Federal Court of Australia

Australian Securities and Investments Commission v Keystone Asset Management Limited (receivers and managers appointed) (in liquidation) (No 5) [2026] FCA 729

File numbers: | VID 536 of 2024 VID 710 of 2025 |

Judgment of: | MOSHINSKY J |

Date of judgment: | 4 June 2026 |

Catchwords: | CORPORATIONS – examination proceeding – where liquidators sought a direction under s 597(9) of the Corporations Act 2001 (Cth) that an examinee produce certain bank statements – where the examinee contended that the application for the direction was an abuse of process – direction made |

Legislation: | Corporations Act 2001 (Cth), ss 9, 86, 53, 596A, 597 |

Cases cited: | Hearne v Street [2008] HCA 36; 235 CLR 125 Re Equititrust Ltd (in liq) (No 3) [2017] FCA 1074 Tomlinson v Ramsey Food Processing Pty Ltd [2015] HCA 28; 256 CLR 507 Walton v ACN 004 410 833 Ltd (formerly Arrium Ltd) (in liq) [2022] HCA 3; 275 CLR 508 |

Division: | General Division |

Registry: | Victoria |

National Practice Area: | Commercial and Corporations |

Sub-area: | Corporations and Corporate Insolvency |

Number of paragraphs: | 51 |

Date of hearing: | 30 April 2026 and 4 June 2026 |

Counsel for the Plaintiff in VID 536 of 2024: | The Plaintiff did not appear |

Counsel for the Liquidators of Keystone: | Dr O Bigos KC with Ms VE Bell |

Solicitor for the Liquidators of Keystone: | Norton Rose Fulbright Australia |

Counsel for Mr Paul Chiodo: | Mr A Segal with Mr MF James (on 30 April 2026); |

Solicitor for Mr Paul Chiodo: | Velocity Legal |

ORDERS

VID 536 of 2024 | ||

| ||

BETWEEN: | AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff | |

AND: | KEYSTONE ASSET MANAGEMENT LIMITED (RECEIVERS AND MANAGERS APPOINED) (IN LIQUIDATION) (ACN 612 443 008) First Defendant PAUL ANTHONY CHIODO Second Defendant | |

order made by: | MOSHINSKY J |

DATE OF ORDER: | 4 JUNE 2026 |

THE COURT ORDERS THAT:

1. Nothing in the second set of orders made on 17 February 2026 (stay orders) prevents the operation of the orders made today in Proceeding VID 710 of 2025.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ORDERS

VID 710 of 2025 | ||

BETWEEN: | KEYSTONE ASSET MANAGEMENT LIMITED (RECEIVERS AND MANAGERS APPOINED) (IN LIQUIDATION) (ACN 612 443 008) Plaintiff | |

AND: | PAUL ANTHONY CHIODO Defendant | |

order made by: | MOSHINSKY J |

DATE OF ORDER: | 4 june 2026 |

THE COURT NOTES THAT:

Mr Paul Chiodo has given an undertaking to pursue any application for leave to appeal and any appeal from these orders expeditiously.

THE COURT ORDERS AND DIRECTS THAT:

1. The further examination of Mr Paul Chiodo be listed on a date to be fixed before a Registrar (for the purpose of production of documents pursuant to these orders).

2. Pursuant to s 597(9) of the Corporations Act 2001 (Cth), Mr Chiodo produce at his examination the books in his possession as set out in the Annexure to this order, other than documents that are in his possession solely by reason of Mr Chiodo (or his representatives) uplifting, inspecting or copying documents produced in response to subpoenas issued on or about 16 December 2025 to three banks in Proceeding VID536/2024.

3. Paragraphs 1 and 2 of these orders be stayed:

(a) until 4.00 pm on 12 June 2026; and

(b) if Mr Chiodo files an application for leave to appeal from these orders by 4.00 pm on 12 June 2026, until the determination of the application for leave to appeal and any appeal.

2. Costs be reserved.

3. There be liberty to apply.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

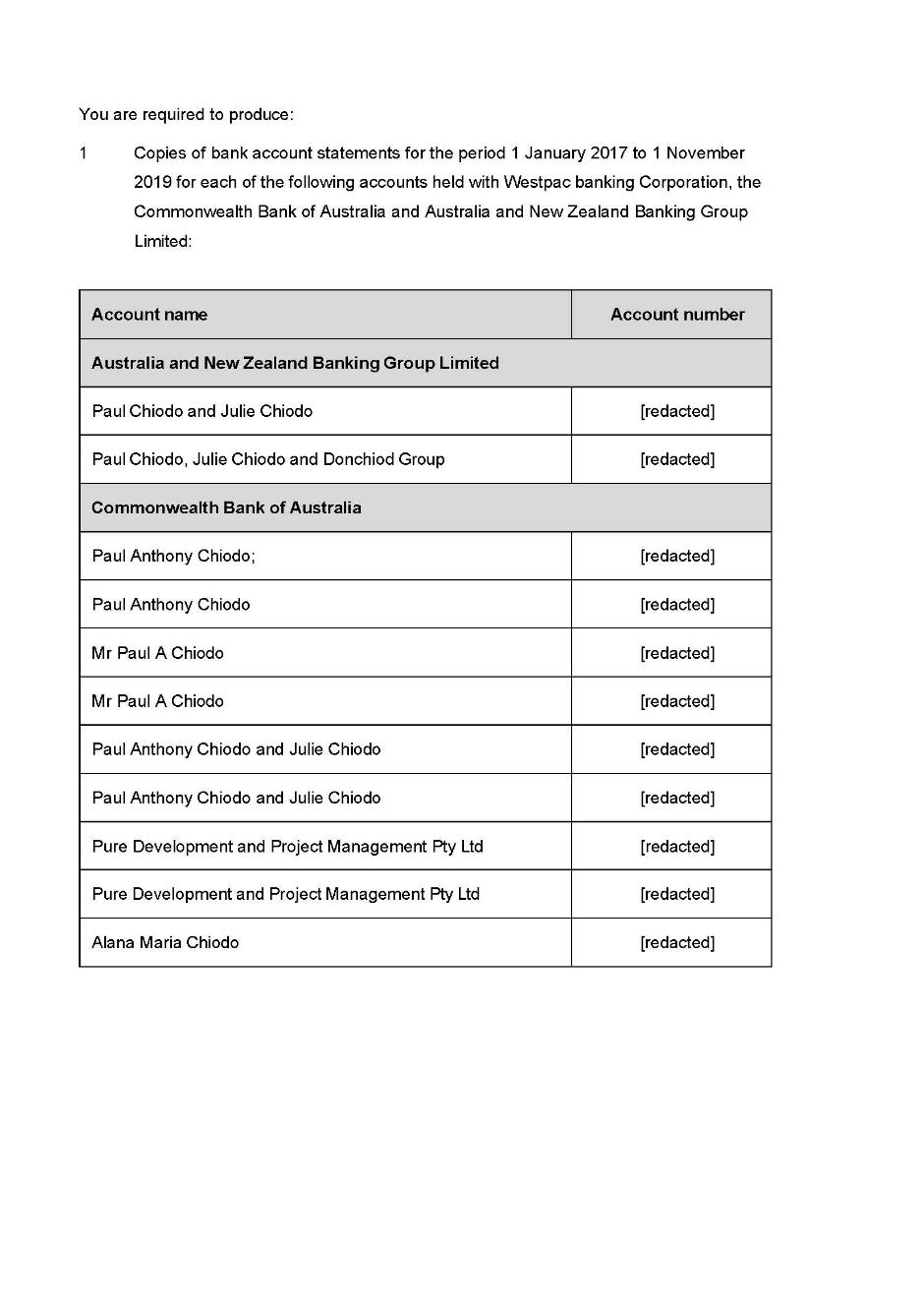

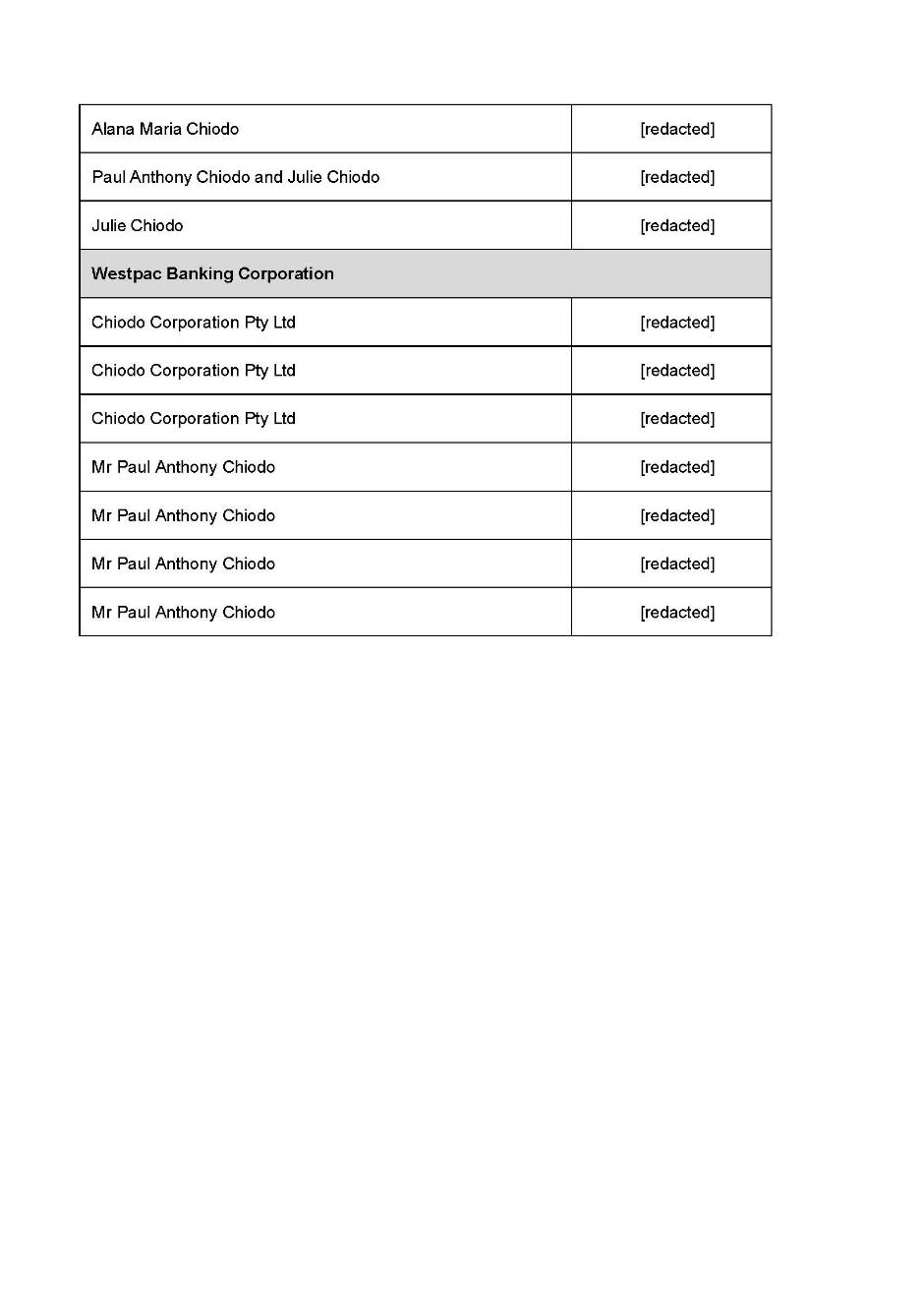

ANNEXURE |

|

REASONS FOR JUDGMENT

MOSHINSKY J:

Introduction

1 Mr Jason Tracy and Mr Glen Kanevsky (the Liquidators), in their capacity as the liquidators of Keystone Asset Management Limited (receivers and managers appointed) (in liquidation) (Keystone) have made an informal application for:

(a) in proceeding VID 710 of 2025 (the Examination Proceeding), a direction under s 597(9) of the Corporations Act 2001 (Cth) for the production by Mr Paul Chiodo of bank statements for certain accounts of Mr Chiodo and his associates for the period 1 January 2017 to 1 November 2019 (the Relevant Period); and

(b) in proceeding VID 536 of 2024 (the ASIC v Keystone Proceeding), an ancillary order,

(together, the Section 597 Application).

2 The Section 597 Application was the subject of a hearing on 30 April 2026. However, the hearing could not be completed on that occasion as one of Mr Chiodo’s contentions (relating to the expression “examinable affairs”) had been raised only a short time before the hearing and the Liquidators had not had a sufficient opportunity to respond. The further hearing of the Section 597 Application was adjourned to 2 June 2026 and orders were made for the filing of additional material by the parties. The hearing on 2 June 2026 was adjourned to 4 June 2026 due to an issue that arose in relation to the obligation discussed in Hearne v Street [2008] HCA 36; 235 CLR 125 (commonly referred to as the “implied undertaking”).

3 In support of the Section 597 Application, the Liquidators rely on an affidavit of Mr Tracy affirmed on 18 May 2026 (the Tracy Affidavit) and outlines of submissions dated 27 April 2026 and 18 May 2026.

4 In opposition to the application, Mr Chiodo relies on outlines of submissions dated 28 April 2026 and 3 June 2026.

5 It is common ground that the documents sought in the Section 597 Application are the same as the bank statements that were the subject of three subpoenas issued to three banks on or about 16 December 2025 in the ASIC v Keystone Proceeding (the Subpoenas). Mr Chiodo made an application to set aside the Subpoenas. On 16 February 2026, the Court dismissed the application to set aside the Subpoenas: Australian Securities and Investments Commission v Keystone Asset Management Ltd (receivers and managers appointed) (in liquidation) (No 4) [2026] FCA 89 (the Subpoena Judgment). Mr Chiodo has applied for leave to appeal from the Subpoena Judgment. That application has not yet been heard.

6 In that procedural context, Mr Chiodo contends that making the orders sought by the Liquidators would bring the administration of justice into disrepute. In other words, he contends that the Section 597 Application is an abuse of process.

7 Mr Chiodo also contends that (subject to one exception) the documents sought by the Liquidators are not related to the “examinable affairs” of Keystone.

The Section 597 Application

8 The orders sought by the Liquidators are annexed to their submissions dated 27 April 2026. In the Examination Proceeding, the Liquidators seek an order that:

Pursuant to section 597(9) of the Corporations Act 2001 (Cth), Mr Chiodo produce at his examination, the books in his control as set out in the schedule to this order.

9 In the course of submissions, senior counsel for the Liquidators adjusted the form of order sought to refer to “possession” rather than “control”, as “possession” is the word used in s 597(9).

10 Section 597(9) provides:

The Court may direct a person to produce, at an examination of that or any other person, books that are in the first-mentioned person’s possession and are relevant to matters to which the examination relates or will relate.

11 The word “possession” is defined in s 86 of the Corporations Act as follows:

A thing that is in a person’s custody or under a person’s control is in the person’s possession.

12 In the ASIC v Keystone Proceeding, the Liquidators seek an ancillary order as follows:

Nothing in the second set of orders made on 17 February 2026 (stay orders) prevents the operation of the orders made this day in proceeding VID 710/2025.

The abuse of process issue

Background and context

13 On or about 16 December 2025, in the ASIC v Keystone Proceeding, the Subpoenas were issued at the request of Keystone to the Australia and New Zealand Banking Group, the Commonwealth Bank of Australia and Westpac Banking Corporation.

14 The documents sought in the Subpoenas were subsequently produced by the banks.

15 On 23 January 2026, Mr Chiodo filed and served an objection letter on Keystone, objecting to the inspection of certain bank statements produced in response to the Subpoenas (the Set Aside Application).

16 On 16 February 2026, the Set Aside Application was dismissed.

17 On 17 February 2026, the Court made an order that the parties have leave to uplift, inspect and copy the documents the subject of the Set Aside Application produced in response to the Subpoenas.

18 On the same day, the Court also made an order that the order for uplift etc be stayed:

(a) until 4.00 pm on 2 March 2026; and

(b) if Mr Chiodo filed an application for leave to appeal from the Subpoena Judgment, until the determination of the application for leave to appeal and any appeal (the Stay Order).

19 Mr Chiodo subsequently filed an application for leave to appeal, which has not yet been heard. It is listed for hearing on 13 July 2026.

The parties’ submissions

20 In that procedural context, Mr Chiodo contends that if the Section 597 Application is granted, the resulting orders would render his application for leave to appeal and any appeal nugatory. He submits that the Liquidators “have proposed a ‘back-door’ method to overcome and sidestep the Stay Order”. Mr Chiodo submits that the direction sought under s 597(9) has both the purpose and the effect of circumventing the Stay Order.

21 Mr Chiodo submits that the Court should not permit the Liquidators to inspect the very same documents that are the subject of the Stay Order by employing another process prior to the determination of the application for leave to appeal and any appeal.

22 Mr Chiodo refers to well-established principles relating to abuse of process, citing Tomlinson v Ramsey Food Processing Pty Ltd [2015] HCA 28; 256 CLR 507 (Tomlinson) at [25] and Walton v ACN 004 410 833 Ltd (formerly Arrium Ltd) (in liq) [2022] HCA 3; 275 CLR 508 (Walton) at [130].

23 Mr Chiodo submits that the direction sought under s 597(9) would be an abuse of process because it would compel production of documents that are presently the subject of the Stay Order, which was made to preserve the integrity of the application for leave to appeal and any appeal.

24 In the course of the hearing today, and in the context of the abuse of process issue, I raised with senior counsel for the Liquidators whether, if I was minded to make a direction under s 597(9), there should be a ‘carve out’ from the direction for documents that are in Mr Chiodo’s possession solely by reason of Mr Chiodo (or his representatives) having uplifted, inspected or copied documents produced in response to Subpoenas. Senior counsel for the Liquidators said that they could “live with” such a carve out, which I took to mean that the Liquidators did not strongly resist such a carve out.

Applicable principles

25 The principles relating to abuse of process have been discussed by the High Court in several recent cases. In Tomlinson, French CJ, Bell, Gageler and Keane JJ stated at [25]-[26]:

25 Abuse of process, which may be invoked in areas in which estoppels also apply, is inherently broader and more flexible than estoppel. Although insusceptible of a formulation which comprises closed categories, abuse of process is capable of application in any circumstances in which the use of a court's procedures would be unjustifiably oppressive to a party or would bring the administration of justice into disrepute. It can for that reason be available to relieve against injustice to a party or impairment to the system of administration of justice which might otherwise be occasioned in circumstances where a party to a subsequent proceeding is not bound by an estoppel.

26 Accordingly, it has been recognised that making a claim or raising an issue which was made or raised and determined in an earlier proceeding, or which ought reasonably to have been made or raised for determination in that earlier proceeding, can constitute an abuse of process even where the earlier proceeding might not have given rise to an estoppel. Similarly, it has been recognised that making such a claim or raising such an issue can constitute an abuse of process where the party seeking to make the claim or to raise the issue in the later proceeding was neither a party to that earlier proceeding, nor the privy of a party to that earlier proceeding, and therefore could not be precluded by an estoppel.

(Footnotes omitted.)

26 In Walton, Gageler J (as his Honour then was) stated at [93]:

“The possible varieties of abuse of process are only limited by human ingenuity and the categories are not closed.” That said, abuses of process “usually fall into one of three categories: (1) the court’s procedures are invoked for an illegitimate purpose; (2) the use of the court’s procedures is unjustifiably oppressive to one of the parties; or (3) the use of the court’s procedures would bring the administration of justice into disrepute”. Those categories can overlap in practice. A pertinent example is where one party invokes a procedure of the court for a purpose unjustifiably oppressive to another. The illegitimacy of the purpose then lies in the unjustifiable oppression. But an invocation of a procedure can be unjustifiably oppressive even if invoked for a legitimate purpose.

(Footnotes omitted.)

See also [130] per Edelman and Steward JJ.

Consideration

27 In my view, the Section 597 Application does not constitute an abuse of process. The application seeks production of the relevant bank statements on a basis which is legally independent of the Subpoenas. In these circumstances, I consider that it is open to the Liquidators to seek production of the documents by way of a direction under s 597(9) even though they initially sought the same documents by way of the issue of the Subpoenas and even though the question whether the Subpoenas should be set aside is the subject of an application for leave to appeal.

28 Further, I am not persuaded that the making of the orders sought by the Liquidators in the present application would be unjustifiably oppressive to Mr Chiodo or would bring the administration of justice into disrepute. This again comes back to the point that a direction under s 597(9) is an independent legal basis to obtain production of documents. If the Liquidators are entitled to production of the documents on this basis, then I do not see why it would bring the administration of justice into disrepute for them to rely on this basis.

29 I accept that, if a direction is made under s 597(9), this may have a practical effect on whether leave to appeal is granted. However, I am not satisfied that any such practical effect would bring the administration of justice into disrepute. The practical effect is merely a consequence of the availability of an independent legal basis to obtain production of the documents.

30 Further, I am not satisfied that the making of the orders sought by the Liquidators would render any appeal from the Subpoena Judgment nugatory. The issue to be determined in any appeal would be whether the Subpoenas should be set aside. That issue is capable of determination regardless of whether the Liquidators have obtained a direction under s 597(9) for production of the same documents.

31 I do not consider that the case falls into the type of cases discussed in Tomlinson at [26] because it would not have been open to the Liquidators to raise an argument based on s 597(9) in the application to set aside the Subpoenas.

32 For these reasons, I reject the abuse of process contention.

The “examinable affairs” issue

33 As noted above, Mr Chiodo contends that (subject to one exception) the documents sought by the Liquidators are not related to the “examinable affairs” of Keystone. The exception is that Mr Chiodo does not press this ground of opposition in relation to the bank account statements of Chiodo Corporation Pty Ltd (Chiodo Corporation) for the account ending x6970.

Applicable provisions

34 Section 596A of the Corporations Act provides that the Court is to summon a person for examination about a corporation’s “examinable affairs” in certain circumstances as there set out.

35 The expression “examinable affairs” is defined in s 9 of the Corporations Act as follows:

“examinable affairs”, in relation to a corporation means:

(a) the promotion, formation, management, administration, restructuring or winding up of the corporation; or

(b) any other affairs of the corporation (including anything that is included in the corporation’s affairs because of section 53); or

(c) the business affairs of any of the following, in so far as those business affairs are, or appear to be, relevant to the corporation or to anything that is included in the corporation’s examinable affairs because of paragraph (a) or (b):

(i) a body corporate that is, or has been, related to the corporation;

(ii) an entity that is, or has been, connected with the corporation.

36 Section 53 of the Corporations Act is also relevant to the meaning of “examinable affairs”. It provides in part:

Meaning of affairs—body corporate other than a CCIV

For the purposes of the definition of examinable affairs in section 9, section 53AA, 232, 233 or 234, paragraph 461(1)(e), section 487, subsection 1307(1) or section 1309, or of a prescribed provision of this Act, the affairs of a body corporate (other than a CCIV) include:

(a) the promotion, formation, membership, control, business, trading, transactions and dealings (whether alone or jointly with any other person or persons and including transactions and dealings as agent, bailee or trustee), property (whether held alone or jointly with any other person or persons and including property held as agent, bailee or trustee), liabilities (including liabilities owed jointly with any other person or persons and liabilities as trustee), profits and other income, receipts, losses, outgoings and expenditure of the body; and

(b) in the case of a body corporate (not being a licensed trustee company or the Public Trustee of a State or Territory) that is a trustee (but without limiting the generality of paragraph (a))—matters concerned with the ascertainment of the identity of the persons who are beneficiaries under the trust, their rights under the trust and any payments that they have received, or are entitled to receive, under the terms of the trust; and

…

(j) where the body has made available interests in a managed investment scheme—any matters concerning the financial or business undertaking, scheme, common enterprise or investment contract to which the interests relate …

37 For the purposes of s 579(9), the Liquidators are not required to establish that the documents sought are relevant “to the potential claim they are investigating”, but rather, “whether, in the terms of s 597(9) of the Corporations Act, the documents are ‘relevant to matters to which the examination relates or will relate’”: Re Equititrust Ltd (in liq) (No 3) [2017] FCA 1074 (Re Equititrust) at [34]. In that regard, the authorities are also clear that the ambit of an examination under Pt 5.9 of the Act is “extremely wide”: Re Equititrust at [34].

The parties’ submissions

38 The Liquidators contend that the bank statements specified in the Schedule to the proposed order are relevant to the “examinable affairs” of Keystone, as the Liquidators wish to investigate each account and determine what funds paid into and out of them may have been sourced from the Chiodo Diversified Property Fund (the CDPF), of which Keystone is the trustee: see the Tracy Affidavit at [66].

39 Mr Chiodo contends that, except in relation to the bank account of Chiodo Corporation ending in x6970, the Liquidators’ material does not provide a sufficient evidentiary basis to establish that the bank account statements relate to the “examinable affairs” of Keystone. In particular, Mr Chiodo submits that Keystone “invites the Court to assume that accounts have received CDPF Funds, without evidence”. Mr Chiodo submits that “[i]t is not sufficient that an account has been shown to receive funds from Chiodo Corporation, or other [Chiodo-related] entities”.

Consideration

40 It is necessary to set out some of the background facts, based on the Tracy Affidavit. As set out in that affidavit:

(a) the CDPF is a trust which was established on 22 August 2016;

(b) the CDPF received substantial amounts of funds from investors;

(c) the original name of the CDPF was the First Guardian Low Density Real Estate Development Fund (the Fund);

(d) the original trustee of the Fund was Falcon Capital Ltd (Falcon);

(e) Mr Chiodo has been a director of Chiodo Corporation at all times since its incorporation on about 18 March 2016;

(f) on or about 18 August 2016, Chiodo Corporation entered into a development agreement with First Guardian Capital Pty Ltd (First Guardian) as representative of the Fund (the Development Agreement); key provisions of the agreement are summarised at [20] of the Tracy Affidavit;

(g) Pure Development & Project Management Pty Ltd (Pure Development) was referred to in the Development Agreement;

(h) Mr Chiodo has been a director of Pure Development at all times since its incorporation;

(i) on or about 10 May 2019, an agreement was entered into between (among others) CF Property Capital Pty Ltd, Falcon and First Guardian (the Funds Management Agreement); key provisions of this agreement are summarised at [24] of the Tracy Affidavit; these included that the Fund would be renamed the “Chiodo Diversified Development Fund” (CDDF); it also provided for the projects relating to certain development vehicles (SPVs) to be held within the CDDF;

(j) CF Property Capital was incorporated on 10 May 2019 and is a related entity of Chiodo Corporation and Mr Chiodo;

(k) on 13 May 2019, a Deed of Variation was executed by Falcon to amend the name of the Fund to the CDDF; despite the name change, the Fund was generally referred to as the Chiodo Diversified Property Fund or CDPF from around this time;

(l) on 11 June 2021, Falcon retired as trustee of the CDPF and was replaced by Keystone;

(m) in early 2022, the Shield Master Fund (SMF) and the Advantage Diversified Property Fund (ADPF) were established;

(n) both the SMF and the ADPF received substantial amounts of funds from investors;

(o) under the SMF, Keystone (as responsible entity) acquired units in the ADPF; and

(p) under the ADPF, Keystone (as trustee) advanced funds to the SPVs.

41 In [34]-[36] of his affidavit, Mr Tracy says that:

34 Based on the above documents and our investigations into Keystone’s examinable affairs so far, it appears that:

(a) both the CDPF and ADPF invested in the same seven projects (identified in paragraph 33 of this affidavit and also referred to in this affidavit as developments), with the CDPF being the beneficial owner of the shares in the SPVs and the ADPF lending money to the SPVs;

(b) Together, the CDPF and the ADPF advanced approximately $385 million to the SPVs. The developments also received significant third party financing, which were often secured by mortgages or other registered security instruments;

(c) Only one project was completed, being the apartments at Red Hill Terraces, Doncaster, known as La Dimora. However, no profit was realised from the La Dimora project and the project remains subject to a loan owed to Keystone as trustee of the ADPF in the amount of $3,691,840 inclusive of interest. The SPV associated with Red Hill Terraces is in receivership, and the shares (which should be beneficially held by the CDPF) have no value;

(d) None of the other projects were completed. Each of the SPVs for those projects has significant debt such that their shares, which should be beneficially held by the CDPF, are likely to be worthless.

35 In light of this, and by reason of the Developer’s Fee only being payable at the end of the project and only in the event of a return of above 8% [being] realised, it appears that Chiodo Corporation was not entitled to payment of any fee in respect of the CDPF. Nevertheless it appears that Chiodo Corporation received substantial amounts, and we wish to investigate this further.

36 Further, it appears that Pure Development may have only been entitled to the project management fee in relation to one of the seven projects, being Red Hill Terrace given the fee was to be calculated on a gross realised value basis. We have also identified invoices issued by Pure Development to the SPVs for “Project Management monthly fee in line with our agreement”. The Development Agreement does not give rise to any entitlement to a monthly fee. Despite this, it appears that Pure Development received substantial amounts, and we wish to investigate this further including to determine whether Keystone and we as liquidators have any proprietary and personal claims against Pure Development.

(Emphasis in original.)

42 In section E of his affidavit (comprising [37]-[65]), Mr Tracy sets out work that has been carried out to trace CDPF funds.

43 In [38] of the affidavit, Mr Tracy identifies outflows from a Falcon account to Chiodo Corporation and to certain SPVs.

44 In [41] of the affidavit, Mr Tracy refers to bank account statements for the SPVs which show transfers during the Relevant Period to Chiodo Corporation, Pure Development and Mr Chiodo. Mr Tracy states at [42]:

A key source (if not the only source) of income of the SPVs during the Relevant Period was CDPF Funds. As such, it appears that the payments made to these entities were made wholly or predominantly using CDPF Funds.

45 In my view, the matters set out above (together with the additional material in relation to Chiodo Corporation at [43]-[48] of the Tracy Affidavit and the additional material in relation to Pure Development at [53]-[56] of the Tracy Affidavit) provide a sufficient basis to conclude that the bank statements sought by the Liquidators for accounts of Chiodo Corporation, Pure Development and Mr Chiodo (whether held by Mr Chiodo alone or together with another or others) relate to the examinable affairs of Keystone. The material set out above provides, in my view, a proper basis to investigate whether funds of the CDPF (of which Keystone is the trustee) made their way (directly or indirectly) into accounts of Chiodo Corporation, Pure Development and Mr Chiodo during the Relevant Period. If funds of the CDPF did make their way (directly or indirectly) into the accounts of Chiodo Corporation, Pure Development and Mr Chiodo during that period, prima facie this involved a misapplication of those trust funds, for the reasons set out in the Tracy Affidavit. For that reason, I am satisfied that there exists a sufficient basis to require the production of those bank statements.

46 The Liquidators seek production of the bank statements for one account of Chiodo Corporation Operations Pty Ltd (Chiodo Corporation Operations). Mr Tracy states at [50] of his affidavit that the Liquidators have identified “claims being made by Chiodo Corporation Operations for GST refunds in respect to costs of the developments incurred”. On the basis of that information, and the provisions of the Funds Management Agreement, Mr Tracy states at [51] that “[i]t appears that Chiodo Corporation Operations received payment of CDPF Funds to which it was not entitled”. While there appears to be a proper basis to contend that if Chiodo Corporation Operations received CDPF funds, it may not have been entitled to those funds, it is not clear to me that there is a sufficient basis to contend that Chiodo Corporation Operations may have received CDPF funds. The one sentence relating to claims for GST refunds appears to be the extent of the evidence on this point. (The evidence in row (f) of the table at [68] of the Tracy Affidavit does not take the matter any further.) Therefore, I am not satisfied on the basis of the present material that there is a sufficient evidentiary basis to require production of the bank statements of Chiodo Corporation Operations for the account ending in x53589.

47 The Liquidators seek production of bank statements for one account in the sole name of Julie Chiodo (ending in x1632). The evidentiary basis for this aspect of the application is at [57]-[61] of the Tracy Affidavit. These paragraphs include that the Liquidators’ investigations to date have identified that ADPF funds were used to pay for renovation costs, property expenses and repaying third party mortgages relating to a property in Julie Chiodo’s name. In my view, this provides a sufficient evidentiary basis to investigate whether ADPF or CDPF funds were paid into her bank account ending in x1632 during the Relevant Period.

48 The Liquidators seek production of bank statements for two bank accounts in the name of a daughter of Paul and Julie Chiodo. The evidentiary basis for this part of the application is at [62]-[65] of the Tracy Affidavit. It appears from this material that payments were made by Pure Development to or for the benefit of the daughter. In circumstances where there is material that suggests that CDPF funds made their way to Pure Development during the Relevant Period (to which it was prima facie not entitled), I consider there to be a proper evidentiary basis to investigate whether any such funds were paid into the two bank accounts of the daughter during the Relevant Period.

49 In summary, I consider that the bank statements sought in the application (other than for the account of Chiodo Corporation Operations) relate to the examinable affairs of Keystone.

Conclusion

50 For these reasons, I will make orders in the Examination Proceeding to the effect that:

(a) The further examination of Mr Chiodo be listed on a date to be fixed before a Registrar (for the purpose of production of documents pursuant to these orders).

(b) Pursuant to s 597(9) of the Corporations Act, Mr Chiodo produce at his examination the books in his possession as set out in the Annexure to the order, other than documents that are in his possession solely by reason of Mr Chiodo (or his representatives) uplifting, inspecting or copying documents produced in response to subpoenas issued on or about 16 December 2025 to three banks in the ASIC v Keystone Proceeding.

51 In the ASIC v Keystone Proceeding, I will make an order that nothing in the second set of orders made on 17 February 2026 (i.e. the Stay Order) prevents the operation of the orders made in the Examination Proceeding.

I certify that the preceding fifty-one (51) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Moshinsky. |

Associate:

Dated: 11 June 2026