FEDERAL COURT OF AUSTRALIA

Bunter v Hardy, in the matter of FT Sydney Pty Ltd (subject to a deed of company) (Application for stay and interlocutory relief) [2026] FCA 742

File number(s): | NSD 910 of 2026 |

Judgment of: | SHARIFF J |

Date of judgment: | 12 June 2026 |

Catchwords: | CORPORATIONS / COMMERCIAL – application by interested parties for stay of proceedings relying upon irrevocable instruments – stay not granted – application for interlocutory and interim relief by creditors seeking to restrain the effectuation of a deed of company arrangement pending final hearing in which various relief is claimed including termination or variation of the deed – prima facie case established but one which has less than moderate prospects – balance of convenience – substantial prejudice to creditors in deprivation of right to seek relief relating to the termination or variation of the deed – prejudice to be balanced against other claims that can continue to be maintained – prejudice to the creditors to be balanced against prejudice to other parties – failure to provide undertakings as to damages – application for interlocutory and interim relief dismissed |

Legislation: | Corporations Act 2001 (Cth) ss 435A, 444D(2), 445D, 447A, 447C, Part 5.3A, Sch 2 (Insolvency Practice Schedule (Corporations)) ss 75-42, 90-15 |

Cases cited: | Air Express Limited v Ansett Transport Industries (Operations) Pty Ltd (1981) 146 CLR 249 Australasian Memory Pty Ltd v Brien [2000] HCA 30; 200 CLR 270 Australian Broadcasting Corporation v Lenah Game Meats Pty Ltd [2001] HCA 63; 208 CLR 199 Australian Broadcasting Corporation v O’Neill [2006] HCA 46; 227 CLR 57 Beecham Group Ltd v Bristol Laboratories Pty Ltd [1968] HCA 1; 118 CLR 618 Capgemini US v Case [2004] NSWSC 674 Castlemaine Tooheys Ltd v South Australia [1986] HCA 58; 161 CLR 148 First Pacific Advisors LLC v Boart Longyear Ltd [2017] NSWCA 116; 320 FLR 78; 121 ACSR 136 Frisken (Trustee) v E K Recruitment Pty Ltd (in liq), in the matter of E K Recruitment Pty Ltd (in liq) [2026] FCA 223 In the matter of Ten Network Holdings Limited (Administrators Appointed) (Receivers and Managers Appointed) and Others [2017] NSWSC 1219 Insurance Australia Ltd t/as CGU Insurance v Capral Ltd [2025] FCAFC 46; 309 FCR 385 Kemppi v Adani Mining Pty Ltd (No 3) [2018] FCA 40; 355 ALR 553 Network Ten Ltd v Fulwood (1995) 62 IR 43 Parkview Constructions Pty Ltd v Tayeh [2009] NSWSC 186; 71 ACSR 65 Patrick Stevedores Operations No 2 Pty Ltd v Maritime Union of Australia [1998] HCA 30; 195 CLR 1 Project Sea Dragon Pty Ltd v Canstruct Pty Ltd [2024] FCAFC 141; 305 FCR 465 QBI Corporation Pty Ltd v Plantation Rise Pty Ltd [2010] QSC 102; 77 ACSR 573 Samsung Electronics Co Ltd v Apple Inc [2011] FCAFC 156; 217 FCR 238 Snowside Pty Ltd as trustee for Snowside Trust v Boart Longyear Ltd [2017] NSWCA 215; 122 ACSR 291 Varley v Varley [2006] NSWSC 1025 Weribone on behalf of the Mandandanji People v State of Queensland [2013] FCA 255 Williment v Federal Commissioner of Taxation [2010] FCA 808; 190 FCR 234 |

Division: | General Division |

Registry: | New South Wales |

National Practice Area: | Commercial and Corporations |

Sub-area: | Corporations and Corporate Insolvency |

Number of paragraphs: | 144 |

Date of hearing: | 9-10 June 2026 |

Counsel for the Plaintiffs: | Mr C Bova SC with Mr J Burnett |

Solicitor for the Plaintiffs: | Maddocks |

Counsel for the First and Second Defendants: | Ms R Mansted with Ms H Zhu |

Solicitor for the First and Second Defendants: | Ashurst Australia |

Counsel for the Sixth Defendant: | Mr R Scruby SC |

Solicitor for the Sixth Defendant: | Henry William Lawyers |

Counsel for the Interested Party: | Mr S J Maiden KC with Ms T Jonker |

Solicitor for the Interested Party: | Arnold Bloch Leibler |

ORDERS

NSD 910 of 2026 | ||

| ||

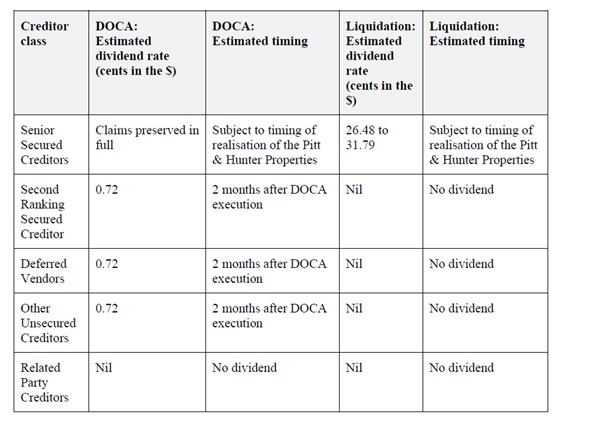

BETWEEN: | ADRIAN MAXWELL BUNTER First Plaintiff 23 HUNTER ST PTY LTD ACN 117 134 951 AS TRUSTEE FOR 23 HUNTER TRUST Second Plaintiff MOIETY PTY LTD ACN 096 505 789 AS TRUSTEE OF THE CHALK & FITZGERALD UNIT TRUST ABN 65 672 406 832 (and others named in the Schedule) Third Plaintiff | |

AND: | DAVID HARDY First Defendant AMANDA CONEYWORTH Second Defendant FT SYDNEY BORROWER PTY LTD (SUBJECT TO A DEED OF COMPANY ARRANGEMENT) (ACN 663 835 756 (and others named in the Schedule) Third Defendant | |

MERRICKS CAPITAL PTY LTD (ACN 126 528 005), MC P&H PTY LTD (ACN 664 068 964) AS TRUSTEE FOR MC P&H FUND, MC PH II PTY LTD (ACN 692 220 812) AS TRUSTEE FOR MC PH II FUND Interested Party | ||

order made by: | SHARIFF J |

DATE OF ORDER: | 12 JUNE 2026 |

THE COURT ORDERS THAT:

1. The interlocutory process filed by the Merricks SPVs seeking a stay dated 5 June 2026 is dismissed.

2. Prayers 5 and 6 of the interlocutory process filed by the Plaintiffs on 5 June 2026 are dismissed.

3. The Merricks SPVs pay the Plaintiffs’ costs of and incidental to the application for a stay.

4. The costs of the Plaintiffs’ claims for interlocutory relief be reserved.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

SHARIFF J:

1. INTRODUCTION

1 There are two applications which have come before me as the Commercial and Corporations list Duty Judge for expedited determination. Some of the background was set out in a rudimentary form in my earlier judgment (Bunter v Hardy, in the matter of FT Sydney Pty Ltd (subject to a deed of company) [2026] FCA 701), and to which I add in what follows.

2 For present purposes, it is sufficient to note that the Plaintiffs are twenty-two of what have come to be known as the Deferred Vendors and were creditors in the administration of the affairs of the fourth defendant (FT Sydney). Effectuation and implementation of the Deed of Company Arrangement dated 25 March 2026 (DOCA) would see their interests as creditors extinguished such that they would have no claims against FT Sydney in the enforcement of the debts they claim. They commenced proceedings seeking relief, including an order that the DOCA be terminated or varied on several grounds, including that it was entered into for an improper purpose and ultimately that their interests as creditors have been unfairly prejudiced. In aid of their claims for final relief, the Plaintiffs seek injunctions to enjoin the defendants from giving effect to the DOCA until the hearing and determination of this proceeding or, alternatively, interim orders seeking to vary the DOCA to forestall the effectuation of the DOCA until the final determination of their claims. They have indicated that they do not give an undertaking as to damages. It is proposed that two further plaintiffs be joined to the proceedings as the 23rd and 24th Plaintiffs, which is not opposed.

3 The other application that belatedly came before me was one made by Merricks Capital Pty Ltd, MC P&H Pty Ltd (ACN 664 068 964) in its capacity as trustee for MC P&H Fund, and MC PH II Pty Ltd (ACN 692 220 812) as trustee for MC PH II Fund (collectively, the Merricks SPVs) for a stay of the applications brought by the Plaintiffs and restraining them from further pressing those applications. The basis of that application are instruments styled as irrevocable undertakings that were entered into between all but two of the Plaintiffs, FT Sydney as purchaser, and the sixth defendant (Mr Milligan) as guarantor (the Undertakings or the Irrevocable Undertakings). I explain below the background and terms to these instruments, but for present introductory purposes, the point is that by those instruments, the relevant Deferred Vendors agreed not only to subordinate their debts and security to (in effect) the Merricks SPVs, but also agreed that they would not seek to take any step in relation to the recovery of the debts owed to them until the Merricks SPVs had been paid. The Merricks SPVs contend that by bringing an action to terminate the DOCA or to vary it, the Plaintiffs have taken action in relation to the recovery of the debts owed to them in breach of the Undertakings. In relation to two proposed Plaintiffs (the proposed 23rd and 24th Plaintiffs), the Merricks SPVs contend that the same conclusion is to be reached by reference to the terms of a Subordination Deed entered into by them. As a result, they claim that the proceedings should be stayed and the Plaintiffs enjoined from further prosecuting them.

4 In the result, I have concluded that both the Merricks SPVs’ application for a stay and prayers 5 and 6 of the Plaintiffs’ applications for interlocutory and interim relief should be dismissed.

5 As the Merricks SPVs’ application for a stay preceded the determination of the application for interlocutory relief, I address those two issues in that order. Before doing so, it is necessary to set out some background facts relevant to the determination of these issues.

6 It goes without saying that I have prepared these reasons with as much expedition as possible and what follows is the best I have been able to do in the time available to set out the essential factual and legal foundation for my reasoning. I should also note that the final hearing of these proceedings is due to commence on Monday, 29 June 2026, before SC Derrington J, and is listed for 3 days.

2. RELEVANT FACTS

7 Much of the facts that follow were drawn from the Administrator’s report to creditors (Creditor’s Report) and facts that were not in dispute for the purpose of the interlocutory applications before me (including from the parties’ various written submissions).

8 There is a present development of property at a site located at Pitt Street and Hunter Street in Sydney (Development Site), comprising 74 amalgamated property titles (the Properties). The Properties are presently owned by FT Sydney and are subject to an approved development application for a high-rise hybrid commercial tower known as the Halo Project. The Development Site formerly consisted of a number of commercial buildings and the Properties were previously owned by a number of persons and entities (primarily in the nature of interests in strata title).

9 From sometime in or about 2018, Mr Milligan, FT Sydney and companies related to FT Sydney (the FT Companies) set about to acquire the 74 separate titles relating to the Properties. Mr Milligan’s original strategy was to consolidate the Properties, obtain initial planning approval for the purpose of the Halo Project by which it is proposed to build a 55-storey timber hybrid commercial tower on the Development Site. Mr Milligan’s original strategy was to sell the Development Site and the rights in the development to another developer or bring in a development partner.

10 Mr Milligan and FT Sydney had been successful in acquiring all the relevant titles in the Properties, and had obtained primary development approval in respect of the Development Site and the Halo Project (though some aspects of the approval remain to be adjusted).

11 Under the respective acquisition terms relating to the sale of the Properties, most of the lot holders’ consideration was payable in two parts:

(a) an upfront payment at settlement (which was typically 80%-90% of the total acquisition price); and

(b) a deferred component (which was typically 10-20% of the total acquisition price) under which the lot holder received an interest rate of 15% of the deferred component and were granted security by way of second ranking mortgages over the respective Properties that had been owned by the respective lot holders. These security interests were managed through units in a trust arranged through the Mezzanine Secured Creditors.

12 The acquisitions were intended to be funded primarily through secured debt facilities provided by the Senior Secured Creditors, who were the Merricks SPVs. The funding provided by the Merricks SPVs was procured through a syndicate of lenders. It appears that these acquisitions were to be funded by the Merricks SPVs through a Senior Secured Debt Facility of $392.4 million, Second Secured Ranking Creditor arrangements of $31 million with the Mezzanine Secured Creditors, a form of vendor finance through Deferred Vendor arrangements in total of $54.3 million and related party debts of $77.4 million.

13 However, the property transactions did not complete in December 2022. FT Sydney was not able to settle in full the upfront settlement payment obligations that were due in December 2022. This led to further unsecured Deferred Vendor obligations, including an agreed interest component of 10%, which were documented in the “Irrevocable undertakings to pay” (referred to above and below as the Undertakings or the Irrevocable Undertakings). As referred to above, and expanded upon below, pursuant to these Undertakings, payment of the Deferred Debt owing to the Deferred Vendors is not due until after the Senior Secured Creditors’ debt is repaid or satisfied in full. The claims of these Deferred Vendors were fully subordinated to those of the Senior Secured Creditors.

14 It is common ground for the purpose of the present applications that, over time, higher interest rates and increases in construction and other development costs adversely affected the feasibility of the Halo Project and increased the amount of capital required to proceed. The FT Companies engaged in an investor process between July and October 2024 in order to obtain funding from a development partner or other sources which did not result in any proposals capable of being progressed to completion.

15 From December 2024, Mr Milligan approached other prospective investors regarding either a sale of the Properties or an investment in the Halo Project. This led to an indicative, non-binding arrangement being signed with Cbus Property C2 Pty Ltd (ACN 688 295 874) (Cbus Property) in March 2025, which contemplated Cbus Property acquiring a 50% interest in the Properties and participating in the Halo Project (the Cbus Property Transaction). Following this development, the Senior Secured Creditors provided additional funding of $27.7 million to progress development approvals and early works to support the Halo Project. Part of these works related to demolition and construction planning.

16 On 4 September 2025, FT Sydney entered into a binding contract to sell Cbus Property a 50% interest in the Properties, subject to conditions (the Cbus Contract). The relevant terms of the Cbus Contract included those which were confidential and which I was satisfied should be the subject of suppression and non-publication orders. Those relevant terms include the following:

(a) the DOCA must be effectuated for the Cbus Contract to be able to complete;

(b) the definitions of default events excludes the FT Companies being placed into voluntary administration or entering into a DOCA, but includes them being placed into liquidation;

(c) the discharge and release of the Mezzanine Security held by the Mezzanine Secured Creditors is necessary for providing “Clear Title” to the Sale Interest, being the 50% interest being acquired by Cbus Property; and

(d) Cbus Property will pay a confidential purchase price, along with a performance fee depending on certain conditions being satisfied, and will fund in part or in whole the development costs of the Halo Project.

17 The Plaintiffs contend that it is significant that the Cbus Contract was entered into some 7 months before the formal administration process specifically contemplated a DOCA similar to that which the defendants have sought to achieve through the DOCA.

18 Meanwhile, sometime before February 2025, Mr Milligan and/or the FT Companies engaged Mr Marcus Ayres (Mr Ayres) of Arcis Advisory Pty Ltd (Arcis), an insolvency advisory firm. Representatives of Arcis and representatives of KPMG started meeting at about that time, some 14 months before the formal administration process was commenced and before FT Sydney entered into the Cbus Property Transaction.

19 From at least February 2026, McGrathNicol, the insolvency adviser of the Merricks SPVs, had telephone calls with KPMG and the first and second defendants (Administrators). During the period from 28 February 2025 to 1 April 2026, there were 30 telephone calls and meetings involving Mr Ayres, McGrathNicol, KPMG and the Administrators.

20 On 1 April 2026, the FT Companies resolved to appoint the Administrators as voluntary administrators of the FT Companies (Resolutions). As explained below, the Plaintiffs contend that, at the time of the Resolutions, Mr Milligan did not genuinely believe, or could not reasonably have believed, that the FT Companies were insolvent, or likely to become insolvent. The reason for this is that it is claimed that:

(a) the Senior Secured Creditors were supporting the FT Companies, and intended to support the FT Companies to complete the Cbus Contract;

(b) following completion of the Cbus Contract, additional financial support was available from Cbus Property; and

(c) the Senior Secured Creditors intended to continue to support the FT Companies for the purpose of facilitating a sale of the remaining 50% interest in the Property (Remaining 50%). It was said that this was consistent with the view expressed by the Administrators that the FT Companies were not insolvent at the time of the voluntary administration, and would be solvent after the administration.

21 On 1 April 2026, the Administrators were appointed as joint and several Administrators of the Companies by Mr Milligan, as sole director of the FT Companies. The stated reason for the appointment was said to be the “unsustainable capital structure and inability to consensually recapitalise the Companies in advance of settling the Cbus Property Transaction”. It appears that this was a reference to the debt obligations owed to the Mezzanine Secured Creditors and the Deferred Vendors (including the debt obligations subject to the Mezzanine Secured Creditors’ security interests) which have continued to increase as a result of capital interest. Further, it appears that by inability to consensually recapitalise the FT Companies in advance of settling the Cbus Property Transaction, it seems that a consensual resolution of all debt obligations was unable to be achieved as the FT Companies did not have access to alternative assets or funding to extinguish these claims. In the absence of the FT Companies being recapitalised, Mr Milligan determined there was a risk that the Cbus Property Transaction would be at risk. The Plaintiffs contended that the link between extinguishing the Plaintiffs’ claims and completing the Cbus Contract was not explained in the Creditor’s Report, and has not been explained since.

22 The Senior Secured Creditors (ie the Merricks SPVs) supported the Administrators through the administration through the Administrators’ Funding Deed. This allowed the Administrators to support the operations of FT Sydney and the progression of the Halo Project.

23 The Plaintiffs contended that the Administrators accepted that the FT Companies were placed into administration by Mr Milligan for the purposes of Mr Milligan proposing a DOCA, as such a course was consistent with the terms of the Cbus Property Transaction. It was submitted that the Administrators were aware that Mr Milligan had intended to prepare a DOCA proposal from the commencement of the administration.

24 On 20 April 2026, the DOCA proposal was received from Mr Milligan. No other DOCA proposal and/or offers for the business and assets were received during the administration. The effect of Mr Milligan’s DOCA proposal, if ultimately effectuated, is that the Plaintiffs are estimated to receive only 0.72c in the dollar. The Plaintiffs contended that this is such a small amount that the practical and commercial effect of the proposal was that the Plaintiffs’ claims would be extinguished for effectively nil consideration.

25 The Administrators formed the view that they considered a formal sale process during the administration but determined that a sale was unlikely to deliver a better outcome than progressing the Cbus Property Transaction. The Administrators formed the view that entry into the DOCA was a better outcome for creditors than a liquidation in the absence of any other proposal. The Administrators noted that a DOCA had been proposed to them by Mr Milligan. The Administrators estimated that the dividends payable to each class of creditor under the proposed DOCA and liquidation scenarios were as follows:

26 The Administrators recommended that the DOCA proposal be accepted by the creditors. The basis for the recommendation was that the DOCA provides a better return to creditors than a liquidation of the FT Companies, and preserves the Cbus Property Transaction and the FT Companies’ ability to continue their existence in line with the objectives of Part 5.3A of the Corporations Act 2001 (Cth) (Corporations Act). The Plaintiffs contended that the FT Companies were never going to be placed into liquidation. The result was pre-determined.

27 On 12 May 2026, at the second meeting of creditors, a resolution was passed that the FT Companies enter into a DOCA as proposed by Mr Milligan. The resolution was passed by the casting vote of the chairperson (being one of the Administrators) in circumstances where:

(a) only 3 creditors voted in favour of the resolution, being the Senior Secured Creditors, the Mezzanine Secured Creditors (voting at the direction of the Senior Secured Creditors) and the beneficiary of a guarantee provided in respect of a loan to a related entity of the FT Companies (which was admitted for $1 only); and

(b) 20 creditors voted against the resolution.

28 The DOCA was executed on 25 May 2026. The relevant terms of the DOCA are as follows:

(a) the “DOCA Contribution” is $1,000,000;

(b) Mr Milligan had procured that the Senior Agent (essentially being the Merricks SPVs parties) consented to $1,000,000 being paid as a “DOCA Contribution” to the Administrators;

(c) the FT Companies are to be treated as one entity, and claims are to be pooled;

(d) completion of the DOCA is made subject to various conditions precedent being fulfilled before 12 June 2026 including that:

(i) the Mezzanine Secured Creditors have provided a full discharge and release of the Mezzanine Security (or relevant court orders have been made);

(ii) the Administrators have received written confirmation from the Senior Agent that the Senior Secured Creditors have consented to completion; and

(iii) if applicable, the Administrators have received a consent to act as a director of each company from each nominee director;

(e) completion will occur no later than two business days following the Administrators confirming in writing that each of the conditions precedent have been satisfied, with the implementation steps set out being effected thereafter;

(f) implementation steps include the following, which are to take place simultaneously and as close in time to each other as possible:

(i) the creditors’ trust deed to be released and take effect;

(ii) payment to the Administrators, and payment and transfer of the “DOCA Contribution” to be administered under the creditors’ trust;

(iii) release of the Mezzanine Security to take effect;

(iv) release of compromised claims;

(v) any appointment documents for any nominee director to come into effect; and

(vi) Administrators to certify that the DOCA has been effectuated;

(g) the Administrators retain day-to-day management and control of each company until the “Termination Date” (being the date that the DOCA is effectuated or terminated in accordance with its terms);

(h) the Administrators must consent to their appointment as trustees of the creditors’ trust and take steps in accordance with the trust deed to ascertain, establish and administer that trust for the benefit of trust creditors;

(i) the “Related Creditors” are not permitted to participate in the distribution of funds from the creditors’ trust;

(j) the Mezzanine Security is to be released and discharged in full at or prior to completion including for the purposes of facilitating settlement and as required under the Cbus Contract;

(k) each Mezzanine Secured Creditor:

(i) remains bound by and must comply with the Intercreditor Deed;

(ii) must not enforce, realise or otherwise deal with the Mezzanine Security;

(iii) is entitled to make a claim against the trust fund as a trust creditor in an amount equal to that creditor’s released claim; and

(iv) all compromised claims are to be forever released, discharged and extinguished and upon all compromised claims being released, each creditor who had a compromised claim is entitled to make a claim against the trust equal in amount to that creditor’s released compromised claim; and

(l) in the event that the deed terminates other than on effectuation, any part of the DOCA contribution must be paid to the Project Account.

29 On 29 May 2026, the Plaintiffs commenced these proceedings. The Plaintiffs have since filed an Amended Originating Process and a Points of Claim. The Amended Originating Process contains the following prayers for relief:

Interlocutory relief

1. Pursuant to r 1.39 of the Federal Court Rules 2011, an order that the time for service of this Originating Application and supporting affidavit be abridged.

2. Pursuant to r 10.24 of the Federal Court Rules 2011, service be effected on:

(a) the first, second, third, fourth and fifth defendants by email to Megan.Lowe@ashurst.com, jacqueline.chan@ashurt.com, and Michael.sloan@ashurst.com; and

(b) the sixth defendant by email to james@milligangroup.com.au and admin@milligangroup.com.au.

3. An order that the matter be listed before the Commercial & Corporations Duty Judge at a time convenient to the Court for initial case management.

4. An order that the notice to produce issued to the First, Second, Third, Fourth and Fifth Defendants be returnable before the Commercial & Corporations Duty Judge at the initial case management hearing.

5. Such further or other interlocutory relief as the Court thinks fit.

Final relief

5A. A declaration pursuant to s 447C of the Corporations Act that the appointment of the First Defendant and Second Defendant as administrators of the Third, Fourth and Fifth Defendants was invalid, void and of no effect.

6. An order pursuant to ss 445D and/or 447A of the Corporations Act, alternatively s 90-15 of the Insolvency Practice Schedule (Corporations) (being Sch 2 to the Corporations Act) (IPS), that the deed of company arrangement entered into by the Defendants and dated 25 May 2026 (DOCA) be terminated from the date it was executed or alternatively from a date the Court considers appropriate.

7. An order pursuant to ss 75-42 and/or 90-15 of the IPS, that each of the resolutions of creditors on 12 May 2026 that the Third, Fourth and Fifth Defendants execute a deed of company arrangement be set aside.

8. An order pursuant to s 447A of the Corporations Act, alternatively s 90-15 of the IPS, that the administration of the Third, Fourth and Fifth Defendants be brought to an end.

9. In the alternative to 6 to 8, an order pursuant to s 447A of the Corporations Act, alternatively 90-15 of the IPS, that the DOCA be amended such that the claims of each of the Deferred Vendors (as defined in the Voluntary Administrators Report in respect of each of the Third, Fourth and Fifth Defendants dated 4 May 2026) are not released.

10. A declaration that the Vendor Deferred Payment (as defined in the Irrevocable Undertakings to Pay between the Plaintiffs, the Fourth Defendant and the Sixth Defendant) payable to each Plaintiff by the Fourth Defendant is secured by an equitable lien over the land sold by that Plaintiff to the Fourth Defendant.

11. A declaration that the DOCA does not bind each Plaintiff so far as concerns the equitable lien securing payment of the Vendor Deferred Payment.

12. Costs.

13. Such further or other orders as the Court thinks fit.

30 The Plaintiffs advance the following claims.

31 The Plaintiffs contend that the voluntary administration was invalid and of no effect because Mr Milligan did not form a bona fide view that the FT Companies were insolvent. In those circumstances, the Court may make declarations under s 447C of the Corporations Act invalidating the administration. The Plaintiffs contend that their claim is consistent with the view expressed by the Administrators.

32 The Plaintiffs next contend that, on the assumption that the administration was valid, the DOCA is liable to be set aside (or that the creditors’ resolution that the FT Companies enter into the DOCA is liable to be set aside). Alternatively, the Plaintiffs claim that the DOCA ought to be varied so that it does not release the claims of the Mezzanine Secured Creditors or the Deferred Vendors. The Plaintiffs contend that the DOCA was entered into for an improper purpose in that the predominant purpose of the DOCA was to strip the FT Companies of unwanted debts and was therefore an abuse of Part 5.3A of the Corporations Act.

33 The Plaintiffs also raise additional contentions which would justify setting aside the DOCA (or the creditors’ resolution) either alone or together with other factors, including that;

(a) the DOCA could not be effectuated without injustice, and the extinguishment of the Plaintiffs’ claims would be unfairly prejudicial or discriminatory; and

(b) the material provided by the Administrators contained material misstatements and omissions (as identified in the Points of Claim at [52]-[71]).

34 The Plaintiffs contended that, in circumstances where the claims of the Mezzanine Secured Creditors and the Deferred Vendors are to be extinguished for de minimis consideration, and the extinguishment of those claims does not appear necessary for FT Sydney to complete the Cbus Contract or to sell the Remaining 50%, their claims are strong ones.

35 Finally, the Plaintiffs raise a claim that they are to be correctly characterised as secured creditors of FT Sydney because they each hold an equitable lien or purchaser’s lien over the Property (or a portion of the Property) to secure repayment of the deferred component of the consideration payable to them by FT Sydney in respect of its purchase of the land. The Plaintiffs say that the effect of the Plaintiffs being characterised as secured creditors is that, by reason of s 444D(2) of the Corporations Act, the DOCA does not bind them so far as concerns the lien securing payment to each Deferred Vendor.

36 Relevantly, s 444D of the Corporations Act provides that:

444D Effect of deed on creditors

(1) A deed of company arrangement binds all creditors of the company, so far as concerns claims arising on or before the day specified in the deed under paragraph 444A(4)(i).

(2) Subsection (1) does not prevent a secured creditor from realising or otherwise dealing with the security interest, except so far as:

(a) the deed so provides in relation to a secured creditor who voted in favour of the resolution of creditors because of which the company executed the deed; or

(b) the Court orders under subsection 444F(2).

…

37 In essence, the Plaintiffs claim that as they have an equitable lien, they are secured creditors who did not vote in favour of the DOCA and therefore are not bound by it in relation to their respective security interests.

3. THE MERRICKS SPVS’ APPLICATION FOR A STAY

38 The Merricks SPVs’ application turns upon the application and operation of the Irrevocable Undertakings and the Subordination Deed, with the latter applicable to the proposed new Plaintiffs.

39 I was taken to one example of the Irrevocable Undertakings, which was on materially similar terms to those entered into by each of the other Plaintiffs who had entered into that instrument. The parties to the Irrevocable Undertaking are each relevant Deferred Vendor, referred to as the Vendor in the document, FT Sydney, who is referred to as Purchaser, and Mr Milligan who is referred to as the Guarantor. The introductory terms of the Irrevocable Undertaking (as set out in Clause 1, Background) identify that the Purchaser has exchanged a “Contract for Sale” with the Vendor in relation to the relevant property in question and that the Purchaser has entered into or will enter into a senior syndicated subscription agreement with the Senior Creditor (which is essentially the Merricks SPVs) and others in connection with the financing of the acquisition of the Property. Clauses 1(c) and (d) provide as follows:

(c) In consideration of the Purchaser entering into this document and agreeing to pay the Vendor the Deferred Payment (as defined below) in accordance with this document, the Vendor has agreed to a reduction in the amount payable to the Vendor at settlement of the Contract, as follows:

I. Settlement sum Deferral of $875,883.00

II. Deferral of Delay Interest calculated to the 15th March 2023 of $242,122.00

(d) In lieu of the amount referred to in paragraph 1(c) that would otherwise be payable under the Contract, following the discharge of the registered first mortgage to be granted by the Purchaser in connection with the Senior Facility Agreement (Senior Mortgage), the Vendor will be entitled to:

I. a deferred payment from the Purchaser in the amount of $1,118,005.00 (Deferred Amount); and

II. interest on the Deferred Amount calculated from 15th March 2023 until the date that the Deferred Amount is paid at the rate of 10% p.a [capitalised monthly] (Deferred Interest)

(the Deferred Amount and Deferred Interest together being the Deferred Payment)

40 What is apparent from the above clauses is that an agreement was entered into to defer payment of a portion of the purchase price, the capitalisation of interest that had accrued up until 15 March 2023, and an entitlement to interest on the deferred amount into the future.

41 The critical operative provisions of the Irrevocable Undertaking are as follows:

2. Operative provisions

(a) Subject to paragraph 2(d) below, the Purchaser must pay the Deferred Payment to the Vendor on or before the date that is 24 months after the date of 22 February settlement under the Contract.

(b) The Purchaser undertakes to pay the Deferred Payment directly to the Vendor (to the account instructed by the Vendor to the Purchaser in writing) from any excess sale proceeds arising from a sale of the Property (whether alone or whether with any other property) to which the Purchaser is entitled after sufficient amounts have been received to fully discharge the Senior Mortgage. It is intended that such payment will be made as a settlement adjustment from the proceeds the Purchaser is directly entitled to from any sale, and prior to the Purchaser receiving any funds.

(c) The Purchaser has irrevocably instructed the Senior Creditor to pay the Deferred Payment directly to the Vendor from such excess proceeds of sale, on the terms of the direction attached to this document.

(d) The Vendor acknowledges and agrees that:

I. notwithstanding anything in this document or the Contract, the Deferred Payment is fully subordinated to all amounts secured by the Senior Mortgage, and is not payable or otherwise capable of satisfaction until the Senior Mortgage has been discharged;

II. until the Senior Mortgage has been discharged, the Vendor must not receive payment of, or take any action or exercise any power against the Purchaser, the Guarantor or any other person in relation to recovery of, the Deferred Payment or any related amount, or otherwise do anything which results in such amounts not being fully subordinated to amounts secured by the Senior Mortgage, including by taking any step to:

* demand payment of all or part of such amount;

* have an administrator appointed to the Purchaser or the Guarantor;

* have the Purchaser or the Guarantor wound up or made bankrupt, or to prove in the winding up or bankruptcy of a Purchaser or the Guarantor; or

* sue or seek to obtain judgment against the Purchaser or the Guarantor;

III. this document does not provide the Vendor with any proprietary right, security interest or caveatable interest in respect of the Property or any other real property;

IV. any funds received by the Vendor in breach of this clause will be held on trust for the Senior Creditor;

V. the Senior Creditor or any other relevant party may exercise their powers under or in connection with the Senior Facility Agreement and the Senior Mortgage as they see fit;

VI. the Vendor must not interfere with any enforcement action taken under or in connection with the Senior Facility Agreement or the Senior Mortgage. If such enforcement action involves the sale of the shares or units in the Purchaser, at the time of disposal the Senior Creditor is irrevocably authorised to release the Purchaser from its obligations to pay all or any part of the Deferred Payment to the extent required to ensure that all amounts secured by the Senior Mortgage can be recovered from such enforcement action (and for valuable consideration the Vendor severally irrevocably appoints the Senior Creditor as its attorney to do anything required to give effect to such release), provided however that (unless contrary to law) any amounts recovered from such enforcement action are otherwise paid in accordance with this document as if they were proceeds realised from a sale of the Property; and VII. this document operates as a deed poll for the benefit of the Senior Creditor and each other party to the Senior Facility Agreement and the Senior Mortgage, and may be enforced by any such party notwithstanding they are not party to this document.

(e) The Guarantor unconditionally and irrevocably guarantees the payment of the Deferred Payment to the Vendor in accordance with this document (Guaranteed Obligation). Any release of all or part of the Purchaser’s obligations to pay the Deferred Payment under paragraph 2(d)VI does not release the Guarantor from its obligations under this guarantee.

(Emphasis added.)

42 It was common ground that by a “Deed Poll”, the Merricks SPVs had the benefit of the terms of the Irrevocable Undertakings and could seek to enforce those terms.

43 The Merricks SPVs advanced three contentions in support of their application for a stay in respect of those Plaintiffs who were parties to the Irrevocable Undertakings.

44 First, it was contended that the relevant Plaintiffs were acting in breach of cl 2(d)(II) of the Irrevocable Undertakings because, by commencing the present proceedings, they had, at a point in time before the Senior Mortgage held by the Senior Creditor was discharged, taken an action or exercised a power against FT Sydney, Mr Milligan, or another person in relation to recovery of the Deferred Payment. The Merricks SPVs submitted that the entire purpose of the proceedings brought by the relevant Plaintiffs was to prevent the extinguishment of their debts, and to keep alive the prospect of the recovery of their debts.

45 Senior Counsel for the Merricks SPVs accepted that there was no evidence that the relevant Plaintiffs had taken any action to seek recovery of the Deferred Debts. However, Senior Counsel for the Merricks SPVs submitted that the sole purpose of the commencement of the present proceedings was a necessary anterior step to recovery of those Debts as it sought the preservation of those Debts for the purpose of recovery.

46 Second, the Merricks SPVs contended that by commencing the present proceedings, the relevant Plaintiffs had taken a step to have the Purchaser (FT Sydney) wound up, as that would be the inevitable consequence if the DOCA were set aside. It was said that this was in breach of cl 2(d)(II) of the Undertakings.

47 Third, the Merricks SPVs contended that the relevant Plaintiffs were acting in breach of cl 2(d)(VI) of the Irrevocable Undertaking because, by seeking to set aside the DOCA which had been supported by the Senior Secured Creditors as a means of enforcing their security to facilitate the restructure and recapitalisation solution constituted by the DOCA and the Cbus Property Transaction, they are interfering with any enforcement action taken in connection with the “Senior Facility Agreement” (essentially, the facility agreements with the Merricks SPVs).

48 I reject these contentions.

49 The Merricks SPVs’ first contention assumes the premise that by bringing the present proceedings, the relevant Plaintiffs have taken an action “in relation to” the recovery of the Deferred Debt. I do not accept that premise.

50 By the present proceedings, as the Merricks SPVs conceded, the relevant Plaintiffs have not taken any step to recover the Deferred Debts. Rather, the proceedings are properly to be characterised as ones where they seek to maintain the existence of those Debts (that is, their preservation) in the face of an instrument that seeks to extinguish those Debts. In my view, that is not an action that is “in relation to” the recovery of the Deferred Debts. No claim has been made for payment of the Deferred Debts presently or in the future. Nor has any claim been made for payment or recovery at a point anterior to the discharge of the Senior Mortgage.

51 By seeking to maintain or preserve the existence of the Deferred Debts, the relevant Plaintiffs are doing no more than that which is manifest from the express terms of the Irrevocable Undertakings. They are owed money. They have taken a step to ensure that this position is maintained.

52 Whilst I accept the words “in relation to” are of broad import, they are to be read in context, having regard to the purpose of the instrument as a whole: eg see Insurance Australia Ltd t/as CGU Insurance v Capral Ltd [2025] FCAFC 46; 309 FCR 385 at [253] (Shariff J). In my view, the objective purpose to be divined from cl 2(d)(II) of the Irrevocable Undertakings, by reference to the whole of the terms of that instrument is that the parties intended the relevant Plaintiffs as Purchasers would not take any action to seek payment of the Deferred Debt, or take any action as to its recovery, or take any action in relation to its recovery until the Senior Mortgage had been discharged. The relevant Plaintiffs are not taking any such action.

53 Nor do I accept the Merricks SPVs’ second contention that the present proceedings are to be characterised as ones whereby the relevant Plaintiffs have otherwise sought to do something that results in the Deferred Debts not being fully subordinated to the amounts secured by the Senior Mortgage. Nothing in these proceedings seeks to secure that result. It seeks to do no more than preserve the existence of the Deferred Debts in the face of the extinguishment of those Debts. That does not alter the fact that the Deferred Debts will remain subordinated to the amounts secured by the Senior Mortgage.

54 I also do not accept that a liquidation of the FT Companies is the result that the Plaintiffs are seeking from bringing of the present proceedings. What the relevant Plaintiffs seek is termination of the DOCA for the purpose of securing a variation to the DOCA or a new DOCA to maintain the existence of the Deferred Debts. I do not accept on the evidence before me that a liquidation of the FT Companies is the result that they are seeking. The liquidation of the FT Companies may arise and, if it does, that will be a result of further discussions or steps taken following the termination of the DOCA or its variation, and much will depend on the position of a number of parties.

55 Finally, I do not accept the central premise of the Merricks SPVs’ third contention that the relevant Plaintiffs have sought to interfere with an enforcement action taken under or in connection with the Senior Facility Agreement. The evidence is that the Merricks SPVs had issued a notice of default on the FT Companies in December 2025. That gave rise to a potential entitlement for the appointment of a receiver and/or other steps that could be taken to enforce the Senior Facility Agreement or the Senior Mortgage. However, that is not what has transpired. Here, there is a DOCA that was proposed by Mr Milligan, which was supported by the Merricks SPVs and the Administrators. The DOCA does not constitute an enforcement action taken under or in connection with the enforcement of the Senior Facility Agreement or Mortgage.

56 Accordingly, I reject the Merricks SPVs’ application for a stay.

57 In relation to two of the new proposed Plaintiffs, the Merricks SPVs relied upon the terms of a Subordination Deed to which those relevant Plaintiffs are a party (again, on materially similar terms). Relevantly, the Merricks SPVs relied upon cl 3.4(c) of the Subordination Deeds, which provide as follows:

3.4 Competing claims

Until the end of the Subordination Period, unless the prior written consent of the Senior Agent is obtained, each Subordinated Creditor is not entitled (in respect of any of the Subordinated Debt) to:

(a) be subrogated to a Senior Creditor or any other Enforcing Party;

(b) claim or receive the benefit of:

(i) any document or deed of which a Senior Creditor has the benefit;

(ii) any money held by a Senior Creditor; or

(iii) any Power of a Senior Creditor or any other Enforcing Party;

(c) make a claim or exercise a right, power or remedy (including under any agreement relating to Subordinated Debt) against a Debtor except as otherwise permitted by this document;

(d) exercise or attempt to exercise any right of set-off against, nor realise any Security Interest from, a Debtor; or

(e) raise any defence or counterclaim in reduction or discharge of any obligation owed by it to a Debtor.

(Emphasis added.)

58 Although the clauses are expressed differently, it is clear that each of the subclauses of clause 3.4 seek to regulate the conduct of the “Subordinated Creditor” in respect of any of the “Subordinated Debt”. For the same reasons as those outlined above, I do not accept that by commencing these proceedings, the relevant proposed Plaintiffs have made a claim or exercised a right or power “in respect of any of the Subordinated Debt”.

59 Accordingly, the Merricks SPVs’ application for a stay fails. It is next necessary to turn to the Plaintiffs’ applications for interlocutory relief.

4. THE PLAINTIFFS’ APPLICATIONS FOR INTERLOCUTORY AND INTERIM RELIEF

60 The two critical questions that arise in the grant of interlocutory relief are:

(a) first, whether the applicant has established that there is a serious question to be tried or a prima facie case, and, in this regard, it suffices to show a sufficient likelihood of success at trial if the evidence remains as it is: Beecham Group Ltd v Bristol Laboratories Pty Ltd [1968] HCA 1; 118 CLR 618 at 622–623 (Kitto, Taylor, Menzies and Owen JJ), as explained by Gummow and Hayne JJ in Australian Broadcasting Corporation v O’Neill [2006] HCA 46; 227 CLR 57 at [65] (Gleeson CJ and Crennan J agreeing with this explanation at [19]); Castlemaine Tooheys Ltd v South Australia [1986] HCA 58; 161 CLR 148 at 153 (Mason ACJ); Australian Broadcasting Corporation v Lenah Game Meats Pty Ltd [2001] HCA 63; 208 CLR 199 at [13] (Gleeson CJ); Samsung Electronics Co Ltd v Apple Inc [2011] FCAFC 156; 217 FCR 238 at [52]–[74] (Dowsett, Foster, Yates JJ); and

(b) second, whether the balance of convenience favours the granting of the injunction, which involves consideration of matters including, among other things, whether the relief will change the status quo, the potential harm that will be caused, whether damages are an adequate remedy, and whether there is any disentitling conduct: Samsung Electronics at [52]–[74].

61 In relation to the first enquiry, a prima facie case does not require the Court to conclude that the Plaintiffs will probably succeed. It requires a sufficient likelihood of success, assessed with the nature of the rights and the practical consequences of grant or refusal, to justify preserving the position until trial or further order: O'Neill at [65], [70]-[72].

62 As to the second inquiry, the Court must balance the inconvenience to the defendant of the grant of the injunction with the inconvenience to the plaintiff of a denial of the grant of an injunction: Samsung Electronics at [62]-[63] (Dowsett, Foster and Yates JJ). Any prejudice and hardship likely to be suffered by third persons if an injunction is granted may also weigh in the balance against the grant of an injunction: Samsung Electronics at [66]; Patrick Stevedores Operations No 2 Pty Ltd v Maritime Union of Australia [1998] HCA 30; 195 CLR 1 at [65]-[66].

63 The two inquiries should not be conducted in isolation from each other. The apparent strength of the parties’ substantive cases will often be an important consideration to be weighed in the balance: Samsung Electronics at [67].

64 The usual practice of courts is to require an undertaking as to damages as a condition of interlocutory relief: see Gibbs J in Air Express Limited v Ansett Transport Industries (Operations) Pty Ltd (1981) 146 CLR 249 at 311-312. It will be necessary to return to this issue below.

4.1 Prima facie case or serious question

65 As set out above, the relief claimed by the Plaintiffs is set out in the Amended Originating Process and the nature of their claims are set out in their Points of Claim. The Plaintiffs submitted that their claims have very good prospects of success so as to establish a prima facie case.

66 The first claim made by the Plaintiffs is that the Resolutions and the voluntary administration were invalid and of no effect, such that they are void ab initio. The Plaintiffs seek a declaration to this effect under s 447C of the Corporations Act invalidating the administration. The basis upon which the Plaintiffs seek this relief is that they contend that there were no grounds upon which Mr Milligan believed, at the time of the Resolutions, that the FT Companies were insolvent or that he could not have had reasonable grounds for such a belief. The essence of the Plaintiffs’ contentions relied upon the following general thread of argument:

(a) at the time of the Resolutions, the FT Companies were being funded by the Merricks SPVs and were able to meet their debts as and when they fell due on a cashflow basis;

(b) the Cbus Contract was to be imminently settled and eventually completed, which would result in a significant cashflow injection from the purchase price specified in that Contract;

(c) further, the Cbus Contract made provision for the funding of ongoing development costs in part or in whole;

(d) additional funding and support would be provided by the Merricks SPVs and also the potential sale of the Remaining 50% interest in the Properties; and

(e) the FT Companies stood to also benefit from a performance fee if certain conditions in the Cbus Contract were satisfied, which would provide further substantial cash injections.

67 The Plaintiffs further contended that the Administrators had formed the same view in that at page 6 of the Creditor’s Report, the Administrators stated as follows:

Based on the Administrators’ investigations, the Companies were solvent on a cashflow basis (being the primary test) up to the date of administration, as they had access to facilities from the Senior Secured Creditors to fund ongoing trading costs. On a balance sheet basis, there is an argument that the Companies may have been insolvent from as early as 30 June 2024, given that the Companies’ liabilities may have exceeded the value of their assets.

68 The opposing parties contended that there was no prima facie case established or, alternatively, that it was a weak case. The opposing parties submitted that the Plaintiffs’ case would have to impugn Mr Milligan’s subjective state of mind and there was no evidence to do so. In addition, the opposing parties submitted that Mr Milligan’s state of mind and/or the objective circumstances had to be informed by the following facts:

(a) the Merricks SPVs had issued notices of default to the FT Companies in December 2025 and there was a threshold enforcement action being taken under the relevant loan facilities;

(b) the debt owing to the Merricks SPVs alone was in excess of $600 million; and

(c) the Cbus Contract was conditional upon the FT Companies entering into a DOCA, such that any funding to be secured from Cbus Property was contingent on this circumstance.

69 At this stage I am not required to determine whether the claim will be successful. I have no evidence at this stage from Mr Milligan. The success of the claim will undoubtedly depend upon the evidence that Mr Milligan gives, an assessment of the views expressed by the Administrators as recorded above, and an examination of the objective circumstances. I am not prepared at this stage to conclude that the Plaintiffs have no prima facie case in this respect. Nor am I able to conclude that such a claim is weak. However, I am also not of the view that the claim is a strong one as contended for by the Plaintiffs, having regard to the objective circumstances. That is because, at least at this stage, there is evidence that the FT Companies were almost entirely reliant upon the Merricks SPVs for funding, which (as explained further below) would eventually run out, and those parties had already issued a notice of default. Doing the best I can, I would assess the prospects of the Plaintiffs succeeding in this cause of action as being greater than weak but less than moderate.

70 However, my assessment of the strength of this aspect of the Plaintiffs’ claims does not weigh heavily on the grant of the interlocutory relief sought by the Plaintiffs. That is because it was common ground between the parties that this aspect of the Plaintiffs’ claims would be able to be maintained irrespective of whether the DOCA is effectuated. That is a matter to which I will return in weighing the balance of convenience.

71 The second claim made by the Plaintiffs is for relief pursuant to s 445D and/or 447A of the Corporations Act, or alternatively s 90-15 of the Insolvency Practice Schedule (Corporations) (IPS), being Schedule 2 to the Corporations Act, that the DOCA be terminated from the date it was executed or alternatively from a date the Court considers appropriate. Additionally, the Plaintiffs seek orders pursuant to ss 75-42 and/or 90-15 of the IPS, that each of the resolutions of the creditors on 12 May 2026 as to the execution of the DOCA be set aside and/or an order pursuant to s 447A of the Corporations Act, or alternatively s 90-15 of the IPS, that the Administration be brought to an end. Alternatively, the Plaintiffs seek orders pursuant to s 447A or s 90-15 of the IPS that the DOCA be amended such that the claims of each of the Deferred Vendors are not released.

72 In support of these claims, the Plaintiffs contended that:

(a) the DOCA was entered into for an improper purpose in that the predominant purpose of the DOCA was to strip the FT Companies of unwanted debts and was therefore an abuse of Part 5.3A of the Corporations Act;

(b) the DOCA could not be effectuated without injustice, and the extinguishment of the Plaintiffs’ claims would be unfairly prejudicial or discriminatory;

(c) the material provided by the Administrators contained material misstatements and omissions (as identified in the Points of Claim at [52]-[71]); and

(d) in circumstances where the Administrators made a casting vote, the power under s 75-42 of the IPS was enlivened, as well as s 447A of the Corporations Act and the general powers under s 90-15 of the IPS.

73 The various threads of the Plaintiffs’ contentions in support of these matters are as follows:

(a) it could be inferred that the purpose for placing the FT Companies into administration and entering into the DOCA was to strip FT Sydney of the debts owing to the Deferred Vendors and to extinguish their rights given:

(i) the extensive involvement of Mr Milligan, Mr Ayres (the restructuring and insolvency advisor for the FT Companies), KPMG (being the entity in which the Administrators are partners or officers), the Merricks SPVs and McGrathNicol (the restructuring and insolvency advisors for the Merricks SPVs);

(ii) the Cbus Contract was entered into in September 2025 in circumstances where a condition precedent to it was that the FT Companies enter into a DOCA and that FT Sydney deliver “Clear Title” in respect of the interests being sold to Cbus Property;

(iii) under the Intercreditor Deed, the Mezzanine Secured Creditors could be directed and were to act at the direction of the FT Companies or the Merricks SPVs, including in relation to removal of their security interests over the Properties, which is what transpired;

(iv) the DOCA proposed by Mr Milligan had clearly been prepared by the solicitors acting for the Merricks SPVs; and

(v) the terms of the DOCA were specifically crafted to extinguish in their entirety the interests held by and the debts owing to the Mezzanine Secured Creditors and the Deferred Vendors;

(b) it could be inferred there was no sensible, commercial, rational or other reason to extinguish the interests held by and/or debts owing to the Mezzanine Secured Creditors and the Deferred Vendors in circumstances where the Merricks SPVs were continuing to provide support and funding to the FT Companies, where further cash injections would come about from the payment of the purchase price under the Cbus Contract, where the costs of the development would be funded by Cbus Property and/or the Merricks SPVs, where the Cbus Contract was not due to complete until the Sunset Date of 30 September 2026, and where, under the Irrevocable Undertakings, the Deferred Vendors were not due to be paid until the mortgage(s) held by or on behalf of the Merricks SPVs are discharged;

(c) further inferences consistent with (a) and (b) above could be drawn from the fact that the Administrators had indicated in the Creditor’s Report that the Merricks SPVs were continuing to support the development and were not insolvent on a cashflow basis;

(d) Cbus Property itself had not insisted on the extinguishment of the interests held by and debts owing to the Mezzanine Secured Creditors and the Deferred Vendors and there was no provision to this effect in the Cbus Contract;

(e) the Mezzanine Secured Creditors and the Deferred Vendors had been treated differently and prejudicially to other creditors, and this was an instance of injustice and discrimination, with the inferred objective being to do no more than strip the FT Companies of all debts owing to the Mezzanine Secured Creditors and the Deferred Vendors;

(f) these inferences could be further supported by the fact that the opposing parties, and particularly the Administrators, had failed to accede to those parts of the present application and/or an open offer that had been made by the Plaintiffs to vary the DOCA so as to preserve the rights of the Deferred Vendors whilst extinguishing the security interests held by them and the Mezzanine Secured Creditors, or to accede to the proposal made by the Plaintiffs that the Administrators approach the Court to seek judicial advice or direction under cl 8.9 of the DOCA or under s 90-15 of the IPS.

74 In further support of the above contentions, the Plaintiffs contended that there had been a belated step taken by the opposing parties to enter into a “Deed of Confirmation and Acknowledgement – related creditors” whereby the related party creditors would also forego their rights and have their claims extinguished, when the DOCA had preserved those rights and treated them differently to the Deferred Vendors and the Mezzanine Secured Creditors.

75 The Plaintiffs contended that it is not the legitimate purpose of a DOCA to simply strip a company of the debts owing to a creditor or a specific class of creditor. In support of this contention, the Plaintiffs relied on the objects of Part 5.3A as specified in s 435A of the Corporations Act, which provides as follows:

435A Object of Part

The object of this Part, and Schedule 2 to the extent that it relates to this Part, is to provide for the business, property and affairs of an insolvent company to be administered in a way that:

(a) maximises the chances of the company, or as much as possible of its business, continuing in existence; or

(b) if it is not possible for the company or its business to continue in existence—results in a better return for the company’s creditors and members than would result from an immediate winding up of the company.

Note: Schedule 2 contains additional rules about companies under external administration.

76 In this respect, the Plaintiffs rely upon Project Sea Dragon Pty Ltd v Canstruct Pty Ltd [2024] FCAFC 141; 305 FCR 465 where Jackman J (O’Callaghan and McElwaine JJ agreeing) said as follows at [84]:

The primary judge then reiterated the conclusion that the DOCA was entered into for the purpose of the Seafarms Group relieving itself of the debt owed by PSD and to continue with the Project as if that debt were never incurred: [182]. The primary judge said that the avoidance of an unwanted indebtedness is not an appropriate purpose for a DOCA, and that no aspect of Pt 5.3A is designed to permit a company to use the DOCA process to rid itself of a liability, merely to restart operations in an almost identical position to the pre-DOCA state save for the existence of the erstwhile debt: [183]. The DOCA in the present case was thus entered into to achieve a purpose which was alien to the objects of Pt 5.3A, which is more than sufficient to warrant setting aside both the administration and the DOCA: [183]. The primary judge said that that conclusion necessarily involves an acceptance of the commercial reality that PSD acted as part of the Seafarms Group, and the purpose of the voluntary administration and DOCA process should be regarded in that light: [184]. That is, the Seafarms Group, or at least SFG and PSD, acted in concert with the intention to orchestrate PSD’s claimed insolvency from February 2023 in order to utilise the voluntary administration and DOCA process to extinguish Canstruct’s debt, and then continue PSD’s business as before: [184]. The primary judge rejected the submission that PSD had to be considered on its own and be regarded as a company which had lost the support of its parent, such that the DOCA was the only option apart from liquidation: [185]. I note that in expressing those conclusions, the primary judge relied only on the first of the alleged improper purposes, namely the purpose of avoiding the debt owed to Canstruct, and not the second alleged improper purpose, namely avoiding scrutiny into possible insolvent trading.

77 Again, the opposing parties contended that no prima facie case had been established or, alternatively, the case is weak. The opposing parties variously contended as follows:

(a) there is nothing novel or improper about parties engaging with reconstruction or insolvency advisors in advance of a company being placed into voluntary administration or a DOCA being proposed;

(b) nor is there anything novel or improper in the eventual administrators being involved in the giving of such advice;

(c) nor is there anything novel in a major secured creditor owed in excess of $600 million being involved in discussions with a borrower, and reconstruction and insolvency advisors in advance of companies being placed into voluntary administration and entry into a DOCA, or in being involved in the formulation of a DOCA to be proposed by a director of a company;

(d) the ongoing support being provided by the Merricks SPVs had already reached its limits, which is corroborated by the fact that a notice of default had been issued in December 2025 and enforcement action had been at least placed on the cards;

(e) given the balance sheet considerations and the fact that Cbus Property would be funding part or all of the development costs, it is unsurprising that Cbus Property had insisted on a condition precedent to its acquisition of 50% of the interest that the company enter into a DOCA and that it receive “Clear Title” of the interest it was acquiring;

(f) the commercial reality by reference to the balance sheet of the FT Companies in view of the enormous debt owed to the FT Companies was that the alternative to the DOCA was liquidation, which was a matter that the Administrators had directly addressed in a Creditor’s Report, and was an alternative that the Deferred Vendors themselves had accepted as being the only alternative to the DOCA as no other proposals had been tabled at the second creditors’ meeting. The alleged ongoing support being provided by the Merricks SPVs was contrary to the evidence before the Court which established that:

(i) the funding provided to the Administrators’ fund would expire on Friday, 12 June 2026;

(ii) the Merricks SPVs’ loan facilities had been fully drawn down and would run out in mid-July 2026; and

(iii) the Merricks SPVs were not prepared to provide any further funding and the unchallenged evidence is that they had taken a view that the FT Companies would need to find funding from another source;

(g) the Deferred Vendors were not treated differentially or discriminately to any other unsecured creditors in their position. It was always intended that the related party creditors would have their debts and rights extinguished as was made clear in the Creditor’s Report, with the DOCA containing an error, which has now been rectified – this was not a belated change of intention, but the correction of an error;

(h) the “Continuing Creditors” (being the ongoing contractors and consultants involved in the demolition, excavation and construction work at the Development Site) were treated differently because they are necessary for the ongoing development of the Development Site as they consist of demolition and excavation contractors, project consultants and the like;

(i) the Plaintiffs’ contentions belied the drastic change in economic circumstances in that the Properties were acquired for approximately $375 million in total, when the value of real estate in the central Sydney CBD was at its height pre-COVID, but subsequently the economic conditions deteriorated with increasing interest rates and capital costs, as well as construction costs;

(j) it was obvious that the FT Companies had struggled to find a development partner, investor or other lender;

(k) the Deferred Vendors entered into the Irrevocable Undertakings and the Subordinated Deeds knowing full well that there was a risk that they would not be paid until the Merricks SPVs were paid and subject to the project being successful;

(l) the fact that the Merricks SPVs had engaged with McGrathNicol indicated that, consistent with the quantum of the debts owing to them, they were actively considering enforcement;

(m) logical, reasonable, commercial, rational reasons existed for the extinguishment of the debts and interests held by the Deferred Vendors and the Mezzanine Secured Creditors, being that it maximised the security owed to the Merricks SPVs, who are by far the greatest creditor, and it further maximised the prospect of the sale of the Remaining 50% or the sale of the shares in the FT Companies over which the Merricks SPVs held security; and

(n) further to the last point, the “cleansing of the balance sheet” for the purposes of a prospective sale was a legitimate purpose for the entry into a DOCA.

78 Met with these contentions, the Plaintiffs submitted that none of these submissions answered the point as to why there was a necessity to extinguish the Deferred Vendors’ debts in circumstances where they clearly will not get paid until the Merricks SPVs get paid. Further, the Plaintiffs latched onto the submission made by Senior Counsel for the Merricks SPVs that at least one purpose for treating the Deferred Vendors differently was to “cleanse the balance sheet” which they submitted was antithetical to the objects of Part 5.3A and the statements made in Project Sea Dragon.

79 There are aspects of the Plaintiffs’ contentions that I regard as having some reasonable prospects of success. Given that the payment of the debts to the Deferred Vendors would be subsidiary to the debts owing to other parties holding security interests in the Properties and FT Companies, it does appear that the reasons for the extinguishment of their debts requires closer interrogation at a final trial than can be conducted at an interlocutory hearing. That is not to say that I accept that these claims will succeed. There are countervailing factors. For example, the Deferred Vendors are not the only parties to have their debts extinguished. The related party creditors are in the same position. It is understandable that the Merricks SPVs were treated differently because of the security interests held and the quantum of the debts owing to them. It is also understandable that the Continuing Creditors were treated differently given that their ongoing cooperation is necessary for the continuing works to be performed at the Development Site.

80 I do not accept that the Plaintiffs have no prima facie case in respect of these claims. However, I cannot say that they are strong claims. That is because, as the opposing parties pointed out, as a matter of fact, the Deferred Vendors were not treated differently to other creditors in a similar position. There are features of the present arrangement that make it potentially distinguishable from the facts of Project Sea Dragon. In that case, there was a single creditor whose debts were extinguished by the exercise of control by a parent/holding company in the face of that creditor having secured a successful arbitrated outcome against the subsidiary entity that had entered into a DOCA. The facts here are that the Deferred Vendors are not the only ones to have their debts extinguished and the facts are also that there is a substantial creditor owed over $650 million who could readily have exercised its enforcement rights to either liquidate the company or to appoint a receiver, where the Administrators regarded liquidation as the only other viable option in the absence of any other DOCA proposal being submitted.

81 The provisions of the IPS relied upon by the Plaintiffs do not change my assessment of the prospects of success of the Plaintiffs’ claims. They require the exercise of discretion on the part of the Court to terminate or vary a DOCA, which necessarily entails similar considerations to those which I have addressed.

82 As a result, I do not regard this aspect of the Plaintiffs’ claims to be especially strong, as contended for by the Plaintiffs. However, I am not prepared to conclude that they are weak. Again, I regard them as being something greater than weak but less than moderate.

83 Finally, the Plaintiffs raise a claim that they are to be correctly characterised as secured creditors of FT Sydney because they each hold an equitable or purchaser’s lien over the Properties or a portion of the Properties. The Plaintiffs say that the effect of the Plaintiffs being characterised as secured creditors is that, by reason of s 444D(2) of the Corporations Act, the DOCA does not bind them so far as concerns the lien securing payment to each Deferred Vendor.

84 The Plaintiffs’ prospects of success in such an action would need to address cl 2(d)(III) of the Irrevocable Undertakings, which provides that the instrument does not provide the Vendors with any proprietary right, security interest or caveatable interest in respect of the Properties or any other real property. There is a live question as to whether that clause displaces any interest held under the original sale contracts, which do not appear to have otherwise been varied by the Irrevocable Undertakings. I do not accept that there is no prima facie case or that it is weak. However, it does not matter much as all the parties accepted that this aspect of the Plaintiffs’ claims would be unaffected by the refusal of interlocutory relief.

4.2 Balance of convenience and discretionary factors

85 It is next necessary to address the factors going to the balance of convenience and related discretionary factors.

86 At this stage, all but one of the conditions precedent to the effectuation of the DOCA have been satisfied. The sole remaining condition to be satisfied requires the Merricks SPVs parties to provide written confirmation to the Administrators as to certain matters, as provided for in cl 4.1(f) of the DOCA. At the close of the hearing before me, Senior Counsel for the Merricks SPVs gave an undertaking that this would not occur before 4:00 pm on Friday, 12 June 2026.

87 In assessing the balance of convenience, it is necessary to consider the prejudice that would be occasioned to the parties if the interlocutory and interim relief claimed is granted or not granted. This requires an assessment as to the effect on the Plaintiffs should the DOCA be effectuated against the consequence for other persons should there be a delay in effectuation of the DOCA.

88 The Plaintiffs submitted that the consequences for them if the DOCA is effectuated are immediate and severe. They submitted that if the DOCA is effectuated, their claims “against FT Sydney will be released and replaced with a right to claim against the creditors trust for the purpose of recovering a de minimis amount”. Additionally, they claimed that as the final relief claimed by the Plaintiffs is that the Administrators were not validly appointed, and, alternatively, that the DOCA be varied or set aside, that relief could be rendered largely nugatory if the DOCA were to be effectuated in the interim.

89 During the course of the hearing, it was largely common ground that if the DOCA is effectuated, the Plaintiffs’ claims and prayers for relief relying upon ss 445D and 447A of the Corporations Act (and the associated provisions of the IPS) seeking a termination or variation of the DOCA would be rendered inutile and unable to be maintained. The one qualification to this area of commonality was whether the power under s 447A of the Corporations Act could be exercised to terminate a DOCA or vary it even after it had been effectuated. Senior Counsel for Mr Milligan properly drew attention to authorities as to the breadth of the power under s 447A (eg Australasian Memory Pty Ltd v Brien [2000] HCA 30; 200 CLR 270 at [26] (Gleeson CJ, McHugh, Gummow, Hayne and Callinan JJ) and at least one authority where the Court had stated that this power could be exercised even after a DOCA had been terminated: QBI Corporation Pty Ltd v Plantation Rise Pty Ltd [2010] QSC 102; 77 ACSR 573 at [46] (Wilson J). However, there are several authorities that are contrary to QBI Corporation: see Parkview Constructions Pty Ltd v Tayeh [2009] NSWSC 186; 71 ACSR 65 at [55]-[72] (Barrett J); and Frisken (Trustee) v E K Recruitment Pty Ltd (in liq), in the matter of E K Recruitment Pty Ltd (in liq) [2026] FCA 223 at [89] (Jackman J).

90 For present purposes, I have proceeded on the weight of the authorities as reflected in the decisions in Parkview and Frisken. Based on these authorities, it follows that if the DOCA is effectuated, the Plaintiffs will lose their right to seek a termination or variation of the DOCA pursuant to ss 445D and 447A of the Corporations Act and the associated provisions of the IPS.

91 I am satisfied that if the DOCA is effectuated, there will be a significant prejudice to the Plaintiffs. The Plaintiffs will be deprived of their right to invoke statutory provisions to seek particular remedies which will not be available to them. It also must be recognised that the Plaintiffs seek to preserve the subject matter of a cause of action that they have validly commenced before the Court. Both the deprivation of a litigant’s right to pursue a cause of action and the need to ensure the preservation of the subject matter of that cause of action are matters that have weighed heavily on me. I accept that the prejudice to the Plaintiffs in this respect is substantial and I reject the contentions to the contrary made by the opposing parties.

92 However, as the opposing parties pointed out, the Plaintiffs have other claims or causes of action that they are pressing and the subject matter before the Court remains unaffected in these respects. Senior Counsel for the Plaintiffs accepted that if the DOCA is effectuated, the Plaintiffs have other claims before the Court that will remain unaffected. That includes the declaration claimed in prayer 1 of the Amended Originating Process (as to the administration and the appointment of the Administrators being invalid and of no effect) and prayers 10 and 11 (which seek declarations to the effect that the Plaintiffs have a vendor’s lien, being an equitable lien over the Properties sold to FT Sydney). The latter of these claims is significant if it is ultimately successful. As noted above, if the claim is established, s 444D(2) of the Corporations Act has the effect that the DOCA would not bind the Plaintiffs in respect of such an equitable lien.

93 Further, as explored during the course of oral submissions, though the proceedings have been litigated with haste to date, with some pause for consideration, the Plaintiffs may have other causes of action against one or more of the defendants or others. As noted above, a substantial part of the Points of Claim relies upon assertions as to false and misleading statements being made, and conduct as between the various defendants intended to deprive them of their rights. None of this need be further explored, but the point to be made is that the Plaintiffs are not left without right or remedy in respect of a contravention of one or other statutory norm, or under a common law or equitable cause.

94 Senior Counsel for the Merricks SPVs further contended that this is a case where damages would be an adequate remedy. By way of example, Senior Counsel submitted that if the Plaintiffs succeeded in establishing that the administration or the appointment of the Administrators was of no effect, they would be entitled to make a claim for damages for the loss of an opportunity to have the Deferred Debts paid. Senior Counsel further submitted that such a loss of opportunity case could be pursued via alternative causes of action, if that is what the Plaintiffs wished to do.