FEDERAL COURT OF AUSTRALIA

Australian Securities and Investments Commission v Brite Advisors Pty Ltd [2024] FCA 69

ORDERS

AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff | ||

AND: | BRITE ADVISORS PTY LTD ACN 135 024 412 Defendant | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. Leave be granted to the plaintiff, who is released from the implied undertaking to the extent necessary, to rely on all of the documents filed in related proceedings, WAD 262/2023, save for:

(a) the confidential affidavit affirmed by Linda Methven Smith on 20 December 2023; and

(b) any affidavit or report filed by Ms Smith marked confidential.

2. Pursuant to s 461(1)(k) of the Corporations Act 2001 (Cth) (Corporations Act), the defendant is wound up on just and equitable grounds.

3. Pursuant to s 472(1) of the Corporations Act, Linda Smith and Robert Kirman of McGrathNicol are appointed joint and several liquidators of the defendant (Liquidators).

4. The defendant is to pay the plaintiff's cost of the proceedings, and such costs as taxed or agreed be reimbursed out of the property of the defendant in accordance with s 466(2) of the Corporations Act.

5. Pursuant to s 57 of the Federal Court of Australia Act 1976 (Cth), Linda Smith and Robert Kirman of McGrathNicol are appointed, jointly and severally, as receivers and managers (Receivers) over the property, assets and undertakings held by the Defendant on trust for another (Trust Assets).

6. The need for the Receivers to file a guarantee under rr 14.21 and 14.22 of the Federal Court Rules 2011 (Cth) is dispensed with.

7. The Receivers are authorised to take possession of, preserve, maintain and sell the Trust Assets.

8. The Receivers have the power:

(a) to do all things (including, but not limited to, the signing of any documents) for the realisation of the Trust Assets;

(b) provided by s 420 of the Corporations Act as if the reference therein to 'the corporation' were to the trust on which the Trust Assets are held, together with the powers that a liquidator has in respect of property of a company (in its role as legal owner and trustee) pursuant to s 477(2) of the Corporations Act;

(c) without limiting the powers granted pursuant to paragraphs 8(a) and (b), and subject to paragraph 11, to do all things necessary to attend to the following identified tasks:

(i) the identification of the Trust Assets and the trust liabilities;

(ii) the identification of trust creditors and distinguishing them from non-trust creditors (if any);

(iii) the ascertaining of the state of the accounts between the beneficiaries and the trustee;

(iv) assessing any request of a client of the Defendant for a superannuation or pension withdrawal and if deemed appropriate by the Receivers processing the withdrawal;

(v) the recovering of, or attempting to recover, the Trust Assets, including debts due to the trust(s);

(vi) the taking of possession of, collecting and protecting the Trust Assets;

(vii) the carrying on of any business of the trust on which the Trust Assets are held;

(viii) the realisation, or attempted realisation, of the Trust Assets;

(ix) the distribution of any proceeds of realisation to meet the claims of the creditors or persons whose debts were incurred in relation to the trust(s); and

(x) any matter in the administration of the trust(s) which is ancillary to the above to the extent to which it had to be undertaken for the purposes of the identified tasks.

9. In the period up to 5:00pm (ACDT) on 4 March 2024, the Receivers would be acting properly and are justified in, for the purposes of exercising their powers under paragraph 8 of these orders:

(a) subject to sub-paragraphs 9(b) to 9(f), assessing and processing only regular superannuation and pension withdrawals that were in place as at 9 November 2023;

(b) declining to assess or process any request for a superannuation or pension withdrawal to the extent that processing the requested withdrawal would result in the total withdrawals processed for an individual beneficiary on and from 9 November 2023 to exceed 30% of the value of the beneficiary's investment recorded in Salesforce as at 9 November 2023;

(c) directing any beneficiary that makes a request of the Receivers for a superannuation or pension withdrawal to submit that request to the relevant Corporate Trustee for that Corporate Trustee to make to the Receivers on the beneficiary's behalf;

(d) declining to assess or process any request for a superannuation or pension withdrawal received directly from a beneficiary, unless the beneficiary is unrepresented by a Corporate Trustee;

(e) requiring any request for a superannuation or pension withdrawal by a Corporate Trustee to be accompanied by such other information as the Receivers consider, in their sole discretion, is necessary to demonstrate to the satisfaction of the Receivers that it is appropriate for the requested withdrawal be processed by the Receivers under Order 8(c)(iv); and

(f) paying any superannuation or pension withdrawal that the Receivers deem appropriate to process in accordance with Order 8(c)(iv), from Trust Assets.

10. In the period up to 5:00pm (ACDT) on 4 March 2024, the Receivers are acting properly and are justified in paying from the Trust Assets:

(a) trading expenses incurred by the defendant on and from 9 November 2023;

(b) trading expenses incurred by the defendant prior to 9 November 2023 but which the Receivers consider necessary to pay in order to continue to carry on the business of the defendant; and

(c) trading expenses incurred by any entity that is an 'associated entity' (as that term is defined in the Corporations Act) of the defendant which the Receivers consider necessary to pay in order to perform and continue to perform their duties arising in or otherwise in connection with their appointment,

to the extent that the cash held in the defendant’s Westpac Operating Accounts is insufficient to meet those expenses.

11. Save for as permitted by these orders (including the orders and directions that apply in these proceedings by virtue of paragraph 9 above), the Receivers are justified and would be acting properly in not distributing any Trust Assets, or any part of them, to or for the benefit of any person asserting a claim to the Trust Assets (including the underlying individual beneficiaries) until further direction or order of the Court.

12. Subject to further order of the Court, WAD262/2023 and WAD13/2024 be case managed together.

Remuneration, costs and expenses

13. The Liquidators shall be entitled to reasonable remuneration properly incurred in the performance of their duties arising in connection with their appointment and in the exercise of their powers as may be approved by the Court on the application of the Liquidators to a Registrar (in such form as the Registrar directs and at no more than 14 day intervals), together with all costs and expenses, to be paid from the property of the defendant.

14. The Receivers shall be entitled to reasonable remuneration properly incurred in the performance of their duties arising in connection with their appointment and in the exercise of their powers as may be approved by the Court on the application of the Receivers to a Registrar (in such form as the Registrar directs and at no more than 14 day intervals), together with all costs and expenses, to be paid from Trust Assets.

15. There be liberty to any party to apply to the Court on 48 hours’ notice.

16. There be liberty to the Liquidators and Receivers to apply to the Court on 48 hours’ notice.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

O’SULLIVAN J:

1 The defendant, Brite Advisors Pty Ltd (Receivers and Managers Appointed) holds an Australian Financial Services Licence and is authorised to carry on a financial services business in Australia including the provision of financial product advice, dealing in certain financial products and operating certain custodial and depository services for retail and wholesale clients Australia.

2 The Australian Securities and Investments Commission (ASIC) applies for orders:

(a) That Brite be wound up pursuant to s 461(1)(k) of the Corporations Act 2001 (Cth) on just and equitable grounds;

(b) The appointment of the current Receivers and Managers to Brite as joint and several Liquidators of Brite pursuant to s 472(1) of the Act; and

(c) The appointment of the current Receivers and Managers jointly and severally as Receivers and Managers of the property, assets and undertakings held by Brite on trust for others (Trust Assets).

3 The application was heard on 6 February 2024. That day orders were made that Brite be wound up, appointing Linda Methven Smith and Robert Kirman as joint and several Liquidators and appointing Ms Smith and Mr Kirman as joint and several Receivers of the Trust Assets held by Brite.

4 When the orders were made, I indicated I would publish reasons for doing so. These are those reasons.

Background

5 This application is the culmination of an extensive investigation commenced by ASIC on 30 June 2021 which led to an application to this Court in October 2023 initially for interim preservation orders and subsequently the appointment of Receivers and Managers to Brite.

6 To understand the process by which ASIC reached this point, it is necessary to set out some of the background.

7 Brite describes itself as a provider of discretionary investment services:

(a) To overseas-based pension schemes (wholesale clients); and

(b) To resident Australian investors investing rolled over United Kingdom Pension Assets through self-managed superannuation funds (retail clients).

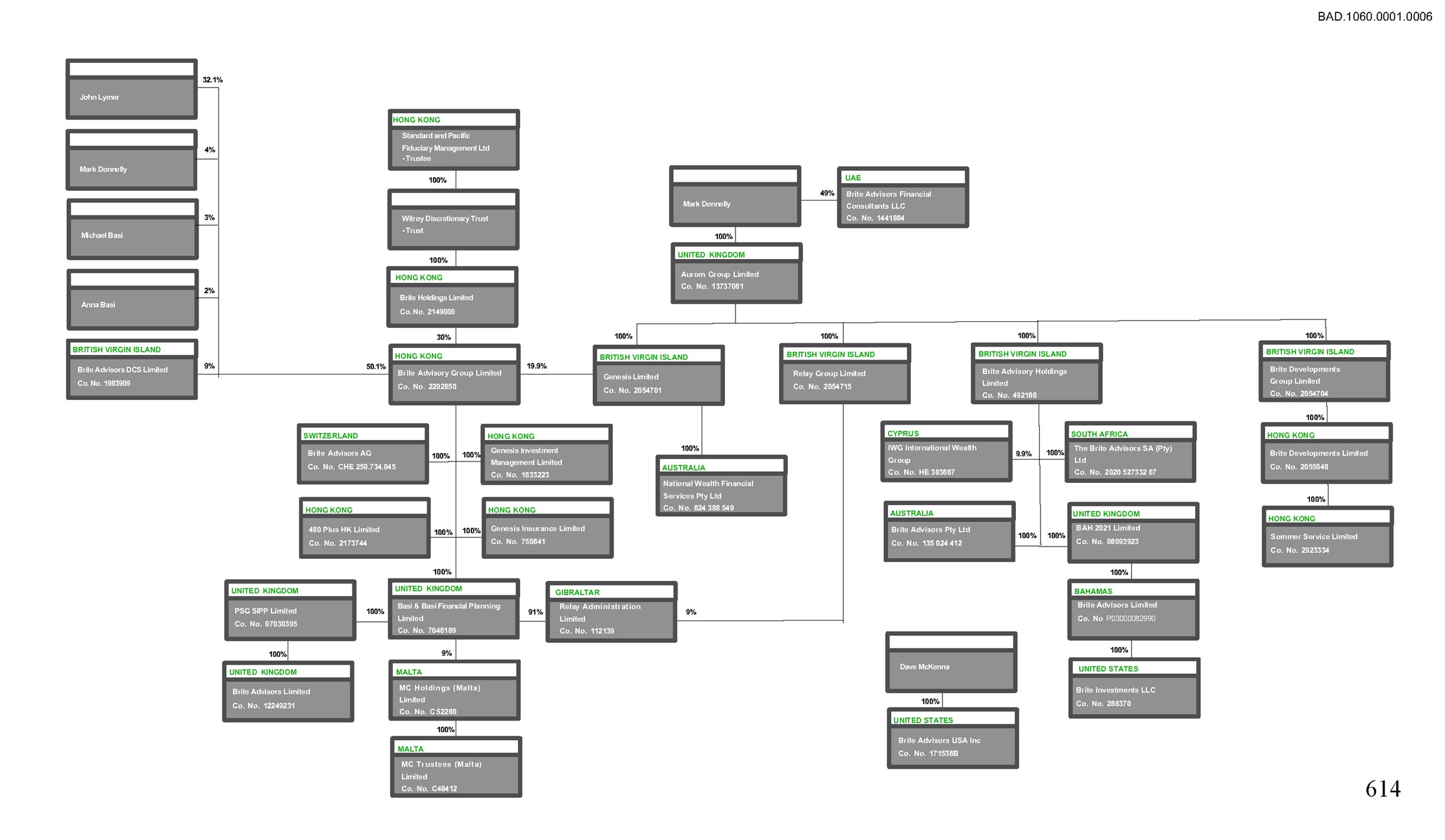

8 Brite forms part of a complicated network of companies incorporated in various countries throughout the world (Brite Group). A copy of the organisational structure of the Brite Group produced to ASIC by Brite, being annexure TRL-07 to the affidavit of Trevor Ross Leach affirmed 22 January 2024 and read on this application, is attached to these reasons as Annexure A. One correction to the organisational structure is that the company identified as “Genesis Investment Management Limited Co No 1633223” in Hong Kong is now known as Brite Hong Kong Limited, a company incorporated in Hong Kong.

9 As is apparent from Annexure A, Brite is a wholly-owned subsidiary of Brite Advisory Holdings Ltd (Brite BVI), a company registered in the British Virgin Islands. The Directors of Brite BVI are Mr Mark Donnelly and Mr David Michael McKenna. The sole shareholder is Aurom Group Limited, a company registered in the United Kingdom.

10 Mr Donnelly is the sole shareholder in Aurom.

11 The ultimate owner of Brite is Aurom.

12 Brite has approximately AUD $1 billion under management, comprised of overseas-based pension schemes or Self-Invested Personal Pensions (SIPP). Brite claims it manages 14 pension schemes. Five of those pension schemes are owned by companies within the Brite Group.

13 On 25 October 2023, ASIC applied ex parte for an urgent interim asset preservation order over the assets of Brite whether held beneficially or otherwise. Banks-Smith J made an interim asset preservation order that day.

14 On 26 October 2023, ASIC issued an originating application seeking the appointment of Receivers and Managers to Brite. It also sought an asset preservation order.

15 At a hearing on 9 November 2023, at which Brite was represented, the Court heard the application for ongoing asset preservation orders. Banks-Smith J made orders by consent not only for the continuation of the asset preservation orders, but also appointing Linda Methven Smith and Robert Kirman of McGrathNicol as Investigative Accountants to address a series of questions concerning the affairs of Brite and to provide a report to the Court on their findings (IA Report).

16 Those questions included the identification of assets and liabilities of Brite and the identification of the amount of beneficiary assets under management by Brite including the whereabouts of those assets. Also included were orders requiring Brite to deliver up immediately to the Investigative Accountants various books and records.

17 On 24 November 2023, the orders made on 9 November 2023 were varied to include a requirement that Brite take all steps necessary to transfer all of its property held by Brite Hong Kong in its accounts held with the Hong Kong and Shanghai Banking Corporation Limited in Hong Kong (HSBC) and a brokerage firm, Interactive Brokers (Hong Kong) (IBHK), part of a worldwide brokerage group, to a “client account” or accounts held by Brite with Westpac Banking Corporation or Interactive Brokers (Australia) (IBA) respectively.

18 Brite were also directed to require Brite Hong Kong to inform IBHK and HSBC not to deal with its property. “Property” had been defined in the orders as including any property for which it was not the sole beneficial owner.

19 The Investigative Accountants filed the IA Report with the Court on 8 December 2023.

20 The IA Report revealed a number of significant concerns, including not only that as from June 2023 Brite had transferred approximately AUD $129 million of beneficiary funds to Brite Hong Kong but also that Brite was unable to account for USD $69 million of those funds.

21 The IA Report also reported that the Investigative Accountants had great difficulty in obtaining books and records from Brite and that the lack of information hampered their ability to make the required investigations.

22 The Investigative Accountants expressed concerns about Brite’s solvency but were unable to give a conclusive answer to the question of whether Brite was solvent because of the lack of books and records provided.

23 On 13 December 2023, at the conclusion of a three-day hearing as to whether Receivers and Managers should be appointed to Brite, the Court made orders appointing Ms Smith and Mr Kirman as Receivers and Managers for the purposes of, amongst other things, identifying, collecting and securing Brite’s Property (as that term is defined in the orders).

24 The Receivers and Managers were ordered to file a report with the Court by 24 January 2024 (Receivers’ Report).

25 On 21 December 2023, on the application of ASIC and the Receivers and Managers, the Directors of Brite were directed to deliver up immediately to the Receivers and Managers Brite’s books and records to allow them to do their task. Those orders required the Directors of Brite to direct various individuals within the Brite Group, including Mr Donnelly, to provide information relating to the beneficiaries’ assets under management to the Receivers and Managers.

26 The Receivers and Managers filed the Receivers’ Report on 24 January 2024.

Legislation

27 Section 461(1)(k) of the Act provides in part:

(1) The Court may order the winding up of a company if:

…

(k) the Court is of opinion that it is just and equitable that the company be wound up.

28 Section 462 of the Act provides in part:

(1) A reference in this section to an order to wind up a company is a reference to an order to wind up the company on a ground provided for by section 461.

(2) Subject to this section, any one or more of the following may apply for an order to wind up a company:

…

(e) ASIC pursuant to section 464.

29 Section 464 of the Act provides:

(1) Where ASIC is investigating, or has investigated, under Division 1 of Part 3 of the ASIC Act:

(a) matters being, or connected with, affairs of a company; or

(b) matters including such matters;

ASIC may apply to the Court for the winding up of the company.

(2) For the purposes of an application under subsection (1), this Act applies, with such modifications as the circumstances require, as if a winding up application had been made by the company.

(3) ASIC must give a copy of an application made under subsection (1) to the company.

30 Section 472(1) of the Act provides:

(1) On an order being made for the winding up of a company, the Court may appoint a registered liquidator to be liquidator of the company.

Winding up on just and equitable grounds

31 There is no issue that ASIC has standing to apply for an order that Brite be wound up pursuant to ss 462(2) and 464(1) of the Act and that a copy of the application has been served on Brite: s 464(3). The Directors have also been served.

32 The principles applying to an application to wind up a company on just and equitable grounds are well-settled.

33 In Australian Securities and Investments Commission v Activesuper Pty Ltd (No 2) (2013) 93 ACSR 189; [2013] FCA 234 at [19]-[24], Gordon J summarised a number of the applicable principles.

19. In the present case, the appointment of a provisional liquidator is sought where the term winding up is sought on the just and equitable ground under s 461(1)(k) of the Act. There is no dispute that ASIC has standing to bring an application to wind up a company on the statutory just and equitable ground: ss 462(2) and 464 of the Act. The classes of conduct which justify the winding up of a company on the just and equitable ground are not closed, and each application will depend upon the circumstances of the particular case: Ebrahimi v Westbourne Galleries Ltd [1973] AC 360 at 374 and 376-379; Australian Securities and Investment Commission v Kingsley Brown Properties Pty Ltd [2005] VSC 506 at [95]-[97]; Nilant v RL & KW Nominees Pty Ltd [2007] WASC 105 at [117]. Nevertheless, it is possible to discern some guiding principles from the authorities.

20. It has long been established that a company may be wound up where there is “a justifiable lack of confidence in the conduct and management of the company’s affairs” and thus a risk to the public interest that warrants protection: Loch v John Blackwood Ltd [1924] AC 783 at 788. In Australian Securities and Investments Commission v ABC Fund Managers (2001) 39 ACSR 443 at [119], Warren J (as her Honour then was) set out three “general fundamental principles”:

First, there needs to be a lack of confidence in the conduct and management of the affairs of the company … Second, in these types of circumstances it needs to be demonstrated that there is a risk to the public interest that warrants protection. Third, there is a reluctance on the part of the courts to wind up a solvent company.

(Citation omitted)

21. In relation to the first, a lack of confidence may arise where, “after examining the entire conduct of the affairs of the company” the Court cannot have confidence in “the propensity of the controllers to comply with obligations, including the keeping of books, records and documents, and looking after the affairs of the company”: Galanopoulos v Moustafa [2010] VSC 380 at [32]; see also Australian Securities Commission v AS Nominees Limited (1995) 62 FCR 504 at 532-3; ABC Fund Managers at [117]-[118]; Australian Securities and Investments Commission v International Unity Insurance Pty Ltd (2004) 22 ACLC 1416 at [135]-[139].

22. …

23. In relation to the second, a risk to the public interest may take several forms. For example, a winding up order may be necessary to ensure investor protection or where a company has not carried on its business candidly and in a straightforward manner with the public: International Unity Insurance at [138]; see also Australian Securities and Investments Commission v Finchley Central Funds Management Ltd [2009] FCA 1110 at [3]. Alternatively, it might be justified in order to prevent and condemn repeated breaches of the law: Kingsley Brown Properties at [96]; see also AS Nominees at 527; Australian Securities and Investments Commission v Chase Capital Management Pty Ltd (2001) 36 ACSR 778 at 793. Again, there is an overlap between matters which would pose a risk to the public interest for the purpose of s 461(1)(k) and which are relevant to the appointment of a provisional liquidator.

24. In relation to the third, it has been said that “a stronger case might be required where the company was prosperous, or at least solvent”: Kingsley Brown Properties at [96]. Solvency, however, is not a bar to the appointment of a liquidator on the just and equitable ground, particularly where there have been serious and ongoing breaches of the Act: ABC Fund Managers at [124]-[130].

34 See also Australian Securities and Investments Commission v Merlin Diamonds Ltd (ACN 009 153 119) [2020] FCA 411; 143 ACSR 426 at [39] (O’Bryan J); ASIC v Chase Capital [2001] WASC 27; (2001) 36 ACSR 778 at 793 (Owen J).

35 There are important public interest considerations when ASIC applies for a winding up order. In Australian Securities and Investments Commission v Finchley Central Funds Management Ltd [2009] FCA 1110, Gilmour J held at [3]:

The plaintiff stands in a somewhat different position to a private applicant for winding up on this ground because the public interest considerations attaching to ASIC as the corporate regulator are relevant to the application. Where companies are engaged in fund management and where there is evidence of serious mismanagement or repeated breaches of the Act so that there is a risk to the public, and in circumstances where ASIC has lost confidence in the company to comply with the relevant law, the court may act to wind up that company on the just and equitable ground.

36 In Australian Securities Commission v AS Nominees Limited (1995) 18 ACSR 459 at p 517 when considering an application by a statutory body applying for the winding up of a company, Finn J observed:

… there seems to be no reason at all why a court entertaining such an application should not have regard to such actual public interest considerations as have … or may have induced the governmental body to seek a just and equitable winding up order.

Consideration

37 The Receivers’ Report reveals a number of serious and in some cases, disturbing matters.

38 First, between June and November 2023, Brite transferred approximately AUD $129.4 million from an account held by it in its IBA accounts to Brite’s Westpac client accounts with those funds then being transferred overseas into an HSBC client account in Hong Kong held by Brite Hong Kong. Those funds were then reinvested into an IBHK account held in the name of Brite Hong Kong.

39 The amount that has been returned to Brite’s Westpac client accounts and IBA accounts from Hong Kong pursuant to the Court’s orders made 24 November 2023 totals approximately AUD $115.8 million.

40 A review of the HSBC statements by the Receivers identified a number of withdrawals and deposits from the HSBC accounts which require further investigation, including payments totalling approximately USD $1.9 million recorded as being paid out of those accounts but which are completely unexplained.

41 Despite numerous requests to the Directors of Brite, the Receivers have not received a full account of the beneficiaries’ assets under management whilst in the custody of Brite Hong Kong.

42 Further, the whereabouts of the balance of the funds transferred to Hong Kong also remains unexplained. In particular, the Receivers have not received any information providing a reconciliation showing the use and allocation of beneficiaries’ assets under management from June 2023 until the funds were returned to Australia. There are no cashiering transactions supporting, amongst other things, any withdrawals from HSBC or IBHK to meet expenses/withdrawals/platform fees, nor details of the expenses paid from the beneficiaries’ assets under management whilst in custody of Brite Hong Kong, nor the documentation relating to any margin loans or other loans secured against the IBHK’s accounts.

43 Second, despite numerous requests to the Directors, the Receivers have not received either a list of the beneficiaries whose funds were moved to Brite Hong Kong nor a list of the beneficiaries referred to as “Rest of World” beneficiaries being those beneficiaries who are located in other than the United Kingdom, the United States of America or Australia. In circumstances where the stated purpose of moving funds to Brite Hong Kong was to segregate funds held for beneficiaries located in the United States of America and United Kingdom, the failure to provide a list of the beneficiaries whose funds were transferred to Brite Hong Kong is of such a fundamental nature that by itself it provides a justifiable lack of confidence in the conduct and management of Brite’s affairs.

44 Third, the receivers located an additional 59 assets listed in AutoRek, a software package which assists in reconciling beneficiaries’ assets under management at an individual beneficiary level, which were not held in IBA’s accounts. These assets are not otherwise disclosed in any financial report or other information provided by the Directors to the Receivers.

45 Fourth, the Receivers identified at least 10 acquisitions made by members of the Brite Group since 2018 at a cost of approximately AUD $8.9 million. Payments for those acquisitions appear to have been made or partly made from beneficiaries’ assets under management using those assets as security. There are a number of other acquisitions which require further investigation.

46 Fifth, Brite does not appear to have maintained proper books and records. The Receivers have not been provided with unfettered access to the books and records of Brite despite numerous requests. Further, there has been a failure to comply with the Court’s orders made on 21 December 2023 requiring Mr Donnelly, Mr Francois Vauville who is Brite Group’s Business Development Officer, and Mr Richard Lissenden who is Head of Advisory of the Brite Group and a Director of Brite Advisory Group Ltd, (a company incorporated in Hong Kong and sole shareholder in Brite Hong Kong) to provide documentation.

47 Sixth, from the information currently available to the Receivers, it is likely that Brite was insolvent from at least 27 October 2023 and likely earlier. Whereas the Court is always reluctant to order the winding up of a company that is or may be solvent, in this matter there are insufficient books and records that have been produced by the Directors to determine that Brite is, in fact, solvent. That in turn, raises concerns about the management of the company and a justifiable lack of confidence in the conduct and management of the company’s affairs.

48 Seventh, the Receivers referred to an email sent 6 October 2023 from a person who appears to be an employee of Brite Hong Kong to Mr Donnelly and Mr John Charles Lymer (a Director of Brite), copied to Mr Lissenden and Ms Erika Nicholson, the latter being Head of Accounts of the Brite Group. The email reports, amongst other things, that the Security and Futures Commission in Hong Kong (SFC) had raised questions concerning the transfer of funds from Brite Hong Kong’s HSBC client accounts to what is referred to as Brite Hong Kong’s house account. The records to which the SFC refer reveal transfers between 27 July 2023 and 23 August 2023 of significant sums of money including GBP £311,271 and USD $177,314. The SFC also requested reasons for withdrawals from Brite Hong Kong’s client account and subsequent deposits back into those accounts some two weeks later between 14 and 18 July 2023 of amounts of USD $18,090,997 and GBP £45,503,638 respectively.

49 Further, on the face of the email, the employee states that not only does he consider that Brite Hong Kong’s actions may constitute violations of SFC rules but goes on to state that the employee will attempt to “make up some documents and present them in a way that SFC may think our acts are controversial, instead of intentional violations.”

50 ASIC submits that this email is a clear admission by Brite staff or management of intentional wrongdoing and misappropriation of client funds. I do not accept that submission but only because it is important to read this passage in the full context of the email and to make allowance for difficulties in expression. It is also from an employee whose authority is unknown. Nonetheless, an explanation is required and at the very least this email raises serious concerns as to the conduct of Mr Lymer who was copied into this email, as well as the operations of Brite Hong Kong and given the other addressees on the email, the Brite Group generally. Since Brite is part of the Brite Group and beneficiaries’ funds were transferred to Brite Hong Kong, this email raises a justifiable lack of confidence in the conduct and management of Brite’s affairs, as well as a risk to the public.

51 Eighth, according to records to which the Receivers have been granted access, in particular the Xero accounting package, there are related party loan accounts owing to Brite totalling approximately AUD $1.1 million. Further, an analysis performed by the Receivers of Brite’s bank statements record that AUD $91 million has been advanced to multiple related parties between May 2016 to October 2023.

52 Again, despite requests, the Receivers have not been provided with supporting documents, including invoices for related party transactions, nor journal entries for significant transactions characterised as related party loans. To the extent that correspondence has been provided explaining there were amounts paid to various Brite Group entities through related party loan accounts, no documents to support these claims have been provided.

53 The absence of documents is of particular significance because the Receivers record that it is the view of Crowe Australasia, an independent accounting and advisory firm retained by the Receivers to prepare an independent report on financial reporting and income tax compliance by Brite (Crowe Horwarth Report), that Brite is a Tier 1 reporting entity. That is because Brite meets the definition of holding “public accountability” meaning that it holds assets in a fiduciary capacity for a broad group of outsiders as one of its primary businesses. The significance is that a Tier 1 reporting entity is obliged to disclose transactions with related parties and outstanding balances, including commitments and relationships with related parties, which may affect assessments of its operations and of its financial statements.

54 Ninth, as at 9 November 2023, there was at least a USD $69 million difference between the funds held in the Brite Group’s Interactive Broker Accounts, Westpac and HSBC Hong Kong accounts compared to the position disclosed in the Salesforce platform. As I understand it, the Salesforce platform allows beneficiaries to view the value of their investments at a particular point in time, or rather it did until its operation was suspended in about November 2023 because the relevant entity within the Brite Group stopped paying the required subscription.

55 At the hearing held in December 2023 at which ASIC applied for the appointment of Receivers and Managers to Brite and at which Mr Lymer, gave evidence, Mr Lymer was unable to provide an explanation as to the USD $69 million difference.

56 Tenth, ASIC refers to an email sent 15 September 2022 sent from Ms Nicholson to Mr Ramon Falzon, Brite’s Chief Financial Officer. The email was located by the Receivers and is referred to in the Receiver’s Report. In it, Ms Nicholson addresses a query from Brite’s auditor as to funds withdrawn from Brite’s IBA accounts.

57 ASIC points to Ms Nicholson’s statement in her email that she was trying to think of the best way to reply to the auditor’s query. Mr Falzon observes that the issue is very sensitive as, “… it will show a lack of process & control gap from our side which would be a big no no for an auditor. I reckon we should review your draft response together tomorrow in our catch up, as we’ve got to be transparent, however this will potentially open up a big can of worms for the auditor.”

58 ASIC submits that the email suggests that funds are withdrawn from Brite’s IBA accounts whenever required, in such amounts as is required and with no correlation between revenue received and amounts withdrawn. I accept that submission.

59 On the basis of the above matters, which are by no means exhaustive, ASIC submits that the Court’s jurisdiction to wind up Brite on just and equitable grounds is clearly enlivened on the basis that there is a justifiable lack of confidence in the conduct and management of the company affairs as well a risk to the public. I accept that submission.

60 It submits further that the facts demonstrate an overwhelming case and observes that Brite’s Directors did not appear before the Court to oppose the application that it be wound up. I accept this submission.

61 Finally, ASIC submits there is clear evidence of misappropriation of beneficiaries’ funds. As to this submission, I make no finding as to whether there has been misappropriation of beneficiaries’ funds but there is sufficient material in the IA Report and the Receivers’ Report to raise very significant, indeed disturbing, concerns such as to amount to a justifiable lack of confidence in the conduct and management of Brite’s affairs. I also consider that the risk to the public is too great not to take action.

62 Further, although I have not gone into detail, the Receivers’ Report sets out a number of suspected contraventions of the Act. I make no findings as to whether there have been any such contraventions, however there is the spectre of not just a number of potential past contraventions, but unless steps are taken, the prospect of further contraventions.

Conclusion

63 It is for these reasons that I am satisfied that an order winding up Brite should be made.

64 ASIC has filed a consent to act as joint and several liquidators signed by Ms Smith and Mr Kirman. There will be an order appointing Ms Smith and Mr Kirman as Liquidators.

The Appointment of a Receiver to Trust Assets-legal principles

65 ASIC also applies, pursuant to s 57 of the Federal Court of Australia Act 1976 (Cth), for the appointment of Receivers and Managers to the Trust Assets.

66 Section 57 provides:

57 Receivers

(1) The Court may, at any stage of a proceeding on such terms and conditions as the Court thinks fit, appoint a receiver by interlocutory order in any case in which it appears to the Court to be just or convenient so to do.

(2) A receiver of any property appointed by the Court may, without the previous leave of the Court, be sued in respect of an act or transaction done or entered into by him or her in carrying on the business connected with the property.

(3) When in any cause pending in the Court a receiver appointed by the Court is in possession of property, the receiver shall manage and deal with the property according to the requirements of the laws of the State or Territory in which the property is situated, in the same manner as that in which the owner or possessor of the property would be bound to do if in possession of the property.

Conclusion

67 Given that Brite holds the beneficiaries’ funds on trust, I consider it is appropriate to make an order that Ms Smith and Mr Kirman be appointed as Receivers and Managers of the beneficiaries’ assets held by Brite on trust.

68 ASIC seeks a number of further orders which I will make.

I certify that the preceding sixty-eight (68) numbered paragraph is a true copy of the Reasons for Judgment of the Honourable Justice O'Sullivan. |

Associate:

Annexure A