Federal Court of Australia

Kwinana, in the matter of Kwinana Wte Pty Ltd as trustee for the Kwinana Wte Holding Trust [2024] FCA 48

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

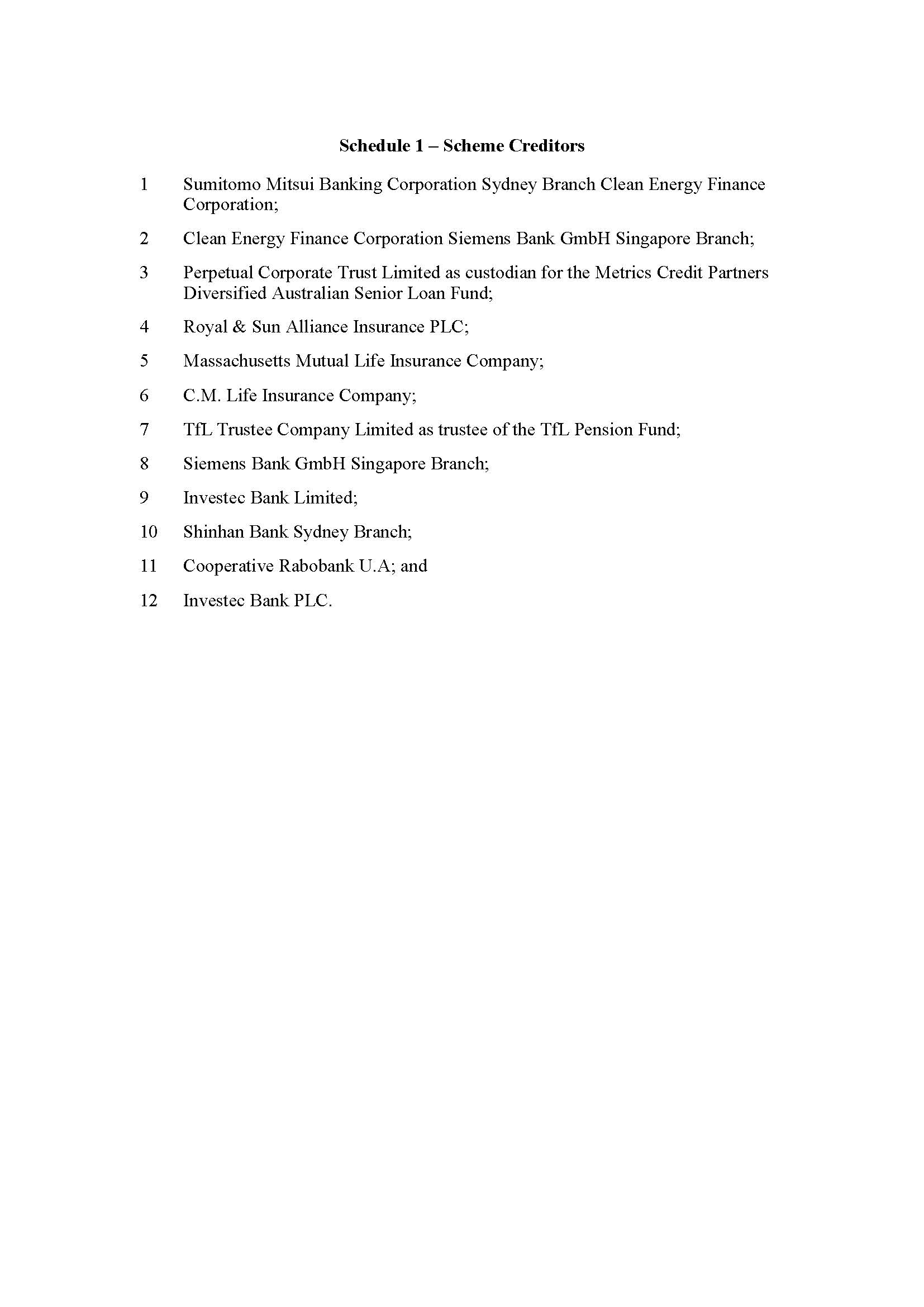

1. Pursuant to s 411(1) of the Corporations Act 2001 (Cth) (Act), the first plaintiff, second plaintiff and third plaintiff (together, plaintiffs) each convene a meeting (collectively, Scheme Meetings) of the parties listed in Schedule 1 (collectively, Scheme Creditors):

(a) for the purpose of considering and, if thought fit, agreeing (with or without modification) to a scheme of arrangement (Scheme) proposed to be made between the plaintiffs and the Scheme Creditors, being a scheme substantially in the form of that contained in Annexure A to the explanatory statement exhibited to the affidavit of John McNamee sworn 30 January 2024 (Scheme Booklet); and

(b) to be held at 3pm (Sydney time) on 21 February 2024 at King & Wood Mallesons, Level 61, 1 Farrer Place, Sydney, New South Wales.

2. The Scheme Meetings be convened by sending on or before 6 February 2024, a copy of the Scheme Booklet substantially in the form of that exhibited to the affidavit of Mr Timothy Michael Klineberg sworn 2 February 2024 by:

(a) registered post to each Scheme Creditors’ address for service of notices in the Finance Documents (as defined in the Scheme); and

(b) email to each Scheme Creditors’ electronic address for service of notices in the Finance Documents (as defined in the Scheme).

3. A Proxy Form in respect of the Scheme Meetings will be valid and effective if, and only if, it is completed and delivered in accordance with its terms by 10am (Sydney time) on 19 February 2024.

4. Mr John McNamee, or failing him, Mr Martin Hanke, be chairperson of the Scheme Meetings.

5. Except for procedural motions, all voting at the Scheme Meetings be by poll as declared by the chairperson.

6. The chair has the power to adjourn the Scheme Meetings in his or her absolute discretion.

7. Compliance with r 2.15 of the Federal Court (Corporations) Rules 2000 (Cth) (Corporations Rules), except insofar as it operates to apply r 75-15(2) of the Insolvency Practice Rules (Corporations) 2016 (Cth) to the Scheme Meetings, be dispensed with.

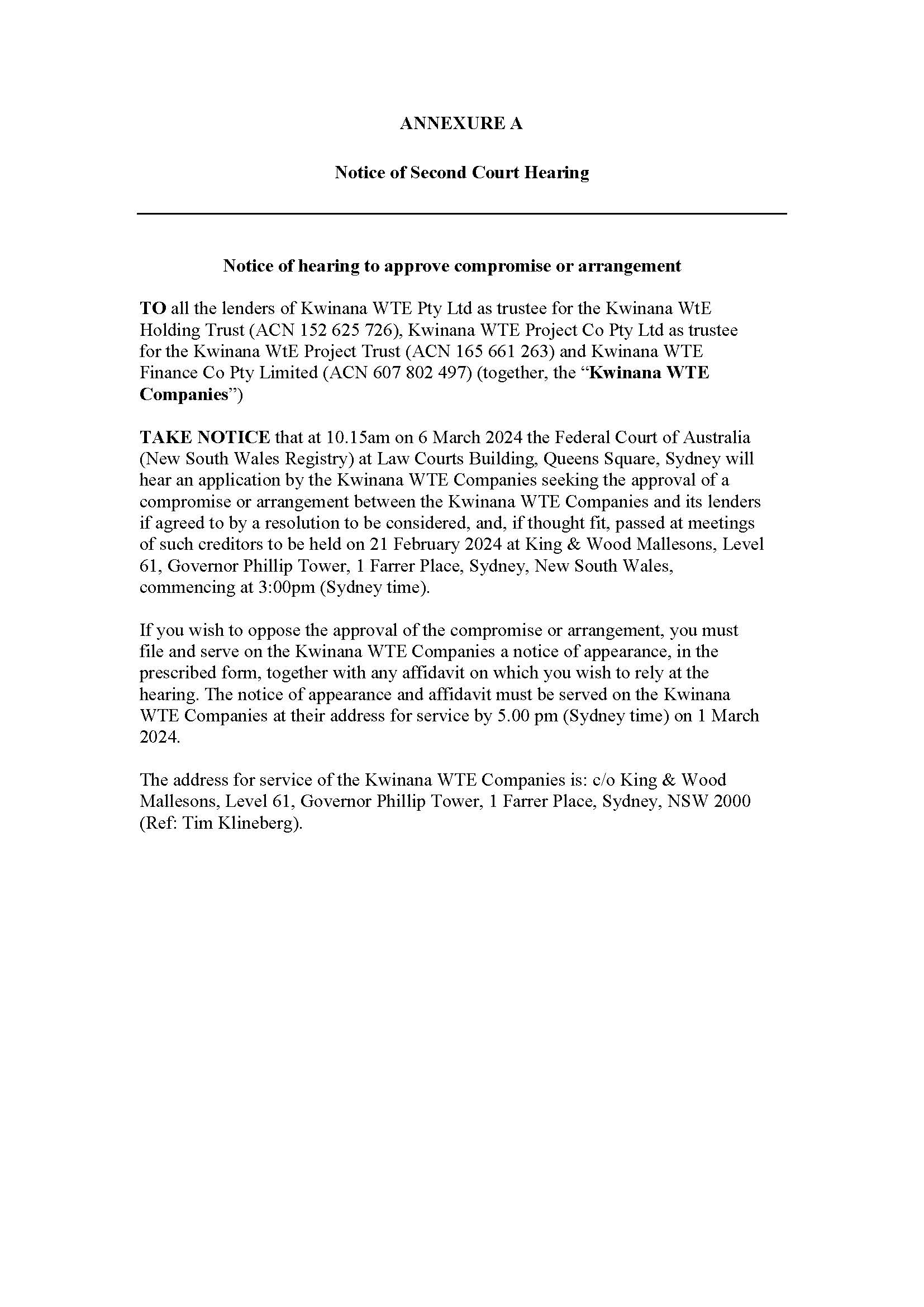

8. Notice of the hearing of an application pursuant to s 411(4)(b) of the Act for orders approving the Scheme be published once in The Australian newspaper, by advertisement substantially in the form of Annexure A to these orders, such advertisement to be published on or before 28 February 2024 and the plaintiffs otherwise be exempted from compliance with r 3.4 of the Corporations Rules.

9. That Mr Richard Tucker and Mr Scott Kershaw be authorised to administer the reorganisation of the assets and affairs of the plaintiffs.

10. The matter be adjourned for a second hearing at 10:15am on 6 March 2024 in Sydney.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

(Delivered ex tempore)

LEE J:

A INTRODUCTION

1 This is an application by Kwinana WtE Pty Ltd (Hold Co), Kwinana WtE Project Co Pty Ltd (Project Co) and Kwinana WtE Finance Co Pty Ltd (Finance Co) (collectively, Scheme Companies).

2 In broad terms, the Scheme Companies, by an originating process (originating process), seek orders pursuant to s 411(1) of the Corporations Act 2001 (Cth) (Corporations Act) to convene meetings of creditors (Scheme Creditors) for the purpose of considering a proposed scheme of arrangement (Scheme) to be made between the Scheme Companies and the Scheme Creditors.

3 This is the first court hearing. If orders are made today to convene meetings of the Scheme Creditors, the Scheme Companies seek further orders at a second court hearing that, among other things, the Scheme be approved pursuant to s 411(4)(b).

4 In support of the originating process, the Scheme Companies rely on:

(1) an affidavit of Mr John McNamee, director, secretary and chairman of the Scheme Companies, sworn on 30 January 2024 (McNamee Affidavit); and

(2) an affidavit of Mr Tim Michael Klineberg, solicitor for the Scheme Companies, sworn on 2 February 2024 (Klineberg Affidavit).

5 For the reasons which follow, I am satisfied that it is appropriate to make orders broadly in the terms sought by the Scheme Companies.

B BACKGROUND

6 The relevant background to the proposed Scheme is set out in the McNamee Affidavit and Klineberg Affidavit. What follows is largely drawn from those affidavits and submissions helpfully provided on the application by Mr Ahmed SC, counsel for the Scheme Companies.

B.1 The Scheme Companies

7 The Scheme Companies are involved in the construction of a thermal treatment plant to produce energy from waste in Western Australia. The original “Target Commercial Operation Date” in respect of that contract was 21 October 2021, which has not been achieved: McNamee Affidavit (at [5], [13]).

8 In order to fund construction, the Scheme Companies have entered into a syndicated facility agreement (Syndicated Facility Agreement). That agreement is entered into by parties including the Scheme Companies, various lenders (that is, the Scheme Creditors) and BTA Institutional Services Australia Limited (in its capacities as agent and security trustee (Security Trustee)). Under the Syndicated Facility Agreement, Finance Co is the principal borrower. Each of Hold Co and Project Co are guarantors: McNamee Affidavit (at [19], Exhibit JM-1).

9 The Scheme Companies have granted security in favour of the Security Trustee under a deed which provides for security over all of the Scheme Companies’ present and after acquired property. The Security Trustee holds that security on trust for the Scheme Creditors: McNamee Affidavit (at [21]).

10 As at 20 December 2023, the amounts that are presently owing by the Scheme Companies to the Scheme Creditors as the secured debt are (McNamee Affidavit (at [22])):

(1) approximately $306 million under Tranche A; and

(2) approximately $88 million under Tranche B.

11 I am informed that there are certain “Events of Default” or “Potential Events of Default” that have occurred under the Syndicated Facility Agreement. The most significant of those Events of Default was the failure to repay the secured debt which matured on 17 October 2023, and which failure triggered an Event of Default under cl 21.1(a) of the Syndicated Facility Agreement: McNamee Affidavit (at [24]).

12 The majority of the Scheme Creditors (10 of 12) have entered into a restructuring support agreement, which is dated 18 December 2023 (Restructuring Support Agreement).

13 Under that agreement, the relevant Scheme Creditors have agreed to forebear from taking any enforcement action in relation to certain Events of Default or Potential Events of Default. That forbearance is conditional on a number of matters, including the proposed Scheme coming into effect by 15 March 2024: McNamee Affidavit (at [25]).

B.2 The Proposed Scheme

14 The proposed Scheme (see Klineberg Affidavit, Exhibit TMK-1) is a creditors’ scheme that would involve the compromise of the debt held by the Scheme Creditors.

15 The debt that is to be compromised is that which is owing under the Syndicated Facility Agreement (Secured Debt).

16 Obviously enough, the anticipated outcome of the proposed Scheme is that the debts owed to the Scheme Creditors will be compromised. The money to be provided to the Scheme Creditors in respect of that compromise will be provided principally by the Acciona Buyer. In exchange, the Acciona Buyer will receive full ownership of Hold Co and a subscription of shares in Finance Co. In addition, part of the funds to compromise the debt will also be funded by an equity contribution.

17 This is illustrated in the following table (McNamee Affidavit (at [55])):

Affected outcome | Before implementation of Scheme (as at 18 October 2023) | After implementation of Scheme |

Secured Debt owed by Scheme Companies to Scheme Creditors | Approximately $395.5 million | Transfer of rights to the Secured Debt of approximately $364.7 million to Acciona Buyer following receipt of the Net Equity Contribution (approximately $13.6 million) and Debt Acquisition Price (approximately $351.1 million). Acciona Buyer releases approximately $30.8 million of the Secured Debt acquired in exchange for $1 for $1 subscription of shares in Finance Co |

Equity Parties (Hold Co and Holding Trust) | Equity Parties - 100% of the interests in Hold Co and the Holding Trust | Acciona Buyer - 100% of the interests in Hold Co and the Holding Trust |

Shareholders (Finance Co) | Project Co - 100% of the interests in Finance Co | Acciona Buyer - > 99.99% of the interests in Finance Co Project Co - < 0.01% of the interests in Finance Co |

18 The key element under the proposed Scheme is that the Scheme Creditors will effectively compromise the Secured Debt in exchange for $0.9222 in the dollar on that debt. The Scheme also provides for certain other inter-conditional transactions to take place. To the extent that those transactions involve performance by third parties other than the Scheme Companies or the Scheme Creditors, that performance will be secured by various deeds which will bind the third parties to the Scheme. The execution of these deeds poll is a condition precedent that must be fulfilled by 8am on the second court hearing date, which is presently listed on 6 March 2024: Klineberg Affidavit (Exhibit TMK-1 (at 164–166, 177)).

19 Aside from the compromise of the Scheme Creditors’ debt, the steps that will occur under the Scheme are set out in cl 9.4 of the Scheme. Those steps will involve the following (McNamee Affidavit (at [54]):

a. the transfer of 100% of the rights, title and interest in and to the Secured Debt commitments totalling approximately $395.5 million to Acciona Buyer for a price equal to 92.22% of the par value of the Secured Debt;

b. certain amendments being made to identified finance documents to give effect to the Secured Debt transfer;

c. the Acciona Buyer subsequently releasing the Scheme Companies from their obligation to pay a portion of the Secured Debt in the amount of the Released Amount of approximately $30.8 million;

d. as consideration for the compromise of the Released Amount, approximately 30.8 million shares in Finance Co being issued to the Acciona Buyer (or its nominee);

e. the transfer of all of the shares in Hold Co and all of the units in the Holding Trust by the parties holding the equity in Hold Co to the Acciona Buyer; and

f. various releases between, among others, certain of the Scheme Companies, the Acciona Parties and any person who is or was, at any time up to and including Scheme Implementation, a director or officer of any Scheme Company and who has executed a deed poll, in respect of any claims relating to any matter that arose or occurred in respect of, or in connection with, the Scheme or any transactions effected under it.

20 Mr McNamee’s evidence is that if the Scheme is not approved and implemented, the Scheme Companies will have no revenue to pay the Secured Debt and will be insolvent. In that circumstance, he considers that the appointment of administrators to the Scheme Companies is likely: McNamee Affidavit (at [35]). On the material before me, this is consistent with the opinions expressed by Mr Strawbridge of FTI Consulting (Australia) Pty Ltd (FTI), an independent expert retained by the Scheme Companies to opine on various scenarios in relation to the proposed Scheme: McNamee Affidavit (at [57](c)), Exhibit JM-1).

B.3 Draft Explanatory Statement

21 A draft explanatory statement (Explanatory Statement) has been provided to the Court which sets out, among other things, a summary of the proposed Scheme, the reasons why the Scheme Creditors may wish to vote in favour, or against, the proposed Scheme, and other information relevant to their consideration of the Scheme: Klineberg Affidavit (Exhibit TMK-1 (at 90)).

22 I am told that a verification process has been undertaken in relation to the draft Explanatory Statement. The process has involved the draft Explanatory Statement being verified by various verifying parties who have the relevant knowledge to provide that verification. A verification guideline was also prepared: McNamee Affidavit (at [71]–[77]).

23 Verification certificates were provided by each verifying party (with the exception of Mr McNamee) in respect of the statements of intention, opinion or belief in the draft Explanatory Statement. Mr McNamee has separately given evidence in respect of those statements that he is not aware of any false or misleading statements in the draft explanatory statement, any material omission in those statements, or anything which causes him to believe that the issue of the relevant statements in the draft Explanatory Statement may involve conduct that is misleading or deceptive: McNamee Affidavit (at [76], [91]).

B.4 ASIC

24 It is also relevant to note that ASIC has been given notice of this hearing pursuant to s 411(2) of the Corporations Act. In December 2023, the Scheme Companies wrote to ASIC, providing it with a copy of the draft explanatory statement, information in relation to the proposed Scheme and an application for relief from cl 8203(a) of Pt 2 of the Corporations Regulations 2001 (Cth) (Corporations Regulations). That application, however, is no longer pursued for reasons set out in Klineberg Affidavit (at [6]).

25 On the evidence before me, in early February this year, ASIC wrote to the Scheme Companies stating that it has had a reasonable opportunity to examine the terms of the proposed Scheme and noted that it did not propose to appear at the first court hearing today or oppose the proposed Scheme: Klineberg Affidavit (Exhibit TMK-1 (at 88)).

C THE RELEVANT LAW

26 The principles on which the Court acts at the convening stage are well known. As Jackman J explained in Catholic Church Insurance Limited, in the matter of Catholic Church Insurance Limited [2023] FCA 1197 (at [10]), the Court’s function is limited to ensuring that:

(a) the statutory and procedural requirements for the holding of the meeting have been satisfied;

(b) there will be available to the creditors all the main facts relevant to the exercise of their judgement;

(c) ASIC has had a reasonable opportunity to examine the proposal; and

(d) the scheme is of such a nature and cast in such terms that, if it achieves the statutory majority at the meeting, the Court would be likely to approve it on a hearing of the petition which is unopposed (and that it is not so blatantly unfair or otherwise inappropriate that it should be stopped in its tracks).

See, in the context of a creditors’ scheme, Re HIH Casualty and General Insurance Limited [2005] NSWSC 1180; (2005) 56 ACSR 295 at [6] (Barrett J) (Re HIH (2005) 56 ACSR 295) and the authorities there cited.

27 Relatedly, in Re Foundation Healthcare Ltd [2002] FCA 742; (2002) 42 ACSR 252 (at 263 [36]), French J emphasised the limited inquiry by the Court at the first hearing, noting that the court, by granting leave to convene the meeting, does not give its imprimatur to the proposed scheme. If the arrangement is one that seems fit for consideration by the meeting of members or creditors and is a commercial proposition likely to gain the court’s approval if passed by the necessary majorities, then leave should be given.

28 Put shortly, it is not the role of the court at the first hearing to wade heavily into the question of whether the arrangement is one which warrants the approval of the court: that question is to be answered when the scheme returns to the court for final approval (Re Foundation at 265 [44]); see also ASIC v Marlborough Gold Mines Ltd (1993) 177 CLR 485 (at 504–505 per Mason CJ, Brennan, Dawson, Toohey and Gaudron JJ).

D CONSIDERATION

29 I am satisfied the statutory and procedural requirements have been met to convene a creditors meeting and that it is appropriate to make orders pursuant to s 411(1) of the Corporations Act, for the following reasons.

30 First, the Scheme Companies are Pt 5.1 bodies under the Corporations Act as they are companies registered under the Act.

31 Secondly, the proposed Scheme is a “compromise” or “arrangement” within the meaning of s 411 of the Corporations Act. The compromise or arrangement in the present case is of a familiar kind. It involves the Scheme Creditors effectively compromising their debts with the Scheme Companies, in exchange for payment of them.

32 Thirdly, I am comfortably satisfied on the evidence before me that there has been proper disclosure of matters to the Scheme Creditors. As set out in Section B.3 above, the Scheme Companies have prepared a draft Explanatory Statement that sets out the details of the proposed Scheme and other relevant matters. A verification process was established to verify the accuracy of the draft Explanatory Statement.

33 Fourthly, as explained above in Section B.4, ASIC has had an opportunity to examine the proposed Scheme and the draft Explanatory Statement, and the requirements of s 411(2) have been fulfilled.

34 Fifthly, the Scheme is bona fide and has been properly proposed. The proposed Scheme is a genuine scheme to effect a reorganisation of the Scheme Companies’ affairs. As noted above (at [21]), Mr Strawbridge, an independent expert, was engaged to assess the proposed Scheme and has expressed his opinion in relation to its effect, and the effect if it is not implemented.

35 Sixthly, the procedural requirements in relation to the proposed Scheme have been met. In this regard, the draft Explanatory Statement (Klineberg Affidavit, Exhibit TMK-1 (at 93–94)) sets out the prescribed disclosure requirements under s 412(1) of the Corporations Act and r 5.1.01 of the Corporations Regulations and the relevant parts of the scheme booklet which contain those disclosures.

36 Accordingly, for the foregoing reasons, I am satisfied that it is appropriate to convene the meetings of creditors. Before concluding, however, I should address two final matters.

37 The first is that strictly speaking, the present application before the Court covers multiple schemes. It has been held, however, that this is not an impediment to the convening of the Scheme meetings. As Finkelstein J noted in Re United Medical Protection Ltd [2007] FCA 631 (at [3]), it used to be the practice to require separate applications or petitions to be filed, one for each company, which would then be heard together as a matter of course. For reasons explained by his Honour, this undesirable practice, which apart from adding unnecessarily to the costs ran the risk of an appeal from one order only, has since fallen by the wayside.

38 The second matter is that the Scheme Companies seek a number of ancillary orders concerning, inter alia, proxy forms, meeting procedures, and publication of an advertisement in relation to the second court hearing date. These are commonplace orders in the context of such applications, and I am satisfied that they should be made broadly in the terms sought by the Scheme Companies.

E CONCLUSION

39 Accordingly, I will make orders convening the proposed Scheme meeting and other orders in the terms I have outlined above.

I certify that the preceding thirty-nine (39) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Lee. |

Associate: