FEDERAL COURT OF AUSTRALIA

Kirk (in his capacity as liquidator of ARG Workforce Pty Ltd (in liq)) v Commissioner of State Revenue, in the matter of ARG Workforce Pty Ltd [2026] FCA 192

File number(s): | NSD 102 of 2025 NSD 103 of 2025 |

Judgment of: | GOODMAN J |

Date of judgment: | 4 March 2026 |

Catchwords: | CORPORATIONS – voidable transactions – good faith defence under s 588FG(2) of the Corporations Act 2001 (Cth) not made out – defendant called witnesses who had no recollection of the salient events – the evidence of those witnesses and the documents tendered did not provide a satisfactory basis from which the Court could be satisfied that the defence had been established |

Legislation: | Corporations Act 2001 (Cth), ss 9, 91, 588FA, 588FC, 588FE, 588FF, 588FG Evidence Act 1995 (Cth), s 140 Payroll Tax Act 1971 (Qld) Taxation Administration Act 1997 (Vic), s 92 Taxation Administration Act 2001 (Qld), ss 7, 11, 87 |

Cases cited: | AHB v NSW Trustee and Guardian [2014] NSWCA 40 Badenoch Integrated Logging Pty Ltd v Bryant [2021] FCAFC 64; (2021) 284 FCR 590 BounceLED Pty Ltd v Clear Skies Corp Pty Ltd (in liq) [2023] NSWSC 121 Briginshaw v Briginshaw [1938] HCA 34; (1938) 60 CLR 336 Capitalink Pty Ltd v Withnall [2024] NSWCA 172 CEG Direct Securities Pty Ltd v Cooper [2025] FCAFC 47; (2025) 309 FCR 66 Cook’s Construction Pty Ltd v Brown (as liqs of DML Resources Pty Ltd (in liq) [2004] NSWCA 105; (2004) 49 ACSR 62 Coshott v Prentice [2014] FCAFC 88; (2014) 221 FCR 450 Cussen v Sultan [2009] NSWSC 1114; (2009) 74 ACSR 496 Dean-Willcocks v Commissioner of Taxation (Cth) [2004] NSWSC 1058; (2004) 51 ACSR 353 Dean-Willcocks v Commissioner of Taxation [2008] NSWSC 1113; (2008) 73 ATR 801 Frigger v Trenfield (No 3) [2023] FCAFC 49 George v Rockett [1990] HCA 26; (1990) 170 CLR 104 GLJ v Trustees of Roman Catholic Church for Diocese of Lismore [2023] HCA 32; (2023) 97 ALJR 857 Ho v Powell [2001] NSWCA 168; (2001) 51 NSWLR 572 Hosking (in his capacity as joint and several liquidator of Evolvebuilt Contracting Pty Ltd (in liq)) v Extend N Build Pty Ltd [2018] NSWCA 149; (2018) 357 ALR 795 In the matter of Portman Securities Pty Ltd (in liq) [2025] NSWSC 1338 Kennedy v Secretary, Department of Industry (No 3) [2016] FCAFC 149 Luck v Chief Executive Officer of Centrelink [2015] FCAFC 75 Pegulan Floor Coverings Pty Ltd v Carter (1997) 24 ACSR 651 Queensland Bacon Propriety Limited v Rees [1966] HCA 21; (1966) 115 CLR 266 Re Ermayne Pty Ltd [1999] SASC 3; (1999) 30 ACSR 330 Sims v Tech Holdings Pty Ltd (trading as Westline Furniture) [1998] SASC 3; (1999) 30 ACSR 330 Shot One Pty Ltd (in liq.) v Day (in liq.) [2017] VSC 741 Smith v Deputy Commissioner of Taxation [1997] FCA 344; (1997) 23 ACSR 611 Stone (in their capacities as joint and several liquidators of Cardinal Project Services Pty Ltd (ACN 090 113 705) (in liq)) v Melrose Cranes & Rigging Pty Ltd (ACN 083 164 845) (No 2) [2018] FCA 530; (2018) 125 ACSR 406 Sutherland (as liquidator of Sydney Appliances Pty Ltd (in liq)) v Eurolinx Pty Ltd [2001] NSWSC 230; (2001) 37 ACSR 477 Trenfield (as joint and several liquidators of ACN 089 008 668 Pty Ltd (in liq) (ACN 089 008 668)) v JMD Park Pty Ltd (ACN 160 743 877) [2019] FCA 2154; (2019) 141 ACSR 277 Walsh v Umoona Tjutagku Health Service Aboriginal Corporation (ICN 7460) (No 2) [2017] FCA 852 White v ACN153 152 731 Pty Ltd (in liq) [2018] WASCA 119; (2018) 53 WAR 234 Williams (as liquidator of Scholz Motor Group Pty Ltd (ACN 108 820 220) (in liq)) v Peters [2009] QCA 180; (2009) 72 ACSR 365 |

Division: | General Division |

Registry: | New South Wales |

National Practice Area: | Commercial and Corporations |

Sub-area: | Corporations and Corporate Insolvency |

Number of paragraphs: | 177 |

Date of hearing: | 2 and 3 December 2025 |

Counsel for the Plaintiffs: | Mr M Hodge KC with Mr S Trewavas |

Solicitor for the Plaintiffs: | Enyo Lawyers |

Counsel for the Defendant: | Mr S C Russell |

Solicitor for the Defendant: | Crown Law |

ORDERS

NSD 102 of 2025 NSD 103 of 2025 | ||

IN THE MATTER OF ARG WORKFORCE PTY LTD ACN 626 211 443 | ||

BETWEEN: | DARRYL EDWARD KIRK IN HIS CAPACITY AS LIQUIDATOR OF ARG WORKFORCE PTY LTD ACN 626 211 443 (IN LIQUIDATION) First Plaintiff ARG WORKFORCE PTY LTD ACN 626 211 443 (IN LIQUIDATION) Second Plaintiff ARG PAYROLL PTY LTD ACN 626 225 232 (IN LIQUIDATION) Third Plaintiff | |

AND: | COMMISSIONER OF STATE REVENUE Defendant | |

order made by: | GOODMAN J |

DATE OF ORDER: | 4 March 2026 |

THE COURT DECLARES THAT:

1. Each of the payments by the second plaintiff to the defendant set out in Schedule 1 to this order is:

(a) an “unfair preference” within the meaning of s 588FA of the Corporations Act 2001 (Cth);

(b) an “insolvent transaction” within the meaning of s 588FC of the Act; and

(c) a “voidable transaction” of the second plaintiff within the meaning of s 588FE of the Act.

2. Each of the payments by the third plaintiff to the defendant set out in Schedule 2 to this order is:

(a) an “unfair preference” within the meaning of s 588FA of the Act;

(b) an “insolvent transaction” within the meaning of s 588FC of the Act; and

(c) a “voidable transaction” of the third plaintiff within the meaning of s 588FE of the Act.

THE COURT ORDERS THAT:

1. Pursuant to s 588FF(1)(a) of the Act the defendant pay the second plaintiff the sum of $2,474,375.01, being the total sum of the voidable transactions set out in Schedule 1.

2. Pursuant to s 588FF(1)(a) of the Act the defendant pay the third plaintiff the sum of $345,791.57, being the total sum of the voidable transactions set out in Schedule 2.

3. Pursuant to s 51A of the Federal Court of Australia Act 1976 (Cth) the defendant pay interest on:

(a) the sum of $2,474,375.01 to the second plaintiff; and

(b) the sum of $345,791.57 to the third plaintiff.

4. The defendant pay the plaintiffs’ costs, as agreed or taxed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

Schedule 1

Date | Workforce payments |

9 August 2021 | $120,355.14 |

18 August 2021 | $119,474.01 |

23 August 2021 | $267,630.92 |

7 September 2021 | $143,756.81 |

21 September 2021 | $267,630.92 |

11 October 2021 | $114,199.27 |

21 October 2021 | $267,630.92 |

11 November 2021 | $138,145.69 |

22 November 2021 | $267,630.92 |

10 December 2021 | $112,305.89 |

31 December 2021 | $267,630.88 |

21 January 2022 | $85,364.11 |

21 January 2022 | $83,269.30 |

21 January 2022 | $84,581.41 |

21 January 2022 | $134,768.82 |

Total | $2,474,375.01 |

Schedule 2

Date | Payroll payments |

23 August 2021 | $40,446.93 |

26 August 2021 | $20,633.11 |

27 August 2021 | $20,633.11 |

7 September 2021 | $20,142.19 |

21 September 2021 | $40,446.93 |

11 October 2021 | $25,393.20 |

21 October 2021 | $19,813.82 |

11 November 2021 | $16,861.22 |

22 November 2021 | $40,446.93 |

10 December 2021 | $26,388.20 |

21 December 2021 | $40,446.93 |

21 January 2022 | $34,139.00 |

Total | $345,791.57 |

[1] | |

[11] | |

[127] | |

[127] | |

[127] | |

[129] | |

[165] | |

[177] |

REASONS FOR JUDGMENT

GOODMAN J:

A. INTRODUCTION

1 The first plaintiff is, and since 2 February 2022 has been, the liquidator of the second plaintiff (Workforce) and the third plaintiff (Payroll).

2 Prior to the appointment of the liquidator, Workforce and Payroll operated a labour hire services business as part of a wider group of companies (ARG group).

3 The liquidator principally seeks an order under s 588FF(1)(a) of the Corporations Act 2001 (Cth), which section provides that upon the application of a company’s liquidator, the Court may make an order that a person pay to that company an amount equal to some or all of the money that the company has paid under a transaction of the company that is voidable because of s 588FE of the Act.

4 Section 588FE of the Act provides in so far as is presently relevant:

588FE Voidable transactions

(1) If a company is being wound up:

(a) a transaction of the company may be voidable because of any one or more of subsections (2) to (6) if the transaction was entered into on or after 23 June 1993; and

…

(2) The transaction is voidable if:

(a) it is an insolvent transaction of the company; and

(b) it was entered into, or an act was done for the purpose of giving effect to it:

(i) during the 6 months ending on the relation-back day; or

(ii) after that day but on or before the day when the winding up began.

5 The relation-back day for the purposes of s 588FE(2)(b)(i) of the Act was the date of the appointment of the liquidator: s 91 of the Act.

6 During the six months ending on the relation-back day, Workforce and Payroll made a series of payments to the Queensland Revenue Office (the QRO which, at that time, was known as the Office of State Revenue) totalling $2,474,375.01 and $345,791.57 respectively. It is common ground that the defendant in each proceeding (Commissioner) is:

(1) a statutory office established under s 7 of the Taxation Administration Act 2001 (Qld);

(2) the relevant officer of the QRO; and

(3) the relevant and responsible authority in relation to matters arising out of the Payroll Tax Act 1971 (Qld).

7 It is also common ground that the payments were transactions of Workforce and Payroll (within the definition of “transaction” in s 9 of the Act) and those transactions were voidable because of s 588FE of the Act.

8 Thus, the payments were voidable transactions and potentially subject to an order under s 588FF(1)(a) of the Act.

9 However, the Commissioner calls in aid s 588FG(2) of the Act, which provides:

588FG Transaction not voidable as against certain persons

…

If transaction entered into for valuable consideration in good faith without grounds for suspecting insolvency

(2) A court is not to make under section 588FF an order materially prejudicing a right or interest of a person if the transaction is not an unfair loan to the company, or an unreasonable director-related transaction of the company, and it is proved that:

(a) the person became a party to the transaction in good faith; and

(b) at the time when the person became such a party:

(i) the person had no reasonable grounds for suspecting that the company was insolvent at that time or would become insolvent as mentioned in paragraph 588FC(b); and

(ii) a reasonable person in the person’s circumstances would have had no such grounds for so suspecting; and

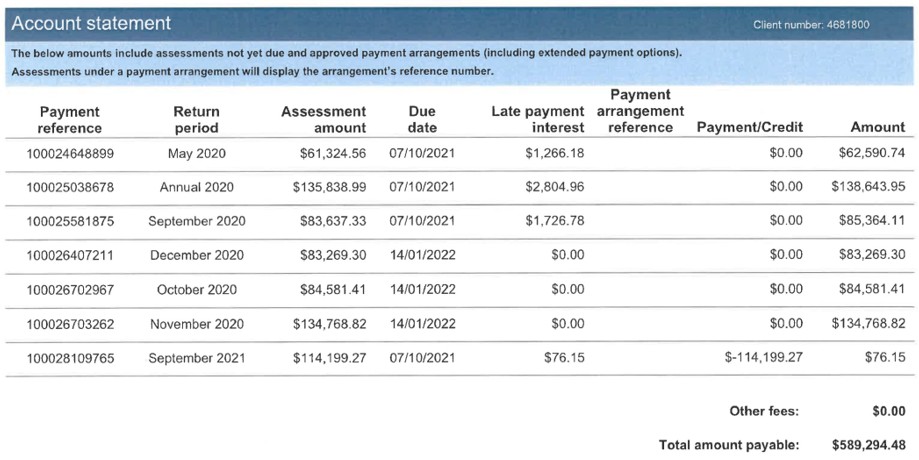

(c) the person has provided valuable consideration under the transaction or has changed his, her or its position in reliance on the transaction.

10 There is no dispute that each transaction was not an “unfair loan” or an “unreasonable director-related transaction”. The liquidator accepts that the QRO provided valuable consideration under each of the transactions. Thus, the issues for determination are whether:

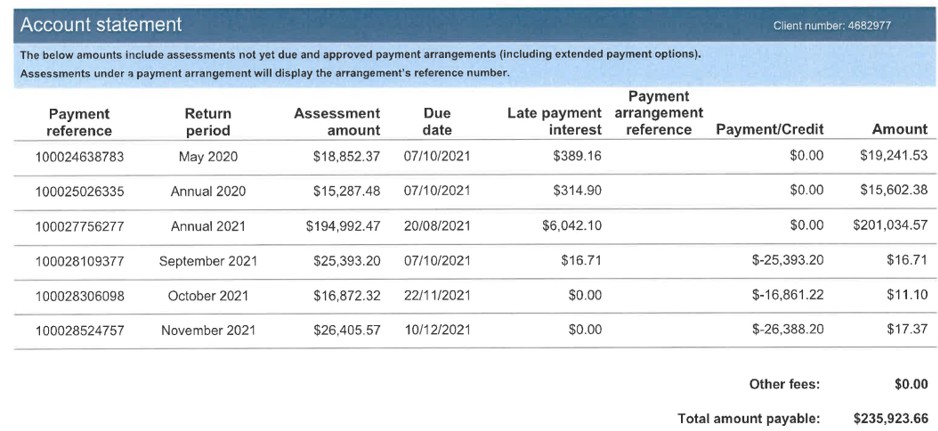

(1) for the purposes of s 588FG(2)(a) of the Act, the QRO became a party to the transactions in good faith;

(2) for the purposes of s 588FG(2)(b) of the Act, at the times when the QRO became a party to the transactions:

(a) the QRO had no reasonable grounds for suspecting that Workforce and Payroll were insolvent or would become insolvent because of matters including entry into the transactions or an act or omission done or made for the purpose of giving effect to the transactions; and

(b) a reasonable person in the QRO’s position would have had no such grounds for so suspecting.

B. FINDINGS OF FACT

11 The liquidator read an affidavit that he made; and tendered reports that he had prepared concerning the solvency of each of Workforce and Payroll.

12 The Commissioner read affidavits from the following persons who were employees of the QRO:

(1) Ms Kelly McKelvey, who was at the relevant times a manager in the Payroll Tax Division of the QRO;

(2) Mr Ieuan Murphy, who was at the relevant times, a Senior Investigations Officer. Part of Mr Murphy’s role was to identify companies that were not, but ought to have been, registered for payroll tax in Queensland;

(3) Ms Tamara Lucas, who was at the relevant times, an Investigations Officer;

(4) Ms Emma Lane, who was at the relevant times, a Debt Resolution Officer. Her role was to attempt to recover outstanding payroll tax debts. In Ms Lane’s position as a Debt Resolution Officer, she had authority to grant a formal payment arrangement application made by a debtor. If payment from a debtor could not be secured (including via a payment arrangement), then the debtor would be referred to a team leader for referral to the legal team for recovery of the debt through legal action;

(5) Ms Jessica Cliffe, who was at the relevant times, a Service Officer. (This role was not explained in her evidence). She had no dealings with Workforce or Payroll or the ARG group more generally; and

(6) Ms Jessica Foo, who was at the relevant times also a Service Officer. (Again, this role was not explained.)

13 No challenge was made to the credit of any of the Commissioner’s witnesses and I accept their evidence.

14 The affidavits of Ms McKelvey, Mr Murphy, Ms Lucas, Ms Lane, Ms Cliffe and Ms Foo principally prove documents held by the QRO.

15 Mr Murphy, Ms Lucas, Ms Lane, Ms Cliffe and Ms Foo also provided evidence that:

(1) QRO’s electronic revenue management system (RMS):

(a) is a computer revenue management system that electronically records interactions between investigating officers and debtors;

(b) contains records of the administration of revenue, grant and tax laws that are administered by QRO. RMS records are used to create work lists that are then allocated to officers for “actioning”; and

(2) all interactions between officers of the QRO and debtors (and any other parts of the Payroll Tax team) were required to be recorded electronically in RMS. This assisted other officers to follow up debtors if debts remained outstanding with knowledge of what had previously occurred with the debtor.

16 Mr Murphy, Ms Lucas, Ms Lane and Ms Foo identified their interactions with Workforce and Payroll that had been recorded on RMS. It appears that Ms McKelvey and Ms Cliffe did not interact directly with Workforce or Payroll.

17 There was also tendered a substantial bundle of documents, including recordings and transcripts of some conversations between employees of the QRO and representatives of Workforce and Payroll.

18 From the above described evidence, I make the following findings of fact.

19 From 30 June 2019, each of Workforce and Payroll was insolvent.

20 On 31 July 2019, Ms Ingrid Mathias, a delegate of the Commissioner of State Revenue, and manager of the Forensics and Information Management Branch of the State Revenue Office of Victoria wrote to Mr Geoff Waite, Acting Commissioner of the QRO. That letter (SRO Victoria letter) provided information under the “Phoenix Taskforce arrangement” and in accordance with s 92(1) of the Taxation Administration Act 1997 (Vic).

21 Ms McKelvey and Mr Murphy explained that:

(1) the “Phoenix Taskforce arrangement” referred to in the SRO Victoria letter is an arrangement that allows each State Revenue office in Australia and other federal government agencies to share information about “phoenixing activity”; and

(2) “phoenixing activity” includes deliberately shutting down a company by deregistration, voluntary administration or liquidation, at a time when, for example, the company’s payroll tax liability is approaching the threshold level at which point the company should be registered for payroll tax purposes, and then forming a new company in its place, to avoid the first company having to pay any future payroll tax liability.

22 In cross-examination, Ms McKelvey and Mr Murphy each accepted that:

(1) “phoenixing activity” was not limited to avoiding payroll tax and extended to the avoidance of other liabilities; and

(2) as at 2019, they understood that businesses engaged in “phoenixing” often had a practice of entering into voluntary administration or liquidation so as to avoid payment of their debts. Ms McKelvey also understood that the ARG group had a past history of engaging in “phoenixing”.

23 The information provided in a schedule to the SRO Victoria letter included:

…

State Revenue Office (SRO) Victoria has recently completed an investigation into ARG Labour Services Pty Ltd (ABN 89 607 112 532) (and any associated entities) to ascertain their compliance with the Payroll Tax Act 2007 (Vic) (the Act).

ARG Labour Services Pty Ltd was identified as a potential labour hire company operating in both Victoria and Queensland, via the Victorian State Revenue Office Phoenix Taskforce activities.

An investigation was commenced on ARG Labour Services Pty Ltd on 14 January 2019, and included the following associated entities under the grouping provisions of the Act –

• Australian Recruiting Group Pty Ltd (ABN 36 126 853 601) (In Liquidation)

• Australian Recruiting Connect Pty Ltd (ABN 75 164 397 399) (In Liquidation)

• ARG Staffing Pty Ltd (ABN 43 131 539 967) (In Liquidation)

Mr Dennis Ting, Manager at ARG Labour Services Pty Ltd confirmed the grouping of the above employers.

Based on the payroll information supplied by Mr Ting and the liquidator’s office, it was determined the group of employers paid taxable wages in excess of the Victorian payroll tax threshold and none of the employers were registered for payroll tax in Victoria, in their own right or as a member of a group.

There is evidence ARG Labour Services Pty Ltd employed in Victoria, Queensland, New South Wales and South Australia.

…

24 Mr Dennis Ting of the ARG group, who is identified in that email, would later become a contact point for the QRO.

25 Ms McKelvey explained that:

(1) each year the Payroll Tax Division of the QRO prepares a campaign program that deals with identifying risks associated with the assessment of payroll tax on behalf of the Commissioner of State Revenue. Some of those risks include:

(a) whether a company:

(i) should be registered for payroll tax purposes;

(ii) is part of a group of related companies, in which case each company of that group is jointly and severally liable for any payroll tax incurred by any of the group companies;

(iii) is reporting inaccurate wage details to QRO or other agencies;

(b) the liability of interstate and national businesses who operate in various jurisdictions, including Queensland, and who avoid having to pay payroll tax in those jurisdictions by engaging in phoenixing activities;

(2) one of Ms McKelvey’s tasks in managing referrals such as the SRO Victoria letter was to detect any non-compliance with payroll tax obligations caused by the manner in which the subject company conducts its affairs, and then assess actual payroll tax liabilities; and

(3) the team that Ms McKelvey managed was more concerned with crystallising actual tax liabilities by way of making the assessments required by s 11 of the Taxation Administration Act, than with recovery of the amounts assessed.

26 On 1 August 2019, Ms McKelvey sent an email to Mr Raymond Chand, then a Senior Investigations Officer and a team leader within the Payroll Tax Division of the QRO, attaching the SRO Victoria letter and requesting Mr Chand to undertake a preliminary review of the entities listed in the SRO Victoria letter and to advise whether those entities were registered, and if so their taxable wages, and whether those entities had been investigated previously.

27 Mr Chand allocated these tasks to Mr Murphy and Ms Lucas, who at the time were investigations officers within the team managed by Ms McKelvey.

28 Mr Murphy and Ms Lucas then carried out the tasks delegated to them and by mid-December 2019, each of Workforce and Payroll was registered for payroll and the subject of notices of assessment. In the course of carrying out those tasks, the following occurred.

29 By 13 November 2019, an ASIC alert had been placed on various companies including Workforce.

30 In the experience of Mr Murphy and Ms Lucas, as part of any investigation into potential phoenixing activities, it was common for investigators to request ASIC to place an ASIC company alert profile upon the companies being investigated and that this would alert the QRO as soon as the company became deregistered or had gone into voluntary administration or liquidation.

31 On 19 November 2019:

(1) Mr Murphy sent an email to Ms McKelvey (copied to Ms Lucas), stating:

In line with our meeting this morning, Tamara will be issuing the New Reg review letter to ARG Workforce Pty Ltd via email (with read receipt) and via registered post (to the ASIC registered business address) today. The initial prompt letter will have a return date of 3 December 2019. Should the client fail to respond to the letter in time, standard practice would be to issue an escalated prompt the day after the initial due date (4 December 2019), with a return date of two weeks (18 December 2019). A strict reading of the Christmas closure procedure (see below) is that officers are not allowed to ‘issue’ assessment notices, reassessments and requisitions from 9 December 2019 to 3 January 2020. Therefore, the standard process is allowed - providing assessments aren’t raised between 9/12/19 - 3/1/20.

In my opinion, there are two treatments we can enact, with treatment ‘1’ being the preferred:

1. Follow due process, issuing the initial prompt letter today and escalated prompt letter on 4 December 2019. Then, where a response:

a. Has not been received before 4 January 2020 – default assess the client on 4 January 2020 on available third party data with penalty tax imposed at a rate of 75%;

b. Is received after 20 December 2019 and before 4 January 2020 – consider whether information submitted by client is reasonable and if so, raise default annual and (where appropriate) periodic assessments on 4 January 2020 with penalty tax imposed at the rate of 5%; or

c. Is received before 20 December 2019, consider whether information submitted by client is reasonable and if so, raise default assessments on 4 January 2020 with no penalty tax imposed.

2. Vary the New Reg process, issuing the prompt letter today and escalated prompt letter on the 4 December 2019 with a final response date of 5 December 2019. Then, where a response:

a. Has not been received on or before 5 December 2019 – default assess the client on 6 December 2019 on available third party data with penalty tax imposed at a rate of 75%; or

b. Is received on or before 5 December 2019, consider whether information submitted by client is reasonable and if so, raise default assessments on 6 December 2020 with no penalty tax imposed.

Please advise if you are agreeable to Tamara proceeding with treatment ‘1’ and/or whether you’d like to discuss further.

…

(bold and underline emphasis in original) ;

(2) Ms McKelvey responded, stating (as written):

Im happy to proceed with option 1 and a default assessment (if required) however, please ensure Dhana and her team are briefed early so we can bank account details on file if we are going to garnishee. ; and

(Ms McKelvey and Mr Murphy explained that the reference to “Dhana” was a reference to Ms Dhana Schofield. Ms McKelvey described Ms Schofield as a member of the QRO’s Resolution Division, and Mr Murphy described her as a member of the QRO’s Collections Team);

(3) Ms Lucas sent an email to Mr Murphy setting out a draft email to Ms Schofield in the following form (as written):

Thank you for your time yesterday afternoon it was appreciated.

Just to recap on our discussion, the letter was issued to the entity today for them to undergo a payroll tax review rather than an investigation.

We are hopeful that they may provide us with a disclosure, however in the event that they do not we will discuss with Kelly in relation to whether we should amend the approach with consideration to the fact that the associated entity may require sensitivity. Tamara will further review this to determine whether the services that are supplied within ARG Workforce Pty Ltd are similar in nature to the potential associated member.

As we discussed, we are still analysing the potential grouping, however if we locate any entities where there is statutory grouping we will notify you as soon as possible so you can issue section 87 notices on those bank records in preparation (just in case).

Due to the office assessment closure from 09/12/2019 to 06/01/2019 this will delay our approach, however our proposed deadlines are as follows;

• Initial letter issued 19/11/2019 Due date of 03/12/2019

• Escalated prompt letter to be issued 04/12/2019 Due date of 18/12/2019

• Default notices to be issued 06/01/2019

Depending on if a response is received, the following may occur on 6 January 2020;

• If response received and no discrepancies, registration and default assessments will be processed as normal in line with a voluntary disclosure

• If no response is received, the matter will progress to default assessment being issued on data available to us

Due to the risk to revenue, we will need to action the recovery process as soon as possible.

Please note, there are other variables that we may nee to consider however we will update you accordingly (where required).

(emphasis added)

32 On 22 November 2019, Mr Murphy asked Ms Lucas to put an ASIC alert on Payroll.

33 On 26 November 2019:

(1) Ms Lucas obtained ASIC historical personal name searches regarding Mr James Campbell (who ceased to be the director of Workforce on 1 November 2019) and Mr Kevin Brady (who replaced him in that position from that date) and an historical extract for Workforce;

(2) Mr Kieran McLaughlin, a Debt Resolution Officer employed by the QRO, caused the issue of a series of notices pursuant to s 87 of the Taxation Administration Act to numerous banks calling for documents regarding Workforce; and

(3) Mr McLaughlin exchanged the following messages with Ms Lucas:

Mr McLaughlin: Hi Tamara, I’m having a look at the entity you were discussing with Dhana last week. I’ve run searches on the previous director and the new director (eff 1/11/2019). I’m assuming the previous director is our concern??

Ms Lucas: Hi Kieran, which director?

Mr McLaughlin: James Campbell

…

Ms Lucas: When you can, could you just send a brief email on who you are section 87 on so that if we need to let you know of others we can jump on them also

Mr McLaughlin: Only banks so far - ANZ, CBA, NAB, WESTPAC plus BANK OF QLD, HSBC, SUNCORP, BENDIGO. It’s unlikely we’ll be issuing s87 requests to any other entities or individuals at this stage…

34 On 29 November 2019, Westpac Banking Corporation provided statements for Workforce for the period between 1 July 2019 and 31 October 2019 in response to the s 87 notice that it received. The other banks served with s 87 notices indicated that they had no documents to produce. The Westpac statements recorded in summary:

Period | Opening Balance | Total Credits | Total Debits | Closing Balance |

28 June-31 July 2019 | $485,776.95 | $2,181,329.97 | $2,598,313.29 | $68,793.63 |

31 July-1 August 2019 | $68,793.63 | $290,000.00 | $46,478.69 | $312,314.94 |

1 August-30 August 2019 | $312,314.94 | $1,807,117.05 | $1,738,324.13 | $381,107.86 |

30 August-30 September 2019 | $381,107.86 | $1,607,035.33 | $1,614,821.02 | $373,322.17 |

30 September-31 October 2019 | $373,322.17 | $2,534,704.80 | $2,865,473.81 | $42,553.16 |

35 The credits recorded in those statements were primarily deposits described as “CASH FLOW FINANCE”. For example, and including only deposits exceeding $100,000:

(1) $292,000 (25 July);

(2) $287,000 (4 July 2019);

(3) $242,000 (5 July 2019);

(4) $307,000 (10 July 2019);

(5) $368,000 (11 July 2019);

(6) $376,000 (18 July 2019);

(7) $292,000 (25 July 2019);

(8) $290,000 (1 August 2019);

(9) 180,000 (5 August 2019);

(10) $252,000 (8 August 2019);

(11) $114,000 (9 August 2019);

(12) $247,377.07 (16 August 2019);

(13) $189,000 (22 August 2019);

(14) $231,000 (23 August 2019);

(15) $170,250 (29 August 2019);

(16) $109,500 (30 August 2019);

(17) $361,500 (5 September 2019);

(18) $221,250 (12 September 2019);

(19) $221,000 (19 September 2019);

(20) $135,000 (26 September 2019);

(21) $224,250 (27 September 2019);

(22) $204,750 (2 October 2019);

(23) $250,000 (4 October 2019);

(24) $252,000 (10 October 2019);

(25) $250,000 (17 October 2019);

(26) $250,000 and $144,715 (23 October 2019); and

(27) $200,000 and $250,000 (30 October 2019).

36 On 6 December 2019, Mr McLaughlin:

(1) sent emails to Ms Schofield:

(a)

Just got Westpac statement through for BP 4681800 ARG Workforce P/L which Tamara Lucas told us about. Significant funds available … ;

(b)

Results from Westpac for ARG Workforce P/L attached. ; and

(2) made a note:

WPAC - statements received - suitable for garnishee

37 On 9 December 2019, and following some assistance from Ms Lucas, Mr Ting completed Workforce’s payroll registration online. In doing so, Mr Ting provided the following information:

(1) Workforce had commenced employing people and paying wages on 1 July 2018;

(2) for the financial year ending 30 June 2019, Workforce had paid $16,671,201 in wages in Queensland and another $6,221,623 elsewhere; and

(3) for the financial year ending 30 June 2020, Workforce had paid, and expected to pay, a total of $14,396,053 in wages in Queensland and another $4,798,684 elsewhere.

38 On 10 December 2019:

(1) notices of default assessment, expressed to be immediately due, were issued to Workforce as follows:

Assessed period | Type of liability | Assessed liability |

1 July 2018-30 June 2019 | Annual | $820,778.05 |

July 2019 | Periodic | $70,734.32 |

August 2019 | Periodic | $70,144.94 |

September 2019 | Periodic | $69,627.00 |

October 2019 | Periodic | $69,091.20 |

November 2019 | Periodic | $68,519.68 |

Total: | $1,168,895.19 |

(2) Mr Murphy and Ms Lucas exchanged messages that included the following (as written):

…

Mr Murphy: great, well the DGE allegedly pays 80% of group wages.

ARG Payroll i believe pays another 19% (so presumably the remaining two GM’s only pay 1% together) ...

Mr Murphy: on that basis, i’m less concerned about sending out assessment notices today for the DGE

Mr Murphy: I look forward to seeing what comes in on Friday :)

Ms Lucas: That was my thoughts too, the risk to those are minimal this one is the big risk. I think if they come in we get them all lined up and ready to go on 06/01/2020 - it will then go in line with the 4 weeks which means that they in theory should get actioned at the same time if we need to garnishee

Ms Lucas: I’m going to avoid using 13000 reference number to avoid triggering anything their end. I’m sure they are familiar that those numbers mean investigation ... even if we do use it for review

…

(emphasis added) ;

(3) Ms Lucas called Mr Ting and confirmed that she was about to email to him the outcome of QRO’s review of Workforce’s application for payroll tax registration. She inquired whether – due to the large size of the payroll tax liability arising from that review – a payment arrangement was required. Mr Ting confirmed that more than likely a payment arrangement would be required. Ms Lucas indicated that she would ensure that this was included in her email to him, as payment arrangements were not handled by Ms Lucas as an Investigating Officer, but were handled by QRO’s Resolutions Division;

(4) Ms Lucas sent an email to Mr Ting which attached letters that:

(a) notified Workforce of the notices of assessments in (1) and included:

2. Penalty tax applied

In accordance with section 58 of the TAA, penalty tax of 75% is automatically imposed on the tax amount on a default assessment, or 75% of the increase in tax on a reassessment.

Section 60 of the TAA provides the Commissioner of State Revenue (the Commissioner) with discretion to remit all or part of the penalty tax.

In this instance, the Commissioner has exercised discretion to remit all penalty tax (a voluntary disclosure was received before an investigation and within 30 days after receiving the Commissioner’s prompt letter) ... ;

(b) confirmed Workforce’s registration for payroll tax from that date, and stated that Workforce’s liability for payroll tax commenced from 1 July 2018,

(That email was sent to an incorrect email address but then sent to the correct address on the following day.); and

(5) Ms Lucas sent an email with the subject line “Notification of large debt – ARG Workforce Pty Ltd …” to Ms Schofield, copied to Mr McLaughlin, Mr Matt Stratford and Ms McKelvey attaching her letter to Workforce, and the Commissioner’s notices of default assessment stating:

As discussed with you, please find attached assessment notices and exit letter issued for ARG Workforce Pty Ltd.

The total amount of the liability (including UTI) is $1,168,895.19 as of today. This debt has been raised as a voluntary disclosure and part of the Compliance New Registration campaign.

I spoke to the client financial controller Mr Ting and he has indicated that they may be required to apply for a payment arrangement – I have included the instructions on this in my exit email (refer to below).

Please note, there is additional group members that will be required to be registered for payroll tax. However these are not expected to be submitted until the end of week and may not be raised until the new year. I will update accordingly.

….

(emphasis in original)

39 On 12 December 2019, Mr Ting completed Payroll’s payroll registration online. In doing so, Mr Ting provided the following information:

(1) Payroll had commenced employing people in Queensland on 1 July 2018;

(2) for the financial year ending 30 June 2019, Payroll had paid $4,201,655 in wages in Queensland plus another $539,360 elsewhere; and

(3) between July and November 2019, Payroll had paid total wages of $1,447,751, in monthly amounts that fluctuated between $251,327 and $337,462.

40 On 17 December 2019:

(1) notices of default assessment, expressed to be immediately due, were issued to Payroll as follows:

Assessed period | Type of liability | Assessed liability |

1 July 2018-30 June 2019 | Annual | $206,965.45 |

July 2019 | Periodic | $14,788.10 |

August 2019 | Periodic | $14,283.37 |

September 2019 | Periodic | $12,648.05 |

October 2019 | Periodic | $16,852.27 |

November 2019 | Periodic | $14,262.13 |

Total: | $279,799.37 |

(2) Ms Lucas sent an email to Mr Ting in which she:

(a) stated that if Payroll was unable to make payment in full and required a payment arrangement, these were handled by QRO’s Resolutions Division, and provided information as to how to contact that Division and apply for a payment arrangement to pay Payroll’s payroll tax liability;

(b) attached:

(i) a letter which set out Payroll’s payroll tax liability for the 2019 financial year, and for the months July to November 2019 based on Payroll’s Online Registration, and which enclosed a copy of the notices of default assessment referred to at (1) above. This letter, as with the earlier letter to Workforce, indicated that the Commissioner had decided to remit all penalty tax; and

(ii) a letter confirming Payroll’s registration for payroll tax purposes as at 17 December 2019.

41 Following the registration of Workforce and Payroll and the issue of notices of default assessment totalling $1,168,895.19 and $279,799.37 respectively, the following occurred.

42 On 6 January 2020, the QRO sent a Payment Overdue notice to:

(1) Workforce. The notice included an Overdue Summary that particularised Workforce’s outstanding payroll tax liability as at that date, comprised of liabilities for the periods July 2018 to June 2019 (Annual 2019); and July to November 2019, in the sum of $1,176,583.39, and stated that such amount was overdue; and

(2) Payroll. The notice included an Overdue Summary that particularised Payroll’s outstanding payroll tax liability as at that date for the periods Annual 2019; and July to November 2019 in the sum of $281,142.29, and stated that such amount was overdue.

43 On 21 January 2020, the QRO sent a Final Payment Reminder to Payroll. The notice included an Overdue Summary that particularised Payroll’s outstanding payroll tax liability as at that date for the periods Annual 2019; and July to November 2019 in the sum of $282,131.81, and requested immediate payment to avoid recovery action being taken.

44 On 6 February 2020, the QRO sent an email to Mr Ting reminding him that Payroll’s January 2020 payroll tax return was due on 7 February 2020.

45 On 7 February 2020:

(1) Mr McLaughlin caused the issue of notices under s 87 of the Taxation Administration Act to various banks regarding Payroll;

(2) Mr McLaughlin sent a Warning Notice to:

(a) Workforce. The notice included an Overdue Summary that particularised Workforce’s overdue amount of payroll tax liability as at that date for the periods Annual 2019; and July to November 2019, as well as the other overdue amounts for the December 2019 period, and the January 2020 liability due as at the date of the notice. The notice stated that the amount owing subject of the notice in the sum of $1,184,862.99, and the total amount overdue of $1,328,484.56, and requested immediate payment to avoid recovery action being taken; and

(b) Payroll. The notice included an Overdue Summary that particularised Payroll’s outstanding payroll tax liability as at that date for the periods Annual 2019; and July to November 2019, as well as other overdue amounts for the liability for the January 2020 period. The notice stated that the amount owing subject of the notice in the sum of $283,121.33, and the total amount overdue of $294,692.95, and requested immediate payment to avoid recovery action being taken.

46 On 12 February 2020, the QRO sent a Final Payment Reminder to Workforce. The notice included an Overdue Summary that particularised Workforce’s outstanding payroll tax liability as at that date for the periods December 2019 and January 2020, as well as the other overdue amounts for the Annual 2019; and July to November 2019 periods. The notice stated that the amount owing subject of the notice in the sum of $118,796.47, and the total amount overdue of $1,305,729.36 and requested immediate payment to avoid recovery action being taken.

47 On 14 February 2020, Westpac provided information (including bank statements) to Mr McLaughlin in answer to the notice it had received under s 87 of the Taxation Administration Act, concerning Payroll. Those statements were not adduced into evidence.

48 On 6 March 2020, the QRO sent an email to Mr Ting reminding him that the February 2020 payroll tax returns for each of Workforce and Payroll were due on 9 March 2020.

49 On 12 March 2020, the QRO sent a Final Payment Reminder to:

(1) Workforce for its February 2020 liability of $78,829.64. The notice also stated a total amount overdue of $1,362,220.09, and requested immediate payment to avoid recovery action being taken; and

(2) Payroll for its February 2020 liability of $12,657.55. The notice also stated a total amount overdue of $298,252.68, and requested immediate payment to avoid recovery action being taken.

50 There appears to be little to no evidence as to events between 12 March 2020 and 19 January 2021. I note that this period corresponded to the first 10 months of the COVID-19 pandemic and that there are some suggestions in the evidence that the debts owed by Workforce and Payroll to the QRO were deferred during this period.

51 On 19 January 2021, the QRO sent a Payment Overdue Notice to:

(1) Workforce. The notice included an Overdue Summary that particularised Workforce’s outstanding payroll tax liability as at that date for the periods Annual 2019; July to December 2019; and July to August 2020, in the sum of $1,448,259.01, and stated that such amount was overdue; and

(2) Payroll. The notice included an Overdue Summary that particularised Payroll’s outstanding payroll tax liability as at that date for the period Annual 2019; and July to November 2019 in the sum of $284,785.58, and requested payment.

52 On 21 January 2021, the QRO sent a notice to Workforce stating that it had not lodged its payroll tax return for the period December 2020 and that it was now overdue.

53 On 29 January 2021, the QRO sent an email to Mr Ting reminding him that Workforce’s December 2020 payroll tax return was due on 14 January 2021.

54 On 3 February 2021, the QRO sent a Final Payment Reminder to:

(1) Workforce. The notice included an Overdue Summary that particularised Workforce’s outstanding payroll tax liability as at that date for the periods Annual 2019; July to December 2019; and July to August 2020, in the sum of $1,452,564.85, and requested immediate payment to avoid recovery action being taken; and

(2) Payroll. The notice included an Overdue Summary that particularised Payroll’s outstanding payroll tax liability as at that date for the periods Annual 2019; and July to November 2019 in the sum of $285,625.44 and requested immediate payment to avoid recovery action being taken.

55 On 5 February 2021, the QRO issued a notice of default assessment for payroll tax liability to Workforce for December 2020 for the sum of $178,874.83.

56 On 5 and 11 February 2021, the QRO sent emails to Mr Ting reminding him that Workforce’s January 2021 payroll tax return was due on 8 February 2021.

57 On 15 February 2021, the QRO sent an Overdue Notice to Workforce stating that it had not lodged its payroll tax return for January 2021 and that it was now overdue.

58 On 22 February 2021, the QRO sent an email to Mr Ting stating that Workforce’s January 2021 payroll tax return was due on 8 February 2021.

59 On 1 March 2021, the QRO issued a notice of default assessment for payroll tax liability to Workforce for January 2021 for the sum of $178,852.28.

60 On 4 March 2021, the QRO sent a Final Payment Reminder to Workforce for its January 2021 liability of $178,852.28. The notice also stated the total amount overdue was $1,640,028.81, and requested immediate payment to avoid recovery action being taken.

61 On 5 and 11 March 2021, the QRO sent emails to Mr Ting reminding him that Workforce’s payroll tax return for February 2021 was due on 8 March 2021.

62 On 15 March 2021:

(1) Mr McLaughlin sent a Warning Notice to Workforce. The notice included an Overdue Summary that particularised Workforce’s outstanding payroll tax liability subject of the notice as at that date for the periods Annual 2019; July to December 2019; and July to August 2020, as well as the other overdue amounts for the liability for the January 2021 period. The notice stated that the amount owing subject of the notice in the sum of $1,465,482.37, and the total amount overdue of $1,644,627.80, and requested immediate payment to avoid recovery action being taken; and

(2) the QRO sent an Overdue Notice to Workforce stating that it had not lodged its payroll tax return for the period February 2021 and that it was now overdue.

63 On 22 March 2021, the QRO:

(1) sent an email to Mr Ting stating that Workforce’s February 2021 payroll tax return was due on 8 March 2021; and

(2) carried out an ASIC search for Workforce.

64 On 29 March 2021, the QRO issued a notice of re-assessment to Workforce for payroll tax liability for the period February 2021, and required immediate payment of $178,852.28.

65 On 1 April 2021, the QRO sent a Final Payment Reminder to Workforce. The notice included an Overdue Summary that particularised Workforce’s outstanding payroll tax liability as at that date for the period February 2021 and October to November 2020, as well as the other overdue amounts for the liability for the Annual 2019; July to December 2019; July to August 2020; and January 2021 periods. The notice stated that the amount owing subject of the notice in the sum of $398,202.51, and the total amount overdue of $2,047,451.85, and requested immediate payment to avoid recovery action being taken.

66 On 6 April 2021, the QRO sent an email to Mr Ting stating that Workforce’s March 2021 payroll tax return was due on 7 April 2021.

67 On 13 April 2021, the QRO sent a Final Payment Reminder to Workforce for its January 2021 liability of $179,776.83. The notice also stated a total amount overdue of $1,952,864.03, and requested immediate payment to avoid recovery action being taken.

68 On 15 April 2021, the QRO:

(1) provided to Workforce notices of re-assessment for the periods December 2020, January 2021 and February 2021;

(2) sent a Final Payment Reminder to:

(a) Workforce. The notice included an Overdue Summary that particularised Workforce’s outstanding payroll tax liability as at that date for the periods March 2020 and April 2020, as well as the other overdue amounts for the Annual 2019, July to December 2019, July to August 2020, and January to February 2021. The notice stated that the amount owing subject of the notice was the sum of $119,847.72, and the total amount overdue of $1,952,864.03 and requested immediate payment to avoid recovery action being taken; and

(b) Payroll. The notice included an Overdue Summary that particularised Payroll’s outstanding payroll tax liability as at that date for the periods March to April 2020, as well as other overdue amounts for the liability for the Annual 2019; and July to November 2019 periods. The notice stated that the amount owing subject of the notice in the sum of $28,025.71, and the total amount overdue of $317,850.45, and requested immediate payment to avoid recovery action being taken.

69 On 19 April 2021, the QRO sent an Overdue Notice to Workforce stating that it had not lodged its payroll tax return for the period March 2021, and that it was now overdue.

70 On 22 April 2021, the QRO sent a Final Payment Reminder to Workforce for its March 2021 liability of $97,807.25. The notice also stated that the total amount overdue was $1,694,061.00 and requested immediate payment to avoid recovery action being taken.

71 A document titled “ARG Workforce – Interaction Action History”, which was produced by the Commissioner, but not otherwise explained, records: “07/05/2021 – Outbound call made to discuss outstanding debt”.

72 On 12 May 2021, the QRO sent a Final Payment Reminder to Workforce for its April 2021 liability of $95,274.70. The notice also stated a total amount overdue of $1,796,783.37, and requested immediate payment to avoid recovery action being taken.

73 On 21 May 2021, the QRO sent a Warning Notice to Workforce. The notice included an Overdue Summary that particularised Workforce’s outstanding payroll tax liability as at that date for the periods March to April 2020, July to August 2020, December 2019, Annual 2019, July to November 2019, as well as the other overdue amounts for the January to April 2021 periods. The notice stated that the amount owing subject of the notice in the sum of $1,605,607.71, and the total amount overdue of $1,944,853.26, and requested immediate payment to avoid recovery action being taken.

74 On 4 June 2021:

(1) the QRO sent an email to Mr Brad Winton of Workforce stating that Workforce’s May 2021 payroll tax return was due on 7 June 2021; and

(2) Mr McLaughlin (who was by then a Senior Debt Resolution Officer) issued further notices under s 87 of the Taxation Administration Act to various banks regarding Workforce.

75 On 8 June 2021, Mr McLaughlin sent a Warning Notice to Payroll. The notice included an Overdue Summary that particularised Payroll’s outstanding payroll tax liability as at that date for the periods March to April 2020, Annual 2019 and July to November 2019. The notice stated that the amount owing subject of the notice in the sum of $321,550.34, and requested immediate payment to avoid recovery action being taken. That notice was received by QRO “Return to Sender” on 22 June 2021.

76 On 10 June 2021, the Commissioner sent a Final Payment Reminder Notice to Workforce for its May 2021 liability of $132,503.88. The notice also included a total amount overdue as $2,136,164.33, and requested immediate payment to avoid recovery action being taken.

77 On 15 June 2021, Westpac provided information (including bank statements) to the QRO in answer to the s 87 notice it had received concerning Payroll and Workforce. The other recipients of the latest s 87 notices indicated that they had nothing to produce.

78 The statements for Workforce recorded:

(1) for the period March to May 2021:

(a) total monthly credits in the order of $4,500,000, $3,500,000 and $4,000,000;

(b) total monthly debits in the order of $3,800,000, $3,000,000 and $3,600,000;

(c) end of month account balances in the order of $1,000,000, $1,600,000 and $2,000,000; and

(2) a balance as at 15 June 2021 of $2,401,002.49.

79 The statements record deposits of “CASH FLOW FINANCE” of:

(1) $247,000, $249,000, $248,000, $164,000 and $250,000 (3 March 2021);

(2) $66,000, $249,000, $248,000 and $250,000 (10 March 2021);

(3) $164,000, $248,000, $250,000 and $249,000 (17 March 2021);

(4) $52,000, $200,000, $249,000 and $250,000 (24 March 2021);

(5) $49,000, $248,000, $249,000 and $250,000 (31 March 2021);

(6) $200,000, $119,000, $230,000, $240,000 and $250,000 (8 April 2021);

(7) $202,000, $249,000 and $250,000 (14 April 2021);

(8) $200,000, $248,000, $100,000 and $250,000 (21 April 2021);

(9) $103,000, $248,000, $250,000, $249,000 (29 April 2021);

(10) $1,111,000 (6 May 2021);

(11) $241,000, $240,000 and $250,000 (12 May 2021);

(12) $62,000, $230,000, $240,000, $220,000 and $250,000 (19 May 2021); and

(13) $204,000, $230,000, $250,000 and $240,000 (26 May 2021).

80 The statements for Payroll, recorded:

(1) for account #738631:

(a) for the period March to May 2021:

(i) total monthly credits in the order of $800,000, $590,000 and $740,000;

(ii) total monthly debits in the order of $825,000, $590,000 and $750,000;

(iii) end of month account balances in the order of $15,000, $19,000 and $10,000;

(b) a balance as at 15 June 2021 of $13,584.95; and

(2) for account number #743617, a nil balance throughout the period March to May 2021.

81 Between 17 June 2021 and 14 July 2021, Mr Christopher White, an accountant engaged by Workforce and Payroll, and Ms Lane engaged in discussions concerning the entry by each of Workforce and Payroll into a payment arrangement in relation to its outstanding payroll tax liabilities.

82 During those discussions:

(1) the initial proposed arrangement focussed upon the debts owed by those companies which, as at 17 June 2021, were $2,139,275.98 for Workforce and $332,013.60 for Payroll;

(2) on 25 June 2021, Mr White provided a completed “Application for Payment Arrangement” form for each company. Each of the applications had been executed by Mr Brady on behalf of the relevant company below a section of the application form which provided:

Verification

By accepting this arrangement, I (or each of us) verify:

1. The information supplied in this form and any supporting documents are true and correct.

2. Payment of the liability noted above would cause me / the company / the trust significant financial hardship.

3. I am not bankrupt / the company is not insolvent / the trust is not insolvent and entry into this arrangement will not cause bankruptcy or insolvency.

…

6. I understand that it is an offence to give the Commissioner information or documents that are false or misleading, and that doing so may result in prosecution under sections 122 and 123 of the Taxation Administration Act 2001

…

(bold emphasis in original)

(Ms Lane treated this text as a standard form and did not turn her mind to anything in it.) ;

(3) the initial payment arrangements were:

(a) for Workforce to pay its outstanding debt of $2,139,275.98 over 24 months, with:

(i) an initial payment of $425,000;

(ii) equal monthly instalments of $71,400;

(iii) the first instalment due on 7 July 2021;

(b) for Payroll to pay its outstanding debt in the sum of $322,013.60 over 24 months, with:

(i) an initial payment of $64,500.00;

(ii) monthly instalments of $10,800.00;

(iii) the first instalment being due to be paid on 7 July 2021;

(4) these initial payment arrangements were varied when:

(a) on 1 July 2021, Ms Lane informed Mr White that the maximum period of time allowed for paying outstanding payroll tax debts under a payment plan was 18 months and that larger initial payments ($573,690.60 for Workforce and $84,818.52 for Payroll) would be required with monthly payments of $71,400 and $10,800 respectively. That arrangement was accepted and on 12 July 2021, Workforce paid $574,000 and Payroll paid $85,000 to the QRO;

(b) on 14 July 2021, Mr White informed Ms Lane with respect to each company that: “[a]fter further review of the businesses’ current financial performance it has been determined that the business could sustain a shorter term to settle the debt” and requested that Ms Lane recalculate the payment so as to reduce the term to six months. Ms Lane did so and payment arrangements were agreed which provided for the following payments by:

(i) Workforce:

Instalment No. 1 | 21 July 2021 | $267,630.92 |

Instalment No. 2 | 23 August 2021 | $267,630.92 |

Instalment No. 3 | 21 September 2021 | $267,630.92 |

Instalment No. 4 | 21 October 2021 | $267,630.92 |

Instalment No. 5 | 22 November 2021 | $267,630.92 |

Instalment No. 6 | 21 December 2021 | $267,630.88 |

Total payable | $1,605,785.48 |

; and

(ii) Payroll:

Instalment No. 1 | 21 July 2021 | $40,446.93 |

Instalment No. 2 | 23 August 2021 | $40,446.93 |

Instalment No. 3 | 21 September 2021 | $40,446.93 |

Instalment No. 4 | 21 October 2021 | $40,446.93 |

Instalment No. 5 | 22 November 2021 | $40,446.93 |

Instalment No. 6 | 21 December 2021 | $40,446.93 |

Total payable | $242,681.58 |

83 On 20 July 2021, the QRO sent an email to Mr Winton stating that Workforce’s payroll tax annual return was due on 21 July 2021.

84 On 21 July 2021:

(1) Workforce’s annual payroll tax for 2021 (Annual 2021) in the amount of $119,841.09 became due and payable;

(2) Workforce paid the first instalment of $267,630.92; and

(3) Payroll paid the first instalment of $40,466.93.

85 On 27 July 2021, the QRO sent a Payment Overdue Notice to Workforce stating that the QRO had not received Workforce’s payment of that amount.

86 On 6 August 2021, the QRO sent an email to Mr Winton of Workforce reminding him that Workforce’s July 2021 payroll tax return was due on 9 August 2021.

87 On 9 August 2021, Workforce paid $120,355.14 to the QRO.

88 On 10 August 2021, the QRO sent a Final Payment Reminder to Workforce for its Annual 2021 liability of $119,841.09. The notice also included an overdue amount for the period July 2021 of $120,355.14, and stated a total amount overdue of $240,196.23. The notice requested immediate payment to avoid recovery action being taken.

89 On 18 August 2021, Workforce paid $119,474.01 to the QRO, being the amount identified in the Overdue Notice dated 27 July 2021 for its Annual 2021 liability.

90 On 23 August 2021, Workforce paid $267,630.92 and Payroll paid $40,446.93 to the QRO, being the amounts due on that date pursuant to the payment plans.

91 On 25 August 2021, the QRO sent a Payment Overdue Notice to Payroll. The notice included an Overdue Summary that particularised Payroll’s outstanding payroll tax liability as at that date for the periods Annual 2021 and July 2021 in the sum of $215,710.68, and stated that such payment was overdue.

92 On each of 26 and 27 August 2021, Payroll paid $20,633.11 to the QRO.

93 On 6 September 2021, the QRO sent an email to Mr Ting reminding him that Payroll’s August 2021 payroll tax return was due on 7 September 2021.

94 On 7 September 2021, Workforce paid $143,756.81 and Payroll paid $20,142.19, to the QRO.

95 On 8 September 2021, the QRO sent a Final Payment Reminder to Payroll with respect to its Annual 2021 liability of $195,673.27. The notice included an Overdue Summary that particularised Payroll’s outstanding payroll tax liability as at that date for the period Annual 2021, as well as a credit amount of $20,633.11 for July 2021. The notice stated the total amount overdue was $175,040.16, and requested immediate payment to avoid recovery action being taken.

96 On 21 September 2021, Workforce paid $267,630.92 and Payroll paid $40,446.93 to the QRO, being the instalments due on that date pursuant to the payment plans.

97 On 11 October 2021, Workforce paid $114,199.27 and Payroll paid $25,393.20 to the QRO.

98 On 12 October 2021, the QRO sent a Final Payment Reminder to:

(1) Workforce. The notice included an Overdue Summary that particularised Workforce’s outstanding payroll tax liability as at that date for May 2020, the year ended 30 June 2020 (Annual 2020), September 2020 and September 2021. The notice stated that the amount overdue was $281,061.16, and requested immediate payment to avoid recovery action being taken; and

(2) Payroll. The notice included an Overdue Summary that particularised Payroll’s outstanding payroll tax liability as at that date for the Annual 2020, May 2020 and September 2021 as $34,179.03. The notice stated the total amount overdue was $231,341.55, and requested immediate payment to avoid recovery action being taken.

99 On 21 October 2021, Workforce paid $267,630.92 to the QRO being the amount due on that date under its payment plan. On the same day Payroll paid $19,813.82 to the QRO.

100 On 5 November 2021, the QRO sent emails to Mr Winton and Mr Ting reminding them that Workforce’s and Payroll’s October 2021 payroll tax returns were due on 8 November 2021.

101 On 11 November 2021:

(1) the QRO sent:

(a) a Final Payment Reminder to Workforce with respect to its October 2021 liability of $138,145.69. The notice also stated that the total amount overdue was $420,934.17, and requested immediate payment to avoid recovery action being taken;

(b) another email to Mr Ting reminding him that Payroll’s October 2021 payroll tax return was due on 8 November 2021; and

(2) Workforce paid $138,145.69 (being its October 2021 liability) and Payroll paid $16,861.22 to the QRO.

102 On 15 November 2021, the QRO sent an Overdue Notice to Payroll stating that it had not lodged its payroll tax return for October 2021 and that it was now overdue.

103 On 22 November 2021:

(1) the QRO sent an email to Mr Ting stating that Payroll’s October 2021 payroll tax return was due on 8 November 2021;

(2) Workforce paid $267,630.92 and Payroll paid $40,446.93 to the QRO, being the instalments due on that date pursuant to the payment plans.

104 On 6 December 2021, the QRO sent:

(1) an email to Mr Winton reminding him that Workforce’s November 2021 payroll tax return was due 7 December 2021; and

(2) an email to Mr Ting reminding him that Payroll’s November 2021 payroll tax return was due on 7 December 2021.

105 On 10 December 2021:

(1) the QRO sent:

(a) an email to Mr Winton of Workforce reminding him that Workforce’s November 2021 payroll tax return was due on 7 December 2021;

(b) an email to Mr Ting of Payroll stating that Payroll’s November 2021 payroll tax return was due on 7 December 2021; and

(2) Workforce paid $112,305.89 and Payroll paid $26,388.20 to the QRO.

106 On 21 December 2021, Payroll paid $40,446.93 to the QRO.

107 As noted above, 21 December 2021 was the due date for Workforce to make the final instalment payment in the sum of $267,630.88 under the Workforce payment arrangement.

108 On 22 December 2021, Mr White notified the QRO of an issue with the direct debit account which prevented that payment being made.

109 On 31 December 2021, Workforce paid $267,630.88 to the QRO.

110 On 11 January 2022, Ms Foo called Mr White concerning that final payment and:

(1) confirmed that the final payment had gone through;

(2) said that she would be remitting late payment interest for the period 26 December 2021 to 9 January 2022 due to the mix-up in relation to receipt of that payment and the direct debit not sweeping due to the holiday shut down period;

(3) said that there were still outstanding payroll tax liabilities for Workforce for the following periods:

(a) May 2020;

(b) September 2020;

(c) Annual 2020; and

(d) September 2021,

in the sum of $286,674.95;

(4) noted that Workforce’s payroll tax liabilities for October to December 2020 had been deferred due to COVID-19, and were not due to be paid until 14 January 2022, and that those amounts were as follows:

(a) October - $84,581.41;

(b) November - $134,768.82; and

(c) December - $83,269.30.

111 Mr White asked why the May 2020 and September 2021 payments were missed because he thought that those payments were part of Workforce’s payment plan, and that he was certain that they had been paid.

112 Ms Foo said to Mr White that she would send to him an account statement for Workforce that would identify its outstanding payroll tax liability.

113 Ms Foo also stated that:

(1) she would also send to Mr White an Account Statement for Payroll that would identify its outstanding payroll tax liability;

(2) Payroll’s outstanding liability was for:

(a) May 2020;

(b) Annual 2020;

(c) Annual 2021;

(d) September to November 2021 ;

(3) the May and September amounts were not included in the payment arrangement; and

(4) perhaps some of the monies used for a down payment were applied towards payment of the above amounts, and if they were not, the monies would have still been applied to Payroll’s account.

114 Mr White in response said this was odd, and that he would await Ms Foo’s email, and he would work with his clients and revert to Ms Foo.

115 On 11 January 2022, Ms Foo sent an email to Mr White concerning Workforce:

As per our phone call today I can confirm that the payment of $267,360.88 has now been processed and applied to your account. Apologies again about the re-sweep not happening it usually goes through overnight but it must not have triggered over our holiday shut down period. As I advised on our phone call I have remitted the late payment interest that automatically accrued over that time from your account.

As of today’s date the account still has an outstanding liability of $286,674.95

The outstanding liability includes:

• May 2020 = $62,590.74

• September 2020 = $85,364.11

• Annual 2020 = $138,643.95

• September 2021 = $76.15

I have attached a copy of the Account Statement as of today’s date, on page 2 you will be able to see a breakdown of these figures.

Please note the Account Statement also includes the liability amounts for October, November and December 2020 which was deferred as a part of the COVID-19 Payroll Tax Deferral application the company was approved for on the 4th of January 2021. These deferral amounts are due on the 14th of January 2022.

To avoid escalated debt recovery action as well as additional late payment interest please pay the outstanding liability as soon as possible.

…

(bold emphasis in original)

116 The attached account statement provided:

117 Also, on 11 January 2022, Ms Foo sent an email to Mr White concerning Payroll:

As per our phone call today, the outstanding liability for ARG Payroll Pty Ltd is $235,923.66.

The outstanding liability includes:

• May 2020 = $19,241.53

• Annual 2020 = $15,602.38

• Annual 2021 = $201,034.57

• September 2021 = $16.71

• October 2021 = $11.10

• November 2021= $17.37

I have attached a copy of the Account Statement as of today’s date, a breakdown of these figures can be found on page 2 of the statement.

To avoid escalated debt recovery action as well as additional late payment interest please pay the outstanding liability as soon as possible.

…

(bold emphasis in original)

118 The attached account statement provided:

119 On 13 January 2022, the QRO sent an email to Mr Ting reminding him that Payroll’s December 2021 payroll tax return was due on 14 January 2022.

120 On 18 January 2022, Mr Lionel Bowden of the QRO, following a conversation with Mr White, sent an email to him attaching a copy of a current account reconciliation for each of Workforce and Payroll. That email included: “I have recorded your intention to make full remittance by 31/01/2022 for each account”.

121 On 19 January 2022, the QRO sent an email to Mr Ting stating that Payroll’s December 2021 payroll tax return was due on 14 January 2022.

122 On 21 January 2022:

(1) Workforce paid to the QRO:

(a) $85,364.11 (an amount corresponding to its liability for September 2020 – see [115] and [116] above);

(b) $84,581.41 (an amount corresponding to its liability for October 2020 – see [110(4)(a)] and [116] above);

(c) $134,768.82 (an amount corresponding to its liability for November 2020 – see [110(4)(b)] and [116] above);

(d) $83,269.30 (an amount corresponding to its liability for December 2020 – see [110(4)(c)] and [116] above);

(2) Payroll paid $34,139.00 to the QRO;

(3) the QRO sent:

(a) an Overdue Payroll Tax Return Notice to Workforce noting that Workforce had not lodged its payroll tax return for the December 2021 period, and that it was now overdue; and

(b) an Overdue Payroll Tax Return notice to Payroll noting that Payroll had not lodged its payroll tax return for the December 2021 period and that it was now overdue.

123 On 2 February 2022, as previously noted, the liquidator was appointed to each of Workforce and Payroll.

124 The chronology set out above refers to numerous reminder letters sent by the QRO to Workforce and Payroll concerning amounts overdue, which are summarised in the tables below.

Workforce

Date of Notice | Type of Notice | Assessment Period | Amount the Subject of the Notice | Cross-reference |

06/01/2020 | Payment Overdue | Annual 2019; July to November 2019 | $1,176,583.39 | [42] |

07/02/2020 | Warning Notice | Annual 2019; July to November 2019 | $1,184,862.99 | [45] |

12/02/2020 | Final Payment Reminder | December 2019; January 2020 | $118,796.47 | [46] |

12/03/2020 | Final Payment Reminder | February 2020 | $78,829.64 | [49] |

19/01/2021 | Payment Overdue Notice | Annual 2019; July to December 2019; July to August 2020 | $1,448,259.01 | [51] |

03/02/2021 | Final Payment Reminder | Annual 2019; July to December 2019; July to August 2020 | $1,452,564.85 | [54] |

04/03/2021 | Final Payment Reminder | January 2021 | $178,852.28 | [60] |

15/03/2021 | Warning Notice | Annual 2019; July to December 2019; July to August 2020 | $1,465,482.37 | [62] |

01/04/2021 | Final Payment Reminder | October to November 2020; February 2021 | $398,202.51 | [65] |

13/04/2021 | Final Payment Reminder | January 2021 | $179,776.83 | [67] |

15/04/2021 | Final Payment Reminder | March to April 2020 | $119,847.72 | [68] |

22/04/2021 | Final Payment Reminder | March 2021 | $97,807.25 | [70] |

12/05/2021 | Final Payment Reminder | April 2021 | $95,274.70 | [72] |

21/05/2021 | Warning Notice | Annual 2019; July to December 2019; March to April 2020; July to August 2020; January to April 2021 | $1,605,607.71 | [73] |

10/06/2021 | Final Payment Reminder | May 2021 | $132,503.88 | [76] |

10/08/2021 | Final Payment Reminder | Annual 2021 | $119,841.09 | [88] |

12/10/2021 | Final Payment Reminder | Annual 2020; May 2020; September 2020; September 2021 | $281,061.16 | [98] |

11/11/2021 | Final Payment Reminder | October 2021 | $138,145.69 | [101] |

Payroll | ||||

Date of Notice | Type of Notice | Assessment Period | Amount the Subject of the Notice | Cross-reference |

06/01/2020 | Payment Overdue | Annual 2019; July to November 2019 | $281,142.29 | [42] |

21/01/2020 | Final Payment Reminder | Annual 2019; July to November 2019 | $282,131.81 | [43] |

07/02/2020 | Warning Notice | Annual 2019; July to November 2019 | $283,121.33 | [45] |

12/03/2020 | Final Payment Reminder | February 2020 | $12,657.55 | [49] |

19/01/2021 | Payment Overdue | Annual 2019; July to November 2019 | $284,785.58 | [51] |

03/02/2021 | Final Payment Reminder | Annual 2019; July to November 2019 | $285,625.44 | [54] |

15/04/2021 | Final Payment Reminder | March to April 2020 | $28,025.71 | [68] |

08/06/2021 | Warning Notice | March to April 2020; Annual 2019; July to November 2019 | $321,550.34 | [75] |

25/08/2021 | Payment Overdue | Annual 2021; July 2021 | $215,710.68 | [91] |

08/09/2021 | Final Payment Reminder | Annual 2021 | $195,673.27 | [95] |

12/10/2021 | Final Payment Reminder | Annual 2020; May 2020; September 2021 | $34,179.03 | [98] |

125 Ms Cliffe explained:

(1) debt management of payroll tax debts starts off in an automated way. A payroll tax assessment gives a due date for payment. Generally, once the due date has passed and payment has not been received, the first reminder letter is automatically printed and sent to the taxpayer;

(2) usually about two weeks later if payment has still not been received, a second reminder letter is automatically printed and sent to the taxpayer. It is a standard letter that warns of steps that might be taken to recover the outstanding debt if payment is not received;

(3) because multiple assessments can be issued to the same person or entity, often more than one set of reminder letters may be issued to the same person or entity;

(4) RMS records are used to create work lists that are then allocated to officers for actioning. It is through the workload allocation process that debts which remain unpaid despite the issue of the automated reminder letters, will typically come to the attention of officers within the QRO. Officers also take action on outstanding matters that are encountered in the course of actioning correspondence and communications received by the QRO; and

(5) work lists are compiled in line with business needs and priorities. The lists are rolling lists where work items that are identified for “actioning” are added and removed. Officers work through their work allocation according to their work priorities. Not all items on a work list will necessarily be “actioned”.

C. CONSIDERATION

C.1 The transactions

126 The impugned payments are set out in their chronological context above and extracted in the table below.

Date | Workforce payments | Payroll payments | Cross-reference |

9 August 2021 | $120,355.14 | [87] | |

18 August 2021 | $119,474.01 | [89] | |

23 August 2021 | $267,630.92 | $40,446.93 | [90] |

26 August 2021 | $20,633.11 | [92] | |

27 August 2021 | $20,633.11 | [92] | |

7 September 2021 | $143,756.81 | $20,142.19 | [94] |

21 September 2021 | $267,630.92 | $40,446.93 | [96] |

11 October 2021 | $114,199.27 | $25,393.20 | [97] |

21 October 2021 | $267,630.92 | $19,813.82 | [99] |

11 November 2021 | $138,145.69 | $16,861.22 | [101] |

22 November 2021 | $267,630.92 | $40,446.93 | [103] |

10 December 2021 | $112,305.89 | $26,388.20 | [105] |

21 December 2021 | $40,446.93 | [106] | |

31 December 2021 | $267,630.88 | [109] | |

21 January 2022 | $85,364.11 | [122] | |

21 January 2022 | $84,581.41 | [122] | |

21 January 2022 | $134,768.82 | [122] | |

21 January 2022 | $83,269.30 | $34,139.00 | [122] |

Total | $2,474,375.01 | $345,791.57 |

C.2 The issues for determination

127 As noted above, the issues for determination are whether:

(1) for the purposes of s 588FG(2)(a) of the Act, the QRO became a party to the transactions in good faith;

(2) for the purposes of s 588FG(2)(b) of the Act, at the times when the QRO became a party to the transactions:

(a) the QRO had no reasonable grounds for suspecting that Workforce or Payroll was insolvent (or would become insolvent because of matters including entry into the transactions or an act or omission done or made for the purpose of giving effect to the transactions); and

(b) a reasonable person in the QRO’s position would have had no such grounds for so suspecting.

C.3 The s 588FG(2)(a) criterion

128 For the purposes of s 588FG(2)(a) of the Act, a person acts in good faith if they act with propriety and honesty; and the test is wholly subjective: White v ACN 153 152 731 Pty Ltd (in liq) [2018] WASCA 119; (2018) 53 WAR 234 at 257 [108] (Murphy and Mitchell JJA and Allanson J). A creditor receiving payment who knows the insolvent circumstances of a debtor, or who suspects insolvency on reasonable grounds, would not ordinarily be acting in good faith: Queensland Bacon Propriety Limited v Rees [1966] HCA 21; (1966) 115 CLR 266 at 287 (Barwick CJ); Sutherland (as liquidator of Sydney Appliances Pty Ltd (in liq)) v Eurolinx Pty Ltd [2001] NSWSC 230; (2001) 37 ACSR 477 at 483 [38] (Santow J); White at 257 [109].

129 In George v Rockett [1990] HCA 26; (1990) 170 CLR 104 at 112 and 115 the High Court of Australia, (Mason CJ, Brennan, Deane, Dawson, Toohey, Gaudron and McHugh JJ) explained:

When a statute prescribes that there must be “reasonable grounds” for a state of mind – including suspicion and belief – it requires the existence of facts which are sufficient to induce that state of mind in a reasonable person.

…

Suspicion, as Lord Devlin said in Hussien v. Chong Fook Kam “in its ordinary meaning is a state of conjecture or surmise where proof is lacking: ‘I suspect but I cannot prove.’” The facts which can reasonably ground a suspicion may be quite insufficient reasonably to ground a belief, yet some factual basis for the suspicion must be shown.

(citations omitted)

130 Further there is no presumption in favour of the party seeking to rely upon s 588FG(2)(a). In the present case, the Commissioner must establish positively that the QRO acted in good faith; the liquidator is not required to prove the absence of good faith. To show that a person became a party to a transaction subjectively in good faith it is necessary to prove that the motive which actuated the person to do so was honest and proper.

131 The inquiry, accordingly, is directed to the party’s state of mind, with regard to their knowledge and belief about the nature of the transaction at the relevant time: Cussen v Sultan [2009] NSWSC 1114; (2009) 74 ACSR 496 at 505 ([33] and [34]) (Nicholas J); Walsh v Umoona Tjutagku Health Service Aboriginal Corporation (ICN 7460) (No 2) [2017] FCA 852 at [40] (Charlesworth J); Shot One Pty Ltd (in liq.) v Day (in liq.) [2017] VSC 741 at [357] (Sloss J); Stone (in their capacities as joint and several liquidators of Cardinal Project Services Pty Ltd (ACN 090 113 705) (in liq)) v Melrose Cranes & Rigging Pty Ltd (ACN 083 164 845) (No 2) [2018] FCA 530; (2018) 125 ACSR 406 at 476 [267] (Markovic J); and In the matter of Portman Securities Pty Ltd (in liq) [2025] NSWSC 1338 at [96] (Black J).

132 As Mansfield J explained in Smith v Deputy Commissioner of Taxation [1997] FCA 344; (1997) 23 ACSR 611 at 621, the concept of good faith “encompasses the state of mind of the creditor as to whether the transaction is to occur in circumstances which will, or may, advantage the creditor over other creditors of the company, so that the state of awareness of the creditor as to the company’s solvency will be directly relevant to that question”.

133 Similarly, in Cussen, Nicholas J explained at 515 [90] that in order to succeed the creditor “must show that there was absent from his mind any suspicion that the company was insolvent at the time he became a party to the impugned transaction, and did not suspect, or did not have an actual apprehension of, insolvency and that such knowledge as he had would not, reasonably considered, have caused him to suspect insolvency. It is difficult to see how the onus could be discharged if the defendant’s evidence does not extend to his state of mind on these matters specifically”.

134 The onus of proof borne by the Commissioner is proof on the balance of probabilities: see s 140 of the Evidence Act 1995 (Cth) and the definition of “case” in the Dictionary to that Act.

135 As Dixon J (as his Honour then was) famously observed in Briginshaw v Briginshaw [1938] HCA 34; (1938) 60 CLR 336 at 361:

The truth is that, when the law requires the proof of any fact, the tribunal must feel an actual persuasion of its occurrence or existence before it can be found. It cannot be found as a result of a mere mechanical comparison of probabilities independently of any belief in its reality.

136 In considering whether the onus has been discharged, an important consideration is the nature and the adequacy of the evidence before the Court. The Court must consider whether the evidence placed before it provides an appropriate basis on which to reach a reasonable decision as to whether that onus has been discharged.

137 In Ho v Powell [2001] NSWCA 168; (2001) 51 NSWLR 572 at 576 ([14] to [15]), Hodgson JA (Beazley JA agreeing) explained: