FEDERAL COURT OF AUSTRALIA

Australian Securities and Investments Commission v Australia and New Zealand Banking Group Limited (Treasury Bonds Case) [2025] FCA 1592

File number: | VID 1212 of 2025 |

Judgment of: | BEACH J |

Date of judgment: | 19 December 2025 |

Catchwords: | CORPORATIONS — primary market for Commonwealth Treasury bonds — secondary market for Commonwealth Treasury bonds — bank acting as duration manager — supply of financial services to the Australian Office of Financial Management, a department of the Commonwealth Treasury — unconscionable conduct concerning the issuance of December 2034 Treasury bonds — hedging strategy of bank — false or misleading representations made to the AOFM about the bank’s secondary market bond turnover — failure to make a report as to a reportable situation in relation to such turnover — breach of Australian financial services licence obligations — contraventions of ss 12CB(1) and 12DB(1) of the Australian Securities and Investments Commission Act 2001 (Cth) — contraventions of ss 912A, 912DAA and 1041H of the Corporations Act 2001 (Cth) — admitted conduct — fixing of pecuniary penalties — penalty principles — orders made |

Legislation: | Australian Securities and Investments Commission Act 2001 (Cth) ss 12BA, 12BAA, 12BAB, 12CB, 12CC, 12DA, 12DB, 12GBA, 12GBB, 12GLA Corporations Act 2001 (Cth) ss 674(2), 761A, 764A, 766D, 912A, 912D, 912DAA, 1041H, 1101B(1), 1105, 1317E, 1317G Evidence Act 1995 (Cth) s 191(3)(a) National Consumer Credit Protection Act 2009 (Cth) ss 29, 31(1), 47(1), 128, 130(1)(c) |

Cases cited: | Australian Building and Construction Commissioner v Construction, Forestry, Mining and Energy Union and Another (2018) 262 CLR 157 Australian Building and Construction Commissioner v Pattinson (2022) 274 CLR 450 Australian Competition and Consumer Commission v J McPhee & Son (Australia) Pty Ltd (No 5) [1998] FCA 310; [1998] ATPR 41-628 Australian Competition and Consumer Commission v Virgin Mobile Australia Pty Ltd [No 2] [2002] FCA 1548 Australian Securities and Investments Commission v AGM Markets Pty Ltd (in liq) (No 3) (2020) 275 FCR 57 Australian Securities and Investments Commission v Australia and New Zealand Banking Group Ltd (2017) 123 ACSR 341 Australian Securities and Investments Commission v Australia and New Zealand Banking Group Limited [2018] FCA 155 Australian Securities and Investments Commission v Australia and New Zealand Banking Group Ltd (No 3) [2020] FCA 1421 Australian Securities and Investments Commission v Australia and New Zealand Banking Group Ltd (2022) 164 ACSR 428 Australian Securities and Investments Commission v Australia and New Zealand Banking Group Limited [2023] FCA 256 Australian Securities and Investments Commission v Australia and New Zealand Banking Group Limited [2023] FCA 1150; (2023) 169 ACSR 649 Australian Securities and Investments Commission v Australia and New Zealand Banking Group Limited (No 3) [2023] FCA 1565 Australian Securities and Investments Commission v Kobelt (2019) 267 CLR 1 Australian Securities and Investments Commission v Superannuation Warehouse Australia Pty Ltd (2015) 109 ACSR 199 Australian Securities and Investments Commission v United Super Pty Ltd [2025] FCA 1453 Australian Securities and Investments Commission v Westpac Banking Corporation (No 2) (2018) 266 FCR 147 Australian Securities and Investments Commission v Westpac Banking Corporation (No 3) (2018) 131 ACSR 585 Australian Securities and Investments Commission v Westpac Securities Administration Ltd (2019) 272 FCR 170 Commonwealth v Director, Fair Work Building Industry Inspectorate (2015) 258 CLR 482 Forster v Jododex Australia Pty Ltd (1972) 127 CLR 421 Productivity Partners Pty Ltd v Australian Competition and Consumer Commission (2024) 419 ALR 30 Societe Civile et Agricole du Vieux Chateau Certan v Kreglinger (Australia) Pty Ltd (2024) 172 ACSR 357; (2024) 179 IPR 226 Volkswagen Aktiengesellschaft v Australian Competition and Consumer Commission [2021] FCAFC 49; 284 FCR 24 |

Division: | General Division |

Registry: | Victoria |

National Practice Area: | Commercial and Corporations |

Sub-area: | Regulator and Consumer Protection |

Number of paragraphs: | 320 |

Date of hearing: | 2 and 3 December 2025 |

Counsel for the Plaintiff: | Mr P Collinson KC, Mr L Livingston SC and Ms J Granger |

Solicitors for the Plaintiff: | Webb Henderson |

Counsel for the Defendant: | Mr J Williams SC and Ms S Palaniappan |

Solicitors for the Defendant: | Herbert Smith Freehills Kramer |

ORDERS

VID 1212 of 2025 | ||

IN THE MATTER OF AUSTRALIA AND NEW ZEALAND BANKING GROUP LIMITED (ACN 005 357 522) | ||

BETWEEN: | AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff | |

AND: | AUSTRALIA AND NEW ZEALAND BANKING GROUP LIMITED (ACN 005 357 522) Defendant | |

order made by: | BEACH J |

DATE OF ORDER: | 19 DECEMBER 2025 |

In these orders, the following definitions apply:

(a) ANZ means Australia and New Zealand Banking Group Limited ACN 005 357 522.

(b) AOFM means the Australian Office of Financial Management, a department of Commonwealth Treasury.

(c) ASIC Act means the Australian Securities and Investments Commission Act 2001 (Cth).

(d) Corporations Act means the Corporations Act 2001 (Cth).

(e) December 2034 Treasury Bonds means the Treasury bonds issued by the AOFM with a maturity date of December 2034 and which were priced on 19 April 2023.

(f) Secondary market bond turnover means the buying and selling of Treasury bonds and other Australian Government Securities to and from intermediaries (market makers) to clients, such as investment funds, asset managers, central banks, and other financial institutions.

(g) SAFA means the statement of agreed facts and admissions signed and tendered by the parties pursuant to s 191 of the Evidence Act 1995 (Cth).

(h) Treasury bonds are medium to long-term debt securities which provide a fixed rate of interest, paid semi-annually to the investor. Treasury bonds are also referred to as Australian Government bonds or Australian Commonwealth Government bonds. Treasury bonds are financial products under s 12BAA of the ASIC Act and s 764A of the Corporations Act.

THE COURT DECLARES THAT:

Unconscionable conduct

1. Between 19 April and 3 May 2023, ANZ contravened s12CB(1) of the ASIC Act by engaging in conduct as a duration manager, in connection with the supply of financial services to the AOFM (representing the Commonwealth of Australia) relating to the issuance of December 2034 Treasury Bonds, in trade or commerce, that was, in all the circumstances, unconscionable:

(a) in the context where: (i) ANZ represented to the AOFM it would be transparent with the AOFM, as set out in the SAFA; (ii) ANZ had the knowledge as set out in the SAFA; and (iii) the AOFM was situationally vulnerable, as a result of ANZ’s failure to disclose to the AOFM ANZ’s trading intentions and pre-hedging progress, ANZ’s failure to inform the AOFM of ANZ’s intention to engage in significant hedging up to and during the pricing call and ANZ’s failure to provide an opportunity to the AOFM to consult regarding the indicative time for the pricing call;

(b) where ANZ’s conduct as duration manager and ANZ’s manner of trading breached ANZ’s own policies for hedging, breached industry guidance and was outside the range of ordinary behaviour of duration managers appointed by the AOFM;

(c) where ANZ failed to inform the AOFM of the state of its hedging when proposing or confirming the time for the pricing call, as set out in the SAFA, failed to propose to delay the pricing call and/or failed to modify its strategy of being fully hedged by the time of pricing, without disclosing that to the AOFM;

(d) where ANZ’s conduct involved (i) trading a low volume of bond futures earlier in the day, despite opportunities being available for it to sell more; (ii) instead, trading a significant volume of bond futures in a compressed time period ahead of and during the pricing call, which it knew would, or was highly likely to, have a downward impact on the price of 10-year Australian bond futures, without disclosing that to the AOFM; and (iii) trading a significant volume of bond futures during the pricing call and placing downward pressure on the reference price at the time of pricing; and

(e) where ANZ made to the AOFM, post-transaction, misleading representations about the circumstances of ANZ’s trading, as set out in the SAFA.

False or misleading representations

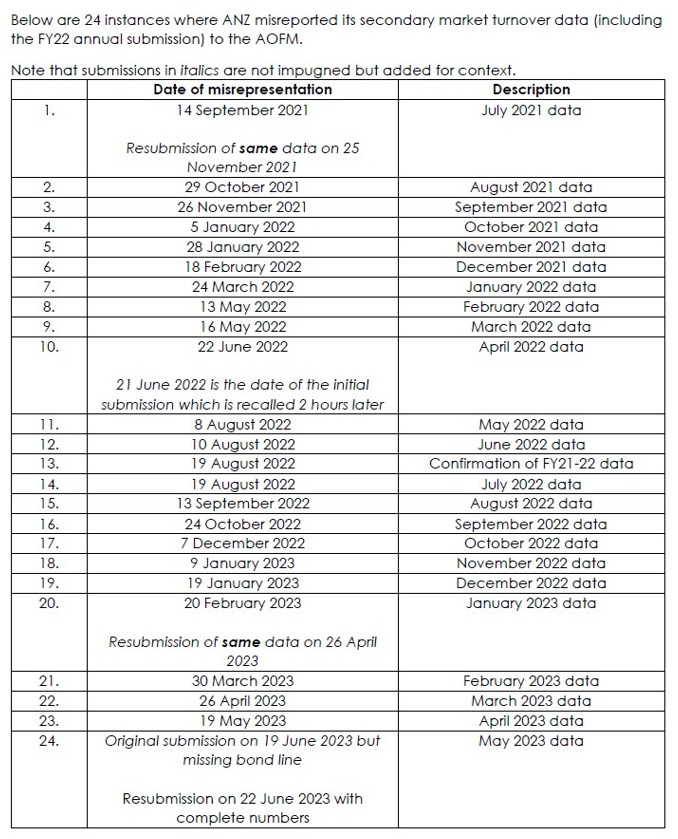

2. On 24 occasions between 14 September 2021 and 22 June 2023, in trade or commerce, in this jurisdiction, and in connection with the supply of financial services, ANZ made representations to the AOFM about its secondary market bond turnover that were false or misleading with respect to the standard, quality, value or grade of those financial services, in contravention of s12DB(1)(a) of the ASIC Act, by submitting to the AOFM:

(a) on 23 occasions, data on a monthly basis about ANZ’s secondary market bond turnover in the period from July 2021 to May 2023;

(b) on 19 August 2022, an annual attestation about ANZ’s secondary market bond turnover for FY22 (July 2021 to June 2022);

which inaccurately represented the volumes of trading, and the counterparties and geographic locations for such trading, conducted by ANZ during the period to which each submission related, as set out in the SAFA.

Misleading or deceptive conduct

3. On 27 occasions between 14 September 2021 and 22 June 2023, in this jurisdiction, ANZ engaged in conduct in relation to financial products or financial services that was misleading or deceptive or likely to mislead or deceive, in contravention of s 1041H(1) of the Corporations Act, by:

(a) on 3 occasions between 20 April 2023 and 3 May 2023, in reports provided by ANZ to the AOFM, making representations which were misleading or deceptive in describing, or were misleading or deceptive by omission in respect of, ANZ’s trading activities as duration manager for the December 2034 Treasury Bond issuance, as set out in the SAFA;

(b) on 23 occasions between September 2021 to June 2023, submitting data on a monthly basis to the AOFM about ANZ’s secondary market bond turnover in the period from July 2021 to May 2023 which inaccurately represented the volumes of trading, and the counterparties and geographic locations for such trading, conducted by ANZ during the period to which each submission related, as set out in the SAFA; and

(c) on one occasion, on 19 August 2022, submitting to the AOFM an annual attestation about ANZ’s secondary market bond turnover which misrepresented that its monthly survey data for FY22 was accurate, as set out in the SAFA.

Failure to report a reportable situation

4. Between 13 September 2023 and 6 June 2024, in this jurisdiction, ANZ did not lodge with ASIC a report in relation to a reportable situation in relation to secondary market bond turnover data reporting, in contravention of s 912DAA(1) and s 912DAA(7) of the Corporations Act, in circumstances where ANZ had reasonable grounds to believe that it had breached a core obligation, and that the breach was significant.

Breach of AFS licensee obligations

5. Between 19 April 2023 and 3 May 2023, ANZ did not do all things necessary to ensure that the financial services covered by its Australian financial services licence were provided efficiently, honestly and fairly, and thereby contravened s 912A(1)(a) and s 912A(5A) of the Corporations Act, by reason of:

(a) engaging in the conduct in connection with the supply of financial services to the AOFM (representing the Commonwealth of Australia) relating to the issuance of December 2034 Treasury Bonds, that was, in all the circumstances, unconscionable;

(b) providing reports to the AOFM between 20 April 2023 and 3 May 2023 which were misleading or deceptive in describing, or were misleading or deceptive by omission in respect of, ANZ’s trading activities as duration manager for the December 2034 Treasury Bond issuance;

(c) failing to adequately prevent, supervise, monitor, review, or identify the conduct set out in paragraphs 1 and 3(a) above; and

(d) failing to adequately implement or enforce its policies and procedures regarding material size transactions, reference price transactions and communications with clients.

6. Between 19 April 2023 and 3 May 2023, ANZ contravened s 912A(1)(ca) and s 912A(5A) of the Corporations Act by failing to take reasonable steps to ensure that its representatives complied with the financial services laws in connection with ANZ’s conduct as duration manager for the issuance of December 2034 Treasury Bonds.

7. Between 19 April 2023 and 3 May 2023, ANZ contravened s 912A(1)(f) and s 912A(5A) of the Corporations Act by failing to ensure that its representatives were adequately trained, and were competent, to provide financial services to the AOFM in connection with ANZ’s role as duration manager for the issuance of December 2034 Treasury Bonds.

8. Between 14 September 2021 and 15 August 2023, ANZ did not do all things necessary to ensure that the financial services covered by its Australian financial services licence were provided efficiently, honestly and fairly, and thereby contravened s 912A(1)(a) and s 912A(5A) of the Corporations Act, by reason of:

(a) making the representations to the AOFM about its secondary market bond turnover that were false or misleading, as set out in paragraph 2 above;

(b) engaging in misleading or deceptive conduct, as set out in paragraphs 3(b) and 3(c) above;

(c) failing to have adequate processes and procedures in place to prepare, review and verify the secondary market bond turnover data being submitted to the AOFM to ensure that it was accurate;

(d) failing to adequately monitor and supervise staff, to ensure that the secondary market bond turnover data was submitted to the AOFM accurately;

(e) failing to ensure that staff who were responsible for the submission of the data were adequately trained or competent;

(f) failing to conduct risk or assurance reviews of the processes and procedures to ensure that misleading information was not provided to the AOFM in connection with ANZ’s secondary market bond turnover data; and

(g) failing to take adequate steps to identify and to address the root causes of the misreporting and failing to escalate the issue for further risk assessment and compliance review, even when the scale of the inaccuracies in the secondary market bond turnover data submitted by ANZ to the AOFM for FY23 was identified and the AOFM was provided updated data for that financial year on 15 August 2023.

9. Between 14 September 2021 and 15 August 2023, ANZ contravened s 912A(1)(ca) and s 912A(5A) of the Corporations Act by failing to take reasonable steps to ensure that its representatives complied with the financial services laws in connection with ANZ’s reporting of secondary market bond turnover data to the AOFM.

10. Between 14 September 2021 and 15 August 2023, ANZ contravened s 912A(1)(f) and s 912A(5A) of the Corporations Act by failing to ensure that its representatives were adequately trained and were competent, to provide financial services in connection with ANZ’s reporting of secondary market bond turnover data to the AOFM.

AND THE COURT ORDERS THAT:

11. Pursuant to s 12GBB(3) of the ASIC Act, and in respect of the contravention the subject of paragraph 1 of these Orders, ANZ pay a pecuniary penalty in the sum of $80 million to the Commonwealth of Australia within 28 days of these Orders.

12. Pursuant to s 12GBB(3) of the ASIC Act, and in respect of the contravention the subject of paragraph 2 of these Orders, ANZ pay a pecuniary penalty in the sum of $40 million to the Commonwealth of Australia within 28 days of these Orders.

13. Pursuant to s 1317G(1) of the Corporations Act, and in respect of the contravention the subject of paragraph 4 of these Orders, ANZ pay a pecuniary penalty in the sum of $2 million to the Commonwealth of Australia within 28 days of these Orders.

14. Pursuant to s 1317G(1) of the Corporations Act, and in respect of the contraventions the subject of paragraphs 5 to 7 of these Orders, ANZ pay a pecuniary penalty in the sum of $5 million to the Commonwealth of Australia within 28 days of these Orders.

15. Pursuant to s 1317G(1) of the Corporations Act, and in respect of the contraventions the subject of paragraphs 8 to 10 of these Orders, ANZ pay a pecuniary penalty in the sum of $8 million to the Commonwealth of Australia within 28 days of these Orders.

16. ANZ pay ASIC’s costs of and incidental to these proceedings fixed in the amount of $1 million.

17. Pursuant to s 1101B(1) of the Corporations Act and s12GLA(2)(b) of the ASIC Act, ANZ undertake a compliance program at its cost which involves the following steps:

(a) Within four months of the date of these Orders or such other time as agreed in writing between ASIC and ANZ, ANZ will undertake a self-assessment and prepare a report (ANZ Report), having regard to relevant Australian laws and Australian and global regulatory and industry guidance, assessing the adequacy and effectiveness of ANZ’s application of the systems, controls, policies, procedures, training, guidance and framework for monitoring and supervision of employees, and governance in ANZ Institutional Bank to prevent, detect and respond to risks of:

(i) trading, in the context of pre-hedging of Australian material size transactions, including reference price transactions, that exerts undue pressure on price or results in materially higher market volatility or disruption of the reference price around the reference time; and

(ii) disclosures to clients before, during and after the pre-hedging of Australian material size transactions including reference price transactions about that pre-hedging which are misleading or not clear, accurate and fulsome.

(b) Within two months of the finalisation of the ANZ Report or such other time as agreed in writing between ASIC and ANZ, ANZ will instruct the independent expert to:

(i) having regard to the ANZ Report, relevant Australian laws and Australian and global regulatory and industry guidance, independently assess the adequacy and effectiveness of ANZ’s application of the systems, controls, policies, procedures, training, guidance and framework for monitoring and supervision of employees, and governance in ANZ Institutional Bank to prevent, detect and respond to risks set out in sub paragraph (a);

(ii) within three months provide a written report (Expert Report) to ASIC and ANZ which sets out the results of the assessment and identifies any deficiencies and make recommendations to address those deficiencies.

(c) In relation to any deficiencies identified in the Expert Report, ANZ will action all reasonable recommendations of the independent expert to address those deficiencies within six months of receiving the Expert Report. Where applicable, ANZ will provide a statement to ASIC explaining why a recommendation has not been adopted or implemented.

(d) The appointment and terms of engagement of the independent expert are to be approved by ASIC in accordance with the terms set out in the Annexure to these orders.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

BEACH J:

1 These reasons deal with one of four cases that I heard over two days concerning proceedings brought by the Australian Securities and Investments Commission against the Australia and New Zealand Banking Group Limited concerning contraventions of various provisions of the corporations legislation and credit legislation. The present reasons concern ANZ’s conduct relating to Treasury bonds. I have delivered a separate set of reasons dealing with the other three cases concerning what I would describe as retail conduct (see Australian Securities and Investments Commission v Australia and New Zealand Banking Group Limited (Retail Cases Omnibus) [2025] FCA 1593). Let me turn to the present case.

2 ANZ is and has been a registered bidder participating in bond tenders conducted by the Australian Office of Financial Management (AOFM), which is a department of the Commonwealth Treasury. AOFM is the issuer of Australian Government Treasury bonds to borrow money on behalf of the Commonwealth government.

3 As part of its role as a registered bidder, ANZ provided information to the AOFM about its monthly turnover in trading Australian Government securities including Treasury bonds in the secondary market.

4 As a registered bidder, ANZ also promoted itself to the AOFM for the role of joint lead manager and duration manager on syndicated issuances of Treasury bonds. The duration manager role is considered prestigious and being awarded the duration manager mandate is conducive to ANZ being perceived as a market leader in the Australian bonds business.

5 ANZ has admitted to engaging in conduct in contravention of ss 12CB and 12DB of the Australian Securities and Investments Commission Act 2001 (Cth) and ss 912A, 912DAA and 1041H of the Corporations Act 2001 (Cth) concerning its activities relevant to the primary bond market as a duration manager and the reporting of its activities in the secondary bond market. The contraventions admitted by ANZ relate to two aspects.

6 The first aspect concerns ANZ’s inappropriate conduct in executing a mandate that it succeeded in obtaining in April 2023 to act as the duration manager for the AOFM’s planned issuance of new 21 December 2034 maturing Treasury bonds via syndication in the week beginning 17 April 2023. I would note here that Treasury bonds are financial products under s 12BAA of the ASIC Act and s 764A of the Corporations Act. Further, I would note that at all relevant times, ANZ provided financial services which were supplied in relation to Treasury bonds and dealt in and made a market in Treasury bonds for the purposes of s 12BAB of the ASIC Act and s 766D of the Corporations Act. ANZ is the holder of an Australian Financial Services Licence (AFSL).

7 The second aspect concerns inaccuracies in the reporting of secondary market bond turnover which ANZ reported to the AOFM in the period from 14 September 2021 to 22 June 2023 and ANZ’s failure to lodge with ASIC a report in relation to a reportable situation in connection with those inaccuracies in circumstances where ANZ had reasonable grounds to believe that it had breached a core obligation, which is a statutory construct.

8 Now ASIC and the ANZ have tendered a statement of agreed facts and admissions (SAFA) setting out facts agreed between the parties pursuant to s 191(3)(a) of the Evidence Act 1995 (Cth). And the parties have put a joint position concerning the orders that they say that I should make concerning the ANZ’s conduct.

9 First, declarations are sought pursuant to s 21 of the Federal Court of Australia Act 1976 (Cth), s 1317E of the Corporations Act and s 12GBA of the ASIC Act.

10 Second, pecuniary penalties are sought pursuant to s 1317G(1) of the Corporations Act and s 12GBB(3) of the ASIC Act in a total amount of $125 million. I should say straight away that I have determined to increase the total amount of the penalties to $135 million for reasons which I will explain later. I would also note that I have imposed penalties in the other three retail cases totalling $115 million.

11 Third, an order for a compliance program is sought pursuant to s 1101B(1) of the Corporations Act and s 12GLA(2)(b) of the ASIC Act.

12 Let me start with some background and then delve more into the factual detail concerning the first aspect of the case dealing with the ANZ’s conduct as the duration manager in April 2023 and which I have synthesised from the SAFA.

AOFM and Treasury bonds

13 As I have said, the AOFM issues Treasury bonds to borrow money on behalf of the Commonwealth government. This is to ensure that the Australian Government can meet its spending, investment and debt payment obligations. Treasury bonds are medium to long term debt securities which provide a fixed rate of interest, paid semi-annually to the investor. Treasury bonds are also referred to as Australian Government bonds or Australian Commonwealth Government bonds.

14 The AOFM is the largest issuer of bonds in the Australian market. Some of its personnel are sophisticated participants in the Australian fixed income market. Notwithstanding this, in April 2023 the AOFM was in a position of situational vulnerability concerning ANZ’s conduct as I will later explain.

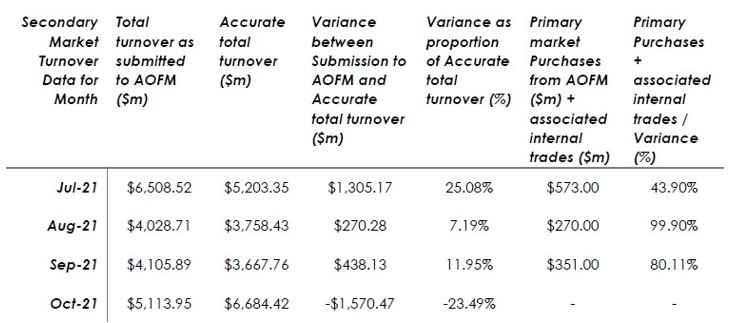

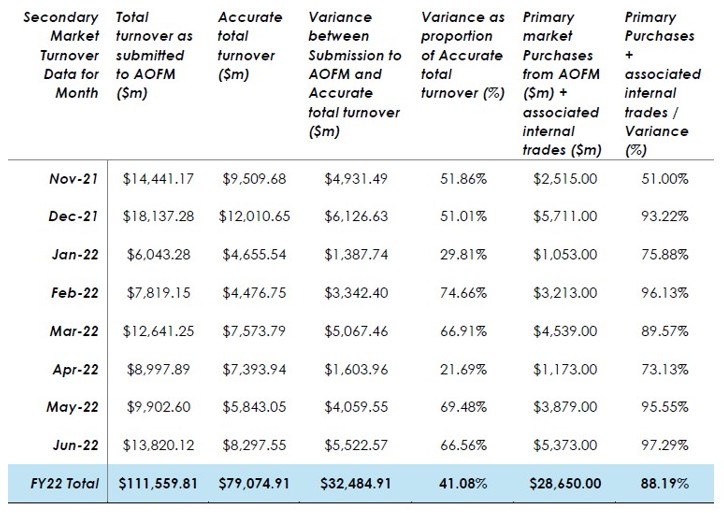

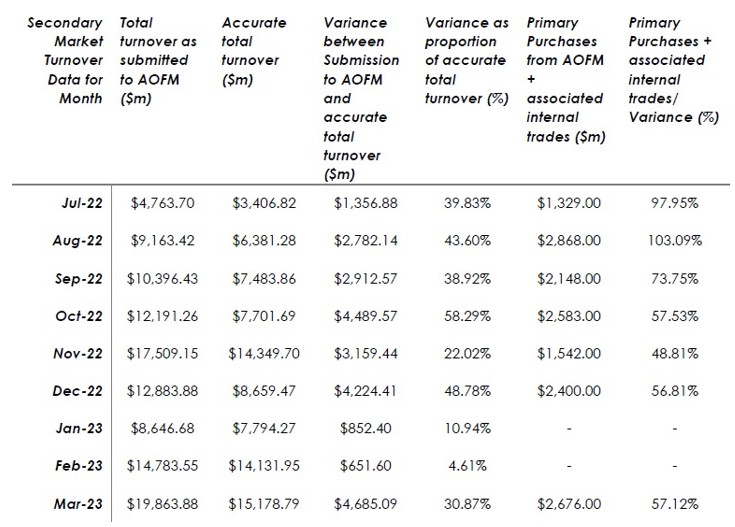

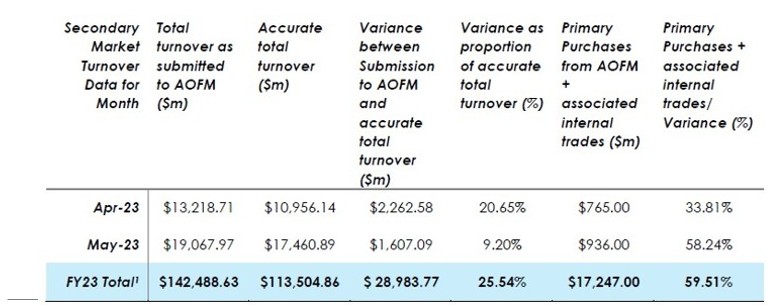

15 The AOFM regularly issues Treasury bonds through periodic auctions conducted by competitive tender, in which registered bidders submit bids.

16 From time to time, the AOFM conducts syndicated issuances of Treasury bonds, typically for a new maturity and for larger volumes than can be obtained through the tender process. A syndication involves the AOFM appointing financial institutions as joint lead managers to support and promote the transaction, with the bonds being placed directly with investors, and appointing one of the joint lead managers as the duration manager to manage the interest rate risks associated with the issuance. The duration manager assumes and manages the risk as principal, and not as agent for the AOFM.

17 In transferring the management of the interest rate risks associated with the issuance to the duration manager, the AOFM relies on the skills and expertise of the financial institution as a sophisticated market participant. Whilst the AOFM is a sophisticated market participant, it does not have the skill set nor expertise to manage this interest rate risk itself. As such, the duration management service is a significant benefit to the AOFM and Commonwealth. The duration manager is not paid a separate fee for this role, beyond the allocated joint lead manager fee. The duration manager has an opportunity to earn a profit if there is a positive spread between the average price at which it sells its futures hedge and the price at which it acquires the bond futures from investors in the bond issuance. If there is a negative spread, the risk manager may incur a financial loss. In providing the duration management, the duration manager may take on significant market risk and deploys its own capital in the management of such risk.

18 Now this all gives rise to an inherent conflict between the financial institution which seeks to manage its risk and make a profit from the provision of the service and the AOFM which will be disadvantaged by any downward price pressure on the reference price. The duration manager manages risk by selling the reference bond futures in the market during the transaction which can place downward pressure on the reference price. Accordingly, whilst the AOFM receives a significant benefit from the services provided by the duration manager, and the AOFM expects that the duration manager will seek to make some profit, it is an expected part of that role that the financial institution will conduct its hedging in such a way as to minimise market disruption, price volatility and price impact; I will elaborate further on the need for and the type of hedging in a moment.

19 At all relevant times, ANZ was a registered bidder participating in tenders conducted by the AOFM. As part of this role, ANZ provided information to the AOFM about its monthly turnover in trading Australian Government securities including Treasury bonds in the secondary market. Secondary market bond turnover refers to the buying and selling of Treasury bonds and other Australian Government Securities to and from intermediaries being the market makers to clients, such as investment funds, asset managers, central banks and other financial institutions.

20 Further, at all relevant times, ANZ promoted itself to the AOFM for the role of joint lead manager and duration manager on syndicated issuances.

ANZ’s role on the 21 December 2034 maturing treasury bond issuance by the AOFM

21 Now towards the end of 2022 and by early 2023, ANZ expected that the AOFM would be conducting a new syndicated bond issuance by April 2023. ANZ had a strong desire to be awarded the duration manager mandate on this transaction.

22 In April 2023, ANZ was appointed by the AOFM as a joint lead manager and as the duration manager for a $14 billion syndicated Treasury bond issuance by the AOFM. But before elaborating on the chronology I need to say a little more about risk and ANZ’s knowledge.

23 Now investors participating in the AOFM’s syndicated bond issuance could do so on either: (a) an outright basis, where the investor purchases the bonds; or (b) an exchange-for-physical (EFP) basis, that is, the investor purchases the bonds combined with a sale of 10-year Australian bond futures. This arrangement allows the investor to hedge the interest rate risk arising from their purchase of the bonds. EFP describes a transaction where one party buys the physical assets and sells Treasury bond futures contracts whilst the opposite party sells the physical assets and buys Treasury bond futures contracts.

24 The role of the duration manager involves accepting the risk associated with the 10-year Australian bond futures which form part of the EFP orders from investors, which may be significant; such bond futures are interest rate derivative contracts traded on the ASX24 under commodity code XT. The duration manager would buy the bond futures from the investors, but this would in turn expose the duration manager to risk. Accordingly, to manage this risk it had to sell bond futures. But of course in selling bond futures, this could place downward pressure on the reference price and the pricing of the Treasury bonds to be issued.

25 Now as part of the duration manager role in April 2023, ANZ knew the following nine matters.

26 First, it would acquire a significant number of 10-year Australian bond futures from investors who were allocated bonds on an EFP basis. This volume was expected to significantly exceed average daily traded volume in 10-year Australian bond futures.

27 Second, it was ANZ’s role, as duration manager, to manage the risk it expected to acquire associated with these bond futures. In doing so, it was permitted by the AOFM to trade before, during, and after pricing. The AOFM disclosed to the market that ANZ could do so.

28 Third, ANZ would be selling 10-year Australian bond futures to pre-hedge the anticipated risk. In doing so, it could also acquire positions in other Australian bond futures, US Treasury futures and foreign exchange positions to offset the risk to ANZ of its pre-hedging position, described as correlated hedges. This trading would be conducted in a segregated portfolio and ANZ would measure the risk of its trading positions in DV01, which is a common approach to managing and measuring risk. This risk metric measures the change in value of a position per each 1 basis point change in yield of the futures contract.

29 Fourth, the AOFM expected, including as a result of ANZ’s representations to the AOFM about how it would undertake the role of duration manager, that ANZ would manage the risk in an orderly manner to minimise market disruption, price volatility and price impact, and in a manner which promoted the fair treatment of the AOFM, and in compliance with ANZ’s policies and industry guidance.

30 Fifth, the price at which ANZ would acquire these bond futures from investors would be set, during the pricing call which commences at a time nominated by ANZ, by ANZ’s nominated trader spotting the prevailing bid-side of the futures price, which is then agreed to by the AOFM and the other joint lead managers. So, the duration manager nominates the time of the pricing call and the AOFM relies on the judgement of the duration manager to select the pricing call time.

31 Sixth, pricing of the bond means the time at which the price or level of the fixed interest rate or yield that will be payable by the AOFM on Treasury bonds for a new bond issuance is set. Pricing is determined by reference to the bid-side spread of the 10 year Australian bond futures contract at the pricing call time and expressed as yield to maturity. The yield of the bond issued by the AOFM on behalf of the Commonwealth is determined by adding a spread, which is predetermined by the AOFM, to the yield implied by the futures bid price agreed on the pricing call. This determined the amount that the Commonwealth would receive from investors who purchased the bonds issued.

32 Seventh, the ANZ would receive no fee or spread for accepting the risk of acquiring the significant number of 10-year Australian bond futures. Instead, it would make a profit or loss from the difference between the price at which it acquired the 10-year Australian bond futures from investors and the price at which it sold an equivalent volume of those contracts in the market during its hedging.

33 Eighth, each basis point reduction in the price of the 10-year Australian bond futures at pricing, and the consequential change in the yield of the bonds, would: (a) disadvantage the Commonwealth because it would reduce the proceeds received by the Commonwealth from the bond issuance; and (b) benefit ANZ because it would pay a lower price to acquire the significant number of 10-year Australian bond futures to be acquired by ANZ from investors in the bond issuance, thereby increasing ANZ’s revenue or reducing its loss associated with managing the EFP risk.

34 Ninth, in managing the risk and to minimise the price impact of its trading activity, a duration manager was expected to liaise with the AOFM on any issues that arose in the course of the trading day which might impact upon its risk management or the timing of the pricing. ANZ also knew that it could: (a) withhold some of its hedging activity, which it was common to do so, until after the time of the bond issuance pricing; and/or (b) adjust the time of the pricing call to occur later in the day to allow itself more time to trade. Withholding some of the hedging activity would cause the duration manager to hold the risk of an unhedged position for a longer period of time. Adjusting the time of the pricing call carries the risk that the reference price may rise in that period.

35 Let me turn to the relevant chronology.

36 On Friday 14 April 2023, the AOFM announced that it planned to issue new 21 December 2034 treasury bonds via syndication in the week beginning 17 April 2023, subject to market conditions; these bonds would have a maturity date of December 2034.

37 Later on the same day, the AOFM appointed ANZ, Commonwealth Bank of Australia, Deutsche Bank and National Australia Bank Limited as joint lead managers. The AOFM also appointed ANZ to be the duration manager.

38 In accepting the appointment as joint lead manager, ANZ agreed to the Syndication Common Terms which required ANZ to: (a) “act efficiently, honestly and fairly in the interests of the Commonwealth during the Bond issuance process” (Clause 7.2(a)); and (b) comply, and ensure its employees comply, with “all Australian laws applicable to the performance of its obligations under the Relevant Agreements” (Clause 17.1). The Terms also record that “The Commonwealth acknowledges that in connection with any offering of Bonds....the Joint Lead Managers … owe no fiduciary duties to, the Commonwealth or any other person.”(Clause 12.2).

39 In accepting the role of duration manager, Mr Sloane on behalf of ANZ informed the AOFM during a telephone call that Mr Christopher Corbett (Head of Rates Trading Australia, Markets) would be the nominated trader and that ANZ would:

certainly try and maintain and manage the risk in a way that is of the least impact to the market and we keep an open and consistent dialogue both with yourselves and myself and the trader who will be looking after the risk.

40 ANZ also agreed to the terms of a document provided by the AOFM titled “Procedural Aspects of Risk Management”. The document noted that the bond would price off the bid side of the 10-year Australian bond futures contract.

41 At 2:15pm on 14 April 2023, Mr Sloane informed Mr Rakesh Jampala (Co-Head of Fixed Income, Markets) in a Bloomberg chat that ANZ had been appointed as joint lead manager and duration manager.

42 At 4:29pm on 14 April 2023, Mr Jampala sent Mr Corbett an email attaching a document titled “Duration Management of Australian Physical Bond Issuance” which was a memo prepared by Mr Jampala in 2020 addressing considerations in acting as a duration manager. The document included the following passage under the heading “Conflicting interests as Duration Manager”:

Duration management execution effectively operates as a reference price transaction, where there is no margin other than being set on the bid side of the futures. ….. There are a number of ways of going about executing this, with important (and often conflicting) considerations. Clearly the least risky approach for ANZ is sell all the risk in as small as possible a window just around time of pricing. However, this course of action will certainly disturb orderly functioning of the market, likely create jump discontinuity in price, and reflect poorly on the overall market, let alone the impact to AOFM in respect of price. The converse would be ANZ selling the risk over a period of days leading into pricing. This would enable a smooth execution with very little impact to the market, but would expose ANZ to very material market risk. Risk which is not priced given we are only getting set off the bid side of futures. The correct approach therefore lies somewhere in the middle, with strategy on any particular occasion subject to market conditions and liquidity at that prevailing time.

43 At 4:31pm on 14 April 2023, Surveillance Senior Manager 1 sent an email to his direct report, Surveillance Manager 2, which forwarded an email chain commencing some time previously discussing a potential approach to intra-day risk limits applicable to the role of duration manager for AOFM transactions. The first email in the forwarded chain was sent by Surveillance Senior Manager 1 stating that he had assumed that ANZ would maintain the “same basic hedging strategy” it had used on recent AOFM transactions to develop appropriate duration manager limits. So, the following was assumed. First, the risk which ANZ would assume at the time of pricing the transaction would be the total size of the deal multiplied by the proportion of investor orders that were on an EFP basis. Second, most of ANZ’s pre-hedging would take place in the 90 minutes prior to pricing time. At the time of pricing, ANZ could typically expect to have pre-hedged up to two thirds of its risk by selling and thereby building a short position in Australian bond futures. Third, ANZ may also acquire partially offsetting positions in other products such as US Treasury futures and AUD/JPY currency trades to mitigate the risk to ANZ as it built the short pre-hedging position; these are described as correlated hedges. Fourth, the aim was to ensure that ANZ’s peak exposure at the time of pricing was kept below 50% of the total deal risk.

ANZ’s material size transaction guidelines, applicable ANZ policies, and industry guidance

44 By 17 April 2023, as required by its material size transaction (MST) guidelines, ANZ had assessed the likely risk it would acquire from the bond issuance transaction. It expected the transaction size to be approximately $10 to 15 billion, with an indicative risk size of $8 to 10 million per basis point, which is referred to in terms of DV01 as I have already said. It assessed the transaction as being material and having a market impact.

45 ANZ established a deal team for the transaction which included Mr Jampala and Mr Corbett.

46 In a call commencing at 2:09pm on 17 April 2023, Mr Jampala described to members of the Desk Risk Management and Compliance teams that: (a) ANZ’s advice to the AOFM will be to launch the transaction the next day (Tuesday), “which means pricing on Wednesday”; and (b) Mr Corbett will be the trader managing the risk of the transaction. Mr Jampala will “be with him pretty closely working – basically, doing it with him and just providing counsel right throughout which is why I’m on the deal team.”

47 ANZ’s MST guidelines and trading practice guidelines in place as at April 2023 required the following.

48 First, traders “should use reasonable endeavours to execute the MST in a manner that: is not disadvantageous to the client” and “is minimally disruptive to the market. You should manage the execution of the MST in a way that promotes the fair treatment of the Client” and pre-hedging “must be carried out insofar as possible in a way that is not detrimental to the Client”.

49 Second, hedging should be aligned with “any applicable ANZ Policy/Procedure/internal guidance and relevant market standard” and in compliance with the following general principles: (a) “When hedging, it should be conducted in a manner that has little influence on market pricing, at a pace consistent with the normal market volumes at that time of day in the relevant instrument, and does not result in undue pressure on pricing around the fixing window/ reference time/ pricing call”; (b) “Trader[s] should ensure that the sole purpose behind hedging is risk mitigation [and] should not be performed for the purpose of influencing or manipulating the fixing rate / reference price / reference rate / reoffer yield”; and (c) “Traders should comply with FMSB’s Risk Management Transactions for New Issuance Standard” and “FMSB’s Reference Price Transactions Standard”.

50 Third, there must be no over-hedging, that is, related hedging should never be more than 100% of ANZ’s risk exposure.

51 Fourth, pre-hedging must only be executed by the MST Trader and that “[t]he Deal Team can include the Senior Trading Manager (if approved by Desk Risk Manager and Compliance). The Deal Team should not include the MST Trader”.

52 ANZ’s Information Flow Guidelines outline principles governing communications from ANZ employees to clients. Relevantly, ‘Principle 3 – Communications’ notes that:

You must communicate in a manner that is clear, accurate, professional, and not misleading.

Sub-principle i) … to support the accuracy and integrity of information, you should: … not communicate false information.

53 Let me set out some other relevant standards.

54 The FICC Markets Standards Board (FMSB) was a UK-based industry body that promotes best practice standards for wholesale markets globally including by developing standards and good practice statements. In November 2016, the FMSB issued the Reference Price Transaction Standard, which relevantly provided: (a) A market participant should “balance the objectives of its hedging strategy against the possibility of putting undue pressure on the reference price, recognising that some price pressure is to be expected as risk is passed, particularly for large transactions or transactions in less liquid markets”; (b) Hedging should generally be “at a pace consistent with normal market volumes at that time of day in the relevant instrument (adjusted as necessary for the volume implicit in the RPT itself, and recognising that this may not be possible for illiquid instruments)” and “Although volatility can be due to many factors, a reasonable hedging strategy would not be expected to induce materially higher volatility of the reference price around the reference time, taking into account the size of the risk being transferred”; (c) Hedging should be designed to neutralize the risk and should not be undertaken for the purpose of creating a new significant open risk position. Further, “Intentional over-hedging (i.e. hedging more than required to cover the firm’s risk) should not take place other than where that is a necessary consequence of appropriate hedging activity, such as where the relevant hedging instrument is only available in a size greater than that required to hedge the RPT”.

55 Further, the Australian Financial Markets Association (AFMA) was a financial markets industry association which maintained codes, policies and procedures for the purpose of regulating its members' conduct in certain financial markets.

56 The AFMA Code of Conduct set out ethical principles for acceptable standards of behaviour in Australian financial markets which members were required to observe and expected to adopt. The Code of Conduct includes: (a) Ethical principle 4, which provides that members were expected to: “Act fairly and honestly when dealing with clients and counterparties”; and (b) Ethical principle 9, which provides that members were expected to: “Observe market standards and conventions, good practice and conduct expected or required of participants in markets when engaging in any form of market dealing”.

57 AFMA’s Guidance on Pre-Hedging and Debt Capital Primary Market Guidelines, which included a section titled Reference Price Transactions, relevantly set out the following: (a) The key characteristic of Reference Price Transactions is the “possibility of market pressure arising from Syndicate Manager risk management activity, and the related potential conflict of interest between the Issuer and the Syndicate Manager”; (b) Dealers should conduct hedging “in a manner that is not intended to disadvantage the Client” and communicate “their hedging practices to the Issuer in a clear manner meant to enable clients to understand their intentions and actions in the market”; (c) The sole intention behind hedging should be “risk mitigation”; and (d) In relation to acceptable hedging practices, the AFMA Guidance included the same matters as set out in the FMSB’s Reference Price Transaction Standard.

18 April 2023: December 2034 Treasury bonds launched

58 At 9:00am on 18 April 2023, the AOFM announced the launch of new Treasury bonds maturing on 21 December 2034, which would be priced on 19 April 2023. The announcement noted that the duration manager “may be involved in hedging activities before, during or after pricing”.

59 To execute the duration manager role, ANZ set up a segregated room on the trading floor. From the time that the deal was launched at 9am on 18 April 2023 until the deal was priced, Mr Corbett, as the nominated trader, and Mr Jampala, as his supervisor, were removed from normal trading activities as required by the MST guidelines. Mr Corbett traded in the segregated room. Mr Jampala was also in the room for most of that period, sitting next to Mr Corbett to provide guidance and supervision. All trades executed in connection with the transaction were recorded in a segregated trading book “R BOND AU”. The trades and offers set out below are those conducted by ANZ, and made in connection with the risk borne by ANZ, in connection with its duration manager role on this transaction.

60 ANZ did not have a documented pre-hedging plan or a formal written hedging strategy for this transaction.

61 Now throughout the course of the transaction, Mr Sloane had a live Bloomberg chat with the AOFM, and Mr Sloane had a further Bloomberg chat with Mr Corbett and Mr Jampala.

62 At about 4:44pm on 18 April 2023, Mr Sloane informed Mr Corbett through Bloomberg chat messages that the size of the bond issuance was likely to be $13 to 15 billion, of which approximately $11 billion would be EFP orders. This is the risk that ANZ would need to manage as duration manager.

63 At about 4:55pm on 18 April 2023, Mr Jampala sought confirmation from Mr Sloane through Bloomberg chat messages that the deal size was not expected to exceed $15 billion and that about 72 percent of the deal would be EFP orders.

64 Mr Corbett had commenced pre-hedging a small volume of the anticipated risk for the transaction on Monday 17 April 2023. By the evening of 18 April 2023, he had accumulated a short position of 13,934 contracts of 10-year Australian bond futures in the R BOND AU portfolio to pre-hedge the anticipated risk. This short position was equivalent to about $1.35 million of DV01 risk, that is, about 13.5 to 16.8% of an anticipated total risk of $8 to 10 million in DV01 terms. He also accumulated a long position of 23,066 contracts of 3-year Australian bond futures, 4,588 contracts of 10-year US Treasury note futures, and 500 contracts of 90-day Australian bank bill futures. His net DV01 position in AU products was equivalent to a short position of about $610,584.

19 April 2023: December 2034 bond pricing date

65 Between 4:46am and 6:10am on 19 April 2023 and before market open, Mr Corbett purchased 1,000 contracts of 10-year Australian bond futures. By buying 10-year Australian bond futures, Mr Corbett reduced his pre-hedging position. This had the effect of increasing the amount of outstanding 10-year bond futures contracts Mr Corbett needed to sell in order to hedge the anticipated number of contracts ANZ would acquire from investors in the bond issuance. Around the same time, he sold 1,000 contracts of 10-year US Treasury note futures. These trades were part of ANZ using correlated hedge products as described above. His net risk position in DV01 terms was largely unchanged as the combined result of these trades.

66 At the end of the SYCOM session on the morning of 19 April 2023, 10-year Australian bond futures were trading at 96.495.

67 ANZ knew, and AOFM reasonably would have expected, that, on this day, in connection with ANZ’s need to hedge its risk associated with a transaction of this kind, ANZ intended to sell a substantial volume of 10-year Australian bond futures between market open at 8:32am and the pricing call time nominated by ANZ which would have, or would be likely to have, the effect of placing downward pressure on the price of the bond futures. The potential for the substantial volume to have downward pressure on the price of 10-year Australian bond futures may be consistent with the need to hedge these types of transactions and risk. However, on 19 April 2023, the AOFM did not know, and could not know, without ANZ informing it, that ANZ would trade a significant volume of bond futures in a compressed time period ahead of and during the pricing call and in a manner that placed undue downward pressure on the reference price at the time of pricing, which was inconsistent with the manner of trading expected by reason of the matters set out above.

68 As a result of the orders, during the time that Mr Corbett was on the pricing call, ANZ had outstanding offers in the market to sell 10-year Australian bond futures at each of the five price levels from 96.465-96.485.

69 ANZ’s trading in the lead up to and during the pricing call applied undue downward pressure on the price of 10-year Australian bond futures at the time of pricing.

70 Shortly prior to and while on the pricing call, the AOFM was observing the market for 10-year Australian bond futures on a Bloomberg screen. The AOFM observed the prevailing price of 10-year Australian bond futures decreasing. Due to the anonymous nature of the futures market, the AOFM did not, and could not without ANZ informing it of its trading activity, know whether, and to what extent, ANZ was responsible for the trading activity in the market. Further, significant selling which was likely to place downward pressure on the price of the reference product by ANZ in close proximity to and at the pricing time would be inconsistent with: (a) the AOFM’s expectations which were understood by ANZ; (b) ANZ’s statements to AOFM about how it would manage duration management roles including this role; and (c) industry guidance including from AFMA and the FMSB.

71 The AOFM had a reasonable expectation that it would be informed if ANZ’s pre-hedging was not sufficiently advanced or if ANZ otherwise encountered difficulties in its pre-hedging prior to the indicative pricing call time, and/or that ANZ would seek to adjust the pricing call to a later time if ANZ was unable to manage its risk in accordance with its policies and industry guidance. The AOFM also relied upon ANZ to nominate the pricing call time.

72 ANZ did not disclose to the AOFM: (a) its intention to seek to be fully hedged by the time of pricing if it could do so at an acceptable price; (b) that its pre-hedging was not sufficiently advanced to achieve that intention without trading a significant volume of 10-year Australian bond futures before and leading into the nominated pricing call time of 1:50pm; and (c) therefore, it intended to engage in such trading which would have, or was highly likely to have, a downward impact on the price of 10-year Australian bond futures as at the time of pricing.

73 ANZ did not provide the AOFM with an opportunity to consult with ANZ about rescheduling the time of the pricing call in light of the progress by ANZ in its hedging. ANZ did not adjust the pricing call time to a later time to allow itself more time to pre-hedge. ANZ did not withhold some of its hedging activity until after the time of pricing.

74 To the contrary, when ANZ had substantial volume of risk still to trade, ANZ’s traders confirmed a pricing call time of 1:50pm and proceeded to sell significant volumes of 10-year Australian bond futures within a compressed time window shortly prior to and during the pricing call time nominated by it, between 1:10pm and 1:54pm.

75 Without knowing ANZ’s specific intentions and trading, and having relied upon ANZ to manage the inherent conflict in accordance with the expected behaviour of a duration manager, at the time of the pricing call, the AOFM was unable to counteract or to protect itself against ANZ’s conduct. To finalise the bond issuance, the AOFM needed to ensure that the issue of $14 billion Treasury bonds would be priced. The AOFM therefore had no alternative but to agree the price which was the bid-side of the 10-year Australian bond futures at the time of pricing on the pricing call. At the time of pricing, the AOFM had no knowledge, and no means of acquiring knowledge without ANZ providing it to the AOFM, of the matters above. As a result and to ANZ’s knowledge, at the time of pricing, the AOFM was in a position of informational and situational disadvantage and vulnerability.

76 ANZ knew, or ought reasonably to have known, that its manner of trading and the undue downward pressure of that trading on the bond futures price was contrary to the AOFM’s reasonable expectations about the pricing of the bond issuance and that ANZ’s conduct exposed the AOFM and the Commonwealth to significant risk of detriment.

77 ANZ earned revenue of $9,979,687 as duration manager and a fee of $2.8 million as joint lead manager.

78 It is convenient to make one other point here. Based on an issuance size of $14 billion, each basis point fall in the futures price, and thereby increase to the yield of the bonds, would detrimentally impact the Commonwealth by reducing the amount received from investors who purchased the bonds issued by about $13.16 million.

Other Issuances

79 Based on data collected by ASIC, between January 2017 and July 2024, the AOFM conducted a total of 21 syndicated bond issuances. Eleven of these issuances had 10-year Australian bond futures as the reference product and an EFP risk of at least $4.2m on a DV01 basis, being approximately 50% of the April 2023 issuance. Having regard only to notional positions in the reference product, that is, not assessed on a DV01 basis, and not including correlated hedging, ANZ’s trading on this transaction when compared to the other 20 issuance transactions, displays the following features.

80 First, except for one transaction in 2018 for which ANZ was also the duration manager, this is the only transaction in which the duration manager had sold reference products equal to the EFP quantity of the reference product at the time of pricing. In all other issuances, the duration manager withheld a portion of the amount of reference product to be sold until after pricing, for purposes including minimising market disruption, protecting the interests of the AOFM, and/or profiting from the anticipated rise in the price of the futures contracts. Of the other 19 transactions including another two previous transactions in which ANZ was the duration manager, the highest proportion that a duration manager sold of the EFP quantity of the reference product by the time of pricing was approximately 85%. ANZ traded a materially higher proportion of its anticipated risk in the 45 minutes prior to pricing.

81 Second, on this transaction, noting that ANZ sold a low volume of the reference product between market open and 1:10pm and a significant volume of the reference product between 1:10pm and pricing, the spotted bid price was 2 basis points lower than the best bid price at market open. Across the 10 other issuances where the reference product was 10-year Australian bond futures and where the EFP risk was greater than $4.2 million in DV01 terms, the median bid price movement was a 2.3 basis point drop and the average was a 2.6 basis point drop. Further, on this transaction, the price of the reference product moved by the widest margin (a decrease of 2 basis points) in the 45 minutes leading to pricing in all 21 issuances.

82 Further, in at least some other transactions, where unanticipated market conditions arose or the duration manager’s pre-hedging was not sufficiently advanced, this was transparently disclosed to the AOFM and a discussion occurred about the timing of the pricing call, the duration manager’s ability to retain a portion of the risk to hedge post pricing, and the potential impact on price of each course of action.

Conduct amounting to unconscionable conduct (s 12CB)

83 As to this conduct that I have elaborated on in a little detail, ANZ admits that in the period 19 April 2023 to 3 May 2023, it contravened s 12CB(1) of the ASIC Act by engaging in conduct, in connection with the supply of financial services to the AOFM representing the Commonwealth of Australia relating to the issuance of December 2034 Treasury bonds, in trade or commerce, that was in all the circumstances unconscionable.

84 Now at all material times, s 12CB(1) prohibited unconscionable conduct in the following terms:

(1) A person must not, in trade or commerce, in connection with:

(a) the supply or possible supply of financial services to a person; or

(b) the acquisition or possible acquisition of financial services from a person;

engage in conduct that is, in all the circumstances, unconscionable.

85 The parties have agreed, which I accept, that the threshold requirements of that section have been met and that the impugned conduct was in “trade or commerce”, as defined in s 12BA, and in “connection with” the supply or possible supply of financial services for the purpose of s 12CB. As s 12CB(4) makes clear, the concept of unconscionability under s 12CB is more wide-ranging than, and not limited by, the concept of unconscionability in equity. And in the context of commercial dealings, the question is whether such conduct is so far “outside societal norms of acceptable commercial behaviour as to warrant condemnation as conduct that is offensive to conscience” (Australian Securities and Investments Commission v Kobelt (2019) 267 CLR 1 at [92] per Gageler J).

86 Section 12CC sets out a non-exhaustive list of factors to which one may have regard in determining whether the conduct answers the description of being unconscionable. But I am not required to evaluate the impugned conduct by reference to the presence or absence of these factors irrespective of the relevance of those factors, but must do so if any of the factors are applicable, noting that the presence or absence of each matter is not a mandatory consideration and the totality of the circumstances dictates whether any such matter is applicable; see Productivity Partners Pty Ltd v Australian Competition and Consumer Commission (2024) 419 ALR 30 at [11] and [55] to [57] per Gageler CJ and Jagot J. I have had regard to the relevant considerations in this case.

87 By reason of the matters above taken together and in all of the circumstances, ANZ’s conduct of its role as duration manager and its manner of trading as set out were contrary to the requirements of its own policies and industry guidance issued by the AFMA and by the FMSB, and were inconsistent with ordinary trading behaviour of duration managers appointed by the AOFM in respect of syndicated bond issuances.

88 I accept, based on the agreed facts, that a trader in the position of ANZ, with the knowledge of ANZ, acting within the range of ordinary trading behaviour of duration managers described above, in all of the circumstances, would have taken one or more of the following steps: (a) sold a greater volume of 10-year Australian bond futures in the period between 8:32am and 1:10pm on 19 April 2023; (b) informed the AOFM prior to the nominated time of the pricing call of some or all of the matters above; (c) revised the chosen hedging strategy to seek to be fully hedged at the time of pricing; (d) adjusted or nominated a different time for the pricing call to allow itself more time to pre-hedge; (e) withheld some of its hedging activity until after the time of pricing; (f) traded in a manner that did not result in the sale of significant volumes of 10-year Australian bond futures in a compressed time window shortly prior to and during the pricing call and did not result in applying undue downward pressure on the price of 10-year Australian bond futures at the time of pricing.

89 But I accept that ANZ’s conduct in its role as duration manager and its manner of trading did not constitute over-hedging or market manipulation.

90 In my view, based on the facts that I have set out and admissions made by the ANZ, ANZ’s conduct in all of the circumstances was unconscionable in contravention of s 12CB(1). Let me elaborate on eight aspects.

91 First, ANZ represented to the AOFM that it would be transparent with the AOFM. It so represented in advance of the appointment as duration manager, when on 29 March 2023, ANZ emailed the AOFM expressing an interest in such an appointment, and attaching a presentation which referred to a key objective for an issuance as “transparency”, specifically a “Transparent process throughout”. And it so represented when accepting the role of duration manager. ANZ told the AOFM that ANZ would “certainly try and maintain and manage the risk in a way that is of the least impact to the market and we keep an open and consistent dialogue both with yourselves and myself and the trader who will be looking after the risk.”

92 Second, ANZ knew on 19 April 2023 that it intended to sell a substantial volume of 10-year Australian bond futures between market open at 8:32am and the pricing call time nominated by ANZ. ANZ knew that this selling would have, or would be likely to have, the effect of placing downward pressure on the price of the bond futures, in its favour and to the detriment of the AOFM. Further, by 9.30am, ANZ knew that the deal size was $14 billion and by about 11.20am that ANZ would receive approximately 84,544 contracts of 10-year Australian bond futures at the time of the issuance. Further, by 12pm, the ANZ traders were aware that they would be seeking to sell about 65,950 contracts of 10-year Australian bond futures in less than two hours until the nominated pricing call time of 1:50pm to fully hedge the contracts ANZ would acquire from investors in the bond issuance. They were also aware that selling this volume within that time period would have, or would be likely to have, a downward impact on the price of 10-year Australian bond futures. Further, by 1pm, the ANZ traders intended to be fully hedged at pricing, if they could do so at an acceptable price, and were aware that they would seek to sell about 63,850 contracts of 10-year Australian bond futures in the next 50 minutes, until ANZ’s nominated pricing call time of 1:50pm, to fully hedge the contracts ANZ would acquire from investors in the bond issuance. They were also aware that selling this volume within that time period would have, or would be likely to have, a downward impact on the price of 10-year Australian bond futures, in its favour and to the detriment of the AOFM.

93 Third, the AOFM was to the ANZ’s knowledge situationally vulnerable, as a result of not knowing ANZ’s specific intentions and trading activity and because, having relied upon ANZ to manage the inherent conflict of interest by conducting itself in accordance with the expected behaviour of a duration manager, the AOFM was unable to counteract or protect itself.

94 Fourth, ANZ breached its own policies for hedging. Those internal policies included ANZ’s MST guidelines and trading practice guidelines in place as at April 2023 which required, inter alia, the following. One aspect was that traders “should use reasonable endeavours to execute the MST in a manner that is not disadvantageous to the client” and “is minimally disruptive to the market. [Traders] should manage the execution of the MST in a way that promotes the fair treatment of the Client” and pre-hedging “must be carried out insofar as possible in a way that is not detrimental to the Client”. And another aspect was that “[w]hen hedging, it should be conducted in a manner that has little influence on market pricing, at a pace consistent with the normal market volumes at that time of day in the relevant instrument, and does not result in undue pressure on pricing around the fixing window/reference time/ pricing call.”

95 Fifth, ANZ breached industry guidance, including the following guidance.

96 The November 2016 Reference Price Transaction Standard issued by the FMSB, which as I have stated is a UK-based industry body that promotes best practice standards for wholesale markets globally including by developing standards and good practice statements, stated that market participants should “balance the objectives of its hedging strategy against the possibility of putting undue pressure on the reference price, recognising that some price pressure is to be expected as risk is passed, particularly for large transactions or transactions in less liquid markets”.

97 Further, AFMA’s Guidance on Pre-Hedging and Debt Capital Primary Market Guidelines, which included a section entitled “Reference Price Transactions”, formed part of the AFMA Code of Conduct. It stated that dealers should conduct hedging “in a manner that is not intended to disadvantage the Client” and communicate “their hedging practices to the Issuer in a clear manner meant to enable clients to understand their intentions and actions in the market”.

98 Sixth, ANZ’s behaviour was outside the range of ordinary behaviour of duration managers appointed by the AOFM. Of the total 21 syndicated bond issuances the AOFM conducted between January 2017 and July 2024 the following may be noted.

99 Except for one transaction in 2018 for which ANZ was also the duration manager, the April 2023 issuance was the only issuance in which the duration manager had sold reference products equal to the EFP quantity of the reference product at the time of pricing. In all other issuances, the duration manager withheld a portion of the amount of reference product to be sold until after pricing, for purposes including minimising market disruption, protecting the interests of the AOFM, and/or profiting from the anticipated rise in the price of the futures contracts. Of the other 19 transactions, including another two previous transactions in which ANZ was the duration manager, the highest proportion that a duration manager sold of the EFP quantity of the reference product by the time of pricing was approximately 85%. ANZ traded a materially higher proportion of its anticipated risk in the 45 minutes prior to pricing on 19 April 2023.

100 In at least some of the other transactions, where unanticipated market conditions arose or the duration manager’s pre-hedging was not sufficiently advanced, this was transparently disclosed by the duration manager to the AOFM and a discussion occurred about the timing of the pricing call, the duration manager’s ability to retain a portion of the risk to hedge post-pricing, and/or the potential impact on price of each course of action. ANZ did not do so on 19 April 2023.

101 Seventh, ANZ failed to take one or more of the following steps. It failed to sell a greater volume of 10-year Australian bond futures in the period between 8.32am and 1.10pm on 19 April 2023. It failed to inform the AOFM of its lack of progress in its hedging in light of its intention to seek to be fully hedged by the time of pricing if it could do so at an acceptable price when proposing or confirming the time for the pricing call. It failed to propose to delay the pricing call. And it failed to modify its strategy of being fully hedged by the time of pricing.

102 Eighth, ANZ was not forthcoming in its reporting to the AOFM about its conduct as duration manager after the issuance, including when the AOFM questioned ANZ about its trading, and instead made inaccurate or incomplete statements which involved misleading conduct about the circumstances of ANZ’s trading.

103 Generally, ANZ traded in the manner set out above and in the context of the circumstances as I have set out. Let me turn to the next topic of misleading and deceptive conduct and false representations.

Misleading conduct and false representations (s 1041H and s 12DB) — introduction

104 ANZ admits that on 27 occasions between 14 September 2021 and 22 June 2023 it engaged in misleading or deceptive conduct contrary to s 1041H of the Corporations Act and it admits that on 24 occasions between 14 September 2021 and 22 June 2023, it made false or misleading representations contrary to s 12DB of the ASIC Act. Those contraventions may conveniently be separated into two categories.

105 First, on and after 19 April 2023, ANZ provided reports to the AOFM which were misleading or deceptive in describing, or were misleading or deceptive by omission in respect of, ANZ’s trading activities as duration manager for the December 2034 Treasury bond issuance. Those reports were provided after the AOFM raised concerns with ANZ as to ANZ’s trading activities as duration manager for the December 2034 Treasury bond issuance and one of those reports was provided in response to queries raised by the AOFM.

106 Second, between 14 September 2021 and 22 June 2023, ANZ provided to the AOFM monthly reports about ANZ’s secondary market bond turnover for the period from July 2021 to May 2023. In those reports, ANZ materially misstated the value of ANZ’s secondary market bond turnover. Further, on 19 August 2022, ANZ provided to the AOFM the annual verification for ANZ’s secondary market bond turnover in FY2021-22. In doing so, ANZ misrepresented to the AOFM that the monthly survey data for the 2021-22 financial year it had previously provided was accurate. I will set out later details as to the 24 occasions on which misrepresentations were made in contravention of s 12DB.

107 But before proceeding further I should say something about the relevant provisions and principles.

108 Section 1041H(1) of the Corporations Act prohibited misleading or deceptive conduct in the following terms:

(1) A person must not, in this jurisdiction, engage in conduct, in relation to a financial product or a financial service, that is misleading or deceptive or is likely to mislead or deceive.

109 Further, s 12DB(1)(a) of the ASIC Act provided:

(1) A person must not, in trade or commerce, in connection with the supply or possible supply of financial services, or in connection with the promotion by any means of the supply or use of financial services:

(a) make a false or misleading representation that services are of a particular standard, quality, value or grade…

110 There are relevant differences between the provisions in respect of certain threshold elements. Section 1041H of the Corporations Act requires the conduct to be “in this jurisdiction” and in relation to either a “financial product” or a “financial service”. By contrast, s 12DB(1)(a) of the ASIC Act applies to representations “in trade or commerce” which are in connection with the supply or possible supply of “financial services”, where those representations are that services are “of a particular standard, quality, value or grade”.

111 Section 1041H(1) applies to conduct “in relation to a financial product or a financial service”. The expression “in relation to” is wide to say the least, and an indirect or less than substantial connection may be sufficient. A “financial service” is defined to include dealing in financial products; see s 766A(1)(b). The term “dealing” is defined to be constituted by, inter alia, issuing, varying or disposing of a financial product; see s 766C(1). And arranging for a person to engage in such conduct is also dealing in a financial product; see s 766C(2).

112 Section 12DB applies to conduct “in connection with the supply or possible supply of financial services, or in connection with the promotion by any means of the supply or use of financial services”. Section 12BAB(1)(g) stipulates that a person provides a financial service if they “provide a service … that is otherwise supplied in relation to a financial product”. The expression “in connection with” may require that the impugned conduct accompany or be involved in the supply of services.

113 In Australian Securities and Investments Commission v Westpac Banking Corporation (No 2) (2018) 266 FCR 147; 127 ACSR 110, I commented on the phrase “in connection with” in the context of s 12CB of the ASIC Act. I considered that whilst the specific degree of connection required understandably varies with the statutory context, a narrow or technical approach was not warranted. I said (at [2172]):

As to the requirement that conduct be “in connection with” the supply or acquisition, or possible supply or acquisition, of financial services, an analogous requirement in s 51AC of the Trade Practices Act was considered in Monroe Topple & Associates Pty Ltd v Institute of Chartered Accountants in Australia (2002) 122 FCR 110. Heerey J held that the expression required that “the conduct impugned ‘accompany, go with or be involved in’ the supply of goods or services” (at [74]). That observation does not support a narrow or technical approach to the expression. It was made in the context of distinguishing conduct directed at the recipient of the relevant goods or services, and conduct directed at (and only said to be unconscionable in relation to) an unrelated third party. Of course, the expression “in connection with” requires a relation between one thing and another, but the specific degree of connection required understandably varies with the statutory context. But a causal relationship is not required. And no narrow approach is warranted having regard to the protective objects of the provision. In particular, I agree with ASIC that there is no basis for implying into the expression “in connection with” a requirement that conduct said to be unconscionable must have occurred prior to the relevant supply or acquisition of financial services. Such a temporal constraint would be artificial and inconsistent with the following matters. First, the generality of the statutory text directs attention to “all the circumstances”. Second, the list of factors expressly identified as relevant to whether s 12CB (or s 12CC) has been breached includes “any conduct that the supplier [or acquirer] or the service recipient [or business supplier] engaged in, in connection with their commercial relationship, after they entered into the contract”; see ss 12CC(2)(j)(iv) and 12CC(3)(j)(iv) (prior to 1 January 2012), and ss 12CC(1)(j)(iv) and s 12CC(2)(j)(iv) (post 1 January 2012). Third, the terms of s 12CB(3)(a) prohibit a court from considering “any circumstances that were not reasonably foreseeable at the time of the alleged contravention”. Such a provision implicitly permits prospective matters to be taken into account. Further, the reference time is not the time of entry into of a dealing but the time of the alleged contravention. Fourth, the very terms of s 12CB(4)(c)(ii) state that “in considering whether conduct to which a contract relates is unconscionable, a court’s consideration of the contract … is not limited to consideration of the circumstances relating to formation of the contract”.

114 Given the similarities between ss 12CB and 12DB, the same approach applies equally to the latter provision.

115 There is little doubt that the threshold elements are satisfied for the alleged contraventions of ss 1041H and 12DB(1)(a). First, the relevant conduct was in this jurisdiction. Second, the relevant conduct was in trade and commerce. Third, the relevant conduct was “in relation to” (for s 1041H(1) of the Corporations Act), or “in connection with the supply of” (for s 12DB(1) of the ASIC Act), financial services.

116 Now subject to the matters just discussed, the applicable legal principles for analysing the conduct are the same under each of s 1041H and s 12DB. There is no material difference between the expression “false or misleading representations” in s 12DB(1) of the ASIC Act and the expression “misleading or deceptive conduct” in s 1041H(1) of the Corporations Act.

117 It is convenient to repeat what I said in ASIC v Westpac (No 2) at [2259] to [2286]:

Let me say the following concerning the elements of s 1041H.

First, the concept of “engaging in conduct” is broad. It is defined inclusively by s 1041H(2)(a) of the Corporations Act to include “dealing in a financial product”. Further, “this jurisdiction” is, relevantly, Australia (s 5(2)).

Second, the expression “in relation to” is of wide ambit. Now it is trite to observe that its meaning will be determined by the context. The phrase signifies the need for there to be a relationship or correlation between the two subjects formally referenced. Moreover, an indirect or less than substantial connection may be sufficient.

More generally, the relevant principles are largely the same as those which apply to s 18 of the Australian Consumer Law. In ACCC v Get Qualified Australia Pty Ltd (in liq) (No 2) [2017] ATPR 42-548 at [25]-[42], I summarised the relevant principles in the following terms which no party in the present proceeding contested.

First, there is no meaningful difference between the words and phrases “misleading or deceptive”, “mislead or deceive” or “false or misleading”.