FEDERAL COURT OF AUSTRALIA

Top Energy Holdings Pty Ltd v Liu [2026] FCA 689

File number(s): | NSD 1165 of 2020 NSD 999 of 2021 |

Judgment of: | GOODMAN J |

Date of judgment: | 4 June 2026 |

Catchwords: | CONTRACTS – whether Business Sale Agreement and Loan Agreement between entities on one side of a joint venture were executed prior to entry into the joint venture, or created after the breakdown of the joint venture – held that each Agreement was created after the joint venture broke down and cannot be relied upon MISLEADING OR DECEPTIVE CONDUCT – whether one side of the joint venture engaged in misleading or deceptive conduct in contravention of s 18 of the Australian Consumer Law by failing to disclose another Loan Agreement – held no misleading or deceptive conduct because of an absence of reasonable expectation of disclosure – held no loss in any event because the non-disclosure was not causative of entry into the joint venture EVIDENCE – evaluation of evidence – primary reliance upon contemporaneous documents – inferences to be drawn from a failure to adduce evidence from signatories to an agreement when the date of execution of the agreement is a central issue |

Legislation: | Competition and Consumer Act 2010 (Cth), Schedule 2, ss 18, 236 Corporations Act 2001 (Cth), ss 180, 181, 182 Evidence Act 1995 (Cth), s 140 |

Cases cited: | Addenbrooke Pty Ltd (ACN 055 973 576) v Duncan (No 2) [2017] FCAFC 76; (2017) 348 ALR 1 Bathurst Regional Council v Local Government Financial Services Pty Ltd (No 5) [2012] FCA 1200 Blatch v Archer (1774) 1 Cowp 63; 98 ER 969 Briginshaw v Briginshaw [1938] HCA 34; (1938) 60 CLR 336 Brown v New South Wales Trustee and Guardian [2012] NSWCA 431 CCL Secure Pty Ltd v Berry [2019] FCAFC 81 Commercial Union Assurance Company of Australia Ltd v Ferrcom Pty Ltd (1991) 22 NSWLR 389 Communications, Electrical, Electronic, Energy, Information, Postal, Plumbing and Allied Services Union of Australia v Australian Competition and Consumer Commission [2007] FCAFC 132; (2007) 162 FCR 466 Effem Foods Pty Ltd (t/as Uncle Ben’s of Australia) v Lake Cumbeline Pty Ltd [1999] HCA 15; (1999) 161 ALR 599 Elanor Funds Management Ltd (ACN 125 903 031) v Alceon Group Pty Ltd (ACN 122 365 986) [2024] FCAFC 121; (2024) 424 ALR 601 Fox v Percy [2003] HCA 22; (2003) 197 ALR 201 Gestmin SGPS SA v Credit Suisse (UK) Ltd [2013] EWHC 3560 Hassan v Minister for Home Affairs [2025] FCAFC 57; (2025) 309 FCR 44 Innes v AAL Aviation Ltd [2017] FCAFC 202; (2017) 259 FCR 246 Jones v Dunkel [1959] HCA 8; (1959) 101 CLR 298 Julstar Pty Ltd v Hart Trading Pty Ltd [2014] FCAFC 151 Kuhl v Zurich Financial Services Australia Ltd [2011] HCA 11; (2011) 243 CLR 361 Les & Zelda Investments Pty Ltd (as trustee for Les & Zelda Family Trust) v Whitehaven Coal Limited (No 4) [2026] NSWSC 107 Ling v Pang [2023] NSWCA 112 Manly Council v Byrne [2004] NSWCA 123 Martin v Norton Rose Fulbright Australia [2021] FCAFC 216; (2021) 395 ALR 413 Neat Holdings Pty Ltd v Karajan Holdings Pty Ltd [1992] HCA 66; (1992) 110 ALR 449 Quintis Ltd (subject to deed of company arrangement) (ACN 092 200 854) v Certain Underwriters at Lloyd’s London Subscribing to Policy Number B0507N16FA15350 [2021] FCA 19; (2021) 385 ALR 639 Roberts-Smith v Fairfax Media Publications Pty Ltd (Reopening Application) [2025] FCAFC 66; (2025) 310 FCR 141 Self Care IP Holdings Pty Ltd v Allergan Australia Pty Ltd [2023] HCA 8; (2023) 277 CLR 186 Watson v Foxman (1995) 49 NSWLR 315 Weissensteiner v The Queen [1993] HCA 65; (1993) 178 CLR 217 |

Division: | General Division |

Registry: | New South Wales |

National Practice Area: | Commercial and Corporations |

Sub-area: | Commercial Contracts, Banking, Finance and Insurance |

Number of paragraphs: | 302 |

Date of last submission/s: | 2 July 2024 |

Date of hearing: | 19 to 22, 25 and 26 March 2024; 3 and 21 June 2024 |

Counsel for the Applicants: | Mr A Kaufmann |

Solicitor for the Applicants: | Coleman Greig Lawyers |

Counsel for the Respondents: | Mr D G Healey with Ms B Ng |

Solicitor for the Respondents: | H & H Lawyers |

ORDERS

NSD 1165 of 2020 | ||

| ||

BETWEEN: | TOP ENERGY HOLDINGS PTY LTD ACN 627 716 410 Applicant | |

AND: | YING LIU First Respondent ZAN HUANG Second Respondent WIN SOLAR ENERGY PTY LTD Third Respondent | |

AND BETWEEN: | WIN SOLAR ENERGY PTY LTD Cross-Claimant | |

AND: | TOP ENERGY HOLDINGS PTY LTD ACN 627 716 410 Cross-Respondent | |

order made by: | GOODMAN J |

DATE OF ORDER: | 4 June 2026 |

THE COURT ORDERS THAT:

1. Within 21 days of the date of these orders, the parties provide to the Associate to Goodman J agreed orders (or failing agreement, competing orders).

2. If the parties are unable to agree on the proposed orders referred to in order 1, then:

(a) within 28 days of the date of these orders each party file and serve written submissions of no more than five (5) pages in support of the orders sought by that party; and

(b) the proceeding be listed for further case management on a date and time to be agreed between the parties and the Associate to Goodman J.

3. The name Ms Ying Lui be corrected to Ms Ying Liu.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ORDERS

NSD 999 of 2021 | ||

BETWEEN: | DE GRANDLAND PTY LTD ACN 615 314 899 Applicant | |

AND: | JOYO HOLDINGS PTY LTD ACN 620 183 011 First Respondent YING LIU Second Respondent ZAN HUANG Third Respondent | |

order made by: | GOODMAN J |

DATE OF ORDER: | 4 JUNE 2026 |

THE COURT ORDERS THAT:

1. Within 21 days of the date of these orders, the parties provide to the Associate to Goodman J agreed orders (or failing agreement, competing orders).

2. If the parties are unable to agree on the proposed orders referred to in order 1, then:

(a) within 28 days of the date of these orders each party file and serve written submissions of no more than five (5) pages in support of the orders sought by that party; and

(b) the proceeding be listed for further case management on a date and time to be agreed between the parties and the Associate to Goodman J.

3. The name Ms Ying Lui be corrected to Ms Ying Liu.

[Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

[1] | |

[28] | |

[28] | |

B.2 Onus and standard of proof and the assessment of evidence | [35] |

B.3 The fallibility of human recollection and primary reliance upon contemporaneous documents | [52] |

[72] | |

[72] | |

[74] | |

[74] | |

[74] | |

[79] | |

[80] | |

[86] | |

[87] | |

[91] | |

[103] | |

[106] | |

[107] | |

[108] | |

[150] | |

[154] | |

[184] | |

C.10 Payment of $330,000 from Top Energy to WSE and removal of Wilson as a director of Top Energy | [192] |

[198] | |

C.12 Lodgement of WSE’s May 2019 Business Activity Statement | [199] |

C.13 Commencement of the De Grandland proceeding | [200] |

[201] | |

[208] | |

[209] | |

[248] | |

[249] | |

[267] | |

[268] | |

[274] | |

[280] | |

E.4 Was the impugned conduct misleading or deceptive or likely to mislead or deceive? | [283] |

E.5 If so, did De Grandland suffer loss by reason of such conduct? | [293] |

[300] | |

F. CONCLUSION | [301] |

REASONS FOR JUDGMENT

GOODMAN J:

A. INTRODUCTION AND OVERVIEW

1 These reasons for judgment concern two related proceedings which, for convenience, I will refer to as the Top Energy proceeding and the De Grandland proceeding. In the reasons which follow, and without intending any disrespect, I follow the course adopted by counsel in these proceedings of referring to various natural persons by their first names.

2 The central players are:

(1) De Grandland Pty Ltd, a company in which the directors and members were Mr Ding (Richard) Li and his business partner Ms Guo Yi (Rebecca) Li;

(2) Ms Ying (Amie) Liu;

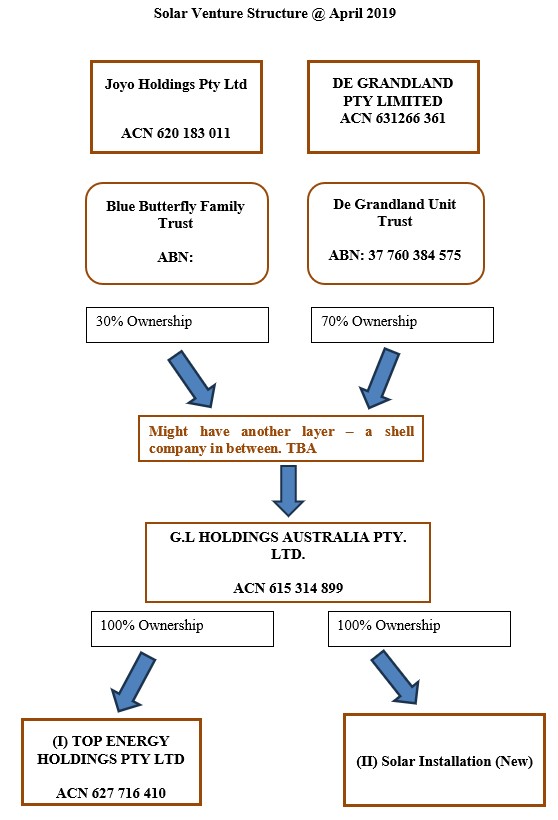

(3) the following companies associated with Amie:

(a) Win Solar Energy Pty Ltd (WSE);

(b) Joyo Holdings Pty Ltd;

(c) Joyo Pty Ltd;

(d) GL Holdings Australia Pty Ltd;

(e) Top Energy Holdings Pty Ltd;

(4) Amie’s husband, Yufeng (Sam) Sun; and

(5) Mr Zan (Wilson) Huang. Wilson assisted Amie with her companies and was a director of some of those companies from time to time.

3 Joyo Holdings was the trustee of the Blue Butterfly Trust. In that capacity, Joyo Holdings held shares in GL Holdings as trustee for the benefit of Amie, Sam and Amie’s son.

4 WSE had a business of selling solar energy products and accessories (such as solar panels, inverters and racks) (WSE business).

5 From about April 2019, there were discussions between Amie and Wilson on the one hand and Richard and Rebecca on the other. Those discussions concerned a joint venture. It is common ground that as part of that joint venture, several events occurred.

6 First, the WSE business was transferred from WSE to Top Energy. The basis on which that transfer occurred is the subject of controversy and at the heart of the proceedings.

7 Secondly, De Grandland invested $2,000,000 in GL Holdings (which held all of the shares in Top Energy) in return for a majority interest in GL Holdings. To that end, on or about 25 June 2019, De Grandland, Joyo Holdings and GL Holdings entered into a Subscription and Shareholders Deed (SSD).

8 Pursuant to the SSD, De Grandland agreed to pay $2,000,000 to GL Holdings in return for the issue to it of 466 shares in GL Holdings, with the result that De Grandland held 466/666 (approximately 70 per cent) and Joyo Holdings held 200/666 (approximately 30 per cent) of the issued shares in GL Holdings.

9 The SSD provided for a trial period of twelve months, with each of De Grandland and Joyo Holdings having an option – exercisable during the period commencing three months prior to the end of the trial period and ending one month prior to the end of the trial period – to terminate the trial period by giving written notice to the other parties requiring De Grandland to sell its 466 shares to Joyo Holdings or GL Holdings.

10 If such notice were provided by De Grandland, then the price payable by Joyo Holdings or GL Holdings for the 466 shares would be $2,000,000.

11 If such notice were provided by Joyo Holdings, then the price payable would be $2,200,000.

12 Neither De Grandland nor Joyo Holdings exercised their option. The trial period expired. Discussions between Richard and Amie ended with a falling out between them (and their respective companies).

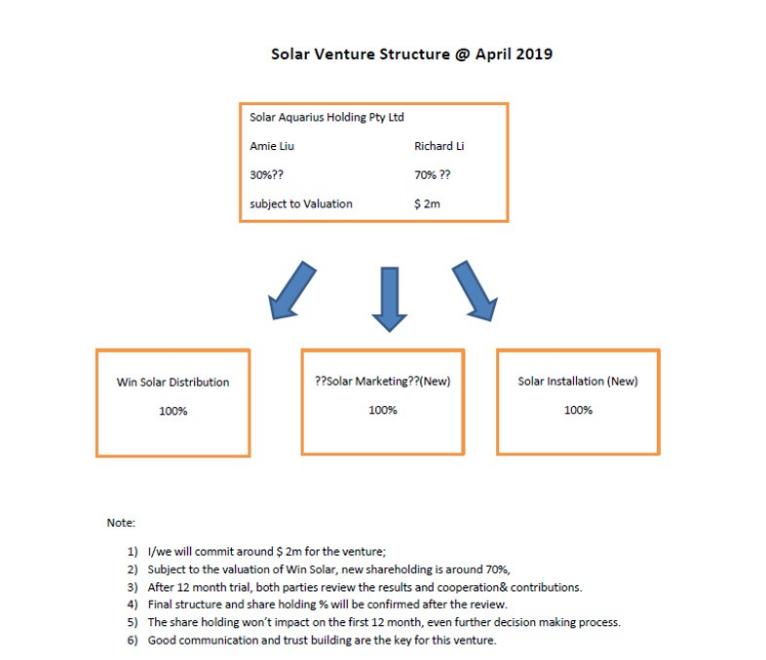

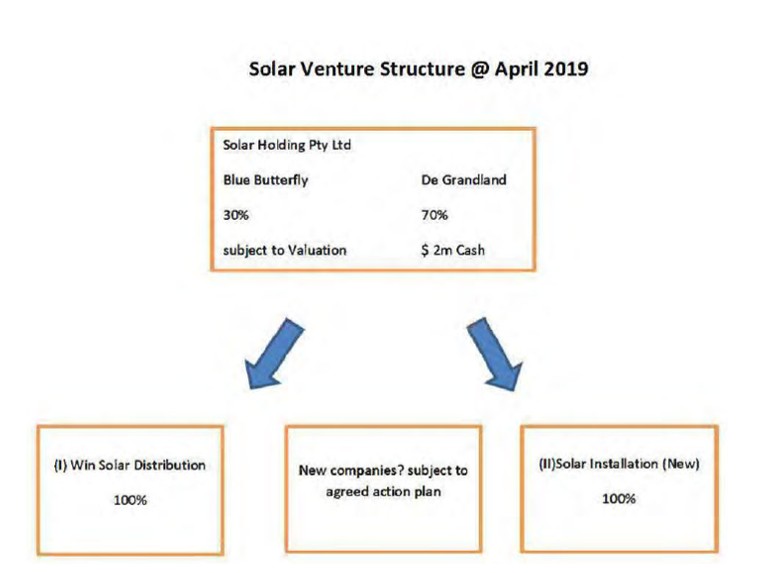

13 During the course of those discussions:

(1) on 30 July 2020 De Grandland, qua member of GL Holdings, called a members’ meeting to be held on 21 August 2020 for the removal of Wilson as a director of GL Holdings;

(2) between 10:00 and 11:00pm on 20 August 2020 (i.e. the night before the scheduled meeting):

(a) WSE demanded payment of $880,000 from Top Energy, purportedly pursuant to a Business Sale Agreement (BSA). The BSA – which was purportedly made on 28 March 2019 between WSE (as seller) and Top Energy (as purchaser) – provided for the sale of the “Business” in return for payment of a Purchase Price of $800,000. (The additional amount of $80,000 demanded was apparently referable to goods and services tax (GST).) The “Business” was defined in the BSA as the “solar system and accessories import and wholesale, trading under the business name Win Solar Wholesale, and running at the domain and website of winsolarwholesale.com.au, excluding the Asset”. The “Asset” was defined in the BSA as meaning “cash, receivables, loan, plant, stock, vehicle, tools and equipment”;

(b) Wilson, qua director of Top Energy caused Top Energy to pay $550,000 to WSE;

(3) on 21 August 2020, De Grandland, using its 70 per cent interest in GL Holdings, removed Wilson as a director of GL Holdings;

(4) on 27 August 2020, De Grandland called a meeting of members of GL Holdings for 17 September 2020 for GL Holdings to pass a resolution, qua sole member of Top Energy, to remove Wilson as a director of Top Energy;

(5) on 15 September 2020,Wilson caused Top Energy to pay a further $330,000 to WSE; and

(6) on 17 September 2020, Wilson was removed as a director of Top Energy.

14 Top Energy then commenced the Top Energy proceeding.

15 In that proceeding, Top Energy seeks an order for the return of the $880,000 ($550,000 plus $330,000) paid to WSE on the basis that the BSA was not a bona fide document and was created not on or about 28 March 2019, but instead in or around August 2020.

16 In this regard, I note that Top Energy’s amended concise statement refers to the BSA as a “sham”. This does not accurately convey the case brought by Top Energy which is, in effect, a case based upon fraud. Further:

(1) the allegation was particularised as one based on fraud. The solicitors for the applicants indicated that “ … the use of the word “sham” refers in respect of each relevant document to a transaction that was fraudulently invented on or about the date referred to above, and not the date recorded in the document, with the intention of it being enforced”. The “date referred to above” for the BSA is 20 August 2020; and

(2) Amie, Wilson and WSE (Top Energy proceeding respondents) have met the case brought against them on the basis that they have been accused of fraudulent conduct. In this regard, there was no greater specificity in the applicants’ case – which was run and defended on the basis of concise statements – as to the precise cause of action (whether in deceit or otherwise) but the case was fought on the basis that if the fraud was established then Amie (via her corporate interests) improperly obtained the $880,000.

17 Each of the Top Energy proceeding respondents denies that the BSA was a fraudulent document and asserts that it recorded a bona fide agreement entered into on 28 March 2019, and thus before the SSD, with its true purpose being to record the terms of a commercial agreement for the sale and purchase of the Business (as defined in the BSA).

18 Top Energy alleges in the alternative – if the BSA was not a fraudulent document – that the payments from Top Energy to WSE totalling $880,000 were made by reason of: (1) a breach of fiduciary duty by Amie; and (2) contraventions of ss 180 to 182 of the Corporations Act 2001 (Cth) by Amie and Wilson (breach of duty case).

19 The essence of the breach of duty case is that the sale of the Business from WSE to Top Energy occurred in circumstances where: (1) there was no due diligence of the Business; (2) no independent valuation of the Business had been obtained; (3) Amie and Wilson knew or ought to have known that the purchase provided little or no benefit to Top Energy; and (4) Amie procured payment, for her own benefit in an amount that she knew or ought to have known was in excess of the value of the Business (as defined in the BSA). Top Energy also alleges that Amie holds moneys allegedly paid to her from the sale of the Business (as defined in the BSA) on trust because she knew that those moneys were the product of her breach of fiduciary duty; and that WSE was knowingly concerned in the contraventions by Amie and Wilson.

20 Each of the Top Energy proceeding respondents contests the allegations made against them on the breach of duty case.

21 WSE brings, in the Top Energy proceeding, a cross-claim in contract against Top Energy for an alleged failure to repay moneys that WSE contends it lent to Top Energy pursuant to a loan agreement purportedly entered into in or about late March or early April 2019 between WSE (as lender) and Top Energy (as borrower) (WSE Loan Agreement), together with interest.

22 Top Energy resists this cross-claim on the bases that:

(1) the WSE Loan Agreement, like the BSA, was not entered into on or about the dates that it bears, but instead was a fraudulent device created on or around 15 September 2022;

(2) alternatively – if the WSE Loan Agreement was not a fraudulent document – then:

(a) the moneys lent were repaid; and

(b) WSE did not advance funds to Top Energy and the only funds advanced to Top Energy were advanced by Joyo Holdings.

23 The De Grandland proceeding was commenced subsequently.

24 In that proceeding, as the case was presented, De Grandland alleges that Joyo Holdings, Amie and Wilson (De Grandland proceeding respondents) engaged in misleading or deceptive conduct or conduct that was likely to mislead or deceive in contravention of s 18 of the Australian Consumer Law (ACL) (being Schedule 2 to the Competition and Consumer Act 2010 (Cth)) by failing to disclose to De Grandland prior to its entry into the SSD, the existence of, relevantly:

(1) the BSA;

(2) the WSE Loan Agreement; and

(3) a loan agreement purportedly entered into in or about late March or early April 2019 between Joyo (as lender) and Top Energy (as borrower) (Joyo Loan Agreement).

25 De Grandland alleges that if it had become aware of these matters, then it would not have entered into the SSD. It seeks damages.

26 The De Grandland proceeding, as presented, is premised upon the BSA, the WSE Loan Agreement and the Joyo Loan Agreement being bona fide documents.

27 For convenience, I will hereafter refer to Top Energy and De Grandland collectively as the applicants, and to Amie, Wilson, WSE and Joyo Holdings collectively as the respondents.

B. THE EVIDENCE AND APPROACH TO FACT FINDING

B.1 The evidence

28 The applicants read lay affidavit evidence of Richard and Rebecca. Richard (but not Rebecca) was cross-examined.

29 The respondents read lay affidavit evidence from:

(1) Mr Donghua Wang, the sole director of Go Solar Group Pty Ltd, a company which carried on a business of solar photovoltaic equipment wholesaling, with offices and warehouses located in various Australian states;

(2) Amie; and

(3) Wilson.

30 The respondents also served lay affidavit evidence from Sam. Sam was the sole director of WSE as at the dates on which the BSA and the WSE Loan Agreement were purportedly signed, and his signature appears on those documents. That evidence was not read, however parts of it were tendered by the applicants.

31 The parties also adduced expert evidence as to the value of:

(1) the Business (as defined in the BSA) as at 28 March 2019 and 30 June 2020;

(2) the shares that De Grandland acquired in GL Holdings as at 25 June and 1 July 2019; and

(3) the shares that Joyo Holdings held in GL Holdings as at 25 June and 1 July 2019.

32 The experts (Ms Michelle Jennings-Jones for the applicants and Mr Ngoc Nguyen for the respondents) also prepared a joint expert report and gave evidence concurrently.

33 There was also a large documentary tender, and the Court Book exceeded 10,000 pages.

34 Before setting out my findings of primary facts, I set out the approach that I have taken to that task.

B.2 Onus and standard of proof and the assessment of evidence

35 As noted above, the applicants allege that the respondents have engaged in fraudulent conduct with respect to the creation of several agreements. As will be seen, the applicants adduce no direct evidence of the commission of such fraud and their case is based upon circumstantial evidence. The following principles are relevant.

36 The onus of proof borne by each of the parties on the cases they seek to prove is proof on the balance of probabilities: see s 140 of the Evidence Act 1995 (Cth) and the definition of “case” in the Dictionary in that Act.

37 However, this does not involve a mere mechanical comparison of probabilities. As Dixon J (as his Honour then was) famously observed in Briginshaw v Briginshaw [1938] HCA 34; (1938) 60 CLR 336 at 361 to 362:

The truth is that, when the law requires the proof of any fact, the tribunal must feel an actual persuasion of its occurrence or existence before it can be found. It cannot be found as a result of a mere mechanical comparison of probabilities independently of any belief in its reality. No doubt an opinion that a state of facts exists may be held according to indefinite gradations of certainty; and this has led to attempts to define exactly the certainty required by the law for various purposes. Fortunately, however, at common law no third standard of persuasion was definitely developed. Except upon criminal issues to be proved by the prosecution, it is enough that the affirmative of an allegation is made out to the reasonable satisfaction of the tribunal. But reasonable satisfaction is not a state of mind that is attained or established independently of the nature and consequence of the fact or facts to be proved. The seriousness of an allegation made, the inherent unlikelihood of an occurrence of a given description, or the gravity of the consequences flowing from a particular finding are considerations which must affect the answer to the question whether the issue has been proved to the reasonable satisfaction of the tribunal. In such matters “reasonable satisfaction” should not be produced by inexact proofs, indefinite testimony, or indirect inferences.

(bold emphasis added)

38 The observations of Mason CJ, Brennan, Deane and Gaudron JJ in Neat Holdings Pty Ltd v Karajan Holdings Pty Ltd [1992] HCA 66; (1992) 110 ALR 449 at 450 are also pertinent:

[T]he strength of the evidence necessary to establish a fact or facts on the balance of probabilities may vary according to the nature of what it is sought to prove. Thus, authoritative statements have often been made to the effect that clear or cogent or strict proof is necessary “where so serious a matter as fraud is to be found”. Statements to that effect should not, however, be understood as directed to the standard of proof. Rather, they should be understood as merely reflecting a conventional perception that members of our society do not ordinarily engage in fraudulent or criminal conduct and a judicial approach that a court should not lightly make a finding that, on the balance of probabilities, a party to civil litigation has been guilty of such conduct. As Dixon J commented in Briginshaw v Briginshaw:

“The seriousness of an allegation made, the inherent unlikelihood of an occurrence of a given description, or the gravity of the consequences flowing from a particular finding are considerations which must affect the answer to the question whether the issue has been proved …”

(italic emphasis in original; bold emphasis added; footnotes omitted)

39 Section 140(2) of the Evidence Act now mandates the taking into account of: (1) the nature of the cause of action propounded; (2) the nature of the subject-matter of the proceeding; and (3) the gravity of the matters alleged.

40 In Communications, Electrical, Electronic, Energy, Information, Postal, Plumbing and Allied Services Union of Australia v Australian Competition and Consumer Commission [2007] FCAFC 132; (2007) 162 FCR 466 at 479 to 482 ([29] to [38]), Weinberg, Bennett and Rares JJ observed:

Standard of proof

29 It follows that proceedings for recovery of pecuniary penalties under the Act are civil proceedings. Accordingly, s 140 of the Evidence Act 1995 (Cth) requires the Court in such proceedings to apply the civil standard of proof on the balance of probabilities. In arriving at a conclusion of satisfaction that a case has been proved on the balance of probabilities, s 140(2) of the Evidence Act provides:

(2) Without limiting the matters that the court may take into account in deciding whether it is so satisfied, it is to take into account:

(a) the nature of the cause of action or defence; and

(b) the nature of the subject-matter of the proceeding; and

(c) the gravity of the matters alleged.

30 The mandatory considerations which s 140(2) specifies reflect a legislative intention that a court must be mindful of the forensic context in forming an opinion as to its satisfaction about matters in evidence. Ordinarily, the more serious the consequences of what is contested in the litigation, the more a court will have regard to the strength and weakness of evidence before it in coming to a conclusion.

31 Even though he spoke of the common law position, Dixon J’s classic discussion in Briginshaw v Briginshaw (1938) 60 CLR 336 at 361-363 of how the civil standard of proof operates appositely expresses the considerations which s 140(2) of the Evidence Act now requires a court to take into account. Dixon J emphasised that when the law requires proof of any fact, the tribunal must feel an actual persuasion of its occurrence or existence before it can be found. He pointed out that a mere mechanical comparison of probabilities independent of any belief in its reality, cannot justify the finding of a fact. But he recognised that (Briginshaw 60 CLR at 361-362):

No doubt an opinion that a state of facts exists may be held according to indefinite gradations of certainty; and this has led to attempts to define exactly the certainty required by the law for various purposes. Fortunately, however, at common law no third standard of persuasion was definitely developed. Except upon criminal issues to be proved by the prosecution, it is enough that the affirmative of an allegation is made out to the reasonable satisfaction of the tribunal. But reasonable satisfaction is not a state of mind that is attained or established independently of the nature and consequence of the fact or facts to be proved. The seriousness of an allegation made, the inherent unlikelihood of an occurrence of a given description, or the gravity of the consequences flowing from a particular finding are considerations which must affect the answer to the question whether the issue has been proved to the reasonable satisfaction of the tribunal. In such matters “reasonable satisfaction” should not be produced by inexact proofs, indefinite testimony, or indirect inferences. Everyone must feel that, when, for instance, the issue is on which of two dates an admitted occurrence took place, a satisfactory conclusion may be reached on materials of a kind that would not satisfy any sound and prudent judgment if the question was whether some act had been done involving grave moral delinquency.

32 Dixon J also pointed out that the standard of persuasion, whether one is applying the relevant standard of proof on the balance of probabilities or beyond reasonable doubt, is always whether the affirmative of the allegation has been made out to the reasonable satisfaction of the tribunal. He said that the nature of the issue necessarily affected the process by which reasonable satisfaction was attained. And, so, he concluded that in a civil proceeding, when a question arose whether a crime had been committed, the standard of persuasion was the same as upon other civil issues. But he added, weight must be given to the presumption of innocence and exactness of proof must be expected (Briginshaw 60 CLR at 362-363).

33 In Rejfek v McElroy (1965) 112 CLR 517 at 520, Barwick CJ, Kitto, Taylor, Menzies and Windeyer JJ held that the criminal standard of proof was inappropriate to the determination of any fact in any civil action tried in any court in Australia where there are no statutory provisions to the contrary. They followed Helton v Allen (1940) 63 CLR 691. They said that the “clarity” of the proof required, where a serious matter such as fraud was to be found, was an acknowledgment that the degree of satisfaction for which the civil standard of proof calls may vary according to the gravity of the fact to be proved (Rejfek 112 CLR at 521). The Court held that it was an error of law for the trial judge to have applied the criminal standard of proof in a civil case. They continued (Rejfek 112 CLR at 521-522):

The difference between the criminal standard of proof and the civil standard of proof is no mere matter of words: it is a matter of critical substance. No matter how grave the fact which is to be found in a civil case, the mind has only to be reasonably satisfied and has not with respect to any matter in issue in such a proceeding to attain that degree of certainty which is indispensable to the support of a conviction on a criminal charge.

…

36 Mason CJ, Brennan, Deane and Gaudron JJ said in Neat Holdings Pty Ltd v Karajan Holdings Pty Ltd (1992) 67 ALJR 170 at 171; 110 ALR 449 at 450 the strength of the evidence necessary to establish a fact or facts on the balance of probabilities at common law may vary according to the nature of that which is sought to be proved. They pointed out that statements in the cases requiring clear, cogent or strict proof as being necessary where a serious matter, such as fraud, is to be found were not to be understood as directed to the standard of proof. They said, rather, those statements should be understood as merely reflecting a conventional perception that members of our society (Neat Holdings 67 ALJR at 171; 110 ALR at 450):

… do not ordinarily engage in fraudulent or criminal conduct and a judicial approach that a court should not lightly make a finding that, on the balance of probabilities, a party to civil litigation has been guilty of such conduct.

(Footnotes omitted.)

Their Honours also said that there were circumstances in which generalisations about the need for clear and cogent evidence to prove matters of the gravity of fraud or crime can be unhelpful or misleading (Neat Holdings 67 ALJR at 171; 110 ALR at 450).

37 In approaching our assessment of the evidence we have borne these principles in mind and have taken into account the matters specified in s 140 of the Evidence Act. The trial judge did so too. Counsel for the CEPU, properly, reminded us of the seriousness of the consequences of a finding that ss 45E(3) and 76(1) of the Trade Practices Act had been contravened, the imposition of a pecuniary penalty and the grant of other forms of relief provided by the Act. We have taken this into account in assessing the evidence and making our findings.

38 Ultimately, because this is a civil, not criminal, proceeding the civil standard of proof applies. Thus, the ACCC had to establish that the circumstances appearing in the evidence gave rise to a reasonable and definite inference, not merely to conflicting inferences of equal degrees of probability, that Edison and the CEPU had made a contract or arrangement or arrived at an understanding within the meaning of s 45E(3) (Trustees of the Property of Cummins (a bankrupt) v Cummins (2006) 227 CLR 278 at [34] per Gleeson CJ, Gummow, Hayne, Heydon and Crennan JJ; see too Bradshaw v McEwans Pty Ltd (1951) 217 ALR 1 at 5 per Dixon, Williams, Webb, Fullagar and Kitto JJ).

(italic emphasis in original; bold emphasis added)

41 See also Brown v New South Wales Trustee and Guardian [2012] NSWCA 431 at [52] (Campbell JA; Bergin CJ in Eq and Sackville AJA agreeing).

42 In Quintis Ltd (subject to deed of company arrangement) (ACN 092 200 854) v Certain Underwriters at Lloyd’s London Subscribing to Policy Number B0507N16FA15350 [2021] FCA 19; (2021) 385 ALR 639 at 669 to 671 ([104] to [106]), Justice Lee made the following observations concerning inferential reasoning:

[104] As Sir Owen Dixon emphasised in a number of cases: (a) when the law requires proof of any fact, the tribunal of fact “must feel an actual persuasion of its occurrence or existence before it can be found” (Briginshaw v Briginshaw (1938) 60 CLR 336; [1938] ALR 334 (at CLR 361)); (b) a party bearing the onus will not succeed unless the whole of the evidence establishes a “reasonable satisfaction” on the preponderance of probabilities such as to sustain the relevant issue (Axon v Axon (1937) 59 CLR 395; [1938] ALR 89 (at CLR 403)); and (c) the “facts proved must form a reasonable basis for a definite conclusion affirmatively drawn of the truth of which the tribunal of fact may reasonably be satisfied” (Jones v Dunkel (at CLR 305)).

[105] However, it is also true that where there is no direct evidence of a fact that a party bearing the onus of proof seeks to prove, “it is not possible to attain entire satisfaction as to the true state of affairs”: Girlock (Sales) Pty Ltd v Hurrell (1982) 149 CLR 155; 40 ALR 45 (at CLR 169; ALR 55 per Mason J). However, in such a case, the law does not require proof to the “entire satisfaction” of the tribunal of fact: see Transport Industries Insurance Co Ltd v Longmuir [1997] 1 VR 125 (Longmuir) (at 141 per Tadgell JA, with whom Winneke P and Phillips JA agreed). Indeed, a party may advance a case relying on circumstantial evidence, on the basis that collectively viewed, a combination of proven facts can provide a sufficient basis for inferring the ultimate fact to be proved. A comprehensive statement as to the sufficiency of circumstantial evidence in a civil case to support proof by inference from directly proved facts was given by the High Court in Bradshaw v McEwans Pty Ltd (1951) 217 ALR 1 (at 5 per Dixon, Williams, Webb, Fullagar and Kitto JJ):

Of course as far as logical consistency goes many hypotheses may be put which the evidence does not exclude positively. But this is a civil and not a criminal case. We are concerned with probabilities, not with possibilities. The difference between the criminal standard of proof in its application to circumstantial evidence and the civil is that in the former the facts must be such as to exclude reasonable hypotheses consistent with innocence, while in the latter you need only circumstances raising a more probable inference in favour of what is alleged. In questions of this sort, where direct proof is not available, it is enough if the circumstances appearing in evidence give rise to a reasonable and definite inference: they must do more than give rise to conflicting inferences of equal degrees of probability so that the choice between them is mere matter of conjecture. But if circumstances are proved in which it is reasonable to find a balance of probabilities in favour of the conclusion sought then, though the conclusion may fall short of certainty, it is not to be regarded as a mere conjecture or surmise …

(Citation omitted).

[106] Furthermore, in assessing a circumstantial case, the question of whether an inference is open and can be drawn as a matter of probability is to be determined by considering the combined weight of all the relevant established facts, rather than by considering each fact sequentially and in isolation: Marriner v Australian Super Developments Pty Ltd [2016] VSCA 141 (Marriner) (at [75] per Tate ACJ, Kyrou and Ferguson JJA). Indeed, as the Full Court of this Court recently stated in Australian Broadcasting Corporation v Wing (2019) 271 FCR 632; 371 ALR 545; [2019] FCAFC 125 (at [134] per Besanko, Bromwich and Wheelahan JJ):

In assessing a circumstantial case, it is important to bear in mind that the facts ultimately to be proven are those that are in issue, and not necessarily all the circumstantial facts themselves. As Dawson J observed in Shepherd v R (1990) 170 CLR 573 at 580; 97 ALR 161 at 165, “[T]he probative force of a mass of evidence may be cumulative, making it pointless to consider the degree of probability of each item of evidence separately.” This invites consideration of the combined weight of circumstantial facts, for it is the essence of a circumstantial case that the combined force of its components should be considered, and proof of some circumstantial facts may be affected by the court’s assessment of other circumstantial facts: Chamberlain v R (No 2) (1984) 153 CLR 521 at 535; 51 ALR 225 at 237 (Gibbs CJ and Mason J). Courts may fall into error by compartmentalising circumstantial facts, rather than standing back and assessing the broader picture.

(italic emphasis in original; bold emphasis added)

43 The following principles concerning the assessment of evidence are also relevant.

44 First, it is well-established that “all evidence is to be weighed according to the proof which it was in the power of one side to have produced, and in the power of the other to have contradicted”: Blatch v Archer (1774) 1 Cowp 63 at 65; 98 ER 969 at 970 (Lord Mansfield).

45 In Weissensteiner v The Queen [1993] HCA 65; (1993) 178 CLR 217 at 227, Mason CJ, Deane and Dawson JJ explained:

We have quoted rather more extensively from the cases than would otherwise be necessary in order to show that it has never really been doubted that when a party to litigation fails to accept an opportunity to place before the court evidence of facts within his or her knowledge which, if they exist at all, would explain or contradict the evidence against that party, the court may more readily accept that evidence. It is not just because uncontradicted evidence is easier or safer to accept than contradicted evidence. That is almost a truism. It is because doubts about the reliability of witnesses or about the inferences to be drawn from the evidence may be more readily discounted in the absence of contradictory evidence from a party who might be expected to give or call it.

46 More recently, in Roberts-Smith v Fairfax Media Publications Pty Ltd (Reopening Application) [2025] FCAFC 66; (2025) 310 FCR 141 at 158 [74], Perram, Katzmann and Kennett JJ observed:

In addressing the evidence relevant to proposed ground 17, it is necessary to keep in mind two important principles which may pull in opposite directions. One is the rule embodied in s 140 of the Evidence Act 1995 (Cth), which was heavily relied upon by the appellant in his submissions in the appeal alleging errors by the primary judge. Here, the allegation concerning Mr McKenzie is pitched at such a level and has such significant consequences that it cannot be taken to have been made out on the basis of what Dixon J referred to in Briginshaw v Briginshaw (1938) 60 CLR 336 at 362 as “inexact proofs, indefinite testimony, or indirect inferences”. The other is the principle in Blatch v Archer (1774) 1 Cowp 63 at 65; 98 ER 969 at 970 (Lord Mansfield CJ) (Blatch v Archer), that evidence on a contested issue is to be weighed according to the relative capacity of the parties to adduce it. Where a matter is particularly within the knowledge of the party that does not bear the onus of proof, relatively slight evidence from the other party may be sufficient to regard the onus as satisfied unless that evidence is rebutted by evidence from the party who has that particular knowledge. Both of these principles can apply at the same time, as discussed recently in Hassan (formerly AFX21) v Minister for Home Affairs (2025) 309 FCR 44 at [52]-[54] (Katzmann & Kennett JJ).

(italic emphasis in original)

47 The concurrent application of the principles in Briginshaw and Blatch v Archer was explained in Hassan v Minister for Home Affairs [2025] FCAFC 57; (2025) 309 FCR 44 by Katzmann and Kennett JJ at 58 [54]:

In making these observations, the primary judge was not inverting principle. The statements in Hampton Court and other cases concerning the parties’ respective capacities to adduce evidence do not provide an exception from the usual principles as to where the onus of proof lies. They concern the weighing of evidence. Here, the onus always lay on the appellant; and the degree of persuasion required to meet that onus was necessarily affected by the principles embodied in s 140(2). Thus, when Dixon CJ said in Hampton Court that “slight evidence may be enough”, his Honour was not excluding the general rule that what is or is not “enough” is affected by the nature of the allegation sought to be proved.

(italic emphasis in original)

48 Secondly, the operation of the rule in Jones v Dunkel [1959] HCA 8; (1959) 101 CLR 298.

49 I respectfully adopt the following summary of relevant principles concerning the drawing of inferences based upon that rule set out by McGrath J in Les & Zelda Investments Pty Ltd (as trustee for Les & Zelda Family Trust) v Whitehaven Coal Limited (No 4) [2026] NSWSC 107 at [76]:

The rule in Jones v Dunkel (1959) 101 CLR 298; [1959] HCA 8, being the principle articulated by Kitto J at 308, Menzies J at 312 and Windeyer J at 320–321, has been distilled, summarised, expanded and explained in a number of authorities in the High Court of Australia, the Federal Court of Australia and the Court of Appeal of this court, principally including (in chronological order): Payne v Parker [1976] 1 NSWLR 191, Glass JA at 201–202; Flack v Chairperson, National Crime Authority (1997) 80 FCR 137, Hill J at 148–149; Adler v Australian Securities and Investments Commission (2003) 179 FLR 1; [2003] NSWCA 131, Giles JA (with whom Mason P and Beazley JA agreed) at [649]; Manly Council v Byrne [2004] NSWCA 123, Campbell J (with whom Beazley JA and Pearlman AJA agreed) at [44]–[61]; Kuhl v Zurich Financial Services Australia Ltd (2011) 243 CLR 361; [2011] HCA 11, Heydon, Crennan and Bell JJ at [63]–[64]; Sagacious Legal Pty Ltd v Wesfarmers General Insurance Ltd [2011] FCAFC 53, Besanko, Perram and Katzmann JJ at [79]; Australian Securities and Investments Commission v Hellicar (2012) 247 CLR 345; [2012] HCA 17, French CJ, Gummow, Hayne, Crennan, Kiefel and Bell JJ at [167]–[169] and Heydon J at [259], [263]–[264]; Jagatramka v Wollongong Coal Ltd [2021] NSWCA 61, Bathurst CJ, Bell P and White JA at [49]; Ling v Pang [2023] NSWCA 112, Kirk JA (with whom Leeming and Mitchelmore JJA agreed) at [20]–[28]; SSABR Pty Ltd v AMA Group Ltd [2024] NSWCA 175 (SSABR appeal decision), Stern JA (with whom Ward P and Price AJA agreed) at [158]–[161]. These authorities support the following legal principles:

(1) The rule in Jones v Dunkel is a principle of judicial reasoning which addresses the drawing of inferences of fact.

(2) The rule in Jones v Dunkel is a principle of plain common sense.

(3) The rule in Jones v Dunkel is that an unexplained failure by a party to call a witness may in appropriate circumstances support an inference that the uncalled evidence would not have assisted the party’s case.

(4) The failure to call a witness may also permit the court to draw, with greater confidence, any inference unfavourable to the party who failed to call the witness, if that uncalled witness appears to be in a position to cast light on whether the inference should be drawn.

(5) The drawing of a Jones v Dunkel inference requires the court to be satisfied that: first, it is expected or natural for the party in question to have called the person; second, the person’s evidence would have elucidated a particular matter that requires explanation, contradiction or an answer; and third, the absence of the person is unexplained.

(6) The rule in Jones v Dunkel only applies once all the evidence in the case is in.

(7) Whether some inference should be drawn, what inference, and with what significance, are all matters of discretion that depend upon the particular case. A particular inference to be drawn will generally only be of material significance where the balance of evidence is equivocal.

(8) In some cases no inference will be drawn merely because corroborative or cumulative witnesses are not called.

(9) The rule in Jones v Dunkel cannot be used to draw a positive inference if the evidence does not otherwise admit of a rationally drawn inference.

(10) The rule in Jones v Dunkel does not permit a court to infer that the uncalled evidence would have been positively damaging to a party’s case.

(11) The rule in Jones v Dunkel does not supply missing gaps in the evidence, or convert conjecture or suspicion into inference; rather, it enables an already available inference to be drawn more comfortably.

(12) The effect of the rule in Jones v Dunkel is not that any inference favourable to the party that failed to call the witness should not be drawn.

(bold and italic emphasis in original)

50 Thirdly, the extension of the rule in Jones v Dunkel in Commercial Union Assurance Company of Australia Ltd v Ferrcom Pty Ltd (1991) 22 NSWLR 389 at 418 to 419, where Handley JA stated:

There appears to be no Australian authority which extends the principles of Jones v Dunkel to a case where a party fails to ask questions of a witness in chief. However I can see no reason why those principles should not apply when a party by failing to examine a witness in chief on some topic, indicates “as the most natural inference that the party fears to do so”. This fear is then “some evidence” that such examination in chief “would have exposed facts unfavourable to the party”: see Jones v Dunkel (at 320-321) per Windeyer J. Moreover in Ex parte Harper; Re Rosenfield [1964-5] NSWR 58 at 62, Asprey J, citing Marks v Thompson 1 NYS 2d 215 (1937) at 218, held that inferences could not be drawn in favour of a party that called a witness who could have given direct evidence when that party refrained from asking the crucial questions.

…

(italic emphasis in original; bold emphasis added)

51 As Heydon, Crennan and Bell JJ explained in Kuhl v Zurich Financial Services Australia Ltd [2011] HCA 11; (2011) 243 CLR 361 at 384 to 385 [63]:

The rule in Jones v Dunkel is that the unexplained failure by a party to call a witness may in appropriate circumstances support an inference that the uncalled evidence would not have assisted the party’s case. That is particularly so where it is the party which is the uncalled witness. The failure to call a witness may also permit the court to draw, with greater confidence, any inference unfavourable to the party that failed to call the witness, if that uncalled witness appears to be in a position to cast light on whether the inference should be drawn. These principles have been extended from instances where a witness has not been called at all to instances where a witness has been called but not questioned on particular topics. Where counsel for a party has refrained from asking a witness whom that party has called particular questions on an issue, the court will be less likely to draw inferences favourable to that party from other evidence in relation to that issue. …

(italic emphasis in original; bold emphasis added; footnotes omitted)

B.3 The fallibility of human recollection and primary reliance upon contemporaneous documents

52 The importance of exercising caution when assessing the veracity of a witness’s recollection of what was said or thought at an earlier time, particularly when the witness has an interest in the outcome of the proceeding, is well-established.

53 As McLelland CJ in Eq observed in the oft-cited passage from Watson v Foxman (1995) 49 NSWLR 315 at 319:

…human memory of what was said in a conversation is fallible for a variety of reasons, and ordinarily the degree of fallibility increases with the passage of time, particularly where disputes or litigation intervene, and the processes of memory are overlaid, often subconsciously, by perceptions or self-interest as well as conscious consideration of what should have been said or could have been said. All too often what is actually remembered is little more than an impression from which plausible details are then, again often subconsciously, constructed. All this is a matter of ordinary human experience.

54 The above passage has been cited with approval by the Full Court of this Court: Julstar Pty Ltd v Hart Trading Pty Ltd [2014] FCAFC 151 at [73] (Dowsett, Rares and Logan JJ); Innes v AAL Aviation Ltd [2017] FCAFC 202; (2017) 259 FCR 246 at 267 to 268 [92] and 274 [125] (Tracey and White JJ), and 285 [186] to 286 [188] (Bromberg J); CCL Secure Pty Ltd v Berry [2019] FCAFC 81 at [44] to [48] (McKerracher, Robertson and Lee JJ); Martin v Norton Rose Fulbright Australia [2021] FCAFC 216; (2021) 395 ALR 413 at 444 [147] (Jagot, Katzmann and Banks-Smith JJ).

55 Thus, the best approach to determining what has in fact occurred “is to place primary emphasis on the objective factual surrounding material and inherent commercial probabilities, together with the documentation tendered in evidence”: Effem Foods Pty Ltd (t/as Uncle Ben’s of Australia) v Lake Cumbeline Pty Ltd [1999] HCA 15; (1999) 161 ALR 599 at 603 [15] to [16] (Gleeson CJ, Gaudron, Kirby and Hayne JJ).

56 In this regard, the earlier statement by Gleeson CJ, Gummow and Kirby JJ in Fox v Percy [2003] HCA 22; (2003) 197 ALR 201 at 210 [31] is also apposite:

Further, in recent years, judges have become more aware of scientific research that has cast doubt on the ability of judges (or anyone else) to tell truth from falsehood accurately on the basis of such appearances. Considerations such as these have encouraged judges, both at trial and on appeal, to limit their reliance on the appearances of witnesses and to reason to their conclusions, as far as possible, on the basis of contemporary materials, objectively established facts and the apparent logic of events. This does not eliminate the established principles about witness credibility; but it tends to reduce the occasions where those principles are seen as critical.

(bold emphasis added; footnotes omitted)

57 Further, as Leggatt J explained in Gestmin SGPS SA v Credit Suisse (UK) Ltd [2013] EWHC 3560 at [22]:

In the light of these considerations, the best approach for a judge to adopt in the trial of a commercial case is, in my view, to place little if any reliance at all on witnesses’ recollections of what was said in meetings and conversations, and to base factual findings on inferences drawn from the documentary evidence and known or probable facts. This does not mean that oral testimony serves no useful purpose — though its utility is often disproportionate to its length. But its value lies largely, as I see it, in the opportunity which cross-examination affords to subject the documentary record to critical scrutiny and to gauge the personality, motivations and working practices of a witness, rather than in testimony of what the witness recalls of particular conversations and events. Above all, it is important to avoid the fallacy of supposing that, because a witness has confidence in his or her recollection and is honest, evidence based on that recollection provides any reliable guide to the truth.

(bold emphasis added)

58 See also Bathurst Regional Council v Local Government Financial Services Pty Ltd (No 5) [2012] FCA 1200 at [1247] to [1248] (Jagot J).

B.4 The reliability of the evidence of the lay witnesses

59 As earlier noted:

(1) Richard, Donghua, Amie and Wilson provided affidavit evidence which was read and they were cross-examined;

(2) Rebecca provided affidavit evidence which was read, but she was not cross-examined; and

(3) Sam provided affidavit evidence which was not read.

60 I accept the evidence of Donghua and Rebecca. No suggestion was made to the contrary.

61 I treat the evidence of Richard, Amie and Wilson – to the extent that it is unsupported by contemporaneous documentary evidence – with great caution for the following reasons.

62 Richard provided many answers that were non-responsive to the questions asked of him and which instead appeared to be directed at arguing his case including the pursuit of proof of particular facts he considered to be favourable to the applicants or unfavourable to the respondents. In doing so, many of his answers were more in the nature of submissions than evidence. By way of example:

Now, and this is on 21 June, this email?---Correct.

Now, you didn’t express any surprise at the time about a loan by Joyo to Top Energy, did you?---So that – that is – answering your question, Mr Healey, that 1.3, second 1.3, is follow with 1.1, 1.2, you know, onwards. So there’s information there. If I can say that 1.1 – say Top Energy purpose Win Solar Wholesale being ..... Win Solar Energy at ..... of 1 million and signed a purchase agreement before 30 September which, of the 800 k is to be paid by Top Energy to Win Solar Energy in instalment of 100 per month after confirming that. So that really contradict to what the BSA say, the goodwill of Win Solar Energy was already done in 2019, either May, June, July. So, at that time, which is a year - - -

HIS HONOUR: Mr Li, I’m going to interrupt you. I will invite you to focus on the question that you’ve been asked about 1.3. I understand there’s a lot of things you want to say about the BSA but your role at the moment is simply to answer the questions that you’re being asked. Mr Kaufmann will make and he has already made a point about - - -?---Okay.

63 Further, in cross-examination he provided a number of answers that cannot be reconciled with the contemporaneous documents. For example, Richard insisted that an email from Amie dated 1 May 2019 ([129(2)] below) which referred to the transfer of “Win Solar Wholesale” to Top Energy was a reference only to a business name and not to the WSE business. Richard’s evidence sought to draw a distinction between the business and the business name which distinction was contrary to the contemporaneous communications between Richard and Amie.

64 A further example is Richard’s evidence that Amie told him on 29 April 2019 that GL Holdings and Top Energy were “clean” companies. Yet, his evidence was that as at that date, he had not heard of Top Energy.

65 Richard also gave evidence which directly contradicted his affidavit. For example, in his affidavit he stated that if Amie could be removed as general manager then he was prepared to maintain his investment. When this was put to him in cross-examination he initially denied this, but accepted it upon being reminded of his affidavit evidence.

66 Amie also provided many answers that were non-responsive to the questions asked of her and which appeared to be directed at arguing her case and identifying facts favourable to the respondents’ case or unfavourable to the cases brought by the applicants.

67 Further, Amie:

(1) in cross-examination made a number of lengthy speeches, typically non-responsive to the question that she had been asked to answer. Those speeches also revealed her animus toward Richard and Rebecca;

(2) in cross-examination repeatedly claimed not to understand the question being asked of her. Even accepting that at times the questions may have been unclear the regularity of the requests for clarification of the questions suggested that Amie was seeking time to compose an answer rather than provide a forthright answer;

(3) in cross-examination, refused to concede obvious points. For example, and as discussed in greater detail below, Amie sent an email to Richard on 21 June 2020 in which she proposed that WSE sell its business to Top Energy, a proposition that is plainly inconsistent with the BSA having been in existence prior to that date. Amie refused to accept that there was such an inconsistency;

(4) in cross-examination claimed to have a clear recollection of a conversation that occurred many years earlier and refused to concede that her recollection could have been mistaken;

(5) in her affidavit evidence claimed that as at 20 August 2020, she believed that it was in the interests of Top Energy to pay WSE’s invoice for the amount payable under the BSA. However, there was no such invoice; and

(6) on 1 December 2018, signed a credit application in which she described herself as a director of WSE. She had ceased to be a director of that company on 1 October 2018.

68 Wilson, in contrast to Richard and Amie, for the most part was more inclined to directly answer the questions put to him and to not advocate a particular position. He also made some concessions as to errors in his evidence. Nevertheless, I have considerable concerns as to the veracity of his evidence where uncorroborated by contemporaneous documentary evidence for reasons including the following.

69 First, Wilson’s affidavit evidence created the clear impression that in June 2019 he had prepared and submitted a Business Activity Statement for WSE for May 2019 which included recognition of an accrued right to $880,000 pursuant to the BSA. That evidence was as follows:

239. When I prepared the May 2019 Business Activity Statement (BAS) for WSE, I included the sale of the goodwill of the Win Solar Wholesale Business to Top Energy. At page 679 of Exhibit ZH-1 is a copy of the May BAS for WSE which was submitted to the ATO. At pages 680 to 707 of Exhibit ZH-1 is a report I generated from WSE’s Dear account on 15 June 2019 which shows the sales which made up the sales reported in the May BAS for WSE, including the sale of the goodwill of the Win Solar Wholesale business. The sale of the business is recorded on the “Summary” worksheet at rows 8 and 9.

240. I included the sale of the goodwill of the Business in the May 2019 BAS because 31 May 2019 was the last day of the month in which the sale occurred (see paragraph 142 above).

241. As the bookkeeper for WSE (via Handy Accounts) I did not issue an invoice for the purchase price in June 2020 or at all because Amie did not ask me to and I was no longer financial controller of WSE.

(bold emphasis in original)

70 This evidence failed to mention that the May 2019 Business Activity Statement was not in fact lodged until March 2021, after these proceedings had been commenced, a fact which came to light by dint of documents produced in answer to a notice to produce. By this omission, and the language used in [239] to [241], Wilson created the clear and false impression that GST referable to the BSA had been paid shortly after May 2019.

71 Secondly, on 1 December 2018, and at a time when he was aware that Amie was not a director of WSE, Wilson signed as a witness to Amie’s signature on a credit application in which she described herself as a director of WSE. Wilson accepted that he knew that Amie was not a director but suggested that he did not sign it knowing that a statement on the credit application that she was a director was wrong. As Wilson acknowledged, this explanation made very little sense.

B.5 Conclusion

72 In circumstances where: (1) the evidence of Donghua and Rebecca is to be accepted but is of limited scope; and (2) the evidence of Richard, Amie and Wilson is to be treated with great caution and covers considerably more ground, the imperative to place greater weight upon the contemporary material, objectively established facts and the apparent logic of events and to place limited reliance upon the recollection of witnesses is heightened.

73 Thus, I have in making the findings of fact set out below placed little weight on the evidence of Richard, Amie and Wilson as to the events that occurred during the period relevant to the determination of the issues in these proceedings. I have little to no confidence in their evidence where it is unsupported by a contemporaneous document to the same effect.

C. FINDINGS OF FACT

C.1 Central players

C.1.1 Richard

74 Richard was born in China and moved to Australia in 1991 in order to study a Bachelor of Economics, majoring in Accounting at Macquarie University.

75 In 2000, he became a Certified Practicing Accountant. In November 2005, he joined Darley Aluminium Trading Pty Ltd as their Business Manager. Darley Aluminium distributes aluminium extrusion products which are used to fabricate, inter alia, solar rails.

76 In 2006, Richard became a Chartered Accountant. In about 2007, he became the General Manager of Darley Aluminium.

77 In or about 2008, Richard became a director and later the sole director of Darley Aluminium.

78 At the time that the SSD was signed on 25 June 2019, Richard was one of two directors of De Grandland, a company which was incorporated in January 2019. His business partner, Rebecca was the other.

C.1.2 Rebecca

79 Rebecca has undertaken a number of business ventures together with Richard, including Darley Aluminium. De Grandland is the investment vehicle that they use for those ventures. Rebecca was a director of De Grandland at the time that the SSD was signed and she signed the SSD.

C.1.3 Amie

80 Amie has an undergraduate degree in International Trade from a university in Nanjing, which was conferred in 1998. She has worked in human resources and then in marketing development as a marketing specialist.

81 In about 2002, she started a fashion business and founded Shanghai Jinying Trading Company Ltd.

82 In 2008 when still in China, Amie started to discover business opportunities in Australia including in the solar industry.

83 In 2009, Amie moved to Australia. She gave up her fashion business because it was difficult to run the business from Australia.

84 In 2011, Amie and Sam bought an accommodation business called Suncoast Backpackers in Maroochydore. They sold the Suncoast Backpackers business at the end of 2013.

85 At all relevant times Amie controlled WSE, Joyo Holdings and Joyo. Amie controlled GL Holdings and Top Energy until the SSD on 25 June 2019 (when De Grandland took a 70 per cent interest).

C.1.4 Sam

86 Sam, as noted earlier, is Amie’s husband. His signature appears on the BSA and the WSE Loan Agreement on behalf of WSE.

C.1.5 Wilson

87 Wilson has a Masters degree in Commerce, majoring in Accounting from the University of Queensland, which was conferred in 2004.

88 Since then he has worked as an accountant and in 2014, he became a Certified Practicing Accountant.

89 On or about 27 March 2015, Wilson became a contractor for Yongxin Accounting Pty Ltd.

90 On 25 January 2017, Wilson caused Handy Accounts Pty Ltd to be incorporated with Wilson as the sole director and sole member.

C.2 October 2018 to March 2019

91 On 1 October 2018, Amie ceased to be a director of WSE and Sam was appointed as the sole director of WSE. Amie remained as the general manager of WSE.

92 In or around October 2018, Donghua and Amie began discussions on WeChat regarding the possibility of integrating the Go Solar business and the WSE business.

93 In November 2018, Donghua introduced Richard, qua director of Darley Aluminium, to Amie.

94 On 1 December 2018, WSE applied for a credit account with Darley Aluminium. The application was signed by Amie who represented that she was a director of WSE. That signature was witnessed by Wilson. This occurred despite Amie no longer being a director of WSE.

95 On 29 January 2019, De Grandland was incorporated. Richard and Rebecca were appointed as directors of De Grandland. They held and continued to hold 49 and 51 per cent respectively of the shares in that company.

96 In early February 2019, Donghua and Amie exchanged WeChat messages regarding Donghua and his wife (Ms Lily Zhou) visiting WSE’s warehouse on the Gold Coast in Queensland. Donghua then conducted an informal due diligence of WSE, during which he and Ms Zhou visited WSE’s warehouse to observe its business operations and inventory management system. During that visit, Donghua and Amie spoke about potentially merging their businesses.

97 Donghua called Amie a few days later and told her that he could probably offer her $1.2 to $1.5 million to acquire the goodwill of the WSE business, but he would need about six to nine months to prepare the acquisition. Amie indicated that she would be exploring her options.

98 Donghua’s evidence was that this was a serious offer which he intended to follow through upon if it were accepted.

99 Donghua made this “offer”, which he described in cross-examination as a “preliminary offer”, in order to acquire the intangible assets of WSE, that is principally its customer base and WSE’s know-how in operating within Queensland. He saw value in those assets in particular, and was not interested in WSE’s other assets such as plant and equipment, inventory, receivables or warehouses. Go Solar had sufficient inventory and other capital – in fact, it supplied such inventory to WSE. Donghua considered WSE’s warehouse to be small, and although Go Solar could make use of it to begin with, he considered it was necessary in the long run to increase warehouse capacity. That being the case, he considered there to be an advantage in commencing operations out of a new warehouse from the beginning, instead of taking over WSE’s existing premises, if he proceeded with acquiring the WSE business.

100 Donghua also believed that there was room to grow the business in Queensland based on his discussions with Amie. In particular, if Go Solar could distribute directly to customers in Queensland (rather than through WSE) it could also take advantage of better margins.

101 However, by mid-March 2019, Donghua had postponed or put on hold the opportunity to purchase the Win Solar Wholesale business because Go Solar was involved in a large project that needed his attention.

102 On 18 March 2019, Wilson replaced Amie as the sole director of Top Energy.

C.3 The BSA

103 The BSA bears a date of 28 March 2019 and as mentioned there is an issue as to whether the BSA was entered into on that date (as the respondents contend) or on or about 20 August 2020 (as the applicants contend). The BSA also bears the signatures of Sam (on behalf of WSE) and Wilson (on behalf of Top Energy), and of Amie as a witness to each of those signatures. There are no dates adjacent to any of the signatures.

104 The BSA includes the following (as written):

BUSINESS SALE AGREEMENT

Business Sale Agreement made 28th March 2019

BETWEEN

(a) Win Solar Energy Pty Ltd of UNIT 813 KAYLEIGH DRIVE, BUDERIM, Queensland, 4556 (‘Vendor’); and

(b) Top Energy Holdings Pty Ltd of Unit 5 54 Newheath Drive, Arundel, Queensland, 4214 (‘Purchaser’)

RECITALS:

A. The Vendor owns and carries on the Business, using the Business Name, at the Premises.

B. The Vendor is the owner of the Intellectual Property.

C. The Vendor is the lessee of the Lease and the Leased Equipment.

D. The Vendor employs the Employees in the Business.

E. The Vendor wishes to sell to the Purchaser, and the Purchaser wishes to buy from the Vendor, the Business is a going concern.

F. The Vendor agrees the Purchaser to run the Business for at most one year before the Purchaser pay the Purchase Price.

THE PARTIES AGREE AND DECLARE AS FOLLOWS:

1. Interpretation

1.1 Definitions

In this agreement unless the context otherwise requires:

Asset means cash, receivables, loan, plant, stock, vehicle, tools and equipment.

Business means solar system and accessories import and wholesale, trading under the business name of Win Solar Wholesale, and running at the domain and website of winsolarwholesale.com.au, excluding the Asset;

...

Completion means completion of the sale and purchase of the Business under clause 5;

Completion Date means the latest of:

(a) 1st May 2019; and

(b) any other date which is agreed in writing before the later of the date referred to in clause (a) by the parties;

...

Premises means the property at Unit 8 13 KAYLEIGH DRIVE, BUDERIM, Queensland, 4556;

...

3. Agreement to sell and buy the Business

3.1 Sale and purchase

On the Completion Date, the Vendor must sell to the Purchaser, and the Purchaser must buy from the Vendor, the Business (including all the right, title, and interest of the Vendor in the Business) free from any security interest or third party interest for the Purchase Price and otherwise on the terms and conditions of this agreement.

3.2 Purchase Price

The Purchase Price payable by the Purchaser for the Business will be $$800,000.

3.3 Purchase Price Payment Date

The Purchase Price Payment Date is 30th June 2020 on which the Purchaser pay to the Vendor the Purchase Price for the Business.

3.4 Title, property and risk

The title to, property in and risk of the Business:

(a) until Completion, remain sole with the Vendor; and

(b) pass to the Purchaser on and from Completion;

and, accordingly, the Vendor is entitled to the takings and profits, and must bear and pay in the proper time all outgoings, of the Business until Completion.

...

5. Completion

5.1 Time and place of Completion

Completion is to occur on the Completion Date at 1st May 2019 at Unit 8 13 Kayleigh Drive, Buderim, Queensland, 4556 or at any other time or place agreed in writing by the parties.

5.2 Obligations of Vendor at Completion

At Completion, the Vendor must give the Purchaser unencumbered title to, and ownership of the Business, and place the Purchaser in effective possession and control of the Business. The Vendor must have taken necessary steps on or before the Completion date to transfer to the Purchaser on Completion (including but not limited to):

(a) ownership of the Business name (if any);

(b) the telephone number, fax number, postal address, email addresses and domain name of the website of the Business; and

(c) licenses, trademarks, patents or other forms of intellectual property rights relating to the Business

5.3 Obligations of the Purchaser at Completion

At Completion the Purchaser must:

(a) Transfer the Business name to under Purchaser;

(b) take possession of the Plant, the Leased Equipment and take over the Lease;

(c) do and execute all other acts and documents that this agreement requires the Purchaser to do or execute at Completion;

(d) On or before the Purchase Price Payment Date, pay all the Purchase Price to the Vendor or as the Vendor may direct by notice to the Purchaser in cash or by bank cheque or in any other form that the parties agree in writing;

(e) the purchaser agreed to use its cash, stock and other form of asset as security of the payment. In case of payment default, the Vendor has the right to possession of the Asset of the Purchaser and cease the Purchaser from using the Intellectual Property.

...

9. GST

9.1 Going concern

The Vendor and Purchaser agree that the supply of the Business is the supply of a going concern pursuant to Subdivision 38-J of the GST Act.

9.2 Taxable Supply

If a party makes a taxable supply to another party under or in connection with this agreement, then (unless the consideration is expressly stated to be inclusive of GST) the consideration for that supply is exclusive of GST, and in addition to paying or providing that consideration the recipient must:

(a) pay to the supplier an amount equal to any GST for which the supplier is liable on that supply, without deduction or set-off of any other amount; and

(b) make that payment as and when the consideration or part of it must be paid or provided, except that the recipient need not pay unless the recipient has received a tax invoice (or an adjustment note) for that supply.

(bold emphasis in original)

105 The evidence of Wilson and Amie is that Wilson prepared the BSA using a precedent he found on the internet.

C.4 The WSE Loan Agreement

106 The WSE Loan Agreement bears two signatures – Wilson’s signature on behalf of Top Energy (next to a handwritten date of 30 March 2019) and Sam’s signature on behalf of WSE (next to a handwritten date of 11 April 2019). As mentioned, there is an issue as to whether it was entered into at about this time (as the respondents contend) or on or about 15 September 2022 (as the applicants contend).

C.5 The Joyo Loan Agreement

107 The Joyo Loan Agreement provides that Joyo is the lender and Top Energy is the borrower. It is otherwise in similar terms to the WSE Loan Agreement.

C.6 Events leading up to the SSD

108 As mentioned, from about April 2019, there were discussions concerning a possible joint venture.

109 On or about 11 to 14 April 2019, an application to transfer the business name “Win Solar Wholesale” from WSE to Top Energy was lodged with the Australian Securities and Investments Commission (ASIC).

110 On 15 April 2019, Richard sent Amie an email attaching a document titled “Solar PV System Distribution and Installation Project”, bearing a date of 13 April 2019. That document included as a project goal: “In 5 years to build business revenue AUD 100m with 5%+ net profit”. At that time, Richard had not been given any financial information about the WSE business and as Richard acknowledged in cross-examination, the lack of a forecast about that business did not stop him imagining the goal of $100 million revenue in five years at five per cent net profit.

111 On 16 April 2019, Richard sent a message to Amie: “When the time is right, I will look at the past financial reports and prepare a high level budget.” In this message, Richard was referring to the previous financial reports of WSE as the operator of the WSE business.

112 On 20 April 2019, Richard sent to Amie documents titled: (1) “Solar PV System Distribution and Installation Project”, bearing a date of 20 April 2019; and (2) “Solar Venture Structure @ April 2019”. His covering email stated:

Please have a look the attached files.

I inserted financial budget as per our Wechat conversations.

With proposed holding company, I suggest we have 12 month trial period then review what we achieved and going to achieve.

Like to have your thoughts and will value your inputs.

...

113 The “Solar PV System Distribution and Installation Project” document was similar to the previous iteration of that document. It included as a project goal: “In 5 years to build business revenue AUD 50m with 5%+ net profit”.

114 The “Solar Venture Structure @ April 2019” was as follows:

115 Richard’s evidence in cross-examination included that as at 20 April 2019:

(1) he had not received any historical financial information from Amie or Wilson;

(2) it was important:

(a) that he had the ability to withdraw from the investment at the end of a 12 month trial period;

(b) to have a review after 12 months and to be able to get his investment back if he chose to, because he did not know if the proposed transaction would work out and he did not want to be locked in; and

(c) to have this “escape route” because it protected him – if the financial position and performance of his investment in WSE was not as he had assumed, he could withdraw from it and get his money back.

116 On 22 April 2019, Richard and Amie exchanged WeChat messages including (as written):

(1) at 7:26am, Amie:

(a)

To ensure that our understanding is ultimately consistent, I have summarised the details of your idea about the joint venture as follows:

1. The trial period of the joint venture is 12 months. Share ratio: Degranand Unit Trust contributes AUD 2 million in cash and takes 70 %shares; Blue Butterfly uses win solar as part of contribution (what is the specific contribution of win solar in your opinion). Subject to a pleasant run-in period (whether there are specific criteria to define a “pleasant run-in”), formal cooperation will commence, and the final shareholder and director structure and share ratio will be determined at that time. If the two companies can’t work together, they will choose to break up after 12 months (what are the breakup details?).

2. In the next 12 months, the joint venture will have three subsidiaries, including a distribution and wholesale company (100%), a branded products company (100%) and an installation company (90%-100%).

What do you mean by “The share holding won’t impact on the first 12 months, even further decision making process”? ; or

(b)

I will continue to sort out the details of your joint venture ideas to ensure that our understanding will not deviate in the end. 1. Use 12 months to test the joint venture, the share ratio is Degranand Unit Trust 2m cash, accounting for 70%, Blue Butterfly uses win soalr as part of contribution (what are the specific win solar contribution in your opinion), if the run-in period is good (whether there are specific criteria for whether the run-in period is good or not), both parties will start formal cooperation, and the final shareholder and director structure and share ratio will be determined at that time. If the two water bottles cannot work together, will choose to break up after 12 months. (What are the details of the break-up?) 2. In the next 12 months, the joint venture company will have three branches, one is the distribution and wholesale company (100%), one is the brand product company (100%), and the other is the installation company (90%-100%) The shareholding won't impact on the first 12 month, even further decision making process. What does this mean.

(2) at 9:35am, Amie:

(a)

1. The trial period of the joint venture is 12 months. Share ratio: Degranand Unit Trust contributes AUD 2 million in cash, taking about 70% shares; Blue Butterfly uses win solar as part of contribution (win solar’s value can be calculated as per the net assets or a multiple of profits). Subject to a pleasant run-in period (whether there is any profit or how much profit is a secondary consideration, and the foundation for long-term cooperation is common values), formal cooperation will commence, and the final shareholder and director structure and share ratio will be determined in light of the actual situation at that time. If the actual situation shows that it is difficult for both parties to have a long-term basis for cooperation during the trial period, Degranand can get back their investment capital if they insist on exiting unilaterally, and if Blue Butterfly asks Degranand to exit, both parties agree that there will be a plan that has the minimal impact on the joint venture.

2. In the next 12 months, the joint venture will have four subsidiaries, including a distribution and wholesale company (100%), a branded products company (100%), an installation company (90%-100%) and a marketing company (100%). ; or

(b)