Federal Court of Australia

Australian Securities and Investments Commission v Keystone Asset Management Ltd [2024] FCA 1019

ORDERS

AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff | ||

AND: | KEYSTONE ASSET MANAGEMENT LTD (ACN 612 443 008) First Defendant PAUL ANTHONY CHIODO Second Defendant | |

DATE OF ORDER: |

THE COURT NOTES THAT:

In these orders:

“ADPF” means the Advantage Diversified Property Fund;

“Corporations Act” means the Corporations Act 2001 (Cth) (Corporations Act);

“Investor Funds” means monies provided to the First Defendant in its capacity as responsible entity of the SMF;

“Property” means all real or personal property, assets or interests in property of any kind, within or outside Australia including choses in action and, by virtue of s 1323(2A) of the Corporations Act, any property held otherwise than as sole beneficial owner;

“Relevant Capacities”, in relation to the First Defendant, means its capacity as responsible entity of the SMF, its capacity as trustee for the ADPF, and its capacity as trustee for the Quantum PE Fund; and

“SMF” means the Shield Master Fund (ARSN 650 112 057).

THE COURT ORDERS THAT:

Leave to amend

1. Pursuant to r 8.21 of the Federal Court Rules 2011, the Plaintiff has leave to file an amended originating process in the form of the proposed amended originating process annexed to the affidavit of Rebecca Jaffe dated 22 August 2024 (Amended Originating Process). The Amended Originating Process is to be filed and served as soon as practicable.

2. The Amended Originating Process be returnable instanter.

Adjournment application

3. The First Defendant’s application for an adjournment be dismissed.

Appointment of receivers

4. Until further order, pursuant to s 1323(1)(h) of the Corporations Act, Jason Tracy and Lucica Palaghia of Deloitte Financial Advisory Pty Ltd be appointed as joint and several receivers and managers (Receivers), without security, of the Property of the First Defendant, for the purposes of:

(a) identifying, collecting and securing the Property of the First Defendant held in any of its Relevant Capacities;

(b) ascertaining the amount of the Investor Funds received by the First Defendant;

(c) identifying any dealings with, payments of, distributions of or uses made of the Investor Funds by the First Defendant;

(d) identifying any Property purchased or acquired, directly or indirectly, with Investor Funds; and

(e) recovering Investor Funds.

5. For the purpose of attaining the objectives for which the Receivers are appointed, the Receivers have the following powers:

(a) the powers set out in s 420(1) and (2)(a), (b), (e), (f), (g), (h), (j), (k), (n), (p), (q), (r), (t) and (u) of the Corporations Act; and

(b) the power to apply to the Court for directions or further orders.

6. The powers in paragraph 5 above shall not extend to the sale of any Property of the First Defendant without prior leave of the Court.

7. The Receivers shall within 28 days of the date of this order provide to the Court and the parties a report as to the receivership of the Property of the First Defendant, including:

(a) a report in relation to the matters referred to in paragraphs 4(a) to (e) above;

(b) an opinion as to the solvency of the First Defendant;

(c) an opinion as to the likely return to creditors and investors in the event that each of the First Defendant and the SMF were to be wound up; and

(d) any other information necessary to enable the financial position of the First Defendant, the SMF and the ADPF to be assessed.

8. In addition to the powers conferred on them by paragraph 5 above, the Receivers have the power to investigate and report on the matters set out in paragraph 7 above.

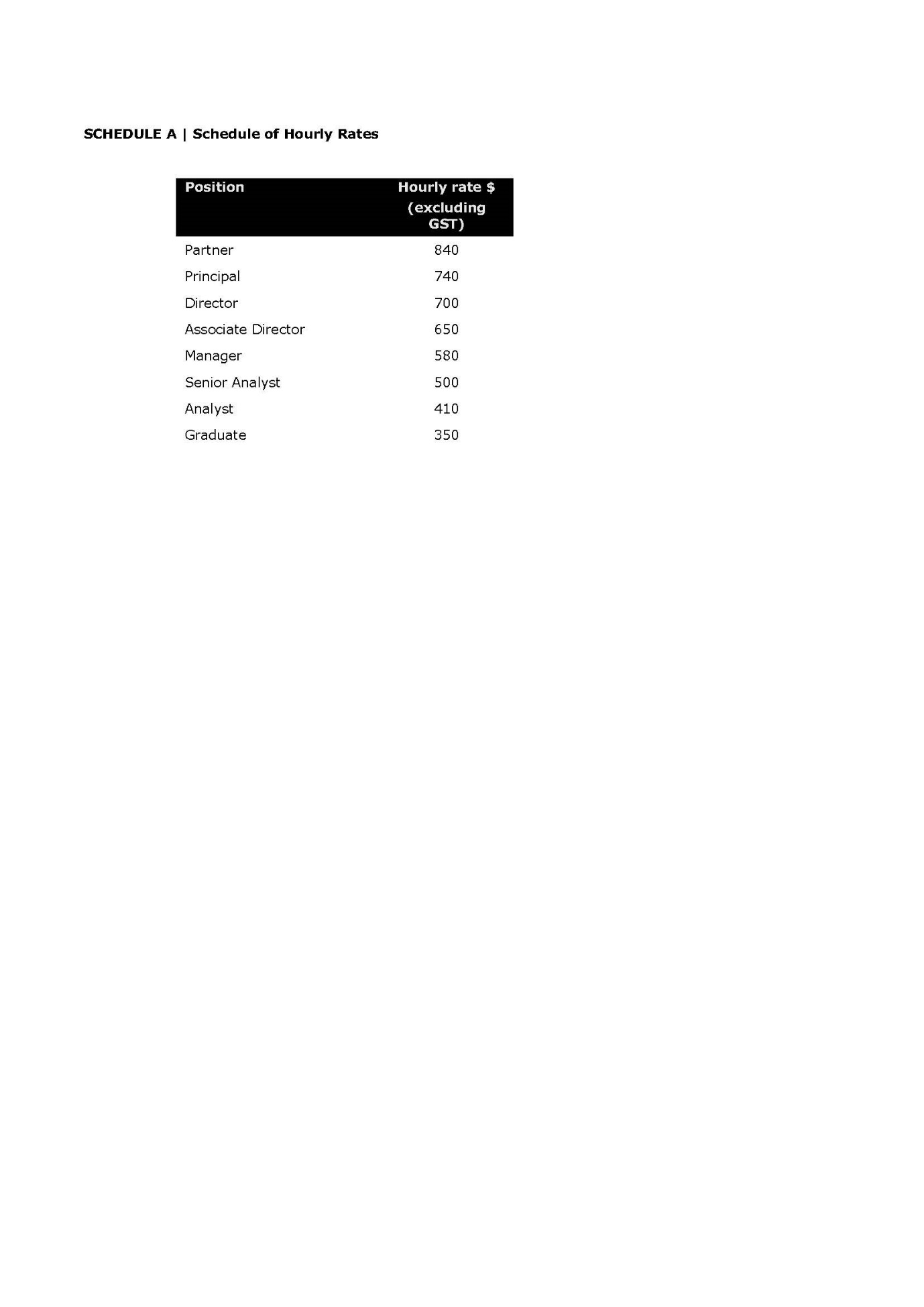

9. The Receivers shall be entitled to reasonable remuneration and reasonable costs and expenses properly incurred in the performance of their duties pursuant to these orders as may be fixed by the Court on the application of the Receivers, such sum to be calculated on the basis of the time reasonably spent by the Receivers, at the rates specified in the Consent to Act at Annexure A to these orders, such fees to be paid out of the Property of the First Defendant.

10. The Receivers shall be entitled to be indemnified out of the Property of the First Defendant for any liability properly incurred in performing their duties and discharging their functions pursuant to these orders.

Books and records

11. The First Defendant shall immediately make available to the Receivers all books and records (including all files, computer records and data in its possession, custody or control) which relate to the Property of the First Defendant.

12. The Plaintiff shall, on the reasonable request of the Receivers, make available to the Receivers all documents and books concerning the First Defendant which have been obtained by the Plaintiff under Division 3 of Part 3 of the Australian Securities and Investments Commission Act 2001 (Cth).

Notice of orders to third parties

13. To the extent necessary, the Plaintiff has leave to give to:

(a) the relevant authorities (domestic and overseas) that record, control and/or regulate the ownership of real property;

(b) the relevant authorities and entities (domestic and overseas) that record, control and/or regulate the ownership of securities;

(c) any bank, building society or other financial institution (domestic and overseas) with which, to the best of the Plaintiff’s knowledge, the First Defendant operates any account;

(d) any other person or entity (domestic and overseas), holding or controlling property which, to the best of the Plaintiff’s knowledge and belief, belongs to the First Defendant or is part of the Property of the First Defendant;

(e) the Australian Prudential Regulation Authority;

(f) Macquarie Investment Management Ltd (ACN 002 867 003; AFSL 237492); and

(g) Equity Trustees Superannuation Limited (ACN 055 641 757; AFSL 229757),

notice of the making of these orders, by delivering a copy of a minute of the orders to that entity or person and/or any person apparently in the employ of that entity or person.

General orders

14. Paragraphs 1 and 3 of the orders made on 26 June 2024 be vacated.

15. The First Defendant pay the Plaintiff’s costs of and incidental to the Originating Process and Amended Originating Process.

16. Paragraphs 4 to 15 of these orders be stayed until 4.00 pm on 28 August 2024.

17. Paragraph 2 of the interlocutory process filed on behalf of Jason Tracy and Lucica Palaghia of Deloitte Financial Advisory Pty Ltd on 12 August 2024 be adjourned to a date to be fixed.

18. There be liberty to apply on 24 hours’ notice.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

MOSHINSKY J:

Introduction

1 The plaintiff, the Australian Securities and Investments Commission (ASIC), commenced this proceeding by originating process dated 17 June 2024. By its originating process, ASIC sought interim and final relief, including the appointment of a receiver and manager to the property of the first defendant (Keystone). On 26 June 2024, the Court made interim orders by consent (the June Orders) appointing Jason Tracy and Lucica Palaghia of Deloitte Financial Advisory Pty Ltd (Deloitte) to a supervisory role in relation to Keystone. ASIC has sought leave to amend its originating process to reflect the relief it now seeks by way of final relief. The proposed amended originating process is annexed to the affidavit of Rebecca Jaffe dated 22 August 2024. At the outset of the hearing, the defendants indicated that the amendments were not opposed and I made an order giving ASIC leave to amend its originating process. I will treat the originating process as so amended.

2 In support of the orders it seeks by way of final relief (in particular, for the appointment of Mr Tracy and Ms Palaghia as receivers and managers of Keystone’s property), ASIC relies on:

(a) an affidavit of Andrea Perrywood affirmed on 17 June 2024 (First Perrywood Affidavit);

(b) an affidavit of Ms Perrywood affirmed on 22 August 2024 (Second Perrywood Affidavit);

(c) ASIC’s outline of submissions dated 17 June 2024; and

(d) ASIC’s outline of submissions dated 23 August 2024 (ASIC’s August Submissions).

3 In opposition to the application, Keystone relies on:

(a) two affidavits of Simon Milne, dated 24 June 2024 and 26 August 2024;

(b) three affidavits of Susanna Ford, dated 15 August 2024, 26 August 2024 and 27 August 2024; and

(c) the second affidavit of Paul Chiodo dated 24 June 2024.

4 Equity Trustees Superannuation Limited (Equity) and Macquarie Investment Management Limited (Macquarie), which represent a large proportion of investors in the relevant funds, have appeared today and support ASIC’s application. Equity relies on an affidavit of Andrej Kocis dated 25 July 2024. Macquarie relies on an affidavit of James Campbell dated 26 August 2024.

5 At the conclusion of the hearing today, I indicated that I would make orders substantially as sought by ASIC and publish my reasons later. Senior counsel for Keystone then asked for a stay of the orders until reasons had been delivered. In light of that request, I said that I would adjourn for a short time and deliver oral reasons today. The reasons that follow are substantially based on ASIC’s August Submissions. In these reasons, I will avoid referring to specific sums of money as they are confidential and disclosure could adversely affect the funds and thus the interests of investors.

Background

6 The Shield Master Fund (SMF) is a registered managed investment scheme. Keystone is the responsible entity of the SMF. Keystone is also the trustee of the Advantage Diversified Property Fund (ADPF) (a wholesale property fund in which a large proportion of the SMF’s funds have been invested). ASIC is investigating the conduct of Keystone, its officers, and related entities.

7 As part of its investigation, ASIC has, among other things, conducted examinations and issued notices for the production of documents. As a result of the information obtained, including what that information revealed about the operation and management of the SMF, and the dissipation of investor funds, ASIC commenced this proceeding.

8 On 18 June 2024, following an urgent ex parte hearing, the Court made various orders sought by ASIC, including for the preservation of assets of Keystone. The proceeding was adjourned until 25 June 2024.

9 On 24 and 25 June 2024, Keystone filed and served four affidavits and written submissions. In its written submissions, Keystone accepted, for the purposes of the hearing of ASIC’s originating process, the desirability of enshrining by Court orders stricter and improved oversight and financial controls on Keystone, under the supervision of independent officers of the Court. Keystone sought the appointment of Mr Tracy and Ms Palaghia of Deloitte to, among other things, validate any proposed payments by Keystone so long as they were satisfied that the payments were in the best interests of investors.

10 ASIC agreed, on an interim basis, to the appointment of Mr Tracy and Ms Palaghia, for the purposes set out in the June Orders, including the preparation of a report on the financial position of the SMF and ADPF (Deloitte Report).

11 A copy of the Deloitte Report was provided to ASIC on 28 July 2024. A copy was also provided to Keystone. By way of further background, senior counsel for ASIC explained at the hearing on 25 June 2024 that the Deloitte Report would also inform ASIC’s consideration of whether to press for the appointment of receivers (T13-14).

12 On 18 August 2024, Mr Tracy wrote to ASIC’s solicitors in response to a request for clarification and questions regarding the Deloitte Report. In answer to a question about what actions were appropriate or necessary to protect investor interests, Mr Tracy stated:

In order to protect the interests of unit holders and underlying investors, we consider a receiver or liquidator should be appointed to Keystone Asset Management.

13 ASIC submits that the findings in the Deloitte Report, and the opinion of Mr Tracy and Ms Palaghia that, at the least, a receiver should now be appointed, support the appointment of receivers and managers as soon as possible.

14 In summary, ASIC submits that the evidence indicates that:

(a) substantial investor funds have been misapplied (including, for example, a large sum paid to “lead generators”);

(e) the value of the assets of the SMF is substantially less than sums invested in the SMF, leaving a significant shortfall for unitholders and underlying investors;

(f) there has been a failure to maintain proper records and books of account, resulting in:

(i) Deloitte not being able to account for a large amount in funds that have been withdrawn from the ADPF bank account, and Deloitte not being able to account for a further sum in ADPF loan funds paid out of the bank accounts of Chiodo Corporation Pty Ltd (Chiodo Corporation);

(ii) significant time and cost being incurred in attempting to allocate amounts spent by Chiodo Corporation using funds loaned by the ADPF; and

(iii) Keystone’s auditor, BDO Audit, lodging breach reports with ASIC;

(g) substantial sums being spent on construction projects using funds loaned from ADPF, without evidence of feasibility studies, a tendering process for contract work, quotations from contractors prior to work commencing, and written contracts specifying what work was to be performed and when payment would be made and in what amounts;

(h) development management agreements which provide for the payment of management fees to Chiodo Corporation (ultimately from funds loaned by ADPF), which were not entered into on arm’s length or commercial terms; and

(i) conflicts of interest, including in relation to the second defendant, Mr Chiodo, who (indirectly) remains a substantial shareholder in Malana Management Pty Ltd, which owns all of the share capital in Keystone.

Applicable principles

15 ASIC’s application is made under s 1323 of the Corporations Act 2001 (Cth) and, to the extent necessary, s 23 of the Federal Court of Australia Act 1974 (Cth).

16 The general principles in relation to s 1323 of the Corporations Act are well established. In summary, there are three preconditions that must be satisfied before a court can exercise the power to grant relief under s 1323: Australian Securities and Investments Commission v MyWealth Management Financial Services Pty Ltd (No 2) [2019] FCA 2107 (Mywealth Management) at [41] per Derrington J. The three preconditions are:

(a) ASIC, or an aggrieved person, has made the relevant application;

(b) one or more of the matters in s 1323(a), (b) or (c) must be satisfied; and

(c) the Court must consider it necessary or desirable to make an order under the section for the purposes of protecting the interests of an aggrieved person to whom the relevant person is, or may be or become, liable.

17 The purpose of s 1323 is to provide a means by which property, that may in due course represent a source of vindication of the rights of aggrieved persons, is preserved for their benefit: Australian Securities and Investments Commission v Burnard [2007] NSWSC 1217; 64 ACSR 360 at [14] per Barrett J. There is no requirement for ASIC to demonstrate a prima facie case of liability under the Corporations Act, or general law, on the part of the relevant person or that the person’s assets may have been or are about to be dissipated: Australian Securities and Investments Commission v Carey (No 3) [2006] FCA 433; 232 ALR 577 (Carey (No 3)) at [26] per French J.

18 With specific reference to s 1323(1)(h) and the appointment of a receiver (or receiver and manager), the touchstone for the exercise of that power is whether it is necessary or desirable in the circumstances: Australian Securities and Investments Commission v Linchpin Capital Group Ltd [2018] FCA 1104 (Linchpin Capital) at [61] per Derrington J. This inquiry focuses upon the protection of aggrieved persons: the needs of aggrieved persons, and the threats or risks to those needs: Australian Securities and Investments Commission v Burke [2000] NSWSC 694 at [6] per Austin J.

19 The fact of dissipation supports the exercise of a discretion in favour of appointing a receiver: Australian Securities and Investments Commission v Adler [2001] NSWSC 451; 38 ACSR 266 at [7(b)] per Santow J; Linchpin Capital at [62]. The existence of a substantial shortfall between moneys invested in a scheme, and moneys left in a scheme, is also a significant factor: Linchpin Capital at [64].

20 A receivership pursuant to s 1323(1)(h) allows for flexibility, including as to the receivers’ powers: Carey (No 3) at [28] per French J.

21 The interests of the aggrieved persons may be protected not only by orders designed to protect against the dissipation of assets, but also by orders which create an opportunity for the assets of the person under investigation to be ascertained: Carey (No 3) at [27] per French J; Australian Securities and Investments Commission v Secure Investments Pty Ltd [2020] FCA 639 (Secure Investments) at [27] per Derrington J; Linchpin Capital at [61] per Derrington J. Receivers may be appointed for purposes including the identification, preservation, securing and recovery of relevant property: see, eg, Australian Securities and Investments Commission v Marco (No 3) [2020] FCA 719; 145 ACSR 265 at order 8; Secure Investments at order 10; MyWealth Management at order 1.

Outline of ASIC’s case

22 In Part C of ASIC’s August Submissions, ASIC provides an outline of the bases upon which it submits that it is necessary and desirable to appoint receivers and managers of the Keystone property. Part C of those submissions sets out the facts and matters relied on by ASIC under the following headings:

(a) C.1 – The Deloitte Report;

(b) C.2 – The financial position of the SMF and the ADPF;

(c) C.3 – Use of funds for ADPF developments;

(d) C.4 – Development management arrangements;

(e) C.5 – Payments by Chiodo Corporation to lead generators;

(f) C.6 – Related party transactions;

(g) C.7 – Mismanagement of the SMF and ADPF.

23 During the hearing today, I was taken to a sample of the evidence to support the propositions set out in Part C of ASIC’s August Submissions. There appears to be a cogent basis for ASIC to have the concerns that it has. Indeed, no submissions were made by Keystone disputing the facts and matters relied on by ASIC in Part C of its August Submissions.

Consideration

24 ASIC submits that, having regard to the matters highlighted in Part C of its August Submissions, and the further matters addressed in the Perrywood affidavits and the Deloitte Report, it is appropriate to make orders for the appointment of receivers and managers over the Keystone property.

25 ASIC submits that, having regard to the significant work performed by Mr Tracy and Ms Palaghia, their familiarity with Keystone, the SMF and the ADPF, their earlier appointment by the Court (at the request of Keystone), and their positions as officers of the Court, Mr Tracy and Ms Palaghia should be appointed as the receivers and managers.

26 Keystone opposes the application on the basis, in summary, that there is a less drastic option available, namely the appointment of an independent person to act as the agent of Keystone, with the agent being tasked with the responsibility of winding up the fund. This alternative is set out in draft orders attached to Keystone’s outline of submissions dated 26 August 2024 in support of an adjournment application. Keystone does not suggest that its alternative orders could be made today, as it does not yet have agreement from an independent person to act in the agent role.

27 For the reasons that follow, I consider that it is appropriate to appoint receivers and managers to Keystone as proposed by ASIC.

28 I am satisfied that the present application satisfies the first two preconditions to the exercise of power under s 1323 of the Corporations Act. The application is made by ASIC in circumstances where ASIC is carrying out an investigation in relation to an act or omission that constitutes or may constitute a contravention of the Corporations Act.

29 I am also satisfied that the evidence establishes that the appointment of receivers and managers is necessary or desirable for the purposes of protecting the interests of aggrieved persons to whom Keystone may be liable (being investors in the SMF and ADPF).

30 ASIC’s investigation indicates that there has been a significant dissipation of SMF funds. This fact strongly supports the exercise of discretion in favour of appointing a receiver and manager.

31 As outlined in Part C.5 of ASIC’s August Submissions, a large sum of ADPF Loan funds has been drawn down and paid (by Chiodo Corporation) to lead generators for the purposes of sourcing new investors for the SMF and/or the ADPF. This is despite “development costs” being the only approved purpose specified by the ADPF loan agreements.

32 A further large sum in ADPF loan funds has been paid to entities related to Keystone, including for expenses that cannot reasonably be characterised as development costs: see Part C.6 of ASIC’s August Submissions.

33 Deloitte has been unable to verify the application of a further large sum of money: see Part C.2 of ASIC’s August Submissions. Further, Deloitte could not allocate a large sum in shared project costs: see Part C.3 of ASIC’s August Submissions.

34 As a consequence of the apparent dissipation referred to above, and the apparent mismanagement of SMF and ADPF funds, there is a substantial shortfall when comparing the moneys invested in the ADPF, against ADPF assets. This also supports the appointment of a receiver and manager.

35 In particular, a large sum of money (excluding redemptions) was invested in the SMF. Of this, the SMF invested a large sum in the ADPF. However, Deloitte assesses that (as at 31 May 2024), the net assets attributable to ADPF unitholders is a significantly lower sum. This indicates a substantial shortfall, and a further shortfall between the sums invested in the SMF by unitholders and the current value of SMF.

36 The extent of Keystone’s mismanagement confirms that there is a need to protect the interests of investors from what appear to be conflicts of interest and breaches of trusts.

37 A large sum in ADPF loan funds was transferred to Chiodo Corporation, apparently pursuant to the Development Management Agreement. Of that amount, it appears that a large sum has been paid to City Built or Mr Filippini (City Built’s director). This is despite Mr Filippini not holding a building licence (until May 2024), City Built not being required to tender or quote for any of the work it undertook, and there being no written contracts.

38 Notwithstanding this and other concerns as to Chiodo Corporation’s role and the performance of its obligations, Keystone entered into a Development Management Fees Reconciliation Agreement on 18 June 2024 (i.e., after this proceeding was commenced). By that agreement, Keystone purports to acknowledge Chiodo Corporation’s entitlement to a large sum in development management fees.

39 On the basis of the material before the Court, I do not have confidence that the SMF and ADPF are being managed in the best interests of investors, or that Keystone is capable of providing such management.

40 Further, the evidence indicates that Keystone’s financial records are incomplete and unreliable. As a result, there are real doubts about the status and value of investments in the SMF and ADPF. The proposed receivership would enable the further ascertainment of the Keystone property.

41 Under ASIC’s proposed orders, the receivers and managers will have three principal tasks:

(a) identifying what Keystone has done with the investor funds it has received;

(b) taking steps to secure the Keystone property and, where possible, to recover investor funds; and

(c) preparing a report that will enable a decision to be made about the future of Keystone and whether the SMF should be wound up.

42 Deloitte has already undertaken much of the work involved in the first task. However, that work is not complete. In particular, the evidence suggests that Deloitte was unable to: verify the use of a sum of money provided by the ADPF to Chiodo Corporation; identify a further sum as relating to a specific project; and verify the use of more than a certain amount paid from ADPF bank accounts.

43 The proposed orders will facilitate the completion of the work involved in the first task, including by requiring Keystone to provide relevant books and records to the receivers, and giving the receivers additional powers to conduct investigations. Further, the proposed orders will require the receivers to address what has occurred since 31 May 2024.

44 The June Orders preserved investor funds by imposing an oversight and approval process as to the transactions that could be undertaken by Keystone. Unlike the June Orders, the further orders proposed by ASIC are concerned to give the receivers an active role in the ongoing operations of Keystone and the SMF. In particular, they give the receivers: the ability to determine the steps that should be taken in the best interests of investors; and powers to take those steps to secure the Keystone property and recover investor funds.

45 The matters identified in the Deloitte Report and the Perrywood affidavits make it appropriate that decisions about the ongoing operations of Keystone should be made by independent officers of the Court, rather than by the management of Keystone. Those matters also confirm the importance of securing the Keystone property where necessary, and otherwise recovering investor funds.

46 ASIC’s proposed orders require the receivers to prepare a further report. This report will deal with the steps that the receivers take in their receivership, and will set out opinions and information that will be relevant to deciding whether Keystone and the SMF should continue in operation or be wound up. Among other things, the report is to include information about the likely returns to creditors and investors in the event that Keystone and the SMF are wound up. The information in the report will be valuable to ASIC, the Court, SMF unitholders and investors, in determining what further steps should be taken in relation to Keystone and the SMF.

47 I do not consider the alternative proposal put forward by Keystone to be a desirable alternative. As already indicated, the proposal cannot be implemented now because no person has yet agreed to act in the agent role. Senior counsel for Keystone submitted that the Court should defer appointing a receiver for two weeks to enable the Keystone proposal to be developed. However, on the material before the Court, I do not consider it realistic that this could be achieved in two weeks. I therefore do not consider the proposal put forward by Keystone to be a realistic one in the near future.

Conclusion

48 For these reasons, I will make orders substantially in the terms sought by ASIC.

[Discussion with counsel then took place regarding a request by Keystone for a stay until 4.00 pm the next day.]

I certify that the preceding forty-eight (48) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Moshinsky. |

Associate: