FEDERAL COURT OF AUSTRALIA

North Limited v Zentree Investments Limited, in the matter of Energy Resources of Australia Ltd [2026] FCA 695

File number: | NSD 787 of 2025 |

Judgment of: | MARKOVIC J |

Date of judgment: | 5 June 2026 |

Catchwords: | CORPORATIONS – application for compulsory acquisition of residual ordinary shares of Energy Resources of Australia Limited – where the applicant is the “90% holder” of the relevant class of securities – where the applicant lodged a compulsory acquisition notice with the Australian Securities & Investments Commission on 11 April 2025 – where at least 10% of the remaining shareholders objected to the compulsory acquisition notice – where the notice relies upon the opinion expressed in an expert’s report dated 2 April 2025 – whether the notice complied with the formal requirements of the Corporations Act 2001 (Cth) or is otherwise deficient – whether applicant has established that the terms set out in the compulsory acquisition notice give a “fair value” for the relevant securities pursuant to s 664F of the Corporations Act – application granted |

Legislation: | Aboriginal Land Rights (Northern Territory) Act 1976 (Cth), s 43 Atomic Energy Act 1953 (Cth), s 41 Corporations Act 2001 (Cth), ss 664A, 664F, 667A, 667AA Federal Court Rules 2011 (Cth), r 9.05 Environmental Protection Act 1986 (WA) Mineral Titles Act 2010 (NT), s 68 |

Cases cited: | Advanced Holdings Pty Ltd atf Demian Trust v Commissioner of Taxation [2021] FCAFC 135 Australian Karting Association Ltd v Karting (New South Wales) Inc [2022] NSWCA 188 Bromley Investments Pty Ltd v Elkington [2003] QCA 407; (2003) 47 ACSR 273 Capricorn Diamonds Investments Pty Ltd v Catto [2002] VSC 105; (2002) 5 VR 61 CCPI Holdings Proprietary Limited v Joan Hose and Ronald Hose [2011] VSC 34 Hudson v National Australia Bank [2022] FCA 1222 Ijack Pty Ltd v Cobb [2018] FCA 1321; (2018) 131 ACSR 418 Macquarie International Health Clinic Pty Ltd v Sydney South West Area Health Service [2010] NSWCA 268; (2010) 383 ALR 577 Pauls Ltd v Dwyer [2002] QCA 545; (2002) 2 Qd R 176 QGold Pty Ltd v Woods [2025] FCA 1201 Re Australian Water Holdings Pty Ltd [2016] NSWSC 254; (2016) 306 FLR 40 Re Navalo Financial Services Group Ltd [2025] NSWSC 317 Teh v Ramsay Centauri [2002] NSWSC 456; (2002) 42 ACSR 354 |

Division: | General Division |

Registry: | New South Wales |

National Practice Area: | Commercial and Corporations |

Sub-area: | Corporations and Corporate Insolvency |

Number of paragraphs: | 469 |

Date of hearing: | 10 – 13, 16 – 18 and 19 – 20 February 2026 |

Counsel for the Plaintiff: | Mr D Thomas SC appears with Mr J Entwisle and Ms M Mellos |

Solicitor for the Plaintiff: | Allens |

Counsel for the First Defendant: | Mr A Sullivan KC appears with Mr A Flick |

Solicitor for the First Defendant: | Piper Alderman |

ORDERS

NSD 787 of 2025 | ||

IN THE MATTER OF ENERGY RESOURCES OF AUSTRALIA LTD | ||

BETWEEN: | NORTH LIMITED ACN 005 233 689 Plaintiff | |

AND: | ZENTREE INVESTMENTS LIMITED First Defendant JIT TSAI LIM (and others named in the Schedule) Second Defendant | |

order made by: | MARKOVIC J |

DATE OF ORDER: | 5 June 2026 |

THE COURT DECLARES THAT:

1. The terms set out in the notice of compulsory acquisition issued to each of the holders of shares in Energy Resources of Australia Ltd ACN 008 558 865 (ERA) by the plaintiff dated 11 April 2025 (Notice) gives a fair value, for the purposes of s 664F(3) and s 667C of the Corporations Act 2001 (Cth), for the shares the subject of the Notice.

THE COURT ORDERS THAT:

2. Pursuant to s 664F of the Corporations Act the acquisition of ERA’s shares by the plaintiff on the terms set out in the Notice be approved.

3. The plaintiff is to file and serve any submissions on the question of costs including in relation to any application to vary the operation of s 664F(4) of the Corporations Act, not exceeding five pages in length, and any affidavits on which it intends to rely by 19 June 2026.

4. The first defendant is to file and serve any submissions in response, not exceeding five pages in length, and any affidavits on which it intends to rely by 3 July 2026.

5. Unless a party seeks an oral hearing, any question arising in relation to the costs of the proceeding will be determined on the papers.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

TABLE OF CONTENTS | |

[7] | |

[22] | |

[23] | |

[40] | |

[54] | |

[56] | |

[56] | |

[58] | |

[64] | |

[89] | |

[94] | |

[102] | |

[127] | |

[154] | |

[155] | |

[158] | |

[164] | |

[172] | |

[176] | |

4.3.3 ERA fixed assets register as at 31 December 2024 (PPE Register) | [179] |

[182] | |

[186] | |

[188] | |

[191] | |

[199] | |

[206] | |

[217] | |

[221] | |

[225] | |

[239] | |

[254] | |

[258] | |

[266] | |

[271] | |

[292] | |

[300] | |

[304] | |

[305] | |

[317] | |

[320] | |

[324] | |

5.4.3.1 Impossibility of opining on the reasonableness of the Rehabilitation Provision | [326] |

[341] | |

[350] | |

[356] | |

[368] | |

[370] | |

[378] | |

[382] | |

5.5 Zentree’s additional objections to the value of the mineral assets | [386] |

[391] | |

[435] | |

[459] | |

[467] | |

ANNEXURE B - LIST OF OBJECTING SHAREHOLDERS (EXCLUDING ZENTREE) |

REASONS FOR JUDGMENT

MARKOVIC J:

1 The plaintiff, North Limited ACN 005 233 689, has a relevant interest in 98.43% of the shares in Energy Resources of Australia Limited ACN 008 558 865 (ERA) via its subsidiary companies. It seeks the Court’s approval, pursuant to s 664F of the Corporations Act 2001 (Cth), to compulsorily acquire the remaining 1.57% of ERA’s shares for $0.002 (or 0.2 cents) per share (Compulsory Acquisition). It must do so because, as explained below, at least 10% of the remaining shareholders in ERA have objected to the Compulsory Acquisition Notice dated 11 April 2025 served by North on them.

2 This proceeding was commenced naming Zentree Investments Limited ACN 681 690 095 as defendant. Following its commencement, by order made on 10 September 2025, eight additional parties were joined to the proceeding as defendants pursuant to r 9.05 of the Federal Court Rules 2011 (Cth). Zentree and each of those parties has provided a notice of their objection to the acquisition by North of their shares in ERA. However, only Zentree took an active role in the proceeding.

3 Based on its grounds of objection filed in the proceeding, Zentree objects to the Compulsory Acquisition of its shares in ERA on the following grounds:

(1) the Notice is invalid and does not comply with:

(a) s 664C(2)(b) of the Corporations Act including because the expert reports served with the Notice do not comply with Pt 6.4A of the Corporations Act because:

(i) the report of Lonergan Edwards & Associates Limited ACN 095 445 560 (LEA) dated 2 April 2025 (LEA Report):

A. does not comply with s 667A of the Corporations Act insofar as it relies in its entirety, or in substantial part, upon a separate expert report; and/or

B. does not comply with s 667C of the Corporations Act and, or alternatively, Australian Securities and Investments Commission (ASIC) Regulatory Guide 111 (RG 111), including by reason of failing to apply the correct, or an appropriate, valuation methodology;

(ii) the report of SRK Consulting (Australasia) Pty Ltd ACN 074 271 720 (SRK) dated 2 April 2025 (SRK Report) does not comply with s 667C of the Corporations Act and, or alternatively, RG 111, including by reason of failing to apply the correct, or an otherwise appropriate, valuation methodology;

(iii) each or both of the LEA Report and the SRK Report:

A. incorrectly relied on subjective decisions made by or at the direction of North and/or ERA to value ERA’s assets at significant undervalue; and/or

B. failed to identify source material, instructions and/or assumptions relied upon by their authors such that the reports cannot be properly understood or fairly interrogated; and

(b) s 664C(1)(e) of the Corporations Act in that it does not comply with the requirement to disclose information known to North and material to shareholders in deciding whether to object to the Compulsory Acquisition, which was information not already disclosed in the expert reports accompanying the Notice; and

(c) Zentree contends that as a result, the jurisdictional threshold to enliven the power under s 664F of the Corporations Act has not been met; and/or

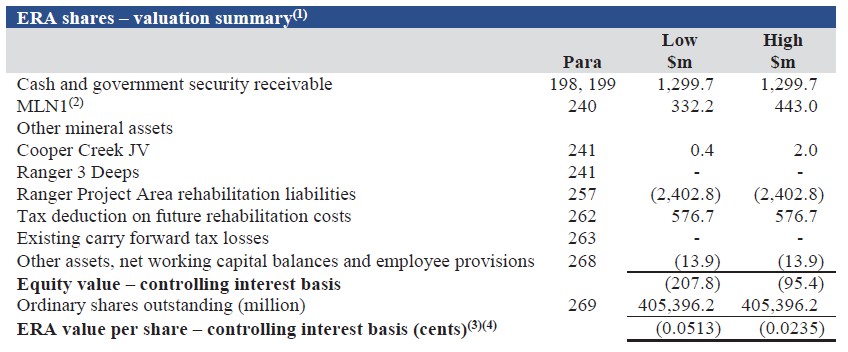

(d) the terms, and/or the cash amount, set out in the Notice do not give fair value for Zentree’s shares within the meaning of Pt 6A.2, or alternatively section 664F(3) of the Corporations Act.

4 As explained below, Zentree abandoned its claim that the LEA Report does not comply with s 664C(2) of the Corporations Act because it refers to another report, the SRK Report (ground (1)(a)(i) of its notice of objection).

5 Having considered the evidence before me and Zentree’s objections (and, to the extent they differ, those of the other objecting shareholders’), I am satisfied that the terms set out in the Notice give a fair value for the shares in ERA. Accordingly, as required by s 664F(3) of the Corporations Act, the Court must approve the acquisition of the remaining ERA shares on the terms set out in the Notice. My reasons for reaching that conclusion follow.

6 To assist the reader, a glossary of defined terms used in these reasons is attached as Annexure A.

1. Statutory framework and legal principles

7 Before proceeding further, it is convenient to set out the applicable statutory framework and legal principles.

8 The compulsory acquisition regime is found in Pt 6A.2 of the Corporations Act which was inserted into the Corporations Law in 2000 following a comprehensive review. The primary intention of the new provisions was to “make it easier for majority shareholders to obtain the benefits of 100 per cent ownership” and to discourage “greenmailing”: see Ijack Pty Ltd v Cobb [2018] FCA 1321; (2018) 131 ACSR 418 at [13] (Moshinsky J).

9 Section 664A of the Corporations Act enables a 90% holder of securities in a particular class of securities to compulsorily acquire all of the shares in that class. Relevantly, a person is a 90% holder in relation to a class of securities of a company if: (1) the securities are shares or convertible into shares; (2) the person’s voting power is at least 90%; and (3) the persons holds, either alone or with a related body corporate, full beneficial interest in at least 90% by value of all the securities of the company that are either shares or convertible into shares: s 664A(2) of the Corporations Act.

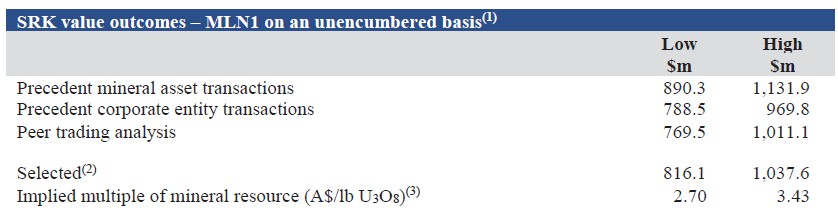

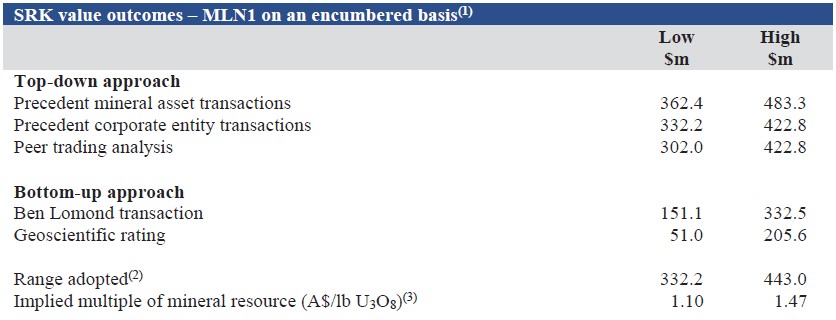

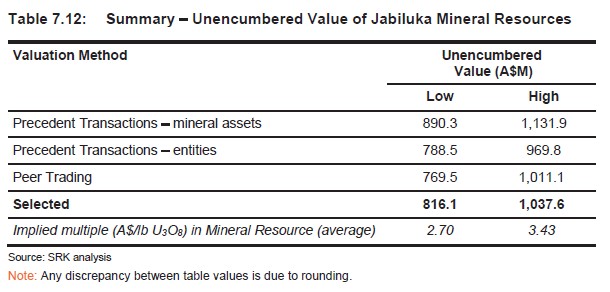

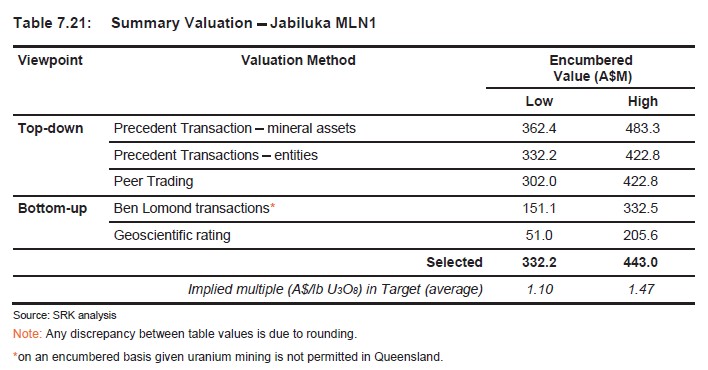

10 The procedure to be adopted by the acquirer is set out in s 644C. The 90% holder must prepare a notice in the prescribed form that, among other things, sets out the cash sum for which the 90% holder proposes to acquire the securities (subs (1)(a)) and discloses any other information that is known to the 90% holder (or any related bodies) that is material to deciding whether to object to the acquisition and is not disclosed in the expert’s report under s 667A of the Corporations Act (subs (1)(e)).

11 The notice in prescribed form must be accompanied by an expert report which has been prepared in accordance with the requirements in s 667A of the Corporations Act: s 664C(2)(b)(ii) of the Corporations Act.

12 An expert report prepared in accordance with s 667A of the Corporations Act must: (1) be prepared by a person nominated by ASIC under s 667AA; (2) state whether in the expert’s opinion the terms proposed in the notice give a fair value for the securities concerned; (3) and set out the reasons for forming that opinion.

13 Where more than 10% of the remaining shareholders object to the notice, as is the case here, s 664A(3)(b) of the Corporations Act requires the acquirer to proceed under s 664F and obtain Court approval. Section 664F of the Corporations Act provides:

(1) If people who hold at least 10% of the securities covered by the compulsory acquisition notice object to the acquisition before the end of the objection period, the 90% holder may apply to the Court for approval of the acquisition of the securities covered by the notice.

(2) The 90% holder must apply within 1 month after the end of the objection period.

(3) If the 90% holder establishes that the terms set out in the compulsory acquisition notice give a fair value for the securities, the Court must approve the acquisition of the securities on those terms. Otherwise it must confirm that the acquisition will not take place.

Note: See section 667C on valuation.

(4) The 90% holder must bear the costs that a person incurs on legal proceedings in relation to the application unless the Court is satisfied that the person acted improperly, vexatiously or otherwise unreasonably. The 90% holder must bear their own costs.

14 While the Corporations Act does not define “fair value”, s 667C sets out how to determine “fair value” for the purposes of Ch 6A of the Corporations Act. It provides:

(1) To determine what is fair value for securities for the purposes of this Chapter:

(a) first, assess the value of the company as a whole; and

(b) then allocate that value among the classes of issued securities in the company (taking into account the relative financial risk, and voting and distribution rights, of the classes); and

(c) then allocate the value of each class pro rata among the securities in that class (without allowing a premium or applying a discount for particular securities in that class).

(2) Without limiting subsection (1), in determining what is fair value for securities for the purposes of this Chapter, the consideration (if any) paid for securities in that class within the previous 6 months must be taken into account.

15 ERA has one class of securities. Thus, the second prescribed step in determining “fair value” in s 667C(1)(b) can be put to one side.

16 The meaning of “fair value” has been considered by courts on a number of occasions. The principles, which were not in dispute and were conveniently summarised by North, are set out below.

17 “Fair” does not mean that there is a search for something which is intrinsically fair according to general notions of fairness: Teh v Ramsay Centauri [2002] NSWSC 456; (2002) 42 ACSR 354 at [12] (Barrett J). There is no scope for the Court to embark upon some general inquiry as to fairness. Rather, “a single and narrow avenue of attack is available” which is “confined to the particular question of adequacy of consideration” and “that question is to be answered solely by reference to the statutory concept of ‘fair value for securities’ defined by s 667C”: Teh at [7] and [9]; Re Navalo Financial Services Group Ltd [2025] NSWSC 317 at [57] (Nixon J).

18 “Fair value” is used in the same sense as “true value”, “real value” and “intrinsic value”: Re Australian Water Holdings Pty Ltd [2016] NSWSC 254; (2016) 306 FLR 40 at [10] (Brereton J). It is to be determined by asking what price would be negotiated in a hypothetical transaction between two willing but not anxious parties: Teh at [14]-[16]; Capricorn Diamonds Investments Pty Ltd v Catto [2002] VSC 105; (2002) 5 VR 61 at [59] (Warren J). Value is to be determined at the date of the compulsory acquisition notice: Teh at [28]-[29].

19 In assessing value, the value of special benefits to the acquirer is not to be included in the calculation of the value of the company as a whole. Nor should an expert add any premium for forcible divestment: Capricorn at [56], [60]-[62].

20 An expert’s opinion is not determinative of whether the terms set out in a compulsory acquisition notice will be endorsed by a court: QGold Pty Ltd v Woods [2025] FCA 1201 at [61] (Derrington J). However, the Court’s decision will ordinarily be largely based on the expert report served with the notice. That report does not need to be beyond criticism for a judge to act on it and conclude that the price was fair: CCPI Holdings Proprietary Limited v Joan Hose and Ronald Hose [2011] VSC 34 at [7] (Davies J), quoting from Bromley Investments Pty Ltd v Elkington [2003] QCA 407; (2003) 47 ACSR 273.

21 There is a range of values which may be said to represent “fair value”: Pauls Ltd v Dwyer [2002] QCA 545; (2002) 2 Qd R 176 at [42] (Davies and Jerrard JJA, Jones J). In Capricorn Warren J observed that “fair value may require a more liberal estimate of value within a range of possible values where there is a compulsory acquisition of property”: at [61]. However, as her Honour also recognised, there is “no hard and fast rule” that some higher value is to be adopted or, as her Honour put it, a “forcing out” premium is to be applied: see Capricorn at [61]; QGold at [183]-[185].

2. The evidence

22 The parties relied principally on documentary and expert evidence. In addition, North relied on one lay witness, Robert Christopher O’Toole, Chief Counsel, Business Development, APAC within the Corporate Legal team of the Legal, Governance and Corporate Affairs function of the Rio Tinto Group (a dual listed structure made up of Rio Tinto Limited ACN 004 458 404, listed on the Australian Securities Exchange (ASX) and Rio Tinto plc, listed on the London Stock Exchange). Mr O’Toole’s evidence was formal in nature, was not challenged and he was not cross-examined.

2.1 North’s expert evidence

23 North relied on the expert reports it served with the Notice, namely the LEA Report and the SRK Report, and further reports prepared by the authors of those reports in reply to Zentree’s expert evidence. The experts and a summary of their qualifications are set out below.

24 Grant Kepler is a director and authorised representative of LEA. Mr Kepler supervised and had overall responsibility for the preparation of the LEA Report on behalf of LEA and was assisted in its preparation by Nathan Toscan, managing director, and other employees of LEA. Mr Kepler joined LEA as a manager in 2002 and was appointed a director in 2008.

25 Prior to joining LEA, Mr Kepler was in the financial advisory services practice of Coopers & Lybrand (which became PricewaterhouseCoopers (PwC)) in 1995, during which time he was seconded to the corporate valuation and strategy group of PwC in London and to PwC’s telecommunications practice in the United States of America (USA). Prior to that Mr Kepler worked in the audit divisions of Price Waterhouse in Sydney and Hall Chadwick in Adelaide.

26 Mr Kepler has a Bachelor of Arts in Accountancy and a Graduate Diploma in Accountancy, both from the University of South Australia. He is a member of Chartered Accountants Australia and New Zealand (CAANZ), an accredited CA Business Valuation Specialist and a Fellow of the Financial Services Institute of Australasia (FINSIA).

27 Jeames McKibben is the principal consultant of SRK. Mr McKibben supervised the preparation of, and had overall responsibility for preparing, the SRK Report. He was assisted in its preparation by other individuals from SRK listed in the report.

28 Mr McKibben joined SRK as a principal consultant in 2016. Prior to joining SRK he held a number of different roles, including:

(1) from 2015 to 2016, technical discipline manager (valuation & property services), SLR Consulting;

(2) from 2009 to 2015, general manager – corporate advisory, Xstract Mining Consultants;

(3) from 2004 to 2009, consultant, senior consultant, then divisional manager – corporate services, Snowden Mining Industry Consultants;

(4) from 2000 to 2002, project manager, Ambase (Morocco) Limited;

(5) from 1998 to 2000, project geologist and project manager, Zamanglo Prospecting;

(6) from 1997 to 1998, project geologist, Consolidated Gold Mines Ltd;

(7) in 1997, project geologist, Johnsons Well Mining NL;

(8) from 1995 to 1996, mineral analyst, Mineral Resources Tasmania; and

(9) from 1994 to 1995, geologist, Normandy Exploration.

29 As a consultant Mr McKibben has specialised in mineral asset valuations and providing independent technical reports for equity and project finance transactions. Mr McKibben has more than 30 years’ experience as a mining professional and has been involved in the preparation of more than 100 independent expert reports (IER) since joining SRK in April 2016.

30 Mr McKibben has a Bachelor of Science (Geology, Geochemistry) from the University of Tasmania and a Masters of Business Administration from Macquarie Graduate School of Management. He is a registered valuer, chartered valuation surveyor and a member of the VALMIN Code Review Committee.

31 Lisa Chandler is a principal consultant at SRK. She assisted in the preparation of parts of the SRK Report, namely location and access for the Ranger Project Area (defined in [58] below) (part 2.1), ownership, land access and tenure of ERA’s mineral assets (part 2.3), permitting and approvals for the Ranger Project (part 3.2), stakeholder engagement (part 3.3), project history for the Jabiluka Project (part 4.1.1) and permitting and approvals for the Jabiluka Project (part 4.2).

32 Ms Chandler joined SRK in 2010 as a principal consultant and remained in that role until 2012. From 2012 to 2014 Ms Chandler was an associate principal consultant with SRK and upon rejoining SRK in 2024 her role reverted to principal consultant. Ms Chandler has over 35 years’ experience as a scientist and engineer in environmental services, including waste geochemistry, due diligence, impact assessment, closure planning, environmental assurance and audit and design.

33 In addition to her roles at SRK Ms Chandler has held a number of other roles including:

(1) from 2008 to 2010 and 2012 to 2024, director and principal consultant, Chandler Redwood Pty Ltd, trading as AEthos Consulting (Ms Chandler’s independent ESG consulting business);

(2) from 2013 to 2017, adjunct senior lecturer in environmental science (especially in relation to environmental management systems, impact assessment, risk management and compliance and audit), Edith Cowan University;

(3) from 2007 to 2008, principal consultant (environmental impact assessment, permitting, mine closure planning, environmental management and audit), Outback Ecology Services; and

(4) from 2004 to 2007, manager audit, West Australian Department of Environment. In that role Ms Chandler was responsible for compliance assessments of significant developments approved under Part IV of the Environmental Protection Act 1986 (WA).

34 Ms Chandler has a Masters of Engineering from the University of Newcastle and a Bachelor of Science (Physical Geography) from McGill University. In 2022 she completed a professional certificate in ESG and Social Responsibility with the Australasian Institute of Mining and Metallurgy (AusIMM), of which she is a member.

35 Raymond Mayne is a principal consultant at SRK. He assisted in the preparation of part 3.4 of the SRK Report which addresses mine closure and rehabilitation costs.

36 Mr Mayne joined SRK in 2022 as a principal consultant. Prior to that he held a number of roles including:

(1) from June 2017 to March 2022, principal environmental scientist, SRK Consulting (South Africa) (Pty) Ltd (SRK SA);

(2) from April 2013 to June 2017, senior environmental scientist, SRK SA; and

(3) from August 2006 to April 2013, environmental scientist, SRK SA.

37 As a consultant Mr Mayne has managed and contributed to closure-related projects as part of multidisciplinary teams, supporting a range of operations with closure liability assessments and the review and updating of mine closure plans. He has also participated in technical reviews of closure aspects as part of due diligence projects.

38 Throughout his professional life, Mr Mayne has regularly managed or contributed to closure cost estimations and liability assessments. He has international experience across a variety of mining commodities and contexts. He has assisted operations internationally in the compilation, updating, or assessment of closure cost estimates. For due diligence projects, Mr Mayne has undertaken reviews and provided opinions on closure aspects, including the appropriateness of cost estimates, the identification of closure risks associated with the operations under review, and, where relevant, any potential opportunities. To date, Mr Mayne has contributed to approximately 10 due diligence projects in which his input has focussed on closure.

39 Mr Mayne has a Bachelor of Science (Environmental Geography) from the University of the Free State in Bloemfontein, South Africa.

2.2 Zentree’s expert evidence

40 Zentree relied on expert reports which responded to the LEA Report and the SRK Report provided by four experts. Those experts and a summary of their qualifications and areas of expertise is set out below.

41 Andrew Ross is a partner of HKA Global Pty Ltd ACN 085 532 047. He has prepared a report in response to the LEA Report in which he addresses the following two questions.

(1) Does the Notice give a “fair value” for the ERA shares described in the Notice when determined pursuant to s 667C of the Corporations Act?

(2) Having reviewed and considered the LEA Report, state whether you agree or disagree with the opinions expressed therein.

42 Mr Ross has been employed as a forensic accountant or been a partner in firms of chartered accountants for more than 35 years. Over that period, he has received training and gained experience in the:

(1) preparation, review and auditing of financial statements for both large and small, listed and unlisted companies;

(2) preparation and review of budgets and forecasts of revenue, costs and profits;

(3) quantification of economic loss and other forms of financial compensation, including the use of tools such as Microsoft Excel to build electronic models which assist in quantifying loss; and

(4) valuation of shares, businesses and other assets or interests in a wide variety of circumstances and industries.

43 Mr Ross has a Bachelor of Commerce (Honours) and a Graduate Diploma in Applied Finance and Investment. He is a Fellow of CAANZ and has been designated as a specialist in both Forensic Accounting and Business Valuation by CAANZ. Mr Ross is also a Fellow of FINSIA.

44 Dr James Burrows is a vice chairman of Charles Rivers Associates (CRA). At Mr Ross’ request he was retained by Zentree to prepare a report to assist in relation to the ERA mineral asset valuation aspects of the SRK Report. Dr Burrows was asked to provide a report that expresses his opinion on the following four matters.

(1) What was the value of the ERA mineral assets (i.e. MLN1, Cooper Creek and R3D) (individually and/or collectively) as at 2 April 2025?

(2) Address whether the values of the ERA mineral assets (individually and/or collectively) set out in the response to the preceding question reflect any particular matters or contingencies, and if so, what are those particular matters or contingencies.

(3) Review the SRK Report and having done so, state whether you agree or disagree with:

(a) the methodology SRK adopted to derive its opinions as to the values of the ERA mineral assets; and

(b) the values derived by SRK through the application of their preferred methodologies for each of the mineral assets.

(4) Paragraph 218 of the LEA Report states that it has cross-checked the findings of the SRK valuation against the implied values attributed to MLN1 based upon the market traded price of ERA shares (over time) as well as the 2023 Interim Entitlement Offer (being the proposed non-underwritten, renouncement offer announced by ERA to the market on 24 June 2022 which aimed to raise approximately $300 million) and the 2024 Entitlement Offer (being the 19.87-for-1 non-underwritten pro-rata renounceable entitlement offer seeking to raise up to approximately $880 million at an offer price of $0.002 or 0.2 cents per share). State whether you agree or disagree with the methodology deployed and conclusions LEA reached in [219] to [240] of the LEA Report.

45 Dr Burrows was formerly chief executive officer (CEO) and president of CRA. He founded CRA’s natural resources practice and managed it for over a decade before becoming head of its dispute resolution practice for about ten years and then President and CEO of CRA for fifteen years. Dr Burrows has authored or co-authored six books, four of which are on metals and minerals markets and policy issues. He has consulted and undertaken research related to the minerals industry over the course of his career, including consulting related to uranium. Dr Burrows’ prior experience relating to the uranium industry includes consulting to the government of Mongolia with respect to negotiating a supply agreement in connection with a uranium mine, consulting to the provincial government of Saskatchewan, Canada with respect to policies and operations of uranium mining in Saskatchewan, and consulting to Freeport-McMoran in connection with clean-up costs and remediation of uranium mines in the USA.

46 Dr Burrows has a Bachelor of Arts in economics from Harvard University and a Ph.D. in economics from the Massachusetts Institute of Technology.

47 Mario Rossi is a mining engineer and a geostatistician with 35 years of industrial, academic, and international experience in the mining industry. Mr Rossi is president and principal geostatistician of GeoSystems International, Inc., a consultancy firm established by Mr Rossi in 1994. Prior to that Mr Rossi held the following roles:

(1) from March 1989 to February 1992, geostatistician at Fluor Daniel Inc., an engineering, procurement, fabrication, construction and maintenance company; and

(2) a consultant with Mineral Resource Development Inc., which operated in geology, resource and reserve estimation and mine planning, and provided consulting services, audits, and reviews to many mining projects and operations around the world.

48 At the request of Dr Burrows, Mr Rossi was asked to:

(1) analyse the Jabiluka Mineral Reserves and Resources;

(2) analyse the Jabiluka mine cash flow spreadsheet; and

(3) analyse the putative comparable uranium properties and companies. In that regard Mr Rossi was instructed to:

(a) identify which of the criteria used by Dr Burrows to define comparability are within his technical expertise, training and experience; and

(b) applying the technical criteria identified in the previous step, evaluate whether each of the uranium projects proposed is comparable to Jabiluka from a technical point of view.

49 Mr Rossi was also instructed in relation to Ranger 3 Deeps (R3D) to:

(1) review documents with respect to the R3D deposit located in the Ranger Project Area;

(2) provide information and data on the mineral resources of R3D; and

(3) provide estimates of mine schedules and capital and operating costs of R3D.

50 Mr Rossi has a mining engineering degree with minors in Project Development and Evaluation, and Metallurgy from the Universidad Nacional de San Juan, Argentina and a Master of Science in Geostatistics from Stanford University. Mr Rossi is a Fellow of AusIMM and a registered member of the Society for Mining, Metallurgy and Exploration, USA.

51 Dr Alexander Lee is a partner at HKA and a chartered geologist, chartered scientist, and chartered European geologist. He was engaged at the request of Mr Ross to provide an expert technical opinion to assist Mr Ross in relation to the rehabilitation cost aspects of the SRK Report. His report addresses the following issues:

(1) the appropriate methodology for assessing the reasonableness of existing cost estimates and the documents and information needed to apply that methodology;

(2) having regard to the preferred methodology, what conclusions can be reached as to the reasonableness of the estimate made by ERA and what issues are material to coming to those conclusions;

(3) where documents or other information are not available, what additional documents or other information would be needed and the reasons why they would be needed, in determining a reasonable cost estimate; and

(4) whether the SRK Report used a suitable methodology, appropriate assumptions and information, and drew appropriate conclusions in 2025 when compiling an ISR related to the Ranger Project Area.

52 Dr Lee has 30 years’ experience assessing land quality liabilities and delivering site remediation and rehabilitation. He has delivered projects internationally and has experience both as a consultant and contractor, with expertise in non-radiological and radiological roles, in both the private and public sectors.

53 Dr Lee has a Ph.D. in Geology and a Masters of Science in Environmental Modelling and Monitoring. He has held or holds the following further professional roles, memberships or affiliations:

(1) served as the elected chair of the UK National Brownfield Forum and is currently its outgoing chair;

(2) member of the Steering Group of the UK National Land Quality Mark Scheme (NQMS) and is NQMS registered as a “suitably qualified and experienced person” and registered as a specialist in land condition;

(3) former chair of the Society of Brownfield Risk Assessors (SoBRA) and is a SoBRA accredited risk assessor holding individual accreditations for human health, permanent gas, vapour, and water environment risk assessments;

(4) director of the Association of Geotechnical and Geoenvironmental Specialists; and

(5) examiner for candidates applying to become a chartered geologist, chartered scientist and SoBRA accredited risk assessor.

2.3 Joint expert reports

54 The parties’ experts prepared a series of joint expert reports having regard to their respective areas of expertise and the questions on which they opined in their individual expert reports. The joint reports relied on by the parties at trial were:

(1) joint report of Mr Rossi and Mr McKibben dated 30 January 2026 which annexes a Microsoft Excel document titled “Copy of Updated_Comparables_Resources JKMR.xlsx”;

(2) joint report of Dr Burrows and Mr McKibben dated 30 January 2026;

(3) joint report of Mr Mayne, Ms Chandler and Mr Lee dated 30 January 2026; and

(4) joint report of Mr Ross and Mr Kepler dated 3 February 2026 which annexes a joint statement of Dr Burrows and Mr Kepler dated the same.

55 The experts gave evidence and were cross-examined in conclaves designed to address the topics covered in their respective reports and the joint reports. Their evidence insofar as it is relevant to the issues to be determined is set out in the balance of these reasons.

3. The facts

3.1 ERA

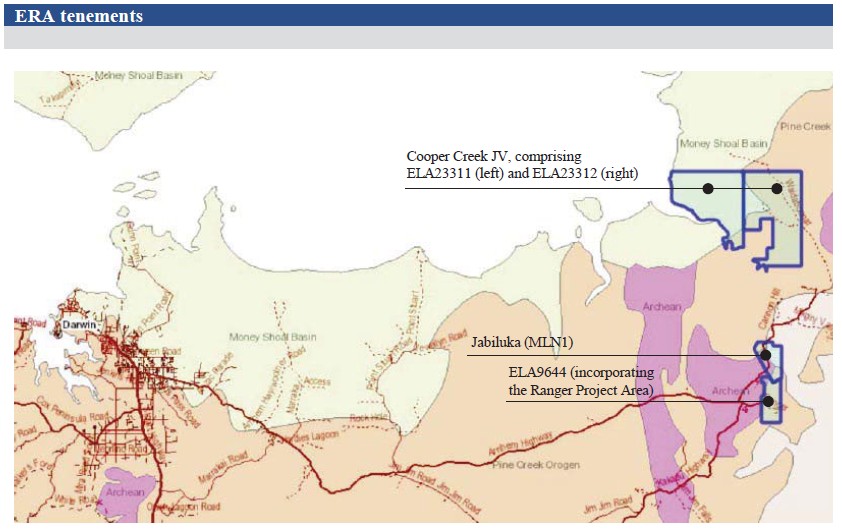

56 ERA is listed on the ASX. It is a uranium miner with operations in the Northern Territory (NT). ERA’s current tenements comprise two exploration licence applications for the Cooper Creek Joint Venture Project (Cooper Creek JV) comprising ELA23311 and ELA23312, MLN1 (also referred to as Jabiluka) and ELA9644 (which incorporates the Ranger Project Area). The tenements are depicted in the map set out below which has been extracted from the LEA Report:

57 As at April 2025 ERA’s principal operation concerned the rehabilitation of the former Ranger uranium mine (see below).

3.1.1 Ranger uranium mine

58 The former Ranger mine lies within the Ranger Project Area which occupies approximately 79 km2 and is surrounded by, but separate from, Kakadu National Park.

59 ERA undertakes its operations in the Ranger Project Area pursuant to an authorisation granted under s 41 of the Atomic Energy Act 1953 (Cth) (s 41 Authority).

60 ERA ceased mining operations at the Ranger mine in 2012 but continued to process stockpiled ore at that site until January 2021, when the s 41 Authority required it to cease. Relevantly, cl 5.1 of the s 41 Authority required ERA to cease or suspend all mining operations by 8 January 2021 and cl 6.1 requires ERA to undertake and complete the rehabilitation of the Ranger Project Area in accordance with Appendix A to the schedule to the s 41 Authority, titled “Environmental Requirements of the Commonwealth of Australia for the Operation of the Ranger Uranium Mine”.

61 In 2009 ERA announced the discovery of the R3D underground resource. However, in 2015 ERA decided not to progress the R3D project, initially placing the exploration into decline and associated infrastructure under care and maintenance. In August 2021 ERA completed backfill works on the R3D decline. No further work is being undertaken on development options for the R3D project. Nor could it given that ERA has no authority to conduct mining operations in the Ranger Project Area and development of R3D is not an authorised activity.

62 Since 1 July 2024 ERA’s operations have been governed by Deemed Mining Licence 0108-18 which comprises Ranger Authorisation 1018-18 and the last approved Ranger Mine Closure Plan (2024 MCP).

63 Activities at the Ranger Project Area are now limited to rehabilitation. Because of the impending expiration of the s 41 Authority, on 12 December 2025 a rehabilitation authority was conferred on ERA by the Commonwealth Minister for Resources pursuant to s 41CA of the Atomic Energy Act which authorises ERA to undertake the rehabilitation work set out in the schedule thereto (s 41CA Authority). The s 41CA Authority requires ERA to rehabilitate the Ranger Project Area as set out in and in accordance with the Environmental Requirements.

3.1.2 Jabiluka

64 Adjacent to the Ranger mine is an area known as Jabiluka, which contains two uranium deposits: Jabiluka I discovered in 1971 and Jabiluka II discovered in 1973. For present purposes, it is the valuation of the Jabiluka II deposit that is in contest. Given North and Zentree’s experts use the term “Jabiluka II” and “Jabiluka deposit” interchangeably in their respective reports and oral evidence, in the balance of these reasons when I refer to the Jabiluka deposit, I am referring to Jabiluka II and vice versa.

65 Since December 1992 ERA has been the holder of MLN1 (being the relevant mining lease) on which the Jabiluka deposit is located.

66 In 1982 Pancontinental Energy NL ACN 003 029 543 and the Northern Land Council (NLC) entered into an agreement under s 43 of the Aboriginal Land Rights (Northern Territory) Act 1976 (Cth) pursuant to the terms of which the NLC consented to the grant of a lease over Jabiluka subject to certain conditions, including making payments to the NLC for the benefit of the local Aboriginal people (Section 43 Agreement).

67 On 12 August 1982 the NT Government granted MLN1 to Pancontinental for a 42-year lease period with an option to renew for 10 years. In 1991 ERA acquired MLN1 from Pancontinental and on 24 December 1991 the Section 43 Agreement was transferred to ERA.

68 A detailed history of the early development of MLN1 is set out in the LEA Report. Relevantly, MLN1 has never been mined.

69 In about February 2005 ERA, the Traditional Aboriginal Owners (Traditional Owners) of the Jabiluka (the Mirarr people) and the NLC entered into a Long Term Care and Maintenance Agreement (LTCMA). The recitals to the LTCMA relevantly include:

A. ERA is the holder of MLNl and is, except as otherwise provided in this Agreement, authorised to develop and mine the Jabiluka Project Area under the Section 43 Agreement, subject to the provisions of the Transfer Agreement.

B. The Traditional Owners are the traditional Aboriginal owners, as defined in the Aboriginal Land Rights (Northern Territory) Act (Cth), of the area that includes the Jabiluka Project Area, being the group which under Aboriginal tradition is responsible for speaking for and making decisions about the Jabiluka Project Area and which asserts native title regarding that area.

…

D. The following issues are of concern to the Traditional Owners and the NLC:

(a) the length of time since MLNl was granted and the current views of the Traditional Owners regarding the Jabiluka Project Area;

(b) the placement of mineralised material above ground on the Jabiluka Project Area; and

(c) the maintenance issues in respect of the Jabiluka Project Area.

E. This Agreement is intended to provide a framework for an agreed phase of long term care and maintenance of the Jabiluka Project Area, and is not intended to set aside or override the effect of Part IV of the Aboriginal Land Rights (Northern Territory) Act (Cth) or the Section 43 Agreement.

F. In the interests of an improved relationship between ERA and the Traditional Owners and the NLC, and ongoing dialogue between the parties as to the management of the Jabiluka Project Area during the proposed care and maintenance phase, the possible end of the proposed care and maintenance phase, and the future management of the Jabiluka Project Area, this Agreement provides, inter alia, that:

(a) ERA will carry out certain rehabilitation and environmental works in relation to the Jabiluka Project Area;

(b) ERA will not carry out further mining development of the Jabiluka Project Area without the approval of the Traditional Owners as provided in this Agreement; and

(c) the NLC and the Traditional Owners will, during the care and maintenance phase, forego certain payments that are claimed to be payable under the Section 43 Agreement and the Deed Poll.

70 Clause 2 of the LTCMA sets out its commencement and term. Relevantly, the LTCMA will remain in force until the later of the end of the “care and maintenance phase”, or the expiry or earlier determination of the Section 43 Agreement. The “care and maintenance phase” is defined to mean “the period starting from the commencement of [the LTCMA] to the date on which approval has been given under clause 6 or the date of expiry or earlier determination of the Section 43 Agreement”.

71 Clause 4.1 sets out ERA’s obligations under the LTCMA including filling and sealing the decline which refers to “the box-cut, main declining tunnel, drive and cross-cut tunnels that have been constructed to uranium ore body no.2” on the Jabiluka Project Area (defined therein), recontouring all disturbed areas providing erosion control and appropriate revegetation, developing and carrying out a water quality program, carrying out a detailed radiation survey at the completion of the works set out in cl 4.1 and carrying out substantial rehabilitation of the Djarr Djarr camp area. Clause 4.2 also requires ERA to remove its infrastructure and equipment located in Jabiluka except as may be required for ERA to comply with its obligations under the LTCMA or any other contractual or statutory obligations or for the purpose of proper environmental management of Jabiluka and surrounds.

72 The NLC and the Traditional Owners’ obligations under the LTCMA are set out in cl 5 of the LTCMA. They agree to forego payments that were otherwise due to them under the Deed Poll (as defined) and the Section 43 Agreement.

73 Clause 6 of the LTCMA is titled “Traditional Owners’ Approval Required”. Clause 6.1 provides:

In further consideration for the NLC and the Traditional Owners entering this Agreement, ERA acknowledges and agrees that prior to ERA undertaking any mining development, or applying for any Authorisation in order to undertake mining development, on the Jabiluka Project Area, ERA will obtain the approval of the Traditional Owners which, if given, is to be in accordance with this clause.

74 Clause 6.2 sets out the manner and circumstances in which the Traditional Owners are to give their approval for the purposes of cl 6.1 and provides:

The approval of the Traditional Owners referred to in clause 6.1 is to be given in the following manner and circumstances:

(a) the Traditional Owners, after having had an opportunity to consider a proposal by ERA for mining development on the Jabiluka Project Area have, as a group, consented to that proposal, and

(b) subject to paragraph (c), a written record of that consideration and consent is prepared which:

(i) is signed by no less than six (6) senior members of the Traditional Owners;

(ii) includes a statement from a legal practitioner that he or she was present when consent was given by the group and that the group was provided with independent legal advice as part of its considerations; and

(iii) includes a statement from the NLC that the NLC is aware of the proposal, had an opportunity to provide advice to the group, were present when consent was given and is satisfied that the decision has been made by the group in accordance with traditional Aboriginal decision-making processes; and

(c) in the event that the number of Traditional Owners who are aged 18 years or over is less than six (6), the written record referred to in paragraph (b):

(i) is to be signed by such number of Traditional Owners as are aged 18 years or over at the time the approval is given; and

(ii) shall include a further statement from the NLC that the number of Traditional Owners who are to sign the written record is appropriate in the circumstances.

75 Clause 6.3 provides for the parties to meet and discuss in good faith the approval referred to in cl 6 within a reasonable time after 1 July 2006 and at least once in every four years thereafter during the term of the LTCMA and at any other time reasonably requested by the Traditional Owners.

76 Clause 10 is titled “Default”. It sets out available remedies for breach of the LTCMA and provides:

10.1 Without limiting the legal or equitable relief or remedies which might be available to them, ERA acknowledges that either or both of the NLC or the Traditional Owners may seek an order for specific performance in relation to the compliance by ERA with the obligations imposed on ERA under clause 4.

10.2 If at any time prior to the giving of written approval in accordance with clause 6 of this Agreement, a breach of clause 6.1 by ERA is found to be proven by a court of competent jurisdiction, being a finding that mining development has been undertaken, or an Authorisation in respect of mining development has been sought or obtained, contrary to that provision, the parties agree that the relief that may be granted for such breach may include any or all of the following;

(a) injunctive relief, which may be indefinite, to prevent the continuation of any application for or grant of any Authorisation, or continuation of any mining development purportedly in accordance with any Authorisation, in breach of this Agreement;

(b) an order that any Authorisation obtained otherwise than in accordance with clause 6 is void and of no effect;

(c) damages; and

(d) an order that specific work be undertaken to restore damage caused by such breach.

77 On 25 February 2005 ERA, the Gundjeihmi Aboriginal Corporation (GAC) and the NLC issued a joint media statement announcing the entry into of the LTCMA. The statement included:

…

While [MLN1] and the [Section 43 Agreement] remain in force, the [LTCMA] obliges ERA (and its successors) to secure Mirarr consent prior to any future mining development of uranium deposits at Jabiluka. The agreement also waives some of ERA's financial obligations flowing from construction of the mine decline in 1998.

…

In welcoming the agreement, Ms Margarula said: “I am pleased that the mining company has listened to the Mirarr people, showing us the respect we deserve as Traditional Owners. This agreement lifts the shadow of Jabiluka off the Mirarr and other Aboriginal people in Kakadu. We now have a chance to solve some of the social problems like alcohol, unemployment and health. Jabiluka will never be mined unless the Mirarr give approval - in future the decision is ours alone for the first time.”

Mr Kenyon-Slaney, said the agreement heralded a new era of cooperation. “The company would like to develop Jabiluka, one of the world's most significant uranium deposits. Under this agreement development would only go ahead with the support of the Traditional Owners and we can now work together to try to find a way forward that meets the expectations of all parties.”

78 As discussed below (see [225]-[238]), the LTCMA effectively gave the Traditional Owners a veto over the right to mine at Jabiluka.

79 Further media statements have been issued by the GAC which reinforce the effect of the LTCMA.

80 On 18 February 2020 the GAC issued a media statement on behalf of the Traditional Owners titled “Rio Tinto majority crucial for Ranger clean-up” which provided:

All investors in [ERA] should understand that the Renounceable Share Entitlement Offer relates solely to funding the vital rehabilitation of the Ranger Project Area at the World Heritage listed Kakadu National Park. The GAC expect that further funds for Ranger’s total clean-up will be needed.

There should be no expectation that any investment in ERA will be recouped from the development of the Jabiluka deposit, for which there is no traditional owner support.

The Mirarr traditional owners applaud the work that ERA has done on the Ranger Mine Closure Plan, with the considerable financial support of its major shareholder, Rio Tinto. ERA and Rio Tinto have demonstrated a clear commitment to working with the traditional owners to address Ranger’s clean-up in a true spirit of corporate social responsibility.

Recent investors in ERA, including Zentree Investments and Willy Packer, should not be speculating about future mining. They are investing in meeting the significant challenge of rehabilitating the traditional land and waters of the Mirarr people and in protecting Kakadu National Park.

81 On 9 April 2022 the GAC issued a media statement which included:

Mirarr Traditional Owners have welcomed statements from mining giant Rio Tinto about the future of the controversial Ranger and Jabiluka sites within the World Heritage listed Kakadu National Park in Australia’s Northern Territory.

Supporters of Mirarr attended Rio Tinto’s London AGM last night Australian time and called on the company to ensure Kakadu is not left with a toxic radioactive legacy given the dramatic increases in the cost and timeframe needed for the rehabilitation of the decommissioned Ranger uranium mine.

Rio Tinto restated its commitment to a comprehensive clean up at Ranger in line with statements at multiple AGMs over the past decade.

“We are happy to hear the commitment from outgoing chair Simon Thompson that Rio Tinto will not walk away from its responsibilities at Kakadu. Mirarr never wanted this mine on our country and we do not want to be left with the poison after it closes” said Mirarr Senior Traditional Owner Yvonne Margarula.

…

In addition to seeking assurance about the Ranger clean up, the Mirarr supporters in London also raised the issue of the future of the Jabiluka site at today’s meeting.

In response to board member Ben Wyatt’s comments [GAC] CEO Justin O’Brien said:

“In recent company statements there is reference to the possible “development or sale” of the Jabiluka deposit. This is of huge concern to us, that place must be permanently protected from mining.

“We are heartened that Rio Tinto has reiterated its support for the wishes of the Mirarr that the Jabiluka site will never be developed without the consent of the Mirarr. We welcome the company’s clear acknowledgement that clear acknowledgement that there is no consent from Mirarr for mining at Jabiluka” Mr O’Brien concluded.

82 That media statement also set out “[b]ackground notes on Rio Tinto and Kakadu uranium mining” which included:

• The Ranger mine and Jabiluka project sites are of enormous cultural heritage significance to the Mirarr Traditional Owners

• Mirarr led a successful international “Stop Jabiluka Mine” campaign to protect their country from mining during the 1990s-2000s. This culminated in:

• no uranium exported from Jabiluka

• mining works being reversed, with mineralised ore returned underground

• extensive rehabilitation works at the site

• a [LTCMA] between Mirarr and Rio Tinto committing the mining company to honour the wishes of the Mirarr

83 On 19 April 2024 the GAC issued a media statement titled ‘Traditional Owners welcome NT Government support at Jabiluka” which included:

Mirarr Traditional Owners of the [Jabiluka Project Area] met with Northern Territory Chief Minister Eva Lawler and Mining Minster Mark Monahan in Darwin today. Senior Traditional Owner Yvonne Margarula, accompanied by her nephew Corben Mudjandi, travelled from Jabiru seeking an end to all talk of mining and certainty about the future of Jabiluka.

This meeting came after mining company [ERA] minority shareholder Willy Packer recently boasted about the prospect of future uranium mining at Jabiluka. Last month, ERA formally applied to extend [MLN1] for 10 years when it expires on 11 August this year.

Senior Traditional Owner Yvonne Margarula said: “We came to this meeting today for an answer. I am happy to say that the Territory Government understands we will never agree to mining at Jabiluka. My father said no, I’ve been saying no for over thirty years.”

…

84 It is also apparent that governments whose permission is required to undertake mining at Jabiluka do not support that course.

85 MLN1 was due to be renewed in August 2024. However, on 26 July 2024, the NT Minister for Mining and Minister for Agribusiness and Fisheries informed ERA that, based on advice from the Commonwealth Minister for Resources and Minister for Northern Australia, ERA’s application to renew MLN1 was refused (Renewal Decision).

86 The advice from the Commonwealth Minister for Resources was contained in a letter dated 25 July 2024 to the NT Minister for Mining which included:

I have considered your correspondence, as well as the views of ERA, the [NLC] and Mirarr Traditional Owners.

I have considered that renewing [MLN1] would be beneficial to ERA, and have considered its submissions including:

• that mining the site could deliver economic benefits for the [NT], the region, and the Mirarr;

• that the site’s uranium, if mined, could be used to produce a significant amount of nuclear energy, contributing to global efforts to lower carbon emissions;

• under the [LTCMA], ERA has committed that mining and development will not occur without the consent of the Mirarr; and

• the arrangements under the [LTCMA] are the best option for all parties.

However, I consider it is significant that the Mirarr strongly object to renewal. I consider it is unlikely that the Mirarr will consent to mining or development within the proposed term of the renewal (ten years). Noting ERA's commitment not to mine without the consent of the Mirarr, I consider the prospects of the site being developed or mined within the proposed term of the renewal are low.

I acknowledge ERA's submission that if the lease is not renewed, future governments and mining proponents may seek to mine the site without Mirarr consent. Decisions about the future of the site should be made at the appropriate time, consistent with the regulatory responsibilities of the Northern Territory and Australian Governments.

I advise you to refuse ERA’s application to renew [MLN1].

…

87 On 27 July 2024 a joint media release was issued by the Commonwealth Minister for the Environment and Water and the Commonwealth Minister for Resources in the following terms:

The Albanese Labor Government has advised the [NT] Government that [MLN1] should not be renewed, allowing the site to be added to Kakadu National Park.

The Commonwealth advice has enabled the Northern Territory Government to decline to extend [MLN1].

The Albanese Government will now begin the process of incorporating the site to the Kakadu National Park, in line with the wishes of the Mirarr Traditional Owners.

Minister for Resources and Northern Australia Madeleine King said the decision would end decades of uncertainty about the project.

“ERA and their major shareholder, Rio Tinto, rightly committed to not developing the site without the support of the Mirarr Traditional Owners, who are completely opposed to the renewal of the lease.

88 On 6 August 2024 ERA commenced a proceeding in this Court against a number of parties including the Commonwealth Minister for Resources and the NT Minister for Mining seeking judicial review of the Renewal Decision. The Renewal Decision is the subject of an interim stay pending the outcome of ERA’s judicial review application. The effect of the stay is that MLN1 continues in force until the decision is made: see Mineral Titles Act 2010 (NT), s 68. It is not necessary or desirable to say more about that proceeding, nor to opine on its merit. For present purposes the position is that MLN1 has not been renewed by the NT Minister for Mining.

3.2 North acquires more than 90% of the shares in ERA

89 North is a wholly owned subsidiary of Rio Tinto. Peko-Wallsend Pty Ltd ACN 000 245 054 is a wholly owned subsidiary of North.

90 Rio Tinto has had a majority interest in ERA since 8 August 2000 and through North and Peko-Wallsend, currently has a relevant interest of 98.43% in the shares in ERA.

91 Commencing in 2019 ERA undertook a series of capital raisings. Most recently, on 29 August 2024 ERA announced its 2024 Entitlement Offer, with net proceeds to be used to fund the planned Ranger Project Area rehabilitation expenditure until “3Q27”.

92 Rio Tinto through its 100% owned subsidiaries, North and Peko-Wallsend, committed those companies to subscribe for their respective pro-rata entitlements but there was limited participation by other existing ERA shareholders and no material participation by new shareholders. Accordingly, approximately 99% of the shares were taken up by Rio Tinto’s subsidiaries and on 21 November 2024, North and Peko-Wallsend were issued a total of 379,916,303,627 ordinary shares in connection with the 2024 Entitlement Offer. On the same day Rio Tinto lodged a substantial holder notice confirming the total number of shares issued with the ASX.

93 Following completion of the 2024 Entitlement Offer North increased its relevant interest in ERA from 86.3% to 98.43%, putting North over the 90% threshold to initiate a compulsory acquisition under Pt 6A.2 of the Corporations Act. The remaining shareholders in ERA hold 1.57% or 6,359,841,384 ordinary shares.

3.3 The Notice

94 On 23 December 2024, after requesting ASIC to nominate an independent expert to prepare a report for the purposes of enabling North to compulsorily acquire the remaining 1.57% of the shares in ERA, North retained LEA to prepare an IER stating whether, in its opinion, the terms proposed in a draft compulsory acquisition notice prepared by North give a fair value for ERA’s shares. LEA was one of three independent experts nominated by ASIC.

95 The draft compulsory acquisition notice provided by North to LEA for the purposes of preparing the IER stated that North intended to acquire the remaining ERA shares for a cash payment of $0.002 or 0.2 cents per share (i.e. the same amount per share as under the 2024 Entitlement Offer).

96 On 16 January 2025 LEA engaged SRK to prepare an ISR to assist with its valuation.

97 LEA completed its IER, being the LEA Report. It annexes the SRK Report.

98 On 11 April 2025 North lodged the Notice to acquire the remaining shares in ERA with ASIC. The Notice provides that:

(1) North proposes to acquire each ordinary share in ERA for the cash amount of $0.002 or 0.2 cents;

(2) the recipient (or anyone who acquired the securities during the objection period) has the right to object to the acquisition of their securities by completing and returning the objection form within one month of receipt of the Notice;

(3) each shareholder has the right to obtain the names and addresses of the other holders from the company register;

(4) North, and its related body corporate, Peko-Wallsend, purchased ordinary ERA shares for $0.002 per new ordinary share pursuant to the 2024 Entitlement Offer and those shares were issued on 21 November 2024; and

(5) North and its related bodies corporate are not aware of any information material to deciding whether to object to the acquisition that had not otherwise been disclosed in the LEA Report and the SRK Report.

99 On the same day ERA lodged the following documents with the ASX:

(1) a letter to its shareholders;

(2) the Notice;

(3) a template objection form; and

(4) a copy of the LEA Report which annexed the SRK Report.

100 On 14 April 2025 all ERA shareholders received copies of the documents referred to in the preceding paragraph.

101 The objection period ended on 19 May 2025. By that date 42.58% of the remaining ERA shareholders holding securities covered by the Notice had objected to the acquisition.

3.4 The LEA Report

102 Mr Kepler, a director and authorised representative of LEA, supervised and had overall responsibility for preparing the LEA Report. As set out above, he was assisted by Nathan Toscan, managing director of LEA and other employees. Mr Kepler’s expertise is set out at [24]-[26] above.

103 At [11] of the LEA Report, LEA summarises its opinion that “the terms of the Compulsory Acquisition give a ‘fair value’ for the ERA shares that are the subject of the Compulsory Acquisition” based on the reasons set out in the report.

104 Under the sub-heading “[a]ssessment of ‘fairness’” the LEA Report provides:

12 ERA conducts no net cash generating activities, with its current operations primarily focused on the rehabilitation of the Ranger Project Area. However, ERA also has other assets, including mineral interest assets (such as MLN1) and cash. Given this, LEA considers the sum of the parts approach to be the most appropriate method for valuing ERA as a whole. This approach allows the value of ERA’s individual assets and liabilities to be separately assessed using the most suitable methodology for each, with the resulting values then aggregated to determine ERA’s overall value. In this regard, we note that:

(a) the future liability for rehabilitating the Ranger Project Area is a finite obligation best assessed using a discounted cash flow (DCF) analysis. LEA has engaged an independent technical specialist, [SRK], to evaluate the reasonableness of the cost estimates prepared by ERA management

(b) ERA’s mineral interest assets (including MLN1, the [R3D] project, and the Cooper Creek JV) are undeveloped mineral interest assets that do not currently generate revenue or cash flow. Given the absence of reliable long-term cash flow projections to support a DCF analysis, LEA has commissioned SRK to independently assess their value

(c) ERA’s other asset and liability items predominantly comprise cash and cash equivalents, or other items that collectively are relatively negligible in value.

(Footnotes omitted.)

105 A summary of the value of ERA’s shares on a 100% controlling basis is set out at [16] of the LEA Report (although I note that the values of MLN1 and the Cooper Creek JV were subsequently updated by Mr McKibben in his supplementary report dated 10 February 2026, which I discuss at [268] below):

106 At [17] of the LEA Report, LEA observed that RG 111 states that “a control transaction is ‘fair’ if the value of the consideration offered is equal to, or greater than, the value of the securities that are the subject of the offer”. Based on its comparison of the value of the consideration proposed by North to the value LEA assessed on a 100% controlling interest basis, and because the former exceeds the latter, LEA concluded that the proposed consideration of 0.2 cents per share is “fair” to ERA shareholders.

107 The LEA Report sets out detailed reasoning to support its opinion summarised above.

108 Part V of the LEA Report is titled “[v]aluation of ERA”. There LEA notes that it has determined the value of the ordinary shares in ERA “by assessing the market value of ERA as a whole,” and then dividing that value by the number of ordinary shares on issue. That is, LEA has assessed the value of ERA shares on a 100% controlling interest basis. LEA explains at [190] of the LEA Report:

Our valuation of ERA as a whole has been undertaken on the basis of market value as a going concern (consistent with the basis of preparation of ERA’s financial statements) where market value is defined as the price that would be negotiated in an open and unrestricted market between a knowledgeable, willing but not anxious buyer and a knowledgeable, willing but not anxious seller acting at arm's length within a reasonable timeframe. ...

(Footnote omitted.)

109 I pause to observe that there is no dispute between the parties and, in particular their respective experts, about this approach to the valuation.

110 At [192] of the LEA Report, LEA points out that ERA conducts no cash generating activities and that its current operations are primarily focussed on rehabilitation of the Ranger Project Area. LEA also notes that ERA has other mineral assets (such as MLN1) and cash. Given this LEA is of the opinion that the “sum of the parts” approach is the most appropriate method for valuing ERA as a whole, a matter which is also agreed between the parties’ relevant valuation experts, Messrs Kepler and Ross. LEA goes on to explain that this method allows the value of ERA’s assets and liabilities to be separately assessed using the most appropriate method for each and the resulting values to be aggregated to determine ERA’s overall value. In that regard LEA says at [192]:

(a) the future liability for rehabilitating the Ranger Project Area is a finite obligation best assessed using a DCF analysis. LEA has engaged an independent technical specialist, SRK, to evaluate the reasonableness of the cost estimates prepared by ERA management

(b) ERA’s mineral interest assets (including MLN1, the Ranger 3 Deeps project and the Cooper Creek JV) are undeveloped mineral interest assets that do not currently generate any revenue or cash flow. Given the absence of reliable long-term cash flow projections to support a DCF analysis, LEA has commissioned SRK to independently assess their value

(c) ERA’s other asset and liability items predominantly comprise cash and cash equivalents, or other items that collectively are relatively negligible in value.

111 At [195] LEA notes that a key aspect of its valuation is that “it is reasonable to expect an acquirer of 100% of the equity of ERA would need to take responsibility for the full rehabilitation of the Ranger Project Area and cover any shortfall that arises between the rehabilitation costs and the value or cash flows that may be generated by ERA’s assets (including MLN1)”.

112 At [198]-[199] LEA addresses “[n]et cash and government security receivable” noting that as at 28 February 2025 ERA had some:

(1) $760 million in cash and cash equivalents and no debt and that its cash balance increased significantly following the receipt of some $766 million (before costs) from the 2024 Entitlement Offer and the issue of new shares under the shortfall facility; and

(2) $539 million in term deposits held with the Department of Industry, Science and Resources and that ERA’s access to these funds is limited to funding the rehabilitation of the Ranger Project Area.

113 Commencing at [200] the LEA Report addresses the value of MLN1. As set out above, to assist it in attributing a value to MLN1, LEA retained SRK. LEA requested that SRK consider both an “unencumbered value of MLN1”, that is unencumbered by the Renewal Decision and the Traditional Owner consent, and an “as is” opinion of the value of MLN1 “reflecting encumbrances arising from the Renewal Decision and position of the Mirarr Traditional Owners and, if considered appropriate, the circumstance that ERA no longer includes MLN1 in reported mineral resources”.

114 LEA summarises SRK’s opinion of the value of MLN1 on both bases:

(1) in relation to the “unencumbered value”, the LEA Report notes at [214]:

(2) in relation to the “as is” or “encumbered value” LEA notes that SRK adopted two valuation approaches, a top-down approach and a bottom-up approach, and sets out the results of SRK’s opinion at [217]:

115 LEA then undertook “cross-checks” of SRK’s valuations against the implied values attributed to MLN1 based on the market traded prices of ERA shares as well as the 2023 Interim Entitlement Offer and the 2024 Entitlement Offer. Insofar as the cross-checks are concerned, at [222] of the LEA Report, LEA notes that throughout the period in which the analysis was undertaken, 31 August 2022 to 21 March 2025, “ERA was a very thinly traded stock and the analysis should therefore be treated with a high degree of caution”. Moreover, LEA says that the trading period also pre-dates ERA’s decision to no longer recognise a mineral resource for MLN1 and “it is not possible to determine the price at which ERA shares may have traded had no mineral resource been reported by ERA for MLN1”.

116 Notwithstanding that, LEA undertook an analysis of the implied value of MLN1 based on the ERA share price in the period 31 August 2022 to 21 March 2025. LEA observed that while it “is not possible to determine with any certainty the current price at which ERA shares would trade in the absence of the Compulsory Acquisition and thus what the current inferred value of MLN1 may be, as a guide” they:

(1) “estimated the value of MLN1 based on LEA’s view of the ‘undisturbed’ share price of ERA … (which takes into account the Renewal Decision, the dilutive impact of the 2024 Entitlement Offer and adjusts for the decline in the spot price of uranium and ERA’s estimated cash burn through to 28 February 2025) and ERA’s 28 February 2025 balance sheet”. That analysis resulted in an implied value of MLN1 of $1,473 million (with a tax deduction available) and $2,049 million (with no available tax deduction); and

(2) considered the implied values as at the period 19 September 2023 to 25 September 2023, when the spot price of uranium was last around A$104/lb, which approximated to $1.1 billion (tax deduction available) and $1.5 billion (tax deduction not available). Having regard to ERA’s announcement on 26 September 2023 that it now expects that total rehabilitation costs will materially exceed the previous estimated range of $1.6 billion to $2.2 billion and that the expected final completion date will also be delayed, LEA reflected the estimated impact of that announcement on the implied value of MLN1 by including a retrospective adjustment of $974 million based upon the final confirmed provision as at 31 December 2024. LEA notes that “[i]f this same retrospective adjustment is extended through to the period of 19 September 2023 to 25 September 2023 the implied value of MLN1 increases to $1.9 billion (tax deduction available) and $2.5 billion (tax deduction not available)”. LEA cautions that these values do not account for factors such as the Renewal Decision and that “[a]djusting these downward by some 17% (tax deduction available) to 13% (tax deduction not available) results in an implied value for MLN1 of $1.6 billion (tax deduction available) to $2.2 billion (tax deduction not available)”.

117 At [226] of the LEA Report, LEA cautions that “[t]hese estimates should be viewed as illustrative and do not represent a definitive assessment of the implied value of MLN1”. That is because there is no certainty that “the market would have assigned, or would currently assign, these values to MLN1 in the absence of the Compulsory Acquisition or with knowledge of ERA’s decision to no longer include MLN1 in reported mineral resources”. Relevantly, LEA also noted that the calculated ranges exceed the encumbered values calculated by SRK and went on to opine that “[s]etting aside potential mispricing issues that likely result from ERA’s status as a very thinly traded stock and the issue pertaining to ERA’s decision to no longer include MLN1 in ERA’s reported mineral resources, in LEA’s view, this discrepancy may be explained by the existence of optionality”.

118 LEA then addressed what it termed “‘in substance’ call-option value” which is the material disconnect between the manner in which traders of minority interest parcels of ERA shares are able to price those shares and the manner in which a purchaser of 100% of the equity in ERA would be able to price 100% of the shares.

119 Having done so, LEA ultimately concluded that the traded market prices for ERA shares are not a reliable reference point for the determination of the market value of the equity in ERA on a 100% controlling interest basis and any implied value of MLN1 that might be derived from that value is also not reliable. LEA reached the same view in relation to the implied value of MLN1 arising from the 2023 Interim Entitlement Offer and the 2024 Entitlement Offer.

120 At [240] of the LEA Report, LEA concluded that in its view the encumbered value attributed to MLN1 by SRK is reasonable and thus adopted the range of $332.2 million (low) to $443.0 million (high) for that asset.

121 In relation to R3D, at [247] of the LEA Report LEA notes that SRK was not able to identify a viable pathway for the grant or exploration and development of R3D and thus considered it no longer had a reasonable basis to assign material value to it. SRK concluded that R3D has negligible to no value associated with it.

122 Commencing at [248] LEA considered the liability associated with the rehabilitation of the Ranger Project Area. LEA observes at [249]:

Mine Closure Plans have been prepared annually by ERA with the 2023 plan receiving Commonwealth Ministerial approval on 6 February 2025. The Ranger Project Area rehabilitation costs were estimated by ERA to be some $3,079 million on an undiscounted, nominal basis as at 31 December 2024. ERA has recognised a provision at 31 December 2024 of $2,422 million assuming a real (pre-tax) discount rate of 2.5% and assumed inflation rates of 0.6% to 2.5% long term. The provision at 28 February 2025 was some $2,403 million (noting that while this is not an audited etc. figure, it is based upon a roll forward of the same methodology and calculation applied in the determination of the provision as at 31 December 2024).

123 As set out above, LEA also engaged SRK to consider the reasonableness of the cost estimates associated with the rehabilitation and mine closure plans. At [254]-[255] of its report, LEA notes:

254 SRK concluded that:

(a) ERA adopting a commercial costing approach rather than a generic liability estimate calculator is a more accurate method and therefore considers that ERA has made the best attempt to understand its liability to the full extent currently possible in the absence of further studies

(b) the approach to closure planning and liability estimating has been undertaken in compliance with good industry practice.

255 SRK also noted:

(a) that the Ranger Project Area rehabilitation is an inherently complex project, with future activities beyond 2027 requiring additional studies and ongoing approvals, and that it is likely that the current provision will need to be revised once these studies are complete and additional approvals granted

(b) a particular area of uncertainty to SRK involves the formal regulatory approval of certain closure criteria and the mechanisms through which relinquishment can be approved and signed off by both NT and Commonwealth regulators

(c) SRK considers the schedule outlined for the Ranger Project Area rehabilitation is aligned with the data currently available, and that the schedule aligns will with the details of the Tranche 1A (to 3Q27 – Phase 1 demolition, Pit 3 initial and secondary capping and further studies – refer paragraph 100 above) – although also noting that the risks and uncertainties associated with activities and timelines beyond 3Q27 should continually be assessed

(d) based on SRK’s experience, there is a potential for under estimation of the provisions throughout the entire post-closure monitoring and maintenance period (beyond 2027 to 2060), and that SRK recommends a legal review of the site’s obligations particularly concerning property holding and continued monitoring programs up to December 2060. LEA notes that to the extent that SRK are correct in their view, any amendment would not be material (in present value terms) in the context of the $2.4 billion provision

(e) the opportunity for costs to reduce under the MSA, but that budgets and forecasts are currently being assessed.

124 LEA considered that the appropriate basis on which to quantify the value of the Ranger Project Area rehabilitation costs is to use the DCF method, with the best available estimate of future costs discounted to present value thus allowing for the time value of money. LEA was of the view that the best available current estimate of the expected future costs of the Ranger Project Area rehabilitation is ERA’s current estimate of the nominal costs reflected in its adopted total Rehabilitation Provision at 28 February 2025 of $2,403 million. This was made of $2,402 million for the Ranger Project Area and $1 million for MLN1. LEA continued at [257]: