FEDERAL COURT OF AUSTRALIA

Xie v Moshav Financial Wholesale Pty Ltd [2025] FCA 250

File number: | NSD 656 of 2021 |

Judgment of: | MARKOVIC J |

Date of judgment: | 26 March 2025 |

Catchwords: | CORPORATIONS – where representative of a holder of an Australian financial services licence (“licensee”) alleged to have contravened provisions in the Corporations Act 2001 (Cth), Australian Securities and Investments Commission Act 2001 (Cth) and/or the Australian Consumer Law – whether licensee liable for conduct of representative – where representative made false and misleading representations and engaged in conduct that was misleading and deceptive – where licensee liable for conduct of representative – orders for damages CONTRACTS – where representative of licensee alleged to have breached employment agreement and/or fiduciary duties and/or engaged in misleading and deceptive conduct – where representative breached employment agreement and fiduciary duties – orders for damages |

Legislation: | Australian Consumer Law, being Sch 2 to the Competition and Consumer Act 2010 (Cth) ss 4, 18, 236 Australian Securities and Investments Commission Act 2001 (Cth) ss 12BAA, 12BAB, 12BB, 12DA, 12DB, 12DF, 12GF, 12GH Corporations Act 2001 (Cth) ss 9, 766C, 769B, 769C, 917A, 917B, 917D, 917E, 917F, 1041E, 1041H, 1041I, 1041N Federal Court of Australia Act 1976 (Cth) s 51A |

Cases cited: | ABN AMRO Bank NV v Bathurst Regional Council (2014) 224 FCR 1 Australian Competition and Consumer Commission v ACM Group Ltd (No 2) [2018] FCA 1115 Australian Competition and Consumer Commission v Woolworths Ltd [2019] FCA 1039 Australian Securities and Investments Commission v AGM Markets Pty Ltd (in liquidation) (No 3) [2020] FCA 208 Australian Securities and Investments Commission v Dover Financial Advisers Pty Ltd [2019] FCA 1932; 140 ACSR 561 Australian Securities and Investments Commission v HCF Life Insurance Company Pty Ltd [2024] FCA 1240 Australian Securities and Investments Commission v Mercer Superannuation (Australia) Ltd [2024] FCA 850 Australian Securities and Investments Commission v Select AFSL Pty Ltd (No 2) (2022) 162 ACSR 1; [2022] FCA 786 Australian Securities and Investments Commission v Vanguard Investments Australia Ltd [2024] FCA 308 BP Refinery (Westernport) Pty Ltd v Shire of Hastings (1977) 180 CLR 266 Care A2 Plus Pty Ltd v Pichardo [2024] NSWCA 35 Cascalang v WealthSure Pty Ltd [2015] FCA 761 Combulk Pty Ltd v TNT Management Pty Ltd (1993) 41 FCR 59 HTW Valuers (Central Qld) Pty Ltd v Astonland Pty Ltd (2004) 217 CLR 640 Kumova v Davison (No 2) [2023] FCA 1 Latol Pty Ltd v Gersbeck (2015) 303 FLR 298; [2015] NSWSC 1631 Lin v Zheng [2023] NSWCA 174 Pegela Pty Ltd & Ors v National Mutual Life Association of Australasia Ltd [2006] VSC 50 Self Care IP Holdings v Allergan Australia [2023] HCA 8; 97 ALJR 388 Selig v Wealthsure Pty Ltd (2015) 255 CLR 661; [2015] HCA 18 Smith v Leveraged Equities Ltd [2020] WASCA 122 Watson v Foxman (1995) 49 NSWLR 315 |

Division: | General Division |

Registry: | New South Wales |

National Practice Area: | Commercial and Corporations |

Sub-area: | Commercial Contracts, Banking, Finance and Insurance |

Number of paragraphs: | 297 |

Date of hearing: | 4-7 March and 19 April 2024 |

Counsel for the Plaintiff: | Mr M Cleary |

Solicitor for the Plaintiff: | Dong & Partners |

Counsel for the First Defendant: | Ms M Castle and Ms V Chan |

Solicitor for the First Defendant: | Swaab Attorneys |

Counsel for the Second Defendant: | The Second Defendant appeared in person. There was no appearance for the Second Defendant on 19 April 2024. |

ORDERS

NSD 656 of 2021 | ||

| ||

BETWEEN: | MR XINWEN XIE Plaintiff | |

AND: | MOSHAV FINANCIAL WHOLESALE PTY LTD First Defendant MR JINYANG (RAYMOND) YU Second Defendant | |

order made by: | MARKOVIC J |

DATE OF ORDER: | 26 March 2025 |

THE COURT ORDERS THAT:

1. Subject to Order 2 below, by 9 April 2025 the parties are to provide draft short minutes of order for the disposition of the proceeding.

2. In the event that the parties cannot agree on the form of orders or any party wishes to vary the proposed orders as to costs:

(a) by 9 April 2025 they are to inform the Associate to Markovic J of the nature and extent of the disagreement between them or of the proposed variation of the costs orders; and

(b) the proceeding will be listed for case management hearing to allow all outstanding matters in dispute to be determined and for final orders to be made.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

MARKOVIC J:

1 In May 2018 Xinwen Xie, the plaintiff, invested in the Hyperbuild Unit Trust. As a result of making that investment Mr Xie brings this proceeding against Moshav Financial Wholesale Pty Ltd and Raymond Yu as first and second defendants respectively.

2 Mr Xie claims damages from Mr Yu who he alleges made certain representations to him in relation to his investment into the Hyperbuild Unit Trust. In making those alleged representations, Mr Xie asserts that Mr Yu breached the Corporations Act 2001 (Cth), the Australian Securities and Investments Commission Act 2001 (Cth) (ASIC Act) and/or the Australian Consumer Law which is Sch 2 to the Competition and Consumer Act 2010 (Cth) (ACL).

3 At the time of the alleged representations Mr Yu was an employee of Moshav and, it is contended, of AXL Financial Pty Ltd, which was, in turn, an authorised representative of Moshav. Mr Xie alleges that Moshav is responsible for the loss and damage he suffered which was caused by Mr Yu and for the actions taken by Mr Yu as an employee of Moshav or, in the alternative, as a representative of Moshav within the meaning of Pt 7.6 of the Corporations Act.

4 Moshav has filed a cross-claim against Mr Yu. It contends that Mr Yu was acting as Moshav’s agent in carrying out investor responsibilities, in that capacity he owed fiduciary duties to Moshav and, in the event that Moshav is found liable to Mr Xie, Mr Yu breached those duties and his employment contract with Moshav. As a result Moshav claims that it has suffered loss and damage.

THE PLEADED CASE

5 Mr Xie relies on a further amended originating process (FAOP) and a further amended statement of claim (FASOC) each filed on 5 March 2024.

6 As against Mr Yu, Mr Xie alleges that:

(1) in about May 2018 Mr Yu made the following Representations to him:

(a) Oliver Roths, who was at all material times the controller of AXL in the role of Group Chief Risk Assessment Officer, planned for AXL, an authorised representative of Moshav, to acquire 51% of the shares in PLC Financial Solutions Limited through Hyperbuild Pty Ltd as trustee for the Hyperbuild Unit Trust. The board of PLC would then be changed so that AXL could control PLC through a backdoor listing by selling the Hyperbuild operations at a combined value of $60 million to PLC (collectively, Hyperbuild Transaction);

(b) the Hyperbuild Transaction would be complete by the end of 2018;

(c) PLC would raise $100 million in a fund for property development;

(d) upon a new unit holder purchasing 500 units in the Hyperbuild Trust (representing 5%) from Hyperbuild for a consideration of $700,000, the new unit holder would be provided with a 5% shareholding in PLC which would lead to a forecast return of at least 6-8 times on its investment; and

(e) the investment was safe because of:

(i) the financial position and management of the Hyperbuild Trust;

(ii) the Hyperbuild Transaction being sure to be “100% successful” as any outstanding matters were “formalities only”; and

(iii) a guaranteed refund of investment if the Hyperbuild Transaction failed;

(2) on or about 8 May 2018 Mr Xie agreed to borrow $170,000 from Mr Yu to invest in the Hyperbuild Trust;

(3) on or about 9 May 2018 Mr Xie invested $700,000 (which included the sum borrowed from Mr Yu) in the Hyperbuild Trust and signed a unit subscription agreement in relation to that investment (Unit Subscription Agreement);

(4) Mr Xie relied upon the Representations, which he believed on reasonable grounds to be true, in agreeing to invest in the Hyperbuild Trust and in transferring funds and signing the Unit Subscription Agreement. If the Representations had not been made and/or if they had not been misleading or deceptive, Mr Xie would not have agreed to invest in the Hyperbuild Trust, transfer the funds or sign the Unit Subscription Agreement;

(5) on or about 17 May 2018 Mr Roths on behalf of Hyperbuild, and without Mr Xie’s knowledge, transferred $150,000 of Mr Xie’s investment in the Hyperbuild Trust into PLC’s solicitors’ trust account;

(6) on 18 May 2018 three million shares in PLC were allotted to Mr Xie and on 13 July 2018 500 units in the Hyperbuild Trust were allotted to Mr Xie;

(7) on or about 15 June 2018 PLC issued 50 million new shares causing Mr Xie’s shareholding to be significantly diluted;

(8) by 16 August 2018 Mr Xie had repaid the loan from Mr Yu, including accrued interest;

(9) the Hyperbuild Transaction did not complete and contrary to the Representations, Mr Xie’s investment in the Hyperbuild Trust was not refunded to him;

(10) on or about 27 August 2019 Hyperbuild went into external administration; and

(11) on or about 6 October 2020 PLC was removed from the official list of the Australian Securities Exchange.

7 Mr Xie further alleges that:

(1) the making of all or some of the Representations was conduct in relation to a financial product or financial service, or both, within the meaning of the Corporations Act and the ASIC Act;

(2) all of the Representations were made with respect to future matters within the meaning of s 769C of the Corporations Act, s 12BB of the ASIC Act and/or s 4 of the ACL and, for the purposes of those sections, Mr Xie relies on the presumption that Mr Yu is taken not to have reasonable grounds for making the Representations unless evidence is adduced to the contrary;

(3) the making of each, some or all of the Representations was conduct in this jurisdiction within the meaning of s 1041H of the Corporations Act and s 12DA of the ASIC Act;

(4) the Representations were misleading or deceptive, likely to mislead or deceive or false in a material particular or materially misleading or were misleading representations that an investment in the Hyperbuild Trust was of a particular standard, quality, value or grade, or was conduct liable to mislead the public as to the nature, characteristics, suitability for purpose or quantity of an investment in the Hyperbuild Trust;

(5) in the alternative, the Representations were likely to induce Mr Xie to apply for or acquire a financial product within the meaning of s 1041E of the Corporations Act and Mr Yu did not care, or ought to have known, that they were false in a material particular or materially misleading. Therefore, in making the Representations Mr Yu engaged in conduct in contravention of s 1041E of the Corporations Act;

(6) further or in the alternative, in making the Representations, Mr Yu engaged in conduct in contravention of s 1041H of the Corporations Act by engaging in conduct in relation to a financial product or financial service that was misleading or deceptive or likely to mislead or deceive; and

(7) further or in the alternative, in making the Representations, Mr Yu engaged in conduct in contravention of ss 12DA, 12DB(1)(a) or 12DF of the ASIC Act or s 18 of the ACL.

8 As against Moshav, Mr Xie alleges that:

(1) Mr Yu’s conduct in making the Representations and contravening s 1041E and/or s 1041H of the Corporations Act was undertaken by Mr Yu as Moshav’s employee, on Moshav’s behalf and within the scope of Mr Yu’s actual or apparent authority and thus is taken, for the purposes of a proceeding under Ch 7 of the Corporations Act, also to have been engaged in by Moshav pursuant to s 769B of that Act. Mr Xie makes the same allegation in respect of the contravention of ss 12DA, 12DB(1)(a) or 12DF of the ASIC Act, relying on s 12GF and s 12GH of that Act; and

(2) further or in the alternative, Moshav was responsible and liable for Mr Yu’s conduct as he was its employee and therefore its representative within the meaning of ss 917B, 917E and 917F of the Corporations Act.

9 Mr Xie claims damages from Mr Yu pursuant to s 1041I of the Corporations Act, s 12GF of the ASIC Act and/or s 236 of the ACL and, further or in the alternative, seeks an order that Moshav pay compensation or damages pursuant to s 917E and s 917F of the Corporations Act.

10 Both Mr Yu and Moshav have filed defences in relation to the allegations raised by Mr Xie, albeit the most recent defence filed by Mr Yu (who at the time of the hearing was not legally represented) was dated 3 September 2021 and responded to the statement of claim filed on 6 July 2021. That defence was prepared with the assistance of a barrister. I do not intend to set out the effect of Mr Yu’s and Moshav’s respective defences at this stage.

11 Consideration of the relief sought by Moshav set out in its cross-claim only arises if Mr Xie is successful in his claim against Moshav. In summary, in its amended notice of cross-claim filed on 19 April 2022 Moshav contends that:

(1) Mr Yu was an employee of Moshav from 18 September 2015 to 31 July 2020 and in the same period was an employee of AXL (or at least performed tasks for AXL at the direction of Mr Roths);

(2) in the course of Mr Yu’s employment with Moshav he was responsible for identifying potential investors willing to invest in mortgage products in Australia and for communicating with potential investors about those financial products (Investor Responsibilities);

(3) by reason of his employment with Moshav and the Investor Responsibilities Mr Yu owed a fiduciary duty to Moshav to:

(a) act in its best interests in his communications with AXL and third parties;

(b) not place himself in a position of conflict;

(c) differentiate any communications he had with AXL and third parties that were in his own capacity from those that were in his capacity as an employee of Moshav; and

(d) act within the scope of his actual or ostensible authority and avoid any personal communications which could give the incorrect impression to a third party that such communications were on behalf of Moshav;

(4) Mr Yu’s contract of employment with Moshav contained certain express and implied terms;

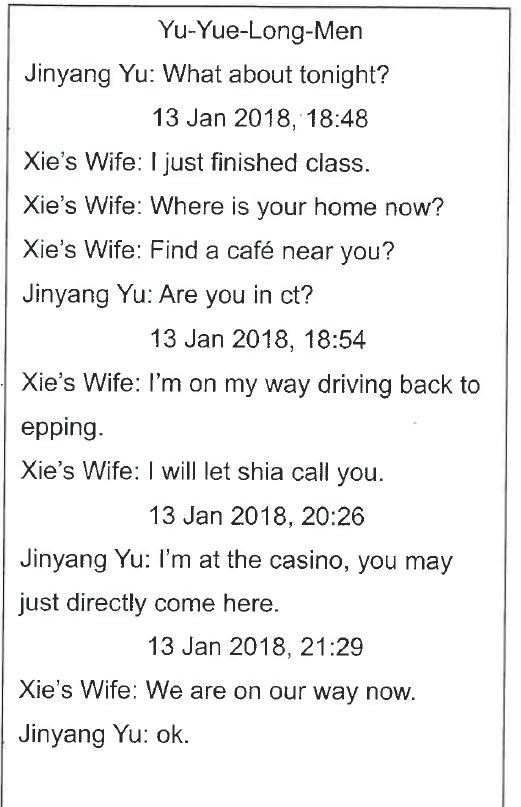

(5) if the Court finds that Moshav is liable to Mr Xie on a cause of action pleaded by him and the cause of action is not apportionable, such that Moshav’s share in the loss and damage is not reduced because it is not found to be a concurrent wrongdoer with others, then Mr Yu is in breach of his fiduciary duties to Moshav and in breach of his contract of employment with Moshav in the ways particularised; and

(6) further and in the alternative, if the Court finds that Mr Yu made the Representations and that Mr Xie has established certain facts pleaded in his statement of claim filed on 6 July 2021 then Mr Yu, in trade or commerce, represented that Moshav was offering an investment opportunity, that representation was misleading or deceptive or likely to mislead or deceive and, in the premises, Mr Yu breached s 18 of the ACL. As a result of that breach, Moshav has suffered loss and damage to the extent of the relief and costs orders which Mr Xie obtains against it in this proceeding.

12 Mr Yu filed a defence to the amended notice of cross-claim at a time when he was legally represented. Once again, I do not intend to set out the contents of that defence at this stage.

WITNESSES

13 Mr Xie relied on:

(1) his own evidence. Mr Xie gave his evidence in chief orally and was cross-examined by Moshav’s counsel, in both cases through an interpreter. Although Mr Xie can write and understand everyday conversations in English, he cannot understand complex language or concepts expressed in English. I found Mr Xie to be an honest witness who attempted to assist the Court by giving considered and frank answers to the questions posed;

(2) evidence given by David Stuart Watt, a chartered accountant, accredited forensic accounting specialist and partner of Hall Chadwick. Mr Watt prepared a report in which he assessed the fair market value of 3 million shares in the business and assets of Irich Financial Solutions Limited (formerly PLC). Mr Watt was not cross-examined; and

(3) evidence given by Wenfu Liu, a National Accreditation Authority for Translators and Interpreters (NAATI) certified translator in Chinese languages. Ms Liu translated a series of WeChat messages from Chinese into English. Ms Liu was not cross-examined.

14 Moshav relied on evidence given by:

(1) Tal Silberman, a director of Moshav. Mr Silberman gave his evidence in chief orally and was cross-examined. Mr Xie submits that I would find Mr Silberman to be an unsatisfactory witness. I do not accept that submission. While there were some aspects of Mr Silberman’s evidence which lacked clarity or required further probing, on balance I found him to be a satisfactory witness; and

(2) Zhuzi Lin, a NAATI certified translator in Chinese languages including Chinese Mandarin. Ms Lin translated a series of documents from Chinese Mandarin to English. She was not cross-examined.

15 Mr Yu gave evidence in his own case. As Mr Yu was self-represented, rather than give his evidence in chief orally, he relied on an outline of his evidence dated 29 July 2022 which had been prepared pursuant to Orders made on 8 June and 13 July 2022 and notified to Mr Xie and Moshav. Mr Yu had legal assistance at the time of the preparation of his outline of evidence.

16 Mr Xie filed and served his FAOP and FASOC after Mr Yu had prepared his outline of evidence. By the FAOP and the FASOC Mr Xie alleges, among other things, that the representations made by Mr Yu were made in relation to future matters within the meaning of s 769C of the Corporations Act, s 12BB of the ASIC Act or s 4 of the ACL and that he relies on the statutory presumption that Mr Yu did not have reasonable grounds for making the representations unless Mr Yu adduces evidence to the contrary.

17 To permit Mr Yu to give evidence relevant to the issues raised by that aspect of the FAOP and the FASOC, counsel for Mr Xie prepared a series of questions designed for that purpose (Additional Questions). The Additional Questions were provided to Mr Yu to consider prior to giving evidence. Mr Yu agreed to proceed with his evidence including by providing answers in the witness box to the Additional Questions. At the hearing I asked each of the Additional Questions and Mr Yu provided answers. Mr Yu was then cross-examined.

18 Mr Yu was not a satisfactory witness. Although he answered the questions put to him, at times his answers were seemingly intentionally vague and at other times he changed his evidence, either in an attempt to place himself in a better light or to meet what he perceived to be a weakness in his defence.

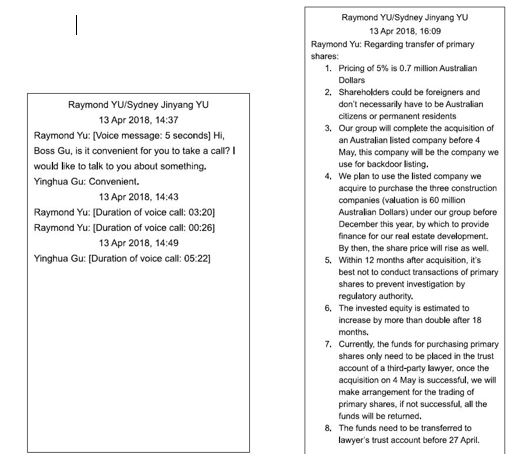

THE FACTS

Mr Xie

19 Mr Xie is a Chinese citizen. He graduated from high school in China in 2008. Mr Xie then attended Shandong Finance and Economics University and, upon graduating, came to Australia to further his studies. Between July 2013 and December 2015 Mr Xie undertook post graduate study in accounting at Macquarie University. When Mr Xie completed his studies, he returned to China to visit his family before returning to Australia in March 2016.

20 Mr Xie presently resides in Australia on a subclass 485 visa. He is sponsored by his current employer, described as a construction materials company, for whom he works as an accountant.

Moshav

21 Moshav is a fund manager. It raises and lends money for the purpose of investing in real property.

22 As a fund manager Moshav derives its capital for investment by issuing units in various managed investment schemes. Upon investment in a scheme and once the scheme is fully subscribed Moshav on lends the funds for commercial property transactions and derives income via interest payments. It returns interest to investors in the relevant scheme. The managed investment schemes are typically secured by a registered first or second mortgage over real property or via general security arrangements.

23 Moshav holds Australian Financial Services Licence (AFSL) no. 439903 (Moshav AFSL). The Moshav AFSL permits Moshav to carry on a financial services business, among other things, to:

(a) provide general financial product advice only, for the following classes of financial products:

…

(iv) interests in managed investment schemes excluding investor directed portfolio services; and

…

(b) deal in a financial product by:

(i) issuing, applying for, acquiring, varying or disposing of a financial product in respect of the following classes of financial products:

(A) interests in managed investment schemes limited to:

(1) own managed investment scheme only; and

(B) securities; and

…

AXL

24 AXL was registered on 16 December 2014. At the time of AXL’s registration, Derek Errol Ziman and Alexander Harmstorf were its directors. Mr Ziman ceased to be a director on 11 May 2015 and Mr Harmstorf ceased to be a director on 24 March 2016 but was reappointed for two further periods: 12 May 2016 to 13 July 2016: and 20 January 2017 to 30 September 2019. AXL has had various other directors since its registration. Relevantly, Mr Roths was appointed a director of AXL on 10 September 2019 and has, since 25 January 2020, been AXL’s sole director.

25 One of the shareholders in AXL was A.C.N. 117 688 356 Pty Ltd, a company of which Mr Silberman is sole director, secretary and shareholder. Mr Silberman explained that A.C.N. 117 688 356 was issued the shares in AXL, at no cost to it, as part of the arrangement for AXL to become an authorised representative of Moshav, as explained below.

26 AXL was an authorised representative under the Moshav AFSL. AXL was issued with a limited authorisation to source investors for Moshav’s funds and for that purpose, on a collaborative basis, Moshav and AXL issued a white label information memorandum to invite investors, via AXL, to invest in one of Moshav’s funds called “premium fund series”. Mr Silberman also described the funds in this series as white label products.

27 In order to put the authorisation in place, by letter dated 15 July 2015 addressed to AXL (Authorisation Letter), Moshav set out the terms on which it had agreed to appoint AXL as its authorised representative under the Moshav AFSL. The Authorisation Letter relevantly provided:

1 Appointment

1.1 [Moshav] agrees to appoint [AXL] as our authorised representative of [Moshav] under the [Moshav AFSL].

1.2 [AXL] accepts the appointment as an authorised representative of [Moshav] under the [Moshav AFSL].

2 Authorisations

[Moshav] authorises [AXL] to provide the financial services as our representative under the authorisations in the [Moshav AFSL] set out in Schedule 1

(the Financial Services).

3 Term

The term of the Agreement shall be 3 year [sic] from the date of this Agreement. Renewal of the Agreement shall be for further terms as agreed between the parties.

4 Sub-authorised Representatives

4.1 [Moshav] gives its consent and authorises [AXL] to appoint the following natural persons to act as sub-authorised representatives so that they may provide one or more of the Financial Services under the [Moshav AFSL] held by [Moshav] (the Sub-Authorised Representatives):

(a) Alexander Gordon Johann Harmstorf

…

28 Schedule 1 to the Authorisation Letter was headed “Authorisation of Authorised Representatives” and provided:

Moshav Financial Wholesale Pty Ltd (ACN 163 365 937) appoints AXL Financial Pty Ltd (ACN 603 393 317) to act as its Authorised Representative for the purposes of providing the following financial services:

1

(a) provide general financial product advice only, for the following classes of financial product:

(i) interests in managed investment schemes excluding investor directed portfolio services,

to wholesale clients.

29 Schedule 2 to the Authorisation Letter was titled “Written Notice to be issued by [AXL] authorising a person to act as a Sub-Authorised Representative of [Moshav]”. Mr Silberman explained that Mr Harmstorf, who he understood was a lawyer who represented Chinese investors looking to invest in Australian funds and who was the person with whom he negotiated in relation to selling the premium fund series, was the only person who signed a letter in accordance with the Authorisation Letter. That is, Mr Harmstorf was the only person AXL appointed as a sub-authorised representative of Moshav.

30 The information memorandum for the premium fund series was issued by AXL. It set out an investment offer to wholesale investors in two funds, a premium mortgage fund and a high yield mortgage fund and included:

(1) information about Moshav, the trustee and custodian of the funds, including its board of directors. At the time its directors were Mr Silberman and Bao Cheng Luo, the latter of whom was described as an executive director;

(2) information about AXL. The information memorandum noted that AXL is “an authorised representative of [Moshav], and is the Manager of the AXL Financial Premium Fund Series”; and

(3) corporate organisation charts for each of AXL and Moshav.

31 Mr Silberman says that when AXL applied to be an authorised representative of Moshav, he would have undertaken a company search to identify its directors and shareholders and completed a credit check. He recalls that he undertook a reasonable amount of due diligence including requiring AXL to complete “know your own client” documents. Mr Silberman’s understanding was that AXL’s only business was the sale of the premium fund series products.

32 At the time that AXL became an authorised representative of Moshav, Mr Harmstorf asked if he could use some of the space in Moshav’s office situated in Double Bay, New South Wales, on a temporary basis. Mr Silberman agreed. Mr Silberman understood that AXL had staff which it temporarily needed to house and Moshav had some capacity to enable what Mr Silberman described as some temporary “hot desking”. The number of AXL staff working from Moshav’s Double Bay office changed but at a maximum it was four to five people. Moshav did not receive any rental or other payment from AXL for the use of its office space.

33 One of the AXL staff members who worked from Moshav’s Double Bay offices from time to time was Izabela Kwoka, Mr Roths’ wife. Ms Kwoka was a registered auditor and, from time to time, she did some work for Mr Silberman. Occasionally, when Ms Kwoka was in the office, Mr Silberman spoke with her, but his discussions did not relate to AXL’s business.

34 Mr Silberman was not aware of AXL’s business interests other than its role as an authorised representative of Moshav and was not aware that it was involved in matters outside of that role, for example, property development. At no stage did Mr Silberman have any form of management role in AXL and he was never a director of AXL. In the absence of a specific business need to do so, including for example for the purpose of AXL introducing prospective borrowers to Moshav (see [38] below), he only spoke with Mr Harmstorf on an ad hoc basis and speculated that over a period of six months he probably spoke to Mr Harmstorf three times.

35 Mr Silberman terminated AXL’s status as an authorised representative of Moshav on about 9 April 2019 because of AXL’s lack of performance. That is, there had been no investors introduced by AXL in its capacity as an authorised representative.

36 AXL was placed into voluntary administration on 18 August 2021 and into liquidation on 22 September 2021.

Mr Silberman and Mr Roths

37 Mr Silberman first met Mr Roths in about 2003. He was aware that Mr Roths had a role in AXL between about 2015 and 2019. He did not know exactly what that role involved but believed that Mr Roths had undertaken credit analysis for Mr Harmstorf.

38 Between about 2015 and 2020 Mr Silberman met with Mr Roths on an ad hoc basis usually in relation to the introduction of potential borrowers from Moshav. Mr Silberman understood that Mr Roths was acting as a finance broker looking to introduce potential borrowers. If there was a particular deal that Mr Roths was seeking to introduce, Mr Silberman might see Mr Roths two to three times per week but otherwise he might not see Mr Roths for several months.

39 Mr Silberman understood that when Moshav was dealing with Mr Roths, he was acting in his capacity as an agent or employee of one of Mr Harmstorf’s companies, of which there were a number, other than AXL.

40 Mr Silberman was unaware of the extent of the businesses in which Mr Roths was involved beyond his involvement in introducing clients to Moshav and undertaking some work with Mr Harmstorf on the credit side.

41 Mr Silberman does not recall when he first became aware of Hyperbuild but he recalls that it was involved in construction on the south coast of New South Wales. He does not recall Hyperbuild ever being the subject of specific discussions between him and Mr Roths, although it was possible that Mr Roths may have sought to introduce Hyperbuild as a potential borrower but no transaction eventuated.

42 Mr Silberman first heard about the Hyperbuild Transaction when he received a letter from Mr Xie’s solicitors, WB Legal.

Mr Yu

43 Mr Yu was born in Shandong Province in 1988. He came to Australia in 2008 to attend university.

44 In 2013 Mr Yu obtained a Bachelor of Accounting from Central Queensland University and in 2014 he obtained a Master of Applied Finance from the University of Western Sydney.

45 In 2014, after Mr Yu had completed his studies, he joined AusLink Investment and, in early 2015, one of his colleagues introduced him to Mr Harmstorf as “the boss of AXL Legal”. At one stage, while in the employ of AusLink, Mr Yu attended AXL Legal’s offices where he met Mr Roths for the first time.

46 During 2015 and 2016 Mr Yu developed a friendship with Mr Roths. They would often go out for a drink or a meal. According to Mr Yu, during their discussions Mr Roths told him that he and Mr Silberman were business partners, and their businesses were “50-50” but he did not specify which business. Mr Roths also told Mr Yu that he was preparing to set up AXL so that the AXL brand could expand from legal, at the time there was a business in existence called AXL Legal, to financial.

Mr Yu’s employment with Moshav

47 In 2015 Mr Yu informed Mr Roths that he needed a new job and an employer sponsor for his visa. Mr Roths later contacted Mr Yu indicating he may have a job opportunity for him and, at the time, mentioned Moshav.

48 At Mr Roths’ instigation in mid to late 2015 Mr Yu attended a meeting with Messrs Silberman and Roths at the Intercontinental Hotel in Double Bay. Mr Yu recalls that at that meeting he was asked questions about his qualifications and his experience. Mr Silberman recalls that he was introduced to Mr Yu but cannot now recall if Mr Roths was at the initial meeting.

49 A few days after the meeting referred to in the preceding paragraph, Mr Roths contacted Mr Yu to inform him that he was successful in obtaining a role with Moshav in sales and marketing focussing on the Chinese market. Mr Roths did not “offer” Mr Yu the job at Moshav, he just told Mr Yu that he got the job.

50 On 18 September 2015 Moshav as “Employer” and Mr Yu as “Employee” entered into an employment agreement (Yu Employment Agreement). The terms of the Yu Employment Agreement relevantly include:

1. ENGAGEMENT

1.1. The Employee is hereby employed by the Employer. The Employee's employment commences on 5 October 2015. The Employee must report for work on 5 October 2015 at 8:30 am at the Employer's premises at 442 New South Head Road Double Bay NSW. The Employee must report to Tal Silberman. In the course of employment the Employee's place of employment may change.

1.2 The Employee is employed in the position of Sales and Marketing Manager (ANZSCO 131112).

1.3 The Employee's duties and responsibilities (“Duties”) in this position include all the duties and responsibilities that would normally attach to that type of position. The Employer may change these Duties during the course of the Employee's employment after consultation with the Employee.

1.4 In addition to the Duties, the Employee is required to fulfill the list of duties and responsibilities set out in Attachment No 1.

…

3. EMPLOYEE’S OBLIGATIONS

3.1 The Employee must at all times in the course of the Employee’s employment:-

(a) act honestly and always in the best interests of the Employer;

(b) promptly follow all lawful and proper directions of the Employer in respect to the carrying out of the Duties;

(c) punctually attend each work day at the designated place of work at the times stipulated by the Employer;

(d) carry out all the Duties carefully, responsibly and competently; and

(e) co-operate and assist management and other employees as and when required.

3.2 Except with the prior consent of the Employer, the Employee must also use computers, telephones, equipment, machinery and vehicles (“Items”) belonging to the Employer for proper and legitimate purposes of carrying on the Employer’s business and in fulfilling the Duties. The Employee must not use any of the Items for the Employee’s personal benefit without the prior written permission of the Employer.

…

18. CONFIDENTIALITY AND TRUST

18.1 During the term of employment the Employee must not work for a competitor of the Employer.

51 I pause to note that in cross-examination Mr Yu accepted that his Moshav email was part of the equipment that belonged to Moshav and that, pursuant to cl 3.2 of the Yu Employment Agreement, he could only use his Moshav email address with Moshav’s prior consent.

52 Attachment 1 to the Yu Employment Agreement is headed “Employee’s duties and responsibilities” and includes:

Sales and Marketing Manager ANZSCO Code 131112

Reporting to: This position reports to the Director

Direct Reports: Future Sales Representatives will be reporting to this position

Tasks Include:

1. The Employee is tasked with developing a product distribution channel for Moshav Financial investment products throughout Chinese speaking markets in Australia, Hong Kong and China.

2. His predominant target product range will be the Moshav Financial and AXL Financial Mortgage Fund Series and direct investments into Property investments as facilitated by Moshav.

…

5. The Employee will be required to promote the Moshav and AXL product range through the WeChat application and other popular media/ advertising solutions in accordance with guidelines set by the Directors from time to time.

53 Mr Yu commenced work at Moshav in about October 2015. His role was to source onshore and offshore Chinese investors to invest in Moshav managed funds. Upon commencing his employment he was trained by Mr Silberman in relation to Moshav’s information memoranda. He was also informed that Moshav held an AFSL, the terms of which were explained to him by Mr Silberman. Mr Yu understood that Moshav was licensed to sell managed investment schemes to wholesale investors but not to retail investors.

54 During the course of Mr Yu’s employment, Mr Silberman met with Mr Yu to discuss marketing to Chinese investors, both Moshav’s products and the AXL premium fund series. As an employee of Moshav, these were the only products that Mr Yu was authorised to sell.

55 Mr Yu also came to learn that AXL was an authorised representative of Moshav, he thinks at about the time AXL obtained that status. Mr Yu understood that as authorised representative of Moshav, AXL was limited to selling the products that Moshav was licensed to sell and that it could not go beyond the terms of its authorised representation.

56 Mr Yu worked at Moshav’s Double Bay office. About four to six weeks after commencing his employment, Mr Yu was given a business card which appeared (both front and back) as follows:

57 Mr Yu attended Moshav’s office almost every morning. However, as Mr Yu’s role was to introduce investors, Mr Silberman’s preference was for him to be “out seeing clients”, rather than in the office. When Mr Yu was in the office Mr Silberman spoke with him regularly about his work in progress and answered any specific questions Mr Yu may have had in relation to particular investors and day to day business matters.

58 Apart from sourcing investors for Moshav’s managed investment schemes, which was his principal role, Mr Yu was, as set out above, also able to facilitate investment in the AXL premium fund series that Moshav was trying to sell. However, Mr Yu only worked for Moshav and, given that his 457 visa was sponsored by Moshav, he was not able to work for any other entity. Despite, Mr Yu believed that his 457 visa did not restrict him from incorporating a company and registering for an Australian Business Number, which he did on multiple occasions for the purpose of doing business in Australia.

59 According to Mr Yu, in late 2015 and early 2016 he often attended AXL’s offices at 1 Market Street, Sydney to meet with Mr Roths. At the time he believed that both Messrs Silberman and Roths were his bosses.

60 Mr Yu said that at times, although not often, Messrs Yu, Silberman and Roths met to discuss how to market products to Chinese investors. In 2015 Mr Yu was, at Mr Roths’ request, marketing products which were not offered by Moshav. According to Mr Yu he did not do so in a secretive way and, while he cannot clearly recall, he thinks he mentioned what he was doing to Mr Silberman.

Mr Xie meets Mr Yu

61 In March 2016 Mr Xie returned to Australia to undertake a NAATI course for translation from Mandarin to English in Sydney. It was at that time that Mr Xie first met Mr Yu in the circumstances described below.

62 Whilst still in China Mr Xie saw a room for rent advertised online. He responded to the advertisement and arranged for rental of the room, dealing at the time with Mr Yu’s then partner. Upon his return to Australia in March 2016 he moved into the room as arranged which was in an apartment located in Epping, New South Wales in which Mr Yu and his then partner lived. Mr Xie continued to lease the room from Mr Yu and his partner until June 2016 (although nothing turns on it, I note that Mr Yu said that he lived in the same apartment as Mr Xie until the end of 2016).

63 After Mr Xie moved out of the room he sublet from Mr Yu, they continued to keep in touch on WeChat.

Mr Xie works for Hyperbuild and AXL

64 Mr Xie did not complete the NAATI course and by September 2016 he had commenced working for Anderson Recruitment, a labour hire company. He continued to work for Anderson Recruitment until the end of 2018.

65 In September 2016 Anderson Recruitment placed Mr Xie at Hyperbuild in the role of assistant accountant, working three to four days per week. In that role, Mr Xie undertook accounting and bookkeeping work for Hyperbuild and AXL. From September 2016 until about April 2017 Mr Xie worked at Hyperbuild/AXL’s office located at New South Head Road, Double Bay, New South Wales and from April 2017 to November 2017 Mr Xie worked at Hyperbuild/AXL’s office located at Shellharbour. In November 2017 Mr Xie returned to China to marry.

66 I pause here to note that there was scant evidence about Hyperbuild. A company search in evidence before me showed that it was registered on 7 January 1998, was placed into external administration on 4 July 2019 and subsequently into liquidation on 1 September 2021. It was deregistered on 11 August 2023. It is apparent that AXL or what appear to be related companies and companies associated with Mr Roths jointly held parcels of different classes of shares in Hyperbuild.

67 Mr Xie understood, from his discussions with Mr Yu in the initial months of his employment with Hyperbuild/AXL, that Mr Roths was “the boss” of AXL and Hyperbuild, AXL was a developer, Hyperbuild undertook building projects for AXL and AXL used Moshav’s AFSL to raise funds for its development projects.

68 In his curriculum vitae Mr Xie describes his duties while working at Hyperbuild/AXL as follows:

* Documenting, reviewing and providing assurance about accuracy and timing of financial transactions by entering account information, creating and updating database and excel spread sheets.

* Applied mathematical abilities on daily basis to calculate and check figures in all areas of accounting systems

* Preparing financial reports, BAS and tax return.

69 At the time Hyperbuild and AXL used MYOB to record transactions. Mr Xie explained that while he was working there, all moneys in Hyperbuild came from AXL by way of loan. As Hyperbuild was a builder, the loan funds were used to pay its expenses. Hyperbuild did not make any profits prior to finalisation of a project.

70 Mr Xie knew that AXL had funds available in its accounts. However, he did not know whether AXL ever made a profit and he did not know from where it sourced its income.

71 As part of Mr Xie’s duties he worked on and did book entries in relation to staff credit cards and staff reimbursement. As a result of that work, Mr Xie knew that AXL reimbursed Mr Yu for his travel costs to China. Mr Xie understood that Mr Yu worked for AXL and Moshav at the same time.

72 Mr Xie reported to Ms Kwoka who was the chief accountant and, as set out above, Mr Roths’ wife. At the end of each week Mr Xie reported by email to Mr Roths in relation to payment of wages, banking reconciliation, credit card usage and bank statements.

73 According to Mr Xie, Hyperbuild/AXL shared its Double Bay office with Moshav. At the time that Mr Xie worked from the Double Bay office there were approximately four staff working for Moshav, one of whom was Mr Yu, who he understood worked as a marketing manager for Moshav, and approximately three staff working for Hyperbuild/AXL.

74 Mr Xie recalls that Mr Roths attended the Double Bay office approximately once per week and that Mr Silberman attended the Double Bay office daily but he rarely spoke to him.

75 Mr Xie often spoke with Mr Yu when he was in the Double Bay office. There were periods of time when Mr Yu was absent in China sourcing investors for Moshav’s project development, including from September to December 2016. Messrs Xie and Yu had lunch together about once a month when Mr Yu was in the Double Bay office, on some occasions, with other staff members.

Mr Roths asks Mr Yu to market products for AXL

76 At a time between 2016 and 2018, Mr Yu can no longer recall precisely when, Mr Roths told Mr Yu to market products not offered by or through Moshav to Chinese investors. Mr Yu recalls that at the time Mr Roths said words to the following effect:

AXL has now become a sub-licensee under Moshav. There will be two lines of products. The original Moshav line is less risky but less reward. The new line will be more risky and more reward. I would like you to try to market some of the new products to Chinese investors.

77 Mr Yu explained that the “new line” referred to by Mr Roths was the premium fund series and, because the return on those products was higher than on the Moshav products, he considered them to be more risky.

78 At the time Mr Yu understood that it was not Moshav asking him to promote the non-Moshav products. This was because Mr Roths offered him 1% commission on successful investment in those products. Mr Yu did not expect to be paid, and was not paid, a salary (in addition to the 1% commission) by AXL or Mr Roths.

79 In cross-examination by Ms Castle, counsel for Moshav Mr Yu gave the following evidence about the request by Mr Roths that he market products for AXL to Chinese investors:

Ms Castle: You gave some evidence yesterday about – and it’s in your outline – about Mr Roths saying that now that AXL was an authorised representative, he had in mind two products. Do you remember that evidence?

Mr Yu: Yes.

Ms Castle: One, the Moshav product, which was less risky, and the other products which were more risky?

Mr Yu: Yes.

Ms Castle: Did you understand the more risky products to be part of the authorised representation that AXL had?

Mr Yu: Yes.

Ms Castle: And did Mr Roths tell you what products they were?

Mr Yu: Yes.

Ms Castle: Was it just what we’ve been referring to as the white-label product?

Mr Yu: Yes.

Ms Castle: And if Mr Roths had wanted AXL to invest in, let’s say, a soft drink bottling plant, did you – would you have considered something like that to be under the terms of the authorised representation?

Mr Yu: No.

Ms Castle: What was your understanding of the products that you saw AXL involved in? So which of the products that you saw AXL involved were authorised as part of its representation?

Mr Yu: From my memory, it’s only the white-label premium fund series. That’s the only products being offered by Moshav to AXL to sell.

Ms Castle: And you were aware, were you, that AXL was involved in doing things other than trying to promote that product?

Mr Yu: Yes.

Ms Castle: Is it true to say that it was your understanding that AXL was involved in a number of separate business interests?

Mr Yu: Yes.

Ms Castle: And was it your understanding that the only one that it was doing as a representative of Moshav was the white-label product?

Mr Yu: Yes.

Ms Castle: And so when you were asked by Oliver to promote other products to investors, was it your understanding that you were doing that outside of the authority of the licence?

Mr Yu: Yes.

Ms Castle: And when you accepted an arrangement to receive a one per cent commission in relation to Hyperbuild, was that – you didn’t tell Mr Silberman about that, did you?

Mr Yu: I didn’t tell Silberman.

80 In about March 2018 Mr Roths arranged an AXL email address for Mr Yu: raymond.yu@axlfinancial.com.au. Mr Yu also had an AXL business card, in addition to his Moshav business card. He does not know if Mr Silberman was aware of his AXL email address, he did not inform Mr Silberman about it . When Mr Yu travelled overseas he gave out either his Moshav or his AXL business card depending on the product he was promoting at the time.

81 In May or June 2018, Mr Yu went to China to seek out investors for the Hyperbuild Transaction. He did not tell Mr Silberman that he was going to China for that purpose as this was an occasion during which Mr Yu was on a period of annual leave.

January 2018

82 On the evening of 13 January 2018 Mr Xie and his wife met with Mr Yu in the lobby of the Star Casino in Sydney for approximately 15 to 30 minutes. Mr Xie explained that the meeting was arranged for two reasons: first, because his wife wanted to meet with Mr Yu as she had not seen him for two or three months; and secondly, because Mr Yu had previously mentioned an investor who came from Mrs Xie’s home town who she might know.

83 At the time of their meeting Mr Xie recalls that he and Mr Yu had a conversation to the following effect (as recounted by Mr Xie through the interpreter):

Mr Xie: Mr Yu long time no see. Where have you been for the past few months?

Mr Yu: I went back to China to look for investors. AXL has borrowed the AFSL to assist with its fundraising for its project development.

Mr Xie recalls that Mr Yu showed him a screenshot of a bank transfer of a large sum exchanged from RMB into Australian dollars.

84 Mr Yu has no recollection of meeting with Mr and Mrs Xie at the Star Casino in early 2018 and disagrees that he had a conversation to the effect set out in the preceding paragraph. Nor does Mr Yu recall ever having any conversation with Mr Xie about the arrangement between Moshav and AXL in relation to Moshav’s AFSL.

85 Despite the fact that Mr Yu cannot recall it, I am satisfied that he did meet with Mr and Mrs Xie on the evening of 13 January 2018 at Star City Casino and that Messrs Yu and Xie had a conversation to the effect set out at [83] above. That finding is reinforced by the exchange of the following WeChat messages between Mr Yu and Mrs Xie on 13 January 2018 between about 6.48 pm and 9.29 pm (as translated):

Mr Roths introduces the Hyperbuild Transaction to Mr Yu

86 According to Mr Yu, Mr Roths first told him about the Hyperbuild Transaction in early 2018. Mr Yu recalls that it was one of the products that Mr Roths asked him to market to Chinese investors. On 20 April 2018 Mr Roths sent Mr Yu two emails, the first of which had a series of attachments, in relation to the Hyperbuild Transaction.

87 According to Mr Yu at some point he mentioned the Hyperbuild Transaction to Mr Silberman, although he cannot recall when he did so or what he said to Mr Silberman about it. Mr Silberman denies ever having a discussion with Mr Yu, or indeed at all, in relation to the Hyperbuild Transaction. The first he heard of the Hyperbuild Transaction was when he received a letter from Mr Xie’s solicitors.

May 2018 – Mr Yu introduces an investment opportunity to Mr Xie

88 At the end of April 2018 Mr Xie’s wife learned that Mr Yu’s new wife was coming to Australia for the first time and so extended an invitation to Mr and Mrs Yu to come to their home, at the time in Epping, New South Wales, on 1 May 2018.

89 Mr and Mrs Yu arrived at Mr and Mrs Xie’s house on 1 May 2018 at about 3 pm. After greeting them at the door Mr and Mrs Xie took Mr and Mrs Yu into their backyard where they had tea. Mr Xie recalls that his wife was sitting at one end and he and Mr and Mrs Yu were sitting on the other side with Mr Yu next to him.

90 Mr Xie recalls that he and Mr Yu had a conversation to the following effect (as recounted by Mr Xie through the interpreter):

Mr Yu: Oliver plans to list his company.

Mr Xie: Which company is that?

Mr Yu: Hyperbuild wants to become a listed company through a backdoor listing. Previously Hyperbuild and AXL borrowed an AFSL from Moshav to do development projects and now Oliver wants to purchase 50% of the shares of a listed company which has a financial services licence. That way he can provide financial services using the listed company’s licence.

Mr Xie: When would Hyperbuild become a listed company?

Mr Yu: Oliver has already acquired over 30% of a listed company’s shares and Oliver will continue to acquire more shares from this company up to 51% before the shareholders’ meeting this week. The whole listing plan will be finalised before September 2018 and Oliver said that if this plan goes successfully, the share price would increase tenfold. According to my estimates even if it’s not as high as tenfold at least six to eight fold is guaranteed.

Mr Xie: How much do I need to invest?

Mr Yu: 5% of the original shares of Hyperbuild amounts to $700,000 and you will be given as a gift 5% of the shares of the listed company. When the shareholders’ meeting is held next week if the stock purchase is finalised and if the contracts are signed then there is no more chance for you to purchase so you have to act quickly if you want to make this investment.

Mr Xie: How many shares has Hyperbuild issued so far?

Mr Yu: Because Hyperbuild is not a listed company yet its shares are called units. Currently it has issued 10,000 units and 500 units equals $700,000.

Mr Xie: What is the name of the listed company?

Mr Yu: This is confidential. What I can tell you is the value of the company is not very big. The market value is only $2 million but this company holds a financial services licence which is the most precious thing.

Mr Xie: So how many shares has this listed company issued?

Mr Yu: About 70 million. You will be given as a gift 3 million stocks which is about 5%.

Mr Xie: Have you invested yourself?

Mr Yu: Yes. I purchased 5% of the shares. This is a very rare universe-opportunity. Only internal could have a chance to invest. Oliver asked me to keep this confidential, but because Oliver knows you that it’s ok to let you know about it. But you have to make a decision quickly because time is tight.

Mr Xie: What is the deadline for the investment?

Mr Yu: Next Tuesday because the shareholders’ meeting is going to be held next week.

Mr Xie: I see. But I need to discuss this with my family. Can you guarantee this listing plan will go successfully, 100%?

Mr Yu: Yes. Because the purchase price of the stocks has already been discussed what needs to be done next week is just signing the contract and then the money used to purchase the stocks will be transferred to the listed company. After that Oliver will change the shareholders of the listed company to his people and he will sell the assets of Hyperbuild into the listed company to finalise the listing process. But these are all formalities, if the listing plan fails Oliver will return all of your money invested.

Mr Xie: Do you confirm that if this fails the money will be returned?

Mr Yu: Yes. Oliver states so in his email and I will forward it to you later.

Mr Xie: Okay. Can you tell me the profit situation of Hyperbuild for the past few years?

Mr Yu: Not including its subsidiaries, Hyperbuild for this financial year – the profits are $3 million.

Mr Xie: Okay. So can you send those documents you just mentioned to me for me to have a look at?

Mr Yu: I will bring those to you in the next few days. Do you know Oliver is working on something big? Oliver has acquired a block of land, a very big block of land, in Sydney and he is going to raise $100 million for developments. So it is trustworthy. If this listing plan goes successfully then the stock will increase tenfold.

91 Mr Yu recalls that the conversation set out above occurred on 2 May 2018 at a meeting which took place at AXL’s Milsons Point offices (see [94] below). Whether it occurred on 1 or 2 May 2018 is in my view of little consequence. Both Messrs Xie and Yu agree that they had an initial conversation about the Hyperbuild Transaction on one of those days. Insofar as Mr Xie’s version of the conversation recorded in the preceding paragraph is concerned, Mr Yu:

(1) denies that:

(a) he said “previously Hyperbuild and AXL borrowed an AFSL from Moshav to do development projects”;

(b) he said “Oliver has already acquired over 30% of a listed company’s shares”. Rather Mr Yu recalls that he said words to the following effect:

Next week, 4 May, the shareholders meeting will be held. We’ve got to take 51% of the shares. Then we will get control of the company”.

(c) he said “according to my estimates even if it’s not as high as tenfold at least six to eight fold is guaranteed”;

(d) he said “5% of the original shares of Hyperbuild amounts to $700,000”. Mr Yu said that he referred to the Hyperbuild Trust, not Hyperbuild shares;

(e) Mr Xie said “[h]ow many shares has Hyperbuild issued so far?” and that he responded “[b]ecause Hyperbuild is not a listed company yet its shares are called units”;

(f) he said: “[w]hat I can tell you is the value of the company is not very big. The market value is only $2 million” or that he described the financial services licence held by the company as “the most precious thing”;

(g) Mr Xie said: “[s]o how many shares has this listed company issued?” and that he responded “[a]bout 70 million” or that 3 million shares was “about five per cent”;

(h) he said “I purchased 5% of the shares”. Mr Yu said that he used the word “invest” not “purchase” and accepted that at that time he had an agreement with Mr Roths about a 5% investment but that no moneys had yet passed to implement the investment;

(i) he said “[t]his is a very rare opportunity. Only internal staff have an opportunity to invest. Oliver asked me to keep this confidential, it is because Oliver knows you that he told me about it. But you have to make a decision quickly because time is tight”;

(j) Mr Xie said “[c]an you guarantee this listing plan will go successfully, 100%?” and he replied “[y]es. Because the purchase price of the stocks has already been discussed what needs to be done next week is just signing the contract and then the money used to purchase the stocks will be transferred to the listed company. After that Oliver will change the shareholders of the listed company to his people”. As to the last sentence, Mr Yu said that he recalls that he said that Mr Roths would change the chairman of the company to his person, not the shareholders;

(k) he said “[b]ut these are all formalities, if the listing plan fails Oliver will return all of your money invested”. Mr Yu recalls that he used the Chinese word “kai shi” which in English means “begin” or commence”. He recalls telling Mr Xie that if the acquisition of PLC was not commenced then his $700,000 investment would be returned and, in that event, Mr Xie would have to return his 3 million shares. However, Mr Yu also gave evidence in cross-examination that at the time of his meeting with Mr Xie, whether on 1 or 2 May 2024, Mr Roths must have already purchased shares in PLC because he was attending a shareholders’ meeting the following week and needed to hold 51% of the shares in PLC before attending that meeting. That is Mr Yu agreed that by the time of his conversation with Mr Xie on 1 or 2 May 2018, Mr Roths had commenced purchasing shares in PLC. In my view it follows that by that time the acquisition of PLC had commenced. When this proposition was put to him in cross-examination, Mr Yu changed his evidence saying that “commenced” means 51% or control of the company. According to Mr Yu, if Mr Roths could not get control of the company, by acquiring 51% of its shares, the acquisition had not commenced and the $700,000 investment would be returned. Mr Yu’s evidence on this issue should be rejected. I accept Mr Xie’s evidence that Mr Yu told him that “if the listing plan fails”, Mr Roths would return his money to him. Indeed, Mr Yu made a similar representation to another investor, Ms Gu (see [98] below);

(l) Mr Xie said “[w]ill you confirm that if this fails the money will be returned?” and that he responded “[y]es. Oliver says so in his email”;

(m) Mr Xie said “Okay. Can you tell me the profit situation of Hyperbuild for the past few years?”;

(n) he said “do you know Oliver is working on something big? Oliver has acquired a block of land, a very big block of land, in Sydney and he is going to raise $100 million for developments. So it is trustworthy” but says that he said something about “raising $100 million through the listing company in the future”; and

(2) cannot recall saying:

(a) “[w]hen the shareholders’ meeting is held next week if the stock purchase is finalised and if the contracts are signed then there is no more chance for you to purchase so you have to act quickly if you want to make this investment”; and

(b) “[n]ext Tuesday because the shareholders’ meeting is going to be held next week”.

92 There were parts of the conversation with Mr Xie which took place on 1 or 2 May 2018 which in cross-examination, Mr Yu agreed that either he or Mr Xie said. For ease I have underlined those parts in the extract at [90] above.

93 After having tea Mr and Mrs Xie and Mr and Mrs Yu dined at a Japanese restaurant. There was no further discussion during the dinner about the investment opportunity.

94 Mr Xie next met with Mr Yu on Wednesday, 2 May 2018. Mr Yu organised the meeting via WeChat. Mr Xie drove to AXL’s Milsons Point office to meet with Mr Yu at about midday. He met Mr Yu downstairs and was taken up to a meeting room. The purpose of the meeting was for Mr Xie to obtain documents about the investment opportunity he had discussed with Mr Yu the previous day. The meeting lasted for about 30 minutes.

95 At the meeting Mr Yu provided two documents to Mr Xie. One was an email from Mr Roths to Mr Yu sent on Friday, 20 April 2018 at 7.18 am with subject “ASX: … Confidential” (20 April 2018 Email) and the other was a letter dated 30 April 2018 on AXL letterhead from Mr Roths, group chief risk assessment officer, to Mr Yu in relation to “The Hyperbuild Unit Trust” (30 April 2018 AXL Letter). In both documents parts of the text had been redacted. Mr Xie’s evidence was that in each case the redacted portions were the parts that identified the company in which Hyperbuild anticipated acquiring a 50% share to achieve its backdoor listing. Mr Yu provided the two documents to Mr Xie by way of further introduction to the investment. Mr Xie recalls that Mr Yu also showed him a draft unit subscription document at the meeting.

96 About halfway through the meeting Mr Roths joined. Mr Xie recalls that Mr Roths asked him if he had any further questions. Mr Xie responded that he did not “because Raymond told [him] everything”.

Mr Yu’s dealings with another potential investor in the Hyperbuild Transaction

97 This was not the first backdoor listing in which Mr Yu was involved. He had earlier been involved in a backdoor listing concerning BIR Financial Limited with Mr Silberman for which he sourced one investor, Ms Yinghua Gu, who invested $1 million.

98 Mr Yu also offered Ms Gu the opportunity to invest in the Hyperbuild Transaction. Set out below are screenshots taken from Mr Yu’s WeChat account on 13 April 2018 (which have been translated into English) of text exchanges with Ms Gu which clearly relate to Mr Yu introducing the Hyperbuild Transaction to Ms Gu:

Mr Yu explained that he referred to Ms Gu as “Boss GU” because she is the director of a company.

Mr Xie considers investing in the Hyperbuild Transaction

99 On the evening of 2 May 2018 Mr Xie telephoned his father in China to discuss the investment opportunity. He recalls that during the conversation he said words to the following effect to his father:

There is a rare investment opportunity. The amount required is $700,000. If the company is successfully listed the profit will be tenfold. The backdoor listing approach will be successful 100%. The boss has already said that if the listing doesn’t work, if it’s not successful, the investment amount will be returned 100%.

At the time Mr Xie did not have $700,000 but was able to borrow $530,000 from his parents for the purposes of making an investment.

100 On 3 May 2018 Messrs Yu and Xie exchanged the following WeChat messages (as translated):

Mr Xie: (at 00:17am) Hi Boss Yu, are you asleep yet?

Mr Yu: (at 8:22am) I was asleep last night.

Mr Xie: (at 10:31am) Ohh.

Mr Xie: (at 1:12pm) Boss Yu, if you and Oliver have made a decision, could you please send me a copy of the contract?

Mr Yu: Yes the decision has been made, and he is preparing the contract.

Mr Xie: (at 1:29pm) Ok (emoji).

Mr Xie: (at 7:25pm) Has the contract been finalised?

Mr Yu: Oliver is working overtime on it.

Mr Xie: Oh god …

101 Mr Xie next spoke with Mr Yu by telephone on 4 May 2018. According to Mr Xie they had a conversation to the following effect:

Mr Yu: Good morning. Have you made a decision about the investment?

Mr Xie: I am very interested in this project. The problem is that the total amount required is $700,000. Well, I currently only have $530,000.

Mr Yu: How about this? You can find another investor or other investors who will jointly hold this 5% of shares with you.

Mr Xie: It’s impossible for me to find another investor in such a short timeframe.

Mr Xie recalls that there was a short pause in the conversation after which it continued to the following effect:

Mr Yu: I have $190,000 at hand currently and I can lend you $170,000 but you have to return this money to me in time because I have a property to settle in September.

Mr Xie: Can I pay it back to you over a three month period?

Mr Yu: Would that be June, July and August?

Mr Xie: Yes.

Mr Yu: Okay but you have to return the money to me on time because I need to settle my property.

Mr Xie: That’s no problem.

And:

Mr Xie: Since I’ve made a decision to invest can you disclose the listed company’s name to me?

Mr Yu: The ASX code for this company is PLC.

Mr Xie: Okay. I will look it up online.

102 Mr Yu does not recall the conversation set out in the preceding paragraph. However, he recalls that Mr Xie told him that he only had $530,00 available and was short $170,000. Mr Yu says that he did not offer to loan Mr Xie the balance of $170,000. Rather, Mr Xie asked whether Mr Yu could loan him $170,000 to make up the funds required for the investment.

103 On 4 May 2018 commencing at 1.29 pm Messrs Yu and Xie also exchanged WeChat messages. As translated the exchange was as follows:

Mr Xie: I have checked it. The market cap for this company is indeed 2 million, with shares worth 75 million.

Mr Yu: Yes.

Mr Yu: It is not a remarkable company.

Mr Yu: Just using it as a shell company.

Mr Xie: Then we merge HB into it.

Mr Xie: Yes, then 3 million shares would equal 4%.

104 Later on 4 May 2018 Mr Yu forwarded three emails with attachments to Mr Xie:

(1) the first email was at 4.24 pm and attached an unredacted version of the 30 April 2018 AXL Letter that had been provided to Mr Xie at the 2 May 2018 meeting. The 30 April 2018 AXL Letter was now addressed to Mr Xie and its date updated to 4 May 2018. That letter provided:

We confirm that we have acquired Hyperbuild Pty Ltd on 1 July 2015 which structure has changed as of 1 July 2016 when the Hyperbuild Units Trust was formed and that we are the majority unit holder in the Hyperbuild Unit Trust since formation.

Hyperbuild Pty Ltd, now acting as trustee of the Hyperbuild Unit Trust, carries on the business know as “Hyperbuild” and effectively controls, through a majority shareholding, the subsidiaries of GLFB Pty Ltd trading as Harvest Homes, Harvest Homes Properties, Hyperbuild Holdings Pty Ltd and HOLZ DC.

It is proposed that all assets of the Hyperbuild Unit Trust will be sold to PLC Financial Services Limited in due course.

Yours faithfully

AXL FINANCIAL PTY LTD

(2) Mr Yu sent the second email to Mr Xie at 4.26 pm. It, in turn, forwarded an email from Mr Roths to Mr Yu dated 20 April 2018 with subject “Commercial in confidence – Hyperbuild Unit Trust”. Mr Roths’ email provided (as written):

Raymond,

As requested please find attached consolidated summary for Hyperbuild and Harvest Homes for the current financial year. We are unable to provide any financial information for Barrington Homes (as we do not own them yet) but we can say that the operation is comparable to our two operations in all aspects and numbers.

I have also attached the proposed unit holder agreement for the issue of units in the Hyperbuild Unit trust which effectively owns GLFB Pty Ltd trading as Harvest Homes, Harvest Homes Properties Pty Ltd, Holz DC Pty Ltd and Hyperbuild Pty Ltd. (The attached ASIC company searches confirm the shareholding of the various companies).

It is proposed that a new unit holder will effectively obtain 5% of unit trust. In the event we proceed with ASX:PLC we will also a lot them 5% on issue in PLC.

If you have any further questions please do not hesitate to call.

With kind regards

Oliver Roths

(3) the third email was also sent by Mr Yu at 4.26 pm. That email forwarded the 20 April 2018 Email, the second of the two documents given by Mr Yu to Mr Xie at the 2 May 2018 meeting, in unredacted form. It provided:

Raymond,

As discussed, following of us obtaining 51% of shares on issue in ASX:PLC on 7 May we anticipate that the board of directors will be changed.

As a shareholder it is my plan to sell into PLC the Hyperbuild operation (including Harvest Homes) together with the Barrington Homes operation at a combined value of $60 million based on a 10x earnings rational which is accepted by the market.

I anticipate this transition will take 3-6 months and should be completed by the end of 2018. I also anticipate that PLC will raise a further $100 million in a development funds which will be used for strategic land purchases south and north of Sydney which will be developed by either of our operations hence maximising profits for shareholders over the next 3-5 years.

With kind regards

Oliver Roths

105 Each of the emails sent by Mr Yu on 4 May 2018:

(1) was sent by Mr Yu from his email address at Moshav, Raymond.Yu@moshavfinancial.com.au; and

(2) included the following sign off by Mr Yu:

106 Mr Yu accepted that it was common for him to use his Moshav email address for non-Moshav business and that he did so throughout the course of his employment with Moshav. He used his Moshav and AXL email addresses interchangeably, without thinking much about their respective use. Mr Yu also accepted that at the time he sent the emails described at [104] above he had no authority from Moshav to use his Moshav email address other than for the business of Moshav.

107 Mr Silberman said that the use by Mr Yu of the Moshav logo and contact details was highly irregular. Mr Silberman’s evidence, which I accept, is that investment in the Hyperbuild Transaction was not a product that Mr Yu was authorised to sell, that to do so was outside Mr Yu’s job description and it was a transaction or product with which Mr Yu should not have been dealing.

108 As set out at [104(2)] above, the second email provided by Mr Yu to Mr Xie attached, among other things, a consolidated financial summary for Hyperbuild and GLFB Pty Ltd trading as Harvest Homes for the period July 2017 to March 2018 (consolidated financial summary). Mr Xie was cross examined about the consolidated financial summary:

(1) in relation to Hyperbuild, it disclosed that its profit to date was $1,277,833. This was contrary to Mr Xie’s evidence that Mr Yu had told him that Hyperbuild had made a profit of $3 million. Despite this, Mr Xie did not raise the difference between the profit figure as disclosed by Mr Yu and that included in the consolidated financial summary with Mr Yu or raise any query with Mr Yu about that matter; and

(2) in relation to Harvest Homes, it showed that its shareholders were Hyperbuild Holdings Pty Ltd as to 51% and Steve Taylor and Dean Turner as to 49%. Mr Xie said that he did not pay attention to this information and, while he read the consolidated financial summary carefully, he may have missed some information that did not seem important to him at the time. He was focussed on the valuation figures, the progress of projects and total values.

Mr Xie decides to invest in the Hyperbuild Trust

109 On 4 May 2018, after his telephone conversation with Mr Yu, and with the knowledge that Mr Yu would loan him $170,000 required to make up the total $700,000 investment, Mr Xie decided that he would invest in the Hyperbuild Transaction. He decided to do so for the following reasons:

(1) the project involved AXL which was a representative of Moshav. For that reason, Mr Xie assumed that the project “would be legal” and “protected by law”;

(2) Mr Yu told him that this was a “rare and precious opportunity” which was only going to be provided to internal staff members;

(3) Mr Yu invested himself;

(4) Mr Yu had often spoken to him about how he successfully sourced investors to make investments into AXL and Moshav projects. Mr Xie was aware that since 2017 Mr Yu had undertaken many successful cases, so he trusted his expertise and advice; and

(5) most importantly Mr Yu told him that the project would be 100% successful and, if it was not, his investment would be returned. Mr Xie trusted Mr Yu and had reason to believe that his investment would be safe.

110 Mr Xie was cross-examined about his conversation with Mr Yu on 1 or 2 May 2018 (see [90] above) and his decision to invest in the Hyperbuild Transaction. He had the following exchange with counsel for Moshav:

Ms Castle: Did you ask for a contract setting out your rights and any promises that you thought had been made to you?

Mr Xie (through interpreter): On 1 May, I requested from him some relevant documents, including the unit subscription agreement to buy original shares from Hyperbuild. But Yu told me the reasons for his confidentiality, and he only showed me two emails from Oliver, and also a draft agreement without Hyperbuild or my personal information.

Ms Castle: And did you read the agreement when a copy was given to you?

Mr Xie (through interpreter): I did, but because it’s not my expertise, so I couldn’t fully understand its clauses.

Ms Castle: And did you ask Mr Yu or a solicitor or anyone else to explain it to you?

Mr Xie (through interpreter): Firstly, I very much trusted Yu. Secondly, it was the end of the week, and by next Monday/Tuesday, I need to get the money ready, because after the shareholders meeting I had no chance to make the investment any more. So I didn’t have sufficient time during that one two-day period to find a lawyer to read this to me.

Ms Castle: Is – was the amount of 700,000 a significant amount to you?

Mr Xie (through interpreter): Of course. I don’t have that available to me. I borrowed it from my parents.

Ms Castle: And so you would take care to ensure that you were comfortable with what – with the investment that was being offered, wouldn’t you?

Mr Xie (through interpreter): Yes, because I triple confirmed with him that this project will be successful. If not, the investment amount will be returned to me 100 per cent. Also, Yu talked to me before, often about the successful stories of his investments. Also, he introduced Anderson to me and through that I got my 457 visa. Plus, his successful investment stories. I trusted him a lot.

Ms Castle: And after hearing successful investment stories, you wanted to get in on a good investment, didn’t you?

Mr Xie (through interpreter): Yes. But this is the first investment in my life. Also, this money was borrowed from my parents. If he didn’t tell me this investment is guaranteed to be 100 per cent successful, if not, it will be returned to me in full, I would have rejected the opportunity.

Ms Castle: And I put it to you that he didn’t say that it would be 100 per cent successful and he didn’t say that if unsuccessful it would be returned to you.

Mr Xie (through interpreter): I’m positive he said those things to me, because I triple confirmed with him. Because this was my first – very first investment and I would like to ensure the risks involved were not very high.

Ms Castle: And anyone who was trying to ensure the risks weren’t high would have done more due diligence; don’t you agree?

Mr Xie (through interpreter): Because Yu told me before next week I need to get the money ready and I need to borrow money in a very short period of time. I had very little time and too much trust in him.

Mr Yu and Mr Xie enter into a loan agreement

111 At some time after 4 May 2018 and before 8 May 2018, probably on 7 May 2018, Mr Xie met with Mr Yu in a café downstairs from AXL’s office in Market Street, Sydney. Mr Xie recalls that during that meeting he had a conversation with Mr Yu to the following effect:

Mr Xie: Raymond I have already decided to make the investment like we discussed on the phone. Can you lend me $170,000?

Mr Yu: Okay. I will draft a loan agreement in between friends.

Mr Yu opened his mobile banking app to show Mr Xie his bank balance and informed Mr Xie that he would bring the agreement to his house for signature.

112 On 8 May 2018 Mr Yu came to Mr Xie’s house. Mr Yu telephoned Mr Xie upon his arrival and asked him to come out to his car, where they met. Once Mr Xie was in the car Mr Yu took out a loan agreement which already included Mr Yu’s signature, address and, as described by Mr Xie, “some of his basic information” (Yu Loan Agreement). Mr Xie recalls that at the time Mr Yu said to him: “this is a standard version of a loan agreement”. Pursuant to the terms of the Yu Loan Agreement, Mr Yu agreed to loan $170,000 to Mr Xie repayable in three instalments.

113 Mr Yu asked Mr Xie to provide a copy of his passport photo page and for him to sign each page of the Yu Loan Agreement. As Mr Yu had informed Mr Xie that it was a standard template, Mr Xie looked at it briefly, signed it and provided Mr Yu with a copy of his passport photo page. In doing so, when Mr Xie saw the payment schedule he discussed with Mr Yu whether he could change the order of payment so that the largest payment would be the final, rather than the first, payment. Mr Yu agreed to that change and it was made in handwriting.

Mr Xie makes his investment in the Hyperbuild Trust

114 Mr Yu next arranged to meet with Mr Xie at 9 am on 9 May 2018 in Double Bay. They met in the public carpark next to Moshav’s Double Bay office. Mr Yu had a unit subscription agreement with him. Mr Xie recalls that Mr Yu informed him that this was “the investment agreement”, asked Mr Xie to sign it and told him that he could only return it after it was signed by other shareholders. Mr Yu says that he described the document as a “unit subscription agreement” not an “investment agreement”. Mr Xie signed the agreement.

115 At approximately 10 am, Mr Xie accompanied Mr Yu to the ANZ bank in Double Bay where Mr Xie and Mr Yu transferred $530,000 and $170,000 respectively to Hyperbuild’s solicitors’, Piper Alderman, trust account held with the ANZ, the details for which Mr Yu provided to Mr Xie.

116 On 14 May 2018 Mr Yu sent Mr Xie photos of two share transfer forms which respectively referred to the transfer of 1 million and 2 million shares in PLC to Mr Xie.

117 On or about 17 May 2018 $150,000 was transferred into the trust account of Nicholas James lawyers, the solicitors for PLC. The narrative in the trust account statement records that those moneys were received from “Xie”.

118 On 15 June 2018 PLC issued 50 million fully paid ordinary shares in PLC, thereby diluting the percentage of shares acquired by Mr Roths or entities associated with him in PLC as at that date. Neither Mr Yu nor Mr Roths told Mr Xie that this had occurred.

Mr Xie repays the loan from Mr Yu