FEDERAL COURT OF AUSTRALIA

Southernwood v Brambles Limited (No 3) [2026] FCA 418

File number(s): | VID 972 of 2018 |

Judgment of: | MURPHY J |

Date of judgment: | 10 April 2026 |

Catchwords: | CORPORATIONS – shareholder class action – representative proceedings – listed securities – earnings guidance for sales revenue and Underlying Profit growth – misleading or deceptive conduct relating to securities – contravention of s 1041H of the Corporations Act 2001 (Cth) – contravention of s 12DA of the ASIC Act 2001 (Cth) – contravention of s 18 of the Australian Consumer Law – whether BXB had reasonable grounds to make representations – continuous disclosure obligations under ASX Listing Rule 3.1 – contravention of s 674 of Corporations Act – loss and damage – market-based or indirect causation |

Legislation: | Australian Securities and Investments Commission Act 2001 (Cth) ss 5, 12BAA, 12BAB, 12BB, 12DA, 12GF, 12GM Corporations Act 2001 (Cth) ss 9, 111AE, 111AL, 111AP, 674, 676, 677, 761A, 764A, 769C, 1041H, 1041I, 1317E, 1317HA, 1317S Competition and Consumer Act 2010 (Cth) s 131A, Sch 2 ss 2, 4, 18, 236 Evidence Act 1995 (Cth) ss 79, 136 Federal Court of Australia Act 1976 (Cth) ss 33Q, 33R, 37M Foreign Evidence Act 1994 (Cth) s 7 Trade Practices Act 1974 (Cth) ss 45D, 51A |

Cases cited: | Australian Competition and Consumer Commission v Colgate-Palmolive Pty Ltd (No 4) [2017] FCA 1590; 353 ALR 460 Australian Competition and Consumer Commission v GlaxoSmithKline Consumer Healthcare Australia Pty Ltd [2019] FCA 676; 371 ALR 396 Australian Competition and Consumer Commission v Mazda Australia [2023] FCAFC 45 Australian Competition and Consumer Commission v Telstra Corporation Ltd [2007] FCA 1904; 244 ALR 470 Australian Competition and Consumer Commission v TPG Internet Pty Ltd [2013] HCA 54; 250 CLR 640 Australian Competition and Consumer Commission v TPG Internet Pty Ltd [2020] FCAFC 130; 278 FCR 450 Australian Competition and Consumer Act v Valve Corp (No 3) [2016] FCA 196; 337 ALR 647 Australian Competition and Consumer Commission v Woolworths Limited [2019] FCA 1039 Addenbrooke Pty Ltd v Duncan (No 2) [2017] FCAFC 76; 348 ALR 1 Allen v The Queen [2014] VSCA 180 Ambergate Ltd v CMA Corp Ltd (Administrators Appointed) [2016] FCA 94; 110 ACSR 642 Arhill Pty Ltd v General Terminal Company Pty Ltd (1990) 23 NSWLR 545 Armory v Delamirie (1722) 1 Stra 505; 93 ER 664 Australian Securities and Investments Commission v Australian Lending Centre Pty Ltd (No 3) [2012] FCA 43; 213 FCR 380 Australian Securities and Investments Commission v Big Star Energy Ltd (No 3) [2020] FCA 1442; 389 ALR 17 Australian Securities and Investments Commission v Cycclone Magnetic Engines Inc [2009] QSC 58; 71 ACSR 1 Australian Securities and Investments Commission v Fortescue Metals Group Ltd (No 5) [2009] FCA 1586; 264 ALR 201 Australian Securities and Investments Commission v Geary and Flugge (Ruling No 5) [2015] VSC 665 Australian Securities and Investments Commission v GetSwift Limited (Liability Hearing) [2021] FCA 1384 Australian Securities and Investments Commission v MacDonald (No 11) [2009] NSWSC 287; 256 ALR 199 Australian Securities and Investments Commission v Narain [2008] FCAFC 120; 169 FCR 211 Australia and New Zealand Banking Group Limited v Australian Securities and Investments Commission [2024] FCAFC 128; 305 FCR 383 Australian Competition and Consumer Commission v Dateline Imports [2015] FCAFC 114 Australian Competition and Consumer Commission v Jones (No 5) [2011] FCA 49 Australian Competition and Consumer Commission v Woolworths Group Ltd [2020] FCAFC 162; 281 FCR 108 Bauer Consumer Media Ltd v Evergreen Television Pty Ltd [2017] FCA 507; 349 ALR 679 Benlist Pty Ltd v Olivetti Australia Pty Ltd [1990] FCA 416; ATPR 41-043 Blatch v Archer [1774] EngR 2; 1 Cowp 63; 98 ER 969 Bonham atf Auchum Super Fund v Iluka Resources Ltd [2022] FCA 71; 404 ALR 15 Brunner v Greenslade [1971] Ch 993 Butcher v Lachlan Elder Realty Pty Ltd [2004] HCA 60; 218 CLR 592 Campbell v Backoffice Investments Pty Ltd [2009] HCA 25; 238 CLR 304 Campomar Sociedad Limitada v Nike International Ltd [2000] HCA 12; 202 CLR 45 Cape Byron Power I Pty Ltd v HSB Engineering Insurance Ltd [2017] NSWSC 1081 CCL Secure Pty Ltd v Berry [2019] FCAFC 81 Ceramic Fuel Cells Limited (in liq) v McGraw-Hill Financial, Inc [2016] FCA 401; 245 FCR 340 Cessnock City Council v 123 259 932 Pty Ltd [2024] HCA 17; 418 ALR 304 City of Botany Bay Council v Jazabas Pty Ltd [2001] NSWCA 94 Claremont Petroleum NL v Cummings [1992] FCA 446; 110 ALR 239 Commonwealth v Amann Aviation Pty Ltd (1991) 174 CLR 64 Communications, Electrical, Electronic, Energy, Information, Postal, Plumbing and Allied Services Union of Australia v Australian Competition and Consumer Commission [2007] FCAFC 132; 162 FCR 466 Crowley v Worley Limited (No 2) [2023] FCA 1613; 171 ACSR 410 Crowley v Worley Limited [2022] FCAFC 33; 293 FCR 438 Cubillo v Commonwealth of Australia (No 2) [2000] FCA 1084; 103 FCR 1 Davis v Wilson [2025] FCA 108 Demagogue Pty Ltd v Ramensky (1992) 39 FCR 31 Digi-Tech (Australia) Ltd v Brand [2004] NSWCA 58; 62 IPR 184 Doppstadt Australia Pty Ltd v Lovick & Son Developments Pty Ltd [2014] NSWCA 158 Downey v Carlson Hotels Asia Pacific Pty Ltd [2005] QCA 199 Euromark Limited v Smash Enterprises Pty Ltd (No 3) [2023] VSC 490 Fabre v Arenales (1992) 27 NSWLR 437 Fink v Fink (1946) 74 CLR 127 Forrest v Australian Securities and Investments Commission [2012] HCA 39; 247 CLR 486 Fraser v NRMA Holdings Limited (1995) 55 FCR 452 Fuller-Lyons (by his tutor Lyons) v New South Wales [2015] HCA 31; 89 ALJR 824 George v Rockett (1990) 170 CLR 104 Gestmin SGPS SA v Credit Suisse (UK) Limited [2013] EWHC 3560 (Comm) Ghazal v Government Insurance Office of New South Wales (1992) 29 NSWLR 336 Global Sportsman Pty Ltd v Mirror Newspapers Ltd (1984) 2 FCR 82 Gloucester (Sub-Holdings 1) Pty Ltd v Chief Commissioner of State Revenue [2013] NSWSC 1419 Google Inc v Australian Competition and Consumer Commission [2013] HCA 1; 249 CLR 435 Grant-Taylor v Babcock & Brown Limited (in liq) [2016] FCAFC 60; 245 FCR 402 Grant-Taylor v Babcock & Brown Ltd (in liq) [2015] FCA 149; 322 ALR 723 Henville v Walker [2001] HCA 52; 206 CLR 459 Ho v Powell (2001) [2001] NSWCA 168; 51 NSWLR 572 Hornsby Building Information Centre Pty Ltd v Sydney Building Information Centre Ltd [1978] HCA 11; 140 CLR 216 Houghton v Immer (No. 155) Pty Ltd [1997] 44 NSWLR 46 Hutchence v South Seas Bubble Co Pty Ltd (1986) 64 ALR 330 James Hardie Industries NV v Australian Securities and Investments Commission [2010] NSWCA 332; 274 ALR 85 Johnson Tiles Pty Limited v Esso Australia Pty Ltd [2000] FCA 1572; 104 FCR 564 Jones v Dunkel [1959] HCA 8; 101 CLR 298 Joye v Beach Petroleum NL (1996) 67 FCR 275 Li v Chief of Army (2012) 261 FLR 226 Lloyd v Belconnen Lakeview Pty Ltd [2019] FCA 2177; 377 ALR 234 Marks v GIO Australia Holdings Ltd [1998] HCA 69; 196 CLR 494 Masters v Lombe (Liquidator); in the matter of Babcock & Brown Limited (In Liq) [2019] FCA 1720 McCartney v Orica Investments Pty Ltd [2011] NSWCA 337 McFarlane as Trustee for the S McFarlane Superannuation Fund v Insignia Financial Ltd [2023] FCA 1628 McGrath; in the matter of Pan Pharmaceuticals Ltd (in liq) v Australian Naturalcare Products Pty Ltd [2008] FCAFC 2; 165 FCR 230 Mealey v Power [2015] NSWSC 1678 Medlin v State Government Insurance Commission [1995] HCA 5; 182 CLR 1 Miller and Associates Insurance Broking Pty Ltd v BMW Australia Finance Ltd [2010] HCA 31; 241 CLR 357 Momcilovic v The Queen [2011] HCA 34; 245 CLR 1 Oran Park Motor Sport Pty Ltd v Fleissig [2002] NSWCA 371 Packer v Cameron (1989) 54 SASR 246 Parkdale Custom Built Furniture Pty Ltd v Puxu Pty Ltd [1982] HCA 44; 149 CLR 191 Payne v Parker [1976] 1 NSWLR 191 Pitcher Partners Consulting Pty Ltd v Neville’s Bus Service Pty Ltd (2019) 271 FCR 392; [2019] FCAFC 119 Potts v Miller (1940) 64 CLR 282 Queensland v Masson [2020] HCA 28; 94 ALJR 785 R (on the application of Bancoult No 3) v Secretary of State for Foreign and Commonwealth Affairs [2018] UKSC 3 R v Myer [2023] QCA 144 Re HIH Insurance Ltd (in liq) (2016) 335 ALR 320; [2016] NSWSC 482 Rivkin Financial Services Ltd v Sofcom Ltd [2004] FCA 1538 Ronchi v Portland Smelter Services Ltd [2005] VSCA 83 RRG Nominees Pty Ltd v Visible Temporary Fencing Australia Pty Ltd (No 4) [2019] FCA 686 Sagacious Legal Pty Ltd v Wesfarmers General Insurance Ltd [2011] FCAFC 53 Schellenberg v Tunnel Holdings Pty Ltd [2000] HCA 18; 200 CLR 121 Schneider v Caesarstone Australia Pty Ltd [2012] VSC 126 Smith v Samuels (1976) 12 SASR 573 Sons of Gwalia Ltd v Margaretic; ING Investment Management LLC v Margaretic [2007] HCA 1; 231 CLR 160 Southernwood v Brambles Limited (Ruling No 1) [2022] FCA 1036 Stemcor (A/asia) Pty Ltd v Oceanwave Line SA [2004] FCA 391 Stone v Chappel [2017] SASCFC 72; 128 SASR 165 Sykes v Reserve Bank of Australia (1989) 88 FCR 511 Taco Co of Australia Inc v Taco Bell Pty Ltd (1982) 42 ALR 177 Tillmanns Butcheries Pty Ltd v Australasian Meat Industry Employees’ Union (1979) 27 ALR 367 Ting v Blanche (1993) 118 ALR 543 TPT Patrol Pty Ltd (as trustee for Amies Superannuation Fund) v Myer Holdings Ltd [2019] FCA 1747; 293 FCR 29 Travel Compensation Fund v Tambree [2005] HCA 69; 224 CLR 627 Venerdi Pty Ltd v Anthony Moreton Group Funds Management Ltd [2013] QSC 219; 1 Qd R 214 Willis v Commonwealth [1946] ALR 349; 73 CLR 105 Woodcroft-Brown v Timbercorp Securities Ltd [2011] VSC 427; 85 ACSR 354 Wotton v Queensland (No 5) [2016] FCA 1457; 157 ALD 14 Zonia Holdings Pty Ltd v Commonwealth Bank of Australia [2024] FCA 477 Zonia Holdings Pty Ltd v Commonwealth Bank of Australia [2025] FCAFC 63 |

Division: | General Division |

Registry: | Victoria |

National Practice Area: | Commercial and Corporations |

Sub-area: | Regulator and Consumer Protection |

Number of paragraphs: | 4171 |

Date of last submission/s: | 27 October 2022 |

Date of hearing: | 8 August - 27 October 2022 |

Counsel for the Applicants | Mr BF Quinn KC with Mr WAD Edwards, Mr TJD Chalke and Mr TA Rawlinson |

Solicitor for the Applicants | Maurice Blackburn Lawyers and Slater & Gordon Lawyers |

Counsel for the Respondents | Mr M Borsky KC with Mr K Loxley and Ms SCB Brenker |

Solicitor for the Respondents | Allens |

Table of Corrections | |

1 May 2026 | Substitution of “Kennett” for “Mackie” in the seventh line of [476] |

1 May 2026 | Removal of duplicate wording at [1592]-[1593] of “Even so, having regard to the fact that the case regarding the October Representations was fully argued, and to the possibility that I may be found to be wrong in relation to the August Representations, it is appropriate that I set out my view as to whether Brambles’ conduct conveyed the October Representations” and splitting of paragraph so as to preserve numbering. |

1 May 2026 | Substitution of “considered” to “did not consider” in the first line of [2664] |

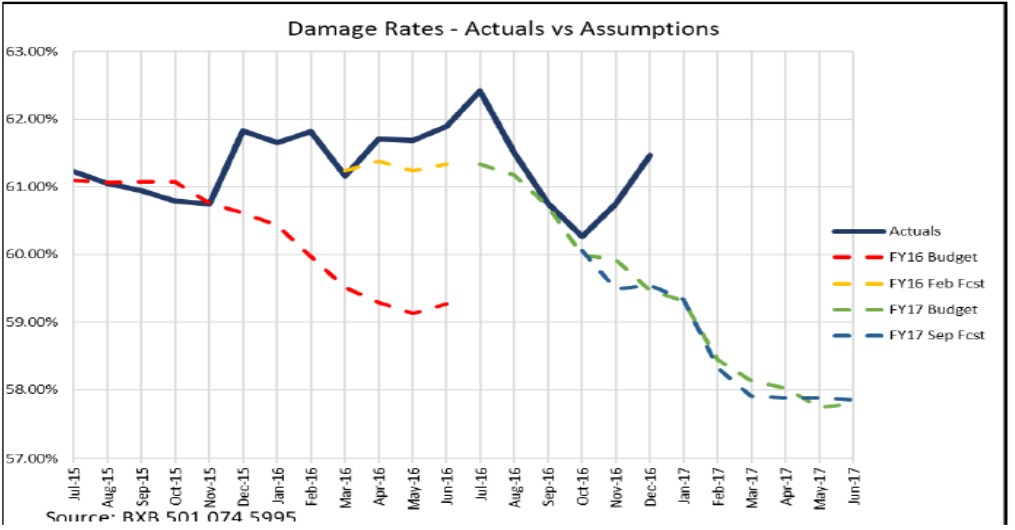

14 May 2026 | Inclusion of relevant graph under [2189] |

14 May 2026 | Substitution of “losses” for “contraventions” at [3063] |

VID 972 of 2018 | ||

BETWEEN: | HOLLY SOUTHERNWOOD Applicant WILLIAM VINCENT KIDD AND MARY AGNES COLLUM AS TRUSTEES FOR THE MAGNESS-BENNETT SUPERANNUATION FUND Applicant | |

AND: | BRAMBLES LIMITED Respondent | |

TABLE OF CONTENTS

REASONS FOR JUDGMENT

MURPHY J

1. INTRODUCTION

1 The first applicant, Holly Southernwood, and the second applicant, William Vincent Kidd and Mary Agnes Collum as Trustees for the Magness-Bennett Superannuation Fund, bring this securities class action on their own behalf and on behalf of all persons who acquired an interest in the ordinary shares of the respondent, Brambles Limited (ACN 118 896 021) (Brambles or the Group), between 18 August 2016 and 17 February 2017 inclusive (Relevant Period) and who suffered loss or damage caused by, or which resulted from, Brambles’ alleged conduct (group members).

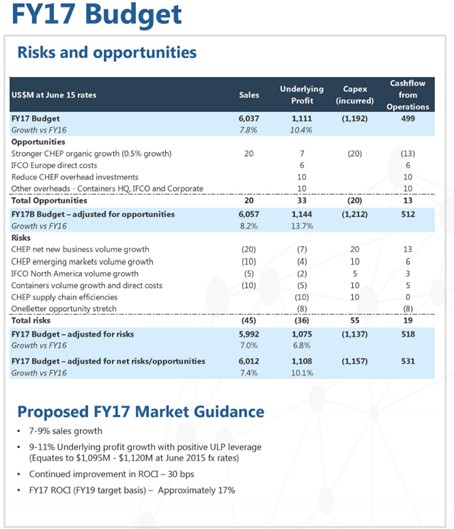

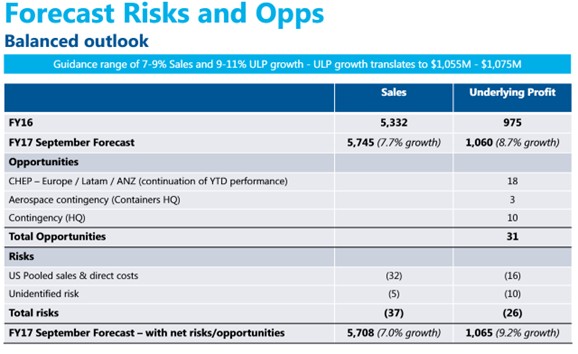

2 The proceeding concerns statements made by Brambles by way of earnings guidance to the market regarding expected sales revenue and Underlying Profit growth in the 2016/17 financial year (FY17 Guidance) and medium-term targets for sales revenue and Underlying Profit growth to FY19 (Medium-Term Targets) and 20% return on capital invested by FY19 (FY19 ROCI Target) (together, the FY19 Targets). The applicants allege that Brambles announced those forecasts to the Australian Securities Exchange (ASX or the market) on 18 August 2016, and reiterated, reaffirmed or maintained them on 20 October 2016 and 16 November 2016. Brambles was unable to achieve its FY17 Guidance and withdrew it on 23 January 2017, and then withdrew the FY19 Targets on 20 February 2017. A significant drop in the price of Brambles shares followed each withdrawal.

3 The applicants allege that Brambles’ earnings guidance announcements to the market were representations in respect of future matters for which there were not reasonable grounds. They allege that on and from each of 18 August, 20 October and 16 November 2016 Brambles contravened the prohibition on misleading or deceptive conduct in trade or commerce in s 1041H(1) of the Corporations Act 2001 (Cth) and its statutory analogues, and that they purchased Brambles shares during the Relevant Period at prices which were inflated as a result of Brambles’ misconduct. They further alleged that, on and from those dates, Brambles was “aware” within the meaning of ASX Listing Rule 3.1 that it was likely that it would not achieve the FY17 Guidance, and that by not immediately disclosing that to the ASX Brambles contravened the continuous disclosure regime under s 674(2) of the Corporations Act.

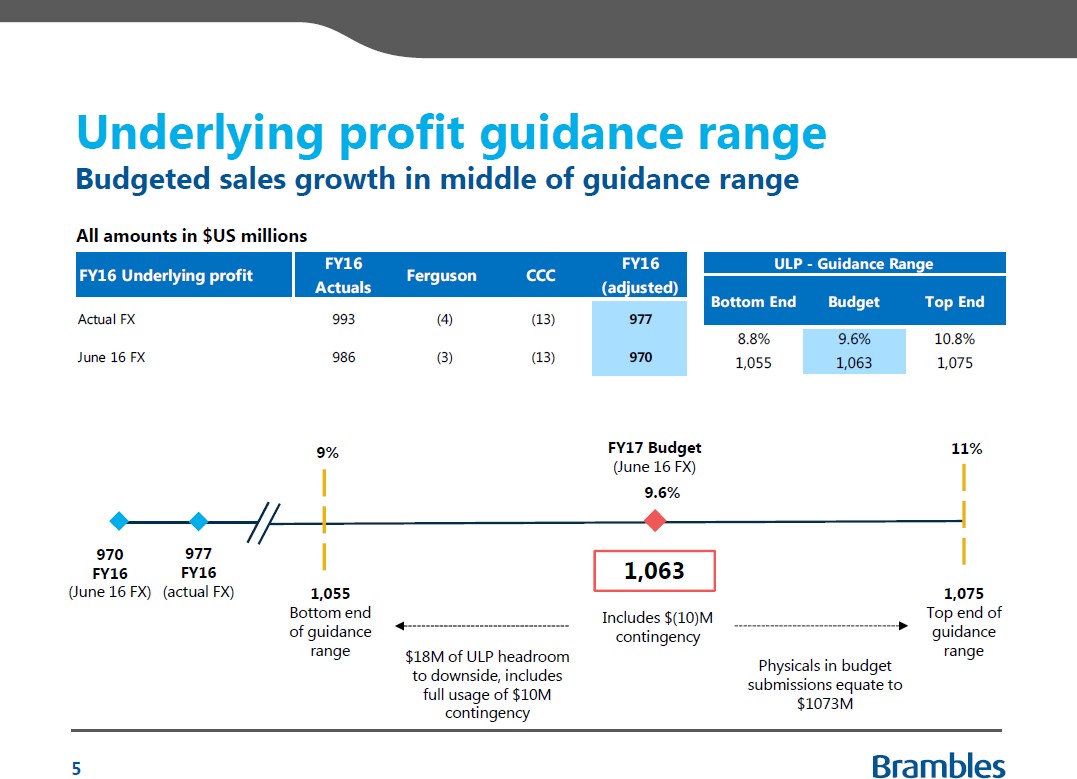

4 At all material times, Brambles was a huge and successful multinational corporation with a portfolio of businesses and operations around the globe. In the 2015/16 financial year, it earned Underlying Profit (defined as profit from continuous operations before finance costs, tax and significant items) of US$970 million, and in the 2016/17 financial year (FY17) it was budgeted to achieve Underlying Profit of US$1,063 million. For FY17, Brambles’ management set an aggressive budget for one of its largest country business units, CHEP North America (CHEP NA) including CHEP NA’s largest business division, US Pooled, as components of the much greater overall Group budget. There was nothing wrong with that; aggressive budgets are a part of commercial life. However, Brambles’ senior management and the Board unwisely set and announced the FY17 Guidance to the market of investors and potential investors in Brambles shares, which guidance left Brambles with little room for any underperformance.

5 The evidence does not show why Brambles set itself such a high bar, and it does not matter in the case. But it I infer that it did so for its own purposes; to optimise its share price. Brambles was, of course, entitled to seek to optimise its share price, but I am satisfied that its earnings guidance announcements were likely to be relied on by investors in deciding whether to buy or dispose of Brambles shares. The problem for Brambles was that a miss to the Underlying Profit budget of less than 1% would mean that it would not achieve the FY17 Guidance.

6 That is what happened. Brambles was forced to withdraw the earnings guidance, which it took too long to do; and when Brambles finally did so it led to two significant share price declines. In the class action the applicants seek to recover their losses suffered by the drop in the price or value of the Brambles share they bought in the Relevant Period; i.e., the amount of the inflation in Brambles’ share price caused by the alleged misleading earnings guidance and failure to disclose that it was, in fact, likely not to achieve its FY17 Guidance.

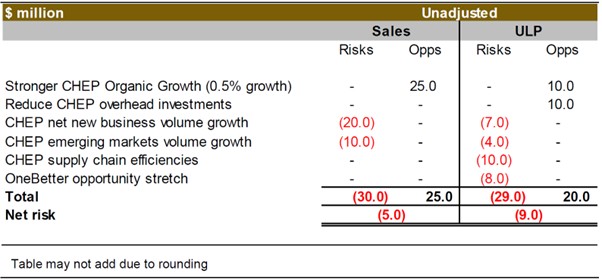

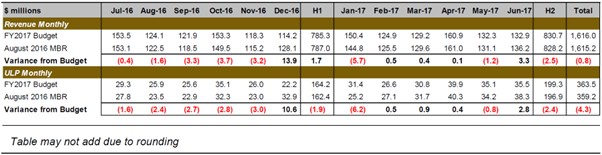

7 The applicants did not establish their claims on and from 18 August 2016 or on and from 20 October 2016. But by 16 November 2016, US Pooled had been unable to achieve its sales revenue budget in any of the first four months of FY17, and because of that and four months of over-budget direct costs, it was unable to achieve its Underlying Profit budget in three out of the first four months of FY17. In September and October FY17, US Pooled and CHEP NA materially missed their respective budgets, and also two reforecasts that had been made to plot a path for their recovery. Upon receipt of the October FY17 results in early November 2016, US Pooled had run up a $(15.9) million sales revenue deficit to budget and a $(25.3) million Underlying Profit deficit to budget year-to-date (or YTD), and largely as a result Brambles had run up a $(15) million sales revenue deficit to budget and an $(18) million Underlying Profit deficit to budget YTD.

8 A reforecast made in September FY17 projected that Brambles would recover to meet its Underlying Profit budget for the full-year largely through a remarkable six months of over-budget performance by US Pooled in the second half of FY17. That reforecast and a revision of it in October FY17 were relied on by Brambles’ management to project that US Pooled and Brambles would recover to achieve budget and the FY17 Guidance for the full year, but US Pooled missed the first months of each of those reforecasts almost immediately after they were made. As it eventuated, US Pooled did not achieve its sales revenue budget in any month from July to December FY17 inclusive, or its Underlying Profit budget in July or any month from September to December FY17 inclusive.

9 Having regard to the aggressive and stretched US Pooled and CHEP NA budgets, months of US Pooled underperformance against budget, the likelihood of continuing US Pooled underperformance against budget, and the unrealistic nature and extent of the projected US Pooled recovery in the second half of FY17, I have found that:

(a) as at and from 16 November 2016 until 23 January 2017 there were not reasonable grounds for the FY17 Guidance in respect of Brambles’ Underlying Profit growth in FY17; and

(b) as at and from 21 December 2016 until 23 January 2017 there were not reasonable grounds for the FY17 Guidance in respect of Brambles’ sales revenue and Underlying Profit growth in FY17.

Brambles thereby engaged in misleading or deceptive conduct as it had made representations in respect of future matters for which lacked reasonable grounds. For similar reasons I have found that, in the same periods, Brambles breached its obligations of timely disclosure to the ASX under the continuous disclosure regime in the Corporations Act.

10 The sales revenue and Underlying Profit performance by US Pooled against budget did not improve in December 2016. The December results, received in early January 2017, showed it had again materially missed budget and reforecasts. Those results continued to translate into materially under-budget results for Brambles overall. In the event that I am later found to have been wrong in the decisions as at 16 November 2016 and 21 December 2016, I find that on and from 5 January 2017 until 23 January 2017 there were not reasonable grounds for the FY17 Guidance in respect of Brambles’ sales revenue and Underlying Profit growth in FY17, and so it had contravened the prohibition against misleading or deceptive conduct. Brambles did not withdraw its FY17 Guidance until 23 January 2017. Again, for similar reasons, I find that over the same period Brambles contravened the continuous disclosure regime.

11 The applicants did not establish their claims in relation the FY19 Targets.

12 The applicants established that they suffered loss and damage as a result of Brambles’ contraventions.

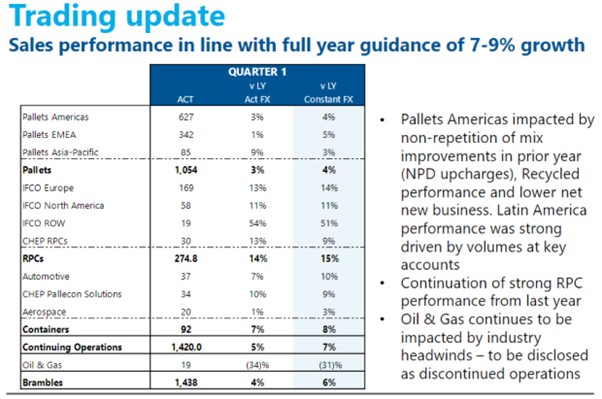

13 The trial ran for five weeks. The case involved a detailed consideration of the budget-setting process for CHEP NA and US Pooled in the first half of calendar year 2016, and the operations of those businesses in the second half of 2016 (being the first half of FY17) with particular emphasis on the reasons for and extent of the sales revenue underperformance and the direct costs overruns. As above, the exercise of determining whether there were reasonable grounds for the earnings guidance to the market are required to be determined as at 20 October 2016, 16 November 2016, 21 December 2016 and 5 January 2017 (and in respect of the FY19 Targets, also as at 23 January 2017). The affidavit evidence on liability ran to more than 1,050 pages, the experts’ reports ran to more than 1,320 pages, the electronic tender bundle comprised around 2,600 documents and the core bundle of documents comprised approximately 500 documents taking up seven lever arch folders. All issues were in dispute, and the parties’ closing submissions totalled 780 pages. As a result, these reasons are necessarily lengthy. No doubt they could be shortened but that would take even longer.

1.1 Notes as to terminology and other matters

14 FY17 refers to the financial year from 1 July 2016 to 30 June 2017, and the same applies, mutatis mutandis, to FY15, FY16, etc. Similarly:

(a) 1H17 and 2H17 refer to the first and second halves (six-month periods) of FY17 respectively and the same notation applies in relation to earlier years;

(b) 1Q17, 2Q17, etc., or Q1, Q2, etc., refer to the corresponding quarters (three-month periods) of FY17, and the same notation applies in relation to earlier years; and

(c) P1, P2, etc., refer to the corresponding monthly reporting periods of FY17 (e.g., P1 of FY17 is the month of July 2016), and the same notation applies in relation to earlier years.

15 I have generally not noted grammatical and spelling errors in emails, in part because English is not the first language of some of the authors.

16 All figures relating to Brambles’ financial results are in US dollars. All figures relating to Brambles’ share price on the ASX are in Australian dollars.

2. BRAMBLES

17 I commence by explaining Brambles’ organisational structure, some relevant Brambles business metrics and the pallets business.

18 Brambles’ business structure and pallets business were not in dispute. I have largely drawn this section of the reasons from the parties’ submissions.

2.1 Brambles’ structure

19 At all material times Brambles’ business was divided into three core business divisions:

(a) The global pallet business, which operated under the Commonwealth Handling Equipment Pool (CHEP) brand and was the dominant pallet pooling business in the world. In FY16, the global pallets business (CHEP Global) accounted for approximately 74% of Brambles’ annual revenue. From 2010, CHEP Global also included a pallet recycling business in North America;

(b) The reusable plastic crates (RPC) pooling business (IFCO), which in FY16 accounted for approximately 18% of Brambles’ annual revenue; and

(c) The containers pooling business (Containers), which in FY16 accounted for approximately 8% of Brambles’ annual revenue. This included an oil and gas business which was deconsolidated and equity accounted upon the creation of the HFG Oil & Gas joint venture (HFG Joint Venture) in FY17 (explained below).

20 CHEP Global was divided into regional “country business units” (CBUs), for operational and reporting purposes. In the Relevant Period, CHEP Global comprised the following five CBUs:

(a) CHEP North America (CHEP NA);

(b) CHEP Europe;

(c) CHEP Latin America (CHEP LATAM);

(d) CHEP Africa, India and the Middle East (CHEP AIME); and

(e) CHEP Asia-Pacific (CHEP APAC).

21 It also included a business called CHEP Aerospace, which was subsequently divested by Brambles on 2 November 2016.

22 Each of those CBUs operated in what were classified within Brambles as either a mature market or an emerging market, based on the saturation of pallet pooling within that region. CHEP NA was a mature market business. CHEP Europe and CHEP APAC were predominantly mature market businesses. CHEP LATAM and CHEP AIME were emerging market businesses.

23 In FY16, within CHEP Global:

(a) CHEP Americas (which included CHEP NA and CHEP LATAM, but of which CHEP NA made up by far the largest percentage of revenue) accounted for approximately 44% of Brambles’ total sales revenue;

(b) CHEP Europe, Middle East and Africa (CHEP EMEA) (which included CHEP Europe and CHEP AIME) accounted for approximately 24% of Brambles’ total sales revenue; and

(c) CHEP APAC accounted for approximately 6% of Brambles’ total sales revenue.

2.2 CHEP North America

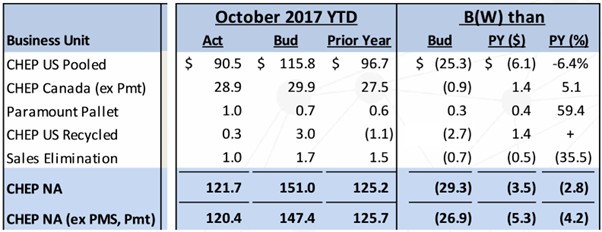

24 The applicants’ case focused on the financial performance of CHEP NA, and more particularly on US Pooled, the largest division within CHEP NA. Brambles estimated that there were over 300 million pooled pallets in North America in 2014, approximately 260 million (84%) of which were in the US Pooled pool. In FY16, CHEP NA earned $2,224.8 million in sales revenue and made $398.1 million in Underlying Profit (defined in section 2.4 below). In FY16 it accounted for approximately 39% of Brambles’ total revenue and 39% of Brambles’ Underlying Profit. In FY17 it was expected to generate approximately 41% of Group Underlying Profit.

25 At all material times CHEP NA comprised the following business units:

(a) US Pooled;

(b) CHEP Canada;

(c) US Recycled; and

(d) Paramount.

26 US Pooled. This business specialised in leasing pallets to manufacturers in the United States for use and return through a pooling model, and it was the largest business unit in CHEP NA. It predominantly issued pallets to manufacturers in the fast-moving consumer goods industry, for which grocery retailers or distributors (such as Walmart, Kroger and Safeway) represented the largest group. Those distributors tended to “turn” their inventories of goods once every 30 to 40 days, which meant that on average a pallet would become available for return to US Pooled after about a month in a distributor’s warehouse.

27 In submissions, Brambles tried to downplay the importance of US Pooled to its achievement of its FY17 earnings guidance. In my view, US Pooled was one of Brambles’ most important CBUs and the performance of US Pooled against its FY17 budget was objectively significant to Brambles achieving its budget for FY17 (Group FY17 budget) and achieving the FY17 earnings guidance.

28 In FY16 US Pooled accounted for:

(a) approximately 67.9% of CHEP NA revenue and approximately 79.1% of CHEP NA Underlying Profit; and

(b) approximately 26.5% of Brambles’ total revenue and approximately 30.1% of Group Underlying Profit.

The Group FY17 budget projected that in FY17 US Pooled would account for:

(a) approximately 68.1% of forecast CHEP NA revenue and 79.2% of forecast CHEP NA Underlying Profit; and

(b) approximately 27.6% of forecast Group revenue; and approximately 34.2% of forecast Group Underlying Profit.

29 That is not to suggest that US Pooled was the only important business unit within Brambles. In FY16, CHEP Europe earned sales revenue of $1,228.2 million compared to US Pooled which earned $1,510.5 million. In that year, CHEP Europe made Underlying Profit of $322.3 million which slightly exceeded US Pooled Underlying Profit of $315 million.

30 CHEP Canada. This business leased pooled pallets to manufacturers in Canada for use and return to the business. It accounted for approximately 8% of Brambles’ total revenue in FY16.

31 US Recycled and Paramount. These businesses were not pallet pooling businesses, and instead were trading businesses that purchased various grades of single use whitewood pallets or cores from retailers and other vendors, repaired them to convert them into pallets of merchantable quality, and then sold the recycled whitewood pallets to customers in the United States and Canada.

32 Together US Recycled and Paramount accounted for approximately 4% of Brambles’ total revenue in FY16.

33 Although US Recycled contributed to CHEP NA’s revenue, due to its lower margins and lower return on capital invested it did not make a material contribution to Underlying Profit. For example, in FY16, annual revenue in US Recycled was $460 million and its Underlying Profit was a loss of $(4.2) million.

2.3 The pallets business

34 A pallet is a flat object that goods are stored on, primarily for the purpose of transportation. They are designed to enable stock to be readily moved by a forklift or hand truck, and their consistent size standardises unit loads for transportation and storage purposes. Pallets typically travel through the supply chain from a product manufacturer to a distributor (either wholesaler or retailer). Most pallets are made from wood. Most CHEP pallets are block pallets, a durable design that can be accessed by a forklift or hand truck from all four directions.

35 A pallet pool is a system by which a “pallet pooler” (such as Brambles) rents pallets to manufacturers of products, which products are then stored and transported on the pallet. The pallet takes a one-way trip “downstream” through the product manufacturer’s supply chain to distributors and retailers. Once emptied of the product, the pallet is returned to the pallet pooler (with different methods applying between different distributors and retailers) for inspection, any necessary repairs and maintenance and then redeployment by the pallet pooler to the next manufacturer.

36 It is useful to understand the typical cycle of a pallet, from its construction, to its delivery to a customer, and then through the pooling cycle until it returns to the pallet pooler; as well as the points in the cycle at which the pallet pooler earns revenue, and incurs capital expenditure and operating costs:

(a) in the event that the pallet pooler purchases a new pallet (as opposed to re-issues an existing pallet):

(i) a pallet is ordered and constructed (often by a third party). The pallet pooler recognises the cost of construction of the pallet (including the cost of delivering the pallet to the manufacturer) as a capital expense;

(ii) the new pallet is delivered either to the pallet pooler or, more commonly, directly to the manufacturer who is the customer of the pooler. If the pallet is delivered to the pallet pooler, and the pooler is required to store the pallet for any period before it is delivered to the manufacturer, the pooler will incur storage costs. If the pallet is not stored before being issued to a manufacturer, then the pallet pooler will not incur any operating costs in relation to that pallet until it goes through the distribution network and returns to the pooler;

(b) when the pallet pooler issues a pallet to a manufacturer (either a new pallet, or more commonly a re-issued pallet previously returned to the pool), the pooler charges the manufacturer an “issue fee”, along with any surcharges, which the pooler recognises as revenue at the time the pallet is issued to the manufacturer;

(c) the manufacturer holds the pallet while it produces its goods, and builds a pallet load for shipment to one of its customers. For each day between issue and the day that the manufacturer transfers the pallet to a distributor, the pallet pooler charges the manufacturer a daily hire fee. CHEP Global commonly refers to this fee as a “Daily Hire Fee”, or more commonly Pallet Days or P-Days;

(d) once the manufacturer has assembled a pallet load of goods, it ships the loaded pallet (under load of those goods) to the manufacturer’s customer (a retailer or distributor). At that point, the pallet pooler takes the pallet off the manufacturer’s account, the pallet is transferred to the distributor’s account, and the pooler charges the manufacturer a “transfer fee”. CHEP Global classified the retailer or distributor to whom the manufacturer transfers the pallet as a “Non-Participating Distributor” (NPD) (explained below). Such manufacturers can be required to pay an “NPD Upcharge”. After the manufacturer transfers the pallet to a retailer or distributor, CHEP Global stops charging the manufacturer a daily hire fee for the pallet;

(e) a retailer or distributor keeps the pallet for as long as it takes to empty the pallet of its load, at which point it is set aside to be returned to the pallet pooler’s Service Centre. The pallet pooler does not generally charge the retailer or distributor a hire fee. Sometimes the pallet pooler may enter an arrangement allowing the retailer or distributor to re-use the pallet while it remains there, which may result in the pallet suffering a higher level of damage; and

(f) the pallet is either returned to the pallet pooler by the retailer or distributor, or collected by the pooler or a third-party contractor. At this point, the end of the pallet cycle, the pallet pooler incurs the bulk of its operating costs in relation to that pallet, namely the cost of transporting, inspecting, washing, repairing and storing the pallet. The cost of repairing damaged pallets can be a material part of operating expenditure.

This describes the cycle of a single pallet, and it should be kept in mind that CHEP Global issued many millions of pallets each year.

37 CHEP Global’s paying customers are the product manufacturers. Manufacturers sign a rental agreement pursuant to which they receive pallets that they are authorised to ship to distributors. In return, manufacturers pay fees to CHEP Global. The delivery of a pooled pallet to a manufacturer is known as an “issue”.

38 In the Relevant Period, the main fees paid to CHEP Global by manufacturers using pooled pallets were:

(a) an issue / delivery charge (for each pallet delivered to the manufacturer);

(b) a daily hire charge (for each day that the pallet was held by the manufacturer);

(c) a transfer fee (for each pallet sent onward to a distributor);

(d) a surcharge for transfer of a pallet to an NPD; and

(e) other surcharges (fuel, lumber, or non-standard delivery costs).

39 Retailers and distributors who receive goods from manufacturers using pooled pallets issued by the pallet pooler to the manufacturer do not typically pay fees to the pooler, but are critical to the pooler’s business model. The efficient recovery of pallets at the end of the supply chain is critical to the success of the pallet pool. Because the manufacturer ceases to pay daily hire fees at the point at which it transfers a pallet to a retailer or distributor, the longer the retailer or distributor holds a pallet, the longer it remains in the cycle without the pallet pooler earning revenue. Moreover, the longer a pallet remains in circulation, the higher the prospect that it will return to the pallet pooler in need of repair or greater repairs, and consequently the greater the operating costs incurred by the pooler.

40 CHEP Global categorised distributors in the following manner:

(a) a Participating Distributor (PD) is a distributor that has signed a “Participating Distributor Agreement” (PDA) or had another arrangement with CHEP Global covering its use of pooled pallets;

(b) a Non-Participating Distributor (NPD) is a distributor authorised to receive pallets from a manufacturer, but which does not have an agreement or contractual relationship governing the return of its pallets after use. Within this group, US Pooled had two specific sub-categories, defined with reference to their “Flow-Through Ratio” (FTR), being the volume of pallets flowing to a distributor compared with the volume recovered from that distributor:

(i) a Semi-Cooperating Distributor (SCD), being an NPD with a flow-through ratio of 70% or higher. Some cooperation from the SCD is likely to occur for a FTR of this level; and

(ii) a Non-Cooperating Distributor (NCD), being an NPD with a flow-through ratio of less than 70%.

In other words, SCDs were easier to recover pallets from than NCDs.

41 The cost to CHEP Global for recovering pallets from a PD was typically lower than from an NPD. The likelihood that a pallet returned to CHEP Global in a damaged state was also lower with a PD than an NPD. As a result, operating expenses associated with pallets that end their journey with a PD were usually lower than with an NPD, particularly an NCD. Pallets were also far more likely to be lost altogether when shipped to an NPD.

42 CHEP NA had another type of pallets business named US Recycled (also known as CHEP Recycled) which involved the construction and sale, or recycling and sale, of different grades of Single Use Whitewood Pallets (whitewood pallets or cores) to manufacturers. The business of recycling whitewood pallets involves purchasing used cores from retailers and other vendors, repairing those cores to convert them into pallets of merchantable quality, and then selling the recycled whitewood pallets to manufacturers. Whitewood pallets are of lower quality than standardised pooled pallets, cheaper to make and less durable than block pallets, and often only accessible by lifting equipment from two of the four directions. For product manufacturers, purchasing whitewood pallets was an alternative to renting a pooled pallet, but such pallets were intended only for a single use. Where products are shipped on a whitewood pallet, ownership of the pallet passes with the product. As a consequence, distributors at the end of the supply chain accumulated used cores that were then typically either sold to or collected by pallet recyclers.

2.4 Brambles’ business terms, metrics and programs

43 The business terms that Brambles used and the metrics that it tracked included the following.

(a) Control ratio: the number of pallets recovered (returned or found) in a given time period as against the number issued (expressed as a percentage). This provides primary information on how effectively the pool is operating - the extent to which the control ratio falls below 100% indicates the degree to which pallets are not being returned to CHEP Global.

(b) Components per Repair or CPR: the average expense for consumption of lumber used to repair a CHEP pooled pallet.

(c) Conversion rate: being the value of customer ‘wins’ as a percentage of the total value of the sales funnel or pipeline.

(d) Cycle time: the average number of days taken for a pallet to return to CHEP Global having been dispatched to the manufacturer. A lower cycle time indicates a more efficient pallet pool, which reduces the need for capital expenditure on new pallets.

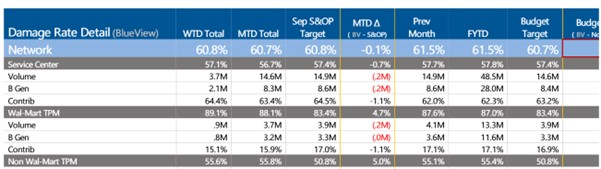

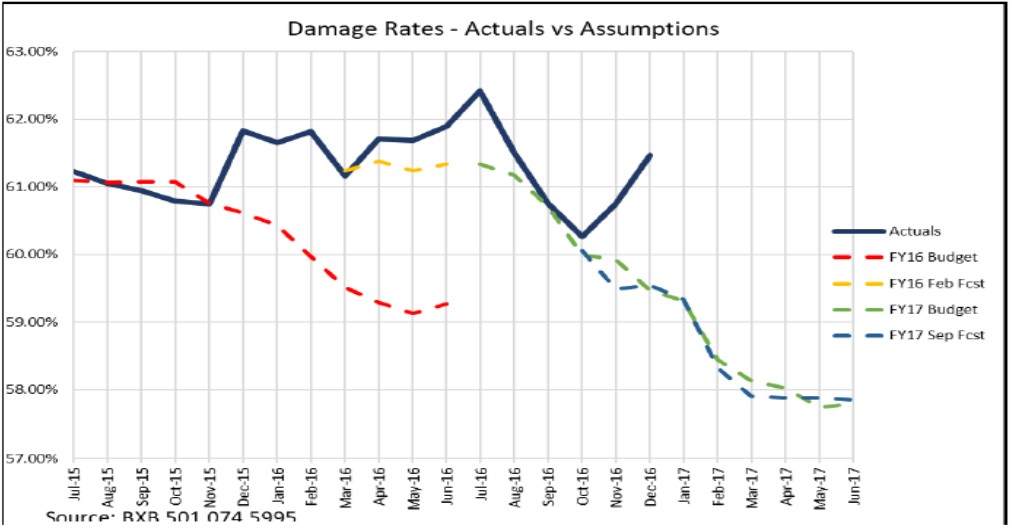

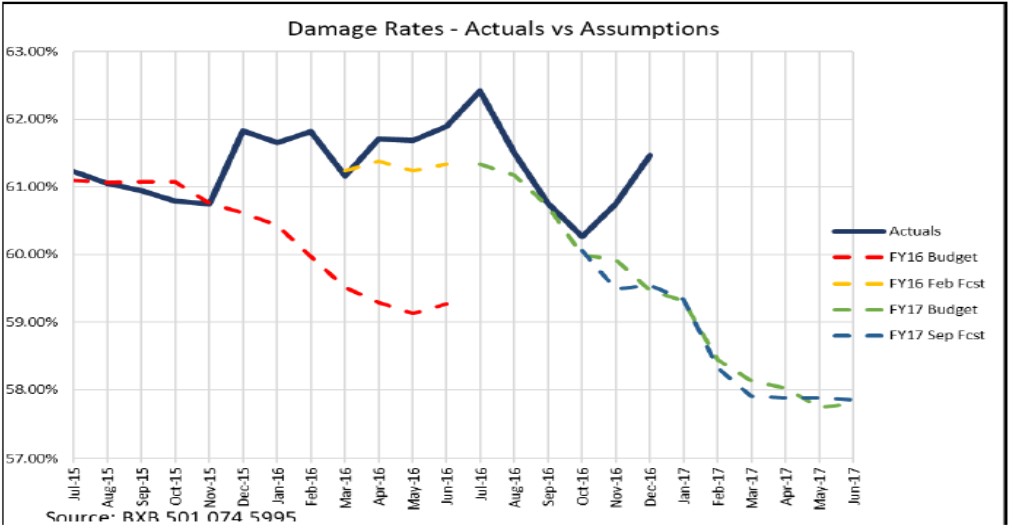

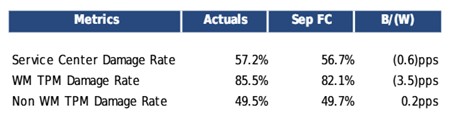

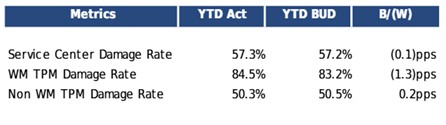

(e) Damage ratio: the percentage of pallets returned to the pool that require conditioning or repair, adjusted for movement in pallets between business units, which includes the following metrics:

(i) the network damage rate: the consolidated US Pooled damage rate;

(ii) the Service Centre damage rate: in FY16, this metric made up the majority (54%) of the contribution to the network damage rate increase that financial year;

(iii) the Walmart damage rate: Walmart pallets had a higher average damage rate than Service Centre and Non-Walmart Total Pallet Management pallets (TPM), due to Walmart's practice of holding on to usable pallets and only returning damaged pallets; and

(iv) the Non-Walmart damage rate: in FY16, TPMs at non-Walmart retailers contributed only a small amount (4%) to the network damage rate increase.

(f) Durability Program: this included two initiatives to increase the durability of pallets within the US Pooled pallet pool which were progressively incorporated across the division:

(i) adding clinched nails to the construction of new pallets and the repair of pallets returned to Service Centres; and

(ii) using nail plates in the construction of new pallets.

The Durability Program also impacted other cost metrics, such as a lower CPR resulting from the pallets needing less repairs.

(g) Durability Study: a pallet durability study conducted at the Pallet Test Track in Orlando, USA which reported in February 2015. The study was intended to simulate the real-world pallet environment, and its results informed the introduction of the Durability Program.

(h) IPEP: Brambles had a policy for managing and appropriately accounting for lost or irrecoverable pallets and other pooled equipment, known as the Irrecoverable Pooling Equipment Provision or IPEP policy. The IPEP was a provision held by Brambles to account for pooling equipment that could not be economically recovered and for which there was no reasonable expectation of receiving compensation, and was reflected on the balance sheet within accumulated depreciation.

(i) OneBetter Program: this program was introduced in around April 2014 for the purpose of reducing overhead costs across the Brambles Group, with its main focus being to centralise functions globally. The program included a dedicated project team who reported to Zlatko Todorcevski on issues including finance, IT, human resources and procurement. At the time the OneBetter Program was introduced, the program was expected to generate a total benefit of approximately $100 million across the Brambles Group by 2020.

(j) NPD upcharge (or surcharge): To account for the risk of higher costs associated with NPD channels, CHEP Global generally charged customers who distributed to NPDs an upcharge fee or surcharge. The NPD upcharge (or surcharge) was priced to accommodate the poor pallet visibility, higher risk of damage and loss, more complexity in collection, and higher costs associated with operating in these channels.

(k) Revenue Per Issue or RPI: the average revenue earned from each pallet issued, calculated as total sales revenue divided by number of pallets issued.

(l) Sales funnel or sales pipeline: the mechanism used by Brambles to organise and track potential new customers. US Pooled did not ‘sell’ pallets but rather leased pallets to customers to use to transport their goods. But US Pooled referred to ‘sales’ because that was the relevant discipline or skillset required to negotiate and enter into leasing contracts with customers.

(m) Sales revenue: what constitutes sales revenue depends upon the nature of the business in the relevant business unit. In US Pooled, sales revenue represented the totality of all fees received from issued pallets.

(n) Stretch: requests for enhanced performance from one level of management of the business to another, so as to enhance or optimise performance, were often referred to as ‘stretch’. The terms ‘go-get’ or ‘white space’ were also used to refer to stretch items within a budget which were not allocated to a specific action item, project or opportunity.

(o) Underlying Profit (also referred to as ULP within Brambles and EBIT (earnings before interest and tax) by some experts and market analysts): calculated by reference to statutory earnings, excluding acquisitions and related costs, restructuring and integration costs, impairment of goodwill and acquisition gains.

(p) Unidentified wins or volume stretch: referred to the total amount of new business Brambles expected to win in a financial year but which was not yet allocated to a specific or potential customer.

(q) Volume growth: referred to as positive or negative revenue growth of pallet volumes (i.e., not changes in price). Brambles recognised two types of volume growth:

(i) New wins: also referred to as new business, comprised of:

(A) Current year wins or CY wins: there are two types of CY wins: New customer contracts: contracts that are entered into in the current financial year; and Lane expansion: refers to securing additional volume in the current financial year under a new agreement with an existing customer, to expand to different products or to provide pallets in additional geographical regions; and

(B) Rollover wins: a contract was considered a rollover win for the portion of the initial 12 months of the contract that fell within the financial year after the year in which the contract was commenced. For example, if a customer signed a 12-month contract in October 2015, that contract would be considered a rollover win for July, August and September of 2016 (the last three months of the contract rollover into FY17); and

(ii) Organic growth: growth from an existing customer under an existing contract (i.e., issuing more pallets to a customer under a contract already in place).

(r) Rollover loss: the opposite of a rollover win, where the portion of the first 12 months of a customer contract loss fell within the financial year following the one in which the loss occurred.

2.5 Dramatis personae

44 The following Brambles officers and executives feature prominently in the case:

(a) Mr Stephen Johns was a non-executive director of Brambles from August 2004 to 30 June 2020. He was the Chair of the Board from 30 September 2014 to 30 June 2020.

(b) Mr Brian Long was a non-executive director of Brambles from 1 July 2014 to 8 October 2020. During that time, he was also a member of the Audit Committee. He was Chair of the Audit Committee from 30 September 2014 to 8 October 2020.

(c) Mr Tom Gorman was the Chief Executive Officer (CEO) of Brambles. He retired from his role as CEO on 20 February 2017.

(d) Mr Graham Chipchase was the CEO-Designate of Brambles from 1 January 2017 to the end of the Relevant Period. He became the CEO of Brambles on 20 February 2017.

(e) Mr Zlatko Todorcevski was the Chief Financial Officer (CFO) of Brambles from October 2012 to 17 November 2016. He retired from his role as CFO on 17 November 2016 but remained available to assist the new CFO until February 2017.

(f) Ms Nessa O’Sullivan was the CFO-Designate of Brambles from 10 October 2016 to 17 November 2016. She took over from Todorcevski as CFO of Brambles from 17 November 2016 to the end of the Relevant Period.

(g) Mr Peter Mackie was the Group President of CHEP Global, a role he held since March 2013. He reported to Gorman.

(h) Mr Philip “Buster” Kennett was the CFO and Senior Vice President of CHEP Global from 6 January 2014 to around the end of the Relevant Period. He reported directly to Mackie and had a functional “dotted-line” reporting structure to Todorcevski (until 16 November 2016) and then to O’Sullivan (from 17 November 2016).

(i) Mr Carmelo Alonso-Bernaola Ruiz was Senior Vice President, Supply Chain, for CHEP Global from September 2013 to the end of the Relevant Period. He reported directly to Mackie and, from early 2017, following a business restructure and realignment of the executive leadership team he reported to Chipchase.

(j) Ms Kim Rumph was the President of CHEP NA until 8 March 2017. She reported to Mackie.

(k) Mr Matthew Lallatin was the CFO of CHEP NA until around 7 October 2016. He reported directly to Rumph.

(l) Mr Bret Hill was the interim CFO of CHEP NA from 18 November 2016 until the end of the Relevant Period. He reported to Rumph.

(m) Ms Laura Nador was the Senior Vice President and General Manager of US Pooled from 1 July 2016 until the end of the Relevant Period. She reported to Rumph.

(n) Mr Daniel Martin (Martin) was the Senior Vice President, Sales and Customer Operations for CHEP NA from around July 2013 until the end of the Relevant Period. He reported to Nador.

2.6 The reporting and monitoring structures

45 The following account of the salient reporting and monitoring structures is drawn almost entirely from Brambles’ submissions:

(a) CHEP weekly volumes report: this report showed a comparison of issues of pallets in the month-to-date (MTD) against the budget or forecast volumes, and level of growth compared to the previous year. The pallet issues were reported on a regional basis within CHEP Global.

(b) ‘Pre-flash’ reports: in the third or fourth week of each reporting period, the Financial Planning and Analysis (FP&A) teams of each CHEP Global CBU prepared a ‘pre-flash’ report based on the data extracted from Brambles Reporting and Consolidation System (BRACS), being the central financial reporting system used by all the business units within Brambles. That report incorporated analysis of the financial results for the first two to three weeks of the reporting period and projections for the balance of the reporting period of each CHEP Global CBU. In FY17, the pre-flash report was due on the third Thursday of each month.

Once settled by the CHEP Global CBUs, the pre-flash reports were sent to the CHEP Global FP&A team. The usual process was then that the CHEP Global FP&A team:

(i) reviewed the pre-flash reports for each CBU and prepared a consolidated CHEP Global pre-flash report; and

(ii) circulated the consolidated pre-flash report to Mackie, Alonso and Kennett, among others.

Due to the time required to prepare the pre-flash report, it being based on an estimate rather than results following close of the month, and the cadence of other financial reporting by CHEP Global, this report was stopped in October 2016.

(c) Submission of monthly results: the final submission of monthly results for each business unit within each CBU was due to be loaded within BRACS four business days after the period end.2327

(d) ‘Flash’ reports: the FP&A team of each CHEP Global CBU usually prepared a flash report of the financial results for the business units of each CBU and sent the data via BRACS to the CHEP FP&A team around four business days following month end. A consolidated flash report for CHEP Global would then be produced and circulated by the CHEP Global FP&A team to Mackie and Kennett, among others.

The flash report provided a preliminary, high-level overview of the financial performance of the Group for the month (broken down into each business division), typically providing details of the revenue and Underlying Profit results from the preceding month and some breakdown of costs. It was prepared shortly after the results for the relevant reporting period became available in BRACS, so they were unaudited and unverified. It did not provide detailed commentary or explanations on the results for the relevant reporting period.

(e) Pallets Performance Review (PPR) reports and meetings: the PPR submission from each CHEP Global CBU was due six days after the period end. The PPR was a template presentation detailing the monthly performance of each CBU and was prepared by the FP&A and management teams of the CBU. Following the submission of the PPRs, around two weeks into each month, a PPR meeting was held with the President and CFO of each CBU and attended by Mackie, Alonso and Kennett to discuss their results for the prior month, including the status of customer negotiations, the competitive landscape and analysis of current and future projected performance.

With respect to the status of customer negotiations, the PPRs set out ‘highlights’ of customer and market opportunities. The purpose of the PPR was not to exhaustively list all wins or prospects.

(f) Business Performance Review (BPR) reports and meetings: each month, two performance review meetings were held for each business division (relevantly, CHEP Global). There was both a CFO BPR meeting and a CEO BPR meeting:

(i) CFO BPRs were held around 10 business days into the month (or around one week after the flash reports were produced). The CFO from the business division (for CHEP Global, being Kennett) would attend and present the results of their division, including data on sales revenue, Underlying Profit and costs for the month and year-to-date (or YTD) to Brambles’ CEO and CFO, Mackie, Alonso and members of the Group FP&A team. The CFO BPR included a discussion of market conditions, including competition, monthly financial results and projections for the balance of the year. Ordinarily, the CFOs (including Kennett) would provide this data one or two days prior to the meeting in the form of a slide deck (CFO BPR Report), prepared following receipt of the PPRs from each CBU.

(ii) CEO BPRs took place around the third week of each month, after the CFO BPRs. These reviews were attended by both the Group President (for CHEP Global, being Mackie) and CFO of the business division, and by Brambles’ CEO and CFO, Kennett, Alonso and members of the Group FP&A team. The purpose of the CEO BPRs was to discuss the safety, financial performance, customers and competition of CHEP Global, as well as strategy and business initiatives, including the outlook for the balance of the financial year. It was usual practice for a slide deck or pack of materials to be circulated in advance of the CEO BPR meetings by members of the business division (CEO BPR Report).

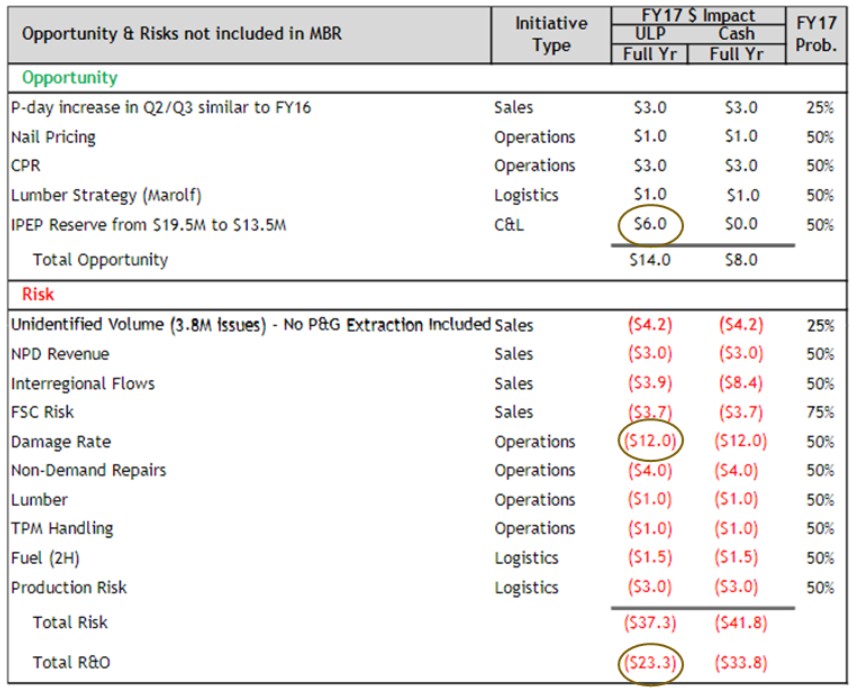

(g) Quarterly reforecasts: in order to monitor its performance against the budget and five-year plan (5YP), Brambles also undertook a quarterly forecast or ‘reforecast’ process in or around September, December and February each year, which assessed current and projected financial results against budget and earnings guidance. The quarterly forecast considered the risks and opportunities known to the business at the time each quarterly forecast was developed. The quarterly forecast involved each CBU again adopting a ‘bottom-up’ approach with ‘top-down’ review by the business division (e.g., CHEP Global). The two reforecasts relevant to this proceeding were prepared by Brambles in September and October 2016 (September Reforecast) and in December 2016 (December Reforecast).

46 Other structured reports and meetings included:

(a) Brambles’ Executive Leadership Team (Brambles’ ELT): Brambles’ ELT comprised the CEO, CFO, the Presidents of each business division, Jean Holley (Group Senior Vice President and Chief Information Officer) and Nicholas Smith (Group Senior Vice President (Human Resources)). On a monthly basis, the ELT (and generally members of the Group FP&A team) met to discuss the financial performance across the Group (including any areas of shortfall in performance), market consensus updates, strategic updates and group governance issues.

(b) At the CHEP Global level:

(i) PLT meetings: on a quarterly basis, the Pallets Leadership Team (CHEP Global PLT) met to discuss the global business performance and strategic direction of CHEP Global; and

(ii) Brambles Strategy Review (BSR) meetings: on a quarterly basis, members of the ELT met to discuss CHEP Global’s progress on the strategic initiatives behind the five-year plan and the long-term strategy for the business division as part of the Group's overall strategic goals.

(c) At the CHEP NA and US Pooled levels:

(i) CHEP NA Executive Leadership Team (CHEP NA ELT): comprised Lallatin, Chris Young (Senior Vice President, Supply Chain, CHEP NA), Daniel Gormley (Vice President, Asset Management, US Pooled), Steve Nebeker (Vice President, Strategic Planning, CHEP NA) and Vishal Patell (Vice President, Retail Solutions, US Pooled).

(ii) US Pooled Executive Leadership Team (US Pooled ELT): comprised Nador (Senior Vice President and General Manager of US Pooled), Martin (Senior Vice President Sales and Customer Operations), Patell, Gormley and Ana Baltasar (Senior Finance Director of US Pooled);

(iii) Monthly Business Review (MBR): the MBR report was a month-in-progress business review of the results for the first two to three weeks of each reporting period, sales pipeline review (of new and existing business) and Risk and Opportunities analysis (R&O schedule). The MBR meeting was generally held during the third week of each reporting period, attended by the CHEP NA leadership team, as well as the key functional leaders of the CHEP NA businesses (including US Pooled) and the business partners in the FP&A team;

(iv) Monthly close deck: the US Pooled close deck was a monthly review of the results for US Pooled for each reporting period. The US Pooled close meeting was held approximately one week after the close of the reporting period, and was where the US Pooled team, together with senior members of the CHEP NA team, discussed the US Pooled close deck;

(v) Monthly Sales Funnel Reports: US Pooled generated monthly Sales Funnel Reports, which set out in significant detail and updated on a rolling basis the opportunities in the sales funnel that were being pursued by US Pooled that underpinned the unidentified new wins assumptions, including annual volumes and the proportion new issues that may be secured in the current year.2345 The Sales Funnel Reports were extracted from the Bluesheet App, a software program that US Pooled used to store, navigate, monitor and update each sales opportunity in the sales funnel, with each opportunity being referred to as a ‘bluesheet’; and

(vi) Monthly Sales and Operations Planning (S&OP) Demand Consensus Reports (Demand Consensus Reports): These were prepared by the US Pooled S&OP team and constituted a demand projection and assessment of individual customer accounts from the sales pipeline, as well as an assessment of organic growth. It also factored in feedback from customers.

(d) Brambles’ Board of Directors (Board): Brambles’ Board met on a monthly basis other than in July. The Board meetings followed a regular cycle which included six in-person meetings and five conference call meetings throughout each financial year. In-person Board meetings were typically scheduled in:

(i) February, when the Board discussed the results for the first half of the financial year and related market disclosures (in Sydney);

(ii) April, when the Board discussed the company’s five-year plan;

(iii) June, when the annual budget was presented to the Board for approval;

(iv) August, when the Board discussed the full-year financial results and related market disclosures (in Sydney);

(v) October, when the Board participated in an annual strategy day; and

(vi) November, shortly before the AGM (in Sydney).

(e) Reporting to the Board generally included the following:

(i) the presentation of a Financial Update at the monthly Board meeting by the CFO. The Financial Update was in the form of a slide deck and was based on the monthly discussions during the CFO BPR and CEO BPR meetings. It included a report on the revenue, Underlying Profit and cash flow results across the Group for the preceding month and the YTD compared against budget and the most recent forecast (if applicable);

(ii) Board packs were provided to the Board in advance of Board meetings, which contained the agenda and Board papers for the relevant meeting, including any slide deck for the Financial Update, and any additional papers for consideration during the relevant Board meeting depending on the time of year (for example, the budget and five-year plan papers for the following financial year would be provided in advance of the June Board meeting); and

(iii) a detailed, monthly Board Report, which was prepared and circulated after the Board meeting (often the following month). It was prepared in a pro-forma template setting out, among other matters, commentary on the Group’s financial results and business performance including developments in geographic markets relating to competition.

3. OVERVIEW OF CLAIMS

47 On 18 August 2016, Brambles published three announcements to the ASX. The applicants alleged that in those announcements, Brambles stated the following earnings guidance to the market:

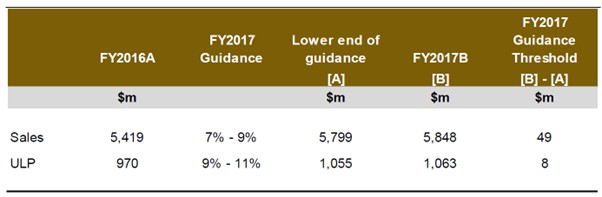

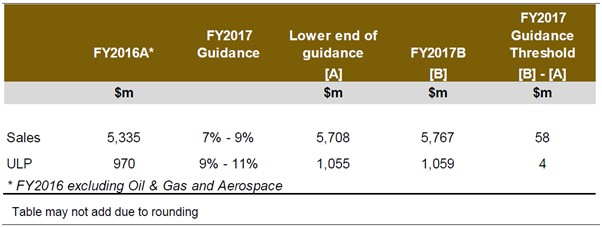

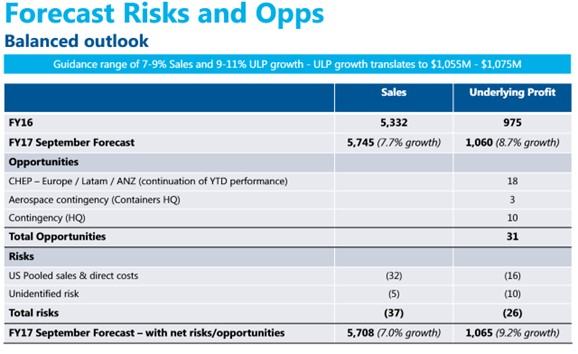

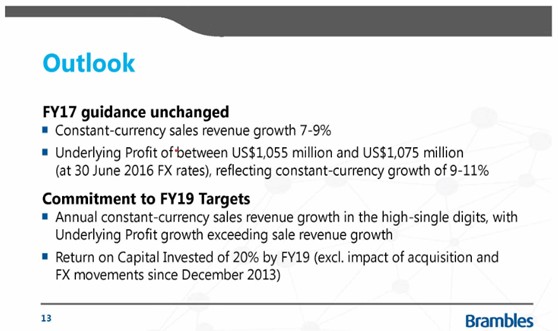

(a) sales revenue growth for FY17 at constant currency of between 7% and 9%; and

(b) Underlying Profit growth in FY17 of between 9% to 11%, equating to a range of between $1,055 million and $1,075 million, at 30 June 2016 foreign exchange rates.

(together, the FY17 Guidance).

48 The applicants also alleged that in those announcements Brambles reaffirmed its target for return on capital invested (ROCI) of 20% by the end of FY19 (excluding foreign exchange impacts and acquisitions made since December 2013 when this target was set) (which I previously identified as the FY19 ROCI Target), and its FY19 targets of constant currency sales revenue growth in the high-single digits, with Underlying Profit growth exceeding sales revenue growth (which I previously identified as the Medium-Term Targets).

49 The Amended Consolidated Statement of Claim (ACSOC) alleged two broad categories of claim.

50 First, that Brambles published its earnings guidance to the market of investors and potential investors in Brambles shares on 18 August 2016, and reaffirmed or maintained that guidance on 20 October and 16 November 2016. On each occasion, Brambles is alleged to have made, reaffirmed or maintained the representations as to each constituent part of the guidance. The representations are alleged to be continuing representations throughout the Relevant Period. The applicants alleged that those representations were misleading and deceptive because they lacked reasonable grounds, having been based on the Group FY17 budget, prepared in substance between February and June 2016, which, among other things, relied on unreasonable assumptions, failed to take adequate account of the predictable negative effects that decisions taken by Brambles in FY16 would have on revenue and costs for US Pooled in FY17, and was infected with unreasonable stretch.

51 The claim of misleading or deceptive conduct does not only turn on Brambles making the representations on 18 August 2016, but also upon Brambles not having revised or corrected those representations during the Relevant Period. The applicants relied upon the totality of Brambles’ conduct, including its reaffirmation of the express representations and its silence in relation to those representations thereafter, as Brambles’ financial performance deteriorated. The applicants also relied on Brambles’ silence in the context that it was bound to comply with the continuous disclosure regime under ASX Listing Rule 3.1 and s 674(2) of the Corporations Act. It is alleged that in that context the market of investors and potential investors in Brambles shares had a reasonable expectation that Brambles would immediately inform the ASX if the representations did not have reasonable grounds.

52 The representations are alleged to be misleading or deceptive or likely to mislead or deceive in contravention of s 1041H(1) of the Corporations Act, s 12DA(1) of the Australian Securities and Investments Commission Act 2001 (Cth) (the ASIC Act) and s 18(1) of the Australian Consumer Law (the ACL) in sch 2 of the Competition and Consumer Act 2010 (Cth) (the CCA), because they were representations as to future matters and Brambles did not have reasonable grounds for making them.

53 Second, that Brambles contravened the obligation of continuous disclosure under ASX Listing Rule 3.1 and s 674(2) of the Corporations Act because it was aware, or ought reasonably to have been aware, on and from 18 August, 20 October or 16 November 2016, that it was likely, or there was at least a material risk, that it would not achieve the FY17 Guidance, FY19 ROCI Target and / or the Medium-Term Targets. That is alleged to be “information” which a reasonable person would expect, if it were generally available, to have a material effect on the price or value of Brambles shares on the ASX, and Brambles was obligated to immediately tell the ASX that information.

54 It is uncontroversial that Brambles did not inform the ASX that it would not achieve the FY17 Guidance until 23 January 2017, and it did not withdraw the FY19 ROCI Target until 20 February 2017.

3.1 The alleged August 2016 contraventions

55 As noted above, the ACSOC alleged that on or about 18 August 2016, Brambles stated to the market that, or to the effect that:

(a) for FY17 Brambles forecast that it would achieve year-on-year growth in sales revenue of between 7% and 9% (defined as the August Sales Revenue Forecast);

(b) for FY17 Brambles forecast that it would achieve year-on-year growth in Underlying Profit of between 9% and 11% (defined as the August Underlying Profit Forecast); and

(c) Brambles reiterated a target for ROCI of 20% by FY19 (defined as the August ROCI Forecast)

(which I collectively call the August Express Representations).

56 The ACSOC further alleged that Brambles made other express representations on 18 August 2016, namely the August Price Representation, and the Medium-Term Targets. However:

(a) the alleged August Price Representation and August Costs Representations were not the subject of detailed submissions by the applicants independent of the August Underlying Profit Forecast. The applicants gave little or no attention to these representations in cross-examination of Brambles’ witnesses or in closing submissions; and

(b) the alleged Medium-Term Targets were not concerned solely with FY17 financial results. It concerned the position in which Brambles expected to be by the end of FY19 (30 June 2020). They alleged that Brambles reaffirmed its FY19 targets of constant currency sales revenue growth in the high-single digits and its FY19 targets of Underlying Profit growth exceeding sales revenue growth. The applicants gave little attention to the Medium-Term Targets in cross-examination of Brambles’ witnesses or in closing submissions. Nor did the applicants take the Court to evidence to rebut Brambles’ contention that there was almost three years between the time the Group FY17 budget was set and when the Medium-Term Targets were due to be met, and that even if Brambles did not meet the FY17 Guidance there was time for Brambles to meet the Medium-Term Targets.

57 In large part, the way in which the applicants’ submissions addressed the August Costs Representations, the August Price Representation, and the Medium-Term Targets representation was just to tack them on to arguments which centrally related to the FY17 Guidance.

58 In a case this large, with so many contested issues, it was inappropriate for the applicants to continue to formally advance those representations but to put on little or nothing by way of evidence or submissions to make them out. If it was not sufficiently important for the applicants to give proper attention to those allegations, then the Court should not be required to deal with them. In my view, given the applicants’ approach to these representations, it is unnecessary to deal with them.

59 I am confirmed in that view because little turns on those alleged representations. If the applicants’ misleading and deceptive conduct claims succeed in relation to the August Sales Revenue Forecast and the August Underlying Profit Forecast, little is added by the August Costs Representations, the August Price Representation, and the Medium-Term Targets. And if the applicants’ claims in relation to the August Sales Revenue Forecast and August Underlying Profit Forecast do not succeed, the applicants are likely to fail on the other pleaded representations.

60 My approach in this regard is not limited to the position as at 18 August 2016. I take the same approach to:

(a) analogous representations to the August Costs Representation such as the October Costs Representation alleged as at 20 October 2016, and the alleged reiteration of the August Costs Representation as at 16 November 2016; and

(b) the Medium-Term Targets representation when picked up as at 20 October 2016 by the October Medium-Term Outlook Representation (as defined later in these reasons) and the alleged reiteration of the Medium-Term Targets representation as at 16 November 2016.

The same applies to the extent that the Medium-Term Targets are integrated into the 23 January Representations as defined later in these reasons, as well as the way they are integrated into the August Information, October Information, and November Information (defined below) in respect of the alleged continuous disclosure contraventions.

61 It is alleged that, by making the express August Sales Revenue Forecast, the August Underlying Profit Forecast and the August ROCI Forecast, Brambles impliedly represented to the market that:

(a) it had undertaken all necessary and reasonable investigations before making any statement or representation as to the state of its business and accounts and had satisfied itself on reasonable grounds following those investigations that the public statements were substantially accurate and not misleading or deceptive in any respect (August All Reasonable Investigations Implied Representation); and

(b) no information had come to the attention of Brambles that meant that there was any material risk that Brambles would not achieve the FY17 Guidance, FY19 ROCI Target or the other alleged representations (August No Material Risk Implied Representation)

(together, the August Implied Representations). The ACSOC pleaded the same implied representations as at 20 October and 16 November 2016.

62 The ACSOC alleged that the alleged express and implied representations (together, the August Representations) were continuing representations. That is, they continued to operate until they were qualified or withdrawn by Brambles. It is alleged that they were not wholly corrected by Brambles until either 23 January 2017 or 20 February 2017.

63 The August Representations are alleged to be:

(a) conduct in trade or commerce;

(b) in relation to a “financial product” and a “financial service” within the meaning of the relevant subsections of the Corporations Act and the ASIC Act;

(c) as to the August Sales Revenue Forecast, August Underlying Profit Forecast and August ROCI Forecast, made in relation to future matters within the meaning of s 769C of the Corporations Act, s 12BB of the ASIC Act, or s 4 of the ACL. On that basis it is alleged the representations are taken to be misleading or deceptive unless there existed reasonable grounds for those representations at the time Brambles made them; and

(d) information that a reasonable person would expect to have a material effect on the price or value of Brambles shares.

64 Then, a plethora of matters are alleged in relation to what is said to be the true state of Brambles’ business as at 18 August 2016, referring to features of Brambles’ performance in FY16 (all in US Pooled and CHEP NA) which are alleged to have meant that Brambles’ growth in sales revenue and Underlying Profit in FY16 was unlikely to be repeated in FY17. I will not set out those allegations. I cover them when dealing with the facts.

65 Then, by reference to a variety of matters, it is alleged that the budget-setting process for the CHEP NA FY17 budget (including the US Pooled FY17 budget), and as a result the CHEP Global FY17 budget and the Group FY17 budget (for Brambles overall), was flawed including because it involved unreasonable assumptions, failed to adequately take account of known or identified risks, and was infected by significant “top-down” pressure from management to impose stretch targets in CHEP NA, and in particular US Pooled. I will not set out those allegations here.

66 Brambles’ Board approved the Group FY17 budget on or about 28 June 2016. The ACSOC alleged that the actual US Pooled and CHEP NA trading results for July 2016 showed below-budget performance in terms of sales revenue and Underlying Profit growth in that month. It is alleged that as at 18 August 2016 (which took into account the actual July 2016 results) a variety of matters including sales revenue, average RPI, the damage rate, direct costs and other metrics meant that it was likely, or alternatively there was a material risk, that in FY17 Brambles would experience a material increase in the costs incurred in US Pooled, and that the revenue earned by Brambles from US Pooled and from CHEP Recycled would decrease, or alternatively would not be sufficient to offset the increase in costs.

67 It is alleged that as at 18 August 2016, it was likely, or alternatively there was a material risk, that Brambles would not achieve, among other alleged representations, the August Sales Revenue Forecast, the August Underlying Profit Forecast and the August ROCI Forecast.

68 The following “information” is alleged to have existed as at and from 18 August 2016:

(a) in respect of sales revenue, it was likely or there was at least a material risk that in Brambles would not achieve year-on-year sales revenue growth of between 7% and 9% in FY17, or its medium term target of constant currency sales revenue growth in the high single digits; and an integral reason for this was that revenue in US Pooled would likely not meet budget in FY17; and

(b) in respect of Underlying Profit, it was likely or there was at least a material risk that Brambles would not achieve year-on-year Underlying Profit growth of between 9% and 11% in FY17, its medium term target of Underlying Profit growth exceeding sales revenue growth or its ROCI target of 20% by FY19; and integral reasons for this were that revenue in US Pooled would likely not meet budget in FY17 and direct costs were going up.

(defined as the August Information). When referred to together with the same information in October and November, this is the Primary Information.

69 It is alleged that (within the meaning of s 674(2) of the Corporations Act):

(a) Brambles had the August Information by no later than 18 August 2016;

(b) the August Information was not generally available; and

(c) a reasonable person would expect the August Information, if it were generally available, to have a material effect on the price or value of Brambles shares.

70 The applicants alleged that Brambles was required by operation of ASX Listing Rule 3.1 to notify that information to the ASX by no later than 18 August 2016, and it did not tell the ASX that information at any time prior to 23 January 2017 or alternatively prior to 20 February 2017. It thereby contravened its continuous disclosure obligation under s 674(2) as at 18 August 2016, and on each day between 18 August 2016 and 23 January 2017 when the August Information was alleged to be partially disclosed, or alternatively at any time prior to 20 February 2017 when it was alleged to be fully disclosed (together with the previous disclosure in January), defined as the August Continuous Disclosure Contraventions.

71 In the alternative, the ACSOC alleged that, as at and from 18 August 2016, Brambles breached its continuous disclosure obligation by failing to disclose certain specified pieces of information (described as Alternative Information) which were available at that time, defined as the Alternative August Continuous Disclosure Contraventions. Brambles also alleged similar contraventions, although based on different pieces of Alternative Information, at and from both 20 October 2016 and 16 November 2016. The applicants, however, abandoned the “Alternative Information” claims during the trial and it is unnecessary to summarise them. Having regard to the applicants’ abandonment of this alternative case I will not further refer to it.

72 Based on the same factual matters that are alleged to underpin the August Continuous Disclosure Contraventions, it is alleged that Brambles:

(a) did not, by 18 August 2016, have reasonable grounds for making the August Sales Revenue Forecast, the August Underlying Profit Forecast or the August ROCI Forecast;

(b) by reason of the matters in (a) did not have reasonable grounds for the representations with respect to future matters in (a) within the meaning of s 769C of the Corporations Act and/or its analogues; and

(c) in the premises, by making the August Representations, engaged in conduct that was misleading or deceptive or that was likely to mislead or deceive in contravention of s 1041H of the Corporations Act and/or its analogues

(the August Misleading Conduct Contraventions).

73 In the period from 18 August 2016 to the end of the Relevant Period, the applicants alleged that the August Continuous Disclosure Contraventions and August Misleading Conduct Contraventions (the August Contravening Conduct) caused the traded price for Brambles shares to be materially higher than their true value or the price that would have existed if the August Contravening Conduct had not occurred.

3.2 The alleged October 2016 contraventions

74 In relation to the alleged contraventions on and from 20 October 2016 the ACSOC adopted the same pleading structure as the alleged August 2016 contraventions.

75 The ACSOC alleged that on 20 October 2016, when Brambles published its First Quarter Trading Update (Q1 Trading Update) to the ASX it stated that, or to the effect that (among other things):

(a) it expected to earn sufficient revenue from new business in US Pooled in 2H17 to achieve the August Underlying Profit Forecast, defined as the October Revenue Representation; and

(b) repeated and thereby reaffirmed the August Underlying Profit Forecast, defined as the October Underlying Profit Representation

(together, the October Express Representations).

76 Again, the ACSOC alleged that Brambles made some other express representations at that time, namely the October Costs Representation and the October Medium-Term Outlook Representation. For the reasons I expressed earlier it is unnecessary to set those representations out when at trial the applicants said little or nothing about them independent of the October Revenue Representation and the October Underlying Profit Representation, and they add little. As earlier noted, having regard to the applicants’ approach to these representations I consider it unnecessary to deal with them.

77 The alleged express representations are alleged to have carried the same implied representations to those conveyed in August (defined as the October Implied Representations). The ACSOC alleged that the alleged express and implied representations (together, the October Representations) were continuing representations. That is, that they continued to operate until they were qualified or withdrawn by Brambles. It is alleged that they were not wholly corrected by Brambles until either 23 January 2017 or 20 February 2017.

78 As with the August Express Representations, the October Express Representations are alleged to be:

(a) conduct in trade or commerce;

(b) in relation to a “financial product” and a “financial service” within the meaning of the relevant subsections of the Corporations Act and the ASIC Act;

(c) made in relation to future matters within the meaning of s 769C of the Corporations Act and/or its analogues. Again, on that basis it is alleged the representations are taken to be misleading or deceptive unless there existed reasonable grounds for those representations at the time Brambles made them; and

(d) information that a reasonable person would expect to have a material effect on the price or value of Brambles shares.

79 Again, a large number of factual matters are alleged regarding the true state of Brambles’ business as at 20 October 2016, including that the indicators as to Brambles’ financial situation, performance and prospects in FY17 had not improved since August 2016, and had in fact worsened. I will not set out those allegations here.