Federal Court of Australia

Australian Securities and Investments Commission v Union Standard International Group Pty Ltd (No 5) [2026] FCA 719

File number: | NSD 2064 of 2019 |

Judgment of: | WIGNEY J |

Date of judgment: | 11 June 2026 |

Catchwords: | CORPORATIONS – proceedings by the Australian Securities and Investments Commission (ASIC) against defendants operating financial services businesses involving contracts for difference and margin foreign exchange contracts – where defendants provided personal advice in contravention of s 911A(1) of the Corporations Act 2001 (Cth) – where defendants made false, misleading or deceptive representations or engaged in misleading or deceptive conduct in contravention of ss 12DB and 12DA of the Australian Securities and Investments Commission Act 2001 (Cth) (ASIC Act) – where defendants found to have engaged in systems of conduct or patterns of behaviour in connection with the supply of financial services that was, in all the circumstances, unconscionable pursuant to s 12CB(1) and (4) of the ASIC Act – where defendants engaged in conduct towards individuals that was, in all the circumstances, unconscionable pursuant to s 12CB(1) of the ASIC Act – where a defendant was held to have contravened s 912A(1)(a) of the Corporations Act 2001 (Cth) by failing to do all things necessary to ensure financial services covered by its AFSL were provided efficiently, honestly and fairly CORPORATIONS – declarations and orders sought for contraventions against provisions in the Corporations Act 2001 (Cth) and the Australian Securities and Investments Commission Act 2001 (Cth) – where ASIC sought declaratory and injunctive relief pursuant to ss 1101B(1) and (4) and 1324(1) of the Corporations Act with respect to contravening conduct – where non-party redress orders sought pursuant to ss 12GNB and 12GNC of the ASIC Act – pecuniary penalties sought pursuant to ss 12GBA(1) and 12GBB(3) of the ASIC Act and s 1317G(1) of the Corporations Act – applicable provisions and principles regarding the fixing of pecuniary penalties – where primary objective of pecuniary penalty is deterrence – consideration of relevant factors in determining appropriate pecuniary penalty – declarations and orders made against defendants |

Legislation: | Australian Consumer Law (contained in Schedule 2 to the Competition and Consumer Act 2010 (Cth)) s 21 Australian Securities and Investments Commission Act 2001 (Cth) ss 12CB, 12CB(1), 12CB(4), 12CB(4)(b), 12DA, 12DA(1), 12DB, 12DB(1), 12GBA, 12GBA(1), 12GBA(1)(a), 12GBA(2), 12GBA(3), 12GBA(4), 12GBB, 12GBB(1), 12GBB(3), 12GBB(5), 12GBC, 12GBCA,12GBCA(1)(a), 12GBCA(2), 12GBCA(2)(a), 12GBCA(2)(b), 12GBCA(2)(c), 12GBCA(2)(c)(i), 12GBCA(2)(c)(ii), 12GBCE, 12GD(1), 12GH, 12GH(2), 12GH(2)(a) 12GLB(1), 12GNB, 12GNC, 12GNC(d), 33 Corporations Act 2001 (Cth) ss 761A, 766B(1)(a), 766B(3)(b), 769B, 769B(1), 769B(1)(a), 911A, 911A(1), 911A(5B), 912A, 912A(1)(a), 912A(5A), 916A, 1023D(3), 1101B(1), 1101B(4)(a), 1317E, 1317E(1), 1317E(2), 1317E(3), 1317E(3)(d), 1317G(1), 1317G(1)(a), 1317G(2), 1317G(4), 1317G(4)(a), 1317G(6), 1324(1) Criminal Code (Cth) (s 3 and Schedule to the Criminal Code Act 1995 (Cth)) s 70.2, 70.2(5), 70.2(5)(b) Evidence Act 1995 (Cth) s 79 Federal Court of Australia Act 1976 (Cth) s 21 Income Tax Assessment Act 1936 (Cth), s 160ZK(5) Corporations Regulations 2001 (Cth) reg 7.8.03(6) ASIC Corporations (Product Intervention Order – Contracts for Difference) Instrument 2020/986 (dated 22 October 2020) |

Cases cited: | Attorney-General v Tichy (1982) 30 SASR 84 Australian Building and Construction Commissioner v Pattinson (2022) 274 CLR 450; [2022] HCA 13 Australian Competition and Consumer Commission v Apple Pty Limited [2012] FCA 646 Australian Competition and Consumer Commission v Cornerstone Investment Aust Pty Ltd (in liq) (No 5) [2019] FCA 1544 Australian Competition and Consumer Commission v Employsure Pty Ltd (2023) 407 ALR 302; [2023] FCAFC 5 Australian Competition and Consumer Commission v Ford Motor Company of Australia Ltd (2018) 360 ALR 124; [2018] FCA 703 Australian Competition and Consumer Commission v Get Qualified Australia Pty Ltd (in liquidation) (No 3) [2017] FCA 1018 Australian Competition and Consumer Commission v Leahy Petroleum Pty Ltd (No 3) (2005) 215 ALR 301; [2005] FCA 265 Australian Competition and Consumer Commission v Leahy Petroleum Pty Ltd (No 2) (2005) 215 ALR 281; [2005] FCA 254 Australian Competition and Consumer Commission v Phoenix Institute of Australia Pty Ltd (Subject to Deed of Company Arrangement) (No 3) [2023] FCA 859 Australian Competition and Consumer Commission v Productivity Partners Pty Ltd (trading as Captain Cook College) (in administration) (No 6) [2025] FCA 542 Australian Competition and Consumer Commission v Reckitt Benckiser (Australia) Pty Ltd (2016) 340 ALR 25; [2016] FCAFC 181 Australian Competition and Consumer Commission v The Construction, Forestry, Mining and Energy Union (2007) ATPR 42-140; [2006] FCA 1730 Australian Competition and Consumer Commission v TPG Internet Pty Ltd (2013) 250 CLR 640; [2013] HCA 54 Australian Ophthalmic Supplies Pty Ltd v McAlary-Smith (2008) 165 FCR 560; [2008] FCAFC 8 Australian Securities and Investments Commission v AGM Markets Pty Ltd (in liq) (No 4) (2020) 148 ACSR 511; [2020] FCA 1499 Australian Securities and Investments Commission v Forex Capital Pty Limited, in the matter of Forex Capital Trading Pty Limited [2021] FCA 570 Australian Securities and Investments Commission v Maxi EFX Global AU Pty Ltd (2020) 148 ACSR 123; [2020] FCA 1263 Australian Securities and Investments Commission v Union Standard International Group Pty Ltd (No 4) [2024] FCA 1481 Commissioner of Taxation of the Commonwealth of Australia v Sun Alliance Investments Pty Limited (in liquidation) (2005) 225 CLR 488; [2005] HCA 70 Commonwealth of Australia v Director, Fair Work Building Industry Inspectorate (2015) 258 CLR 482; [2015] HCA 46 Johnson v The Queen (2004) 205 ALR 346; [2004] HCA 15 Maxi EFX Global AU Pty Ltd v Australian Securities and Investments Commission (2021) 284 FCR 643; [2021] FCAFC 59 Mill v The Queen (1988) 166 CLR 59 at 63; [1988] HCA 70 R v Jacobs Group (Australia) Pty Ltd (2023) 280 CLR 170; [2023] HCA 23 Singtel Optus Pty Ltd v Australian Competition and Consumer Commission (2012) 287 ALR 249; [2012] FCAFC 20 Trade Practices Commission v CSR Ltd (1991) ATPR ¶41-076; [1990] FCA 521 Walsh v Rother District Council [1978] 1 All ER 510 |

Division: | General Division |

Registry: | New South Wales |

National Practice Area: | Commercial and Corporations |

Sub-area: | Corporations and Corporate Insolvency |

Number of paragraphs: | 273 |

Date of hearing: | 1-2 July 2025 |

Counsel for the Plaintiff: | Mr L Livingston SC with Mr D Birch |

Solicitor for the Plaintiff: | Clayton Utz |

Counsel for the | Ms M Painter SC with Mr F Tao and Ms C Brain |

Solicitor for the | Piper Alderman |

ORDERS

NSD 2064 of 2019 | ||

| ||

BETWEEN: | AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff | |

AND: | UNION STANDARD INTERNATIONAL GROUP PTY LTD First Defendant MAXI EFX GLOBAL AU PTY LTD Second Defendant BRIGHT AU CAPITAL PTY LTD Third Defendant | |

order made by: | WIGNEY J |

DATE OF ORDER: | 11 June 2026 |

THE COURT DECLARES THAT:

A. AS AGAINST THE SECOND DEFENDANT

1. From 15 August 2018 to 12 March 2019, Maxi EFX Global AU Pty Ltd trading as EuropeFX (EuropeFX) contravened:

(a) s 911A(1) of the Corporations Act 2001 (Cth) (Corporations Act) by conducting a financial services business providing personal advice on 142 occasions when it did not hold an Australian Financial Services Licence (AFSL), and was not acting as a corporate authorised representative of the holder of an AFSL that permitted the provision of personal advice;

(b) s 12DB(1) of the Australian Securities and Investments Commission Act 2001 (Cth) (ASIC Act) by making false and misleading representations to customers on 72 occasions regarding:

(i) the profits its customers might expect to make;

(ii) the risks its customers were exposed to;

(iii) the withdrawal of funds from customers’ trading accounts;

(iv) the recovery of losses;

(v) the returns to be made by reducing investment with equities and increasing investment with EuropeFX;

(vi) the returns to be made by investing with EuropeFX compared with a bank account;

(vii) a plan that would be or had been developed, which had been designed to meet a customer’s objectives, or needs and improve the customer’s financial position; or

(viii) EuropeFX being regulated by the Australian Securities and Investments Commission such that the customer was exposed to less risk than would otherwise be the case.

(c) s 12DA(1) of the ASIC Act by engaging in misleading or deceptive conduct on nine occasions regarding:

(i) the location of its main officers, headquarters, or offices from which it conducted a substantial part of its business, located in Australia; or

(ii) how EuropeFX earned revenue and account managers earned commission.

(d) s 12CB(1) and (4) of the ASIC Act by engaging in a system of conduct and a pattern of behaviour in connection with the supply of financial services that was, in all the circumstances, unconscionable including by:

(i) engaging in the following system of conduct:

A. utilising misleading and deceptive online advertisements, promotions and marketing techniques which were likely to attract customers with little or no relevant knowledge in contracts for difference (CFDs) and margin foreign exchange contracts (Margin FX Contracts) with the targeting of such people being systemic and deliberate;

B. having an “onboarding” system that was not genuinely intended or employed to weed out or discourage inexperienced or vulnerable customers from trading risky products through EuropeFX with that system being, at best indiscriminate and possibly deliberate;

C. deriving its revenue, or the bulk of its revenue, from its customers’ trading losses;

D. having a system of remuneration for its account managers which provided an incentive for them to encourage and pressure customers to trade more and deposit more funds into their trading accounts and which effectively gave rise to a conflict of interest; and

E. having a customer base in which a significant proportion of people were relatively ignorant of and inexperienced in the trading of CFDs and Margin FX Contracts, which was known to EuropeFX and its account managers; and

(ii) account managers engaging in a pattern of behaviour whereby they:

A. failing to give customers any sensible or adequate explanations about the relevant financial products and the risks involved in trading in them;

B. consistently and pervasively providing personal advice in contravention of s 911A(5B) of the Corporations Act in circumstances where they knew they were not permitted to do so and EuropeFX management knew they were doing so and failed to act in respect of it;

C. consistently and pervasively making false, misleading or deceptive representations for the general or common purpose of the customer trading more and depositing more funds than they otherwise would have;

D. encouraging and fostering a relationship whereby the customer relied and depended almost entirely on the account manager in respect of their trading and trading account;

E. pressuring vulnerable customers to trade and deposit more funds into their trading accounts, which conduct was known to EuropeFX management;

F. employing other inappropriate, unfair or sharp practices, including discouraging or impeding withdrawals, advising customers to engage in inappropriate and unfair trading strategies and encouraging ongoing trading by misleading references to the trading balance in the trading account;

(iii) providing no or almost no training to the account managers;

(iv) failing to deal with the consistent and pervasive misconduct of account managers, which was known to EuropeFX management;

(v) having an unfair complaints resolution process;

(e) s 12CB(1) of the ASIC Act on four occasions by engaging in conduct towards four customers that was, in all the circumstances, unconscionable.

2. From 13 March 2019 to 31 January 2020, EuropeFX contravened:

(a) s 911A(1) and (5B) of the Corporations Act by conducting a financial services business providing personal advice on 143 occasions when it did not hold an AFSL, and was not acting as a corporate authorised representative of the holder of an AFSL that permitted the provision of personal advice;

(b) s 12DB of the ASIC Act by making the false and misleading representations referred to in 1.(b) above to customers on 80 occasions;

(c) s 12DA(1) of the ASIC Act by engaging in misleading or deceptive conduct on nine occasions as referred to in 1.(c) above;

(d) s 12CB(1) and (4) of the ASIC Act by engaging in a system of conduct and a pattern of behaviour in connection with the supply of financial services that was, in all the circumstances, unconscionable, by engaging in the conduct referred to in 1.(d) above; and

(e) s 12CB(1) of the ASIC Act on four occasions by engaging in conduct towards four customers that was, in all the circumstances, unconscionable.

B. AS AGAINST THE THIRD DEFENDANT

3. From 12 December 2018 to 12 March 2019, Bright AU Capital Pty Ltd trading as TradeFred (TradeFred) contravened:

(a) s 911A(1) of the Corporations Act by conducting a financial services business providing personal advice on one occasion when it did not hold an AFSL, and was not acting as a corporate authorised representative of the holder of an AFSL that permitted the provision of personal advice;

(b) s 12DB of the ASIC Act by making false and misleading representations to customers on three occasions regarding:

(i) the risks its customers were exposed to; and

(ii) the profits they might expect to make;

(c) s 12CB(1) and (4) of the ASIC Act by engaging in a system of conduct and a pattern of behaviour in connection with the supply of financial services that was, in all the circumstances, unconscionable by:

(i) engaging in the following system of conduct:

A. utilising or taking advantage of online advertising or promotional material which was likely to attract customers who were likely to be inexperienced and unsophisticated in respect of trading in complex derivatives;

B. utilising an onboarding process that facilitated or encouraged the opening of accounts by inexperienced or vulnerable customers;

C. largely deriving its income from customers’ trading losses in circumstances where its customers were unlikely to have been aware of that fact;

D. remunerating its account managers in a way which provided an incentive for them to encourage and pressure customers to deposit more funds into their trading accounts;

E. failing to appropriately train its sales or account managers; and

F. failing to prevent and respond to instances where account managers engaged in inappropriate and improper conduct towards customers; and

(ii) account managers engaging in a pattern of behaviour whereby they:

A. knew that they were generally dealing with inexperienced, financially unsophisticated and therefore vulnerable customers;

B. generally failed to give any, or any adequate, explanations concerning the complex financial products that were being offered to their customers, and the nature and extent of the risks involved in trading in those products;

C. frequently gave the customers personal advice in circumstances where they either knew, or ought to have known, that TradeFred was not authorised or permitted to provide such advice;

D. frequently made misleading or deceptive representations to customers;

E. encouraged customers to depend on them and rely on their advice, despite the fact that they were not permitted to give personal advice;

F. often recommended and pressured the customers to trade and deposit further funds; and

G. employed other inappropriate, unfair or sharp practices, including encouraging customers to deposit further money by employing illusory promotions, encouraging customers to employ inappropriate or unfair trading strategies, encouraging use of funds from inappropriate sources and discouraging or impeding withdrawals; and

(d) s 12CB(1) of the ASIC Act on one occasion by engaging in conduct towards one customer that was, in all the circumstances, unconscionable.

4. From 13 March 2019 to 17 December 2020, TradeFred contravened:

(a) s 911A(1) and (5B) of the Corporations Act by conducting a financial services business providing personal advice on 19 occasions when it did not hold an AFSL, and was not acting as a corporate authorised representative of the holder of an AFSL that permitted the provision of personal advice;

(b) s 12DB of the ASIC Act by making false and misleading representations to customers on 42 occasions regarding:

(i) the risks its customers were exposed to;

(ii) the profits they might expect to make;

(iii) the withdrawal of funds from customers’ trading accounts;

(iv) the recovery of losses;

(v) the returns to be made by reducing investment with equities and increasing investment with TradeFred;

(vi) a customer receiving and being able to access bonus credits after depositing a certain amount of money in their trading account;

(vii) the returns to be made by investing with TradeFred compared with a bank account;

(viii) a plan that would be or had been developed, which had been designed to meet a customer’s objectives, or needs and improve the customer’s financial position; or

(ix) TradeFred being regulated by the Australian Securities and Investments Commission such that the customer was exposed to less risk than would otherwise be the case;

(c) s 12DA(1) of the ASIC Act by engaging in misleading or deceptive conduct on one occasion as to how TradeFred earned revenue;

(d) ss 12CB(1) and (4) of the ASIC Act by engaging in a system of conduct and a pattern of behaviour in connection with the supply of financial services that was, in all the circumstances, unconscionable by engaging in the conduct referred to in 3.(c) above; and

(e) contravened s 12CB(1) of the ASIC Act on three occasions by engaging in conduct towards three customers that was, in all the circumstances, unconscionable.

C. AS AGAINST THE FIRST DEFENDANT

5. From 15 October 2018 to 12 March 2019, Union Standard International Group Pty Ltd (USG) contravened s 12DB of the ASIC Act by making false and misleading representations to customers on four occasions regarding:

(a) the profits they might expect to make;

(b) the reports prepared by an analyst for USG; or

(c) an analyst who prepared reports for USG.

6. From 15 August 2018 to 12 March 2019, USG engaged in the contraventions of EuropeFX and TradeFred set out in paragraphs 1 and 3 above as EuropeFX and TradeFred were at all relevant times the corporate authorised representatives of USG and acting as its agents within their apparent authority (by operation of s 769B(1) of the Corporations Act and s 12GH(2) of the ASIC Act), and thereby engaged in:

(a) 143 contraventions of s 911A(5B) of the Corporations Act;

(b) 75 contraventions of s 12DB(1) of the ASIC Act;

(c) nine contraventions of s 12DA of the ASIC Act;

(d) the contraventions of ss 12CB(1) and 12CB(4)(b) of the ASIC Act set out in paragraphs 1.(d) and 3.(c) above by engaging in a system of conduct and a pattern of behaviour in connection with the supply of financial services that was, in all the circumstances, unconscionable; and

(e) five contraventions of s 12CB(1) of the ASIC Act by engaging in conduct towards customers that was, in all the circumstances, unconscionable.

7. From 13 March to 13 December 2019, USG contravened s 12DB of the ASIC Act by making false and misleading representations referred to in paragraph 5 above to customers on 24 occasions.

8. From 13 March 2019 to 31 January 2020, USG engaged in the contraventions of EuropeFX and TradeFred set out in paragraphs 2 and 4 above as EuropeFX and TradeFred were at all relevant times the corporate authorised representatives of USG and acting as its agents within their apparent authority (by operation of s 769B(1) of the Corporations Act and s 12GH(2) of the ASIC Act), and thereby engaged in:

(a) 162 contraventions of s 911A(5B) of the Corporations Act;

(b) 122 contraventions of s 12DB(1) of the ASIC Act;

(c) 10 contraventions of s 12DA of the ASIC Act;

(d) the contraventions of ss 12CB(1) and 12CB(4)(b) of the ASIC Act set out in paragraphs 2.(d) and 4.(d) above by engaging in a system of conduct and a pattern of behaviour in connection with the supply of financial services that was, in all the circumstances, unconscionable; and

(e) seven contraventions of s 12CB(1) of the ASIC Act by engaging in conduct towards seven customers that was, in all the circumstances, unconscionable.

9. From 11 April 2019 to May 2020, USG contravened ss 912A(1)(a) and (5A) of the Corporations Act by failing to do all things necessary to ensure that the financial services covered by its AFSL were provided efficiently, honestly and fairly, in that it continued to actively solicit customers in China for its Margin FX Contracts and CFDs and issue those customers with Margin FX Contracts and CFDs when it knew, or ought reasonably to have known, that its customers in China were likely to be contravening Chinese law in trading in its financial products, and it failed to take any, or any reasonable steps, to warn its customers that it was exposing them to potential criminal and civil liability in China.

THE COURT ORDERS THAT:

A. AS AGAINST THE SECOND DEFENDANT (EuropeFX)

Pecuniary penalties for misconduct prior to 13 March 2019

1. EuropeFX pay to the Commonwealth a pecuniary penalty of $4,200,000 for its contraventions of s 12DB(1) of the ASIC Act set out in declaration 1.(b), pursuant to s 12GBA(1) of the ASIC Act.

2. EuropeFX pay to the Commonwealth a pecuniary penalty of $2,800,000 for its contraventions of s 12CB(1) of the ASIC Act set out in declaration 1.(e), pursuant to s 12GBA(1) of the ASIC Act.

Pecuniary penalties for misconduct on and from 13 March 2019

3. EuropeFX pay to the Commonwealth a pecuniary penalty in the amount of $17,500,000 for the contraventions of s 911A(5B) of the Corporations Act set out in declaration 2.(a), pursuant to s 1317G(1) of the Corporations Act.

4. EuropeFX pay to the Commonwealth a pecuniary penalty of $14,000,000 for its contraventions of s 12DB of the ASIC Act set out in declaration 2.(b), pursuant to s 12GBB(3) of the ASIC Act.

5. EuropeFX pay to the Commonwealth a pecuniary penalty of $70,000,000 for its contraventions of s 12CB(1) and (4) of the ASIC Act set out in declaration 2.(d), pursuant to s 12GBB(3) of the ASIC Act.

6. EuropeFX pay to the Commonwealth a pecuniary penalty of $5,600,000 for its contraventions of s 12CB(1) of the ASIC Act set out in declaration 2.(e), pursuant to s 12GBB(3) of the ASIC Act.

Other orders

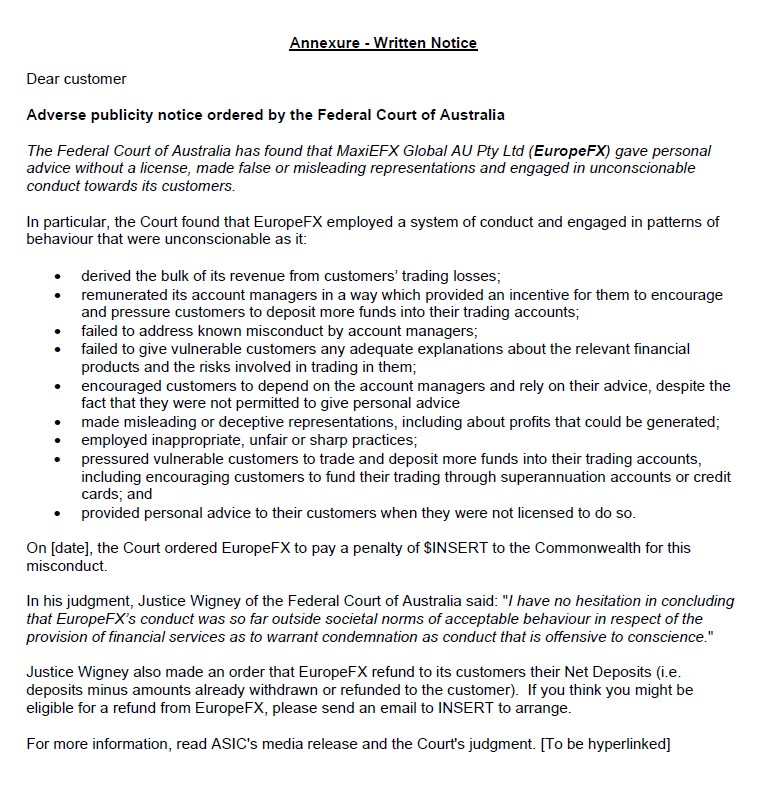

7. Pursuant to s 12GLB(1) of the ASIC Act, within six months of the date of this order, EuropeFX is to cause to be published, at its own expense, a notice in the terms set out in the Annexure to these orders (Written Notice) by sending (by ordinary post or email) to each customer who held a trading account with EuropeFX between 15 August 2018 and 31 January 2020 an email or letter and including within the body of that correspondence the terms of the Written Notice.

8. Pursuant to ss 1101B(4)(a) and 1324(1) of the Corporations Act and s 12GD(1) of the ASIC Act EuropeFX is permanently restrained from carrying on a financial services business, or carrying on a business related to, concerning or directed to financial products or financial services within the meaning of s 761A of the Corporations Act, or otherwise providing financial product advice.

9. Pursuant to ss 12GNB and 12GNC(d) of the ASIC Act, EuropeFX refund to its clients their Net Deposits, being:

(a) the total amount that the client deposited to the client’s trading account(s) with EuropeFX; less

(b) any amounts withdrawn, or already refunded to the client, from the client’s trading account(s); less

(c) any amounts refunded to the client as a result of any arrangement or agreement; less

(d) any amounts which the client in fact receives, pursuant to reg 7.8.03(6) of the Corporations Regulations 2001 (Cth).

B. AS AGAINST THE THIRD DEFENDANT (TradeFred)

Pecuniary penalties for misconduct prior to 13 March 2019

10. TradeFred pay to the Commonwealth a pecuniary penalty of $350,000 for its contraventions of s 12DB(1) of the ASIC Act set out in declaration 3.(b), pursuant to s 12GBA(1) of the ASIC Act.

11. TradeFred pay to the Commonwealth a pecuniary penalty of $350,000 for its contraventions of s 12CB(1) of the ASIC Act set out in declaration 3.(d), pursuant to s 12GBA(1) of the ASIC Act.

Pecuniary penalties for misconduct on and from 13 March 2019

12. TradeFred pay to the Commonwealth a pecuniary penalty in the amount of $1,400,000 for the contraventions of s 911A(5B) of the Corporations Act set out in declaration 4.(a), pursuant to s 1317G(1) of the Corporations Act.

13. TradeFred pay to the Commonwealth a pecuniary penalty of $7,000,000 for its contraventions of s 12DB of the ASIC Act set out in declaration 4.(b), pursuant to s 12GBB(3) of the ASIC Act.

14. TradeFred pay to the Commonwealth a pecuniary penalty of $17,500,000 for its contraventions of s 12CB(1) and (4) of the ASIC Act set out in declaration 4.(d), pursuant to s 12GBB(3) of the ASIC Act.

15. TradeFred pay to the Commonwealth a pecuniary penalty of $2,800,000 for its contraventions of s 12CB(1) of the ASIC Act set out in declaration 4.(e), pursuant to s 12GBB(3) of the ASIC Act.

C. AS AGAINST THE FIRST DEFENDANT (USG)

Pecuniary penalties for misconduct prior to 13 March 2019

16. USG pay to the Commonwealth a pecuniary penalty of $400,000 for its contraventions of s 12DB of the ASIC Act set out in declaration 5, pursuant to s 12GBA(1) of the ASIC Act.

17. USG pay to the Commonwealth a pecuniary penalty of $7,700,000 for its contraventions of s 12DB and s 12CB(1) of the ASIC Act set out in declaration 6, pursuant to s 12GBA(1) of the ASIC Act.

Pecuniary penalties for misconduct on or after 13 March 2019

18. USG pay to the Commonwealth a pecuniary penalty of $4,800,000 for its contraventions of s 12DB of the ASIC Act set out in declaration 7, pursuant to s 12GBB(3) of the ASIC Act.

19. USG pay to the Commonwealth a pecuniary penalty of $135,800,000 for its contraventions of s 911A of the Corporations Act and ss 12DB, 12CB(1) and (4) of the ASIC Act set out in declaration 8, pursuant to s 12GBB(3) of the ASIC Act and s 1317G(1) of the Corporations Act.

20. USG pay to the Commonwealth a pecuniary penalty of $8,000,000 for its contraventions of s 912A(1)(a) and (5A) of the Corporations Act set out in declaration 9, pursuant to s 1317G(1) of the Corporations Act.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

WIGNEY J:

1 Between about 2017 and early 2020, the defendants in this proceeding, Union Standard International Group Pty Ltd (USG), Maxi EFX Global AU Pty Ltd (EuropeFX or EFX) and Bright AU Capital Pty Ltd (TradeFred) operated financial services businesses. Those services included offering retail customers the opportunity of trading in highly risky over-the-counter derivative products known as contracts for difference (CFDs) and margin foreign exchange contracts (Margin FX Contracts). Each of USG, EuropeFX and TradeFred profited handsomely from the provision of those services. Their customers did not.

2 The applicant, the Australian Securities and Investments Commission (ASIC) commenced this proceeding alleging that EuropeFX and TradeFred engaged in systems of conduct or patterns of behaviour in the conduct of their respective businesses which were unconscionable, and also engaged in unconscionable conduct in their dealings with several identified customers, in contravention of s 12CB of the Australian Securities and Investments Commission Act 2001 (Cth) (ASIC Act). ASIC also alleged that EuropeFX and TradeFred repeatedly gave personal advice to customers when not permitted to do so and thereby contravened s 911A of the Corporations Act 2001 (Cth) (Corporations Act) and that USG, EuropeFX and TradeFred made false or misleading representations to their customers on many occasions in contravention of s 12DA or s 12DB of the ASIC Act. USG, who held an Australian Financial Services License (AFSL), was also alleged to be liable in respect of the contravening conduct of EuropeFX and TradeFred, who were USG’s corporate authorised representatives (CARs), and to have contravened s 912A(1)(a) of the Corporations Act by failing to do all things necessary to ensure that the financial services covered by its AFSL were provided efficiently, honestly and fairly.

3 On 20 December 2024, I handed down a judgment in which I held that USG, EuropeFX and TradeFred had engaged in virtually all the contravening conduct as alleged by ASIC: Australian Securities and Investments Commission v Union Standard International Group Pty Ltd (No 4) [2024] FCA 1481 (liability judgment or LJ). The matter was adjourned to allow the parties to file evidence and advance submissions in relation to the declarations and orders that should be made and any other relief that should be granted consequent upon those findings.

4 The relief sought by ASIC in respect of the contravening conduct included declaratory relief and injunctive relief pursuant to ss 1101B(1) and (4)(a) and 1324(1) of the Corporations Act and s 12GD(1) of the ASIC Act, non-party redress orders pursuant to ss 12GNB and 12GNC of the ASIC Act and pecuniary penalties pursuant to ss 12GBA(1) and 12GBB(3) of the ASIC Act and s 1317G(1) of the Corporations Act.

5 USG and TradeFred, who were being wound-up in insolvency at the time, did not file any evidence and submissions and their liquidators effectively submitted to any orders the Court may make in respect of relief. EuropeFX did not oppose any of the relief sought by ASIC, though it did submit that the pecuniary penalties that were sought by ASIC in its submissions were too high. ASIC submitted that it would be appropriate for the Court to make pecuniary penalties in respect of EuropeFX’s contraventions which totalled $114.1 million. EuropeFX submitted that the pecuniary penalties sought by ASIC were excessive and that pecuniary penalties that totalled about $40 million would be appropriate.

6 For the reasons that follow, it is appropriate for the Court to make the declarations and orders sought by ASIC against USG, EuropeFX and TradeFred. In relation to the size of the appropriate pecuniary penalties to be imposed on EuropeFX, while EuropeFX argued to the contrary, EuropeFX’s contraventions were unquestionably egregious, deliberate and flagrant. By its conduct, EuropeFX systematically exploited many vulnerable and financially naïve and gullible customers for its own financial gain. Only very substantial pecuniary penalties will effectively deter the likes of EuropeFX and those who stand behind them from engaging in such conduct in the future. The penalties proposed by ASIC are, in all the circumstances, entirely appropriate.

7 References to statutory provisions in these reasons may be taken to be references to the text of those provisions as at the time of the relevant contraventions. It should be noted in that context that the contraventions span a lengthy period during which there were significant changes to the applicable provisions, including those concerning the maximum pecuniary penalties that the Court can order.

Overview and summary of findings in respect of contraventions

8 This judgment should be read together with the liability judgment. It is assumed that readers of this judgment will be familiar with the detailed reasons and findings of fact made in the liability judgment. I do not propose to rehearse that reasoning or repeat those findings in this judgment other than where necessary to address the competing submissions made by ASIC and EuropeFX in respect of the appropriate pecuniary penalties. What follows is no more than a thumbnail sketch of the key findings made in the liability judgment. It is not intended to replace or supplant in any way the findings in the liability judgment. If there is any inconsistency, the findings in the liability judgment prevail. The focus of the following summary is mainly on the findings concerning EuropeFX given that only EuropeFX appeared and adduced evidence and advanced submissions in respect of the appropriate relief. As is clear from the liability judgment, the business conducted by TradeFred was relevantly similar to the business conducted by EuropeFX, though TradeFred’s business was perhaps smaller in scale.

9 USG obtained its AFSL in 2016. The AFSL permitted USG to provide general financial product advice to retail clients. It did not permit it to provide personal financial advice. USG’s business mainly involved dealing in derivatives by issuing and making a market for CFDs and Margin FX Contracts. USG was the principal and counterparty to all the CFD and Margin FX contract positions it made available to its customers.

10 Mr John Martin was a director of USG and was its “Responsible Manager” and Head of Compliance.

11 USG appointed EuropeFX and TradeFred as its CARs and authorised them to provide specified financial services on its behalf. That authority did not extend to permit EuropeFX and TradeFred to provide personal financial product advice to their customers.

12 EuropeFX’s director during the period 2018 to 2020 was Mr Pedro Sasso, though he was briefly replaced by Mr Martin in the period from September 2018 to April 2019. It was readily apparent from the evidence adduced during the trial that Mr Sasso was little more than a puppet director who took instructions from others, though mainly a man named Mr Gal Amar. Mr Amar resided overseas and controlled a company based in either Cyprus or Israel which in turn controlled EuropeFX.

13 The financial services business conducted by EuropeFX as USG’s CAR involved offering CFDs and Margin FX Contracts to customers through an online trading platform. CFDs and Margin FX Contracts are complex and highly risky over-the-counter derivative financial products which effectively enable an investor to profit from movements in the price of an underlying asset (a commodity or share or stock market index) or currency pairing (in the case of Margin FX Contracts). Of course, investors could also incur losses from those movements in price, depending on the position they opened and the direction the price moved. At the time, CFDs and Margin FX Contracts could be highly leveraged, which meant that small financial outlays could generate large profits or, conversely, result in substantial losses well beyond the amount outlaid. The evidence adduced at trial indicated that the nature of those financial products was such that inexperienced or unsophisticated investors in CFDs and Margin FX Contracts were almost certain to lose the money that they invested, often within a very short space of time.

14 USG was the principal and counterparty to all the CFD and Margin FX contract positions opened by EuropeFX’s customers. It profited when EuropeFX’s customers incurred losses. Similarly, by virtue of its arrangements with USG, EuropeFX generated revenue when its customers made losses as a result of closing positions that had moved against them.

15 EuropeFX outsourced almost the entirety of its day-to-day business to foreign entities and individuals. It retained a company based in Belize to source and “onboard” customers. Financially unsophisticated and naïve customers were clearly targeted, including by online promotions which included false celebrity endorsements and misleading claims concerning the profits that could be earned by a system of automatic trading in Bitcoin. Prospective customers were onboarded by, or on behalf of, EuropeFX despite it being obvious from the information provided by those customers that they were wholly unqualified and unsuited to investing in complex and risky leveraged financial products.

16 EuropeFX outsourced all its trading and trading account customer interactions to a business based in Israel which provided call centre services. Employees of that business acted as EuropeFX account managers and, in that capacity, regularly spoke with EuropeFX’s customers over the telephone in relation to their trading and trading activities. Those employees regularly gave the customers personal financial advice in respect of their trading, despite the fact that EuropeFX was not permitted to provide such advice and despite the fact that the account managers well knew that they were not permitted to give personal financial advice. The account managers also frequently made false, misleading or deceptive representations to the customers to encourage them to trade and frequently pressured the customers to trade and deposit more and more funds into their trading accounts. That was hardly surprising given that the account managers received commission based on the amount of money their customers deposited.

17 Those supposedly responsible for management at USG (as the AFSL holder) and EuropeFX were well aware of misconduct on the part of the outsourced foreign account managers. While that misconduct was discussed at supposed compliance meetings, little or nothing was actually done to remedy it. That again was hardly surprising given the sizeable revenue that was being derived by EuropeFX from its customers’ losses. It had no incentive whatsoever to put a stop to the misconduct. Indeed, the available and obvious inference was that it was more than content for the misconduct to continue. Such steps as were taken by USG to address the misconduct were obviously either ignored or were, at best, ineffectual.

18 EuropeFX’s complaint and dispute resolution processes were also largely outsourced to a foreign-based person or entity. Those processes turned out to be one-sided and unfair. The primary aim of the processes, such as they were, was to dissuade complainants from lodging complaints with external regulators and pressuring them to accept paltry confidential settlements. EuropeFX was no doubt anxious to avoid its disaffected customers from approaching the regulators because that would put at risk the continuance of their profitable enterprise.

19 Overall, the systems of conduct and patterns of behaviour employed by EuropeFX in the conduct of their businesses were manifestly unconscionable. The indicia of the unconscionable systems of conduct and patterns of behaviour included: misleading advertising and promotions directed to naïve, financially unsophisticated and vulnerable customers; the deliberate onboarding of customers known to have been inexperienced and unsuitable for investing in risky leveraged derivatives; a system of remuneration by which profits were directly referrable to and derived from customers’ losses, unbeknownst to the customers; the inadequate (or non-existent) training of account managers; and the known patterns of inappropriate behaviour of account managers which included: the provision of personal financial advice; the failure to give adequate explanations in respect of CFD and Margin FX trading and its inherent risks; the making of false, misleading and deceptive representations; the pressuring of customers to deposit funds (in circumstances where account managers received commission based on their customers’ deposits) and engage in more and more trading; offering unfair promotions to encourage the customers to make further deposits and continue trading; encouraging the use of inappropriate funds (including borrowed money and superannuation); and the giving of advice in respect of inappropriate or unfair trading strategies.

20 EuropeFX’s unconscionable systems of conduct and patterns of behaviour were shown to have been specifically employed in the case of eight identified customers who were referred to as the EFX8. The EFX8 were all, to some extent, vulnerable because they had relatively limited financial means and no relevant experience in respect of trading in sophisticated and risky financial products. None of them had an adequate understanding of CFDs or Margin FX Contracts and the inherent risks involved in trading in those products. None of them were given any adequate or intelligible explanations or information about the relevant products or the inherent risks in trading in them. They were nonetheless onboarded by EuropeFX and encouraged to deposit more and more money and engage in more and more trading. They were all subjected to egregious account manager misconduct. One need only listen to the recordings of some of the exchanges between the EFX8 and their account managers to appreciate the gravity of the misconduct. They were all given personal advice, misled and deceived, encouraged to rely and depend on their account managers, given inappropriate trading advice and pressured to deposit more and more into their trading accounts, including funds from inappropriate sources. Each of them effectively lost most, if not all, of the money they had deposited into their trading accounts. Those who subsequently complained about their dealings with EuropeFX and its account managers were discouraged from lodging complaints with the regulator and pressured to accept modest settlements.

21 EuropeFX profited handsomely from its business. As adverted to earlier, USG essentially profited or derived revenue from the losses incurred by EuropeFX’s customers and EuropeFX’s arrangements with USG were that it received a very large proportion of those profits or that revenue. Not surprisingly, the losses incurred by EuropeFX’s customers were huge and therefore EuropeFX’s revenue was huge. Evidence tendered during the trial revealed that, between April 2019 and January 2020, EuropeFX received payments from USG which totalled $55,500,616.89. Those payments reflected EuropeFX’s share of the losses made by its customers from trading in CFDs and Margin FX Contracts made available by USG.

22 TradeFred’s business was conducted in a very similar manner to EuropeFX’s businesses. Like EuropeFX, TradeFred, as USG’s CAR, offered CFDs and Margin FX Contracts to customers through an online trading platform. Like EuropeFX, TradeFred outsourced almost all its day-to-day business activities to offshore service providers. Like EuropeFX, TradeFred essentially derived its revenue or income from its customers’ losses. And like EuropeFX, the systems of conduct and patterns of behaviour by which TradeFred conducted its business were manifestly unconscionable. TradeFred’s unconscionable systems of conduct and patterns of behaviour were shown to have been specifically employed in the case of four identified customers who were referred to as the TF4.

23 USG conducted its own financial services business as well as authorising its CARs, EuropeFX and TradeFred, to provide financial services on its behalf. Like its CARs, USG was found to have made false, misleading and deceptive statements to some of its customers in Australia. USG also actively promoted itself and its CFDs and Margin FX Contracts to Chinese citizens in China, despite the fact that in doing so it not only breached Chinese law, but also exposed its Chinese customers to contraventions of Chinese law and possible penalties for doing so.

Findings in respect of contraventions by EuropeFX

24 In the liability judgment I found, in short summary, that EuropeFX had:

(1) contravened s 911A(1) of the Corporations Act on 285 occasions by providing personal advice to customers, through its account managers or representatives, in circumstances where it was not licensed to do so;

(2) contravened s 12DB(1) of the ASIC Act on 190 occasions by making, in trade or commerce, in connection with the supply or possible supply of financial services, or in connection with the promotion of such services, false or misleading representations that the services were of a particular standard or quality, or that the services had certain performance characteristics or benefits;

(3) contravened s 12DA(1) of the ASIC Act on 18 occasions by engaging in conduct, in trade or commerce, and in relation to financial services, where that conduct was misleading or deceptive, or likely to mislead or deceive;

(4) contravened s 12CB(1) of the ASIC Act on one occasion by engaging in conduct, in trade or commerce, and in connection with the supply or possible supply of financial services, where that conduct comprised or constituted a system of conduct or pattern of behaviour that was, in all the circumstances, unconscionable; and

(5) contravened s 12CB(1) of the ASIC Act on eight occasions by engaging in conduct, in trade or commerce, and in connection with the supply or possible supply of financial services to a person, where that conduct was, in all the circumstances, unconscionable.

Findings in respect of contraventions by TradeFred

25 In the liability judgment I found, in short summary, that TradeFred had:

(1) contravened s 911A(1) of the Corporations Act on 20 occasions by providing personal advice to customers, through its account managers or representatives, in circumstances where it was not licensed to do so;

(2) contravened s 12DB(1) of the ASIC Act on 54 occasions by making, in trade or commerce, in connection with the supply or possible supply of financial services, or in connection with the promotion of such services, false or misleading representations that the services were of a particular standard or quality, or that the services had certain performance characteristics or benefits;

(3) contravened s 12DA(1) of the ASIC Act on two occasions by engaging in conduct, in trade or commerce, and in relation to financial services, where that conduct was misleading or deceptive, or likely to mislead or deceive;

(4) contravened s 12CB(1) of the ASIC Act on one occasion by engaging in conduct, in trade or commerce, and in connection with the supply or possible supply of financial services, where that conduct comprised or constituted a system of conduct or pattern of behaviour that was, in all the circumstances, unconscionable; and

(5) contravened s 12CB(1) of the ASIC Act on four occasions by engaging in conduct, in trade or commerce, and in connection with the supply or possible supply of financial services to a person, where that conduct was, in all the circumstances, unconscionable.

Findings in respect of contraventions by USG

26 In the liability judgment, I found, in short summary, that USG had:

(1) contravened s 12DB(1) of the ASIC Act on 56 occasions by making, in trade or commerce, in connection with the supply or possible supply of financial services, or in connection with the promotion of such services, false or misleading representations that the services were of a particular standard or quality, or that the services had certain performance characteristics or benefits;

(2) contravened s 911A(1) of the Corporations Act on 306 occasions, those being contraventions arising from the fact that, on each of the occasions when EuropeFX and TradeFred engaged in conduct that contravened s 911A(1) of the Corporations Act, they did so as agents of USG by reason of s 769B(1)(a) of the Corporations Act;

(3) contravened:

(a) s 12DB(1) of the ASIC Act on 282 occasions;

(b) s 12DA(1) of the ASIC Act on 20 occasions; and

(c) s 12CB(1) of the ASIC Act on 14 occasions;

those being contraventions arising from the fact that, on each of the occasions when EuropeFX and TradeFred engaged in conduct that contravened ss 12DB(1), 12DA(1) and 12CB(1) of the ASIC Act, they did so as agents of USG by reason of s 12GH(2)(a) of the ASIC Act; and

(4) contravened s 912A(1)(a) of the Corporations Act by failing to do all things necessary to ensure that the financial services covered by its financial services licence were provided efficiently, honestly and fairly.

DECLARATIONS in respect of contraventions

27 It is convenient to first consider the declaratory relief sought by ASIC. EuropeFX did not submit that the Court could not or should not make declarations in respect of its contraventions of the Corporations Act and the ASIC Act. As already noted, USG and TradeFred did not make any submissions in respect of the relief sought by ASIC.

28 As a result of material amendments to both the Corporations Act and the ASIC Act that had effect from 13 March 2019, it is necessary to distinguish between those contraventions that occurred before 13 March 2019 and those contraventions that occurred after that date.

Pre-13 March 2019 Corporations Act contraventions

29 Subsection 1317E(1) of the Corporations Act provided that “[i]f a Court is satisfied that a person has contravened a civil penalty provision, it must make a declaration of contravention”. Subsection 1317E(2) provided that a declaration of contravention must specify, among other things, the civil penalty provision that was contravened, the person who contravened the provision and the conduct that constituted the contravention.

30 Subsections 911A(5B) and 912A(5A) of the Corporations Act were not specified as being civil penalty provisions prior to 13 March 2019. They were specified as being a civil penalty provision after that date. It follows that s 1317E(1) of the Corporations Act does not apply in respect of EuropeFX’s and TradeFred’s contraventions of s 911A(5B), USG’s contraventions of s 911A(5B) by virtue of s 769B of the Corporations Act and USG’s contravention of s 912A(5A), that occurred before 13 March 2019.

31 The Court nevertheless has a wide discretionary power to make declarations under s 21 of the Federal Court of Australia Act 1976 (Cth) (FCA Act). The exercise of that discretion in respect of contraventions of legislative provisions is generally accepted to be appropriate because such declarations serve to: record the Court’s disapproval of the contravening conduct; vindicate the regulator’s claim that the defendant contravened the provision; and assist the regulator to carry out its duties and deter other persons from contravening the provisions: see Australian Competition and Consumer Commission v The Construction, Forestry, Mining and Energy Union (2007) ATPR 42-140; [2006] FCA 1730 at [6] and the cases cited therein.

32 It is, in all the circumstances, appropriate to make declarations in respect of the pre-March 2019 Corporations Act contraventions. No party submitted otherwise. For reasons that will be explained later, the declarations ultimately sought by ASIC in respect of the contraventions of s 911A of the Corporations Act, both prior to and after 13 March 2019, did not reference all the contraventions identified in the liability judgment.

Post-13 March 2019 Corporations Act contraventions

33 In the case of EuropeFX’s and TradeFred’s contraventions of s 911A(5B), USG’s contraventions of s 911A(5B) by virtue of s 769B of the Corporations Act and USG’s contravention of s 912A(5A) that occurred after 13 March 2019, the Court is required by s 1317E(1) to make declarations in respect of those contraventions. The declarations sought by ASIC in respect of the contraventions of s 911A(5B) by EuropeFX, TradeFred and USG and the contravention of s 912A(5A) by USG will accordingly be made.

Pre-13 March 2019 ASIC Act contraventions

34 Prior to 13 March 2019, there was no section in the ASIC Act which provided for the making of declarations in respect of contraventions of provisions in the ASIC Act. As noted above in the context of the Corporations Act contraventions, however, the Court has the discretionary power to make declarations in respect of contraventions of the ASIC Act which occurred prior to 13 March 2019 pursuant to s 21 of the FCA Act.

35 It is appropriate to make declarations in respect of the pre-March 2019 ASIC Act contraventions. No party submitted otherwise. For reasons that will be explained later, the declarations ultimately sought by ASIC in respect of the contraventions of ss 12DA and 12DB of the ASIC Act, both prior to and after 13 March 2019, did not reference all the contraventions identified in the liability judgment.

Post-13 March 2019 ASIC Act contraventions

36 From 13 March 2019, s 12GBA(3) of the ASIC Act provided that the Court must make a declaration if (following an application by ASIC) it is satisfied that a person has contravened a civil penalty provision in the ASIC Act. While s 12GBA(3) does not apply in the case of contraventions of s 12DA of the ASIC Act, which is not a civil penalty provision, the Court nevertheless has the power under s 21 of the FCA Act to make declarations in respect of contraventions of that provision. No party submitted that the Court should not make declarations in respect of the s 12DA contraventions.

37 The Court will accordingly make the declarations sought by ASIC in respect of the contraventions of ss 12CB, 12DA and 12DB of the ASIC Act by EuropeFX, TradeFred and USG.

Applicable STATUTORY PROVISIONS AND principles in respect of fixing pecuniary penalties

38 It is necessary to separately consider the applicable provisions concerning the fixing of pecuniary penalties for contraventions of the Corporations Act and the ASIC Act.

Penalties for Corporations Act contraventions

39 As has already been noted, ss 911A(5B) and 912A(5A) of the Corporations Act were not civil penalty provisions prior to 13 March 2019. It is therefore only necessary to have regard to the post-13 March 2019 provisions of the Corporations Act relating to pecuniary penalties.

40 Subsection 1317E(3) of the Corporations Act incorporated a table which specified and categorised the provisions of the Act which were civil penalty provisions. Subsections 911A(5B) and 912A(5A) were “uncategorised” civil penalty provisions because they were neither “corporation/scheme civil penalty provision[s]” or “financial services civil penalty provision[s]”: s 1317E(3)(d).

41 Subsection 1317G(1) of the Corporations Act relevantly provided that a Court may order a person to pay to the Commonwealth a pecuniary penalty in relation to the contravention of a civil penalty provision if a declaration of contravention of the civil penalty provision by the person had been made under s 1317E: s 1317G(1)(a). Subsection 1317G(2) provided that the pecuniary penalty must not exceed the pecuniary penalty applicable to the contravention of the civil penalty provision.

42 Subsection 1317G(4) provided as follows:

Pecuniary penalty applicable to the contravention of a civil penalty provision—by a body corporate

The pecuniary penalty applicable to the contravention of a civil penalty provision by a body corporate is the greatest of:

(a) 50,000 penalty units; and

(b) if the Court can determine the benefit derived and detriment avoided because of the contravention—that amount multiplied by 3; and

(c) either:

(i) 10% of the annual turnover of the body corporate for the 12‑month period ending at the end of the month in which the body corporate contravened, or began to contravene, the civil penalty provision; or

(ii) if the amount worked out under subparagraph (i) is greater than an amount equal to 2.5 million penalty units—2.5 million penalty units.

43 ASIC’s submissions regarding the appropriate penalty to be imposed in respect of the contraventions of s 911A of the Corporations Act by EuropeFX, TradeFred and USG and USG’s contravention of s 912A of the Corporations Act proceeded on the basis that s 1317G(4)(a) was the applicable provision in determining the maximum pecuniary penalty for those contraventions.

44 Subsection 1317G(6) of the Corporations Act provided as follows:

Determining pecuniary penalty

In determining the pecuniary penalty, the Court must take into account all relevant matters, including:

(a) the nature and extent of the contravention; and

(b) the nature and extent of any loss or damage suffered because of the contravention; and

(c) the circumstances in which the contravention took place; and

(d) whether the person has previously been found by a court (including a court in foreign country) to have engaged in similar conduct.

Penalties for ASIC Act contraventions

45 It is necessary to consider the applicable ASIC Act provisions concerning pecuniary penalties both before and after 13 March 2019, when significant amendments to those provisions came into force, because the ASIC Act contraventions by EuropeFX, TradeFred and USG straddled that date.

Pre-13 March 2019 contraventions

46 In the relevant period prior to 13 March 2019, s 12GBA(1)(a) of the ASIC Act relevantly provided that, if the Court was satisfied that a person had contravened, inter alia, a provision of Subdivision C (which included s 12CB) and Subdivision D (which included s 12DB) other than s 12DA, the Court could order the person to pay to the Commonwealth such pecuniary penalty, in respect of each act or omission by the person to which s 12GBA applied, as the Court determined to be appropriate.

47 Subsection 12GBA(2) of the ASIC Act provided as follows:

In determining the appropriate pecuniary penalty, the Court must have regard to all relevant matters including:

(a) the nature and extent of the act or omission and of any loss or damage suffered as a result of the act or omission; and

(b) the circumstances in which the act or omission took place; and

(c) whether the person has previously been found by the Court in proceedings under this Subdivision to have engaged in any similar conduct.

48 Subsection 12GBA(3) of the ASIC Act provided (at all relevant times before 13 March 2019) that the pecuniary penalty payable was not to exceed, in the case of acts or omissions in contravention of Subdivisions C or D (which respectively included ss 12CB and 12DB), 10,000 penalty units if the person who engaged in those acts or omissions was a body corporate. A penalty unit at the time was $210.00.

49 It follows that the maximum penalty that could be imposed for each of the contraventions of ss 12CB and 12DB of the ASIC Act by EuropeFX, TradeFred and USG that occurred before 13 March 2019 was $2.1 million.

50 Prior to 13 March 2019, s 12GBA(4) provided as follows:

If conduct constitutes a contravention of 2 or more provisions referred to in paragraph (1)(a):

(a) a proceeding may be instituted under this Act against a person in relation to the contravention of any one or more of the provisions; but

(b) a person is not liable to more than one pecuniary penalty under this section in respect of the same conduct.

51 Subsection 12GBA(4) was repealed on 13 March 2019. EuropeFX’s submissions concerning the operation or effect of s 12GBA(4) in respect of its contraventions are discussed in detail later.

Post-13 March 2019 contraventions

52 Following the amendments to the ASIC Act which came into effect on 13 March 2019, the relevant provisions concerning the imposition of pecuniary penalties were contained in s 12GBB of the ASIC Act. Subsection 12GBB(1) of the ASIC Act provided that ASIC could apply to a Court for an order that a person who was alleged to have contravened a civil penalty provision pay the Commonwealth a pecuniary penalty. Subsection 12GBB(3) provided in effect that, where the Court made a declaration under s 12GBA (in the form it took after 13 March 2019 as discussed earlier in the context of declaratory relief) that the person had contravened a civil penalty provision, the Court could “order the person to pay to the Commonwealth a pecuniary penalty that the Court considers is appropriate (but not more than the amount specified in section 12GBC)”.

53 Subsection 12GBB(5) provided as follows:

Determining pecuniary penalty

In determining the pecuniary penalty, the Court must take into account all relevant matters, including:

(a) the nature and extent of the contravention; and

(b) the nature and extent of any loss or damage suffered because of the contravention; and

(c) the circumstances in which the contravention took place; and

(d) whether the person has previously been found by a court (including a court in a foreign country) to have engaged in any similar conduct.

54 Section 12GBC provided that the pecuniary penalty must not be more than “the pecuniary penalty applicable to the contravention of the civil penalty provision”. While there appears to have been a legislative glitch in respect of the specification of penalties for civil penalty provisions for a short period after 13 March 2019, ASIC proceeded on the basis that the applicable provision was s 12GBCA(2) of the ASIC Act, which provided as follows in respect of the pecuniary penalty applicable to a contravention of a civil penalty provision by a body corporate:

Pecuniary penalty applicable to the contravention of a civil penalty provision—by a body corporate

The pecuniary penalty applicable to the contravention of a civil penalty provision by a body corporate is the greatest of:

(a) 50,000 penalty units; and

(b) if the Court can determine the benefit derived and detriment avoided because of the contravention—that amount multiplied by 3; and

(c) either:

(i) 10% of the annual turnover of the body corporate for the 12‑month period ending at the end of the month in which the body corporate contravened, or began to contravene, the civil penalty provision; or

(ii) if the amount worked out under subparagraph (i) is greater than an amount equal to 2.5 million penalty units—2.5 million penalty units.

55 ASIC contended that the penalty applicable to the contraventions of s 12DB of the ASIC Act by EuropeFX, TradeFred and USG that occurred after 13 March 2019 was the penalty specified in s 12GBCA(2)(a), namely 50,000 penalty units, which equated to $10.5 million. The basis of that contention appeared to be that: the Court could not determine the benefit derived because of those contraventions and therefore s 12GBCA(2)(b) did not apply; $10.5 million was more than the amount calculated pursuant to s 12GBCA(2)(c)(i); and s 12GBCA(2)(c)(ii) was not applicable in the circumstances of the case. EuropeFX did not appear to dispute ASIC’s contentions in that regard.

56 While the determination of the maximum penalty for a contravention of s 12DB of the ASIC Act in the period between 13 March 2019 and mid-2020 is by no means easy to work out due to the obscurity of the relevant statutory provision, in the absence of any dispute in respect of this issue I will proceed on the basis proposed by ASIC. Accordingly, the maximum penalty for the contraventions of s 12DB of the ASIC Act by EuropeFX, USG and TradeFred that occurred after 13 March 2019 was $10.5 million. In any event, as discussed later, the maximum penalty for a single contravention of s 12DB was somewhat academic given the multiplicity of contraventions.

57 The penalty applicable to the contraventions of s 12CB of the ASIC Act by EuropeFX that occurred after 13 March 2019 was a matter of contention. ASIC contended that the Court could determine the benefit derived by EuropeFX because of the contraventions and that amount multiplied by three exceeded $10.5 million. The penalty applicable to the contraventions was accordingly to be calculated pursuant to s 12GBCA(2)(b) of the ASIC Act. EuropeFX submitted that the Court could not determine the amount it derived because of the contraventions on the evidence before the Court and therefore the penalty applicable to the contraventions of s 12CB was $10.5 million in accordance with s 12GBCA(2)(a) of the ASIC Act. That issue will be addressed and determined later in these reasons.

Applicable principles in respect of pecuniary penalties

58 There was little, if any, disagreement between the parties in respect of the principles which bind the Court in fixing pecuniary penalties for contraventions of civil penalty provisions in the Corporations Act and the ASIC Act. The key principles derived from the authorities may be summarised as follows.

The primacy of deterrence

59 It might surprise the victims and persons otherwise affected by the contravening conduct in this case that the Court’s purpose in imposing a pecuniary penalty for a contravention of a civil penalty provision is not to punish or denounce the conduct. Rather it is to deter and promote compliance. That is, however, unquestionably the current state of the law. The purpose of a civil penalty is “primarily if not wholly protective in promoting the public interest in compliance”: Commonwealth of Australia v Director, Fair Work Building Industry Inspectorate (2015) 258 CLR 482; [2015] HCA 46 at [55] approving the statement by French J in Trade Practices Commission v CSR Ltd (1991) ATPR ¶41-076 at 52,152; [1990] FCA 521 at [40]; see also Australian Building and Construction Commissioner v Pattinson (2022) 274 CLR 450; [2022] HCA 13 at [15], [16], [42].

60 It follows that the “appropriate” pecuniary penalty (to use the word used in the relevant provisions in both the Corporations Act and the ASIC Act) is one that serves the object of deterrence, both specific and general. The Court must “attempt to put a price on contravention that is sufficiently high to deter repetition by the contravener and by others who might be tempted to contravene”; and the penalty must not be one which would be “regarded by [the] offender or others as an acceptable cost of doing business”: Pattinson at [15] and [17]; Australian Competition and Consumer Commission v TPG Internet Pty Ltd (2013) 250 CLR 640; [2013] HCA 54 at [66] citing with approval Singtel Optus Pty Ltd v Australian Competition and Consumer Commission (2012) 287 ALR 249; [2012] FCAFC 20 at 265 [62]. The penalty must also not be greater than is necessary to achieve the object of deterrence because “severity beyond that would be oppression” and the penalty must therefore be one which “strikes a reasonable balance between deterrence and oppressive severity”: Pattinson at [40]-[41].

Relevant factors

61 As the earlier consideration of the relevant pecuniary penalty provisions in both the Corporations Act and the ASIC Act revealed, both sets of provisions include a list of the “relevant matters” that the Court must take into account in determining a pecuniary penalty. The relevant matters in that list include: the nature and extent of the contravention; the nature and extent of any loss or damage suffered because of the contravention; the circumstances in which the contravention took place; and whether the person has previously been found by a court to have engaged in any similar conduct. The statutory list of relevant matters is, however, clearly not exhaustive. The Court must have regard to “all relevant matters”.

62 The matters or factors which might inform the assessment of such a penalty have been said to include both matters pertaining to the nature and character of the contravening conduct and matters pertaining to the character of the contravener: Pattinson at [18]-[19], [57]. The factors pertaining to the former generally include the circumstances in which the conduct took place, the deliberateness of the contravention and the period over which it extended. The factors pertaining to the latter generally include whether the contravener has shown a disposition to cooperate with the relevant regulator and, where the contravener is a company, the size of the company and whether the contravention arose out of the conduct of senior management or at a lower level. There is, however, no “rigid catalogue of matters for attention”: Pattinson at [19], citing with approval Australian Ophthalmic Supplies Pty Ltd v McAlary-Smith (2008) 165 FCR 560; [2008] FCAFC 8 at [91].

63 It is important to emphasise that, given that the purpose of imposing a pecuniary penalty is to deter, not to punish, the types of factors to which reference has been made are only relevant to the extent that they relate to deterrence: Pattinson at [44]. For example, the fact that a contravention of a civil penalty provision was particularly serious because it was deliberate, planned, concealed and carried out by senior management would tend to indicate that a higher penalty should be imposed because only a high penalty would be effective to deter contravening conduct of that nature. The fact that the contravening conduct was serious does not in and of itself compel a higher penalty because, unlike the imposition of sentences for criminal offending, pecuniary penalties are not imposed to punish or ensure that an offender gets his or her “just deserts”.

Relevance of the maximum penalty

64 While the maximum penalty that is prescribed for a contravention may be a relevant consideration when it comes to determining an appropriate pecuniary penalty, the maximum penalty does not constrain the exercise of the discretion beyond requiring “some reasonable relationship between the theoretical maximum and the final penalty imposed”: Pattinson at [55], citing with approval Australian Competition and Consumer Commission v Reckitt Benckiser (Australia) Pty Ltd (2016) 340 ALR 25; [2016] FCAFC 181 at [155]-[156]. The “reasonable relationship”, it would appear, is to be determined having regard to the fact that the maximum penalty is intended “to be imposed in respect of a contravention warranting the strongest deterrence within the prescribed cap” (Pattinson at [58]), not by reference to the fact that the maximum penalty is reserved for the worst category of contravening conduct, as is generally the case when imposing a sentence for a criminal offence: Pattinson at [49]-[51].

Double punishment, course of conduct and totality

65 Cases concerning the imposition of pecuniary penalties frequently refer to the principles that are said to apply when multiple civil penalty contraventions are committed during a single course of conduct. Similarly, reference is frequently made to the so-called “totality principle” which is said to apply when the Court is fixing pecuniary penalties for multiple contraventions. Both the course of conduct principle and the totality principle are derived from the principles that apply when sentencing for criminal offences. They address similar issues but are nevertheless conceptually distinct.

66 When sentencing for criminal offences, the course of conduct principle requires that, where an offender is to be sentenced for a “number of technically identifiable offences”, but the offender was “truly engaged upon one multi-faceted course of criminal conduct”, the sentencing court should avoid double punishment by ordering that the sentences for the separate offences be served concurrently, or partly concurrently, or by lowering the individual sentences: Attorney-General v Tichy (1982) 30 SASR 84 at 92-93; cited with approval in Johnson v The Queen (2004) 205 ALR 346; [2004] HCA 15 at [4].

67 The totality principle in criminal sentencing, on the other hand, requires the sentencing court, when passing a series of sentences in respect of separate offences, to review the aggregate sentence to ensure that it is “just and appropriate”, or “look at the totality of the criminal behaviour and ask itself what is the appropriate sentence for all the offences”: Mill v The Queen (1988) 166 CLR 59 at 63; [1988] HCA 70 at [8], adopting what was said in Thomas, Principles of Sentencing (Heinemann, 2nd ed, 1979) at 56-57.

68 As can be seen, both the course of conduct and totality principles are inextricably linked to the overarching principle that, when sentences are to be imposed for multiple offences, the sentencing court must be astute to avoid doubly punishing the offender in respect of overlapping offences and equally astute to ensure that the overall or effective sentence imposed on the offender is proportionate to the gravity of the offending conduct.

69 The course of conduct and totality principles do not directly apply to the fixing of pecuniary penalties. That is not only because, as has already been noted, pecuniary penalties are not imposed to punish, but also because the notion, drawn from the criminal law, that a penalty must be proportionate to the seriousness of the conduct that constituted the contravention does not apply when fixing pecuniary penalties: Pattinson at [38]. The course of conduct and totality concepts or principles may nevertheless be employed as “analytical tools” that might assist in the assessment of what penalty may be considered reasonably necessary to deter further contraventions: Pattinson at [45]. While the role that those principles may play as analytical tools was not explored in any real depth in Pattinson, the only logical or principled role they could play would appear to be to ensure that, in the case of multiple contraventions, the total penalty is not oppressive or unreasonable, in the sense that it is greater than necessary to achieve the object of deterrence.

Evidence in respect of penalty

70 The parties and the Court proceeded on the basis that all the evidence that was adduced at the liability stage was relevantly before the Court and could be considered in determining the appropriate pecuniary penalty. That evidence was discussed in considerable detail in the liability judgment. I do not propose to refer at length to that evidence in these reasons other than where it is necessary to resolve competing submissions concerning the nature and extent of EuropeFX’s contraventions. ASIC and EuropeFX did, however, tender some additional evidence which was said to be relevant to the fixing of appropriate penalties. It is accordingly necessary to briefly refer to that evidence.

ASIC’s evidence

71 ASIC adduced affidavit evidence from one of its officers which concerned EuropeFX’s compliance with document production notices issued to it pursuant to s 33 of the ASIC Act. ASIC submitted that the evidence of the officer was relevant to the question whether EuropeFX had cooperated with ASIC during its investigation. EuropeFX objected to that evidence on the basis of relevance. It submitted that the evidence was not relevant to the pecuniary penalties that the Court should impose essentially because it did not contend that cooperation should be taken into account as a mitigating factor. Nor, it was submitted, should any lack of cooperation be considered to be an aggravating factor.

72 I admitted the evidence of the ASIC officer concerning compliance with the production notices over EuropeFX’s objection, essentially because I consider that EuropeFX’s lack of cooperation with ASIC is a relevant factor to consider in determining the appropriate penalty. As discussed later, the language of mitigation and aggravation is not entirely apposite when it comes to determining pecuniary penalties. While EuropeFX’s lack of cooperation may not be a particularly weighty consideration in all the circumstances, in my view the evidence concerning cooperation was, and is, nonetheless of some relevance.

73 ASIC also adduced evidence from another officer which, in broad terms, concerned the size of the over-the-counter derivatives market in Australia and USG’s position in that market. The relevance and significance of that evidence is discussed later.

EuropeFX’s evidence

74 EuropeFX tendered a report prepared by a solicitor and “compliance consultant”, Ms Regina (Gina) Block, which purported to contain expert opinion evidence in respect of two broad issues or topics. The first issue concerned the legislative and regulatory regime in respect of holders of AFSLs and CARs and more specifically the duties and obligations that AFSL holders have in respect of their CARs. The second issue concerned whether USG had failed to adequately perform or fulfil its duties and obligations towards EuropeFX. ASIC objected to the tender of Ms Block’s report. I upheld that objection. My reasons for rejecting the evidence of Ms Block were and are as follows.

75 There were several fundamental problems with Ms Block’s evidence. The first problem was relevance. It may be accepted that the statutory and regulatory regime that governed the relationship between USG, as the holder of an AFSL, and EuropeFX, as USG’s CAR, was generally relevant not only to the question of liability, but also to the determination of the appropriate penalties to be imposed. The relevant statutory and regulatory regime was the subject of submissions at the liability stage of the proceeding and was addressed in the liability judgment to the extent that it was relevant to the issues that arose in respect of EuropeFX’s liability. More will be said about that shortly. The general nature of the legislative and regulatory regime, however, is not really a matter for expert opinion evidence and was largely not in dispute or contest. The relevant provisions of the Corporations Act and the ASIC Act speak for themselves and their operation is tolerably clear. ASIC’s published Regulatory Guide 105, which was addressed by Ms Block, also essentially speaks for itself and the content and operation of the guide was not in dispute. What was in issue, however, was Ms Block’s evidence concerning USG’s failure to adequately perform or fulfil its duties and obligations towards EuropeFX and the relevance of that evidence to the question of the appropriate pecuniary penalties that should be imposed on EuropeFX.

76 When pressed to explain the relevance of Ms Block’s evidence to the question of the pecuniary penalties to be imposed on EuropeFX, senior counsel for EuropeFX submitted that the evidence was relevant in two ways. First, the evidence was said to be relevant to EuropeFX’s culpability and the deliberateness of its contravening conduct. In short, it was submitted that Ms Block’s evidence was that the relevant “compliance systems” were USG’s responsibility, not EuropeFX’s responsibility, and that EuropeFX’s contraventions were a result of USG’s failings, not EuropeFX’s failings. Second, it was said that Ms Block’s evidence was relevant to the relationship between the penalties to be imposed on USG and EuropeFX respectively. It was, in short, submitted that Ms Block’s evidence supported the proposition that the penalties to be imposed on EuropeFX should be less than the penalties to be imposed on USG.