FEDERAL COURT OF AUSTRALIA

Australian Securities and Investments Commission v BSF Solutions Pty Ltd (Liability) [2024] FCA 553

ORDERS

DATE OF ORDER: |

THE COURT:

1. Grants leave to the applicant to amend the Concise Statement in the form handed to the Court on 30 April 2024.

2. Adopts the following defined terms in the paragraphs which follow:

Term | Definition |

ACL | Australian Credit Licence pursuant to s 35 of the Credit Act |

BSF | BSF Solutions Pty Ltd, the first respondent |

Cigno | Cigno Australia Pty Ltd, the second respondent |

Cigno Services | The following Services: (a) processing loan applications for proposed credit contracts with BSF, and providing to consumers the proposed credit contracts with BSF after the applications were approved; (b) receiving and processing loan repayments, either directly from consumers or by entering into agreements with direct debit providers to arrange for consumers’ accounts to be directly debited and paid to Cigno, monitoring those payments and taking steps to recover debts from defaulting consumers; (c) monitoring repayments and defaults of the loans, including arranging changes to consumers’ repayment schedules and notifying consumers about upcoming payments and defaults; (d) sending account statements, reminders and other communications to consumers and receiving and responding to all consumer enquiries concerning the loans; and (e) remitting to BSF funds received from consumers. |

Cigno Fees | Account Keeping Fee, Default Fee, and Change of Payment Schedule Fee as referred to in the Services Agreements |

Credit Act | National Consumer Protection Act 2009 (Cth) |

Credit Code | National Credit Code, being Schedule 1 to the Credit Act |

Harrison | Brenton James Harrison, the third respondent |

Loan Agreement | The agreements entered into by consumers with BSF entitled “No Fee for Credit Loan Agreement” or “No Upfront Charge Loan Agreement” |

Loan Management Facilitation Agreement | The agreement dated 20 July 2022 between BSF and Cigno bearing that name |

No Upfront Charge Loan Model | The business model implemented during the Relevant Period whereby Cigno marketed small loans to consumers, processed loan applications and managed repayments, and BSF advanced those loans, as part of which: (a) pursuant to the Loan Management Facilitation Agreement, BSF charged Cigno an assessment fee of $19.99 for the assessment and approval of each loan application that BSF received, irrespective of whether the application was approved; (b) BSF required consumers to enter into a Loan Agreement; and (c) Cigno required consumers to enter into a Services Agreement |

Relevant Period | The period from July 2022 to 3 October 2023 |

Services Agreements | The agreements entered into by Cigno with consumers described as “Account Keeping Agreements”, of which Cigno entered into 150,112 |

Swanepoel | Mark Swanepoel, the fourth respondent |

3. Declares that, in the Relevant Period, on each occasion that BSF entered into or performed a Loan Agreement, BSF contravened s 29(1) of the Act by engaging in a credit activity without holding an ACL authorising BSF to engage in that activity, being the activity of being a credit provider under a credit contract (for the purpose of Item 1(a) of s 6(1) of the Credit Act), the activity of carrying on a business of providing credit, being credit the provision of which the Credit Code applies to (for the purpose of Item 1(b) of s 6(1)), and the activity of performing the obligations, or exercising the rights, of a credit provider in relation to a credit contract or proposed credit contract (for the purpose of Item 1(c) of s 6(1)), in that:

(a) BSF was, and remained during the Relevant Period, a credit provider to consumers pursuant to the No Upfront Charge Loan Model;

(b) BSF entered into, performed and gave effect to 150,112 Loan Agreements with consumers; and

(c) BSF advanced loan amounts and sought recovery of loan amounts.

4. Declares that, in the Relevant Period, on each occasion that BSF demanded, received or accepted a fee described as a “Late Payment Fee”, BSF contravened s 32(1) of the Credit Act by demanding, receiving or accepting fees, charges or other amounts from consumers for engaging in a credit activity without holding an ACL authorising BSF to engage in that activity, being:

(a) the credit activity of carrying on a business of providing credit, being the provision of which the Credit Code applies to (for the purpose of Item 1(b) of s 6(1) of the Credit Act); and

(b) the credit activity of performing the obligations, or exercising the rights, of a credit provider in relation to a credit contract (for the purpose of Item 1(c) of s 6(1) of the Credit Act).

5. Declares that, in the Relevant Period, on each occasion that Cigno provided any of the Cigno Services pursuant to the No Upfront Charge Loan Model, Cigno contravened s 29(1) of the Credit Act by engaging in a credit activity without holding an ACL authorising Cigno to engage in the credit activity, in that in relation to each customer who entered into a Loan Agreement with BSF:

(a) in performing a Services Agreement with a consumer, Cigno exercised the rights of a credit provider (BSF) on behalf of BSF in relation to a credit contract or a proposed credit contract (for the purpose of Item 1(c) of s 6(1) of the Credit Act); and

(b) Cigno provided a credit service (as defined in s 7 of the Credit Act), by:

(i) providing credit assistance (as defined in s 8 of the Credit Act) to consumers by:

A. suggesting that they apply for a particular credit contract with a particular credit provider (being BSF); and

B. assisting them to apply for a particular credit contract with a particular credit provider (being BSF); and

(ii) acting as an intermediary (as defined in s 9(a) of the Credit Act) between consumers and BSF for the purposes of securing a provision of credit for the consumer under a credit contract with the credit provider (being BSF).

6. Declares that, in the Relevant Period, on each occasion that Cigno demanded, received or accepted the Cigno Fees, Cigno contravened s 32(1) of the Credit Act by demanding, receiving or accepting fees, charges or other amounts from consumers for engaging in a credit activity without holding an ACL authorising Cigno to engage in that activity, being the credit activity of:

(a) exercising the rights of a credit provider (being BSF) on behalf of BSF in relation to a credit contract (for the purpose of Item 1(c) of s 6(1) of the Credit Act);

(b) to the extent that Cigno demanded, received or accepted the Account Keeping Fee, providing a credit service (as defined in s 7 of the Credit Act) by:

(i) providing credit assistance (as defined in s 8 of the Credit Act) to consumers by:

A. suggesting that they apply for a particular credit contract with a particular credit provider (being BSF);

B. assisting them to apply for a particular credit contract with a particular credit provider (being BSF); and

(ii) to the extent that Cigno demanded, received or accepted the Account Keeping Fee, acting as an intermediary (as defined in s 9(a) of the Credit Act) between consumers and BSF for the purposes of securing a provision of credit for the consumer under a credit contract with the credit provider (being BSF).

7. Declares that Harrison was involved in BSF’s contraventions of:

(a) s 29(1) of the Credit Act and, by virtue of s 169(b) of the Credit Act, thereby himself contravened s 29(1) of the Credit Act; and

(b) s 32(1) of the Credit Act and, by virtue of s 169(b) of the Credit Act, thereby himself contravened s 32(1) of the Credit Act.

8. Declares that Swanepoel was involved in Cigno’s contraventions of:

(a) s 29(1) of the Credit Act and, by virtue of s 169(b) of the Credit Act, thereby himself contravened s 29(1) of the Credit Act; and

(b) s 32(1) of the Credit Act and, by virtue of s 169(b) of the Credit Act, thereby himself contravened s 32(1) of the Credit Act.

9. Orders that BSF be permanently restrained (whether by servants, agents or employees) from:

(a) demanding, receiving or accepting fees, charges or other amounts from consumers (including the “Late Payment Fee” and amounts of principal) in respect of Loan Agreements entered into during the Relevant Period for as long as it does not hold an ACL authorising it to engage in the credit activities of:

(i) carrying on a business of providing credit, being credit the provision of which the code applies to (for the purpose of Item 1(b) of s 6(1) of the Credit Act); and

(ii) performing the obligations, or exercising the rights, of a credit provider in relation to a credit contract (for the purposes of Item 1(c) of s 6(1) of the Credit Act);

(b) engaging in the credit activities of being a credit provider under a credit contract (for the purpose of Item 1(a) of s 6(1) of the Credit Act), carrying on a business of providing credit, being credit the provision of which the Credit Code applies to (for the purpose of Item 1(b) of s 6(1) of the Credit Act), and performing the obligations, or exercising the rights, of a credit provider in relation to a credit contract or a proposed credit contract (for the purpose of Item 1(c) of s 6(1) of the Credit Act) for so long as it does not hold an ACL authorising it to engage in credit activities by:

(i) entering into or performing agreements with consumers on the same or substantially the same terms as the Loan Agreement;

(ii) providing credit to consumers pursuant to a model the same or substantially the same as the No Upfront Charge Loan Model;

(iii) entering into or performing any agreement on the same or substantially the same terms as the Loan Management Facilitation Agreement; and

(iv) implementing a model on the same or substantially the same terms as the No Upfront Charge Loan Model.

10. Orders that Cigno be permanently restrained (whether by its servants, agents or employees) from:

(a) in respect of Services Agreements entered into during the Relevant Period, engaging in credit activities by exercising the rights of a credit provider (being BSF) on behalf of BSF in relation to a credit contract (for the purpose of Item 1(c) of s 6(1) of the Credit Act) by providing the Cigno Services;

(b) in respect of Services Agreements entered into during the Relevant Period, demanding, receiving or accepting fees, charges or other amounts from consumers, including the Cigno Fees and amounts of principal owing to BSF;

(c) exercising the rights of a credit provider in relation to a credit contract or proposed credit contract (for the purpose of Item 1(c) of s 6(1) of the Credit Act) and providing a credit service (as defined in s 7 of the Credit Act) for as long as it does not hold an ACL authorising it to engage in the credit activities, including by:

(i) entering into or performing agreements with consumers on the same or substantially the same terms as the Services Agreements;

(ii) entering into or performing any agreement on the same or substantially the same terms as the Loan Management Facilitation Agreement; and

(iii) implementing a model which is the same or substantially the same as the No Upfront Charge Loan Model; and

(d) demanding, receiving or accepting fees, charges or other amounts from consumers, including the Cigno Fees and amounts of principal owing to BSF, for as long as it does not hold an ACL authorising it to engage in the credit activities, including:

(i) the credit activity of exercising the rights to a credit provider (including BSF) on behalf of the credit provider in relation to a credit contract (for the purpose of Item 1(c) of s 6(1) of the Credit Act) by providing the Cigno Services;

(ii) in relation to the Account Keeping Fee, the credit activity of providing a credit service (as defined in s 7 of the Credit Act) by providing credit assistance (as defined in s 8 of the Credit Act) to consumers by:

(1) suggesting that they apply for a particular credit contract with a particular credit provider (including BSF); and

(2) assisting them to apply for a particular credit contract with a particular credit provider (including BSF); and

(iii) in relation to the Account Keeping Fee, acting as an intermediary (as defined in s 9(a) of the Credit Act) between consumers and a credit provider for the purposes of securing a provision of credit for the consumer under a credit contract with a credit provider (including BSF).

11. Orders that Harrison be permanently restrained from:

(a) being involved in any conduct by BSF demanding, receiving or accepting fees, charges or other amounts from consumers (including the “Late Payment Fee” and amounts of principal) in respect of Loan Agreements entered into during the Relevant Period for so long as BSF does not hold an ACL authorising it to engage in the credit activities of:

(i) carrying on a business of providing credit, being credit the provision of which the code applies to (for the purpose of Item 1(b) of s 6(1) of the Credit Act); and

(ii) performing the obligations, or exercising the rights, of a credit provider in relation to a credit contract (for the purposes of Item 1(c) of s 6(1) of the Credit Act);

(b) being involved in any conduct by BSF engaging in the credit activities of being a credit provider under a credit contract (for the purpose of Item 1(a) of s 6(1) of the Credit Act), carrying on a business of providing credit, being credit the provision of which the Credit Code applies to (for the purpose of Item 1(b) of s 6(1) of the Credit Act), and performing the obligations, or exercising the rights, of a credit provider in relation to a credit contract or a proposed credit contract (for the purposes of Item 1(c) of s 6(1) of the Credit Act) for so long as BSF does not hold an ACL authorising it to engage in the credit activities by:

(i) entering into or performing agreements with consumers on the same or substantially the same terms as the Loan Agreement;

(ii) providing credit to consumers pursuant to a model the same or substantially the same as the No Upfront Charge Loan Model;

(iii) entering into or performing any agreement on the same or substantially the same terms as the Loan Management Facilitation Agreement; and

(iv) implementing a model on the same or substantially the same terms as the No Upfront Charge Loan Model.

12. Orders that Swanepoel be permanently restrained from:

(a) being involved in any conduct by Cigno, in respect of Service Agreements entered into during the Relevant Period:

(i) engaging in credit activities by exercising the rights of a credit provider (being BSF) on behalf of BSF in relation to a credit contract (for the purpose of Item 1(c) of s 6(1) of the Credit Act) by providing any of the Cigno Services; and

(ii) demanding, receiving or accepting fees, charges or other amounts from consumers, including the Cigno Fees and amounts of principal due to BSF;

(b) being involved in any conduct by Cigno:

(i) exercising the rights of a credit provider in relation to a credit contract or proposed credit contract (for the purpose of Item 1(c) of s 6(1) of the Credit Act) and providing a credit service (as defined in s 7 of the Credit Act) for so long as Cigno does not hold an ACL authorising it to engage in the credit activities, including by:

A. entering into or performing agreements with consumers on the same or substantially the same terms as the Services Agreements;

B. entering into or performing any agreement on the same or substantially the same terms as the Loan Management Facilitation Agreement; and

C. implementing a model which is the same or substantially the same as the No Upfront Charge Loan Model; and

(ii) being involved in any conduct by Cigno demanding, receiving or accepting fees, charges or other amounts from consumers, including the Cigno Fees and amounts of principal owing to BSF, for so long as Cigno does not hold an ACL authorising it to engage in the credit activities, including:

A. the credit activity of exercising the rights of a credit provider (being BSF) on behalf of the credit provider in relation to a credit contract (for the purpose of Item 1(c) of s 6(1) of the Credit Act) by providing the Cigno Services; and

B. in relation to the Account Keeping Fee, the credit activity of providing a credit service (as defined in s 7 of the Credit Act) by:

(1) providing credit assistance (as defined in s 8 of the Credit Act) to consumers by:

(a) suggesting that they apply for a particular credit contract with a particular credit provider (being BSF); and

(b) assisting them to apply for a particular credit contract with a particular credit provider (being BSF); and

(2) acting as an intermediary (as defined in s 9(a) of the Credit Act) between consumers and a credit provider for the purposes of securing a provision of credit for the consumer under a credit contract with a credit provider (being BSF).

13. Directs that the applicant serve and send to my Associate by 31 May 2024 proposed adverse publicity orders pursuant to s 182 of the Credit Act and proposed orders for the further conduct of the proceedings.

14. Directs that the respondents serve and provide to my Associate by 7 June 2024 its response to the proposed orders referred to in para 13 above, together with any written submissions in support.

15. Directs the applicant to serve and provide to my Associate by 14 June 2024 any proposed revisions to its proposed orders pursuant to para 13 above, together with any written submission support.

16. Lists the matter for a case management hearing in relation to the terms of the adverse publicity orders and further orders for the case management of the matter at 9.30 am on 21 June 2024.

17. Reserves the question of the costs of the proceedings to date.

(10

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

JACKMAN J:

Introduction

1 In these proceedings, the Australian Securities and Investments Commission (ASIC) alleges contraventions by the first respondent (BSF) and the second respondent (Cigno) of the National Consumer Credit Protection Act 2009 (Cth) (Credit Act), having regard to the provisions of the National Credit Code (Credit Code), being Schedule 1 to the Credit Act. ASIC also alleges that the third respondent, Mr Harrison, was involved in BSF’s contraventions, and that the fourth respondent, Mr Swanepoel, was involved in Cigno’s contraventions.

2 The central thrust of ASIC’s allegations is that BSF and Cigno established a lending business model (referred to as the No Upfront Charge Loan Model), which they implemented from about July 2022 to 3 October 2023 (Relevant Period). Under that model, Cigno marketed small loans to consumers, processed loan applications and managed repayments, and BSF advanced those loans to consumers (BSF Credit). Although loans ceased being written pursuant to the No Upfront Charge Loan Model from 21 December 2022, BSF and Cigno have continued to demand, receive and accept fees, charges and other amounts from consumers pursuant to agreements entered into before that date. Neither BSF nor Cigno held an Australian Credit Licence (ACL). ASIC alleges that both have contravened, and continue to contravene, the prohibition against engaging in a credit activity without a licence, contrary to s 29(1) of the Credit Act, and the prohibition against demanding, receiving or accepting fees, charges or other amounts from a consumer for engaging in a credit activity, contrary to s 32(1) of the Credit Act. Mr Harrison and Mr Swanepoel were during the Relevant Period, and remain, the sole director and secretary of BSF and Cigno respectively. ASIC alleges that they were “involved in” the respective contraventions by BSF and Cigno, within the meaning of s 5(1) of the Credit Act.

3 A central issue in the proceedings is whether either of the fees described by Cigno as the “Account Keeping Fee” or the “Change of Payment Schedule Fee” was “a charge [that] is or may be made for providing the” BSF Credit, within the meaning of s 5(1)(c) of the Credit Code. In this regard, it should be noted that on 27 June 2022 (that is, in the month before the Relevant Period began), the Full Court delivered judgment in Australian Securities and Investments Commission v BHF Solutions Pty Ltd [2022] FCAFC 108; (2022) 293 FCR 330 (the BHF Proceeding), in which it was held that an earlier model established by parties related to BSF and Cigno was unlawful. In particular, the Full Court in the BHF Proceeding held that the “Financial Supply Fee” charged by Cigno Pty Ltd in that case was “a charge [that] is or may be made for providing the credit”. I deal with the Full Court’s reasoning in the BHF Proceeding in detail below.

4 In broad terms, ASIC contends that, pursuant to the No Upfront Charge Loan Model, if a consumer borrowed money from BSF, and repaid the loan in accordance with the terms of the loan agreement with BSF (Loan Agreement) without defaulting, the consumer would not be required to pay any amounts to BSF other than to repay the principal. ASIC accepts that there was, pursuant to the terms of the Loan Agreement, no requirement to pay BSF interest or any other fees or charges for the provision of the credit. ASIC contends that it was because of the consumer’s entry into an “Account Keeping Agreement” with Cigno (Services Agreement) that the consumer paid anything for their loans. ASIC contends that it was pursuant to the Services Agreements that the consumers were charged for the provision of the credit they obtained pursuant to the No Upfront Charge Loan Model.

5 ASIC contends that the Account Keeping Fee (and any Change of Payment Schedule Fee) paid by consumers to Cigno was the fee by which consumers paid for the loan. ASIC submits that if a consumer repaid their loan in accordance with the terms of their Loan Agreement without defaulting and without requesting any change to their payment schedules under the Loan Agreement, the only fee they would be required to pay, pursuant to the No Upfront Charge Loan Model, was the Account Keeping Fee paid by the consumer to Cigno. If, in addition, a consumer requested any change to their payment schedules under the Loan Agreement, the only fees they would be required to pay pursuant to the No Upfront Charge Loan Model were the Account Keeping Fee and the Change of Payment Schedule Fee paid by the consumer to Cigno. In addition, a “Default Fee” was payable if the consumer defaulted on loan repayments.

6 The question of pecuniary penalties sought against all four respondents, and questions of final injunctive relief against Mr Harrison and Mr Swanepoel from carrying on or being involved in the carrying on of any business engaged in credit activity, have been ordered to be heard separately and subsequently to the other questions in the proceedings.

Salient Legislative Provisions

7 Section 29(1) of the Credit Act, which is a civil penalty provision, prohibits a person from “engag[ing] in a credit activity if the person does not hold a licence authorising the person to engage in the credit activity”.

8 “Credit activity” is defined in the table in s 6 of the Credit Act, which provides relevantly:

(1) The following table sets out when a person engages in a credit activity.

Meaning of credit activity | ||

Item | Topic | A person engages in a credit activity if: |

1 | credit contracts | (a) the person is a credit provider under a credit contract; or (b) the person carries on a business of providing credit, being credit the provision of which the National Credit Code applies to; or (c) the person performs the obligations, or exercises the rights, of a credit provider in relation to a credit contract or proposed credit contract (whether the person does so as the credit provider or on behalf of the credit provider); or |

2 | credit service | the person provides a credit service; or |

9 In the present case, ASIC alleges that BSF engaged in the credit activity specified in items 1(a), 1(b) and/or 1(c) and that Cigno engaged in the credit activity specified in items 1(c) and/or 2.

10 For the purposes of s 6(1) of the Credit Act, “credit contract” has the same meaning as in s 4 of the Credit Code, which provides:

For the purposes of this Code, a credit contract is a contract under which credit is or may be provided, being the provision of credit to which this Code applies.

11 The Credit Code applies to the provision of credit as described in s 5(1) of the Code:

5 Provision of credit to which this Code applies

(1) This Code applies to the provision of credit (and to the credit contract and related matters) if when the credit contract is entered into or (in the case of precontractual obligations) is proposed to be entered into:

(a) the debtor is a natural person or a strata corporation; and

(b) the credit is provided or intended to be provided wholly or predominantly:

(i) for personal, domestic or household purposes; or

(ii) to purchase, renovate or improve residential property for investment purposes; or

(iii) to refinance credit that has been provided wholly or predominantly to purchase, renovate or improve residential property for investment purposes; and

(c) a charge is or may be made for providing the credit; and

(d) the credit provider provides the credit in the course of a business of providing credit carried on in this jurisdiction or as part of or incidentally to any other business of the credit provider carried on in this jurisdiction.

12 Section 6 of the Credit Code provides a number of exclusions from the application of the Credit Code. The respondents submit that if I find that the Account Keeping Fee is not a charge for the provision of credit but that the Change of Schedule Payment Fee is such a charge, than the exemption in s 6(5) of the Credit Code applies (T374.27–375.08). However, for the reasons given below, I have found that both those fees are charges for the provision of credit. Accordingly, there is no need for me to consider s 6(5) of the Credit Code. In any event, s 6(5) applies only to the provision of credit under a “continuing credit contract”, which is defined in s 204 as requiring that the credit contract contemplates multiple advances of credit. The Loan Agreements in the present case contemplated only a single advance of credit.

13 By s 13(1) of the Credit Code, in any proceedings in which a party claims that a credit contract is one to which the Credit Code applies, it is presumed to be such unless the contrary is established. It follows that the Loan Agreements in the present case are presumed to be credit contracts to which the Credit Code applies unless the contrary is established by the respondents.

14 For the purposes of s 6(1) of the Credit Act, a person provides a “credit service” if the person either provides “credit assistance” to a consumer or “acts as an intermediary”: s 7 of the Credit Act.

15 Section 8 of the Credit Act defines “credit assistance” as follows:

8 Meaning of credit assistance

A person provides credit assistance to a consumer if, by dealing directly with the consumer or the consumer’s agent in the course of, as part of, or incidentally to, a business carried on in this jurisdiction by the person or another person, the person:

(a) suggests that the consumer apply for a particular credit contract with a particular credit provider; or

(b) suggests that the consumer apply for an increase to the credit limit of a particular credit contract with a particular credit provider; or

(c) suggests that the consumer remain in a particular credit contract with a particular credit provider; or

(d) assists the consumer to apply for a particular credit contract with a particular credit provider; or

(e) assists the consumer to apply for an increase to the credit limit of a particular credit contract with a particular credit provider; or

(f) suggests that the consumer apply for a particular consumer lease with a particular lessor; or

(g) suggests that the consumer remain in a particular consumer lease with a particular lessor; or

(h) assists the consumer to apply for a particular consumer lease with a particular lessor.

It does not matter whether the person does so on the person’s own behalf or on behalf of another person.

16 Section 9 of the Credit Act defines “acts as an intermediary” as follows:

9 Meaning of acts as an intermediary

A person acts as an intermediary if, in the course of, as part of, or incidentally to, a business carried on in this jurisdiction by the person or another person, the person:

(a) acts as an intermediary (whether directly or indirectly) between a credit provider and a consumer wholly or partly for the purposes of securing a provision of credit for the consumer under a credit contract for the consumer with the credit provider; or

(b) acts as an intermediary (whether directly or indirectly) between a lessor and a consumer wholly or partly for the purposes of securing a consumer lease for the consumer with the lessor.

It does not matter whether the person does so on the person’s own behalf or on behalf of another person.

17 In the present case, ASIC alleges that Cigno both “provide[d] credit assistance to a consumer” (ss 7(a) and 8) and/or “acted as an intermediary” (ss 7(b) and 9).

18 Section 32(1) of the Credit Act, which is also a civil penalty provision, deals with the consequences of charging fees where s 29(1) is contravened. It provides:

32 Prohibition on charging a fee etc.

Prohibition on charging a fee etc.

(1) A person must not demand, receive or accept any fee, charge or other amount from a consumer for engaging in a credit activity if, by engaging in that credit activity, the person contravenes, or would contravene, section 29 (which deals with the requirement to be licensed).

Civil penalty: 5,000 penalty units.

19 In the present case, ASIC alleges that BSF contravened s 32(1) by demanding, receiving and/or accepting a fee described as a “Late Payment Fee” for engaging in the credit activity specified in either or both items 1(b) or 1(c) of s 6(1). ASIC also alleges that Cigno contravened s 32(1) by demanding, receiving and/or accepting the Account Keeping Fee, the Default Fee and/or the Change of Payment Schedule Fee for engaging in the credit activity specified in either or both items 1(c) or 2 of s 6(1).

20 Section 169 of the Credit Act provides that a person who is involved in a contravention of a civil penalty provision is taken to have contravened the provision. The term “involved in” is defined in s 5(1) of the Credit Act as follows:

A person is involved in a contravention of a provision of legislation if, and only if, the person:

(a) has aided, abetted, counselled or procured the contravention; or

(b) has induced the contravention, whether by threats or promises or otherwise; or

(c) has been in any way, by act or omission, directly or indirectly, knowingly concerned in or party to the contravention; or

(d) has conspired with others to effect the contravention.

21 The concepts used in that definition of “involved in” are also adopted in s 177(1)(c)–(f) in relation to the power of the Court to grant injunctions.

Salient Contractual Provisions

The Loan Management Facilitation Agreement

22 On 20 July 2022, Cigno and BSF entered into a “Loan Management Facilitation Agreement”. Recital B stated that BSF offers credit to customers under Loan Agreements, and does not charge any person any fees or any other charge for the provision of credit under Loan Agreements, and that the only fees payable by the customer to BSF are Late Payment Fees. Recital C stated that BSF assesses and approves loan applications from prospective customers and chooses whether to disburse funds to any prospective customer according to BSF’s own procedures. Recital D stated that Cigno is in the business of assisting its customers managing customers’ accounts. Recital E stated that Cigno may charge fees at its discretion to its customers for its services associated with assisting its customers in sourcing short term funding and managing customers’ accounts. Recital F stated that Cigno “does not provide credit to its customers and does not charge any fees to its customers for the provision of credit and will not do so”.

23 The provisions of the Loan Management Facilitation Agreement included the following, noting that the term “Referrals” is defined in cl 1.18 as customers of BSF which have been referred to it by Cigno:

(a) Cigno will pay BSF an assessment fee for each Referral assessed by BSF, which Cigno will pay regardless of the outcome of BSF’s assessment (cl 3.3); the assessment fee was an amount of $19.99 (as stipulated in the BSF Handbook: first affidavit of Ms Balding at [46] and CB 1126); I note that Mr Swanepoel gave evidence in his ASIC examination that the assessment fee was $10 (CB 559 line 15), but I regard the documentary evidence in the BSF Handbook as more reliable;

(b) Cigno warranted that it would not pass on the assessment fee to customers either directly or indirectly (cl 3.4);

(c) BSF agreed not to charge Referrals for the provision of credit and to only charge a Late Payment Fee if the Referral defaults under the loan agreement (cll 4.1–4.2);

(d) Cigno promised to act on behalf of the Referral to facilitate repayment of all amounts owing to BSF under its Loan Agreement with the Referral (cll 6.3–6.6);

(e) if a potential customer communicated to Cigno a request not to use the services of Cigno and, instead, to deal directly with BSF, Cigno promised to immediately provide the customer with the usual contact details for a customer to deal directly with BSF at no charge (cll 9.1–9.2);

(f) Cigno and BSF disavowed any agreement between them for Cigno to undertake customer identification and verification procedures on behalf of BSF, and confirmed that information or documents supplied by Cigno to BSF relating to the Referral’s identity was done by Cigno on the Referral’s behalf (cl 13.1); and

(g) Cigno and BSF confirmed that they were unrelated parties and that the agreement did not create an agency relationship, partnership or joint venture between the parties (cll 12–13).

24 In relation to the last point, cl 12.1 provided as follows:

Notwithstanding the provisions of this Agreement, nothing in this Agreement will create an ongoing relationship between the parties and neither party will in any way pledge that the parties have an ongoing relationship, are related, associated or incur any obligation on behalf of the other, except for the obligations specifically referred to in this Agreement.

25 In addition, cl 13.1 provided as follows:

Nothing in this Agreement will create an agency relationship, partnership or joint venture between the parties, including that no agreement or arrangement exists between the Lender [i.e. BSF] and Referrer [i.e. Cigno] for the Referrer to undertake customer identification and verification procedures of the Referral on behalf of the Lender. Where the Referrer supplies the Lender with information or documents relating to the Referral’s identity, the Referrer is doing so on behalf of the Referral.

The Loan Agreement

26 From July 2022 until 21 December 2022, BSF entered into agreements with individual customers known as a “No Fee for Credit Loan Agreement”, which after a short period, had its name changed to “No Upfront Charge Loan Agreement” (Loan Agreement). The terms of the two agreements are the same.

27 Under the Loan Agreement between BSF and its customer, BSF promised to provide a Loan Amount to the customer in return for a promise to repay the Loan Amount and any fees payable under the Loan Agreement (cl 1.1). BSF did not charge interest or any other fees for the provision of credit to customers (cl 2.1).

28 The Loan Agreement provided for a Late Payment Fee of $20 if the borrower failed to make a required payment when due to BSF (cl 2.2). However, BSF retained a discretion to waive the Late Payment Fee (cl 2.3), or to apply a 50% discount to that fee (cll 2.4, 3.1–3.4), including in circumstances where the borrower gave advance notice of an impending late payment before the relevant date for payment.

29 The customer agreed to pay the Loan Amount in instalments (cll 1.1, 2.2) subject to the customer’s express right to make early repayments at any time before the instalment due date, without penalty (cl 6.7). Any unpaid fees were capitalised and became part of the Loan Amount (cl 2.5).

The Services Agreements

30 Between 18 July 2022 and 21 December 2022, Cigno entered into Services Agreements with individual customers. There were two versions of the Services Agreements, both of which were entitled “Account Keeping Agreement”. The first of them was used for only three days, from 18 to 20 July 2022 (Version 1). A total of 2,450 consumers entered into Version 1 agreements (CB 5713). The second version was then used from 21 July 2022 to 21 December 2022. (Version 2). A total of 99,562 consumers entered into Version 2 agreements (CB 5713).

31 The principal difference between the two versions concerns the way in which the Services are described in cl 1.1. In Version 1 of the Services Agreement, cl 1.1 provided as follows:

We agree to provide you with the following account keeping services (Services):

a. assist you to source credit from a Lender;

b. conduct a preliminary assessment of your credit application with a Lender;

c. facilitate all communications between you and the Lender concerning your Loan Agreement;

d. provide management services concerning your Cigno Account;

e. process payments owed by you to us and the Lender on your behalf; and

f. facilitate all other services related to the Loan Agreement.

32 In Version 2 of the Services Agreement, cl 1.1 provided as follows:

We agree to provide you with the following account keeping services from the Commencement Date of this Account Keeping Agreement (this excludes any services performed by any party relating to the Loan Agreement prior to the Commencement Date) (Services):

a. facilitate all communications between you and the Lender concerning your Loan Agreement;

b. provide management services concerning your Cigno Account;

c. process payments owed by you to us and the Lender on your behalf; and

d. facilitate all other account keeping services related to the Loan Agreement from the Commencement Date.

33 The term “Commencement Date” is defined in Recital B as the day immediately following the date when the customer enters into a Loan Agreement to which the Services Agreement relates. The amendments made to cl 1.1 after the initial three-day period of 18 to 20 July 2022 were plainly intended to make it clear that the Services Agreement did not apply to any services which may have been provided by Cigno to the customer before the customer entered into a Loan Agreement. In saying that, I am not finding that the contractual stipulations are determinative of any issue in these proceedings.

34 An Account Keeping Fee was payable by the customer to Cigno for the provision of the Services provided to the customer under the Services Agreement (cl 3.1). The Account Keeping Fee was expressed to be payable by the customer to Cigno “for costs associated with maintaining your Cigno Account including but not limited to communications between us and you, communications between us and the Lender and various reconciliations” (cl 3.3). The Account Keeping Fee was payable weekly in advance (cl 3.1 and Item 4 of the details). The Account Keeping Fee continued until the “Total Amount Owing” under the Services Agreement, and any amount owing under the Loan Agreement (including if the customer chose to deal directly with the “Lender”), was repaid or Cigno terminated the Services Agreement (cll 3.3, 8.1– 8.4 and 9). The customer could close his or her Cigno Account only if he or she repaid the Total Amount Owing under the Services Agreement, and any amount owing under the Loan Agreement: cl 8.2. In effect, whether the initial term was shortened or extended, once there was no customer account to keep, no Account Keeping Fee was charged. There was no penalty or fee payable under the Services Agreement for early repayment of the Total Amount Owing.

35 The amount of the Account Keeping Fee was identified in Item 4 of the details of the Services Agreement for each customer, and reduced to a weekly fee of $5.95 after the “Initial Period Finalisation Date” (being the date when the final instalment was due) specified in Item 6 of the details (cll 3.2 and 3.7). The Services Agreement does not disclose how the amount stated in Item 4 of the details was calculated, nor would one ordinarily expect that such an agreement would do so. ASIC engaged an expert accountant, Ms Oliver, to provide an explanation of the methodology by which the Account Keeping Fee was calculated, and Ms Oliver gave unchallenged evidence that the code used by Cigno calculated the weekly Account Keeping Fee as:

(a) a fixed amount of $5.95; plus

(b) if the payment date is before the date for payment of the final instalment (referred to as the Initial Period Finalisation Date in the Services Agreements), an additional variable fee calculated as follows:

(i) the sum of:

(A) the loan amount multiplied by a “Configuration Percentage” (ranging from 35% to 85% depending on the number of repayments and whether they were made weekly or fortnightly); and

(B) a fixed component of $13;

(ii) dividing (i) by the length of the loan in weeks.

36 The Default Fee was payable to Cigno if the customer defaulted on loan repayments (cl 3.4). This was initially $67 as at 18 July 2022 (CB 1093). It remained $67 throughout the Relevant Period, and the evidence of customers’ account statements shows that each time a Default Fee was charged, it was in the amount of $67. There is some evidence that the Default Fee (or “Dishonour Fee”) was $79 as at 21 July 2022 (CB 1085, and see screenshots of Cigno’s websites as at 27 July 2022 at CB 2036 and as at 17 August 2022 at CB 2363), and then reduced to $67 (see screenshots of Cigno’s websites as at 5 October 2022 at CB 2613, 26 October 2022 at CB 2952 and 21 December 2022 at CB 3233). However, ASIC submits, and I accept, that the reference in the template draft of Version 2 and on the Cigno websites were errors, and the Default Fee remained at $67 throughout the Relevant Period.

37 The Change of Payment Schedule Fee was payable to Cigno if the customer requested a change in his or her schedule of loan repayments (cl 3.6). This was $15 as at 18 July 2022 (CB 1093) and remained at that level throughout the Relevant Period (see screenshots of Cigno’s websites referred to in the preceding paragraph).

38 Cigno agreed to facilitate collection of all payments due to it and the Lender in intervals and amounts as set out in the Loan Agreement (cl 5.1). In receiving or collecting repayment on behalf of the customer in accordance with the payment schedule and the Loan Agreement, Cigno agreed to allocate repayments proportionately between the amount owing to the Lender and the amount owing to Cigno, and if there was a shortfall in amounts owing, then payments would be applied between the respective obligations in Cigno’s reasonable discretion (cl 5.3). Cigno would retain a copy of the Loan Agreement to enable it to calculate and collect repayments from the customer to forward to the Lender (cl 5.4).

The Websites of Cigno

39 The evidence includes screenshots taken by officers of ASIC of the two Cigno websites during the Relevant Period on various dates. Although the websites changed from time to time, the salient aspects remained consistent in their essential content. It is convenient to refer to the screenshots taken on 5 October 2022 (CB 5/2590–2909). That set of screenshots begins with a page headed “Short Term Cash Loans Up to $1,000” with a scale ranging from $50 to $1,000 and the words “APPLY NOW” in a box on which the potential customer could click (CB 2590). The next page is headed “Why Choose Cigno?”, and included in the answer to that question is a reference to “EMERGENCY cash when you need it”, below which appeared the following:

Sometimes waiting days (or even weeks) for a loan just isn’t good enough. With Cigno, you can get cash within hours. Our 24/7 online platform lets you apply anywhere, anytime – even on weekends. It’s the easiest way to get fast cash loans in Australia.

40 The “Cigno Loan Options” were set out (CB 2592–3), and included payday loans, bad-credit loans, Centrelink loans, and emergency loans. A page headed “How it Works” (CB 2596–7) referred to three steps, namely easy online application, fast approval, and same day cash. Pausing there, the reference to “Cigno Loan Options” may have the led some readers to think that Cigno was the lender, reinforced by what appears in the following paragraph of these reasons to “a Cigno Loan”. However, an astute reader would have picked up from the material in the next two paragraphs that Cigno and the Lender were different entities.

41 A section headed “FAQs” (CB 2598) included the question “What is the cost of a Cigno loan?” to which the answer is given: “Fees vary depending on the length of your specific loan and the terms of the relevant payday lender. You can visit our Costs page for more information about this.” (CB 2600). The reference to the Costs page appears to be a reference to the page headed “How Much Does it Cost?” (CB 2613–4). ASIC submits, and I accept, that the pronoun “it” in that question refers to the loan, or to use the language of the Credit Act, the provision of credit. The answer to that question is given as follows:

Once you have chosen a loan amount to suit your needs and submitted your application, we will work with our lenders to get you pre-approval. You will then be given the opportunity to choose from a variety of loan and flexible repayment options that you can afford.

There are no costs payable by you to the Lender for the provision of the loan however should you choose to use the Cigno Account Keeping Service you will be required to pay a Weekly Account Keeping Fee.

We believe in being up-front about our fees and have no hidden charges. The Weekly Account Keeping Fee is calculated based on several factors. Be assured however that we will make sure you are fully aware of exactly how much you will need to pay before you are locked into any contract. Until you agree to the contract, you are under no obligation. You can choose to not proceed at any time without any penalty.

EXAMPLE: a loan of $250 with the Cigno Account Keeping Service may incur a weekly Account Keeping Fee of $28.50.

WARNING: This calculation is an example only for a contract period of 10 weeks. It is solely for illustrative purposes. It does not constitute a quote and does not take into account your personal needs and financial circumstances.

It’s important to make your payments in accordance with your payment schedule so that you don’t incur extra fees or have any defaults added to your credit record.

42 It is then stated that there are no early payment or early termination fees payable to Cigno or the Lender should the customer choose to make an early or additional payment or pay out his or her contract early. Reference is then made to the circumstance of the customer needing to change or postpone the payment schedule, and the customer is told to let Cigno know at least one business day before the relevant payment is scheduled. It is then stated that although the Lender does not allow a change of payments and a missed payment is an event of default, Cigno will communicate with the Lender on the customer’s behalf and secure a 50% reduction to the Lender’s dishonour fee, and Cigno may charge a Change of Payment Schedule Fee of $15. It is then stated that if the customer does not let Cigno know that he or she needs to change a payment and “your payment dishonours”, Cigno may charge a dishonour fee of $67, and in addition, the Lender may charge a default fee of $20. The statement is then made that “as your agent”, Cigno will email the customer the repayment dates and send repayment reminders.

43 A page headed “How it Works” (CB 2608) states the following:

Cigno is an emergency cash specialist. Our role is to act as your agent in relation to applying for and managing loans. Our services include:

• Assisting you to secure credit from a lender using Cigno’s quick and easy application process;

• Collecting and collating your details and verification documents required to submit a credit application with a lender on your behalf;

• Conducting an assessment of your credit application prior to submitting to a lender;

• Presenting the finalised credit application to a lender in a particular format to ensure the fastest response possible;

• Communicating with a lender concerning your credit application;

• Agreeing with the lender to make payments on your behalf as and when due under the Loan Agreement; and

• Provide ongoing management services to you, including:

• Ongoing access to the Cigno customer service team;

• Ongoing access to all Cigno online resources and the member portal;

• Corresponding on your behalf with the lender regarding your loan agreement;

• Collecting and processing payments owed by you to the lender;

• Providing regular payment reminders via email and SMS;

• Providing regular account statements and upon request;

• Assisting you to change or modify your payment schedule; and

• Facilitating all other services and reconciliations related to your Cigno account and the loan agreement

Through us you can receive up to $1,000 in your account today with manageable repayment options.

44 ASIC submits, and I accept, that the list of services indicates that the services actually provided by Cigno included services performed for the customer before the customer entered into the Loan Agreement. In my view, that is clearly correct in relation to the first five bullet points in the above extract. There is then set out a diagram showing the three steps of easy online application, fast approval, and same day cash.

45 The evidence of screenshots taken by officers of ASIC of the Cigno websites during the Relevant Period did not include screenshots of what was displayed if one clicked on one of the boxes with the words “APPLY NOW”. However, evidence concerning that matter was included in an interlocutory affidavit of Ms Moore, the solicitor for the respondents, dated 3 November 2023. ASIC tendered certain paragraphs of that affidavit as admissions. However, Ms Moore was careful to identify on each occasion when she gave evidence on information and belief whether the information had been provided by Mr Harrison, being the sole director of BSF, or by Mr Swanepoel, the sole director of Cigno. Where evidence had been given on the instructions of Mr Harrison, I admitted that evidence only against BSF and Mr Harrison, and where the evidence had been given on instructions by Mr Swanepoel, I admitted that evidence only against Cigno and Mr Swanepoel. I admitted the screenshots at Tab 4 of the annexures to Ms Moore’s affidavit only against Cigno and Mr Swanepoel. However, the opening and closing written submissions on behalf of all four respondents contained an extensive discussion of the evidence in Ms Moore’s affidavit concerning the additional material on the Cigno websites which had not been included in the screenshots obtained by officers of ASIC. ASIC did not make any submission to the effect that the relevant portion of the respondents’ opening and closing written submissions did not fairly set out the effect of the additional elements of the Cigno websites and indeed sought to tender the underlying evidence of Ms Moore against all respondents. Accordingly, I proceed on the basis that it is common ground between all four respondents and ASIC that those portions of the respondents’ opening written submissions (being paras 30 to 42) and the respondents’ closing written submissions (paras 47 to 59) are correct. The respondents accepted the appropriateness of that approach (T242.37–38, 392.19–42). I set out in the following paragraphs the effect of those portions of the respondents’ written submissions.

46 To apply for a loan via the Cigno website, a potential customer clicked one of the APPLY NOW icons displayed on the Cigno website. Alternatively, if the potential customer had previously used Cigno’s services, they could click the LOGIN icon and sign in to Cigno’s member portal.

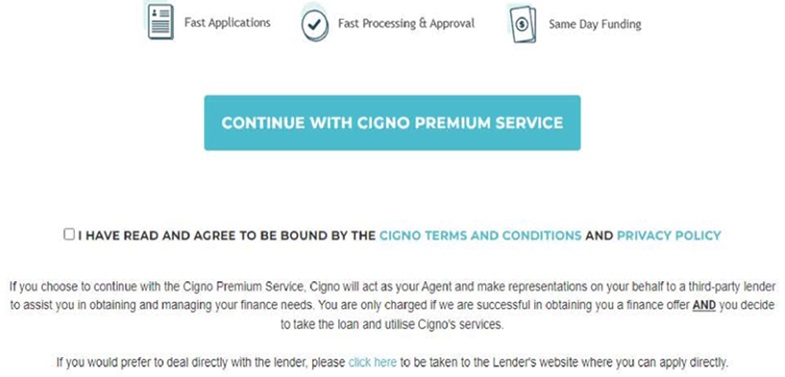

47 If the potential customer clicked the APPLY NOW icon, they were redirected to a webpage entitled “Cigno: Warning About Borrowing”. That page stated that it can be expensive to borrow small amounts of money, and borrowing may not solve the customer’s money problems. It then directed the reader to a telephone number for information about other options for managing bills and debts, and recommended talking to various providers of services to see if a payment plan could be worked out. The reader was also told about the possibility of an advance from Centrelink if the person was on government benefits, and also referred to the Government’s MoneySmart website for information as to how small amount loans work and other options.

48 If the potential customer chose to continue with the loan application process, they would be required to click the Continue icon, which would take them to the next webpage titled New Client – Choose Option, which showed the following:

Pausing there, I note that the final sentence appeared in relatively small print, and was located after the box marked CONTINUE WITH CIGNO PREMIUM SERVICE and after the box to be ticked evidencing the customer having read and agreed to be bound by the Cigno terms and conditions and privacy policy.

49 If the potential customer chose to deal directly with the lender by clicking the click here hyperlink, the customer was taken to a webpage that displayed the following text:

You have chosen to deal directly with the lender.

We can direct you to proceed with: BSF Solutions Pty Ltd

Note, this is still optional for you. You can continue to their website in which you will be subject to their normal loan application process. Do [sic] wish you all the success in your findings for a cash solution!

BSF Solutions can be contacted via: www.bsfsolutions.com.au

If you would prefer to use the Cigno Premium Services, please click here: New Cigno Loan

I note that customers who choose to deal directly with BSF entered into agreements with BSF on different terms from the Loan Agreement, and which provided that the cost of the loan was 5% of the loan amount (Tab 2 of MM-1). As I say later in these reasons, there were only two customers who did so, and their transactions are not part of the case brought by ASIC.

50 If the potential customer initially chose to engage Cigno’s services by clicking Continue with Cigno Premium Service (and ticking the box to indicate that they had read and agreed to be bound by Cigno’s terms and conditions and privacy policy), or subsequently clicked the hyperlink New Cigno Loan after considering the option to deal directly with BSF, the potential customer was taken to an online form titled Cigno — New Application.

51 Returning Cigno customers who logged into the member portal to apply for a loan were previously provided with the new customer disclosures during their initial loan obtained through Cigno. They were not provided with that information again.

52 The potential customer completed the online form by inputting personal and contact details, as well as loan details, including the amount sought and the reason for requesting the loan. Once the form was completed, the potential customer was required to upload proof of identity and bank statements.

53 If the potential customer successfully completed the form and uploading steps, Cigno gave the potential customer’s loan application to BSF using an application programming interface, unless the potential customer owed money to Cigno, in which case Cigno would notify the potential customer that the application was not forwarded to the lender.

54 Upon receipt of the application, BSF assessed the application against BSF’s lending criteria and communicated to Cigno whether the application was approved or declined.

55 If the potential customer’s application was approved, Cigno advised the potential customer of the approval and invited them to accept their agreements by clicking a link that took the potential customer to the member portal on the Cigno Website.

56 Once at the Cigno website, the potential customer was advised of BSF’s loan approval amount, was asked to consider whether proceeding was the right choice, and was reminded that they could choose to deal directly with the lender by clicking on the hyperlink to the lender’s website.

57 If the potential customer chose to proceed with Cigno, they were:

(a) presented with a series of choices regarding their desired loan amount and payment schedule;

(b) advised of the total Cigno Account Keeping Charges;

(c) presented with two separate web frames containing a proposed Services Agreement and Loan Agreement, respectively; and

(d) invited to agree to the Services Agreement and Loan Agreement by separately clicking a box that confirmed their acceptance of each agreement.

58 If the potential customer accepted the Services Agreement and the Loan Agreement, they were again provided with a summary of their payment schedule and notified that a copy of their agreements had been sent to their email.

Evidence of Individual Consumers

59 ASIC tendered documentary evidence giving details of 16 consumers who entered into Loan Agreements and Service Agreements, and the fees that they were charged in relation to those agreements. Affidavits by two of those consumers were read by ASIC, one of whom (Ms Kim) was cross-examined. ASIC does not suggest that those 16 consumers are a representative sample of the entire class of about 100,000 consumers who entered into Loan Agreements and Service Agreements. However, it may assist in understanding the transactions in question to set out the evidence concerning one of those consumers, Ms McDougall, being the first in the list of 16 consumers annexed to ASIC’s Concise Statement, and one of the two deponents to affidavits.

60 On 26 August 2022, Ms McDougall conducted a Google search for quick cash loans and obtained several results, including Cigno, and clicked on a link to its website. Ms McDougall followed a link on Cigno’s website to start the application process and applied for a $250 loan. She submitted the personal information and bank statements required for the loan application, and received approval for the loan about one hour later. Within about five minutes of accepting the loan terms, Ms McDougall received an email from Cigno attaching the Loan Agreement and the Services Agreement, and later the same day she received the $250 loan into her bank account. The covering email of 26 August 2022 set out a payment schedule with fortnightly payments of $124 due on 1, 15 and 29 September 2022, with a final payment of $120.13 due on 13 October 2022. The Loan Agreement provided that BSF would lend her the BSF Credit of $250, Ms McDougall promised to pay a Late Payment Fee of $20 each time a payment amount was not paid on or before the payment date, and Ms McDougall was required to repay the BSF Credit in instalments. The Services Agreement with Cigno provided that the Loan Amount was $250, the Account Keeping Fee was $34.59 payable weekly in advance, and fees that may be payable were a Default Fee of $67 and a Change of Payment Schedule Fee of $15.

61 Ms McDougall made the fortnightly repayments on the due dates in September and October 2022, and on 15 October 2022 received an email from Cigno which said that her account had been finalised and attached an account statement. The account statement showed that she had paid weekly account keeping fees of $34.59 which totalled $242.13, and that she had paid Cigno a total of $492.13 for the $250 loan.

62 On 16 October 2022, Ms McDougall applied for a second loan of $250 with Cigno, by logging into the member portal on the Cigno website. Since her personal details were already in the portal, she only needed to select the amount that she wanted to apply for and to follow a link to a secure portal, from which she logged into her bank account to provide Cigno with access to her bank statements. About one hour after submitting the loan application on the Cigno website, she received an email from Cigno which said that Cigno had secured a loan for her from BSF, and contained a link which required her to read and accept the agreements. Ms McDougall did not accept the agreements at that time, as she was still contemplating if it was worthwhile taking out the new $250 loan, and Cigno sent her a number of reminders over the following four weeks.

63 Late on 23 November 2022, Ms McDougall decided to click on a link on one of the follow-up emails from Cigno and accept the loan. At about 1 am on 24 November 2022, Ms McDougall received an email from Cigno which confirmed that her loan application had been finalised, and attached a Loan Agreement and a Services Agreement. The covering email set out the payment schedule for $125 to be paid on each of 8 December 2022, 22 December 2022 and 5 January 2023, with a final payment of $123.08 payable on 19 January 2023. The Loan Agreement with BSF provided that BSF would lend her the BSF Credit of $250, she agreed to pay a Late Payment Fee of $20 each time a payment amount was not paid on or before the payment date, and she was required to repay the BSF Credit in fortnightly instalments. The Services Agreement with Cigno provided that the Loan Amount was $250, the Account Keeping Fee was $31.01 payable weekly in advance, and fees that may be payable were a Default Fee of $67 and a Change of Payment Schedule Fee of $15. On 24 November 2022, within about two or three hours of receiving the 1 am email from Cigno, Ms McDougall received the $250 loan into her bank account.

64 In December 2022, Ms McDougall tried to contact Cigno on the phone to reschedule her upcoming payments, and received an automated message asking her to contact Cigno by email or chat. Ms McDougall did not do so. During January and early February 2023, Ms McDougall received a number of emails from Cigno informing her that her scheduled repayments had failed, and some of the emails attached default notices. On 18 February 2023, Ms McDougall received an email from Cigno telling her that her repayment had failed because of insufficient funds, and attached a default letter entitled “Third and Final Notice Further Action Pending”. That default letter said that her total outstanding balance was $723.83. On 20 February 2023, Ms McDougall sent an email to Cigno asking if Cigno could organise a payment plan as she was experiencing financial difficulties. A further exchange of emails between Ms McDougall and Cigno took place, and on 20 February 2023 a payment plan of $60 per fortnight beginning on 1 March 2023 was agreed. Ms McDougall began making repayments to Cigno of $60 per fortnight from 1 March 2023, but then experienced difficulties in March and April 2023 in logging into her Cigno member portal. On 12 May 2023, Ms McDougall received an email from Cigno saying that it had been notified that its direct debit authority had been cancelled by Ms McDougall or by her bank, and requested that she make manual payments to its bank account, which Ms McDougall did not do. On 12 May 2023, Ms McDougall received an email from Cigno attaching a default notice. On about 24 May 2023, Ms McDougall’s fortnightly $60 payments to Cigno resumed, although she had not taken steps to reactivate the direct debit.

65 At the time of affirming her affidavit on 20 October 2023, Ms McDougall was still being charged with fortnightly repayments of $60 to Cigno. Her account statement dated 8 August 2023 showed that for the second loan of $250, Ms McDougall had been charged $828.63 in fees, and had repaid Cigno a total of $785. The fees charged to Ms McDougall comprised:

(a) the weekly Account Keeping Fee, initially in the amount of $31.01 per week, but from 19 January 2023 in the amount of $5.95 per week;

(b) four Change of Payment Schedule Fees of $15 each;

(c) four Default Fees of $67 each; and

(d) six Late Payment Fees, two of which were charged at $20 each, and four of which were discounted by 50% to $10 each.

66 The outstanding balance as at 20 October 2023 was $59.08, which Ms McDougall expected to be debited on 25 October 2023.

Evidence of ASIC Examinations

67 ASIC tendered portions of transcripts of examinations conducted pursuant to s 253 of the Credit Act of Mr Harrison, Mr Swanepoel and Mr Hussein (of Mantaq Solutions Pty Ltd (Mantaq)). Section 303(1) provides that a statement that a person makes at an examination is admissible in evidence against the person in proceedings subject to various exceptions. One of those exceptions is where the statement is not admissible in evidence against the person in the proceedings because of subs 295(3). That provision applies where, before making an oral statement giving information or signing a record, the person (other than a body corporate) claims that the statement, or signing the record, as the case may be, might tend to incriminate the person or make the person liable to a penalty. Subsection 295(3) provides that the statement is not admissible in evidence against the person in criminal proceedings or proceedings for the imposition of a penalty, other than proceedings in relation to the falsity of the statement, or the falsity of any statement contained in the record. The examinees all made claims for that privilege in answering questions at their examinations.

68 I note that an objection on the ground of hearsay had been made in the respondents’ schedule of objections to the tender of the examination transcripts of the three examinees, but no argument was put to me at the hearing on that ground (see T207.45–211.14 and 224.39–40). Counsel for the respondents stated that, in the case of Mr Harrison and Mr Swanepoel, if the examinee who claimed the privilege had the benefit of a limitation order under s 136 of the Evidence Act 1995 (Cth) to the effect that the transcript was not admitted against him, then the tender of the transcripts was not controversial (T210.21–22). The objections to the tender of the transcript of Mr Hussein’s examination were resolved by agreement (T224.39–40). Accordingly, there was no need for me to rule on the objection previously foreshadowed on the ground of hearsay.

69 Accordingly, I admitted the identified portions of the examination transcript of Mr Harrison subject to a limitation under s 136 that it was not admitted against Mr Harrison. Similarly, I admitted the identified portions of the examination transcript of Mr Swanepoel subject to a limitation under s 136 that it was not admitted against Mr Swanepoel (T220.5-11). I admitted the identified passages of Mr Hussein’s transcript without any s 136 limitation, given that Mr Hussein is not a party to the proceedings (T226.5-13).

Aggregated Customer Numbers and Aggregated Payments

70 The total number of customers who entered into Loan Agreements with BSF in the period 18 July 2022 to 26 June 2023 (being the date of the relevant notice by ASIC under s 253 of the Credit Act) was 100,583 (CB 1049, 1055). The total number of such Loan Agreements was 150,114 (CB 1049, 1055). The figures show that some customers entered into more than one Loan Agreement, as illustrated by the case of Ms McDougall to whom I have referred above.

71 The total number of customers who entered into Loan Agreements with BSF in the period from 18 July 2022 to 26 June 2023 after Cigno referred their loan application to BSF was 100,581 (CB 1049, 1055). The total number of such Loan Agreements originating from loan applications that Cigno referred to BSF was 150,112 (CB 1049, 1055).

72 It follows that only two customers out of about 100,000 customers entered into Loan Agreements without having been referred to BSF by Cigno. Thus, while it is true to say that the Cigno website offered a choice between using Cigno’s services and approaching BSF directly, only a very small number of customers chose the latter. I have referred at para 48 above to the way in which the option of dealing directly with the lender appeared in relatively small print, and was located after the boxes to be clicked on for continuing with the Cigno service and for having read and agreed to the Cigno terms and conditions and privacy policy. Those features of the website, in my view, were not designed to enhance the prospect of customers deciding to deal directly with the lender. I infer from the nature of those features of the website that the very small number of customers who chose to deal directly with BSF was consistent with the expectations and intentions of Cigno and BSF, and of Mr Swanepoel and Mr Harrison as their sole directors respectively.

73 In the period from July 2022 to 30 May 2023 (being the date of Mr Swanepoel’s examination), Cigno did not refer its customers to any lenders other than BSF (CB 528). That evidence was given as part of Mr Swanepoel’s examination, which, as I have indicated above, was not admitted against Mr Swanepoel himself. However, as I have indicated at paragraph 49 above, if a customer chose to deal directly with the lender by clicking on the relevant hyperlink on the Cigno website, the customer was taken to a page on the Cigno website that identified only one such lender, namely BSF. I infer from that page on the Cigno website that during the Relevant Period, Cigno did not refer its customers to any lenders other than BSF. As the material in para 49 above is common ground among all respondents and ASIC, I draw that inference against all respondents, including Mr Swanepoel.

74 Mr Harrison gave evidence in his examination that Cigno was the only entity that referred borrowers to BSF for loans in the period July to December 2022 (CB 387 lines 12–14, CB 395 lines 1–5). That evidence was admitted against all respondents other than Mr Harrison. However, I draw an inference against all respondents, including Mr Harrison, that Cigno was the only entity that referred borrowers to BSF for loans in the period July to December 2022, based on the fact (to which I have referred above) that only two customers out of about 100,000 customers entered into Loan Agreements without having been referred to BSF by Cigno. It is theoretically possible that those two customers had been referred by another broker or intermediary, but there is no evidence to indicate that that was a realistic possibility. In my view, it is more likely than not that those two customers had taken up the option presented by the Cigno website (see paras 48 and 49 above) to deal directly with the lender, namely BSF.

75 It follows from the above material that the businesses of Cigno and BSF were closely intertwined. With only two exceptions, the customers who entered into Loan Agreements with BSF (numbering more than 100,000) had their loan applications referred to BSF by Cigno. Further, Cigno did not refer its customers to any lenders other than BSF. Accordingly, I regard it as appropriate to refer, consistently with ASIC’s contentions, to BSF and Cigno having established and implemented a lending business model, namely the No Upfront Charge Loan Model. The elements of that model are set out in the Loan Facilitation Management Agreement, the Loan Agreements and the Services Agreements, and also in the aspects of the Cigno websites to which I have referred above.

76 The conclusion that BSF and Cigno participated in an overarching business model does not depend on any finding that they were in a relationship of agency, partnership or joint venture or any other kind of ongoing legal relationship apart from the contractual relationship under the Loan Management Facilitation Agreement, and I do not make any such finding. Accordingly, the conclusion that BSF and Cigno participated in the No Upfront Charge Loan Model is not contradicted by cll 12 and 13 of the Loan Management Facilitation Agreement (in which Cigno and BSF confirmed that they were unrelated parties and that the agreement did not create an agency relationship, partnership or joint venture between the parties).

77 There are some inconsistencies between the agreements, on the one hand, and the Cigno websites, on the other hand, which I resolve in the following way. As to the amount of the Default Fee, as I have indicated above, I find that that fee was charged in the amount of $67 throughout the Relevant Period, despite references on the Cigno websites in the early stages of the Relevant Period to the fee (referred to as “Dishonour Fee”) being $79. Second, I find that the Cigno websites correctly described the services provided by Cigno as including a range of services which pre-dated the entry by the customer into a Loan Agreement. That is a matter which is reflected in Version 1 of the Services Agreement. While I accept that the limitation in the description of services in Version 2 of the Services Agreement provides an accurate statement of the binding contractual promise on the part of Cigno under Version 2, limiting its contractual promise to provide services to those which were provided after the Commencement Date, I do not regard that as an accurate statement of the services in fact provided by Cigno. That does not require me to find that Version 2 of the Services Agreement was a sham, but merely that the binding contractual promises by Cigno did not correspond to what Cigno told potential customers who read its websites it would provide, and what Cigno did in fact provide, by way of services.

78 In terms of the aggregated amounts of payments made pursuant to the No Upfront Charge Loan Model, the 100,581 consumers who entered into 150,112 Loan Agreements borrowed a total of $34,709,015 from BSF. As at 3 October 2023, those customers were charged fees in the following amounts:

(a) in excess of $63,426,811.85 charged by Cigno, comprising:

(i) Account Keeping Fees of $33,961,220.31;

(ii) Default Fees of $24,682,034.55; and

(iii) Change of Payment Schedule Fees of $4,783,557; and

(b) in excess of $6,588,660 charged by BSF, being the Late Payment Fees.

79 In addition, Cigno paid to BSF assessment fees in the period 18 July 2022 to 26 June 2023 (being the date of ASIC’s s 253 notice) in the total amount of $9,196,120, there having been 460,036 loan applications referred by Cigno to BSF in that period (CB 1076 and 1100; CB 1050 and 1056). It will be recalled that assessment fees were payable irrespective of whether the customer entered into a Loan Agreement with BSF, and the evidence thus indicates that about one third of loan applications lodged with Cigno resulted in Loan Agreements.

Operation of Integrated and Automated Systems and BSF and Cigno

80 ASIC relied on a number of aspects of the business operations of Cigno and BSF to demonstrate that those companies did not operate independent and separate businesses, but should be regarded as having collaborated in implementing a shared business model in the No Upfront Charge Loan Model. Some of those aspects, taken on their own, may not be regarded as particularly significant. However, in my view, the evidence to which I refer in the paragraphs below is an illustration of the principle that a true picture may emerge from the overall accumulation of detail viewed from a distance, and thus the overall effect of the detail is not necessarily the same as the sum total of the individual details: Transport Industries Insurance Co Ltd v Longmuir [1997] 1 VR 125 at 141 (Tadgell JA, with whom Winneke P and Phillips JA agreed), cited with approval in Seven Network (Operations) Ltd v Fairfax Media Publications Pty Ltd [2023] FCAFC 185 at [40] (Wheelahan, Anderson and Jackman JJ).

81 Pursuant to the No Upfront Charge Loan Model, Cigno collected information from consumers in support of their loan applications and provided those applications electronically to BSF. Bank statements were required to support a loan application. Cigno performed a preliminary assessment of loan applications before referring customers to BSF (CB 654–5, not admitted against Mr Swanepoel). Cigno’s websites described its services as including an assessment of credit applications prior to submitting them to the lender (CB 1710, 2032, 2357, 2608, 2948 and 3226). That performance assessment functionality was built into the software used for the purposes of the No Upfront Charge Loan Model (CB 655, not admitted against Mr Swanepoel).

82 As set out below, BSF and Cigno used the same service provider to support their information technology systems. BSF was a small company with only two employees (CB 1461). BSF did not have the internal infrastructure to collect the principal amounts which were owed to it by its customers who dealt with it through Cigno (CB 12456, not admitted against Cigno and Mr Swanepoel).

83 Cigno had a computer system for managing loan applications and the loans themselves. Mr Hussein acknowledged in his ASIC examination that this system was called “Barcasoft”, and said that it was known as the “LMS” or “loan management system” (CB 772), and he took part in creating it in 2014 (CB 774-5). Mr Hussein said that, among other things, during the Relevant Period that system calculated costs and fees charged to clients (CB 775–7).