Federal Court of Australia

Twinza Oil Limited (Receivers and Managers Appointed), in the matter of Twinza Oil Limited (Receivers and Managers Appointed) (No 2) [2025] FCA 1325

File number: | WAD 247 of 2025 |

Judgment of: | BANKS-SMITH J |

Date of judgment: | 31 October 2025 |

Catchwords: | CORPORATIONS – creditors’ scheme of arrangement – application for approval of scheme under s 411 of the Corporations Act 2001 (Cth) – debt for equity scheme – single class of lenders – where effect of scheme is to dilute ordinary shares and cancel preference shares – objectors hold ordinary or preference shares – whether objectors have economic interest in scheme – contested expert valuation evidence of economic interest – where independent expert report prepared for purpose of informing scheme stakeholders relied upon for purpose of establishing valuation – application of principles in Dasreef Pty Ltd v Hawchar (2011) 243 CLR 588 – where experts rely on work of others – tender of report prepared for the scheme company by technical consultant not called as a witness – whether Court can be satisfied to requisite standard that objectors have no economic interest such that scheme should be approved – onus – application for approval refused |

Legislation: | Corporations Act 2001 (Cth), ss 411, 553, 563A, 600H Evidence Act 1995 (Cth), ss 60, 79, 102, 135, 136 Federal Court Rules 2011 (Cth), rr 23.11, 23.13 |

Cases cited: | ASIC v Rich [2005] NSWSC 999 Atlas Iron Limited, in the matter of Atlas Iron Limited [2016] FCA Australian Securities and Investments Commission v Rich [2005] NSWCA 152; (2005) 218 ALR 764 BE Australia WD Pty Ltd (subject to a Deed of Company Arrangement) v Sutton (2011) 82 NSWLR 336 Bodney v Bennell [2008] FCAFC 63; (2008) 167 FCR 84 Createc Pty Ltd v Design Signs Pty Ltd [2009] WASCA 85 Dasreef Pty Ltd v Hawchar [2011] HCA 21; (2011) 243 CLR 588 Harrington-Smith v Western Australia (No 7) [2003] FCA 893; (2003) 130 FCR 424; Herron v HarperCollins Publishers Australia Pty Ltd [2022] FCAFC 68 HG v R [1999] HCA 2; (1999) 197 CLR 414 In the matter of Boart Longyear Limited (No 2) [2017] NSWSC 1105 In the matter of Centro Properties Limited and CPT Manager Limited in its capacity as responsible entity of Centro Property Trust [2011] NSWSC 1465 In the matter of Nexus Energy Ltd (subject to deed of company arrangement) [2014] NSWSC 1910 Lang v The Queen [2023] HCA 29; (2023) 278 CLR 323 Malone on behalf of the Western Kangoulu People v State of Queensland (No 3) [2022] FCA 827 Minerology Pty Ltd v Sino Iron Pty Ltd (No 5) [2015] FCA 571 Netdeen Pty Ltd t/as GJ Gardner Homes v Lindfield NSW Pty Ltd [2025] NSWCA 196 One Funds Management Limited, in the matter of One Funds Management Limited (No 2) [2025] FCA 602 Phosphate Co-Operative Co of Australian Pty Ltd [1989] VR 665 Re Tea Corporation Ltd [1904] 1 Ch 12 Re Bluebrook Ltd [2009] EWHC 2114; [2010] 1 BCLC 338 Re Boart Longyear Ltd [2021] NSWSC 982 Re Opes Prime Stockbroking Ltd [2009] FCA 813; (2009) 179 FCR 20 Re Seven Network Ltd [2010] FCA 400 Roach v Page (No 11) [2003] NSWSC 907 Rush v Nationwide News Pty Ltd (No 5) [2018] FCA 1622 Tiger Resources Limited, in the matter of Tiger Resources Limited (No 2) [2020] FCA 266 Twinza Oil Limited (Receivers and Managers Appointed) [2025] ATP 30 Twinza Oil Limited (Receivers and Managers Appointed), in the matter of Twinza Oil Limited (Receivers and Managers Appointed) [2025] FCA 939 Twinza Oil Ltd (Receiver and Managers Appointed) v WM Clough Pty Ltd as trustee for the WM Clough Family Trust [2025] FCA 1165 White in the matter of Twinza Oil Limited [2025] FCA 1054 Williams v Spautz (1992) 174 CLR 509 Woods v T&FS Woods Pty Ltd [2023] FCA 1108 |

Division: | General Division |

Registry: | Western Australia |

National Practice Area: | Commercial and Corporations |

Sub-area: | Corporations and Corporate Insolvency |

Number of paragraphs: | 276 |

Date of hearing: | 17 October 2025 |

Counsel for the Plaintiff: | Mr SK Dharmananda SC with Mr LN Firios and Mr L Pham |

Solicitor for the Plaintiff: | Lavan |

Counsel for the First and Second Interested Persons: | Mr C Belyea |

Solicitor for the First and Second Interested Persons: | Clayton Utz |

Counsel for the Third to Seventh Interested Persons: | Mr E Heenan SC |

Solicitor for the Third to Seventh Interested Persons: | Bennett |

ORDERS

WAD 247 of 2025 | ||

IN THE MATTER OF TWINZA OIL LIMITED (RECEIVERS AND MANAGERS APPOINTED) (ACN 111 551 403) | ||

TWINZA OIL LIMITED (RECEIVERS AND MANAGERS APPOINTED) (ACN 111 551 403) Plaintiff | ||

TOR ASIA CREDIT OPPORTUNITY MASTER FUND LP First Interested Person TOR ASIA CREDIT MASTER FUND LP Second Interested Person WM CLOUGH PTY LTD AS TRUSTEE FOR THE WA CLOUGH FAMILY TRUST AND AS TRUSTEE FOR THE WM CLOUGH SUPERANNUATION FUND Third Interested Person MCRAE CLOUGH PTY LTD Fourth Interested Person MCRAE INVESTMENTS PTY LTD Fifth Interested Person PROCURO PTY LTD ATF SECURITY BLANKET SUPER FUND Sixth Interested Person DILATO HOLDINGS PTY LTD ATF THE HINDSIGHT INVESTMENT TRUST Seventh Interested Person | ||

order made by: | BANKS-SMITH J |

DATE OF ORDER: | 31 OcTOber 2025 |

THE COURT ORDERS THAT:

1. The application that the scheme be approved is dismissed.

2. The parties provide a joint minute of proposed orders dealing with costs within seven days.

3. Absent agreement, separate minutes as to costs may be filed and the parties will be heard as required.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

BANKS-SMITH J:

Introduction

1 This is an application by the plaintiff, Twinza Oil Limited (Receivers and Managers Appointed) pursuant to s 411 of the Corporations Act 2001 (Cth) for orders approving a proposed scheme of arrangement between it as scheme company and a single class of its creditors.

2 On 6 August 2025 I made orders approving the convening of a meeting of scheme creditors for the purpose of considering and, if thought fit, agreeing to the proposed scheme and approving the dispatch of the scheme materials to scheme creditors (convening hearing): Twinza Oil Limited (Receivers and Managers Appointed), in the matter of Twinza Oil Limited (Receivers and Managers Appointed) [2025] FCA 939 (Twinza (No 1)). No alternative proposal to the scheme had been received by Twinza at that time, and that remains the position.

3 Following the convening hearing, the scheme materials were duly dispatched.

4 The scheme meeting was held on 12 September 2025. As provided by the terms of the scheme, there was only one class of voters and relevantly it did not include shareholders. The members of the class were certain senior lenders (see [19] below), all of whom are parties to a syndicated facility agreement and have a community of interest in the outcome.

5 The scheme creditors approved the scheme; 100% by value and by number present and voting at the scheme meeting voted in favour of the scheme. The scheme was thus agreed to in the manner contemplated by s 411(4)(a)(i) of the Corporations Act. In that and all other respects, procedural steps relevant to the grant of approval by the Court under s 411(4)(b) were duly and properly taken so that, at the level of procedure and process, there is no obstacle to the grant of that approval.

6 However, the approval of the scheme by the Court is challenged.

7 A challenge on the basis of class was foreshadowed by three related objectors at the convening hearing, who on the day of the hearing sought an adjournment. Between them, the objectors hold ordinary shares and preference shares in Twinza. However, Twinza opposed the late adjournment application and sought to progress the convening of the meeting. It did so cognisant of the risk that the issue may arise again at the approval hearing. I refused the adjournment application, noting Twinza's request that any remaining issue of class be dealt with at the approval hearing, and its observation that such an approach had previously been taken by this Court in One Funds Management Limited, in the matter of One Funds Management Limited [2025] FCA 475.

8 The identified risk eventuated.

9 The challenge to the scheme in fact escalated after the convening hearing, with objectors taking a number of separate steps which have occupied the time of the parties and the Court (expanded upon below). Two additional objectors sought to be heard at the approval hearing.

10 In summary, the challenge by the objectors to the approval of the scheme is on two bases.

11 The first rests on whether the objectors have an economic interest in the scheme such that they should have been entitled to vote at the scheme meeting. Twinza's contention is that due to its financial position, neither holders of convertible redeemable preference shares (CRPS) nor ordinary shareholders have any economic interest in the scheme. The absence of an economic interest is well-recognised as a basis for obviating the need for consent from a shareholder in the context of a reconstruction or amalgamation: Re Tea Corporation Ltd [1904] 1 Ch 12; Re Opes Prime Stockbroking Ltd [2009] FCA 813; (2009) 179 FCR 20 at [76]; Re Bluebrook Ltd [2009] EWHC 2114; [2010] 1 BCLC 338 at [25]; In the matter of Centro Properties Limited and CPT Manager Limited in its capacity as responsible entity of Centro Property Trust [2011] NSWSC 1465 at [112]; In the matter of Boart Longyear Limited (No 2) [2017] NSWSC 1105 at [281]. The objectors maintain they have an economic interest in the scheme and that Twinza has not met its onus of establishing otherwise.

12 Twinza accepted that on the approval application it bore the onus to the usual civil standard of establishing that the objectors do not have an economic interest in the scheme. If there is a dispute about whether there is an economic interest, as observed by Mann J in Re Bluebrook at [25]:

… then the court is entitled to ascertain whether a purported class actually has an economic interest in a real, as opposed to a theoretical or merely fanciful, sense, and act accordingly – see the reasoning in Re MyTravel Group plc [2005] 2 BCLC 123 at first instance. Where things have to be proved, the normal civil standard applies.

13 The second challenge is the contention that the scheme cannot extinguish the rights of the CRPS holders without a separate members' scheme of arrangement. This challenge rests on statutory construction, and in particular whether rights as a member can be compromised by a creditors' scheme, having regard to the text of s 411(5A) of the Corporations Act.

14 For the reasons set out below Twinza has not persuaded me that its financial position is such that the objectors have no economic interest in the company. Accordingly, and after careful consideration, I have declined to approve the scheme. It has not been necessary to determine the second challenge.

15 As a preliminary matter, I note the urgency with which this matter has proceeded. For example, the evidence disclosed that any delay to the approval and implementation of the scheme would result in Twinza incurring interest on its senior debt of approximately USD2.4 million per week. Twinza stated that it has avoided being wound up only because the senior lenders have supported it by a Standstill Agreement predicated on the scheme. The senior lenders have indicated they will continue to support Twinza only if the scheme is approved and implemented. Delay has the very real potential to prejudice all stakeholders. I appreciate that all parties have addressed the issues in this application under some time pressure, as must the Court.

16 Before turning to the challenges, it is appropriate to briefly describe the interested parties, the operations and financial position of Twinza and the key components of the scheme.

Interested parties

17 There are some 359,219,659 shares on issue in Twinza. There are some 38,091,403 CRPS on issue across seven classes. No party suggested the difference between CRPS classes was of any real significance.

18 Seven entities have over the course of events filed notices under r 2.9 of the Federal Court (Corporations) Rules 2000 (Cth) of their intention to appear at the respective hearings. Those parties and their respective Twinza stakeholder interests (based on information in the affidavit evidence of Mr Stephen Quantrill, the executive chair and director of Twinza) are as follows:

Party | Name | Interest |

First interested party | Tor Asia Credit Opportunity Master Fund LP | Secured creditor (senior lender with 46.78% of the total senior debt) |

Second interested party | Tor Asia Credit Master Fund LP | Secured creditor (senior lender with 45.88% of the total senior debt) |

Third interested party | WM Clough Pty Ltd ATF WM Clough Family Trust | Shareholder (CRPS and ordinary shares) Creditor (USD10,538 subordinated to senior debt) |

Fourth interested party | McRae Clough Pty Ltd | Potentially CRPS holder (unclear) Creditor (USD330,935 due and payable) |

Fifth interested party | McRae Investments Pty Ltd | Shareholder (CRPS and ordinary) Creditor (USD5,353, subordinated to senior debt) |

Sixth interested party | Procuro Pty Ltd ATF Security Blanket Super Fund | Ordinary shareholder |

Seventh interested party | Dilato Holdings Pty Ltd ATF Hindsight Investment Trust | Ordinary shareholder |

19 The first and second interested parties, referred to as the senior lenders, are represented by Clayton Utz. Generally when I refer to the position of the senior lenders, it is a reference to the first and second interested parties. However, there are 'other senior lenders': Henry Edmund Aldorf (0.58%), Pacific World Energy Ltd (3.86%) and Hendale PNG Limited (2.90%). The scheme proposed and endorsed at the scheme meeting is made between Twinza and these five senior lenders.

20 The third, fourth and fifth interested parties are referred to for convenience as the Clough parties, and are represented by Bennett. The sixth and seventh interested parties filed notices only shortly before the approval hearing and are also represented by Bennett. I was informed that the sixth and seventh interested parties are not related to the Clough parties, and that they did not seek to make any separate submissions.

Kerogen

21 The scheme is supported by the senior lenders (who were represented at the hearing) and by Kerogen Investments No 6 (Singapore) Pte Ltd, an independent commercial party. Kerogen and three other investors for which it is agent hold the majority of the CRPS (approx 77.5%). They do not constitute the majority of CRPS holders by number; there are 37 CRPS holders (Quantrill affidavit p 469). It would therefore appear that the Kerogen interests would not hold the statutory headcount majority for a resolution by a class of CRPS holders, if such a class had been established.

22 Kerogen also holds 100,000 ordinary shares in Twinza (27.84%).

23 Kerogen has provided an undertaking to Twinza which expires on 31 December 2025 to support the scheme, absent a superior proposal.

Chronology and summary of proposed scheme

24 As described in Twinza (No 1), Twinza is an Australian public company which for several years has been pursuing through its subsidiary an offshore gas liquids and condensate project in the Gulf of Papua, offshore Papua New Guinea, known as the Pasca A project.

25 The relevant subsidiary is Twinza Oil (PNG) Ltd (Twinza PNG), a company incorporated under the laws of the British Virgin Islands and registered as a PNG overseas company.

26 Twinza PNG is the operator and 95% equity holder of the Pasca A project. A PNG state-owned enterprise, Mineral Resources Development Company Limited (MRDC), holds the remaining 5% of the project through an entity called Hevehe Petroleum Limited. MRDC has an entitlement to acquire up to 50% in the project subject to certain conditions, pursuant to the terms of a sale and purchase agreement made between Twinza PNG, MRDC and Hevehe made 29 May 2024 (SPA).

27 In December 2024, Twinza PNG, the Government of Papua New Guinea and MRDC entered into a gas agreement in relation to the Pasca A project which is central to attracting investment in Twinza.

28 Twinza is in the process of launching the second phase of its front-end engineering design (FEED) process, which will involve a series of technical and other studies to confirm the requirements and estimated cost of the project. The targeted date for completion of FEED is on or before 30 June 2026.

29 The market engagement phase of FEED was due to commence on 1 October 2025, but is expected to be delayed pending the approval and implementation of the scheme.

30 The anticipated date for completion of the final investment decision (FID) is not confirmed but, pursuant to the gas agreement, must occur by 19 June 2027 (subject to extension).

31 According to Mr Quantrill, termination rights under the gas agreement may be triggered if targeted dates for FEED and FID are not met. Further, downstream agreements with MRDC, said to be crucial to the ongoing operation of the Pasca A project, are similarly at risk of termination.

32 Under the facility agreement, four separate tranches of funding were made available to Twinza by the senior lenders. Until the maturity date of 15 December 2024, the interest rate was set at 23% per annum on tranches A, B, and C, and 30% per annum on tranche D. From 15 December 2024, the interest rate increased to 35% per annum on tranches A, B, C, and D.

33 Twinza is in default to its various senior lenders and interest continues to accrue on the principal amount.

34 The senior lenders appointed the receivers on 19 February 2025. The outstanding senior debt owed by Twinza is approximately USD351,350,796 (at 12 September 2025), an amount which is said by Twinza to exceed the value of its assets.

35 The senior lenders therefore proposed a restructure of Twinza's debt and equity by way of the creditors' scheme, the key components of which were that tranches A, B and C of the funding would be exchanged for equity in Twinza. The interest rate for tranche D would be reduced to 10% per annum (with a default rate of 12% per annum).

36 From as early as February 2025, Mr Clough (an alternate director of Twinza) was on notice that a reconstruction was proposed.

37 On 19 February 2025 Twinza and its senior lenders entered into a scheme implementation agreement (SIA) and agreed the terms under which they would implement the scheme.

38 The scheme's key components are as follows:

(a) the senior lenders will provide a release of up to 92% of the senior debt. The senior debt will be reduced from the amount then due (approximately USD324 million) to USD30 million;

(b) as consideration for the senior lenders' partial release of the senior debt, Twinza will issue new ordinary shares to the senior lenders. The senior lenders will post-scheme hold 85% of the ordinary shares on issue;

(c) Twinza will issue new ordinary shares to holders of CRPS by which the preference shares will be replaced and substituted with ordinary shares in the company. The holders of preference shares will post-scheme hold 10% of the ordinary shares on issue;

(d) current shareholders will post-scheme hold 5% of the ordinary shares on issue;

(e) the facility agreement will be amended by reducing the senior debt, reducing the interest rate on the balance of the debt, removing a subset of senior lenders, removing the existing fee structure and associated amendments; and

(f) there will be provisions that ensure the scheme, if implemented, will not affect employees or certain creditors (ordinary course of trade creditors).

39 If the scheme completes, the senior lenders (first and second interested parties) will hold 78.12% of the issued capital of Twinza.

40 On 10 April 2025 the receivers lodged with ASIC a Report on Company Activities and Property (ROCAP). The ROCAP valued the assets of Twinza at between USD458 million and USD528 million (both values being greater than the approximately USD324 million then owed by Twinza to the senior creditors).

41 On 24 June 2025 BDO Corporate Finance Australia provided their independent expert report in relation to the scheme. The BDO report valued the assets of Twinza, in the event the scheme does not proceed and Twinza were to be wound up within six months, at between (rounded) USD180 million and USD250 million in a low and high scenario respectively, being a shortfall of between USD145 million and USD70 million in assets over liabilities. BDO also opined that Twinza's total debt is likely to hinder it from securing finance or attracting investment for the project.

42 It appears that the draft scheme booklet documents were provided to Mr Clough on or about 11 July 2025 (Mills Oakley letter 16 July 2025). Mr Clough was made aware of the proposed timetable for the scheme by (at least) 25 June 2025 (letter Lavan to Mr Clough of that date).

43 The first court hearing for orders to convene the scheme meeting and dispatch the scheme booklet, including the BDO report and annexures, proceeded on 6 August 2025.

Potential challenge to the scheme disclosed at the convening hearing

44 I have already referred to the Clough parties' adjournment application made at the convening hearing on 6 August 2025.

45 I refused the late adjournment application (Twinza (No 1) at [43]-[48]) and made orders convening the meeting. However, as suggested by senior counsel for Twinza, resolution of the class issue was deferred to any approval hearing (at [49]).

46 Of particular relevance was the fact that Mr Clough apparently had knowledge of the BDO report since around late April 2025 and so had an opportunity to raise issues or objections in relation to it sooner.

47 It is true that Mr Clough required consent to use information he had obtained in his capacity as an alternate director of Twinza in order to take steps relating to the BDO report on behalf of the Clough parties, but it is also apparent that agreements with the receivers were negotiated and executed that permitted access to the 'Twinza data' by third parties nominated by Mr Clough. Further it is apparent that by email of 1 May 2025 the receivers had informed Mr Clough that if any of the directors of Twinza wished to seek a second independent valuation they were welcome to do so.

48 At the convening hearing, a date was scheduled for the approval hearing, that date being 23 September 2025. The Clough parties therefore had a further six weeks to obtain valuation evidence and the parties had six weeks to program and organise how the matter might proceed at the approval hearing. Having regard to the evidence relied on for the convening hearing and the position of the secured creditors, it would have been apparent to the Clough parties that it was highly likely that the scheme creditors would conditionally approve the scheme at the scheme meeting. It would have been imprudent on the part of the Clough parties to postpone preparation for any opposition to its approval until after the scheme meeting.

Notice of general meeting issued by Clough parties

49 After the convening hearing, the Clough parties took other steps before filing any evidence for the purpose of the approval hearing.

50 By notice dated 14 August 2025, WM Clough gave notice to Twinza under s 203D of the Corporations Act of its intention to move a resolution to remove three directors at a general meeting of the company. The directors the subject of the notice were Mr Quantrill, Mr Stefan White and Mr Stuart Brown. Mr Quantrill had an important role in negotiating key agreements relating to the Pasca A project. He has provided affidavits on behalf of Twinza for the purpose of the convening and approval hearings.

51 On 18 August 2025 WM Clough gave Twinza a notice of general meeting, purportedly called by it as a member holding at least 5% of the issued shares in the company under s 249F, together with proposed resolutions to remove the three directors and replace them with three other directors at a meeting to be held on 17 September 2025 (including Mr Clough and Mr Anthony Samaha).

52 The timing of the proposed general meeting was such that it would have taken place prior to the approval hearing (originally listed for 23 September 2025). On its face, the risk of a general meeting on that date placed the scheme at risk, as it had the potential to prevent Twinza from satisfying certain conditions of the SIA.

Orders made that proceedings by receivers justified

53 The receivers therefore brought urgent proceedings before a duty judge seeking an order pursuant to s 424 of the Corporations Act, that they would be justified in commencing proceedings. The application was determined on 27 August 2025: White in the matter of Twinza Oil Limited [2025] FCA 1054 (Feutrill J).

54 Orders were made to the effect that the receivers were justified in causing Twinza to bring proceedings to seek a declaration that any decision of the directors to postpone the general meeting called by WM Clough was valid and effective and to injunct WM Clough from conducting a general meeting.

Injunction proceeding to restrain general meeting

55 The receivers then commenced the anticipated proceeding. An interlocutory application seeking injunctive relief was heard on an urgent basis by O'Sullivan J on 12 September 2025. His Honour granted an injunction restraining the conduct of any general meeting called by WM Clough or its servants or agents pending the outcome of the approval hearing or further order: Twinza Oil Ltd (Receiver and Managers Appointed) v WM Clough Pty Ltd as trustee for the WM Clough Family Trust [2025] FCA 1165.

The statutory demand

56 Meanwhile the fourth interested party, McRae Clough, issued a statutory demand to Twinza relying on a claimed debt in the sum of $496,395.

57 Unsurprisingly, the solicitors for Twinza wrote to Bennett referring to what was said by Martin CJ in Createc Pty Ltd v Design Signs Pty Ltd [2009] WASCA 85 at [50], citing Williams v Spautz (1992) 174 CLR 509, in relation to circumstances where the issue of a statutory demand is an abuse of process.

58 As I understand it, an application was brought to set aside the statutory demand but in any event, the receivers decided in the interests of efficiency to determine that McRae Clough be a List A Creditor under the scheme, such that it would be paid following implementation of the scheme.

59 It would appear that the application to set aside the statutory demand has been adjourned.

The Takeovers Panel

60 By application to the Takeovers Panel dated 20 August 2025 WM Clough sought a declaration of unacceptable circumstances: Twinza Oil Limited (Receivers and Managers Appointed) [2025] ATP 30.

61 WM Clough submitted that the effect of the scheme was to dilute the voting power of the ordinary shareholders of Twinza from 100% to 5% while providing control of Twinza to the senior lenders, without the ordinary shareholders of Twinza being given any opportunity to either participate in the transaction or vote as to whether the transaction should be approved. It submitted that one of the unacceptable circumstances was that:

[t]he shareholders of Twinza will not have a reasonable and equal opportunity to participate in any benefits accruing from [the Scheme], nor indeed are they being afforded any opportunity to participate in any benefits, contrary to the purpose set out in section 602(c) of the Corporations Act.

62 WM Clough sought an order that Twinza obtain approval from its ordinary shareholders for the proposed issue of shares to the senior lenders under the scheme.

63 On 8 September 2025 (reasons published to parties on 19 September 2025), the Takeovers Panel declined to conduct a proceeding, stating that (footnotes omitted):

[29] Where no equity value remains in the shares of a given company, the relevance of the objectives of Chapter 6 may be limited. In the case of a creditors' scheme of arrangement, that is principally because the interests of creditors assume greater weight in comparison with members who (in such a case) have no real economic interest in the company.

[30] The Panel has not previously considered a creditors' scheme. The Panel has considered several matters where a company is in receivership or administration and has entered into a deed of company arrangement. In those matters, the Panel has noted that there is no exception from section 606 for deeds of company arrangement and therefore, the requirements of Chapter 6 cannot be ignored. Even so, the Panel has stated that "proceedings will generally be unlikely to be conducted where a company is in administration, and no equity value remains in its shares. The exercise of discretion to conduct proceedings depends on whether we consider there is any reasonable prospect that we would declare the specific circumstances before us to be unacceptable circumstances taking into account relevant public interest considerations.

…

[33] The applicant raised concerns with the valuation in the Independent Expert's Report. The Independent Expert concluded that, among other things, 'In the event the Scheme does not proceed, the total debts owing to the Senior Lenders and Other Senior Lenders exceeds the value of Twinza's assets by between US$55 million and US$128 million'. The independent expert also compared the book value of Twinza's assets as at 30 June 2024 (US$281 million) to Twinza's debt of US$324 million as at 31May 2025 and noted 'we do not consider there to be a material difference between book value and fair value'.

[34] The Panel applies a high threshold to question the correctness of an expert's report. In our view, the report provides a basis for the conclusion reached by the Independent Expert, while recognising that different experts may form different views in relation to key judgments (including risk adjustments) and accordingly reach a different conclusion.

[35] In any event, we consider in this case that the Court is the more appropriate forum in which this issue should be challenged. The Independent Expert's Report forms part of the scheme booklet lodged with and reviewed by ASIC and approved for distribution by the Court.

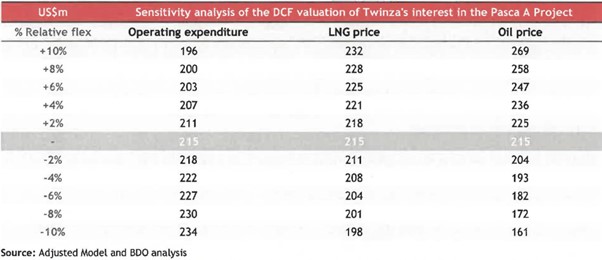

The adjournment of the approval hearing

64 As indicated in the introduction, the Clough parties challenge the opinion of BDO that provides the foundation for Twinza's submissions (and those of the senior lenders).

65 When I had heard nothing from the parties (including the Clough parties) following the date of the proposed scheme meeting, my Chambers made inquiries as to whether the scheme resolution had been passed and what the parties intended in relation to the programming of any evidence. I was concerned as to whether the Clough parties maintained their challenge to the scheme and if so, how it was intended that evidence be adduced in that regard in a time frame that would permit any response from Twinza and the filing of respective submissions. The parties did not agree programming orders.

66 On 17 and 18 September 2025 the Clough parties filed three affidavits which provided critiques of the BDO report and one of its attachments, being a technical report prepared by RISC Advisory Pty Ltd dated 23 June 2025. Those affidavits were provided by Anthony Samaha (chartered accountant), Robert Mountjoy (director Mountjoy Project Management, former Twinza employee and CRPS holder) and David Lim (principal reservoir engineer at Odin Reservoir Consultants) (together the critique reports). Although the deponents commented on aspects of the BDO and RISC reports, it was not immediately apparent whether they were purporting to provide independent expert opinion evidence. Their reports attached to their affidavits did not comply with the requirements of r 23.13 of the Federal Court Rules 2011 (Cth) relating to expert evidence.

67 On 22 September 2025 each of those deponents provided a further affidavit, which contained reference to r 23.13 and at that point it was apparent that indeed the Clough parties were seeking to rely on the critique reports as expert opinion evidence.

68 A solicitor from Bennett, Ms Jessica Chapman, also filed an affidavit that annexed documents referred to by the deponents, including a version of Twinza's 'Open Book Economic Model' dated 26 February 2025; and a modified version of Twinza's 'Open Book Economic Model' dated 11 July 2025, referred to by Mr Samaha.

69 Ms Chapman also deposed that on 18 September 2025 Lavan had provided copies of all the materials that had been provided to BDO and RISC to each of Mr Clough, Mr Mountjoy, Mr Samaha and Mr Lim. Those documents were not tendered by Twinza or the Clough parties.

70 On the basis of the 'sources of information' listed in appendix 2 of the BDO report, Lavan had provided BDO with copies of legal, financing and project agreements; the relevant expert evidence practice note; ASIC regulatory guides, company searches and records; and numerous company books and records. Those books and records included cashflow forecasts; 'key drivers/assumptions for the FY26 forecasts' by way of a Twinza cashflow (120325); '2023.01.20 Pasca A Economic Model Inputs.pdf'; and '2025-02-26 Pasca Project OBEM Investor Model.xlsm'. BDO also listed the RISC report.

Hearing on 23 September 2025

71 At the commencement of the original listing of the approval hearing, senior counsel for Twinza objected to the tender of the Samaha, Mountjoy and Lim affidavits on the basis that they were filed late so as to cause prejudice to Twinza, and on the basis of admissibility having regard to s 79 of the Evidence Act 1995 (Cth). Twinza had taken steps to obtain preliminary responses to those affidavits but had expressed caution about use of those preliminary responses, having regard to the short time afforded to BDO and RISC to respond. In the circumstances I refused to exclude the Samaha, Mountjoy and Lim affidavits on the basis that they were filed late, as it appeared to me the fairer course was to adjourn the hearing for a short period so that Twinza could invite BDO and RISC to respond more fully to the critiques. However, I preserved Twinza's ability to pursue objections in relation to admissibility and weight (ts 12).

72 In the end the hearing was adjourned to Friday, 17 October 2025 with Monday, 20 October 2025 also reserved.

73 A number of other matters were discussed at the 23 September 2025 hearing.

74 It was clear that Twinza intended to rely on the BDO report but, expressed generally, that report was prepared for a specific purpose (and in accordance with identified guidelines), being to include in the scheme booklet so as to assist the scheme creditors in assessing how they should vote in relation to the proposed scheme.

75 BDO are an experienced provider of such reports for use in schemes and other company arrangements, and no doubt the report was also prepared with knowledge it would be read and considered by the Court for the purpose of the convening hearing. As Brooking J said in Phosphate Co-Operative Co of Australian Pty Ltd [1989] VR 665 at 684, 'generally speaking, the outcome of an application for approval of a scheme of arrangement is not to be determined by whether the judge finds the expert’s report persuasive: whether the report is persuasive is a question for the members'. As his Honour continued, however, 'if the judge takes the view that the report has a tendency to mislead or confuse, that is another matter'.

76 At the approval hearing, the BDO report was relied upon for a different purpose; to respond to the Clough parties' argument that there should be a separate class, a question that would arguably be determined by whether the ordinary and preference shareholders had any economic interest in Twinza.

77 This issue was referred to generally as the 'valuation' issue, although it is important to acknowledge that the real question being addressed was that of economic interest on the part of shareholders and holders of CRPS. Twinza accepted that it bore the onus of establishing that the ordinary and preference shareholders had no economic interest such as would entitle them to vote in relation to the scheme (whether by a separate members' scheme, a class in the creditors' scheme or otherwise).

78 With this in mind, I asked at the hearing whether it was intended to cross examine the experts, observing that such a course is often of assistance to the Court in the context of technical opinion evidence.

79 Having regard to the flurry of affidavits filed immediately ahead of the 23 September 2025 hearing, I also directed that the parties would require leave to file further evidence (apart from the foreshadowed reply affidavits). It was noted that the Clough parties had already filed their submissions, including submissions objecting to the admissibility or weight of the BDO and RISC reports, so that further submissions that it might seek to file were confined to responding to the reply affidavits.

80 All of this was done having regard to the significance of the issues to the parties, but also acknowledging the need to resolve the challenge as efficiently as possible, taking into account the many other litigious steps that had proceeded between the parties in a short period of time, the rapidly accruing interest liability and the risk to Twinza's interest in the Pasca A project and the stakeholders if funding was withdrawn and securities otherwise enforced.

81 On 9 October 2025 the Clough parties filed submissions opposing the admission of the BDO and RISC reports on two grounds that, viewed objectively, had not been exposed in their previous submissions. Twinza's response was to seek leave to file further responsive affidavits to address the matters in those submissions. I granted Twinza such leave.

82 The Clough parties also complained that the BDO report included reference to an 'Adjusted Model' that had not been provided to them. There was no suggestion that any prior request had been made by them for the document. Twinza agreed to produce it to the parties forthwith. I also generally granted liberty to apply.

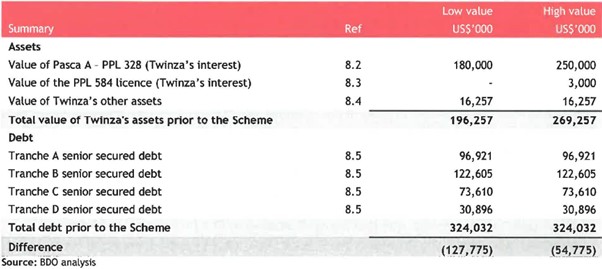

The approval hearing

83 The hearing proceeded on 17 October 2025. No party sought to utilise the reserved second hearing day. There was no request by either party to cross examine the witnesses. I was informed relevantly that Mr Andrawes of BDO had been present in Court during the hearing and available for cross examination.

84 It was apparent that the outcome in relation to the issue of economic interest rested on challenges made by the Clough parties to the admissibility and weight of evidence relied upon by Twinza. In particular the challenges focussed on the BDO report, the RISC report, a third-party document relied upon by RISC referred to as the Gaffney Cline (GCA) report and the Adjusted Model. The GCA report on Pasca A resources was prepared in April 2023 on the instructions of Twinza.

85 The Clough parties did not adduce any separate independent valuation. They tendered the critique reports.

86 The proceedings have been conducted under time constraints, but that is at times a regrettable necessity of proceedings involving commercial urgency.

Preliminary comment – different task to that undertaken by ASIC and the Takeovers Panel

87 Twinza made a number of submissions about the veracity of the BDO report, having regard to ASIC guidelines and applicable standards required of an expert opinion intended to inform security-holder decisions.

88 I do not find (and do not need to find) that there was any failure on the part of BDO to comply with those standards and guidelines. On the contrary, on the face of the report considerable care and expertise was deployed.

89 However, as both ASIC and the Takeovers Panel indicated, the issue of class (and so the underlying question of economic interest) falls to be determined by the Court. It is the Court that is tasked by s 411 to approve a scheme. The Court must apply the usual rules of evidence and standards of proof must be met.

90 In saying that, the position of ASIC and the Takeovers Panel is important. If either drew attention to any particular issue or reservation about the scheme, that is a matter to which I would have given close attention.

Mr Andrawes and Mr Craig

91 Twinza tendered affidavits of Mr Sherif Andrawes of BDO and Mr Adam Craig of RISC which attached their respective expert reports. Mr Andrawes provided by his affidavits the BDO report from the scheme booklet, verifying its contents. He also provided two supplementary reports replying to matters raised by the Clough parties' critiques. Mr Craig provided by his affidavit the RISC report which had formed an annexure to BDO's report. He also provided a supplementary report replying to matters raised by the Clough parties' critiques.

92 There was no issue taken as to the specialised expertise of Mr Andrawes or Mr Craig, and nor could there sensibly have been. Both are eminently qualified to address the matters in their respective reports.

93 Mr Andrawes is a partner of BDO in the global and national natural resources and energy team, a role which involves providing advice to clients in the mining, oil and gas and renewables sectors across the globe. He has provided over 750 public independent expert reports and acted as investigating accountant for over 100 initial public offerings. He is acknowledged by Chartered Accountants Australia as a recognised business valuation specialist and has extensive valuation experience in the mining and exploration sector, including for the purpose of schemes of arrangement. In both the first and supplementary reports, Mr Andrawes confirms that he has read and understood the Federal Court's Expert Evidence Practice Note and used his best endeavours to comply with that note. He also states that the reports have been prepared in accordance with the Accounting Professional & Ethical Standards Board professional standards APES 225 'Valuation Services' and having regard to ASIC Regulatory Guide 111 ('Content of expert reports') (RG 111) and Regulatory Guide 112 ('Independence of experts') (RG 112). Mr Andrawes declares that BDO are independent in accordance with RG 111 and RG 112 and have complied with those guides.

94 Mr Andrawes briefed RISC to provide an independent technical specialist's report to assist it in providing the advice contained in the BDO report. It is expressly disclosed in the BDO report that BDO have relied on the RISC report. The RISC report was prepared by Mr Craig.

95 Mr Craig does not refer to the Federal Court's Expert Evidence Practice Note. Any non-compliance with the note or r 23.13 of the Federal Court Rules does not of itself prevent its admission, although it can go to weight: Minerology Pty Ltd v Sino Iron Pty Ltd (No 5) [2015] FCA 571 at [11].

96 Twinza relies on the BDO report as the primary valuation expert evidence, but Twinza does not purport to treat the RISC report merely as a third-party source of information. Through Mr Craig's affidavit, evidence of the RISC report was separately adduced by its author.

97 The RISC report in turn refers to the GCA report, which was never prepared as an independent expert report. Rather, it was prepared for Twinza in 2023. The GCA report was also provided by the Clough parties to their own experts.

98 Mr Craig is a geoscientist and manager with over 30 years' experience in the upstream oil and gas sector and has undertaken many petroleum and resources evaluations and audits. Having held senior roles for energy companies including Woodside Energy and Cooper Energy, he transitioned from KUFPEC (an international oil company), where he was responsible for all Australian sub-surface activities, to RISC in 2020.

99 RISC is an independent advisory firm that provides business consultancy services to the oil and gas industry. It has experience in providing independent technical specialist's reports compliant with RG 111 and RG 112. RISC states that reserves and resources are reported in its advice in accordance with the definitions of reserves, contingent resources and prospective resources and guidelines set out in the Petroleum Resources Management System prepared by the Oil and Gas Reserves Committee of the Society of Petroleum Engineers.

100 Accepting their expertise, the question is whether the opinion evidence of Mr Andrawes and Mr Craig is admissible under s 79 of the Evidence Act as an exception to the rule excluding opinion evidence.

Mr Samaha, Mr Mountjoy and Mr Lim

101 Twinza submitted that little weight should be accorded to the reports of Mr Samaha and Mr Mountjoy due to their (undisclosed) impartiality. Mr Samaha was a person put forward alongside Mr Clough as a proposed replacement director in the proceeding before O'Sullivan J. Mr Mountjoy is a CRPS holder. Complaints were also made that the reports do not comply with r 23.11 of the Federal Court Rules and it is not possible for the Court to discern whether the opinions expressed are wholly or substantially based on their expert knowledge. The independence of Mr Samaha and Mr Mountjoy as experts is said to be compromised as reflected in certain communications with Mr Clough.

102 Twinza made no complaint about the independence of Mr Lim, but contended that the utility of his report was undermined by its limited scope.

103 I will deal with these matters further when I address the complaints made by the Clough parties about the RISC report.

Principles – admissibility of opinion evidence

104 The starting point is that the opinion evidence is said to be relevant because it could rationally affect the assessment of the probability that, absent the scheme, the shareholders will have no economic interest. In the end I have to feel an actual persuasion of the fact in issue.

105 Section 79(1) of the Evidence Act relevantly provides that if a person has specialised knowledge based on the person's training, study or experience, the opinion rule does not apply to evidence of an opinion of that person that is wholly or substantially based on that knowledge.

106 There was some difference in emphasis between the parties as to the applicable principles, and so it is appropriate to recall the principles that emerge from the judgment of the plurality (French CJ, Gummow, Hayne, Crennan, Kiefel and Bell JJ) in Dasreef Pty Ltd v Hawchar [2011] HCA 21; (2011) 243 CLR 588:

(a) To be admissible under s 79(1) the evidence that is tendered must satisfy two criteria. The first is that the witness who gives the evidence has specialised knowledge based on the person’s training, study or experience; the second is that the opinion expressed in evidence by the witness is wholly or substantially based on that knowledge (at [32]).

(b) Ordinarily the expert’s evidence must explain how the field of specialised knowledge in which the witness is expert, and on which the opinion is wholly or substantially based, applies to the facts assumed or observed so as to produce the opinion propounded. Although those elements are drafted in s 79 in a lengthy manner, fulfilment of the requirement can often be met quickly and easily, such as in the case of a specialist medical practitioner expressing a diagnostic opinion in his or her relevant field of specialisation (at [37]).

(c) The admissibility of opinion evidence is to be determined by application of the requirements of the Evidence Act rather than by any attempt to parse and analyse particular statements in decided cases divorced from the context in which those statements were made (at [37]).

(d) The opinion expressed by a witness must be connected with the witness’s specialised knowledge based on training, study or experience. A failure to demonstrate that an opinion expressed by a witness is based on the witness’s specialised knowledge based on training, study or experience is a matter that goes to the admissibility of the evidence, not its weight (at [41]-[42]).

107 The High Court revisited the admissibility of an expert opinion in Lang v The Queen [2023] HCA 29; (2023) 278 CLR 323. Although concerned with admissibility at common law, Kiefel CJ and Gageler J confirmed (at [11]) that the principles, whether under the uniform legislation or common law, require that:

… in order to satisfy the condition of admissibility that the opinion of an expert be demonstrated to be based on specialised knowledge or experience, the inference drawn by the expert which constitutes the opinion be supported by reasoning on the part of the expert sufficient to demonstrate that the opinion is the product of the application of the specialised knowledge of the expert to facts which the expert has observed or assumed.

108 The difference in emphasis to which I referred was that although the Clough parties were careful not to suggest that s 79 incorporates the common law basis rule, they emphasised the role of the so-called 'proof of assumptions rule'. They suggested that it remains necessary for each underlying fact assumed by BDO or RISC to be proved in order for their opinions to be admissible, and that such rule 'informs the exercise of considering admissibility'.

109 The Clough parties' contention as to the importance of proof of underlying facts relied upon by the experts was said to be drawn from the reasons of Lee J in Herron v HarperCollins Publishers Australia Pty Ltd [2022] FCAFC 68 at [500]-[501] (Rares J and Wigney J agreeing at [147] and [265]).

110 In circumstances quite different to those of the present matter, the Court considered in Herron whether reports of 'dead experts' (deceased doctors, whose reports were never prepared as expert reports) were admissible. Lee J referred to three 'factual basis rules' said to apply for the purpose of s 79, being: (1) are the facts and assumptions on which the expert’s opinion is founded disclosed (assumption identification rule); (2) is there evidence admitted, or to be admitted before the end of the tendering party’s case, capable of proving matters sufficiently similar to the assumptions made by the expert to render the opinion of value (proof of assumptions rule); and (3) is there a statement of reasoning showing how the facts and assumptions relate to the opinion stated to reveal that that opinion is based on the expert’s specialised knowledge (statement of reasoning rule).

111 In doing so, Lee J referenced Heydon J's detailed reasons in Dasreef. In this respect, Heydon J contended that these common law rules survived into the uniform evidence scheme and were not abolished by it: Dasreef at [101], [127] and [130].

112 Different views have been expressed in relation to the 'proof of assumptions' rule: Dasreef at [103] (Heydon J), and see discussions in Freckleton and Selby, Expert Evidence Law, Practice, Procedure and Advocacy (5th ed, Thomson Reuters 2013) at [2.20.140]; and Odgers, Uniform Evidence Law (20th ed, Thomsons Reuters, 2025) at [EA.79.240].

113 In Herron, Lee J was careful to point out that such 'rules' go to the utility of an expert opinion, and that there was little to be gained from 'rehearsing the cases as to admissibility' (at [501]). His Honour specifically referred to the proof of assumptions 'rule' in the context of the value to be attributed to a report. His Honour also referenced the reasons of Spigelman CJ (with whom Giles and Ipp JJA agreed) in Australian Securities and Investments Commission v Rich [2005] NSWCA 152; (2005) 218 ALR 764. Relevantly, Spigelman CJ made reference to (and emphasised) at [98] the statement by Gleeson CJ in HG v R [1999] HCA 2; (1999) 197 CLR 414 at [41], that expert evidence:

… required identification of the facts [the expert] was assuming to be true, so that they could be measured against the evidence; and … demonstration or examination of the scientific basis of the conclusion.

114 I also note Jagot J's observation in Lang that insofar as the common law has regard to whether evidence has been or will be admitted to prove primary facts, or sufficiently likely facts to make the opinion useful, it is a factor that has been said to go to weight rather than admissibility: Lang at [431].

115 I approach the consideration of the expert evidence in this matter on the basis that where evidence is admissible in accordance with what was said in Dasreef and Lang, there remains the evaluative task of assessing whether and to what extent the opinion assists the court. The Full Court in Herron did not go so far as to say that under s 79 an expert opinion will be inadmissible if the factual basis for the opinion is not proved by admissible evidence. What is said in Herron reflects the evaluative task to be undertaken in relation to the opinion and any evidence that is before the court, a task that goes to the weight to be attributed to the opinion.

116 Similarly, an evaluation of the evidence will inevitably be required if the court is asked to consider whether an opinion should be excluded on the ground that its probative value is outweighed by its prejudicial effect: Lang at [15]-[17].

117 Separate objection was taken by the Clough parties to reliance by RISC on the GCA report. A particular issue therefore arises as to reliance by one expert on material produced by others.

118 In Bodney v Bennell [2008] FCAFC 63; (2008) 167 FCR 84, the Full Court observed that under the common law rules of evidence, experts were entitled to rely upon reputable publications as a basis for their opinions and could give evidence about the matters stated in such publications, notwithstanding that the publications constituted hearsay. The Full Court explained:

[92] Before the Evidence Act it was well established that experts are entitled to rely upon reputable articles, publications and material produced by others in the area in which they have expertise, as a basis for their opinions. In Borowski v Quayle [1966] VR 382 at 386 (Borowski) Gowans J, quoting Wigmore on Evidence 3rd ed, vol 2 at 784-785, said that to reject expert opinion because some facts to which the witness testifies are known only upon the authority of others, 'would be to ignore the accepted methods of professional work and to insist on finical and impossible standards'. Experts may not only base their opinions on such sources, but may give evidence of fact which is based on them. They may do this although the data on which they base their opinion or evidence of fact will usually be hearsay information, in the sense they rely for such data not on their own knowledge but on the knowledge of someone else. The weight to be accorded to such evidence is a matter for the court. See generally Borowski at 385-387, PQ v Australian Red Cross Society [1992] 1 VR 19 at 34-35, H v Schering Chemicals [1983] 1 WLR 143 at 148-149, Millirrpum v Nabalco Pty Ltd (1971)17 FLR 141 at 161-163 and Jango (No 4) at [8].

[93] There is nothing in the Evidence Act that displaces this body of law. The Australian Law Reform Commission, on whose report the Act was based, said:

Under existing law hearsay evidence that is admissible for a non-hearsay purpose is not excluded, but may not be used by the court as evidence of the facts stated. This involves the drawing of unrealistic distinctions. The issue is resolved by defining the hearsay rule as preventing the admissibility of hearsay evidence where it is relevant by reason only that it would affect the court’s assessment of the facts intended to be asserted. This would have the effect that evidence relevant for a non-hearsay purpose – eg to prove a prior consistent or inconsistent statement, or to prove the basis of the expert’s opinion – will be admissible also as evidence of the facts stated.

See Interim Report No 26, Evidence (1985) vol 1 at para 685.

119 In Malone on behalf of the Western Kangoulu People v State of Queensland (No 3) [2022] FCA 827, O'Bryan J said at [40]:

… is accommodated by s 60(1) of the Evidence Act which provides that the hearsay rule does not apply to evidence of a previous representation that is admitted because it is relevant for a purpose other than proof of an asserted fact. Under that provision, hearsay basis material referred to in an expert report is rendered admissible for the purpose of showing the basis or foundation for the opinions expressed in the report: Quick v Stoland Pty Ltd (1998) 87 FCR 371 at 377 per Branson J and 382 per Finkelstein J; Neowarra at [38] per Sundberg J. Unlike the position at common law, hearsay evidence admitted under s 60 is admitted for all purposes (including proof of a fact asserted in such evidence): Lee v R (1998) 195 CLR 594 at [39]-[40]. The Court may, however, exclude such hearsay evidence under s 135 of the Evidence Act if its probative value is substantially outweighed by the danger that the evidence might be unfairly prejudicial to a party, might be misleading or confusing or might cause or result in undue waste of time. The Court may also limit the use to be made of such hearsay evidence under s 136 if there is a danger that a particular use of the evidence might be unfairly prejudicial to a party or might be misleading or confusing.

120 See also Roach v Page (No 11) [2003] NSWSC 907 at [74(j)] (care must be taken to avoid a disadvantage through 'happenstance' by reference to other materials); Harrington-Smith v Western Australia (No 7) [2003] FCA 893; (2003) 130 FCR 424 at [38] (s 136 may be invoked if there is a suggestion that the hearsay form was chosen to prove the asserted facts by hearsay evidence); and Netdeen Pty Ltd t/as GJ Gardner Homes v Lindfield NSW Pty Ltd [2025] NSWCA 196 at [203]-[207] (citing Malone with approval).

121 This line of cases is of particular importance because BDO refer to the evidence of RISC as explaining some of the assumptions on which their opinion is based. In turn, RISC relied on (relevantly) the GCA report as explaining some of the assumptions on which RISC's opinion is based.

The GCA report

122 The GCA report was tendered by Twinza through an affidavit of Mr Myles Allen, a Lavan solicitor, which attached copies of documents that were provided to Lavan by Bennett in response to a notice to produce. It is relevant and admissible on the basis that it was relied upon by RISC. However, because of the operation of s 60 of the Evidence Act, care must be taken to assess the weight of such hearsay material and whether s 136 should be invoked to prevent unfairness.

123 I reject the Clough parties' credibility objection to the GCA report being tendered. It is not relied upon by Twinza to challenge the credibility of the Clough witnesses. It is a document referred to in the BDO report and the RISC report as a source document upon which assumptions are based. Clough's own expert witness, Mr Mountjoy, also referred to it on a number of occasions in his critique of the RISC report and described (relevantly) work including the GCA work as 'robust'.

124 As observed, the GCA report is part of the material relied on by Mr Craig of RISC to form his expert opinion, with the result that it is admissible under s 60 of the Evidence Act. The Clough parties complain about the source of information in the GCA report, but they are matters that go to weight, rather than to admissibility. I accept that GCA are reputable and experienced, and that the report in evidence appears to have been carefully prepared in accordance with accepted standards. In circumstances where Mr Craig (who can be expected with his skills to understand and assess the GCA report) and Mr Mountjoy (who says production profiles certified by GCA and other GCA work should not be departed from, and states that GCA 'is globally recognised with a strong reputation') have both in effect endorsed the GCA report, I am satisfied that I can give it weight when considering the RISC report. I would not exclude it under s 135, having regard to Mr Mountjoy's reference to and endorsement of GCA's work.

Tender of the Adjusted Model

125 The Clough parties also objected to the tender of the Adjusted Model on the basis that I should exercise my discretion under s 135 to exclude it on the ground that it was provided late and to permit its tender would be unfairly prejudicial. The Adjusted Model forecasts cash flows for Twinza and, as will be seen, is central to BDO's valuation of the company's assets.

126 The Adjusted Model is said to be derived from the 26 February 2025 Model provided by Twinza to BDO and to RISC. RISC stated that it provided comments to BDO on the Model. It described the Model as '2025-02-26 Pasca Project OBEM Investor Model.xlsm'. The Model is also in evidence. I referred above to the affidavit of Ms Chapman read by the Clough parties. It annexed (JSC-3) printed copies of a document described as 'Twinza's Open Book Economic Model dated 26 February 2025'. As the printed copies of the annexure were largely illegible (being Excel format), electronic copies were provided separately to the parties and the Court. Bennett have renamed the Excel document in its electronic form to 'JSC-03.xlsm'. However, the date and descriptions are otherwise similar and the references to the document by Mr Craig sufficiently persuade me this is the underlying Model. I have also reviewed both versions in electronic form, and the similarity of the Excel documents, with certain matters highlighted in the Adjusted Model, supports this conclusion (I note that RISC and Mr Mountjoy refer to further versions of an economic model, and a July 2025 version is also in evidence through the affidavit of Ms Chapman (JSC-5)).

127 I consider the Adjusted Model is relevant and admissible, albeit that the entries within it are founded in part on the books and records of Twinza and in part on adjustments that follow BDO's own assessments and those of RISC. It provides the basis upon which certain assumptions were drawn by BDO and RISC. The fact that it was not attached to the BDO report is explained by Mr Andrawes – see [168(c)] below.

128 Insofar as the Adjusted Model incorporates the adjustments that are explained in the body of the BDO report, the veracity of those adjustments is linked to the RISC report, a matter to which I will return.

129 I also note that parts of the Adjusted Model have been extracted by BDO from the Excel spreadsheets and copied into the BDO report (an example is the sensitivity model at [159] below).

130 I decline to exclude the Adjusted Model under s 135 of the Evidence Act. I do not consider the Clough parties were relevantly prejudiced by its late production in circumstances where it was clearly referred to as a source material and particular details were disclosed in the BDO report. The Clough parties could have requested it at an earlier point in the proceeding.

The nature of the objections to the BDO and RISC reports

131 The Clough parties objected to the affidavits of Mr Andrawes on the basis that the opinions in the BDO reports did not disclose the manner in which they were based on his skill, knowledge and experience and so were said to be inadmissible under s 79, with the objection said to go to the 'final conclusion' on value and risk.

132 It was acknowledged that the primary BDO report and the primary RISC report were in fact already admitted into evidence for the purpose of the convening hearing and were reviewed by the Court for that purpose.

133 However, in the end, as a practical matter little rests on this. Senior counsel for the Clough parties submitted that if, but for the fact those reports were admitted previously, they do not meet the admissibility threshold having regard to objections and submissions now made, they could not be given weight. Twinza did not seek to rely on the tender and admission of the reports at the convening hearing as a basis to deny the Clough parties the opportunity to make submissions at the approval hearing as to admissibility for the purpose of the economic interest argument. This issue does not arise in relation to the supplementary BDO or supplementary RISC reports, as they had not been previously tendered.

134 The Clough parties disclosed a number of objections to the BDO report in their written submissions. At the approval hearing, senior counsel also worked through the BDO report raising a number of matters.

135 The various objections are addressed later in these reasons.

The BDO opinion

136 The BDO report is detailed and takes the form of independent expert reports frequently seen and reviewed by the court in the context of schemes.

137 Having summarised the scheme, BDO set out the six matters as to which Twinza's solicitors had sought their opinion:

1 The value of the assets of the Company relative to the debts owing to the Senior Lenders and Other Senior Lenders in the event the Scheme does not proceed;

2 The solvency of the Company immediately following the implementation of the Scheme;

3 The expected amount that would be available to Senior Lenders, Other Senior Lenders, CRPS holders, all other creditors and Shareholders if the Scheme did not proceed and the Company were to be wound up within six months of the hearing of the application for an order under section 411 (1) and (1A) of the [Corporations] Act;

4 The expected amount that would be paid to Senior Lenders, Other Senior Lenders, CRPS holders, all other creditors and Shareholders if the Scheme was implemented;

5 The extent, if any, to which the expected amount that would be paid to CRPS holders, differs between either of the scenarios outlined above; and

6 The consequences of not approving the Scheme.

138 The respective answers were:

1 In the event the Scheme does not proceed, the total debts owing to the Senior Lenders and Other Senior Lenders exceeds the value of Twinza's assets by between US$55 million and US$128 million.

2 Following the implementation of the Scheme, the Company does not appear to be insolvent. Although the Company is expected to remain cash flow solvent through to at least April 2026, it remains loss making in the short term and is reliant on ongoing external funding.

3 In the event the Scheme does not proceed, the expected dividend that would be available to Senior Lenders and Other Senior Lenders is between US$179 million (55% of the amount owing) and US$254 million (78% of the amount owing). The expected dividend to all Priority Creditors would be US$123k (100% of the amount owing), while unsecured creditors, CRPS holders and Shareholders would not receive any return.

4 In the event the Scheme proceeds, the Senior Debt will reduce to a balance of US$35 million. Therefore, the Senior Lenders and Other Senior Lenders would be satisfied with equity and the new US$35 million facility. We note that as a result of the Scheme, the Senior Lenders and Other Senior Lenders will also collectively hold at least 85% of the Company's issued capital. Priority Creditors and Unsecured Creditors will also be paid in full (under the ordinary course of business). All CRPS on issue will be replaced and substituted with ordinary shares. The estimated surplus cash available to ordinary shareholders (including those holding new shares issued pursuant to the Scheme) is between US$135 million and US$208 million.

5 If the Scheme does not proceed, CRPS holders would receive US$ nil. If the Scheme is implemented, the CRPS on issue will be cancelled and replaced with ordinary shares. We have estimated the surplus cash that would be available to shareholders post-Scheme, with outcomes ranging from US$135 million to US$208 million. However, we note that shareholders do not receive a dividend following implementation of the Scheme, instead they retain their shareholding, albeit diluted in a going concern business.

6 If the Scheme is not implemented, and without additional funding, the Company will be insolvent and will need to enter applicable insolvency procedures in the various jurisdictions of its subsidiaries. If the Scheme is not implemented, there would also be a reduced return for Senior Lenders and Other Senior Lenders.

139 BDO then addressed their valuation methodology. They noted that:

… the valuation is being conducted under the assumption that the scheme proceeds and the assumption that it does not proceed in order to determine whether the shareholders and the CRPS holders hold an economic interest in Twinza.

140 That is, the valuation opinion expressly addresses the question that Twinza contends I am to resolve for the purpose of the so-called class issue.

141 BDO's profile of Twinza notes its flagship asset is the Pasca A project (PPL 328). BDO stated that Twinza was awarded PPL 328 in 2011. An appraisal in 2017 confirmed the field had enough resources for commercial development. Four wells have been drilled. BDO referred to the GCA report. They said GCA assessed the recoverable resources volume in April 2023, and reproduced details of those amounts. GCA also validated the potential of storing carbon dioxide, suggesting the capacity to offset carbon emissions.

142 BDO set out Twinza's intended development phases, noting that concept and pre-FEED were completed and that it was currently preparing the FEED for the first phase of development, which would involve drilling three wells connected to an offshore platform with processing facilities. Condensate and LPG would be stored on a floating vessel with excess gas reinjected.

143 BDO noted that PPL 584, which surrounds the Pasca A project, has been held by Twinza since 2020.

144 BDO also recited the financing arrangements, including the facility agreement, the tranches of funding drawn and noted there have been some 14 amendment deeds entered into, increasing draw-downs and maturity dates, observing that senior lenders had debt for equity conversion rights under the facilities.

145 Details of borrowings were set out, together with historical statements of the company's financial position (based on audited financial accounts to the year ended June 2024) and historical profit and loss statements.

146 BDO analysed the economic context and outlook for Papua New Guinea in order to consider the implications for the oil and gas industry, and also considered the economic outlook for Australia. They provided an analysis of the oil and gas industry, being the industry in which Twinza operates.

147 BDO then turned to the valuation task and methodologies. Having discussed different methodologies they said the following:

In our assessment of the value of the Company's assets and liabilities, we have chosen to employ a Sum-of-Parts approach. In assessing the Sum-of-Parts value of Twinza's assets relative to its debts, we have used the following methodologies:

• The core value of Twinza lies in the future cash flows to be generated from its interest in the Pasca A PPL 328 licence. These cash flows have a finite life and vary substantially from year to year, rendering it most appropriately valued using a DCF [discounted cash flow] approach, while having reliance on the technical inputs verified by the independent technical specialist, RISC. Based on discussions with RISC, and in accordance with Regulatory Guide 170 Prospective Financial Information ('RG 170') and Information Sheet 214 Mining and resources - Forward-looking statements ('IS 214'), we consider there to be sufficient reasonable grounds to estimate the future cash flows to be generated from the Pasca A PPL 328 licence. Therefore, we consider the application of a DCF approach to be an appropriate valuation approach for this asset.

• The value of the Company's exploration potential of the PPL 584 licence not included in the DCF valuation, is valued using alternative valuation methodologies by RISC, as contained in the ITAR in Appendix 5.

• Twinza's other assets and liabilities were valued using the NAV [net asset value] approach.

148 Valuations were done on a going concern basis:

Both the valuations of the Company's assets under the assumption that the Scheme does not proceed and our valuation following the implementation of the Scheme have been conducted on a going concern basis.

In accordance with RG 111, fair market value should be determined on the basis of a knowledgeable and willing, but not anxious seller. The funding requirements for the development of the project are taken into account in the same way under both scenarios. Therefore, we do not consider it appropriate, nor in accordance with RG 111, to assess the value of the Pasca A project on the basis of the Company being under financial distress.

149 In Part 8 of the report BDO set out their valuation opinions and explained their reasons for their opinion.

150 In summary, BDO concluded that the value of the assets of Twinza relative to the debts owing to the senior lenders and other senior lenders, assuming the scheme does not proceed, is as follows:

151 It therefore follows, on this analysis, that assuming the scheme does not proceed, there will be a shortfall to the senior lenders and other senior lenders.

152 BDO explained that in relation to the valuation of Pasca A PPL 328, performing a DCF valuation requires the determination of:

(a) the future cash flows that the PPL 328 licence is expected to generate that are attributable to Twinza's ownership interest; and

(e) an appropriate discount rate to apply to the cash flows of the PPL 328 licence to convert them into their present value equivalent.

153 BDO explained (in the second supplementary report) that the starting point for assessing the future cash flow model is Twinza's own cash flow model:

In valuing the Pasca A project we explain in the [principal report] why we have selected the discounted cash flow methodology as being the most appropriate valuation approach to adopt. In order to apply the discounted cash flow methodology we must have a reliable cash flow model. RG 111.113 states that the cash flow model must be prepared on a reasonable basis and further that 'It is important that those producing such information to the expert have used methods of analysis and presentations previously used by the company'. As such it is common practice for an expert to use the Company's own cash flow model as a basis for their valuation and if there are any major variations then the expert adjusts for them and comments on them in the report.

154 BDO undertook the discounted cash flow methodology as follows:

(a) management of Twinza had prepared and provided a detailed forecast cashflow Model;

(b) the Model estimated the future cash flows expected from production over the life of PPL 328 which incorporates Phase 1 and Phase 2 operations. The Model reflects forecasts of nominal, after-tax cash flows over the forecast period on a calendar year basis in USD terms. The Model shows cash flows assuming a 50% interest in the Pasca A project;

(c) BDO assessed the reasonableness of the Model prepared by Twinza;

(d) they adjusted the Model where they considered appropriate, to produce the Adjusted Model;

(e) the Adjusted Model incorporated the payments Twinza would receive from the sale of a 45% interest in the Pasca A project pursuant to the SPA; reflected any changes to the technical assumptions as a result of RISC's review; and reflected any changes to the economic and other input assumptions that BDO considered appropriate as a result of their research;

(f) from its review of the technical assumptions, RISC recommended that adjustments be made to the Model. Those adjustments were increases to abandonment and decommissioning costs; a delay of up to two years to the schedule (with a best estimate being a one-year delay); and an increase to the capital expenditure profile by up to 50%, with a best estimate being a 25% capital expenditure increase;

(g) BDO considered and adjusted RISC's recommendations in forming their DCF valuation range in order to satisfy themselves that once the required adjustments were made, the Adjusted Model formed a reasonable basis for the valuation; and

(h) the Model was prepared based on estimates of the production profiles, operating costs and capital expenditure. The main assumptions underpinning the Model and the Adjusted Model include gas, condensate and LPG production volumes; oil and gas prices; operating costs; capital expenditure; royalties and levies; corporate and other taxes; and discount rates. Each of these was addressed in further detail.

155 Further, BDO explained that they analysed the Model to confirm its integrity and mathematical accuracy; appointed RISC as technical expert to review, and where required, provide changes to the technical assumptions underpinning the Model; conducted independent research on certain economic and other inputs such as oil prices, inflation, and the discount rate applicable to the future cash flows of Pasca A, specifically PPL 328; held discussions with RISC to confirm the reasonableness of the technical inputs underpinning the Model; and performed sensitivity analysis on the value of PPL 328 by flexing key assumptions and inputs.

156 As to RISC's involvement, BDO stated that:

RISC was engaged to prepare a report providing a technical assessment of the assumptions underlying the Model. RISC's assessment involved the review and provision of opinion on the reasonableness of the assumptions adopted in the Model, including but not limited to:

• gas, condensate and LPG production profiles

• reserves and resources included in the Model

• operating costs (comprising operating expenses, general and administrative expenses, royalties, and selling costs)

• capital expenditure (development and sustaining capital required) including decommissioning and abandonment costs

• other relevant assumptions.

157 BDO then moved through a consideration of a number of matters, explaining the assumptions upon which their opinion is based – economic assumptions, gas production assumptions, operating expenditure, capital expenditure, identification of the appropriate discount rate, and the identification of the appropriate interest of Twinza for the purpose of valuation (50% or 95%, as addressed below).

158 As to the appropriate discount rate to apply to the cash flows to convert them into their present value equivalent, BDO said: