FEDERAL COURT OF AUSTRALIA

Australian Mud Company Pty Ltd v Globaltech Corporation Pty Ltd (No 5) [2024] FCA 58

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The proceeding be adjourned to a date to be fixed (after hearing from the parties) for the making of final orders.

2. The parties be heard as to any other orders.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

BESANKO J:

Introduction

1 These reasons deal with a claim for pecuniary relief by way of damages and an account of profits in relation to the infringement of an Australian Standard Patent.

2 Liability was heard and determined before relief. The issue of liability included the determination of a claim for infringements of the patent and a cross-claim that the patent is invalid. I delivered reasons on 26 November 2018 (Australian Mud Company Pty Ltd v Globaltech Corporation Pty Ltd [2018] FCA 1839; (2018) 138 IPR 33) and made orders on 14 December 2018. I made declarations of infringements of the patent, granted injunctions and dismissed the cross-claim. My decision was the subject of an appeal to the Full Court of this Court which was dismissed (Globaltech Corporation Pty Ltd v Australian Mud Company Pty Ltd [2019] FCAFC 162; (2019) 145 IPR 39). There was then an application to the High Court for special leave to appeal which was also dismissed.

3 The applicants are Australian Mud Company Pty Ltd (Australian Mud) and Reflex Instruments Asia Pacific Pty Ltd (Reflex). Australian Mud is the owner of the relevant patent, being Australian Standard Patent No 2010200162 entitled “Core Sample Orientation” (the Patent). Reflex is the exclusive licensee of the Patent and it manufactured and supplied the core sample orientation tools which are the embodiment of the invention described in the Patent (ACT Tool). Australian Mud neither manufactured nor supplied the ACT Tool in Australia or overseas during the relevant period. In those circumstances, it will be sufficient for me to refer to Reflex.

4 The respondents are Globaltech Corporation Pty Ltd (Globaltech Corporation) and Globaltech Pty Ltd. Globaltech Corporation manufactured and supplied the infringing tools. The infringing core orientation tools were developed and sold under the names “Orifinder v3A”, “Orifinder v3B” and “Orifinder v5”. The relevant versions for the purposes of these reasons are the Orifinder v3B and the Orifinder v5. It is sufficient in the circumstances to refer to Globaltech Corporation as Globaltech.

5 Section 122(1) of the Patents Act 1990 (Cth) (the Act) provides that the relief a court may grant for the infringement of a patent includes an injunction and, at the option of the plaintiff, either damages or an account of profits.

6 On 21 September 2022, the applicants notified the Court and Globaltech that they made the following election with respect to the pecuniary relief it sought for the infringement of the Patent:

1. In respect of Orifinder Tools (as defined in order 4(a) made by Besanko J on 14 December 2018) supplied by the Respondents that have been used in Australia, the Applicants elect to claim damages.

2. In respect of Orifinder Tools supplied by the Respondents that have been exported from Australia, the Applicants elect to claim an account of profits.

3. If there are any other Orifinder Tools supplied by the Respondents that are not covered by 1 or 2 above, the Applicants elect to claim damages in respect of those tools.

7 Globaltech has made a submission that this “split” election is not valid and effective and this submission is addressed below.

8 Both the applicants and the respondents are part of a larger group of companies. Australian Mud and Reflex are wholly owned subsidiaries of Imdex Pty Ltd (Imdex) and form part of the Imdex Group. Globaltech Corporation and Globaltech Pty Ltd are part of the Boart Longyear Group which includes Boart Longyear Australia Pty Ltd (BLYA).

9 In order to understand how the applicants put their claim for damages and for an account of profits it is necessary to describe, at this stage at a general level, the business models adopted by Globaltech and BLYA on the one hand, and Reflex on the other. Initially, the relevant period in terms of the supply of infringing tools was said to be from May 2015 to January 2019. However, as the matter developed it became clear that the relevant period is from May 2015 to April 2019.

10 There are two agreements between Globaltech and BLYA which are relevant in terms of Globaltech’s business model. The first agreement is dated 31 October 2013 and entitled “Equipment Distribution Agreement” and the second agreement is undated and entitled “Amended and Restated Equipment Distribution Agreement”. The first agreement applied from at least May 2015 to December 2015 and the second agreement applied from 1 January 2016 to at least April 2019. The first agreement was amended and restated by the second agreement according to the recitals in the second agreement. I will refer to these agreements together as the Distribution Agreements.

11 XXXXXX X X X X X XX X X X X X X X X X XXX X X X X X X X X X X X XX X XXX X XXXXXXXXXXXXXXXXXXX XXXXXXXXXXXXXX XXXXXXXXXXX XXXXXX XXXXXXXXXXXXXXXXXXXXXXXX XXXXXXXXXXXX XXXXXXXX XXXX X X XXXXXXXXXXXXXXXXXXXXX XXXXXXXXXXXXXXXXXXX XXXX XXXXX XXXXXXXXXXXXXXXXX XXXXXXXXXXXXXXXXX XXXXXXXXX XXX XX X X X X X XXXXXXXXXXXXXXXX XXXXXXXXXXX X XXXXXXXXX XXXXX XXXXXXXXXXXXXXXXXXXXXX X XXXXXXXXXXXXX X X X X X X X X XXXXXXX XXXXXXXXXXXXXXXX XXXXXXXXXXXXXX XXXXXXXXXX XXXXXX XXXXXXXXXXXXXXXXXXXX XXXXXXXXXXXXX XXXXXXXXX X XXXXXX XXXXXXXXXXXXXXXXXXXXXX XXXXXXXXXXXXX XXX X X X XX X XXXXXXXXXXXXXXXXX XXXXXXXXXXXXXXX XXXXXXXXXX XXXXXXXX XXX XXXXXXXXXXXXXXXXXX XXXXXXXXXXXXXXXXXXXXX XXXXXXXXX XX XXXXXXXXXXXXXXXXXXXXXXXXX XXXXXXXXXXXXXXXXXX X X X X XXXXX XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX XXXXXXXXXXXXXX XXX XXXXXXXXXXXXXXXXXXXXXXX XXXXXXXXXXXXXXXXXX XXXXXXXX XXXX XXXXXXXXXXXXXXXXX XXXXXXXXXXXXXX X X X XX XXXXXXXXXXXXXXXXX

12 Mr Khaled Hejleh is the managing director of Globaltech and he gave unchallenged evidence that Globaltech manufactured the Orifinder v5 Tools and sold them to BLYA at “cost price”. Mr Hejleh also gave unchallenged evidence that the advantage of this business model is that it enabled Globaltech to take advantage of BLYA’s extensive and expensive global distribution channel and networks. As he saw it, Globaltech paid an amount of what would otherwise be part of the rental revenue in order to utilise the BLYA distribution channel.

13 The rental model used by BLYA involved the imposition of a daily charge based on the tool being used. Reflex’s model also involved the imposition of a daily charge, but its charge applied to the period the tool was out of its possession irrespective of whether the customer was using it on a particular day. Dr Michelle Lisa Carey, who was employed by Imdex as the Chief of Product Management and Marketing, said that Reflex charged on a daily basis whilst the customer had possession of the tool.

14 Reflex manufactures and supplies downhole instruments, including a digital core orientation tool or system known as the Reflex Advanced Core Tool or Reflex ACT. There have been various versions of the Reflex ACT. Reflex has a manufacturing facility at Balcatta in the State of Western Australia where it manufactures the tools it supplies, including the ACT Tool. It provides a number of its ACT Tools globally and domestically by way of hiring which it finds more profitable than sale. Its business in this area has grown.

15 Reflex seeks relief from Globaltech in relation to infringing tools which Globaltech sold to BLYA and which BLYA then rented to customers within Australia.

16 Reflex’s claim for damages is that it lost a number of rental opportunities by reason of Globaltech’s sale of the infringing Orifinder Tools to BLYA and that BLYA’s history of renting tools to its Australian customers reflects Reflex’s loss of opportunities on a one to one basis. Reflex’s damages are the lost profits from the rental transactions it would otherwise have entered into, but for Globaltech’s infringing conduct. This is one aspect of Reflex’s claim and I will refer to it as Reflex’s lost profits claim.

17 Globaltech also sold a number of infringing tools to BLYA which BLYA then provided to overseas entities which were related companies. These were tools which were shipped overseas by BLYA to be used as part of the Boart Longyear Group of companies’ overseas fleet. As with all the rental arrangements, Globaltech received royalty payments with respect to these tools and with respect to the tools “shipped overseas by BLYA to its related companies for their use”, Reflex claims an account of profits.

18 Reflex’s split election is based on what happened to the infringing tools after Globaltech sold them to BLYA and, in particular, whether they were used in Australia or exported from Australia.

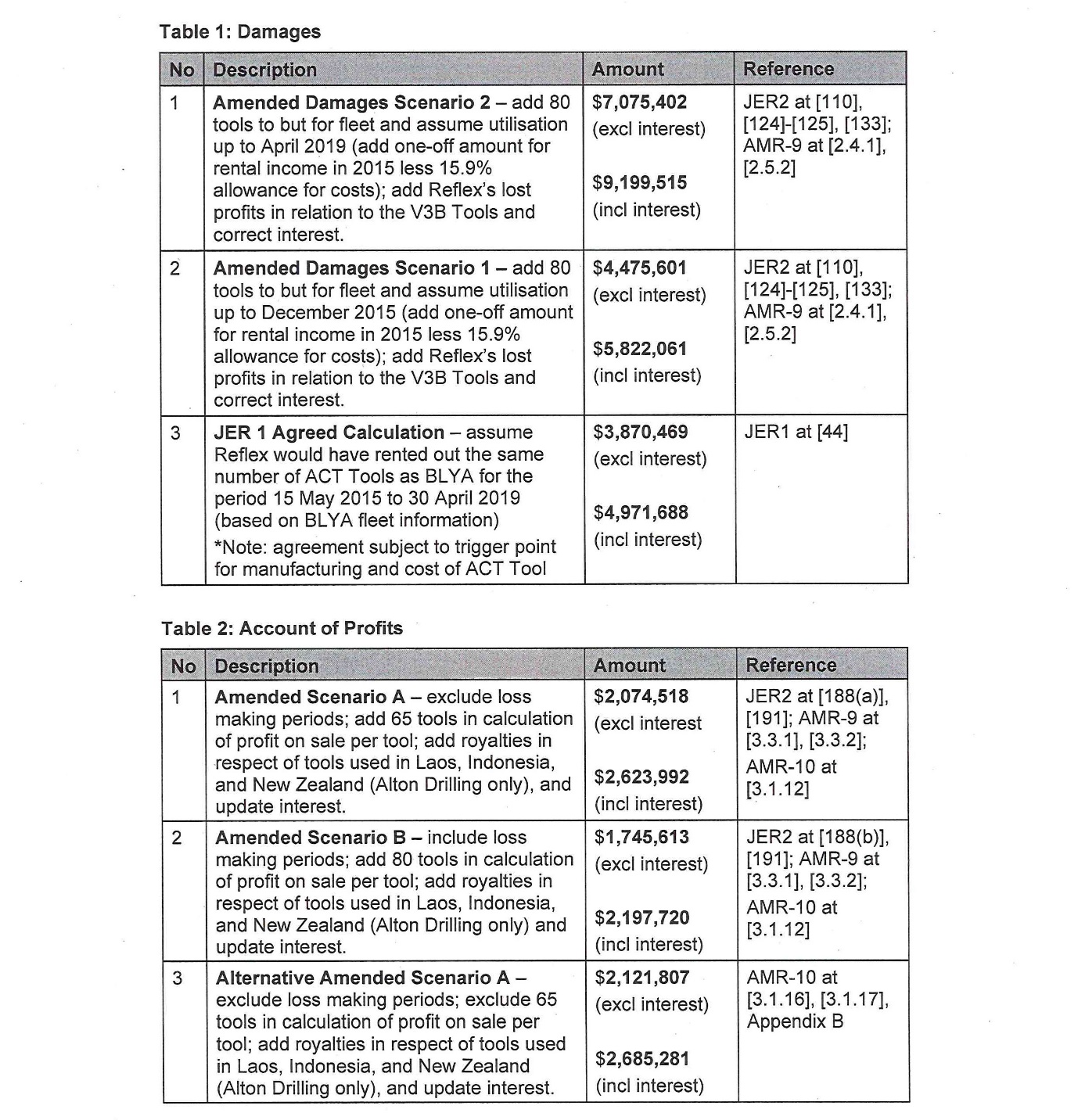

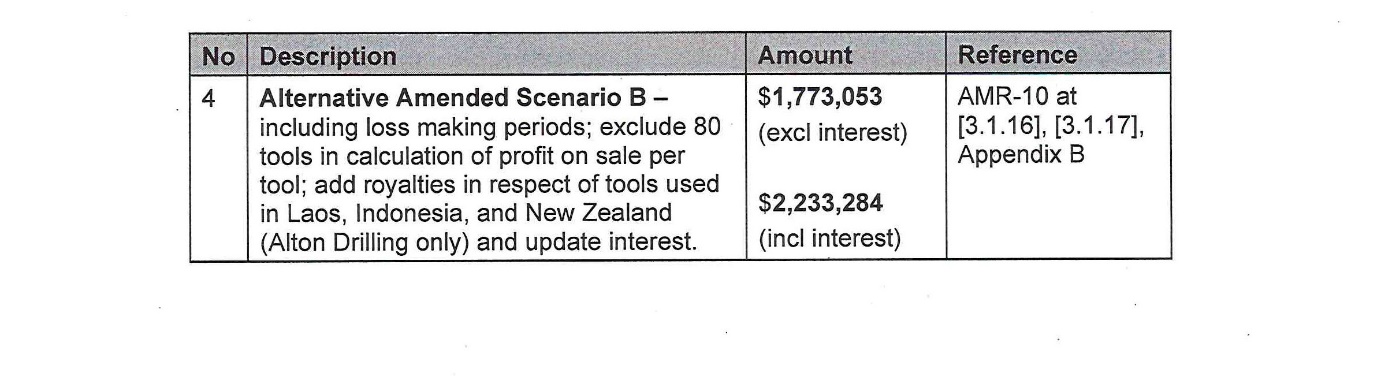

19 A summary of Reflex’s claims is as follows. Reflex’s primary case on damages is that it is entitled to the amount of $7,075,402 before interest. It has also put forward calculations of its damages which are lower than this figure and which are based on different assumptions. Reflex’s primary case on its claim for an account of profits is that it is entitled to $2,074,518 before interest. Again, it has put forward other calculations of its account of profits as alternatives. The document attached to these reasons and marked “Revised Annexure A” was prepared by Reflex and it sets out the alternatives advanced by Reflex with respect to its claims for damages and with respect to its claim for an account of profits.

The Validity of Reflex’s Split Election

20 The evidence establishes that between 2015 and 2019, Globaltech supplied at least 1,177 infringing Orifinder v5 Tools to BLYA. I put to one side for the purposes of considering the validity of the election, the supply by Globaltech of 16 infringing Orifinder v3B Tools in 2012. I also put to one side for the purposes of considering the validity of the election, the supply of 80 Orifinder v4 Tools by Globaltech to BLYA and the subsequent conversion of those tools by Globaltech to Orifinder v5 Tools in 2015. The issues arising in relation to those matters will be addressed later in these reasons.

21 The evidence establishes that of the 1,177 infringing Orifinder v5 Tools supplied by Globaltech to BLYA, 412 tools were used in Australia and 763 tools were exported from Australia. The small discrepancy in the figures of two tools is not material for present purposes.

22 Reflex’s election is to the effect that it claims the remedy of damages with respect to the 412 infringing tools used in Australia and it claims the remedy of an account of profits with respect to the 763 infringing tools which were exported from Australia.

23 Reflex submits that its election is valid. It submits that whilst it is true that s 122(1) of the Act refers to either damages or an account of profits, the right to elect arises in relation to each and every infringement and it is clear on the authorities that each and every supply of an infringing tool is a separate and distinct infringement. It claims that this is also illustrated by the way in which the limitation period provided for in s 120(4) of the Act is applied where there is a course of supply of an infringing product over time, some supplies within and some supplies outside the limitation period. Supplies outside the limitation period which, but for this circumstance would be actionable, cannot be the subject of relief, whereas within the limitation period can be the subject of relief. Reflex also pointed out that Globaltech had not identified a general principle in support of its submission.

24 Reflex relied on two authorities in which this Court has proceeded on the basis that a split election is valid and effective: LED Builders Pty Ltd v Eagle Homes Pty Ltd [1999] FCA 584; (1999) 44 IPR 24 (LED Builders) at [18] per Lindgren J and Aristocrat Technologies Australia Pty Ltd v Konami Australia Pty Ltd (No 3) [2022] FCA 1373; (2022) 170 IPR 42 (Konami) at [10] per Nicholas J.

25 Globaltech submits that Reflex’s split election is invalid. Some of its arguments seemed to be directed to the proposition that a split election can never be valid in any circumstances. As an alternative, Globaltech put a more limited proposition. As I understood the more limited proposition, it is that where there have been multiple infringements of a patent by the supply of the same or a similar product over a period of time, there needs to be some distinguishing feature between the supplies for which damages are claimed and the supplies for which an account of profits is claimed before a split election will be considered valid. Globaltech submits that there is no such distinguishing feature in this case. All supplies of the infringing tools were made by Globaltech to BLYA pursuant to the Distribution Agreements and no distinction was drawn in those agreements between tools which were to be used in Australia and tools which were to be exported from Australia. Furthermore, Globaltech submits that the two cases relied on by Reflex do not assist its argument because in both cases, there was no argument about the validity of the split election and in both cases there was a relevant distinguishing feature between the infringements.

26 Before considering these arguments, I record a submission made by Reflex to the effect that it had an alternative claim for damages should its election be invalid. It will not be necessary for me to deal with the submission and claim in this context because I hold Reflex’s election to be valid. Reflex contends that if the split election is invalid, it nevertheless has a claim for damages with respect to the 763 infringing Orifinder v5 Tools which were exported from Australia. Reflex does not put this claim for damages on the same basis as its claim for damages in relation to the 412 tools used in Australia. It submits that there are two, or at least one, other methods of calculating damages with respect to the 763 infringing Orifinder v5 Tools depending on the facts. The first of these other methods is a calculation of damages based on royalties under assumed licences of the 763 tools or some number thereof. To proceed to calculate damages in this way, there would ordinarily need to be evidence of licences and the royalties payable thereunder. The second of these other methods is a calculation of damages by reference to what has been called a reasonable user charge, it being assumed that Reflex would not have allowed another party to use its intellectual property rights without charge.

27 These alternative approaches to determining damages have been considered in a number of cases, including in Watson, Laidlaw & Co Ltd v Pott, Cassels & Williamson [1914] 31 RPC 104 at 117–120 per Lord Shaw; General Tire and Rubber Company v Firestone Tyre and Rubber Company Limited [1975] 2 All ER 173; (1975) 1B IPR 713 at 725–728 per Lord Wilberforce; [1976] 93 RPC 197 (General Tire); Meters Ltd v Metropolitan Gas Meters Ltd [1911] 28 RPC 157 at 163–165 per Fletcher Moulton LJ; Pearce v Paul Kingston Pty Ltd (1992) 25 IPR 591 at 592; and Winnebago Industries Inc v Knott Investments Pty Ltd (No 4) [2015] FCA 1327; (2015) 241 FCR 271 at [12]–[100] per Yates J.

28 Reflex submits that there is evidence of a reasonable royalty or (if necessary) reasonable user charge in the form of the royalty received by Globaltech as set out in the Distribution Agreements and that the experts could readily calculate the loss should that become necessary.

29 Globaltech submits that it is not open to Reflex to advance either of these methods of calculating damages with respect to the 763 tools because it is not how Reflex conducted its case at trial and this means that Globaltech has not adduced evidence that it might otherwise have done. Furthermore, Globaltech submits that even if Reflex is permitted to advance the claims, the evidence is not sufficient to establish the claims. If Globaltech is correct and Reflex’s election is invalid and if it is correct and it is not open to Reflex to put an alternative case based on a royalty under a licence or a reasonable user charge or such a case fails because of a lack of evidence, then subject to the issue concerning the 80 tools, Reflex’s case concerning the infringing Orifinder v5 Tools is limited to the 412 tools supplied by Globaltech to BLYA and used in Australia.

30 As I will now explain, I hold that Reflex’s election is valid and there is no need to consider Relex’s alternative argument in this context. I will need to return to the argument in a different and more limited context.

31 Reflex has elected between damages and an account of profits with respect to each infringement of the Patent, being the manufacture and sale or supply of an infringing tool. It is well established that an applicant cannot receive both damages and an account of profits for the infringement of a patent. The applicant must choose one or the other (Colbeam Palmer Ltd v Stock Affiliates Pty Ltd [1968] HCA 50; (1968) 122 CLR 25 (Colbeam Palmer v Stock Affiliates) at 32 per Windeyer J). It is equally well established that each act of patent infringement is a separate cause of action, being a statutory tort. The patentee or the exclusive licensee has a separate right to recover in relation to each act of infringement (Leplastrier & Co Ltd v Armstrong-Holland Ltd (1926) 26 SR (NSW) 585 at 591–592 per Harvey CJ; Black & Decker Inc v GMCA Pty Ltd (No 5) [2008] FCA 1738; (2008) 79 IPR 450 at [14] per Heerey J).

32 In both LED Builders and Konami, pecuniary relief was assessed and awarded on the basis of an account of profits for profit generating arrangements and damages for infringements which did not result in a profit. It is true that in neither case was the validity of the split election in dispute. That is one point of difference from this case. Globaltech submits that there is another point of difference. In Konami, the wrongdoer chose to make some supplies of infringing products (i.e., conversion of existing gaming machines) on a no charge basis and with respect to those supplies, Aristocrat claimed damages, and in LED Builders, the difference between the “account of profits infringements” and the “damages infringements” turned on whether or not the wrongdoer had commenced constructing houses using the infringing plans. Globaltech’s submission is that in this case, there is nothing in its conduct as the wrongdoer to distinguish between any of the supplies to BLYA. It supplied infringing tools to BLYA and it was up to BLYA and outside Globaltech’s control to determine whether the tools were used in Australia or exported from Australia. That is a point of difference, but it was never made clear how that was a material difference in terms of the innocent party’s right of election.

33 Globaltech submits that there is no case where the issue of a split election was disputed and the Court decided that a split election was valid. That appears to be true so far as my researches and those of counsel have been able to ascertain, but equally there is no case which has held that a split election is invalid. Globaltech sought to place some reliance on the way in which hearings as to liability (including any cross-claim alleging invalidity) and relief are ordinarily conducted in this Court. Where liability and relief are split, as they often are, the Court will not ordinarily in the liability hearing involve itself in identifying each and every infringement where the applicant’s case is of an allegedly infringing product being supplied over a period of time. That is probably correct, but I cannot see how that circumstance bears on whether or not split elections are valid. It seems to me that both LED Builders and Konami, and the latter in particular, provide good examples of why a split election ought to be allowed. Konami was not able to avoid the consequences of its infringements because its commercial arrangements resulted in it converting electronic gaming machines free of charge.

34 I am not persuaded by the other two major arguments advanced by Globaltech in support of its contention that Reflex’s election is invalid.

35 First, Globaltech submits that in some way, never clearly identified, there is an inconsistency between, on the one hand, the assumption underlying a claim for damages that 412 tools had not been supplied (i.e., as if the statutory tort had not been committed) and the assumption underlying a claim for an account of profits that 763 tools had been supplied and the statutory tort had been waived and the innocent party was entitled to the profits made by the infringer. The two remedies do proceed on a different basis, but I am unable to see how that affects the right of election.

36 Secondly, Globaltech submits that in some way, again never clearly identified, Reflex’s election was inconsistent with Reflex’s own business model of not differentiating between the revenue received from the supply of ACT Tools in Australia and the supply of ACT Tools in the rest of the Asia Pacific or APAC region. I am unable to see how the circumstance of Reflex’s treatment of revenue in its accounts affects the right of election.

37 In my opinion, absent leading authority or a clear general principle grounded in logic and sound policy considerations, the general principle that each infringement is a separate cause of action in respect of which the applicant has a right of election determines this issue. An applicant is entitled to exercise that right in a way that best suits its interests (Edelman J, McGregor on Damages (20th ed, Sweet & Maxwell, 2018) at [14-014]). It is not bound to exercise the election in a way that mitigates loss to the infringer. If an applicant chooses a split election that creates a difficulty for it in terms of the assumptions to be made and the facts that it must prove, then that is a problem for the applicant to resolve.

The Witnesses at the Hearing

38 Reflex called three witnesses at the hearing.

39 Mr Andrew Murray Ross is a chartered accountant and partner in the Sydney office of KordaMentha which is an investment and advisory firm. He practices as a forensic accountant. Mr Ross has over 30 years’ experience in the provision of financial advice, valuation and forensic accounting and his curriculum vitae indicates that he has assisted in quantifying economic loss in a wide variety of industries. Furthermore, he has substantial experience in providing expert evidence in cases before the courts.

40 Mr Ross has provided no less than five reports dealing with Reflex’s claims. The large number of reports came about for one or more of the following reasons: Mr Ross’ instructions being changed, including instructions about the assumptions he was to make, further documents being provided or further non-documentary evidence being put forward.

41 Mr Ross’ first report relates to Reflex’s claim for damages and his second report relates to Reflex’s claim for an account of profits. His third report relates to both claims, and his fourth report relates to the claim for an account of profits. Mr Ross’ fifth report was provided in response to a note prepared by Ms Dawna Kathleen Wright (exhibit R13), who was the expert called by Globaltech.

42 Mr Ross conferred with Ms Wright about the issues and they prepared two confidential joint experts’ reports. They gave concurrent evidence (or evidence in joint session) during the hearing and it is true (as Reflex submits) that there is a substantial measure of agreement between them as to the financial and accounting issues raised, including in relation to the overall methodology for both the claim for damages and the claim for an account of profits. There was no issue about the honesty of either of the experts.

43 Reflex also adduced evidence from two Imdex employees. The evidence-in-chief of these witnesses was given by way of affidavits and each of them was then the subject of short cross-examinations. There were objections to parts of the evidence-in-chief of these witnesses, but for the most part I overruled the objections holding that the objections really went to the weight to be accorded to the evidence.

44 Mr Leslie James McGill is employed by Imdex as the Operations Support Manager. At the time he swore his first affidavit, his position was that of Commercial Manager. He has sworn two affidavits, one on 2 April 2021 and the other on 23 March 2023 in connection with an order for discovery. The important affidavit is the first one.

45 At the time Mr McGill swore his first affidavit, he was responsible for managing all aspects of the commercial affairs of Reflex and Australian Mud, including “commercial analysis, management reporting, legal and operational support globally, and evaluating [the] performance of Reflex and AMC”. He said that he was also involved in supporting the product management and development function, amongst other duties. Mr McGill said that he had worked for Imdex for over 12 years in total and that during that time, he held various commercial and financial roles which he identified. They included Commercial Manager, Group Financial Controller, Group Reporting Manager and Assistant Company Secretary. Mr McGill described Reflex’s business and the accounting system of the Imdex Group. He also described the ACT Toolkit and the cost of the toolkit. Mr McGill prepared a spreadsheet which shows, among other things, the rental revenue generated by ACT kits in the APAC region for the period from July 2013 to January 2020. He described various aspects of the spreadsheet, including revenue and the utilisation rate.

46 The other Imdex employee was Dr Michelle Lisa Carey. Dr Carey affirmed two affidavits. As I have said, she is the Chief of Product Management and Marketing at Imdex. Dr Carey has been an employee of Imdex since 2012. She described her qualifications and experience. Dr Carey said that in her present role, she is responsible for making decisions as to which products will be developed by Imdex. This research and development process involves, among other matters, Dr Carey approving development of products and software, supervising and monitoring development of products and software, reviewing the product development cycle and deciding if a particular product or software should be commercialised once it has been developed.

47 Dr Carey’s responsibility during her time as an employee of Imdex included responsibility for monitoring the performance of instruments in the Reflex rental fleet. Dr Carey gave evidence as to the implementation and success of the Reflex rental fleet, the manufacture of ACT Tools, the management of the rental fleet, the composition and operation of the sales teams, market trends and conditions and the capacity of Reflex to manufacture additional ACT Tools. In her second affidavit, Dr Carey described the components in an ACT kit and the itemised cost of the components.

48 Mr McGill and Dr Carey were honest and straightforward witnesses. Globaltech did not suggest otherwise. Nor did Globaltech suggest that they were not qualified in the fields which they identified. Globaltech did criticise their evidence, but not on these grounds. Globaltech’s point was different. It accepted that some rental opportunities had been lost to Reflex as a result of its infringing conduct, but in calculating the extent of those lost opportunities, the general nature of the evidence adduced by Reflex, and the fact that it was not the best evidence otherwise available, weighed heavily against Reflex.

49 Globaltech also called three witnesses at the hearing.

50 I have already mentioned Ms Wright. She is a chartered accountant and a senior managing director of the forensic and litigation consulting practice at FTI Consulting. In that role, she provides services in the areas of forensic accounting, valuation and financial investigation. She has more than 20 years of experience and her experience includes as an expert witness, consulting expert and an expert determiner. Ms Wright prepared two reports and was the author of the note referred to earlier (exhibit R13). Ms Wright’s first report relates to Reflex’s claim for an account of profits and her second report relates to Reflex’s claim for damages. As I have already said, Ms Wright conferred with Mr Ross and there is a substantial measure of agreement between them. She is a co-author of the joint experts’ report and gave evidence with Mr Ross in the joint session.

51 Mr Khaled Hejleh is the managing director of Globaltech. He is familiar with all aspects of Globaltech’s business and technology. Seven affidavits and answers to interrogatories affirmed by Mr Hejleh were tendered and formed his evidence-in-chief.

52 Reflex submits that a number of Mr Hejleh’s affidavits were only required because he needed to correct or provide key qualifications to conclusions in other affidavits he had sworn. Reflex gave examples of where this had occurred, the most notable of which was his correction in his affidavit of 14 June 2023 of a statement he had made in his affidavit of 2 June 2023. Further, Reflex submits that this correction is evidence of the fact that Mr Hejleh was willing to rely on his recollection in the absence of business records on matters perceived to assist Globaltech’s case with the result that further details were required to present a full picture. Mr Hejleh’s evidence was that BLYA’s v5 Tools located overseas were returned to Globaltech and destroyed by it. Reflex issued a Notice to Produce dated 8 June 2023 in respect of that subject matter and that notice led to a return of only three handwritten documents. Reflex submits that Mr Hejleh then revealed in his oral evidence that some of the 763 Orifinder v5 Tools exported overseas may have remained overseas after September 2019. This is important because if that were so, then those tools would continue to result in the payment of royalty revenue to Globaltech and could have formed part of Reflex’s claim for an account of profits. The relevant passage in Mr Hejleh’s evidence is as follows:

And so what date, then, were all the v5 tools, located overseas, returned to Globaltech? ---They returned in bits and pieces with – we have no control on that. When they turn up, we – they get warranty immediately and then get destroyed after that date. We don’t – we have no control when they come back. All what we did is replaced everything. We – we supplied the replacement, new stock replacement for everything that was out there.

So it’s the case, is it, that there could be still some v5 tools located overseas that haven’t been returned?---Could be.

Yes?---No control on it.

53 Reflex submits that the inaccuracies and lack of detail in Mr Hejleh’s affidavits with respect to key matters, such as the total of tools manufactured as opposed to supplied, and the dates of revenue from the supply of infringing tools, had material costs consequences for it because it had to seek particulars and query details of various assertions or conclusions made by Mr Hejleh. It was submitted that these difficulties for Reflex were compounded by the fact that Globaltech’s business records were incomplete in some respects and production of material on relevant issues by Globaltech to Reflex was very slow, with some material only being served on the last day of evidence.

54 Reflex asks the Court to prefer the objective documentary evidence, being the financial records of Globaltech and BLYA, the evidence of the expert witnesses based on those records and the evidence of Mr Cameron, to the evidence of Mr Hejleh where there are any inconsistencies.

55 As I will explain later in these reasons, I found a number of aspects of Mr Hejleh’s evidence to be unsatisfactory.

56 Globaltech adduced evidence from a BLYA employee, Mr Joshua Brent Cameron, who is the Instrumentation Regional Manager APAC, Geological Data Services, of BLYA. He has affirmed three affidavits. Mr Cameron’s knowledge of BLYA’s activities prior to January 2016 was limited. The v3B Tools were supplied and sold in 2012 and Mr Cameron said that during the period from March 2012 to June 2014, he was an assistant driller/researcher. In other words, he was part of BLYA’s drilling services team and involved in deploying tools, including core orientation tools down holes. Mr Cameron agreed that in 2012, BLYA used Reflex’s Ace core orientation tools. From June 2014 to November 2019, Mr Cameron’s role at BLYA was as a Technical Representative – Geographical Data Services. He agreed that he was not involved in negotiating agreements on behalf of BLYA with manufacturers of downhole equipment and he agreed that he had no personal knowledge of the extent of any use or supply of any v4 or v5 Tools by BLYA before January 2016. He agreed that the first date upon which he became aware of BLYA supplying the tool called “TruCore” was in January 2016.

57 Mr Cameron produced a spreadsheet showing what he asserted was the total number of tools in BLYA’s total fleet of v5 Tools available for rent in Australia during the period from January 2016 to 30 April 2019 and the status of those tools, that is to say, whether they were on hire, out of service for repair etc., in a given month in that period. Mr Cameron produced a similar spreadsheet in a later affidavit.

58 Mr Cameron was an honest witness whose knowledge was limited. He was asked to address a number of precisely framed questions.

The Facts

59 I propose to deal with the facts in two parts or sections. First, I will set out my findings of fact in relation to a number of general matters and, in the course of doing so, I will also identify areas where there is a dispute as to the facts. Secondly, I will then deal with the specific factual disputes between the parties in the context of the particular issues to which they relate.

Reflex and Imdex

60 As I have said, Australian Mud and Reflex are wholly owned subsidiaries of Imdex and are part of the Imdex Group. Imdex is listed on the Australia Stock Exchange and it has related corporate bodies worldwide. The Imdex Group is a large group and it employs approximately 500 staff globally.

61 The Reflex ACT Tools form part of Reflex’s rental fleet which operates worldwide and includes Australia. For the purposes of Imdex’s accounting system, its operations are divided into five geographical regions as follows:

(1) Asia Pacific;

(2) Northern America

(3) South America;

(4) Europe;

(5) Middle East and Africa.

62 The Asia Pacific geographical region includes Australia, Papua New Guinea, Indonesia, Mongolia, Philippines, New Zealand and Cambodia.

63 Mr McGill has used APAC information in circumstances where Australia specific information is not identified within Imdex’s accounting and transactional system as this is the best information for the Australian market “that is available to me”.

64 In or about 2012, Imdex was moving the entirety of the Reflex instrument fleet to a rental model. Reflex hired a number of products both globally and domestically and those products included the ACT II and ACT III tools. I accept Dr Carey’s evidence that since 2012, the rental fleet, which includes the ACT Tools and other tools, has continued to grow in relation to rental based income and to establish itself as a market leader in the mining industry. That growth in the rental fleet is reflected in the annual reports for the period between 2015 and 2018. I also accept Dr Carey’s evidence that since 2012 and throughout the period from 2015 to 2019, the ACT Tools have been one of the most successful product lines in the rental fleet. The ACT Tools and their associated IP are treated by Imdex as Reflex’s most important assets.

65 Imdex continues to invest in research and development and has developed a next generation ACT Tool which is intended to replace the Reflex ACT III. The ACT-IQ was commercially demonstrated during the relevant period, but it was not contributing revenue as part of the rental fleet.

66 ACT Tools are among the most mature and durable products in the Reflex rental fleet. The durability and longevity of the tool means that, in relation to manufacturing, Reflex does not increase the fleet size in anticipation of older tools becoming unreliable, or a large number of older tools failing at the same time. Dr Carey described the ACT Tools as “low-touch, when compared to other rental tools, as the ACT Tools typically require little maintenance and few repairs”. ACT Tools are developed to withstand the harsh downhole environment. ACT Tools are built with no moving parts as the internal components are soldered together to reduce the likelihood of faults. I accept that evidence.

67 Since 2012, the ACT Tools have been supplied in kits which comprise two tools. It is a “two-tool system”. This mode of supply has now become industry standard. The Orifinder v5 Tool is also supplied in kits which comprise two core orientation tools.

68 There are significant peaks and troughs in the mineral exploration industry. The exploration phase of the mining life cycle generally occurs over a series of campaigns across a period of anywhere between two and ten years and each of the campaigns typically lasts for around three to six months. During this time, an ACT kit is usually required to remain onsite, depending on the type and length of the exploration campaign. The remaining phases of the mining cycle, post-exploration, may last decades depending upon the size of the mine. A diamond exploration drilling rig can work for up to 24 hours a day and during this time, each individual core orientation tool, assuming there is a two-tool system, may be required to perform for up to 12 hours a day. A core orientation tool performs an average of between 10 to 20 orientation readings per day, depending on the hardness of the drilling environment and the length and diameter of the core involved.

69 In the Australian market, an ACT kit is typically hired two to four times a year depending on the length of the drilling campaign. The tool remains in the rental fleet and is continuously hired to different customers throughout its lifespan. A typical rental agreement between Reflex and a customer includes the “Master Customer Agreement” and customers are responsible for all costs associated with renting the Reflex tools, including, among other costs, freight, service charges, consumable items and repairs and recalibration of the tools that are misused or damaged as a result of negligence on the part of the customer. Rental charges are incurred from the time a customer collects an ACT kit or the time the kit is dispatched from the Reflex facility or warehouse until the time it is returned. The rental rate is charged daily and under the terms of the Master Agreement, can be charged regardless of whether the tool is being used. ACT kits delivered in Australia typically reach the nominated site within approximately a week of being dispatched by Reflex. It follows from what I said earlier that Reflex charges for this period as the daily rental rate is applied from the time the ACT kit leaves the Reflex facility or warehouse until it is returned. Customers are not required to return the ACT kit to any particular Reflex facility. Reflex instead gives customers the option to return the kit to any Reflex warehouse or facility.

70 Both Mr McGill and Dr Carey described the components in an ACT kit. Their descriptions are not inconsistent. I accept both accounts, although I found Dr Carey’s description the clearer of the two.

71 Mr McGill said that ACT Tools are supplied in kits consisting of two ACT Tools, being downhole units, one controller and a selection of running gear, being equipment and consumables relevant to the operation of the ACT Tools in the field. Mr McGill produced data which identified the current range of ACT kits, the accompanying components and the associated manufacturing costs as at January 2021. That data was in the form of a spreadsheet which he said was used to calculate the total standard material costs of an ACT kit and for the purposes of reporting and budgeting. The material produced by Mr McGill did not include other costs of goods sold, expense items such as repairs, consumables and freight. His evidence was that an ACT kit comprises components which fall into two categories, being optional or compulsory. He described the compulsory components as referring to components that must be supplied in each ACT kit and that includes the two ACT Tools. The optional components refer to components that may vary in the ACT kit which includes running gear, consumables and handheld devices. In the case of handheld devices, such a component is required for the operation of the ACT Tools, but the customer has a choice to select from different models. In those circumstances, the handheld devices are classified as optional. Mr McGill said that running gear and consumables are also classified as optional components as these components may vary from each ACT kit depending on the size of the ACT Tool. Mr McGill’s instructions were to the effect that certain optional components were only included in an ACT kit when expressly requested by a customer and those components included the ACT III docking station and the ori-auditor and core removal tool componentry. The cost of the controller varies. The manufacturing costs also vary depending upon the core size with the core size “H” being the most expensive size ACT Tool in the range.

72 One of the documents produced by Mr McGill was a schedule showing the total price for “a common kit type” and that includes a figure identified as “running gear” or “optional items” with notations against that figure as follows: “Assume all running gear” and “assume all optional items are taken”.

73 Dr Carey said that an ACT kit consists of the following:

(1) a Pelican case;

(2) two downhole units, being the two ACT Tools;

(3) a handset controller, being either the Reflex ACT II or ACT III controller;

(4) a barrel extension;

(5) a marking jig;

(6) a user guide;

(7) a docking station; and

(8) miscellaneous consumables.

74 Dr Carey produced a spreadsheet generated by Imdex’s computer system which identifies the current components of an ACT kit and other related products that are sold separately. This is the same document produced by Mr McGill. Reflex offers its customers the option to purchase additional components that are set out in the ACT kit schedule which are not supplied in a standard ACT kit. These components are not essential for the use of the ACT Tools in core drilling operations. However, they provide a stream of revenue for Reflex. For example, a customer can purchase a core removal tool which is used to remove a core sample that is stuck inside a lifter case while protecting the end of the core sample from damage.

75 There is a dispute between the parties about the manufacturing costs of an ACT kit which is addressed in the next section which deals with the specific issues.

76 Mr McGill produced a spreadsheet showing, among other things, the rental revenue generated by ACT kits in the APAC region, including Australia, for the period July 2013 to January 2020 (Confidential Annexure LJM-5). The utilisation of tools is a percentage figure representing the relationship between the number of tools on hire and the number of tools in the fleet. Before Reflex manufactures an ACT Tool, a capital expenditure request must be raised and approved by the management of Imdex. Capital expenditure requests are considered by Imdex management with respect to overall ACT fleet availability and once approved, instructions are given to the Imdex facility in Balcatta to commence the manufacture of ACT Tools.

77 The figures for rental revenue generated from the ACT kits are figures for the APAC region, including Australia. APAC ACT customers are charged a daily rental rate as well as an additional loss or damage protection “coverage rate”, if so, elected by the customer, per ACT kit which is invoiced monthly. A coverage rate is an additional daily charge paid by customers to protect against the risk of accidental damage or loss. The customer can elect to pay a coverage charge which increases the daily rental rate. If the coverage charge is applied, Reflex assumes the risk and customers are not liable for the cost of replacing the tool where it is lost or damaged in the ordinary course of business. In the event that the customer does not pay the coverage rate and the tool is lost or damaged in the ordinary course of business, the customer is liable to pay for the cost of replacing the tool as determined by Reflex or as agreed between the parties.

78 Mr McGill agreed in cross-examination that he could have details of the revenue for ACT Tools in Australia.

79 ACT Tools are manufactured at Imdex’s manufacturing facility at Balcatta.

80 Reflex maintains an inventory of the components for ACT Tools at its facility in Perth for the purposes of repairs, servicing and manufacturing. Dr Carey expressed the opinion, which I accept, that the manufacture of an ACT Tool is relatively simple as the tool is modular and the parts are largely preassembled. In her experience, a single Reflex technician can assemble several ACT Tools in a day, including any calibrations required. Reflex typically stores at least three months’ anticipated supply of components for its rental tools onsite in inventory to avoid any shortages. In cross-examination, Dr Carey said that she could have provided by way of evidence, more detail of the inventory held by Reflex, such as the number of parts held in any particular month.

81 Reflex controls both the labour and materials involved in the manufacturing process for ACT Tools and it does not experience capacity restraints in relation to the manufacture of additional tools. Imdex has an established framework that streamlines supply chains and ensures that it is able to adjust to rapid changes in sourcing volumes and changing customer needs. Reflex has continued to review all aspects in relation to warehouse locations, inventory turns, risk management of key products and logistics and customer service to improve its supply chain.

82 Reflex is the sole manufacturer of ACT Tools. It controls their manufacture, supply and distribution. The tools are distributed to customers through Reflex’s national and global offices, warehouses, and authorised agents and distributors.

83 Dr Carey believes that during the relevant period, the supply of ACT Tools was impacted by rentals of infringing Orifinder core sample orientation tools supplied by Globaltech that would otherwise have been supplied by Reflex. Dr Carey expressed the belief that Reflex would have been able to ensure capacity to manufacture additional ACT Tools, if necessary, in a short period of time by adopting two strategies. First, Reflex could have diverted resources, including stopping all non-essential work, to focus on manufacturing ACT Tools. Dr Carey gave an example. If an unexpected request meant that ACT Tools were required within a month, production for other tools, such as the Reflex EZ-GYRO and Reflex EZ-TRAC survey tools, could have been stopped and resources be reallocated strictly to the manufacture of ACT Tools. Servicing and repair teams could have been instructed to assist with manufacturing and the sales and sales support team could have assisted with packaging ACT kits. Secondly, in Dr Carey’s experience, demand for ACT Tools was typically limited to the most popular sizes, such as the N2 and HQ. It was therefore possible to resize the ACT Tools stored in inventory. This process is relatively quick and simple as the internal electronic components for all ACT Tools are the same. The manufacturing and service departments can resize a tool by removing the internal electronic components and simply placing them into a different outer casing.

84 Reflex has procedures in place for tools to be transferred from different countries to account for any shortfalls in the rental fleet. Reflex considers that all of its tools are global. However, the transfer of ACT Tools and rental tools in general is not a common practice to satisfy a small one-off demand due to the additional costs involved.

85 There is a dispute between the parties as to Reflex’s capacity to manufacture additional ACT Tools in the manner Reflex asserts which is addressed in the next section which deals with the specific issues.

86 I have already referred to the concept of utilisation of tools and to the fact that this refers to the number of ACT kits “on hire” expressed as a percentage of the total APAC ACT rental fleet each month. It is related to an area of substantial dispute between the parties.

87 The way in which Reflex operates its business is that ACT kits are classified into three categories. First, “available” refers to ACT kits that are ready and available to be hired to customers. These include tools which are stored in Reflex’s warehouses or the warehouses of distributors. Secondly, “unavailable” refers to ACT kits that are not available for rent due to a range of reasons, including being in transit between locations, undergoing service or repair, or being held on a customer’s site as a spare tool. Thirdly, “on hire” refers to ACT kits that are currently being hired by customers and generating revenue.

88 Mr McGill said that in his experience the maximum practical utilisation percentage that Imdex typically reaches for the APAC region is between 55 to 60%. He referred to this as the Utilisation Threshold. He explained that at this threshold, it will typically become difficult in practical terms to operate because ACT kits are dispersed across multiple customer sites, often in remote locations, multiple Reflex warehouses (Perth, Kalgoorlie and Brisbane) and across nine different size variants, making it difficult to ensure that the correct size ACT kit can quickly be made available in the correct location to meet customer demand. Mr McGill said that the remaining 40 to 45% of ACT kits are recorded as either unavailable or available, but not on hire due, for example, to the kit being in the incorrect location or of the wrong size. Mr McGill said that a utilisation of 100% is therefore not practically possible. He said that once the Utilisation Threshold was reached, there will typically be an increase in the number of capital expenditure requests coming from the Reflex general managers. A capital expenditure request is a request to build additional ACT Tools and hence expand the fleet to meet customer demand.

89 The information produced by Mr McGill in relation to the topic of the cost of goods sold related to the APAC region between July 2014 and January 2020 inclusive. Mr McGill said that he was satisfied that the APAC cost of goods sold was representative of Australia. He formed the conclusion that Australia represented such a large percentage of APAC revenue and that since all Reflex tool types were offered across the whole APAC region, he was satisfied that the APAC cost of goods sold is representative of Australia.

90 Both Mr McGill and Dr Carey gave evidence about selling costs in relation to the tools and the activities of sales and sales support staff. Their evidence was not inconsistent. Dr Carey’s evidence was more detailed. I accept the evidence, subject to a consideration of the complaints made about it by Globaltech.

91 Mr McGill prepared information for the relevant sales and sales support staff for the APAC region, including Australia. The sales and sales support staff are employed on a fixed salary basis and not on a commission basis. Mr McGill described them as core members of the Reflex team. His evidence was that the team had undergone little change over the relevant period despite Reflex’s product offering expanding over the relevant period and thereby increasing business complexity.

92 Dr Carey said that Imdex has a separate sales and sales support team for each geographical region. The composition of the sales team since 2012 has remained static despite market volatility and both seasonal and cyclical changes in customer demand. The sales team has the capability to service a large number of customers without additional assistance as the rental fleet operates efficiently with minimal intervention once the rental agreement and the rental details are entered into the system and the status of the tool is changed. It is common for a single customer to hire several ACT kits at a time so that not every new hire requires significant involvement from the sales team. Furthermore, ACT Tools do not often fail and customers are familiar with the product and the sales team is rarely required to arrange for replacements to be sent to customers or organise training demonstrations. The work of a sales representative cannot be performed by a contractor or a consultant because of the level of expertise required. If there is a spike for customer demand for ACT Tools, the sales team is typically required to work harder and longer to service customers rather than additional members joining the team. In cross-examination, Dr Carey agreed that she was not involved in the actual negotiation of rental contracts and that she could have provided details such as the names and hours worked of sales staff.

The Market for Electronic Core Orientation Tools

93 During the period from a time in 2015 to 2019, the ACT Tools were the only electronic core sample orientation tools available on the Australian market other than the infringing electronic core orientation tool referred to as the Orifinder v5 Tool or the TruCore Tool. There was at one point another orientation tool known as the ORIshot and supplied by a company called Coretell Pty Ltd, but that tool was held to infringe certain innovation patents (Australian Mud Company Pty Ltd v Coretell Pty Ltd (No 4) [2015] FCA 1372).

94 Globaltech does not dispute that between 2015 and 2019 and up to the present day, the majority of exploration mining companies use electronic core orientation tools to orientate recovered drill samples. A small proportion of the core orientation market has not transitioned to electronic methods and continues to use mechanical methods to orientate core. This small proportion of the market primarily relates to mining exploration companies who are drilling vertical or near vertical holes. This small proportion of the Australian market would have been unlikely to have ever rented an Orifinder v5 Tool or any other electronic tool during the relevant period. If the Orifinder v5 Tool had not been in the market and such a customer needed to rent a core orientation tool, they would have rented another mechanical device and did not have to rent an electronic tool from Reflex.

Globaltech

95 Globaltech supplied Orifinder v3A kits between October 2011 and approximately April 2012 to potential customers outside Australia only. They are not part of Reflex’s claim in this proceeding. The Orifinder v3B kits were supplied between April 2012 to approximately 31 October 2012 to customers both in Australia and overseas. According to Mr Hejleh, sales of the Orifinder v5 Tools commenced in May 2015 and ceased in January 2019. “Orifinder income” generated within the period 1 November 2012 to 30 April 2015 was in relation to a tool known by the parties as the Orifinder “v4” Tool which does not form part of these proceedings. The development by Globaltech of the Orifinder Tools commenced in 2009.

96 During the relevant period, according to Mr Hejleh, Globaltech’s sole customer for the sale of the Orifinder v5 Tools in Australia was BLYA and Globaltech did not sell or rent the Orifinder v5 Tools to any other customers in Australia. BLYA branded the Orifinder v5 Tools it purchased from Globaltech as “TruCore”. Globaltech has never used a rental model for its Orifinder Tools. It manufactured and sold those tools to BLYA at cost price, but it did not retain any property rights in the Orifinder v5 Tools upon their delivery to BLYA. It was a matter for BLYA as to what it did with those tools.

97 Mr Hejleh said that BLYA has an extensive and expensive distribution channel and networks which are very costly as they require hundreds of personnel, multiple warehouses in many countries, global logistics, legal support and the like. Globaltech does not have such a network. It sells its tools at cost price and it derives a percentage of BLYA’s rental revenue. This made commercial sense to Globaltech as it effectively paid an amount of the rental revenue it might otherwise have received to utilise the BLYA distribution channel. I have already referred to this evidence. I accept it in general terms.

98 Globaltech supplied 18 v3B kits between April 2012 and approximately 31 October 2012. Mr Hejleh said that 1,276 Oritool v5’s were supplied by Globaltech and 924 Oripad v5’s were supplied by Globaltech. Before it commenced the supply of the Orifinder v5 Tools, Globaltech supplied a tool known as the v4 Tool. Australian Mud and Reflex, or their parent and subsidiary companies, alleged that the v4 Tool infringed Patent No 2008229644 in proceeding number NSD 142 of 2015. That is a different patent to the one which is the subject of the present proceedings. Globaltech denied infringement. On 21 September 2015, Globaltech and Imdex Global BV executed a Deed of Settlement which granted a release to Globaltech in relation to the supply of v4 Tools. On 19 October 2015, a judge of this Court made orders by consent in the v4 proceedings whereby Globaltech was required to cease making, hiring, selling or otherwise disposing of, offering to make, hire, sell or otherwise dispose of, using or importing, or keeping for the purpose of doing any of those things, the core orientation tool marketed or sold under the name of Orifinder version 4. Those orders were made after the Court was informed by Globaltech that sales of the v4 Tool had ceased several months earlier and Globaltech was willing to abandon the v4 Tool and settle the proceedings since it had developed a new core orientation tool, being the v5 Tool.

99 A spreadsheet in Globaltech’s business records indicates that it supplied BLYA with a total of 80 v4 Tools. In expectation of the settlement of the v4 proceedings, BLYA returned the v4 Tools to Globaltech and Globaltech replaced those tools with v5 Tools. Mr Hejleh’s recollection is that the replacement with the v5 Tools occurred in or about July to August 2015 which was about one to two months before the Deed of Settlement was signed. However, Globaltech does not have any records to allow him to be more precise with the exact dates of receipt of the v4 Tools and replacement with the v5 Tools. The dates are matters of dispute.

100 Mr Hejleh says that to the best of his knowledge all sales, revenue and royalties relating to Globaltech’s supply of v5 Tools to BLYA was included in the figures he previously provided in answers to interrogatories and in his previous affidavits. Mr Hejleh produces invoices for royalty payments for use by BLYA of what he says were v4 Tools between January 2015 and July 2015. He said that none of the invoices relate to the v5 Tools as the v5 Tools had not been developed, manufactured or supplied to BLYA during the periods identified in the invoices. Mr Hejleh asserts that Globaltech does not have any records showing where or when the replaced v5 Tools were used by BLYA. He does say that Globaltech’s business records do not show that it received any royalties for BLYA’s use of the v5 Tools until February 2016. In other words, no royalties were received before February 2016.

101 There is a substantial dispute between the parties as to how, if at all, the 80 tools affects Reflex’s lost profits claim and this dispute is addressed in the next section of these reasons.

102 Mr Hejleh asserted in his evidence that following orders made in the present proceedings and in or around February 2019, Globaltech began replacing v5 Tools which had been supplied to BLYA with an alternative core orientation tool which was known as the “UPIX” Tool. He said that BLYA’s v5 Tools that were located in Australia were returned to Globaltech’s Forrestfield premises and destroyed by Globaltech’s production staff. Replacement UPIX Tools were shipped to BLYA. He states that by March 2019, all v5 Tools located within Australia had been replaced by the UPIX Tool. BLYA’s v5 Tools that were located overseas were returned to Globaltech’s Singapore premises and destroyed by Globaltech’s production staff in Singapore. A replacement UPIX Tool was shipped from Singapore to BLYA outside of Australia. He said that by September 2019, all v5 Tools located overseas had been replaced by the UPIX Tool. As I have already indicated, under cross-examination, it is apparent that Mr Hejleh was no longer able to assert this. He said that no royalties were received by Globaltech in respect of the use of the v5 Tools by BLYA within Australia after March 2019, and outside Australia after September 2019. Royalties after those dates resulted from the use by BLYA or its customers of the UPIX Tool. Mr Hejleh corrected one of his statements in a later affidavit. He said that BLYA’s v5 Tools that were located overseas were returned to Globaltech’s Australian premises and destroyed by Globaltech’s production staff in Australia. A replacement UPIX Tool was shipped from Singapore by BLYA outside of Australia.

BLYA

103 Mr Cameron states that the BLYA fleet of v5 TruCore Tools was in use by BLYA in the sense that the product fleet was rented or available to rent by BLYA’s customers in Australia from January 2016 through to 30 April 2019 because the records he had indicated usage of tools from January 2016 (albeit only one unit) ending in April 2019. Mr Cameron was asked by those instructing him to provide data in respect of the utilisation rates of the BLYA fleet during that period. In his response, his focus was on the period from January 2016 through to 30 April 2019. He refers to this as the v5 TruCore fleet period. Mr Cameron produced a document from BLYA’s records which shows the total number of tools in BLYA’s total fleet of v5 TruCore Tools available for rent in Australia during the v5 TruCore fleet period and the status of those tools, that is to say, whether they were on hire, out of service for repair etc., in a given month in the v5 TruCore fleet period. Again, by reference to the period from January 2016 to 30 April 2019, Mr Cameron identified the number of v5 TruCore Tools BLYA purchased from Globaltech as 1,176 tools or 588 kits. He identified the number of those tools which remained in Australia to be used as part of BLYA’s Australian based fleet as 412 tools or 206 kits. BLYA also hired out tools in the wider APAC region which, in BLYA’s case, means Australia, Laos, Indonesia and New Zealand and Mr Camerson identified that it supplied by way of export 42 tools or 21 kits to Indonesia, Laos and New Zealand. Finally, Mr Cameron identified the number of tools which were shipped overseas by BLYA to be used as part of the Boart Longyear Group of companies overseas based fleet and were not at any time used in Australia as 763 tools.

104 In his third affidavit, Mr Cameron corrected a statement he made previously about the number of tools “on hire” in a given month. He said that he did not mean to suggest that the number of tools identified as being “on hire” for any given month were each on hire for the full 30 or 31 days in each such identified month. He said that in any given month, some or all of those tools which he identified as being “on hire” may have been hired for a lesser number of days within that month. The number of days that a tool is on hire in a month at a given customer is recorded in the BLYA monthly royalty reports and Mr Cameron was responsible for generating these reports during the period from January 2016 to January 2019. Mr Cameron produces the monthly royalty reports for these months. In addition, he has extracted data from BLYA’s records for the months of February 2019 to April 2019.

105 The two matters referred to in the last two paragraphs are disputed issues in the case: the first as to whether the total tools “sold” included the 80 tools and the second as to whether the days on hire for BLYA should be reflected in Reflex’s loss of opportunities.

An Introduction to the Issues

106 This is a case where substantial efforts were made, particularly by the experts, to identify issues for the Court’s resolution without the need for evidence in proof of facts which upon careful consideration could be the subject of agreement. As I have said, by the time the hearing had finished, Mr Ross had provided no less than five expert’s reports and Ms Wright had provided two reports and her note. Furthermore, in the second half of 2022, the parties had identified what each of them considered to be the issues. Following that, the experts conferred on at least two occasions and following those conferences, they produced joint experts’ reports containing a statement of the matters upon which they agreed and a statement of those matters upon which they disagreed. That was all done with a view to identifying the issues at the hearing as precisely as possible. That result was largely achieved and, to the extent it was not, that seemed to be because of changes in instructions, including as to assumptions, or the production of further evidence, including documents.

107 I mention these circumstances because they mean that I can approach the matters requiring determination by reference to the issues as defined by the parties, and not by, in effect, “starting from scratch” with Mr Ross’ first report.

108 There were some matters raised earlier in the proceeding which were in dispute that are no longer in dispute.

109 First, there is no longer an issue about whether royalties payable in relation to the use of the infringing tools overseas which use does not infringe the Australian Patent can be taken into account in Reflex’s account of profits claim. Globaltech now accepts that those royalties can be taken into account. Secondly, whilst there is a remaining issue about interest, the experts agree about the methodology to be used. Thirdly, there was an issue as to whether, and to what extent, taxation should be taken into account in the award of pecuniary relief. That matter is no longer in dispute because Globaltech accepts that an award of pecuniary relief in this proceeding is to be made on a pre-tax basis. There remains a relatively minor issue about whether a small discount on the award for an account of profits should be made on the basis that Globaltech has in all likelihood paid tax on the profits it received and (so it is contended) may have difficulty recovering that tax or will experience delay or incur costs on doing so.

110 I turn now to address each of the issues. As I understand it, both parties accept that should any one or more of my conclusions mean that there is a need for further calculations to be performed, that can be done relatively quickly by the experts by appropriate variations to the modelling they have already carried out.

Damages

Introduction

111 Leaving aside the effect of Ms Wright’s note (exhibit R13) which I will come back to, the starting point for the damages claim is the JER1 Agreed Calculation set out in Revised Annexure A. This is a calculation about which the experts agree, subject to certain qualifications. The qualifications are as follows.

112 First, there is an assumption in the JER1 Agreed Calculation of a one to one relationship between the number of rentals of infringing tools and the rentals which would have been achieved by the innocent party in the “but-for” counterfactual that is said by Globaltech to be unrealistic. There must be, according to Globaltech, a reduction for contingencies and uncertainties. That reduction can be applied at the level of the one to one assumption or at the end of the overall calculation, but in either case, it should be a substantial discount.

113 Secondly, there is an assumption in the JER1 Agreed Calculation about the Utilisation Threshold, that is, the point at which Reflex would have needed to manufacture additional tools and, therefore, incur additional costs, in order to meet the additional demand for tools envisaged in the but-for counterfactual. There is a dispute between the parties about the appropriate assumption in that respect.

114 Thirdly, there is an assumption in the JER1 Agreed Calculation about the cost of manufacturing each new ACT Tool which must be taken into account in the but-for counterfactual. There is a dispute between the parties about the appropriate assumption in that respect.

115 Finally, there is a dispute about whether there are lost profits in relation to the Orifinder v3 Tools which should be added to the JER1 Agreed Calculation.

116 I turn now to the other two scenarios in Revised Annexure A. Reflex has abandoned any claim for a one-off amount for rental in 2015 less 15.9% allowance for costs and so that may be put to one side. The claim for Reflex’s lost profits in relation to the v3B Tools speaks for itself.

117 The major difference between the JER1 Agreed Calculation on the one hand, and the two Scenarios on the other, is the 80 tools being an assumption that, in addition to the tools on hire assumed in the JER1 Agreed Calculation, there are another 80 tools on hire in the but-for counterfactual until December 2015 in the case of Scenario 1 and until April 2019 in the case of Scenario 2. The issue concerning the additional 80 tools is described in detail and addressed below. There are also a number of issues involving the 80 tools and those issues include the following: (1) whether the 80 tools should be taken into account at all; (2) whether they should be taken into account until December 2015 or until April 2019; (3) whether it should be assumed that the 80 tools were fully utilised or partially utilised; and (4) whether they should be included in the cost per Orifinder v5 Tool for the purposes of the calculation of the account of profits.

118 Before leaving this general introduction, I return briefly to Ms Wright’s note. That was a substantial issue raised by Globaltech late in the course of the proceeding. The note was prepared by Ms Wright following her receipt of the third affidavit of Mr Cameron affirmed on 14 June 2023. In that affidavit, Mr Cameron referred to his earlier affidavits in which he produced documents showing the infringing tools “on hire” in a given month. I have already referred to his evidence. Nevertheless, his precise evidence is worth setting out. It is as follows:

6. In doing so, I did not mean to suggest that the number of tools identified as being “on hire” for any given month were each on hire for the full 30 or 31 days in each such identified month. In any given month, some or all of those tools which I identified as being “on hire” may have been hired for a lesser number of days within that month.

7. The number of days that a tool is on hire in a month at a given customer is recorded in the BLYA Monthly Royalty Reports. I was responsible for generating these reports during the period January 2016 through to January 2019. Annexed to this affidavit and marked Confidential Annexure JBC-4 is a copy [of] these reports for each of these months. I did not generate these reports from February 2019 onwards, and so I also annex as part of Confidential Annexure JBC-4 data that I have extracted from the EZRentOut system for the months February 2019 to April 2019.

119 Ms Wright adjusted her damages calculation in the JER1 Agreed Calculation ($3,870,469 before interest) by apportioning for the days the kits were actually hired based on the Monthly Royalty Reports produced by Mr Cameron. This results in a reduction from $3,870,469 to $1,695,221 in the JER1 Agreed Calculation. Mr Ross disagreed with this approach and is of the opinion that there should be no reduction for this reason. This dispute is addressed below. As I understood Globaltech’s submission, it was that even if this matter did not support a precise reduction of the order put forward by Ms Wright, it did support, together with other factors, a substantial discount in the order of 30 to 40% to the amount that might otherwise be awarded.

One to One Assumption and Discounts

120 Reflex’s business model was to manufacture a fleet of electronic core orientation tools which it hired or rented out to customers in Australia. It made profits on those transactions. Globaltech’s business model was different. It manufactured the infringing tools and sold them (at cost according to Mr Hejleh) to BLYA. It was BLYA which then assembled a fleet of tools and made those tools available to be hired or rented out in Australia. Reflex seeks to use BLYA’s hiring out or rental figures to establish its loss of hiring or rental opportunities. There is nothing inherently flawed in approaching the matter in that way.

121 The experts agreed as to the appropriate general methodology for the determination of Reflex’s loss of profits as a result of Globaltech’s infringements and that was the identification and then comparison of actual cashflows to Reflex and the “but-for” cashflows. The but-for cashflows involve an identification of the position Reflex would have been in had the infringements not occurred and the cashflows which would have resulted.

122 The starting point in the analysis is the identification of the relevant principles in circumstances where the Court is dealing with a but-for counterfactual. I do not think that the parties were in dispute about the relevant principles, as distinct from their application to the facts of this case. Reflex submits that the one to one assumption is justified on the facts of the case, whereas Globaltech submits that absent a practical certainty (which is not shown here), there must always be discounts for contingencies and the uncertainties.

123 The matter which is the subject of the Court’s consideration is a state of affairs which is a hypothetical or a counterfactual. It is not a historical fact. The law takes a different approach in the case of a hypothetical or a counterfactual. The distinction was identified by Brennan J (as his Honour then was) and Dawson J in Malec v JC Hutton Pty Ltd [1990] HCA 20; (1990) 169 CLR 638 in the following passage (at 639–640):

The fact that the plaintiff did not work is a matter of history, and facts of that kind are ascertained for the purposes of civil litigation on the balance of probabilities: if the court attains the required degree of satisfaction as to the occurrence of an historical fact, that fact is accepted as having occurred. By contrast, earning capacity can be assessed only upon the hypothesis that the plaintiff had not been tortiously injured: what would he have been able to earn if he had not been tortiously injured? To answer that question, the court must speculate to some extent. As the hypothesis is false — for the plaintiff has been injured — the ascertainment of earning capacity involves an evaluation of possibilities, not establishing a fact as a matter of history. Hypothetical situations of the past are analogous to future possibilities: in one case the court must form an estimate of the likelihood that the hypothetical situation would have occurred, in the other the court must form an estimate of the likelihood that the possibility will occur. Both are to be distinguished from events which are alleged to have actually occurred in the past. Lord Diplock said in Mallett v. McMonagle:

“The role of the court in making an assessment of damages which depends upon its view as to what will be and what would have been is to be contrasted with its ordinary function in civil actions of determining what was. In determining what did happen in the past a court decides on the balance of probabilities. Anything that is more probable than not it treats as certain. But in assessing damages which depend upon its view as to what will happen in the future or would have happened in the future if something had not happened in the past, the court must make an estimate as to what are the chances that a particular thing will or would have happened and reflect those chances, whether they are more or less than even, in the amount of damages which it awards.”

(Citation omitted.)

124 Justices Deane, Gaudron and McHugh made a similar point when their Honours said (at 642–643):

A common law court determines on the balance of probabilities whether an event has occurred. If the probability of the event having occurred is greater than it not having occurred, the occurrence of the event is treated as certain; if the probability of it having occurred is less than it not having occurred, it is treated as not having occurred. Hence, in respect of events which have or have not occurred, damages are assessed on an all or nothing approach. But in the case of an event which it is alleged would or would not have occurred, or might or might not yet occur, the approach of the court is different. The future may be predicted and the hypothetical may be conjectured. But questions as to the future or hypothetical effect of physical injury or degeneration are not commonly susceptible of scientific demonstration or proof. If the law is to take account of future or hypothetical events in assessing damages, it can only do so in terms of the degree of probability of those events occurring. The probability may be very high — 99.9 per cent — or very low — 0.1 per cent. But unless the chance is so low as to be regarded as speculative — say less than 1 per cent — or so high as to be practically certain — say over 99 per cent — the court will take that chance into account in assessing the damages. Where proof is necessarily unattainable, it would be unfair to treat as certain a prediction which has a 51 per cent probability of occurring, but to ignore altogether a prediction which has a 49 per cent probability of occurring. Thus, the court assesses the degree of probability that an event would have occurred, or might occur, and adjusts its award of damages to reflect the degree of probability. The adjustment may increase or decrease the amount of damages otherwise to be awarded. See Mallett v. McMonagle; Davies v. Taylor; McIntosh v. Williams. The approach is the same whether it is alleged that the event would have occurred before or might occur after the assessment of damages takes place.

(Citations omitted; see also Sellars v Adelaide Petroleum NL [1994] HCA 4; (1994) 179 CLR 332 at 349–351 per Mason CJ, Dawson, Toohey and Gaudron JJ; at 365–368 per Brennan J.)