Federal Court of Australia

Australian Securities and Investments Commission v RAMS Financial Group Pty Ltd [2025] FCA 1087

File number(s): | NSD 885 of 2025 |

Judgment of: | SHARIFF J |

Date of judgment: | 4 September 2025 |

Catchwords: | PRACTICE AND PROCEDURE – interlocutory application for third party to be granted leave to intervene or to be appointed as an amicus curiae or contradictor in civil penalty proceedings – where case management stay sought in the alternative – where the proposed intervenor is the lead applicant in representative proceedings involving the respondent – where parties to the civil penalty proceedings have agreed to facts and admissions made by the respondent and also agreed on penalty – where the proposed intervener disputes facts agreed between the parties – where the proposed intervener accepts it has no direct legal interest in the determination of the civil penalty proceedings – whether the interests of the proposed intervener will be sufficiently impacted by a declaration in these proceedings – application dismissed COSTS – where the proposed intervenor submits that no order should be made as to costs – particular circumstances do not justify deviation from the ordinary rule as to costs – orders made |

| |

Legislation: | Australian Securities and Investments Commission Act 2001 (Cth) s 12CB Competition and Consumer Act 2010 (Cth) s 51ACB, Sch 2 (Australian Consumer Law) s 21 Federal Court of Australia Act 1976 (Cth) ss 5, 23, 37AF, 37AG(1)(a), 37M, 37N, 43 National Consumer Credit Protection Act 2009 (Cth) ss 31, 47, 73 Federal Court Rules 2011 (Cth) r 9.12(1) |

Cases cited: | Ashby v Slipper [2014] FCAFC 15; 219 FCR 322 Australian Competition and Consumer Commission v Dataline.net.au Pty Ltd [2006] FCA 1427; 236 ALR 665 Australian Competition and Consumer Commission v MSY Technology Pty Ltd [2012] FCAFC 56; 201 FCR 378 Australian Securities and Investments Commission v AGM Markets Pty Ltd (in liq) (No 3) [2020] FCA 208; 275 FCR 57 Australian Securities and Investments Commission v Australia and New Zealand Banking Group Limited [2023] FCA 256 Australian Securities and Investments Commission v Commonwealth Bank of Australia [2020] FCA 790 Australian Securities and Investments Commission v Commonwealth Bank of Australia [2022] FCA 1422 Australian Securities and Investments Commission v Westpac Banking Corporation [2018] FCA 1733; 132 ACSR 230 Australian Securities and Investments Commission v Whitebox Trading Pty Ltd [2017] FCAFC 100; 251 FCR 448 Bauer Media Pty Ltd v Wilson [2018] VSCA 68 Environment Council of Central Queensland Inc v Minister for the Environment and Water (No 2) [2024] FCAFC 97 Firebird Global Master Fund II Ltd v Republic of Nauru (No 2) [2015] HCA 53; 327 ALR 192 George v Fletcher (Trustee) (No 2) [2010] FCAFC 71 Hua Wang Bank Berhad v Commissioner of Taxation [2013] FCAFC 28 Levy v Victoria [1997] HCA 31; 189 CLR 579 Minister for Industry, Tourism & Resources v Mobil Oil Australia Pty Ltd [2004] FCAFC 72 Northern Territory v Sangare [2019] HCA 25; 265 CLR 164 NW Frozen Foods Pty Ltd v Australian Competition and Consumer Commission [1996] FCA 1134; 71 FCR 285 Orica Australia Pty Ltd v Coal Mining Industry (Long Service Leave Funding) Corporation [2024] FCA 1104 Roadshow Films Pty Ltd v iiNet Ltd [2011] HCA 54; 248 CLR 37 Sharman Networks Ltd v Universal Music Australia Pty Ltd [2006] FCAFC 178; 155 FCR 291 Sydney Trains v Australian Rail, Tram and Bus Industry Union [2024] FCA 1466 Volkswagen Aktiengesellschaft v ACCC [2021] FCAFC 49; 284 FCR 24 |

Division: | General Division |

Registry: | New South Wales |

National Practice Area: | Commercial and Corporations |

Sub-area: | Commercial Contracts, Banking, Finance and Insurance |

Number of paragraphs: | 77 |

Date of hearing: | 26 August 2025 |

Counsel for the Applicant | Mr M Brady KC with Mr S Cleary |

Solicitor for the Applicant | Gadens |

Counsel for the Respondent | Mr S Lawrance SC with Ms E Bathurst |

Solicitor for the Respondent | Allens |

Counsel for Top Ryde Financial Services Pty Ltd | Ms T Epstein with Mr S Gerber |

Solicitor for Top Ryde Financial Services Pty Ltd | Morris Mennilli |

ORDERS

NSD 885 of 2025 | ||

| ||

BETWEEN: | AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Applicant | |

AND: | RAMS FINANCIAL GROUP PTY LTD ACN 105 207 538 Respondent | |

TOP RYDE FINANCIAL SERVICES PTY LTD Interlocutory Applicant | ||

order made by: | SHARIFF J |

DATE OF ORDER: | 4 September 2025 |

THE COURT ORDERS THAT:

1. The interlocutory application filed by Top Ryde Financial Services Pty Ltd on 23 June 2025 be dismissed.

2. Top Ryde Financial Services Pty Ltd pay the costs incurred by the applicant and respondent in responding to the interlocutory application, as agreed or taxed.

3. Pursuant to s 37AF of the Federal Court of Australia Act 1976 (Cth) and on the ground specified in s 37AG(1)(a), namely that the order is necessary to prevent prejudice to the proper administration of justice, for a period of 10 years from the date of this Order, the following information be suppressed and not published:

(a) references, in connection with Federal Court proceeding number NSD 885/2025, to the names (excluding references to the name Top Ryde Financial Services Pty Ltd), and locations, where applicable, of the RAMS Franchises, RAMS Franchise principals and loan writers, including their initials, as referred to at paragraphs 59(b), 59(c), and 75 to 77 and pages 34 to 56 of the Statement of Agreed Facts and Admissions and contained at Annexure SC-01 of the affidavit of Scott Couper dated 3 June 2025.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

SHARIFF J:

1. INTRODUCTION

1 These reasons deal with an application made by Top Ryde Financial Services Pty Ltd (TRFS) to, amongst other things, intervene or be appointed as a contradictor or an amicus curiae in the substantive civil penalty proceedings as between the applicant (ASIC) and the respondent, Rams Financial Group Pty Ltd (RFG) (the Civil Penalty Proceedings). RFG is a wholly-owned subsidiary of Westpac Banking Corporation (Westpac).

2 In the Civil Penalty Proceedings, ASIC seeks declaratory relief and the imposition of pecuniary penalties against RFG for contraventions of the National Consumer Credit Protection Act 2009 (Cth) (the Credit Act). The relief sought by ASIC is set out in the Originating Application filed on 3 June 2025.

3 The gravamen of the allegations made by ASIC relate to RFG’s conduct in its capacity as the holder of an “Australian credit license” (ACL) under the Credit Act, under which license it was authorised to engage in credit activities other than as a credit provider, and under which it assisted consumers to obtain home loans financed by Westpac (albeit those loans were branded as “RAMS Home Loans”). At all relevant times, RFG operated a Franchise Network (RAMS Franchise Network) by which its franchisees (RAMS Franchisees) used the RAMS business name to provide credit assistance to consumers in relation to the distribution of RAMS-branded home loans. RFG appointed RAMS Franchisees and their staff as Authorised Credit Representatives (ACRs) of RFG for the purposes of providing that credit assistance.

4 ASIC and RFG have reached an agreement in relation to the disposition of the Civil Penalty Proceedings as reflected in the Updated Statement of Agreed Facts and Admissions on Liability dated 30 July 2025 (Liability SAFA), the Statement of Agreed Facts on Relief dated 11 July 2025 (Penalty SOAF) and the joint submissions as to penalty filed on 5 August 2025 (Joint Submissions). The hearing of the Civil Penalty Proceedings is listed before me on 21 October 2025 for determination of the appropriate penalty to impose in light of the admitted facts and contraventions.

5 TRFS wishes to be heard in the Civil Penalty Proceedings. It is one of the RAMS Franchisees. It is also the lead applicant in proceedings NSD 671/2024 in this Court, being representative proceedings brought on behalf of some but not all of the former RAMS Franchisees against RFG (the Class Action Proceedings). The Class Action Proceedings arise in the context of the fact that RFG terminated the representative and franchise agreements of TRFS and group members. TRFS brings claims on its own behalf, and on behalf of group members, alleging that RFG breached a contractual and statutory obligation to deal with them in good faith, engaged in unconscionable conduct within the meaning of s 21 of the Australian Consumer Law (as set out in Sch 2 of the Competition and Consumer Act 2010 (Cth) and/or s 12CB of the Australian Securities and Investments Commission Act 2001 (Cth) (ASIC Act), and contravened cl 6 of the (now superseded) Franchising Code of Conduct and thereby contravened s 51ACB of the Competition and Consumer Act.

6 TRFS contends that there is an overlap between the Civil Penalty Proceedings and the Class Action Proceedings and that its interests are sufficiently affected such that it should be granted leave to intervene in these proceedings, or at least be appointed as a contradictor or as an amicus curiae. Alternatively, it contends that there should be a “case management stay” of the Civil Penalty Proceedings pending the final determination of the Class Action Proceedings.

7 For the reasons that follow, TRFS’ application should be dismissed.

2. THE APPLICABLE PRINCIPLES

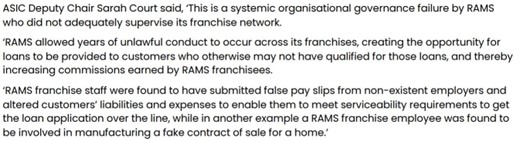

8 Sections 5(2) and 23 of the Federal Court of Australia Act 1976 (Cth) (FCA Act) and r 9.12(1) of the Federal Court Rules 2011 (Cth) (FC Rules) empower the Court to exercise a discretion to grant a person leave to intervene. Rule 9.12 of the FC Rules provides as follows:

(1) A person may apply to the Court for leave to intervene in a proceeding with such rights, privileges and liabilities (including liabilities for costs) as may be determined by the Court.

(2) The Court may have regard to:

(a) whether the intervener's contribution will be useful and different from the contribution of the parties to the proceeding; and

(b) whether the intervention might unreasonably interfere with the ability of the parties to conduct the proceeding as the parties wish; and

(c) any other matter that the Court considers relevant.

(3) When giving leave, the Court may specify the form of assistance to be given by the intervener and the manner of participation of the intervener, including:

(a) the matters that the intervener may raise; and

(b) whether the intervener's submissions are to be oral, in writing, or both.

9 In Roadshow Films Pty Ltd v iiNet Ltd [2011] HCA 54; 248 CLR 37 at [2], French CJ, Gummow, Hayne, Crennan and Kiefel JJ identified the circumstances in which a person may be granted leave to intervene. Their Honours observed:

A non-party whose interests would be directly affected by a decision in the proceeding, that is one who would be bound by the decision, is entitled to intervene to protect the interest likely to be affected. A non-party whose legal interest, for example, in other pending litigation is likely to be affected substantially by the outcome of the proceedings in this Court will satisfy a precondition for leave to intervene. Intervention will not ordinarily be supported by an indirect or contingent affection of legal interests following from the extra-curial operation of the principles enunciated in the decision of the Court or their effect upon future litigation.

10 In respect of this statement, Snaden J recently observed in Orica Australia Pty Ltd v Coal Mining Industry (Long Service Leave Funding) Corporation [2024] FCA 1104 at [9] that:

As to the final of those three scenarios, it is significant to note the qualifier, “ordinarily”. There is no blanket rule by which a person must be denied leave to intervene if his or her rights stand to be affected only in the ways that the third category contemplates: ASF17 v Commonwealth (2024) 98 ALJR 782, 786 [16] (Gageler CJ, Gordon, Steward, Gleeson, Jagot and Beech-Jones JJ), 798 [83] (Edelman J).

11 In Sydney Trains v Australian Rail, Tram and Bus Industry Union [2024] FCA 1466, in refusing the ACTU’s application to intervene, Wheelahan J adopted the Victorian Court of Appeal's distillation of principle in Bauer Media Pty Ltd v Wilson [2018] VSCA 68 where the Court of Appeal (Tate and Beach JJA) relevantly reasoned at [7]:

The principles upon which a court may grant leave to intervene are not in dispute. The governing principles may be briefly summarised as follows:

(1) A non-party whose interests would be affected directly by a decision in a proceeding is entitled to intervene to protect the interest liable to be affected.

(2) Where the legal interests of a person may be affected by the operation of precedent or by the doctrine of stare decisis, a court may grant leave to intervene if the interest is sufficiently substantial.

(3) Where a person having the necessary legal interest to apply for leave to intervene can show that the parties to the particular proceeding may not present fully the submissions on a particular issue, being submissions which the Court should have to assist it to reach a correct determination, the Court may exercise its jurisdiction by granting leave to intervene.

(4) A grant of leave may be limited, and subject to such conditions as to costs or otherwise as will do justice as between the parties.

(5) A non-party must satisfy the Court that its contribution, as an intervener, will be useful and different from the contribution of the parties, and that the intervention will not unreasonably interfere with the conduct of the proceeding.

12 Separately to intervention, the circumstances in which the Court may appoint a person as a contradictor or amicus curiae were also considered in Roadshow Films, where their Honours stated at [4] and [6]:

The grant of leave for a person to be heard as an amicus curiae is not dependent upon the same conditions in relation to legal interest as the grant of leave to intervene. The Court will need to be satisfied, however, that it will be significantly assisted by the submissions of the amicus and that any costs to the parties or any delay consequent on agreeing to hear the amicus is not disproportionate to the expected assistance.

…

In considering whether any applicant should have leave to intervene in order to make submissions or to make submissions as amicus curiae, it is necessary to consider not only whether some legal interests of the applicant may be indirectly affected but also, and in this case critically, whether the applicant will make submissions which the Court should have to assist it to reach a correct determination. Ordinarily then, in cases like the present where the parties are large organisations represented by experienced lawyers, applications for leave to intervene or to make submissions as amicus curiae should seldom be necessary or appropriate and if such applications are made it would ordinarily be expected that the applicant will identify with some particularity what it is that the applicant seeks to add to the arguments that the parties will advance.

(Emphasis added.)

13 There is an important distinction between an intervener and a person appointed as an amicus curiae. As the Full Court explained in Sharman Networks Ltd v Universal Music Australia Pty Ltd [2006] FCAFC 178; 155 FCR 291 at [7] to [9] (Branson, Lindgren and Finkelstein JJ):

There can be a degree of confusion in the use of the terms ‘amicus curiae’ and ‘intervener’. At the extremes, the distinction is clear enough. Where a court invites a legal practitioner to assist it by ensuring that its attention is drawn to all relevant law and arguments, the legal practitioner is an amicus curiae, not an intervener. On the other hand, where a person's interests may be affected by the outcome, the person, if permitted by the court, becomes an ‘intervener’, not an amicus curiae.

There is, however, a large intermediate area. A non-lawyer entity may seek to become involved in litigation. It may be an official body, such as the Australian Competition and Consumer Commission or the Australian Securities and Investments Commission (we leave to one side any special statutory power to intervene or to apply for leave to intervene). It may be an organisation that puts itself forward as acting in the public interest. The Amici so characterised themselves. Yet a further class of case is illustrated by an industry, trade or professional association, whose members' interests may be affected, directly or indirectly, by the outcome of the litigation.

While it is easy to see the first of these three intermediate categories as comprising entities acting in the public interest, entities in the second and third classes may be acting, to various degrees, both in the public interest and in private interests.

14 The Full Court observed in Minister for Industry, Tourism & Resources v Mobil Oil Australia Pty Ltd [2004] FCAFC 72 at [77] (Branson, Sackville and Gyles JJ) that, “whatever the position in criminal cases, in a civil penalty case where there is no contradictor, the Court may request assistance from an amicus curiae or a potential intervenor”: see, e.g., Volkswagen Aktiengesellschaft v ACCC [2021] FCAFC 49; 284 FCR 24 at [5] (Wigney, Beach and O'Bryan JJ); Australian Securities and Investments Commission v Whitebox Trading Pty Ltd [2017] FCAFC 100; 251 FCR 448 at [4] (Allsop CJ, Middleton and Bromwich JJ); Australian Securities and Investments Commission v Westpac Banking Corporation [2018] FCA 1733; 132 ACSR 230 (Perram J).

3. AN OVERVIEW OF THE RESPECTIVE PROCEEDINGS

15 In order to make sense of the submissions advanced before me, it is necessary to identify the relevant issues raised in the Civil Penalty Proceedings and those raised in the Class Action Proceedings.

3.1 The Civil Penalty Proceedings

16 In the Civil Penalty Proceedings, the focus is on RFG’s obligations under the Credit Act. Relevantly, those obligations include primarily ss 31 and 47(1) of the Credit Act.

17 Section 31(1) of the Credit Act provides:

Prohibition on conducting business with unlicensed persons

(1) A licensee must not:

(a) engage in a credit activity; and

(b) in the course of engaging in that credit activity, conduct business with another person who is engaging in a credit activity;

if, by engaging in the credit activity, the other person contravenes section 29 (which deals with the requirement to be licensed).

Civil penalty: 5,000 penalty units.

18 The prohibition in s 31(1) is on a licensee conducting business with an unlicensed person. As I will return to below, the relevant licensee is RFG. Neither TRFS nor any of the group members are licensees.

19 Section 47(1) of the Credit Act provides as follows:

General conduct obligations

(1) A licensee must:

(a) do all things necessary to ensure that the credit activities authorised by the licence are engaged in efficiently, honestly and fairly; and

(b) have in place adequate arrangements to ensure that clients of the licensee are not disadvantaged by any conflict of interest that may arise wholly or partly in relation to credit activities engaged in by the licensee or its representatives; and

(c) comply with the conditions on the licence; and

(d) comply with the credit legislation; and

(e) take reasonable steps to ensure that its representatives comply with the credit legislation; and

(ea) comply with the Reference Checking and Information Sharing Protocol; and

(f) maintain the competence to engage in the credit activities authorised by the licence; and

(g) ensure that its representatives are adequately trained, and are competent, to engage in the credit activities authorised by the licence; and

(h) have an internal dispute resolution procedure that:

(i) complies with standards and requirements made or approved by ASIC in accordance with the regulations; and

(ii) covers disputes in relation to the credit activities engaged in by the licensee or its representatives; and

(ha) give to ASIC the same information it would be required to give under subparagraph 912A(1)(g)(ii) of the Corporations Act 2001 if it were a financial services licensee; and

(i) be a member of the AFCA scheme; and

(j) have compensation arrangements in accordance with section 48; and

(k) have adequate arrangements and systems to ensure compliance with its obligations under this section, and a written plan that documents those arrangements and systems; and

(l) unless the licensee is a body regulated by APRA:

(i) have available adequate resources (including financial, technological and human resources) to engage in the credit activities authorised by the licence and to carry out supervisory arrangements; and

(ii) have adequate risk management systems; and

(m) comply with any other obligations that are prescribed by the regulations.

20 The focus of the general obligations in s 47(1) is on the conduct of the licensee which, here, is relevantly, RFG. The relevant paragraphs of s 47(1) focus on whether the licensee had in place policies and procedures, undertook training, and took other steps to ensure that it, and its representatives, comply with the credit legislation. In relation to s 47(1)(a), it has been held that it is “not in doubt that a contravention of the ‘efficiently, honestly and fairly’ standard does not require a contravention or breach of a separately existing legal duty or obligation”: Australian Securities and Investments Commission v AGM Markets Pty Ltd (in liq) (No 3) [2020] FCA 208; 275 FCR 57 at [512] (Beach J). Rather, it is a provision that looks at the licensee’s behaviour more generally rather than with regard to any one person: AGM Markets at [525]. In this regard, it has been held that the use of the word “ensure” in s 47(1)(a) imports a forward-looking element into the obligation. It is necessary not only to act efficiently, honestly and fairly from day to day, but to take steps to guard against lapses from that standard by employees or representatives: Australian Securities and Investments Commission v Commonwealth Bank of Australia [2022] FCA 1422 at [146] (Downes J).

21 Similarly, it has been held that s 47(1)(e) “is concerned with the processes and procedures implemented by a licensee”: Australian Securities and Investments Commission v Australia and New Zealand Banking Group Limited [2023] FCA 256 at [52] (O’Bryan J).

22 In the Civil Penalty Proceedings, ASIC contends, and RFG accepts, that during the period 3 June 2019 to 30 April 2023 (the Relevant Period), Westpac and RFG undertook investigations, through Westpac’s Group Investigations (GI) and Secured Lending Taskforce (SLTF) teams, into allegations of misconduct relating to RAMS Franchisees. The nature of the alleged misconduct investigated by Westpac varied widely. It included allegations relating to:

(a) the acceptance of referrals from unaccredited referrers in breach of the RAMS Referrer Policy (Unaccredited Referrer Misconduct);

(b) engagement in credit activities where there was a conflict of interest in breach of the RAMS Conflict of Interest Policy (Conflict of Interest Misconduct);

(c) the submission of loan applications which included false information and/or documents (False Documentation Misconduct);

(d) transferring funds in relation to loans, including by facilitating the payment of customer arrears payments, with the result that the RAMS Franchise continued to receive commission payments and making a payment to a customer for the purpose of satisfying the customer’s settlement fees and the first year of the annual package fee (Transfer of Funds Misconduct);

(e) misusing information and IT systems (Privacy and IT Misconduct); and

(f) other types of misconduct in breach of RAMS policies.

23 The GI and SLTF teams found that much of that alleged misconduct was substantiated.

24 On the basis of the outcome of these investigations, ASIC was satisfied that RFG had contravened the Credit Act. To that end, the Originating Application seeks the following relief:

1. A declaration, pursuant to section 166 of the National Consumer Credit Protection Act 2009 (Cth) (Credit Act) that, between 3 June 2019 and 30 April 2023, the Respondent (RFG) contravened section 31(1) of the Credit Act on 84 occasions (as identified in Schedule 2 to the Statement of Agreed Facts and Admissions that is Annexure SC-1 to the Affidavit of Scott Couper filed 3 June 2025), by its representatives accepting referrals of consumers for loans, in circumstances where the referrers were contravening s 29 of the Credit Act in making the referrals.

2. A declaration, pursuant to section 166 of the Credit Act that, between 3 June 2019 and 30 April 2023, RFG, while engaging in credit activities, failed to do all things necessary to ensure that the credit activities authorised by its licence were engaged in efficiently, honestly and fairly, in contravention of sections 47(1)(a) and 47(4) of the Credit Act, by failing to:

(a) implement effective controls to ensure that its representatives complied with relevant policies and procedures;

(b) establish adequate compliance audit and routine loan file review procedures to detect misconduct;

(c) adequately respond to possible misconduct within the RAMS Franchise Network;

(d) have in place adequate arrangements to ensure that its clients were not disadvantaged by any conflict of interest that might have arisen wholly or partly in relation to credit activities engaged in by it or its representatives, in contravention of section 47(1)(b) of the Credit Act;

(e) comply with the credit legislation, in contravention of section 47(1)(d) of the Credit Act;

(f) take reasonable steps to ensure that its representatives complied with the Credit Act, in contravention of section 47(1)(e) of the Credit Act; and

(g) comply with section 31(1) of the Credit Act as described in Declaration 1 herein.

3. A declaration, pursuant to section 166 of the Credit Act that, between 3 June 2019 and 30 April 2023, RFG, while engaging in credit activities, contravened sections 47(1)(b) and 47(4) of the Credit Act by failing to have in place adequate arrangements to ensure that its clients were not disadvantaged by any conflict of interest that might have arisen wholly or partly in relation to credit activities engaged in by it or its representatives.

4. A declaration, pursuant to section 166 of the Credit Act that, between 3 June 2019 and 30 April 2023, RFG, while engaging in credit activities, failed to take reasonable steps to ensure that its representatives complied with the Credit Act, in contravention of sections 47(1)(e) and 47(4) of the Credit Act, by failing to:

(a) implement effective controls to ensure that its representatives complied with relevant policies and procedures;

(b) establish adequate compliance audit and routine loan file review procedures to detect misconduct;

(c) adequately respond to possible misconduct within the RAMS Franchise Network; and (d) have in place adequate arrangements to ensure that its clients were not disadvantaged by any conflict of interest that might have arisen wholly or partly in relation to credit activities engaged in by it or its representatives.

5. A declaration, pursuant to section 21 of the FCA Act that, between 3 June 2019 and 30 April 2023, RFG contravened section 47(1)(d) of the Credit Act by failing to comply with each of sections 31(1), 47(1)(a), 47(1)(b) and 47(1)(e) of the Credit Act.

(Emphasis added.)

25 It will be immediately evident that each of these proposed declarations is directed to the conduct of RFG. It will also be immediately apparent that there is a distinction in the prayers for relief relating to contraventions of s 31(1) of the Credit Act (prayer 1) and those relating to contraventions of s 47(1) (prayers 2 to 5). In relation to the former, ASIC’s case against RFG (which is admitted) proceeds on the basis that the contravention is established by conduct established to be contrary to the statutory norm stipulated in s 31(1), namely, acceptance of referrals from unaccredited persons and, specifically, where it was RFG’s representatives (not RFG itself) that are said to have accepted such referrals. By contrast, the latter contraventions of s 47(1) all relate to conduct (which is admitted) that is said to establish a failure in systems or policies, or inadequacies in relation to them. Whilst that too is said to be conduct that is contrary to the statutory norm in s 47(1), it is a qualitatively different norm to that contained in s 31(1) of the Credit Act.

26 As set out below, TRFS contends that, irrespective of the different quality of the conduct on the part of RFG that is said to give rise to the contravening conduct, both sets of contraventions have (in the main) a necessary predicate fact that it was the conduct of RFG’s representatives, and specifically, the relevant RAMS Franchisees, that provides the factual foundation to the respective contraventions.

3.2 The Class Action Proceedings

27 The pleadings in the Class Action Proceedings comprise TRFS’ Amended Statement of Claim filed 10 June 2025 and RFG’s Amended Defence filed 4 July 2025.

28 The pleadings in the Class Action Proceedings put in issue the nature and quality of the investigations conducted by Westpac and RFG that led to the “substantiated findings of misconduct” as against RAMS Franchisees. TRFS alleges that the process of conducting the relevant investigations by Westpac:

(a) was flawed;

(b) did not provide a proper basis for finding the alleged anomalies existed;

(c) further or alternatively, identified issues which, according to the RAMS policies, were within the responsibility of RFG and not TRFS or group members to detect and remedy;

(d) further or alternatively, did not demonstrate any systemic issues or any material fault by TRFS or group members.

29 It is clear to me that a central factual dispute in the Class Action Proceedings is whether the investigations in fact identified any wrongdoing on the part of TRFS, or on the part of group members. TRFS submits that the alleged misconduct or anomalies were either, inter alia, not anomalies or, even if they were, they were not anomalies that the RAMS franchise systems gave RAMS Franchisees the tools to detect. TRFS further contends in the Class Action Proceedings that Westpac and RFG’s investigations did not provide for an adequate (or any) opportunity for TRFS and group members to respond to the allegations or to the extent that responses were given, they were not properly considered. It is said that this and other conduct establishes that RFG did not comply with its obligations of good faith arising under the franchise agreements and the Franchising Code, and otherwise engaged in unconscionable conduct in contravention of the Competition and Consumer Act and the ASIC Act.

30 The various assertions made by TRFS in the Class Action Proceedings are denied by RFG. For present purposes, TRFS draws attention to the fact that a live issue in the Class Action Proceedings is whether the TRFS and group members engaged in any of the alleged conduct so as to substantiate the findings of misconduct including the same or similar matters that are the subject of the Civil Penalty Proceedings. TRFS also draws attention to the fact that RFG in its defence relies upon the fact that particular breach reports were reported to ASIC as a basis upon which it seeks to justify its decision to revoke and/or terminate the relevant arrangements with the RAMS Franchisees. TRFS also points out that in its defence that RFG has reserved the right to rely upon other matters that existed at the time of revocation or termination which would have justified the same decision that it made (had those reasons been known to RFG at the relevant time). TRFS submitted that these aspects of RFG’s defence highlighted the overlap between the two proceedings and the need for it to be heard in the Civil Penalty Proceedings.

4. TRFS’ SUBMISSIONS

31 TRFS accepted that it did not have a direct legal interest in the determination of the Civil Penalty Proceedings, but submitted that its interests were sufficiently affected to justify the grant of leave to intervene or, at least, by its appointment as amicus curiae.

32 TRFS submitted that, if the Court adopted the matters contained in the Liability SAFA and made the declarations sought, “…it will have put its imprimatur on the facts agreed, including on facts in dispute in the Class Action and misconduct which TRFS denies”.

33 TRFS’ contentions proceeded on the premise that if the Court makes the declarations sought, the Court would be accepting the reasonableness of the investigations conducted by Westpac and RFG and the correctness of the findings made at the conclusion of those investigations, especially as to the substantiated findings that TRFS and group members engaged in serious misconduct, including being complicit in the provision of false documentation in support of loans. Given that TRFS and group members deny those allegations, it was submitted that there were serious questions raised as to whether such findings should be made without hearing from TRFS especially given that ASIC had not conferred with TRFS or group members about these allegations, and a central issue in the Class Action Proceedings is whether RFG acted in good faith in the conduct of the relevant investigations.

34 TRFS points out that the Liability SAFA takes as its central premise that the findings of Westpac’s and RFG’s investigations are to be accepted as fact (i.e., that the misconduct occurred and/or is established) and require the Court to accept that RFG’s failure to prevent the alleged misconduct gave rise to certain contraventions. In this regard, in the oral argument before me, Counsel for TRFS drew attention to particular aspects of the Originating Application and the Liability SAFA which proceeded on predicate facts that RAMS Franchisees (including TRFS and group members) had actually engaged in misconduct (as opposed to there being a finding to that effect). It was submitted that these assertions were not merely inviting the Court to make findings of fact that Westpac and RFG’s investigations concluded that the allegations of misconduct were substantiated but were asking the Court to accept that the RAMS Franchisees in fact engaged in that misconduct.

35 TRFS submitted that in relation to prayer 1 of the Originating Application and Schedule 2 of the Liability SAFA, ASIC and RFG were seeking that the Court make findings that RFG’s representatives (which include TRFS and group members) had in fact engaged in misconduct by dealing with unaccredited referrers. For example, TRFS pointed out that the Liability SAFA at [7] contains the following agreed fact:

The schedules to the SAFA comprise:

(a) Schedule 1, being a table summarising the findings of misconduct made by Westpac’s GI team following investigations into allegations of misconduct at a number of RFG franchises between at least 1 January 2018 and April 2023; and

(b) Schedule 2, being a table summarising findings made by Westpac's GI team of occasions on which RFG franchisees and employees dealt with unaccredited referrers in circumstances where those dealings resulted in contraventions of s 31(1) of the Credit Act by RFG as licensee.

(Emphasis added.)

36 TRFS emphasised that these parts of the Liability SAFA, which relate to the alleged contraventions of s 31 of the Credit Act, were cast in terms of actual findings of misconduct that involved the conduct of RFG Franchisees, not just substantiated findings. It also drew attention to the Liability SAFA at [59] and [61] which also made reference to findings of misconduct as set out in Schedule 1 of that SAFA.

37 In relation to the False Documentation Misconduct, TRFS submitted that the Liability SAFA proceeded on the basis that there were occasions where RFG Franchisees had knowingly submitted false documents. TRFS pointed out that the Liability SAFA at [63] provides as follows:

63. Cases involving concerns about false documentation that were investigated by GI and SLTF included occasions where loan applications submitted to RFG by RAMS Franchises were found by Westpac's GI team to have been supported by false documentation in respect of which:

(a) the false documentation was provided to RFG presumably in order to increase the prospects of the loan application being approved by RAMS Credit on behalf of Westpac;

(b) one example of a case involving false documentation as found by Westpac's GI team was described as a “staged wages” case, which occurred when loan applications were found to have been supported by misleading documentation (such as false pay slips from non-existent employers, supported by bank account statements which showed payments into those accounts of amounts coinciding with the false pay slips) which gave the impression (or “staged”) that the loan applicant was receiving wages of a particular amount from a particular employer, where those representations were untrue;

(c) where GI and/or SLTF undertook investigations into concerns about false documentation, it was sometimes the case that GI and/or SLTF was satisfied that false documentation had been provided in support of a loan application, but did not then proceed to, or were not able to, determine which party or parties (from among the loan applicant, the referrer and the RAMS Franchisee or their employees) knew that false documents had been supplied in support of a loan application. Accordingly, the False Documentation Misconduct described in paragraph 69 below does not capture all instances where false documentation may have been provided to RFG in support of loan applications, only those instances where GI and/or SLTF made findings that RAMS Franchisees or their employees were involved in the misconduct; and

(d) the False Documentation Misconduct described in paragraph 69 below captures those occasions where, in the opinion of the GI investigator, it could be established that RAMS Franchisees or their employees had themselves knowingly submitted loan applications supported by false documentation or information or were complicit in doing so. In a number of the investigations undertaken by GI and SLTF during the Relevant Period, GI and/or SLTF was unable to determine whether the RAMS Franchisee or their employees knew that the documents supplied were false.

(Emphasis added.)

38 TRFS submitted that these matters of fact were not limited to those which Westpac and RFG’s investigations had determined to be “substantiated findings” of misconduct, but included instances where the investigators found that the RFG Franchisees or their employees were involved in the misconduct, in that they were complicit in submitting false documentation.

39 TRFS also drew attention to the fact that, although the factual basis of the alleged contraventions of s 47(1) of the Credit Act were expressed as being tied to misconduct substantiated by Westpac and RFG’s investigations, the facts agreed in the Liability SAFA made clear that the factual basis assumed that the RFG Franchisees had actually engaged in conduct that was a predicate to such substantiated findings. By way of example, TRFS referred to the Liability SAFA at [73], which provides as follows:

RFG’s Failings Failure to comply with RAMS Policy and Procedure Compliance Responsibilities and RAMS

Misconduct Investigation Responsibilities

73. During the Relevant Period, RFG failed to:

(a) take adequate steps to ensure that RAMS Franchises and their staff did not breach RAMS Policies in the manner described in Schedule 1;

(b) prior to Project Guardian (as defined in sub-paragraph 77(b) below), create adequate policies and procedures for responding to possible misconduct, including by:

(i) adopting a consequence management process where decisions about consequences for misconduct by RAMS ACRs rested with the RAMS Head of Sales and the RAMS Head of Risk and Compliance and only if those two senior managers disagreed on the consequence would the Managing Director have the final decision right, in circumstances where the Head of Sales had a competing interest between promoting sales and growth verses penalising a RAMS Franchisee, and where that competing interest was not clearly mitigated; and

(ii) failing to create an effective consequence management policy which:

(A) set out parameters about when concerns about possible misconduct should be referred by RFG to SLTF or GI for investigation; and

(B) set out processes for addressing those matters described in subparagraph (f) below;

(c) implement effective controls to ensure that RFG representatives did not breach the policy requirement not to deal with unaccredited referrers, including by failing to:

(i) satisfy itself that there were adequate processes in place to verify that a referrer was accredited;

(ii) put in place controls to monitor the accuracy of an Accredited Referrer’s unique referrer identifier code which was required to be entered in Symmetry by the RAMS Franchise as part of the home loan application process; and

(iii) include Welcome Calls as a control in JUNO, as a result of which, RFG management was unable to assess and confirm whether that control was operating effectively, in circumstances where Welcome Calls were the key control used by RFG for identifying the use of unaccredited referrers;

(d) take adequate steps to ensure that RAMS Franchisees and their employees adhered to the process for a prospective referrer to become accredited under the Accreditation Process, which failure led to the use of referrers who:

(i) did not hold a current ACL under Part 2-2 of the Credit Act;

(ii) were not an authorised representative of an ACL holder under Part 2-3 of the Credit Act; or

(iii) not exempt from being required to hold an ACL under the credit legislation;

(e) establish adequate compliance audit and routine loan file review procedures to detect misconduct, including by:

(i) establishing compliance audits with a very narrow focus that, among other things, were not designed to identify misconduct, and which excluded higher risk loan applications (such as declined or withdrawn files) from sampling processes; and

(ii) establishing an inappropriately undemanding paper file review process (5 files, every 6 months) undertaken by the RAMS Field Franchise sales team and was not focused on detecting misconduct issues; and

(f) adequately respond to possible misconduct within the RAMS Franchise Network, including by virtue of failing to:

(i) record all incidents of misconduct in a central location and to include sufficient information in JUNO to enable analysis of those incidents;

(ii) review incidents of misconduct with a view to determining whether they were indicative of systemic issues within the RAMS Franchise Network;

(iii) implement an adequate mechanism to monitor, consider and respond to incidents of misconduct;

(iv) impose consistent consequences for misconduct, and failing to adequately record consequences imposed for misconduct;

(v) adequately document the rationale for approving the extension of the term of a Franchise Agreement, having regard to incidents of misconduct in respect of that RAMS Franchise; and

(vi) identify systemic misconduct issues arising from investigations into misconduct at individual franchises.

(Emphasis added.)

40 TRFS pointed out that, whilst some of the abovementioned facts referred to RFG having failed to have adequate policies and systems to guard against possible misconduct, other facts tied RFG’s contravening conduct to the conduct and failures of the RFG Franchisees. In this regard, it was submitted that the Court could not sensibly make findings as to whether there had been inadequacies in, or non-compliance with, RFG’s relevant systems and policies unless it made antecedent findings of fact as to the conduct of the relevant representatives.

41 TRFS submitted that given that RFG maintained in the Class Action Proceedings that it “may rely upon other reasons that existed at the time of revocation or termination which could have justified the same action (had those reasons then been known)” and that it “reserve[d] the right to rely on further reasons including following the resolution of any exemption application made to AUSTRAC”, RFG could rely upon the findings made in the Civil Penalty Proceedings to provide support for its position in the Class Action Proceedings.

42 By reason of these matters, TRFS submitted that there was an overlap with the matters in issue in the Class Action Proceedings and that there was an indirect impact upon its legal rights. It was submitted that this was an exceptional case where the contravener, RFG, was not only making admissions as to its own conduct but also relying upon the conduct of the third party RFG Franchisees to support those admissions. TRFS contended that the Court was being asked to make serious findings of misconduct that warranted leave to intervene being granted, especially in circumstances where ASIC has not sought the views of the RFG’s Franchisees and where RFG and TRFS are in dispute as to whether the alleged conduct had occurred. TRFS submitted that the role of the Court in findings of fact in civil penalty proceedings was not limited to simply adopting the facts agreed between the parties. In support of these contentions, TRFS relied upon the observations made by the Full Court in Mobil Oil where their Honours considered the principles to be derived from the judgment of Burchett and Keifel JJ (Carr J agreeing) in NW Frozen Foods Pty Ltd v Australian Competition and Consumer Commission [1996] FCA 1134; 71 FCR 285 at 291and stated at [48] that:

First, Burchett and Kiefel JJ do not say that the Court is precluded from requesting further information in order to determine whether the agreed penalty is a proper one in the circumstances. In particular, their Honours do not suggest that the Court is bound to act without further inquiry on the statement of facts presented by the parties.

(Emphasis added.)

43 TRFS also relied upon the fifth proposition in Mobil Oil that Burchett and Kiefel JJ drew from NW Frozen Foods at [51(v)]:

In determining whether the proposed penalty is appropriate, the Court examines all the circumstances of the case. Where the parties have put forward an agreed statement of facts, the Court may act on that statement if it is appropriate to do so.

(Emphasis added.)

44 Relying upon these passages, TRFS submitted that the Court was not bound to accept the facts as presented in the Liability SAFA and it was not appropriate to do so in circumstances where the facts agreed between ASIC and RFG as to the conduct of the RFG Franchisees were in dispute in overlapping proceedings.

45 Further, TRFS submitted that leave to intervene was warranted where there was a reputational effect on the interests of TRFS and group members. It submitted that the reputational effects on TRFS and group members were particularly pronounced in circumstances where (a) RFG’s defence in the Class Action Proceedings includes reliance on the fact that RFG made breach reports to ASIC to justify its decision to revoke and/or terminate the contractual arrangements with them, (b) despite these reports being made to ASIC, TRFS and group members had not been consulted by ASIC prior to accepting the facts contained in the Liability SAFA, (c) ASIC could take action under s 73(1) of the Credit Act to give information to another licensee about the RFG Franchisees (i.e., licensees other than RFG), which had the prospect of curtailing any work that those Franchisees could perform as ACRs for other lending organisations such that it could impair the ability to earn income altogether, (d) ASIC had made public statements about the conduct of RFG which referred to the conduct of RFG Franchisees, and (e) the initial version of the Liability SAFA identified the relevant RFG Franchisees in respect of whom factual allegations were said to have been proved or substantiated in Schedules 1 and 2 (though these references have now been anonymised in the present version of the Liability SAFA).

46 As for the public statement made by ASIC, it recorded as follows:

47 During the oral hearing before me, ASIC indicated that this public statement was no longer being published (albeit it does appear on ASIC’s website). Nevertheless, TRFS submitted that such public statements affected its reputation. TRFS submitted that in Ashby v Slipper [2014] FCAFC 15; 219 FCR 322, Mansfield and Gilmour JJ at [143] concluded (on the unique facts of that case) that the denial of an opportunity for a solicitor to be heard as to serious allegations relating to his professional integrity warranted those allegations to be put to the solicitor (cf Siopis J). By analogy, TRFS submitted that it should be given an opportunity to be heard in circumstances where serious allegations were being made that necessarily impugned its reputation.

48 During the oral hearing, when pressed about what assistance TRFS would provide to the Court, if it was granted leave to intervene or was otherwise appointed as an amicus curiae or contradictor, Counsel for TRFS indicated that it would (a) wish to make submissions as to what factual findings the Court should or should not make from the Liability SAFA, and (b) lead limited evidence that put in issue the nature of the findings from the investigations undertaken by Westpac and RFG. As to the latter matter, Counsel for TRFA submitted that the evidence it would seek to lead would not necessarily be adduced for the purpose of falsifying the facts in the Liability SAFA but to provide a factual basis upon which the Court would not make certain findings consistent with those contained in the Liability SAFA.

49 ASIC and TRFS disputed central aspects of TRFS’ submissions. They otherwise submitted that TRFS’ proposal to call evidence to dispute the agreed facts contained in the Liability SAFA would result in the Civil Penalty Proceedings being “hijacked” and turn into a “dress rehearsal” of the Class Action Proceedings.

5. CONSIDERATION

5.1 No warrant for leave to intervene

50 I am not satisfied that TRFS has established any ground upon which leave to intervene should be granted.

51 First, as a starting position, TRFS accepts that it has no direct legal interest that is or will be affected by the Civil Penalty Proceedings.

52 Second, nothing to be decided in the Civil Penalty Proceedings is intended to, or will, decide any question of law that arises in the Class Action Proceedings. This requires some explanation.

53 The declarations sought in ASIC’s Civil Penalty Proceeding are directed to the conduct of RFG. It is RFG’s conduct that would, if the declarations are made, be the subject of the Court’s censure. The declarations would not, and could not, affect TRFS’ interests, either directly or indirectly. This is clear because:

(a) it is not in contest that RFG was required to comply with its statutory obligations as a licensee pursuant to ss 31(1), 47(1)(a), 47(1)(b), 47(1)(d) and 47(1)(e) of the Credit Act;

(b) in relation to s 31(1) of the Credit Act, it is RFG, as licensee, that was required not to accept referrals from the unaccredited referrers – the question of law that arises is whether RFG contravened this obligation by accepting such referrals (assuming that to be accepted as a matter of fact);

(c) in relation to s 47(1) of the Credit Act, TRFS accepted that a contravention could be established by a licensee’s failure to have in place adequate policies or systems. As such, it was not in contest that to comply with s 47(1), RFG was required to take certain steps by way of policies and systems to promote or ensure compliance. Specifically:

(i) in order to comply with s 47(1)(a) of the Credit Act, RFG was required to, amongst other things, create adequate policies and procedures for the operation of the RAMS Franchise Network; take reasonable steps to ensure that those policies and procedures were complied with by RFG and ACRs; adequately investigate and respond to possible misconduct within the RAMS Franchise Network; comply with its obligations pursuant to ss 47(1)(b) and 47(1)(e), and its obligations pursuant to s 31(1) of the Credit Act;

(ii) in order to comply with s 47(1)(b) of the Credit Act, RFG was required to, amongst other things, have in place adequate arrangements to ensure that consumers were not disadvantaged by any conflict of interest that may arise wholly or partly in relation to credit activities undertaken by it; and

(iii) in order to comply with s 47(1)(e) of the Credit Act, RFG was required, amongst other things, to have in place adequate arrangements to ensure that ACRs complied with policies and procedures that were implemented for the purposes of ensuring those ACRs complied with the Credit Act, including to: conduct adequate compliance audit and routine loan file review procedures to detect misconduct in relation to loan applications received from RFG Franchisees; and adequately investigate and respond to possible misconduct within the RFG Franchise Network.

54 The questions as to the content of the relevant statutory obligations and whether RFG complied with them (assuming the facts can be established) are ones which arise uniquely to RFG. Those questions of law do not bear upon any legal obligation imposed on the RFG Franchisees.

55 Third, the questions of fact that arise in the Civil Penalty Proceedings need to be viewed in their context. The facts that have been agreed in the Liability SAFA are those which have been agreed as between ASIC and RFG. Any factual findings that are made do not give rise to res judicata or issue estoppel as between RFG and TRFS and the group members, and TRFS accepted this to be the case.

56 Whilst it is correct, as TRFS pointed out by reliance upon Mobil Oil, that the Court is not bound to accept findings of fact, it is also necessary to bear in mind that those facts have been agreed for the purpose of s 191 of the Evidence Act 1995 (Cth). As a result, absent any questions I have about those facts, I will not be called upon to adjudicate any factual controversies as between ASIC and RFG. The position is therefore as Beach J described it in Australian Securities and Investments Commission v Commonwealth Bank of Australia [2020] FCA 790 at [12]:

…I have not been required to determine any factual question on its merits. Accordingly, the recitation of what follows is premised on the relevant facts not being in issue between the parties, which is the consequence of invoking s 191 of the Evidence Act 1995 (Cth). To so invoke s 191 provides a sufficient factual foundation to support my exercise of power to impose a penalty and to make the required declarations without any necessity to receive evidence let alone independently adjudicate on whether those facts exist. Accordingly, all that I need to be satisfied of is whether the agreed facts on their face provide a sufficient foundation for the declarations and orders sought. The text of s 191(2)(a) makes this plain.

57 In the present case, without descending into detail, it is relevant that the agreed facts as contained in the Liability SAFA arise in circumstances where, in relation to the alleged contraventions of s 47(1) of the Credit Act, during the Relevant Period:

(a) Westpac and RFG undertook investigations into allegations of misconduct relating to certain of the RFG Franchisees which resulted in 35 reports which contained what it described as “substantiated” findings of misconduct relating to RAMS Franchises (GI Reports);

(b) Westpac and RFG’s investigations found several matters to have given rise to “substantiated misconduct” as revealed in the GI Reports; and

(c) RFG failed to take the steps necessary for it to comply with its statutory obligations in respect of that substantiated misconduct.

58 The description in the Liability SAFA of the relevant findings of misconduct as being “substantiated” reflects the language of the GI Reports. In these circumstances, for the purpose of the contraventions of s 47(1) of the Credit Act, the Court is not being asked to find that the “substantiated” conduct actually occurred and such findings are, in fact, unnecessary for the purpose of the relief that is sought by ASIC. That is because RFG’s contraventions of s 47(1) will have occurred whether or not the “substantiated” misconduct actually occurred.

59 It is true, as TRFS pointed out, some of the facts in this respect proceed on the basis that RFG Franchisees had breached one or more of RFG’s relevant policies or systems, but in my view these matters do no more than reflect the investigatory findings made by Westpac and RFG and, in any event, are findings that do not bind the RFG Franchisees. Thus, in the Class Action Proceedings, TRFS and group members will not be precluded from disputing these and other matters. Further, even if in the Class Action Proceedings it is ultimately found that some, or even all, of the underlying “substantiated misconduct” did not occur, that could have no impact on whether RFG had contravened s 47(1) of the Credit Act.

60 Although the contraventions of s 31(1) of the Credit Act proceed on a different factual predicate, the position is essentially no different. Unlike the contraventions of s 47(1), the contraventions of s 31(1) of the Credit Act require the Court to be satisfied that RFG accepted referrals from unaccredited referrers. The factual premise for that contravention proceeds on the accepted basis that RFG did receive such referrals. TRFS’ submissions that there is scant detail of these in the Liability SAFA is a criticism that is, at this stage, well made. As I observed during the course of the hearing before me, I may need to be satisfied as to that factual predicate as an essential basis upon which to be satisfied that RFG contravened s 31(1) of the Credit Act. Again, to the extent that I am satisfied as to these matters, the acceptance of those facts would not bind TRFS and group members.

61 Fourth, as a result of each of the above matters, I am not satisfied that there is a relevant overlap between the Civil Penalty Proceedings and the Class Action Proceedings to warrant leave to intervene being granted. That is not to say that there is no overlap at all. In one sense, both proceedings relate to a similar subject matter, but that is to cast a simplistic eye over both Proceedings and place a gloss on the substantive legal and factual differences between them. More importantly, to speak in terms of an overlap between the two proceedings fails to recognise that (irrespective of the apparent overlap) the interests of TRFS and the other group members are not directly or indirectly affected by the Civil Penalty Proceedings. As RFG pointed out in its submissions, a later judge may follow an earlier judge on a question of law and may be bound to follow a higher court’s determination of a question of law. However, the same considerations do not apply to findings of fact. Thus, even if a relevant factual overlap existed, it would not give rise to a substantial affection of TRFS’s legal interests of the type required to support intervention: Levy v Victoria [1997] HCA 31; 189 CLR 579 at 601–602. To put this in crude terms, TRFS and the other group members will have their day in Court and will not be affected by anything that is found and determined in the Civil Penalty Proceedings.

62 Further, the facts and admissions agreed between ASIC and RFG as set out in the Liability SAFA have been agreed solely for the purpose of the Civil Penalty Proceedings. If there was any doubt about this, I am prepared to make that clear in my determination of the Civil Penalty Proceedings: see, e.g., Australian Competition and Consumer Commission v Dataline.net.au Pty Ltd [2006] FCA 1427; 236 ALR 665 at [59] (Kiefel J). This course will be available to me in the determination of the Civil Penalty Proceedings, if necessary, to ensure the public is not under the mistaken impression that there was an adjudication by the Court on facts affecting TRFS and group members.

63 Fifth, as to the reputational impact on TRFS and group members, the incontrovertible fact is that by reason of the Class Action Proceedings, it is now a matter of public record that RFG relevantly revoked and/or terminated its arrangements with TRFS and group members. Further, by reason of RFG’s defence in the Class Action Proceedings, it is a matter of public record that it is alleged that TRFS and group members engaged in particular forms of conduct that are in issue in those Proceedings. I do not regard the potential for ASIC to provide information to other licensees under s 73 of the Credit Act as taking things much further. It is inconceivable to me that any other licensee that has appointed TRFS or group members as ACRs would not be aware of the Class Action Proceedings or the matters that are the subject of those Proceedings. It is also a matter of public record that TRFS and group members deny the allegations made by Westpac and RFG.

64 Further, in the oral hearing before me, RFG expressly disclaimed that it would be relying upon the declarations made or penalties imposed in the Civil Penalty Proceedings as being post-fact discovered matters seeking to advance its defence of the Class Action Proceedings.

65 Accordingly, given the current state of play, I regard the reputational issues (if any) arising from the Civil Penalty Proceedings as adding only marginally to those that already exist and not giving rise to a sufficient interest to warrant leave to intervene being granted.

66 Finally, I am satisfied that the course proposed by TRFS would introduce a substantial and unwarranted burden upon the Court and the parties in the Civil Penalty Proceedings. In substance, it would require the Court to adjudicate on factual controversies which are otherwise not in dispute in the Civil Penalty Proceedings and would impose the burden upon the Court to do so in advance of the Class Action Proceedings. I do not regard this as being consistent with the overriding dictates of case management under ss 37M and 37N of the FCA Act.

5.2 No grounds to appoint TRFS as amicus curiae or contradictor

67 Whilst I accept that the Court may appoint an amicus curiae or contradictor where the Court is concerned about particular matters, I am not satisfied that there is such a need in this case.

68 In any event, in my view, TRFS would provide a partisan view that would not assist me as an amicus. Nor am I satisfied that RFG is not a proper contradictor to ASIC’s application. RFG is well-advised and well-resourced and had an interest in opposing the declaratory relief sought: see eg Australian Competition and Consumer Commission v MSY Technology Pty Ltd [2012] FCAFC 56; 201 FCR 378 at [30] (Greenwood, Logan and Yates JJ). In the present case, to the extent that there is a need for a contradictor or further assistance, I am satisfied that I will receive it. If that position changes, I will raise it with the parties and review the position further if the need arises.

5.3 No grounds for case management stay

69 A case management stay is the exercise of a discretionary power. Case management stays have typically been granted where proceedings are pending in another court and the Court determines that it is desirable that those proceedings proceed to their conclusion first. The exercise of the discretion to grant a case management stay is informed by the general principle that it is undesirable that two courts should determine the same dispute, and practical considerations based on common-sense and fairness guide which action should proceed first. The person seeking the case management stay bears the onus of showing that it is just and convenient to interfere with the other party’s ordinary rights. The Court’s discretion is to be exercised in accordance with the overarching purpose of civil practice found in s 37M of the FCA Act.

70 I am not satisfied that a case management stay should be ordered where the outcome of the Class Action Proceeding could have no impact on whether the relief sought in ASIC’s Civil Penalty Proceedings ought to be granted. And likewise, the effect of any orders made in ASIC’s Civil Penalty Proceeding could not impact the relief sought in the Class Action Proceeding. Both matters should continue to appropriate resolution on their current trajectories.

6. COSTS

71 ASIC and RFG sought their costs of the application on the basis that costs should follow the event. TRFS submitted that there should be no order as to costs given that it has nevertheless made submissions that have assisted the Court and drawn attention to matters upon which the Court will be able to better focus during the hearing and in determination of the Civil Penalty Proceedings. TRFS further submitted that its application was not gratuitous and that costs do not invariably follow the event in an application for leave to intervene: citing Hua Wang Bank Berhad v Commissioner of Taxation [2013] FCAFC 28 at [65] (Logan, Jagot and Robertson JJ).

72 Costs are at the discretion of the Court. This is made plain by s 43 of the FCA Act. However, the ordinary position in civil litigation is that costs follow the event: Firebird Global Master Fund II Ltd v Republic of Nauru (No 2) [2015] HCA 53; 327 ALR 192 at 193 [6] (French CJ, Kiefel, Nettle and Gordon JJ); George v Fletcher (Trustee) (No 2) [2010] FCAFC 71 at [12] (Ryan, Marshall and Logan JJ); Environment Council of Central Queensland Inc v Minister for the Environment and Water (No 2) [2024] FCAFC 97 at [61] (Colvin and Horan JJ). The general principle as to costs, which has been described as “one of the most, if not the most important” principles, is that a successful party is entitled to its costs, unless there are special circumstances which warrant a departure from that position: Northern Territory v Sangare [2019] HCA 25; 265 CLR 164 at [25] (Kiefel CJ, Bell, Gageler, Keane and Nettle JJ per curiam).

73 In Hua Wang Bank Berhad, Logan, Jagot and Robertson JJ observed that public interest considerations can attend intervention and amicus applications. Their Honours expressed the view that the public interest would not be served if costs generally followed the event where such an application was unsuccessful. I accept that in certain circumstances the public interest attendant upon an application for leave to intervene or to assist the Court in a proceeding as an amicus curiae may, together with other factors, contribute to a conclusion that special circumstances justify deviating from the ordinary rule as to costs. However, this will not always be the case, even where one is granted leave to intervene and acts to vindicate the public interest – see Kingdom of Spain v Infrastructure Services Luxembourg S.à.r.l. (No 3) [2021] FCAFC 112; 392 ALR 443 at [28] where Allsop CJ (with whom Perram and Moshinsky JJ agreed) queried rhetorically why private parties should have to pay for the costs incurred by reason of the unsuccessful intervention of an international body.

74 I do not consider that a sufficient public interest attends the present case, if any exists at all. TRFS did not identify any such interest in its submissions. It seems to me, as ASIC points out, that the object of TRFS’ application to intervene and its application for a stay of the proceedings was to vindicate its own interests and perhaps those of the group members in the Class Action Proceedings.

75 TRFS has failed in its application. Whilst TRFS’ submissions have assisted me in focussing on particular matters in the Civil Penalty Proceedings, it remains the case that, despite its helpful written and oral submissions, it has failed in its application and increased the costs of the parties to the proceedings. Although costs do not invariably follow the event in an application of this kind, I am not satisfied that in the particular circumstances there is any reason to depart from the usual order as to costs.

7. SUPPRESSION AND NON-PUBLICATION ORDERS

76 During the course of the oral hearing before me, it became apparent that aspects of the evidentiary materials before me had inadvertently provided sufficient information to enable the identification of one or more of the RAMS Franchisees, RAMS Franchisee principals and loan writers, when that was not the intent of ASIC, RFG or TRFS. It was accepted that this was an oversight and that it was unnecessary for me for the purpose of the determination of the present application or the Civil Penalty Proceedings to be able to identify any of these persons. Each of ASIC, RFG and TRFS agreed that this material should be the subject of suppression and non-publication orders under s 37AF(1) of the FCA Act.

77 I am satisfied that the evidentiary materials that make it possible to identify the RAMS Franchisees, RAMS Franchisee principals and loan writers was included by way of oversight. It was not intended to be disclosed and it is not necessary for the Court to have this material to determine the present application or the Civil Penalty Proceedings. Obviously, this does not apply to the actual identity of TRFS, which is a matter of record. Other than this, I am satisfied that it “is necessary to prevent prejudice to the proper administration of justice” as referred to in s 37AG(1)(a) of the FCA Act to make the orders sought by ASIC, RFG and TRFS, and I will make those orders.

I certify that the preceding seventy-seven (77) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Shariff. |

Associate:

Dated: 4 September 2025