FEDERAL COURT OF AUSTRALIA

Australian Securities and Investments Commission v Walker Stores Pty Ltd (In Liquidation) [2026] FCA 665

File number: | VID 647 of 2025 |

Judgment of: | BEACH J |

Date of judgment: | 18 May 2026 |

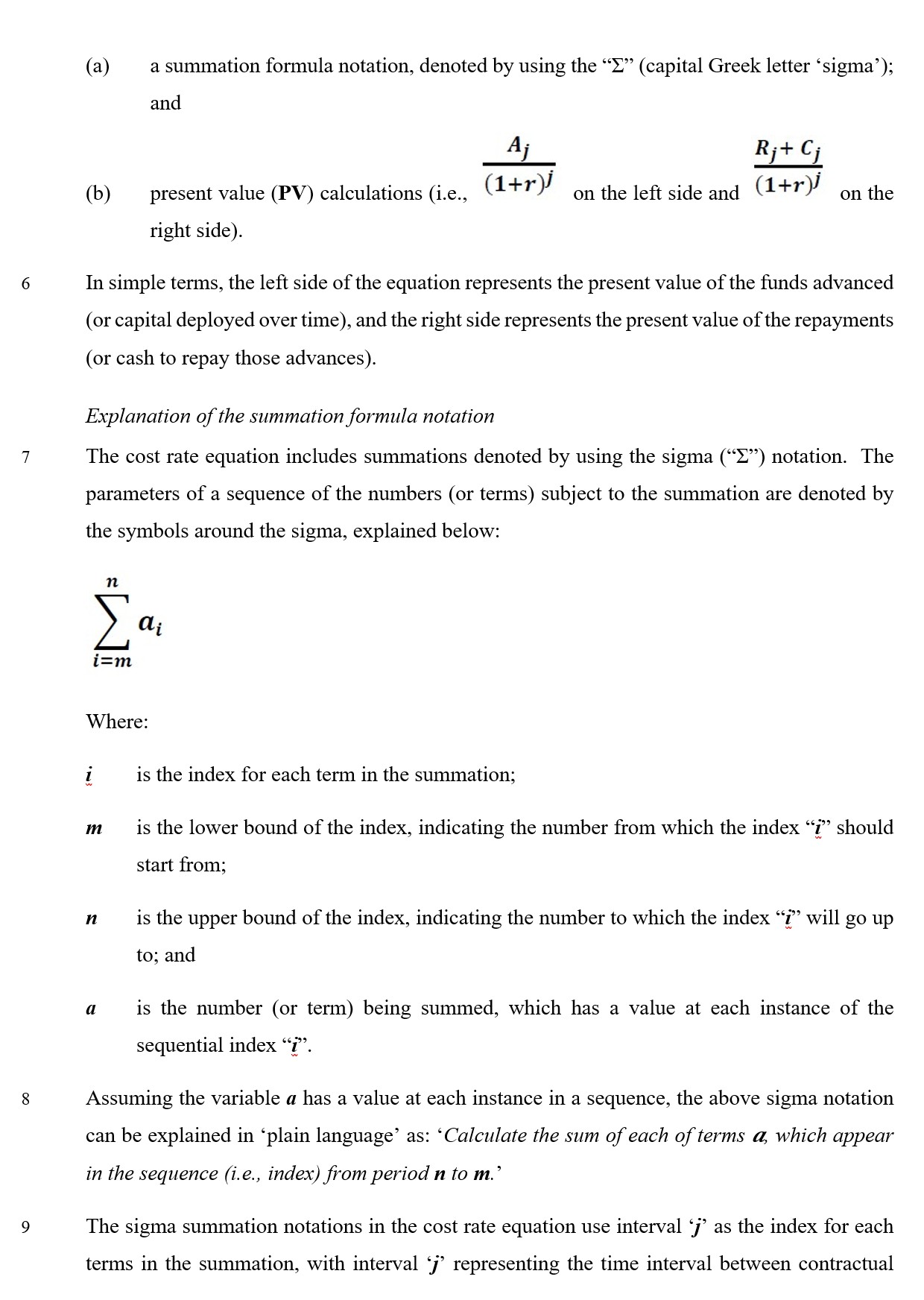

Date of publication of reasons: | 29 May 2026 |

Catchwords: | CORPORATIONS — consumer credit — credit contracts — cap on the cost of credit by way of the annual cost rate (ACR) — contravention of s 24(1) and s 32A of the National Credit Code — observations on the calculation of the ACR — respondent markups — meaning of “amount of credit” — meaning of “cost of credit” — meaning of “credit fees or charges” — alternative constructions of s 32B of the Code — observations on credit cost construction — observations on cash price construction — meaning and application of the term “cash price” — rate cap contraventions under s 32A of the Code — whether disclosure contraventions under s 17(3) of the Code — interest rate calculations — use of flat rate calculation method — contravention of s 28 of the Code — key requirements provisions — declarations under s 166 of the National Consumer Credit Protection Act 2009 (Cth) — pecuniary penalties under s 167 of the Act for breach of the Code — application of ss 167A and 167B of the Act — penalties fixed — adverse publicity notice — s 182 of the Act — orders made |

Legislation: | Banking Act 1959 (Cth) s 5 Consumer Credit Legislation Amendment (Enhancements) Act 2012 (Cth) Schedule 4 s 13 Corporations Act 2001 (Cth) ss 553B, 1317E, 1101B National Consumer Credit Protection Act 2009 (Cth) s 5, Division 3 of Part 2, ss 166, 167, 167A, 167B, 175, 182, Schedule 1 (National Credit Code) ss 3, 4, 5, 6, 11, 13, 17, 23, 24, 27A, 28, Division 4A of Part 2, 32A, 32B, Part 6, 113, 116, 204 Consumer Credit Legislation Amendment (Enhancements) Bill 2012 (Cth) Explanatory Memorandum to the National Consumer Credit Protection Bill 2009 (Cth) National Consumer Credit Protection Bill 2009 (Cth) Revised Explanatory Memorandum to the Consumer Credit Legislation Amendment (Enhancements) Bill 2012 (Cth) Consumer Credit (New South Wales) Act 1995 (NSW) Credit (Commonwealth Powers) Act 2010 (NSW) Schedule 3, cl 7 Consumer Credit (Queensland) Act 1994 (Qld) Credit (Commonwealth Powers) Act 2010 (Qld) Part 6 s 34 Consumer Credit (Victoria) Act 1995 (Vic) s 39(1) Credit (Commonwealth Powers) Act 2010 (Vic) s 22(4) Consumer Credit (New South Wales) Special Provisions Regulation 2002 (NSW) regs 7, 8 Consumer Credit (Queensland) Special Provisions Regulation 2008 (Qld) Consumer Credit (New South Wales) Amendment (Maximum Annual Percentage Rate) Bill 2005 (NSW) Schedule 2 New South Wales, Gazette: Legislation, Allocation of Administration Acts, No 133, 23 August 2002 New South Wales, Minutes of the Proceedings, Legislative Council, 27 August 2002 New South Wales, Parliamentary Debates, Legislative Assembly, 19 October 2005 New South Wales, Parliamentary Debates, Legislative Assembly, 9 November 2005 Victoria, Parliamentary Debates, Legislative Assembly, 4 May 1995 |

Cases cited: | Australian Competition and Consumer Commission v Australian Institute of Professional Education Pty Ltd (in liquidation) [2017] FCA 521 Australian Competition and Consumer Commission v Aveling Homes Pty Ltd [2017] FCA 1470 Australian Competition and Consumer Commission v Dataline.Net.Au Pty Ltd (in liquidation) (2007) 161 FCR 513 Australian Competition and Consumer Commission v Get Qualified Australia Pty Ltd (in liquidation) (No 3) [2017] FCA 1018 Australian Securities and Investments Commission v AGM Markets Pty Ltd (in liq) (No 4) [2020] FCA 1499; (2020) 148 ACSR 511 Australian Securities and Investments Commission v Australia and New Zealand Banking Group Ltd [2023] FCA 1150; (2023) 169 ACSR 649 Australian Securities and Investments Commission v BHF Solutions Pty Ltd (2022) 293 FCR 330 Australian Securities and Investments Commission v Darranda Pty Ltd (Penalty) [2025] FCA 938 Australian Securities and Investments Commission v Kobelt [2016] FCA 1327 Australian Securities and Investments Commission v Rent 2 Own Cars Australia Pty Ltd (2020) 147 ACSR 598 Australian Securities and Investments Commission v Westpac Banking Corporation (Omnibus) [2022] FCA 515; (2022) 407 ALR 1 Australian Securities and Investments Commission v Westpac Banking Corporation (No 3) [2018] FCA 1701; (2018) 131 ACSR 585 Australian Securities and Investments Commission v Westpac Banking Corporation [2026] FCA 651 BSF Solutions Pty Ltd v Australian Securities and Investments Commission [2025] FCAFC 88 Bull v Attorney-General (NSW) (1913) 17 CLR 370 Commissioner of State Revenue (Victoria) v Lend Lease Development Pty Ltd (2014) 254 CLR 142 Kwik Finance (Sydney) Pty Ltd v Walker [2014] NSWCA 73 Re Make it Mine Finance Pty. Ltd [2015] FCA 393; (2015) 238 FCR 562 Re Make it Mine Finance Pty. Ltd (No 2) [2015] FCA 1255 The Queen v Khazaal (2012) 246 CLR 601 Walker v Consumer, Trader and Tenancy Tribunal (NSW) [2013] NSWSC 1432 |

Division: | General Division |

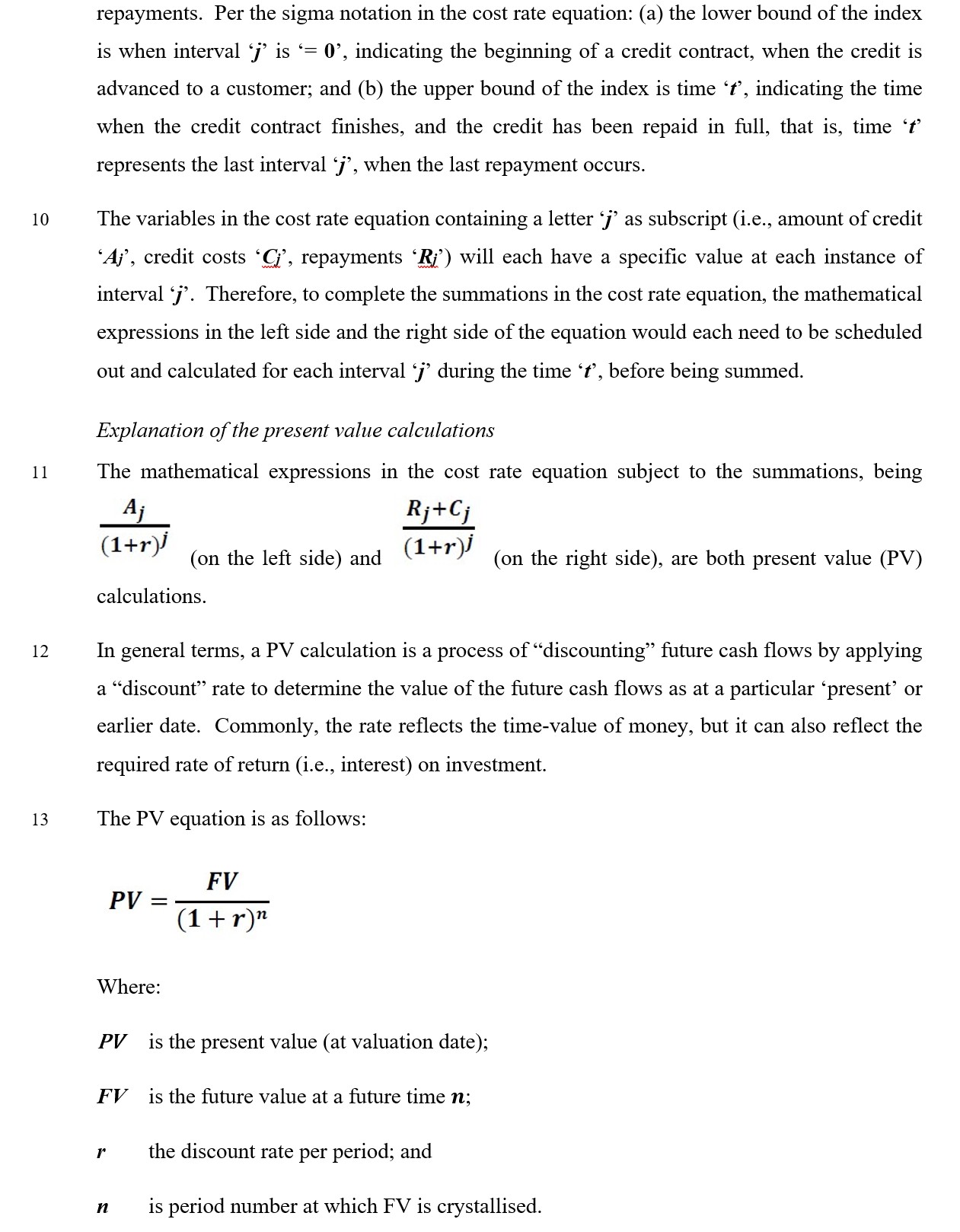

Registry: | Victoria |

National Practice Area: | Commercial and Corporations |

Sub-area: | Regulator and Consumer Protection |

Number of paragraphs: | 323 |

Date of hearing: | 20 February and 18 May 2026 |

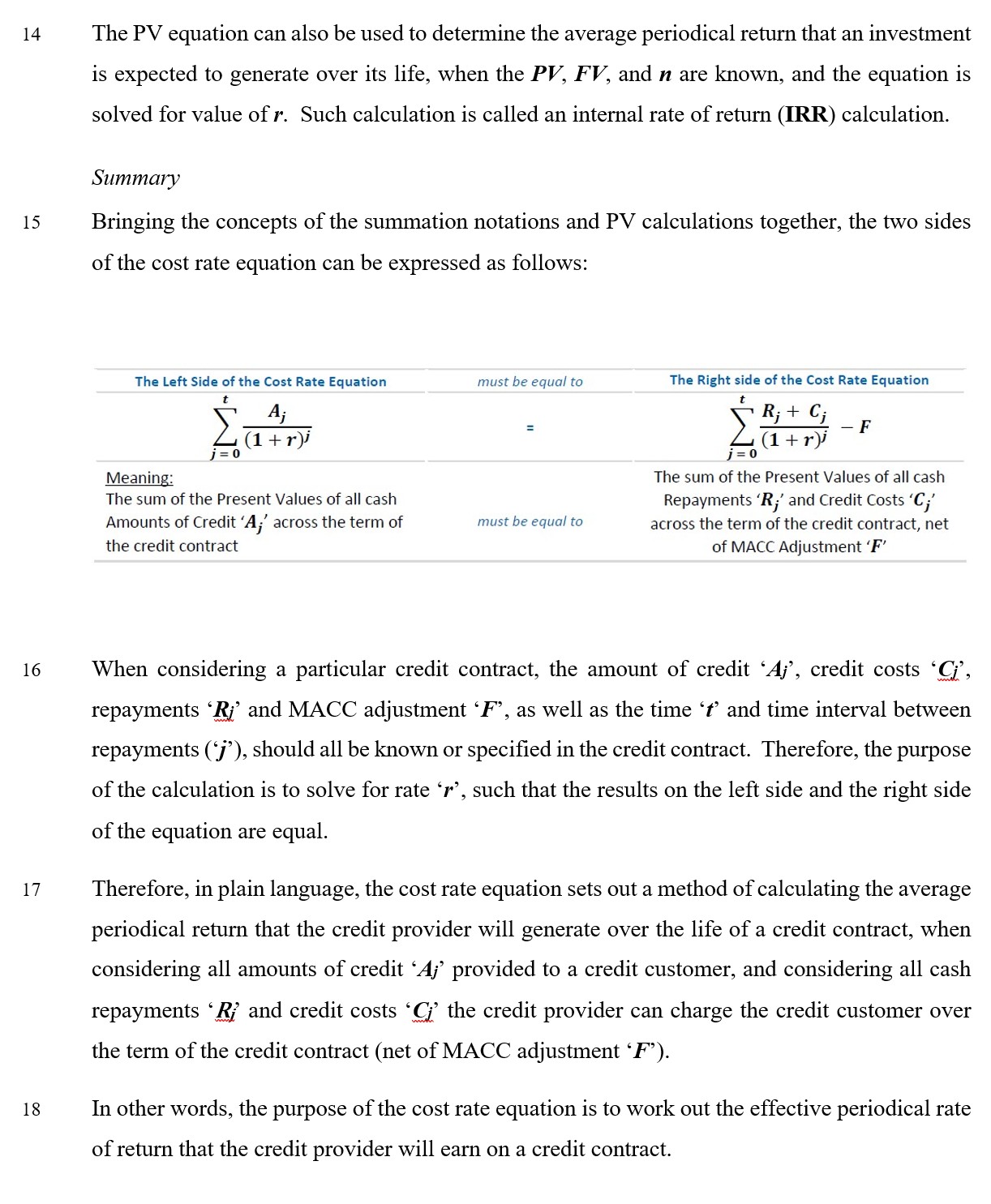

Counsel for the Applicant: | Ms K O’Gorman SC, Ms E Levine and Mr G Rees |

Solicitor for the Applicant: | DLA Piper |

Counsel for the Respondent: (Receivers) | Ms V Bell (20 February 2026 only) |

Solicitor for the Respondent: (Receivers) | Jones Day |

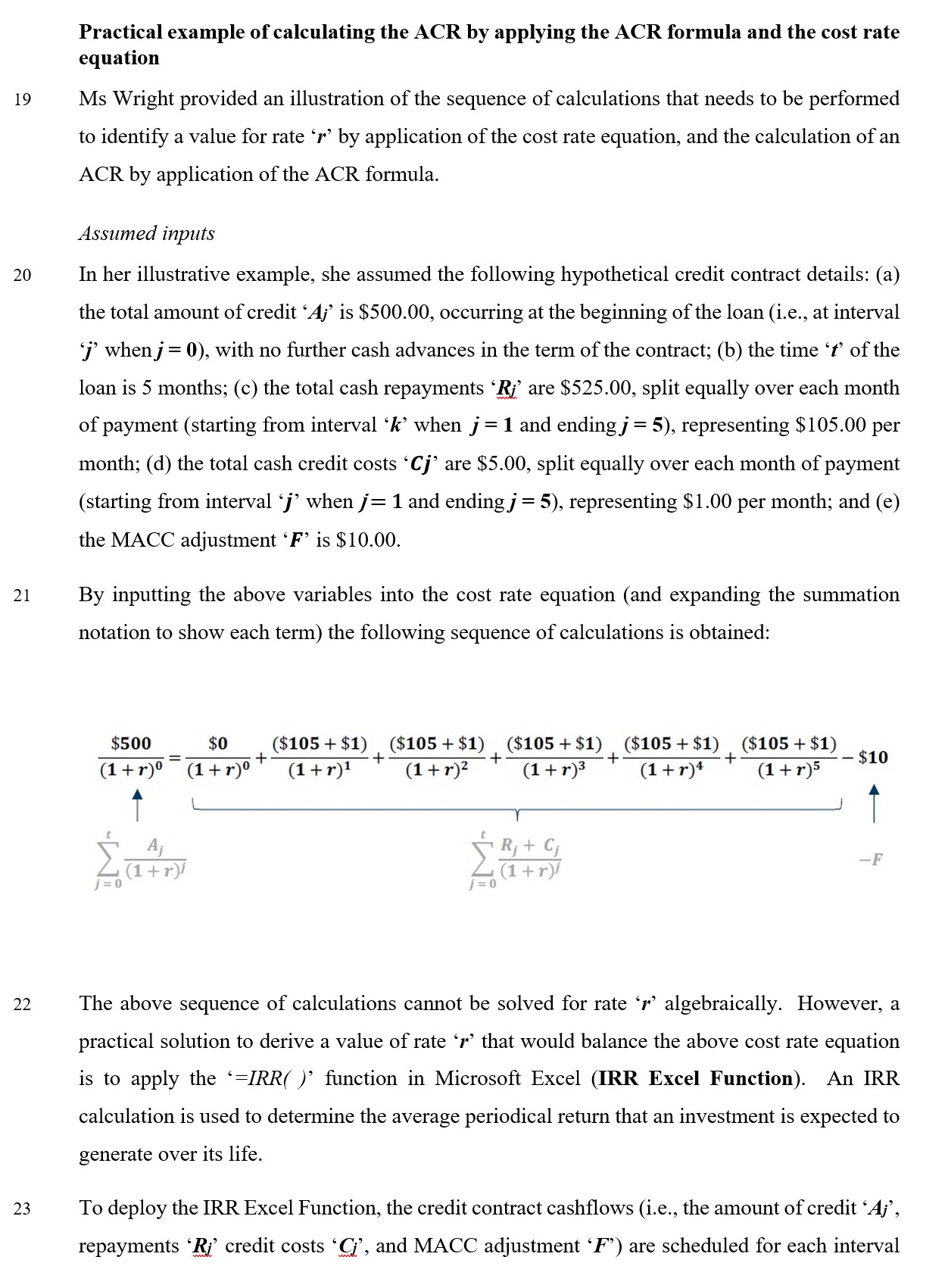

ORDERS

VID 647 of 2025 | ||

| ||

BETWEEN: | AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Applicant | |

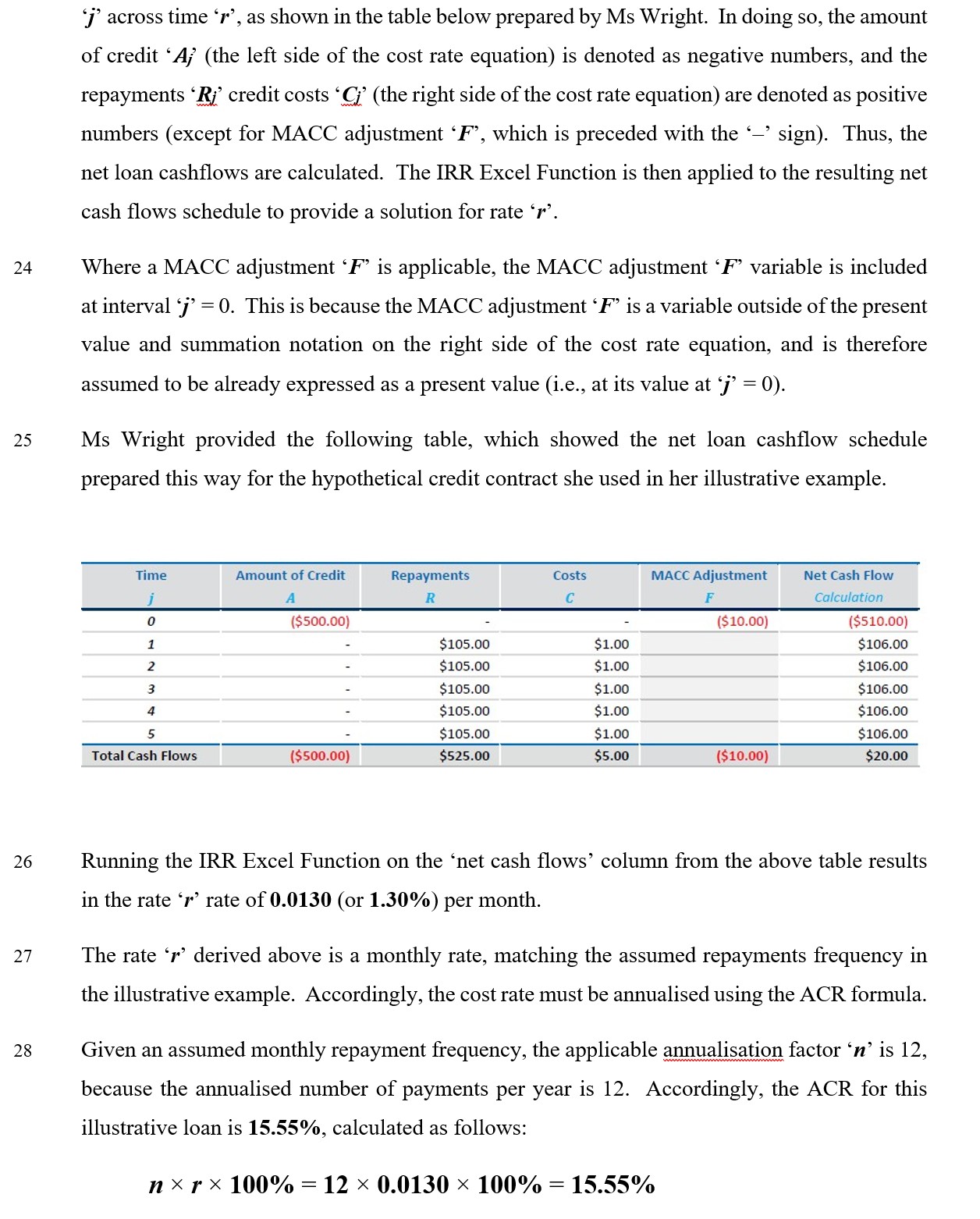

AND: | WALKER STORES PTY LTD ACN 007 973 962 (IN LIQUIDATION) Respondent | |

order made by: | BEACH J |

DATE OF ORDER: | 18 MAY 2026 |

OTHER MATTERS:

A. References to Contract A are references to the contract a consumer entered into with Walker Stores on 2 July 2024 for the purchase of a Haier 7.5kg Front Load Washing Machine model HWF75AW3, with payment required to be made to Walker Stores in weekly instalments of $9.93 over a term of 3 years.

B. References to Contract B are references to the contract a consumer entered into with Walker Stores on 5 July 2024 for the purchase of an LG 315L Top Mount Frost Free Silver Fridge model GT-3S, with payment required to be made to Walker Stores in weekly instalments of $15 over a term of 3 years.

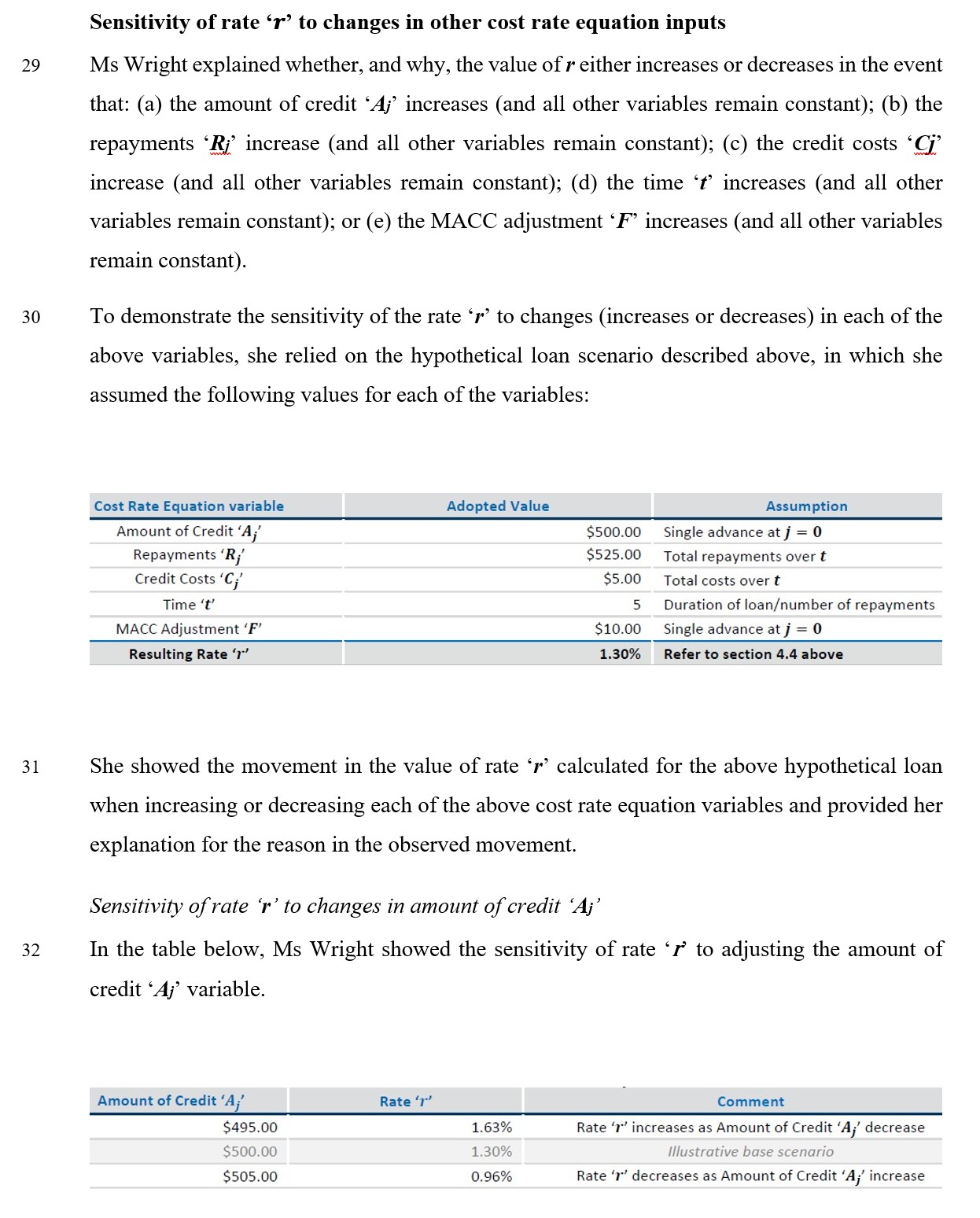

C. References to Contract C are references to the contract a consumer entered into with Walker Stores on 1 July 2024 for the purchase of an Apple iPhone 15 256GB Pink model MTP73ZP/A, with payment required to be made to Walker Stores in fortnightly instalments of $54.44 over a term of 3 years.

D. References to the Credit Act are references to the National Consumer Credit Protection Act 2009 (Cth).

E. References to the Credit Code are references to Schedule 1 to the Credit Act.

DECLARATIONS

Rate Cap Contraventions

Pursuant to s 113(1) of the Credit Code, the Court declares that:

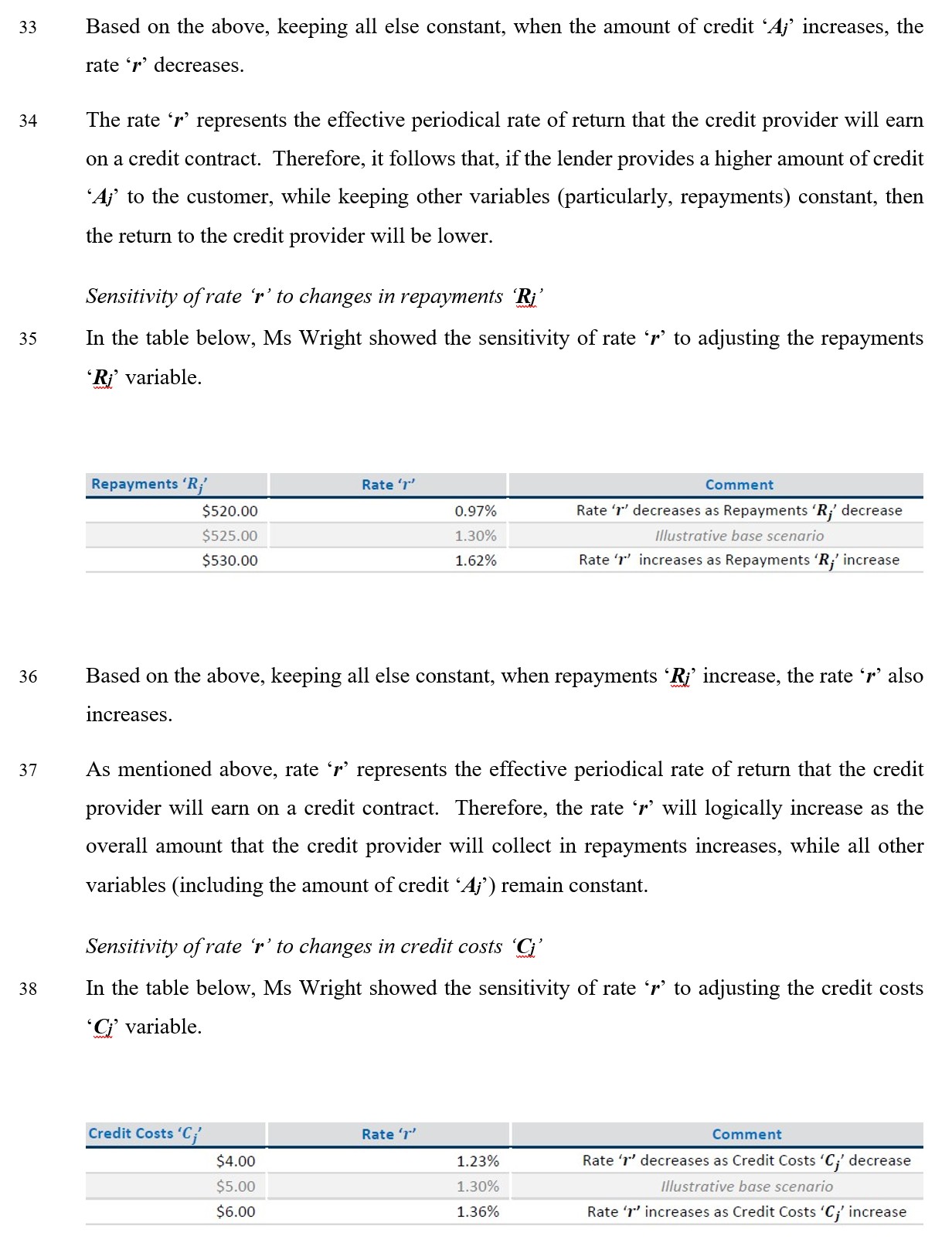

1. Between September 2021 and 27 February 2025 (Relevant Period), the respondent (Walker Stores), trading as “Snaffle”, entered into each of Contracts A, B, and C which were credit contracts that imposed an annual cost rate that exceeded the maximum rate of 48% (Rate Cap) in contravention of the key requirement contained in s 32A(1) of the Credit Code.

Pursuant to s 166 of the Credit Act, the Court declares that:

2. During the Relevant Period, Walker Stores contravened s 24(1)(a) of the Credit Code by entering into Contracts A, B, and C on terms imposing a monetary liability prohibited by s 23(1) of the Credit Code in that the amount payable under each contract exceeded the Rate Cap.

Interest Calculation Contraventions

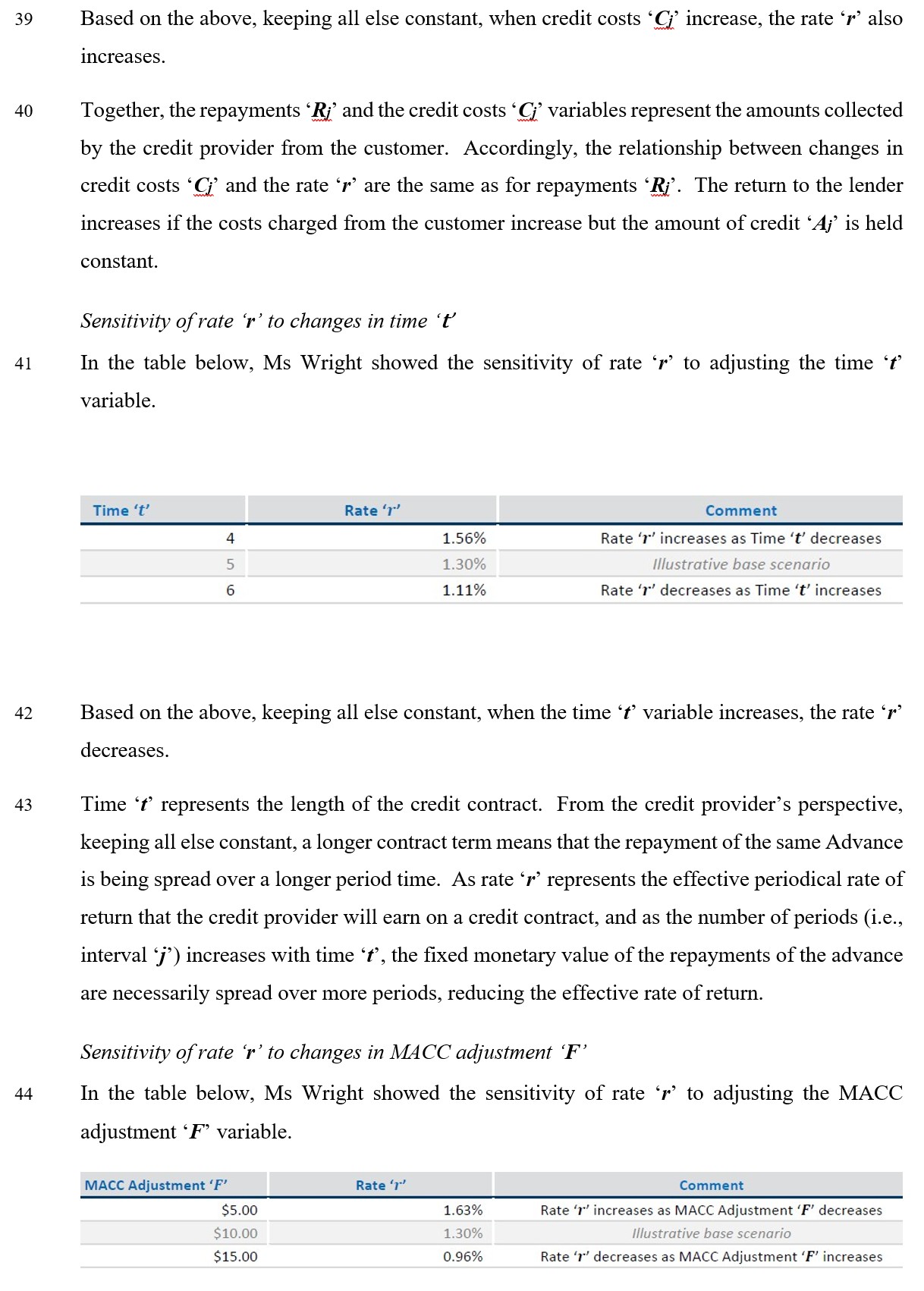

Pursuant to s 166(2) of the Credit Act, the Court declares that:

3. During the Relevant Period, Walker Stores contravened s 24(1)(a) of the Credit Code by entering into 38,562 credit contracts (including Contracts A, B, and C) on terms imposing a monetary liability prohibited by s 23(1) of the Credit Code in that each contract applied interest calculated by applying the applicable interest rate to the total contract amount rather than the unpaid amount owing at any given time, contrary to s 28 of the Credit Code.

4. During the Relevant Period, Walker Stores contravened s 24(1)(b) of the Credit Code, by requiring or accepting payment of interest under each of 38,562 credit contracts (including Contracts A, B, and C), where that interest was calculated on the total contract amount, rather than the unpaid amount owing at any given time, resulting in an amount greater than that permitted under s 28 of the Credit Code.

AND THE COURT ORDERS THAT:

Pecuniary Penalties

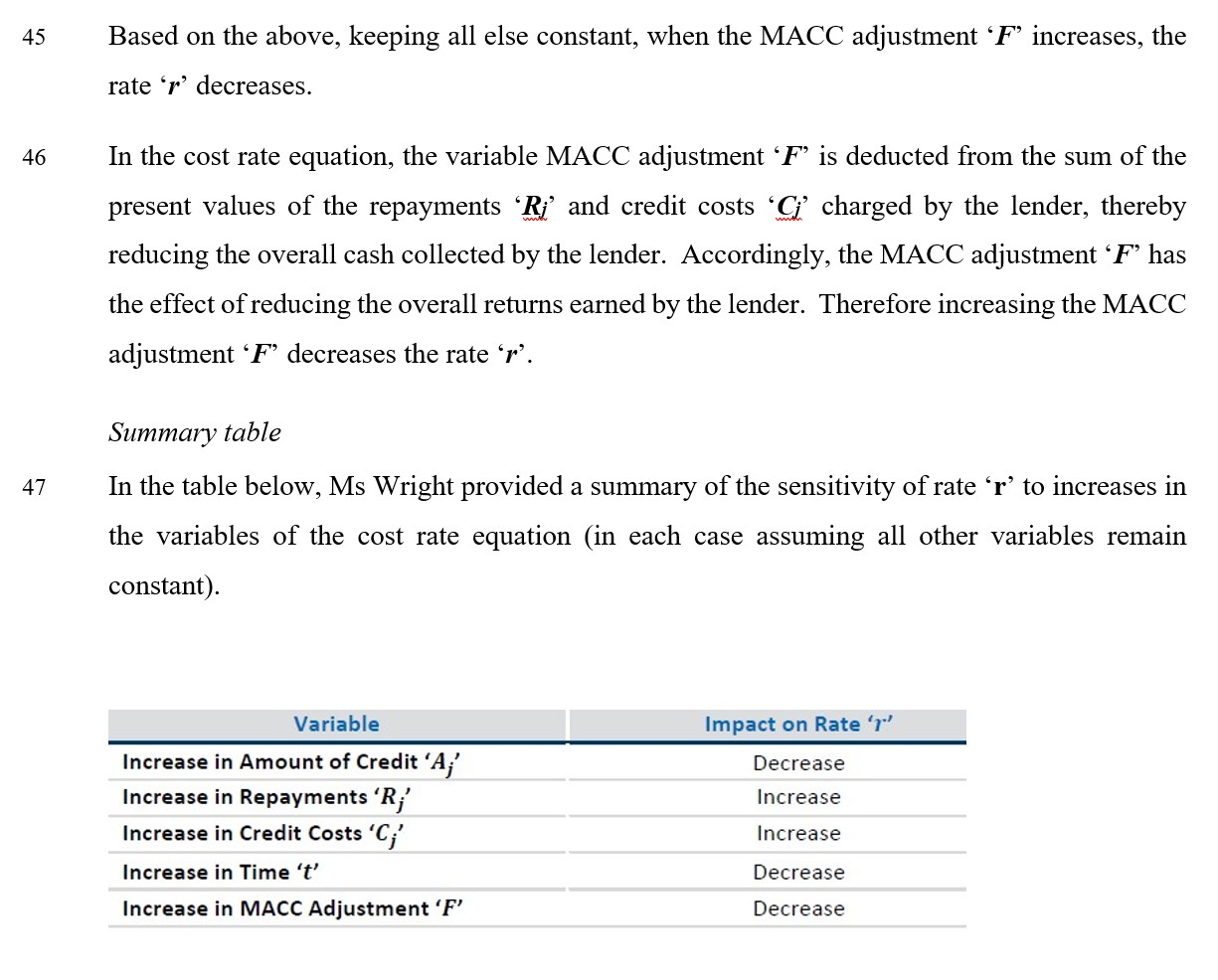

5. Walker Stores pay to the Commonwealth of Australia a pecuniary penalty of $1.5 million in respect of the contraventions of s 24(1) of the Credit Code referred to in paragraph 2 above being the Rate Cap Contraventions.

6. Walker Stores pay to the Commonwealth of Australia a pecuniary penalty of $32 million in respect of the contraventions of s 24(1) of the Credit Code referred to in paragraphs 3 and 4 above being the Interest Calculation Contraventions.

Adverse Publicity Orders

7. Within 14 days of the date of these orders, Walker Stores must:

(a) request Addis Holdings Pty Ltd (Addis Holdings), as the entity which controls and/or operates the websites located at:

(i) https://www.snaffle.com.au (Snaffle Website); and

(ii) https://aspire42.com.au (Aspire42 Website),

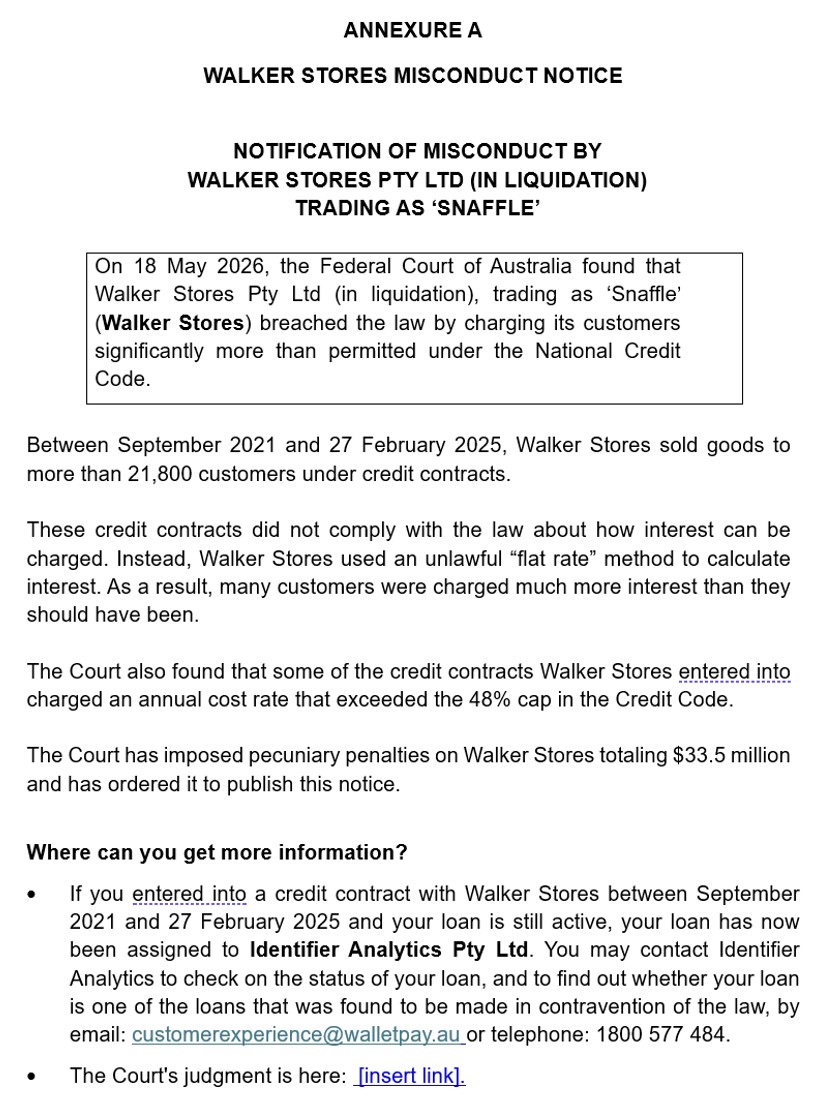

to publish, at Walker Stores' expense, a written adverse publicity notice in the terms set out in Annexure A to these orders; and

(b) take all steps reasonably available to it to procure publication of that notice by Addis Holdings in accordance with order 8 below.

8. The notice referred to in order 7 above must be:

(a) published in an immediately visible area of the home page on the Snaffle Website and the Aspire42 Website under a banner titled ‘Notification of Misconduct by Walker Stores trading as Snaffle’;

(b) published in font no less than 14 point; and

(c) displayed on each of the Snaffle Website and the Aspire42 Website for a period of no less than 365 days.

Costs

9. Walker Stores pay the applicant’s costs of and incidental to the proceeding, to be taxed if not agreed, without prejudice to the applicant’s right to apply for a lump sum costs order.

10. Liberty to apply.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

BEACH J:

1 Walker Stores Pty Ltd (in liquidation) previously carried on an online business supplying consumer goods including home appliances and furniture to consumers by way of “credit contracts”, as defined in s 4 of the National Credit Code (the Code), being Schedule 1 to the National Consumer Credit Protection Act 2009 (Cth) (the Credit Act), with repayments by instalments over 12, 24 or 36 months.

2 Between September 2021 and 27 February 2025, Walker Stores entered into 38,562 credit contracts, including three specific sample contracts that I will identify later.

3 ASIC has alleged that by charging consumers significantly more under those credit contracts than it was permitted to, and by failing to disclose to consumers information about those credit contracts, Walker Stores contravened the requirements of the Code. ASIC’s case is that during the relevant period Walker Stores engaged in the following three categories of contraventions.

4 First, it is said that by entering into the sample contracts pursuant to which it sold goods at marked-up prices, Walker Stores breached s 32A of the Code, which imposes a cap on the cost of credit by way of the annual cost rate or ACR, and thereby contravened s 24(1) of the Code.

5 Second, it is said that the contract documents comprising each sample contract failed to set out the cash price and amount of credit provided, and thereby contravened ss 17(3)(a)(i) and 17(3)(c) of the Code, which is a “key requirement” contravention but not a civil penalty contravention. Section 17 does not include the words “civil penalty” or “penalty units” and so does not meet the definition in s 5(1) of the Credit Act of “civil penalty provision”. It instead refers to Part 6, which provides for penalties for contraventions of “key requirements”. Section 113 of the Code allows for penalties to be imposed for breaches of a “key requirement”. Further, s 116(2) of the Code provides that “section 167B of the National Credit Act [which provides for maximum civil penalties] applies in the same way in relation to the contravention of a key requirement as it would apply in relation to a civil penalty provision under that Act”.

6 Third, it is said that with respect to all 38,562 credit contracts entered into during the relevant period including the sample contracts, Walker Stores imposed an interest charge in excess of the maximum amount permitted under s 28 of the Code. ASIC’s case is that Walker Stores determined the amount of interest on a flat rate basis, contrary to the method for applying interest required by s 28 of the Code. Accordingly, ASIC says that Walker Stores contravened s 24(1) of the Code.

7 ASIC has sought declarations of the rate cap contraventions and the disclosure contraventions in respect of the sample contracts. It has sought declarations of the interest calculation contraventions for all 38,562 contracts which includes the sample contracts. And it has sought pecuniary penalties for each category of contravention, adverse publicity notices and costs.

8 ASIC has not now pressed for the injunctions sought in its originating application because Walker Stores assigned its interest in 24,444 active credit contracts to a related entity and retained other credit contracts which are no longer active.

9 It is useful at this point to say something about the external administrations that Walker Stores has been and is now subject to.

10 On 9 July 2025, Walker Stores entered into voluntary administration and became the subject of a receivership. In the proceeding before me, the receivers have filed a concise response to ASIC’s concise statement on Walker Stores’ behalf, which admitted all of ASIC’s factual allegations.

11 On 3 March 2026, Walker Stores’ creditors resolved to wind up the company. On 17 March 2026, I granted ASIC leave to proceed against Walker Stores now in liquidation.

12 Based on Walker Stores’ concise response it is not in dispute that: (a) Walker Stores priced its credit contracts in the manner alleged and in particular, by aggregating five amounts (the respondent markups) to derive the Walker Stores price, to which it then added GST; (b) interest was calculated using the flat rate calculation method of multiplying the Walker Stores price including GST by the number of years of the contract by the interest rate; (c) the sample contracts were governed by the Code; (d) the sample contracts were priced by way of successive addition of the respondent markups to the acquisition cost; and (e) interest was calculated by the flat rate calculation method across all credit contracts entered into by Walker Stores during the relevant period.

13 ASIC has relied on the documentary evidence annexed to its investigator’s affidavits and various affidavits of its external solicitor. The documentary evidence before me also includes a list of contract particulars for 38,562 contracts provided by the receivers on 3 March 2026.

14 ASIC has also tendered an expert report of Ms Dawna Wright, a forensic accountant and principal of FTI Consulting, who prepared a report explaining the operation of the formulae in issue, as well as calculating the total amount overcharged with respect to the rate cap and interest calculation contraventions; annexed to these reasons are some extracts from her report.

15 On 18 May 2026, I imposed on Walker Stores a total pecuniary penalty of $33.5 million and made various other declarations and orders. These are my reasons for so doing.

Some relevant background

16 Walker Stores holds an Australian credit licence, which was first issued on 22 March 2011 and which authorises it to carry on a business of providing credit.

17 Walker Stores is a member of what is known as the Aspire 42 corporate group, as is Aspire 42 Financing Pty Ltd (Aspire 42). Aspire 42 and Walker Stores are related entities. Further, United Wholesale Solutions Pty Ltd (UWS) is a member of a corporate group of companies that has over-lapping shareholders, directors and management executives with the Aspire 42 corporate group.

18 From at least around late September 2021, Walker Stores traded under the name “Snaffle” and operated exclusively online through the website “Snaffle.com.au”. Trading as Snaffle, Walker Stores offered consumers products such as electronics, furniture and household appliances, to be purchased on 12, 24 or 36 month credit contracts with weekly or fortnightly repayment terms. It also offered consumers the option to pay for those goods for cash, and Walker Stores claimed that this formed the retail arm of the Snaffle business. But these cash sales were negligible. In either case, the purchase price of the goods, or the price which was financed with credit, was the same as the Walker Stores price.

19 Now the process by which Walker Stores determined the Walker Stores price is central to this matter.

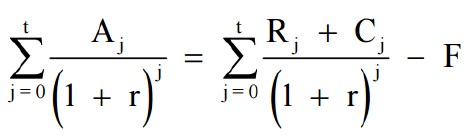

20 Walker Stores obtained the goods it sold on credit from wholesale or retail suppliers such as JB Hi-Fi and the Good Guys. They were obtained for Walker Stores by way of two associated entities pursuant to a supply agreement dated 13 March 2020.

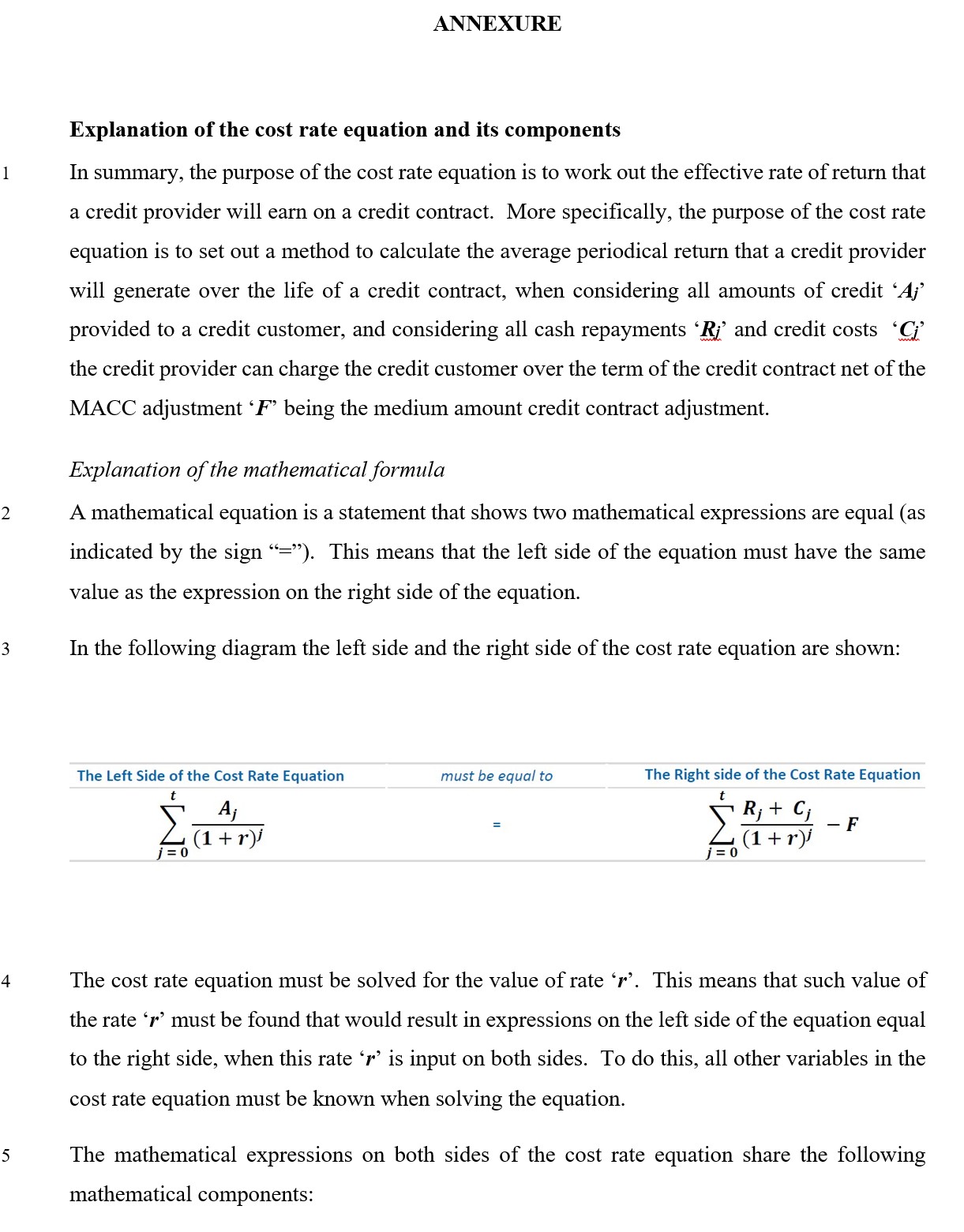

21 The supply agreement was made between Aspire 42 and UWS. It describes Aspire 42 as a service company engaged by Walker Stores, though it does not specify what that engagement is or whether it is in writing. The services required of Aspire 42 include to manage the ordering, delivery, payment and resupply of the household goods to Walker Stores.

22 By the supply agreement, Aspire 42 appointed UWS as its exclusive supplier of household goods for a term of 36 months. Upon Walker Stores requiring a household good to on-sell to the consumer under a credit contract, it was to inform Aspire 42 and Aspire 42 would order those goods from UWS. UWS was to source the household goods from its selected suppliers, and order and pay for those goods and inform Aspire 42 when the goods were available for delivery. UWS was then to deliver the goods as directed by Aspire 42 and issue it a tax invoice. For this service, Aspire 42 was to pay UWS the price charged by the supplier, plus a margin on that price, plus GST and delivery.

23 The supply agreement was silent as to the quantum of the margin to be applied to pay for UWS’s services. But it would seem that the margin Walker Stores paid UWS for its services was 10%. The supply agreement also did not state how Aspire 42 was to be paid, if at all, for its services.

Respondent markups

24 The price UWS paid to purchase the good from a supplier is termed the acquisition cost. The 10% of that acquisition cost that Walker Stores paid to UWS for the services of sourcing, managing and delivering the good to the consumer was the UWS markup, being the first markup applied by Walker Stores.

25 To the acquisition cost, raised by 10% by the UWS markup, Walker Stores added a succession of further markups.

26 First, Walker Stores imposed a global 3% markup on the acquisition cost, to cover its operating expenditure including personnel, marketing, sales, occupancy, administration and IT. This markup is termed the operating costs markup.

27 Second, a flat $35 fee described as a delivery fee was added. However, this figure was charged irrespective of whether Walker Stores (or UWS on its behalf) incurred any delivery fee, and the credit contracts did not specify any amount for delivery. This is termed the delivery fee.

28 Third, Walker Stores imposed a further markup on top of the acquisition cost raised by the UWS markup, operating costs markup, and delivery fee, as “profit” or a “margin”. This is termed the profit margin. This markup was determined on a per-product basis, with margins ranging from approximately 5% to 30%, and was further subject to a “dynamic margin pricing process” by reference to factors such as supply conditions, demand, seasonality and promotional considerations. This process was directed to producing a retail price that provided for a profit margin on the retail activity. Walker Stores approached pricing on the basis that the retail sale of the goods and the provision of credit were separate and independent business transactions, with the goods price set so as to achieve a desired retail margin. Interest was then applied as a distinct component of the overall transaction.

29 The sub-total of the acquisition cost and each of these respondent markups is the Walker Stores price. That is, acquisition cost + UWS markup + operating costs markup + delivery fee + profit margin, or algebraically (assuming a 30% profit margin) ((acquisition cost + (acquisition cost x .1) + (acquisition cost x .03) + delivery fee) x 1.3). Walker Stores charged GST on the Walker Stores price, and to this amount added interest.

Walker Stores’ interest charges

30 For each credit contract, Walker Stores applied flat interest. The interest rate it applied increased from 15% at the start of the relevant period to 25 July 2023, to 22.5% between 25 July 2023 and 8 December 2023, and finally to 25.75% from 8 December 2023 to at least the end of the relevant period.

31 It calculated interest by simply taking the Walker Stores price, with GST, and multiplying that figure by the then-current interest rate for each year of the contract. Taking the terms of contract A as an example, a consumer taking out a 3 year instalment contract at a 25.75% interest rate would have to pay Walker Stores 77.25% of the principal (the Walker Stores price with GST) in interest alone. In other words, Walker Stores did not impose reducible interest, by which the interest is calculated only on the remaining outstanding principal.

32 This method of calculation of interest, the flat rate calculation method, was put in place in September 2021, that is, in the period immediately prior to its first offer of credit contracts under the Snaffle brand in October 2021, which is the start of the relevant period.

33 The application of the flat rate calculation method across Walker Stores’ entire loan book is the subject of ASIC’s case concerning the interest calculation contraventions.

The sample contracts

34 For the purposes of its rate cap contraventions and disclosure contraventions cases, ASIC relies on the particulars of the three sample contracts. Under each sample contract the Walker Stores price was determined according to the methodology set out above, that is: (a) the acquisition from a retail supplier by UWS (or Aspire 42) on behalf of Walker Stores at the acquisition cost; (b) the addition to the acquisition cost of the respondent markups; (c) the charging of GST; and then (d) the application to the Walker Stores price + GST of interest calculated using the flat rate calculation method. Of course ASIC alleges that this method was applied to Walker Stores’ entire loan book.

35 The sample contracts were selected by ASIC to present a clear and confined case in respect of the rate cap contraventions and disclosure contraventions.

36 The documents comprising each sample contract and its terms were produced by Walker Stores as “client files”. In respect of each customer, all of Walker Stores’ client files produced to ASIC comprise the same suite of documents being: (a) a document titled “Pre-Contractual Statement (Financial Table), Line of Credit Agreement Schedule and Tax Invoice” (Schedule); (b) a document containing terms and conditions; (c) a credit guide; and (d) a list of payments received to the date of the provision of the contracts to ASIC.

37 The Schedule contains the essential integers of the credit contract. It names Walker Stores, trading as Snaffle under its Australian credit licence, as the credit provider. It gives the contract a unique loan number. It then sets out a description of the goods financed, giving a “unit price” (the Walker Stores price) plus GST as the “total purchase price”.

38 Each sample contract and its accompanying terms and conditions describe the credit product offered to consumers as a “line of credit”.

39 Consistently, the Schedule for each sample contract records that the consumer was approved to borrow a specified maximum amount of credit per month. The Schedules refer to this specified amount as the “amount of credit – line of credit facility (maximum amount of credit approved)”. Although an annual subscription fee was provided for in each Schedule, the subscription fee under each sample contract was $0.

40 Next, the Schedule lists the terms of credit: an annual percentage rate of 25.75%, “calculated for the Term and added to the purchase price of the Goods and divided by the number of months as selected by you for [sic] as the Term”.

41 The Schedule then lists various essential terms under the heading “Repayments”, being: (a) the amount of each repayment; (b) the total number of repayments; (c) the term of the contract in months; (d) when repayments are to be made – in the case of each sample contract, this was monthly in arrears; and (e) the total amount of interest to be paid.

42 The Schedule also provides for an establishment fee (which is “$nil” in all sample contracts), and other contingent fees (such as dishonour fees) which are not relevant.

43 Finally, the Schedule states a grand total payable under each sample contract, which is labelled as the “total credit fees and charges”. This amount is the total of the Walker Stores price, with GST, plus the total amount of interest to be paid.

44 Pursuant to the terms and conditions documents issued with each sample contract, the consumer acquired title to the purchased good, albeit subject to an “Encumbrance” in favour of Walker Stores. Walker Stores stated in those terms and conditions in addition to the Schedule as noted above, contrary to its actual practice for calculating and charging interest, that interest would be “calculated daily by applying the daily percentage rate to the daily outstanding balance (excluding the Subscription Fee) on your account. The daily percentage rate is the Interest Rate divided by 365”.

Contract A

45 Contract A was entered into on 2 July 2024 with consumer A and was made for the purchase by consumer A of a Haier 7.5kg front load washing machine model, with payments by consumer A required under contract A to be made to Walker Stores in equal weekly instalments of $9.93 over a term of 3 years, as implied by there being 156 instalments over a three-year term stated in the Schedule.

46 The Schedule for contract A stated that the “total purchase price” was $873.95, the “total amount of interest” was $675.13, and the “total credit fees and charges” amount was $1,549.08.

47 As with each sample contract, this terminology is both at odds with s 17 of the Code and inapt. The “total purchase price” is not the total payable to purchase the good by instalments but instead denotes the Walker Stores price plus GST. It is the price that would be payable for cash and without interest. The “total credit fees and charges” is not a reference to the statutory term “credit fees and charges” as defined in s 204 of the Code, but instead is the total amount payable by the consumer over the life of the contract, excluding any contingent fees such as dishonour fees.

48 Walker Stores, via UWS and Aspire 42, acquired the washer from Appliances Online, an online seller of appliances, for $539 inclusive of GST. That amount is $334.95 less than the Walker Stores price with GST, and $1,010.08 less than the total amount payable by the consumer over the life of the contract. Consumer A therefore stood to pay almost triple the amount payable for the washer had they purchased it directly from Appliances Online or a similar retailer. Consumer pricing is changeable across retailers and there is evidence before me of competitor online retailers for the same good for a comparable amount to the acquisition cost.

49 The $873.95 Walker Stores required for the washer on credit (before interest) was priced by adding to the $539 acquisition cost the following respondent markups: (a) the UWS markup of $53.90, which UWS applied to the acquisition cost and Walker Stores paid UWS; (b) the operating costs markup of $16.17, being 3% of the acquisition cost; (c) the delivery fee of $35; and (d) the profit margin of $150.43, which was a 23.4% increase on $644.07, being the sum of the acquisition cost plus the UWS markup plus the operating costs markup plus the delivery fee. The sum of the respondent markups was $255.50, and then adding GST of 10% on the Walker Stores price achieved the total purchase price of $873.95.

50 Walker Stores then added interest of 25.75%, which was calculated using the flat rate calculation method, to the principal Walker Stores price plus GST for each of the three years of the contract, being $225.05 each year irrespective of whatever consumer A paid down on the principal over that time.

51 Upon the contract being executed, UWS acquired the washer from Appliances Online and had Appliances Online deliver it to consumer A, for a total payment to Appliances Online of $539, inclusive of GST and with no charge paid by UWS for delivery.

52 Consumer A had, at the time the list of contracts was provided by the receivers on 3 March 2026, paid 85 of 156 instalments against contract A, equal to $844.05.

53 Contracts B and C are similar in form to contract A.

Contract B

54 Contract B was entered into on 5 July 2024 with consumer B and was made for the purchase by consumer B of an LG 315L top mount frost-free silver fridge, with payments by consumer B required under the contract to be made to Walker Stores in equal weekly instalments of $15 over a term of 3 years, as implied by there being 156 instalments over a three-year term stated in the Schedule.

55 The Schedule for contract B stated that the “total purchase price” (the Walker Stores price plus GST) of the fridge was $1,320.17, the “total amount of interest” was $1,019.83, and the “total credit fees and charges” (or really, total payable) was $2,340.

56 Walker Stores, via UWS and Aspire 42, acquired the good from Appliances Online for $925 (inclusive of GST), $395.17 less than Walker Stores priced the fridge, and $1,415 less than the total amount payable by the consumer over the life of the contract. Consumer B therefore stood to pay more than 2.5 times the amount payable for the fridge had they had purchased it directly from Appliances Online or a similar retailer.

57 The Walker Stores price for the fridge was priced by adding to the $925 acquisition cost the following respondent markups: (a) the UWS markup of $92.50; (b) the operating costs markup of $27.75, being 3% of the acquisition cost; (c) the delivery fee of $35; and (d) the profit margin of $119.90, which was an 11.1% increase on $1,080.25, being the sum of the acquisition cost plus the UWS markup plus the operating costs markup plus the delivery fee. The sum of the respondent markups was $275.15, and then adding GST of 10% on the Walker Stores price achieved the total purchase price of $1,320.17.

58 Walker Stores then added interest of 25.75% or $339.94, which was calculated using the flat rate calculation method, for each of the three years of the contract.

59 Upon the contract being executed, UWS acquired the fridge from Appliances Online and had Appliances Online deliver the fridge to consumer B, for a total payment to Appliances Online of $925, inclusive of GST and with no charge for delivery.

60 Consumer B had, at the time the list of contracts was provided by the receivers, paid 83 of 156 instalments against contract B, equal to $1,395.

Contract C

61 Contract C was entered into on 1 July 2024 with consumer C and was made for the purchase by consumer C of an Apple iPhone 15 256GB, with payments by consumer C required under the contract to be made to Walker Stores in equal fortnightly instalments of $54.44 over a term of 3 years, as implied by there being 78 instalments over a three-year term stated in the Schedule.

62 The Schedule for contract C stated that the “total purchase price” (the Walker Stores price plus GST) of the phone was $2,395.67, the “total amount of interest” was $1,850.65, and the “total credit fees and charges” (or really, total payable) was $4,246.32.

63 Walker Stores, via UWS and Aspire 42, acquired the phone from Xtreme Communications, an online retailer mainly of refurbished phones, for $1,733 (inclusive of GST), $662.67 less than Walker Stores priced the phone, and $2,513.32 less than the total amount payable by the consumer over the life of the contract. Consumer C therefore stood to pay more than 2.5 times the amount payable for the phone had they purchased it directly from Xtreme or a similar retailer.

64 The Walker Stores price for the phone was priced by adding to the $1,733 acquisition cost the following respondent markups: (a) the UWS markup of $173.30; (b) the operating costs markup of $51.99, being 3% of the acquisition cost; (c) the delivery fee of $35; and (d) the profit margin of $184.59, which was an 9.3% increase on $1,992.29, being the sum of the acquisition cost plus the UWS markup plus the operating costs markup plus the delivery fee. The sum of the respondent markups was $444.88 and then adding GST of 10% on the Walker Stores price achieved the total purchase price of $2,395.67.

65 Walker Stores then again added interest of 25.75% or $616.89 on that figure by way of interest, which was calculated using the flat rate calculation method, for each of the three years of the contract.

66 Upon the contract being executed, UWS acquired the phone from Xtreme and had Xtreme deliver the phone to consumer C. Unlike under contracts A and B, Xtreme charged UWS a delivery fee, so that the total UWS paid to Xtreme (and Walker Stores paid to UWS) was $1,758, being $1,733, inclusive of GST, plus $25 delivery.

67 Consumer C had, at the time the list of contracts was provided by the receivers, paid 8 of 78 instalments against contract C, totalling $435.52, with a number of dishonoured and failed payments recorded.

The remaining contracts

68 For the interest calculation contraventions case, ASIC further relies on particulars of the 38,562 contracts entered by Walker Stores over the course of its trading. These contracts have not been individually reviewed by ASIC. Instead, it relies on their particulars as set out in the list of contracts provided by the receivers. Contracts A, B and C are part of this set.

69 I should say here that I am prepared to find that each of the 38,562 contracts was a credit contract to which the Code applies. This is so for four reasons. First, Walker Stores’ business model was selling consumer goods on credit. Second, Walker Stores admitted entering credit contracts to which the Code applies. Third, the receivers of Walker Stores provided the list of contracts in response to ASIC’s request for an Excel document containing various particulars of all credit contracts Walker Stores entered in the relevant period, which it represented were credit contracts subject to the Code. Fourth, one has the statutory presumption in s 13(1) of the Code that each contract in the list of contracts was a credit contract to which the Code applies. That presumption applies given that there is no evidence to the contrary.

Walker Stores’ retail arm

70 From 22 January 2024, Walker Stores offered a “Pay Now” option on the Snaffle website, by which consumers could purchase a good for cash, being the Walker Stores price, plus GST. Before 22 January 2024, Walker Stores allowed consumers to purchase goods for cash by contacting Walker Stores by phone. But few consumers ever paid Walker Stores the Walker Stores price to purchase a good for cash. Walker Stores produced only 96 invoices for recorded cash sales, and confirmed that 53 of the 96 invoices were for cash purchases made by staff employed by the Aspire 42 corporate group, which involved promotional discounts, rather than to consumers. It would seem on the evidence that few consumers purchased goods from Walker Stores with cash for the Walker Stores price. And in my view the Walker Stores price was not a price which a cash purchaser could reasonably be expected to pay.

The rate cap contraventions

71 ASIC contends that by reason of Walker Stores’ pricing practice, Walker Stores contravened s 32A of the Code in respect of each sample contract. ASIC says that Walker Stores embedded within the stated price of goods sold under sale by instalments contracts, amounts that are, in substance, charges for the provision of credit. Further, it says that as a result, the ACR under those contracts exceeded the maximum ACR of 48% prescribed by s 32A.

72 Section 32A(1) prohibits a credit provider entering into a credit contract with an ACR of greater than 48%. Section 32B(2) of the Code provides the mathematical formula for calculating the ACR of a credit contract. The formula compares the “amount of credit” (Aj) against the “repayments” (Rj) and “credit cost amount” (Cj). I will set out the statutory provision in a moment. I should note that the integers of ss 32A and 32B of the Code have not been the subject of any detailed judicial attention. Greenwood J considered breaches of s 32A in Australian Securities and Investments Commission v Rent 2 Own Cars Australia Pty Ltd (2020) 147 ACSR 598, although there was no debate before his Honour as to the proper construction of s 32B.

73 Now it is obvious that where the credit provided is in the form of money, the identification of the “amount of credit”, “repayments” and “credit cost amount” is straightforward. But where, as here, the “credit” advanced pursuant to a “credit contract” entails the provision of title to a consumer good, with consideration for that title to be made over a term, the identification of the “amount of credit” is less straightforward. Goods do not have a single value that may be expressed in dollar figures, as money does. Payments of instalments toward the purchase of a good may mix payments for the purchase of the good, payments toward interest, and payments for fees or services relating to the credit, without obvious distinction.

74 Moreover, this complexity is compounded in this case by Walker Stores’ application of the respondent markups. The Walker Stores price, being inclusive of the respondent markups, was in each case substantially greater than the price that Walker Stores paid for the goods, and the price each consumer could have paid for the same goods from other retailers, albeit not under credit contracts. Put simply, ASIC’s case is that the Walker Stores price cannot be treated as being the “amount of credit”.

75 An additional complexity is that the terms “amount of credit” and “cost of credit”, which are integers in the formula used in s 32B(1) to define r, and thus the ACR, do not have obvious application to credit contracts of the type under consideration in the present case. There is therefore some opacity in how those terms are to be construed.

The competing constructions

76 ASIC has identified two alternative candidate constructions of s 32B which can conveniently be referred to as:

(a) the credit cost construction; and

(b) the cash price construction.

77 On the credit cost construction, ASIC says that the “amount of credit” is exclusive of the respondent markups, because they are in substance “credit fees or charges” or “fee[s] or charge[s] payable by” the consumer to reimburse Walker Stores for its services of, and in relation to, the provision of goods on credit and thus form part of the “credit cost amount”; see the definition of “credit cost amount” in s 32B(3) of the Code. Being costs of credit, they are thereby excluded from forming part of the “amount of credit”. As a result, on this construction, the “amount of credit” is equal to the Walker Stores price plus GST, less the respondent markups.

78 Alternatively, on the cash price construction, ASIC says that the “amount of credit” is the “cash price” for the goods as defined by s 204(1) of the Code. As a result, the Walker Stores price is not, by reason of the respondent markups, a price a consumer would reasonably be expected to pay from the supplier and so is not the “cash price” and thus is not the “amount of credit”.

79 ASIC says that on either of its two constructions, the phrase “cost of credit” captures a sum that is referable to the cost to consumers of the good being provided on “credit”, which cost is calculated in different ways by reference either to s 32B(3)(b) or s 204(1) of the Code. ASIC says that this phrase should be interpreted so as to prevent credit providers from avoiding the operation of s 32A of the Code by defining the “amount of credit” as whatever the credit contract defines it to be.

80 ASIC says that each of its constructions is supported by the text and context of ss 32A and 32B of the Code and in light of the purpose and history of Division 4A of Part 2 in which those provisions appear. Let me delve more deeply into s 32B.

Part 2 Division 4A – the ACR

81 Division 4A of Part 2 imposes a limit on the ACR of certain credit contracts and gives the means of its calculation. The ACR provides a single annualised expression of the relationship in any regulated credit contract between the amount of credit provided, on the one hand, and the total of all repayments and payments of the cost of credit, on the other, in each case over the life of the contract.

82 The ACR combines two formulae in ss 32B(1) and (2).

83 Section 32B(1) provides the annualisation formula of the ACR in the following terms:

(1) The annual cost rate of a credit contract must be calculated as a nominal rate per annum, together with the compounding frequency, using the formula:

n x r x 100%

where:

n is the number of repayments per annum to be made under the credit contract (annualised if the term of the contract is less than 12 months), except that:

(a) if repayments are to be made weekly—n is 52.18; and

(b) if repayments are to be made fortnightly—n is 26.09; and

(c) if the contract does not provide for a constant interval between repayments—n is to be derived from the interval selected for the purposes of the definition of j in subsection (2).

r is the solution of the equation specified in subsection (2).

84 Section 32B(2) is a cost rate equation that provides the r input to that annualisation formula, in the form of an equation of two different summations:

(2) The equation for the purposes of the definition of r in subsection (1) is:

where:

Aj is the amount of credit to be provided under the credit contract at time j (the value of j for the provision of the first amount of credit is taken to be zero).

Cj is the credit cost amount (if any) for the credit contract that is payable by the debtor at time j in addition to the repayments Rj.

F is:

(a) if the credit contract is a medium amount credit contract—$400 (or such other amount as is prescribed by the regulations); or

(b) if the credit contract is not a medium amount credit contract and an amount is prescribed by the regulations in relation to the contract—that amount; or

(c) otherwise—$0.

j is the time, measured as a multiple (not necessarily integral) of:

(a) if the credit contract does not provide for a constant interval between contractual repayments—an interval of any kind selected by the credit provider as the unit of time; or

(b) otherwise—the interval between contractual repayments that will have elapsed since the first amount of credit is provided under the credit contract.

Rj is the repayment to be made at time j.

t is the time, measured as a multiple of the interval between contractual repayments (or other interval so selected), that will elapse between:

(a) the time when the first amount of credit is provided under the credit contract; and

(b) the time when the last repayment is to be made under the contract.

85 The equation in essence equating two summations has the following interesting features relevant to its construction.

86 The cost rate equation includes summations denoted by the capital sigma (“Σ”) notation, which indicates that a summation of a sequence of numbers (or terms) is to be performed. The sequence is bounded by the lower and upper bounds shown below and above the sigma, respectively. Each expression in the cost rate equation subject to the summations, being the left and right sides of the equals sign, is a present value calculation of, respectively, the “amount of credit”, and of the amount of all “repayments” and “credit cost amounts”. Of course, a present value calculation is a process of discounting future cash flows by applying a discount rate to determine the value of the future cash flows as at a particular present or earlier date. Commonly, the rate reflects the time-value of money, but it can also reflect the required rate of return on an investment.

87 Now adopting the defined terms in s 32B, the following may be noted.

88 The left hand side of the cost rate equation gives the sum of the present values of all cash amounts of credit ‘Aj’ across the term of the credit contract from interval j=0 (the initial provision of credit) to t (the time for final repayment).

89 The right hand side summation formula gives the sum of the present values of all cash repayments ‘Rj’ and credit costs ‘Cj’ across the term of the credit contract, from interval j=0 (the initial provision of credit) to t (the time for final repayment), net of the medium amount credit contract (MACC) adjustment ‘F’.

90 The rate r is the rate which, added to 1 in the denominator of each summation formula, reduces those formulae so that each is equal to the other.

91 Now in each of the sample contracts, there is one provision of credit at time j=0, by reason of the definition of Aj in s 32B(2), such that the denominator on the left hand side formula resolves down to (1+r)0 or 1 obviously, such that the entire left hand side equation becomes equal to Aj (when j=0) or simply A, the “amount of credit”.

92 So, the cost rate equation sets out a method of calculating the average periodical return that the credit provider will generate over the life of a credit contract, when considering all amounts of credit ‘Aj’ provided to a credit customer, and considering all cash repayments ‘Rj’ and credit costs ‘Cj’ the credit provider can charge the credit customer over the term of the credit contract (net of the medium amount credit contract adjustment ‘F’).

93 In simple terms then, the ACR equation measures the proportion between the “amount of credit”, and the sum of all “repayments” and payment of any “credit cost amounts”, weighted over the life of the contract. So, the purpose of the cost rate equation is to work out the effective periodical rate of return that the credit provider will earn on a credit contract. The greater the sum of repayments and payments over a given amount of credit, the higher the r rate must be to equalise the two.

94 A lower r corresponds to a smaller “gap” between what is lent and what is recovered. The rate r is therefore a measure of the total “cost” of the credit. This “cost” is then annualised by the simple formula in s 32B(1) to give a single percentage figure showing the “cost” as an annualised rate being the annual cost rate or ACR.

95 The right-hand side of the equation refers to both “repayments’’ (Rj) and “credit cost amounts’’ (Cj). As a result, the fees and charges that are within the definition of “credit cost amount” are treated as a cost of credit. For the purposes of calculating the ACR they therefore are an input only in the right-hand side of the equation.

96 As I have indicated, I have set out in an annexure to these reasons a more detailed explanation given by Ms Wright.

97 Now the “credit cost amount” is defined in broad terms in ss 32B(3) to (4A) as follows:

Credit cost amount

(3) The credit cost amount for the credit contract is the sum of the following amounts if they are ascertainable:

(a) the amount of credit fees and charges payable in relation to the contract;

(b) the amount of a fee or charge payable by the debtor (whether or not payable under the contract) to:

(i) any person (whether or not associated with the credit provider) for an introduction to the credit provider; or

(ii) any person (whether or not associated with the credit provider) for any service if the person has been introduced to the debtor by the credit provider; or

(iii) the credit provider for any service relating to the provision of credit, other than a service referred to in subparagraph (ii);

(c) any other amount prescribed by the regulations.

(4) For the purposes of subsection (3), the amounts referred to in that subsection:

(a) include an amount that is payable even if the credit is not provided; but

(b) do not include an amount of a government fee, charge or duty payable in relation to the credit contract.

(4A) Despite subsection (3), the regulations may provide that a specified amount, or an amount included in a specified class, is not an amount referred to in paragraph (3)(a) or (b).

98 The “credit fees and charges” that are a component of the “credit cost amount” are defined in s 204(1) in the following terms:

credit fees and charges means fees and charges payable in connection with a credit contract or mortgage, but does not include:

(a) interest charges (including default charges); or

(b) any fees or charges that are payable to or by a credit provider in connection with a credit contract in connection with which both credit and debit facilities are available if the fees or charges would be payable even if credit facilities were not available (not being annual fees or charges in connection with credit card contracts); or

(c) government charges, or duties, on receipts or withdrawals; or

(d) enforcement expenses.

99 But contrastingly, neither “fees” nor “charges” is separately defined. But s 32B(4) counts such fees and charges even if not actually paid (just payable) and excludes from their definition government fees, charges or duties payable in relation to the credit contract. This suggests that but for this exception, government fees, charges or duties would otherwise have fallen into the meaning of “credit cost amount”, and as a consequence that “fees” and “charges” have their ordinary, broad meaning.

100 Likewise, “services” is defined in s 204(1) to include: (a) rights in relation to, and interests in, real property; (b) insurance; (c) professional services; or (d) a right to services, but does not include “the provision of credit or a right to credit or services provided under a consumer lease”.

101 In one sense therefore, the term “credit cost amount” is apt to capture amounts which are in substance fees or charges attending the provision of credit, to abbreviate the definitions set out above from s 32B(3) and s 204(1). And in directing attention to whether amounts are in substance fees charged to consumers, the “credit cost amount” definition further assists in defining what “amount of credit” is actually provided to consumers.

102 Now in general it would seem readily apparent that the statutory purpose of this Division is to impose a cap on the cost of credit, that is, the costs charged for providing an “amount of credit”, which, together with the prohibitions in ss 23(1) and 24 of the Code concerning a credit provider exceeding that cap, limit the permissible cost to consumers of credit. But one is also to some extent enlightened as to the statutory purpose by considering the specific history of the ACR which I will now briefly address.

History and purpose of the ACR

103 The Code other than Division 4A of Part 2 is in substance an adoption by Commonwealth law of the earlier Uniform Consumer Credit Code (UCCC); see the explanatory memorandum to the National Consumer Credit Protection Bill 2009 (Cth) which described the Code as “largely replicat[ing]” the UCCC at pp 3, 6 and 239. The UCCC did not cap credit costs or interest but allowed each jurisdiction to do so; see for example the Consumer Credit (Victoria) Act 1995 (Vic), where s 39(1) provided that a credit contract with an annual percentage rate over 48% was unenforceable.

104 The legislative history of s 32B is as follows.

105 Clearly, the purpose of the UCCC, the predecessor to the Code, was to increase transparency and inform consumers of the true cost of credit; (Victoria, Parliamentary Debates, Legislative Assembly, 4 May 1995, 1234). Indeed, the idealistic mantra of “truth in lending” has sometimes been used to describe this objective.

106 In Re Make it Mine Finance Pty. Ltd [2015] FCA 393; (2015) 238 FCR 562, I discussed this mantra (at [36] to [41]) in the following terms:

ASIC has contended that the purpose of the relevant provisions is to protect consumers and that they should be interpreted in that light. It says that the Code's predecessor legislation was the Consumer Credit (Queensland) Act 1994 (Qld), which was re-enacted in various jurisdictions. It asserts that the predecessor legislation was based on the principle of “truth in lending”. Accordingly, it says that a similar foundation applies in the present case because of the similarity between the Code and the predecessor legislation.

ASIC's submissions suggested that I should take a modern purposive approach to interpretation. And it emphasised non-textual material.

It need hardly be said that “it is the text, construed according to such principles of interpretation as provide rational assistance in the circumstances of the particular case, that is controlling” (Carr v Western Australia (2007) 232 CLR 138 (Carr) at [6] per Gleeson CJ).

Now there is no bright line between a textual approach and the modern purposive approach to interpretation; to suggest otherwise is to assert a false dichotomy. Rather, to begin with the text is necessary to ascertaining purpose. Indeed, there is no clearer manifestation of legislative purpose. A top down approach of starting with non-textual material has little to commend it. Starting with the text is self-evidently advantageous, so long as the broader context and extrinsic material are always considered, rather than being artificially filtered out if textual ambiguity or uncertainty is not shown; sometimes only the extra textual will reveal the latent textual equivocacy. Moreover, the textual approach is not sensibly described using epithets such as “black letter”, “semantic”, “strict” or “literal”. Rather, what is being identified is the starting point, rather than the finishing point to determine purpose.

The extrinsic material put before me (Ch 8 of the Explanatory Memorandum to the National Consumer Credit Protection Bill 2009 (Cth)) was underwhelming, except on one aspect. Moreover, this is not a case where there is any lack of clarity as to the objectives sought to be achieved or the vice sought to be addressed.

ASIC drew my attention to Australian Finance Direct Ltd v Director of Consumer Affairs (Vic) (2006) 16 VR 131 where predecessor legislation, the Consumer Credit (Victoria) Code, was considered. Reference was made to the manifest purpose of that Code being to ensure “truth in lending” (Neave JA at [166]-[168] and [188]-[189]). See also, on appeal, Australian Finance Direct Ltd v Director of Consumer Affairs (Vic) (2007) 234 CLR 96 at [19] per Gleeson CJ, Gummow, Hayne and Crennan JJ where it was said, in the context of construing that Code, that “[w]ider considerations of ‘truth in lending’ are not to be disregarded, but they tend to divert the argument into unproductive speculation about the importance or possible importance to debtors of knowledge of the holdback”. I have not disregarded “truth in lending”, but it does not assist my task. The various competing views of the meaning of the text debated before me are all consistent with that goal and none is a better fit than any other. Moreover, such phraseology does not answer the question as to the potential relevance and importance of the information said to be omitted to the potential debtor class (and their assumed level of sophistication, education and comprehension) and whether disclosure to such a class meaningfully provides “truth” or non-disclosure its converse. Indeed, putting to one side the context of the falsity of a proposition, which is not a context relevant for present purposes, the significance of the absence of information or the level of generality or specificity of information is not appropriately analysed through an epistemological concept or by interlarding an analysis of the statutory text with a catch-phrase; the vernacular of social philosophy ought not distort the task identified by Gleeson CJ in Carr. Let me then turn to the more meaningful textual analysis.

107 The earliest form of the ACR was added by regulation into the New South Wales enactment of the UCCC, and then followed by Queensland, specifically to capture fees in that State’s cap on the maximum amount that could be charged under smaller credit contracts. That regulation was then expanded by the parliament of New South Wales and subsequently Queensland to increase the scope of its application to all credit contracts.

108 The ACR as adopted into the Code expands again the scope of fees and charges captured in the cost rate equation.

109 The previous legislative regimes assist in the constructional exercise insofar as they evince a legislative intention to prevent credit being provided at excessive cost to consumers. As such, they support a construction of “amount of credit” that in respect of the sale of goods by instalments is not dependent on the terms of the credit contract and that prevents avoidance of the ACR cap in s 32A.

110 The legislative history of the ACR evinces, in state-based predecessors to the Code, a parliamentary concern to address avoidance tactics by lenders in bundling fees and charges into credit, and, increasingly in the years immediately before the enactment of the ACR, to count all fees and charges associated with credit as part of its overall cost, and to thereby limit that cost.

111 Courts may use prior forms of legislation to construe later forms. The same may be said of legislation dealing with the same subject matter across jurisdictional boundaries. Further, construction of Commonwealth legislation with State legislation which is in pari materia is permissible. This is all the more so when the Commonwealth law is in effect a re-enactment or consolidation of the earlier state laws, and for which the constructional approach to consolidation legislation is apposite.

112 The first form of the ACR calculation, which combines both interest and charges together in a single weighted sum, was passed as regs 7 and 8 of the Consumer Credit (New South Wales) Special Provisions Regulation 2002 (NSW) (the 2002 special provision).

113 Regulation 7 set a maximum annual percentage rate (an interest rate) of 48%. Regulation 8 went on to provide how the maximum annual percentage rate was to be calculated in terms very similar to those now found in s 32B of the Code. Regulation 8(1) provided that:

For the purposes of section 11(1A) of the Act [which was a power to set a maximum annual percentage rate by regulation], interest charges and all credit fees and charges under a short term credit contract are to be included for the purpose of calculating the maximum annual percentage rate under a short term credit contract. For that purpose, the maximum annual percentage rate under a short term credit contract is to be calculated in accordance with subclauses (2)–(7).

114 Other than referring to “annual percentage rate”, which is a term now used in a more limited capacity in the Code to refer to the annual interest rate specified in the contract, regs 8(2) and (3) are very similar to ss 32B(1) and (2). Regulations 8(4) to (6) provide tolerances and assumptions substantially similar to ss 32B(5) to (7).

115 Regulation 8(7) provides a definition of “amount of credit” which is arguably as opaque as that in s 3 of the Code, as “the amount (or the maximum amount) required by the debtor”.

116 The most significant differences are as to fees and charges. Regulation 8 only includes fees and charges in the interest calculation for short term credit contracts. The definition of Cj is more simply, and less inclusively, drafted at reg 8(3):

Cj is the fee or charge (if any) payable by the debtor at time j (j is taken to be zero for any such fee or charge payable before the time of the first amount of credit provided) in addition to the repayments Rj, being a credit fee or charge that is ascertainable when the annual percentage rate is calculated.

117 It would seem that there is no record of any explanation, debate, or other reasoned consideration for its insertion into the New South Wales credit legislation. The 2002 special provision was gazetted into law with minimal explanation on 23 August 2002 (New South Wales, Gazette: Legislation, Allocation of Administration Acts, No 133, 23 August 2002) and tabled without comment in the Legislative Council of New South Wales on 27 August 2002 (New South Wales, Minutes of the Proceedings, Legislative Council, 27 August 2002).

118 Now in 2005, the Consumer Credit (New South Wales) Amendment (Maximum Annual Percentage Rate) Bill 2005 (NSW) was introduced. The objects of the Bill were inter-alia to amend the Consumer Credit (New South Wales) Act 1995 (NSW) “to enable the making of regulations that require the calculation for determining the maximum annual percentage rate to include interest charges and all credit fees and charges for all credit contracts covered by the Code”, and to amend the 2002 special provision “to provide that interest charges and all credit fees and charges are to be included for the purposes of calculating the maximum annual percentage rate for all credit contracts covered by the Code”.

119 Schedule 2 of the Bill amended clause 7 of the 2002 special provision to remove the limitation to short term credit contracts and so require that the ACR formula set out in the 2002 special provision, which was unchanged, would apply to all credit contracts.

120 In the second reading speech, the relevant Minister identified fringe lenders providing relatively small high-cost loans who would impose fees and charges far in excess of reasonable costs (New South Wales, Parliamentary Debates, Legislative Assembly, 19 October 2005 at 18907 to 18908). Further, it was said that the Bill was a response to credit providers imposing fees and charges, which were in the nature of interest charges, but which previously had fallen outside the interest rate cap calculation, and thereby had avoided the cap (New South Wales, Parliamentary Debates, Legislative Assembly, 9 November 2005 at 19328).

121 In 2008, Queensland adopted this language into its own form of the UCCC (Consumer Credit (Queensland) Special Provisions Regulation 2008 (Qld)).

122 So, it would seem that the apparent intention of the NSW Parliament in 2005 in expanding the reach of the form of the ACR was to impose a cap that captured the true cost of a credit contract by requiring credit costs to be accounted together with interest repayments.

123 This is reflected in the evolving statutory language. It was initially only the interest rate which was capped; by the 2002 special provision, at least for short term contracts (for which Parliament expressed a particular concern regarding overcharging and predatory practices), all fees and charges were included in the “annual percentage rate”. This was later extended to all credit for the reasons addressed to the NSW House: the avoidance of cost caps by building fees and charges into lending which were “in the nature of interest” (New South Wales, Parliamentary Debates, Legislative Assembly, 9 November 2005 at 19328). That is to say, the evident concern was that credit could be made more expensive to the consumer in a way which avoided existing regulatory limits. The remedy was to seek to capture credit costs more broadly.

124 Each of NSW and Queensland maintained their “annual percentage rate” formulae upon the commencement of the Credit Act and Code; see the Credit (Commonwealth Powers) Act 2010 (NSW) at Schedule 3, cl 7(2), and the Credit (Commonwealth Powers) Act 2010 (Qld) at Part 6 s 34(2). The Consumer Credit (Queensland) Special Provisions Regulation 2008 had implemented a provision substantially the same as that of NSW. The Credit Act and the Code, being an adoption by Commonwealth law of the UCCC, maintained the UCCC’s emphasis on transparency and disclosure, rather than proscription of particular fees or charges, but did not, on commencement, contain Division 4A of Part 2 or otherwise cap credit costs. Victoria maintained its own 48% cap on interest only (Consumer Credit (Victoria) Act 1995 (Vic) s 39(1), as amended by the Credit (Commonwealth Powers) Act 2010 (Vic) s 22(4)).

125 In 2012, s 13 of Schedule 4 to the Consumer Credit Legislation Amendment (Enhancements) Act 2012 (Cth) (Enhancements Act) inserted Division 4A into Part 2 of the Code, which contained the now present forms of ss 32A and 32B.

126 The revised explanatory memorandum to the relevant Bill explained that s 32A “introduce[d] a cap on costs for all other contracts other than small amount credit contracts” (revised explanatory memorandum to the Consumer Credit Legislation Amendment (Enhancements) Bill 2012 (Cth) at [5.46]). It went on to state that the s 32B formula “largely adopts the model currently in force in New South Wales … The use of an existing formula avoids the need for changes by credit providers who currently have developed practices to comply with the New South Wales cap on costs” (at [5.54] to [5.55]).

127 However, the definition of Cj was redrafted and also included s 32B(4A). The revised memorandum explained (at [5.56] and [5.58]):

… The introduction of this regulation-making power will enable the Government to quickly respond to attempts to circumvent the objective of these reforms.

…

This regulation-making power is included in recognition, in the Australian jurisdictions that have a cap on costs, of the development of a diverse range of methods of charging the borrower additional amounts that do not meet the definition of costs to be included in calculating the cap in State or Territory legislation. Credit providers have adopted a range of practices in order to be able to generate a return of more than 48 per cent while still complying with the cap.

128 So, it would seem that the statutory intention to the ACR formula, insofar as it may be drawn from these extrinsic materials, is to capture the substantive cost of credit to a consumer by requiring amounts that are in substance credit costs, that is, the cost of providing credit, to be disclosed and measured, whether or not they are framed as such in the credit contract, and to address avoidance practices by broadly defining the costs of credit.

129 But it must be said that this history does not elucidate the meaning of the phrases “amount of credit” and “credit cost amount” in specific ways. Let me now return to the construction of s 32B.

Construction of s 32B

130 As I have already touched on, the equation in s 32B(2) balances the “amount of credit” (i.e., Aj, which appears on the left-hand side of the equation) against the “credit cost amount” and “repayments” (i.e., Rj, which appears on the right-hand side of the equation). In this equation, “credit cost amount”, being the sum of the credit fees and charges and other fees and charges payable for any service relating to the provision of credit (i.e., Cj, which appears on the right-hand side of the equation), and “repayments” sit together on the right-hand side formula as capturing the amounts required to be paid or repaid by the consumer, in fees and charges or in payments of principal with interest.

131 But the “amount of credit” in the present context is a tricky concept, and it is the construction of this term which is central to the constructional choice between the two possible constructions that ASIC has advanced.

132 Of course the construction of “amount of credit” must begin with the statutory text, read in its context and in light of its statutory purpose. And the Code is remedial legislation with its overarching purpose being “to protect consumers from unscrupulous and unfair lending practices” (Australian Securities and Investments Commission v BHF Solutions Pty Ltd (2022) 293 FCR 330 at [169] per O’Bryan J). It is not in doubt that the Code should be construed broadly so as “to give the fullest relief which the fair meaning of its language will allow” (Isaacs J in Bull v Attorney-General (NSW) (1913) 17 CLR 370 at 384).

133 Now the “amount of credit” is defined in s 3 of the Code in terms that are not particularly helpful. “Credit” is defined in s 3(1) as debt deferred, and in s 3(2) the “amount of credit” is “the amount of the debt actually deferred”. Section 3(2) excludes from the “amount of credit” (a) “any interest charge under the contract”, and “(b) any fee or charge (i) that is to be or may be debited after credit is first provided under the contract; and (ii) that is not payable in connection with the making of the contract”.

134 The meaning of the first exclusion in s 3(2)(a), being interest under the contract, is obvious. It delineates between credit and proportional charges on its repayment.

135 Section 3(2)(b) excludes “any fee or charge” which answers the description of being debited or which may be debited after credit is first provided and is not payable in connection with the making of the contract. “Fees” and “charges” are not defined, but these terms are broad and unconstrained, and should take their ordinary meaning as any amount imposed on, or charged to, the consumer for some purpose. An amount answering the broad description of a “fee or charge” is therefore not “credit”.

136 Now clearly the ambit of excluded fees and charges in s 3(2) is not exactly the same as in s 32B(3), and a given fee or charge could conceivably answer the definition in s 3(2) but not that in s 32B(3), or vice versa. But according to ASIC, this does not speak against its construction of the exclusion of “fees or charges” as “credit cost amounts” from the “amount of credit”. Section 3(2) is a definitional provision of general application, intended to identify the existence of credit to which the Code applies. Section 32B(3) is a measuring provision intended to measure with specificity the cost of that credit. There may conceivably be cases in which the two do not align exactly, but this is simply an artefact of the statutory drafting.

Credit cost construction

137 ASIC’s credit cost construction works in the following way.

138 ASIC says that the “amount of credit” or Aj in the equation in s 32B(2) is to be construed as the amount of debt deferred, less amounts that are in substance payments of “credit cost amounts” or Cj. The “deferred debt” is the sum of the contractual price Walker Stores charged for the good less a deduction for amounts that satisfy the definition of “credit cost amount”. Any amount which is in substance a “credit cost amount” must be so excluded, as a charge required from consumers, rather than credit provided to them, and so exclusive of credit by reason of ss 3(2) and 32B(3).

139 ASIC says that each of the respondent markups was a “credit fee or charge” relating to the contract within the meaning of s 32B(3)(a), or a “fee or charge payable by” the consumer to Walker Stores (i.e., “the credit provider”) for “any service relating to the provision of credit” within the meaning of s 32B(3)(b)(iii) of the Code. ASIC says that together the respondent markups were therefore the “credit cost amount” for the purposes of s 32B(3)(a) and (b)(iii). But ASIC accepts that the GST charged on the Walker Stores price did not, by reason of s 32B(4)(b), form part of the “credit cost amount”.

140 ASIC says that as each of the respondent markups was a charge to consumers for services relating to credit, none of the respondent markups was part of the credit extended to the consumer, and so not part of the “amount of credit” or Aj for the purposes of s 32B(2), and neither was any part of the “repayments” of the “amount of credit” or Rj (being repayment of the principal with interest, but not credit cost amounts).

141 So, ASIC says that the “amount of credit” or Aj was equal to the Walker Stores price plus GST, less the respondent markups. In other words, recognition of the respondent markups as “credit cost amounts” leaves the “amount of credit” as effectively the acquisition cost plus GST. On this analysis, the GST payable on the respondent markups remains treated as credit received by the consumer, by reason of the specific exception in s 32B(4)(b). ASIC says that this results in a small decrease in the ACR favourable to Walker Stores, as against the counterfactual case in which no respondent markups were added, Walker Stores offered goods at its acquisition cost, and recovered its costs and profit by way of interest or expressly nominated fees.

142 Now I accept that the definition of “credit cost amount” in s 32B(3) is broad. The “credit cost amount” includes two relevant definitions: (a) “credit fees and charges”, and (b)(iii) fees or charges payable to “the credit provider for any service relating to the provision of credit”. Both limbs of the definition cover “fees or charges”. “Fees or charges” are terms used throughout the Code to refer to any charge imposed of whatever kind. Fees and charges have their ordinary, broad meaning and should also be read consistently with the purpose and structure of the Code.

143 Of the two relevant limbs, the term “credit fees and charges” is defined to mean “fees and charges payable in connection with a credit contract”, but not “interest charges” and certain other fees including government charges. It must also logically exclude the fees or charges identified in s 32B(3)(b)(i) to (iii).

144 Provided an amount can be properly characterised as a fee or charge in the broad sense, and is not excluded from the definition of “credit fee or charge”, the remaining criterion for identification of a charge as a credit fee or charge is its being payable “in connection with” a credit contract or “in relation to” the contract in the context of s 32B(3)(a).

145 Now both relevant limbs of the “credit cost amount” definition use linking terms being “for” and “relating to” for s 32B(3)(b)(iii), and “in relation to” for s 32B(3)(a). These words are significant, as they constrain the otherwise unbounded “fees or charges” into those which have a specific character or purpose.

146 The word “for”, in relation to the purpose of “charge for credit” (as that term appears in the application provision s 5 of the Code) was considered in ASIC v BHF in the context of the phrase “charge … for providing the credit”. O’Bryan J (with whom Besanko and Lee JJ agreed) preferred ASIC’s broad reading of “for” as better achieving the purpose of the Code. He expressed the following view (at [172]):

A broader construction of the phrase “charge … made for providing the credit” is to be preferred. Giving the statutory language its full ordinary meaning, the Code would apply if a charge is made in exchange for, on account of or by reason of the provision of credit, applied in a commercially practical manner. There is nothing strained in construing the preposition “for” in s 5(1)(c) in that manner. The construction requires a direct relationship between the charge and the provision of credit by looking to the circumstances in which, or conditions on which, the charge is made or imposed and the reason for the charge. It looks to the substance of the credit arrangements rather than their contractual form and ensures that the remedial provisions of the Code are not easily avoided by carefully structured credit arrangements.

147 It is also to be noted that French CJ in The Queen v Khazaal (2012) 246 CLR 601 at [31] stated:

Relational terms such as “connected with” appear in a variety of statutory settings. Other examples are: “in relation to”; “in respect of”; “in connection with”; and “in”. They may refer to a relationship between two subjects which may be the same or different and may encompass activities, events, persons or things. They may denote relationships which are causal or temporal or relationships of similarity or difference. The task of construing such terms does not involve the resolution of ambiguity. They are ambulatory words and may be designed to cover a variety of subjects and a variety of relationships between those subjects. The nature and breadth of the relationships they cover will depend upon their statutory context and purpose. Generally speaking it is not desirable, in construing relational terms, to go further than is necessary to determine their application in a particular case or class of cases. A more comprehensive approach may be confounded by subsequent cases.

148 Ultimately, O’Bryan J regarded the approach to s 5 as (at [179]) “an evaluative task that requires the relevant charge to be characterised by reference to the statutory criterion”. So, the concept of a charge for providing the credit is a broad one, and informed by the statutory purpose, which is remedial in nature and directed to consumer protection. And it must be assessed in the particular case by looking at the substance or essence of the matter. Further, it must also be accepted that a charge for credit may also have other purposes or functions such as to meet administrative expenses.

149 The essential question on identifying a charge for credit is “what it actually is that the consumer pays or promises to pay in order to obtain a provision of credit” (ASIC v BHF at [4] per Lee J); see also BSF Solutions Pty Ltd v Australian Securities and Investments Commission [2025] FCAFC 88 at [35] and [37] per Anderson, Cheeseman and Rofe JJ.