Federal Court of Australia

Secretary of the Department of Health, Disability and Ageing v Key Promotional Products Pty Ltd [2026] FCA 510

File number(s): | QUD 288 of 2024 |

Judgment of: | LONGBOTTOM J |

Date of judgment: | 30 April 2026 |

Catchwords: | HEALTH LAW – Therapeutic goods – Application for declaration of contraventions of the Therapeutic Goods Act 1989 (Cth) – Import and supply of medical devices not of a kind included in the Australian Register of Therapeutic Goods – Where false or misleading representations made as to registration of medical devices – Where contraventions by a company were aided, abetted, counselled and procured by Second Respondent – Where hearing proceeded by Statement of Agreed Facts and Issues – Where Respondents admit to contraventions – Power of Court to impose civil penalty and grant declaratory relief sought. |

Legislation: | Acts Interpretation Act 1901 (Cth), s 2B Corporations Act 2001 (Cth), s 500(2) Crimes Act 1914 (Cth), s 4AA Evidence Act 1995 (Cth), s 191 Federal Court of Australia Act 1976 (Cth), ss 21(1), 43(1) Therapeutic Goods Act 1989 (Cth), ss 3, 4, 9A, 41BBA, 41BD(1), 41MIB(1), 41MLA, 41MLA(1), 41MLA(2), 42MLA(2), 42Y, 42Y(1), 42Y(2), 42Y(3), 42YC, 42YC(2), Ch 4, Pts 4-5, Div 1 Federal Court Rules 2011 (Cth), r 40.02 |

Cases cited: | Australian Building and Construction Commissioner v Construction, Forestry, Mining and Energy Union [2017] FCAFC 113; (2017) 254 FCR 68 Australian Competition and Consumer Commission v Australian Institute of Professional Education Pty Ltd (in liq) [2017] FCA 521 Australian Competition and Consumer Commission v Coles Supermarkets Australia Pty Ltd [2014] FCA 1405 Australian Competition and Consumer Commission v Fisher & Paykel Customer Services Pty Ltd [2014] FCA 1393 Australian Competition and Consumer Commission v MSY Technology Pty Ltd [2012] FCAFC 56; (2012) 201 FCR 378 Australian Securities and Investments Commission v BHF Solutions Pty Ltd [2022] FCAFC 108; (2022) 293 FCR 330 Australian Securities and Investments Commission v Westpac Banking Corporation [2019] FCA 2147 BMW Australia Ltd v Australian Competition & Consumer Commission [2004] FCAFC 167; (2004) 207 ALR 452 Coal Mining Industry (Long Service Leave Funding) Corporation v Hitachi Construction Machinery (Australia) Pty Ltd (Penalty) [2023] FCA 1187 Comcare v Linfox Australia Pty Ltd [2015] FCA 61; (2015) 144 ALD 593 Construction, Forestry, Mining and Energy Union v Cahill [2010] FCAFC 39; (2010) 194 IR 461 Dawson v Deputy Commissioner of Taxation (1984) 71 FLR 364 Director, Fair Work Building Industry Inspectorate v Construction, Forestry, Mining and Energy Union [2015] FCAFC 59; (2015) 229 FCR 331 Forster v Jododex Australia Pty. Limited [1972] HCA 61; (1972) 127 CLR 421 Hobart International Airport Pty Ltd v Clarence City Council [2022] HCA 5; (2022) 276 CLR 519 Mornington Inn Pty Ltd v Jordan [2008] FCAFC 70; (2008) 168 FCR 383 Productivity Partners Pty Ltd (trading as Captain Cook College) v Australian Competition and Consumer Commission [2024] HCA 27; (2024) 281 CLR 338 R v Bull [1974] HCA 23; (1974) 131 CLR 203 Royer v The State of Western Australia [2009] WASCA 139; (2009) 197 A Crim R 319 Ruddock v Vadarlis (No 2) [2001] FCA 1865; (2001) 115 FCR 229 Rural Press Limited v Australian Competition & Consumer Commission [2003] HCA 75; (2003) 216 CLR 53 Secretary, Department of Health and Aged Care v Vapor Kings Pty Ltd [2023] FCA 1297 Secretary, Department of Health and Ageing v Prime Nature Prize Pty Ltd (in liq) [2010] FCA 597 Secretary, Department of Health v Evolution Supplements Australia Pty Ltd (No 2) [2021] FCA 872 Secretary, Department of Health v Medtronic Australasia Pty Ltd [2024] FCA 1096; (2024) 305 FCR 433 Secretary, Department of Health v Oxymed Australia Pty Ltd [2021] FCA 1518 Secretary, Department of Health v Peptide Clinics Australia Pty Ltd [2019] FCA 1107; (2019) 137 ACSR 494 Symes v Stewart [1920] HCA 73; (1920) 28 CLR 386 Volkswagen Aktiengesellschaft v Australian Competition and Consumer Commission [2021] FCAFC 49; (2021) 284 FCR 24 |

Division: | General Division |

Registry: | Queensland |

National Practice Area: | Commercial and Corporations |

Sub-area: | Regulator and Consumer Protection |

Number of paragraphs: | 61 |

Date of last submission/s: | 15 September 2025 |

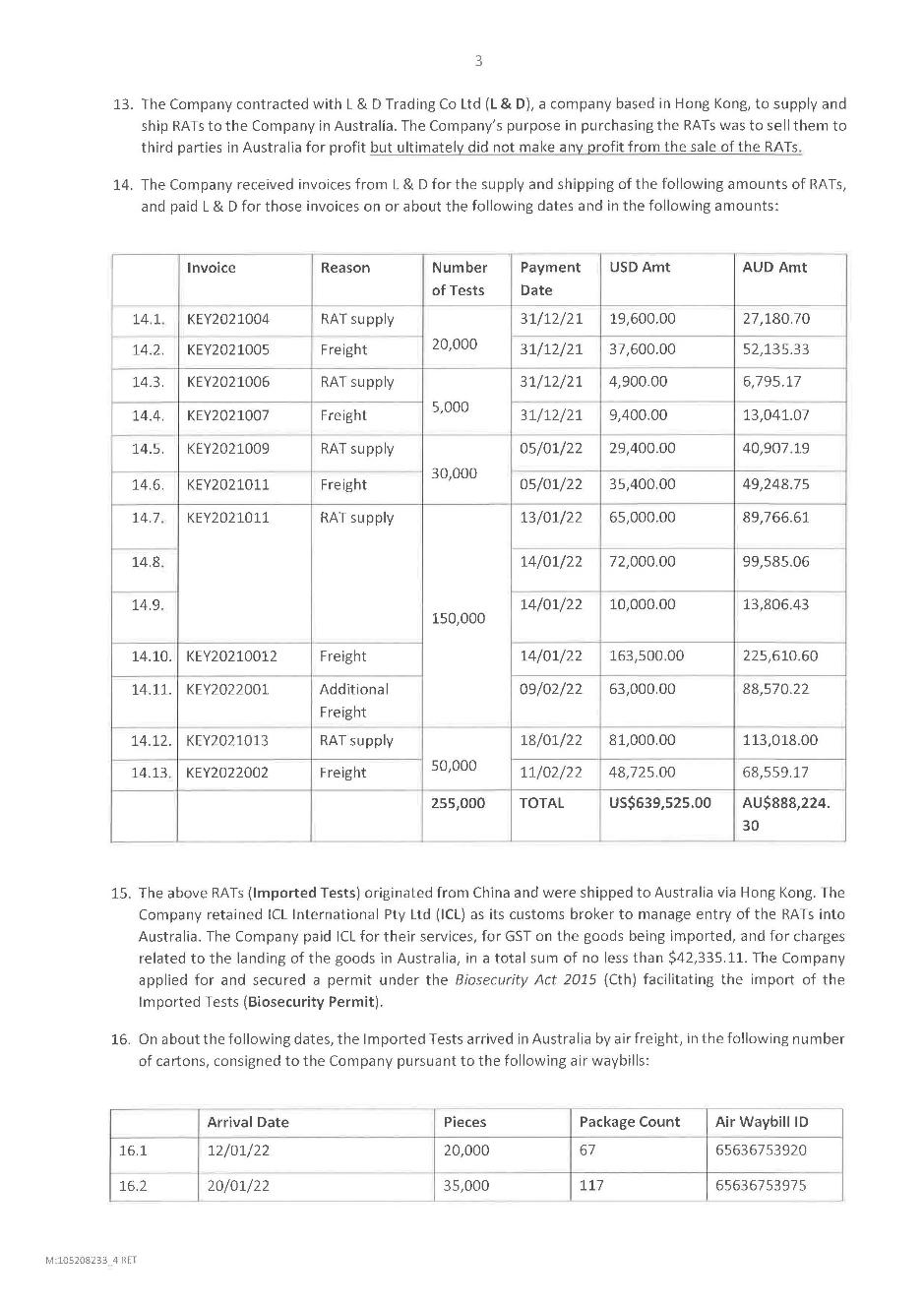

Date of hearing: | 1 September 2025 |

Counsel for the Applicant: | Mr M A Taylor |

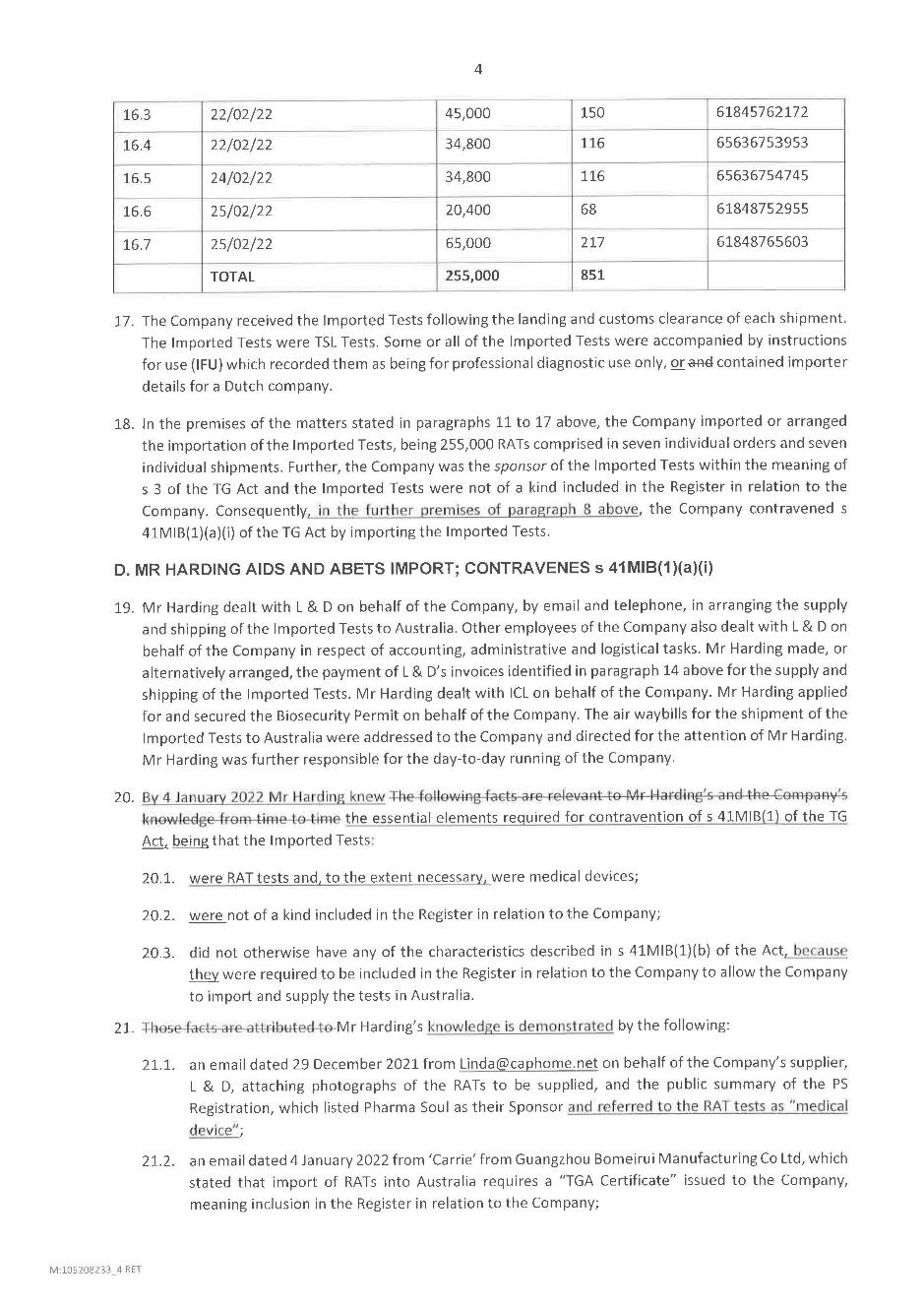

Solicitor for the Applicant: | Holding Redlich |

Counsel for the First Respondent: | No appearance |

Counsel for the Second Respondent: | Mr P G Jeffery |

Solicitor for the Second Respondent: | Affinity Lawyers |

ORDERS

QUD 288 of 2024 | ||

| ||

BETWEEN: | SECRETARY OF THE DEPARTMENT OF HEALTH, DISABILITY AND AGEING Applicant | |

AND: | KEY PROMOTIONAL PRODUCTS PTY LTD (ACN 614 074 770) First Respondent CRAIG SHANE HARDING Second Respondent | |

order made by: | LONGBOTTOM J |

DATE OF ORDER: | 30 april 2026 |

THE COURT NOTES THAT:

A. So far as the following orders concern the penalty to be imposed on the First Respondent (Key Promotional), they are made with the consent of the liquidator of Key Promotional (Mr Matthew John Bookless).

B. So far as the following orders affect the interests of the Second Respondent (Mr Craig Harding), they are made by consent between the Applicant (Secretary) and Mr Harding.

THE COURT ORDERS THAT:

1. Pursuant to s 500(2) of the Corporations Act 2001 (Cth), the Secretary has leave to proceed with this proceeding against Key Promotional on the condition that the Secretary does not take any step to enforce against Key Promotional any order for the payment of any amount of money, whether by way of penalty, costs or otherwise, without further leave of the Court.

THE COURT DECLARES THAT:

2. Between 12 January 2022 and 25 February 2022, Key Promotional contravened s 41MIB(1)(a)(i) of the Therapeutic Goods Act 1989 (Cth) (TG Act) by importing 255,000 medical devices into Australia, to which none of the provisions of s 41MIB(1)(b) of the TG Act applied.

3. Between on or about 12 January 2022 and on or about 28 March 2022, Key Promotional contravened s 41MIB(1)(a)(iii) of the TG Act by supplying 240,720 medical devices in Australia, to which none of the provisions of s 41MIB(1)(b) of the TG Act applied.

4. Mr Harding aided, abetted, counselled or procured Key Promotional’s contraventions of s 41MIB(1)(a)(i) and s 41MIB(1)(a)(iii) of the TG Act (as referred to in orders 2 and 3) and was, therefore, involved in those contraventions for the purpose of s 42YC of the TG Act.

5. Between 29 December 2021 and 3 March 2022, Key Promotional contravened s 41MLA(1) and s 41MLA(2)(a) of the TG Act by making 2,303 false or misleading representations that the medical devices were of a kind included in the Australian Register of Therapeutic Goods maintained under s 9A of the TG Act.

6. Between 4 January 2022 and 3 March 2022, Mr Harding aided, abetted, counselled or procured Key Promotional’s contraventions of s 41MLA(1) and s 41MLA(2)(a) of the TG Act in relation to 1,183 of the false or misleading representations referred to in order 5 and was, therefore, involved in those contraventions for the purpose of s 42YC of the TG Act.

THE COURT ORDERS THAT:

7. Pursuant to s 42Y(2) of the TG Act, Key Promotional pay a pecuniary penalty to the Commonwealth of $1,750,000 in respect of the contraventions that it committed.

8. Pursuant to s 42Y(2) of the TG Act, Mr Harding pay a pecuniary penalty to the Commonwealth of $250,000 in respect of the contraventions that he committed, within 21 days of the date of these Orders, subject to order 9(a) below.

9. In respect of the penalty against Mr Harding:

(a) $70,000 of that penalty is suspended on the condition that Mr Harding does not commit any further civil penalty contravention under, or any offence against, any provision of the TG Act for a period of 10 years from the date of these Orders; and

(b) if there is no such contravention or offence by Mr Harding, enforcement of the suspended amount shall be permanently stayed.

10. Key Promotional and Mr Harding pay the Secretary’s costs as follows:

(a) Key Promotional: $60,000; and

(b) Mr Harding: $40,000, to be paid within 21 days of the date of these Orders.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

LONGBOTTOM J:

1 The First Respondent (Key Promotional) admits to contraventions of the Therapeutic Goods Act 1989 (Cth) (TG Act) relating to the import and supply of certain rapid antigen test kits (RATs) and representations with respect to their quality. The Second Respondent (Mr Craig Harding) was an employee of Key Promotional and married to the director of the company. Mr Harding admits to aiding, abetting, procuring or counselling Key Promotional in its contraventions of the TG Act.

2 The hearing proceeded by way of a statement of agreed facts and issues that had been agreed between the Applicant (Secretary) and Key Promotional (SOAF) and an amended statement of agreed facts and issues that had been agreed between the Secretary and Mr Harding (ASOAF). The SOAF and ASOAF are reproduced at Annexures A and B. The summary that follows is taken from those documents.

3 Shortly after it signed the SOAF, Key Promotional went into liquidation. As such, the Secretary requires leave to continue the proceeding against the company: Corporations Act 2001 (Cth), s 500(2). The liquidator (Mr Matthew Bookless) neither consents nor opposes the grant of leave.

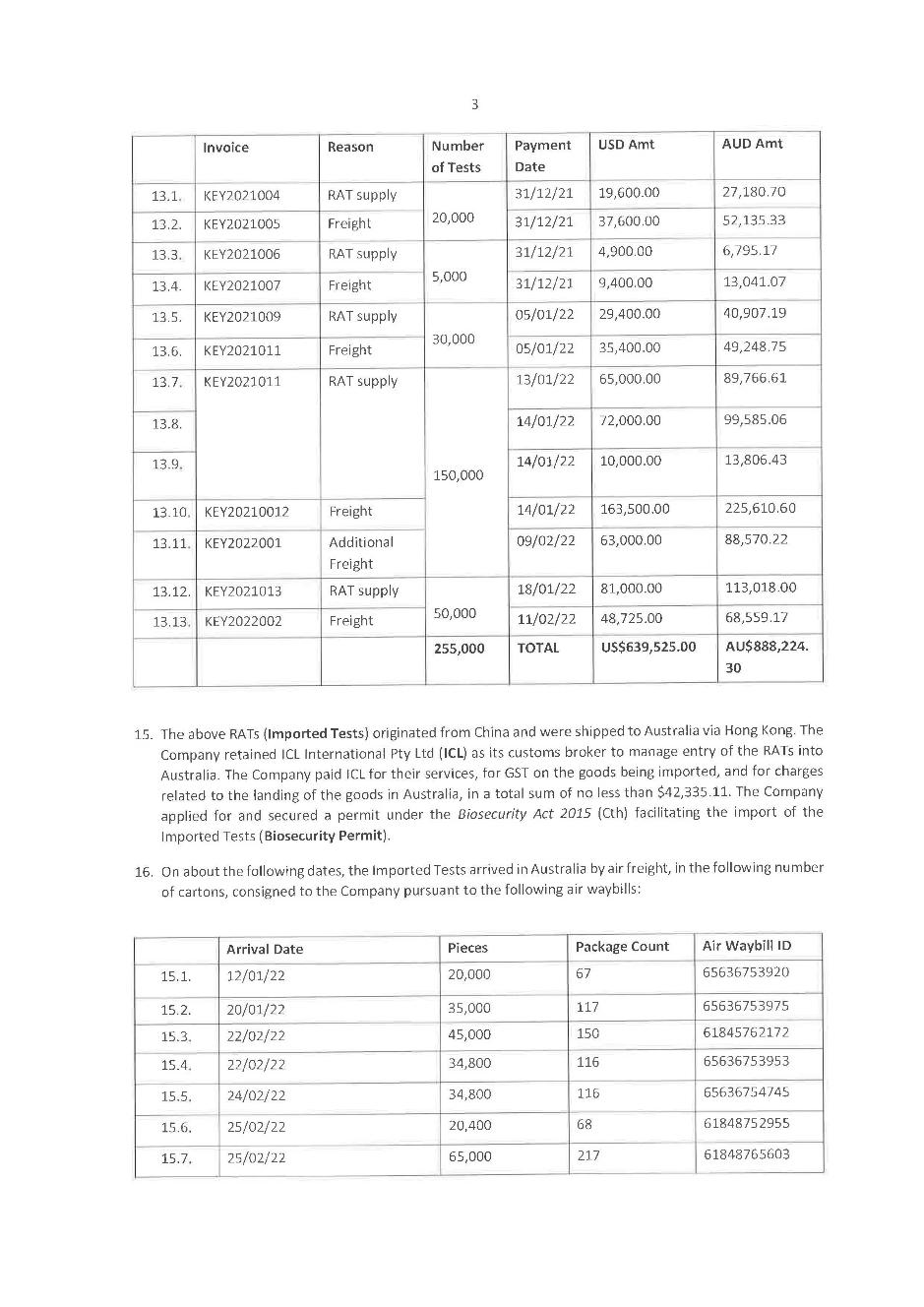

4 Key Promotional agrees that between 12 January 2022 and 25 February 2022, it imported 255,000 RATs not included in the Australian Register of Therapeutic Goods maintained by the Secretary: TG Act, s 9A. Key Promotional further agrees that it made false or misleading representations that the RATs were of a kind included in the Register (by stating they were “TGA approved” or attaching the record of a medical device that was in the Register) and supplied no less than 240,720 of the RATs to customers in Australia.

5 Each of the RATs were a “medical device” within the meaning of the TG Act because they were an apparatus intended to be used for human beings for the purpose of diagnosing a disease, namely, COVID-19: TG Act, s 41BD(1)(a)(i). A person will contravene the TG Act if they import into or supply a medical device in Australia that is not of a kind included in the Register in relation to the person, or if they make a false or misleading representation that the medical device is of a kind that is included in the Register: TG Act, ss 41MIB(1)(a)(i), 41MIB(1)(a)(iii), 41MIB(1)(b)(i), 41MLA(1) and 41MLA(2)(a). A contravention of any of those sections of the TG Act attracts the imposition of a civil penalty.

6 Mr Harding agrees that by 4 January 2022, he knew the essential matters that went to make up the above described contraventions of the TG Act by Key Promotional. As such, Mr Harding agrees that from that date, he aided, abetted, counselled or procured those contraventions: TG Act, s 42YC.

7 Mr Harding and the Secretary have agreed to proposed orders which include a pecuniary penalty payable by Mr Harding, pursuant to s 42Y of the TG Act, in the amount of $250,000 (with $70,000 of that suspended on the condition that Mr Harding does not commit any further contravention of or offence against any provision of the TG Act, including any civil penalty provision for a period of 10 years). Mr Harding and the Secretary jointly seek a declaration or declarations reflecting the conduct by Mr Harding that gave rise to his liability to pay a civil penalty.

8 The liquidator has agreed to the proposed penalty against Key Promotional pursuant to s 42Y of the TG Act ($1,750,000) in respect of the contraventions of the TG Act. The Secretary also seeks declarations that Key Promotional contravened the TG Act by importing the RATs into and supplying the RATs in Australia, and made false or misleading statements that the RATs were of a kind included in the Register or, otherwise, made false or misleading representations within the meaning of s 41MLA: TG Act, ss 41MIB(1)(a)(i), 41MIB(1)(a)(iii) and 41MLA.

9 For the following reasons, I will grant the Secretary leave to continue against Key Promotional pursuant to s 500(2) of the Corporations Act and make declarations and orders substantially in the form sought by the Secretary and consented to, or agreed, by Key Promotional and Mr Harding.

leave to proceed

10 The principles to be applied in determining an application by a regulator for leave to proceed under s 500(2) of the Corporations Act were helpfully summarised by Bromwich J in Australian Competition and Consumer Commission v Australian Institute of Professional Education Pty Ltd (in liq) [2017] FCA 521 at [22]-[24] and [26]. These reasons assume that the reader is familiar with that summary.

11 The TG Act is relevantly concerned with establishing and maintaining a national system of controls relating to the quality, safety and efficacy of therapeutic goods including medical devices used in Australia: TG Act, s 4(1)(a). The facts agreed in the SOAF are serious. They raise a matter of public interest involving contraventions of the TG Act with respect to that “national system of controls” in connection with a medical device to be used for the detection of the COVID-19 antigen in humans in response to the public health crisis that was the pandemic.

12 The Secretary, as regulator of the TG Act, has a real interest in seeking relief to vindicate a public right that the TG Act has been breached: cf, Institute of Professional Education at [26(4)]. That outcome would also serve the independent public interest in there being a public record of contraventions and penalties as an aid to deter future contraventions by others: cf, Secretary, Department of Health and Ageing v Prime Nature Prize Pty Ltd (in liq) [2010] FCA 597 at [22] (Stone J). That general deterrent function is not defeated by the fact that Key Promotional is in liquidation and unable to pay penalties: cf, Prime Nature at [22] and the authorities there cited.

13 I accept that those factors – together with the fact the Secretary cannot pursue relief by way of lodging a proof of debt – support the grant of leave in this case. Section 500(2) of the Corporations Act contemplates that the Court may impose terms upon the grant of leave. The orders sought by the Secretary envisage a condition that he must not take any step to enforce any order for payment of money against Key Promotional, without further leave of the Court. Such a condition is appropriate in the circumstances. I will, therefore, grant the Secretary leave to continue on those terms.

declarations

Guiding principles

14 The Court has a wide discretionary power to make declarations under s 21(1) of the Federal Court of Australia Act 1976 (Cth): Forster v Jododex Australia Pty. Limited [1972] HCA 61; (1972) 127 CLR 421 at 435-436 (Gibbs J). Declarations relating to contraventions of legislative provisions are likely to be appropriate where they serve to record the Court’s disapproval of the contravening conduct, vindicate the claim that the respondent contravened the provisions, assist the regulator to carry out its duties and deter other persons from contravening the provisions: Australian Building and Construction Commissioner v Construction, Forestry, Mining and Energy Union [2017] FCAFC 113; (2017) 254 FCR 68 at [93] (Dowsett, Greenwood and Wigney JJ).

15 Before granting declaratory relief, a court should be satisfied that the question is real (not hypothetical or theoretical) and that an applicant has a sufficient or real interest in raising the issue and that there is a proper contradictor: Forster at 437-438; see also, Hobart International Airport Pty Ltd v Clarence City Council [2022] HCA 5; (2022) 276 CLR 519 at [32]-[34] (Kiefel CJ, Keane and Gordon JJ).

16 The facts necessary to support a declaration may be established by agreed facts: Australian Competition and Consumer Commission v Fisher & Paykel Customer Services Pty Ltd [2014] FCA 1393 at [52] (Wigney J). But “close attention” should be given to the form of proposed declarations, particularly those “by consent”: Rural Press Limited v Australian Competition & Consumer Commission [2003] HCA 75; (2003) 216 CLR 53 at [90] (Gummow, Hayne and Heydon JJ).

17 Moreover, the declaration should “disclose the basis on which” a contravention has occurred and provide “sufficient indication of how and why the relevant conduct is a contravention” of the TG Act: BMW Australia Ltd v Australian Competition & Consumer Commission [2004] FCAFC 167; (2004) 207 ALR 452 at [35] (Gray, Goldberg and Weinberg JJ) and Australian Competition and Consumer Commission v Coles Supermarkets Australia Pty Ltd [2014] FCA 1405 at [77] (Gordon J), as cited in Comcare v Linfox Australia Pty Ltd [2015] FCA 61; (2015) 144 ALD 593 at [12] (Flick J).

Material

18 As already noted, the primary facts were set out in the SOAF and ASOAF. The Secretary filed supplementary evidence including:

(a) an affidavit of Mr David Jack Jenvey dated 27 March 2025. Mr Jenvey is the Acting Director of the Product Investigation Section in the Regulatory Practice and Support Division, Health Products Regulation Group, Regulatory Compliance Branch of the Australian Government Department of Health and Aged Care; and

(b) affidavits of Mr Howard Rapke respectively dated 4 June 2025, 29 August 2025 and two dated 15 September 2025. Mr Rapke has conduct of the proceeding on behalf of the Secretary.

19 I am satisfied that the agreed facts as contained in the SOAF and ASOAF are to be accepted as true for the purpose of this proceeding: Evidence Act 1995 (Cth), s 191 and Australian Securities and Investments Commission v BHF Solutions Pty Ltd [2022] FCAFC 108; (2022) 293 FCR 330 at [24] (O’Bryan J, with whom Besanko and Lee JJ agreed). To the extent to which the statements contained in the SOAF or ASOAF are statements as to law, or statements of mixed fact and law, I will treat those statements as formal admissions by Key Promotional or Mr Harding (as relevant) for the purposes of this proceeding: Secretary, Department of Health v Medtronic Australasia Pty Ltd [2024] FCA 1096; (2024) 305 FCR 433 at [21] (Needham J).

Disposition

20 I am satisfied that this is an appropriate case to grant declaratory relief against Key Promotional and Mr Harding in substantially the same terms as sought by the Secretary. That is for the following reasons.

21 Even though Key Promotional has admitted that it contravened s 41MIB and s 41MLA of the TG Act, and Mr Harding has admitted that he aided, abetted, counselled or procured those contraventions, I am independently satisfied that the agreed facts amount to contraventions of each of those provisions. That includes satisfaction that insofar as the SOAF or ASOAF refers to terms defined by the TG Act (such as a “medical device” or “supply”) or terms having a specific legal meaning (such as “import” and “false or misleading”), the facts, as agreed, satisfy those definitions.

Key Promotional

22 Insofar as it concerns Key Promotional, I am satisfied that:

(a) Import: between 12 January 2022 and 25 February 2022, Key Promotional imported 255,000 medical devices into Australia that were not of a kind included in the Register, in contravention of s 41MIB(1)(a)(i) of the TG Act. The expression “import” is not defined by the TG Act. The Secretary submits, and I accept, that the RATs were “imported” into Australia when they were brought into the country: cf, R v Bull [1974] HCA 23; (1974) 131 CLR 203 at 254 (Gibbs J); see also, at [212] (Barwick CJ), [248] (Menzies J), [265]-[266] (Stephen J), and [273] Mason JJ); cf, [242]-[243] (McTiernan J in dissent). The SOAF records that the RATs arrived in Australia on various dates between 12 January 2022 and 25 February 2022;

(b) Supply: between on or about 12 January 2022 and on or about 28 March 2022, Key Promotional supplied 240,720 of the medical devices referred to in [22(a)] above in Australia, in contravention of s 41MIB(1)(a)(iii) of the TG Act. That timeframe reflects the agreement that the RATs were delivered following payment and their receipt into Australia. A “supply” is relevantly defined by the TG Act as “supply by way of sale”: TG Act, s 3. As the Secretary highlights, while the meaning of “supply” depends on its statutory context, in its narrowest sense it means physical delivery: see, Symes v Stewart [1920] HCA 73; (1920) 28 CLR 386 at 389 (Knox CJ, with whom Isaacs and Rich JJ agreed) and Dawson v Deputy Commissioner of Taxation (1984) 71 FLR 364 at 371 (King CJ with whom Cox J agreed); cf, 375 (Legoe J). Therefore, the Secretary submits, and I accept, that the supplies occurred when the RATs were delivered to customers. The first of the RATs arrived in Australia on 12 January 2022. The SOAF does not record the date the last of the RATs were delivered. But [24] of the SOAF incorporates by reference Annexure B to the concise statement filed by the Secretary on 3 June 2024. It is there recorded that the last payment received for the RATs was on 28 March 2022. Given that the precise dates of delivery are not recorded, I will declare the contraventions as occurring between those approximate dates; and

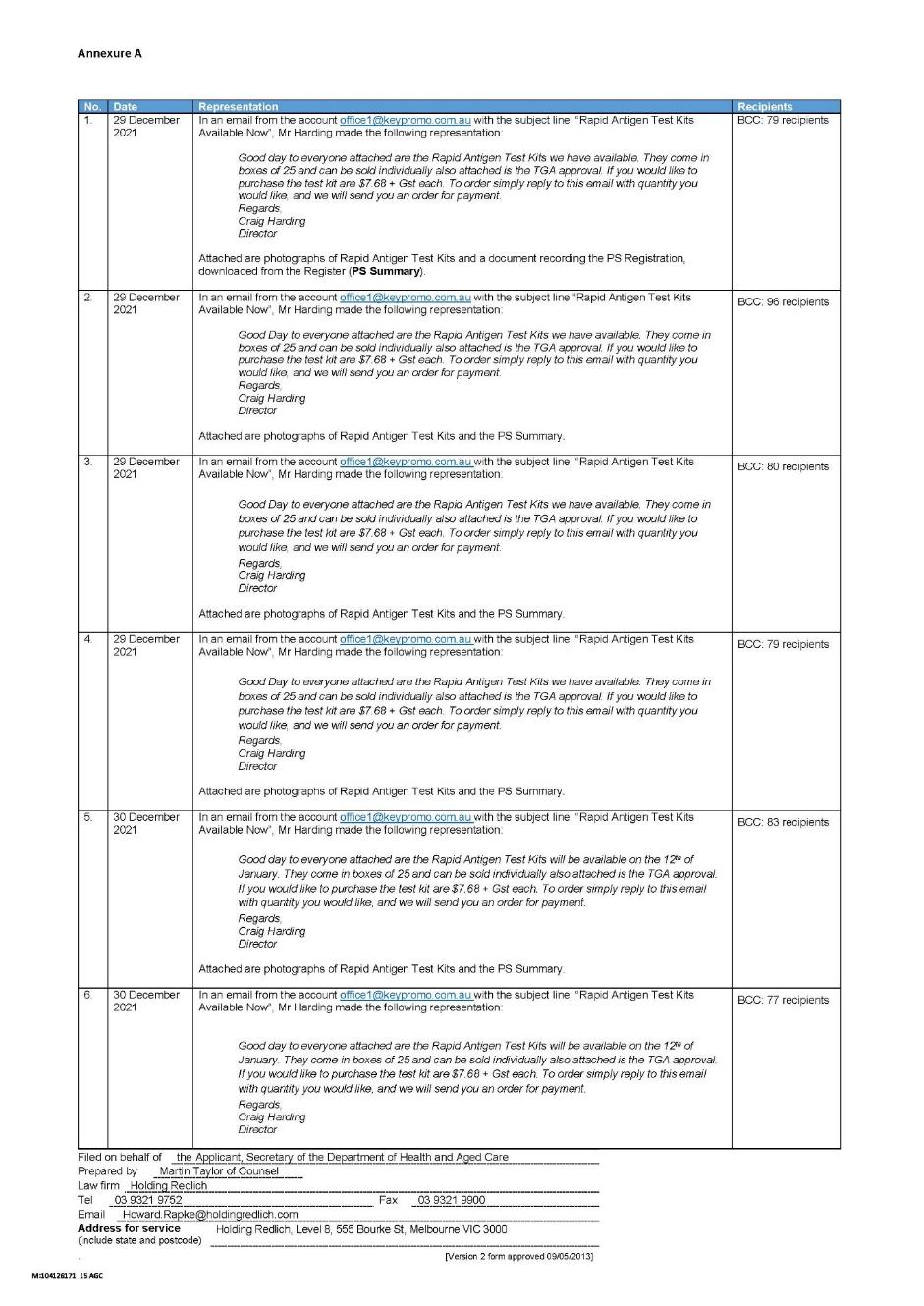

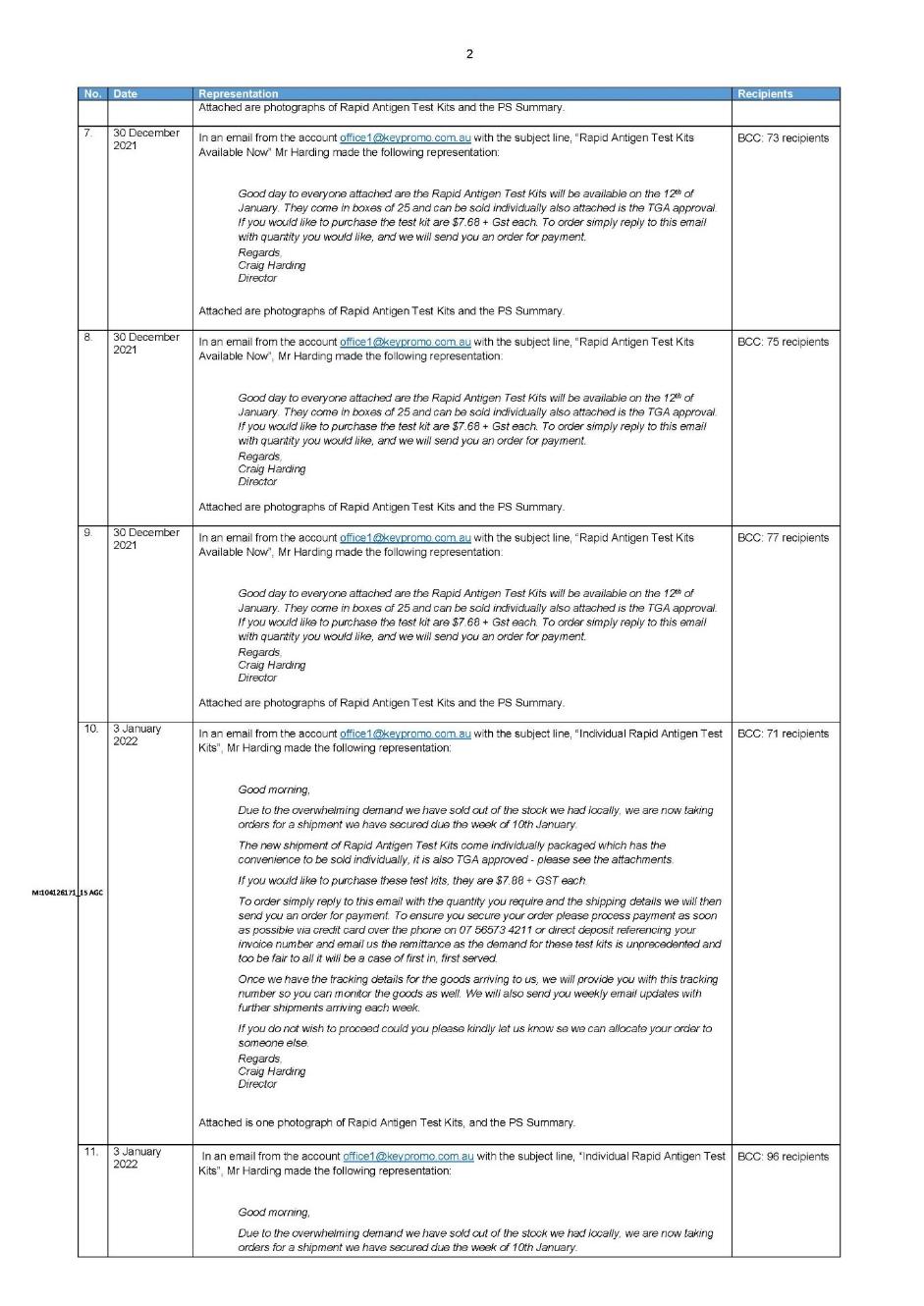

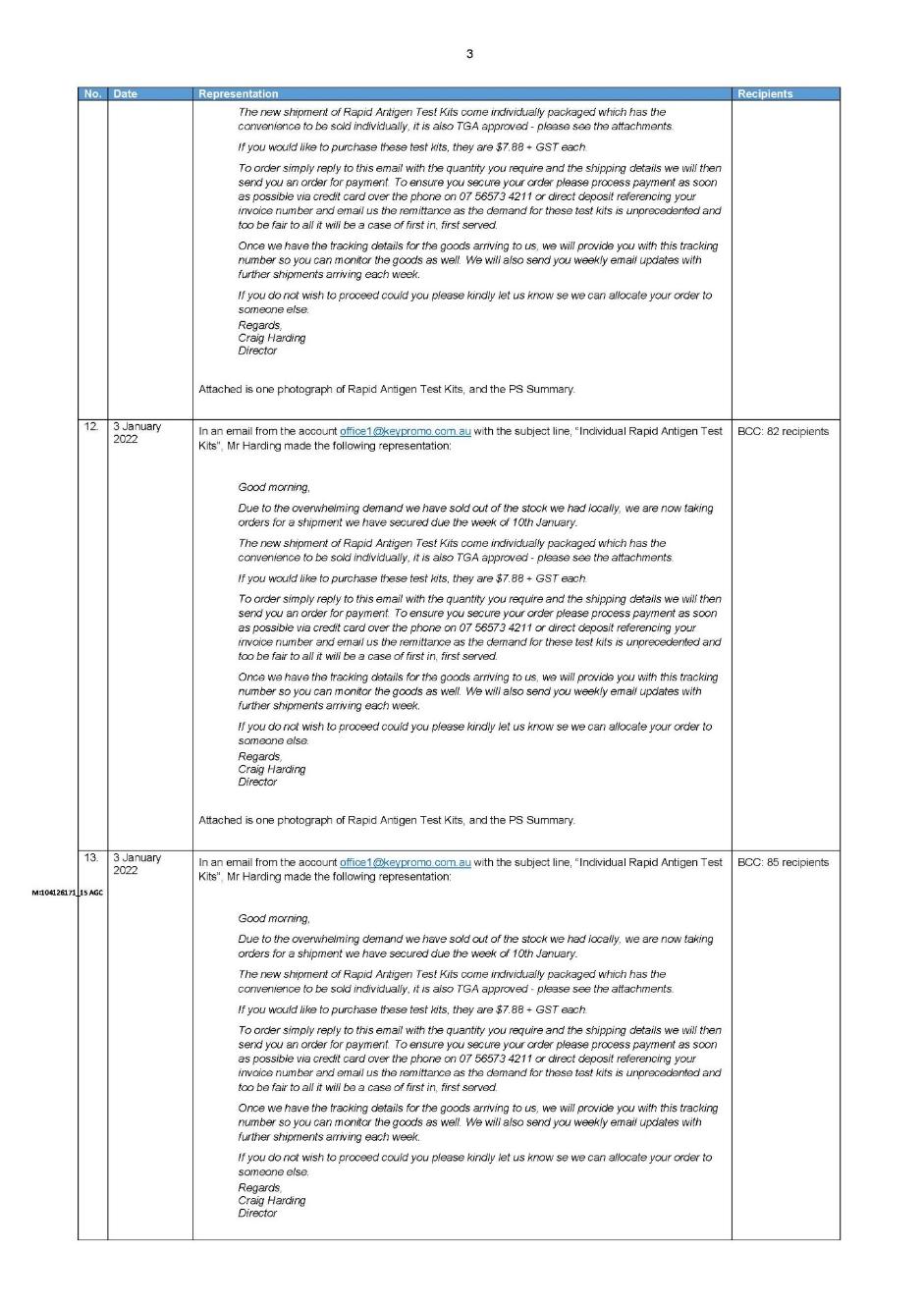

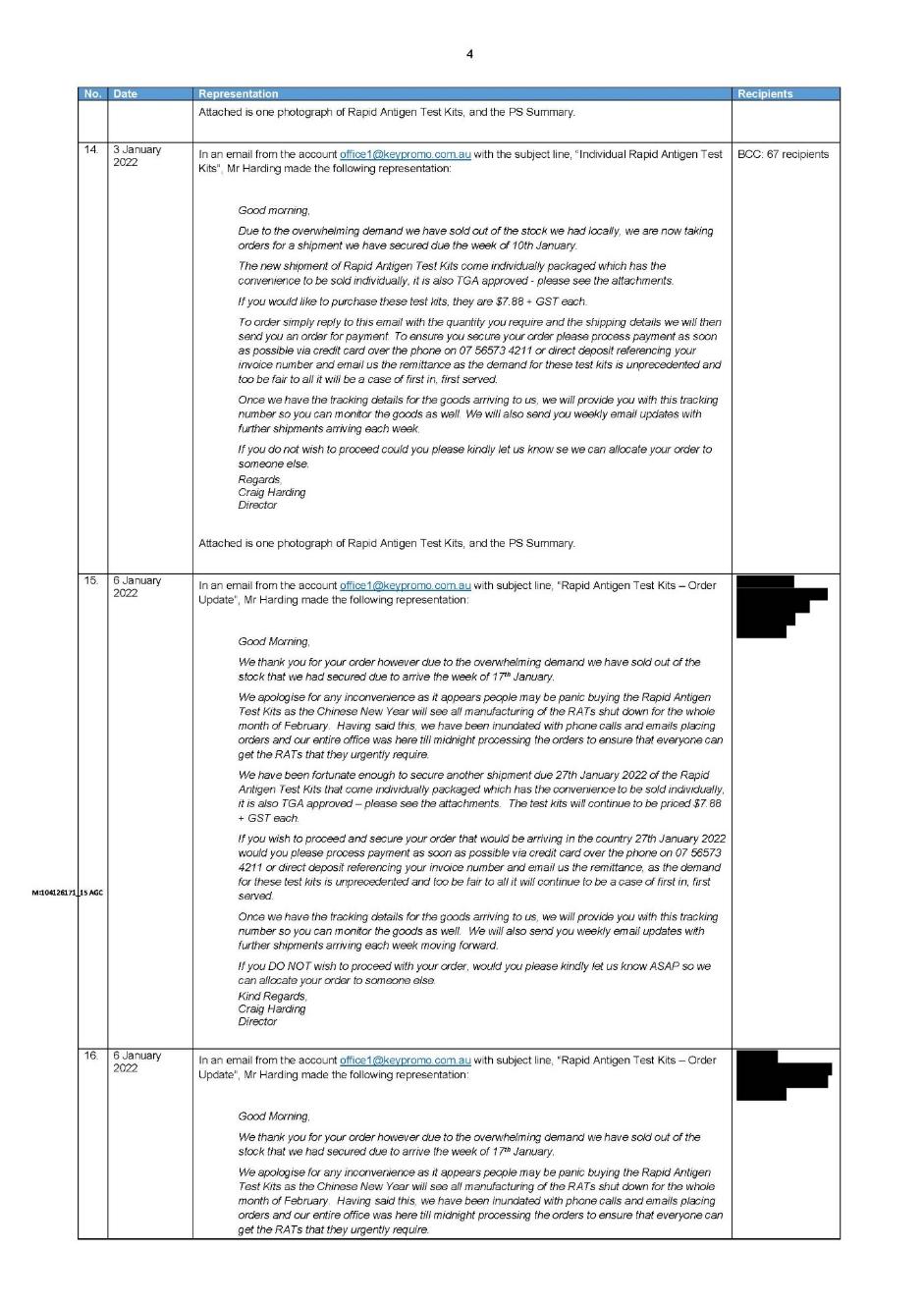

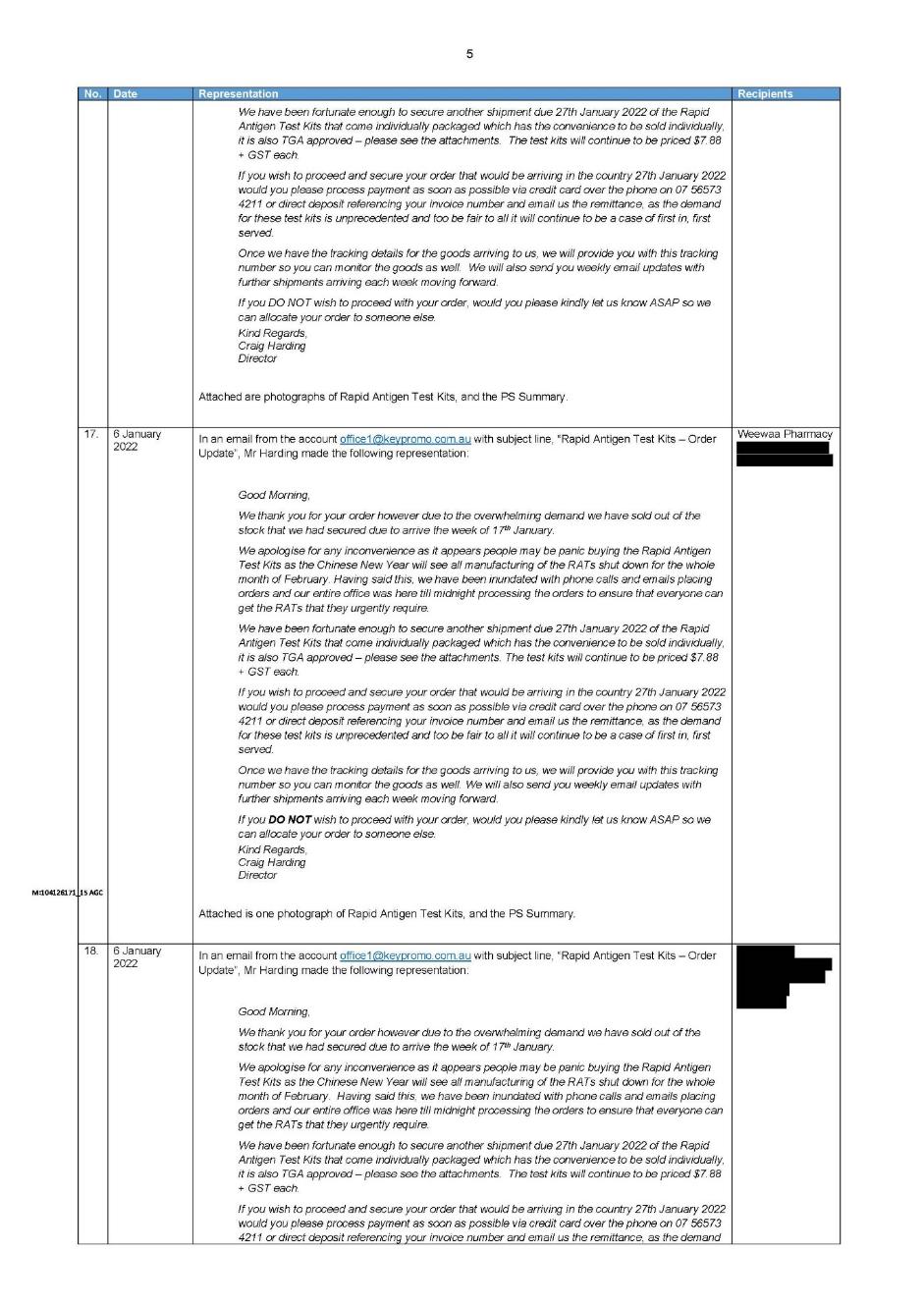

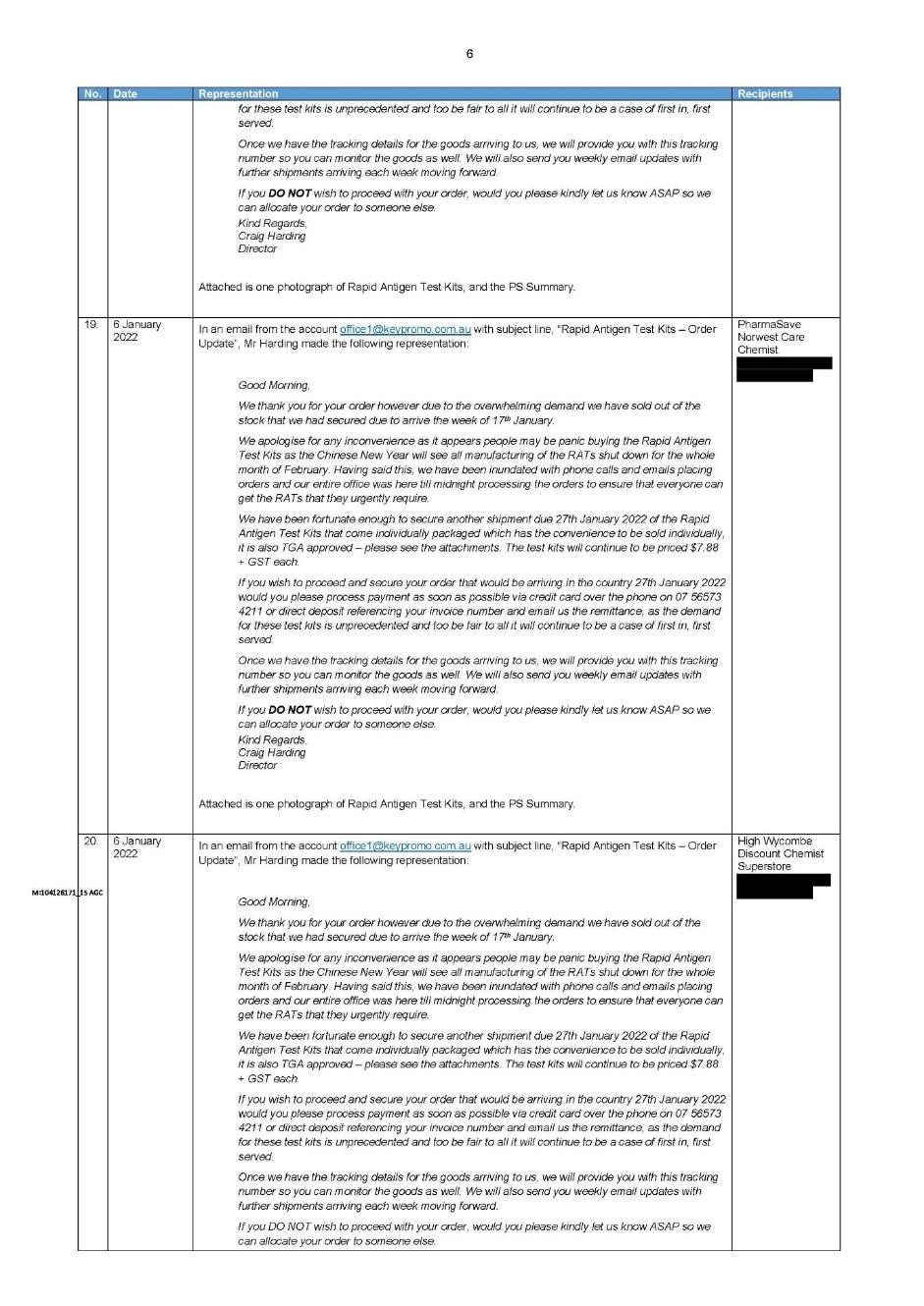

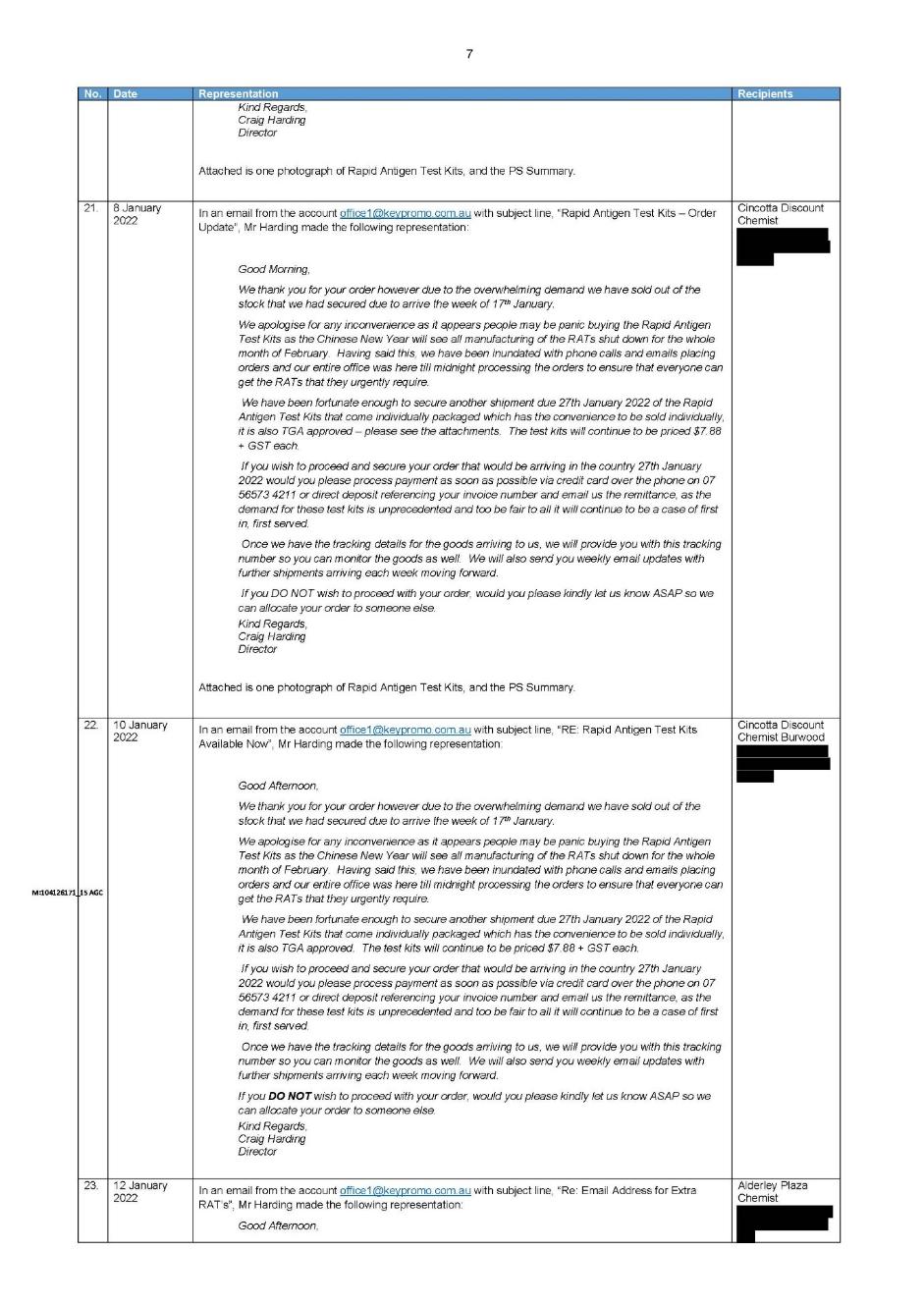

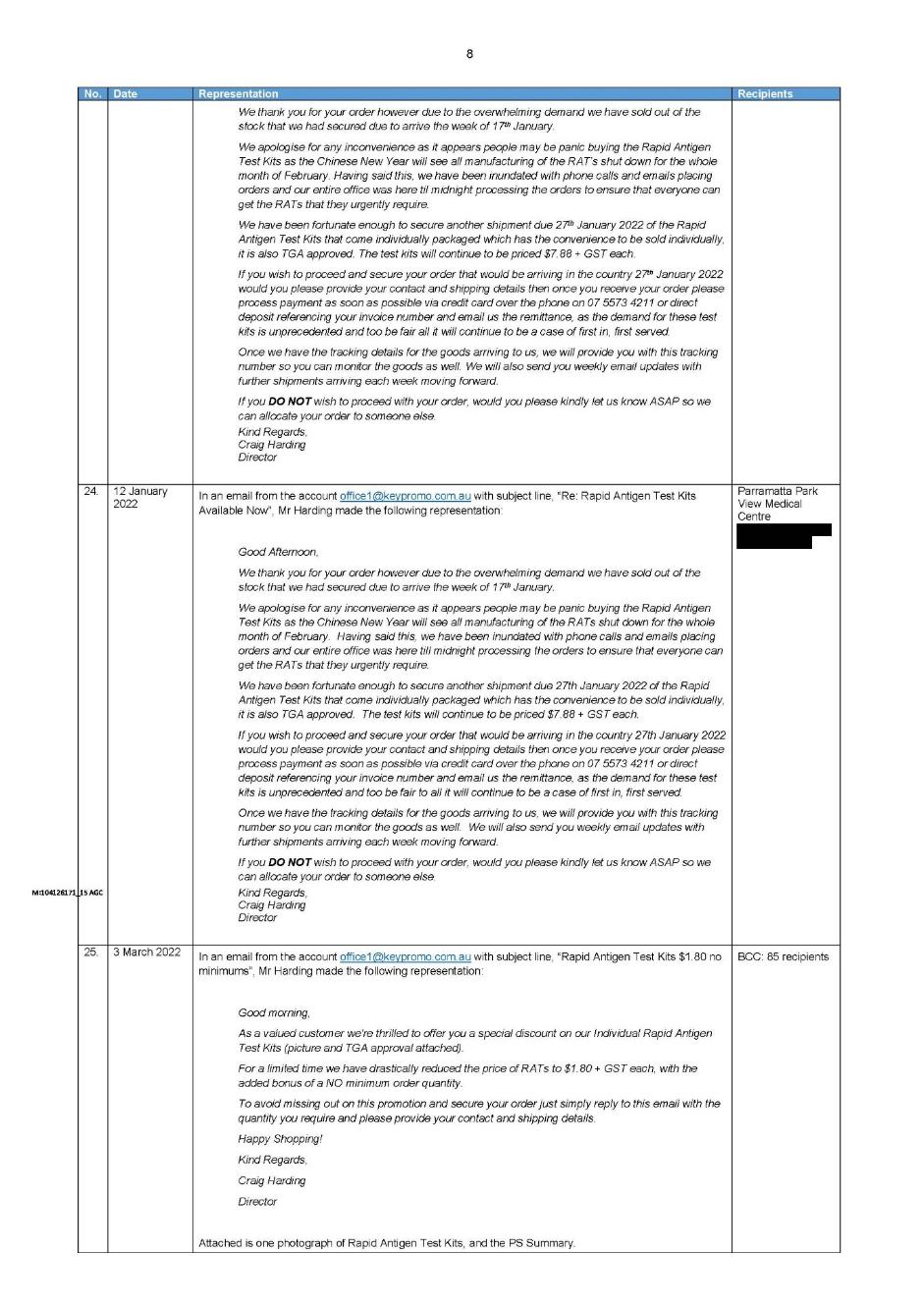

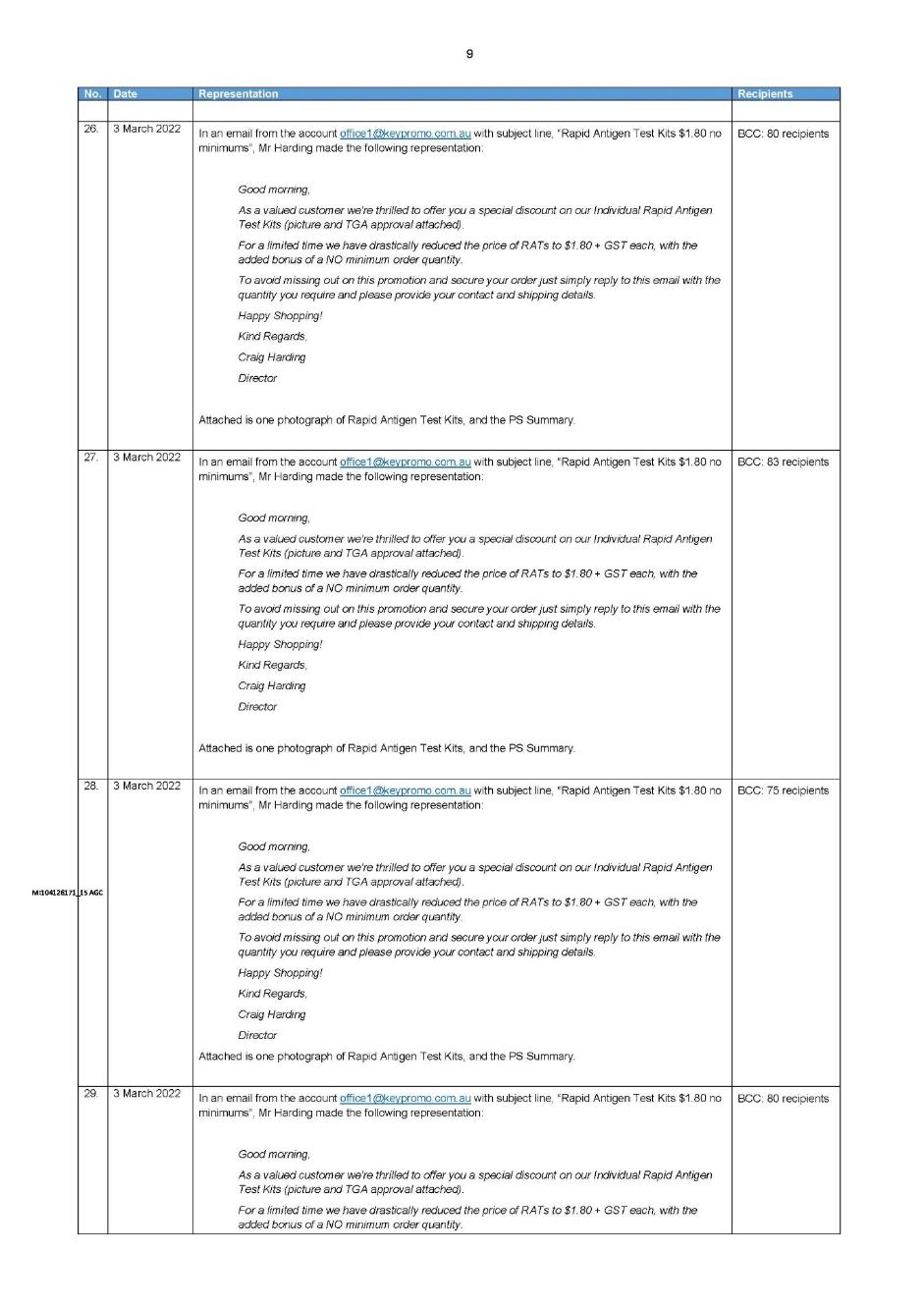

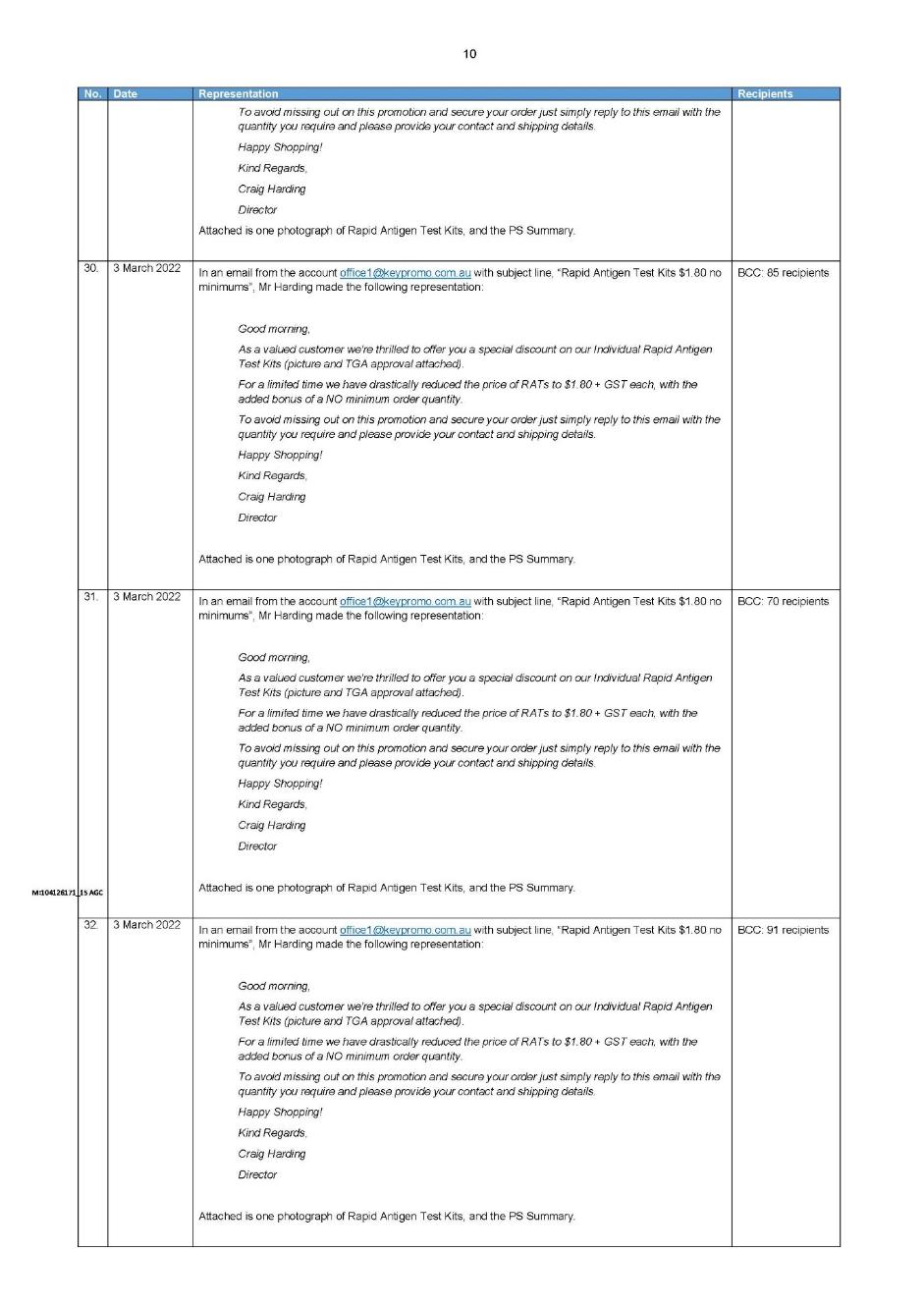

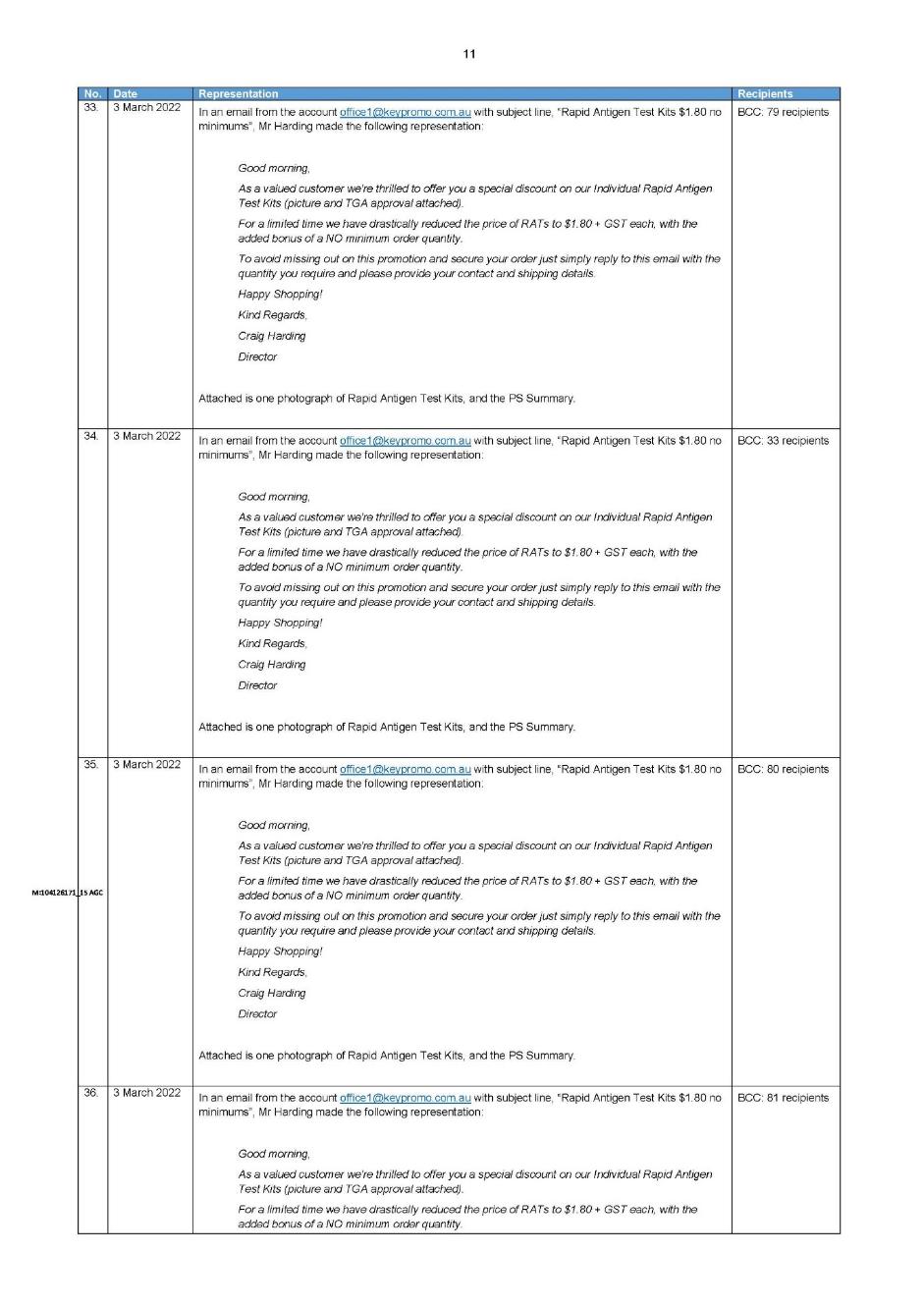

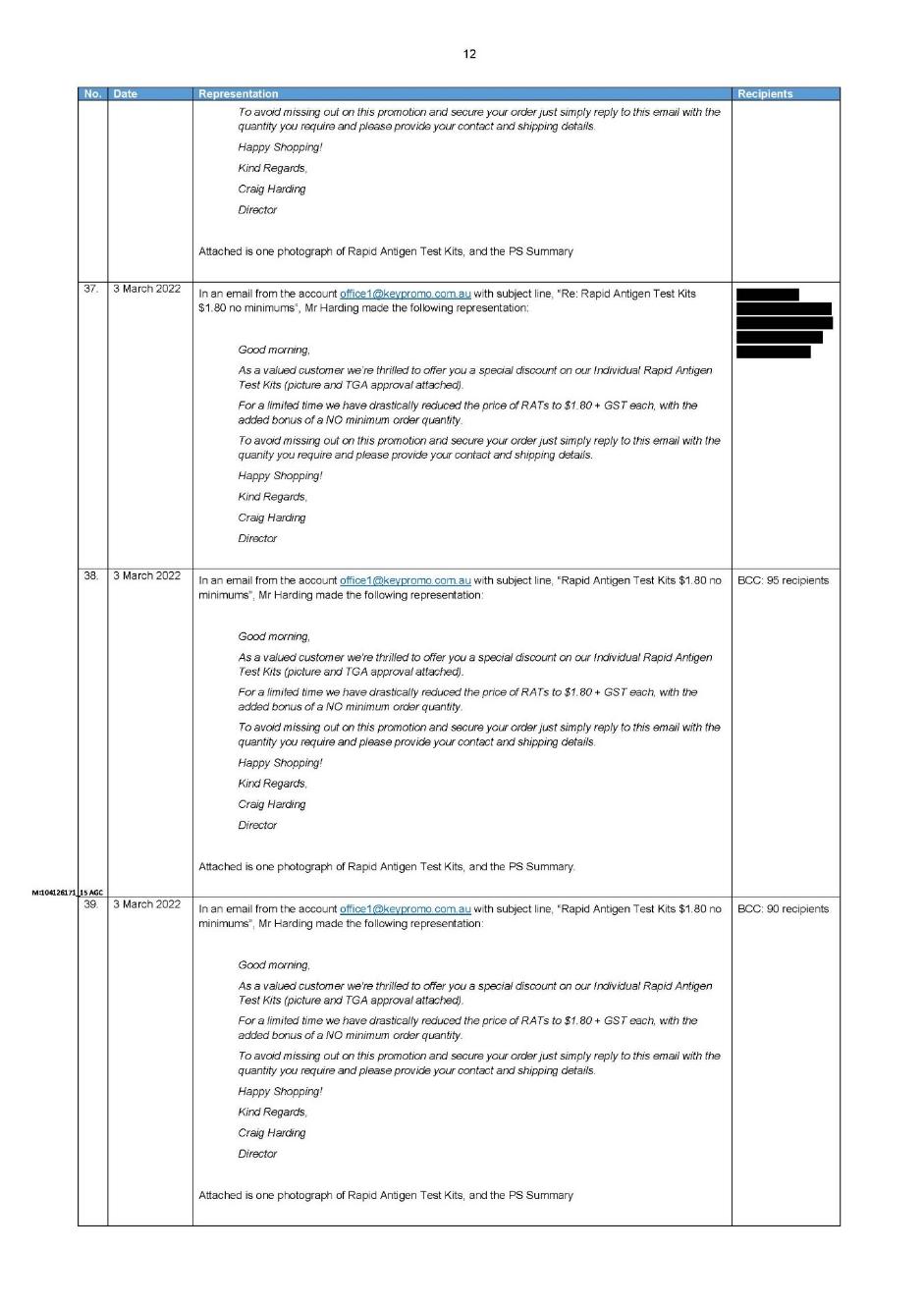

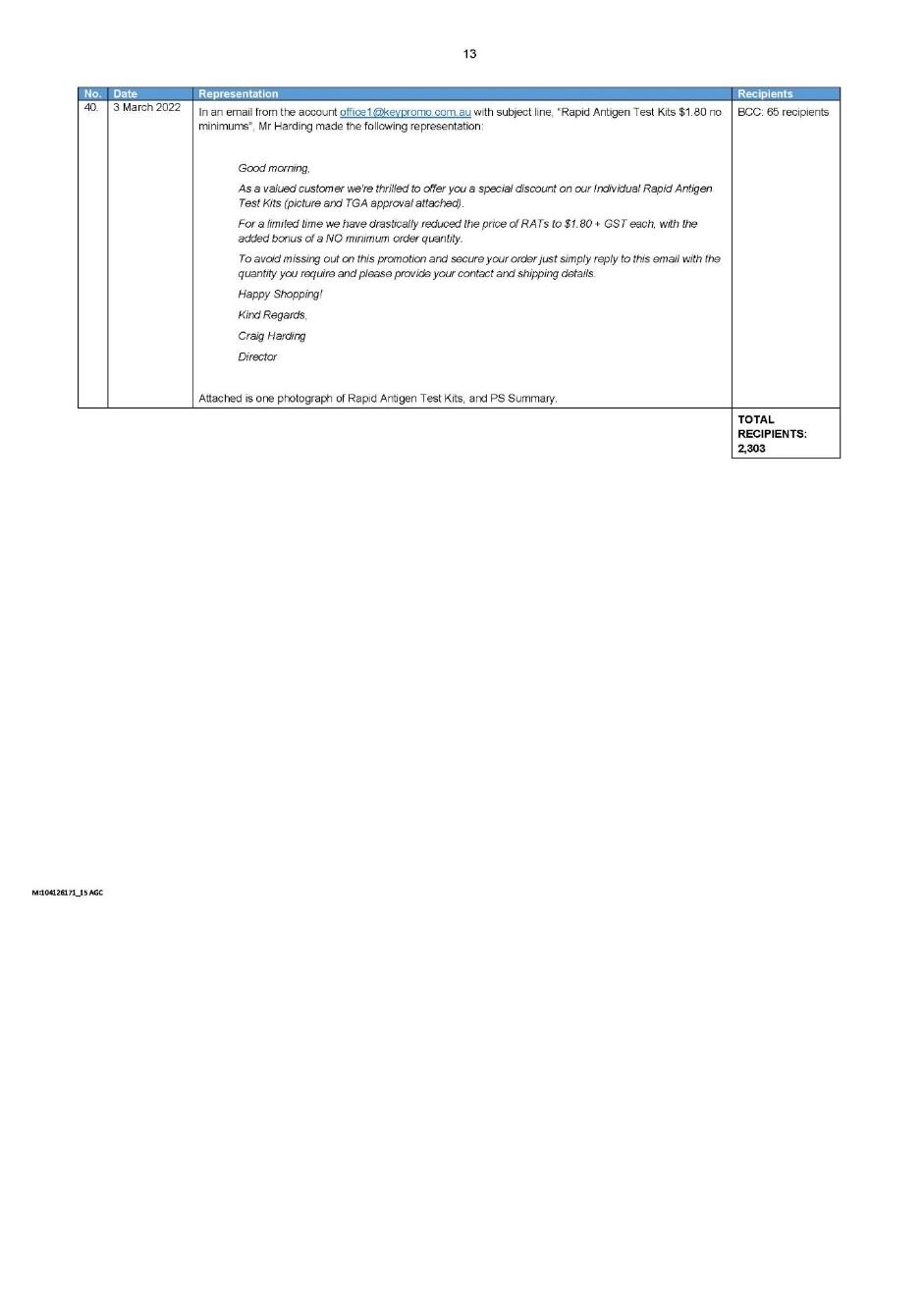

(c) Representations: Between 29 December 2021 and 3 March 2022, Key Promotional made 2,303 false or misleading representations in the manner described in the SOAF that the medical devices it imported into Australia were of a kind included in the Register, in contravention of s 41MLA(1) and s 41MLA(2)(a) of the TG Act. I pause to note that the SOAF does not identify the date or the number of the representations made by the company, but that figure is incorporated by reference at [27] of the SOAF. That paragraph refers to Annexure A of the concise statement, which sets out 40 emails that were sent to a total of 2,303 recipients between the relevant dates (email representations). A copy of the annexure containing the email representations is reproduced as Annexure C to these reasons.

23 There is one aspect of declaratory relief sought by the Secretary against Key Promotional that I am not prepared to make. The Secretary seeks a declaration that the email representations were false or misleading because they represented that the RATs were of a kind included in the Register maintained under s 9A of the TG Act, or were “otherwise false and misleading representations to which s 41MLA of the TG Act applies”. I am satisfied that the email representations were false or misleading because they represented that the RATs were medical devices of a kind included in the Register: TG Act, s 42MLA(2)(a). But, in the absence of specificity as to how s 41MLA of the TG Act “otherwise” applied to those representations, I am not prepared to make the further declaration sought by the Secretary: cf, BMW Australia at [35].

Mr Harding

24 Insofar as it concerns Mr Harding, I am satisfied that he aided, abetted, counselled or procured contraventions of the material provisions of the TG Act by Key Promotional: TG Act, s 42YC. That liability arises by reason of his knowledge of the essential matters constituting the contraventions by Key Promotional of those provisions of the TG Act: Productivity Partners Pty Ltd (trading as Captain Cook College) v Australian Competition and Consumer Commission [2024] HCA 27; (2024) 281 CLR 338 at [82] (Gageler CJ and Jagot J), [148]-[149] (Gordon J), [266] (Edelman J) and [339] (Beech-Jones J).

25 The Secretary and Mr Harding are agreed that Mr Harding had the requisite knowledge by 4 January 2022: cf, Medtronic Australasia at [21]. On that date Mr Harding received an email informing him that the importation of the RATs into Australia required a “TGA Certificate” issued to Key Promotional. Mr Harding admits that from that date he knew that the RATs were medical devices not of a kind included in the Register in relation to Key Promotional and that they did not otherwise have the characteristics prescribed in s 41MIB(1)(b) of the TG Act that would render their importation into and supply in Australia, permissible under the terms of the legislation.

26 As appears from the matters set out above, Key Promotional’s contraventions of the provisions of the TG Act dealing with importation and supply of the RATs commenced after 4 January 2022. However, its contraventions of the provisions of the TG Act with respect to false or misleading representations about the RATs commenced beforehand, on 29 December 2021. Given those matters, the Secretary submits, and I accept, it is apt to frame the declaration against Mr Harding in terms of the number of false or misleading representations made after 4 January 2022. As appears from Annexure C to these reasons, there were 1,183 such representations.

Declaratory relief ought to be granted

27 There is an important public service to be served by granting declarations substantially in the terms sought by the Secretary. So much is made clear by s 4 of the TG Act, as referred to above. An aspect of that “national system of controls” is the Register, inclusion in which requires satisfaction of prescribed criteria: cf, TG Act, Ch 4, Pts 4-5, Div 1. Mr Jenvey gave evidence on behalf of the Secretary that the conduct of Key Promotional (as described in the SOAF) created a risk to end-users. That was because the RATs were potentially ineffective or unsafe, not suitable for testing, or not accompanied by adequate instructions for use. As Mr Jenvey explains, the contraventions are of particular concern in the context of the statutory scheme because they occurred shortly after the approval of self-administered COVID-19 rapid antigen tests (in November 2021), as part of the response to the public health emergency that was the COVID-19 pandemic.

28 For those same reasons, I am satisfied that the question is real (not hypothetical or theoretical) and that the Secretary, given his function, has a real interest to raise it: cf, Forster at 437-438. Key Promotional and Mr Harding are proper contradictors because each of them has a “true interest to oppose” the declarations sought: Forster at 437-438; see also, Australian Competition and Consumer Commission v MSY Technology Pty Ltd [2012] FCAFC 56; (2012) 201 FCR 378 at [14]-[18] (Greenwood, Logan and Yates JJ). While the liquidator did not appear at the hearing, the SOAF was agreed prior to the company going into liquidation, and I am satisfied from the communications with Mr Bookless that he has been served with the material upon which the Secretary relies. I will, therefore, make declarations in the terms outlined above.

civil penalties

29 The Secretary is empowered to apply on behalf of the Commonwealth for an order that both Key Promotional and Mr Harding pay the Commonwealth pecuniary penalties because the application was made within six years after the relevant contraventions of the TG Act: TG Act, s 42Y(1).

30 Section 42Y(3) of the TG Act provides:

(3) In determining the pecuniary penalty, the Court must have regard to all relevant matters, including:

(a) the nature and extent of the contravention; and

(b) the nature and extent of any loss or damage suffered as a result of the contravention; and

(c) the circumstances in which the contravention took place; and

(d) whether the person has previously been found by the Court in proceedings under this Act to have engaged in any similar conduct.

31 The principles relevant to the imposition of civil penalties, including in the context of the TG Act, are well-settled and need not be restated here: Secretary, Department of Health v Evolution Supplements Australia Pty Ltd (No 2) [2021] FCA 872 at [52]-[59] and [66]-[69] (Burley J); see also, Secretary, Department of Health v Peptide Clinics Australia Pty Ltd [2019] FCA 1107; (2019) 137 ACSR 494 at [28]-[34] (Jagot J). These reasons assume the reader is familiar with those principles, which I refer to below, as appropriate in dealing with the submissions made by the parties.

32 Where, as here, the penalties are agreed, “the proper approach in synthesising the relevant factors is to assess the proposed figure against [the relevant factors], determine whether it fits within the permissible range and, if no particular figure can be said to be more appropriate than another … accept it as appropriate”: Medtronic Australasia at [116] (Needham J), citing Volkswagen Aktiengesellschaft v Australian Competition and Consumer Commission [2021] FCAFC 49; (2021) 284 FCR 24 at [127] (Wigney, Beach and O’Bryan JJ). Even where satisfied that the proposed orders are within the Court’s power and are appropriate, the Court should “exercise a degree of restraint when scrutinising the proposed settlement terms, particularly where both parties are legally represented and able to understand and evaluate the desirability of the settlement”: Coles Supermarkets at [72] (Gordon J), as cited in Medtronic Australasia at [116].

assessment of penaltIES

Contravention of civil penalty provisions

33 I am satisfied for the reasons outlined at [22] and [24]-[26] above, that each of Key Promotional and Mr Harding have contravened ss 41MIB(1)(a)(i), 41MIB(1)(a)(iii) and 41MLA(1) of the TG Act, thereby enlivening the discretionary power of the Court to make a civil penalty order: TG Act, s 42Y(2).

34 In the case of Mr Harding, the consequence of his aiding, abetting, counselling or procuring the contraventions by Key Promotional of those civil penalty provisions, is that the TG Act applies as if Mr Harding had contravened the provisions in question: TG Act, s 42YC(1)(a) and s 42YC(2).

Maximum Penalty

35 The maximum penalty for a company’s contravention of ss 41MIB(1)(a)(i), 41MIB(1)(a)(iii) or 41MLA(1) of the TG Act is 50,000 penalty units. For an individual, the maximum penalty for contravention of each of those provisions is 5,000 penalty units. The value of a penalty unit at the relevant time (1 July 2020 to 31 December 2022) was $222: Crimes Act 1914 (Cth), s 4AA; Acts Interpretation Act 1901 (Cth), s 2B; and Notice of Indexation of the Penalty Unit Amount (Cth) (14 May 2020). Thus, the maximum penalty for each contravention of the TG Act by Key Promotional was $11,100,000, and for each contravention by Mr Harding was $1,100,000.

Nature and extent of the contraventions (s 42Y(3)(a)) and course of conduct

36 The contraventions of the TG Act were numerous, comprising the importation of 255,000 RATs (s 41MIB(1)(a)(i)), the supply of 240,720 RATs in Australia (s 41MIB(1)(a)(iii)) and the making of 2,303 false or misleading representations that the RATs were a medical device of a kind included in the Register (s 41MLA(1) and s 41MLA(2(a)) of which Mr Harding aided, abetted, counselled or procured 1,183.

37 The Secretary and Mr Harding submit that the maximum penalties available against Key Promotional and Mr Harding are “so large as to have no practical bearing on the appropriate penalties to be finally imposed”. They also submit that “at a minimum” it would be appropriate to treat each type of contravention of the TG Act (import, supply and false or misleading representations) as a course of conduct.

38 The course of conduct principle is a discretionary tool of analysis that may be applied where “there is an interrelationship between the legal and factual elements of two or more offences”, so as to ensure that the offender is not punished twice for what is essentially the same conduct: Construction, Forestry, Mining and Energy Union v Cahill [2010] FCAFC 39; (2010) 194 IR 461 at [39] (Middleton and Gordon J).

39 That interrelationship “may be legal, in the sense that it arises from the elements of the contraventions, or factual, because of a temporal or geographic link or the presence of other circumstances compelling the conclusion that the contraventions arise out of substantially the same act, omission or occurrences”: Coal Mining Industry (Long Service Leave Funding) Corporation v Hitachi Construction Machinery (Australia) Pty Ltd (Penalty) [2023] FCA 1187 at [24] (Raper J), citing Royer v The State of Western Australia [2009] WASCA 139; (2009) 197 A Crim R 319 at [22] (Owens JA).

40 I accept that there is an interrelationship between the legal and factual elements of each of the importations, supplies and representations made by Key Promotional with respect to the RATs, such that it is appropriate to treat each category of contravention of the TG Act as a course of conduct, rather than individual contraventions of the relevant provisions of the TG Act. In the case of import and supply, those contraventions involved the same (or substantially the same) medical device and occurred over a confined period. In the case of the representations, those contraventions were made with respect to the same (or substantially the same) medical device, the representations were of a substantially similar kind and occurred over a confined period. Those same considerations apply to Mr Harding’s aiding, abetting, counselling or procuring of those contraventions.

41 The Secretary and Mr Harding propose further delineated courses of conduct by reference to both the email of 4 January 2022 referred to above, as well as the following emails described in the ASOAF:

21.3. Mr Harding’s emails of 6 and 7 January 2022 that the Company sought a Biosecurity Permit for RATs that were “NOT ARTG approved”, meaning not of a kind included in the Register in relation to the Company nor within any other exclusion in s 41MIB(l)(b) of the Act;

21.4. an email dated 20 January 2022 from Stephanie Golman of Pharma Soul to Mr Harding, in which he was informed that it was “illegal to import and sell” the TSL Tests in Australia because they were neither approved by the TGA nor “approved by Pharma Soul for import”; and

21.5. an email dated 22 January 2022 from sales@testsealabs.com to Mr Harding in response to his request for a manufacturer’s certificate, in which he was advised that “Australia market [sic] is special, you can not import illegally”.

(Emphasis in original; underlining removed)

42 The “TSL Tests” referred to in that extract are diagnostic medical devices for severe acute respiratory syndrome-associated coronavirus, which are manufactured by a company on the Register, including a company identified in the above emails as “Pharma Soul”.

43 The Secretary and Mr Harding contend that, viewed as a course of conduct, and before considering the “totality principle”, the appropriate civil penalties with respect to Mr Harding are as follows:

47.1. in respect of the import of 230,000 tests purchased on or after 5 January 2022: knowledge or gross recklessness as to contravention given the supplier’s 4 January email. $175,000 in relation to the second respondent;

47.2. in respect of supply of the approximately 55,000 tests which were imported / landed on 12 and 20 January 2022 and inferred to have been supplied on or about those dates, with only the knowledge demonstrated by the 4, 6 and 7 January emails: reckless or grossly reckless. $125,000 in respect of the second respondent;

47.3. in respect of the supply of approximately 185,720 Imported Tests from about the date of their arrival on 22 February 2022: Knowledge that these supplies were made in contravention of TG Act following emails of 20 and 22 January 2022. Although the Company had pre-sold those to third parties and received funds, the Company’s decision to continue to supply (rather than cancel and refund the sales) demonstrates prioritisation of at least recouping the Company’s “investment” over compliance with the law and maintaining public safety. $250,000 in relation to the second respondent;

47.4. in relation to 10 individual or group email misrepresentations from 6 January 2022 to 12 January 2022: made directly contrary to Mr Harding's acknowledgement to Department of Agriculture that “NOT ARTG approved”, making these misrepresentations to try and profit or recoup the Company’s investment. $200,000 in respect of the second respondent;

47.5. In relation to 16 individual or group email misrepresentations on 3 March 2022: made with above knowledge and knowledge of later emails. Again, misrepresentations to try and recoup the Company’s investment. $200,000 in respect of the second respondent.

(Emphasis in original; underlining removed)

44 I am not persuaded that it is useful to further delineate the courses of conduct as the Secretary and Mr Harding contend. Mr Harding is taken to have aided, abetted, counselled or procured the contraventions of the TG Act by Key Promotional by reason of his knowledge of the essential matters constituting those contraventions. Mr Harding admits in the ASOAF that he had that knowledge as a consequence of the email of 4 January 2022, by which he was informed that the RATs were medical devices not of a kind included in the Register. I accept those contraventions were serious. I am not satisfied that the emails between 6 and 22 January 2022, as extracted above, compel the conclusion that there should be a further delineation of his conduct on the grounds of seriousness because of an attempt to try and recoup the investment of Key Promotional.

45 The Secretary further submits that viewed as a course of conduct, and before considering the “totality principle”, the appropriate civil penalties with respect to Key Promotional are as follows:

141.1. in respect of the import of 25,000 tests ordered and paid for before 5 January 2022: recklessness as to contravention, although no contravention …: $750,000 against the Company;

141.2. in respect of the import of 230,000 tests purchased on or after 5 January 2022: knowledge of the essential elements, and knowledge or gross recklessness as to contravention given the supplier’s 4 January email. $1.5M Company; and $175,000 in relation to …;

141.3. in respect of supply of the approximately 55,000 tests which were imported / landed on 12 and 20 January 2022 and inferred to have been supplied on or about those dates, with only the knowledge demonstrated by the 4, 6 and 7 January emails: reckless or grossly reckless; $1 M Company, and $125,000 in respect of …;

141.4. in respect of the supply of approximately 185,720 Imported Tests from about the date of their arrival on 22 February 2022: Knowledge that these supplies were made in contravention of TG Act following emails of 20 and 22 January 2022. Although the Company had pre-sold those to third parties and received funds, the Company’s decision to continue to supply (rather than cancel and refund the sales) demonstrates prioritisation of at least recouping the Company’s “investment” over compliance with the law and maintaining public safety. $1.75M Company, and $250,000 in relation to …;

141.5. in relation to 14 individual or group email misrepresentations made prior to 4 January 2022 where there was no contravention by …: $1 million in relation to the Company;

141.6. in relation to 10 individual or group email misrepresentations from 6 January 2022 to 12 January 2022: made directly contrary to … acknowledgement to Department of Agriculture that the Imported Tests were “NOT ARTG approved”, making these misrepresentations to try and profit or recoup the Company’s investment. $1.5M Company, $200,000 in respect of …;

141.7. In relation to 16 individual or group email misrepresentations on 3 March 2022: made with above knowledge and knowledge of later emails. Again, misrepresentations to try and recoup the Company’s investment. $1.5M Company, $200,000 in respect of … .

(Footnotes omitted)

46 I am not persuaded that it is useful to further delineate the courses of conduct as the Secretary proposes. As appears from the declarations with respect to Key Promotional, the only contraventions of the TG Act that occurred prior to 4 January 2022, are the 1,120 false or misleading representations under s 41MLA(1) and s 41MLA(2)(a) between 29 December 2021 and 3 January 2022. There is, therefore, a disconnect between the courses of conduct identified in the extract set out above and the declarations that will be made (eg, with respect to the import of the RATs). That disconnect is understandable because the submissions were filed prior to the hearing, and following the hearing the Secretary filed further submissions seeking alternative dates for the declarations, having regard to the meaning of “import” and “supply”. Nonetheless, it highlights the difficulty in at least two of the further delineated courses of conduct the Secretary contends for (141.1 and 141.2). In any event, the “facts” relied on to support the further delineated courses of conduct in 141.4, 141.6 and 141.7 are not agreed to by Key Promotional in the SOAF. For those reasons, and those otherwise identified above with respect to the emails between 6 and 22 January 2022, I am not persuaded that there is a basis, or it is useful in this instance, to further delineate the course of conduct with respect to the company as the Secretary urges.

47 Irrespective, the contraventions were serious as is underscored by the public health context in which they occurred. Key Promotional did not make a profit from the import and sale of the RATs. Indeed, it is agreed that the company made a financial loss. Nonetheless, the Secretary submits, and I accept, that by their conduct, Key Promotional and Mr Harding attempted to take advantage of a public health emergency for financial gain. Those matters not only call attention to the seriousness of the contraventions, but also highlight the need for general deterrence with respect to such conduct.

Nature and extent of any loss and damage suffered as a result of the contraventions (s 42Y(3)(b))

48 Mr Jenvey gives evidence, based on an examination of the records of the purchase and seizure of the RATs, that their quality, safety and performance has not been established because they were not assessed. Mr Jenvey outlines that the RATs were imported by a Dutch company and at least some of them were labelled as being intended for use in the Netherlands. In addition to the absence of information enabling their assessment and approval, Mr Jenvey emphasises that the actual quality, safety and performance of the tests were not established by the evidence, including whether they were suitable for the Australian climate. At least some of the RATs were also accompanied by instructions for use which recorded them as being for professional (as opposed to public) diagnostic use. Mr Jenvey gives evidence that both these and the other imported RATs gave rise to a “substantial risk of harm” because they did not meet the labelling, ease-of-use and support requirements that were a fundamental feature of the approval of COVID-19 self-tests introduced in November 2021, under the Therapeutic Goods (Medical Devices – Excluded Purposes) Specification 2020 made under s 41BEA of the TG Act. Mr Jenvey further deposes that because the RATs were outside the regulatory regime, the Therapeutic Goods Administration (TGA) was unable to monitor or trace the tests or perform actions such as the recall for sub-standard tests.

49 Mr Harding emphasises, and I accept, that there is no evidence of actual harm resulting from the contraventions of the TG Act by him and Key Promotional. That said, I am persuaded that the potential for risk outlined by Mr Jenvey, specifically with respect to the inability of the TGA to perform its functions in furtherance of the objects of the TG Act with respect to medical devices imported into and supplied in Australia, is a matter that accentuates the need for general deterrence.

Circumstances in which the contraventions took place (s 42Y(3)(c))

50 The facts relevant to this consideration are detailed in those parts of the reasons above dealing with s 42Y(3)(a) and s 42Y(3)(b) of the TG Act. The Secretary submits, and I accept, that the circumstances in which the contraventions took place, that is the COVID-19 pandemic, is a matter that is relevant to both specific and general deterrence. The conduct of Key Promotional and Mr Harding is properly characterised as prioritising financial gain over compliance with the law and maintaining public safety in the context of the COVID-19 pandemic affecting the community.

Whether the person has previously been found to have engaged in similar conduct (s 42Y(3)(d))

51 There is no evidence before me that either Key Promotional or Mr Harding have previously been found by a court in proceedings under the TG Act to have engaged in similar conduct to that considered in this proceeding.

Other considerations

52 Mr Harding and Key Promotional (until its liquidation) have cooperated with the Secretary in the conduct and resolution of this proceeding. It is an agreed fact that Mr Harding is a long-term sufferer of bipolar affective disorder and alcohol use disorder and was suffering acute symptoms in the period shortly prior to the contraventions. I am informed by the parties that this circumstance informed the agreement reached by the Secretary and Mr Harding in proposing the civil penalty to be imposed on Mr Harding, as well as its partial suspension, to which I turn below.

Comparable cases

53 The Secretary, in his written submissions, referred the Court to four other cases involving the imposition of a civil penalty under the TG Act: Secretary, Department of Health and Aged Care v Vapor Kings Pty Ltd [2023] FCA 1297 at [46] (Abraham J); Secretary, Department of Health v Oxymed Australia Pty Ltd [2021] FCA 1518; Evolution Supplements; and Peptide Clinics. As the Secretary submits, none is a true comparator in the sense that there are such similar circumstances that they give me guidance as to penalty: cf, Medtronic Australasia at [131].

Totality principle

54 The Court will generally have regard to the “totality principle” in determining the appropriate penalty for a large number of contraventions: Coal Mining Industry at [27]. This involves a final consideration of whether the cumulative total of the penalty is just and appropriate and not excessive, having regard to the totality of the relevant contravening conduct: Coal Mining Industry at [27], citing Australian Securities and Investments Commission v Westpac Banking Corporation [2019] FCA 2147 at [272], [308] (Wigney J). It is not mandatory to apply the “totality principle” and, if applied, it does not require any effective reduction in penalty: Coal Mining Industry at [27], citing Cahill at [41]-[42] (Middleton and Gordon JJ); Mornington Inn Pty Ltd v Jordan [2008] FCAFC 70; (2008) 168 FCR 383 at [58]-[59] (Stone and Buchanan JJ); and Director, Fair Work Building Industry Inspectorate v Construction, Forestry, Mining and Energy Union [2015] FCAFC 59; (2015) 229 FCR 331 at [40]-[42] (Dowsett, Greenwood and Wigney JJ).

Agreed penalties

55 The penalty is agreed as between the Secretary and Key Promotional and as between the Secretary and Mr Harding. In the case of Key Promotional, that agreement takes the form of the consent given by the liquidator to the proposed penalty. In the case of Mr Harding, that agreement is reflected in the ASOAF.

56 The agreed penalty with respect to:

(a) Key Promotional is $1,750,000, reflecting the highest of the proposed penalties set out at [45] above; and

(b) Mr Harding is $250,000, reflecting the highest of the proposed penalties set out at [43] above. It is proposed that $70,000 of that penalty be suspended on the condition Mr Harding does not commit any further civil penalty contravention or offence against the TG Act for a period of 10 years. An order is sought that the pecuniary penalty be paid within 21 days of the date of the Orders I make today.

57 It seems to me that the proposed penalties as agreed are suitable, having regard to the totality of the conduct, the significance of the contraventions by Key Promotional and Mr Harding, as well as the considerations prescribed by the TG Act, and otherwise detailed above. Insofar as it concerns the suspension of part of the penalty proposed for Mr Harding, I am satisfied that I have the power to make that order and that in the circumstances described under the heading “other considerations” it is appropriate to do so: Vapor Kings at [46].

disposition

58 For all of the above reasons, I am prepared to make the following orders:

7. Pursuant to s 42Y(2) of the TG Act, Key Promotional pay a pecuniary penalty to the Commonwealth of $1,750,000 in respect of the contraventions that it committed.

8. Pursuant to s 42Y(2) of the TG Act, Mr Harding pay a pecuniary penalty to the Commonwealth of $250,000 in respect of the contraventions that he committed, within 21 days of the date of these Orders, subject to order 9(a) below.

9. In respect of the penalty against Mr Harding:

(a) $70,000 of that penalty is suspended on the condition that Mr Harding does not commit any further civil penalty contravention under, or any offence against, any provision of the TG Act for a period of 10 years from the date of these Orders; and

(b) if there is no such contravention or offence by Mr Harding, enforcement of the suspended amount shall be permanently stayed.

costs

59 The Secretary seeks an order that Key Promotional and Mr Harding pay a proportion of his costs on a lump sum basis. Mr Harding has agreed to a lump sum costs order against him in the amount of $40,000. The Secretary seeks a lump sum costs order of $60,000 against Key Promotional. As the solicitor for the Secretary (Mr Howard Rapke) acknowledges in his affidavit dated 15 September 2025, it is not clear from the correspondence with Mr Bookless whether the liquidator has agreed to the costs order. In any event, the Secretary has filed a further affidavit from Mr Rapke dated 15 September 2025, which addresses the matters required by Practice Note GPN-COSTS in support of a lump sum costs order sought against each of Key Promotional and Mr Harding, including relevantly, how the lump sum has been calculated: cf, Practice Note GPN-COSTS at [4.10]; see also, Federal Court Rules 2011 (Cth), r 40.02(b).

60 The Court has a broad discretion to award costs under s 43(1) of the Federal Court Act. Ordinarily, a successful party is entitled to an award of costs in its favour in the absence of special circumstances that would justify some other order: Ruddock v Vadarlis (No 2) [2001] FCA 1865; (2001) 115 FCR 229 at [11] (Black CJ and French J). The general rule assumes that where an applicant succeeds in a proceeding, it will have incurred costs because the respondent’s conduct made it necessary for the applicant to bring the proceeding: Ruddock at [12].

61 I am satisfied that there are no special circumstances that would justify a departure from the ordinary position that costs follow the event. In light of the matters Mr Rapke deposes to, I am also persuaded that it is appropriate to make a lump sum costs order in the terms sought by the Secretary.

I certify that the preceding sixty-one (61) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Longbottom. |

Associate:

Dated: 30 April 2026

ANNEXURE A

Statement of Agreed Facts and Issues

ANNEXURE B

Amended Statement of Agreed Facts and Issues

ANNEXURE C

Email Representations