Federal Court of Australia

Satterley Property Group Pty Ltd v Federal Commissioner of Taxation [2024] FCA 421

ORDERS

WAD 64 of 2023 | ||

SATTERLEY PROPERTY GROUP PTY LTD Applicant | ||

AND: | FEDERAL COMMISSIONER OF TAXATION Respondent | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The appeal be dismissed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

BESANKO J:

Introduction

1 There are two appeals under s 14ZZ of the Taxation Administration Act 1953 (Cth) (TAA) before the Court. The appellant in each case is Satterley Property Group Pty Ltd (SPG) and the respondent is the Federal Commissioner of Taxation (the Commissioner). SPG in each case was dissatisfied with the Commissioner’s objection decision and lodged an appeal to this Court against those decisions. Under s 14ZZO of the TAA, SPG has the burden of proving that the assessment in each case was excessive, or otherwise incorrect, and what the assessment should have been. The two appeals are closely related in terms of the facts and issues and the appeals have been consolidated.

2 SPG lodged an objection on 4 May 2021 to its income tax assessment for the 2020 income year. On 8 March 2022, the Commissioner advised SPG that its objection had not been allowed. SPG had sought the excision from its taxable income for the income year ended 30 June 2020 of the amount of $2,557,897 and the setting aside of the objection decision in full. I will refer to this as the first appeal as it was the first in time.

3 SPG lodged an objection on 9 January 2023 to its income tax assessment for the 2020 income year. On 14 March 2023, the Commissioner advised SPG that its objection had not been allowed. By its objection, SPG had sought the excision from its taxable income for the income year ended 30 June 2020 of the amount of $761,738 and the setting aside of the objection decision in full. I will refer to this as the second appeal.

4 In the first appeal, SPG repeats the facts and circumstances set out in its objection dated 4 May 2021 together with the grounds of objection stated in that objection. The arguments have been put on the appeal and, in those circumstances, there is no need for me to set out the facts and circumstances in the objection.

5 In the first appeal, SPG’s case is that the amount of $2,557,897 is deductible pursuant to s 8-1(1) or, in the alternative, s 40-880 of the Income Tax Assessment Act 1997 (Cth) (ITAA 1997). Those sections are set out below. SPG claims that the amount of $2,557,897 was paid to a group of shareholders referred to as small investors and described in the evidence as “Participating Shareholders” and that this amount represented 50% of payments described as Top-Up Payments in the Share Sale Agreements (SSAs) with each shareholder and that this amount is deductible under s 8-1(1) of the ITAA 1997. SPG claims that the amount of $2,557,897 was necessarily incurred by SPG in carrying on its business for the purpose of gaining or producing assessable income (see s 8-1(1)(b)). SPG claims that such payments to the Participating Shareholders were made to overcome the negative impact on investors in respect of the losses they sustained from investing, indirectly via a chain of trusts and companies, in certain land development projects known as the Austin Cove Joint Venture (Austin Cove JV) and the Beacham Road Joint Venture (Beacham Road JV), both of which had been promoted by SPG and in respect of which SPG had received management and selling fees. SPG claims that the payment was also made for the purposes of attracting investors to invest in future property development projects. SPG claims that the expenditure maintained its fee income from such future projects and its reputation and goodwill and the expenditure was incurred on revenue account and deductible, not being capital or of a capital nature. SPG refers to the legal test as to whether a loss or outgoing is incurred on revenue account or on capital account and in that context refers to Hallstroms Pty Ltd v Federal Commissioner of Taxation [1946] HCA 34; (1946) 72 CLR 634 (Hallstroms); Sun Newspapers Ltd v Federal Commissioner of Taxation [1938] HCA 73; (1938) 61 CLR 337 (Sun Newspapers); and Commissioner of Taxation v Sharpcan Pty Ltd [2019] HCA 36; (2019) 269 CLR 370 (Sharpcan).

6 In the alternative to its first argument, SPG contends that it is entitled to a deduction under s 40-880 of the ITAA 1997 on the ground that the capital expenditure does not fall into the category of expenditure incurred which could, apart from s 40-880, be taken into account in working out the amount of a capital gain or a capital loss from a CGT event within s 40-880(5)(f) and nor would it be taken into account in calculating any capital gain or capital loss made on future CGT events because it does no more than preserve the value of SPG’s goodwill within s 40-880(6).

7 The Notice of appeal in the second appeal is more detailed, but is broadly to the same effect. Nevertheless, it is of assistance in identifying the issues and I will summarise it. SPG claims that the amount of $761,738 is deductible pursuant to s 8-1 or, in the alternative, s 40-880 of the ITAA 1997. SPG claims that the amount of $761,738 is a portion of the payments it made during the income year ended 30 June 2020. The payments were made in November 2019 to certain shareholders in Yunderup Holdings Pty Ltd (formerly known as TRGP Austin Cove Pty Ltd (Yunderup)) together with portions of payments made to shareholders in Satterley Austin Bay Limited (SABL) and Satterley Beacham Road Limited (SBRL) which portions SPG has characterised as “Top-Up Payments” and which total $2,431,337.

8 SPG claims that the Top-Up Payments were made on capital or revenue account. If the payments were made on revenue account, then they were allowable deductions under s 8-1 of the ITAA 1997. If, in the alternative, the payments were made on capital account, then they were nevertheless allowable deductions under s 40-880 of the ITAA 1997. SPG claims that the Bowman Waters Trust (BWT) owned a 50% interest in Yunderup in addition to being an equal joint venturer in the Austin Cove JV between BWT and Yunderup. SPG claims that a number of investors in the Austin Cove JV also invested in Yunderup. SPG’s case is that the remaining land and other assets of the Austin Cove JV and the Beacham Road JV were sold and a method for the full, but staggered refund of capital investment was implemented to certain shareholders in Yunderup (and in SABL and SBRL). This followed the issue of an Information Memorandum dated 22 May 2018 (IM) to investors followed by the necessary shareholder approvals in June 2018. In accordance with that approval, numerous SSAs were entered into with the Participating Shareholders in Yunderup (and in SABL and SBRL) which dealt with the sale of the shares in Yunderup (and the shares in SABL and SBRL) to SPG provided that a number of Conditions Precedent were satisfied.

9 The IM was prepared and issued by SPG in its capacity as the project manager of each of the Austin Cove JV and the Beacham Road JV respectively and at the direction, and with the authority of, the Management Committees of each of the JVs.

10 The proposal in the IM was two-fold. First, the proposal involved the disposal of the landholdings and other assets of the joint ventures. Secondly, the proposal involved, subject to that disposal, a refund to Participating Shareholders in each of SABL, SBRL and Yunderup of the full amount of their original capital investment in the companies at the time and in the way specified in the IM.

11 SPG claims that in the case of the Yunderup shares, the SSA entered into between SPG and the Participating Shareholders provided that the “Purchase Price” of the Yunderup shares was the market value of those shares and that at the completion of the sale and purchase of the shares, subject to the SSA, sellers of the Yunderup shares would also be paid, in addition to the Purchase Price, a “Top-Up Payment” which was an amount to be paid by SPG to the Participating Shareholders over three payments in a two year period, to ensure those shareholders were refunded the full value of their initial investment. SPG makes a number of claims about how it conducts its business and the importance of investors to the successful operation of its business. It also refers to its business model. SPG states that the development projects had failed financially and could not be financially supported in the future. SPG claims that its primary position is that the Top-Up Payments to Participating Shareholders are deductible in accordance with s 8-1(1)(a) or (b) of the ITAA 1997 and are not within s 8-1(2)(a) or any other provision of s 8-1 of the ITAA 1997. SPG claims, among other things, that the purpose of the expenditure was to minimise negative publicity, class actions or other threats of legal action, so maintaining its good reputation and its ability to continue to earn fees by way of management and selling fees from current and future customers. SPG also claims that the shares acquired from the Participating Shareholders in Yunderup (and SABL) had no value to it and that the acquisition by SPG of shares in Yunderup (and SABL and SBRL) was not the purpose for which the expenditure was directed. SPG claims that the Top-Up Payments did not form part of the consideration for the shares in Yunderup (or in SABL or SBRL).

12 SPG claims in the alternative, that the Top-Up Payments were not payments which could, apart from s 40-880, be taken into account in working out the amount of a capital gain or a capital loss from a CGT event because the payments could not form part of the cost base, or reduced cost base, for the shares that it acquired from the Participating Shareholders because, in turn, those payments did not constitute monies paid, or required to be paid, in respect of its acquisition of the shares and were instead ex gratia payments made by it to each of the Participating Shareholders. SPG claims that the payments comprised capital expenditure incurred in relation to its goodwill and, therefore, s 40-880(5)(f) of the ITAA 1997 did not apply.

13 In the further alternative, SPG claims that if the expenditure could be taken into account in working out the amount of capital gain or capital loss from a CGT event, nevertheless, it falls within an exception to the exception contained in s 40-880(6). That subsection provides that previous subparagraphs, including s 40-880(5)(f), do not apply to expenditure a taxpayer incurs to preserve (but not to enhance) the value of goodwill if the expenditure incurred is in relation to a legal or equitable right and the value to the taxpayer of the right is solely attributable to the effect that the right has on goodwill.

14 As I have said, the same facts and issues arise in the case of the Participating Shareholders in SABL, SBRL and Yunderup and the same arguments are put by both SPG and the Commissioner. The SSA is in materially the same terms in the case of each of the three companies.

The Relevant Legislative Provisions

15 Section 8-1 of the ITAA 1997 is in the following terms:

8‑1 General deductions

(1) You can deduct from your assessable income any loss or outgoing to the extent that:

(a) it is incurred in gaining or producing your assessable income; or

(b) it is necessarily incurred in carrying on a *business for the purpose of gaining or producing your assessable income.

Note: Division 35 prevents losses from non‑commercial business activities that may contribute to a tax loss being offset against other assessable income.

(2) However, you cannot deduct a loss or outgoing under this section to the extent that:

(a) it is a loss or outgoing of capital, or of a capital nature; or

(b) it is a loss or outgoing of a private or domestic nature; or

(c) it is incurred in relation to gaining or producing your *exempt income or your *non‑assessable non‑exempt income; or

(d) `a provision of this Act prevents you from deducting it.

For a summary list of provisions about deductions, see section 12‑5.

(3) A loss or outgoing that you can deduct under this section is called a general deduction.

For the effect of the GST in working out deductions, see Division 27.

Note If you receive an amount as insurance, indemnity or other recoupment of a loss or outgoing that you can deduct under this section, the amount may be included in your assessable income: see Subdivision 20‑A.

Section 40-880 is in the following terms:

40‑880 Business related costs

Object

(1) The object of this section is to make certain *business capital expenditure deductible over 5 years, or immediately in the case of some start‑up expenses for small businesses, if:

(a) the expenditure is not otherwise taken into account; and

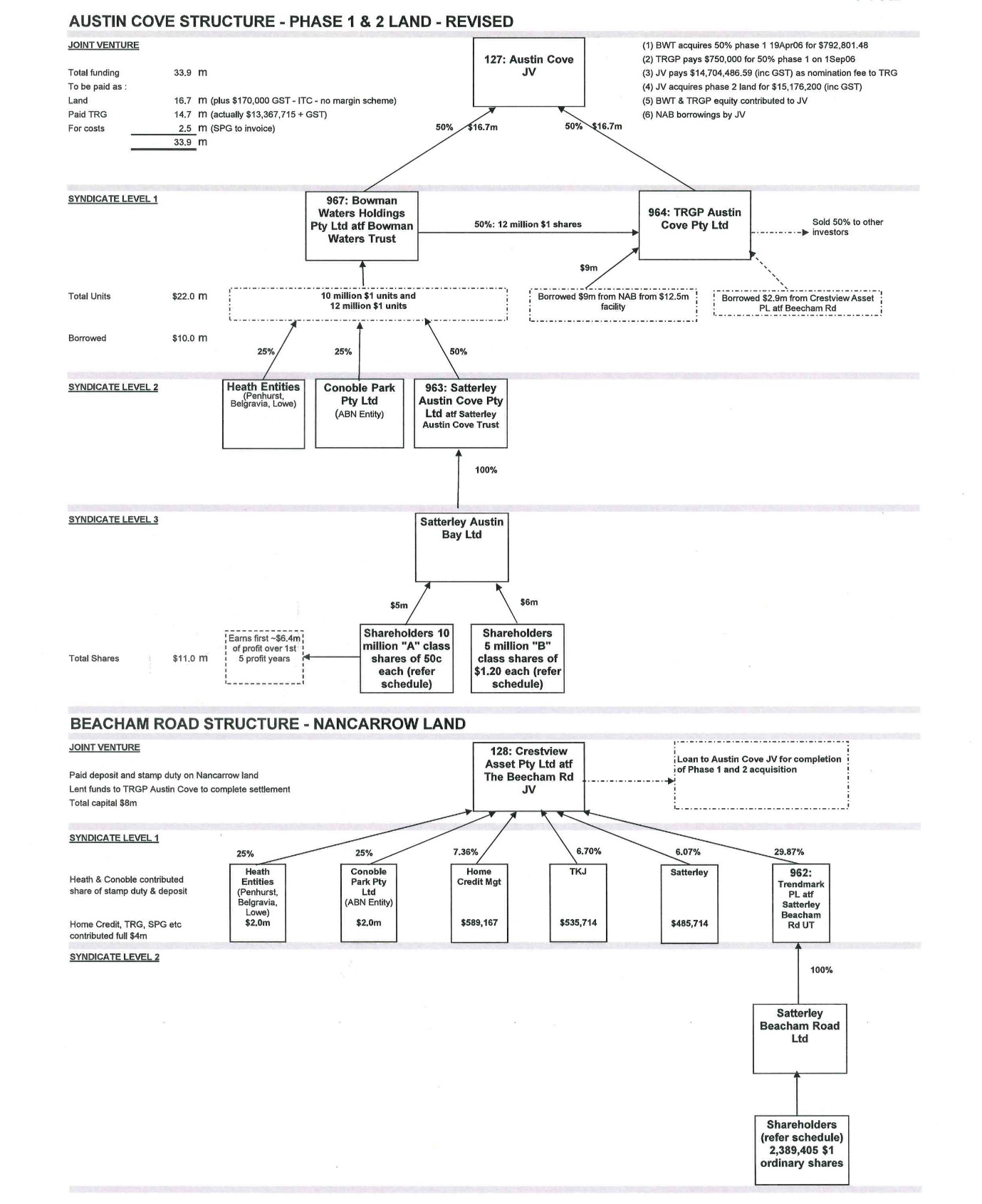

(b) a deduction is not denied by some other provision; and

(c) the business is, was or is proposed to be carried on for a *taxable purpose.

Note: If Division 250 applies to you and an asset:

(a) if section 250‑150 applies—you cannot deduct an amount for capital expenditure you incur in relation to the asset to the extent specified under subsection 250‑150(3); or

(b) otherwise—you cannot deduct an amount for such expenditure.

Deduction

(2) You can deduct, in equal proportions over a period of 5 income years starting in the year in which you incur it, capital expenditure you incur:

(a) in relation to your *business; or

(b) in relation to a business that used to be carried on; or

(c) in relation to a business proposed to be carried on; or

(d) to liquidate or deregister a company of which you were a *member, to wind up a partnership of which you were a partner or to wind up a trust of which you were a beneficiary, that carried on a business.

…

Limitations and exceptions

…

(5) You cannot deduct anything under this section for an amount of expenditure you incur to the extent that:

…

(f) it could, apart from this section, be taken into account in working out the amount of a *capital gain or *capital loss from a *CGT event; ..

(6) The exceptions in paragraphs (5)(d) and (f) do not apply to expenditure you incur to preserve (but not enhance) the value of goodwill if the expenditure you incur is in relation to a legal or equitable right and the value to you of the right is solely attributable to the effect that the right has on goodwill.

…

16 Section 110-25 is in the following terms:

110-25 General rules about cost base

(1) The cost base of a *CGT asset consists of 5 elements.

Note 1: You need to keep records of each element: see Division 121.

Note 2: The cost base is reduced by net input tax credits: see section 103‑30.

Note 3: An amount that makes up all or part of an element of the cost base of an asset may be determined under section 230‑505, if the amount is provided for acquiring a thing, and you start or cease to have a Division 230 financial arrangement as consideration for the acquisition of the thing.

5 elements of the cost base

(2) The first element is the total of:

(a) the money you paid, or are required to pay, in respect of *acquiring it; and

(b) the *market value of any other property you gave, or are required to give, in respect of acquiring it (worked out as at the time of the acquisition).

Note 1: There are special rules for working out when you are required to pay money or give other property: see section 103‑15.

Note 2: This element is replaced with another amount in many situations: see Division 112.

…

17 The issues which arise under the legislative provisions are as follows. First, there is an issue as to whether the Top-Up Payments are deductions within s 8-1 of the ITAA 1997. SPG submitted that logically the first question is whether the payments fall within that subsection and then whether the payments are payments of capital or of a capital nature within s 8-1(2)(a). SPG submitted that the payments fall within s 8-1(1) and they are not of capital or of a capital nature within s 8-1(2)(a). The Commissioner started with the issue of whether the payments were payments of capital or of a capital nature and, in the course of submissions on that topic, submitted that the payments did not fall within s 8-1(1). The Commissioner submitted that the payments were of capital or of a capital nature and did not fall within s 8-1(1). Either the approach of SPG or that of the Commissioner is permissible (Ausnet Transmission Group Pty Ltd v Federal Commissioner of Taxation [2015] HCA 25; (2015) 255 CLR 439 at [13]).

18 The second main issue arises if the payments are payments of capital or of a capital nature (and/or do not fall within s 8-1(1)).

19 The question which then arises is whether the payments fall within s 40-880 which addresses business capital expenditure not otherwise taken into account and a deduction not denied by some other provision. I do not think there was any dispute that, assuming the payments were of capital or of a capital nature, they fell within s 40-880(1) and (2) of the ITAA 1997. However, there are a number of exceptions in s 40-880. One such exception is expenditure which could, apart from s 40-880, be taken into account in working out the amount of a capital gain or a capital loss from a CGT event (s 40-880(5)(f)). This, in turn, directs attention to the first element of the cost base of a CGT asset and, in particular, the money the taxpayer paid or was required to pay, “in respect of acquiring it”, that is, the CGT asset (s 110-25(2)(a)). The Commissioner submits that the payments fall within this provision and SPG denies that. SPG submits that even if that be so, the Top-Up Payments fall within the exception to the exception, being expenditure incurred to preserve, but not enhance, the value of goodwill if the expenditure incurred is in relation to a legal or equitable right and the value of the right to the taxpayer is solely attributable to the effect that right has on goodwill in which case s 40-880(5)(f) does not apply.

20 I should say at this point that initially there was some uncertainty about the amount of Top-Up Payments. That uncertainty has been resolved by the Statement of Agreed Facts and Issues (SOAF). The total amount of Top-Up Payments to Participating Shareholders is $2,431.337 comprised as follows: (1) SABL $1,519,768; (2) SBRL $149,831; and (3) Yunderup $761,738.

Three Key Documents

21 SPG entered into approximately 103 SSAs with the minor shareholders of SABL, SBRL and Yunderup respectively. It is convenient to take the agreement involving a Participating Shareholder between SPG and the shareholder as a representative example. The minor shareholders are referred to in the SSA as the “Participating Shareholders”. The major investors are identified by name in the SSA and are designated as the “Non-Participating Shareholders”.

22 The SSA is governed by a number of Conditions Precedent. The Conditions Precedent are set out in clause 3.2 and included the Non-Participating Shareholders signing and delivering to the relevant joint venture company a waiver of any pre-emptive rights they may have had in respect of the shares subject to the agreement, and the sale and settlement of all of the land remaining subject to the Austin Cove JV or the Beacham Road JV.

23 Clause 2 of the SSA is a key clause in the SSA. It is entitled “SALE” and provides as follows:

Subject to clause 3 [i.e., the Conditions Precedent]:

(a) the Seller agrees to sell to the Buyer and the Buyer agrees to buy the Sale Shares:

(i) for the Purchase Price;

(ii) with all attached or accrued rights, including the right to receive any dividend which is unpaid as at the date of this document; and

(iii) free from all Encumbrances; and

(b) the Buyer agrees to pay the Seller the Top-Up Payment in the way and at the times specified in clause 6,

in each case on the terms and conditions in this document.

24 The definitions in clause 1 provide that the Purchase Price means the amount specified in item 7 of the Reference Schedule. That item refers to the “SABL Share Price” refers (relevantly) to $0.001 per SABL share which is the “Market Value of the SABL Shares”. Market Value is, in turn, defined to mean “an amount per share that is equal to their Market Value on the ACJV Settlement Date being an amount of $0.001 per SABL Share”.

25 Item 7 also refers to a method of payment of the Purchase Price being the full Purchase Price on completion which is 30 days after the satisfaction of the last of the Conditions Precedent.

26 The term “SABL Top-Up Payment” is defined in the SSA to mean:

… the ex gratia amount the Buyer is offering to pay to the SABL Participating Shareholders (who are, for the avoidance of doubt, also shareholders in SBRL) for their shares in SABL on the terms specified in this document. It is an amount per share equal to the:

(a) SABL A Class Issue Price;

plus

(b) SABL B Class Issue Price;

less

(c) the aggregate of the:

(i) SABL Share Price; and

(ii) the SBRL Premium (if any).

27 The Top-Up Payment is an amount paid in three instalments over a two year period to ensure that the Participating Shareholders were refunded the full value of their initial investment.

28 The reason for the difference in the figures between the Notice of appeal in the first appeal and the figures now put forward (see [20] above) is as follows. SPG’s Notice of Objection was lodged on 4 May 2021 and a decision with respect to the objection was notified to SPG by notice dated 8 March 2022. SPG lodged its Notice of appeal on 9 May 2022. There was then a dispute between the parties as to whether the grounds stated in SPG’s objection dated 4 May 2021 included payments made by SPG in the 2020 income year to certain shareholders in Yunderup up to an amount of $761,737.50 were also deductible from SPG’S assessable income for that year pursuant to s 8-1(a) or (b), or alternatively pursuant to s 40-880 of the ITAA 1997. With respect to the second appeal, SPG’s Notice of Objection was lodged on 9 January 2023. SPG was advised of the decision on the objection on 14 March 2023. That decision referred to the objection to the income tax assessment for the 2020 income year which was decided on 8 March 2022. The objection dated 14 March 2023 states that it is in regard to a further particular, being an additional deduction amount also for the 2020 income year which was not part of the previous objection decided on 8 March 2022. On 21 March 2023, SPG lodged its Notice of appeal in the second appeal. The two proceedings were consolidated by order dated 4 April 2023. SPG has produced the financial documents in SABL, SBRL and Yunderup to whom it has paid a Purchase Price and a Top-Up Payment and that reveals that the figures set out above are correct.

29 Finally, I note that the SSA has an entire agreement clause (clause 14.4).

30 The Commissioner agreed that neither s 8-1(2)(b) nor (c) of the ITAA 1997 applies.

31 The next document to be considered is the Project Management and Exclusive Selling Agency Agreement Austin Cove Joint Venture (PMA). There was a similar document in the case of the Beacham Road JV. Under these agreements, SPG was appointed as the project manager of each of the joint ventures and exclusive selling agent of the developed lots as they became available. As I will explain, although SPG received distributions and dividends from companies involved in the joint venture, the bulk of its income came from project management and selling fees.

32 It will be recalled that although the definition of SABL Top-Up Payment refers to an “ex gratia” amount, it refers to the amount being “for the shares” in SABL. The Commissioner argues that this supports the proposition that the Top-Up Payment was part of the consideration for the shares. SPG disputes this and submits that when read as a whole, the SSA supports the proposition that the consideration for the acquisition of the shares was the Purchase Price and this was quite clear from the ex gratia payment which is the Top-Up Payment.

33 SPG submits that if the proposition it advances is not clear from a consideration of the SSA read as a whole, reference may also be made to the IM.

34 I have already referred to the IM and the proposal with which it deals. The IM explains the proposal in some detail. That proposal required the approval of shareholders. The matters in the IM upon which SPG relies are as follows.

35 First, SPG relies on the definition of SABL Top-Up Payments which does not include the phrase “for their shares”. It is as follows:

SABL Top-Up Payments means the ex gratia amount Satterley is offering to pay to the SABL Participating Shareholders (who are, for the avoidance of doubt, also shareholders in SBRL) on the terms specified in section 4.2 of this IM. It is an amount per share equal to the:

(a) SABL A Class Issue Price;

plus

(b) SABL B Class Issue Price;

less

(c) the aggregate of the:

(i) SABL Share Price; and

(ii) the SBRL Premium (if any).

36 Secondly, SPG relies on the section in the IM which identifies the “Background and Purpose of the Proposal”. The relevant paragraphs in relation to SABL and Yunderup shares are as follows:

It is proposed to sell all of the landholdings and other assets of the JVs and subject to settlement of these sales, to Refund to Participating Shareholders the aggregate amount of their original investments in the Companies in the way and at the time specified in this IM.

…

SABL and Yunderup Share Purchase Offer and Top-Up Payment

The net proceeds from the sale of the ACJV land and other assets will not deliver any return to the SABL Participating Shareholders or the Yunderup Participating Shareholders.

Accordingly, subject to the sale of the ACJV’s assets and each relevant Participating Shareholder entering into the SABL Share Sale Agreement and or the Yunderup Share Sale Agreement (as the case may be), Satterley offer to pay to the:

(a) SABL Participating Shareholders, an aggregate amount equal to the SABL Share Price and the SABL Top-Up Payment; and

(b) Yunderup’s Participating Shareholders, an aggregate amount equal to the Yunderup Share Price and the Yunderup Top-Up Payment.

37 I should say that the terms of the paragraphs dealing with SBRL shares are in different terms to those dealing with SABL and Yunderup shares. That was because the latter shares were viewed as having no market value and in the SSAs were assigned a nominal value of $0.001 per share, whereas the SBRL shares were viewed as having a market value. I did not understand either party to suggest this difference was material to the characterisation of the Top-Up Payments.

38 The SABL A Class Share Price was the issue price of the A Class Shares, being an amount of $0.50 per share and the issue price of the B Class Shares was $1.20 per share.

39 There was a confidentiality clause (in 10) whereby the parties are not to disclose the contents of the SSA or the transactions contemplated by it.

40 There is no covenant by the Participating Shareholders not to sue SPG or, indeed, any other party involved in the joint ventures.

Summary of the Facts and Arguments of the Parties

41 A number of affidavits were filed by SPG and none of the deponents were required for cross-examination by the Commissioner. The Commissioner did not tender any material or documents “in addition to what has already gone in”. SPG tendered the following affidavits: (1) affidavit of Nigel Frank Satterley and annexures dated 7 November 2022; (2) affidavit of Nigal Frank Satterley dated 19 December 2022; (3) affidavit of Russell John Gibbs and annexures dated 18 August 2022; (4) affidavit of Russell John Gibbs dated 7 November 2022; (5) affidavit of Anthony Robert Carr and annexures dated 17 August 2022; (6) affidavit of Anthony Robert Carr and annexures dated 3 November 2022; (7) affidavit of Michael Ian Lurie and annexures dated 4 November 2022; (8) affidavit of Rossmore James Carmichael and annexures dated 19 December 2022; (9) SOAF dated 18 May 2023; (10) Information Memorandum; (11) Share Sale Agreement for SABL dated 2 June 2018; (12) Two Project Management and Exclusive Selling Agency Agreements; (13) Schedule of Share Agreement payment to Shareholders; (14) Notice of Objection and Reasons for Decision; and (15) Austin Cove Structure – Phase 1 & 2 Land-Revised. The structure of the Austin Cove Structure is complex and I attach to these reasons the diagrams showing that structure.

42 Mr Satterley is the founder and chief executive officer SPG. Mr Gibbs is and was at the relevant time a non-executive director of SPG. Mr Carr is a non-executive director of SPG. Between 2006 and 2019, he was the chief financial officer of SPG and subsequently the deputy managing director. Mr Lurie is SPG’S solicitor. Mr Carmichael is the general manager, finance, employed by SPG. It is unnecessary to make other than brief reference to the affidavit material because almost all of the relevant facts are set out in the SOAF.

43 It is agreed that for more than 40 years, SPG has been in the business of property development, acting as a developer, land manager and sales agent and carrying out the following: (1) identifying large parcels of land for residential development; (2) acquiring land through special purpose vehicles (companies or trusts); (3) raising capital through equity investments to fund the acquisition and development of the land, with supplementary support from debt finance; (4) acting as project manager, managing projects as directed by the board of management committee; and (5) acting as sales agent for projects by undertaking sales of new land allotments. It is agreed that SPG raises capital for its land development projects by promoting its projects to investors and that it derives its income from project management fees which are charged to the special purpose vehicles in which the investors invest and selling fees charged on the sale and settlement of the developed land.

44 SPG submits that the appeal turns on whether the Top-Up Payments it paid to small investors in one of its projects (Austin Cove Project) which had been performing poorly for a number of years were deductible under s 8-1 of the ITAA 1997, or if not that section, s 40-880(2). In November 2019 and subsequently, SPG paid sums totalling several million dollars to those small investors. The sums were paid pursuant to a series of SSAs. Two samples of an SSA were put before the Court, one in first appeal involving SABL and SBRL, and the other in the second appeal involving Yunderup. As I have said, the SSAs are materially the same. SPG’s contention is that the monies paid to each investor consisted of the Purchase Price and the Top-Up Payment. The Purchase Price was the amount which corresponded with the figure SPG had calculated as the market value of the shares acquired and that it was intended by SPG to be the consideration for their purchase. I have already set out the definition of the SABL Top-Up Payment. The definition contains a statement that the Top-Up Payment is an ex gratia amount. In each case, it is an amount per share equal to the Issue Price less the Share Price.

45 SPG’s contention is that the Top-Up Payments were not made for the purchase of acquiring the shares. SPG contends that it made those payments to protect its brand name, reputation and its continued ability to raise money from investors. SPG contends that prior to entering into the SSAs, it was under no obligation to repurchase the shares of the Participating Shareholders or to compensate for any loss they had sustained on the sale of the shares. SPG submitted that it was appropriate to characterise the Top-Up Payments as voluntary ex gratia payments which SPG intended as a marketing exercise to enable the small investors to get their money back.

46 SPG contends that without the payments, it was at risk of incurring advertising, marketing and possibly legal costs to achieve its desired outcomes. SPG contends that the payments fall within either para (a) or para (b) of s 8-1(1). In the alternative, it contends that the payments are deductible under s 40-880(2) because they do not fall within the exception to subs (2) in subs (5)(f). Even if this be wrong, at least in the case of the Top-Up Payments paid to investors in SABL and Yunderup, which as SPG pointed out, constitute approximately 94% of the value of the deductions claimed in the appeals fall within the exception to the exception within subs (6) of s 40-880. The Share Price in the case of SABL and Yunderup was a nominal amount.

47 The background to the appeals is as follows. In 2006, SPG became interested in acquiring land for development at South Yunderup in Western Australia. It arranged to establish two entities, being BWT and Yunderup (formerly TRGP). Each of those entities acquired a 50% interest in a 20 hectare parcel of land in South Yunderup. That parcel of land comprised 152 lots. SPG named the land “Austin Cove” and it was intended by SPG that the development at Austin Cove consist of two phases. Bowman Water Holdings Pty Ltd as trustee for the BWT (Bowman Waters) and Yunderup acted as equal joint venturers of the Austin Cove JV with the main purpose to develop, manage and sell land. The Austin Cove JV also acquired a further parcel of land in Austin Cove for the purpose of developing 2,678 individual lots, schools and mixed retail and commercial areas. This development did not proceed.

48 The Austin Cove JV was funded by initial capital of approximately $33.9 million through a layered investment structure. External investors held shares in SABL which was established to hold, indirectly, 50% of the BWT. A number of investors in the Austin Cove JV also invested in Yunderup. In about 2006, SPG also arranged for land near Austin Cove (known as Beacham Road) to be acquired by Crestview Asset Pty Ltd (Crestview). This land joined the main Austin Cove development and was purchased at a cheaper price and treated as part of the same project. Crestview was bare trustee for the Beacham Road JV. The joint venture was made up of several entities, each holding a percentage share in the joint venture and its land assets. The Beacham Road JV was funded by initial capital of $8 million contributed by its joint venturers, one being Trendmark Pty Ltd as trustee for the SBRUT which trust held a 29.87% interest in the Beacham Road JV and SBRL held all the units in SBRUT. The Austin Cove JV and the Beacham Road JV did not perform as had been forecast. The joint venturers incurred trading losses despite further capital injections from major investors (Non-Participating Shareholders) and, in the case of the Austin Cove JV, those losses were substantial. By 2016, there had been a number of complaints by the smaller investors (Participating Shareholders) about the poor performance of their investments. SPG caused the IM to be prepared and it was sent to small investors holding shares in SABL, SBRL and Yunderup. The IM contained a proposal to dispose of the Austin Cove JV and the Beacham Road JV landholdings. The proposal was that the small investors would be repaid the full amount of their original capital investments in SABL, SBRL and Yunderup and that a top-up amount would be made as part of any amount paid by SPG to each small investor. In June 2018, the shareholders agreed to the proposal to dispose of the Austin Cove JV and Beacham Road JV landholdings and other assets. In June 2018, SPG and small investors entered into the SSAs. The Top-Up Payments were made to those shareholders in three payments over a two year period after certain conditions were satisfied.

49 It is convenient to note at this point that the Commissioner filed an amended appeal statement pursuant to an order of the Court. The Commissioner contends that the loss or outgoing was not necessarily incurred in carrying on a business for the purpose of gaining or producing assessable income within s 8-1(1)(b) and that further, the Top-Up Payments form part of the cost base of the acquired shares and by reason of s 8-1(2)(d), they cannot be deducted. That paragraph provides that there cannot be a deduction of a loss or outgoing where a provision in the Act prevents the taxpayer from deducting it. This argument was not repeated in the Commissioner’s written submissions. SPG contends that acceptance of the implicit proposition would necessarily mean that the Top-Up Payments were outgoings of capital, or of a capital nature. Section 8-1(2)(d) will have no role to play should SPG prove that the Top-Up Payments were outgoings made on revenue account.

50 SPG submits that whether the payments are characterised as being on capital account or revenue account depends primarily on “what the outgoing is calculated to effect from a practical and business point of view”. SPG submits that outgoings incurred in “gaining or producing assessable income” are outgoings on revenue account. Furthermore, outgoings “necessarily” incurred in carrying on a business for the purpose of doing so are outgoings incurred on revenue account. In Ronpibon Tin NL v Federal Commissioner of Taxation [1949] HCA 15; (1949) 78 CLR 47, the High Court said (at 56):

The word “necessarily” no doubt limits the operation of the alternative, but probably it is intended to mean no more than “clearly appropriate or adapted for”: cf per Higgins J in Commonwealth v Progress Advertising & Press Agency Co Pty Ltd.

51 In Federal Commissioner of Taxation v Snowden & Willson Pty Ltd [1958] HCA 23; (1958) 99 CLR 431 (Snowden & Willson), Dixon CJ referred to the Ronpibon Tin case and said the following (at 437):

What is meant by the qualification is that the expenditure must be dictated by the business ends to which it is directed, those ends forming part of or being truly incidental to the business.

52 Justice Fullagar, with whom Williams J agreed, followed the observations of the Court in the Ronpibon Tin case about the meaning of “necessarily” (at 144). In Magna Alloys & Research Pty Ltd v Federal Commissioner of Taxation [1980] FCA 150; (1980) 33 ALR 213 (Magna Alloys & Research), Deane and Fisher JJ said (at 232):

The requirement that the claimed outgoing be “necessarily” incurred in carrying on the relevant business does not, in the context, mean that the outgoing must be either “unavoidable” or “essentially necessary”. Nor does the word “necessarily” import a requisite of logical necessity. What is required is that the relevant expenditure be appropriate and adapted for the ends of the business carried on for the purpose of earning assessable income (see, Ronpibon Tin NL v Federal Commissioner of Taxation; Federal Commissioner of Taxation v Snowden & Willson Pty Ltd).

(Citations omitted.)

53 In Sharpcan; Kiefel CJ, Bell J, Gaegler J (as his Honour then was), Nettle and Gordon JJ said that the test of whether an outgoing is incurred on revenue account or capital account primarily depends on what the outgoing is calculated to effect from a practical and business point of view. Their Honours referred to the well-known passage of Dixon J (as his Honour then was) in Sun Newspapers where his Honour said (at 363):

There are, I think, three matters to be considered: (a) the character of the advantage sought, and in this its lasting qualities may play a part; (b) the manner in which it is to be used, relied upon or enjoyed, and in this and under the former head recurrence may play its part; and (c) the means adopted to obtain it; that is by providing a periodical reward or outlay to cover its use or enjoyment for periods commensurate with the payment or by making a final provision or payment so as to secure future use or enjoyment.

54 Justice Dixon also referred to the difficulty of distinguishing between revenue and capital in the case of intangible property can be difficult. With respect to goodwill, his Honour said the following (at 360-361):

In the beginning the goodwill may have been established by a great initial outlay upon a widespread advertising campaign carried out upon a scale which it was not intended to maintain or repeat. The outlay might properly be considered to be of a capital nature. On the other hand, the goodwill may have been gradually established by continual advertisement over a period of years growing in extent as it proved successful. In that case the expenditure upon advertising might be regarded as an ordinary business outgoing on account of revenue. More often than not an outlay of capital in establishing an organisation or obtaining an asset of an intangible nature does not produce a permanent condition or advantage. Its effects are exhausted over a period of time.

55 Earlier, his Honour had referred to the elements constituting goodwill as “widespread or general reputation, habitual patronage by clients or customers, and an organised method of serving their needs” (at 360) (see also Latham CJ at 356).

56 SPG submits that the value of goodwill may be diminished when there is adverse publicity concerning the business. However, the mere fact that adverse publicity may have this effect does not mean expenditure is automatically on “capital” account if it is incurred to protect the reputation of a business.

57 In Snowden & Willson, Taylor J said (at 450):

But it is one thing to say that unless a particular expenditure is outlaid the goodwill of a business will or may suffer and another to assert that this very circumstance alone will brand the expenditure, when made, as an expenditure of a capital nature for it is not only capital expenditure which is ultimately reflected in the value of the goodwill of a business since every step in the day to day operations of a business may tend to enhance, preserve, or destroy it. It may, I think, be said that the true character of the expenditure in question in this case is to be sought in a consideration of its immediate purpose as revealed by an appreciation of the occasion which was thought to call for it and of the circumstances in which it was made.

58 Outgoings incurred on advertising and marketing are often part of the daily activities of those engaged in the business. In Magna Alloys & Research , Brennan J said (at 229):

Though goodwill is a capital asset of a business it is frequently earned and maintained by the daily activities of those engaged in the business. The valuable if intangible asset of goodwill frequently grows out of activities the cost of which is a charge on revenue account: see Sun Newspapers. Supra, 61 CLR at 360–1; 1 AITR at 411. Expenditure incurred in attempting to vindicate the business methods of the taxpayer, overcoming the obstacle to its trading which had been raised by the prosecutions is properly to be regarded as a cost on revenue account.

(Citation omitted.)

59 SPG submits that how it derived its income is significant in terms of the characterisation of the outgoings. It derived its income by way of project management and selling fees by raising capital for its project. Its ability to maintain SPG’s brand, good reputation and relationships with investors was critical to “this essential, regular and ongoing feature” of SPG’s business and the Top-Up Payments were made in this context. The Top-Up Payments were made in the course of a poorly performing project and they were paid to the very investors from whom capital had been raised. They were directed at meeting a “continuous demand” (see Sun Newspapers at 362 per Dixon J).

60 SPG then moved to the issue of whether the Top-Up Payments were deductible under s 40-880(2) on the assumption that they were made on capital account. SPG’s submission is that they were a deduction by reason of subs (2) and they did not fall within the terms of subs (5)(f). In the alternative, they fell within the exception to the exception in s 40-880(6).

61 SPG submits that whether the expenditure fell within the terms of subs (5)(f) turned on whether the first element of the cost base of a CGT asset applied to the Top-Up Payments, that is to say, whether the Top-Up Payments are monies SPG paid or was required to pay in respect of acquiring the shares. Whether the Top-Up Payments fell within subs (6) is only an issue with respect to the Top-Up Payments made to investors in SABL and Yunderup. The issue, in those circumstances, is whether the expenditure was incurred to preserve, but not to enhance, the value of goodwill and is incurred in relation to a legal or equitable right and the value of the right to SPG is solely attributable to the effect that the right has on goodwill.

62 SPG submits that the words in s 110-25(2)(a) “in respect of acquiring” must be taken to mean “to acquire” or “for acquiring” the CGT asset in question. It submits that the terms of the section requires a consideration of the purpose for which the taxpayer paid the monies and, in particular, whether the taxpayer paid the monies to acquire the CGT asset. SPG submits that that question should be answered in the negative.

63 SPG’s first submission is that it made the Top-Up Payments to protect its brand name, reputation and continued ability to raise money from investors and that it did not make the Top-Up Payments in respect of acquiring any CGT asset. SPG’s case is that the only monies it paid “in respect of acquiring” the relevant shares, being the CGT asset in question, was the Purchase Price under each of the SSAs.

64 SPG submits in support of those propositions that regard may be had to the proper construction of the IM and to the SSAs read as a whole. With respect to the SSA, SPG relies on the definitions of the SABL Top-Up Payment, the SBRL Top-Up Payment and the Yunderup Top-Up Payment, and the definition of “Refund”. The definition of this last term is as follows:

Refund means the aggregate amount each Participating Shareholder paid for their shares in the Company when they made their original investment and that Participating Shareholders will be entitled to receive arising from the purchase of their shares and, if applicable, the amount the Buyer [SPG] pays by way of the Top-Up Payment, on the terms and conditions in this IM.

65 SPG also relies on the definition of Refund in the IM and the discussion of Refund Proposal in paras 4.1, 4.2 and 4.3 of the IM. It relies on the description of the “Proposal” in section 1 of the IM. It seems that SPG also relies on the reference to refund and the distinction drawn between the share price and the Top-Up Payment. SPG points to section 1.8 which refers to the payment of the share price and the Top-Up Payment “in order to Refund to Participating Shareholders the aggregate amount of their combined initial investment in the Companies”. Finally, SPG relies on the last two rows of the column headed “Event” in the table headed “Indicative Timetable of the Offer” in the IM. Those last two rows are as follows:

Event | Expected date |

Notify Shareholders of the market value and the: purchase price Satterley will pay each Participating Shareholder for their shares in each Company; and Top-Up amount Satterley will pay each Participating Shareholder | Within 30 days after Settlement Date |

Satterley pays the purchase price and first instalment of the Top-Up Payments to those Participating Shareholders who have given Satterley a signed share sale agreement and transfer form | Within 30 days after Settlement Date |

66 With respect to the SSAs, SPG relies on a number of matters. First, SPG relies on para 7 which is in the following terms:

7. PURCHASE PRICE

The Purchase Price is the SABL Share Price (excluding GST, if any) which the Buyer must pay to the Seller at Completion in the way set out in clause 5.4(a).

67 Secondly, SPG relies on Recital B which is the following effect:

B. The Buyer has agreed to:

(a) buy and the Seller has agreed to sell to the Buyer the Sales Shares for the Purchase Price; and

(b) pay the Top-Up Payment to the Seller,

on the terms and conditions in this document.

68 Thirdly, SPG relies on the following definitions: Market Value of the SABL Shares, SABL Share Price, Market Value of the SBRL Shares, SBRL Share Price, Market Value of the Yunderup Shares, Yunderup Share Price, Purchase Price and Refund. The definitions are as follows:

Market Value of the SABL Shares means an amount per share that is equal to their market value of the ACJV Settlement Date, being an amount of $0.001 per SABL Share.

Market Value of the SBRL Shares means an amount per share that is equal to their market value on the BRJV Settlement Date.

Market Value of the Yunderup Shares means an amount per share that is equal to their market value on the ACJV Settlement Date, being an amount of $0.001 per Yunderup Share.

The definitions relating to Share Price are as follows:

SABL Share Price means the price the Buyer is offering to pay to the Participating Shareholders for their shares in SABL, being $0.001 per SABL share, which is the Market Value of the SABL Shares.

SBRL Share Price means the price the Buyer is offering to pay to the Participating Shareholders for their shares in SBRL. It is $0.001 per share, which is the Market Value of the SBRL Shares.

Yunderup Share Price means the price the Buyer is offering to pay to the Participating Shareholders for their shares in Yunderup, being $0.001 per Yunderup share, which is the Market Value of the SABL Shares.

69 I have already referred to clause 2 in the SSA. SPG also relies on clause 6 which is headed “Top-Up Payment” and is as follows:

6. TOP-UP PAYMENT

(a) The Buyer must pay to each of:

SABL’s Participating Shareholders, the SABL Top-Up payment in 3 instalments as follows:

(i) the first instalment, being an amount equal to the aggregate of the SABL Share Price and 50% of the SABL Top-Up Payment respectively, on the Completion Date;

(ii) the second instalment, being an amount equal to 25% of the SABL Top-Up Payment, on or before the first anniversary of the ACJV Settlement Date; and

(iii) the third and final instalment, being an amount equal to the full remaining balance of 25% of the SABL Top-Up Payment, on or before the second anniversary of the ACJV Settlement Date.

(b) No interest is payable on the SABL Share Price or the SABL Top-Up Payment unless any instalment is not paid on or before the due date for payment. In that case, the Buyer must pay interest on the full amount of the overdue instalment at the Default Rate, from the date on which the amount was due to and including the date on which it is paid in full, together with all interest, fees, costs, charges and expenses then due and owing. Default interest is calculated on the basis of a 365-day year and compounds monthly, on the last day of each month, until the full amount outstanding is paid.

70 SPG relies on aspects of the evidence of Mr Carr, Mr Lurie and Mr Carmichael, including contemporaneous correspondence exchanged between the first two of those witnesses to make good its argument that the Top-Up Payments were not in respect of acquiring the shares.

71 With respect to SPG’s alternative argument concerning the preservation, but not enhancement of goodwill, it submits that the exception to the exception was introduced to confine deductibility under s 40-880(2) to expenditure in relation to goodwill that could not otherwise be brought to account under the ITAA (see Sharpcan at [43] and [44]–[47]). SPG submits that the payments were made to preserve the goodwill of the business, that is to say, its brand and reputation. SPG submits that should its argument that the money paid or required to be paid was in respect of acquiring the shares, then those payments would have been made in relation to a legal or equitable right being its right to acquire the relevant shares under the SSAs or the bundle of rights afforded to it as holder of the shares following the completion of those agreements. Finally, SPG claims that the value to it of the right is solely attributable to the effect that the right has on goodwill. SPG paid only a nominal market value for the shares in SABL and Yunderup, namely $0.001 per share. That amount may be contrasted with the amounts it paid by way of Top-Up Payments to the Participating Shareholders who held shares in SABL or Yunderup. SPG submits that its proposed evidence in relation to making the Top-Up Payments supports the conclusion that the shares acquired by it in both SABL and Yunderup had no value to it in and of themselves and the value to it of any rights which it acquired in relation to those shares was solely attributable to the effect which those rights had on SPG’s goodwill.

72 The Commissioner defined the three issues for determination as follows:

(1) Were the Top-Up Payments made on capital or revenue account?

(2) If made on revenue account, are they allowable deductions under s 8-1(1)(a) or s 8-1(1)(b)?

(3) If made on capital account, are they allowable deductions as “blackhole expenditure” under s 40-880?

The Commissioner addressed issue (1) and issue (2) together.

73 The Commissioner submitted that the Top-Up Payments were on capital account and were, therefore, not deductible by reason of s 8-1(2)(a). He further submitted that if it is found that the payments were on revenue account, then they are not deductible under either s 8-1(1)(a) or (b).

74 With respect to the first matter, the Commissioner submitted that the expenditure needs to be characterised objectively from a practical and business perspective of the taxpayer, but also having regard to the legal nature of the various rights created or otherwise obtained by that expenditure. In Hallstroms, Dixon J said the following (at 648):

What is an outgoing of capital and what is an outgoing on account of revenue depends on what the expenditure is calculated to effect from a practical and business point of view, rather than upon the juristic classification of the legal rights, if any, secured, employed or exhausted in the process.

To be clear, that does not mean that the legal rights and their classification are irrelevant (Clough Limited v Commissioner of Taxation [2021] FCAFC 197 at [69].)

75 The Commissioner submits that on the proper construction of the SSAs, the Top-Up Payments form part of the consideration SPG paid for the acquisition of a capital asset, namely, the shares of the Participating Shareholders in SABL, SBRL and Yunderup. The Commissioner contends that in construing the SSA regard should be had to the text of the document alone. He submits that any ambiguity should be subject to the contra proferentem rule having regard to the sophistication of the agreement, legal advice having been clearly sought in the drafting, and the lack of opportunity for the Participating Shareholders to make amendments or negotiate the terms.

76 The Commissioner refers to clause 2 of the SSAs. The simple submission is that, subject to the satisfaction of the Conditions Precedent, which included the sale of relevant land, SPG undertook to pay the Purchase Price and the Top-Up Payment calculated in accordance with the relevant formula. The Commissioner submits that the Purchase Price is unambiguous and susceptible of only one meaning and that there is no cause to consult the IM which is not referred to in the SSA and was created for an entirely different purpose.

77 The Commissioner submits that there are other reasons why the Top-Up Payments should be considered as having been made on capital account. A key part of SPG’s business is attracting investors to its land development processes and an essential component of the infrastructure or framework of SPG’s business is its investors within the special purpose vehicles which are created by it. As a result of the investment in a number of land developments, SPG is able to generate income through project management fees which are charged to the special purpose entities in which the investors invest and selling fees which are charged and recovered on the sale and settlement of the developed land. The fee arrangements are governed by PMAs. SPG’s business is one of “longstanding with a well-established existing framework” and it can be inferred from this that its name and reputation are, at least, contributing factors to a potential investor’s decision to invest funds in the special purpose vehicles.

78 The Commissioner submits that by reference to the three matters identified by Dixon J in Sun Newspapers, it is clear that the Top-Up Payments should be characterised as an outlay of capital, or of a capital nature, for three reasons.

79 First, the Commissioner submits that the Top-Up Payments were a means to secure or protect part of the infrastructure of SPG’s business as the payments sought various advantages. The advantages were the preservation of goodwill amongst the Participating Shareholders and goodwill is considered to be a capital asset. The nature of goodwill was considered by the High Court in Federal Commissioner of Taxation v Murry [1998] HCA 42; (1998) 193 CLR 605. The plurality in that case, in turn, referred to the descriptions of goodwill by Lord Lindley and by Lord Macnaghten in Inland Revenue Commissioners v Muller & Co’s Margarine Ltd [1901] AC 217 at 223–224 and 235 respectively. Lord Macnaghten made the following well-known observations:

What is goodwill? It is a thing very easy to describe, very difficult to define. It is the benefit and advantage of the good name, reputation, and connection of a business. It is the attractive force which brings in custom. It is the one thing which distinguishes an old-established business from a new business at its first start. The goodwill of a business must emanate from a particular centre or source. However widely extended or diffused its influence may be, goodwill is worth nothing unless it has power of attraction sufficient to bring customers home to the source from which it emanates. Goodwill is composed of a variety of elements. It differs in its composition in different trades and in different businesses in the same trade.

80 The High Court also referred to the observations of Judge Swan in Haberle Crystal Springs Brewing Co v Clarke (1929) 2 F 2d 219 at 221-2 as follows:

A going business has a value over and above the aggregate value of the tangible property employed in it. Such excess of value is nothing more than the recognition that, used in an established business that has won the favour of its customers, the tangibles may be expected to earn in the future as they have in the past. The owner’s privilege of so using them, and his privilege of continuing to deal with customers attracted by the established business, are property of value. This latter privilege is known as goodwill.

81 The Commissioner submitted that the Top-Up Payments, which involved a refund of the entire value of the Participating Shareholders’ investment in the Yunderup Development over a period of two years was meant to appease those shareholders. SPG sought to protect a component of its business structure, being the “minor” investors who are deployed as part of the framework to earn SPG its income. Satisfied investors are more likely to invest in SPG’s land development business in the future than disgruntled investors. The Commissioner’s contention is that the payments were targeted payments aimed at the organisation or arrangement of the profit earning structure of SPG’s business, rather than an incident of the operations which it carried on. The other advantage was the likely immunity from potential litigation of the Participating Shareholders related to the commercial failure of the Yunderup Development. The Top-Up Payments made it less likely that the Participating Shareholders would sue and was ultimately designed to protect the infrastructure of SPG’s business model as a whole.

82 Secondly, the Commissioner submitted that the Top-Up Payments were effectively made by one lump sum to secure an enduring change. The change was the extraction of the Participating Shareholders from the underperforming Yunderup Development. This freed up the Participating Shareholders to invest in other things, including other developments of SPG. It followed that the expenditure was for the enduring benefit of SPG’s business as a whole and not just in respect of running the Yunderup Development.

83 Thirdly, the Commissioner contended that the payments were unusual and that no similar payment had been made before. They were not in the nature of ordinary working expenses. They were made for the purpose of restructuring the focus of SPG’s business away from the Yunderup Development so as to put it in the best position to earn more profits in the future.

84 The Commissioner referred to the observations of the Full Court in Commissioner of Taxation v Healius Ltd [2020] FCAFC 173; (2020) 281 FCR 57 (Healius) at [68] to the effect that the question of whether expenditure is on revenue account or capital account requires the consideration of a counterfactual, that is to say, the expected structure of the business but for the outgoing, compared to the expected structure of the business after the outgoing. The Commissioner submits that the expected structure but for the outgoing was that the shares would still be owned by the Participating Shareholders and the Yunderup Development would have continued to incur substantial losses and require a further injection of capital. Although SPG would still have earnt an income from the Yunderup Development as properties were sold and from ongoing management fees, as one of the major investors it was unlikely to have earned a profit according to the projections made in 2018 in the IM. The structure of the business after the outgoing was that the Participating Shareholders in the Yunderup Development were removed, the threat of litigation was reduced and SPG acquired more control of the special purpose vehicles to allow it to focus its business on more commercially viable land developments.

85 It was at this point that the Commissioner addressed s 8-1(1). He submitted that there was no evidence of a discernible nexus between the Top-Up Payments and SPG’s income such as to engage s 8-1(1)(a). He submits that there is insufficient evidence to engage s 8-1(1)(b). He submits that all SPG asserts is that the ends of its business required the payments to be made. In Magna Alloys & Research, Deane and Fisher JJ said the following (at 235):

The controlling factor is that viewed objectively the outgoing must, in the circumstances, be reasonably capable of being seen as desirable or appropriate from the point of view of the pursuit of the business ends of the business being carried on for the purpose of earning assessable income. Provided it comes within that wide ambit, it will, for the purposes of s 51(1), be necessarily incurred in carrying on that business if those responsible for carrying on the business so saw it.

86 The Commissioner submitted that the expenditure is not like marketing or advertising expenses, but rather, formed part of a considered restructure or reorganisation of SPG’s business. The argument that the expenditure was similar to advertising or marketing expenses is difficult to make, having regard to the presence of a confidentiality clause in the SSAs.

87 With respect to the third issue advanced on the assumption that the payments were made on capital account, the Commissioner submits that the shares are CGT assets which could be the subject of a future CGT event and that on the proper construction of the SSAs and s 110-25(2)(a), the Top-Up Payments form part of the cost base of the acquired shares. In those circumstances, no deduction is permitted for the Top-Up Payments under s 40-880(2) by reason of the exclusion provided in s 40-880(5)(f). The argument that the Top-Up Payments formed part of the cost base of the shares has been set out in the Commissioner’s argument that the Top-Up Payments were on capital account. SPG’s argument to the contrary is incorrect because it relies on the subjective purpose for which it paid the Top-Up Payments. The Commissioner also points to the fact that all s 40-880(5)(f) requires is that the expenditure incurred could be taken into account in working out the amount of a capital gain or a capital loss from a CGT event (emphasis added).

88 With respect to the argument relating to s 40-880(2) and (6), the Commissioner submits that the preservation in s 40-880(6) was necessary as the Tax Laws Amendment (2006) Measures No 1 Act 2006 (Cth) abolished the ability to include expenditure in relation to goodwill in the fourth element of the cost base of a CGT asset.

89 The legal right was the acquired shares and it is not solely attributable to the preservation of goodwill because SPG gained apparent immunity from litigation in respect of the failed Yunderup Development, the silence of Participating Shareholders in respect of the failed Yunderup Development and the ability to restructure its business to focus on other ventures. Furthermore, the expenditure has a value in that the acquired shares can be identified and quantified in SPG’s accounts which have a value from any contribution that their acquisition might have had on goodwill in that they could be sold to third parties irrespective of their perceived nominal value (see Sharpcan at [52]).

90 SPG made a number of submissions in reply. In relation to the first issue as to whether the expenditure was revenue or capital, SPG relied on its earlier submissions and the submissions it made in relation to the third issue, that is to say, if capital, the Top-Up Payments are deductible under s 40-880(2). Although SPG accepts that there is less risk of it being sued by dissatisfied shareholders because the Top-Up Payments were made, it does not accept that it enjoyed likely immunity from potential litigation. The SSA contains no forbearance from suit covenants or incorporation provisions purporting to release SPG from claims associated with investments made by the Participating Shareholders. Nor do they contain provisions purporting to indemnify SPG against any such claims. The submission that the shareholders extracted from the Yunderup Development would invest in, among other things, other developments of SPG does not rise above speculation. The submission that the expenditure incurred in making the Top-Up-Payments was not analogous to an advertising or marketing expense because of the presence of a confidentiality clause within the SSAs takes the matter nowhere because SPG’s case is that the payments were made to limit adverse publicity, that is, the purpose of the payments was to protect SPG’s brand name, reputation and continued ability to raise money from its investors. In other words, the payments were made to ensure SPG’s brand and good reputation were maintained.

91 The Commissioner’s submissions that if the Top-Up Payments were on revenue account, then they are not deductible under s 8-1(1)(a) or s 8-1(1)(b) of the ITAA 1997 is not supported by reasons. SPG’s submission is that once it is accepted that the Top-Up Payments were on revenue account, it necessarily follows that they fall within s 8-1(1)(a) or s 8-1(1)(b).

92 With respect to the first argument in relation to s 40-880(2) and s 110-25(2)(a), SPG submitted that the position taken by the Commissioner requires consideration of the role of any construction of the SSA in ascertaining SPG’s purpose in making the Top-Up Payments. SPG had previously submitted that the statutory inquiry to which s 110-25(2)(a) of the ITAA 1997 was directed invites attention to the purpose for which the taxpayer paid the money, relevantly, whether the taxpayer did so to acquire the CGT asset. SPG pointed to the difference between motive and purpose. The motive for a person’s conduct is the person’s reason for engaging in it and, by contrast, the purpose of a person’s conduct is the end that is sought to be accomplished by it (see Sharpcan at [49]).

93 SPG drew a distinction between an inquiry into a taxpayer’s purpose in incurring an expense and an inquiry into the meaning of a provision in a commercial instrument. These inquiries serve different functions. In the case of the first, the inquiry is to ascertain the purpose of one person in incurring an expense and, in the latter, the inquiry is to ascertain the common intention of two or more parties to the instrument. In the case of an inquiry into the common intention of the parties to the instrument, that is to be ascertained by reference to what “a reasonable person would understand by the language used by the parties to express their agreement” (Wilson v Anderson [2002] HCA 29; (2002) 213 CLR 401 at 418). In the ordinary case, the terms of the instrument cannot be contradicted, altered or added to by oral evidence because of the parol evidence rule. The rule applies not only to oral evidence, but to extrinsic evidence in other forms.

94 The inquiry under s 110-25(2)(a) is as to the purpose of the taxpayer in incurring the expense in question. The parol evidence rule has no role to play in this inquiry. It follows that the SSAs, although plainly relevant to the drawing of possible inferences as to SPG’s purpose in making the Top-Up Payments, their proper construction is not necessarily determinative.

95 In the alternative, the process of construction does not involve reading the various definitions in isolation. A commercial contract must be construed as a whole in order to ascertain the common intention of the parties to it. SPG pointed to the difference drawn in Recital B between the Purchase Price and the Top-Up Payment. Furthermore, the Purchase Price is expressly identified as consideration for the subject matter of the transaction, namely, the shares held by the Participating Shareholders. SPG submitted that the repeated maintenance in the SSAs of the distinction between Purchase Price and Top-Up Payments supports an inference that each payment was intended for a separate purpose. The Top-Up Payment was intended as a separate, ex gratia payment to compensate the Participating Shareholder for any difference between the Purchase Price and the price originally paid by the shareholder in connection with the acquisition of the shares. It followed, so SPG submitted, that the Top-Up Payment was not intended to form part of the consideration for the acquisition of the shares. SPG makes the point that although the phrase “for their shares” in the definition (for example) of SABL Top-Up Payment in the SSAs, that phrase does not appear in any of the definitions in the IM.

96 With respect to the argument based on s 40-880(6), SPG made the following submissions in response to the four matters referred to by the Commissioner.

97 First, as to the apparent immunity from litigation, the SSAs contain no forbearance from suit and nor do they release SPG from claims associated with investments made by Participating Shareholders. Nor do they contain provisions purporting to indemnify SPG against any such claims.

98 Secondly, with respect to the silence of Participating Shareholders and the confidentiality clause, SPG submits that it is difficult to see how the shareholders’ agreement not to disclose the information in question could have had any value to SPG in and of itself. In any event, clause 10 merely prevented the Participating Shareholders disclosing information about the SSAs. It did not prevent them from making adverse remarks about either the failed Yunderup Development or their own failed investments.

99 Thirdly, with respect to the argument that as a result of the rights acquired under the SSAs, SPG was able to restructure its business to “focus on other ventures”, SPG submits that this does not rise above speculation. Furthermore, SPG submits that even if this was not the case, it is not apparent how any such “ability” might be capable of translating into “value” within the meaning and for the purpose of s 40-880(6).

100 Finally, with respect to the argument by the Commissioner that the shares were capable of being sold to third parties irrespective of their “perceived nominal value”, that argument is again, speculative.

Analysis

Preliminary matters

101 First, I will start with an analysis of the issue raised by the Commissioner’s reliance on s 8-1(2)(a). I have reached the conclusion that the Top-Up Payments are on capital account. In those circumstances, there is no need for me to consider whether the Top-Up Payments fall within either para (a) or (b) of s 8-1(1).

102 Secondly, the way in which SPG put its submission about the effect of the SSAs was stated in its amended appeal statement at para 7.3.5.3 as follows:

the Top-Up Payments did not form part of the consideration paid by the Applicant for the shares in any of SABL, SBRL or Yunderup;

103 Neither party suggested that, as a matter of law, where one asset moves from one contracting party to the other, in this case the shares, the consideration moving from the other contracting party cannot be divided into the Purchase Price for the shares and an ex gratia payment which is said to relate to goodwill. I note that goodwill as such is not referred to in the SSAs.

104 Thirdly, the Commissioner referred to the parol evidence rule to meet the argument of SPG that the Court should look beyond the SSAs to other evidence in order to determine the nature of the transactions contained in the SSAs. There is a potential difficulty here in that one of the contracting parties is not involved in the dispute and is not before the Court.

105 Finally, it is necessary to distinguish between the parol evidence rule and the rule as to the circumstances in which the Court may consider extrinsic evidence for the purposes of resolving ambiguities in a contract. The leading case remains Codelfa Construction Pty Ltd v State Rail Authority of NSW [1982] HCA 24; (1982) 149 CLR 337 and, in particular, the judgment of Mason J (as his Honour then was). His Honour referred to the parol evidence rule in the following terms (at 347):

The broad purpose of the parole evidence rule is to exclude extrinsic evidence (except as to surrounding circumstances), including direct statements of intention (except in cases of latent ambiguity) and antecedent negotiations, to subtract from, add to, vary or contradict the language of a written instrument (Goss v Lord Nugent). Although the traditional expositions of the rule did not in terms deny resort to extrinsic evidence for the purpose of interpreting the written instrument, it has often been regarded as prohibiting the use of extrinsic evidence for this purpose. No doubt this was due to the theory which came to prevail in English legal thinking in the first half of this century that the words of a contract are ordinarily to be given their plain and ordinary meaning. Recourse to extrinsic evidence is then superfluous. At best it confirms what has been definitely established by other means; at worst it tends ineffectively to modify what has been so established.

(Footnote omitted.)

106 As to the use of extrinsic evidence to resolve ambiguities in a contract, Mason J said the following (at 352):

The true rule is that evidence of surrounding circumstances is admissible to assist in the interpretation of the contract if the language is ambiguous or susceptible of more than one meaning. But it is not admissible to contradict the language of the contract when it has a plain meaning. Generally speaking facts existing when the contract was made will not be receivable as part of the surrounding circumstances as an aid to construction, unless they were known to both parties, although, as we have seen, if the facts are notorious knowledge of them will be presumed.

Substantive issue

107 As I have said, I have reached the conclusion that the Top-Up Payments were made on capital account. I accept the Commissioner’s arguments.

108 The Top-Up Payments, whether they be Top-Up Payments for SABL, SBRL or Yunderup, are all defined as being Top-Up Payments “for their shares”. I do not think that this circumstance is outweighed by the reference in the definition to “an ex gratia amount” as there is no reason why an ex gratia amount cannot be included in the consideration for the shares.

109 The key clause is section 2 in the SSAs. The definition of Top-Up Payment is to be read into clause 2. It is true that clause 2 separately refers to the Purchase Price and the Top-Up Payment, but those two payments are linked by the word “and”. Furthermore, the purchase of the shares and the obligation to pay the Purchase Price and Top-Up Payment are both conditional on the sale of the land and this would be unnecessary if the Top-Up Payment was, in reality, a voluntary payment (ex gratia or as a favour) to preserve goodwill.

110 I do not consider that any of the matters raised by SPG contradict this conclusion. It is true that Recital B is suggestive of the proposition advanced by SPG as is the separation of terms used in the SSA of Market Value and Purchase Price on the one hand, and Top-Up Payments on the other. SPG’s reliance on clause 5.4 does not advance the matter in its favour. That clause simply indicates that at completion, SPG must pay the Purchase Price and the first instalment of the Top-Up Payment. The fact that the Top-Up Payment is made in instalments leads nowhere.