FEDERAL COURT OF AUSTRALIA

Commissioner of State Revenue v Gleeson, in the matter of Dalma Form Specialist Pty Ltd (subject to deed of company arrangement) [2024] FCA 908

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. Pursuant to s 445D(1) of the Corporations Act 2001 (Cth), the deed of company arrangement entered into by Dalma Form Specialist Pty Ltd and dated 3 May 2024 be terminated.

2. Bruce Gleeson and Daniel Robert Soire be appointed as joint and several liquidators of the second defendant.

3. The plaintiff’s further amended originating process is otherwise dismissed.

4. The Deputy Commissioner of Taxation’s interlocutory process filed on 17 May 2024 is dismissed.

5. The parties are to confer and within 14 days of the date of publication of these reasons:

(a) if the parties can agree upon proposed orders for costs of the proceeding, they are to provide draft orders to the Associate to Markovic J to be made by consent in Chambers; or

(b) if the parties cannot agree upon proposed orders for costs of the proceeding, they are each to provide to the Associate to Markovic J their proposed orders and any submissions, not exceeding two pages in length, and the proceeding is to be listed at a mutually convenient time for hearing on the question of costs.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

MARKOVIC J:

1 On 21 December 2023 the second defendant, Dalma Form Specialist Pty Ltd (administrators appointed, subject to deed of company arrangement), was placed into voluntary administration. The first defendants, Bruce Gleeson and Daniel Robert Soire, were appointed as its Voluntary Administrators.

2 On 12 April 2024, at the reconvened second creditors’ meeting, the creditors of Dalma Form passed a resolution approving an amended proposal for a deed of company arrangement, the proponents of which were the third, sixth and seventh defendants, Dalma Constructions Pty Ltd, Incline Hire Pty Ltd and Jason Ivan Andrijic (collectively, DOCA proponents).

3 The plaintiff, the Chief Commissioner of State Revenue, is a creditor of Dalma Form. At the second meeting his proof of debt (POD), which on its face was for more than $11 million, was admitted by the Administrators for $1 and he voted against the resolution referred to in the preceding paragraph.

4 On 3 May 2024 the Administrators, Dalma Form, the DOCA proponents and the fourth and fifth defendants, Dalma Hire Pty Ltd, and Dalma Services NSW Pty Ltd, entered into a deed of company arrangement (DOCA) and the Administrators became Deed Administrators. Insofar as the parties to the DOCA, other than the Administrators, are concerned: Incline Hire is a related company of Dalma Form; Mr Andrijic is the sole director and shareholder of Dalma Form and Incline Hire, Rade Cikes is the sole director of Dalma Constructions and Dalma Services; and Igor Cikes, Rade Cikes’ son, is the sole director of Dalma Hire.

5 On 3 May 2024 the Chief Commissioner commenced this proceeding. In his further amended originating process filed on 17 May 2024 (FAOP) he seeks the following orders:

(1) leave be granted to him pursuant to s 444E of the Corporations Act 2001 (Cth) to begin or proceed with a proceeding against Dalma Form;

(2) pursuant to s 90-15 of the Insolvency Practice Schedule (Corporations) being Sch 2 to the Corporations Act (IPS) the decision of the Administrators to admit the Chief Commissioner’s POD for only $1 be set aside and pursuant to s 75-41 and/or s 90-15 of the IPS the resolution passed at the second meeting in favour of the amended proposal for a deed of company arrangement be set aside; and

(3) pursuant to subs 445D(1)(c), (e), (f) and/or (g) and/or s 447A of the Corporations Act the DOCA be terminated.

6 Although his standing to appear is disputed by the second to seventh defendants (who I will refer to collectively as the Dalma Defendants), the Deputy Commissioner of Taxation appears in the proceeding in support of the Chief Commissioner’s application. On 17 May 2024, the Deputy Commissioner filed an interlocutory process seeking the following relief:

(1) an order pursuant to subs 445D(1), (f) and/or (g) of the Corporations Act that the DOCA be terminated;

(2) a declaration that, consequent upon making an order in terms of (1) above and pursuant to s 446AA of the Corporations Act, Dalma Form is taken to have passed a special resolution under s 491(2) of the Corporations Act that it be wound up voluntarily;

(3) an order pursuant to s 499(2D)(a) of the Corporations Act that Stephen Hathway of Helm Advisory, a registered liquidator, be appointed as liquidator of Dalma Form; and

(4) in the alternative to (1) to (3) above, an order pursuant to s 447A of the Corporations Act and/or s 90-15 of the IPS that Part 5.3A of the Corporations Act is to operate in relation to Dalma Form such that:

(a) the DOCA is terminated;

(b) Dalma Form is taken to have passed a special resolution under s 491(2) of the Corporations Act that it be wound up voluntarily; and

(c) Mr Hathway be appointed as liquidator of Dalma Form for the purposes of the winding up.

7 I make two observations about the Deputy Commissioner’s interlocutory process. First, in the course of the hearing the Deputy Commissioner informed the Court that he did not press the prayers for relief in which he sought that Mr Hathway be appointed as liquidator of Dalma Form (paras (3) and (4)(c)). Secondly, there is commonality in the relief sought by the Deputy Commissioner and the Chief Commissioner in that they both seek to have the DOCA terminated. In effect, the Deputy Commissioner appeared in the proceeding to support the Chief Commissioner’s application and indicated in the course of the hearing that if the Chief Commissioner was successful in obtaining the relief he sought in relation to termination of the DOCA, there would be no need to consider his interlocutory process.

8 As set out above, the Administrators are the first defendants. It is convenient to set out their position on the Chief Commissioner’s application. They recognise that they are obliged to act in the best interests of Dalma Form. In that regard and consistently with their position to date (as described below) they remain of the view that a winding up is in the best interests of Dalma Form’s creditors. It follows that the Administrators do not oppose the Chief Commissioner’s application for the DOCA to be terminated (albeit only on certain of the grounds articulated by the Chief Commissioner) and, as a consequence, that Dalma Form be wound up.

9 The Administrators note that the Chief Commissioner contends that he makes no criticism of their conduct of the administration but, notwithstanding that, he puts in issue two aspects of the Administrators’ conduct: first, that the Administrators ought to have admitted the Chief Commissioner’s POD for its full value for voting purposes at the second meeting; and secondly, that the Administrators ought to have informed creditors that the Chief Commissioner’s POD was an assessment pursuant to s 11 of the Tax Administration Act 1996 (NSW) (TA Act) and it was a material omission to have failed to do so. The Administrators invited the Chief Commissioner to withdraw these contentions and to seek termination of the DOCA on a narrow basis relying only on subs 445D(1)(e), (f) and/or (g) noting that if he did so they would file a submitting appearance. The Chief Commissioner declined to do so.

10 Accordingly, while the Administrators sought to assist the Court with the relevant facts, including by providing an evaluation of the return to creditors under the DOCA and in a liquidation scenario, the primary focus of their submissions was on the two contentions raised by the Chief Commissioner, both of which concern his POD.

BACKGROUND

11 Dalma Form was incorporated on 27 November 2013. It provides formwork services on construction projects.

12 On 21 October 2021 the Chief Commissioner informed Dalma Form that it was registered for payroll tax with a start date of 1 July 2017 and monthly payment frequency.

13 By email sent on 25 October 2021 Revenue NSW provided Mr Andrijic with a Notice of Investigation and Audit questionnaire and asked him to complete and return the questionnaire with the requested documentation.

The Administrators’ appointment to Dalma Form

14 As set out above, on 21 December 2023 the Administrators were appointed to Dalma Form.

15 On 22 December 2023 the Administrators sent a letter to Revenue NSW informing it of their appointment and inquiring whether Dalma Form owed any payroll tax.

The first meeting of creditors

16 On 5 January 2024 the Administrators held the first meeting of creditors of Dalma Form by video conference. Mr Soire was the chairperson. In light of a discussion held shortly prior to that meeting with representatives from the Australian Taxation Office (ATO) and Mr Hathway of Helm Advisory, the liquidator of Admin Form Pty Ltd (In Liquidation), which claimed to be a creditor, the first meeting was adjourned for one week to 12 January 2024 to permit the ATO and Admin Form to pursue their proposal for replacement of the Administrators.

17 On 12 January 2024 the first meeting of creditors was resumed. Once again, the meeting was held by video conference and chaired by Mr Soire. A resolution was put to the meeting and moved on behalf of the ATO that the Administrators be removed as administrators and that Mr Hathway be appointed as administrator of Dalma Form in their place. That resolution was not passed.

The Administrators’ first report to creditors

18 On 30 January 2024 the Administrators issued their first report to creditors. Among other things, the first report:

(1) confirmed that PODs had been received from 14 creditors of Dalma Form. The Chief Commissioner, who at that time had not lodged any POD or claim against Dalma Form and had not issued any correspondence to the Administrators, was not one of the known creditors as at the date of the first report;

(2) included a proposal for a deed of company arrangement made by Incline Hire and Mr Andrijic;

(3) referred to the fact that the ATO and Mr Hathway on behalf of Admin Form had informed the Administrators that their investigations suggested that Dalma Form may be part of a group of over 30 companies that had, over the past 15 years, allegedly operated to defraud the ATO of $150 million in unpaid taxes (Alleged Scheme);

(4) noted that the Administrators had carried out preliminary investigations but, without documentary evidence, it was premature for them to draw any conclusions about the alleged conduct and they could not express any conclusions on the allegations of fraud;

(5) asked that if any creditor had any information or documents regarding the Alleged Scheme or that may assist with the investigations, they provide that information to the Administrators immediately;

(6) noted that, in light of the serious allegations raised about the Alleged Scheme, the Administrators intended to adjourn the second meeting for the maximum period of 45 days to allow time for further investigations into the affairs of Dalma Form; and

(7) informed creditors that the Administrators were of the opinion that it would be in their interests for Dalma Form to be wound up. The Administrators formed that opinion despite Mr Andrijic and Incline Hire’s early proposal for a deed of company arrangement.

Early correspondence with the Revenue NSW

19 By email sent on 31 January 2024 Revenue NSW informed the Administrators that (as written):

The abovementioned company is registered for Payroll Tax (RNSW Ref: 164659550).

A Payroll Tax liability may have been identified and a Proof of Debt will be submitted in due course if appliable. The company does not appear to be registered for Land Tax or other state taxes in NSW.

lf you are aware of an additional liability to Revenue NSW, please advise accordingly.

20 On 7 February 2024 the second meeting was convened and adjourned by Mr Gleeson, who acted as chairperson, for 45 business days until 12 April 2024.

21 By email sent on 12 March 2024 Misty Andrews, assistant coordinator for insolvency – tax debt, taxes and grants, Revenue NSW, informed the Administrators that:

Further to our email below, we wish to advise that an investigation into potential Payroll Tax liabilities owed by the abovementioned entity are yet to conclude, however, we anticipate that it is likely RNSW will lodge a claim in this Administration.

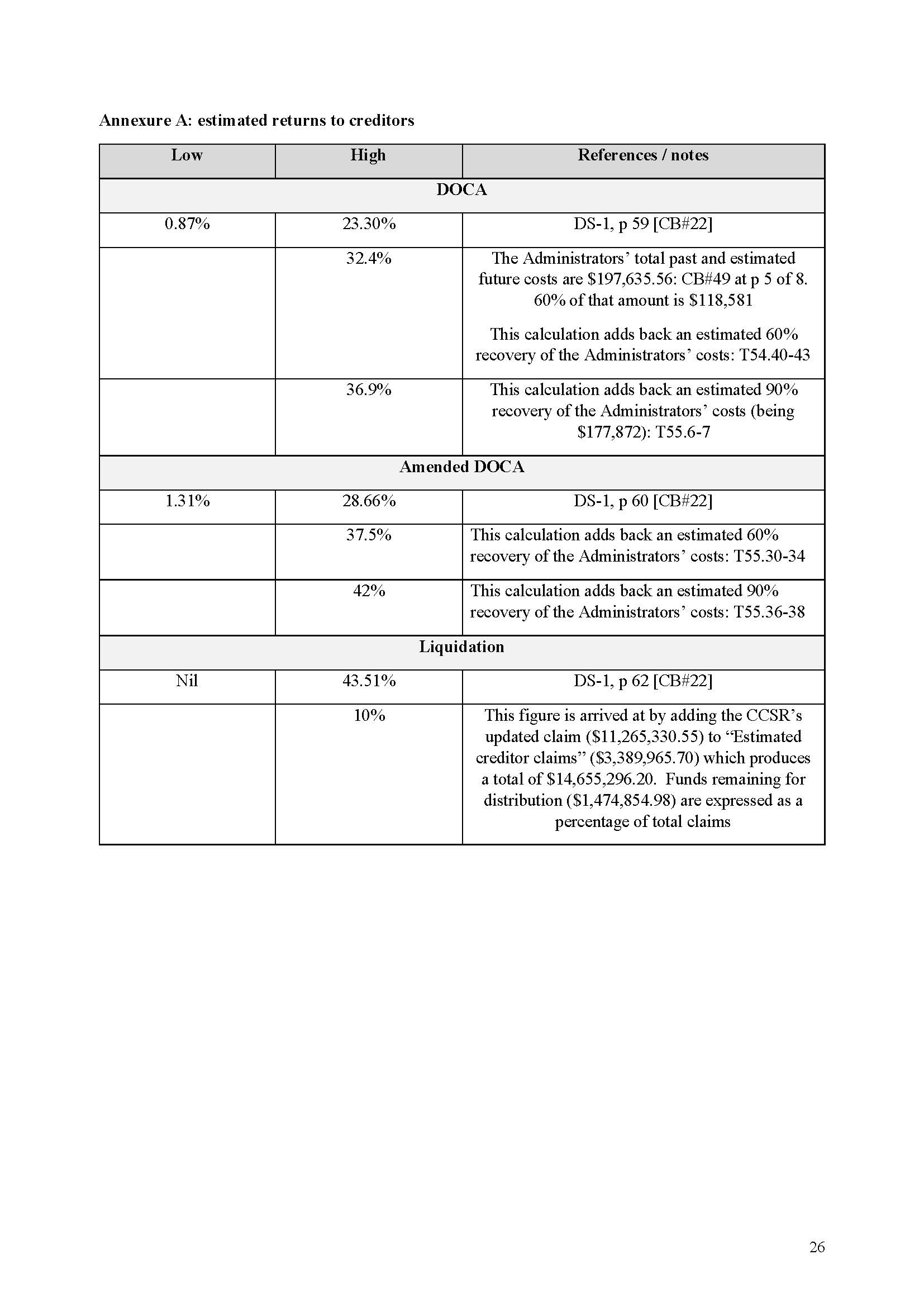

In the interim, may we kindly request a copy of the Voluntary Administration Report and Statement Of Administrator’s Opinion at your earliest convenience.

22 On 13 March 2024 Revenue NSW sent an email to the Administrators in which it asked the Administrators to “confirm if [Dalma Form] will continue to trade during the administration period so an Administrator Trading account can be established if required”.

Production of books by Dalma Form

23 On 19 March 2024 Gillis Delaney Lawyers, Dalma Form’s former solicitors, produced books and records in answer to a notice issued by the Administrators pursuant to s 438C of the Corporations Act. Mr Soire explained that the documents produced by Gillis Delaney disclosed that it appeared that the Chief Commissioner had commenced an investigation into Dalma Form’s payroll tax obligations in 2021 and had sought certain information from Dalma Form. The records produced did not disclose that the Chief Commissioner had made any assessment of payroll tax as at the date of the Administrators’ appointment.

24 Mr Soire noted that the production of the documents by Gillis Delaney was, other than the reference in Revenue NSW’s email dated 12 March 2024 (see [21] above), the first time that the Administrators had received any documents referring to an investigation by Revenue NSW. Notwithstanding that Revenue NSW did not lodge a formal POD until 10 April 2024 (see below), from that point on the Administrators provided Revenue NSW with all documents that they provided to Dalma Form’s creditors.

The Administrators’ supplementary report to creditors

25 On 4 April 2024 the Administrators issued a supplementary report to creditors. In the executive summary to that report, among other things, the Administrators stated:

…

• To enable us to recover a retention from Aqualand and better investigate the affairs of the Company including whether or not the Company, its Director, other entities or persons were participants in the Alleged Scheme, the second meeting of creditors that was held on 7 February 2024 was unilaterally adjourned by us for the maximum period of forty-five (45) business days.

• Since the adjournment, we have undertaken significant work, attended numerous meetings and conducted substantial investigations into the Company’s financial affairs. We have also received requests for information and documents from creditors and attended to respond to same. Please refer to Section 4 of this Report for details regarding such work.

…

• The Australian Taxation Office has raised concerns that the Company was part of a group of companies that have undertaken its business operations in such a way as to deprive the ATO of PAYG tax over a ten year period. It is alleged that within the group of companies the Company was one of the client facing companies which performed the construction work or formwork (the Construction Companies). Other companies within the group of companies were labour hire companies which employed the various employees of the group (the Labour Hire Companies) and made the employees available to the Construction Companies.

• The Labour Hire Companies, most of whom have been wound up over the past 10 years, were required to pay the wages, annual leave, superannuation and PA YG tax of their employees, however the Labour Hire Companies have been wound up leaving the ATO as a significant unsecured creditor on each occasion in relation to unpaid PAYG. It is alleged that the Construction Companies (including the Company) only paid sufficient labour hire fees to cover the wages, annual leave and superannuation, leaving the Labour Hire Companies with insufficient funds to pay the PAYG tax (the Alleged Scheme).

• Our investigations reveal that other companies within the group provided administrative and hiring services to the Construction Companies (the Admin Companies) and charged the Construction Companies fees. Based on the information presently available, we have concerns as to whether the fees charged by the Admin Companies may be disproportionate to the services provided or above market rates.

• We have also recently received an amended DOCA proposal from the Proponents.

• We are required to provide creditors with information regarding the amended DOCA proposal and the estimated returns to creditors in both a DOCA scenario and a Liquidation which are contained in Sections 6 and 7 of this Report.

26 The “amended DOCA proposal” referred in the supplementary report (DOCA Proposal) was made by the DOCA proponents. The “key terms” of the DOCA Proposal were recorded in the supplementary report as follows:

• The Deed Administrators will establish a Deed Fund for the Company

• The Company Deed Fund will consist of:

(a) Deed Contribution of $250,000 payable by the Proponents as follows:

- $25,000 within 60 days after the date of execution of the DOCA

- Nine (9) monthly payments of $25,000 commencing one month after the first payment is made

(b) Any amounts owing/recoverable from retentions due to the Company;

(c) Any refunds received or receivable by the Company, the Administrators or the Deed Administrators, including workers compensation premium refunds.

• The Company Deed Fund will be applied to pay the costs and disbursements of the Administrators (and Deed Administrators) in relation to the Company in full and provide a return to the Admitted Creditors of the Company.

• The Deed Administrators will have the power to recover retentions owing to the Company.

27 The Administrators said the following about the DOCA Proposal:

Advantages and disadvantages of the DOCA proposal

Having regard to the results of our investigations into the financial affairs of [Dalma Form], we have considered the advantages and disadvantages of the DOCA proposal and set them out as Annexure “H” of this Report.

Funding of the proposal

The amended DOCA proposal provides for $250,000 to be paid in ten (10) instalments over a period of approximately eleven (11) months from the date of execution of the DOCA. The Proponents are [Mr Andrijic], Incline Hire and Dalma Constructions. As noted in this Report, we have sought information from Dalma Constructions regarding its financial position, however we have not received a response to date.

Accordingly, there is no certainty regarding the Proponents’ ability (particularly Dalma Constructions) to fund the Deed Contribution. We therefore cannot provide any comment regarding the likelihood of the funds being received for the Deed Fund .

Final comments

We note that whilst the attached DOCA proposal does not indicate that the funds currently held by us as [Administrators] forms part of the Deed Fund, it is our understanding that it is the intention of the Proponents to include same and accordingly, this amount has been included in the analysis attached as Annexure “G”. If this is not the case, we will inform creditors immediately.

Based on the above analysis and our investigations to date, it is our view that the DOCA proposal does not provide creditors with greater return than an optimistic Liquidation scenario. Further, we are of the view that investigations are warranted (including conducting public examinations) regarding the aspects outlined throughout this Report and specifically in Section 4(c). These investigations can only be conducted should [Dalma Form] be placed into Liquidation.

For these reasons, we believe that creditors should not resolve to accept the Proponent’s proposal for a DOCA and [Dalma Form] should be wound up.

28 In the supplementary report, in summary, the Administrators also reported that:

(1) they held $3,064.54 in cash;

(2) of three possible retention claims referred to in the first report, one had materialised. That was a claim of $649,000 from Aqualand Constructions Pty Ltd;

(3) they had estimated ordinary unsecured creditors to be between $1,305,273.70 and $2,815,381.46;

(4) they had not been provided with all of the books and records of Dalma Form, a matter of significant concern to the Administrators. Relevantly the Administrators reported (as written):

We have made several requests to the Director to obtain books and records and other information, and , in particular, Company emails. Whilst the Director has purported to comply with such requests, we have not been provided with all books and records of the Company without any proper explanation. This is of significant concern to us.

We have engaged a forensic IT expert to review the outlook data files and MYOB back-up file provided to our office. We have been advised that upon review that:

• The outlook data files provided is a pst file which is created by a user on a local computer to manually save copies of emails, calendar items etc. This means it is not a file (such as an ost file) which is automatically created by the email client application (i.e . Outlook) to store an offline synchronised copy of an online email account. This means that this file is not a duplicate backup of the entire email account and folders.

• There are no emails in the ‘Sent Items’ folder.

• The MYOB file provided is a back-up file used by MYOB Account Right and the first journal entry was entered on 28 November 2013 and the last journal entry was entered on 20 December 2023.

(5) there were a number of potential claims that may be available to Dalma Form in a liquidation including for unfair preferences, uncommercial transactions/unreasonable director related transactions, creditor defeating dispositions, insolvent trading and breach of directors’ duties;

(6) they had identified certain areas of concern which warranted further significant investigations being undertaken including by way of examinations under s 596A and s 596B of the Corporations Act; and

(7) they had undertaken an investigation in relation to the Alleged Scheme which disclosed that Dalma Form had, during the period in which it traded, engaged numerous labour hire companies which had gone into liquidation. The Administrators noted that if Dalma Form “goes into Liquidation, we are of the view that a public examination will enable further information and evidence to be obtained to consider whether there is a claim that [Dalma Form] may have against [Mr Andrijic], Rade Cikes and Igor Cikes and other entities as a result of [Dalma Form] potentially incurring liabilities to the ATO as a participant in the Alleged Scheme”.

The Chief Commissioner submits a POD

29 On 10 April 2024 at 11.37 am Revenue NSW submitted a POD in the amount of $11,374,884.13, for estimated payroll tax liabilities for the 2018 to 2021 financial years. The covering letter, signed by Rochelle Nicholson, a delegate of the Chief Commissioner, stated that “[t]he proof of debt is based on an estimate of Payroll Tax and is authorised under section 11 of the [TA Act]”.

30 On 10 April 2024 by email sent at 2.11 pm the Administrators sought “further information and documents in support of the basis and quantum of the claimed payroll tax liability” in the Chief Commissioner’s POD from Revenue NSW.

31 By email sent on 11 April 2024 at 2.57 pm Revenue NSW responded to the Administrators’ request for further information as follows, with its answers to the Administrators’ queries recorded in italics (as written):

I make reference to your request for further information to support our claim. I have sought advice from our Compliance team who have provided their calculations (attached) and summarised the following to your points below;

1. Copies of the payroll tax assessments; Not issued as yet; POD is based on estimated liability.

2. The basis of the claimed payroll tax liability and the reasons why the payroll tax is an “estimate”;

Payments to labour providers by customer (identified in working papers attached) to be assessed as liable under s42 of the Payroll Tax Act 2007. Penalty tax rate proposed to be applied to assessments is 75%, as CCSR likely to be satisfied that tax default was caused in part by the intentional disregard of the PTA by the taxpayer, as per s27(2) of the Taxation Administration Act 1996.

3. All correspondence with the Company regarding the payroll tax liabilities; Copy of NOI can be provided; finalisation letter not yet issued.

4. Calculations. working papers, or analysis of the Company’s taxable wages for the purposes of the quantification of the Company’s payroll tax liability; Working papers with estimated liability attached.

5. If the Proof of Debt is based on estimated, details and information used by Revenue NSW to calculate the payroll tax See response above.

6. If the Company has been grouped, details regarding:

a. The basis of the grouping;

b. The entities or companies within the group;

c. The taxable wages for each entity that has been assessed/grouped.

Grouping analysis not yet finalised.

Kind confirm receipt of this information and confirmation that our claim will be admitted.

32 On 11 April 2024, after receipt of the email referred to in the preceding paragraph, the Administrators requested that Revenue NSW provide “the NOI referred in point 3 and/ or the notice of determination pursuant to s 42 of the Payroll Tax Act”.

33 Also on 11 April 2024 Revenue NSW provided a proxy form to the Administrators in advance of the second meeting.

34 On the afternoon of 11 April 2024 Mr Soire discussed the Chief Commissioner’s POD and the information received earlier that day from Revenue NSW with Martin Vu, a principal of Jones Partners, who was working on Dalma Form’s administration. Mr Soire recalls that they discussed the following matters:

(1) the working papers including a list of 27 companies whose services were not limited to labour providers but included architectural, bookkeeping, supply and recruitment;

(2) the Chief Commissioner’s claim appeared to be based on a determination under s 42 of the Payroll Tax Act 2007 (NSW) by which the Chief Commissioner determined that certain persons were deemed to be employees of Dalma Form and/or deemed certain payments as wages for the purposes of the Payroll Tax Act;

(3) they ought to inform creditors before the resumption of the second meeting of the Chief Commissioner’s POD and the claim that he made, especially as it was for a very large sum; and

(4) they ought to obtain urgent legal advice about the Chief Commissioner’s POD, including whether it ought to be admitted for voting purposes at the resumption of the second meeting.

35 In light of the Chief Commissioner’s POD and the further information received from Revenue NSW, Mr Soire had a Circular to Creditors prepared and sent. The Circular, sent at 5.25 pm on 11 April 2024, informed creditors that a POD had been received from the Chief Commissioner and another creditor, Lendlease. In relation to the Chief Commissioner’s POD it provided (emphasis in original):

We advise creditors that on 10 April 2024, Revenue NSW lodged a Proof of Debt with our office in the amount of $11,374,884.13 for estimated payroll tax liabilities, interest and penalties for the financial years ended 30 June 2018 to 30 June 2021. We have recently received from Revenue NSW calculations for its estimated payroll tax liabilities and the basis of its claim. We are urgently obtaining legal advice regarding the claim of Revenue NSW.

This claim is significant and if admitted in full or in part, would have an impact on the estimated dividends to creditors in both the DOCA and Liquidation scenarios provided in the Supplementary Report. If the claim is admissible, there will be an equivalent increase in the Company’s creditor claims in both a DOCA and Liquidation scenario. There may also be further claims available against the Director in a Liquidation.

36 In an email sent at 8.57 am on 12 April 2024, the Administrators followed up on their email sent the previous afternoon (see [32] above) and again requested that Revenue NSW provide, as a matter of urgency, the “NOI” and/or the notice of determination. Later that morning, Revenue NSW provided a copy of the Notice of Investigation. It included:

We’ve commenced an investigation of the payroll tax obligations of [Dalma Form] and any other businesses grouped under the Payroll Tax Act 2007.

You’ve been selected for an investigation because we are currently reviewing businesses in your industry to correct common errors, such as incorrectly declared contractor payment and employment agency arrangements. Our compliance program detects these types of errors to help you comply with your tax obligations.

The focus of our investigation will be on payroll tax for the financial years ended 30 June 2018, 2019, 2020, 2021 and the current financial year. Compliance with the Jobs Action Plan, land tax, duties, and other state tax legislation may also be reviewed, where applicable.

37 Mr Soire has since seen the letter and email from the Chief Commissioner and Revenue NSW addressed to Mr Andrijic referred to respectively at [12] and [13] above. He had not seen that correspondence before being provided with the Commissioner’s evidence in this proceeding and, as far as he is aware, the Administrators were not, prior to its receipt on 12 April 2024, provided with the Notice of Investigation (including as part of the material produced by Dalma Form’s former solicitors referred to at [23] above).

38 On the morning of 12 April 2024, the Administrators sought urgent legal advice in relation to the Chief Commissioner’s POD from their solicitors, Polczynski Robinson, including by instructing their solicitors to brief counsel.

39 By email sent at 10.03 am on 12 April 2024 to Revenue NSW the Administrators sought a copy of the notice of determination that was made in relation to Dalma Form and the reasons for the determination. As far as Mr Soire is aware neither he, Mr Gleeson nor any of their staff received any notice of determination as requested at that time or at any time prior to the resumption of the second meeting. The first time that Revenue NSW provided a notice of determination was on 29 April 2024 (see below).

40 At about midday on 12 April 2024, Ms Andrews of Revenue NSW telephoned the Administrators’ office and spoke with Messrs Soire and Vu. Mr Soire recalls that they discussed the following matters in relation to the Chief Commissioner’s POD:

(1) Ms Andrews stated that Revenue NSW’s audit team was finalising its investigations and that she was waiting on information and findings to be reviewed;

(2) Mr Soire asked whether a notice of determination had been issued and, if so, whether it could be provided urgently. Ms Andrews informed them that no notice of determination had yet been issued;

(3) Mr Soire asked for a draft notice or something similar, but Ms Andrews said that could not be provided; and

(4) Ms Andrews stated that if, hypothetically, the Chief Commissioner’s claim was rejected, she would be seeking to have it admitted at least for $1 for voting purposes.

41 Mr Vu made a file note of the discussion with Ms Andrews referred to in the preceding paragraph which Mr Soire observes is consistent with his recollection of the call. Mr Vu’s file note includes (as written):

Dalma Form Specialist

Revenue NSW, Misty, DS and MV, 12:02pm incoming call from Misty.

DS noted the reports that were provided and asked whether there was anything Revenue NSW wished to ask us Concerns around the likelihood of claim being admitted in full.

Estimate POD, audit team finalising their investigations.

Waiting on information and findings to be reviewed.

Notice of determination s42 not yet issued.

In lien of wages being declared, basing claim on contractor payments being made.

Questions:

…

Anything else? Notice of assessment? No.

…

Hypothetically, claim rejected, will be seeking claim be admitted for $1.

42 On 12 April 2024 at about 2.00 pm Messrs Soire and Vu met with the Administrators’ solicitors to discuss the legal issues associated with the Chief Commissioner’s POD. Given the urgency associated with the advice required, Polczynski Robinson provided their advice orally at that meeting. Mr Soire does not recall making a file note of what was said but recalls that the substance of the legal advice was as follows:

(1) the Chief Commissioner’s claim is stated to be based on an “estimate of payroll tax”;

(2) the claim is based on a determination under s 42 of the Payroll Tax Act, but no formal or final notice of determination has been made;

(3) Revenue NSW is raising questions about the relationships between Dalma Form and other entities and it appears that some of those entities that were subcontractors may be treated as employees (and payments to them may be treated as wages) under the Payroll Tax Act, but it is difficult to say in the absence of a determination;

(4) no “notice of assessment” has been issued by Revenue NSW, which means that the conclusive evidence provisions, to the effect that the fact of a notice provides conclusive evidence that the debt is owing, do not apply to the Chief Commissioner’s claim, at least at present;

(5) the Chief Commissioner’s claim is not a debt payable within the meaning of s 44 of the TA Act;

(6) in circumstances where Revenue NSW has indicated an intention to issue a notice of assessment based on a determination to be made under s 42 of the Payroll Tax Act the claim is either a contingent claim or a debt the value of which had not been established;

(7) thus, for the purposes of r 75-85(4) of the Insolvency Practice Rules (Corporations) 2016 (IP Rules), the Administrators will need to make a just estimate of the claim;

(8) according to the Bovis case, in making a just estimate the Administrators are not required to undertake any detailed enquiry but should do so on the basis of the material provided by the Chief Commissioner and the facts known to the Administrators based on their own investigations as at that date;

(9) given that:

(a) no notice of assessment had been issued by Revenue NSW;

(b) Revenue NSW’s investigations were not complete;

(c) no notice of determination had been issued in accordance with s 42(2) of the Payroll Tax Act; and

(d) Dalma Form’s books and records (at least on their face) disclosed that Dalma Form did not employ any employees,

the Administrators, acting impartially and in accordance with r 75-100(3) of the IP Rules, ought to admit the Chief Commissioner’s POD for voting purposes for $1 and mark it as “objected to”, subject to the vote being declared invalid if the objection is sustained; and

(10) it was suggested to counsel that, subject to further and final consideration, the Administrators were minded to admit the Chief Commissioner’s POD for voting purposes for $1 and she did not suggest that this was in any way inappropriate in the circumstances.

43 Mr Soire said that he decided to admit the Chief Commissioner’s POD for voting purposes for $1 and mark it as “objected to” for the following reasons:

(1) the legal advice provided by Polczynski Robinson (and counsel), including that the Administrators ought to admit the Chief Commissioner’s POD for voting purposes for $1 (and the reasoning provided);

(2) Dalma Form’s books and records did not suggest that it had any employees and any liability for payroll tax, including that:

(a) in the course of the administration, no persons had asserted that they were employees; and

(b) Dalma Form did not lodge any payroll tax returns;

(3) in accordance with r 75-95 of the IP Rules, the Administrators were required to ask creditors to give evidence in writing in relation to a debt claimed by a creditor to establish the liability of the company for the debt where it is necessary to do so. However, other than the limited working papers no reasons were otherwise given or particulars supplied with the Chief Commissioner’s POD to demonstrate how s 42 of the Payroll Tax Act was to apply to Dalma Form’s particular circumstances;

(4) the fact that no final determination had in fact been made by the Chief Commissioner under s 42 of the Payroll Tax Act, which he considered was a necessary precursor to establishing that Dalma Form owed a liability under that provision;

(5) the working papers provided by Revenue NSW contained a schedule itemising 27 “contractors” and payments to those persons appeared to be grouped and deemed as wages. But the Administrators were in no position to undertake any detailed factual enquiry as to the relationship between those parties and the “contractors” in the limited time available;

(6) the Administrators were otherwise not in a position to undertake any other factual enquiry given the second meeting had been convened and was due to commence at 2.30 pm on 12 April 2024 (which was the final day of the maximum period of 45 business days since the second meeting was initially held); and

(7) having regard to the available information, he was satisfied that the claim should be admitted (that is, that the Chief Commissioner was a creditor of Dalma Form) but he was unable to ascribe a proper figure to the claim (because of the uncertainties and contingencies involved). Thus, he concluded that it was appropriate to admit the claim for voting purposes at a nominal value of $1.

44 By email sent on 12 April 2024 the Administrators informed Revenue NSW that they intended to admit the Chief Commissioner’s POD for $1 for voting purposes.

The reconvened second meeting

45 The second meeting commenced shortly after 2.30 pm on 12 April 2024. It was a hybrid meeting conducted by video conference and in person. Mr Soire acted as chairperson.

46 Mr Soire recalls that during the meeting Mr Vu, on behalf of the Administrators, announced the creditors in attendance and the adjudication of their claims. Among other things, he noted that the Chief Commissioner had lodged a claim in the amount of $11,374,884.13 which related to an estimate of payroll tax and that no notice of assessment or formal notice of determination with reasons had been issued for that claim. He also stated that, for voting purposes, the Chief Commissioner’s claim had been admitted for $1 and marked objected to pursuant to r 75-100(3) of the IP Rules. All proofs of debt submitted by creditors were tabled at the meeting and no creditor sought to inspect any of them.

47 Mr Soire also recalls that Ms Andrews, who attended the meeting on behalf of the Chief Commissioner, confirmed that the Chief Commissioner’s claim was based on an estimate and that further investigations under anti-avoidance provisions were taking place. She said that she was confident that the anti-avoidance provisions would be applied and that assessments would be raised in the coming weeks. Ms Andrews also said that the Chief Commissioner was yet to make a formal determination, although she noted that Revenue NSW considered the evidence to be strong. In response to a question by Mr Xenos, an observer from the ATO, Mr Soire said that it was not possible to make a just estimate of the quantum of the Chief Commissioner’s claim and, on that basis, it was admitted for $1.

48 In relation to the Chief Commissioner’s POD, the minutes of the second meeting record:

Ms Misty Andrews requested that she be the proxy holder for Revenue NSW and Rowena Masoe is an observer on behalf of Revenue NSW. The Chairperson noted same.

Ms Andrews noted that Revenue NSW’s claim is based on an estimate and these particulars have been provided to the Administrators’ office whilst further investigations under anti-avoidance provisions are taking place. She noted that these anti avoidance provisions are only applied in exceptionally rare circumstances and only where the Chief Commissioner is likely to be satisfied that it is warranted and necessary. She noted that they are confident that these provisions will be applied and assessments raised in the coming weeks.

Mr Xenos asked whether that means a just estimate was made or the whole amount should be admitted. The Chairperson advised that there is no basis for a just estimate.

Mr Polczynski noted that a Proof of Debt was submitted and an estimate provided but no reasons had been provided by Revenue NSW although they had been sought.

Mr Hathway asked Ms Andrews to comment on same. Ms Andrews advised that their investigations have been impacted by the evidence and the agreements in place with the Company were to avoid payroll tax, but Revenue NSW have yet to make a formal determination. However, their evidence is strong and they have provided to the Chairperson and Mr Vu with the particulars of those calculations. Ms Andrews advised that they believe that they may object to the decision regarding the adjudication to that claim.

Mr Vu noted that Revenue NSWs claim was marked objected to. The Chairperson advised that Ms Andrew’s comments were noted.

49 Mr Soire does not recall Ms Andrews saying that the Chief Commissioner’s claim constituted an assessment by way of estimate and as best he can recall Ms Andrews did not say words to that effect. Nor does Mr Soire recall Ms Andrews referring to s 11 of the TA Act and his recollection is that she did not make any reference to any specific section of the TA Act, including s 11.

50 Mr Soire did not refer to the Chief Commissioner’s POD as having constituted an “assessment” because at the time he was not aware of the significance, if any, of whether or not the Chief Commissioner’s POD did constitute an assessment. As far as Mr Soire can recall, this was not something that was discussed in the conference with Polczynski Robinson earlier that day. Mr Soire focused on the fact that:

(1) the Chief Commissioner’s claim was an estimate based on a determination but that determination was yet to be finalised; and

(2) no notice of assessment had been issued by Revenue NSW.

51 At the second meeting creditors were asked to vote on two competing resolutions: one in favour of the DOCA Proposal; and one in favour of a winding up of Dalma Form. Mr Soire informed the meeting that the Administrators recommended against a resolution that Dalma Form execute the proposed deed of company arrangement and, rather, recommended that Dalma Form be wound up.

52 Notwithstanding that, a resolution that “the DOCA be approved by creditors” (DOCA Resolution) was passed on a poll, both by number of creditors and value of claims. Mr Soire notes, and the minutes of the second meeting confirm, that eight creditors with a value of $1,218,403.01 voted in favour of the DOCA Resolution and seven creditors with a value of $551,508.08 voted against it. The minutes of the second meeting record the following results on a poll taken of the vote on the DOCA Resolution:

(1) creditors who voted in favour of the DOCA Resolution:

Number | Creditor name | Voting amount ($) |

1 | Auswood International Pty Ltd | 196,988.00 |

2 | Burgess Arnott & Grava Pty Ltd | 78,160.00 |

3 | Dalma Hire Pty Ltd | 66,525.81 |

4 | Doka Formwork Australia Pty Ltd | 577,544.58 |

5 | Elite QS Consulting Pty Ltd | 22,816.86 |

6 | Gillis Delaney Lawyers | 37,177.70 |

7 | Incline Hire Pty Ltd | 225,940.56 |

8 | Taylor & Co | 13,249.50 |

Total | 1,218,403.01 |

(2) creditors who voted against the DOCA Resolution:

Number | Creditor name | Voting amount ($) |

1 | Acrow Formwork & Scaffolding Pty Ltd | 280,872.86 |

2 | Admin Form Pty Ltd (In Liquidation) | 50,466.60 |

3 | Australian Taxation Office | 66,666.74 |

4 | Plus Form NSW Pty Ltd (In Liquidation) | 98,018.21 |

5 | Revenue NSW | 1.00 |

6 | Shorehire Pty Ltd | 52,919.07 |

7 | Workers Compensation Nominal Insurer | 2,563.60 |

Total | 551,508.08 |

No creditors abstained.

53 In terms of those creditors who voted in favour of the DOCA Resolution:

(1) Incline Hire is a related company of Dalma Form;

(2) Robert Grava was the proxy holder for Mr Andrijic, Incline Hire, Auswood International Pty Ltd, Burgess Arnott & Grava Pty Ltd and Elite QS Consulting Pty Ltd. Mr Grava worked for Dalma Form until an unspecified date in 2023 and then commenced work for Incline Hire;

(3) the directors of Dalma Hire are Rade Cikes and Igor Cikes, both of whom the Administrators consider may have been shadow directors of Dalma Form; and

(4) Stephen Taylor, trading as Taylor & Co, is Dalma Form’s accountant.

54 Mr Soire did not exercise his casting vote as chairperson. Had he been required to do so, he would have exercised it against the DOCA Resolution and in favour of a resolution that Dalma Form be wound up, consistent with the recommendation of the Administrators in the supplementary report and his opinion expressed at the second meeting.

Chief Commissioner issues assessments to Dalma Form

55 By email sent on 29 April 2024 Mercelita Gabrillo Compliance Officer, Customer Service -Taxes & Grants, Revenue NSW, informed the Administrators that:

During the payroll tax investigation of [Dalma Form], payments to numerous contractors were identified in the records and information provided by Dalma Form and obtained from other sources.

As a result of the records and information reviewed, I have made a determination, as Delegate of the Chief Commissioner of State Revenue, under s42 of the Payroll Tax Act 2007 (“PTA”), that the payments to those contractors are wages for the purposes of the PTA and that Dalma Form is the employer. The wages are taxable wages for the purposes of s6 of the PTA, and Dalma Form is liable to pay the payroll tax on the taxable wages under s7 of the PTA.

A copy of the s 42 determination, accompanied by a statement of facts and reasons, and the notices of assessment (Assessments) were attached to the email. The Assessments assessed the following amounts for financial years 2018 to 2021 inclusive for payroll tax, interest and penalty tax:

1 July 2017 to 30 June 2018 for $2,955,755.96;

1 July 2018 to 30 June 2019 for $2,533,666.07;

1 July 2019 to 30 June 2020 for $3,363,584.57;

1 July 2021 to 30 June 2021 for $2,412,303.95.

56 Mr Soire observes that this was the first occasion on which a notice of determination or a notice of assessment had been provided by the Chief Commissioner in relation to the external administration of Dalma Form and that the total claimed in the Assessments is $109,553.58 less than was claimed in the Chief Commissioner’s POD.

57 Dalma Form has filed notices of objection to the Assessments. The Deed Administrators’ consent was not sought by any party in relation to the preparation or lodgement of those objections nor have the Deed Administrators provided their consent.

The DOCA is executed

58 In accordance with their obligations under s 444B(2)(a) of the Corporations Act, namely that Dalma Form must execute the deed of company arrangement within 15 business days of the second meeting, the DOCA was executed on 3 May 2024. That being so, on that day:

(1) the Administrators became Deed Administrators; and

(2) pursuant to cl 7(a) of the DOCA, control of Dalma Form returned to Mr Andrijic.

59 On 2 July 2024, in accordance with cl 5(b) of the DOCA, the first payment was made.

Proposal to vary the DOCA

60 On 17 June 2024 the DOCA proponents submitted a proposal to the Deed Administrators seeking to vary the DOCA (variation proposal). Among other things the variation proposal increases the “Deed Contributions” from $250,000 to $350,000 and adds two additional “Proponents”, namely Dalma Services and Dalma Hire.

Updated analysis of expected returns to creditors

61 The Deed Administrators have reviewed the variation proposal and have provided an updated analysis of estimated returns to creditors (calculated as at 19 June 2024) based on three different scenarios: the DOCA; an amended DOCA based on the variation proposal; and if the DOCA is terminated and Dalma Form wound up. That analysis, which was in evidence before me, was undertaken without any final adjudication of creditor claims or any further work in relation to possible claims available in a liquidation.

62 In summary the updated analysis provides for the following estimated dividends to creditors (expressed as a percentage return) in a “low” and “high” scenario in each case:

Scenario | Low estimate | High estimate |

DOCA | 0.87% | 23.30% |

Amended DOCA | 1.31% | 28.66% |

Liquidation | Nil | 43.51% |

63 Mr Soire was cross-examined about the updated analysis. He gave the following evidence:

(1) he accepted that in each case, the “low” scenario assumes lower returns and higher creditor claims and the “high” scenario assumes higher returns and lower creditor claims;

(2) he accepted that if the Administrators recover their costs of this proceeding, the amount recovered would be added to the funds available for distribution in the DOCA and amended DOCA scenarios. As set out in the Deed Administrators’ report dated 1 July 2024, he accepted both the Administrators’ own estimate of percentage recovery of actual legal costs incurred in this proceeding in the range of 60-90% and the costs incurred as at 1 July 2024 and future estimated costs of the proceeding which at the time were together $197,635.56;

(3) he explained the amount available under the DOCA in a low scenario has decreased since 19 June 2024 such there would likely be less than the estimated $138,000 available for distribution in that scenario;

(4) he agreed, on the assumption that Dalma Form goes into liquidation, that if some or all the voidable transaction claims identified are successful, the amount available for distribution will be “vastly more than 100,000 or 150,000”. However, he was not able to estimate how high the figure might be;

(5) he explained that in an optimistic liquidation scenario, the liquidators’ legal fees are higher because more work would need to be done to make the higher recoveries assumed in that scenario; and

(6) he accepted that if upon examination the liquidators formed a view that there was no or little prospect of a successful claim, they would not incur the legal fees associated with pursuing such a claim.

64 Based on their revised analysis, the Administrators’ view expressed in the supplementary report, that it is in the interests of creditors that Dalma Form be wound up, remains unchanged.

The Deputy Commissioner’s evidence

65 The Deputy Commissioner relied on an extensive amount of evidence in support of his application. However, given my approach to resolution of the questions for determination and the conclusion I have reached in relation to the Chief Commissioner’s FAOP, it is not necessary for me to set out that evidence.

LEGISLATIVE FRAMEWORK AND SOME LEGAL PRINCIPLES

Corporations Act

66 Part 5.3A of the Corporations Act concerns company administrations. The object of Pt 5.3A is set out in s 435A which provides:

The object of this Part, and Schedule 2 to the extent that it relates to this Part, is to provide for the business, property and affairs of an insolvent company to be administered in a way that:

(a) maximises the chances of the company, or as much as possible of its business, continuing in existence; or

(b) if it is not possible for the company or its business to continue in existence—results in a better return for the company’s creditors and members than would result from an immediate winding up of the company.

(Note omitted.)

67 Div 10 of Pt 5.3A is titled “Execution and effect of deed of company arrangement”. It includes s 444E which provides, among other things, that a person bound by a deed of company arrangement cannot, until the deed terminates, bring or proceed with a proceeding against the company except with the leave of the Court.

68 Section 445D of the Corporations Act is in Div 11 of Pt 5.3A which is titled “Variation, termination and avoidance of deed”. Section 445D relevantly provides:

(1) The Court may make an order terminating a deed of company arrangement if satisfied that:

…

(c) there was an omission from such a document and the omission can reasonably be expected to have been material to such creditors in so deciding; or

…

(e) effect cannot be given to the deed without injustice or undue delay; or

(f) the deed or a provision of it is, an act or omission done or made under the deed was, or an act or omission proposed to be so done or made would be:

(i) oppressive or unfairly prejudicial to, or unfairly discriminatory against, one or more such creditors; or

(ii) contrary to the interests of the creditors of the company as a whole; or

(g) the deed should be terminated for some other reason.

(2) An order may be made on the application of:

(a) a creditor of the company; or

(b) the company; or

(ba) ASIC; or

(c) any other interested person.

69 In Decon Australia Pty Ltd v TFM Epping Land Pty Ltd [2022] FCAFC 54 a Full Court of this Court (Yates, O’Callaghan and Halley JJ) relevantly said at [144]:

Section 445D involves a two stage process. The first stage is to determine whether one of the grounds referred to in sub-s (1) has been established and, if it has, the second stage is to decide whether to exercise the discretion to terminate the DOCA based on that ground. See Britax Childcare Pty Ltd v Infa Products Pty Ltd [2016] FCA 848; (2016) 115 ACSR 322 (Burley J) at 342 [90]; Shafston Avenue Construction Pty Ltd v McCann [2019] FCA 1426; (2019) 138 ACSR 299 at 336 [130] (Reeves J). …

70 That is, the Court has a discretion whether to terminate a deed of company arrangement even if it is satisfied that a ground under s 445D(1) of the Corporations Act is established. That discretion is to be exercised having regard to all of the relevant circumstances viewed as a whole including the interests of creditors as a whole and the public interest: see Decon Australia at [145]; TNT Building Trades Pty Ltd v Benelong Developments Pty Ltd (admins apptd) [2012] NSWSC 766; (2012) 91 ACSR 17 at [27].

71 In Sino Group International Limited v Toddler Kindy Gymbaroo Pty Ltd [2023] FCAFC 110; 168 ACSR 311 at [71]-[73] a Full Court of this Court (Farrell, Cheeseman and Feutrill JJ) relevantly said in relation to the exercise of the discretion under s 445D:

71 There are many factors that the Court will take into account when considering if the discretion to terminate a DOCA, once enlivened, should be exercised. Many of the relevant factors in the authorities relate to the interests of creditors as a whole on the one hand, and the public interest on the other. Public interest may be understood as whether the continuation of the DOCA is conducive or detrimental to commercial morality and to the interests of the public at large. The Court must carefully balance the interests of creditors with the public interest in considering whether it is appropriate to exercise the discretion to terminate a DOCA.

72 The following non-exhaustive list of factors, drawn from the authorities, are relevant to the exercise of the Court’s discretion:

(1) Whether the creditors voted to enter into a DOCA, noting that creditors are generally taken to be in a better position to judge what is in their best interests than the Court;

(2) Whether the vote is carried by the votes of related creditors whose interests are not aligned with the unrelated creditors;

(3) Whether the information base upon which the creditors voted was materially flawed whether because it was false, misleading or otherwise omitted information;

(4) The degree to which false, misleading or omitted information had, or is likely to have had, an influence on the manner in which creditors voted;

(5) Whether creditors would be better off under a DOCA or in a liquidation;

(6) Whether the dividend under a DOCA is likely to be insignificant;

(7) Whether the continuation of the DOCA would have the effect of eroding commercial morality or public confidence in financial systems; and

(8) Whether the effect of the DOCA, once implemented, would be to permit an insolvent company to continue to trade, contrary to the public interest.

…

73 The list of factors relevant to the Court’s exercise of the discretion is not closed. As s 445D(1) involves a discretion that must be exercised judicially, any factor that is relevant to the exercise of the discretion, having regard to the purpose of Pt 5.3A of the Act, may be taken into account. There are many factors that the Court will take into account when considering if the discretion to terminate a DOCA, once enlivened, should be exercised. Some of the relevant factors are the same or similar to those which are taken into account in determining if the deed or a provision of it is oppressive, unfairly discriminatory, unfairly prejudicial or contrary to the interest of the company’s creditors as a whole under s 445D(1)(f) of the Act.

72 Section 446AA relevantly provides:

(1) This section applies if a company has executed a deed of company arrangement and:

(a) the Court, at a particular time, makes an order under section 445D terminating the deed of company arrangement; or

…

(2) The company is taken:

(a) to have passed, at the time referred to in paragraph (1)(a) or subparagraph (1)(b)(ii), as the case may be, a special resolution under section 491 that the company be wound up voluntarily; and

(b) to have done so without a declaration having been made and lodged under section 494.

(1) The Court may make such order as it thinks appropriate about how this Part is to operate in relation to a particular company.

(2) For example, if the Court is satisfied that the administration of a company should end:

(a) because the company is solvent; or

(b) because provisions of this Part are being abused; or

(c) for some other reason;

the Court may order under subsection (1) that the administration is to end.

(3) An order may be made subject to conditions.

(4) An order may be made on the application of:

(a) the company; or

(b) a creditor of the company; or

(c) in the case of a company under administration—the administrator of the company; or

(d) in the case of a company that has executed a deed of company arrangement—the deed’s administrator; or

(e) ASIC; or

(f) any other interested person.

74 Section 499 relevantly provides:

…

(2D) If section 446AA applies in relation to the company because of paragraph 446AA(1)(a):

(a) the Court may, immediately after it makes the order referred to in that paragraph, appoint a person to be the liquidator for the purpose of winding up the affairs and distributing the property of the company; and

(b) if no appointment is made under paragraph (a) of this subsection:

(i) the company is taken to have appointed the administrator of the deed of company arrangement referred to in section 446AA to be the liquidator for the purpose of winding up the affairs and distributing the property of the company; and

(ii) the appointment takes effect at the time referred to in paragraph 446AA(1)(a).

IPS

75 Section 90-15(1) of the IPS provides that the Court may make such orders as it thinks fit in relation to the external administration of a company. It may do so on its own initiative or on an application under s 90-20 of the IPS. Section 90-15(3) sets out a non-exhaustive list of the types of orders the Court can make and relevantly includes:

(a) an order determining any question arising in the external administration of the company;

(b) an order that a person cease to be the external administrator of the company;

…

76 Section 90-15(4) sets out a non-exhaustive list of the matters which can be taken into account in considering whether to make an order under s 90-15(1) and provides:

(4) Without limiting the matters which the Court may take into account when making orders, the Court may take into account:

(a) whether the liquidator has faithfully performed, or is faithfully performing, the liquidator’s duties; and

(b) whether an action or failure to act by the liquidator is in compliance with this Act and the Insolvency Practice Rules; and

(c) whether an action or failure to act by the liquidator is in compliance with an order of the Court; and

(d) whether the company or any other person has suffered, or is likely to suffer, loss or damage because of an action or failure to act by the liquidator; and

(e) the seriousness of the consequences of any action or failure to act by the liquidator, including the effect of that action or failure to act on public confidence in registered liquidators as a group.

77 Section 90-20(1) provides for those persons who may apply for an order under s 90‑15 of the IPS. For present purposes they include “a person with a financial interest in the external administration of the company”. A person has a financial interest in the external administration if the person is, relevantly, a creditor: see s 5-30 of the IPS.

IP Rules

78 Rule 75-85 sets out a creditor’s right to vote at a creditors’ meeting. Rule 75-85(4) provides:

A creditor must not vote in respect of:

(a) an unliquidated debt; or

(b) a contingent debt; or

(c) an unliquidated or a contingent claim; or

(d) a debt the value of which is not established;

unless a just estimate of its value has been made.

79 Rule 75-100 concerns decisions in relation to entitlement to vote at a creditors’ meeting. It provides:

(1) The person presiding at a meeting may determine any question that arises as to the entitlement of a person to vote.

(2) In deciding whether a person is entitled to vote at a meeting of creditors, the person presiding must:

(a) have regard to the merits of the person’s claim; and

(b) act impartially and independently.

(3) If the person presiding is in doubt whether a proof of debt or claim should be admitted or rejected, her or she must mark that proof as objected to and allow the creditor to vote, subject to the vote being declared invalid if the objection is sustained.

(4) A decision by the person presiding to admit or reject a proof of debt or claim for the purposes of voting may be appealed against to the Court within 10 business days after the decision.

TA Act

80 Section 7 of the TA Act provides that the purpose of the Act “is to make general provision with respect to the administration and enforcement of the other taxation laws”.

81 The term “assessment” is defined in s 3 to mean:

assessment means an assessment made by the Chief Commissioner under Part 3 of the tax liability of a person under a taxation law, and includes—

(a) a reassessment and a compromise assessment under Part 3, and

(b) an assessment by the Supreme Court or the Civil and Administrative Tribunal on an application for a review.

82 Section 4 sets out the meaning of “taxation laws” and prescribes those Acts that are taxation laws for the purposes of the TA Act. They include the Payroll Tax Act.

83 Section 8 is titled “General power to make assessment” and provides:

(1) The Chief Commissioner may make an assessment of the tax liability of a taxpayer.

(2) An assessment of a tax liability may consist of a determination that there is not a particular tax liability.

(3) For the avoidance of doubt, an assessment of tax liability is taken to have been made when the Chief Commissioner calculates the tax liability of a taxpayer based on a return under the Payroll Tax Act 2007 or any other Act prescribed by the regulations for the purposes of this subsection (whether or not the Chief Commissioner issues a notice of assessment as a result of that calculation or otherwise notifies the taxpayer of the calculation).

84 Section 11 sets out the information on which an assessment is made and provides:

(1) The Chief Commissioner may make an assessment on the information that the Chief Commissioner has from any source at the time the assessment is made.

(2) If the Chief Commissioner has insufficient information to make an exact assessment of a tax liability, the Chief Commissioner may make an assessment by way of estimate.

Payroll Tax Act

85 Section 4 of the Payroll Tax Act provides that “[t]his Act is to be read together with the [TA Act] which provides for the administration and enforcement of this Act and other taxation laws”.

86 Part 2 of the Payroll Tax Act is titled “Imposition of payroll tax”. Sections 6 and 7 respectively provide that payroll tax is imposed on all taxable wages and that the liability to pay payroll tax is on the “employer by whom taxable wages are paid or payable”. Payroll tax is usually payable within seven days after the end of the month in which the taxable wages were paid or payable except in the month of June when they are to be paid within 28 days after the end of the month in relation to taxable wages paid or payable in June: s 9.

87 Section 42 is titled “Agreement to reduce or avoid liability to payroll tax” and provides:

(1) If the effect of an employment agency contract is to reduce or avoid the liability of any party to the contract to the assessment, imposition or payment of payroll tax, the Chief Commissioner may—

(a) disregard the contract, and

(b) determine that any party to the contract is taken to be an employer for the purposes of this Act, and

(c) determine that any payment made in respect of the contract is taken to be wages for the purposes of this Act.

(2) If the Chief Commissioner makes a determination under subsection (1), the Chief Commissioner must serve a notice of the determination on the person taken to be an employer for the purposes of this Act.

(3) The notice must set out the facts on which the Chief Commissioner relies and the reasons for the determination.

(4) This section has effect in relation to agreements, transactions and arrangements made before, on or after the commencement of this section.

QUESTIONS TO BE RESOLVED

88 The following questions arise on the Chief Commissioner’s FAOP:

(1) does the Deputy Commissioner have standing to pursue his interlocutory process?

(2) should leave be granted to the Chief Commissioner pursuant to s 444E of the Corporations Act to begin or proceed with this proceeding?

(3) assuming the answer to (2) is yes:

(a) should the Administrators’ decision to admit the Chief Commissioner’s POD for $1 be set aside?

(b) if the answer to (a) above is yes, should the DOCA Resolution be set aside?

(c) should the DOCA be terminated?

89 As set out above and assuming the answer to (1) above is “yes”, the Deputy Commissioner appears to support the Chief Commissioner in his application to terminate the DOCA or, if the Chief Commissioner is unsuccessful in obtaining that relief, he seeks the same relief in his own right.

A PRELIMINARY ISSUE: THE DEPUTY COMMISSIONER’S STANDING

90 The Dalma Defendants challenge the Deputy Commissioner’s standing.

91 Rule 2.13 of the Federal Court (Corporations) Rules 2001 (Cth) relevantly provides that:

(1) The Court may grant leave to any person who is, or who claims to be:

(a) a creditor, contributory or officer of a corporation; or

(b) an officer of a creditor, or contributory, of a corporation; or

(c) any other interested person;

to be heard in a proceeding without becoming a party to the proceeding.

92 Similarly s 445D(2) and s 447A(4) of the Corporations Act each permit an application to be brought for relief by a creditor or “any other interested person” (see [68] and [73] above). Section 90-20(1) of the IPS provides that a person with “a financial interest” in the external administration of the company has standing to bring an application for orders pursuant to s 90-15 of the IPS. Such a person includes a creditor (see 0 above).

93 It was not in dispute that:

(1) at the time the Deputy Commissioner filed his interlocutory process, he was a creditor of Dalma Form in that Dalma Form owed a debt which was due and payable to the Deputy Commissioner in the sum of $126,672.83 (DCT Debt). The amount due was a running balance account (RBA) deficit debt for the purposes of s 8AAZH of the Taxation Administration Act 1953 (Cth);

(2) according to Stephen Taylor, Dalma Form’s accountant, on 18 June 2024 he reviewed the ATO’s online portal and found that there were multiple accounts for Dalma Form including:

(a) an account described as “Activity statement 003 DFS” which had a zero balance; and

(b) an account styled “Activity statement (Administration) 001 DFS” (Administration Account) which had a debit balance of $279,805.39. Mr Taylor understands that upon Dalma Form entering into administration the ATO created the Administration Account;

(3) on 19 June 2024 Dalma Form made payment of $283,000 into the account styled “Activity statement 003 DFS” (DCT Payment);

(4) on 21 June 2024 Mr Taylor ascertained that a credit of $283,000 was applied to the account styled “Activity statement 003 DFS”. Immediately after doing so Mr Taylor sent a request to the ATO on its online portal requesting that the credit be transferred to the Administration Account so that the amount owing was cleared and Dalma Form recorded as being in credit to the ATO; and

(5) the Deputy Commissioner accepts that on 20 June 2024 he received the DCT Payment which was allocated to the RBA established for Dalma Form.

94 As a result, the Deputy Commissioner accepts that the DCT Debt has been discharged. It follows that the Deputy Commissioner at the time of the hearing was not, and since 20 June 2024 has not been, a creditor of Dalma Form.

95 However, the Deputy Commissioner contends that by reason of the DCT Debt and the claims he has, or is likely to have, in respect of the Alleged Scheme, he was each of a creditor, an interested person and a person with a financial interest in the external administration of Dalma Form at the time that he sought leave to be heard in the proceeding and when he filed the interlocutory application.

96 The Deputy Commissioner submits that even if payment of the DCT Debt has the effect that he is no longer a creditor of Dalma Form, he has a material economic interest in the administration or subsequent liquidation of Dalma Form and, consequently, the outcome of this proceeding. The Deputy Commissioner submits that whether assessed through s 445D(2)(c) or s 447A(4)(f) of the Corporations Act, s 90-15 of the IPS or r 2.13(e) of the Corporations Rules, he is an “interested person” in the relevant sense.

97 The Deputy Commissioner was a creditor of Dalma Form as at the date of commencement of the proceeding and thus had standing to file and ventilate his interlocutory process. However, if the relevant time to assess the question of standing is the time of the hearing, the question to be determined is whether the Deputy Commissioner had and continues to have standing on and from 20 June 2024, including at the hearing. Whether he does will depend on the time at which the question of standing is to be determined or put another way, whether standing can be lost in the way the Dalma Defendants allege.

98 In Shangri-La Construction Pty Ltd v GVE Hampton Pty Ltd (in liq) & Ors [2021] VSC 161; (2021) 152 ACSR 19 a group of creditors, referred to as ‘Opposing Creditors” challenged the plaintiff’s standing to bring an application for the appointment of a special purpose liquidator (SPL) under s 90-15 of the IPS. Detailed submissions were made by the parties in relation to that issue. In the result, Connock J dismissed the plaintiff’s application because his Honour was not satisfied that the plaintiff had established that it was just and beneficial for the winding up, or the creditors as a whole, for the SPL to be appointed or that there was otherwise utility or good reason in the circumstances of the case to appoint the SPL. That being so, his Honour did not need to address the question of the plaintiff’s standing.

99 However, in light of the detailed submissions that had been made, Connock J considered it appropriate to state briefly the conclusion he had reached on that question. His Honour said at [190]-[191] and [193]:

[190] I do not accept the Opposing Creditors’ submission that, although the application was commenced with standing as a creditor, the plaintiff would lose that standing and the right to continue with the application if (as was contended by the plaintiff) the plaintiff ceased to be a creditor of the Company prior to the making of final orders.

[191] There is nothing in the language of s 90-15 or s 90-20 of Sch 2 to the Act, or the related provisions earlier referred to in these reasons, that lends support for the contention that standing can be lost depending upon the purpose of the applicant or application, or depending upon whether the application is properly to be characterised as relating to future or past dealings in the external administration. That is not what the section says, there is no contextual or textual support for it, and it is not supported by any authority. The language of the Act is clear and ss 90-15 and 90-20 do not provide for such qualifications. There is in my view no legitimate basis for seeking to imply or inject into the provisions the suggested qualifications, and so to do also falls foul of well-established principles of statutory construction.

…

[193] Given the above, and noting that the Opposing Creditors did not ultimately maintain their submission that standing under s 90-15 would be lost in all cases where creditor status was lost, it is neither necessary nor desirable to seek to consider or address the many other submissions made by the parties in connection with standing. However, for completeness, I add that had the submission that standing would be lost in all cases been maintained, I would not have accepted that submission. Again, it is not what the sections say; there is no textual or contextual support for the contention, and it is not supported by any authority. This conclusion sits well with the conclusions reached in Boart, Complete Liquid Transport, and Re Living Australia, and the cases there cited. It is also well accepted that s 90-15 has and is intended to have a broad operation.

(Footnotes omitted.)

100 The Dalma Defendants submit that the authorities relied on by Connock J in his Honour’s obiter remarks at [193] did not “deal squarely” with the issue that they seek to raise. While those authorities do not involve the application of s 445D(2) of the Corporations Act or provisions which are in identical terms, they squarely address the question of whether a creditor with standing to bring an application at the time of the filing of the application will lose that standing if they cease to be a creditor after the commencement of the proceeding or the filing of the application and prior to the making of final orders. They are therefore relevant by analogy and instructive in determination of the issue that was before the Court in Shangri-La. In each of Re Boart Longyear Ltd (2019) 370 ALR 30; [2019] FCA 62, Deputy Commissioner of Taxation v Complete Liquid Transport Pty Ltd [2010] FCA 1067 and Mutton v Living Australia Pty Ltd [2020] FCA 739; (2020) 145 ACSR 82 cited at [193] of Shangri-La, it was found that the standing of the creditors in question turned on their status as a creditor as at the commencement of the proceeding rather than at the time of the hearing.

101 In my view the conclusion reached by Connock J in Shangri-La is compelling and, as his Honour observed, sits well with the authorities to which his Honour referred. The Deputy Commissioner was a creditor as at the commencement of the proceeding and when he filed his interlocutory process. Despite payment of the DCT Debt, he did not lose his standing. That is a complete answer to the Dalma Defendants’ contention that the Deputy Commissioner has no standing.

102 In the alternative the Deputy Commissioner contends that he is an “other interested person” for the purposes of the s 445D(2)(c) or s 447A(4)(f) of the Corporations Act.

103 In Allatech Pty Ltd v Construction Management Group Pty Ltd (2002) 167 FLR 324 the plaintiff, Allatech, sought orders under s 445D(1) of the Corporations Act terminating a deed of company arrangement and appointing a liquidator to Construction Management Group Pty Ltd (CMG). Allatech alleged that there was a failure to disclose certain matters to creditors in the voluntary administrator’s report. One of the issues that arose was Allatech’s standing to bring the application. Allatech alleged that it had standing under s 445D(2) as an “other interested person”.

104 In considering whether that was so, Austin J observed (at [16]) that “other interested person” was not defined in the Corporations Act but expressed the view (at [18]) that they are “words of wide scope”, a view which was reinforced by comparing s 445D(2) with other provisions of Pt 5.3A of the Corporations Act which confer standing to make applications of various kinds, for example s 447A. His Honour continued at [19]-[20]:

19 Sections 445D(2) and 447A(4) may be contrasted with ss 447E(3) and 449D(3), as well as with s 445G(1). Standing to make applications under these latter sections, where the subject of the application is rather more specific than the subject of the former sections, is confined to creditors, members, officers (in the case of s 449D(3)) and the commission. The comparison suggests that the words “other interested person”, where they are added to the list, are inserted to broaden the class of potential applicants.