FEDERAL COURT OF AUSTRALIA

Australasian Centre for Corporate Responsibility v Santos Limited [2026] FCA 96

File number: | NSD 858 of 2021 |

Judgment of: | MARKOVIC J |

Date of judgment: | 17 February 2026 |

Catchwords: | CORPORATIONS – “greenwashing” – where representations made by a publicly listed company are alleged to be misleading or deceptive or likely to mislead or deceive in contravention of provisions in the Corporations Act 2001 (Cth) and the Australian Consumer Law – whether representations made with respect to future matters – characteristics of the target audience – whether reasonable grounds for making assumptions underpinning objectives – where representations relate to long term objectives – where satisfied the representations were not misleading or deceptive in the manner alleged – application dismissed |

Legislation: | Australian Consumer Law being Sch 2 to the Competition and Consumer Act 2010 (Cth) ss 4, 18, 33 Carbon Credits (Carbon Farming Initiative – Carbon Capture and Storage) Methodology Determination 2021 (Cth) Corporations Act 2001 (Cth) ss 769C, 1041H National Greenhouse and Energy Reporting Act 2007 (Cth) Federal Court Rules 2011 (Cth) rr 16.42, 16.43 United Nations Framework Convention on Climate Change (UNFCCC) Paris Agreement 2015 |

Cases cited: | Addenbroke Pty Ltd v Duncan (No 2) (2017) 348 ALR 1 AHG WA (2015) Pty Ltd v Mercedes-Benz Australia/Pacific Pty Ltd (2023) 303 FCR 479 Australian Competition and Consumer Commission v ACM Group Limited (No 2) [2018] FCA 1115 Australian Competition and Consumer Commission v Coles Supermarkets Australia Pty Ltd (2015) 327 ALR 540 Australian Competition and Consumer Commission v Dateline Imports Pty Ltd [2015] FCAFC 114 Australian Competition and Consumer Commission v Google LLC (No 2) [2021] FCA 367; (2021) 391 ALR 346 Australian Competition and Consumer Commission v Mazda Australia Pty Ltd [2023] FCAFC 45 Australian Competition and Consumer Commission v TPG Internet Pty Ltd (2020) 278 FCR 450 Australian Competition and Consumer Commission v Woolworths Group Ltd (2020) 281 FCR 108; [2020] FCAFC 162 Australian Competition and Consumer Commission v Woolworths Limited [2019] FCA 1039 Australian Consumer and Competition Commission v HJ Heinz Co Australia Ltd (2018) 363 ALR 136 Bonham atf Auchman Super Fund v Iluka Resources Ltd (2022) 404 ALR 15; [2022] FCA 71 Campomar v Nike International (2000) 202 CLR 45 City of Botany Bay Council v Jazabas Pty Ltd [2001] NSWCA 94 Commercial Union Assurance Co of Australia Ltd v Ferrcom Pty Ltd (1991) 22 NSWLR 389 Crowley v Worley Limited (2022) 293 FCR 438 Doppstadt Australia Pty Ltd v Lovick & Son Developments Pty Ltd [2014] NSWCA 158 Forrest v Australian Securities and Investments Commission (2012) 247 CLR 486; [2012] HCA 39 Husseini v Girchow Enterprises Pty Ltd [2024] FCAFC 143 Ireland v WG Riverview Pty Ltd (2019) 101 NSWLR 658 Jones v Dunkel (1959) 101 CLR 298 Kuhl v Zurich Financial Services Australia Ltd (2011) 243 CLR 361 Liberty Mutual Insurance Company Australian Branch trading as Liberty Specialty Markets v Icon Co (NSW) Pty Ltd [2021] FCAFC 126; (2021) 396 ALR 193 Lin v Zheng [2023] NSWCA 174 Minister for the Environment v Sharma [2022] FCAFC 35 Pabai v Commonwealth of Australia (No 2) [2025] FCA 796 Self Care IP Holdings Pty Ltd v Allergan Australia Pty Ltd [2023] HCA 8; (2003) 277 CLR 186 Sykes v Reserve Bank of Australia (1998) 88 FCR 511 at 520 Taco Company of Australia Inc v Taco Bell Pty Ltd (1982) 42 ALR 177 |

Division: | General Division |

Registry: | New South Wales |

National Practice Area: | Commercial and Corporations |

Sub-area: | Regulator and Consumer Protection |

Number of paragraphs: | 854 |

Date of hearing: | 28 – 31 October 2024, 1, 4, 5, 7, 8, 11, 12, 14 and 15 November 2024 and 3 and 6 December 2024 |

Counsel for the Applicant: | Mr N Hutley SC, Mr S Hartford-Davis, Mr J Entwisle and Ms Z Bush |

Solicitor for the Applicant: | Environmental Defenders Office Ltd |

Counsel for the Respondent: | Mr N Young KC, Mr B Lim and Ms C Trahanas |

Solicitor for the Respondent: | Herbert Smith Freehills Kramer (formerly Herbert Smith Freehills) |

ORDERS

NSD 858 of 2021 | ||

| ||

BETWEEN: | AUSTRALASIAN CENTRE FOR CORPORATE RESPONSIBILITY Applicant | |

AND: | SANTOS LIMITED (ACN 007 550 923) Respondent | |

order made by: | MARKOVIC J |

DATE OF ORDER: | 17 February 2026 |

THE COURT ORDERS THAT:

1. The further amended originating process and the further amended concise statement each filed by the applicant on 26 August 2023 are dismissed.

2. The applicant is to pay the respondent’s costs of the proceeding.

3. Any party that wishes to apply to vary Order 2 is to notify the Associate to Markovic J of their intention to do so by 3 March 2026.

4. The text of the reasons for judgment published today is to be published and disclosed only to the parties and their legal advisors.

5. By midday AEDT on 20 February 2026 the parties are to confer and to inform the Associate to Markovic J of any redactions that they propose are to be made to the reasons as a result of and in accordance with orders made to date in this proceeding pursuant to s 37AF of the Federal Court of Australia Act 1976 (Cth).

THE COURT NOTES THAT:

6. The reasons for judgment will be published on 23 February 2026 at 10 am AEDT and any redactions made in the reasons are made in accordance with the orders made to date in this proceeding pursuant to s 37AF of the Federal Court Act.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

MARKOVIC J:

1 “Greenwashing”, a term coined relatively recently, occurs when a company makes itself, its products or services appear more environmentally friendly, sustainable or ethical than they are in fact. It is that concept which is at the heart of this proceeding.

2 The applicant, Australasian Centre for Corporate Responsibility (ACCR), is an incorporated not for profit. It is, according to its website, a “shareholder advocacy and research organisation” which uses “shareholder strategy to enable investors to escalate engagements with heavy-emitting companies in their portfolios”. ACCR’s mission is “to influence changes to the strategies of [its] portfolio companies to decrease absolute, real world emissions”.

3 ACCR is and was at all material times a shareholder in the respondent, Santos Limited, a leading producer and supplier of natural gas in Australia and a publicly listed company whose shares are traded on the Australian Securities Exchange (ASX).

4 ACCR contends that Santos engaged in conduct that was misleading or deceptive or likely to mislead or deceive in contravention of s 1041H of the Corporations Act 2001 (Cth) and s 18 and s 33 of the Australian Consumer Law being Sch 2 to the Competition and Consumer Act 2010 (Cth) (ACL). That conduct was, according to the ACCR, engaged in by Santos via Santos’ Investor Day Presentation published on 1 December 2020, its Annual Report published on 18 February 2021 (2020 Annual Report) and its Climate Change Report published on 18 February 2021 (2021 Climate Change Report).

5 In summary, the ACCR alleges that:

(1) in the 2020 Annual Report Santos represented that it is a producer of “clean energy” and that natural gas provides “clean energy”, whereas in fact gas is not “clean” and Santos is a heavy emitter of greenhouse gases (GHG); and

(2) in the Investor Day Presentation and 2021 Climate Change Report Santos represented that:

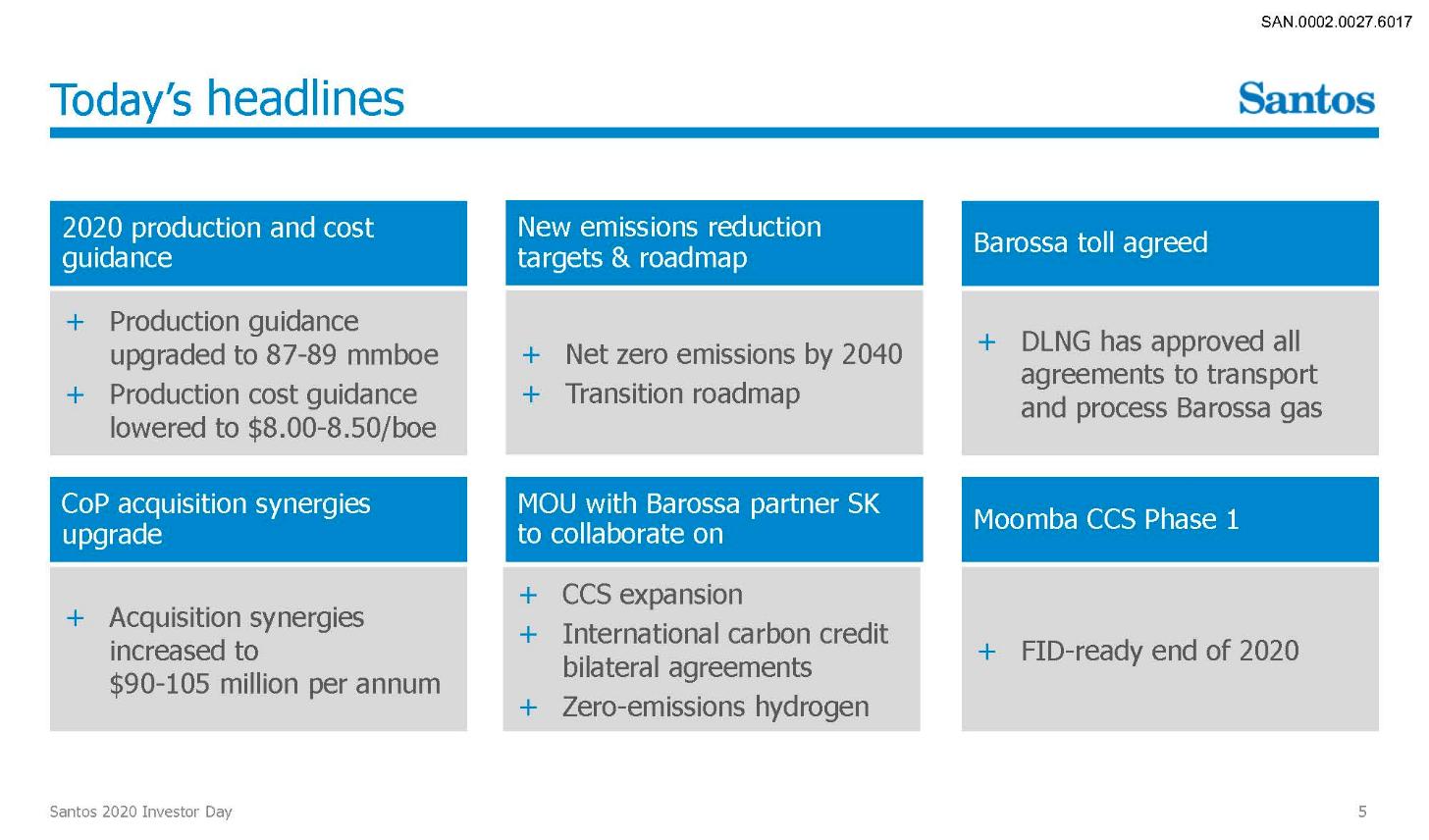

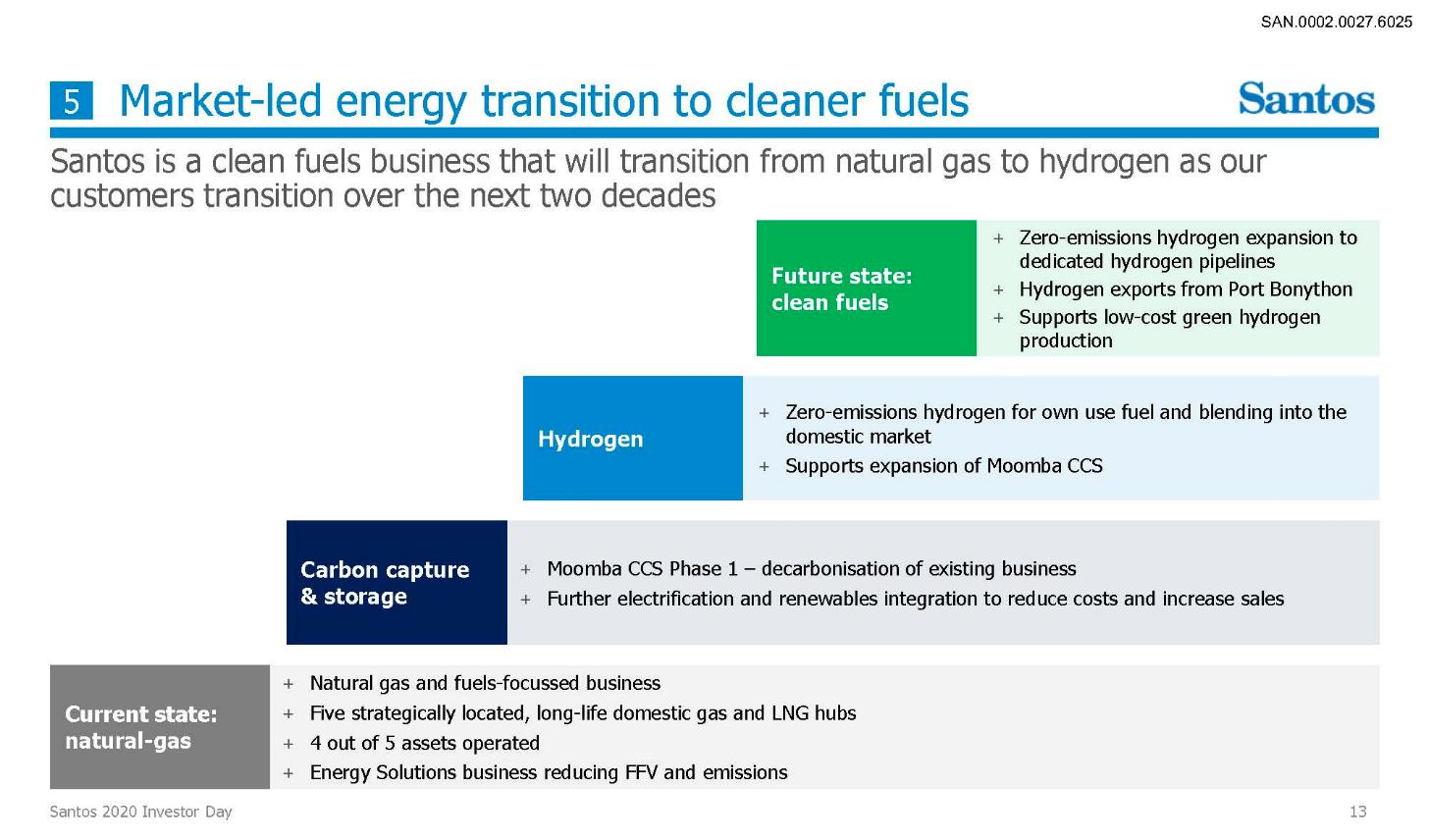

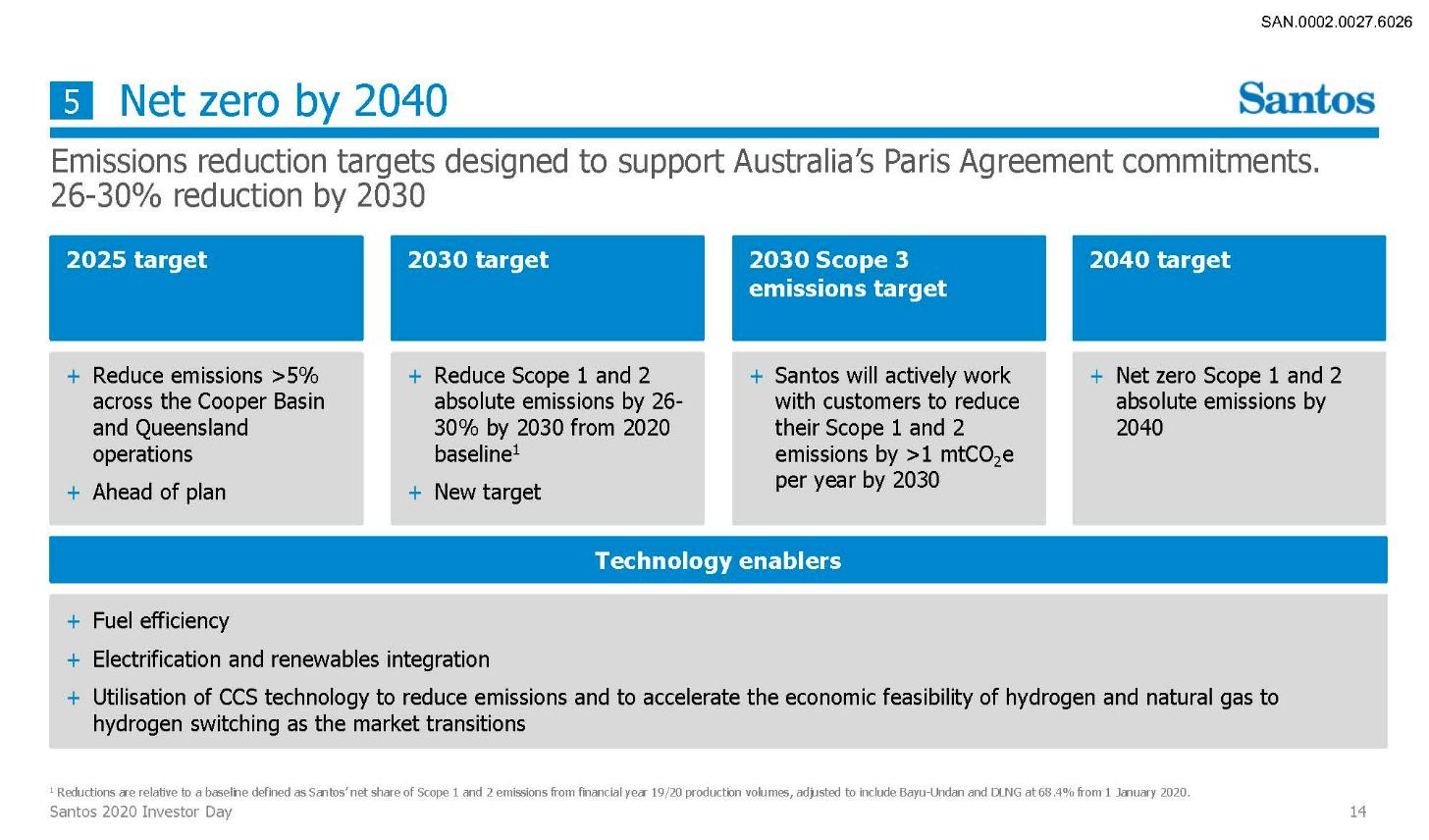

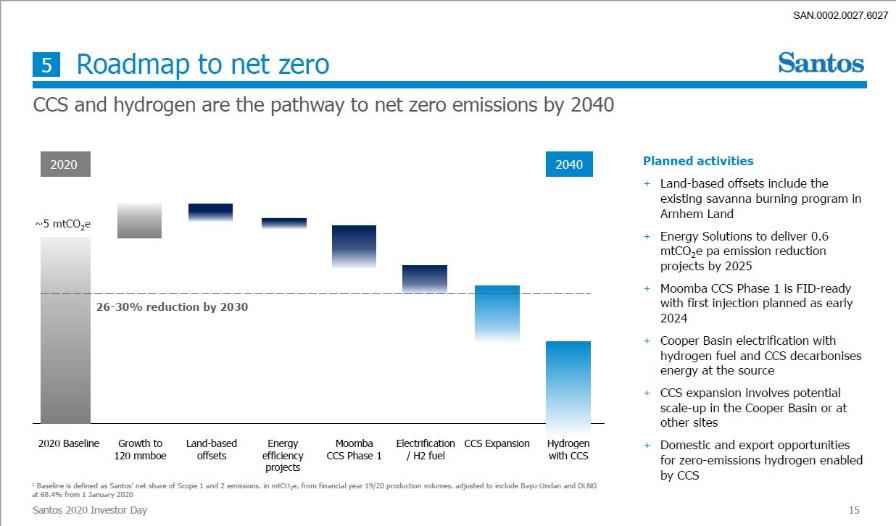

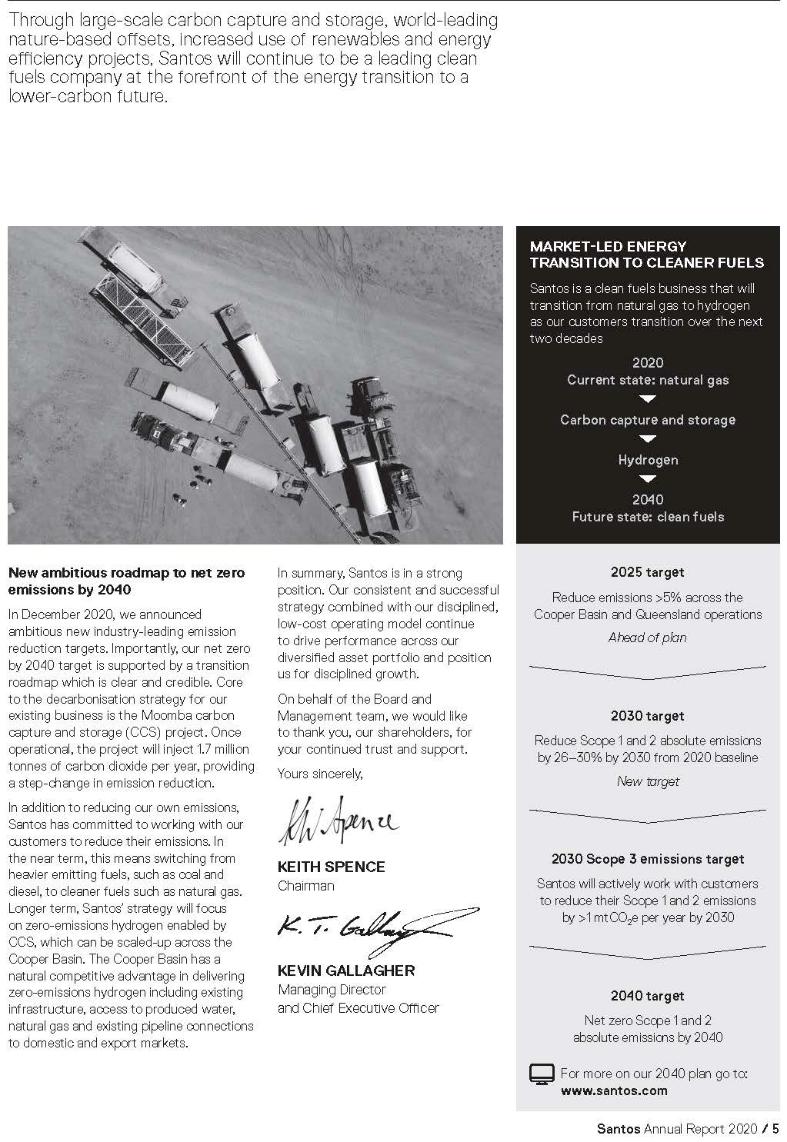

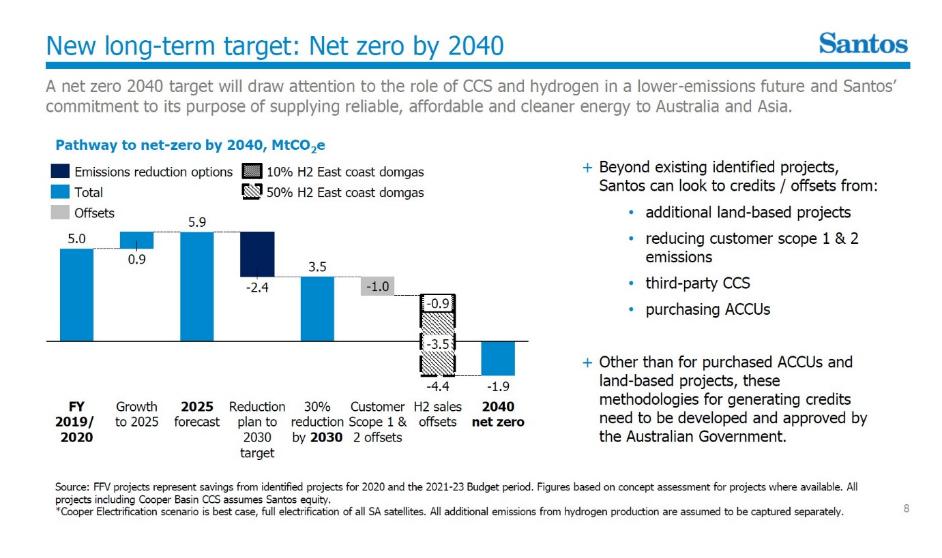

(a) it has a credible and clear plan, based upon reasonable assumptions, to reduce Scope 1 and 2 GHG emissions by 26-30% by 2030 (from its 2019-2020 financial year baseline) (2030 Target) and achieve “net zero” Scope 1 and 2 GHG emissions by 2040 (as depicted in slide 15 of the Investor Day Presentation) (Net Zero Roadmap) but that Santos did not disclose that:

(i) the 2030 Target and Net Zero Roadmap did not account for additional Scope 1 and 2 emissions associated with expected hydrocarbon growth and exploration opportunities beyond 2025, and Santos’ proposed carbon capture and storage (CCS) and hydrogen produced from natural gas using CCS (blue hydrogen) production plans; and

(ii) the 2030 Target and Net Zero Roadmap depend upon a range of undisclosed and/or unreasonable qualifications and assumptions to reduce or offset Santos’ Scope 1 and 2 GHG emissions, including reductions or offsets which are “nominal”, “notional” and “speculative”; and

(b) it can, in future, deliver “zero-emissions” or “clean” hydrogen, and hydrogen with “no emissions in its production (‘Scope 1 and 2’)”, whereas in fact Santos is proposing to produce blue hydrogen, which generates material additional emissions.

6 The ACCR seeks declarations of contravention and an injunction. It does not seek damages. It explains, in line with its stated mission, that it brings its claim to vindicate the public interest in ensuring that commitments by Australian companies regarding climate change are reasonably based and not misleading.

7 Santos contends that its statements were not misleading or deceptive as alleged. In summary it contends:

(1) in relation to the alleged “clean energy” representation that it did not convey that consumption of natural gas produced no emissions and that no reasonable member of the target audience could have been led into that error;

(2) in relation to zero-emissions hydrogen, it did not convey that it could produce hydrogen with literally no emissions. Rather, at the relevant time “zero-emissions” as a descriptor of hydrogen was synonymous with other adjectives like “clean” and “carbon neutral” which referred to hydrogen produced from natural gas with CCS and with the use of offsets for residual emissions; and

(3) in the Net Zero Roadmap, it was setting long term targets which were based on assessments about potential developments and opportunities in a highly uncertain future in an industry marked by rapid changes in markets, technology, economics and regulation. The reasonable member of the target audience would have understood this and would not have otherwise been misled. Santos says that it exercised judgements about potential developments that would favour development of CCS hubs and the emergence of a market for hydrogen and that its climate change targets were the result of many years work, reflection on its competitive advantages in evolving energy markets and the continual adjustment of its strategies to adapt to changing circumstances.

8 I have included definitions for all terms used in these reasons. In order to assist the reader, I also attach to these reasons, as Annexure A, a glossary of the more often used defined terms and a dramatis personae which includes a description of the roles of the various key Santos employees who either gave evidence before me or are referred to in these reasons.

1. The Facts

9 I set out below a summary of the relevant facts, some of which were agreed.

1.1 The witnesses

10 I commence with a description of the backgrounds, and, to the extent necessary, my impressions of the lay witnesses relied on by Santos and the experts relied on by each of the ACCR and Santos. The ACCR did not call any lay witnesses.

1.1.1 Santos’ lay witnesses

11 The following lay witnesses gave evidence on behalf of Santos.

12 Brett Kenneth Woods who has over 25 years’ experience in the oil and gas industry, commencing in 1994 as a contractor for Woodside Energy.

13 Mr Woods commenced his employment with Santos in 2013:

(1) prior to May 2020 he held the role of Executive Vice President (VP), Developments; and

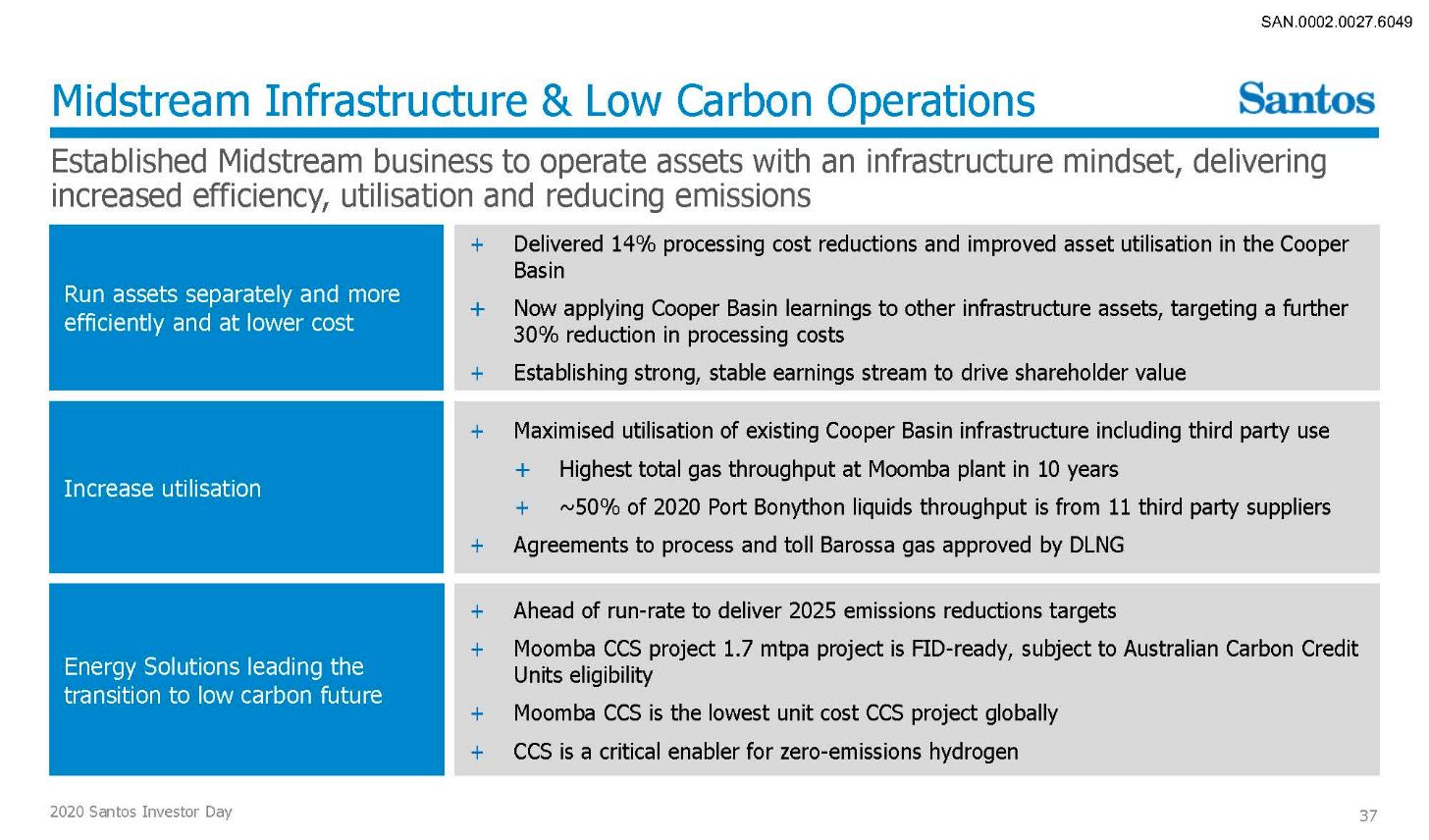

(2) from May 2020 to February 2022 (which is the period relevant to this proceeding), he held the role of EVP, Midstream Infrastructure and Low Carbon Operations although, from May 2021 to February 2022, Mr Woods’ title was Chief Operating Officer, Midstream Infrastructure & Clean Fuels but his role was functionally the same as when he was VP.

14 In his role as VP, Midstream Infrastructure and Low Carbon Operations, Mr Woods reported to Kevin Gallagher, Santos’ managing director and chief executive officer (CEO), and was involved in overseeing Santos’:

(1) midstream gas processing facilities, which process both natural gas and liquified natural gas (LNG), at Moomba, Port Bonython and Darwin LNG;

(2) Energy Solutions team;

(3) CCS projects; and

(4) joint venture, the Papua New Guinea (PNG) LNG project.

15 In overseeing the Energy Solutions team and CCS projects, Mr Woods received regular written updates and detailed technical reviews and had regular team meetings and one-on-one briefings with team members about the progress of projects and studies being undertaken.

16 Mr Woods was involved in the development of projects to support the emissions targets announced by Santos at its Investor Day on 1 December 2020 (see below) being:

(1) the 2030 Target which, as set out above, was a target for Santos to reduce its Scope 1 and 2 emissions by 26-30% by 2030; and

(2) a 2040 Scope 1 and 2 net zero emissions target (2040 Target),

(referred to collectively as Targets).

17 Mr Woods was responsible for ensuring that the Targets reflected Santos’ CCS projects and the activities of the Energy Solutions team, including proposed or possible future activities, and the analysis conducted by that team. He was also involved in discussions about the Targets during their development and provided input to ensure they were aligned to Santos’ corporate strategy, including its clean energy strategy.

18 From February 2022 to 1 September 2023, when he went on “gardening” leave, Mr Woods was President, Midstream and Clean Fuels at Santos and, in that role, was a member of Santos’ Executive Committee (ExCom) and also reported to Mr Gallagher.

19 Since February 2024 Mr Woods has been the CEO of Beach Energy Limited.

20 Mr Woods graduated from Curtin University with a Bachelor of Science with Honours in geology and geophysics in 1996 and is a graduate of the Harvard Business School Advanced Management Program, which he undertook in 2018.

21 Mr Woods was cross-examined.

22 Angus John Jaffray who joined Santos in February 2016 as a consultant. From shortly after his appointment until 2023 Mr Jaffray held the following roles:

(1) from May 2016, Executive VP, Strategy and Corporate Services. In 2017, while in that role, Mr Jaffray established the Energy Solutions team;

(2) from September 2018, VP, Organisation Integration at Santos. In that role, Mr Jaffray focused on the integration of Quadrant Energy, which Santos acquired in August 2018;

(3) from about March 2019 to January 2021, VP, People and Sustainability, reporting to Mr Gallagher. In that role, Mr Jaffray’s responsibilities included human resources, remuneration and performance, organisational and learning development, public affairs, sustainability and organisational integration. Insofar as sustainability was concerned, Mr Jaffray’s responsibilities included:

(a) managing the team with carriage of reporting on sustainability matters, including consolidating and reporting on emissions data, preparing Santos’ Climate Change Reports and engaging with local communities. That team was headed by Alicia Genet who at the time held the position of Head of Public Affairs and Sustainability, who reported to Mr Jaffray, and included Anshul Jain, Manager Carbon and Sustainability, who reported to Ms Genet; and

(b) presenting to Santos’ Environment, Health, Safety and Sustainability Board Committee on sustainability-related matters; and

(4) from January 2021, VP, People, Culture and Transformation. Mr Jaffray’s responsibilities in this role were the same as in his previous role save that he was no longer responsible for public affairs and sustainability. Responsibility for the sustainability team, headed by Ms Genet, moved to Jodie Hatherly, at the time Santos’ general counsel. Notwithstanding this change, Mr Jaffray continued to be involved in the finalisation of the 2021 Climate Change Report.

23 Prior to joining Santos Mr Jaffray held various leadership and consulting roles: from 1991 to 1999 he held various roles in the United Kingdom (UK), French and German offices of Crown Cork and Seal, a global packaging group; in 2001, after obtaining his Master of Business Administration (MBA), he joined The Boston Consulting Group where he was a member of the Mining and Metals Practice, the Energy Practice and the Operations Practice. He became a partner of The Boston Consulting Group in 2011 and headed up its West Australian office from 2010 to 2014; and in May 2014 until he joined Santos in 2016, he was a director of Azure Consulting Australia where he worked on projects involving operations, transformation and strategy for industrial clients.

24 Mr Jaffray holds a Bachelor of Arts with Honours in geography from the University of Cambridge and an MBA from the Australian Graduate School of Management, University of New South Wales.

25 Mr Jaffray was cross-examined.

26 Ying Luo who joined Santos in February 2009. From that time until September 2021, she held various positions as an engineer, an operations supervisor, an analyst, and a project and strategy lead. In particular, from November 2017 to September 2021 Ms Luo held the position of Project and Strategy Lead, Energy Solutions. In that capacity her role included:

(1) leading a team of engineers to deliver emissions reduction and renewable integration projects across Santos’ portfolio;

(2) implementing aspects of Santos’ strategy for positioning its business for a low carbon future (Clean Energy Strategy);

(3) leading the development of hydrogen project opportunities across Santos’ portfolio; and

(4) embedding emissions reduction into the day-to-day operations of Santos’ business.

27 In this role Ms Luo reported to Rowan Mackay, Manager Strategy Energy Solutions, until March 2020 and Chad Wilson, VP Energy Solutions, from April 2020 until September 2021.

28 From October 2021 to April 2023, Ms Luo was a Senior Advisor Hydrogen Development at Australian Gas Infrastructure Group (AGIG) and in May 2023 she commenced her current role as Chief Advisor and General Manager Strategy at Cooper Energy Ltd.

29 Ms Luo holds a Bachelor of Engineering and Bachelor of Science from Monash University, which she obtained in 2008, an MBA from the University of South Australia, which she obtained in 2013 and a Graduate Certificate, Energy and Resources: Policy and Practice from University College London, which she obtained in 2013.

30 Ms Luo was cross-examined.

31 Nicholas Hugh James Harley who from February 2020 to August 2024 held the role of Project Manager, Carbon Capture and Storage within the Energy Solutions division. In that role Mr Harley was responsible for the development and delivery of a large-scale CCS project at Santos’ gas fields in the Cooper Basin (Moomba CCS Project). He was accountable for bringing the Moomba CCS Project online, including the engineering, procurement, construction and commissioning of the CCS facility, the transport pipeline and the field injection wells and oversaw a team tasked with delivering the Moomba CCS Project (Moomba CCS Project Team). At the time Mr Harley gave evidence, the Moomba CCS Project Team comprised approximately 30 people but during 2020 was smaller, comprising approximately six people.

32 In August 2024, Mr Harley’s title changed to Subsurface and Approvals Manager as part of a restructure. Mr Harley became responsible for managing subsurface elements of the Moomba CCS Project and project approvals. He is no longer responsible for the development and delivery of the whole of the Moomba CCS Project.

33 From February 2007 to August 2010 Mr Harley was employed by Santos as an engineer. After completing an MBA in 2011 Mr Harley worked at McKinsey & Company in London in their oil and gas practice, working across Africa, the UK, Europe and South East Asia.

34 In about August 2013 Mr Harley rejoined Santos. Since that time and until taking on his current role he held the following roles:

(1) from August 2013 to March 2015, Strategy and Commercial Advisor, Exploration;

(2) from April 2015 to October 2015, Team Leader Southern Assets;

(3) from November 2015 to July 2017, Transformation Program Lead/Manager; and

(4) from July 2017 to February 2020, Field Development Planning Manager which involved early-stage concept planning for various upstream projects for the extraction of natural gas in the Cooper Basin and eastern Queensland assets.

35 Mr Harley holds a Bachelor of Engineering (Hons, Mechatronics) and a Bachelor of Economics from the University of Adelaide, obtained in 2006, and an MBA from Judge Business School, University of Cambridge, obtained in 2011.

36 Mr Harley was cross-examined.

37 The ACCR submits that in making factual findings about what “grounds” Santos had at the time of the announcements in question I should adopt the “helpful working hypothesis” that “contemporaneous documents written in the ordinary course of business are of great importance” (citing Liberty Mutual Insurance Company Australian Branch trading as Liberty Specialty Markets v Icon Co (NSW) Pty Ltd [2021] FCAFC 126; (2021) 396 ALR 193 at [239] (Allsop CJ, Besanko and Middleton JJ)) and that Santos’ decision-making process can be seen through those contemporaneous documents to have materialised relatively spontaneously and organically. Coupled with that the ACCR submits that I should place little to no weight upon what Santos’ lay witnesses purport to recall thinking at the time of the announcements in December 2020 and January 2021, except where the recollection is supported by a contemporaneous document.

38 While I accept that the contemporaneous documents created at the relevant time are of “great importance”, I also accept that it does not follow that, in light of the documents that were relied on before me, I would give little or no weight to the oral evidence. The documents are to be viewed in context. That is having regard not only to the whole of the documentary record but also where relevant to the oral evidence.

39 As Santos submits, this is not a case where the oral evidence is superfluous or might be rejected because it is inconsistent with the contemporaneous documents. The documents reveal and record the roles of the various individuals within Santos and the development of material by those with relevant responsibility. Material was submitted to senior management and discussed. Evidence of those discussions is not always evident on the face of the documents, and the oral evidence serves to fill the gaps.

40 The oral evidence given by the lay witnesses also explained why and how certain options were developed and/or included in the material, particularly in the Net Zero Roadmap. Evidence of that nature can assist in providing context and background.

41 That said, I am acutely aware of the caution given against “reliance on subjective evidence from the representor as being necessarily likely to give an accurate picture of what information the representor ‘had’ as a basis for any prediction or forecast made”: see Australian Competition and Consumer Commission v Woolworths Limited [2019] FCA 1039 at [135] (Mortimer J as her Honour then was). I will proceed with that caution in mind and having regard to the overall circumstances of the case.

42 As to the evidence given by Santos’ lay witnesses, the ACCR submits that I would have little confidence in the affidavits of Messrs Woods and Jaffray and Ms Luo given they were sworn in late November 2023, around three years after the relevant events. It contends that the ordinary processes of human recollection would make it virtually impossible to recall what set of considerations were playing upon a person’s mind at the time of making a decision three years ago and that the affidavits adopt “a dubious trope” with the witnesses purporting to recall precisely what he or she did or did not believe or think at the time the Targets were announced.

43 That the affidavits were sworn three years after the relevant events is not an uncommon occurrence and of little moment or indeed, relevance. As Santos submits, the ACCR did not suggest to the witnesses in cross-examination that their key recollections were only formed at the time their affidavits were sworn. Their recollections were not challenged on that basis, and the ACCR cannot sustain such a submission having not taken that step.

44 The ACCR also challenges the reliability of each of Messrs Woods and Jaffray and Ms Luo as witnesses based on their demeanour and the evidence they each gave in cross-examination.

45 The ACCR submits that Mr Woods’ evidence should not be accepted unless it was against interest or corroborated by a contemporaneous document. It supports that submission based on the following contentions: first, Mr Woods could not remember a whole range of important details, for example whether he spoke to Ms Luo about hydrogen emissions, whether he told Ms Luo in about mid July 2020 that it was important that the proposal be “zero emissions hydrogen” and which Santos employee had suggested that Santos calculate 50% market share by volume of hydrogen; secondly, Mr Woods was otherwise argumentative and unreliable and was shown to be a partisan witness including by using his time in cross-examination to deflect attention away from areas in which he perceived Santos’ case may be weak; thirdly, Mr Woods was prone to giving pre-prepared speeches that were non-responsive to questions; fourthly he repeatedly sought clarification of questions which needed no clarification, instead of giving frank answers; and finally, on several occasions he contradicted himself where his perception of Santos’ interest changed.

46 I did not find Mr Woods to be argumentative, unreliable or partisan. Certainly, Mr Woods held his ground when challenged on aspects of his evidence. But that is not a reason why I would not accept any of his evidence. While Mr Woods may in some respects have been defensive, I did not find him to be partisan. That Mr Woods, or any other witness, could not recall particular matters is also not a reason to discount the totality of that persons’ evidence. Human memory is fallible and more so as time passes. Overall, I found Mr Woods to be a satisfactory witness who did his best to assist the Court.

47 The ACCR accepts that Ms Luo was generally an honest and intelligent witness, a sentiment with which I agree. However, it goes on to submit that the frequency with which Ms Luo could not recall important events and circumstances again means that the Court should place little weight on what she claims in her affidavit to have had in mind at particular points in time, illustrating that point by reference to examples. I disagree. As I have said, that a witness may not recall the answer to a specific question does not undermine the whole of their evidence. Ms Luo gave evidence four years after the relevant events and a year after she completed her affidavit. That she could not recall some matters of detail or events is hardly surprising. As I have already observed I found Ms Luo to be an honest witness, who did her best to assist the Court and who gave her evidence in a considered way.

48 The ACCR describes Mr Jaffray’s evidence as relatively inconsequential in the context of the case but submits that, to the extent he purported to give evidence of what he subjectively had in mind in 2020, the Court should place little weight on that evidence for the reasons set out at [37] above. I do not accept that Mr Jaffray’s evidence is “inconsequential”. His evidence discloses that, given his role at Santos as VP of People and Sustainability during the relevant period, he had a significant role overseeing the preparation of papers submitted to the Santos Board about the Targets and the Net Zero Roadmap. Mr Jaffray’s evidence, supplemented by documentary evidence, provides a fuller chronology of the development of the Targets and the Net Zero Roadmap.

49 I have no reason to doubt that Mr Jaffray is anything other than a truthful witness whose evidence was largely not challenged and which I would accept.

1.1.2 The expert witnesses

50 The parties relied on extensive expert evidence which covered different fields of specialised knowledge including, described at a high level: hydrogen production; hydrogen transportation; carbon credit schemes; climate change and the meaning of net zero; lifecycle analysis of GHG emission; CCS; corporate strategy; and economics. I note that the ACCR and Santos did not necessarily engage experts in the same fields of expertise nor did they both engage experts to address all areas. For example, only Santos engaged experts in the latter two fields.

51 I set out below a short biography for each of the experts relied on and, where relevant or necessary, my observations of them.

52 The ACCR relied on the following experts.

53 Paul Martin who is a consultant at Spitfire Research Inc. Mr Martin obtained Bachelors and Masters degrees in Applied Science (Chemical Engineering) from the University of Waterloo, Ontario Canada in 1990 and 1991 respectively. Since 1993 he has been a Licensed Professional Engineer in the province of Ontario (as well as in other provinces from time to time). Since 1991 Mr Martin has worked in the field of chemical engineering.

54 From 1996 to 2022 Mr Martin:

(1) was a program manager and senior technical fellow at Zeton Inc where, as senior or principal project engineer and project manager or senior project manager/mentor, he was responsible for the completion of pilot and demonstration plant projects and engineering/cost studies for plants for chemicals, polymers, primary metals/hydrometallurgy and alternative energy/alternative chemical feedstocks sectors. He also acted as a design consultant for the early stages of process development work, including in the design teams of client firms as they developed intellectual property related to new process technology; and

(2) maintained a private scientific/technical consultancy practice, Spitfire. Spitfire undertakes work related to decarbonisation of production and energy projects, early stage technology development assistance, technoeconomics, evaluation of technological readiness level, expert witness work, assistance with strategy for scale-up and path to commercialisation, and evaluation of research and development claims as part of investment due diligence.

55 Mr Martin claims he has expertise in relation to hydrogen and its derivatives in terms of their manufacture and use as chemicals and their roles in the decarbonisation of the economy. He has been responsible for the selection of construction materials for corrosion service, and for the design and construction of piping systems for fuel gas, hydrogen, synthesis gas mixtures containing hydrogen, and hydrogen-derived products handled at both low and very high temperatures and pressures, as well as piping systems to convey other chemicals and mixtures. He wrote and served as gatekeeper of the corporate piping specifications for Zeton Inc.

56 Mr Martin prepared three reports addressing the blending of hydrogen into existing gas networks.

57 It became apparent in cross-examination that Mr Martin was opposed to hydrogen playing any part in the decarbonisation of energy and that he had both expressed and defended that view. He expressed the view in an article published on LinkedIn on 6 November 2024 titled “Distilled Thoughts on Hydrogen” (Martin LinkedIn Article) and accepted in cross-examination that he “stridently” objects to the use of hydrogen as a fuel, including its use as an industrial fuel in industrial processes.

58 The Martin LinkedIn Article included by way of summary:

Why do you hate hydrogen so much? I DON’T HATE HYDROGEN! I think it’s a dumb thing to use as a fuel, or as a way to store electricity. That’s all. It’s too expensive, for reasons that are structural and which can’t be fixed by innovation. Even black hydrogen, made from fossils with over 10 kg CO2 and perhaps 14 kg CO2e/kg emissions going right to the free atmospheric sewer, for the low-low price of $1.50/kg, is already $11/MMBTU or $11/GJ of higher heating value (HHV). It’s just too expensive to waste as a fuel for heating or transport. It’s expensive because it’s inefficient, but the real deal killer is that it is also ineffective as a fuel, i.e. difficult and expensive to move and store.

I also think it’s part of a bait and switch scam being put forward by the fossil fuel industry. And what about the electrolyzer and fuelcell companies, the technical gas suppliers, natural gas utilities and the renewable electricity companies that are pushing hydrogen for energy uses? They’re just the fossil fuel industry’s unwitting accomplices- their “useful idiots” in this regard.

59 Santos submits that in light of Mr Martin’s publicly held views, his evidence about the reasonableness of solving the challenges associated with the transmission and transport of hydrogen domestically and internationally should be accorded no weight. It says that the views he expresses on this topic very much resemble those expressed in the Martin LinkedIn Article and, in any event, he has no experience in Australia or in large scale infrastructure investment and did not conduct any detailed study to support his views about “economic sensibility”. As to the latter after accepting that it was technically possible to build a new transmission pipeline to transmit hydrogen from Moomba to Port Bonython, but not economically sensible, Mr Martin had the following exchange with senior counsel for Santos, Mr Young KC, in cross-examination:

Mr Young: Not only. Now, in point of fact, you have not done any analysis of the cost of building, for instance, a new transmission pipeline between Melbourne and the East Coast of Australia, have you?

Mr Martin: No.

Mr Young: No. Your concern is simply that it would be a very large capital expenditure, a vast sum of money; correct?

Mr Martin: My concern is that it’s a vast sum of money per unit of delivered energy, and hence it would be a considerable cost to whoever is using that material for energy, that hydrogen for energy.

Mr Young: Yes. Well, it may depend on the volume of the market, may it not, Mr Martin?

Mr Martin: Of course.

Mr Young: Yes. And it may depend upon demand in the market, and whether any alternatives exist and at what cost, may it not?

Mr Martin: Correct. Yes.

Mr Young: Yes.

Mr Martin: Fair enough.

Mr Young: And you haven’t analysed any of that?

Mr Martin: Well, I have looked at the cost of each of the steps. They’re laid out in the various reports.

Mr Young: Yes. You haven’t looked at any kind of financial analysis of the net present value of infrastructure that might need to be built between Moomba and the East Coast, have you?

Mr Martin: I was not retained

Mr Young: Yes.

Mr Martin: for that purpose. No.

60 On the one hand, Mr Martin’s steadfast and publicly aired beliefs about the use of hydrogen as a fuel undermine his impartiality and thus the assistance he can give the Court. On the other, Mr Martin was prepared to make concessions in cross-examination and, as the extract above demonstrates, accept weaknesses or gaps in his own analysis. For that reason, while I would decline to accept Santos’ invitation to accord no weight to Mr Martin’s evidence, I would give it only limited weight.

61 Malte Meinshausen who is an Associate Professor in the School of Geography, Earth and Atmospheric Sciences at the University of Melbourne. Associate Professor Meinshausen holds a Ph.D. in Climate Science & Policy from the Swiss Federal Institute of Technology (ETH Zurich) and an M.Sc. in Environmental Change and Management from the University of Oxford. He has written on topics relating to climate change and the Paris Agreement (see [117]-[119] below).

62 Associate Professor Meinshausen has held and/or continues to hold the following positions:

(1) from 2000 to 2005 he worked as a freelance consultant for government bodies and environmental non-government organisations on climate policy issues;

(2) from 2005 to 2015 he was a Scientific & Technical Advisor for the German Ministry of Environment on international climate policy. In that role he was a member of the German delegation to the Intergovernmental Panel on Climate Change meetings and the United Nations Framework Convention on Climate Change (UNFCCC) negotiations;

(3) from 2007 to 2009 he also held the position of founding co-director of the not-for-profit research institute and think tank, Climate Analytics, Berlin; and

(4) since 2020 he has been a co-director of a new start-up, Climate Resource.

63 Associate Professor Meinshausen provided three expert reports addressing whether the production, distribution and end-use of natural gas contribute to anthropogenic climate change and global warming, the current and expected impacts of anthropogenic climate change and global warming on the environment, the accounting system for GHG emissions as it existed in February 2021 and whether the documents provided to him (including the Net Zero Roadmap, the 2021 Climate Change Report and the Investor Day Presentation) disclosed a reasonable basis for Santos to have claimed, as at February 2021, that it could achieve “net-zero” Scope 1 and 2 GHG emissions by 2040.

64 Fiona Beck who is a senior lecturer at the School of Engineering, College of Engineering and Computer Science at the Australian National University (ANU). Associate Professor Beck holds a Ph.D. in “[d]esigning plasmonic nanoparticles for light trapping applications in solar cells” from the Research School of Engineering, ANU and a M.Sc. (Physics), 1st Class from the University of Glasgow. Her research focuses on clean energy technologies.

65 Among other things, Associate Professor Beck:

(1) is the convener of the ANU’s Hydrogen Fuels project and the Hydrogen Economy research cluster for the Institute of Climate, Energy and Disaster Solutions;

(2) leads a research group designing new ways to selectively drive chemical reactions to capture carbon dioxide (CO2) from the atmosphere and produce solar fuels;

(3) convened the Hydrogen Fuels project for “ZCEAP - ANU’s Zero-Carbon Energy for the Asia-Pacific Grand Challenge” and in that role she published academic articles and provided submissions to government regarding zero carbon industries and exports; and

(4) has authored or contributed to analysis about hydrogen’s role in the energy transition.

66 Associate Professor Beck provided three expert reports outlining calculations on the emissions intensity and the amount of emissions associated with the production of hydrogen. Santos submits that a number of the assumptions underpinning Associate Professor Beck’s evidence, in particular her calculations on the emissions intensity and amount of emission associated with the production of hydrogen, were unsound. To the extent necessary I address that submission below when considering Associate Professor Beck’s evidence in context.

67 Shohini Parker who is the principal and founder of Carbon Transition Consulting. Ms Parker holds a B.Sc. (1st Hons) and Bachelor of Chemical Engineering (1st Hons) from Monash University. She has over 15 years of consulting experience working with resource sector companies and across the industrial and financial sectors in Australia.

68 Ms Parker has held the following positions:

(1) from 2002 to 2006 she worked at ExxonMobil Corporation as a Gas Reservoir Surveillance Engineer (2002 to 2005) and a Production Planner (2003 to 2004); and

(2) from 2006 to 2015 she worked at Energetics Pty Ltd where she held various roles including consultant, senior consultant, Victorian regional manager and principal consultant.

69 Ms Parker provided two expert reports in relation to company strategies to reduce GHG emissions and plans to achieve net zero emissions. She opined on whether reliance on carbon credits or offsets was a material consideration for companies and their investors in achieving those plans and whether it was reasonable or credible for Santos to make certain of the assumptions it made as a part of its net zero plan.

70 Santos submits that I would find Ms Parker to be an unreliable witness. It says that Ms Parker provided opinions for which she had no expertise or foundation and failed to make appropriate concessions about those matters when challenged.

71 In support of that submission Santos points to Ms Parker’s claim to work on behalf of investors. Relevantly, Ms Parker says at [20] of her first report:

In my work on behalf of investors reviewing companies’ net zero plans during this time, I was specifically asked to provide my views on whether the plans were aligned with the latest science on emissions reduction pathways required to limit global temperature goals to 1.5°C by the end of the century.

a. In forming my views, I drew on the most recent science-based emissions reduction pathways available during 2020, which were from the IPCC 1.5°C Special Report (released June 2018).

b. In this IPCC report, ‘carbon removals’ were a necessary contributor to reach a global net zero emissions position for ‘hard-to-abate’ sectors by 2050. However, the pathways and report conclusions indicated that carbon removals should not be used as an alternative to the implementation of decarbonisation technologies wherever these technologies were available, notwithstanding the need for substantial investment to ‘scale-up’ these technologies to commercially viable levels.

c. In my reports delivered to my investor clients during this time, I therefore considered and commented on the scale of carbon offset use in the net zero plan of the company I was reviewing and whether this scale was aligned with the IPCC 1.5°C Special Report. I also reviewed and commented on how the scale of carbon offset use compared to net zero targets published by other companies in the sector.

(Footnotes omitted.)

72 Santos submits that Ms Parker has not undertaken work on behalf of investors as claimed in her report and is not qualified to opine on their attributes, views or expectations.

73 In order to test Ms Parker’s claim to have undertaken work on behalf of investors, Santos served a subpoena on Ms Parker seeking documents relevant to [20] of her first report. In response Ms Parker produced two documents relating to a single entity, Regnan Pty Ltd. Those documents are a proforma document titled “engagement guide – climate change XYZ Company Inc” and an invoice made out to that entity. The invoice from Ms Parker’s consulting firm to Regnan disclosed that Ms Parker’s work was to undertake environmental, social, and governance (ESG) assessment scores for two different entities.

74 Ms Parker described Regnan as an investor research and engagement firm which provides services to the investment community but is not itself an investor. Regnan develops reports and disseminates a range of different materials to its clients who are institutional investors, asset managers and banks. Ms Parker was a contractor to Regnan for several years and undertook her work for it using its servers. Thus, she did not have further documents to produce in answer to the subpoena served on her. Ms Parker’s evidence was that that work gave her insight into what investors were interested in, based on what those investors asked Regnan to produce.

75 That evidence clearly supports Santos’ submission that Ms Parker has not undertaken work on behalf of investors and is not qualified to opine on their attributes, views or expectations. Based on the documents produced in answer to the subpoena served on her, the closest she came was the limited work she undertook for a research firm which, in turn, produced material for investors. Even accepting that Ms Parker was a contractor to the research firm for “several years” does not assist to qualify her to provide an opinion about investors’ views or expectations. Ms Parker did not refer to that work in her curriculum vitae, and it is impossible to assess her qualifications in that regard. I would reject Ms Parker’s asserted expertise about investors.

76 There were also other aspects of Ms Parker’s evidence which were troubling.

77 Ms Parker expressed opinions in areas where she did not have the requisite expertise and/or the proper foundation. For example, she gave evidence about the availability of carbon credits including by reference to the development of future policy. However, in cross-examination she conceded that she had not read the “relevant Australian government reports concerning the gas industry”. In another example Ms Parker said that she had no opinion on whether “as a potential supplier of hydrogen, … Santos would have substantial bargaining power in the circumstances of those industries as one of the only credible large scale suppliers of such services … likely to emerge” but then went on to deny, in my view somewhat implausibly, that such matters would have any bearing on Santos’ bargaining power.

78 Ms Parker also expressed a view in her first report (at [38]) that it was “likely that many of Santos’ industrial natural gas customers in Australia using gas for heating and other industrial purposes are likely to exceed 100,000 tonnes CO2-e of operational emissions annually and therefore be captured under the [Safeguard Mechanism]”. In cross-examination Ms Parker accepted that she had not undertaken any investigation or analysis to support that opinion. She said that it was “a general statement based on the size of the gas facilities”. Despite the fact that in a later joint report Ms Parker accepted the analysis of Santos’ expert, Mr Snow, which impacted the opinion she expressed at [38] of her first report, she refused to accept or concede that her opinion was erroneous. Rather, she came up with a new and alternative basis to justify her opinion.

79 Ms Parker was also shown to be selective in her evidence. In her first report at [19] she gave evidence about the stakeholder concerns that she recommends her clients consider in relation to carbon offsets. However, she did not include in her report by way of balance the benefits perceived by stakeholders in relation to carbon offsets. This omission was highlighted by an advice she in fact gave to one of her clients which included both the negative and positive features of offsets perceived by stakeholders. In cross-examination Ms Parker tried to explain the disparity in an unconvincing and argumentative way.

80 Santos also raised concerns about Ms Parker’s understanding of the Taskforce for Climate-Related Financial Disclosures (TCFD) and contends that she misrepresented the TCFD framework. I address the TCFD framework and Santos’ submissions in relation to Ms Parker’s evidence below.

81 The ACCR submits that Ms Parker was a careful witness who properly acknowledged when she did not have expertise to answer a question. That was not the impression I had of her as a witness. While on a few occasions Ms Parker said she did not have the relevant expertise to answer a question, more frequently she tried to explain away evidence that she did not perceive would assist the opinion she gave in her reports in an unconvincing and argumentative way. She was not prepared to make concessions. I have set out some examples above. Overall, I did not find Ms Parker to be a satisfactory witness and would place very little weight on her evidence.

82 Timonthy Grant who is the founder and director of Lifecycles, a supplier of life cycle assessments and circular economy services across Australia. Mr Grant established Lifecycles in 2003. He holds a Master of Engineering (Cleaner Production) from RMIT University and a Bachelor of Applied Science in Environmental Assessment and Land Use Policy from Deakin University.

83 Mr Grant has also held the following positions:

(1) from 1996 to 2003 he was a program manager, LCA, Centre for Design, RMIT University;

(2) in 2003 he was an assistant director, Centre for Design, RMIT University;

(3) from 2005 to 2013 he was an adjunct research fellow, CSIRO Division of Atmospheric Research; and

(4) from 2008 to 2010 he was an adjunct professor, Centre for Design, RMIT University.

84 Mr Grant provided two expert reports in relation to lifecycle GHG emissions assessment for different energy sources.

85 Santos relied on the following experts.

86 Peter Cook who is an earth scientist in the areas of energy, resources, and GHG technologies. Professor Cook holds the degrees of B.Sc. (Hons) (University of Durham), M.Sc. (ANU), Ph.D. (University of Colorado) and D.Sc. (University of Durham). He is a Fellow of the Academy of Technological Sciences and Engineering.

87 Professor Cook is currently a Professorial Fellow, University of Melbourne, a position he has held since 2012. He is also a Consultant and Chair (Expert Panel) to the New South Wales (NSW) Government on Gas, a consultant to BHP on CCS and the Victorian Government on unconventional gas, Chair of the BHP-sponsored GeoCquest Project involving Melbourne, Stanford and Cambridge Universities, Distinguished Scientist CO2CRC, a member of the CarbonNet Advisory Board and Chair of the Academies (ACOLA) Review of Unconventional Gas.

88 Prior to 2012 Professor Cook held the following positions:

(1) from 1968 to 1976 he was a Senior Geologist, Bureau of Mineral Resources;

(2) from 1976 to 1982 he was a Senior Research Fellow, RSES, ANU;

(3) from 1982 to 1990 he was a Division Chief/Associate Director, Bureau of Mineral Resources;

(4) from 1988 to 1989 he was a Professor at Université Louis Pasteur;

(5) from 1990 to 1998 he was a Director, British Geological Survey;

(6) from 1998 to 2003 he was a Director, Australian Petroleum CRC; and

(7) from 2003 to 2011 he was Chief Executive, CO2CRC.

89 Professor Cook prepared one report concerning CCS. There was no dispute that Professor Cook is an acknowledged expert in CCS and that his evidence should be accepted to the extent it is relevant.

90 David Collis who since 1986 has been a professor of strategy at the Harvard Business School specialising in corporate and global strategy. From 1997 to 2002 Professor Collis was a professor at the Yale School of Management and from 1985 to 1986 and in the Autumn of 2003 at Columbia Business School. In those roles he taught and continues to teach MBA students across the full range of strategy courses and has developed corporate and global strategy courses. Professor Collis also teaches strategy in all of Harvard’s Executive Programs, including specialised courses on corporate and global strategy. From 1978 to 1982 Professor Collis was a management consultant with The Boston Consulting Group in London where he specialised in corporate strategy.

91 Professor Collis has a Bachelor of Arts (in economics) and M.A. (Cambridge University), an MBA (Harvard Graduate School of Business Administration) and a Ph.D. in business economics (Harvard University).

92 Professor Collis prepared one report in relation to long term corporate strategy. Once again, there was no dispute that Professor Collis is an acknowledged expert and that his evidence should be accepted to the extent it is relevant.

93 James Arthur Snow who since 2008 has been an executive director at Oakley Greenwood, a consulting firm.

94 Among other things, Mr Snow has led, designed, and implemented extensive renewable gas and energy projects for groups such as the Commonwealth Department of Industry, Science, Energy and Resources (DISER), Water Authorities (Yarra Valley Water, BAWB), the Energy Network Association, Australian Hydrogen Council, APA Group, Victorian Department of Environment, Land, Water and Planning, Tasmanian State Development Department and the New Zealand Gas Network Businesses. He has also led the development of stretch goals for the Low Emissions Technology Statement (LETS) working with the LETS Taskforce (Messrs Finkel, Clarke and King) focussing on energy storage and the role of renewable gases (hydrogen and renewable methane). Mr Snow is also engaged with developments related to hydrogen markets and how hydrogen technology can be monetised, including as dispatchable (demand side) load, liquid fuel replacement and through methanation, and has assisted State Governments and the Federal Government on renewable gas policy matters.

95 Mr Snow has been involved in the design, construction and operation of gas pipelines, gas distribution systems, coal, naphtha and natural gas fuelled steam methane reforming (SMR) plants producing hydrogen syngas and towns gas, LNG and compressed natural gas facilities, natural gas, diesel, CSG and LNG power stations, high voltage electricity power lines, heavy trucking motive power such as mine trucks, gas cleaning equipment including CO2 extraction, coal handling and coke oven facilities in steelmaking, ammonium nitrate plants, brown coal gasification and the gasification of biomass, water and waste water treatment facilities and associated biomass rendering plants and anerobic diesters. He also has a background in the production, distribution, storage and end use of hydrogen through his work with ammonia, SMR, towns gas, coal to gas, and liquids to gas.

96 Prior to joining Oakley Greenwood Mr Snow held the following roles:

(1) from 1978 to 1990 he had various roles at AGL;

(2) from 1990 to 1991 he was marketing director, Energetics Pty Ltd (Newcastle);

(3) from 1991 to 1992 he was the CEO of Hunter Electricity;

(4) from 1993 to 2001 he held roles of CEO Consulting/CFO/General Manager at Energetics Pty Ltd;

(5) from 2001 to 2004 he was VP, Charles River Associates, Asia Pacific;

(6) from 2005 to 2006 he was executive GM development, Energy Developments Ltd; and

(7) from 2006 to 2008 he was a senior advisor, Charles River Associates, International.

97 Since 2016 Mr Snow has been an adjunct professor at the University of Queensland, Energy Initiative, although this honorary title and departmental affiliation is under review given the recent establishment of the ARC Centre of Excellence for Green Electrochemical Transformation of Carbon Dioxide (GETCO2), where Mr Snow is a key Industry Participant, and the closure of the Energy Initiative.

98 Mr Snow is also a Fellow of the Institution of Chemical Engineers, Past Chair of the Australian Chemical College and Fellow of the Institute of Engineers Australia. He has a B.E. (Chemical) Honours.

99 Mr Snow prepared one report which addressed a number of areas including a life cycle analysis, the meaning of net zero emissions, the domestic and export hydrogen markets, infrastructure for hydrogen and blue hydrogen.

100 While the ACCR accepts that Mr Snow has a long history working in or with the gas industry, it submits that I would treat his evidence with caution and only accept it where it was supported by other experts or documentary evidence. This approach is urged because the ACCR says that Mr Snow was willing to venture opinions on topics on which he had no expertise and without a proper basis.

101 Mr Snow provided an extensive report (as well as participating in the preparation of a number of joint reports – see below). Overall, I found him to be a frank witness who had a deal of practical experience which he brought to bear in his report and in giving evidence. Where a question strayed into an area that was not within his area of expertise, he informed the cross-examiner accordingly or, as necessary, informed the Court and the cross-examiner of his source of the information relied on to address the gap in his own expertise, for example in relation to the material used to construct a pipeline to transport hydrogen.

102 The ACCR refers to Mr Snow’s evidence about the meaning of the term “zero emissions hydrogen” which is set out in Part 4.2 below. In summary, he expressed the view in his report that at the relevant time the Australian energy industry used that term to refer to green and blue hydrogen. In cross-examination Mr Snow frankly accepted that he could not locate any published work that expressed that view and also acknowledged that in an article he had co-authored he and his junior colleague had referred to blue hydrogen as “low net emissions”. He conceded these matters without prompting or the need for repeated questions from the cross-examiner.

103 The view expressed by Mr Snow and his co-author in November 2021 is at odds with the view Mr Snow expressed when asked about the definitions at an earlier but proximate point in time. That evidence is addressed further below (see [557]). However, it does not cause me to discount the whole of Mr Snow’s evidence or treat it in the manner the ACCR contends.

104 Sanjay Unni who is the managing director of the Berkeley Research Group (BRG), an expert services firm specialising in economics and financial analysis. Dr Unni leads BRG’s securities practice which addresses a wide range of issues relating to transactions in financial instruments. Dr Unni joined BRG in October 2010. From May 2000 to September 2010 he worked at LECG LLC, another expert services firm, in the positions of senior economist (May to December 2000), managing economist (January to December 2001), senior managing economist (January 2002 to April 2006), principal (April 2006 to November 2007) and director in the securities practice (November 2007 to September 2010).

105 From August 1984 to May 2006 Dr Unni had various teaching roles at Southern Methodist University, Dallas, Texas, University of Texas at Dallas, University of Strathclyde, Glasgow and University of California, Berkeley.

106 Dr Unni has a B.A. (Honours), Economics, University of Delhi (1984), M.A., Economics, Southern Methodist University (1994) and Ph.D., Economics, Southern Methodist University (1994).

107 Dr Unni prepared two reports. In his first report he addressed three questions: first, what if any impact did the announcements at the Investor Day Presentation of the target to reduce Scope 1 and Scope 2 absolute emissions by 26‐30% by 2030 from a 2020 baseline, a target of net zero Scope 1 and Scope 2 absolute emissions by 2040 and the Net Zero Roadmap (together Target Information) have on the price of Santos’ shares; secondly, what if any impact did the restatement of the Target Information in the 2020 Annual Report and the 2021 Climate Change Report and/or statements made in relation to the Target Information in those reports have on the price of Santos’ shares; and thirdly, from an economic perspective why did the Target Information, when provided to the market, affect or not affect (as the case may be) the price of Santos’ shares as set out in the answers to questions 1 and 2? In his second report Dr Unni responded to aspects of Ms Parker’s evidence.

108 Dr Unni was of the opinion that neither the announcement of the Target Information on 1 December 2020 or the restatement of that information on 18 February 2021 had any impact on the stock price of Santos’ shares. Dr Unni set out the bases on which he had formed those views including by carrying out event studies which, he explains, is a methodology developed by financial economists to analyse whether an event that discloses information to market participants about a company affected the price of the company’s shares. More particularly, an event study examines the returns on a company’s shares (i.e. percentage change in share price from one day to the next) and identifies how much of the return is attributable to the events in issue, after controlling for other factors influencing the share price on the same day.

109 The event study for 1 December 2020 showed that:

(1) the market index increased by 1.08%;

(2) the industry index declined by -0.08%;

(3) based on the historical relationship between Santos and the market and industry indices, the predicted return for Santos was -0.57%;

(4) by close of trade on 1 December 2020 Santos’ share price increased by 0.81%; and

(5) since the predicted return on 1 December 2020 was -0.57%, the abnormal return was 1.38% (0.81% - (-0.57%)), which was not statistically significant under the terms provided by the event study model.

110 An event study was undertaken for 18 February 2021 on two bases: one by reference to the ASX200 and the ASX200 Energy and the other with those same indices but removing two companies: Origin Energy; and Woodside. Those event studies showed abnormal returns of 3.16% and 2.36% respectively. Once again, those returns were not statistically significant.

111 Dr Unni was cross-examined about the event study as at 1 December 2020. He had the following exchange with senior counsel for the ACCR, Mr Hutley SC:

Mr Hutley: Yes. Now, there’s a table there. And that records your event study analysis for 1 December 2020, is that correct?

Dr Unni: That is correct, yes.

Mr Hutley: And your model predicted that Santos’ shares would decrease by 0.057 per cent – 0.57 per cent, I’m sorry?

Dr Unni: Yes, that is correct.

Mr Hutley: But in fact, the shares went up by 0.81 per cent, is that correct?

Dr Unni: The shares went up by 0.81 per cent

…

Mr Hutley: Therefore, you observed an abnormal return on that date, of 1.38 per cent?

Dr Unni: Yes, that is correct.

Mr Hutley: However, your view is that this return was not statistically significant, under the test provided by the event study model, correct?

Dr Unni: Yes, that’s right.

Mr Hutley: And that is because it was less than 1.96 per cent, correct?

Dr Unni: That is because the figure described in this chart as the: T statistic Was less than 1.96.

Mr Hutley: Quite. And that meant that you could not exclude, to a 95 per cent degree of confidence level, that the abnormal return you observed was caused by factors other than the release of the information by the company. Is that correct?

Dr Unni: Yes, that’s correct.

Mr Hutley: It may have been caused by the release of the information by the company, if the company released fresh information. But you can’t tell, because it may have been caused by other factors, correct?

Dr Unni: This abnormal return is within a range of fluctuations that one observes, even on days without any news released by the company. And so, we don’t have an objective basis to conclude that this return was attributable to the release of news.

Mr Hutley: Quite. So what you’re saying – it may have been, but you can’t say whether it was, or it wasn’t, because it may have been caused by what you call ordinary fluctuations, correct?

Dr Unni: I think a more precise statement would be that I had no basis to say that it was caused by the news.

Mr Hutley: You had no basis to say it wasn’t, also, correct?

Dr Unni: The nature of the hypothesis being tested here, is whether we have a basis to know that this news – this price was – reaction was caused by information. And so that’s

Mr Hutley: Yes?

Dr Unni: the reason I’m – that I’m reporting the test of that hypothesis. Yes.

Mr Hutley: Now would you address my question, if you would be so kind. You have no basis for saying it wasn’t caused by the release of the information, have you?

Dr Unni: I have no basis to identify any particular causal factor for this fluctuation. Yes.

Mr Hutley: So is the answer to my question “yes”?

Dr Unni: To – yes, to the extent it’s consistent with what I said. Yes

112 In relation to the event study carried out for 18 February 2021 Dr Unni accepted in cross-examination that there was an abnormal return, but he could not say one way or the other whether that was caused by the release of the information he was studying.

113 The effect of Dr Unni’s evidence was that any movement in the Santos share price was small, i.e. not statistically significant, and, in effect, the cause of the movement was not known. That result and Dr Unni’s evidence based on the event studies, namely that there was no meaningful change in the share price at the time of the announcement, was consistent with analysts’ commentary at the time which Dr Unni also examined.

114 The ACCR submits that I would give limited weight to Dr Unni’s evidence because he is not an expert in disclosures of the type in question in this case and, ultimately, he accepted that he could not say one way or the other whether the share price movement was or was not caused by the release of the relevant information. I do not accept that Dr Unni does not have the expertise to give the evidence he gave in the context of this case nor do I accept that his evidence should be given limited weight for the reasons given by the ACCR. Dr Unni answered the questions about the result of the event studies and how they are to be understood thoughtfully and frankly. I have referred above to the effect of his evidence. Ultimately the question of the role of and weight to be given to Dr Unni’s evidence is dependent on its relevance to, and what assistance, if any, it provides, in the resolution of the questions before the Court.

115 The parties also relied on joint expert reports which were prepared following conferral between the parties’ independent experts identifying the matters upon which the experts agree and disagree. Joint reports were provided by:

(1) Mr Grant and Mr Snow;

(2) Associate Professor Meinshausen, Professor Cook and Mr Snow;

(3) Associate Professor Beck and Mr Snow;

(4) Ms Parker and Mr Snow;

(5) Mr Martin and Mr Snow; and

(6) Ms Parker and Professor Collis.

1.2 Some background

116 Before proceeding further, it is convenient, in order to understand the evidence and to put it and the representations in context, to set out the prevailing policy backdrop, some background about Santos, the nature of the production of natural gas and the process and purpose of CCS.

1.2.1 The Paris Agreement

117 The United Nations Framework Convention on Climate Change (UNFCCC) Paris Agreement 2015 (Paris Agreement) entered into force in Australia and globally in 2016. It establishes both temperature and emission goals to address climate change. The objective of the Paris Agreement is set out in Art 2.1 which relevantly provides:

1 This Agreement, in enhancing the implementation of the Convention, including its objective, aims to strengthen the global response to the threat of climate change, in the context of sustainable development and efforts to eradicate poverty, including by:

(a) Holding the increase in the global average temperature to well below 2°C above pre-industrial levels and pursuing efforts to limit the temperature increase to l .5°C above pre-industrial levels, recognizing that this would significantly reduce the risks and impacts of climate change;

(b) Increasing the ability to adapt to the adverse impacts of climate change and foster climate resilience and low greenhouse gas emissions development, in a manner that does not threaten food production; and

(c) Making finance flows consistent with a pathway towards low greenhouse gas emissions and climate-resilient development.

…

118 Article 4 of the Paris Agreement requires all parties to prepare, communicate and maintain nationally determined contributions aimed at reducing emissions so that GHG emissions reach net zero in the second half of this century (i.e. 2050 or later). Article 4 of the Paris Agreement relevantly provides:

1. In order to achieve the long-term temperature goal set out in Article 2, Parties aim to reach global peaking of greenhouse gas emissions as soon as possible, recognizing that peaking will take longer for developing country Parties, and to undertake rapid reductions thereafter in accordance with best available science, so as to achieve a balance between anthropogenic emissions by sources and removals by sinks of greenhouse gases in the second half of this century, on the basis of equity, and in the context of sustainable development and efforts to eradicate poverty.

2. Each Party shall prepare, communicate and maintain successive nationally determined contributions that it intends to achieve. Parties shall pursue domestic mitigation measures, with the aim of achieving the objectives of such contributions.

3. Each Party’s successive nationally determined contribution will represent a progression beyond the Party’s then current nationally determined contribution and reflect its highest possible ambition, reflecting its common but differentiated responsibilities and respective capabilities, in the light of different national circumstances.

4. Developed country Parties should continue taking the lead by undertaking economy-wide absolute emission reduction targets. Developing country Parties should continue enhancing their mitigation efforts, and are encouraged to move over time towards economy-wide emission reduction or limitation targets in the light of different national circumstances.

…

13. Parties shall account for their nationally determined contributions. In accounting for anthropogenic emissions and removals corresponding to their nationally determined contributions, Parties shall promote environmental integrity, transparency, accuracy, completeness, comparability and consistency, and ensure the avoidance of double counting, in accordance with guidance adopted by the Conference of the Parties serving as the meeting of the Parties to this Agreement.

…

119 Article 6 relevantly provides:

1. Parties recognize that some Parties choose to pursue voluntary cooperation in the implementation of their nationally determined contributions to allow for higher ambition in their mitigation and adaptation actions and to promote sustainable development and environmental integrity.

2. Parties shall, where engaging on a voluntary basis in cooperative approaches that involve the use of internationally transferred mitigation outcomes towards nationally determined contributions, promote sustainable development and ensure environmental integrity and transparency, including in governance, and shall apply robust accounting to ensure, inter alia, the avoidance of double counting, consistent with guidance adopted by the Conference of the Parties serving as the meeting of the Parties to this Agreement.

3. The use of internationally transferred mitigation outcomes to achieve nationally determined contributions under this Agreement shall be voluntary and authorized by participating Parties.

4. A mechanism to contribute to the mitigation of greenhouse gas emissions and support sustainable development is hereby established under the authority and guidance of the Conference of the Parties serving as the meeting of the Parties to this Agreement for use by Parties on a voluntary basis. It shall be supervised by a body designated by the Conference of the Parties serving as the meeting of the Parties to this Agreement, and shall aim:

(a) To promote the mitigation of greenhouse gas emissions while fostering sustainable development;

(b) To incentivize and facilitate participation in the m1t1gation of greenhouse gas emissions by public and private entities authorized by a Party;

(c) To contribute to the reduction of emission levels in the host Party, which will benefit from mitigation activities resulting in emission reductions that can also be used by another Party to fulfil its nationally determined contribution; and

(d) To deliver an overall mitigation in global emissions.

5. Emission reductions resulting from the mechanism referred to in paragraph 4 of this Article shall not be used to demonstrate achievement of the host Party’s nationally determined contribution if used by another Party to demonstrate achievement of its nationally determined contribution.

…

7. The Conference of the Parties serving as the meeting of the Parties to this Agreement shall adopt rules, modalities and procedures for the mechanism referred to in paragraph 4 of this Article at its first session.

8. Parties recognize the importance of integrated, holistic and balanced non-market approaches being available to Parties to assist in the implementation of their nationally determined contributions, in the context of sustainable development and poverty eradication, in a coordinated and effective manner, including through, inter alia, mitigation, adaptation, finance, technology transfer and capacity building, as appropriate. These approaches shall aim to:

(a) Promote mitigation and adaptation ambition;

(b) Enhance public and private sector participation in the implementation of nationally determined contributions; and

(c) Enable opportunities for coordination across instruments and relevant institutional arrangements.

9. A framework for non-market approaches to sustainable development is hereby defined to promote the non-market approaches referred to in paragraph 8 of this Article.

120 Although the Paris Agreement has legal effect in Australia under international law, no Federal legislation has been enacted to create a source of rights and obligations under Australian domestic law: Minister for the Environment v Sharma [2022] FCAFC 35 at [5] (Allsop CJ, Beach and Wheelahan JJ); Pabai v Commonwealth of Australia (No 2) [2025] FCA 796 at [8] (Wigney J).

1.2.2 The TCFD

121 The TCFD is a body established by the International Bank of Settlements and comprises senior executives of major corporations from around the world. The TCFD describes its remit to be “to develop climate-related disclosures that ‘could promote more informed investment, credit [or lending], and insurance underwriting decisions’ and, in turn, ‘would enable stakeholders to understand better the concentrations of carbon-related assets in the financial sector and the financial system’s exposures to climate-related risks’”. The TCFD developed four recommendations in relation to climate related financial disclosures around four thematic areas that “represent core elements of how organisations operate”. They are: governance; strategy; risk management; and metrics and targets.

122 The 2021 Climate Change Report referenced the TCFD recommendations and was expressed to be “TCFD aligned”.

123 There is some disagreement between the parties about the scope or role of the TCFD framework. It concerns “financial filings” and “financial reporting”. For example, the TCFD “believes disclosures related to the Governance and Risk Management recommendations should be provided in annual financial filings”, “[f]or disclosures related to the Strategy and Metrics and Targets recommendations, the [TCFD] believes organizations should provide such information in annual financial filings when the information is deemed material” and “[c]ertain organizations—those in the four nonfinancial groups that have more than one billion USDE in annual revenue—should consider disclosing information related to these recommendations in other reports when the information is not deemed material and not included in financial filings”.

124 Ms Parker suggested that financial disclosure was one of “four different pillars of disclosure” in the TCFD. I do not accept that evidence. The four “pillars” of the TCFD are as set out above. It is clear on a review of the TCFD framework document each “pillar” concerns financial disclosure.

1.2.3 Santos’ operations

125 As set out above, Santos in a leading producer and supplier of natural gas in Australia.

126 Santos’ operations were organised around five core asset hubs:

(1) Cooper Basin in northeast South Australia and southwest Queensland;

(2) Queensland and NSW;

(3) PNG;

(4) Northern Australia and Timor-Leste; and

(5) Western Australia (WA).

1.2.4 Natural gas

127 The parties were agreed about the following properties in relation to the production, use and emissions of and from natural gas.

128 The production and end use of natural gas involves the release of greenhouse gases, mostly CO2 as well as methane (CH4), into the atmosphere. The emission of CO2 and CH4, together with nitrous oxide (N2O), into the earth’s atmosphere, contributes to the harms associated with the impacts of climate change, otherwise known as anthropogenic climate change.

129 A company’s GHG emissions can be classified into three “scopes”:

(1) Scope 1 emissions are direct emissions from a company’s activities;

(2) Scope 2 emissions are indirect emissions from the generation of energy purchased or acquired by the company; and

(3) Scope 3 emissions are all indirect emissions (not included in Scope 2) that occur in a company’s value chain but are not directly owned or controlled by a company, including both upstream and downstream emissions.

130 Reduction of Scope 1 and 2 emissions reduces the amount of GHG emissions released into the atmosphere. If CCS is used successfully to capture and permanently store Scope 1 emissions, it reduces the amount of Scope 1 emissions that a company releases into the atmosphere.

131 Emissions are reported in units of CO2 equivalent (CO2e) in order to take into account the warming effects of different types of GHGs. This is achieved by assigning each GHG a global warming potential (GWP) relative to the warming potential of CO2. Therefore, CO2 has a GWP of 1. Over a 100-year time period, CH4 has a GWP of 28. Over a 20-year time period, it has a GWP of 86.

132 During the lifecycle of natural gas, GHGs can be released into the atmosphere due to:

(1) a process known as venting, which involves the deliberate release of gases into the atmosphere as part of the gas production process. The main source of venting for many gas processing facilities around the world is CO2 that is removed from an unprocessed gas stream;

(2) a process known as flaring, which involves waste gases containing hydrocarbons being combusted, releasing gases into the atmosphere;

(3) the combustion of fossil fuels to provide energy, for example, to generate electricity or compress gas; and

(4) fugitive emissions, which are the unintentional release of GHGs into the atmosphere, such as through leaks.

133 The quantum of GHG emissions associated with the lifecycle of natural gas varies depending on a range of factors including extraction approach, raw gas composition, processing technologies, transportation methods and end use.