Federal Court of Australia

TAL Life Insurance Services Limited, in the matter of TAL Life Insurance Services Limited [2025] FCA 130

ORDERS

TAL LIFE INSURANCE SERVICES LIMITED (ABN 31 003 149 157) First Applicant TAL LIFE LIMITED (ABN 70 050 109 450) Second Applicant | ||

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. Pursuant to section 194 of the Life Insurance Act 1995 (Cth), the scheme for the transfer of the life insurance business of TAL Life Insurance Services Limited, the First Applicant, to TAL Life Limited, the Second Applicant, in the form of Annexure A to these orders (Scheme), be confirmed without modification.

2. The Scheme takes effect on and from 11:59PM AEDT on 31 March 2025.

3. TAL Dai-ichi Life Australia Pty Limited pay the costs of the proceeding of the Australian Prudential Regulation Authority as agreed or, if no agreement can be reached, as assessed.

4. There be liberty to apply.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ANNEXURE A

Scheme under Part 9 of the Life Insurance Act 1995 (Cth) for the transfer of the life insurance business of TAL Life Insurance Services Limited ABN 31 003 149 157 to TAL Life Limited ABN 70 050 109 450

The meaning of words in title case is set out in clause 8.1.

(a) This is a scheme prepared pursuant to Part 9 of the Life Act and operates only on, and subject to, its confirmation by the Federal Court (Scheme).

(b) This Scheme gives effect to the transfer deed between TAL Life Limited (TAL Life), TAL Life Insurance Services Limited (TLISL) and TAL Dai-ichi Life Australia Pty Ltd ABN 97 150 070 483 (TAL Dai-ichi) entered into on or around 3 September 2024 (Transfer Deed), under which TLISL has agreed to transfer its Life Business to TAL Life, subject to confirmation by the Federal Court of this Scheme and satisfaction of certain conditions.

(c) TAL Life and TLISL are registered as life companies under the Life Act. TAL Life and TLISL are incorporated in New South Wales. The sole shareholder of each of TAL Life and TLISL is TAL Dai-ichi. The ultimate parent company of both TAL Life and TLISL is Dai-ichi Life Holdings, Inc.

(d) The objective of this Scheme is to transfer the Life Business from TLISL to TAL Life in the manner provided for by this Scheme.

2 Transfer of the Life Business

Subject to the Federal Court confirming the Scheme, this Scheme takes effect on and from 11:59pm (AEDT) on 31 March 2025 or on such other date as the Federal Court may determine (Effective Time).

2.2 Transfer of the Life Business

At the Effective Time, the Life Business is transferred from TLISL to TAL Life, and TAL Life obtains and assumes all rights and benefits, and all obligations and liabilities of the Life Business on the basis, and in the manner, set out in this Scheme.

2.3 Consequences of the transfer of the Life Business

Without limiting clause 2.2, the happenings and consequences set out in clauses 3 to 6 occur at and from the Effective Time unless otherwise stated.

3 Consequences of the transfer of the Life Business

TAL Life becomes the issuer of the TLISL Policies and TLISL ceases to be the issuer of the TLISL Policies.

(a) TAL Life becomes the issuer of the TLISL Policies in place of TLISL and the TLISL Policy Owners become TAL Life Policy Owners. For the avoidance of doubt, the TLISL Policies will remain in-force and there will be no cessation of the TLISL Policies as a result of the Scheme.

(b) The rights and liabilities of the TLISL Policy Owners will be the same in all respects as they would have been if:

(1) the applications on which the TLISL Policies were based had been made to, or accepted by, TAL Life instead of TLISL; and

(2) the TLISL Policies had originally been issued by TAL Life instead of TLISL (subject to the variations set out in this Scheme).

3.3 Assumption of policy liabilities

TAL Life assumes all liabilities and obligations of TLISL under, or in respect of, the TLISL Policies.

3.4 Release of policy liabilities

TLISL is released and discharged from all liabilities and obligations under, or in respect of, the TLISL Policies.

TAL Life, as issuer of the TLISL Policies pursuant to clause 3.1, is entitled to all rights and benefits of TLISL under, or in respect of, the TLISL Policies, including:

(a) the right to receive any fees payable under, or in respect of, the TLISL Policies;

(b) the right to receive premiums payable under, or in respect of, the TLISL Policies; and

(c) the right to enforce all rights and remedies available under the TLISL Policies, including in respect of any non-payment of such premiums or fees.

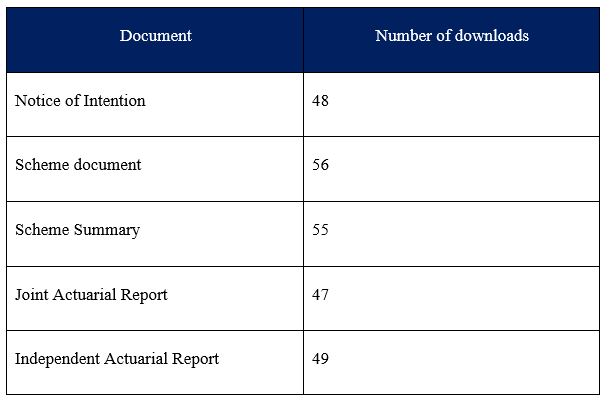

(a) to deduct premiums or fees payable in respect of the TLISL Policies (including by debiting a bank account, through automatic payroll deductions or through electronic bank transfer); or

(b) to disclose or obtain information in the course of carrying on the Life Business of TLISL,

are deemed to be given to TAL Life instead of TLISL.

Any person having a claim on or obligation to TLISL under, or in respect of, a TLISL Policy, has the same claim on or obligation to TAL Life instead of TLISL, irrespective of when such claim or obligation arose.

Any proceedings in connection with a TLISL Policy that are pending, or that commence, whether by or against TLISL, in any court, tribunal or entity dealing with complaints, must be continued by or against TAL Life instead of TLISL and must be amended to that effect.

TAL Life will assume the conduct and administration of, and the liability for, any policy owner remediation programs being conducted by TLISL prior to the Effective Time but which have not been completed at the Effective Time.

3.10 Applications

Any application for a TLISL Policy which has not been accepted by TLISL at the Effective Time is, for all intents and purposes, to be treated as an application to TAL Life, and any policy resulting from such an application takes effect as a TAL Life Policy.

TAL Life:

(a) bears the obligation to pay commissions payable to any person in respect of a TLISL Policy; and

(b) is entitled to seek repayment of commission (whether originally paid by TAL Life or TLISL) in excess of the recipient’s entitlement, instead of TLISL.

(a) TAL Life, as the life company that is to assume all the rights and liabilities in respect of the TLISL Policies, assumes the position of TLISL under all TLISL Contracts as if TAL Life was the original party to those contracts in place of TLISL. The TLISL Contracts will continue in full force and effect on this basis.

(b) Without limiting clause 3.12(a):

(1) TAL Life assumes all rights, powers, privileges, and all liabilities and obligations of TLISL under the TLISL Contracts, whenever occurring;

(2) TAL Life assumes the position of TLISL under the TLISL Contracts in respect of any proceedings pending by, or against, TLISL in respect of the TLISL Contracts;

(3) all references to TLISL in a TLISL Contract will be read as a reference to TAL Life;

(4) all references to TLISL Statutory Fund No.1 in a TLISL Contract will be read as a reference to TAL Life Statutory Fund No.1; and

(5) all references to TLISL Statutory Fund No.2 in a TLISL Contract will be read as a reference to TAL Life Statutory Fund No.2.

(a) all references to TLISL in a TLISL Policy are replaced with TAL Life;

(b) all references to TLISL Statutory Fund No.1 in a TLISL Policy will be read as a reference to TAL Life Statutory Fund No.1;

(c) all references to TLISL Statutory Fund No.2 in a TLISL Policy will be read as a reference to TAL Life Statutory Fund No.2; and

(d) the terms and conditions of TLISL Policies will not change as a result of the Scheme.

3.14 Consequences for TAL Life Policies

The terms and conditions of TAL Life Policies will not change as a result of the Scheme.

(a) Each TLISL Policy referable to TLISL Statutory Fund No.1 becomes a TAL Life Policy referable to TAL Life Statutory Fund No.1.

(b) Each TLISL Policy referable to TLISL Statutory Fund No.2 becomes a TAL Life Policy referable to TAL Life Statutory Fund No.2.

(a) The TLISL Assets of TLISL Statutory Fund No.1 become assets of TAL Life Statutory Fund No.1.

(b) The TLISL Assets of TLISL Statutory Fund No.2 become assets of TAL Life Statutory Fund No.2.

(a) The TLISL Liabilities of TLISL Statutory Fund No.1 become liabilities of the TAL Life Statutory Fund No.1.

(b) The TLISL Liabilities of TLISL Statutory Fund No.2 become liabilities of the TAL Life Statutory Fund No.2.

(c) The liabilities of the TLISL Statutory Fund No.1 and TLISL Statutory Fund No.2 will be transferred individually for an amount equal to the carrying value in TLISL financial records at the Effective Time.

(a) On and from the Effective Time, TAL Life will maintain such policies and practices as are required to enable it to conduct the Life Business in a manner which is consistent with its legal and regulatory obligations, and which satisfies the contractual rights and benefits of the TLISL Policy Owners.

(b) For the purposes of this clause 5, “policies and practices” includes any policies and practices relating to:

(1) the method of determining premium rates and charges;

(2) underwriting and claims management;

(3) each insurer’s capital management framework;

(4) each insurer’s reinsurance management framework;

(5) each insurer’s risk management framework;

(6) each insurer’s business continuity and material outsourcing framework;

(7) each insurer’s data risk framework (including cyber security and data risk management);

(8) each insurer’s dispute resolution framework; and

(9) each insurer’s remediation programs, including the “TAL Enterprise Remediation Guiding Principles”, which is aligned to the ASIC Regulatory Guide RG 277 Consumer Remediation and the ASIC best practice field guide titled “Making it Right: how to run a consumer centred remediation”.

(c) TAL Life must review its policies and practices periodically to ensure that they remain appropriate. Where appropriate, TAL Life will adjust the policies and practices to take better account of its legal and regulatory obligations and with due regard to maintaining the contractual rights and benefits of the TLISL Policy Owners.

TAL Life and TLISL will do all such things and execute all such deeds, instruments, transfers or other documents as may be necessary or desirable to give full effect to the provisions of this Scheme and the transactions contemplated by them.

7 Costs of the Scheme

All costs, including any stamp duty, associated with the transfer of the Life Business of TLISL will be paid by TAL Dai-ichi and not by TLISL Policy Owners or TAL Life Policy Owners.

8 Interpretation

In this Scheme:

APRA means the Australian Prudential Regulation Authority.

Australian Policy Owners’ Retained Profits has the meaning given in the Life Act.

Capital Adequacy Requirement means in the case of a statutory fund or a shareholders' fund, the capital adequacy requirement as determined in accordance with APRA Prudential Standard LPS 110 Capital Adequacy.

Effective Time has the meaning given in clause 2.1.

Federal Court means the Federal Court of Australia.

Life Act means the Life Insurance Act 1995 (Cth).

Life Business means all of TLISL’s life insurance business including the TLISL Assets and the TLISL Liabilities.

life insurance business has the meaning given in the Life Act.

Reinsurance Treaty means a contract under which a party, the reinsurer, agrees to indemnify another party, the cedant, for a specified share of the risk that arises from a specified class of insurance policies issued by the cedant.

TAL Life means TAL Life Limited ABN 70 050 109 450.

Transfer Deed has the meaning given in clause 1(b).

TAL Life Policies means the policies issued by TAL Life that are referable to a TAL Life Statutory Fund immediately prior to the Effective Time.

TAL Life Policy Owner means an owner of a TAL Life Policy.

TAL Life Statutory Fund means a fund established by TAL Life that relates solely to the life insurance business of TAL Life or a particular part of that business.

TLISL means TAL Life Insurance Services Limited ABN 31 003 149 157.

TLISL Assets means all assets referable to the Life Business immediately prior to the Effective Time, including:

(a) the assets supporting any Australian Policy Owners’ Retained Profits in relation to the TLISL Statutory Funds immediately prior to the Effective Time;

(b) the assets supporting the policy liabilities in respect of the TLISL Policies immediately prior to the Effective Time;

(c) the assets supporting any other liabilities of the TLISL Statutory Funds immediately prior to the Effective Time; and

(d) all other assets of the TLISL Statutory Funds immediately prior to the Effective Time.

For the avoidance of doubt, TLISL Assets do not include any assets of the TLISL Shareholders’ Fund.

TLISL Contracts means all contracts entered into by TLISL in relation to the Life Business prior to the Effective Time, excluding the Reinsurance Treaties.

TLISL Liabilities means all liabilities (actual and contingent) referable to the Life Business immediately prior to the Effective Time, including:

(a) the policy liabilities in respect of the TLISL Policies immediately prior to the Effective Time; and

(b) all other liabilities of the TLISL Statutory Funds immediately prior to the Effective Time.

For the avoidance of doubt, TLISL Liabilities do not include any liabilities of the TLISL Shareholders’ Fund.

TLISL Policies means the policies issued by TLISL that are referable to a TLISL Statutory Fund immediately prior to the Effective Time.

TLISL Policy Owner means an owner of a TLISL Policy.

TLISL Shareholders’ Fund means the TLISL fund maintained separately from the TLISL Statutory Funds that holds, among other assets, the minimum amount of capital required to be held outside the TLISL Statutory Funds in accordance with the Capital Adequacy Requirement.

TLISL Statutory Fund means a fund established by TLISL that relates solely to the Life Business of TLISL or a particular part of that business.

8.2 Interpretation

Headings are for convenience only, and do not affect interpretation. The following rules also apply in interpreting this document, except where the context makes it clear that a rule is not intended to apply:

(a) A reference to:

(1) a legislative provision or legislation (including subordinate legislation) is to that provision or legislation as amended, re-enacted or replaced, and includes any subordinate legislation issued under it;

(2) a document (including this document) or agreement, or a provision of a document (including this document) or agreement, is to that document, agreement or provision as amended, supplemented, replaced or novated;

(3) a party to this document or to any other document or agreement includes a successor in title, permitted substitute or a permitted assign of that party;

(4) a person includes any type of entity or body of persons, whether or not it is incorporated or has a separate legal identity, and any executor, administrator or successor in law of the person; and

(5) anything (including a right, obligation or concept) includes each part of it.

(b) A singular word includes the plural, and vice versa.

(c) If a word or phrase is defined, any other grammatical form of that word or phrase has a corresponding meaning.

(d) A reference to information is to information of any kind in any form or medium, whether formal or informal, written or unwritten, for example, computer software or programs, concepts, data, drawings, ideas, knowledge, procedures, source codes or object codes, technology or trade secrets.

(e) The expression this document or this Scheme includes the agreement, arrangement, understanding or transaction recorded in this document, including any schedule to this document or this Scheme.

(f) A reference to time is a reference to Sydney, New South Wales, Australia time.

JACKMAN J:

Introduction

1 In these proceedings the applicants, TAL Life Insurance Services Limited (TLISL) and TAL Life Limited (TAL Life) make an application under s 193 of the Life Insurance Act 1995 (Cth) (Life Act) for an order under s 194 of the Life Act confirming a scheme for the transfer of the life insurance business of TLISL to TAL Life (the Scheme).

2 The transfer is of some scale, involving more than 430,000 in-force TLISL policies and the transfer of more than $2 billion in assets. TAL Life is currently the largest life insurer in Australia and will become larger and more diversified. As a result, its capital requirements will reduce. The actuarial evidence is that TAL Life will remain in a sound financial and capital position such that the security of the benefits of both TLISL and TAL Life policy owners will be adequately maintained, as I discuss in detail below.

3 On 17 September 2024 I made orders dispensing with the requirements of s 191(2)(c) of the Act for the purpose of the Scheme (Dispensation Orders). The Dispensation Orders and other procedural requirements under the Life Act have been complied with, as I address in detail below.

4 The actuaries have updated their evidence since the dispensation hearing, taking into account updated financial information and planned distributions in excess of target capital. Each of the actuaries has maintained his opinion that the Scheme is not expected to have a material adverse impact on policy owners, as I discuss in detail below.

Background to and Overview of the Scheme

5 Both TLISL and TAL Life are authorised under the Life Act to conduct life insurance business and do so through their various statutory funds as prescribed under the Life Act.

6 The proposed Scheme involves an intra-group transfer of life insurance business within the TAL Group. The TAL Group is comprised of eight wholly owned subsidiary companies (including TLISL and TAL Life), held by TAL Dai-ichi Life Australia Pty Ltd (TDA), the ultimate parent company of which is Dai-ichi Life Holdings, Inc, which is listed on the Tokyo Stock Exchange.

7 TLISL was acquired by TDA from Westpac Banking Corporation (Westpac) in August 2022. Specifically, TDA and Westpac entered into a share sale deed in August 2021 for the acquisition, and completion of the sale occurred in August 2022. Upon acquisition, TLISL changed its name from Westpac Life Insurance Services Limited.

8 Since the acquisition, as a member of the TAL Group, TLISL has been undertaking a program of integration with TAL Life’s life insurance business. As part of this integration:

(a) TLISL employees have been transferred from TLISL to TAL Services (another wholly owned subsidiary within the TAL Group);

(b) support functions (such as operational and information technology functions) provided by the TAL Group have been progressively introduced to support TLISL’s life insurance business;

(c) the systems which held policy owner information for policies issued by TLISL have been migrated to systems operated by TAL Life;

(d) TLISL is now governed by several of the same TAL Group frameworks which apply to TAL Life including its Risk Management Framework, Risk Appetite Statement and Reinsurance Management Policy; and

(e) the transitional services that were provided by Westpac have concluded.

9 Since August 2022, TLISL has operated its life insurance business as a functional business unit within the TAL Group, with a number of TAL Group functional business areas providing infrastructure and support services to TLISL. TLISL is currently closed to new business for all product lines.

The life insurance business of TLISL

10 TLISL has been a registered life insurer since 1986. It currently operates its life insurance business through two statutory funds:

(a) Statutory Fund No 1 (TLISL SF1) which contains individual and group life risk business and fixed and lifetime immediate annuities; and

(b) Statutory Fund No 2 (TLISL SF2) which contains ordinary and superannuation investment-linked policies. All of TLISL’s investment-linked business is issued from TLISL SF2.

TLISL also maintains a Shareholders’ Fund separately from TLISL SF1 and TLISL SF2. No business is issued from this Fund.

11 TLISL carries on the following categories of life insurance business:

(a) life risk insurance business which comprises death cover, total and permanent disablement (TPD) cover, critical illness or trauma cover and income protection benefits resulting from sickness or an accident;

(b) deferred, allocated, term and lifetime annuity business; and

(c) ordinary and superannuation investment-linked business.

TLISL does not have any participating business.

12 As of 1 August 2022, TLISL has been closed to new business for all product lines. The creation of new policies for either individual or group business is not permitted, although changes to existing policies, policy reinstatements, and the addition of new members to group schemes are permitted. Prior to closing to new business, TLISL distributed its product through independent and aligned financial advisers, directly to the public and through group arrangements.

13 Reinsurance for TLISL is managed in accordance with TDA’s Reinsurance Management Policy. TLISL’s largest reinsurance exposure is with Pacific Life Re Australia, which came into effect on 1 October 2022. TLISL also has a number of less material reinsurance arrangements, only one of which is with a foreign-domiciled reinsurer.

The life insurance business of TAL Life

14 TAL Life has been a registered life insurer since 1973. It is currently the largest life insurer in Australia with total assets of more than $8.5 billion and net assets of near $1 billion. TAL Life currently operates its life insurance business through two statutory funds:

(a) Statutory Fund No 1 (TAL Life SF1) which contains business for individual and group risk policies, participating traditional and investment account policies, non-participating traditional and investment account policies and immediate annuities; and

(b) Statutory Fund No 2 (TAL Life SF2) which contains ordinary and superannuation investment-linked policies and allocated annuity and allocated pension investment-linked policies. All of TAL Life’s investment-linked policies are currently issued from TAL Life SF2.

TAL Life also maintains a separate Shareholders’ Fund. No business is issued from this Fund.

15 TAL Life’s business is segmented into retail, group, direct and investment business units for profit reporting purposes. Retail business is primarily sold via independent financial advisers including dealer groups. Group business is distributed via superannuation schemes, master trust platforms and corporate superannuation schemes. Products are also sold directly to individuals through the TAL and InsuranceLine brands, as well as through alliance partner distribution channels.

16 Through its statutory funds, TAL Life carries on the following categories of life business:

(a) life risk insurance business which comprises death and terminal illness cover, TPD cover, critical illness or trauma cover and income protection benefits resulting from sickness or accident;

(b) participating and non-participating traditional (whole of life and endowment cover) business;

(c) ordinary and superannuation investment-linked business; and

(d) deferred, allocated, term and lifetime annuity business.

17 As at 31 March 2024, TAL Life’s annuities, participating and non-participating, conventional and investment account businesses are closed, with only group retirement income arrangements open to new business.

The proposed Scheme and Transfer

18 Whilst both companies are managed within the same corporate group and share many processes, management of two life insurance entities within the same group increases operational complexity, costs and capital in insurance operations. The TDA board has identified that rationalisation of the existing legal entities and statutory fund structures across the two insurers will help TDA achieve its objectives by simplifying the business, thereby reducing costs, operational risk and capital. This, it is anticipated, will ultimately create a better customer experience through greater scale, a higher level of benefit security, better quality reporting and more opportunities for legacy system upgrades and legacy product simplification.

19 Accordingly, the Scheme is proposed to rationalise and simplify the TAL Group’s structure by transferring all of TLISL’s life business to TAL Life pursuant to a scheme under Pt 9 of the Life Act. The proposed effective time of transfer under the Scheme is 11:59pm AEDT on 31 March 2025 (the Scheme Effective Time).

20 The Scheme gives effect to a transfer deed dated 5 September 2024 under which TLISL has agreed to transfer its life business to TAL Life, subject to confirmation by the Court (the Transfer Deed). The Transfer Deed is also conditional upon a “no objection” decision by the Treasurer of the Commonwealth of Australia (the Treasurer) under the Insurance Acquisitions and Takeovers Act 1991 (Cth) (IATA): see cl 2.1(b).

21 The Scheme is based on the joint actuarial report prepared by Mr Corrigan and Mr Ch’ng (the Joint Actuarial Report), and the independent actuarial report prepared by Mr Merten (the Independent Actuarial Report).

22 The key elements of the Scheme are as follows:

(a) all of the policies issued by TLISL that are referable to TLISL SF1 and TLISL SF2 immediately prior to the Scheme Effective Time will become TAL Life policies, referable respectively to TAL Life SF1 and TAL Life SF2 (cll 2.2 and 4.1);

(b) the assets and liabilities from TLISL SF1 and TLISL SF2 will be transferred respectively to TAL Life SF1 and TAL Life SF2 (cll 2.2, 4.2 and 4.3);

(c) TAL Life will become the issuer of all TLISL life policies (cl 3.1);

(d) the rights and liabilities of TLISL policy owners will be the same as they would have been if the applications on which their policies are based had been accepted by TAL Life instead of TLISL (cl 3.2);

(e) any person having a claim on or obligation to TLISL under or in respect of a TLISL policy will have the same claim on or obligation to TAL Life instead of TLISL irrespective of when the claim or obligation arose (cl 3.7);

(f) any proceedings in connection with a TLISL policy must be continued by or against TAL Life instead of TLISL (cl 3.8);

(g) TAL Life will assume the conduct and administration, and the liability for, any policy owner remediation programs being conducted by TLISL which have not been completed by the time the Scheme takes effect (cl 3.9); and

(h) all reinsurance treaties to which TLISL is a party and other contracts in relation to its life business will transfer to TAL Life (cl 3.12).

23 The terms and conditions of TLISL life policies will not change as a result of the Scheme. References to TLISL will be replaced with TAL Life and references to the TLISL Statutory Fund will be read as references to the respective TAL Life Statutory Fund (cl 3.13).

24 The terms and conditions of TAL Life policies will not change as a result of the Scheme (cl 3.14).

25 All costs associated with the transfer will be paid by TDA and not by TLISL policy owners or TAL Life policy owners (cl 7).

Relevant principles for Confirmation

26 The provisions applicable to the curial supervision of schemes of transfer of life insurance business are contained in Pt 9 of the Life Act. Section 190(1) of the Life Act provides that no part of the life insurance business of a life company may be transferred to another life company except under a scheme confirmed by the Court.

27 Section 193 of the Life Act relates to the application to the Court for confirmation and provides as follows:

(a) Any of the companies affected by a scheme may apply to the Court for confirmation of the scheme.

(b) An application for confirmation must be made in accordance with the regulations.

(c) APRA is entitled to be heard on an application.

28 Under s 194 of the Life Act, the Court has the discretion to confirm the scheme with or without modification, or to refuse to confirm it. Section 194(2) of the Life Act sets out the factors to which the Court must have regard in deciding whether to confirm the scheme. They are:

(a) the interests of the policy owners of a company affected by the scheme; and

(b) if a report relevant to all or part of the scheme has been filed with the Court under section 175 – that report; and

(c) any other matter the Court considers relevant.

29 I recently considered the principles relevant to s 194 of the Life Act in Integrity Life Australia Ltd, in the matter of Integrity Life Australia Ltd [2024] FCA 92 at [49] and following, and the following paragraphs repeat that analysis insofar as it is pertinent to the present application.

30 As the permissive language of s 194 of the Life Act makes clear, the confirmation of the scheme is a matter for the Court’s discretion; however, confirmation is not a matter of course, nor is it a mere formality: St Andrew’s Insurance (Australia) Pty Ltd, in the matter of St Andrew’s Insurance (Australia) Pty Ltd [2024] FCA 881 at [8] (St Andrew’s) (Jackman J); AIA Australia Limited, in the matter of AIA Australia Limited (No 2) [2023] FCA 1305 at [30] (AIA Australia Limited No 2) (Derrington J); Asteron Life & Superannuation Limited, in the matter of Asteron Life & Superannuation Limited (No 3) [2021] FCA 1148; (2021) 394 ALR 89 at [126] (Asteron Life No 3) (Allsop CJ).

31 While the Court’s discretion is broad, it is not unfettered and must be exercised on the evidence and having regard to the objects of the Life Act, principally the protection of the interests of policy owners in a manner consistent with the continued development of a viable, competitive and innovative life insurance industry: s 3(1) of the Life Act; In the Application of Commonwealth Insurance Holdings Ltd and the Colonial Mutual Life Assurance Society Ltd [2007] FCA 1012 at [12] (Commonwealth Insurance Holdings) (Edmonds J); OnePath Life Limited, in the matter of OnePath Life Limited (No 2) [2022] FCA 811 at [17]–[18] (OnePath Life No 2) (Jagot J). The regime for the supervision of the transfer or amalgamation of life insurance businesses by the Court is one of the means adopted to achieve this object: Colonial Mutual Life Assurance Society Limited, in the matter of Colonial Mutual Life Assurance Society Limited [2021] FCA 394 at [26] (Colonial Mutual Life) (Allsop CJ); Re Royal & Sun Alliance Life Assurance Ltd [2000] FCA 1259; (2000) 104 FCR 37 at [3] (Royal & Sun) (Katz J); Asteron Life No 3 at [82].

32 As Allsop CJ explained in Asteron Life No 3 at [127]-[129], drawing upon the reasons of Edmonds J in Commonwealth Insurance Holdings at [13], there are two main dimensions to the protection of the interests of policy owners:

(a) first, the procedural dimension by which the Court considers whether the process undertaken in connection with the scheme has been properly executed in accordance with the requirements of the Life Act, the Life Insurance Regulations 2024 (Cth) (Life Regulations) and any orders made by the Court pursuant to s 191(5) of the Act: see St Andrew’s at [9]; and

(b) second, the substantive dimension in which the Court is concerned to see that the scheme will not be prejudicial to the interests of policy owners, and that policy owners are properly safeguarded, ie there is not likely to be any material detriment to policy owners affected by the scheme: see AIA Australia Limited No 2 at [32].

33 The question as to whether policy owners will be adversely affected is to be answered predominantly by reference to the actuarial evidence. It involves a comparison of the security of those policy owners’ benefits and their reasonable benefit expectations as they stood prior to the implementation of the scheme (ie without the scheme), and as they would stand following the implementation of that scheme: Commonwealth Insurance Holdings at [14]; Asteron Life No 3 at [129]; St Andrew’s at [10].

Compliance with the Dispensation Orders and the procedural dimension

34 The Dispensation Orders required the applicants to take a number of detailed steps and processes intended to notify policy owners and others of the Scheme and the application for confirmation of the Scheme. Several of these steps overlap with the requirements under the Life Act as amended.

35 The applicants have complied with the Dispensation Orders. In particular:

(a) on 23 September 2024, the Notice of Intention (as approved by APRA) was published in The Australian newspaper and from that date made available for viewing and download on the dedicated Scheme webpages on each of the “TAL Life” and “BT Life” branded websites of TDA (the Scheme webpages) (Orders 2(a), (b) and (c));

(b) from 23 September 2024, the Scheme document, the Scheme Summary (as approved by APRA), the Joint Actuarial Report and the Independent Actuarial Report (the Scheme documents) were made available for viewing and download on the Scheme webpages (Orders 2(b) and (c));

(c) from 23 September 2024, a link to an online enquiry form to submit enquiries about the Scheme was included on the Scheme webpages (Order 2(d));

(d) from 23 September 2024, the applicants established a dedicated email address (as specified in the Notice of Intention and Scheme Summary) to receive enquiries about the Scheme (Order 2(e));

(e) between 1 October and 7 November 2024, the applicants arranged for the mail-out of the Scheme Summary to TLISL policy owners, other than those for whom TLISL has no record of a current mailing address (Order 2(g)). Prior to the mail-out, staff attempted to contact TLISL policy owners for whom no current mailing address was held to update their mailing addresses (Order 2(f)) and staff followed the returned mail procedure described in David Lees’ affidavit sworn 10 September 2024 in respect of posted material returned undelivered (Order 2(h))];

(f) from 25 September 2024, the applicants arranged for the operation of a call centre to handle calls about the Scheme, having trained staff to handle calls relating to the Scheme (Orders 2(i) and (j));

(g) on request, copies of the Scheme documents were made available to 27 TLISL and TAL Life policy owners (Order 2(k));

(h) summaries were also sent to persons who became TLISL policy owners after the date for the extraction of addressed for the mailout (Order 2(l));

(i) the applicants sent, by email, a link to the Scheme documents alongside a general overview of the Scheme:

(i) on 25 September 2024, to independent financial advisers and financial advice licensees on the applicants’ distribution list as at 25 September 2024 (Order 2(m)); and

(ii) on 20 September 2024, to policy owners of TAL Life Group policies (Order 2(n)).

36 As set out above, the applicants arranged for publication of the Notice of Intention in The Australian newspaper. While not strictly necessary to do so under the current requirements of the Life Act, and the experience of the applicants (including in previous scheme processes) being that digital disclosure is now a more effective and widely accessible form of disclosure in the Australian market, the additional publication in The Australian (a newspaper of national circulation) was designed to increase the prominence of the proposed Scheme and provide a form of print disclosure about the proposed Scheme for those affected policy owners who may not have access to, or regularly access, digital communication channels.

37 All in all, the applicants arranged for the mail-out of 341,567 copies of the Scheme Summary. Some 5,442 letters were returned undelivered and became subject to the prescribed returned mail procedure. Through that procedure, the postal or email addresses of 1,568 policy owners were identified such that, in total a copy of the Scheme Summary remained undelivered to only 1.15% of policy owners for whom the applicants or third parties held a record of a mailing address.

38 The evidence is that the Scheme webpages were collectively visited 1,010 times, with the following number of downloads for each Scheme Document:

39 Each of the Notice of Intention and the Scheme Summary are required to be published in a manner that results in them being “accessible to the public” and “reasonably prominent”: subss 191(2A) and (2F) of the Life Act. The publication of these documents on Scheme webpages resulted in them:

(a) being accessible to the public. There were no restrictions to accessing the Scheme webpages. The number of visits to the Scheme webpages and the downloads of the Scheme documents demonstrate this accessibility. The Notice of Intention was also published in The Australian, a newspaper with a national circulation; and

(b) being reasonably prominent. The Scheme webpages were accessible via click-through files on the homepages of the “TAL Life” and “BT Life Insurance” branded websites. On both mobiles and desktops, this click-through was clearly displayed on the website landing page, comprising an image with the title “Scheme Transfer” and subtitle “Transfer of TLISL’s life insurance business to TAL Life”, emboldened and with differentiated font size.

40 Otherwise, as required by s 191(2)(a) of the Life Act, the actuarial reports on which the Scheme is based, have been given to APRA.

41 As at 30 June 2024, there were approximately 18,260 financial advisers across 1,682 advice licensees on the distribution lists maintained by TLISL and TAL Life, as well as approximately 240 policy owners who were the owners of group policies issued by TAL Life, comprising the trustees of the registrable superannuation entities and other corporate policy owners. Arrangements were made on 20 September 2024 and 25 September 2024 to provide a general overview of the proposed Scheme and links to the Scheme documents via email to each of these three cohorts. As at 6 February 2025, less than 1% of these emails were returned to the applicants with a message that the email could not be delivered.

42 As indicated above, it is a condition precedent of the Transfer Deed dated 5 September 2023 that TAL Life obtain a “go-ahead” decision from the relevant Minister under the IATA, providing notice that the Commonwealth Government has no objection to the proposed transfer: cl 2.1. TAL Life received approval to that effect by email on 29 January 2025 from APRA, as the delegate of the Minister in relation to the proposed transfer.

Actuarial Evidence, Reinsurance and Remediation

43 The Scheme is based on the Joint Actuarial Report and the Independent Actuarial Report. The actuaries have supplemented these reports by preparing a detailed “Addendum” in which they have updated their opinions by reference to financial information as at 31 December 2024 (as opposed to 31 March 2024) and intervening events (the Joint Actuarial Addendum and the Independent Actuarial Addendum). In each case, the actuaries maintain their opinion that the Scheme will not materially prejudice the interests of policy owners of TLISL or TAL Life, and that the statutory funds of TLISL and TAL Life as a whole will remain in a sound financial position after the transfer under the Scheme.

44 Each of the actuaries presenting expert evidence to the Court is a highly experienced professional in the field and agreed to be bound by the Expert Evidence Practice Note. At the time of preparing the Joint Actuarial Report, Mr Ch’ng was the appointed actuary of TLISL. On 3 February 2025, as part of the ongoing harmonisation of the regulatory affairs of the applicants, Mr Corrigan, the appointed actuary of TAL Life, was also appointed the appointed actuary of TLISL. Mr Ch’ng remains part of the TAL Group actuarial team and is now the alternative appointed actuary of both TLISL and TAL Life in the event of a temporary absence of Mr Corrigan. Mr Merten is a partner of Deloitte Touche Tohmatsu, practising in its Actuarial Team.

Financial Security and Profitability

45 The Scheme involves the transfer of assets and liabilities in TLISL SF1 and TLISL SF2, including insurance contract liabilities and associated reinsurance, and including assets sufficient to support 100% of target capital requirements. As described above, these are assets in excess of prudential requirements and the additional internal target capital levels approved by the TDA board to provide added protection against breaching the regulatory capital requirements as a result of unanticipated adverse events; these assets represent resources that are available for alternative productive use. As indicated in the Joint Actuarial Report, any excess assets above target capital requirements would be transferred to the TLISL shareholders’ fund prior to the Scheme taking effect.

46 Each of the initial actuarial reports was prepared with financial information as at 31 March 2024. The planned distributions of assets in excess of target capital requirements in TLISL (which were outlined at the dispensation hearing) have been made since that time, and have been taken into account in the Joint Actuarial Addendum and the Independent Actuarial Addendum to the actuarial reports. The distributions have been effected by dividend payments from TLISL to its parent TDA of $370 million in May 2024 and $240 million in November 2024. TAL Life has also made a distribution of excess assets to TDA by a dividend payment of $460 million in November 2024. These distributions largely explain the changes in capital in excess of Prescribed Capital Amount (PCA) and the Capital Adequacy Multiples (CAM) from the position as at 31 March 2024.

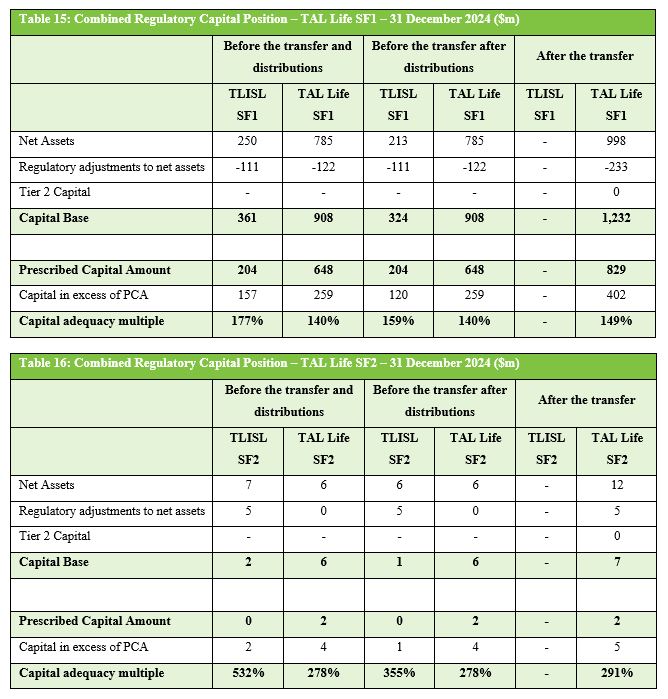

47 The combined regulatory capital position before and after the proposed transfer on the updated 31 December 2024 accounts, and before and after the excess capital distributions, is set out in Tables 15 and 16 at [6.2.1] of the Joint Actuarial Addendum as follows:

48 There is an overall $13 million reduction in the combined PCA following the transfer mainly driven through additional capital efficiencies of diversification. It is noted that the reductions in CAM for TLISL policy owners (177% in TLISL SF1 to 149% in TAL Life SF1 and 532% in TLISL SF2 to 291% in TAL Life SF2) are related to the excess assets held at 31 December 2024 and assets in excess of 100% of target capital being available for distribution to shareholders.

49 On the basis of their analysis in the Joint Actuarial Addendum, Messrs Corrigan and Ch’ng observe that:

• following the transfer, each transferring statutory fund and TAL Life as a whole will remain in a sound financial position and TAL Life policy owners’ benefit security will remain adequate after the Proposed Transfer;

• immediately after the Proposed Transfer the statutory funds of TAL Life as a whole will continue to satisfy the requirements of the applicable prudential capital standards;

• TAL Life is projected to be profitable on an ongoing basis with relatively stable capital coverage; and

• the risk profile considerations and expected profitability of the TAL Life statutory funds and TAL Life as a whole, will maintain the security of policy owners’ benefits.

TLISL is also expected to retain sufficient assets to cover any outstanding liabilities and capital requirements after the proposed transfer.

50 Messrs Corrigan and Ch’ng make the following observations in relation to the capital reserving levels impacting TLISL and TAL Life policies in the Joint Actuarial Addendum at [7.4.3.1]:

• as set out in Section 6.2.1, TLISL policy owners are currently insured with an entity which has $160m of capital in excess of the PCA. Existing TAL Life policy owners are currently insured with an entity which has $263m of capital in excess of the PCA;

• it is noted that, assets in excess of those required to meet the target capital requirements can, by Board approval (and subject to certain other constraints), be paid as a dividend to shareholders. Hence capital levels at a single point in time do not necessarily reflect the ongoing likely capital position;

• following the Proposed Transfer, the TLISL and TAL Life policy owners will be part of an entity with capital in excess of PCA of $407m as set out in Section 6.2.1. There will be a reduction in the PCA required to support the transferring TLISL business due to the increased diversification benefits within a larger statutory fund. Distributions to the TLISL shareholders’ fund are expected to occur prior to the Proposed Transfer of any excess capital above a target capital ratio of 100% from TLISL SF1 and SF2; and

• the current capital adequacy levels for TLISL SF1 and SF2 and TAL Life SF1 and SF2 are all greater than 100%. As per Section 6.2.1, the indicative capital adequacy multiple for post-transfer TAL Life Statutory Funds No. 1 and No. 2 are 149% and 291% respectively. These ratios remain sufficiently high to provide adequate security, exceed the minimum prudential capital requirements and do not adversely impact the level of prudential protection for the transferring TLISL policy owners or existing TAL Life policy owners.

Given the above, it can be concluded that the post-transfer capital reserving levels of TAL Life SF1 and SF2 will not adversely impact the transferring TLISL and TAL Life existing policy owners’ benefit security.

51 Similar conclusions are reached in the detailed analysis prepared by Mr Merten in the Independent Actuarial Addendum at [5.4], [6.3.2] and [7.3.2]. Mr Merten makes the salient point that TLISL is closed to new business whereas TAL Life is open to new business. The proposed transfer into TAL Life will mitigate the risks related to the stand-alone TLISL entity in this regard, such as a reducing pool of policy owners leading to an increased volatility in claims experience which may impact future premium rates. Mr Merten also notes at [5.4] in his analysis of the capital implications before and after the Scheme:

…that TLISL and TAL Life were each expected to be in strong capital generating positions over the next 3 years based on each entity’s FCR [Financial Condition Report] projections as at 31 March 2024. This provides comfort that post-transfer neither TLISL or TAL Life policies would be expected to be subsidising capital losses on the other business.

Premium Rates, Policy Administration and Other Reasonable Benefit Expectations

52 The fundamental expectation of policy owners is that they will receive their contractual benefit entitlements when due. Nonetheless, there are a number of areas identified by the actuaries that involve some discretion being exercised by TLISL historically and by TAL Life in the future. These have the potential, in theory, to affect policy owners’ reasonable benefit expectations. The discretions that the actuaries have considered relate to premium rate changes, claims handling, policy administration, underwriting, and product improvements and policy maintenance.

53 It is important to appreciate when considering these issues, that since August 2022 TLISL has already operated its life insurance business as a functional business unit within TDA. Consequently, many administrative processes and policies have already been aligned as between the two insurers. As Mr Merten observes, many key decisions in relation to harmonisation have already been made.

(1) Premium Rates

54 In terms of premium rate changes, which can be of particular significance to policy owners, Messrs Corrigan and Ch’ng observe that:

As TLISL and TAL Life are both entities owned by TDA, the approaches in which premium rates are set follow a consistent philosophy. There will be no changes in this approach as a result of the Proposed Transfer.

Management has advised that the premium rates currently adopted by TLISL were set after considering a number of factors, including claims experience, customer impacts, relative competitor positioning and the expected return on capital for the portfolio. Management has indicated that their primary goal is to provide value for customers and that premiums continue to support the long-term sustainability of the portfolio. …

There will be no increase in the TLISL premium rates as a result of the Proposed Transfer as profitability of the TLISL policies will remain at least in line with pre-transfer levels. This reflects:

• no changes to the reinsurance terms and commission terms applying to the transferring policies as a result of the transfer; and

• claims experience analysis will continue to be assessed separately to the TAL Life products.

55 In relation to premium rates for TAL Life policy owners, they conclude:

TAL Life’s current policy owners are unlikely to be affected by the transfer since the business will continue to be priced accordingly to the TAL Life Product Pricing Policy, and profitability assessment will continue to be separate from the former TLISL policies.

56 Mr Merten reaches the same conclusion.

(2) Claims Handling

57 As TLISL and TAL Life are both entities owned by TDA, their approaches to claims handling follow a consistent philosophy, and they use consistent policies and adopt consistent practices. Both companies operate under the Life Insurance Code of Practice. TLISL and TAL Life claims are managed separately but under an aligned philosophy, and both entities use aligned policies and have adopted aligned practices with reporting to the same executive manager. This will not change as a result of the proposed transfer.

58 Messrs Corrigan and Ch’ng have provided detailed dispute reporting statistics as reported to APRA in Table 24 of the Joint Actuarial Report. They observe that the number of disputes for both entities relative to the number of policies and number of lives insured are low, with the number of disputes lodged being in the 0.02% to 0.03% range of number of lives insured for both entities. They note that the absolute number of disputes for TAL Life is much larger due to the large group portfolio, which comprises a number of industry superannuation funds supporting members in the millions. They conclude that policy owners’ reasonable expectations for both TLISL and TAL Life policy owners are expected to be met with regard to the claims handling philosophy and any ongoing remediation programs. Similar conclusions are reached in the Independent Actuarial Report.

59 Mr Merten separately considers customer service levels as an aspect of the reasonable expectations of policy owners. He has observed that currently the wait times across the contact centres for each insurer are very similar. He concludes that there will be no material changes to customer service levels for TAL Life and TLISL customers as a consequence of the proposed transfer.

(3) Policy Administration

60 The majority of TLISL policies are managed through the Computations Life Office Administration System (CLOAS). This administration system for TLISL policies will be directly transferred to TAL Life as part of the proposed transfer. No changes will be made to these systems as a result of the proposed transfer. Similarly, no changes will be made to the administration of legacy products as a result of the proposed transfer.

61 No functional changes will be made to the systems that administer the TAL Life products as a result of the proposed transfer. Accordingly, reasonable benefit expectations of both sets of policy owners are expected to be met with regard to policy administration. Mr Merten has reached the same conclusion.

(4) Underwriting

62 As TLISL is closed to new business, underwriting will be limited to benefit changes for existing policies. TLISL policy owners who currently have the option to increase their sum insured will continue to have that option and will be assessed against TLISL’s underwriting standards. TLISL’s underwriting system is ringfenced within TAL Life’s “ecosystem” in accordance with TLISL underwriting agreements and policies. This will not be impacted as a result of the proposed transfer.

63 There will be no impact on the existing TAL Life underwriting philosophy and rules as a result of the proposed transfer. TAL Life’s management intends to harmonise the TLISL and TAL Life practices so that, in time, a consistent approach can be adopted for both TLISL and TAL Life customers.

64 Messrs Corrigan and Ch’ng consider that transferring policy owners should not have specific expectations regarding how policies will be underwritten, save that underwriting should be performed fairly and on a basis that is not more conservative than that adopted at the time the policy was originally underwritten. On this basis, given that TLISL’s underwriting is ringfenced, with an intention to harmonise the practices in the future, the reasonable benefit expectations of both TLISL and TAL Life policy owners are expected to be met with respect to underwriting approach and philosophy. Similar conclusions were reached by Mr Merten in the Independent Actuarial Report.

(5) Product improvements and policy maintenance

65 Given that TLISL is currently closed to new business, future product changes are likely to be limited. As such, TLISL can only make enhancements to product features or changes to policy definitions which do not adversely impact current policy owners and do not result in an increase in the premiums. This approach aligns with TAL Life and its treatment of its own legacy businesses and will not change as a result of the proposed transfer. There are no changes as a result of the Scheme to the TAL Life approach to product improvements.

Reinsurance

66 Reinsurance for TLISL is managed in accordance with TDA’s Reinsurance Management Policy (RMP). This is the same RMP under which TAL Life manages its reinsurance so as to meet its obligations to policy owners, effectively manage capital and risk, and comply with regulatory requirements.

67 TLISL has provided notice to all of its reinsurers about the proposed Scheme and that their treaties will transfer to TAL Life under the Scheme. Only one of TLISL’s reinsurers, namely, Transamerica Premier Life Insurance Company Inc (Transamerica), is foreign-domiciled. Transamerica reinsures 0.5% of TLISL’s portfolio with an annual reinsurance premium paid of $2.4 million. Transamerica has agreed with the applicants to novate all relevant treaties and agreements with TLISL as part of their contract renewal process in order to give effect to the transfer of those reinsurance arrangements under the Scheme.

68 For the balance of TLISL’s reinsurance arrangements, there is no need to novate any of its reinsurance treaties, as those arrangements will be transferred to TAL Life pursuant to the proposed Scheme (see cl 3.12(d) of the Scheme).

69 On this basis, the benefit security of TLISL and TAL Life policy owners will not be adversely affected by the impact of the Scheme on existing reinsurance arrangements.

Remediation

70 At the time these proceedings were commenced, TLISL was undertaking two material policy owner remediation programs. These related to:

(a) the incorrect benefit period expiry date in the CLOAS; and

(b) an issue in respect of flexible linked benefit policies that led to stamp duty being applied in NSW after the first year of cover.

71 Both of these programs have now been completed.

72 TLISL is undertaking an additional two material policy owner remediation programs. These programs are being undertaken in accordance with the “TAL Enterprise Remediation Guiding Principles” and relate to:

(a) the incorrect application of Consumer Price Index to Living Reinstatement and Repurchased Death covers; this has led to affected policy owners being overcharged in premiums. There are approximately 150 policy owners to be remediated under this program, which is expected to be completed by 31 July 2025; and

(b) the incorrect inclusion on policy schedules of a “Loyalty Benefit” (involving a small increase to the sum insured) on renewal notices for certain types of buyback cover for which the policy owner is not eligible under the policy terms and conditions. There are approximately 1,971 policy owners to be remediated under this program, which is expected to be completed by 30 August 2025.

73 TAL Life was undertaking three remediation programs when these proceedings were commenced. These programs have now been completed.

74 TAL Life will assume the conduct and administration of the remaining TLISL remediation programs under cl 3.9 of the Scheme. TAL Life will not make any changes to the design or resourcing of these remediation programs as a result of the proposed Scheme. In particular, TAL Life intends that the same project teams will remain responsible for each remediation program to its conclusion. As noted, these remediation programs are already being conducted under the “TAL Enterprise Remediation Guiding Principles” to which express reference is made in cl 5(b)(9) of the Scheme.

75 In these circumstances, the actuaries have concluded that the Scheme will not affect the remaining remediation programs and that policy owners will not be disadvantaged or inequitably treated as a result of the proposed transfer.

Actuarial Conclusions

76 Messrs Corrigan and Ch’ng conclude that:

In summary, the proposed Scheme will not result in any unfairness to the owners of the policies referable to any of the statutory funds involved in the proposed Scheme. In addition, the proposed Scheme will not materially prejudice the interests of TAL Life policy owners. Further, immediately after the proposed transfer, TAL Life will continue to satisfy regulatory capital standards and remain in a sound financial position.

77 With respect to the transferring TLISL policy owners, Mr Ch’ng expresses his opinion that:

(a) the proposed Scheme will not adversely impact the contractual benefits and rights of the transferring TLISL policy owners;

(b) TAL Life’s intended basis of determining and implementing the non-contractually specified and discretionary aspects of the transferring TLISL policies will continue to meet the overall reasonable benefit expectations of the transferring TLISL policy owners; and

(c) TAL Life will remain in a sound financial position and the transferring TLISL policy owners’ benefit security will remain adequate after the proposed Scheme.

78 With respect to the existing TAL Life policy owners, Mr Corrigan states his opinion that:

(a) there will be no impact to the contractual benefits and rights of the existing TAL Life policy owners as a result of the proposed Scheme;

(b) there will be no impact to the reasonable benefit expectations of the existing TAL Life policy owners as a result of the proposed Scheme;

(c) each of the statutory funds of TAL Life, and TAL Life as a whole, will remain in a sound financial position and the existing policy owners’ benefit security will remain appropriate after the proposed Scheme; and

(d) there will be no disadvantages to the existing TAL Life policy owners as a result of the proposed Scheme.

79 Moreover, Messrs Corrigan and Ch’ng have concluded that the proposed transfer in fact will benefit policy owners. They state at [1.4] of the Joint Actuarial Report:

The Proposed Transfer will benefit Policy Owners through:

• Scale – The Proposed Transfer will result in expense synergies from having lower external costs such as lower investment management fees due to the scale of the combined investment portfolio and the ability to be more competitive in the market through pricing.

• Operational Risk – The Proposed Transfer will reduce overall operational risk. The integration program that has been underway since TLISL was acquired has reviewed processes across the business within both TAL Life and TLISL to end up with harmonised processes. Overall, this leads to more streamlined processes and a better policy owner experience. The combining of two companies into one also reduces and streamlines the number of reporting tasks that are required from a regulatory perspective as these will be combined within TAL Life leading to better quality reporting.

• Benefit Security – The Proposed Transfer will also result in increased diversification of insurance and asset risks providing a higher level of benefit security for policy owners. In addition, the increased size of the combined portfolio will result in a lower overall volatility of insurance risk experience across the portfolio which may result in greater pricing stability for policy owners.

80 Mr Merten has conducted a detailed analysis of the Scheme in the Independent Actuarial Report and in the Independent Actuarial Addendum. He has concluded that the proposed Scheme will not materially adversely affect any group of transferring TLISL policy owners or TAL Life policy owners, nor does he anticipate material adverse impacts in respect of their:

(a) contractual rights;

(b) reasonable benefit or other policy owner expectations; or

(c) benefit security.

81 In coming to these conclusions, Mr Merten found that:

Overall, the TLISL Policy Owners [and in a corresponding paragraph the TAL Life Policy Owners] will become part of a larger and more diverse company that is open to new business. The Proposed Transfer is likely to result in unit cost savings due to economies of scale. The cost of integration of the TLISL business has been and continues to be funded via TDA, thereby, not impacting the Policy Owners of TLISL or TAL Life. Any expense savings achieved, together with greater diversification of risk within the fund, would ensure that benefit security is not weakened.

82 Mr Merten helpfully summarises his more detailed observations in relation to TLISL policy owners at [8.1] of the Independent Actuarial Addendum as follows:

1. There will be no changes to the contractual benefits and other rights of TLISL Transferring Policy Owners.

2. In relation to areas where decisions are being made that could impact Transferring Policy Owner expectations, TLISL operations have mostly been harmonised with those of TAL Life through common ownership and staff in shared services. All key decisions related to harmonisation have been already made, and so I am comfortable any remaining decisions regarding harmonisation with respect to the Proposed Transfer will not adversely impact Policy Owners.

3. Service provided to TLISL Transferring Policy Owners in future by TAL Life should be at least at levels experienced while Policy Owners of TLISL, given TAL Life’s commitment to take on staff and systems and its largely completed integration plan.

4. TLISL Transferring Policy Owners will not be exposed to the costs of transition as a result of the Proposed Transfer being implemented. Costs relating to the Proposed Transfer will be met by the shareholder of TLISL and TAL Life, TAL Dai-ichi Life Australia Pty Limited (TDA).

5. Security of Policy Owner benefits should not be adversely impacted by the Proposed Transfer. The capital position of TAL Life after the Proposed Transfer is sound with the merged capital position indicating that after the Proposed Transfer benefit security is maintained.

6. TLISL is closed to new business and TAL Life is open to new business. The Proposed Transfer into TAL Life will mitigate the risks related to the standalone TLISL entity in this regard, such as a reducing pool of Policy Owners leading to increased volatility in claims experience which may impact future premium rates.

7. TLISL does not hold any participating insurance policies so there is no need to consider reasonable benefit expectations of any Transferring Policy Owners contracts with regards to participation in profits of the entity.

83 Mr Merten then summarises his observations in relation to the TAL Life policy owners at [8.2] of the Independent Actuarial Addendum as follows:

1. There will be no changes to the contractual benefits and other rights of TAL Life Policy Owners.

2. There are no adverse changes proposed to the TAL Life products, product strategy, customer service levels or claims management.

3. TAL Life Policy Owners will not be exposed to the costs of transition as a result of the Proposed Transfer being implemented. Costs relating to the Proposed Transfer will be met by TDA. Ultimately, successful integration is expected by TAL Life to lead to unit cost savings due to economies of scale.

4. TAL Life participating Policy Owners will continue to be managed via a separate sub-fund with no changes to investment policy, profit allocation approach, expense allocation approach and bonus policy.

5. The capital position of TAL Life, for each Statutory Fund and the entity overall, post transfer is expected to remain sound after completion of the Proposed Transfer with no diminution in benefit security for Policy Owners as a result of the Proposed Transfer.

Policy Owner Response and Objections to the Scheme

84 Policy owners have been given notice of the Scheme through the various channels required by the Dispensation Orders as set out above. This has resulted in over 342,000 Scheme Summaries being provided, and the Scheme documents being published on the Scheme webpages for close to five months. The applicants have also provided a general overview of the Scheme to a large number of financial service licensees and advisers.

85 By 6 February 2025, the applicants had received 3,166 telephone calls relating to the proposed Scheme through a dedicated toll-free number and had received 199 emails to the dedicated email address. The subject matter of these calls and emails, insofar as they related to the Scheme, comprised:

(a) queries about the nature and effect of the proposed Scheme including whether the proposed Scheme will result in any changes to the terms or premiums applicable to a policy, and if any action is required on the part of the policy owner;

(b) requests for clarification and an explanation of the Scheme Summary in simple terms;

(c) requests to opt out of the mail-out process related to the proposed Scheme and to update contact details;

(d) requests for information about the sale of TLISL to TDA;

(e) queries about TAL due to a lack of familiarity with the TAL brand;

(f) requests to cancel a policy; and

(g) two objections to the proposed Scheme which are addressed in further detail below.

86 Enquiries in respect of the Scheme were also received by the applicants’ solicitors, Herbert Smith Freehills (HSF). As at 10 February 2025, HSF had received enquiries from 22 policy owners about the proposed Scheme and had responded, or attempted to respond, to each of them by a return telephone call. These enquiries mostly related to questions about the impact of the Scheme either in a general way or specific to the policy. Two policy owners expressed concern about TAL Life not being an Australian company unlike “Westpac” and their lack of familiarity with the “TAL” brand. One of these policy owners has objected to the Scheme in writing and this objection is addressed below.

Objections to the Scheme

87 Two policy owners have expressed an objection to the Scheme by way of emails to the applicants. Neither appeared at the confirmation hearing. The applicants accept that these objections reflect genuine concerns and have addressed them in correspondence with each policy owner.

88 The first policy owner, who is currently under claim on the basis of serious health issues, has objected to the proposed Scheme on the basis that they did not want “TAL” to be their insurer, as this may result in changes to their policy terms or to the quality of customer service.

89 The second policy owner stated that they did not want their life insurance policy to be transferred to a foreign entity or parent organisation entity; that they did not want to contract with a foreign entity; that their trust and arrangement was made with Westpac in 1999; that they did not wish to contract with TAL Life; and that they did not know what legal jurisdiction TAL Life falls under. This policy owner considered the transfer to be a security issue under the Constitution and questioned how a foreign owned entity could be trusted to ensure it was investing in Australian organisations and keeping its funds’ money in Australia and securely. The policy owner appears to have requested HSF to convey these objections to the Court.

90 It is convenient to address these objections and some of the concerns expressed by other policy owners together.

91 First, the general objection that the policy owners do not want their insurer changed is not a valid objection to the Scheme because that consequence is inherent in the very nature of a Scheme under Pt 9 of the Life Act. As Rimer J said in Re Hill Samuel Life Assurance Limited [1998] 3 All ER 176,179 [d]–[e] in dealing with objections to the sanction of a Scheme under Sch 2C to the Insurance Companies Act 1982 (UK):

There are in evidence a number of representations from various policyholders who have expressed concern and some element of dissatisfaction about the proposed schemes, for a number of different reasons. I do not think it is necessary to go through their objections in any close detail. Certain of them express, perhaps understandably, the complaint that having, for example, taken out a Hill Samuel policy, and having chosen not to take an Abbey Life policy, they feel a degree of dissatisfaction in finding themselves locked into Abbey Life. I have some sympathy with that, but it seems to me that that is inherent in the very nature of the scheme involving the transfer of life business from one company to another.

92 A similar view was expressed by Stone J in National Mutual Life Association of Australasia Limited v Challenger Life No 2 Ltd [2009] FCA 1 at [22]–[23]:

It is entirely understandable that people who had invested in one company should be concerned and even resentful when, without their consent, their investment is transferred to another company. It is also understandable that these concerns should be exacerbated in the current climate of severe financial instability. Nevertheless, Parliament in providing in the Life Insurance Act for such transfers clearly regarded them as consistent with the principal object of the Act…

… Consistent with the principal object of the Act, however, the Court is not directed to consider only the interests of policyholders or to consider [their] interests as paramount. Their interests must be considered in the context identified in s 3(1). Moreover, it should be assumed that the interests of policyholders are necessarily identical with their preferences.

See also the acknowledgement by Allsop CJ in Asteron Life No 3 at [121] and [129] that such “somatic considerations…fall outside the somewhat clinical terms of Part 9 of the Act”.

93 Second, the concern expressed that the Scheme may result in a change to the policy terms or the quality of service is not persuasive in respect of the proposed Scheme. Save for the identity of the insurer and relevant statutory fund, the terms and conditions of transferring policies will not change under the Scheme: see cll 3.2(b), 3.7, 3.8, 3.9 and 3.13 of the Scheme. Further, the actuarial evidence is to the effect that the quality of customer service, as manifested by claims handling practices, policy administration, underwriting and product improvements, are not expected to be adversely impacted by the Scheme. Mr Merten found that there would be no material changes to customer service levels. Rather, policy owners can expect to experience benefits from the Scheme through scale, operational risk and benefit security as explained above.

94 Third, an objection to the Scheme on the basis that the policies or business of TLISL will be transferred to a non-Australian insurer or parent entity do not constitute a proper basis for not confirming the Scheme. Similar objections were addressed and rejected by Allsop CJ in Asteron Life No 3 at [120][124] involving the same transferee under analogous circumstances. While it may be a frustrating and disappointing experience for policy owners to have their insurer changed (without their consent), the discretion to confirm the Scheme is to be exercised having regard to the interests of policy owners, which are not necessarily synonymous or identical with the preferences of each and every one of them. Nevertheless, the actuarial evidence shows that the Scheme will not be prejudicial to these interests, and indeed will be beneficial to them.

95 In the United Kingdom, similar objections have been characterised as “subjective” and rejected as irrelevant to the exercise of the discretion to “sanction” a Scheme under Pt VII and s 111 of the Financial Services and Markets Act 2000 (UK) (FSMA): Re Prudential Assurance Company Limited and Rothesay Life plc [2020] EWCA Civ 1626; [2021] Lloyd’s Law Reports 623 (Re Prudential Assurance) at [111]–[121]. In Re Prudential Assurance the English Court of Appeal at [117] agreed with what Warren J said in Re Scottish Equitable plc and Rothesay Life plc [2017] EWHC 1439 (Ch) as follows:

63. [fairness] is not the subjective view of a policyholder or even of the judge. An objective view must be formed, a view reached against the objective standards and the factors appropriate to take into account. To take an extreme example, a scheme would not be unfair because it transferred business from a Scottish company to an English company even though a particular policyholder selected the company in the first place precisely because it was Scottish rather than English. …

114. … Miss Hutchins emphasises the unfairness, as she sees it, of compelling her elderly father to transfer to a new company from the venerable SE which he deliberately chose. He wants to be given a choice, in particular to transfer to LGAS rather than to RL.

115. There are two points to make. Firstly, the venerable position of SE is not, I am afraid, of itself a relevant factor. Even venerable institutions can fail as those who work in this area of the law are well aware. …

116. Secondly, a newish body, that is to say, RL, is not to be regarded as an unsuitable provider simply because it is new otherwise we could never have new entrants into the market for transfers. The question is not its age but its financial strength, record and expectations. (emphasis added)

96 In Re Prudential Assurance, the Court found that subjective factors relied on by objecting policy owners on the basis of the transferor’s age, venerability and established reputation, and their assumption that the transferor would provide their annuity throughout its lengthy term, were not relevant to be taken into account in the exercise of the Court’s discretion: Re Prudential Assurance at [119].

97 There are other underlying difficulties with the objection and concerns that the business is to be transferred to a foreign entity. The transfer of the business to be effected has been the subject of Government approval. The substance of the “go-ahead” decision made by APRA as a delegate of the Minister (referred to above) under s 41(1) of the IATA is that the Commonwealth Government has no objection to, and it would not be contrary to the public interest for, TAL Life to acquire the life business of TLISL by means of a scheme under Pt 9 of the Life Act. Further, the transaction received two approvals from the Treasurer as being in the national interest, namely pursuant to the Foreign Acquisitions and Takeovers Act 1975 (Cth) and the Financial Sector Shareholdings Act 1998 (Cth).

98 Moreover, insofar as there are concerns about the security of assets and funds in TAL Life post-transfer, the distribution of retained profits of the statutory fund and of shareholders’ capital in relation to a statutory fund, is governed by the provisions in Pt 4, Div 6 of the Life Act. These provisions limit distributions which would have the result of capital adequacy or solvency standards not being satisfied in relation to the fund. The general requirements regarding the establishment and operation of the statutory funds of TAL Life under Pt 4, Div 1 of the Life Act and the actuarial evidence of the capital position of TAL Life, if the proposed Scheme is confirmed, also address concerns about the security of the benefits of transferring policy owners post-Scheme.

99 Finally, because of the sale of the shares of TLISL to TDA, since August 2022 TLISL’s ultimate holding company has been domiciled in Japan and would continue to be even if the Scheme were not confirmed.

100 Mr Hollo SC submits, and I accept, that the admittedly genuine objections and concerns expressed by policy owners do not form a basis for not confirming the Scheme.

The Position of APRA

101 The applicants have consulted extensively with APRA since March 2024 in respect of the proposed Scheme. APRA has been provided with drafts of the Scheme documents, and, as set out above, has given its approval to the Notice of Intention and the Scheme Summary.

102 APRA was represented at both the dispensation hearing and the confirmation hearing and supports the confirmation of the Scheme without modification.

Conclusion and Orders

103 In my view, it is appropriate to confirm the Scheme without modification, and to make orders in the form proposed. Those proposed orders do not depart from existing practice.

104 Order 3 of the proposed orders provides that TDA pay APRA’s costs of the proceedings as agreed, or if an agreement cannot be reached, as assessed. Under cl 7 of the Scheme, all costs associated with the transfer of the life insurance business of TLISL are to be paid by TDA.

105 The Court has the power to make an order for the payment of costs by a non-party. TDA is aware of the proposed order and has a sufficient connection to the proceedings to be the subject of the costs order proposed: see OnePath Life Limited, in the matter of OnePath Life Limited [2022] FCA 406 at [20] (Jagot J).

106 I wish also to express my gratitude to Mr Hollo SC, Ms Lyons (who appeared for APRA), and to the solicitors, actuaries and lay witnesses involved in this matter, for the clear and efficient way in which the matter has been presented and argued.