FEDERAL COURT OF AUSTRALIA

Esso Australia Resources Pty Ltd v Commissioner of Taxation [2024] FCA 87

ORDERS

ESSO AUSTRALIA RESOURCES PTY LTD Applicant | ||

AND: | Respondent | |

DATE OF ORDER: | 16 February 2024 |

THE COURT ORDERS THAT:

1. Within 14 days, the parties file any agreed minute of proposed orders to give effect to the reasons (including as to costs).

2. If the parties cannot agree, within 21 days each party file and serve a minute of proposed orders to give effect to the reasons (including as to costs) together with an outline of submissions (of no more than three (3) pages) in support of those proposed orders.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

HESPE J:

INTRODUCTION

1 The applicant, Esso Australia Resources Pty Ltd, is the operator of an unincorporated 50/50 joint venture between it and BHP Billiton Petroleum (Bass Strait) Pty Ltd which included petroleum processing facilities to process petroleum extracted from the Gippsland Basin into commercial products including sales gas, liquid petroleum gas and condensate (Gippsland Basin Joint Venture) (GBJV).

2 The applicant, as operator of the GBJV, entered into an agreement pursuant to which the GBJV would process raw petroleum for another joint venture. These proceedings concern the assessability under the Petroleum Resource Rent Tax Assessment Act 1987 (Cth) (PRRTA Act) of certain amounts which relate to that agreement and were receivable by the applicant in the financial years ended 30 June 2013 to 30 June 2017 (the relevant years).

3 The issues in these proceedings are:

(1) Were amounts of Monthly Reservation Fees receivable by the applicant in the relevant years “assessable tolling receipts” for the purposes of s 24A of the PRRTA Act?

(2) If not, were Monthly Reservation Fee amounts receivable by the applicant in the relevant years “assessable property receipts” for the purposes of s 27(1)(d) of the PRRTA Act?

(3) Was the amount paid to the applicant pursuant to clause 3.6 of a Deed of Amendment, Restatement and Release made on 18 July 2013 (the Settlement Sum) an “assessable tolling receipt” or alternatively an “assessable property receipt”?

(4) If the Monthly Reservation Fee amounts and/or Settlement Sum were “assessable tolling receipts” or “assessable property receipts” were those assessable receipts derived by the applicant in the relevant years?

4 The parties were agreed that if the Monthly Reservation Fee amounts and/or Settlement Sum were “assessable property receipts”, the matter ought to be remitted to the Commissioner of Taxation, the respondent, for reassessment taking into account s 30 of the PRRTA Act.

5 At the commencement of the hearing, the applicant withdrew its appeal in relation to an amount of “Switching Fees” on which it had been assessed in the original assessment issued to it in respect of the year ended 30 June 2017.

EVIDENCE

6 The applicant relied upon affidavits from two witnesses, both of whom were cross-examined:

(a) Ms Johanne Brown, appointed in January 2004 by the applicant on behalf of the GBJV as the lead negotiator in relation to the development of the Kipper gas field. Ms Brown was responsible for the negotiation of the commercial agreements underpinning the development of the Kipper gas field until she left Australia in July 2006. From mid-2011, Ms Brown again became involved in negotiations to resolve issues that had arisen in relation to the Kipper gas field development. Ms Brown ceased to be involved in these negotiations in around mid-April or early May 2013.

(b) Ms Elly Thorne, who commenced to undertake work in relation to the Kipper gas field in late 2015 or the start of 2016 on behalf of the applicant. Ms Thorne was involved in the processes for the implementation of the processing agreement in relation to the Kipper gas field. Ms Thorne left Australia in 2018 but returned in August 2020 and was given responsibility for overseeing contracts relating to the management of the Kipper gas field.

7 No attack was made on the credit of the witnesses. However, their evidence added little to the contemporaneous documents annexed to their affidavits. The following findings of fact are based primarily on those documents.

BACKGROUND

8 A number of production licences over petroleum fields in the Gippsland Basin were held within the GBJV structure.

9 In addition to being the operator of the GBJV, the applicant was also a joint venturer in a number of petroleum exploration and production joint ventures in respect of a number of oil and gas fields in the Gippsland Basin. One of these joint ventures was called the RL2JV. By the start of 2004, the participants of the RL2JV included the applicant, a subsidiary of BHP, a subsidiary of Woodside Energy Group Limited and two subsidiaries of Santos Ltd.

The Gippsland Basin

10 Petroleum fields in the Gippsland Basin consist of oil and gas fields. Whether a field is described as a gas field or an oil field is dependent on whether the field consists primarily of gaseous hydrocarbons (such as methane and ethane, with other light hydrocarbons) or primarily of heavier, liquid hydrocarbons (such as crude and condensate). Oil fields generally contain some quantity of gaseous hydrocarbons and gas fields generally contain some liquid hydrocarbons.

11 The GBJV processing facilities, comprising offshore wells, platforms, offshore and onshore pipelines, plants at Longford and facilities at Long Island Point, are used to process petroleum recovered from fields in the Gippsland Basin. In Esso Australia Resources Pty Ltd v Commissioner of Taxation [2011] FCA 360; (2011) 194 FCR 32, Middleton J described this process as follows (at [24]–[26]):

[24] Esso recovers petroleum from wells on a series of offshore platforms in Bass Strait. Esso conducts an integrated process involving the platforms, the Longford Gas Processing and Crude Stabilisation Plant (‘Longford’ or ‘the Longford Plant’) and Long Island Point Fractionation Plant (‘LIP’), separating the recovered petroleum into a number of hydrocarbon products for commercial exploitation. The process to which the petroleum recovered from Bass Strait is subjected to produce these products is one of separating the petroleum into its constituent hydrocarbons and removing impurities (such as water, hydrogen sulphide and other non-hydrocarbon substances).

[25] Esso’s platforms, pipelines and processing facilities are designed to produce commercially saleable oil and gas products from the raw petroleum recovered from petroleum pools beneath the seabed in Bass Strait. The process is one of successive stages of separation and filtration commencing with the raw petroleum and finishing with the production of the commercially saleable products.

[26] In summary, the process is integrated and continuous, involving the following steps:

(a) The use of wells on the Bass Strait platforms to recover liquid and gaseous raw petroleum from the petroleum pools.

(b) Some separation of the recovered petroleum on the platforms into substantially liquid and substantially gaseous streams, which is then piped to shore. In some cases, these streams are recombined prior to being piped to shore.

(c) Further separation and filtering of the substantially gaseous petroleum stream in the gas plants at Longford so as to produce the commercial product ‘sales gas’ and a raw LPG stream (condensate) of propane, butane and ethane. Some liquid petroleum extracted from this stream is added to the stabilised crude oil stream from the Longford. The sales gas is sold at the exit of the Longford Plant.

(d) Further separation and filtering of the substantially liquid petroleum stream in the Longford Plant so as to produce the commercial product stabilised crude oil and to remove the raw LPG and gas that is piped across to the gas plants.

(e) Transport of the raw LPG and stabilised crude oil by pipeline to the LIP. At that plant the stabilised crude oil is stored for sale while the raw LPG stream is further separated (fractionated) into the commercial products ethane, propane and butane for sale. Ethane is not sold at Long Island Point; it is transported by pipeline to Altona where it is sold.

12 This description was consistent with the responses given to questions in cross-examination by Ms Thorne.

13 The commercially saleable products produced from petroleum recovered from the Gippsland Basin fall into three general categories:

(1) commercially saleable gas, which primarily consists of methane (with traces of ethane, propane and butane) and which is sold at the exit of the Longford plants;

(2) natural gas liquids, which primarily consist of ethane, propane and butane (these last two together are known as LPG) and which are piped to Long Island Point Fractionation Plant (LIP) to be fractionated and sold; and

(3) stabilised crude, which is primarily condensate, and which is piped to LIP and sold.

14 There is a physical limit to how much petroleum can be transported to and processed by the GBJV’s processing facilities.

The Kipper gas field

15 The Kipper gas field, a petroleum gas field in the Gippsland Basin, straddles two production licences, one of which was held by the GBJV parties and one of which was held by the RL2JV. Although there was significant overlap between the parties to the GBJV and the parties to the RL2JV, the parties were not identical. The development and the commercialisation of the Kipper gas field required agreement between the two joint ventures.

16 The applicant did not consider the Kipper gas field to be a high priority field for development compared with other fields in the Gippsland Basin to which it had rights, for two reasons. First, petroleum from the Kipper gas field was expected to produce comparatively lower levels of liquid petroleum products, such as liquefied petroleum gas (LPG) and condensate, which were of higher commercial value than commercially saleable gas. Second, the gaseous petroleum from the Kipper gas field contained higher levels of carbon dioxide than gas from other petroleum fields. At that time the Longford plants did not have the capability to remove the requisite amount of carbon dioxide from the gaseous petroleum from the Kipper gas field to meet relevant sales specifications and standards. Investment in further infrastructure was required before petroleum from the Kipper gas field could be processed into a commercial gas product which could be sold to customers.

17 Commercial pressure mounted on the applicant to progress the development of the Kipper gas field from two sources:

(1) Since 1993, the interest of the RL2JV in the Kipper gas field had been in the form of a retention lease which had been renewed twice. The latest renewal was set to expire in December 2003. The Victorian Government had indicated that a further renewal of that retention lease was unlikely.

(2) Santos and Woodside were placing pressure on the applicant to progress with the development of the Kipper gas field.

18 The parties to the two joint ventures negotiated the terms of various agreements to underpin the development, management and commercialisation of the Kipper gas field. Because the applicant and BHP were parties to both joint ventures, Santos and Woodside were the negotiators for the RL2JV.

19 One of the matters to be negotiated and resolved by the GBJV and the RL2JV parties was whether to use the GBJV’s processing facilities to process petroleum from the Kipper gas field or to construct new processing facilities, which would result in the Kipper gas field being a stand-alone development rather than integrated with other Gippsland Basin field developments.

20 To address the fact that the Kipper gas field was subject to production licences held by each of the RL2JV and the GBJV, it was proposed that a new unincorporated joint venture be formed between the parties to the RL2JV and the GBJV. This new joint venture was referred to as the Kipper Unit Joint Venture (KUJV).

Chronology of Negotiations

21 The RL2JV rejected initial proposals made by the GBJV for the KUJV to use the GBJV’s processing facilities to process petroleum from the Kipper gas field.

22 The first proposal was recorded in a letter dated 30 May 2002 from the GBJV to the RL2JV. The proposal provided for an integrated development of the Kipper gas field through the GBJV’s infrastructure. The proposal provided for the GBJV to receive raw petroleum from the Kipper gas field and process it producing sales gas, condensate and LPG. The commercially saleable gas was to be delivered to the KUJV and the GBJV was to purchase the LPG and condensate in their unprocessed state. In supplementary information provided on the same day by the GBJV to the RL2JV, it was recorded at the time that “significant modifications” to the GBJV’s existing infrastructure might be required to support the Kipper gas field. In the context of this proposal, the GBJV was described as “Provider” / “Buyer” and the KUJV was described as “User” / “Seller”.

23 The first proposal provided for three payments:

(a) A “Monthly Reservation Fee” to be paid by the [KUJV] to the [GBJV] for every month during the term of the agreement except in cases where the agreement is suspended or terminated.

(b) A “Condensate Purchase Price” to be paid by the [GBJV] for all quantities of condensate based on the price of North West Shelf condensate (adjusted for freight and differences in composition), less A$10/bbl fee.

(c) A “LPG Purchase Price” to be paid by the [GBJV]. The purchase price was to be the [GBJV’s] weighted average export value of propane and butane volumes less A$12/T fee.

24 The “Monthly Reservation Fee” was to be calculated by multiplying an escalated “Processing Service Tariff” by a “Maximum Daily Quantity” (MDQ) and the number of days in the month:

(a) The Processing Service Tariff was expressed in 01/01/2002 A$ per MDQ/Day and was said to include “compensation to the [GBJV] for the fact that unprocessed Liquids are purchased at the Receipt Point”. The Processing Service Tariff was to be increased over time from A$ 1.97 /MDQ/Day to A$ 2.18 /MDQ/Day.

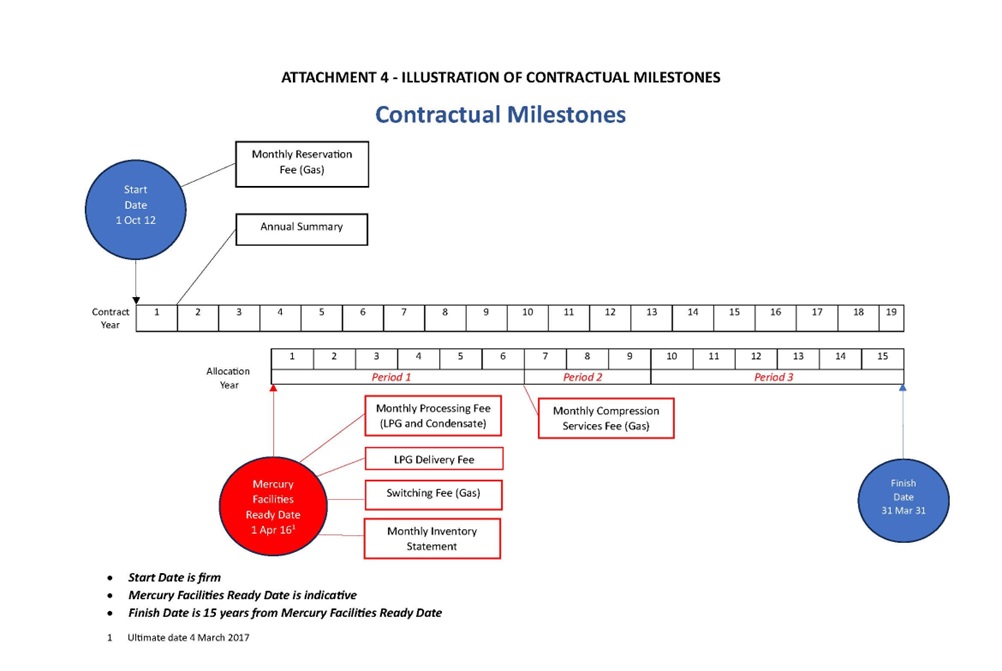

(b) The MDQ was defined in that proposal as the “maximum daily quantity” up to which the KUJV could nominate and the GBJV would be obliged to offer the processing service.

25 The first proposal was characterised by Woodside and Santos as “unattractive” as the proposed tariffs constituted 98% of the prevailing Victorian gas price and was not regarded as based on a realistic cost of service. Woodside considered that a mutually acceptable outcome needed to provide all parties with an appropriate return on their investment that took into account the risks involved. Woodside sought further information on the nature and magnitude of any investment required to be made by the GBJV to provide the Kipper processing service and the cost of providing that service. The GBJV responded that its proposal was based on an assessment of the alternative development options.

26 In developing proposals in relation to the Kipper gas field, one of the factors the applicant took into account was to estimate how much of its processing capacity it would need to allocate to Kipper petroleum.

27 In early 2003, the RL2JV considered a potential stand-alone development that would have involved it using processing infrastructure other than that of the GBJV.

28 By letter dated 10 September 2003 to the RL2JV, the GBJV put forward a revised proposal for the integrated development of the Kipper gas field. The GBJV described the main differences between the previous proposal and this proposal as that the “Receipt Point” was moved further up-stream, LPG was delivered in-kind and there was splitting out of tariffs associated with liquids handling to account for the fact that the GBJV was to deliver LPG to the KUJV. The GBJV was to process the Kipper petroleum into sales gas, sales LPG and condensate. The sales gas and sales LPG would be delivered to the KUJV and the GBJV would purchase the condensate after processing.

29 The proposal included the following proposed payments:

(a) An “Up-front Tariff” as follows:

Amount (expressed in 01/01/2002 A$) | Due Date |

A$ 47 Million | 01/01/2005 |

A$ 20 Million | 01/01/2006 |

A$ 81 Million | 01/01/2007 |

(b) A “Monthly Reservation Fee” to be paid by the [KUJV] to the [GBJV] “during the Term of the Agreement except where the Agreement is terminated”. The Monthly Reservation Fee was to be calculated by multiplying the MDQ, the number of days in the month and an escalated sales gas capacity reservation tariff (SGCRT).

(c) A “Monthly Processing Fee” to be paid by the [KUJV] to the [GBJV] calculated as:

MPF = QLPG x LPGPST + QCond x CondPST

where:

QLPG means the amount of LPG allocated to the [KUJV] during the previous month; and

QCond means the amount of Condensate allocated to the [KUJV] during the previous month.

30 Each of the SGCRT, LPGPST (LPG Processing Service Tariff) and CondPST (Condensate Processing Service Tariff) were tariffs expressed in 01/01/2002 A$ as follows:

SGCRT A$ 1.40 /MDQ/Day for Period 1;

A$ 1.60 /MDQ/Day for Period 2 and Period 3;

LPGPST: A$ 12 /tonne of Sales LPG;

CondPST A$ 10 /stabilised barrel of Condensate

Each was to be indexed at CPI relative to 01/01/2002.

31 By letter dated 28 October 2003, the RL2JV made a counterproposal. The counterproposal put forward two alternatives, resulting in the same effective internal rate of return after tax which Santos and Woodside could support. Santos and Woodside (as negotiators for the RL2JV) stated that any proposed terms by the GBJV that provided a lower effective internal rate of return would be rejected. The first alternative involved reducing the up-front tariff by $65m pro-rata. The second alternative was for the GBJV to purchase the raw petroleum at an inlet. Under this second alternative no fees would be paid to the GBJV.

32 By letter dated 11 December 2003 the GBJV made a counterproposal. Part of the proposal was for “the previously considered pre-payments [to be] rolled into the gas processing toll”. The indicative terms provided for an increase in the SGCRT to A$1.82/MDQ/Day for Period 1 and A$2.02/MDQ/Day for Period 2 and Period 3.

33 In January 2004, a draft “memorandum of understanding of indicative terms and conditions for the processing of Kipper gas, purchase of liquids and provision of operation services” was exchanged between the GBJV parties and the RL2JV parties. The proposal was for the KUJV as “User” to pay a Monthly Reservation Fee based on a predetermined MDQ. The RL2JV proposed that the Monthly Reservation Fee be reduced for those periods where the processing facilities were not available or where the available capacity of the facilities fell below 95%. The KUJV were to also pay a Monthly Processing Fee based on the quantities of LPG and condensate produced and allocated to the KUJV during the previous month. All condensate and excess quantities of LPG were to be purchased by the GBJV parties.

34 Under the January 2004 indicative terms, the proposed tariffs (subject to indexation) were:

SGCRT A$ 1.63/MDQ/Day for Period 1;

A$ 1.83/MDQ/Day for Period 2 and Period 3;

LPGPST: A$ 120/tonne of Sales LPG;

CondPST A$ 10/stabilised barrel of Condensate

35 On 29 June 2004, Santos expressed concern about the “Fixed toll payments” in the memorandum of understanding. The MDQ had to that point been based on reserves estimated at a 50% probability of being recovered. Santos wanted to change it to reserves estimated based on a 90% probability (resulting in a lower MDQ).

36 Between July and December 2004, the parties continued to negotiate the terms of the memorandum of understanding including:

(1) The level of SGCRT. Woodside sought a reduction in the SGCRT, stating that the value of the Kipper resource “at present is heavily determined by the level of Processing Services Tariffs”. The value of the project was also being impacted by a rise in the value of the Australian dollar at the time, which meant that the $A value of gas sales and capital expenditure was falling. The reference date from which the $A was to be measured for the purposes of calculating fees was commercially important.

(2) A variation to the MDQ reservation. Woodside was concerned that the MDQ reservation be such “as to ensure the project meets minimum investment criteria in a P90 case”.

(3) The impact of a force majeure event on the KUJV’s liability to pay the Monthly Reservation Fee.

37 By December 2004, further analysis of another of Esso Australia group’s interests (relating to the Marlin field) had resulted in an upgrade of the level of recoverable reserves. This upgrade of higher value reserves (compared to the Kipper gas field) increased the opportunity cost to the applicant of dedicating processing capacity to Kipper petroleum, which could otherwise be used to process the more valuable petroleum from the Marlin field.

38 By letter dated 3 December 2004, the applicant informed the RL2JV that the applicant could not continue to support the memorandum of understanding in its then present form.

39 In January 2005, the GBJV parties had been working on preparing a revised proposal for the development of the Kipper gas field.

40 In February 2005, the RL2JV and GBJV discussed an alternative development concept for the Kipper gas field. The proposal involved the applicant and BHP delaying taking their full entitlement of Kipper gas for up to four years. This would enable the Kipper gas field to be developed in stages by increasing the number of wells drilled over time (with two wells to be drilled in the first stage and two further wells to be drilled in the second stage). The GBJV was to provide the same processing services to the RL2JV as had been previously proposed.

41 On 2 June 2005, the GBJV and RL2JV parties entered into:

(1) Memorandum of Understanding – Indicative Terms and Conditions for Processing of Kipper Gas and Purchase of Liquids (KGPA MOU). Under this agreement, relevantly the KUJV parties were to pay a Monthly Reservation Fee and Monthly Processing Fee to the GBJV;

(2) Memorandum of Understanding – Indicative Terms for Provision of Operating Services; and

(3) Indicative Terms and Conditions for Kipper Field Unitisation and Unit Operating Agreement. The purpose of this agreement was to form the KUJV, being the unincorporated joint venture between the parties to the GBJV and the RL2JV, to develop the Kipper gas field.

42 The KGPA MOU provided for the following payments:

(1) A Monthly Processing Fee to be calculated as follows: MPF = QLPG x LPGPST + QCond x CondPST.

(2) A Monthly Reservation Fee calculated by multiplying the User’s Maximum Daily Quantity (UMDQ) by the indexed SGCRT and the number of days in the month.

43 The “Processing Service Tariffs” were expressed as follows:

SGCRT A$ 1.82/GJ of MDQ for Period 1;

A$ 2.02/GJ of MDQ for Period 2 and Period 3;

LPGPST A$ 12/tonne of Sales LPG;

CondPST A$ 10 /stabilised barrel of Condensate.

Each of the Processing Service Tariffs were subject to indexation.

44 In May 2006, Woodside sold its share in the RL2JV to Santos. This meant that the remaining parties to the RL2JV by 2006 were Santos, BHP and the applicant.

45 On 17 July 2006, the RL2JV parties obtained a production licence in relation to the Kipper gas field. A condition of the grant of that licence was ongoing consideration of the development of the field.

Original KGPA

46 On 31 October 2006, the GBJV and RL2JV parties entered into the following agreements:

(1) a Kipper Field Unitisation and Unit Operating Agreement, establishing the new KUJV unincorporated joint venture, with the participants being each of the GBJV and RL2JV parties. The effect of the agreement was to unitise each parties’ interest in the Kipper gas field with the result that the applicant and BHP held between them 65% of the economic interest in the Kipper gas field and Santos held the remaining 35%.

(2) a Gas Processing Agreement (Original KGPA), under which the GBJV parties (as Providers) were to provide processing services and the KUJV parties (as Users) were to have raw petroleum from the Kipper gas field processed into gas, LPG and condensate. Because the applicant and BHP were parties to both the joint ventures, each of BHP and the applicant entered into the agreement in two capacities — as a Provider and as a User.

(3) an Operating Services Agreement, which set out the terms upon which the GBJV would provide operating services to the KUJV and would manage KUJV assets; and

(4) a Liquid Sales and Purchase Agreement, which set the terms upon which Santos effectively agreed to sell condensate and excess quantities of LPG produced from the Kipper gas field to the applicant and BHP.

47 Because the petroleum from the Kipper gas field would be mixed with petroleum from other fields as it was being processed, it was not practically possible to trace petroleum hydrocarbons recovered from the Kipper gas field into particular products. Under the Original KGPA, the parties agreed that different components recovered from the Kipper gas field would be taken to result in different products. For example, to the extent that the petroleum recovered was comprised of methane, the petroleum would be taken to result in the production of sales gas.

48 Under the Original KGPA, prior to the “Start Date”, there was no obligation on the KUJV (as Users) to make payments or to make raw petroleum available or on the GBJV (as Providers) to make services available to the Users: cl 3.1. The “Start Date” was somewhat tautologically defined as the date from which the obligations of the Users to make payments and the Providers to provide services was to commence: cl 4.2.

49 Clause 5 of the Original KGPA provided:

5.1 User's Obligations

Subject to this Agreement, on and from the Start Date and for the remainder of the Term, each User agrees to:

(a) make Petroleum available at the Receipt Point; and

(b) take back custody of Gas, LPG and Condensate made available for delivery by a Provider at the Delivery Points; and

(c) pay the Monthly Reservation Fee, Monthly Compression Services Fee and the Step-Out Monthly Reservation Fee (if applicable) in accordance with the terms and conditions of this Agreement; and

(d) purchase and pay for the Services in the quantities, at the price, and in accordance with the other terms and conditions of this Agreement.

5.2 Provider's Obligations

Subject to this Agreement, on and from the Start Date and for the remainder of the Term, each Provider agrees to:

(a) take custody of each User's Petroleum at the Receipt Point; and

(b) make available the Services to each User; and

(c) make available Gas, LPG and Condensate at the Delivery Points to each User.

50 Clause 8 of the Original KGPA relevantly provided:

8. PROCESSING SERVICES AND MDQ

8.1 Processing Services

Commencing on the Start Date and subject to other terms and conditions of this Agreement, each Provider…shall provide the following services ("Processing Services") to each User during the Term of this Agreement:

…

(c) process that Petroleum (except that Petroleum received for Fuel and Flare) into Gas, LPG and Condensate;

…

8.2 MDQ and UMDQ

Subject to Clause 8.3, the MDQ will be the Max.MDQ and each User's UMDQ will be that User's Max.UMDQ, each as set out in Exhibit A Item 1.1.

51 A User could request a reduction or increase in its UMDQ in respect of any year after contract year 5 in certain circumstances: cl 8.3.

52 Pursuant to cl 17.2, Providers were required to convert a quantity of petroleum made available by the Users, into quantities of sales gas, LPG and condensate and allocate the quantities derived (based on the agreed components described at [47]).

53 Clause 22 of the Original KGPA relevantly provided:

22.2 Processing Service Tariffs

(a) The "Gas Capacity Reservation Tariff” in the Contract Year "n" (“GCRTn”) shall be calculated throughout the Term of the Agreement in accordance with the following formula:-

GCRTn = $1.8200 x (CPIn / 138.5)

Where:-

$1.8200 is the Gas Capacity Reservation Tariff (per GJ of UMDQ) expressed in Reference Date A$;

CPIn is CPI in respect of the September quarter of the immediately preceding Contract Year; and

138.5 is the CPI at the Reference Date.

(b) The "LPG Process Servicing Tariff” in the Contract Year "n" (“LPGPSTn”) shall be calculated in accordance with the following formula:-

LPGPSTn = $12.0000 x (CPIn/138.5)

Where:-

$12.0000 is the LPG Processing Service Tariff (per tonne) expressed in Reference Date A$;

CPIn is CPI in respect of the September quarter of the immediately preceding Contract Year; and

138.5 is the CPI at the Reference Date.

(c) The “Condensate Processing Service Tariff” in the Contract Year "n" (“CondPSTn”) shall be calculated in accordance with the following formula:-

CondPSTn = $10.0000 x (CPIn/138.5)

Where:-

$10.0000 is the Condensate Processing Service Tariff (per barrel) expressed in Reference Date A$;

CPIn is CPI in respect of the September quarter of the immediately preceding Contract Year; and

138.5 is the CPI at the Reference Date.

…

22.3 Monthly Reservation Fee

(a) Subject to Clause 27.3(d), the “Monthly Reservation Fee” (“MRFn”) to be paid each Month by each User with effect from the Start Date shall be equal to MRFn, in Contract Year “n” in which that Month occurs, and shall be calculated in accordance with the following formula:

MRFn = GCRTn x (UMDQn - RSOUMDQn) x 30.4375

where:

GCRTn is defined in Clause 22.2(a);

UMDQn is the applicable UMDQ (GJ/Day) for that User in Contract Year “n”;

RSOUMDQn is the applicable User’s Requested Step-Out UMDQ (GJ/Day) for that User in Contract Year “n” in accordance with Clause 8.3(b); and

30.4375 is the average number of Days per month over the Term.

For the avoidance of doubt, if the Start Date does not occur on the first Day of the first Month, the MRF for the first Month will be pro-rated by dividing the number of Days from the Start Date to the end of the first Month by the total number of days in that Month.

…

22.4 Monthly Processing Fee

The "Monthly Processing Fee" ("MPFn") to be paid each Month by each User with effect from the Start Date shall be equal to MPFn in Contract Year "n" in which that Month occurs, shall be calculated in accordance with the following formula:

MPFn = (LPGPSTn x LPGQn) + (CondPSTn x CondQn)

where:

LPGPSTn is defined in Clause 22.2(b);

CondPSTn is defined in Clause 22.2(c);

LPGQn is the quantity of LPG (in tonnes) allocated to that User in accordance with Clause 17 in the Month of Contract Year "n"; and

CondQn is the quantity of Condensate (in barrels) allocated to that User in accordance with Clause 17 in the Month of Contract Year "n".

54 Clause 23 of the Original KGPA required each Provider to render to each User a statement (Monthly Statement). The Monthly Statement was to relevantly show:

(a) that Provider's Proportionate Share of the User's Monthly Reservation Fee for that Month;

…

(c) that Provider's Proportionate Share of the User's Monthly Processing Fee for the quantity of LPG and Condensate allocated to the User in accordance with Clause 17 on each Day in the preceding Month;

…and;

(j) the due date for payment.

The net sum set out in the Monthly Statement was to be paid by the later of the 20th day of the month in respect of which a Monthly Statement was issued by a Provider or 10 days after receipt of the Monthly Statement (whichever was later): cl 23.5.

55 Clause 23.8 of the Original KGPA relevantly provided:

23.8 Payment Dispute

(a) When any amount included within a Monthly Statement issued by a Provider to a User is the subject of a bona fide dispute, that User or that Provider (as the case may be) shall immediately Notify the other of the amount in dispute and the reasons for the dispute.

(b) The undisputed portion shall promptly be paid and after settlement of the dispute any amount agreed, adjudged or determined to be due shall be included in the next Monthly Statement to be given under this Agreement together with interest measured and accrued daily, and compounded monthly at a rate equivalent to the Interest Rate of each month or part month for which interest is to be calculated for the period starting from and including the due date for payment of the net sum payable under the relevant provisional Monthly Statement and ending on the date of the payment of the adjustment…

56 Clause 27.3 of the Original KGPA provided for a modification to the calculation of the Monthly Reservation Fee to be made in certain circumstances for a month in a contract year in which certain kinds of force majeure events occurred. If the force majeure event occurred at the Providers’ facilities, the effect of the modification was to relieve a User from its obligation to pay its “Proportionate Share of that User’s Monthly Reservation Fee”: cl 27.3(b)(i). If the force majeure event occurred at the User’s end, the effect of the modification (if it applied) was that the Monthly Reservation Fee was to be calculated by reference to the User’s “Field Capacity UMDQ” (rather than the UMDQ): cl 27.3(d).

57 Exhibit A set out the maximum and minimum MDQ allocations for each contract year. The maximum MDQ allocations were set out in Exhibit A.1.1 as follows:

A.1 MDQ Reservation Schedule and Flowing Pressure

A.1.1 Maximum MDQ Allocation

Contract Year | Max. MDQ (GJ/Day) | Santos Max. UMDQ (GJ/Day) | KUJV BHPBMax. UMDQ (GJ/Day) | KUJV Esso Max. UMDQ (GJ/Day) | Receipt Point Flowing Pressure at Max. MDQ (kPaa) | Fuel and Flare (GJ/Day) | |

1-4 | 92,000 | 64,750 | 13,625 | 13,625 | 14,400 | 5,000 | |

1 | 5 | 185,000 | 64,750 | 60,125 | 60,125 | 12,200 | 10,000 |

6 | 185,000 | 64,750 | 60,125 | 60,125 | 12,200 | 10,000 | |

2 | 7 | 185,000 | 64,750 | 60,125 | 60,125 | 7,200 | |

8 | 185,000 | 59,500 | 62,750 | 62,750 | 7,200 | 15,000 | |

9 | 185,000 | 47,250 | 68,875 | 68,875 | 7,200 | ||

3 | 10 | 165,000 | 40,850 | 62,075 | 62,075 | 5,500 | 14,000 |

11 | 135,000 | 33,850 | 50,575 | 50,575 | 4,500 | 11,000 | |

12 | 115,000 | 28,600 | 43,200 | 43,200 | 4,000 | 10,000 | |

13 | 95,000 | 19,850 | 37,575 | 37,575 | 3,500 | 8,000 | |

14 | 80,000 | 0 | 40,000 | 40,000 | 2,000 | 6,000 | |

15 | 55,000 | 0 | 27,500 | 27,500 | 2,000 | 5,000 |

58 Each User’s MDQ allocations in each year did not marry each User’s proportionate interest in the KUJV. Despite Santos having a 35% proportionate unitised interest in the KUJV (and therefore a 35% economic interest in the Kipper gas field), Santos was entitled to 70% of the MDQ allocation in years 1 to 4.

59 By deed of amendment dated 14 December 2007, the definition of “Start Date” was amended to 1 April 2011 or such other date as agreed between parties.

Restated KGPA

60 In about 2010, unexpected high levels of mercury were discovered in petroleum recovered from the Kipper gas field. The GBJV processing facilities had not been designed to process petroleum with that level of mercury. The discovery meant that petroleum from the Kipper gas field could not commence to be processed through the GBJV processing facilities without modifications to those facilities and the introduction of additional processes. There was a resulting delay to the processing of petroleum.

61 The delay to processing gave rise to a dispute between Santos and the GBJV. Santos had been issued with monthly invoices for the Monthly Reservation Fee commencing 1 April 2011. Santos was disputing its liability to pay these invoices. The GBJV was seeking payment in order to commence recovering the costs it had already incurred in making the GBJV facilities able to handle the higher carbon dioxide levels in Kipper petroleum. The GBJV was also seeking funding from the KUJV participants for the construction of mercury handling facilities.

62 On 18 July 2013, the parties entered into a series of agreements to resolve issues that had arisen as a result of the unexpected high levels of mercury. The agreements included:

(1) the Kipper Mercury Facilities Cost Recovery Agreement; and

(2) the Kipper Gas Processing Agreement – Deed of Amendment, Restatement and Release (the Deed).

63 Pursuant to the Deed:

(1) The terms of the Original KGPA were amended and restated, as Annexure A to the Deed (Restated KGPA): cl 2.1.

(2) The payment by Santos of specified amounts, the execution of the Deed and the execution of the Kipper Mercury Facilities Cost Recovery Agreement and the Kipper Project Services Agreement – Deed of Amendment No 1, were in full and final satisfaction of the dispute between the parties relating to:

(a) the mercury content of petroleum from the Kipper gas field to be processed under the KGPA;

(b) whether the Monthly Reservation Fee was payable as at 1 April 2011 or subsequently at all; and

(c) the Start Date: cl 3.1.

(3) As a consequence of the amendment of the Start Date, each of the Providers agreed to cancel the Monthly Statements issued in respect of the period from 1 April 2011 to 30 September 2012 inclusive: cl 3.4.

(4) The parties “confirm[ed] the validity” of the Monthly Statements issued by each of the Providers for the period from 1 October 2012 to the date of the Deed and Santos acknowledged receipt of those Monthly Statements (cl 3.5). Santos agreed to pay to each Provider the amounts shown as being due, together with any amounts in respect of a Monthly Statement issued between 10 June 2013 and the “Effective Date” (being the date all parties signed the Deed), within 30 days of the Effective Date: cl 3.6.

(5) The parties acknowledged and agreed that after the Effective Date, Monthly Statements would issue and be paid in accordance with the KGPA: cl 3.9.

64 The Restated KGPA provided for:

(a) The “Start Date” as 1 October 2012.

(b) A new concept of the “Mercury Facilities Ready Date”:

“Mercury Facilities Ready Date” means the date of the Notice issued by GBJV Esso for the purposes of Clause 4.5 of the Kipper Mercury Facilities Cost Recovery Agreement, notifying the Parties that the Kipper Mercury Facilities and the GCP Mercury Infrastructure are ready to receive Petroleum.

(c) A new concept of an “Allocation Year”:

“Allocation Year” means, for the first Allocation Year, the period from the start of the Day on the Mercury Facilities Ready Date until the start of the Day which is twelve months after the first Day of the month in which the Mercury Facilities Ready Date occurs (the “Allocation Anniversary Date”), and thereafter each successive period of twelve consecutive months during the Term beginning with the start of the Day on the Allocation Anniversary Date in any year until the start of the Day on the Allocation Anniversary Date in the succeeding year…

(d) Attached as Attachment 4 to the Restated KGPA was a diagrammatic illustration of contractual milestones which “illustrates the relationship between the Start Date, the Allocation Year and the Mercury Facilities Ready Date”: cl 4.2. A slightly modified version of that attachment is reproduced in the annexure to these reasons.

65 Clause 5 was amended as follows:

5. OBLIGATIONS OF THE PARTIES

5.1 User’s Obligations

Subject to this Agreement and the Amendment Deed:

(a) on and from the Start Date and for the remainder of the Term, each User agrees to pay the Monthly Reservation Fee; and

(b) on and from the Mercury Facilities Ready Date and for the remainder of the Term, each User agrees to:

(i) make Petroleum available at the Receipt Point; and

(ii) take back custody of Gas, LPG and Condensate made available for delivery by a Provider at the Delivery Points; and

(iii) pay the Monthly Compression Services Fee and the Step-Out Monthly Reservation Fee (if applicable) in accordance with the terms and conditions of this Agreement; and

(iv) purchase and pay for the Services in the quantities, at the price, and in accordance with the other terms and conditions of this Agreement.

5.2 Provider’s Obligations

Subject to this Agreement, on and from the Mercury Facilities Ready Date and for the remainder of the Term, each Provider agrees to:

(a) take custody of each User’s Petroleum at the Receipt Point; and

(b) make available the Services to each User; and

(c) make available Gas, LPG and Condensate at the Delivery Points to each User.

66 Clause 8 of the Restated KGPA relevantly provided (emphasis added):

8.1 Processing Services

(a) Commencing on the Mercury Facilities Ready Date and subject to other terms and conditions of this Agreement, each Provider, in its Proportionate Share, shall provide the following services (“Processing Services”) to each User during the Term of this Agreement:

(i) …take custody at the Receipt Point of each User’s Petroleum (including Petroleum for Fuel and Flare) made available by that User up to but not exceeding that User’s UMDQ of that Allocation Year;

(ii) meter the quantity of Petroleum received pursuant to Clause 8.1(a);

(iii) process that Petroleum (except that Petroleum received for Fuel and Flare) into Gas, LPG and Condensate (excluding services provided under the Kipper Project Services Agreement);

(iv) return custody of Gas, LPG and Condensate by making available at the Delivery Points the corresponding quantities of Gas, LPG and Condensate, derived from the User’s Petroleum in accordance with Clause 17, to each User or to another person for that User’s account;

…

(b) The Providers will provide Processing Services to the Users in accordance with Max. UMDQs specified in Exhibit Al.1 and Min. UMDQs specified in Exhibit Al.2 during the Allocation Years specified in those Exhibits. The MDQ Processing Allocations specified in Exhibit A1.1 and A1.2 represent the Users’ reservation of gas processing capacity under this Agreement.

8.2 MDQ and UMDQ

Subject to Clause 8.3, the MDQ will be the Max.MDQ and each User’s UMDQ will be that User’s Max.UMDQ, each as set out in Exhibit A Item 1.1.

8.3 Changes to MDQ and UMDQ after Allocation Year 5

(a) A User may request a reduction in its UMDQ below its Max.UMDQ in respect of any Allocation Year after Allocation Year 5 by giving Notice to the Providers at least two Allocation Years before the start of the relevant Allocation Year. The Providers shall not withhold consent to a User’s proposed decrease in UMDQ provided that:

(i) the resulting MDQ shall be greater than or equal to the Min.MDQ set out in Exhibit A Item 1.2 or, if no Min.MDQ is set out in Exhibit A Item 1.2 for an Allocation Year, the resulting MDQ shall be greater than or equal to the Providers’ economically feasible minimum MDQ; and

(ii) the resulting User’s UMDQ shall be greater than or equal to that User’s Min.UMDQ set out in Exhibit A Item 1.2.

(b) A User may request an increase in its UMDQ above its Max.UMDQ in respect of any Allocation Year after Allocation Year 5 by giving Notice to the Providers at least two Allocation Years before the start of the relevant Allocation Year. The Providers shall not unreasonably withhold consent to the proposed increase in UMDQ provided that:

(i) the request from the User is made as a result of an increase in Recoverable Petroleum; or

(ii) the request is made following a User Force Majeure Event which prevented the User from making Petroleum available at the Receipt Point, in whole or in part, and provided further that it only applies to those Days for which the User has previously paid to each Provider its share of the Monthly Reservation Fee and Monthly Compression Services Fee applicable to that UMDQ for the period of that User Force Majeure Event to the extent required under Clause 27.3 (“Pre paid UMDQ Days”); or

(iii) the request from the User is made as a result of the first Allocation Year being less than 365 Days;

and:

(iv) all other Users consent to the User’s UMDQ increase, such consent not to be unreasonably withheld; and

(v) the resulting MDQ shall be less than or equal to the MDQ in the prior Allocation Year and, in any case, less than or equal to 185,000 GJ/Day; and

(vi) the resulting MDQ shall be greater than or equal to an economic threshold to be agreed. For the purpose of determining the economic threshold for requests made under paragraph (ii) above, the Parties shall assume that the full Monthly Reservation Fee at the date of the request will be payable by the User in respect of the quantity of the requested increase, as opposed to the Step-Out Monthly Reservation Fee.

…

(c) A User may request an increase in its UMDQ above its Max.UMDQ in respect of any Allocation Year after Allocation Year 5 by giving Notice to the Providers. The Providers shall consider in good faith a User’s requested increase in UMDQ provided that:

(i) the request is made as a result of that User forecasting insufficient remaining UMDQ to enable it to achieve its KUJV Petroleum entitlement depletion by the Planned Depletion Date; and

(ii) all other Users consent to the User’s UMDQ increase; and

(iii) the resulting MDQ for any Allocation Year shall not exceed 185,000 GJ/Day; and

(iv) the sum of all the Users’ UMDQ shall be greater than an economic threshold to be agreed.

(d) To the extent that the Providers agree to a User’s request under this Clause 8.3, the User’s UMDQ, the User’s Max.UMDQ and the MDQ, each as set out in Exhibit A Item 1, will be amended accordingly with effect from the date of such agreement and such amended quantities shall be used in calculating the Monthly Reservation Fee payable by a User pursuant to Clause 22.3 thereafter. Where the amounts paid in respect of the Monthly Reservation Fee for the period prior to such agreement exceeds the amount that would have been due if the such amended quantities had been applicable at the time the relevant Monthly Reservation Fee was calculated, then each Provider shall make an adjustment in the manner provided by Clause 23.3 (b).

(e) For the purposes of ascertaining any adjustment in respect of Clause 8.3(d), Monthly Statements issued to Users during the first Contract Year relate to Petroleum to be produced and supplied to Users under this Agreement during the first Allocation Year, and Monthly Statements issued to Users during each subsequent Contract Year shall relate to Petroleum to be produced and supplied to Users under this Agreement during each corresponding Allocation Year in accordance with the 15 year profile set out in Exhibit A.1.1.

8.4 No over-commitment

Each Provider shall not enter into any new or additional Third Party Agreement if that Provider is aware at the date of that additional commitment that it is unable to fulfil its contractual obligations in respect of gas processing capacity (as specified in Exhibit A Item 1.1) under all Third Party Agreements and this Agreement.

67 Clause 22 of the Restated KGPA relevantly provided:

22.1 Fee Components

(a) In accordance with Clause 23.5, each User shall pay to each Provider that Provider’s Proportionate Share of the Monthly Reservation Fee applicable for that User for each Month during a Contract Year as set out in Exhibit A.1.3. The Monthly Reservation Fee applicable during a given Contract Year shall be calculated under Clause 22.3(a).

…

(c) In accordance with Clause 23.5, each User shall pay to each Provider that Provider’s Proportionate Share of the Monthly Processing Fee applicable for that User for each Month during the Term. The Monthly Processing Fee applicable during a given Allocation Year shall be calculated under Clause 22.4.

…

22.2 Processing Service Tariffs

(a) The “Gas Capacity Reservation Tariff” in the Contract Year “n” (“GCRTn”) shall be calculated throughout the Term of the Agreement in accordance with the following formula:-

GCRTn = $1.8200 x (CPIn /138.5)

Where:

$1.8200 is the Gas Capacity Reservation Tariff (per GJ of UMDQ) expressed in Reference Date A$;

CPIn is CPI in respect of the September quarter of the immediately preceding Contract Year; and

138.5 is the CPI at the Reference Date.

(b) The “LPG Processing Service Tariff” in the Allocation Year “n” (“LPGPSTn”) shall be calculated in accordance with the following formula:-

LPGPSTn = $12.0000 x (CPln / 138.5)

Where:-

$12.0000 is the LPG Processing Service Tariff (per tonne) expressed in Reference Date A$;

CPIn is CPI in respect of the September quarter of the immediately preceding Allocation Year; and

138.5 is the CPI at the Reference Date.

(c) The “Condensate Processing Service Tariff” in the Allocation Year “n” (“CondPSTn”) shall be calculated in accordance with the following formula:-

CondPSTn = $10.0000 x (CPIn /138.5)

Where: -

$10.0000 is the Condensate Processing Service Tariff (per barrel) expressed in Reference Date A$;

CPIn is CPI in respect of the September quarter of the immediately preceding Allocation Year; and

138.5 is the CPI at the Reference Date.

…

22.3 Monthly Reservation Fee

(a) Subject to Clause 27.3(d), the “Monthly Reservation Fee” (“MRFn”) to be paid each Month by each User with effect from the Start Date shall be equal to MRFn in Contract Year “n” in which that Month occurs, and shall be calculated in accordance with the following formula, using the values provided in Exhibit A.1.3:

MRFn = GCRTn x (UMDQn - RSOUMDQn) x 30.4375

where:

GCRTn is defined in Clause 22.2(a);

UMDQn is the applicable UMDQ (GJ/Day) for that User in Contract Year “n”.

RSOUMDQn is the applicable User’s Requested Step-Out UMDQ (GJ/Day) for that User in Allocation Year “n” in accordance with Clause 8.3(b); and

30.4375 is the average number of Days per month over the Term.

For the avoidance of doubt, if the Start Date does not occur on the first Day of the first Month, the MRF for the first Month will be pro-rated by dividing the number of Days from the Start Date to the end of the first Month by the total number of days in that Month.

…

22.4 Monthly Processing Fee

The “Monthly Processing Fee” (“MPFn”) to be paid each Month by each User with effect from the Mercury Facilities Ready Date shall be equal to MPFn in Allocation Year “n” in which that Month occurs, shall be calculated in accordance with the following formula:

MPFn = (LPGPSTn x LPGQn) + (CondPSTn x CondQn)

where:

LPGPSTn is defined in Clause 22.2(b);

CondPSTn is defined in Clause 22.2(c);

LPGQn is the quantity of LPG (in tonnes) allocated to that User in accordance with Clause 17 in the Month of Allocation Year “n”; and

CondQn is the quantity of Condensate (in barrels) allocated to that User in accordance with Clause 17 in the Month of Allocation Year “n”.

68 Clause 23 of the Restated KGPA relevantly provided:

23.1 Monthly Statement

In the Month in which the Start Date occurs and in each Month thereafter, each Provider shall…render to each User a statement (“Monthly Statement”)…showing for that Month:

(a) that Provider’s Proportionate Share of the User’s Monthly Reservation Fee for that Month;

…

(c) that Provider’s Proportionate Share of the User’s Monthly Processing Fee for the quantity of LPG and Condensate allocated to the User in accordance with Clause 17 on each Day in the preceding Month;

…

(f) that Provider’s Proportionate Share of the User’s Monthly Compression Services Fee for that Month;

…

(h) any other sum due and owing to or by that Provider under this Agreement in respect of that Month and the reason why that sum is due and owing;

…and;

(j) the due date for payment.

…

23.3 Adjustment of Statements

…

(b) In the event that an adjustment is required for the purposes of Clause 8.3(d), then within ninety (90) Days of the agreement referred to in Clause 8.3(d), each Provider shall render to each User a statement of adjustment showing the appropriate adjustments to the Monthly Reservation Fee payable for the period prior to such agreement together with an Adjustment Note. The amount resulting from the adjustment shall be paid by the relevant Party ten days after receipt of the statement of adjustment in accordance with this Clause 23.3(b). Interest shall be measured and accrued daily, and compounded monthly at a rate equivalent to the Interest Rate of each month or part month for which interest is to be calculated for the period starting from and including the due date for payment of the net sum payable in respect of the adjustments to the Monthly Reservation Fee and ending on the date of the payment of the adjustment.

…

23.5 Payment Due Date

(a) On or before the 20th day of the Month in respect of which a Monthly Statement is issued by a Provider or ten Days after receipt of the Monthly Statement, whichever is the later, the User or the Provider (as the case may be) shall pay to the other the net sum, if any, set out in that Monthly Statement.

(b) If the application of Clause 23.5(a) would result in the date of payment being a Day which is not a Business Day, then payment will be due on the immediately preceding Business Day.

…

69 Exhibit A.1.1 was amended to provide:

A.1.1 Maximum MDQ Allocation

Period | Allocation Year | Max. MDQ (GJ/Day) | Santos Max. UMDQ (GJ/Day) | KUJV BHPB Max. UMDQ (GJ/Day) | KUJV Esso Max. UMDQ (GJ/Day) | Receipt Point Flowing Pressure at Max. MDQ (kPaa) | Fuel & Flare (GJ/Day) |

0 | Start Date to Mercury Facilities Ready Date | 0 | 0 | 0 | 0 | 0 | 0 |

1 to 4 | 92,000 | 64,750 | 13,625 | 13,625 | 14,400 | 5,000 | |

1 | 5 | 185,000 | 64,750 | 60,125 | 60,125 | 12,200 | 10,000 |

6 | 185,000 | 64,750 | 60,125 | 60,125 | 12,200 | 10,000 | |

7 | 185,000 | 64,750 | 60,125 | 60,125 | 7,200 | 15,000 | |

2 | 8 | 185,000 | 59,500 | 62,750 | 62,750 | 7,200 | 15,000 |

9 | 185,000 | 47,250 | 68,875 | 68,875 | 7,200 | 15,000 | |

10 | 165,000 | 40,850 | 62,075 | 62,075 | 5,500 | 14,000 | |

11 | 135,000 | 33,850 | 50,575 | 50,575 | 4,500 | 11,000 | |

3 | 12 | 115,000 | 28,600 | 43,200 | 43,200 | 4,000 | 10,000 |

13 | 95,000 | 19,850 | 37,575 | 37,575 | 3,500 | 8,000 | |

14 | 80,000 | 0 | 40,000 | 40,000 | 2,000 | 6,000 | |

15 | 55,000 | 0 | 27,500 | 27,500 | 2,000 | 5,000 |

70 Exhibit A was amended to include A.1.3 which provided as follows:

A.1.3 MDQ for calculation of Monthly Reservation Fee

Contract Year | Max. MDQ (GJ/Day) | Santos Max UMDQ (GJ/Day) | KUJV BHPB Max UMDQ (GJ/Day) | KUJV Esso Max. UMDQ (GJ/Day) |

1 | 92,000 | 64,750 | 13,625 | 13,625 |

2 | 92,000 | 64,750 | 13,625 | 13,625 |

3 | 92,000 | 64,750 | 13,625 | 13,625 |

4 | 92,000 | 64,750 | 13,625 | 13,625 |

5 | 185,000 | 64,750 | 60,125 | 60,125 |

6 | 185,000 | 64,750 | 60,125 | 60,125 |

7 | 185,000 | 64,750 | 60,125 | 60,125 |

8 | 185,000 | 59,500 | 62,750 | 62,750 |

9 | 185,000 | 47,250 | 68,875 | 68,875 |

10 | 165,000 | 40,850 | 62,075 | 62,075 |

11 | 135,000 | 33,850 | 50,575 | 50,575 |

12 | 115,000 | 28,600 | 43,200 | 43,200 |

13 | 95,000 | 19,850 | 37,575 | 37,575 |

14 | 80,000 | 0 | 40,000 | 40,000 |

15 | 55,000 | 0 | 27,500 | 27,500 |

For each Contract Year after 15 | 0 | 0 | 0 | 0 |

Subsequent Developments

71 By deed made on 3 March 2016, Santos assigned its interest in the KUJV to MEPAU A Pty Ltd (Mitsui).

72 Issues with the development of the Kipper gas field continued to emerge. The Kipper gas processing agreements had been negotiated on the basis that four wells would be drilled. By deed dated 17 September 2019, the parties recognised that the Users were considering changing the Kipper gas field development so that only one additional well would be drilled (rather than two). Changing to the three well development resulted in further changes to the gas processing agreement. These changes were recorded in deeds dated 11 December 2019 and 3 July 2020. Relevantly:

(a) The circumstances in which a reduction to a User’s UMDQ under cl 8.3 could be made were further amended. A User’s UMDQ could be reduced in respect of any day where one or more Kipper gas field wells were not expected to produce petroleum. However, that reduction would not affect the Monthly Reservation Fee calculated under cl 22.3: cl 3.10 of deed dated 3 July 2020.

(b) Changes were agreed to be made to Exhibit A.1.1 and Exhibit A.1.2 to recognise less production. Following the deed of 3 July 2020, Exhibit A.1.1 provided:

A.1.1 Maximum MDQ Allocation

Period | Allocation Year | Max. MDQ (GJ/Day) | Mitsui Max UMDQ (GJ/Day) | KUJV BHP Max UMDQ (GJ/Day) | KUJV Esso Max UMDQ (GJ/Day) | WTN Separator Pressure at Max. MDQ (kPaa) | Fuel & Flare (GJ/Day) |

0 | Start Date to Mercury Facilities Ready Date | 0 | 0 | 0 | 0 | 0 | 0 |

1 to 4 | - | - | - | - | - | - | |

1 | 5 | 124,284 | 64,290 | 29,997 | 29,997 | 11,460 | 10,000 |

6 | 124,285 | 64,331 | 29,977 | 29,977 | 11,460 | 10,000 | |

7 | 181,067 | 62,963 | 59,052 | 59,052 | 11,460 | 15,000 | |

2 | 8 | 176,008 | 56,242 | 59,883 | 59,883 | 5,920 | 15,000 |

9 | 153,093 | 38,848 | 57,123 | 57,123 | 5,320 | 15,000 | |

10 | 130,345 | 32,061 | 49,142 | 49,142 | 4,670 | 14,000 | |

11 | 111,935 | 27,885 | 42,025 | 42,025 | 4,050 | 11,000 | |

3 | 12 | 94,733 | 23,407 | 35,663 | 35,663 | 3,630 | 10,000 |

13 | 83,000 | 17,230 | 32,885 | 32,885 | 3,050 | 8,000 | |

14 | 74,300 | 0 | 37,150 | 37,150 | 2,590 | 6,000 | |

15 | 64,088 | 0 | 32,044 | 32,044 | 2,130 | 5,000 |

(c) Importantly, no changes were made to the table set out in Exhibit A.1.3: cl 3.4 of each of the deeds dated 11 December 2019 and 3 July 2020. There was no change to the MDQ for calculation of the Monthly Reservation Fee payable.

ASSESSABLE TOLLING RECEIPTS

73 The first issue is whether the Monthly Reservation Fees were amounts receivable in relation to the processing of petroleum as defined in s 24A of the PRRTA Act. That section provides:

For the purposes of this Act, a reference to assessable tolling receipts derived by a person in relation to a petroleum project is a reference to the consideration receivable by the person in relation to the processing of external petroleum, or internal petroleum, in relation to the project.

74 There was no dispute that the petroleum processed from the Kipper gas field was “internal petroleum”. The relevant petroleum project was the subject of a combination certificate issued pursuant to s 20 of the PRRTA Act which specified the production licences held by the GBJV and the KUJV and by a third 50/50 joint venture between BHP and the applicant (called the Blackback Joint Venture).

Submissions of the Parties

Applicant Submissions

75 The applicant submitted that the Monthly Reservation Fee amounts were not “assessable tolling receipts” because they were not consideration receivable in relation to the processing of petroleum. The applicant submitted that Monthly Reservation Fees were paid for the reservation of processing capacity.

76 The applicant relied upon the description of the Monthly Reservation Fees as a “reservation fee” as provided for in both the Original KGPA and the Restated KGPA. The applicant sought to rely on elements of the formula provided for in cl 22.3(a) for the calculation of the fee and, in particular, from the use of the term “UMDQ” which, as a daily quantity expressed in gigajoules, was said to be “a capacity concept, being the User’s Maximum Daily Quantity, and not a reference to or description of the volume of petroleum actually processed”.

77 The applicant contended that the Monthly Reservation Fee amount was calculated using a formula that was not referable to the quantity of petroleum processed. The Monthly Reservation Fee amount was payable before any processing was obliged to be undertaken and there was no refund of the Monthly Reservation Fees if processing did not occur.

78 The applicant submitted that the Monthly Reservation Fee was to be contrasted against the Monthly Processing Fee which was calculated by reference to actual quantities of condensate and LPG produced from processing and was payable during periods in which processing occurred.

Respondent Submissions

79 The respondent submitted that the Monthly Reservation Fee amounts were “assessable tolling receipts” receivable as consideration in relation to the processing of petroleum. The respondent contended that the phrase “in relation to” required that the payment be “in substance one for processing”, relying upon Esso Australia Resources Pty Ltd v Commissioner of Taxation [2011] FCAFC 154; (2011) 199 FCR 226 at [163] (Esso (Full Court)).

80 The respondent contended that the Monthly Reservation Fee amounts were “in substance” a payment for the processing of gas based on the integers in the formula for the calculation of the Monthly Reservation Fee. The GCRT integer was defined in cl 22.2(a) of the Original KGPA and the Restated KGPA. Clause 22.2 was headed “Processing Service Tariffs”. The heading was said to support his contention that fees calculated using the tariffs set out in cl 22.2 were fees for the processing of petroleum. The GCRT and UMDQ were both expressed by reference to a quantity of gas (expressed in gigajoules). As a factual matter, gas output was a function of petroleum processed. The Monthly Reservation Fee amounts were thus to be understood as amounts calculated by reference to quantities of gas to be processed.

81 The respondent submitted that describing the Monthly Reservation Fee as a fee to reserve capacity did not mean it was not a fee for gas processed. It was submitted that whether or not a User elects to utilise all of the Provider’s capacity to provide processing services, the relevant fee was still a fee for processing. The respondent sought to draw an analogy with a take or pay obligation like that the subject of the decision in Esso where, at first instance, Middleton J did not consider the obligation to pay to arise from a failure to take gas but, rather (at [496]–[497]) there was an obligation to pay at the outset for the gas taken in a particular year. The consideration for the gas taken in a particular year was thus a “certain sum no matter how much gas [was] in fact taken”.

82 The respondent submitted that commercially, the Monthly Reservation Fee ought to be regarded as a fee for processing petroleum into gas. It was submitted that if the Monthly Reservation Fee was not characterised as a fee receivable for processing petroleum into gas, there would be no monetary consideration passing in relation to the processing of petroleum which results in the production of gas in circumstances where the agreement is entitled a “gas processing agreement”. This was said to be a commercial nonsense.

83 The respondent submitted that the Monthly Reservation Fee amounts represented a prepayment for processing, assessable as soon as it was receivable. Reference was made to paragraphs [3.7]–[3.8] of the Explanatory Memorandum to the Petroleum Resource Rent Tax Assessment Amendment Bill 2011 (Cth), including example 3.1. Those paragraphs state:

[3.7] The PRRT is being extended to onshore projects and the North West Shelf project from 1 July 2012. The time from which assessable receipts can be derived for the North West Shelf project and onshore projects has been set at 1 July 2012 [Schedule 2, items 9 and 10]. This ensures that onshore projects are not taxed on receipts received prior to the PRRT applying onshore. When the look back starting base approach has been adopted certain assessable receipts can be derived prior to 1 July 2012.

[3.8] However, any prepayment of assessable receipts is taken to have been derived in the financial year in which the activity is undertaken [Schedule 2, item 13]. This ensures that payment of receipts received before 1 July 2012 for petroleum or marketable petroleum commodities not recovered or produced until after 1 July 2012 is assessable.

Example 3.1: Pre-payment of an assessable tolling receipt

Thorsouth Oil and Gas Limited operate the Whenrangy petroleum project. Thorsouth Oil and Gas Limited entered into a contract on 1 July 2011 with Haskicdoyle Gas Limited to process their gas through the Whenrangy petroleum project’s gas processing plant for the next five years. Haskicdoyle Gas Limited prepaid Thorsouth Oil and Gas $15 million on 1 July 2011 ($3 million per year) to undertake this toll processing. The proportion of the activity that was undertaken prior to 1 July 2012 will not generate an assessable tolling receipt for example, $3 million. The proportion of the activity undertaken after 1 July 2012 will generate an assessable tolling receipt when the tolling activity is undertaken of $3 million per year for the next four years.

84 That Bill was enacted as the Petroleum Resource Rent Tax Assessment Amendment Act 2012 (Cth) which in clause 13(1) of Schedule 2 provides:

For the purposes of applying section 31 of the Petroleum Resource Rent Tax Assessment Act 1987 to an onshore petroleum project or the North West Shelf project, treat any receipts:

(a) of a kind referred to in that section; and

(b) derived before 1 July 2012 in relation to activities undertaken in relation to the project on or after that day;

as having been derived in the financial year in which the activities are undertaken.

CHARACTER OF THE MONTHLY RESERVATION FEES

Construction of s 24A

85 In applying s 24A of the PRRTA Act to the Monthly Reservation Fee amounts, the following principles apply:

(1) The character of the Monthly Reservation Fee is to be determined by reference to its character in the hands of the recipient. This flows from the statutory language. What must be determined is whether the Monthly Reservation Fee amounts are consideration receivable in relation to processing.

(2) The phrase “in relation to” is to be construed in context. In the context of s 24A, the phrase is limited by the word “consideration”. Just as the use of the word “consideration” in s 24, in the context of sales, controlled the meaning and scope of the phrase “assessable petroleum receipts”, so too the word “consideration” controls the meaning and scope of the phrase “assessable tolling receipts” in s 24A, irrespective of whether the textual nexus is provided by the words “in relation to” or “for”: Woodside Energy Ltd v Commissioner of Taxation [2009] FCAFC 12; (2009) 174 FCR 91 at [62].

(3) Consideration in s 24A is not used in the sense of consideration moving from one party to another to make the contract binding. Adapting the statement of Dixon J in Archibald Howie Pty Ltd v Commissioner of Stamp Duties (NSW) [1948] HCA 28; (1948) 77 CLR 143 at 152, consideration in the context of s 24A looks to that which moves the processing of petroleum. The question is whether the Monthly Reservation Fee amounts were receivable as a quid pro quo for “processing”. The issue requires an examination of the connection between the Monthly Reservation Fee amounts receivable and the processing of petroleum: Esso at [495]; Esso (Full Court) at [200].

(4) It follows that not every payment required to be made under a contract entitled “gas processing agreement” is consideration receivable in relation to processing. In determining the character of the amount entitled to be received it is necessary to identify the source of the entitlement to the receipt.

(5) The word “processing” in s 24A is a reference to the performance of activities which are in the nature of “processing”. Section 2 defines “processing of internal petroleum” in inclusive terms as including the “stabilisation, transportation, storage or recovery of internal petroleum in relation to the project”. It is apparent from the statutory language that a receipt is not an assessable tolling receipt if it is not receivable as consideration for performance of an activity.

(6) Caution must be exercised in determining the character of a receipt by reference to an integer in the calculation of its quantum. It has long been established that the manner of calculation does not determine the character of the amount for taxation purposes: Glenboig Union Fireclay Co Ltd v Inland Revenue Commissioners (1922) 12 TC 427 at 464; Commissioner of Taxes (Vic) v Phillips [1936] HCA 11; (1936) 55 CLR 144 at 156; Commissioner of Taxation v Northumberland Developments (1995) 59 FCR 103 at 120.

86 The respondent’s reliance on the phrase “in substance” in Esso (Full Court) at [163] is not a substitute for the statutory language. As the Full Court’s reasoning demonstrates, the question of characterisation is to be drawn from a close analysis of the contractual basis for the receipt.

87 The applicant became entitled to the Monthly Reservation Fee in the relevant years pursuant to the terms of the Restated KGPA. It is the terms of that contract which must be considered.

Construction of the Restated KGPA

88 The respondent sought to draw inferences in relation to the character of the Monthly Reservation Fee from the terms of the proposals exchanged between the parties in the course of their negotiations leading up to the Original KGPA. In particular, the respondent sought to contend that the Monthly Reservation Fee had its origin in proposals for processing that were concerned with processing fees.

89 The Court does not accept the submission of the respondent that the character of the Monthly Reservation Fee can be determined by reference to the terms of proposals which were never agreed.

90 Nor does the Court accept the contention of the applicant that the character of the Monthly Reservation Fee must necessarily be the same under the Original KGPA as under the Restated KGPA, as explained further below.

91 Although termed a “gas processing agreement”, what was to be processed under the Restated KGPA was “petroleum”. The contract provided for a firm commitment basis for processing rather than processing as and when capacity was available. In other words, the Providers undertook to provide processing services for the production of gas up to a maximum reserved capacity, rather than providing those processing services as capacity became available.

92 As originally provided for in the Original KGPA, the Monthly Reservation Fee was essentially a fixed fee payable during each month when processing services were obliged to be performed. The MDQ concept recognised the capacity in the GBJV’s processing facilities that was being reserved for the processing of petroleum from the Kipper gas field. As a fixed sum, the Monthly Reservation Fee meant that the Users generally bore the risk that the Kipper development reserves of gas were less than expected, as reflected in the MDQ. What was less clear was who was to bear the risk if the facilities were not capable of processing, at all, the petroleum extracted from the Kipper gas field.

93 Having regard to the dispute that arose when processing did not commence on the Start Date in relation to Monthly Reservation Fee amounts that had been invoiced, it is apparent that notwithstanding the execution of the Original KGPA, the Providers and Users did not have a common understanding of what the Monthly Reservation Fee amounts were really for.

94 From its refusal to pay the Monthly Statements issued to it, it is inferred that the Users (and in particular, Santos) viewed the Monthly Reservation Fee as a fixed fee for processing services in fact provided (albeit irrespective of how much gas in fact resulted from the provision of those services). From its stance that the Monthly Statements were payable notwithstanding no petroleum from the Kipper gas field had been processed, it is inferred that the applicant regarded the Monthly Reservation Fee as a monthly fixed fee payable irrespective of whether gas processing services were in fact provided. So understood, the monthly fixed fee compensated the applicant for the fact that it had to dedicate processing capacity to processing Kipper gas when it could have used that processing capacity to process more valuable petroleum from other gas fields and for the fact that it needed to earn a return on the capital investment it had made to modify the processing facilities to process Kipper gas field petroleum with its higher levels of carbon dioxide.

95 The discovery of high mercury levels in the Kipper gas field petroleum changed the parties’ understanding of the project risks and the resulting delay to processing crystallised the lack of common understanding of the role and function of the Monthly Reservation Fee. Whatever the objective character of the Monthly Reservation Fee that may have been discerned from the terms of the Original KGPA, it was the Restated KGPA terms which reflected the agreement of the parties following the discovery of the high mercury levels and which reflected the agreed basis for the receipt and payment of the Monthly Reservation Fee. The character of the Monthly Reservation Fee is thus to be ascertained by reference to the terms of that amended and restated agreement in light of the objective circumstances known to the parties at the time of the restatement of the KGPA.

96 Under the terms of the Restated KGPA:

(a) Users were obliged to pay the Monthly Reservation Fee on and from the Start Date (1 October 2012).

(b) The quantum of the Monthly Reservation Fee was based on values described as UMDQ amounts set out in Exhibit A.1.3. The UMDQ values provided for in Exhibit A.1.3 were not the UMDQ values representing the capacity reserved pursuant to cl 8.1(b). Gas processing capacity was reserved for an allocation year by reference to maximum and minimum UMDQs specified in Exhibit A.1.1 and Exhibit A.1.2: cl 8.1(b).

(c) Providers were obliged to provide Processing Services from the Mercury Facilities Ready Date (which turned out to be 4 March 2017, nearly some five years after the Start Date).

(d) It was only from the Mercury Facilities Ready Date that Users could nominate the quantity of gas which the User required to be made available at the Delivery Point. The Users could nominate their desired output from processing up to a MDQ specified in Exhibit A.1.1 (not Exhibit A.1.3) and MDQ was open to adjustment within certain parameters (albeit not for the first 5 Allocation Years).

(e) Under the agreement it was petroleum that was to be processed and it was gas that was to be produced. The object of the gas processing services to be provided was to produce the output of gas requested by the User. Based on that requested output, the Providers made a petroleum nomination: cl 16.5. This was the amount of petroleum which the User was required to make available at the receipt point. In this way Providers determined the required petroleum input in order to produce the Users’ nominated gas output. The UMDQ in Exhibit A.1.1 was not a quantity of petroleum to be processed but a maximum quantity of output gas that could be requested.

(f) The UMDQ value set out in Exhibit A.1.3 (which was used to calculate the Monthly Reservation Fee) was not a daily quantity of output gas that could be requested in the year in which the Monthly Reservation Fee was paid. Nor as matters transpired, having regard to the 2019 and 2020 deeds, did the values in Exhibit A.1.3 represent a quantity of gas that could come to be requested in a future year. The UMDQ figures in Exhibit A.1.3 used to calculate the Monthly Reservation Fee was a fixed number that did not correlate to the quantity of gas to be produced or to the petroleum processing capacity in fact reserved.

(g) On and from the Mercury Facilities Ready Date, the Users were obliged to pay “Monthly Processing Fees” calculated by reference to the quantity of condensate and liquified petroleum in fact produced. The processing fee payable under cl 22.4 was not calculated by reference to the quantity of sales gas produced. The processing fees commenced on the Mercury Facilities Ready Date, at the same time as the Providers became obliged to provide processing services. The Monthly Processing Fee was a variable fee — it was not based on a fixed value but was calculated by reference to the quantity of some of the products actually produced from the raw petroleum.

97 Limited assistance is gained from the terms used to describe the integers in the formula for calculating the Monthly Reservation Fee amounts. The fact that the Monthly Reservation Fee is calculated by a formula that uses an integer that is described as a quantity of gas is not determinative of the character of the Monthly Reservation Fee particularly in circumstances where the quantity of gas is a fixed figure and is not a measure of the quantity of the petroleum in fact processed or the quantity of gas in fact produced.

98 Nor is assistance gained from the description of the Monthly Reservation Fee as a “reservation fee” rather than a “processing fee”. Parties cannot by a label determine the character of an amount: Radaich v Smith [1959] HCA 45; (1959) 101 CLR 209 at 214 (McTiernan J); Construction, Forestry, Maritime, Mining and Energy Union v Personnel Contracting Pty Ltd [2022] HCA 1; (2022) 275 CLR 165 at [184] (Gordon J). Affixing a label to the payment does not assist in ascertaining what the payment is for. That is a matter that is to be ascertained by reference to the contract terms. Nothing in the terms of the Original KGPA or the Restated KGPA provided that the Monthly Reservation Fee was for “capacity sterilised” any more than the payment in Esso was for “take or pay” obligations or entitlements.