FEDERAL COURT OF AUSTRALIA

DC Rd DC Pty Ltd v Zhang (Trial Judgment) [2026] FCA 16

File number(s): | NSD 247 of 2023 |

Judgment of: | JACKMAN J |

Date of judgment: | 23 January 2026 |

Catchwords: | EQUITY – application for equitable relief and personal remedies for breaches of fiduciary duties – where applicant relied on respondents (property developers and an accountant) identifying and proposing properties to be purchased on applicants’ behalf – where respondents informed applicants that property would be purchased in applicant-company’s name for $45m – where respondents fashioned a back-to-back contract to purchase property in own name for $14m and misappropriated remaining $33m profit into various entities and properties owned by respondents EQUITY – whether first respondent personally owed fiduciary duties – where fiduciary duties owed by director to a company not concurrent with duties owed to shareholders on same subject matter – where any implicit undertaking was done so in capacity as director of company – where first respondent not a de facto director of applicant – where first respondent did not personally receive property that would render him constructive trustee with associated fiduciary duties – where knowing assistance not pleaded – no personal fiduciary duty owed by first respondent as distinct from those owed by company EQUITY – whether second respondent personally owed fiduciary duties – where legal principles of accountant-client relationship considered – where second respondent required to comply with tax agents’ code of professional conduct and certified practising accountants’ code of ethics – where second respondent personally undertook activities to considerable extent – second respondent did not undertake fiduciary obligations as distinct from accounting company – accounting company undertook fiduciary duties – whether second respondent knowingly assisted in generating proceeds – where dishonest and fraudulent design found – where actual knowledge of back-to-back contracts found – where no traceable money received personally by second respondent (as distinct from entities under his control) – knowing assistance found in relation to second respondent’s role as constructive trustee of sale proceeds and subsequent breaches EQUITY – consideration of tracing principles – consideration of volunteer in Black v Freeman trust (defined in reasons) being personally liable from time of knowledge – where mixed trust money – where re-mortgaging property in breach of constructive trustee duties – where inability to trace into debt – where lowest intermediate balance rule applied – where bona fide purchasers for value without notice – where trustee who pays off mortgage entitled to equitable subrogation to position of original mortgagee – where equitable subrogation available on pro rata basis – respondents’ actual knowledge imputed to entities controlled by them and tracing available where entities breached fiduciary duties CONSUMER LAW – application for relief for misleading or deceptive conduct under s 18 of the ACL (defined in reasons) concerning development potential and value of property – whether circumstances objectively gave rise to reasonable expectation that relevant facts would have been disclosed to applicants – disclosures and non-disclosures made by first respondent, second respondent (including entities) and fourteenth respondent found to be misleading or deceptive – causation and reliance found – measure of loss calculated by price paid less true value of what was acquired – apportionment applied pursuant to s 87CD(1) of the CC Act (defined in reasons) and s 35(1) of the CLA (defined in reasons) CONSUMER LAW – whether contributory negligence defence applicable under s 137B of the CC Act – where findings of intention to cause loss or damage – where applicants exercised reasonable care in the circumstances – defence not available |

Legislation: | Competition and Consumer Act 2010 (Cth) Corporations Act 2001 (Cth) Evidence Act 1995 (Cth) Federal Court of Australia Act 1976 (Cth) Tax Agent Services Act 2009 (Cth) Civil Liability Act 2002 (NSW) Fair Trading Act 1987 (NSW) Law Reform (Miscellaneous Provisions) Act 1965 (NSW) Professional Standards Act 1994 (NSW) Real Property Act 1900 (NSW) Mercantile Act 1867 (Qld) |

Cases cited: | ABN Amro Bank NV v Bathurst Regional Council [2014] FCAFC 65; (2014) 224 FCR 1 Addenbrooke Pty Ltd v Duncan (No 2) [2017] FCAFC 76; (2017) 348 ALR 1 Aged Care Services Pty Ltd v Kanning Services Pty Ltd [2013] NSWCA 393; (2013) 86 NSWLR 174 Agip (Africa) Ltd v Jackson [1990] Ch 265 Amann Aviation Pty Ltd v Commonwealth (1990) 22 FCR 527 Austin v Royal [1999] NSWCA 222; (1999) 47 NSWLR 27 Australian Conference Association Ltd v Mainline Constructions Pty Ltd (in liq) [1978] HCA 45; (1978) 141 CLR 335 Barclays Bank Ltd v Quistclose Investments Ltd [1970] AC 567 Barnes v Addy (1874) LR 9 Ch App 244 BCEG International (Australia) Pty Ltd v Xiao [2022] NSWSC 972; (2022) 162 ACSR 601 Birmingham and District Land Company v London and North Western Railway Company (1886) 34 Ch D 261 Bishopsgate Investment Management Ltd (in liq) v Homan [1995] Ch 211 Black v S Freedman & Co (1910) 12 CLR 105 Bofinger v Kingsway Group Ltd [2009] HCA 44; (2009) 239 CLR 269 Boscawen v Bajwa [1996] 1 WLR 328 Briginshaw v Briginshaw [1938] HCA 34; (1938) 60 CLR 336 Brunninghausen v Glavanics [1999] NSWCA 199; (1999) 46 NSWLR 538 Burston Finance Ltd v Speirway Ltd (in liq) [1974] 1 WLR 1648 Buzzle Operations Pty Ltd (in liq) v Apple Computer Australia Pty Ltd [2011] NSWCA 109; (2011) 81 NSWLR 47 Byrnes v Kendle [2011] HCA 26; (2011) 243 CLR 253 Caron v Jahani (No 2) [2020] NSWCA 117; (2020) 102 NSWLR 537 Chetwynd v Allen [1899] 1 Ch 353 Chu v Lin, in the matter of Gold Stone Capital Pty Ltd (Trial Judgment) [2024] FCA 766 Cochrane v Cochrane (1985) 3 NSWLR 403 Cohen v Cohen [1929] HCA 15; (1929) 42 CLR 91 Day v Tiuta International Ltd [2014] EWCA Civ 1246 DC Rd DC Pty Ltd v Zhang (No 3) [2024] FCA 221 Demagogue Pty Ltd v Ramensky (1992) 39 FCR 31 Director of the Serious Fraud Office v Lexi Holdings plc [2008] EWCA Crim 1443; [2009] QB 376 Eastern Shipping Company v Quah Beng Kee [1924] AC 177 Elanor Funds Management Ltd v Alceon Group Pty Ltd [2024] FCA 121; (2024) 424 ALR 601 Eugenie Holdings Pty Ltd v Stratford (unreported, Supreme Court of New South Wales, Giles J, 12 November 1991) 61–66 Farah Constructions Pty Ltd v Say-Dee Pty Ltd [2007] HCA 22; (2007) 230 CLR 89 Federal Commissioner of Taxation v BHP Billiton Limited [2019] FCAFC 4; (2019) 263 FCR 334 Fistar v Riverwood Legion and Community Club Ltd [2016] NSWCA 81; (2016) 91 NSWLR 732 Gandel Meats Pty Ltd, in the matter of Centennial Mining Ltd (subject to a deed of company arrangement) v Centennial Mining Ltd (No 2) [2020] FCA 633 Grimaldi v Chameleon Mining NL (No 2) [2011] FCAFC 6; (2011) 200 FCR 296 Hagan v Waterhouse (No 2) (1991) 34 NSWLR 308 Harstedt Pty Ltd v Tomanek [2018] VSCA 84; (2018) 55 VR 158 Hasler v Singtel Optus Pty Ltd [2014] NSWCA 266; (2014) 87 NSWLR 609 Heperu Pty Ltd v Belle [2009] NSWCA 252; (2009) 76 NSWLR 230 Herrod v Johnston [2012] QCA 360; [2013] 2 Qd R 102 Hopcraft v Close Brothers Ltd [2025] UKSC 33; [2025] 3 WLR 423 Hospital Products Limited v United States Surgical Corporation [1984] HCA 64; (1984) 156 CLR 41 HTW Valuers (Central Qld) Pty Ltd v Astonland Pty Ltd [2004] HCA 54; (2004) 217 CLR 640 In re Stapleford Colliery Company (1880) 14 Ch D 432 In the matter of Fellmane Pty Ltd (in liq) [2020] NSWSC 595 Independent Trustee Services Ltd v GP Noble Trustees Ltd [2012] EWCA Civ 195; [2013] Ch 91 John Alexander’s Clubs Pty Ltd v White City Tennis Club Ltd [2010] HCA 19; (2010) 241 CLR 1 Johnson v Mackinnon [2021] NSWCA 152 Jones v Dunkel [1959] HCA 8; (1959) 101 CLR 298 Korda v Australian Executor Trustee (SA) Ltd [2015] HCA 6; (2015) 255 CLR 62 Kuhl v Zurich Financial Services Australia Ltd [2011] HCA 11; (2011) 243 CLR 361 Legal Services Board v Gillespie-Jones [2013] HCA 35; (2013) 249 CLR 493 Lewis v Nortex Pty Ltd (in liq) [2006] NSWSC 480 Li v Ye [2025] NSWCA 227 Michael Wilson & Partners Ltd v Nicholls [2011] HCA 48; (2011) 244 CLR 427 Miller & Associates Insurance Broking Pty Ltd v BMW Australia Finance Ltd [2010] HCA 31; (2010) 241 CLR 357 Mitchell v Al Jaber [2025] UKSC 43; [2025] 3 WLR 849 Naaman v Jaken Properties Australia Pty Ltd [2025] HCA 1; (2025) 421 ALR 227 Nadilo v Souris [2019] NSWSC 108 Nguyen v Sage Consultant Group Pty Ltd [2021] NSWSC 753; (2021) 20 BPR 41,989 Oliver v Renwick Street Pty Ltd [2024] NSWSC 346 Padovan v MCG Group Pty Ltd (in liq) [2011] NSWSC 1080 Patten v Bond (1889) 60 LT 583 Paul A. Davies (Australia) Pty Ltd (in liq) v Davies [1983] 1 NSWLR 440 Paul v Speirway Ltd [1976] Ch 220 Pilmer v Duke Group Ltd (in liq) [2001] HCA 31; (2001) 207 CLR 165 Porter v Mulcahy & Co Accounting Services Pty Ltd [2021] VSC 572 Potts v Miller [1940] HCA 43; (1940) 64 CLR 282 Re Diplock [1948] Ch 465 Re Elizabethan Theatre Trust; Lord v Commonwealth Bank of Australia (1991) 30 FCR 491 Re Global Finance Group Pty Ltd (in liq); Ex parte Read [2002] WASC 63; (2002) 26 WAR 385 Re Goldcorp Exchange Ltd [1995] 1 AC 74 Re Hallett’s Estate (1880) 13 Ch D 696 Re Montagu’s Settlement Trusts [1987] Ch 264 Re Oatway [1903] 2 Ch 356 Re Sirrah Pty Ltd (in prov liq) [2021] NSWSC 413; (2021) 152 ACSR 212 Re Sutherland; French Caledonia Travel Service Pty Ltd (in liq) [2003] NSWSC 1008; (2003) 59 NSWLR 361 Robb Evans of Robb Evans & Associates v European Bank Ltd [2004] NSWCA 82; (2004) 61 NSWLR 75 Roscoe (Bolton) Ltd v Winder [1915] 1 Ch 62 Russell Gould Pty Ltd v Ramangkura [2014] NSWCA 310; (2014) 87 NSWLR 552 Scott v Scott [1963] HCA 65; (1963) 109 CLR 649 Shalson v Russo [2003] EWHC 1637 (Ch); [2005] Ch 281 Silversea Cruises Australia Pty Ltd v Abellanoza [2019] NSWCA 306 Sinclair v Brougham [1914] AC 398 Smits v Cugola [2022] QCA 262 State Bank of New South Wales v Geeport Developments Pty Ltd (1991) 5 BPR 11,947 Sze Tu v Lowe [2014] NSWCA 462; (2014) 89 NSWLR 317 Torlonia v Wright [2016] NSWSC 1139 Turner v O’Bryan-Turner [2022] NSWCA 23; (2022) 107 NSWLR 171 United States Surgical Corporation v Hospital Products International Pty Ltd [1983] 2 NSWLR 157 Walker v Corboy (1990) 19 NSWLR 382 Walsh v Permanent Trustee Australia Ltd (1996) 21 ACSR 213 Westdeutsche Landesbank Girozentrale v Islington London Borough Council [1996] AC 669 Wilkes v Spooner [1911] 2 KB 473 Xiao v BCEG International (Australia) Pty Ltd [2023] NSWCA 48; (2023) 111 NSWLR 132 Yeung Kai Yung v Hong Kong and Shanghai Banking Corporation [1981] AC 787 Zervas v Burkitt (No 2) [2019] NSWCA 236 |

Division: | General Division |

Registry: | New South Wales |

National Practice Area: | Commercial and Corporations |

Sub-area: | Commercial Contracts, Banking, Finance and Insurance |

Number of paragraphs: | 478 |

Date of hearing: | 10 December – 23 December 2025 |

Counsel for the Applicants: | Mr C Colquhoun SC with Mr B Smith and Ms M Kearney |

Solicitors for the Applicants: | Corrs Chambers Westgarth |

Counsel for the 1st, 5th, 9th and 15th Respondents: | Mr V Bedrossian SC with Mr D Elliott |

Solicitors for the 1st, 5th, 9th and 15th Respondents: | Amberlake Lawyers |

Counsel for the 2nd, 3rd, 6th, 10th, 11th, 12th, 13th and 16th Respondents: | Mr D Pritchard SC with Mr J Parrish and Mr N Lennings |

Solicitors for the 2nd, 3rd, 6th, 10th, 11th, 12th, 13th and 16th Respondents: | Kells |

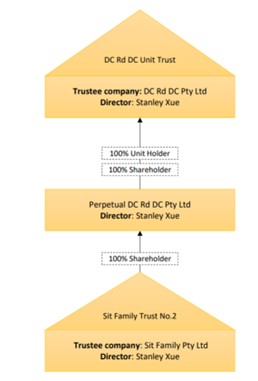

Counsel for the 14th Respondent: | Mr M Condon SC with Mr A Smith |

Solicitors for the 14th Respondent: | Emerson Lewis Lawyers |

ORDERS

NSD 247 of 2023 | ||

| ||

BETWEEN: | DC RD DC PTY LTD First Applicant STANLEY XUE Second Applicant SIT FAMILY PTY LTD ACN 617 947 065 Third Applicant FAI KEUNG (PHILLIP) SIT Fourth Applicant | |

AND: | DONG (TONY) ZHANG First Respondent ZHENGJUN (BOB) CAI Second Respondent CENTRAL ADVISORY GROUP PTY LTD ACN 163 958 843 Third Respondent (and others named in the Schedule) | |

order made by: | JACKMAN J |

DATE OF ORDER: | 23 January 2026 |

THE COURT:

1. Notes that defined terms and abbreviations used in these orders bear the same meaning as set out in the Glossary in the reasons for judgment dated 23 January 2026 at [1].

Tony Parties

2. Orders Tony to pay damages to DC Rd pursuant to s 236 of the ACL in the amount of $36,866,947.94, plus interest pursuant to s 51A of the FCA Act.

3. Orders Link to account to DC Rd in the amount of $19,739,471.93, plus compound interest at the FCA Interest Rates with yearly rests.

4. Orders Belrose COB to account to DC Rd in the amount of $18,299,990, plus compound interest at the FCA Interest Rates with yearly rests.

5. Declares that Belrose COB holds the whole of the Belrose Property on constructive trust for DC Rd.

6. Declares that DC Rd is entitled to an equitable charge over the proceeds of sale of lots in the Smithfield Property to secure the amount of $3,718,601 plus simple interest at the FCA Interest Rates.

Bob Parties and Lian Parties

7. Orders Bob to pay equitable compensation to DC Rd in the amount of $36,866,947.94, plus compound interest at the FCA Interest Rates with yearly rests.

8. Orders each of Bob and CATA to pay damages to DC Rd pursuant to s 236 of the ACL in the amount of $36,866,947.94, plus interest pursuant to s 51A of the FCA Act.

9. Orders CTD to account to DC Rd in the amount of $12,073,962, plus compound interest at the FCA Interest Rates with yearly rests.

10. Orders CAC to account to DC Rd in the amount of $5,000,000, plus compound interest at the FCA Interest Rates with yearly rests.

11. Orders CAGA to account to DC Rd in the amount of $5,357,657.21 plus compound interest at the FCA Interest Rates with yearly rests.

12. Orders Lian to account to DC Rd in the amount of $1,571,000, plus interest pursuant to s 51A of the FCA Act from 14 February 2023.

13. Declares that Lian holds the Turramurra Property on constructive trust for DC Rd to the extent of securing the amount of $1,571,000 plus interest as referred to in the previous order.

14. Declares that Lian holds $1,000,000 plus simple interest at the FCA Interest Rates in the Lian CBA Account 7759 as a constructive trustee for DC Rd and orders that Lian pay that amount to DC Rd.

15. Declares that DC Rd has an equitable charge over the Herbert Street Property to secure the amount of $590,000 plus simple interest at the FCA Interest Rates.

16. Declares that Saiala holds the Saiala Property on constructive trust for DC Rd to the extent of securing the amount of $1,900,000 plus simple interest at the FCA Interest Rates from 14 February 2023, and is liable to account to DC Rd for that amount including interest.

17. Declares that Clarence 104 holds the Clarence 104 Property on constructive trust for DC Rd to the extent of securing the amount of $266,657.21 plus simple interest at the FCA Interest Rates, and is liable to account to DC Rd for that amount plus interest.

18. Declares that DC Rd is entitled to an equitable charge over the DSZ Clarence Street Properties to secure the amount of $930,000 plus simple interest at the FCA Interest Rates.

Joinder of Mortgagees and Caveator

19. Grants leave to the Applicants to join as respondents NAB, CBA and Green Route Pty Ltd, and directs that they be served with an amended originating application joining them by 30 January 2026.

20. Directs that NAB, CBA and Green Route Pty Ltd file and serve any affidavits and written submissions in relation to whether there should be an order for the sale by Court-appointed trustees of the Belrose Property and the DSZ Clarence Street Properties (in the case of NAB), the Turramurra Property and the Herbert Street Property (in the case of CBA), and the Clarence 104 Property (in the case of Green Route Pty Ltd), or any other relief by 16 February 2026.

21. Directs that the Applicants and respondents file and serve any affidavits and written submissions in response by 23 February 2026.

22. Fixes the matter for further hearing in relation to the matters raised in those affidavits and submissions on 27 February 2026 at 9.30am.

John

23. Orders John to pay damages to DC Rd pursuant to s 236 of the ACL in the amount of $5,530,042.19, plus interest pursuant to s 51A of the FCA Act.

24. Orders John to account to DC Rd in the amount of $150,000, plus interest pursuant to s 51A of the FCA Act from 13 December 2024.

Costs

25. Directs the Applicants to file and serve any affidavits and written submissions in relation to costs by 6 March 2026.

26. Directs the respondents to file and serve any affidavits and written submissions in relation to costs by 10 April 2026.

27. Directs the Applicants to file and serve any affidavits and written submissions in reply in relation to costs by 1 May 2026.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

JACKMAN J:

Glossary

1 In these reasons, I have used the following capitalised terms with the following meanings (noting that in using first names for the principal protagonists I am merely following the practice adopted by the parties and do not intend any disrespect).

Defined Term | Meaning |

4FASOC | Fourth Further Amended Statement of Claim |

30 Denham | 30 Denham Pty Ltd, the purchaser of the Denham Court Property from Khengs |

132 Irwins Rd East Kurrajong | 132 Irwins Rd East Kurrajong Pty Ltd |

471 Hunter Street Newcastle | 471 Hunter Street Newcastle Pty Ltd |

Accounting WeChat Group | HYG Accounting Circle WeChat Group, which from 8 July 2019 included Bob, Tony, John, Phillip, Stanley and two employees of CATA (Ms Sissi Qu and Mr Kevin Zhao) |

ACL | Australian Consumer Law, being Sch 2 to the Competition and Consumer Act 2010 (Cth) in relation to corporations, and the same text as applies to natural persons under ss 27–32 of the FTA. |

Alice | Ms Yu Chun (Alice) Lam, the wife of Phillip and mother of Stanley |

ANZ | Australia and New Zealand Banking Group Ltd |

ANZ Turramurra Loan Account 8143 | A home loan account with ANZ in the names of Bob and Lian for the Turramurra Property, being BSB 012217 and account number 6852 78143 |

Applicants | DC Rd, Stanley, Sit Family and Phillip |

Arthur Street Property | The property located at 6 Arthur Street, Ryde NSW 2112 |

ASIC | Australian Securities and Investments Commission |

ATO | Australian Taxation Office |

Back-to-Back Contracts | The First Contract and the Second Contract whereby 30 Denham purchased the Denham Court Property from Khengs for $14 million plus GST on 25 July 2019 and sold it on 25 July 2019 to DC Rd for $45 million plus GST |

Belrose COB | Belrose COB Pty Ltd, the registered proprietor of the Belrose Property |

Belrose Property | The property located at 3 Minna Close, Belrose NSW 2085 |

Bob | Mr Zhengjun (Bob) Cai, the second respondent |

Bob 1 | Bob’s first affidavit dated 1 August 2024 |

Bob 2 | Bob’s second affidavit dated 1 August 2025 |

Bob 3 | Bob’s third affidavit dated 5 December 2025 |

Bob Parties | Bob, CAG, CAC and CATA |

Bob and Lian ANZ Account 1814 | An ANZ bank account in the name of Bob and Lian, being BSB 012 217 and account number 4231 91814, and is an offset account linked to the ANZ Turramurra Loan. |

Bob and Lian St George Account 7741 | A St George bank account in the name of Bob and Lian, being BSB 112 879 and account number 4894 17741, and is an offset account linked to the St George Arthur Street Loan. |

Bob St George Account 8334 | A St George bank account in the name of Bob, being BSB 112 879 and account number 442538334, and is an offset account |

Burwood Development | The development at 17–23 Esher Street, Burwood NSW 2134 |

CAC | Central Advisory Capital Pty Ltd, the sixth respondent |

CAC Account | The ANZ bank account in the name of CAC, being BSB 012 071 and account number 2304 85648 |

Caddens Development | The development at 29 and 46–66 O’Connell Street, Caddens NSW 2747 |

CAG | Central Advisory Group Pty Ltd, the third respondent |

CAGA | Central Advisory Group Asia Ltd, a company incorporated in Hong Kong, and the seventh respondent |

CAGA Account | The ANZ bank account in the name of CAGA, being BSB 012 013 and account number 4653 92227 |

Capitive | Capitive Pty Ltd, now known as HYG Property Pty Ltd |

CATA | Central Accounting and Taxation Advisory Pty Ltd, the tenth respondent |

CB | Court Book |

CBA | Commonwealth Bank of Australia |

CBA Arthur Street Loan Account | A home loan account with the CBA in the name of Bob and Lian for the Arthur Street Property, being BSB 062 370 and account number 5680 79321 |

CBA Herbert Street Loan Account | A home loan account with the CBA in the name of Bob and Lian for the Herbert Street Property, being BSB 062 370 and account number 5680 38861 |

Central Quarry | Central Quarry Project Pty Ltd |

CIA | Central Institute Advisory Pty Ltd |

CLA | Civil Liability Act 2002 (NSW) |

Clarence 104 | Clarence 104 Pty Ltd, the thirteenth respondent and registered proprietor of the Clarence 104 Property |

Clarence 104 Property | The property located at 104/50 Clarence Street, Sydney NSW 2000 |

Code of Ethics | Code of Ethics for Professional Accountants (APES 110) |

Coombes Contractors | Coombes Contractors Consulting C Pty Ltd, being the trustee of the Coombes Trust |

Corporations Act | Corporations Act 2001 (Cth) |

CC Act | Competition and Consumer Act 2010 (Cth) |

CSSS Holdings | CSSS Holdings Pty Ltd |

CTD | Charm Team Development Ltd, a company incorporated in Hong Kong and the fourth respondent |

CTD Account | The ANZ bank account in the name of CTD, being BSB 012 071 and account number 2327 21923 |

DC Rd | DC Rd DC Pty Ltd, the first applicant |

DC Rd Proceeds (or DCP) | The net proceeds of $33,232,962 from the Back-to-Back Contracts received by 30 Denham |

Denham Court Property | The property located at 30 Denham Court, Denham Court NSW 2565, comprising about 82 hectares of land |

Deposit | The deposit of $4.5 million paid on or about 18 July 2019 by DC Rd for the purchase of the Denham Court Property |

DSZ Accountants | DSZ Accountants Pty Ltd, the sixteenth respondent, and registered proprietor of the DSZ Clarence Street Properties |

DSZ ANZ Loan Account | A loan account with the ANZ in the name of DSZ Accountants in its own capacity and as trustee for DSZ Partners Trust, being BSB 012 402 and account number 4005 29026 |

DSZ ANZ Mortgage | The mortgage granted over the DSZ Clarence Street Properties |

DSZ Clarence Street Properties | The properties situated at 78, 105 and 106/50 Clarence Street, Sydney NSW 2000 |

East Kurrajong Development | The development of 132 Irwins Road, East Kurrajong NSW 2758 and 157, 159–283 and 300 Irwins Road, Blaxlands Ridge NSW 2758 |

Elton Report | Draft Report by Elton Consulting in relation to the Denham Court Property dated 26 June 2019 |

EOI | Expression of Interest |

Evidence Act | Evidence Act 1995 (Cth) |

FCA Act | Federal Court of Australia Act 1976 (Cth) |

FCA Interest Rates | The rates set out in para 2.2 of the Interest on Judgments Practice Note (GPN-INT) issued on 18 September 2017 |

First Contract | The contract for the purchase of the Denham Court Property for $14 million plus GST between 30 Denham and Khengs dated 25 July 2019 |

First EOI | The EOI submitted by Tony on behalf of Vantager to purchase the Denham Court Property for $12 million plus GST on or about 4 July 2019 |

First Loan Agreement | Loan Agreement dated 15 July 2019 between 30 Denham and CTD |

FTA | Fair Trading Act 1987 (NSW) |

Harvest Land | Harvest Land Group Pty Ltd |

He Charis | He Charis Investments Pty Ltd |

Herbert Street Property | The property located at 48/20 Herbert Street, West Ryde NSW 2114 |

His Charis Investments | His Charis Investments Pty Ltd |

Howard 1 | Mr Howard’s first expert report dated 26 March 2025 |

Howard 2 | Mr Howard’s second expert report dated 26 September 2025 |

Howard 3 | Mr Howard’s third expert report dated 29 October 2025 |

HYG | Hong Yang Group |

ING | ING Bank (Australia) Ltd |

Investx | Investx Investments Pty Ltd |

Investx Holding | Investx Investments Holding Pty Ltd |

John | Mr Fan (John) He, the fourteenth respondent |

John 1 | John’s first affidavit dated 21 October 2025 |

John 2 | John’s second affidavit dated 16 December 2025 |

John Loan | The interest-free loan of $2 million advanced by Sit Family to John on 29 October 2019 for the purchase by John of the Warrawee Property |

Khengs | Khengs Pty Ltd, the registered proprietor of the Denham Court Property until its sale to 30 Denham |

KOB001 Pty Ltd ITF Cai & Li Family CBA Account 4601 | A CBA account in the name of KOB001 Pty Ltd ITF Cai & Li Family, being BSB 067 167 and account number 10914601 |

KPL | KPL Lawyers, the solicitors for 30 Denham in relation to the Back-to-Back Contracts |

Langkawi | Langkawi Investments Ltd, a company incorporated in the British Virgin Islands |

Lian | Ms Lian Li, the wife of Bob and the eleventh respondent |

Lian 1 | Lian’s first affidavit dated 9 August 2024 |

Lian 2 | Lian’s second affidavit dated 1 August 2025 |

Lian 3 | Lian’s third affidavit dated 16 December 2025 |

Lian ANZ Account 2964 | An ANZ bank account in the name of Lian, being BSB 012 306 and account number 6472 92964 |

Lian CBA Account 2814 | A CBA bank account in the name of Lian, being BSB 062 799 and account number 1359 2814, and an offset linked to the Arthur Street Property |

Lian CBA Account 7759 | A CBA bank account in the name of Lian, being BSB 062 799 and account number 1358 7759, and an offset account |

Lian CBA Account 7767 | A CBA bank account in the name of Lian, being BSB 062 799 and account number 1358 7767, and an offset account |

Lian NAB Account 2340 | A NAB bank account in the name of Lian, being BSB 082 062 and account number 8610 22340 |

Lian Parties | Lian, Saiala, Clarence 104, and DSZ Accountants |

Lian St George Account 7185 | A St George bank account in the name of Lian, being BSB 112 879 and account number 433587185 |

LIB | Lowest intermediate balance |

Link | Link Investments Ltd, a company incorporated in Hong Kong, and the fifth respondent |

Management WeChat Group | HYG Management Circle WeChat Group, which from 8 July 2019 included Phillip and his two sons (Stanley and Henry), John, Tony and Alice |

Miriam Park | Miriam Park West Ryde Pty Ltd |

Miriam Park Facility | Miriam Park’s loan facility with ING Bank |

Miriam Park Property | The property located at 4 and 6–8 Miriam Road, West Ryde NSW 2114 |

Newcastle Development | The development at 471 Hunter Street, Newcastle NSW 2300 |

Nguyen 1 | Mr Anh Nguyen’s first expert report dated 25 August 2025 |

Nguyen 2 | Mr Anh Nguyen’s second expert report dated 23 September 2025 |

Oasis | Oasis International Pty Ltd |

O’Connell Street Caddens | O’Connell Street Caddens Pty Ltd |

Perpetual Burwood | Perpetual Burwood Pty Ltd |

Perpetual DC Rd | Perpetual DC Rd DC Pty Ltd |

Perpetual Pymble | Perpetual Pymble Pty Ltd |

Phillip | Mr Fai Keung (Phillip) Sit, the fourth applicant, and the father of Stanley |

Phillip 1 | Phillip’s first affidavit dated 16 May 2024 |

Phillip 2 | Phillip’s second affidavit dated 8 October 2024 |

Phillip 3 | Phillip’s third affidavit dated 14 August 2025 |

Phillip 4 | Phillip’s fourth affidavit dated 18 November 2025 |

Phillip 5 | Phillip’s fifth affidavit dated 4 December 2025 |

Pleasant Land | Pleasant Land Pty Ltd |

PS Act | Professional Standards Act 1994 (NSW) |

Pymble Stage 1 Development | The development at 14 Park Crescent, Pymble NSW 2073 |

Pymble Stage 2 Development | The development at 16 Park Crescent, Pymble NSW 2073 |

QBI Burwood | QBI Burwood Pty Ltd |

Ryde Development | The development at 270–272 Quarry Road, Ryde NSW 2122 |

SAF | Statement of Agreed Facts |

Saiala | Saiala Holdings Pty Ltd, the twelfth respondent |

Saiala Property | The land located at 32 Saiala Road, East Killara NSW 2071 |

Scheme | CPA Australia Ltd Professional Standards (Accountants) Scheme |

Second Contract | The contract for the purchase of the Denham Court Property between 30 Denham and DC Rd for $45 million plus GST dated 25 July 2019 |

Second EOI | The EOI submitted by Tony on behalf of Vantager to purchase the Denham Court Property for $14 million plus GST on or about 12 July 2019 |

Settlement Sum | The amount of $30,162,735.03 paid by DC Rd pursuant to the Second Contract on or about 5 September 2019 |

Simultaneous Settlement | The completion of the First Contract and the Second Contract on 5 September 2019 |

Sit Family | Sit Family Pty Ltd, the third applicant |

SL2 | Secured Lending 2 Pty Ltd |

SL2 Facility | Loan Facility between Smithfield 40 and SL2 entered into on 27 September 2023 |

Smithfield 40 | Smithfield 40 Pty Ltd, the fifteenth respondent |

Smithfield Property | The property located at 40 Pavesi Street, Smithfield NSW 2164, which on 10 April 2024 was subdivided into Lots 1 to 33 and Common Property in Strata Plan 107847 |

Supp CB | Supplementary Court Book |

SPV | Special purpose vehicle |

Stanley | Mr Stanley Xue, the second applicant, and the son of Phillip |

Stanley 1 | Stanley’s first affidavit dated 19 May 2024 |

Stanley 2 | Stanley’s second affidavit dated 8 October 2024 |

Stanley 3 | Stanley’s third affidavit dated 17 November 2025 |

St George | St George Bank |

St George Arthur Street Loan Account | A home loan account with St George in the names of Bob and Lian for the Arthur Street Property, being BSB 112 912 and account number 2245 32700 |

St George Herbert Street Loan Account | A home loan account with St George in the name of Bob for the Herbert Street Property, being BSB 112 912 and account number 2285254000 |

TAS Act | Tax Agent Services Act 2009 (Cth) |

TECP Burwood | TECP Burwood Pty Ltd |

TECP Family | TECP Family Pty Ltd |

TECP Pymble | TECP Pymble Pty Ltd |

Tony | Mr Dong (Tony) Zhang, the first respondent |

Tony 1 | Tony’s first affidavit dated 8 August 2024 |

Tony Parties | Tony, Link, Belrose COB and Smithfield 40 |

Turramurra Property | The property located at 36 Warrangi Street, Turramurra NSW 2074, of which Lian is the registered proprietor |

Vantage Pymble | Vantage Pymble Pty Ltd |

Vantager | Vantager Group Pty Ltd (now known as HYG Development Pty Ltd) |

Vantager Burwood Development | Vantager Burwood Development Pty Ltd |

Vantager Construction | Vantager Construction Pty Ltd |

Vantager Development | Vantager Development Consolidation Group Pty Ltd (now known as Pacific Oasis Consolidation Group Pty Ltd) |

Vantager Esher | Vantager Esher Development Pty Ltd |

Vantager Pymble Development | Vantager Pymble Development Pty Ltd |

Vantager Pymble Park | Vantager Pymble Park Pty Ltd |

Vantager Pymble Park Development | Vantager Pymble Park Development Pty Ltd (now known as Sit Family Pacific Pymble Park Development Pty Ltd) |

Variation Agreement | Variation of Loan Agreement dated 30 July 2019 between 30 Denham and CTD |

Warrawee Property | The property located at 45 Cherry Street, Warrawee NSW 2074, of which John is the registered proprietor |

Yanquin Holdings | Yanquin Holdings Pty Ltd |

Introduction

2 These proceedings concern the purchase of the Denham Court Property by DC Rd. DC Rd is controlled by Stanley and Phillip and ultimately owned by Sit Family, as the trustee of the Sit Family Trust No 2. The directors of Sit Family are Stanley and Alice, his mother. Phillip is the father of Stanley and the husband of Alice.

3 On 25 July 2019, DC Rd agreed to purchase the Denham Court Property for $45 million plus GST. Phillip and Stanley were introduced to the Denham Court Property by Tony and John. John and Tony each made representations and, as I find in these reasons, omitted to disclose matters about the Denham Court Property, and its potential for development, to Phillip and Stanley, and accordingly to DC Rd.

4 At the time that DC Rd agreed to purchase the Denham Court Property on 25 July 2019, Bob (through his company, CATA) was Stanley, Phillip and DC Rd’s accountant, appointed by them on the recommendation of Tony. Bob (through CATA) was also Tony and John’s accountant, and had been since prior to 2016.

5 In the period from 2016 to 2019, Phillip had invested in a number of property developments with Tony and John (through the Vantager group) such that by the time Tony and John recommended the Denham Court Property to Phillip and Stanley, Phillip and Stanley trusted Tony and John and the representations they made about the Denham Court Property and its potential for development.

6 When purchasing the Denham Court Property, Phillip and Stanley were not aware of the following matters:

(a) Tony had already negotiated to purchase the Denham Court Property from Khengs for $14 million plus GST through a company incorporated for that purpose, 30 Denham. The director of 30 Denham was an associate of Bob’s, Mr Derrick De Souza;

(b) the Denham Court Property was sold by Khengs to 30 Denham by a contract which exchanged and settled simultaneously with DC Rd’s purchase from 30 Denham. Funds paid by DC Rd to purchase the Denham Court Property were used by 30 Denham to pay Khengs; and

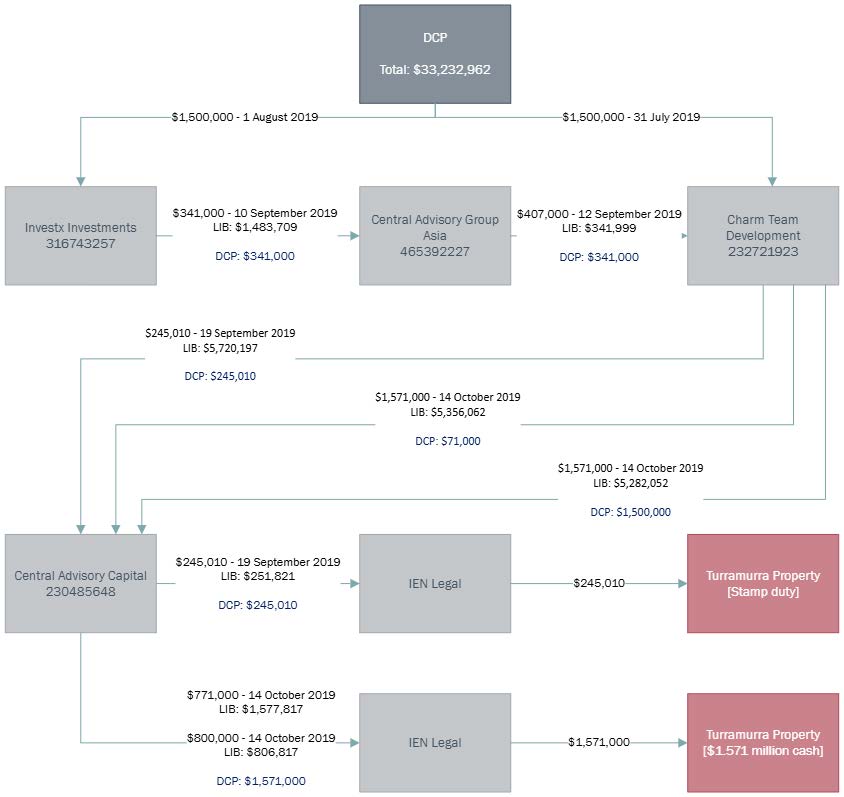

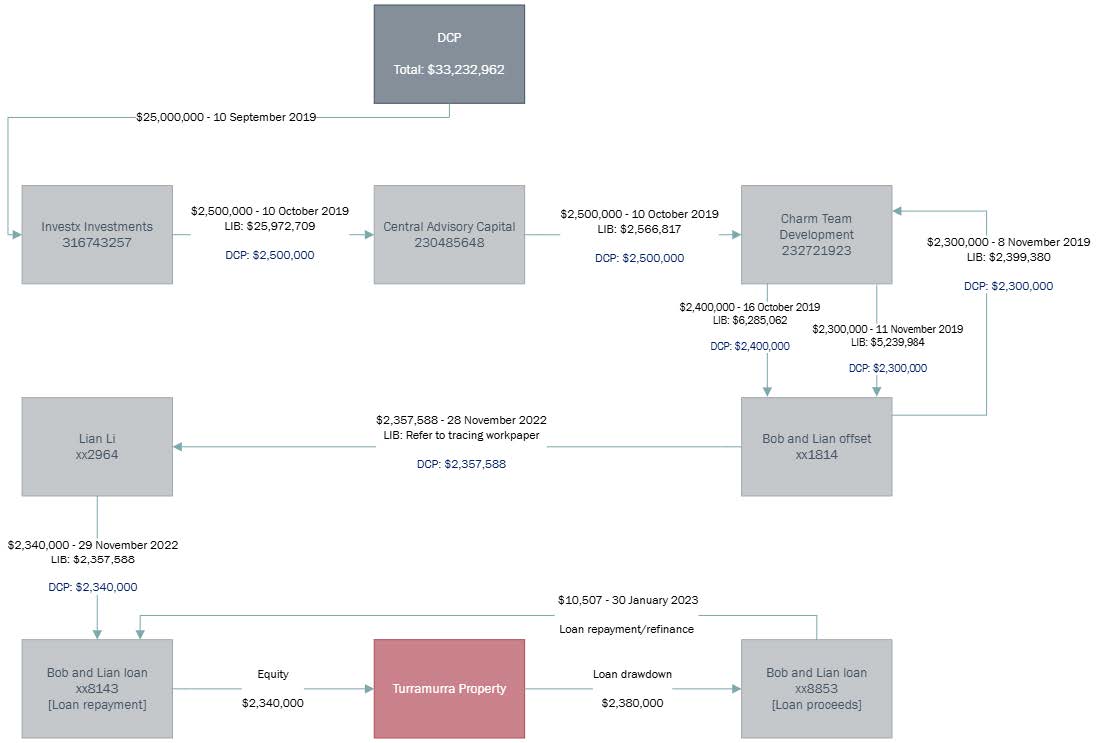

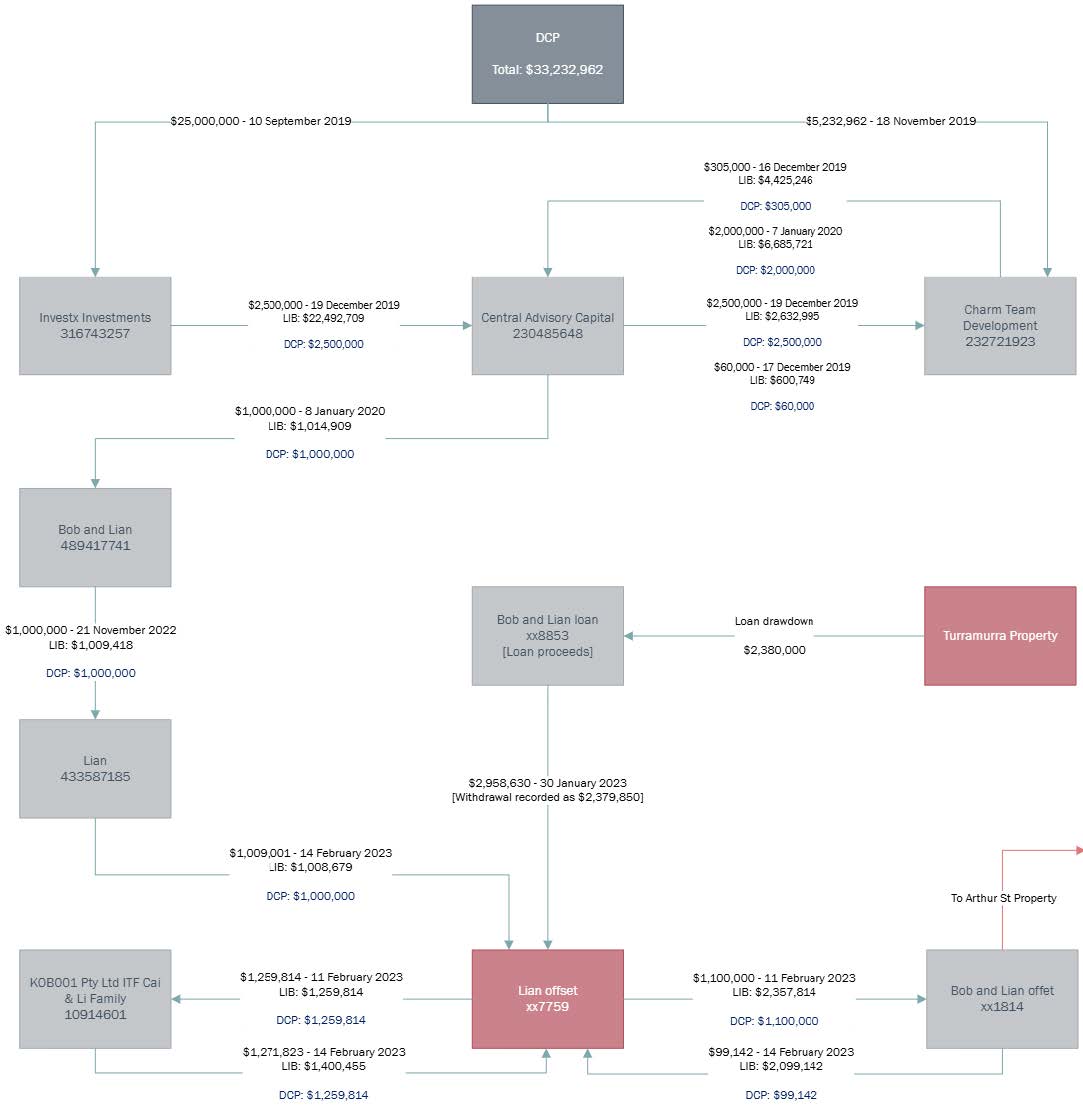

(c) the DC Rd Proceeds of about $33 million, being the difference between the $14 million plus GST paid by 30 Denham to Khengs and the $45 million plus GST paid by DC Rd to 30 Denham, were funnelled through entities controlled by Tony and Bob respectively:

(i) $26.5 million of the DC Rd Proceeds was transferred to Investx, a company controlled by Tony; and

(ii) $6,732,961 from the DC Rd Proceeds was paid to CTD, a company incorporated in Hong Kong and controlled by Bob.

7 The parties agree that, as at 25 July 2019, the Denham Court Property was not worth $45 million but was worth $10,800,000: Ex I. As at 2 April 2025 and 22 July 2025, the parties agree that the Denham Court Property was worth $15,312,500 (Ex I), although I do not regard the valuation at that date as relevant.

8 The Applicants contend that Tony, Bob and other entities (including 30 Denham as constructive trustee) breached fiduciary duties owed to the Applicants (or that Bob knowingly assisted Tony’s and 30 Denham’s breaches) by reason of their involvement in the Back-to-Back Contracts through which about $33 million was misappropriated from the Applicants and transferred to companies controlled by Tony and Bob. The Applicants seek equitable relief, including personal remedies (by way of equitable compensation and account) and proprietary remedies (by way of constructive trusts and equitable subrogation) in relation to assets acquired with the misappropriated funds.

9 The Applicants also contend that Tony, Bob and John engaged in misleading or deceptive conduct (including by omission) concerning the Denham Court Property and its development potential, on which Phillip, Stanley and DC Rd relied in entering the contract to purchase the Denham Court Property and thereby suffered loss.

10 That summary is intended to provide a very short overview of the matters dealt with in detail below. As the summary indicates, the case involves brazen fraud and dishonesty perpetrated by Tony through 30 Denham towards the Applicants, which even the most morally calloused reader will find breathtaking in its audacity. Bob knew of and assisted in Tony’s and 30 Denham’s fraud and dishonesty. In making findings as to those matters, I bear in mind the nature of the causes of action, the subject matter of the proceedings, and the gravity of the matters alleged: s 140 of the Evidence Act; Briginshaw v Briginshaw [1938] HCA 34; (1938) 60 CLR 336 at 362 (Dixon J). While John also acted wrongfully, the Applicants do not allege that he was fraudulent or dishonest, or that he knowingly assisted in Tony’s and 30 Denham’s fraud and dishonesty. For the reasons given below, the Applicants have succeeded in very large (but not complete) measure in seeking the relief which they claim. I should also emphasise at the outset that no issue has been raised concerning the competence or integrity of the two firms of solicitors engaged by the purchasers in the transactions, namely Dentons and KPL.

Credibility of Witnesses

11 I note at the outset that Tony did not give evidence. To the extent that I have drawn inferences against Tony, I have drawn them with greater confidence because Tony did not give evidence in circumstances where he was in a position to cast light on whether such inferences should be drawn: Jones v Dunkel [1959] HCA 8; (1959) 101 CLR 298 at 308 (Kitto J), 312 (Menzies J) and 320–21 (Windeyer J); Kuhl v Zurich Financial Services Australia Ltd [2011] HCA 11; (2011) 243 CLR 361 (Kuhl) at [63] (Heydon, Crennan and Bell JJ).

Stanley

12 I regard Stanley as an honest and credible witness. He accepted candidly that the quality of his memory of events in 2019 was variable, depending on how important matters were to him at the time: T93.11–15. In general, I accept his evidence. There was, however, an internal inconsistency in his evidence concerning what he recalls John saying in the voice call on 4 July 2019, as to which I prefer the evidence given in his affidavits over that given in cross-examination, as I explain at [110] below. I regard Stanley’s evidence as much more reliable than that of Bob or John where their evidence is in conflict.

Phillip

13 Phillip was an impressive witness, who was clear and precise in his evidence. He has an unusually good memory of the detail of events in 2019 and thereafter. Phillip showed some understandable frustration at times with the repetitious nature of some of his cross-examination, but I do not regard that as adversely affecting his credibility. There was, however, an inconsistency between the evidence in his affidavits and that given in cross-examination concerning what he recalls John saying on 3 and 4 July 2019, as to which I prefer Phillip’s affidavit evidence (see [108]–[110] below). I regard Phillip’s evidence as much more reliable than that of Bob or John where their evidence is in conflict.

Bob

14 I regard Bob as a thoroughly unreliable witness. His cross-examination was riddled with self-contradiction and inconsistency with his affidavits, his previous testimony in his public examination, and with contemporaneous documents sent to or by him. He refused to accept the plain and obvious meaning of a number of documents. He was evasive and non-responsive. His cross-examination descended into theatre of the absurd when he solemnly denied knowing who Phillip was in 2019 (T406.16–409.35), in direct contradiction of his affidavit evidence (for example, Bob 1 at [35] and [44]). That contradiction cannot be explained away by reference to confusion over Anglicised Chinese names, as Bob referred to Phillip by that name in his affidavits and those affidavits are presumably in Bob’s own words (except perhaps for matters of legal jargon which Bob had translated for him: T321.29–323.37). I also find that Bob gave knowingly false instructions to CTD’s solicitor when preparing a proof of debt in the winding up of 30 Denham to the effect that $4.5 million had actually been drawn down under the loan facility from CTD to 30 Denham: CB11/6861 and T472.22–477.2. In sum, Bob would say anything that he thought would be to his forensic or commercial advantage. I reject his evidence except where it was uncontroversial, or consisted of admissions against interest, or was corroborated by contemporaneous documents.

Lian

15 I do not regard Lian as a reliable witness. Lian gave implausible evidence as to her reaction to being served with freezing orders on 14 February 2023, to the effect that she did not read past the first page or look through the freezing orders and only wanted to understand the orders “very briefly”, despite being distressed by the orders and regarding them as a serious matter: T519.34–522.36. Lian also implausibly denied that Bob told her that the freezing orders related to a property transaction he had been involved in at Denham Court and an allegation that he had received money from the Back-to-Back Contracts: T522.41–523.2. Lian struck me as a shrewd, intelligent and financially sophisticated person who would have demanded an explanation from Bob, who in turn would probably have told her what had led to the freezing orders, namely the Back-to-Back Contracts and the use of DC Rd Proceeds. Further, as I discuss in detail below at [321]–[324], Lian’s evidence concerning the purported gift of $4.4 million from her mother-in-law is beset with difficulties.

John

16 John was also an unreliable witness, whose evidence I do not accept except where it is uncontroversial, consists of admissions or is corroborated by contemporaneous documents. He was hesitant before agreeing with propositions, was frequently evasive and non-responsive, and at times refused to accept the plain meaning of documents. There were inconsistencies between his affidavit evidence and his cross-examination concerning his recollection of events, and he had a poor memory of events and conversations in mid-2019 and generally. Indeed, he accepted that he had no real memory of the conversations on 3 and 4 July 2019: T597.1–20. An example of his lack of credibility was when he claimed in his cross-examination that Phillip had asked him and Tony to look for land banking in addition to development land (T548.33–549.12), which is not mentioned in his affidavits.

Cheng Lu, Hongguang (Steve) Shen, Mark Ma and Mario Quintiliani

17 These witnesses made affidavits which were read by the Bob Parties and the Lian Parties, but they were not required for cross-examination. In the absence of any challenge to their affidavit evidence, I accept that evidence.

Mr Andrew Howard and Mr Anh Nguyen

18 Mr Howard and Mr Nguyen were called as expert accountants in relation to tracing. I have relied heavily on Mr Howard’s tracing analysis in ways that were not the subject of any criticism by Mr Nguyen. It is not necessary for me to form a view as to their respective credibility as experts compared with each other. The main issue which divided them concerned the treatment of Lian’s claim for a beneficial interest in certain bank accounts, which does not arise on the factual findings which I have made at [321]–[327] below.

Mr Anthony Rowan, Mr David Lunney and Mr Galanos

19 Mr Rowan is an expert town planner, and Mr Lunney and Mr Galanos are expert valuers of real property. None of them were required for cross-examination, and I accept their evidence. The parties agreed to adopt the mid-point between the respective opinions as to the value of the Denham Court Property as an agreed fact: Ex I; see [7] above.

Relevant persons and entities

The Sit family and their related entities

20 DC Rd was incorporated on 16 July 2019. Since 6 September 2019, DC Rd has been the registered proprietor of the Denham Court Property. The sole shareholder of DC Rd is Perpetual DC Rd: SAF [1].

21 Stanley is the sole director of DC Rd and Perpetual DC Rd: SAF [2].

22 Sit Family was incorporated on 14 March 2017. Sit Family is the sole shareholder of Perpetual DC Rd and is the trustee of the Sit Family Trust No 2. Stanley is also a director and shareholder of Sit Family: SAF [3]. Alice is the other director of Sit Family: Stanley 1 at [5].

23 Phillip is Stanley’s father and Alice’s husband. Phillip was born in Fujian Province in South–East China. He first travelled to Australia in 1992: Phillip 1 at [4], [9]. He moved his young family to Australia in 2001, but continued to operate his Chinese businesses between Australia and China from that time: Phillip 1 at [12]–[15]. Phillip has lived in Australia since 2021: Phillip 1 at [15].

24 Phillip is the director of Oasis, which was incorporated for the purpose of investing in property development in Australia during the period 2015 to 2023: Stanley 1 at [4]; CB14/8673. It was through Oasis that Phillip invested in his first Sydney property development project in Ryde with Tony and John (referred to below at [59]–[61]).

Tony and his related entities

25 Tony and John founded the Vantager group of companies in about 2016, which identified and developed properties for profit: SAF [5].

26 In this capacity, Tony was a director of Vantager from 3 August 2016 to 30 July 2019 and Vantager Development from 11 May 2018 to 30 July 2019: SAF [6].

27 Tony was also the sole director and shareholder of TECP Family, which held 50% of the shares in Vantager, Vantager Development and Capitive until 30 July 2019. Tony was also the sole director and shareholder of FS Vantager Pty Ltd (now deregistered), which held 50% of the shares in Vantager Development and Capitive until 30 July 2019: SAF [7].

28 Investx and Investx Holding were incorporated on 18 July 2019. Until at least 30 July 2020, Tony was the sole director of Investx and Investx Holding, Investx Holding was the sole shareholder in Investx and Tony was the sole shareholder in Investx Holding: SAF [8].

29 Link was incorporated in Hong Kong on 10 September 2019. Tony is the sole director of Link. Tony is also the sole director of Langkawi, a company incorporated in the British Virgin Islands, which is the sole shareholder of Link: SAF [9]. At the time of the incorporation of Link, CAGA was its company secretary: Supp CB2/769 at 772. Bob was a (or the) director of CAGA at the time (as indicated by his resignation as director in a notice filed on 7 December 2022 but purportedly, and I find (at [38]) falsely, dated 1 October 2022: CB12/7619).

30 Belrose COB was incorporated on 16 April 2020. Belrose COB is, and since 13 October 2020 has been, the registered proprietor of the Belrose Property. Tony is the sole director of Belrose COB and, until at least 27 January 2023, was its sole shareholder: SAF [10].

31 Smithfield 40 was incorporated on 2 November 2021. Smithfield 40 was the registered proprietor of the Smithfield Property until 10 April 2024, at which time the land was subdivided into Lots 1 to 33 and Common Property in Strata Plan 107847. Tony and John are the directors of Smithfield 40: SAF [11].

Bob, Lian and their related entities

32 Bob is a certified practising accountant and chartered tax adviser. He is, and has been at all times relevant to the allegations made against the respondents in the 4FASOC, a member of CPA Australia who held a current public practice certificate issued by CPA Australia. Bob is also a member of NTAA Plus Ltd and The Tax Institute and is registered with the Tax Practitioners Board: SAF [12].

33 Tony met Bob in around 2015 through a mutual business acquaintance (Bob 1 at [22]), and since that time Tony has engaged Bob to establish companies and unit trusts for Tony and John and to attend to the accounting work for those companies: Bob 1 at [23]. Bob was also introduced to John in 2016: Bob 1 at [23]. Shortly afterwards, in 2017, Bob’s accountancy company, CATA, attended to the incorporation of various entities and trusts on behalf of the Sit family on the instructions of John, including Sit Family itself: Bob 1 at [38]–[39]; CB13/7840–7842.

34 Bob is, and has been since 31 December 2019, a registered proprietor of the Arthur Street Property. Bob is, and has been at all times relevant to the allegations made against the respondents in the 4FASOC, the registered proprietor of the Herbert Street Property: SAF [13].

35 CAG was incorporated on 27 May 2013, and Bob is the sole director of CAG: SAF [14]. CAG has never traded: Bob 1 at [15]. The Applicants submit that Bob has previously admitted that CAG is a vehicle through which he operates a business (citing his public examination at CB13/7834, lines 14–17), but the relevant question was put by reference to “an organisation known as the Central Advisory Group”, which is also the second registered business name of CATA (see at [39] below), and I regard Bob as having understood the question to relate to CATA rather than to CAG. There is thus no evidence that CAG has ever traded.

36 CTD was incorporated in Hong Kong on 12 June 2015, and Bob was the sole director and shareholder of CTD until at least 15 June 2022: SAF [15]. The Applicants submit, and I accept, that any changes in control of CTD were not effected until 28 November 2022, being the date on the relevant form which was filed on 7 December 2022: CB12/7654, 7656.

37 CAC was incorporated on 18 August 2017. Bob is the sole director of CAC. The sole shareholder of CAC is CIA. Bob is the sole director and shareholder of CIA: SAF [16].

38 CAGA was incorporated in Hong Kong on 25 April 2016. Bob was the sole director and shareholder of CAGA until at least 1 October 2022: SAF [17]. Given that the document recording Bob’s resignation as a director purportedly on 1 October 2022 was not lodged until 7 December 2022 (CB12/7619), it was probably back-dated.

39 CATA operates an accounting practice under the registered business names “Central Accounting Taxation Advisory” and “Central Advisory Group”. CATA is also registered with the Tax Practitioners Board. Bob is the sole director and shareholder of CATA, as well as an employee: SAF [18]. From 2017 to 2024, CATA had about eleven staff (including Bob) and provided accounting services to about 1,900 clients per year: Bob 1 at [11]. In 2017 to 2019, Bob was not personally involved in the services which CATA provided to many of those clients: Bob 1 at [12]. I accept those aspects of Bob’s evidence. The evidence is also supported by Mr Shen’s unchallenged affidavit as to matters of general practice by Bob. Bob’s primary role within CATA was to create and maintain relationships with clients and referrers, and Bob says that he is only involved in complex accounting and tax work: Bob 2 at [13]. However, I do not accept that the last sentence was true of Bob and CATA’s approach to their work for the Applicants, as explained at [98]–[102] below.

40 At all times relevant to the allegations made against the respondents in the 4FASOC, CATA generated total fee income of $10 million or less in each financial year and held a professional indemnity insurance policy insuring it and its employees (including Bob) up to a limit of indemnity of $2 million for any one claim: SAF [19].

41 Bob is the husband of Lian. Lian is, and since 16 October 2019 has been, the registered proprietor of the Turramurra Property: SAF [20].

42 Saiala was incorporated on 15 March 2021. Saiala is, and has been since about 12 May 2021, the registered proprietor of the Saiala Property. The sole director of Saiala is Lian and its sole shareholder is Lian Studio Pty Ltd. The sole director of Lian Studio Pty Ltd is Lian and its sole shareholder is Lian Equity Pty Ltd. Lian is the sole director and shareholder of Lian Equity: SAF [21].

43 Clarence 104 was incorporated on 8 September 2021. Clarence 104 is, and since about 22 October 2021 has been, the registered proprietor of the Clarence 104 Property. The sole director of Clarence 104 is Lian and its sole shareholder is Pang Equity Investments Pty Ltd. The sole director of Pang Equity Investments and its sole shareholder is Pang Equity Pty Ltd. Lian is the sole director and shareholder of Pang Equity: SAF [22].

44 DSZ Accountants was incorporated on 8 November 2012. DSZ Accountants is, and has been at all times relevant to the allegations made against the respondents, the registered proprietor of the DSZ Clarence Street Properties. Lian is, and has been since at least 22 October 2022, the director of DSZ Accountants: SAF [23].

John

45 John has been an acquaintance of Phillip’s since John was a child. Phillip was close friends with John’s mother (a pastor) through their church in Fujian: Phillip 1 at [20]. Phillip and John became reacquainted in around 2008 in Australia: Phillip 1 at [21]. Phillip lent money to John in about 2012 to 2014 to purchase his first residential property development in West Ryde: Phillip 1 at [22]. Phillip later advanced John $2 million to purchase the Warrawee Property on an interest free basis and without any repayment date: Phillip 3 at [10]–[15]; John 1 at [64], [236]. John introduced Phillip to Tony in 2016: Phillip 1 at [23]. Phillip trusted John’s advice and judgment: Phillip 1 at [24].

46 John was a director of Vantager from 3 August 2016 to 30 July 2019. He was a director of Vantager Development from 11 May 2018 to 30 July 2019. He was a director of Capitive from 25 October 2018 to 30 July 2019. He was a director of Vantager Construction from 7 August 2019 to 30 March 2021. He is also (currently) the sole director and shareholder of He Charis, which held 50% of the shares in Vantager until 30 July 2019. He is also a director of Smithfield 40. John is the sole shareholder of Pleasant Land and has been its sole director since its registration on 11 December 2019: Supp CB3/1597–8. He is, and has been since 2 December 2019, the registered proprietor of the Warrawee Property: SAF [24].

The Vantager Group

Operation of the Vantager group of companies

47 From about 2016, Tony and John conducted a property development business through the Vantager group of companies. The Vantager group of companies included the following companies, which did not hold any land assets:

(a) Vantager, which was incorporated on 3 August 2016;

(b) Vantager Development, which was incorporated on 11 May 2018, to act as the ultimate holding company for each development management company. TECP Family was the sole shareholder of Vantager Development from incorporation until 15 January 2019, at which time TECP Family and FS Vantager became 50% shareholders;

(c) Vantager Pymble Development, which was incorporated on 11 May 2018 to manage the development (along with Vantager) of the Pymble Stage 1 Development and was wholly owned by Vantager Development;

(d) Vantager Pymble Park Development, which was incorporated on 11 May 2018 to manage the development (along with Vantager) of the Pymble Stage 2 Development and was wholly owned by Vantager Development; and

(e) Vantager Esher, which was incorporated on 11 May 2018 to manage the development of the Burwood Development and was wholly owned by Vantager Development: SAF [44].

48 The Vantager group of companies also included:

(a) Capitive, which was incorporated on 25 October 2018 and acted as the sales agent in respect of certain developments.

(b) Vantager Construction, which was incorporated on 9 July 2019 and provided construction services in respect of certain developments. Vantage Pymble as trustee for the Vantage Pymble Unit Trust entered into a written construction agreement on 30 September 2019 with Vantager Construction for construction of the Pymble Stage 1 Development: SAF [45]

(c) In addition, SPVs were incorporated to hold the land in respect of developments. The SPVs acted as corporate trustees of unit trusts in respect of the developments. Investors in each development would acquire shares in the SPVs and units in the unit trusts: SAF [46].

49 Ordinarily, the Vantager group of companies charged at least the following fees (SAF [47]):

(a) a development management fee; and

(b) a sales commission.

50 Vantager’s development management fee was usually 2% plus GST of total sales value, and the sales commission was usually 2.25% plus GST of each sale: Stanley 1 at [34]. Ordinarily, the Vantager group also charged a construction management fee usually of 10% plus GST of the construction cost: Stanley 1 at [34].

51 Prior to Stanley commencing work for the Vantager group of companies, Tony was primarily responsible for identifying properties for development, undertaking feasibility analysis, financial matters, researching zoning requirements, obtaining DA approval and marketing and sales, whereas John was primarily responsible for construction: SAF [48]. One of Tony’s roles was to identify potential properties for Phillip to purchase and provide details to Phillip, including the advantages and disadvantages and significant or important matters relating to potential properties for purchase: T538.46–539.19. As for John, the advice he gave Phillip sometimes extended beyond construction, such as in relation to East Kurrajong in August 2019: T540.24–542.21. As discussed below, at [105]–[110] and elsewhere, the Denham Court Property provides another example. In June 2019, Phillip wanted Tony and John to identify land that could be developed by subdivision, building and sale: T543.34–42.

52 The Applicants submitted that Vantager was not involved in any pre-acquisition activities in relation to properties, but only in the development and sale of properties once they were purchased, as a step towards their submission that Tony (rather than Vantager) owed duties to the Applicants in relation to the pre-acquisition phase. I reject that submission. It is contrary to the fact that Vantager was Elton Consulting’s client in Elton Consulting preparing and sending the Elton Report on 26 June 2019, about a month before contracts were exchanged for the Denham Court Property: CB8/4706. It was Vantager which paid Elton Consulting’s invoice: Ex F. It is also contrary to the agreed fact that on or about 4 July 2019, Tony submitted the First EOI “on behalf of Vantager” to purchase the Denham Court Property for $12 million plus GST (SAF [70]), and submitted the Second EOI on or about 12 July 2019 on behalf of “Vantager Group Pty Ltd or nominated”: SAF [71]. It is also contrary to the normal scope of operations of a “property development business”, as the business of the Vantager group of companies is described in SAF [44]. Indeed, it is an agreed fact that the Vantager group of companies not only developed properties for profit but also identified such properties: SAF [5].

53 Stanley commenced working for the Vantager group of companies (on around 5 July 2018), initially working three to four days a week (after he completed his university studies) before moving to full time shortly thereafter (SAF [49]: the bracketed words are established by Stanley 1 at [7] and Stanley 2 at [8]–[9].)

Investments by the Sit family in Vantager developments

54 Before 2021, Phillip spent most of his time living in China, travelling to Australia multiple times a year to visit his wife, Alice and their sons, Stanley and Henry: Phillip 1 at [15]. From 2016, Phillip began investing in Australian property development at the invitation of John, his long–term acquaintance. As noted above, John introduced Phillip to Tony: Phillip 1 at [23].

55 From about 2016 to around mid–2019, Phillip and Stanley invested (through entities associated with them) in the Ryde Development, Pymble Stage 1 Development, Pymble Stage 2 Development, Burwood Development, Caddens Development, East Kurrajong Development and Newcastle Development: SAF [50].

56 The investments referred to above were made by Sit Family, Oasis and other companies controlled by Phillip and Stanley:

(a) owning shares in SPV companies incorporated for the purpose of the developments; and

(b) owning units in unit trusts established for the purpose of the developments: SAF [51].

57 Tony, John, Phillip and Stanley held interests in the Ryde Development, the Pymble Stage 1 Development, the Pymble Stage 2 Development and the Burwood Development (through entities associated with them) and shared (or intended to share) in the profit from them. In addition, Phillip and Stanley (through Sit Family or Oasis) paid development management fees, construction fees and sales commissions in respect of these developments: Phillip 1 at [42], [49], [61].

58 As Phillip did not speak English very well, was spending most of his time in China and was not familiar with the Australian property market, he trusted John and Tony to make decisions about investing in and developing property in Australia: Phillip 1 at [24].

Ryde Development

59 The Ryde Development was the first project developed by Tony and John through Vantager: Phillip 1 at [23]. John introduced Phillip to the Ryde Development in 2016: Phillip 1 at [23]. The planning and development of the Ryde Development were undertaken by John and Tony through Vantager: Phillip 1 at [38].

60 In respect of the Ryde Development:

(a) the Ryde Development consisted of 10 residential townhouses located at 270–272 Quarry Road, Ryde NSW 2112;

(b) the His Charis Investments Trust was established for the purposes of the Ryde Development pursuant to a Unit Trust Deed made on 29 April 2016, with His Charis Investments as trustee. The His Charis Investments Trust and His Charis Investments were set up by CATA;

(c) the original unitholders of the units in the His Charis Investments Trust were He Charis and TECP Family, with one unit each. Subsequently, on 30 June 2016, further units were issued such that TECP Family held two units, He Charis held 3 units, Central Quarry (a company controlled by Bob) held one unit, the trustee for the Lunlun Chan Company Trust held two units and Oasis as trustee for the Pacific Oasis Trust held four units. Later, on 30 November 2018, Oasis became the sole unitholder in the His Charis Investments Trust when Oasis paid the unitholders the value of their original investment plus 10% and their units were cancelled;

(d) the original shareholders in His Charis Investments were TECP Family with two shares, He Charis with three shares, Oasis with four shares, Central Quarry with one share and Coria and Samuel Chan with two shares. Later, on 30 November 2018, the shareholding in His Charis Investments changed, such that TECP Family held two shares, He Charis held two shares and Oasis held four shares;

(e) His Charis Investments as trustee for the His Charis Investments Trust purchased the land the subject of the Ryde Development for $5.17 million. His Charis Investments entered into a loan facility with NAB for the Ryde Development in or about February 2017. Phillip also advanced funds to His Charis Investments for the Ryde Development by way of loan;

(f) the Ryde Development commenced in 2016 and was completed in 2020, with gross sales of around $15 million; and

(g) following the completion of the Ryde Development, John and Tony (through entities associated with them) received a total of 50% of the total profit derived from this development, by TECP Family receiving 50% of the profits of the project to be held on trust for John and Tony. The total profit was $540,000: SAF [53].

61 The other 50% of the profit was paid to Phillip’s benefit (presumably via Oasis), and Phillip had provided most of the $5.17 million for the purchase of the land, and most of the additional funds for the construction costs: Phillip 1 at [36], [38].

Pymble Stage 1 Development

62 In 2017, Tony and John asked Phillip if he would be interested in investing in a property development project at Pymble, which became the Pymble Stage 1 Development: Phillip 1 at [39]. Phillip agreed to invest 50% of the purchase price through Sit Family, on the understanding that Tony and John would provide the remaining 50%: Phillip 1 at [40], Stanley 1 at [24]. Tony and John undertook the development of the Pymble Stage 1 Development.

63 In respect of the Pymble Stage 1 Development:

(a) the Pymble Stage 1 Development consisted of 10 residential apartments located at 14 Park Crescent, Pymble NSW 2073;

(b) the Vantager Pymble Unit Trust was established for the purposes of the Pymble Stage 1 Development pursuant to a Unit Trust Deed dated 25 May 2017, with Vantage Pymble as trustee;

(c) the original unitholder of the Vantager Pymble Unit Trust was Sit Family as trustee for the Sit Family Trust No 2, with one unit. On 26 May 2017, one unit was issued to each of TECP Family as trustee for TECP Family Trust and He Charis as trustee for Charis Investments Trust. From 4 June 2017, the unitholders were TECP Family with five units, He Charis with five units, Sit Family with fifty units, and Naturalwell Commercial Pty Ltd with nineteen units. On 6 June 2017, ZL Investment Group Pty Ltd subscribed for nineteen units. On 21 June 2021, AUD Advance Alliance Pty Ltd as trustee for the Aus Advance Alliance Trust subscribed for two units;

(d) the original shareholder in Vantage Pymble was Sit Family with one share. Subsequently, from 26 May 2017, the shareholders were Sit Family with ten shares, TECP Family with nine shares and He Charis with one share. From 21 June 2018, Sit Family increased its shareholding to fifty shares, TECP Family decreased its shareholding to five shares and He Charis increased its shareholding to five shares. From 26 June 2018, AUD Advance Alliance Pty Ltd held two shares, Naturalwell Commercial Pty Ltd held 19 shares and ZL Investment Group Pty Ltd held nineteen shares;

(e) Vantage Pymble as trustee for the Vantager Pymble Unit Trust purchased the land the subject of the Pymble Stage 1 Development for $6.75 million. The Sit family contributed to that purchase price. A loan was obtained from ING to pay for the construction costs;

(f) the Pymble Stage 1 Development commenced in 2017 and was completed in 2021, with gross sales of around $19 million;

(g) Vantage Pymble as trustee of the Vantager Pymble Unit Trust entered into a written construction agreement on 30 September 2019 with Vantager Construction for construction of the Pymble Stage 1 Development;

(h) the final distribution of profits from the Pymble Stage 1 Development was governed by a Settlement Deed executed on 31 October 2022 to which Tony, John, Stanley, Vantager, Vantage Pymble, Sit Family and Sit Family Pacific Pymble Development Pty Ltd, amongst others, were parties; and

(i) all of the units in the Vantager Pymble Unit Trust and all of the shares in Vantage Pymble are presently owned by entities controlled by the Applicants: SAF [54].

64 Sit Family received approximately 50% of the $1.45 million profit: Phillip 1 at [44].

Pymble Stage 2 Development

65 In 2018, Tony and John invited Phillip to invest in another development project in Pymble, which became the Pymble Stage 2 Development. Phillip ultimately invested 60% of the purchase price through Sit Family, with other investors contributing the remaining 40%: Phillip 1 at [46]–[47]; Stanley 1 at [25].

66 In respect of the Pymble Stage 2 Development:

(a) the Pymble Stage 2 Development consisted of twenty residential apartments, located at 16 Park Crescent, Pymble NSW 2073;

(b) the Vantager Pymble Park Unit Trust was formed for the Pymble Stage 2 Development, with Vantager Pymble Park Pty Ltd as trustee, pursuant to a Unit Trust Deed dated 20 April 2018;

(c) the original unit holders of the Vantager Pymble Park Unit Trust were Perpetual Pymble Pty Ltd with five units, CSSS Holdings with one unit, Yanqin Holdings Pty Ltd with one unit, T&L Yang Pty Ltd with one unit and TECP Pymble with two units. By 25 July 2019, Perpetual Pymble held six units in the Vantager Pymble Park Unit Trust;

(d) the original shareholders in Vantager Pymble Park were Sit Family Pty Ltd with five shares from incorporation until 25 September 2017; TECP Family with one share from incorporation until 25 September 2017; He Charis with one share from incorporation until 25 September 2017; and Legend Investment 101 Pty Ltd with one share from incorporation until 23 April 2018. Subsequently, the shareholders in Vantager Pymble Park were Perpetual Pymble with five shares from 25 September 2017, which increased to six shares from 27 May 2019 and then to ten shares from 1 June 2022; TECP Pymble with one share from 25 September 2017 until 1 June 2022; QBI Pymble Pty Ltd with one share from 3 October 2017 until 23 April 2018; Yangqin Holdings with one share from 20 April 2018 until 1 June 2022; T&L Yang with one share from 20 April 2018 until 1 June 2022; and CSSS Holdings with one share from 20 April 2018 until 27 May 2019;

(e) Vantager Pymble Park as the trustee for Vantager Pymble Park Unit Trust purchased the land the subject of the Pymble Stage 2 Development for $14.5 million. The Sit Family contributed to that purchase price;

(f) the development commenced in 2018 and was completed in 2022, with gross sales of around $44 million;

(g) the final distribution of profits from the Pymble Stage 2 Development was governed by a Settlement Deed executed on 2 June 2022, to which Tony, John, Stanley, Vantager, Vantager Pymble Park, Vantager Construction, Sit Family Pacific Pymble Park Development, amongst others, were parties; and

(h) all of the units in the Vantager Pymble Park Unit Trust and all of the shares in Vantager Pymble Park are presently owned by entities controlled by the Applicants: SAF [55].

67 Sit Family received approximately 60% of the profit of about $2.8 million: Phillip 1 at [50].

Burwood Development

68 In early 2017, Tony and John identified an opportunity to enter into an option to purchase land in Burwood: Phillip 1 at [51]. Tony subsequently invited Phillip to join the Burwood Development inviting him to invest in a 1/3 share, with Tony and John also holding a 1/3 share each: Phillip 1 at [52]. Subsequently, it was agreed between Phillip, Tony and John that Phillip would have a 95% interest, with Tony and John holding 5%.

69 In respect of the Burwood Development:

(a) the Burwood Development consists of a site of approximately 1681 square metres located at 17–23 Esher Street, Burwood NSW 2134;

(b) the Burwood Development was acquired subject to a put and call option in 2017;

(c) the Vantager Burwood Development Unit Trust was formed for the Burwood Development, with Vantager Burwood Development as trustee, pursuant to a Unit Trust Deed dated 28 February 2017;

(d) by 25 July 2019, Sit Family held 95% of the units in the Vantager Burwood Development Unit Trust, with TECP Burwood and QBI Burwood each holding 2.5% of the units;

(e) Vantager Burwood Development had 200 shares, with 190 owned by Perpetual Burwood until 12 October 2022, when it acquired the five shares owned by TECP Burwood and QBI Burwood;

(f) the purchase price for the site at Burwood was approximately $22 million and was subject to a specified Floor Space Ratio. Settlement has not yet completed. Vantager Burwood paid an option fee of around $2.2 million; and

(g) all of the units in the Vantager Burwood Development Unit Trust and all of the shares in Vantager Burwood Development are presently held or owned by entities controlled by the Applicants: SAF [56].

Caddens

70 In early 2019, John and Tony identified a property for Phillip to purchase in Caddens. John told Phillip it was a good investment for Phillip (Phillip 1 at [57]), so Phillip proceeded with the purchase: Phillip 1 at [58]. The Caddens Development was the first property investment by Sit Family or Oasis without outside investors, but it was still to be developed by Tony and John through Vantager: Phillip 1 at [61].

71 In respect of the Caddens Development:

(a) the Caddens Development consists of properties located at 46–66 O’Connell Street, Caddens and 29 O’Connell Street, Caddens NSW 2747;

(b) the land the subject of the Caddens Development was purchased by O’Connell Street Caddens as trustee for the O’Connell Street Caddens Unit Trust for $28.2 million pursuant to a contract for sale dated 13 March 2019;

(c) the ultimate sole shareholder of O’Connell Street Caddens is Sit Family and the sole director is Stanley: SAF [57].

72 An additional fee of $1.8 million was paid for the acquisition of the Caddens Property, which Tony told Phillip was required to be paid as an agent’s fee. John and Tony took responsibility for the acquisition of the Caddens Property, including dealing with the agents (Savills) and lawyers: Phillip 1 at [58].

East Kurrajong Development

73 In mid–July 2019, Tony and John recommended to Phillip that he purchase properties in East Kurrajong: Phillip 1 at [59]–[60]. Phillip purchased the properties in East Kurrajong on Tony and John’s recommendation, and also on the basis that Vantager would undertake the development of the East Kurrajong Development: Phillip 1 at [61]–[62].

74 In respect of the East Kurrajong Development:

(a) the East Kurrajong Development consists of properties located at 132 Irwins Road, East Kurrajong NSW 2758 and 157, 159–283 and 300 Irwins Road, Blaxlands Ridge NSW 2758;

(b) the land the subject of the East Kurrajong Development was purchased by 132 Irwins Rd East Kurrajong as trustee for the 132 Irwins Rd East Kurrajong Unit Trust for $12.6 million pursuant to a contract for sale dated 9 August 2024; and

(c) the ultimate sole shareholder of 132 Irwins Rd East Kurrajong is Sit Family and the sole director is Stanley: SAF [58].

Newcastle Development

75 In around August 2019, Tony and John introduced Phillip to a property at 471 Hunter Street Newcastle 2300, which Phillip purchased through Sit Family: Phillip 1 at [140].

76 In respect of the Newcastle Development:

(a) the Newcastle Property consists of a property located at 471 Hunter Street, Newcastle 2300;

(b) the land the subject of the Newcastle Development was purchased by 471 Hunter Street Newcastle as trustee for the 471 Hunter Street Newcastle Unit Trust, for $5,250,000 pursuant to a contract for sale dated 13 August 2019; and

(c) the ultimate sole shareholder of 471 Hunter Street Newcastle is Sit Family and the sole director is Stanley: SAF [59].

Acquisition of Vantager group of companies

77 By 2019, Phillip had invested substantial sums in Vantager group developments, and as such he expected Tony and John to mentor Stanley in property development: Phillip 1 at [63], [66]. However, when Phillip returned to Australia at the end of June 2019, he formed the view that Tony and John were doing little to mentor Stanley: Phillip 1 at [66]–[69]. Phillip had a conversation with John about this, which Phillip recorded in his diary for 29 June 2019: Phillip 1 at [68], CB8/4744. Phillip’s diary notes indicate he said to John that the options included separating his dealings from Tony and John. Phillip was also unhappy about the payment of fees to Vantager, which he thought were excessive, and he expressed that unhappiness to Tony and John: Phillip 2 at [14].

78 On 1 July 2019, Phillip and John spoke again at Phillip’s home, at which time Phillip gave John options as to how their property dealings could continue: Phillip 1 at [69]–[70]. Ultimately it was agreed between Phillip, Tony and John on 2 July 2019 that Sit Family would acquire the Vantager group of companies and Tony and John would be paid an annual salary of $300,000 each for providing services to Vantager, together with a 20% share of the profits: Phillip 1 at [71]; Phillip 2 at [18]. That agreement was then documented in a set of minutes of a meeting between Phillip, Tony and John on 8 July 2019: CB8/4841.

79 Thus, in early July 2019:

(a) Phillip, John and Tony agreed that Sit Family would acquire the Vantager group of companies, including the shares held in Vantager, Vantager Development and Capitive by TECP Family and FS Vantager Pty Ltd: SAF [60(a)];

(b) as part of the acquisition, $300,000 per annum each was to be paid to Tony and John as a salary, as well as a 20% share of dividends: Phillip 1 at [71], [75]; and

(c) Tony was aware that Sit Family would be acquiring the interest he held in the Vantager group of companies through the shareholdings of TECP Family in Vantager and Vantager Development and the shareholding of FS Vantager Pty Ltd in Capitive: SAF [60(b)].

80 On 30 July 2019 the acquisition of the Vantager group of companies by Sit Family completed, such that:

(a) Sit Family became the sole shareholder of Vantager;

(b) Stanley became the sole director of Vantager;

(c) Sit Family became the sole shareholder of Vantager Development;

(d) Stanley became the sole director of Vantager Development;

(e) Sit Family became the sole shareholder of Capitive; and

(f) Stanley became the sole director of Capitive: SAF [61].

81 I note that that series of transactions took place five days after the Back-to-Back Contracts were entered into.

82 Following the acquisition, $300,000 per annum was paid to entities associated with each of Tony and John whilst they continued to provide services to Vantager. That can be inferred from the fact that the evidence does not reveal any complaint about the agreement to that effect not having been performed.

83 On 30 July 2019, Tony sent an email to Bob confirming the change in the Vantager group ownership: CB9/5581. Bob arranged the restructure: Phillip 1 at [76]–[78].

84 From 30 July 2019 to August 2021, the following properties were identified by Tony for potential purchase and/or development:

(a) 845 Pacific Highway, Chatswood;

(b) 5 Wongala Crescent, Beecroft;

(c) 211 Northumberland Street, Liverpool;

(d) 219–231 Botany Road, Waterloo;

(e) 727 & 731–733 Hunter Street, Newcastle West;

(f) 498 King Street, Newcastle West;

(g) 27–29 Argyle Street, Parramatta.

(h) 76–90 Evaline Place and 21–23 Claremont Street, Campsie NSW 2194; and

(i) 16–18 Wentworth Street, Parramatta: SAF [63].

Retainer of CATA

Retainer of CATA by Tony

85 From around 2013 or 2014 to January 2023, CATA provided accounting and taxation services to Tony and companies of which Tony was a director: SAF [64].

86 From around mid-2016 to January 2023, CATA provided accounting and taxation services to the Vantager group of companies: SAF [65].

Retainer of CATA by Sit Family

87 In around May or June 2019, Phillip and Stanley interviewed accountants in Australia to manage the affairs of Sit Family: Stanley 1 at [41]; Phillip 1 at [80]. One of the accountants recommended to Phillip by Tony was Bob (Phillip 1 at [82]), who at that time was the accountant for Tony, John and Vantager. A WeChat message recorded a meeting taking place between Tony, Phillip and Bob shortly after 6 May 2019: CB8/4644.