Federal Court of Australia

Australian Securities and Investments Commission v Macquarie Investment Management Limited [2026] FCA 303

File number(s): | VID 1280 of 2025 |

Judgment of: | WHEELAHAN J |

Date of judgment: | 20 March 2026 |

Catchwords: | CORPORATIONS – duty of a financial services licensee under s 912A(1)(a) of the Corporations Act 2001 (Cth) to do all things necessary to ensure that the financial services covered by the licence are provided efficiently, honestly and fairly – defendant was the trustee of the Macquarie Superannuation Plan – plaintiff alleges that the defendant contravened s 912A(1)(a) and s 912A(5A) of the Act in relation to the facilitation of investments in the Shield Master Fund on behalf its members – Shield Master Fund terminated – application for declarations of contravention – contraventions admitted by defendant – no application for pecuniary penalty – whether Court should make declarations sought – orders appropriate – relief granted |

Legislation: | Australian Securities and Investments Commission Act 2001 (Cth) s 93AA Corporations Act 2001 (Cth) ss 760A, 912A(1)(a), 912A(5A), 1317E Evidence Act 1995 (Cth) s 191(2)(a) Superannuation Industry (Supervision) Act 1993 (Cth) ss 10(1), 19(1) |

Cases cited: | Australian Building and Construction Commission v Construction, Forestry, Mining and Energy Union [2017] FCAFC 113; 254 FCR 68 Australian Competition and Consumer Commission v MSY Technology Pty Ltd [2012] FCAFC 56; 201 FCR 378 Australian Securities and Investments Commission v AGM Markets Pty Ltd (in liq) [2020] FCAFC 208; 275 FCR 57 Australian Securities and Investments Commission v AustralianSuper Pty Ltd [2025] FCA 102; 172 ACSR 615 Australian Securities and Investments Commission v Commonwealth Bank of Australia [2022] FCA 1422 Australian Securities and Investments Commission v Keystone Asset Management Ltd [2024] FCA 1019 Australian Securities and Investments Commission v National Australia Bank Limited [2022] FCA 1324; 164 ACSR 358 Australian Securities and Investments Commission v Westpac Securities Administration Ltd [2019] FCAFC 187; (2019) 272 FCR 170 Commonwealth v Director, Fair Work Building Industry Inspectorate [2015] HCA 46; 258 CLR 482 Forster v Jododex Australia Pty Ltd [1972] HCA 61; 127 CLR 421 |

Division: | General Division |

Registry: | Victoria |

National Practice Area: | Commercial and Corporations |

Sub-area: | Regulator and Consumer Protection |

Number of paragraphs: | 32 |

Date of hearing: | 20 March 2026 |

Counsel for the plaintiff: | Mr S Parmenter KC with Ms A Mobrici |

Counsel for the defendant: | Mr D Sulan SC |

Solicitors for the defendant: | Allens |

ORDERS

VID1280 of 2025 | ||

IN THE MATTER OF MACQUARIE INVESTMENT MANAGEMENT LTD (ACN 002 867 003) IN ITS CAPACITY AS TRUSTEE OF THE MACQUARIE SUPERANNUATION PLAN | ||

BETWEEN: | AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff | |

AND: | MACQUARIE INVESTMENT MANAGEMENT LTD (ACN 002 867 003) IN ITS CAPACITY AS TRUSTEE OF THE MACQUARIE SUPERANNUATION PLAM Defendant | |

order made by: | WHEELAHAN J |

DATE OF ORDER: | 20 MARCH 2026 |

THE COURT NOTES THAT:

Terms used in the declarations below are to be construed in the context of the Court’s reasons for judgment in this proceeding published this day.

THE COURT DECLARES THAT:

1. By 1 March 2022 (being the date on which the Conservative, Balanced and Growth classes of the Shield Master Fund were added to Macquarie Wrap), the defendant ought to have placed each of those classes of the Shield Master Fund on a watch list, such as the Watch List referred to in its Investment Governance Framework, in order that they could be subject to further monitoring action, including in accordance with the provisions of the Investment Governance Framework, additional reporting, due diligence, performance monitoring or other follow up action, but did not do so.

2. In the period between 1 March 2022 and 5 June 2023 (being the period during which the Conservative, Balanced and Growth classes of the Shield Master Fund were investment options on Macquarie Wrap), the defendant ought to have placed each of those classes of the Shield Master Fund on a watch list, such as the Watch List referred to in the Investment Governance Framework, in order that they could be subject to further monitoring action, including in accordance with the provisions of the Investment Governance Framework, additional reporting, due diligence, performance monitoring or other follow up action, but did not do so.

3. By 6 May 2022 (being the date on which the High Growth class of the Shield Master Fund was added to Wrap), the defendant ought to have placed that class of the Shield Master Fund on a watch list, such as the Watch List referred to in the Investment Governance Framework, in order that it could be subject to further monitoring action, including in accordance with the provisions of the Investment Governance Framework, additional reporting, due diligence, performance monitoring or other follow up action, but did not do so.

4. In the period between 6 May 2022 and 5 June 2023 (being the period during which the High Growth class of the Shield Master Fund was an investment option on Wrap), the defendant ought to have placed that class of the Shield Master Fund on a watch list, such as the Watch List referred to in the Investment Governance Framework, in order that it could be subject to further monitoring action, including in accordance with the provisions of the Investment Governance Framework, additional reporting, due diligence, performance monitoring or other follow up action, but did not do so.

5. By reason of the matters referred to in each of declarations 1, 2, 3 and 4 above, at all times between 1 March 2022 and 5 June 2023, the defendant failed to do all things necessary to ensure that the financial services covered by its financial services licence were provided efficiently, honestly and fairly, and the defendant thereby contravened s 912A(l)(a) of the Corporations Act 2001 (Cth).

6. By reason of each of the contraventions referred to in declaration 5 above, the defendant contravened s 912A(5A) of the Corporations Act 2001 (Cth).

THE COURT ORDERS THAT:

7. The defendant is to pay the plaintiff’s costs of the proceeding as agreed, or in the absence of agreement, to be taxed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

WHEELAHAN J:

1 This regulatory proceeding arises out of the collapse in late 2024 of a registered management investment scheme known as the Shield Master Fund. The responsible entity for the Shield Master Fund was Keystone Asset Management Ltd (Keystone). On 27 August 2024, on the application of the plaintiff, the Australian Securities and Investments Commission (ASIC), the Court appointed receivers and managers to all property of Keystone held otherwise than as sole beneficial owner: Australian Securities and Investments Commission v Keystone Asset Management Ltd [2024] FCA 1019 (Moshinsky J). Keystone is now in liquidation, and the Shield Master Fund has been terminated.

2 The defendant, Macquarie Investment Management Ltd (Macquarie), is the trustee of the Macquarie Superannuation Plan which invested in the Shield Master Fund on behalf of its members. ASIC alleges that Macquarie contravened s 912A(1)(a) and s 912A(5A) of the Corporations Act 2001 (Cth) in relation to its facilitation of these investments and seeks declarations of contravention accordingly.

The Macquarie Superannuation Plan

3 The Macquarie Superannuation Plan is a regulated superannuation fund within the meaning of s 19(1) of the Superannuation Industry (Supervision) Act 1993 (Cth), which in turn makes it a registrable superannuation entity within the meaning of s 10(1) of that Act. Macquarie, as trustee of the Macquarie Superannuation Plan, is subject to various requirements under the Superannuation Industry (Supervision) Act, such as compliance with a prudential standard relating to investment governance titled Superannuation Prudential Standard SPS 530 - Investment Governance. Macquarie is also subject to obligations and duties that attach to it as trustee under general law and under the terms of the trust deed.

4 Macquarie is the holder of an Australian financial services licence. The terms of Macquarie’s financial services licence authorise it to deal in financial products such as interests in managed investment schemes, investor directed portfolio services, and superannuation. As the holder of a financial services licence Macquarie is subject to the obligation of financial services licensees under s 912A(1)(a) of the Corporations Act. That obligation is to –

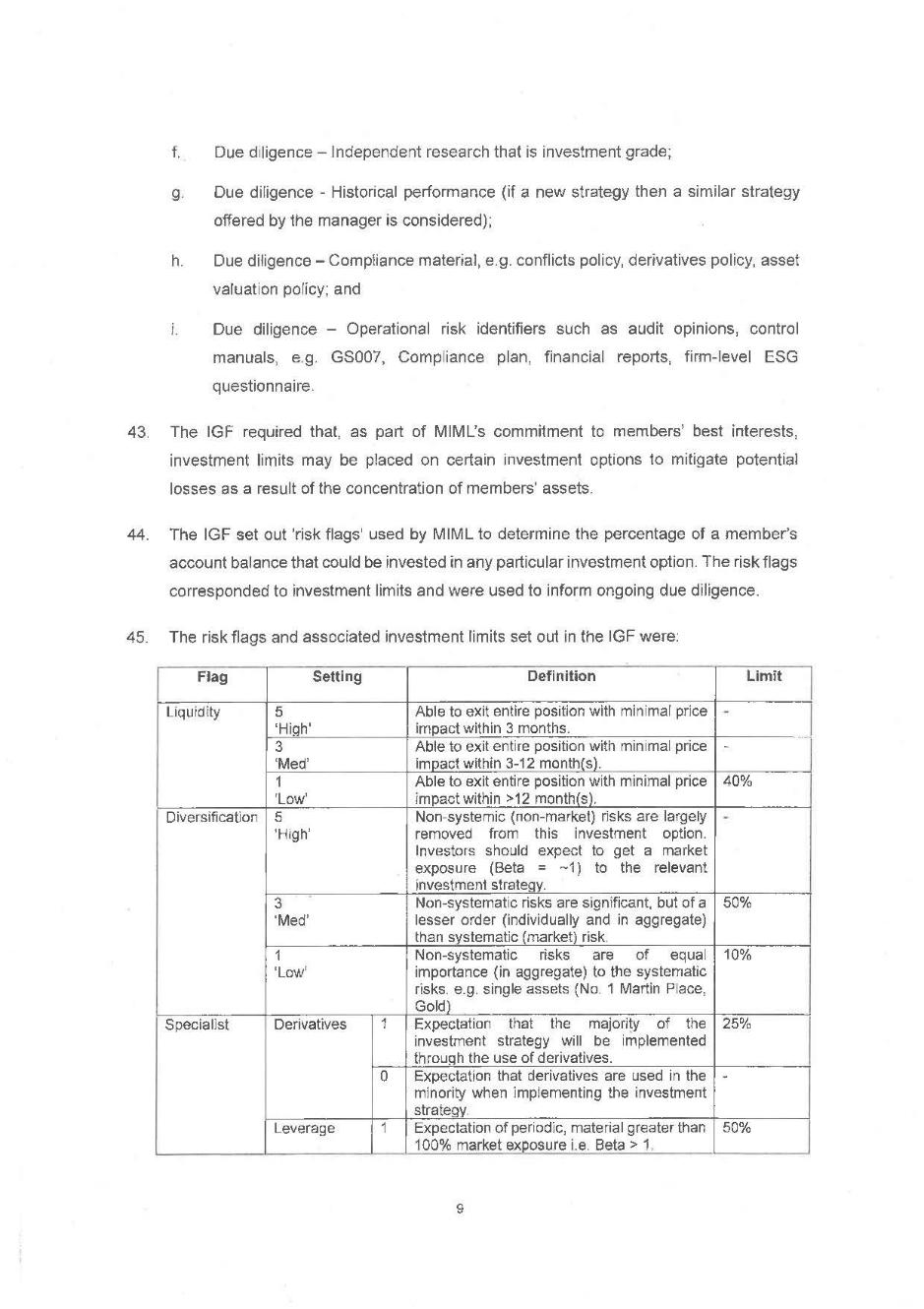

do all things necessary to ensure that the financial services covered by the licence are provided efficiently, honestly and fairly;

5 A person who contravenes s 912A(1)(a) contravenes s 912A(5A), which is a civil penalty provision.

6 At 31 August 2025, the Macquarie Superannuation Plan had 123,620 members and net assets of $50.78 billion. The Macquarie Superannuation Plan formed part of a broader investment platform operated by Macquarie known as the Macquarie Wrap. The Wrap provided members of the Superannuation Plan with investment options including managed funds, separately managed accounts, international and domestic securities, term deposits and insurance options. There were hundreds of managed funds available as investment options under the Wrap.

7 Macquarie included investment in the Shield Master Fund as one of the options available under its Wrap. The effect of that inclusion was that members or financial advisers on their behalf could direct Macquarie to invest in the Shield Master Fund as one of the options on the investment menu for the Wrap.

8 Between 1 March 2022 and 5 June 2023, approximately 3,060 Macquarie Superannuation Plan accounts held investments in the Shield Master Fund. Some of the Shield Master Fund units held in those accounts have since been redeemed. At 24 September 2025, 2,833 Macquarie Superannuation Plan accounts held investments in the Shield Master Fund. These accounts had a total net capital invested in the Shield Master Fund of approximately $321 million.

The duty under s 912A(1)(a) of the Corporations Act

9 The applicable principles relating to the duty of a financial services licensee under s 912A(1)(a) of the Corporations Act were not in issue in this proceeding and the following account reflects a broad acceptance of the parties’ submissions.

10 The duty under s 912A(1)(a) is to do all things necessary to ensure that the financial services covered by the licence are provided efficiently, honestly and fairly. The provision is itself a source of legal obligation and a contravention of the provision does not require a contravention or breach of a separately existing legal duty or obligation: Australian Securities and Investments Commission v AGM Markets Pty Ltd (in liq) [2020] FCA 208; 275 FCR 57 (AGM Markets) at [512] (Beach J). The statutory obligation does not require a standard of absolute perfection but imposes a reasonable standard of performance: Australian Securities and Investments Commission v National Australia Bank Limited [2022] FCA 1324; 164 ACSR 358 at [364] (Derrington J); Australian Securities and Investments Commission v Commonwealth Bank of Australia [2022] FCA 1422 at [152] (Downes J). The parties submitted that the obligation requires that there be adherence to social and commercial norms or standards of behaviour: Australian Securities and Investments Commission v Westpac Securities Administration Ltd [2019] FCAFC 187; (2019) 272 FCR 170 at [173] (Allsop CJ). However, I note the observations of Beach J in AGM Markets at [514]–[519] and his Honour’s acceptance of the more limited proposition that the provision enshrines a statutory norm to be read conformably with s 760A and the other provisions of the Corporations Act and the Australian Securities and Investments Commission Act 2001 (Cth) (ASIC Act), and is to be applied to an infinite variety of corporate delinquency and self-interested commerciality.

11 The words “efficiently, honestly and fairly” connote a requirement of competence in complying with relevant statutory obligations: AGM Markets at [507] (Beach J). As for the requirement of efficiency, this has been recognised as requiring that the licensee is “adequate in performance, produces the desired effect, is capable, competent and adequate”, and if the performance of a licensee’s functions falls short of the reasonable standard of performance that the public is entitled to expect, then the efficiency requirement will not have been met: AGM Markets at [508] (Beach J). A contravention of the section requires the identification of what was necessary for the licensee to do, but which it omitted to do: Australian Securities and Investments Commission v AustralianSuper Pty Ltd [2025] FCA 102; 172 ACSR 615 at [143] (Hespe J).

Macquarie’s contraventions

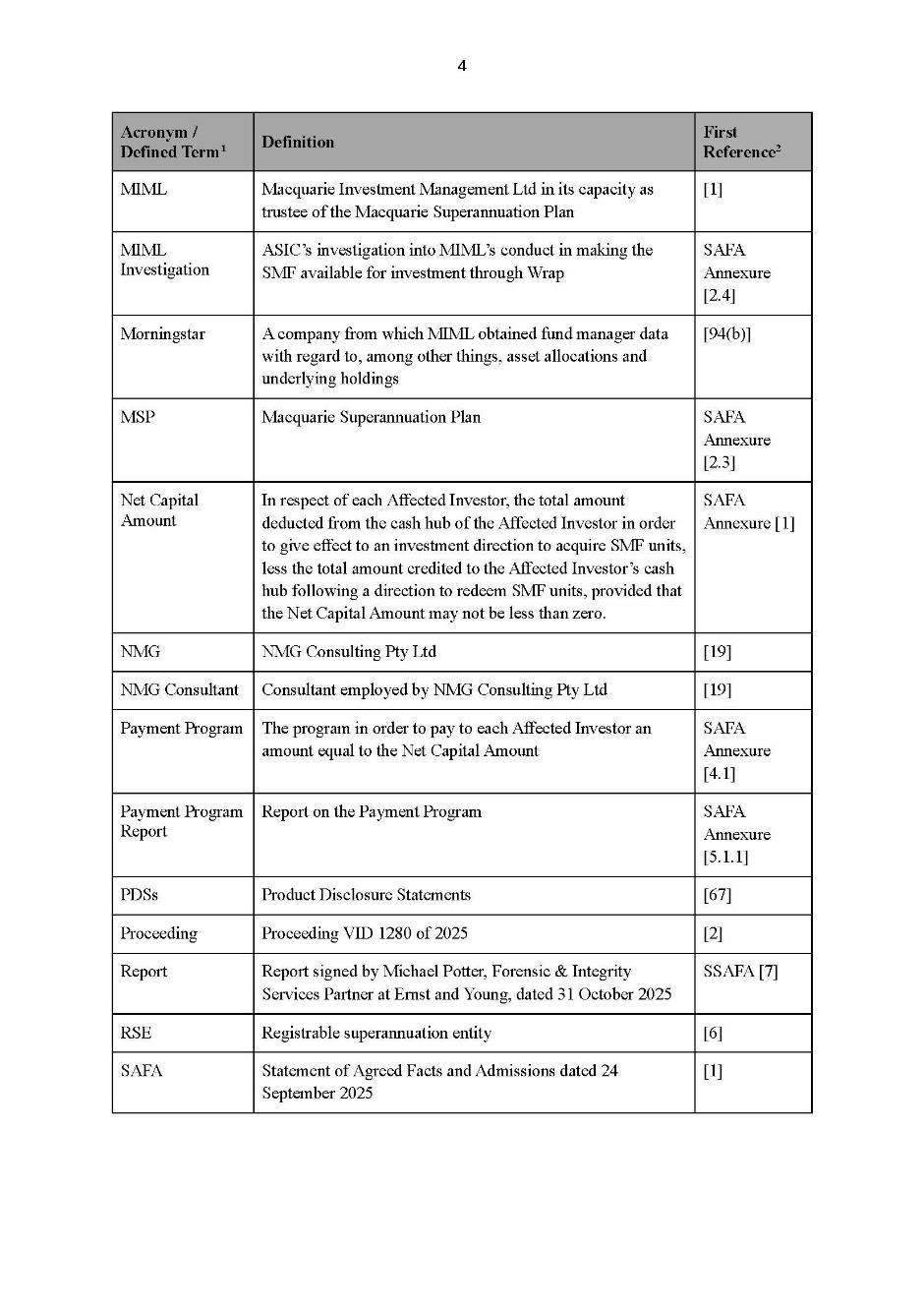

12 Macquarie admits that it contravened s 912A(1)(a) and s 912A(5A) of the Corporations Act in relation to the circumstances of the inclusion and maintenance on the Macquarie Wrap of the option to invest in the Shield Master Fund. The admissions are contained in a statement of agreed facts and admissions which was filed with the originating process and received into evidence together with two supplementary statements of agreed facts. The statements of agreed facts are annexed to these reasons. Further, all the documents in the proceeding are available on the Court’s website as part of an online file.

13 A feature of the statements of agreed facts and the parties’ written submissions is the prolific use of bespoke acronyms. Acronyms of this type are letters without apparent meaning and impair the efficient reading and comprehension of documents. The Court ordered ASIC to file a glossary of acronyms and defined terms, and the glossary is also annexed to these reasons.

14 An essential feature of the contraventions by Macquarie and the failure of the Shield Master Fund was the identity of two individuals behind the Fund, Mr Paul Chiodo and Mr Ilya Frolov, and the relationship between the Fund and vehicles associated with those individuals in which it invested its funds. As I stated at the outset, Keystone was the responsible entity of the Shield Master Fund. From there, the following connections are relevant –

(a) 100% of the shares in Keystone were owned by Malana Management Pty Ltd (ACN 633 213 948) (Malana);

(b) the shareholders of Malana were Chiodo Corporation Pty Ltd (ACN 611 404 909) (Chiodo Corp) and the Frolov Family Trust;

(c) the directors of Malana were Mr Chiodo and Mr Frolov;

(d) the investment manager of the Shield Master Fund was CF Capital Pty Ltd (CF Capital);

(e) the shareholders of CF Capital were Chiodo Corp and the Frolov Family Trust;

(f) the sole director of Chiodo Corp was Mr Chiodo;

(g) the sole shareholder of Chiodo Corp was Pure Development & Project Management Pty Ltd (ACN 141 910 581);

(h) the sole director and shareholder of Pure Development & Project Management Pty Ltd was Mr Chiodo;

(i) Keystone was the trustee of the Chiodo Diversified Property Fund and the Advantage Diversified Property Fund, and CF Capital was the investment manager of both Funds;

(j) both the Chiodo Diversified Property Fund and the Advantage Diversified Property Fund were wholesale unregistered unit trusts that invested funds in various property developments; and

(k) a large proportion of the funds in the Shield Master Fund were invested in the Advantage Diversified Property Fund.

15 The Shield Master Fund relevantly included four investment classes described as follows –

(a) the Conservative class;

(b) the Balanced class;

(c) the Growth class; and

(d) the High Growth class.

16 At the relevant times Macquarie had governance procedures including an Investment Governance Framework with respect to investment options made available through the Macquarie Superannuation Plan. The operation of the Framework and identification of the various teams and consultants involved are set out in the statement of agreed facts and admissions. Of particular relevance is that the Investment Governance Framework provided for the maintenance of a Watch List which was presented to monthly meetings of an Investment Governance Team of Macquarie and which highlighted investment options which were at thresholds where the Team was considering further action, for example, applying limits, conducting further due diligence, fund closure, or strategy changes.

17 The contraventions by Macquarie relate to the inclusion of the Shield Master Fund on the Macquarie Wrap in two stages. The first stage was the addition of the Conservative, Balanced, and Growth classes of the Shield Master Fund in March 2022. The second stage was the inclusion of the High Growth class of the Shield Master Fund in May 2022.

18 Various characteristics of the Conservative, Balanced and Growth classes of the Shield Master Fund that were known to Macquarie warranted the inclusion of those classes by Macquarie on a watch list for further monitoring, follow-up actions, and due diligence. The characteristics included that –

(1) The Shield Master Fund was a new fund with no funds under management.

(2) The product disclosure statements for the Conservative and Balanced classes of the Shield Master Fund contained differing statements regarding target asset allocations.

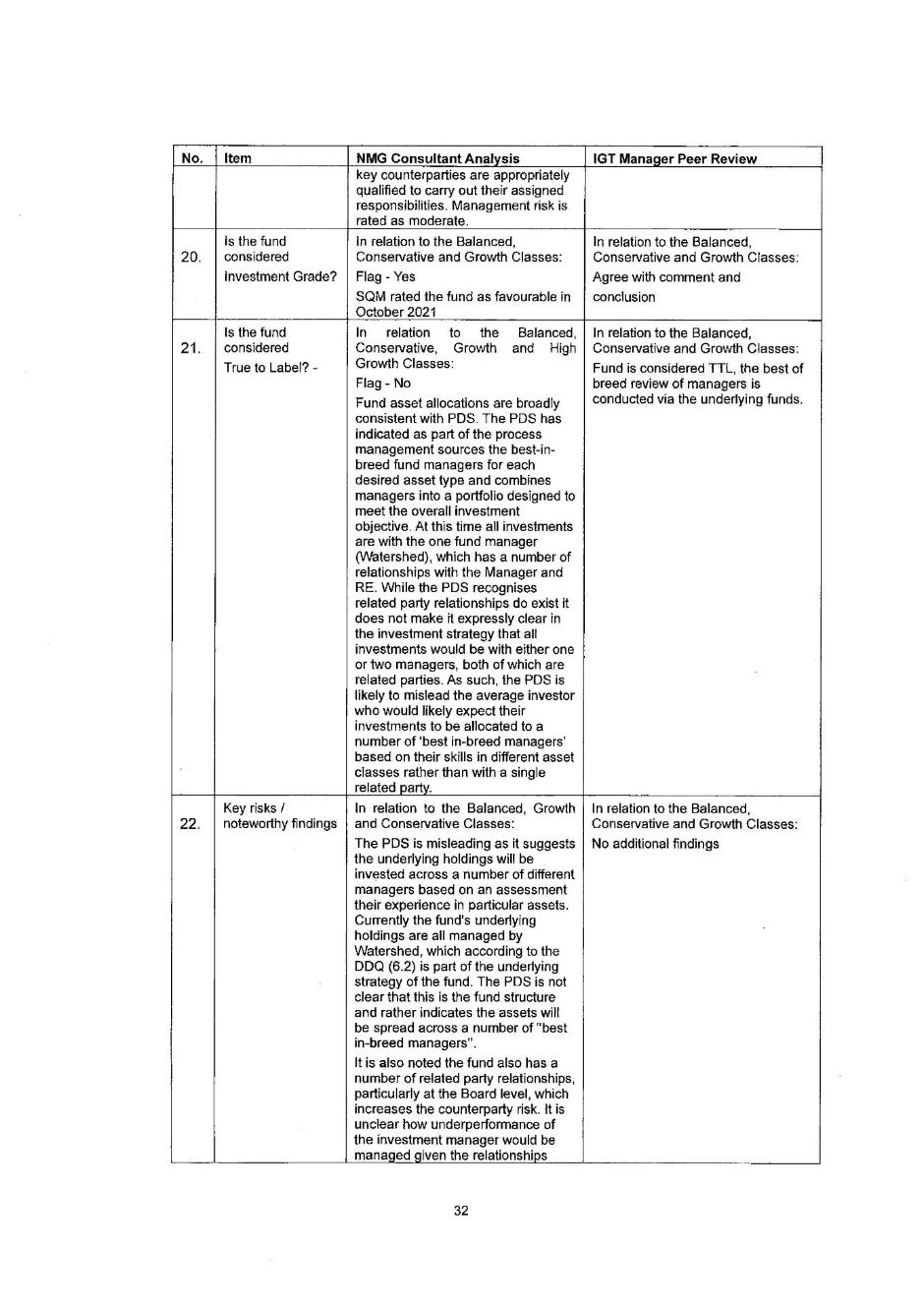

(3) The product disclosure statements and other documents provided to Macquarie contained inconsistent statements regarding the identities of the fund managers for the underlying holdings of the Shield Master Fund.

(4) There were liquidity risks arising from the proposed investment in a property development fund known as the Chiodo Diversified Property Fund, given that it was an illiquid asset.

(5) There was the potential for conflicts of interest to arise given the related party relationships involving Keystone, CF Capital Pty Ltd, which was the investment manager of both the Shield Master Fund, and the Chiodo Diversified Property Fund. This potential for conflict included Keystone and CF Capital Pty Ltd having common directors and shareholders, and the fact that Chiodo Corporation Pty Ltd was identified as the manager of the underlying property developments that some of the funds would be invested in, with that investment being managed by Mr Chiodo through CF Capital Pty Ltd.

19 Various characteristics of the High Growth class of the Shield Master Fund that were known to Macquarie also warranted the inclusion of that class on a watch list for closer monitoring. The characteristics included the matters referred to in [18] above in relation to the other classes, and similarly inconsistent statements in the documents relating to the High Growth class regarding the identities of the underlying fund managers.

20 I find that the contraventions by Macquarie were as follows, based upon the agreed facts and the admissions which Macquarie has made in this proceeding –

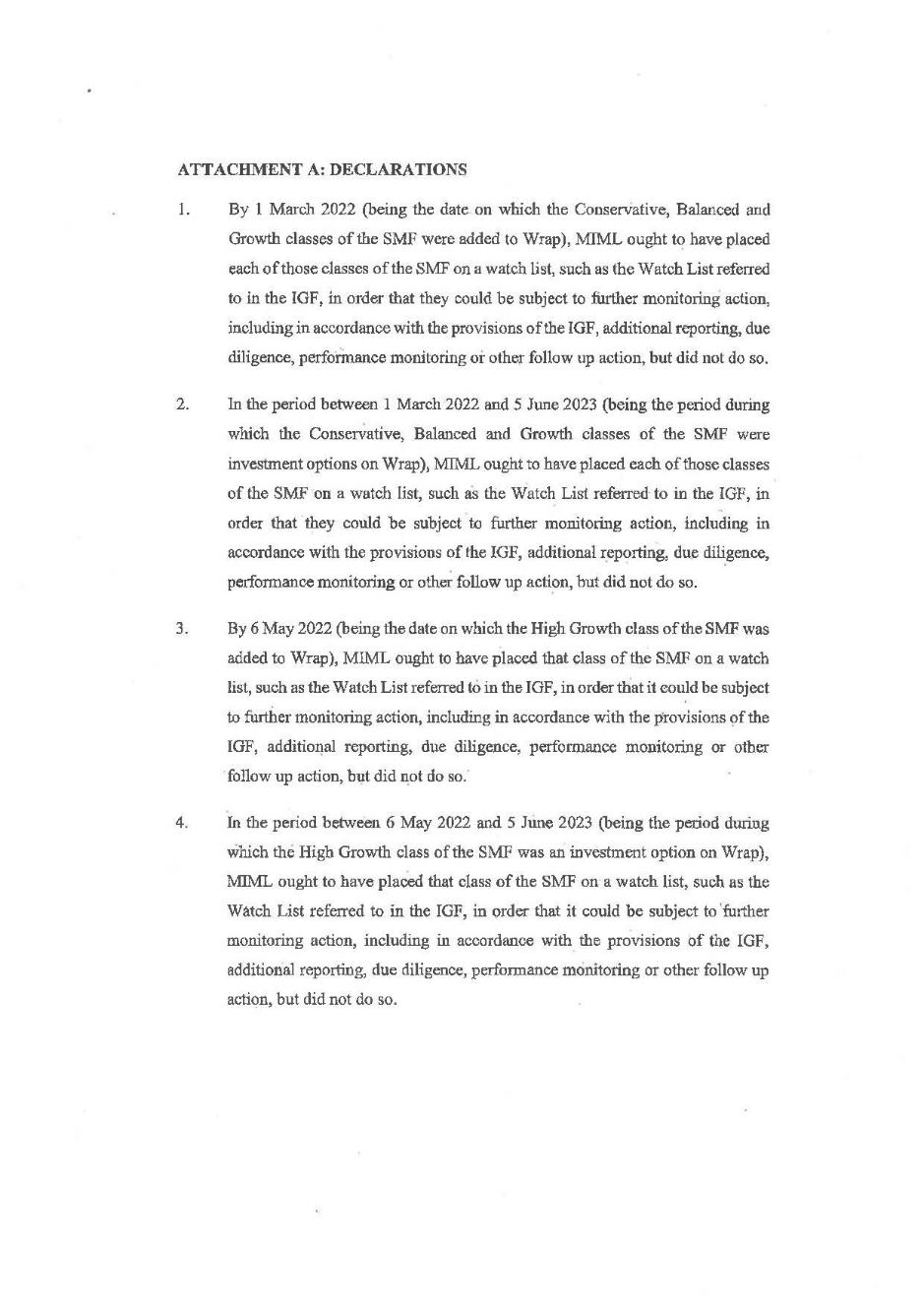

(1) By 1 March 2022 (being the date on which the Conservative, Balanced and Growth classes of the Shield Master Fund were added to the Wrap), Macquarie ought to have placed each of those classes of the Shield Master Fund on a watch list, such as the Watch List referred to in its Investment Governance Framework, in order that they could be subject to further monitoring action, including in accordance with the provisions of the Investment Governance Framework, additional reporting, due diligence, performance monitoring or other follow up action, but did not do so.

(2) In the period between 1 March 2022 and 5 June 2023 (being the period during which the Conservative, Balanced and Growth classes of the Shield Master Fund were investment options on the Wrap), Macquarie ought to have placed each of those classes of the Shield Master Fund on a watch list, such as the Watch List referred to in its Investment Governance Framework, in order that they could be subject to further monitoring action, including in accordance with the provisions of the Investment Governance Framework, additional reporting, due diligence, performance monitoring or other follow up action, but did not do so.

(3) By 6 May 2022 (being the date on which the High Growth class of the Shield Master Fund was added to the Wrap), Macquarie ought to have placed that class of the Shield Master Fund on a watch list, such as the Watch List referred to in its Investment Governance Framework, in order that it could be subject to further monitoring action, including in accordance with the provisions of the Investment Governance Framework, additional reporting, due diligence, performance monitoring or other follow up action, but did not do so.

(4) In the period between 6 May 2022 and 5 June 2023 (being the period during which the High Growth class of the Shield Master Fund was an investment option on the Wrap), Macquarie ought to have placed that class of the Shield Master Fund on a watch list such as the Watch List referred to in its Investment Governance Framework, in order that it could be subject to further monitoring action, including in accordance with the provisions of the Investment Governance Framework, additional reporting, due diligence, performance monitoring or other follow up action, but did not do so.

(5) By reason of the matters referred to in each of paragraphs (1) to (4) above, at all times between 1 March 2022 and 5 June 2023, Macquarie failed to do all things necessary to ensure that the financial services covered by its financial services licence were provided efficiently, honestly and fairly, and Macquarie thereby contravened s 912A(1)(a) of the Corporations Act.

(6) By reason of each of the contraventions referred to in paragraph (5) above, Macquarie contravened s 912A(5A) of the Corporations Act.

Remediation by Macquarie

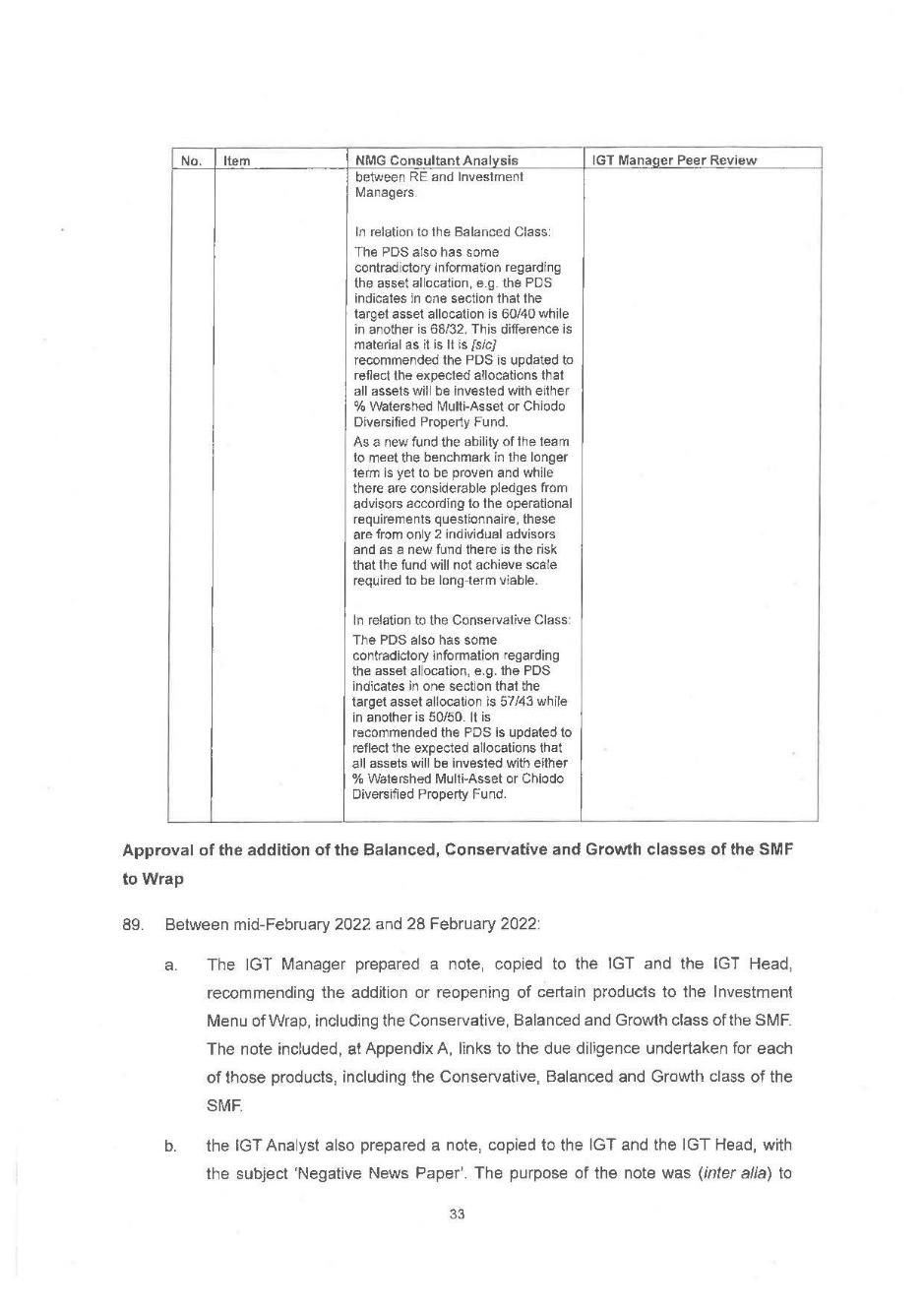

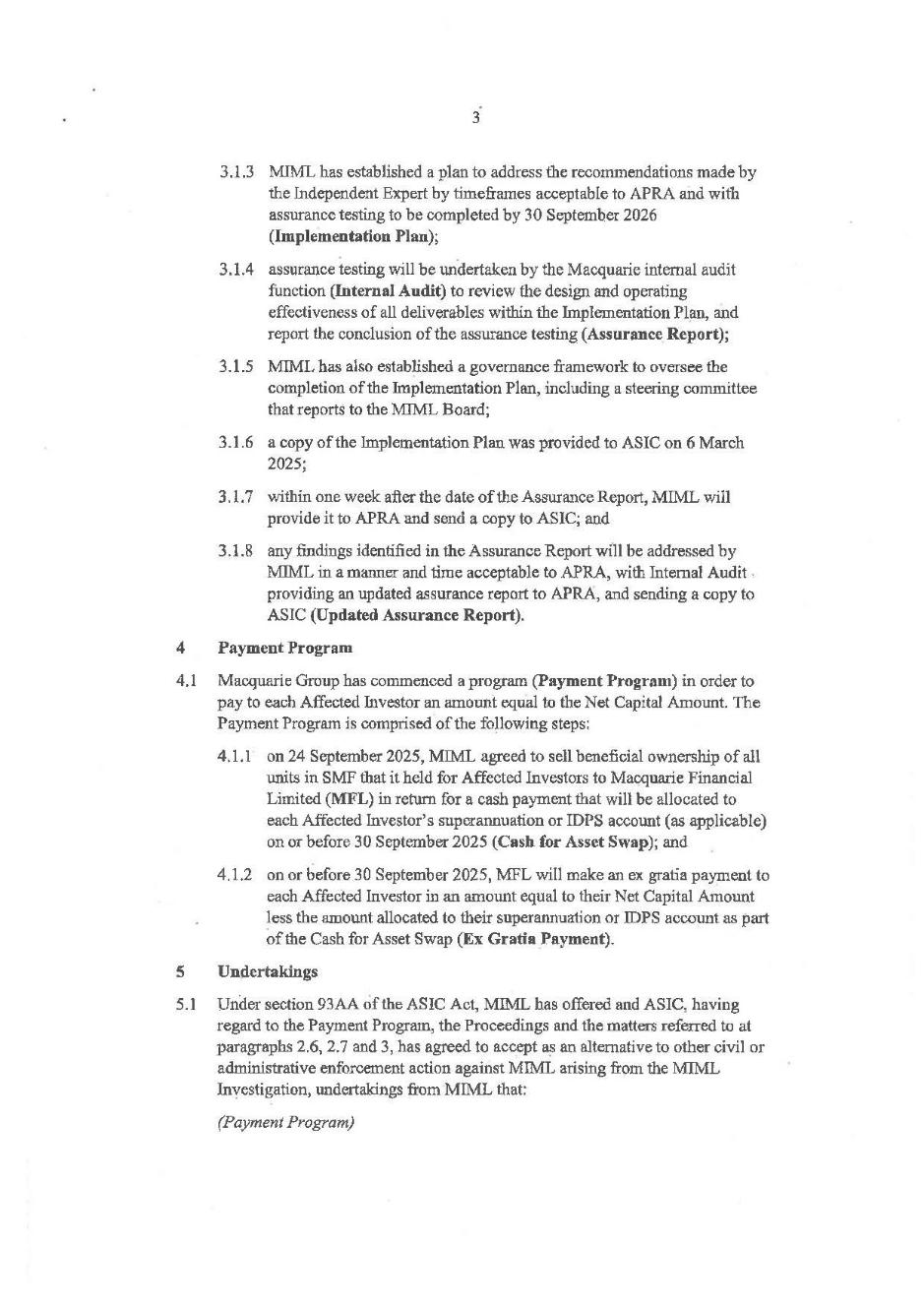

21 On 24 September 2025, Macquarie offered to ASIC, and ASIC accepted, a Court Enforceable Undertaking under s 93AA of the ASIC Act in the form annexed to the statement of agreed facts and admissions which is annexed to these reasons for judgment. The Undertaking provided for a payment program which required the return to Macquarie’s “Affected Investors” (as defined in clause 1 of the Undertaking) of an amount equal to 100% of the net capital amount they invested in the Shield Master Fund. The mechanism for doing so is described in the Undertaking, and included –

(a) a cash for asset swap involving Macquarie Financial Limited (Macquarie Financial) agreeing to purchase all units in the Shield Master Fund held by Macquarie for its Affected Investors in exchange for a cash payment to their superannuation or Investor Directed Portfolio Service account, as applicable, by 30 September 2025;

(b) a further payment by Macquarie Financial to its Affected Investors by 30 September 2025, described as an ex gratia payment, which reflected any shortfall between the net capital amount and the cash for asset swap; and

(c) the preparation of a report by a suitably qualified third party, by 31 October 2025, assessing whether any Affected Investors had been paid less than the net capital amount which they had invested in the Shield Master Fund, and if so to arrange for the payment of any shortfall.

22 The Undertaking also noted that Macquarie, at the request of the Australian Prudential Regulation Authority (APRA), is to address the findings from an independent review of the design and operating effectiveness of Macquarie’s Investment Governance Framework in a manner and time acceptable to APRA.

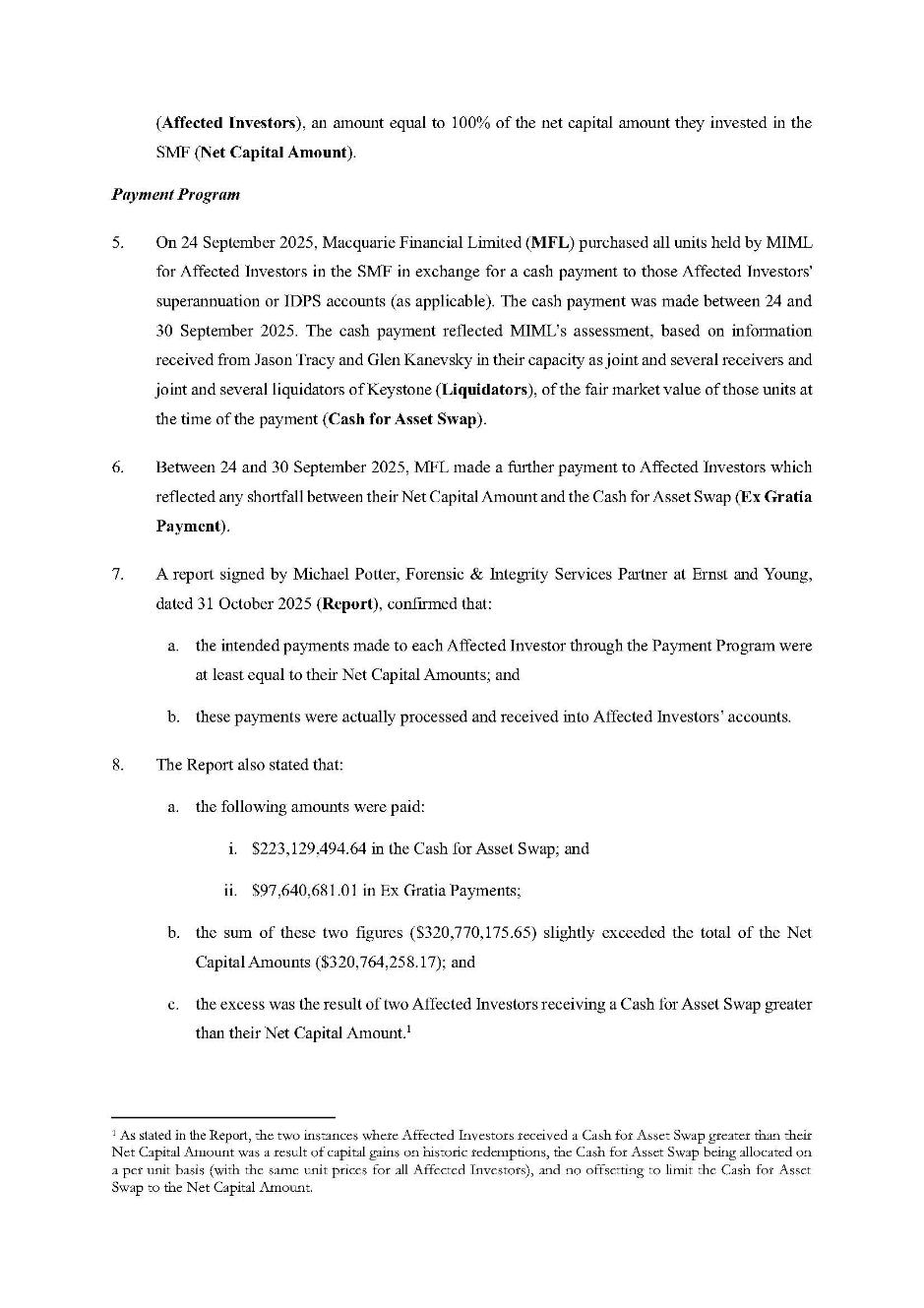

23 A report signed by Michael Potter of Ernst and Young dated 31 October 2025 confirmed that the intended payments made to each Affected Investor through the payment program were at least equal to their net capital amounts and these payments were processed and received into investor accounts. Mr Potter’s report also stated that –

(a) $223,129,494.64 was paid in the cash for asset swap;

(b) $97,640,681.01 in ex gratia payments were paid;

(c) the sum of these two figures, being $320,770,175.65, slightly exceeded the total of the net capital amounts, being $320,764,258.17; and

(d) the excess was the result of two Affected Investors receiving a cash for asset swap greater than their net capital amount.

24 The result of the cash for asset swap is that Macquarie’s Affected Investors have had paid into their superannuation or Investor Directed Portfolio Service accounts an amount reflecting the assessed value of their holdings in the Shield Master Fund, with Macquarie Financial being left to wait for any remaining or recovered assets of the Shield Master Fund to be realised and distributed to it. The upshot of the performance of the Undertaking is that Macquarie Financial instead of the Affected Investors will bear any loss. The net total realisation from the sale of a significant proportion of the equities held by Keystone as responsible entity of the Shield Master Fund amounted to $195,890,964.71 and is currently held in interest-bearing accounts.

The remedies sought by ASIC in this proceeding

25 The only remedies sought by ASIC against Macquarie in the originating process are declarations of contravention. Although s 912A(5A) of the Corporations Act is a civil penalty provision, ASIC does not seek any penalty.

26 ASIC stated to the Court that it agreed with Macquarie not to seek any pecuniary penalty having regard to what it described as the following exceptional circumstances –

(a) the Court Enforceable Undertaking given by Macquarie to ASIC, the performance of which has resulted in all Affected Investors having recovered the net capital amount they invested in the Shield Master Fund;

(b) Macquarie admitting to having contravened s 912A(1)(a) of the Corporations Act, on the basis of the facts set out in the statement of agreed facts and admissions, prior to the commencement of this proceeding;

(c) the strong public interest in prioritising the prompt return of the capital invested by members of APRA regulated super funds where this is possible, thus providing them with a degree of certainty and comfort;

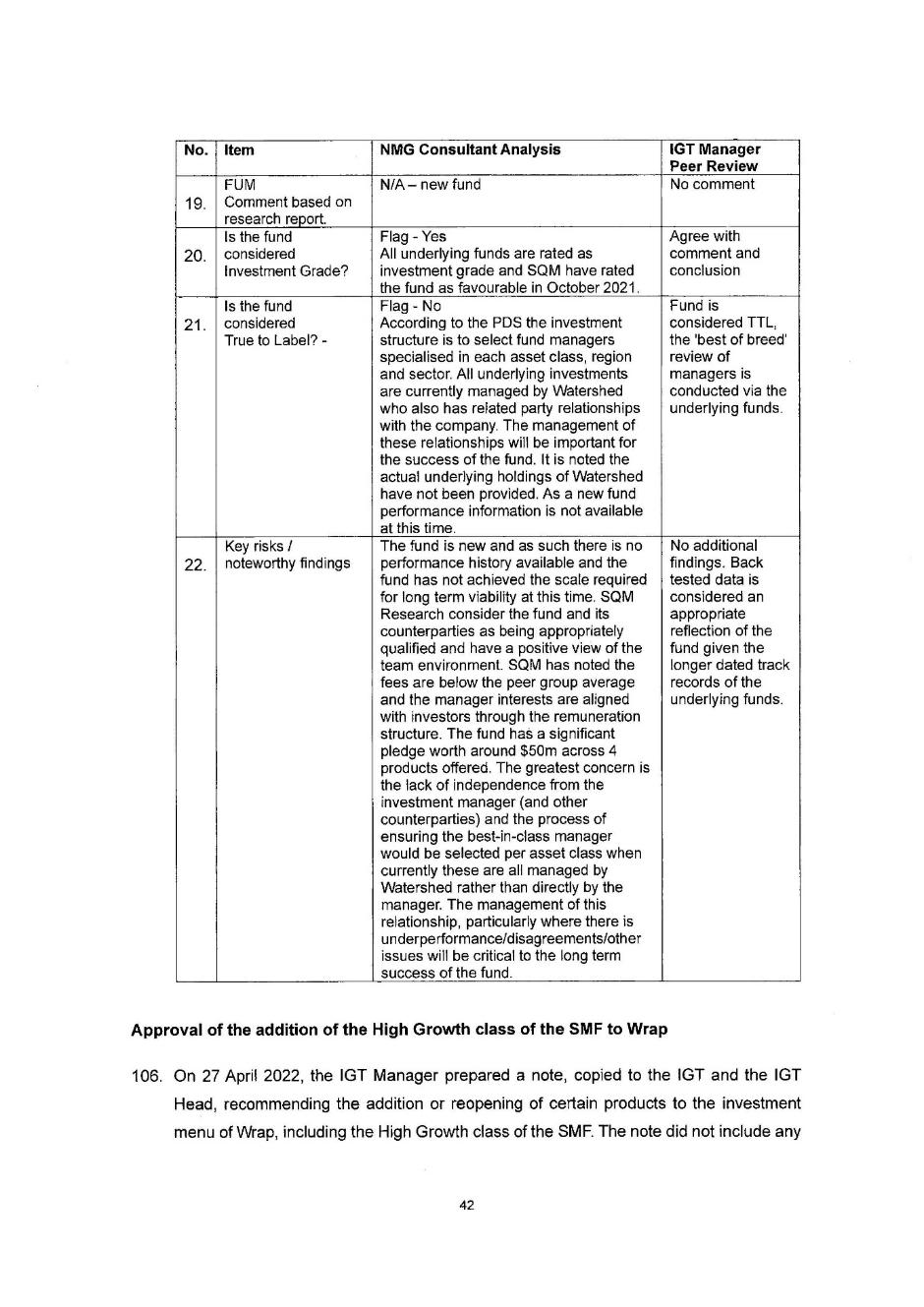

(d) the contrition shown by Macquarie by its entry into the Undertaking and making the admissions in the statement of agreed facts and admissions;

(e) the significance of the admissions by Macquarie in making clear to trustees of choice superannuation funds that their obligations under s 912A(1)(a) of the Corporations Act require them to take active steps to assess and monitor funds which they make available on their platforms; and

(f) to encourage other parties in like circumstances voluntarily to give undertakings to ASIC, including to undertake remediation measures.

27 ASIC also stated to the Court that no order for a compliance program was sought because questions of compliance are covered by Macquarie addressing the recommendations made by the independent review of the design and operating effectiveness of Macquarie’s Investment Governance Framework which is noted in section 3.1 of the Undertaking and referred to at [22] above.

28 Because no pecuniary penalty is sought by ASIC in what is an adversarial proceeding, no occasion arises for the Court to consider whether a penalty should be imposed, and if so, an appropriate amount. Nor is there any occasion for the Court to express an opinion on the absence of any order for a compliance program, save that the Court acknowledges the public benefit in the resolution of civil proceedings by agreement.

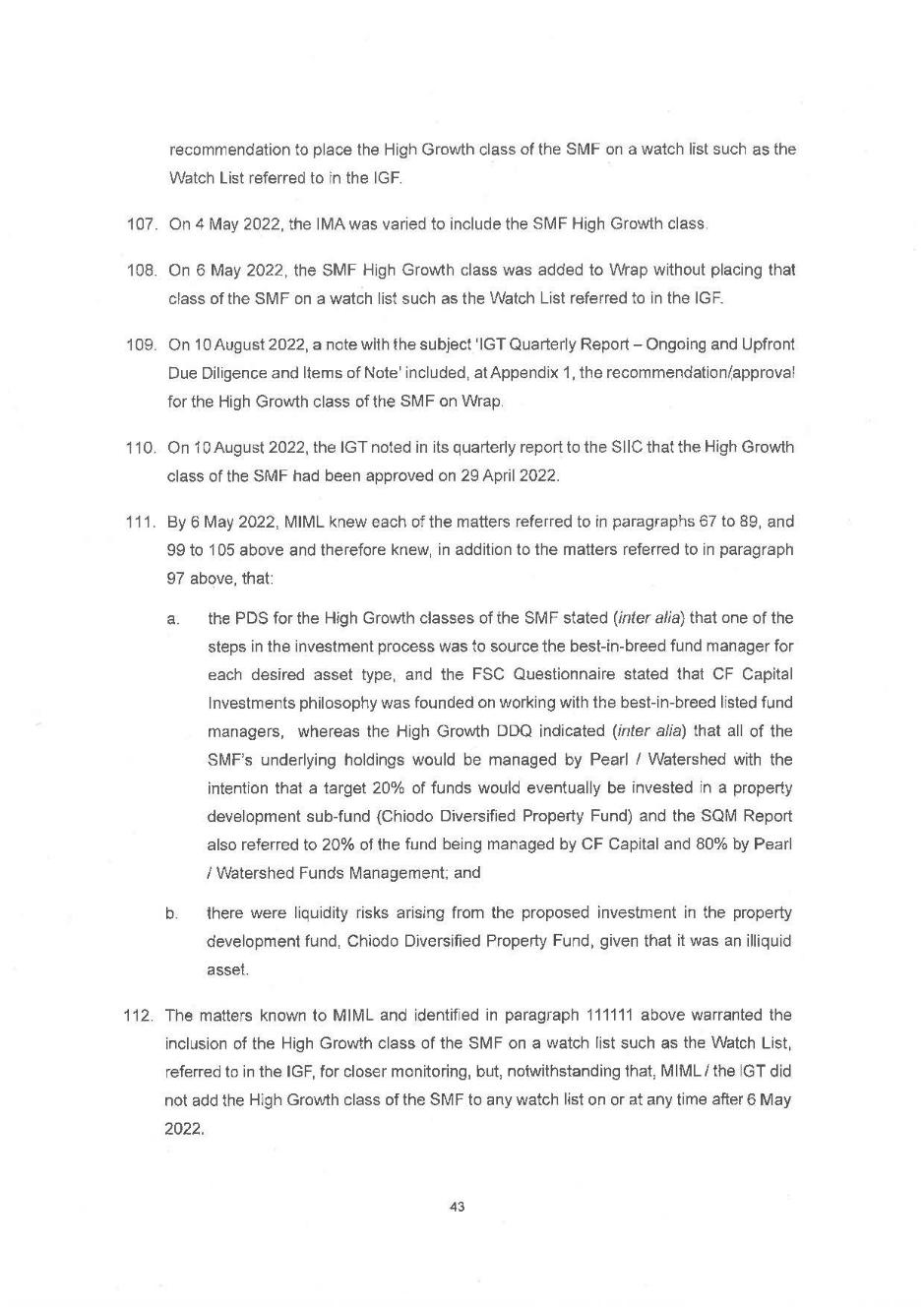

29 I turn now to the question of declarations. The declarations are sought in the exercise of judicial power, and they are sought by consent. However, although sought by consent the Court must still be persuaded that what is proposed is appropriate: Commonwealth v Director, Fair Work Building Industry Inspectorate [2015] HCA 46; 258 CLR 482 (Agreed Penalties Case) at [57] –[58] (French CJ, Kiefel, Bell, Nettle and Gordon JJ).

30 In Forster v Jododex Australia Pty Ltd [1972] HCA 61; 127 CLR 421 at 437–438, Gibbs J cited the speech of Lord Dunedin in Russian Commercial and Industrial Bank v British Bank for Foreign Trade Ltd [1921] 2 AC 438 at 448 who summarised the principles applied by Scottish courts to the action of declarator and identified the following requirements –

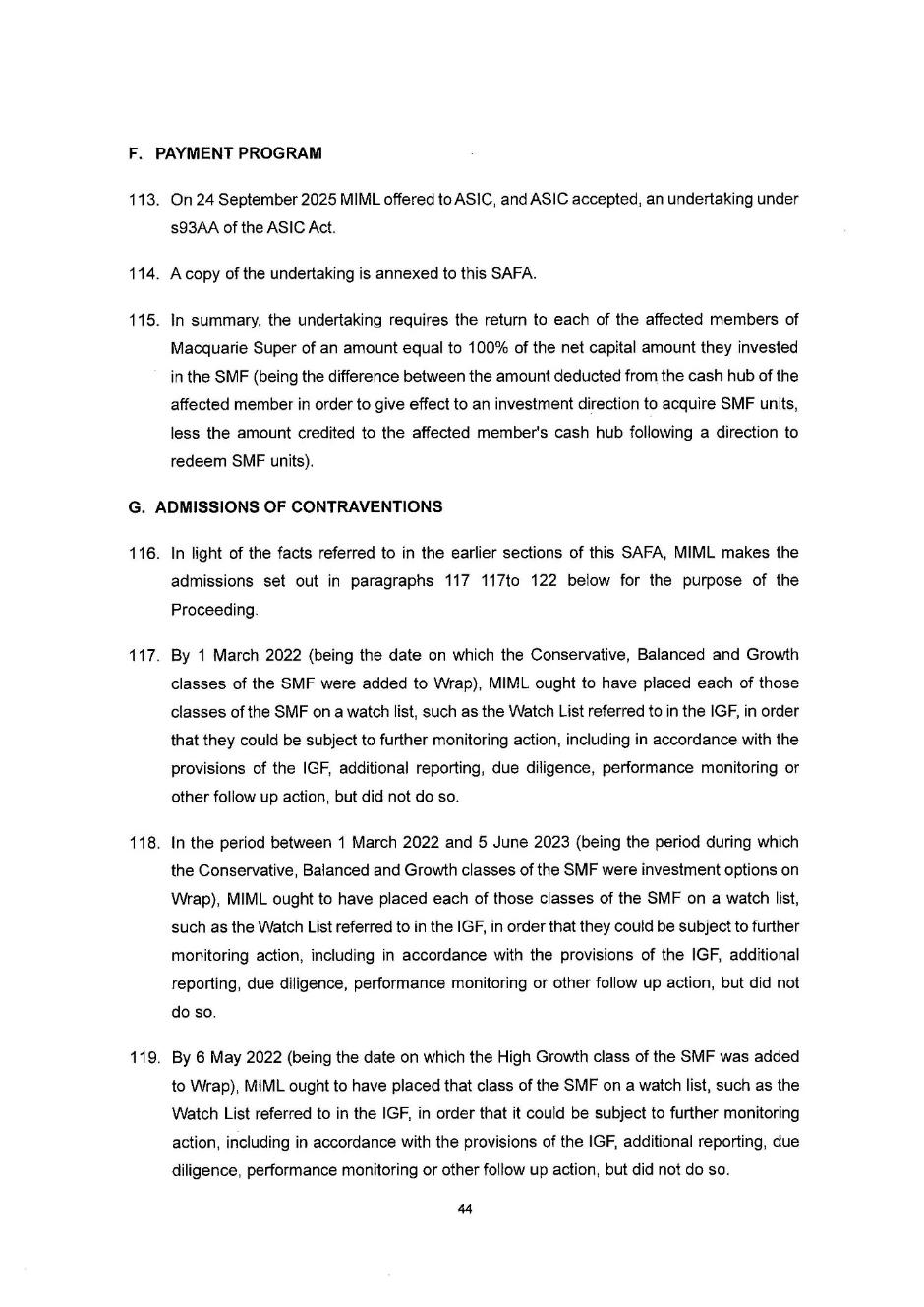

The question must be a real and not a theoretical question; the person raising it must have a real interest to raise it; he must be able to secure a proper contradictor, that is to say, some one presently existing who has a true interest to oppose the declaration sought.

31 I am satisfied that these requirements are met in this proceeding, and in determining to make the declarations sought by ASIC I have had regard to the following –

(1) Because this is an adversarial proceeding of a civil nature there is considerable scope for the parties to agree on facts and consequences, including upon the appropriate remedy provided that it is an appropriate remedy: Agreed Penalties Case at [57].

(2) There is a significant legal controversy between ASIC and Macquarie which is to be resolved by ASIC applying to the Court to make declarations of contravention based on findings supported by the statements of agreed facts and admissions where, pursuant to s 191(2)(a) of the Evidence Act 1995 (Cth), evidence is not required to prove an agreed fact.

(3) The significant legal controversy between ASIC and Macquarie is evidenced by the terms of the Court Enforceable Undertaking which is annexed to the statement of agreed facts and admissions. The controversy existed before this proceeding commenced and, like the Agreed Penalties Case, is to be resolved by ASIC prosecuting the proceeding on the basis of the admissions which Macquarie agreed to make in support of ASIC’s claim for declaratory relief.

(4) There is a public interest in the settlement of the controversy between ASIC and Macquarie in relation to Macquarie’s contraventions of s 912A(1)(a) and (5A) of the Corporations Act. In this respect, being a civil proceeding, it is entirely consistent with the nature of civil proceedings for a court to make orders by consent and to approve a compromise of proceedings on terms proposed by the parties, provided the Court is persuaded that what is proposed is appropriate: Agreed Penalties Case at [57].

(5) It is in the public interest for ASIC, as the regulator, to seek the declarations and for the declarations to be made. The public interest in making declarations of contravention of civil penalty provisions of the Corporations Act is enshrined in s 1317E of the Act which provides that if the Court is satisfied that a person has contravened a civil penalty provision, it must make a declaration of contravention.

(6) Correspondingly, Macquarie has an interest in opposing the declarations and is a proper contradictor: Australian Competition and Consumer Commission v MSY Technology Pty Ltd [2012] FCAFC 56; 201 FCR 378 (MSY Technology) at [30] (Greenwood, Logan and Yates JJ).

(7) I am therefore satisfied that there is a justiciable controversy and that the Court has the power to make the declarations sought.

(8) I am satisfied that the facts and admissions in the statements of agreed facts and admissions provide a sufficient factual foundation for making the declarations.

(9) I am satisfied that the terms of the proposed declarations relate to conduct that contravened the Corporations Act and the matters in issue have been identified with sufficient precision: MSY Technology at [35].

(10) Finally, and not losing sight of the requirement in s 1317E(1) of the Corporations Act to make a declaration if the Court is satisfied that a person has contravened a civil penalty provision of the Act, I am satisfied that the proposed declarations sought by ASIC are appropriate. They are appropriate because they serve to record the Court’s disapproval of the contravening conduct, they vindicate the ASIC’s claim that Macquarie contravened the Corporations Act, they assist ASIC to carry out the duties conferred upon it by the ASIC Act and the Corporations Act in relation to other similar conduct, they inform the public of the harm arising from Macquarie’s contravening conduct, and they deter other corporations from contravening the Corporations Act: Australian Building and Construction Commission v Construction, Forestry, Mining and Energy Union [2017] FCAFC 113; 254 FCR 68 at [93] (Dowsett, Greenwood and Wigney JJ).

Conclusions

32 I will make declarations substantially in the terms sought. I will order that Macquarie pay ASIC’s costs of the proceeding.

I certify that the preceding 32 (thirty-two) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Wheelahan. |

Associate:

Dated: 20 March 2026

Annexure A

Annexure B

Annexure C

Annexure D