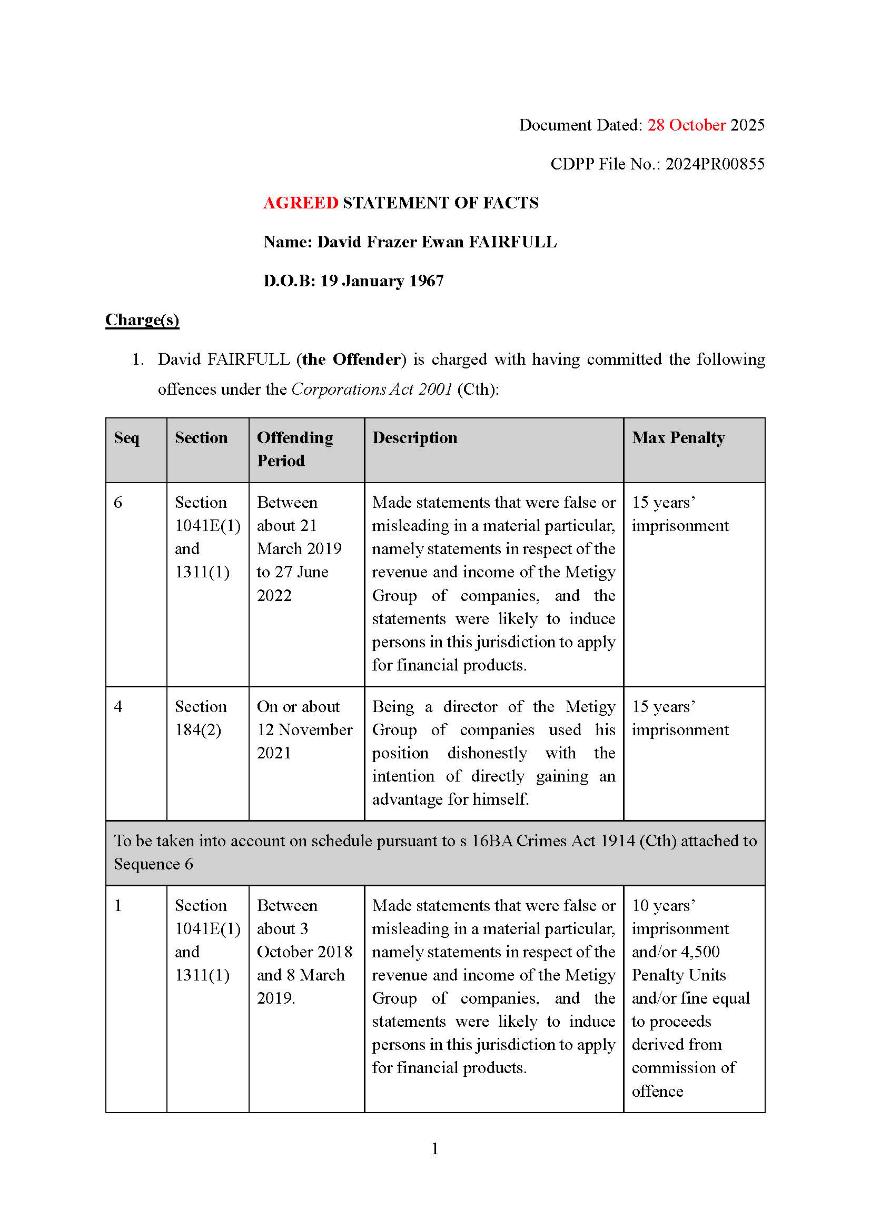

1 The offender, Mr David Frazer Ewan Fairfull, falls to be sentenced for two offences:

(1) Count 1 - sequence 6: that, between about 21 March 2019 and 27 June 2022, at North Sydney and elsewhere in New South Wales, the offender made statements that were false or misleading in a material particular, namely statements in respect of the revenue and income of the Metigy Group of companies, and the statements were likely to induce persons in this jurisdiction to apply for financial products, contrary to ss 1041E(1) and 1311(1) of the Corporations Act 2001 (Cth) (Corporations Act).

(2) Count 2 - sequence 4: that, on or about 12 November 2021, at North Sydney and elsewhere in New South Wales, being a director of the Metigy Group of companies, the offender used his position dishonestly with the intention of directly gaining an advantage for himself, contrary to s 184(2) of the Corporations Act.

2 In addition, Mr Fairfull admitted to the following offence which is to be taken into account on count 1, pursuant to s 16BA of the Crimes Act 1914 (Cth) (Crimes Act):

Sequence 1: that, between about 3 October 2018 and 8 March 2019, the offender made statements that were false or misleading in a material particular, namely statements in respect of the revenue and income of the Metigy Group, and the statements were likely to induce persons in this jurisdiction to apply for financial products, contrary to ss 1041E(1) and 1311(1) of the Corporations Act.

3 Mr Fairfull pleaded guilty on 4 November 2025 in the Local Court of New South Wales, with his pleas being maintained in this Court. This matter proceeded by way of an agreed statement of facts (ASOF) (with the reference to sequences above reflecting the identification of the relevant conduct in that statement).

Facts

4 The following is only an overview of the offences, with more detail being in the ASOF attached to these reasons as attachment A. The ASOF attached does not include annexures B, C, and D which detail the individual amounts invested into the Metigy Group, and by whom. The information contained in those annexures is unnecessary to include given the purpose of attaching the ASOF is to enable the reader to better understand the details and scale of the offending. In particular, the ASOF together with annexure A therein contains a list of the falsifications relating to count 1 and the scheduled offence. This better reflects the volume and range of the false information Mr Fairfull provided in committing count 1, and the steps he undertook in doing so.

5 Mr Fairfull was the Chief Executive Officer (CEO) and a director of Metigy Pty Limited (in liquidation) (Metigy), and a director of Metigy Administration Pty Ltd (in liquidation) (Metigy Administration), and Metigy Global Pty Ltd (in liquidation) (collectively, the Metigy Group). At all relevant times, the Metigy Group was developing a software platform that intended to use machine learning and artificial intelligence to allow small-to-medium enterprises to develop and deploy digital marketing strategies. It was a software-as-a-service business that depended on paying subscribers and venture capital funding for its operation and growth.

6 Acting on behalf of Metigy, Mr Fairfull raised, or attempted to raise, capital by the following means:

(1) an initial seed round, raising $2.2 million during March, May and July 2019;

(2) a seed+ round, raising $1.2 million, completed in December 2019;

(3) a convertible note issuance, raising $20 million, completed in October 2020;

(4) a partial sale of Metigy shares belonging to Mr Fairfull (through Fairfull Holdings) and other foundation shareholders’ associated entities, which raised $15,684,396 in July 2021 (the secondary share sale); and an attempted Series B capital raise of approximately $50 million between about April and July 2022, not completed because Metigy entered voluntary administration on 29 July 2022.

7 The completed capital raisings and the secondary share sale together totalled approximately $39.08 million. The attempted Series B capital raise sought a further $50 million.

8 In each completed capital raising, and in the attempted Series B capital raise, Mr Fairfull knowingly provided false financial information to investors. In the secondary share sale, he provided false financial information to the purchasers of the shares.

9 Between October 2018 and July 2022, Mr Fairfull exclusively controlled the flow of financial and subscriber information given to potential investors and to purchasers of shares in the secondary share sale, through data rooms, emails and investor briefings. The falsified financial information and forged documents, which included revenue, monthly recurring revenue (MRR), annual recurring revenue (ARR), and bank statements, were for the purpose of persuading investors to invest in Metigy.

The s 16BA schedule offence (sequence 1)

10 The scheduled offence is part of the context in which Mr Fairfull undertook the conduct which forms count 1.

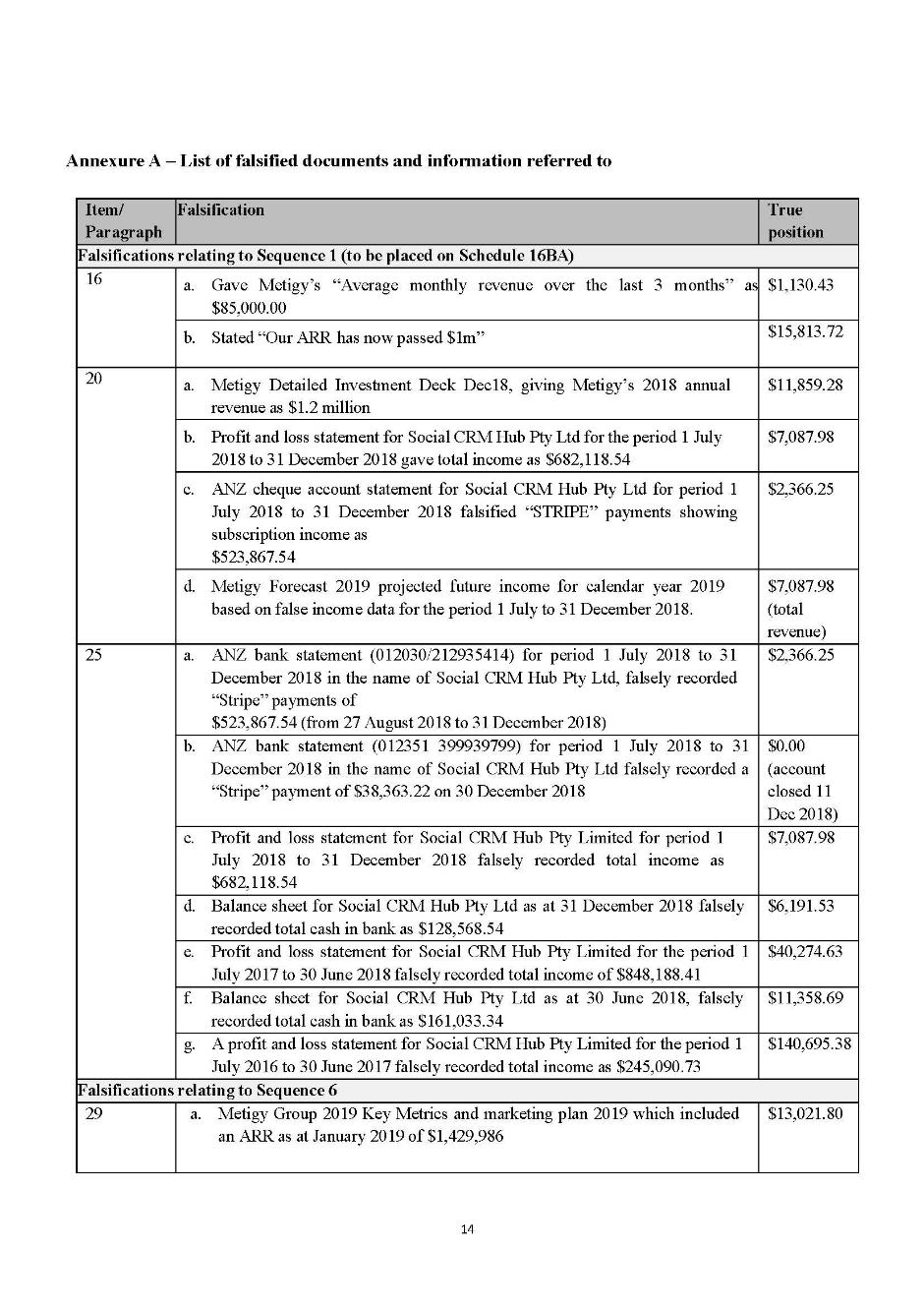

11 In late 2018, CP Ventures Pty Limited (CP Ventures) invited Mr Fairfull to apply for funding, which he did on 3 October 2018, by completing an online application form. The application provided information he knew was false relating to Metigy’s average monthly revenue and ARR. The application represented Metigy’s average monthly revenue over the previous three months as $85,000 when the true figure was $1,130.43 and represented ARR as having passed $1 million, when the true annualised figure was $15,813.72. Acting on the false information, CP Ventures informed Mr Fairfull it was prepared to invest by purchasing newly allotted shares. He then created and uploaded documents to a data room established by CP Ventures and another one established by himself purportedly on behalf of Metigy, including profit-and-loss statements, balance sheets, ANZ bank account statements, and investor presentation material – knowing the true financial position was substantially worse than represented and that investors would rely on these documents. These documents were provided to enable potential investors to undertake their due diligence. At all relevant times, Mr Fairfull was the only person to create and upload company records to the data rooms.

12 In late 2018, Mr Fairfull was introduced to Cygnet Capital Pty Ltd (Cygnet). On 4 March 2019, Mr Fairfull sent Cygnet a document titled “Metigy Detailed Investment Deck Mar 19” which falsely represented Metigy’s 2018 financial year revenue as $1.2 million, when the true revenue was no more than $11,859.28. On 8 March 2019, Mr Fairfull gave Cygnet a folder which contained further falsified information he had created (including false bank statements) and access to the Metigy data room which contained falsified information.

Count 1 – False and misleading statements (sequence 6)

Initial seed and seed+ rounds

13 During the initial seed and seed+ rounds, Mr Fairfull continued to provide documents which falsely overstated Metigy’s ARR, revenue, costs and profit-and-loss position. In reliance on the false financial information, investors associated with CP Ventures and Cygnet subscribed for newly allotted ordinary shares in Metigy in the initial seed and seed+ rounds, contributing a total of $3,399,983.21. Had they known Metigy’s true financial state, they would not have subscribed.

The convertible note issuance

14 On 21 May 2020, Mr Fairfull provided Cygnet with updated financial information representing that Metigy’s revenue for May 2020 was $750,000. The true figure was $1,083.16. To provide documentation to substantiate the false figures, Mr Fairfull forged two National Australia Bank (NAB) bank account statements and a term deposit statement for the Metigy Group, using PDF editing software to alter recorded deposits and balances. The forged documents were uploaded to the Metigy data room for the purposes of sharing them with Regal Funds Investment Pty Ltd (Regal), Five V Capital Pty Ltd (Five V), Cygnet, and other investors.

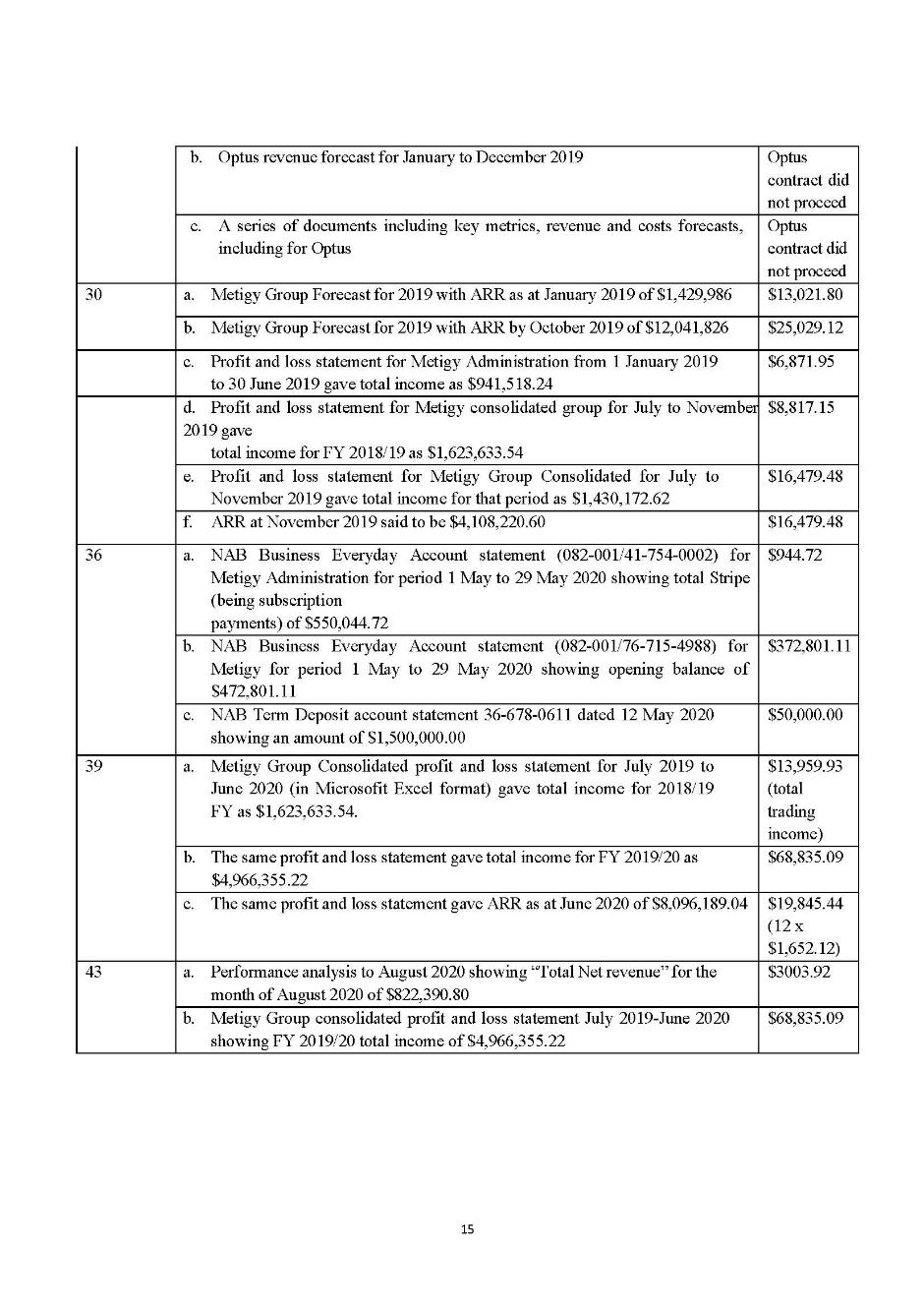

15 Further false profit-and-loss documents and forecasts were sent to investors in August and September 2020, including an investment summary which falsely claimed the full-year revenue for 2019/2020 was $5 million and the ARR as at August 2020 was $9.8 million.

16 On 29 September 2020, Metigy completed the convertible note issuance, raising $20 million from 27 separate investors. The investors relied on the false representations. Had they known Metigy’s true position, they would not have purchased convertible notes.

Investor updates and the secondary share sale

17 Following the convertible note issuance, Mr Fairfull was required by the convertible note subscription deed to send investors quarterly updates about Metigy’s financial performance. Each update was created by him and contained materially false information about Metigy’s financial performance. Mr Fairfull’s intention was to avoid current investors seeking a return of their investment, and to induce further investment.

18 On 24 February 2021, Mr Fairfull sent investors a quarterly update falsely representing Metigy Administration’s “Total net revenue” for July to December 2020 as $6,160,567.22, when the true figure was $12,522.27. The same update falsely represented net revenue for January 2021 as $1,512,000, when the true figure was $2,277.70.

19 In May 2021, Mr Fairfull approached investors who had subscribed for shares in 2019, and the convertible notes in 2020, with the possibility of the secondary share sale.

20 On 2 June 2021, Mr Fairfull sent investors a further financial performance update falsely representing Metigy Administration’s revenue for April 2021 as $2,206,119.54, with the true figure being $1,543.89. The secondary share sale ultimately raised $15,684,396. Had purchasers known the true financial position, they would not have purchased the shares.

Attempted Series B capital raise

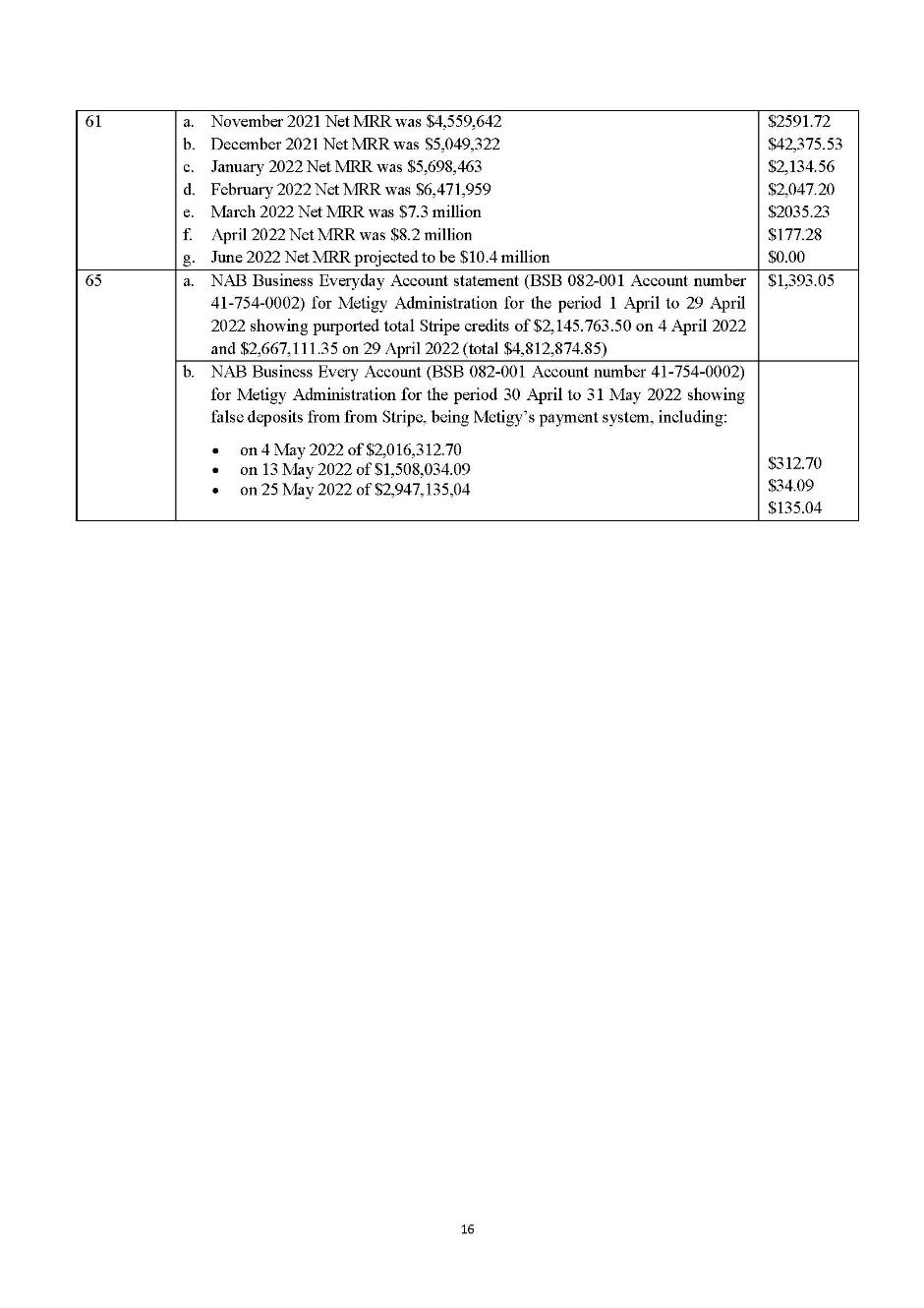

21 By September 2021, Mr Fairfull was proposing a further Series B capital raise of approximately $50 million. On 30 September 2021, he circulated a business update falsely representing Metigy Administration’s MRR for August 2021 as $3,304,958. The true figure was $2,086.78. The same material included further false MRR and ARR figures, and forecasted the ARR to be approximately $135 million by the end of the 2021 financial year and approximately $175 million by December 2022.

22 In April and June 2022, Mr Fairfull continued to provide materially false financial information to Cygnet, Regal, Five V and potential investors. The profit-and-loss statement for May 2022 falsely showed total net revenue of $8,953,060.02, generating a false ARR figure of $107,436,720.24. The actual revenue for May 2022 was $0.00. To support the figures presented for the Series B capital raise, Mr Fairfull forged three further bank statements using PDF editing software and uploaded the altered documents to the Metigy data room.

23 On 27 July 2022, Regal was advised by Metigy’s Chief Financial Officer (CFO) that the June 2022 ARR figure of $107 million was false. On 28 July 2022, representatives of Regal and Five V confronted Mr Fairfull at his home. On that occasion, Mr Fairfull admitted the June 2022 ARR figure of $107 million was completely false; that the management accounts provided for the convertible notes were false; and that the NAB bank statement for the period from 30 April – 31 May 2022 and Silicon Valley Bank statement for the period from 1 May – 31 May 2022 had been doctored by him.

24 On 29 July 2022, Mr Fairfull’s conduct was reported to the Australian Securities and Investments Commission (ASIC) by a representative of Regal. The same day, the Metigy Group entered voluntary administration, owing approximately $39 million to creditors.

Count 2 – Dishonest use of position (sequence 4)

25 On 12 November 2021, Mr Fairfull withdrew $7.7 million from the Metigy bank account. The transaction was recorded as a loan to Fairfull Holdings, his privately-owned company (the Director Loan). The loan agreement was executed by Mr Fairfull on behalf of Metigy and Fairfull Holdings. Neither Mr Fairfull nor Fairfull Holdings provided any security for the loan. The money in the Metigy bank account almost entirely comprised funds raised in the convertible note issuance. The Director Loan accordingly involved the diversion of investor funds.

26 The loan agreement was dated 14 November 2021 and executed by Mr Fairfull. The loan breached cl 4.5 of the note subscription agreement, which required the proceeds of the notes to be used “to fund the growth and development of [Metigy] and to meet [Metigy’s] general working capital requirements”.

27 The loan was uncommercial and, according to the administrator of the Metigy Group, caused the group to become insolvent from 14 November 2021.

28 Between 19 January 2022 and 13 July 2022, Mr Fairfull made repayments towards the Director Loan totalling $2,940,000. Approximately $4.76 million accordingly remained outstanding at the date of administration on 29 July 2022.

29 Mr Fairfull stated in his interview with the authorities that the Director Loan was intended to provide short-term finance to allow him and his wife to purchase residential real estate. The funds were used to help acquire a $10.5 million home in Mosman, NSW, and a $7.7 million property in Wattamolla, Kangaroo Valley, NSW. Both properties were purchased in the names of Mr Fairfull and his wife. He admitted he used his position as a director dishonestly with the intention of directly gaining an advantage for Fairfull Holdings, and indirectly for himself, in circumstances where he was aware that the funds were derived from the convertible notes and could only be used as working capital for the software-as-a-service business.

Sentencing principles

30 Mr Fairfull is to be sentenced in accordance with Pt IB of the Crimes Act, which requires that the sentence imposed by the Court be of a “severity appropriate in all the circumstances of the offence”: s 16A(1) of the Crimes Act.

31 In determining the sentence, in addition to any other matters, the Court must take into account the matters set out in s 16A(2) as far as they are relevant and known to the Court.

32 The sentencing process involves the judge weighing all the relevant circumstances and making a judgment as to what is the appropriate sentence. It involves the balancing of many different and conflicting features in a process known as “instinctive synthesis”: Wong v The Queen [2001] HCA 64; (2001) 207 CLR 584 at [75]; Markarian v The Queen [2005] HCA 25; (2005) 228 CLR 357 at [51].

33 That said, general deterrence is generally of particular importance in “white collar” offending because offending of this nature is difficult to detect, investigate and prosecute successfully.

34 The importance of general deterrence in white collar crime is emphasised in Director of Public Prosecutions (Cth) v Gregory [2011] VSCA 145; (2011) 34 VR 1 (Gregory) at [53]:

In seeking to ensure that proportionate sentences are imposed, the courts have consistently emphasised that general deterrence is a particularly significant sentencing consideration in white collar crime and that good character cannot be given undue significance as a mitigating factor and plays a lesser part in the sentencing process. ... Moreover, general deterrence is likely to have a more profound effect in the case of white collar criminals. White collar criminals are likely to be rational, profit seeking individuals who can weigh the benefits of committing a crime against the costs of being caught and punished. Further, white collar criminals are also more likely to be first time offenders who fear the prospect of incarceration.

35 As succinctly explained by Wood J in R v Pantano (1990) 49 A Crim R 328 at 330:

... those involved in serious white collar crime must expect condign sentences. The commercial world expects executives and employees in positions of trust ... to conform to exacting standards of honesty. It is impossible to be unmindful of the difficulty of detecting sophisticated crimes of the kind here involved, or of the possibility for substantial loss by the public… The element of general deterrence is an important element of sentencing for such offences…

36 When greater weight is attached in the balancing process to general deterrence, it necessarily follows, at least in a relative sense, that less weight will be accorded to what might otherwise be significant mitigating factors: R v Gajjar [2008] VSCA 268; (2008) 192 A Crim R 67 at [28]; Tran v The Queen [2021] VSCA 292 at [7]; Forrest v Commonwealth Director of Public Prosecutions [2026] FCAFC 69 (Forrest) at [164].

37 Further, it is a feature of white collar crimes that offenders are likely to have no prior convictions, are of good character and have good prospects of rehabilitation: Director of Public Prosecutions (Cth) v Page [2006] VSCA 224 at [37]. However, such factors may be of lesser significance for white collar crimes, since it is that factor which normally places the offender in a position where they are able to commit the offence: R v Rivkin [2004] NSWCCA 7; (2004) 59 NSWLR 284 (Rivkin) at [410]; Forrest at [236].

38 Offences of the type committed in this case undermine the integrity of Australia’s financial markets and system of corporate regulation, and erode the confidence of participants in the commercial world. Victims of these types of crimes are not confined to those who directly suffered through loss of their funds, but extend to the investing public at large, “the injury being that related to the loss of confidence in the efficacy and integrity of the market in public securities”: Rivkin at [412]; Commonwealth Director of Public Prosecutions v Kirby [2025] FCA 757 (Kirby) at [73].

39 As observed in Joffe v R; Stromer v R [2012] NSWCCA 277; (2012) 82 NSWLR 510 at [34], the objects of chapter 7 of the Corporations Act include, “as a central element, the promotion of public confidence in the fairness and honesty of markets for financial products. An important feature of that promotion of confidence is the presence of criminal offences for recognised market misconduct” and “[c]onfidence in the honesty and integrity of the financial markets is of the utmost importance in an economy and a society which depend significantly for their well-being on the efficient operation of such markets”.

40 The maximum penalty is also a relevant consideration. Recently, in Hurt v The King [2024] HCA 8; (2024) 281 CLR 286, Gageler CJ and Jagot J at [27], reiterated its relevance:

[W]hen a statute specifies a maximum sentence the specified maximum has two functions. It confines the power of the court to impose any sentence greater than the maximum. It also informs the sentencing process by conveying the Commonwealth Parliament’s view of the relative seriousness of the offence. In Markarian v The Queen, for example, Gleeson CJ, Gummow, Hayne and Callinan JJ said that “careful attention to maximum penalties will almost always be required, first because the legislature has legislated for them; secondly, because they invite comparison between the worst possible case and the case before the court at the time; and thirdly, because in that regard they do provide, taken and balanced with all of the other relevant factors, a yardstick”. In other words, the maximum sentence reflects the Commonwealth Parliament’s view of the appropriate sentence for the worst possible case constituting the offence.

41 There has been a steep increase in the maximum penalties for the offences. The maximum penalty for the s 1041E(1) offences increased from 5 years to 10 years imprisonment on 24 November 2010, and then to 15 years imprisonment on 13 March 2019. The maximum penalty for the s 184(2) offence increased from 5 years imprisonment to 15 years imprisonment on 13 March 2019: Treasury Laws Amendment (Strengthening Corporate and Financial Sector Penalties) Act 2019 (Cth) sch 1 item 140.

42 An increase in the maximum penalty for an offence reflects a legislative view about the seriousness of the offence. An increase in the maximum penalty for an offence is an indication that sentences for that offence should be increased: Muldrock v The Queen [2011] HCA 39; (2011) 244 CLR 120 at [31].

43 The increased maximum penalties necessarily impact on the usefulness of comparative sentences which have been imposed where a lower maximum penalty applied.

44 Count 1 is a rolled-up count. That is, a count in which more than one contravention of the relevant offence provision, or more than one episode of criminality, is particularised as part of the charge. This approach is adopted in some cases where there is a guilty plea and consent from the offender’s counsel because otherwise the counts would offend the rule against duplicity: R v Jones [2004] VSCA 68 at [13]; Director of Public Prosecutions (Cth) v Nippon Yusen Kabushiki Kaisha [2017] FCA 876; (2017) 254 FCR 235 at [206]-[207]. The maximum penalty for the offence remains the same as if it were a single offence. However, the objective criminality of the offence is greater for the offender than if there was only one count: Forrest at [220].

45 There is also an offence to be taken into account on count 1 under s 16BA of the Crimes Act. That involves an admission of guilt but there is no conviction: Attorney-General’s Application under s 37 of the Crimes (Sentencing Procedure) Act 1999 (No 1 of 2022) [2002] NSWCCA 518; (2002) 56 NSWLR 146 (AG’s Application) at [23]. It follows that in taking the s 16BA offences into account, the sentencing judge is not imposing any punishment for those offences: AG’s Application at [29]. Rather, when taking the other (s 16BA) offence into account, the Court is concerned only with imposing a sentence for “the principal offence”; it is no part of the sentencing court’s task to determine appropriate sentences for a s 16BA offence or to determine the overall sentence that would be appropriate for all the offences and then apply a “discount” for the use of the procedure under s 16BA: AG’s Application at [39]. It may be expected that the use of the procedure set out in s 16BA will result in a lower effective sentence than that which would have been imposed if an offender had been sentenced for the principal offence and separately sentenced for each of the offences included in the s 16BA schedule: AG’s Application at [34]. That said, “[i]t does not follow, however, that the increase to the penalty as a result of taking the two s 16BA offences into account will necessarily be small”: Director of Public Prosecutions (Cth) v Wallenius Wilhelmsen Ocean AS [2021] FCA 52; (2021) 368 ALR 98 (WWO) at [233]; Forrest at [221].

46 It is important to recall that in sentencing, a court may not take into account facts adverse to the interests of the offender unless those facts are established beyond reasonable doubt. For facts in favour of the offender, it is enough that those facts are proved on the balance of probabilities: R v Olbrich [1999] HCA 54; (1999) 199 CLR 270 at [27]. The onus is on the offender to establish those mitigating factors. That said, as noted above at [31], s 16A of the Crimes Act requires that those matters be taken into account so far as they are “relevant and known to the court”. That phrase is not to be construed as imposing a universal requirement that matters urged in sentencing hearings be either formally proved or admitted: Weininger v The Queen [2003] HCA 14; (2003) 212 CLR 629 at [21]-[22].

The evidence relied on

47 The Crown tender bundle included the:

(1) agreed statement of facts dated 2 November 2025; and

(2) sentencing assessment report dated 6 January 2026.

48 Mr Fairfull relies on:

(1) a psychological report from Mr Chafi Awit dated 30 January 2026;

(2) a letter of apology from Mr Fairfull dated 3 April 2026; and

(3) medical records, comprising a Royal North Shore discharge summary dated 30 July 2025 and Mater Hospital discharge summary dated 29 November 2022.

49 Mr Fairfull gave evidence at the sentencing hearing.

Consideration

The offences

50 The offending conduct in count 1 was committed against the background of the offending taken into account on the s 16BA schedule offence. That offence reflects the conduct in count 1 was not the beginning of the dishonest course of conduct. Rather, as the prosecution submitted, count 1 was the continuation, and then the escalation, of an established method: false revenue statements, false recurring revenue statements, false financial accounts and false investor-facing documents.

51 The offence is a rolled-up count reflecting a continuing course of conduct which occurred over 3 years and 3 months. When the schedule offence is considered, the conduct occurred over nearly four years, only stopping when it was detected by others. As detailed above, the ASOF and annexure A thereto detail the numerous individual false statements that have been rolled-up into count 1.

52 Mr Fairfull was the CEO of Metigy and a director of all three Metigy Group companies. He occupied a position of trust and control within the group, and was exclusively responsible for and had control of investor-facing information. He abused this position of trust with both the companies and investors, whom he invited to rely on the financial information he provided. The financial information presented to investors – revenue, MRR, ARR, and bank balances – were core markers of whether the business was performing, whether its valuation could be supported, and whether further capital should be deployed. The false information went to the heart of what investors and shareholders were being asked to fund. He forged and falsified banking documentation to lend credibility to the false financial information being provided to investors, to persuade them to invest (and not withdraw their investment). They relied upon it to conduct their due diligence before making an investment in Metigy. Mr Fairfull’s falsehoods did not remain static but escalated in scale and the financial amounts he sought to acquire. They grew overtime. Mr Fairfull progressed from making false application forms and investor decks, to creating false profit-and-loss statements and forecasts, to forged bank statements, to investor updates asserting MRR and ARR figures entirely divorced from reality. For example, the May 2022 profit-and-loss statement falsely showed total net revenue of $8.95 million and ARR of $107.4 million, when the actual revenue for May 2022 was zero. Mr Fairfull knew the information was false. He knew the true financial position was substantially worse than represented. He knew investors and purchasers would rely on the information, and they did. Had they known the true position, they would not have invested or purchased shares. The completed investment and share-sale transactions identified in the ASOF totalled approximately $39.084 million. The attempted Series B capital raise sought a further $50 million.

53 The conduct was sophisticated, involving a high degree of planning and premeditation.

54 During this course of conduct, Mr Fairfull withdrew $7.7 million, the subject of count 2. The Director Loan was unsecured and uncommercial. The administrator considered this caused the Metigy Group to become insolvent from 14 November 2021, being the date the money was withdrawn. The money consisted almost entirely of funds raised in the convertible note issuance, and therefore the Director Loan breached cl 4.5 of the note subscription agreement. The funds had been raised based on false statements, for the growth and development of the business and for working capital. The loan was used to help finance the acquisition of residential real estate in the names of Mr Fairfull and his wife: a $10.5 million Mosman home and a $7.7 million Wattamolla property. That said, I accept that he had made repayments totalling approximately $2.94 million, and I take that into account.

55 The objective seriousness of the offending conduct is self-evident. As explained further below, it was for Mr Fairfull’s benefit.

56 Mr Fairfull’s submissions do not grapple with the serious nature of the conduct undertaken in the offending. Mr Fairfull’s written submission pointed to facts which he submitted the offending did not include, in an attempt to distinguish it with what was suggested to be more serious offending. The submission was as follows:

the agreed facts do not disclose the existence of offshore concealment structures, sophisticated laundering arrangements, destruction of evidence, coordinated offending involving others, or broader criminal enterprise of the kind sometimes seen in the most serious forms of corporate fraud. Nor did the offending involve public securities trading, insider trading, market manipulation, or the corruption of public trading markets in the conventional sense. Rather, the conduct occurred in the context of private capital raisings involving sophisticated commercial and venture capital participants, all of whom were nevertheless plainly entitled to honesty and transparency in the information provided to them.

57 The submission attempts to minimise the severity of the conduct. It is unclear what the significance is of the submission that the victims of the conduct were sophisticated participants. Leaving aside the accuracy of that description, as the submission acknowledges, all participants were entitled to honesty and transparency. Further, the comparison of this conduct with other types of offences (e.g. insider trading) which appear to be characterised as more serious, is flawed. The seriousness of any offence necessarily depends on its facts and circumstances. Those offences, as with this one, are all directed to ensuring public confidence in the fairness and honesty of markets for financial products. The submission fails to recognise that count 1 is an offence directed to prohibiting false or misleading information being provided which is likely to induce others to apply for financial products. In this case, Mr Fairfull committed that offence with premeditated and sophisticated conduct, over a significant period of time, where he repeatedly provided knowingly false information to persuade participants to contribute funds where they would not have if they knew the true financial state of the companies. As explained further below, he did so to obtain funds for his use and benefit. He obtained $39 million, and was attempting to obtain a further $50 million.

58 The same approach, focussing on what was said to be the absence of the features of more serious offending was taken by Mr Fairfull in the description in his written submissions of count 2, which omitted reference to the amount of money he obtained, being $7.7 million, the motivation for the conduct, or the use to which it was put.

59 Mr Fairfull is to be sentenced for the conduct he undertook, taking into account all the relevant facts and circumstances. As he accepted, the absence of aggravating factors is not mitigating.

Victim impact statement

60 Given Mr Fairfull’s submission recited at [56] above, including his characterisation of the nature of the investors, it is timely at this stage to refer to the victim impact statement from the co-founder and managing partner of CP Ventures. This details the impact of Mr Fairfull’s offending which includes, inter alia: financial loss, including $1.3 million invested by CP Ventures in Metigy across four rounds in 2019, personal investments in Metigy by CP Venture’s managing partners, and millions of dollars invested by investors introduced to Metigy by CP Ventures; relationship impacts, including the loss of trust in CP Ventures by their investors; and reputational damage caused to CP Ventures by Mr Fairfull’s deception. The statement is illustrative of the type of loss that Mr Fairfull’s offending has caused for the investors and purchasers of shares, who relied upon the false information he provided. This included “hard working Australians saving for retirement and wanting to back Australian businesses”.

61 In addition, it is important to also recall the broader implications of such offending, in that it undermines the integrity of Australia’s financial markets and system of corporate regulation and erodes the confidence of participants in the commercial world, as described above.

Mr Fairfull’s submissions in relation to moral culpability and the offending

62 Mr Fairfull in written submissions “accepted that the offending is objectively grave and involved serious and sustained dishonesty committed in a corporate and investment context over a prolonged period” which represented a serious breach of trust. But Mr Fairfull also submitted:

the offending should not be characterised as archetypal predatory corporate criminality motivated solely by personal greed. The offending occurred in the context of a genuine operating technology start-up under escalating commercial pressure, and reflected progressively entrenched concealment, distorted decision-making and deteriorating psychological functioning on the part of the offender rather than inherently predatory conduct driven by anti-social attitudes or purely by greed.

63 As to count 1, Mr Fairfull submitted that:

the offending occurred in the context of an emerging technology start-up dependent upon recurring venture capital investment and future-oriented product development. Metigy was a genuine operating business with actual employees, genuine technology development, commercial operations and clients. [His] conduct was directed toward maintaining the viability of the business and continuing development of what he believed to be a commercially valuable product which would ultimately generate profits for those who invested, rather than the systematic extraction of investor funds for personal enrichment throughout the offending period.

64 As to count 2, Mr Fairfull, while accepting it was serious, submitted “the conduct did not involve the permanent misappropriation or clandestine diversion of company funds in the conventional sense”. The transaction was recorded as a loan, repayments totalling approximately $2.94 million were subsequently made, and the ASOF supports the inference that he contemplated repayment at the time the funds were advanced, albeit in circumstances where the conduct remained dishonest and constituted a serious breach of duty.

65 He submitted there are substantial mitigating factors, and when all the factors are considered a sentence of imprisonment of less than 3 years would serve all purposes of sentencing.

66 At this stage it is appropriate to address Mr Fairfull’s submissions relating to the assessment of his moral culpability.

67 Mr Fairfull gave evidence that he accepted responsibility and was not making any excuses for his conduct. However, the submission and evidence of Mr Fairfull’s purported motivation does seek to minimise the seriousness of his conduct. Mr Fairfull’s approach in relation to his conduct in count 1 was that the ends justified the means. That is, he believed he would ultimately make the business succeed with the development of the product in 4-5 years. However, he had trouble raising capital. Mr Fairfull justified making false statements to persuade investors to invest in his business because he believed the product would be successful, and investors would not lose out in the end. Mr Awit recorded Mr Fairfull “was convinced that all investors would be reimbursed their investments down the track”.

68 Mr Fairfull submitted his history and psychological assessment, as described by Mr Awit, a psychologist, is relevant to understanding the offending and the context in which he committed the offences. He did not submit that the psychological context meant he was “incapable of understanding the wrongfulness of his conduct”. Rather, he relied on Mr Awit’s opinions to support a submission he had lower moral culpability for his offending conduct, albeit it was described at hearing as justifying only a moderate reduction. Where the state of a person’s mental health contributes to the commission of the offence in a material way, the offender’s moral culpability may be reduced. Reduced moral culpability for the offending may affect the issue of just punishment and denunciation, such that the element of general deterrence is moderated or eliminated as a sentencing consideration: see e.g. Directory of Public Prosecutions (Cth) v De La Rosa [2010] NSWCCA 194; (2010) 79 NSWLR 1 (De La Rosa); R v Verdins [2007] VSCA 102; (2007) 16 VR 269.

69 Mr Awit recorded the history provided by Mr Fairfull. This included that he had previously owned and run another business which, through no fault of his, ceased trading and led to him being declared bankrupt. Thereafter he separated from his wife for some time. Mr Awit recorded Mr Fairfull was a founding director of Metigy which he ran for eight years up until the end of 2022. Mr Awit’s opinion was that Mr Fairfull was suffering from Generalised Anxiety Disorder and Major Depressive Disorder at the time he saw him, in January 2026. I note he opined the testing results at that time showed Mr Fairfull was suffering from moderate levels of depression, anxiety and stress. Given the history provided by Mr Fairfull, Mr Awit provided a probable diagnosis during the period of the offending of Major Depressive Disorder with anxious distress. He recorded that Mr Fairfull reported his symptoms were worse during the offending period but were at their peak in 2022 to 2023, the year that followed the discovery of Mr Fairfull’s offending and the Metigy Group going into administration.

70 Mr Awit described that Mr Fairfull advised him that the need to succeed and not fail again (after his previous company ceased to trade and he was declared bankrupt) “drove his anxiety through the roof”. He was fearful of the impact failure may have on his marriage and family. Mr Fairfull advised him “that if production stopped due to the inability to raise capital, then someone else in the market could take over, and the business would be dead”. He advised that his belief in his product (which was essentially providing a marketing technology platform, using generative AI to assist, even before AI became popular) compelled him to push forward in his attempts to raise capital.

71 Mr Awit recorded that Mr Fairfull advised he found himself “blurring the lines between what was right and what was wrong, in order to achieve the success of the product so that everyone could benefit.” Mr Awit then opined that Mr Fairfull, struggling to find the capital to allow the product to be completed, “blurred the lines between right and wrong when he initially committed the offence in 2019”. He “continued with his behaviour, in part out of fear of failure and what this would mean not only to himself, but to his family, staff and investors. The writer also notes that Mr. Fairfull’s aversion to failing again (and potentially losing his marriage) and a need to prove himself were all motivating factors”. He opined Mr Fairfull’s depression and anxiety weakened his “resolve and ability to sort his problems out”, and that he became trapped rather than confronting his situation. He opined the conditions he diagnosed Mr Fairfull with are documented to correlate with impaired decision-making. Mr Awit also recorded that “[Mr Fairfull] accepts that his actions (no matter how well-intended they were) were wrong”.

72 A number of observations can be made about Mr Awit’s report.

73 First, and most tellingly, when count 2 is considered, it is plain the motivation in respect to the effect of the possible failure of the business on employees and investors advanced by Mr Fairfull to Mr Awit cannot be accepted. Taking $7.7 million as a Director Loan was solely for his personal benefit. It was to assist in purchasing what the parties described as two luxury real estate properties. Mr Fairfull admitted as much when giving evidence. He also accepted that the withdrawal could not, in any way, have helped the business. Nonetheless, that the transfer of the money is recorded as a loan, and he is said to have had an intention at the time that he would repay the money, does not diminish the seriousness of this offence. He chose to take $7.7 million when he knew the financial state of the companies and that the money he took had been obtained from investors (based on false statements) for a specific purpose (and so was in breach of cl 4.5 of the note subscription agreement). The withdrawal of that money resulted in the companies becoming insolvent. He chose to withdraw this money regardless of the consequences to the Metigy Group and its employees and investors. He did so dishonestly, with the intention of advantaging his company, Fairfull Holdings, with the money to be used for his own personal benefit.

74 This conduct cannot fall within any explanation given by Mr Fairfull to Mr Awit of his motivation. In giving evidence, Mr Fairfull said he took the $7.7 million because he “was trying to do something good for [his] family”. That motivation plainly does not cohere with the explanation for the offending in Mr Awit’s report. Nor does it fit within the opinions Mr Awit expressed as to Mr Fairfull’s psychological state. Mr Awit described Mr Fairfull as “intermittently” depressed and anxious throughout the period of 2019-2022, and that this would to some degree have weakened his resolve and ability to sort his problems out. He opined that it can often be easier to go along with already established patterns of behaviour than to force oneself to deal with a difficult situation. Leaving aside that opinion does not fit comfortably with the deliberate, repeated and sophisticated falsifications that form the basis of count 1, it also cannot sit with Mr Fairfull’s conduct for count 2, a separate, distinct and one-off act of dishonesty to assist him in purchasing two luxury real estate properties. There is nothing linking Mr Awit’s opinions in respect to anxiety and depression with Mr Fairfull’s conduct for count 2. I note during the hearing in answer to a question from the Court, Mr Fairfull’s counsel conceded that his conduct in relation to the $7.7 million was different from that in count 1, and it cannot be understood in the context of his anxiety and the need to succeed. He further submitted that it “[cannot] be properly and fully explained, other than, perhaps, part of his psychological matrix that having a big home or a luxurious home was part of that overall character and pressure that he felt”. The problem with that submission is that it is not supported by anything Mr Fairfull has said, or any other material. It is entirely speculative.

75 The dishonest conduct of withdrawing the $7.7 million for his own benefit in the circumstances in which that occurred is inconsistent with Mr Fairfull’s case as to the nature of his offending.

76 The failure of Mr Awit’s report to address the $7.7 million withdrawal significantly impacts on the weight that can be attributed to his opinions, in particular his causal opinions, given he was purporting to comment on the motivation for all of Mr Fairfull’s offending conduct. If Mr Awit was not informed of Mr Fairfull’s motive for count 2, he did not have all the relevant facts to make an accurate evaluation. Regardless, I note that Mr Awit was provided with the ASOF which included reference to the $7.7 million withdrawal and the use to which Mr Fairfull put it. Nonetheless, he provided an opinion without any reference to it. To do so adversely impacts on the weight of the opinions provided.

77 Second, Mr Awit’s opinions are based on Mr Fairfull’s description of his conduct (e.g. an acceptance of Mr Fairfull’s claim he was blurring the lines), which is inconsistent with what occurred. Mr Fairfull’s description of the offending “blurring the lines” cannot be accepted. Mr Fairfull’s acts were premeditated, knowingly false and dishonest. Count 1 involved repeated false statements and the creation of false documents to support his lies about the financial position of the companies. The acts were designed to persuade investors to part with their money, by investing or otherwise providing capital for the business. Count 2 was a dishonest act for personal financial gain. In addition, Mr Awit’s opinions are based on an acceptance of Mr Fairfull’s description of his motivation for his conduct. For example, although Mr Fairfull in evidence denied he thought his conduct was well-intended, it appears Mr Awit interpreted what he was told by Mr Fairfull as being just that. That appears to be based on Mr Fairfull reporting that, at the time he “[blurred] the lines” in 2019, his intention was to create a successful product so everyone could benefit.

78 Third, in that context, Mr Awit’s analysis is based on Mr Fairfull’s self-serving description of his condition during the relevant period. Mr Fairfull’s references to anxiety and depression are lay descriptions of how he felt. Although Mr Awit described the basis of the diagnoses, his opinion is dependent on Mr Fairfull’s descriptions of symptoms and how he was feeling, provided after the offending conduct. It depended on his own reporting of the existence, timing, nature and extent of symptoms, and the effect thereof. Although Mr Fairfull gave evidence that what he told Mr Awit was the truth, and that could be tested at the hearing, he provided no supporting evidence of his condition at the time. Mr Fairfull gave evidence that during the period of offending he did on occasion get sleeping medication from his doctor, but there is no evidence (including from him) that there was any complaint about anxiety or depression to his doctor, or that his doctor referred him to professional assistance on that account.

79 Mr Fairfull submitted Mr Awit’s opinions are “materially consistent with the objective chronology of the offending”. That submission fails to grapple with the conduct undertaken, including the use of the $7.7 million to assist in the purchase of his properties. It ignores that the opinions are underpinned by an acceptance of Mr Fairfull’s version of the events. It is also premised on an assertion there was a “prolonged and escalating … concealment” of his conduct, which attributes a motive for the repeated nature of the offending in count 1 that is not borne out by the material. As described above, he acted on the premise that the ends justified the means. That is not concealment, but a course of conduct to achieve a purpose. That said, undoubtedly for the conduct to remain undetected it did require ongoing concealment. Again, the submission cannot sit with count 2.

80 Mr Fairfull also submitted there is a “general consistency” in the material tendered on his behalf, including the “independently prepared” sentence assessment report. However, the content of the sentence assessment report is very limited, particularly in regard to the commission of the offences. It does not address the reason for the offending, beyond that Mr Fairfull was experiencing “an overwhelming sense of need to make the business work regardless of why or how” and felt “a need to ‘prove his worthiness’”. It too is based on the self-serving statements of Mr Fairfull. The sentence assessment report does not assist in considering the weight to be attached to the opinions of Mr Awit.

81 Further, Mr Fairfull’s written submissions based on Mr Awit’s report tended to overstate its contents. They also do not address the limitations of the report, including the lack of consideration of the nature of and motivation for the conduct in count 2.

82 Given the evidence, I do not accept that Mr Fairfull continued his offending because of a weakened resolve or inability to deal with his problems.

83 Mr Fairfull may have been anxious when the capital for his company became hard to source, and he may well have feared his business would fail, and did not want that to occur. Once he began offending he may have felt a sense of anxiety at the possibility of his conduct being revealed. Nonetheless, he deliberately provided false information to overcome that difficulty and chose repeatedly to do so to achieve his own purposes. He believed in his business and he wanted to succeed. When he began the offending he believed the project of developing a software platform to harness AI, on his own evidence, would take 4-5 years to reach fruition. Mr Fairfull may have justified his conduct to himself by telling himself the investors would not lose out because the project would ultimately be successful, but he was not committing the offences for their benefit. Nor was he doing so, “so that everyone could benefit”. Investors provided approximately $39 million based on his false statements. Whilst he was in the process gaining more and more investments based on repeatedly providing false financial information, he chose to withdraw $7.7 million of the funds raised, for his own benefit. In the circumstances, this reflects he chose to put himself above others. It could only have harmed the existing investors and the business. That exposes the flaw in any suggestion his offending conduct was for the benefit of others. Then in April 2022, by using false statements he sought to obtain a further $50 million for his company. His conduct only stopped in July 2022 when it was exposed by others. Mr Fairfull had difficulty raising capital for his business, which he considered had a solid product in development that if completed would make the company a considerable profit. To overcome the difficulty, he obtained capital by undertaking the conduct in count 1. This was to enable the companies’ success and by extension his own, with all that this entails. I am satisfied Mr Fairfull’s conduct in committing the offences was to obtain money for his own use and benefit. As counsel for Mr Fairfull properly conceded during the sentencing hearing, in answer to a question from the Court, both offences were committed for his financial benefit. Undoubtedly, Mr Fairfull made bad decisions, but not ones that have a lower moral culpability on that account.

84 Mr Fairfull gave evidence that his belief he could make the business work and everybody would be repaid was not a rational one. But there is a rational explanation for his conduct. His acts were deliberate, premeditated, sophisticated and rational ones to achieve a purpose. They were dishonest acts designed for personal gain. In relation to count 1, he considered the ends justified the means. It is difficult to understand how it can be said that his conduct in relation to count 2 was not rational, as his actions led to the outcome he intended (i.e. to obtain money to enable him to purchase the properties).

85 Mr Fairfull has not established anxiety and depression materially contributed to the commission of his offences, such as to lessen his moral culpability. Even if Mr Fairfull was fearful of failure and felt a need to prove himself, that does not diminish his moral culpability. I am not persuaded that Mr Fairfull has established that his moral responsibility for the offending is moderated in the manner contended. That said, I accept that his anxiety and depression is otherwise relevant to his subjective case, to which I return below.

86 In my view, given the nature of the conduct undertaken by Mr Fairfull and the manner in which it was undertaken, general deterrence is a primary sentencing consideration in this case.

Subjective features

87 I have already addressed some aspects of Mr Fairfull’s subjective case, in referring to Mr Awit’s evidence.

88 I take into account his history and background as it is recorded in Mr Awit’s report. That includes his history of having a previous business fail through no fault of his own, him becoming bankrupt and the effect of that on his family. I take into account his childhood experiences, as described by him to Mr Awit. These matters provide, amongst other things, a context for the offending.

Guilty plea

89 Mr Fairfull pleaded guilty on 4 November 2025 at the Downing Centre Local Court and was committed for sentence to this Court. He confirmed that plea at the sentencing hearing. The Crown accepted there is utilitarian value to the plea, and the admissions also are relevant to remorse and the facilitation of the administration of justice.

90 In relation to the utilitarian value of the plea, although it is not required under the Crimes Act to quantify and specify an amount attributed to this consideration, in my view it is desirable to do so: see Forrest [152]. The Crown accepted the plea should attract a 25% discount.

91 The remaining subjective matters which may be reflected by the plea, being remorse and the facilitation of the administration of justice, are taken into account in the instinctive synthesis process. During that, care must be taken not to double count a consideration.

Cooperation

92 Mr Fairfull submitted that he participated in an interview with investigators in which he made admissions concerning the offending conduct. This occurred on 15 December 2023. Mr Fairfull submitted this assistance and cooperation warrants a separate discrete discount in the order of at least 5%.

93 The context and timing are important. This occurred after representatives of Regal and Five V confronted Mr Fairfull at his home on 28 July 2022, after they had been advised by the CFO of Metigy that the June 2022 ARR of $107 million provided to them was completely false. On or around 28 July 2022, Regal became aware there were further irregularities and misrepresentations in documents provided to them during various capital raisings, including very significant overstatements in Metigy’s financial position from 2020 to 2022. When confronted, Mr Fairfull admitted, inter alia, that the management accounts were false, that bank statements from 30 April 2022 to 31 May 2022 had been doctored by him and that the June 2022 ARR figure of $107 million was completely false. On 29 July 2022, Regal informed ASIC that Mr Fairfull had provided them, and other investors, with false financial information which significantly overstated the revenue of the Metigy Group. On the same day, the Metigy Group entered voluntary administration owing approximately $39 million to creditors.

94 There is no evidence before me that quantifies or describes the level of assistance, apart from Mr Fairfull making admissions to the offending. There is no evidence as to the significance of that cooperation to the investigation. While s 16A(2)(h) identifies that cooperation with law enforcement can be taken into account, it does not require that the Court specify a discount for this consideration. I do not propose to do so, but rather it is a matter that I will take into consideration in the process of instinctive synthesis.

Prior good character

95 Mr Fairfull is a 58 year old with no relevant prior convictions, and he was a person who was otherwise of good character. However, as already explained, good character may be of lesser significance for white collar crimes, since it is that factor which normally places the offender in a position where they are able to commit the offence: Rivkin at [410]. It is said that the fact that people of otherwise good character and compelling personal circumstances are tempted to engage in such conduct emphasises the need for a clear deterrent for offending of this nature: see e.g. R v Glynatsis [2013] NSWCCA 131; (2013) 203 A Crim R 99 at [79] (McCallum J); Gregory at [53]; Forrest at [236], [253]. Mr Fairfull accepted that good character in this case, in and of itself, may be given reduced weight.

96 In this case, Mr Fairfull’s good character put him in the position to commit these offences. The position of a director and CEO has within it certain character criteria, which lent support to the trustworthiness of Mr Fairfull in holding out the false representations and documentation.

97 Further, Mr Fairfull was not a first-time offender from the time he committed the second offence. It was only that he had not yet been caught out: see e.g. R v Smith [2000] NSWCCA 140; (2000) 114 A Crim R 8 (R v Smith) at [21]; R v Phelan (1993) 66 A Crim R 446 at 448. It follows that the mitigating effect of good character is lessened in circumstances where an offender has engaged in the commission of a number of offences over a long period of time: R v Smith at [21]-[22].

98 I take Mr Fairfull’s good character into account and that he did not commit his first offence until he was in his 50s, but in my view, in the circumstances of the offending in this case, it has less weight than otherwise might be the case.

Health

99 Mr Fairfull relies on his psychological condition and physical health as relevant matters pursuant to s 16A(2)(m) of the Crimes Act. As already discussed, he submitted the psychological material assists in understanding his moral culpability, impaired decision-making and entrenched avoidance behaviour during the offending period. As explained, I am not persuaded the evidence moderates his moral culpability. That said, I accept it has some relevance in the assessment of his subjective case. Further, I accept that Mr Fairfull has suffered from anxiety and depression since his offending was revealed. I also note that the sentencing assessment records that Mr Fairfull said he has spoken to a psychologist on several occasion since the offending was uncovered. He has expressed a willingness to engage in psychological treatment in his letter of apology to the Court. However, there is no evidence or submission to suggest that any psychological condition by itself would result in him doing his time harder if imprisoned.

100 There is evidence of Mr Fairfull’s cardiac issues and medication he takes to manage this. I take this fact into account. However, Mr Fairfull accepted that in the absence of further expert evidence, it has not been established these cardiac conditions alone mean prison would be unusually onerous or that the conditions are incapable of management in prison.

Other considerations

101 I accept that Mr Fairfull has expressed remorse for his conduct. He repeatedly said he has taken full responsibility for his actions and sincerely regrets the damage and suffering caused to investors. Mr Fairfull submitted that the sentence assessment report independently confirms matters such as insight and remorse. It records that he “was able to demonstrate insight into the impact of the offending, particularly for his family, friends and adult children” and “he was also able to identify that he ‘broke trust’ for his staff and that he caused ‘stress and trouble for investors and staff’. He reported that investors lost money which would impact the performance of their funds”. He has provided a letter of apology that expresses his sincere remorse and apology for his actions.

102 I accept Mr Fairfull’s admissions to the authorities and his early guilty pleas reflect he is remorseful for his conduct and demonstrate an intention to facilitate the course of justice. I accept his evidence that he is remorseful for his conduct. That said, although he has some insight into the offending, what is noticeable in his letter of apology and in his evidence is the failure to acknowledge the offending was for his benefit. I also note that, as described above, his description of his conduct as “blurring the lines” and not being rational downplays its seriousness, and reflects on the degree of his insight.

103 I also accept he has good prospects of rehabilitation, and is at a very low risk of reoffending. As a result, I consider while specific deterrence is of less relevance, it still has some role in the sentencing process, albeit relatively limited.

104 Mr Fairfull submitted that any term of imprisonment will weigh more heavily upon him by reason of a combination of factors including his age, it being his first custodial sentence, his cardiac condition, psychological functioning, current mental state, and the dramatic collapse in his personal and professional circumstances. I take this combination of factors into account.

105 Mr Fairfull also submitted that he has:

…additionally suffered very substantial ramifications arising from the collapse of the Metigy business, the destruction of his professional reputation, financial ruin, public humiliation, strain upon his family relationships and the ongoing psychological burden associated with the present proceedings.

106 He acknowledged that these effects do not rise to the level of extra-curial punishment and are appropriately categorised as “the natural devastating consequences of his own conduct”, but submitted they are still relevant to the overall instinctive synthesis. As previously explained, given his use of his position and good reputation in committing these offences, this submission, while relevant, carries relatively little weight. These consequences are also not uncommon for this type of offending. That said, I take the effects into account.

107 I note that there is very little before me about his family. Information about them only appears in his history as relayed to Mr Awit, and what is recorded in the sentencing assessment report. These reports refer to his wife and three children, one or two of whom reside with him. I note he has worked in his son’s gardening business over the past few years. I note a daughter and his sister attended the sentence hearing. There is no evidence relied on, or any submission made as to the impact of the offending on his family, although I can infer there obviously has been some impact, and his imprisonment will have a further impact on them.

Comparative cases

108 The increase in the maximum penalty impedes the usefulness of prior sentences as comparative cases. The maximum penalty was increased twice in a limited time, with the last increase being 50%. This is in the context of the sentences which had to date been imposed for this type of offending: Forrest at [244].

109 In that context it is important to recall care must always be taken in using what has been done in other cases: Hili v The Queen [2010] HCA 45; (2010) 242 CLR 520 (Hili) at [53]. As recognised, the range of past sentences does not fix “the boundaries within which future judges must, or even ought, to sentence”. Sentences imposed in other cases “are no more than historical statements of what has happened in the past. They can, and should, provide guidance to sentencing judges, and to appellate courts, and stand as a yardstick against which to examine a proposed sentence”: Hili at [54] (emphasis included) citing De La Rosa at [304]. It is also recognised that consistency in federal sentencing is important, but that consistency relates to the application of relevant legal principles rather than numerical equivalence and is to be achieved through the work of the intermediate courts of appeal: Hili at [18], [56]; R v Pham [2015] HCA 39; (2015) 256 CLR 550 at [28].

110 The cases referred to by the Crown, including Kirby, Sigalla v R [2021] NSWCCA 22 (Sigalla), R v Donald [2013] NSWCCA 238, R v Silver [2020] QCA 102, Regina v Shawn Darrell Richard [2011] NSWSC 866 and R v Moylan [2014] NSWSC 944, all dealt with offences at a time of significantly lower maximum penalties. The Crown submitted that Kirby was of particular relevance, as the features that informed the disposition in that case are present in this case, and several are present in materially aggravated form. Mr Fairfull only addressed Sigalla, submitting it is distinguishable. Nonetheless, although fact specific, these cases, inter alia, illustrate the nature and type of considerations which have been taken into account in sentencing for this type of offence.

Disposition

111 The objective seriousness of each offence is substantial. It is important to recall that count 1 is a rolled-up count, and includes a s 16BA offence taken into account on schedule. It is also important to recall the maximum penalties that apply for these offences, and that they have increased significantly.

112 Mr Fairfull’s conduct occurred over a period of 3 years and 8 months (including the offence taken into account on schedule). Mr Fairfull knew investors and purchasers would rely on the information he provided and that, had they known the true position, they would not have invested or purchased. That was the very purpose of providing the false information. He engaged in multiple acts of dishonesty using his position of trust and control, which included forging banking documentation to induce others to invest and provide capital for his business. The completed transactions on the ASOF approached $39 million in subscribed capital and share-purchase consideration, with an attempt for a further $50 million. His deception escalated over time. He took the approach of the ends justified the means; it enabled the companies to continue working towards the product being produced, and its success from which he would benefit. Knowing the financial circumstances of the companies, he nonetheless provided to himself a substantial personal benefit of $7.7 million through the Director Loan to acquire residential luxury properties. On the conduct being revealed, the Metigy Group entered voluntary administration owing approximately $39 million to creditors.

113 For the reasons already explained, given the nature of the conduct undertaken by Mr Fairfull and the manner in which it was undertaken, general deterrence is a primary sentencing consideration. I do not accept Mr Fairfull’s submission his moral responsibility is reduced. It necessarily follows less weight can be given to matters personal to Mr Fairfull.

114 The most significant of the matters in mitigation are the early pleas of guilty with all that entails. I place great weight on that factor. As explained above, for the utilitarian aspect of the pleas of guilty, I allow a 25% discount for each offence. In addition, the other factors taken from the plea (the subjective factors of remorse, contrition, and the willingness to facilitate the course of justice) have been taken into account in his favour in the instinctive synthesis process. I have also taken into account the subjective features relied on, as explained above.

115 This Court is to impose a sentence of the severity appropriate in all the circumstances of the offence. The obligation in s 16A(1) applies to the determination of a non-parole period: Hili at [40]; R v Hatahet [2024] HCA 23; (2024) 282 CLR 392 at [28]. The intention of the legislature in providing for the fixing of minimum terms is to provide for mitigation of the punishment of the prisoner in favour of his rehabilitation through conditional freedom, when appropriate, once the prisoner has served the minimum time that a judge determines justice requires that he must serve having regard to all the circumstances of his offence: Bugmy v The Queen [1990] HCA 18; (1990) 169 CLR 525 (Bugmy) at 536 referring to Power v The Queen [1974] HCA 26; (1974) 131 CLR 623 at 629 and Deakin v The Queen [1984] HCA 31; (1984) 58 ALJR 367 at 766; and see Hili at [40]. While all matters are to be taken into account in both the head sentence and any non-parole period to be imposed, the weight to be attached to them can vary given the role or purpose of a non-parole period: Bugmy at 531. The deterrent and punitive effects of sentences for a particular offence must be reflected both in the head sentence and non-parole period: Hili at [41], [63].

116 Taking into account and weighing the relevant considerations by the process of instinctive synthesis, including the factors in s 16A(2) of the Crimes Act that are relevant and known to the Court, I impose the following sentences.

117 The sentence in relation to count 1 is 7 years and 6 months imprisonment, which reflects a 25% discount for the utilitarian value of the plea of guilty. In relation to count 2, a sentence of 3 years which reflects a 25% discount.

118 It may be accepted that the second offence occurred during the commission of the first, but the nature of the conduct is different. Mr Fairfull submitted that “[a]ll offences arose during the same broader period of deterioration within the Metigy business and occurred within the same commercial and psychological context.” The premise of the submission has been dealt with above. Suffice to say that context does not adequately account for the nature of the two offences. In particular, for the reasons already explained, it does not account for the conduct in count 2. I do not accept Mr Fairfull’s submission that there is a substantial degree of overlap between counts 1 and 2. It may be accepted that they occurred during the same period of time, and that he used the same position within the Metigy Group in respect to each. However, count 2 is blatant and deliberate conduct, involving separate criminality to the offending in count 1. There is overlap in each as he abused his position within the companies, but that does not detract from the conduct being two separate and distinct offences. In count 2 Mr Fairfull used funds that he obtained as a result of the count 1 offending conduct which were provided by investors for the growth and development of the business, to assist him in purchasing two luxury properties. He did so knowing the true financial circumstances of the companies.

119 I do propose to order some concurrency, but there also needs to be accumulation: see, for example, the oft cited Cahyadi v The Queen [2007] NSWCCA 1; (2007) 168 A Crim R 41 at [37]. I am mindful of the principle of totality which obliges a judge “who is sentencing an offender for a number of offences to ensure that the aggregation of the sentences appropriate for each offence is a just and appropriate measure of the total criminality involved”: Postiglione v The Queen [1997] HCA 26; (1997) 189 CLR 295 at 307-308, citing Mill v The Queen [1988] HCA 70; (1988) 166 CLR 59 at 63.

120 I also note the sentence on count 1, given it is a rolled-up count with an offence taken into account by the schedule, has an inherent element of leniency: e.g. Forrest at [257].

121 I consider there should be 18 months served concurrently, which results in an aggregate sentence of 9 years imprisonment.

122 There is to be a single non-parole period imposed, being 5 years and 4 months imprisonment.

I certify that the preceding one hundred and twenty-two (122) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Abraham. |

Associate:

Dated: 19 June 2026

ANNEXURES

Attachment A — Agreed Statement of Facts