FEDERAL COURT OF AUSTRALIA

Australian Securities and Investments Commission v RAMS Financial Group Pty Ltd (Penalty) [2025] FCA 1304

File number(s): | NSD 885 of 2025 |

Judgment of: | SHARIFF J |

Date of judgment: | 24 October 2025 |

Catchwords: | CONSUMER LAW – admitted contraventions of ss 31(1), 47(1)(a), 47(1)(b), 47(1)(d), 47(1)(e) and 47(4) of the National Consumer Credit Protection Act 2009 (Cth) – joint position and submissions as to pecuniary penalties to be imposed – whether contraventions established on agreed facts – whether declarations should be made – whether quantum of penalties appropriate |

Legislation: | Corporations Act 2001 (Cth) s 912A(1)(a) National Consumer Credit Protection Act 2009 (Cth) ss 5(1), 6, 7, 8, 29, 31(1), 47(1)(a), 47(1)(b), 47(1)(d), 47(1)(e), 47(4), 166, 167B(2) Evidence Act 1995 (Cth) s 191 Federal Court of Australia Act 1976 (Cth) ss 37AF(1), 37AG(1)(a) Treasury Laws Amendment (Strengthening Corporate and Financial Sector Penalties) Act 2019 (Cth) National Consumer Credit Protection Regulations 2010 (Cth) |

Cases cited: | Australian Building and Construction Commissioner v Construction, Forestry, Mining and Energy Union [2017] FCAFC 113; 254 FCR 68 Australian Building and Construction Commissioner v Construction, Forestry, Mining and Energy Union [2018] HCA 3; 262 CLR 15 Australian Building and Construction Commissioner v Pattinson [2022] HCA 13; 274 CLR 450 Australian Competition and Consumer Commission v Hillside (Australia New Media) Pty Ltd trading as Bet365 (No 2) [2016] FCA 698 Australian Competition and Consumer Commission v Multimedia International Services Pty Ltd [2016] FCA 439; 243 FCR 392 Australian Competition and Consumer Commission v Optus Mobile Pty Ltd [2019] FCA 106 Australian Competition and Consumer Commission v Telstra Corporation Ltd [2010] FCA 790; 188 FCR 238 Australian Competition and Consumer Commission v TPG Internet Pty Ltd [2013] HCA 54; 250 CLR 640 Australian Competition and Consumer Commission v Universal Music Australia Pty Ltd (No 2) [2002] FCA 192; 201 ALR 618 Australian Securities and Investments Commission v AGM Markets Pty Ltd (in liq) (No 3) [2020] FCA 208; 275 FCR 57 Australian Securities and Investments Commission v AMP Financial Planning Pty Ltd (No 2) [2020] FCA 69; 377 ALR 55 Australian Securities and Investments Commission v Australia and New Zealand Banking Group Limited [2023] FCA 256 Australian Securities and Investments Commission v Australia and New Zealand Banking Group Limited [2023] FCA 1150; 169 ACSR 649 Australian Securities and Investments Commission v BT Funds Management Limited [2021] FCA 844 Australian Securities and Investments Commission v Camelot Derivatives Pty Ltd (in liq) [2012] FCA 414; 88 ACSR 206 Australian Securities and Investments Commission v Citigroup Global Markets Australia Pty Limited (ACN 113 114832) (No. 4) [2007] FCA 963; 160 FCR 35 Australian Securities and Investments Commission v Commonwealth Bank of Australia [2020] FCA 790 Australian Securities and Investments Commission v Commonwealth Bank of Australia [2022] FCA 1422 Australian Securities and Investments Commission v Ferratum Australia Pty Limited (in liq) [2023] FCA 1043 Australian Securities and Investments Commission v Layaway Depot Pty Ltd [2023] FCA 1685 Australian Securities and Investments Commission v MLC Nominees Pty Ltd [2020] FCA 1306; 147 ACSR 266 Australian Securities and Investments Commission v National Australia Bank Ltd [2020] FCA 1494 Australian Securities and Investments Commission v National Australia Bank Ltd [2022] FCA 1324 Australian Securities and Investments Commission v RAMS Financial Group Pty Ltd [2025] FCA 1087 Australian Securities and Investments Commission v Westpac Banking Corporation (Omnibus) [2022] FCA 515 Australian Securities and Investments Commission v Westpac Banking Corporation (No 3) [2018] FCA 1701 Australian Securities and Investments Commission v Westpac Banking Corporation [2019] FCA 2147 Australian Securities and Investments Commission v Westpac Securities Administration Limited, in the matter of Westpac Securities Administration Limited [2021] FCA 1008 Australian Securities Investments Commission v Membo Finance Pty Ltd (No 2) [2023] FCA 126 Barbaro v The Queen [2014] HCA 2; 253 CLR 58 Commonwealth v Director, Fair Work Building Industry Inspectorate [2015] HCA 46; 258 CLR 482 Competition and Consumer Commission v Woolworths Limited [2016] FCA 44; ATPR-42-521 Construction, Forestry, Mining and Energy Union v Cahill [2010] FCAFC 39; 269 ALR 1 Flight Centre Ltd v Australian Competition and Consumer Commission (No 2) [2018] FCAFC 53; 260 FCR 68 Green v The Queen [2011] HCA 49; 244 CLR 462 Hili v The Queen [2010] HCA 45; 242 CLR 520 Lacey v Attorney-General (Qld) [2011] HCA 10; 242 CLR 573 Mayfair Wealth Partners Pty Ltd v Australian Securities and Investments Commission [2022] FCAFC 170; 295 FCR 106 NW Frozen Foods Pty Ltd v Australian Competition and Consumer Commission [1996] FCA 1134; 71 FCR 285 Singtel Optus Pty Ltd v Australian Competition and Consumer Commission [2012] FCAFC 20; 287 ALR 249 Trade Practices Commission v CSR Limited [1990] FCA 521; ATPR 41-076 |

Division: | General Division |

Registry: | New South Wales |

National Practice Area: | Commercial and Corporations |

Sub-area: | Commercial Contracts, Banking, Finance and Insurance |

Number of paragraphs: | 195 |

Date of hearing: | 21 October 2025 |

Counsel for the Applicant | Mr M Brady KC with Mr S Cleary |

Solicitor for the Applicant | Gadens |

Counsel for the Respondent | Mr S Lawrance SC with Ms E Bathurst |

Solicitor for the Respondent | Allens |

ORDERS

NSD 885 of 2025 | ||

| ||

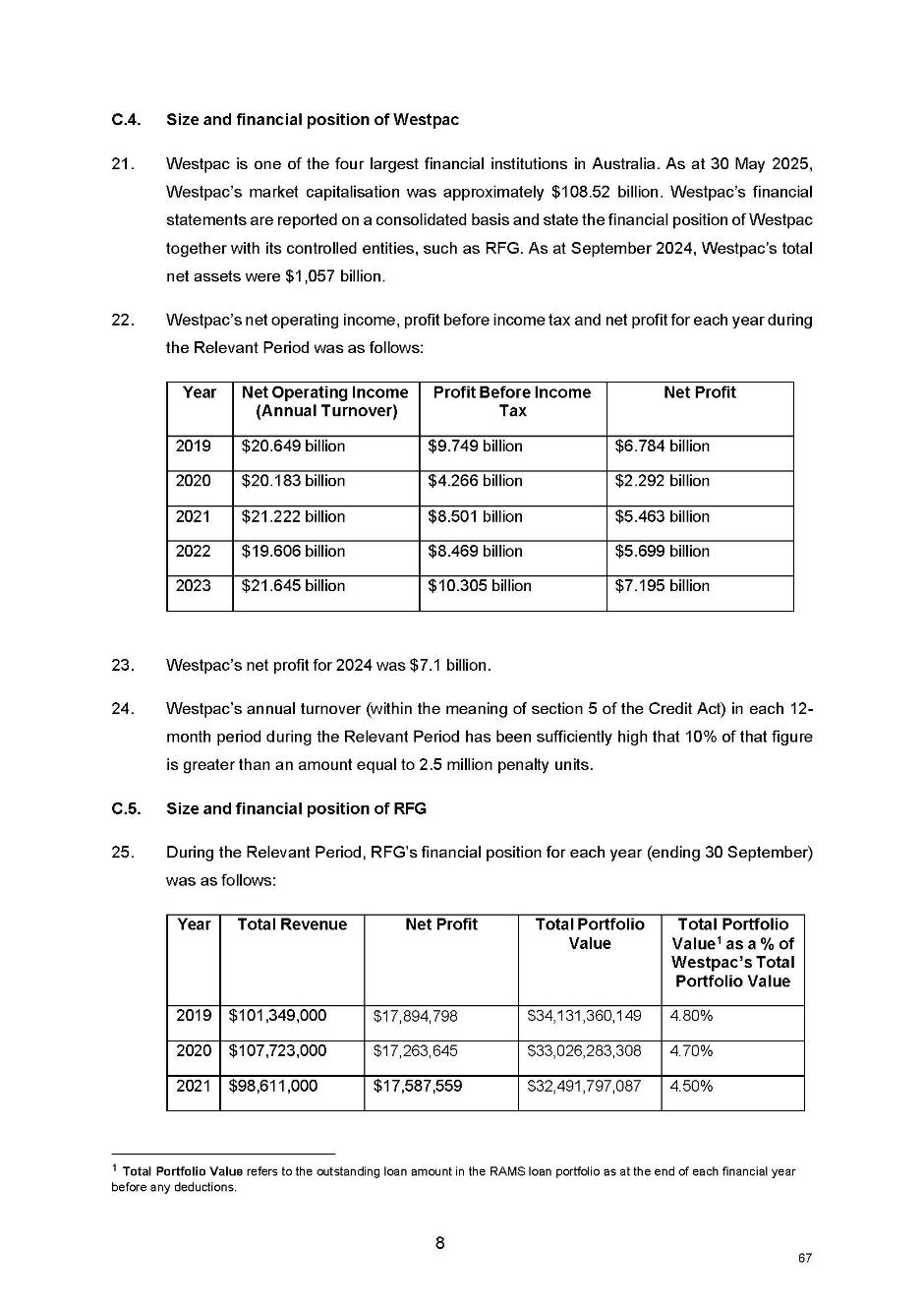

BETWEEN: | AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Applicant | |

AND: | RAMS FINANCIAL GROUP PTY LTD ACN 105 207 538 Respondent | |

order made by: | SHARIFF J |

DATE OF ORDER: | 24 October 2025 |

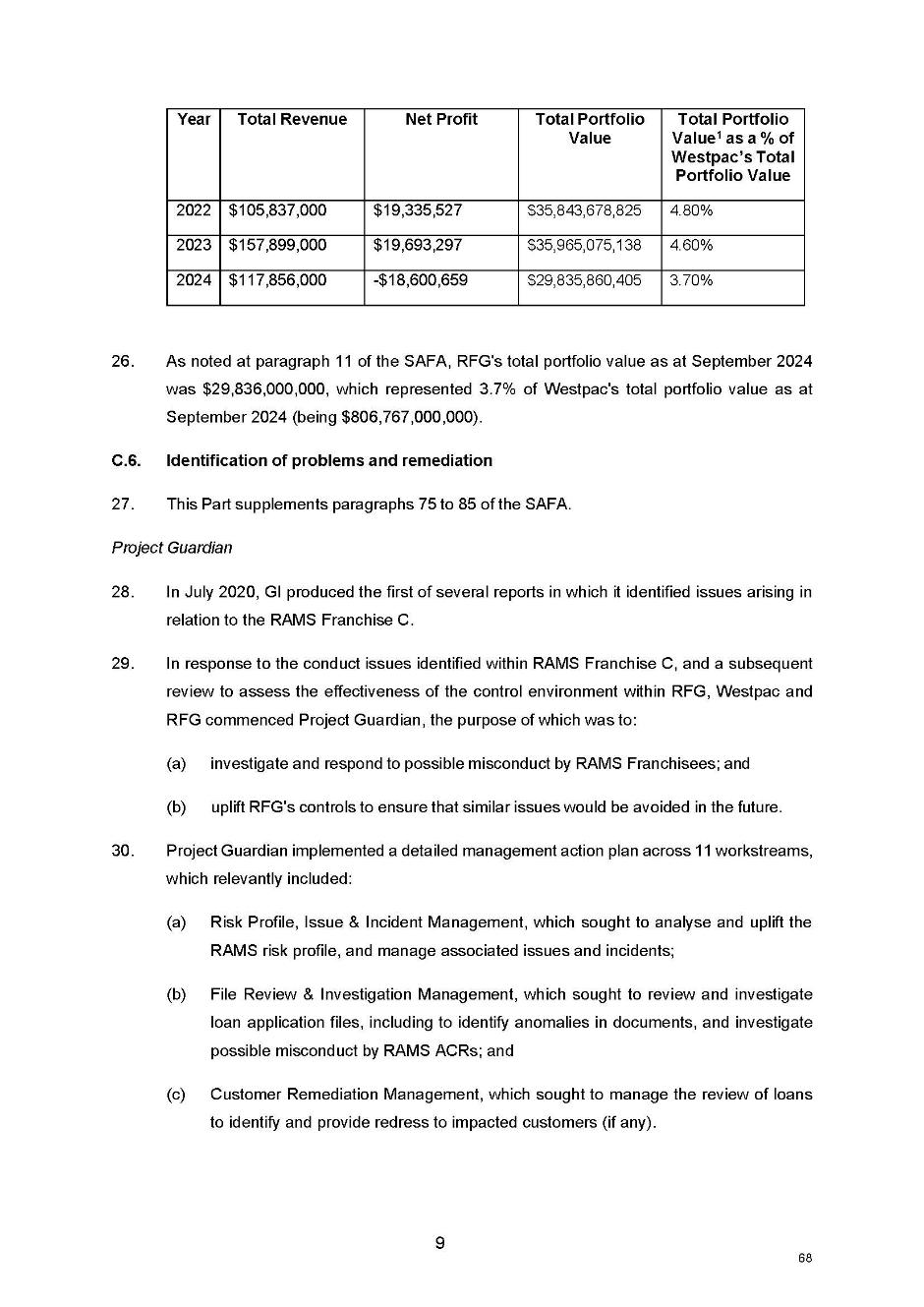

THE COURT ORDERS THAT:

1. The parties confer and provide short minutes of order to the Associate to Justice Shariff which give effect to the reasons for judgment dated 24 October 2025 in respect of the declarations of contravention required to be made under s 166 of the National Consumer Credit Protection Act 2009 (Cth) (the Credit Act).

2. Within 30 days, the Respondent (RFG) pay to the Commonwealth an aggregate pecuniary penalty of $20 million in respect of RFG’s conduct found to have contravened ss 31(1), 47(1)(a), 47(1)(b), 47(1)(e), and 47(4) of the Credit Act.

3. RFG pay the Applicant’s costs as agreed or taxed.

4. Pursuant to s 37AF of the Federal Court of Australia Act 1976 (Cth) (the FCA Act), and on the ground specified in s 37AG(1)(a), namely, that it is necessary to prevent prejudice to the proper administration of justice, for a period of 10 years from the date of this Order, the following information, in connection with Federal Court proceeding number NSD 885 of 2025, be suppressed and not published:

(a) references to the names and locations of RAMS Franchises, RAMS Franchise principals and loan writers, including their initials, as referred to in:

(i) page 31 of the hyperlinked Statement of Agreed Facts and Admissions on Liability, which is tendered and marked Exhibit 1 (Hyperlinked SAFA); and

(ii) columns B and C contained at Annexure KAB-01 of the affidavit of Kristina Andrea Belci affirmed on 20 October 2025 (Belci Affidavit); and

(b) references to the unlicensed unaccredited referrers as referred to in the Belci Affidavit, being:

(i) the names of unlicensed unaccredited referrers in column D contained at Annexure KAB-01;

(ii) the name, CRN, ABN, and ACN of the entity the subject of the search at Annexure KAB-02; and

(iii) the name of the individual the subject of the email correspondence at Annexure KAB-03; and

(c) the redacted information in the documents set out in Schedule 1 to these Orders, as hyperlinked to the Hyperlinked SAFA, being:

(i) references to the names and locations of the RAMS Franchises, RAMS Franchise principals and loan writers, including their initials;

(ii) references to the names of the unlicensed unaccredited referrers;

(iii) references to the personal information of RAMS customers including names, contact information, property addresses, bank account numbers, BSB numbers and bank card numbers; and

(iv) references to the names and contact information of Westpac employees.

5. Pursuant to s 37AI of the FCA Act, all material contained in the documents set out in Schedule 1 of these Orders, as attached to, and accessible by hyperlinks in, the Hyperlinked SAFA, be suppressed and not published pending completion of the redactions referred to in order 4(c) of these Orders.

SCHEDULE 1

# | Document Name | Date | Document ID |

1 | GI Report | 17 August 2019 | RAM.001.032.3971 |

2 | GI Report | 27 September 2019 | RAM.001.152.0017 |

3 | GI Report | 30 September 2019 | RAM.001.038.1065 |

4 | GI Report | 24 October 2019 | RAM.001.038.3139 |

5 | GI Report | 1 May 2020 | RAM.001.032.3850 |

6 | GI Report | 5 May 2020 | RAM.001.032.3953 |

7 | GI Report | 7 May 2020 | RAM.001.032.4089 |

8 | GI Report | 19 May 2020 | RAM.001.032.3942 |

9 | GI Report | 17 June 2020 | RAM.001.037.6866 |

10 | GI Report | 29 July 2020 | RAM.001.038.3685 |

11 | GI Report | 24 November 2020 | RAM.001.038.3495 |

12 | GI Report | 20 May 2021 | RAM.001.038.3393 |

13 | GI Report | 21 July 2020 | RAM.001.038.3559 |

14 | GI Report | 1 September 2021 | RAM.001.038.3413 |

15 | GI Report | 15 September 2021 | RAM.001.012.0199 |

16 | GI Report | 30 September 2021 | RAM.001.012.0191 |

17 | GI Report | 25 March 2022 | RAM.001.037.0602 |

18 | GI Report | 29 March 2022 | RAM.001.037.0610 |

19 | GI Report | 29 March 2022 | RAM.001.037.0722 |

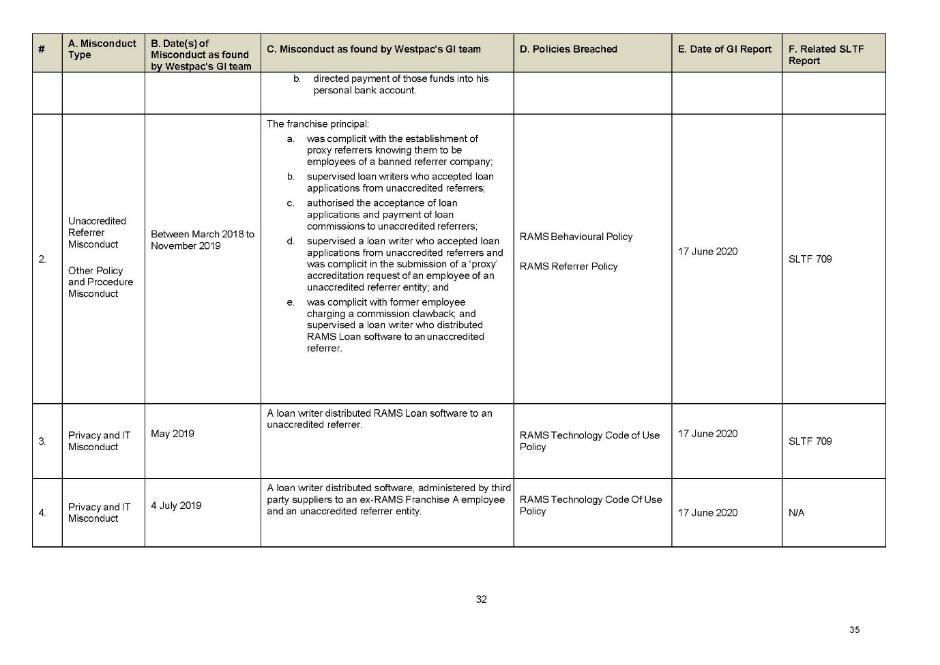

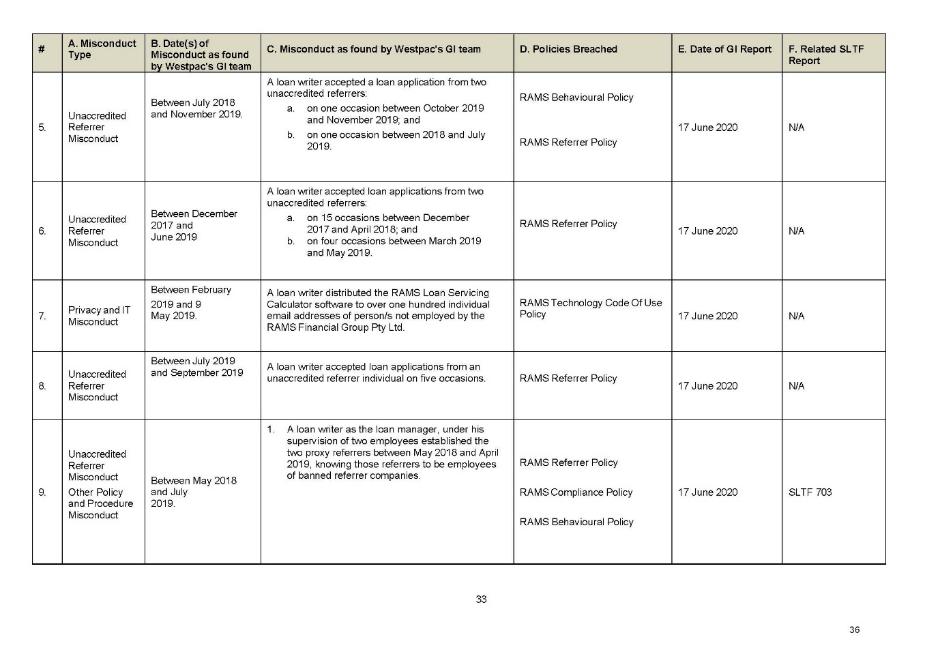

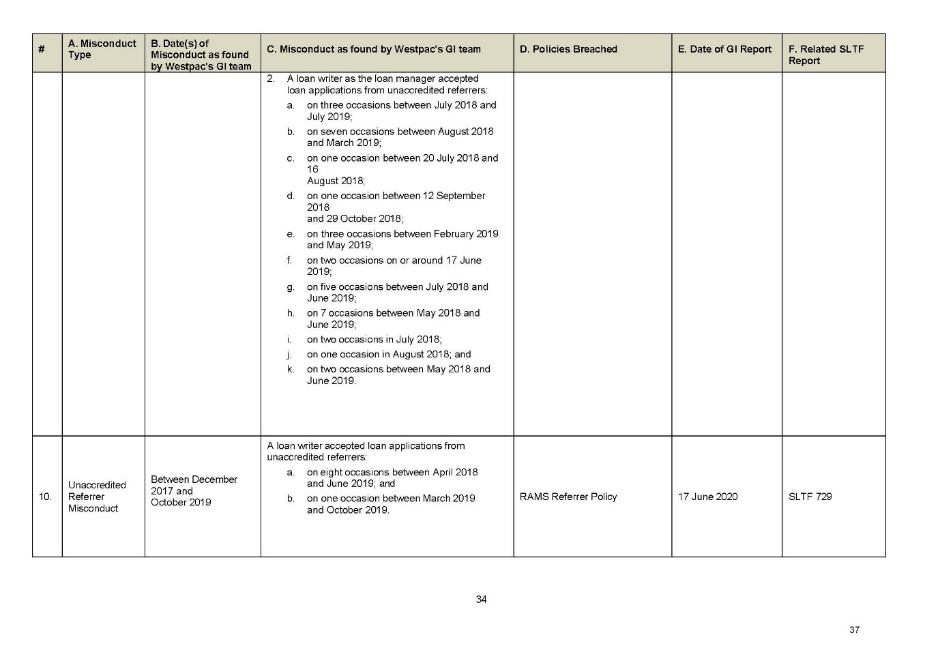

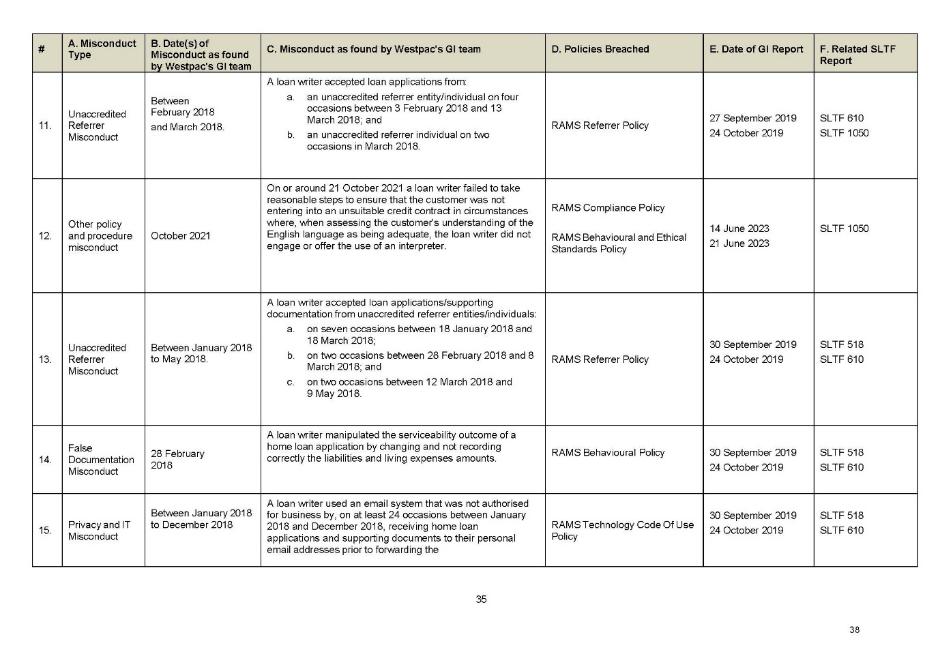

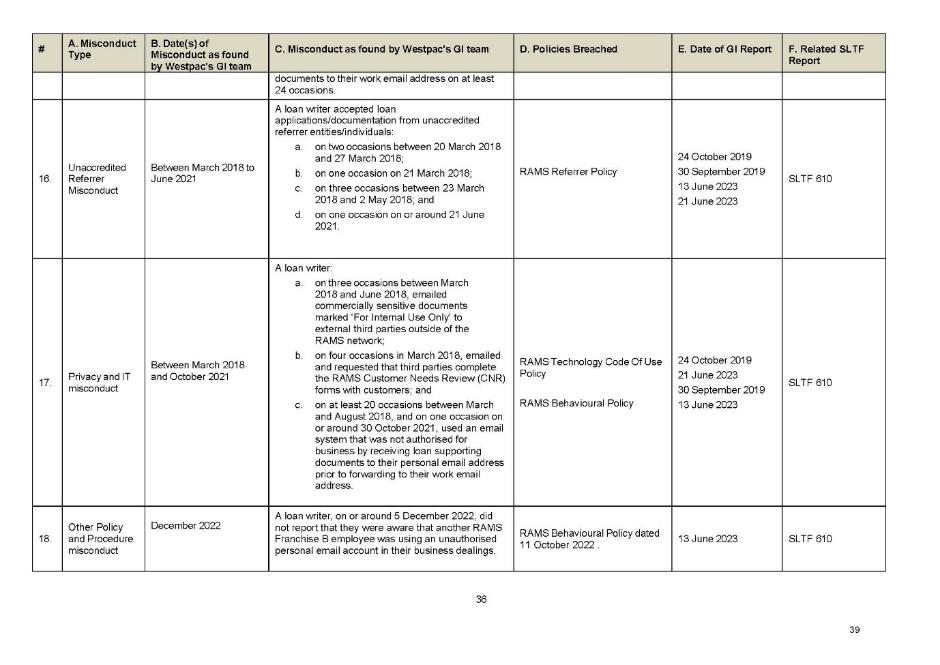

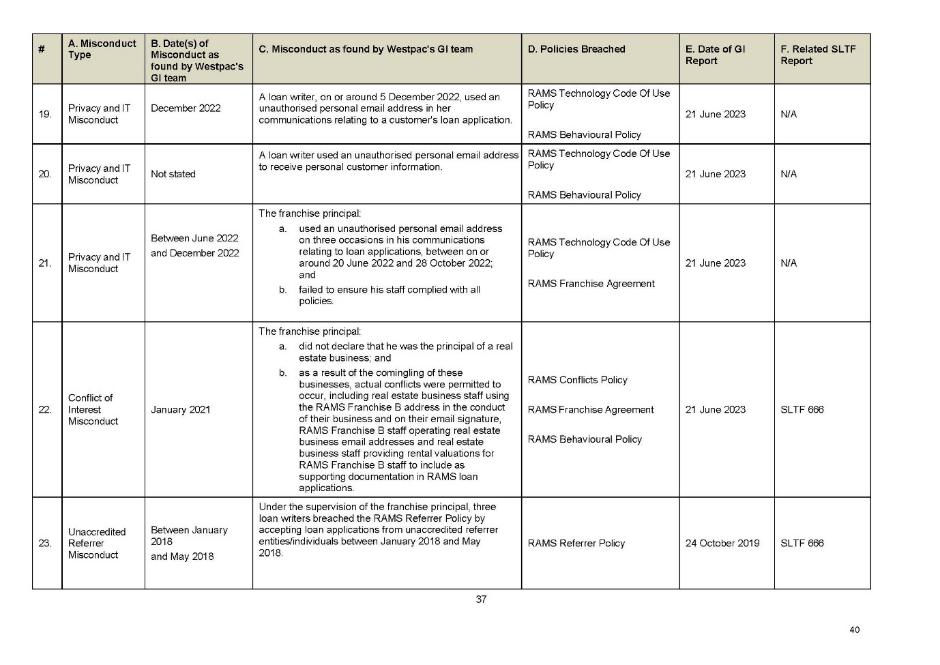

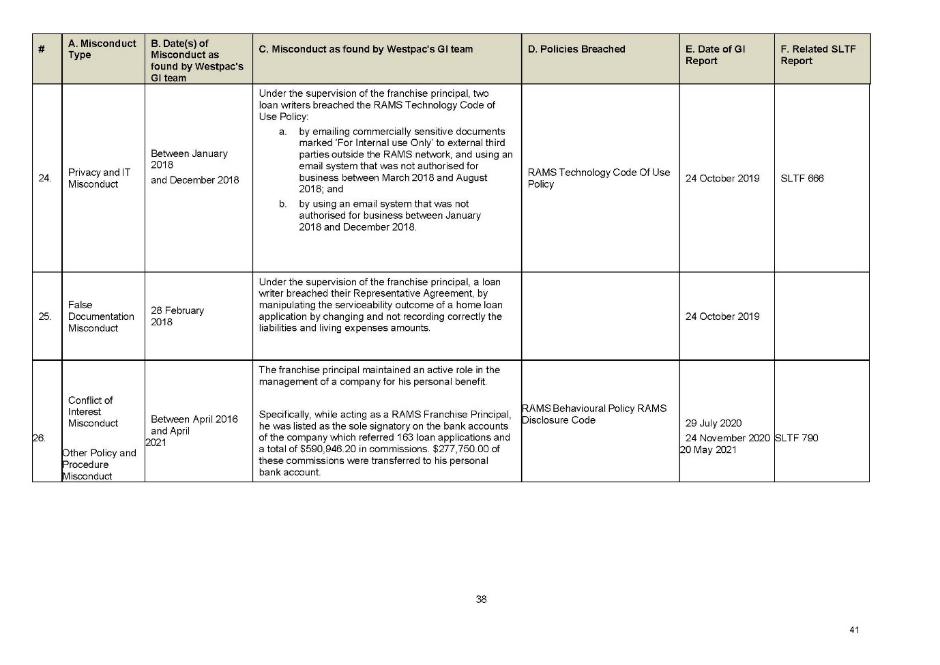

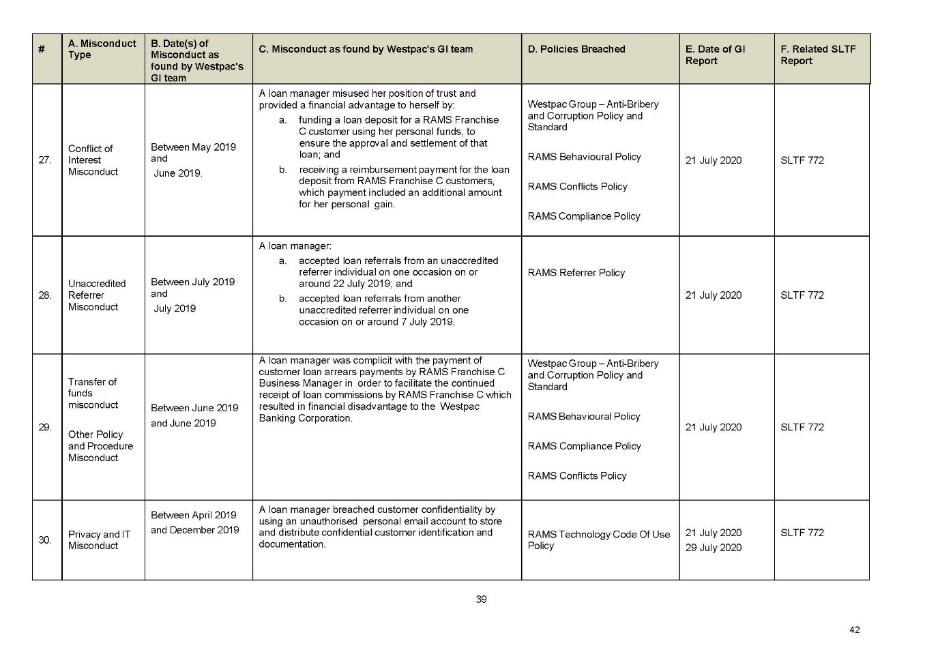

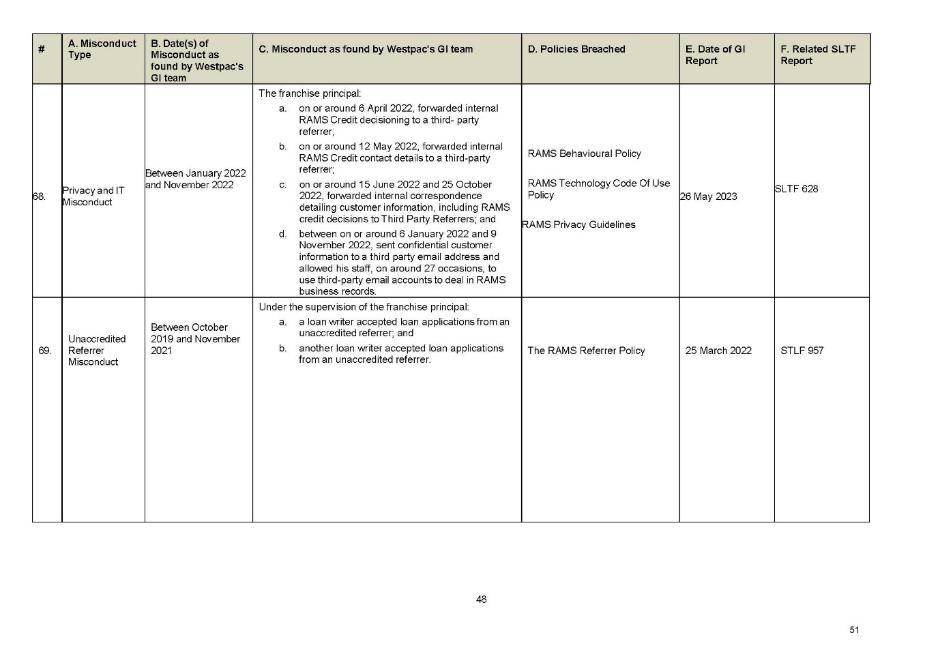

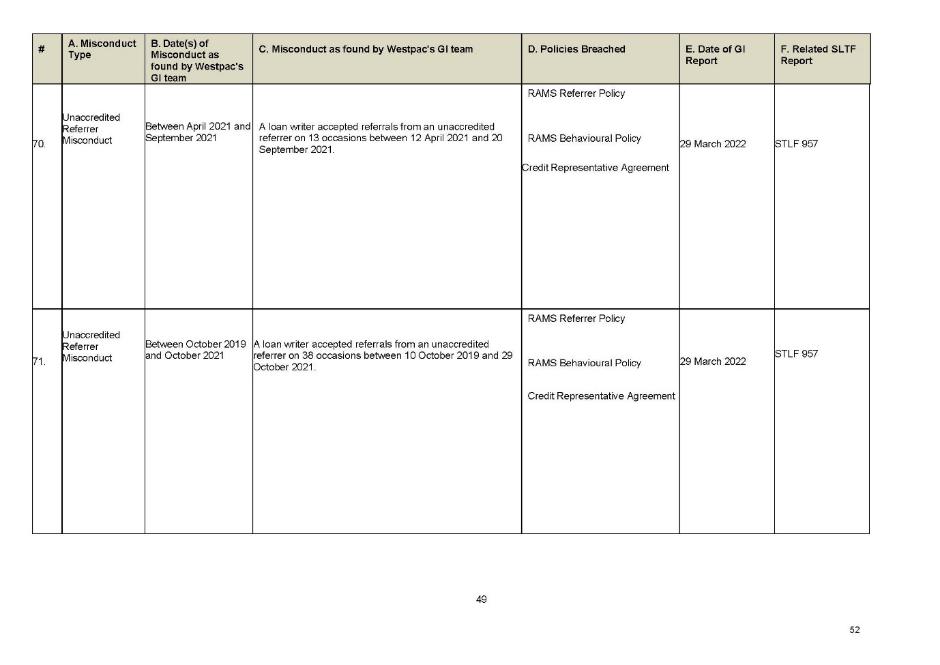

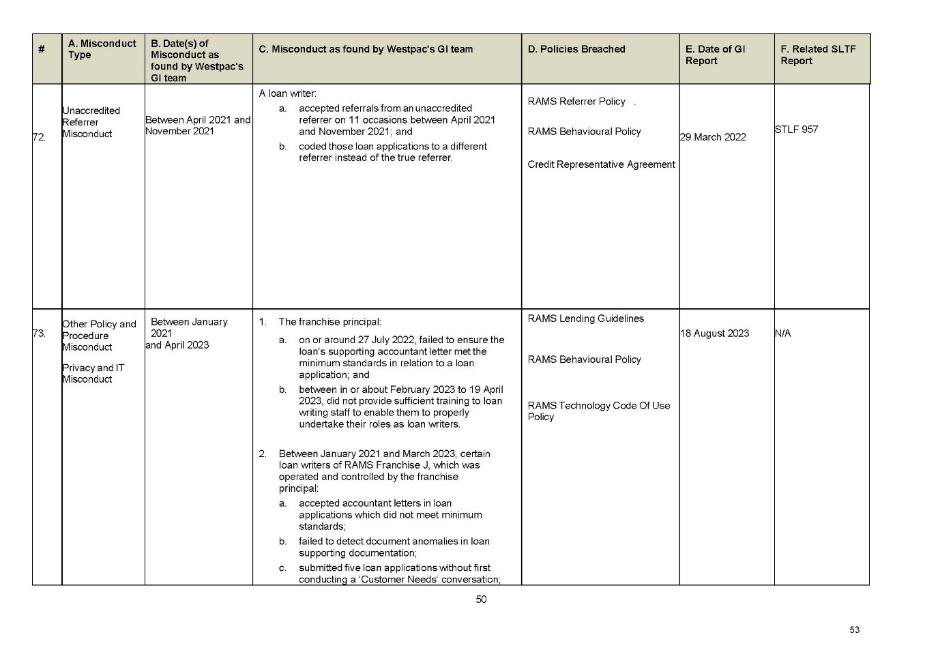

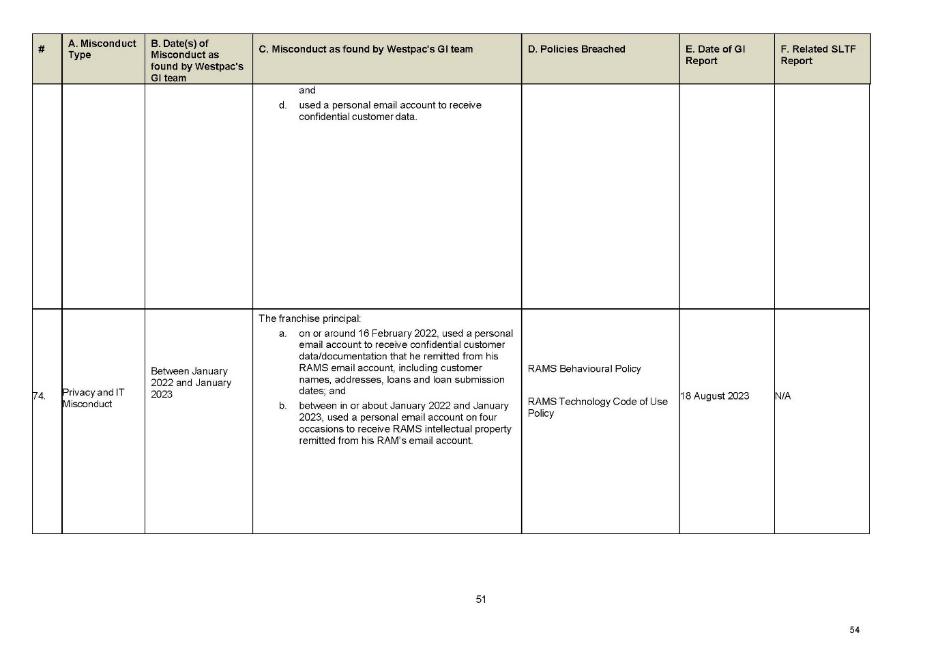

20 | GI Report | 4 August 2022 | RAM.001.037.0400 |

21 | GI Report | 4 August 2022 | RAM.001.113.0031 |

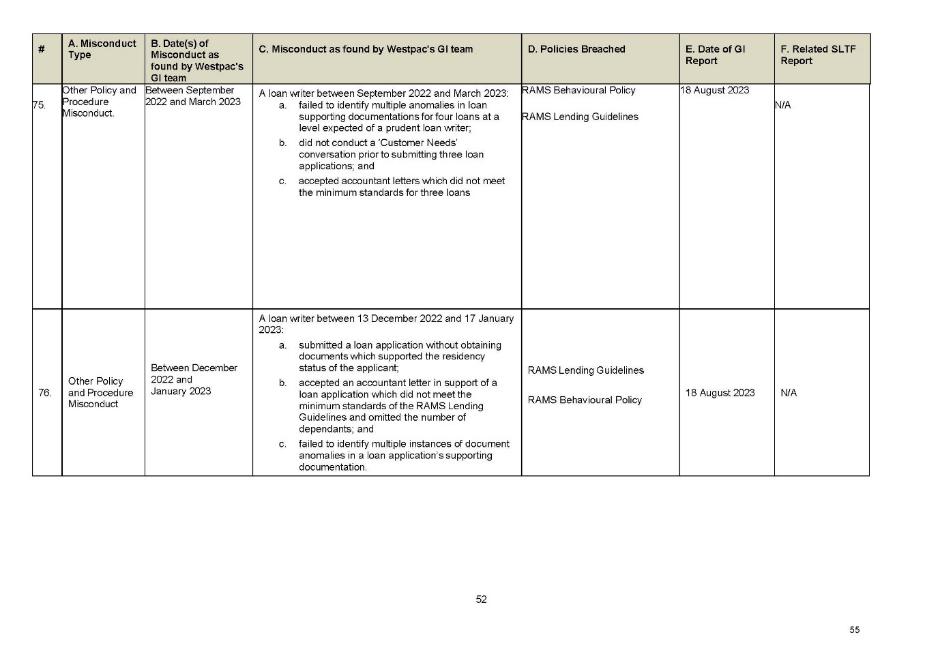

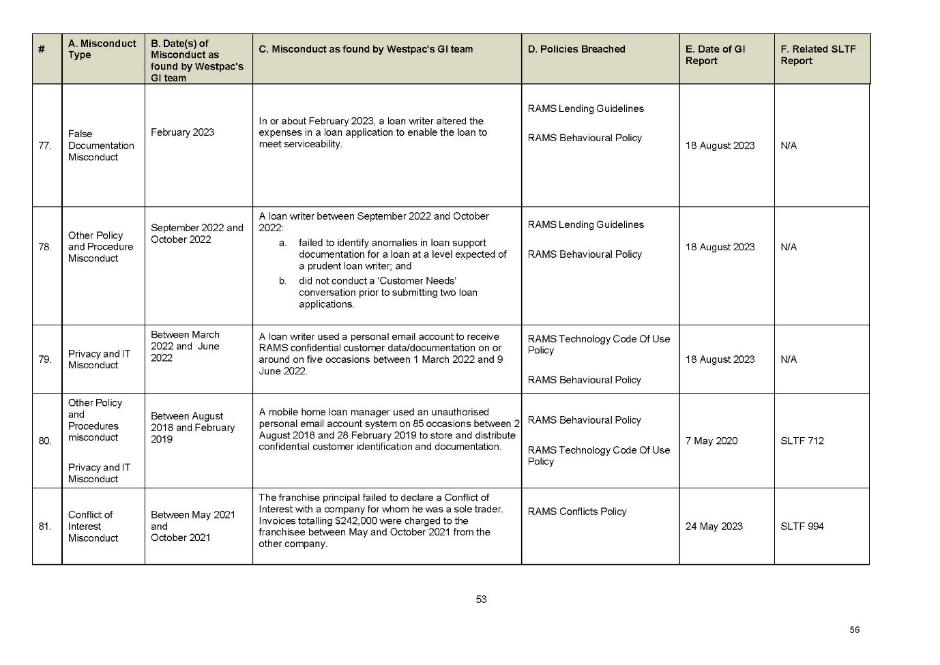

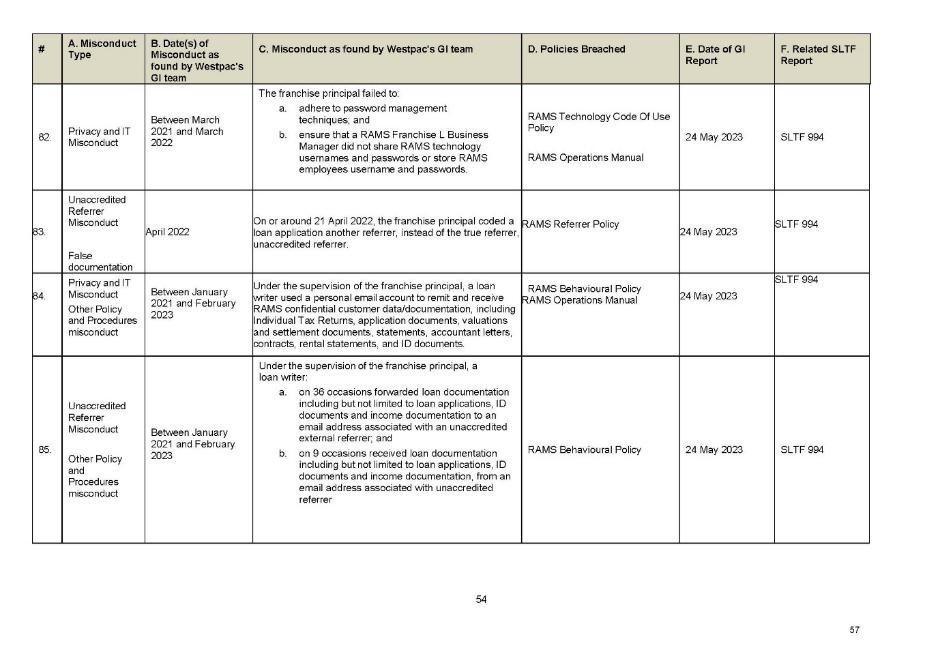

22 | GI Report | 7 February 2023 | RAM.001.113.0730 |

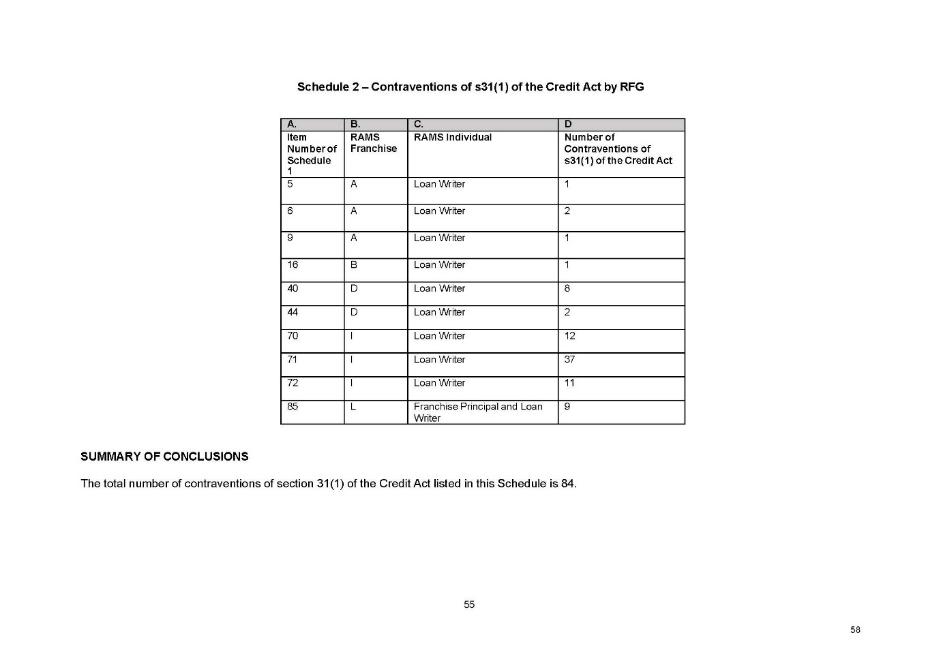

23 | GI Report | 7 February 2023 | RAM.001.113.0738 |

24 | GI Report | 24 May 2023 | RAM.001.006.1093 |

25 | GI Report | 26 May 2023 | RAM.001.006.1080 |

26 | GI Report | 13 June 2023 | RAM.001.011.9365 |

27 | GI Report | 14 June 2023 | RAM.001.011.9336 |

28 | GI Report | 21 June 2023 | RAM.001.006.1123 |

29 | GI Report | 18 August 2023 | RAM.001.006.1141 |

30 | GI Report | 18 August 2023 | RAM.001.011.9396 |

31 | GI Report | 18 August 2023 | RAM.001.011.9413 |

32 | GI Report | 18 August 2023 | RAM.001.011.9445 |

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011

REASONS FOR JUDGMENT

SHARIFF J:

1. INTRODUCTION

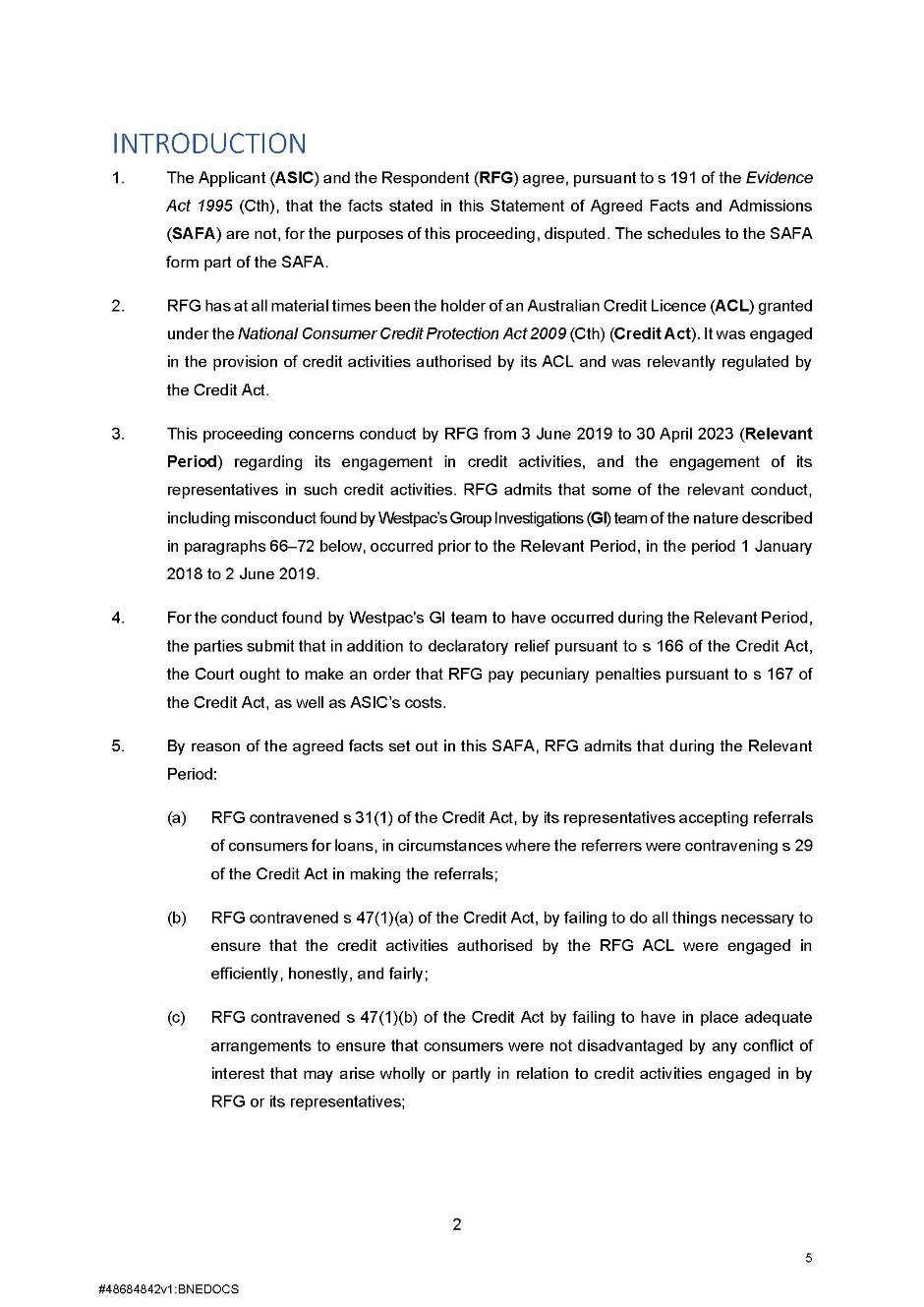

1 These proceedings involve an examination as to whether the respondent, RAMS Financial Group Pty Ltd (RFG), contravened important provisions of the National Consumer Credit Protection Act 2009 (Cth) (the Credit Act). Although RFG has admitted liability and has agreed to pay a civil penalty of $20 million, it is nevertheless necessary for the Court to decide whether contraventions have occurred and, if so, whether the agreed penalty is appropriate.

2 RFG was, and is, a wholly-owned subsidiary of Westpac Banking Corporation (Westpac). Westpac acquired RFG in 2008. RFG was, and is, the holder of an “Australian credit license” (ACL) granted under the Credit Act. RFG sought to provide credit services, and to assist, consumers through a franchise network (the RAMS Franchise Network) by which its franchisees (RAMS Franchisees) used the RAMS business name to provide credit assistance to consumers in relation to the distribution of RAMS-branded home loans which were, in fact, home loans with Westpac (albeit those loans were branded as “RAMS Home Loans”). RFG appointed RAMS Franchisees and their staff as authorised credit representatives (ACRs) of RFG for the purposes of providing credit assistance.

3 One of the central purposes of the Credit Act is to protect consumers and to do so by the regulation of the conduct of licensees. An essential aspect of this regulatory scheme is that persons involved in the provision of a “credit service” to consumers, including by providing “credit assistance” to them, must be licensed. As I explain below, a further essential aspect of the scheme is that, as provided for by s 31(1) of the Credit Act, a licensee is prohibited from engaging in a credit activity and, in the course of doing so, conducting business with a person who is also engaging in a credit activity without an Australian credit licence authorising them to do so. The purpose of this prohibition is to ensure that the overall objectives of the statutory scheme are not frustrated by “licensees engaging with unlicensed persons to subvert its intent”: Australian Securities and Investments Commission v National Australia Bank Ltd [2020] FCA 1494 (ASIC v NAB) at [90] (Lee J).

4 A further important aspect of the regulatory scheme enacted under the Credit Act is found in s 47(1). That section relevantly requires a licensee to do all things necessary to ensure that the credit activities authorised by the licence are engaged in “efficiently, honestly and fairly” (s 47(1)(a)), that adequate arrangements are in place to ensure that clients are not disadvantaged by conflicts of interest (s 47(1)(b)), and that reasonable steps are taken to ensure that representatives of the licensee comply with credit legislation (s 47(1)(e)).

5 I am satisfied on the facts that the parties have agreed to in the present case that RFG failed to comply with these basal obligations. On 84 occasions, RFG (through its franchise representatives) accepted referrals of consumers from third parties who were not licensed. There were yet further occasions when RFG accepted referrals of consumers from third parties who were not accredited by RFG in accordance with its own policies and procedures. The facts further demonstrate that, whilst RFG had policies and procedures in place, they were inadequate in several fundamental respects including in seeking to avoid conflicts of interest and breaches of privacy. I am satisfied that RFG failed to ensure that certain of its franchise representatives complied with the Credit Act and RFG’s applicable policies including as to dealing only with accredited referrers, conflicts of interest, privacy, use of information technology systems, and other behaviour.

6 The conduct that lies at the heart of the proceedings came to light when RFG and Westpac commenced investigating potential instances of misconduct that were alleged to have occurred within the RAMS Franchise Network. Some of the investigations were commenced at RFG’s initiative, and others were commenced following one or more complaints being made. Those investigations expanded over time, and there were many of them. RFG and Westpac determined in various respects that the allegations of misconduct were substantiated, and that in other respects they were not. Amongst other things, RFG and Westpac’s investigations substantiated allegations that some RAMS Franchisees had failed to comply with various of RFG’s policies and the Credit Act.

7 RFG disclosed the various findings of its investigations to ASIC and thereafter ASIC commenced its own investigation into RFG. RFG co-operated with ASIC in its investigation. RFG and Westpac have taken other commendable steps such as embarking upon reviews and audits to improve their systems and policies and have taken a conservative approach to the payment of compensation to consumers by way of remediation.

8 Nevertheless, the facts here establish that (as acknowledged by RFG and Westpac’s Board Risk Committee) the “root causes” of the contraventions were that RFG was conducted as an “autonomous business with a unique risk profile” which was borne of its franchise model, and, further, RFG had an immature risk culture, a deficient control environment and there was insufficient oversight of its non-standard methods of business. In the circumstances, it is important that the penalty to be imposed must serve the object of deterrence and promote compliance with the regulatory regime.

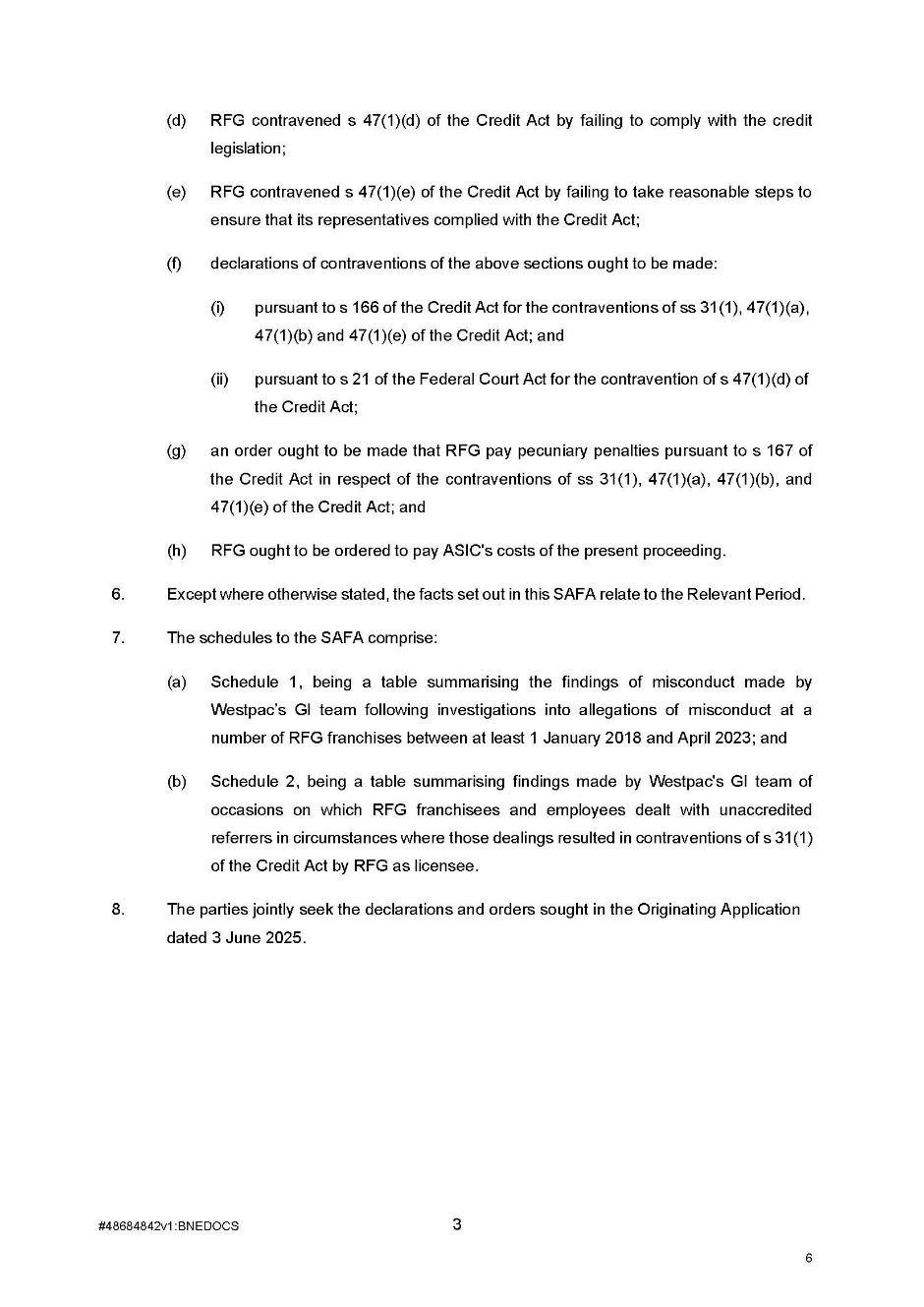

9 By the time that these proceedings were commenced, the parties had reached agreement as to the facts relevant to RFG’s admissions of liability. Specifically, based on those agreed facts, RFG admitted that it had contravened the Credit Act during the period from 3 June 2019 to 30 April 2023 (the Relevant Period). As a result, ASIC seeks declaratory relief and the imposition of pecuniary penalties against RFG in respect of contraventions of ss 31(1), 47(1)(a), (b), (d) and (e) and 47(4) the Credit Act. RFG agrees that orders should be made to this effect. The parties have subsequently reached agreement as to the facts relevant to penalty and as to the form of relief that should be granted including as to the quantum of the penalty to be imposed.

10 The parties’ position as to these matters is set out in the Updated Statement of Agreed Facts and Admissions on Liability dated 30 July 2025 (Liability SAFA), the Updated Statement of Agreed Facts on Relief dated 30 July 2025 (Penalty SOAF), and the joint submissions as to penalty filed on 5 August 2025 (Joint Submissions).

11 There is a recognised public interest in the settlement of proceedings under regulatory regimes in order to avoid lengthy and complex civil litigation. However, the fact that the parties have agreed that a declaration of contravention should be made does not relieve the Court of the obligation to satisfy itself that the making of the declaration is appropriate: Commonwealth v Director, Fair Work Building Industry Inspectorate [2015] HCA 46; 258 CLR 482 (FWBII) (French CJ, Kiefel, Bell, Nettle and Gordon JJ) at [59]. The role of the Court is not merely to “rubber stamp” orders agreed between a regulator and a person who has admitted contravening a statute: FWBII at [30]–[31], [48], [58]. It is necessary for the Court to determine whether the declarations and pecuniary penalty orders are appropriate and should be made: FWBII at [59]. In this respect, the Court is assisted by joint submissions, especially where they are advanced by a specialist regulator able to offer “informed submissions as to the effects of contravention on the industry and the level of penalty necessary to achieve compliance”: FWBII at [60]–[61]; Australian Securities and Investments Commission v Westpac Banking Corporation (Omnibus) [2022] FCA 515 at [100]–[101] (Beach J).

12 For the reasons set out below, I have concluded that having regard to the agreed facts and all the relevant circumstances, with some exceptions, the declarations sought by the parties should be made and that the aggregate agreed penalty of $20 million falls within the permissible range of penalties for the contraventions which RFG has admitted. Before turning to my reasons for so concluding, it is necessary for me at the outset to mention three matters.

13 First, there are other proceedings before the Court that involve RFG (NSD 671/2024) (the Class Action Proceedings). The Class Action Proceedings relate to RFG’s conduct in terminating the franchise agreements of the RAMS Franchisees. I addressed the subject matter of the Class Action Proceedings in my separate reasons for declining an application for leave to intervene in these proceedings made by the lead applicant of those proceedings: see Australian Securities and Investments Commission v RAMS Financial Group Pty Ltd [2025] FCA 1087. As I said in those reasons, the findings made in these proceedings are based on the agreed facts that are before me and do not give rise to any determination of any factual or legal issue as between RFG and the group members in the Class Action Proceedings. It is necessary for me to again reiterate that:

(a) to the extent that RFG has admitted contraventions of ss 47(1)(a), (b) and (e) of the Credit Act, it has done so on the basis that the investigations conducted by RFG and Westpac substantiated allegations that some (but not all) of the RAMS Franchisees engaged in misconduct;

(b) it is based on the fact of RFG and Westpac substantiating allegations of misconduct (as opposed to establishing the underlying fact of that misconduct), that RFG has admitted that it failed in various ways to comply with its obligations under ss 47(1)(a), (b), (d) and (e) of the Credit Act;

(c) ASIC and RFG jointly submit that the obligation under ss 47(1)(a), (b), (d) and (e) of the Credit Act as applicable to RFG (as licensee) may be established by RFG accepting (as it has done here) that its relevant processes and systems were deficient in various ways; and

(d) to the extent that RFG has admitted contraventions of s 31(1) of the Credit Act, those admissions are based on the agreed facts before me and do not preclude those facts being contradicted or challenged in the Class Action Proceedings.

14 Second, it is also necessary for me to reiterate that given the parties tendered the Liability SAFA and the Penalty SOAF, I have not been required to determine any factual question on its merits which is a consequence of s 191 of the Evidence Act 1995 (Cth). As Beach J mentioned in Australian Securities and Investments Commission v Commonwealth Bank of Australia [2020] FCA 790 at [12], “all that I need to be satisfied of is whether the agreed facts on their face provide a sufficient foundation for the declarations and orders sought. The text of s 191(2)(a) makes this plain”.

15 Third, both as a result of certain matters arising in the Class Action Proceedings and because of the nature of some of the sensitive nature of the materials that were before me (such as the personal details of consumers), I was satisfied that it was necessary to make suppression and non-publication orders under s 37AF(1) of the Federal Court of Australia Act 1976 (Cth) (the FCA Act) in order to prevent prejudice to the administration of justice (as specified in s 37AG(1)(a)). I did not make orders in the terms sought by ASIC, which would have suppressed and prevented the publication altogether of certain of the investigation reports as were referenced in hyperlinks to the Liability SAFA. Instead, I have limited the operation of the suppression and non-publication orders to names, identities, locations and personal or information relating to the RAMS Franchises, particular managers, and consumers. My orders under s 37AF(1) will operate for a period of 10 years but are subject to further order.

2. THE RELEVANT PROVISIONS OF THE CREDIT ACT

16 Chapter 2 of the Credit Act contains a licensing regime for those seeking to engage in a “credit activity”, as defined in the Credit Act. There is no dispute between the parties that RFG is, and was at all material times, the holder of ACL number 388065 (RFG’s ACL) and, therefore, a licensee for the purposes of the Credit Act.

17 Section 6 of the Credit Act provides that a person engages in a “credit activity” if the person is a credit provider under a credit contract or carries on a business of providing credit to which the National Credit Code (being Sch 1 of the Credit Act) applies. A person also engages in a “credit activity” if the person provides a “credit service”, which is defined in s 7 as providing “credit assistance” to a consumer or acting as an “intermediary”. Relevantly, s 8 of the Credit Act defines “credit assistance” as follows:

A person provides credit assistance to a consumer if, by dealing directly with the consumer or the consumer’s agent in the course of, as part of, or incidentally to, a business carried on in this jurisdiction by the person or another person, the person:

(a) suggests that the consumer apply for a particular credit contract with a particular credit provider; or

…

(d) assists the consumer to apply for a particular credit contract with a particular credit provider; or

…

18 Section 9 of the Credit Act defines “acts as an intermediary” as follows:

A person acts as an intermediary if, in the course of, as part of, or incidentally to, a business carried on in this jurisdiction by the person or another person, the person:

(a) acts as an intermediary (whether directly or indirectly) between a credit provider and a consumer wholly or partly for the purposes of securing a provision of credit for the consumer under a credit contract for the consumer with the credit provider; or

…

19 Part 2–1 of Ch 2 of the Credit Act prohibits persons from engaging in credit activities and related activities without an ACL. As has been observed, the purpose of these prohibitions is to ensure that credit activities (as defined) are regulated by the Credit Act, and that those engaging in credit activities are subject to the requirements imposed on licensees under the Act: Australian Securities and Investments Commission v Australia and New Zealand Banking Group Limited [2023] FCA 256 (ASIC v ANZ) at [12] (O’Bryan J).

20 Section 31(1) of the Credit Act provides:

31 Prohibition on conducting business with unlicensed persons

Prohibition on conducting business with unlicensed persons

(1) A licensee must not:

(a) engage in a credit activity; and

(b) in the course of engaging in that credit activity, conduct business with another person who is engaging in a credit activity;

if, by engaging in the credit activity, the other person contravenes section 29 (which deals with the requirement to be licensed).

Civil penalty: 5,000 penalty units.

21 As will be apparent from the text, the prohibition in s 31(1) is reliant upon the “other person contravening section 29”. Section 29 of the Credit Act provides as follows:

29 Prohibition on engaging in credit activities without a licence

Prohibition on engaging in credit activities without a licence

(1) A person must not engage in a credit activity if the person does not hold a licence authorising the person to engage in the credit activity.

Civil penalty: 5,000 penalty units.

22 The interaction between ss 29 and 31 has the effect that a licensee is prohibited from engaging in a credit activity by conducting a business with another person who is said to be engaging in a credit activity but where in fact that other person is not licensed to do so. As I will explain later in these reasons, the facts before me establish, and it is admitted, that RFG engaged in conduct in this regard that was prohibited by s 31(1).

23 In ASIC v ANZ, O’Bryan J referred to the observations made about the statutory scheme by Lee J in ASIC v NAB, and stated as follows at [13]–[15]:

As observed by Lee J in Australian Securities and Investments Commission v National Australia Bank Ltd [2020] FCA 1494 (ASIC v NAB) (at [90]), the section seeks to ensure that the overall objectives of the credit regime are not frustrated by licensees engaging with unlicensed persons to subvert its intent.

Section 110(1)(b) of the Credit Act provides that the regulations may exempt a “credit activity” from certain provisions of the Credit Act. Relevantly, reg 25 of the National Consumer Credit Protection Regulations 2010 (Cth) (Credit Regulations) exempts certain credit activities from the requirement in s 29 to hold an Australian credit licence. The exemptions include where a person (a referrer) refers a consumer to a licensee (such as a bank) which is able to provide a particular credit activity to the consumer (such as a home loan). The limits of the activities in which the referrer may engage are prescribed by reg 25. Relevantly, reg 25(2) allows a licensee to receive from an unlicensed person, and the unlicensed person to provide to a licensee, the name and contact details of a consumer and a short description of the purpose for which the consumer may want a provision of credit...

Part 2.2 of Ch 2 of the Credit Act regulated the issue of, and compliance with, Australian credit licences. The key aims of the licensing regime are to regulate credit industry participants and enhance consumer protection: ASIC v NAB at [83]. Further, the licensing regime assisted in ensuring that those who engage in “credit activity” are subject to the responsible lending requirements in Ch 3 of the Credit Act. In ASIC v NAB (at [85]), Lee J observed:

Those requirements aim to protect consumers (both from conduct of lenders and from consumers making poor borrowing decisions) by imposing standards of behaviour on licensees prior to and when entering into a credit contract. The conduct requirements apply only to persons who are licensed under the National Credit Act (that is, holders of an ACL). Relevantly, licensees are required to test the suitability of the proposed credit contract and assess the consumer’s ability to meet their financial obligations under the proposed credit contract. To do so requires direct dealings between the lender and the putative borrower, hence the prohibition on an unlicensed intermediary.

24 Separately, but also relatedly, s 47(1)(a), (b), (d) and (e) of the Credit Act provide as follows:

47 General conduct obligations of licensees

General conduct obligations

(1) A licensee must:

(a) do all things necessary to ensure that the credit activities authorised by the licence are engaged in efficiently, honestly and fairly; and

(b) have in place adequate arrangements to ensure that clients of the licensee are not disadvantaged by any conflict of interest that may arise wholly or partly in relation to credit activities engaged in by the licensee or its representatives; and

…

(d) comply with the credit legislation; and

(e) take reasonable steps to ensure that its representatives comply with the credit legislation; and

…

25 Section 47(4) of the Credit Act provides that:

Civil penalty for non-compliance

(4) The licensee must not contravene paragraph (1)(a), (b), (e), (ea), (f), (g), (h), (i), (j), (k), (l) or (m).

Civil penalty: 5,000 penalty units.

Note: Contravening paragraphs (1)(c) (obligation to comply with conditions on the licence) and (d) (compliance with the credit legislation) has consequences under other provisions.

26 As I explain below, RFG admits that, by reason of the conduct that it has found to be substantiated, it contravened these provisions. It should also be noted, as identified in the notation to s 47(4), that a failure to comply with s 47(1)(d) (being the general obligation to “comply with the credit legislation”) does not itself constitute a contravention of s 47(4).

3. THE AGREED FACTS

27 For completeness, I have attached the Liability SAFA and the Penalty SOAF to these reasons. They are marked respectively as Annexures A and B.

28 For convenience and so that these reasons cohesively explain the relevant factual basis upon which I am satisfied that the orders sought by the parties should be made (with exceptions relating to the alleged contravention of s 47(1)(d) and certain other matters), I have set out below the facts that I considered to be relevant to my determination. In doing so, I have borrowed from the Liability SAFA and the Penalty SOAF where I have considered it appropriate to do so.

3.1 Background to the Franchise Arrangements

29 RFG was acquired by Westpac in 2008. During the Relevant Period, RFG provided credit assistance to consumers:

(a) between at least 1 January 2018 and 15 December 2020:

(i) in relation to RAMS-branded home loans financed by Westpac; and

(ii) in relation to home loans with other lenders on the “RAMS Choice” (a third party aggregator) panel; and

(b) from 16 December 2020, only in relation to RAMS-branded home loans financed by Westpac.

30 RFG operated a franchise model through the RAMS Franchise Network whereby RAMS Franchisees used the RAMS business name to provide credit assistance to consumers in relation to the distribution of RAMS-branded home loans. The RAMS-branded home loans were credit contracts with Westpac and were loans to which the Credit Act applied.

31 There were a total of 73 RAMS Franchisees from time to time within the RAMS Franchise Network during the course of the Relevant Period, though the number of RAMS Franchisees operating at any one time varied.

32 The RAMS Franchisees operated under individual RAMS franchise agreements with RFG (Franchise Agreement), which were amended from time to time and were subject to the Franchising Code of Conduct, as enacted by the Competition and Consumer (Industry Codes—Franchising) Regulation 2014 (Cth).

33 The RAMS Franchisees employed their own staff, including staff involved in submitting loan applications (Loan Writers). The Loan Writers were ACRs of RFG.

3.2 The policies and practices applicable to RFG and RAMS Franchisees

34 During the Relevant Period, Westpac Group and Consumer Division policies (Westpac Policies) applied to RFG's Head Office staff. RAMS Franchisees and their employees (including Loan Writers) were required to comply with the RAMS Franchise Network’s Operations Manual, as amended by RFG from time to time (RAMS Operations Manual) and incorporated by reference into the Franchise Agreement.

35 In addition, RAMS Franchisees were required to comply with policies, guidelines, and procedures as amended by RFG from time to time (RAMS Policies), which relevantly included:

(a) the RAMS Compliance Policy – National Consumer Protection Act 2009 (Cth) Policy;

(b) the RAMS Conflict of Interest Policy and the RAMS Conflicts of Interest Procedure (the RAMS Conflict of Interest Policy);

(c) the RAMS Franchise Behavioural and Ethical Standards Policy;

(d) the RAMS Franchise Third Party Referrer Policy (the RAMS Referrer Policy);

(e) the RAMS Referrer Procedure;

(f) the RAMS Franchise Technology Code of Use Policy;

(g) the RAMS Customer Identification Procedure;

(h) the RAMS Privacy Operating Guidelines;

(i) the RAMS Lending Guidelines;

(j) the RAMS Disclosure Document 2014 Code;

(k) the RAMS Franchise Sales Procedure; and

(l) the RAMS Customer Identification Policy.

3.3 RAMS authorised credit representatives (ACRs)

36 Prior to, and during, the Relevant Period, RFG appointed RAMS Franchisees, and certain employees of the RAMS Franchisees, as its ACRs, within the meaning of s 64 of the Credit Act (RAMS ACRs). These appointments were made pursuant to the Credit Act and documented in written Corporate Credit Representative Agreements with corporate RAMS Franchisees and written Credit Representative Agreements with non-corporate RAMS Franchisees and employees of RAMS Franchisees (collectively, the Credit Representative Agreements). Pursuant to the Credit Representative Agreements, RFG appointed RAMS ACRs as:

(a) its credit representatives under the Credit Act, and authorised them to engage in credit activities on its behalf; and

(b) sub-agents of Westpac to carry out identification procedures on Westpac’s behalf for the purposes of the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 (Cth) and the Verification of Identity Regulations (being any requirements to identify a person in connection with the granting of a mortgage).

37 The Credit Representative Agreements authorised RAMS ACRs to carry out, relevantly, the following activities:

(a) to follow up on leads provided by RFG, the RAMS Franchisee or self-generated leads;

(b) to provide a credit guide to a customer in accordance with RFG’s instructions;

(c) to conduct interviews to make reasonable inquiries about a customer’s financial situation, and their requirements and objectives, using tools provided by RFG;

(d) to take reasonable steps to verify a customer’s financial situation in accordance with RAMS Policies;

(e) to make a preliminary assessment about whether a facility or variation to an existing facility is not unsuitable for a customer, using tools provided by RFG; and

(f) to assist a customer to complete an application or variation application for facilities that are determined to be not unsuitable by the preliminary assessment, using tools provided by RFG.

38 The parties agreed, and I am satisfied that, that when carrying out the activities described in the preceding paragraph, RAMS ACRs engaged in a “credit activity” for the purposes of the Credit Act. I am also satisfied that RAMS ACRs were, pursuant to subparagraph (a)(iii) of the definition of “representatives” in s 5(1) of the Credit Act, representatives of RFG.

39 RFG required RAMS ACRs to:

(a) complete initial training to satisfy training standards as determined by RFG prior to acting under their ACR appointment;

(b) complete ongoing training, as specified by RFG and set out in the RAMS Operations Manual;

(c) comply, relevantly, with the RAMS Policies, and to use the information technology and other operational systems provided to them by RFG, including RFG’s systems infrastructure;

(d) deal only with accredited referral partners in accordance with the RAMS Operations Manual and the RAMS Referrer Policy; and

(e) disclose details of any actual or perceived conflicts of interest, in particular where the RAMS ACR had a personal interest which could be inconsistent with the interests of RFG or its customers, such that it could influence or compromise, or appear to influence or compromise, the RAMS ACR's duties and responsibilities to RFG or its customer, in accordance with the RAMS Operations Manual and the RAMS Conflict of Interest Policy.

3.4 RFG’s requirements relating to Accredited Referrers

40 During the Relevant Period, RAMS Franchisees and their employees received referrals of prospective customers from third parties (referrals).

41 RAMS Franchisees and their employees were only permitted by RFG to accept referrals from third parties who were, with limited exceptions, referrers who had been accredited (Accredited Referrers) in accordance with the requirements of the RAMS Operations Manual, the RAMS Referrer Policy and the “RAMS Franchise Referrer Procedure” (the RAMS Accreditation Process). Throughout the Relevant Period, RAMS Franchisees received induction training about the policies and procedures in place that applied to the use of Accredited Referrers, and their associated responsibilities under the RAMS Accreditation Process.

42 Pursuant to the RAMS Accreditation Process, only the following three types of referrers could be accredited:

(a) an entity that held an ACL under Part 2–2 of the Credit Act or who was an ACR of an ACL holder under Part 2–3 of the Credit Act, and who conducted a referral business;

(b) an entity that was exempt under the National Consumer Credit Protection Regulations 2010 (Cth) and conducted a business in which providing referrals was incidental to its main activities (Exempt Referrer); or

(c) a Westpac-approved broker that held an ACL or was an ACR (Westpac-Approved Broker).

3.5 RFG’s process for accrediting referrers

43 In order for a prospective referrer to become accredited under the RAMS Accreditation Process, a RAMS Franchisee or employee was required to:

(a) gather information about the identity of the prospective referrer;

(b) gather information to confirm whether the prospective referrer held a current ACL, was a current ACR of an ACL-holder, was a Westpac-Approved Broker, or was an Exempt Referrer;

(c) conduct searches in relation to the prospective referrer, including a company search (where relevant) and searches to determine whether the prospective referrer had been banned or disqualified by ASIC; and

(d) undertake any other steps set out in the RAMS Operations Manual, RAMS Referrer Policy and RAMS Franchise Referrer Procedure in relation to the prospective referrer.

44 Next, the RAMS Franchisee or employee was required to submit the accreditation request to RFG for determination. Westpac would then perform additional checks on the prospective referrer and related individuals prior to determination (including ABN and ASIC searches, verification of the prospective referrer’s business address, and checks against Westpac’s internal databases, which included the names of individuals with known misconduct, financial crime links, or involvement in fraud).

45 A team within RFG called “RAMS Franchise Field Compliance” would notify the relevant RAMS Franchisee of the outcome of the accreditation request and, if approved, a “Referrer Agreement” was required to be entered into between the relevant RAMS Franchisee and the prospective referrer. If accredited, and subject to the type of referrer (eg, an Exempt Referrer or Westpac-Approved Broker), Accredited Referrers would:

(a) provide consumer details, including the consumer’s name, contact details, and a short description of their purpose for seeking the provision of credit, if known, to the RAMS Franchisee;

(b) conduct an initial lending conversation with the consumer; and/or

(c) provide completed home loan application forms and supporting documents to the RAMS Franchisee.

46 In the event a consumer who wished to apply for a RAMS-branded home loan was referred to a RAMS Franchisee by an Accredited Referrer, the RAMS Franchisee or RAMS ACR was required to inform RFG that the loan application had been so referred, including by providing details of the Accredited Referrer’s unique referrer identifier code in the relevant electronic lodgement system (known as Symmetry) as part of the home loan application process.

3.6 Loan application process

47 During the Relevant Period, consumers approached RAMS Franchisees:

(a) through a central RAMS phone number for consumer enquiries, being 13RAMS (137 267), which referred consumers to the RAMS Franchisees;

(b) through Accredited Referrers; or

(c) by directly approaching a RAMS Franchisee or a Loan Writer.

48 Having been approached by consumers, RAMS Franchisees or their Loan Writers obtained information and documents from the consumers for the purpose of submitting loan applications to RFG for RAMS-branded home loans.

49 Prior to lodging home loan applications on behalf of consumers, during the Relevant Period RAMS Franchisees and their Loan Writers were required:

(a) pursuant to the Franchise Agreement, to ensure the consumer’s information was accurately captured, and that the information was a true and accurate reflection of the consumer’s circumstances;

(b) pursuant to the Credit Representative Agreement, to take reasonable steps to correctly collate and convey any information provided to RFG or any lender (including information in relation to any application), and not provide any information that the RAMS Franchisee or its officers, employees, agents or contractors knows (or should know) is false, misleading or forged;

(c) pursuant to the RAMS Policies:

(i) to identify the consumer;

(ii) to assess whether the consumer was eligible for a RAMS-branded home loan, in accordance with the RAMS Lending Guidelines, as amended from time to time;

(iii) to perform a preliminary suitability assessment about the consumer, in the course of which they were required to ascertain the consumer’s financial situation by:

(A) identifying and recording accurately the consumer’s requirements and objectives and ensuring any recommended loan met their requirements;

(B) collecting accurate, relevant and complete information about the consumer, including their financial information; and

(C) checking, verifying and assessing the consumer's information, including financial information, carefully to ensure RFG had a complete picture of the consumer’s financial situation, including income, expense, employment status, and exit strategy should the loan term exceed the consumer’s expected retirement age; and

(iv) in the course of performing the suitability assessment, to:

(A) obtain supporting documents to confirm the consumer’s financial and personal situation as described and set out in the RAMS Lending Guidelines, as amended from time to time and the Operations Manual including documents required for Pay As You Go employees, loan statements, documents required for self-employed consumers and documents to substantiate the consumer’s funds to complete the transaction such as a deposit;

(B) review the consumer’s supporting documentation in accordance with the RAMS Lending Guidelines;

(C) validate the consumer’s declared liabilities (and were strongly recommended to obtain a report from a credit reporting body);

(D) optionally obtain valuations;

(E) assess the capacity of the consumer to service the loan; and

(v) before submitting a loan application, check all the consumer’s information carefully to ensure RFG had a complete picture of the consumer's financial position.

50 Once the above steps were complete, the RAMS Franchisee or Loan Writer was required to submit the loan application to a team comprised of Westpac employees called “RAMS Credit & Loan Operations” (RAMS Credit), which, on behalf of Westpac, processed applications for approved products from receipt of the application until they instructed solicitors to prepare loan documents for settlement.

51 Upon receipt of a loan application, RAMS Credit first undertook a “triage” process (which throughout the Relevant Period, was undertaken by a team called “RAMS Home Ownership Services”) to ensure that the loan application was in a state ready for assessment by a RAMS Credit Manager. As part of the “triage” process, RAMS Credit was required to:

(a) ensure that all supporting documents were provided in accordance with the RAMS Policies;

(b) assess whether there was any missing information or documents;

(c) verify information in the loan application by cross-checking it against supporting documents;

(d) undertake “Requirements and Objectives checks”, including to ensure that the loan application included a full and complete preliminary assessment; and

(e) use triage “checklists” to perform their functions.

52 If, following the “triage” process, the loan application was determined to be in a state ready for assessment by a RAMS Credit Manager, it was allocated to a RAMS Credit Manager within RAMS Credit to conduct, on behalf of the credit provider, a substantive assessment of whether the credit contract would be unsuitable for the customer.

53 The assessment by a RAMS Credit Manager involved:

(a) reviewing the loan application and ensuring it complied with policy, verifying the income documents, and checking for red flag indicators that could indicate fraud;

(b) considering the comprehensive credit report information as well as security information contained within the valuation report;

(c) reviewing financial statements that could indicate non-disclosure of information;

(d) performing an unsuitability assessment on behalf of Westpac;

(e) completing a “credit memorandum” which referenced the credit calculations, as well as completing servicing calculations; and

(f) sending the loan to the Settlement Team for settlement if approved.

54 On some occasions, as an additional step within the process, the loan application was referred to the RAMS Risk and Fraud Operations team (RAMS Risk and Fraud), including where there were anomalies or concerns about information or consumers in respect of an application.

55 Once a RAMS Credit Manager assessed the application, the RAMS Credit Manager, on behalf of Westpac as the credit provider, would approve the application conditionally, approve the application unconditionally, defer the application for the purpose of obtaining further information, or decline the application.

56 Since at least June 2019, RFG also conducted post-loan settlement “Welcome Calls” with consumers, in respect of which:

(a) the calls were outsourced to a contact centre at Unisys Mortgage Processing (UMP);

(b) the callers were required to collect information from consumers;

(c) the information collected permitted UMP to determine whether there were anomalies in the manner in which RAMS ACRs discharged their obligations under the RAMS’ ACL (including whether the consumer had been referred from a third party other than an Accredited Referrer); and

(d) in the event of an anomaly, UMP was required to refer the Welcome Calls to RAMS Compliance for further review.

3.7 Investigations Process

57 During the Relevant Period, misconduct concerns relating to a RAMS Franchise could be investigated by one RFG or by:

(a) a group within Westpac called the Secured Lending Taskforce (SLTF), which could have received the request to investigate from either RFG or Westpac; or

(b) a group within Westpac called Group Investigations, which could have received the request to investigate from either RFG or Westpac.

58 Where SLTF undertook an investigation into misconduct concerns relating to a RAMS Franchise, it provided the findings of that investigation to relevant groups, which included Group Investigations. Those findings could be incorporated by Group Investigations (also referred to as GI) into its investigation.

59 From around mid-2022, having regard to information sharing restrictions imposed by relevant laws, RFG was provided with only a summary of SLTF's findings, and only in instances where termination and/or revocation of the Franchise Agreement and/or Credit Representative Agreement was recommended by Westpac.

60 Where GI undertook an investigation into misconduct concerns relating to a RAMS Franchise it would, on completion of its investigation, prepare a report which included its findings about whether the misconduct was “substantiated” (GI Report).

61 Of the 35 GI Reports that informed Schedules 1 and 2 of the Liability SAFA, 24 GI Reports were addressed, or copied, to RFG’s Managing Director. In relation to the remaining GI Reports, all were addressed, or copied, to either the Head of Risk and Compliance and/or in-house lawyers supporting the RAMS business.

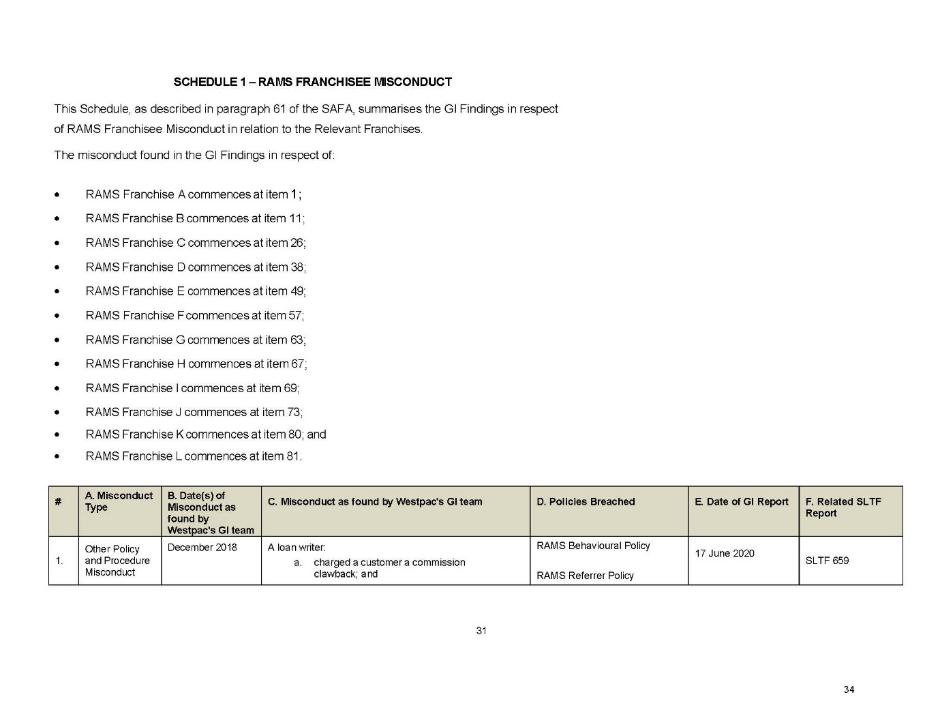

62 During the Relevant Period, RFG used Westpac’s risk and compliance system, known as “JUNO”, to record and manage risk and compliance issues.

3.8 The findings of misconduct within the RAMS Franchise Network

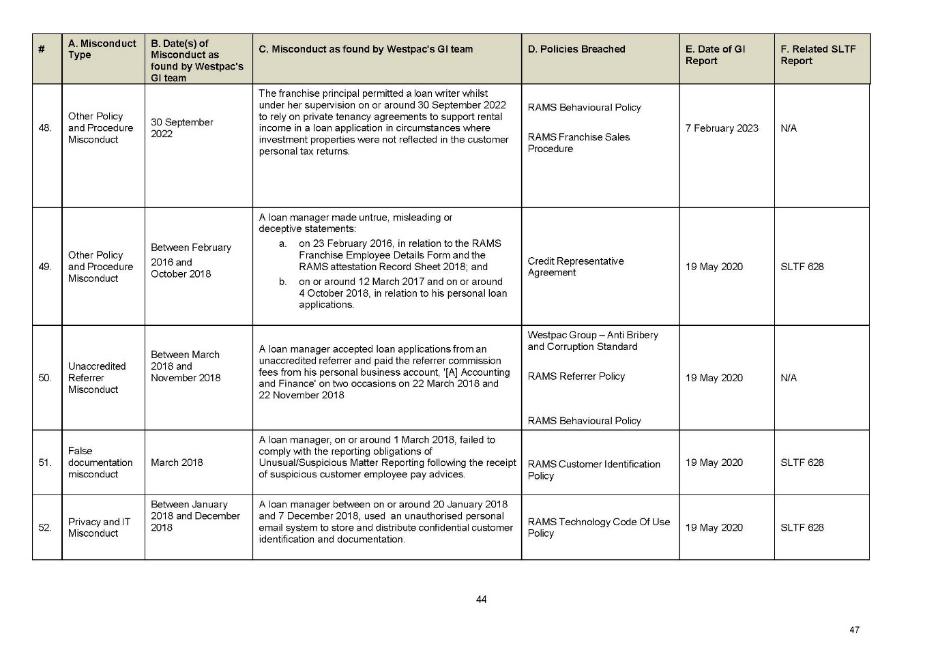

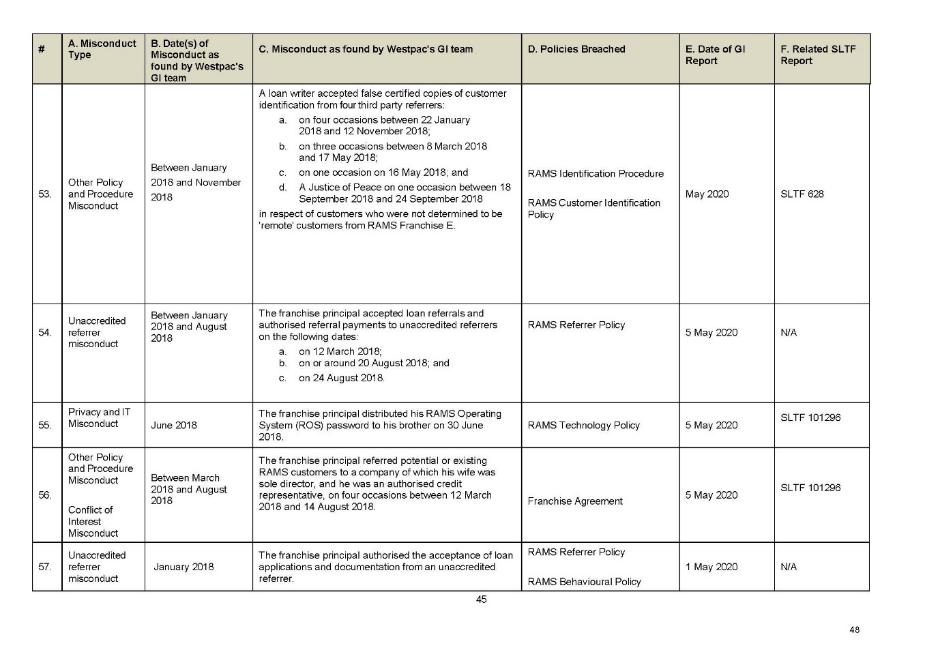

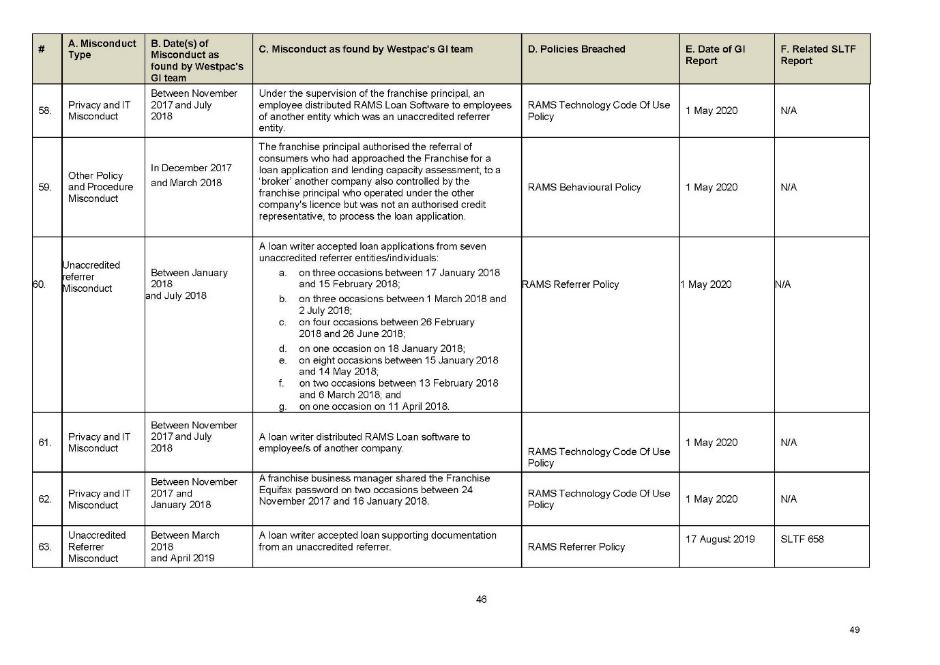

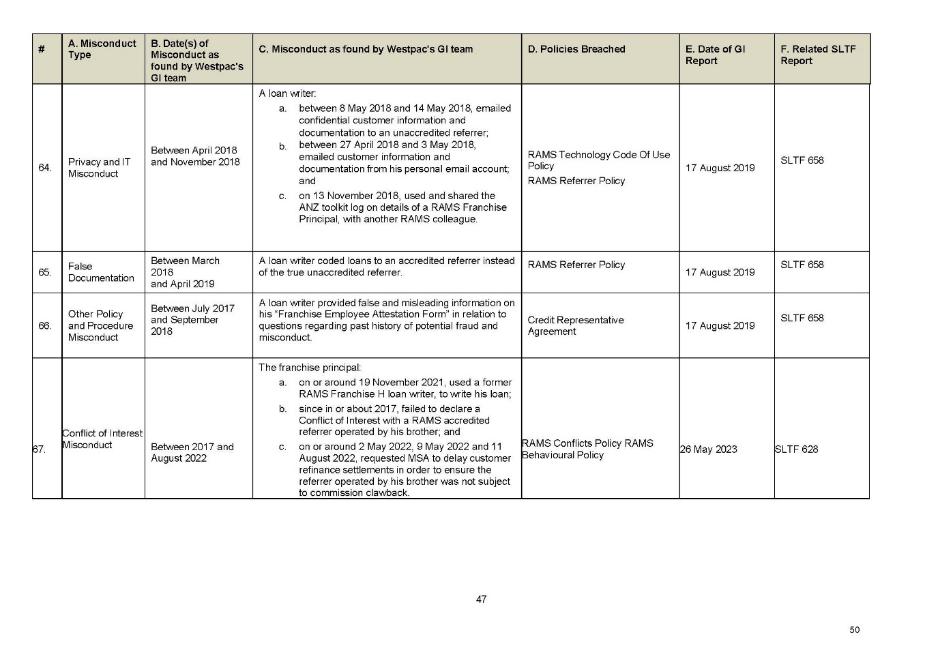

63 During the Relevant Period, Westpac and RFG undertook investigations, including through GI and SLTF, into allegations of misconduct relating to the RAMS Franchises.

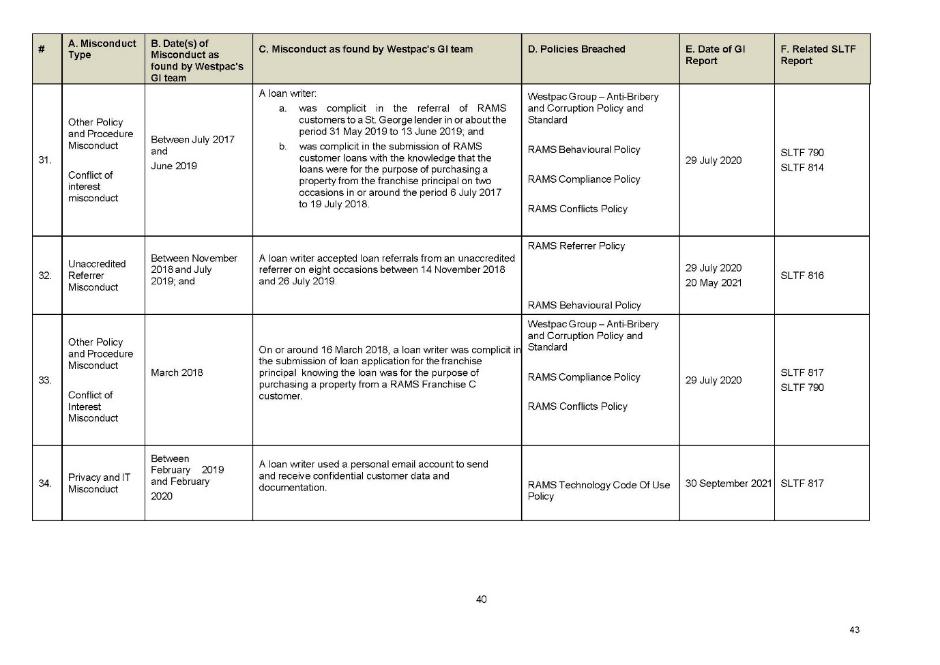

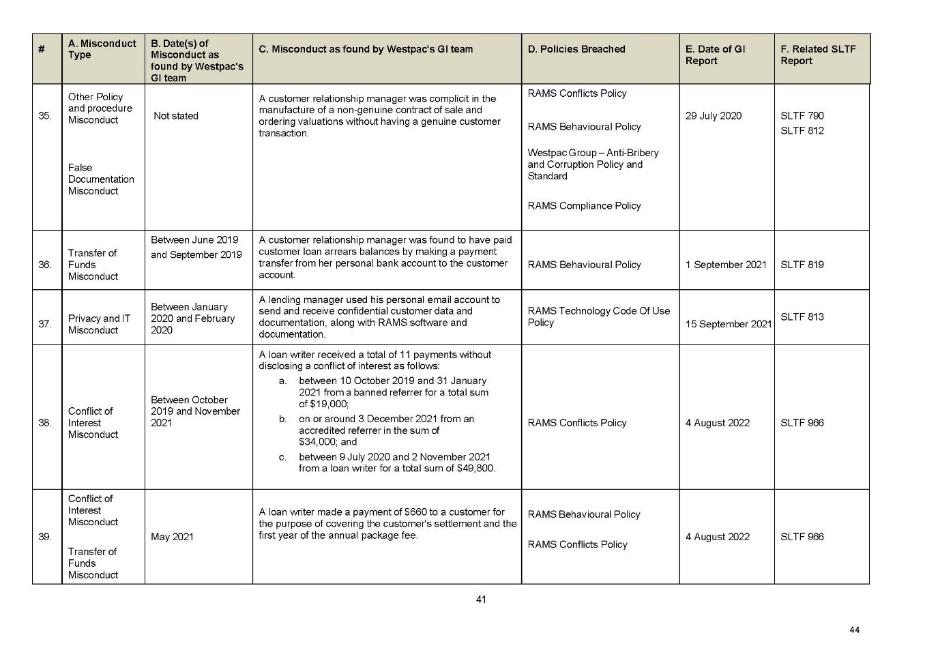

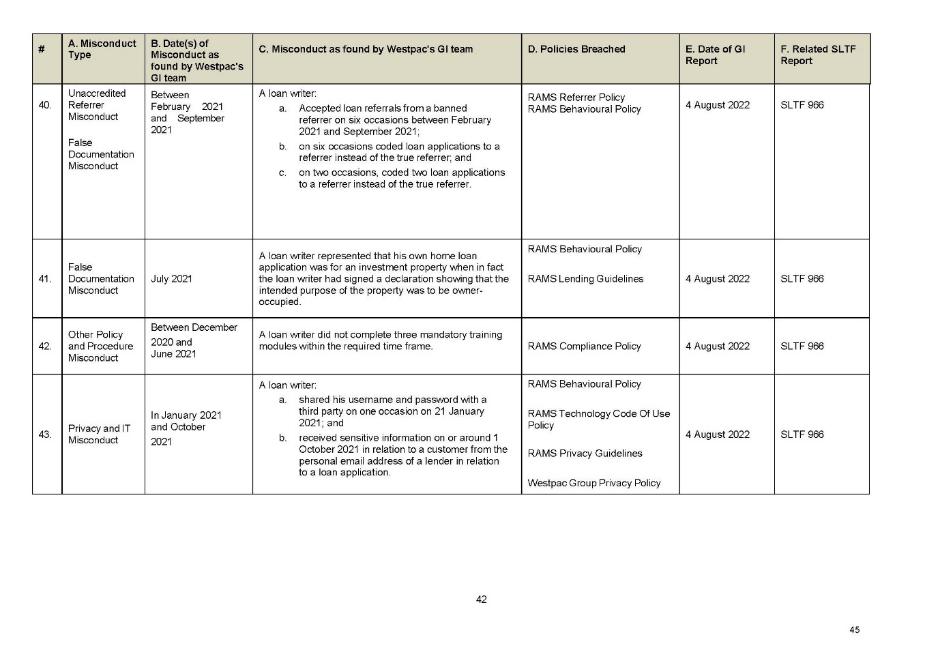

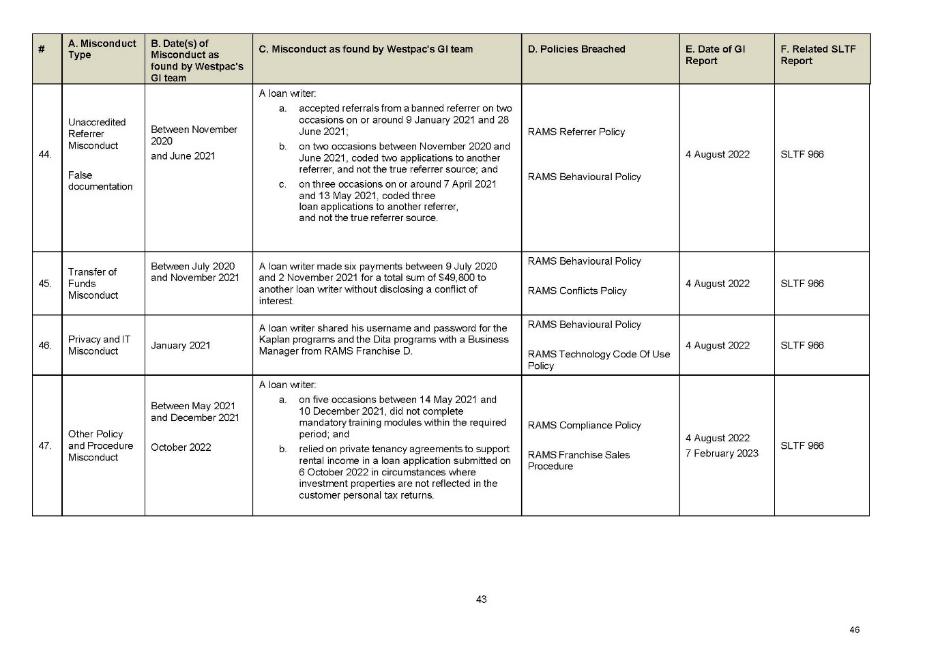

64 The nature of the alleged misconduct investigated by GI and SLTF varied widely. Schedules 1 and 2 to the Liability SAFA summarise substantiated findings of misconduct made by GI (GI Findings). The GI Findings:

(a) relate to conduct that occurred over the course of a 5-year period from at least 1 January 2018 to April 2023;

(b) involve staff, including RAMS Franchisees and Loan Writers, at 12 RAMS Franchises (being RAMS Franchises A, B, C, D, E, F, G, H, I, J, K, and L) (Relevant Franchises); and

(c) are set out in 35 GI Reports, the first of which is dated 17 August 2019 (RAMS Franchise G) and the last of which is dated 18 August 2023 (RAMS Franchise J).

65 RFG was made aware of the GI Findings, including through the provision of GI reports to its Managing Director, Head of Risk and Compliance, and/or in-house lawyers supporting the RAMS business.

66 Schedule 1 of the Liability SAFA summarises the GI Findings in relation to the Relevant Franchises. Specifically:

(a) the first column sets out the item number;

(b) column A identifies the category of misconduct with reference to one or more of the categories of misconduct as discussed below;

(c) column B identifies the time period over which the misconduct occurred;

(d) column C summarises the particular misconduct in respect of each item number;

(e) column D identifies the RAMS or Westpac Policies that GI found had been breached by virtue of the misconduct;

(f) column E identifies the date of the relevant GI Report; and

(g) column F identifies whether there was a related SLTF Report, and the number of that Report.

67 Schedule 2 of the Liability SAFA summarises the GI Findings of the “Unlicensed Referrer Misconduct” (see [71] below) in relation to the Relevant Franchises that involved contraventions of s 31(1) of the Credit Act. Specifically:

(a) column A identifies the item number in Schedule 1 that relevantly deals with Unaccredited Referrer Misconduct;

(b) column B identifies the Relevant Franchise;

(c) column C identifies the name of the Relevant Franchise staff member that accepted the referral; and

(d) column D identifies the number of contraventions of s 31(1) of the Credit Act referrable to the item number.

68 In addition, I have received a further revised version of Schedule 2 in an Affidavit of Ms Kristina Andrea Belci affirmed 20 October 2025 at Annexure KAB-01. This was a non-anonymised version of Schedule 2 of the Liability SAFA. As I have addressed above, I have made suppression and non-publication orders in respect of the content that reveals identifying information.

3.9 The categories of misconduct

69 The misconduct which is the subject of the GI Reports is categorised for the purposes of Column A of Schedule 1 of the Liability SAFA as follows:

(a) Unaccredited Referrer Misconduct;

(b) Conflict of Interest Misconduct;

(c) False Documentation Misconduct;

(d) Transfer of Funds Misconduct;

(e) Privacy and IT Misconduct; and

(f) Other Policy and Procedure Misconduct.

70 For present purposes, it is convenient to provide a brief summary of each category of misconduct.

3.9.1 Unaccredited Referrer Misconduct

71 RFG and Westpac found substantiated instances of some RAMS Franchises accepting referrals from unaccredited referrers. In those instances, RFG and Westpac were satisfied that the relevant RAMS Franchises breached the RAMS Referrer Policy (Unaccredited Referrer Misconduct): see Schedule 1 of the Liability SAFA at rows 1, 2, 5, 6, 8, 9, 10, 11, 13, 16, 23, 28, 32, 40, 44, 50, 54, 57, 60, 63,64, 65, 69, 70, 71, 72, and 83.

3.9.2 Unlicensed Referrer Misconduct

72 Where representatives at the Relevant Franchises accepted referrals from unaccredited referrers who did not hold an ACL under Part 2–2 of the Credit Act or who were not an authorised representative of an ACL holder under Part 2–3 of the Credit Act at the time of the referral (Unlicensed Referrer Misconduct), RFG contravened s 31(1) of the Credit Act, as addressed in further detail below and in Schedule 2 of the Liability SAFA.

3.9.3 Conflicts of Interest Misconduct

73 During the Relevant Period, the types of conduct identified by GI in respect of particular Relevant Franchises included that they were found by RFG and Westpac to have:

(a) engaged in credit activities where there was a conflict of interest or relationships between representatives at the Relevant Franchises and other commercial businesses which provided services or referrals to the Relevant Franchises as described in Schedule 1 of the Liability SAFA at rows 22, 26, 27, 31, 33, 38, 39, 56, 67, and 81, including by:

(i) while acting as a principal at a Relevant Franchise, being listed as the sole signatory on the bank accounts of a company which referred loan applications to the Relevant Franchise and personally receiving commissions from those referrals;

(ii) personally, receiving monies from referrers; and

(iii) while acting as a principal at a Relevant Franchise, failing to declare a conflict of interest with an Accredited Referrer operated by that principal’s brother; and

(b) thereby, breached the RAMS Conflict of Interest Policy.

3.9.4 False Documentation Misconduct

74 During the Relevant Period, the types of conduct identified by GI in respect of particular Relevant Franchises included that they were found by RFG and Westpac to have:

(a) submitted loan applications prepared by representatives at the Relevant Franchises which included, likely in order to increase the prospects of the loan application being approved, false information and/or documents in support of the loan applications in the manner identified in Schedule 1 of the Liability SAFA at rows 14, 25, 35, 40, 41, 44, 51, 65, 77, and 83, including by:

(i) altering the declared expenses in loan applications to enable the loan to meet serviceability requirements;

(ii) representing that their own home loan application was for an investment property when in fact it was to be owner-occupied; and

(iii) coding loan applications to a party other than the true referrer; and

(b) thereby, breached the policies described in the corresponding column D of those rows in Schedule 1.

3.9.5 Transfer of Funds Misconduct

75 During the Relevant Period, the types of conduct identified by GI in respect of particular Relevant Franchises included that they were found by RFG and Westpac to have:

(a) Transferred funds in relation to loans in the manner identified in Schedule 1 of the Liability SAFA at rows 29, 36, 39, and 45, including by:

(i) facilitating the payment of customer arrears payments with the result that the Relevant Franchise continued to receive commission payments; and

(ii) making a payment to a customer for the purpose of satisfying the customer’s settlement fees and the first year of the annual package fee; and

(b) thereby, breached the policies described in the corresponding coplumn D of those rows in Schedule 1.

3.9.6 Privacy and IT Misconduct

76 During the Relevant Period, the types of conduct identified by GI in respect of particular Relevant Franchises included that they were found by RFG and Westpac to have:

(a) misused information or IT systems in the manner described in Schedule 1 of the Liability SAFA at rows 3, 4, 7, 15, 17, 19, 20, 21, 24, 30, 34, 37, 43, 46, 52, 55, 58, 61, 62, 64, 68, 73, 74, 79, 80, 82 and 84, including by:

(i) distributing RFG software to unaccredited referrers or persons not employed by RFG;

(ii) using unauthorised personal email accounts to store and distribute confidential customer identification and documentation; and

(iii) sharing a username and password with a third party; and

(b) thereby, breached the policies described in the corresponding column D of those rows in Schedule 1.

3.9.7 Other Policy and Procedure Misconduct

77 During the Relevant Period, the types of conduct identified by GI in respect of particular Relevant Franchises included that they were found by RFG and Westpac to have:

(a) breached other policies and procedures, or guidelines, not otherwise described in one of the categories described above, in the manner described in Schedule 1 of the Liability SAFA at rows 1, 2, 9, 12, 18, 26, 29, 31, 33, 35, 42, 47, 48, 49, 53, 56, 59, 66, 73, 75, 76, 78, 80, 84, and 85, including by:

(i) establishing proxy referrers knowing them to be employees of banned referrer companies;

(ii) failing to identify multiple anomalies in supporting documentation for loan applications at a level expected of a prudent loan writer; and

(iii) failing to identify customers themselves (but rather accepting false certified copies of customer identification from referrers); and

(b) thereby, breached the policies described in the corresponding column D of those rows in Schedule 1.

3.10 Franchisee Oversight Controls Review and Project Guardian

78 In response to concerns identified with the conduct of a particular RAMS Franchise, Westpac:

(a) on 5 October 2022, commenced a review into RFG’s Franchisee Oversight Controls (Franchisee Oversight Controls Review), to assess the effectiveness of the control environment within RAMS, specifically focussed on the oversight of certain franchisee conduct, being conflicts of interest, the use of unaccredited referrers, and the misrepresentation of loan application information; and

(b) on 25 November 2022, commenced “Project Guardian”, the purpose of which was to investigate and respond to possible misconduct by other franchisees within the RAMS Franchise Network and uplift RAMS controls to ensure that similar issues would be avoided in the future.

79 Project Guardian ran over the course of approximately 22 months at a cost of approximately $46 million. Project Guardian included monitoring and targeted reviews of all RAMS Franchisees, reviews of historical and new loan applications referred by RAMS Franchisees, the engagement of an external expert to conduct an independent review of the RAMS control environment, and the implementation of associated control uplifts.

80 Westpac and RFG committed over 200 employees and external consultants to Project Guardian. In the course of this project:

(a) RFG enhanced relevant policies, procedures and controls, developed and updated training modules, and completed an enhancement of the RFG risk profile and supervision and monitoring framework; and

(b) there was an increase in the number of investigations conducted by GI and SLTF into RAMS Franchisees as evidenced in Schedule 1 of the Liability SAFA. These investigations were conducted in tandem with RFG's uplift of its policies, procedures, and controls, and resulted in the termination of Franchise Agreements with RAMS Franchisees and Credit Representative Agreements with RAMS ACRs.

81 As part of Project Guardian, Westpac also undertook a broad review exercise which involved a review of the entire portfolio of RAMS loans settled in the period December 2016 to December 2022.

82 The process resulted in Westpac remediating 48 customer loans to a value of $7,567,418. In determining whether a loan required remediation, Westpac did not require evidence of any actual misconduct by RAMS Franchisees (that is, customers were remediated even if it could not be established that any financial harm they may have suffered was the result of conduct of RAMS ACRs).

83 The loans requiring remediation represented approximately 0.05% of all loans originated through the RAMS Franchise Network between December 2016 and December 2022.

84 The total remediation value represented 0.025% of the RAMS total portfolio value as at September 2024 and 0.0009% of the Westpac total portfolio value as at September 2024.

3.11 Other audits and reviews

85 On 13 December 2022, the Executive Manager (Credit Quality and Regulatory Change) at Westpac delivered a report on the findings of the Franchisee Oversight Controls Review to the Managing Director (Mortgages).

86 On 14 April 2023, Westpac’s Group Audit team finalised its “RAMS Franchisee Management and Oversight Audit Report” which reported on the findings of its audit.

87 On 15 September 2023, the Westpac Board Risk Committee received a Memorandum reporting to it on Westpac management’s analysis of “Root Causes relating to RAMS Matters”, in which four root causes were identified as contributing to the deficiencies in RFG, being:

(a) an autonomous business with a unique risk profile;

(b) an immature risk culture and capability within RFG;

(c) a deficient control environment and controls testing; and

(d) insufficient oversight of a non-standard end-to-end business unit.

3.12 Closing the RAMS business

88 Following commencement of Project Guardian, having regard to the findings of the investigations conducted by GI and SLTF into RAMS Franchisees and their employees, RFG terminated Credit Representative Agreements with ACRs who had been the subject of substantiated findings of misconduct.

89 RFG wound down the RAMS Franchise Network in its entirety, effective 6 August 2024, which included the termination of all remaining Franchise Agreements and the termination of the remaining Credit Representative Agreements.

3.13 ASIC's investigation

90 Commencing in September 2022, RFG and Westpac reported to ASIC on multiple occasions potential breaches of ss 31(1) and 47 of the Credit Act pursuant to the requirement in s 50B of the Credit Act.

91 ASIC commenced its investigation into the conduct the subject of these reports in mid-2023.

92 RFG fully cooperated with ASIC in its investigation, and has engaged constructively with ASIC in relation to several voluntary requests for information and documents.

4. THE CONTRAVENTIONS

93 Based on the agreed facts, I am satisfied that RFG contravened the Credit Act for the reasons set out below.

4.1 Contraventions of s 31(1) of the Credit Act

94 As set out at [22] above, the interaction between ss 29 and 31 has the effect that a licensee, in the course of engaging in a credit activity, is prohibited from engaging in that credit activity by conducting a business with another person where that other person is not licensed to engage in a credit activity.

95 Relevantly, as applied to the circumstances here, the question that arises is whether on the agreed facts, RFG, during the course of being engaged in a credit activity, conducted business with another person who was engaging in a credit activity without a licence authorising that activity.

96 The agreed and admitted facts demonstrate that there were 84 instances where consumers were referred to RAMS Franchisees by third parties who were not licensed to provide credit activity. Those third parties included accountants, tax agents, and other types of advisors. The fact that those persons were not licensed at the relevant times is established by evidence adduced by ASIC which establishes that:

(a) ASIC maintains a database of the names and details of all individuals who hold, or held, an ACL;

(b) ASIC also maintains a database of the names and details of all individuals who are, or have been, authorised credit representatives of an ACL holder under Part 2–3 of the Credit Act;

(c) subject to one qualification, a search of these databases disclosed that none of the entities or persons identified in a suppressed and redacted version of Schedule 2 of the Liability SAFA are recorded as being the holders of an ACL or an authorised representative of an ACL holder; and

(d) in one instance, although the corporate entity was recorded as an authorised credit representative of a different ACL holder, there is no evidence that the individual person who provided the referral to the relevant RFG Franchisee was an authorised credit representative of any ACL holder or sub-authorised by the relevant corporate entity to provide credit services.

97 I am satisfied that in each of these instances RFG was dealing with a person who was not licensed to provide a credit activity.

98 As to whether in each such instance, the other person (being the referrer) was engaged in a “credit activity”, the parties submitted that the broad definitions of “credit activity” and “credit assistance” in ss 7 and 8 of the Credit Act encompassed such activities. I am satisfied that by referring a consumer to a RAMS Franchisee for the purpose of obtaining a home loan, the “other person” was at the very least (in the course of, or incidentally, to a business carried on by that person) providing “credit assistance” to that consumer as provided for in s 8 of the Credit Act. In each such instance, the “other person” had in one or another way advised or suggested that the relevant consumer apply for or obtain a home loan through the relevant RAMS Franchisee.

99 Accordingly, I am satisfied that RFG contravened s 31(1) on each of the 84 occasions identified in Schedule 2 of the Liability SAFA.

4.2 Contraventions of s 47(1)(a) of the Credit Act

100 As set out above, s 47(1)(a) required RFG to “do all things necessary to ensure that the credit activities authorised by its licence were” engaged in “efficiently, honestly and fairly”.

101 The meaning of the phrase “efficiently, honestly and fairly” in s 47(1)(a) is informed by cases on s 912A(1)(a) of the Corporations Act 2001 (Cth) (the Corporations Act), which uses the same expression: Australian Securities Investments Commission v Membo Finance Pty Ltd (No 2) [2023] FCA 126 at [37] (Yates J). The parties in their joint submissions provided a useful summary of the relevant propositions to be drawn from those cases, from which I have borrowed as they are both accurate and an efficient summation of those propositions.

102 The authorities in relation to the obligation in s 912A(1)(a) of the Corporations Act (“to do all things necessary to ensure that the financial services covered by the licence are provided efficiently, honestly and fairly”) include the following propositions (per Foster J in Australian Securities and Investments Commission v Camelot Derivatives Pty Ltd (in liq) [2012] FCA 414; 88 ACSR 206 at [69] (with citations omitted)):

(a) the words “efficiently, honestly and fairly” must be read as a compendious expression, meaning a person who goes about their duties efficiently having regard to the dictates of honesty and fairness, honestly having regard to the dictates of efficiency and fairness, and fairly having regard to the dictates of efficiency and honesty;

(b) the words “efficiently, honestly and fairly” connote a requirement of competence in providing advice and in complying with relevant statutory obligations. They also connote an element not just of even handedness in dealing with clients but a less readily defined concept of sound ethical values and judgment in matters relevant to a client’s affairs;

(c) the word “efficient” refers to a person who performs his duties efficiently, meaning the person is adequate in performance, produces the desired effect and is capable, competent and adequate. Inefficiency may be established by demonstrating that the performance of a licensee’s functions falls short of the reasonable standard of performance by a dealer that the public is entitled to expect;

(d) it is not necessary to establish dishonesty in the criminal sense. The word “honestly” may comprehend conduct which is not criminal but which is morally wrong in the commercial sense; and

(e) the word “honestly” when used in conjunction with the word “fairly” tends to give the flavour of a person who not only is not dishonest, but also a person who is ethically sound.

103 A contravention of the “efficiently, honestly and fairly” standard does not require a contravention or breach of a separately existing legal duty or obligation, whether statutory, fiduciary, common law or otherwise given that the statutory standard itself is the source of the obligation: Australian Securities and Investments Commission v AGM Markets Pty Ltd (in liq) (No 3) [2020] FCA 208; 275 FCR 57 at [512] (Beach J). Section 912A(1)(a) of the Corporations Act has been described as “a statutory norm to be read conformably with s 760A and the other provisions of the Corporations Act and the ASIC Act”: AGM Markets at [519] (Beach J).

104 The word “ensure” as contained in the statutory text imports a forward-looking element into the obligation. It is necessary not only to act efficiently, honestly and fairly from day to day, but to take steps to guard against lapses from that standard by employees or representatives: Australian Securities and Investments Commission v Commonwealth Bank of Australia [2022] FCA 1422 at [146] (Downes J), citing Australian Securities and Investments Commission v AMP Financial Planning Pty Ltd (No 2) [2020] FCA 69; 377 ALR 55 at [105] (Lee J), cited with approval in Australian Securities and Investments Commission v Ferratum Australia Pty Limited (in liq) [2023] FCA 1043 at [49] (Kennett J) (ASIC v Ferratum).

105 Although the subjective intention of the alleged contravener may clearly be relevant, the standard may be unintentionally breached. Contravention is generally a matter for objective analysis: Australian Securities and Investments Commission v National Australia Bank Ltd [2022] FCA 1324 at [352] (Derrington J) cited with approval in ASIC v Ferratum at [49] (Kennett J).

106 As applicable to RFG, and based on the agreed facts, I am satisfied that in the operation of the RAMS Franchise Network, RFG was required to take particular steps to comply with s 47(1)(a) of the Credit Act. Although those steps themselves were not prescribed in s 47(1)(a) of the Credit Act, given that RFG was engaged in credit activities through the RAMS Franchise Network it was imperative that it took appropriate and adequate steps to “ensure” that the RAMS Franchisees could, and did, comply with its own policies in providing efficient, honest and fair services to consumers who were seeking to enter into, and did enter into, home loans.

107 In particular, as the parties submitted, I am satisfied that this obligation required RFG to:

(a) create adequate policies and procedures for the operation of the RAMS Franchise Network;

(b) take reasonable steps to ensure that those policies and procedures were complied with by RFG and RAMS ACRs;

(c) adequately investigate and respond to possible misconduct within the RAMS Franchise Network including:

(i) in relation to non-compliance with the RAMS Policies;

(ii) in response to investigations by the SLTF and GI; and

(iii) by implementing appropriate controls to manage identified risks, where those risks were identified in the course of the relevant investigations; and

(d) conduct adequate compliance audit and routine loan file review procedures to detect misconduct in relation to loan applications received from RAMS Franchisees.

108 The parties also agreed and jointly submitted that RFG was required by s 47(1)(a) to comply with its obligations pursuant to ss 31(1), 47(1)(b) and 47(1)(e) of the Credit Act. I have doubts about this submission and do not consider it necessary to accept the joint position of the parties in this respect, or to make such a finding. The effect of the parties’ joint position in this respect is that RFG was required by s 47(1)(a) to comply with other provisions of the Credit Act, which would add little, if anything, to those other obligations. This submission is to be contrasted to the separate contention, which I do accept, that s 47(1)(a) extends to a licensee ensuring that it has adequate policies and procedures in place to discharge its obligations under ss 31(1), 47(1)(c), (d), and (e). The separate contention focusses on the adequacy of systems, policies and procedures directed to ensuring compliance, as opposed to merely requiring compliance with another obligation. However, in respect of s 47(1)(b) it is to be observed that it is an obligation which already requires a licensee to have in place “adequate arrangements” to ensure that its clients are not disadvantaged by conflicts of interest. Generally, I share the views that O’Bryan J expressed in respect of a similar issue that arose in ASIC v ANZ where his Honour stated at [57]:

It cannot be doubted that the stipulation in s 47(1)(a), that a licensee must do all things necessary to ensure that the credit activities authorised by the licence are engaged in efficiently, honestly and fairly, is important. There is a body of case law in respect of the analogous provision in s 912A(1)(a) of the Corporations Act 2001 (Cth), although there has been limited appellate consideration of the provision (there was limited discussion in Australian Securities and Investments Commission v Westpac Securities Administration Ltd (2019) 272 FCR 170). In my view, the question whether ANZ’s conduct in this case constitutes a contravention of s 47(1)(a) is not free from doubt. The relationship between each of the paragraphs of s 47(1), and how paragraph (a) should be construed in light of the other paragraphs, may need consideration. An overly broad construction of paragraph (a), as propounded by ASIC, may render otiose the other paragraphs. In the circumstances of the present case, I am not willing to make a declaration of contravention of s 47(1)(a) solely on the basis of ANZ’s admission and without contest. The admission has no practical consequences for ANZ as the admission, and proposed declaration, would be merely duplicative of the other admissions.

109 Despite some of the infelicity in the parties’ position and the declarations that they proposed, I am nevertheless satisfied that RFG contravened s 47(1)(a) by:

(a) failing to take reasonable and adequate steps to ensure that RAMS Franchises and their staff complied with RAMS Policies;

(b) failing to create and establish adequate policies and procedures for responding to possible misconduct;

(c) failing to create an effective consequence management policy which set out parameters about when concerns about possible misconduct should be referred by RFG for investigation; and

(d) failing to implement effective controls to ensure that RFG representatives did not breach the policy requirement not to deal with unaccredited referrers, including by failing to:

(i) satisfy itself that there were adequate processes in place to verify that a referrer was accredited;

(ii) put in place controls to monitor the accuracy of an Accredited Referrer’s unique referrer identifier code which was required to be entered in Symmetry by the RAMS Franchise as part of the home loan application process; and

(iii) include post-loan settlement “Welcome Calls”, as described in paragraph 51 of the Liability SAFA, to consumers as a control in JUNO, as a result of which RFG management was unable to assess and confirm whether that control was operating effectively, in circumstances where Welcome Calls were the key control used by RFG for identifying the use of Unaccredited Referrers;

(e) failing to take adequate steps to ensure that RAMS Franchisees and their employees adhered to the process for a prospective referrer to become accredited under the Accreditation Process, which failure led to the use of referrers who:

(i) did not hold a current ACL under Part 2–2 of the Credit Act;

(ii) were not an authorised representative of an ACL holder under Part 2–3 of the Credit Act; or

(iii) not exempt from being required to hold an ACL under the credit legislation;

(f) failing to establish adequate compliance audit and routine loan file review procedures to detect misconduct, including by:

(i) establishing compliance audits with a very narrow focus that, among other things, were not designed to identify misconduct, and which excluded higher risk loan applications (such as declined or withdrawn files) from sampling processes; and

(ii) establishing an inappropriately undemanding paper file review process (5 files, every 6 months) undertaken by the RAMS Field Franchise sales team and was not focused on detecting misconduct issues; and

(g) failing to adequately respond to possible misconduct within the RAMS Franchise Network, including by virtue of failing to: