FEDERAL COURT OF AUSTRALIA

Australian Securities and Investments Commission v Cohen [2025] FCA 1255

File number(s): | NSD 1114 of 2021 |

Judgment of: | GOODMAN J |

Date of judgment: | 16 October 2025 |

Catchwords: | CORPORATIONS – conflicted remuneration - Division 4 of Part 7.7A of the Corporations Act 2001 (Cth) – incentives offered to sales agents – requirement to plead with specificity and prove the elements of s 766B of the Act – existence of conflicted remuneration not established – alleged involvement of the first and second respondents in alleged contraventions of provisions of Division 4 not established CORPORATIONS – first respondent’s duties under s 180 of the Act – contended breaches of duty arising from conduct relating to the availability of the incentives offered to sales agents and from alleged omissions with respect to such incentives – consideration of the circumstances of the corporation and the first respondent’s offices and responsibilities – breaches of duty by the first respondent not established |

Legislation: | Corporations Act 2001 (Cth), ss 9, 50, 180, 761A, 761G, 763A, 763C, 764A, 766B, 910A, 912A, 916A, 916B, 917C, 922A, 963A, 963AA, 960, 961P, 963E, 963F, 963J, 963L, 1324,1549A, 1549B Corporations Amendment (Life Insurance Remuneration Arrangements) Act 2017 (Cth) Evidence Act 1995 (Cth), s 140 Federal Court of Australia Act 1976 (Cth), s 37M Life Insurance Act 1995 (Cth), s 9 Corporations Amendment (Life Insurance Remuneration Arrangements) Regulations 2017 (Cth) Corporations Regulations 2001 (Cth), regs 7.6.05, 7.7A.11B, 7.7A.11C, 7.7A.16H |

Cases cited: | Australian Securities and Investments Commission v Commonwealth Bank of Australia [2023] FCAFC 135; (2023) 299 FCR 604 Australian Securities and Investments Commission v Drake (No 2) [2016] FCA 1552; (2016) 340 ALR 75 Australian Securities and Investments Commission v MacDonald (No 11) [2009] NSWSC 287; (2009) 256 ALR 199 Australian Securities and Investments Commission v Noumi Limited (No 4) [2024] FCA 1192 Australian Securities and Investments Commission v Rich [2009] NSWSC 1229; (2009) 75 ACSR 1 Australian Securities and Investments Commission v Select AFSL Pty Ltd (ACN 151 931 618) (No 2) [2022] FCA 786; (2022) 162 ACSR 1 Australian Securities and Investments Commission v Westpac Banking Corporation (ACN 007 457 141) [2022] FCA 515; (2022) 159 ACSR 381 Briginshaw v Briginshaw [1938] HCA 34; (1938) 60 CLR 336 Diakyne Pty Ltd (ACN 099 168 402) v Ralph [2009] FCA 721; (2009) 72 ACSR 450 Shafron v Australian Securities and Investments Commission [2012] HCA 18; (2012) 247 CLR 465 Termite Resources NL (ACN 112 036 398) (in liq) v Meadows [2019] FCA 354; (2019) 135 ACSR 45 |

Division: | General Division |

Registry: | New South Wales |

National Practice Area: | Commercial and Corporations |

Sub-area: | Corporations and Corporate Insolvency |

Number of paragraphs: | 423 |

Date of last submissions: | 29 April 2025 |

Date of hearing: | 17-21 July 2023 and 24-28 July 2023 |

Counsel for the Plaintiff: | Mr E Nekvapil SC with Mr T Kane and Ms M O’Brien |

Solicitor for the Plaintiff: | Australian Securities and Investments Commission |

Counsel for the First Defendant: | Mr J C Hewitt SC with Mr A R Langshaw |

Solicitor for the First Defendant: | Maddocks Lawyers |

Solicitor for the Second Defendant: | The second defendant appeared in person |

ORDERS

NSD 1114 of 2021 | ||

BETWEEN: | AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff | |

AND: | KEITH CHARLES COHEN First Defendant ROBERT RAFEC OAYDA Second Defendant | |

order made by: | GOODMAN J |

DATE OF ORDER: | 16 october 2025 |

THE COURT ORDERS THAT:

1. The originating process be dismissed.

2. By 31 October 2025, the parties are to confer as to the appropriate orders for costs and are to provide to the Court a joint set of orders that may be made by consent or, absent agreement, competing orders.

3. If the parties lodge competing orders, then the proceeding is to be listed for case management at a date and time convenient to the Court and the parties.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

[1] | |

[19] | |

[218] | |

[218] | |

[219] | |

[223] | |

[224] | |

[227] | |

[229] | |

C.3.3.1 Was the FPP a “financial product of a particular class”? | [231] |

C.3.3.2 Was access to the prizes dependent upon the number of FPPs acquired by retail clients? | [239] |

[241] | |

[269] | |

[270] | |

[271] | |

[273] | |

[274] | |

C.4.4 Provision of financial product advice to persons as retail clients | [275] |

[277] | |

[290] | |

C.5 ASIC’s further alternative contention – s 963AA of the Act and reg 7.7A.11B(1) | [291] |

[292] | |

[295] | |

[298] | |

[299] | |

[300] | |

[301] | |

C.5.3.4 Was information given to persons in relation to the FPP? | [306] |

[308] | |

[310] | |

[312] | |

[316] | |

[317] | |

[318] | |

[319] | |

D. DID MR COHEN CONTRAVENE S 180 OF THE ACT? | [340] |

[341] | |

[343] | |

[344] | |

[346] | |

[347] | |

[348] | |

[349] | |

[350] | |

[363] | |

[365] | |

[366] | |

[378] | |

D.4.1 Mr Cohen’s knowledge concerning the First Bali Sales Incentive | [381] |

[383] | |

D.4.3 Mr Cohen’s knowledge concerning the Second Bali Sales Incentive | [385] |

[387] | |

[392] | |

D.5 Has a contravention of s 180 of the Act been established? | [401] |

[402] | |

[404] | |

[422] | |

[423] |

REASONS FOR JUDGMENT

GOODMAN J:

A. INTRODUCTION AND OVERVIEW

1 The plaintiff (ASIC) seeks declaratory relief, injunctive relief, disqualification orders, and orders for pecuniary penalties against the defendants, Mr Keith Cohen and Mr Robert Oayda.

2 Mr Cohen was a director of various companies within the Freedom group of companies, which during the relevant period – namely 15 November 2017 to 2 October 2018 – included Freedom Insurance Group Ltd (FIG), Freedom Insurance Pty Ltd, Freedom Administration Pty Ltd and Insurance Network Services Australia Pty Ltd (INSA).

3 References in these reasons for judgment to Freedom are references to the group of companies generally or to the business they conducted. Greater precision is not required, other than to record that: (1) Freedom Insurance held an Australian Financial Services Licence (Freedom AFSL); (2) INSA was the employer of the sales agents who worked for the Freedom group; and (3) FIG was, from December 2016, an entity listed on the Australian Stock Exchange (ASX).

4 Mr Oayda was engaged by INSA as a consultant to deliver services to INSA and Freedom Insurance during the period from about 7 September 2016 to about 17 September 2018 and acted as the Quality Assurance (QA) Manager for Freedom Insurance from about late 2016 or early 2017 to about January 2018. In that position, he was responsible for the management of Freedom Insurance’s QA team and QA processes.

5 As noted above, Freedom Insurance held the Freedom AFSL. During the relevant period, it sold an insurance product known as the Freedom Protection Plan (FPP). The FPP was sold by the sales agents who worked from a call centre.

6 During September 2017, Freedom suffered a significant downturn in its sales of the FPP. From November 2017, Freedom sought to address this slump by conducting incentive programs referred to herein individually as the Vespa Incentive, the First Bali Sales Incentive and the Second Bali Sales Incentive, and collectively as the Incentives. The Incentives each had a prize: the Vespa Incentive involved the award of a Vespa motorcycle to the winner; and each of the Bali Sales Incentives offered travel to and from, and accommodation in Bali, Indonesia to those sales agents who met their sales targets, referred to herein as the Bali 1 package and the Bali 2 package.

7 Mr Adam Walker was the sole recipient of the Vespa. There were 28 recipients of the Bali 1 package (First Bali Sales Incentive prize-winners) and eight recipients of the Bali 2 package (Second Bali Sales Incentive prize-winners). The recipients of the Vespa, the Bali 1 package and the Bali 2 package (together, the prizes) are referred to herein collectively as the prize-winning sales agents.

8 ASIC contends that during the relevant period Freedom Insurance and INSA contravened provisions within Part 7.7A of the Corporations Act 2001 (Cth). I address the issues and evidence below by reference to ASIC’s pleaded case. In circumstances where: (1) Mr Cohen, by his senior counsel, made clear that he was defending the case as pleaded; and (2) Mr Oayda is a litigant in person, it is appropriate that ASIC be held to its pleaded case.

9 First, ASIC contends that Freedom Insurance contravened s 963E(2) of the Act which provided:

963E Licensee must not accept conflicted remuneration

...

(2) A financial services licensee contravenes this section if:

(a) a representative, other than an authorised representative, of the licensee accepts conflicted remuneration; and

(b) the licensee is the, or a, responsible licensee in relation to the contravention.

10 In essence, ASIC contends that Freedom Insurance contravened s 963E(2) of the Act because: (1) it was a “financial services licensee”; (2) its representatives, namely the prize-winning sales agents, accepted “conflicted remuneration” in the form of the prizes; and (3) it was the “responsible licensee” in relation to the contraventions.

11 Secondly, ASIC contends that Freedom Insurance contravened s 963F of the Act, which provided:

963F Licensee must ensure compliance

A financial services licensee must take reasonable steps to ensure that representatives of the licensee do not accept conflicted remuneration.

12 ASIC contends that Freedom Insurance, as a financial services licensee, failed to take reasonable steps to ensure that the prize-winning sales agents (as its representatives) did not accept conflicted remuneration in the form of the prizes.

13 Thirdly, ASIC contends that INSA contravened s 963J of the Act, which provided:

963J Employer must not give employee conflicted remuneration

An employer of a financial services licensee, or a representative of a financial services licensee, must not give the licensee or representative conflicted remuneration for work carried out, or to be carried out, by the licensee or representative as an employee of the employer.

14 In essence ASIC contends that INSA, as the employer of the prize-winning sales agents (being representatives of a financial services licensee, namely Freedom Insurance), gave those agents conflicted remuneration in the form of the prizes for work carried out or to be carried out by those agents as employees of INSA.

15 ASIC does not seek relief against Freedom Insurance or INSA, each of which has been deregistered, with respect to the contended contraventions. Instead, it proceeds only against Mr Cohen and Mr Oayda.

16 ASIC alleges that:

(1) Mr Cohen was “knowingly concerned in, or party to” within the meaning of s 1324(1) of the Act, contraventions of:

(a) ss 963E(2) and 963F of the Act by Freedom Insurance;

(b) s 963J of the Act by INSA; and

(2) Mr Oayda was “knowingly concerned in, or party to” contraventions of ss 963E and 963F of the Act by Freedom Insurance, within the meaning of s 1324(1)(e) of the Act.

17 In the remainder of these reasons, I set out my principal findings of fact (Part B) before considering the centrally relevant question of whether the prizes were “conflicted remuneration” for the purposes of the Act (Part C). As I reach the conclusion that ASIC has not established that any of the prizes were conflicted remuneration, it is not necessary to address whether Freedom Insurance contravened s 963E(2) or 963F of the Act or INSA contravened s 963J of the Act; or whether Mr Cohen and Mr Oayda were knowingly concerned in, or party to the pleaded contraventions.

18 ASIC also alleges that Mr Cohen, qua director of Freedom Insurance and INSA, contravened s 180 of the Act, in broad terms, by failing to take reasonable steps to prevent Freedom Insurance and INSA from engaging in contraventions (actual or potential) of ss 963E(2), 963F, and 963J of the Act. For the reasons developed below at Part D, I am not persuaded that Mr Cohen contravened s 180 of the Act.

B. PRINCIPAL FINDINGS OF FACT

19 ASIC read affidavit evidence from:

(1) Mr Malcolm McCool, a solicitor who was employed by Freedom as its Head of Legal & Product Development during the relevant period;

(2) Ms Lisa Delahunty, who was employed by Freedom as a risk and compliance manager during the relevant period;

(3) Mr Adrian Turner, who was employed by Freedom and managed Freedom’s sales team during the relevant period;

(4) Mr Daniel Saphra, who was employed by INSA from 22 January 2018 and who worked as a sales agent selling FPPs; and

(5) Ms Rachel Perla, a lawyer in the employ of ASIC.

20 ASIC also adduced evidence, under compulsion of a subpoena, from Ms Jennifer Andrews, a former chief financial officer (CFO) of Freedom.

21 Each of these witnesses, with the exception of Ms Perla, was cross-examined.

22 Each of Mr Cohen and Mr Oayda provided affidavit evidence and was cross-examined.

23 Mr Cohen also adduced affidavit evidence from Ms Isabella Heath, a solicitor in the employ of Mr Cohen’s solicitor and Mr Gavin Bellamy, a process server. Ms Heath and Mr Bellamy were not cross-examined. The evidence of Mr Bellamy and Ms Heath was relevant only to the question of whether Mr Cohen should be allowed to adduce evidence of a transcript of an examination of Mr Walker in circumstances where Mr Walker apparently was not available for cross-examination. I have decided that such evidence should not be admitted.

24 In addition to the several thousand pages tendered with the affidavits, there was a separate documentary tender in the order of 11,000 pages.

25 From this evidence, the salient facts are set out below.

26 I pause to note that there are several areas in respect of which some witnesses differ in their recollections. Many of these differences were not explored or tested in cross-examination, and some are, at most, of peripheral relevance to the issues requiring determination on the pleaded case.

27 There are, however, some areas of tension between the evidence of Mr Cohen and the evidence of Mr McCool which are of some importance to ASIC’s case that Mr Cohen contravened s 180 of the Act.

28 To the extent that there are differences between the evidence of Mr Cohen and Mr McCool, I prefer the evidence of Mr Cohen, particularly in circumstances where: (1) ASIC did not contend that Mr Cohen’s evidence should not be accepted; (2) contemporaneous documents are more consistent with Mr Cohen’s evidence than with Mr McCool’s evidence; and (3) Mr McCool shifted during cross-examination, at times significantly, away from aspects of his affidavit evidence. For example:

(1) evidence in his affidavit that he “did not take on any responsibilities for the compliance function and in particular, operational compliance” yielded in cross-examination to evidence that:

(a) part of his role as Freedom’s Head of Legal was to apply his legal skills to ensure that there was no non-compliance with any applicable financial services laws that related to Freedom’s business;

(b) in his role as Freedom’s Head of Legal, it was incumbent upon him to be aware of what was happening in the business, to apply his decades of experience as a financial services lawyer so as to identify any risks, and to take appropriate steps to address any identified risks;

(2) evidence in his affidavit suggesting that his role was limited to specific tasks when requested by Mr Cohen and that he had no involvement in, or responsibility with respect to the Incentives yielded in cross-examination to evidence that:

(a) he had been tasked by Mr Cohen with considering the effect of the legislative changes to be introduced by the Corporations Amendment (Life Insurance Remuneration Arrangements) Bill 2016 (LIF Reforms) upon, inter alia, the arrangements between Freedom and its sales agents; and

(b) it was his responsibility to consider all aspects of the LIF Reforms including non-monetary incentives.

29 Nothing in these reasons for judgment should be taken as suggesting that Mr McCool was negligent. No such case was brought by ASIC, nor is such a case addressed herein. The observations and findings made with respect to Mr McCool are made in the context of the s 180 case brought by ASIC against Mr Cohen.

30 Returning to the salient facts, Freedom commenced in 2009 with the incorporation of INSA and INSA Distribution Pty Ltd (which was renamed on 1 September 2010 to Freedom Insurance) and grew over time with the incorporation of, relevantly, Freedom Administration (in July 2013) and FIG (in October 2015).

31 Freedom was established to market and distribute life insurance products. Mr Cohen, Mr Harvey Light and Mr Brian Pillemer were the founders and founding directors of INSA and INSA Distribution. Mr Light and Mr Pillemer had previously worked with Mr Cohen at Australian Life Insurance Group Pty Ltd (ALI). Ms Yolande De Torres joined Freedom at an early stage and worked in establishing Freedom’s business.

32 Mr Cohen was the managing director, Mr Light was head of operations, Mr Pillemer was CFO and Ms De Torres worked on the financial services licensing requirements. In those early days, they were the only four permanent employees and they did not adhere to a strict organisational structure and instead were all involved in doing whatever needed to be done.

33 On 14 August 2009, Dr Tamsin Clarke of Auron Consulting Pty Ltd provided a detailed letter of advice to INSA (Mr Pillemer and Mr Cohen) titled “General Advice re Principles to apply in offering insurance policies”. The letter contained the following “Background”:

Background

INSA has recently been established to act as an independent distributor of insurance products to retail clients.

(a) INSA proposes to use advertising to attract phone and email enquiries from retail clients. The enquiries will generally be answered by ‘call centre’ telephone and/or email operators.

(b) INSA will provide clients with its own FSG and with the issuers’ PDSs for the relevant insurance product(s) offered.

(c) INSA does not wish or intend to provide anything other than general product advice, although some of its business may relate to the provision of replacement insurance products.

(d) INSA is in the process of obtaining an AFSL covering the appropriate authorisations which it will need to carry on this business through ‘call centre’ telephone and/or email operators and will carry out the appropriate training of those operators.

Generally, the Corporations Act regulates the marketing of insurance products, which come within the definition of ‘financial products’ (with some specific exemptions such as funeral benefits).

Insurance provided to individual persons relating to motor vehicle, home building, home contents, sickness and accident, consumer credit, travel or personal and domestic property (see Corporations Regulations 7.1.11 to 7.1.17) is deemed under the Corporations Act to be provided to a ‘retail’ client (s 761G(5)).

The INSA activities described above therefore involve two potential ‘financial services’ (see s 766A) for the purposes of the Corporations Act:

• giving general financial product advice to ‘retail’ clients, and

• arranging for a ‘retail’ client to acquire a financial product offered by an insurer.

References in this advice to sections are to sections in the Corporations Act unless indicated otherwise.

(emphasis in original; footnotes omitted)

34 On 17 September 2009, INSA Distribution applied for an Australian Financial Services Licence. Mr Cohen was involved in the preparation of this application, including ensuring the veracity of the information included in it. That application included:

(1) an overview of INSA Distribution’s business that included:

4.0 Details of how the business is operated. |

4.1 The Applicant will enter into an arrangement with existing life & general insurers to distribute their risk life & general insurance products.

4.2 Distribution will be via phone through a centralised call centre which will receive inquiries in response to advertising on television and in other media. Marketing material may contain straightforward general advice such as highlighting the benefits of taking out a particular type of insurance. All general advice contained in any such advertising or marketing material will be reviewed by an RG 146 qualified person within the group and checked by our external legal counsel.

4.3 Call centre staff will perform the task of offering the products to customers. All INSA’s call centre staff will be direct employees of INSA Group and will be subjected to a rigorous selection process and extensive training program. Sales staff will be supervised and monitored by team leaders who in turn will be supervised and monitored by the head of Human Resources & Training (Annexure 1 Organisational Chart).

4.4 Customers will not be provided with any personal advice. Essentially a “no advice” offer process will be followed, although the call centre scripting and general marketing will contain a limited amount of general advice. Customers requiring personal advice will be told that they should contact an independent financial adviser.

…

6.0 Outsourced operations – details of who performs these and in what location, if other than the principal place of business. |

6.1 The following services will be outsourced by the Applicant:

• External auditor (Baskin & Clarke, Chartered Accountants)

• External Dispute Resolution Scheme (Financial Ombudsman Service)

• Legal services re licensing & compliance (Auron Consulting Pty Ltd)

• IT support & development services as required

6.2 All operations sourced from outside the Company will be done in a manner consistent with INSA’s Outsourcing Policy and Procedures.

6.3 A set of compliance and risk management protocols will be established by the Company. These have been designed to minimize the risk of potential breaches of the AFS Licence Conditions.

…

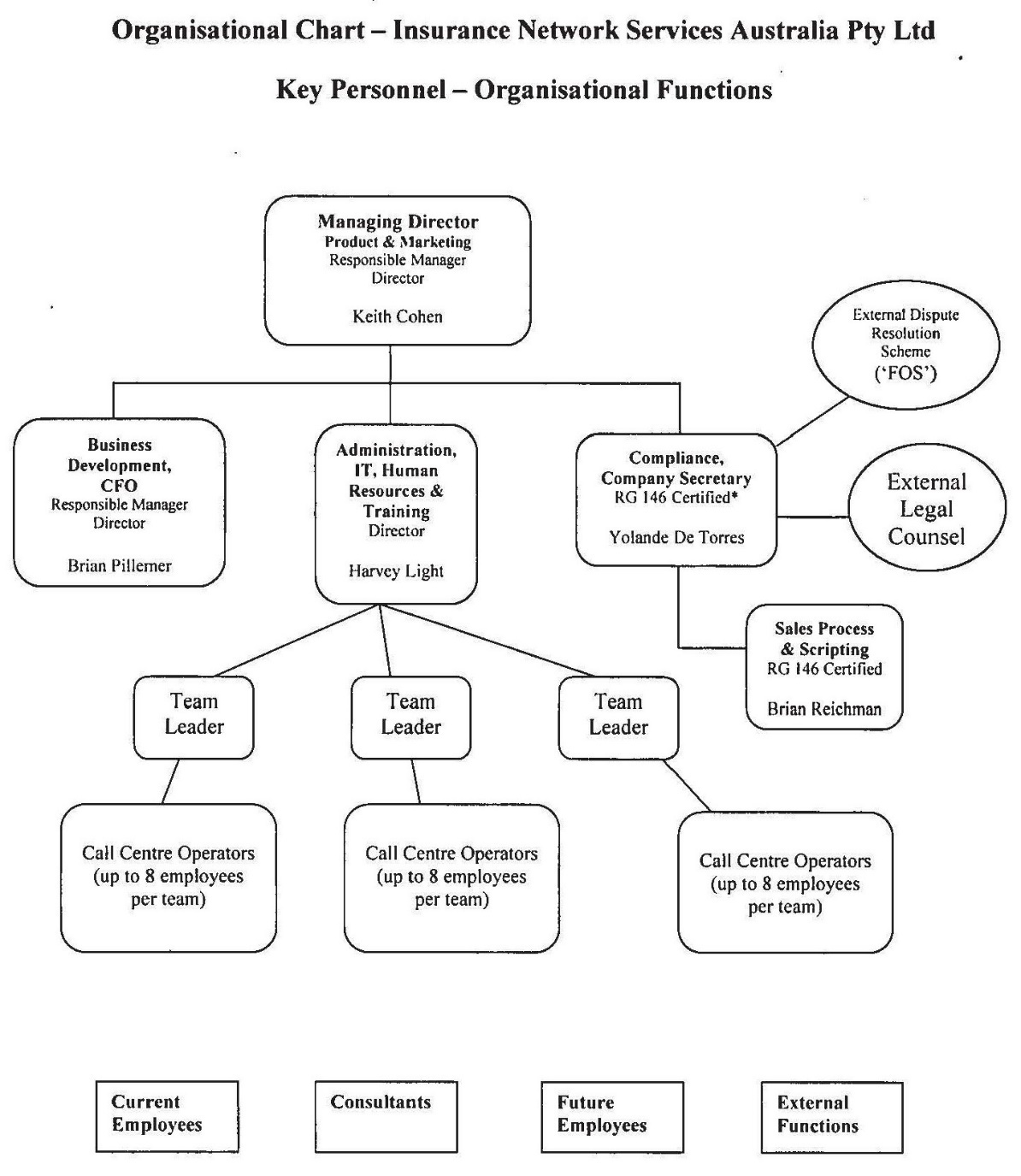

10.0 Organisational Chart and relevant information |

10.1 See Annexure 1 Organisational Chart – Insurance Network Services Australia Pty Ltd, Key Personnel – Organisational Functions

10.2 The Compliance Manager is responsible for ongoing compliance with AFS obligations and is also responsible for reporting breaches directly to ASIC.

10.3 The Compliance Manager is currently enrolled to do Kaplan Professional’s Tier 1 Compliance Solutions course which will lead to RG 146 certification upon completion*.

…

(emphasis in original);

(2) an organisational chart in the following terms:

(3) a table of organisational competence which set out, inter alia, details of Mr Cohen’s experience as follows:

Details of Responsible Manager(s) | Keith Charles Cohen Relying on RG 105 Option 5 |

Qualifications | Bachelor of Science University of Cape Town, South Africa, Completed 1983 (This course is NOOSR verified -please see appendix B 1.8) Membership of Professional Associations • Fellow of the Institute of Actuaries of Australia • Fellow of the Institute of Actuaries (UK) • Member of the Actuarial Society of South Africa • Associate of the Society of Actuaries (US)

|

Experience in providing: Dealing services on behalf of another in applying for life risk and general insurance products. | Dates in Role: August 2002 to February 2009 Dealing Entity Name: A.L.I. Group Pty Ltd/Australian Life Insurance Business Description: Life Insurance and General Insurance distribution and administration. Around 50 staff and more than 2,500 sales per month. Position: Managing Director and Founder Clients: Over 200 retail mortgage broking business relationships resulting in over 4,500 brokers being accredited as authorised representatives of the company. The company had over 50,000 retail customers. Products: Life risk products and Home & Contents insurance. Role : Involved directly in all aspects of the business set up and operations including distribution, administration, legal, marketing, actuarial and finance. Products were distributed both through the company’s authorised representatives and through its call centre. All products were distributed on a no advice basis. Deal Experience: • Life risk products. A.L.I. customers applied for cover on applications provided to them by ALI Distribution’s authorised representatives who were mortgage brokers. These applications were submitted centrally for processing. The insurer for the majority of these products was Tower Life Ltd who outsourced the administration of these policies to A.L.I Administration Pty Ltd which was part of the A.L.I. Group. Policies were issued by ALI Administration on behalf of Tower Life. Income Protection policies were inputted directly onto the Macquarie Life policy system and Macquarie handled all the administration. Customers who wished to cancel or vary their products/policies would call a central call centre at A.L.I. • General Insurance products. All Home & Contents products were initially offered by A.L.I.’s authorised representatives with all applications processed centrally directly onto the systems provided by Insurer QBE. QBE handled all policy administration. • All client monies were collected and held by the Insurers Tower, Macquarie or QBE Keith Cohen had 7 years of dealing experience at A.L.I. As a founder of the business he was involved in the setup of all processes. Some particular instances or circumstances are as follows: • Participated in the development of and signed off on all retail customer correspondence templates. • Signed off on all client communications. • Ran a monthly Compliance meeting that reviewed any breaches or complaints. • Developed the broker training programs for both life risk and home & contents products and facilitated signoff from the Head of Compliance. • Participated in the training of brokers as required to ensure the adequacy and appropriateness of the training materials. • Would listen into calls made by the call centre operators on a ad hoc basis to ensure calls being made were compliant and that operators were providing a high level of customer service. • Developed and facilitated signoff of a DVD to be used by mortgage brokers to educate their retail customers directly on A.L.I. products. • Thoroughly reviewed daily and monthly lodgments, lapses, cancellations and retention rates to ascertain if there were any trends requiring investigation. • Presented on a regular basis to call centre and processing staff to increase their understanding of the total business. • Ran focus groups for over 100 authorised representatives using external consultants over a 3 month period. • Ran regular twice weekly management team meetings. At INSA, all insurance products will be processed directly onto the systems of the product issuers in a similar fashion to that at A.L.I. Dates in Role: 1996 to 2002 Entity Name: Westpac Life Insurance Services Position: Principal Executive Officer (1998-2002) Chief Actuary (1996-1998) |

(4) a submission concerning Mr Cohen’s competence as a responsible manager; and

(5) a statement of personal information for Mr Cohen in which he agreed to be a responsible manager for INSA Distribution.

35 On 29 October 2009, Compact Compliance & Corporate Training wrote to ASIC in the following terms:

Re: Corporations Act Knowledge

This letter is to confirm that Brian Pillemer and Keith Cohen have today attended a training course for AFSL Responsible Managers conducted by our firm.

The objective of this particular course is to provide participants with an overview of their obligations as Responsible Managers, the Licensee’s obligations under its Australian Financial Services’ Licence, and to refresh some of the fundamental features of the financial services reform regime.

The learning outcomes of the course are that upon completion of the course, participants should be able to:

• explain their obligations as Responsible Managers;

• explain key regulatory obligations in relation to the provision of financial services;

• explain the business’ authorisations under its AFS licence;

• consider and explain potential personal liability arising from their role as a Responsible Manager; and

• identify and explain developments and trends that have, and are, taking place in the financial services industry which might impact on their role as Responsible Managers.

In terms of content, the course looks at the following:

a) basic concepts in both the Corporations Act and ASIC Act, and the changes brought about to the Corporations Act by virtue of the Financial Services Reform Act 2001;

b) consideration of why a financial services business may require an AFS Licence;

c) what constitutes a financial product;

d) consideration of the participants’ AFS licence authorisations in relation to both products and services;

e) distinction between wholesale and retail clients, and what this means to a financial services provider;

f) the obligations of the Licensee, both generally and specifically in relation to its authorisations, including disclosure requirements, conflicts of interests, risk management, etc;

g) the key requirements and responsibilities pertaining to their role as Responsible Managers; and

h) some activities which are prohibited under the Corporations Act.

In addition to being trainers and having conducted this course to many Responsible Managers from a wide range of AFSL holders over the last 4 years, both Grant Holley and I are lawyers practising in financial services and providing advice to licensees and their senior management in relation to obligations arising pursuant to the conduct of the financial services.

(emphasis in original)

36 On 30 October 2009, ASIC issued an AFSL to INSA Distribution. From that time, it was a financial services licensee. It was also the entity which entered into distribution agreements with insurers from time to time, providing the arrangements for the marketing and distribution of those insurers’ products by Freedom.

37 The AFSL included authorisation as follows:

1. This licence authorises the licensee to carry on a financial services business to:

(a) provide general financial product advice for the following classes of financial products:

(i) general insurance products; and

(ii) life products limited to:

(A) life risk insurance products as well as any products issued by a Registered Life Insurance Company that are backed by one or more of its statutory funds; and

(b) deal in a financial product by:

(i) arranging for another person to apply for, acquire, vary or dispose of financial products in respect of the following classes of financial products:

(A) general insurance products; and

(B) life products limited to:

(1) life risk insurance products as well as any products issued by a Registered Life Insurance Company that are backed by one or more of its statutory funds;

to retail clients.

38 On 1 September 2010, INSA Distribution changed its name to Freedom Insurance and on 6 September 2010, ASIC issued the Freedom AFSL to Freedom Insurance in that name.

39 Mr Cohen remained a responsible manager under the Freedom AFSL until October 2018. As will be seen, others also became responsible managers under the Freedom AFSL as Freedom’s business grew.

40 In late 2010, Freedom launched its first product. From that time, it gradually took on more employees and, over time, it developed more formal business structures and reporting lines as the business grew.

41 In 2011: (1) Mr McCool (with whom Mr Cohen had worked at both ALI and Westpac Banking Corporation) joined Freedom, as a part-time legal consultant; and (2) Mr Turner joined Freedom, as its contact centre manager.

42 In about 2012, Mr Pillemer left as an executive of Freedom and Ms Jennifer Andrews joined Freedom as its CFO. Mr Cohen had worked with Ms Andrews at ALI and Westpac.

43 As at 30 June 2012, Freedom had 29 staff (which included 12 call centre sales staff, seven customer service staff and two administration/quality assurance staff).

44 On 18 July 2013, Freedom Administration was incorporated. It carried out administration – such as premium collection and customer service – for the insurers whose products Freedom distributed.

45 By 2014, the business of Freedom involved:

(1) distributing insurance products to consumers via its in-house call centre, on behalf of insurers with whom Freedom had distribution arrangements;

(2) undertaking marketing and lead generation activities for those insurance products;

(3) undertaking in-house policy administration services on behalf of the insurers with which Freedom had distribution arrangements; and

(4) managing customer relationships post-sale including through premium collection, retention, cancellations, renewals and claim processing.

46 In about 2014, Freedom entered into a distribution agreement with NobleOak Life Limited, pursuant to which Freedom marketed and sold insurance products issued by NobleOak. Freedom also undertook policy administration services for NobleOak. NobleOak’s policies were fully reinsured by Swiss Re Life & Health Australia Limited and, as a result, Freedom dealt with both NobleOak and Swiss Re in relation to these arrangements. Freedom also took an equity stake in NobleOak and Mr Cohen was a director of NobleOak between about 2016 and 2017.

47 In about 2015, Ms Jennifer Davitt was employed by Freedom as its chief operating officer (COO).

48 On 10 July 2015, Mr Cohen entered into an employment contract with Freedom Insurance as its full-time managing director. Clause 1.4 of the employment contract indicated that Mr Cohen’s duties would be those described in item 4 of the Schedule to that contract, which in turn described Mr Cohen’s responsibilities in the role of managing director as follows:

4.1 Specific

To direct and control the Freedom group of companies operations and to give strategic guidance and direction to the business, including:

• implementing company policy

• developing strategic plans

• directing and controlling the work and resources of the group

• controlling group finances including preparation and implementation of budgets building and maintaining an effective management team

• establishing and maintaining effective formal and informal links with major customers

• maintaining a dialogue between shareholders and the board

• accountability to the board for all company operations

4.2 General

During your employment you will:

(1) work faithfully and diligently for Freedom;

(2) act at all times in Freedom’s best interests;

(3) use all reasonable means to protect and promote Freedom, its property and its reputation;

(4) perform the duties assigned to you from time to time to the best of your abilities;

(5) comply with the lawful directions and instructions made or given to you by Freedom’s Board, Freedom’s senior management and your manager in relation to your duties;

(6) devote the whole of your time and attention during your normal working hours and during such other reasonable hours as Freedom’s business may reasonably require from time to time; and

(7) act at all times in a manner which will ensure a safe and healthy work environment for all employees and contractors of Freedom.

49 On the same day, Mr McCool entered into an employment contract with Freedom Insurance as its “Head of Legal & Product Development, Company Secretary”. His specific responsibilities under that contract were described as:

4.1 Specific

• Legal, contractual, licensing and product development and related tasks as requested.

• Legal advice and guidance on contractual, licensing, product, operational and HR issues as requested

• Company secretarial and record retention services to Freedom group companies

• Management services as part of the senior management team

50 Mr McCool’s designated general responsibilities were similar to those set out in Mr Cohen’s employment contract.

51 In around 2015 or 2016, Freedom’s sales and customer service functions were separated into distinct teams and Mr Turner’s role shifted to the day-to-day management of the sales team only.

52 From about 2016, Freedom operated from premises at Bond Street in the central business district of Sydney. The business occupied two inter-connected floors, with all of the sales agents on the upper floor. The finance and marketing teams, risk and compliance teams, the COO, Mr Cohen and Mr McCool, as well as meetings rooms, were on the lower floor.

53 On 17 February 2016, Mr Wesley Chan of Swiss Re forwarded to Mr Cohen and others an email from Ms Bianca Richardson, a senior policy manager with the Financial Services Council indicating that the Corporations Amendment (Life Insurance Remuneration Arrangements) Bill 2016 had been introduced in the House of Representatives on 11 February 2016 and providing a summary of key components covered in the Bill.

54 Mr Cohen forwarded that email to Mr McCool.

55 On 11 April 2016, Mr McCool prepared and signed a notification to ASIC that Freedom Insurance wished to add him as a responsible manager on the Freedom AFSL. The notification identified that: (1) Mr McCool was employed by Freedom Insurance as a legal adviser; (2) it was proposed that financial services for which he would be responsible would be “provide financial product advice” and “deal in financial product”; (3) he would spend one to three days per week on duties related to the provision by Freedom Insurance of such services; and (4) his experience included experience in banking, general insurance, life insurance, “law firm/legal” and management with an overall type of experience as a technical adviser and in management with relevant industry experience exceeding five of the previous eight years.

56 Mr McCool was added as a responsible manager.

57 Mr McCool accepted in cross-examination that he represented that he was capable of giving legal advice in relation to Freedom’s products, as to the provision of financial product advice, and dealing in financial products.

58 As at 30 June 2016, Freedom had 171 staff (which included 90 call centre sales staff, 27 customer service/retention staff and 17 administration/quality assurance staff).

59 From about August 2016, FIG was the ultimate holding company of Freedom Insurance, Freedom Administration and INSA.

60 On or about 7 September 2016, Mr Oayda, who was a friend of Mr Cohen, commenced as a consultant to Freedom. Mr Oayda began working at Freedom in the role of QA Manager. He worked within the operations department and reported to Ms Davitt initially, and then Mr Mark Weinstein when Mr Weinstein was operations manager, and later to Mr Craig Orton as COO.

61 On 21 October 2016, Freedom and Swiss Re entered into a Product Development and Distribution Agreement.

62 Prior to entry into this agreement, Swiss Re undertook a due diligence process. Swiss Re’s due diligence report included, with respect to, inter alia, “sales and retention” a recommendation to “proceed with no critical show stoppers identified”.

63 Pursuant to this agreement Swiss Re could conduct regular audits of Freedom’s business to ensure compliance with the agreements and applicable laws. Such audits subsequently took place.

64 On 28 October 2016, FIG issued a prospectus for an initial public offering.

65 Freedom’s management structure at that time was described as follows:

(1) Mr Cohen was the managing director and chief executive officer (CEO);

(2) Ms Andrews was the CFO, reporting directly to Mr Cohen;

(3) Ms De Torres was the Head of Marketing, reporting directly to Mr Cohen;

(4) Mr McCool was the Head of Legal and Product Development, reporting directly to Mr Cohen;

(5) Ms Davitt was the COO, reporting directly to Mr Cohen. Among other things, the sales team and the compliance/QA teams fell within the operations group under Ms Davitt’s supervision. Mr Turner (Head of Sales) and Mr Light reported to Ms Davitt; and

(6) Mr Mark Schroeder was the managing director of Spectrum, an adviser distribution business acquired by Freedom.

66 Mr Cohen was described in the prospectus as:

Mr Keith Cohen is the CEO, Executive Director and founder of Freedom.

Keith has been responsible for leading the development and execution of the Company’s long term strategy with a view to creating shareholder value. He is responsible for the day-to-day management decisions and has been critical to the success of the Company including the development of insurer relationships from inception to the more recent acquisition of Spectrum.

Keith has extensive experience in the life insurance industry and was also the founder and Managing Director of Australian Life Insurance Group (ALI Group) from September 2002 to March 2009. Prior to this, Keith was also a Director of various Westpac companies (WBC.ASX), including Westpac Life Insurance Services Limited, Westpac General Insurance Limited, Westpac Financial Services Limited, Westpac Financial Consultants Limited and Westpac Custodian Nominees Limited. Before joining Westpac as the Chief Actuary in 1996, Keith was Deputy General Manager - Development Actuary at Sage Life Limited in South Africa. Keith is also a Non-Executive Director on the NobleOak Board.

Keith holds a Bachelor of Science degree from the University of Cape Town and is a Fellow of the Institute of Actuaries of Australia and the UK.

67 Ms Andrews was described in the prospectus as:

Ms Jenny Andrews is the CFO of Freedom.

Jenny is responsible for financial planning, reporting and managing all financial risks of the Company. She is a senior finance executive with strong expertise in actuarial, financial and operational management across life insurance, superannuation and wealth management.

From June 2009 to October 2012, Jenny was Head of Pricing and Profitability with ANZ Wealth Management (part of ANZ.ASX). She is also experienced in start-up companies and was another founding member of Australian Life Insurance where during the period 2003 to 2009 she was CFO and Chief Actuary for the group. Jenny was responsible for the financial and operational management of the company and established the group’s financial systems and reporting infrastructure

During the period 1998 to 2003, Jenny was the Financial Control Actuary at Westpac Financial Services Ltd (part of WBC.ASX) where she was responsible for leading the actuarial team. From 1994 to 1998, Jenny held the roles of Valuation Actuary and Associate Actuary Marketing (Pricing and Product Development) with TOWER Life Australia Ltd (now TAL).

Jenny holds a Bachelor of Science degree and is a Fellow of the Institute of Actuaries of Australia.

68 Ms Davitt was described in the prospectus as:

Mrs Jennifer Davitt is the COO of Freedom.

Jennifer joined Freedom in 2015 and has been instrumental in providing senior management to all aspects of operations including but not limited to marketing, sales, training, human resources, compliance and systems. She has been integral in the project management of the Spectrum acquisition and the successful listing of Freedom on the ASX. She is a senior executive in the banking and finance sector with a broad skill base across multiple disciplines including business transformation, project management, change management, financial management, mergers and acquisitions, risk, procurement, technology, process excellence, HR and governance.

From 2006-2015, Jennifer held various head of department and executive roles in which she displayed a focus on execution and the creation of high performing teams. During her time at ANZ Limited (ANZ ASX), Bankwest Ltd (subsidiary of CBA.ASX), Qantas Loyalty (part of QAN ASX) and multiple appointments at Westpac Banking Corporation Ltd (WBC.ASX), Jennifer successfully led major programmes of work, involving process improvement, cultural transformation, technical integration and major capital works.

As a former Naval Officer in the Royal Australian Navy, Jennifer is recognised for the structure and discipline she brings to the organisations for which she works, whilst also understanding the importance of customer centricity, stakeholder management and fiscal efficiency.

Jennifer holds a MBA, Master of Project Management and a Bachelor of Arts (Economics).

69 Mr McCool was described in the prospectus as:

Mr Malcolm McCool is the Group General Counsel of Freedom.

Malcolm initially joined Freedom in 2011 to help facilitate the next phase of its development and has primarily been involved in project type initiatives relating to relationships with insurers and reinsurers and product and benefit fund design.

He is a senior lawyer with 30 years’ experience in a range of corporate legal and management positions in the financial services industry. For much of that period he has been involved in the life insurance industry and has developed a unique mix of legal, product, process development and business and management skills that are ideally suited to a specialist life insurance business such as the Freedom group.

Malcolm was a founding member of ALI Group. Prior to the commencement of ALI Group in 2002, Malcolm held senior legal positions for 4 years with Westpac Banking Corporation (WBC.ASX) and became a leading practitioner in the financial services reform laws that now regulate the insurance industry. From 1990 Malcolm spent 8 years with Citibank group in various legal roles.

Malcolm holds a Bachelor degree in both Law and Commerce from the University of NSW.

(emphasis added)

70 Mr McCool accepted in cross-examination that this description was accurate. He also accepted that:

(1) he was a senior lawyer with 30 years’ experience in a range of corporate, legal and management positions in the financial services industry;

(2) he was a leading practitioner in the financial services reform laws that regulate the insurance industry;

(3) in issuing the prospectus, Freedom was representing to prospective investors that Mr McCool, as the general counsel of Freedom, would exercise all of the skills that are described in that part of the prospectus in discharging his responsibilities as the group general counsel and would be applying his legal skills to ensure that there was no non-compliance with any applicable financial services laws that related to Freedom’s business; and

(4) one of the ways that he would discharge his responsibilities would be to ensure that there was no non-compliance with any applicable financial services laws.

71 Mr McCool also gave evidence that:

(1) he and Mr Cohen worked well as a team and their familiarity with each other, which had developed over years, allowed Mr McCool a high degree of autonomy;

(2) Mr Cohen did not try to micro-manage Mr McCool’s work;

(3) he understood that Mr Cohen had a high regard for Mr McCool’s skill and competence as a lawyer;

(4) he was aware of the general conflicted remuneration provisions in the Act; and

(5) it was his view in 2017 that the conflicted remuneration provisions of the Act did not apply to incentives such as the First Bali Sales Incentive and the Vespa Incentive. This was based on his understanding that Freedom operated on a “no advice” model.

72 As to the “no advice” model, Mr McCool gave evidence that:

(1) prior to 1 January 2018:

The understanding was that we – that the business was doing a no advice model and that sales agents were not permitted to provide advice in those calls. I think we confirmed in the scripts that there was no advice in the scripts. They were purely factual. And, therefore, the conflicted remuneration provisions that related to advice which I think came into effect early in that decade didn’t apply to the Freedom – to the Freedom business. ;

(2) and:

I recall saying to Mr Cohen, prior to March 2018 and based on the scripts I had seen to that point, words to the effect, “from what I have seen, we don’t have general advice in our scripts”. From what I had seen prior to March 2018, the content of the scripts was primarily factual, but I was unaware of the context, such as training, and management instructions that might impact how the scripts were utilised…

(emphasis in original)

73 Mr Light was described in the prospectus as:

Harvey is a founding member of Freedom and was a member of the Board and Director of Freedom Insurance until October 2016. Harvey is responsible for the shared service functions of the business. His primary responsibilities include management of the customer service, collections, claims, underwriting and retention teams. In addition, Harvey is also responsible for enterprise wide functions including facilities, procurement. systems and technology.

Harvey has over 25 years’ experience in IT and administration management. primarily in the insurance environment working for companies such as HIH (formerly HIH.ASX) and Allianz Australia Limited. Harvey was part of the management team that founded and ran ALI Group from September 2002 until March 2009.

74 Ms De Torres was described in the prospectus as:

Ms Yolande De Torres is the Head of Marketing of Freedom.

Yolande has been with Freedom since its inception and was instrumental in obtaining Freedom’s AFSL. In her current role as Head of Marketing, she has overall responsibility for the strategic planning and execution of all marketing and media activity, liaising closely with relevant external and internal stakeholders.

Until May 2016, she also held the position of Head of Compliance. In this role Yolande was responsible for designing the overall compliance framework for the business as well as overseeing the day to day implementation of best practices ensuring high standards of quality and compliance are met.

Prior to joining Freedom, Yolande held senior roles in business administration, compliance and marketing including 4 years at Insession Pty Ltd (now ACI Worldwide) and 5 years at Falkiner Global Investors Ltd (FGIL) where she was also a Director.

Yolande holds a Bachelor Degree in Arts from Sydney University.

75 Ms Diane Osborne was described in the prospectus as:

Ms Diane Osborne is the Head of Risk Management and Compliance for Freedom.

Diane joined Freedom in 2016 and is responsible for overseeing all regulatory requirements, risks and the day-to-day compliance issues of the Company. Her responsibilities for the Company is to ensure all staff including management and employees adhere strictly to the Company compliance policies and procedures.

Diane comes from a background of more than 20 years’ experience in financial services as a senior legal, company secretarial and compliance manager. Prior to her current role, Dianne was General Counsel and Compliance Manager at Uniting Financial Services, General Counsel and Company Secretary at Cuscal Limited, Legal Head of Retail & Business Distribution at Westpac Banking Corporation (WBC.ASX), Legal Head of Product & Compliance at St. George Bank (subsidiary of WBC.ASX) and Global Head of Legal & Compliance at AMP Ltd (AMP.ASX).

Diane holds a Bachelor of Arts and a Bachelor of Law from Macquarie University.

(emphasis added)

76 On 17 November 2016, and in connection with its proposal to list on the ASX, Freedom issued a compliance policy, which included:

4. Responsibilities and Organisation

Responsibility for Compliance at Freedom is normally divided as follows:

a) Board

Ultimate responsibility for Compliance within Freedom resides with its Board of Directors. The role of the Board is to provide strategic guidance for Freedom and effective oversight of Management.

b) Committees

The Audit and Risk Committee is responsible for ensuring that Freedom has an appropriate Compliance Framework and Policies to manage compliance risks in accordance with its risk appetite and monitors Freedom’s adherence with its Compliance Policies and Procedures and considers the effectiveness of internal control systems as well as to set and review any internal audit plan and outcomes.

The Remuneration and Nomination Committee provides appropriate corporate governance by identifying the mix of skills and individuals required in Directors to allow the Board to contribute to the successful oversight and stewardship of Freedom and discharge their duties under the law diligently and efficiently; and aligns Freedom’s remuneration approach with shareholder interests to allow it to attract, motivate and retain its staff and enhance Freedom’s performance in a manner that supports the long-term financial soundness of Freedom.

The responsibilities of the Committees are set out in more detail in their respective Charters.

c) Managing Director

The Managing Director ensures that Freedom’s compliance framework is fit for purpose and operational and that Senior Managers and Team Leaders are aware of their obligations and have implemented processes to adhere to and sustain compliance.

The Managing Director is able to bring material and relevant compliance matters to the appropriate Committee and Board in a timely manner, in consultation with the Senior Managers and Team Leaders and in particular the Head of Risk and Compliance.

d) Head of Risk and Compliance (“HRC”)

The HRC must have a direct reporting line to the Managing Director, and have regular and unfettered access to the Board and the Audit and Risk Committee.

The role will include:

• Involving in, and having the authority to provide effective challenge to activities and decisions that may materially affect Freedom’s risk profile.

• Reviewing the key business risks and risk reports and recommending internal control enhancements

• Being a custodian of any risk appetite statements, risk frameworks, policies and charters and facilitating updates and developments of those documents on an on-going basis as required for Board oversight and approvals.

• Ongoing monitoring and reporting of Risk and Compliance functions,

e) Head of Legal

The Head of Legal’s compliance obligations include providing specific, general and compliance advice and guidance to business units, management, Team Leaders and the Board.

f) Senior Managers and Team Leaders

Senior Managers and Team Leaders are responsible for the day to day management of compliance risks and for ensuring that the procedures and guidance in support of Freedom’s integrity and ethical standards are adhered to in the areas for which they are responsible, including by ensuring appropriate training. This also includes responsibility for ensuring that appropriate remedial or disciplinary action is taken according to the relevant procedures if breaches are identified.

g) All Employees

Each individual in Freedom (including any contractor and agent) is expected to comply with all Freedom Policies and Procedures and be responsible for familiarising themselves with the Policies and Procedures that are relevant to their particular circumstances.

…

6. Framework Governance

a) Framework Governance

Freedom must ensure that the “Three Lines of Defence” model is understood and applied consistently to enable an effective governance and internal control environment. Accountability for Compliance is structured within this model as follows:

• Line 1: Business – owners of the compliance obligations, related compliance risks and compliance behaviours within their business;

• Line 2: Risk & Compliance Team – provide advice, review and oversight of obligations and ensure the compliance framework is fit for purpose; and

• Line 3: Audit – independent review of the Compliance framework and internal controls.

Freedom’s Three (3) Lines of Defence

Independent Review (3rd Line) Independent experts engaged to validate effectiveness of the compliance management systems. | |

Audit | |

Compliance Team (2nd Line Compliance personnel or subject matter experts that ensure compliance is done adequately and appropriately. Responsible for the Compliance Framework. | |

Risk & Compliance | Legal |

Business (1st Line) Owns compliance as part of their strategy, structure and day-to-day operations. Are responsible for behavioural compliance. | |||

Managing Director | Senior Management | Team Leaders | All Employees |

b) Compliance Forum

The line 2 Risk & Compliance Team and Head of Legal must meet on a regular basis to ensure that the Compliance framework is fit for purpose and is being consistently implemented. This Compliance forum should consider compliance obligations, risks, breaches and other compliance information and be attended by all line 2 Freedom compliance professionals.

(bold emphasis in original; underline emphasis added)

77 Mr McCool agreed in cross-examination that the description of Mr Cohen’s role as managing director accorded with his understanding; and that the description of his responsibilities as Head of Legal was accurate.

78 Mr McCool regularly spoke with Ms Osborne and later Ms Delahunty as the “line 2 risk and compliance team”.

79 On 1 December 2016, FIG was listed on the ASX. Mr McCool was heavily involved in the process that led to the listing of FIG, including providing assistance with the preparation of the prospectus. From this time, the companies within Freedom operated as one business, with business and management matters relating to the respective companies being reported to the directors of FIG. The directors of the subsidiary companies acted only to approve administrative or process matters, such as company accounts or a change of auditor, and did not receive management reports on the day-to-day operations of the particular subsidiary company.

80 Mr Cohen continued as the managing director and CEO of each of the companies within Freedom after the listing of FIG on the ASX.

81 In 2017 and following FIG’s public listing, Mr Cohen devoted less time to the day-to-day operations of Freedom and devoted more of his time to more strategic issues within Freedom. For example, his time was devoted to investor relations, pursuing acquisition opportunities for Freedom, developing new products and managing the relationship with Swiss Re.

82 In an average week he spent: (1) between 20 and 30 per cent of his time on investor relations; (2) about 10 to 20 per cent of his time on relationship management issues with Swiss Re; (3) between 10 to 30 per cent of his time developing new products; and (4) between 10 to 30 per cent of his time dealing with board and management related issues. At various times in 2017 and early 2018 between 20 and 80 per cent of his time was spent on a proposed transaction by which Freedom would acquire St Andrews Life and General Insurance companies from the Bank of Queensland (St Andrews acquisition).

83 Mr Cohen had confidence in his senior executive team to focus on the day-to-day operations of Freedom as most of them had worked for him (either at Freedom or in earlier roles) for a reasonably long time. Mr Cohen considered them to be competent executives with relevant experience and he felt that they worked well together.

84 In early 2017, Ms Davitt ceased working for Freedom. Freedom did not hire a replacement COO immediately and she was not replaced until February 2018, when Mr Orton commenced with Freedom as its COO. As a result, for most of 2017, the sales and operations managers reported directly to Mr Cohen (rather than reporting to him through the COO, as had been the case when Ms Davitt held that position).

85 On 18 January 2017, Mr McCool sent an email to Ms De Torres and Mr Light, which he copied to Mr Cohen, with the subject line “FSG – Freedom Protection Plan (1 February 2017)”, as follows:

Hi

Just updated the FSG - tiny changes as marked. Otherwise it seems ok. Not sure if you really want to give to Swiss Re for a look, otherwise we can look to print.

Note I didn’t put in anything about clawbacks or variable commission as per existing FSG.

86 The email attached a Financial Services Guide for the FPP, which included:

What services are provided?

Our representatives are authorised by us to:

• make you aware of the availability of the insurance protection provided by the Freedom Protection Plan.

• provide you with information on the product including a premium quote and a copy of the PDS.

• answer any questions that you may have about the product features.

• arrange for you to apply for the product and obtain an authority for the Insurer to obtain premium payments.

• assist with changes that you might request to your insurance after it has commenced.

We may also provide you with information and general advice about the product through our representatives or by means of additional promotional material.

…

How are our representatives paid?

Our representatives that arrange your insurance or make changes to it after it commences, are provided with the usual employee benefits such as salary and superannuation. They may also qualify for additional remuneration based on performance criteria that can include volume of sales. We may also pay a fee to people or organisations who refer customers to us.

(emphasis in original)

87 Mr McCool accepted in cross-examination that at this time he needed to, and did, understand how Freedom’s representatives were paid.

88 On 1 February 2017:

(1) an Administration Agreement between Freedom Administration and Swiss Re commenced. Under this agreement, Freedom Administration provided certain administrative services to Swiss Re in relation to the insurance products;

(2) a Services Agreement between INSA and Swiss Re commenced. This agreement also concerned the insurance products and provided for certain services in respect of these products to be provided by INSA to Swiss Re; and

(3) a product specification for the FPP was approved by Swiss Re and Freedom and signed by Mr Cohen. The product specification included:

2.6 Method of Distribution

The product will be offered through a combination of inbound and outbound calls through Freedom’s call centre. A simple, convenient no-advice process will be followed with no forms to complete or medical examinations required. All calls are recorded and the recording will form the basis of the application.

Initially, it is not intended that prospective customers will be able to apply directly through the Freedom Insurance website or by submitting an application contained in direct mail packs. However, these mediums will be used to promote the product and obtain expressions of interest by means of inbound calls.

2.7 Financial Product Advice

The product will be distributed by on a predominantly “no advice” basis. Call centre staff may be permitted by Freedom to provide limited general financial product advice to customers or prospective customers. Where Freedom permits the provision of general advice in this manner it will be fully scripted by Freedom. Promotional material may also contain basic general advice in connection with the product.

No personal financial product advice will be provided by Freedom or call centre staff to customers or prospective customers.

…

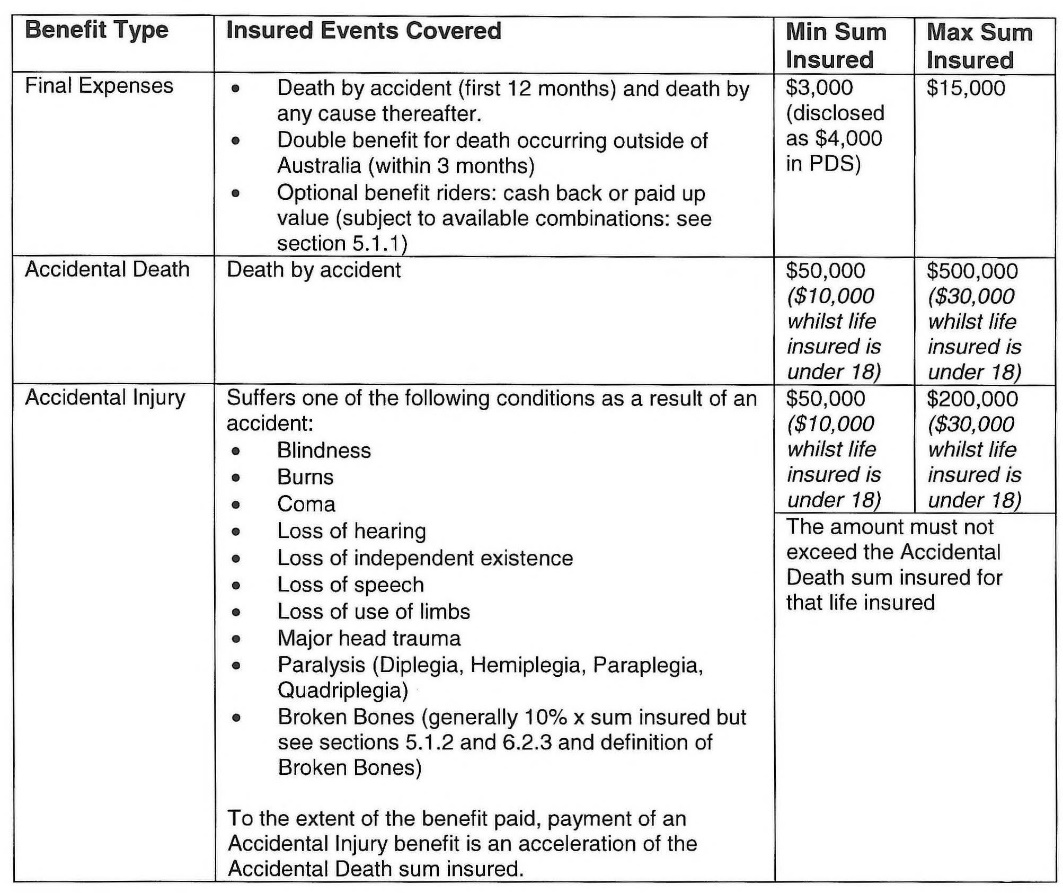

5.1 Benefit Overview

(bold emphasis in original; underline emphasis added)

89 As is apparent, the FPP provided three types of benefit or cover. In summary, those three types of benefit or cover were as follows:

(1) Final Expenses Cover (FEC) was a core benefit option, with cover of up to $15,000 payable upon death. This benefit could be used for any purpose once received, including the payment of funeral expenses, and was payable as a lump sum;

(2) Accidental Death Cover (ADC) was a core benefit option, with cover of up to $500,000 payable upon death by accident (subject to exclusions). The benefit payable was the amount of the sum insured that applied on the date of death, which was to be paid as a lump sum; and

(3) Accidental Injury Cover (AIC) – which could only be obtained if ADC was also obtained – provided cover of up to $200,000 payable upon the occurrence of particular specified injuries suffered as a result of an accident (as an advance of the accidental death benefit, and with the same exclusions).

90 The agreements between Freedom and Swiss Re entitled Freedom to commissions and fees payable by Swiss Re in connection with the distribution of the FPPs and the provision of associated services.

91 Freedom distributed the FPP on behalf of Swiss Re, through a combination of inbound and outbound telephone calls to or from Freedom’s call centre. Sales agents working in the call centre were provided with scripts to follow in their calls which prescribed the information that the sales agents were required to provide to potential customers during the course of the call.

92 It was Mr Cohen’s intention when establishing Freedom and developing the funeral insurance product that the FPP would be distributed by Freedom’s call centre on a “no advice” basis, in that neither general nor personal advice would be provided by call centre staff to the customer. Mr Cohen understood that the scripts that were provided to sales agents were developed on that basis.

93 From time to time when Mr McCool was discussing product documentation, scripts and other issues within Freedom’s business with Mr McCool, Mr McCool told Mr Cohen that Freedom did not have any general advice in its scripts.

94 The sales agents were supervised directly by team leaders, who had responsibility for several agents each, and ultimately reported to Mr Turner. The number of sales agents at Freedom fluctuated, but between 2016 and 2018, there were approximately 90 to 100 such agents.

95 The sales agents comprised a combination of Australian residents, sponsored agents and agents on working holiday visas. Many of the sales agents were from the United Kingdom and they were relatively young, often in their 20s. Many had university degrees and were working at call centres as relatively short-term employment to fund their travels.

96 Leads for the sales agents were generated by the marketing team and loaded into the dialer by the “Dialer Manager”. The Dialer was the system Freedom used to manage and optimise leads. Calls to customers were initiated by the Dialer and the sales agent took the calls and spoke with the customer using a Freedom sales script. There were certain things that a sales agent was required to say to a potential customer on any call and these were specified in the sales script.

97 On 17 February 2017, Freedom Insurance notified ASIC of the addition of Ms Osborne as a responsible manager on the Freedom AFSL.

98 On 30 May 2017, Ms Osborne provided to Ms De Torres a checklist that Mr McCool had prepared of AFSL requirements to be used in checking scripts. In an earlier email to Ms De Torres, Mr McCool stated:

Further to our meeting last week about the script, I have prepared a script AFSL checklist to assist with review/updating of the scripts.

Diane is just finishing a few bits and pieces and will send it you before long. It is more a list of the requirements at this stage and we will turn it into something that looks more like a checklist in due course so that we can retain a record of approving each script. It follows the legislation/regulations very closely.

We can add other obligations in the future to cover other obligations

99 On about 14 June 2017, Ms Osborne prepared a Risk Management Framework Review document, which included:

Recommended Resolution

The Board resolved that:

1. The current risk management framework continues to be sound and sufficient for the financial year ending 30 June 2017.

2. Statements be included in FIG’s annual report confirming that the Board reviewed FIG’s risk management framework during FY17 and was satisfied that it continues to be sound

Background

In accordance with Recommendation 7.2 of the ASX Corporate Governance Principles and Recommendations, prior to 30 June 2017 the Board or the Audit and Risk Committee should:

(a) undertake an annual review of FIG’s risk management framework to satisfy itself that it continues to be sound; and

(b) disclose in its FY17 Corporate Governance Statement, whether such a review has taken place.

Overview

Freedom has a number of policies, practices and processes which currently ensures that there are:

• Adequate procedures for identifying risks;

• Policies that are a reasonable balance between cost and risk; and

• Measures to ensure the organisation is adequately protected.

This paper seeks to provide the Board with an overview of the current risk management processes within FIG.

Controls and Management of Risks

Current controls used to manage risks include:

• Small hands-on management team aware of the primary risks facing the business and responsible for managing and monitoring those risks;

• Management structures that enable immediate and decisive action to be taken to address risks as they arise;

• Regular management meetings and interactions to enable identification of issues and risks:

• Corporate decision making which includes a discussion of the potential risks embedded in those decisions.

• Alignment of interests between management and the business

• Expertise in all relevant areas of the business including legal and financial

• Tight controls on expenditure with authorities generally limited to CEO and CFO

…

• Checklists for ensuring legal compliance

• Review and sign off approval process for documentation and processes

• Comprehensive sales agent training and Scripting for all sales calls

Audits and reviews (External)

Recent reviews and audits have confirmed no adverse findings. Improvements suggested have been implemented, where required, to address any issues or gaps identified. These include:

• AFSL Audits of both Spectrum and Freedom by Crowe Horwath

• A financial audit by Crowe Horwath of both Freedom and Spectrum

• A due diligence review by Swiss Re of the distribution and administration processes and controls prior to product launches

• A due diligence process conducted by Piper Alderman as part of the IPO and ASX listing process in 2016

Recent Enhancements

…

• employment of a Head of Risk and Compliance

(bold and italic emphasis in original; underline emphasis added)

100 In Mr Cohen’s view, the underlined controls were consistent with the way in which the Freedom senior executive team operated.

101 Mr McCool understood from reading the Risk Management Framework Review document that he and other executives of Freedom were required to take immediate and decisive action where necessary to address risks as they arose and to have regular management meetings and interaction to enable the identification of issues and risks.

102 The Risk Management Framework Review document also referred to “Recent Enhancements”, stating:

As part of its aim for continuous improvement considerable progress has been made in the previous 9 months towards formally documenting and implementing the risk management process ...

103 This was consistent with Mr Cohen’s view of the way in which Freedom was moving. Freedom began to develop more formal practices and procedures as the organisation grew and in particular after the listing of FIG. Mr Cohen recalled numerous conversations with Mr McCool about the development of these practices and procedures within Freedom in which Mr McCool told Mr Cohen that controls and processes would be added as the organisation grew, with controls that were appropriate for its size.

104 On 8 September 2017 at 9:33am, Mr Cohen and Mr Turner (among many others) received a regular sales report which indicated a significant downturn in Freedom’s sales. At 9:57am, Mr Cohen sent an email to Mr Turner: “What’s happening? When do you see turnaround & any specific/urgent action plans”. At 10:15am, Mr Turner responded indicating that he had been investigating the issue, and would report back to Mr Cohen the following Monday (11 September 2017). Later in the evening of 8 September 2017 (at 8:02pm), Mr Turner sent a further email to Mr Cohen describing several possible reasons for the downturn in sales, including the quality of sales leads that had been used to initiate calls by sales agents.

105 In this regard, Freedom acquired leads which were used by the Dialer to initiate calls on behalf of sales agents. The leads purchased by Freedom varied in quality and cost. High quality leads were, for example, people who had called directly asking for a funeral insurance policy. Such leads were more expensive but typically had high conversion rates. An example of a lower quality lead is someone who had taken part in a survey and ticked a box indicating that they were content to receive a call about funeral insurance. Such leads were less expensive and typically had lower conversion rates.

106 The slump in sales caused a drop in the morale, and the commission earnings, of the sales agents.

107 Also on 8 September 2017, Mr Cohen forwarded to Mr McCool an email he had received from Ms Bronwyn Kirwan of Swiss Re concerning the LIF Reforms and a proposed review to be conducted by Swiss Re concerning remuneration. Ms Andrews, Mr McCool and Ms Norma Pezikian were involved in that review on behalf of Freedom.

108 Mr McCool understood the LIF Reforms to be an important piece of legislation and that Mr Cohen, by forwarding the email to Mr McCool expected Mr McCool to take appropriate steps with respect to the email. He also understood that the proposed changes affected remuneration for sales agents. Mr McCool familiarised himself with the proposed changes.

109 Mr Cohen:

(1) was involved in numerous discussions about the LIF Reforms and the impact they would have on Freedom’s business, both with executives at Freedom and with people at Swiss Re (and Ms Kirwan in particular);

(2) understood in 2017 that the most significant way in which the LIF Reforms could potentially impact Freedom’s business was through the introduction of a cap on upfront commissions and new minimum periods for “clawbacks” of commissions where policies had lapsed;

(3) was concerned that although the LIF Reforms capped, but did not completely ban, upfront commissions, a wholesale ban on upfront commissions could be introduced in the near future. Upfront commissions were a significant proportion of Freedom’s business and so a ban on upfront commissions would affect Freedom’s entire business; and

(4) expected that Mr McCool would be considering the LIF Reforms and their impact on Freedom’s business and based on his discussions with Mr McCool in 2017, believed he was doing that.

110 Mr Cohen was also involved in numerous discussions with Mr McCool and other members of Freedom’s senior executive team and Swiss Re about whether changes would have to be made to the commission arrangements between Freedom and Swiss Re in order to comply with the new legislation. Mr McCool was advising Freedom about the impact of the LIF Reforms and working with Swiss Re to consider the impact that the reforms might have on the commission arrangements between Swiss Re and Freedom.

111 In October 2017, Ms Delahunty commenced with Freedom as a risk and compliance officer. She reported to Mr McCool and worked with Ms Osborne within the “compliance function” of Freedom.

112 On 4 October 2017, Mr Cohen sent a report to the board of FIG, identifying the cause of the problem with sales as the quality of sales leads.

113 Thereafter, the low-quality leads were removed from the Dialer. Some of the lead suppliers also compensated Freedom by providing additional better quality leads. However, this took a month or two to resolve.

114 Mr Cohen also indicated in his 4 October 2017 report that he anticipated that Freedom’s September 2017 results would be significantly below forecasts.

115 On 13 October 2017, Ms Kirwan of Swiss Re sent an email to Mr Cohen and Mr McCool indicating that Swiss Re had been working through the proposed LIF Reforms and was working towards providing a formal opinion to Freedom before the end of October 2017.

116 On 18 October 2017, Mr Cohen presented a detailed report to the directors of FIG concerning the decline in sales. The board resolved to closely monitor this issue and to determine at the end of October 2017 whether an announcement to the market should be made.

117 On 25 October 2017, Mr Weinstein sent an email to Mr Light, which was copied to Mr Turner, Mr Cohen and Ms De Torres, in which he suggested various ways of boosting sales, including incentives.

118 On 3 November 2017, FIG published an ASX market announcement downgrading its revenue forecasts for the first half of the financial year ending 30 June 2018.

119 On 6 November 2017, Ms Pezikian sent an email to various persons and copied it to Mr Cohen and Mr McCool (among others), which referred to the work that Freedom was doing with Swiss Re in order to confirm the changes that needed to be made as a result of the LIF Reforms.

120 On the same day, Mr McCool sent an email to Mr Cohen and Ms Pezikian indicating that he had not heard back from Herbert Smith Freehills (HSF) on the “life insurance commission advice” and that it was important to receive that advice so that Freedom could “get a move on”.

121 On 8 November 2017, Ms Pezikian sent an email to Mr Josh Hunt of Swiss Re (copied to Mr McCool) asking if he had received external advice on the LIF Reforms.