FEDERAL COURT OF AUSTRALIA

Australian Competition and Consumer Commission v Coles Supermarkets Australia Pty Ltd [2026] FCA 598

File number(s): | VID 973 of 2024 VID 1247 of 2024 |

Judgment of: | O’BRYAN J |

Date of judgment: | 14 May 2026 |

Catchwords: | CONSUMER LAW – prohibitions against misleading or deceptive conduct and false or misleading representations – supermarket pricing ticket stating ‘was/now’ prices – whether ticket was false, misleading or deceptive – whether the ticket represented to consumers that the product’s current price was a genuine reduction to, or discount from, the product’s previous price – whether the ticket represented to consumers that the product had been offered for sale at the previous price for a reasonable period – where the product had been offered for sale at the previous price for only four weeks in circumstances where prices for manufactured and packaged grocery products were relatively stable over time – ticket found to be misleading because the discount represented on the ticket was not genuine in circumstances where the product had not been sold at the previous price stated on the ticket for a reasonable period |

Legislation: | Competition and Consumer Act 2010 (Cth) s 155, Sch 2 (Australian Consumer Law) ss 18(1), 29(1)(i) Evidence Act 1995 (Cth) s 140 Federal Court of Australia Act 1976 (Cth) Trade Practices Act 1974 (Cth) Competition and Consumer (Industry Codes—Food and Grocery) Regulation 2015 (Cth) Competition and Consumer (Industry Codes—Food and Grocery) Regulations 2024 (Cth) |

Cases cited: | AA v The Trustees of the Roman Catholic Church for the Diocese of Maitland-Newcastle [2026] HCA 2; 427 ALR 67 Ascot Four Pty Ltd v Australian Competition and Consumer Commission (2009) 176 FCR 106 Australian Competition and Consumer Commission v Allans Music Group Pty Ltd [2002] FCA 1552 Australian Competition and Consumer Commission v Ascot Four Pty Ltd [2008] FCA 1295; 250 ALR 467 Australian Competition and Consumer Commission v Carrerabenz Diamond Industries Pty Ltd [2008] FCA 1103; (2008) ARPR 42-248 Australian Competition and Consumer Commission v Coles Supermarkets Australia Pty Ltd [2014] FCA 634; 317 ALR 73 Australian Competition and Consumer Commission v Jewellery Group Pty Ltd [2012] FCA 848; 293 ALR 335 Australian Competition and Consumer Commission v Kogan Australia [2020] FCA 1004; 145 ACSR 609 Australian Competition and Consumer Commission v Prouds Jewellers Pty Ltd [2008] FCA 75; 75 IPR 306 Australian Competition and Consumer Commission v Prouds Jewellers Pty Ltd [2008] FCAFC 199 Australian Competition and Consumer Commission v Prouds Jewellers Pty Ltd (No 2) [2008] FCA 476 Australian Competition and Consumer Commission v TPG Internet Pty Ltd (2013) 250 CLR 640 Australian Competition and Consumer Commission v TPG Internet Pty Ltd (2020) 278 FCR 450 Australian Securities and Investments Commission v Vanguard Investments Australia Ltd [2024] FCA 308 Bed Bath ‘N’ Table Pty Ltd v Global Retail Brands Australia Pty Ltd [2025] HCA 50; 100 ALJR 57 Briginshaw v Briginshaw (1938) 60 CLR 336 Butcher v Lachlan Elder Realty Pty Limited (2004) 218 CLR 592 Campomar Sociedad, Limitada v Nike International Limited (2000) 202 CLR 45 Demery v Coles Supermarkets Australia Pty Ltd [2025] FCA 1016 Ducret v Chaudhary’s Oriental Carpet Palace Pty Ltd (1987) 16 FCR 562 G v H (1994) 181 CLR 387 Global Sportsman Pty Ltd v Mirror Newspapers Pty Ltd (1984) 2 FCR 82 Google Inc v Australian Competition and Consumer Commission (2013) 249 CLR 435 Hornsby Building Information Centre Pty Ltd v Sydney Building Information Centre Ltd (1978) 140 CLR 216 Jewellery Group Pty Ltd v Australian Competition and Consumer Commission [2013] FCAFC 144 Neat Holdings Pty Ltd v Karajan Holdings Pty Ltd [1992] HCA 66; 110 ALR 449 Noone (Director of Consumer Affairs Victoria) v Operation Smile (Australia) Inc (2012) 38 VR 569 Parkdale Custom Built Furniture Pty Ltd v Puxu Pty Ltd (1982) 149 CLR 191 Roberts-Smith v Fairfax Media Publications Pty Limited & Others (Appeal) (2025) 310 FCR 170 Self Care IP Holdings Pty Ltd v Allergan Australia Pty Ltd (2023) 277 CLR 186 Taco Co of Australia Inc v Taco Bell Pty Ltd (1982) 42 ALR 177 Trade Practices Commission v Cue Design Pty Ltd (1996) 85 A Crim R 500; (1996) ATPR 41-475 |

Division: | General Division |

Registry: | Victoria |

National Practice Area: | Commercial and Corporations |

Sub-area: | Regulator and Consumer Protection |

Number of paragraphs: | 523 |

Date of last submissions: | 5 March 2026 |

Date of hearing: | 16-20 and 25-26 February 2026 |

Counsel for the Applicant (VID973/2024): | G Rich SC with E Bathurst, S McLeod and S Rajanayagam |

Solicitor for the Applicant (VID973/2024): | Johnson Winter Slattery |

Counsel for the Applicant (VID1247/2024): | P Cashman with D Townsend |

Solicitor for the Applicant (VID1247/2024): | Gerard Malouf and Partners |

Counsel for the Respondent (VID 973/2024 and VID1247/2024): | J Sheahan KC with N De Young KC, A Barraclough and S Hogan |

Solicitor for the Respondent (VID 973/2024 and VID1247/2024): | Allens |

ORDERS

VID 973 of 2024 | ||

| ||

BETWEEN: | AUSTRALIAN COMPETITION AND CONSUMER COMMISSION Applicant | |

AND: | COLES SUPERMARKETS AUSTRALIA PTY LTD (ACN 004 189 708) Respondent | |

order made by: | O’BRYAN J |

DATE OF ORDER: | 14 May 2026 |

THE COURT ORDERS THAT:

1. By 29 May 2026, the parties provide to the chambers of O’Bryan J agreed or, if not agreed, competing proposed orders giving effect to these reasons and for the further disposition of the proceeding.

2. If the parties are unable to agree on the proposed orders referred to in order 1, by 5 June 2026 the parties are to file and serve written submission limited to 5 pages in support of the orders proposed by that party.

3. Pursuant to ss 37AF(1)(b) and 37AG(1)(a) of the Federal Court of Australia Act 1976 (Cth), access to and disclosure (by publication or otherwise) of section C.6 of the reasons for judgment delivered today be restricted to the parties until further order of the Court.

4. By 29 May 2026, the respondent file and serve any application under ss 37AF(1)(b) and 37AG(1)(a) of the Federal Court of Australia Act 1976 (Cth) for ongoing suppression of any confidential financial information contained in section C.6 of the reasons for judgment, supported by an affidavit and submissions limited to 5 pages.

5. The proceeding be listed for further case management at 10.15 am on 10 June 2026.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ORDERS

VID 1247 of 2024 | ||

| ||

BETWEEN: | BENJAMIN GLENN DEMERY Applicant | |

AND: | COLES SUPERMARKETS AUSTRALIA PTY LTD (ACN 004 189 708) Respondent | |

order made by: | O’BRYAN J |

DATE OF ORDER: | 14 may 2026 |

THE COURT ORDERS THAT:

1. By 29 May 2026, the parties provide to the chambers of O’Bryan J agreed or, if not agreed, competing proposed orders giving effect to these reasons and for the further disposition of the proceeding.

2. If the parties are unable to agree on the proposed orders referred to in order 1, by 5 June 2026 the parties are to file and serve written submission limited to 5 pages in support of the orders proposed by that party.

3. Pursuant to ss 37AF(1)(b) and 37AG(1)(a) of the Federal Court of Australia Act 1976 (Cth), access to and disclosure (by publication or otherwise) of section C.6 of the reasons for judgment delivered today be restricted to the parties until further order of the Court.

4. By 29 May 2026, the respondent file and serve any application under ss 37AF(1)(b) and 37AG(1)(a) of the Federal Court of Australia Act 1976 (Cth) for ongoing suppression of any confidential financial information contained in section C.6 of the reasons for judgment, supported by an affidavit and submissions limited to 5 pages.

5. The proceeding be listed for further case management at 10.15 am on 10 June 2026.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

O’BRYAN J:

[1] | |

[1] | |

[21] | |

[30] | |

[36] | |

[46] | |

[47] | |

[49] | |

[64] | |

[67] | |

[74] | |

[79] | |

[113] | |

[133] | |

[189] | |

[364] | |

[364] | |

[367] | |

[373] | |

[404] | |

[406] | |

E.2 What did the Down Down tickets convey to ordinary consumers? | [408] |

E.3 Were the Down Down tickets for the sample products misleading or deceptive? | [435] |

[518] | |

[] |

A. INTRODUCTION

A.1 ACCC proceeding

1 On 23 September 2024, the Australian Competition and Consumer Commission (ACCC) commenced a proceeding (VID 973 of 2024) against Coles Supermarkets Australia Pty Ltd (Coles) alleging that, between February 2022 and May 2023 (the relevant period), Coles temporarily increased the retail prices of 245 products (affected products) before placing those products on ‘Down Down’ promotions at prices which, although lower than the temporarily increased prices, were higher than, or the same as, the price at which each product had ordinarily been offered for sale prior to the temporary increase.

2 The Down Down promotional program was introduced by Coles in 2010 and continued until (at least) the end of the relevant period. At all relevant times, Down Down was a well-known promotional program. When introduced in 2010, the promotion was heavily marketed with a memorable jingle “Down down, prices are down” sung by the British rock group Status Quo to the tune of their 1975 popular song “Down Down”. The marketing of the promotional program was also associated with a large red hand pointing downwards. Although features of the marketing changed over the years, the Down Down promotional program continued to be a well-recognised promotional program associated with Coles in the relevant period. In broad terms, the Down Down promotional program was a program by which Coles offered to customers a range of commonly purchased products at reduced prices. As illustrated below, a central feature of the promotion was the use of ‘was/now’ pricing, by which the Down Down promotional price was compared to an earlier higher price.

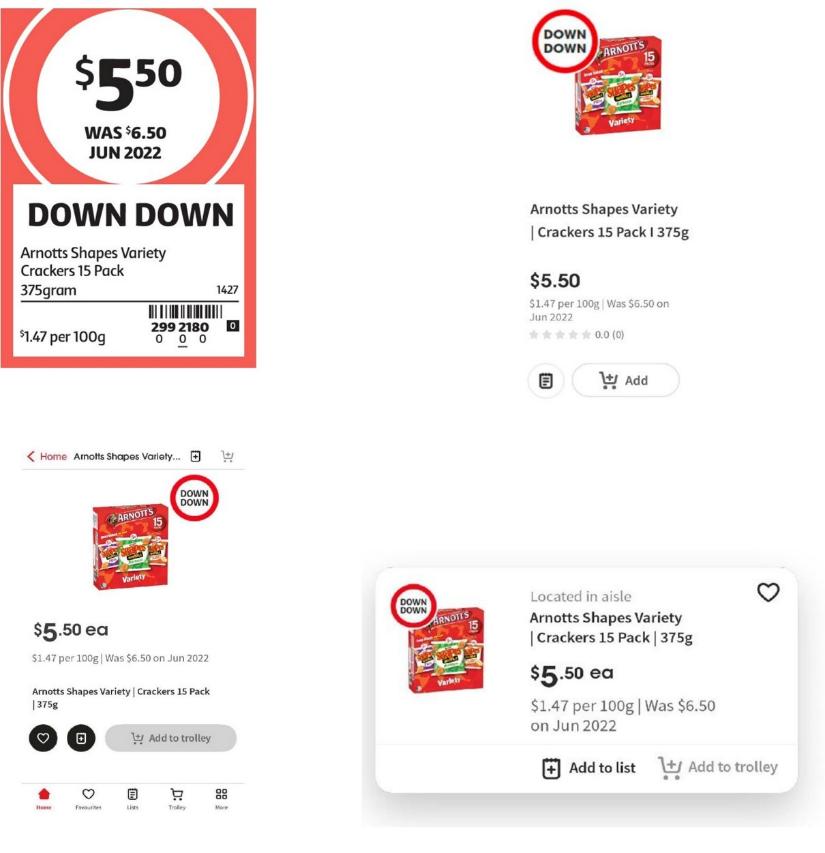

3 Coles communicated the price and, if applicable, the promotional status of products offered in-store and online through pricing labels or product tiles respectively (referred to collectively as tickets). Where a product was not on promotion, the product was promoted using a ‘standard shelf edge ticket’ (often referred to in the evidence as a white ticket). Products on a Down Down promotion were identified by Coles in-store and online using a specific form of pricing label (for products offered in-store) and product tile (for products offered online) to distinguish them from products that were not on promotion and from products on other forms of promotion. The Down Down label for a product offered in-store was displayed on the shelf immediately below the relevant product (or otherwise physically near the relevant product); and the Down Down tile for a product offered online was displayed near the picture of the relevant product. The Down Down tickets displayed by Coles in its stores and online respectively included the following features:

(a) a red and white colour scheme, coupled with the words “Down Down” in large bold font;

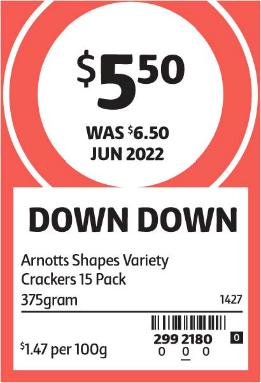

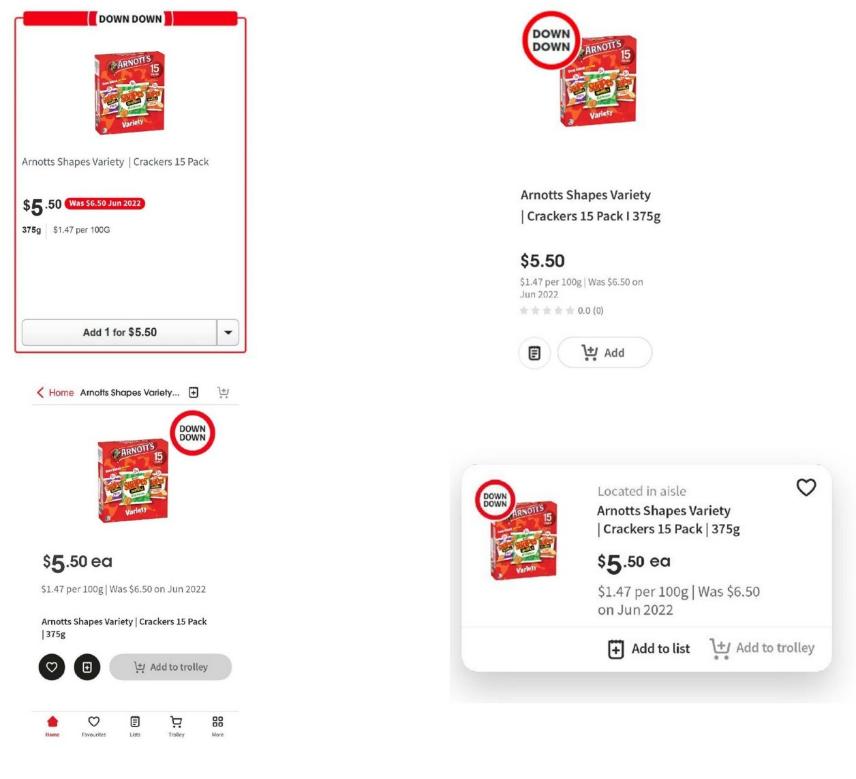

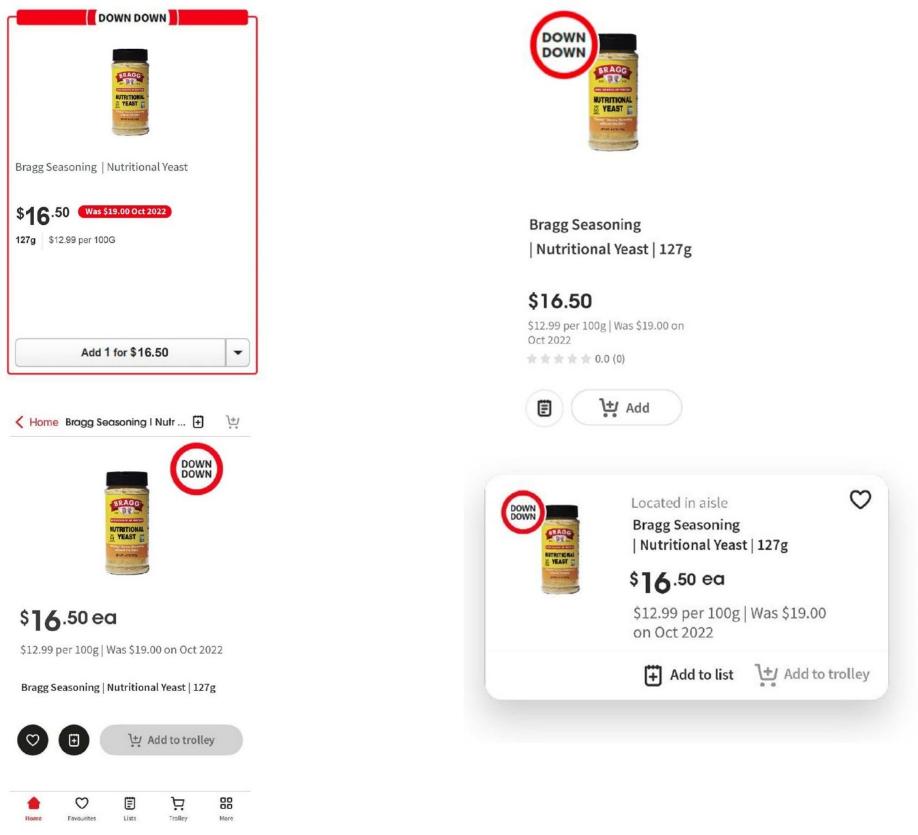

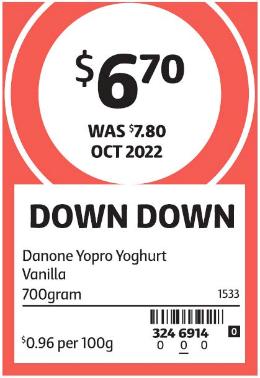

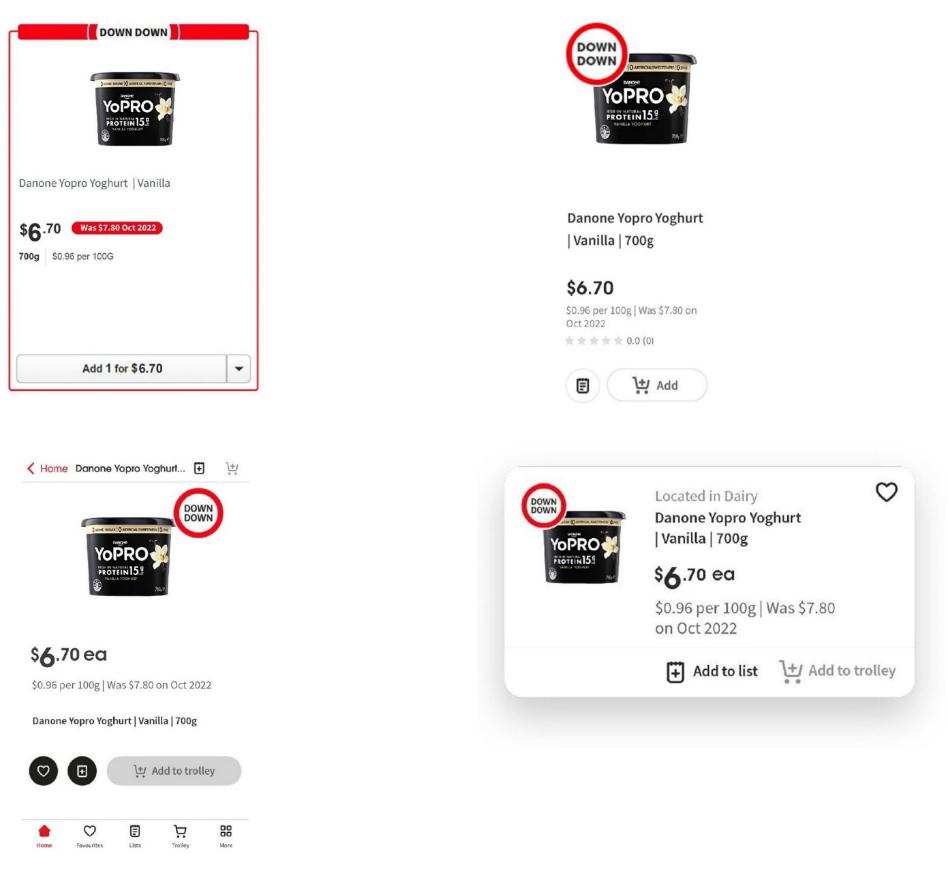

(b) the name of the relevant product (for example, “Arnotts Shapes Variety Crackers 15 Pack 375gram”);

(c) the price at which the product was available for sale during the Down Down promotion (the Down Down price), displayed in prominent font; and

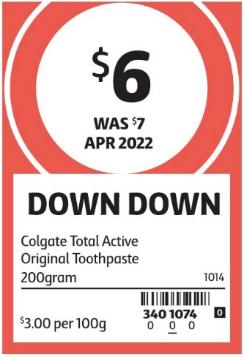

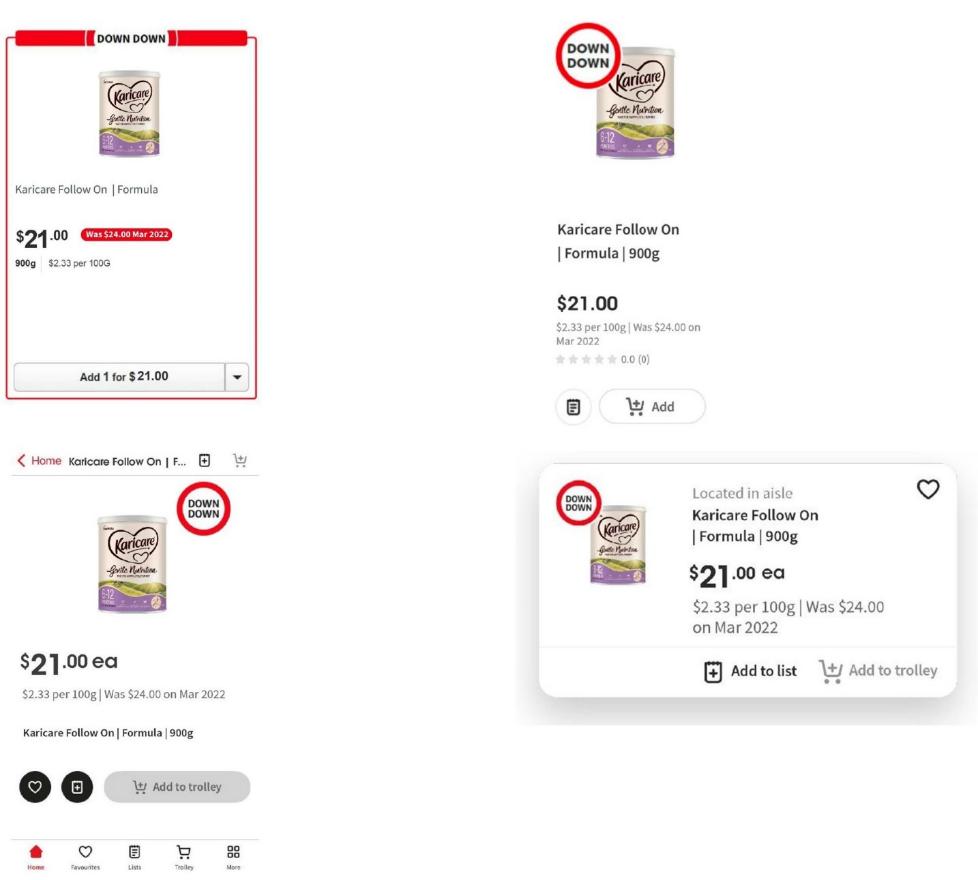

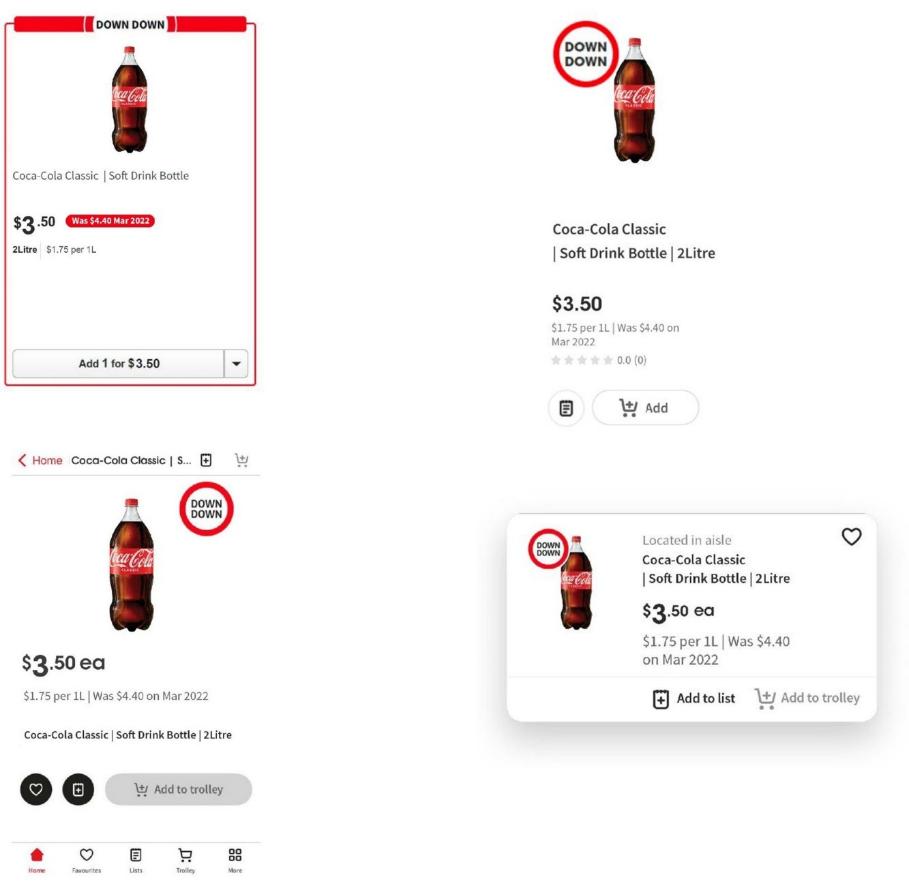

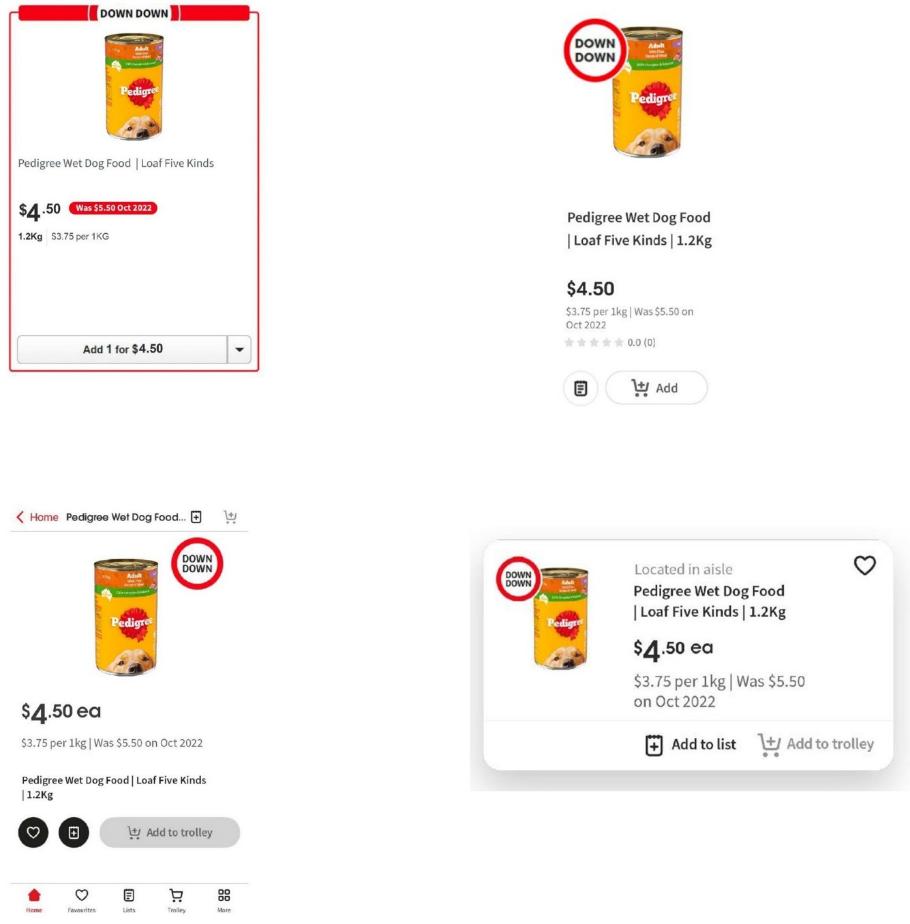

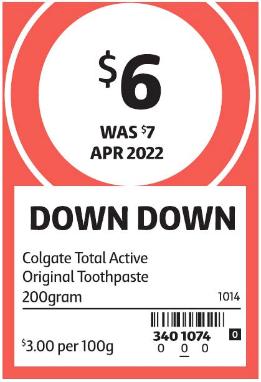

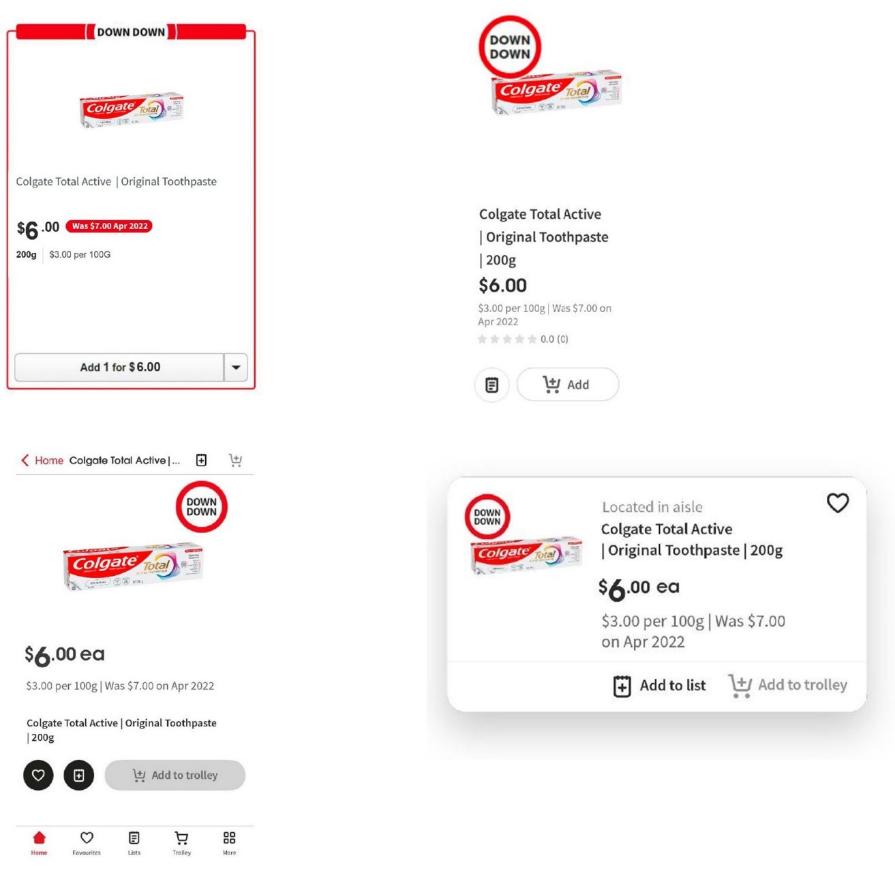

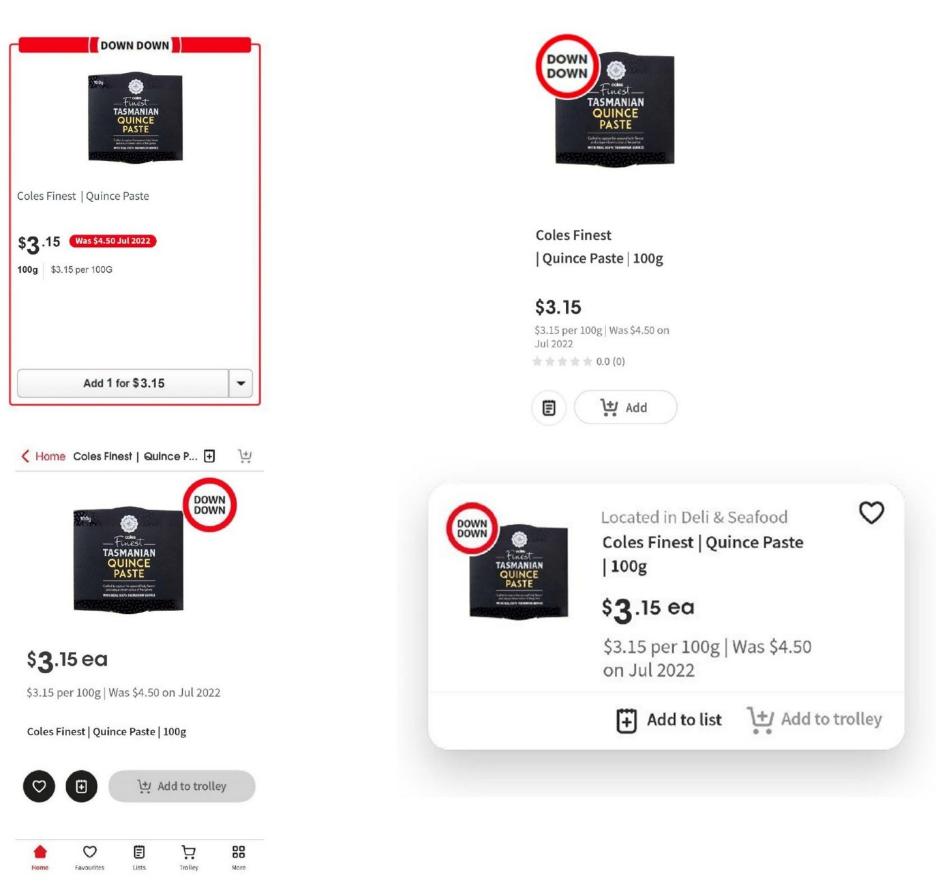

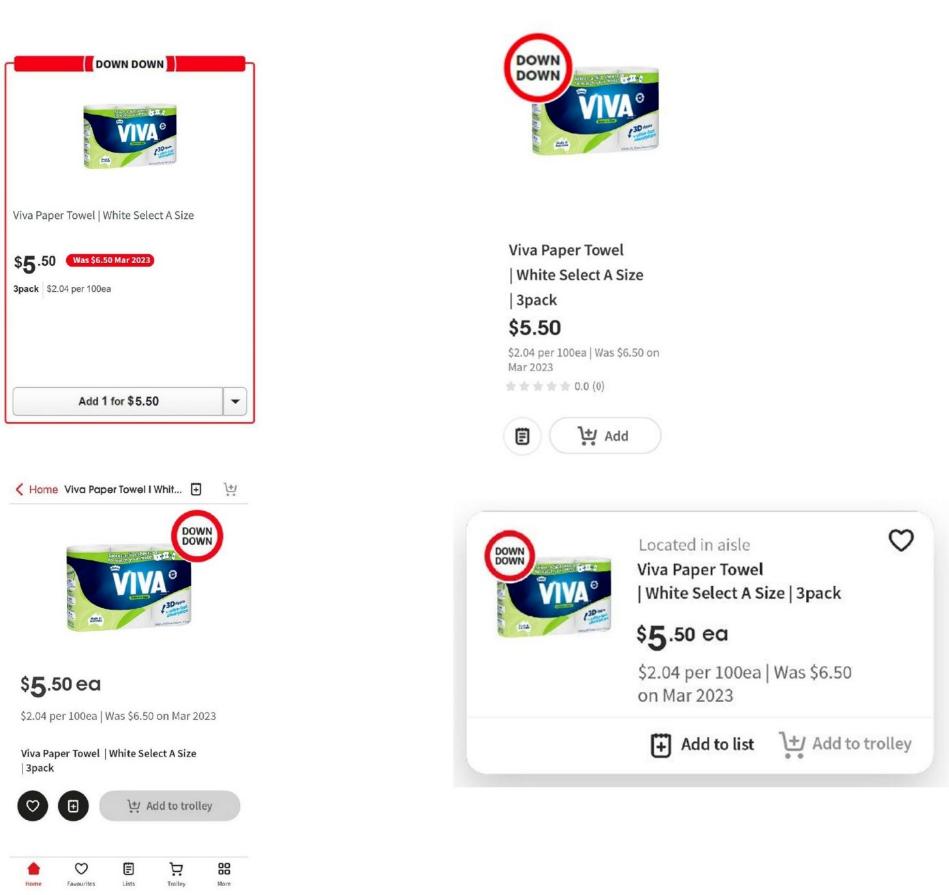

(d) in most cases, a ‘Was’ price for the product, displayed in smaller font, together with the date of the ‘Was’ price (for example, “Was $6.50 June 2022”).

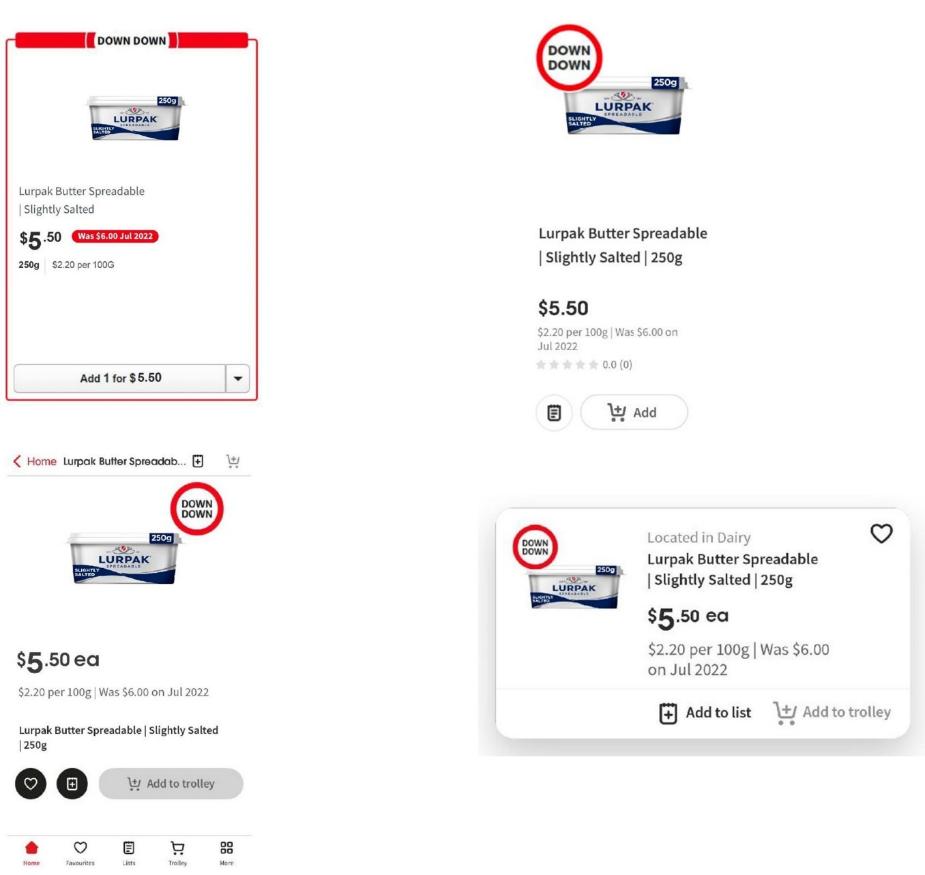

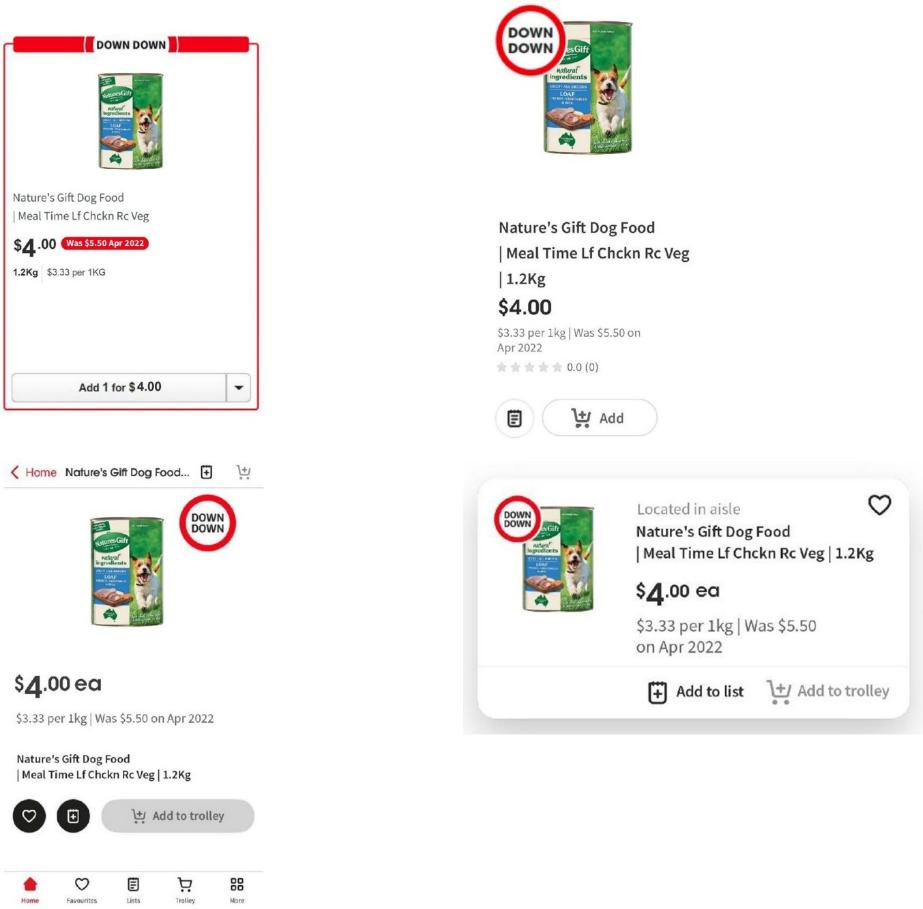

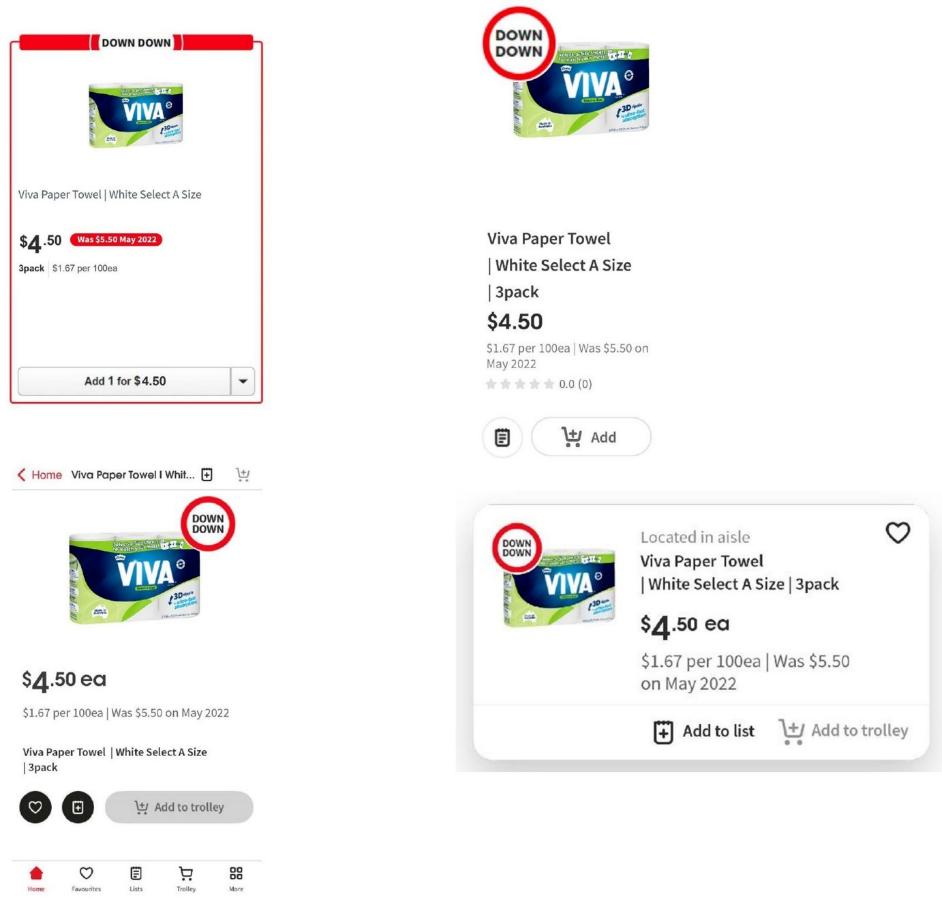

4 Examples of the Down Down tickets as they appeared in-store and online during the relevant period are as follows:

5 In its Concise Statement, the ACCC alleged that, in respect of each of the affected products, the information displayed on the Down Down ticket for the product represented to consumers that the product’s Down Down price was “a genuine reduction to, or discount from, the product’s previous regular price” (the genuine discount representation). In its opening written submissions at trial, the ACCC stated that the phrase ‘previous regular price’ means “the price at which that product was ordinarily offered for sale for a reasonable period prior to the promotion”.

6 The ACCC further alleged in its Concise Statement that the genuine discount representations were false or misleading because:

(a) Coles had increased the price of each affected product for only a relatively short period of time (which the ACCC referred to as the ‘price spike period’) prior to placing the product on the Down Down promotion and, in most cases, advertising that higher price as the relevant ‘Was’ price on the product’s Down Down ticket; and

(b) the price at which Coles offered each affected product for sale during the Down Down promotion was:

(i) in 249 instances, higher than; and

(ii) in 6 instances, the same as,

the affected product’s previous regular price (which the ACCC alleged was the price at which Coles had previously offered the product for sale prior to the ‘price spike period’, excluding any short-term specials or promotions).

7 For some affected products, there was more than one occasion during the relevant period on which the product was placed on a Down Down promotion following an alleged price spike period. For this reason, the total number of separate instances referred to in the preceding paragraph is 255, which is greater than the total number of affected products (being 245).

8 The ACCC’s allegations concern three prices at which each of the affected products was sold, which the parties generally referred to as Price 1, Price 2 and Price 3. Price 1 was the price prior to the price increase; Price 2 was the price during the alleged price spike period; and Price 3 was the Down Down price following the alleged price spike period. That terminology is used occasionally in these reasons.

9 The ACCC alleged that Coles’ conduct in offering the affected products on the Down Down tickets was misleading or deceptive, or likely to mislead or deceive, in contravention of s 18(1) of the Australian Consumer Law (the ACL), and that each Down Down ticket conveyed a representation which was false or misleading with respect to the price of the affected products in contravention of s 29(1)(i) of the ACL. As discussed later in these reasons, there is no material difference in the meaning of the phrases ‘misleading or deceptive’ and ‘false or misleading’ as used in ss 18(1) and 29(1) respectively. In these reasons, the word ‘misleading’ is used as a shorthand when referring to the ACCC’s allegations that the Down Down tickets were misleading or deceptive or likely to mislead or deceive contrary to s 18(1) and false or misleading contrary to s 29(1).

10 Significantly, the ACCC’s case disregarded any changes in the list (wholesale) prices paid by Coles for the affected products. The ACCC contended that the Down Down ticket for each affected product conveyed the genuine discount representation and that the representation was misleading because the ‘Was’ price had been in effect for only a relatively short period of time (the ‘price spike period’ or Price 2) and therefore was not the product’s previous regular price. Rather, the product’s previous regular price was the price prior to the ‘Was’ price (Price 1), which in almost all cases was lower than the Down Down price (Price 3). On the case advanced by the ACCC, changes in the list prices for the affected products are irrelevant because the Down Down tickets do not refer to the list prices and consumers are unaware of the list prices.

11 In its Concise Response, Coles said that, during the relevant period, Coles and its suppliers were experiencing significant cost increases including, but not limited to, a surge in global commodity prices, and in the cost of packaging, freight, utilities and international shipping. In response to requests from its suppliers for cost price alterations (abbreviated as CPA), which are also referred to as cost price increases (abbreviated as CPI), or changes to the promotional funding arrangements, Coles (with the supplier) reassessed the promotional and non-promotional pricing of the supplier’s products, including in relation to the affected products. Where an affected product had been on a Down Down program, the affected product was taken off the Down Down program and sold at a non-promotional (white ticket) price which was typically at or below the supplier’s new recommended retail price (often abbreviated to RRP). Later, these affected products returned to the Down Down program at a new promotional price. Coles says that the non-promotional (white ticket) price was a genuine, undiscounted shelf price, and that the subsequent Down Down program price was therefore a genuine discount from that shelf price.

12 Coles denied that the Down Down tickets conveyed the genuine discount representation in the form alleged by the ACCC and said further that the concept of a ‘previous regular price’, being a component of the ACCC’s alleged representation, is unclear. Coles said that the Down Down tickets conveyed that the Down Down price was a genuine reduction from its previous non-promotional (white ticket) price. Another way of expressing the same contention is that the Down Down ticket represented to consumers that the Down Down price was a reduction to, or discount from, the price at which the product had last been genuinely offered for sale and sold by Coles.

13 Coles said that, so understood, the Down Down tickets for the affected products were not misleading. In every case, the price of the affected product had been increased following a request by a supplier either to increase its wholesale price to Coles (with a consequential increase to its recommended retail price), or to reduce its promotional funding offered to Coles, and following Coles’ agreement to the request in whole or in part. The product was then offered by Coles at a non-promotional (white ticket) price at or below the supplier’s recommended retail price for a period before placing the product on a Down Down promotion. Coles says that the ‘Was’ price on the Down Down ticket was the immediately preceding non-promotional (white ticket) price for the product which was a genuine undiscounted price.

14 On Coles’ case, the relevant enquiry is whether the ‘Was’ price stated on each Down Down ticket was a genuine price at which the product had been last offered for sale by Coles prior to being placed on the impugned Down Down promotion. On that case, the genuineness of the price must be assessed by a range of factors including the commercial circumstances in which the price was determined, the period over which the product was offered at that price and the volume of sales at that price.

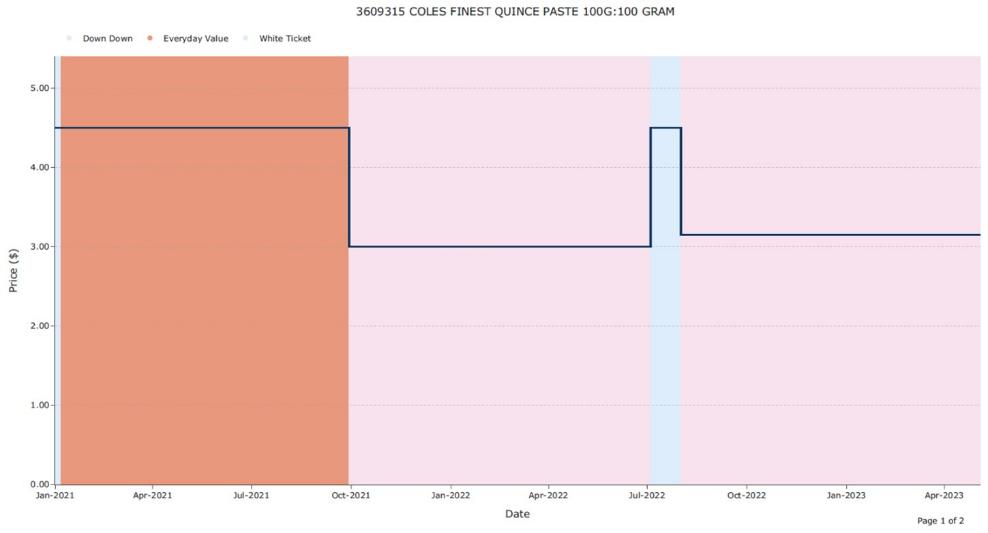

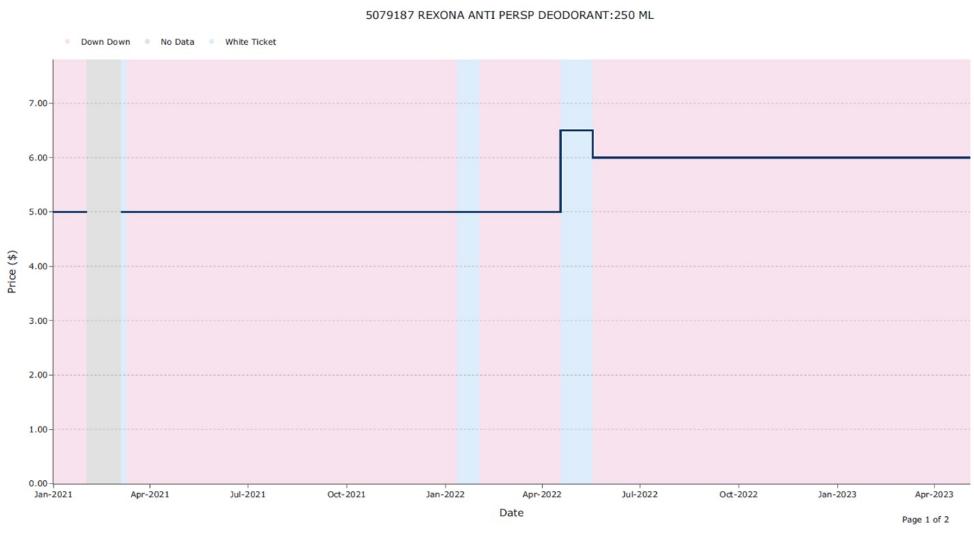

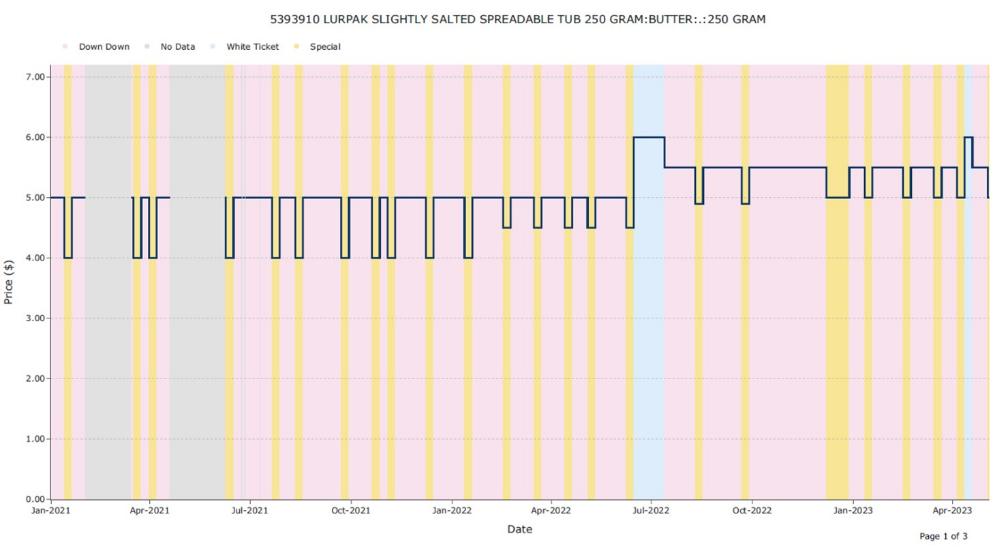

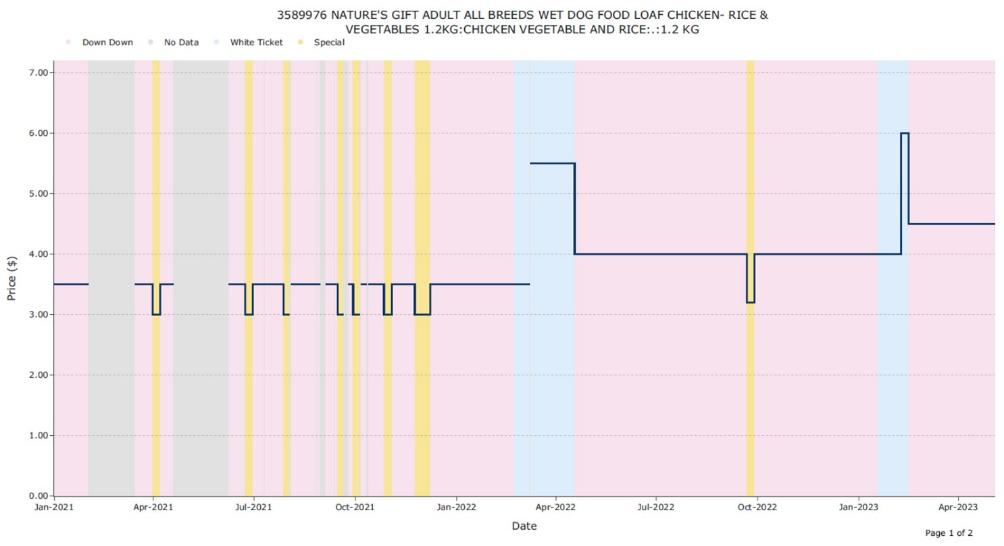

15 The Court made orders that a trial on all issues of liability would be conducted with respect to a sample of affected products as agreed between the parties or determined by the Court. The parties agreed 12 sample products which are as follows:

(1) Karicare Follow On Formula (900 gram) (Karicare Formula);

(2) Coca-Cola Soft Drink (2 litre) (Coca-Cola 2 litre);

(3) Pedigree Adult Wet Dog Food With 5 Kinds Of Meat Loaf (1.2 kg can) (Pedigree Dog Food);

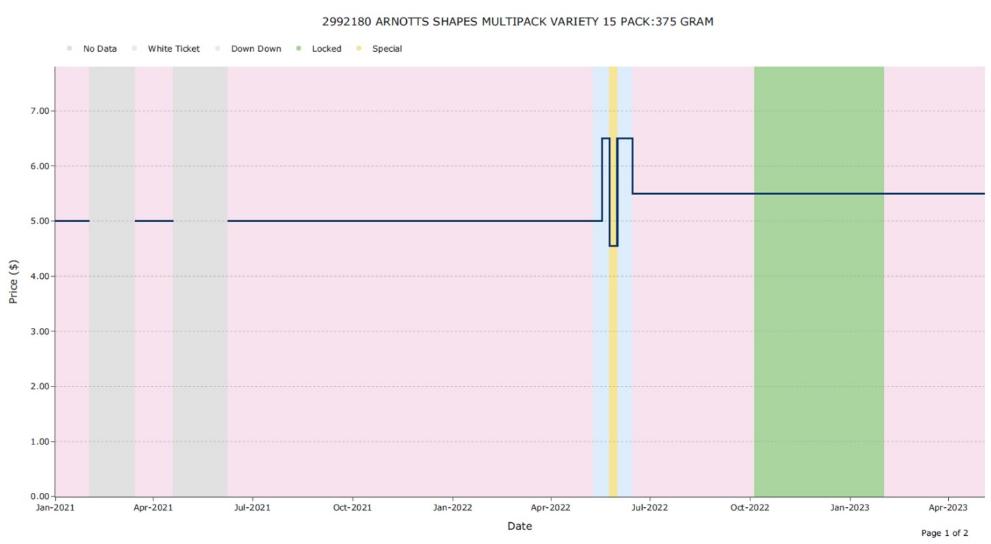

(4) Arnott’s Shapes Multipack Variety 15 Pack (375 gram) (Arnott’s Shapes Multipack);

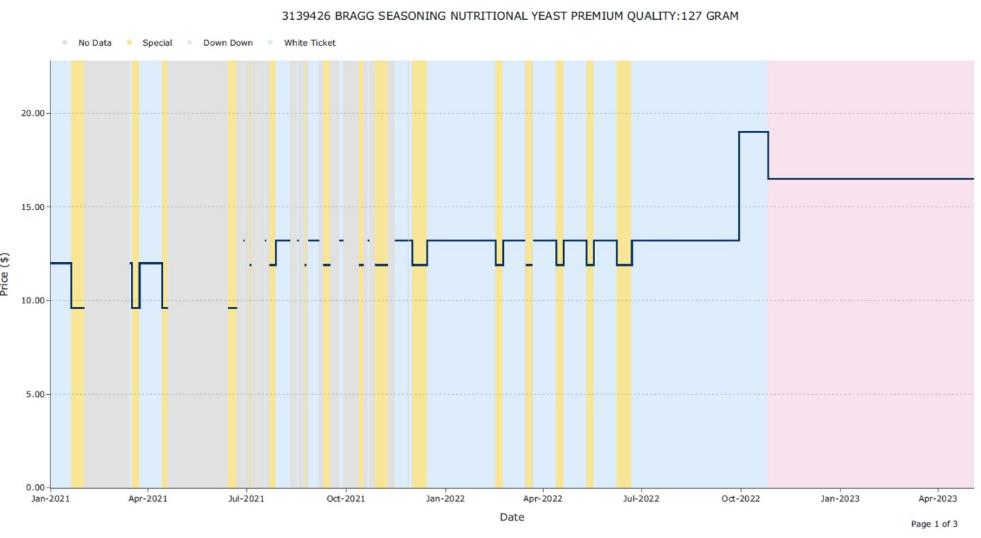

(5) Bragg Seasoning Nutritional Yeast Premium Quality (127 gram) (Bragg Yeast);

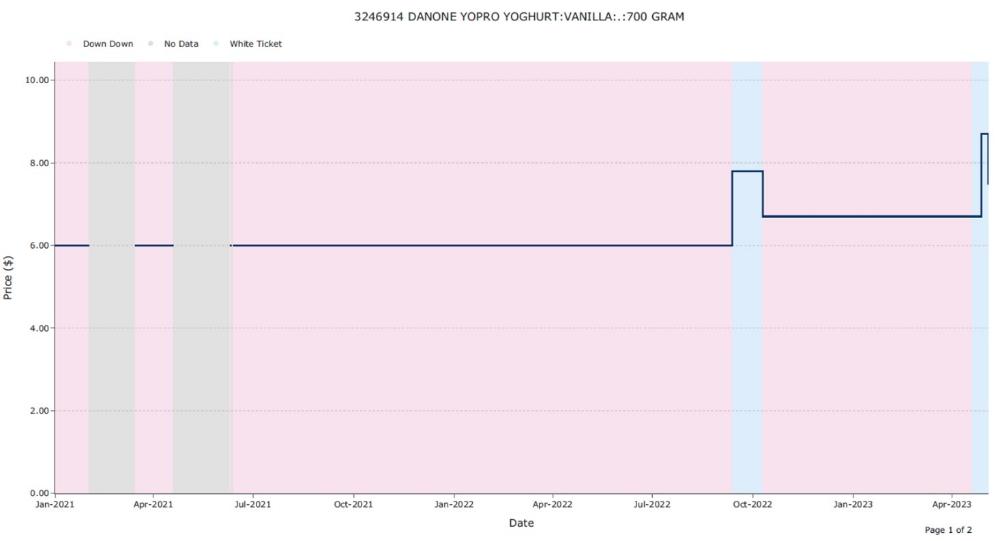

(6) Danone Yopro Yoghurt Vanilla (700 gram) (Yopro Yoghurt);

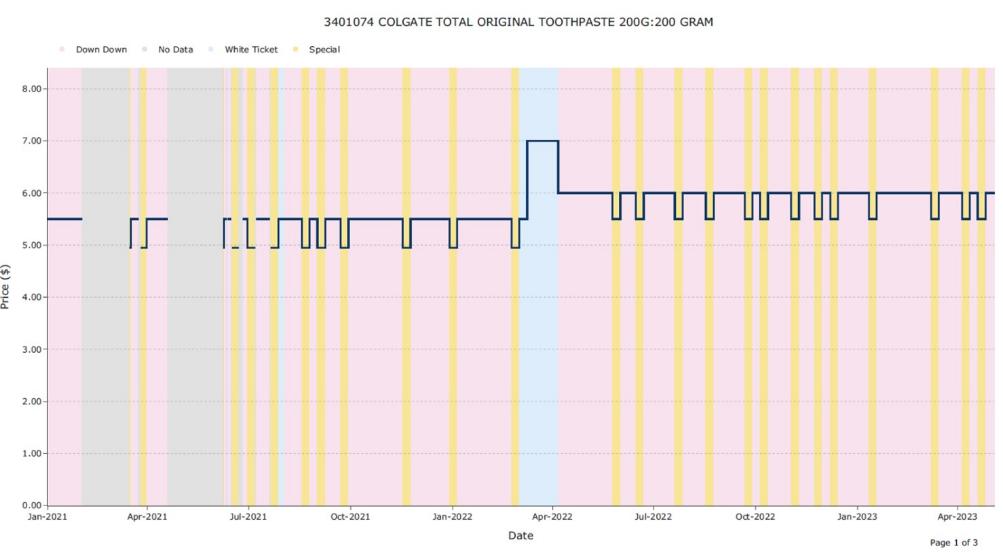

(7) Colgate Total Original Toothpaste (200 gram) (Colgate Toothpaste);

(8) Coles Finest Quince Paste (100 gram) (Coles Quince Paste);

(9) Rexona Anti Persp Deodorant (250 ml) (Rexona Deodorant);

(10) Lurpak Slightly Salted Spreadable Tub (250 gram) (Lurpak Butter);

(11) Nature’s Gift Adult All Breeds Wet Dog Food Loaf Chicken Rice & Vegetables (1.2 kg) (Nature’s Gift Dog Food); and

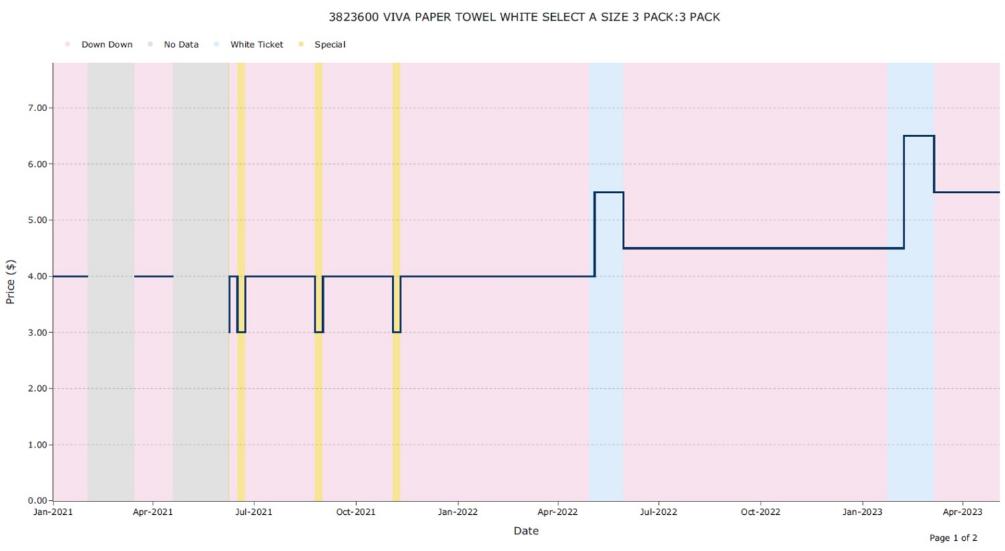

(12) Viva Paper Towel White Select A Size (3 Pack) (Viva Paper Towels).

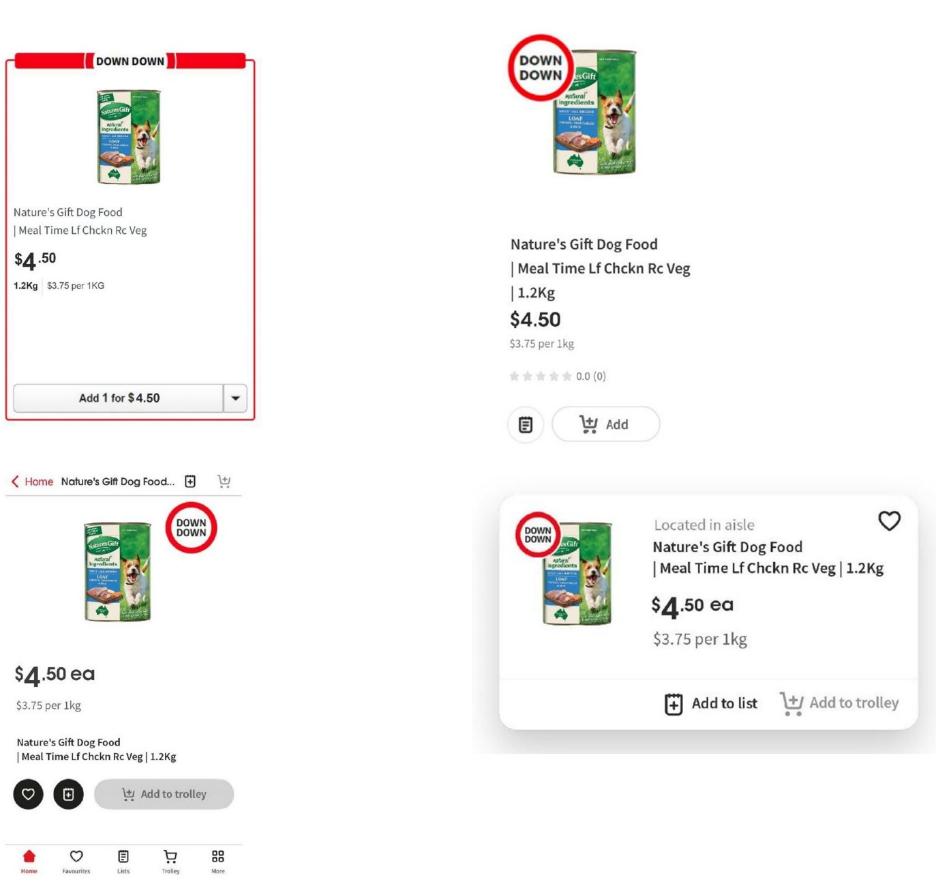

16 Two of the sample products, the Nature’s Gift Dog Food product and the Viva Paper Towels product, each involved two separate Down Down tickets. Thus, these reasons concern 14 Down Down tickets in total.

17 Each of the sample products is a manufactured and packaged grocery product. The proceeding does not concern fresh food grocery products.

18 The evidence adduced by the parties with respect to each of the sample products and Down Down tickets was detailed and voluminous. It included not only the retail prices for the sample products during the relevant period, but also the negotiations between the relevant supplier and Coles with respect to increases in the list (wholesale) prices for the sample products, the promotional plan proposed by the supplier (including proposed retail prices), Coles’ retail sales margins based upon the proposed retail prices and Coles’ retail sales volumes.

19 A great deal of the evidence adduced by the parties is irrelevant to the ACCC’s primary case. As already noted, the ACCC’s primary case disregards changes in the list prices paid by Coles for the affected products because it alleges the Down Down tickets do not refer to the list prices and consumers are unaware of the list prices. Most of the evidence is, however, relevant to Coles’ case in defence. Coles contends that the Down Down ticket represented to consumers that the Down Down price was a reduction to, or discount from, the price at which the product had last been genuinely offered for sale and sold by Coles. If Coles is correct, it becomes necessary to consider whether the ‘Was’ price stated on the Down Down ticket was a genuine price at which the product had been last offered for sale by Coles, which requires consideration of the factors referred to above, including the commercial circumstances in which the price was determined, the period over which the product was offered at that price and the volume of sales at that price.

20 The nature and scope of the arguments advanced by the parties has necessitated the making of factual findings about many aspects of Coles’ supermarket business including its management structure, retail pricing policies and practices, purchase arrangements with suppliers, the Down Down promotional program and the commercial negotiations between Coles and relevant suppliers with respect to the sample products.

A.2 Class action proceeding

21 On 14 November 2024, Benjamin Demery commenced a representative proceeding (VID 1247 of 2024) against Coles advancing materially the same allegations as made in the ACCC proceeding. Mr Demery claims damages on his own behalf and on behalf of other persons (group members) who purchased one or more affected products during the relevant period from Coles.

22 On 23 May 2025, orders were made in the representative proceeding in the same terms as the ACCC proceeding: that an initial trial on all issues of liability would be conducted with respect to a sample of affected products as agreed between the parties or determined by the Court. The parties were informed that the Court proposed to conduct a joint trial on liability issues in both proceedings. The parties raised no objection to that course. Timetabling orders were made in each proceeding to prepare the proceedings for trial.

23 On 20 June 2025, Coles filed an application seeking security for costs from Mr Demery in the representative proceeding. Ultimately, Coles and Mr Demery reached a compromise on the disposition of the security for costs application, and the parties requested the Court to make orders reflecting the compromise. After considering the compromise and proposed orders, the Court gave effect to the compromise by making orders on 26 August 2025. The Court’s reasons for making the orders are published in Demery v Coles Supermarkets Australia Pty Ltd [2025] FCA 1016. As explained in those reasons, the parties’ intention was to enable the issues of liability to be determined in the most efficient manner possible and without incurring unnecessary or duplicative costs. The elements of the agreement were:

(a) all issues of liability in the representative proceeding would be determined in accordance with the judgment on liability in the ACCC proceeding;

(b) the applicant and group members in the representative proceeding, except those who opt out, would be bound by findings made in the determination of issues of liability in the ACCC proceeding;

(c) the representative proceeding would be stayed until the Court delivers judgment on liability in the ACCC proceeding, although the applicant would have liberty to apply to lift the stay if liability is resolved in the ACCC proceeding other than by trial and judgment;

(d) all extant trial preparation orders in the representative proceeding would be vacated;

(e) the applicant would have liberty to apply for an order for access to the evidence and submissions filed in the ACCC proceeding; and

(f) the security for costs application would be adjourned indefinitely.

24 The orders made on 26 August 2025 included orders that:

(a) the initial trial on liability issues in the representative proceeding be heard together with the initial trial on liability issues in the ACCC proceeding (joint liability trial);

(b) the applicant in the representative proceeding was to take no step in the representative proceeding or in the ACCC proceeding (and including at the joint liability trial) except:

(i) upon application for leave of the Court, for which reasonable prior notice is provided to Coles; and

(ii) with the specific leave of the Court; and

(iii) without prejudice to Coles’ right to submit that leave should not be granted until the determination of any application by Coles for security for costs (should Coles exercise its liberty to re-enliven its application); and

(c) at the joint liability trial, the evidence in the ACCC proceeding be evidence in the representative proceeding.

25 As part of the compromise, Mr Demery, on his own behalf and on behalf of group members (except persons who opt out of the representative proceeding), gave an undertaking to the Court and to Coles that he and the group members (except persons who opt out) will be bound by all findings of fact, findings of law and mixed findings of fact and law made in the determination of liability issues in the initial trial in the ACCC proceeding, and will consent to corresponding findings being made in the representative proceeding, without prejudice to the right of Mr Demery to appeal, or seek leave to appeal, any such finding.

26 On 9 September 2025, orders were made pursuant to s 33J(1) of Federal Court of Australia Act 1976 (Cth) (FCA Act) fixing 21 November 2025 as the date by which group members may opt out of the representative proceeding. A number of opt out notices have been received by the Court.

27 On 23 February 2026, shortly prior to the hearing of closing submissions at the joint liability trial, Mr Demery filed an interlocutory application seeking leave to make a closing submission. The application was supported by an affidavit of Gregory Mackey (Mr Demery’s solicitor) sworn the same day. A copy of the proposed closing submission was exhibited to the affidavit, together with some correspondence between Mr Demery and Coles. The closing submission principally concerned the application of the Briginshaw principle in the class action proceeding. Leave was granted for Mr Demery to make the closing submission and Mr Demery filed and served the written submission, to which Coles replied in writing on 25 February 2026. The parties’ submissions with respect to the application of the Briginshaw principle are addressed below.

28 Mr Demery’s written submission also referred to correspondence with Coles, exhibited to the supporting affidavit, in which Mr Demery sought to qualify the undertaking that had been given to the Court and that was recorded in the orders made on 26 August 2025 (that Mr Demery and group members agreed to be bound by all findings of fact, findings of law and mixed findings of fact and law made in the determination of liability issues in the initial trial in the ACCC proceeding). The submission stated that Mr Demery sought leave of the Court to qualify the undertaking. No such leave was sought in Mr Demery’s interlocutory application. Nor did Mr Demery advance any submissions in writing or orally as to why such leave should be granted at that late stage (the hearing of closing submissions in the joint liability trial). Nor was any explanation proffered as to the nature and terms of the qualification sought by Mr Demery. Coles opposed any such leave, submitting that:

(a) the nature of the qualification was wholly unclear and would be impractical in effect;

(b) when the undertaking was given, Mr Demery was aware that the ACCC proceeding was a civil penalty proceeding to which the Briginshaw principle applied; and

(c) the undertaking was given in the context of an application for security for costs and as part of a compromise which established the framework for the joint hearing of the two proceedings consistently with the overarching purpose set out in s 37M of the FCA Act.

29 I accept Coles’ submissions. To the extent that Mr Demery pressed an application to qualify the undertaking given to the Court as recorded in the orders made on 26 August 2025, the application is refused. The qualification sought by Mr Demery was undefined, likely to be impractical in effect, and would be unjust to Coles in circumstances where Coles’ security for costs application had been compromised on the basis of the undertaking.

A.3 Submissions concerning the Briginshaw principle

30 Section 140 of the Evidence Act 1995 (Cth) (Evidence Act) prescribes the standard of proof in civil proceedings in the following terms:

(1) In a civil proceeding, the court must find the case of a party proved if it is satisfied that the case has been proved on the balance of probabilities.

(2) Without limiting the matters that the court may take into account in deciding whether it is so satisfied, it is to take into account:

(a) the nature of the cause of action or defence; and

(b) the nature of the subject-matter of the proceeding; and

(c) the gravity of the matters alleged.

31 Section 140 reflects the civil standard of proof at common law, which was explained by Dixon J in Briginshaw v Briginshaw (1938) 60 CLR 336 (Briginshaw) at 361-362:

The truth is that, when the law requires the proof of any fact, the tribunal must feel an actual persuasion of its occurrence or existence before it can be found. It cannot be found as a result of a mere mechanical comparison of probabilities independently of any belief in its reality. … Except upon criminal issues to be proved by the prosecution, it is enough that the affirmative of an allegation is made out to the reasonable satisfaction of the tribunal. But reasonable satisfaction is not a state of mind that is attained or established independently of the nature and consequence of the fact or facts to be proved. The seriousness of an allegation made, the inherent unlikelihood of an occurrence of a given description, or the gravity of the consequences flowing from a particular finding are considerations which must affect the answer to the question whether the issue has been proved to the reasonable satisfaction of the tribunal. In such matters “reasonable satisfaction” should not be produced by inexact proofs, indefinite testimony, or indirect inferences.

32 In reliance upon those principles, Coles submitted that, in deciding whether the alleged contraventions of the ACL had been proved on the balance of probabilities, the Court must have regard to: (a) the nature of the cause of action; (b) the nature of the subject matter of the proceeding; and (c) the gravity of the matters alleged. Coles submitted that:

Since the alleged contravention of s 29 of the ACL may expose Coles to a civil penalty, a high level of satisfaction should be reached before finding the contraventions proved.

33 While accepting that the Court is required to take into account the matters referred to in s 140(2) of the Evidence Act and, more broadly, apply the Briginshaw principle, Mr Demery submitted that the consequences of a finding of contravention of the ACL differed between the ACCC proceeding and the class action. The ACCC proceeding seeks to penalise Coles by the imposition of a civil penalty, whereas the class action seeks only to compensate Mr Demery and group members. In other words, the class action only seeks to put the parties back in the position that they would have been in if the contravening conduct had not occurred. Mr Demery submitted that the Court cannot take into account the fact that a civil penalty may be imposed in the ACCC proceeding in determining whether the proven conduct is misleading for the purposes of the class action in which compensation – and not a form of sanction or punishment – is sought.

34 Mr Demery’s submission cannot be accepted. The effect of the Briginshaw principle is that “the strength of the evidence necessary to establish a fact or facts on the balance of probabilities may vary according to the nature of what it is sought to prove”: Neat Holdings Pty Ltd v Karajan Holdings Pty Ltd [1992] HCA 66; 110 ALR 449 at 450 (Mason CJ, Brennan, Deane and Gaudron JJ); G v H (1994) 181 CLR 387 at 399 (Deane, Dawson and Gaudron JJ). A significant aspect of the principle is that it affects the process of fact finding in cases where no criminal or other penal consequences will be imposed. That is because it is sufficient to attract the operation of the principle that the conduct complained of in a proceeding might be characterised as illegal, capable of attracting a penalty or otherwise of grave consequence, even if no such correlative consequences would flow from those findings in that proceeding. Indeed, that was the context in which Briginshaw was decided. The case concerned a petition for divorce on the ground of adultery. While the proceeding raised a civil matter, it was the recognition that the allegation entailed “grave moral delinquency” (at 362 per Dixon J), “a serious matter” (at 350 per Rich J) or a “serious allegation” (at 347 per Latham CJ and 353 per Starke J) that justified the stricter requirement that “reasonable satisfaction” should not be produced by inexact proofs, indefinite testimony, or indirect inferences. The Briginshaw principle is routinely and appropriately applied in civil proceedings that involve grave allegations of wrongdoing, but which do not attract penal consequences: see for example Roberts-Smith v Fairfax Media Publications Pty Limited & Others (Appeal) (2025) 310 FCR 170 at [23] (where it was necessary to prove the truth of alleged war crimes, but the proceeding was for the recovery of damages for defamation) and AA v The Trustees of the Roman Catholic Church for the Diocese of Maitland-Newcastle [2026] HCA 2; 427 ALR 67 at [219] (where it was sought to prove child sexual abuse, but the proceeding was for the recovery of damages for negligence).

35 In any event, this is not a case in which the evidentiary burden of proof is significant. There was little, if any, dispute as to the primary facts. No challenge was made to the credit of any witness. The issue in dispute principally concerns what the Down Down tickets conveyed to ordinary and reasonable consumers, and whether what was conveyed was misleading. These questions are to be determined objectively by reference to largely undisputed facts.

A.4 Summary of conclusions

36 The issues raised in this proceeding are finely balanced. By way of summary, I have reached the following conclusions on the issues for determination.

37 I have concluded that the Down Down tickets for the sample products conveyed a representation to ordinary consumers that Coles had reduced the price of the product from the ‘Was’ price and, implicitly, that the reduction in price involved a real or genuine discount. The vast majority of ordinary consumers, when shopping, would not have formed any conscious belief about the period for which the product had been offered for sale by Coles at the ‘Was’ price, beyond an intuitive sense that the discount being promoted was genuine and not artificial. Nevertheless, incorporated within the notion of a genuine discount from an identified previous price is the notion that the identified previous price was a price at which the product had been ordinarily offered for sale by Coles for a reasonable period.

38 In assessing whether each of the Down Down tickets for the sample products was misleading, it is necessary to evaluate all of the factors that bear upon the question whether the ‘Was’ price shown on the ticket was a price at which the product had been ordinarily offered for sale for a reasonable period, such that the discount shown on the ticket can be regarded as a genuine discount. Those factors include the commercial circumstances in which the price of the product had been increased, the level at which the ‘Was’ price was set, the period for which the product was sold at the ‘Was’ price, and the volume of products sold at that price.

39 Having evaluated the circumstances in which Coles increased the retail prices of the sample products before placing those products on the impugned Down Down tickets, I have concluded that the price increases all resulted from supplier cost price increases, and that Coles increased the prices in a commercially justifiable manner. Coles did not select an artificially high ‘Was’ price for the sample products in order to increase the perceived discount on the Down Down ticket. The sample products were offered for sale at the ‘Was’ price in the ordinary course of Coles’ business and the sample products were sold in commercial volumes at the ‘Was’ price.

40 The remaining factor that must be considered is the period for which the sample products were offered at the ‘Was’ price. The question that must be answered is whether the discount stated on the Down Down tickets was not a genuine discount because the sample products were only offered for sale at the ‘Was’ price for a short period, typically four weeks and sometimes less? In this industry context, involving manufactured and packaged grocery products sold in a large supermarket, what is the minimum period that the product must have been offered for sale at the ‘Was’ price in order to conclude that the product had been offered for sale at that price for a reasonable period and the discount stated on the Down Down ticket was genuine? The answer to that question is necessarily an evaluative judgment on which reasonable minds may differ.

41 In answering that question, I have taken into account a number of matters. Coles’ supermarkets are open for extended trading hours every day of the week and each store is visited by thousands of consumers every day. Nevertheless, the evidence indicates that, aside from products sold on Special or other short-term promotions, the prices that Coles charged for manufactured and packaged products (with which this proceeding is concerned) were relatively stable from month to month, with relatively infrequent changes. The Down Down and Every Day Price promotional mechanics required prices to remain stable for twelve weeks and six months respectively. The evidence indicates that Down Down prices were typically stable for much lengthier periods. The evidence with respect to white ticket prices also suggests that those prices were relatively stable. I have also taken into account Coles’ own assessment, as reflected in its internal policies as at January 2022, that a product could not be sold on a Down Down promotion, showing a discount from a previous price, unless the product had been offered for sale at the previous price for a minimum period of twelve weeks. Although Coles subsequently relaxed that internal policy in March 2022, it did so in response to perceived competitive pressure from Woolworths.

42 Taking those matters into account, I have concluded that the Down Down tickets for the sample products would not have been misleading if the products had been sold at the ‘Was’ price for a minimum period of twelve weeks immediately preceding the Down Down promotion. This reflects a conclusion that, if an ordinary consumer were told that the product had been ordinarily sold by Coles at the ‘Was’ price for a period of twelve weeks immediately prior to the Down Down promotion, the consumer would believe that the Down Down price was a genuine discount to the ‘Was’ price. Conversely, if the ordinary consumer were told that the product had been ordinarily sold by Coles at the ‘Was’ price for a period that was materially shorter than twelve weeks, the consumer would not believe that the Down Down price was a genuine discount to the ‘Was’ price.

43 On that basis, I have concluded that 13 of the 14 Down Down tickets that were the subject of consideration in the joint liability trial were misleading because the relevant products were not sold at the ‘Was’ price stated on the ticket for a reasonable period and, as a consequence, the discount represented on the ticket was not genuine. It follows that, in offering the sample products on those Down Down tickets, Coles:

(a) engaged in conduct in trade or commerce that was misleading, in contravention of s 18(1) of the ACL; and

(b) made a misleading representation with respect to the price of the sample products in connection with the promotion of the supply of the sample products in trade or commerce, in contravention of s 29(1)(i) of the ACL.

44 I have concluded that the Down Down ticket for the Nature’s Gift Dog Food product, which offered the product at a price of $4.50, was not misleading because it did not include a ‘Was’ price on the Down Down ticket.

45 The reasons for those conclusions follow.

B. OVERVIEW OF THE EVIDENCE

46 As noted earlier, although the trial was confined to the sample products, the parties adduced an extensive volume of evidence at trial.

B.1 ACCC’s evidence

47 In its case, the ACCC tendered:

(a) four statements of facts that had been agreed between the parties for the purposes of s 191 of the Evidence Act, the first of which was dated 13 June 2025 (First SOAF), the second was dated 21 August 2025 but was replaced by an amended version dated 16 February 2026 (Amended Second SOAF), the third was dated 17 November 2025 (Third SOAF) and the fourth was dated 12 February 2026 but was replaced by an amended version dated 15 February 2026 (Amended Fourth SOAF);

(b) admissions made by Coles in response to requests for information made by the ACCC pursuant to s 155 of the Competition and Consumer Act 2010 (Cth) (CCA) and admissions made by Coles voluntarily in responses to requests for information made by the ACCC; and

(c) documents produced by Coles in response to requests made by the ACCC pursuant to s 155 of the CCA.

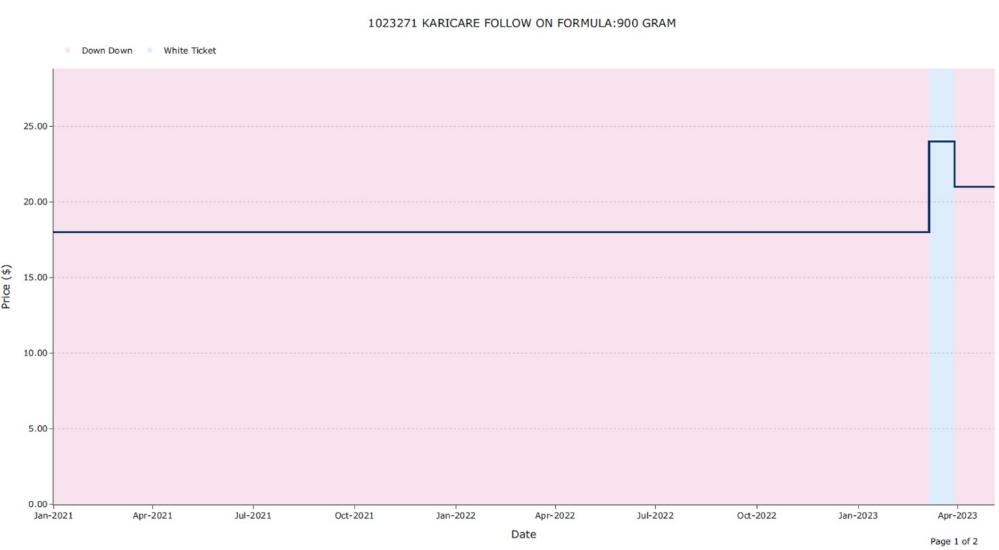

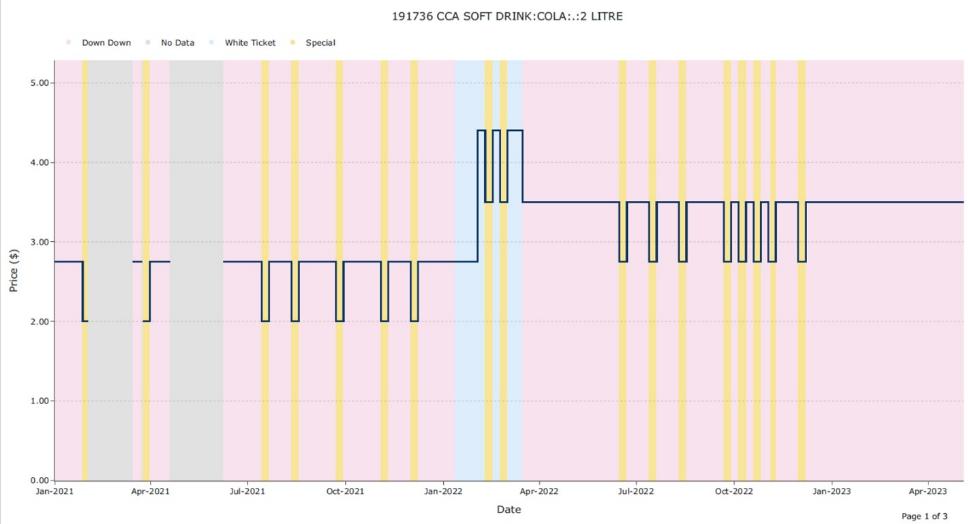

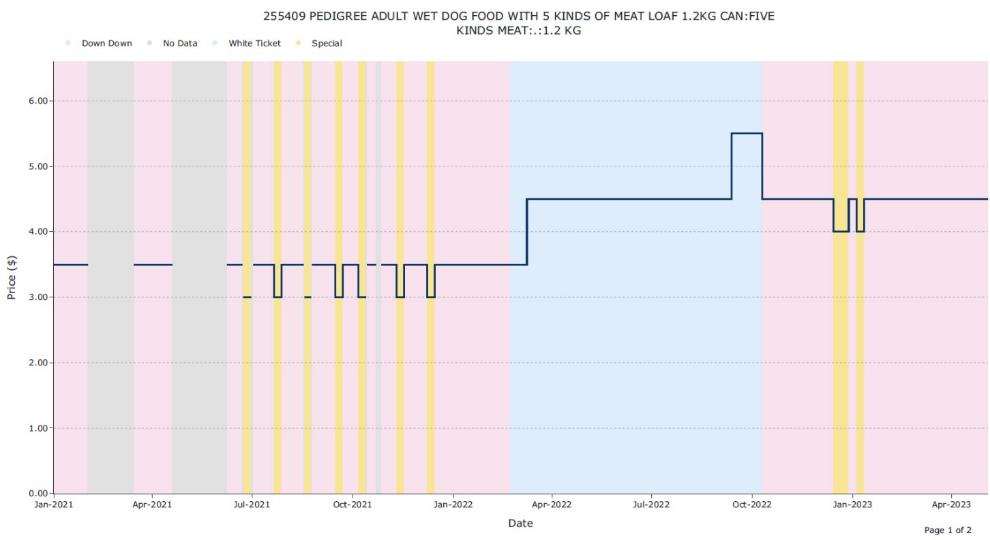

48 The ACCC also tendered an expert report of Dawna Wright of FTI Consulting dated 3 September 2025 (Wright Report). Ms Wright is a qualified Chartered Accountant and a Senior Managing Director and Head of Forensic and Litigation Consulting, Australia, at FTI Consulting. In this role, Ms Wright provides forensic accounting, valuation and financial investigation services. The Wright Report includes graphs and tables of the prices at which Coles offered the sample products for sale between January 2021 and May 2023, including the classification of the relevant price as either non-promotional (that is, a white ticket) or promotional (and, in that case, identifying the specific promotion that applied to the price being one of ‘Down Down’, ‘Special’, ‘Every Day Value’ or ‘Locked’). In certain limited periods of time, no pricing data was available. The data was agreed between the parties and Ms Wright was not required for cross-examination.

B.2 Coles’ evidence

49 In its case, Coles adduced affidavit evidence from employees or former employees within relevant business divisions of Coles. During the relevant period, Coles’ business was organised by reference to business units, business categories and product categories. Coles had six business units: Grocery; Produce; Bakery; Dairy, Frozen & Convenience; Meat Deli & Seafood; and Health & Home. Each business unit was divided into a number of business categories. For example, the Health & Home business unit comprised four business categories: Health, Beauty and Baby; Homecare; General Needs; and Telco, Tobacco and Entertainment. Each business category in turn comprised multiple product categories. For example, the Health, Beauty and Baby business category comprised various product categories such as Soaps and Body Wash. Product categories often comprised sub-categories (eg Handwash). The employees or former employees who gave evidence on behalf of Coles were as follows.

50 Debra Galle made two affidavits, the first dated 21 November 2025 and the second dated 13 February 2026, and was cross-examined. Ms Galle is the General Manager, Own Brand at Coles. Ms Galle has been employed at Coles since 2019 and has held several positions since then. She has also previously worked at Mars Petcare Australia, SPC Ardmona and Coca-Cola Amatil. During the relevant period, Ms Galle held three roles. From July 2019 to March 2022, Ms Galle was the Business Category Manager of Breakfast and Health Foods. From April 2022 to October 2022, Ms Galle was the General Manager of Business Unit Strategy & Commercial Excellence. In this role, Ms Galle was responsible for supporting the delivery of Coles’ overall commercial strategy and had oversight of several teams, including relevantly, the Pricing and Value team and the Supplier Relations team. From October 2022 to December 2024 Ms Galle was the General Manager of the Health and Home business unit. Ms Galle gave evidence about the structure of Coles’ business, the use of category budgets to measure performance in each product category, the considerations that affect retail pricing and product ranging, tickets and pricing mechanics, promotions and the promotional guardrails. In her second affidavit, Ms Galle made several corrections to her initial affidavit and gave further evidence on the promotional guardrails. Ms Galle was a knowledgeable witness who gave clear answers to questions. I accept her evidence in full.

51 Rebecca Thompson made an affidavit dated 24 November 2025 and was cross-examined. Ms Thompson was employed at Coles from January 2022 until January 2026. Most recently, she was the Head of Transformation and Delivery (Health and Home Unit) and during the relevant period held the role of Senior Category Manager of the Biscuits and Cookies category. Ms Thompson gave evidence about the Biscuits and Cookies category, the considerations that affect retail pricing and promotions and the process of negotiating cost price increase requests with suppliers. Ms Thompson also gave evidence about the Arnott’s Shapes Multipack product, including the CPA request made by Arnott’s and Coles’ response to that request and its pricing decisions. Overall, I consider that Ms Thompson was a knowledgeable witness who sought to assist the Court with her answers. At times, Ms Thompson became unnecessarily defensive in providing answers, and felt the need to provide additional information or explanation when answering questions. This created a degree of tension during her cross-examination. Despite that, I considered that Ms Thompson was an honest and reliable witness and I have no reason to doubt her evidence.

52 Eleftheria (Via) Lavdas made an affidavit dated 18 November 2025 and was cross-examined. Ms Lavdas is currently the Head of Commercial Trade Activation at Coles. Ms Lavdas first started work at Coles in 2002 and has held many positions within Coles over the years. Ms Lavdas has also worked for periods at Franklins Supermarkets and Woolworths. In the relevant period, she was the Manager of the Impulse business category. Ms Lavdas gave evidence concerning the Impulse business category, Coles’ pricing decisions and promotional plans, Coles’ trading terms with suppliers including the management and assessment of CPA requests received from suppliers. Ms Lavdas also gave evidence about the Arnott’s Shapes Multipack product, including the CPA request made by Arnott’s and Coles’ response to that request, including its pricing decisions. Ms Lavdas was an impressive witness who gave clear answers to questions. I accept her evidence in full.

53 Katherine Bailey made an affidavit dated 21 November 2025 and was cross-examined. Ms Bailey is currently the General Manager of Brand and Marketing at Coles. Ms Bailey has been employed by Coles since 2011 and has held numerous positions which variously concern Coles’ marketing, branding and media. Ms Bailey gave evidence about the Down Down program, including its key marketing features and how these have changed over time. Ms Bailey also gave evidence about the various channels used to communicate pricing mechanics, including by tickets, in-store signage, and by advertising methods such as catalogues, television, radio and online advertisements, and emails to customers. Ms Bailey was an impressive witness who gave clear answers to questions. I accept her evidence in full.

54 Paul Carroll made an affidavit dated 18 November 2025 and was cross-examined. Mr Carroll is currently the Commercial Lead of e-Commerce at Swaggle, an online pet specialty retailer owned by Coles. Mr Carroll has been employed by Coles since October 2019 and during the relevant period held the role of Senior Category Manager of Pet, a role which he officially finished on 29 January 2023. Mr Carroll begun his new role at Swaggle on 30 January 2023, but was asked to perform both roles until 20 February 2023. Mr Carroll gave evidence about the Pet category, considerations that affect price setting and promotional planning and the assessment of CPA requests from suppliers. Mr Carroll also gave evidence about the Nature’s Gift Dog Food product, including two CPA requests during the relevant period from the supplier, Real Pet Food. Mr Carroll also gave evidence about the Pedigree Dog Food product and the CPA request made by Mars in relation to that product. I consider that Mr Carroll was an honest witness who endeavoured to assist the Court with his answers. However, cross-examination revealed some inconsistencies between his affidavit evidence and the underlying documentary record with respect to the Nature’s Gift Dog Food and Pedigree Dog Food products. In the course of cross-examination, Mr Carroll gave additional evidence with respect to certain inconsistencies. Whilst Mr Carroll insisted that his evidence was based on his actual recollection of events, I am not persuaded that that was always correct. I consider that aspects of Mr Carroll’s evidence involved unconscious reconstruction (in other words, Mr Carroll was not conscious of the fact that he had reconstructed his memory from the documentary record). In making that finding, I make no criticism of Mr Carroll. It is unsurprising that Mr Carroll’s recollection of events that occurred some four years ago in respect of a pricing decision with respect to two products is limited, if non-existent. In respect of those products, I place primary reliance upon the documentary record.

55 Matthew Hankin made an affidavit dated 21 November 2025 and was cross-examined. Mr Hankin is currently the Head of Coles 360 Commercial Integration. He has been employed by Coles and its related entities since 1987 and has held numerous roles, including as a Business Category Manager for various categories since 2009. During the relevant period, Mr Hankin was the Business Category Manager for Health, Baby and Beauty. Mr Hankin gave evidence about the Health, Baby and Beauty business category and CPA requests in relation to two products, Colgate Toothpaste and Rexona Deodorant. Mr Hankin was a knowledgeable witness who gave clear answers to questions. I accept his evidence in full.

56 Edward McCutchan made an affidavit dated 20 November 2025 was cross-examined. Mr McCutchan is currently the Category Manager of Deli Entertainment at Coles. He has been employed at Coles since 2018 and has held various roles. During the relevant period, Mr McCutchan was the Assistant Category Manager of Deli Cheese and Antipasto from January 2022 to March 2023, and the Category Manager of Deli Specialty and Dry Goods from March 2023 to July 2024. Mr McCutchan gave evidence about the Deli Cheese and Antipasto category and the factors that affect promotional pricing. Mr McCutchan also gave evidence about the Coles Quince Paste product and the CPA request received from the supplier in relation to that product. Mr McCutchan was a knowledgeable witness who gave clear answers to questions. I accept his evidence in full.

57 Jack Jorgensen made an affidavit dated 20 November 2025. Mr Jorgensen was not required for cross-examination. Mr Jorgensen is currently the Senior Category Manager for Biscuits and Cookies at Coles. He has been employed by Coles since 2015 and has held various roles, including as Category Manager and Senior Category Manager for various product categories. During the relevant period, Mr Jorgensen was the Category Manager for Coffee, Tea and Milk Additives from March 2020 to March 2022 and the Senior Category Manager for Health Foods from March 2022 to April 2025. Mr Jorgensen gave evidence about the Health Foods category and the process of making pricing and promotional decisions following a CPA request from a supplier. Mr Jorgensen also gave evidence about the Bragg Yeast product and the CPA request made during the relevant period in relation to that product.

58 James Cubbon made an affidavit dated 20 November 2025. Mr Cubbon was not required for cross-examination. Mr Cubbon is currently the Commercial Development Manager of BU Strategy and Commercial at Coles. Mr Cubbon has been employed by Coles since 2011 and has held numerous roles, including as a category manager for various product categories. During the relevant period, Mr Cubbon was the Senior Category Manager of Soft Drinks, Cold Drinks, Energy and Sports from February 2021 to September 2022 and the Category Manager of Pasta, Rice and Noodles from September 2022 to October 2025. Mr Cubbon gave evidence about the Soft Drinks, Cold Drinks, Energy and Sports categories, how retail pricing and promotional decisions were made, and also gave evidence in relation to the CPA request made in relation to the Coca-Cola 2 litre product, and the price increase that followed.

59 Massimo Palmisciano made an affidavit dated 24 November 2025. Mr Palmisciano was not required for cross-examination. Mr Palmisciano is currently the Senior Category Manager for the Chilled Desserts and Chilled Spreads categories at Coles. He has been employed at Coles since April 2020 and has held various roles as a category manager. During the relevant period, Mr Palmisciano was the Category Manager of Cheese and Entertainment from October 2020 to July 2022, immediately after which he entered into his current role. Mr Palmisciano gave evidence about the Chilled Desserts and Chilled Spreads categories and the factors that influence decisions concerning promotions and CPA requests. Mr Palmisciano also gave evidence about the Yopro Yoghurt product and the CPA request received in relation to that product during the relevant period.

60 Tony Bullock made an affidavit dated 1 December 2025. Mr Bullock was not required for cross-examination. Mr Bullock is the General Manager Finance of Commercial, Customer and Digital at Coles. Mr Bullock gave evidence that explained the pricing data extracted from Coles’ Enterprise Data Platform in relation to the sample products.

61 Saurav Sachdev made an affidavit dated 16 February 2026. Mr Sachdev was not required for cross-examination. Mr Sachdev is the Head of Technology in the Data and AI Platform team at Coles. He gave evidence about Coles’ databases, including the Enterprise Data Platform and the Business Information Warehouse. Mr Sachdev also provided sales figures data for the Coca-Cola 2 litre product during the relevant period.

62 Coles also tendered an expert report of Dr Geoff Edwards dated 4 December 2025 (Edwards Report). Dr Edwards was not required for cross-examination. Dr Edwards is an economist specialising in industrial organisation and competition economics. He is a Vice President of Charles River Associates, a global consulting firm providing expertise in economics, finance and strategy, with offices in Australia and throughout Europe and North America. In his report, Dr Edwards confirmed that he agreed with the pricing data for the sample products presented by Ms Wright in her report. Dr Edwards supplemented that pricing data with data concerning the prices charged by suppliers to Coles (referred to as the ‘cost price’) for the sample products and the promotional funding agreed to be provided by suppliers (referred to as ‘supplier funding’). Dr Edwards presented the data in two forms. Appendix B to the Edwards Report was an excel spreadsheet which compiled the daily retail price, cost price and supplier funding for each of the sample products. Appendix C presented that data in the form of three graphs for each sample product showing, relative to date (on the x-axis):

(a) the retail price charged by Coles, including the classification of the price, in the same form as presented by Ms Wright;

(b) the retail price charged by Coles, the cost price charged by the supplier and the supplier funding; and

(c) the retail price charged by Coles and the net cost price charged by the supplier (being the cost price less the supplier funding).

63 Coles also tendered a range of other documents.

C. FACTUAL FINDINGS

64 This section of the reasons contains my factual findings based on the evidence adduced at trial. Despite the large volume of evidence that was adduced at trial, there was little dispute between the parties with respect to the primary facts.

65 As stated earlier, the parties agreed four statements of facts for the purposes of s 191 of the Evidence Act. Section 191(2) stipulates that, unless the Court grants leave, evidence is not required to prove the existence of an agreed fact and evidence may not be adduced to contradict or qualify an agreed fact. Some of the witness and documentary evidence traverses the same topics as addressed by the statements of agreed facts. However, none of the parties submitted that the witness and documentary evidence adduced at trial contradicted or qualified the agreed facts, and I have proceeded on the basis that the evidence supplements and elaborates upon the agreed facts. The factual findings set out below are based upon both the agreed facts and the additional witness and documentary evidence.

66 Unless indicated to the contrary, all of the factual findings set out below apply to the relevant period.

C.1 Coles Supermarkets

67 Coles is a subsidiary of Coles Group Limited (Coles Group). During the relevant period, ‘Supermarkets’ was a business segment for the purposes of Coles Group’s financial reporting.

68 Coles is the operator of the second largest supermarket chain in Australia, which (as at June 2023) had more than 840 supermarkets nationwide, including around 21 small-format ‘Coles Local’ stores. The ‘Coles Local’ stores have a smaller range of standard grocery items compared to a usual Coles supermarket. There are Coles supermarkets located in every Australian state and territory.

69 Coles also operates an online retail platform called ‘Coles Online’. This offers consumers the ability to shop for groceries online, with the choice of home delivery or pick up from ‘Click&Collect’ locations. Coles Online may be accessed by consumers via the Coles website (www.coles.com.au) or the Coles App (which may be used on mobile phones, tablets and similar devices).

70 A typical Coles supermarket ranged approximately 18,000 to 24,000 products in any given week. The products offered for sale by Coles comprised both:

(a) proprietary or ‘branded’ products, being products with brands that were owned by Coles’ suppliers, such as Coke and Pepsi; and

(b) Coles ‘Own Brand’ products, being products with brands that were owned by Coles such as ‘Coles Finest’ and ‘Coles Nature’s Kitchen’.

71 Coles’ customers come from all walks of life: from highly paid professionals to persons who are unemployed; from teenagers to elderly pensioners; from all levels of education. They are as varied as is the population of Australia. Most consumers want to spend as little time shopping for groceries as possible. They are often in a hurry and are shopping for many different products during the same visit. Most consumers do not shop at Coles for the purpose of browsing, but because there are specific products that they need or want.

72 Coles operates on the basis that consumers typically shop for groceries once a week. However, there are many consumers who shop at Coles less than once a week, and there are lots of products (including the sample products and other affected products) that most consumers buy less than once a month or even less frequently.

73 Coles competes with a range of retailers. Woolworths, Aldi and independent supermarkets (including IGA) offer the same or similar products as Coles across a number of categories, although Aldi does not offer many branded products. In some categories, Coles has additional competitors, such as Chemist Warehouse and Priceline in relation to health and beauty products, Amazon in relation to non-food products (such as toilet paper and nappies) and Bunnings in relation to cleaning products.

C.2 Coles’ business structure

74 The ‘Merchandise’ division within Coles was primarily responsible for sourcing the products that Coles supplied to customers. The Merchandise division was organised by reference to ‘product categories’, ‘business categories’ and ‘business units’. Product categories sat within business categories and business categories sat within business units.

75 Coles had six business units during the relevant period: Grocery; Produce; Bakery; Dairy, Frozen & Convenience; Meat Deli & Seafood; and Health & Home. Each business unit was led by a general manager, and was divided into a number of business categories. Each business category was led by a business category manager, and comprised multiple product categories. Each product category was typically led by a category manager.

76 Category managers had primary responsibility for determining the products that Coles offered for sale in their categories, the retail prices Coles charged for those products, planning and implementing promotional programs for those products, and negotiating and agreeing with suppliers on matters such as the suppliers’ ‘list’ prices (the prices they charged to Coles before any discounts, rebates, offsets or other adjustments) and promotional plans (including suppliers’ contribution to funding promotions).

77 Each category manager reported to a business category manager, who was responsible for a portfolio of product categories comprising a business category. Business category managers provided guidance on, and became involved in, decisions made by category managers from time to time.

78 Business category managers, in turn, reported to the general manager who had responsibility for their business category. For example, the category manager for Soft Drinks reported to the business category manager for Beverages, who in turn reported to the general manager of Grocery.

C.3 Coles’ retail pricing policies and practices

State-based pricing policy

79 Coles had state-based pricing during the relevant period. This means that, subject to limited exceptions, it charged the same price for each product that it offered for sale across all stores in a particular geographic region. These geographic regions reflected state and territory boundaries, save that Broken Hill (located in New South Wales) was included in the South Australia region, and Western Australia was split into two different geographic regions.

80 Again, subject only to limited exceptions, products offered for sale via Coles Online were priced consistently with products sold in Coles’ physical stores.

81 Notwithstanding Coles’ policy of state-based pricing, the majority of products were priced on a national basis, so the retail prices of products supplied by Coles were typically the same across Coles’ physical stores nationally and Coles Online, with some exceptions. An example of these exceptions is that some beverage products were subject to particular legislative requirements, namely the container deposit schemes which varied by states and territories. The exceptions are not material to the issues of liability in this proceeding. The prices at which Coles offered the affected products for sale throughout the relevant period, both in Coles’ physical stores and via Coles Online, were agreed between the parties and set out at Annexure 1 to the First SOAF.

Business and pricing strategies

82 A number of witnesses gave evidence about Coles’ business and pricing strategies. The following aspects of Coles’ strategies have relevance to the issues in the proceeding.

83 An important aspect of Coles’ business strategy is its customer ‘value proposition’. Ms Lavdas explained that Coles’ value proposition is to offer a “great” range of quality products at attractive prices and for those products to be available in-store or online when customers want them. Ms Lavdas emphasised that it was not enough to offer a great range of products if those products were not sold for attractive prices or if there was no stock available for Coles’ customers to buy. Ms Lavdas said that she aimed to deliver on Coles’ value proposition by (amongst other things) developing Coles’ product range so as to offer a range of products that suited different customer needs and desires throughout the year and to include products of different quality levels at a range of prices so that there was a choice available for every customer.

84 Coles adopted a ‘good, better, best’ ranking system within most categories. The products within the ‘best’ tier were usually premium offerings with higher prices, while the ‘better’ tier comprised mid-range products and the ‘good’ tier reflected more entry-level offerings with lower prices. Category managers were instructed to apply this product classification system when making ranging and pricing decisions, to ensure customers generally had choice across all tiers and at a range of price points. The tiering system also assisted category managers with deciding which pricing mechanic (described below) would be most appropriate for a given product.

85 A number of witnesses agreed that Coles’ business strategy was not only to provide value to its customers but was also to deliver a ‘value message’ to customers; that is, to communicate to customers that the price of the product was good value. The value message was communicated through Coles’ marketing and advertising, but also through Coles’ pricing mechanics. Relevantly to this proceeding, the Down Down pricing mechanic, discussed in more detail below, conveyed a value message through the use of a ‘was/now’ pricing ticket.

86 Coles sought to provide value to its customers, and to convey a value message to its customers, through the use of promotional (discounted) pricing strategies. Coles and its suppliers benefitted from promotions because they typically drove additional sales volumes. However, as stated by Ms Lavdas during cross-examination, whether a promotion resulted in increased sales volumes depended upon whether the promotional price was “relevant and appropriate”. For suppliers, placing products on promotion was also an effective way for their brand and their products to be drawn to the attention of customers due to the use of prominent tickets and (in some instances) displays in high visibility locations in-store. Products sold on promotion were also often included in Coles’ catalogues and other advertising material (including television and radio), which helped to advertise the discounted price of the product, the product and the supplier’s brand. As discussed further below, promotions were usually jointly funded by Coles and its suppliers. The expression ‘funding’ describes bearing the cost of a promotional discount – ie the difference between the product’s undiscounted price and its promotional price. Suppliers typically provided funding by paying to Coles an amount for each unit of the product that Coles sold (which was referred to as a ‘scan deal’). Coles typically funded the promotion by accepting a lower gross margin on the product (compared to the gross margin Coles received when the product was sold at its undiscounted price).

87 During cross-examination, the ACCC suggested to a number of Coles’ witnesses that the reason that Coles chose to sell certain products at a promotional (discounted) price was because Coles expected that the promotional price (supported by promotional funding) would be optimal for Coles’ business. By ‘optimal’, the ACCC meant profit-maximising: that is, the expected increase in sales volumes offsets the decrease in gross margin earned at the promotional price. A number of Coles’ witnesses agreed with that proposition, as illustrated by the following exchange with Mr McCutchan:

In setting promotional prices for a sustained period, you are making a judgment call that that promotional price is likely to generate a better return for Coles than a higher retail price; correct? --- Yes. I mean, otherwise, we wouldn’t – we probably wouldn’t do it. There wouldn’t be a reason to do it.

88 However, a number of witnesses noted that Coles’ objective was profit-maximisation of its whole business, which required it to consider the pricing of each product relative to other products within the same range or category (as the sales of one product may affect the sales of another), and the broader commercial effects of the pricing of individual products. The following exchange with Mr McCutchan is illustrative:

What you are trying to do in making retail pricing decisions about individual products within your category is to find a price which is likely to generate the best return for Coles; correct? --- Yes. The best return can be a number of things. Could be increasing the amount of customers. It could be ensuring we’ve got a breadth of range. It’s not necessarily just focused on we’re making more profit.

Pricing practices or ‘mechanics’

89 During the relevant period, Coles had in place a range of pricing practices, which it referred to internally as pricing ‘mechanics’.

90 Coles communicated the price and, if applicable, the promotional status of products offered to consumers in-store and online through pricing tickets. Where a product was not on promotion, the product was promoted using a standard shelf edge ticket (white ticket). In-store tickets took the form of physical paper labels and were typically displayed on the shelf immediately below the relevant product, or otherwise physically near the relevant product. Online tickets took the form of individual product tiles which displayed a photograph of, and information about, a particular product on the Coles website or in the Coles App. Both in-store and online tickets included certain details about a product, including the product name, the price of the product and, if applicable, any promotional offer for that product. The price of a product was in some instances also communicated to consumers through advertising channels such as catalogues, TV and outdoor media.

91 Most of the products that Coles ranged at any point in time were offered for sale at a ‘white ticket’ price. The name ‘white ticket’ was used because products sold at white ticket prices were accompanied by tickets that were white with black text. White tickets sat entirely within the edge of supermarket shelves. They contained no colours or promotional markings. White ticket prices were undiscounted (ie non-promotional) prices and were usually set at or around the suppliers’ recommended retail prices. They were first set when a supplier’s product was first included in Coles’ range and usually only changed when the supplier changed the list price for the product, or one of Coles’ competitors changed the price it charged for the product. Within Coles, ‘list price’ refers to the wholesale price charged by a supplier to Coles for each SKU (stock keeping unit, being the unique article code used to identify a specific product) supplied, exclusive of any discounts, rebates, offsets, allowances, adjustments and supplier funding that might be agreed between Coles and the supplier. An illustration of an in-store white ticket, taken from Ms Bailey’s evidence, is as follows:

92 Coles also used the following types of promotional pricing mechanics when offering products for sale:

(a) ‘Specials’, being short-term promotions which typically lasted for a week, where the customer was offered a short-term discount such as $2 or 20% off (Coles also internally referred to these promotions as ‘HiLo’ promotions);

(b) ‘Multi-buy’, being a promotion where the customer was offered a saving when they bought two or more of the same item;

(c) ‘Mix ‘N Save’, being a promotion where the customer was offered a saving when they bought multiple products within the same range;

(d) ‘Down Down’, being a long-term promotional program on which the affected products were promoted and which is described below;

(e) ‘Dropped & Locked’, being a promotion that involved discounting a product from its white ticket price and ‘locking in’ the reduced price until a date that was specified on the ticket (during the relevant period, products on Dropped & Locked were required to remain on the program for at least twelve weeks); and

(f) ‘Every Day Price’ (also referred to as ‘Every Day Low Price’ and ‘Every Day Value’), which involved selling products at a consistent price for a period of at least six months.

93 Other than Every Day Price, each of these pricing mechanics involved offering products for sale at a stated discount or saving compared to the price at which Coles offered the product for sale immediately before the start of the promotion. For mechanics other than Specials, that was the product’s white ticket price. For Specials, it was either the product’s white ticket price or a Down Down price.

94 Throughout the relevant period, Coles had internal policies governing the conduct of the different types of promotions used by Coles. These policies were referred to internally at Coles as ‘promotional guardrails’. The guardrails were amended from time to time. Ms Galle explained that the promotional guardrails were business rules that category managers were instructed to follow when setting retail prices. The promotional guardrails formed part of Coles’ legal and compliance framework and were the responsibility of the Legal and Compliance teams. The promotional guardrails included a statement that the rules were required to be followed to “ensure” that the promotion “is not considered misleading and deceptive advertising”.

95 There were three significant differences between the Down Down and the Every Day Price mechanics, as reflected in the promotional guardrails that applied to each type of promotion. First, the Down Down mechanic involved a price comparison between the Down Down price and an earlier ‘Was’ price, whereas the Every Day Price mechanic did not have a price comparison. Second, the promotional guardrails required the Every Day Price promotion to be conducted for a minimum period of six months (that is, once a product was promoted on an Every Day Price, that price was required to be maintained for a period of six months), whereas the Down Down promotion was only required to be conducted for a minimum period of twelve weeks. Third, while a product was on the Every Day Price mechanic, it could not be sold on Special at a lower price, whereas the Down Down mechanic permitted a product to be sold on Special for one week out of every four weeks. This was referred to within Coles as ‘pulsing’ the price.

96 The different pricing mechanics were typically applied to different types of products. Ms Galle explained that:

(a) premium products (eg in the ‘best’ tier) were often better suited to the Specials mechanic that offered shorter-term steeper discounts, to incentivise customers to trial or ‘trade up’ to that product;

(b) products that consumers tended to purchase impulsively (known as ‘impulse’ products), such as chocolates and snacks, also tended to be better suited to the Specials mechanic, because it drew customers’ attention to products when shopping in-store or online that they may not have planned in advance to purchase;

(c) the Mix ‘N Save mechanic was best suited to products that customers often purchased in different variations or flavours (for example, yoghurt or pet food), because customers were more likely to buy multiples of those products; and

(d) the Down Down mechanic was best suited to frequently purchased staple products as well as those in larger pack sizes because it gave customers discounted prices for a longer period.

97 During oral testimony, Ms Galle explained that the Every Day Price mechanic was intended by Coles to be a flat price (that is, it does not have a ‘was/now’ saving message) and was generally applied to products at the entry level or basket essentials (items which customers would buy week in, week out). In comparison, the Down Down mechanic tended to be applied to mid-tier products. Further, the Every Day Price was required to be maintained for a minimum period of six months, thus guaranteeing that price for a lengthy period. However, this meant that the Every Day Price mechanic was relatively inflexible and not well-suited to the high inflationary environment during the relevant period when Coles was receiving many CPA requests. In contrast, the Down Down price was required to be maintained for only twelve weeks and also permitted further discounts, which afforded greater pricing flexibility.