Federal Court of Australia

Crawford, in the matter of Pro-Pac Packaging Limited (administrators appointed) [2025] FCA 1357

File number: | VID 1447 of 2025 |

Judgment of: | BEACH J |

Date of judgment: | 5 November 2025 |

Date of publication of reasons: | 6 November 2025 |

Catchwords: | CORPORATIONS — insolvency — voluntary administration of Pro-Pac group of companies — Part 5.3A of the Corporations Act 2001 (Cth) — extension of convening period for second meeting of creditors — Daisytek order — ss 439A(6) and 447A of the Act — directions to enter into funding agreements — s 90-15 of the Insolvency Practice Schedule (Corporations) (IPS) — orders concerning liabilities and limitations on the administrators’ personal liability — ss 443A and 447A of the Act — orders dealing with funds handling — directions concerning payment of funds out of the administration account — directions concerning ss 65-25, 65-45 and 90-15 of the IPS and s 447A of the Act — extension of time to deal with requests of creditors — s 90-15 of the IPS and s 447A of the Act — rule 70-1(2)(a) of the Insolvency Practice Rules (Corporations) 2016 (Cth) — orders made |

Legislation: | Corporations Act 2001 (Cth) ss 435A, 439A(2), 439A(6), 443A, 447A Insolvency Practice Rules (Corporations) 2016 (Cth) rule 70-1(2)(a) Insolvency Practice Schedule (Corporations) (IPS) ss 60-10, 65-5(1), 65-15, 65-25, 65-45, 90-15 |

Cases cited: | Parbery, in the matter of NewSat Limited (Administrators Appointed) (Receivers and Managers Appointed) [2015] FCA 435 Re Ansett Australia Ltd [2001] FCA 1439; (2001) 39 ACSR 355 Re Ansett Australia Ltd (No 1) [2001] FCA 1806; (2002) 115 FCR 376 Re Ansett Australia Ltd (No 3) [2002] FCA 90; (2002) 115 FCR 409 Re Daisytek Australia Pty Ltd (Administrators Appointed) (2003) 45 ACSR 446 Re Grocon Pty Ltd (admins apptd) (No 1) [2020] VSC 833 Re Mentha (in their capacities as joint and several administrators of the Griffin Coal Mining Company Pty Ltd) (admins apptd) (2010) 82 ACSR 142 Re Riviera Group Pty Ltd (Administrators Appointed) (Receivers and Managers Appointed) (2009) 72 ACSR 352 Secatore, in the matter of In-Fusion Management Pty Ltd (Administrators Appointed) [2016] FCA 1072 Stimpson, in the matter of Eagle Boys Dial-A-Pizza Australia Pty Ltd (Administrators Appointed) [2016] FCA 935 Wight, in the matter of Responsible Entity Services Limited (in liquidation) [2025] FCA 1219 |

Division: | General Division |

Registry: | Victoria |

National Practice Area: | Commercial and Corporations |

Sub-area: | Corporations and Corporate Insolvency |

Number of paragraphs: | 89 |

Date of hearing: | 5 November 2025 |

Counsel for the Plaintiffs: | Mr L Freckelton |

Solicitor for the Plaintiffs: | Norton Rose Fulbright Australia |

ORDERS

VID 1447 of 2025 | ||

IN THE MATTER OF PRO-PAC PACKAGING LIMITED (ADMINISTRATORS APPOINTED (ACN 112 971 874 | ||

KEITH ALEXANDER CRAWFORD AND ROBERT BRUCE SMITH IN THEIR CAPACITY AS JOINT AND SEVERAL ADMINISTRATORS OF PRO-PAC PACKAGING LIMITED (ADMINISTRATORS APPOINTED) ACN 112 971 874 First Plaintiff PRO-PAC PACKAGING LIMITED ACN 112 971 874 Second Plaintiff PRO-PAC GROUP PTY LTD ACN 095 393 776 (and others named in the Schedule) Third Plaintiff | ||

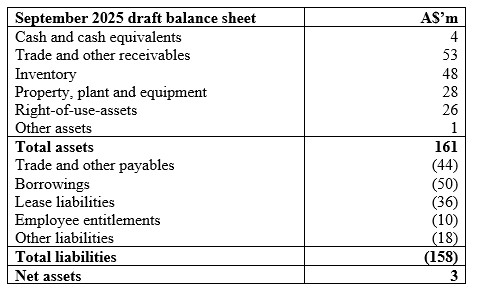

order made by: | BEACH J |

DATE OF ORDER: | 5 NOVEMBER 2025 |

THE COURT NOTES THAT:

“Administrators” means Keith Crawford and Robert Smith, in their capacity as the voluntary administrators of the Second to Twenty Fourth Plaintiffs, being the First Plaintiffs in the proceeding;

“Pro-Pac Companies” means the Second to Twenty-Fourth Plaintiffs in this proceeding;

“Australian ScotPac Funding Deed” means the Funding Variation Letter (including the Voluntary Administration Addendum) between the Administrators, the Second to Fourteenth Plaintiffs, the Sixteenth to Twenty-Fourth Plaintiffs, the New Zealand Pro-Pac Companies, and Scottish Pacific Business Finance Pty Ltd ACN 008 636 388 being substantially in the form of Tab B of confidential annexure RBS-A to the Smith Affidavit;

“New Zealand Pro-Pac Companies” means Integrated Packaging Ltd NZBN 372943 (Administrators Appointed) and Pro-Pac Finance (NZ) Limited NZBN 6515713 (Administrators Appointed);

“NZ ScotPac Funding Deed” means the Funding Variation Letter (including the Voluntary Administration Addendum) between the Administrators, the Second to Fourteenth Plaintiffs, the Sixteenth to Twenty-Fourth Plaintiffs, the New Zealand Pro-Pac Companies and Scottish Pacific Business Finance Ltd NZ BN 535333 being substantially in the form of confidential exhibit FKM-1 to the affidavit of Fiona Murray-Palmer affirmed on 5 November 2025;

“Kin Funding Deed” means the Administration Support Deed between the Administrators, the Second to Fourteenth Plaintiffs, the Sixteenth to Twenty-Fourth Plaintiffs, the New-Zealand Pro-Pac Companies and Kin Group Pty Ltd ACN 095 313 714 being substantially in the form of Tab A of confidential annexure RBS-A to the Smith Affidavit;

“Smith Affidavit” means the affidavit of Robert Bruce Smith affirmed on 5 November 2025 and filed in this proceeding.

THE COURT ORDERS THAT:

1. Pursuant to s 439A(6) of the Corporations Act 2001 (Cth) (Act), the period within which the Administrators must convene the second meeting of creditors of the Pro-Pac Companies required under s 439A of the Act be extended to Wednesday, 20 May 2026.

2. Pursuant to s 447A of the Act, Pt 5.3A of the Act is to operate in relation to the Pro-Pac Companies such that, notwithstanding the provisions in s 439A(2) of the Act, the second meetings of the creditors of the Pro-Pac Companies required under s 439A of the Act may be convened and held at any time during, or within, five business days after the convening period as extended by order 1 above, provided that the Administrators give notice of the meeting to creditors of each of the Pro-Pac Companies (including the persons or entities claiming to be creditors of the Pro-Pac Companies) at least five business days before the meeting.

3. Pursuant to s 447A(1) of the Act that Part 5.3A of the Act is to operate in relation to the Administrators and the Pro-Pac Companies as if s 443A(1) of the Act provides that:

(a) all liabilities of the Administrators and the Pro-Pac Companies incurred in connection with, or with respect to, any obligations arising out of the Kin Funding Deed, the Australian ScotPac Funding Deed or the NZ ScotPac Funding Deed, including monies borrowed, interest incurred in respect of monies borrowed, and borrowing costs or expenses are in the nature of debts incurred by the Administrators in the performance and exercise of the Administrators’ functions and powers as administrators of each of the Pro-Pac Companies; and

(b) notwithstanding that the liabilities in subparagraph (a) are debts or liabilities incurred by the Administrators in the performance and exercise of their functions as joint and several administrators of the Pro-Pac Companies, the Administrators will not be personally liable to repay such debts or satisfy such liabilities (including any interest incurred in respect of monies borrowed, interest incurred in respect of monies borrowed, and any borrowing costs or expenses) to the extent that the Administrators’ right of indemnity out of the property of the Pro-Pac Companies is insufficient to satisfy such debts or liabilities.

4. Pursuant to s 65-45(1) of the Insolvency Practice Schedule (Corporations) being Schedule 2 to the Act (IPSC), and further or alternatively s 90-15 of the IPSC, or further or alternatively s 447A of the Act, that s 65-25(1) of the IPSC is to operate such that the Administrators must not pay any money out of the PPG Administration Account (as that term is defined in the Smith Affidavit) otherwise than:

(a) for purposes related to the external administration of the Pro-Pac Companies and their related entities in New Zealand; or

(b) in accordance with the Act; or

(c) in accordance with any further direction of the Court.

5. Pursuant to s 447A(1) of the Act, and further or in the alternative, s 90-15 of the IPSC, r 70-1(2)(a) of the Insolvency Practice Rules (Corporations) 2016 (Cth) is to operate in relation to the Pro-Pac Companies as if:

(a) the words ‘5 business days after receiving the request’ be read as ‘10 business days after receiving the request’; and

(b) the Administrators may provide the information, report, or document requested by a creditor by publishing that information, report, or document on the creditor portal maintained by the Administrators accessible on the website https://www.mcgrathnicol.com/creditors/pro-pac-packaging-group.

AND THE COURT DIRECTS THAT:

6. Pursuant to s 90-15 of the IPSC, the Administrators are justified and acting reasonably in carrying on their duties as Administrators in:

(a) causing the Pro-Pac Companies (other than Integrated Machinery Pty Ltd, the Fifteenth Plaintiff) to enter into and perform the Australian ScotPac Funding Deed;

(b) causing the Pro-Pac Companies (other than Integrated Machinery Pty Ltd) to enter into and perform the NZ ScotPac Funding Deed; and

(c) causing the Pro-Pac Companies (other than Integrated Machinery Pty Ltd) to enter into and perform the Kin Funding Deed.

AND THE COURT FURTHER ORDERS THAT:

7. Pursuant to ss 37AF and 37AG of the Federal Court of Australia Act 1976 (Cth) that, until further order, the following documents be marked confidential on the Court file and not be published, disclosed or accessed except by Court staff, the plaintiffs or their advisors on the ground that this order is necessary to prevent prejudice to the proper administration of justice:

(a) paragraphs 53, 55(part), 57(part) and 68(b)-(c) of the Smith Affidavit;

(b) confidential annexure RBS-A to the Smith Affidavit;

(c) paragraphs 21 and 28 (part) of the written outline of submissions dated 5 November 2025 and filed in support of the Administrators’ originating process dated 4 November 2025 (as amended); and

(d) the affidavit of Fiona Murray-Palmer affirmed on 5 November 2025 together with confidential exhibit FKM-1.

8. The Administrators within 2 business days of these orders are to take all reasonable steps to give notice of these orders to:

(a) the creditors of the Pro-Pac Companies (including the persons claiming to be creditors) by means of a circular:

(i) to be sent by email transmission to creditors for whom the Administrators currently have an email address; or

(ii) to be sent by ordinary post to creditors for whom the Administrators currently only have a postal address; and

(b) the Australian Securities and Investments Commission, by its street address or email address.

9. Liberty be granted to any person demonstrating a sufficient interest to apply to vary or discharge any orders made above, on two (2) business days’ written notice being given to the Plaintiffs and to the Court.

10. The Administrators’ costs of and incidental to this application be costs in the administrations of the Pro-Pac Companies.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

BEACH J:

1 On 23 October 2025, Mr Keith Crawford and Mr Robert Bruce Smith were appointed as joint and several administrators of Pro-Pac Packaging Limited and its Australian subsidiaries.

2 On the same date as their appointment to the Australian companies, Mr Crawford, Mr Andrew Grenfell and Mr Kare Johnstone were appointed as joint and several administrators to two additional companies in the corporate group that are registered in New Zealand, being Integrated Packaging Limited and Pro-Pac Finance (NZ) Limited.

3 The Australian companies and the New Zealand companies, together with one company registered in Malaysia and another registered in the USA, constitute the Pro Pac Group. The Malaysian and American entities are not the subject of external appointments at this stage.

4 The administrators have sought the following orders.

5 First, they have sought orders relieving the administrators from personal liability for funding arrangements to be entered into to allow the administrators to manage the administration of the companies.

6 Second, they have sought orders extending the period within which the administrators are required to convene the second meetings of creditors of the Australian companies by 6 months. Further, they have sought a consequential order enabling the meetings of the creditors of the Australian companies to be convened under s 439A of the Corporations Act 2001 (Cth) at any time during the convening period or within 5 business days thereafter.

7 Third, they have sought directions relieving the administrators from the requirement of strict compliance with Division 65-45 of the Insolvency Practice Schedule (Corporations) (IPS), in relation to using funds in the account of one company for purposes related to other companies in the group.

8 Fourth, they have sought an order extending the time in which the administrators must respond to any creditor requests for information from 5 business days to 10 business days and permitting that information to be provided by way of a creditor portal established on the McGrathNicol website.

9 The New Zealand administrators have made a similar application to the High Court of New Zealand in parallel to this application.

10 Now given that the New Zealand administrators are also making such an application for orders concerning the New Zealand companies, the administrators considered whether the present application before me should be brought under the UNCITRAL Model Law on Cross-Border Insolvency. But they were informed by solicitors engaged by the New Zealand administrators that the New Zealand court is not a party to the Judicial Insolvency Network (as the Federal Court is) and therefore the New Zealand court may not have subscribed to the JIN’s guidelines to cross-border cooperation between courts. The New Zealand administrators were concerned that if the applications in both jurisdictions were brought under the Model Law, this may cause delay to the hearing of the most time sensitive aspects of the New Zealand application, being relief sought in relation to certain employee entitlements under New Zealand law. For that reason, an application under the Model Law has not been made.

11 I do not propose to comment on the advice given to the administrators. And in any event cross-border co-operation can easily take place with New Zealand outside the parameters of the Model Law and the JIN as it has done very effectively in the past. One notable example was the joint sitting between a Full Court of this Court of which I was a member and the NZ Court of Appeal in Loo v Kelly [2021] FCAFC 186; (2021) 156 ACSR 194 involving the insolvency of various Halifax Australian and NZ entities; similar co-operation took place at first instance between Markovic J and Venning J. In any event, the fact is that no application has been made under the Model Law and I will proceed accordingly.

12 I should note one other matter before proceeding further. At 11.00 am on 3 November 2025, the first meeting of creditors of each of the Australian companies was held. Mr Smith was the chair of each meeting. Approximately 130 people attended the meetings. The creditors resolved to establish a committee of inspection for Pro-Pac Group Pty Ltd (PPG); 12 people have been appointed to the committee.

Overview of the Pro-Pac Group

13 Pro-Pac Packaging Limited is an ASX-listed company which, itself and through its subsidiaries, develops, manufactures and distributes packaging products in Australia and internationally.

14 The Australian subsidiaries are the following: PPG; Perfection Packaging Pty Ltd; Integrated Packaging WA Pty Ltd; Integrated Recycling Pty Ltd; Pro-Pac Packaging (Aust) Pty Ltd; Pro-Pac Packaging Manufacturing (Syd) Pty Ltd; Pro-Pac Packaging Manufacturing (Melb) Pty Ltd; Pro-Pac Packaging Manufacturing (Bris) Pty Ltd; Pro-Pac Finance Pty Ltd; Integrated Packaging Group Pty Ltd; Goodstone International Pty Ltd; Pro-Pac Industrial Group Pty Limited; Integrated Machinery Pty Ltd; Creative Packaging Pty Ltd; Pro-Pac (GLP) Pty Ltd; ACN 003 940 921 Pty Limited; Great Lakes Moulding Pty Ltd; ACN 002 431 898 Pty Limited; Finpact Pty Ltd; ACN 002 029 852 Pty Limited; ACN 108 620 506 Pty Limited; and ACN 087 226 631 Pty Limited.

15 The Pro-Pac Group’s business is divided into four key business units (the businesses).

16 First, there is Integrated Packaging (Australia) which comprises three main divisions being Integrated Packaging, Integrated Machinery and Integrated Recycling. According to Integrated Packaging Australia’s website it is Australia’s largest specialist manufacturer and distributor of stretch film wrap and associated products. It manufactures and distributes printed polyethylene and PVC food films and services industrial and agricultural markets.

17 Second, there is Integrated Packaging (New Zealand) which conducts a similar business to Integrated Packaging Australia, but located in New Zealand.

18 Third, there is Perfection Packaging which manufactures and distributes flexible packaging for fast-moving consumer goods, food, health and personal care industries. It has contracts with large customers such as Arnott’s.

19 Fourth, there is Speciality Packaging which imports and distributes specialty packaging supplies such as modified atmosphere packaging trays for various industries, most predominantly the food sector.

20 Based on the administrators’ preliminary investigations it would seem that a number of entities to which they are appointed are not trading and largely dormant. This appears to be a result of businesses that were run out of the now-dormant entities having been transferred to the active companies in 2020. From their investigations it would seem that trading predominantly occurs via one entity in Australia, being PPG, and one entity for New Zealand, being Integrated Packaging Limited. Further, some of the dormant entities continue to be parties to property leases that have not been novated to PPG and there appear to be a number of inter-company loans.

21 The most recent management accounts prepared by the companies are as at 30 September 2025, which can be summarised as follows:

22 In relation to the above table, trade and other receivables include those debtors subject to various security interests (the majority of debtors), and a small balance of intercompany debtors. Further, all premises are leased. Further, trade and other payables, lease liabilities and other liabilities are expected to constitute unsecured creditor claims, with this balance expected to increase as claims are crystallised when formal proofs of debt are called for.

23 The administrators have identified that there are approximately 545 employees, 139 secured creditors (4 with All PAAP registrations and 135 with other security interests) and approximately 1,200 unsecured creditors, resulting in a significant, but as yet unknown quantum of creditor claims.

24 Further, most funds received including from the New Zealand companies are received into PPG’s bank account in Australia and from that account PPG pays liabilities of the companies, including paying from time to time the wages of the New Zealand employees and New Zealand suppliers and other creditors. Further, there are also accounts held with New Zealand banks. The New Zealand bank accounts receive cash from New Zealand customers and those funds are used to pay local suppliers and employees.

25 Further, the group’s significant secured creditors are Scottish Pacific Business Finance Pty ltd (ScotPac) and Australia and New Zealand Banking Group Limited which each have registered AllPAAP security interests arising under General Security Deeds with the companies, other than Integrated Machinery Pty Ltd. The companies have granted AllPAAP security interests to both ScotPac and its related NZ entity (ScotPac NZ).

26 Further, Bennamon Pty Ltd, a company related to Kin Group Pty Ltd, a major shareholder of Pro-Pac Packaging Limited, has advanced funds to the Group for the purpose of, amongst others, meeting employee obligations, and so has priority under s 560 for repayment of those amounts. It has also registered AllPAAP security interests against eight of the companies.

The financing of the Pro-Pac Group by ScotPac

27 On 28 November 2022, PPG and Pro-Pac Finance Pty Ltd (the borrowers) entered into a facility agreement with ScotPac under which ScotPac provided a debtor finance facility to the borrowers. ScotPac agreed to advance funds of up to AUD30,000,000.00. ScotPac also entered into a NZD3,000,000 facility.

28 Under the ScotPac facility agreement, ScotPac purchases present and future book debts of the companies in return for which it makes cash available to the companies. The amount of cash which ScotPac pays in respect of each purchased invoice depends on a number of factors including the age of the debt.

29 As security for the ScotPac facility agreement, the various companies within the Group, save for Integrated Machinery Pty Ltd, each guaranteed and provided indemnities in relation to the borrowers’ obligations under the facility agreement.

30 Pursuant to a general security deed dated 1 December 2022, each of the borrowers and guarantors granted to ScotPac a security interest in all its present and after-acquired property to secure its obligations under the ScotPac facility agreement and the guarantees and indemnities provided therein. The security interests provided by the Australian companies were registered on the Personal Property Securities Register.

31 The ScotPac facility agreement has subsequently been amended as follows: (a) variation deed dated 17 January 2023 under which various clarifying changes were made to both the facility agreement and general security deed; (b) variation deed dated 21 June 2023 which increased the “Early Payment Percentage” in the facility agreement from 60% to 75%; (c) variation deed dated 28 March 2024 which increased the “Early Payment Percentage” in the facility agreement from 75% to 80%; and (d) variation deed dated 28 March 2024 which increased the “Early Payment Percentage” in the facility agreement to 80%.

32 Relevantly, under the Scot Pac facility agreement, the appointment of an administrator to any transaction party, which includes the borrowers and the guarantors, is a default event. Further, whilst a default event is continuing, ScotPac may end the facility agreement, disapprove all approved accounts and demand that the borrowers immediately repay all amounts to which ScotPac is entitled.

33 On 14 October 2024, PPG entered into a further facility agreement with ScotPac under which ScotPac agreed to provide a chattel mortgage facility to PPG. Pursuant to the chattel mortgage facility, ScotPac agreed to advance funds of up to AUD5,000,000 to PPG.

34 The chattel mortgage facility is the subject of a priority deed between ScotPac, the various companies other than Integrated Machinery Pty Ltd, ScotPac NZ and ANZ. The priority deed gives ScotPac priority ahead of ANZ in respect of its security over: (a) the book debts of PPG, Pro-Pac Finance Pty Ltd and Integrated Packaging Limited; and (b) the equipment listed in annexure A of the chattel mortgage schedule the subject of the facility. Further, the chattel mortgage facility is secured by a guarantee and indemnity given by the various companies save for Integrated Machinery Pty Ltd.

35 Generally, the various companies have been reliant on access to the ScotPac facilities to provide working capital to the businesses.

36 In order to fund the administration of the companies, the administrators intend to enter into a further variation deed with ScotPac, comprising a facility variation letter incorporating a voluntary administration addendum (Australian ScotPac funding deed) under which funds will continue to be available to the companies on revised terms.

37 But so as not to lose ScotPac’s priority as agreed with ANZ under the priority deed, the funds are to be provided under a varied version of the existing facilities rather than by way of a new facility arrangement. This also avoids the companies having to pay a fee to ScotPac that would otherwise arise on termination of the existing ScotPac facility. The administrators, the various Australian companies (save for Integrated Machinery Pty Ltd) and the New Zealand companies will be party to the ScotPac funding deed, together with ScotPac.

38 A similar suite of documents on substantially similar terms will be entered into by the New Zealand administrators, the Australian companies (other than Integrated Machinery Pty Ltd), the New Zealand companies and the administrators in respect of an NZD facility to be provided by ScotPac (NZ funding deed).

39 If the administrators are not able to finalise a deal on satisfactory terms with ScotPac, they will not execute the ScotPac funding deed, in which case ScotPac will cease to make funds available under the ScotPac facilities.

40 The administrators seek orders which have the effect of relieving them from personal liability for the funds advanced to the companies under the ScotPac facilities, as amended by the Australian ScotPac funding deed and the NZ funding deed.

41 Further, in addition to the funding that it is contemplated will be provided by ScotPac under the proposed ScotPac funding deeds, the administrators have had some discussions with Kin Group about the possibility of Kin Group providing alternative or supplementary funding. It has been agreed that in exchange for the Australian administrators entering into an administration support deed (Kin group deed), it will support the administrators in continuing to trade the businesses.

42 Now under the ScotPac funding deeds, and the consequent amendments to the ScotPac facility agreement, the companies will have access to up to AUD20,000,000 and NZD3,000,000, being a total of approximately AUD22,600,000.

43 The administrators are of the opinion that it is necessary to obtain funding to allow the companies to continue to trade, rather than immediately ceasing to trade. In order to trade the businesses as a going concern in the immediate future and provide certainty to employees, customers and suppliers, sufficient liquidity needs to be available. The administrators currently anticipate that the estimated monthly costs of the Australian companies will be between AUD15 million to AUD25 million not including remuneration and disbursements of the administrators.

44 The ScotPac funding deeds are unlikely to adversely affect the rights of creditors, and will in fact maximise returns for creditors given that the employee wages, rent and other critical expenses will continue to be paid during the administration whilst they work towards improving the cash flow of the companies. If a recapitalisation or sale(s) of the businesses is achieved, it is anticipated that a substantial number of employees will either remain with the companies, or transfer their employment to a purchaser(s), thereby avoiding the crystallisation of termination payments for most employees and other key contracts may remain on foot or be novated, which ensures ongoing payments to the counterparties. The terms of the facility are more favourable if the facility continues (as varied) than if it terminates.

45 The terms of the ScotPac funding deeds include the following matters.

46 First, ScotPac will provide access to funds up to approximately AUD22,600,000 according to the modified terms of the facility agreement for the purpose of covering the costs of the administrators, including the New Zealand administrators, trading the companies, including to meet employee wages, PAYG, payroll tax, superannuation, rent and critical trading expenses (the administration funding).

47 Second, the administrators have agreed that ScotPac may receive repayment of its debts as a priority ahead of the administrators’ entitlements from proceeds from book debts the subject of ScotPac’s security and proceeds available from the equipment the subject of ScotPac's security, after satisfaction of the administrators’ remuneration, costs and expenses of preserving and realising that equipment.

48 Third, ScotPac has agreed not to enforce a pre-existing entitlement to a compensatory administration fee, which was triggered by the appointment of the administrators and due and payable to ScotPac, in exchange for an arrangement fee that is considerably lower than the compensatory administration fee.

49 Fourth, the administration funding is on a limited recourse basis, in that the administrators’ personal liability for the debts and liabilities incurred under the ScotPac funding deeds and the varied facility will be limited to the extent that they can be indemnified from the assets of the companies to which they are appointed; an analogous position applies to the NZ administrators.

50 The terms of the proposed Kin group deed are in large part confidential and it is not necessary to set them out. The parties to the deed will be Kin Group, the Australian companies save for Integrated Machinery Pty Ltd, and the administrators of the Australian companies.

51 Generally speaking, I accept the administrators’ position that it is necessary and reasonable to cause the Australian companies to enter into the ScotPac funding deeds and the Kin group deed and it is in the best interests of creditors.

52 First, the finance provided under the administration funding deeds will enable the administrators to trade on the businesses and permit them to make urgent payments and receive income, until a decision is made regarding the recapitalisation or sale of the businesses and will lead to an increased pool of funds being available to creditors than if the companies were immediately wound up.

53 Second, operating the businesses will maximise the value of the businesses and the chance that the Australian companies, or part of their businesses, will continue after administration.

54 Third, the provision of funding by ScotPac will not disturb pre-existing priorities of pre-appointment debts. Further, as I have indicated ScotPac has agreed to the limited recourse provisions in the ScotPac funding deeds and Kin Group has indicated it will agree to limited recourse provisions in the Kin group deed.

55 Fourth, the funding provides an opportunity for the companies to continue trading and for employees to continue to be paid and otherwise avoids the immediate termination of employees, obviating the crystallisation of termination entitlements for hundreds of employees, which they estimate may exceed AUD20,000,000, including redundancy and payments in lieu of notice, in the event of closure of the group. In addition, it provides an opportunity for the longer-term employment of a significant part of the companies’ workforce. Further, it avoids crystallisation of claims by client customers under service contracts entered with the companies.

56 Finally, it would seem that the terms are commercial, in that they are on usual terms and, in the administrators’ view, reflect the current market for funding of this nature and provide for more favourable financial outcomes for the companies overall if the ScotPac facility continues (as varied) than if it terminates; fees that would be payable on termination of the ScotPac facilities will not be payable.

57 So, the administrators consider that entry into the administration funding deeds is in the best interests of the companies and the companies’ creditors. But that being said, given the risk of exposure to personal liability, the administrators are not willing or able to enter into the administration funding deeds or draw down on the facilities thereunder without the protection of the orders sought.

Some relevant provisions and principles

58 The object of Pt 5.3A of the Act and the IPS insofar as it relates to Pt 5.3A is set out in s 435A, which provides:

435A Object of Part

The object of this Part, and Schedule 2 to the extent that it relates to this Part, is to provide for the business, property and affairs of an insolvent company to be administered in a way that:

(a) maximises the chances of the company, or as much as possible of its business, continuing in existence; or

(b) if it is not possible for the company or its business to continue in existence—results in a better return for the company’s creditors and members than would result from an immediate winding up of the company.

59 Section 443A provides:

443A General debts

(1) The administrator of a company under administration is liable for debts he or she incurs, in the performance or exercise, or purported performance or exercise, of any of his or her functions and powers as administrator, for:

(a) services rendered; or

(b) goods bought; or

(c) property hired, leased, used or occupied, including property consisting of goods that is subject to a lease that gives rise to a PPSA security interest in the goods; or

(d) the repayment of money borrowed; or

(e) interest in respect of money borrowed; or

(f) borrowing costs.

(2) Subsection (1) has effect despite any agreement to the contrary, but without prejudice to the administrator’s rights against the company or anyone else.

60 So, an administrator is liable for debts they incur in the performance, or purported performance or exercise, of any of their functions and powers as administrator, including for the repayment of money borrowed. The correlative entitlement to the imposition of personal liability under s 443A is the right of administrators under s 443D to be indemnified from the company’s property for debts or liabilities incurred during the administration.

61 Now the power under s 447A to make orders limiting the personal liability of administrators under s 443A is well-established. Section 447A of the Act provides the Court with a broad power to make such orders as it thinks appropriate about how Part 5.3A of the Act is to operate in relation to a particular company. That power is to be exercised consistently with the purpose of Part 5.3A, namely to provide for the business, property and affairs of an insolvent company to be administered in a way that maximises the chances of the company, or as much as possible of its business, continuing in existence, or, if that is not possible, results in a better return for the company’s creditors than would result from an immediate winding up of the company.

62 In Re Mentha (in their capacities as joint and several administrators of the Griffin Coal Mining Company Pty Ltd) (admins apptd) (2010) 82 ACSR 142, Gilmour J explained (at [30]):

The principles governing the granting of an application for orders under s 447A to vary the liability of administrators under s 443A can be summarised as follows:

a) the proposed arrangements are in the interests of the company's creditors and

b) typically the arrangements proposed are to enable the company's business to continue to trade for the benefit of the company’s creditors;

c) the creditors of the company are not prejudiced or disadvantaged by the types of orders sought and stand to benefit from the administrators entering into the arrangement;

d) notice has been given to those who may be affected by the order.

(citations omitted)

63 Further, the Court is empowered under s 90-15 of the IPS to make such orders as it sees fit in respect of the administration of the group. The function of such orders, or judicial directions, is not to determine the rights and liabilities associated with a particular transaction, but rather to confer a level of protection on the administrator. But the fact that a s 90-15 direction may relate to a decision or action of a commercial character does not prevent such a direction being made. I have recently discussed the relevant principles concerning s 90-15 and would incorporate that discussion (see Wight, in the matter of Responsible Entity Services Limited (in liquidation) [2025] FCA 1219 at [95] to [99]).

64 Now both the subject matter and the desirability of the proposed financing strategy require commercial judgments to be made by the administrators that are matters primarily for them rather than the Court. But as Goldberg J explained in a trilogy of cases with which I have more than a passing familiarity concerning the administration of the Ansett group of companies in 2001 and 2002 (Re Ansett Australia Ltd [2001] FCA 1439; (2001) 39 ACSR 355 at [57] to [82], Re Ansett Australia Ltd (No 1) [2001] FCA 1806; (2002) 115 FCR 376 at [42] to [54] and Re Ansett Australia Ltd (No 3) [2002] FCA 90; (2002) 115 FCR 409 at [42] to [67]), the Court is nevertheless not precluded from giving the necessary directions or making the appropriate declarations so as to protect administrators from claims that they have acted unreasonably in entering into particular transactions or, more generally, engaging in particular conduct or refraining to so act. I propose to adopt a similar proportionate and practical approach.

65 Now limiting the administrators’ personal liability in the manner proposed will enable the administrators to access the funding required to preserve and operate the business as a going concern, for the purposes of maximising the return to creditors. It is consistent with the objectives of Part 5.3A to preserve the companies’ assets and maximise the potential return to creditors. And if the liability limitation orders are not made, it is likely that no alternative funding will be obtained and the companies would cease trading, resulting in a less favourable outcome for creditors.

66 Further and more generally, there is unlikely to be any material prejudice or disadvantage to creditors by limiting the personal liability of the administrators. The orders simply relieve the administrators from the identified personal liabilities in circumstances where the continued trading of the companies is likely to be for the benefit of the creditors.

67 More generally, the orders relieving the administrators from personal liability will facilitate them making commercial decisions in the best interests of the companies and creditors uninfluenced by concerns of personal liability.

68 Generally, the orders and directions sought concerning the subject matter that I have discussed are appropriate, including the orders to vary the application of s 443A by the utilisation of s 447A. Moreover, the orders for prompt service of these orders and the reservation of liberty to apply preserve the rights of affected parties to be heard should they object to the orders made.

PPG administration account

69 The companies largely use the PPG account as one of the key bank accounts for all the businesses. To the extent practicable, the administrators have not sought to disturb how the companies had previously operated within the group, including in relation to the operation of the banking function. So, they are using the bank account set up for the administration of PPG as the account from which they will pay employees, suppliers etc, including from time to time the employees and suppliers of the New Zealand companies, and the lessors under leases which remain in the names of the otherwise dormant Australian companies.

70 The administrators seek an order which relieves them from the requirement of strict compliance with Division 65-45 of the IPS so that they can use funds in the account of PPG for purposes related to other companies in the group.

71 Now s 65-5(1) of the IPS provides that an external administrator of a company must pay all moneys received by the external administrator on behalf of or in relation to the company into an administration account as defined by s 60-10 for the company within five business days after receipt. Section 65-15 requires an administrator not to pay other moneys into an administration account. Further, s 65-25 prohibits an administrator from paying money out of an administration account other than for purposes related to the administration of that company.

72 Now s 65-45 of the IPS provides a plenary power to make orders modifying the arrangements with respect to the operation of administration accounts. I will make orders under s 65-45 dispensing with the requirements for administration accounts to be opened and operated for all of the companies. There should be only one such account. In Re Grocon Pty Ltd (admins apptd) (No 1) [2020] VSC 833, in similar circumstances to those obtaining here, Gardiner AsJ granted relief of this nature (at [46] to [48]). I would adopt similar reasoning which by analogy justifies the orders that are now sought.

Provision of information to creditors

73 Given the size and complexity of the group, the administrators also request orders which vary the regime under the Act for the provision of information to creditors. The administrators would like the timeframe for any information to be provided to be extended from 5 business days to 10 business days.

74 The administrators have created a “creditor portal” on the McGrathNicol website where creditors can obtain information specific to the companies. Where a creditor requests information and the administrators consider the requested information to be relevant to all (or a large sub-set) of creditors, they propose that such information could be provided to the creditors via the creditor portal. This would avoid the administrators going to the time and expense of posting or sending the information to multiple individual creditors.

Convening period for second meeting of creditors

75 As I observed in Parbery, in the matter of NewSat Limited (Administrators Appointed) (Receivers and Managers Appointed) [2015] FCA 435 and in Secatore, in the matter of In-Fusion Management Pty Ltd (Administrators Appointed) [2016] FCA 1072, the Court has power to extend the convening period under ss 439A(6) and 447A, but in exercising this power the Court must have regard to the objects set out in s 435A, which seek to maximise the chance of the particular company under administration or as much as possible of its business continuing in existence, or if that is not possible, to achieve a better return for the company’s creditors than would result from an immediate liquidation. A central question is whether additional time is likely to enhance the return to creditors, particularly unsecured creditors. But the power to extend the time should not be exercised lightly, let alone as a matter of course. But Pt 5.3A should be given a commercial construction and application which reflects the reality of the setting in which both the relevant company under administration and the administrator find themselves. The Court must balance the expectation that administration will be a relatively speedy and summary matter against the consideration that undue speed should not be allowed to prejudice constructive commercial actions directed to maximising the return for creditors. The perspective from which Pt 5.3A should be applied should not be narrow, and its application should not be refracted through the pessimistic lens of an insolvency technician. And in that context, generally there is usually greater upside than downside in granting an extension for a reasonable period, where the reasonableness of the duration of the extension is contextualised by the particular circumstances.

76 Now as to the well accepted factors that may justify an extension, these were set out by Austin J in Re Riviera Group Pty Ltd (Administrators Appointed) (Receivers and Managers Appointed) (2009) 72 ACSR 352 at [13] and by Edelman J in Stimpson, in the matter of Eagle Boys Dial-A-Pizza Australia Pty Ltd (Administrators Appointed) [2016] FCA 935 at [8] to [10]. I do not need to repeat them.

77 In my view, applying such factors to the evidence before me, the extension sought is readily justified. Further, I will also make a Daisytek order under s 447A to deal with the operation of s 439A(2) (see Re Daisytek Australia Pty Ltd (Administrators Appointed) (2003) 45 ACSR 446 at [10] to [14] per Lindgren J). Such an order allows the administrators to hold the second meeting of creditors for each of the companies at any time during the extended convening period or within five days of its conclusion. This allows for the possibility that if the relevant steps can be completed earlier than anticipated in respect of one or more of the companies, then the administrators could hold the second meetings of creditors more promptly in a particular case.

78 The administrators consider that the prospect of a recapitalisation or sale of the businesses at optimal value will be improved by the continuation of the administrations during the period of stabilising the businesses and conducting the sale processes. It will also allow the administrators to undertake their investigation and reporting obligations more effectively.

79 The benefits of the ongoing administrations include: (a) the application of moratoria under the Act, which allows the administrators to better manage the working capital required to stabilise the businesses and reduce disruptions to the administrators’ work; (b) the availability of options for potential purchasers of the businesses to recapitalise the businesses through a deed of company arrangement and/or for the sale of the businesses or key parts of it to include a DOCA. Further, an extended convening period will also allow the administrators and their staff the time to properly undertake their statutory obligations.

80 Now pursuant to ss 439A(1) and (5), the administrators are required to convene the second meeting of creditors of the Australian companies by no later than 20 November 2025 with the meeting to be held not later than 27 November 2025. Pursuant to rule 75-225(3) of the Insolvency Practice Rules (Corporations) 2016 (Cth), the administrators are also required to prepare and provide a report about the business of each of the Australian companies, its property, affairs and financial circumstances. The administrators are also required to express an opinion in relation to the Australian companies about whether it would be in the interests of the Australian companies’ creditors for: (a) the administration of the Australian companies to end and control to be returned to the directors; or (b) the Australian companies to execute any deeds of company arrangement; or (c) the Australian companies to be wound up; and (d) the reasons for the opinion and such other information known to the administrators which will enable the creditors to make an informed decision. The administrators consider that it will be difficult to make an informed and comprehensive recommendation to creditors on the future of the Australian companies, and in turn, the creditors will be unable to make an informed decision, until the administrators’ investigations are more advanced. The administrators consider that completion of their stabilisation and possible sales processes will be necessary to allow a full understanding of the Australian companies’ positions prior to the second meeting of creditors.

81 Further, given the nature of the companies’ assets most of which are debtors, plant and equipment or stock, Mr Smith anticipates that the sale of the businesses and assets on a going concern basis will exceed the realisations available in an immediate shut-down scenario, where those assets will be sold or collected on a “fire sale” basis.

82 Further, it is currently estimated that the completion of a sale of the Australian businesses may not occur until the end of April 2026. The administrators’ request for a 6-month extension of the convening period takes this into account and allows a few weeks “buffer” in case any of the steps in the sales process take longer than anticipated. The administrators consider that the completion of all their sales processes will be necessary to allow a full understanding the companies’ positions at the second meeting of creditors. Naturally, the administrators will seek to expedite their sales processes wherever possible.

83 Ultimately, the various matters set out above are manifestations, in one way or another, of the Riviera factors which conventionally justify extensions of convening periods.

84 First, the Australian companies comprise part of an integrated corporate group with considerable size and scope of activities.

85 Second, the Australian companies form part of a corporate structure with complexity, including as a result of substantial offshore activities.

86 Third, more time is required for the administrators to execute an orderly disposal of the Australian companies’ assets, and to allow a potential sale of the businesses on a going concern basis.

87 Fourth, more generally, the additional time is likely to enhance the return to unsecured creditors.

88 For all of the above reasons, the proposed extension of the convening period for the second meetings of creditors of the Australian companies is appropriate and justified.

Conclusion

89 For the foregoing reasons I made the necessary orders yesterday.

I certify that the preceding eighty-nine (89) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Beach. |

Associate:

Dated: 6 November 2025

SCHEDULE OF PARTIES

VID1447 of 2025 | |

Plaintiffs | |

Fourth Plaintiff | PERFECTION PACKAGING PTY LTD ACN 108 256 042 |

Fifth Plaintiff | INTEGRATED PACKAGING WA PTY LTD ACN 130 895 822 |

Sixth Plaintiff | INTEGRATED RECYCLING PTY LTD ACN 141 456 386 |

Seventh Plaintiff | PRO-PAC PACKAGING (AUST) PTY LTD ACN 059 499 660 |

Eighth Plaintiff | PRO-PAC PACKAGING MANUFACTURING (SYD) PTY LTD ACN 068 689 412 |

Ninth Plaintiff | PRO-PAC PACKAGING MANUFACTURING (MELB) PTY LTD ACN 068 689 458 |

Tenth Plaintiff | PRO-PAC PACKAGING MANUFACTURING (BRIS) PTY LTD ACN 073 304 524 |

Eleventh Plaintiff | PRO-PAC FINANCE PTY LTD ACN 622 519 073 |

Twelfth Plaintiff | INTEGRATED PACKAGING GROUP PTY LTD ACN 132 697 664 |

Thirteenth Plaintiff | GOODSTONE INTERNATIONAL PTY LTD ACN 070 661 460 |

Fourteenth Plaintiff | PRO-PAC INDUSTRIAL GROUP PTY LIMITED ACN 104 805 361 |

Fifteenth Plaintiff | INTEGRATED MACHINERY PTY LTD ACN 070 099 811 |

Sixteenth Plaintiff | CREATIVE PACKAGING PTY LTD ACN 114 020 405 |

Seventeenth Plaintiff | PRO-PAC (GLP) PTY LTD ACN 104 645 981 |

Eighteenth Plaintiff | ACN 003 940 921 PTY LIMITED ACN 003 940 921 |

Nineteenth Plaintiff | GREAT LAKES MOULDING PTY LTD ACN 090 886 105 |

Twentieth Plaintiff | ACN 002 431 898 PTY LIMITED ACN 002 431 898 |

Twenty-First Plaintiff | FINPACT PTY LTD ACN 003 977 982 |

Twenty-Second Plaintiff | ACN 002 029 852 PTY LIMITED ACN 002 029 852 |

Twenty-Third Plaintiff | ACN 108 620 506 PTY LIMITED ACN 108 620 506 |

Twenty-Fourth Plaintiff | ACN 087 226 631 PTY LIMITED ACN 087 226 631 |