Federal Court of Australia

Australian Securities and Investments Commission v Australian Unity Funds Management Limited [2025] FCA 1679

File number: | VID 736 of 2025 |

Judgment of: | MOSHINSKY J |

Date of judgment: | 23 December 2025 |

Date of publication of reasons: | 30 January 2026 |

Catchwords: | CORPORATIONS LAW – distribution of financial products – target market determinations – where the defendant on 89 occasions issued interests in a fund to retail clients without requiring them to submit a completed questionnaire to enable determination of whether the applicants were within the target market – where the defendant on 239 occasions issued interests in a fund to retail clients without reviewing questionnaires submitted by the applicants to enable determination of whether the applicants were within the target market – where the defendant admitted to contravening s 994E(3) of the Corporations Act 2001 (Cth) – where ASIC and the defendant jointly proposed that the Court make a declaration of contravention and impose a pecuniary penalty of $7,125,000 – agreed declaration made and agreed penalty imposed |

Legislation: | Corporations Act 2001 (Cth), ss 761A, 761G, 764A, 766C, 912D, 994A-994Q, 1011B, 1317E, 1317G Trade Practices Act 1974 (Cth), s 76 |

Cases cited: | Australian Building and Construction Commissioner v Construction, Forestry, Mining and Energy Union [2018] HCA 3; 262 CLR 157 Australian Building and Construction Commissioner v Pattinson [2022] HCA 13; 274 CLR 450 Australian Competition and Consumer Commission v Cement Australia Pty Ltd [2017] FCAFC 159; 258 FCR 312 Australian Competition and Consumer Commission v Coles Supermarkets Australia Pty Ltd [2014] FCA 1405 Australian Competition and Consumer Commission v Coles Supermarkets Australia Pty Ltd [2015] FCA 330; 327 ALR 540 Australian Competition and Consumer Commission v Multimedia International Services Pty Ltd [2016] FCA 439; 243 FCR 392 Australian Competition and Consumer Commission v Murray Goulburn Co-Operative Co Ltd [2018] FCA 1964 Australian Securities and Investments Commission v American Express Australia Limited [2024] FCA 784 Australian Securities and Investments Commission v Austal Ltd [2022] FCA 1231 Australian Securities and Investments Commission v Australia and New Zealand Banking Group Ltd [2018] FCA 155 Australian Securities and Investments Commission v Australia and New Zealand Banking Group Ltd [2023] FCA 1150; 169 ACSR 649 Australian Securities and Investments Commission v AustralianSuper Pty Ltd [2025] FCA 102; 172 ACSR 615 Australian Securities and Investments Commission v Firstmac Ltd [2025] FCA 12 Australian Securities and Investments Commission v Hollista Colltech Ltd [2024] FCA 244 Australian Securities and Investments Commission v iSignthis Ltd (Penalty) [2025] FCA 917 Australian Securities and Investments Commission v MLC Nominees Pty Ltd [2020] FCA 1306; 147 ACSR 266 Australian Securities and Investments Commission v National Australia Bank [2025] FCA 947 Australian Securities and Investments Commission v Vanguard Investments Australia Ltd (No 2) [2024] FCA 1086 Australian Securities and Investments Commission v Westpac Banking Corporation [2019] FCA 2147 Australian Securities and Investments Commission v Westpac Banking Corporation (No 3) [2018] FCA 1701; 131 ACSR 585 Chief Executive Officer of the Australian Transaction Reports and Analysis Centre v Westpac Banking Corporation [2020] FCA 1538; 148 ACSR 247 Commonwealth v Director, Fair Work Building Industry Inspectorate [2015] HCA 46; 258 CLR 482 Construction, Forestry, Mining and Energy Union v Cahill [2010] FCAFC 39; 269 ALR 1 Flight Centre Ltd v Australian Competition and Consumer Commission (No 2) [2018] FCAFC 53; 260 FCR 6 Mayfair Wealth Partners Pty Ltd v Australian Securities and Investments Commission [2022] FCAFC 170; 295 FCR 106 Minister for Industry, Tourism and Resources v Mobil Oil Australia Pty Ltd [2004] FCAFC 72; (2004) ATPR 41-993 NW Frozen Foods Pty Ltd v Australian Competition and Consumer Commission [1996] FCA 1134; 71 FCR 285 Singtel Optus Pty Ltd v Australian Competition and Consumer Commission [2012] FCAFC 20; 287 ALR 249 Trade Practices Commission v CSR Ltd [1991] FCA 762; (1991) ATPR 41-076 Volkswagen Aktiengesellschaft v Australian Competition and Consumer Commission [2021] FCAFC 49; 284 FCR 24 |

Division: | General Division |

Registry: | Victoria |

National Practice Area: | Commercial and Corporations |

Sub-area: | Regulator and Consumer Protection |

Number of paragraphs: | 124 |

Date of last submissions: | 18 December 2025 |

Date of hearing: | 25 November 2025 |

Counsel for the Plaintiff: | Dr MD Rush KC with Ms M Hardinge |

Solicitor for the Plaintiff: | Australian Securities and Investments Commission |

Counsel for the Defendant: | Ms WA Harris KC with Mr A Di Stefano |

Solicitor for the Defendant: | King & Wood Mallesons |

ORDERS

VID 736 of 2025 | ||

| ||

BETWEEN: | AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff | |

AND: | AUSTRALIAN UNITY FUNDS MANAGEMENT LIMITED (ACN 071 497 115) Defendant | |

order made by: | MOSHINSKY J |

DATE OF ORDER: | 23 DECEMBER 2025 |

THE COURT NOTES THAT:

In these declarations and orders:

Contravention Period means the period between 5 October 2021 and 5 October 2023.

Fund means the Australian Unity Select Income Fund (ARSN: 091 886 789).

Fund TMDs means the target market determinations that Australian Unity Funds Management Limited made for the Fund and published on 5 October 2021, 21 December 2022 and 24 May 2023.

Red-flag investors means the 144 investors referred to in paragraph 22 of the Statement of Agreed Facts dated 30 September 2025, being the subset of the 239 investors who were issued interests in the Fund in circumstances where their Questionnaires were not reviewed who provided at least one response that indicated they were not in the target market for the Fund.

THE COURT DECLARES THAT:

1. Pursuant to s 1317E(1) of the Corporations Act 2001 (Cth) (Corporations Act), the defendant contravened s 994E(3) of the Corporations Act by engaging in retail product distribution conduct during the Contravention Period in circumstances where it failed to take reasonable steps that would have resulted in, or would have been reasonably likely to have resulted in, the defendant’s retail product distribution conduct being consistent with the Fund TMDs, by:

(a) on 89 occasions, issuing interests in the Fund to retail clients without requiring them to submit, as part of their application, a completed questionnaire with answers to questions to determine whether they were within the target market described in the Fund TMDs; and

(b) on 239 occasions, issuing interests in the Fund to retail clients without reviewing submitted questionnaires that had been completed by them to determine whether they were within the target market described in the Fund TMDs.

THE COURT ORDERS THAT:

2. Pursuant to s 1317G(1) of the Corporations Act, the defendant pay to the Commonwealth of Australia a pecuniary penalty of $7,125,000 in respect of the contraventions of s 994E(3) of the Corporations Act referred to in the declaration set out above.

3. The pecuniary penalty referred to in paragraph 2 be paid within 30 days of the date of this order.

4. Pursuant to s 1101B(1)(a) of the Corporations Act, within 30 days of the publication of the Court’s reasons for judgment, the defendant publish, at its own expense, a written adverse publicity notice (Written Notice) in the terms set out in Annexure A to this order, by:

(a) for a period of no less than 90 days, maintaining a copy of the Written Notice, in font no less than 10-point, on the Australian Unity Wealth & Capital Markets website available in a prominent area of the following web address: https://www.australianunity.com.au/wealth (webpage); and

(b) sending a copy of the Written Notice to the last known email or postal address of each retail client referred to in paragraph 1(a) of the declaration above and the red-flag investors.

5. The defendant pay the plaintiff’s costs of the proceeding, as agreed or assessed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

MOSHINSKY J:

Introduction

1 The defendant (AUFM) is a public company registered under the Corporations Act 2001 (Cth) and a wholly-owned subsidiary of Australian Unity Limited (AUL), a mutual company with mutual capital instruments and simple corporate bonds listed on the Australian Securities Exchange. AUFM is a member of the Australian Unity group of companies (the Group), providing fund management services within the Group’s business platform known as “Wealth & Capital Markets”.

2 At all relevant times, AUFM:

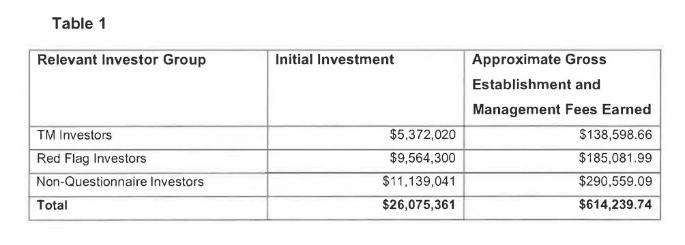

(a) held an Australian Financial Services licence which authorised AUFM, as a responsible entity, to operate registered managed investment schemes holding mortgages and incidental property; and

(b) was the responsible entity and investment manager for, and issuer of interests in, the Australian Unity Select Income Fund (the Fund).

3 The Fund was (and remains):

(a) a registered managed investment scheme under Ch 5C of the Corporations Act; and

(b) a contributory mortgage scheme, providing clients with an opportunity to invest in a range of syndicate-funds, each of which provides exposure to a specific registered first mortgage loan procured by Australian Unity’s Wealth & Capital Markets mortgages team.

4 It is common ground that an interest in the Fund is a “financial product” within the meaning of s 764A of the Corporations Act.

5 Between 5 October 2021 and 5 October 2023 (the Contravention Period), AUFM made three target market determinations (TMDs) for the Fund, on 5 October 2021 (First TMD), 21 December 2022 (Second TMD) and 24 May 2023 (Third TMD) (collectively, the Fund TMDs). The Fund TMDs defined AUFM’s target market for the Fund.

6 The plaintiff (ASIC) alleges, and AUFM admits, that:

(a) on 89 occasions, AUFM issued interests in the Fund to retail clients without requiring them to submit, as part of their application, a completed questionnaire with answers to questions to determine whether they were within the target market described in the Fund TMDs; and

(b) on 239 occasions, AUFM issued interests in the Fund to retail clients without reviewing submitted questionnaires that had been completed by them to determine whether they were within the target market described in the Fund TMDs.

7 ASIC alleges, and AUFM admits, that AUFM thereby contravened s 994E(3) of the Corporations Act by engaging in retail product distribution conduct in circumstances where it failed to take reasonable steps that would have resulted in, or would have been reasonably likely to have resulted in, AUFM’s retail product distribution conduct being consistent with the Fund TMDs.

8 The parties have prepared a statement of agreed facts dated 30 September 2025 (SOAF). The parties jointly propose that the Court make a declaration of contravention (to the effect of [6]-[7] above) and impose a pecuniary penalty of $7,125,000 on AUFM. It is also proposed that the Court make orders requiring AUFM to publish a notice about the Court’s decision and requiring AUFM to pay ASIC’s costs of the proceeding.

9 At the hearing of the application on 25 November 2025, I raised a concern that the SOAF did not provide an adequate explanation of how the contraventions happened. I also raised a concern that the material did not make clear whether any of the affected applicants had suffered loss as a result of the contraventions. A third concern was that a remediation plan had not yet been finalised. I indicated that I considered these matters to be relevant to the Court’s consideration of whether the proposed penalty was appropriate. The parties were given leave to file further material. Subsequently, AUFM filed an affidavit of Jose (Joe) Fernandes, Group Chief Investment Officer and Executive General Manager – Funds Management at AUL, dated 16 December 2025 (Fernandes Affidavit), which addressed these matters. ASIC did not seek to cross-examine Mr Fernandes on the affidavit. In response to a request from the Court, ASIC provided to my chambers a supplementary submission dated 18 December 2025 in which ASIC set out its position of AUFM’s proposed remediation plan. ASIC stated that it was satisfied that AUFM’s remediation plan was “an available approach”.

10 Following my consideration of that additional material, on 23 December 2025 I made a declaration and orders substantially in the terms proposed by the parties (including the imposition of a penalty of $7,125,000) and said that I would provide my reasons for judgment later. The following are my reasons for making the declaration and orders.

Legislative context

11 Part 7.8A of the Corporations Act (comprising ss 994A-994Q) imposes design and distribution obligations on distributors of financial products for retail clients (the DDO regime). The regime commenced operation on 5 October 2021.

12 The DDO regime was “designed to assist consumers to obtain appropriate financial products by requiring issuers and distributors to have a customer-centric approach to designing, marketing and distributing financial products”: Parliament of the Commonwealth of Australia, Revised Explanatory Memorandum for the Treasury Laws Amendment (Design and Distribution Obligations and Product Intervention Powers) Bill 2019, [1.5].

13 Broadly, Pt 7.8A requires certain persons to make a TMD by, among other things, identifying the class of retail clients that comprises the target market for their products.

14 Division 3 of Pt 7.8A deals with distribution of financial products. Within that division, s 994E broadly requires distributors to take reasonable steps to ensure that their “retail product distribution conduct” – which includes issuing a financial product – is consistent with their TMD in relation to that product.

15 During the Contravention Period, s 994E(3) provided:

If:

(a) a target market determination for a financial product has been made; and

(b) the product is on offer for acquisition by issue, or for regulated sale, to retail clients; and

(c) a regulated person engages in retail product distribution conduct in relation to the product; and

(d) the regulated person failed to take reasonable steps that would have resulted in, or would have been reasonably likely to have resulted in, the retail product distribution conduct being consistent with the determination;

the regulated person contravenes this subsection unless the retail product distribution conduct is excluded conduct.

…

Note 3: This subsection is also a civil penalty provision (see section 1317E). For relief from liability to a civil penalty relating to this subsection, see section 1317S.

16 The expression “reasonable steps” in s 994E(3)(d) was defined in s 994E(5):

Without limiting subsections (1) and (3), reasonable steps in relation to a person are steps that, in the circumstances, the person is reasonably able to take that will, or are reasonably likely to, result in retail product distribution conduct in relation to the financial product being consistent with the target market determination for the product, taking into account all relevant matters, including:

(a) the likelihood of any such conduct being inconsistent with the determination; and

(b) the nature and degree of harm that might result from an issue or regulated sale of the financial product:

(i) to retail clients who are not in the target market; or

(ii) that is inconsistent with the determination; and

(c) what the person knows, or ought reasonably to know, about:

(i) the matters referred to in paragraphs (a) and (b); and

(ii) ways of eliminating or minimising the likelihood and the harm; and

(d) the availability and suitability of ways to eliminate or minimise the likelihood and the harm.

Background facts

17 The following statement of the background facts is based on the SOAF and the Fernandes Affidavit. I accept the facts set out in the SOAF and the Fernandes Affidavit.

Preparation for the DDO regime

18 Prior to the commencement of the DDO regime on 5 October 2021, within the Group:

(a) there existed a DDO Steering Committee, which was a body with high-level oversight across the Group’s preparatory work for the commencement of the DDO regime (DDO Project), including the preparatory work of the Wealth & Capital Markets platform’s business; its members included the then-General Manager of Customer & Product, who was present at meetings during which the question of whether application questionnaires in general were needed was debated; and

(b) there existed a DDO Working Group, the role of which was readying relevant business units to comply with the DDO regime; its members included the Fund Product Manager and DDO Project Manager at the time.

19 At the time that the DDO regime commenced, AUFM had in place a draft Product Governance Framework, which set out AUFM’s policies with respect to compliance with the DDO regime.

Fund TMDs

20 As noted in the Introduction, during the Contravention Period, AUFM made three target market determinations for the Fund (referred to in these reasons as the “Fund TMDs”). Copies are annexed to the SOAF.

21 The Fund TMDs defined AUFM’s target market for the Fund by, firstly, identifying a potential class of consumers who may invest in the Fund by reference to their:

(a) investment objective (capital growth, capital preservation, capital guaranteed, or income distribution);

(b) intended use of the financial product as a percentage of the consumer’s investable assets (solution/standalone: 75-100%, core: 25-75%, or satellite/small: <25%);

(c) investment timeframe (short ≤2 years, medium >2 years, or long >8 years);

(d) risk and return profile (low, medium, high, or very high); and

(e) need to withdraw money (daily, weekly, monthly, quarterly, annually or longer).

22 Using this framework from the Fund TMDs, AUFM determined the types of consumers who were within, potentially within, or outside, the Fund’s target market, having regard to the nature and characteristics of the Fund itself. The results were then summarised in each Fund TMD.

23 The target market of the First TMD was summarised as follows:

This product is likely to be appropriate for a consumer seeking income distribution to be used as a satellite/small or a core component within a portfolio where the consumer has a medium or long investment timeframe, medium or high risk/return profile and needs annually or longer access to capital.

24 The target market of the Second TMD and Third TMD was summarised as follows:

This product is likely to be appropriate for a consumer seeking income distribution to be used as a satellite/small allocation within a portfolio where the consumer has a short, medium or long investment timeframe, high risk/return profile and needs annually or longer access to capital.

Application process and questionnaires

25 In order to acquire an interest in the Fund, prospective investors were required to undertake an application process which involved the investor submitting an application form which could be completed online (Online Application) or by paper (Paper Application).

26 Where a prospective investor completed an Online Application during the Contravention Period, they were required to answer a series of questions titled “Target Market Criteria” (Online Questionnaire). These questions were intended to elicit information about whether or not the prospective investor fell within the Fund’s target market and whether the investment was therefore appropriate to their objectives, financial situation and needs.

27 During the Contravention Period, default responses would automatically populate the Online Questionnaire so that a prospective investor would be assessed as falling within the target market of the Fund if the investor submitted the Online Questionnaire with the default responses. The Online Questionnaire disclosed this to prospective investors as follows:

Please note if you don’t select at least one option, the form provides default answers which will assume the product is suitable for you / meets your investment objective.

28 The SOAF states at [19] that where a prospective investor completed a Paper Application prior to 30 September 2022, they were not provided with any questionnaire which assessed whether they fell within the Fund’s target market. The SOAF does not explain why a paper questionnaire was not provided.

29 Where a prospective investor completed a Paper Application between 30 September 2022 and 5 October 2023, the Paper Application included a page titled “Target Market Determination Questions” (Paper Questionnaire). These questions were intended to elicit information about whether or not the prospective investor fell within the Fund’s target market and whether the investment was therefore appropriate to their objectives, financial situation and needs. The content of the Paper Questionnaire was substantively similar to that of the Online Questionnaire. The SOAF states at [20] that AUFM did not require prospective investors completing a Paper Application to complete the Paper Questionnaire as part of their application for an interest in the Fund. The SOAF does not explain why AUFM did not require the Paper Questionnaire to be completed.

30 The SOAF states at [21] that, despite receiving responses to the Online Questionnaire and the Paper Questionnaire (together, the Questionnaires) submitted by prospective investors, during the period between 5 October 2021 and 21 August 2023, AUFM did not review any of the responses to the Questionnaires. By way of partial explanation for AUFM’s failure to review the responses to the Questionnaires, the SOAF contains the following facts at [27]:

(a) AUFM provided staff training on the DDO regime in or around September or October 2021. The then-DDO Project Manager knew by at least 11 October 2021 that the team receiving responses to the Questionnaires had not been trained as to what to do with the information received. AUFM did not begin offering an online DDO compliance training module for its employees until around November 2022.

(b) AUFM’s failure to review the responses to the Questionnaires came to the attention of Wealth & Capital Markets’ Risk & Compliance team in or around November 2022. The matter was considered again when the then-Fund Product Manager and their supervisor, the then-General Manager of Customer & Product, completed an assessment in February 2023 in response to a request by AUL’s Group Audit team.

(c) An independent control test (or “ICT”) was conducted in February 2023 by a former Risk & Compliance Manager in the Risk & Compliance team, as part of regular assurance activities under Australian Unity’s Enterprise Risk Management Policy and Procedure.

(d) On 20 March 2023, AUFM’s then-Chief Executive Officer for the Wealth & Capital Markets business was informed that the product team for the Fund did not get data for the responses to the Questionnaires and therefore the outcome of the control self-assessment was “partially ineffective”.

(e) Following ICTs conducted in February and April 2023, in May 2023 it was recommended that the responses to the Questionnaire be reviewed.

31 The SOAF states at [28], and I accept, that the conduct in issue took place in the context of a newly introduced regulatory regime and AUFM’s conduct entailed a failure to implement appropriate systems and procedures to ensure compliance with its obligations under that regime; that is, it is not the case that AUFM deliberately failed to comply with the law.

32 The Fernandes Affidavit, at [25] and following, provides further details on the factors which Mr Fernandes believes led to the contraventions and explains why Mr Fernandes believes those factors have now been addressed by AUFM. Mr Fernandes states:

26. Through my review of documents, including the transcript of an examination of the then-DDO Project Manager conducted by ASIC on 29 May 2025 (transcript), and enquiries I have made, I believe that the contravention was due to competency and process deficiencies which I describe below, including a deficiency in training of relevant staff, in the context of a newly introduced regulatory regime. …

27. As appears from pages 6 to 7 and 27 to 28 of the transcript …, the then-DDO Project Manager, who was charged with delivery of the project for the establishment of AUFM’s DDO compliance regime at inception, did not have any prior experience in, and had not received any formal training on, the requirements of the DDO regime. While he received briefings from his direct supervisor and did his own research on what the new regime required, the lack of formal training in relation to this new regime was a clear process failure, which, I believe, in turn led to the then-DDO Project Manager not adequately understanding the purpose of the Questionnaires at the commencement of the DDO regime. As he said at page 56 of the transcript at line 25-26, “... I didn’t even consider the questions or application forms as part of DDO”. Nor did he seem to appreciate the relationship between the answers in the Questionnaires and AUFM’s TMD: see, for example, page 17 at line 37 to page 18 at line 11 of the transcript.

28. Further, and consequently, he did not appreciate that the team receiving responses to the Questionnaires ought to have been trained on what to do with them for the purposes of compliance with the DDO regime.

29. As set out in paragraph 27c of the [SOAF], the then-DDO Project Manager knew by at least 11 October 2021 that the team receiving responses to the Questionnaires had not been trained or instructed as to the significance of, or what to do with, the information received.

30. This problem was compounded by the fact that not only was this a new regime but because of deficiencies in [AUFM’s Product Governance Framework], there were insufficient documented procedures embedded into the organisation at the commencement of the DDO regime. This lack of documented procedures contributed to the situation whereby – notwithstanding that appropriate training was made available in respect of other matters referrable to the establishment of the DDO regime – the then-DDO Project Manager did not adequately understand the purpose of the Questionnaires, and therefore did not arrange for training for the team receiving the responses on their significance or what to do with them. Nor did he identify, or realise the significance of the fact that, for a time, Questionnaires were not provided with Paper Applications: see page 78 at line 45 to page 79 at line 20 of the transcript.

31. The former DDO Project Manager left the organisation in May 2023. As noted, while the immediate cause of AUFM’s failure to administer and/or review Questionnaires was a lack of knowledge of the requirements of the DDO regime and the significance of the processes required to comply with it, and consequential failures to arrange for training in the implementation of those processes, a key underlying cause was deficiencies in AUFM’s product and project governance architecture (both as to structure and implementation) and components of its control environment. In this regard, too much reliance was placed on the then-DDO Project Manager who was not in fact adequately supported to discharge the expectations of the organisation with regards to DDO compliance.

(Emphasis added.)

33 Insofar as Mr Fernandes provides evidence about improvements in AUFM’s processes and governance systems, I set out those aspects of his affidavit later in these reasons.

34 In or around August 2023, AUFM engaged a data entry specialist for the purpose of reviewing past responses to the Questionnaires submitted during the period between 1 October 2021 and 17 August 2023 (the Review). This data entry exercise and subsequent analysis led to the identification of responses to the Questionnaires which indicated that certain investors fell outside of the target market (see further below).

35 Between the completion of the Review and the end of the Contravention Period, AUFM received and did not review 16 Online Questionnaires and 1 Paper Questionnaire.

36 On 28 September 2023, AUFM lodged a breach report with ASIC pursuant to s 912D of the Corporations Act.

Summary of the contraventions

37 During the Contravention Period (5 October 2021 to 5 October 2023), 328 non-advised retail investors (the Relevant Investors) were issued with interests in the Fund. Of the 328:

(a) 89 investors had not completed a Questionnaire (Non-Questionnaire Investors); and

(b) 239 investors had completed a Questionnaire (Questionnaire Investors), but their responses had not been reviewed. Within this group:

(i) 144 investors had provided at least one response that indicated they were not in the target market for the Fund (Red Flag Investors);

(ii) the balance (95 investors) had not provided a response indicating they were outside the target market (TM Investors).

38 I note that, while the SOAF refers to 87 investors being in the category of Non-Questionnaire Investors, that figure has been revised to 89 in the Fernandes Affidavit: see the affidavit at [16]. Consequently, the total number of Relevant Investors is 328 rather than 326 (which is the figure that appears in the SOAF).

39 In relation to the Non-Questionnaire Investors, Mr Fernandes states at [13] of his affidavit that, because they did not submit a Questionnaire, it is impossible to tell whether they were outside the target market for the Fund. I take this to mean it is not practicable now to determine this.

40 It is an agreed fact, and I accept, that on each occasion that AUFM issued interests in the Fund to a retail client during the Contravention Period, it engaged in retail product distribution conduct within the meaning of s 994A of the Corporations Act.

Events subsequent to the Contravention Period

41 On 6 October 2023, AUFM lodged a second breach report with ASIC. On the same day, AUFM updated the Fund TMD to include new distribution conditions, which required AUFM to review responses to the Questionnaires prior to issuing interests in the Fund to prospective investors.

42 On 10 October 2023, AUFM lodged a significant dealing notification pursuant to s 994G of the Corporations Act.

43 Since October 2023, it has been compulsory for prospective investors to complete the Questionnaires as part of both a paper-based and online application.

44 From October 2023 to around June 2024, AUFM manually reviewed all responses to the Questionnaires. From 7 July 2024, knock-out questions were put in place for Online Questionnaires, meaning that a prospective investor cannot proceed with their Online Application if they provide a response which indicates they fall outside the target market. Since 7 July 2024, in respect of Paper Applications, Paper Questionnaire responses have been entered into AUFM’s systems manually by AUFM staff when they are received but, as with Online Applications, knock-out questions are in place such that if a prospective investor provides a response indicating that they fall outside the target market for the Fund, they are not issued interests in the Fund.

45 In June 2024, AUFM made further changes to the questionnaire process as detailed in [33] of the SOAF. At [34], the SOAF states that AUFM has made changes to uplift (or improve) its product governance framework.

46 In his affidavit, Mr Fernandes provides the following evidence about improvements in AUFM’s processes and governance systems:

26. … I consider the uplift in AUFM’s Product Governance Framework (PGF) (referred to below and in paragraphs 26c and 34 of the [SOAF]) and improvements in governance relating to project management and delivery within W&CM (which I explain further in paragraph 37 below) has substantially mitigated the possibility of a recurrence of the contravention in other organisational contexts within W&CM and/or AUFM.

…

32. W&CM has since then [i.e. since May 2023] appointed a full-time employee who holds the role of Product Governance Lead & DDO Officer. This staff member is appropriately experienced, legally qualified, and has received training on the DDO. This role involves supporting the W&CM business in respect of DDO compliance and the provision or the procuring of DDO related advice as needed. Further, and more broadly, the organisation has now embedded procedures in the (uplifted) PGF, which applies across product governance and is not limited to DDO. In this regard, for the purposes of the PGF, W&CM allocates accountabilities to the various phases of the product lifecycle as follows: Product Design - Senior Product & Innovation Manager and the General Manager, Strategy Execution; Product Distribution – General Manager, Distribution & Marketing; and Product Monitoring: General Manager, Operations.

33. As noted at paragraph 34 of the [SOAF], significant uplifts have already been made to the PGF addressing, amongst other things, the lack of documented procedures which contributed to the failure to arrange for training of the team who reviewed Questionnaire responses and the omission of the Questionnaire from paper-based application forms. A further, substantially uplifted version of the PGF was most recently adopted across the organisation on 8 September 2025. All staff in W&CM were informed via email of the uplifted PGF on 10 September 2025, and training for teams within W&CM was delivered in October and November 2025.

34. The PGF:

(a) comprises a High-Level Description document, Product Design Stage Procedures document, Distribution Stage document and Monitoring Stage Procedures document. Together these documents set out the framework for the governance lifecycle of all products issued by W&CM businesses, including that of AUFM; and

(b) is, amongst other things, intended to support all relevant stakeholders within W&CM by providing a detailed understanding around each stage of the product lifecycle from design, distribution, and ongoing monitoring and review including in relation to the discharge of the significant dealing obligations under the DDO regime (that is, the obligations to notify ‘significant dealings’ in financial products which are not consistent with the [products’] target market determination). All relevant W&CM staff are required to complete a DDO Learning Management System module. The module was updated following the most recent uplift of the PGF to include specific information about the purpose of the PGF, staff responsibilities under the PGF, significant dealings, and the purpose of DDO legislation in terms of how W&CM products are designed and distributed to customers.

35. In addition, as referred to at paragraph 26 above, there have been improvements in governance relating to project management and delivery within W&CM. In this regard, there is now a Platform Steering Committee, the membership of which comprises … the W&CM Chief Executive Officer and the W&CM leadership team, as well as standing attendees from the Australian Unity Group, including the Australian Unity Group Risk & Compliance Manager, Group Chief of Audit and the Group Executive – Technology. This governance body provides greater discipline, oversight and control of the delivery of major projects within W&CM.

36. Further, I believe that the organisation has learned from this experience through a reinforced understanding of the importance of ensuring that, across the business, persons with appropriate competencies are appointed (especially to important governance and compliance roles), and are otherwise provided with appropriate training and support. With the changes implemented, I am confident that AUFM has taken all reasonable steps to mitigate the risk of a recurrence of the type of failure described above in this affidavit.

Harm to consumers and benefit to AUFM

47 The SOAF states at [39] that during the Contravention Period, AUFM accepted initial investments of up to $9,564,300 into the Fund from investors who had returned responses to the Questionnaires indicating that they may have been, or were, outside the Fund’s target market (i.e. the 144 Red Flag Investors). The SOAF states that further amounts were invested by the investors who did not return a Questionnaire (i.e. the Non-Questionnaire Investors) but the amount does not appear in the SOAF.

48 The SOAF states at [40] that these investors (i.e. the Red Flag Investors and the Non-Questionnaire Investors) were exposed to the risk that they might have obtained a financial product that was not appropriate to their objectives, financial situation or needs, and to the risk of financial loss; that is, while all investments are subject to the risk of loss (assuming they are not capital-guaranteed) or lower-than-expected returns, AUFM’s contraventions may have resulted in particular investors being exposed to greater risk than they were suited to.

49 The SOAF states at [41] that AUFM benefited from these investments by receiving application and management fees (which were paid by borrowers, not investors in the Fund) and gaining an increased ability to capitalise loans within the Fund. The gross application and management fees generated over the Relevant Period from the $9,564,300 in initial investments (that is, investments from the Red Flag Investors) is estimated to be approximately $174,630.88. The SOAF states that additional fees were earned from the investors who were not required to complete a Questionnaire (i.e. the Non-Questionnaire Investors) but these are not set out in the SOAF.

50 The Fernandes Affidavit provides further information about these matters. At [14], the affidavit provides the following details of the initial investments and the establishment fees (or application fees) and management fees for each cohort:

51 The Fernandes Affidavit explains at [15] that, upon further analysis, the correct figure for the fees earned from the Red Flag Investors is approximately $185,081.99 rather than the $174,630.88 figure referred to in the SOAF.

52 Mr Fernandes deals with the historical performance of the Fund since December 2014 at [19]-[20] of his affidavit. Then, at [21] and following, Mr Fernandes deals with the performance of the Fund during the Contravention Period insofar as it affected Relevant Investors. The focus of the analysis in the affidavit is the Red Flag Investors and the Non-Questionnaire Investors (a total of 233 investors). I consider this to be a logical approach because those investors either were or may have been outside the target market. Conversely, the TM Investors do not appear to have been outside the target market. The analysis is set out in Table 3 of the affidavit. In [24] of his affidavit, Mr Fernandes provides a summary and explanation of Table 3. The endpoint of the analysis is as follows:

Red Flag Investors and Non-Questionnaire Investors did not necessarily invest solely in the Syndicate-Funds that are treated as non-performing for the purpose of Table 3 (being Syndicate-Funds 621 and 633). Rows 12-13 show that, when accounting for the distributions that those investors received in relation to the Fund as a whole (that is, from all Syndicate-Funds in which they invested and not limited only to Syndicate-Funds 621 and 633), only 1 investor account incurred an overall loss. The total of this loss is estimated to be $88,812. This investor is a Non-Questionnaire Investor so it is not clear whether they were within the target market for the Fund.

(Emphasis added.)

AUFM’s remediation plan

53 The Fernandes Affidavit sets out (at [37] and following) details of AUFM’s customer remediation plan. The plan was developed after consultation with ASIC: see the affidavit at [39]. Under the plan, certain cohorts of investors will be able to obtain financial advice from a third party financial adviser. The groups of investors who will be able to participate in the remediation plan are the 144 Red Flag Investors and the 89 Non-Questionnaire Investors (together, Eligible Investors).

54 Mr Fernandes explains at [41] that the TM Investors will not be within the scope of the customer remediation plan because, although their Questionnaire responses were not reviewed prior to their investment in the Fund, a subsequent review of their Questionnaire responses found that they were within the target market for the Fund and so are not regarded as having been exposed to the risk of a product that was not suitable for them. I consider it reasonable for the remediation plan not to include the TM Investors.

55 Under the remediation plan, Eligible Investors will be able to seek financial advice about the following:

(a) in relation to those Eligible Investors who remain invested in the Fund, financial advice as to how to redeploy the amounts they currently have invested in the Fund after their current Syndicate-Fund investment(s) mature; and

(b) in relation to those Eligible Investors who are no longer invested in the Fund, but have not yet redeployed some or all of their previous investment in the Fund, how to redeploy those funds.

56 AUFM has engaged Bridges Financial Services Pty Ltd (Bridges Financial), which is part of the Insignia Financial Group, as the third party to provide financial advice under the remediation plan.

57 AUFM will pay Bridges Financial directly for the cost of the advice Bridges Financial provides to Eligible Investors within the scope of the remediation plan such that Eligible Investors who elect to participate in the customer remediation plan will not be out of pocket for doing so.

58 It will not be compulsory for Eligible Investors to participate in the remediation plan. Eligible Investors will have a period of 4 months from the date on which the adverse publicity notice is published to decide whether they wish to participate in the remediation plan and to notify AUFM of this. If an Eligible Investor’s investment matures after that time, they will still be able to participate in the customer remediation plan if they have informed AUFM of their desire to do so by that time (i.e. within the period of 4 months referred to earlier). That is, they do not have to obtain the remedial advice within the 4-month period; they are merely required to inform AUFM of their desire to do so.

59 If all Eligible Investors take up the opportunity for remedial financial advice, the total cost of the remediation plan to AUFM will be in the approximate range of $1,146,950 – $1,263,450.

Applicable principles

60 The following summary of the applicable principles is substantially based on the parties’ joint submissions.

Approach where parties to regulatory proceedings propose orders by consent

61 The proper approach to civil regulatory orders which are sought on an agreed basis is explained in Commonwealth v Director, Fair Work Building Industry Inspectorate [2015] HCA 46; 258 CLR 482 (FWBII). The High Court there reaffirmed the practice of acting upon agreed penalty submissions, as explained in NW Frozen Foods Pty Ltd v Australian Competition and Consumer Commission [1996] FCA 1134; 71 FCR 285 (NW Frozen Foods) and Minister for Industry, Tourism and Resources v Mobil Oil Australia Pty Ltd [2004] FCAFC 72; (2004) ATPR 41-993.

62 The plurality in FWBII emphasised the “important public policy involved in promoting predictability of outcome in civil penalty proceedings” which “assists in avoiding lengthy and complex litigation and thus tends to free the courts to deal with other matters and to free investigating officers to turn to other areas of investigation that await their attention”: at [46] per French CJ, Kiefel, Bell, Nettle and Gordon JJ. The plurality also noted that in civil proceedings there is generally “very considerable scope” for the parties to agree upon the appropriate remedy and for the court to be persuaded that it is an appropriate remedy: at [57]. Their Honours went on to state at [58]:

Subject to the court being sufficiently persuaded of the accuracy of the parties’ agreement as to facts and consequences, and that the penalty which the parties propose is an appropriate remedy in the circumstances thus revealed, it is consistent with principle and … highly desirable in practice for the court to accept the parties’ proposal and therefore impose the proposed penalty.

63 These principles are not confined to agreed submissions on pecuniary penalties but apply equally to agreement on other forms of relief. The High Court’s conclusions as to the desirability of acting upon agreed penalty submissions were made in the context of its broader recognition that civil penalties were but one of numerous forms of relief which a regulator could choose to pursue as a civil litigant in civil proceedings including by making submissions as to that relief: see FWBII at [24], [57]-[59], [63], [103] and [107]. This is consistent with the long-standing judicial support for agreed positions on declarations, injunctions and other relief in civil regulatory proceedings, having regard to the public interest explained in NW Frozen Foods at 291, 298-299.

64 In considering whether the agreed and jointly proposed penalty is an appropriate penalty, it is necessary to bear in mind that there is no single appropriate penalty. Rather, there is a permissible range of penalties within which no particular figure can necessarily be said to be more appropriate than another. The permissible range is determined by all the relevant facts and consequences of the contravention and the contravenor’s circumstances: see, for example, Australian Competition and Consumer Commission v Coles Supermarkets Australia Pty Ltd [2014] FCA 1405 (Coles Supermarkets) at [72], [75] per Gordon J. Where the penalty proposed by the parties is within the permissible range, the Court will not depart from the submitted figure “merely because it might otherwise have been disposed to select some other figure”: NW Frozen Foods at 291. In Australian Securities and Investments Commission v National Australia Bank [2025] FCA 947 (ASIC v NAB), Neskovcin J stated at [45]:

In considering whether the proposed agreed penalty is an appropriate penalty, the Court should generally recognise that the agreed penalty is most likely the result of compromise and pragmatism on the part of the regulator, and can be expected to reflect, amongst other things, the regulator’s considered estimation of the penalty necessary to achieve deterrence and the risks and expense of the litigation had it not been settled: Volkswagen Aktiengesellschaft v Australian Competition and Consumer Commission (2021) 284 FCR 24; [2021] FCAFC 49 at [129] (Wigney, Beach and O’Bryan JJ), referring to [FWBII] at [109] (Keane J).

65 In Coles Supermarkets, Gordon J noted at [72] that once the Court is satisfied that orders are within power and appropriate, it should exercise a degree of restraint when scrutinising the proposed settlement terms, particularly where both parties are legally represented and able to understand and evaluate the desirability of the settlement.

Principles concerning declaratory relief

66 ASIC seeks a declaration pursuant to s 1317E of the Corporations Act. That section requires the Court to make a declaration of contravention if the Court is satisfied that a person has contravened a civil penalty provision.

67 In Australian Securities and Investments Commission v Hollista Colltech Ltd [2024] FCA 244 at [45], Sarah C Derrington J observed in relation to s 1317E, referring to the decision of the Full Court in Mayfair Wealth Partners Pty Ltd v Australian Securities and Investments Commission [2022] FCAFC 170; 295 FCR 106 at [184] per Jagot, O’Bryan and Cheeseman JJ, that the “mandatory terms of the section necessarily override the discretionary considerations to which a court might otherwise have given weight, in declining to make a declaration”.

Principles concerning pecuniary penalties

68 At all relevant times, s 994E(3) of the Corporations Act was a civil penalty provision: see s 994E(3), Note 3. The Court therefore has power to order that AUFM pay a pecuniary penalty under s 1317G(1)(a) of the Corporations Act once it has made a declaration under s 1317E.

69 Parliament has left it to the Court to decide what penalty is “appropriate” in all the circumstances, having regard to the Court’s own independent opinion: Australian Securities and Investments Commission v MLC Nominees Pty Ltd [2020] FCA 1306; 147 ACSR 266 at [117] per Yates J. The fact that the regulator and the contravenor have agreed on a proposed penalty “is plainly a relevant and important matter which the Court must have regard to in determining an appropriate penalty”: Volkswagen Aktiengesellschaft v Australian Competition and Consumer Commission [2021] FCAFC 49; 284 FCR 24 at [131] per Wigney, Beach and O’Bryan JJ.

70 Section 1317G(6) of the Corporations Act provides that in determining the pecuniary penalty, the Court must take into account all relevant matters, including:

(a) the nature and extent of the contravention; and

(b) the nature and extent of any loss or damage suffered because of the contravention; and

(c) the circumstances in which the contravention took place; and

(d) whether the person has previously been found by a court (including a court in a foreign country) to have engaged in similar conduct.

71 It is well established that deterrence, both specific and general, is the primary purpose of civil penalties and that they are “primarily if not wholly protective in promoting the public interest in compliance”: FWBII at [55]; Australian Building and Construction Commissioner v Pattinson [2022] HCA 13; 274 CLR 450 (Pattinson) at [15] per Kiefel CJ, Gageler, Keane, Gordon, Steward and Gleeson JJ. A penalty must have the necessary “sting or burden” to secure “the specific and general deterrent effects that are the raison d’être of its imposition”: Australian Building and Construction Commissioner v Construction, Forestry, Mining and Energy Union [2018] HCA 3; 262 CLR 157 at [116] per Keane, Nettle and Gordon JJ. The penalty must be at a level that ensures that the penalty is not regarded as a “mere cost of doing business”: Australian Securities and Investments Commission v Australia and New Zealand Banking Group Ltd [2023] FCA 1150; 169 ACSR 649 at [96] per Beach J.

72 The High Court reiterated in Pattinson that it has long been recognised that “civil penalties are imposed primarily, if not solely, for the purpose of deterrence”: at [15]. In that case, the plurality cited with approval the statement of French J in Trade Practices Commission v CSR Ltd [1991] FCA 762; (1991) ATPR 41-076 (CSR Ltd) at 52,152 that the object of imposing civil penalties under s 76 of the Trade Practices Act 1974 (Cth) was to “attempt to put a price on contravention that is sufficiently high to deter repetition by the contravenor and by others who might be tempted to contravene the Act”. It is a question of balancing the need for deterrence against the need to avoid an oppressive penalty: Pattinson at [40].

73 In addition to deterrence and the matters listed in [70] above, the case law refers to the following “French factors” as relevant to assessing what is an appropriate penalty (see CSR Ltd at 52,152-52,153; NW Frozen Foods at 292-295; Pattinson at [18]):

(a) the size and financial position of the contravening company;

(b) the deliberateness of the contravention and the period over which it extended;

(c) whether the contravention arose out of the conduct of senior management or at a lower level;

(d) whether the contravenor has a corporate culture conducive to compliance with the law, as evidenced by educational programs and disciplinary or other corrective measures in response to an acknowledged contravention; and

(e) whether the contravenor has shown a disposition to co-operate with the authorities responsible for the enforcement of the law in relation to the contravention and taken steps to remediate.

74 The plurality in Pattinson relevantly observed at [19] that:

It may readily be seen that [the list of factors identified by French J in CSR Ltd] includes matters pertaining both to the character of the contravening conduct … and to the character of the contravenor … It is important, however, not to regard the list of possible relevant considerations as a “rigid catalogue of matters for attention” as if it were a legal checklist. The court’s task remains to determine what is an “appropriate” penalty in the circumstances of the particular case.

(Footnotes omitted.)

75 Additional factors that may be relevant to penalty include (see, eg, Australian Securities and Investments Commission v Westpac Banking Corporation (No 3) [2018] FCA 1701; 131 ACSR 585 at [49] per Beach J; Australian Securities and Investments Commission v AustralianSuper Pty Ltd [2025] FCA 102; 172 ACSR 615 (AustralianSuper) at [214] per Hespe J; Australian Securities and Investments Commission v iSignthis Ltd (Penalty) [2025] FCA 917 at [36] per McEvoy J):

(a) the existence within the contravenor of compliance systems, including provisions for and evidence of education and internal enforcement of such systems;

(b) remedial and disciplinary steps taken after the contravention and directed to putting in place a compliance system or improving existing systems and disciplining officers responsible for the contravention;

(c) whether the directors of the corporation were aware of the relevant facts and, if not, what processes were in place at the time or put in place after the contravention to ensure their awareness of such facts in the future;

(d) the extent of any profit or benefit derived as a result of the contravention; and

(e) whether the contravenor has been found to have engaged in similar conduct in the past.

76 The appropriateness of the amount of a penalty must be assessed by reference to the specific civil penalty provision which has been contravened in light of its context and purpose, and the objects of the relevant statute as a whole: Australian Securities and Investments Commission v Australia and New Zealand Banking Group Ltd [2018] FCA 155 at [22(5)] per Middleton J.

77 The process of having regard to the various relevant factors in deriving a penalty figure has been described in many cases as one of intuitive synthesis: see, eg, Australian Competition and Consumer Commission v Murray Goulburn Co-Operative Co Ltd [2018] FCA 1964 at [36] per Beach J. The process requires a holistic consideration of all factors taken together, rather than the consideration of each factor in a sequential, mathematical process (such as starting from some pre-determined figure and making incremental additions or subtractions for each separate factor).

78 Pursuant to s 1317G(2) of the Corporations Act, a pecuniary penalty must not exceed the maximum pecuniary penalty applicable to the contravention of the relevant civil penalty provisions.

79 Section 1317G(4) of the Corporations Act sets out the relevant formula for the calculation of the applicable maximum. The value of a penalty unit changed during the course of the Contravention Period. The details are set out in the parties’ submissions at [50].

80 In this case, 89 of the contraventions occurred between 5 October 2021 and 30 September 2022, when retail clients who submitted a Paper Application did not submit a Paper Questionnaire. The other 239 contraventions occurred across the three periods in which the value of penalty units changed, although primarily within the first two of those periods.

81 The parties submit, and I accept, that in this case the relevant maximum penalty is to be calculated by reference to s 1317G(4)(a), rather than s 1317G(4)(b) or (c). That is because:

(a) as between the calculation methods in ss 1317G(4)(a) and (c), the application of s 1317G(4)(a) results in the “greatest” pecuniary penalty (for the reasons explained in the parties’ submissions); and

(b) it is not possible to precisely quantify the benefit derived and detriment avoided (per s 1317G(4)(b)).

82 The total maximum penalty in the present case is extremely large. Assuming (for the purposes of simplifying the calculation) that all contraventions occurred during the first part of the Contravention Period (when the value of a penalty unit was lowest), the total maximum penalty is approximately $3.6 billion.

83 It has been observed that in cases where there are a large number of contraventions, the theoretical maximum penalties may be so high as to become “practically meaningless”: Australian Securities and Investments Commission v Vanguard Investments Australia Ltd (No 2) [2024] FCA 1086 at [110] per O’Bryan J; ASIC v NAB at [59]. Nevertheless, the theoretical maximum penalties are relevant in at least a general sense in that they highlight the seriousness of the conduct in question: ASIC v NAB at [59].

84 In Pattinson, Kiefel CJ, Gageler, Keane, Gordon, Steward and Gleeson JJ considered that the statutory maximum penalty is but one yardstick that ordinarily must be applied, and must be treated as one of a number of relevant factors to inform the assessment of a penalty of appropriate deterrent value: at [53]-[55]. Their Honours rejected an approach that “[treated] the statutory maximum [penalty] as implicitly requiring that contraventions be graded on a scale of increasing seriousness, with the maximum to be reserved exclusively for the worst category of contravening conduct”: at [49].

85 Multiple contraventions may be treated as one or more “course of conduct” where there is an interrelationship between the legal and factual elements of each of the offences: see Construction, Forestry, Mining and Energy Union v Cahill [2010] FCAFC 39; 269 ALR 1 (Cahill) at [39] per Middleton and Gordon JJ. Whether separate contraventions should be treated as a course of conduct is a question of fact having regard to the circumstances of the case: Cahill at [39].

86 The “course of conduct” principle is a “tool of analysis” which can, but need not, be used in any given case: Cahill at [39]-[42]; Australian Competition and Consumer Commission v Cement Australia Pty Ltd [2017] FCAFC 159; 258 FCR 312 at [421]-[424] per Middleton, Beach and Moshinsky JJ.

87 Where the Court treats multiple contraventions as a single course of conduct, it does not follow that the maximum penalty for the course of conduct is limited to the maximum penalty for a single contravention, or that the Court must impose the cumulative total of each of the penalties: Australian Competition and Consumer Commission v Coles Supermarkets Australia Pty Ltd [2015] FCA 330; 327 ALR 540 at [15]-[16], [20], [84] per Allsop CJ. Rather, the course of conduct principle is “a tool to assist the Court in arriving at the appropriate penalty for the contraventions” (Australian Securities and Investments Commission v Westpac Banking Corporation [2019] FCA 2147 (ASIC v Westpac) at [268] per Wigney J), and the Court retains its discretion to impose the penalty that best reflects the seriousness of the conduct taken as a whole.

88 In determining the appropriate penalty for multiple related contraventions the Court will also have regard to the “totality” principle, as a final consideration of whether the cumulative total of the penalty is just and appropriate and not excessive having regard to the totality of the relevant contravening conduct: ASIC v Westpac at [272], [308]. It enables the Court to consider whether the final penalty is in proportion to the nature, quality and circumstances of the conduct involved. The Court may apply the principle to “alter the final penalties to ensure that they are just and appropriate”: Chief Executive Officer of the Australian Transaction Reports and Analysis Centre v Westpac Banking Corporation [2020] FCA 1538; 148 ACSR 247 at [69] per Beach J.

89 Differences in the facts and circumstances which underlie different cases mean caution must be exercised and there may be little to be gained by comparing the penalties imposed in other cases where the facts differ: see, eg, Singtel Optus Pty Ltd v Australian Competition and Consumer Commission [2012] FCAFC 20; 287 ALR 249 at [60] per Keane CJ, Finn and Gilmour JJ.

90 However, this does not mean that penalties imposed in other cases are never relevant: Australian Competition and Consumer Commission v Multimedia International Services Pty Ltd [2016] FCA 439; 243 FCR 392 at [123] per Edelman J. Comparable cases may give the Court some broad guidance: Flight Centre Ltd v Australian Competition and Consumer Commission (No 2) [2018] FCAFC 53; 260 FCR 68 at [69] per Allsop CJ, Davies and Wigney JJ. In Australian Securities and Investments Commission v Austal Ltd [2022] FCA 1231, O’Bryan J stated at [84]:

[T]he Court is not usually assisted by the citation of penalties imposed in other cases with different circumstances as establishing an appropriate “range” for the penalty to be imposed: Singtel at [60]. Nonetheless, assessments of penalty in analogous cases are capable of providing guidance to the Court in so far as they may ensure parity of treatment of similar circumstances: “there should not be such an inequality as would suggest that the treatment meted out has not been even-handed” (NW Frozen Foods Pty Ltd v Australian Competition and Consumer Commission (1996) 71 FCR 285 at 295; see also Australian Competition and Consumer Commission v Cornerstone Investment Australia Pty Ltd (in liq) (No 5) [2019] FCA 1544 at [55] per Gleeson J).

Adverse publicity orders

91 Section 1101B(1)(a)(i) of the Corporations Act gives the Court power to make any orders it thinks fit if, on the application of ASIC, it appears to the Court that a person has contravened a provision of Ch 7 of the Corporations Act, or any other law relating to dealing in financial products or providing financial services. This Court has accepted that power extends to the making of adverse publicity orders: see, eg, AustralianSuper at [250]-[254].

92 The purpose of adverse publicity orders is both punitive and protective (in the sense of dispelling incorrect or false impressions and/or alerting the public and customers to the fact of contravening conduct). Such orders serve to support the primary orders and prevent repetition of the contravening conduct: ASIC v NAB at [90]. In ASIC v NAB, Neskovcin J stated at [91]:

It is not uncommon for the Court to order that corrective notices or adverse publicity notices be mailed or emailed directly to affected persons and also be published on the contravener’s website –– doing so is more likely to bring the notice to the affected person’s attention than doing so solely via the contravener’s website: Australian Securities and Investments Commission v Colonial First State Investments Limited [2021] FCA 1268 at [86(d)] (Murphy J).

Consideration

Contraventions

93 I will first consider whether s 994E(3) was contravened in the present case.

94 As submitted in the parties’ joint submission, I am satisfied that each of the elements of s 994E(3) is made out here:

(a) s 994E(3)(a): AUFM made three TMDs during the Contravention Period.

(b) s 994E(3)(b): the product (being an interest in the Fund) was a financial product (as defined in ss 994A, 994AA(1)(a), and 761A), which was on offer for acquisition by issue to retail clients (as they are defined in s 761G).

(c) s 994E(3)(c): AUFM was a regulated person (as defined in s 1011B) because it was both an issuer of a financial product and a financial services licensee, and it engaged in retail product distribution conduct (RPD Conduct) in relation to the product (as defined in s 994A) by dealing in the product in relation to a retail client and, more particularly, by issuing the financial product to retail clients (see s 766C(1)(b)). Thus, on each occasion AUFM issued interests in the Fund to retail clients, it engaged in RPD Conduct.

(d) s 994E(3)(d): AUFM failed to take the reasonable steps to achieve the result required by s 994E(3)(d) as follows:

(i) on 89 occasions during the Contravention Period, by issuing interests in the Fund to retail clients who had applied by way of a Paper Application and had not been required to, and did not, submit a Questionnaire to determine whether the retail client was within the target market described in the Fund TMD; and

(ii) on 239 occasions during the Contravention Period, by issuing interests in the Fund to retail clients without reviewing submitted Questionnaires to determine whether the retail client was in the target market described in the Fund TMD.

95 Accordingly, I am satisfied that AUFM contravened s 994E(3) of the Corporations Act because it failed to take reasonable steps that would have, or would have been reasonably likely to have, resulted in its retail distribution conduct being consistent with its TMDs.

96 It is common ground that each of the 328 occasions on which AUFM issued interests in the Fund involved a separate contravention of s 994E(3).

Declaration

97 I will next consider whether it is appropriate to make the declaration proposed by the parties, namely:

Pursuant to s 1317E(1) of the Corporations Act 2001 (Cth) (Corporations Act), the defendant contravened s 994E(3) of the Corporations Act by engaging in retail product distribution conduct during the Contravention Period in circumstances where it failed to take reasonable steps that would have resulted in, or would have been reasonably likely to have resulted in, the defendant’s retail product distribution conduct being consistent with the Fund TMDs, by:

(a) on 89 occasions, issuing interests in the Fund to retail clients without requiring them to submit, as part of their application, a completed questionnaire with answers to questions to determine whether they were within the target market described in the Fund TMDs; and

(b) on 239 occasions, issuing interests in the Fund to retail clients without reviewing submitted questionnaires that had been completed by them to determine whether they were within the target market described in the Fund TMDs.

98 The two provisos in s 1317E(1) are established in this case. First, for the reasons set out above, I am satisfied that AUFM contravened s 994E(3) of the Corporations Act. Secondly, s 994E(3) of the Corporations Act is a civil penalty provision.

99 Finally, s 1317E(2) sets out what the declaration must specify. Relevantly for this proceeding, the proposed declaration which the parties have agreed satisfies the requirements of s 1317E(2) because it is a declaration which:

(a) is to be made by the Federal Court of Australia: s 1317E(2)(a);

(b) identifies s 994E(3) as the civil penalty provision that was contravened: s 1317E(2)(b);

(c) specifies that AUFM contravened s 994E(3): s 1317E(2)(c); and

(d) specifies the conduct of AUFM that constituted the contravention of s 994E(3): s 1317E(2)(d).

100 For these reasons, I am satisfied that it is appropriate to make a declaration in the terms proposed by the parties.

Penalty

101 For the reasons that follow, I consider that the total penalty proposed by the parties in respect of the admitted contraventions of s 994E(3) of the Corporations Act, namely $7,125,000, is appropriate.

Nature, extent and circumstances of the conduct

102 While AUFM’s contraventions of s 994E(3) took place in the context of a newly introduced regulatory regime, I consider that this factor is only of limited mitigatory significance. The applicable provisions came into operation more than two years after they were introduced into the Corporations Act. There was, therefore, a substantial lead time for AUFM to prepare itself for the new requirements.

103 AUFM’s contravening conduct related to a significant number – 328 – of non-advised investors who acquired interests in the Fund during the Contravention Period.

104 In respect of 89 investors in the Fund (the Non-Questionnaire Investors), being those investors who completed a Paper Application prior to 30 September 2022, AUFM failed to provide them with a questionnaire which assessed whether they fell within the Fund’s target market. In respect of 239 investors (the Questionnaire Investors), being those investors who completed a Questionnaire, AUFM failed to review their questionnaires to determine whether they fell within the Fund’s target market. These failings are serious. Moreover, there is no satisfactory explanation for how they came about. Insofar as the Fernandes Affidavit seeks to explain how the contraventions came about, the explanation is essentially that the person tasked with ensuring compliance with the DDO regime (the DDO Project Manager) did not have appropriate experience or training. This reflects poorly on the ‘compliance culture’ of AUFM at the time. It suggests that AUFM did not take its regulatory obligations sufficiently seriously; otherwise, it would have ensured that an appropriately qualified person was tasked with implementing the DDO regime. Further and in any event, it remains hard to understand how the DDO Project Manager (or others within AUFM) failed to appreciate that the questionnaires that applicants completed as part of the application process needed to be reviewed by AUFM personnel. This would seem to be a matter of common sense.

Size and resources of AUFM

105 The size and financial resources of the contravenor are relevant considerations in assessing whether a penalty is sufficient to achieve deterrence.

106 In the financial year ending 30 June 2025, the Group reported consolidated revenue and other income of $2.6 billion and $136.2 million in adjusted EBITDA. In 2025, the Wealth & Capital Markets business had a total of $15.2 billion gross funds under management, administration and advice. For the financial year ending 2025, AUFM reported total revenue of $75 million and reported losses after tax of $32.6 million. These figures demonstrate that AUFM is a substantial company and part of a substantial corporate group. Having regard to these matters, a large penalty is required to serve the object of specific deterrence.

Impact of the contraventions

107 During the Contravention Period, AUFM accepted initial investments of approximately $26,075,361 into the Fund from Relevant Investors. Further, AUFM earned establishment and management fees of approximately $614,240 in respect of those investments.

108 In considering whether any of the Relevant Investors suffered loss as a result of AUFM’s contraventions of s 994E(3), it is appropriate to focus on the Red Flag Investors and the Non-Questionnaire Investors rather than the TM Investors. In the case of the Red Flag Investors, a subsequent review of their answers to the Questionnaires they completed indicates that they each provided at least one response that indicated that they were not within the target market for the Fund. In the case of the Non-Questionnaire Investors, in circumstances where they were not required to (and did not) complete a Questionnaire, it is not practicable now to assess whether they fell within the target market for the Fund. The position, therefore, in respect of the Non-Questionnaire Investors, is that some or all of them may have fallen outside the target market for the Fund. On the other hand, in the case of the TM Investors, a subsequent review of their Questionnaires did not indicate that they fell outside the target market for the Fund. In these circumstances, it does not appear that the contraventions impacted the TM Investors.

109 At the very least, it can be said that, as a result of the contraventions, the Red Flag Investors and possibly some or all of the Non-Questionnaire Investors were exposed to the risk that they might have obtained a financial product that was not appropriate to their objectives, financial situation or needs, and to a risk of financial loss.

110 It does not appear practicable to determine definitively whether any of the Red Flag Investors or Non-Questionnaire Investor suffered loss as a result of AUFM’s contraventions. This would probably require a counterfactual analysis that takes into account facts and matters pertaining to each investor, that is, an examination of what the particular investor would have done if their application for an interest in the Fund had been rejected. In my opinion, the analysis contained in the Fernandes Affidavit is sufficient for present purposes. This approaches the question in a broad brush way by considering whether any of the Red Flag Investors and Non-Questionnaire Investors are likely to suffer an overall cash loss. Approaching the matter on this basis, it appears that relatively few investors are likely to suffer such a loss.

111 In view of the impacts and potential impacts described above, a substantial penalty is required to achieve the object of deterrence.

Deliberateness of the conduct

112 I accept that the contraventions were not deliberate.

Seniority of persons involved

113 ASIC does not allege that senior management of AUFM or AUL were involved in the contraventions.

Prior contraventions

114 AUFM has not previously been found to have engaged in any similar conduct to the contraventions that are the subject of this proceeding.

Co-operation

115 AUFM has co-operated with ASIC in the course of this proceeding, including by:

(a) proposing a joint approach to resolving the dispute at the earliest possible opportunity;

(b) making admissions of contraventions; and

(c) agreeing to the imposition of an appropriate penalty, as well as declaratory and other relief sought by ASIC.

116 AUFM has thereby demonstrated a significant level of co-operation with the regulator. This is a relevant factor in considering the appropriate penalty and supports the imposition of a lower penalty than would otherwise be imposed.

Remediation

117 AUFM’s remediation plan is outlined at [53]-[59] above. As noted in the Introduction to these reasons, in response to a request from the Court, ASIC provided a supplementary submission dated 18 December 2025 in which ASIC set out its position in relation to AUFM’s proposed remediation plan. ASIC stated that it was satisfied that AUFM’s remediation plan was “an available approach”.

118 The fact that AUFM has adopted the remediation plan is relevant to penalty, in that it ameliorates the impact of the contraventions on the affected investors, and demonstrates that AUFM appreciates the need to address the contraventions.

Improvements

119 In considering the penalty required for the purpose of specific deterrence, it is relevant to take into account the improvements in AUFM’s processes and governance systems outlined at [46] above. These improvements make it less likely that another similar contravention will occur.

Parity

120 The parties’ joint submissions draw attention to two cases. The first is Australian Securities and Investments Commission v Firstmac Ltd [2025] FCA 12, in which Downes J imposed a penalty of $8 million on Firstmac Ltd for 831 contraventions of s 994E(3) of the Corporations Act following a contested hearing. The second is Australian Securities and Investments Commission v American Express Australia Limited [2024] FCA 784, in which Jackman J imposed an agreed penalty of $8 million on American Express Australia Ltd for two contraventions of s 994C(4) of the Corporations Act. The facts of the cases are briefly described in the parties’ joint submissions. Only limited assistance is provided by those cases.

Conclusion on penalty

121 In the circumstances of this case, I do not consider it necessary to consider whether the contraventions constituted one or more “courses of conduct”.

122 Having regard to the matters set out above, I am satisfied that the penalty proposed by the parties is appropriate. I consider that the penalty is sufficient to achieve the objects of specific and general deterrence.

Adverse publicity order

123 The parties submit, and I accept, that it is appropriate for the Court to make an adverse publicity order in this case in the form annexed to the proposed orders. It provides for a notice, expressed in clear and straight-forward terms:

(a) to be placed on a prominent part of the Australian Unity Wealth & Capital Markets website; and

(b) to be sent directly to the last known email or postal address of the Non-Questionnaire Investors and the Red Flag Investors.

Conclusion

124 For these reasons, I made the declaration and orders proposed by the parties.

I certify that the preceding one hundred and twenty-four (124) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Moshinsky. |

Associate:

Dated: 30 January 2026