FEDERAL COURT OF AUSTRALIA

Australian Securities and Investments Commission v Nuix Limited, in the matter of Nuix Limited [2026] FCA 490

File number(s): | NSD 827 of 2022 |

Judgment of: | GOODMAN J |

Date of judgment: | 23 April 2026 |

Catchwords: | MISLEADING OR DECEPTIVE CONDUCT – whether the first defendant (Nuix Limited) engaged in misleading or deceptive conduct in contravention of s 1041H(1) of the Corporations Act 2001 (Cth) or s 12DA(1) of the Australian Securities and Investments Commission Act 2001 (Cth) (ASIC Act) in making announcements to the Australian Securities Exchange (ASX) or by failing to disclose particular information to the ASX in connection with its financial performance – whether, for the information not disclosed, there was a reasonable expectation of disclosure of that information – held: no contravention established CORPORATIONS – continuous disclosure – whether Nuix contravened s 674(2) of the Corporations Act by not disclosing particular information to the ASX – whether the information was information to which Listing Rule 3.1 of the ASX Listing Rules applied – whether the exception in Listing Rule 3.1A applied – held: no contravention established DIRECTORS’ DUTIES – alleged contraventions of s 180 of the Corporations Act by each of the directors of Nuix – case dependent upon establishment of contravention of the Corporations Act or ASIC Act by Nuix – no contravention by Nuix established – held: case dismissed |

Legislation: | Australian Securities and Investments Commission Act 2001 (Cth), ss 12BB, 12DA Competition and Consumer Act 2010 (Cth), Sch 2, s 18 Corporations Act 2001 (Cth), ss 9, 180, 674, 676, 677, 769C, 1041H, 1362A Corporations (Coronavirus Economic Response) Determination (No. 2) 2020 (Cth) Corporations (Coronavirus Economic Response) Determination (No. 4) 2020 (Cth) Trade Practices Act 1974 (Cth), s 51A |

Cases cited: | Addenbrooke Pty Ltd (ACN 055 973 576) v Duncan (No 2) [2017] FCAFC 76; (2017) 348 ALR 1 Australian Competition & Consumer Commission v Dateline Imports Pty Ltd [2015] FCAFC 114 Australian Competition and Consumer Commission v Jones (No 5) [2011] FCA 49 Australian Competition and Consumer Commission v Mazda Australia Pty Limited [2023] FCAFC 45 Australian Securities and Investments Commission v Diversa Trustees Limited [2023] FCA 1267 Australian Securities and Investments Commission v Rich [2009] NSWSC 1229; (2009) 75 ACSR 1 Bonham (as trustee for the Aucham Super Fund) v Iluka Resources Ltd [2022] FCA 71; (2022) 404 ALR 15 Crowley v Worley Ltd [2022] FCAFC 33; (2022) 293 FCR 438 Cruikshank v Australian Securities and Investments Commission [2022] FCAFC 128; (2022) 292 FCR 627 Elanor Funds Management Ltd (ACN 125 903 031) v Alceon Group Pty Ltd (ACN 122 365 986) [2024] FCAFC 121; (2024) 424 ALR 601 George v Rockett [1990] HCA 26; (1990) 170 CLR 104 Masters v Lombe (in his capacity as liquidator of Babcock & Brown Ltd (in liq) (ACN 108 614 955) [2021] FCAFC 161; (2021) 392 ALR 326 Parkdale Custom Built Furniture Proprietary Limited v Puxu Proprietary Limited [1982] HCA 44; (1982) 149 CLR 191 Self Care IP Holdings Pty Ltd v Allergan Australia Pty Ltd [2023] HCA 8; (2023) 277 CLR 186 Sykes v Reserve Bank of Australia [1998] FCA 1405; (1998) 88 FCR 511 TPT Patrol Pty Ltd v Myer Holdings Ltd [2019] FCA 1747; (2019) 293 FCR 29 |

Division: | General Division |

Registry: | New South Wales |

National Practice Area: | Commercial and Corporations |

Sub-area: | Regulator and Consumer Protection |

Number of paragraphs: | 956 |

Date of hearing: | 20-24, 27-30 November and 5, 8 and 11-15 December 2023 |

Counsel for the Plaintiff: | Mr J Giles SC with Mr J Hewitt SC and Ms B Ng |

Solicitor for the Plaintiff: | Minter Ellison |

Counsel for the First Defendant: | Mr M J Darke SC with Mr J Entwisle |

Solicitor for the First Defendant: | Gilbert and Tobin |

Counsel for the Second Defendant: | Mr D F C Thomas SC with Ms M Ellicott |

Solicitor for the Second Defendant: | Corrs Chambers Westgarth |

Counsel for the Third and Fourth Defendants: | Mr N C Hutley SC with Ms A Zheng |

Solicitor for the Third and Fourth Defendants: | Jones Day |

Counsel for the Fifth Defendant: | Mr P M Knowles SC with Ms E Steer |

Solicitor for the Fifth Defendant: | MBC Lawyers Pty Ltd |

Counsel for the Sixth Defendant: | Mr D Roche SC with Ms K Dyon |

Solicitor for the Sixth Defendant: | Horton Rhodes Legal Pty Ltd |

ORDERS

NSD 827 of 2022 | ||

IN THE MATTER OF NUIX LIMITED | ||

BETWEEN: | AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff | |

AND: | NUIX LIMITED ACN 117 140 235 First Defendant RODNEY GRAHAM VAWDREY Second Defendant JEFFREY LAURENCE BLEICH (and others named in the Schedule) Third Defendant | |

order made by: | GOODMAN J |

DATE OF ORDER: | 23 april 2026 |

THE COURT ORDERS THAT:

1. The originating process filed on 28 September 2022 be dismissed.

2. Subject to order 3, the plaintiff pay the defendants’ costs of the proceeding, as agreed or taxed.

3. Any party seeking a different costs order is to notify the Associate to Goodman J within 21 days of the date of these orders.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

GOODMAN J

A. INTRODUCTION

1 The first defendant, Nuix, is an Australian based company in the business of providing investigative analytics and intelligence software to customers worldwide.

2 On 18 November 2020, Nuix issued a prospectus for an initial public offering (IPO) of its shares. The prospectus contained, relevantly, two forecasts (Prospectus Forecasts), being forecasts that Nuix’s:

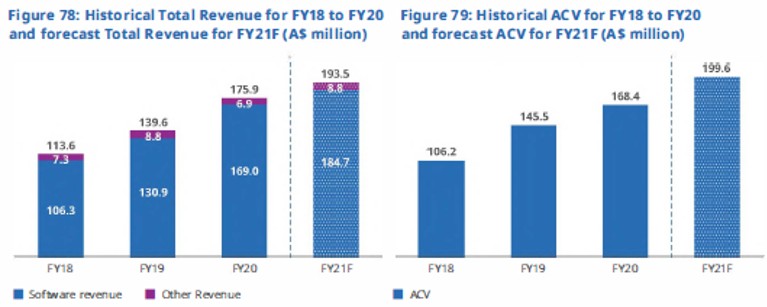

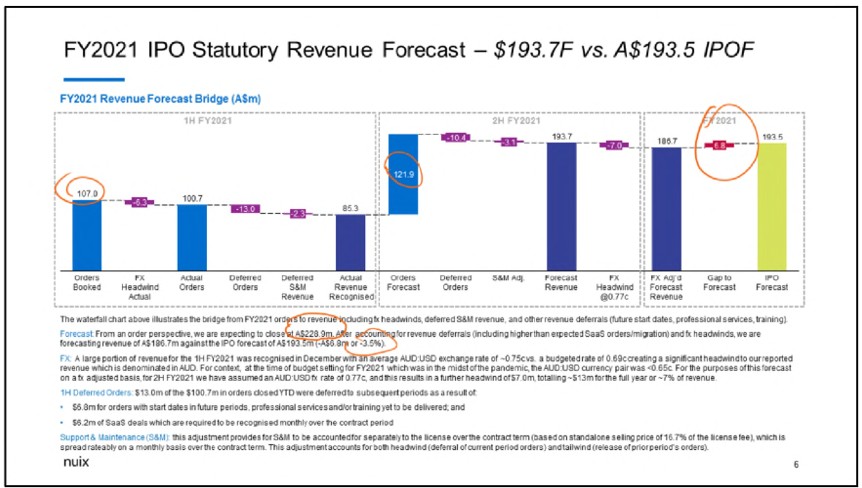

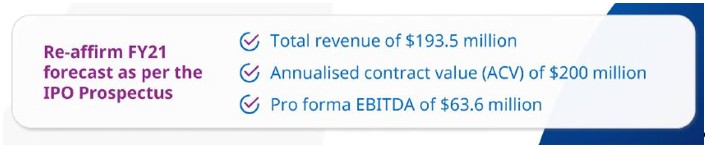

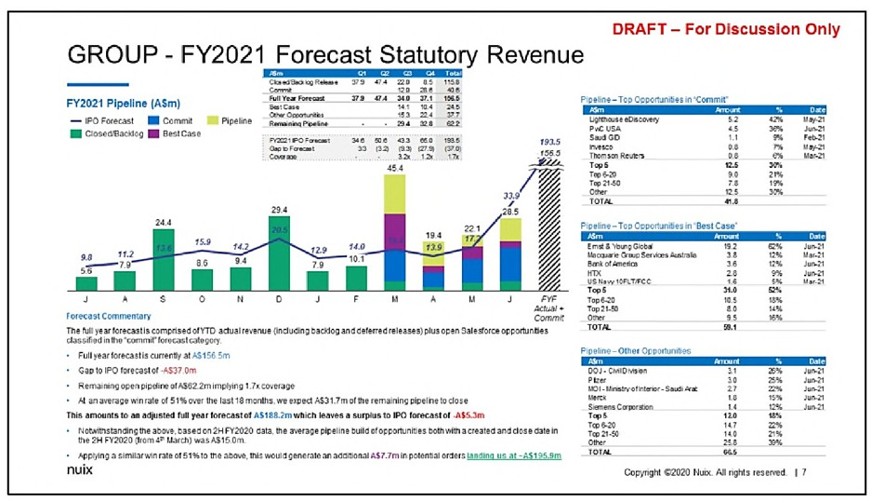

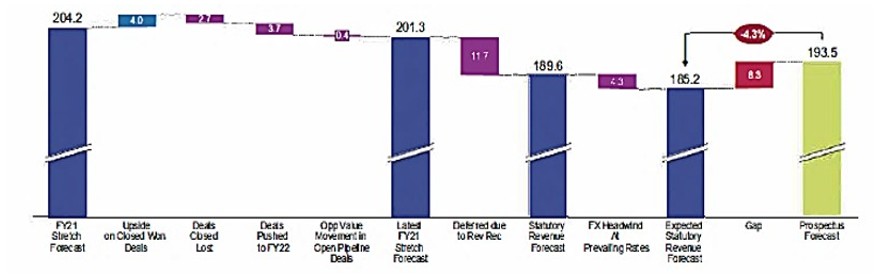

(1) revenue for the year ended 30 June 2021 (FY21) would be $193.5 million (Prospectus Revenue Forecast); and

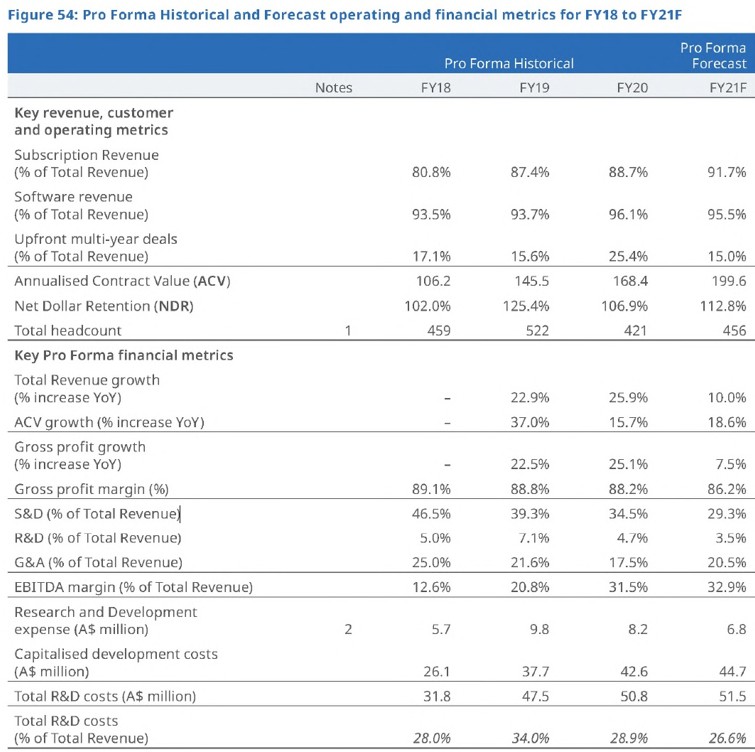

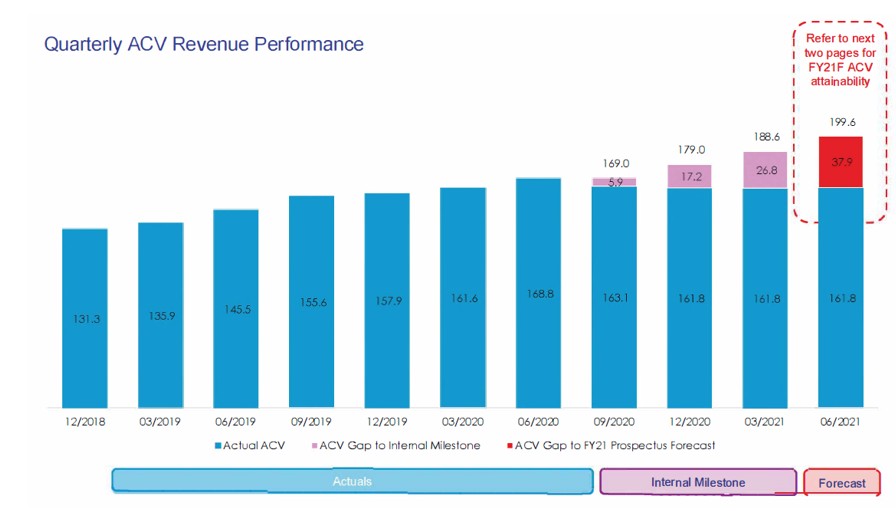

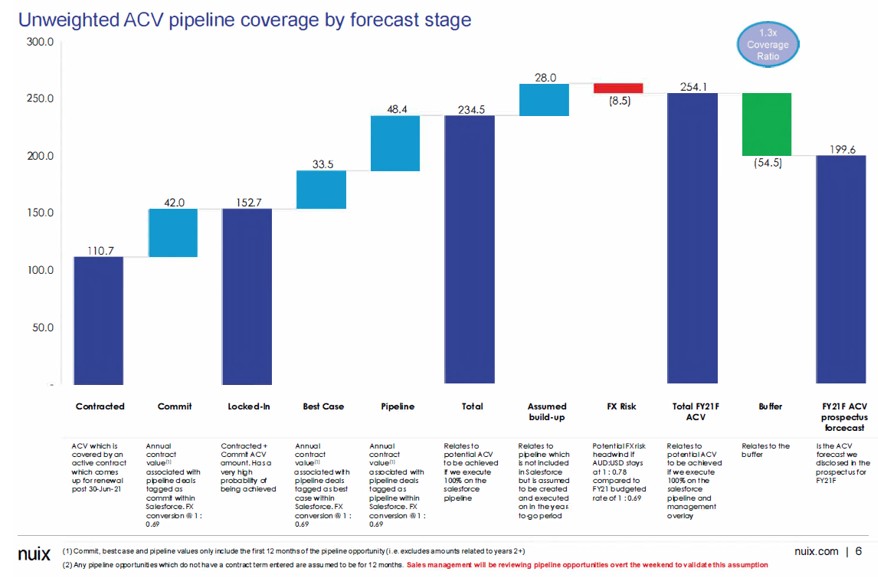

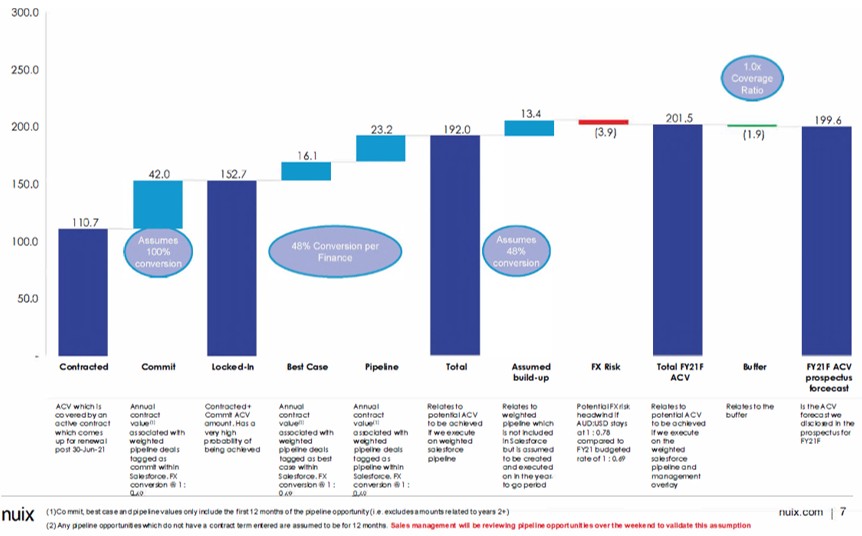

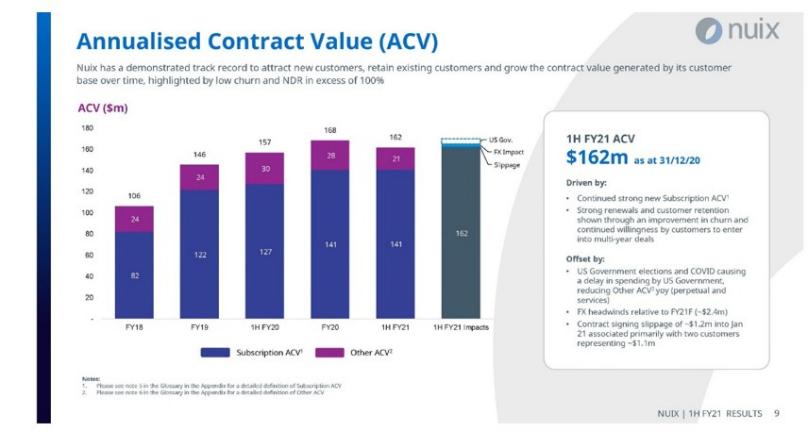

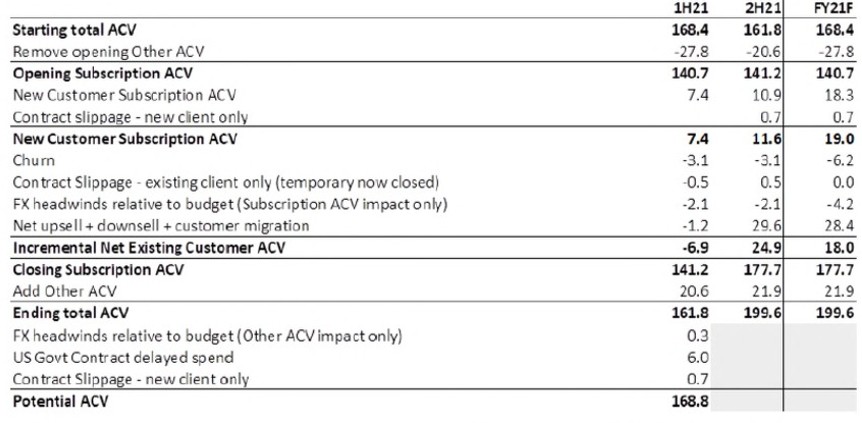

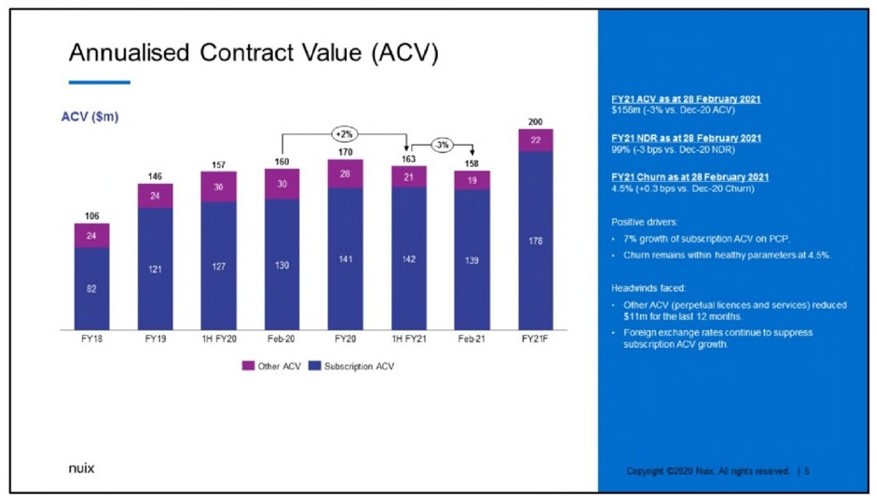

(2) annualised contract value (ACV) as at 30 June 2021 would be $199.6 million (Prospectus ACV Forecast). ACV is a financial metric used by Nuix which is explained in some detail below.

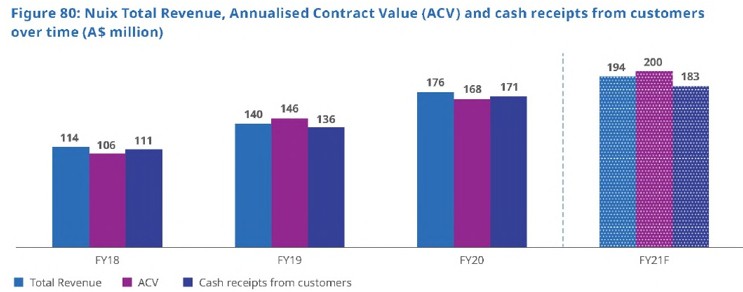

3 In the six months or so which followed, Nuix released three sets of announcements to the Australian Securities Exchange Limited (ASX). In the first two – the 26 February ASX Announcements and the 8 March ASX Announcement, Nuix re-affirmed both the Prospectus Revenue Forecast and the Prospectus ACV Forecast. In the third – the 21 April ASX Announcement – Nuix downgraded its revenue forecast for FY21 from $193.5 million to a range of $180 to $185 million. The 21 April ASX Announcement also conveyed a revised forecast of ACV as at 30 June 2021 in the range of $168 to $177 million.

4 The plaintiff (ASIC) alleges that during the period from 18 January to 21 April 2021 (relevant period) Nuix:

(1) engaged in misleading or deceptive conduct in contravention of s 1041H(1) of the Corporations Act 2001 (Cth) and s 12DA(1) of the Australian Securities and Investments Commission Act 2001 (Cth) (ASIC Act) by making the 26 February and 8 March ASX Announcements and by failing to disclose particular information to the ASX; and

(2) contravened s 674(2) of the Corporations Act by failing to disclose particular information to the ASX.

5 ASIC also alleges that each of the directors of Nuix during the relevant period – Mr Rodney Vawdrey (Nuix’s Chief Executive Officer (CEO) and its only executive director), Mr Jeffrey Bleich, Sir Iain Lobban, Mr Daniel Phillips and Ms Susan Thomas – contravened s 180 of the Corporations Act by failing to exercise the degree of care and diligence that a reasonable person acting as a director of a company in Nuix’s circumstances would have exercised.

6 ASIC seeks a range of relief including:

(1) declarations that Nuix contravened:

(a) ss 674(2) and 1041H(1) of the Corporations Act;

(b) s 12DA(1) of the ASIC Act;

(2) declarations that the directors of Nuix each contravened s 180 of the Corporations Act;

(3) an order for the imposition of pecuniary penalties upon Nuix for each contravention of s 674(2) of the Corporations Act;

(4) orders for the imposition of pecuniary penalties upon each of the directors of Nuix for each contravention of s 180 of the Corporations Act; and

(5) orders for the disqualification of each director from managing corporations.

7 The defendants were pellucid and unwavering in their stance that they were defending the proceeding on the basis of the case as pleaded and did not agree to any departure from that case.

8 The observations of Button J in Australian Securities and Investments Commission v Diversa Trustees Limited [2023] FCA 1267 at [13] to [16] are apposite:

13 Pursuit of a civil penalty case is not without consequence. The authorities recognise that pursuit of such proceedings has consequences in a number of areas: the framing and specificity of the allegations advanced; the nature of the proof required to make out the case; and the approach to be adopted in construing legislation.

14 A civil penalty proceeding of this kind is a serious kind of case, bearing a penal nature: Naismith v McGovern (1953) 90 CLR 336 at 341. To adopt observations made by the Full Court (Logan, Bromberg and Katzmann JJ) in Construction, Forestry, Mining and Energy Union v BHP Coal Pty Ltd (2015) 230 FCR 298 (BHP Coal) at [63], albeit in the context of the Fair Work Act 2009 (Cth), “[i]n this class of case, it is especially important that those accused of a contravention know with some precision the case to be made against them. Procedural fairness demands no less”. In a civil penalty proceeding, it is incumbent on the regulator to be clear and consistent regarding the allegations made; a “clear and tolerably stable body of allegations of contraventions of law” is required: Federal Commissioner of Taxation v Ludekens (2013) 214 FCR 149 (Ludekens) at [20]. It is not appropriate for the regulator to plant “a forest of forensic contingencies”, or to alter the basis of the allegation of the alleged contraventions on a rolling basis in the leadup to, and during, the trial: see Ludekens at [20] (Allsop CJ, Gilmour and Gordon JJ).

15 Civil penalty proceedings generally involve allegations of some gravity. ... The gravity of the allegations involved is reflected in the application of the civil burden of proof: Briginshaw v Briginshaw (1938) 60 CLR 336 (Briginshaw) at 362 (Dixon J); Australian Securities and Investments Commission v Westpac Banking Corporation [2019] FCA 2147 at [225] (Wigney J). As stated by the Full Court (Logan, Bromberg and Katzmann JJ) in BHP Coal at [63] (quoting Dixon J in Briginshaw), “where … the resolution of an issue exposes a respondent to a penalty, satisfaction on the balance of probabilities is not achieved by ‘inexact proofs, indefinite testimony, or indirect inferences’”. The conclusions I set out below do not depend on the application of any elevated standard of proof but, naturally, application of an elevated standard would only reinforce those conclusions.

16 ASIC’s pursuit of a civil penalty case also brings with it the need to construe the legislation in question having regard to its penal character, and to exercise caution before accepting any “loose, albeit ‘practical’, construction”: Stevens v Kabushiki Kaisha Sony Computer Entertainment (2005) 224 CLR 193 at [45] (Gleeson CJ, Gummow, Hayne and Heydon JJ); see also Australian Competition and Consumer Commission v Quantum Housing Group Pty Ltd (2021) 285 FCR 133 at [88] (Allsop CJ, Besanko and McKerracher JJ); Paccioco v Australia and New Zealand Banking Group Ltd (2015) 236 FCR 199 at [300] (Allsop CJ, with whom Besanko J and Middleton J agreed). Precision of the kind referred to by Moshinsky J in Australian Securities and Investments Commission v RI Advice Group Pty Ltd (No 2) (2021) 156 ACSR 371; [2021] FCA 877 (RI Advice) at [410]–[411] is also of particular importance in civil penalty proceedings.

(bold and italic emphasis in original)

9 The analysis undertaken in these reasons for judgment addresses the case as pleaded.

10 It has taken some time to finalise these reasons for judgment. I commenced writing them during the course of the hearing. The writing continued thereafter, with the assistance of the written submissions filed by the parties (in excess of 1,000 pages) and by reference to the evidence (in excess of 11,000 pages). The writing was interrupted from time to time by the demands of other cases that had to be addressed. Nevertheless, I apologise to the parties for the time taken to complete these reasons.

B. THE LEGAL AND REGULATORY FRAMEWORK

11 I turn now to consider the legal and regulatory framework within which ASIC’s allegations fall to be assessed.

B.1 Introduction

12 As noted above, ASIC alleges that Nuix:

(1) engaged in misleading or deceptive conduct in contravention of:

(a) s 1041H(1) of the Corporations Act;

(b) s 12DA(1) of the ASIC Act; and

(2) failed to disclose information to the ASX, in contravention of s 674(2) of the Corporations Act.

B.2 Statutory provisions concerning misleading or deceptive conduct

13 ASIC relies upon the following statutory provisions for its misleading or deceptive conduct case:

(1) s 1041H(1) of the Corporations Act which provided that:

A person must not, in this jurisdiction, engage in conduct, in relation to a financial product or a financial service, that is misleading or deceptive or is likely to mislead or deceive.

(2) s 12DA(1) of the ASIC Act which provided that:

A person must not, in trade or commerce, engage in conduct in relation to financial services that is misleading or deceptive or is likely to mislead or deceive.

14 It is common ground between ASIC and Nuix in respect of the conduct the subject of ASIC’s allegations that:

(1) Nuix was required to comply with s 1041H(1) of the Corporations Act and s 12DA(1) of the ASIC Act; and

(2) the impugned conduct to the extent that it occurred, occurred “in relation to a financial product or a financial service” (for s 1041H(1)) and “in trade or commerce” and “in relation to financial services” (for s 12DA(1)).

15 Where ASIC alleges that Nuix’s conduct involved representations as to future matters (Part F below), it also relies upon:

(1) s 769C of the Corporations Act, which provided:

769C Representations about future matters taken to be misleading if made without reasonable grounds

(1) For the purposes of this Chapter, or of a proceeding under this Chapter, if:

(a) a person makes a representation with respect to any future matter (including the doing of, or refusing to do, any act); and

(b) the person does not have reasonable grounds for making the representation;

the representation is taken to be misleading.

(2) Subsection (1) does not limit the circumstances in which a representation may be misleading.

(3) In this section:

proceeding under this Chapter has the same meaning as it has in section 769B. ; and

(bold and italic emphasis in original)

(2) s 12BB of the ASIC Act, which provided:

12BB Misleading representations with respect to future matters

(1) If:

(a) a person makes a representation with respect to any future matter (including the doing of, or the refusing to do, any act); and

(b) the person does not have reasonable grounds for making the representation;

the representation is taken, for the purposes of Subdivision D (sections 12DA to 12DN), to be misleading.

(2) For the purposes of applying subsection (1) in relation to a proceeding concerning a representation made with respect to a future matter by:

(a) a party to the proceeding; or

(b) any other person;

the party or other person is taken not to have had reasonable grounds for making the representation, unless evidence is adduced to the contrary.

(3) To avoid doubt, subsection (2) does not:

(a) have the effect that, merely because such evidence to the contrary is adduced, the person who made the representation is taken to have had reasonable grounds for making the representation; or

(b) have the effect of placing on any person an onus of proving that the person who made the representation had reasonable grounds for making the representation.

(4) Subsection (1) does not by implication limit the meaning of a reference in this Division to:

(a) a misleading representation; or

(b) a representation that is misleading in a material particular; or

(c) conduct that is misleading or is likely or liable to mislead;

and, in particular, does not imply that a representation that a person makes with respect to any future matter is not misleading merely because the person has reasonable grounds for making the representation.

(bold and italic emphasis in original)

B.3 Statutory provisions concerning continuous disclosure

16 As noted above, ASIC alleges that Nuix contravened s 674(2) of the Corporations Act.

17 During the relevant period, that section imposed disclosure obligations upon each “listed disclosing entity”, such as Nuix.

18 However, the operation of s 674 of the Corporations Act was affected by the legislative response to the COVID-19 pandemic and, in particular, the Corporations (Coronavirus Economic Response) Determination (No. 2) 2020 (Cth), which was made pursuant to s 1362A of the Corporations Act on 25 May 2020 and extended by the Corporations (Coronavirus Economic Response) Determination (No. 4) 2020 (Cth) on 22 September 2020 (together, the Determinations). The latter Determination ceased to operate with effect from 23 March 2021.

19 As a result of the Determinations, s 674 of the Corporations Act is to be read as follows:

(1) during the period from 18 January 2021 (being the commencement of the relevant period) until 22 March 2021:

674 Continuous disclosure—listed disclosing entity bound by a disclosure requirement in market listing rules

Obligation to disclose in accordance with listing rules

(1) Subsection (2) applies to a listed disclosing entity if provisions of the listing rules of a listing market in relation to that entity require the entity to notify the market operator of information about specified events or matters as they arise for the purpose of the operator making that information available to participants in the market.

(2) If:

(a) this subsection applies to a listed disclosing entity; and

(b) the entity has information that those provisions require the entity to notify to the market operator; and

(c) that information is not generally available; and

(d) the entity knows or is reckless or negligent with respect to whether that information would, if it were generally available, have a material effect on the price or value of ED securities of the entity;

the entity must notify the market operator of that information in accordance with those provisions.

...

(bold and italic emphasis in original)

(2) from 23 March 2021:

674 Continuous disclosure—listed disclosing entity bound by a disclosure requirement in market listing rules

Obligation to disclose in accordance with listing rules

(1) Subsection (2) applies to a listed disclosing entity if provisions of the listing rules of a listing market in relation to that entity require the entity to notify the market operator of information about specified events or matters as they arise for the purpose of the operator making that information available to participants in the market.

(2) If:

(a) this subsection applies to a listed disclosing entity; and

(b) the entity has information that those provisions require the entity to notify to the market operator; and

(c) that information:

(i) is not generally available; and

(ii) is information that a reasonable person would expect, if it were generally available, to have a material effect on the price or value of ED securities of the entity;

the entity must notify the market operator of that information in accordance with those provisions.

...

(bold and italic emphasis in original)

20 It is common ground as between ASIC and Nuix that during the relevant period Nuix was required to comply with s 674(2) of the Corporations Act and that the shares in Nuix were “ED securities” of Nuix.

21 As is apparent, the effect of the Determinations was to introduce into s 674 of the Corporations Act a fault element (recklessness or negligence) which was operative from (relevantly) 18 January 2021 until 22 March 2021. Only negligence is presently relevant.

22 Throughout the relevant period, section 676 of the Corporations Act provided as follows:

676 Sections 674 and 675 – when information is generally available

(1) This section has effect for the purposes of sections 674 and 675.

(2) Information is generally available if:

(a) it consists of readily observable matter; or

(b) without limiting the generality of paragraph (a), both of the following subparagraphs apply:

(i) it has been made known in a manner that would, or would be likely to, bring it to the attention of persons who commonly invest in securities of a kind whose price or value might be affected by the information; and

(ii) since it was so made known, a reasonable period for it to be disseminated among such persons has elapsed.

(3) Information is also generally available if it consists of deductions, conclusions or inferences made or drawn from either or both of the following:

(a) information referred to in paragraph (2)(a);

(b) information made known as mentioned in subparagraph (2)(b)(i).

(bold emphasis in original)

23 Section 677 of the Corporations Act was also affected by the Determinations. The effect of the Determinations upon s 677 is that it is to be read as follows:

(1) from 18 January 2021 until 22 March 2021:

677 Sections 674 and 675—material effect on price or value

For the purposes of sections 674 and 675, an entity knows or is reckless or negligent with respect to whether information would have a material effect on the price or value of ED securities of the entity if the entity knows or is reckless or negligent with respect to whether the information would, or would be likely to, influence persons who commonly invest in securities in deciding whether to acquire or dispose of the ED securities.

(bold emphasis in original)

(2) from 23 March 2021:

677 Sections 674 and 675—material effect on price or value

For the purposes of sections 674 and 675, a reasonable person would be taken to expect information to have a material effect on the price or value of ED securities of a disclosing entity if the information would, or would be likely to, influence persons who commonly invest in securities in deciding whether to acquire or dispose of the ED securities.

(bold emphasis in original)

B.4 The Listing Rules

24 Throughout the relevant period, s 674(1) of the Corporations Act provided that s 674(2) of that Act applied to a listed disclosing entity such as Nuix if “provisions of the listing rules of a listing market in relation to that entity [required] the entity to notify the market operator of information about specified events or matters as they [arose] for the purpose of the operator making that information available to participants in the market”.

25 The Listing Rules published by the ASX imposed such a requirement upon Nuix. Of central relevance are Listing Rules 3.1 and 3.1A:

Immediate notice of material information

General rule

3.1 Once an entity is or becomes aware of any information concerning it that a reasonable person would expect to have a material effect on the price or value of the entity’s securities, the entity must immediately tell ASX that information.

Exception to rule 3.1

3.1A Listing rule 3.1 does not apply to particular information while each of the following requirements is satisfied in relation to the information:

3.1A.1 One or more of the following 5 situations applies:

• It would be a breach of a law to disclose the information;

• The information concerns an incomplete proposal or negotiation;

• The information comprises matters of supposition or is insufficiently definite to warrant disclosure;

• The information is generated for the internal management purposes of the entity; or

• The information is a trade secret; and

3.1A.2 The information is confidential and ASX has not formed the view that the information has ceased to be confidential; and

3.1A.3 A reasonable person would not expect the information to be disclosed.

(bold emphasis in original)

26 Other relevant parts of the Listing Rules are as follows.

27 Listing Rule 19 addressed the interpretation of the Listing Rules and provided, relevantly:

Principles on which the listing rules are based

19.1 The listing rules are based on the principles set out in the Introduction.

Entity must comply with spirit, intention and purpose etc of rules

19.2 An entity must comply with the listing rules as interpreted:

• in accordance with their spirit, intention and purpose;

• by looking beyond form to substance; and

• in a way that best promotes the principles on which the listing rules are based.

…

General principles of interpretation

19.3 In these rules unless the context otherwise requires:

(a) Expressions that are not specifically defined in the listing rules, but are given a particular meaning in the Corporations Act, have the same meaning in the listing rules.

…

Definitions

19.12 The following expressions have the meanings set out below.

…

aware an entity becomes aware of information if, and as soon as, an officer of the entity ... has, or ought reasonably to have, come into possession of the information in the course of the performance of their duties as an officer of that entity.

…

information for the purposes of Listing Rules 3.1 3.1B (sic), information includes:

(a) matters of supposition and other matters that are insufficiently definite to warrant disclosure to the market; and

(b) matters relating to the intentions, or likely intentions, of a person.

…

(bold emphasis in original)

28 The Introduction to the Listing Rules (which is referred to in Listing Rule 19.1) included:

The principles on which the Listing Rules are based

The Listing Rules serve the interests of listed entities and investors, both of whom have a vital interest in maintaining the reputation and integrity of the ASX market and ensuring that it is internationally competitive and facilitates efficient capital raising.

The principles which underpin the obligations imposed on listed entities by the Listing Rules include:

…

• Timely disclosure should be made of information which may have a material effect on the price or value of an entity’s +securities.

…

B.5 Guidance Note 8

29 An important part of the regulatory framework is Guidance Note 8, which was republished by the ASX on 9 December 2020.

30 The purpose of Guidance Note 8 is described therein as being to assist listed entities to understand and comply with the continuous disclosure obligations under, inter alia, Listing Rules 3.1 and 3.1A (at [1]).

31 Paragraph [4] of Guidance Note 8 deals with the obligation to disclose “market sensitive information” immediately. The expression “market sensitive information” is used in Guidance Note 8 to describe information concerning an entity that “a reasonable person would expect to have a material effect on price or value of the entity’s securities”([4.1]).

32 At paragraph [4.2], it is noted that the test to determine whether information is market sensitive and thus needs to be disclosed under Listing Rule 3.1 is set out in s 677 of the Corporations Act. Under that section a reasonable person is taken to expect information to have a material effect on the price or value of an entity’s securities if that information “would, or would be likely to, influence persons who commonly invest in securities in deciding whether to acquire or dispose of” the entity’s securities. It is noted that this test is an objective one and this may give rise to inevitable practical difficulties because entities are effectively required to predict how investors will react to particular information when it is disclosed. It is also noted that entities may find “the 5/10% parameters mentioned [at paragraph 8.7] below that ASX uses for determining whether or not to refer a potential breach of Listing Rule 3.1 to ASIC helpful in understanding the order of magnitude of the likely change in price or value of their securities that ASX considers will trigger a disclosure obligation under Listing Rule 3.1”.

33 At paragraph [4.3], it is noted that in making an assessment as to whether or not information is market sensitive and thus needs to be disclosed, the information in question needs to be looked at in context.

34 Paragraph [4.4] addresses the question: “[w]hen does an entity become aware of information?”.

35 Paragraph [4.5] deals with the meaning of the word “immediately” in Listing Rule 3.1. It provides:

Under Listing Rule 3.1, market sensitive information must be disclosed to ASX immediately upon the entity becoming aware of the information, unless it falls within the carve-outs from disclosure in Listing Rule 3.1A.

Judicial authority in analogous situations confirms that the word “immediately” should not be read as meaning “instantaneously”, but rather as meaning “promptly and without delay”:

“The words forthwith and immediately have the same meaning. They are stronger than the expression within a reasonable time, and imply prompt, vigorous action, without any delay, and whether there has been such action is a question of fact, having regard to the circumstances of the particular case.”

Doing something “promptly and without delay’’ means doing it as quickly as it can be done in the circumstances (acting promptly) and not deferring, postponing or putting it off to a later time (acting without delay).

A period of time will necessarily pass between when an entity first becomes obliged to give information to ASX under Listing Rule 3.1 and when it is able to give that information to ASX in the form of a market announcement. This passing of time, of itself, does not mean that there has been a “delay” in the provision of the information to ASX. Some announcements may be able to be prepared and given to ASX relatively quickly, while others may take longer to complete. The question is (sic) each case is whether the entity is going about this process as quickly as it can in the circumstances and not deferring, postponing or putting it off to a later time.

ASX recognises that how quickly an entity can give an announcement of particular information to ASX will be dictated by the circumstances confronting it at the time. Relevant factors may include:

• where and when the information originated;

• the forewarning (if any) the entity had of the information;

• the amount and complexity of the information concerned;

• the need in some cases to verify the accuracy or bona fides of the information;

• the need for an announcement to be carefully drawn so that it is accurate, complete and not misleading;

…

• the need in some cases for an announcement to be approved by the entity’s board or disclosure committee.

ASX will take these factors into account in assessing whether an entity has complied with its obligation to disclose information under Listing Rule 3.1 promptly and without delay.

…

ASX will expect an entity to act particularly quickly if ASX asks it to make an announcement under Listing Rule 3.1B because of a sudden and significant movement in the market price or traded volumes of its securities or otherwise to correct or prevent a false market in its securities. In such cases, if the entity is not in a position to issue its announcement to the market straight away, ASX will generally expect it to request a trading halt.

ASX will also expect an entity to act particularly quickly if the information to be announced is especially damaging and likely to cause a significant fall in the market price of the entity’s securities (eg, information that the board of the entity has resolved to appoint an administrator or that a lender has declared an event of default and appointed a receiver). Again, in such a case, if the entity is not in a position to issue its announcement to the market straight away, ASX will generally expect the entity to request a trading halt.

Given the requirement in Listing Rule 3.1 for immediate disclosure and the significant legal and financial consequences that can follow from a breach of that rule, it is important that entities have in place appropriate compliance systems to ensure that information which is potentially market sensitive is promptly assessed to determine whether it requires disclosure under that rule and, if it does, that it is promptly given to ASX.

...

(italic and underline emphasis in original; bold emphasis added; footnotes omitted)

36 Paragraph [4.8] addresses the question: “[d]oes the board need to approve an announcement under Listing Rule 3.1?”. It includes:

The courts have acknowledged that it is appropriate for some particularly significant continuous disclosure announcements to be considered and approved by the board of directors of an entity before they are released. They have also made it clear, however, that this is not legally necessary in all cases.

Given the requirement for announcements under Listing Rule 3.1 to be issued immediately, an entity should have suitable arrangements in place to enable this to occur. Such arrangements may include giving appropriate delegations to senior management to release some announcements of their own accord and, if the matter falls outside those delegations, having a disclosure committee that can meet by phone or on short notice to consider the announcement.

Where an entity considers an announcement to be so significant that it ought to be approved by its full board before release, it needs to think carefully about how it will manage its disclosure obligations. This will require a close consideration of the nature of the information to be disclosed, the applicability of the exceptions in Listing Rule 3.1A and whether the circumstances warrant requesting a trading halt.

Where it is the decision of the board itself that is the information to be disclosed under Listing Rule 3.1 (such as a decision by the board to declare a dividend, to implement a scheme of arrangement or to appoint an administrator), the obligation to disclose generally will not arise until the board has made that decision. It usually will not be necessary to request a trading halt ahead of that decision (although that could change if there are signs that information about the impending board decision has leaked and this has had or could have a material impact on the market price or traded volumes of the entity’s securities).

Where the information to be disclosed falls within the exceptions to immediate disclosure in Listing Rule 3.1A but the board determines that it is now appropriate and timely to announce the matter to the market, it will be that decision of the board that is the trigger for the announcement rather than any legal obligation under Listing Rule 3.1. Again, it usually will not be necessary to request a trading halt ahead of that decision (although that could change if there are signs that information about the matter has leaked ahead of the announcement and this has had or could have a material impact on the market price or traded volumes of the entity’s securities).

Where, however, the information to be disclosed relates to something that has already happened and:

• it does not and never did fall within the exceptions to immediate disclosure in Listing Rule 3.1A, or

• it originally fell within those exceptions but has since ceased to do so,

the obligation to disclose will usually already have arisen before the board comes to consider the matter – in the former case at the point when the entity first became “aware” of the information and in the latter case at the point when Listing Rule 3.1A ceased to apply. To comply with the timing requirements of Listing Rule 3.1, an announcement with that information must be given to ASX promptly and without delay. In turn, this means that the requisite board meeting to consider the announcement must be convened and the board must settle and approve the announcement promptly and without delay. Consideration of the announcement cannot be delayed to a previously scheduled regular board meeting or to a meeting to be convened at a future date.

In addition, if the market will be trading at any time after the entity first became obliged to give market sensitive information to ASX under Listing Rule 3.1 and before the board can approve the giving of an announcement with that information to ASX for release to the market, the entity should consider carefully whether it ought to request a trading halt to prevent the market trading on an uninformed basis over that period, applying the guidance above in ‘4.6 The use of trading halts and voluntary suspensions to manage disclosure issues’.

Again, ASX would strongly encourage an entity which is unsure about whether it should be requesting a trading halt to cover the time required for the board to approve an announcement, to contact its listings adviser at ASX to discuss the situation.

(bold emphasis added; footnotes omitted)

37 Paragraph [4.10] addresses the question: “[h]ow does Listing Rule 3.1 interact with other disclosure obligations?”:

…

The continuous disclosure obligations in Listing Rule 3.1 also operate in parallel with:

• the periodic disclosure obligations in Chapters 4 and 5 of the Listing Rules;

• the half-yearly and annual financial reporting requirements in the Corporations Act; and

• the disclosure obligations in relation to a prospectuses, PDSs, cleansing notices, bidders’ statements, targets’ statements and scheme documents under the Corporations Act,

(together, “periodic disclosure documents”).

Once these periodic disclosure documents have been released to the market, the information in them is regarded by ASX as “generally available” and therefore not something that requires a separate disclosure under Listing Rule 3.1.

Generally speaking, an entity is not expected to release the information in a periodic disclosure document ahead of the scheduled release date for that document. Sometimes, however, in the course of preparing a periodic disclosure document, market sensitive information may become apparent that ought to be disclosed immediately under Listing Rule 3.1. Two areas where this issue commonly arises are market sensitive “earnings surprises” and market sensitive material post-balance date events.

If, in the course of preparing a periodic disclosure document, it becomes apparent to an entity that its reported earnings will differ so significantly from market expectations that a reasonable person would expect information about its reported earnings to have a material effect on the price or value of its securities, the entity must disclose that information to ASX immediately under Listing Rule 3.1. It cannot wait until the periodic disclosure document is released. The same is true for information about a material post-balance date event that a reasonable person would expect to have a material effect on the price or value of its securities.

Entities should also be aware of Listing Rule 4.3D, which requires an entity to tell ASX immediately of any circumstances which are likely to affect the results or other information contained in its preliminary final report and to explain their effect on the entity’s current or future financial performance or financial position. This rule reflects the primacy of continuous disclosure obligations over periodic disclosure obligations. If particular information is market sensitive, it must be disclosed immediately and cannot be withheld until the scheduled release date for a periodic disclosure document.

(bold emphasis added; footnotes omitted)

38 Paragraph [5] deals with Listing Rule 3.1A and the exceptions to immediate disclosure. At [5.1], the following general comments are made:

Listing Rule 3.1A sets out exceptions to the requirement to make immediate disclosure of market sensitive information under Listing Rule 3.1. These exceptions seek to balance the legitimate commercial interests of entities and their security holders with the legitimate expectations of investors and regulators concerning the timely release of market sensitive information. They also seek to ensure that information is not disclosed prematurely when, rather than inform the market, it could misinform or mislead the market.

Unless the requirements in all three of Listing Rules 3.1A.1, 3.1A.2 and 3.1A.3 are satisfied in respect of particular market sensitive information, Listing Rule 3.1A does not apply and the entity must disclose the information immediately under Listing Rule 3.1.

If the requirements in all three of Listing Rules 3.1A.1, 3.1A.2 and 3.1A.3 are initially satisfied in respect of particular market sensitive information but any one of them ceases to be satisfied thereafter, Listing Rule 3.1A ceases to apply at that point and the entity must then disclose the information immediately under Listing Rule 3.1.

(bold emphasis added; footnotes omitted)

39 Paragraphs [5.2] to [5.7] address the categories of information identified in the first limb of Listing Rule 3.1A, namely 3.1A.1, which deals with, inter alia, “[i]nformation generated for the internal management purposes of the entity”.

40 Paragraph [5.6] provides:

This category of information is excluded from disclosure because of the prejudice it could cause to an entity and its security holders, as well as the administrative burden it would create, if it was required to disclose information generated for internal management purposes.

To fall within this category, the information must have been “generated for the internal management purposes of the entity”. The expression “entity’’ here is to be read in a commercial rather than a legal sense. It includes not only information generated for the internal management purposes of the entity itself, but also for the internal management purposes of any child entity or other entity in which the entity may have an economic interest.

Information does not have to be generated internally to fall within this category. Information generated externally (eg, by an adviser or consultant) may fall within this category provided it is going to be used for the internal management purposes of the entity (eg, to help inform a management decision).

Management documents such as budgets, forecasts, management accounts, business plans, strategic plans, contingency plans, decision papers, minutes of management meetings and the like clearly fall within this category, as do board papers and board minutes. Professional advice (eg, from lawyers, accountants and financial advisers) will also usually fall within this category.

However, for the avoidance of doubt, the mere fact that information may happen to be mentioned in a document generated for internal management purposes does not mean that the information itself falls within this category. Management documents often include information about potentially market sensitive events or circumstances, where those events or circumstances (as distinct from the document that refers to them) could not fairly be described as being information generated for internal management purposes. Information about such events or circumstances is not protected from disclosure by this category.

(bold emphasis added)

41 Paragraph [5.8] deals with the second limb of Listing Rule 3.1A, namely 3.1A.2, which deals with the requirement that the information be confidential.

42 Paragraph [5.9] addresses the third limb of Listing Rule 3.1A, namely 3.1A.3 which deals with the information that a reasonable person would not expect to be disclosed. Paragraph [5.9] provides:

The third requirement for Listing Rule 3.1A to apply is that a reasonable person would not expect the information to be disclosed.

The reasonable person test is an objective one. It is to be judged from the perspective of an independent and judicious bystander and not from the perspective of someone whose interests are aligned with the entity or with the investment community.

As a general rule, information that falls within the prescribed categories in Listing Rule 3.1A.1 and that meets the confidentiality requirements in Listing Rule 3.1A.2 will also satisfy the reasonable person test in Listing Rule 3.1A.3. The very reason why the categories in Listing Rule 3.1A.1 are prescribed is because they reflect a value judgment on the part of ASX that a reasonable person would not expect that type of information to be disclosed, at least while it remains confidential.

Consequently, the reasonable person test in Listing Rule 3.1A.3 has a very narrow field of operation. It will only be tripped if there is something in the surrounding circumstances sufficient to displace the general rule described above. Two prime examples would be:

• where an entity has “cherry-picked” its disclosures, disclosing “good” information of a particular type that is likely to have a positive effect on the price or value of its securities but then declining to disclose “bad” information of the same type that is likely to a negative effect on the price or value of its securities, on the pretence that it is not market sensitive or protected from disclosure by Listing Rule 3.1A – Example H5 in Annexure A is an illustration; or

• where the information needs to be disclosed in order to prevent an announcement of other information under Listing Rule 3.1 from being misleading or deceptive.

The reasonable person test also performs two subsidiary purposes: it reinforces the fact that Listing Rule 3.1A does not operate to protect information from disclosure if it has ceased to be confidential or if it is required to correct or prevent a false market. In the former case, this is because a reasonable person would expect that once information has become known to, and is being traded on by, some in the market (as evidenced, for example, by a sudden and significant movement in the market price or traded volumes of an entity’s securities), that information should be disclosed immediately to the whole market. In the latter case, this is because a reasonable person would expect an entity, acting responsibly, to immediately disclose any information necessary to correct or prevent a false market in its securities.

ASX is aware that some entities and their advisers have taken the view that the reasonable person test may have a broader operation than ASX has suggested above and require the disclosure of information that is of a particular type or quality. ASX does not agree. The issue of whether information is of a type or quality that is protected from immediate disclosure under Listing Rule 3.1A is answered by whether it falls within or outside the prescribed categories in Listing Rule 3.1A.1. If it falls within those categories, it will only require immediate disclosure if it does not meet the confidentiality requirements in Listing Rule 3.1A.2 or if there is something in the surrounding circumstances sufficient to displace the general rule described above.

…

(bold emphasis added; footnotes omitted)

43 Paragraph [7] deals with “[p]articular disclosure issues”.

44 The first of these is [7.1] titled “[e]arnings guidance”, which provides:

Generally speaking, an entity is not required by Listing Rule 3.1 to release its internal budgets or earnings projections to the market. They are generated for internal management purposes and, provided they remain confidential, clearly fall within the carve-outs to immediate disclosure in Listing Rule 3.1A. Accordingly, subject to the exceptions mentioned below, it is perfectly acceptable for an entity to have a policy of not providing earnings guidance to the market.

Notwithstanding this, some entities have a practice of providing periodic earnings guidance to the market in order to assist investors in assessing the value of their securities. Some entities also give “one-off’ earnings guidance in disclosure documents, such as prospectuses, PDSs, bidders’ statements, targets’ statements and scheme documents.

Without wishing in any way to discourage this practice, ASX would remind entities of the regulatory issues that need to be considered when issuing earnings guidance.

As a forward-looking statement, earnings guidance must be based on reasonable grounds or else it will be deemed to be misleading, with all the significant legal consequences that entails. For this reason, appropriate due diligence needs to be applied to the preparation of earnings guidance. The underlying figures and assumptions should be carefully vetted and signed off at a suitably senior level before the guidance is released.

Since it is the directors who are ultimately responsible for confirming that an entity’s financial statements have been prepared in accordance with applicable accounting standards and give a true and fair view of its financial performance, it will also generally be appropriate for the guidance to be approved by the board before it is released.

(bold emphasis added; footnotes omitted)

45 The third particular disclosure issue is dealt with in [7.3], titled “[m]arket sensitive earnings surprises”. This is a lengthy section of Guidance Note 8 and it is necessary to set out the relevant parts in some detail:

Generally speaking, an entity’s earnings for a particular reporting period are not required to be reported to the market until the due date for the release of that information under Chapter 4 of the Listing Rules.

However, for many entities, the market’s expectations of its earnings over the near term may be a material driver of the price or value of its securities. Those expectations may have been informed by:

• earnings guidance the entity has given to the market;

• in the case of entities covered by sell-side analysts, the earnings forecasts of those analysts; or

• the entity’s pcp earnings.

Those expectations may also have been informed or modified by:

• “outlook statements” made by the entity in its last annual report or at its last results announcement or annual general meeting;

• other disclosures the entity has made to the market over the reporting period; and

• market-wide or sector-wide events that can reasonably be expected to affect the entity.

If an entity becomes aware that its earnings for the current reporting period will differ materially (downwards or upwards) from market expectations, it needs to consider carefully whether it has a legal obligation to notify the market of that fact. This obligation may arise under Listing Rule 3.1 and section 674, if the difference is of such magnitude that a reasonable person would expect it to have a material effect on the price or value of the entity’s securities – referred to in this Guidance Note as a “market sensitive earnings surprise”. Alternatively, in the case of an entity which becomes aware that its earnings for a reporting period will differ materially from earnings guidance it has published to the market, it may arise under section 1041H, because failing to inform the market that its published guidance is no longer accurate could constitute misleading conduct on its part.

This raises a number of important questions:

1. How does an entity determine what the market is expecting its earnings for the current reporting period to be?

There are three base indicators to which the market may have regard in forming its expectations for an entity’s earnings for the current reporting period. They are (in decreasing order of relevance and reliability):

• if the entity has published earnings guidance for the current reporting period, that guidance;

• if the entity is covered by sell-side analysts, the earnings forecasts of those analysts for the current reporting period; and

• the entity’s pcp earnings.

Of these three indicators, the first will usually be the most authoritative, since it comes from the source that can reasonably be expected to have the most accurate and up-to-date information about an entity’s likely earnings for the current reporting period – the entity itself.

...

In the case of all three measures above, as mentioned previously, market expectations can be informed or modified by the disclosures the entity makes to the market over the reporting period and by market-wide or sector-wide events affecting an entity. ...

3. How large does an earnings surprise have to be to trigger a disclosure obligation?

An earnings surprise will need to be disclosed to the market under Listing Rule 3.1 if it is market sensitive – that is, it is of such a magnitude that a reasonable person would expect information about the earnings surprise to have a material effect on the price or value of the entity’s securities. In this regard, it is important to note that the determining factor for whether a disclosure obligation arises is the materiality of the effect that information about the earnings surprise will have on the price or value of the entity’s securities, not the materiality of the size of the earnings surprise. The fact that an entity may disclose that it expects its earnings to be X% lower (or higher) than market expectations will not necessarily translate into an X% fall (or rise) in the price or value of its securities – the fall (or rise) in price or value could be more or less than X%. This makes providing broadly applicable percentage guidelines on when a difference in actual or projected earnings compared to market expectations might be considered market sensitive (and therefore required to be disclosed under Listing Rule 3.1) challenging.

Assessing whether or not information about a potential earnings surprise is market-sensitive will require a consideration of factors such as:

• the extent of the earnings surprise (in both percentage and absolute terms);

• whether the market has an expectation that the entity’s earnings will be stable or volatile;

• whether near term earnings is a material driver of the value of the entity’s securities;

• whether the earnings surprise is attributable to a non-cash item (such as depreciation, amortisation or an impairment charge) that may not impact on underlying cash earnings;

• whether the earnings surprise is a permanent one or is simply due to a timing issue (eg, a material revenue or expense item that was expected to be booked in one reporting period is booked in a different reporting period);

• whether the earnings surprise is attributable to one-off or recurring factors;

• whether the earnings surprise is attributable to a change in accounting standards or policies;

• whether the earnings surprise will affect the entity’s expected dividend for the current reporting period or future periods;

• whether the relative outlook for the entity in coming financial periods is positive or negative; and

• the extent to which the earnings surprise may have been signalled to the market in previous announcements by the entity, or is attributable to known market-wide or sector-wide events, that the market has already factored into the price or value of the entity’s securities.

It will also depend upon whether the earnings surprise relates to:

• earnings guidance published by the entity;

• the earnings forecasts of analysts covering the entity’s securities; or

• the entity’s pcp earnings.

In this regard, as mentioned previously, the relevance and reliability of these measures as an indicator of the market’s expectations for an entity’s earnings decreases from the first to the second and from the second to the third. Hence, all other things being equal, it is likely to take a comparatively smaller variation between the entity’s actual or projected earnings and the first measure above for that to be considered market sensitive. It is likely to take a somewhat larger variation between the entity’s actual or projected earnings and the second measure above, and a larger variation again between the entity’s actual or projected earnings and the third measure above, for that to be considered market sensitive. This underpins the percentage guidelines ASX suggests in response to question 4 below.

4. What guidance can ASX give on when an earnings surprise should be disclosed…

(a) ... where an entity has published earnings guidance on foot?

Where an entity has published earnings guidance on foot for the current reporting period, ASX would recommend that the entity carefully consider updating its published guidance if and when it expects there to be a material difference between its actual or projected earnings for the period and the guidance it has given to the market. For these purposes, ASX would suggest that entities apply the guidance on materiality that formerly appeared in the Australian Accounting Standards, that is:

• treat an expected variation in earnings compared to its published guidance equal to or greater than 10% as material and presume that its guidance needs updating; and

• treat an expected variation in earnings compared to its published guidance equal to or less than 5% as not being material and presume that its guidance therefore does not need updating,

unless, in either case, there is evidence or convincing argument to the contrary.

Where the expected variation in earnings compared to its published earnings guidance is between 5% and 10%, the entity needs to form a judgment as to whether or not it is material. Entities in the ASX 300 or that normally have very stable or predictable earnings should consider applying a materiality threshold of 5% rather than 10%. Entities outside the ASX 300 that have relatively variable earnings may consider it more appropriate to apply a materiality threshold of 10%.

This recommendation has regard to the fact that entities that have published earnings guidance on foot have made a positive representation to the market that will serve to set the market’s expectations for their earnings. If they subsequently expect their earnings to differ from their published guidance, not only will they need to consider their potential disclosure obligations under Listing Rule 3.1 and section 674 (ie, whether information about the difference is market sensitive in all of the circumstances), they will also need to consider their potential liability under section 1041H for having misled the market as to their likely earnings. By contrast, entities that do not have published earnings guidance on foot will generally only need to consider their potential disclosure obligations under Listing Rule 3.1 and section 674.

Where an entity has published its earnings guidance as a range rather than a single figure, ASX will generally interpret that as a composite representation that its earnings will not be less than the lower point of the range, nor more than the higher point of the range. Accordingly, the 5%/10% guidance above should be applied by reference to the lower point of the range (in the case of a negative earnings surprise) or the higher point of the range (in the case of a positive earnings surprise).

ASX hastens to add that the guidance above on earnings surprises is not intended in any way to discourage listed entities or their boards from issuing earnings guidance. It is simply intended to ensure that the market is kept properly informed if an entity’s actual or projected earnings is expected to differ materially from its guidance.

(b) … where an entity does not have published earnings guidance on foot and it is covered by sell-side analysts?

...

(c) … where an entity does not have published earnings guidance on foot and it is not covered by sell-side analysts?

…

(d) In all three cases above?

The guidelines in (a), (b) and (c) above are purely ASX’s suggestions to assist entities in determining if and when they should consider notifying the market of a potential earnings surprise. The mere fact that an entity may expect its actual or projected earnings to differ from market expectations by more (or less) than those particular percentages will not necessarily mean that information about the difference is (or is not) market sensitive or, where the entity has published earnings guidance on foot, that its guidance is (or is not) misleading.

…

ASX would also note that negative earnings surprises tend to be more problematical than positive earnings surprises. Experience shows that negative earnings surprises, when disclosed, will often have an immediate negative impact on the price or value of an entity’s securities. Positive earnings surprises, on the other hand, when disclosed, will not necessarily have a positive impact on the price or value of an entity’s securities, particularly if the market regards them as attributable to “one-off” factors or they are accompanied by a less positive outlook statement. Further, class action litigation for continuous disclosure breaches relating to earnings surprises has to date only arisen in relation to negative earnings surprises, not positive earnings surprises.

ASX would therefore recommend that the board and management of listed entities take particular care when it comes to making a decision on whether or not to disclose a negative earnings surprise and, if there is any doubt in their mind on whether it is disclosable, that they err on the side of caution and disclose it to the market.

5. When does an entity become aware of a market sensitive earnings surprise?

In ASX’s opinion, for an entity to have to disclose under Listing Rule 3.1 market sensitive information about an expected difference in its earnings for the current reporting period compared to market expectations, there needs to be a reasonable degree of certainty that there will be such a difference.

The fact that an entity’s earnings may be comparatively ahead of or behind market expectations part way through a reporting period does not mean that this situation will prevail at the end of the reporting period. Its earnings may change due to changes in the many variables that can affect an entity’s earnings over a reporting period. They may also change because the entity adjusts its business plans in response.

The market’s expectations also may change over the course of a reporting period as it factors in relevant marketwide or sector-wide events and absorbs the various disclosures the entity has made over that period.

Consequently, disclosure issues about potential earnings surprises are generally more likely to arise towards the end of the reporting period than at the beginning, when there will be comparatively greater certainty as to whether or not the entity’s earnings for the period are going to differ from market expectations.

Whether and when an entity is aware of a market sensitive earnings surprise ultimately requires an exercise of judgment by the entity and its directors and other officers. In some cases, they may have sufficient information before the end of the reporting period to have the requisite degree of certainty that the entity is facing a market sensitive earnings surprise. In other cases, they may not have the requisite degree of certainty until after the end of the reporting period, when the entity is in the course of finalising its financial statements for the period and having them audited.

6. What should be included in an announcement about a market-sensitive earnings surprise?

Subject to the rider below, in most circumstances, ASX would expect an announcement that an entity anticipating its earnings for the current reporting period will differ materially from market expectations to include:

• if the earnings surprise relates to the entity’s published guidance and:

• the announcement is made before the end of the reporting period:

• a statement to the effect that the entity is updating its earnings guidance for the current reporting period;

• the amount or range of earnings it was previously guiding for the current reporting period and the date it gave that guidance; and

• the amount or range of earnings it is now guiding for the current reporting period;

• the announcement is made after the end of, and prior to the publication of its financial statements for, the reporting period:

• a statement to the effect that the entity is expecting its earnings for the current reporting period to differ materially from its published guidance;

• the amount or range of earnings it was previously guiding for the current reporting period and the date it gave that guidance; and

• the amount or range of earnings it is now expecting to report for the current reporting period;

…

Whether or not such an announcement is described in this way, it will effectively constitute earnings guidance. It should therefore be subject to the same due diligence in its preparation, and to the same vetting and sign-off processes at a senior level, as any earnings guidance.

Again, since it is the directors who are ultimately responsible for confirming that an entity’s financial statements have been prepared in accordance with applicable accounting standards and give a true and fair view of its financial performance, it will also generally be appropriate for an announcement that an entity is expecting its earnings for the current reporting period to differ materially from market expectations to be approved by the board before it is released.

The one rider to the above is that earnings guidance is a forward-looking statement and must therefore be based on reasonable grounds or else it will be deemed to be misleading, with all the significant legal consequences that entails. There may be extraordinary circumstances where market, sector or entity-specific events mean that an entity is not able to forecast its earnings with any degree of confidence. In those cases, the entity legally will not be able to include in an announcement about a market sensitive earnings surprise any updated earnings projections or guidance. In such a case, it will suffice if the entity explains why it is not able to include any updated earnings projections or guidance in the announcement.

7. When should an announcement be made about a market-sensitive earnings surprise?

Where Listing Rule 3.1 applies, information about a market sensitive earnings surprise has to be released “immediately”. As indicated above, this does not mean “instantaneously” but rather “promptly and without delay”.

In assessing whether an entity has acted immediately under Listing Rule 3.1, ASX will make due allowance for the fact that any announcement that an entity’s earnings will be less than the market is expecting will be of such import that it will likely need to be approved by the entity’s board before it is released to the market. Where the announcement is to be accompanied by new or updated earnings guidance, ASX will also make due allowance for the fact that the preparation of such guidance will take time and will need to be properly vetted and signed off by the entity’s CEO and CFO, and most likely again approved by the board, before it is released to the market.

Nonetheless, an entity in this situation should be working diligently to ensure that the announcement and any new or updated guidance is approved and released to the market as quickly as reasonably practicable in the circumstances.

Concluding remarks on earnings surprises

ASX acknowledges that the issues addressed in questions 1, 2 and 3 above can be difficult ones for an entity and its officers. Forecasting its earnings for the current reporting period with an appropriate degree of confidence, assessing what the market is expecting its earnings to be and then predicting how the market will react if its earnings differ materially from those expectations involves many variables and requires considerable judgment. ASX is mindful of this when it considers whether it should refer a potential breach of Listing Rule 3.1 to ASIC involving a market sensitive earnings surprise. The matters ASX refers to ASIC usually involve an obviously significant difference in earnings compared to the relevant base used to measure market expectations mentioned in question 1 above and where the announcement of the entity’s results in fact triggers a material change in the market price of its securities.

…

(bold and italic emphasis in original; underline emphasis added; footnotes omitted)

46 Paragraph [8] deals with ASX’s enforcement practices. Paragraph [8.7] is titled “[r]eferrals to ASIC” and provides:

If ASX suspects that an entity has committed a significant contravention of the Listing Rules, or that an entity or any other person (such as a director, secretary or other officer of the entity) has committed a significant contravention of the Corporations Act, it is required under that Act to give a notice to ASIC with details of the contravention. The purpose of such a notice is so that ASIC can then consider what action, if any, it may wish to take in relation to the suspected contravention.

Given the critical importance of timely disclosure of market sensitive information to the integrity and efficiency of the market, ASX will regard any contravention of Listing Rule 3.1 or of section 674 as a “significant’’ contravention for these purposes and refer the matter to ASIC.

In deciding whether or not to refer a potential contravention of Listing Rule 3.1 and/or section 674 to ASIC, ASX will need to form a view on whether the information in question was market sensitive. As mentioned previously, the test for determining this is set out in section 677 of the Corporations Act. Under that section, a reasonable person is taken to expect information to have a material effect on the price or value of an entity’s securities if the information “would, or would be likely to, influence persons who commonly invest in securities in deciding whether to acquire or dispose of” those securities. Applying this test literally would require ASX to put itself into the shoes of persons who commonly invest in securities at the time the information was required to be disclosed under Listing Rules 3.1 and 3.1 A and hypothetically form a view on whether the information would have influenced their decision to acquire or dispose of the entity’s securities at that time.

Instead of undertaking that hypothetical task, ASX will generally look to the actual effect that the information had on the market price of the entity’s securities when it was finally announced to the market and assess for itself whether or not the information in fact had a material effect on the market price. For these purposes, ASX will generally apply the materiality guidelines that formerly appeared in the Australian Accounting Standards as a reasonable measure of materiality. Thus, if the information appears to ASX to have moved the market price of the entity’s securities (relative to prices in the market generally or in the entity’s sector) by roughly:

• 10% or more, ASX will generally regard that as confirmation that the information was market sensitive and therefore refer a potential breach of Listing Rule 3.1 and section 674 to ASIC;

• 5% or less, ASX will generally regard that as confirmation that the information was not market sensitive and therefore not refer the matter to ASIC.

Where the price movement is between 5% and 10%, ASX will have regard to a number of factors to determine whether the information should be regarded as market sensitive. This includes the nature and significance of the information, the market capitalisation of the entity, the beta of its securities, the bid-offer spread at which its securities normally trade, and whether there was a noticeable spike in the volume of its securities traded in the lead up to and shortly after the announcement. For smaller entities outside of the ASX 300, ASX would generally expect the application of these factors to result in it applying a materiality threshold that is 10% or close to it. For larger entities within the ASX 300, ASX would generally expect the application of these factors to result in it applying a materiality threshold that is closer to 5% than to 10%.

It should be noted that the fact that ASX takes this approach in assessing whether or not to refer a potential breach of Listing Rule 3.1 and section 674 to ASIC does not displace the test for materiality of information in section 677, nor does it preclude ASIC or a litigant taking a different view to ASX as to the materiality of information. If ASIC institutes criminal or civil penalty proceedings against, or a litigant institutes civil proceedings to recover damages from, an entity for breaching section 674, it will have to prove its case using the test for materiality of information in section 677, regardless of any view that ASX may have taken on the issue of materiality.

...

(bold emphasis added; footnotes omitted)

B.6 Regulatory Guide 230

47 Another relevant item of regulatory guidance is Regulatory Guide 230 – Disclosing non-IFRS financial information (RG230) which was issued by ASIC in December 2011 and was operative during the relevant period.

48 RG230 relevantly provided:

Disclosing non-IFRS financial information

RG230.1 Financial information that is presented other than in accordance with all relevant accounting standards as defined in s9 of the Corporations Act 2001 (Corporations Act) (described in this guide as ‘non-IFRS financial information’) is being used increasingly in financial reports and other documents, such as transaction documents and market announcements.

Note 1: International Financial Reporting Standards (IFRS) are issued by the International Accounting Standards Board (IASB). When ‘IFRS’ is used to describe an item of information (e.g. ‘IFRS profit’), that item should be taken to be prepared in accordance with IFRS.

Note 2: ‘Financial report’ means the documents referred to in s295 and 303 of the Corporations Act, being financial statements, notes to the financial statements and the directors’ declaration about the statements and notes.

RG230.2 In this guide, we give guidance on when non-IFRS financial information may or may not be used and what additional disclosure should be made so that the information is not misleading. The purpose of our guidance is to:

(a) promote more meaningful communication of financial information to investors and other users of financial reports;

(b) assist directors in ensuring that the financial information disclosed is not misleading; and

(c) provide greater certainty in the market about ASIC’s views on disclosure of non-IFRS financial information.

…

What is non-IFRS financial information?

RG230.5 We define ‘non-IFRS financial information’ as:

financial information that is presented other than in accordance with all relevant accounting standards.

…

RG230.7 We consider there are three main types of documents in which non-IFRS financial information is commonly disclosed:

(a) financial reports;

(b) documents other than financial reports and transaction documents (e.g. documents accompanying financial reports, market announcements, presentations to investors and briefings to analysts); and

(c) transaction documents, such as prospectuses, scheme documents and takeover documents.

…

Documents other than financial reports and transaction documents

RG230.10 It may be necessary or appropriate to include non-IFRS financial information in documents accompanying the financial report ( e.g. the directors’ report), market announcements, presentations to investors and briefings to analysts: see Section D.

RG230.11 Such information can provide meaningful insights into the financial condition or performance of a business. ASIC is not seeking to prohibit the use of nonIFRS financial information in documents related to the financial result, but considers guidance will reduce the risk that such information is misleading.

…

Definition of non-IFRS financial information and related terms

RG230.14 ‘Non-IFRS financial information’ is financial information that is presented other than in accordance with all relevant accounting standards.

…

Scope of non-IFRS financial information

RG230.20 This regulatory guide provides guidance on when users may or may not include non-IFRS financial information in financial reports and other corporate documents. …

…

D Documents other than financial reports and transaction documents

Users of financial reports may ask for financial information in addition to the financial report to better understand aspects of the performance of an entity.

There are cases where non-IFRS financial information in documents accompanying the financial report, market announcements, presentations to investors and briefings to analysts, is necessary or useful to investors and other users of the information.

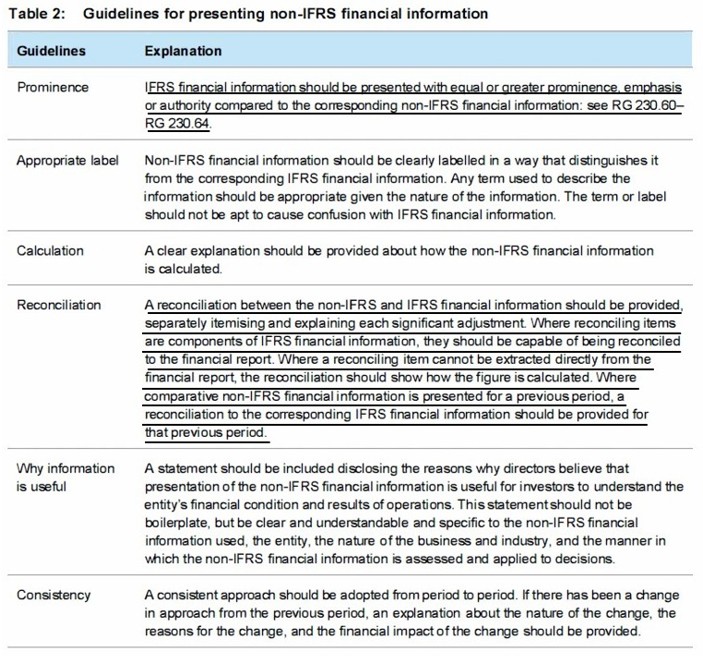

This information must not be misleading. In this regard, important considerations include that:

• IFRS financial information should be given equal or greater prominence compared to non-IFRS financial information, in particular IFRS profit; and

• non-IFRS financial information should:

- be explained and reconciled to the IFRS financial information;

- be calculated consistently from period to period; and

- be unbiased and not used to remove ‘bad news’.

…

Use of non-IFRS financial information

RG230.52 There may be demands from users of financial reports for information to better understand aspects of the performance of an entity, including information on the drivers of the business and external influences, and more information on the items comprising the reported result. It is possible for this information to be included in documents accompanying the financial report (e.g. the directors’ report), market announcements, presentations to investors, briefings to analysts, advertisements and financial reviews sent to shareholders.