FEDERAL COURT OF AUSTRALIA

Fair Work Ombudsman v Sushi Bay Pty Ltd (in liq) (No 2) [2024] FCA 76

ORDERS

DATE OF ORDER: | 14 February 2024 |

THE COURT ORDERS THAT:

1. Within 14 days, the Ombudsman file and serve a document setting out the declarations and orders reflecting the reasons for judgment.

2. If the fifth respondent, being the only active respondent, contends that any of the proposed declarations or orders does not reflect the reasons for judgment, by 13 March 2024 she identify the basis for her contention and provide supporting submissions limited to five (5) pages.

3. The matter be listed for case management of the remaining questions at 9:30am on 18 March 2024.

4. There be liberty to apply on two (2) days’ notice.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

KATZMANN J:

1 This is a case about the conduct of four companies (Sushi Bay Pty Ltd, Sushi Bay ACT Pty Ltd, Auskobay Pty Ltd and Auskoja Pty Ltd (the corporate respondents)) and one person, Ms Yi Jeong (also known as Rebecca) Shin (collectively the respondents), all of whom are said to have contravened the Fair Work Act 2009 (Cth) (FW Act) and the Fair Work Regulations 2009 (Cth) (FW Regulations) in numerous respects.

2 The corporate respondents are members of the Sushi Bay group of companies (Sushi Bay Group). At all relevant times they employed staff to run, and serve in, restaurants in New South Wales, the Australian Capital Territory and the Northern Territory. Ms Shin was the sole director and shareholder of each of the corporate respondents throughout that time. She was also their Chief Executive Officer.

3 The Fair Work Ombudsman alleges that the respondents contravened the FW Act and Regulations by paying some 163 employees (the Employees) below award rates; failing to pay annual leave or annual leave loading; unreasonably requiring employees to repay or refund money paid to them by the corporate respondents; making and keeping records which were false or misleading in a material particular; giving pay slips to employees which they knew to be false or misleading; and providing the Ombudsman or a Fair Work Inspector information or documents which they knew to be false or misleading. Some of the alleged contraventions are said to be “serious contraventions” within the meaning of the FW Act because they were committed knowingly and as part of a systematic pattern of conduct. The Employees represent about 73% of the corporate respondents’ workforce. Approximately 85% of them were temporary visa holders.

4 The contraventions are said to have occurred over a period of nearly four years, from 29 February 2016 to 26 January 2020 (the Contravention Period).

5 The Ombudsman seeks declaratory relief, orders requiring the corporate respondents to reimburse the affected employees (with interest), and pecuniary penalties. This judgment is concerned with liability only.

6 Separate defences were filed by the corporate respondents on the one hand and Ms Shin on the other. At the time the defences were filed, all respondents were represented by Hillard & Berry Solicitors.

7 Thousands of pages of evidence were filed and served by the Ombudsman. None of the respondents filed any evidence.

8 After the Ombudsman filed and served her evidence and the time for the respondents to file their evidence had expired, each of Sushi Bay, Sushi Bay ACT and Auskoja was wound up in insolvency and a liquidator appointed. Auskobay was wound up earlier, about two weeks before its evidence was due to be filed. After Auskobay was wound up, Hillard & Berry served notices of ceasing to act. The liquidator informed the Ombudsman that he did not intend to defend the proceeding or file any evidence and that he did not require any witnesses for cross-examination. On 1 June 2023, Wigney J granted the Ombudsman leave to proceed against the corporate respondents under s 471B of the Corporations Act 2001 (Cth): Fair Work Ombudsman v Sushi Bay Pty Ltd [2023] FCA 548.

9 On 31 May 2023, Ms Shin advised the Ombudsman that she did not intend to appear at the hearing. Accordingly, the hearing proceeded in the absence of all respondents. In considering whether the Ombudsman’s allegations have been made out, I have borne in mind that she carries the onus of satisfying the Court that the contraventions have been committed, that the allegations she makes are serious, and that findings against her will in all likelihood result in the imposition of civil penalties. For this reason, although she only needs to prove that the allegations are made out on the balance of probabilities, the necessary state of satisfaction should not be produced by “inexact proofs, indefinite testimony or indirect inferences”: Briginshaw v Briginshaw (1938) 60 CLR 336 at 362 (Dixon J). See, too, Evidence Act 1995 (Cth), s 140.

10 On the other hand, the fact that Ms Shin did not adduce evidence or make submissions is not without consequences.

11 Ms Shin had every opportunity to answer the Ombudsman’s allegations. If they were contestable, she could have filed evidence disputing some or all of the allegations and answering the Ombudsman’s evidence. She could have appeared by a lawyer or in person. A document entitled “Statement of facts and legal issues” filed on her behalf by her then lawyers, MathasLaw, and prepared by a principal of that firm, includes the following assertions. First, the reason she did not give evidence is a concern that she may make admissions that could be used against her in criminal proceedings as contemplated by s 554 of the FW Act, which provides that criminal proceedings may be commenced against a person for conduct that is substantially the same as conduct constituting a contravention of a civil remedy provision. Second, she cannot give evidence of this concern because in so doing she may be open to be cross-examined on other grounds and that reason is sufficient to displace a Jones v Dunkel inference that might otherwise be drawn against her.

12 Jones v Dunkel (1959) 101 CLR 298 is authority for several propositions. The first is that the unexplained failure of a party to give evidence or call witnesses may lead to an inference that the missing evidence or absent witness would not have assisted that party’s case (at 308 (Kitto J), 312 (Menzies J) and 321 (Windeyer J)). The second is that a court may take that circumstance into account in deciding whether to accept particular evidence that relates to a matter on which the absent witness could have spoken: Heydon JD, Cross on Evidence (12th ed, LexisNexis Butterworths, 2021) at [1215]. It does not matter that the party who could have called the evidence does not carry the onus of proof: O’Donnell v Reichard [1975] VR 916 at 921 (Gillard J); Steele v Mirror Newspapers Ltd [1974] 2 NSWLR 348 at 367 (Hutley JA). The third is that evidence the witness might have contradicted can be accepted more readily: Jones v Dunkel at 312 (Menzies J). And the fourth is that any inference favourable to the other party for which there is a foundation in the evidence can more comfortably be drawn: Jones v Dunkel at 308 (Kitto J); at 312 (Menzies J). While a Jones v Dunkel inference cannot fill gaps in the evidence and cannot convert conjecture or suspicion into inference, if the inference is drawn it can “weigh the scales, however slightly, in favour of the opposing party”: Adler v Australian Securities and Investments Commission [2003] NSWCA 131; 21 ACLC 1810; 46 ACSR 504; 179 FLR 1 at [649] (Giles JA, Mason P and Beazley JA agreeing at [1] and [2] respectively).

13 In his textbook, Cases and Materials on Evidence (Butterworths, 1975) at 62, Heydon observed:

[A] party’s failure to give any satisfactory explanation of a prima facie case against him may suggest that the case is sound, either because silence is assent – an implied admission, or because it shows a consciousness of guilt or liability, or because inferences from the prima facie case, being unchallenged, are thereby strengthened. The presumption is the stronger where the facts are particularly within his knowledge.

14 The fact that the proceedings are proceedings for a pecuniary penalty is not a satisfactory explanation: Australian Securities and Investments Commission v Adler [2002] NSWSC 171; 41 ACSR 72; 20 ACLC 576; 168 FLR 253 at [504] (Santow J); Adler at [664]–[669]. The proceedings are still civil proceedings. The Court is expressly charged with applying the rules of evidence for civil matters when hearing proceedings relating to a contravention of a civil remedy provision: FW Act, s 551.

15 It is not clear whether in the Statement Ms Shin was referring to any inference that may be drawn from her failure to give evidence, but I will proceed on the basis that she was.

16 There are difficulties with both her assertions she makes.

17 As to the first assertion a concern that she might make admissions that could be used against her in subsequent criminal proceedings is not a legitimate explanation: Cross on Evidence at [1215].

18 If, by the first assertion, Ms Shin is to be taken to have been invoking the privilege against self-incrimination, that can only be claimed by a witness and then only under oath or affirmation: Chong v CC Containers Pty Ltd (2015) 48 VR 402 at [236] (Redlich, Santamaria and Kyrou JJA). Besides, that is not an explanation sufficient to displace a Jones v Dunkel inference if it is otherwise available. As Hill J said in Australian Competition and Consumer Commission v Universal Music Australia Pty Ltd (2001) 115 FCR 442 at [33]:

Where the proceedings are criminal (and the present proceedings are not; they are proceedings, inter alia, for the recovery of a civil penalty) it might be thought that the failure of the accused to go into evidence should not lead to the drawing of Jones v Dunkel inferences. After all it is clear that a witness can not be compelled to give evidence which is likely to incriminate the witness or expose the witness to a penalty. However, even in criminal cases it has been held that the failure of the accused, who is in a position to deny, explain or answer the evidence adduced by the prosecution, to give evidence will permit the jury to draw inferences adverse to the accused more readily: see Azzopardi v The Queen (2001) 205 CLR 50; 179 ALR 349, affirming Weissensteiner v The Queen (1993) 178 CLR 217. A fortiori, therefore, the failure of a respondent to proceedings for recovery of a pecuniary penalty to give evidence on a matter relevant to an issue in the proceeding and deny, explain or answer the evidence adduced against the respondent will permit the Court more readily to draw the inferences to which the decision in Jones v Dunkel refers.

19 In any case, as Ms Shin acknowledged, s 555 of the FW Act would generally prevent the use in any subsequent criminal proceedings of any evidence she might give or documents she might produce in this proceeding where the conduct alleged to constitute the offence is substantially the same conduct. The only exception is where the criminal proceeding relates to the giving of false evidence in this proceeding.

20 The second assertion, it will be recalled, was that if Ms Shin were to give evidence on oath or affirmation about her concern, she would expose herself to the risk of cross-examination. That is obviously so. But fear of cross-examination is also an unsatisfactory explanation.

21 The Ombudsman read affidavits from nine witnesses. Three were members of the staff of the Office of the Fair Work Ombudsman. Those witnesses were Evan Richard Brownell, Investigator, Compliance and Enforcement and a former Fair Work Inspector (FWI) and Team Leader; Radha Kumbhari, a Calculations Team Officer in the Calculations Team; and FWI Yoomin Lee, the Compliance and Enforcement Branch. Four were former employees of Sushi Bay. From one of those employees, Yongho (also known as Phillip) Kim, was a long-time employee and a member of the corporate respondents’ management team from 2016 as Human Resources (HR) and Management Team Manager. The remaining two witnesses were interpreters who had translated certain affidavits.

22 Amongst other things, FWI Lee’s evidence detailed the respondents’ previous interactions with the Ombudsman, including an audit in 2009 of Sushi Bay, an audit in 2014 of Sushi Bay QLD Pty Ltd (another entity in the Sushi Bay Group), an audit in 2019 of Sushi Bay ACT, and an investigation in 2019 into the respondents. FWI Lee also deposed to a site visit to the corporate respondents’ head office in Eastwood, New South Wales (Head Office) and the Belconnen “store” or “branch” (restaurant) on 4 February 2020. A good deal of the documentary evidence upon which the Ombudsman relied was contained in a single exhibit to FWI Lee’s affidavit. The exhibit included company searches; correspondence with officers of the corporate respondents including Ms Shin; documents obtained by Fair Work inspectors on site visits to Sushi Bay entities; documents produced to the Ombudsman in response to notices to produce (NTP) issued to the corporate respondents; and documents produced by the Department of Home Affairs, MYOB (a business management platform) and St George Bank. Various Excel spreadsheets created by the corporate respondents were also exhibited to that affidavit.

23 Mr Brownell’s evidence related to the course of a 2016 investigation into Sushi Bay ACT and Ms Shin that led to proceedings in the Federal Circuit Court of Australia (FCCA) in 2017.

24 Ms Kumbhari calculated the amounts of the alleged underpayments.

25 Sushi Bay was incorporated on 29 September 2006. It has long been on the Ombudsman’s radar.

26 On 24 July 2009, the Ombudsman wrote to Ms Shin advising that Sushi Bay, trading as Robina Sushi Bay, had been selected for an audit of its time and wages records. To facilitate the audit, the Ombudsman requested that Ms Shin provide certain information, including time and wage records for each employee for the month of June 2009. Upon inspection of the records Ms Shin produced in response to that request, the Ombudsman determined that Sushi Bay had contravened the predecessor to the FW Act, the Workplace Relations Act 1996 (Cth), by underpaying hourly rates to three employees.

27 On 5 November 2009 the Ombudsman sent a “Determination of Contravention” letter to Ms Shin as the director of Sushi Bay outlining the findings from the audit and requiring Sushi Bay to rectify the contraventions by taking certain action, including reviewing the wage rates paid to all current and former staff and providing evidence of any “back payments”. The letter contained a warning that the Ombudsman might bring enforcement action, including litigation, against Sushi Bay to recover any outstanding amounts and obtain penalties against both the company and any individual involved in the contraventions.

28 On 26 November 2009, after receiving notification that the underpayments had been rectified, the Ombudsman wrote to Ms Shin advising that a decision had been made to take no further compliance action. That letter included the following advice:

To assist you to comply with current and future obligations, further information can be accessed at www.fwa.gov.au or by calling the Fair Work Infoline on 13 13 94.

IMPORTANT INFORMATION

From 1 January 2010 employers should be aware of changes to the national workplace relations system under the Fair Work Act 2009. From this date, the National Employment Standards (NES) and modern awards come into effect. The NES are a set of 10 minimum standards of employment, and apply to all employees in the national system, regardless of any industrial instrument or contract of employment.

In association with the NES, modern awards will make up a new safety net for employees. Modern awards will apply to employees based on particular industries or occupations. Employers should make sure they are aware of their rights and obligations under the Fair Work Act 2009 by contacting the Fair Work Infoline on 13 13 94, or visiting www.fairwork.gov.au.

(Original emphasis.)

29 Sushi Bay ACT was incorporated on 15 October 2012, Auskobay on 13 March 2012 and Auskoja on 9 September 2012.

30 In 2014, the Ombudsman conducted an audit of Sushi Bay Qld. On 13 November 2014, FWI Christine Polzin advised Ms Shin by email of the results of that audit, attaching a letter setting out the Ombudsman’s findings. On the same date infringement notices were sent to Sushi Bay Qld and each of the corporate respondents. In short, each of these companies was found to have failed to keep employee time and wage records before June/July 2014 and Sushi Bay Qld was found to have underpaid employees by paying below award rates in contravention of s 45 of the FW Act in that employees were incorrectly classified, paid below the prescribed hourly rates, not paid penalty rates for working weekends or public holidays, not paid annual leave loading, and not given the opportunity to negotiate part-time hours agreements. Each of the corporate respondents and Sushi Bay Qld were penalised $2,550 and Sushi Bay Qld was required to “rectify the contraventions”. The audit findings included detailed information about the Restaurant Industry Award 2010 (Restaurant Award or Award), the classification of employees under the Award and the minimum rates that should have been paid.

31 On 1 December 2014, Daniel Oh, Chief Operational Officer for the Sushi Bay Group, responded to the audit, attaching what he referred to as “the rectified wage conditions of employees in compliance with the [FW] Act”. The Ombudsman was dissatisfied with the response and on 2 December 2014 FWI Polzin emailed Mr Oh attaching a letter to “the Proper Officer” of Sushi Bay Qld pointing out numerous deficiencies in the response (“contraventions that remain outstanding”). Mr Oh replied on 31 December 2014 with evidence of payments made to current and former employees and new employment contracts for current part-time employees. But the Ombudsman remained concerned that several employees who began their employment at the introductory level were kept at that level for more than the maximum period of three months and that no pay slips were supplied. FWI Polzin wrote to Mr Oh and Ms Shin on 5 January 2015, referring to these matters, among other things, and insisting on receiving pay slips to confirm the rectification of the underpayments.

32 On 1 May 2015, the Ombudsman sent Ms Shin, in her capacity as director of Sushi Bay Qld, a “letter of caution” the express purpose of which was to encourage voluntary compliance and ensure that the activities of non-compliant employers were monitored “in the event of subsequent non-compliance”. The Ombudsman informed Ms Shin of her opinion that Sushi Bay Qld had contravened s 45 of the FW Act by failing to classify employees in accordance with Schedule B to the Restaurant Award; by failing to pay the prescribed hourly rates; by failing to pay employees the prescribed rates of pay for Saturday and Sunday work, or work performed on public holidays; by failing to pay employees annual leave loading on taken leave; and by failing to negotiate part-time hours agreements with employees engaged on a part-time basis. While she did not consider it was in the public interest to bring civil proceedings at this time, the Ombudsman warned Ms Shin that the fact that Sushi Bay Qld had already been issued with a letter of caution would be taken into account in deciding whether it would be in the public interest to commence proceedings if there were future contraventions.

33 In about February 2016 the Ombudsman started a “Fast Food and Restaurant Campaign” targeting employers in the ACT. As part of that campaign, she began investigating compliance with the FW Act by Sushi Bay ACT. In the course of that investigation FWI Michelle Reid served Sushi Bay ACT with a notice to produce under s 712 of the FW Act (April 2016 NTP). Documents were produced in response to the April 2016 NTP and various email exchanges ensued. Between May 2016 and April 2017 there was extensive correspondence between FWI Reid and Ms Shin. In June 2016, Ms Shin was invited to attend an interview with FWI Reid but she declined the invitation.

34 On 26 May 2017 FWI Reid wrote to Ms Shin informing her of the outcome of the investigation and the Ombudsman’s findings that Sushi Bay ACT had contravened various provisions of the FW Act (ss 44, 45, 90, 96, 323, 535), the FW Regulations (reg 3.33) and the Restaurant Award (cll 12, 13, 15, 20, 30.1, 34.1, 35.2) and foreshadowing enforcement action. Joseph Lee, Chief Administrative Officer for Sushi Bay ACT, replied on Ms Shin’s behalf, admitting the contraventions, although quibbling with some of the Ombudsman’s calculations. That reply included the following statements:

During the last two weeks of extensive review performed on the fourteen contraventions listed in the same email, we came to realize that Sushi Bay ACT Pty Ltd has made unintended breaches of a number of sections in Fair Work Act 2009 since we has had a poor understanding for details of the award so far. It is our sincere regret that our negligence has caused underpayment toward our employees’ hard work and effort. We value our employees more than any assets in our business and therefore we owe them our deepest apology. We consider it a serious matter and we have taken this time as an opportunity to educate the existing payroll team. Going forward, this issue will well be· documented internally to avoid it being repeated in the course of our future business.

35 With respect to remediation Mr Lee advised:

1. Hall staff will be categorized at least level 2 in Sushi Bay ACT Pty Ltd according to the definition of Food and Beverage attendant grade 2 (Level 2) ; noting that Level 1 does not include service to customers.

2. Kitchen staff with prior industry experience would at least be classified at the Kitchen Attendant Grade l (Level 1) according to the job description set out B.3.1 of the Award.

3. All employees categorized at Introductory Level would continue to be categorized at this level only for a maximum period of three months.

4. All employees working 38 hours or less in a week whose working hours vary from one week to another that their shifts is not reasonably predictable will be categorized as Casual according to sub-clause 12.6 and clause 13.

5. For all employees other than casual employees, all relevant leaves will accrue and be paid accordingly.

6. Leave loading of 17.5% will need to be paid in addition to the payment for annual leave.

Sushi Bay ACT Pty Ltd will at all times abide by the laws and regulations set forth by the authorities including Fair Work. In order for us to be fully knowledgeable however, we need the guidance of your good office on correctly computing for the underpayment amount of the 22 employees in the list.

36 On 28 June 2017, FWI Reid responded to Mr Lee, explaining why the Ombudsman’s calculations were correct.

37 On 23 October 2017, the Ombudsman advised Ms Shin that she intended to bring proceedings against Sushi Bay ACT and Ms Shin to seek rectification of underpayments, imposition of civil penalties and other orders. Proceedings of that nature were commenced in the FCCA on 3 November 2017 (the 2017 Proceedings).

38 On 28 June 2019, the FCCA made the following declarations and orders based on a statement of agreed facts:

THE COURT DECLARES THAT:

(1) The first respondent contravened the following civil remedy provisions of the Fair Work Act 2009 (Cth) (“the Act”):

(a) Section 44(1) by contravening the following provisions of the National Employment Standards contained in Part 2-2 of the Act;

(i) Failing to pay annual leave entitlements in accordance with section 90(2);

(ii) Failing to accrue paid personal/carers leave in accordance with section 96;

(b) Section 45 by contravening the following clauses of the Restaurant Industry Award 2010:

(i) Failing to pay adult minimum wages as required by clause 20;

(ii) Failing to pay junior minimum wages as required by clause 20.3;

(iii) Failing to pay casual loading as required by clause 13.1;

(iv) Failing to pay penalty rates as required by clause 34.1;

(v) Failing to make part-time agreements as required by clause 12.3; and

(c) Section 535(1) by failing to keep records of the kind prescribed by the Fair Work Regulations 2009 (Cth).

(2) The second respondent was involved in the first respondent’s contraventions as set out above, within the meaning of section 550 of the Act.

THE COURT ORDERS THAT:

(3) Pursuant to section 546(1) of the Act and within 42 days, the first respondent is to pay a pecuniary penalty of $103,680 in respect of the contraventions as set out above.

(4) Pursuant to section 546(1) of the Act and within 42 days the second respondent is to pay a pecuniary penalty of $20,736 in respect of her involvement (within the meaning of section 550 of the Act) in the first respondent’s contraventions as set out above.

(5) Pursuant section 545(1) of the Act, the first respondent will, within three months of the date of this order, provide for workplace relations compliance training (“training”) on the following terms:

(a) The first respondent must engage, at its own expense, a person or organisation with expertise in workplace relations, and approved by the applicant, to conduct the training;

(b) The training must relate to compliance with the Act and the Restaurant Award, including the first respondent’s obligations in respect of minimum wages, casual loading, penalty rates, personal leave and annual leave entitlements, part-time agreements and record-keeping;

(c) The training must be undertaken by:

(i) All persons employed or engaged by the first respondent whose duties relate to the management of employees, the administration of payroll, and the administration and compliance with Australian workplace laws; and

(ii) The second respondent.

(d) Within 30 days of completing the training, the first respondent must provide the applicant, in writing, with a report specifying the date(s) on which the training was completed, the details of the delivery and content of the training and the names and positions of all persons who undertook the training;

(6) Pursuant to section 545(1) of the Act, the first respondent will, at its own expense, engage a third party, or third parties, with appropriate qualifications in accounting and workplace relations to undertake an audit of the first respondent’s compliance with the Act and the Restaurant Award on the following terms:

(a) The audit period will be the first accounting quarter commencing after the making of the orders;

(b) The audit is to be completed within 30 days of the end of the audit period;

(c) The audit will apply to all employees employed by the first respondent at any time during the audit period;

(d) The audit will assess the first respondent’s compliance with the following obligations according to each employee’s classification of work, category of employment and hours worked during the audit period:

(i) Wages and work related entitlements under the Restaurant Award; and

(ii) Accrual and payment of entitlements under the National Employment Standards in Part 2-2 of the Act.

(e) Within 14 days of the audit being completed, the first respondent will rectify any contraventions identified in the audit;

(f) Within 30 days of the audit being completed, the first respondent will provide to the applicant:

(i) A copy of the audit report, which will include a statement of the methodology used in the audit;

(ii) A copy of the source materials used to audit the times worked by employees (including but not limited to rosters, time cards and time sheets) and the amounts paid to the employees (including but not limited to pay slips and pay reports);

(iii) Written details of any contraventions identified in the audit;

(iv) Evidence of rectification by the first respondent of any contraventions identified in the audit.

(7) The applicant has liberty to apply on seven days’ notice in the event that any of the preceding orders are not complied with.

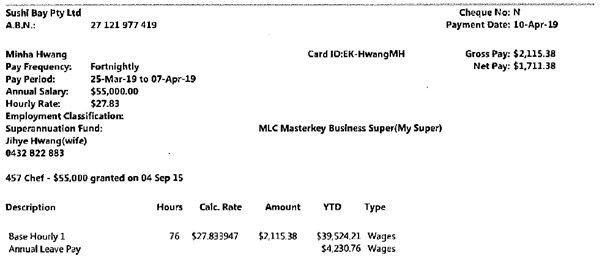

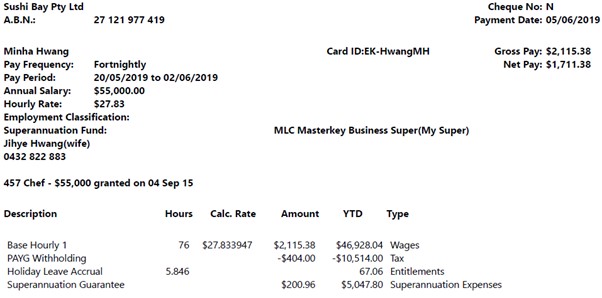

39 The following month the Ombudsman received requests for assistance from two former employees – Minha and Jihye Hwang – who claimed that they had failed to receive their proper entitlements, including overtime, weekend penalty rates, annual leave loading and superannuation.

40 The Ombudsman then began an investigation into their employment between 1 January 2014 to 31 July 2019 (the 2019 Investigation). In about August 2019, the 2019 Investigation was expanded to include other employees engaged by the other corporate respondents. As part of that investigation notices to produce were served and site visits were conducted at Sushi Bay restaurants and offices. One such notice was served on Sushi Bay on 29 August 2019 for records and documents relating to the employment of Mr and Mrs Hwang, including time and wage records (August 2019 NTP) to which Sushi Bay responded in September and October 2019.

41 On 17 October 2019, in accordance with the Training Order, Ms Shin, Sol Shin (Sushi Bay’s COO from 2017) and Mr Lee (among others) participated in a half day workplace relations training conducted by Australian Industry Group, which included training on the FW Act, National Employment Standards, the Restaurant Award (including classifications, minimum rates, allowances, penalty rates and overtime payable under the Restaurant Award), record keeping obligations, and “serious contraventions” under the FW Act.

42 On 3 November 2019, Kenneth Hong, principal of H & H Lawyers, emailed to the Office of the Ombudsman a number of documents relating to a “self-audit” conducted by UG Accountants for Sushi Bay ACT for the period 1 July to 6 October 2019 (Audit Period) in respect of eight Sushi Bay ACT employees (Audit Employees). Those documents included a report from the accountants, a document containing “recalculations” of the hourly rates and total hours worked by the Audit Employees during the Audit Period, and payroll advices purporting to record, amongst other things, the total number of hours worked by, and the gross and net amounts paid to, those employees in that period.

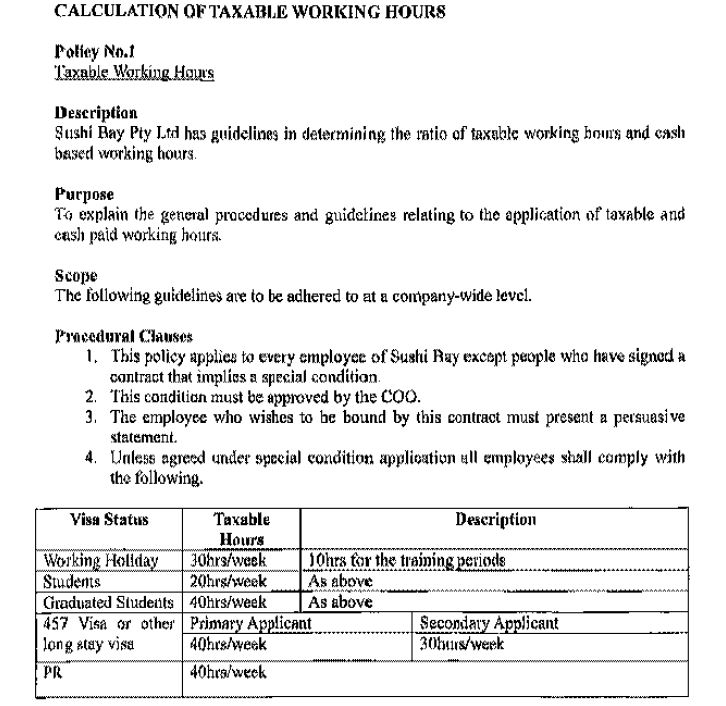

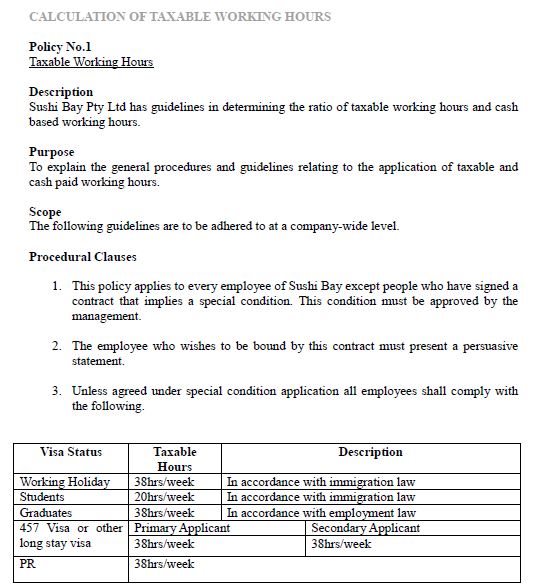

43 On 4 February 2020 a number of Fair Work inspectors conducted an unannounced site visit on the Sushi Bay Group Head Office and the Sushi Bay restaurant in Belconnen where they obtained a number of records.

44 On 24 April 2020, FWI Edward Skeels issued a NTP to MYOB requiring production of records or documents relating to any MYOB products used by the respondents to record the payment of wages to various employees during the period 1 June 2016 and 31 January 2020 (MYOB NTP). MYOB produced documents to the Ombudsman on 29 June 2020 (MYOB Records).

45 On 3 July 2020, FWI Skeels issued a NTP to St George Bank which required production of bank statements for all accounts held by the respondents during the period 1 March 2016 to 29 January 2020. The relevant documents were produced in July 2020.

46 On 6 October 2020, FWI Skeels issued a NTP to Sushi Bay which required production of payroll records and documents relating to the Ombudsman’s investigation into the respondents (October 2020 NTP). On 2 November 2020, Mr Simon Berry of Hilliard & Berry, sent emails to the Ombudsman attaching documents in response to the October 2020 NTP.

47 Based on the admissions, I make the following findings.

48 Each of the corporate respondents is a “constitutional corporation” and “national system employer” within the meaning of ss 12 and 14(1)(a) of the FW Act, respectively. They were part of the Sushi Bay Group that shared a common sole director and shareholder (Ms Shin) and were collectively managed out of the Head Office from which a centralised payroll system operated. The corporate respondents operated sushi restaurants in the following relevant locations: Belconnen, ACT; Darwin, NT; Carlingford, NSW; Campbelltown, NSW; Charlestown, NSW; Forster, NSW; Glendale, NSW; Liverpool, NSW; Merrylands, NSW; Miranda, NSW; Miranda Westfield, NSW; Parramatta, NSW; Penrith, NSW; Rouse Hill, NSW; Shellharbour, NSW and Wollongong, NSW (the Sushi Bay Restaurants).

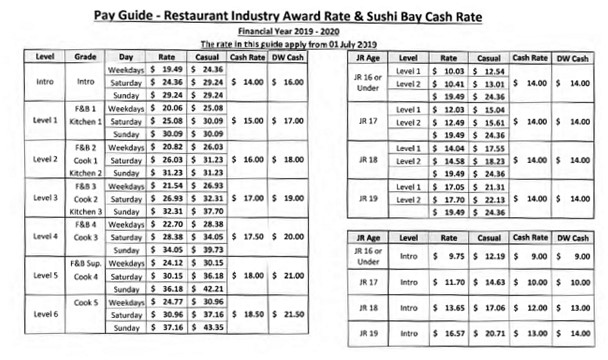

49 At the relevant times each of Sushi Bay and Auskoja was an “approved work sponsor” within the meaning of the Migration Act 1958 (Cth) and employed persons to work on Temporary Work (skilled) visas (subclass 457 visas) in the Sushi Bay Restaurants.

50 The corporate respondents held various bank accounts with St George Bank. Ms Shin was the sole signatory on those accounts.

51 At various times during the Contravention Period, Sushi Bay employed the 66 people listed in Table 1 in Annexure A to these reasons (Sushi Bay Employees):

(a) Mr Hwang from, relevantly, 29 February 2016 to 14 July 2019;

(b) Mrs Hwang from 29 February to 19 June 2016, and then from on or about 29 June 2017 to 9 September 2018;

(c) the 22 persons listed at lines 2 to 23 of Table 1 of Annexure A (Sushi Bay 457 Employees) at various times during the period 6 May 2019 to 26 January 2020 (457 Period); and

(d) the 42 persons listed at lines 25 to 66 of Table 1 of Annexure A (Sushi Bay Dual Rate Employees) at various times during the period 21 October 2019 to 26 January 2020.

52 At various times from 21 October 2019 to 26 January 2020, Sushi Bay ACT employed the 15 people listed in Table 2 in Annexure A (Sushi Bay ACT Employees). Each of these employees worked at the Belconnen restaurant and was employed for the period or periods set out in column B of Table 2 in Annexure A.

53 Auskobay employed the 46 people listed in Table 3 of Annexure A to these reasons (Auskobay Employees) during the following periods:

(a) Mrs Hwang from 20 June to 31 December 2016; and

(b) the 45 people listed at lines 2 to 46 in column A, Table 3 in Annexure A at various times during the period 21 October 2019 to 26 January 2020.

54 Each of the Auskobay Employees was engaged to perform work at the Sushi Bay restaurant locations set out in column C of Table 3 of Annexure A and was employed during the periods set out in column B.

55 At various times from 6 May 2019 to 26 January 2020, Auskoja employed the 37 persons listed in Table 4 of Annexure A (Auskoja Employees). They were:

(a) the three people listed at lines 1 to 3 in Table 4, who were each on 457 visas (Auskoja 457 Employees); and

(b) the 34 people listed at lines 4 to 37 in Table 4 (Auskoja Dual Rate Employees).

56 Each of the Auskoja Employees was engaged to perform work at the Sushi Bay restaurant locations set out in column C of Table 4 in Annexure A and were employed during the periods set out in column B.

57 The Restaurant Award applied to the employment of each of these Employees.

58 In September 2022, the affidavits of Phillip Kim, Minha and Jihye Hwang, and Kitae Kim were served on Simon Berry of Hilliard & Berry. At the hearing, I granted Phillip Kim a certificate under s 128 of the Evidence Act 1995 (Cth).

59 There is no reason why I should not accept any of this evidence. Apart from minor objections to certain paragraphs of the affidavits taken by Ms Shin, it was unchallenged. Moreover, much of the evidence is supported by the contemporaneous documents produced by the respondents in response to the Ombudsman’s notices to produce or obtained by the Ombudsman at site visits. Unless otherwise indicated, the narrative below is drawn from their affidavits.

60 Mr Kim was employed by Sushi Bay (and at times Sushi Bay ACT) from 8 May 2005 to 19 April 2020. He started work as a kitchen attendant in the Castle Hill restaurant and was later promoted to restaurant supervisor. In or about 2008, he was promoted, along with Mr Oh, to positions in the Sushi Bay Group’s management team. On some days he worked as a supervisor at the Castle Hill restaurant and on others he worked at the Sushi Bay Group Head Office in Eastwood.

61 From the middle of 2013, Mr Kim visited various restaurants to discuss operations, including hiring employees and staff complaints, with the relevant supervisors.

62 Mr Kim was appointed to the position of HR Manager in 2016. Even though he was employed by Sushi Bay, because the Group’s operations were managed by a centralised system he performed duties as HR Manager on behalf of a number of companies in the Sushi Bay Group. He reported to Sushi Bay’s COO who, in turn, reported to Ms Shin.

63 The corporate respondents admitted that Mr Kim was the person responsible for arranging and signing employment contracts on behalf of the corporate respondents; hiring, transferring or discussing pay and conditions with employees; and determining, in conjunction with the relevant restaurant managers, the status and classification of employees.

64 Around 11 March 2020, Mr Kim accepted an offer of voluntary redundancy made by Ms Shin. His last day of work was 19 April 2020.

The other members of the management team

65 Daniel Oh was employed by Sushi Bay as COO from about 2005 until at least July 2017 and was responsible for arranging and signing employment contacts on behalf of the corporate respondents. Mr Oh had prior experience operating a Japanese restaurant and working in an immigration lawyer’s office such that he was aware of Australian labour and immigration laws. From about 2016, Mr Kim reported to Mr Oh who in turn reported directly to Ms Shin .

66 Joseph Lee was employed by Sushi Bay as Chief Administrative Officer from early 2017. He was authorised to direct the payroll team in the performance of their duties on behalf of each of the corporate respondents.

67 Sol Shin was employed by Sushi Bay as COO from about 2017. He was also the sole director of Auskosu Pty Ltd, another entity in the Sushi Bay group, and Ms Shin’s son. He reported directly to his mother. From time to time, Mr Kim would seek direction from Mr Shin in relation to the Operational Guidelines (discussed below), visa sponsorship procedures, contract forms and matters regarding specific employees.

68 Mr Hwang first came to Australia in 2010 on a “working holiday visa”. In March 2014 he obtained a student visa which continued until about July 2015. During this time he studied business at a private educational college.

69 In early March 2014 Mr Hwang started working for Sushi Bay at the restaurant in Liverpool as a kitchen hand and cook. In about October or early November 2014, Mr Hwang was transferred to work at the Rouse Hill restaurant. He returned to the Liverpool restaurant in early 2015 and worked there until about early 2016.

70 The evidence indicates that Mr Hwang signed two employment contracts. One, which I infer was the first in time, is undated. Amongst other things, it stated that he was employed in the position of “cook”, described his duties and hours of work, acknowledged that he was employed subject to the terms of the Restaurant Award, and represented that he would be paid in accordance with the Award.

71 In early 2015, Phillip Kim and Daniel Hwang (another member of the management team) visited the Liverpool restaurant and asked Mr Hwang whether he was interested in Sushi Bay sponsoring him for a Temporary Work (Skilled) (subclass 457) visa (457 visa).

72 On 24 July 2015, Mr Hwang signed a new employment contract which “replace[d] and supersede[d]” the first. Amongst other things, it stated that the agreement had to be read in conjunction with the Restaurant Award which also applied to his employment contract, described his position as “chef”; provided that his ordinary hours of work would be an average of 38 per week plus “reasonable overtime as required” for which (absent any “Award flexibility agreement”) he would be paid in accordance with the Award; and stipulated that he would receive a base salary of $55,000 a year which would be paid by electronic funds transfer (EFT). Nevertheless, he was told by one of the managers that he was expected to work around 50-55 hours a week and that he would be paid according to Sushi Bay’s “internal policy”. He was told that it would be difficult for him to get overtime pay or take sick leave but that it would be possible for him to take annual leave.

73 The second employment contract also provided that Mr Hwang’s employment was subject to the condition that he held a valid visa, which allowed him to be employed under the terms and conditions in that contract, and that Sushi Bay agreed to support his application for the grant of a 457 visa. Importantly, it stated that Sushi Bay “also agrees to give all undertakings imposed under the Migration Act 1958 and Migration Regulations 1994 in connection with the sponsorship”. The contract was expressed to take effect upon the grant of the 457 visa and to last four years from the commencement of employment unless otherwise terminated in accordance with the contract.

74 Around 4 September 2015, Mr Hwang was emailed a copy of a letter from the Department of Immigration and Border Protection notifying him that he had been granted a 457 visa. Mrs Hwang was included on his visa application as his dependant.

75 Sushi Bay arranged for Mr Hwang to obtain a Certificate III in Asian Cookery and a Diploma in Hospitality Management.

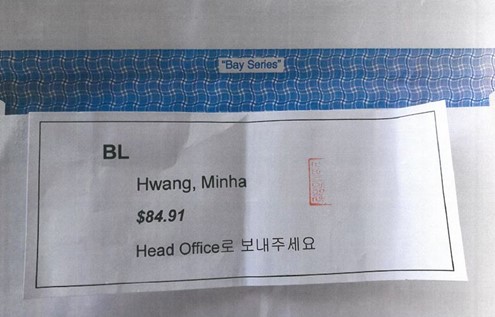

76 Around February 2016 a manager told Mr Hwang that he would be transferred to the Campbelltown restaurant. He worked there from about 8 February 2016 until August 2018. In about February 2017, Phillip Kim informed him that he was going to be appointed as a “key person”. As a result of the appointment he became second-in-charge at the Campbelltown restaurant and was responsible for supporting the restaurant supervisor and training staff, in addition to his duties as a chef. In about September 2018, he was transferred to the Belconnen restaurant to be that restaurant’s supervisor.

77 Mr Hwang resigned from his position with Sushi Bay on 14 July 2019.

78 Mrs Hwang first came to Australia in about November 2013 on a “working holiday” visa. She started working for Sushi Bay on a full-time basis on about 1 October 2014. She worked at the Campbelltown restaurant in the kitchen and on the floor, greeting customers and taking orders.

79 About one month after Mrs Hwang started working at the Campbelltown restaurant, she signed an employment contract that stated she was to be employed as a cook, that her ordinary hours of work would be an average of 38 hours per week and that she would be paid, by EFT, an amount “as per applicable industry award”.

80 In or about August 2015, Mrs Hwang asked to be transferred to a different restaurant and in or about September 2015 she was transferred the Merrylands restaurant. While working at the Merrylands restaurant she received pay slips from Auskobay.

81 From about 31 December 2016 to 29 June 2017 she was absent from work for health reasons. She returned to work for Sushi Bay at the Rouse Hill restaurant. She was later transferred to work at various Sushi Bay restaurants in Parramatta.

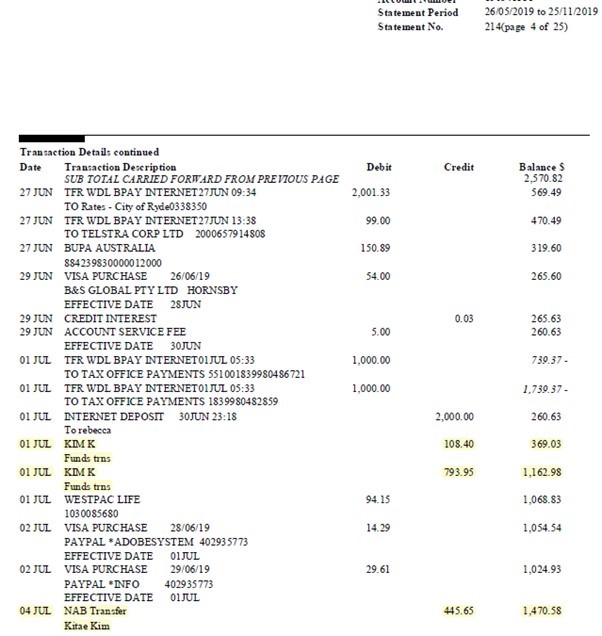

82 In about September 2018 Mrs Hwang resigned from the employ of Sushi Bay.

83 Mr Kitae Kim first came to Australia on a “working holiday” visa in around August 2012. About a month later he started working at the Parramatta restaurant and in October 2012 he transferred to the new Merrylands restaurant. He flew home in around July 2013 to finish his university studies and returned to Australia in late February 2016 on a student visa. He resumed employment with Sushi Bay in mid-April 2016 at the Campbelltown restaurant. While working at the Campbelltown restaurant he also worked occasionally at other Sushi Bay restaurants. In around August 2017, Sushi Bay sponsored him for a 457 visa.

84 In mid-April 2018 Mr Kim was transferred to Darwin. He began work at the Darwin restaurant on 23 April 2018. At first he worked as a cook but was later promoted to the position of “supervisor”. He began working as a supervisor on about 12 August 2019, although he signed his “supervisor contract” some eight days later. As a supervisor his responsibilities included supervising kitchen and floor staff; preparing rosters; overseeing food preparation; ordering stock; interviewing and training new staff; seeking approval from Head Office in relation to upgrading staff levels; processing staff leave requests and resignations; paying supplier invoices from cash sales; overseeing hygiene; and assessing employees to “level up”, that is to say to prepare for being assessed for a new level. He resigned on 18 July 2020.

Knowledge of the Restaurant Award

85 From at least 13 November 2014, when Ms Shin received the email from FWI Polzin, she was aware that the Restaurant Award applied to the corporate respondents and to employees working in the Sushi Bay Restaurants. She knew that the Award prescribed minimum rates of pay. She also knew that pay rates depended on the classifications of the employees. And she knew that different, higher, rates applied for working on weekends and public holidays, that an annual leave loading applied to all periods of taken annual leave and accrued annual leave untaken at the end of employment, and that accrued untaken annual leave must be paid out when the employment ceases.

86 From at least 2014, Phillip Kim was also aware that the Restaurant Award prescribed minimum wages, casual rates, weekend and public holiday penalties, and overtime rates. Like Ms Shin, he certainly knew about these things after the Ombudsman began investigating Sushi Bay Qld. Around late 2014 to early 2015, Mr Kim helped Mr Oh prepare responses to the Ombudsman inquiries about records kept by that company.

87 During his time at Sushi Bay, Mr Kim learned that some of the hours worked by some employees were not paid in accordance with the Restaurant Award. He deposed that he did not raise this with restaurant managers or other employees because “that was decided by the CEO and [he] was in no position to give an explanation”.

88 Mr Kim undertook training on Australian employment laws and the Restaurant Award. In or around 2017 or 2018, he attended a seminar conducted by the Ombudsman about modern awards, and “allowances” for sick leave and annual leave. Ms Shin and Mr Lee also attended. On 17 October 2019 Mr Kim attended internal training arranged at Head Office conducted by the Australian Industry Group. That training covered many subjects including awards, penalty rates, sick leave, annual leave and holiday (presumably public holiday) leave.

THE RECORD-KEEPING AND PAYROLL SYSTEM

89 The Ombudsman alleged that the contraventions arose out of two features of the operation of the Sushi Bay Group’s centralised payroll system.

90 The first feature was called the “Dual Rate Method”. By this method the Ombudsman claimed that certain employees were paid for a set number of “contracted hours” per fortnight in accordance with rates which were compliant with the Restaurant Award but that any additional hours worked were paid in cash at rates below the Award rates. Those employees were Mrs Hwang, the Sushi Bay Dual Rate Employees, the Sushi Bay ACT Employees, the Auskobay Employees and the Auskoja Dual Rate Employees (collectively, the Dual Rate Employees).

91 The second feature was called the “Deduction Method”. It was applied to the calculation of wages paid to sponsored employees of Sushi Bay and Auskoja on subclass 457 visas (the 457 Employees). The Ombudsman alleged that these employees were paid a gross fortnightly salary consistent with their employment contract but were required to pay particular amounts back to their employer during some fortnights.

92 The Ombudsman submitted that the apparent object of the system was to conceal from the relevant authorities that employees were paid below the minimum rates and entitlements prescribed by the Restaurant Award and, in many cases, were working more hours than their visa conditions permitted.

93 In their defences, the corporate respondents largely admitted that the Dual Rate Method and Deduction Method were features of its payroll system. The affidavits of Phillip Kim, Mr and Mrs Hwang and Kitae Kim explain how the Sushi Bay Group’s record-keeping and payroll system operated. I make the following findings based on their evidence, the admissions made by the corporate respondents and the documents obtained from them by the Ombudsman and tendered in evidence.

94 The Sushi Bay Group employed a payroll team which operated out of Head Office. The team generally consisted of about eight or nine staff members who reported to, and were directed by, Joseph Lee. When Phillip Kim became HR Manager, he began working more closely with the payroll team.

95 The payroll team processed the fortnightly payroll for each of the companies in the Sushi Bay Group. Their work included generating pay slips and emailing them to employees, paying employees by EFT, and paying and collecting cash from employees.

96 From time to time, the payroll team asked Mr Kim to give them instructions about how specific employees should be paid. The instructions covered such subjects as the appropriate rate to pay an employee, the correct ratio of “taxable wages” and “cash wages” (see Dual Rate Method below), and whether an employee was subject to deductions (see Deduction Method below). On other occasions, Mr Kim directed the payroll team based on requests from other members of the management team. Mr Kim would only issue such directions after he had obtained approval from the COO and Ms Shin or other relevant members of the management team. He did not otherwise have authority to issue directions to the payroll team.

97 The payroll system was operated from Head Office. The corporate respondents determined and recorded the following matters with respect to each of the Employees: their status and purported classification under the Restaurant Award in an Excel spreadsheet (Classification Document); a standard number of hours per fortnight (Award Hours) for which they were paid the hourly rate prescribed by the Restaurant Award for their designated classification, including any applicable minimum rates, Saturday rates, Sunday rates, public holiday rates and casual loadings (Award Rates); and an hourly rate, referred to as the “Sushi Bay Cash Rate” of between $14 to $18.50 (Base Cash Rate), which was the base rate to be paid for hours that each employee worked in excess of the Award Hours in a fortnight (Cash Hours). While the corporate respondents disputed this, I find (as Ms Shin admitted) that the Base Cash Rates applicable to the Employees during the relevant periods are those set out in column H of Tables 1 to 4 in Annexure A of the Ombudsman’s pleadings.

98 In relation to those Employees who held student visas or were engaged on a part-time basis, the Award Hours were 40 hours per fortnight, including up to six hours a week for Saturday work and six hours a week for Sunday work. In relation to all other Employees, the Award Hours were 76 hours per fortnight, including up to six hours a week for Saturday work and six hours a week for Sunday work.

99 Every fortnight, the managers of each of the Sushi Bay Restaurants prepared and signed records of the days and hours worked by each of the Employees during that fortnight and faxed them to Head Office. The payroll team would then create an Excel spreadsheet for each fortnightly pay period for each corporate respondent (Total Hours Worked Spreadsheets) on which they recorded the names of the Employees who worked that fortnight; the actual hours worked in each week of the fortnight and on each day, derived from the records kept by the relevant restaurant; the prescribed number of Award Hours for the fortnight; and the way in which the actual hours worked were to be apportioned and therefore paid as Award Hours and Cash Hours per week, including which of those hours were worked on a Saturday, Sunday and public holiday.

100 The Total Hours Worked Spreadsheets and the Classification Document were obtained following the Ombudsman’s visit to Head Office in February 2020.

101 The effect of the admissions of the corporate respondents is that the Total Hours Worked Spreadsheets accurately record the hours worked by the Employees as well as the proportion of those hours that were “taxable hours” paid by EFT and those that were “cash hours”.

102 The payroll team prepared the Total Hours Worked Spreadsheets using records prepared by restaurant supervisors that were sent to Head Office. These records included fortnightly rosters; timesheets recording the hours and days worked by employees over a fortnightly period; and records of the cash wages received from Head Office by employees of the particular restaurant.

103 In mid-2013 Sushi Bay developed “Operational Guidelines” (2013 Operational Guidelines). The evidence indicates that they were prepared by Daniel Oh and updated by him in 2017 (2017 Operational Guidelines). Mr Oh provided training about different policies in the Operational Guidelines at regular monthly meetings called “Key Person Incentive Program” (KPIP) meetings. KPIP meetings took place at Head Office. They were attended by restaurant supervisors and the management team. Mr Hwang also attended approximately six or seven KPIP meetings while working as the supervisor of the Belconnen restaurant. On the occasions he attended he recalled “Head Office managers” discussing, amongst other topics, sales targets, customers service issues and hiring.

104 Phillip Kim attended several “Head Managers’ meetings” with Ms Shin during which the 2017 Operational Guidelines were discussed and in which Ms Shin directed the management team to inform restaurant supervisors that they should be followed. As supervisor of the Darwin restaurant, Kitae Kim was told to familiarise himself with the Operational Guidelines.

105 In or about June 2013 the corporate respondents codified the distinction between Award Hours and Cash Hours in the Operational Guidelines in a policy called “Calculation of Taxable Working Hours” (Working Hours Policy). While the corporate respondents made no such admission, their own records demonstrate as much.

106 The table at the bottom of the Working Hours Policy set out the visa status of an employee and the number of “taxable hours” an employee holding that visa could work. An employee’s “taxable hours” were paid at the rate set out in the Restaurant Award. If an employee worked more than their “taxable hours”, the additional hours were to be paid at the Base Cash Rate, which was invariably below the Award Rates.

107 This is the version of the policy which appeared in the 2013 Operational Guidelines:

108 This is the version in the 2017 Operational Guidelines:

109 “Working holiday” visa holders were usually full-time employees. “Students” were part-time or casual employees. “Graduated Students” or “graduates” were full-time employees. Employees who held 457 visas or had obtained permanent residency were also full-time employees.

110 The Ombudsman alleged that, from at least November 2015, the corporate respondents made and kept a pay guide which prescribed the applicable Award Rates to be paid for Award Hours and the Base Cash Rates payable for Cash Hours (SOC/ASOC [25]). The corporate respondents denied the allegation (Defence [23]). But the evidence (including their own records) belies the denial. On the basis of the evidence I make the following findings.

111 The rates which all employees of the Sushi Bay Group were paid were set out in a document entitled “Pay Guide – Restaurant Industry Award Rate & Sushi Bay Cash Rate”. The payroll department was required to apply the rates set out in the Pay Guide.

112 This is an example of a Pay Guide, prepared by Phillip Kim for the 2019–2020 financial year that was obtained during the unannounced site visit to Head Office in February 2020:

113 The legal hourly rates for the “taxable hours” worked appear under the column headed “Rate” and lower hourly rates under the column headed “Cash Rates” and “DW Cash” (for employees in Darwin). The lower cash hourly rates were paid for overtime hours.

114 The system of paying employees for overtime hours (at lower rates and in cash) was in place before Phillip Kim started working for Sushi Bay.

115 From around November 2015, Phillip Kim was responsible for preparing and updating the Pay Guide. The rates were based on the minimum hourly rates under the Restaurant Award. When the Ombudsman announced increases in minimum rates, Mr Kim, the COO and other managers working at the Head Office would discuss the appropriate increase in the “taxable rates” and “cash rates” at a management team meeting. A draft Pay Guide was then presented to Ms Shin for her approval.

116 On these occasions the COO would confirm that the rates were based on the rates in the Restaurant Award. Ms Shin would then approve the draft or direct that a number in the guide be changed. Once approved, Mr Kim would communicate the new rates to restaurant managers who would then announce the increase to employees. Mr Lee would share the Pay Guide with the payroll team.

117 During the periods of employment set out in Annexure A, each of the relevant corporate respondents paid the respective Dual Rate Employees according to the Dual Rate Method. That is to say, in respect of the Award Hours, the Dual Rate Employees were paid at Award Rates and in respect of any Cash Hours worked during each fortnight at Cash Rates. As recorded in the Total Hours Worked Spreadsheets, the Dual Rate Employees were paid:

(a) at their Base Cash Rate for any Cash Hours worked Monday to Friday;

(b) at 125% of their Base Cash Rate for any Cash Hours worked Saturdays;

(c) at 150% of their Base Cash Rate for any Cash Hours worked Sundays; and

(d) at 200% of their Base Cash Rate for any Cash Hours worked on public holidays,

(collectively, Cash Rates).

118 From time to time during their employment, 33 of the Dual Rate Employees were paid for all hours worked in certain periods at the Cash Rates, as indicated in the table below:

Name | Cash Rate Period |

Sushi Bay | |

Yujeong Bae | 20/01/2020 to 26/01/2020 |

Keonwoo Baek | 18/11/2019 to 01/12/2019 |

Donggeun Choi | 11/11/2019 to 17/11/19 |

Solie Choi | 11/11/2019 to 16/112020 |

Jihye Hwang | 29/06/2017 to 17/07/2017 |

Geonwoo Kim | 06/01/2020 to 12/01/2020 |

Jisu Lee | 13/01/2020 to 26/01/2020 |

Pyeonghwa Lee | 06/01/2020 to 12/01/2020 |

Yeeun Lee | 06/01/2020 to 12/01/2020 |

Capa Lileth | 04/11/2019 to 17/11/2019 |

Jihyeok Park | 06/01/2020 to 12/01/2020 |

Ga Hee Son | 25/11/2019 to 15/12/2019 |

Sushi Bay ACT | |

Yeji Hong | 25/11/2019 to 01/12/2019 |

Hyemin Hwang | 21/10/2019 to 17/11/2019 |

Taewook Kang | 25/11/2019 to 01/12/2019 |

Bokyung Lee | 28/10/2019 to 03/11/2019 |

Auskobay | |

Juhwan Maeng | 06/01/2020 to 12/01/2020 |

Seongjin Cheon | 21/12/2019 to 27/12/2019 |

Yeonju Jang | 11/11/2019 to 17/11/2019 |

Deokryeong Jeong | 06/01/2020 to 12/01/2020 |

Heejoon Jo | 06/01/2020 to 12/01/2020 |

Minkyu Jo | 06/01/2020 to 12/01/2020 |

Chulmin Kim | 06/01/2020 to 12/01/2020 |

Geumjong Kim | 11/11/2019 to 24/11/2020 |

Kiryang Kim | 30/12/2020 to 12/01/2020 |

Kyoungsuo Kim | 11/11/2019 to 17/11/2019 |

Hyebeen Rim (Lim) | 06/01/2020 to 12/01/2020 |

Seongho Shin | 06/01/2020 to 12/01/2020 |

Auskoja | |

Nahyun Choi | 20/01/2020 to 26/01/2020 |

Dareum Jang | 25/11/2019 to 01/11/2020 |

Kyounghee Jang | 06/01/2020 to 12/01/2020 |

Minjong Lee | 11/11/2019 to 18/11/2019 |

Jinjoo Park | 6/01/2020 to 26/01/2020 |

119 Each fortnight the payroll team paid the Dual Rate Employees on behalf of their respective employing corporate respondent by:

(a) using the hours set out in the Total Hours Worked Spreadsheets to calculate the gross amounts payable to each Dual Rate Employee for their Award Hours by applying the relevant Award Rates;

(b) calculating the withholding tax and net amount to be paid to each Dual Rate Employee by EFT in respect of the Award Hours;

(c) arranging for payment by EFT to each Dual Rate Employee of the net amounts for the Award Hours and the applicable tax amount to be withheld;

(d) using the hours set out in the Total Hours Worked Spreadsheets to calculate the amount payable to each Employee for the Cash Hours worked, by applying the relevant Cash Rates; and

(e) creating, in Sushi Bay’s MYOB payroll account, a record for each pay period of the Award Hours and amounts paid in respect of those hours, which generated the following records of the Award Hours, the Award Rates and the gross and net amounts paid in respect of the Award Hours:

(i) “Payroll Activity [Detail]” records;

(ii) “Payroll Activity [Summary]” spreadsheets;

(iii) “Payroll Advice” records; and

(iv) from time to time, pay slips in respect of the Dual Rate Employees.

120 The only matter not admitted by the corporate respondents was the Ombudsman’s allegation (made in [31](e) of the SOC/ASOC) that the payroll team facilitated cash payments to the Dual Rate Employees by sending faxes to the Sushi Bay Restaurants requiring managers to pay certain specified employees in cash or by sending cash in particular denominations to Sushi Bay Restaurants to be paid to specified employees. But the affidavits of Mr and Mrs Hwang and Kitae Kim support the allegation. On the basis of their uncontested evidence, I find the allegation proved and make the following additional findings.

121 Mr Hwang was paid partly by EFT and partly in cash. Most fortnights, Sushi Bay would pay the same amount (reflecting his “taxable hours”) into his bank account. The amount of cash wages he received varied depending on the number of “cash hours” he worked.

122 Each fortnight a courier delivered envelopes from Head Office to the restaurant he was working at (Campbelltown and then Belconnen). The envelopes were addressed to individual employees and contained, amongst other things, cash wages and paper slips (relevant to the Deduction Method). While working as a supervisor at the Belconnen restaurant, he was responsible for distributing the envelopes to employees. He would ask employees to sign a paper record to confirm the cash amount they received.

123 Each fortnight, Mr Hwang would prepare a document which recorded the total hours worked by employees on weekdays, Saturdays and Sundays. Mr Hwang prepared these records by referring to “employee timesheets” that were completed by employees at the end of each shift. They recorded the hours the employees worked that day. Mr Hwang would then send a copy of the record, along with the employee timesheets, to Head Office with the courier who came to deliver the envelopes containing the cash payments. When he worked at the Campbelltown restaurant, Mr Hwang saw his supervisors carry out the same process. A similar practice was followed in the Darwin restaurant when Kitae Kim was the supervisor there, although he would fax the records to Head Office.

124 At the end of each day of work, Mrs Hwang was required to record on paper her start and finish times. Every fortnight when she was working at the Campbelltown restaurant, the paper records of working hours were sent to Head Office by fax and the originals were delivered to Head Office by the courier Sushi Bay used to deliver envelopes containing cash and other documents. While working at the Merrylands, Rouse Hill and Parramatta restaurants she observed this same process.

125 Every fortnight, on a Thursday or Friday when she was rostered for work, Mrs Hwang saw a person deliver items in a plastic bag to the restaurant supervisor, sometimes along with other documents. At times, Mrs Hwang was the person who accepted delivery of the bag, which she then deposited in the safe. When Mrs Hwang looked into the bag she noticed that it contained envelopes with employees’ names written on them, some of which contained cash.

126 Each fortnight Mrs Hwang generally received part of her pay directly into her bank account and part in cash. The amount paid into her bank account was usually the same amount recorded on the pay slips she received. She understood that the hourly Cash Rates she was paid were lower than the rates recorded on her pay slip and below the minimum Award Rates.

127 As a supervisor, Kitae Kim was responsible for distributing cash payments to employees. Each fortnight he was instructed by the payroll team at Head Office to pay certain employees their “cash wages”. He received his instructions by faxes which identified the relevant employees and the cash wage amounts. He made the cash payments from cash derived from “branch cash sales”, which was kept in the safe at the restaurant. He put the relevant amount of cash for each individual employee in an envelope and handed the envelopes to the employees at the end of their shifts. He required employees who received cash envelopes to count the cash in their envelopes and sign a logbook to verify the amount of cash they received. When he did not have enough cash from sales to pay employees, he was instructed by someone from the payroll team to tell those employees that they would receive their cash wages in a few days.

128 The Sushi Bay Group had a policy that required the 457 Employees to pay cash back to Head Office during some pay periods, depending on the number of hours they worked. The policy appears to have been developed by Daniel Oh in consultation with Ms Shin and was ultimately approved by Ms Shin.

129 Each fortnight, one or more of the payroll team, on behalf of the relevant employing corporate respondent, calculated payments to the 457 Employees and caused them to be paid using the following method:

(a) paying the 457 Employees a gross fortnightly salary consistent with their employment contracts (including additional amounts for leave loadings during periods of annual leave) (457 Gross Salary) by paying the net component by EFT to each 457 Employee, and withholding the relevant taxation component;

(b) calculating and recording in Excel spreadsheets (Deduction Spreadsheets) the following:

(i) the 457 Gross Salary;

(ii) amounts referred to as “Actual 457 Gross”, which were generally the amounts the 457 Employees would have been entitled to receive for their Award Hours at the Award Rates (by applying the Award Rates to the Award Hours recorded in the Total Hours Worked Spreadsheets) (Actual Gross);

(iii) the differences between the 457 Gross Salary and the Actual Gross (the 457 Gross Salary minus the Actual Gross) paid to each 457 Employee (457 Difference);

(iv) a notional “to be deducted amount” (Notional Deduction Amount), being the total of:

(A) the 457 Difference;

(B) 9.5% of the 457 Difference for superannuation;

(C) 5.45% of the 457 Difference plus superannuation for payroll tax;

(D) 3% of the 457 Difference plus superannuation for workers compensation;

(E) (from in or about November 2018) for periods in which annual leave loading was paid, an additional deduction calculated in respect of annual leave loading paid as part of the 457 Gross Salary and annual leave loading the relevant employer calculated would have been payable on the Actual Gross;

(v) the amount which, according to the respondents’ modus operandi, the 457 Employee was entitled to be paid for any Cash Hours worked in the fortnight, by multiplying the relevant Cash Rates by the Cash Hours worked (Cash Amount); and

(vi) the difference between the Notional Deduction Amount and the Cash Amount;

(c) depending on whether the Notional Deduction Amount was higher or lower than the Cash Amount, either:

(i) paying the 457 Employees the difference in cash for the Cash Hours (if the Notional Deduction Amount was lower than the Cash Amount); or

(ii) requiring the 457 Employees to pay back a portion of the amount paid by EFT (if the Notional Deduction Amount was higher than the Cash Amount), being the Actual Deduction Amounts.

130 The Deduction Spreadsheets were obtained by the Ombudsman during the site visit to Head Office in February 2020.

131 Each fortnight, one or more of the payroll team created a record in Sushi Bay’s MYOB payroll account of the gross and net amount of the 457 Gross Salary for each pay period, which generated the following records:

(1) Payroll Activity [Detail] records;

(2) Payroll Activity [Summary] spreadsheets;

(3) Payroll Advice records; and

(4) from time to time, pay slips in respect of the 457 Employees.

132 The effect of the policy was that, if a sponsored employee did not work their full-time contracted hours (76 hours per fortnight), the employee would be paid their contracted hours but would have to repay, by bank transfer or in cash, the amounts attributed to the hours they did not in fact work.

UNREASONABLE REQUIREMENTS TO SPEND OR PAY CONTRAVENTIONS (SECTION 325)

133 Since 15 September 2017, s 325 of the FW Act has relevantly provided:

Unreasonable requirements to spend or pay amount

(1) An employer must not directly or indirectly require an employee to spend, or pay to the employer or another person, an amount of the employee’s money or the whole or any part of an amount payable to the employee in relation to the performance of work, if:

(a) the requirement is unreasonable in the circumstances; and

(b) for a payment—the payment is directly or indirectly for the benefit of the employer or a party related to the employer.

Note: This subsection is a civil remedy provision (see Part 4‑1).

134 Previously the section relevantly provided as follows:

(1) An employer must not directly or indirectly require an employee to spend any part of an amount payable to the employee in relation to the performance of work if the requirement is unreasonable in the circumstances.

Note: This subsection is a civil remedy provision (see Part 4‑1).

135 The amendment was made by the Fair Work Amendment (Protecting Vulnerable Workers) Act 2017 (Cth) (Protecting Vulnerable Workers Amendment Act).

136 Section 327 relevantly provides that, in proceedings for the recovery of an amount payable to an employee in relation to the performance of work, any amount an employee is required to spend (or pay) contrary to s 325(1) is taken never to have been paid to the employee.

137 A detailed discussion of the legislative history, context and purpose of s 325 and the related provisions appears in Australian Education Union v Victoria (Department of Education and Early Childhood Development) (2015) 239 FCR 461 (Bromberg J). It is unnecessary for present purposes to say anything about those matters here.

138 The purpose of the 2017 amendment was “to clarify the operation” of the section: Explanatory Memorandum (EM) on the Fair Work Amendment (Protecting Vulnerable Workers) Bill 2017 (Protecting Vulnerable Workers Amendment Bill) [82].

139 As I observed in Fair Work Ombudsman v Foot & Thai Massage Pty Ltd (in liquidation) (No 4) [2021] FCA 1242 at [523], the effect of s 327 is that, if an employee is required to spend (or pay) any part of his wages in contravention of s 325, then the amount so spent (or paid) can be recovered from the employer as an underpayment of wages claim.

140 “Require” and “spend” bear their ordinary meanings: Foot & Thai at [525]. In the absence of a statutory definition, “pay” must also bear its ordinary meaning. An employer may require payment without making a demand. Consistent with the remedial purpose of the section, a beneficial interpretation should be given to it. An authoritative request would suffice: Foot & Thai at [528]. There is little practical difference between the verbs “spend” and pay” in this context. “Spend” is relevantly defined in The Macquarie Dictionary (1st ed, Macquarie Library, 1981) as “to pay out, disburse, or expend; dispose of (money, wealth, resources, etc.)”. That definition remains unchanged in the most recent edition of the Macquarie Dictionary, published almost 40 years later: Macquarie Dictionary (8th ed, Macquarie Dictionary Publishers, 2020). As I found in Foot & Thai at [564], a requirement to refund to an employer a portion of monies earned from the performance of work is prima facie unreasonable and amounts to a contravention of s 325.

141 The Ombudsman pleaded (at SOC/ASOC [78]) that, by reason of the Deduction Method:

(a) during the Contravention Period, Sushi Bay required Mr Hwang and the Sushi Bay 457 Employees set out in Annexure B, Table 1, to spend or pay the Actual Deduction Amounts, being amounts of their own money or money payable to them for the performance of work, in respect of fortnightly pay periods and in the amounts detailed in Annexure B, Table 1; and

(b) during the 457 Period, Auskoja required the Auskoja 457 Employees to spend or pay the Actual Deduction Amounts, being amounts of their own money or money payable to them for the performance of work, in respect of the fortnightly pay periods and in the amounts detailed in Annexure B, Table 2.

The tables are annexed to these reasons.

142 As a result, the Ombudsman pleaded (at SOC/ASOC [79]–[80]), Sushi Bay and Auskoja contravened s 325 because it was unreasonable for them to require the 457 Employees to spend or pay the Actual Deduction Amounts and because the requirement was directly or indirectly for the benefit of the respondents.

143 None of the respondents disputed that the 457 Employees were paid in accordance with the Deduction Method. The only question, then, is whether the requirement that each of the affected employees pay the Actual Deduction Amounts was unreasonable in the circumstances. While the corporate respondents denied the allegation, Ms Shin admitted it was. For the reasons which follow, I find that it was.

144 Minha Hwang gave the following evidence about his own experience. I make the following findings based on that evidence.

145 During the time Mr Hwang worked at the Campbelltown and Belconnen restaurants while sponsored on a 457 visa (8 February 2016 to 14 July 2019) he usually worked between five and six days each week for a total of between 50 and 55 hours. On most days he worked 11 to 11.5 hours per day, from the time the restaurant opened until it closed, excluding a one-hour unpaid lunch break. He usually worked at least one day on weekends and regularly worked on public holidays.

146 During his initial interview to work at the Sushi Bay restaurant in Liverpool, Mr Kim told him that he would be paid as a full-time employee and would work full-time hours but would be paid a “tax wage” and a “cash wage” because he was on a student visa and subject to work restrictions. In some fortnights, Mr Hwang was required to pay back part of his wage to Head Office, which I take to be a reference to his employer. Generally, if he worked over 50 hours per week and each day on the weekend, he did not need to pay anything.

147 When the envelopes containing cash wages and pay slips were delivered to him (and others) each fortnight at the restaurant where he worked, Mr Hwang also received envelopes containing paper slips which recorded the deduction amount he was required to pay back to Head Office. An example such a paper slip appears at page 807 of volume 1 of the Court Book:

148 The figure of $84.91, shown on this paper slip, aligns with an entry in the Deduction Spreadsheet for Mr Hwang for the pay period 25 March 2019 to 7 April 2019:

149 When he received a paper slip in his envelope, Mr Hwang would withdraw the specified amount in cash from his bank account and put it in the envelope. When he worked at the Belconnen restaurant, he gave the courier envelopes containing the deduction amounts from himself and other employees sponsored on 457 visas to return to Head Office.

150 Mr Hwang was given four weeks paid annual leave a year. He took annual leave on multiple occasions. Each time, his “taxable wage” was deposited into his bank account. When he returned to work he would then receive an envelope containing a paper slip directing him to pay an amount back to Sushi Bay. For two weeks annual leave the deduction was around $700.

151 Kitae Kim’s experience was similar. He was required to return to Sushi Bay part of his wages during fortnights in which he worked less than 50 to 55 hours per week. Like Mr Hwang, when Mr Kim received an envelope which contained a paper slip with an amount and words in Korean to the effect of “please pay back to Head Office”, he would withdraw the amount in cash, put the money in the envelope and, when he next had a shift, he would put the envelope in the safe in the restaurant.

152 On multiple occasions during his employment at the Parramatta, Merrylands and Campbelltown restaurants when the courier from Head Office came to drop off cash envelopes on Thursdays, Kitae Kim saw the restaurant supervisor take envelopes from the safe (including the envelope containing cash that he had put into the safe) and hand them to the courier along with other documents.

153 Some repayments were made directly into Ms Shin’s personal bank account by EFT. Ms Shin agreed that she received five such payments during the 457 Period pursuant to the Deduction Method from two Employees. Kitae Kim deposed that while working at the Darwin restaurant, he would receive a call from the accounts department instructing him to transfer a deduction amount by EFT to a St George bank account. That was Ms Shin’s personal bank account. Although only five such transactions occurred during the 457 Period, Ex YL-1 (between pages 8454 and 8493 of the Court Book) contains additional evidence of 39 occasions during 2018 and 2019, showing transfers of the so-called “deduction amounts” from the accounts of Sushi Bay employees into her personal account.

154 Kitae Kim took four weeks’ annual leave in June 2019. When he returned to work, he was informed by Head Office over the phone that he had to pay the deduction amounts which related to the pay periods in which he did not work.

155 The following, by way of example, is an extract of transactions from Ms Shin’s personal bank account records that on 1 July 2019, Kitae Kim transferred to Ms Shin $108.40 and $793.95 and that on 4 July 2019 he transferred to her $445.65:

The Deduction Spreadsheets for the pay periods 20 May to 2 June 2019, 3 June to 16 June 2019, and 17 June to 30 June 2019 respectively record that Kitae Kim was required to repay the same amounts as he transferred: