Federal Court of Australia

Cameron v Commissioner of Taxation [2026] FCA 609

File number(s): | WAD 325 of 2023 WAD 326 of 2023 WAD 327 of 2023 WAD 184 of 2024 WAD 185 of 2024 WAD 186 of 2024 |

Judgment of: | HILL J |

Date of judgment: | 19 May 2026 |

Catchwords: | TAXATION – six appeals brought under s 14ZZ of the Taxation Administration Act 1953 (Cth) in respect of objection decisions of Commissioner – issue in WAD325-327/2023 is whether interest on sub-trust loans paid by a family trust is deductible under s 8-1(1)(a) of the Income Tax Assessment Act 1997 (Cth) – issue in WAD184-186/2024 is whether a valid family trust election was made in respect of the Cameron Family Trust for the purposes of Sch 2F to the Income Tax Assessment Act 1936 (Cth) – appeals dismissed |

Legislation: | Income Tax Assessment Act 1936 (Cth) Sch F Div 271 Income Tax Assessment Act 1997 (Cth) s 8-1(1)(a) Taxation Administration Act 1953 (Cth) s 14ZZO Taxation Laws Amendment (Trust Loss and Other Deductions) Act 1998 (Cth) Sch items 22(3) and 23(3) Taxation Laws Amendment Act (No 2) 2000 (Cth) Sch 11 |

Cases cited: | Allied Pastoral Holdings Pty Ltd v Commissioner of Taxation [1983] 1 NSWLR 1 Amalgamated Zinc (De Bavay’s) Ltd v Federal Commissioner Taxation [1935] HCA 81; (1935) 54 CLR 295 AusNet Transmission Group Pty Ltd v Federal Commissioner of Taxation [2015] HCA 25; (2015) 255 CLR 439 Australian Competition and Consumer Commission v Bluescope Steel Ltd (No 5) [2022] FCA 1475 Australian Competition and Consumer Commission v Olex Australia Pty Ltd [2017] FCA 222 Australian Securities and Investments Commission v Whitebox Trading Pty Ltd (No 7) [2019] FCA 849; (2019) 137 ACSR 61 Automotive Invest Pty Ltd v Commissioner of Taxation [2024] HCA 36; (2024) 419 ALR 324 Charles Moore & Co (WA) Pty Ltd v Federal Commissioner of Taxation [1956] HCA 77; (1956) 95 CLR 344 Clough Limited v Commissioner of Taxation [2021] FCAFC 197; (2021) 114 ATR 1 Commissioner of Taxation v Cassaniti [2018] FCAFC 212; (2018) 266 FCR 385 Commissioner of Taxation v Hall [2026] FCAFC 43 Commissioner of Taxation v Roberts [1992] FCA 363; (1992) 37 FCR 246 ET-China.com International Holdings Ltd v Cheung [2021] NSWCA 24; (2021) 388 ALR 128 Federal Commissioner of Taxation v Day [2008] HCA 53; (2008) 236 CLR 163 Federal Commissioner of Taxation v Munro [1926] HCA 58; (1926) 38 CLR 153 Federal Commissioner of Taxation v Payne [2001] HCA 3; (2001) 202 CLR 93 Federal Commissioner of Taxation v Riverside Road Lodge Pty Ltd (in liq) [1990] FCA 205; (1990) 23 FCR 305 Federal Commissioner of Taxation v Smith [1981] HCA 10; (1981) 147 CLR 578 Federal Commissioner of Taxation v Total Holdings (Australia) Pty Ltd [1979] FCA 30; (1979) 43 FLR 217 Fletcher v Commissioner of Taxation [1991] HCA 42; (1991) 173 CLR 1 Fox v Percy [2003] HCA 22; (2003) 214 CLR 118 Gestmin SGPS SA v Credit Suisse (UK) Ltd [2013] EWHC (Comm) 3560 Hallstroms Pty Ltd v Commissioner of Taxation (Cth) (1946) 72 CLR 634 Hayden v Commissioner of Taxation [1996] FCA 1690; (1996) 68 FCR 19 J Hutchinson Pty Ltd v Australian Competition and Consumer Commission [2024] FCAFC 18; (2024) 302 FCR 79 Luxton v Vines [1952] HCA 19; (1952) 85 CLR 352 Magna Alloys and Research Pty Ltd v Federal Commissioner of Taxation (1980) 33 ALR 213 Martin v Norton Rose Fulbright Australia [2021] FCAFC 216; (2021) 289 FCR 369 McCormack v Commissioner of Taxation [1979] HCA 18; (1979) 143 CLR 284 Pennytel Australia Pty Limited v Engelke [2025] FCA 1384 Service v Commissioner of Taxation [2000] FCA 188; (2000) 97 FCR 265 Spassked v Commissioner of Taxation [2003] FCAFC 282; (2003) 136 FCR 441 Spriggs v Federal Commissioner of Taxation [2009] HCA 22; (2009) 239 CLR 1 Trautwein v Federal Commissioner of Taxation [1936] HCA 77; (1936) 56 CLR 63 Trustees of the Property of Cummins (a bankrupt) v Cummins [2006] HCA 6; (2006) 227 CLR 278 Turner v Richards [2025] NSWCA 83 Watson v Foxman (1995) 49 NSWLR 315 |

Division: | General Division |

Registry: | Western Australia |

National Practice Area: | Taxation |

Number of paragraphs: | 133 |

Date of last submission/s: | 28 April 2026 |

Date of hearing: | 5-6 May 2026 |

Counsel for the Applicant: | Ms C Burnett SC and Mr D Lewis |

Solicitor for the Applicant: | McWilliams Davis Lawyers |

Counsel for the Respondent: | Mr M O’Meara SC and Ms E Luck |

Solicitor for the Respondent: | Gadens Lawyers |

ORDERS

WAD 325 of 2023 | ||

| ||

BETWEEN: | CHARMAINE CAMERON Applicant | |

AND: | COMMISSIONER OF TAXATION Respondent | |

order made by: | HILL J |

DATE OF ORDER: | 19 may 2026 |

THE COURT ORDERS THAT:

1. The appeal is dismissed with costs.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ORDERS

WAD 326 of 2023 | ||

| ||

BETWEEN: | BRUCE CAMERON Applicant | |

AND: | COMMISSIONER OF TAXATION Respondent | |

order made by: | HILL J |

DATE OF ORDER: | 19 may 2026 |

THE COURT ORDERS THAT:

1. The appeal is dismissed with costs.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ORDERS

WAD 327 of 2023 | ||

| ||

BETWEEN: | ADJUVANT PTY LTD Applicant | |

AND: | COMMISSIONER OF TAXATION Respondent | |

order made by: | HILL J |

DATE OF ORDER: | 19 may 2026 |

THE COURT ORDERS THAT:

1. The appeal is dismissed with costs.

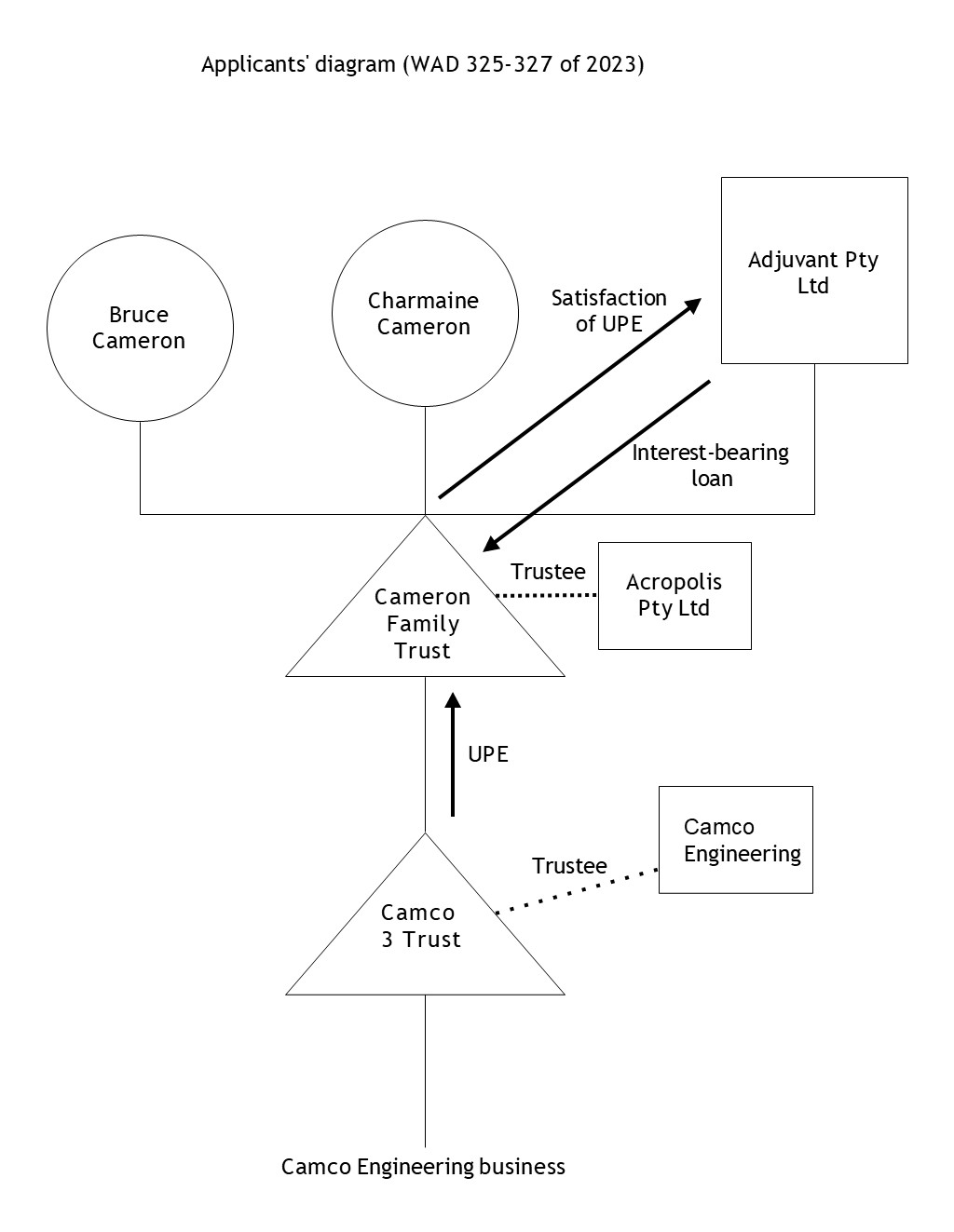

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ORDERS

WAD 184 of 2024 | ||

| ||

BETWEEN: | BRUCE JOHN CAMERON Applicant | |

AND: | COMMISSIONER OF TAXATION Respondent | |

order made by: | HILL J |

DATE OF ORDER: | 19 may 2026 |

THE COURT ORDERS THAT:

1. The appeal is dismissed with costs.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ORDERS

WAD 185 of 2024 | ||

| ||

BETWEEN: | ACROPOLIS PTY LTD AS TRUSTEE FOR THE CAMERON FAMILY TRUST Applicant | |

AND: | COMMISSIONER OF TAXATION Respondent | |

order made by: | HILL J |

DATE OF ORDER: | 19 may 2026 |

THE COURT ORDERS THAT:

1. The appeal is dismissed with costs.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ORDERS

WAD 186 of 2024 | ||

| ||

BETWEEN: | CHARMAINE ANN CAMERON Applicant | |

AND: | COMMISSIONER OF TAXATION Respondent | |

order made by: | HILL J |

DATE OF ORDER: | 19 may 2026 |

THE COURT ORDERS THAT:

1. The appeal is dismissed with costs.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

HILL J:

A. introduction

1 These six proceedings are appeals brought under s 14ZZ(1)(a) of the Taxation Administration Act 1953 (Cth) (TA Act) against objection decisions of the Respondent (Commissioner) dated 17 October 2023 (for proceedings WAD325-327/2023) and 16 May 2024 (for proceedings WAD184-186/2024). The proceedings all concern the Cameron Family Trust.

Proceedings WAD325-327/2023 concern whether certain interest payments by the Family Trust in the income years ended 30 June 2019 and 30 June 2020 (IY 2019 and IY 2020) are deductible under s 8-1 of the Income Tax Assessment Act 1997 (Cth) (ITAA97). That issue in turn depends on whether those interest payments were incurred in gaining or producing assessable income.

Proceedings WAD184-186/2024 concern whether the three Applicants (Mr and Mrs Cameron and the trustee of the Family Trust) are liable to pay family trust distribution tax (FTD Tax) for IY 2019, IY 2020 and IY 2021. That issue in turn depends on whether there is in fact a valid and effective family trust election in respect of the Family Trust for the purposes of Sch 2F of the Income Tax Assessment Act 1936 (Cth) (ITAA36). The Family Trust’s income tax return for the income year ended 30 June 1999 (IY 1999) referred to a family trust election being made for IY 1995. Mr Cameron and Mr Cook, his accountant, say that no family trust election was ever made.

2 For the reasons set out below, each appeal is dismissed with costs.

3 Evidence: The parties filed a court book for proceedings WAD325-327/2023, and a separate court book for proceedings WAD184-186/2024. After the hearing, the parties filed an agreed list of tendered documents.

4 The Applicants in WAD325-327/2023 rely on an affidavit of Bruce Cameron affirmed on 15 August 2024 (Cameron WAD325-327 affidavit). The Applicants in WAD184-186/2024 rely on affidavits of Lawrence Cook, the accountant and registered tax agent for the Family Trust, affirmed on 6 March 2025 (first Cook affidavit) and 28 August 2025 (second Cook affidavit); and on an affidavit of Bruce Cameron affirmed on 3 June 2025 (Cameron WAD184-186/2024 affidavit). The Applicants also filed an affidavit of Paul Fletcher affirmed on 24 April 2026.

b. Background

B.1 Overview of WAD325-327/2023

5 Applicants: The three Applicants are beneficiaries of the Family Trust. Adjuvant Pty Ltd is a private proprietary company. Bruce Cameron and Charmaine Cameron are directors of Adjuvant, and are also directors of Acropolis Pty Ltd, which is the corporate trustee of the Family Trust.

6 Camco Engineering, Camco Trusts: Camco Engineering Pty Ltd was incorporated in 1994. Camco Engineering is the trustee of five trusts (collectively, the “Camco Trusts”), which are titled the “Camco 1 Trust” through “Camco 5 Trust”. Each of these trusts is related to one of the directors and shareholders (or “Principals”) of Camco Engineering, who include Mr Cameron.

7 The trust relating to Mr Cameron is the Camco 3 Trust. It was established by deed on 9 June 1995, with Camco Engineering as the corporate trustee and Bruce Cameron as the appointed guardian and appointor. Bruce Cameron, Charmaine Cameron and the Family Trust are beneficiaries of the Camco 3 Trust.

8 1995 and 1997 “partnership agreements”: In 1995, Camco Engineering executed a document titled “Partnership: The Camco Partnership”, acting in its capacities as the trustee of the Camco 1 Trust through Camco 4 Trusts (1995 Deed). In July 1997, Camco Engineering executed a document titled “Partnership Agreement”, which added the “Camco 5 Trust” (of which Camco Engineering was also the trustee) (1997 Deed). (The version of the 1997 Deed in the Court Book is unsigned; however, Mr Cameron’s affidavit states that this document was signed in July 1997 by the Principals and this evidence is not challenged.) The Applicants accept that a partnership was not formed in law by either of these documents (because there was only a single legal person, Camco Engineering), but contend that each of these documents operates as a deed that is binding on Camco Engineering. It is agreed between the parties that the engineering business of Camco Engineering is carried on by the Camco Trusts collectively. It is convenient to call this the “Camco business”.

9 In the period IY 2013 to IY 2018, the Family Trust’s income consisted entirely of distributions from the Camco 3 Trust. In IY 2019 and IY 2020, distributions from the Camco 3 Trust provided the major proportion of the Family Trust’s income, although the Trust received some other income (those distributions being $3.996 million of $4.108 million in IY 2019; and $5.465 million of $5.560 million in IY 2020).

10 Sub-trust Loans (2013-2015, 2018-2020): In IY 2013 to IY 2015 and IY 2018 to IY 2020, the unpaid present entitlements of Adjuvant to distributions from the Family Trust were set aside and placed on separate sub-trusts of which Acropolis was trustee (Adjuvant sub-trust). These amounts were converted to interest-only loans (Sub-trust Loans) from the Adjuvant sub-trust to the Family Trust on terms consistent with Option 1 in the Australian Taxation Office’s (ATO’s) (now withdrawn) Law Administration Practice Statement PS LA 2010/4. That is, interest was payable on the Sub-trust Loans by the Family Trust to the Adjuvant sub-trust annually at the relevant benchmark rates (see ITAA 1936 s 109N(2)), and the term of the loans was seven years (see s 109N(3)(b)).

The amount of these Sub-trust Loans entered into in 2013, 2014, 2015 and 2018 ranged between $0.98 million and $1.2 million. The amount of the Sub-trust Loans entered into in 2019 and 2020 were $2 million and $3.5 million, respectively.

The amount of interest paid by the Family Trust on these Sub-trust Loans was $11,154 for IY 2013 and $80,888 for IY 2014, then ranged between $179,820 and $191,101 for IY 2015 to IY 2018, and was $251,089 for IY 2019 and $356,171 for IY 2020.

11 The amount to which the Family Trust was entitled under the sub-trust borrowing for a year was set off against Adjuvant’s unpaid present entitlement from the Family Trust for that year. That is, no money was actually advanced by the Adjuvant sub-trust to the Family Trust. In each of IY 2019 and IY 2020, the Family Trust returned the interest payments made under the Sub-trust Loans (the Interest Payments) as deductible outgoings.

12 The role of these Sub-trust Loans, in the context of the business of Camco Engineering, and the activities of the Camco Trusts and the Family Trust, is considered in section C.2 below.

13 Objection process: The Applicants’ income tax returns for IY 2019 and IY 2020 reported the Interest Payments as income. After a review, the Commissioner raised concerns regarding the Interest Payment expenses claimed as a deduction from the Family Trust’s income in each of those years.

14 On 18 November 2022, the Family Trust self-amended its trust tax returns for IY 2019 and IY 2020 to remove the Interest Payment deductions claimed in relation to the Sub-Trust Loans, and amended its statements of distribution. Consequently, each of the Applicants amended their income tax returns to increase their declared trust income from the Family Trust.

15 Commissioner amends Applicants’ assessments (Nov 2025): The increased trust income declared by the Applicants was commensurate with the Family Trust disallowed Interest Payment deductions. Accordingly, on 24 and 25 November 2022, the Respondent issued notices of amended assessments to each of the Applicants in respect of IY 2019 and IY 2020.

16 Applicants’ objections disallowed (Jan, Oct 2023): On 23 January 2023, the Applicants each lodged an objection to the notices of amended assessments for IY 2019 and IY 2020, contending that the Interest Payments made by the Family Trust under the Sub-Trust Loans were deductible outgoings. On 17 October 2023, the Commissioner made separate decisions in relation to each Applicant disallowing their objection.

17 Appeal under s 14ZZ (Dec 2023): The Applicants filed these appeals against the Commissioner’s decisions under s 14ZZ of the TA Act on 13 December 2023.

B.2 Overview of WAD184-186/2024

18 Applicants and the Family Trust: The Family Trust is a discretionary trust established on 14 July 1988, and varied by deed dated 17 June 1993. Bruce and Charmaine Cameron are part of the class of “general beneficiaries” of the Family Trust. Bruce Cameron is both the guardian and appointor of the Family Trust during his lifetime.

19 As noted, Acropolis is the corporate trustee of the Family Trust. Bruce and Charmaine Cameron are directors and the sole shareholders of Acropolis.

20 Family Trust income tax return IY 1999 (Nov 2000): On 1 November 2000, Acropolis’ registered tax agent, Mr Lawrence Cook, lodged electronically with the Australian Taxation Office an income tax return for IY 1999 for Acropolis as trustee for the Family Trust. This income tax return included a completed schedules headed “1999 Family Trust Election and/or Family Trust Revocation” and “1999 Interposed Entity Election”.

21 Reference to a family trust election: The Family Trust Election section of the Schedule to the IY 1999 income tax return stated that the trust is the Family Trust; the trustee is Acropolis; the income year specified is 1995; and the “specified individual” (whose family group is to be taken into account in relation to the election) is Mr Bruce Cameron. This part of the Schedule included the following declaration:

Declaration:

I/We declare all the particulars and information required in this schedule are included in this schedule and any attachments to this schedule and that the particulars and information provided in this schedule and any attachments are true and correct in every detail, and

i. *that the trust is making a family trust election specifying the 1998-99 income year, the details of which are set out above, for the purposes of section 272-80 of the Income Tax Assessment Act 1936 and that the trustees(s) is/are* able to make the election in accordance with that section; and

ii. *that the trust has made a family trust election specifying an income year before the 1998-99 income year, the details of which are set out above, for the purposes of section 272-80 of the Income Tax Assessment Act 1936 and that the trustee(s) was/were* able to make the election in accordance with that section and item 22 of Schedule 1 to the Taxation Laws Amendment (Trust Loss and Other Deductions) Act 1998, and

iii. *that the trust is revoking a family trust election, the details of which are set out above, for the purposes of subsections 272-80(6)-(8) of the Income Tax Assessment Act 1936 ad that the trustee(s) is/are* able to revoke the election in accordance with those subsections and if applicable subitem 22(6) of Schedule 1 to the Taxation Laws Amendment (Trust Loss and Other Deductions) Act 1998;

*Cross out whichever is not applicable

22 The signature block for the trustee (Acropolis) is dated 18 September 2000. Mr Cook (the registered tax agent for the Family Trust) accepted that, if a family trust election had been made, the applicable part was (ii) above (relating to a family trust election before IY 1999).

23 Reference to an interposed entity election: The Interposed Entity Election section of the Schedule to the Family Trust’s IY 1999 income tax return stated that the entity was the Family Trust; the family trust in respect of which the interposed entity election was made was the Camco 3 Trust; the income year specified in the family trust election was 1995 (with a commencement time of 19 May 1995); and the specified individual was Bruce Cameron.

24 The issue in WAD184-186/2024 is the legal effect of these statements in the Family Trust’s IY 1999 income tax return, when weighed against the other evidence: see section D.3 below.

25 Family Trust income tax return FY 2019-2021: On 30 June 2020, Acropolis’ tax agent, Mr Matthew Cook, lodged the Family Trust’s income tax return for the financial year ending 30 June 2019 (FY 2019), recording trust distributions made to members of the Cameron family group.

26 On 26 and 28 July 2021, Mr Matthew Cook lodged the Family Trust’s income tax return for IY 2020, and an amended income tax return in respect of IY 2019, respectively. The amended 2019 income tax return and the 2020 income tax return disclosed various trust distributions from the Family Trust to the Robot Trust (of $58,000 in IY 2019 and $60,000 in IY 2020) and Lumitex (of $4.99 million in IY 2020). On 4 August 2022, Mr Matthew Cook lodged the Family Trust’s income tax returns for FY 2021. The 2021 income tax return disclosed a trust distribution from the Family Trust to the Robot Trust (of $60,000).

27 It is common ground that Robot Trust and Lumitex Ltd are outside Mr Cameron’s family group.

28 Objection process: In December 2021, the Commissioner commenced a review of Bruce Cameron’s and related parties’ tax affairs, including the Family Trust.

29 FTD tax payment advices (Nov 2022): Around 18 November 2022, Acropolis as trustee for the Family Trust made a voluntary disclosure, and Family Trust Distribution Tax Payment Advices were lodged, in respect of the Family Trust’s trust distributions to the Robot Trust and to Lumitex in each of IY 2019, 2020 and 2021. The Family Trust Distribution Tax Payment Advices:

noted the Family Trust Election dated 18 September 2000, with a commencement time of 9 May 1995;

declared distributions to the Robot Trust in IY 2019 to 2021 in amounts totalling almost $180,000; and to Lumitex in IY 2020 in the amount of $5,000,000.

30 Amended income tax returns for FY 2019-2021 (Nov 2022, Jan 2023): On 18 November 2022, Acropolis’ tax agent, Mr Lawrence Cook also lodged the Family Trust’s amended income tax return for FY 2019 and 2020. On 19 January 2023, Acropolis’ tax agent, Mr Lawrence Cook, lodged the Family Trust’s amended income tax return for FY 2021.

31 Notices of liability (Jan 2023): On 25 January 2023, the Respondent issued Notices of Liability – Family Trust Distribution Tax (FTD Tax Notice) pursuant to s 271-90 of Sch 2F of the ITAA 1936, to Bruce Cameron and Charmaine Cameron (as directors of Acropolis) and to Acropolis (as trustee of the Family Trust). These Notices stated that the Applicants were jointly and severally liable to pay FTD tax for IY 2019, 2020 and 2021 (for amounts totalling approximately $2.4 million), and were jointly and severally liable to pay general interest charge on any amounts of FTD tax that remained unpaid after the due date for payment.

32 Applicants’ objections disallowed (Mar 2023, May 2024): On 23 March 2023, the Applicants each lodged an objection to their FTD Notice. On 16 May 2024, the Commissioner made separate decisions disallowing the Applicants’ objections to the FTD Tax Notices.

33 Appeal under s 14ZZ (Jul 2024): The Applicants filed these appeals against the Commissioner’s decisions under s 14ZZ of the TA Act on 15 July 2024.

C. WAD325-327/2023: deductibility of interest payments

34 As noted, the issue in proceedings WAD325-327/2023 is whether the Interest Payments made by the Family Trust on the Sub-trust Loans are deductible for IY 2019 and IY 2020.

C.1 ITAA 1997 s 8-1: general deductions

35 ITAA 1997 s 8-1(1): By s 8-1(1)(a) of the ITAA 1997, a loss or outgoing may be deducted from a taxpayer’s assessable income “to the extent that … it is incurred in gaining or producing [the taxpayer’s] assessable income”. It is common ground that the further ground of deductibility in s 8-1(1)(b), and the exclusions from deductibility in s 8-1(2), are not relevant.

36 “In the course of”: In Federal Commissioner of Taxation v Day [2008] HCA 53; (2008) 236 CLR 163, Gummow, Hayne, Heydon and Kiefel JJ made the following points about s 8-1(1)(a):

The words “incurred in gaining or producing … assessable income” have long been held to mean incurred “‘in the course of’ gaining or producing” income: Day at [21]. There must be a connection between the expenditure and deriving (in the sense of gaining or producing) assessable income: Day at [22].

The question posed by s 8-1(1)(a) is whether the occasion of the outgoing is “found in whatever is productive of actual or expected income”: Day at [30], quoting Federal Commissioner of Taxation v Payne [2001] HCA 3; (2001) 202 CLR 93 at [11] (Gleeson CJ, Kirby and Hayne JJ).

Essential to that inquiry is determining what it is that is productive of assessable income: Day at [31]. No narrow approach is taken to determining what is productive of a taxpayer’s income, and account should be taken “of the whole of the operations of the business concerned”: Day at [33].

The breadth of the language in s 8-1(1) and the generality of its application mean that there is no formula that can be applied to the circumstances of every case. Cases are helpful to show the connection found on the facts of those cases, but do not always explain how the search for the requisite connection is to be undertaken: Day at [30].

37 It is convenient to begin with four general points about the application of s 8-1(1).

38 “Activities or operations”: First, the Commissioner emphasises a line of cases (beginning with Amalgamated Zinc (De Bavay’s) Ltd v Federal Commissioner Taxation [1935] HCA 81; (1935) 54 CLR 295 at 309 (Dixon J)) which state that there must be a connection between an outgoing and the “operations or activities” of the taxpayer that gain or produce assessable income: see, for example, Commissioner of Taxation v Roberts [1992] FCA 363; (1992) 37 FCR 246 at 254 (Hill J, with Jenkinson J agreeing), citing Charles Moore & Co (WA) Pty Ltd v Federal Commissioner of Taxation [1956] HCA 77; (1956) 95 CLR 344 at 351 (the Court) (which referred to “operations”) and Federal Commissioner of Taxation v Smith [1981] HCA 10; (1981) 147 CLR 578 at 585-586 (Gibbs CJ, Stephen, Mason and Wilson JJ); Federal Commissioner of Taxation v Total Holdings (Australia) Pty Ltd [1979] FCA 53; (1979) 43 FLR 217 at 224 (Lockhart J, with Northrop and Fisher JJ agreeing). The Commissioner contends that there are no relevant “operations or activities” of the Family Trust.

39 However, these statements have largely if not exclusively been made in the context of a continuing business, which can be expected to have operations and activities. Section 8-1(1)(a) (unlike s 8-1(1)(b)) is not confined to cases where income is derived from carrying on a business: see Federal Commissioner of Taxation v Riverside Road Lodge Pty Ltd (in liq) [1990] FCA 205; (1990) 23 FCR 305 at 312 (the Court); Spriggs v Federal Commissioner of Taxation [2009] HCA 22; (2009) 239 CLR 1 at [56] (French CJ, Gummow, Heydon, Crennan, Kiefel and Bell JJ). I would not analyse the reference to “operations and activities” as adding more to the meaning of s 8-1(1)(a) or narrowing its operation. Rather, like the use of the phrase “incidental and relevant”, the expression “operations and activities” describes a part of the relevant circumstances in a particular case, rather than being a test to ascertain the outer limits of the provision: see Day at [29]. The same point is addressed by identifying what it is that is productive of assessable income (the inquiry posed in Day at [31]). In many cases, the thing or matter that is productive of assessable income can be described as an activity or operation.

40 Deductibility of interest: Second, this case concerns the deductibility of interest payments in particular. I adopt the analysis in Roberts at 255-256 on this point (see also Hayden v Commissioner of Taxation [1996] FCA 1690; (1996) 68 FCR 19 at 24-25 (Spender J)).

(a) The mere act of borrowing money, burdened with the obligation to pay interest, does not of itself gain or produce assessable income. The amount borrowed is not assessable income.

(b) In the ordinary case, the necessary connection between the outgoing for interest and the activities which more directly gain or produce assessable income will be found in the use to which the borrowed funds are put. However, a rigid tracing of funds will not always be necessary or appropriate. (In other words, in many cases the objective relationship between an expenditure and that which is productive of income will provide a sufficient answer to whether the outgoing is deductible, without any reference to the taxpayer’s subjective purpose or motives: Day at [39].)

(c) However, “[t]hat is not to say that there may not be cases where [the taxpayer’s] motivation or subjective purpose” will be relevant to the characterisation of the outgoing, at least where the outgoing was voluntarily incurred. For example, motive or purpose could be relevant to a case where no assessable income could be identified at the time the outgoing was incurred, or where the relevant assessable income was less than the amount of the outgoing.

41 In that last situation (either no or very little assessable income), the question will be whether the outgoing is to be characterised as genuinely and not colourably incurred in gaining or producing assessable income. The interest will not be deductible if the outgoing is explained by reference to the independent pursuit of some other objective: see Fletcher v Commissioner of Taxation [1991] HCA 42; (1991) 173 CLR 1 at 18-19 (the Court); see also Hayden at 28 (referring to a “purpose quite independent of the [income-producing] property”).

42 Relevance of purpose: Third, as will be seen, the Applicants’ arguments look particularly to the purpose of incurring expenditure. In Commissioner of Taxation v Hall [2026] FCAFC 43 at [5], Thawley J (with McElwaine and Wheatley JJ agreeing) stated that “[i]t is necessary to look to the essential character of the expenditure, rather than the subjective purpose for which an item of expenditure has been incurred”. It might be thought that there is some tension between this statement (rejecting subjective purpose), and the apparent relevance given to “motivation or subjective purpose”, at least in some cases, in Roberts at 255: see [40](c) above.

43 Any tension is resolved by the High Court’s discussion of purpose and related concepts in Automotive Invest Pty Ltd v Commissioner of Taxation [2024] HCA 36; (2024) 419 ALR 324. That case concerned the A New Tax System (Luxury Car Tax) Act 1999 (Cth) (LCT Act), which provided in s 9-5(1) that a taxpayer was entitled to quote the taxpayer’s Australian Business Number in relation to a supply or importation of a luxury car if, at the time of quoting, the taxpayer “ha[s] the intention of using the car for one of the [specified] purposes, and for no other purpose”. The majority judgment of Edelman, Steward and Gleeson JJ made the following points of principle relevant to this case:

(a) The majority in Automotive Invest distinguished between “motive”, “means” and “purpose”. A person’s purpose is usually the ultimate end, object or goal that the person seeks to achieve. A person’s motive is the reason that the person seeks to achieve that purpose or end. And a person’s means are the way in which the purpose is to be achieved: Automotive Invest at [110]. It is necessary to characterise the relevant person’s purpose or end at the proper level of generality, as distinct from any motive for that purpose or the intended means of achieving that purpose: Automotive Invest at [111].

(b) Section 9-5(1) of the LCT Act directs attention explicitly to the taxpayer’s subjective purpose: Automotive Invest at [65], [126]. By contrast, the majority referred with apparent approval to the proposition that s 8-1(1) of the ITAA 1997 is concerned with “objective purpose”; that is, the object which the incurring of the expenditure is apt to achieve: see Automotive Invest at [109]. In determining objective purpose, “what the taxpayer says are the character and scope of his business or undertaking is evidence of what its character and scope are in fact”; however, whether an act is “apt to achieve” an object can be proved only by inference from “known circumstances”: Automotive Invest at [116]-[117], quoting Magna Alloys and Research Pty Ltd v Federal Commissioner of Taxation (1980) 33 ALR 213 at 215, 222 (Brennan J).

44 Automotive Invest indicates that, to the extent that purpose is relevant when applying s 8-1(1) of the ITAA 1997, this is an objective purpose. This objective purpose determines the essential character of the outgoing. However, a taxpayer’s subjective purpose is evidence of what the character and scope of the business is in fact, which is relevant to determining the objective purpose or essential character of the expenditure. That analysis is supported by previous cases such as Service v Commissioner of Taxation [2000] FCA 188; (2000) 97 FCR 265 at [55]-[57] (the Court) and Spassked v Commissioner of Taxation [2003] FCAFC 282; (2003) 136 FCR 441 at [75] (Hill and Lander JJ).

45 Relevance of legal form: Fourth, the Applicants contend that questions of legal form are not determinative of whether an outgoing has a necessary connection to the taxpayer gaining or producing assessable income. They rely on the statement in Roberts at 261 that the characterisation of an outgoing depends on “what the expenditure is calculated to effect from a practical and business point of view, rather than upon the juristic classification of the legal rights”, quoting Hallstroms Pty Ltd v Commissioner of Taxation (Cth) (1946) 72 CLR 634 at 648 (Dixon J).

46 It may be accepted that questions of legal form are not determinative, but they are a relevant part of the background circumstances. To characterise expenditure from a practical and business perspective is not to disregard the legal nature of any liability that is discharged by the making of that expenditure, nor is it to inquire into whether the expenditure is similar or economically equivalent to expenditure that might have been incurred in some other transaction. Rather, it is to have regard to the “whole picture” of the commercial context within which the particular expenditure is made: AusNet Transmission Group Pty Ltd v Federal Commissioner of Taxation [2015] HCA 25; (2015) 255 CLR 439 at [74] (Gageler J); see also [22] (French CJ, Kiefel and Bell JJ); Clough Limited v Commissioner of Taxation [2021] FCAFC 197; (2021) 114 ATR 1 at [68]-[69] (Thawley J, with Kenny and Davies JJ agreeing).

C.2 Camco Trusts, Family Trust and Sub-trust loans

47 The structures at issue (the Camco Trusts, the Family Trust, and the Sub-trust Loans) arise out of the means for distributing profits of the business carried on by the Camco Trusts collectively. The Applicants provided a diagram to represent these structures, which is annexed to these reasons for judgment.

48 1995 Deed cl 9: The 1995 Deed provides in cl 9 that “net profits of the Partnership … shall belong to the Partners in such shares as are specified in Item 8 of the First Schedule or in such shares as shall from time to time be unanimously agreed in writing by the Partners.” The default position in item 8 of the First Schedule is for net profits to be distributed “in accordance with the capital contributions of the Partners [ie the Principals]”. Clause 9 of the 1997 Deed is to the same effect.

49 The Applicants observe here that Camco Engineering, as the trustee of each of the Camco Trusts, has broad powers to deal with property of the various trusts in its different capacities as trustee: see Camco 3 Trust deed, cls 6.29-6.31.

50 Camco Engineering: Mr Cameron states in his WAD325-327 affidavit that he was responsible for the financial modelling for the business carried on by the “Partnership” (in truth, the Camco business carried on by the Camco Trusts collectively: see [8] above). In each year (including between IY 2013 and IY 2020), the Principals of Camco Engineering agreed on a different basis for sharing the net profit between the Camco Trusts. Mr Cameron presented a “profit sharing schedule” to the annual meeting of the “partnership”, and (subject to one disagreement relating to the retirement of Mr Fusco) his proposed distribution was approved by the other Principals without disagreement and that decision was recorded in minutes.

51 Mr Cameron states that he took the view that all of the surplus funds of the Camco business should remain with the business, and that the Principals should only take from the business sufficient monies to fund their living needs and to pay tax. This was so that the Camco business could retain the maximum funds while minimising external debt. He states that the other Principals agreed with him.

52 Family Trust was entitled to all of Camco 3 Trust’s net income IY 2013-2020: After the annual meeting of the “partnership”, there was an annual formal meeting of each of the Camco Trusts. At the latter, the relevant Camco Trust would identify the entity or entities that would be entitled to receive the net income of the trust fund (under cl 3 of the Camco 3 Trust deed). From IY 2013 to IY 2020, Camco 3 Trust chose the (Cameron) Family Trust as the entity that was entitled to receive all of the trust income of the Camco 3 Trust.

53 Distribution of Family Trust’s income: The net income of the Family Trust was in turn distributed by the trustee (Acropolis) under cl 3 of the Family Trust deed. In IY 2013 to IY 2020, Acropolis made Adjuvant one of the beneficiaries entitled to some of the income of the Family Trust for that year; for example, in IY 2013, Adjuvant was entitled to the next $1.2 million, after the distribution of net capital gains and franking credits to Mrs Cameron, and the distribution of the first $270,000 to another family-related trust.

54 Sub-trust borrowings to deal with Adjuvant’s UPEs: Mr Cameron explains the reasons for the Sub-trust Loans as follows. He states that he understood that where an entity (such as the Family Trust) was made entitled to the income of a Camco Trust, that entitlement would remain wholly or substantially unpaid due to the arrangement agreed between the Principals for the Camco business to retain as much money as possible. Mr Cameron understood further that the unpaid amount would be subject to the published views of the ATO on the application of Pt III Div 7A of the ITAA 1936 (distributions to entities connected with a private company) to “unpaid present entitlements” (UPEs).

55 Mr Cameron understood that the consequences of the above matters would be as follows:

The effect of the Principals’ policy that they would not seek access in cash to all of their share of the profit of the Camco business (see [50] above) was that the Camco 3 Trust did not have enough cash to satisfy in full the Family Trust’s entitlement to the income of the Camco 3 Trust. That in turn meant that the Family Trust did not have enough cash to satisfy in full the entitlement of the beneficiaries of the Family Trust (including Adjuvant) to their share of the income of the Family Trust.

Any UPE held by Adjuvant would give rise to a tax liability, because it would be a deemed dividend paid by Adjuvant to the Family Trust. However, Mr Cameron understood that the effect of the ATO’s then PS LA 2010/4 (see [10] above) was that there would not be a deemed dividend if the UPE were placed on a “sub-trust arrangement”.

56 Mr Cameron states that he caused “sub-trust arrangements” to be entered into for IY 2013 to 2015, and IY 2018 to 2020. Under those arrangements, Adjuvant’s entitlement to income of the Family Trust was set aside on a sub-trust for Adjuvant, and then lent back to the Family Trust for a term of 7 years and bearing interest: see [10]-[11] above.

57 Purpose of sub-trust arrangements: Mr Cameron’s WAD325-327 affidavit gives the following evidence about the purpose of the Sub-trust Loans. (Again, references in his affidavit to the “Partnership” must be understood as references to the Camco business carried on by the Camco Trusts collectively: see [8] above.)

(a) Mr Cameron states that he wanted to keep the amount of external debt of the Camco Trust’s business to a minimum, to reduce the risk of any of the Principals losing their family home in the event of default by Camco Engineering.

(b) Mr Cameron states that his understanding was that the annual profits of a partnership (which he believed the Camco Trusts to be in) automatically belong to the partners in their respective shares, and that the partners are entitled to call for payment of their respective shares of the profit (unless they have agreed otherwise).

(c) Mr Cameron states that it was of significant importance to him that the “Partnership” not pay out those shares of profits to the Partner Trusts (such as the Camco 3 Trust) unless the Principals at the time were agreed that the financial position of the business of the “Partnership” could accommodate such a payment, as this way that business would have the maximum funds available to it to fund growth with the minimum external debt.

(d) Mr Cameron states that the “Partnership” collectively retaining as much as possible of the funds representing profits was foremost in his mind as, in his view, the business of the “Partnership” “was a voracious beast that required as much funding as it could get for it to continue to grow successfully”. He states that, because the monies owed to the Partner Trusts by the “Partnership” were being used for capital purchases and to fund working capital demand, it was not possible for the partner trusts to be repaid in circumstances where the “Partnership” did not have surplus cash at bank without the “Partnership” increasing loan funding from other sources.

(e) Mr Cameron states that his paramount concern was to ensure that the “Partnership” collectively retained as much as possible of the funds representing its profits so that the “Partnership” could be as profitable as possible which in his view would, in turn, maximise the future profit shares of each of the Partner Trusts (including the Camco 3 Trust) and which would, in turn, maximise the future income of the Family Trust. He states that it was also his preference that Adjuvant and other entities associated with him should not have to pay the additional income tax that would be payable if there were a deemed dividend, “while still ensuring that the Partnership retained as much as possible of the funds representing its profits”.

C.3 Analysis of whether Interest Payments on Sub-trust Loans were deductible

58 The question is whether the Interest Payments on the Sub-trust Loans were incurred in the course of the Family Trust gaining or producing assessable income.

This question requires determining what it is that is productive of assessable income, and its connection to the outgoing: Day at [21], [30]-[31]; see [36] above.

Interest payments usually take their character from the use to which the borrowed money is put, although in some situations the purpose of the borrowing (meaning the objective purpose) is relevant: see [40]-[41], [44] above.

59 Sub-trust Loans are not directly productive of income for the Family Trust: Here, the Sub-trust Loans were not used to produce income for the Family Trust directly. As noted, the amounts lent by Adjuvant under the Sub-Trust Loans were set off against UPEs held by Adjuvant in respect of the Family Trust. It was common ground that the direct effect of these arrangements from the Family Trust’s perspective was to convert one type of liability into another: the Trust’s liability to pay Adjuvant’s UPE (an immediate liability, not bearing interest) was converted into a debt liability (a non-current liability to repay the principal in seven years, and to pay interest in the meantime). In other words, this is not a case where the borrowed moneys were invested in an income-producing asset, where the connection between interest payments and gaining or producing assessable is obvious from the use of the moneys.

60 Instead, the Applicants contend that the connection between the Interest Payments and the derivation of assessable income by the Family Trust arises out of the connection between the Sub-trust Loans and the derivation of income by the Camco 3 Trust in the Camco business. In oral argument, the Applicants’ senior counsel stated that, in broad terms, the effect of the Sub-trust Loans was to make approximately an extra $7 million available to the Camco 3 Trust over 2013 to 2020 to be used in the Camco business. The Applicants contend that the Interest Payments are deductible, because:

(1) the Family Trust was foregoing a present right to payment from the Camco 3 Trust (which could have been used to satisfy Adjuvant’s UPEs in respect of the Family Trust), in return for the expectation of obtaining greater payments from the Camco 3 Trust in the future (relying on Total Holdings); and

(2) by not calling on the Family Trust’s right to payment from the Camco 3 Trust, the Family Trust was preserving the capital that was being used by the Camco 3 Trust in the Camco business (relying on Roberts).

61 Neither argument can be accepted.

62 Sub-trust Loans to increase distributions to Family Trust? The Applicants’ first argument proceeds in the following steps: (i) the Family Trust not calling on the Camco 3 Trust increases the amount of money available to the Camco 3 Trust; (ii) increasing the amount of funds available to the Camco 3 Trust would boost the profitability of the Camco business generally; (iii) that would increase the amounts that would be distributed to the Camco 3 Trust; (iv) that, in turn, would increase the amounts to be distributed to the Family Trust: see [57](e) above. This is said to provide a sufficient connection between the Interest Payments and the gaining or producing of assessable income by the Family Trust.

63 This first argument relies on Total Holdings.

In Total Holdings, the taxpayer company lent money to its subsidiary (TAL) between 1960-1968 on loans that were interest free and repayable on demand: Total Holdings at 220. The evidence was that the purpose of this interest free loan was to make TAL profitable as quickly as possible: Total Holdings at 226-227. The question was whether the taxpayer could deduct the interest payable on its borrowings (which it had used by making the interest free loans to TAL).

Lockhart J held that the interest payments were deductible: the taxpayer’s activities were designed to render TAL profitable as soon as commercially feasible and to promote the generation of income by TAL and its subsequent derivation by the taxpayer. The liability for interest of the taxpayer under its loans was incidental and relevant to the derivation of its income and was part of its business activities: Total Holdings at 229.

64 Total Holdings is distinguishable: I accept the Commissioner’s submission that Total Holdings is distinguishable. In that case, the taxpayer had taken positive steps to invest in TAL: the taxpayer purchased shares (see Total Holdings at 224) and entered into loan arrangements with TAL. Those steps were taken to gain or produce assessable income from TAL in the form of dividends. There is no comparable step here: for example, the Family Trust has not lent money to Camco 3 Trust. Even accepting that “operations and activities” is not a separate requirement to engage s 8-1(1) (see [39] above), in Total Holdings the taxpayer took steps that were productive of assessable income.

65 The Applicants contend that the comparable step is that the Family Trust has not called on its unpaid present entitlement as against the Camco 3 Trust, and that any difference between Total Holdings and this case is one of legal form only. As noted, legal form is a relevant part of the circumstances (even if it is not determinative), and it is not sufficient for a taxpayer to show that the outgoing is similar or economically equivalent to an expenditure that might have been incurred: Ausnet at [74]; see [46] above. Choosing not to call on a present entitlement under a trust is very different from purchasing shares and entering into loans.

66 This is not to impose any standard of “busyness” in order for an outgoing to be deductible. It is rather to require there to be a sufficient connection between the outgoing and what is productive of the Family Trust gaining or producing assessable income: see [36] above. As the Commissioner’s submits, it is not open to ignore the different structures in place, and to treat the Camco Trusts (such as the Camco 3 Trust) and the various family trusts (such as the Family Trust) as an aggregate entity with aggregate activities. Here, any connection between the Interest Payments and what is productive of the Family Trust deriving assessable income would have to be provided by the purpose of the Sub-trust Loans, meaning the objective purpose: see [44] above. On the Applicants’ argument, a beneficiary of a trust would have the (objective) purpose of gaining or producing assessable income by not calling on its entitlement to receive money under the trust, simply because the trust now has more resources with which to derive assessable income to make future distributions to the beneficiary. That argument is not supported by Total Holdings (and, as explained below, nor is it supported by Roberts).

67 Indeed, the Applicants’ argument, if correct, would mean that interest on a borrowing would be deductible, even if the Family Trust’s borrowings were used for a purpose entirely unconnected with the Camco business. That is because, even then, the Family Trust would be preserving the amount of money that was available to the Camco 3 Trust to be used to derive assessable income (from which it could make increased future distributions to the Family Trust). But that result is contrary to Federal Commissioner of Taxation v Munro [1926] HCA 58; (1926) 38 CLR 153, applied in Hayden at 28 and Riverside Road at 314. That analysis reveals that the asserted connection between the Sub-trust Loans and the gaining or producing of assessable income by the Family Trust is too remote.

68 Is greater distributions to the Family Trust a purpose in fact? It might be noted that Mr Cameron’s evidence, taken as a whole, shows that he was very concerned about the size of distributions to the various Camco Trusts, and wanted to maximise the funds that were available to the Camco business to fund growth: see [57](c) and (d) above; cf [57](e). This might have raised questions about whether steps (iii) and (iv) in the Applicants’ argument (set out in [62] above) were correct as a matter of fact. However, the Commissioner did not make any argument along these lines, and I do not consider this issue any further. The Applicants’ first argument should be rejected, for the reasons given above.

69 Sub-trust Loans preserve the capital available to the Camco 3 Trust? The Applicants’ second argument is that the Family Trust entering into the Sub-trust Loans preserves the capital available to the Camco 3 Trust (and the Camco business), similar to the loan considered in Roberts.

70 In Roberts, a partnership (a law firm) sought to reduce the value of the partnership, to enable a new partner to join, by paying the existing partners $25,000 each. The partnership borrowed $125,000 to make these payments: Roberts at 248. The issue was whether the interest on this loan was deductible. Hill J (with Jenkinson J agreeing) held that the interest may be deductible, depending on the facts, and that the matter should be remitted to the Tribunal to make the necessary findings of fact: Roberts at 260.

71 The Applicants rely on the following statement of Hill J in Roberts at 257, considering the position if a partnership had taken out a loan to fund the repayment to a partner of undrawn partnership distributions:

The funds to be withdrawn in such a case were employed in the partnership business; the borrowing replaces those funds and the interest incurred on the borrowing will meet the statutory description of interest incurred in the gaining or production by the partnership of assessable income.

72 The Applicants contend that the borrowing entered into by the Family Trust ensures that the funds of the Camco 3 Trust are not diminished, and that taking steps not to diminish funds is the same in substance as “replacing” those funds (which, it is said, Roberts holds is deductible).

73 Roberts is not applicable: However, it is clear from the remainder of Roberts that Hill J did not mean to suggest that the interest on a loan used to replace any funds used by a partnership would be deductible. His Honour later distinguished between a repayment that reduced a partner’s equity in the partnership (that is, including the partner’s share of profits), and a repayment of a capital contribution made by the partner constituting their share of the “partnership capital”: see Roberts at 259-260. Hill J expressly held in Roberts at 260 that interest on a loan used to return a partner’s equity in the partnership would not be deductible:

The provision of funds to the partners in circumstances where that provision is not a repayment of funds invested in the business [that is, the “partnership capital”], lacks the essential connection with the income producing activities of the partnership or, in other words, the partnership business. Likewise, the interest incurred on the borrowing will not be incidental and relevant to the partnership business. (emphasis added)

74 That is, the reasoning set out in [71] above applies to the replacement of capital contributions, and the reference to “undrawn partnership distributions” has to be understood in that light.

75 So understood, Roberts does not assist the Applicants, for two separate reasons. First, in no sense has the Family Trust invested in the Camco 3 Trust, let alone in a manner comparable to partnership capital contributions. Second, on the evidence, the Sub-trust Loans are not entered into to preserve the capital contributions made by the Principals: rather, Mr Cameron refers to the Sub-trust Loans ensuring that the Camco business “retained as much as possible of the funds representing its profits” (emphasis added): see [57](e) above.

76 Again, it is not sufficient that paying interest on a loan is necessary in a general sense to preserve income-producing assets: see [67] above.

77 Other arguments: It is not necessary to rule on the Commissioner’s other arguments as to why the Interest Payments are not deductible; for example, the Commissioner contended a separate basis for refusing deductibility was that the Family Trust, as the beneficiary of a discretionary trust, never had an entitlement to receive any money from the Camco 3 Trust, and its receipt of income from the Camco 3 Trust was passive and did not involve any “activities or operations”.

78 Conclusions in WAD325-327/2023: For these reasons, the appeals under s 14ZZ of the TA Act in WAD325-327/2023 are dismissed.

D. WAD184-186/2024: was a family trust election made in respect of the family trust?

79 As noted, the issue in proceedings WAD184-186/2024 is whether a valid family trust election was made in respect of the Family Trust.

D.1 ITAA 1936 Sch 2F: Family Trust Elections

80 Div 271: Division 271 of Sch 2F to the ITAA 1936 (added in 1998) deals with family trust distribution tax. The key provisions for present purposes are as follows.

81 Circumstances attracting tax liability (ss 271-15, 271-20): By s 271-15, there is a tax liability if a family trust makes distributions outside the family group, in the circumstances specified in s 271-15(1). One of those circumstances is that a trustee “makes a family trust election in relation to a trust” (s 271-15(1)(a)). A trust is a “family trust” at any time when a family trust election is in force (s 272-75).

82 By s 271-20, there is a tax liability if an interposed trust makes a distribution outside the family group. The section applies if the trustee of a trust has made an interposed entity election for the trust “to be included in the family group of the individual specified in a family trust election”; and the trust confers a present entitlement on a person outside that family group (s 271-20(1)). That is, any interposed entity election presupposes that a family trust election has been made.

83 Family trust election (s 272-80): The requirements for a family trust election are set out in s 272-80. Generally, the requirements include that the election is in writing and in the approved form (s 272-80(2)), and that the trust passes the family control test in s 272-87 at all times in the specified income year (see s 272-80(1) and (4)). However, this general position is affected by transitional provisions, discussed next.

84 By s 272-80(5), a family trust election generally cannot be varied or revoked, except in the circumstances set out in s 272-80(5A)-(5C), (6) and (6A).

85 Interposed entity election (s 272-85): The requirements for an interposed entity election are set out in s 272-85. An essential precondition is that a trustee has made a family trust election, because the effect of an interposed entity election is to include (at all times after a specified day in a specified year) a partnership or trust in the family group of an individual specified in a family trust election (see s 272-85(1)). Generally, an interposed entity election cannot be revoked (see s 272-85(5), (5A) and (5B)).

86 Transitional provisions: Schedule 2F (including Div 271) was added to the 1936 ITAA by the Taxation Laws Amendment (Trust Loss and Other Deductions) Act 1998 (Cth) (1998 Amendment Act), Sch item 1.

87 Original transitional provisions: Item 22 of the Schedule to the 1998 Amendment Act, as enacted, made provision for family trust elections to be made for income years before IY 1998. Relevantly, item 22(3) provided (emphasis added):

(3) If a family trust election can, in accordance with this item, specify the 1997-98 year of income or an earlier year of income:

(a) …

(b) the election must be in writing in a form approved by the Commissioner; and

(c) the election must be made:

(i) if the trustee is required to furnish a return for the 1997-98 year of income—by the time when the trustee furnishes the return; or

(ii) if the trustee is not required to furnish a return for that year of income—before the end of 2 months after the end of that year of income or before the end of such later day as the Commissioner allows.

88 Item 23 of the Schedule to the 1998 Amendment Act, as enacted, made similar provision for interposed entity elections to be made for the income years before IY 1998. In particular, any interposed entity election had to be in writing in an approved form (item 23(3)(b)).

89 These original transitional provisions permitted a family trust election to be made for the 1995 income year (the income year referred to in the IY 1999 income tax returns).

90 Amended transitional provisions: The transitional provisions in item 22 of the Schedule to the 1998 Amendment Act were themselves amended by the Taxation Laws Amendment Act (No 2) 2000 (Cth) (2000 Amendment Act), Sch 11 (which also added a new item 22A). However, item 11 of Sch 11 to the 2000 Amendment Act preserved the operation of the enacted version of item 22 of the Schedule to the 1998 Amendment Act. It is common ground that the relevant transitional provision is item 22 of the Schedule to the 1998 Amendment Act, as enacted.

D.2 Evidence relating to a family trust election

91 Income tax returns for IY 1999: The Commissioner relies on information included in income tax returns for IY 1999 for the Family Trust, Camco 3 Trust and Adjuvant; and also information included in income tax returns for the Camco 5 Trust, the Wilson Family Trust and Cresslane Pty Ltd (entities associated with another principal of the Camco business, Mr Wilson).

92 Family Trust IY 1999 income tax return (FTE and IEE): As noted, the Family Trust’s IY 1999 income tax return refers to a family trust election being made in respect of the Family Trust, and also to an interposed entity election: see [21]-[23] above. As noted, the making of an interposed entity election presupposes that a valid family trust election has been made.

93 Camco 3 Trust income tax return IY 1999 (FTE and IEE): The Camco 3 Trust’s IY 1999 income tax return also refers to a family trust election and an interposed entity election. This return was lodged around 1 November 2000 by Mr Lawrence Cook on behalf of Camco Engineering as the trustee of the Camco 3 Trust.

The family trust election referred to in the Camco 3 Trust’s 1999 return is in respect of the Camco 3 Trust. The return states that the specified income year was 1995, and that the specified individual was Bruce Cameron. The “FTE Declaration Details” page states that the trustee making the declaration was Camco Engineering, and included the date 18 September 2000.

The interposed entity election referred to in the Camco 3 Trust’s 1999 return is made in respect of the Camco 3 Trust. The return states, relevantly, that the family trust for which the interposed entity election was made was the (Cameron) Family Trust, that the income year specified in the family trust election for that trust was 1995 (with an election time of 19 May 1995), and that the specified individual’s name was Bruce Cameron.

94 Adjuvant income tax return IY 1999 (IEEs): The IY 1999 income tax return for Adjuvant (a beneficiary of the Family Trust) refers to two interposed entity elections.

The first is an interposed entity election made in respect of the Camco 3 Trust. The specified income year for the family trust election for the Camco 3 Trust is 1995 (with an election commencement date of 19 May 1995), and the specified individual is Bruce Cameron. The “IEE Declaration Details” states that the person making the declaration is Bruce Cameron, which is dated 18 September 2000.

The Adjuvant 1999 return also refers to an interposed entity election being made in respect of the (Cameron) Family Trust. The specified income year for this election is 1995 (with a specified day of 19 May 1995). The income year specified in the family trust election for the Family Trust is said to be 1995 (with an election commencement time of 19 May 1995). The specified individual is Mr Cameron.

95 Camco 5 Trust income tax return IY 1999 (FTE and IEE): The Camco 5 Trust’s IY 1999 income tax return provides information about a family trust election in respect of that trust, specifying the 1997 income year and identifying Mr Wilson as the specified individual whose family group is to be taken into account in respect of that trust. The Camco 5 Trust’s 1999 return also refers to an interposed entity election made by the Camco 5 Trust in relation to the Wilson Family Trust, again specifying the 1997 income year and Mr Wilson as the specified individual. The family trust election and interposed entity election in respect of the Camco 5 Trust (made by Camco Engineering) are both dated 18 September 2000.

96 Wilson Family Trust income tax return IY 1999 (FTE and IEE): The Wilson Family Trust’s IY 1999 income tax return refers to a family trust election being made in respect of that Trust, and also to an interposed entity election made in respect of the Camco 5 Trust.

The family trust election referred to in the Wilson Family Trust’s return specifies the 1995 income year, and the specified individual as Mr Wilson. The declaration is said to be made by Crosstown Pty Ltd (the trustee of the Wilson Family Trust), and dated 18 September 2000.

The interposed entity election referred to in the Wilson Family Trust’s return states that the trust for which this election is made is the Camco 5 Trust, and specifies the income year of 1997 (with a specified day of 13 June 1997). The specified individual is Mr Gregory. Again, the declaration is said to be made by Crosstown, and dated 18 September 2000.

97 Cresslane income tax return IY 1999 (IEEs): Cresslane’s IY 1999 income tax return refers to two interposed entity elections.

The first is an interposed entity election made in respect of the Camco 5 Trust. The specified income year for this election is said to be 1998 (with a specified day of 25 June 1998). The return refers to a family trust election being made in respect of the Camco 5 Trust, with a specified income year of 1997 (and election commencement time of 13 June 1997). The person making the declaration is said to be Mr Wilson, with a date of 18 September 2000.

Cresslane’s 1999 return also refers to an interposed entity election being made in respect of the Wilson Family Trust. The income year specified for this election is 1998 (with a specified day of 25 June 1998). The income year in the family trust election for the Wilson Family Trust is said to be 1995 (with an election commencement time of 19 May 1995), and the specified individual is Mr Wilson. The declaration for the interposed entity election is said to be made by Mr Wilson on 18 September 2000.

98 Applicants’ evidence: The Applicants rely on the evidence of Lawrence Cook, the accountant for the Family Trust and Camco 3 Trust at the time, and of Mr Cameron. The Applicants also refer to the Family Trust’s tax returns from IY 2000 onwards.

99 Mr Cook’s affidavit evidence: The key points in Mr Cook’s first affidavit are as follows:

(a) Mr Cook states that, since their inception, he “ha[s] hated” family trust elections, and that he would rarely recommend their use to a client unless there was a specific and compelling reason to make the election.

(b) On the rare occasions on which a client has caused a trustee of a trust they controlled to make a family trust election, Mr Cook “may also have recommended” that an interposed entity election be made for another entity so that it could receive distributions from the trust that made the family trust election without adverse tax consequences.

(c) Mr Cook states that his understanding in 1998 was that a family trust election had to be made using a form provided by the ATO, rather than in a tax return, and that if a trustee wanted to make a family trust election then it had to complete the form and hold onto it, rather than give it to the ATO. Mr Cook recalls obtaining a stack of the ATO forms for making a family trust election around the time they were introduced in 1998. He recalls placing a stack of these forms in an office cabinet and states that, to the best of his recollection, he never took them out to fill one in. He states he is completely certain that he never had a client sign one of those forms.

(d) Mr Cook recalls that there was an amendment to income tax legislation in around 2000 affecting family trust elections. He recalls that “from around this time family trust elections had to be made in a trust’s income tax return (or as a schedule to that return) rather than on a separate form that was not given to the ATO”.

(e) Mr Cook does not have a specific recollection of lodging the income tax return for the Family Trust for IY 1999. The ATO lodgment receipt shows that the return was lodged a little after 11pm. Although the return gives the name “M L Cook” (Mr Cook’s son) as the contact person, Mr Cook states that his practice was to lodge personally all returns for which he was responsible as the registered tax agent until around 2010.

(f) Mr Cook states that he cannot think of any reason why he would have recommended that the Family Trust make a family trust election. He states that the only explanation that occurs to him is that it was an accidental error that he made working late at night and under time pressure.

(g) Mr Cook states that he used the information provided by the ATO to complete the Family Trust Distribution Tax Payment Advices (see [29] above). He states that, in filling in these forms, he did not consider that the Family Trust had made a family trust election.

100 Mr Cook’s second affidavit adds the following points:

(a) Mr Cook recalls that, around June 1999, he attempted to familiarise himself with how family trust elections could be made in new software. He thinks that, while he cannot be sure of the details given the time that has elapsed, in the course of familiarising himself with how family trust elections could be made using this software he created a “template” form of family trust election data. He thinks that the error he made in the IY 1999 Family Trust income tax return was either accidentally to include, or accidentally to fail to remove, the template form of family trust election data.

(b) Mr Cook states that, while he cannot be sure, this accidental inclusion or failure to remove a template form of family trust election resulted in the same 18 September 2000 date being shown in the return for the Cameron Family Trust, the Camco 3 Trust and the Camco 5 Trust.

101 Mr Cook’s oral evidence: Mr Cook made the following new points during cross examination.

(a) Mr Cook was taken to an ATO form which was the 1998 approved form for making a family trust election (1998 FTE form), and a 1999 document from the ATO titled “family trust election and/or family trust revocation: form and notes” (1999 ATO notes).

• Mr Cook agreed that the notes to the 1998 FTE form stated that it must be used to make a family trust election specifying an income year before 1998. The election was required to be made within a certain period of the trust lodging a return for IY 1998 (if a return was required that year). A copy of the election was required to be retained by the taxpayer for 5 years.

• Mr Cook agreed that the notes in the 1999 ATO notes stated that certain information about a family trust election had to be provided in the IY 1999 tax return, if (relevantly) the trustee had already made a family trust election specifying an income year before IY 1998.

• Mr Cook agreed that the effect of these forms was that a family trust election specifying an income year before 1998 was made by completing the 1998 FTE form.

(b) Mr Cook accepted that 14 other clients of his had made family trust elections. He stated that, with each of these clients, there was a reason for the client to complete a family trust election. Mr Cook stated that family trust elections were useful if it was intended to carry forward tax losses, or to deal with franking credits of more than a certain amount of more than $5,000. He stated that neither of these factors was present in the case of the entities associated with Mr Cameron. When asked if a family trust election might have been made for the Family Trust to guard against the risk of future losses, Mr Cook stated that a family trust election could be made in the relevant year if required.

(c) Mr Cook stated that the 14 other family trust elections were not a mistake. However, he stated that he had never completed the 1998 FTE form. He stated that he had thought that it was possible to make a valid family trust election by providing the information in the 1999 income tax return. There was a discussion of whether this meant that the family trust elections apparently made by the 14 clients who intended to make an election were in fact invalid.

(d) Mr Cook accepted that the details about family trust elections and interposed entity elections referred to in the IY 1999 returns of the Camco 3 Trust, the Family Trust and Adjuvant were not added inadvertently, or automatically by a computer. Mr Cook accepted that the 1995 date could be explained as the date on which the Camco business started operation.

• Mr Cook stated that he believed he must have put this information into a draft assessment for each of these entities, with a view to obtaining instructions from Mr Cameron on whether to make these elections. He believed that he must have inadvertently forgot to delete this information when lodging the 1999 returns.

• Mr Cook stated that none of the income tax returns for Camco 3 Trust (and the other entities associated with Mr Cameron) from 2000 until 2022 referred to a family trust election having been made. He stated that the Camco 3 Trust had made distributions in 2006 to the Let 3 Trust, which would have attracted FTD tax if a family trust election had been made. Mr Cook stated that these actions showed that he and Mr Cameron had never acted on the basis that a family trust election had been made in respect of the Family Trust.

(e) Mr Cook accepted that the details about family trust elections and interposed entity elections referred to in the IY 1999 returns for the entities associated with Mr Wilson were not added inadvertently. He accepted that the 1997 date referred to in these forms could be explained as the (later) date on which Mr Wilson joined the Camco business. He also accepted that the returns for the entities associated with Mr Wilson were lodged at different times from the returns for the entities associated with Mr Cameron, and that Mr Cook was not under the same time pressure when he lodged the returns for the Wilson entities.

102 Mr Cameron’s evidence: Mr Cameron states in his WAD184-186 affidavit that, to the best of his recollection, he has never discussed the concept of making a “family trust election” or an “interposed entity election” for the Family Trust or for any other entity, and had heard of neither concept before this dispute. He states that, to the best of his recollection, he has never been aware that he signed a document that purported to make either of these kinds of election for the Family Trust or any other entity. He states that he would generally follow any recommendation of Mr Cook, if Mr Cameron found the explanation of the reason for that recommendation sensible.

103 Mr Cameron’s oral evidence was largely to the same effect. He stated that he would sometimes take a tax issue to Mr Cook. Mr Cameron stated that, although he could not remember every form he had signed over the last 20 years, he could remember every type of form he had signed. His practice was to read any new type of document “front to back” before signing it.

104 Contemporary returns: As stated by Mr Cook in cross-examination, the tax returns for the Family Trust for IY 2000 to IY 2022 do not refer to a family trust election having been made.

In the income tax return for IY 2000, the return stated: “Family trust/interposed entity election status-insert appropriate code”. No code was entered.

In the income tax return for IY 2001, the return stated: “If the trustee(s) has/have made or is/are making or revoking a family trust election and/or made or making one or more interposed entity elections for the 2000-01 income year or an earlier income year, print the appropriate election status code for the trust”. No code was entered.

The returns since 2007 have stated that, “If the trustee has made … a family trust election, write the four-digit income year specified of the election”. No year has been added.

105 Mr Cook also stated in cross-examination that the Family Trust made distributions to the Let 3 Trust in IY 2006 (which is shown by the Family Trust’s tax return). Mr Cook stated that he was of the view that there was no family trust election at that point, because in his view a distribution to the Let 3 Trust would have attracted FTD Tax (because at that time there was no retrospective election available under s 99 of the ITAA 1936).

D.3 Analysis of whether a valid family trust election was made

106 The sole question in dispute in these appeals is whether a valid family trust election was made in respect of the Family Trust.

107 Approach to fact-finding: The Applicants accept that they bear the onus of proof in these proceedings (TA Act s 14ZZO). However, they draw attention to the five propositions made by Steward J (with Greenwood J agreeing) in Commissioner of Taxation v Cassaniti [2018] FCAFC 212; (2018) 266 FCR 385 at [88], derived from Allied Pastoral Holdings Pty Ltd v Commissioner of Taxation [1983] 1 NSWLR 1. Those propositions include that the ordinary civil standard applies in these proceedings, and an applicant need only succeed in weighing the metaphorical scales “ever so slightly in his favour” to discharge the burden of proof. On the other hand, the Commissioner observes, correctly, that he does not have any burden to show that an assessment was correctly made: see for example McCormack v Commissioner of Taxation [1979] HCA 18; (1979) 143 CLR 284 at 303 (Gibbs J), 306 (Stephen J), 323 (Murphy J). Further, any gap in the documentary records cannot work in the taxpayer’s favour: Trautwein v Federal Commissioner of Taxation [1936] HCA 77; (1936) 56 CLR 63 at 87 (Latham CJ).

108 Here, the affidavit evidence of Mr Cameron and Mr Cook is given many years after any election would have taken place. The Commissioner relies particularly on the contemporary documentary evidence, consisting of income tax returns filed for IY 1999. As well as their affidavit evidence, the Applicants refer to different documentary evidence, including the Family Trust’s tax returns from IY 2000 onwards.

109 Many cases have stated that ordinary human experience is that human memory is fallible, and the degree of fallibility increases over time. That is particularly so where disputes or litigation intervene, and the processes of memory are overlaid, often subconsciously, by perceptions or self-interest as well as conscious consideration of what should have been said or could have been said: see Watson v Foxman (1995) 49 NSWLR 315 at 319 (McLelland CJ in Eq); Martin v Norton Rose Fulbright Australia [2021] FCAFC 216; (2021) 289 FCR 369 at [147] (the Court). Similarly, in Fox v Percy [2003] HCA 22; (2003) 214 CLR 118 at [31], Gleeson CJ, Gummow and Kirby JJ stated that scientific research has cast doubt on the ability of judges (or anyone else) to tell truth from falsehood accurately on the basis of a witness’s demeanour. These considerations have encouraged judges “to limit their reliance on the appearances of witnesses and to reason to their conclusions, as far as possible, on the basis of contemporary materials, objectively established facts and the apparent logic of events” (emphasis added).

110 That is not to say that no use can be made of oral evidence and affidavit evidence based on current recollection. In Gestmin SGPS SA v Credit Suisse (UK) Ltd [2013] EWHC (Comm) 3560 at [22], Legatt J stated:

[T]he best approach for a judge to adopt in the trial of a commercial case is, in my view, to place little if any reliance at all on witnesses’ recollections of what was said in meetings and conversations, and to base factual findings on inferences drawn from the documentary evidence and known or probable facts. This does not mean that oral testimony serves no useful purpose – though its utility is often disproportionate to its length. But its value lies largely, as I see it, in the opportunity which cross-examination affords to subject the documentary record to critical scrutiny and to gauge the personality, motivations and working practices of a witness, rather than in testimony of what the witness recalls of particular conversations and events. Above all, it is important to avoid the fallacy of supposing that, because a witness has confidence in his or her recollection and is honest, evidence based on that recollection provides any reliable guide to the truth. (emphasis added)

This passage has been quoted with approval in Australia: see for example ET-China.com International Holdings Ltd v Cheung [2021] NSWCA 24; (2021) 388 ALR 128 at [27] (Bell P, with Bathurst CJ agreeing); Turner v Richards [2025] NSWCA 83 at [60] (Payne JA, with Leeming and Adamson JJA agreeing); Pennytel Australia Pty Limited v Engelke [2025] FCA 1384 at [194] (Needham J), and the cases cited.

111 The Applicants’ reply submissions appear to contend that these principles are confined to legal issues where the precise form of words is important (such as cases about misleading or deceptive conduct). However, the reasoning in Fox v Percy and Gestmin is not so confined.