FEDERAL COURT OF AUSTRALIA

United Petroleum Pty Ltd v Perth Airport Pty Ltd (No 2) [2026] FCA 620

File number(s): | VID 260 of 2022 |

Judgment of: | ANDERSON J |

Date of judgment: | 20 May 2026 |

Catchwords: | CONSUMER LAW – misleading and deceptive conduct – whether statements in information brochure and in-person meeting as to when Qantas would relocate terminals at Perth Airport were misleading – representations were with respect of future matter and not merely statements as to an expectation or state of mind – whether applicant relied on representations – whether representations caused applicant to enter into transaction – whether applicant would have sought to agree alternative transaction. LOSS AND DAMAGE – which party bears the legal and evidentiary onus – consideration of Potts v Miller analysis in an alternative transaction case – what is the relevant loss claimed – whether applicant needs to show value of income-producing asset. EVIDENCE – where misleading conduct plead on part of corporation – consideration of relevant decision-maker within corporation and attribution of knowledge for the purposes of reasonable grounds in s 4 of the Australian Consumer Law– where no board member from respondent gave evidence – consideration of Jones v Dunkel and Blatch v Alder. PLEADINGS AND PROCEDURE – whether loss of opportunity case advanced by applicant prior to closing submissions – whether any denial of procedural fairness for plaintiff to rely on loss of opportunity case. |

Legislation: | Competition and Consumer Act 2010 (Cth), sch 2 (Australian Consumer Law) ss 18, 236, 237. Trade Practices Act 1974 (Cth) |

Cases cited: | Ackers v Austcorp International Ltd [2009] FCA 432 Aldi Foods Pty Ltd v Moroccanoil Israel Ltd (2018) 261 FCR 301; [2018] FCAFC 93 Attard v James Legal Pty Ltd (2010) 80 ACSR 585; [2010] NSWCA 311 Australian Competition and Consumer Commission v Danoz Direct Pty Ltd (2003) 60 IPR 296; [2003] FCA 881 Australian Competition and Consumer Commission v ACM Group Ltd (No 2) [2018] FCA 1115 Australian Competition and Consumer Commission v Kimberly-Clark Australia Pty Ltd [2019] FCA 992 Australian Competition and Consumer Commission v TPG Internet Pty Ltd (2013) 250 CLR 640 Australian Competition and Consumer Commission v Woolworths Group Limited (2020) 281 FCR 108; [2020] FCAFC 162 Australian Competition and Consumer Commission v Woolworths Ltd [2019] FCA 1039 Australian Securities and Investments Commission v GetSwift Ltd [2021] FCA 1384 Australian Securities and Investments Commission v Retail Employees Superannuation Pty Ltd [2024] FCA 1081 Auswest Timbers Pty Ltd v. Secretary to the Department of Sustainability & Environment [2010] VSC 389 Bathurst Regional Council v Local Government Financial Services Pty Ltd (No 5) [2012] FCA 1200 Berry v CCL Secure Pty Ltd (2020) 271 CLR 151; [2020] HCA 27, Blatch v Archer (1774) 1 Cowp 63; (1774) 98 ER 969 Brambles Holdings Ltd v Carey (1976) 15 SASR 270 Butcher v Lachlan Elder Realty Pty Ltd (2004) 218 CLR 592; [2004] HCA 60 Campbell v Backoffice Investments Pty Ltd (2009) 238 CLR 304; [2009] HCA 25 Cash Bazaar Pty Ltd v RAA Consults Pty Ltd (No 2) (2020) 381 ALR 668; [2020] FCA 636 City of Botany Bay Council v Jazabas Pty Ltd [2001] NSWCA 94 Crowley v Worley Ltd (2022) 293 FCR 428; [2022] FCAFC 33 Demagogue Pty Ltd v Ramensky (1992) 39 FCR 31 Digi-Tech (Australia) Ltd v Brand [2004] NSWCA 58; (2004) 62 IPR 184 Fox v Percy (2003) 214 CLR 118; [2003] HCA 22 Fraser v NRMA Holdings Ltd (1995) 55 FCR 452 Gates v City Mutual Life Assurance Society Ltd (1986) 160 CLR 1; [1986] HCA 3 Girchow Enterprises Pty Ltd v Ultimate Franchising Group Pty Ltd (Final Hearing) [2023] FCA 420 GlaxoSmithKline Australia Pty Ltd v Reckitt Benckiser (Australia) Pty Ltd (No 2) (2018) 133 IPR 190; [2018] FCA 1 Gould v Vaggelas (1985) 157 CLR 215; [1985] HCA 75 Henville v Walker (2001) 206 CLR 459; [2001] HCA 52 HTW Valuers (Central Qld) Pty Ltd v Astonland Pty ltd (2004) 217 CLR 640; [2004] HCA 54 Husseini v Girchow Enterprises Pty Ltd [2024] FCAFC 143 Ingot Capital Investments Pty Ltd v Macquarie Equity Capital Market Ltd (2008) 73 NSWLR 653 International Assets Pty Ltd (as Trustee for Stavroula Family Trust) v Rubin [2025] VSC 454 Ireland v WG Riverview Pty Ltd (2019) 101 NSWLR 658; [2019] NSWCA 307 Jafari v 23 Developments Pty Ltd [2018] VSC 404 JLW (Vic) Pty Ltd v Tsiloglou [1994] 1 VR 237 Jones v Dunkel (1959) 101 CLR 298; [1959] HCA 8 Krakowski v Eurolynx Properties Ltd 183 CLR 563; [1995] HCA 68 Lam v Ausintel Investments Australia Pty Limited (1989) 97 FLR 458 Lantrak Holdings v Yammine [2023] FCAFC 156 Lloyd v Belconnen Lakeview [2019] FCA 2177; (2019) 142 ACSR 445 Lonergan v JQZ Eleven Pty Ltd (2022) 21 BPR 44,211; [2022] NSWSC 1461 MA & J Tripodi Pty Ltd v Swan Hill Chemicals Pty Ltd [2019] VSCA 46 Marks v GIO Australia Holdings Ltd (1998) 196 CLR 494; [1998] HCA 69 Martin v Norton Rose Fulbright Australia (2021) 289 FCR 369; [2021] FCAFC 216 McGrath v Australian Naturalcare Products Pty Ltd (2008) 165 FCR 230; [2008] FCAFC 2 Miller & Associates Insurance Broking Pty Ltd v BMW Australia Finance Limited (2010) 241 CLR 357; [2010] HCA 31 North East Equity Pty Ltd v Proud Nominees Pty Ltd (2010) 269 ALR 262; [2010] FCAFC 60 Potts v Miller (1940) 64 CLR 282 Protec Pacific Pty Ltd v Steuler Services GmbH & Co KG [2014] VSCA 338 QVB Pharmacy Pty Ltd v Le [2022] NSWSC 1612 Re Day (2017) 340 ALR 368; [2017] HCA 2 Re HIH Insurance Ltd (in liq) (2016) 335 ALR 320 Ricochet Pty Ltd v Equity Trustees Executor & Agency Co Ltd (1993) 41 FCR 229 Samsung Electronics Australia Pty Ltd v LG Electronics Australia Pty Ltd (2015) 113 IPR 11; [2015] FCA 227 Self Care IP Holdings Pty Ltd v Allergan Australia Pty Ltd (2023) 277 CLR 186; [2023] HCA 8 Sidhu v van Dyck (2014) 251 CLR 505; [2014] HCA 19 Taco Co of Australia Inc v Taco Bell Pty Ltd (1982) 42 ALR 177 TPT Patrol Pty Ltd v Myer Holdings Ltd (2019) 293 FCR 29; [2019] FCA 1747 Viterra Malt Pty Ltd & Others v Cargil Australia Ltd (2023) 74 VR 1; [2023] VSCA 157 Watson v Foxman (1995) 49 NSWLR 315 Wilson v Arwon Finance Pty Ltd [2020] WASC 137 Wormald v Maradaca Pty Ltd [2020] NSWCA 289 |

Division: | General Division |

Registry: | Victoria |

National Practice Area: | Commercial and Corporations |

Sub-area: | Commercial Contracts, Banking, Finance and Insurance |

Number of paragraphs: | 613 |

Date of last submission/s: | 2 October 2025 |

Date of hearing: | 8-11, 15, 17, 23-25 September 2025 |

Counsel for the Applicants: | Mr N de Young KC and Mr S Jenkins |

Solicitor for the Applicants: | Norton Rose Fulbright |

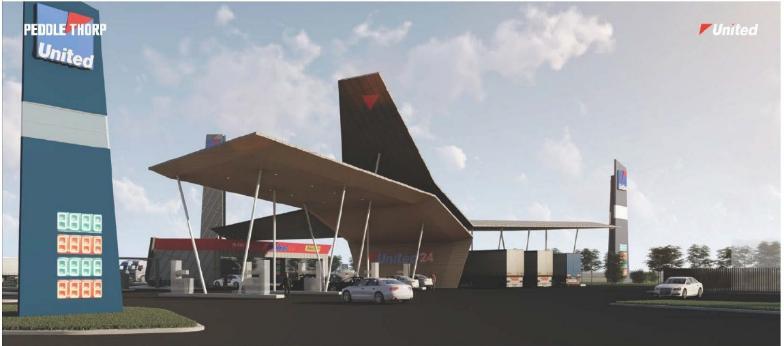

Counsel for the Respondent: | Ms J Taylor SC, Mr P Walker and Mr B Willesee |

Solicitor for the Respondent: | Allens |

ORDERS

VID 260 of 2022 | ||

| ||

BETWEEN: | UNITED PETROLEUM PTY LTD (ACN 085 779 255) First Applicant UNITED PETROLEUM AUSTRALIA PTY LTD (ACN 164 398 832) Second Applicant | |

AND: | PERTH AIRPORT PTY LTD (ACN 077 153 130) Respondent | |

order made by: | ANDERSON J |

DATE OF ORDER: | 20 May 2026 |

THE COURT ORDERS THAT:

1. Judgment is entered in favour of the Applicants.

2. The parties are to confer and submit to the chambers of the Honourable Justice Anderson proposed minutes of orders that reflect and give effect to the reasons for judgment published today and quantify United’s loss and damage, interest and costs by 20 July 2026.

3. In the event the parties are unable to reach agreement, the parties are to file, in mark up, draft orders identifying the points of difference each proposes together with written submissions limited to 4 pages in support of their respective positions.

4. The proceeding be stood over for case management at 9:30 am on 28 July 2026.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

ANDERSON J:

INTRODUCTION | [1] |

BACKGROUND | [8] |

UNITED’S PLEADED CASE | [38] |

PAPL’S DEFENCE | [41] |

AGREED LIST OF ISSUES FOR DETERMINATION AT TRIAL | [42] |

UNITED’S LAY EVIDENCE | [43] |

Avi Silver | [43] |

Eddie Hirsch | [77] |

Gary Brinkworth | [95] |

David Szymczak | [142] |

Adam Marsland | [185] |

Claude Mestrov | [186] |

PAPL’S LAY EVIDENCE | [188] |

David Skinner | [188] |

Steve Holden | [233] |

Ian Barker | [263] |

Natasha Boshard | [267] |

EXPERT EVIDENCE | [285] |

Valuation evidence | [286] |

Economic Evidence | [325] |

Quantity Surveyors | [333] |

GENERAL PRINCIPLES ON MISLEADING AND DECEPTIVE CONDUCT | [339] |

ISSUES 1 TO 3 - WHETHER PAPL MADE THE REPRESENTATIONS TO UNITED | [346] |

The Information Brochure | [347] |

The Oral Representations | [395] |

Post AFSL Representations | [419] |

Conclusion on Issues 1 to 3 | [436] |

ISSUE 4: REPRESENTATIONS WITH RESPECT TO FUTURE MATTERS | [439] |

ISSUES 5 AND 6: DID PAPL HAVE REASONABLE GROUNDS TO MAKE THE REPRESENTATIONS? | [448] |

Applicable principles | [448] |

PAPL’s Submissions | [454] |

Consideration | [460] |

ISSUE 7 – DID PAPL ENGAGE IN MISLEADING OR DECEPTIVE CONDUCT BY SILENCE? | [513] |

Relevant Principles | [514] |

ISSUES 8 TO 11 – DID UNITED RELY ON PAPL’S REPRESENTATIONS? | [526] |

General principles on reliance | [526] |

United’s pleaded case on reliance | [531] |

United’s key decision makers | [534] |

ISSUES 12 TO 14: DID UNITED SUFFER LOSS AND DAMAGE BECAUSE OF PAPL’S CONDUCT | [552] |

Principles on causation and loss | [552] |

United’s case on loss and damage | [557] |

Expert evidence on loss and damage | [569] |

Analysis of loss and damage | [580] |

Factual findings on causation and the counterfactual | [594] |

Excess rent | [611] |

Excess construction costs | [612] |

DISPOSITION | [613] |

ANNEXURE A – GLOSSARY OF TERMS |

INTRODUCTION

1 This proceeding is brought by United Petroleum Pty Ltd, together with one of its related entities, United Petroleum Australia Pty Ltd (collectively, United or the United Parties), against Perth Airport Pty Ltd (PAPL) for damages alleged to arise out of PAPL’s misleading or deceptive conduct in contravention of s 18 of the Australian Consumer Law (ACL), being Sch 2 of the Competition and Consumer Act 2010 (Cth).

2 The proceeding concerns PAPL and United entering into an Agreement for Sublease dated 17 April 2019 (AFSL), and a sublease dated 17 May 2021 (Sublease), to lease and develop, a service station site on Airport Drive at Perth Airport in Western Australia (Site). This type of lease is known as a Ground Lease – being a lease where the tenant is responsible for developing and maintaining any buildings and improvements to the land; whilst the lessor owns the land, the lessee owns any improvements and buildings on the land. United leased the Site for an initial term of 15 years from July 2020 at $900,000 per annum, with a 3% increase per annum until 2035. The United service station was designed and constructed by United at a cost of $7,721,182.67 (Perth Airport Service Station).

3 The United Parties allege that PAPL made representations to the effect that Qantas Airways Ltd (Qantas) will or is expected to relocate all its domestic and international terminals from Airport West to Airport Central by 2025 or the mid to late 2020s (Qantas Relocation) which will or is expected to result in certain traffic volumes at the site on Airport Central. The United Parties allege that the written request for tender documents provided to United by PAPL represented that traffic volumes will “almost double” on Airport Drive where the Site is located once the Qantas Relocation occurs.

4 The United Parties allege that PAPL’s representations were misleading and deceptive. In addition, the United Parties allege that PAPL engaged in misleading or deceptive conduct because PAPL withheld certain information from United that was critical to the representations. The United Parties allege that PAPL did not have the expectations represented. The United Parties contend that this was because the Qantas Relocation and the traffic volumes as represented were matters of mere assumption, planning or conjecture, and those matters would have been revealed had PAPL disclosed all relevant matters to United.

5 United alleges that it has suffered loss and damage because of PAPL’s misleading or deceptive conduct. The alleged misleading and deceptive conduct is said to have occurred primarily prior to the execution of the AFSL and Sublease. But for the impugned conduct, United asserts it would not have gone ahead with the AFSL and Sublease in their current form but would instead have negotiated with PAPL and agreed to a more favourable transaction. United alleges that under this alternative transaction, it would have constructed a smaller, cheaper service station and agreed to a lower rent of not more than $500,000 per annum.

6 PAPL denies that it engaged in any misleading or deceptive conduct in connection with the AFSL or the Sublease. PAPL contends that United entered into the transaction with PAPL without reliance on any alleged representation or failure by PAPL to disclose any relevant matters.

7 PAPL contends that United now holds a valuable long-term leasehold interest in an area the subject of continued commercial development and that United cannot prove any actionable loss by reason of the misleading or deceptive conduct that it alleges.

BACKGROUND

8 Perth Airport is located about 30 minutes from the Perth central business district and is spread over 2,000 ha. The terminals that make up Perth Airport have undergone significant change over the last decade or so.

9 Perth Airport was historically separated into the International Precinct and the Domestic Precinct. As of 2023 , the area of the airport contained (a) the ‘Airport Central’ precinct (Terminals 1 and 2); and (b) the ‘Airport West’ precinct (Terminals 3 and 4).

10 Qantas is the largest airline operating at the airport. Currently it operates its domestic and international services from the Airport West precinct (Terminals 3 and 4). Jetstar, which is a wholly-owned subsidiary of Qantas, operated its domestic services from Terminal 3 in the Airport West precinct and its international services from Terminal 1 in Airport Central until 2 September 2024 when Jetstar started operating its domestic services from Terminal 2 in Airport Central. Network Aviation, another wholly-owned subsidiary of Qantas, operates domestic services from Airport West. It also operates some charter flights from what is known as the ‘General Aviation’ area.

11 Since the 1980s, there have been plans to consolidate all commercial passenger services at the Perth Airport into one terminal. The 1985 Airport Master Plan included, under the heading “Terminal Area Concept”, a statement that the “Eastern Terminal Area – is the preferred location for airline terminals … The Master Plan therefore is based on the ultimate location of all airline passenger terminal facilities in the Eastern Terminal Area”. The Eastern Terminal Area is what is now known as Airport Central. This concept of relocating all passenger terminal facilities to Airport Central is referred to as either Consolidation or, in the context of this proceeding, the Qantas Relocation.

12 On or about 1 May 2008 PAPL released a paper entitled, “Vision for the Future”, identifying the plan to merge Perth Airport into a single hub around the existing International Terminal, also being Airport Central.

13 By November 2009, PAPL had released the 2009 Master Plan identifying the plan to consolidate all large regular passenger transport air services into the current International Precinct (ie, the Eastern Terminal Area) in stages, commencing 2012.

14 In 2014, PAPL released its 2014 Master Plan stating that “the final stage of consolidation of all commercial air services will occur early 2020s, when new facilities are constructed in Airport Central for Qantas Airways Group operations” and that “Consolidation … will dramatically alter where and how vehicles and people access Perth Airport.”

15 On 10 December 2016, PAPL and Qantas entered into a Heads of Agreement in which they agreed, amongst other things, to use “Best Endeavours … to achieve Consolidation, on commercial terms to be agreed, by no later than 31 December 2025” (Qantas Heads of Agreement).

16 On 22 February 2017, the PAPL board approved “Airport Central Master Plan 16”, which included steps to achieve Consolidation and relocation of Qantas to Airport Central by 31 December 2025, and “endorsed expenditure of $5.2 million to progress projects through the initial phase”.

17 In April 2017, United engaged Peddle Thorp Architects to design the service station to be built at the Site (that is, the Perth Airport Service Station). That design, with distinctive ‘wings’ was at times referred to as the Millennium Concept. The image below, from a Peddle Thorp planning document, demonstrates the distinctiveness of the design:

18 On 4 May 2017, PAPL and Qantas entered into the Terminal 3 Development Agreement, which included a mutual obligation on the parties to use “Best Endeavours” to achieve Consolidation by 31 December 2025 (Development Agreement).

19 On 30 May 2017, the PAPL board approved capital plans based on Consolidation occurring by 2025.

20 On 6 July 2017, Mr David Skinner, the Senior Property Manager in the Property Team at PAPL (whose job title was Senior Leasing & Development Manager up to May 2023), sent by email to United, the following documents:

(a) a document entitled “Request for Proposals – Airport Central Precinct Service Station” (the RFP); and

(b) a document entitled “Information Brochure – Airport Service Station Opportunity” (the Information Brochure).

21 The Information Brochure invited tender recipients to submit a proposal for either a:

(a) Building Lease (also known as a Top Lease), whereby PAPL would construct and lease a base building to the tenant and the tenant would be responsible for the fit out and operation of the service station; or

(b) Ground Lease, whereby PAPL would lease the land to the tenant, and the tenant would construct, fit out, and operate the service station.

22 The Information Brochure said PAPL “will require a minimum initial lease of 15 years”, and “has a preference of a Ground Lease”. The proposed site was to be located within the Airport Central Precinct, at the corner of Airport Drive and Paltridge Road, where the Site is now located – although the Site is larger than the proposed site in the Information Brochure (being 8,879 m2).

23 On 14 July 2017, Mr Skinner emailed a document called “Addenda 1” (Addenda 1) to Mr Sam Carmeli, the National Acquisitions Manager at United. The Addenda 1 contained questions that PAPL had been asked by various parties that were interested in submitting a tender and PAPL’s answers to those questions. Addenda 1 also annexed a copy of the Perth Airport’s design guidelines (Design Guidelines).

24 On 4 August 2017, Darren Searle, who was the Executive General Manager of United, sent an email to Mr Skinner submitting United’s tender for the Site.

25 On 1 October 2017, PAPL released a Capital Expenditure Plan reflecting Consolidation by December 2025.

26 On 22 November 2017, PAPL provided a lease proposal to United.

27 A meeting occurred on 27 February 2018, which assumed importance in this proceeding. The meeting occurred in-person at Perth Airport. Mr Gary Brinkworth, United’s Chief Executive Officer (CEO) at the time, attended on behalf of United. Mr Skinner attended on behalf of PAPL. A matter of controversy between the parties was whether Mr Steve Holden, PAPL’s Chief Commercial Officer (COO) at the time also attended on behalf of PAPL, and if so for how long, and whether Mr Geoff Manolitsa, United’s General Counsel at the time attended the meeting. Mr Skinner and Mr Holden are alleged to have made misleading representations at this meeting concerning the Qantas Relocation. The meeting predated the execution of the AFSL (April 2019) and the Sublease (May 2021). On 13 April 2018, PAPL and United executed a Heads of Agreement for a sublease for the Site.

28 On 17 April 2019, PAPL and United executed the AFSL.

29 On 30 October 2019, PAPL informed United that it had satisfied PAPL’s Approvals Condition under the AFSL.

30 On 13 January 2020, United informed PAPL that it had satisfied United’s Approvals Condition under the AFSL.

31 On 3 July 2020, PAPL issued Notices of Practical Completion for PAPL’s works under the AFSL.

32 On 23 July 2020, PAPL wrote to United, giving notice that the Sublease Commencement Date would be 24 July 2020.

33 On 17 May 2021, PAPL and United executed the Sublease.

34 These reasons define the Relevant Period as 6 July 2017, the date Mr Skinner sent the tender documents to United, to 17 April 2019, the date that PAPL and United executed the AFSL. Whilst United has alleged misleading and deceptive conduct in respect of conduct after this date, I have found that the misleading conduct lapsed upon the execution of the AFSL, and for that reason I define the Relevant Period as ending on 17 April 2019.

35 It is helpful at this stage to set out who the key players are from each party to the dispute:

(a) Mr Avi Silver: co-founder and director of United;

(b) Mr Eddie Hirsch: co-founder and director of United;

(c) Mr Gary Brinkworth: Group CEO of United from October 2016, until 31 January 2020;

(d) Mr David Szymczak: current CEO of United (and has held that position since July 2020). Prior to that he was the COO of United;

(e) Mr David Skinner: Senior Property Development Manager in PAPL’s Property team, a position he has held since 2012 (although under different titles); and

(f) Mr Steve Holden: COO/Chief Property Officer at PAPL until he left United in April 2022.

36 These reasons use the term the Perth Airport Project when referring to the consideration and work by United of its tender for the Site.

37 It is also helpful at this point to understand the layout of the Perth Airport area and the Site. The below image shows the Perth Airport area as at September 2017 (about 2 months after United received the tender documents), showing the Airport West and Airport Central precincts and the Site (at that point, still prospective).

UNITED’S PLEADED CASE

38 In its Amended Statement of Claim filed on 8 December 2023 (ASOC), United alleges the following claims:

(a) Before United entered into the AFSL and before United entered into the Sublease, PAPL represented to United that:

(i) As part of PAPL’s consolidation of commercial air services in Airport Central, Qantas will relocate all its domestic and international flights from Terminals 3 and 4 in Airport West to Airport Central (being the Qantas Relocation) by:

(A) 2025; and

(B) further and alternatively, by the mid to late 2020s.

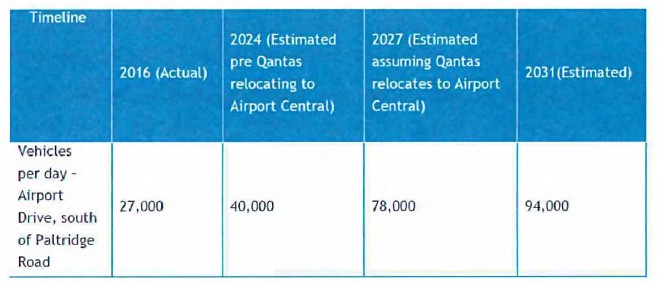

(ii) When the Qantas Relocation is complete, traffic volumes on Airport Drive, a road abutting the Site, will almost double from the estimated 40,000 vehicles per day in 2024 to 78,000 vehicles per day, and ultimately to an estimated 94,000 vehicles per day by 2031.

(collectively, the Qantas Representations).

(b) Further or alternatively, before United agreed to the AFSL and entered into the Sublease, and in order to induce the United Parties to do so, PAPL represented to the United Parties that:

(i) Qantas Group is expected to relocate all international and domestic flights from Terminal 3 and Terminal 4 located at Airport West, to Airport Central in the mid to late 2020s completing the consolidation of commercial air services in Airport Central; and

(ii) When Qantas relocates from Airport West to Airport Central in the mid to late 2020s it is expected that traffic volumes will almost double on Airport Drive from 40,000 to 78,000 per day;

(iii) PAPL in fact held the expectations, opinions or states of mind set out in (a) and (b); and

(iv) PAPL had reasonable grounds for the expectations, opinions or states of mind (the Further Representations).

(c) The Qantas Representations and Further Representations (collectively the Representations) were continuing representations;

(d) United entered into the AFSL in April 2019 and the Sublease in May 2021 in reliance on the Representations;

(e) The Representations were:

(i) representations with respect to future matters within the meaning of s 4 of the ACL;

(ii) misleading or deceptive, in that PAPL:

(A) did not expect Qantas to relocate to Airport Central in the mid to late 2020s and did not expect that traffic volumes would almost double on Airport Drive from 40,000 to 78,000 per day; and

(B) did not have reasonable grounds to hold such an expectation, opinion or state of mind;

(f) At no time prior to the execution of the AFSL and the Sublease did PAPL disclose the matters set out in Annexure A (Relevant Matters) to United, which may be summarised as:

(i) PAPL had not identified the person or persons within PAPL who held the belief that Qantas would relocate by 2025, or by the mid to late 2020s and the grounds upon which they held that belief;

(ii) Qantas’ refusal to provide a binding commitment to achieve Consolidation by 2025;

(iii) Qantas needed to reach, but had not reached, agreement with PAPL on the commercial terms for Consolidation by 2025;

(iv) after reaching agreement on the commercial terms, there were a number of steps required by Qantas and PAPL to achieve Consolidation, including significantly, agreement on design plans, the expected cost to Qantas, and the forecast demand of the new terminal;

(v) by March 2018, Qantas and PAPL had only agreed to use best endeavours and work in good faith to reach agreement on commercial terms for Consolidation;

(vi) numerous and ongoing disputes between Qantas and PAPL from at least April 2018, including in relation to the expenditure on the Terminal 1 upgrade (referred to as STEP), whether Qantas should be liable for capital expenditure on non-aeronautical upgrades required for Consolidation, and the use and cost of Terminal 3, which culminated in proceedings being commenced by PAPL against Qantas in the Supreme Court of Western Australia on 17 December 2018;

(vii) in or around 2018, Qantas raised concerns with PAPL about the references to Qantas relocating to Airport Central in 2025 in PAPL’s Exposure Draft of the Perth Airport 2020 Master Plan;

(viii) as at June 2018, PAPL had only prepared a roadmap for Consolidation, which required completion of a number of significant steps, and Qantas and PAPL failed to meet those milestones after June 2018;

(ix) PAPL and Qantas’ continuing disagreements about Consolidation layouts in 2018 through to December 2021;

(x) between December 2018 and 13 September 2021, Qantas maintained there was no enforceable obligation requiring it to relocate to Airport Central by 31 December 2025, that PAPL was neither proposing nor able to effect such a relocation by that date, and that Qantas had sufficient capacity to continue operating from Terminals 3 and 4 until at least 2030; and

(xi) disputes between PAPL and Qantas in 2020 and onwards in relation to Consolidation, including pricing, construction and leasing arrangements, and the useful life of Terminals 3 and 4.

(g) By making the Representations and by failing to disclose the Relevant Matters, PAPL contravened s 18(1) of the ACL; and

(h) United has suffered loss and damage, because of PAPL’s misleading or deceptive conduct.

39 The pleaded Qantas Representations are said to have been conveyed by the following conduct:

(a) the provision of the Information Brochure and the RFP as part of the tender process;

(b) statements made by PAPL representatives to United representatives in the course of negotiations for the Sublease, in particular at a meeting on 27 February 2018;

(c) written correspondence sent by PAPL to United dated 7 August 2020; and

(d) the publication of a press release by PAPL on its website dated 10 March 2020 (and published on or around 10 or 11 March 2020).

40 In contrast, the Further Representations are only pleaded as having been conveyed by the provision of the Information Brochure and the RFP as part of the tender process.

PAPL’S DEFENCE

41 By its Amended Defence, filed on 22 December 2023, PAPL denies that it engaged in any misleading or deceptive conduct in connection with the AFSL or the Sublease, and contends that United entered into the transaction with PAPL without reliance on any of the alleged Representations or failure by PAPL to disclose the Relevant Matters.

AGREED LIST OF ISSUES FOR DETERMINATION AT TRIAL

42 The parties agreed that the following list of issues arise out of the pleadings and identified the matters requiring determination (using the parties’ exact wording):

# | Issue | ||

Was there misleading conduct? | |||

1 | Was there a representation made by PAPL to United as pleaded at ASOC [11] or [11A]? If so, when was it made? | ||

(a) | Did the Information Brochure convey the Qantas Representations or the Further Representations to United? | ||

(b) | Did Mr Skinner or Mr Holden convey the Qantas Representations to United at a meeting on 27 February 2018? | ||

(c) | Did the 11 March 2020 press release convey the Qantas Representations to United? | ||

(d) | Did the 7 August 2020 letter from PAPL to Lavan convey the Qantas Representations or the Further Representations to United? | ||

2 | If one or more of the Qantas Representations were made to United, were they a representation to the effect that Qantas will relocate: | ||

(a) | by 2025; or | ||

(b) | by the mid to late 2020s? | ||

3 | If one or more of the Qantas Representations or Further Representations were made to United, were they representations of a continuing nature? If so – | ||

(a) | Did any representation continue beyond the date United submitted its tender (4 August 2017)? | ||

(b) | Did any representation continue beyond the date the AFSL was signed (17 April 2019)? | ||

(c) | Did any representation continue beyond the date the Sublease commenced (24 July 2020)? | ||

4 | If one or more of the Qantas Representations or Further Representations were made to United, were they representations with respect to a future matter for the purposes of s 4(1) of the ACL? | ||

5 | If one or more of the Qantas Representations or Further Representations were made to United, and if one or more of the Representations was with respect to a future matter: | ||

(a) | has evidence been adduced by PAPL to the contrary of the proposition that PAPL did not have reasonable grounds for making the Representations as required by s 4(2) of the ACL as alleged in the Defence [16A(b)(ii)]; | ||

(b) | if so, has United otherwise proven that the PAPL did not have reasonable grounds for making the Representations as alleged in ASOC [16A(c)]? | ||

(c) | [PAPL proposes the following additional sub-issue] Whose grounds, within PAPL, are relevant in determining whether PAPL had reasonable grounds for making the Representations? | ||

6 | If one or more of the Further Representations were made to United: and if one or more of the Representations were not with respect to a future matter, did PAPL hold the expectation reflected in the statements as alleged in ASOC [16A(a)] and [16A(b)]: see Defence [16A(b)(i)]. | ||

7 | Did PAPL engage in misleading or deceptive conduct by silence? | ||

(a) | Was there a reasonable expectation that PAPL would disclose any or all of the Relevant Matters to United? | ||

(b) | If so: | ||

(i) | which Relevant Matters that PAPL should have disclosed to United did it not disclose; and | ||

(ii) | was the failure to disclose such Relevant Matters misleading or deceptive? | ||

If there was misleading conduct, did United rely on it? | |||

8 | [United proposes this issue. PAPL considers it is covered by issue 9 below] If one or more of the Qantas Representations or Further Representations were made to United, did United rely on the representation in: | ||

(a) | entering into the AFSL; | ||

(b) | entering into the Sublease; and/or | ||

(c) | carrying out the Lessee’s Works in accordance with the AFSL? | ||

9 | But for the Qantas Representations and/or the Further Representations, would the United Parties: | ||

(a) | not have entered the AFSL; | ||

(b) | not have entered into the Sublease; | ||

(c) | not have agreed to carry out the Lessee’s Works in accordance with the AFSL in their current form but rather or would they have only agreed to build a substantially smaller and cheaper service station, or not have commenced the works at all from 23 July 2020; | ||

(d) | have sought to negotiate more favourable terms in respect of the Sublease, as to lower rent and United Parties’ standard lease terms (including a force majeure clause); and/or | ||

(e) | not have agreed to lease the Site in respect of the Sublease unless the rent was reduced to approximately $500,000 per annum? | ||

If so, how and at what point in time? | |||

10 | If PAPL had disclosed to United any of the Relevant Matters that should have been disclosed, would United have taken any of the steps in (a) to (d) above? If so, how and at what point in time? | ||

11 | If or to the extent that, by reason of the Qantas Representations and/or the Further Representations, or the alleged non-disclosure of the Relevant Matters, the United Parties would have wished to do any or all of (a) to (d) above following entry into the AFSL and/or Sublease, could the United Parties have done so in light of the terms of the AFSL and/or Sublease (pleaded in the Defence at [8]-[10])? | ||

Causation and loss/damage | |||

12 | But for the Representations and/or PAPL's failure to disclose any Relevant Matters that should have been disclosed: | ||

(a) | would United and PAPL have entered any transaction? | ||

(b) | alternatively, would United and PAPL have entered an alternative commercial transaction – and if so, on what terms? | ||

13 | If United and PAPL would not have entered the transaction at all, what loss, if any, has United proved that it has suffered by entering the transaction that it did? | ||

14 | Alternatively, if United and PAPL would have entered an alternative commercial transaction, what loss, if any, has United proved that it has suffered by not entering that transaction as compared to the one it did enter? | ||

UNITED’S LAY EVIDENCE

Avi Silver

43 Avi Silver (Mr Silver) gave evidence that he is a director of both applicants, collectively, the United Parties, having held that position since both companies were incorporated in 1999 in the case of United Petroleum, and in 2013, in the case of United Petroleum Australia. United Petroleum Australia is the holding company of United Petroleum. United tendered one witness statement of Mr Silver dated 12 July 2023.

44 Mr Silver’s evidence was that United is an Australian fuel retailer and importer. United has a network of approximately 450 service stations across Australia and employs approximately 330 employees throughout Australia.

45 United’s business was established in 1993 with the opening of a chain of service stations and convenience stores in South Australia by Mr Silver’s business partner, Mr Eddie Hirsch. Mr Silver and Mr Hirsch expanded its operations into Victoria and over the next two years built networks in New South Wales, the Australian Capital Territory, and Queensland. United now runs a vertically integrated business after acquiring fuel import terminals in the mid-2000s in Victoria, New South Wales, Queensland, Northern Territory and Tasmania. United both constructs petrol stations as well as purchasing existing petrol stations. United is a privately held corporation which is owned equally by Mr Silver and Mr Hirsch (through their respective wholly-owned corporate vehicles). The key business decisions are made by both Mr Silver and Mr Hirsch. United’s business is structured so that key management personnel report to Mr Silver and Mr Hirsch. These management roles are occupied by the CEO, COO, and various other senior managerial positions.

46 Mr Silver holds a commercial building licence and an associated entity of United also holds a builder’s licence. Between 2018 and 2020, United completed the construction of 29 service stations throughout Australia under design and construct contracts. The construction costs for these service stations varied between $1.8 million and $5.7 million depending upon the size and the facilities offered at the service station site.

47 The Perth Airport Service Station is a flagship service station of United. It was designed by architects, Peddle Thorp, to have a unique design, being aeroplane wings as a canopy and an aeroplane tail to display United’s name and logo (ie, the Millennium Concept). Mr Silver said that United wanted to build the Millennium Concept designed by Peddle Thorp as a selling point so as to try and win the tender from PAPL for the new service station.

48 From around mid-2017, the Perth Airport Project was managed by United’s then CEO, Mr Brinkworth. Mr Brinkworth would inform Mr Silver of the progress of the project on a regular basis or when Mr Silver’s approval was required for significant items relating to the tender. Mr Silver would discuss the progress with the tender on a regular basis with Mr Hirsch. The meetings were informal as Mr Silver and Mr Hirsch had adjoining offices with a conference room and they would talk on, or close to, a daily basis about United’s business, including the tender for the Perth Airport Service Station. Prior to Mr Brinkworth commencing at United, Mr Carmeli and Mr Searle had been working on the tender, with Mr Brinkworth assuming responsibility as the CEO.

49 Mr Silver’s evidence was that United has a standard feasibility process that it undertakes when assessing the viability of a prospective service station site. That process involves assessing the site location and using that assessment to project fuel volume, shop sales and other revenue that United believes a United service station could achieve on the prospective site, and estimates the expenses associate with the site. Based on those projected numbers, United then determine the projected net profit which that site would return. Mr Silver said that those numbers are populated in a pro forma excel spreadsheet. That population task is performed by staff at United, under the supervision of management, who then report to Mr Silver.

50 Mr Silver directs management to use conservative figures to populate the feasibility spreadsheet. Mr Silver used the feasibility spreadsheet for the Perth Airport Service Station to discuss the tender with United’s senior management. Mr Silver uses the feasibility spreadsheet to understand the return that a particular project will deliver. Mr Silver would decide whether the return was sufficient or not based on the projected numbers to justify United committing to the project. The ultimate decision as to whether United would proceed with the project or not was made by Mr Silver and Mr Hirsch who rely upon their respective 42 and 50 years’ experience in the petroleum retail business.

51 Mr Silver’s evidence was that central to United’s decision to submit a tender for the Perth Airport Service Station was the location of the Site, the forecast traffic numbers; the exclusivity that would be afforded to United, and the design (being the Millennium Concept).

52 Mr Silver read PAPL’s Information Brochure prior to United submitting a tender for the Site. Mr Brinkworth told Mr Silver that Qantas was relocating all its international and domestic terminals to Airport Central by 2025, and that, as a result of the relocation, the traffic that would pass the Site would nearly double in 2025, with a continued increase each year thereafter. Whilst Mr Silver could not recall the exact detail and dates of discussions he had with Mr Brinkworth about the Perth Airport tender, he had many discussions with Mr Brinkworth. Mr Silver had a clear recollection of Mr Brinkworth advising him of the Qantas Relocation and the increase in traffic numbers past the Site on multiple occasions during his discussions with Mr Brinkworth. Mr Silver’s written evidence was that those discussions occurred prior to United submitting a tender and prior to the execution of the AFSL and the Sublease because these matters were relevant to the design and construction costs of the Site and what rent United was prepared to pay PAPL for the Site.

53 Mr Silver agreed for United to sublease the Site and build the Perth Airport Service Station because he believed that the Perth Airport Service Station would be profitable, based on his experience and the sales that he and Mr Hirsch believed United could achieve. Mr Silver considered the Perth Airport Service Station to be a good business opportunity as it provided access to flight passengers, airport staff, ride share drivers and taxi drivers as well as delivery truck drivers delivering goods to shops at the airport. Mr Silver believed that a significant number of vehicles would pass the Site each day. United has service stations at Adelaide Airport and also at Launceston Airport, and the opportunity of being able to open a service station at Perth Airport was of interest to United.

54 Mr Silver’s evidence was that an important component of the attractiveness of the Site was the expected Qantas Relocation, which would place the Qantas and Jetstar terminals in direct proximity to the Site. Based on the statements in the Information Brochure, Mr Silver expected to nearly double the traffic at the Site after the Qantas Relocation, which would be good for United’s business.

55 Mr Silver’s evidence was that the Qantas Relocation was absolutely key to determining the rent and capital expenditure for the Site, given it would increase the number of customers who purchased fuel and other products from United. For this reason, the Qantas Relocation was a significant factor in Mr Silver’s decision to offer the rental amount of $1 million per annum (excl GST) in United’s tender proposal – which was ultimately negotiated down to $900,000 per annum (excl GST) but with a bank guarantee to secure the rent payable.

56 The Qantas Relocation was also a significant factor in Mr Silver’s decision to agree to build a flagship service station using the architects, Peddle Thorp, to create a unique, aeroplane inspired, airport service station – the Millennium Concept.

57 Mr Silver said that the initial construction cost for the Perth Airport Service Station was estimated to be $6.5 million, however the cost ultimately ended up being in excess of $8.6 million, which was mainly due to the impact of the Covid-19 pandemic, which extended the construction time and costs. Mr Silver was emphatic in his evidence that, were it not for the Qantas Relocation and the associated doubling of traffic past the Site, he would not have offered to design and build the Perth Airport Service Station. Instead, Mr Silver would have designed and built a smaller and simpler style of service station which would have cost approximately $4 million to $4.5 million. Mr Silver’s evidence was that he would not have offered or agreed to pay $900,000 (excl GST) per annum in rent, instead, he would have only agreed to pay an amount up to $500,000, presumably exclusive of GST, in rent.

Cross-examination

58 Mr Silver, under cross-examination, said that he initially offered PAPL $1 million dollars per year in rent but, after negotiations and a requirement by PAPL for United to provide a bank guarantee, United negotiated the rent down to $900,000 with a bank guarantee.

59 In relation to the feasibility spreadsheet for the Site, which Mr Silver agreed was prepared by Mr Carmeli in or about July 2017, two of the critical inputs were the vehicles per day and the projected monthly fuel sales. Mr Silver accepted that the feasibility spreadsheet anticipated traffic volumes of around 800 movements per day into the proposed service station. That figure came from 2.5% of the 31,550 vehicles passing the Site each day – known as the ‘turn-in’ rate.

60 Mr Silver said the vehicles per day figure of 31,550 came from the Information Brochure and was the actual number of vehicles which travelled past the Site as at March 2017 (being the total of the figures 16,100 and 15,450 included at page 7 of the Information Brochure). That is, that was the figure at the commencement of the lease and did not incorporate any increased traffic from the Qantas Relocation.

61 The spreadsheet also included a volume of fuel sales per month of 1,183,125 litres. It was put to Mr Silver that the fuel sales figure of 1,183,125 litres was worked out by multiplying the vehicles per day (31,550) by the average volume of a tank (50 l) by the days in a month (30) by the turn-in rate (2.5%). Mr Silver accepted that the 1.2 million litre figure corresponded with that calculation, and appeared to therefore accept that monthly fuel sales were being calculated by reference to the vehicles per day figure of 31,550. Mr Silver accepted that the feasibility spreadsheet was one of the things he took into account in considering how much to put in the tender proposal but emphasised that there were many versions of this spreadsheet – noting he had discussed with Mr Carmeli that this version had the wrong shop sales figure included. Mr Silver accepted that United’s tender proposal stated that “United anticipate traffic volumes of around 800 movements per day into the service centre”. Mr Silver accepted that that was the actual number at commencement and did not incorporate any increased traffic from the Qantas Relocation.

62 Mr Silver accepted that he signed a tender both for a ground lease and also for a building lease (Top Lease) but said that because of the number of deals which he undertook for United, he relied on his in-house legal counsel and real estate managers to review the documentation, such that he does not read the whole of the documents presented to him because he would not be able to undertake any other work if he did.

63 Mr Silver said that the design of the service station was not dependent on the expected 800 vehicles per day. The design was to create a landmark that would enhance United’s ability to win the tender. The design was not to attract customers.

64 Mr Silver was not aware that the tender documents required a business plan from United for the Site.

65 Mr Silver recalled discussing with Mr Brinkworth, the numbers in the feasibility spreadsheets but he could not remember the detail of the numbers in the different spreadsheets presented to him.

66 Mr Silver could not remember the specific date upon which construction of the Perth Airport Service Station commenced, but he believed that it was at the start of the Covid-19 pandemic lock down in very late 2019 or early 2020. Mr Silver accepted that the business model being put forward on 9 March 2018 was that United would achieve fuel sales of 14.4 million litres in the first operative year of the Site, which was based on 31,550 vehicles passing the Site per day, with incremental increases in the following four years that did not factor in the Qantas Relocation.

67 Mr Silver said that based on the actual figure of 31,550 vehicles per day, the Site was not sufficiently profitable. Mr Silver said that he believed the Qantas Relocation would happen in the mid-2020s. Mr Silver said that most service stations had no volume growth. The Site was attractive because of the volume growth with increased traffic due to the Qantas Relocation. The Qantas Relocation was central to the business case for the Site. The timing for the Qantas Relocation was to be in the second half of the 15-year term of the lease. Mr Silver believed that sometime in the second half of the 15-year term, Qantas would relocate. That was the basis for the rental of $900,000 which United offered in the proposal it put forward.

68 Mr Silver said that Mr Brinkworth had, on many occasions between 2017 and the day that contracts were exchanged, discussed, in many meetings in corridors and conference rooms, the Qantas Relocation and the increased traffic numbers that were expected to occur. However, as I have said above, under cross-examination Mr Silver accepted that Mr Brinkworth did not work on the Perth Airport Project until after the tender had been submitted. Counsel for PAPL informed Mr Silver, by reference to the relevant documents, that the tender was submitted on 4 August 2017 and that Mr Brinkworth only became the CEO around mid-2017. On that basis, Mr Silver conceded that, whilst he did not recall the specific dates, Mr Brinkworth only began informing Mr Silver of the progress of the Perth Airport Project on a regular basis or when his approval was required for significant items relating to the tender, after United submitted its tender proposal. However, later on in his cross-examination Mr Silver rejected the proposition that the conversations that he had with Mr Brinkworth about Qantas’ Relocation and the expected increased traffic, occurred only after the tender had been submitted to PAPL.

69 Mr Silver rejected that he did not know when Qantas would relocate. Mr Silver was adamant that he was told that Qantas would relocate in the mid-2020s. Mr Silver rejected the proposition that he had recreated a date by which Qantas would relocate for the purpose of giving his evidence.

70 Mr Silver was adamant that he took into account Qantas’ Relocation by the mid-2020s in determining the rent which United would offer and the capital expenditure which United would incur on the Site. Mr Silver said that he understood that the Qantas Relocation would take place around the mid-2020s, although there was not yet a specific date.

71 Mr Silver said that the reason he decided to build the Millennium Concept was to win the tender by creating a landmark service station. That was the reason he spent the additional money to create a unique facility which would be something which would be attractive to PAPL as lessor.

72 Mr Silver rejected the proposition that the rent he offered of $900,000 was not based on the Qantas Relocation by mid-2020s. Mr Silver said that Qantas was the biggest user of the airport and that it would be silly for him not to have considered the Qantas Relocation in his decision to offer the $900,000 rent.

73 Mr Silver rejected the proposition that he wanted to win the tender and was prepared to pay a premium. Mr Silver said “I wanted to win the site because in any tender I participate in, I want to win, but my main goal is to make money … It’s all about the return”. Mr Silver said he wanted to do the special design (the Millennium Concept) to win the tender, but the main motivator was to make a sufficient profit.

74 Mr Silver rejected the proposition that his offer of a rental of $900,000 had more to do with winning the tender, than with determining whether or not the Site would be profitable. Mr Silver said that he would never do that. Mr Silver said that he would “never go into a business that doesn’t make money because it’s got exposure”. Mr Silver said that is not what he does.

Findings

75 I find Mr Silver to be a truthful and reliable witness who was forthright in answering questions put to him under cross-examination. I am satisfied that he made appropriate concessions when he could not recall the detail of events and matters which occurred more than six years ago. I accept Mr Silver’s evidence that he would not have submitted a request for tender offering a rent of $900,000 for the Site, had he not believed that Qantas would relocate to the new central terminal in the mid-2020s. I also accept Mr Silver’s evidence that he believed the traffic volume past the Site would dramatically increase after the Qantas Relocation in the mid-2020s. I accept Mr Silver’s emphatic denial that he agreed to pay a premium rent in order to win the tender for the Site. I accept Mr Silver’s evidence that he would never go into a business proposition which was not profitable. I accept Mr Silver’s evidence when he stated that he believes everything in business is about the return on investment.

76 In relation to the involvement of Mr Brinkworth and the conversations alleged to have occurred between him and Mr Silver, I accept Mr Silver’s evidence that he had conversations with Mr Brinkworth prior to the submission of the tender. Properly understood, Mr Silver’s evidence was that United had been working on the Perth Airport Project from around at least late-2016, with primary responsibility resting with Mr Carmeli and Mr Searle; Mr Brinkworth became involved in the Perth Airport Project from mid-2017; the tender was submitted on 4 August 2017; and his involvement became more active after the tender submission. I accept that evidence. As I have outlined earlier, United received the RFP material from PAPL on 6 July 2017. Therefore, I accept Mr Silver’s evidence that he had conversations with Mr Brinkworth regarding the Perth Airport Project generally prior to the tender submission. As I discuss later, this is also largely consistent with Mr Brinkworth’s evidence. I also accept that given the effluxion of time, it was correctly acknowledged by Mr Silver that he did not precisely recall when particular people became involved in or undertook specific steps in the project, and this does not reflect negatively on the credibility or reliability of his evidence.

Eddie Hirsch

77 Eddie Hirsch (Mr Hirsch) gave evidence that he is a co-founder and a 50% co-owner of United Petroleum and United Petroleum Australia, along with Mr Silver. United tendered one witness statement of Mr Hirsch dated 17 July 2023.

78 Mr Hirsch gave evidence that he and Mr Silver were both involved in the day-to-day running of the United business, however, they have separate areas of responsibility. Mr Hirsch is responsible for the “upstream” – being the fuel importation and distribution – part of the United business. This involves sourcing the fuel, bringing it to different shipping terminals, and negotiating deals with major oil companies. Mr Silver is responsible for the retail part of United’s business – being the buying and leasing of property for service stations, constructing service stations, and operating the service stations.

79 Mr Hirsch and Mr Silver keep each other updated on significant issues and developments in their respective areas of responsibility. Sometimes they seek each other’s opinion on a particular issue. On smaller issues, they advise each other after the event, whilst on bigger issues they discuss the matter before a final commitment is made by United. Mr Hirsch said that he and Mr Silver do not interfere in each other’s areas of responsibility or second guess each other’s decisions. He relies on Mr Silver to do the property deals for acquisition and leasing of property for service stations. It is Mr Silver’s call to do the property deals, just like it is his call to do the deals for the acquisition of fuel. Mr Hirsch said that if a lease came to him which has Mr Silver’s signature already on it, he would sign it.

80 Mr Hirsch signed the AFSL and the Sublease for the Perth Airport station.

81 Mr Hirsch’s involvement in the decision to submit a request for tender for the Perth Airport site was limited. Mr Silver kept him updated about the project but otherwise Mr Hirsch relied upon Mr Silver to get the deal done and did not seek to second guess Mr Silver’s opinion. Mr Hirsch said that Mr Silver was the ultimate decision maker in respect of the lease of the Site. Mr Hirsch said that it was Mr Silver’s call and that he executed the AFSL and Sublease because Mr Silver had made the call that United should enter into those agreements. Mr Hirsch did not recall being provided with any of the tender documents from the landlord, PAPL. Mr Hirsch did not recall being provided with the feasibility spreadsheets for the project. Mr Hirsch did not get involved in property deals at that level of detail but, rather, relied upon Mr Silver and his property expertise.

82 Mr Hirsch was not involved in formulating United’s response to the RFP for the Site. Mr Silver briefed Mr Hirsch before the bid was submitted but did not seek his approval. Mr Hirsch said that the bid for the Site was a matter for Mr Silver.

83 On several occasions before the AFSL was executed, Mr Silver briefed Mr Hirsch on the project. Mr Hirsch could not recall the precise dates or occasions on which this occurred. At least one of these briefings took place in a conference room at United’s office where Mr Silver showed Mr Hirsch the map of Perth Airport on Google Earth. Mr Brinkworth was present on some of these occasions. Mr Szymczak, the then COO, may have been present at some of these discussions but Mr Hirsch was not certain about that.

84 During these briefings, Mr Silver told Mr Hirsch that Qantas was relocating its terminals to the area of the airport containing the proposed Perth Airport Service Station – being the Qantas Relocation. Mr Silver told Mr Hirsch that the Qantas Relocation would occur by mid-2025. Mr Silver also told Mr Hirsch that United would have exclusivity in the airport precinct and that United would have the only petrol station at the airport. Mr Hirsch said that, based on these briefings, he understood that as a result of the Qantas Relocation, every car carrying passengers to Perth Airport would come past the Perth Airport Service Station. Mr Hirsch did not recall Mr Silver mentioning specific figures in terms of the vehicles per day before and after the Qantas Relocation. Mr Hirsch said that he was not generally involved in these sorts of details.

85 Mr Hirsch regarded the Qantas Relocation as being an important factor driving the deal. Mr Hirsch had dealings with Qantas in Melbourne, where United supplies jet fuel to Qantas, and he knew that Qantas had a big share of the air passenger market.

86 Mr Hirsch regarded the rental United agreed to pay for the Perth Airport of $900,000 (excl GST) per annum to be a hefty rent. Mr Hirsch said, to his mind, this amount was justified by the impending Qantas Relocation. Mr Hirsch said that, but for the Qantas Relocation, he would expect the rent to have been dramatically lower but would have deferred to Mr Silver on the specific amount of rent that United should pay.

87 Mr Hirsch said that the Perth Airport Service Station constructed by United was massive. But for the expected Qantas Relocation, based on Mr Hirsch’s experience, he would expect that United would have wanted to build a much smaller service station, but would have deferred to Mr Silver on the specifics.

Cross-examination

88 Mr Hirsch said, under cross-examination, that, whilst he does not recall the exact dates or occasions on which his briefings with Mr Silver (and others) took place in relation to the Perth Airport Project, he and Mr Silver have adjoining rooms at their office with a conference room in the middle and “probably meet basically every day, three or four days a week”: [T211.42-44]. In particular, Mr Hirsch remembered the occasion when he and Mr Silver went into the conference room and Mr Silver showed him a map of the Perth Airport site on Google Earth and where the service station would be built and where Qantas was relocating. Mr Hirsch said that Mr Brinkworth may have been in the room (which I take to be the conference room) at some of the meetings between him and Mr Silver, including the Google Earth meeting, but that it was Mr Silver providing the briefing. Mr Hirsch did not squarely answer whether he was able to remember whether this meeting took place before or after the AFSL was executed. However, Mr Hirsch was adamant that he and Mr Silver “speak about major deals all the time” and that Mr Silver briefs and concurs with him before “the final signing”: at [T214.3-14].

89 Mr Hirsch accepted that he relied upon Mr Silver to get the deal done in relation to the Perth Airport Project. Mr Hirsch said that Mr Silver was very strong on the Perth Airport Project and that he did not second guess Mr Silver. However, Mr Hirsch was emphatic that whilst he left the details of the deal to Mr Silver, such as the underlying economics, he and Mr Silver had many discussions about the Perth Airport Project and that Mr Silver came with the final proposal and discussed it with Mr Hirsch. Mr Hirsch said Mr Silver “was very strong on it, that he wanted the deal” and Mr Hirsch agreed with Mr Silver that with the expected traffic flows, it would be a good deal: [T215.14-16]. Mr Hirsch said that he knew that there were some negotiations going on regarding rent as part of the final deal, but he did not concern himself with those matters, leaving them to Mr Silver.

90 Mr Hirsch was emphatic in rejecting the proposition that he could not actually remember the briefings on the Perth Airport Project. Mr Hirsch said he could remember being told specifically about the Qantas Relocation and that this was a major part of the deal. Mr Hirsch said that he was confident in knowing that around 2025, he was told by Mr Silver that Qantas would relocate (at [T217.36-37]) – I take this to mean that Mr Hirsch was confident that Mr Silver told him that Qantas would relocate by around 2025. Mr Hirsch said there was no doubt about that in his mind.

91 Mr Hirsch stated that the Qantas Relocation was very important to the deal because Qantas was not a minor airline, Qantas was a massive airline. Qantas was an important factor driving the deal because Qantas had a big share of the passenger market in Australia. Mr Hirsch said that if Qantas were relocating, like Mr Silver had told him, then the Perth Airport Service Station’s volume would dramatically increase.

92 Mr Hirsch accepted in cross-examination that he left the details of the economics of the Perth Airport service station to Mr Silver, but said (at [T219.11-17]) that:

There has been many a time where I haven’t agreed with Mr Silver, because all major deals are discussed between the two of us. It’s not one person doing it. For a major deal to happen, we have robust discussions where I have actually in other areas probably said no, but in this case, Mr Silver’s pointing to me how strong this – this deal was with the Qantas relocation, I agreed with him. But it’s not a sole director that signs off. It’s two directors.

Findings

93 I accept Mr Hirsch as an honest and reliable witness. Mr Hirsch made appropriate concessions during the course of cross-examination and was forthright in his evidence of what he could and could not recall. As to his discussions with Mr Silver regarding the Perth Airport Project, Mr Hirsch was emphatic in his evidence of the importance of the Qantas Relocation to United submitting a response to the RFP. I accept Mr Hirsch’s evidence that he believed the Qantas Relocation would result in dramatically increasing the traffic flows past the Site and that this was what made the transaction a good deal for United.

94 I also accept Mr Hirsch’s evidence that he believed that the Qantas Relocation would take place around 2025 and that the relocation was an important driving factor of the deal.

Gary Brinkworth

95 Gary Brinkworth (Mr Brinkworth) was employed as the Group CEO for United from October 2016 to 31 January 2020. He was hired by United for the specific purpose of guiding United through its proposed initial public offering (IPO) and listing on the Australian stock exchange. The IPO did not proceed, and Mr Brinkworth remained employed as United’s CEO until 31 January 2020. United tendered two witness statements of Mr Brinkworth dated 14 July 2023 and 25 June 2024.

96 During Mr Brinkworth’s tenure as CEO of United, he was involved in the contracting and/or establishment of over 100 service stations, including highway service centres.

97 Mr Brinkworth said that during his time at United, Mr Silver and Mr Hirsch were the directors and co-owners of United and oversaw and directed the operations of United’s business. Mr Brinkworth’s role at United was to work with Mr Silver and Mr Hirsch, take responsibility for the day-to-day operations, lead the key strategic opportunities, and make recommendations on projects requiring capital expenditure. Mr Silver and Mr Hirsch held the exclusive authority for all capital investments made by United.

98 Mr Brinkworth, in his role as CEO of United, had ready access to Mr Silver and Mr Hirsch and would often speak to them multiple times each day. United had a flat management structure so meetings were frequently spontaneous and originated from informal discussions with Mr Silver and Mr Hirsch.

99 At the time Mr Brinkworth joined United in October 2016, United was already working on the Perth Airport Project. Mr Brinkworth was not involved in the project at that stage. Mr Sam Carmeli, who was the National Acquisitions Manager, worked with Mr Silver on the project.

100 In around July 2017, Mr Darren Searle was engaged as Executive General Manager and took over from Mr Carmeli in working on the Perth Airport Project. It was from about this time that Mr Brinkworth gradually became more involved in the project.

101 On 6 July 2017, PAPL’s Senior Leasing and Development Manager, Mr David Skinner, sent an email to United’s acquisitions team, and also to Mr Carmeli, which attached the RFP and the Information Brochure.

102 On 14 July 2017, Mr Skinner emailed the Addenda 1 to Mr Carmeli. Mr Carmeli forwarded the Addenda 1 to Mr Brinkworth on 16 July 2017. Addenda 1 included the following question and answer:

103 In about late July or early August 2017, before United submitted its response to the RFP, Mr Searle provided Mr Brinkworth with a detailed briefing on the Perth Airport Project and the proposed response to the RFP. Mr Searle took Mr Brinkworth through the history of the RFP process and provided to Mr Brinkworth all relevant documents from PAPL, including the RFP and the Information Brochure, which Mr Brinkworth then reviewed. Mr Searle took Mr Brinkworth through the feasibility spreadsheet for the proposed service station and briefed Mr Brinkworth on United’s proposal and the next steps required to obtain Mr Silver’s sign off for the proposal.

104 Mr Brinkworth, prior to being briefed on the Perth Airport Project, was not involved in formulating United’s proposed tender submission. Mr Brinkworth’s active involvement commenced only after United’s tender submission had been sent to PAPL. Mr Brinkworth did say, however, that the design included in the proposal (being the Millennium Concept) was very different from United’s standard service stations, which typically have an area of 3,000 m2 (compared to the Site’s 8,879 m2).

105 Between 22 November 2017 and 13 April 2018, United and PAPL negotiated the Heads of Agreement. Mr Brinkworth was involved in these negotiations on behalf of United. Through these negotiations, Mr Brinkworth negotiated a reduction in rent from $1.19 million per annum to the final rent of $900,000 per annum (excl GST) with a bank guarantee.

106 In January 2018 Mr Brinkworth obtained a copy of the feasibility spreadsheet for the Perth Airport Project which Mr Carmeli had prepared, which was dated 21 July 2017. On 31 January 2018, Mr Brinkworth caused the spreadsheet to be updated to include the updated rent of $900,000 (excl GST) per annum and with an updated shop sales margin of 16% instead of 10%. Mr Brinkworth said the spreadsheet aimed to define the average performance across the first term of the lease to provide an indicative return on the capital and cost. Mr Brinkworth explained that the spreadsheet contained a sensitivity analysis, whereby the Site was compared to other sites, in this case United’s Westgate service stations in Melbourne. The table has data for: vehicles per day; the percentage of traffic which are heavy (ie commercial) vehicles; the fuel margin in cents per litre; the estimated turn-in rate; volume of fuel sales per month; the percentage of shop sales (in dollars) for every litre of fuel sold; and sales at the shop in dollars. For the latter three inputs an actual figure is used for the comparison sites, whilst an estimate is used for the Site. Mr Brinkworth said the spreadsheet revenue figures were heavily based on the assumption of the Qantas Relocation.

107 In particular, Mr Brinkworth said the estimated fuel sales of 1.2 million litres per month represented an assessment of the volume of fuel sales the Perth Airport Service Station could generate over time taking into account the Qantas Relocation and the associated increase in traffic. Mr Brinkworth said this is reflected in the turn-in rate in the sensitivity analysis of 2.5%, which would be more than three times higher than the actual turn-in rates for United’s Westgate sites. In other words, to achieve the estimated fuel sales of 1.2 million litres per month with only 31,550 vehicles per day of traffic, the Perth Airport Service Station would need to have a turn-in rate that is over three times higher than the actual turn-in rates for United’s Westgate service stations. However, if the traffic increased to 78,000 vehicles per day after the Qantas Relocation (as set out in the Information Brochure), a 1% turn-in rate would be sufficient to achieve 1.17 million litres per month in fuel sales. If traffic further increased to 94,000 vehicles per day (as predicted in the Information Brochure for 2031), a turn-in rate of 0.85% would be sufficient to achieve 1.2 million litres per month in fuel sales.

108 Thus, Mr Brinkworth said that absent the expectation of the Qantas Relocation, he would not have considered the January 2018 spreadsheet to be a realistic estimate of the expected profitability of the service station. Without the Qantas Relocation, in his view, the Site and the Perth Airport Service Station could not support a rent of $900,000 per annum (excl GST) and capital expenditure of $6.5 million.

109 In about February 2018, Mr Brinkworth had a telephone discussion with Mr Skinner during which it was agreed that a meeting should be held in Perth with Mr Holden, to discuss the terms being negotiated for the Sublease and for Mr Holden to provide greater detail on the development plans for the airport. Mr Brinkworth referred to Mr Holden as PAPL’s Chief Property Officer, but at the time he was PAPL’s COO. That meeting took place on 27 February 2018 at PAPL’s offices in Perth.

110 Mr Brinkworth said that apart from himself, Mr Manolitsa, United’s General Counsel, and Mr Holden and Mr Skinner, of PAPL were present at the meeting. Mr Brinkworth’s evidence was that the meeting started with a review of the overall strategic plan with PAPL’s representatives taking Mr Brinkworth and Mr Manolitsa through the expected growth projections and some of the development opportunities so that United could get a better appreciation of why PAPL expected the traffic and activity at the airport to grow, and why PAPL’s view that a third runway could potentially be required within ten years. Mr Brinkworth’s evidence was that he said that from United’s perspective, given the scale of the development at the Site and the nature of the agreement, a ten-year term was inadequate to generate a return on United’s investment and that United would need to make sure that it had as much time as possible post the Qantas Relocation to justify the expenditure on the project.

111 Mr Brinkworth said that he made it “really clear” to Mr Holden and Mr Skinner that United were hoping to get, at a minimum, “that requirement” extended to 15 years, in line with the first term, so as to maximise the time-frame with the increased Qantas Relocation traffic and activity: [T225.45-47]-[T226.1-4]. Mr Brinkworth clarified that by “that requirement” he was referring to resumption of the Site by PAPL, in the event of a third runway being required: [T226.7-13]. Mr Brinkworth also discussed how United could start to accelerate and leverage some of the benefits to the employees that would occur with the Qantas Relocation within that 2025 window.

112 Mr Brinkworth said he and Mr Manolitsa “stressed the importance” of the Qantas Relocation to the Perth Airport Project and that Mr Holden said the Qantas Relocation would occur “somewhere between 2025”: [T226.16-22]. Mr Brinkworth said he responded that it “was imperative that it happen as quickly as possible, so that [United] could realise the benefit of the relocation as part of that lease term” and that Mr Holden and Mr Skinner acknowledged “their expectation was or their view was that it would happen between 2025”: [T226.25-32].

113 On 13 April 2018 PAPL and United executed the final Heads of Agreement.

114 Mr Brinkworth understood the position to be that PAPL was expecting to complete the Qantas Relocation in the early 2020s and by 2025, and that given the number of references to early and mid-2020s, the reference to late 2020s in the Information Brochure did not accurately reflect PAPL’s plans but rather was there because PAPL wanted to leave itself some wriggle room.

115 In relation to the answer to Question 7 in Addenda 1 extracted above, Mr Brinkworth understood it to mean that no exact date had been set for the Qantas Relocation (consistently with the other materials, which did not suggest there was an exact date).

116 Mr Brinkworth was then involved in the negotiations related to the terms of the AFSL, between 13 April 2018 and 17 April 2019 (when the AFSL was executed).

117 Mr Brinkworth said he had numerous discussions with Mr Silver in the period between July 2017 and April 2019. These included one-on-one meetings, although Mr Brinkworth did not expand on when these meetings occurred, the frequency or what was discussed. Mr Brinkworth also referred to a specific conversation as part of a United executive meeting, also attended by Mr Szymczak and Mr Geroge Svinos (the then Group Chief Financial Officer – now deceased), which including looking at a Google Earth map of the Perth Airport area and reviewing the layout of the airport, the location of the Site and the proximity of the Qantas terminal and commercial businesses. Finally, Mr Brinkworth refers to a conversation regarding the Site during a trip to Perth in 2018, where he and Mr Silver inspected multiple service stations sites in Perth, including the Site. Mr Brinkworth said that in each conversation there was a discussion to the effect that the Qantas Relocation was expected to occur by the early to mid-2020s.

118 Further, sometime in the first half of 2019, Mr Brinkworth agreed with PAPL on the contents of a joint press release about the Perth Airport Service Station but does not remember the details of these discussions or when exactly they took place. The press release is dated 10 March 2020 and included the following:

With Terminals 3 & 4 scheduled to be relocated by 2025, the Airport Central Precinct will increasingly become the focus for aeronautical operations and the design of this development will help to create a great first impression for visitors to Western Australia.

119 Mr Brinkworth said the wording of the press release reflected his understanding that Qantas would relocate all of its international and domestic flights from Terminal 3 and Terminal 4 to Airport Central by 2025 at the latest and that no representatives of PAPL ever said anything to suggest that the Qantas Relocation would not occur or would be delayed.

120 Mr Brinkworth said he regarded the Qantas Relocation as critical to ensure the Site was sustainable. First, this was because traffic volumes are critical to the revenue that can be derived from a service station, and the Qantas Relocation was expected to bring about a large increase in traffic volume (and therefore a large increase in revenue). Mr Brinkworth assumed that the Qantas Relocation was a primary reason for the increase in the Information Brochure from the forecast of 40,000 vehicles per day in 2024 to 94,000 vehicles per day by 2031.

121 Mr Brinkworth was clear that he did not recall any mention from PAPL representatives that the Qantas Relocation was conditional, qualified or in any way uncertain; nor that PAPL and Qantas only had an agreement to use “best endeavours” to achieve Consolidation by 2025; nor that the Qantas Relocation was subject to PAPL reaching an agreement for Qantas to relocate on “commercial terms”.

122 Mr Brinkworth said that the topic of the construction works required to achieve Consolidation were never raised in his discussions with Mr Skinner and Mr Holden.

123 Mr Brinkworth said that based on (a) his 36 years of professional experience and over 25 years’ experience in senior leadership positions, and (b) key features in the Information Brochure being the Qantas Relocation occurring by 2025 and the increase in traffic numbers, he would have expected to be informed by PAPL of the following:

(a) that it did not have a firm agreement with Qantas that obligated Qantas to relocate its terminals to Airport Central by 2025;

(b) any other relevant matters that could have affected the Qantas Relocation date or that could have affected the represented increase in traffic numbers on Airport Drive; and

(c) any change in position represented by PAPL before United executed the AFSL in April 2019. This is particularly the case where United had negotiated its position based on the information provided to it by PAPL.

Cross-examination

124 Mr Brinkworth said that the exact date for when Qantas would relocate was yet to be finalised.

125 Mr Brinkworth understood that United, as a tenderer, was required to rely on its own enquiries in submitting a tender but that that related to data points or secondary inputs, it was not his expectation that it related to any core tenet of the proposal. Mr Brinkworth accepted that those provisions would relate to the traffic volume data provided in the Information Brochure, but did not believe they applied to the expectation that the Qantas Relocation would occur by the mid to late 2020s.

126 Mr Brinkworth understood that the tender documents contained a clause that no person had been authorised to make any representations or warranties in connection with the tender documents but, at a practical level, Mr Brinkworth said he needed to be able to work with the PAPL personnel to progress the negotiation.