FEDERAL COURT OF AUSTRALIA

Cody Gemtec Retail Pty Ltd v Underwriting Members of Syndicate 2003 at Lloyd’s (Declassing Applications) [2024] FCA 1098

ORDERS

DATE OF ORDER: | 20 September 2024 |

THE COURT ORDERS THAT:

1. Each proceeding be adjourned for a case management hearing on a date to be fixed for the making of orders in conformity with these reasons, including:

(a) approving notices to group members under s 33X(5) of the Federal Court of Australia Act 1976 (Cth) (FCA Act);

(b) the making of orders pursuant to s 33ZB of the FCA Act;

(c) the making of declassing orders pursuant to s 33N of the FCA Act (following the making of any s 33ZB orders and the service of approved notices in each proceeding to group members);

(d) any orders as to costs; and

(e) as to the future conduct of each of the declassed proceedings and any related proceeding.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

LEE J:

A INTRODUCTION AND BACKGROUND

1 The operation of Pt IVA of the Federal Court of Australia Act 1976 (Cth) (FCA Act) is now well into its fourth decade. As was recently remarked upon by the Full Court (Murphy, Beach and Lee JJ) in R&B Investments Pty Ltd (Trustee) v Blue Sky (Reserved Question) [2024] FCAFC 89 (at [102]–[103], [121]), there are evident public policy benefits in the existence of the open class action regime provided for by Pt IVA, being those foreshadowed by the Australian Law Reform Commission in its seminal report entitled Grouped Proceedings in the Federal Court (Report 46, December 1988) upon which Pt IVA of the FCA Act was largely, but not wholly, based (at 44):

The main objective of [the class action regime] … is to secure a single decision on issues common to all and to reduce the cost of determining all related issues arising from the wrongdoing. To achieve maximum economy in the use of resources and to reduce the cost of proceedings, everyone with related claims should be involved in the proceedings and should be bound by the result.

2 Consistently with this, in describing the general objectives of the Bill which inserted Pt IVA in the FCA Act, the then Attorney-General stated that it would:

[P]rovide a new representative action procedure in the Federal Court. The new procedure will enhance access to justice, reduce the costs of proceedings and promote efficiency in the use of court resources … The Bill gives the Federal Court an efficient and effective procedure to deal with multiple claims. Such a procedure is needed for two purposes. The first is to provide a real remedy where, although many people are affected and the total amount at issue is significant, each person’s loss is small and not economically viable to recover in individual actions. It will thus give access to the courts to those in the community who have been effectively denied justice because of the high cost of taking action. The second purpose of the Bill is to deal efficiently with the situation where the damages sought by each claimant are large enough to justify individual actions and a large number of person wish to sue the respondent. The new procedure will mean that groups of person, whether they are shareholders or investors, or people pursuing consumer claims, will be able to obtain redress and do so more cheaply and efficiently than would be the case with individual actions.

Commonwealth, Second Reading Speech, House of Representatives, 14 November 1991, 3174–3175 (Attorney-General)

3 The class action regime is an example of major law reform that has achieved its intended aim. It has not only provided a mechanism by which access to justice has been achieved for countless group members with small claims against those who have engaged in various forms of contravening conduct, but has also provided a flexible, efficient and cost-effective mechanism by which large numbers of disparate claims with some element of commonality can be determined in a staged process whereby a common issue or issues bind not only the parties to the class action, but all those whose claims are affected by the class action, being group members.

4 As part of the Full Court in Gill v Ethicon Sàrl (No 3) [2019] FCA 587; (2019) 369 ALR 175, I described (at 176 [4]) how a claim of a group member is determined in whole or in part and highlighted the most important provision within Pt IVA, being s 33ZB, noting that this provision provides that a judgment given in a class action must describe or otherwise identify the group members affected by it and binds all such persons other than any person who has opted-out under s 33J.

5 The “statutory estoppel” arising upon the making of a s 33ZB order is the mechanism by which non-party group members are bound by the determination of questions in a class action. It is critical to keep firmly in mind that the scheme contemplates that binding answers to common questions or issues of commonality inform the later bespoke determination of the varying, individual (and sometimes quite disparate) claims of group members.

6 For reasons that have never been adequately explained, when faced with a miscellany of individual claims, which gave rise to common issues concerning persons who alleged that they suffered interruption or interference to a business conducted by them consequent upon the COVID-19 pandemic (and had a contract of insurance alleged to respond to such claims), a group of insurers the subject of the claims made a decision to eschew the procedural mechanism which would have allowed any findings in litigation to become legally binding upon all those potentially affected (and then allowed individual claims to be resolved pursuant to a Court supervised process).

7 Rather, as will become evident, the insurers fastened upon a process that antedated the development of modern class action regimes. They sought to identify “test cases”, ran them in two Courts, and then put in place “private” processes of assessment, not subject to court supervision, which were said to be informed by the principles emerging from those test cases.

8 It is not suggested that this course was adopted by the insurers otherwise than in good faith and based on considered advice, but despite submissions on these applications to the contrary, there was no obstacle to the insurers seeking the cooperation of one or more insureds for a Pt IVA representative proceeding to be commenced and all declaratory relief sought by the insurers in test cases being able to be determined by way of cross-claim on an expedited basis. Individual claims could then have been resolved under the supervision of the Court.

9 The relevant claims against the insurers were plainly “claims” as that term is used in s 33C of the FCA Act. There is also no doubt orders could have been fashioned to ensure that any findings of law and fact said to be common to the various insureds would have become binding upon those insureds (subject to the insureds not taking the active step to opt-out of such proceedings). If at the time there were (for reasons I do not understand) concerns as to the jurisdiction of this Court, this could have been accommodated by commencing the class action in the Supreme Court of New South Wales.

10 Both this Court and the Supreme Court of New South Wales did cooperate with the insurers and did provide speedy determination, at intermediate Court of Appeal level, to resolve many issues between the parties. The difficulty that has emerged is that the result of these test cases is not binding on those who were not a party to those proceedings.

11 This has resulted in the present disputation which would have been unnecessary if different forensic choices had been made at the outset of this controversy.

12 One can only infer that the insurers, given the quality of legal representation they engaged, would have turned their minds to alternatives to the test case approach adopted. It is also reasonable to infer that the test case regime was adopted because the insurers perceived it to be in some way superior to using the class action regime. I will not speculate as to why the insurers thought the course they adopted was superior.

13 It suffices to note that the collateral litigation caused by the duplication of litigation and the commencement of applications to “declass” the four class actions suggests the decision to adopt a test case regime (although providing some of the same benefits achievable by use of the class action procedure), did not constitute the optimal way of facilitating the just resolution of the disputes between the insurers and the insureds according to law, and as quickly, inexpensively and efficiently as possible.

14 But unlike Lot’s wife, for present purposes, we must not look back – what has happened has happened. The Court is now faced with the need to deal with the declassing applications based upon the evidence adduced on the applications and by reference to the circumstances that existed as at the time of the hearing of the applications. It is no part of the Court’s function to penalise the insurers because different forensic decisions could have obviated the disputation that now exists.

B THE CLASS ACTIONS AND DECLASSING APPLICATIONS

15 There are four open class actions being case managed together with the intention that a concurrent initial trial take place (together with at least one additional individual claim). The class actions the subject of the declassing applications are as follows:

(1) Cody Gemtec Retail Pty Ltd v The Underwriting Members of Syndicate 2003 at Lloyd’s (NSD 637 of 2021) (Lloyd’s class action);

(2) Strand Fitness Pty Ltd v QBE Insurance (Australia) Limited (NSD 638 of 2021) (QBE class action);

(3) CMC Hospitality Pty Ltd v Insurance Australia Ltd (NSD 893 of 2021) (IAL class action); and

(4) Vicki Field Swim School Pty Ltd v Hollard Insurance Company Pty Ltd (NSD 1048 of 2021) (Hollard class action).

16 As discussed below, a registration regime has been put in place for the class actions pursuant to an order made following the filing of the declassing applications, fixing a date by which group members could take an active step to provide an expression of interest for their claim to be determined in the class action.

B.1 QBE Class Action

17 In this class action, the group members are identified as all persons who, relevantly:

(1) were insured at any time during the period 19 January 2020 to the date of commencement under a contract of insurance with QBE that provided cover under specified policy wordings; and

(2) suffered interruption or interference to the business conducted by a named insured occurring consequent upon the COVID-19 pandemic.

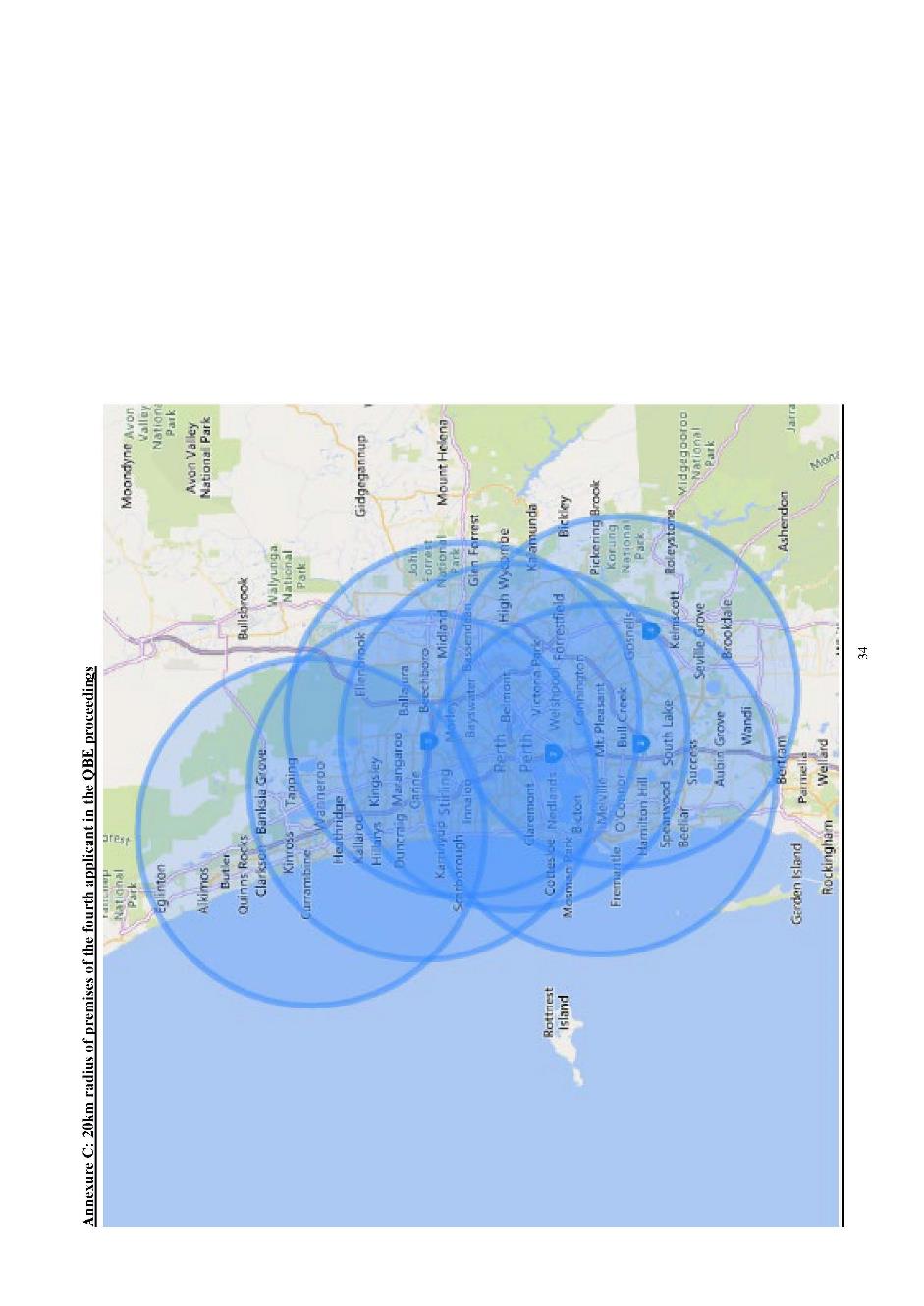

18 The QBE class action involves (or is proposed to involve) 28 policy wordings, and there are four types of insuring clauses being:

(1) infectious disease clauses, which respond to interruption to or interference with the business as a result of the “outbreak of a human infections or contagious disease occurring within a 20 kilometre radius of the situation” (QBE amended statement of claim (QBE ASOC) (at [17]));

(2) hybrid outbreak clauses, which respond to interruption to or interference with the business due to closure or evacuation of the whole or part of the premises by order of a relevant authority as a result or in consequence of an “outbreak” of an infectious or contagious human disease occurring within a 20 kilometre radius (or in some policies “within the immediate vicinity”) of the premises (QBE ASOC (at [18]));

(3) disease hybrid clauses, which respond to interruption to or interference with the business in consequence of closure or evacuation of all or part of the premises by order of a relevant authority as a result of infectious or contagious human disease (in some policies within a 50 kilometre radius, in other policies 20 kilometres, in one policy within 15 kilometres, and in the remaining policies no radius requirement is imposed at all) which prevents or hinders the use of the building or access thereto or results in a cessation or diminution of trade due to temporary falling away of potential custom (QBE ASOC (at [19], [20A]));

(4) discovery hybrid clauses, which respond to interruption to or interference with the business because of closure or evacuation of the business by order of a relevant authority consequent on the discovery of an organism likely to result in a human infectious or contagious disease. In one policy the discovery must occur within a 15 kilometre radius, but no proximity requirement is imposed in the others (QBE ASOC (at [20], [20A])).

19 Although the precise number of group members is not known, there appear to be approximately 36,000 insureds holding the relevant type of policy. There have been 4,133 registrations for the class actions (plus 241 “late” registrations).

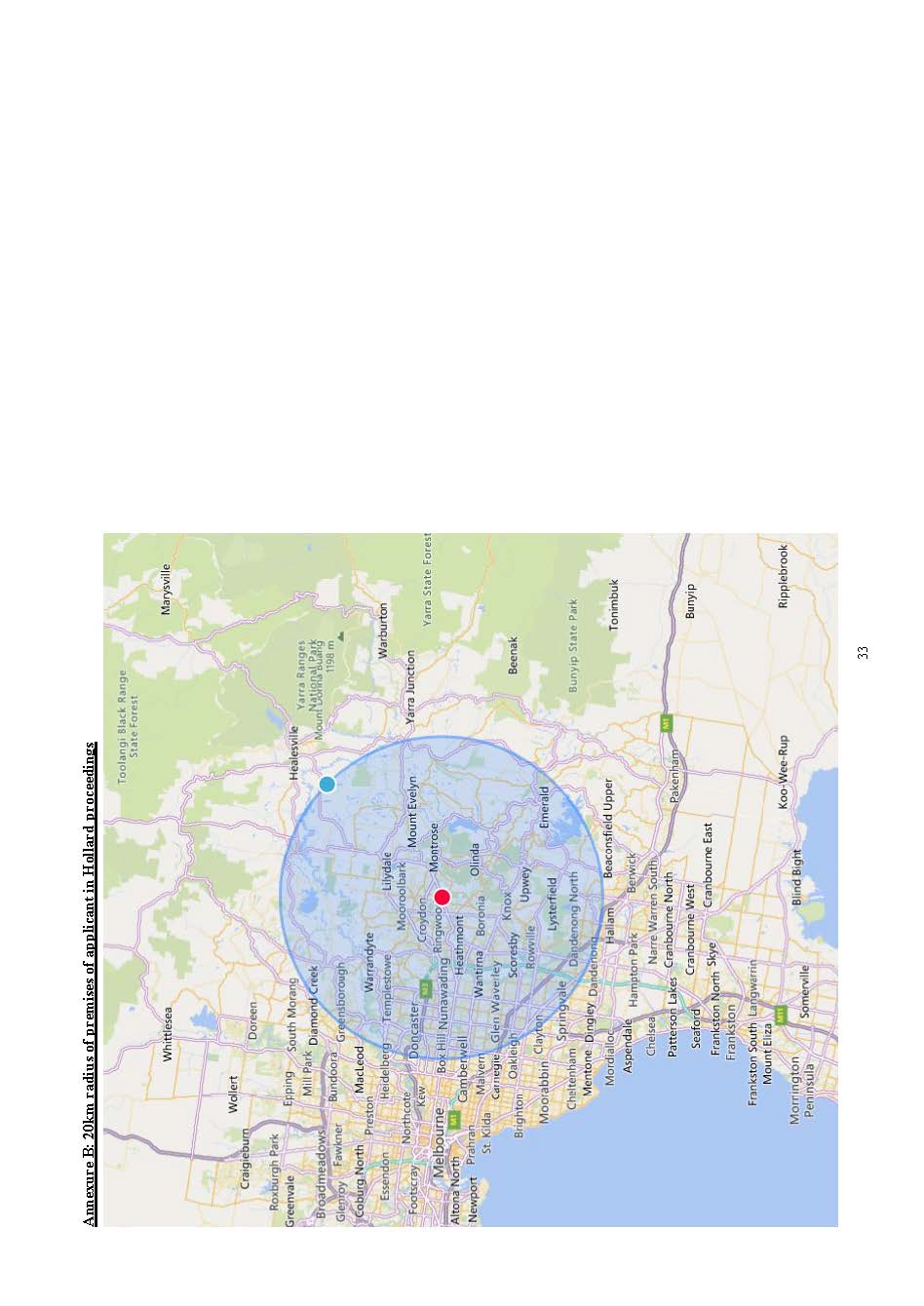

B.2 Lloyd’s Class Action

20 In this class action, the group members are identified as all persons who, relevantly:

(1) were insured at any time during the period 18 January 2020 to the date of commencement under a contract of insurance with Lloyd’s that provided cover for business interruption under one of four policy wordings; and

(2) suffered interruption or interference to the business conducted by a named insured occurring consequent upon the COVID-19 pandemic.

21 Each of the four policy wordings have the same relevant insuring clause, being an infectious disease clause, which responds to interruption to or interference with the business because of the “outbreak of a notifiable human infections or contagious disease occurring within a [20 kilometre] radius of the Situation” (Lloyd’s further amended statement of claim (Lloyd’s FASOC) (at [13(d), (e)])).

22 There are 77 individual relevant Lloyd’s policies that apply to 110 insured locations. In total, 46 businesses (43 plus three “late” registrations) responded to the Court’s notice. Of those 46 registrants, 44 recorded in their registrations that they had suffered loss of the kind pleaded in the Lloyd’s FASOC.

B.3 IAL and Hollard Class Actions

23 By their respective originating applications filed in 2021, the applicants identified the group members as being persons who or which:

(1) were named as an insured under a contract of insurance with IAL/Hollard which contained a reference to the Quarantine Act 1908 (Cth) (Quarantine Act) in force at any time during the period from 19 January 2020 to the date of commencement;

(2) operated a business in any part of Australia during the period from 19 January 2020 to the date of the commencement which experienced interruption or interference because of SARS-CoV-2 and/or COVID-19 (and/or restrictions imposed by Commonwealth, State or Territory governments and public authorities in connexion with SARS-CoV-2 and/or COVID-19); and

(3) have not, as at the date of commencement of this proceeding, been paid by IAL/Hollard, under a relevant policy, the full amount of any losses resulting from that interruption or interference.

24 There were 1,480 registered interested group members in the IAL class action and 1,255 registered interested group members in the Hollard class action as at the nominated registration date. A further 35 “late” registrations in the IAL class action and 31 in the Hollard class action were received.

B.4 The Declassing Applications

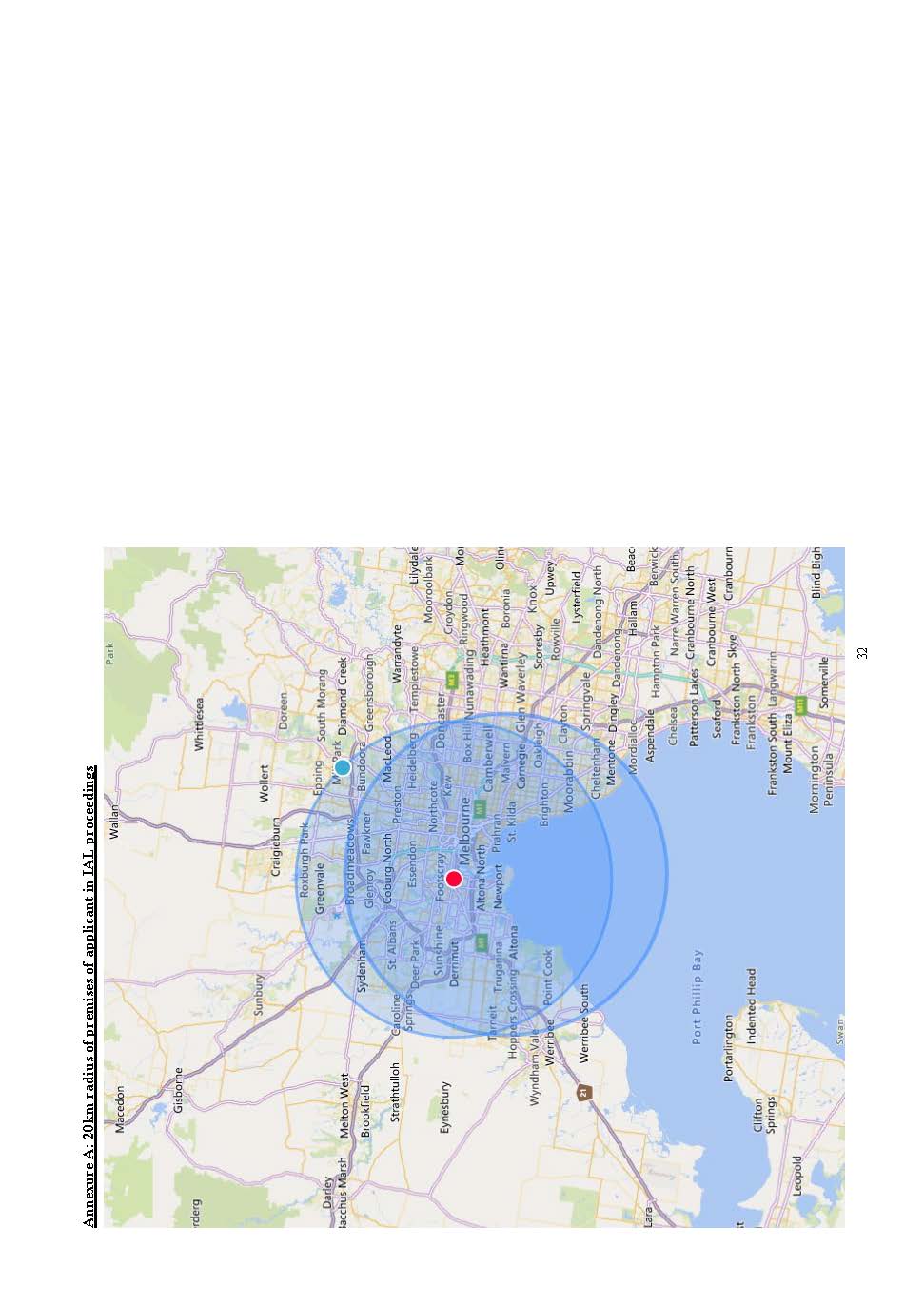

25 As noted above, the present reasons involve the determination of “declassing” applications brought in relation to each of the four class actions.

26 I will turn shortly to the precise way in which each of the insurers put their argument that the relevant class action be declassed, but shorn of unnecessary complications, the primary contention is that test cases (including what I describe below as the Second Test Case) resolved all common issues in each of the class actions and this Court should now declass and leave all residual issues to be determined pursuant to internal claims processes set up by the insurers which, it is asserted, would facilitate the resolution of the claims of the insureds, including all group members, quickly, cheaply and fairly.

27 Before coming to the details of each of the individual applications and the individual bases upon which each of the insurers put their argument, it is convenient to turn initially to the principles attending resolving applications to declass under s 33N of the FCA Act.

C DECLASSING APPLICATIONS GENERALLY

28 Section 33N of the FCA Act is in the following terms:

33N Order that proceeding not continue as representative proceeding where costs excessive etc.

(1) The Court may, on application by the respondent or of its own motion, order that a proceeding no longer continue under this Part where it is satisfied that it is in the interests of justice to do so because:

(a) the costs that would be incurred if the proceeding were to continue as a representative proceeding are likely to exceed the costs that would be incurred if each group member conducted a separate proceeding; or

(b) all the relief sought can be obtained by means of a proceeding other than a representative proceeding under this Part; or

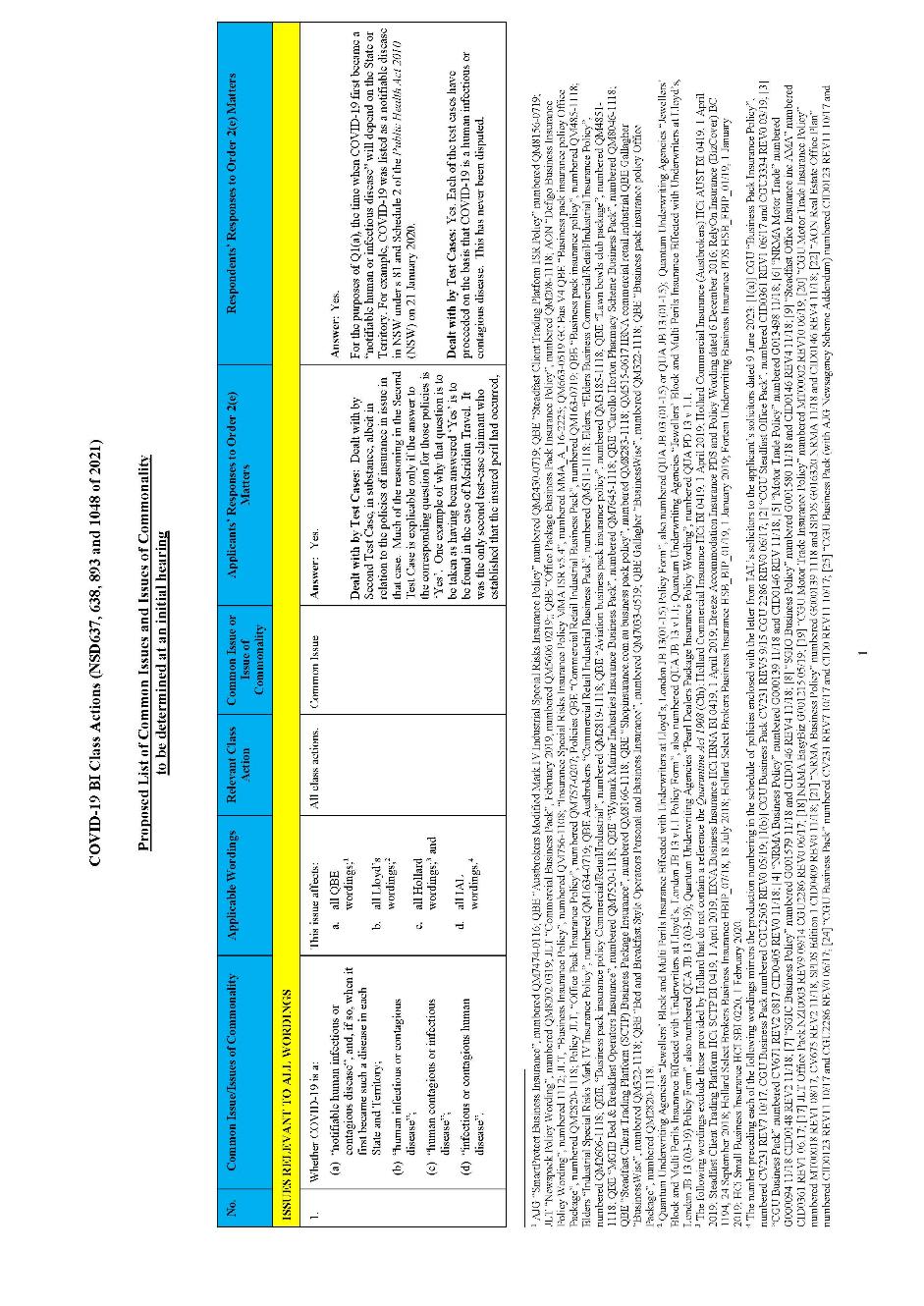

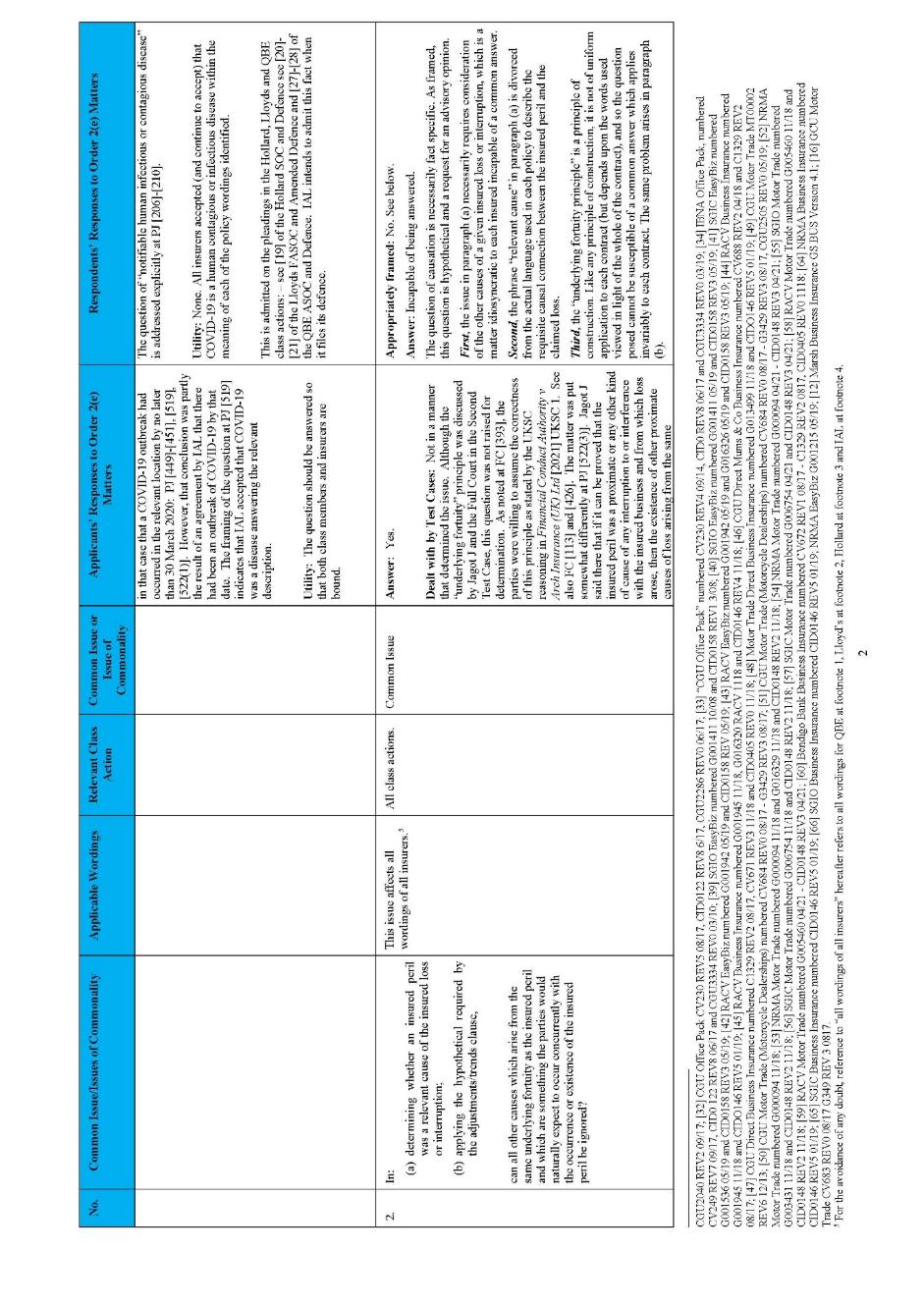

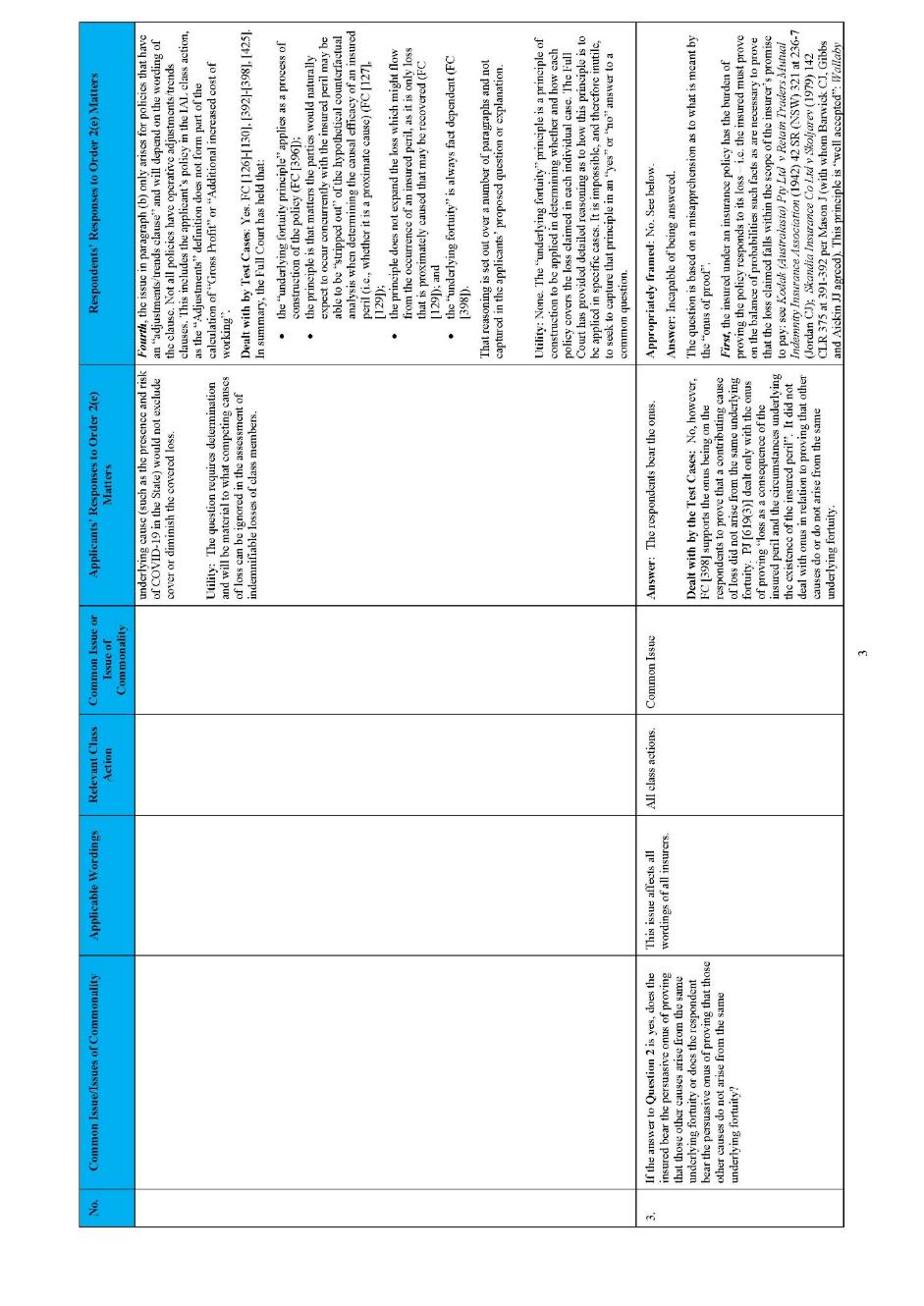

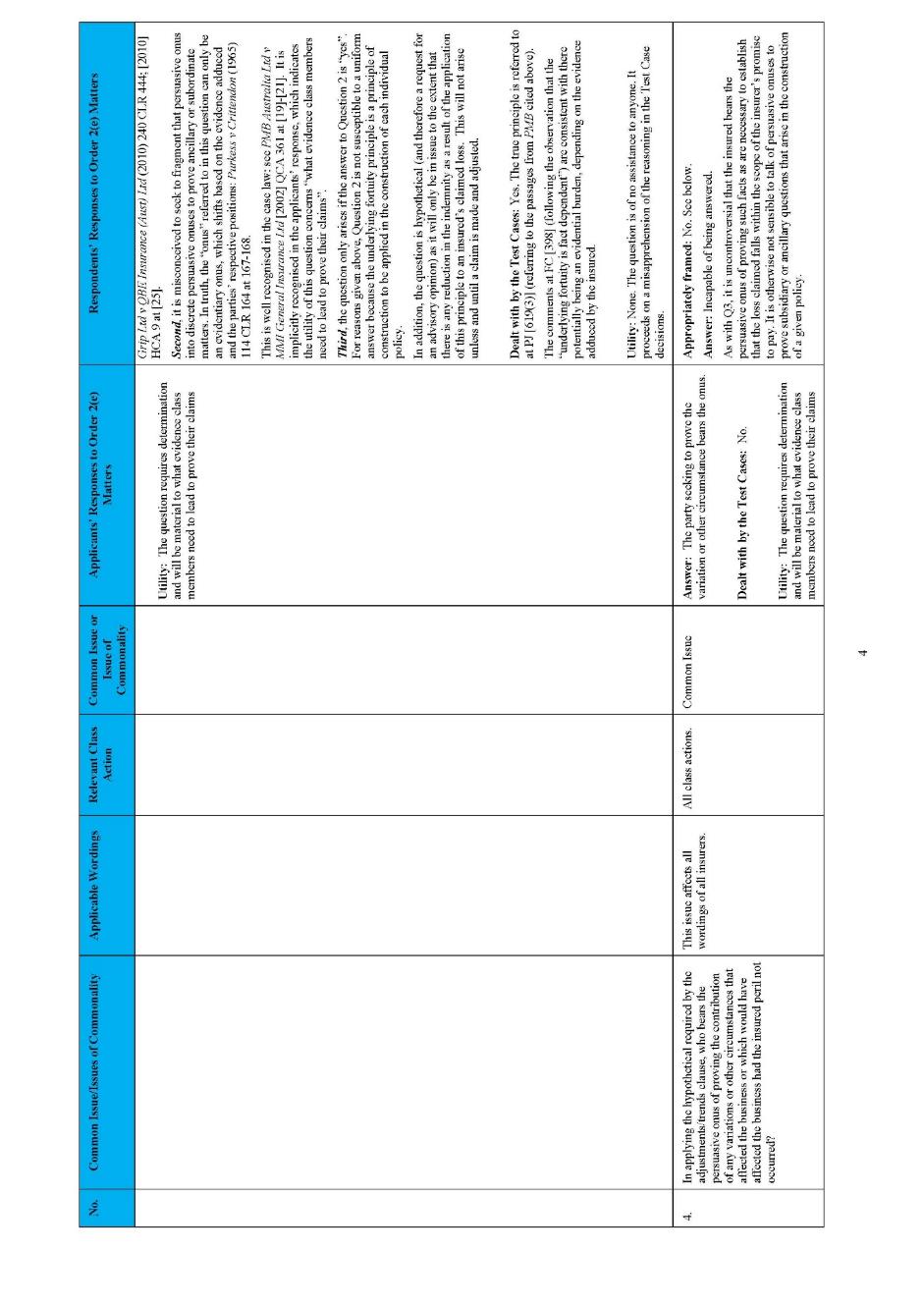

(c) the representative proceeding will not provide an efficient and effective means of dealing with the claims of group members; or

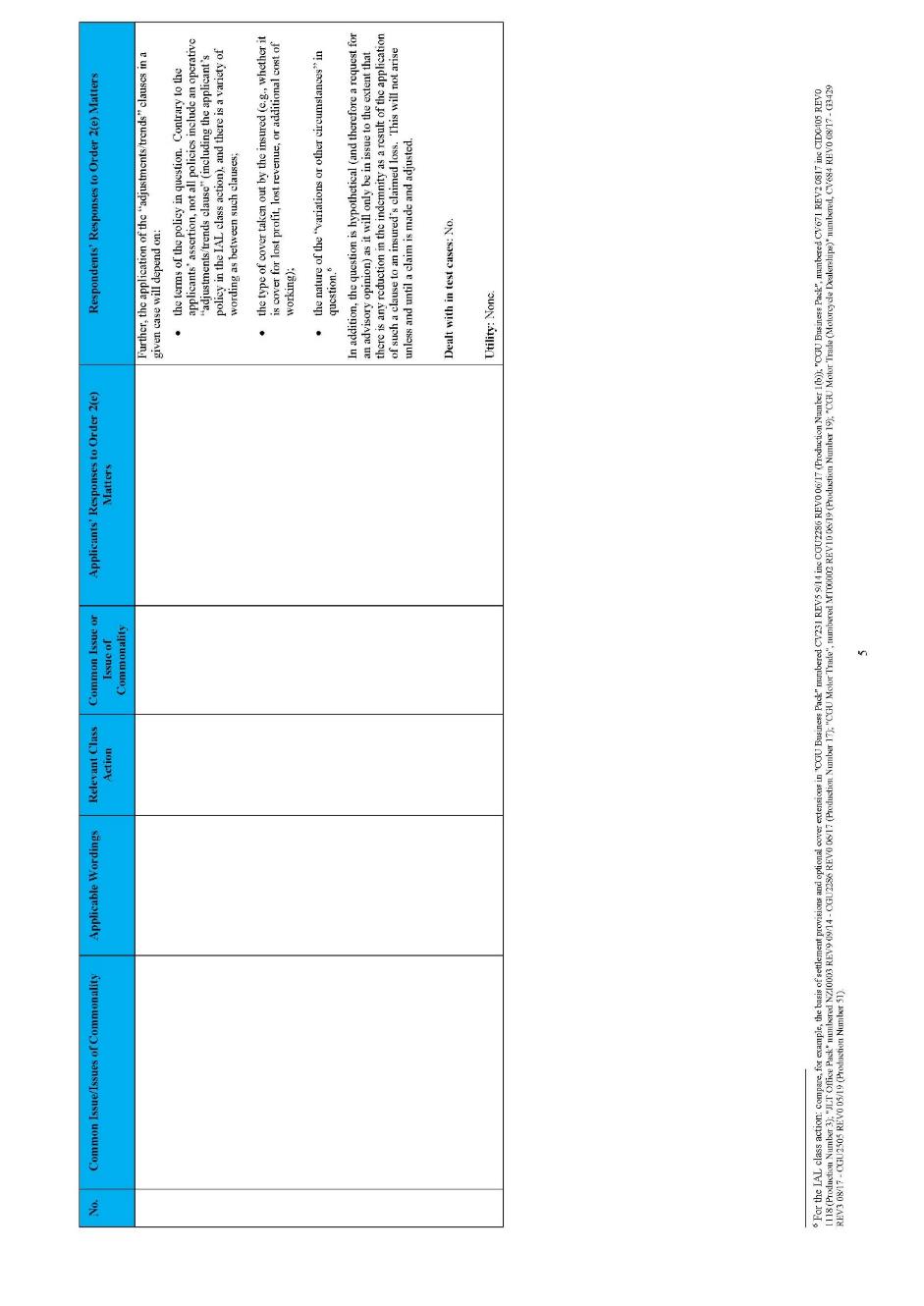

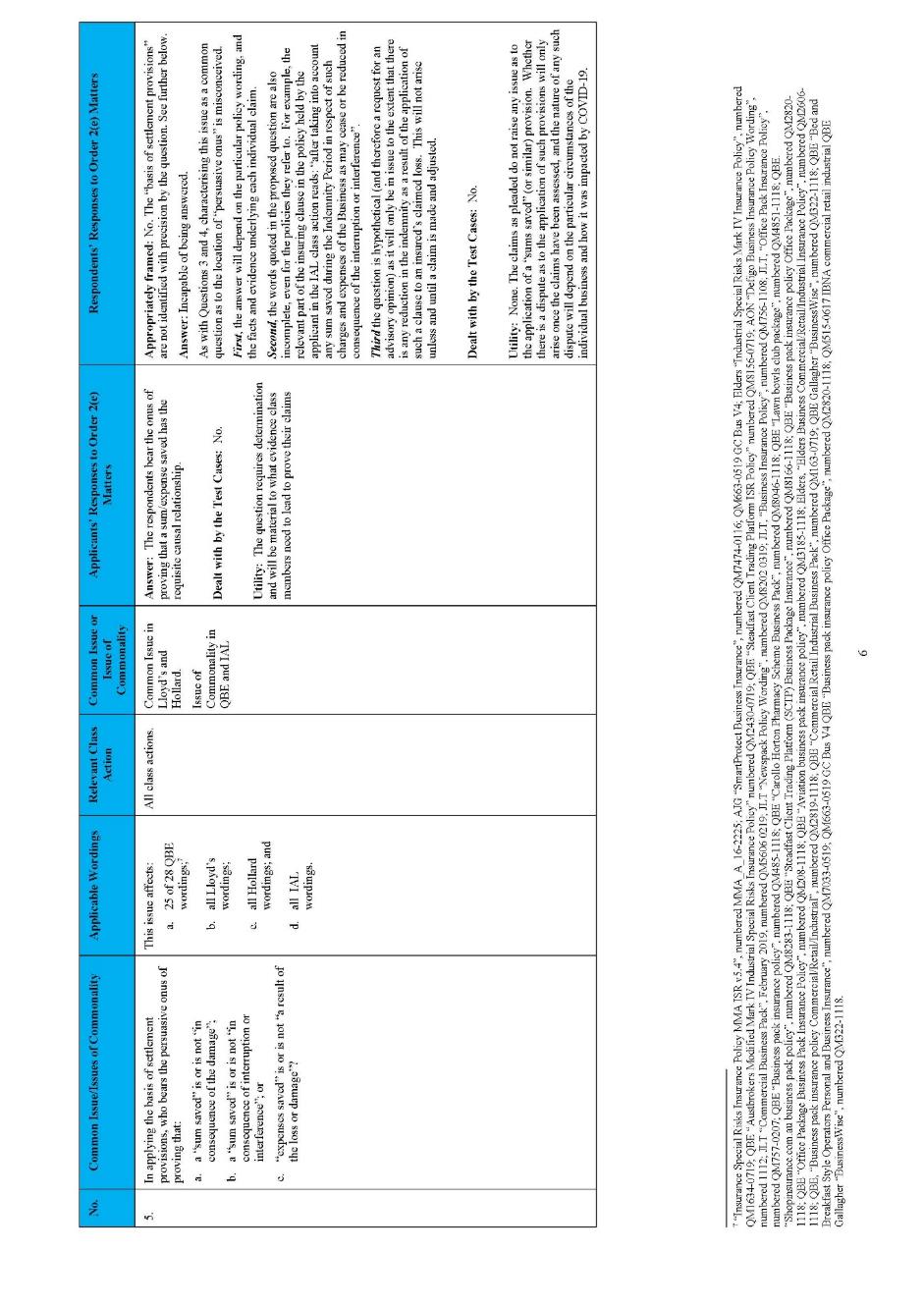

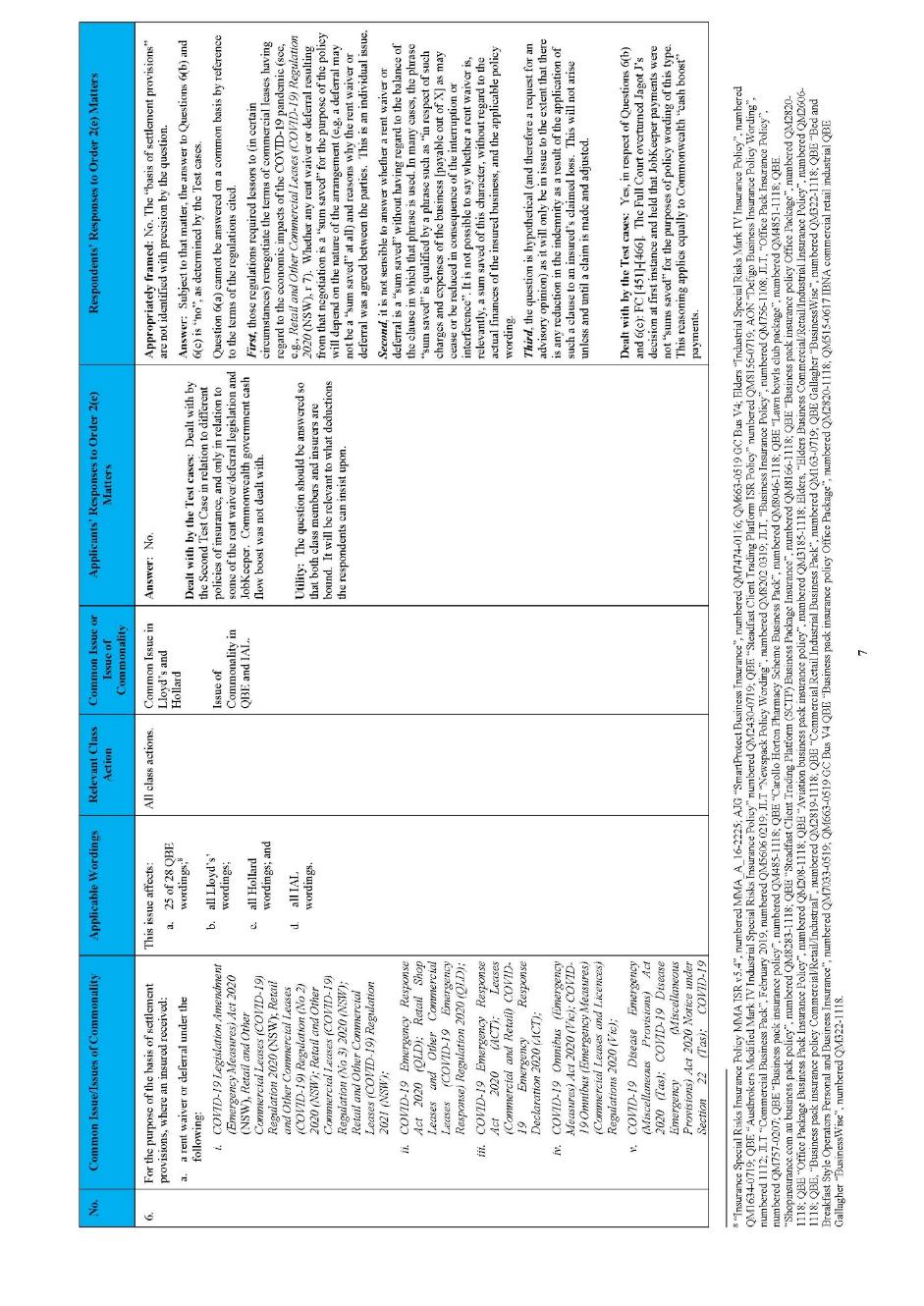

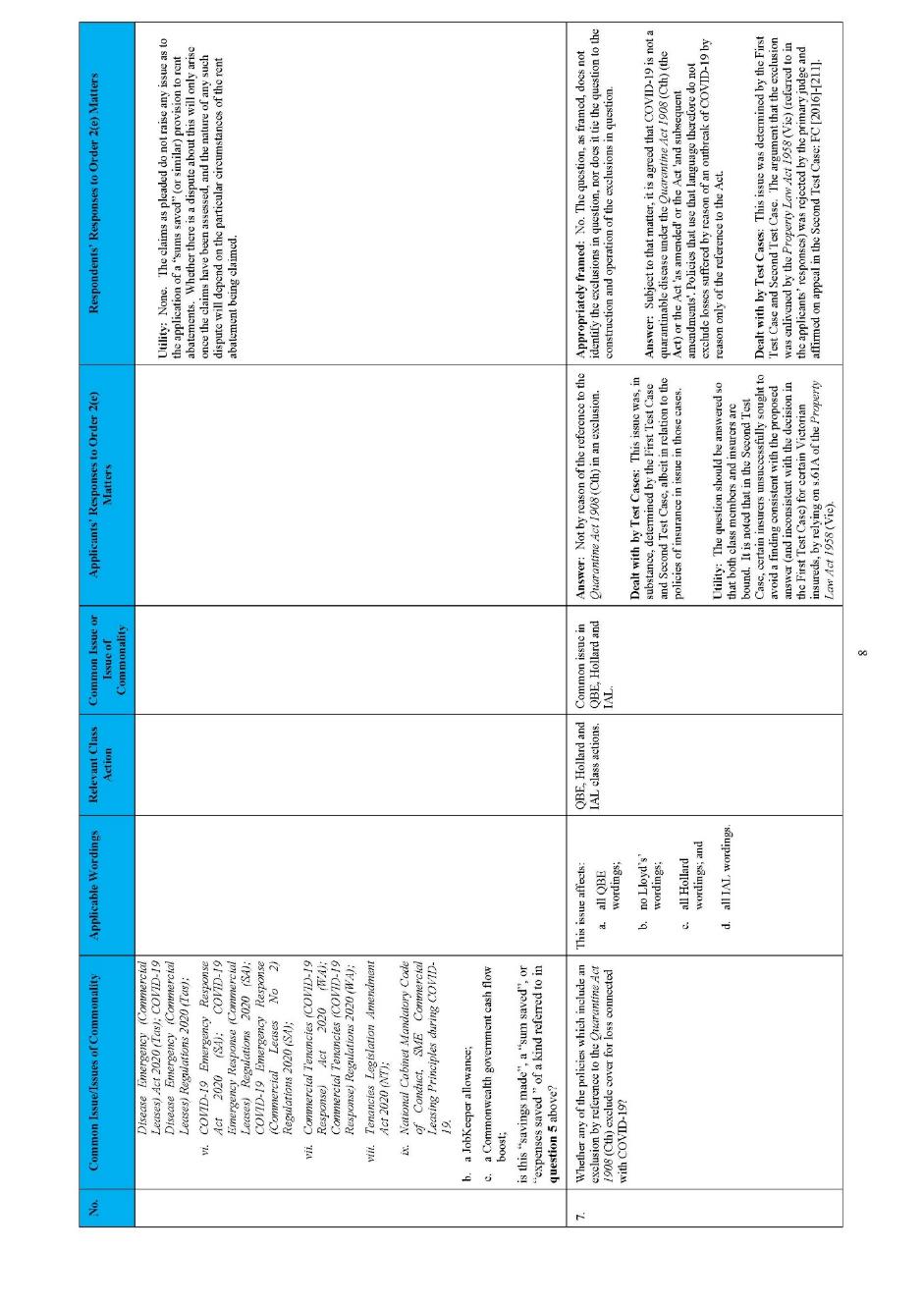

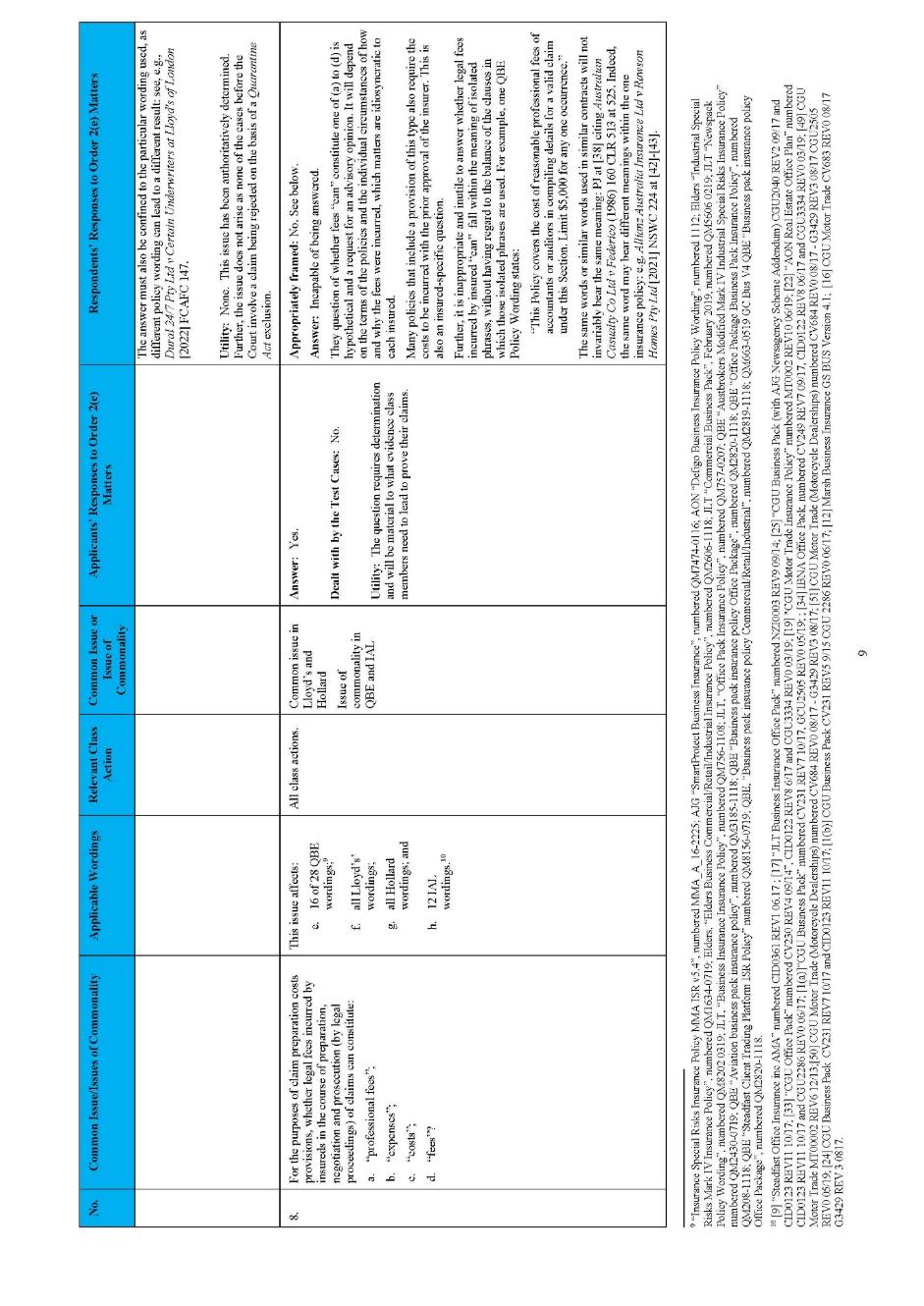

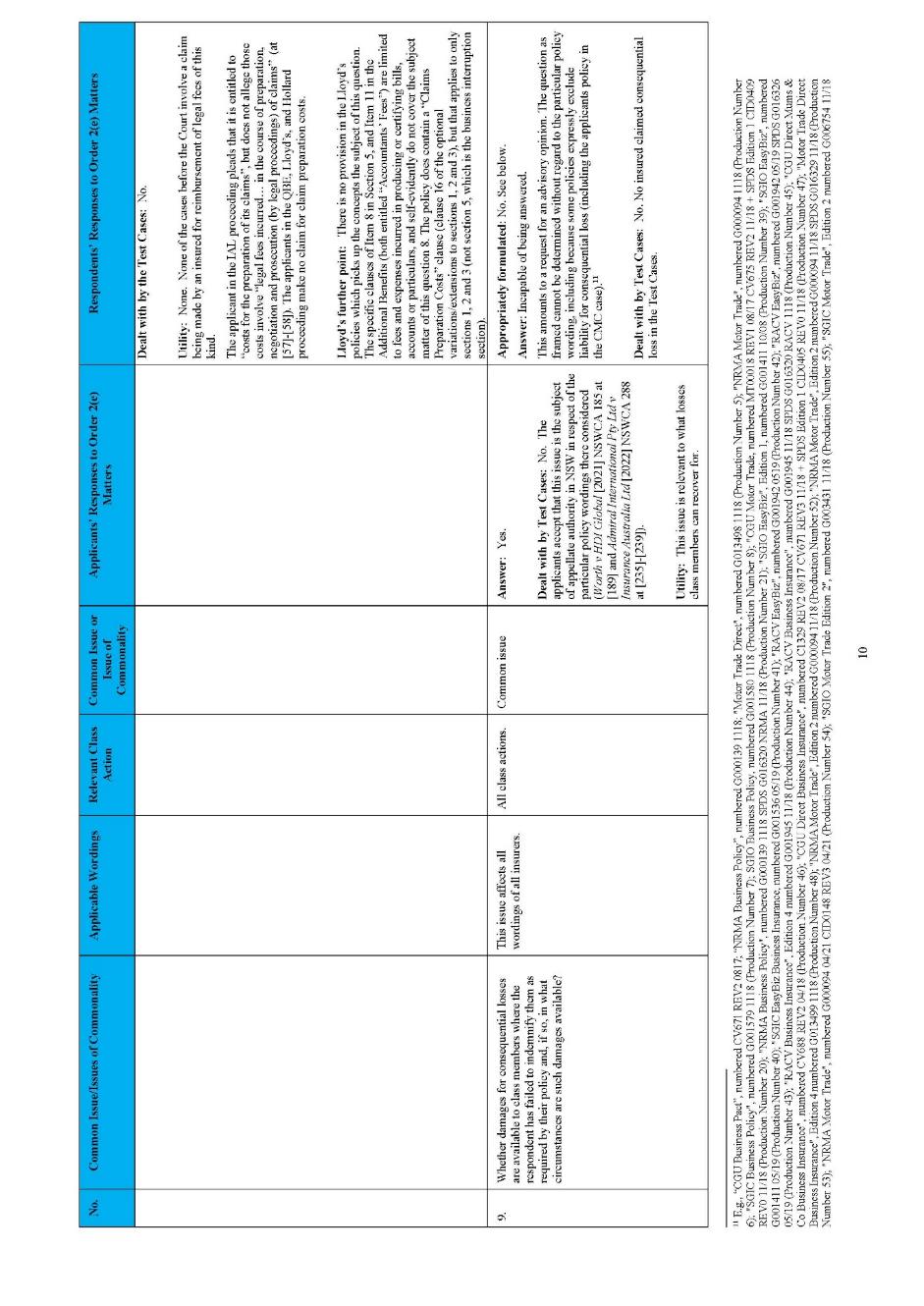

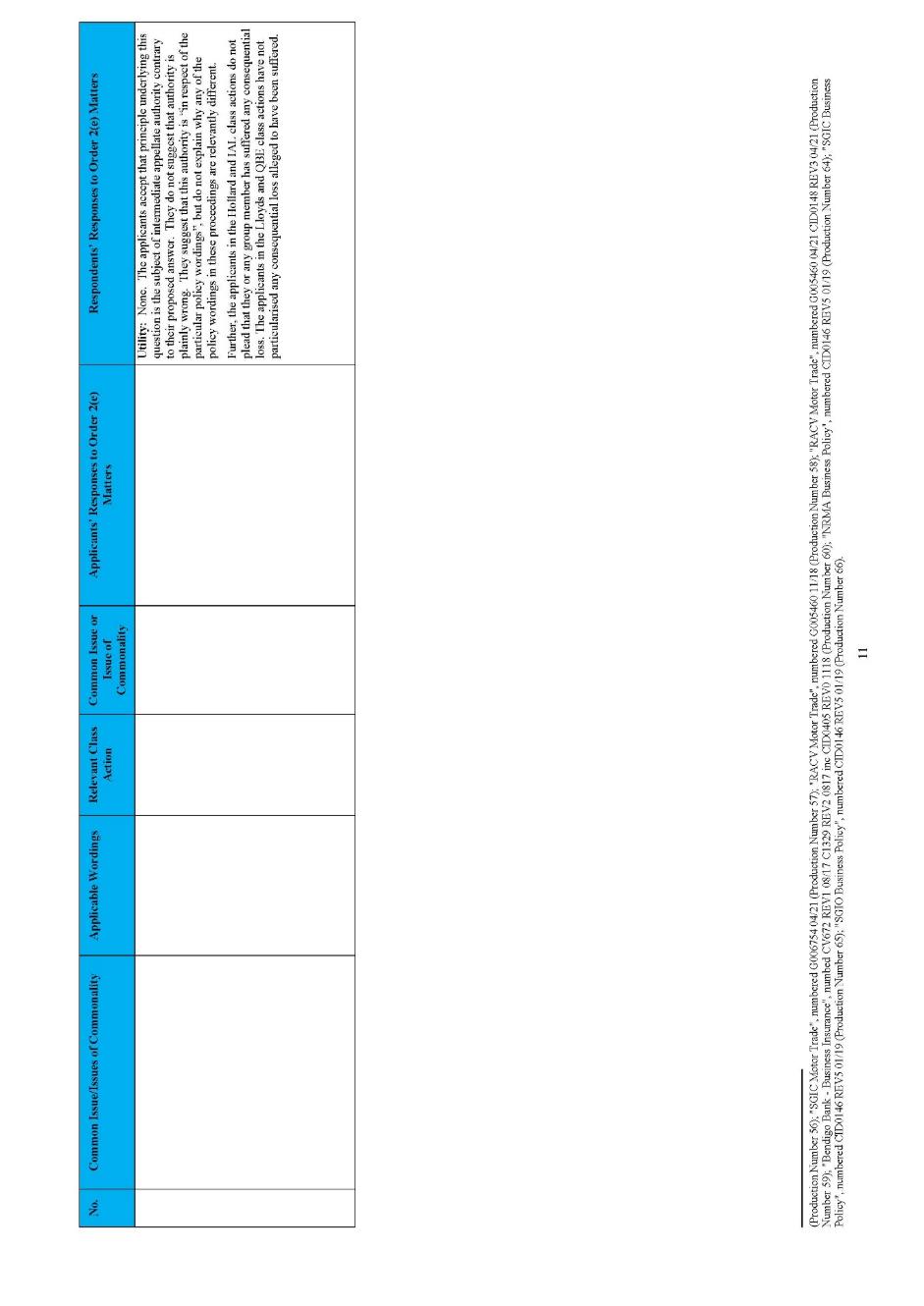

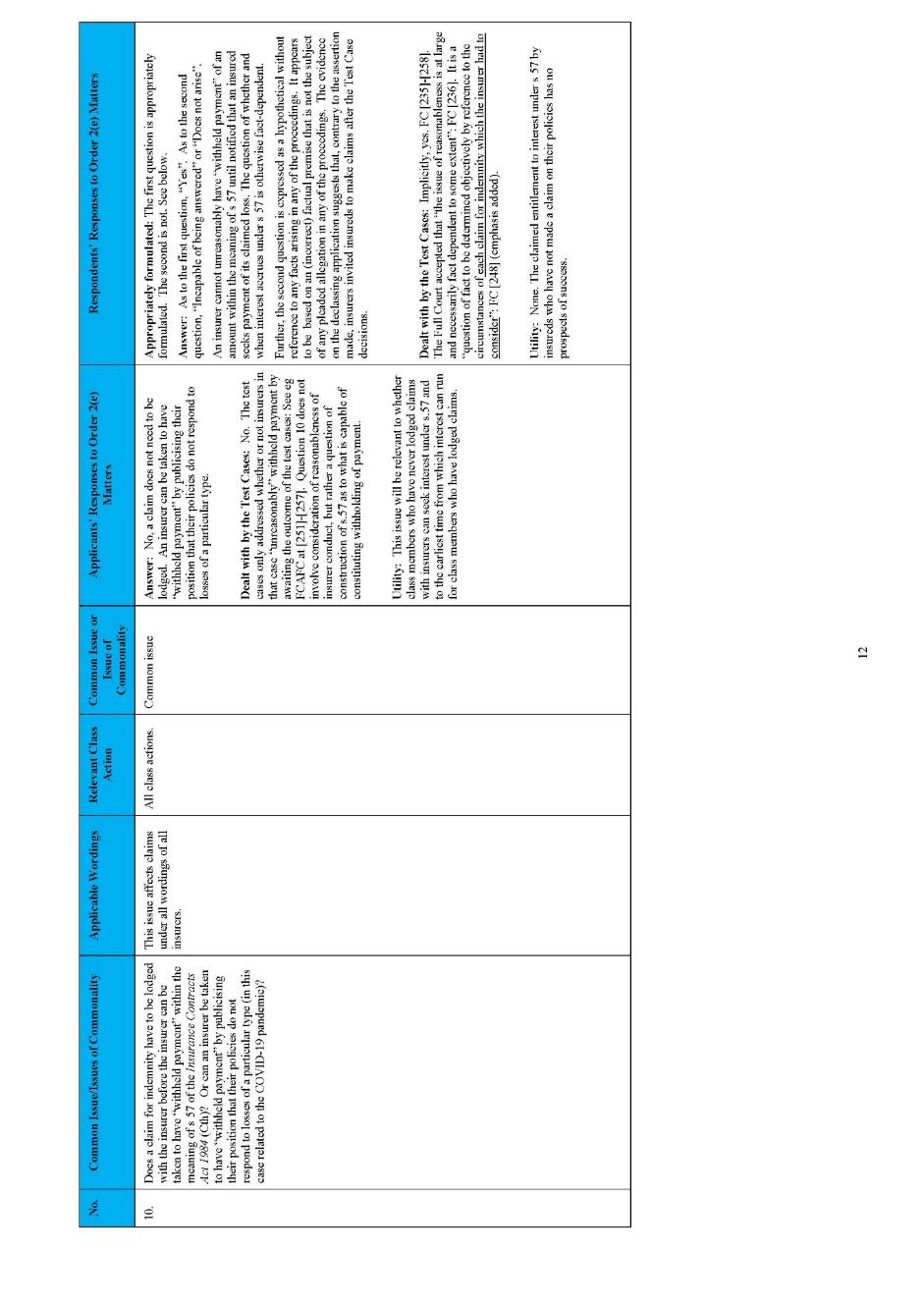

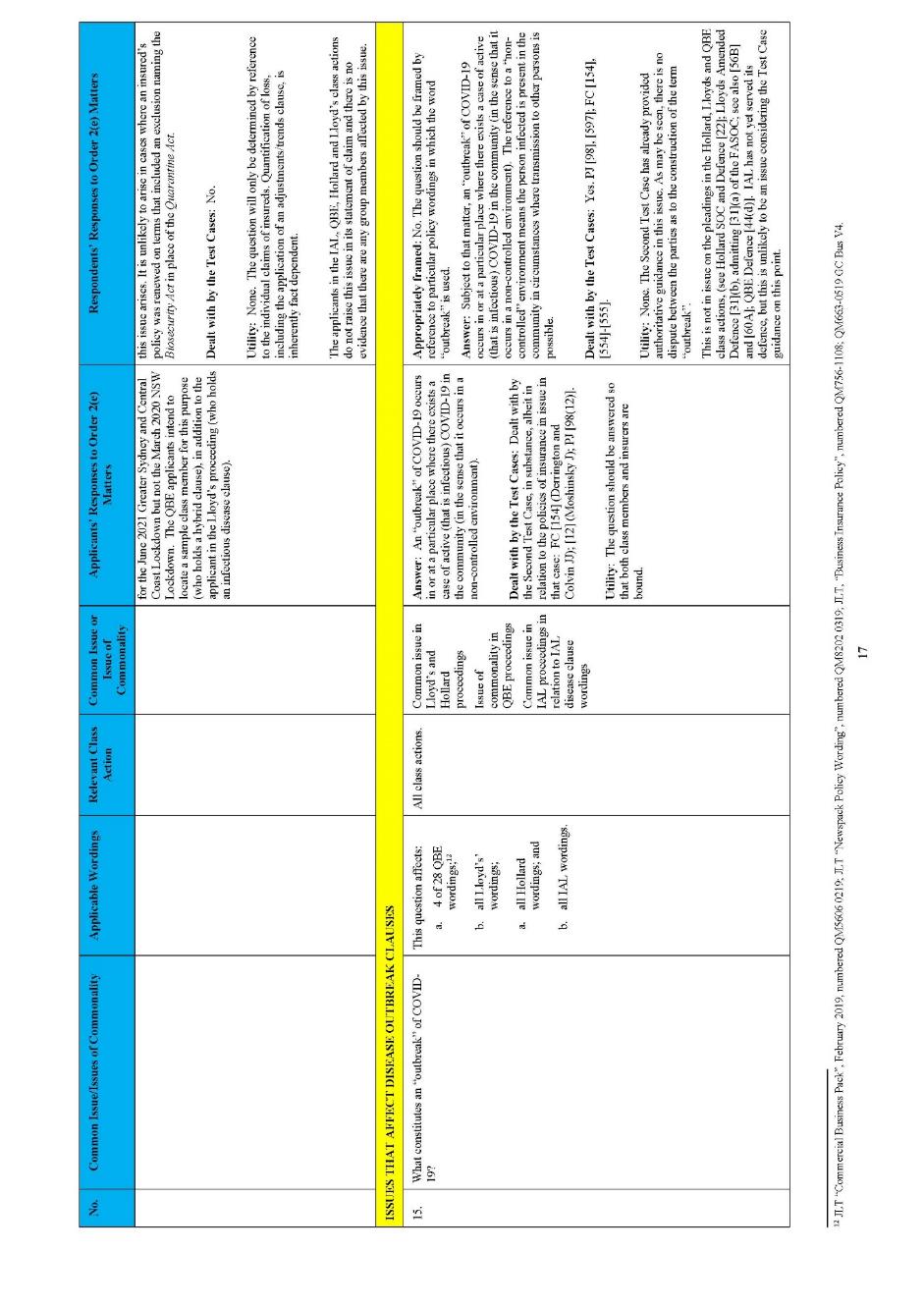

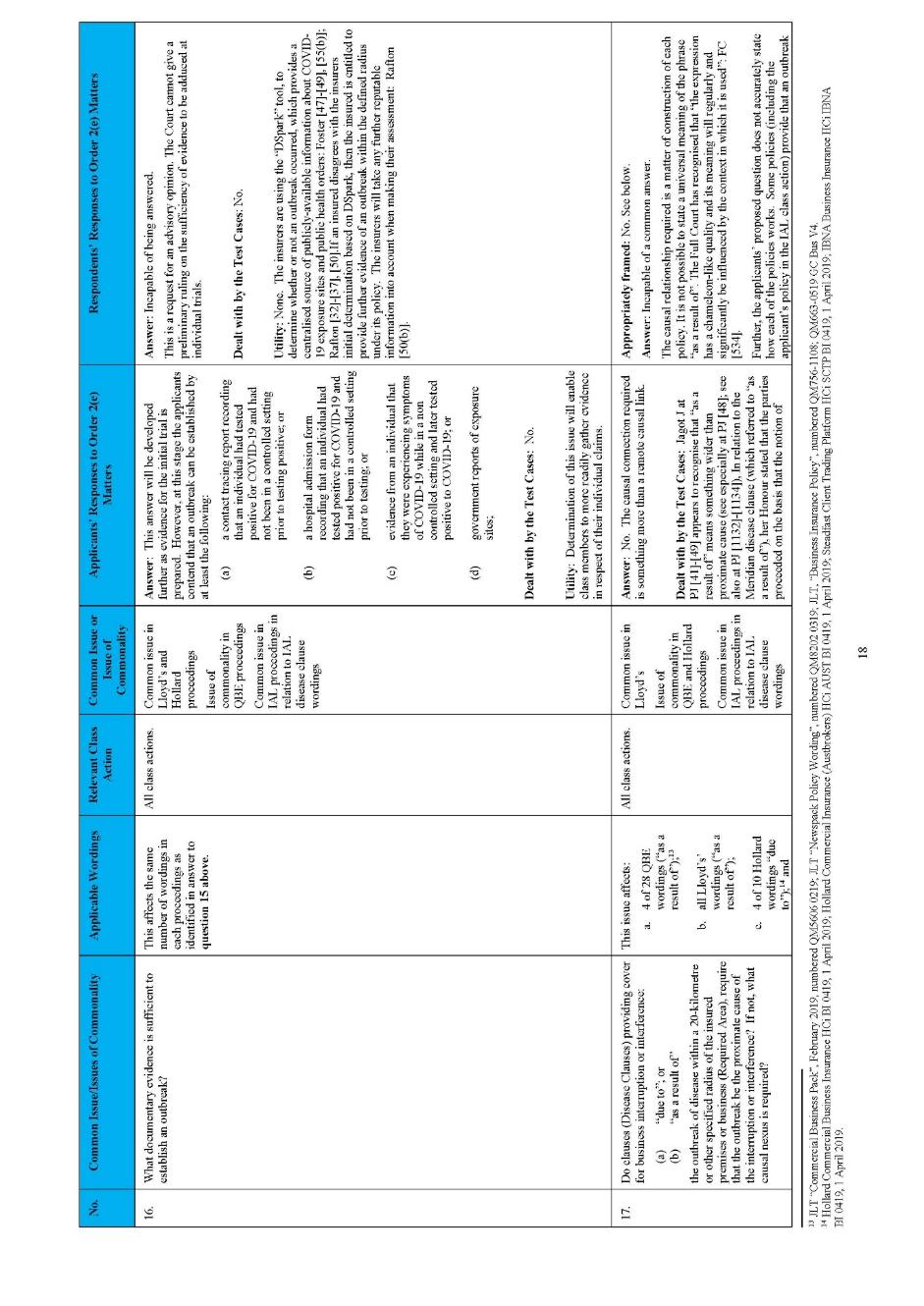

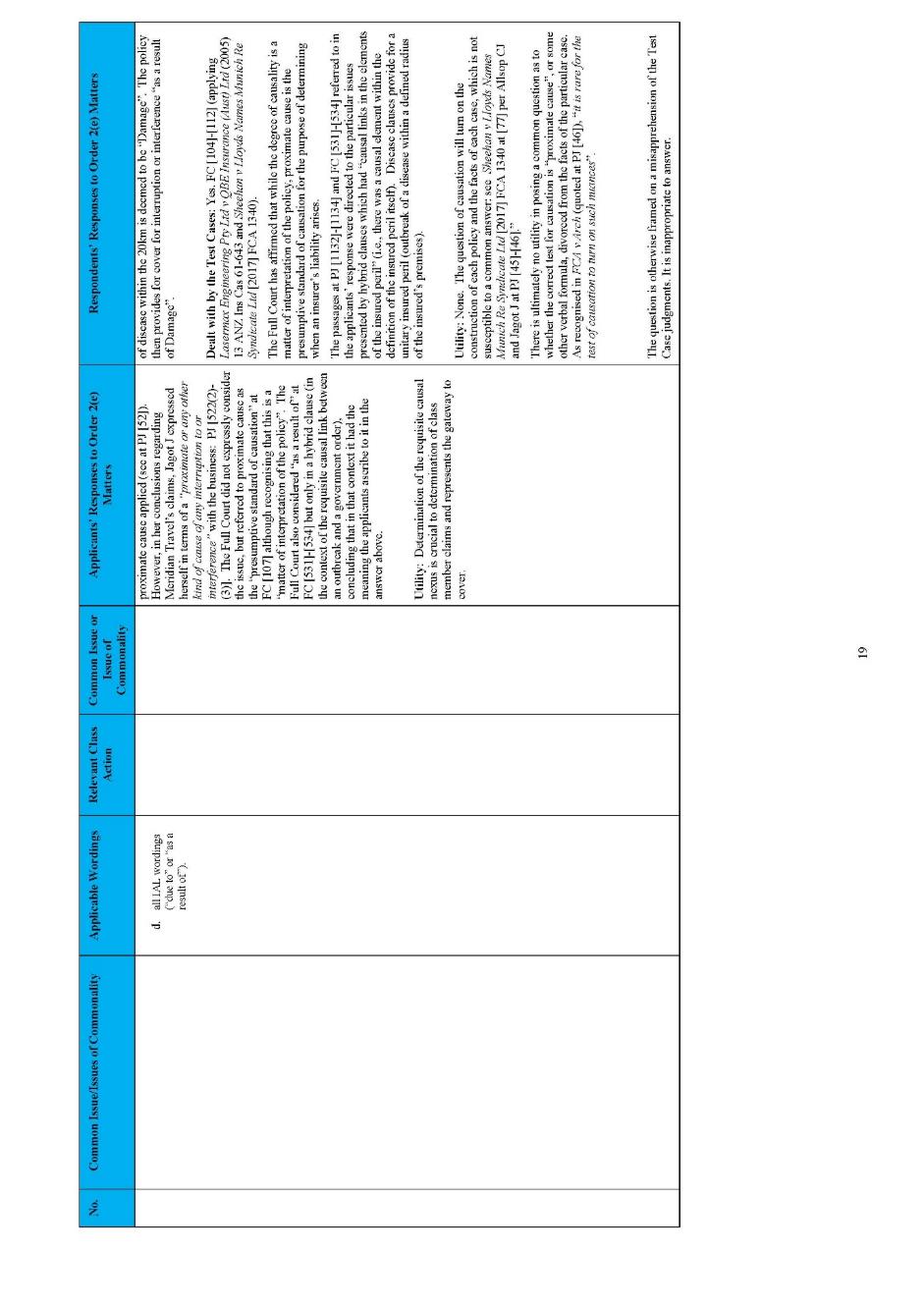

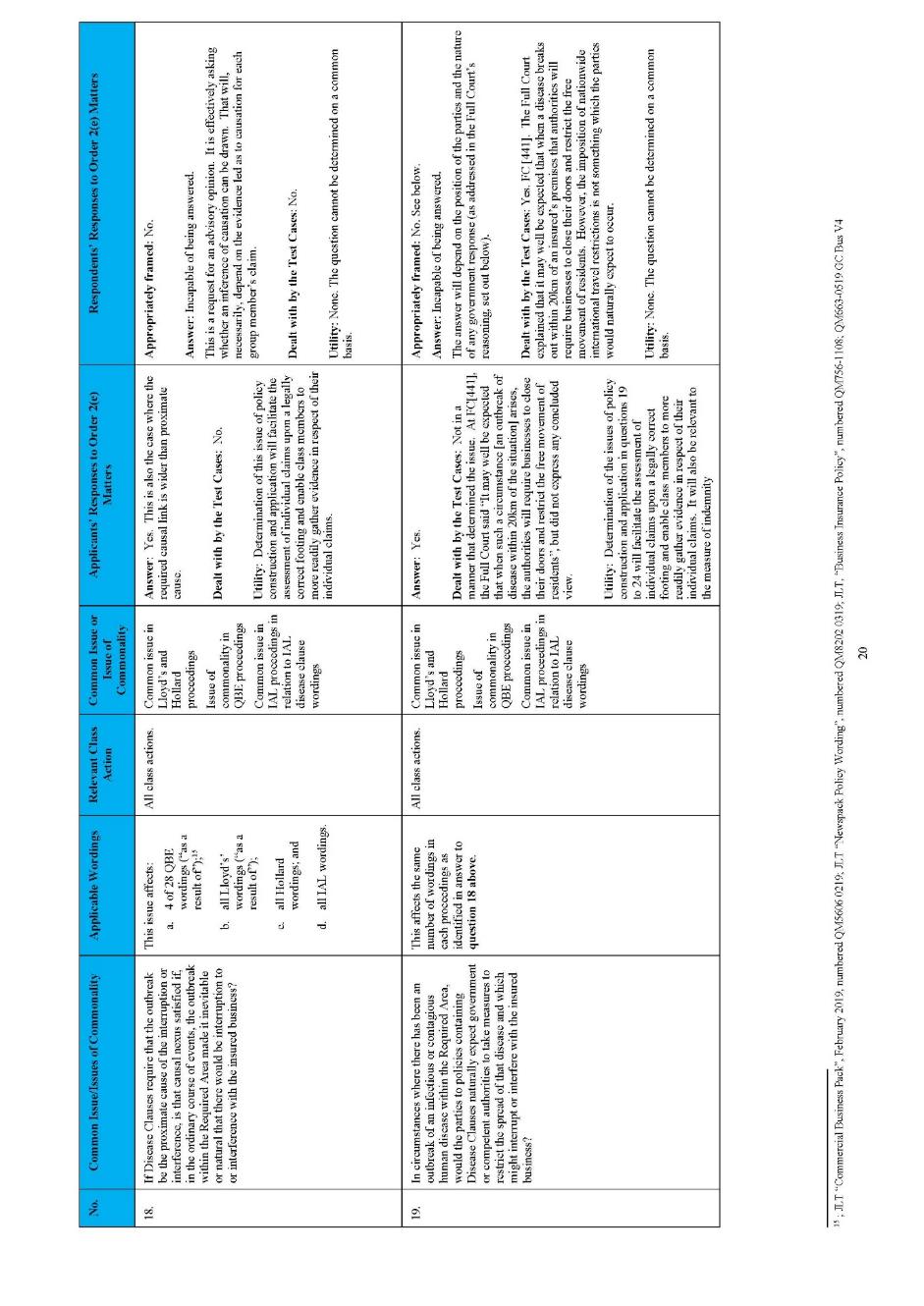

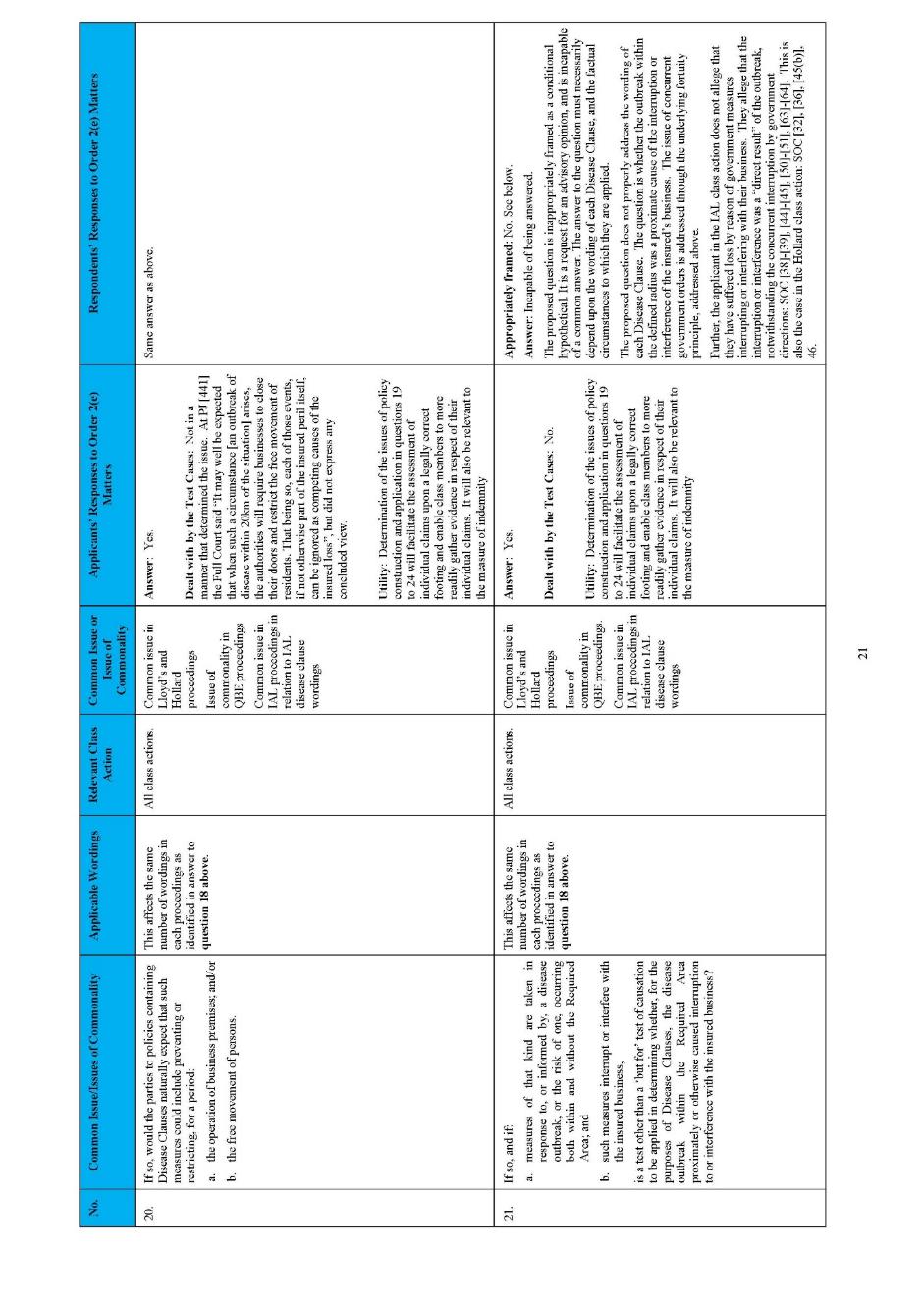

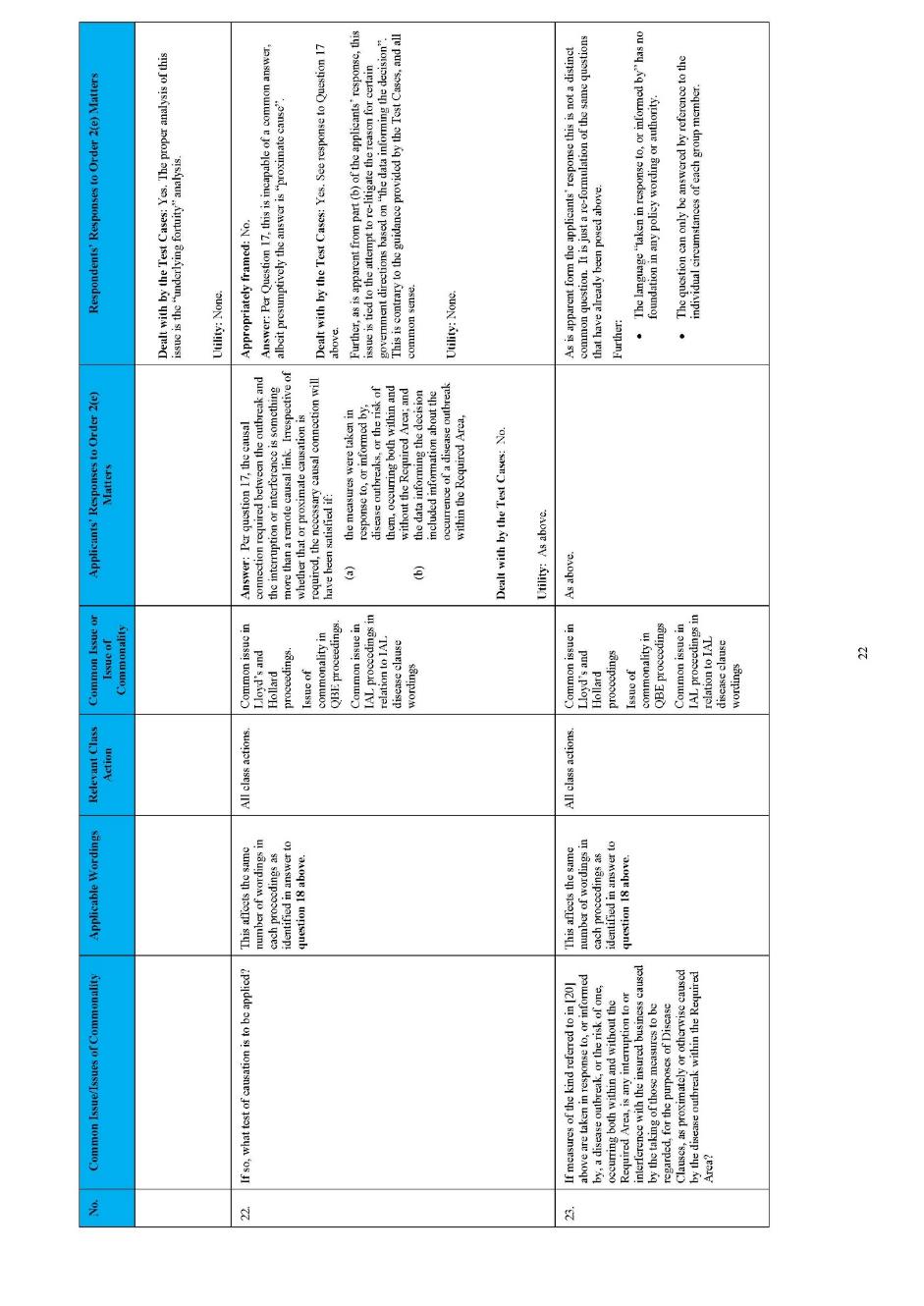

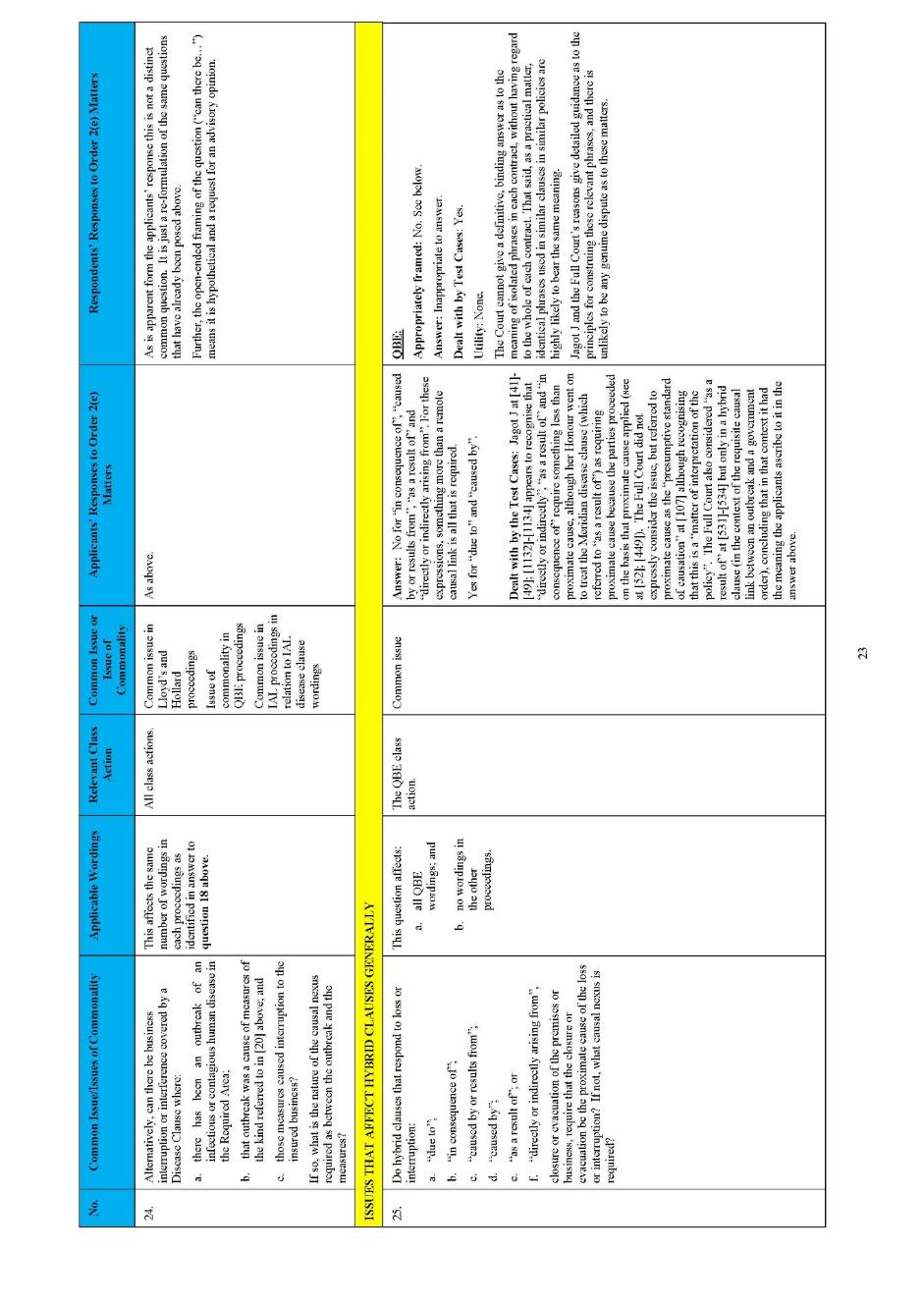

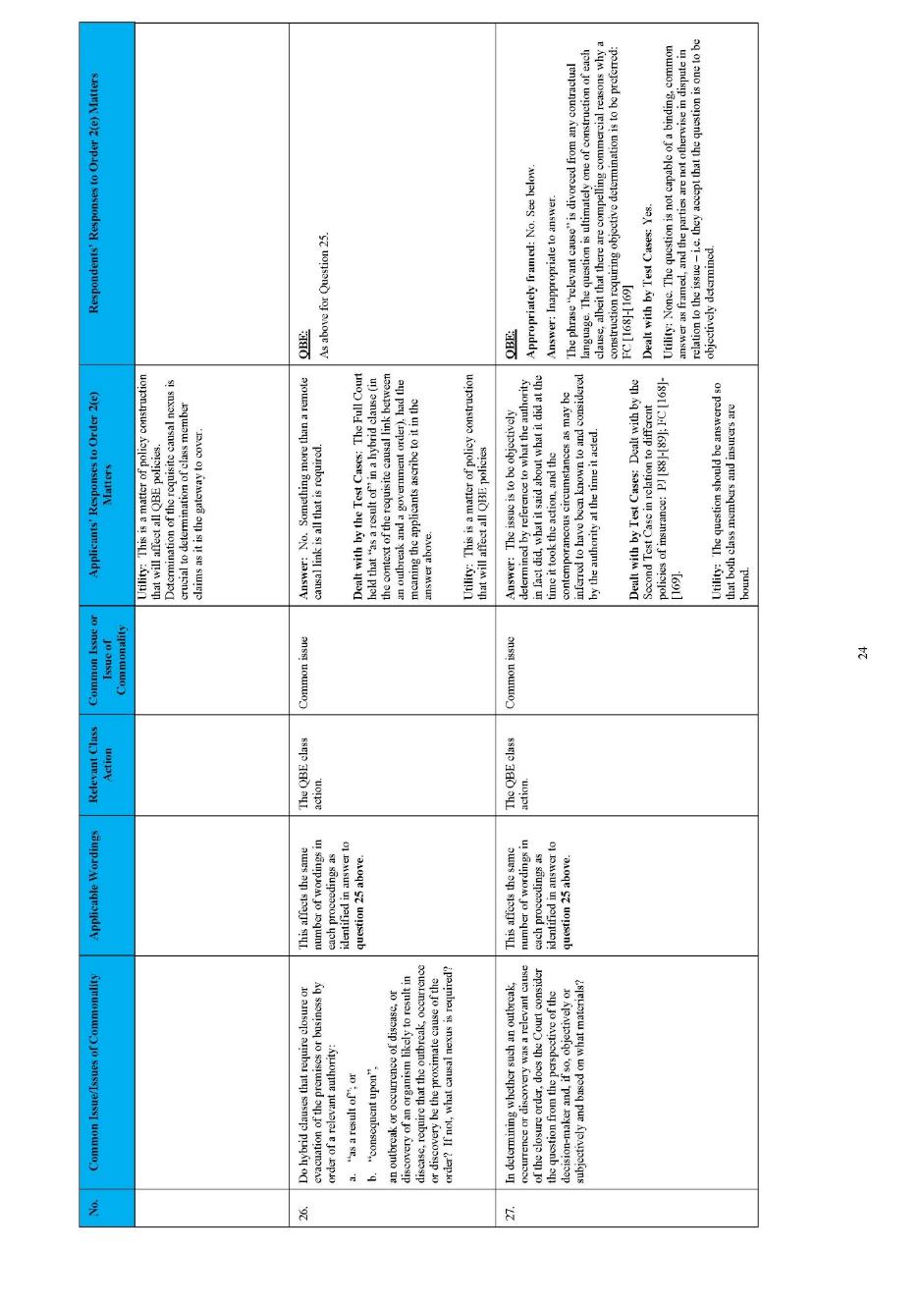

(d) it is otherwise inappropriate that the claims be pursued by means of a representative proceeding.

(2) If the Court dismisses an application under this section, the Court may order that no further application under this section be made by the respondent except with the leave of the Court.

(3) Leave for the purposes of subsection (2) may be granted subject to such conditions as to costs as the Court considers just.

29 As the arguments developed on these applications, the insurers contend that I ought to be satisfied that it is in the interests of justice to declass the proceedings because all the following grounds are established on the evidence or, alternatively, one or two of them:

(1) the costs that would be incurred if the proceedings were to continue as representative proceedings are likely to exceed the costs that would be incurred if each group member conducted a separate proceeding (Costs Ground);

(2) all the relief sought can be obtained by means of a proceeding other than a representative proceeding under Pt IVA (Individual Proceeding Ground);

(3) the representative proceedings will not provide an efficient and effective means of dealing with the claims of group members (Efficiency Ground); or

(4) it is otherwise inappropriate that the claims be pursued by means of a representative proceeding (Alternative Ground).

30 As was explained by the Full Court in ISG Management Pty Ltd v Mutch [2020] FCAFC 213; (2020) 385 ALR 146 (at 150–151 [17] per White, Lee and SC Derrington JJ), it is important not to elide the nature of the task the Court is undertaking in dealing with the s 33N enquiry, which logically involves three steps:

First, whether or not any or all of the matters specified in s 33N(1)(a) to (c) (the Costs Ground and/or the Individual Proceeding Ground and/or the Efficiency Ground) are made out; secondly, consideration as to whether there was another, that is, different reason why it is inappropriate that the claims be pursued by means of a class action (that is, whether the Alternative Ground is made out); and thirdly, if one or other of the grounds are made out whether, because of that established ground or grounds, the primary judge should reach a level of satisfaction that it is in the interests of justice to declass the proceeding.

31 Further, as the Full Court further explained (at 151 [20]), the reason why it is important not to elide the distinct aspects of a s 33N application is that such an elision can obscure the nature of the preliminary findings and ultimate decision called to be made by the exercise of the discretion.

32 After determining whether one or more of the grounds called in aid by the insurers are made out (which findings demand a unique outcome), I then turn to the logically subsequent question as to whether “because” of the ground or grounds I have found made out, I have reached the state of satisfaction that the interests of justice warrant declassing.

33 This determination involves “a degree of subjectivity” such that the decision could, in a “broad sense” be described as a discretionary decision: Coal and Allied Operations Pty Limited v Australian Industrial Relations Commission [2000] HCA 47; (2000) 203 CLR 194 (at 205 [20] per Gleeson CJ, Gaudron and Hayne JJ); Minister for Immigration and Border Protection v SZVFW [2018] HCA 30; (2018) 264 CLR 541 (at 563 [49] per Gageler J). This is reinforced by the subsection providing that “the Court may” make a declassing order; the word “may” suggesting that the Court can make a declassing order “at the discretion of the … Court” (Acts Interpretation Act 1901 (Cth), s 33(2A)).

34 Despite a faintly pressed contention made on behalf of Hollard that this approach did not reflect the appropriate test (for reasons which were undeveloped), there was no real dispute as to the correctness of the approach mandated by the Full Court in Mutch.

35 Although, as it turns out, it is possible to resolve the substance of this application on a relatively narrow ground, for completeness, it is appropriate I record the precise way that each of the insurers put their application.

C.1 QBE Class Action

36 QBE relies upon each of the s 33N grounds.

37 In relation to the Costs Ground, QBE apparently submits that the costs of continuing as a class action are likely to exceed those of hypothetical separate proceedings for three reasons (although it is evident each of these reasons more properly relate to the Efficiency Ground).

38 First, the only real common issues between QBE and its insureds have been resolved authoritatively by the test cases. To the extent that the applicants seek to keep some of those issues alive in the proceeding, they are an attempt to re-litigate aspects of those test cases (and, I infer, this will mean unnecessary costs are incurred).

39 Secondly, the only real areas of potential dispute between QBE and group members that are left outstanding after the test cases are issues of causation and loss and any individual defences that may be available to QBE. These are issues which QBE says require individualised analysis of each group member’s circumstances and which cannot be resolved at any initial trial of the applicants’ claims.

40 Thirdly, QBE makes the point that a group member, with carriage of their own claim in a separate proceeding, is necessarily likely to be able to prosecute that claim in a more efficient and targeted fashion, than will the representative applicants who cannot have the same degree of familiarity with every group member’s claim.

41 Regarding the Individual Proceeding Ground, the third point (mentioned in the preceding paragraph) was apparently called in aid and QBE further submits the relief sought in the class action consists of declarations, damages, interest, and costs. QBE states that all such relief can be obtained by proceedings other than representative proceedings.

42 But, as was accepted in oral address by senior counsel for QBE, the real arguments related to the other two grounds.

43 In terms of the Efficiency Ground, QBE asserts the QBE class action is likely to be neither an efficient, nor an effective, means of dealing with group member claims, when compared with the alternatives. To this end, QBE states that it is unlikely that an initial trial of this proceeding would be conducted and determined within the next 12 months. Following any initial trial, QBE submits, “it is conceivable, if not likely, that there would then follow appeals as to any common questions”. It is only after that time, that individual group member claims would fall for determination. QBE asserts the operation of an ordinary claims assessment process is liable to be far more efficient.

44 As to the Alternative Ground, QBE submits that it is otherwise inappropriate that the claims be pursued by means of a representative proceeding. This submission is premised on arguments relating to the re-litigation of matters which have been determined and “a lack of federal jurisdiction over some or all group member claims” (although it was again accepted in oral submissions by QBE that there must have been more than seven claims at the time the QBE class action commenced and it was licitly commenced as it passed through the s 33C and s 33K “gateway” provisions).

C.2 Lloyd’s Class Action

45 Lloyd’s relies upon the Efficiency Ground and that it is “otherwise inappropriate that the claims be pursued by means of a representative proceeding”, that is, the Alternative Ground.

46 As to the Efficiency Ground, Lloyd’s adopts submissions made by Hollard (noted below) and submits there are no issues of commonality of any real substance, the determination of which will improve the efficiency of the resolution of disputes. It is not efficient, it is said, within the meaning of s 33N(1)(c), to employ the resources of the Court to administer insurance claims (or any other contractual claims) which are not and may never be the subject of dispute through a reference process of the kind contemplated. Absent any such dispute, it is doubtful that there would be a justiciable controversy grounding the Court’s (and thus any proposed referee’s) “jurisdiction”. The Efficiency Ground invites a comparison between the efficiency and effectiveness of a class action as opposed to the resolution of claims on an individual basis and a reference process of the kind contemplated is almost certain to involve the reference of large numbers of uncontroversial claims and this is “manifestly inefficient”.

47 As to the Alternative Ground, it is said to be inappropriate to employ the procedures provided under Pt IVA to administer the diverse claims of a class of persons that are parties to insurance policies (or any other form of contract) absent common issues. The powers of the Court under Pt IVA are said to be “for the purpose of facilitating the efficient resolution of common issues arising in claims of [seven] or more persons” and absent “any common issue in the claims of such of the group members as have claims, the continuation of the proceedings as a representative action constitutes a misuse of those powers”. It is further said to be unjust, and accordingly “otherwise inappropriate” to expose Lloyd’s to a litigated conflict with insureds with whom it may never have any dispute concerning their entitlement to indemnity.

48 In addition to these submissions made in the Hollard class action, and specifically relevant to the Lloyd’s class action, Lloyd’s submits that the following two factors engage the Efficiency Ground, or alternatively the Alternative Ground, and favour exercising the discretion to de-class the Lloyd’s proceeding, being: (1) the relatively small size of the group member cohort; and (2) the geographical diversity of the group members.

49 Despite previously conceding issues relating to jurisdiction, Lloyd’s withdrew this submission orally and made an argument that the Court lacked jurisdiction to deal with group member claims.

C.3 IAL Class Action

50 IAL also relies upon the Efficiency Ground and the Alternative Ground and summarises its threefold reasons as follows.

51 First, the class action has no ongoing utility as there are no substantial common issues left for determination. The claims the subject of the proceeding are claims under insurance policies, which have different terms and conditions and different types and levels of cover. To the extent those policies contain policy wording that suggest commonality, those issues were resolved by the test cases in which the applicant in the IAL class action did not seek to intervene. What is left over are questions of causation and loss, which are inherently individualised.

52 Secondly, that group members have other processes available to make claims under their policies and resolve any disputes. IAL gave extensive notification to policy holders of the existence of the test case process and its outcome, and invited claims to be submitted, well before the IAL class action was re-enlivened in late 2022. Claims by IAL’s insureds are currently being made, assessed, and adjusted in accordance with the policies, utilising the services of a third-party expert loss adjuster. To the extent there is any objection by a policy holder to the results of that determination, then that dispute will concern individualised issues of causation and loss that are inappropriate for resolution by means of a class action. Those issues are more appropriately resolved by IAL’s internal claims resolution process or the Australian Financial Complaints Authority (AFCA).

53 Thirdly, the continuation of the class action is not in group members’ interests. Due to the lack of commonality and alternate processes for claims to be resolved, the only person who will benefit from this class action is the applicant’s litigation funder. Of note is that the funder has not agreed to fund all individual assessments but only “those claims it thinks are worthwhile”.

C.4 Hollard Class Action

54 Hollard also contends the Efficiency Ground and the Alternative Ground have been made out.

55 Its submissions have already been noted above and again relate to the contention the findings of the Full Court in the Second Test Case, including findings resolving the important questions of legal principle concerning, for example, the construction of policy provisions and that there is no practical necessity for an order under s 33ZB to bind Hollard and the group members to relevant findings. The formulation and making of orders under s 33ZB will require a notification, opt-out and registration process which is, in the circumstances set out above, inappropriately burdensome and not cost efficient. Further, given the guidance provided by the test cases, there are no issues of commonality of any real substance, and it is not efficient to employ the resources of the Court to administer insurance claims (or any other contractual claims) which are not and, following the usual claims process, may never be the subject of dispute through a reference process of the kind contemplated.

56 As to the Alternative Ground, it is submitted inappropriate to administer the diverse claims of a class of persons that are parties to insurance policies (or any other form of contract) absent common issues.

57 Although relied upon as part of the arguments said to make out the Alternative Ground, another contention made by Hollard reflects arguments made by other insureds and goes to what is properly seen as a separate point. It is submitted the Court “does not have jurisdiction in respect of the proceeding because the claims under s 57 of the Insurance Contracts Act 1984 (Cth) (ICA) are colourable”. The applicant has not informed Hollard of the extent of loss it claims and therefore there are no prospects of the applicant in the Hollard class action establishing “that it has been unreasonable for Hollard to have withheld payment so as to engage s 57(2) of the ICA, and there is no other basis of jurisdiction available”.

D THE REGISTRATION PROCESS

58 The determination of these applications has had a long history. The applications first came before me for hearing approximately a year ago. After hearing extensive argument at that time, it became evident there were two matters which required further examination.

59 The first was that argument as to the utility of the class actions was of limited assistance without understanding the extent of interest of the individual insureds as to whether they wished their claims to be determined in the class actions. Put another way, there was a way of testing the submission then advanced by the insurers that it was “unfair” to group members to allow the class actions to continue and that group members would act “rationally” and therefore be “uninterested” in pursuing the class actions because they had available to them the various internal dispute mechanisms.

60 Following the hearing of extensive argument, I proposed to the parties that orders be made providing for the issue of a notice to group members informing them of their options and permitting them to register with the applicants’ solicitors if they were interested in the relevant class action continuing.

61 In the end, all parties agreed to this course and the content of the notices to group members was settled by the Court following extensive toing and froing. As Annexure A to these reasons, I set out a copy of the notice in the QBE class action as a representative example.

62 The notices set out, in a way consistent with the protective and supervisory duty of the Court to group members, the existence of the relevant class action, including the basis upon which the class action was to be funded and information concerning legal costs. The notices also provided information about the relevant internal claims processes. The notices were distributed to all group members by a variety of means which were utilised to maximise the prospect of the relevant notice reaching all group members. This notification and subsequent registration process took considerable time, partly because several insureds did not have reliable contact details for all policyholders.

63 It was important to adopt this course because while the class actions are on foot, the Court needs to protect the interests of group members and an important aspect of fulfilling this role is the mechanism chosen by the legislature (ss 33X and 33Y of the FCA Act) by which important matters relevant to group members are to be communicated to them “as soon as practicable after the happening of the event to which the notice relates”: see s 33X(5) and (6).

64 My underlying reason for requiring notification was not only to inform group members as to their rights and as to the extant applications, but I was cognisant that if there was minimal interest in group members having their claims determined in a class action then this would be a potentially determinative factor in the exercise of any discretion under s 33N.

65 As will be further discussed below, it is evident, following the completion of this registration of interest process, there is significant interest in each class action by group members. It is worth noting that if one reviews the submissions made in July 2023, any suggestions that the vast bulk of group members would reject the notion they should be involved in the class actions (because they apparently knew had an internal review mechanism available to them at no cost), is contradicted by what has happened in response to the notices.

66 The second aspect of the applications that required further clarification relates to the Efficiency Ground and arose because of the need of the class action applicants to be far more specific in identifying the common issues and issues of commonality that they say remain to be determined in the class actions.

67 In Dillon v RBS Group (Australia) Pty Ltd [2017] FCA 896; (2017) 252 FCR 150, I explained in some detail (in a way that has been the subject of discussion in a number of authorities since), the notion of a “claim” in a Pt IVA class action; how group membership comprises persons and not claims of persons; and the disparate nature of claims that can be encompassed within a class action. I also explained (at 164 [63]ff) the use of case management techniques to identify questions that went beyond strictly common questions (as that concept is used in s 33C and 33H of the FCA Act).

68 I also explained that it is well established that the Court conducts class actions in a practical manner and ensures, to the extent otherwise advisable, that at an initial trial as many questions of law and fact having a degree of commonality are decided and noted (at 164 [66]):

What this approach demonstrates is the flexibility which the extensive case management powers in s 33ZF and s 37P provide for the efficient management of class actions. I said at the outset of these reasons that the expression an “initial trial of common issues” is a misnomer. This is because experience demonstrates that in many cases of quite different types of class actions, the Court has found it expedient to not only deal with the claim of the representative applicant at the initial trial but also with common questions (properly so called) and also questions which have utility in resolving aspects of the claims of a subset of the group members, which, to adapt Gillard J’s phrase, may be called issues of commonality.

69 After referring to several authorities, I then noted (at 166–167 [75]):

The boundaries of what can be determined at the initial trial are the boundaries of the principled exercise of judicial power, being questions or facts in issue which are neither abstract nor hypothetical. Case management imperatives, procedural fairness and the mandate of the overarching purpose inform what should be determined. This approach informed the issues selected to be determined in this case …

70 Following the applicants belatedly attending to the task of comprehensively setting out the common issues and issues of commonality that they say remain to be determined, I required the respondents to provide a detailed response indicating whether the proposed question was appropriately framed; whether it was dealt with by the test cases; and whether there was utility in answering it.

71 This has proved a useful exercise and set out as Annexure B to this judgment is a schedule of the questions identified by the applicants marked MFI-3 and the principal submission made on behalf of the relevant respondent as to why that issue is insufficiently common or otherwise lacks utility.

72 Regrettably, obtaining clarity as to these two matters has significantly delayed the resolution of the declassing applications. But having identified the level of group member interest and having obtained clarity as to the remaining issues said to have a degree of commonality, a firmer basis has been established by which the Court can make an assessment as to whether, in particular, the Efficiency Ground is established, and whether the Court should proceed to declass the proceedings. I will return to both these matters below.

E THE INTERNAL REVIEW PROCESS

73 Before coming to more general relevant findings, as is evident from their submissions, each of the insurers have set up a form of internal review process. It is worth explaining the nature of these processes and, in broad terms, these processes (and their legal consequences) can be summarised as follows.

74 If a customer is dissatisfied with QBE’s response to a complaint, the customer can ask QBE to refer the complaint to the Customer Relations team or the customer can contact the team directly. As part of the complaints process, a so-called “Dispute Resolution Specialist” within Customer Relations is to conduct what is said to be an “independent” review of the customer’s complaint and will: (a) contact the customer to acknowledge receipt of the complaint by phone, email, or letter; (b) review the complaint and all relevant information; (c) update the customer on the progress of the review; (d) endeavour to provide a final decision in writing within 30 calendar days; and (e) will contact the customer if the team requires more information or the complaint requires further investigation, explain what is required, and outline the reasons for any delay. The team is to then confirm a new timeframe for the decision and is to notify the customer of their right to contact AFCA or another relevant external dispute scheme.

75 Under Lloyd’s internal dispute resolution process, there are two stages. First, Lloyd’s will respond to a customer’s complaint with a decision within 15 business days of its receipt, if Lloyd’s has all information necessary to complete the investigation. Secondly, if this decision does not resolve the complaint to the customer’s satisfaction, the complaint will be “reviewed” by Lloyd’s Australia if it falls within the Terms of Reference of the Australian Financial Ombudsman. Otherwise, it will be referred to the Complaints Team at Lloyd’s based in the United Kingdom. If the dispute remains unresolved, the customer may be referred to the Financial Ombudsman Service Limited under the terms of the General Insurance Code of Practice.

76 IAL’s internal dispute resolution process requires the dissatisfied customer to contact it about their concerns. Its consultants then attempt to resolve complaints at first instance or shortly thereafter. If the consultant is unable to resolve the concern, the customer may be referred to a manger, or the customer may request to speak to a manager. The manager will attempt to resolve the complaint as soon as possible, or within 15 days of receipt of the complaint if more information is required. If the complaint cannot be resolved speedily, the customer can ask for it to be escalated to the Customer Relations team, who will contact the customer if they require additional information or have reached a decision. Customer Relations are then to advise the customer of the progress of their complaint and the timeframe for a decision in relation to the complaint.

77 If a person is not satisfied with Hollard’s response to their complaint, it may be referred in writing to Hollard’s Internal Dispute Resolution Committee. The Committee is to acknowledge the complaint in writing within two business days of its receipt, requesting any further information if it is necessary. The Committee is then to investigate all details of the complaint; provide a written response outlining any reason for the decision; and inform the person of any action Hollard intends to take in resolution of the complaint. The Committee will respond within 30 days but may request a later response date.

78 Each of the review processes are subject to an internal review and a “appeal process” to AFCA. The rules of AFCA are in evidence. Rule A.1.2 provides:

These rules form part of a contract between AFCA and Financial Firms and Complainants. AFCA may develop Operational Guidelines setting out how AFCA interprets and applies these rules.

79 Further, Rule A.15.3 provides:

In the case of any other complaint, a Determination by an AFCA Decision Maker is final, and is binding upon the parties if accepted by the Complainant within 30 days of the Complainant’s receipt of the Determination.

If Rule A.15.3 applies, the Financial Firm may ask the Complainant to provide it with a binding release from liability in respect of the matters resolved by the Determination, provided the release:

a) is limited to the matters dealt with in the Determination,

b) is consistent with the Determination; and

c) is provided to the Complainant within a timeframe specified by AFCA. If a Financial Firm asks a Complainant to provide it with a binding release in accordance with this rule, the Complainant must complete the release. The release shall be effective from the date on which the Financial Firm fulfils all of its obligations under the Determination.

80 Despite some earlier uncertainty, it is now common ground that should a person who is a group member accept a determination made by AFCA, they will be bound as a matter of contract from seeking further relief. Although it may be that the insurers do not propose to take this point if subsequent litigation took place.

81 None of the parties asserted that an insured who happens to be group member would be bound at law or in equity by a “determination” made at an earlier or different stage of the internal dispute resolution process (and I was not asked to make findings in relation to this point which would require examination of the policies and related material).

F RELEVANT FINDINGS

F.1 Introduction and Registrations

82 I have already set out the number of registrations received in each of the class actions, although it may be that some of those who have registered may not be able to establish that they suffered any relevant loss (and hence would not be group members). The numbers may not be arithmetically correct, but they are sufficiently accurate for present purposes, which is to gauge whether group members generally have an interest in pursuing their claims by way of the class actions in circumstances where it was suggested, at least initially, that it is unlikely that there would be any such interest.

83 It is neither necessary nor appropriate, in a declassing application, to engage in any form of micro-analysis of individual group member claims.

84 There are two further important topics requiring findings. The first is recording what has occurred procedurally relating to the test cases; and the second relates to what is left of common issues and issues of commonality following the test cases.

F.2 The Test Cases

85 There have been two test cases conducted in Australia. Unimaginatively, they have been called the First Test Case and the Second Test Case. As noted above, both were organised by the insurers, or more specifically, the Insurance Council of Australia (ICA) with the consent of AFCA, the external dispute resolution scheme with power to make determinations of up to $542,500 (prior to 1 January 2024) for direct financial loss, which determinations are not binding unless the insured accepts the determination. That limit has since increased for complaints lodged on or after 1 January 2024 to $631,500, according to the AFCA webpage entitled “Outcomes AFCA Provides”.

86 The First Test Case was announced in July 2020. It related to whether exclusions which referenced the repealed Quarantine Act rather than the current Biosecurity Act 2015 (Cth) excluded claims arising from the COVID-19 pandemic. In November 2020, the decision in the First Test Case was delivered by the Court of Appeal of New South Wales, being HDI Global Specialty SE v Wonkana [2020] NSWCA 296; (2020) 104 NSWLR 634. The Court of Appeal found that the exclusions did not apply to COVID-19. Special leave to appeal was refused.

87 After judgment in the First Test Case, the ICA announced that it was considering a further test case “that explores outstanding policy matters, including proximity and prevention of access, relating to the pandemic and business interruption insurance”.

88 The Second Test Case, then comprising nine individual proceedings, was commenced in this Court in February 2021, with a further proceeding commenced by QBE in April 2021.

89 The Second Test Case was heard by Justice Jagot at first instance, with her Honour being asked to consider certain questions relating to policy response (no case involved a loss or quantum assessment). Judgment was delivered in October 2021 in Swiss Re International SE v LCA Marrickville Pty Ltd [2021] FCA 1206; (2021) 394 ALR 461. In nine of the ten cases, it was found that the insured’s policy did not respond. In the tenth case (Meridian v IAL), which concerned an infectious disease clause, Jagot J found that the insuring clause was triggered. I am informed that this case has recently settled.

90 There were then appeals and cross-appeals in respect of five of the cases, with the Full Court (Moshinsky, Derrington and Colvin JJ) delivering judgment in LCA Marrickville Pty Limited v Swiss Re International SE [2022] FCAFC 17; (2022) 290 FCR 435. The Full Court largely upheld the conclusions of Jagot J. Special leave to appeal was subsequently refused.

91 The Second Test Case, obviously enough, was determined in relation to the policies, and on the facts (both agreed and proven), before the Court. Although the applicants “embrace the reasoning in the Second Test Case in relation to policy construction in so far as it can be applied by analogy” they contend “substantial common issues of law and fact” remain.

92 What has become increasingly evident is whether this contention of the applicants has sufficient substance is at the core of the resolution of these declassing applications.

F.3 Common Issues and Issues of Commonality

93 I have already referred to the fact that MFI-3 contains, after many efforts, the applicants’ best attempt to identify common issues and issues of commonality (and also summarises the response of the insurers to those contentions).

94 I have reached the conclusion that it is a significant overstatement to contend “substantial common issues of law and fact” remain. This is evident for several reasons.

95 First, Issues 6(b) and (c), 7, 15, 28, 38 and 42 are said to give rise to issues required to be determined, but really do no such thing. There is no real extant controversy as to these matters for the reasons identified by the insurers in MFI-3.

96 Secondly, and more generally, although it may be accepted that the policies contain policy wording that suggest common issues or a degree of commonality, to the extent that it could be done so, and those common issues were of real significance, they were addressed and resolved by the test cases.

97 It is the nature of the individual claims of group members that they arise under insurance policies – with differing terms and types and levels of cover. Looked at as a matter of substance, the real remaining disputation relates to questions of individualised causation and loss. As I will explain below, there is some utility in binding all parties to some of the answers to common issues identified during the process of argument, but this is different from identifying whether there are any common issues of real substance left to be argued and then determined at an initial trial.

98 Thirdly, reflecting the last point, there is a high degree of artificiality about the alleged commonality of some of the issues identified: without being exhaustive, it is evident that Issues 8, 9, 11, 12, 13, 14, 17, 18, at least in part, are individually fact dependent; are not the subject of an identified dispute between an applicant and an insurer; or are really questions of construction of different policies with different wordings.

99 Fourthly, it is unnecessary to go through each issue because the applicants accepted that Issues 19–23 were the high watermark of the issues of commonality requiring determination. The difficulty with Issues 19 and 20 is that although it might be said they raise questions of policy construction, it is likely that there will be a range of disparate circumstances (both temporarily and geographically) informing any answer. An answer will necessarily turn on findings as to particular facts and it is difficult to see why it would be more specific than those produced, in the circumstances of that case, by the Full Court in LCA Marrickville (at 565–566 [441] per Derrington and Colvin JJ) as referenced in MFI-3.

100 With Issues 21–23, which follow on from 19 and 20, it proposes a question as to whether a test other than a “but for” test of causation is to be applied, but the relevant causation principles are tolerably plain. As Allsop J (with whom Kiefel and Stone JJ agreed) observed in McCarthy v St Paul International Insurance Co Ltd [2007] FCAFC 28; (2007) 157 FCR 402 (at 430–431 [91]), if there are two concurrent proximate causes, “one falling within the policy, the other simply not covered by the terms of the policy”, the insured may recover. Further, it is difficult to see the utility of such an abstract question when there can be no real dispute as to the accuracy of Allsop CJ’s general summary of the causal inquiry in insurance law in Sheehan v Lloyds Names Munich Re Syndicate Ltd [2017] FCA 1340; (2017) 19 ANZ Ins Cas ¶62–158 (at [77]) as follows:

The causal inquiry in insurance law is directed to the proximate cause of the relevant loss or damage. This means proximate in efficiency, not the last in time: Leyland Shipping Co Ltd v Norwich Union Fire Insurance Society Ltd [1918] AC 350 at 369 per Lord Shaw; Global Process Systems Inc v Syarikat Takaful Malaysia Berhad (The “Cendor MOPU”) [2011] UKSC 5; 1 Lloyds Rep 560 at 564 [19] per Lord Saville and 568 [49] per Lord Mance. A proximate cause is determined based upon a judgment as to the “real”, “effective”, “dominant” or “most efficient” cause: see Leyland Shipping [1918] AC at 370 per Lord Shaw; Wayne Tank and Pump Co Ltd v Employers Liability Assurance Corp Ltd [1974] QB 57 at 66 per Lord Denning MR. What is the proximate cause is to be decided as a matter of judgment reached by applying the commonsense knowledge of a business person or seafarer: see The “Cendor MOPU” [2011] l Lloyds Rep at 564 [19] per Lord Saville and 568 [49] and 576 [79] per Lord Mance. There does not need to be a single dominant, proximate or effective cause of loss or damage: McCarthy v St Paul International Insurance Co Ltd [2007] FCAFC 28; 157 FCR 402 at 430 [90]. In City Centre Cold Storage Pty Ltd v Preservatrice Skandia Insurance Ltd (1985) 3 NSWLR 739 (referred to in McCarthy 157 FCR at 430 [90]), Clarke J at 745 approached the question as follows:

… to determine in the first instance whether there is one effective cause. But, recognising that in the present case there are a number of contributing causes, I do not propose straining to isolate one if it seems to me that two or more causes operated with approximately equal effect.

101 I accept I have not dealt with each issue identified. Clearly there remain some real or potential disputes, which might be thought to have some degree of commonality. For example, as to Issues 35, 36 and 40, there is clearly an issue and the parties have been unable to agree an answer. Further there are a series of questions which have a similar theme and have elicited a common response from the insurers: see Issues 2–5, 7–9, 14, 15, 17 (linked to 25), 26–32, 37, 39, 41 and 43.

102 But the point is not whether it is possible, with effort, to divine questions with some degree of commonality or whether a class action passed through the s 33C “gateway”. The reality is that following the test cases, what remains to be resolved are some potential issues which transcend individual claims, but upon close analysis I accept the insurers’ submission that they cannot be properly characterised as substantial common issues of law and fact which necessitate a contested hearing.

103 Having reached these conclusions, it is necessary to turn to the application of s 33N to each class action.

G AN EVALUATION OF EACH SECTION 33N ARGUMENT

G.1 Introduction

104 Consistently with the Full Court’s reasoning in Mutch (at 150–151 [17]), one would usually approach the s 33N task by the process of three steps: first, identifying whether any or all of the Costs Ground and/or the Individual Proceeding Ground and/or the Efficiency Ground are made out; secondly, considering whether there was another, that is, different reason why it is inappropriate that the claims be pursued by means of a class action (that is, whether the Alternative Ground is made out); and thirdly, deciding whether because of that established ground or grounds, I should reach a level of satisfaction that it is in the interests of justice to declass the proceeding.

105 Many of the submissions made on behalf of the insurers did not follow these logical steps. Various factual matters were called in aid, for example, to establish the Efficiency Ground but were also relied upon to establish the Alternative Ground even though the submission was directed to matters of efficiency.

106 Although the applications have been heard together, plainly it is necessary to consider each class action individually. No party disputed the reality, however, that despite some subtle differences, there was a dominant, common or general thread that ran through each of the insurers’ arguments as declassing being justified by reason of a lack of remaining substantial common questions.

107 Accordingly, in the light of my findings in the preceding section, it is only necessary to consider the application of s 33N by reference to two of the contentions made by the insurers:

(1) That there may be a lack of jurisdiction to deal with the claims of group members (Lack of Jurisdiction Contention).

(2) There is no utility in the class action because all real common issues have been determined in the test cases and that there are insufficient common issues or issues of commonality to resolve (Lack of Common Issue Contention).

108 Because the issue of jurisdiction is logically anterior to all other issues it is worth dealing initially with the arguments based upon jurisdiction, before turning to what I consider to be the determinative issue (which was sometimes made in the context of the Efficiency Ground or in relation to the Alternative Ground).

G.2 Jurisdiction Contention

109 There is no substance to this contention raised by Hollard and QBE.

110 The first point to be made is that the submissions of the insurers tend to conflate concepts which are distinct. When it comes to denial of indemnity under a policy of insurance, the position is clear. As Rares J explained in Sagacious Legal Pty Ltd v Wesfarmers General Insurance Limited (No 4) [2010] FCA 482; (2010) 268 ALR 108 (at 111 [5]):

This matter has been in federal jurisdiction since at least the time of the insurer’s refusal of indemnity. It involved rights and liabilities under a contract of insurance that owed their existence to a federal law, namely the Insurance Contracts Act: compare Agtrack (NT) Pty Ltd v Hatfield (2005) 223 CLR 251; 218 ALR 677; [2005] HCA 38 at [29] and [32] per Gleeson CJ, McHugh, Gummow, Hayne and Heydon JJ. As Gibbs CJ, Mason, Wilson, Brennan, Deane and Dawson JJ explained in LNC Industries Ltd v BMW (Aust) Ltd (1983) 151 CLR 575 at 581; 49 ALR 599 at 602:

When it is said that a matter will arise under a law of the Parliament only if the right or duty in question in the matter owes its existence to a law of the Parliament that does not mean that the question depends on the form of the relief sought and on whether that relief depends on federal law. A claim for damages for breach or for specific performance of a contract, or a claim for relief for breach of trust, is a claim for relief of a kind which is available under State law, but if the contract or trust is in respect of a right or property which is the creation of federal law, the claim arises under federal law. The subject matter of the contract or trust in such a case exists as a result of the federal law.

111 But of course, we are here dealing with the claims of group members; many of whom have not had indemnity denied. These people have claims within the meaning of s 33C. This is not to say they have a right or entitlement to relief; but rather that facts, circumstances and legal rights exist anterior to and independent of the class action, which may ground a right or entitlement to relief if that person’s claim is ultimately heard and determined by the Court. They all have an interest in obtaining definitive answers to any common questions which, in essence, operate as declarations of right.

112 There was some confusion arising from the relevant insurers submissions in conflating the issue of whether a claim existed and the distinct constitutional notion of a “matter”, including the suggestion that a “matter” must exist between each group member and the relevant insurer. However, as I observed as part of the Full Court in Elliott-Carde v McDonald’s Australia Limited [2023] FCAFC 162; (2023) 301 FCR 1 (at 57 [366], Beach and Colvin JJ agreeing):

In Williams v Toyota Motor Corporation Australia Limited [2021] FCA 1425; (2021) 288 FCR 282 (at 293–294 [56]–[57]), I had cause to consider, and doubt the correctness of, the observation of Wilcox J in Nixon v Philip Morris (Australia) Ltd [1999] FCA 1107; (1999) 95 FCR 453 (at 484 [52]) that Pt IVA provides a mechanism for determining, in the one proceeding, individual claims, each of which must be a “matter” within the meaning of ss 76 and 77 of the Constitution. For my part, to assert in an a priori way that each claim in a class action must be an individual “matter”, or that all of the claims as grouped in the class action must be part of the one “matter”, is difficult to reconcile with the breadth of the concept of what can constitute a “matter” (see Re Wakim; Ex parte McNally (1999) 198 CLR 511 (at 585–586 per Gummow and Hayne JJ)) but also gives insufficient recognition to the different extents of commonality that can exist in (and within) claims grouped in a Pt IVA proceeding. All that is necessary is that the claims be in a “matter” or “matters” within the subject matter jurisdiction of the Court.

113 There was no suggestion that any of the representative applicants’ claims were not within federal jurisdiction, and it is, of course, a heresy to suggest some form of concurrent state and federal jurisdiction. If each of the claims for declaratory type relief in relation to the common questions advanced by the relevant representative applicant is in federal jurisdiction, the claims of their privies in interest, the represented persons, who also have an interest in (and be entitled to take the benefit of), declaratory relief, are part of the same overall justiciable controversy (and constitutional “matter”) and hence are within the jurisdiction of the Court.

114 In any event, although it does not matter, when it comes to the Hollard class action for example, and without seeking to be exhaustive, the following federal matters are raised on the applications and pleadings: (a) claims by the applicant and on behalf of group members for interest under s 57 of the ICA; (b) to the extent that group members who are Disease Clause Covered Insureds were not parties to the policies under which they were insured, s 48(1) of the ICA conferred rights of recovery upon those group members; and (c) the applicant, in reply, relies upon s 54(1) of the ICA. Similarly, in the QBE class action, there is also a claim made under s 57 for interest on behalf of both the applicant and group members and there is no proper basis for finding that the s 57 interest claims are made against an insurer for the improper purpose of fabricating jurisdiction and it is not incapable on its face of legal argument: see Citta Hobart Pty Ltd v Cawthorn [2022] HCA 16; (2022) 276 CLR 216 (at 234 [35] per Kiefel CJ, Gageler, Keane, Gordon, Steward and Gleeson JJ).

G.3 Lack of Common Issue Contention

115 The real issue is the consequence that flows from my finding that what remains cannot be properly characterised as amounting to substantial common issues of law and fact which necessitate a contested hearing.

116 The focus is on “the claims” of the group members. What is required to enliven the Efficiency Ground is a consideration of the efficiency of the claims in the existing representative proceeding, recognising that the inquiry is a wide one, as was explained by Kiefel J in Bright v Femcare Ltd [2002] FCAFC 243; (2002) 195 ALR 574 (at 601 [130]).

117 Although the consequences of such a finding were said by the insurers to enliven various grounds specified in s 33N(1), I am satisfied that in all the circumstances, the real issues in each of the class actions are now overwhelmingly individual and that each of the representative proceedings will not now provide an efficient and effective means of dealing with the claims of group members.

118 It is worth stressing that I am not dealing with this issue tabula rasa. Although in each case I think a class action with a speedy initial trial leading promptly to a Court supervised assessment process would have been more efficient (and fairer) if adopted at the outset, the well-advanced private assessment processes have now become a more efficient mechanism of dealing with the residuum of issues left following the test cases. I am satisfied the alternative of the Court proceeding now to have a very limited initial trial of a few relatively vague issues of commonality and then creating a different Court supervised reference process for individual assessment would be more costly, slower and less efficient.

119 It follows the Efficiency Ground is made out. I can leave aside the other grounds.

H THE EXERCISE OF THE DISCRETION

120 As I have explained in Section C above, given the Efficiency Ground has been established, it follows that I am required to determine whether it is “in the interests of justice” to declass the proceedings because of the ground. Needless to say, as is evident by the use of the word “may”, the making of s 33N orders is discretionary, even where the conditions for the exercise of power have been made out in each class action: see above (at [33]); Guglielmin v Trescowthick (No 2) [2005] FCA 138; (2005) 220 ALR 515 (at 531 [71] per Mansfield J).

121 The lodestar expression “the interests of justice” is, obviously enough, a very broad one, informed by the consideration of fairness to all concerned, and hence it is important to recall that in the exercise of the discretion, it is necessary to have regard to all relevant considerations, not merely upon the matters which have been determinative in establishing the Efficiency Ground (which, in this case, has triggered the exercise of the discretion).

122 It is worth focussing initially on matters that militate against the declassing of each of the proceedings.

123 First, as I noted in the introduction, I am far from convinced that the approach of running various test cases, rather than arranging for class actions to have been commenced, is a course which is consistent with modern case management imperatives referred to in Pt VB of the FCA Act and the reality that class actions are the manifestly optimal way by which matters common to a number of small claims are best determined in this Court. Moreover, contrary to the unified position of the insurers when this matter first came before me, the reaction of the group members to the registration process – which had the benefit of identifying people who wished to advance claims – suggests a class action process adopted at the outset would have been fairer.

124 Having said this, each case falls to be considered depending upon its own circumstances at time of the exercise of the discretion and here, the horse has bolted. As far as I am concerned, insurers should not assume that in future cases adopting a test case procedure (which they no doubt consider most attractive from their perspective) is one that would be looked upon favourably – particularly given the maturity the class action regime has now reached in providing an effective procedural mechanism which delivers access to justice for individuals with small claims in a binding and costs effective way.

125 Secondly, there is the existing and important protective and supervisory role I currently have regarding group members. Because of the course the insurers adopted, it seems a significant number of claimants were unaware of their ability to maintain claims against the insurers or did not know how to go about it. Despite the insurers’ submissions to the contrary, when the Court approved simple messages that could be understood by group members, the notification process showed how many were interested in pursuing claims and indicated their willingness to participate in the class action, notwithstanding that that would involve some cost to them. This seems to me to be a salutary lesson reinforcing the notion that a Court-approved notification scheme to group members is likely to be more effective than a notification given by insurers relating to private resolution schemes.

126 Thirdly, related to the last point about the Court’s role towards non-party group members, the private resolution schemes of the insurers are ones which do not have any direct Court oversight. In making this comment, I am not doubting the integrity of those involved in the process and their competence in assessing claims, but a Court-appointed referee system would give claimants comfort that the assessment process is subject to the close supervision of the Court in not only providing a fair outcome but an outcome that is perceived to be disinterested.

127 Balanced against these matters are the factors that favour declassing.

128 First, and most importantly, as I have explained, there is the lack of subsisting common issues of real substance left in the wake of the determination of the test cases. The Court’s role is to resolve controversies by the exercise of judicial power dealing with issues bona fide in dispute. Although it has a protective role in the present context, it should not put aside time to hear an initial trial of dubious utility and then become a clearinghouse to determine individual issues simply because class actions, when these controversies first arose, would have been a better mechanism for the resolution of common issues.

129 Secondly, although the test case approach meant no statutory estoppel arose upon determination of common issues, to the extent the applicants (given their duties to group members) consider it desirable, it is still possible to use s 33ZB as a mechanism by which the group members as well as the insurers are bound to determinations of issues which are no longer controversial and may be relevant for their individual claims. During oral argument I explored with the insurers those questions in respect of which there seemed to be no substantial dispute, which could be the subject of s 33ZB orders. I intend to put in place a mechanism by which this can occur and so this matter does not stand in the way of reaching a state of satisfaction that it is in the interests of justice to declass the proceedings.

130 Thirdly, although the comparator of private determination of claims through the processes adopted by the insurers is not the same as those claims being determined through the court system, there is nothing on the evidence for me to conclude that the process will not be conducted bona fide and there are some measures of review protection for the insureds if they are dissatisfied with an initial determination.

131 Fourthly, as noted above, the private claim process is well advanced and will be able to be completed earlier than if the Court was to put in place a reference process from scratch after an initial trial.

132 Fifthly, provided group members are notified of their ability to make claims and given all necessary information in order to do so (a matter to which I will return), there is a potential cost benefit in participating in the private claim process for group members (in that outgoings will not be required to be deducted from any amount recovered to reflect the costs associated with maintaining the claim through the class action).

133 Sixthly, although I did consider whether it may be possible for aggregate damages to be awarded, the circumstances of these cases are such that there does not seem to me to be any realistic ability for any aggregate damages award to be made – the reality is that individual assessment is necessary.

134 Seventhly, although those promoting the class actions will no doubt experience some loss by reason of the declassing, that is an inevitable consequence of the vicissitudes of class action litigation and, in any event, is partly a consequence of the class actions not being commenced quickly (and then firmly and vigorously opposing the test case procedure when it was first proposed or pressing for an initial trial be held concurrently with the test cases).

135 For these reasons, I am satisfied it is in the interests of justice to make s 33N orders in relation to each proceeding. Although I well recognise each class action has some differences, I have explained my reasons in an omnibus fashion because of the commonality of relevant and determinative factors in each class action. Notwithstanding this, I have separately exercised my discretion in relation to each proceeding.

I DISPOSITION, ORDERS AND FUTURE STEPS

136 Two further steps are required prior to making orders to declass each of the proceedings.

137 First, giving a notice to all group members of what is going to happen and a clear statement of their rights to pursue any claim they have, and how it can be pursued if they wish to do so.

138 Secondly, making any relevant s 33ZB orders proposed by the applicants which seem to me to reflect the results of their test cases and may be for the benefit of group members for the determination of their individual claims. Although technically the fact I propose to make s 33ZB orders and an order for notification would be a basis for rejecting the unqualified relief sought in the interlocutory applications, this would be a triumph of form over substance, and I note the course of making s 33ZB orders before declassing is not unprecedented: see Zhang de Yong v Minister for Immigration, Local Government & Ethnic Affairs (1993) 45 FCR 384 (at 405 per French J).

139 I have notified the parties that these proceedings together with all related proceedings are to be re-docketed to another Judge of the Court for ultimate disposition. But I should resolve all outstanding matters concerning the declassing before that reallocation occurs.

140 The parties should confer as to appropriate orders to give effect to these reasons. In those circumstances, the only order I propose to make is that the matter be adjourned and that a case management hearing be fixed after consultation with the parties upon delivery of these reasons.

I certify that the preceding one hundred and forty (140) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Lee. |

Associate:

Dated: 20 September 2024

ANNEXURE A

ANNEXURE B