Federal Court of Australia

AIM Mining Corporation Limited v Wiluna Mining Corporation Limited [2026] FCA 697

File number(s): | WAD 149 of 2026 |

Judgment of: | VANDONGEN J |

Date of judgment: | 14 May 2026 |

Date of publication of reasons | 5 June 2026 |

Catchwords: | CORPORATIONS - application for interlocutory injunction restraining resolution from being put to members at general meeting under s 1324 of the Corporations Act 2001 (Cth) and s 23 of the Federal Court of Australia Act 1976 (Cth) - whether there is a serious question to be tried - application dismissed |

Legislation: | Corporations Act 2001 (Cth) ss 9, 232, 233, 606, 608, 611, 1041H, 1324 Evidence Act 1995 (Cth) ss 79, 135 Federal Court of Australia Act 1976 (Cth) s 23 |

Cases cited: | Armstrong World Industries (Australia) Pty Ltd v Parma [2014] FCA 743; (2014) 101 ACSR 150 Australian Broadcasting Corporation v Lenah Game Meats Pty Limited [2001] HCA 63; (2001) 208 CLR 199 Australian Competition and Consumer Commission v TPG Internet Pty Ltd [2020] FCAFC 130; (2020) 278 FCR 450 Australian Securities and Investments Commission v Merhi (No 2) [2025] FCA 1343 Australian Securities and Investments Commission v Vanguard Investments Australia Ltd [2024] FCA 308 Beecham Group Limited v Bristol Laboratories Pty Limited (1968) 118 CLR 618 Bulfin v Bebarfald's Limited (1938) 38 SR (NSW) 423 Campbell v Backoffice Investments Pty Ltd [2009] HCA 25; (2009) 238 CLR 304 Ceni Enterprises Pty Ltd (in liq) v Sykes, in the matter of Ceni Enterprises Pty Ltd (in liq) [2024] FCA 842 Chequepoint Securities Ltd v Claremont Petroleum NL (1986) 11 ACLR 94 Chowder Bay Pty Ltd v Paganin [2018] FCAFC 25 Clarke v Australian Computer Society Incorporated [2019] FCA 2175 Devereaux Holdings Pty Ltd v Pelsart Resources NL (No 2) (1985) 9 ACLR 956 Fraser v NRMA Holdings Limited (1995) 55 FCR 452 Global Sportsman Pty Ltd v Mirror Newspapers Pty Ltd (1984) 2 FCR 82 Kahler v Castle Hill Country Club Ltd [2017] NSWSC 851 Lion Nathan Australia Pty Ltd v Coopers Brewery Ltd [2005] FCA 1426; (2005) 55 ACSR 583 Minister for Immigration and Multicultural Affairs v MZAPC [2025] HCA 5; (2025) 185 ALD 427 Samsung Electronics Company Ltd v Apple Inc [2011] FCAFC 156; (2011) 217 FCR 238 Smart EV Solutions Pty Ltd v Guy [2023] FCA 1580 Yorke v Lucas (1985) 158 CLR 661 |

Division: | General Division |

Registry: | Western Australia |

National Practice Area: | Commercial and Corporations |

Sub-area: | Corporations and Corporate Insolvency |

Number of paragraphs: | 124 |

Date of hearing: | 14 May 2026 |

Counsel for the Plaintiff: | Mr B Roberts KC with Mr S Tomasich |

Solicitor for the Plaintiff: | Lavan |

Counsel for the Defendant: | Mr B Dharmananda SC with Mr PA Walker |

Solicitor for the Defendant: | Mallesons |

Counsel for the Interested Party: | Mr AJ Papamatheos SC with Mr JD Birch |

Solicitor for the Interested Party: | HWL Ebsworth Lawyers |

ORDERS

WAD 149 of 2026 | ||

| ||

BETWEEN: | AIM MINING CORPORATION LIMITED Plaintiff | |

AND: | WILUNA MINING CORPORATION LIMITED Defendant | |

BYRNECUT AUSTRALIA PTY LTD Interested Party | ||

order made by: | VANDONGEN J |

DATE OF ORDER: | 14 MAY 2026 |

THE COURT ORDERS THAT:

1. The interlocutory process filed by the plaintiff on 12 May 2026 is dismissed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

VANDONGEN J:

1 The defendant in these proceedings, Wiluna Mining Corporation Limited (Wiluna), is an unlisted public gold mining company. Wiluna entered voluntary administration in July 2022 and executed a deed of company arrangement (DOCA) in July 2023, which effectuated in December 2025. Control of the company was then returned to its board.

2 On 23 February 2026, a substantial shareholder of Wiluna, Byrnecut Australia Pty Ltd (Byrnecut), entered into share purchase agreements with two minority shareholders of Wiluna to acquire a total of approximately 17.7 million ordinary Wiluna shares at a price of $0.725 per share (SPAs). As I will shortly explain, because those transactions would see Brynecut's voting power in Wiluna increase from 24.26% to 29.50%, the acquisition by Byrnecut of Wiluna shares under the SPAs required approval by Wiluna shareholders by resolution passed at a general meeting.

3 In late April 2026, Wiluna issued a notice for a general meeting to take place on 15 May 2026 (NoM). It was intended that several resolutions would be put to Wiluna shareholders at that meeting to consider and, if thought fit, pass, including two resolutions giving approval for the acquisition of shares by Byrnecut under the SPAs (Resolutions).

4 The plaintiff, AIM Mining Corporation Limited (AIM), is a member of the 'Creasy Group' which is a privately-run group of companies that have interests in mining and resources. AIM, which holds approximately 8.80% of the issued shares in Wiluna, has over time expressed interest in transacting with Wiluna including as a potential acquirer of Wiluna.

5 By an originating process filed on 12 May 2026, AIM sought orders permanently restraining Wiluna from putting the Resolutions to its shareholders. By an interlocutory process, also filed on 12 May 2026, AIM sought an interlocutory injunction to similar effect.

6 AIM's application for an interlocutory injunction came on for an urgent hearing before me as duty judge. As senior counsel for AIM confirmed at the hearing, AIM's case for interlocutory injunctive relief was based on one or more of the following grounds:

(1) Wiluna had failed to comply with, or was proposing not to comply with, item 7(b) of s 611 of the Corporations Act 2001 (Cth).

(2) Wiluna had contravened, or was proposing to contravene, s 1041H of the Corporations Act, by engaging in conduct, in relation to its shares, that was misleading or deceptive or was likely to mislead or deceive.

(3) The directors of Wiluna had failed to provide full and fair disclosure of information material to its shareholders making an informed judgment on the Resolutions.

7 At the hearing I granted leave to Byrnecut to appear as an interested party.

8 After hearing submissions from all parties, I decided to dismiss AIM's application for an interlocutory injunction. What follows are my reasons for reaching that decision.

9 It is convenient to begin by identifying the uncontentious principles that must be applied when determining an application for an interlocutory injunction.

The relevant legal principles to be applied

10 AIM's application relied on the Court's power to grant an interim injunction under s 1324(4) of the Corporations Act 2001 (Cth), pending determination of its application for final injunctive relief under s 1324(1). AIM also relied on the Court's power under s 23 of the Federal Court of Australia Act 1976 (Cth).

11 The parties approached AIM's application for an interlocutory injunction on the basis that it fell to be resolved according to the well-established principles that apply to the exercise of this Court's equitable jurisdiction to grant an injunction: Smart EV Solutions Pty Ltd v Guy [2023] FCA 1580 at [28]. However, insofar as AIM sought to rely on s 1324(4) of the Corporations Act, it should be noted that, as Beach J observed in Armstrong World Industries (Australia) Pty Ltd v Parma [2014] FCA 743; (2014) 101 ACSR 150 at [22], the jurisdiction that the Court may exercise under s 1324(4) differs from the equitable jurisdiction as there is at least one additional factor that should be taken into account. That additional factor is whether the injunction would have some utility, or would serve some purpose, within the contemplation of the Corporations Act such as preventing or ameliorating a threatened contravention of that Act: see also Australian Securities and Investments Commission v Merhi (No 2) [2025] FCA 1343 at [50]; and Ceni Enterprises Pty Ltd (in liq) v Sykes, in the matter of Ceni Enterprises Pty Ltd (in liq) [2024] FCA 842 at [71].

12 Nevertheless, as it was not suggested by any party that AIM's application for an interlocutory injunction turned on whether it would have some utility, or would serve some purpose, within the contemplation of the Corporations Act, I dealt with the application under s 1324(4) on the basis that the traditional considerations that apply in the context of applications for interlocutory injunctions were the only relevant considerations.

13 Turning to those traditional considerations. In Minister for Immigration and Multicultural Affairs v MZAPC [2025] HCA 5; (2025) 185 ALD 427 at [23], Gageler CJ, Gordon, Gleeson and Jagot JJ (with whom Edelman J agreed at [54] and Beech-Jones J agreed at [107]) explained that the primary purpose of an interlocutory injunction is to keep matters in status quo until the rights of the parties can be determined at trial. Their Honours also said, quoting Australian Broadcasting Corporation v Lenah Game Meats Pty Limited [2001] HCA 63; (2001) 208 CLR 199 (Lenah Game Meats) at [11] (Gleeson CJ), that:

[t]he condition precedent remains that 'a plaintiff seeking an interlocutory injunction must be able to show sufficient colour of right to the final relief, in aid of which interlocutory relief is sought', the usual description of the sufficiency of that colour of right being the establishment of a serious question to be tried or a prima facie case.

14 In support of that proposition, their Honours also referred to the passage in Lenah Game Meats at [13], where Gleeson CJ referred to the following passage from the reasons of Mason ACJ in Castlemaine Tooheys Limited v The State of South Australia (1986) 161 CLR 148 at 153:

In order to secure such an injunction the plaintiff must show (1) that there is a serious question to be tried or that the plaintiff has made out a prima facie case, in the sense that if the evidence remains as it is there is a probability that at the trial of the action the plaintiff will be held entitled to relief; (2) that [the plaintiff] will suffer irreparable injury for which damages will not be an adequate compensation unless an injunction is granted; and (3) that the balance of convenience favours the granting of an injunction.

15 When an interlocutory injunction is sought in respect of private rights, it is necessary to identify the legal or equitable rights which are to be determined at trial, and in respect of which final relief is sought: Samsung Electronics Company Ltd v Apple Inc [2011] FCAFC 156; (2011) 217 FCR 238 at [52], citing Lenah Game Meats at [8] to [21] (Gleeson CJ), [59] to [61] (Gaudron J), [86] to[92], [98] to[100], [105] (Gummow and Hayne JJ). Accordingly, what will be a sufficient likelihood of success will depend on the nature of the rights asserted and the practical consequences that are likely to flow from the order sought: Beecham Group Limited v Bristol Laboratories Pty Limited (1968) 118 CLR 618 at 622.

16 Whether there is a prima facie case, and whether the balance of convenience and justice favours the grant of an injunction, are related inquiries and they should not be considered in isolation from each other. The apparent strength of the substantive cases of the parties will often be an important consideration to be weighed in the balance: Samsung at [67]. Further, the interaction between the Court's assessment of the likely harm to the applicant if no injunction is granted, and its assessment of the adequacy of damages as a remedy, will always be an important factor in the Court's determination of where the balance of convenience and justice lies: Samsung at [63].

17 Having summarised the relevant principles to be applied it is convenient at this stage to identify the relevant rights which are to be determined at trial and in respect of which final relief is sought by AIM.

The rights to be determined at trial

18 In its originating process, AIM applies for orders that Wiluna be restrained from putting the Resolutions to its members, relying on ss 232, 233, 1041H and/or 1324 of the Corporations Act, as well as on the 'inherent power of this Court'. In that regard, AIM claims that:

(1) The NoM omits material information in contravention of item 7(b) of s 611 of the Corporations Act.

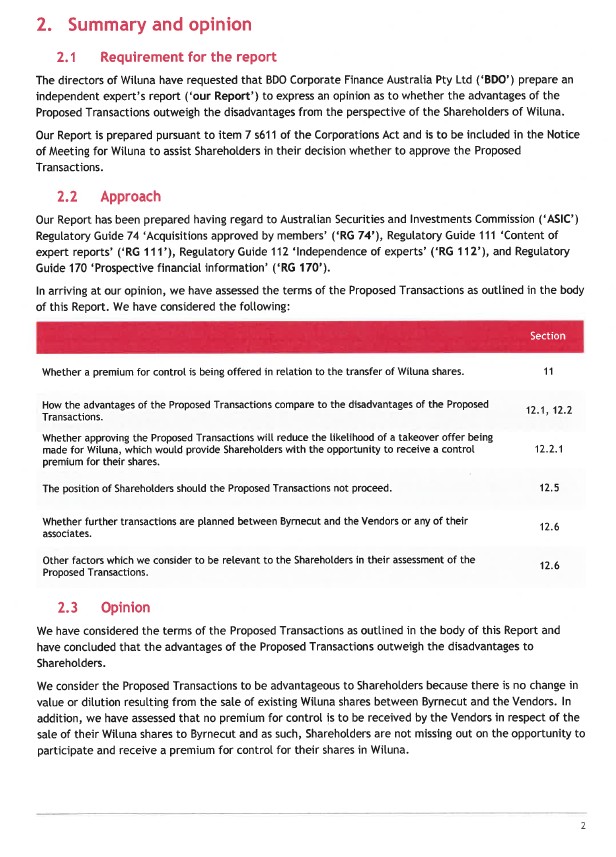

(2) The NoM is misleading or deceptive, or is likely to mislead or deceive, in relation to a financial product or a financial service, contrary to s 1041H of the Corporations Act.

(3) Full and fair disclosure of matters, material to an informed judgment by Wiluna shareholders has not been given by Wiluna's directors.

(4) If the Resolutions are passed it will constitute conduct that is contrary to the interests of Wiluna shareholders as a whole, or are oppressive to, unfairly prejudicial to, or unfairly discriminatory against, a Wiluna shareholder or shareholders, in contravention of s 232 of the Corporations Act.

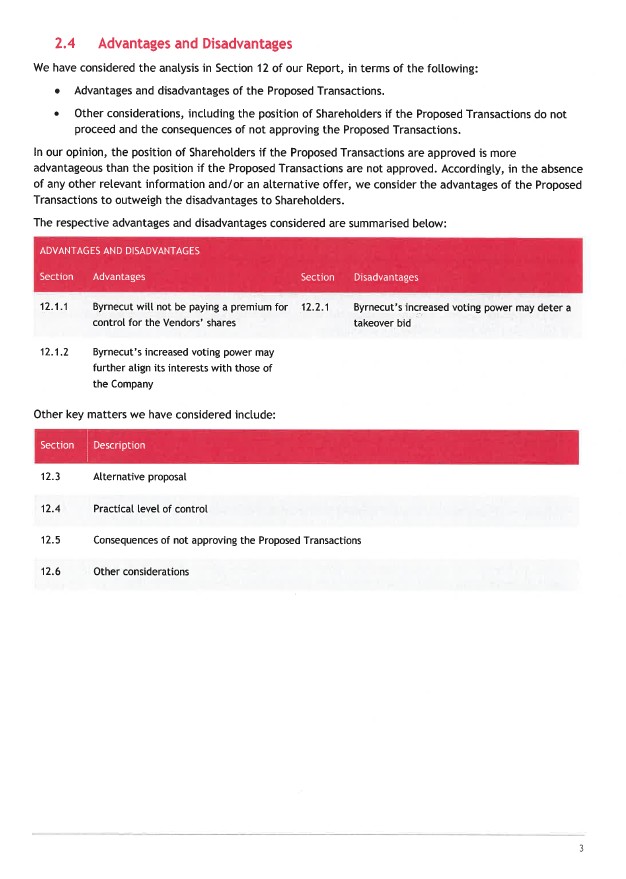

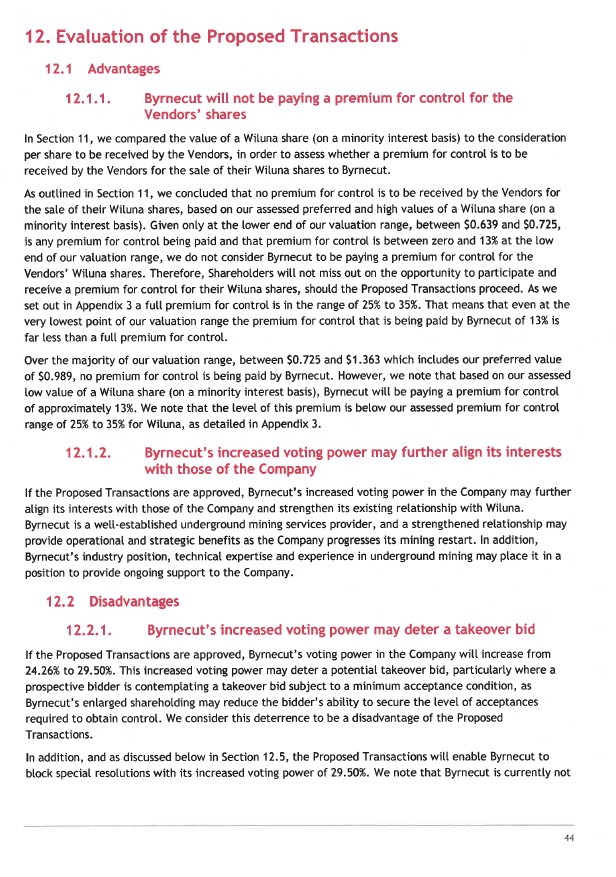

19 By its originating process, AIM also seeks various forms of declaratory relief as well as orders under s 233 of the Corporations Act. However, senior counsel for AIM informed the Court that it did not seek an interlocutory injunction in aid of any claims made under s 232, or any orders under s 233, of the Corporations Act. As AIM's interlocutory process itself made clear, AIM's application for an interlocutory injunction was based on the first three claims identified at [18] of these reasons.

20 As I have already alluded to, the first of those claims is concerned with a purported contravention of s 611 of the Corporations Act. To properly understand this aspect of AIM's case, to which I will return later in these reasons, it is necessary to reproduce some relevant parts of s 606:

606 Prohibition on certain acquisitions of relevant interests in voting shares

Acquisition of relevant interests in voting shares through transaction entered into by or on behalf of person acquiring relevant interest

(1) A person must not acquire a relevant interest in issued voting shares in a company if:

(a) the company is:

(i) a listed company; or

(ii) an unlisted company with more than 50 members; and

(b) the person acquiring the interest does so through a transaction in relation to securities entered into by or on behalf of the person; and

(c) because of the transaction, that person's or someone else's voting power in the company increases:

(i) from 20% or below to more than 20%; or

(ii) from a starting point that is above 20% and below 90%.

....

(1A) However, the person may acquire the relevant interest under one of the exceptions set out in section 611 without contravening subsection (1).

21 For the purposes of this matter, a person has a 'relevant interest' in securities, such as shares, if they are the holder of the securities: s 608(1)(a). A 'voting share' is, relevantly, an issued share in a company that carries certain voting rights: s 9.

22 Section 606(4A) provides that a person commits an offence if they contravene s 606(1).

23 Section 611, which is expressly referred to in s 606(1A), contains a table that identifies the types of acquisitions of relevant interests in a company's voting shares that are exempt from the prohibition in s 606(1). For the purposes of these proceedings, it is only necessary to reproduce item 7 of that table:

Approval by resolution of target

7 An acquisition approved previously by a resolution passed at a general meeting of the company in which the acquisition is made, if:

(a) no votes are cast in favour of the resolution by:

(i) the person proposing to make the acquisition and their associates; or

(ii) the persons (if any) from whom the acquisition is to be made and their associates; and

(b) the members of the company were given all information known to the person proposing to make the acquisition or their associates, or known to the company, that was material to the decision on how to vote on the resolution, including:

(i) the identity of the person proposing to make the acquisition and their associates; and

(ii) the maximum extent of the increase in that person's voting power in the company that would result from the acquisition; and

(iii) the voting power that person would have as a result of the acquisition; and

(iv) the maximum extent of the increase in the voting power of each of that person's associates that would result from the acquisition; and

(v) the voting power that each of that person's associates would have as a result of the acquisition.

24 AIM's application for an interlocutory injunction focussed on para (b) of item 7. Put simply, AIM's case was that before being asked to consider and, if thought fit, pass the Resolutions, the Wiluna shareholders would not have been given all the information known to Wiluna that would be material to the decision on how to vote on the Resolutions. More specifically, AIM's case was that the information in the NoM that was given to the members of Wiluna was misleading or omitted material information.

25 The second and third claims on which AIM relied also concentrated on the information in the NoM and relied upon substantially the same contention that the information was misleading and that there had been a failure to disclose all material information.

26 The second claim relied on s 1041H(1) of the Corporations Act, which is in the following relevant terms:

1041H Misleading or deceptive conduct (civil liability only)

(1) A person must not, in this jurisdiction, engage in conduct, in relation to a financial product or a financial service, that is misleading or deceptive or is likely to mislead or deceive.

27 As I will explain in more detail later in these reasons, AIM's case was that, by issuing the NoM to its shareholders, Wiluna had engaged in conduct, and continued to engage in conduct on an ongoing basis, in relation to its shares that was misleading or deceptive or likely to mislead or deceive.

28 Insofar as the third claim is concerned, AIM's case was that the directors of Wiluna owe a fiduciary duty not to mislead its shareholders and to make full disclosure of all of material facts so as to fully and fairly inform those shareholders about the Resolutions. In that regard, AIM relied on various statements of principle in cases such as Devereaux Holdings Pty Ltd v Pelsart Resources NL (No 2) (1985) 9 ACLR 956; Bulfin v Bebarfald's Limited (1938) 38 SR (NSW) 423; Lion Nathan Australia Pty Ltd v Coopers Brewery Ltd [2005] FCA 1426; (2005) 55 ACSR 583; and Kahler v Castle Hill Country Club Ltd [2017] NSWSC 851.

29 All of these grounds were primarily concerned with an independent expert report authored by two directors of BDO Corporate Finance Australia Pty Ltd (BDO) dated 21 April 2026, which was annexed to the NoM (BDO Report). AIM's case was also concerned with the fact that the NoM informed Wiluna shareholders that, if they were to appoint the Chair of the meeting as their proxy, any undirected proxies would be taken to amount to a direction, and express consent, for the Chair to vote in favour of the Resolutions.

30 Before summarising the relevant parts of the BDO Report, and explaining in more detail AIM's case in relation to the undirected proxies, it is convenient to identify the evidence on which the parties relied.

The evidence

31 AIM relied on the following affidavits:

Affidavit affirmed on 11 May 2026 by Hui Guo

32 Ms Guo is a director and the company secretary of AIM, and the group general manager of the Creasy Group. In her affidavit, Ms Guo provided a brief description of the Creasy Group's activities and outlined various takeover activity that has occurred with respect to Wiluna, including details of several proposals to acquire Wiluna that the Creasy Group has put since early 2024. Ms Guo also summarised what she described as the 'significant interest' that has been shown by other parties in acquiring Wiluna.

33 According to Ms Guo, Wiluna issued an announcement to its shareholders on 12 March 2026 regarding a proposed acquisition by Byrnecut of shares in Wiluna from certain Wiluna shareholders. Further, Ms Guo attested that the NoM was issued on 22 April 2026, in which approval was sought for several resolutions, including the Resolutions seeking shareholder approval for the acquisition of Wiluna shares by Byrnecut. Ms Guo gave evidence that the NoM was accompanied by a letter to shareholders from the Chairman of Wiluna (Letter to Shareholders) together with the BDO Report. Copies of all of those documents were annexed to Ms Guo's affidavit. I will return to describe the NoM, Letter to Shareholders and BDO Report in more detail later in these reasons. At this stage it is enough to note that the Resolutions sought approval from Wiluna shareholders for the acquisition of Wiluna shares by Byrnecut pursuant to the SPAs, which would result in Byrnecut holding 29.50% of the voting power in Wiluna.

34 Ms Guo also gave evidence that, based on her professional experience, if Byrnecut were to acquire Wiluna shares pursuant to the SPAs:

(1) Byrnecut would then be able to block special resolutions, and would thereby be able to block any takeover of Wiluna via a scheme of arrangement under Pt 5.1 of the Corporations Act;

(2) the acquisition would impair AIM's ability to offer to acquire further shares in Wiluna; and

(3) the acquisition would have a 'significant deterrent' effect on AIM and on any other bidder for Wiluna.

Affidavits of Myles David Allen affirmed on 11, 12 and 13 May 2026

35 Mr Allen is a solicitor employed by Lavan, the solicitor for the plaintiff in these proceedings. To his first affidavit, Mr Allen annexed copies of Wiluna's constitution as well as company searches for AIM and Wiluna. To both his first and his second affidavits, Mr Allen attached a significant amount of correspondence that had passed between Lavan and Mallesons, the solicitor for Wiluna. It is unnecessary to summarise that correspondence.

36 In his third affidavit, Mr Allen gave evidence about effecting service of the documents filed on behalf of AIM in these proceedings on Byrnecut as well as on the other parties to the SPA.

Affidavits of Simon Powell James, affirmed on 12 May 2026, and Evan William Wright, affirmed on 13 May 2026

37 Mr James is a partner of HLB Mann Judd, and is a chartered accountant and registered company auditor. Mr Wright is a senior managing director in the Disputes and Economics practice of Ankura Consulting (Australia) Pty Ltd, and an authorised representative of that company. Both Mr James and Mr Wright were engaged by Lavan, on behalf of the plaintiff, to prepare independent expert reports containing answers to four specific questions. Their reports were annexed to their respective affidavits.

38 Objections were raised to the admissibility of the affidavits of Mr James and Mr Wright. I will deal with those objections later in these reasons.

39 Wiluna relied on two affidavits that were affirmed on 13 May 2026 by Samuel James Dundas, a partner of Mallesons:

Samuel James Dundas' first affidavit

40 In the first of his affidavits, Mr Dundas gave evidence about:

(1) the various proceedings in which AIM and Wiluna have been involved since around October 2025, in the Supreme Court of Western Australia and the Takeovers Panel;

(2) the correspondence that had passed between Lavan and Mallesons;

(3) AIM's previous proposals to acquire Wiluna; and

(4) the number of undirected proxies that had been submitted in advance of the general meeting.

41 Mr Dundas also referred to Wiluna's engagement with the Australian Securities and Investments Commission (ASIC) regarding the NoM and the general meeting. In that regard, Mr Dundas attested that, on 10 April 2026, Mallesons lodged a draft NoM and a draft of the BDO Report with ASIC for the purpose of seeking feedback in relation to Wiluna's intention to seek approval at a general meeting for the acquisition of shares by Byrnecut under the SPAs pursuant to item 7 of s 611 of the Corporations Act. According to Mr Dundas, ASIC informed Mallesons on 20 April 2026 that it had no further comments in relation to those documents.

42 Mr Dundas also said that ASIC had been informed about the dispatch of the NoM, that ASIC had been advised about comments AIM made about the BDO Report, and that ASIC had been provided with BDO's response to AIM's comments.

43 Finally, Mr Dundas annexed a copy of an independent expert report prepared by HLB Mann Judd for a general meeting of another company, Takoradi Limited, in 2014.

Samuel James Dundas' second affidavit

44 To his second affidavit Mr Dundas annexed a letter from the authors of the BDO Report dated 13 May 2026. In that letter, the authors provided responses to the reports of Mr James and Mr Wright and confirmed that, having considered the contents of those reports, they were of the view that no material matters had been raised that were not appropriately disclosed in the BDO Report and, as such, no supplementary report was required.

45 Byrnecut did not read any affidavit material.

46 Having identified the evidence on which the parties sought to rely, I will now turn to the question of whether AIM established that there was a serious question to be tried.

Is there a serious question to be tried?

47 Before explaining why I was ultimately not satisfied that there was a serious question to be tried, it is necessary to say something more about AIM's case. In that regard, a major focus of AIM's case for an interlocutory injunction was on the NoM and, more specifically, the BDO Report that was annexed to the NoM.

48 The NoM comprised the following documents:

(1) the Letter to Shareholders;

(2) a document headed 'Attendance and Voting Information';

(3) a Notice of General Meeting;

(4) an Explanatory Statement; and

(5) two annexures, comprising a statement by Byrnecut and the BDO Report.

49 The Letter to Shareholders relevantly included the following summary of the Resolutions:

RESOLUTIONS 1 & 2 - NO RECOMMENDATION FROM THE BOARD

These resolutions seek to approve Byrnecut Australia Pty Ltd acquiring a combined ~17.7 million Shares from two existing shareholders at $0.725 per share. No new shares are being issued. If the Proposed Transactions are approved, Byrnecut will increase its Voting Power from the current 24.26% to 29.50%.

[Wiluna] engaged [BDO] to prepare and provide an independent expert's report in relation to the Proposed Transactions. [BDO] has concluded that the advantages outweigh the disadvantages for non-associated shareholders. A copy of the [BDO Report] is attached to the Explanatory Statement as Annexure B. I urge you to read the [BDO Report] in full.

The Directors of [Wiluna] have determined not to give a recommendation on how non-associated Shareholders should vote on [the Resolutions], for the reasons set out in section 1.10 of the Explanatory Statement in the Notice of Meeting.

However, if you appoint the Chair as your proxy, and you do not include an express voting direction on your Proxy Form, you will be directing, and expressly consenting to the Chair voting in favour of [the Resolutions].

50 The Attendance and Voting Information document also included a statement to the effect that the Chair of the meeting intended to vote all undirected proxies in favour of the Resolutions.

51 The Notice of General Meeting set out the Resolutions in full, together with the following information relating to the Resolutions:

Independent Expert's Report. Shareholders should carefully consider the report prepared by [BDO] for the purposes of the Shareholder approval. The [BDO Report] comments on whether the advantages of the Sale contemplated by Resolution 1 outweigh the disadvantages of the Sale to the non-associated Shareholders.

The opinion of [BDO] is that the advantages of the Sale of the [relevant] Shares to Byrnecut and the resulting increase in the Voting Power of Byrnecut in [Wiluna] outweigh the disadvantages of the Sale to the non-associated Shareholders.

52 Further information about the Resolutions was set out in the Explanatory Statement. Relevantly, there was information about the statutory and commercial context in which the Resolutions were being put to Wiluna shareholders, as well as the following statement about the BDO Report:

[Wiluna] engaged [BDO] to prepare and provide an independent expert's report (a copy of which is attached to this Explanatory Statement as Annexure B). Shareholders are urged to carefully read the [BDO Report] to understand the scope of the report, the methodology of the valuation and the sources of information and assumptions made.

The [BDO Report] is also available on [Wiluna's] website at www.wilunamining.com.au.

53 The Explanatory Statement also included information about the SPAs, including the conditions of the proposed transactions, the scheduled completion date and the fact that the SPAs would both automatically terminate after three months, in the event the relevant transaction had not completed.

54 Under a heading 'Advantages - Resolutions 1 and 2', the Explanatory Statement read:

The Directors are of the view that the following non-exhaustive list of advantages may be relevant to a Shareholder's decision on how to vote on [the Resolutions].

(a) Byrnecut is a strong supporter of [Wiluna]. It has supported [Wiluna's] strategic goals through its external administration process, including by providing funding for: (i) working capital under the Byrnecut Notes early in the deed administration process in 2023; and (ii) payment to the [Wiluna's] Creditors' Trust (which enabled [Wiluna's] participating former unsecured creditors to be paid 100 cents in the dollar) near the end of the external administration process in 2025. A Byrnecut Associate, Byrnecut Offshore Pty Ltd, also agreed to amend the terms of the secured loan to [Wiluna] to allow the Creditors' Trust to be repaid before the secured loan is paid off. The Proposed Transactions will further the strategic alignment of interests between [Wiluna] and Byrnecut. In addition, as stated in the Byrnecut Statement, it supports [Wiluna's] current direction and does not intend to seek any change to the business of [Wiluna].

(b) [BDO] has concluded that non-associated Shareholders are not missing out on the opportunity to participate and receive a premium for control for their Shares, as Byrnecut is not paying a premium for control for [its purchase of Wiluna shares]. Shareholders should read the [BDO Report] in full for further information in relation to this conclusion.

(c) [BDO] has concluded that the advantages of the Proposed Transactions outweigh the disadvantages to the non-associated Shareholders.

55 The Explanatory Statement also included an indication by the Directors that they were of the view that a further list of disadvantages may be relevant to a shareholder's decision on how to vote on the Resolutions, namely:

(1) The purchase by Byrnecut of shares under the SPAs would increase its voting power from 24.26% to 29.50%. This increase may deter a potential takeover bid by a third party and make Byrnecut's power to block special resolutions definite. However, in any event, Byrnecut would also be able to acquire another 3% of shares in the future as permitted by the exemption in item 9 of s 611 of the Corporations Act, under the so-called 'creep rule'.

(2) By increasing its voting power, Byrnecut might see an incremental increase in its ability to influence Wiluna's business, operations and financial performance, and the interests of Byrnecut may not always be consistent with the interests of all other Wiluna shareholders.

56 The Explanatory Statement made further reference to the BDO Report in the following terms:

1.9. Independent Expert's Report

[Wiluna] engaged [BDO] to prepare and provide an independent expert's report (a copy of which is attached to this Explanatory Statement as Annexure B).

The [BDO Report] includes an independent examination of the Proposed Transactions, to assist non-associated Shareholders to assess the merits of, and decide whether to approve each Proposed Transaction.

The [BDO Report] concludes that the advantages of the Proposed Transactions contemplated by [the Resolutions] outweigh the disadvantages of the Sale to the non-associated Shareholders.

[BDO] notes certain key advantages and disadvantages of the proposal raised in [the Resolutions] to [Wiluna] and to Shareholders not associated with Byrnecut. Those advantages and disadvantages are set out in Section 12 of the [BDO Report].

Shareholders should carefully consider the full [BDO Report] prepared by [BDO] for the purposes of the Shareholder approval pursuant to [the Resolutions] to understand the scope of the report, the methodology of the valuation and the sources of information and assumptions made.

Shareholders should read the [BDO Report] in its entirety before deciding how to vote on [the Resolutions].

57 The Explanatory Statement also included the following concerning the recommendations of the Wiluna directors in connection with the Resolutions:

1.10. Recommendation of the Directors

The Directors do not have any material interest in the Proposed Transactions.

The Directors of [Wiluna] have determined not to give a recommendation on how non-associated Shareholders should vote on [the Resolutions], for the reasons below:

[various reasons were set out here]

The Directors are not aware of any other information, other than as set out in this Explanatory Statement and the accompanying [BDO Report] that would reasonably be required by Shareholders to allow them to make a decision as to whether it is in the best interests of [Wiluna] to pass [the Resolutions].

If you appoint the Chair as your proxy, and you do not include an express voting direction on your Proxy Form, you will be directing, and expressly consenting to the Chair voting in favour of [the Resolutions].

58 Also annexed to the NoM was a statement by Byrnecut given to Wiluna to facilitate its preparation and prompt dispatch of the NoM. It is unnecessary to summarise the Byrnecut statement, other than to note that it included a statement that, as an underground mining service provider, to the extent that a tender may be issued by Wiluna for those sorts of services, Brynecut would look to submit a tender in a market competitive tender process. Otherwise, there were no contracts or proposed contracts between Wiluna and Byrnecut. The Byrnecut statement also set out Byrnecut's present intentions with respect to Wiluna in the event shareholders approved the acquisition of shares. In summary, Byrnecut indicated that it supported Wiluna's current direction and did not seek to make any change to Wiluna's business, and that it had no other relevant present intentions with respect to Wiluna.

59 The final document to which reference must be made is the BDO Report itself.

60 The BDO Report noted that the directors of Wiluna had requested that BDO provide an independent expert's report to express an opinion as to whether the advantages of the proposed acquisition of shares by Byrnecut outweigh the disadvantages from the perspective of Wiluna shareholders. Given the centrality of the BDO Report to AIM's case, I have attached the relevant passages taken from that report in an annexure to these reasons.

61 According the BDO Report, regard was had to various ASIC regulatory guides in its preparation, including ASIC Regulatory Guide 111 (ASIC RG 111). ASIC RG 111 provides guidance on the content of expert reports, and how an expert can help security holders make informed decisions about transactions, including transactions involving the acquisition of issued voting shares for the purposes of ss 606(1) and 611 of the Corporations Act. Relevantly, ASIC RG 111 provides that, for the purposes of the approval for the sale of shares that is required by item 7 of s 611, an expert should identify the advantages and disadvantages of a relevant proposal to security holders not associated with the transaction. In that regard, the ASIC RG 111 indicates that the expert should provide an opinion either: (a) that the advantages of the proposal outweigh the disadvantages; or (b) that the disadvantages of the proposal outweigh the advantages.

62 ASIC RG 111 further provides that a specific issue the expert should determine is whether the vendor is to receive a premium for control, stating that:

[t]he greater the control premium, the greater the advantages of the transaction to the non-associated holders would need to be to support a finding that the advantages of the proposal outweighed the disadvantages. These other advantages may come, for example, from a better long-term profit outlook as the incoming security holder offers superior management skills.

63 As may be seen from the extracts taken from the BDO Report that are annexed to these reasons, BDO identified that there were two advantages of the proposed acquisition of Wiluna shares by Byrnecut:

(1) Byrnecut will not be paying a premium for control in its acquisition of the shares; and

(2) Byrnecut's increased voting power may further align its interests with those of Wiluna.

64 One disadvantage was identified in the BDO Report, namely that Byrnecut's increased voting power may deter a takeover bid.

65 On this basis, an opinion about the 'Proposed Transactions' (namely, Byrnecut's acquisition of Wiluna shares under the SPAs) was expressed in the BDO Report in the following terms:

We have considered the analysis in Section 12 of our Report, in terms of the following:

• Advantages and disadvantages of the Proposed Transactions.

• Other considerations, including the position of Shareholders if the Proposed Transactions do not proceed and the consequences of not approving the Proposed Transactions.

In our opinion, the position of Shareholders if the Proposed Transactions are approved is more advantageous than the position if the Proposed Transactions are not approved. Accordingly, in the absence of any other relevant information and/or an alternative offer, we consider the advantages of the Proposed Transactions to outweigh the disadvantages to Shareholders.

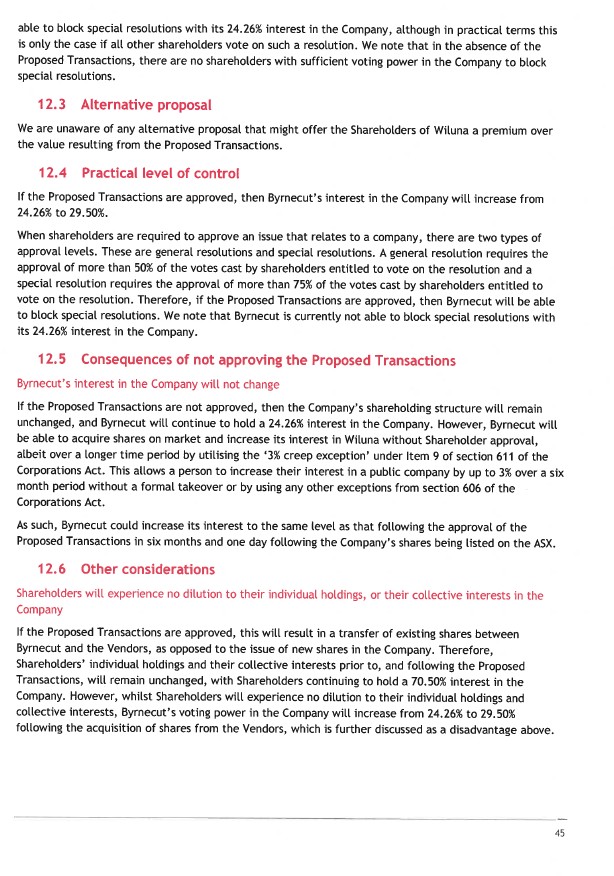

66 The 'other considerations' to which reference was made were the fact that:

(1) the practical level of control that would flow from Byrnecut's proposed acquisition, in the sense that Byrnecut would then be in a unilateral position to block special resolutions;

(2) if the acquisition did not proceed then, under the exemption in item 9 of s 611, Byrnecut could, in six months and one day following Wiluna shares being listed on the ASX, increase its interest to the same level as that following the acquisition;

(3) Wiluna shareholders would not experience any dilution to their individual holdings or collective interest in the company;

(4) Byrnecut had stated that it supported Wiluna's current direction and did not intend to seek any change to the company's business; and

(5) no further transactions were planned between Byrnecut and Wiluna.

67 It was submitted on behalf of AIM that the conclusion reached in the BDO report was 'irrational, confused and confusing' and that it 'lacks sufficient reasoning to justify the opinion stated'. On that basis it was submitted that the presentation of this opinion to the Wiluna shareholders was misleading. AIM submitted that, when the BDO Report is closely considered, the proposed acquisition of Wiluna shares by Byrnecut is of no advantage to Wiluna members. It was further submitted that the BDO Report failed to engage in a relevant and proper weighting of the factors to which it referred, and that it thereby failed to give the Wiluna members relevant and material information required for making a decision as to whether to approve an increase in Byrnecut's voting power. In support of those submissions, senior counsel for AIM undertook a detailed examination of the purported advantages and disadvantages that were identified in the BDO Report.

68 Although AIM did not dispute the conclusion reached by BDO that Byrnecut will not be paying a premium for control, it was submitted that the first purported advantage identified in the BDO Report was not an advantage to members. In that regard, it was submitted that the fact non-associated Wiluna shareholders will not miss out on the opportunity to receive a premium for control should be understood as a lack of a disadvantage, as opposed to an advantage. It was submitted that the non-associated Wiluna shareholders would be no better off so far as a control premium goes, whether the transactions under the SPAs do or do not proceed.

69 In relation to the second purported advantage identified in the BDO Report, it was submitted that the conclusion that 'Byrnecut's increased voting power in [Wiluna] may further align its interests with those of [Wiluna] and strengthen its existing relationship with Wiluna' lacks cogency or reasoning and that it amounts to little more than conjecture. In that regard, it was submitted that the conclusion relied on a mere assertion that, as Byrnecut is an established underground mining services provider, 'a strengthened relationship may provide operational and strategic benefits as [Wiluna] progresses its mining restart'. However, AIM contended that there is no basis for that opinion as Byrnecut had merely indicated that it would look to tender in a competitive process if Wiluna issues a tender for underground mining services, and that it otherwise supports Wiluna's current direction. AIM also relied on the fact that an increase from a 24.26% stake to a 29.50% stake would not, in and of itself, give rise to a greater alignment of interests between Wiluna and Byrnecut.

70 As to the disadvantage referred to in the BDO Report, AIM embraced the conclusion reached by BDO that the proposed increase in Byrnecut's voting power may deter potential takeover bids for Wiluna. In that regard, AIM noted that an increase in voting power to 29.50% would give Byrnecut the ability to block special resolutions and that there would then be an increased ability on the part of Byrnecut to form a bloc of voting power with other shareholders that would deter any takeover bidder, including from AIM.

71 It was submitted on behalf of AIM that, having identified that the increase in Byrnecut's voting power might deter a takeover bid, which would have an impact on the value of Wiluna's shares, it was then necessary for BDO to weigh that against any advantages. According to AIM, when it is appreciated that the two purported advantages that were identified by BDO are 'illusory, at best', BDO's conclusion that 'the position of Shareholders if the Proposed Transactions are approved is more advantageous than the position if the Proposed Transactions are not approved' is unsustainable.

72 AIM also contended that the directors of Wiluna exacerbated the problems with the conclusions expressed in the BDO Report. In that regard, AIM accepted that the directors expressly declined to offer any recommendation to members as to how to vote in relation to the Resolutions. However, it was submitted that, despite the obvious problems with the BDO Report, the directors of Wiluna nevertheless highlighted the conclusion reached in that report that the advantages of the proposed acquisition of shares by Byrnecut outweighed the disadvantages. Further, AIM submitted that, when coupled with the fact that the Chair of the meeting had indicated that he would direct all undirected proxies in favour of the Resolutions, the directors were in fact conveying to the shareholders that the board was of the view that Byrnecut's acquisition of shares was in their best interests.

73 In summary, AIM submitted that the:

directors have represented to members, through highlighting the conclusion in the [BDO Report] and the direction of undirected proxies in favour of [the Resolutions], that the increase in Byrnecut's voting power is advantageous to members. However, as submitted above, that conclusion is unclear and unsupported. Thus, there is a serious question to be tried as to whether members have been given materially misleading information and material information omitted from the [NoM].

74 As senior counsel for AIM accepted at the hearing, AIM's contention that there is a serious question to be tried as to whether the Wiluna shareholders have been given materially misleading information boils down to a proposition that they have been told, via the BDO Report, that they will be better off after Byrnecut has acquired shares under the SPAs than they would have been had that transaction not taken place.

75 AIM made a further, but related submission which concerned the references in the NoM to the fact that if the Chair of the meeting was appointed as a shareholder's proxy, then any undirected proxies would be directed in favour of the Resolutions. It was submitted that this rendered misleading the other statements that appeared in the NoM to the effect that the directors of Wiluna had determined not to make any recommendation to members about voting on the Resolutions. It was contended that those other statement were rendered misleading (or confusing) because the indication that undirected proxies would be directed in favour of the Resolutions represented that the Resolutions were in the best interest of shareholders when the directors were saying, at the same time, that they had decided not to make any recommendations.

76 Having summarised the submissions made on behalf of AIM, I will now deal with the three claims made by AIM that I have earlier discussed at [18] to [29] of these reasons, in aid of which an interlocutory injunction was sought.

The NoM omits material information in contravention of item 7(b) in s 611 of the Corporations Act

77 This claim can be dealt with in short order. Contrary to the approach that was taken by all parties, item 7 in s 611 of the Corporations Act is not a source of legal rights in respect of which AIM could seek final relief against Wiluna, in aid of which an interlocutory injunction could be granted to restrain Wiluna to put the Resolutions. This is because item 7 of s 611 does not impose any relevant obligation on Wiluna in the circumstances of this case.

78 Under s 611 an acquisition of a relevant interest in a company's voting shares that would otherwise contravene s 606(1) will be exempt from the prohibition in s 606(1), but only if certain conditions are met. Those conditions are provided for in the various items in the table that appears in s 611. In this case the focus of AIM's application for an interlocutory injunction was on the condition in para (b) of item 7, namely, that Wiluna shareholders be given all information known to Wiluna that was material to the decision on how to vote on the Resolutions. However, Wiluna would not contravene s 611 or item 7 by failing to comply with that requirement. Instead, the consequence of a failure to give the requisite information would be that Byrnecut would not be able to avail itself of an exemption under s 611 and, if it proceeded to acquire shares under the SPAs, may thereby commit an offence.

79 In those circumstances, I formed the view that AIM's reliance on item 7 of s 611 as source of legal rights in respect of which it could seek final relief against Wiluna was misplaced and that, as a consequence, there was no serious question to be tried as to whether Wiluna failed to comply with item 7 of s 611.

80 AIM did not seek an injunction against Byrnecut.

Wiluna had contravened, or was proposing to contravene, s 1041H of the Corporations Act by engaging in conduct, in relation to its shares, that was misleading or deceptive or was likely to mislead or deceive

81 As O'Bryan J observed in Australian Securities and Investments Commission v Vanguard Investments Australia Ltd [2024] FCA 308 at [21] (Vanguard):

The prohibitions against making false or misleading representations in s 12DB [of the Australian Securities and Investments Commission Act 2001 (Cth) (ASIC Act)] and against conduct that is liable to mislead the public in s 12DF of the ASIC Act are part of a suite of legislative prohibitions of misleading conduct in trade or commerce which originated in the Australian Consumer Law (through its statutory predecessor, Part V of the Trade Practices Act 1974 (Cth)) and are now also contained in the ASIC Act and the Corporations Act 2001 (Cth) (Corporations Act). The central conception of misleading conduct, which lies at the heart of each of the prohibitions, has been interpreted in a consistent manner across the various prohibitions. The applicable principles were most recently summarised by the High Court (Kiefel CJ, Gageler, Gordon, Edelman and Gleeson JJ) in the context of ss 18 and 29 of the Australian Consumer Law in Self Care IP Holdings v Allergan Australia [2023] HCA 8; 97 ALJR 388 as follows (citations omitted):

'[80] The principles are well established. Determining whether a person has breached s 18 of the ACL involves four steps: first, identifying with precision the "conduct" said to contravene s 18; second, considering whether the identified conduct was conduct "in trade or commerce"; third, considering what meaning that conduct conveyed; and fourth, determining whether that conduct in light of that meaning was "misleading or deceptive or … likely to mislead or deceive".

[81] The first step requires asking: "what is the alleged conduct?" and "does the evidence establish that the person engaged in the conduct?". The third step considers what meaning that conduct conveyed to its intended audience. As in this case, where the pleaded conduct is said to amount to a representation, it is necessary to determine whether the alleged representation is established by the evidence. The fourth step is to ask whether the conduct in light of that meaning meets the statutory description of "misleading or deceptive or … likely to mislead or deceive"; that is, whether it has the tendency to lead into error. Each of those steps involves "quintessential question[s] of fact".

[82] The third and fourth steps require the court to characterise, as an objective matter, the conduct viewed as a whole and its notional effects, judged by reference to its context, on the state of mind of the relevant person or class of persons. That context includes the immediate context - relevantly, all the words in the document or other communication and the manner in which those words are conveyed, not just a word or phrase in isolation - and the broader context of the relevant surrounding facts and circumstances. It has been said that "[m]uch more often than not, the simpler the description of the conduct that is said to be misleading or deceptive or likely to be so, the easier it will be to focus upon whether that conduct has the requisite character". That said, the description of the conduct alleged and identified at the first step should be sufficiently comprehensive to expose the complaint, because it is that conduct that will ultimately, as a whole, be determined to be or not to be misleading or deceptive.

[83] Where the conduct was directed to the public or part of the public, the third and fourth steps must be undertaken by reference to the effect or likely effect of the conduct on the ordinary and reasonable members of the relevant class of persons. The relevant class of persons may be defined according to the nature of the conduct, by geographical distribution, age or some other common attribute, habit or interest. It is necessary to isolate an ordinary and reasonable "representative member" (or members) of that class, to objectively attribute characteristics and knowledge to that hypothetical person (or persons), and to consider the effect or likely effect of the conduct on their state of mind. This hypothetical construct "avoids using the very ignorant or the very knowledgeable to assess effect or likely effect; it also avoids using those credited with habitual caution or exceptional carelessness; it also avoids considering the assumptions of persons which are extreme or fanciful". The construct allows for a range of reasonable reactions to the conduct by the ordinary and reasonable member (or members) of the class.'

82 In Vanguard, O'Bryan J also noted that in Australian Competition and Consumer Commission v TPG Internet Pty Ltd [2020] FCAFC 130; (2020) 278 FCR 450 at [22], the Full Court observed that:

[t]he central question is whether the impugned conduct, viewed as a whole, has a sufficient tendency to lead a person exposed to the conduct into error (that is, to form an erroneous assumption or conclusion about some fact or matter)

83 At a high level of generality, the conduct of Wiluna that AIM alleges was misleading is the provision of the NoM to Wiluna shareholders. However, as I understood the submissions that were made on behalf of AIM, it was alleged more specifically that it is Wiluna's conduct in:

(1) adopting and endorsing the opinions, as well as the rationale for those opinions, that were expressed in the BDO Report about the advantages and the disadvantage of Byrnecut's acquisition of shares under the SPAs, including the opinion that if the acquisition is approved the position of Wiluna shareholders will be more advantageous than if it were not approved; and

(2) independently conveying those opinions as propositions in the NoM,

that was or is misleading or deceptive, or was likely to mislead or deceive.

84 It is necessary to deal with both aspects of Wiluna's alleged misleading conduct in turn. However, the starting point to is to recognise that the premise of AIM's claim is that the relevant opinions, and the rationale for those opinions, expressed in the BDO Report concerning the advantages and disadvantages of Byrnecut's proposed acquisition of Wiluna shares, were misleading or deceptive.

85 It is, of course, well settled that a statement of opinion can amount to misleading or deceptive conduct. However, a statement of opinion cannot be regarded as such simply because it turns out that the opinion is incorrect: Global Sportsman Pty Ltd v Mirror Newspapers Pty Ltd (1984) 2 FCR 82 at 88. Nevertheless, as French CJ observed in Campbell v Backoffice Investments Pty Ltd [2009] HCA 25; (2009) 238 CLR 304 at [33]:

Opinions may carry with them one or more implied representations according to the circumstances of the case. There will ordinarily be an implied representation that the person offering the opinion actually holds it. Other implied representations may be that the opinion is based upon reasonable grounds, which may include the representation that it was formed on the basis of reasonable enquiries. In the case of a person professing expertise or particular skill or experience the opinion may carry the implied representation that it is based upon his or her expertise, skill or experience.

86 See also, Chowder Bay Pty Ltd v Paganin [2018] FCAFC 25 at [30] to [31].

87 Unfortunately, and no doubt because of the speed with which AIM's application for an interlocutory injunction came on for hearing, the representations that are alleged to have been made by the authors of the BDO Report that were said to be misleading or deceptive were not clearly identified.

88 Senior counsel for AIM made trenchant criticisms of the opinion expressed in the BDO Report that there were advantages to the non-associated shareholders of Wiluna. Most of the focus of those criticisms was on the opinion in the BDO Report that the absence of a premium for control represented an advantage to the non-associated members. The essential point that was made by senior counsel was that, while a transaction in which a purchaser of shares is required to pay a premium for control may properly be understood as being disadvantageous to non-associated shareholders, because those shareholders would miss out on an opportunity to receive a similar premium, the lack of any premium for control is a neutral factor. It was also submitted, in effect, that as the other advantage that was identified in the BDO Report was speculative, the non-associated shareholders were in reality left only with a disadvantage, namely the deterrent effect on any takeover bid.

89 However, senior counsel never suggested that the authors of the BDO Report did not honestly hold their opinions or that their opinions were not based on their expertise, skill or experience. Instead, AIM's complaints about the opinions expressed in the BDO Report focussed on the rationale, or the grounds, for those opinions. Accordingly, AIM's case appeared to be that the authors of the BDO report made a misleading implied representation that their opinion that the advantages of Byrnecut's proposed acquisition of Wiluna shares outweighed the disadvantages to non-associated Wiluna shareholders was based on reasonable grounds. It is, however, unnecessary to further consider the precise nature of AIM's case. That is because the critical question was whether AIM had established that there was a serious question to be tried that Wiluna had engaged in conduct that was misleading or deceptive, or that was likely to mislead or deceive.

90 It was submitted on behalf of AIM that, by publishing the NoM to its shareholder, Wiluna did more than merely pass on misleading representations that were expressly or impliedly made in the BDO Report, in the sense referred to in Yorke v Lucas (1985) 158 CLR 661 at 666. As senior counsel explained, AIM's case was that Wiluna had adopted or endorsed, in the NoM, the misleading representations made by the authors of the BDO Report. At the hearing, senior counsel took me to various passages in the NoM that he submitted supported this conclusion. I have reproduced those passages earlier in these reasons at [51], [54], [56] and [57].

91 In Google Inc v Australian Competition and Consumer Commission [2013] HCA 1; 249 CLR 435 at [15], French CJ, Crennan and Kiefel JJ said that it had been established:

in relation to intermediaries or agents that the question whether a corporation which publishes, communicates or passes on the misleading representation of another has itself engaged in misleading or deceptive conduct will depend on whether it would appear to ordinary and reasonable members of the relevant class that the corporation has adopted or endorsed that representation. It has also been established that, if that question arises, it will be a question of fact to be decided by reference to all the circumstances of a particular case

(citations omitted)

92 Having regard to all of the circumstances, and based on the evidence before me, I was ultimately not satisfied there was a serious question to be tried that it would appear to ordinary and reasonable non-associated Wiluna shareholders that Wiluna had adopted or endorsed any representations made by the authors of the BDO Report.

93 Firstly, the NoM contains several prominent statements that very clearly convey that the directors of Wiluna had determined not to give any recommendations on how non-associated shareholders should vote on the Resolutions. In my view it would appear to an ordinary and reasonable non-associated shareholder considering those statements, and the NoM as a whole, that the directors of Wiluna were therefore not endorsing or adopting any opinions, including those expressed in the BDO Report, that suggested that a vote in favour of the Resolutions would be to the shareholder's advantage.

94 Secondly, there are repeated references to the BDO Report in the NoM as an 'Independent Expert Report'. In my view, those references clearly convey to non-associated shareholders that the BDO Report contains opinions reached independently of Wiluna and its directors, and that those opinions were formed by someone who was impartial, unbiased and objective. That conclusion is reinforced by the following passage that appears in section 1.9 of the Explanatory Statement:

The Independent Expert's Report includes an independent examination of the Proposed Transactions, to assist non-associated Shareholders to assess the merits of, and decide whether to approve each Proposed Transaction.

(emphasis added)

95 It is true that the NoM contained an accurate summary of the opinion of the authors of the BDO Report that the advantages to non-associated shareholders of Byrnecut's acquisition of shares outweighed its disadvantages. However, I was not satisfied that there was a serious question to be tried that ordinary and reasonable non-associated shareholders would understand that, by merely summarising that opinion, the directors of Wiluna were therefore of thereby endorsing or adopting those conclusions. In that regard, non-associated shareholders were expressly urged to read the BDO Report 'in full' and 'in its entirety' for themselves, to 'carefully consider the report prepared by the Independent Expert for the purposes of the Shareholder approval', and to 'carefully read the Independent Expert's Report to understand the scope of the report, the methodology of the valuation and the sources of information and assumptions made'.

96 Thirdly, it may be accepted that section 1.6 of the Explanatory Statement conveys that the directors of Wiluna formed the view that the proposed acquisition of shares by Byrnecut will further the strategic alignment of interests between Wiluna and Byrnecut, and that this was consistent with the views reached by the authors of the BDO Report that this was an advantage that may be relevant to non-associated shareholders. However, what is made clear by the references in that section of the Explanatory Statement to the conclusions reached in the BDO Report that non-associated shareholders would not miss out on the opportunity to receive a premium for control and that the advantages of the proposed transaction outweighed the disadvantages, is that they were conclusions reached by the independent authors of the BDO Report not the directors. When section 1.6 of the Explanatory Statement is considered in the context of the NoM as a whole, ordinary and reasonable non-associated Wiluna shareholders would not understand that what was being conveyed was that the directors were endorsing or adopting those opinions, or the rationales for those opinions.

97 Fourthly, an ordinary and reasonable non-associated Wiluna shareholder would not understand the references in the NoM to the fact that if a non-associated shareholder decided to appoint the Chair of the meeting as their proxy, and did not include an express voting direction in their proxy form, they would be taken to have directed, and consented to, the Chair voting in favour of the Resolutions, as amounting to an endorsement or adoption by the directors of the opinions expressed in the BDO Report or the rationale for those opinions. In a context in which, as I have already said, the NoM repeatedly stated that the directors had determined not to make any recommendation about how non-associated shareholders should vote on the Resolutions, an ordinary and reasonable non-associated shareholder would understand that they were merely being informed about what would happen to any undirected proxies given to the Chair.

98 For essentially the same reasons, I was also not satisfied that there was a prima facie case that Wiluna had independently represented that the advantages of the proposed transaction outweighed the disadvantages to non-associated shareholders.

99 AIM also appeared to contend that Wiluna had engaged in, or was proposing to engage in misleading or deceptive conduct, by representing in the NoM that its board of directors declined to make a recommendation in relation to the Resolutions. AIM appeared to argue that such conduct was misleading because the NoM simultaneously contained a 'de facto recommendation to members to approve [the Resolutions]' because it indicated that undirected proxies would be voted by the Chair in favour of the Resolutions. In support of that submission, AIM referred to the decision of Goldberg J in Lion Nathan Australia at [69], where his Honour held that if directors inform shareholders of their intention to vote in favour of a resolution it is 'tantamount to a recommendation to do the same; it has the same effect'.

100 Those submissions must be rejected. In my view, there was no serious question to be tried that the NoM had a tendency to lead a non-associated shareholder into forming an erroneous assumption or conclusion that the directors were making a form of subliminal recommendation that the shareholder's should support for the Resolutions.

101 As I have already noted, the NoM contained several clear statements to the effect that the directors had decided not to make any recommendations concerning the Resolutions. Those statements stand in stark contrast to other statements that were made in the NoM about other resolutions in respect of which the directors did make clear recommendations. Further, at section 1.10 of the Explanatory Statement, several reasons were given for not making recommendations in relation to the Resolutions. In that context, it is difficult to see how statements about how the Chair of the meeting intended dealing with undirected proxies could realistically be seen to have had a tendency to lead any non-associated shareholder into falsely concluding that Wiluna's directors were, in fact, recommending that the associated shareholders support of the Resolutions in the face of express statements to the contrary.

102 In any event, even if it were open to infer from the stated intention to deal with undirected proxies that the Chair of the meeting was in favour of the Resolutions, that could not be a serious question to be tried as to whether there was a tendency to lead non-associated shareholders into erroneously but reasonably concluding that the board, and therefore Wiluna, was implicitly recommending that they vote in favour of the Resolutions.

Wiluna's directors did not give Wiluna shareholders full and fair disclosure of matters material to an informed judgment

103 It is settled that information provided in a notice of general meeting must enable shareholders to judge for themselves whether to attend the meeting and vote for or against the proposal, or whether to leave the matter to be determined by the majority attending and voting at the meeting: Clarke v Australian Computer Society Incorporated [2019] FCA 2175 at [142]. Further, there is an equitable principle that it is the fiduciary duty of directors not to mislead members who are to consider whether to pass a resolution at a general meeting by providing them with material that is other than substantially full and true, especially where the directors themselves may benefit from the passing of the resolution: Devereaux at 958.

104 In Lion Nathan Australia at [37], Goldberg J expressed the principle in the following way:

In general terms it may be said that where a general meeting of the shareholders of a company has been called to consider, and if thought fit, pass a resolution which affects the company and its shareholders the directors are bound to make a full and fair disclosure of all matters which are within their knowledge and which would enable the shareholders to make a properly informed judgment on the issue in question: Peters’ American Delicacy Co Ltd v Heath (1939) 61 CLR 457; [1939] ALR 124 at 486 per Latham CJ; Bulfin v Bebarfald’s Ltd (1938) 38 SR (NSW) 423 at 432-438. The obligation upon directors in this respect is even more significant where they have either made a recommendation to shareholders as to what they should do or have advised shareholders as to how they (the directors) propose to vote.

105 Similar expressions of the principle can be found in Chequepoint Securities Ltd v Claremont Petroleum NL (1986) 11 ACLR 94 at 96 to 97 and in Kahler at [33] to [39], both of which were relied on by AIM.

106 In ENT Pty Ltd v Sunraysia Television Ltd [2007] NSWSC 270; (2007) 25 ACLC 399 at [20], Austin J (quoting Devereaux) said that the question is not whether the explanatory documents provided to shareholders could have been drafted differently, but what effect the documents will have on 'the ordinary shareholder who scans or reads the document quickly, not as a lawyer, but as an ordinary man or woman in commerce or as an ordinary investor'. If a deficiency is identified, the court considers whether there is any reasonable ground for supposing that the deficiency would cause shareholders to vote, or abstain from voting, under a serious misapprehension of the position.

107 As I understood senior counsel's submissions, AIM's case was that there is a serious question to be tried as to whether, in breach of their fiduciary duties, the directors of Wiluna failed to make a full and fair disclosure in the NoM of all matters that would enable shareholders to make a properly informed judgment in deciding how to vote on the Resolutions. More specifically, it was submitted that there was a serious question to be tried as to whether Wiluna shareholders had been given materially misleading information and whether material information had been omitted from the NoM.

108 To the extent that this aspect of AIM's case relied on a contention that there was a serious question to be tried that the directors of Wiluna breached their fiduciary obligation not to provide misleading information to shareholders, for the reasons I have already given at [81] to [102] of this judgment, that contention must be rejected.

109 The precise basis of AIM's submission that there is a serious question to be tried that the directors breached their fiduciary obligation by failing to provide Wiluna shareholders with material information was somewhat elusive. Beyond bare assertions that material information had been 'omitted' from the NoM, no real attempt was made in written submissions filed in advance of the hearing to identify that information.

110 In his oral submissions at the hearing of the application for an interlocutory injunction, senior counsel for AIM appeared to submit that the directors had omitted to include information in the NoM that the opinions about the advantages and disadvantage of Byrnecut's acquisition of shares that were reached by the authors of the BDO Report were wrong. The main focus of that contention was on the opinion that the lack of any payment by Byrnecut of a premium for control was an advantage to shareholders. Senior counsel also appeared to submit that the NoM should have, but did not, include a more fulsome 'explication' of the disadvantage that was identified in the BDO Report, namely the deterrent effect of Byrnecut's increased voting power particularly in a context in which the lack of a premium for control, properly understood, was not an advantage for shareholders.

111 Senior counsel also relied on the reports produced by Mr James and by Mr Wright, and took the Court to answers they gave to questions about the effect or consequences on the market for the shares in Wiluna if the Resolutions were to be passed at the meeting on 15 May 2026. As I understood it, the purpose of referring the Court to that evidence was to submit that the various answers given by Mr James and Mr Wright constituted information that ought to have been disclosed to shareholders.

112 In relation to Mr James' report, the Court's attention was drawn to his opinions that, from a market perspective:

(1) there would be no dilution or change to economic interests affecting non-associated shareholders;

(2) Byrnecut's increased stake may reduce the likelihood of a successful third-party takeover bid as it contributes to a pathway by which effective control may be consolidated over time without payment of a control premium, raising the risk that minority shareholders may be deprived of any future opportunity to realise a control premium;

(3) Byrnecut's increased stake raised the prospect of two major shareholders with substantial holdings (that is, Byrnecut and another major shareholder) having the ability to influence the outcome of major corporate actions and materially reducing effective contestability for control; and

(4) an increase in Byrnecut's shareholding furthers its position within the share register and reduces the relative influence of minority shareholders over Wiluna's future strategic and capital decisions.

113 In relation to Mr Wright's report, the Court's attention was drawn to the following opinion:

If the Resolutions are approved, Byrnecut's ownership in Wiluna will increase from 24.3% to 29.5%. This increased ownership level enhances Byrnecut's ability to influence, or veto, key corporate decisions, however in my view it provides no clear economic benefit or advantages to remaining shareholders. In my view, Byrnecut increasing its shareholding is likely to have an adverse effect on other shareholders in Wiluna.

114 Reference was also made to Mr Wright's opinion that approving the Resolutions would likely have an adverse effect on the market for Wiluna's shares because an increase in Byrnecut shareholding to 29.50%:

(1) gives Byrnecut the ability to block special resolutions;

(2) further concentrates the ownership of Wiluna;

(3) could result in a higher minority interest discount on Wiluna shares;

(4) may reduce the prospect of a takeover bid for Wiluna; and

(5) may set a price benchmark for future share transactions,

and that those factors are likely to reduce the attractiveness of Wiluna's shares to both existing and prospective investors, and may potentially constrain the upside potential for minority shareholders.

115 The Court was also referred to Mr Wright's opinions that there is no tangible financial, operational or strategic benefit to shareholders from Byrnecut's increased shareholding interest, and that the absence of a premium for control is not an advantage to other shareholders but simply avoids an unfair outcome to those other shareholders.

116 As I have already said, both Wiluna and Byrnecut objected to the reports of Mr James and Mr Wright. It was contended that the various opinions expressed in those reports were not wholly or substantially based on the relevant author's specialised knowledge, or on their training, study or experience, as required by s 79 of the Evidence Act 1995 (Cth). A further objection was raised by Byrnecut on the basis that the Court should exercise its discretion under s 135 of the Evidence Act to refuse to admit those reports in evidence because their probative value was substantially outweighed by the danger the evidence might be unfairly prejudicial, misleading or confusing, or cause or result in undue waste of time. However, as will be seen, it is unnecessary to deal with those objections.

117 One difficulty with AIM's contention that there was a serious question to be tried about whether the directors had breached their fiduciary obligation to make a full and fair disclosure was that none of the directors appeared at the hearing of AIM's interlocutory application. Presumably it was thought that their interests would be adequately protected by Wiluna. However, that difficulty can be set to one side. That is because there was a more fundamental difficulty with the proposition that, on a prima facie basis, the directors of Wiluna had failed to comply with their fiduciary obligation of disclosure.

118 As can be seen from the statement of principle in the extract taken from the judgment of Goldberg J in Lion Nathan Australian at [104] of this judgment, directors are bound to make a full and fair disclosure of all matters that are within their knowledge and that would enable the shareholders to make a properly informed judgment on the issue in question. However, AIM never suggested, and I was taken no evidence that could establish, even on a prima facie basis, that the information AIM submitted should have been disclosed to shareholders was known to any director of Wiluna. In my view, it necessarily followed that AIM had failed to establish that there was a serious question to be tried as to whether the directors of Wiluna had breached their fiduciary obligation to provide full and fair disclose to the Wiluna shareholders.

119 I should note that in ENT Pty Ltd, reference was made, at [21], to the decision of the Full Court in Fraser v NRMA Holdings Limited (1995) 55 FCR 452, and to the fact that it is authority for the proposition that '[a] proper discharge of the duty may require that the directors take reasonable steps to ascertain relevant information for communication to members if that information is not known to the board'. Whether such duty would arise in circumstances in which a notice is given for a general meeting to consider a resolution that, if passed, would qualify as an exemption under item 7 of the table in s 611 of the Corporations Act raises interesting questions. This is because the condition expressed in item 7(b) is relevantly that members be given all information 'known to the company'.

120 However, that question does not need to be resolved here. Even if the Wiluna directors were required to take reasonable steps to ascertain relevant information for communication to shareholders, it was never suggested and I was not taken to any evidence that was capable of establishing, on a prima facie basis, that the directors had failed to take reasonable steps to obtain and disclose to Wiluna shareholders the information that AIM contended had not been disclosed in the NoM.

121 For these reasons, I was not satisfied that AIM had established that there was a serious question to be tried in relation to any of the three claims on which it relied in support of its application for an interlocutory injunction.

The balance of convenience

122 In circumstances in which I concluded that AIM had failed to establish that there was a serious question to be tried, it was unnecessary for me to address the question of whether the balance of convenience favoured the grant of an interlocutory injunction.

Conclusion

123 For these reasons I concluded that AIM's urgent application for an interlocutory injunction must be dismissed.

124 I will hear from the parties further about the question of the costs of the application.

I certify that the preceding one hundred and twenty-four (124) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Vandongen. |

Associate:

Dated: 5 June 2026

Annexure - relevant passageS from BDO Report