Federal Court of Australia

Rosemont Capital Investments Pty Ltd v Weinberg [2026] FCA 224

File number(s): | NSD 1146 of 2021 |

Judgment of: | CHEESEMAN J |

Date of judgment: | 9 March 2026 |

Catchwords: | TRUSTS – whether payment subject to trust of the character described in Barclays Bank Ltd v Quistclose Investments Ltd [1970] AC 567 – whether objective mutual intention was for funds to be used for specific and exclusive purpose of “regulatory capital” – whether funds to be “ring-fenced” in term deposit – whether funds could be used as working capital. Held: Quistclose trust found. KNOWING RECEIPT – whether related company under control of sole director common to both the immediate payer and the payee was a knowing recipient of funds under first limb of Barnes v Addy (1874) LR 9 Ch App 244. Held: knowing receipt found. ACCESSORIAL LIABILITY – where director had knowledge of the essential matters indicating that applying funds for a different purpose would be a breach of trust – where director applied funds to own benefit in breach of trust – whether director liable as accessory for procuring breach of trust. Held: accessorial liability found. MISLEADING OR DECEPTIVE CONDUCT – where claim under s 18 of the Australian Consumer Law – s 1041H of the Corporations Act 2001 (Cth) – s 12DA of the Australian Securities and Investments Commission Act 2001 (Cth) – whether representations made as to sole purpose and intended use of funds – whether representation made as to status of related company as that of a wholly owned subsidiary – whether liability should be reduced for contributory negligence or proportionate liability. Held: misleading or deceptive conduct found – contributory negligence and proportionate liability not applicable. TORTS – deceit – whether false representation knowing it to be false – whether intention that applicant rely on false representation. Held: deceit found. EVIDENCE – admissibility – where tender of partial audio recording – whether to exercise discretion in s 135 of the Evidence Act 1995 (Cth) to reject the tender of the recording. Held: tender rejected. |

Legislation: | Australian Securities and Investments Commission Act 2001 (Cth) s 12DA Competition and Consumer Act 2010 (Cth) Sch 2, Australian Consumer Law s 18 Corporations Act 2001 (Cth) s 1041H Evidence Act 1995 (Cth) s 135 Federal Court of Australia Act 1976 (Cth) s 37M |

Cases cited: | Aon Risk Services Australia Limited v Australian National University [2009] HCA 27; 239 CLR 175 Australian Super Developments Pty Ltd v Marriner [2014] VSC 464 Banque Commerciale SA (in liq) v Akhil Holdings Ltd [1990] HCA 11; 169 CLR 279 Barclays Bank Ltd v Quistclose Investments Ltd [1970] AC 567 Barnes v Addy (1874) LR 9 Ch App 244 Bathurst Regional Council v Local Government Financial Services Pty Ltd (No 5) [2012] FCA 1200 Briginshaw v Briginshaw [1938] HCA 34; 60 CLR 336 Butcher v Lachlan Elder Realty Pty Ltd [2004] HCA 60; 218 CLR 592 Byrnes v Kendle [2011] HCA 26; 243 CLR 253 China Life Trustees Ltd v China Energy Reserve and Chemical Group Overseas Co Ltd [2024] HKCFA 15 Dare v Pulham [1982] HCA 70; 138 CLR 658 Effem Foods Pty Ltd v Lake Cumbeline Pty Ltd [1999] HCA 15; 161 ALR 599 Farah Constructions Pty Ltd v Say-Dee Pty Ltd [2007] HCA 22; 230 CLR 89 Fox v Percy [2003] HCA 22; 214 CLR 118 Gould v Vaggelas [1985] HCA 85; 157 CLR 215 Grimaldi v Chameleon Mining NL (No 2) [2012] FCAFC; 200 FCR 296 Henville v Walker [2001] HCA 52; 206 CLR 459 Ho v Powell [2001] NSWCA 168; 51 NSWLR 572 Hughes v St Barbara Mines Ltd (No 4) [2010] WASC 160 Krakowski v Eurolynx Properties Ltd [1995] HCA 68; 183 CLR 563 Magill v Magill [2006] HCA 51; 226 CLR 551 Marks v GIO Australia Holdings Ltd [1998] HCA 69; 196 CLR 494 Neilson v Overseas Projects Corporation of Victoria Ltd [2005] HCA 54; 223 CLR 331 Pittmore Pty Ltd v Chan [2020] NSWCA 344; 104 NSWLR 62 Regie National des Usines Renault SA v Zhang [2002] HCA 10; 210 CLR 491 Twinsectra Ltd v Yardley [2002] 2 AC 164 Watson v Foxman (1995) 49 NSWLR 315 |

Division: | General Division |

Registry: | New South Wales |

National Practice Area: | Commercial and Corporations |

Sub-area: | Regulator and Consumer Protection |

Number of paragraphs: | 171 |

Date of last submission/s: | 3 July 2024 |

Date of hearing: | 5-6 and 11 June 2024 |

Counsel for the Applicant: | Mr E Ball |

Solicitor for the Applicant: | Gillis Delaney Lawyers |

Counsel for the Respondent: | The Respondent appeared in person |

ORDERS

NSD 1146 of 2021 | ||

| ||

BETWEEN: | ROSEMONT CAPITAL INVESTMENTS PTY LTD Applicant | |

AND: | MR PHILLIP WEINBERG Respondent | |

order made by: | CHEESEMAN J |

DATE OF ORDER: | 9 March 2026 |

THE COURT ORDERS THAT:

1. By 12.00pm on 13 March 2026, the parties are to email to the Associate to Cheeseman J joint proposed short minutes of order addressed to the making of final orders (marked-up to show any areas of disagreement between the parties).

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

CHEESEMAN J:

INTRODUCTION

1 The applicant, Rosemont Capital Investments Pty Limited, claims against the respondent, Mr Phillip Weinberg, in respect of a payment of $1 million it made to BestEx Pty Ltd on 30 December 2016 and which BestEx subsequently paid to BestEx Asia Ltd. The purpose for which Rosemont advanced the $1 million to BestEx and how the funds were in fact used by BestEx, and in turn by BestEx Asia, is the subject of this dispute.

2 The relief claimed by Rosemont against Mr Weinberg is framed as a claim in respect of: procuring a breach of trust; misleading or deceptive representations in contravention of one or more of s 18 of the Australian Consumer Law (ACL), which is in Schedule 2 of the Competition and Consumer Act 2010 (Cth), s 1041H of the Corporations Act 2001 (Cth), and s 12DA of the Australian Securities and Investments Commission Act 2001 (Cth) (the ASIC Act); and the tort of deceit.

3 Rosemont identifies the claim in relation to procuring a breach of trust as its primary claim with the consequence that if it succeeds Mr Weinberg will be required to reconstitute the trust fund and thereafter the funds will be returned to Rosemont. The primary allegation is that the $1 million advanced to BestEx was impressed with a Quistclose trust (taking its name from the decision in Barclays Bank Ltd v Quistclose Investments Ltd [1970] AC 567 (Wilberforce LJ, with whom the other Law Lords agreed) as expounded by Millett LJ in Twinsectra Ltd v Yardley [2002] 2 AC 164 and subsequent authorities). In the case of BestEx Asia, Rosemont contends that the alleged trust is either a Quistclose trust or that BestEx Asia is liable under the first limb of Barnes v Addy (1874) LR 9 Ch App 244 based on BestEx Asia’s receipt of the funds with knowledge (attributed to it through Mr Weinberg) of BestEx’s breach of trust. Rosemont relies on this as a further and separate basis upon which Mr Weinberg must reinstate the trust and that the funds thereafter be returned to Rosemont.

4 The directors and shareholders of Rosemont are Mr David Klinger and Ms Tricia Klinger. Mr Klinger is the sole company secretary of Rosemont. Mr Klinger is the only witness on whom Rosemont relies.

5 Mr Weinberg was a director and sole company secretary of BestEx from the date of its incorporation. Mr Christopher Jenkins was a director of BestEx between 19 January 2017 and 6 May 2019. Mr Weinberg was otherwise the sole director of BestEx. Mr Weinberg appeared and gave evidence remotely. Mr Weinberg is legally qualified. He appeared as a litigant in person. He did not rely on any evidence from witnesses other than himself in his defence of this proceeding. Mr Weinberg chose to participate in the proceeding remotely. He appeared via a Microsoft Teams link. He was evidently well versed in the legal principles that were relevant to the matters raised in this proceeding and to my observation was able to fully participate in the hearing and effectively present his evidence and make his submissions to the Court.

6 The critical document for the purpose of each of Rosemont’s claims is an email sent by Mr Weinberg to Mr Klinger on 29 December 2016. In this email, Mr Weinberg requested Mr Klinger to transfer $1 million to BestEx’s bank account in Australia and said that BestEx would issue a convertible note for the full amount with a coupon payment to cover Mr Klinger’s funding costs. Mr Weinberg then set out what BestEx would do as a consequence of the transfer, including how the funds would be used by BestEx Asia which was described as a “wholly owned subsidiary of [BestEx]”.

7 This email, amongst other evidence of the surrounding circumstances known to both parties, is relied on to support Rosemont’s trust-based claims as evidence of the parties’ mutual intention objectively ascertained as to the purpose for which the funds were to be used. This email is also relied on as conveying the material representations that are alleged to be misleading or deceptive for the purpose of Rosemont’s statutory claims for misleading or deceptive conduct as well as relied on to convey a false representation for the tort of deceit.

8 Mr Weinberg admits that on 30 December 2016 he caused the $1 million that had been advanced by Rosemont to BestEx to be transferred to BestEx Asia. The Commonwealth Bank International Money Transfer is in evidence. It is dated 30 December 2016. The beneficiary is identified as BestEx Asia and the “description/purpose of payment” is described as “equity investment”. Mr Weinberg is identified as the sender. The form bears his signature. The sender’s account number is that which is identified in the 29 December 2016 email as BestEx’s account.

9 Rosemont’s claim against Mr Weinberg rather than against BestEx and BestEx Asia is explained by BestEx entering into voluntary administration pursuant to a creditor’s voluntary winding up application under s 436A of the Corporations Act on 5 March 2020, then into liquidation on 15 April 2020, and BestEx Asia ceasing its business at around the same time. I have relied on the Australian Securities and Investments Commission register for the date of the creditor’s voluntary winding up rather than the later date alleged in the Statement of Claim. Nothing turns on the difference between these two dates.

EVIDENCE and PRINCIPLES APPLICABLE TO FACT-FINDING

10 Rosemont relied on two affidavits of Mr Klinger and the exhibits to those affidavits. Mr Klinger gave evidence and was cross-examined by Mr Weinberg. Mr Weinberg relied on his own affidavit and the exhibit to that affidavit. Mr Weinberg gave evidence at the hearing and was cross-examined by counsel appearing for Rosemont. In addition to the Courtbook, a number of documents were tendered during the proceedings.

11 In undertaking the fact‑finding task, I apply the civil standard of proof but recognise that a fact is not to be found by a mechanical comparison of probabilities. Instead, the Court must feel an actual persuasion of the occurrence or existence of the fact before it can be found: Briginshaw v Briginshaw [1938] HCA 34; 60 CLR 336 at 361-362 (Dixon J). The strength of the evidence necessary to establish facts on the balance of probabilities varies according to the nature of what it is sought to prove.

12 In assessing contested oral dealings and disputed events from years earlier, I bear in mind the recognised fallibility of human memory, and that fallibility increases with the passage of time, particularly where disputes or litigation intervene: Watson v Foxman (1995) 49 NSWLR 315 at 319 (McLelland CJ in Eq).

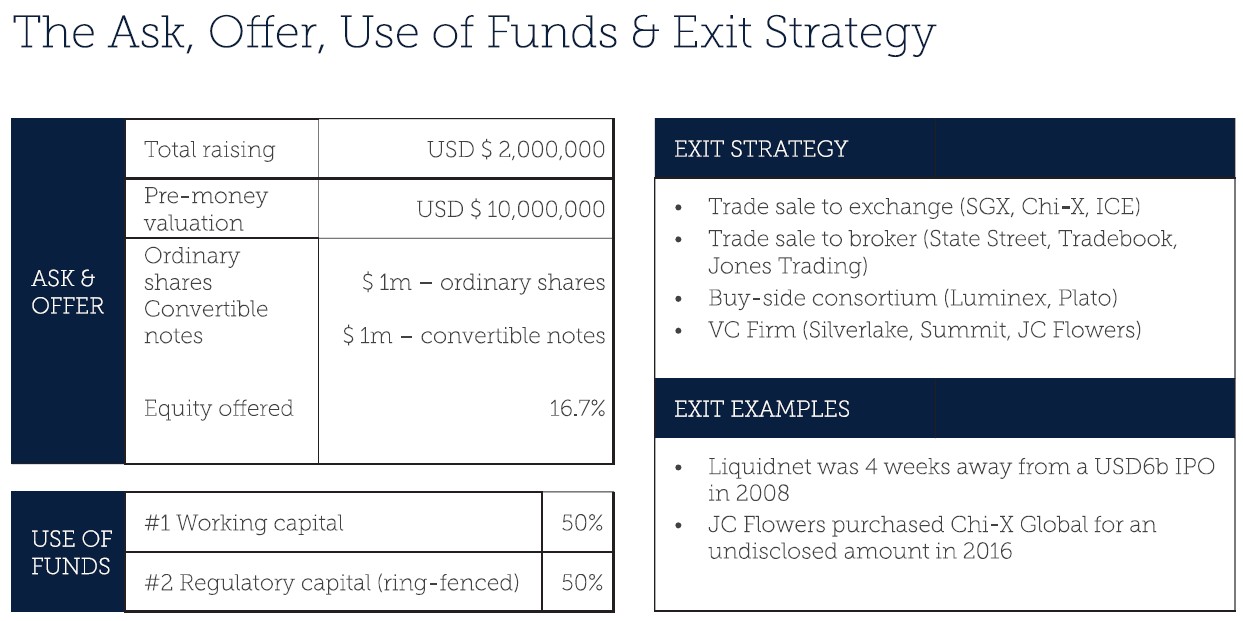

13 I have placed primary emphasis on the objective factual surrounding material and the inherent commercial probabilities, together with the contemporaneous documentation tendered in evidence: Effem Foods Pty Ltd v Lake Cumbeline Pty Ltd [1999] HCA 15; 161 ALR 599 at [15] (Gleeson CJ, Gaudron, Kirby and Hayne JJ); Fox v Percy [2003] HCA 22; 214 CLR 118 at [31] (Gleeson CJ, Gummow and Kirby JJ). It is well recognised in the authorities that contemporaneous documents generally provide a safer repository of reliable fact: Bathurst Regional Council v Local Government Financial Services Pty Ltd (No 5) [2012] FCA 1200 at [1247] (Jagot J); Hughes v St Barbara Mines Ltd (No 4) [2010] WASC 160 at [157] (Martin J).

14 Finally, in determining facts under the civil standard, I must consider not just what are the probabilities on the limited material which the Court has, but also whether that limited material is an appropriate basis on which to reach a reasonable decision: Ho v Powell [2001] NSWCA 168; 51 NSWLR 572 at [14]-[15] (Hodgson JA, Beazley JA agreeing).

FINDINGS ON THE EVIDENCE

15 Before turning to the legal questions, I make findings of fact which supply the relevant context for the objective assessment of the parties’ mutual intentions in relation to the $1 million transfer and for determining what was conveyed by the 29 December 2016 email. Unless otherwise indicated, I am satisfied of the following matters.

Corporate structure and ownership

16 BestEx was incorporated in 2012. In around October 2012, BestEx was granted an Australian Financial Services Licence (AFSL). The Australian Securities Exchange required BestEx to maintain certain minimum regulatory capital requirements in order to conduct business in Australia. It later came to operate the Australian arm of the business that was described in the evidence as “Block Event”. By early 2015, BestEx had an agreement in place with Pershing Securities Australia Pty Ltd which was addressed to meeting its regulatory capital requirements in Australia.

17 BestEx Asia was incorporated in Hong Kong in or about April 2016 for the purpose of expanding the Block Event business to Hong Kong. Mr Weinberg arranged its incorporation. Mr Klinger was not involved in establishing BestEx Asia and left those steps to Mr Weinberg.

18 From its incorporation, Mr Weinberg was the sole director of BestEx Asia. By resolution of Mr Weinberg in his capacity as sole director, dated 30 April 2016, 10,000 shares were issued to Mr Weinberg. I accept Mr Klinger’s evidence that he was not shown that resolution at the time and only became aware of it later. Mr Weinberg was the sole shareholder of BestEx Asia from its incorporation. In January 2017, following the payment by Rosemont on 30 December 2016, BestEx Asia’s issued share capital increased through the provision of AUD 1 million in funds, noted on the notice of alteration of share capital to be by the existing sole shareholder, namely Mr Weinberg. Mr Weinberg took up the whole of the new issue. Mr Weinberg was at all times the sole shareholder of BestEx Asia.

19 I reject Mr Weinberg’s evidence that it was agreed between him and Mr Klinger that Mr Weinberg would hold the shares in BestEx Asia in his own name on trust for BestEx (whether because of Mr Klinger’s reputational issues or otherwise).

20 Subject to one exception, Mr Weinberg’s assertion is unsupported by contemporaneous documents and is inconsistent with repeated contemporaneous descriptions of BestEx Asia as intended to be, and represented as being, a wholly owned subsidiary of BestEx.

21 The exception is an email dated 12 December 2016, which was sent by Mr Weinberg to Mr Mark Nelligan and blind-copied to Mr Klinger. This email was sent in the context of the termination of BestEx’s negotiations with Pershing entities in Singapore where BestEx was seeking to secure settlement and execution services from Pershing.

22 After conducting due diligence of BestEx, Pershing determined not to provide settlement and execution services to BestEx. Mr Weinberg deposes to being informed in a telephone call on or around 6 December 2016 “that Pershing LLC will not agree to provide services to BestEx because of concerns about Mr Klinger's character”.

23 Mr Weinberg and Mr Klinger requested to speak to the Pershing decision-makers in New York. A meeting was organised for December 2016. Ultimately, Pershing did not change its position.

24 Mr Weinberg sent the 12 December 2016 email in a last ditch effort to persuade Pershing to reverse its decision. Mr Weinberg says he drafted this email in consultation with Mr Klinger. This email is relied on by Mr Weinberg to demonstrate that Mr Klinger was on notice that Mr Weinberg was the sole shareholder of BestEx Asia. The email includes an express statement to that effect. The whole tenor of the letter is to seek to minimise Mr Klinger’s involvement with BestEx and BestEx Asia to alleviate Pershing’s concerns regarding Mr Klinger’s character which were understood to be the driver for Pershing’s decision not to do business with BestEx.

25 In his affidavit Mr Klinger said that he did not recall reading this email and he did not recall Mr Weinberg discussing it with him. In his oral evidence, Mr Klinger was more equivocal about whether he had read the email. He said that at the time of this email, everything was in a heightened state of flux and that he did not pick up on the fact that Mr Weinberg had represented that he was the sole shareholder of BestEx Asia. He said that if he had appreciated this it would have rung alarm bells for him. Given the importance of the subject matter of this email at the time, as a last-ditch effort to persuade Pershing to provide settlement and execution services, I find that Mr Klinger did read this email. However, he did not hone in on the statement about Mr Weinberg being the sole shareholder of BestEx Asia. This passing isolated reference is not consistent with the repeated earlier descriptions which can only be understood as conveying that BestEx Asia was intended from inception to be, and was, a wholly owned subsidiary of BestEx. It was also contradicted by further written communications after 12 December 2016 to which Mr Weinberg and Mr Klinger were privy including the 29 December 2016 email which was expressly addressed to confirmation of the arrangement in relation to the payment of the $1 million and expressly described BestEx Asia as a wholly owned subsidiary of BestEx.

26 I accept Mr Klinger’s evidence that at the relevant time he was unaware that BestEx Asia was owned personally by Mr Weinberg and was not a subsidiary of BestEx.

27 The business venture involving Mr Klinger and Mr Weinberg appears to have been established in early 2015. It used the name Block Event. An internet domain – “blockevent” was used in connection with the Block Event business. Block Event was not registered as a company. The Block Event business operated in Australia through BestEx and relied on BestEx’s AFSL.

28 As part of establishing the Block Event business, in around April 2015, Mr Klinger was appointed Chief Executive Officer (CEO) of BestEx and Mr Weinberg was appointed Chief Operating Officer of BestEx. Mr Klinger did not become a director or shareholder of BestEx at this time or at any subsequent time.

Capital-raising context and the “regulatory capital” theme

29 This is a theme in the evidence that provides essential context known to both Mr Weinberg and Mr Klinger that relates to the circumstances in which the 29 December 2016 email was sent. During 2015-2016, Mr Klinger and Mr Weinberg explored expansion of the business into Asia. The evidence shows that, in that period, they explored obtaining settlement and execution services for Asian equities and considered the capital that would be required for those arrangements and for regulatory licensing.

30 A recurring theme in contemporaneous communications to which both men were privy was a distinction between: (a) capital described as “regulatory” (or otherwise required to satisfy settlement collateral or licensing-related requirements); and (b) capital described as “working capital” for operating expenses. In those communications, capital described as regulatory capital was repeatedly characterised as segregated, low-risk, and not to be used for operations.

31 Those communications form part of the objective factual matrix against which the December 2016 arrangement must be assessed. They are not, of themselves, determinative of the parties’ mutual intention at the time the $1 million was advanced, but they explain why the parties treated the December 2016 funding step as directed to securing the licence and satisfying minimum liquidity requirements.

32 In October 2015, Mr Klinger travelled to Singapore to meet with Mr Mark Nelligan, managing director of Pershing Securities Pte Ltd, to discuss Pershing’s services for executing and settling transactions for clients in Asia. At the meeting, Mr Nelligan said that to use Pershing Securities to settle trades would require approximately 2% of the value traded in liquid assets for settlement capital. In a discussion between Mr Klinger and Mr Weinberg following the Pershing Securities meeting, they discussed that based on an initial budget for a trading value of $50 million per day, they would need to hold settlement capital (collateral) of around $1 million. This appears to be the genesis of the idea that BestEx Asia would need $1 million in capital to support the business operations that it intended to operate in Hong Kong under a licence from the Hong Kong Securities and Futures Commission (HKSFC).

33 On 12 January 2016, Mr Weinberg and Mr Klinger participated in a call with Mr Alex Duperouzel and Mr Charles French of Compliance Asia Consulting Limited, a firm which advised financial services providers in respect of regulatory matters in Asia. Compliance Asia’s advice was that the company would require a Type 1 licence from the HKSFC in order to undertake the proposed trading business. Compliance Asia further informed them that if the company intended to physically operate in Hong Kong, it would require a Type 7 licence. BestEx could not apply for a HKSFC licence because it was not incorporated in Hong Kong. Compliance Asia also advised that if a Type 1 licence was approved, the company would need to be capitalised with HKD 5 million and thereafter maintain HKD 3 million in liquid capital. This information, to which both Mr Weinberg and Mr Klinger were privy, is relevant to ascertaining objectively what they mutually understood as to the HKSFC’s Financial Resources Rules (FRR) requirements.

34 On 7 March 2016, Mr Weinberg sent Mr Klinger a proposal received from Compliance Asia in relation to preparing a licence application to submit to the HKSFC for Type 1 and Type 7 licences and for ongoing support services. In his email forwarding the Compliance Asia proposal, Mr Weinberg stated:

We will need to register a wholly owned HK subsidiary, with an office in HK (TORA or serviced office) and have a HK resident Director (Chris Jenkins or whoever TORA put on our board). By the end of the application process, we would need to fund it to meet min reg cap requirements in order to be licensed.

(Bold emphasis added)

35 This is the first written communication between Mr Weinberg and Mr Klinger concerning the need to fund “min cap” requirements, which I infer to mean minimum regulatory capital requirements, as opposed to the settlement collateral which was anticipated to be required for the proposed Pershing arrangements. The other point of significance is that Mr Weinberg expressly states that the entity to be licensed will be a “wholly owned HK subsidiary”.

36 One of the ideas that Mr Klinger and Mr Weinberg had in relation to the means by which regulatory capital could be raised was by issuing a convertible note. Mr Klinger says that in one of their conversations, either he or Mr Weinberg said words to the effect, “we will wind up the business before we ever touch the [r]egulatory [c]apital.” He says that in this same conversation, Mr Weinberg then said to him words to the effect, “the [r]egulatory [c]apital will be as safe as money in the bank.” Mr Weinberg denies this. He also denies that he and Mr Klinger had discussions during and from about mid-2016 about “the need to raise two different kinds of capital” as Mr Klinger contends.

37 Mr Weinberg denies that he ever said that “the regulatory capital will be as safe as money in the bank”. His denial is premised on what he says was his practice to refer to the two tranches of capital to be raised as “settlement capital/collateral” and “working capital” respectively, consistent with the primary intended purposes of the separate tranches. The contemporaneous documents which passed through Mr Weinberg’s hands and were authored or approved by him do not reflect what he now asserts to be his practice in relation to referring to the two tranches of capital to be raised as “settlement capital/collateral” and “working capital”. Mr Weinberg’s evidence to this effect is patent reconstruction.

38 On this issue, where there is a conflict between the evidence of Mr Weinberg and Mr Klinger, I prefer Mr Klinger’s evidence. It follows that I reject Mr Weinberg’s denials. In reaching this conclusion I have afforded weight to the contemporaneous documents to which Mr Klinger and Mr Weinberg were privy. The contemporaneous documents in the main support the conclusion that Mr Klinger’s account reflects what was communicated between the parties at the time.

39 The following contemporaneous documents illustrate the conclusion I have reached that the contemporaneous record aligns with Mr Klinger’s evidence. This is not an exhaustive canvas of the contemporaneous documents that support this conclusion.

40 On 18 May 2016, Mr Klinger copied Mr Weinberg into an email sent to Mr Richard Macfarlane which included details of Mr Macfarlane’s employment offer. Amongst other things, Mr Weinberg noted that Mr Macfarlane’s role would be to “manage the Asian equities part of the business” and would include “liaising with regulatory bodies and exchanges when appropriate.” The letter concluded with an invitation for Mr Macfarlane to participate in the capital raising, referencing a convertible note structure:

We also need to raise approximately US 1 mil for regulatory capital that will sit in T-Bonds and will not be used for working capital. This capital is effectively risk free unless we have a major error. There are a couple of different ways we can fund this but one option is that it is funded by existing staff who could borrow money to invest in a convertible note structure that paid a coupon which covered the borrowing cost and had an exercise price of around US$10mil valuation.

(Bold emphasis added)

41 This is the first contemporaneous document that refers to a proposal for BestEx to issue convertible notes for the purpose of raising “US 1 mil for regulatory capital that will sit in T-Bonds and will not be used for working capital”. It is a communication to which both Mr Weinberg and Mr Klinger were privy. It distinguishes between “regulatory capital” which is to be placed in T-Bonds, which I take to be Treasury or government bonds, and which “will not be used for working capital”. It proposes that the mechanism to raise the funds to be purposed as “regulatory capital” will be a convertible note with a coupon to cover the payer’s borrowing costs and an exercise option timed to the company achieving a “US$10 mil valuation”. There are obvious similarities between what Mr Weinberg has proposed in this letter, copied to Mr Klinger, and the proposal contained in the 29 December 2016 email to which I will come.

42 In early July 2016, Mr Weinberg and Mr Klinger circulated various iterations of investor presentations to potential investors. Mr Weinberg says that Mr Klinger was the one who created and maintained the presentations. But the evidence demonstrates that he was also responsible for presenting the information derived from the presentations to investors and that he liaised with Mr Klinger in relation to keeping their messaging consistent.

43 On 5 July 2016, Mr Weinberg sent Mr Klinger an email with the subject “Cap Raising” which included an extract from the investor presentations. Mr Weinberg asked:

Just to confirm, is this what we're going to investors with (from the preso)?

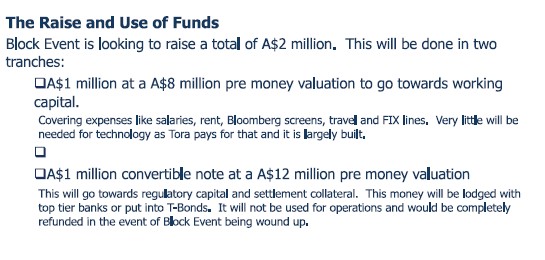

44 This email was in relation to what Mr Weinberg and Mr Klinger would tell potential investors about the arrangements to be put in place to support BestEx Asia’s licence. In it they draw a distinction between “working capital” on the one hand and “regulatory capital and settlement collateral” on the other hand. Moreover, they drew a distinction between the use to which particular tranches of the capital raising could be put. Funds raised for the purpose of “regulatory capital and settlement collateral” are to be raised by the issue of convertible notes at a $12 million pre money valuation. At the time of this email, Mr Weinberg and Mr Klinger were still liaising with Pershing in relation to the prospect of Pershing providing settlement and execution services. They expected that BestEx would be required to place US $1 million by way of a bond with Pershing. The reference to “regulatory capital and settlement collateral” is understood in that context. Importantly, the expressed future intention in relation to these funds on which they both agree at this time is that once the $1 million for “regulatory capital and settlement collateral” is raised, this money will be “lodged with top tier banks or put into T-Bonds. It will not be used for operations and would be completely refunded in the event of Block Event being wound up”. This reference is consistent with Mr Klinger’s evidence that Mr Weinberg told him that “we will wind up the business before we ever touch the [r]egulatory [c]apital” and that “the [r]egulatory [c]apital [would] be as safe as money in the bank.”

45 Mr Weinberg says that the wording in the investor presentation, which he copied into the email, was entirely Mr Klinger's and not his own. Mr Weinberg’s evidence is self-serving and not to the point. The communication is relevant in that it demonstrates that at least at this time, Mr Weinberg confirmed to Mr Klinger that he intended to provide information to investors that confirmed that he shared Mr Klinger’s understanding and intention as to BestEx seeking to raise $1 million for “regulatory capital and settlement collateral”, as well as the means by which it would be raised, to what purpose it would be applied once raised (and the purpose for which it would not be used, viz. working capital) and how it would be segregated from BestEx Asia’s other assets and protected in the event the business failed.

46 The evidence establishes that in the months following July 2016, Mr Weinberg and Mr Klinger each sent various iterations of the investor presentations to potential investors. For example, on 6 July 2016, Mr Klinger provided the investor presentation to Mr Christopher Ryan. On the slide entitled “Use of Funds” the wording from the 5 July 2016 email referred to above is repeated. Namely, that $1 million would “go towards regulatory capital”.

47 Mr Weinberg sought to distance himself from the content of the investor presentations. I do not accept his evidence on this topic. Mr Weinberg emailed Mr Klinger on 30 August 2016 and attached a short and a long version of the investor pack. In his covering email he said that he had “updated the investor pack and made it look nicer”. Mr Weinberg said that he updated the presentation on the basis of Mr Klinger’s instructions to update the presentation with a graphic designer. He said that he could not recall any changes being made to the substantive content of the presentation.

48 The updated investor pack attached to Mr Weinberg’s email included the following slide:

49 On this slide under the heading “The Ask, Offer, Use of Funds & Exit Strategy”, it is again stated that $1 million (now described as 50% of the total raising of $2 million) would be used for “[r]egulatory capital (ring-fenced)”. I draw the inference that the funds purposed to supply regulatory capital were to be raised by the issue of a convertible note whereas the funds purposed to supply working capital were to be raised by an offer of ordinary shares. This is consistent with the earlier materials and is reflected in the demarcation between rows #1 and #2 dealing with “use of funds”. This is the first reference in the contemporaneous documents to the funds used for the purpose of supplying regulatory capital being “ring-fenced”. The antecedent proposal for Pershing to supply settlement services was based on BestEx supplying settlement collateral that was similarly segregated pursuant to the requirement to deposit the amount required as settlement collateral in a bond-like arrangement.

December 2016: crystallisation of the arrangement and objective mutual intention

50 By September 2016, Mr Weinberg and Mr Klinger had not been able to raise funds for regulatory capital. The references in the investor materials to regulatory capital were removed after Mr Weinberg and Mr Klinger decided in September 2016 that the funds required for this purpose would be sourced internally from the employees of the business.

51 The shift in the target of the capital raising to be used for regulatory capital to employees, instead of third party investors, is reflected in the contemporaneous documents to which Mr Weinberg and Mr Klinger were privy.

52 Mr Klinger’s evidence was that around this time he decided that he would make the investment himself or use a company under his control to do so. He explained his rationale for making this decision as his consideration that it would be both a safe and worthwhile investment. He understood that it would be safe because the funds were to be used for regulatory capital and not as working capital. He understood that this meant that the funds would be “as safe as money in the bank”. He considered it to be a worthwhile investment because Block Event had been operating successfully in Australia and the benefit of a convertible note and the coupon payment were in his opinion a good return on what was a low-risk investment.

53 By November 2016, Mr Weinberg and Mr Klinger’s attempts to raise capital for the purpose of BestEx Asia’s working capital had not succeeded.

54 In December 2016, BestEx Asia had received in-principle approval for the grant of its Type 1 licence under the HKSFC’s FRR. Contemporaneous communications in that period to which both men were privy (including communications with advisers and the bank at which BestEx Asia had opened its account) addressed the need to inject capital and to retain a minimum liquidity amount, including by placing a specified amount on term deposit.

55 On 1 December 2016, Mr Weinberg and Mr Klinger attended a meeting with Mr Darren Sommers of KHQ Lawyers. On 5 December 2016, Mr Weinberg emailed Mr Sommers (copying Mr Klinger) stating they were proceeding on the basis of a holding company with two wholly owned operating subsidiaries, referring to the requirement that the Hong Kong operating company retain a minimum amount of liquid capital. That email sought advice on how the investment by “David and I” could be best protected.

56 At this stage, it appears that Mr Weinberg and Mr Klinger were contemplating imposing a holding company above BestEx and BestEx Asia. They also appear to have been contemplating that although Mr Klinger, through Rosemont, would fund the $1 million injection into BestEx, that $500,000 of that investment would be made on Mr Weinberg’s behalf and that they would each equally take up any convertible note issued in consequence of the investment. On the documents, it does not appear that Mr Sommers was favoured with the information that Mr Klinger would fund Mr Weinberg’s part of the investment. This is apparent from the repeated references to the investment being by Mr Weinberg and Mr Klinger. The reference to “two wholly owned operating subsidiaries, one for Australia and the other for HK” refers to BestEx and BestEx Asia respectively. Mr Weinberg does not reveal in this email that he in fact owns the whole of the shares in BestEx Asia.

57 On 7 December 2016, Mr Sommers responded with a proposed structure, including a simple loan (or alternatively a convertible note), security, and guarantees. This exchange forms part of the documentary context in which the later 29 December 2016 email is to be construed objectively.

58 On 23 December 2016, Mr Weinberg emailed Mr Sommers (copying Mr Klinger) confirming that the holding company would not on-lend to the Hong Kong subsidiary but would instead purchase equity to meet the relevant capital requirements for the issue of the Type 1 licence. This email is significant. Read with the preceding correspondence, this communication manifests an outwardly expressed intention that the $1 million would be advanced to BestEx and would be applied to capitalise BestEx Asia by share acquisition, with such shares to be issued to BestEx. It demonstrates that Mr Weinberg and Mr Klinger mutually intended by 23 December 2016 that the arrangement would be as follows:

(1) the $1 million advance by (at that stage) Mr Klinger and Mr Weinberg would be paid to the holding company – BestEx (which was being held out to be the holding company of BestEx Asia, notwithstanding the true position known to Mr Weinberg);

(2) a commercial decision would be made as to whether that advance was to be by way of a simple loan agreement or by way of a convertible note subscription;

(3) a series of general security agreements would be put in place to create security interests over the assets of the payees in favour of the payors, including relevantly, Mr Klinger and Mr Weinberg;

(4) the $1 million received by BestEx would not be on-lent to BestEx Asia – it would instead be used by BestEx to purchase shares in BestEx Asia to meet the capital requirements in Hong Kong (which BestEx Asia had to satisfy to convert the in principle approval it had received to the grant of a licence); and

(5) the paperwork necessary to document the final arrangements would be put in place after the $1 million was advanced to BestEx and applied by it to acquire shares in BestEx Asia and that would be some time after 9 January 2017 (when Mr Sommers returned from leave).

59 The instructions given to Mr Sommers in writing, and to which Mr Weinberg and Mr Klinger were both privy, manifests their mutual intention as to each of those matters.

60 I find that on or about 27 December 2016, Mr Klinger told Mr Weinberg he was ready to transfer the $1 million and asked Mr Weinberg to confirm in writing the bank account details, what was to be done with the money, and what would happen afterwards. That request prompted Mr Weinberg’s email of 29 December 2016.

61 On 29 December 2016, Mr Weinberg emailed Mr Klinger with the subject “Bank Account Details for Transfer and Confirmation of Arrangement” requesting that Mr Klinger transfer $1 million to BestEx. The subject line of the email is consistent with it being sent in response to Mr Klinger’s oral request for confirmation of the arrangement. The 29 December 2016 email provides (as written):

From: Phillip Weinberg

Sent: Thursday, 29 December 2016 11:30 AM

To: David Klinger

Subject: Bank Account Details for Transfer and Confirmation of Arrangement

Hi David,

Please transfer AUD 1m to the following account:

Account Name: BestEx Pty Ltd

BSB:06 [XXXX]

Acc: 1046 [XXXX]

This is the bank account of BestEx Pty Ltd in Australia which will issue a convertible note for the full amount with a coupon payment to cover your funding costs.

The funds will be used to capitalise BestEx Asia Ltd (a wholly owned subsidiary of BestEx Pty Ltd) and placed on term deposit with DBS Bank in HK to meet the SFC’s FRR rules. Once the funds are received I will be able to provide a bank statement to the SFC so that the license can be granted.

The company’s solicitors will prepare the documentation to issue the convertible note and secure the funds upon their return on 9th January 2017.

Regards,

Phillip Weinberg

62 The email closely mirrors the email chain between Mr Weinberg, Mr Klinger and Mr Sommers.

63 By 29 December 2016, Mr Weinberg and Mr Klinger had agreed that instead of a simple loan agreement the funds would be advanced to subscribe for a convertible note with a coupon covering Mr Klinger’s funding costs. This was consistent with what Mr Weinberg and Mr Klinger had promoted to employees when seeking to solicit investment which was intended to be used for the same purpose, that is, as regulatory capital to support BestEx Asia’s licence application. It was mutually intended that the $1 million would be paid to BestEx before the convertible note was issued (or indeed drawn up).

64 The penultimate substantive paragraph is key. It is slightly ambiguous.

65 The first part of the opening sentence is plain in its meaning. It conveys that funds once received by BestEx were to be used to capitalise BestEx Asia. That is, to acquire shares in BestEx Asia by BestEx. In this way, BestEx Asia, which had been represented by Mr Weinberg to be a wholly owned subsidiary of BestEx from its inception, would continue to be a wholly owned subsidiary of BestEx, albeit with a greatly increased issued share capital. Once the $1 million additional share capital had been issued, BestEx Asia would be in a position to demonstrate to the HKSFC that it had satisfied the regulatory capital requirements for the grant of its Type 1 licence.

66 The latter part of the opening sentence is where some ambiguity seeps in on the face of the document if read in isolation. On the face of the document alone, it is not clear whether the parties’ mutual intention was for the whole of the $1 million applied to acquire the BestEx Asia shares was to be used by BestEx Asia by being “placed on term deposit with DBS Bank in HK to meet the SFC’s FRR rules” or whether the parties’ mutual intention was for only the part of the funds required to satisfy the minimum liquidity requirements of the HKSFC’s FRR be placed on term deposit. This ambiguity is resolved by reference to the surrounding context and what had passed between the parties concerning what they understood to be the minimum liquidity requirements of the HKSFC’s FRR. In particular, Mr Weinberg’s email dated 20 December 2016, copied to Mr Klinger, which identified that the amount of the term deposit would be HKD 3 million (in USD or AUD equivalent).

67 On 30 December 2016, Rosemont transferred $1 million to BestEx. On the same day, Mr Weinberg caused the $1 million to be transferred to BestEx Asia by international money transfer, nominating himself as sender.

68 It is common ground that upon receipt of the $1 million, BestEx Asia’s share capital was increased and Mr Weinberg subscribed for all of the newly issued shares. BestEx did not subscribe for any shares.

69 On 31 December 2016, Mr Macfarlane emailed Mr Weinberg, copying Mr Klinger, for a “loan from BE on official terms” to pay a Hong Kong tax bill said to be due on 20 January 2017. Mr Klinger replied, copying Mr Weinberg, on 1 January 2017. In that email Mr Klinger informed Mr Macfarlane that “[w]e do have the extra cash but it is in AUD at the moment” but that it would take time to convert to HKD. Mr Klinger proposed instead to lend the money to Mr Macfarlane using his personal redraw facility against his house which allowed him to borrow in HKD. Had Mr Klinger believed the whole of the $1 million was going to sit in a term deposit he would not have alluded to the availability of extra cash in AUD at that moment. The only “extra cash in AUD” in BestEx Asia was that which had been subscribed to the issue of its shares. I find that both Mr Klinger and Mr Weinberg intended that the term deposit would be limited to the amount of HKD 3 million.

70 By notice of alteration of share capital dated 10 January 2017, BestEx Asia notified the Hong Kong Companies Register that its issued share capital had been increased through provision of AUD $1 million by the existing shareholder.

71 Having regard to the contemporaneous documents, I find that by late 2016 the parties’ common understanding changed from what it had been during their earlier capital-raising endeavours because their attempts at external capital raising had not succeeded and the business still needed to secure the licence. In December 2016, following in-principle approval, the parties’ objectively manifested intention was that the $1 million supplied by Rosemont would be advanced to BestEx, applied by BestEx to acquire shares in BestEx Asia and thereby capitalise it, and that from the $1 million injected into BestEx Asia an amount equivalent to HKD 3 million would be placed on term deposit to satisfy the minimum liquidity requirement which they understood to apply.

72 Further support for the inference I have drawn as to the parties’ mutual intention that only the equivalent of HKD 3 million be placed in term deposit arises as a matter of commercial necessity. In circumstances where no separate working capital funding had been secured, I infer that the parties objectively intended that the balance of the $1 million not required to be placed on term deposit for liquidity purposes would be available to meet BestEx Asia’s working capital needs.

73 In reliance on the confirmation supplied by the 29 December 2016 email, Mr Klinger caused Rosemont to advance the $1 million. He did this in accordance with the parties’ mutual intention that a convertible note would be agreed and issued at a later time. It was mutually intended that BestEx would apply those funds to acquire shares in BestEx Asia. Instead, the shares were issued to Mr Weinberg personally, without Mr Klinger’s knowledge or concurrence and contrary to the parties’ shared objective intention as to the use to which the funds were to be put at the time the funds were advanced. BestEx Asia was granted a Type 1 licence by the HKSFC on 18 January 2017. A copy of that licence was not in evidence.

ISSUES FOR DETERMINATION

74 The factual findings relevant to the issues that arise for determination are set out above. Those findings address:

(1) the ownership and corporate structure of BestEx Asia: [16]-[28];

(2) the capital‑raising context in 2016: [29]-[49]; and

(3) the arrangement objectively manifested between the parties in December 2016, culminating in the transfer of $1 million on 30 December 2016: [50]-[73].

75 Against that factual foundation, the issues for determination are whether, on those findings, Rosemont has established its trust‑based claims, its claims for misleading or deceptive conduct, and its claim in deceit. The sub-issues which arise in relation to each category of claim are articulated in the consideration of each category of claim.

TRUST-BASED CLAIMS

Issues

76 In resolving the trust‑based claims, I proceed by reference to the findings at [16]-[28] (ownership and knowledge) and [50]-[73] (December 2016 objective mutual intention and application of funds).

77 In relation to the trust-based claims the central issue is whether the intention of Rosemont and BestEx (and relatedly, BestEx Asia upon receipt of the funds), objectively ascertained, was for the $1 million to be used exclusively for the specific purpose of providing BestEx Asia with “regulatory capital” for the purpose of it obtaining a licence to operate in Hong Kong. Leaving issues of onus aside for the moment, the parties have not sought to establish as a matter of fact the content of any regulatory capital requirements for the grant of the relevant licence by the HKSFC. That is so notwithstanding that Rosemont positively pleads that the $1 million was to be used “by BestEx for the sole purpose of providing regulatory capital to BestEx Asia in accordance with the [HKSFC]’s [FRR]”: Statement of Claim [31(a)].

78 Rosemont’s pleaded allegation, which Mr Weinberg denies, is that at the time the $1 million payment was made, there existed a shared and outwardly manifested intention between Mr Weinberg, BestEx, BestEx Asia, Mr Klinger and Rosemont as to the use and treatment of the contributed funds. The substance of that intention, it is said, was that the funds:

(1) would be applied solely for the purpose of providing regulatory capital to BestEx Asia in accordance with the HKSFC’s FRR;

(2) would, for that purpose, be placed in a term deposit with a bank in Hong Kong;

(3) would be ring‑fenced from other monies controlled by BestEx or BestEx Asia;

(4) would not be used for working capital or other operational expenses of those entities; and

(5) would not otherwise be at the free disposal of Mr Weinberg, BestEx, or BestEx Asia.

79 Rosemont relies on a series of communications and documents said to evidence that intention.

80 The way in which Rosemont frames its case begets the question of what “regulatory capital” BestEx Asia was required to have under the HKSFC’s FRR. As mentioned, neither party sought to prove the applicability or the content of the HKSFC’s FRR in relation to BestEx Asia. Nor did either party submit that in the absence of proof, the presumption of similarity between the law of Hong Kong and the law of the forum should apply: Neilson v Overseas Projects Corporation of Victoria Ltd [2005] HCA 54; 223 CLR 331 at [125] (Gummow and Hayne JJ). The approach taken by the parties in this regard may be contrasted with the orthodox approach to the proof of foreign law: Regie National des Usines Renault SA v Zhang [2002] HCA 10; 210 CLR 491 at [70] (Gleeson CJ, Gaudron, McHugh, Gummow and Hayne JJ); Neilson at [115] (Gummow and Hayne JJ).

81 The way in which Rosemont ran its case was directed to the Court finding that the evidence established that the parties’ mutual intention, objectively determined, was that funds were to be applied for an exclusive purpose which the parties understood to be in accordance with the HKSFC’s FRR. What is important in determining if the funds were impressed with a Quistclose trust is not whether the parties’ understanding of what was required by the HKSFC’s FRR was correct, but rather whether the Court may infer that the parties objectively had a mutual intention that the funds be used exclusively for a specific purpose and no other. If Rosemont establishes that the parties to the trust had a mutual intention for the funds to be used exclusively for that specific purpose, it matters not whether the specific purpose was in fact a requirement of the HKSFC’s FRR. Ascertaining what the objective mutual intention of the parties was in relation to the $1 million payment will be informed by an objective assessment of their manifested mutual understanding of what was required to meet the HKSFC’s FRR.

82 Both Mr Klinger and Mr Weinberg gave evidence about their own understanding of what was required by the HKSFC’s FRR as they applied to BestEx Asia. Their respective subjective uncommunicated understanding of the requirements of the HKSFC’s FRR do not assist in ascertaining objectively what the parties’ mutually understood as to the relevant requirements of the HKSFC’s FRR. Determining what the parties mutually understood about the HKSFC’s FRR in their application to BestEx Asia is relevant to the broader task of ascertaining objectively the parties’ mutual intention in relation to the use of funds and whether the use was for a specific purpose and exclusively for that purpose. The focus must be on an objective assessment of what their mutual understanding was in respect of the relevant requirements of the HKSFC’s FRR. That is ascertained by drawing inferences from the language used in the parties’ communications with each other and third parties to which Mr Weinberg and Mr Klinger were both party, the nature of the transaction, and from the circumstances attending the relationship between the parties as well as commercial necessity.

83 Rosemont contends that the parties’ outwardly manifested mutual intention warrants the conclusion that the $1 million was impressed with a Quistclose trust to the effect that it could only be used for the purpose of providing regulatory capital to support the licence required by BestEx Asia to operate in Hong Kong and that in turn required the funds to be placed in a term deposit with a bank in Hong Kong; be ring‑fenced from other monies controlled by BestEx or BestEx Asia; not be used for working capital or other operational expenses; and not otherwise be at the free disposal of Mr Weinberg, BestEx, or BestEx Asia.

84 Rosemont maintains that the specific purpose for which the funds were exclusively to be used was immediately breached by Mr Weinberg causing BestEx to use the funds for a purpose which was not authorised and accordingly, the alleged trust was breached on the very day the funds were advanced.

85 Rosemont carries the onus of proving the trust and that the parties’ mutual intention, objectively ascertained, was to the effect it alleges. Rosemont seeks relief directed to requiring Mr Weinberg to restore to it the funds it paid to BestEx to the trust.

86 Fundamental to the determination of Rosemont’s claims in this proceeding is what the parties objectively intended as to the use of the funds advanced and whether their objective intention operated as a constraint on the use to which the $1 million advance would be applied. That is an issue that must be objectively ascertained as a matter of the mutual intention of the parties to the alleged trust – that is Rosemont and BestEx, and by extension, BestEx Asia, in so far as Rosemont claims that there was a secondary trust which bound BestEx Asia upon its receipt of the relevant funds from BestEx.

87 In its closing submissions, Rosemont submitted that the success of its claims premised on inducing a breach of trust does not depend upon it establishing the entirety of the matters it has pleaded in relation to the manifestation of the objective intention as to the exclusive purpose for which the funds were to be used. The relevant part of the Statement of Claim is paragraph [31], the effect of which is captured at paragraph [78] above. Rosemont closed its case on the basis that it was open to the Court to find that a trust existed, but that the terms of the trust were, for example, for less than the full $1 million to be held on trust or that the funds were not required to be held in a term deposit at all times. On this basis, Rosemont submits that if it falls short in establishing that the parties’ mutual intention was as it contends, then Mr Weinberg is still liable in relation to the lesser amount.

88 Mr Weinberg describes the $1 million payment as an “investment”. Mr Weinberg’s position is that the most that can be said about the mutual intention of the parties at the time of the funds transfer is that some part of the funds were to be used to provide regulatory capital to BestEx Asia, and that this was only one of several mutually intended purposes to which the $1 million could be applied.

89 Mr Weinberg maintains that in the context of the regulatory capital requirements which BestEx Asia was required to meet, the regulatory capital purpose posited by Rosemont is inherently uncertain. Mr Weinberg submits that properly understood in the context of BestEx Asia, the so-called regulatory capital purpose was ambiguous. He submits that it could be limited to mean only the requirement for BestEx Asia to have a minimum paid-up share capital to support the grant of its licence. Mr Weinberg gave evidence to the effect that he understood that under the HKSFC’s FRR the money received by BestEx Asia to subscribe for its shares was immediately available to it and at its free disposal but that BestEx Asia had an ongoing obligation to comply with ongoing liquid capital requirements and report on its compliance during the currency of its licence. Mr Weinberg’s subjective understanding in this regard, and whether it was a correct understanding of the application and content of the HKSFC’s FRR, is not the point in issue. The point in issue, as I have exposed above, is the parties’ mutual understanding, assessed objectively, in relation to the requirements of the HKSFC’s FRR and whether that informs the parties’ mutual intention relied on to support the imposition of a Quistclose trust.

90 Mr Weinberg further submitted that the regulatory capital purpose posited by Rosemont could extend to the liquidity requirement imposed under the HKSFC’s FRR pursuant to which he says that BestEx Asia was required to maintain a minimum amount of liquid capital. Mr Weinberg says that the uncertainty of the regulatory capital purpose posited by Rosemont is evident from the fact that it could mean both the capitalisation requirement and the liquidity requirement. For these reasons, Mr Weinberg submits that Rosemont’s contention as to the parties’ mutual intention is lacking in the requisite certainty to establish a Quistclose trust.

91 Mr Weinberg maintains that properly understood the regulatory capital purpose of the $1 million payment was effectuated and the trust was performed. Mr Weinberg’s submission that the trust was performed is premised on the regulatory capital purpose being capable of being satisfied in various ways and not inherently requiring a long-term segregation of the $1 million to be used only for the regulatory capital purpose for which Rosemont contends. Mr Weinberg maintains that as a result any beneficial interest Rosemont may have had under the alleged trust fell away upon BestEx Asia obtaining the relevant licence.

92 Mr Weinberg in his closing submissions raised additional defences which were broadly based on claims of waiver or release, laches and unclean hands. Mr Weinberg did not plead these defences in his defence and had not otherwise exposed his reliance on these matters in the materials he served before the hearing. He did not put the basis for these claims to Mr Klinger when Mr Klinger gave evidence. These issues raised by Mr Weinberg were not covered by the list of issues for determination that was agreed between the parties in revised form shortly before the hearing. In these circumstances, having regard to the requirement of procedural fairness, contemporary case management, and the overarching purpose embodied in s 37M of the Federal Court of Australia Act 1976 (Cth), Mr Weinberg is not permitted to rely on these matters in defence over Rosemont’s objection: Dare v Pulham [1982] HCA 70; 138 CLR 658; Banque Commerciale SA (in liq) v Akhil Holdings Ltd [1990] HCA 11; 169 CLR 279; Aon Risk Services Australia Limited v Australian National University [2009] HCA 27; 239 CLR 175.

Consideration – trust based claims

93 Rosemont’s trust-based claims fall to be determined by applying the relevant legal principles to the findings of fact set out at [16]-[73], in particular the findings as to the parties’ objective mutual intention in December 2016 and the subsequent application of the $1 million at [50]-[73].

94 Rosemont’s primary claim against Mr Weinberg is that he procured a breach of trust by each of BestEx and – by extension – BestEx Asia. Rosemont contends that in the case of BestEx, the alleged trust was a Quistclose trust. In the case of BestEx Asia, Rosemont contends that the alleged trust is either a Quistclose trust or that BestEx Asia is liable under the first limb of Barnes v Addy based on BestEx Asia’s receipt of the funds with knowledge of BestEx’s breach of trust (attributed to it through Mr Weinberg). Rosemont relies on this as a further and separate basis upon which Mr Weinberg must pay equitable compensation to Rosemont. Rosemont acknowledges that its claim based on Mr Weinberg procuring a breach of trust by BestEx Asia ultimately does not matter to the success of its claims if it succeeds against Mr Weinberg on the basis of its claim that Mr Weinberg procured a breach of trust by BestEx.

95 Rosemont contends that if it establishes that Mr Weinberg procured a breach of trust by BestEx and BestEx Asia respectively, then Mr Weinberg must pay equitable compensation to Rosemont to restore the funds alleged to be the subject of the trust(s).

96 Rosemont’s claims based on procurement of a breach of trust are dependent on Rosemont establishing the basal proposition that the $1 million it paid to BestEx was impressed with a Quistclose trust.

97 There does not appear to be a dispute between the parties as to the applicable legal principles. The contest is as to the application of the relevant principles to the facts. The focal point of the factual controversy is whether Rosemont has established the requisite mutual intention as to the specific and exclusive purpose to which the funds were to be applied.

Applicable legal principles

98 Whether a Quistclose trust arises depends upon the objective mutual intention of the parties, assessed by reference to their outward manifestations and the surrounding circumstances known to both parties at the time of the transaction. Uncommunicated subjective intentions are irrelevant: Byrnes v Kendle [2011] HCA 26; 243 CLR 253 at [113]-[115] (Heydon and Crennan JJ).

99 The critical question is whether the parties intended that the funds advanced were to be applied exclusively for a specific purpose, such that they were not at the free disposal of the recipient. Where that intention is established, equity treats the recipient as bound by a fiduciary obligation to apply the funds only for that purpose, and to return the funds if the purpose fails or is departed from: Twinsectra at [74] (Millett LJ); China Life Trustees Ltd v China Energy Reserve and Chemical Group Overseas Co Ltd [2024] HKCFA 15 at [147]-[148] (Gummow NPJ, Cheung CJ, Ribeiro, Fok and Lam PJJ agreeing).

100 It is not necessary that the transferor positively intend to retain a beneficial interest in the funds. The retention of beneficial interest is the legal consequence of the parties’ restrictive intention as to use, not a separate requirement for the creation of a Quistclose trust: China Life at [147]-[148].

101 Where a Quistclose trust is established, its breach occurs if the funds are applied for a purpose other than that for which they were advanced. If the funds are transferred onward with knowledge of the trust obligation, the recipient may likewise be bound, or alternatively subject to a constructive trust. It is sufficient that the third party had knowledge of the essential facts constituting the trust obligation and intentionally participated in conduct that brought about its breach under the first limb of Barnes v Addy.

102 A third party who knowingly induces or procures a breach of trust or breach of fiduciary duty may also be rendered accountable in equity as a “constructive trustee”: Grimaldi v Chameleon Mining NL (No 2) [2012] FCAFC; 200 FCR 296 at [245] (Finn, Stone and Perram JJ); Pittmore Pty Ltd v Chan [2020] NSWCA 344; 104 NSWLR 62 at [152] (Leeming JA, Bell P and Brereton JA agreeing).

103 These principles are applied below by reference to the findings at [50]-[73], which identify the purpose for which the funds were advanced and how they were in fact applied.

Issue 1: Purpose of the $1 million payment

104 Issue 1 is resolved by the findings at [50]-[73]. Those findings establish that, viewed objectively, the parties mutually intended that the $1 million advanced by Rosemont would be paid to BestEx, applied by BestEx to acquire shares in BestEx Asia, thereby capitalising that entity, and that from the injected funds an amount equivalent to HKD 3 million would be placed on term deposit to satisfy the minimum liquidity requirement which the parties understood to apply.

105 As found at [53], in circumstances where no separate working‑capital funding had been secured, the parties also objectively intended that the balance of the $1 million which was not required to be placed on term deposit would be available to meet BestEx Asia’s working capital needs.

Issue 2: Existence of a Quistclose trust

106 Given the findings at [50]-[73] as to the exclusive mandate governing the application of the $1 million, the question whether the funds were impressed with a Quistclose trust turns on whether that mandate constrained BestEx’s freedom of disposition.

107 Having regard to my conclusion in relation to Issue 1, I further conclude that the $1 million advanced by Rosemont was impressed with a Quistclose trust. The relevant purpose or mandate which supplied the trust obligation was that those funds when advanced (and before being applied as the subscription for a future proposed convertible note) had to be applied for the specific and exclusive purpose of BestEx acquiring shares in BestEx Asia. Had that been done, BestEx Asia would thereafter have been required to place the equivalent of HKD 3 million on term deposit to satisfy what the parties mutually understood to be the minimum liquidity requirement imposed under BestEx Asia’s Type 1 licence. Again, had that been done, BestEx Asia would have been able to apply the balance of the share subscription capital to its working capital. However, the BestEx Asia shares were not issued to BestEx resulting in breach of the trust and triggering the obligation to return the $1 million to Rosemont.

Issues 3 and 4: Use of funds and breach

108 For the reasons given at [50]-[73], the $1 million was not applied consistently with the exclusive purpose for which it was advanced. The application of the funds to the issue of shares in BestEx Asia to Mr Weinberg personally constituted a breach of that trust. By Mr Weinberg immediately causing BestEx to release the funds to his control and by expending the $1 million to acquire BestEx Asia shares in his own right (and not for BestEx) Mr Weinberg caused both BestEx and BestEx Asia to breach the specific and exclusive purpose for which the funds had been advanced. This specific and exclusive purpose was known to each of the BestEx entities by reason of Mr Weinberg’s knowledge being relevantly attributed to each of them.

Issues 5 and 6: Trust in BestEx Asia’s hands

109 The funds were subject to a Quistclose trust in BestEx Asia’s hands. If I am wrong in making that conclusion, the funds were subject to a constructive trust in BestEx Asia’s hands.

110 There was an immediate breach of the relevant trust by reason of the funds being applied to issue BestEx Asia shares in Mr Weinberg’s name.

111 Given that I have found that breach occurred at the point in time when Mr Weinberg caused BestEx to advance $1 million for the purpose of Mr Weinberg being issued with BestEx Asia shares, it is not necessary to determine whether the use of the funds received by BestEx Asia involved further and additional breaches. Had such an analysis been necessary it would be undertaken by reference to the earlier finding I have made as to the parties’ mutual intention that the portion of the $1 million that exceeded that which was to be held on term deposit to satisfy BestEx Asia’s Type 1 liquidity requirements could be used as working capital.

Issue 7: Procurement of breach by Mr Weinberg

112 The principles in relation to the accessorial liability of a person in Mr Weinberg’s position if it is established that he procured BestEx and/or BestEx Asia to breach the trusts for which Rosemont contends are well established. A third party who knowingly induces or procures a breach of trust or breach of fiduciary duty whether for his or her own, or for another person’s, benefit may be rendered accountable in equity as a “constructive trustee”. Unlike the second limb of Barnes v Addy, it is not necessary to show any dishonest or fraudulent design: Grimaldi at [245]; Farah Constructions Pty Ltd v Say-Dee Pty Ltd [2007] HCA 22; 230 CLR 89 at [161] (Gleeson CJ, Gummow, Callinan, Heydon and Crennan JJ); Pittmore at [152]; Australian Super Developments Pty Ltd v Marriner [2014] VSC 464 at [284]-[310] (Sloss J). On the findings at [16]-[73], Mr Weinberg had knowledge of the essential matters constituting the trust obligation and controlled the application of the funds.

113 Mr Weinberg had knowledge of the essential matters which, to a reasonable person, would indicate that applying the money for different purposes would be a breach of trust: Pittmore at [194]. Mr Weinberg also intended that his actions would have the consequence that the money would be applied for those different purposes: Pittmore at [193]. Mr Weinberg cannot avoid accessorial liability by claiming that he was acting merely as a director of BestEx; he has acted other than in that capacity as Chief Operating Officer, sole shareholder, and secretary of BestEx Asia, by which he caused the money advanced from Rosemont to be applied to issue further share capital to himself: Pittmore at [166]. I am satisfied that Mr Weinberg knowingly procured the breaches of trust by BestEx and BestEx Asia.

114 Mr Weinberg controlled each of BestEx and BestEx Asia. He knowingly caused each of them to engage in the conduct that was relevantly in breach of their trust and/or fiduciary obligations and in doing so, he had knowledge of the specific and exclusive purpose for which the funds were advanced and that in using it to take up shares in BestEx Asia himself he was acting contrary to that purpose. As a result, Mr Weinberg is rendered accountable in equity as a constructive trustee as an accessory for procuring a breach of trust for his own benefit.

Issue 8: Equitable compensation

115 Mr Weinberg is liable to pay equitable compensation.

MISLEADING OR DECEPTIVE CONDUCT CLAIM

Issues

116 The misleading or deceptive conduct claims fall to be determined by reference to the findings at [16]-[28] (ownership of BestEx Asia) and [50]-[73] (the content and effect of the 29 December 2016 email and the subsequent transfer and application of funds).

117 Rosemont alleges that Mr Weinberg made three material representations in his 29 December 2016 email when requesting Mr Klinger to cause $1 million to be paid to BestEx while stating that in return BestEx would issue a convertible note.

118 First, a representation to the effect that the $1 million would be used by BestEx for the sole purpose of providing regulatory capital to BestEx Asia in accordance with the HKSFC’s FRR; and for that purpose, the $1 million be placed in a term deposit with a bank in Hong Kong. Rosemont defines this as the Capitalisation Representation.

119 Second, a representation to the effect that BestEx Asia was a wholly owned subsidiary of BestEx. Rosemont defines this as the Subsidiary Representation.

120 Third, a representation to the effect that it was Mr Weinberg’s intention that the $1 million be used in accordance with the Capitalisation Representation. Rosemont defines this as the Intention Representation.

121 Mr Klinger’s evidence is that he would not have caused Rosemont to advance the $1 million if he had known the truth about any of the alleged representations. He contends that had he known the true position, he would have been concerned that the $1 million payment would have been at risk and not protected by a “ring-fenced” term deposit which could not be used for working capital, and otherwise be within the control of the broader Block Event business conducted through BestEx which he understood to be a wholly owned subsidiary of BestEx, namely BestEx Asia.

122 The three representations are pleaded in the Statement of Claim: [12]-[13]. Mr Weinberg’s defence to these paragraphs are in the corresponding paragraphs of the Defence: [12]-[13].

123 Mr Weinberg relies on his assertion that the convertible note referred to was intended to be issued in two equal parts, with Mr Klinger funding Mr Weinberg’s share by way of non-recourse loan. Mr Weinberg denies that the Capitalisation Representation and the related Intention Representation were conveyed by the 29 December 2016 email. He advances a positive case as to what he maintains were the representations that were conveyed by the 29 December 2016 email and the way in which he alleges that Mr Klinger necessarily understood the representations made in the 29 December 2016 email in light of the surrounding context of which the parties were aware.

124 Mr Weinberg’s stance in relation to the Subsidiary Representation is different. He accepts that it was conveyed in his 29 December 2016 email but says that the shares in BestEx Asia were then held by him on trust for BestEx in accordance with the instructions given to him by Mr Klinger. Mr Weinberg alleges that Mr Klinger’s instructions were motivated by Mr Klinger’s acceptance that his reputational baggage had proved to be an impediment to BestEx securing Pershing’s settlement and execution services and further that to have his name associated with BestEx Asia may be an impediment to BestEx Asia obtaining a licence to operate in Hong Kong.

125 Mr Klinger’s reputation was tainted by his alleged past conduct which had been the subject of an investigation and litigation involving the Australian Taxation Office in this Court and involving the New South Wales Crime Commission in the Supreme Court of New South Wales. It was common ground that Mr Klinger did not want to be named as a responsible officer of BestEx Asia for the purpose of its licence application. Mr Weinberg claimed that even if Mr Klinger was not named as a responsible officer, Mr Klinger’s reputation could impact BestEx Asia’s licence application by the mere fact that he was shareholder of BestEx. Mr Weinberg did not adduce evidence beyond his own speculation based on what he said Mr Klinger had said to him (and which Mr Klinger denied). He did not seek to establish for example, that Mr Klinger was at the relevant time a substantial shareholder of BestEx who would have had to be named in BestEx Asia’s licence application if BestEx Asia had been a subsidiary of BestEx. Mr Weinberg did not seek to prove the relevant foreign law as to what comprised being a “substantial shareholder” for the purpose of the licence application. Moreover, the evidence as to the percentage shareholding that Mr Klinger held in BestEx at the relevant time was less than clear.

126 The following issues arise for determination in relation to Rosemont’s misleading or deceptive conduct claims. I will use continuous numbering following on from the numbering of the trust-based claims:

(9) Did the 29 December 2016 email contain any of the “Capitalisation Representation”, “Subsidiary Representation”, and “Intention Representation”?

(10) If the answer to Issue 9 is “yes”, were any of the representations found to be conveyed misleading or deceptive (or likely to mislead or deceive)?

(11) If the answer to Issue 10 is “yes”, did Rosemont rely on any of the representations found to be conveyed, and as a result suffer loss?

(12) If the answer to Issue 11 is “yes”, should the amount of compensation payable by Mr Weinberg to Rosemont be reduced on account of Rosemont’s contributory negligence and to reflect the proportionate liability of BestEx?

Consideration – misleading or deceptive claims

Applicable legal principles

127 Before turning to consider the issues raised for determination, I will briefly address the relevant legal principles. There is no dispute between the parties as to the applicable principles.

128 The prohibitions in s 18 of the Australian Consumer Law, s 1041H of the Corporations Act, and s 12DA of the ASIC Act are materially similar. Each directs attention to whether the respondent engaged in conduct that was misleading or deceptive, or likely to mislead or deceive. There is no requirement to establish any intention to mislead.

129 Whether conduct is misleading or deceptive is an objective question of fact. The conduct must be assessed as a whole, in its context, by reference to what it would convey to a reasonable person in the position of the representee. Where the conduct involves representations, they may be express or implied from the circumstances, and their meaning is determined by what the conduct conveys, not by what the representor subjectively intended: Butcher v Lachlan Elder Realty Pty Ltd [2004] HCA 60; 218 CLR 592 at [39] (Gleeson CJ, Hayne and Heydon JJ), [109] (McHugh J).

130 Where misleading conduct is established, it is sufficient that the representation played a material part in inducing the representee to enter the transaction. It need not be the sole or dominant cause. Loss is established where the representee is worse off by reason of acting on the misleading conduct: Henville v Walker [2001] HCA 52; 206 CLR 459 at [95], [144]-[145] (McHugh J, Gummow J agreeing at [153]); Marks v GIO Australia Holdings Ltd [1998] HCA 69; 196 CLR 494 at [42] (McHugh, Hayne and Callinan JJ).

Issue 9: Did the 29 December 2016 email convey any of the “Capitalisation Representation”, “Subsidiary Representation”, and “Intention Representation”?

131 Rosemont claims that each of the representations are misleading or deceptive within the meaning of one or more of s 18 of the ACL, s 1041H of the Corporations Act, and s 12DA of the ASIC Act.

132 The Capitalisation Representation alleged by Rosemont is to the effect that the $1 million would be used by BestEx for the sole purpose of providing regulatory capital to BestEx Asia in accordance with the HKSFC’s FRR; and for that purpose, be placed in a term deposit with a bank in Hong Kong. For the reasons already given, I am not satisfied that this representation was substantively conveyed by the 29 December 2016 email when considered in the relevant context known to both parties. The 29 December 2016 email conveyed that the $1 million would be used by BestEx to acquire shares in BestEx Asia and that once so applied the equivalent of HKD 3 million would be placed on term deposit. The combined effect of these two things would – according to the parties’ mutual understanding – satisfy the requirements that BestEx Asia was required to meet to support its Type 1 licence in accordance with the HKSFC’s FRR.

133 I am not satisfied that objectively construed in the whole of the surrounding circumstances, including that BestEx Asia had not raised any capital to be applied to its working capital, that the 29 December 2016 email conveyed that the whole of the $1 million once received by BestEx Asia in consideration for the issue of its shares would thereafter be held in a term deposit and not be available to utilise as working capital. The constraint in relation to placing the funds on term deposit and not using the funds to supply working capital was limited to the equivalent of HKD 3 million which was a portion only of the funds paid for the BestEx Asia shares.

134 Rosemont has not established that the Capitalisation Representation was conveyed by the 29 December 2016 email.