FEDERAL COURT OF AUSTRALIA

Australian Securities and Investments Commission v BPS Financial Pty Ltd (Penalty) [2026] FCA 18

File number(s): | QUD 380 of 2022 |

Judgment of: | DOWNES J |

Date of judgment: | 27 January 2026 |

Catchwords: | CONSUMER LAW – established contraventions of s 911A(1) and s 911A(5B) Corporations Act 2001 (Cth) – whether defendant should be relieved from liability pursuant to s 1317S Corporations Act – established contraventions of s 12DA(1) and s 12DB(1) Australian Securities and Investments Commission Act 2001 (Cth) – where defendant carried on a financial services business in issuing a financial product, and providing financial product advice in relation to that product, without being licensed – where defendant made attempts to comply with the law – where financial product was called the Qoin Wallet which allowed user to make non-cash payments using Qoin Tokens or Qoin – where defendant made false or misleading representations on its website and in a White Paper available on its website – where no direct evidence that any consumer relied on the representations and suffered loss or damage – dispute as to quantum of penalty to be imposed – corrective advertising ordered – injunctive relief granted STATUTORY INTERPRETATION – meaning of “benefit” in s 1317G(f)(b) Corporations Act – whether “benefit” means revenue or profit – meaning of “benefit derived” |

Legislation: | Australian Securities and Investments Commission Act 2001 (Cth) ss 12DA(1), 12DB, 12GBCA(2) Corporations Act 2001 (Cth) ss 763A, 911A, 1101B(1), 1317G(4), 1317S, 1324(1) Criminal Code Act 1995 (Cth) s 70.2(5) |

Cases cited: | Australian Competition and Consumer Commission v BlueScope Steel Ltd (No 6) [2023] FCA 1029 Australian Competition and Consumer Commission v High Adventure Pty Ltd (2006) ATPR 42-091; [2005] FCAFC 247 Australian Competition and Consumer Commission v Hillside (Australia New Media) Pty Ltd trading as Bet365 (No 2) [2016] FCA 698 Australian Securities and Investments Commission v Bit Trade Pty Ltd (No 2) [2024] FCA 1422 Australian Securities and Investments Commission v BPS Financial Pty Ltd [2024] FCA 457 Australian Securities and Investments Commission v BPS Financial Pty Ltd (2025) 309 FCR 542; [2025] FCAFC 74 Australian Securities and Investments Commission v Cassimatis (No 8) (2016) 336 ALR 209; [2016] FCA 1023 Australian Securities and Investments Commission v Ferratum Australia Pty Ltd (in liq) (No 2) [2024] FCA 701 Australian Securities and Investments Commission v Firstmac Limited (Penalty Hearing) [2025] FCA 12 Australian Securities and Investments Commission v Healey (No 2) (2011) 196 FCR 430; [2011] FCA 1003 Australian Securities and Investments Commission v La Trobe Financial Asset Management Ltd (2021) 158 ACSR 363; [2021] FCA 1417 Australian Securities and Investments Commission v Web3 Ventures Pty Ltd (Penalty) [2024] FCA 578 Director of Consumer Affairs Victoria v Hocking Stuart (Richmond) Pty Ltd [2016] FCA 1184 Flight Centre Ltd v Australian Competition and Consumer Commission (No 2) (2018) 260 FCR 68; [2018] FCAFC 53 Gould v Vaggelas (1985) 157 CLR 215 I & L Securities Pty Ltd v HTW Valuers (Brisbane) Pty Ltd (2002) 210 CLR 109; [2002] HCA 41 Its Eco Pty Ltd v BPS Financial Limited (Settlement Approval) [2025] FCA 545 R v Jacobs Group (Australia) Pty Ltd (2023) 280 CLR 170; [2023] HCA 23 Singtel Optus Pty Ltd v Australian Competition and Consumer Commission (2012) 287 ALR 249; [2012] FCAFC 20 |

Division: | General Division |

Registry: | Queensland |

National Practice Area: | Commercial and Corporations |

Sub-area: | Commercial Contracts, Banking, Finance and Insurance |

Number of paragraphs: | 180 |

Date of hearing: | 20–21 November 2025 |

Counsel for the Plaintiff: | Mr M Brady KC with Mr R Strong |

Solicitor for the Plaintiff: | Australian Securities and Investments Commission |

Counsel for the Defendant: | Ms S McLeod |

Solicitor for the Defendant: | NXT Legal |

ORDERS

QUD 380 of 2022 | ||

BETWEEN: | AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff | |

AND: | BPS FINANCIAL PTY LTD (ACN 604 899 381) Defendant | |

order made by: | DOWNES J |

DATE OF ORDER: | 27 january 2026 |

THE COURT ORDERS THAT:

PENAL NOTICE

TO: BPS FINANCIAL PTY LTD (ACN 604 899 381)

IF YOU (BEING THE PERSON BOUND BY THIS ORDER):

(A) REFUSE OR NEGLECT TO DO ANY ACT WITHIN THE TIME SPECIFIED IN THIS ORDER FOR THE DOING OF THE ACT; OR

(B) DISOBEY THE ORDER BY DOING AN ACT WHICH THE ORDER REQUIRES YOU NOT TO DO;

YOU WILL BE LIABLE TO IMPRISONMENT, SEQUESTRATION OF PROPERTY OR OTHER PUNISHMENT.

ANY OTHER PERSON WHO KNOWS OF THIS ORDER AND DOES ANYTHING WHICH HELPS OR PERMITS YOU TO BREACH THE TERMS OF THIS ORDER MAY BE SIMILARLY PUNISHED.

THE COURT ORDERS THAT:

Pecuniary Penalties

1. Within 7 days, the parties are to confer and provide to the chambers of Downes J an agreed form of order giving effect to the reasons for judgment concerning the payment of pecuniary penalties and any agreed payment instalment plan.

2. If the parties are unable to agree upon a form of order:

(a) the parties shall each provide their proposed draft of the same to the chambers of Downes J within 10 days accompanied by any written submissions not exceeding three (3) pages and the form of order will be determined on the papers;

(b) the date on which the order is made concerning the payment of pecuniary penalties and any agreed payment instalment plan is described in this Order and Annexure A to this Order as the ‘penalty order’.

Injunctions

3. Pursuant to section 12GD(1) of the Australian Securities and Investments Commission Act 2001 (Cth) (‘ASIC Act’), the defendant (‘BPS’) is permanently restrained from contravening section 12DB of the ASIC Act by making any false or misleading representation, in written statements:

(a) concerning the number of holders of the Qoin Wallet (‘Qoin Wallet Holders’), including the number of Qoin Wallet Holders who have advised BPS that they are willing to accept full or part payment for goods and services via Qoin;

(b) concerning the ability of Qoin Tokens to be exchanged for fiat or other crypto-assets using the Qoin Wallet; and

(c) that the Qoin Wallet has been officially approved and/or officially registered.

4. Pursuant to section 1101B(1) and section 1324 of the Corporations Act 2001 (Cth), BPS is restrained for a period of 10 years from the date of this Order from carrying on a financial services business in this jurisdiction without holding an Australian financial services licence, except as permitted by the Corporations Act.

Adverse publicity orders

5. Pursuant to section 1101B of the Corporations Act and section 12GLB of the ASIC Act, BPS take the following steps:

(a) within 14 days of the date of the penalty order being made, send correspondence to the operator of the website https://qoin.com (‘Qoin Website’) enclosing a copy of these Orders and the associated judgment and request that the operator of the Qoin Website cause a copy of the notice in the form of Annexure A to this Order (the ‘Notice’) to be published on the Qoin Website such that:

(i) the Notice shall be viewable by clicking a ‘click through’ banner located on the Qoin Website;

(ii) the ‘click-through’ banner is to be:

A. located in the top half of the Qoin Website; and

B. not obscured, blocked or interfered with by any operation of the Qoin Website, other than during periods of IT outages or maintenance;

(iii) the ‘click-through’ banner shall contain the words “Notice ordered by the Federal Court of Australia – unlicensed conduct and false or misleading representations” in at least size 12, bold, black and sans-serif font centred on a white background;

(iv) the ‘click-through’ banner is to operate in the form of a one-click hyperlink to the Notice;

(v) the Notice shall occupy the entire webpage that is accessed via the ‘click-though’ banner;

(vi) the Notice shall be in size 12, bold, black and sans-serif font that is on a white background and in a black bordered box;

(vii) the ‘click-through’ banner is to remain on the Qoin Website for a period of no less than 90 days;

(viii) the Qoin Website is to be maintained or otherwise kept active for the period during which the Notice is required to remain on the Qoin Website, other than during periods of IT outages or maintenance; and

(ix) the Qoin Website shall not have in place any mechanism which would preclude search engines from indexing the pages or scanning the pages for links to follow.

(b) within 28 days of the date of the penalty order being made, file and serve an affidavit enclosing a copy of the correspondence referred to in Order 5(a) confirming that the correspondence was sent, together with any response.

6. Pursuant to section 1101B of the Corporations Act and section 12GLB of the ASIC Act, within 14 days of the date of the penalty order being made, BPS is to publish, or cause to be published, the Notice on the Qoin Wallet App such that:

(a) the Notice shall be viewable by accessing a link displayed in a ‘pop-up message’ appearing in the Qoin Wallet App after a person has opened the Application;

(b) the ‘pop-up message’ shall contain the words “Notice ordered by the Federal Court of Australia – unlicensed conduct and false or misleading representations – tap here for more information about an important recent Federal Court decision. No action is required’;

(c) the ‘pop-up message’ is to operate in the form of a one-click hyperlink to the Notice; and

(d) the ‘pop-up message’ is to display in the Qoin Wallet App a period of no less than 90 days from the date that the Notice is first published on the Qoin Wallet App.

7. Subject to Order 8 below, BPS pay 90% of the plaintiff’s costs of the proceeding up to and including 3 May 2024, and the plaintiff’s costs after 3 May 2024, all such costs to include reserved costs but excluding any costs of the appeal in proceeding QUD 331 of 2024, with all such costs to be assessed on the standard basis if not agreed.

8. BPS be entitled to set-off the amount it is entitled to claim against the plaintiff by way of costs thrown away pursuant to paragraph 6 of the Orders made on 21 June 2023 (to be assessed if not agreed) against the amount payable to the plaintiff pursuant to Order 7 above.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ANNEXURE A

ADVERSE PUBLICITY NOTICE

The Federal Court of Australia has ordered BPS Financial Pty Ltd (ACN 604 899 381) (BPS) to publish this notice.

Following action by the Australian Securities and Investments Commissions (ASIC), on 22 May 2024, the Federal Court of Australia declared that:

Between 30 January 2020 and 4 November 2020 and between 1 September 2021 to 19 October 2023, BPS carried on a financial services business by dealing in a financial product and providing financial product advice without holding an Australian Financial Services Licence.

Between 30 January 2020 and 21 November 2021, BPS represented in trade and commerce in connection with the promotion and supply of financial services that a person who purchased Qoin could be confident that, if and when they wished to do so, they would be able to exchange Qoin that they held for fiat currency through independent exchanges (the Fiat Trade Representation), which was false or misleading as to the performance characteristics, uses or benefits of the Qoin Wallet.

Between 30 January 2020 and 20 July 2023, BPS represented in trade and commerce in connection with the promotion and supply of financial services that a person who purchased Qoin could be confident that, if and when they wished to do so, they would be able to exchange Qoin that they held for other crypto-assets through independent exchanges (the Crypto Trade Representation), which was false or misleading as to the performance characteristics, uses or benefits of the Qoin Wallet.

Between 8 October 2021 and 24 October 2022, BPS represented in trade and commerce in connection with the promotion and supply of financial services that Qoin could be used to purchase goods and services from an increasing number of Qoin Merchants (the Merchant Growth Representation) which was false and misleading as to the performance characteristics, uses or benefits of the Qoin Wallet.

Between 30 January 2020 and 24 October 2022, BPS represented in trade and commerce in connection with the promotion and supply of financial services that the Qoin Wallet had been officially approved and/or officially registered (the Approval / Registration Representation), which was false and misleading.

Following an appeal by ASIC on 30 May 2025, the Full Court of the Federal Court of Australia, declared that between 5 November 2020 and 30 August 2021, BPS carried on a financial services business by dealing in a financial product and providing financial product advice without holding an Australian Financial Services Licence.

As a consequence, the Federal Court has found that, between 30 January 2020 and 19 October 2023, BPS carried on a financial services business by dealing in a financial product and providing financial product advice without holding an Australian Financial Services Licence (Unlicensed Conduct).

On 27 January 2026, the Federal Court determined that BPS should pay total pecuniary penalties of $14 million to the Commonwealth for engaging in the Unlicensed Conduct and making the Fiat Trade, Crypto Trade, Merchant Growth and Approval / Registration Representations.

On 27 January 2026, the Federal Court ordered that BPS be restrained from:

carrying on a financial services business without an appropriate Australian Financial Services Licence for a period of 10 years.

further making the Fiat Trade, Crypto Trade, Merchant Growth or Approval / Registration Representations.

Further information

BPS’s conduct contravened the following financial services laws:

sections 911A(1) and 911A(5B) of the Corporations Act 2001 (Cth); and

sections 12DA and 12DB of the Australian Securities and Investments Commission Act 2001 (Cth).

For further information about the conduct, see the following links:

Justice Downes’ judgment of 3 May 2024 [https://www.judgments.fedcourt.gov.au/judgments/Judgments/fca/single/2024/2024fca0457]; [to be hyperlinked]

The Full Federal Court’s judgment of 30 May 2025 [https://www.judgments.fedcourt.gov.au/judgments/Judgments/fca/full/2025/2025fcafc0074]; [to be hyperlinked]

Justice Downes’ judgment of 27 January 2026 [to be hyperlinked]

ASIC’s media release of [insert date of media release] [to be hyperlinked].

REASONS FOR JUDGMENT

DOWNES J:

Synopsis

1 From January 2020 until mid-2023 the defendant, BPS Financial Pty Ltd (BPS) engaged in serious and unlawful misconduct. During that period, without holding an Australian Financial Services Licence (AFSL), BPS carried on a financial services business in the course of which it issued a non-cash payment facility called the Qoin Wallet and provided financial product advice in relation to that product. BPS also published false and misleading representations about the ability of Qoin Tokens to be exchanged for fiat currency and other crypto-assets, the growing number of Qoin merchants, and the official approval and registration status of the Qoin Wallet. During the same period, BPS issued more than 96,000 Qoin Wallets and derived substantial revenues totalling over $42 million from the sale of Qoin Tokens.

2 This judgment relates to the question of relief following a decision on liability which was handed down on 3 May 2024: Australian Securities and Investments Commission v BPS Financial Pty Ltd [2024] FCA 457 (Liability Judgment or LJ).

3 These reasons assume familiarity with the Liability Judgment, and I will adopt the defined terms used in it, unless indicated otherwise. The term “Qoin Wallet” is used interchangeably with the term “Qoin NCP Product” as it was used in the Liability Judgment, reflecting the finding made as to the identity of the relevant financial product (noting the parties accepted that nothing turns on this): LJ [112].

4 In summary, the critical findings in the Liability Judgment were as follows:

(1) BPS contravened ss 911A(1) and 911A(5B) of the Corporations Act, other than in relation to the period from 5 November 2020 and 30 August 2021 (being the PNI Period): LJ [205];

(2) BPS contravened ss 12DA(1) and 12DB(1) of the ASIC Act in relation to the Trade Representation, the Merchant Growth Representation and the Approval / Registration Representation: LJ [317], [360] and [397].

5 ASIC brought an appeal from the Liability Judgment, contending that BPS should also be found liable for contravention of ss 911A(1) and 911A(5B) during the PNI Period. The Full Court delivered its judgment on 30 May 2025 and upheld ASIC’s appeal: Australian Securities and Investments Commission v BPS Financial Pty Ltd (2025) 309 FCR 542; [2025] FCAFC 74 (Collier, Markovic and Shariff JJ) (Appeal Judgment or AJ).

6 In total, this Court has made seven declarations of contravention against BPS. Three of those declarations relate to contraventions of s 911A of the Corporations Act. In combination they establish that, in contravention of ss 911A(1) and 911A(5B) of the Corporations Act, BPS carried on a financial services business from 30 January 2020 to 19 October 2023 without holding an AFSL, being a business of:

(1) dealing in a financial product being the Qoin Wallet; and

(2) providing financial product advice by publishing on the Qoin Website, and in promotional material accessible to the public, statements of opinion which were intended to influence persons in making a decision in relation to the Qoin Wallet.

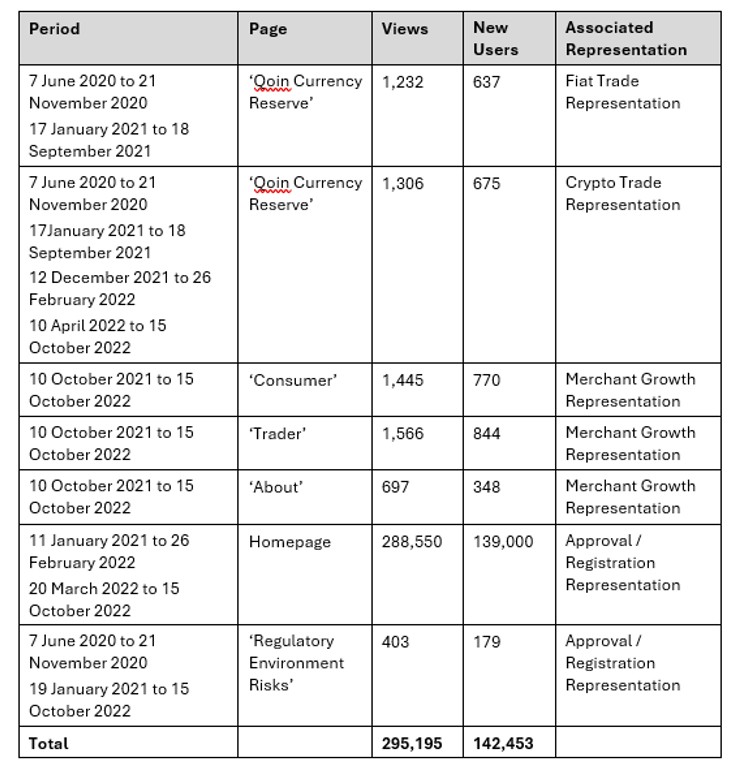

7 The remaining four declarations relate to contraventions of s 12DB of the ASIC Act. They establish that, by statements made on the Qoin Website and in promotional material available on that website during the periods specified in the first column of the table below, BPS made the representations in trade or commerce in connection with the promotion and supply of financial services set out in the second column that were false and misleading in the respects specified in the third column:

Period | Detail of Representation | Respect in which false and misleading |

30 Jan 2020 to 21 Nov 2021 | A person who purchased Qoin could be confident that, if and when they wished to do so, they would be able to exchange Qoin that they held for fiat currency through independent exchanges (the Fiat Trade Representation). | False or misleading as to the performance characteristics, uses or benefits of the Qoin NCP Product in that throughout that period: (a) it was not possible to exchange Qoin for fiat currency on any independent exchange; (b) in so far as the Fiat Trade representation was a representation as to a future matter, BPS did not have reasonable grounds for making that representation. |

30 Jan 2020 to 20 July 2023 | A person who purchased Qoin could be confident that, if and when they wished to do so, they would be able to exchange Qoin that they held for other crypto-assets through independent exchanges (the Crypto Trade Representation). | False or misleading as to the performance characteristics, uses or benefits of the Qoin NCP Product in that throughout that period: (a) it was not possible to exchange Qoin for other crypto-assets on any independent exchange; and (b) in so far as the Crypto Trade Representation was a representation as to a future matter, BPS did not have reasonable grounds for making that representation. |

8 Oct 2021 to 24 October 2022 | Qoin could be used to purchase goods and services from an increasing number of Qoin Merchants (being the Merchant Growth Representation). | False and misleading as to the performance characteristics, uses or benefits of the Qoin NCP Product in that the number of Qoin Merchants was in an overall and persistent state of decline from 8 October 2021. |

30 Jan 2020 to 24 Oct 2022 | The Qoin NCP Product had been officially approved and/or officially registered (being the Approval/Registration Representation). | False and misleading as to: (a) the standard, quality, value and grade of the Qoin NCP Product; (b) the approval or benefits of the Qoin NCP Product, in that the Qoin NCP Product was not a product that had been officially approved or officially registered. |

8 The central issue which remains to be determined is the quantum of the civil penalty to be imposed on BPS, which can be divided into the following sub-issues:

(1) whether BPS should be relieved of liability for the claims proven as part of the Unlicensed Conduct Case pursuant to s 1317S of the Corporations Act;

(2) if the answer to (1) is “no”, the quantum of any penalty for the claims proven as part of the Unlicensed Conduct Case against BPS; and

(3) the quantum of any penalty for the claims proven as part of the Misleading Conduct Case against BPS.

9 By way of overview, ASIC’s position is that BPS should not be relieved of liability for the Unlicensed Conduct Contravention and it should be ordered to pay total pecuniary penalties of $21 million, whereas BPS’s position is that it should be relieved of liability in relation to the Unlicensed Conduct Case (or that no penalty be imposed) and that it should be ordered to pay total pecuniary penalties of $600,000.

10 For the following reasons, I have determined that BPS should not be relieved from liability to pay any pecuniary penalty in relation to the Unlicensed Conduct Contravention and that an appropriate total pecuniary penalty to be paid by BPS in this case is the amount of $14 million. I have also determined it to be appropriate to order relief in the form of injunctions and corrective advertising substantially in the terms proposed by the parties, and to impose a slight discount on the costs order made in favour of ASIC and to exclude the costs of the appeal.

11 As the parties agreed that they should be given an opportunity to confer, or failing agreement to provide written submissions, as to the appropriate form of orders giving effect to the pecuniary penalty as found in these reasons and payment of it by way of an instalment plan, I will make such orders. Because this will have the consequence that the date of the Order containing the penalty is not yet known, I have modified the proposed orders relating to the corrective advertising and the wording of Annexure A to reflect this fact. I have also made other minor amendments.

Should BPS be relieved of liability for the unlicensed conduct under s 1317S?

12 Section 1317S of the Corporations Act relevantly provides as follows:

(1) In this section:

“eligible proceedings”:

(a) means proceedings for a contravention of a civil penalty provision (including proceedings under section 588M, 588W, 961M, 1317GA, 1317GB, 1317H, 1317HA, 1317HB, 1317HC or 1317HE); and

(b) does not include proceedings for an offence (except so far as the proceedings relate to the question whether the court should make an order under section 588K, 1317H, 1317HA, 1317HB, 1317HC or 1317HE).

(2) If:

(a) eligible proceedings are brought against a person; and

(b) in the proceedings it appears to the court that the person has, or may have, contravened a civil penalty provision but that:

(i) the person has acted honestly; and

(ii) having regard to all the circumstances of the case (including, where applicable, those connected with the person's appointment as an officer, or employment as an employee, of a corporation or of a Part 5.7 body), the person ought fairly to be excused for the contravention;

the court may relieve the person either wholly or partly from a liability to which the person would otherwise be subject, or that might otherwise be imposed on the person, because of the contravention.

13 Section 911A(5B) is a civil penalty provision: s 1317E. Accordingly, the Unlicensed Conduct Case is an eligible proceeding for the purpose of s 1317S.

14 Section 1317S operates as a dispensing power to excuse the contravener of the liability resulting from the finding of contravention: Australian Securities and Investments Commission v Healey (No 2) (2011) 196 FCR 430; [2011] FCA 1003 at [86], [94] (Middleton J). It does not operate to remove the contravention itself: Healey (No 2) at [86].

15 Section 1317S involves three stages of inquiry: Healey (No 2) at [84]. They are:

(1) whether the applicant has acted honestly;

(2) whether the applicant ought fairly to be excused in all the circumstances; and

(3) whether the applicant be relieved from liability wholly or in part.

Did BPS act honestly?

16 The first stage of the inquiry requires the court to be positively satisfied that the applicant has acted honestly and, therefore, a mere absence of dishonesty is insufficient: Healey (No 2) at [87]. A person acts honestly if their conduct is without moral turpitude in the sense that it is without deceit or conscious impropriety, without intent to gain an improper benefit or advantage, and without carelessness or imprudence that negates the performance of the duty in question: Healey (No 2) at [88]. The final element was interpreted by Jackman J in Australian Securities and Investments Commission v Web3 Ventures Pty Ltd (Penalty) [2024] FCA 578 at [7] as meaning “without carelessness or imprudence to such a degree as to demonstrate that no genuine attempt at all has been made to comply with the duty”.

17 BPS began to develop the idea of the Qoin Project in mid-to-late 2019. At that time, its director, Mr Wiese, formed the view that the relevant regulations, laws and licensing requirements were very complex and, accordingly, he decided to obtain legal advice from HWL Ebsworth (HWLE) to ensure that the Qoin Project was fully compliant.

18 On or around 17 October 2019, BPS obtained a written advice from Mr Anastas, a partner at HWLE who specialises in financial services, about the relevant regulatory framework. Mr Wiese understood from that advice that, to the extent that the Qoin Project would involve providing a non-cash payment facility, this would constitute the provision of a financial service for the purposes of the Corporations Act and, therefore, would need to be properly licensed.

19 At the same time, Mr Anastas also provided oral advice to Mr Wiese and Mr Quinn, Bartercard’s Risk and Compliance Manager, that given the unclear state of the law in relation to cryptocurrency, it may be useful to try to engage directly with ASIC to get an understanding of its views on the subject.

20 On 4 November 2019, via teleconference, Mr Wiese, Mr Quinn and Mr Anastas met with Mr McMahon, a Senior Manager at ASIC, to discuss regulation. During that meeting, Mr Wiese and Mr Anastas outlined the business of the Qoin Project, including the proposed issue of Qoin Wallets and how they would function, and explained that Bartercard intended to apply for an AFSL to cover the provision of financial services associated with the product, but understood that this could take some time. Although it was made clear that he could not provide advice, Mr McMahon outlined that it was potentially permissible for BPS to rely on the intermediary authorisation exemption in the interim before being granted an AFSL. Mr Wiese took away from that discussion that, while it waited for ASIC to process its AFSL, it would be possible for BPS to issue Qoin Wallets under an intermediary authorisation, provided it was compliant.

21 On 4 December 2019, BPS received from HWLE a template agreement for use in respect of both the Intermediary Authorisation and Corporate Authorised Representative Arrangements.

22 On 10 December 2019, BPS received advice from Mr Anastas about:

…the separate obligations that will apply to BPS Financial Limited (BPS) and Billzy Pty Ltd (Wallet Provider) (together, parties) in respect of the proposed Wallet and Payment Facility (together, facilities). …

The parties will be required to satisfy certain financial services obligations in respect of the Payment Facility. In particular:

(a) in order for BPS to issue the Payment Facility:

(i) BPS will be required to hold an appropriate Australian financial services licence (AFSL) or enter into an appropriate intermediary authorisation arrangement with an appropriate AFSL holder for BPS to issue the Payment Facility to consumers; and

(ii) BPS will be required to prepare and (through the Wallet Provider) provide a Product Disclosure Statement in respect of the Payment Facility; and

(b) in order for both parties to promote the Payment Facility (assuming both the Wallet Provider and BPS will promote the Payment Facility):

(i) BPS will be required to hold an appropriate AFSL or enter into an authorised representative arrangement with an appropriate AFSL holder to provide general advice in respect of the Payment Facility; and

(ii) the Wallet Provider, and BPS (as authorised representative of an appropriate AFSL holder), will be required to prepare and provide a Financial Services Guide in respect of its financial services.

(Emphasis in original.)

23 On or around 16 December 2019, BPS entered the First Billzy AR Agreement and the First Billzy Intermediary Agreement with Billzy, the holder of an AFSL with authorisation to deal in non-cash payment facilities. Billzy required that its versions of the agreements be used. BPS paid Mr Banks of Billzy, through his company PNI, and his solicitors, MLC Legal, to draft those agreements. In total, BPS paid Mr Banks $38,500 for his services.

24 Mr Wiese was satisfied that the arrangements described in the advice from HWLE on 10 December 2019 was consistent with what was being proposed by Mr Banks.

25 In mid-2020, Mr Wiese became aware of social media posts criticising the Qoin Project and making various allegations about its compliance with financial services laws. In response, BPS engaged HWLE in June 2020 and October 2020 to advise whether Qoin was a derivative and whether the Qoin Project complied with the relevant laws and regulations.

26 On 13 October 2020, BPS lodged its application for an AFSL, with the assistance of HWLE.

27 In total, the fees paid by BPS to HWLE for advice and assistance between September 2019 and October 2020 in relation to regulatory compliance issues was approximately $66,903.95.

28 In around October 2020, Mr Wiese was informed that:

(1) Billzy had been approached for a commercial transaction with a possible consequence that Billzy may not be able to authorise BPS beyond the initial 12-month period provided for under the First Billzy Arrangement; and

(2) Mr Holmes had spoken to Mr Banks, who was the director of PNI, and Mr Banks had advised Mr Holmes that PNI was willing to authorise BPS to continue issuing and providing financial advice in relation to the Qoin Wallet on materially the same commercial terms as had been agreed between BPS and Billzy.

29 BPS paid Mr Banks (through PNI) a further $3,850 for the preparation of the PNI AR Agreement.

30 On around 4 November 2020, BPS entered the PNI AR Agreement.

31 In around mid-March 2021, Mr Wiese was told by Mr Quinn that he had been informed by Mr Anastas that ASIC was investigating BPS.

32 On or around 8 June 2021, HWLE forwarded Mr Wiese a letter received from Ms Harper of ASIC, advising that ASIC would not be able to make a decision on BPS’s AFSL application due to the ongoing investigation.

33 On or around 1 September 2021, BPS entered the Second Billzy AR Agreement and the Second Billzy Intermediary Agreement.

34 Having regard to these matters, I am satisfied that BPS acted honestly, and ASIC does not contend otherwise. There is no evidence of deceit or conscious impropriety, nor intent to gain an improper benefit or advantage. In light of the legal advice obtained by BPS and its engagement with ASIC, it also cannot be said that BPS acted carelessly or imprudently to such a degree as to demonstrate no genuine attempt to comply with s 911A.

Ought BPS fairly be excused?

35 The second stage of the inquiry requires the question of whether the applicant ought fairly to be excused be addressed having regard to all the circumstances of the case.

36 In Web3 Ventures at [13], Jackman J observed that the breadth of the expression “ought fairly be excused” is capable of incorporating reasonableness as a consideration, citing Australian Securities and Investments Commission v Cassimatis (No 8) (2016) 336 ALR 209; [2016] FCA 1023 at [810] (Edelman J).

37 In Web3 Ventures, the applicant relied on the following seven considerations as the basis for it being excused from liability under s 1317S:

(1) its contravening conduct was not a serious departure from the requirements of the Corporations Act and arose from an honest view about the application of technical legal definitions;

(2) no loss or damage was suffered by investors by reason of its contravention;

(3) the benefit obtained from the contravention was modest;

(4) its contravention arose in an uncertain regulatory environment where government bodies were unsure as to the extent to which the financial product regime of the Corporations Act applied to cryptoasset service providers;

(5) it was subject to adverse media coverage in the sense that it was unfair or incorrect;

(6) it had never previously been found by a court to have engaged in similar conduct; and

(7) it had actively engaged with key industry participants and regulators.

38 In oral submissions, BPS structured its application for relief around those seven considerations. Although it accepted that each application must be decided on its own facts, it submits that those considerations provide a useful framework to guide the Court’s analysis in this case given its factual similarities to Web3 Ventures.

39 As to the first consideration, Jackman J found at [14] that the applicant’s contravening conduct arose from an honest view about the application of technical legal definitions because it “formed the unchallenged view, after obtaining advice from a leading law firm, that there was no identified risk that the … product would breach any laws or regulations”.

40 BPS submits that it is in the same position as a result of the advice which it obtained for the following reasons.

41 First, even if it had used the template supplied by HWLE for these agreements, it would not have made any difference as that template also “contemplated an arrangement in which BPS (in different capacities) would have been both the product provider and maker of offers to arrange for the issue of the relevant financial product and, in addition, the AFSL holder would have appointed BPS as an authorised representative to both provide general financial product advice and issue non-cash payment products”.

42 Secondly, it obtained the advice from HWLE on 21 October 2020 which stated that, in HWLE’s view, BPS was compliant with financial services laws as they concerned the Qoin Project because, relevantly, “in respect of that Payment Facility (being a non-cash payment facility), BPS is authorised to … issue non-cash payment facilities to retail clients as a representative under Billzy’s AFSL” (emphasis removed.). BPS further submits that it engaged PNI to draft the agreements. It submits that the drafting was done by Mr Banks, who was qualified to provide advice on the basis that he was, as an AFSL holder, a “responsible manager” and “key person” as required by ASIC, with assistance of his solicitors, MLC Legal. BPS submits that, in these circumstances, “a lay person may reasonably have expected that if Mr Banks and his solicitors were not qualified to advise BPS about relevant regulatory requirements, he would have said so rather than charge BPS $38,500.00 for it” (emphasis in original, referring to the payment for the First Billzy AR Agreement and First Billzy Intermediary Agreement).

43 Finally, it is uncertain what further instructions it may realistically have been expected to give to its advisers in order to ensure that it obtained the advice which ASIC appears to suggest that it should have sought. It contends that “a client cannot be expected to have sufficient expertise to ask detailed and specific questions about possible nuances of statutory construction which themselves require some degree of legal knowledge and acuity to identify”. BPS submits that it is unsurprising that it did not seek specific advice about “the necessity for financial services to be provided in a representative capacity” in circumstances where the “necessity” was only established by the Appeal Judgment and that even now, there is no one clear answer to the question of whether, in circumstances where BPS always intended to the sole product issuer, an authorised representative exemption might permit it to issue the Qoin NCP Product, given that ASIC’s invitation to determine whether it is a general principle was declined in the Appeal Judgment.

44 However, these submissions do not take sufficient account of the critical findings in the Liability Judgment and the Appeal Judgment. In light of these findings, it cannot be said that there was not a serious departure by BPS from the requirements of the Corporations Act.

45 BPS was found not to be exempt during the Billzy Periods because:

(1) BPS did not provide the services of issuing the Qoin NCP Product and providing financial product advice in relation to that product as a representative of Billzy: LJ [156]–[172]. That is because:

(a) the First and Second Billzy AR Agreements restricted the financial services which BPS was authorised to provide to services in relation to financial products issued by Billzy and this did not include the Qoin Wallet;

(b) in any event, the First and Second Billzy AR Agreements did not authorise BPS to issue any financial product, but only to “arrange for a client to apply for, acquire or dispose of” such products;

(2) BPS did not provide the services of issuing the Qoin Wallet pursuant to an intermediary authorisation within the terms of the exemption under s 911A(2)(b) because that did not extend to arrangements under which the product provider referred to in sub-paragraph (ii) of that provision was also the authorised representative referred to in sub-paragraph (i). This was because the plain language of s 911A(2)(b) contemplates that the offers in sub-paragraph (i) will be made by someone other than the product provider in sub-paragraph (ii). That is because, if the authorised representative and the product provider are the same person (even if the same person but acting in different capacities), there would not be any “arrangement” or an “intermediary authorisation”. The words “arrangement” and “intermediary” connote at least two parties being involved: LJ [181]. There was no ambiguity in the provision: LJ [189];

(3) the terms of the Billzy AR Agreements did not authorise BPS to make offers to arrange the issue of a financial product: LJ [194].

46 BPS was found not to be exempt during the PNI Period because:

(1) BPS was not exempt under s 911A(2)(a) because it was not issuing the Qoin Wallet or providing financial product advice in its capacity as a representative of PNI, but was, in truth and in substance, doing so in its own right: AJ [106]–[116];

(2) the PNI AR Agreement did not record any arrangement under which PNI and its authorised representatives are to make offers to arrange the issue of the Qoin Wallet. That is to say, the agreement did not appoint PNI as intermediary as contemplated by s 911A(2)(b). The appointment of BPS as authorised representative to arrange the issue of its own product and authorisation to make offers to do so was not supported: LJ: [199]. On its face, therefore, the PNI AR Agreement did not record any arrangement or intermediary authorisation under which PNI and its authorised representatives would make offers to arrange for the issue of the Qoin NCP Product by BPS: LJ [200];

(3) in any event, the arrangement between PNI and BPS was that BPS would make offers to arrange the issue of the product by BPS. This was not an arrangement which meets the requirements of s 911A(2)(b) of the Corporations Act: LJ [201].

47 In circumstances where BPS knew that it could not lawfully carry on its intended business without an AFSL unless an exemption applied to the services it was to provide, BPS commenced and continued to carry on its business on the assumption that it was compliant with the Corporations Act by entering the agreements entered with Billzy and PNI. However, the exemptions upon which BPS sought to rely were not engaged just by entering those agreements, but on the factual circumstances applicable to each provision of a financial service said to be within the exemption. In other words, BPS could not meet its statutory obligations simply by the execution of agreement that did not reflect the reality of the arrangements between the parties. Critically, none of the legal advice obtained by BPS addressed these matters.

48 Thus, while it may be accepted that BPS did not necessarily need to use the template agreement supplied by HWLE, it was unreasonable for BPS not to have obtained independent legal advice about whether the agreements entered with Billzy and PNI were, by their terms, sufficient to bring it within the exemptions having regard to the manner in which BPS intended to operate or had been operating its business.

49 This is a significant matter which tells against relief from liability.

50 As to the second consideration, it was common ground between the parties that there was no evidence either way as to whether investors suffered loss or damage by reason of the breach. As a result, I treat this consideration as neutral.

51 As to the third consideration, BPS makes two submissions. First, it submits that the measure of the benefit obtained from its contravention should be the profit it received, rather than the revenue it generated. Secondly, it submits that, regardless of whether profit or revenue is used as the measure of the benefit, the benefit obtained by BPS was modest as compared to other cases. However, whether the appropriate measure of the benefit to BPS is by reference to revenue or profit, the benefit to BPS could not be said to be modest. That BPS made commercial decisions which reduced the benefit retained by it does not affect this conclusion.

52 As to the fourth consideration, BPS submits that its contravention arose in an uncertain regulatory environment where government bodies were unsure as to the extent to which the financial product regime of the Corporations Act applies to cryptoasset service providers. It advances three arguments.

53 First, while it accepts that a court is not a government body as such, BPS submits that different views were taken at first instance and on appeal in the Federal Court in the liability phase of the proceeding. However, those different views were taken about the PNI Arrangement which was in place for less than a year, and does not relate to the entire period in question. Further, the views concerned the peculiar facts underlying the PNI Arrangement, and not the broader issues concerning the application of the financial product regime of the Corporations Act to cryptoasset service providers: AJ [118]–[119].

54 Secondly, BPS observes that ASIC accepted that the arguments it raised and ultimately succeeded upon on appeal were “more refined and different to those advanced at first instance”.

55 Thirdly, BPS observes that, in its media release, ASIC specifically stated that it appealed the Liability Judgment “with the intention of clarifying when a provider of a financial product who is an authorised representative of an Australian financial services licensee is exempt from the requirement to hold an AFSL”.

56 There is some force in the submission that the contravention by BPS during the PNI Period arose in an uncertain regulatory environment. However, such uncertainty only serves to fortify my view that, in such circumstances, BPS should have obtained its own legal advice about the precise agreements that it was proposing to enter having regard to the manner in which it was proposing to or was operating its business, and it was not reasonable for it to fail to do that. This is especially as the precise manner in which BPS operated its business was the basis upon which the Full Court determined that BPS was not exempt under s 911A(2)(a) during the PNI Period.

57 As to the fifth consideration, it was common ground that this consideration was irrelevant in this case because the media release issued by ASIC was neither unfair nor incorrect.

58 As to the sixth consideration, it was common ground that BPS had never previously been found by a court to have engaged in similar conduct. However, ASIC submits that there was no evidence either way as to whether Bartercard has engaged in similar conduct. Notwithstanding this, this consideration weighs in BPS’s favour.

59 As to the seventh consideration, BPS submits that it was actively involved, or at the very least had attempted to be involved, in policy discussions with ASIC. To substantiate that claim, it points the fact that it met with ASIC prior to launching the Qoin Project to confirm that there was no in principle problem with it seeking to operate under one of the s 911A(2) exemptions while it awaited the outcome of its AFSL application, requested a meeting with ASIC in early 2021 to provide an update on its activities, which was denied, and then requested a further meeting with ASIC soon after the commencement of this proceeding in an attempt to comply, which was also denied.

60 However, the policy discussions referred to in Web3 Ventures at [29] concerned policy discussions with key industry participants and regulators, and active participation in industry bodies, which is different conduct to that relied upon by BPS. Having said that, the fact of the actual and attempted consultations with ASIC provides some support to BPS’s application to be relieved from liability because it demonstrates that BPS sought to conduct its business in a lawful manner and has not consciously sought to contravene the Corporations Act.

61 However, on balance and notwithstanding that, to some extent, certain of the Web3 Ventures considerations support the application by BPS to be relieved from liability, others do not apply or tell against such relief being granted. For these reasons, I am not persuaded that BPS ought fairly to be excused from liability for the Unlicensed Conduct Case.

62 As BPS has failed at the second stage of the inquiry, it is unnecessary to address the third stage.

The quantum of any penalty for the Unlicensed Conduct Case

63 The Court’s power to make a pecuniary penalty order in respect of a contravention of civil penalty provisions in each Act is conferred respectively by s 1317G of the Corporations Act and s 12GBB of the ASIC Act. The legal framework applicable to the Court’s power to impose civil pecuniary penalties is outlined in Australian Securities and Investments Commission v Firstmac Limited (Penalty Hearing) [2025] FCA 12 at [5]–[14] (Downes J).

Maximum Penalty

64 Since 22 June 2020, ss 1317G(4) of the Corporations Act and 12GBCA(2) of the ASIC Act have made identical provision for the pecuniary penalty applicable to a contravention of a civil penalty provision by a corporation. They each provide that:

The pecuniary penalty applicable to the contravention of a civil penalty provision by a body corporate is the greatest of:

(a) 50,000 penalty units; and

(b) if the Court can determine the benefit derived and detriment avoided because of the contravention—that amount multiplied by 3; and

(c) either:

(i) 10% of the annual turnover of the body corporate for the 12‑month period ending at the end of the month in which the body corporate contravened, or began to contravene, the civil penalty provision; or

(ii) if the amount worked out under subparagraph (i) is greater than an amount equal to 2.5 million penalty units—2.5 million penalty units.

65 BPS engaged in the contravening conduct throughout the overall period spanning the dates encompassed by the three declarations made by the Federal Court, which conduct is properly considered as a single course of conduct.

66 It is common ground that the turnover approach under s 1317G(4)(c) is inapplicable to this case because the value of 50,000 penalty units exceeded 10% of BPS’s annual turnover at all relevant times.

67 BPS submits that the benefit approach under s 1317G(4)(b) is inappropriate because the benefit which it derived from the contravention cannot properly be determined. Rather, it contends that the penalty unit approach under s 1317G(4)(a) should be used. On that basis, it submits that the maximum penalty for the contravention is $15,650,000 reflecting the applicable penalty unit value of $313 per unit. BPS’s alternative position is that, if the benefit approach is to be applied, the measure of benefit should be regarded as $18,172,481 being the profit which BPS obtained from the contravention. On this basis, the maximum penalty would be $54,517,443, which is equal to the profit derived by BPS multiplied by three.

68 ASIC submits that the benefit approach under s 1317G(4)(b) is applicable and contends that revenue derived by BPS during the overall period (that is, between 30 January 2020 and 19 October 2023) is the appropriate measure of benefit derived from the contravention. On that basis, so ASIC submits, the maximum penalty for the contravention would be $126,785,313, which is equal to the revenue which BPS derived from the sale of Qoin Tokens throughout the overall period in the amount of $42,261,771, multiplied by three.

69 Section 1317GAD defines “benefit derived” as “the total value of all benefits obtained by one or more persons that are reasonably attributable to the contravention”.

70 As to whether the benefit derived by BPS from the contravention can be determined, ASIC submits that the definition of “benefit derived” requires a reasonable connection between the contravention and the benefit but it does not require that the contravention caused or resulted in the benefit. Additionally, it submits that the construction of the section should be informed by the principal purpose of civil penalty provisions being to deter contraventions, referring generally to I & L Securities Pty Ltd v HTW Valuers (Brisbane) Pty Ltd (2002) 210 CLR 109; [2002] HCA 41 at [26] (Gleeson CJ). Applying this approach, ASIC argues that “the acquisition of a [Qoin Wallet] was an essential preliminary step for any buyer of Qoin Tokens”. In other words, but for the contravening conduct, BPS would not have been able to sell the Qoin Tokens and derive revenue. Ultimately, ASIC submits that this satisfies the “reasonably attributable” requirement.

71 BPS accepts that there is “some merit” to ASIC’s submission. However, it submits that “it would be incorrect to say that all of the revenue which BPS derived from the sale of these tokens is reasonably attributable to its contravention of s 911A”. According to Mr Wiese, the only revenue which BPS has generated directly has been through the sale of Qoin Tokens and that it has stopped earning any trade revenue from Qoin since 30 June 2022, when it stopped selling Qoin Tokens. BPS emphasises that it was always possible for a person to be issued a Qoin Wallet without ever purchasing any Qoin Tokens, and that it never charged a fee for issuing a Qoin Wallet or facilitating transactions between Qoin Wallets.

72 The manner in which the Qoin Facility operated, and the interaction between the Qoin Tokens and the Qoin Wallets, is addressed at LJ [30]–[68]. The Qoin Facility is not the Qoin NCP Product: LJ [107]. Rather, the financial product within the meaning of s 763A of the Corporations Act is the Qoin Wallet alone: LJ [112]. It was in relation to the Qoin Wallet that I found that BPS was not exempt under s 911A(2)(a): LJ [172]; AJ [117].

73 The Qoin Wallet was a necessary component of the Qoin Facility, and BPS derived the revenue from the sale of Qoin Tokens, which were another essential component of the Qoin Facility. For that reason, there is a reasonable connection between these two components, and it would draw an artificial distinction to conclude otherwise. This has the consequence that the revenue derived by BPS from the sale of the Qoin Tokens in the course of its operation of the Qoin Facility is reasonably attributable to the contravention by BPS of s 911A(1) of the Corporations Act.

74 For these reasons, the benefit derived by BPS from the contravention can be determined with the consequence that the benefit approach under s 1317G(4)(b) is applicable.

75 The next issue is whether revenue or profit is the appropriate measure of the benefit derived by BPS. This question turns on the meaning of “benefit”.

76 The statutory definition of benefit in s 9 is an expansive one, being “any benefit, whether by way of payment of cash or otherwise”.

77 ASIC submits that “those words plainly describe the receipt by BPS of over more than $42 million from the sale of Qoin Tokens”. It relies on the High Court’s reasoning in R v Jacobs Group (Australia) Pty Ltd (2023) 280 CLR 170; [2023] HCA 23 (Kiefel CJ, Gageler, Gordon, Steward, Gleeson and Jagot JJ). In that case, s 70.2(5) of the Criminal Code Act 1995 (Cth), a similarly worded but not identical provision to s 1317G(4), was interpreted as requiring, in ASIC’s words, a “gross receipts approach”. I address that decision in further detail below.

78 In response, BPS makes three submissions. First, referring to Australian Competition and Consumer Commission v BlueScope Steel Ltd (No 6) [2023] FCA 1029 at [41]–[44] (Thomas J), it contends that “benefit” is not concerned with theoretical notions and that profit is therefore the proper measure because it reflects the value which BPS obtained. Secondly, it points to the accepted penalty factor of “the extent of any profit or benefit derived” from the contravention, submitting that this supports a profit-based approach. Thirdly, it argues that a penalty need only exceed the profit made to avoid being treated as a tolerable cost of doing business, and that using revenue would go beyond what is necessary for that purpose. It was this latter submission which received particular emphasis at the hearing.

79 As observed above, the statutory definition of benefit is an expansive one, and encompasses the receipt of money in payment for Qoin Tokens as part of the Qoin Project. Like the provision in Jacobs Group, the focus in the statutory definition of benefit and in s 1317G(4)(b) itself is the obtaining of the advantage, and there is no reference to any disadvantage or burden or risk that might have been involved in the obtaining of the benefit or advantage.

80 In Jacobs Group at [30], [37]–[39], [50] and [53] the plurality made the following observations, many of which have equal application to the relationship between s 1317G(4)(a), (b) and (c):

Further, s 70.2(5)(b) is part of a scheme which includes s 70.2(5)(a) and (c). These paragraphs involve a mutually exclusive hierarchy, given that it is the greatest amount of the fine yielded by application of all paragraphs which is the maximum penalty. While the value of the benefit obtained in s 70.2(5)(b) is different from the annual turnover in s 70.2(5)(c), nothing in the language of the scheme suggests that the “value of the benefit … obtained” involves some netting off process of any kind. If, in the case of money received, the value of the benefit obtained is no more and no less than the money in fact obtained (irrespective of any costs, expenses or risks in obtaining that money), the two integers – value of the benefits obtained and turnover – are not the same. Section 70.2(5)(b), relating to the value of the benefit obtained, focuses on the advantage obtained from the bribery offence, if it can be determined. Section 70.2(5)(c), relating to annual turnover, focuses on the “turnover period” which is the period of 12 months ending at the end of the month in which the conduct constituting the offence occurred. Accordingly, it should not be assumed that s 70.2(5)(b) does not mean the gross amount of money a body corporate received from a bribery offence because annual turnover involves gross amounts received as specified in s 70.2(6). The temporal focus of the paragraphs is different. Moreover, not every advantage obtained will be the payment of money. The expansive language of s 70.2(5)(b) is sufficient to capture the value of all benefits obtained, if that value can be determined.

…

It is also relevant that, unlike s 70.2(5)(c), which is supported by the details in s 70.2(6) prescribing how annual turnover is to be ascertained, there is no hint in s 70.2(5)(b) that the value of the benefit is to be ascertained by some specific process of valuation. In the absence of legislative specificity, the process of valuation would be highly contestable.

Valuation processes have been described, rightly, as an “imprecise, opinionative activity involving the consideration of many variables, sometimes with equally legitimate outcomes”. Where legislation requires a type or process of valuation, whether the valuation be judicial or otherwise, “there must be room for inferences and inclinations of opinion which, being more or less conjectural, are difficult to reduce to exact reasoning or to explain to others” involving a “lack of demonstrative proof”, potentially “abounding with uncertainties” and leaving “more than ordinary room for … guesswork”. Such a process is profoundly unsuited to a provision such as s 70.2(5)(b) which is part of a scheme for the imposition of a maximum penalty for an offence, and where the Crown must establish the maximum penalty.

These textual considerations all point to the “value of the benefit … obtained” in s 70.2(5)(b) meaning, in the case of the receipt of money, no more and no less than the sum of the money in fact received.

…

Second, and equally important, s 70.2(5)(b) would become a potentially highly contested field of battle in and of itself. It is not that a court is incapable of determining a highly contestable issue. It is that to introduce a new highly contested field of battle, the resolution of which does no more than fix the maximum penalty, would tend to undermine the purpose of ensuring “effective, proportionate and dissuasive” penalties for bribery offences as required by the OECD Convention. As discussed, while it may be accepted that, in many statutory and other contexts, the concept of the “value” of something calls up for consideration a specific type and process of valuation, s 70.2(5)(b) does not suggest that it is concerned with any type or process of valuation. At the least, it does not do so if, by value, what is meant is deducting the costs, expenses, and risks incurred in providing or receiving a corrupt benefit. Given the expansive reach of s 70.2(5)(b) to capture direct and indirect advantages obtained by both the offender and its related bodies corporate, a construction of “value of the benefit … obtained” as requiring a process of valuation involving deductions to identify a “net benefit” would significantly expand the width and depth of the contestable field.

…

Another important consideration that weighs against adopting a “net benefit” construction of the “value of the benefit … obtained” in s 70.2(5)(b) is that, as has been said above, s 70.2(5) sets a maximum penalty only. The actual sentence to be imposed is to be determined on the basis of an instinctive synthesis of many considerations. This includes: (a) as set out in s 16A(1) of the Crimes Act 1914 (Cth), that the sentence imposed must be “of a severity appropriate in all the circumstances of the offence”; and (b) under s 16A(2), that the court must take into account “[i]n addition to any other matters … such of the following matters as are relevant and known to the court” including, in s 16A(2)(a), “the nature and circumstances of the offence” and, in s 16A(2)(e), “any injury, loss or damage resulting from the offence”. These provisions involve ample scope for a body corporate defendant to prove its “net benefit” or even its loss as a result of performing a contract secured by a bribery offence. A trial judge can calibrate the relevance of those circumstances, in the context of all other factors to be considered, to ensure the penalty imposed is proportionate to all circumstances of the offence. There is no basis, however, to conclude that s 70.5(2)(b) operates by embedding the same considerations into the setting of the maximum penalty. If that were so, the same considerations would dictate both the setting of the maximum penalty and the fixing of the actual penalty as part of the overall circumstances of the case. Again, that “double” operation of the same considerations would tend to undermine the statutory objects of achieving effective, proportionate, and dissuasive penalties.

(Citations omitted.)

81 While Jacobs Group was decided in a different statutory context, the High Court’s reasoning is apposite because it concerns legislation which is drafted in very similar terms to that under consideration in this case. It thus provides strong support for ASIC’s construction.

82 In my view, ASIC’s posited construction is therefore the correct one.

83 Thus, “benefit” in s 1317G(f)(b) means, in the case of the receipt of money by BPS, the gross revenue in fact received by BPS during the period that it engaged in the contravening conduct.

84 It follows that revenue is the appropriate measure of the benefit derived by BPS within the meaning of s 1317G(f)(b) with the consequence that the maximum penalty for the Unlicensed Conduct Case is $126,261,771.00.

Nature, extent and circumstances of the contravention

85 As to this matter, ASIC’s submissions are largely subsumed within the issues addressed above in relation to s 1317S and the findings of fact in the Liability Judgment and the Appeal Judgment.

86 In response, BPS’s submissions addressed certain submissions made by ASIC.

87 First, BPS submits that ASIC’s criticism that it did not “wait… until it had obtained an AFSL” is unfair on the basis that a Senior Manager at ASIC had expressly told it that there was no in principle difficulty with it relying on the exemption while it waited to obtain an AFSL. However, considering my findings in relation to the application under s 1317S, BPS did not do enough to ensure that its conduct fell within an exemption.

88 Secondly, BPS submits that the implication that it somehow acted improperly by proceeding on the assumption it could bring itself within the scope of the authorised representative exemption “by simply executing” a relevant agreement is also unfair. While it accepts that its assumption was wrong, it contends that it does not automatically mean that it was unreasonable. Again, this has been addressed.

89 Thirdly, BPS contends that it is unclear whether ASIC’s references to it executing “documents that did not reflect the reality of the arrangements, and the actual operation of those arrangements, between the parties”, and it proceeding “without regard to whether what was being done in the actual provision of the financial services conformed with the intended operation of those documents” are intended to refer to the findings in the Liability Judgment that BPS did not fall within either of the exemptions in ss 911A(2)(a) or 911A(2)(b) or something more nefarious. However, there was no suggestion by ASIC that any of the agreements executed by BPS were a sham, and any suggestion that ASIC was advancing such a case was expressly disavowed by its senior counsel.

Previous similar conduct

90 This matter has also been addressed above in the context of the application for relief under s 1317S.

Nature and extent of any loss or damage

91 It was common ground that there was no evidence as to whether investors suffered loss or damage by reason of the contravention of s 911A. This is a factor which supports a lesser penalty than might otherwise have been imposed.

Whether contravention deliberate or reckless

92 BPS accepts that its contravention of s 911A was deliberate in the sense that the actions taken by it were brought about by conscious decision and not by accident. However, it submits that none of its conduct was deliberate or intentional in the sense that at no point was BPS prepared to court the risk of contravening the Corporations Act. I accept this submission.

93 As outlined above, BPS did take some steps to seek to comply with the law and, therefore, its contravention cannot be characterised as deliberate or reckless. This is a factor which supports a lesser penalty than might otherwise have been imposed.

Seniority of individuals responsible for contravention

94 BPS accepts that the conduct resulting in the contravention was primarily the responsibility of its directors including, in particular, Mr Wiese.

Capacity to pay and size

95 The objective of general deterrence may require the imposition of a penalty that is beyond the respondent’s financial capacity to pay and which may cause insolvency: see Australian Competition and Consumer Commission v High Adventure Pty Ltd (2006) ATPR 42-091; [2005] FCAFC 247 at [11] (Heerey, Finkelstein and Allsop JJ). In Director of Consumer Affairs Victoria v Hocking Stuart (Richmond) Pty Ltd [2016] FCA 1184 at [32]–[33], Middleton J observed:

Therefore, the amount of penalty should, in general, be set having regard to an amount the contravener can realistically be expected to discharge and should not be unnecessarily oppressive. This is not determinative, but is a factor. Of course, if the contravener has organised his or her affairs to render themselves beyond sanction, different considerations will apply.

Nevertheless, a penalty should not be set so low that it does not meet the goal of general deterrence, even if that low penalty acts in the circumstances as a specific deterrent having regard to the individual financial circumstances of the contravener.

96 The evidence reveals that BPS is currently the subject of a small business restructuring plan under Pt 5.3B of the Corporations Act. Mr Wiese’s evidence is that the imposition of any significant pecuniary penalty would likely result in BPS’s insolvency, it being wound up, it being unable to maintain the Qoin App or Q Shop for the benefit of Qoin Wallet users, and a reduction in the liquidity and value of Qoin Tokens held by individuals and businesses (including those who received 4.3 million Qoin Tokens as part of the settlement of the class action proceedings earlier this year). As to this last matter, see Its Eco Pty Ltd v BPS Financial Limited (Settlement Approval) [2025] FCA 545 (Downes J). ASIC does not dispute that BPS would enter liquidation if a total penalty of $21 million, or even $10 million, was imposed.

97 ASIC submits that the size of the company may be relevant in determining the size of a pecuniary penalty that would operate as an effective specific deterrent citing Australian Securities and Investments Commission v Bit Trade Pty Ltd (No 2) [2024] FCA 1422 at [28] (Nicholas J). BPS agrees with this but submits that it is of limited significance when the contravener’s business has shut down citing Australian Securities and Investments Commission v Ferratum Australia Pty Ltd (in liq) (No 2) [2024] FCA 701 at [13] (Kennett J). Having said that, BPS also accepts that the need for general deterrence remains, which is the case. It accepts that it is necessary that penalties which are imposed are, and are seen to be, more than just the cost of doing business.

98 In my view, to impose no penalty upon BPS for the Unlicensed Conduct, being what it proposes, would be incapable of deterring contraveners “from the cynical calculation involved in weighing up the risk of penalty against the profits to be made from contravention”: Singtel Optus Pty Ltd v Australian Competition and Consumer Commission (2012) 287 ALR 249; [2012] FCAFC 20 at [62]–[63] (Keane CJ, Finn and Gilmour JJ).

99 The fact that several years after the contraventions occurred, BPS is now on the “brink of insolvency” (according to Mr Wiese) does not change the primary purpose of the imposition of pecuniary penalties. What is to be deterred is contravening conduct.

Existence of compliance systems

100 The legal advice obtained by BPS with respect to the Unlicensed Conduct Case has been addressed above. This is a factor which supports a lesser penalty than might otherwise have been imposed.

Cooperation with ASIC

101 BPS sought to engage with ASIC both before and after the institution of these proceedings.

102 Upon the Liability Judgment being delivered, BPS amended the AR Agreement with Billzy to reflect the reasons in that judgment.

103 BPS cooperated by voluntarily providing information and documents requested by ASIC in relation to penalty. Those documents included:

(1) copies of all relevant legal advices which BPS received, and the instructions provided in relation to those advices;

(2) documents detailing Qoin Token sales, and the revenue generated from those sales, between 30 January 2020 and 19 October 2023; and

(3) financial reports for the financial years ending 30 June 2020 to 30 June 2025.

104 ASIC submits that BPS did not voluntarily provide information or materials to ASIC during the course of ASIC’s investigation or prior to these proceedings, and points to an email which Mr Wiese sent to ASIC on 10 February 2022 attaching a letter from BPS’s then legal representatives which stated that BPS was not encouraging its employees to participate in voluntary interviews with ASIC. ASIC characterised this letter as BPS “discouraging” its employees from voluntary interviews.

105 However, the letter received from BPS’s legal representatives on 10 February 2022 stated, “our clients are unfortunately unable to recommend to their employees that they accept ASIC’s invitation to participate in voluntary interviews” and instead requested that ASIC proceed to issue examination notices to any persons it wished to interview. That BPS’s legal representatives did not consider it advisable to recommend that employees attend voluntary interviews with ASIC is unremarkable in circumstances where the conduct of a formal interview under s 19 grants an examinee certain protections which a voluntary interview would not. Further, BPS made at least two employees available for voluntary interviews. The letter of 10 February 2022 also requested that ASIC issue s 19 notices in respect of any person that it wished to interview — demonstrating a willingness to facilitate such examinations rather than a desire to hinder ASIC’s investigations.

106 ASIC also submits that BPS contested all of the alleged contraventions in its pleadings and at trial. While it is true that BPS contested both phases of the proceeding (liability and relief), BPS filed a submitting notice in and did not actively contest the appeal, and it also made important concessions throughout the liability hearing which helped to narrow the issues in dispute. Whilst I accept that such conduct, like BPS’s cooperation with ASIC in response to its statutory obligations, is not worthy of specific reduction of any penalty—noting BPS is not seeking a “cooperation discount” for them—it remains relevant to the overall consideration of BPS’s degree of cooperation.

107 ASIC submits that BPS has not expressed contrition. However, following receipt of the submissions by ASIC, Mr Wiese stated in his fourth affidavit that BPS “is genuinely remorseful for its conduct”, and emphasises that BPS has endeavoured to communicate openly and constructively with ASIC and the Court, and to attempt compliance. The expression of remorse was not challenged on the basis that it was not genuine.

108 As to Mr Wiese’s evidence in his first affidavit that he “cooperated fully during ASIC’s 18-month investigation” and concerning cooperation generally, ASIC seeks a finding that Mr Wiese’s evidence is not credible, or should be given little weight, in light of evidence given by Mr Wiese about a text which he sent to Mr Quinn asking him to have his executive assistant delete an email. However, the circumstances surrounding the text message were “incredibly vague” (as BPS submits) and the precise content of the email to be deleted is unknown and could not be recalled by Mr Wiese. Overall, I consider Mr Wiese gave evidence of his best recollection of the circumstances relating to the text message, being more than three years ago and when he was unwell and at home, with the result that I decline to make the finding sought.

109 Overall, BPS’s conduct provides some support for a lesser penalty than might otherwise have been imposed.

Prospective negative impact on third parties

110 As observed in the Liability Judgment, the value of Qoin Tokens is effectively linked to and may be affected by disruptions in the merchant ecosystem and overall market for Qoin. In light of this conclusion and accepting that the imposition of a significant penalty would likely result in BPS’s insolvency, I agree with BPS that it would be unfortunate for there to be a negative impact on third parties holding Qoin Tokens, especially those claimants who received Qoin Tokens in lieu of money in the settlement of the class action proceedings.

111 The real question is whether the evidence established that there would be such a negative impact.

112 By his first affidavit, Mr Wiese sought that the “punitive actions in this matter, while important to highlight the dangers of operating an unlicensed business (albeit unwittingly) not be excessive to the extent that the current business is completely destroyed, with resultant harm to the businesses who rely on Qoin for a proportion of their trading”. He also stated that he believed that “penalties and further adverse publicity will oppress BPS, making it impossible to service and support thousands of current users and their migration to other digital wallet providers”.

113 During cross-examination, it was put to Mr Wiese that, because BPS’s involvement in the Qoin Project has been wound back and overtaken in most ways by the Qoin Foundation, the liquidation of BPS would be unlikely to have any impact on the confidence in or liquidity of the value of Qoin Tokens. Mr Wiese’s response was that negative impacts could still arise because he along with Mr Pathak and others would no longer be involved in the oversight of the Qoin Project. In my view, this answer sounded somewhat speculative and so I place little weight on this evidence.

114 Without clearer evidence that a substantial pecuniary penalty would necessarily have a corrosive effect on the market for Qoin and therefore disadvantage third parties, this factor carries little weight in this case.

Extent of any remedial steps taken

115 By its written submissions, BPS submits that it “is not in a financial position to pay any sums in remediation because it had previously utilised most of the profits it received from the sale of the Qoin Tokens to re-buy that Qoin from community members in order to set up the BTX Exchange” and “largely emptied its inventory of Qoin Tokens […] as part of the settlement of the Qoin class action”. At the hearing, however, BPS’s counsel argued that the act of paying out almost all of the Qoin Tokens received from BTX to members of the class action was itself a remedial step because it effectively involved BPS disgorging any benefit it obtained back to the Qoin users.

116 However, as ASIC submits, the act of paying out the Qoin Tokens to members of the class action “cannot sensibly be described as remediation” because it was a commercial decision made by BPS in order to settle that legal proceeding.

Extent of any profit or benefit derived

117 BPS submits that it has retained essentially none of the profit that it generated in FY20 and FY21 as a result of paying out the Qoin Tokens to members of the class action to settle that proceeding.

118 However, BPS made a commercial decision to settle the class action, and the fact that this affected the amount of profit which it retained has no bearing upon the quantum of the appropriate penalty to be imposed.

119 BPS also submits that at no point did it receive any fees for its issue of Qoin Wallets or the facilitation of transactions between Qoin Wallet holders. This submission has been addressed above with the consequence that it is relevant to take into account the revenue derived by BPS from the sale of Qoin Tokens.

Specific and general deterrence

120 BPS submits that there is no need for specific deterrence in this case given:

(1) BPS is no longer involved in any of the activities which gave rise to the Unlicensed Conduct and there is no reason to expect that it will resume those activities;

(2) even if it did re-embark on those activities, it has consented to injunctions which would expose it to punishment for contempt in the event that it engaged in the same or similar conduct in the future;

(3) given the financial circumstances of both itself and its parent company, a penalty of any amount will be sufficient to ensure the potential costs of non-compliance cannot be regarded by BPS or its parent company as an acceptable cost of doing business; and

(4) the steps which BPS took to obtain advice about the relevant regulatory framework both before, and in the course of, embarking on the Qoin Project evidences a company that is genuinely concerned with ensuring compliance with the law — albeit one that has been found to have fallen short in those endeavours.

121 However, as ASIC submits, specific deterrence does have a role to play in this case because:

(1) although specific deterrence may be of minimal significance if a business has shut down, Mr Wiese wants BPS to continue operating. If it does, its continued operation will still be connected with the Qoin Project (i.e., the running of the Qoin Shop);

(2) the senior officers of BPS most closely involved in and responsible for contraventions continue to operate BPS and continue to have some ongoing involvement in the wider Qoin Project, which is a relevant factor.