FEDERAL COURT OF AUSTRALIA

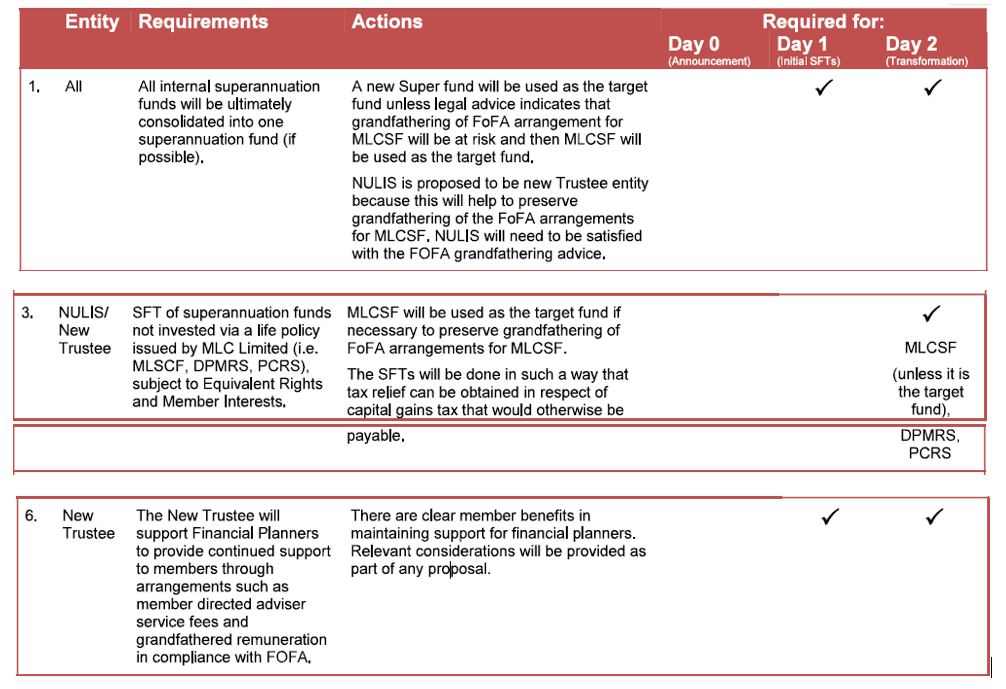

Brady v NULIS Nominees (Australia) Limited in its capacity as trustee of the MLC Super Fund (No 4) [2024] FCA 1374

ORDERS

Applicant | ||

AND: | NULIS NOMINEES (AUSTRALIA) LIMITED (ACN 008 515 633) IN ITS CAPACITY AS TRUSTEE OF THE MLC SUPER FUND Respondent | |

DATE OF ORDER: | 2 December 2024 |

THE COURT ORDERS THAT:

1. Subject to Order 2 below, on or before 16 December 2024 the parties are to provide draft orders for the disposition of the proceeding, including by providing proposed answers to the common questions at Annexure B to these reasons.

2. In the event that the parties cannot agree on the matters referred to in Order 1:

(a) by 16 December 2024 they are to inform the Associate to Markovic J of the nature and extent of the disagreement between them; and

(b) the proceeding will be listed for case management hearing to allow all outstanding matters in dispute to be determined and for final orders to be made.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

MARKOVIC J:

1 Before 1 July 2016 Mervyn Lawrence Brady, the applicant, was a member of The Universal Superannuation Fund Scheme (TUSS), the trustee of which was MLC Nominees Pty Ltd (MLCN). On 1 July 2016 the members of TUSS, including Mr Brady, were transferred by a successor fund transfer (SFT) to the MLC Super Fund, the trustee of which from the time it was established has been NULIS Nominees (Australia) Limited, the respondent to this proceeding. At all relevant times National Australia Bank (NAB) was the ultimate holding company of NULIS.

2 Mr Brady brings this proceeding under Pt IVA of the Federal Court of Australia Act 1976 (Cth) on his own behalf and as representative party for and on behalf of certain members of the MLC Super Fund whose memberships and benefits were transferred on 1 July 2016 by SFT from TUSS to the MLC Super Fund (Group Members). He seeks damages or equitable compensation from NULIS for amounts he and Group Members allegedly lost from being charged fees from 1 July 2016 from which they say they derived no benefit.

3 At the heart of the proceeding are two decisions made prior to the SFT by NULIS on 10 June 2016 and 16 June 2016, referred to respectively as the Grandfathering Decision and the LRA Approval Decision (together, Decisions). The Grandfathering Decision was a decision by NULIS to charge Mr Brady and Group Members fees to fund commissions to financial services licensees following the proposed SFT. The LRA Approval Decision was a decision by NULIS to bind itself to pay those commissions from the date of the SFT by way of the Licensee Remuneration Agreement (LRA) and an amending deed to the Internal Remuneration Agreement (IRA). Mr Brady seeks to impugn the Decisions as well as various aspects of NULIS’ conduct in connection with the payment of certain sums, which I will refer to as commissions, to financial services licensees in the period 1 July 2016 to 23 September 2020.

1. A summary of Mr Brady’s claims

4 Mr Brady’s claims are set out in a fifth further amended statement of claim (5FASOC) which is a lengthy and detailed pleading, parts of which I set out below in the course of resolving Mr Brady’s claims. At a high level Mr Brady’s claims fall into three main categories.

5 First, Mr Brady contends that NULIS lacked power under the MLC Super Fund Trust Deed to charge fees insofar as they represented revenue to NULIS that may ultimately form part of a pool of funds used to pay commissions.

6 Secondly, Mr Brady contends that NULIS breached its duties as trustee under the Superannuation Industry (Supervision) Act 1993 (Cth) (SIS Act) by making the Decisions and by implementing the Grandfathering Decision. As to the latter Mr Brady alleges that NULIS breached its duties by paying or allowing commissions to be paid to financial services licensees and their authorised representatives on and from 1 July 2016 to 23 September 2020 that were funded by fees charged to his and Group Members’ superannuation accounts.

7 Thirdly, Mr Brady contends that NULIS breached s 963K of the Corporations Act 2001 (Cth) by paying commissions after 1 July 2016 with the consequence that the charging of fees to fund the payment of those commissions was a breach of the Trust Deed because those fees were not for the “administration and operation” of the MLC Super Fund.

8 Mr Brady claims that NULIS should pay damages under s 55(3) of the SIS Act or equitable compensation for its breaches to him and Group Members (or at their election restore their superannuation accounts) or, in the alternative, the Court should make an order requiring NULIS to pay compensation or restore his and Group Members’ accounts or to pay compensation to them.

9 NULIS has filed a detailed defence to the 5FASOC. In short it denies that it lacked power to charge fees for the purpose of funding commissions or that it has breached the Trust Deed either because, in turn, it breached the SIS Act or s 963K of the Corporations Act as alleged.

10 In these reasons I address the facts followed by a consideration of each of the three categories of claim made by Mr Brady and, to the extent relevant, the sample group member, Sophia Margaretha Atkinson, who represents those Group Members described at [13] below.

11 For ease of reference, Annexure A to these reasons is a glossary of the defined terms used in these reasons.

12 It is convenient first to provide a description of the witnesses (other than experts) relied on by the parties followed by a summary of the relevant facts.

13 Mr Brady relied on his own evidence and evidence given by Ms Atkinson, who was appointed as sample group member for non-vested Group Members. That is, a member of the MLC Super Fund who, in contrast to Mr Brady, was not entitled to access his or her benefits at the relevant time: see Brady v NULIS Nominees (Australia) Limited in its capacity as trustee of the MLC Super Fund [2021] FCA 999. Ms Atkinson relies on a second further amended points of claim which sets out the material facts in relation to her personal circumstances and otherwise substantially repeats the matters pleaded in the fourth amended statement of claim, which has been superseded by, and which I will take to be a reference to, the 5FASOC.

14 Neither Mr Brady nor Ms Atkinson were cross-examined.

15 NULIS relied on evidence given by the following witnesses.

16 Peggy Yvonne O’Neal AO was a non-executive director of NULIS from 14 February 2011 to 31 March 2020 and a non-executive director of MLCN and PFS Nominees Pty Limited (PFSN) from 14 February 2011 to 14 February 2017. PFSN was a wholly owned subsidiary of NAB and the trustee of superannuation funds collectively referred to in these reasons as the Plum Funds (see [61] below).

17 Ms O’Neal was admitted as a solicitor in Australia in September 1991 and was a partner of law firm Freehills (now Herbert Smith Freehills) specialising in superannuation and financial services law from 1 July 1995 to 30 June 2009; a consultant with Freehills from 1 July 2009 to 1 June 2011; and has been a consultant with law firm Lander & Rogers, continuing to specialise in superannuation and financial services law, since 1 June 2011.

18 Ms O’Neal has also held and/or continues to hold a number of other roles including:

(1) member of the Law Council of Australia Superannuation Committee since 1996 and now an emeritus member of that committee. From 2002 to 2006 she was chair of the committee;

(2) consultant to the Commonwealth Treasury on the Superannuation System review (known as the Cooper Review) as a member of the secretariat to the expert panel;

(3) member of the peak consultative group advising the Commonwealth government on the “Stronger Super” reform package in 2011. This was a voluntary position which involved Ms O’Neal advising the Commonwealth government on strategies for modernising the governance, efficiency, structure and operation of Australia’s superannuation system;

(4) fellow of the Australian Institute of Company Directors;

(5) on boards and committees in the superannuation industry (other than NULIS, MLCN and PFSN):

(a) independent consultant to the Audit, Risk and Compliance Committee of UniSuper Limited from August 2009 to June 2020;

(b) independent member of the External Compliance Committee of Vanguard Investments Australia Limited from August 2009 to June 2020;

(c) director of the Commonwealth Superannuation Corporation from 1 July 2011 to 30 June 2020; and

(d) director and chair of Vanguard Super Pty Ltd since 1 August 2021;

(6) director of Women’s Housing Limited since July 2013; Infrastructure Specialist Asset Management Limited since July 2018; Dementia Australia Network since December 2020; and the Australia-American Educational Foundation (Fulbright Commission) since January 2021;

(7) director of Richmond Football Club Limited since November 2005 and president since October 2013;

(8) chair of an inquiry “Women and Girls in Sport and Active Recreation” for the Victorian Minister of Sport in 2014-15; and

(9) member of Victoria’s Ministerial Council on Women’s Equality from August 2017 to June 2020.

19 In 2018 Ms O’Neal was awarded an Honorary Doctor of Laws by Swinburne University. In June 2019 she was appointed an Officer of the Order of Australia for distinguished service to Australian Rules Football, to superannuation and finance law, and to the advancement of women in leadership roles. In 2021 she was named Melburnian of the year. Since 1 January 2022 Ms O’Neal has been the chancellor of the Royal Melbourne Institute of Technology (RMIT) University.

20 Ms O’Neal was cross-examined.

21 Mr Brady submits that Ms O’Neal’s evidence was a “highly reconstructed, self-serving exercise of seeking to persuade the Court of NULIS’ case” and that Ms O’Neal was not a forthright witness and that she sought to avoid answering, or prevaricated, in relation to questions which she considered were adverse to NULIS’ interests. In short, Mr Brady urges that I would not rely on Ms O’Neal’s evidence save insofar as it is adverse to NULIS’ interests.

22 That was not my impression of Ms O’Neal as a witness. The events the subject of this proceeding took place some eight years ago, and some seven years prior to Ms O’Neal giving evidence. That being so, it can be accepted that some of Ms O’Neal’s evidence was her best recollection of the events based on her review of the material made available to her. To that end, it might be classified as a reconstruction. In other respects, given the passage of time, Ms O’Neal could not clearly recall some matters. It is hardly surprising that Ms O’Neal could not recall the detail of board papers or of discussions.

23 But those aspects of Ms O’Neal’s evidence did not undermine the totality of her evidence. In my opinion, Ms O’Neal endeavoured to assist the Court by answering the questions she was asked in cross-examination to the best of her ability and with a degree of precision. That is unsurprising given both Ms O’Neal’s role over many years as a NULIS non-executive director and her significant experience in the superannuation industry. Ms O’Neal was also prepared to make concessions where appropriate and to reconsider her answers to questions over the course of the three days during which she gave evidence. Taken together my overall impression of Ms O’Neal was as a thoughtful witness who gave her evidence in as full and frank a way as made possible by the passage of time.

24 It is convenient to address at this stage Mr Brady’s criticism of Ms O’Neal’s evidence on the basis that she had not accessed, let alone reviewed, “the full suite of documents (to determine what was of relevance) when preparing her affidavit”. I pause to observe that in this case the “full suite of documents” likely amounted to many thousands of pages. For example, the court book in the form tendered (in two exhibits) comprised over 1,700 documents and many thousands of pages.

25 Ms O’Neal gave evidence about the process she underwent in preparing her affidavit. She said:

… it started with discussions about what I did recall, and then because I have no documents of my own, I asked for those documents to be collected over time and that I would read them, the minutes for the meeting.

26 Ms O’Neal identified the categories of documents she wished to review. They were what she described as “official documents”, namely board papers, workshop packs and minutes of meetings. Ms O’Neal also asked to see the letter from NAB dated 29 October 2015.

27 It is not of any moment nor a matter of concern that Ms O’Neal was not given, nor requested, access to NULIS’ discovery as part of her preparation of her evidence. Ms O’Neal is an experienced non-executive director who had served for many years on the MLCN, PFSN and NULIS boards and understood the way those boards operated. In those circumstances, as NULIS submits, that Ms O’Neal was able to identify the material she required for review in preparing her evidence is not surprising.

28 Kellie Maree Stansell holds a Bachelor of Mathematics and Finance from the University of Wollongong. She joined MLC, the NAB’s wealth management business, in August 2014 and has held the following roles since that time:

(1) from August 2014 to December 2015 she was a product manager under the MLC brand responsible for leading, driving and delivering key corporate super product initiatives across MasterKey Business Super (MKBS) and the Plum Superannuation Fund;

(2) from January 2016 to June 2016 she was responsible for leading the “trustee approval” stream for the implementation of the SFTs that occurred on 1 July 2016 for the transfer of members and assets of five superannuation funds, one of which was TUSS, into the MLC Super Fund as described later in these reasons;

(3) from 1 July 2016 she was responsible for implementing the proposed trade-ups of legacy superannuation products from a product delivery point of view and in January 2017 her title changed to senior manager, transformation delivery as part of NAB’s decision to establish a dedicated team responsible for implementing the trade-ups (referred to in these reasons as the Trade-up Program);

(4) from January 2018 to May 2019 she was reassigned from her role implementing the Trade-up Program from a product delivery perspective to work on another program within the business relating to MySuper but retained some supervision and leadership responsibilities for the components of the Trade-up Program being implemented during that period;

(5) from May 2020 to May 2022 she was head of platform enablement. Ms Stansell remained responsible for implementing the commitments made by NAB from a product delivery point of view but her responsibilities also included overseeing other product initiatives within the MLC Super Fund. During that period Ms Stansell’s employer changed to Insignia Financial Limited as a result of the sale by NAB on 31 May 2021 of its wealth business; and

(6) from 1 May 2022 she has been head of MasterTrust product transformation. In that role Ms Stansell is responsible for driving the MasterTrust product transformation for Insignia.

29 By way of further explanation, in her role leading the trustee approval stream for the SFTs Ms Stansell was responsible for drafting the papers presented to both the transferring (MLCN and PFSN) and receiving (NULIS) trustees addressing equivalency of members’ rights and members’ best interests.

30 These papers sought to collate all of the issues that the transferring and receiving trustees had to consider in order to approve the SFTs. Ms Stansell also drafted what she referred to as “noting” papers which provided an update to the transferring and receiving trustees on the status of the issues to be considered. Ms Stansell recalls that some issues were dealt with separately from the trustee approval stream and had their own papers which she did not prepare. Included in these issues was whether to continue grandfathered commissions.

31 From December 1998 to June 2014, prior to joining MLC, Ms Stansell was employed by AMP Services Limited where she held various roles including head of product for AMP’s retail superannuation, retirement and investment portfolio of products, head of product strategy and research and head of MySuper product solutions. In that latter role, Ms Stansell was involved in SFTs including transferring an AMP superannuation fund and its members into another of their existing funds. As a result, she developed an understanding of the issues and the work involved in undertaking SFTs.

32 Ms Stansell was cross-examined.

33 As Mr Brady acknowledges, Ms Stansell gave her evidence directly and without prevarication. Ms Stansell was an impressive witness. She gave detailed evidence in relation to her role and the steps involved in the Trade-up Program with which she was involved and answered questions put to her in cross-examination directly, clearly and with care. Contrary to a further submission made by Mr Brady I was not left with any impression that Ms Stansell sought to avoid answering questions or that she prevaricated when she perceived to do otherwise would be contrary to NULIS’ case, either in relation to the exchange between senior counsel for Mr Brady and Ms Stansell relied on by Mr Brady or otherwise.

34 Martin James Dickson who is associate director, finance in the deputy chief financial officer change team at NAB. Mr Dickson has held that role since March 2017 save for the period from January 2021 to December 2021, when he was seconded to the NAB Group External Reporting Team. Mr Dickson commenced employment with NAB in August 2008. From August 2008 to March 2017, he held various roles in the NAB group finance team including from March 2010 to March 2017 the role of senior manager. In those roles, Mr Dickson was responsible for overseeing the process by which the accounts of NAB and its subsidiaries were consolidated at the end of each month using the system known as Hyperion Financial Management (HFM) for the purpose of financial reporting which is a finance system used to consolidate accounting data for data flows between NAB Group entities. Mr Dickson was part of the team that consolidated the accounts at the end of each month and prepared the consolidated financial reports for the NAB Group.

35 Among other things, Mr Dickson gave evidence about the HFM system and the processes through which intercompany transactions in the NAB Group are consolidated through the HFM system for the purpose of statutory and management reporting.

36 Mr Dickson was cross-examined.

37 Daniel John Atwell who is head of group financial control at Insignia and has been in the role since the sale by NAB of the MLC Wealth segment of its business to Insignia in October 2021. Mr Atwell is responsible for the accounting and financial reporting processes of MLC Wealth Limited (formerly known as National Wealth Management Services Limited (NWMSL)). Prior to that, commencing on 30 June 2016, Mr Atwell held roles in the MLC Wealth Corporate Financial Control team where he was responsible for the accounting and financial reporting processes of NWMSL. He gave evidence about the process by which payments of commissions and other types of adviser payments were made to financial services licensees by NWMSL on behalf of NULIS, MLC Investments Limited and MLC Limited in the period 1 July 2016 to 23 September 2020. Mr Atwell was not cross-examined.

38 Sharon Irene Blanche King, who since June 2021 has been the head of fund reporting (Super) at Insignia and in that role is responsible for accounting and financial reporting processes in relation to certain superannuation funds including the MLC Super Fund. From November 2015 to June 2021 Ms King held the equivalent role of head of external reporting (Super) at NAB. Ms King has been responsible for overseeing the accounting and financial reporting processes of the MLC Super Fund since the SFT on 1 July 2016. She gave evidence about the accounting treatment of fees payable to the MLC Super Fund and payment by the MLC Super Fund to NULIS of fees for administration services. Ms King was not cross-examined.

39 Anna Faith Dow, who is head of governance and reporting at Insignia. From January 2019 to October 2021 Ms Dow was an associate director in the MLC financial control investments team. In that role she was responsible for leading the financial control investments team in the provision of financial and statutory reporting and the preparation and co-ordination of annual financial statements for all superannuation product-issuing companies and asset management companies within the MLC Wealth group. One of the companies she was responsible for overseeing was NULIS (in its corporate capacity). Ms Dow gave evidence about two processes in relation to NULIS of which she had direct knowledge given her role: first, the process by which NULIS charged fees to the MLC Super Fund; and secondly, the process by which NULIS paid expenses which it owed in its corporate capacity, including amounts owed to MLC Wealth Limited in respect of the payment of commissions and other adviser payments to financial services licensees on behalf of NULIS. She also gave evidence about how those fees and expenses were treated in the financial statements of NULIS. Ms Dow was not cross-examined.

40 Michael Esber, who is a senior analyst engineer at Insignia. Mr Esber extracted daily transaction statements and daily balance reports from a product administration system known as “Compass” for Mr Brady and Ms Atkinson. Compass is the product administration system used by Insignia to store information regarding, among other things, the accounts of members who hold MasterKey Pension Fundamentals and MKBS. Mr Esber gave evidence about the steps he took in each case to extract those reports from the Compass system. Mr Esber was not cross-examined.

41 Sandra Owen, who is an analyst, investment control at Insignia. Ms Owen is part of the finance department and her team provides a daily review of unit prices for the MLC business. In her role Ms Owen uses the system known as “Unison” on a daily basis to view and extract information. The Unison system stores data in respect of the daily unit prices of MLC investment funds. Ms Owen extracted an Excel spreadsheet (converted into PDF format) that contains data in respect of the daily “buy”, “mid” and “sell” unit prices of the “GTGP” and “GTINC” investment funds on each day in the period 1 July 2016 to 5 June 2020. She gave evidence about the steps she took to extract the data contained in the spreadsheet. Ms Owen was not cross-examined.

42 Rajan Rodrigo, who is a senior consultant, solution design at Insignia. His role involves designing technology solutions for the MLC business. As part of his role, Mr Rodrigo uses the system known as “MasterKey” on a day-to-day basis and is familiar with the types of data stored on the system. Mr Rodrigo gave evidence about how the MasterKey system operates. Mr Rodrigo was not cross-examined.

43 Jean York, who is a technical analyst/programmer at Insignia. Her role involves computer programming in relation to a system known as “AMANDA” which is used in the MLC Wealth business. Ms York gave evidence about the data which she caused to be extracted from the AMANDA system and the process she undertook to extract the data and create spreadsheets containing datasets. Ms York was not cross-examined.

44 Murray Alan Bartram, who is a senior analyst engineer at Insignia. His role involves extracting and analysing data. He is familiar with the use of the “Mainframe Archive User Interface” (MAUI) to access and extract data relating to accounts which were administered on the “CAPSIL” system until their trade-up to the “Compass” system. He gave evidence about the data he caused to be extracted from the MAUI system and the process he undertook to extract the data and create spreadsheets containing datasets. Mr Bartram was not cross-examined.

2.2 Employees within the NAB group

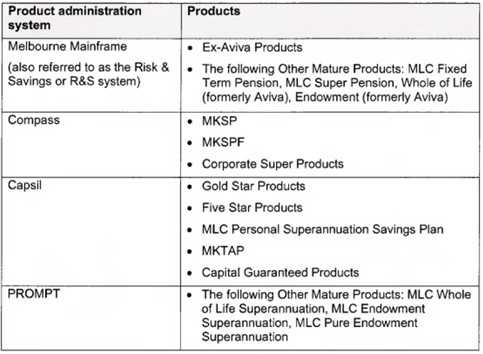

45 In order to assist in understanding the evidence and facts as they were developed before me it is convenient to set out in one place the various NAB Group employees who were involved in assisting the NULIS, MLCN and PFSN boards prior to the SFTs and the NULIS board after the SFTs. Many of them held more than one job title during those periods. For ease I have, for most of the employees listed, only referred to their most relevant in time job title. The relevant employees included (in alphabetical order):

(1) Paul Carter – executive general manager, super and investment platforms. Prior to holding this position, Mr Carter was executive general manager, corporate and institutional wealth. In that role, he was responsible for sales, client relationships, member experience, product management and claims management for the NAB Wealth businesses that service corporate and institutional clients across the Plum, Business Super and MLC Insurance brands. Prior to that, Mr Carter was executive general manager of business operations and strategy at NAB Wealth and managing director of Plum Financial Services. He also held senior roles in financial services and strategy at Citigroup and the Boston Consulting Group;

(2) Michelle Finlay – senior consultant, actuarial, pricing & profitability, retail super and investment platforms, NAB CPS Wealth;

(3) Tom Garde – general manager, product, corporate and institutional wealth;

(4) Justine Gorman – head of risk, wealth transformation program, NAB;

(5) Tim Gorste – senior manager, NAB Wealth Transformation;

(6) Andrew Hagger – group executive, NAB Wealth;

(7) Andrew Lawless – product development manager, retail platforms, MLC;

(8) Matthew Lawrance – executive general manager, NAB Wealth and CEO of MLC Super;

(9) Daniel Levy – general manager, portfolio development, NAB Wealth;

(10) Brian Marriott – chief operating officer of NULIS, MLCN and PFSN for a period of 11 years and, as set out below, the Office of Trustee (OTT). Mr Marriott held various executive roles in superannuation and investment spanning more than 25 years, including leading service delivery and operations at Colonial First State. He also held a number of senior roles in the wealth division of NAB across operations and strategic changes projects;

(11) Damian Murphy – chief risk officer, NAB Wealth;

(12) Lisa Neaves – senior product manager, product strategy and development, NAB Wealth;

(13) Brad Tallents – head of business transformation, NAB Wealth; and

(14) Kathy Vincent – general manager, retail super & investments. Ms Vincent joined MLC in November 2012 and was responsible for driving development and management of MLC’s retail superannuation and investment platforms. Prior to joining MLC Ms Vincent spent 20 years at Macquarie Group Ltd in a number of leadership roles in the area of product development.

46 The following persons were executive officers of NULIS within the meaning of s 10 of the SIS Act and “Responsible Persons” of NULIS within the meaning of SPS 520 Fit and Proper at [11]:

(1) Mr Marriott from 1 May 2015 to 23 September 2020;

(2) Ms Vincent from 1 May 2015 to 24 November 2017;

(3) Mr Carter from 1 May 2015 to 31 January 2017;

(4) Mr Lawrance from 1 May 2015 to 16 November 2018; and

(5) Mr Murphy from 1 May 2015 to 5 April 2019.

47 There are three relevant trustees: NULIS, MLCN and PFSN.

48 From 14 February 2011 and at all times prior to the SFT the directors of NULIS, MLCN and PFSN were the same and it was often the case that the meetings of the three boards were convened at the same times (referred to in these reasons as combined board meeting).

49 For most of the period from 1 July 2015 to 30 June 2016 (Pre-SFT Period) the directors of NULIS, MLCN and PFSN were Nicole Smith, John Reid, Trevor Hunt, Evelyn Horton, Terry McCredden and Ms O’Neal. Michael Clancy was also a director of NULIS, MLCN and PFSN for part of that period, resigning on 15 December 2015.

50 In the period from 1 July 2016 to 31 March 2020 (Post-SFT Period) Ms Smith, Ms Horton, Ms O’Neal and Messrs Reid, Hunt and McCredden each remained as directors of MLCN and PFSN for various periods of time. From 26 August 2016 the boards of NULIS, MLCN and PFSN were no longer the same: Andrew Gale was appointed as a director of NULIS. The board of NULIS was wholly comprised of non-executive directors during both the Pre-SFT Period and the Post-SFT Period.

51 Meetings of the boards of NULIS, MLCN and PFSN were held at least quarterly, and usually more frequently, whilst Ms O’Neal was a director. In the period from March 2016 to 30 June 2016, in the lead up to the SFTs, board meetings were held at least fortnightly. In the Post-SFT Period the NULIS board met at least every two months and usually more often.

52 Board workshops were held from time to time in the Pre and Post-SFT Periods. They were attended by the directors of NULIS, individuals from the OTT, representatives of the administrator and, where relevant, other service providers to the MLC Super Fund.

53 Workshops allowed the directors, prior to any formal proposal being presented at a board meeting, to request and be provided with information by representatives of the relevant service providers in relation to the particular topic for consideration and discussion. In turn, this allowed “deep dives” into issues or strategies, provided extended time for the directors to consider complex issues in a less formal setting, facilitated more in-depth discussions than could be accommodated at a formal board meeting and allowed the directors to identify any issues which required further work. For example, often workshops would be held in relation to potential options for product improvements providing a forum where directors could be given details of the benefits to members and any other impacts of a proposal prior to preparation of a board paper and making a decision.

54 Minutes were not taken at board workshops, although from time to time informal notes were taken of the discussions and of any action items to be progressed.

55 The OTT was a dedicated office established by the boards of NULIS, MLCN and PFSN to support those trustee companies in meeting corporate governance and trustee and fiduciary responsibilities, including managing conflicts of interest.

56 The OTT was governed by a Charter which set out its roles and responsibilities and the authorities under which it operated. The Charter was approved by the boards of each of MLCN, NULIS and PFSN.

57 The OTT comprised a relatively small number of staff (referred to as members in the Charter) and, from time to time, was supported by external consultants. The members of the OTT were employed by NAB and its subsidiaries and seconded to MLCN, NULIS and PFSN.

58 During the time that Ms O’Neal was a director of NULIS, MLCN and PFSN, Mr Marriott was the chief operating officer of the OTT. Ms O’Neal saw the function of the OTT as the “arms and legs” of the trust. She had a good working relationship with Mr Marriott and other members of the OTT and found that OTT staff members were responsive to requests she made for information or assistance as a director.

59 From time to time Ms O’Neal sought information from Mr Marriott or other OTT staff members and they were sometimes asked to give their views to the NULIS board. In circumstances where a decision was required to be made and Ms O’Neal did not think she had sufficient information, Ms O’Neal’s practice was to request, usually via the chair of the NULIS board, that the OTT obtain additional information.

60 NULIS was the trustee of a number of Registrable Superannuation Entities (RSEs) during the Pre-SFT Period and the Post-SFT Period. It was appointed trustee of the MLC Super Fund upon execution of the Trust Deed on 9 May 2016 (see below).

61 The MLC Super Fund was set up to be the successor fund of five superannuation funds which were the subject of SFTs:

(1) TUSS, which was under the trusteeship of MLCN; and

(2) four superannuation funds which were under the trusteeship of PFSN, namely:

(a) The Plum Superannuation Fund;

(b) The National Australia Bank Superannuation Fund A;

(c) The BHP Billiton Superannuation Fund; and

(d) The Worsley Alumina Superannuation Fund,

(collectively, Plum Funds).

62 The day to day operation of the MLC Super Fund was facilitated by personnel employed by or seconded to NWMSL or by NULIS’ ultimate shareholder, NAB. NWMSL provided the services and resources required by NULIS to operate the MLC Super Fund pursuant to a services agreement dated 30 June 2016 between NULIS and NWMSL, which was varied on 22 June 2017 and 14 February 2018.

63 MLCN invested the assets of TUSS in investment linked insurance policies issued by MLC Limited to MLCN in its capacity as trustee of TUSS. According to Ms O’Neal the structure of investments in the Pre-SFT Period was complex. It had been established historically as a tax effective way to invest the assets of TUSS and reflected the origin of the MLC business as a life company before it expanded into superannuation.

64 In the Pre-SFT Period MLC Limited also acted as the administrator of TUSS.

65 MLC Limited maintained various investment options with different investment objectives and tax characteristics in which TUSS assets were invested. MLCN did not have direct control over any of these investment options. MLC Limited was able to vary the investment objectives, profile, underlying assets or manager of an investment as it thought appropriate but was required to give notice to MLCN of any variation given the potential disclosure obligations to members of TUSS.

66 MLC Limited was entitled to:

(1) deduct investment costs and investment expenses from the assets of each investment option, which were taken into account when calculating the unit price and performance figures for each investment option each day; and

(2) charge fees, including by way of deduction from an investment option or by allocating the fee as a deduction to the value of the account maintained by it for a particular member.

67 Ms O’Neal understood that the unit prices set by MLC Limited included a profit margin and that its various costs and expenses were taken into account when daily unit prices were calculated. The value of the units would, in effect, be the market value of the investment less the fees charged by MLC Limited.

68 As trustee of TUSS, MLCN did not make any profit. All revenue from fees charged to members of TUSS was revenue of MLC Limited. Each member of TUSS had their account attached to a particular superannuation “product”. Products are vehicles for holding members’ superannuation each of which have different fee structures, investment menus and insurance arrangements. Some of the superannuation products in TUSS charged members fees from which commissions were paid to financial services licensees.

2.6.1 TUSS Commission Products

69 In the Pre-SFT Period TUSS comprised various retail superannuation products which could be acquired by members directly or through a financial adviser and a corporate superannuation product known as MKBS.

70 While Ms O’Neal was a director of MLCN the product disclosure statements (PDS) issued for on-sale products in TUSS were reviewed by the Disclosure Governance Committee, of which Ms O’Neal was a member and chair at various times.

71 The commission paying products in TUSS as at June 2016 (TUSS Commission Products) comprised:

(1) a cohort of products acquired from Aviva Australia Holdings Limited (Ex-Aviva Products);

(2) retail products, being product offerings which an individual could invest in, known as:

(a) MasterKey Superannuation Gold Star and MasterKey Allocated Pension Gold Star (together, Gold Star Products);

(b) MasterKey Superannuation Five Star and MasterKey Allocated Pension Five Star (together, Five Star Products);

(c) MLC Personal Superannuation Savings Plan;

(d) MasterKey Term Allocated Pension (MKTAP); and

(e) MasterKey Super and Pension (MKSP);

(3) MKBS, a corporate product which was a superannuation arrangement established by an employer in order to satisfy its superannuation guarantee requirements for employees that do not choose their own superannuation fund; and MasterKey Personal Super (MKPS) which was the product to which a member of MKBS was automatically transferred after ceasing employment (together, Corporate Super Products);

(4) products where MLC Limited provided a guarantee, known as MLC Capital Guarantee Personal Super Savings Products Series 1 (ex-Capita) and MLC Capital Guarantee Personal Super Savings Products Series 2 (Accumulus); and

(5) products where MLC Limited issued a life policy under which the member was insured.

72 The TUSS Commission Products were “accumulation” style products into which a member’s superannuation contributions were made and invested. In general terms, a member’s account balance was the amount of contributions plus investment earnings or less investment losses, as applicable, and net of any fees or costs. There were no defined benefit members in TUSS.

73 With the exception of the Corporate Super Products, the TUSS Commission Products were off-sale by 1 July 2014 such that new members were not permitted to invest in those products. The Corporate Super Products remained on-sale, in that they were available to new and existing members, in the period following the SFTs. However, the commission arrangements (namely, adviser contribution fees and insurance commissions) only applied to members who joined the product prior to 29 November 2013.

74 Some of the TUSS Commission Products had a number of series or product variants as a result of trade-ups which occurred before the SFTs. This happened because in some of the previous trade-ups, certain product features had been “grandfathered” or carried over to the target or destination product which led to the “umbrella” product having series or variants. For example, in MasterKey Superannuation Gold Star there were ten product series and in MasterKey Superannuation Five Star there were four product series.

75 By the time Ms Stansell commenced working on the Trade-up Program, all of the TUSS Commission Products, other than MKSP and the Corporate Super Products, were classified as legacy products. The legacy products were administered on a product administration system that was not the “go-forward” system, that is the system which was used for new products. This included products that were administered on the Melbourne Mainframe and Capsil systems (see below).

76 As a non-executive director of MLCN in the Pre-SFT Period, Ms O’Neal:

(1) had a general understanding of the various groupings of the TUSS Commission Products (see [71] above);

(2) did not have a detailed understanding of the specific terms and features of the TUSS Commission Products as many were off-sale and not active; and

(3) Ms O’Neal’s knowledge of the TUSS Commission Products was gained from discussions at board meetings and workshops, in particular, in the context of proposals to improve the features of legacy products.

77 Ms O’Neal considered that certain of the legacy products were outside MLCN’s risk appetite. This was primarily because they were off-sale products lagging behind contemporary standards. In cross-examination Ms O’Neal explained in relation to the legacy products that:

(1) they were not up to date and did not sit on a digital platform that could be easily administered which meant there was a chance of human error in their administration;

(2) they had features to which members had agreed originally but which were unattractive when compared to modern on-sale product offerings;

(3) there was a risk that the trustee (and its board) no longer understood the products in the way that it should; and

(4) they were outside the trustee’s risk appetite because they were relatively high fee products compared to more modern products being offered first, by MLCN and later, by NULIS. The higher costs were partly caused by the fact that the products were held on old platforms and, as the number of members declined, there were fewer members across whom the costs of maintaining those platforms could be spread.

78 The view that these legacy products were outside MLCN’s risk appetite was recorded in an MLCN board paper titled “Project Mars – Retail Product Strategy” dated 25 November 2015 (Retail Product Strategy Paper) which was presented to a combined board meeting on 2 December 2015. “Project Mars” was the internal name for the proposed SFTs and the then proposed Trade-up Program. It aimed to simplify the superannuation business by reducing the number of superannuation funds, products and product administration systems that would be within the TUSS Division of the MLC Super Fund.

79 In addition to the TUSS Commission Products, there were two on-sale retail products available to the TUSS Division of the MLC Super Fund which did not pay commissions: MasterKey Super Fundamentals (MKSF); and MasterKey Pension Fundamentals (together, MKSPF). As explained below, these were the products to which the TUSS Commission Products were upgraded in the Post-SFT Period.

80 The TUSS Commission Products and MKSPF were administered on four different product administration systems, each of which housed member data and records, as follows:

81 Compass became the “go-forward” system because it was the product administration system that MLC Limited used to administer products that were open to new members.

82 As set out above, Ms O’Neal understood that the functionality of some of these administration systems was outdated and they were expensive. She recalls this was discussed in the Pre-SFT Period on various occasions among MLCN directors with the objective of transitioning members’ records to a contemporary product administration system, Compass, and closing the legacy systems, including:

(1) section 4 of the Trustee Business Plan for October 2015 to September 2018 (approved by MLCN’s board at its meeting on 23 September 2015) identified the need to deal with the complexity and cost of the legacy product administration systems as a key focus for MLCN as trustee; and

(2) the legacy product administration systems on which certain TUSS Commission Products were administered, and the contemporary Compass administration system, were referred to in the Product Mars Retail Product Strategy Paper included in the meeting pack for the 2 December 2015 combined board meeting in the context of the proposed product upgrade strategy following the SFTs.

2.6.3 Commissions on the TUSS Commission Products

83 Ms O’Neal understood that in the Pre and Post-SFT Periods there were three primary types of commissions paid in respect of the TUSS Commission Products:

(1) asset-based or “trail” commissions, which were commission payments made to financial services licensees that were referable to the balance of the member’s account and which became payable when a member acquired an interest in a product and which continued to be paid while the member held an interest in the product;

(2) contribution-based commissions, which were commission payments made to financial services licensees which were calculated based on contributions made to a member’s account; and

(3) insurance commissions (applicable to the Corporate Super Products only), which were commission payments made to financial services licensees calculated as a percentage of the insurance premium payable in respect of insurance cover acquired through those products.

84 As a director of MLCN Ms O’Neal understood that in the Pre-SFT Period, MLC Limited paid commissions to financial services licensees, set the fees and determined the unit prices of the investment options for members of TUSS. As set out at [68] above, those fees were revenue of MLC Limited and the commissions were paid to financial services licensees from this fee revenue.

85 Ms O’Neal understood, both as a director of MLCN and NULIS, that the commissions for the TUSS Commission Products were embedded in the cost of the product to the member, were paid for upon the initial acquisition of the product and that there was no legal requirement for a financial services licensee to provide any ongoing service to a member in exchange for the commission.

86 In the Pre and Post-SFT Periods Ms O’Neal understood that certain of the TUSS Commission Products had fees which were paid to financial services licensees for the provision of service, or access to service (that is, “fee for service” arrangements), separate to the commission arrangements described at [83] above. These included “adviser service fees” and “plan service fees” which were not grandfathered commissions. Throughout the period that Ms O’Neal was a director of MLCN and NULIS, she understood that the terms “commissions” and “fees” were used in PDSs to differentiate between amounts which were embedded as part of the cost of the product to a member (that is, commissions) and amounts which were paid separately and related to the provision of, or access to, ongoing services (that is, fees).

87 The Plum Funds generally comprised large employer-sponsored superannuation plans. Certain assets of the Plum Funds were held directly by the Plum Pooled Superannuation Trust, which was a special type of RSE and was wound up following the SFTs as it was no longer necessary. Other assets of the Plum Funds were invested by PFSN in investment-linked insurance policies issued by MLC Limited.

88 Each employer sub-plan in the Plum Funds had a legal agreement known as a “Participation Agreement” which formed part of the governing rules of the fund. A Participation Agreement set out detailed rules for investments and usually could not be amended without the agreement of the employer-sponsor. Each of the sub-plans which had more than 50 members was required to have a policy committee which had equal representation from the employer and members. These committees provided feedback to the trustee on behalf of the sub-plan members.

89 In the Pre-SFT Period Ms O’Neal was aware, from her role as a director of PFSN and her role as a solicitor at Freehills providing advice to PFSN for many years, that PFSN became the trustee of most of these sub-plans because of various SFTs which occurred in the period from approximately 2002 onwards from standalone corporate superannuation funds or competitor master trusts. During this time, many employers no longer wished to operate their own fund because of the significant and frequent increases in regulatory requirements.

90 Ms O’Neal explains that the Plum Funds comprised both accumulation plans, defined benefit plans and hybrid plans. In contrast, TUSS had accumulation plans only.

91 Ms O’Neal recalls that there were no commissions paid in respect of products in the Plum Funds. That was because the products were usually employer-sponsored, were not distributed to retail investors in the same manner as the retail products in TUSS (for example, through a financial adviser) and the majority of members in the Plum Funds were not directly advised by a financial adviser. All of the sub-plans in the Plum Funds had a relationship manager, who assisted employers in managing their obligations. Thus, as Ms O’Neal explains, the target markets of TUSS and the Plum Funds were fundamentally different.

2.8 Mr Brady invests in superannuation with MLC

92 Mr Brady is 85 years old. He completed his third year of secondary school before becoming an apprentice electrical fitter (radio). Mr Brady was self employed as a television serviceman repairing televisions, video recorders and radios from 1970 until his retirement in 2001.

93 The manager of the Mullumbimby branch of NAB introduced Mr Brady to Maurice James, who he understood to be a financial adviser, in late 1998. Mr Brady recalls visiting Mr James’ office for the first time in late 1998. I understand that at the time (and in any event as at 2004) Mr James was at MK Financial Planning Services Pty Ltd which was an authorised representative of GWM Adviser Services Limited trading as Garvan Financial Planning, an Australian financial Services Licensee.

94 By letter dated 7 December 1998 Mr James provided Mr Brady and his wife, Sheila Brady, with an investment plan dated 3 December 1998. In summary, the investment plan recommended that Mr and Mrs Brady’s investment portfolio of $169,800 be invested across a range of allocated pension/annuities, cash based investments and direct equities. Mr Brady cannot recall receiving or reading Mr James’ letter or the enclosed investment plan.

95 In about 1999 Mr Brady and his wife sold their home. They had about $155,000 to invest for their retirement.

96 Mr Brady recalls that he went to see Mr James who at that time provided him with some MLC Limited documentation. Mr and Mrs Brady were shown applications for MLC superannuation, copies of which he no longer has. Mr Brady did not pay much attention to the documents but recalls that he was investing his money into MLC superannuation.

97 It is apparent that in 1999 Mr Brady opened a TUSS National Personal All in One Super account and that he signed an application form for that account dated 3 February 1999.

98 Insofar as Mr Brady can recall, before investing in MLC superannuation he did not receive any written advice, advice in relation to particular or alternative superannuation investment options or advice about fees, charges or commission that might be charged, paid or negotiated or other financial advice from Mr James or anyone else at NAB or MLC Limited or on their behalf. Upon searching his records, Mr Brady was unable to find any records of advice.

99 On a number of occasions Mr James asked Mr and Mrs Brady to visit his office in Tweed Heads to sign documentation. When they did so the documents to be signed were already filled in and Mr James asked for them to be signed. Once again, Mr Brady does not recall receiving any written or verbal advice in relation to those documents.

100 In December 2001 Mr Brady received:

(1) from NAB a document titled “THE UNIVERSAL SUPER SCHEME NATIONAL PERSONAL ALL IN ONE SUPER Statement of benefits as at 30 November 2001 Exit statement”, which is the earliest written record Mr Brady has in relation to his MLC superannuation; and

(2) from MLC Limited a document titled “MLC MasterKey Superannuation upgrade investment confirmation as at 1 December 2001 Entry statement” which recorded that his superannuation was transferred to MasterKey Superannuation Five Star (Nil entry fee version).

101 As best as Mr Brady can recall:

(1) he did not receive any advice or communication from Mr James in relation to the transfer of his superannuation to MasterKey Superannuation Five Star (Nil entry fee version); and

(2) after making his initial investment Mr Brady never received any written or oral financial advice from Mr James or from any other MLC Limited or NAB employee or representative in relation to his superannuation.

102 On 7 September 2004 Mr James provided a “Statement of Advice (incorporating a financial plan)” to MR and Mrs Brady. The recommendations included combining “current MLC super with Colonial policy and convert to an allocated pension to provide retirement income”, namely MasterKey Allocated Pension.

103 Mr Brady was shown a MasterKey Allocated Pension application form dated 8 September 2004 which bears his and Mrs Brady’s signatures on pages 6 and 5 respectively. Other than the signatures, he does not recognise the handwriting on the form, does not know who completed the form, and does not recall discussing its contents or receiving any advice about it. On 8 September 2004 Mr Brady also signed a “Request to transfer funds ‘to the MLC MasterKey Allocated Pension’ authorising the transfer of funds to the MasterKey Allocated Pension which is invested in The Universal Super Scheme”. Despite Mr Brady’s lack of recollection, it is clear that from about September 2004 he had an MasterKey Allocated Pension Gold Star account.

104 In about March 2005 Mr Brady received from MLCN an “MLC MasterKey Portfolio Summary” and “Statement of Account” as at 31 December 2005 for his MasterKey Allocated Pension Gold Star account which showed that his portfolio comprised units held in MLC IncomeBuilder and MLC MasterKey Horizon 5 – Growth Portfolio. Mr Brady explained that his portfolio remained the same throughout the period he held his MasterKey Allocated Pension Gold Star Account, namely 2004 to 2020.

105 Subject to the following, after 2006 the only further documents and services Mr Brady can recall receiving in relation to his superannuation were annual notifications by letter and/or statements from MLC Limited, MLCN and then NULIS notifying his account balances. Mr Brady cannot recall receiving any service from a financial adviser in relation to his superannuation from 2005 to 2020.

106 James & Young Wealth Management, which I infer is a firm of which Mr James is or was a principal, produced documents in answer to a subpoena served on it in this proceeding. Some of the documents produced suggest that Mr Brady received various communications in relation to his accounts held with MLC Limited that he neither had in his possession nor could recall. Mr Brady acknowledged that the documents produced on subpoena suggest that he received various documents from Mr James in relation to his MLC accounts that he did not previously hold or recall. Mr Brady has carried out a search and, other than the documents produced on subpoena, he does not have copies of any other documents from Mr James’ office in respect of any advice concerning his MLC accounts.

107 As well as the letter dated 7 December 1998 and its enclosure referred to at [94] above, a number of other documents were produced by James & Young Wealth Management in relation to Mr and Mrs Brady and their MLC superannuation including statements of advice, diary notes of meetings, questionnaires, tax invoices, email exchanges with Mr James and correspondence enclosing portfolio reports. In summary Mr Brady cannot recall receiving, reading and, in some cases, understanding the correspondence and/or advice he received as evidenced by those documents. However, he does recall generally contacting Mr James to discuss what he should do prior to his retirement at age 65.

108 While Mr Brady has an imperfect recollection, it was not in dispute, and the evidence shows, that he invested in MasterKey Allocated Pension Gold Star in 2004.

109 An annual statement to 30 June 2016 was issued by MLCN as the trustee of TUSS, just prior to the SFT, for Mr Brady’s MasterKey Allocated Pension Gold Star account. It showed an account start date of 10 September 2004, included Mr Brady’s account and customer numbers, named Mr Brady’s adviser, Mr James, and provided a summary of his account including its opening balance, payments out, fees paid directly from the account and movement in investment value to arrive at a closing balance.

110 The annual statement as at 30 June 2016 also included an investment summary which showed that Mr Brady owned two investments in MasterKey Allocated Pension Gold Star: MLC Horizon 5, with “inception date” of 4 June 1998; and MLC IncomeBuilder, with “inception date” of 31 July 1997.

111 By letter dated September 2016 Mr Brady was informed that a PDS “summarising the features and terms of [his] account in MLC MasterKey Allocated Pension Gold Star” was available to him either online, by email or in hard copy if he so requested.

112 An annual statement to 30 June 2017 for Mr Brady’s MasterKey Allocated Pension Gold Star account provided exactly the same information save that the statement was issued by the trustee of the MLC Super Fund, NULIS, and the amounts shown for the opening balance, payments out, fees paid directly, movement in investment value and closing balance differed as did the opening and closing balances for the two products in which Mr Brady had invested.

113 By letter dated 9 April 2020 Mr Brady was informed that his MasterKey Allocated Pension Gold Star account was moving to MasterKey Pension Fundamentals as part of NULIS’ “ongoing program to modernise and simplify its products to benefit members overall”. That letter informed Mr Brady that there was “[g]ood news” because his “annual fees are expected to decrease by approximately $825.15 pa, based on [his] account balance of … and investments at 5 March 2020” and that:

MLC MasterKey Pension Fundamentals has a different fee structure and doesn’t pay commission to advisers. …

If you wish to consult your financial adviser, you may pay a fee for the services you receive. You can choose how to pay for these services, including having the fee deducted from your account, which would be an additional cost to you.

114 On 5 June 2020 Mr Brady was transferred to MasterKey Pension Fundamentals.

2.10 Ms Atkinson invests in superannuation with MLC

115 Ms Atkinson is 62 years old. She is a part-time secretary and part-time teacher. She became a member of TUSS on 10 October 1994. At the time she was employed by her husband’s business, Accounting & Business Consulting Services Pty Ltd (ABC). She is currently employed by the same business part-time and is also employed part-time as a teacher. As at March 2022 she anticipated that she would continue to work for the next two to three years.

116 In 1994 ABC subleased premises from Bridgeport Sydney which was a provider of financial services and a client of ABC. Neither Ms Atkinson nor her husband, Hugh Atkinson, were clients of Bridgeport.

117 Ms Atkinson and her husband set up MLC Limited superannuation accounts at the same time. Ms Atkinson cannot now recall whether she or her husband filled in any application forms at the time. Her listed Plan adviser in the Statements of Account provided to her by MLCN in July 2009 and July 2010 was Bridgeport.

118 Ms Atkinson does not recall receiving any written or oral financial advice from Bridgeport or any financial adviser at that time or at any subsequent time from 1994 to 30 June 2021.

119 Ms Atkinson invested in the MKBS product. Ms Atkinson, like Mr Brady, had an imperfect recollection of her superannuation matters in the thirty years since she first established her superannuation account.

120 In about July 2009 Ms Atkinson received from MLCN an MKBS statement of account recording her investments as at 30 June 2009. That statement recorded her investments at the time as being equally split three ways between MLC Horizon 5, BT Balanced Fund (Closed) and INVESTCO Growth Fund (Closed).

121 Ms Atkinson’s investment options remained as they were until 2014 when MLCN unilaterally moved her investment in the BT Balanced Fund (Closed) to MLC Horizon 3 – Conservative Growth Portfolio and her investment in INVESTCO Growth Fund (Closed) to MLC Horizon 4 – Balanced Portfolio. Her future contributions and rollovers continued from then until 2021 to be invested in equal shares in MLC Horizon 3 – Growth Portfolio, MLC Horizon 4 – Balanced Portfolio and MLC Horizon 5.

122 Ms Atkinson does not recall receiving any financial advice from any financial adviser nor any contact from MLCN about her investment options nor the fees and commissions charged in relation to her account, with the exception of the communications from MLCN referred to in the preceding paragraph notifying her of the changes to her investment options.

123 By letter dated April 2016, Ms Atkinson was notified by MLC of “Important changes to [her] super”, relevantly, the proposed SFT. The letter indicated that MKBS products would be moved to a new fund by SFT, if the SFT proposal was approved, and was accompanied by a flyer providing further information regarding the proposed SFT, including a list of “Fees and other charges”. There was no mention of financial adviser fees in the flyer. However, it noted that “[f]or more information about your current fees, transaction costs and how they are calculated, please log in to your account with your customer number on mlc.com.au or see the Product Disclosure Statement (PDS) on mlc.com.au/pds/mkbs”.

124 An annual statement to 30 June 2016 for Ms Atkinson’s MKBS account was accompanied by a covering letter which notified her of “[t]he movement of [her] super to the MLC Super Fund” which took effect on 1 July 2016. Ms Atkinson was then sent a copy of the PDS for her MKBS account by MLC in September 2016. Ms Atkinson does not recall receiving correspondence regarding changes to her MKBS product in the Post-SFT Period.

125 To the best of Ms Atkinson’s knowledge, she did not receive any services from a financial adviser in relation to her superannuation investment.

2.12 Product disclosure statements

126 The PDS for MasterKey Allocated Pension Gold Star dated 23 September 2016 was in evidence before me. It includes in that part describing “Fees and other costs”:

(1) the following explanation:

This document shows fees and other costs that you may be charged. These fees and other costs may be deducted from your money, from the returns on your investment or from the assets of the superannuation entity as a whole.

Other fees, such as activity fees or advice fees for personal advice may also be charged, but these will depend on the nature of the activity or advice chosen by you.

Taxes are set out in another part of this document.

You should read all the information about fees and other costs because it is important to understand their impact on your investment.

The fees and costs for each investment option offered by the superannuation entity are set out below and in the Investment Menu section starting on page 20.

(2) a table describing types of fees, amounts payable for each fee type and how and when each fee type is paid; and

(3) a worked example of annual fees and costs based on a $50,000 balance held in MLC Horizon 4.

2.13 The events leading up to the SFTs

127 The SFTs occurred in the context of NAB’s sale of 80% of its shareholding in MLC Life to Nippon Life Insurance Company which was announced in October 2015. That transaction was referred to within the NAB Group as Project Astro. The boards of MLCN and PFSN as trustees respectively of TUSS and the Plum Funds were first briefed on Project Astro on 31 July 2015.

128 From at least August 2015 Ms O’Neal became aware, and discussed with her fellow board members, that as part of Project Astro the transfer of the assets and members of TUSS and the Plum Funds would occur through SFTs of those funds into a new superannuation fund. This was as an alternative to cancelling the investment-linked insurance policies issued by MLC Limited and transferring the underlying investments or proceeds from the sale of assets to the existing superannuation funds.

129 As Ms O’Neal explains, an SFT is effectively a transfer of members and their benefits from one superannuation fund to another, without their consent. Ms O’Neal estimates that during her career as a solicitor and as a director of NULIS, MLCN and PFSN, including as chair of the Successor Fund Transfer Committee, she provided legal advice on, or considered as a trustee director, in the range of 90 to 100 SFTs. Ms O’Neal advised on what she believes was the first SFT in Australia when Telstra merged two superannuation funds in around 1997.

130 Ms O’Neal was supportive of transferring the assets and members to a new superannuation fund, rather than to the existing superannuation funds. Ms O’Neal was of this view primarily because the latter method would have incurred capital gains tax (CGT), and she was aware, having provided legal advice as a solicitor on previous SFTs, that CGT rollover relief was available where all members and all assets of a superannuation fund were moved from one fund to another in the same tax year. As a director of MLCN and PFSN, Ms O’Neal considered that the CGT rollover relief was a significant factor in considering the proposed SFT and a fundamental consideration in assessing whether the SFT was in the best interests of members.

131 Ms O’Neal considered that proceeding by way of SFT was the only practical option available. The alternative, which would result in payment of CGT, was not an attractive option given the amount of CGT that would have been payable out of the assets of the relevant fund and because the transfers to TUSS and the Plum Funds would also have been subject to contributions tax payable by the members.

132 Various board meetings and workshops which, as I have already observed, as a matter of practice were generally held jointly between MLCN, PFSN and NULIS, were held in the second half of 2015 at which the proposal in respect of the SFTs was developed and discussed.

2.13.1 Combined board workshop – 12 August 2015

133 On 12 August 2015 a combined board workshop was held. A workshop pack titled “Project Astro: Confidential Trustee Workshop” was provided for it. One of the items on the agenda was “[t]he preferred structure and how to implement it”. In relation to that agenda item, among other things, the workshop pack identified:

(1) the recommended preferred structure was as one superannuation fund, to be split into divisions to separate the different types of member offering, into which the existing super funds (TUSS and the Plum Funds) would transfer. That structure was recommended because “[a] simple transfer of the assets from MLC Limited to each of the super funds would incur capital gains tax” and the tax position therefore required that all members of TUSS and the Plum Funds be moved via an SFT to another super fund;

(2) none of the superannuation funds that invest in investment-linked life policies issued by MLC Limited (that is, TUSS or the Plum Funds) could be used as the target receiving fund meaning that either a new superannuation fund was required, or one of the other existing RSEs could be used. The identified preference was a new fund with a new trustee; and

(3) as a matter for consideration the issue of losing grandfathered commissions.

2.13.2 Combined board workshop – 14 September 2015

134 On 14 September 2015 a combined board workshop was held. The documents provided in the workshop pack were “works in progress” ahead of the upcoming 14 October 2015 combined board meeting. The emphasis was “on the opportunity to discuss direction and align expectations” with the workshop purpose stated to be to address the “latest thinking from management on the Mars Proposal in order to [h]elp Directors understand the direction of the proposal” and “[s]eek formal feedback from Directors to guide actions over the next few weeks leading up to a formal proposal for consideration”.

135 The workshop pack included a draft letter from MLCN to NAB for Project Astro. The draft letter referred to NAB’s proposal “in the wake of the Transaction”, that a new superannuation fund be established with NULIS as its trustee and that a number of specified funds including TUSS amalgamate into the new fund by way of an SFT. After referring to the “Principles” which would apply to the amalgamation, the draft letter continued:

I confirm that, subject to the Principles, [MLCN], as trustee of TUSS, is supportive of the proposed Amalgamation and confirms its in-principle support to undertake the following steps in relation to the proposed Amalgamation:

• Assess, in accordance with its statutory and general law duties, the detailed terms of the SFT proposal and a Business Case for the amalgamation of TUSS into the New NAB Fund by way of a SFT.

• Obtain independent advice in relation to the SFT proposal and Business Case.

• Subject to [MLCN] being reasonably satisfied that the SFT proposal is in the best interests of the beneficiaries of TUSS after taking into consideration the terms of the SFT proposal and the Business Case, implementing an amalgamation of TUSS into the New NAB Fund by way of a SFT, including:

• cancelling its existing investment insurance contract with MLC and

• requesting that the policy proceeds be paid by way of in-specie transfer to the trustee of the New NAB Fund (or as it may direct in writing).

• A release by [MLCN] of MLC as administrator of TUSS from all MLC’s historic liabilities and obligations as administrator of TUSS prior to the SFT date on the condition that these liabilities are assumed by NAB.

The initial support of [MLCN] outlined above is based on the information that you have provided about the benefits of the Amalgamation for members of TUSS.

However, as you would expect, further work needs to be undertaken to confirm this as the details of the Amalgamation are developed.

136 The workshop pack also:

(1) identified that the “window” of time for the SFTs to take place was through to 30 June 2017, which was the “End of Tax Relief”. At that time, CGT rollover relief available in relation to the merger of superannuation funds and the treatment of assets related to the merger applied only to mergers occurring before 1 July 2017; and

(2) included a document titled “Mars Principles (Discussion Document)” which set out (in two columns) certain “Principles” and “Outworking”. One of the stated principles under the heading “New Fund and New Trustee” was that “Grandfathering of FoFA status in respect of the MLCSF is important”. “FoFA” is a reference to the Future of Financial Advice reforms which came into effect by amendments to the Corporations Act and Corporations Regulations 2001 (Cth) described below. The related “Outworking” column in relation to the item “New Fund and Trustee” which included this principle, included that “[a] new Super fund will be used as the target fund unless legal advice indicates that grandfathering of FoFA arrangement for MLCSF will be at risk and then MLCSF will be used as the target fund” and “NULIS will be the new Trustee entity because this will help to preserve grandfathering of the FoFA arrangements for MLCSF”.

137 As to the latter matter, the references to “MLCSF” were references to the MLC Superannuation Fund which was an entirely different superannuation fund that was ultimately not the subject of the SFTs and is not involved in this proceeding. As NULIS points out the option identified in this draft discussion document, that NULIS be the receiving trustee for the SFTs on the basis this may assist to preserve the continuation of grandfathered arrangements which existed for products in the MLC Superannuation Fund, fell away in 2015 together with the early proposal that that fund might be transferred as part of the SFTs. This document does not support a conclusion that the consideration in 2015 of NULIS being the potential receiving trustee for the SFTs had any connection to the grandfathered commission arrangements which existed in TUSS.

2.13.3 Combined board workshop – 30 September 2015

138 A further workshop was held on 30 September 2015 in relation to the Project Mars proposal. The workshop pack included a paper authored by Mr Marriott titled “Project Astro / Mars – COO Overview”, which provided a perspective from the OTT on the proposed SFTs. Under the heading “Purpose” Mr Marriott stated:

The purpose of this paper is to provide additional insight around the work currently being undertaken in response to NAB’s decision to substantially divest itself of its life insurance business and its downstream impacts to the Trustee entities.

My role is unique in the organisation in that I do not act at any time for or perform work for any other entity in the group except the superannuation Trustee entities, I have no reporting line to management, the shareholder, the administrator or the life company. In that capacity, I have in the lead up to any public announcement, embedded myself in the Astro/Mars program to ensure that the Trustee’s (and its members) interests are appropriately dealt to ensuring all relevant matters are escalated to the Trustee free of any conflicts or constraints. This paper is written from that vantage point.

139 Mr Marriott’s paper also noted that he and Ashleigh Crittle of the OTT had “been involved in or engaged on every aspect of the draft proposal being considered at today’s workshop”, including:

(1) “[t]he re-design of the ‘Principles’ document that was discussed at the 14 September 2015 Trustee workshop”, which had been “sharpened to provide a clearer view of what is required when and by which entity at the right level of detail for the Trustee”; and

(2) the initial drafting of the letters that the Trustee would expect from the shareholder, its administrators and the life company and then the “subsequent management and oversight of all iterations and consultation”.

140 The workshop pack also included a draft of a paper to be presented at the upcoming 14 October 2015 board meeting titled “Superannuation entity amalgamation & rationalisation – Project Mars” which provided “an overview of management’s proposal to simplify NAB Wealth’s super fund structures, servicing and governance (the Mars Proposal) as a key component of [NAB’s] intention to substantially divest ownership and control of the life insurance business currently carried out by MLC Limited to ‘Neptune’ (Project Astro)” (original emphasis).

2.13.4 NAB letter dated 9 October 2015

141 By letter dated 9 October 2015 from Andrew Thorburn, Group CEO and Managing Director, NAB, to MLCN and PFSN (9 October 2015 Letter) NAB referred to Project Astro and set out its proposal for a “series of amalgamation and transformation activities” for its superannuation business within NAB Wealth. The details and key requirements of the proposal were included in a document attached to the 9 October 2015 Letter (Key Requirements). Under the heading “Benefits to Members” the 9 October 2015 Letter provided:

The Initial SFTs have been proposed as a means of providing the following key benefits for members of the transferring. RSEs:

1. significantly increased scale with expected cost reduction benefits;

2. funding of Operational Risk Financial Requirements (ORFR) through shareholder capital, enabling the removal of existing ORFR levies and release of existing ORFR member reserves for the benefit of members;·

3. the opportunity to provide more efficient and seamless transition of members through different life stages including accumulation phase, transition to retirement and post-retirement, as part of a single RSE environment;

4. the opportunity to provide a more co-ordinated approach to investment menu construction across funds, utilising the strongest components from each of the current separate menus; and

5. the opportunity to significantly reduce complexity and operational risk in the administration and investment environment.

In addition, the Initial SFTs will provide a platform which will enable NAB to invest in on-going product improvement including the trade-up of legacy business and enhanced member services. It is NAB’s current intention to pursue these strategies and, in the case of the trade-up of the legacy business, for this to be done within 3 years of completion of the Transaction.

142 The Key Requirements included, among other things:

143 In the 9 October 2015 Letter NAB requested that, “subject to the Principles and the Requirements”, MLCN and PSFN as “trustees of the transferring RSEs” confirm their in-principle support for the proposed “Initial SFTs”. The “Initial SFTs” referred to the proposal that TUSS and the Plum Funds be amalgamated into a new superannuation fund by way of SFTs and that a NAB Wealth entity be appointed as trustee and administrator of the fund.

2.13.5 Combined board meeting – 14 October 2015

144 A combined board meeting was held on 14 October 2015.

145 At that meeting the directors noted a further draft of the paper they had considered at the 30 September 2015 workshop (see [138] above) dated 8 October 2015 prepared by Mr Carter now titled “Superannuation Entity Initial SFT’s & Transformation Proposal – Project Mars” and resolved to approve the issue of letters by MLCN and PFSN to NAB “substantially in the form contained in the Legal Advice, subject to receipt of the signed letter from NAB, substantially in the form contained in Appendix 2”.

146 Under the heading “Purpose”, the paper provided:

This paper provides an overview of the [NAB’s], as shareholder, proposal to simplify NAB Wealth’s super find structures, servicing and governance (the Mars Proposal) as a key component of its intention to substantially divest ownership and control of the life insurance business currently carried out by MLC Limited to ‘Neptune’ (Project Astro). Note there has been extensive Trustee briefing and consultation on the nature and impact of the Mars proposal.

It is requested that considering the operating arrangements currently in place with MLC Limited, each of [MLCN] and [PFSN] provide a letter to the [NAB] confirming their in-principle agreement to the Mars Proposal and to undertake the steps required to implement the change subject to compliance with their statutory and general law duties.

147 The paper included an overview of the elements of Project Mars, outlined the benefit to members and annexed the proposed letter setting out MLCN’s and PFSN’s (as transferring trustees) in principle agreement as sought in the 9 October 2015 Letter, a Project Mars workplan and a summary of legal, tax and risk management advice. As described in the paper, Ms O’Neal understood that the proposal for the SFTs came from NAB and was made in the context of its sale of 80% of MLC Life for some $2.4 billion. That is, the superannuation investments had to be removed from MLC Limited to allow that sale to occur.

148 Under the heading “Proposed letter of in-principle agreement sought from MLCN and PFSN” the paper provided:

In relation to Day 0 Astro transaction communications and specifically in consideration of the current investment arrangements between MLCN, PFSN and MLC Limited, NAB has requested that MLCN and PFSN provide a letter of in-principle support (included in the legal advice) to the proposed Initial SFTs.

To assist MLCN and PFSN in providing this in-principle support, NAB is providing them with a letter (refer to Appendix 2) that includes, amongst other things:

• an acknowledgement of their commitment to operating a successful superannuation business within NAB Wealth;