FEDERAL COURT OF AUSTRALIA

Australian Securities and Investments Commission v Westpac Banking Corporation [2026] FCA 651

File number(s): | VID 695 of 2023 |

Judgment of: | MCEVOY J |

Date of judgment: | 26 May 2026 |

Catchwords: | CORPORATIONS – where defendant holds an Australian financial services licence – where defendant has contravened s 72(4) of the National Credit Code and s 47(1)(a) and (4) of the National Consumer Credit Protection Act 2009 (Cth) (Credit Act) – where defendant failed to respond to hardship notices within prescribed timeframes or at all – where defendant failed to have in place adequate systems, processes and controls – where contravening conduct was substantially admitted – where defendant was under a continuing obligation to respond to hardship notices and committed a separate contravention on each day that it failed to respond pursuant to s 175A of the Credit Act – pecuniary penalties sought against defendant – where contraventions were serious and grossly negligent – where contraventions impacted vulnerable customers and some caused irreparable harm – where defendant has remediated customers and demonstrated contrition and cooperation – consideration of appropriate penalty in the circumstances – penalty of $26 million found to be appropriate – consideration of adverse publicity order – adverse publicity order made in form of a press release |

Legislation: | Australian Securities and Investments Commission Act 2001 (Cth) ss 12GBCM Bankruptcy Act 1966 (Cth) Pt IX Corporations Act 2001 (Cth) ss 1317QA, 912A(1)(a) Crimes Act 1914 (Cth) s 4AA Evidence Act 1995 (Cth) ss 191, 191(2) Federal Court of Australia Act 1976 (Cth) s 21 Insurance Contracts Act 1984 (Cth) s 75R National Consumer Credit Protection (Transitional and Consequential Provisions) Act 2009 (Cth) Sch 8, Pt 2, item 3 National Consumer Credit Protection Act 2009 (Cth) ss 6, 47, 47(1)(a), 47(4), 166(2), 167, 167(1), 167(2), 167(3), 167B(2), 175, 175A, 177, 182 National Consumer Credit Protection Act 2009 (Cth) Sch 1, National Credit Code ss 4, 72, 72(1), 72(2), 72(4), 72(5), 73, 88, 89A Superannuation Industry Act 1993 (Cth) s 108A Treasury Laws Amendment (Strengthening Corporate and Financial Sector Penalties) Act 2019 (Cth) Sch 3, Pt 4 National Consumer Credit Protection Regulations 2010 (Cth) National Credit Protection Bill 2009 (Cth) |

Cases cited: | Australian Building and Construction Commission v Construction, Forestry, Mining and Energy Union [2018] HCA 3; 262 CLR 157 Australian Building and Construction Commissioner v Construction, Forestry, Mining and Energy Union [2017] FCAFC 113; 254 FCR 68 Australian Building and Construction Commissioner v Pattinson [2022] HCA 13; 274 CLR 450 Australian Competition and Consumer Commission v Australian Safeway Stores Pty Ltd [1997] FCA 450; 145 ALR 36 Australian Competition and Consumer Commission v Coles Supermarkets Australia Pty Ltd [2015] FCA 330; 327 ALR 540 Australian Competition and Consumer Commission v Dell Australia Pty Ltd (No 2) [2023] FCA 983 Australian Competition and Consumer Commission v Get Qualified Australia Pty Ltd (in liq) (No 3) [2017] FCA 1018 Australian Competition and Consumer Commission v Leahy Petroleum Pty Ltd (No 3) [2005] FCA 265; 215 ALR 301 Australian Competition and Consumer Commission v Murray Goulburn Co-Operative Co Ltd [2018] FCA 1964 Australian Competition and Consumer Commission v Optus Mobile Pty Limited [2019] FCA 106 Australian Competition and Consumer Commission v Reckitt Benckiser (Australia) Pty Ltd [2016] FCAFC 181; 340 ALR 25 Australian Competition and Consumer Commission v TPG Internet Pty Ltd [2013] HCA 54; 250 CLR 640 Australian Competition and Consumer Commission v Yazaki Corporation [2018] FCAFC 73; 262 FCR 243 Australian Ophthalmic Supplies Pty Ltd v McAlary-Smith [2008] FCAFC 8; 165 FCR 560 Australian Securities and Investments Commission v AMP Financial Planning Proprietary Limited [2022] FCA 1115; 164 ACSR 64 Australian Securities and Investments Commission v Australia and New Zealand Banking Group Limited [2023] FCA 256 Australian Securities and Investments Commission v Adler [2002] NSWSC 483; 42 ACSR 80 Australian Securities and Investments Commission v AGM Markets Pty Ltd (in liq) (No 3) [2020] FCA 208; 275 FCR 57 Australian Securities and Investments Commission v AGM Markets Pty Ltd (In Liq) (No 4) [2020] FCA 1499; 148 ACSR 511 Australian Securities and Investments Commission v AMP Financial Planning Pty Ltd (No 2) [2020] FCA 69; 377 ALR 55 Australian Securities and Investments Commission v AMP Superannuation Limited [2023] FCA 488; 168 ACSR 206 Australian Securities and Investments Commission v Australia and New Zealand Banking Group Limited (Retail Cases Omnibus) [2025] FCA 1593 Australian Securities and Investments Commission v Australia and New Zealand Banking Group Ltd (No 3) [2020] FCA 1421 Australian Securities and Investments Commission v Australia and New Zealand Banking Group Limited [2023] FCA 1150; 169 ACSR 649 Australian Securities and Investments Commission v AustralianSuper Pty Ltd [2025] FCA 102; 172 ACSR 615 Australian Securities and Investments Commission v BT Funds Management Ltd [2021] FCA 844 Australian Securities and Investments Commission v Camelot Derivatives Pty Ltd (in liq) [2012] FCA 414; 88 ACSR 206 Australian Securities and Investments Commission v Commonwealth Bank of Australia [2020] FCA 790 Australian Securities and Investments Commission v Commonwealth Bank of Australia [2022] FCA 1422 Australian Securities and Investments Commission v Commonwealth Bank of Australia [2021] FCA 423 Australian Securities and Investments Commission v Commonwealth Bank of Australia [2020] FCA 1543 Australian Securities and Investments Commission v Commonwealth Bank of Australia (No 2) [2021] FCA 966 Australian Securities and Investments Commission v Darranda Pty Ltd (Liability) [2024] FCA 1015 Australian Securities and Investments Commission v Ferratum Australia Pty Limited (in liq) [2023] FCA 1043; 169 ACSR 553 Australian Securities and Investments Commission v Ferratum Australia Pty Ltd (in liq) (No 2) [2024] FCA 701 Australian Securities and Investments Commission v Financial Circle [2018] FCA 1644; 131 ACSR 484 Australian Securities and Investments Commission v iSignthis Limited (Penalty) [2025] FCA 917 Australian Securities and Investments Commission v Lanterne Fund Services Pty Ltd [2024] FCA 353 Australian Securities and Investments Commission v LGSS Pty Ltd (No 3) [2025] FCA 205; 173 ACSR 641 Australian Securities and Investments Commission v Macquarie Bank Limited [2024] FCA 416 Australian Securities and Investments Commission v Mercer Financial Advice (Australia) Pty Ltd [2023] FCA 1453 Australian Securities and Investments Commission v MLC Limited [2023] FCA 539; 168 ACSR 122 Australian Securities and Investments Commission v MLC Nominees Pty Ltd [2020] FCA 1306; 147 ACSR 266 Australian Securities and Investments Commission v National Australia Bank [2025] FCA 947 Australian Securities and Investments Commission v National Australia Bank Ltd [2022] FCA 1324; 164 ACSR 358 Australian Securities and Investments Commission v National Australia Bank Ltd [2021] FCA 1013 Australian Securities and Investments Commission v National Australia Bank Limited [2020] FCA 1494 Australian Securities and Investments Commission v Noumi Ltd (No 3) [2024] FCA 862 Australian Securities and Investments Commission v OnePath Custodians Pty Ltd [2023] FCA 1485 Australian Securities and Investments Commission v RACQ Insurance Limited [2023] FCA 1503 Australian Securities and Investments Commission v RI Advice Group Pty Ltd [2022] FCA 496; 160 ACSR 204 Australian Securities and Investments Commission v Statewide Superannuation Pty Ltd [2021] FCA 1650 Australian Securities and Investments Commission v Westpac Banking Corporation (No 2) [2018] FCA 751; 266 FCR 147 Australian Securities and Investments Commission v Westpac Banking Corporation (Omnibus) [2022] FCA 515; 407 ALR 1 Australian Securities and Investments Commission v Westpac Banking Corporation [2019] FCA 2147 Australian Securities and Investments Commission v Westpac Banking Corporation (No 3) [2018] FCA 1701; 131 ACSR 585 Australian Securities and Investments Commission v Westpac Banking Corporation (Penalty Hearing) [2024] FCA 52 Australian Securities and Investments Commission v Westpac Banking Corporation (The Consumer Credit Insurance Case) [2022] FCA 359; 158 ACSR 647 Australian Securities and Investments Commission v Westpac Securities Administration Ltd [2019] FCAFC 187; 272 FCR 170 Australian Securities and Investments Commission v Westpac Securities Administration Limited [2021] FCA 1008; 156 ACSR 614 Chief Executive Officer of the Australian Transaction Reports and Analysis Centre v Westpac Banking Corporation [2020] FCA 1538; 148 ACSR 247 Commonwealth of Australia v Director, Fair Work Building Industry Inspectorate [2015] HCA 46; 258 CLR 482 Construction, Forestry, Maritime, Mining and Energy Union v Fair Work Ombudsman [2023] FCA 72; 322 IR 233 Construction, Forestry, Mining and Energy Union v Cahill [2010] FCAFC 39; 269 ALR 1 Fair Work Ombudsman v Blakely [2023] FCA 1121 Flight Centre Limited v Australian Competition and Consumer Commission (No 2) [2018] FCAFC 53; 260 FCR 68 Forster v Jododex Australia Pty Ltd [1972] HCA 61; 127 CLR 421 Markarian v The Queen [2005] HCA 25; 228 CLR 357 Minister for the Environment, Heritage and the Arts v PGP Developments Pty Limited [2010] FCA 58; 183 FCR 10 Mornington Inn Pty Ltd v Jordan [2008] FCAFC 70; 168 FCR 383 NW Frozen Foods Pty Ltd v Australian Competition and Consumer Commission [1996] FCA 1134; 71 FCR 285 R v De Simoni [1981] HCA 31; 147 CLR 383 Singtel Optus Pty Ltd v Australian Competition and Consumer Commission [2012] FCAFC 20; 287 ALR 249 Story v National Companies and Securities Commission (1988) 13 NSWLR 661 Trade Practices Commission v CSR Ltd [1990] FCA 762; [1991] ATPR 41-076 Australian Securities and Investments Commission v Membo Finance Pty Ltd (No 2) [2023] FCA 126 Volkswagen Aktiengesellschaft v Australian Competition and Consumer Commission [2021] FCAFC 49; 284 FCR 24 |

Division: | General Division |

Registry: | Victoria |

National Practice Area: | Commercial and Corporations |

Sub-area: | Commercial Contracts, Banking, Finance and Insurance |

Number of paragraphs: | 203 |

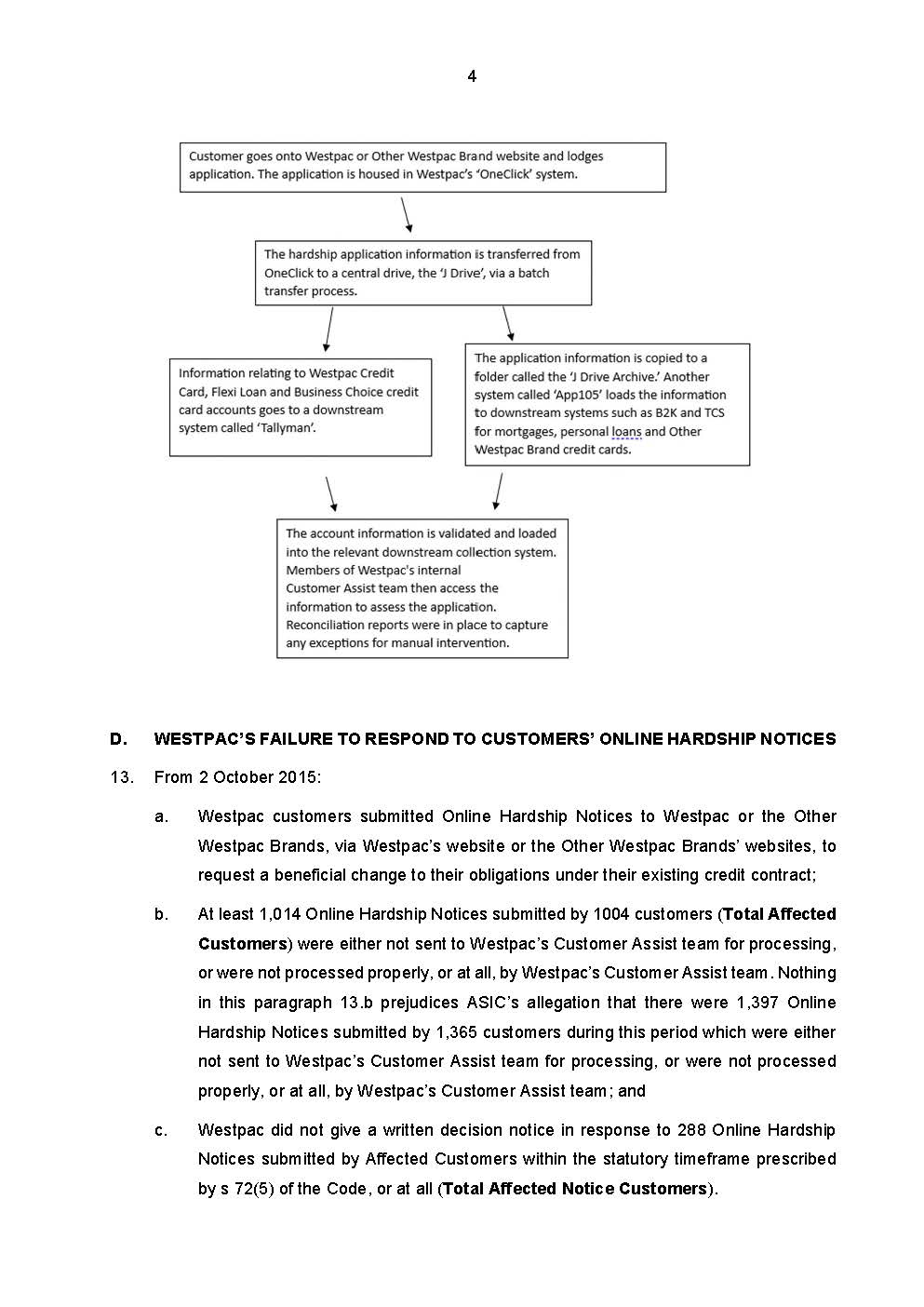

Date of last submission/s: | 29 August 2025 |

Date of hearing: | 26 May 2025 |

Counsel for the Applicant: | C H Truong KC and A Storey |

Solicitor for the Applicant: | Australian Securities and Investments Commission |

Counsel for the Respondent: | K C Morgan SC and A Ilic |

Solicitor for the Respondent: | Clayton Utz |

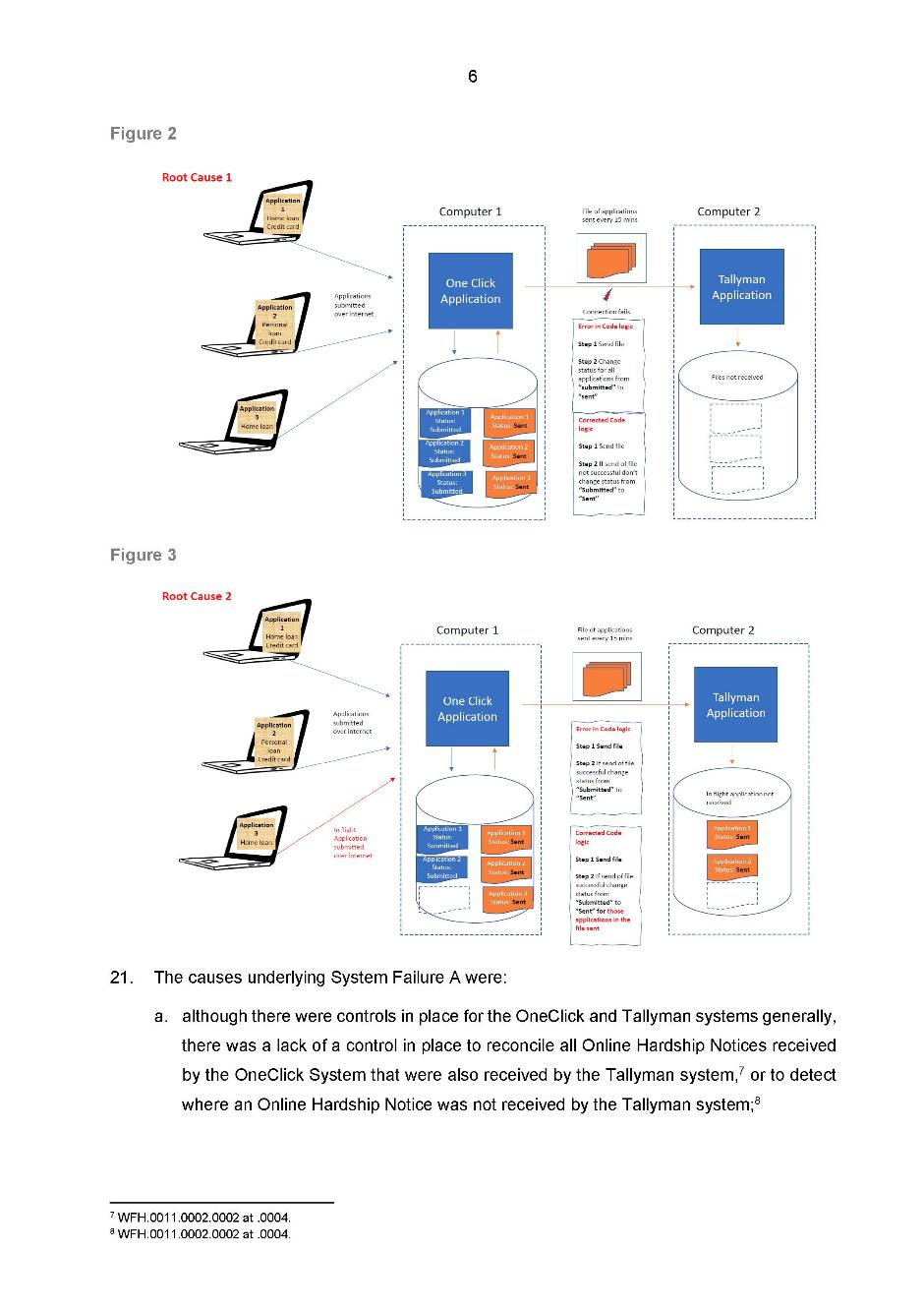

ORDERS

VID 695 of 2023 | ||

| ||

BETWEEN: | AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Applicant | |

AND: | WESTPAC BANKING CORPORATION ACN 007 457 141 Respondent | |

order made by: | MCEVOY J |

DATE OF ORDER: | 26 May 2026 |

DEFINITIONS

In these declarations and orders, terms have the following meanings:

(a) Agreed Contravention Period means 4 September 2017 to 8 May 2023.

(b) Code means the National Credit Code, being Schedule 1 to the Credit Act, as in force during the Relevant Period and the Agreed Contravention Period.

(c) Credit Act means the National Consumer Credit Protection Act 2009 (Cth) as in force during the Agreed Contravention Period and the Relevant Period.

(d) Credit Licence means Australian Credit Licence.

(e) Online Hardship Notice means a hardship notice submitted to Westpac by a customer (who had entered into a credit contract, within the meaning of s 4 of the Code, with Westpac or the Other Westpac Brands) by completing an online form via the public websites of Westpac and the Other Westpac Brands.

(f) Other Westpac Brands mean St George, BankSA and Bank of Melbourne, which operated under Westpac’s Credit Licence and were trading brands of Westpac during the Relevant Period and the Agreed Contravention Period.

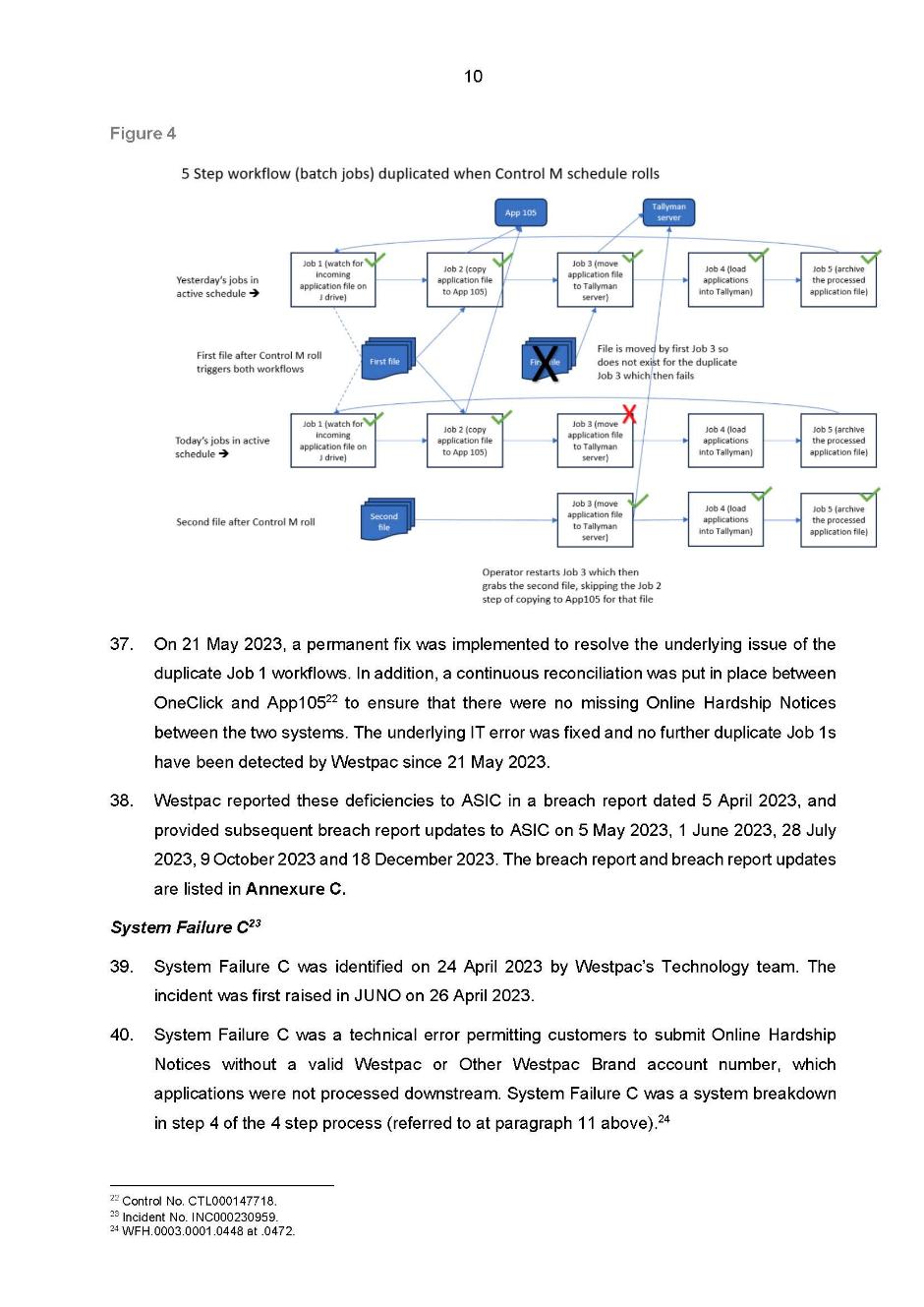

(g) Relevant Period means 2 October 2015 to 7 June 2023.

(h) Westpac means the respondent, Westpac Banking Corporation (ACN 007 457 141).

(i) Westpac Customer Assist Team means the team at Westpac which actioned the Online Hardship Notices.

(j) Written Decision Notice means a written notice in response to a customer’s Online Hardship Notice as required by s 72(4) of the Code.

THE COURT DECLARES THAT:

1. From 2 October 2015, Westpac failed to give a Written Decision Notice in response to customers’ Online Hardship Notices, within the timeframe required by s 72(4) and (5) of the Code, or at all, and thereby contravened s 72(4) of the Code:

(a) on each occasion 223 Online Hardship Notices were submitted by a customer during the Agreed Contravention Period; and

(b) on each occasion 277 Online Hardship Notices were submitted by a customer during the Relevant Period (which includes the 223 Online Hardship Notices referred to in subparagraph (a)).

2. During the Relevant Period, for each customer who submitted an Online Hardship Notice prior to 4 September 2017 and who did not receive a Written Decision on or after 13 March 2019, pursuant to s 175A(1) of the Credit Act Westpac:

(a) was under a continuing obligation to respond to each Online Hardship Notice by giving a Written Decision Notice;

(b) committed a separate contravention of s 72(4) of the Code each day it failed to give a Written Decision Notice in response to each Online Hardship Notice, within the timeframe required by s 72(4) and (5) of the Code; and

(c) is deemed to have contravened section 72(4) of the Code on and after 13 March 2019 in relation to each relevant customer.

3. In the period from 13 March 2019 to 7 June 2023, Westpac failed to do all things necessary to ensure that the credit activities authorised by the credit licence are engaged in efficiently, honestly and fairly, and thereby contravened s 47(1)(a) and (4) of the Credit Act, in that during that period Westpac:

(a) did not maintain adequate systems, controls and processes which ensured that:

(i) Online Hardship Notices submitted by customers were received by the Westpac Customer Assist team; and

(ii) Written Decision Notices were given to customers within the timeframes prescribed by s 72(4) and (5) of the Code; and

(b) did not conduct adequate risk reviews, investigations, monitoring and analysis of its Online Hardship Notice systems and processes to enable it to identify any issues with its systems or processes, or to otherwise ensure that its Online Hardship Notice systems and processes enabled compliance with s 72(4) and (5) of the Code.

THE COURT ORDERS THAT:

1. Westpac pay to the Commonwealth of Australia a pecuniary penalty of $26 million, within 30 days of the date of these orders, in respect of Westpac’s contraventions of s 72(4) of the Code and s 47(1)(a) and (4) of the Credit Act as identified in declarations 1 to 3 above.

2. Pursuant to s 182 of the Credit Act, within 14 days of the date of these orders, Westpac publish, at its own expense, a written adverse publicity notice (Written Publicity Notice) in terms set out in Annexure A to these orders, for a period of no less than 90 days, maintaining a copy of the Written Publicity Notice, in 10 point font or larger, in an immediately visible area of the following web addresses:

(a) https://www.westpac.com.au/;

(b) https://www.stgeorge.com.au/;

(c) https://www.bankofmelbourne.com.au/; and

(d) https://www.banksa.com.au/.

3. Pursuant to s 177 of the Credit Act, Westpac, at its own cost:

(a) within one month, implement system, operational and process changes that are adequate to ensure Online Hardship Notices are responded to within the time limits specified by s 72(4) and (5) of the Code; and

(b) within one month of implementing the changes referred to in subparagraph (a):

(i) appoint a suitably qualified independent expert agreed between Westpac and the Australian Securities and Investments Commission (ASIC) (or, failing agreement, determined by the Court); and

(ii) instruct the expert to prepare and provide to ASIC a written report on the outcome of the implementation of the changes referred to in subparagraph (a), including as to whether and to what extent the changes have been fully and effectively implemented in accordance with these orders, and provide recommendations to Westpac to remedy any aspects of Westpac’s systems, operations and processes to ensure compliance with s 72(4) and (5) of the Code;

(c) within six months after appointing the expert referred to in subparagraph (b):

(i) provide to ASIC a copy of the report referred to in subparagraph (b) above; and

(ii) state what steps Westpac has taken to give effect to the expert’s recommendations.

4. Westpac pay ASIC’s costs of the proceeding, to be agreed or assessed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ANNEXURE A

Adverse Publicity Order

The Federal Court of Australia has ordered Westpac Banking Corporation to publish this written adverse publicity notice.

On 26 May 2026 Justice McEvoy of the Federal Court of Australia ordered Westpac Banking Corporation (Westpac) to pay a total pecuniary penalty of $26 million in connection with Westpac’s failure to receive, and respond to, customers’ online hardship notices within the timeframes required by law throughout the period of 2 October 2015 to 7 June 2023 (Relevant Period). Affected customers include Westpac customers and St George, BankSA and Bank of Melbourne customers, who operated under Westpac’s Australian credit licence.

Justice McEvoy imposed the $26 million pecuniary penalty after declaring that, by that conduct:

(a) Westpac had failed to do all things necessary to ensure that the credit activities authorised by the credit licence were engaged in efficiently, honestly and fairly; and

(b) Westpac had failed to comply with consumer credit law.

Westpac failed to give a written response to 277 customers’ online hardship notices during the Relevant Period.

Westpac made admissions of contravention in the proceeding. Westpac also cooperated with ASIC in the investigation and during the proceeding.

Prior and during the proceeding, Westpac conducted a remediation program in which it paid a total of $1,735,126.81 in remediation to impacted customers and apologised for its conduct. This remediation program was broader than the 277 customers that were subject to the proceeding.

Westpac has committed to funding and implementing new technology systems and processes for receiving and responding to online hardship notices.

Further information

The above conduct contravened the following consumer credit laws:

Section 72(4) and (5) of the National Credit Code, being Schedule 1 to the National Consumer Credit Protection Act 2009 (Cth); and

Section 47(1)(a) and (4) of the National Consumer Credit Protection Act 2009 (Cth).

For further information about the conduct, see the following:

The court’s judgment on penalty [hyperlink];

Australian Securities and Investments Commission media release [hyperlink]; and

Statement of facts agreed between the parties to the proceeding which is Annexure A to the court’s judgment [hyperlink].

REASONS FOR JUDGMENT

MCEVOY J:

1 The applicant in this proceeding, the Australian Securities and Investments Commission (ASIC), alleges that Westpac Banking Corporation (Westpac) has contravened s 72(4) of the National Credit Code (Code) and s 47(1)(a) and (4) of the National Consumer Credit Protection Act 2009 (Cth) (Credit Act) by failing to respond to online financial hardship requests made by vulnerable customers who were unable to meet their repayment obligations under a credit contract. The reasons for these requests varied, but they included serious health issues, unemployment during the COVID-19 pandemic, and family violence.

2 ASIC alleges that at least between 4 September 2017 and 8 May 2023 (Agreed Contravention Period) Westpac did not, either within the period prescribed by s 72(5) of the Code or at all, respond to certain online hardship notices submitted by its retail customers. ASIC also alleges that in the period between 13 March 2019 and 7 June 2023 Westpac failed to do all things necessary to ensure that the credit activities authorised by its credit licence were engaged in efficiently, honestly and fairly. Westpac substantially admits the conduct alleged by ASIC, and admits that it has contravened s 72(4) of the Code during the Agreed Contravention Period and that it has contravened s 47(1)(a) and (4) of the Credit Act during the period 13 March 2019 to 7 June 2023. Westpac also accepts that its conduct was serious.

3 There is, however, a dispute between the parties as to two matters. The first is the form of the declarations which are to be made by the court in respect of Westpac’s contraventions. The issue relates principally to the number of online hardship notices that are properly to be the subject of the declaration of contravention of s 72(4) of the Code. This dispute falls to be resolved through a determination of the proper construction and effect of s 175A of the Credit Act. ASIC’s construction of s 175A of the Credit Act, and the additional notices in respect of which it seeks declarations of contravention, encompass a broader period of time than the Agreed Contravention Period. This period is from 2 October 2015 to 7 June 2023 (Relevant Period).

4 In addition to declarations of contravention, compliance orders and an adverse publicity order, ASIC seeks that Westpac be required to pay a pecuniary penalty for its contraventions in the amount of $30 million. This is comprised of $20 million for the contraventions of s 72(4) of the Code and $10 million for the contraventions of s 47 of the Credit Act. Westpac’s position as to penalty is that a total penalty in this amount would be excessive and inappropriate, and that a penalty in the order of $10 million would be more appropriate. This is the second dispute between the parties.

5 The parties have jointly prepared and filed a statement of agreed facts (SOAF) pursuant to s 191 of the Evidence Act 1995 (Cth) (Evidence Act). While the court is not required to accept the SOAF uncritically, in this case I accept it as credible and cogent, and proof of the facts it contains. The effect of the SOAF is that evidence to prove the facts that it contains is not necessary, and the court has before it a sufficient factual foundation to support the exercise of its power to make declarations and impose a penalty: Evidence Act s 191(2); Minister for the Environment, Heritage and the Arts v PGP Developments Pty Limited [2010] FCA 58; 183 FCR 10 at [35] (Stone J); Australian Securities and Investments Commission v Commonwealth Bank of Australia [2020] FCA 790 at [12] (Beach J) (ASIC v Commonwealth Bank of Australia).

6 In addition to the SOAF, in support of its position regarding liability and penalty ASIC relies upon:

(a) the affidavit of Mr Andrew Fleming affirmed on 29 April 2024 (Fleming Affidavit);

(b) the affidavit of Mr Michael Dorman affirmed on 17 July 2024;

(c) written submissions on liability and penalty dated 19 March 2025;

(d) written submissions in reply dated 6 May 2025; and

(e) supplementary written submissions dated 29 August 2025.

7 In support of its position regarding liability and penalty Westpac relies upon:

(a) the affidavit of Mr Alexander McNab Stewart affirmed on 24 June 2024 (Stewart Affidavit);

(b) the affidavit of Ms Ananya Roy affirmed on 27 June 2024; (Roy Affidavit)

(c) written submissions on liability and penalty dated 23 April 2025; and

(d) supplementary written submissions dated 29 August 2025.

8 For the reasons that follow there will be declarations and orders substantially in the form sought by ASIC. Insofar as pecuniary penalty is concerned, I have determined that Westpac should be ordered to pay a total penalty of $26 million.

THE LEGISLATIVE SCHEME

9 Before turning to the underlying facts and contraventions themselves, it is useful to commence with an overview of the relevant legislative scheme under the Code and the Credit Act. The specific provisions relevant to Westpac’s conduct will be the subject of later consideration.

10 The Code is contained in Schedule 1 to the Credit Act. It provides a consumer protection framework for consumer credit and related transactions. The Code relevantly provides debtors with a right to seek that credit contracts be amended or varied on the basis of financial hardship: see Explanatory Memorandum, National Credit Protection Bill 2009 (Cth) at [8.2], [8.159]–[8.162].

11 Section 72 of the Code provides a procedural mechanism by which debtors may notify credit providers of financial hardship and seek to make changes to their credit contracts where such contracts are regulated by the Code. As Yates J accepted in Australian Securities and Investments Commission v Membo Finance Pty Ltd (No 2) [2023] FCA 126 at [29] (Membo Finance (No 2)), this section provides an important formal mechanism to protect consumers who may be vulnerable when experiencing financial hardship.

12 Pursuant to s 72(1) of the Code, a debtor who considers that they are unable to meet their obligations under a credit contract, may give notice to the credit provider of that inability. Such notice is generally referred to as a hardship notice.

13 After receiving a hardship notice, a credit provider must give written notice to the debtor that advises them of the outcome of their hardship notice in accordance with the content and timing requirements in s 72(4) and (5) of the Code (decision notice). A credit provider may request further information from the debtor with respect to their hardship notice under s 72(2) of the Code. Relevantly, s 89A of the Code provides that in certain circumstances where a hardship notice has been given by a debtor, a credit provider must not begin enforcement proceedings against that debtor unless the credit provider has given the debtor a written decision notice stating that the credit contract will not be changed, and 14 days has expired since such notice was given.

THE RELEVANT FACTS

14 As has been mentioned, the facts agreed by the parties for the purposes of this proceeding are set out in the SOAF, which is annexed to these reasons. I will not therefore describe the facts in any more detail than is necessary to resolve the outstanding liability issue and the question of appropriate penalty.

15 At all material times Westpac held an Australian credit licence which authorised it to engage in credit activities within the meaning of s 6 of the Credit Act and provide credit pursuant to credit contracts to which the Code applies. St George, BankSA and Bank of Melbourne (Other Westpac Brands) also operated under Westpac’s Australian credit licence and were, and continue to be, trading brands of Westpac. It is sometimes necessary to refer specifically to the Other Westpac Brands in these reasons, but a reference to Westpac should be taken to be a reference to the respondent entity that held the credit license under which its subsidiaries operated.

16 From 16 July 2015 to 28 February 2023 “financial hardship” was described in Westpac’s financial hardship policies (as well as those of the Other Westpac Brands) as occurring when a customer is “willing but unable to meet their existing financial obligations for a period of time”. Examples of situations which might cause financial hardship were listed in these policies, and included unemployment, reduced income, injury or illness (including carer responsibilities), death of a family member, natural disaster, over commitment or indebtedness and vulnerability. The types of financial assistance offered to customers were described at various times in these policies as including: loan extensions; short term reduced payments; short term moratorium; interest rate reduction; debt settlement; debt waiver; and any contractual rearrangement that Westpac considered appropriate.

17 The policies recognised also that customers may experience “extreme hardship” as a result of circumstances including “severe or terminal illness, disablement, long term unemployment [and] long-term loss of contract or supplier”. They provided that customers experiencing incurable or permanent financial hardship “may be candidates for long-term or permanent collection arrangements”. Such arrangements included long term payment plans, partial write-offs and the allowance of time for customers to sell their property (after 1 July 2019).

18 During the Relevant Period, the policies stated that Westpac would respond to a hardship notice submitted by a customer in respect of which no further information was required within 21 days of the date that the notice was received. The policies set out the procedure by which further information could be requested if necessary. Pursuant to the policies, once a hardship notice had been assessed, as was required under the Code, Westpac was to provide the customer with a written decision notice and provide reasons.

19 The policies provided that in circumstances where Westpac had or had cause to issue a default notice to a customer under s 88 of the Code, Westpac would not take enforcement action unless it had given a written decision notice to a customer and a period of 14 days had elapsed. This aspect of the policies essentially mirrored s 89A of the Code.

20 Westpac’s financial hardship policies incorporated, in their appendices, commitments under the Australian Banking Association’s Banking Code of Practice (Banking Code of Practice) as they applied from time to time. Westpac (and the Other Westpac Brands) have been signatories to the Banking Code of Practice since 1 February 2014. The Banking Code of Practice is a voluntary set of commitments which includes commitments to customers experiencing financial difficulty. ASIC submits, and I accept, that each relevant credit contract in this proceeding incorporated the terms of the Banking Code of Practice. Westpac did not contend that the position was otherwise.

21 From 2 October 2015, customers who entered into a credit contract within the meaning of s 4 of the Code with Westpac or the Other Westpac Brands could give a hardship notice by completing an online form via the public websites of Westpac and the Other Westpac Brands. It will be apparent that these online hardship notices were, relevantly, the means by which Westpac’s customers notified Westpac that they were unable to meet their obligations under a credit contract. Westpac’s systems were intended to work such that after submission, the online hardship notice would be processed by a certain automated system known as the “OneClick” system, then transferred to other automated systems and then to Westpac’s “Customer Assist” team, which was the team responsible for determining the customer’s request. The system(s) to which an online hardship notice was transferred depended on the credit product(s) to which the hardship notice related. The details of the relevant Westpac systems and processes are set out in Part C of the SOAF.

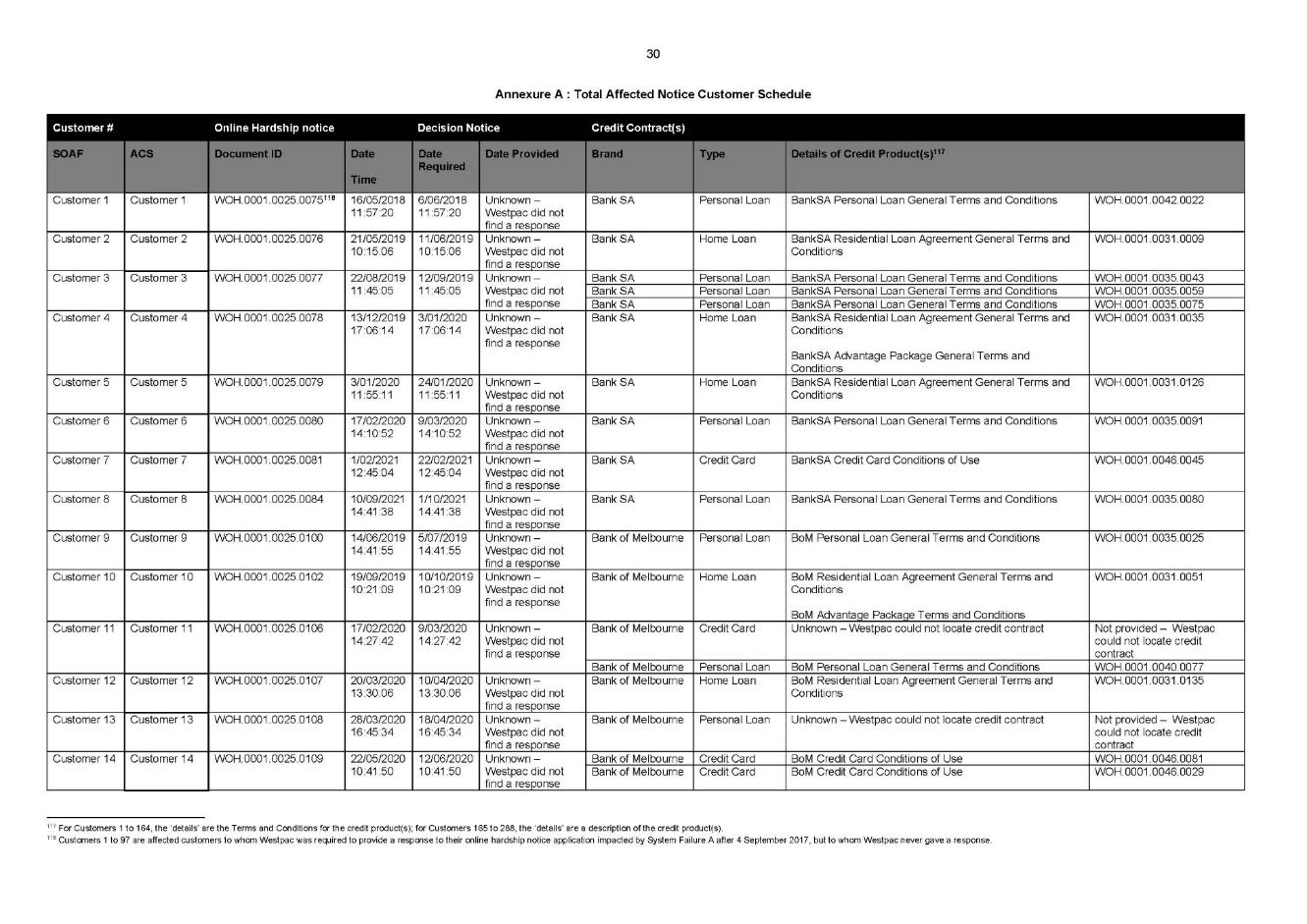

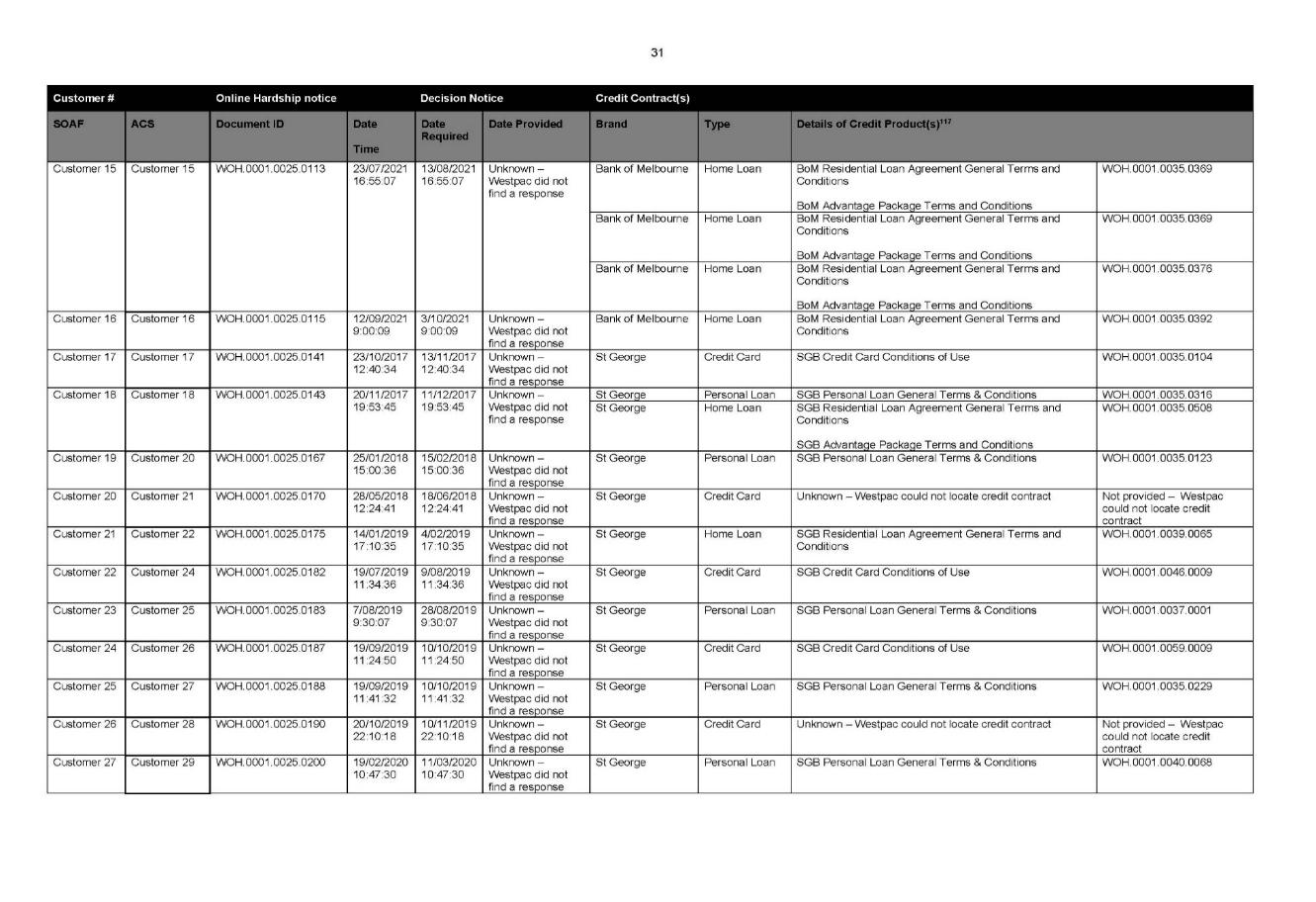

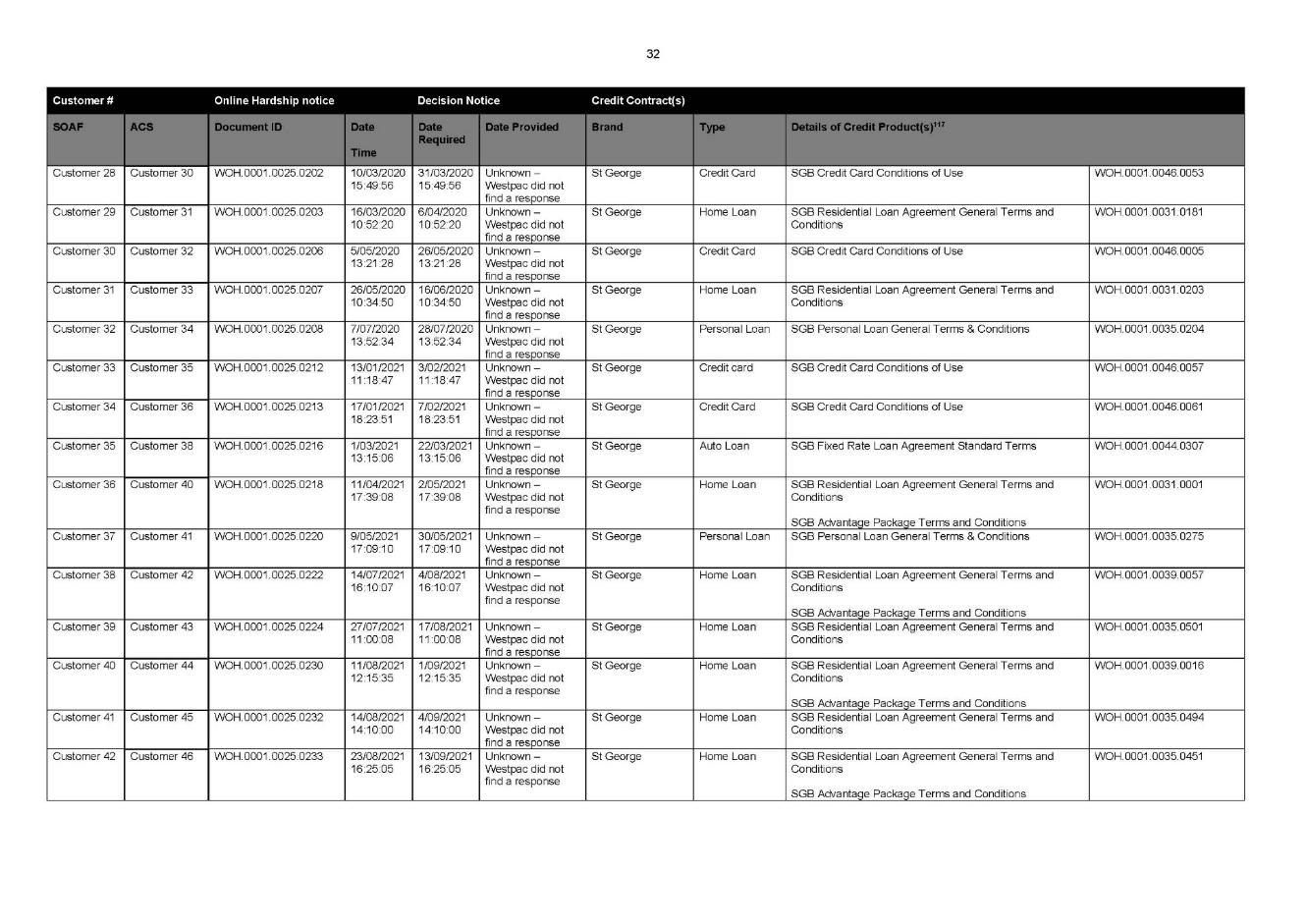

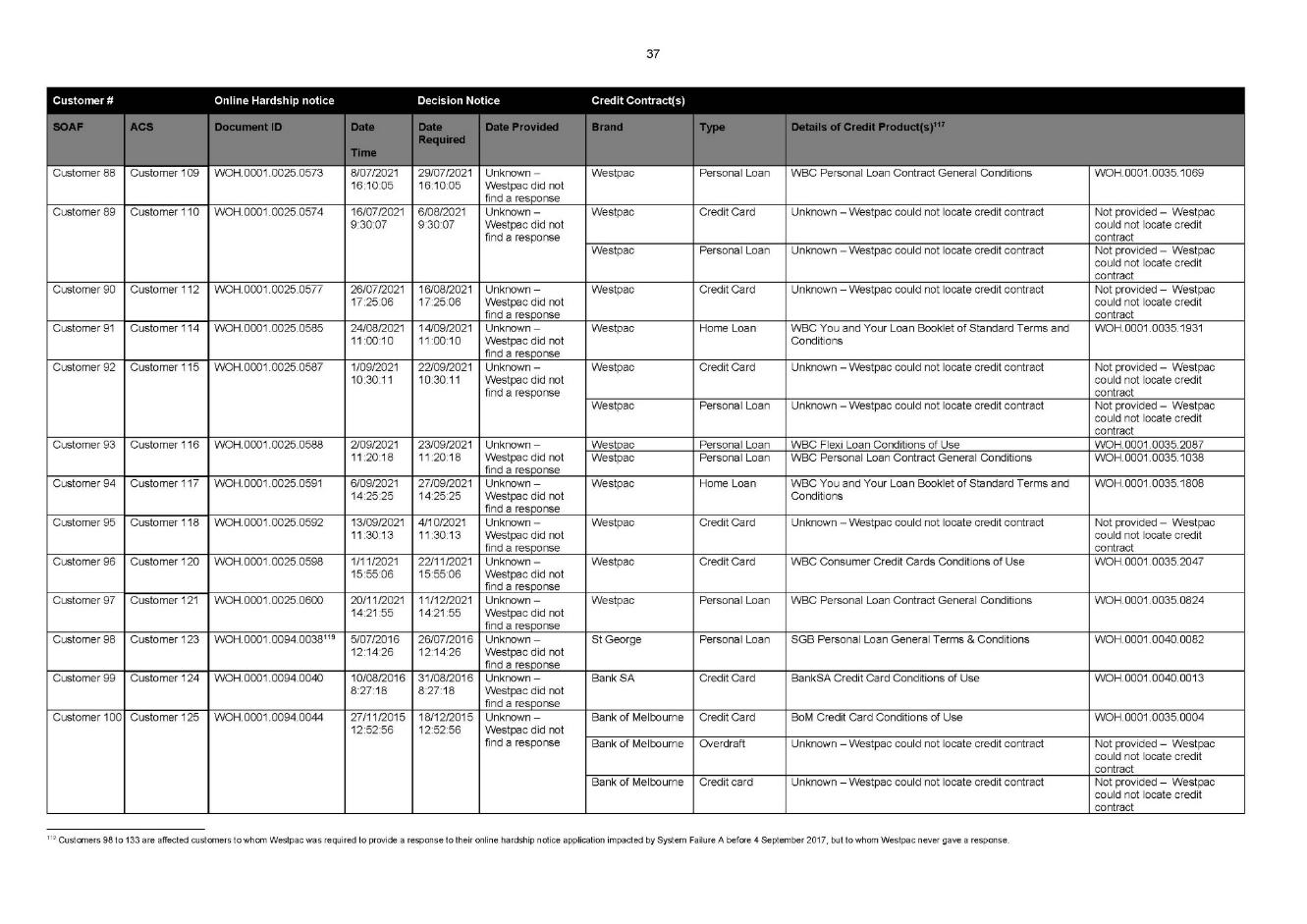

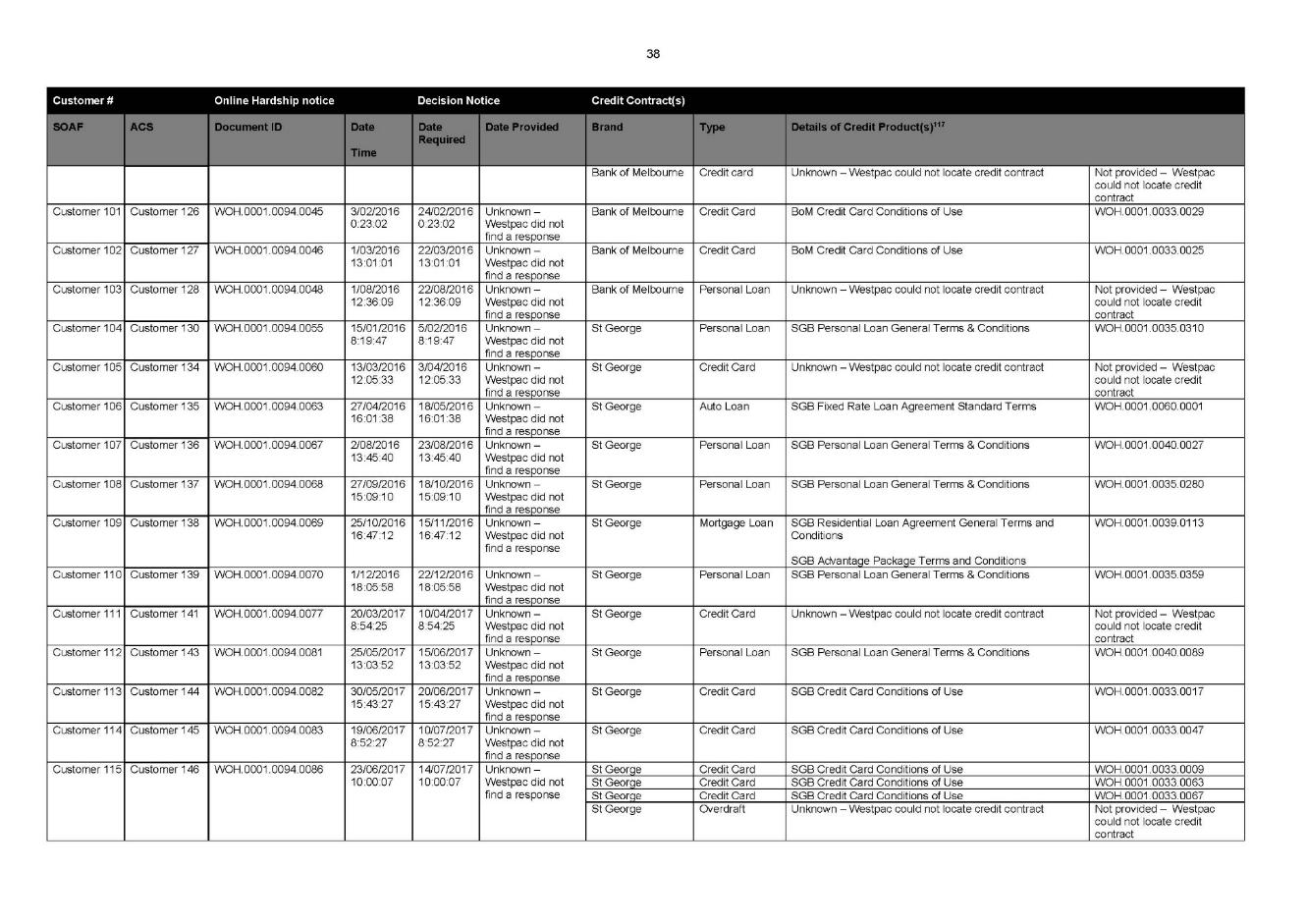

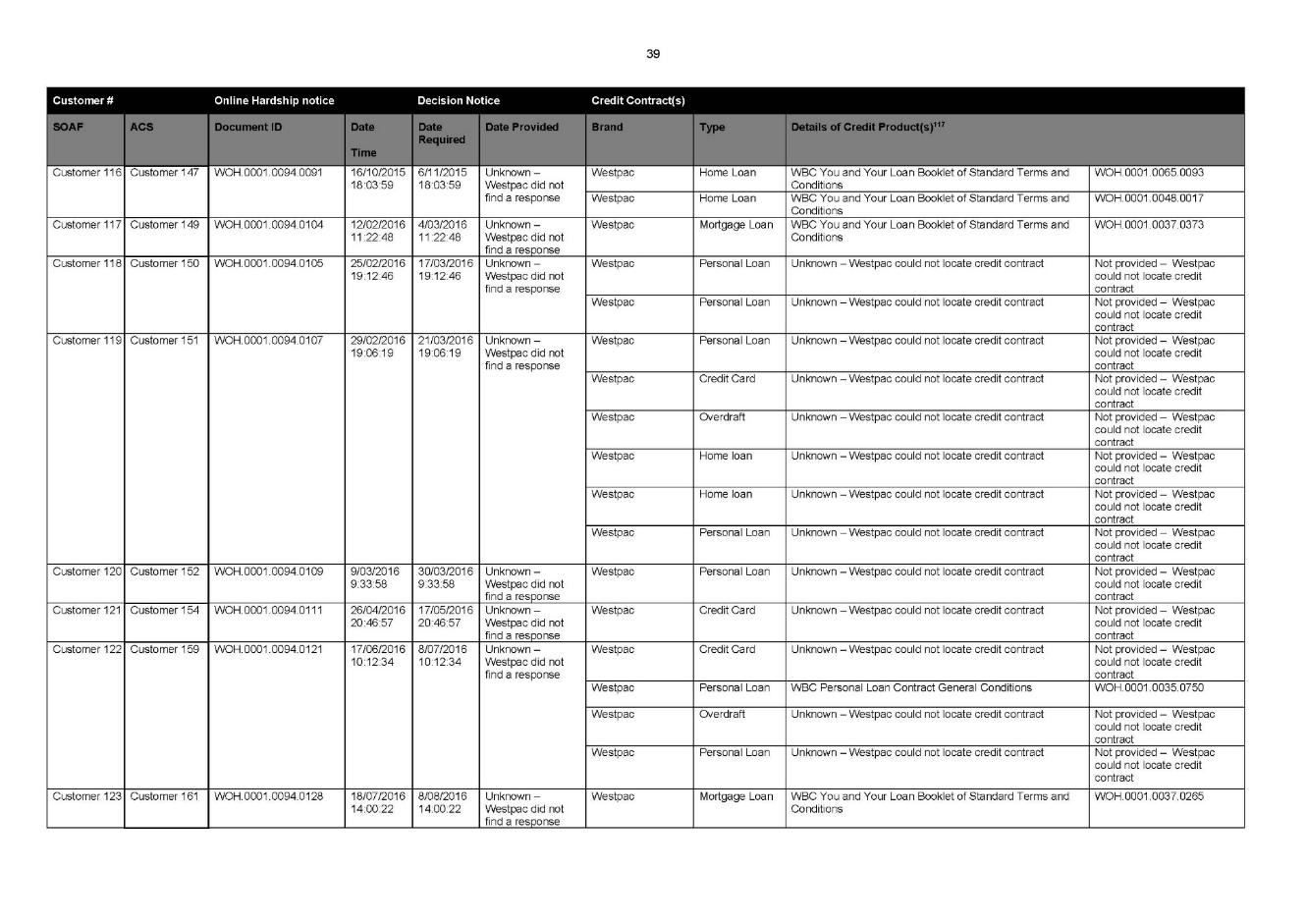

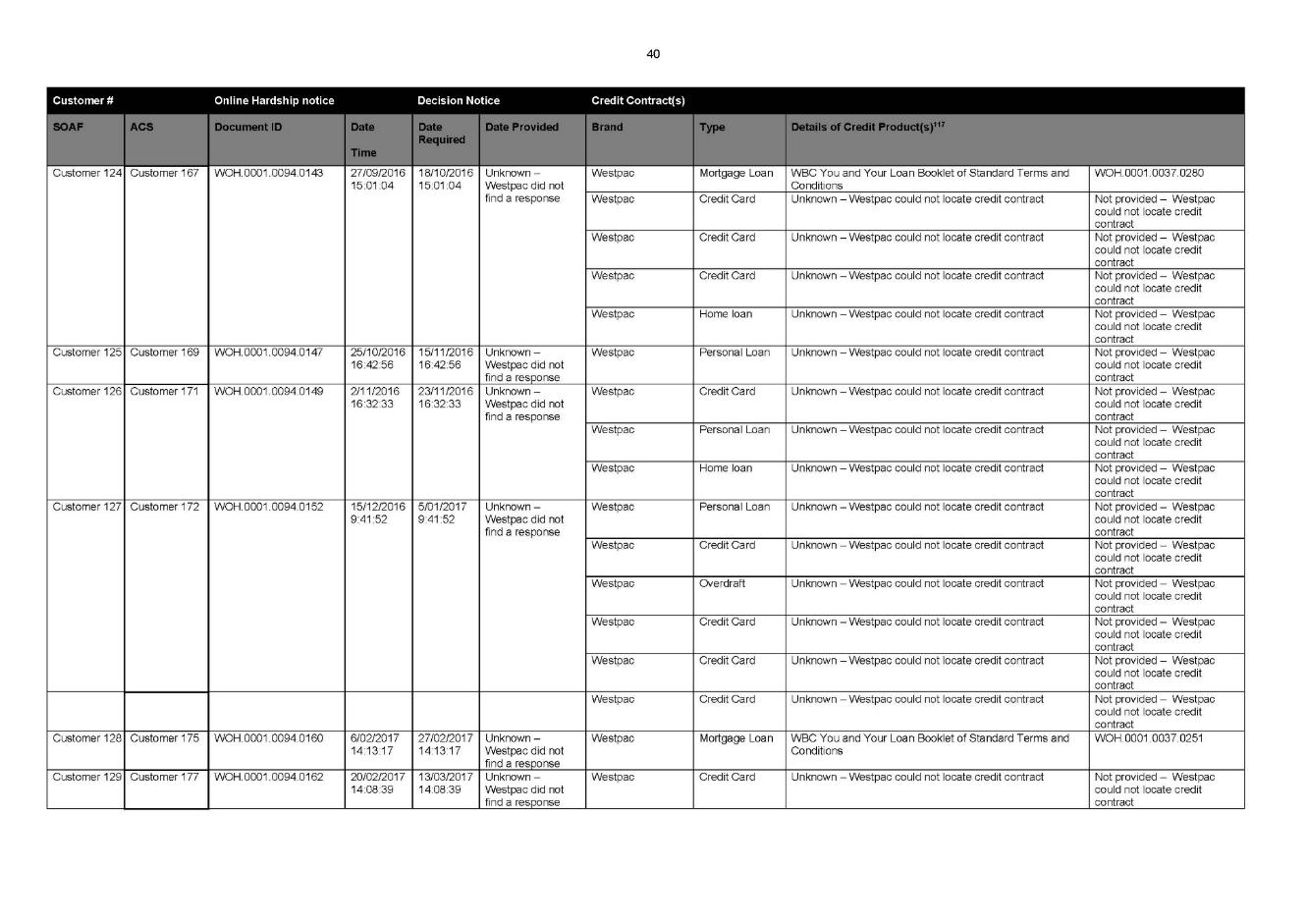

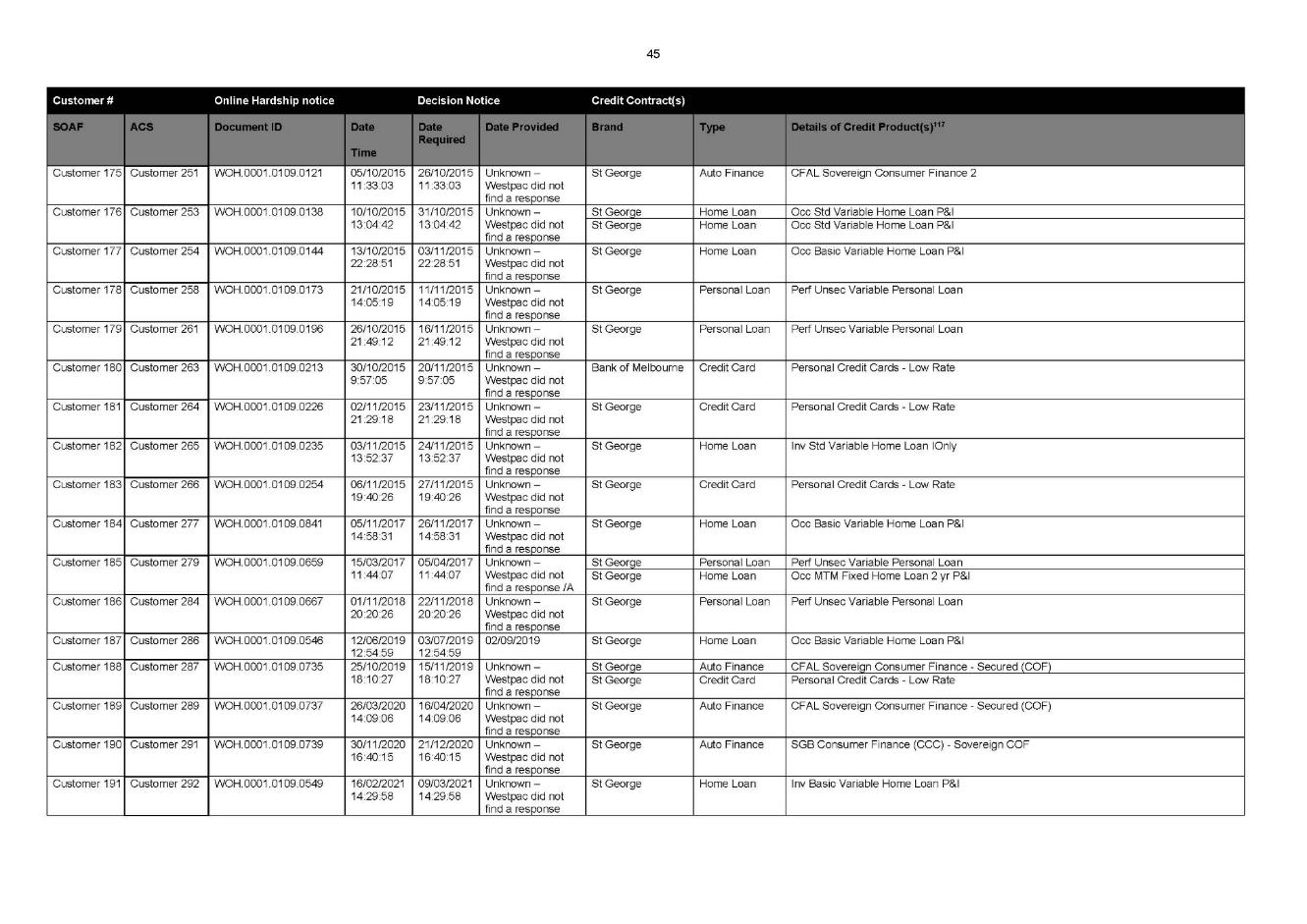

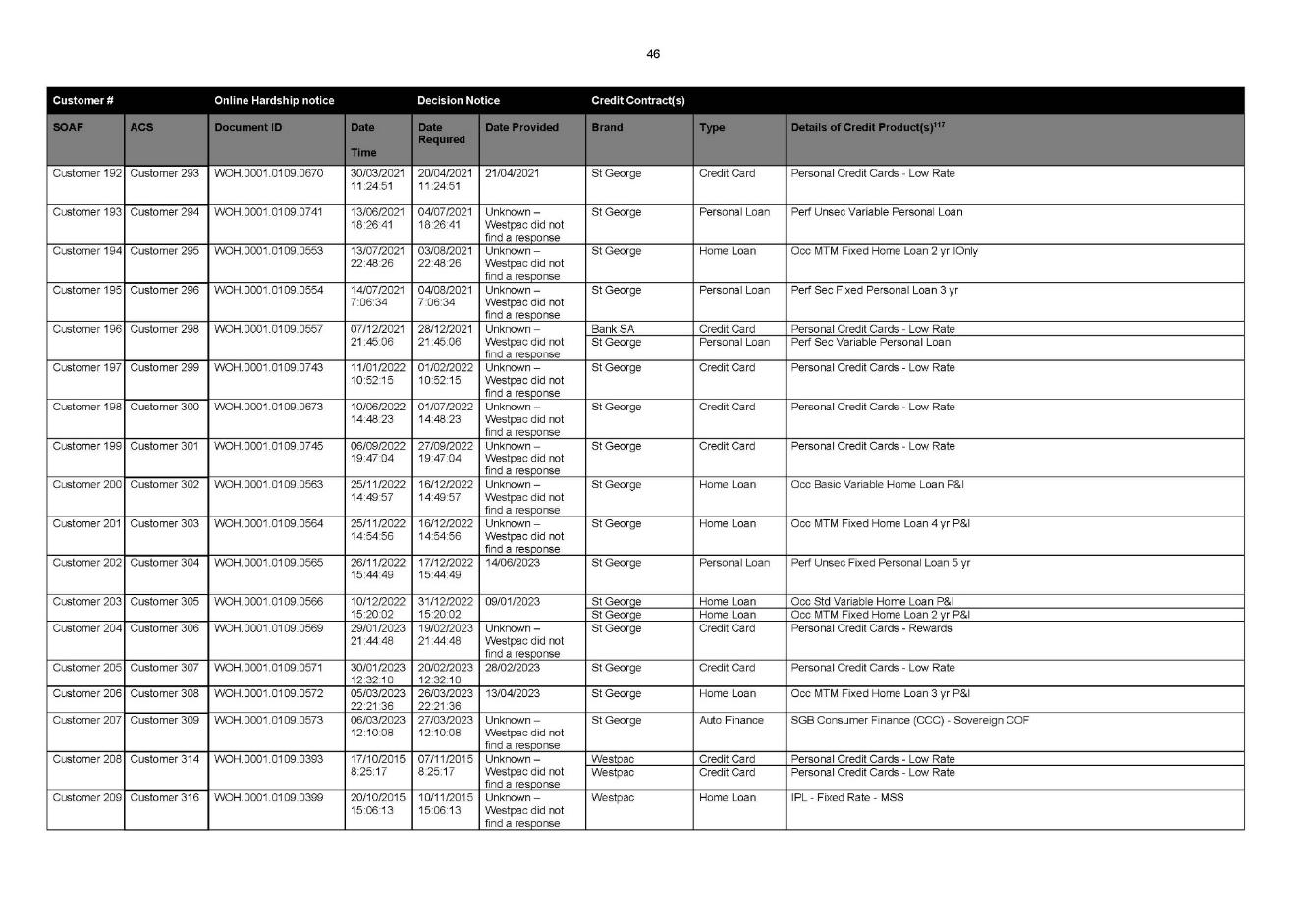

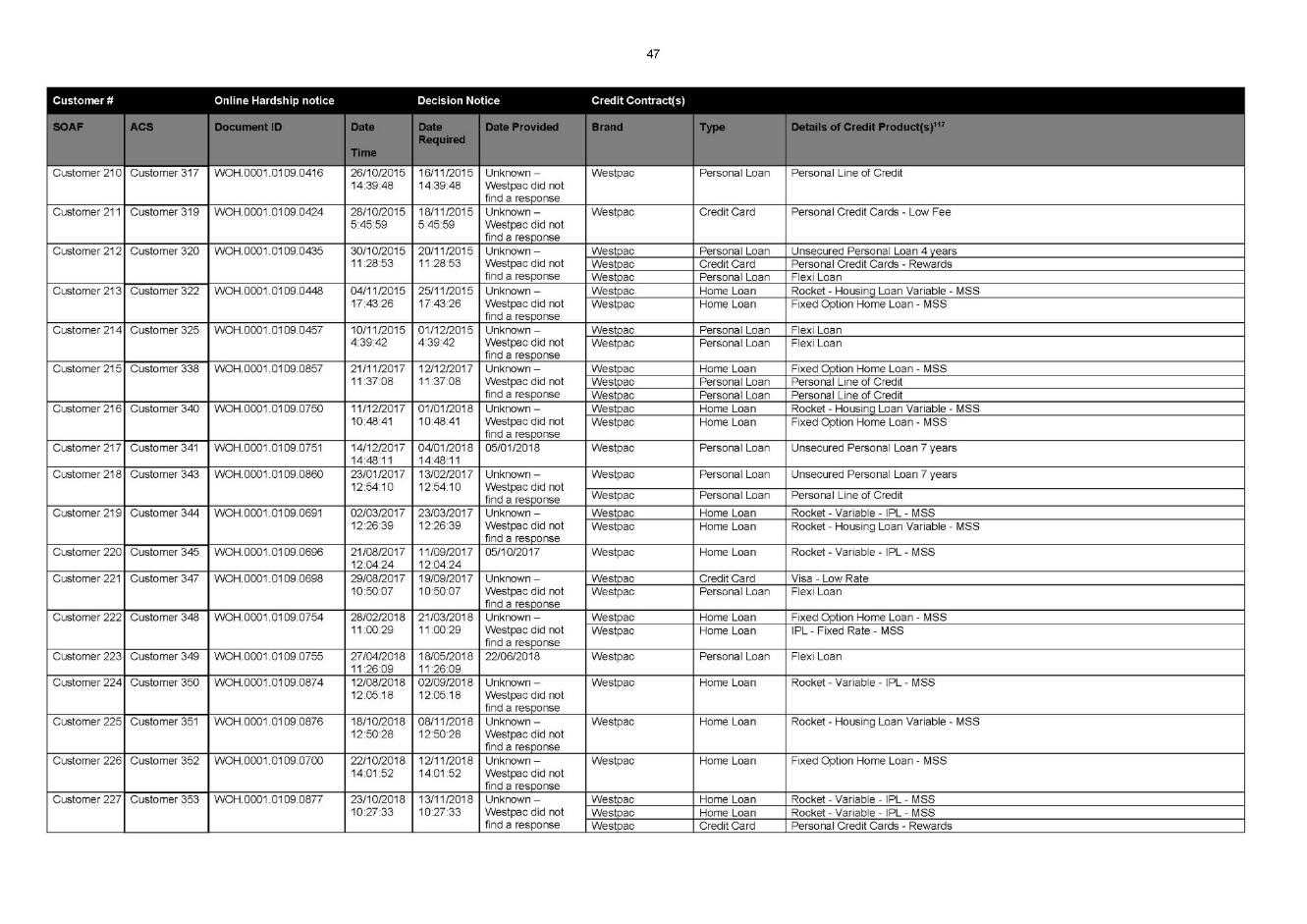

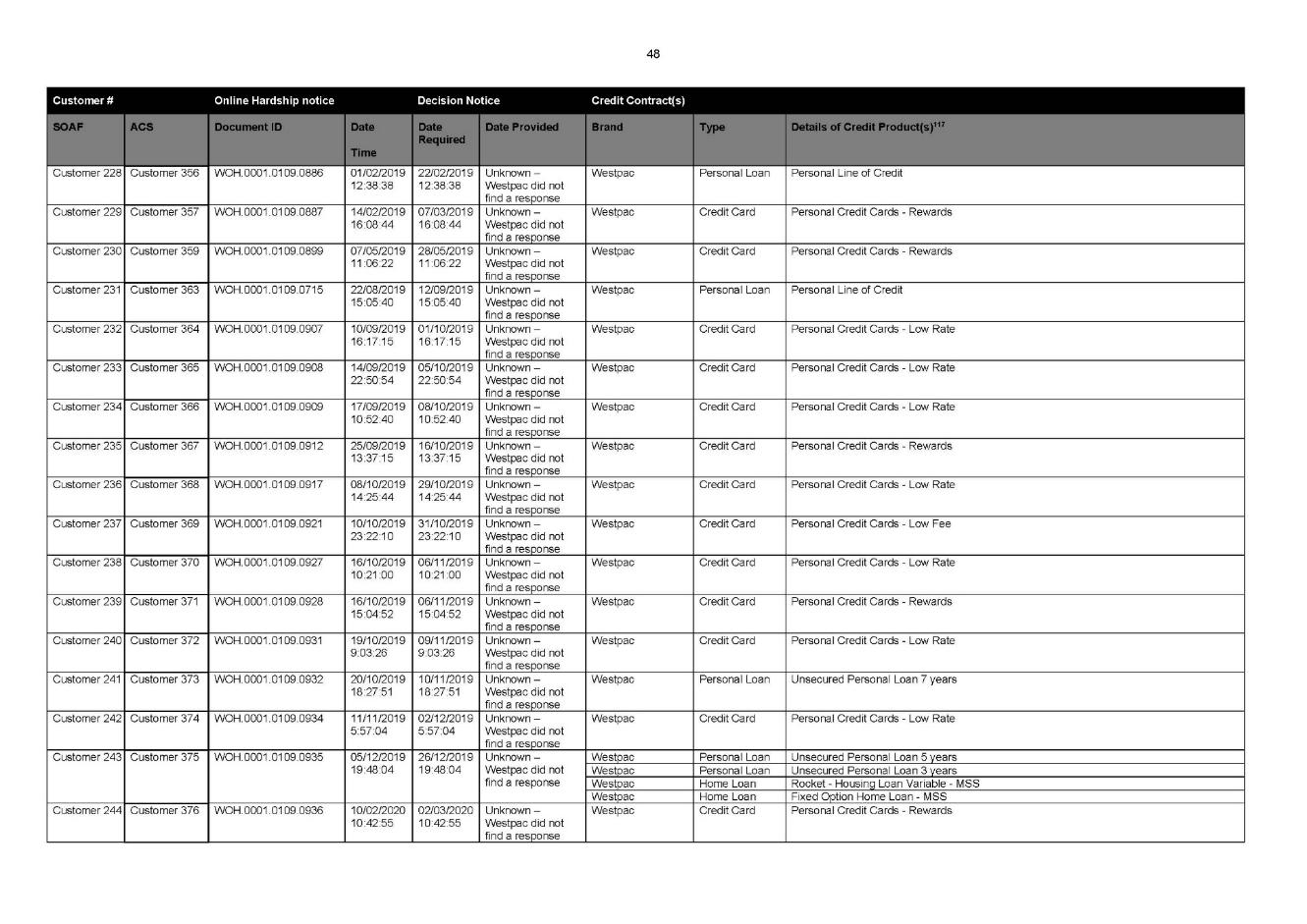

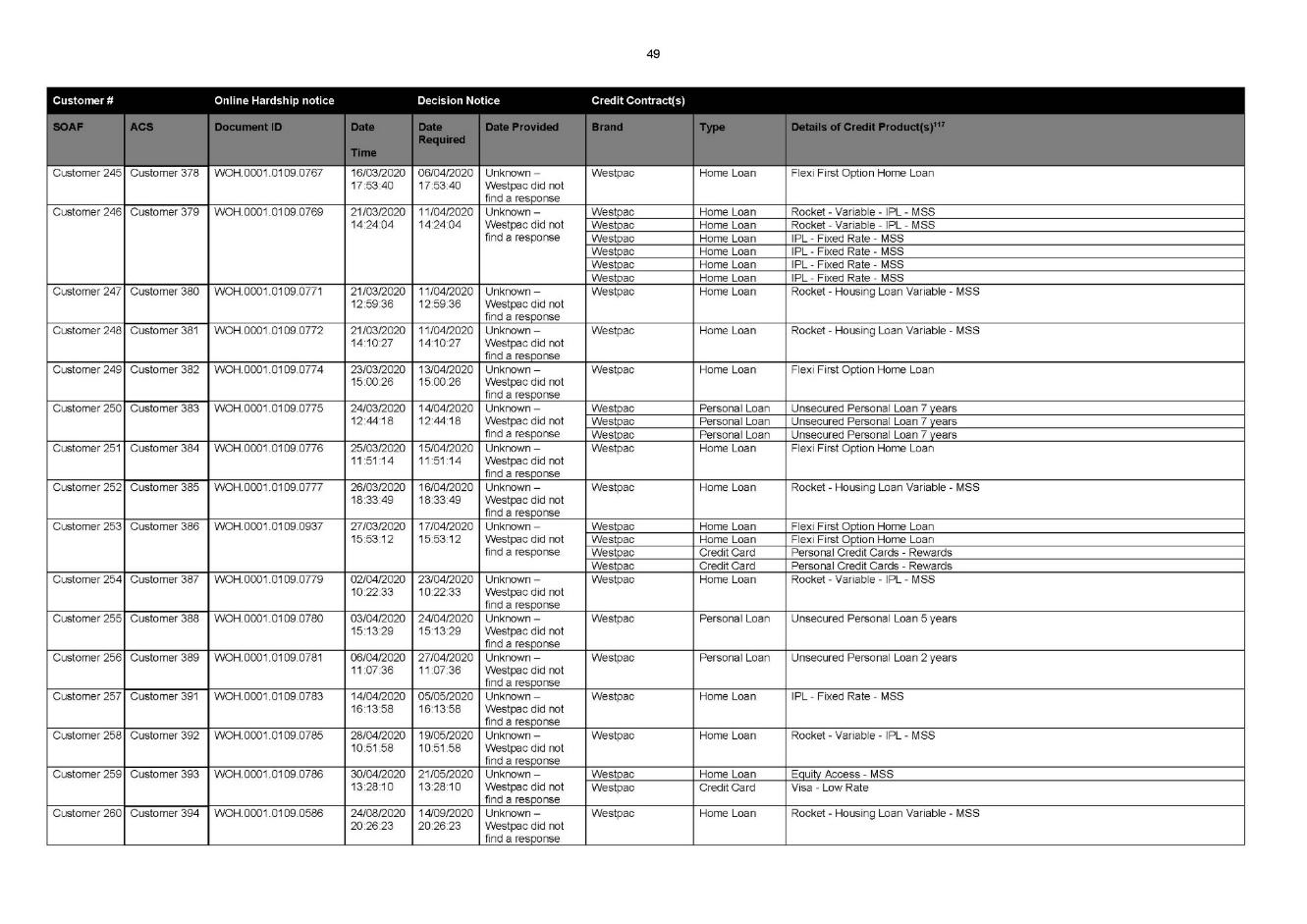

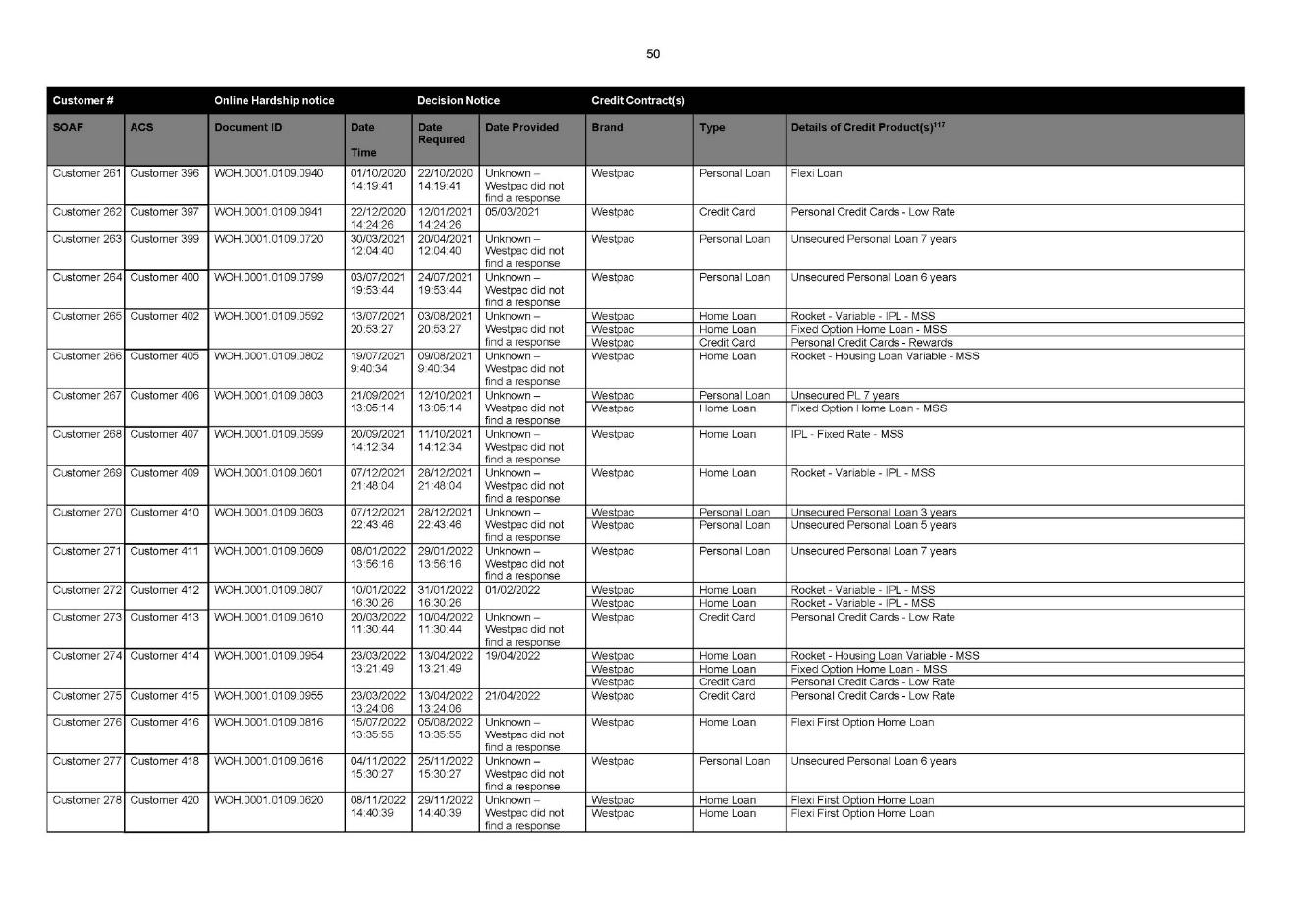

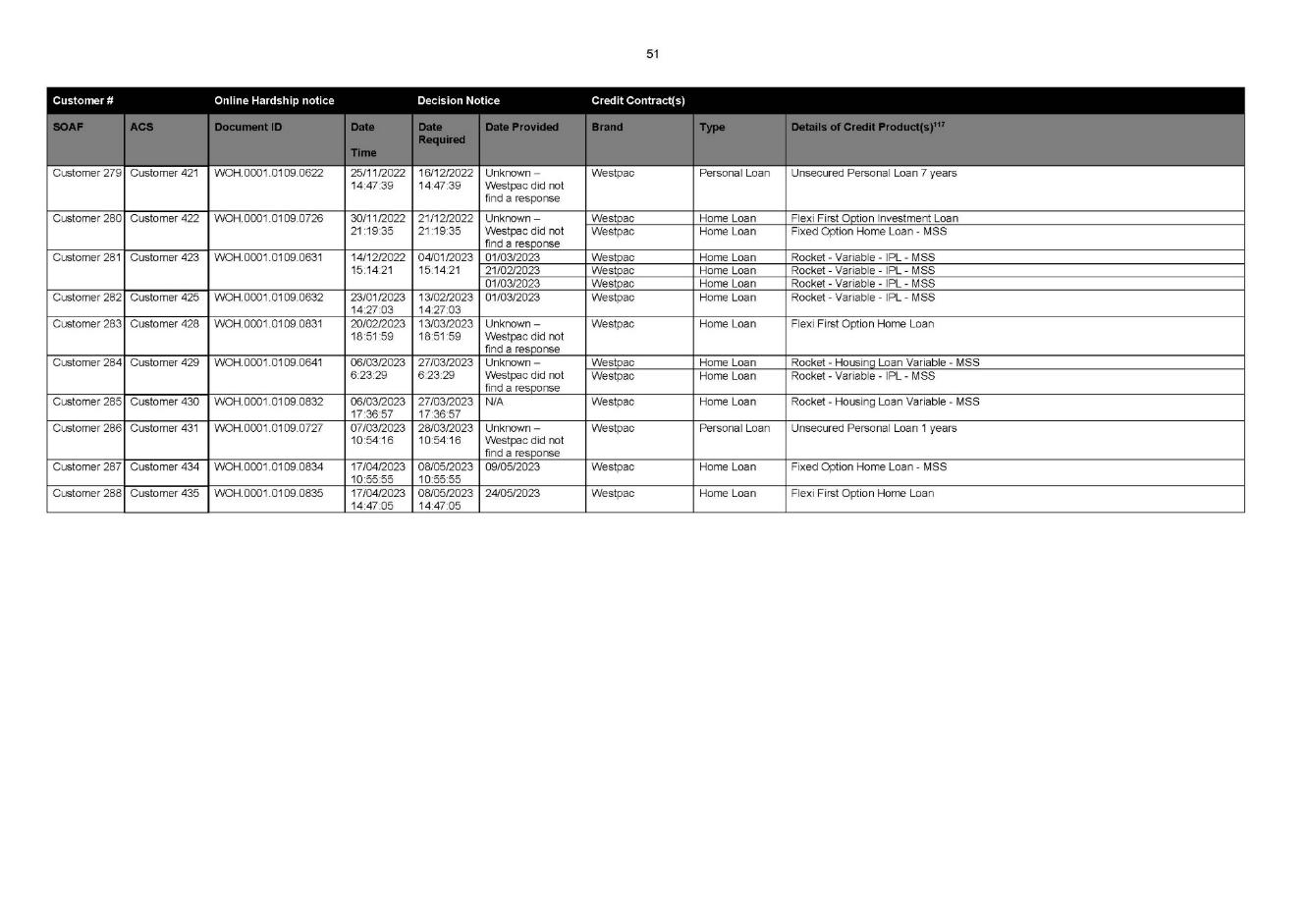

22 Also from 2 October 2015, at least 1,013 online hardship applications submitted by 1,003 customers were either not sent to Westpac’s Customer Assist team for processing, or were not processed properly, or at all, by Westpac. Westpac did not give a written decision notice in response to 277 of these online hardship notices submitted by affected customers within the statutory timeframe prescribed by s 72(5) of the Code, or at all. The parties agree that 223 online hardship notices fall within the Agreed Contravention Period. Westpac’s failures in this regard are set out in Parts D and E of the SOAF.

23 It is to be noted that the references in Part D of the SOAF to 1,014 online hardship notices submitted by 1,004 customers and to Westpac not having given a written decision notice in response to 288 online hardship notices in total, are incorrect. The parties agree, due to circumstances that are unnecessary to describe here but which are explained in the Roy Affidavit, that this aspect of the SOAF was incorrect. They agree that the correct number of online hardship applications submitted, the number of customers, and the number that were not responded to, are those that have been set out above. It is also apparent that the reference to Westpac not having given a written decision notice in response to 224 online hardship notices at paragraph [14] of the SOAF is a typographical error.

24 During the Agreed Contravention Period Westpac accepts that its systems and processes for online hardship notices were deficient in several material respects. These include system failures, IT errors, and operational or processing deficiencies. Indeed Westpac accepts that its “OneClick” system which was supposed to process and transfer online hardship notices to other systems, as well as its other systems processes and operations for online hardship notices, were defective. The details of the deficiencies and failures in the systems are set out in Part E of the SOAF.

25 In its written submissions ASIC summarises Westpac’s contraventions as arising from the following four system failures and three operational failures:

(a) network connectivity failures and a batching process error affecting the transfer of online hardship applications from Westpac’s OneClick system database to a central drive called the “J Drive” (System Failure A);

(b) a file transfer batch configuration error affecting the transfer of online hardship applications from the J Drive to the “App105” system (System Failure B);

(c) a technical error permitting customers to submit an online hardship application without a valid Westpac account number which applications were not transferred further (System Failure C);

(d) data formatting issues in the online application form which prevented some forms from loading in collections systems for action to be taken (System Failure D);

(e) human error in that missing applications appearing in a reconciliation report were not raised with the correct teams for action to be taken (Operational Failure A);

(f) human error in that those responsible for sending missing applications forming part of System Failure A did not send those applications through (Operational Failure B); and

(g) various other human errors resulting in action not being taken in relation to hardship applications (Operational Failure C).

26 ASIC submits that although each System and Operational Failure has different underlying causes, each failure and delay in rectification stemmed from what it describes as Westpac’s “complex, aging and inadequate IT platforms, systems and processes” and Westpac’s “chronic underfunding to improve them.”

27 Westpac identified System Failure A on 31 January 2022. The circumstances in which the System Failure was identified are set out in the SOAF and it is unnecessary to repeat them, save to note that the identification was due to a customer having called Westpac to request information regarding their online hardship application. Westpac identified the other System and Operational Failures at certain times between 31 January 2022 and 7 June 2023.

28 Between 12 September 2017 and 31 January 2022, Westpac had received 16 customer complaints regarding online hardship notices that had not been responded to, and had itself identified “missing” online hardship notices during that time.

29 As is set out in Part F of the SOAF, a number of internal IT “tickets” and other internal incident reports were raised within Westpac, including in its risk and compliance management system, identifying that online hardship notices were “missing” or had not been received by the Customer Assist team. The issues and failures with the automated systems were, however, not substantially investigated until the investigation that led to the identification of System Failure A in January 2022.

30 The consequences of Westpac’s failures, the remediation that has been provided, and the action Westpac has otherwise taken to address the system failures will be addressed further below. These matters are described more fully in the SOAF. It is relevant to note, however, that during the Relevant Period Westpac took action in relation to certain customers’ debt despite them having submitted an online hardship notice. That action included the recording of adverse credit information and default on some affected customer’s credit files, and referring certain customers to third-party debt collectors who then pursued the debts.

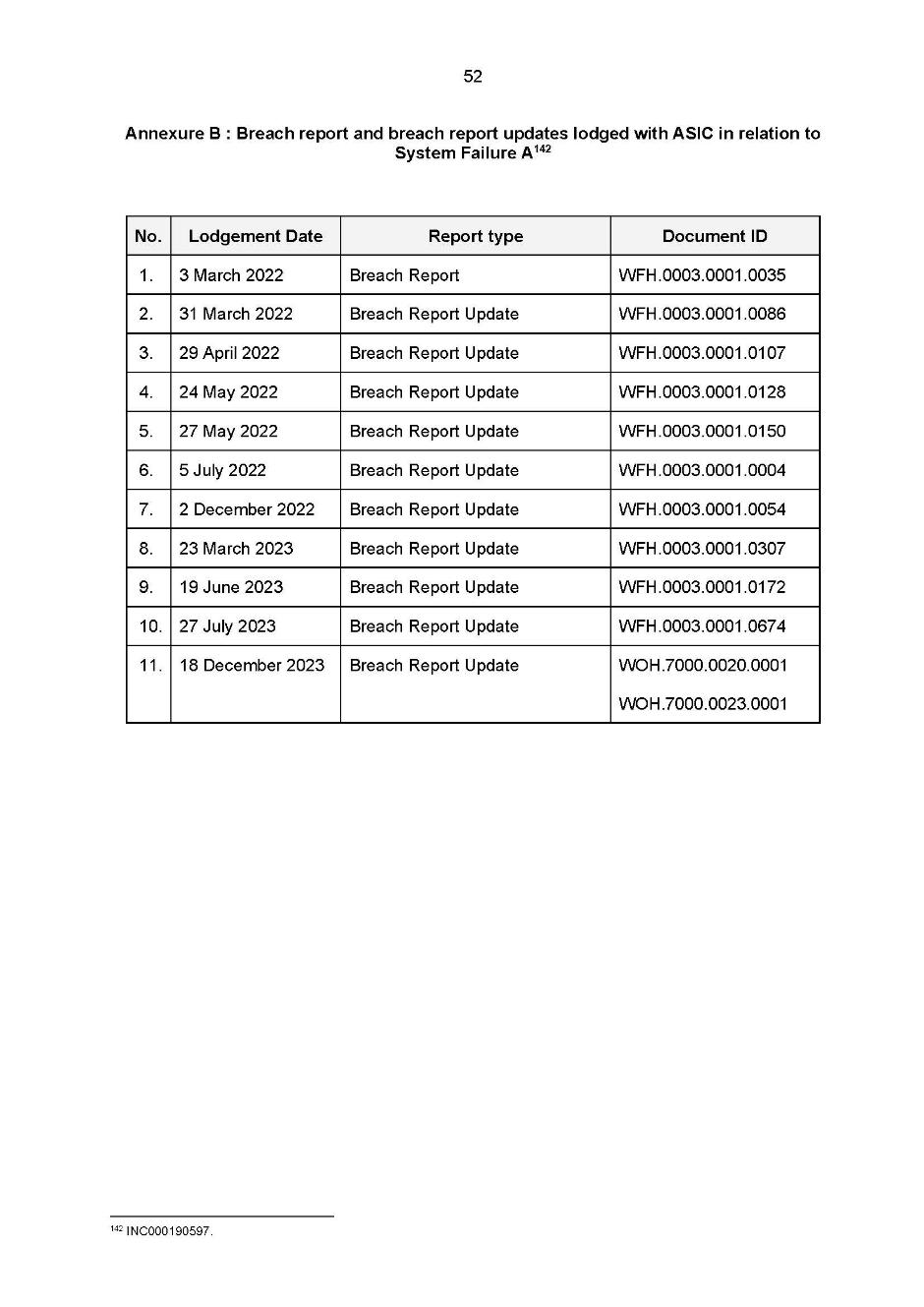

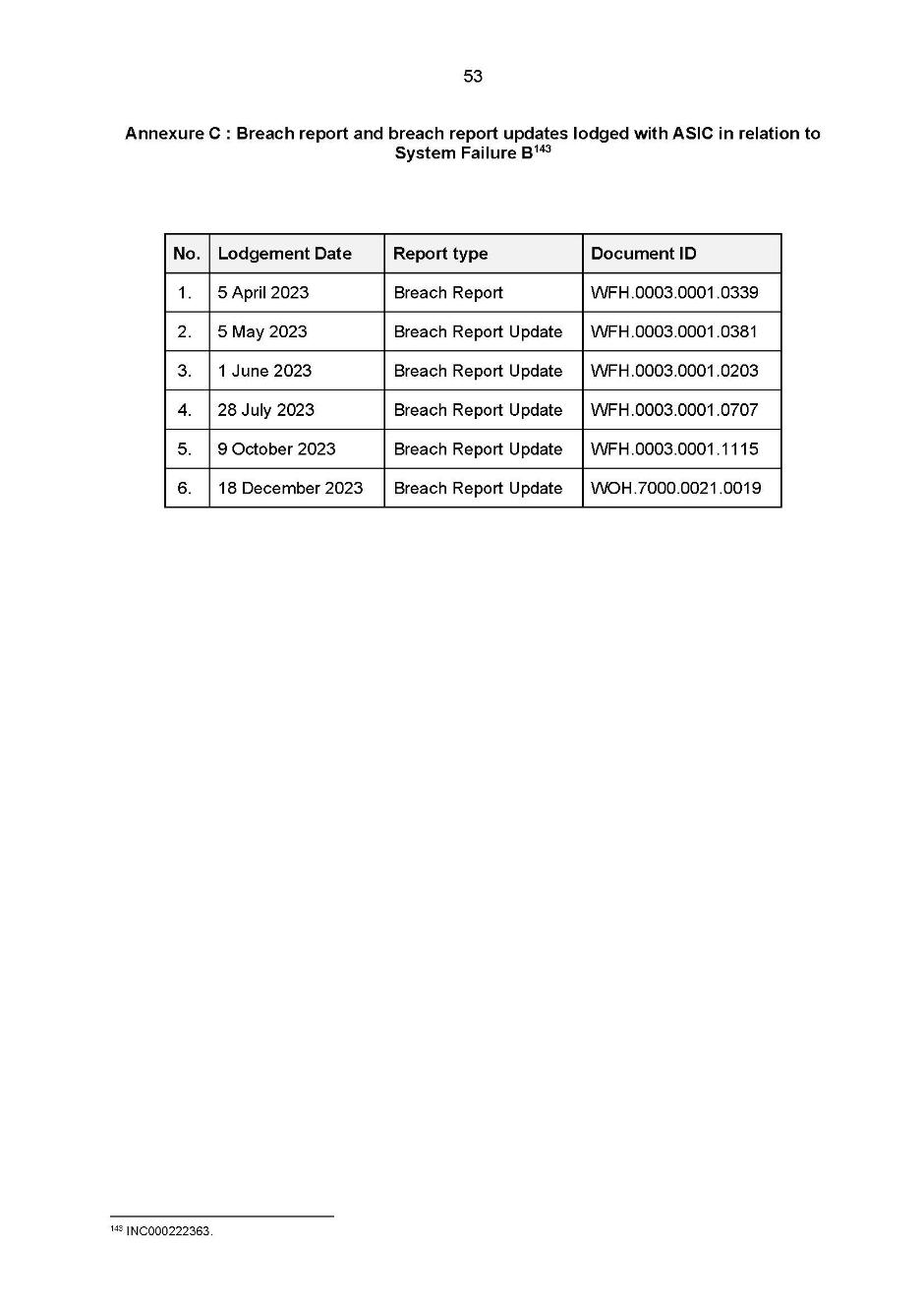

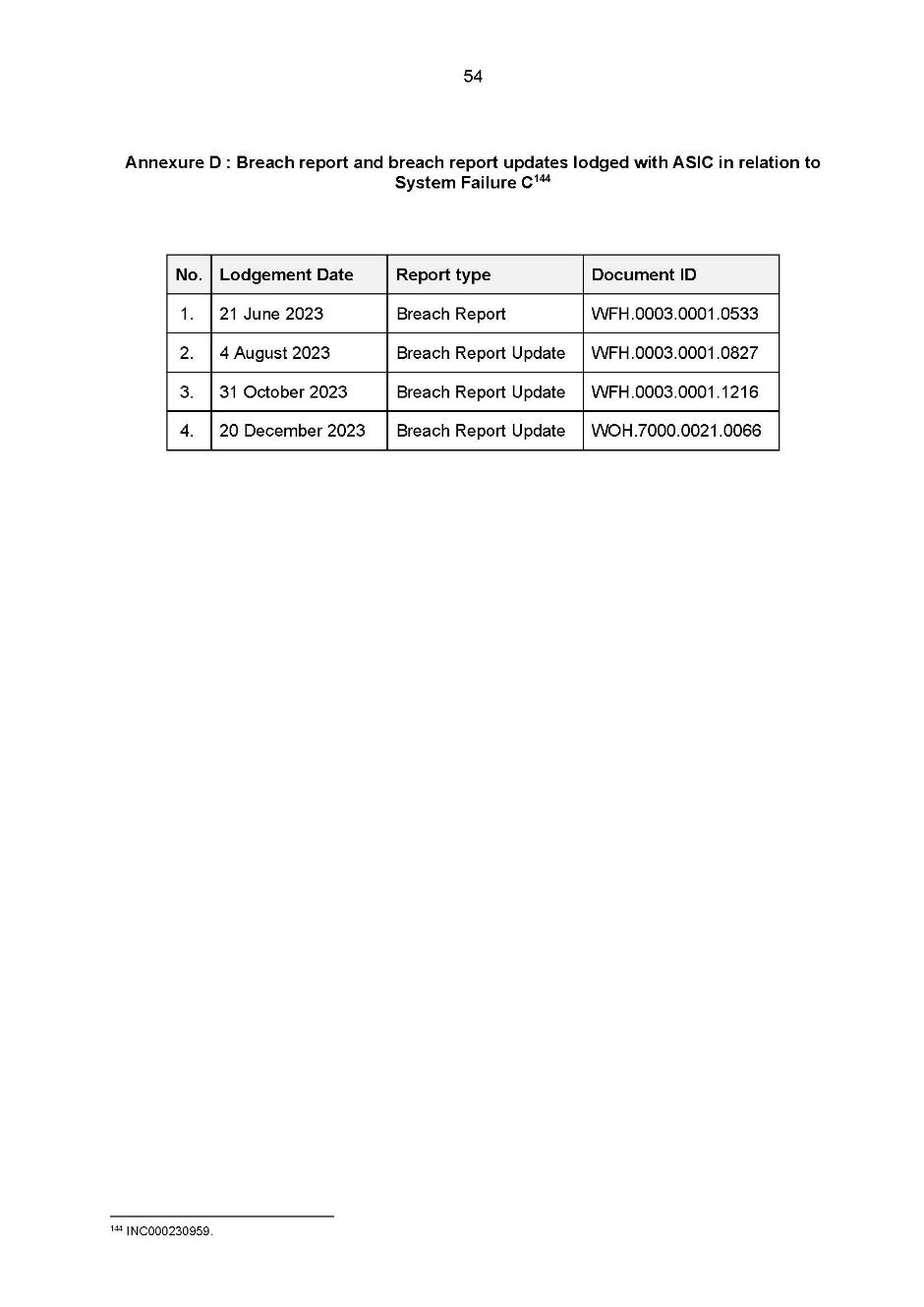

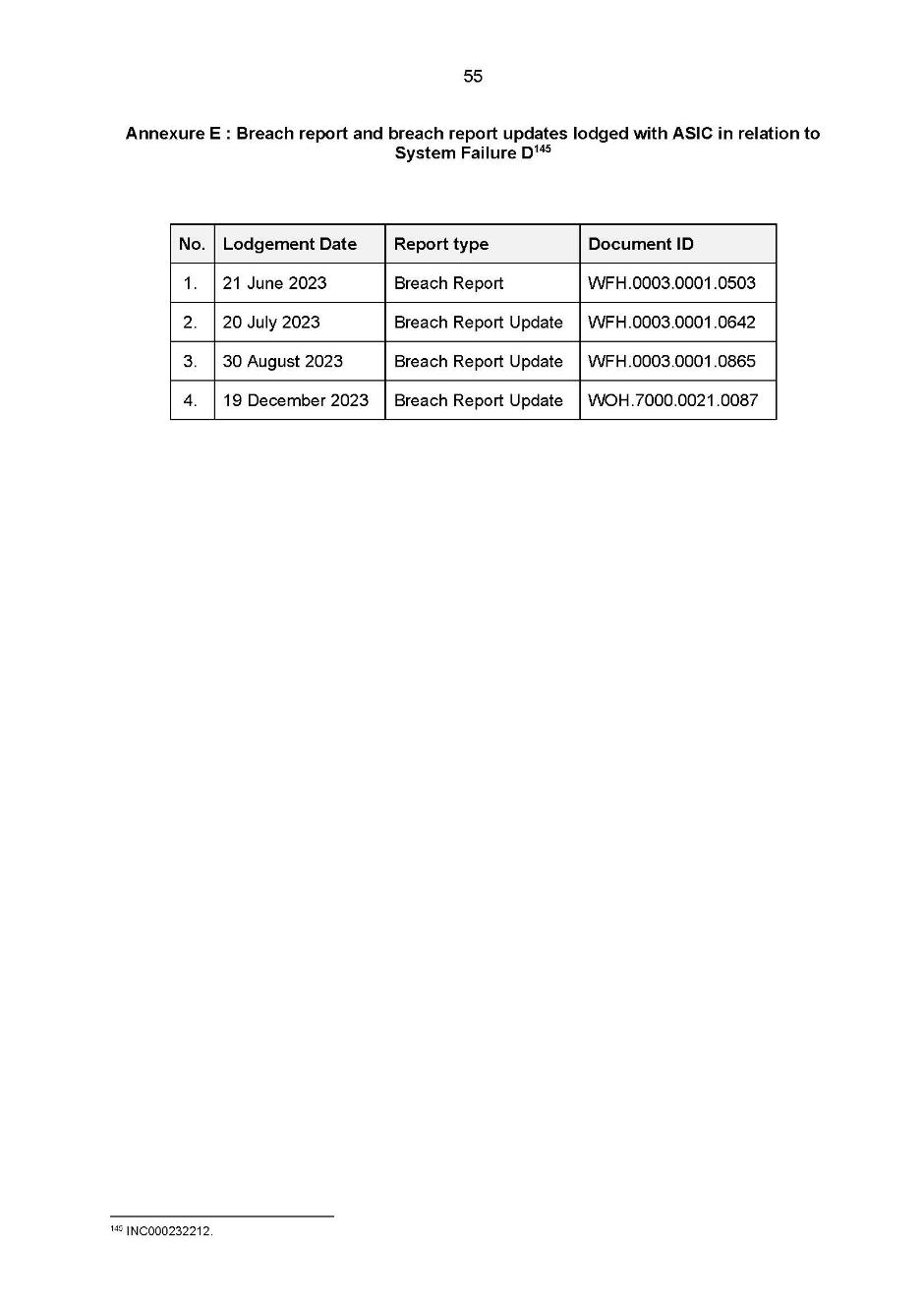

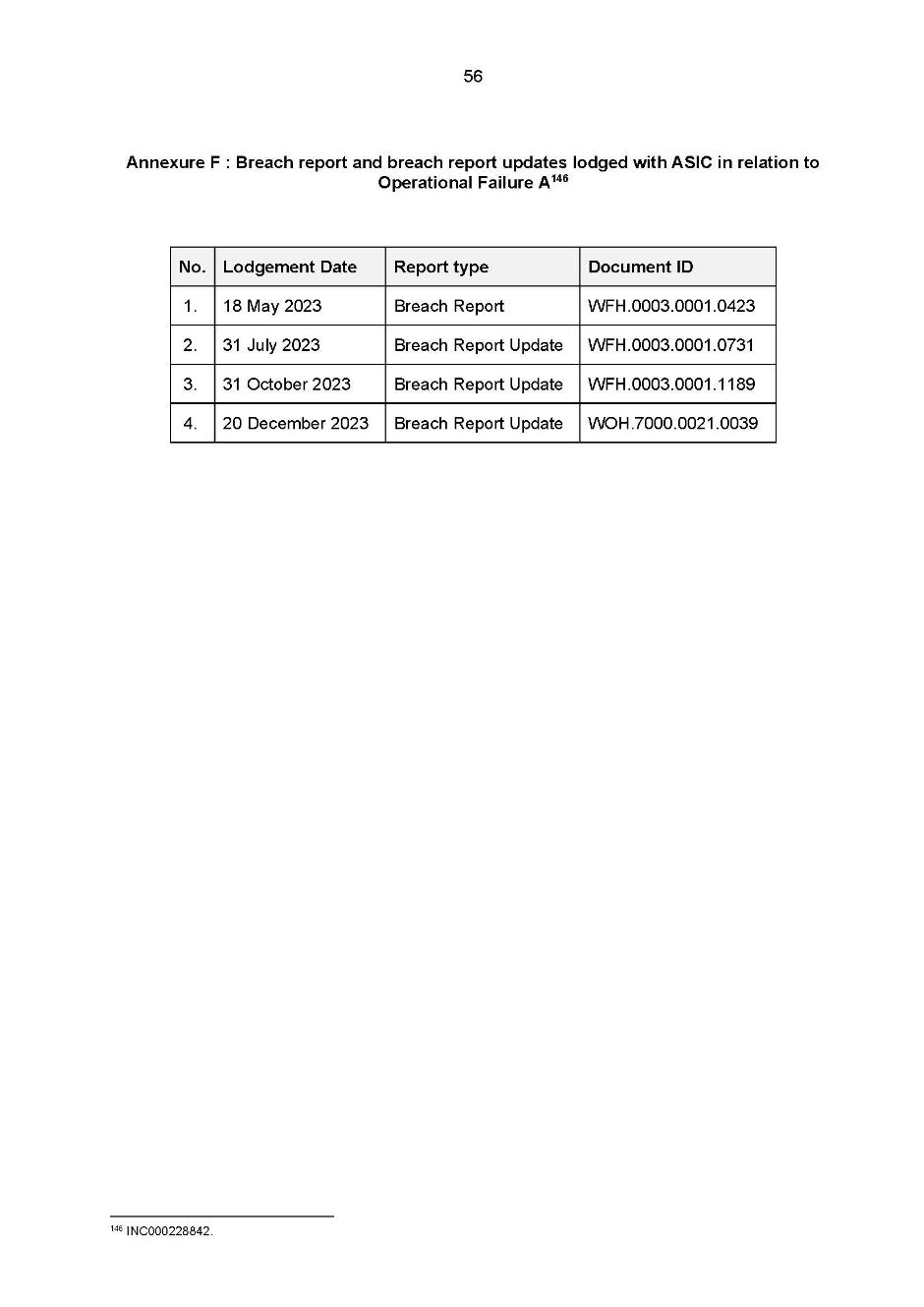

31 Westpac reported the deficiencies in its systems in relation to System Failure A to ASIC on 3 March 2022. It also subsequently reported the deficiencies in relation to the other System and Operational Failures to ASIC, and provided several breach report updates. These are set out in detail at paragraphs [27], [38], [48], [57], [66], [73], [79] and Annexures B to H to the SOAF.

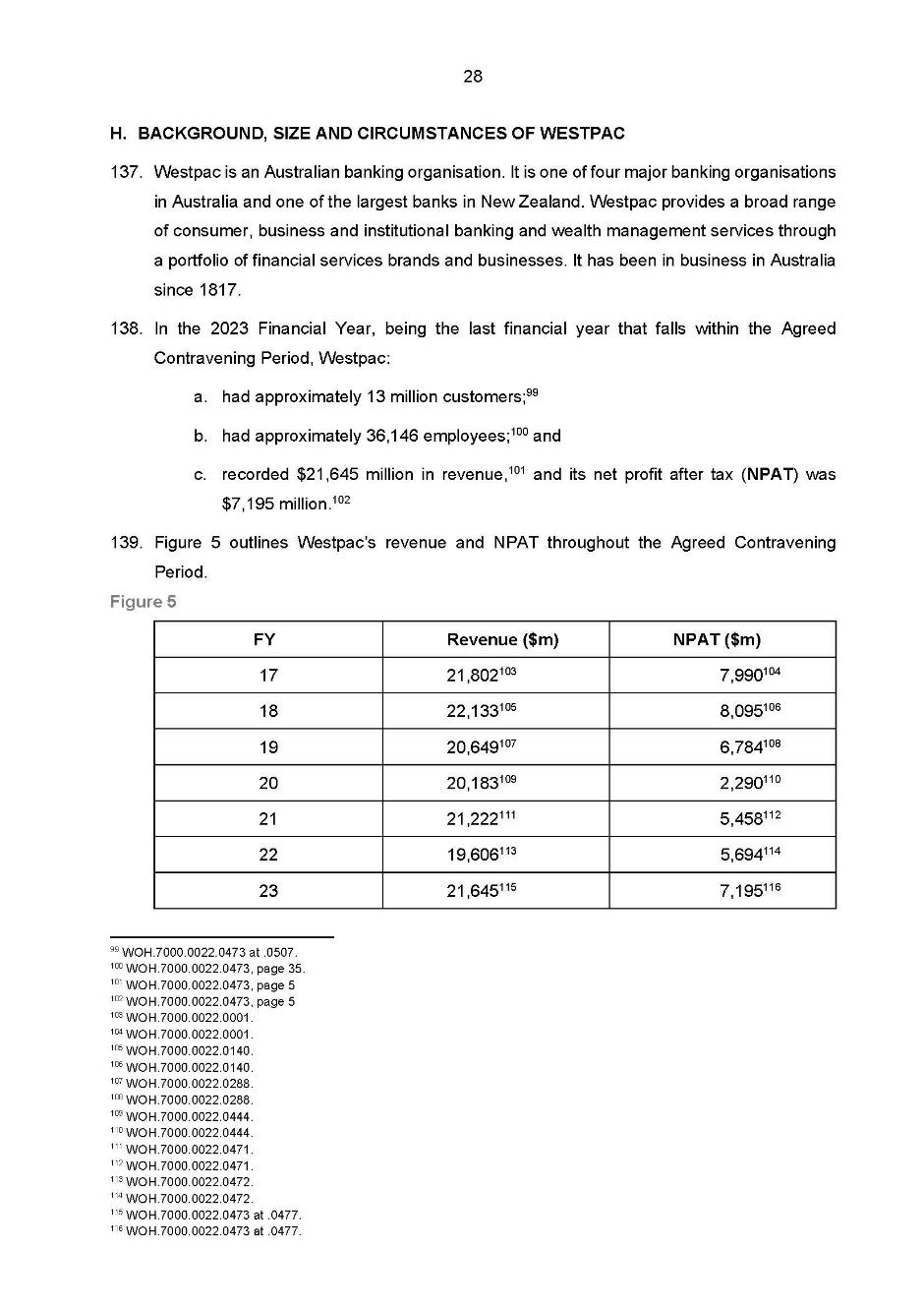

32 As has been mentioned, Westpac accepts that the contravening conduct was serious. Westpac also acknowledges that the time taken to identify the issues with its online hardship process and the customers affected as a consequence is “disappointing”. Those affected, particularly those the subject of adverse credit reporting and debt recovery action, may have used stronger language.

THE CONTRAVENTIONS

33 Despite Westpac having substantially admitted the contraventions, it is necessary to consider the contraventions which have been alleged. It is convenient first to consider Westpac’s contraventions of s 72 of the Code, including the total number of hardship notices relevant to those contraventions by reference to s 175A the Credit Act, before turning to Westpac’s contraventions of s 47 of that Act.

Westpac’s contraventions of s 72 of the Code

The terms of s 72 of the Code

34 Section 72 of the Code is in the following terms:

72 Changes on grounds of hardship

Hardship notice

(1) If a debtor considers that he or she is or will be unable to meet his or her obligations under a credit contract, the debtor may give the credit provider notice (a hardship notice), orally or in writing, of the debtor’s inability to meet the obligations.

Note: If the debtor gives the credit provider a hardship notice, there may be requirements (beyond those in section 88) that the credit provider must comply with before beginning enforcement proceedings—see section 89A.

Further information

(2) Within 21 days after the day of receiving the debtor’s hardship notice, the credit provider may give the debtor notice, orally or in writing, requiring the debtor to give the credit provider specified information within 21 days of the date of the notice stated in the notice. The information specified must be relevant to deciding:

(a) whether the debtor is or will be unable to meet the debtor’s obligations under the contract; or

(b) how to change the contract if the debtor is or will be unable to meet those obligations.

(3) The debtor must comply with the requirement.

Note: The credit provider need not agree to change the credit contract, especially if the credit provider:

(a) does not believe there is a reasonable cause (such as family violence, illness or unemployment) for the debtor’s inability to meet his or her obligations; or

(b) reasonably believes the debtor would not be able to meet his or her obligations under the contract even if it were changed.

Notice of decision on changing credit contract

(4) The credit provider must, before the end of the period identified under subsection (5), give the debtor a notice:

(a) that is in the form (if any) prescribed by the regulations and records the fact that the credit provider and the debtor have agreed to change the credit contract; or

(b) that is in the form (if any) prescribed by the regulations and states:

(i) the credit provider and the debtor have not agreed to change the credit contract; and

(ii) the reasons why they have not agreed; and

(iii) the name and contact details of the AFCA scheme; and

(iv) the debtor’s rights under that scheme.

Civil penalty: 5,000 penalty units.

(4A) Subsection (4) does not apply if the credit provider and the debtor agree to a change to the credit contract that defers or otherwise reduces the obligations of the debtor under that contract for a period not exceeding 90 days.

(5) The credit provider must give the notice before the end of the period identified using the table.

Period for giving notice | ||

| If: | The period is: |

1 | The credit provider does not require information under subsection (2) | 21 days after the day of receiving the hardship notice |

2 | The credit provider requires information under subsection (2) but does not receive any information in compliance with the requirement | 28 days after the stated date of the notice under subsection (2) |

3 | The credit provider requires information under subsection (2) and receives information in compliance with the requirement | 21 days after the day of receiving the information |

Regulations may prescribe shorter periods for credit contracts

(6) The regulations may provide for subsections (2), (3), (4) and (5) to have effect in relation to credit contracts prescribed by the regulations as if a particular reference in subsection (2) or (5) to a number of days were a reference to a lesser number of days prescribed by the regulations.

35 The current version of s 72(4) of the Code came into effect on 1 March 2013 and applies to credit contracts entered into after that date. Save for an increase in penalty units, the amendments that were made during the Agreed Contravention Period were minor and are unnecessary to describe in these reasons.

36 As ASIC submits, there are four elements required to establish a contravention of s 72(4) of the Code as follows:

(1) the contract was a credit contract within the meaning of s 4 of the Code;

(2) a hardship notice has been given pursuant to s 72(1) of the Code;

(3) the credit contract to which the hardship notice related was entered into on or after 1 March 2013; and

(4) the credit provider did not provide to the debtor a decision notice within the relevant statutory timeframe set out in s 72(5) of the Code.

37 The National Consumer Credit Protection Regulations 2010 (Cth) (Regulations) do not prescribe the form that a hardship notice provided by a debtor to a creditor pursuant to s 72(4) of the Code should take. However, the case law indicates that such a notice must be in writing: Membo Finance (No 2) at [32]. Further, as ASIC notes, the Code does not prescribe the changes that may be made to a credit contract as a result of a creditor determining that a debtor is suffering hardship in the relevant sense, however s 73 of the Code does require that the particulars of any change be provided to a debtor in writing no later than 30 days after there has been agreement to the change or changes.

The admitted contraventions

38 Westpac admits that during the Agreed Contravention Period it failed to respond to 223 online hardship notices which were submitted by customers of Westpac and the Other Westpac Brands within the period prescribed in s 72(5) of the Code, or at all. With respect to each of these occasions it accepts that the four elements of s 72(4) (as set out in paragraph 36) are established. It therefore admits that it has contravened s 72(4) with respect to these 223 hardship notices.

39 Having regard to the SOAF and the evidence tendered by the parties, in particular the information and documents contained in the Fleming Affidavit, as well as the admissions made by Westpac, I am satisfied that Westpac contravened s 72 on at least 223 occasions as alleged by ASIC.

Westpac’s further contraventions of s 72 of the Code

40 As has been mentioned, Westpac does not admit to the totality of the contraventions of s 72 of the Code alleged by ASIC. That is to say that ASIC alleges that Westpac has contravened s 72 of the Code with respect to an additional 54 online hardship notices the subject of ASIC’s proposed declaration, and Westpac denies this. As has also been mentioned, the difference in the number of hardship notices alleged by ASIC and agreed to by Westpac results from the parties having taken differing positions as to the proper construction and effect of s 175A of the Credit Act. Westpac’s position in essence is that ASIC is unable to seek declarations with respect to the additional 54 online hardship notices because they were provided to Westpac prior to the Agreed Contravention Period and are therefore outside the limitation period for this proceeding.

41 In these circumstances, the main liability issue for the court to determine is the effect of s 175A of the Credit Act and, in consequence, whether a declaration of a contravention of s 72(4) of the Code should be made in respect of the 223 affected notice customers (as Westpac contends) or the 277 affected notice customers (as ASIC contends).

The effect of s 175A of the Credit Act

42 Section 175A of the Credit Act is in the following terms:

(1) If an act or thing is required under a civil penalty provision to be done:

(a) within a particular period; or

(b) before a particular time;

then the obligation to do that act or thing continues until the act or thing is done (even if the period has expired or the time has passed).

(2) A person who contravenes a civil penalty provision that requires an act or thing to be done:

(a) within a particular period; or

(b) before a particular time;

commits a separate contravention of that provision in respect of each day during which the contravention occurs (including the day the relevant pecuniary penalty order is made or any later day).

43 Section 175A of the Credit Act was introduced as part of the Treasury Laws Amendment (Strengthening Corporate and Financial Sector Penalties) Act 2019 (Cth) (Strengthening Penalties Act) and commenced on 13 March 2019. That Act introduced almost identical continuing contravention provisions in s 1317QA of the Corporations Act 2001 (Cth) (Corporations Act), s 12GBCM of the Australian Securities and Investments Commission Act 2001 (Cth) (ASIC Act), and s 75R of the Insurance Contracts Act 1984 (Cth).

44 Schedule 3, Pt 4 of the Strengthening Penalties Act sets out the transitional provisions for s 175A of the Credit Act, which relevantly states:

Subject to this Part, the amendments made by Schedule 3 to the [Strengthening Penalties Act] apply in relation to the contravention of a civil penalty provision if the conduct constituting the contravention of the provision occurs wholly on or after the commencement day.

See also National Consumer Credit Protection (Transitional and Consequential Provisions) Act 2009 (Cth) Sch 8, Pt 2, item 3 (Transitional Provisions Act).

45 The Explanatory Memorandum to the Strengthening Penalties Act at [1.113] explains the operation of s 175A as follows:

Contravening a civil penalty provision does not relieve the person of their obligations under the provision. If an act or thing is required to be done, the obligations continue until the act or thing is done. This means that if the act or thing is not done, the civil penalty provision is initially contravened, and a separate contravention is then committed each day until the act or thing is done.

46 Section 175A of the Credit Act does not operate retrospectively. The Revised Explanatory Memorandum to the Strengthening Penalties Act provides at [1.248]:

The amendments made by this Bill in relation to a contravention of a civil penalty provision apply to contraventions that occur wholly on or after the commencement day of this Bill.

47 At the time of the hearing in this proceeding, there had been no judicial consideration of s 175A of the Credit Act and limited judicial consideration of the transitional provisions. Section 175A of the Credit Act has subsequently been considered in Australian Securities and Investments Commission v National Australia Bank [2025] FCA 947 (Neskovcin J) (ASIC v NAB) and Australian Securities and Investments Commission v Australia and New Zealand Banking Group Limited (Retail Cases Omnibus) [2025] FCA 1593 (Beach J) (ASIC v ANZ (Retail Omnibus)). In both cases, their Honours found that s 175A of the Credit Act provides that a credit provider’s obligation to give a notice under s 72(4) of the Code continues until that act is done, and that a credit provider who contravenes s 72(4) of the Code commits a separate contravention of that provision in respect of each day during which the contravention occurs (including the day the relevant pecuniary penalty order is made or any later day): ASIC v NAB at [26]; ASIC v ANZ (Retail Omnibus) at [63]. In both these cases, however, the declarations of contravention related only to conduct that had occurred after 13 March 2019. It remains that there has been no judicial consideration of the application of s 175A of the Credit Act to s 72(4) of the Code that is of assistance in circumstances where ASIC seeks declarations with respect to conduct that occurred in part prior to 13 March 2019.

48 Westpac contends that the judicial consideration of the transitional provisions does not offer any adequate guidance as to the effect of s 175A on s 72(4) of the Code in the present context. By contrast, ASIC submits that a number of these cases are informative as to the effect of s 175A. First ASIC draws attention to Australian Securities and Investments Commission v AustralianSuper Pty Ltd [2025] FCA 102; 172 ACSR 615 (ASIC v AustralianSuper), in which AustralianSuper had admitted that in the period 1 July 2013 to 19 June 2022 it failed to establish rules as required by s 108A of the Superannuation Industry Act 1993 (Cth). In that case ASIC had sought civil penalties under s 912A(1)(a) and (5A) of the Corporations Act for failures that occurred between 13 March 2019 to 20 June 2022. Justice Hespe observed (at [164]) that:

It is only conduct occurring wholly on or after the commencement date which results in the contravention of s 912A(5A) and which attracts the civil penalty provision. However, the fact that contravening conduct commenced occurring prior to the commencement date and continued after the commencement date does not prevent a determination of a contravention in respect of the conduct that occurred after the commencement date. Such an outcome is consistent with the approach adopted in Australian Securities and Investments Commissioner v Westpac Banking Corporation [2022] FCA 515 at [409]–[412] (Beach J) and in Australian Securities and Investments Commission v Macquarie Bank Limited [2024] FCA 416 at [69] (Wigney J).

49 ASIC also referred the court to the treatment of analogous substantive provisions, namely s 1317QA of the Corporations Act. This section was discussed briefly in Australian Securities and Investments Commission v Statewide Superannuation Pty Ltd [2021] FCA 1650 (Statewide Superannuation) and Australian Securities and Investments Commission v Noumi Ltd (No 3) [2024] FCA 862 (Noumi). In Statewide Superannuation at [88]–[89], Besanko J held that in the context of the defendant failing to lodge a written breach report with ASIC within the statutory timeframe under the Corporations Act there was a separate contravention on each day that the defendant failed to lodge the report. In Noumi at [49]–[50], Jackman J held that by operation of s 1317QA of the Corporations Act separate and continuing contraventions of s 674(2) of the Corporations Act occurred on each trading day in the relevant periods. However, the issue of whether contraventions occurred “wholly” after 13 March 2019 did not arise in either proceeding.

50 Turning then to the parties’ submissions on this issue, ASIC contends that s 175A of the Credit Act enlivens penalties for contraventions that would otherwise be barred by the limitation in s 167 of that Act. Its position is that where a contravention of s 72 of the Code (being the obligation to give a decision notice under s 72(4) by the prescribed timeframes) occurred prior to six years before these proceedings were commenced (being prior to 4 September 2017) but continued on or after 13 March 2019, s 175A of the Credit Act allows ASIC to seek penalties in respect that contravention.

51 Westpac submits, however, that the usual limitation period of six years ought to apply in this proceeding, precluding both the making of a declaration or the imposition of a pecuniary penalty on Westpac in relation to contraventions that occurred prior to 4 September 2017. Westpac contends that ASIC’s submission that s 175A of the Credit Act has the effect of permitting it to allege contraventions outside the limitation period should not be accepted.

52 Westpac submits that to apply s 175A of the Credit Act to s 72(4) of the Code it is necessary to determine whether each constituent element of a contravention occurred wholly on or after 13 March 2019. It submits that for the purpose of that analysis the elements of a contravention of s 72(4) of the Code are:

(a) that the debtor gave the hardship notice (s 72(1) of the Code); and

(b) that the credit provider failed to give notice of their determination of the hardship notice within the prescribed time (ss 72(2), (4) and (5) of the Code).

53 Westpac illustrates its submission by way of an example in which a customer provided an online hardship notice to Westpac on 5 July 2016. Westpac was required to respond to that notice on 27 July 2016. Thus, in Westpac’s submission, the contravention was complete on 28 July 2016 (the day after compliance was required). Other than by operation of s 175A, the contravention did not continue despite the written decision not being given by that date, or at all. Westpac contends that the words “occur wholly on or after” in the transitional provisions expressly limit the operation of s 175A of the Credit Act such that each contravention of s 72(4) that occurred prior to 13 March 2019 was completed and concluded on the day the credit provider failed to comply with its obligations to provide a determination of the hardship notice. Westpac submits that ASIC’s interpretation of s 175A of the Credit Act finds no support in the drafting of the section, is contrary to the express language of the transitional provisions, and is inconsistent with ss 166 and 167 of the Credit Act.

54 Nonetheless, for the following reasons, and having regard to the explanatory memoranda and the authorities set out above, I prefer ASIC’s submissions as to the effect of s 175A of the Credit Act. I accept, as ASIC submits, that the transitional provisions which have been referred to apply to s 175A of the Credit Act and not s 72 of the Code. The focus of the enquiry is whether the relevant conduct constitutes a contravention of s 175A of the Credit Act, and whether that conduct occurred wholly on or after 13 March 2019. The conduct to which s 175A of the Credit Act applies is a continuing obligation to do an act or thing. Here that is the giving of a decision notice by the timeframes prescribed by the Code, until that act or thing has been performed: ASIC v NAB at [26]; ASIC v ANZ (Retail Omnibus) at [63].

55 I accept, as ASIC submits, that Westpac’s continuing failure to give a decision notice under s 72(4) within the prescribed timeframe was the “conduct constituting the contravention”. For the 54 affected customers in question, that conduct occurred each day wholly on or after 13 March 2019 until Westpac issued the affected customer a decision notice: Credit Act s 175A(2); Statewide Superannuation at [88]–[89]; Noumi at [49]–[50], [69]. As ASIC submits, it does not matter if the customer submitted a hardship notice prior to 13 March 2019, or if Westpac failed to give a decision notice prior to 13 March 2019; the contravening conduct is the continuing failure to give a decision notice. It also does not matter that the initial contravention of s 72(4) of the Code occurred prior to 4 September 2017, provided that Westpac continued to contravene its obligation to give a decision notice on and after 13 March 2019. It is not open to Westpac to avoid liability for its failure to provide written decision notices under s 72(4) of the Code simply and only because the obligation to do so first arose prior to 13 March 2019.

56 It is on this basis that the total number of online hardship notices and total affected customers the subject of declaration one will be 223 and 277, respectively. It is appropriate also that the period referred to is the Relevant Period, that is 2 October 2015 to 7 June 2023.

57 Nevertheless, even if I am not correct in the above analysis, and Westpac’s position as to the effect of 175A of the Credit Act is to be preferred, the number of affected customers in the declaration (an additional 54, out of 277) does not materially affect my determination of the appropriate penalty to be imposed. The parties appear to accept that this is so.

58 With this in mind I note that Westpac makes a number of further detailed submissions on the subject of whether s 72(4) of the Code was a continuing contravention prior to the enactment of s 175A of the Credit Act. I accept ASIC’s submission, however, that it is unnecessary to engage with those submissions or to determine that question in circumstances where I have accepted ASIC’s position as to the effect of s 175A of the Credit Act. This is particularly so in circumstances where, even if my analysis as to s 175A of the Credit Act were to be regarded as incorrect, and Westpac’s submissions with respect to the contraventions not being “continuing” were to be accepted, that would have no material impact on the appropriate pecuniary penalty I have decided to impose.

Westpac’s contraventions of s 47 of the Credit Act

59 ASIC alleges that Westpac has contravened s 47 of the Credit Act during the Agreed Contravention Period. Westpac admits that this is so.

60 Section 47(1)(a) of the Credit Act is in the following terms:

General conduct obligations of licensees

General conduct obligations

(1) A licensee must:

(a) do all things necessary to ensure that the credit activities authorised by the licence are engaged in efficiently, honestly and fairly; and

61 Section 47 of the Credit Act is a civil penalty provision where the contravening conduct occurred wholly on or after 13 March 2019: Transitional Provisions Act Sch 8, Pt 2, item 3.

62 ASIC draws attention to the principles applicable to determining contravention set out by Foster J in Australian Securities and Investments Commission v Camelot Derivatives Pty Ltd (in liq) [2012] FCA 414; 88 ACSR 206 at [69] (in the context of s 912A(1)(a) of the Corporations Act) as follows:

(a) The words “efficiently, honestly and fairly” must be read as a compendious indication meaning a person who goes about their duties efficiently having regard to the dictates of honesty and fairness, honestly having regard to the dictates of efficiency and fairness, and fairly having regard to the dictates of efficiency and honesty.

(b) The words “efficiently, honestly and fairly” connote a requirement of competence in providing advice and in complying with relevant statutory obligations. They also connote an element not just of even handedness in dealing with clients but a less readily defined concept of sound ethical values and judgment in matters relevant to a client’s affairs.

(c) The word “efficient” refers to a person who performs his [or her] duties efficiently, meaning the person is adequate in performance, produces the desired effect, is capable, competent and adequate. Inefficiency may be established by demonstrating the performance of a licencee’s functions falls short of the reasonable standard of performance that the public is entitled to expect.

(d) It is not necessary to establish dishonesty in the criminal sense. The word “honestly” may comprehend conduct which is not criminal but which is morally wrong in the commercial sense.

(e) The word “honestly” when used in conjunction with the word “fairly” tends to give the flavour of a person who not only is not dishonest, but also a person who is ethically sound.

(Citations omitted)

See also Australian Securities and Investments Commission v Westpac Banking Corporation (No 2) [2018] FCA 751; 266 FCR 147 at [2347]–[2348] (Beach J) (ASIC v Westpac (No 2)); Australian Securities and Investments Commission v AGM Markets Pty Ltd (in liq) (No 3) [2020] FCA 208; 275 FCR 57 at [505]–[510] (Beach J); Story v National Companies and Securities Commission (1988) 13 NSWLR 661 (Young J).

63 ASIC submits that the following additional principles are also relevant in the present case:

(a) A contravention of the “efficiently, honestly and fairly” standard does not require a contravention or breach of a separately existing legal duty or obligation, whether statutory, fiduciary, common law or otherwise. The statutory standard itself is the source of the obligation: ASIC v Westpac (No 2) at [2350].

(b) Breach of another provision may itself be sufficient to constitute a violation of general obligations: see, for example, Australian Securities and Investments Commission v Westpac Banking Corporation (Omnibus) [2022] FCA 515; 407 ALR 1 at [71]–[73] (Beach J) (ASIC v Westpac (Omnibus)).

(c) The word “ensure” imports a forward-looking element into the obligation. It is necessary not only to act efficiently, honestly and fairly from day to day, but to take steps to guard against lapses from that standard by employees or representatives: Australian Securities and Investments Commission v Commonwealth Bank of Australia [2022] FCA 1422 at [146] (Downes J), citing Australian Securities and Investments Commission v AMP Financial Planning Pty Ltd (No 2) [2020] FCA 69; 377 ALR 55 at [105] (Lee J) (ASIC v AMP Financial Planning Pty Ltd (No 2)).

(d) The standard may be unintentionally breached. Contravention is generally a matter of objective analysis: Australian Securities and Investments Commission v National Australia Bank Ltd [2022] FCA 1324; 164 ACSR 358 at [352] (Derrington J); Australian Securities and Investments Commission v Ferratum Australia Pty Limited (in liq) [2023] FCA 1043; 169 ACSR 553 at [49] (Kennett J) (ASIC v Ferratum).

(e) Some conduct is appropriate to assess through a public expectation lens: for example, fees charged for no service, or providing financial advice without consideration of the client’s best interests: Australian Securities and Investments Commission v RI Advice Group Pty Ltd [2022] FCA 496; 160 ACSR 204 at [49] (Rofe J), referring to Australian Securities and Investments Commission v MLC Nominees Pty Ltd [2020] FCA 1306; 147 ACSR 266 (Yates J) and Australian Securities and Investments Commission v Westpac Securities Administration Ltd [2019] FCAFC 187; 272 FCR 170 (Allsop CJ, Jagot and O'Bryan JJ).

(f) Where the contravening conduct occurred prior to 1 March 2019 and continued after that date, that does not prevent a determination of a contravention in respect of conduct that occurred on or after 1 March 2019: ASIC v AustralianSuper at [164] (Hespe J) citing ASIC v Westpac (Omnibus) at [409]–[412] and Australian Securities and Investments Commission v Macquarie Bank Limited [2024] FCA 416 at [69] (Wigney J).

(g) Dishonesty in the criminal sense is not required: Australian Securities and Investments Commission v Lanterne Fund Services Pty Ltd [2024] FCA 353 at [93] (McEvoy J).

64 ASIC submits that while the authorities to which reference has been made have largely considered the meaning of the phrase “efficiently, honestly and fairly” in the context of s 912A(1)(a) of the Corporations Act, the principles essayed in these cases are equally applicable to s 47(1)(a) of the Credit Act: see Australian Securities and Investments Commission v Darranda Pty Ltd (Liability) [2024] FCA 1015 at [240] (Hespe J) citing Membo Finance (No 2) at [37]. I accept that this is so.

65 ASIC alleges, and Westpac admits, that in the period from 13 March 2019 to 7 June 2023 Westpac failed to do all things necessary to ensure that the credit activities authorised by its credit licence were engaged in efficiently, honestly and fairly, and that Westpac thereby contravened s 47(1)(a) and (4) of the Credit Act by failing to:

(a) maintain adequate systems, controls and processes which ensured that:

(i) online hardship notices given by customers were received by the Customer Assist team; and

(ii) written decision notices were given to customers within the timeframes prescribed by s 72(4)and (5) of the Code; and

(b) conduct adequate risk reviews, investigations, monitoring and analysis of its online hardship notice systems and processes to enable it to identify any issues with its systems or processes, or to otherwise ensure that its online hardship notice systems and processes enabled compliance with s 72(4) and (5) of the Code.

66 On the subject of whether Westpac’s activities were engaged in efficiently, ASIC makes a number of submissions which it is unnecessary to describe in detail. In substance, however, ASIC contends that Westpac’s online hardship systems, processes and operations were inefficient in eight respects which it says had a cumulative and compounding effect. Those eight matters may be summarised as follows:

(a) First, ASIC submits that from 1 October 2015 to 6 June 2023, Westpac had a complex, multi-system environment with aging technology which created an unacceptable risk (of which Westpac was aware) that online hardship notices would not be received and processed, including timely requests for customer information, within the timeframes prescribed by s 72(4) and (5) of the Code.

(b) Secondly, ASIC submits that Westpac had a heavy reliance on manual workarounds to its aging and complex IT systems which made its online hardship notices process vulnerable to human error and process deficiencies as evidenced by what has been termed Operational Failure A and Operational Failure C.

(c) Thirdly, ASIC submits that the manual interim control that Westpac put in place to rectify System Failure A caused what has been termed Operational Failure B in that it resulted in a number of online hardship notices not being received until 15 days after they were originally submitted by the customer. This, ASIC submits, was inefficient having regard to the timeframes stipulated by s 72(5) of the Code and Westpac’s financial hardship policies, which required Westpac to provide a written decision notice within 21 days of receiving the online hardship notice.

(d) Fourthly, ASIC submits that prior to the identification of System Failure A in 2022 Westpac adopted a siloed approach to fixing the root cause of this failure, evidenced by several internal incident and service tickets raised in 2018, 2020 and 2021 in respect of missing hardship notices and a 2023 audit report.

(e) Fifthly, ASIC submits that Westpac could have, but did not, undertake an end-to-end review of the processes from a systems and processes perspective prior to April 2023.

(f) Sixthly, ASIC submits that Westpac’s sustained underinvestment in what ASIC considers to be outdated and failing IT systems caused Westpac to remain technologically complex in comparison to its peers.

(g) Seventhly, ASIC notes that Westpac admits that on at least 61 occasions it declined an affected customer’s hardship notice on the basis that the customer had not provided sufficient information to assess their request, in circumstances where the customer’s online hardship notice, as affected by the system failures and/or operational failures, had provided sufficient information. ASIC submits that five of these occasions relate to the admitted contraventions of s 72(4) of the Code.

(h) Eighthly, ASIC submits that despite receiving 13 customer complaints between 13 March 2019 and 31 January 2022 (when System Failure A was formally identified) about ignored online hardship notices, including customers who complained twice, Westpac did not take any steps to determine whether there was a systemic issue. ASIC submits that this demonstrates that Westpac’s risk management processes were inadequate and ineffective at this time.

67 Further, ASIC submits that Westpac’s online hardship systems, processes and operations were unfair in two respects:

(a) First, ASIC contends that Westpac’s online hardship systems, processes and operations impacted a class of customers experiencing a personal or financial crisis of varying severity and there was also a level of randomness as to whether a customer’s hardship application would be impacted by any of the system and operational failures.

(b) Secondly, ASIC submits that because of the deficiencies in Westpac’s online hardship systems, processes and operations, Westpac issued default letters, recorded a default on a customer’s credit file, commenced enforcement proceedings and, or alternatively, referred a customer to third party debt collection despite those customers having previously applied for hardship relief.

68 ASIC submits that Westpac exacerbated affected customers’ personal and financial stress, and exposed those customers to further financial harm. ASIC notes that Westpac received several customer complaints in relation to default letters and notices as early as July 2018. In respect of enforcement proceedings, ASIC submits that Westpac risked contravening, or did in fact contravene, s 89A of the Code, and did not comply with the terms of its financial hardship policies in force between 16 July 2015 to 28 February 2023.

69 Finally, as to the matter of whether Westpac’s online hardship systems, processes and operations were honest, ASIC submits that Westpac was (or should have been) aware of the deficiencies in its systems, processes and operations, and its potential to affect customers experiencing financial hardship, and yet it persisted with those systems, processes and operations which exclusively impacted customers who were experiencing financial hardship. ASIC does not otherwise contend that Westpac’s conduct displayed actual dishonesty.

70 For substantially the reasons that ASIC submits, I accept that Westpac’s conduct fell well short of the reasonable standard of a credit licence holder which the public is entitled to expect, especially given Westpac’s size and resources and the commitments it has made under the Banking Code of Practice. In particular, I accept that Westpac failed to ensure that its credit activities were engaged in efficiently, honestly and fairly because Westpac:

(a) did not prioritise the funding and investment to upgrade and simplify its complex legacy IT systems until 2024, despite being on notice that online hardship notices were not being properly sent or received, including in circumstances where it had received multiple complaints on the subject; and

(b) delayed undertaking an end-to-end review of the processes from a systems and processes perspective until April 2023, and in this way did not take sufficient steps to guard against the risk that it would not give a written decision in response to an online hardship notice within the statutory timeframe prescribed by s 72(5) of the Code, or at all.

71 I am satisfied also that, as Westpac accepts, Westpac has contravened s 47(1)(a) by failing to:

(a) maintain adequate systems, controls and processes which ensured that online hardship notices given by customers were received by the Customer Assist team and written decision notices were given to customers within the timeframes prescribed by s 72(4) and (5) of the Code and to ensure as far as practicable that the contravening conduct did not occur; and

(b) conduct adequate risk reviews, investigations, monitoring and analysis of its online hardship notice systems and processes to enable it to identify any issues with its systems or processes, or otherwise to ensure that its online hardship notice systems and processes enabled compliance with s 72(4) and (5) of the Code.

DECLARATIONS

72 ASIC seeks declarations pursuant to s 21 of the Federal Court of Australia Act 1976 (Cth) (FCA Act) and s 166(2) of the Credit Act in respect of Westpac’s contravening conduct.

73 The court has a wide discretionary power to make declarations pursuant to s 21 of the FCA Act: ASIC v Commonwealth Bank of Australia at [152]; Australian Securities and Investments Commission v Financial Circle [2018] FCA 1644; 131 ACSR 484 at [155] (O’Callaghan J); Australian Securities and Investments Commission v Mercer Financial Advice (Australia) Pty Ltd [2023] FCA 1453 at [49] (McEvoy J) (ASIC v Mercer).

74 In Forster v Jododex Australia Pty Ltd [1972] HCA 61; 127 CLR 421, Gibbs J set out (at 437–438) the three requirements that should be satisfied before the discretion is exercised in favour of making a declaration as follows:

(a) the question must be a real and not a hypothetical or theoretical one;

(b) the applicant must have a real interest in raising it; and

(c) there must be a proper contradictor.

75 The language of s 166(2) of the Credit Act is mandatory. It requires the court to make a declaration of contravention if it is satisfied that a person has contravened a civil penalty provision of the Credit Act: see Australian Securities and Investments Commission v Australia and New Zealand Banking Group Limited [2023] FCA 256 at [41]–[46] (O’Bryan J).

76 The parties largely agree as to form of the declarations. As has been explained, there is a dispute in respect of the total number of online hardship notices specified in the declaration of a contravention of s 72 of the Code, and therefore about the period within which it is to be specified that Westpac’s contraventions of both s 72 of the Code and s 47 of the Credit Act occurred. For the reasons I have outlined, I accept ASIC’s submission that there was a total of 277 affected notice customers between the period of 2 October 2015 and 7 June 2023.

77 I have determined that the contraventions that are the subject of the proposed declarations are established by the facts set out in the SOAF and the admissions made by Westpac. I am satisfied, therefore, that declarations of contravention must be made: s 166(2) of the Credit Act. I accept also that there is utility in making declarations in the form proposed by ASIC and substantially agreed by Westpac. Their terms identify the contravening conduct with specificity and record the court’s disapproval of it. There will therefore be declarations substantially in the terms that ASIC proposes.

PECUNIARY PENALTY

Relevant principles

78 Sub-sections 167(1) and (2) of the Credit Act give the court power to order a pecuniary penalty in respect of a contravention of a civil penalty provision where a declaration of contravention pursuant to s 166 has been made.

79 The discretion to be applied in setting a pecuniary penalty must be guided by the relevant statutory provisions. Nevertheless, the legal principles that govern the assessment of the quantum of a pecuniary penalty that should be imposed for civil contraventions are well established. These principles may be summarised as follows.

80 First, the power to impose a penalty must be exercised judicially; that is, fairly and reasonably: Australian Building and Construction Commissioner v Pattinson [2022] HCA 13; 274 CLR 450 at [40] (Kiefel CJ, Gageler, Keane, Gordon, Steward and Gleeson JJ) (Pattinson).

81 Secondly, the primary or sole purpose of civil penalties is deterrence, both specific and general: Pattinson at [9]–[10], [15]–[18]; Commonwealth of Australia v Director, Fair Work Building Industry Inspectorate [2015] HCA 46; 258 CLR 482 at [55] (French CJ, Kiefel, Bell, Nettle and Gordon JJ) (Agreed Penalties Case), referring to Trade Practices Commission v CSR Ltd [1990] FCA 762; [1991] ATPR 41-076 at 52,152 (French J) (CSR). See also Australian Securities and Investments Commission v Adler [2002] NSWSC 483; 42 ACSR 80 at [125]–[126] (Santow J). As I observed in ASIC v Mercer at [64], specific deterrence is concerned with deterring repetition of the contravening conduct by the contravener and general deterrence is concerned with deterring others who might be tempted to engage in similar contraventions: see Pattinson at [9], [15], [42], [47]–[48]. Penalties will be imposed to promote the public interest in compliance, and should be no greater than necessary to achieve the objectives of deterrence: Agreed Penalties Case at [55], referring to CSR at 52,152; Pattinson at [10], [40]. It is trite to observe that the object of pecuniary penalties does not include retribution, denunciation or rehabilitation: Pattinson at [15]–[16].

82 Thirdly, while the civil penalty should not be so high that it is oppressive, it should not be so low as to be regarded by the contravener as “an acceptable cost of doing business”: ASIC v Mercer at [65], citing Pattinson at [17], [40]–[41]; Australian Building and Construction Commission v Construction, Forestry, Mining and Energy Union [2018] HCA 3; 262 CLR 157 at [116] (Keane, Nettle and Gordon JJ); Australian Competition and Consumer Commission v TPG Internet Pty Ltd [2013] HCA 54; 250 CLR 640 at [66] (French CJ, Crennan, Bell and Keane JJ); Singtel Optus Pty Ltd v Australian Competition and Consumer Commission [2012] FCAFC 20; 287 ALR 249 at [62]–[63] (Keane CJ, Finn and Gilmour JJ) (Singtel Optus); NW Frozen Foods Pty Ltd v Australian Competition and Consumer Commission [1996] FCA 1134; 71 FCR 285 at 293 (Burchett and Kiefel JJ) (NW Frozen Foods); Australian Securities and Investments Commission v Westpac Banking Corporation [2019] FCA 2147 at [255] (Wigney J) (ASIC v Westpac Banking). The penalty must be “proportionate” and “appropriate” in the sense that it strikes a reasonable balance between oppressive severity and deterrence in the circumstances of the case: Pattinson at [40]–[41], [46].