FEDERAL COURT OF AUSTRALIA

Pascoe v Voukidis Holdings Pty Ltd [2024] FCA 915

ORDERS

Applicant | ||

AND: | VOUKIDIS HOLDINGS PTY LTD (ACN 067 238 144) First Respondent ZV ASSET MANAGEMENT PTY LTD (ACN 132 620 378) Second Respondent CHRISTOS VOUKIDIS Third Respondent | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. By 23 August 2024, the parties are to provide draft orders to chambers to give effect to these reasons.

2. If the parties disagree as to the appropriate outcome as to costs, each party must file and serve any submissions on costs (limited to four pages) by 28 August 2024, with any responsive submissions (limited to two pages) by 30 August 2024.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

[1] | |

[4] | |

[18] | |

[19] | |

[32] | |

[38] | |

[46] | |

[50] | |

[50] | |

60 Belmore St, Burwood, and Peter and Kathy’s claims to be creditors of COV in its liquidation | [51] |

Receipts into, and payments from, Voukidis Holdings’ bank account | [60] |

[68] | |

[70] | |

[72] | |

[75] | |

[77] | |

[79] | |

[80] | |

[81] | |

[82] | |

[83] | |

[88] | |

[101] | |

[107] | |

[113] | |

[115] | |

[119] | |

[122] | |

[123] | |

[152] | |

[152] | |

[158] | |

[161] | |

[168] | |

[170] | |

[186] | |

[190] | |

[196] | |

[208] | |

[211] | |

[217] | |

[223] | |

[235] | |

[250] | |

[250] | |

[277] | |

IF THE TRANSFER OF PETER AND KATHY’S SHARES IN VOUKIDIS HOLDINGS TO ZVAM WAS EFFECTIVE, WAS ZVAM’S TRANSFER OF THE SHARES TO CHRISTOS VOID PURSUANT TO S 37A OF THE CONVEYANCING ACT 1919 (NSW)? | [282] |

[289] | |

[294] | |

[299] |

BUTTON J

1 The Applicant is the trustee in bankruptcy of Peter Voukidis and Kathy Voukidis. They are the mother and father of Christos Voukidis. Given their common surname, I will refer to them as Peter, Kathy and Christos. Christos’ sister is Penny Calagis.

2 The Applicant brought the proceeding, advancing claims in respect of the following principal issues:

(1) The date on which Peter and Kathy entered into the Loan Agreement (defined below) with Voukidis Holdings Pty Ltd (Voukidis Holdings).

(2) Whether Voukidis Holdings was a secured creditor of Peter and Kathy (with security over their home at 3 Wyatt Avenue, Burwood NSW (the Property) pursuant to the Loan Agreement, notwithstanding that no mortgage in registrable form was provided by Peter and Kathy until 2021.

(3) Whether Voukidis Holdings’ rights as a creditor of Peter and Kathy are an asset of the KEPP CO Unit Trust (the KC Trust), or held by Voukidis Holdings in its own right.

(4) Whether the Loan Agreement should be set aside on the ground of unconscionable conduct and/or undue influence.

(5) The amount for which Voukidis Holdings should be admitted as a creditor of the bankrupt estates of Peter and Kathy.

(6) Whether Peter and Kathy authorised the transfer of their 1003 ordinary shares in Voukidis Holdings to ZV Asset Management Pty Ltd (ZVAM) in May to August 2020 and, if so, whether the transfer should be avoided under s 120 or s 121 of the Bankruptcy Act 1966 (Cth) (the Act).

3 The factual background to the present issues arising is as follows.

Peter, Kathy, Christos and the loans

4 The Property was Peter and Kathy’s home. In 2007, they took out a loan with AMP Bank (AMP). In August 2009, Peter and Kathy applied to AMP to refinance their existing loan (which then stood at $162,000) into a new, interest only loan of $720,000. False statements were made in the application as to their income. There is no suggestion AMP was aware of the false statements when it approved their application.

5 Christos deposed that his parents entered into the 2009 loan with AMP so as to provide funds (he said by loan) to enable him to pay legal expenses associated with legal proceedings in the Supreme Court of Victoria. I will refer to that particular proceeding (being proceeding No 2014 of 2005) as the Joint Venture Proceeding. The Applicant relied on documents filed in that proceeding in impugning Christos’ credit. I return to the Joint Venture Proceeding below.

6 As at August 2009, Peter was 77 and Kathy was 72. Both Peter and Kathy were retired and depended on Christos to assist them with their living expenses, which he did. Both Peter and Kathy were born in Greece. Kathy could not read English. Peter previously worked as a courier between 1990 and 2000, and had some work as a pedestrian crossing supervisor after he retired in 2000. Kathy worked in a café run by the family, and retired from work in or about 2000.

7 On taking out the 2009 loan with AMP, Peter and Kathy provided $550,000 to Christos between September and December 2009. He needed funds for legal expenses in litigation. Christos did not repay the sums advanced by his parents.

8 On the Respondents’ case, the payments to Christos were advanced pursuant to a loan agreement dated 5 September 2009 (the 2009 Loan Agreement). The Applicant disputed that the 2009 Loan Agreement was entered into on 5 September 2009, and contended that it was in fact created by Christos in 2016 to enable Peter and Kathy to be admitted as creditors of Christos for an inflated amount when Christos was seeking to enter into a personal insolvency agreement instead of becoming a bankrupt. I say more about the 2009 Loan Agreement at paragraphs 113 to 114 below.

9 Initially, Peter and Kathy met their obligations to pay interest to AMP by drawing down on funds under the 2009 AMP loan but, by late 2010, their capacity to fund the interest payments in that way was close to being exhausted.

10 The apparent solution was for Peter and Kathy to enter into a loan agreement with Voukidis Holdings and pay interest on the AMP loan from those loaned funds. A written loan agreement, dated 1 October 2010 on its face (the Loan Agreement), was signed by Peter, Kathy and Voukidis Holdings. Under the Loan Agreement, Voukidis Holdings was to lend $3 million to Peter and Kathy. Whether Voukidis Holdings obtained a security interest in the Property pursuant to this agreement is disputed, as is the date the document was signed; the Respondents said it was signed on 1 October 2010, but the Applicant contended the Loan Agreement was backdated, and in fact only signed some time in 2020 as it became clear that Peter and Kathy were headed for bankruptcy.

11 Under the Loan Agreement, the standard interest rate was 12% per annum and the default interest rate was 24% per annum. Interest was calculated monthly, and unpaid interest was capitalised monthly.

12 Voukidis Holdings has claimed to be a secured creditor in the bankruptcies of Peter and Kathy. Between 4 November 2010 and 20 July 2021 (being the date of Peter and Kathy’s bankruptcies), Voukidis Holdings advanced around $373,650 to Peter and Kathy. A transfer of $95,000 from Peter and Kathy to Voukidis Holdings on 7 December 2020 was treated by Voukidis Holdings as a partial repayment. A further transfer of $10,000 by Peter to Voukidis Holdings on 16 July 2021 was also treated by the Applicant as reducing the net balance advanced by Voukidis Holdings to Peter and Kathy. While the $10,000 sum was not recorded as reducing the balance in all schedules produced by Voukidis Holdings, it was recorded as reducing the balance owing in the schedule addressed to Peter and Kathy and dated 11 July 2022. If both of these sums are included, that brings the net total advanced over that time to about $268,650.

13 With the application of interest compounding monthly at 12% and then at 24% (from July 2011), the gross total amount claimed by Voukidis Holdings in the bankruptcies of Peter and Kathy was $1,852,200 (although that amount was claimed to be owing as at 31 August 2021). The asserted justification for the application of the default rate of interest was the failure of Peter and Kathy to provide a mortgage in registrable form.

14 Voukidis Holdings did not lodge a caveat on the title to the Property until on or about 25 August 2020 (caveat AQ339359). The caveat stated that the interest claimed was a “mortgage” pursuant to the Loan Agreement.

15 The due date for repayment stipulated in the Loan Agreement was 30 June 2021. On or about 31 March 2021, Peter and Kathy signed a loan deed with Voukidis Holdings as lender (the Loan Deed). The Applicant did not contend this document was backdated. It was, unlike the earlier Loan Agreement, witnessed by an independent third party. The principal sum under the Loan Deed included sums advanced under the earlier Loan Agreement.

16 Peter and Kathy executed a mortgage in registrable form dated 22 March 2021 (the Mortgage). The Applicant did not contest the dating of that document.

17 Under the 2021 Loan Deed and Mortgage, the date for repayment was the earlier of the sale of the Property or the deaths of Peter and Kathy.

The corporate entities and share transfers

18 Some matters concerning the relevant corporate entities need to be explained.

19 Voukidis Holdings was incorporated on 21 November 1994. Its initial directors were Peter, Kathy, Christos and Olga Sclavenitis, who at that time (and until February 2018) adopted her married name: Olga Voukidis. I will refer to Ms Sclavenitis as Olga. Olga was married to Christos. They separated in 2013 and divorced in 2017.

20 At incorporation, the shares in Voukidis Holdings were divided into ordinary shares and dividend variable shares. The shares were held as follows:

(a) C&O Voukidis Pty Ltd (COV) held one dividend variable share and 1000 ordinary shares; and

(b) Christos, Olga, Peter and Kathy each held one dividend variable share and one ordinary share.

21 COV was the trustee of the Voukidis Family Trust and the Voukidis Family No. 2 Trust. The capacity in which COV held its shares in Voukidis Holdings was not clear on the evidence, however, nothing turns on that.

22 On 20 June 2013, Olga ceased to be a director of Voukidis Holdings.

23 On 1 May 2014, Peter and Kathy resigned as directors of Voukidis Holdings and, on the same day, COV transferred its 1000 ordinary shares in Voukidis Holdings to Peter and Kathy in equal shares (ie 500 shares each), and transferred its one dividend variable share to Peter. COV went into liquidation on 27 May 2014, shortly after transferring its shares in Voukidis Holdings to Peter and Kathy.

24 On 29 April 2016, Christos ceased to be formally recorded as a director of Voukidis Holdings, although the Applicant contended Christos continued to control Voukidis Holdings. Also on 29 April 2016, Christos transferred his one ordinary share and one dividend variable share in Voukidis Holdings to Peter. Peter was also appointed Voukidis Holdings’ sole director. Four days after transferring his shares in Voukidis Holdings to Peter, Christos became a bankrupt on 3 May 2016.

25 Peter and Kathy claimed in Christos’ bankruptcy for over $2.8 million. That claim was made on the basis of amounts advanced by Peter and Kathy to Christos, purportedly pursuant to the 2009 Loan Agreement.

26 Just as Christos divested his shares in Voukidis Holdings just before his bankruptcy, and COV divested its shares just before its liquidation, Peter and Kathy transferred their shares in Voukidis Holdings shortly before their bankruptcies.

27 On 5 August 2020, an ASIC Form 484 was lodged in respect of Voukidis Holdings. Christos, in his capacity as a director of Voukidis Holdings, certified that the information in the form was “true and complete”. The form recorded that it was “signed” on 5 August 2020 but did not bear any signature.

28 A second copy of the ASIC form dated 4 August 2020 — and which the evidence established had not been lodged with ASIC — was in evidence. That copy was signed by both Christos and Peter, apparently on 5 October 2020.

29 On their face, both forms recorded the resignation of Peter as a director and secretary of Voukidis Holdings on 15 May 2020, and the appointment of Christos in his place. They also recorded the transfer of 502 ordinary shares in Voukidis Holdings from Peter to ZVAM, and 501 ordinary shares from Kathy to ZVAM. The “earliest date of change” in respect of those transfers was recorded as 15 May 2020.

30 Whether Peter and Kathy in fact transferred their shares in Voukidis Holdings to ZVAM prior to their bankruptcies was in issue in this proceeding.

31 In some apparent housekeeping, a Transfer of Shares document dated 15 May 2020 was prepared that purported to transfer Olga’s one ordinary share and one dividend variable share in Voukidis Holdings to Christos for $2. Christos did not dispute that he applied Olga’s signature to this document, but Olga maintained she had not authorised Christos to do so. Olga also said that she had reverted to her maiden name — Sclavenitis — in 2018, so was not signing as “Olga Voukidis” at the time her “Voukidis” signature was applied by Christos in 2020.

32 COV was incorporated on 13 May 1994. At the time, its directors were Christos and Olga. Christos and Olga each held one dividend variable share and one ordinary share in COV.

33 As mentioned above, COV acted as the trustee of both the Voukidis Family Trust and the Voukidis Family No. 2 Trust.

34 On 20 June 2013, Olga ceased to be a director of COV. On 10 March 2015, Olga ceased to be a shareholder of COV.

35 On 27 May 2014, COV entered into liquidation.

36 On 4 May 2016, following his bankruptcy, Christos ceased to be a director of COV.

37 COV was deregistered on 22 November 2020.

38 ZVAM was incorporated on 7 August 2008. Its directors at the time were Christos and Maurizio Zappacosta, who together owned all of the share capital in ZVAM (each holding one ordinary share).

39 Mr Zappacosta is an accountant and was a business associate of Christos.

40 On 4 July 2013, Christos transferred his ordinary share in ZVAM to MM Asset Management Pty Ltd.

41 On 29 April 2016, a few days before his bankruptcy, Christos ceased to be a director of ZVAM, and Robert Leidl was appointed in his place.

42 On 16 June 2014, Mr Zappacosta resigned as a director of ZVAM, leaving Mr Leidl as its sole director. Mr Leidl was a business associate of Christos. Mr Zappacosta retained his shareholding in the company, and remained a shareholder at least to 20 December 2022 (being the date of the ASIC register search in evidence), as to one ordinary share.

43 As noted above, the Respondents claim that on 15 May 2020 Peter and Kathy transferred their shares in Voukidis Holdings to ZVAM. I address these purported share transfers in more detail below.

44 On 8 January 2021, Mr Leidl resigned as a director of ZVAM, and Peter Christopher Voukidis, Christos and Olga’s son, was appointed in his place.

45 On 16 March 2021, a form was lodged with ASIC notifying that MM Asset Management Pty Ltd had transferred its ordinary share in ZVAM to Voukidis Management Pty Ltd (Voukidis Management), and that a further three ordinary shares had been issued to Voukidis Management. The form specified 28 February 2021 as the earliest date of change.

46 On 25 August 1998, the KC Trust was established. The initial trustee was Con Calagis, Ms Calagis’ husband, and the sole unitholder was COV in its capacity as trustee for the Voukidis Family Trust.

47 Sometime between 25 August 1998 and 15 March 2001, Mr Calagis retired as trustee of the KC Trust and Kepp Co Pty Ltd (Kepp Co) was appointed in his place.

48 On 30 June 2003, Kepp Co retired as trustee of the KC Trust and Voukidis Holdings was appointed in its place.

49 The authenticity of the (very limited) financial records produced by Voukidis Holdings in the present proceeding is disputed, as is whether it entered into the Loan Agreement and made advances to Peter and Kathy in its own right, or as trustee of the KC Trust.

Properties, bank accounts and transactions: the AMP accounts and advances from Voukidis Holdings to Peter and Kathy

50 Peter and Kathy owned and lived at the Property, which is 3 Wyatt Avenue, Burwood. Christos and Olga lived next door, at 5 Wyatt Avenue. Christos and Olga moved out of 5 Wyatt Avenue and, from August 2005, rental income in respect of 5 Wyatt Avenue was received by Voukidis Holdings. Olga’s evidence was that they lived at 5 Wyatt Avenue until about 2000, before moving to 5 Appian Way, Burwood, and then to 37 Thompson St, Drummoyne. Christos gave evidence that rent only began to be received in respect of 5 Wyatt Avenue from August 2005 because until that point he and Olga resided there. Nothing turns on whether Olga and Christos moved from the property in 2000 or 2005.

60 Belmore St, Burwood, and Peter and Kathy’s claims to be creditors of COV in its liquidation

51 60 Belmore St, Burwood, was another property owned by Peter and Kathy (the Belmore St Property). That property was transferred to COV in April 2003. The Belmore St Property was sold in March 2012. Break Fast Investments Pty Ltd (Break Fast) was COV’s principal creditor. In June 2017, Peter and Kathy pursued their claim to be creditors of COV, entitled to the proceeds of sale of the Belmore St Property, by litigation in the Supreme Court of Victoria (the COV Proceeding).

52 Peter and Kathy’s entitlement was said to arise pursuant to a letter dated 12 February 2003, recording the terms of a loan from them to COV (as trustee for the Voukidis Family No. 2 Trust) upon the transfer of their interest in the Belmore St Property. The Applicant in this proceeding contended that the 2003 loan letter was backdated and only devised to support a claim being made in COV’s liquidation to the proceeds of sale of the Belmore St Property, and to thwart Break Fast’s claim to the proceeds of sale of the Belmore St Property.

53 Break Fast, on behalf of COV (then in liquidation) contested Peter and Kathy’s claim. On 14 June 2018, Sloss J (having delivered reasons for judgment on 24 May 2018) dismissed Peter and Kathy’s claim and ordered that Peter and Kathy pay the defendant’s costs of the proceeding to Break Fast, to be taxed if not agreed.

54 In reliance on the costs order, on 4 May 2020 Break Fast caused a summons for taxation of costs to be filed, by which it claimed $347,372.35 in costs. In seeking to oppose the taxation, Peter and Kathy authorised Christos to provide instructions to a costs solicitor.

55 Relevantly, a title search of the Property (being Peter and Kathy’s residence) performed on 4 May 2020 revealed that the only encumbrance on the title to that property (aside from an easement for drainage) as at that date was a mortgage in favour of AMP.

56 On 14 July 2020, the Supreme Court of Victoria issued a “Notice of Estimate” which informed the parties that, if subject to taxation, the costs likely to be payable by Peter and Kathy would be $223,130. Interim orders were then made on 27 July 2020, requiring Peter and Kathy to pay $100,000 to Break Fast.

57 Shortly thereafter, and as mentioned above, on or about 25 August 2020, a caveat was lodged on the title to the Property on behalf of Voukidis Holdings. The caveat claimed that Voukidis Holdings’ interest arose pursuant to a mortgage dated 20 August 2020 between Voukidis Holdings and Peter and Kathy. The caveat referred to a supporting document described as “Loan Agreement dated 1 Oct 2010”.

58 On 27 October 2020, the Supreme Court of Victoria fixed the costs payable to Break Fast by Peter and Kathy in the sum of $264,965.47.

59 Peter and Kathy’s liability to Break Fast for the costs of the failed litigation then led to their bankruptcies.

Receipts into, and payments from, Voukidis Holdings’ bank account

60 Between 2001 and March 2012, monthly rental payments in respect of the Belmore St Property were deposited in Voukidis Holdings’ bank account.

61 Christos’ evidence was that Voukidis Holdings received rents from 5 Wyatt Avenue and the Belmore St Property in some kind of managerial capacity. There were no documents concerning this arrangement in evidence, and Christos’ evidence did not detail the nature of that arrangement. However, nothing presently turns on the capacity in which Voukidis Holdings received those rents.

62 In addition to the rental receipts from those two properties, Voukidis Holdings received transfers from other entities associated with Christos: T-Pay Australia Pty Ltd, Meet Me Introductions Pty Ltd and Gravity Ventures Pty Ltd.

63 The bank account statements of Voukidis Holdings’ account show that Peter and Kathy received $2,500 per month from that account from (at least) March 2001 to June 2008. Prior to February 2004, those transfers out of the Voukidis Holdings bank account had narrations that referred to Peter and Kathy. While those narrations no longer appeared from February 2004, it was accepted that the transfers were to Peter and Kathy.

64 The amount of the regular transfers then increased to $3,500 per month from June 2008. Those regular transfers continued during and after November 2010, until April 2016 (although no transfers were made in June 2009 and November 2013, and there was an additional transfer of $5,000 in February 2012). The Respondents contended that, from November 2010, the transfers were made pursuant to the Loan Agreement, which they contended was entered into on 1 October 2010.

65 The transfers to Peter and Kathy recommenced in August 2016, mostly in the sum of $3,000, although the amount varied and was higher in some months.

66 Between August 2019 and January 2021, five payments of $4,200 each were made to Peter and Kathy.

67 From September 2009, the monthly transfers out of Voukidis Holdings’ bank account can be reconciled with Peter and Kathy’s AMP bank statements, confirming that they were in fact paid to Peter and Kathy.

Servicing the AMP loan and the offset account

68 Bank statements for Peter and Kathy’s offset account with AMP were in evidence. Those statements show draw downs and payments out by cheque, being the means by which the funds referred to in paragraph 7 above were provided to Christos.

69 Peter and Kathy’s interest payments were made by deductions from the offset account. Initially, they made small drawdowns against the loan to fund the interest payments. Then, from 4 November 2010, transfers from Voukidis Holdings into the offset account provided the means by which Peter and Kathy met their interest obligations under the AMP loan.

70 The COV Proceeding, referred to above, was not the only litigation in which the Voukidis family was engaged.

71 I refer to other litigation in addressing matters concerning Christos’s credit.

THE WITNESSES, ISSUES OF CREDIT AND HEARSAY

72 The Applicant relied on: two affidavits sworn by him, dated 21 February 2023 and 12 April 2023; two affidavits of his solicitor, Alan James Foster, dated 15 June 2023 and 10 October 2023; two affidavits of Greg Joseph Taylor, a director of Break Fast, dated 16 August 2023 and 5 September 2023; an expert report of Andrew Le, dated 22 August 2023; a further expert report of Mr Le, dated 5 September 2023; an expert report of John Ganas, dated 21 January 2024; and a further expert report of Mr Ganas, dated 29 May 2024.

73 The Applicant also called Olga, to whom a subpoena to give evidence had been issued. Olga was cross-examined. The Applicant’s other witnesses, and the two experts, were not cross-examined.

74 The Respondents relied on: two affidavits of Christos, dated 14 September 2023 and 9 May 2024; an affidavit of Ms Calagis, dated 22 March 2024; and an affidavit of Mr Zappacosta, dated 13 June 2024. Christos, Ms Calagis and Mr Zappacosta were cross-examined.

Hearsay evidence of Peter and Kathy

75 The Applicant sought to adduce hearsay evidence of Peter and Kathy pursuant to s 67 of the Evidence Act 1995 (Cth) (the Evidence Act) on the basis that Peter and Kathy were not available to give evidence. Peter is deceased. Kathy is elderly and in ill-health. It was accepted that she was unable to give evidence.

76 Some of the documents tendered as hearsay evidence were not objected to. I ruled against the Respondents’ objection to one document tendered as hearsay evidence of Peter and Kathy (being a joint affidavit they swore in a proceeding in the Supreme Court of Victoria). Some additional hearsay evidence (transcript extracts of evidence given by Gerard O’Hea and Theo Baker in Supreme Court of Victoria proceedings) was also tendered pursuant to s 64 of the Evidence Act, without objection.

77 The Applicant sought to adduce tendency evidence, being evidence adduced to prove that Christos has or had a tendency to create false documents, backdate documents, knowingly give false evidence on oath and give false instructions to lawyers.

78 The tendency evidence was sought to be adduced after notice was given under s 97(1) of the Evidence Act. I granted a dispensation under s 100(1) of the Evidence Act from the notice requirement in s 97 in relation to a document that was not referred to in the tendency notice served on the Respondents, and admitted the tendency evidence over the Respondents’ objections, for reasons recorded in the transcript.

79 Olga was called by the Applicant. She gave evidence on subpoena concerning her relationship with Christos and their homes, her involvement (or lack thereof) with the activities of COV and Voukidis Holdings, and the application of her signature to various documents. She was cross-examined. I accept Olga as a witness of truth, although her evidence on some matters (referred to below) was of limited probative value.

80 Ms Calagis was called by the Respondents, and was cross-examined. With the Applicant’s agreement, Ms Calagis was cross-examined by video link from New South Wales as she had caring responsibilities for Kathy. Ms Calagis’ evidence focused on the execution of the Loan Agreement and, in particular, whether it was executed in 2010. I have accepted her evidence, as detailed below.

81 The Respondents called Mr Zappacosta. He was cross-examined, also by video link from New South Wales. His evidence concerned whether Voukidis Holdings entered into the Loan Agreement and made advances to Peter and Kathy as trustee of the KC Trust or in its own capacity. I have rejected his evidence. Mr Zappacosta made himself the uncritical mouthpiece of Christos and gave baseless evidence.

82 To a large extent, the Respondents’ case relied on evidence given, and documents produced, by Christos. The Applicant urged the Court to find that Christos is an unreliable witness, whose evidence should not be accepted unless it is independently corroborated by documents or other witnesses whose evidence is also accepted. In aid of that submission, the Applicant adduced the tendency evidence referred to above. I address this evidence below.

83 The Joint Venture Proceeding involved Ambridge Investments Pty Ltd and Break Fast, which was controlled at the relevant time by Christos.

84 On 24 August 2009, Christos swore an affidavit in the Joint Venture Proceeding in his capacity as a director of Break Fast, the sixth defendant to the proceeding. Christos gave evidence that Break Fast had discovered bank statements in the Joint Venture Proceeding. Christos had manipulated those bank statements. Christos sought to explain his conduct in manipulating the bank statements in his 24 August 2009 affidavit. He said as follows (emphasis added):

Some of the statements which have been discovered are incorrect or incomplete. I have altered some of these statements prior to them being discovered in this proceeding. I provide this affidavit in explanation of alterations of those statements which I performed and apologise to the Court.

85 Christos went on to explain the reasons why he amended the bank statements (emphasis added):

By about August 2007 and at the time I first made some of these alterations I was getting extremely frustrated at the intrusion placed upon Break Fast’s business activities and business relationships by the activities of the plaintiff and particularly the actions of Greg Taylor.

…

Because of this frustration and the fact that, in my view, the plaintiff had no right to know what the ongoing business was of Break Fast until they had established any interest in the company, which is expressly denied, I altered some of the transactions that had occurred. This was in an effort to avoid endless investigations and continuing each and every transaction entered into by Break Fast which I viewed as being premature and an abuse of process.

I now realise that my actions were not appropriate. The extreme seriousness of the conduct I have engaged in has been thoroughly explained to me by my lawyers. I am deeply regretful of my actions and sincerely wish to apologise to this Honourable Court.

86 Christos’ affidavit exhibited a table setting out the alterations he had made. Some were as to the description of the transaction concerned, and some were as to the amount of the transaction. In total, there were more than 85 alterations admitted to. Some of the amounts altered were substantial. For example, Christos deposed to having changed an entry in a bank statement from $20,000 to $180,000.

87 On his own admission, Christos falsified evidence in a Supreme Court of Victoria proceeding. The gravity of this conduct alone, exhibiting, as it does, Christos’ willingness to falsify documents to serve his personal and business ends, would lead me to conclude that Christos is not an honest and truthful person whose evidence can be taken at face value. But the litany of Christos’ misdeeds goes on, reinforcing that conclusion.

88 On 24 August 2009, Christos swore a further affidavit in the Joint Venture Proceeding deposing to the circumstances surrounding his non-compliance with orders made in that proceeding on 3 May 2007.

89 Paragraph 2(a) of the 3 May 2007 orders directed that the sum of $320,210 be paid into an interest-bearing trust account with Rigby Cooke solicitors, and provided that such amount could only be withdrawn for two purposes: payment of costs associated with compliance with orders made in a related proceeding for the removal of cladding from the property at 176 Wellington Parade, East Melbourne (the Wellington Parade Property); or the payment of such sum into Court pending the hearing of an appeal against the orders made in the related proceeding.

90 The 3 May 2007 orders also provided, by paragraph 2(b), for payment of a further $340,000 into the Rigby Cooke interest-bearing trust account and that such funds were only to be withdrawn for payment of legal costs incurred by Break Fast in the Joint Venture Proceeding.

91 In his second 24 August 2009 affidavit, Christos deposed that while the funds the subject of the orders were not paid into a Rigby Cooke trust account, they had only been applied for purposes permitted by the orders. The relevant paragraphs of the affidavit are as follows:

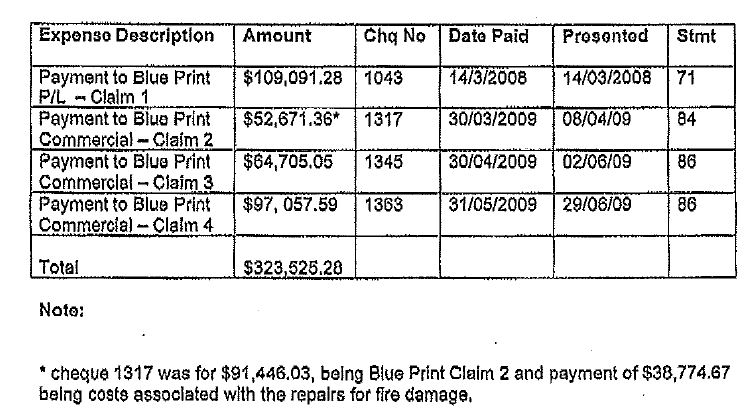

7. All of the funds which were the subject of the Orders made on 3 May 2007 were expended consistent with those Orders. For the cladding removal as provided for in order 2 (a), $323,526.28 was paid to Blue Print Commercial or to third parties at their direction. Each of the cheque requisition documents, invoices, bank accounts and general ledgers reflecting these payments have been discovered (including documents numbered 42, 93, 135 and 136 in the Defendants Supplementary Discovery). A further amount of $459,932.81 has been paid to Rigby Cooke lawyers and to G.W Meldrum Barristers Clerk. The Defendants maintain a claim of legal professional privilege over the Rigby Cooke invoices. I am informed and verily believe that Rigby Cooke will verify the amount paid for legal expenses in a separate affidavit. The cheque requisition documents and bank statements have been discovered. The rest of the monies released were applied to the Sixth Defendant's funds as working capital.

8. The payments referred to in paragraph 7 (save for $120,000 referred to below) were made from an interest bearing cash management account in the name of the sixth defendant account number 87-401-8316 which was not a Rigby Cooke trust account. I am informed by my solicitors and verily believe that in October 2008 a trust account was opened at Rigby Cooke in the name of Break Fast Investments Pty Ltd. An amount of approximately $120,000 was paid into that account by Break Fast Investments Pty Ltd and applied to outstanding legal invoices. This made up part of the $459,932.81 referred to above. Because the monies were spent consistently with the Orders made 3 May 2007 I did not think that it was necessary for all the monies to go into the Rigby Cooke trust account.

9. I deeply regret the failure to comply with the Orders by paying the funds out of an account which was not a Rigby Cooke trust account, although the funds were paid out only to the parties for which the funds were permitted by the Orders.

92 Exhibited to the affidavit at CV-1 was a document titled “Summary of Application of Funds Referred to in paragraph 2(a) [of the 3 May 2007 orders] being $320,210”. Exhibit CV-1 comprised the following table:

93 As can be seen, the first payment recorded in the table was an amount of $109,091.28 paid on 14 March 2008. It was described as “Payment to Blue Print P/L – Claim 1” and was said to be associated with cheque number 1043 and bank statement 71.

94 The payment of $109,091.28 and cheque number 1043 were the subject of evidence in a further proceeding in the Supreme Court of Victoria involving Break Fast, Christos and Gravity Ventures Pty Ltd (the Gravity Proceeding). In the Gravity Proceeding, Break Fast tendered evidence including:

(a) a copy of a Break Fast cheque requisition dated 14 March 2008 in relation to cheque number 1043;

(b) a copy of a Valleyclad Pty Ltd (Valleyclad) “tax invoice” dated 3 December 2007 addressed to Break Fast as “client” and in the amount of $109,091.29;

(c) a copy of a National Australia Bank (NAB) bank statement numbered 71 with two relevant entries on 14 March 2008 for “Bank Cheque Issue Fee” in the amount of $8.00 and “Miscellaneous Debit” in the amount of $109,091.28; and

(d) a copy of a NAB bank cheque dated 14 March 2008, payable to “R Romano” in the sum of $109,091.28.

95 The director of Valleyclad, Mr O’Hea, gave evidence in the Gravity Proceeding to the effect that Valleyclad had not prepared or issued the “tax invoice” dated 3 December 2007 and that, despite what the documents produced by Break Fast indicated, Valleyclad had not worked for, and did not receive payment from Break Fast.

96 Mr Baker, a former director of Break Fast, also gave evidence in the Gravity Proceeding. Mr Baker explained that it would be inconsistent for Valleyclad to issue a tax invoice directly to Break Fast in circumstances where the relevant works were contracted to Break Fast by Blue Print Commercial (for whom Valleyclad was a subcontractor). Mr Baker also gave evidence that he had come to understand that the $109,091.28 cheque had been applied by Christos to purchase a property at 8 Third Avenue, Lane Cove NSW (the Lane Cove Property) from “R Romano”. Mr Baker’s evidence was that Christos had used the funds without the consent of Break Fast.

97 The evidence of Mr O’Hea was admitted as hearsay evidence in this proceeding after the Applicant served a notice as to the hearsay evidence. The Respondents withdrew their objection to the admission of the hearsay evidence of Mr O’Hea, and that of Mr Baker.

98 Christos was cross-examined in this proceeding about the evidence tendered by Break Fast in the Gravity Proceeding and his second 24 August 2009 affidavit, filed in the Joint Venture Proceeding. Christos accepted that:

(a) the sum of $109,091.28 was “probably” used by him to purchase a bank cheque in the name of R Romano in order to purchase the Lane Cove Property;

(b) the evidence which he had given at paragraphs 7 to 9 of his affidavit was “false” and “inaccurate”; and

(c) he knew, at the time of making the affidavit, that the representations contained at CV-1 as to the payment of $109,091.28 to Blue Print Commercial on 14 March 2008 were inaccurate.

99 When pressed as to his knowledge of the 3 May 2007 orders, Christos accepted that he “did know of the orders” but sought to minimise his understanding of them, claiming to recall there having been “a significant amount of confusion as to exactly how those orders were to be executed” and suggesting that he had not been intimately aware of how to comply with them.

100 It is frankly staggering that, on the very same day he was swearing an affidavit confessing to, and apologising for, having manipulated bank statements, Christos swore another affidavit riddled with mistruths. This second affidavit falsely claimed that the funds that Christos had, in breach of court orders, put towards buying the Lane Cove Property had been applied to a purpose sanctioned by the Court’s orders (cladding removal works).

101 The principal issue in the Joint Venture Proceeding was whether Break Fast was acting as a company in its own right, or as the manager of an unincorporated joint venture, in relation to its investment in the Wellington Parade Property.

102 On 4 September 2008, Christos swore a “further supplementary affidavit of documents” in his capacity as a director of Break Fast. The affidavit discovered, as document 63, a copy of a document described as a “facsimile from Graham Jacobs to Anthony Fink” dated 13 September 2001.

103 As it happened, another copy of the fax from Mr Jacobs to Mr Fink dated 13 September 2001 was discovered in the Joint Venture Proceeding. The two versions of the fax appeared identical at first glance, both bearing the date “13/09/01” and time “10:17:19 AM”. However, the two documents differed in the following important respects:

(a) on the first page, in the first paragraph of the letter, the words “joint venture” had been replaced with the word “company” in the version discovered by Christos;

(b) on the second page, in the draft balance sheet, the words “Partners’ Equity” had been replaced with the words “Shareholders’ Equity” in the version discovered by Christos;

(c) in the draft balance sheet, references to “Ambridge Investments Pty Ltd Capital” and “Total Ambridge Investments Pty Ltd” had been replaced by references to “Mark Stanley Capital” and “Total Mark Stanley” in the version discovered by Christos; and

(d) on the third page, the words “Total Partners’ Equity” had been replaced with the words “Total Shareholders’ Equity” in the version discovered by Christos.

104 Christos was cross-examined in the Joint Venture Proceeding regarding the “altered” version of the fax but denied that he had manufactured the version discovered by his affidavit of documents dated 4 September 2008.

105 Christos was again cross-examined about this document in this proceeding. He accepted that the characterisation of the activities of Break Fast as those of a manager of an unincorporated joint venture — as opposed to a company — was of central importance to the outcome of the Joint Venture Proceeding. It was put to Christos that, at the time of making the affidavit of documents in September 2008, he knew that the document was false and nonetheless put it forward as a genuine document. Christos gave evidence that he did not recall knowing the document to be false at the time it was put forward, nor how he came to have the document.

106 Christos’ evidence was not persuasive. It was evasive. I do not accept Christos’ evidence in this proceeding that he did not recall knowing the document to be false at the time he put it forward in giving discovery in the Joint Venture Proceeding.

COV Proceeding and the tax returns

107 As outlined above, in around June 2017 Peter and Kathy commenced the COV Proceeding.

108 On 23 May 2017, in a separate proceeding before the Supreme Court of Victoria, the liquidator of COV had obtained orders that they were justified in not further investigating Peter and Kathy’s claim and would be justified in not defending, and in causing the company not to take further steps to defend, any proceeding commenced by Peter and Kathy in relation to that claim. As such, the COV Proceeding was defended by Break Fast who, as the only other significant creditor of COV, was granted leave to defend the proceeding for and on behalf of COV.

109 Peter and Kathy’s entitlement was said to arise pursuant to a letter dated 12 February 2003, recording the terms of a loan from them to COV upon the transfer of their interest in the Belmore St Property. I return to this letter below.

110 As mentioned above, Peter and Kathy took out a loan from AMP in 2009. The loan application enclosed documents described as Peter and Kathy’s tax returns in respect of the 2007 and 2008 income years. Christos was cross-examined about these documents in the COV Proceeding. He gave evidence that:

(a) he, in conjunction with a finance broker, filled out the home loan application form on behalf of Peter and Kathy;

(b) the income tax returns were “draft” returns prepared for the purpose of the loan application, and the information in the returns was provided by him;

(c) he knew the information would be relied upon by AMP to increase the facility to $720,000; and

(d) the rental income shown in the tax returns (being Peter and Kathy’s sole source of income described in the returns) was inaccurate in that it was not properly attributable to Peter and Kathy.

111 Christos was also cross-examined about the AMP loan application documents in this proceeding. He accepted that AMP would require information about Peter and Kathy’s ability to service the debt, and that the tax returns enclosed with the application (whether or not they were in draft or final form) made representations as to Peter and Kathy’s income in respect of the 2007 and 2008 income years. However, when pressed on the accuracy of the returns, and despite his previous evidence in the COV Proceeding, Christos seemed to suggest that the returns were not, by reason of their being in draft form, inaccurate. At one point during his cross-examination, Christos sought to shift the blame to AMP for not having requested income tax assessments (cf returns). Ultimately, Christos accepted that the returns provided in support of the loan application were false when viewed against Peter and Kathy’s tax returns as ultimately filed. His evidence on this topic was evasive and unconvincing.

112 I find that Christos:

(a) provided the income figures contained in the tax returns;

(b) knew that AMP would rely on the income figures provided in the tax returns for the purposes of assessing whether to advance the loan, whether or not they were in fact “draft” returns; and

(c) knew the income figures in the tax returns were inaccurate and deliberately overstated them in order to secure the loan, which was taken out entirely for his benefit.

113 As noted above, the Applicant disputed that Christos and his parents entered into the 2009 Loan Agreement in 2009. In support of his submission that the 2009 Loan Agreement was in fact created in 2016, the Applicant relied on the following evidence:

(1) In the COV Proceeding, Peter gave evidence (in September 2017) that about two or three years prior, he had adopted a “curl” to his signature. However, that “curl” was present on the 2009 Loan Agreement, whereas it was not present on, for example, his signature on the AMP loan application, dated 10 August 2009. The Applicant also pointed to other documents signed by Peter in 2016 and 2017 which contained the “curl”, in relation to which Peter gave evidence. The signature appearing on the 2009 Loan Agreement was as follows:

Peter’s signatures appearing on the 2009 AMP home loan application were as follows:

An example of the “curl” appearing in Peter’s signature on other documents signed in 2017 included the following:

(2) The Applicant also relied on a discrepancy between the figure disclosed by Christos on oath to be owing to his parents as at 30 September 2014 ($750,000) and the amount purportedly owing at that date, calculated pursuant to the provisions of the 2009 Loan Agreement, according to the Schedule enclosed to Peter and Kathy’s proof of debt lodged in Christos’ bankruptcy ($1,985,913.65).

114 The evidence supports a conclusion that the 2009 Loan Agreement was not signed in 2009 due to the changes to Peter’s signature. Christos had Peter’s electronic signature, and a strong motive to backdate the document (to inflate the amount for which his parents would be admitted in his bankruptcy, and maximise their resulting voting power in the decision to enter into a personal insolvency agreement). I accept the Applicant’s contention that the 2009 Loan Agreement is an example of a document backdated by Christos.

115 As explained above, the 12 February 2003 letter was put forward by Peter and Kathy in the COV Proceeding in support of their claim to part of the proceeds of sale of the Belmore St Property in priority to Break Fast.

116 The Applicant submitted that the letter was put forward in the COV Proceeding as a genuine document when in fact it had not been created in 2003, having instead been created by Christos for the purposes of that proceeding. In support of his submission, the Applicant relied on the following evidence:

(1) Olga’s evidence that the first time she had seen the letter was in the months prior to the trial of this proceeding, when she was shown a copy by the Applicant’s solicitor. While identifying the signature on the document as her own, Olga gave evidence that she doubted that she had signed the document. Olga explained that it was unlikely she would have been with her father (whose signature appears on the document as a witness) on a school night, that she did not consider it plausible that her father would have signed “in the air” as opposed to on the line, and that — on the assumption that her father, Peter and Kathy were in the same room when the document was signed — she did not believe Peter, Kathy and her father would have discussed each other’s assets with one another.

(2) That Olga had not authorised anyone to apply her digital signature to this document.

(3) The second expert report of Mr Ganas, which concluded that it was most likely that Olga’s signature on the letter was a digital signature produced by a process of “cut and paste forgery”.

(4) That the letter features Peter’s “curl” signature, however (and as explained at paragraph 113(1) above), Peter gave evidence in the COV Proceeding that he had only adopted that form of signature in approximately 2014.

117 Christos was cross-examined about the genuineness of this document in this proceeding. He rejected any suggestion that the letter had been “concocted” by him sometime between 2014 and 2017 to enable Peter and Kathy to put forward a claim to the proceeds of sale of the Belmore St Property, or that he had applied Olga’s signature to the document in order to create the appearance that it had been signed by her. Christos appeared to maintain that Olga’s signature on the letter was not a digital signature at all.

118 On the basis that the letter features Peter’s “curl” signature and not the signature he was using before about 2014, I accept the Applicant’s contention that this document was backdated. I do not base that conclusion on Olga’s evidence regarding the location of her father’s signature relative to the signing line.

119 In this proceeding, the Respondents produced a document purporting to be a letter from Voukidis Holdings to Peter and Kathy dated 11 July 2022. The letter said: “Please find below the statement for the period 1 July 2021 to 30 June 2022 regarding your loan facility.” The letter then set out, in table form, transaction details (draw down amounts, interest charged, repayments and loan balances).

120 The expert evidence of Mr Le was that the document itself was created on 23 May 2023, by the user “CV”, and that the document contained two embedded pdf images, the second of which (setting out the transaction details) was created on 29 May 2023. The creation of this image six days after the creation of the principal document shows the document was not an original, but was created in May 2023, I infer by Christos.

121 This document is a further instance of Christos creating a backdated document and using it in litigation without disclosing the circumstances of its creation.

Conclusion on Christos’ credit

122 I do not accept Christos as a witness of truth. His willingness to fabricate documents (particularly the bank statements noted above) and give false evidence (particularly in relation to the application of funds in accordance with a court order for cladding removal purposes) means that I do not accept Christos’ evidence on contested facts unless supported by the evidence of a witness whose disposition to dishonesty has not been established (such as Ms Calagis) or reliable documentary evidence. In addition, I found Christos’ evidence in cross-examination to often be evasive and non-responsive. In my assessment, in answering questions in cross-examination, Christos’ evidence was directed to what he perceived to be to the Respondents’ advantage. He sought to side-step or minimise the significance of evidence put to him regarding his history of falsification of documents and false evidence.

WHEN WAS THE LOAN AGREEMENT EXECUTED?

123 The Applicant’s position was that the Loan Agreement was entered into in 2020, and not on the date stated on the face of the document, being 1 October 2010.

124 The Applicant submitted that, even putting to one side Christos’ history of document falsification, the terms of the Loan Agreement (which in the Applicant’s submission created an “absurdly inflated liability” of Peter and Kathy to Voukidis Holdings of more than $1,800,000 on advances (net of repayments) of $268,650 over a period of more than 10 years) and the timing of the lodgement of the caveat in support of it (on or about 25 August 2020, when Peter and Kathy were aware of the imminent costs order in the COV Proceeding) should invite the most serious scepticism as to the date of the Loan Agreement’s execution.

125 In an annexure to his closing submissions, the Applicant relied on further pieces of evidence as supporting his contention that the Loan Agreement was not executed on 1 October 2010, including:

(1) The fact that no native file of the unexecuted document was ever produced, with no credible explanation given for the absence of the native file.

(2) The earliest evidenced date of existence of the document (other than Christos and Ms Calagis’ evidence) was 5 August 2020, being the “date content created” and “date content last modified” date identified in respect of the document by Mr Le.

(3) The fact that no mortgage was provided by Peter and Kathy until 22 March 2021, despite it being a condition precedent to any advances under the Loan Agreement, and the absence of any good reason for a mortgage not being provided earlier.

(4) The absence of any credible explanation by Christos for the failure to lodge a caveat until August 2020, when he well knew the caveat procedure to protect unregistered security interests.

(5) The absurdity of the assertion by Christos that Voukidis Holdings notified Peter and Kathy of the imposition of default interest from 1 July 2011, while at the same time making a further 84 advances of money to Peter and Kathy between 1 July 2011 and 20 July 2021.

(6) That in 2016, Christos prepared a pension application on Peter’s behalf and ticked “no” in respect of the question: “In the last 12 months have you (and/or your partner) [being Peter and Kathy] borrowed an amount which is secured against your home”.

126 The Respondents’ position was that the Loan Agreement was entered into on the date stated on its face, being 1 October 2010. They relied on:

(a) Christos’ evidence;

(b) Ms Calagis’ evidence;

(c) the transfer of substantial funds from Voukidis Holdings to Peter and Kathy, which transfers commenced on 4 November 2010; and

(d) Mr Ganas’ evidence that: “There is no evidence to support the proposition that the [Loan Agreement] is not an original document.”

127 Unlike many other documents, which were only produced in pdf copy format, the Loan Agreement was produced in “original”, with inked signatures. The year 2010 was part of the typed document, but “1 October” was inserted in ink. There were two signed originals. Ms Calagis said that was because Peter was not happy with how his signature appeared on the first version he signed, so he signed another copy. Nothing turns on whether Ms Calagis’ explanation should be accepted as the terms of the two versions were the same.

128 I also note that Peter’s signature appears without the “curl” (explained above at paragraph 113(1)). If, as the Applicant alleged, the Loan Agreement was only executed in 2020, Peter must have consciously signed the document adopting the “old” version of his signature (without the “curl”). There is no reason to conclude that Peter was so cunning as to adopt his “old” signature when signing the document.

129 Mr Le examined a pdf version of the Loan Agreement that was produced by the Respondents. That pdf version was created on 5 August 2020 and the pdf file was also last modified on that date. However, as dating a pdf does not date the document from which the pdf file was created, Mr Le’s evidence only goes as far as establishing that the earliest pdf copy of the Loan Agreement was made in 2020.

130 Mr Ganas examined an original of the Loan Agreement. He was unable to determine when it was created.

131 That leaves the lay witness evidence concerning when the Loan Agreement was created and signed.

132 As mentioned above, it was common ground that neither Peter nor Kathy could give evidence, Peter being deceased and Kathy being aged and infirm in a nursing home.

133 Christos gave evidence that the Loan Agreement was signed on or about 1 October 2010. He stated that he had provided a soft copy template document to Peter, who filled out details (after having consulted with a solicitor friend of his) such as the parties, and some details around the definitions and recitals. Christos said he could not recall specifically the changes Peter made.

134 Christos stated that on 1 October 2010 (or thereabouts), he went to his parents’ house, that Ms Calagis was already there when he arrived, and that he did not bring the hard copies of the Loan Agreement to the house.

135 Given Christos’ chequered history of fabricating documents and giving untrue evidence on oath, I place no weight on his evidence.

136 Unlike Christos, Ms Calagis does not have an established history of fabricating documents and giving false evidence. Her evidence was that, in the afternoon of 1 October 2010, she received a call from Peter asking her to “come over to [Peter and Kathy’s] house and witness my signature, and your mother’s, signatures to a loan agreement. We are getting a loan from Chris’s company”. In cross-examination, Ms Calagis gave evidence that when she arrived at her parents’ house, her parents were there and Christos arrived shortly after she did. Ms Calagis said that two copies of the Loan Agreement were on the table when she arrived.

137 Ms Calagis recalled Peter saying to Kathy: “‘Remember seeing a solicitor, remember going to a solicitor’ that sort of thing, about a loan.” Ms Calagis gave evidence that she quickly read the document before witnessing the signatures, but did not see how much the loan was for, what interest rate would be payable, or when it would have to be repaid. However, Ms Calagis said that she could recall seeing the date “1 October 2010” written on the Loan Agreement before she witnessed the signatures. She also gave evidence that this was the only document signed by her parents that she witnessed between 2000 and 2022.

138 Ms Calagis explained that her father signed the first copy of the Loan Agreement, but was not happy with his signature, and so he signed a second copy of the Loan Agreement.

139 In re-examination, the following exchange occurred:

Now right at the end of your cross-examination, Mr Evans put to you that it wasn’t until 2020 that you witnessed the signatures on this document, and you said you disagree. Why do you disagree?---Because it wasn’t – it wasn’t four years ago. Because four years ago my dad was -was sick. He broke his femur, and it was way before that. So it was, yes, back in 2010.

140 Ms Calagis gave evidence that, in 2010, she was working part-time as a learning support officer and worked Mondays through to Thursdays. That is relevant as 1 October 2010 was a Friday. Accordingly, Ms Calagis’ work schedule was consistent with her evidence regarding having received a call from her father to come around to the Property that afternoon.

141 I accept that Ms Calagis is likely loyal to her family and that the family’s interests lie in maximising the amounts that can be claimed by family entities, including Voukidis Holdings, in Peter and Kathy’s bankruptcies. I also accept that Ms Calagis did not have an independent recollection that the Loan Agreement was executed on 1 October 2010, nearly 14 years ago, but fixed the date of the events to which she deposed by reference to the date stated on the Loan Agreement. While she did not, in my assessment, have an independent recollection of the specific date on which the documents were signed, she had a good recollection of the signing gathering and surrounding circumstances, which recollections would be impossible to reconcile with the Loan Agreement only having been signed in 2020 (as the Applicant alleged).

142 Ms Calagis’ evidence was consistent and not shaken in cross-examination. Aspects of her evidence had the ring of truth, in particular her recollection that she witnessed her parents signing this document long before Peter broke his leg, which happened in 2020, some ten years after 2010. Ms Calagis was also not much involved in her parents’ financial affairs. The fact that she only witnessed their execution of one document means that it is unlikely that her evidence about the execution of the Loan Agreement was merely the product of mixing up the circumstances of the execution of the Loan Agreement with the execution of some other document.

143 I do not consider that, as the Applicant submitted, I could reject Ms Calagis’ evidence without impugning her credit. As I have explained, I do not consider her evidence to be the product of innocent confusion.

144 Olga gave evidence that she was not made aware of the Loan Agreement in 2010. She said that she “had no knowledge of what went on within their family”, and explained that she was first shown the Loan Agreement within the preceding two months by the Applicant’s solicitor. While Olga was a director of Voukidis Holdings in 2010, I do not consider that her lack of awareness of the Loan Agreement in 2010 (or at any time before 2024) suggests it was not entered into in 2010. That is because Olga had little to no involvement in the running of Voukidis Holdings.

145 In addition, the objectively verified circumstances are that Peter and Kathy had a need for funds to meet their interest obligations to AMP on the 2009 loan and had exhausted their capacity to meet the interest payments by drawing down on the AMP loan itself by mid to late 2010. In other words, there was a clear need for them to have a source of funds from which to meet the interest obligations. Of course, the need for funds does not dictate that a formal loan be entered into as their son, Christos, was already supporting them financially. He could have simply provided them with further funds without entry into a formal loan. Nevertheless, the need to meet their interest obligations provides an identifiable impetus that would explain entering into a loan agreement in 2010.

146 That does not explain, however, the quantum of the loan. Interest payments on the AMP loan were in the order of only around $3,000 to $4,000 per month, yet the loan agreement was for up to $3 million. That quantum is more readily explicable if, as the Applicant contended, the Loan Agreement was entered into in 2020 when it became clear that Peter and Kathy would have non-family creditors arising out of the failed litigation in the Supreme Court of Victoria. Nevertheless, I do not consider that the fact that the quantum is more readily explicable if the loan were entered into in 2020 outweighs the other evidence in support of the 2010 date.

147 While I note that the pension application completed by Christos for Peter stated that there was no secured loan taken out against the Property, given Christos’ propensity to misstate matters when convenient (eg in stating his parents’ income in applying for the AMP loan), the pension form does not constitute compelling evidence that the Loan Agreement was in fact not entered into in 2010, but only in 2020.

148 By his Originating Application, the Applicant sought (inter alia) declarations that the Loan Agreement did not create any security interest in respect of the Property or, if it did, that any security interest so created is void pursuant to ss 120 and/or 121 of the Act. In pleading the basis for the claims for relief under ss 120 and/or 121 of the Act in relation to the Loan Agreement, the Statement of Claim advanced those claims “if it is established that the Loan Agreement was entered into at a date after 23 May 2017” (in respect of the s 120 claim) and “22 March 2016, alternatively 17 June 2016, alternatively 20 July 2016” (in respect of the s 121 claim).

149 In my view, on the balance of probabilities, the Loan Agreement was entered into in 2010. My acceptance of Ms Calagis’ evidence is central to this conclusion.

150 As I have concluded that the Loan Agreement was not entered into after the dates listed at paragraph 148 above, it is not necessary to determine whether ss 120 or 121 apply to the Loan Agreement.

151 For completeness, I note that I do not accept that the Respondents had the burden of establishing that the Loan Agreement was entered into in 2010 and not, as the Applicant suggested, 2020. Given that it was the Applicant who invoked ss 120 and 121 of the Act to avoid any security interest conferred by the Loan Agreement and to do so on the basis of the Loan Agreement having been entered into after a particular date, I do not accept that Voukidis Holdings bears the onus of establishing the date on which the Loan Agreement was entered into simply because it is the entity claiming in the bankruptcies of Peter and Kathy, or because the Applicant also sought relief for the removal of Voukidis Holdings’ caveats.

DID THE LOAN AGREEMENT CREATE A SECURITY INTEREST?

152 The parties agreed that, if the Loan Agreement was entered into in 2010 and did not create a security interest, then the Loan Deed and Mortgage are void under ss 120 and 122 of the Act.

153 Given my conclusion on the date issue, it is necessary to proceed to consider the question of whether the Loan Agreement created a security interest.

154 In order for an equitable mortgage or equitable charge to come into existence, “there must be an intention to create an immediate proprietary interest or immediate right of recourse to identifiable, present, or in the case of a charge, future property”: Roberts v Investwell Pty Ltd (in liq) (2012) 88 ACSR 689; [2012] NSWCA 134 (Investwell) at [29] (Bathurst CJ, Beazley JA and Tobias AJA agreeing). This is a question of the construction of the agreement in issue.

155 In concluding that there was no intention to grant an immediate security interest in Investwell, Bathurst CJ drew attention to the features of the agreement in question at [32]:

First, the obligation to grant the mortgage [is] expressed to be upon request. Second, the proposed security is expressed as alternatives, the third alternative being security that Mr Roberts may consider necessary. Third, the form of security is not settled but is required to be in a form acceptable to the legal advisers to Mr Roberts. These matters taken cumulatively seem to me to lead to the conclusion that there was no intention to grant an immediate equitable interest of charge.

156 In my view, the Loan Agreement did not create a security interest.

157 The question of whether or not Voukidis Holdings held a security interest pursuant to the Loan Agreement rests on the terms of the Loan Agreement governing the provision of security. The relevant provisions were in the following terms:

3. Conditions Precedent and Subsequent

3.1 Conditions

The obligations of the Lender to provide the funds under this Facility and not require such funds to be repaid immediately is conditional upon the Lender having received the following in form and substance reasonably satisfactory to the Lender:

(a) a mortgage in registerable [sic] form over the Property on terms acceptable to the Lender;

(b) written confirmation from the Borrower in a form reasonably satisfactory to the Lender that the Warranties are true, correct and accurate as at each Drawdown Date; and

(c) the Guarantor and Borrower complying with all of their obligations hereunder.

3.2 Best Endeavours

The Borrower must use its best endeavours to obtain the fulfilment of the conditions set out in Clause 3.1.

158 The Respondents contended that Peter and Kathy were in default under the Loan Agreement because they did not use their “best endeavours” (clause 3.2) to provide a mortgage in registrable form to Voukidis Holdings. They also contended that, notwithstanding Peter and Kathy’s failure to provide a mortgage in registrable form, the terms of the Loan Agreement created an immediate equitable security interest in the Property.

159 The Applicant submitted that clause 3.1 is properly to be regarded as a “contingent condition”, in that it merely provides that the performance of two of the obligations of the lender (to provide funds, and to observe the requirement regarding the timing of repayment under clause 6.1) are subject to the contingency that the lender has received the documents prescribed by sub-clauses 3.1(a)–(b). He submitted that this construction is supported by the best endeavours clause, on the basis that if clause 3.1 was a “promissory term” there would be no need for a best endeavours clause.

160 The Applicant further submitted, by reference to Joseph Finance and Investment Pty Ltd v Eastwood Retirement Pty Ltd [2023] VSC 731, that a best endeavours clause does not impose an absolute obligation, with the result that the appropriate remedy is damages and not specific performance. The Applicant concluded that: “The provision of a mortgage in registrable form would have effected the creation of an equitable security, but a less than absolute obligation to provide it does not achieve the same result”.

161 As noted above, based on the authorities (principally Investwell) the critical question is whether the Loan Agreement evinces an intention to create an immediate proprietary interest or an immediate right of recourse to identifiable property.

162 Clause 3.1 did not create an equitable mortgage or equitable charge. The Loan Agreement does not evince an intention on the part of the parties for the creation of an immediate proprietary interest or right of recourse against the Property. Rather, the effect of clause 3.1 was that Voukidis Holdings was not obliged to advance funds to Peter and Kathy if no mortgage in registrable form was provided. The clause did not itself purport to create a security interest in the Property. The evident intention of the clause was to entitle Voukidis Holdings to insist on provision of a mortgage in registrable form before advancing funds under the Loan Agreement.

163 The fact that the Loan Agreement did not specify the terms of the proposed mortgage, but instead referred to it being “on terms acceptable to the Lender” also tends against any conclusion that the parties intended to create an immediate interest in the Property (as was the case in Investwell at [32]).

164 The existence of a best endeavours obligation, imposed by clause 3.2, does not assist the Respondents. It does not impose an absolute obligation. All that clause does is to require Peter and Kathy to use their best endeavours to provide (inter alia) a mortgage in registrable form which, had it been provided, would have created a security interest in the Property.

165 Consequently, and in accordance with the position agreed by the parties, the Loan Deed and Mortgage are void and Voukidis Holdings stands as an unsecured creditor.

166 It also follows that the first caveat (lodged on or about 25 August 2020) was not supported by the Loan Agreement, which was the stated basis for the interest claimed.

167 However, it is still necessary to determine whether the Loan Agreement should be set aside, as the sum for which Voukidis Holdings can prove in the bankruptcies of Peter and Kathy as an unsecured creditor depends on the interest rate to be applied. If the Loan Agreement is not set aside, the amount will be calculated in accordance with the contractual terms of the Loan Agreement (including as to compounding interest).

SHOULD THE LOAN AGREEMENT BE SET ASIDE ON THE BASIS OF HAVING BEEN PROCURED BY UNCONSCIONABLE CONDUCT AND/OR UNDUE INFLUENCE?

168 The Applicant contended that the Loan Agreement should be set aside on the basis that it was procured by unconscionable conduct and/or undue influence.

169 On the basis of my earlier finding that the Applicant has not established that the Loan Agreement was not entered into on the date on the face of the document, the circumstances relevant to whether a presumption of undue influence arises, and the facts relevant to whether the Loan Agreement was procured by unconscionable conduct, are to be established as at 2010. (If that finding is wrong and the Loan Agreement was entered into in 2020, then it was common ground that the Loan Agreement would be void under s 120 of the Act and it would not be necessary to consider undue influence or unconscionable conduct.)

170 The Applicant contended that the Loan Agreement was procured by unconscionable conduct on the part of Voukidis Holdings, acting via Christos. That claim was advanced in equity and also pursuant to statute. While the Applicant pleaded reliance on s 12CA of the Australian Securities and Investments Commission Act 2001 (Cth) (the ASIC Act), he made an oral application for leave to also rely on the equivalent provisions of the Australian Consumer Law (ACL) in the event that the Respondents were correct in their contention that the ASIC Act provisions did not apply because Voukidis Holdings did not provide a “financial service” pursuant to s 12BAB(9) of the ASIC Act. The grant of leave was not resisted beyond counsel for the Respondents submitting that Voukidis Holdings was not acting “in trade or commerce” in entering into the Loan Agreement.

171 The principles concerning unconscionable conduct in equity are reasonably well-established. Those principles were summarised by the plurality in Thorne v Kennedy (2017) 263 CLR 85; [2017] HCA 49 (Thorne v Kennedy) at [37]–[40] (Kiefel CJ, Bell, Gageler, Keane and Edelman JJ) (citations omitted):

Unconscionable conduct

There was no controversy on this appeal concerning the principles of unconscionable conduct in equity. Those principles were recently restated by this Court in Kakavas v Crown Melbourne Ltd.

A conclusion of unconscionable conduct requires the innocent party to be subject to a special disadvantage “which seriously affects the ability of the innocent party to make a judgment as to [the innocent party’s] own best interests”. The other party must also unconscientiously take advantage of that special disadvantage. This has been variously described as requiring “victimisation”, “unconscientious conduct”, or “exploitation”. Before there can be a finding of unconscientious taking of advantage, it is also generally necessary that the other party knew or ought to have known of the existence and effect of the special disadvantage.

In Commercial Bank of Australia Ltd v Amadio, Deane J said that the equitable principles concerning relief against unconscionable conduct are closely related to those concerned with undue influence. The same circumstances can result in the conclusion that the person seeking relief (i) has been subject to undue influence, and (ii) is in a position of special disadvantage for the purposes of the doctrine concerned with unconscionable conduct. For instance, in Diprose v Louth [No 1], the trial judge, King CJ, observed that both doctrines were satisfied where the defendant “was in a position of emotional dominance which gave her an influence over the [plaintiff] which she exercised unconscientiously to procure the gift of the house”. Before the High Court in that case, Mr Diprose relied only upon the ground of unconscionable conduct.

Although undue influence and unconscionable conduct will overlap, they have distinct spheres of operation. One difference is that although one way in which the element of special disadvantage for a finding of unconscionable conduct can be established is by a finding of undue influence, there are many other circumstances that can amount to a special disadvantage which would not establish undue influence. A further difference between the doctrines is that although undue influence cases will often arise from the assertion of pressure by the other party which might amount to victimisation or exploitation, this is not always required. In Commercial Bank of Australia Ltd v Amadio, Mason J emphasised the difference between unconscionable conduct and undue influence as follows:

“In the latter the will of the innocent party is not independent and voluntary because it is overborne. In the former the will of the innocent party, even if independent and voluntary, is the result of the disadvantageous position in which he is placed and of the other party unconscientiously taking advantage of that position.”

172 A party seeking to set aside a transaction on the basis of unconscionable conduct in equity must establish: (1) that one party to the transaction is placed at a “special disadvantage” vis-à-vis the other by reason of some condition or circumstance which seriously affects the ability of the innocent party to make a judgement as to their own best interests; and (2) that the other party unconscientiously took advantage of that special disadvantage: Commercial Bank of Australia Ltd v Amadio (1983) 151 CLR 447 (Amadio) at 462 (Mason J); Thorne v Kennedy at [38] (Kiefel CJ, Bell, Gageler, Keane and Edelman JJ). For a finding of unconscientious taking of advantage to be made, it is also generally necessary that the other party knew or ought to have known of the existence and effect of the special disadvantage: Thorne v Kennedy at [38], citing Amadio at 462.

173 Determining cases of unconscionable conduct:

[C]alls for a precise examination of the particular facts, a scrutiny of the exact relations established between the parties and a consideration of the mental capacities, processes and idiosyncrasies of the [weaker party]. Such cases do not depend upon legal categories susceptible of clear definition and giving rise to definite issues of fact readily formulated which, when found, automatically determine the validity of the disposition … “A court of law works its way to short issues, and confines its views to them. A court of equity takes a more comprehensive view, and looks to every connected circumstance that ought to influence its determination upon the real justice of the case”.

(Jenyns v Public Curator (Qld) (1953) 90 CLR 113 at 118–9 (Dixon CJ, McTiernan and Kitto JJ), quoting The Juliana (1822) 2 Dods 504 at 522 (Lord Stowell). See also Tanwar Enterprises Pty Ltd v Cauchi (2003) 217 CLR 315; [2003] HCA 57 at [23] (Gleeson CJ, McHugh, Gummow, Hayne and Heydon JJ); Kakavas v Crown Melbourne Ltd (2013) 250 CLR 392; [2013] HCA 25 at [122]–[123] (the Court); Thorne v Kennedy at [43] (Kiefel CJ, Bell, Gageler, Keane and Edelman JJ); Australian Securities and Investments Commission v Kobelt (2019) 267 CLR 1; [2019] HCA 18 at [150] (Edelman J).)

174 The relevant circumstances in which the Loan Agreement was entered into include the following.

175 At the time the Loan Agreement was entered into, Peter and Kathy were already elderly. In 2010, they were 78 and 73 years old, respectively, and had retired in 2000. Peter and Kathy had run a café, which was sold in about 1989, and Peter had then worked as a courier from 1990 to 2000. After his retirement in 2000, Peter had worked from time to time as a pedestrian crossing supervisor. Given his background, work history and the absence of any evidence that Peter was financially sophisticated, I infer that he was not financially sophisticated (contrary to the Respondents’ contention that Peter had “substantial business acumen” and that he and Kathy were “savvy business people”).

176 While Peter and Kathy were, on Olga’s evidence, “sharp as a tack” around 2010, her perception of their “sharpness” in relation to the ordinary interactions between a woman and her parents-in-law does not suggest that Peter and Kathy were financially sophisticated. There was no suggestion that Olga had any engagement with Peter and Kathy in relation to their financial affairs.

177 Peter and Kathy trusted Christos with their financial affairs and had, prior to 2009, already advanced significant funds ($500,000) to Christos to invest on their behalf, without questioning how he was investing the funds or requiring him to sign any documents in respect of the transaction.

178 Kathy was particularly vulnerable. She could not read English and left her business affairs to Peter and Christos.