FEDERAL COURT OF AUSTRALIA

Probis Financial Services Pty Ltd (administrators appointed) v Kong [2023] FCA 1398

ORDERS

DATE OF ORDER: | 14 november 2023 |

THE COURT ORDERS THAT:

Freezing order

1. Upon the undertakings given to the Court by the applicants set out in Schedule A to the (second) set of orders made on 14 September 2023, the freezing order made by those orders be extended until further order of the Court.

Disclosure affidavit

2. Order 3 of the orders made on 11 October 2023 be vacated.

3. The respondent serve the affidavit of the respondent filed in accordance with order 2 of the orders made on 11 October 2023 upon the applicants forthwith.

Case management

4. The parties have liberty to apply.

5. Costs be reserved.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

GOODMAN J

1 On 14 September 2023, on an ex parte application brought by the applicants – Probis Financial Services Pty Ltd (administrators appointed) and its administrators – Yates J made an interim world-wide freezing order against the assets of the respondent, Mr Kong, together with ancillary orders, including an order that Mr Kong file and serve an affidavit providing disclosure of his assets. The freezing order was subsequently continued until the determination of applicants’ application for the continuance of the freezing order.

2 On 11 October 2023, on Mr Kong’s application, Shariff J made orders pursuant to which the asset disclosure affidavit to be filed by Mr Kong with the Court would be subject to suppression and non-publication, with the issue of whether that affidavit should be served on the applicants reserved for determination together with the aforementioned application for the continuance of the freezing order. Mr Kong subsequently filed a disclosure affidavit.

3 The issues for present determination are whether the freezing order should be continued; and whether the applicants should have access to the disclosure affidavit.

4 The following summary is taken from the affidavit evidence read on this application, namely: (1) the affidavits of Mr Jonathan O’Loughlin (the solicitor for the applicants) sworn 13 September 2023 and 20 October 2023; (2) the affidavit of Mr Richard Albarran (one of the administrators) sworn 20 October 2023; and (3) the affidavits of Mr David Jenaway (the solicitor for Mr Kong) sworn 11 and 30 October 2023. Mr Kong’s disclosure affidavit was not read and I have had no regard to it.

5 Until 28 July 2023, Probis, the holder of an Australian Financial Services Licence (AFSL) conducted a financial services business.

6 Mars Cap Limited (MCL), a company incorporated in New Zealand, engaged in business as a provider of various financial services (see [9(1)] below for further detail). Mr Kong was at all material times the sole shareholder and director of MCL.

7 Mr Chen (James) Yu was a director of Probis from 1 March 2018 until 15 May 2023. The evidence suggests that he was also engaged by MCL as its compliance manager, although the precise period of such engagement is not clear.

8 Between 15 July 2019 and 23 August 2019, a series of emails was exchanged between Mr Yu (from an MCL email address), Mr Kong, and solicitors from Chapman Tripp, a law firm in New Zealand retained by MCL, concerning an Anti-Money Laundering and Countering Financing of Terrorism Risk Assessment and Compliance Programme (Policy). The emails suggest that Mr Yu and Mr Kong were actively involved in the formation of the Policy and that various drafts of the Policy were created and circulated for comment before a final version was approved for lodgement with the New Zealand Financial Markets Authority.

9 The Policy includes the following:

(1)

RISK ASSESSMENT AND COMPLIANCE PROGRAMME (THE POLICY)

PART 1: BACKGROUND

This Policy contains a Risk Assessment and Compliance Programme for the purposes of the Anti-Money Laundering and Countering Financing of Terrorism Act 2009 (the Act).

The Policy has been prepared for Mars Cap Limited (MCL) in respect of its financial activities that are subject to the Act.

1 About MCL

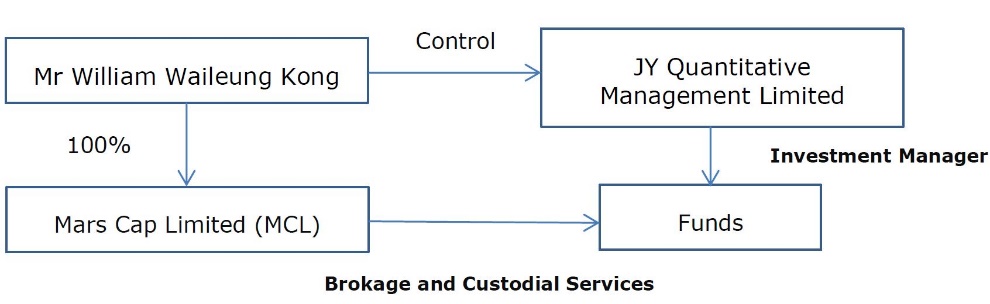

MCL has been established as a brokerage and custodial company to better service the JY Quantitative Management Limited (JY) group of companies. MCL is a limited liability company incorporated in New Zealand and registered on the New Zealand Financial Service Providers Register.

JY and its affiliates currently provide custodian services for a number of products including funds, shares, structured products and other financial products for overseas investors. The investors are based in a range of jurisdictions including the Cayman Islands, Hong Kong, the United States and Japan. MCL will provide brokerage and custodial services to JY and its affiliates, and to their investors.

MCL’s sole shareholder is Mr William Waileung Kong, who is also the co-founder of JY and is internationally qualified (CFA, CAIA). JY currently has 6 Hedge Funds based in the Cayman Islands under management, with a total fund size of over USD $600 million.

The following corporate structure summarises MCL’s business:

2 MCL is registered on the New Zealand Financial Service Providers Register

MCL is registered on the Financial Service Providers Register (FSPR). Under its FSPR Registration, MCL is registered to provide the following financial services to its clients:

a) brokering service (including a custodial service);

b) keeping, investing, administering, or managing money, securities, or investment portfolios on behalf of other persons; and

c) trading financial products or foreign exchange on behalf of other persons.

MCL will also provide administrative support associated with the services above.

MCL is a member of the Financial Dispute Resolution Scheme.

MCL currently plans to provide its Services to wholesale clients in New Zealand, and financial institutions and managed funds around the world, in particular, Japan, United Kingdom, Cyprus, Hong Kong and Australia. The majority of other wholesale clients will be residents of Taiwan, Hong Kong, Singapore and Mainland China. The targeted managed funds will be based in the Cayman Islands and underlying investment products within the portfolio are based across the globe. MCL will also be trading financial products and foreign exchange on behalf of its clients.

A summary of MCL’s clients and its geographical locations are listed below:

• Types of MCL’s clients: wholesale clients, financial institutions, managed funds, and high net worth individuals;

• Geographical locations: New Zealand, Cayman Islands, Japan, United Kingdom, Cyprus, Hong Kong, Australia, Taiwan, Hong Kong, Singapore and Mainland China

MCL does not intend to provide its Services to retail clients based in New Zealand. MCL may consider providing its Services to New Zealand based retail investors should its operations expand, and is fully aware of the regulatory requirements if it wishes to provide such Services. Should MCL provide its services to retail clients based in New Zealand, MCL will update this Policy to reflect the risks of these additional business activities accordingly.

Because MCL will hold client money and property on their behalf, MCL is required to meet the brokers and custodian obligations under the Financial Advisers Act 2008 (FAA).

MCL will initially on-board existing hedge funds managed by JY. Once the funds are on-boarded by MCL, they will trade through MCL. The platforms offered will include JY’s proprietary trading platform and MT4/MT5. Before the clients can start to trade, they will deposit funds with MCL for settlement with the counterparties. MCL will hold the funds on trust for its clients. MCL will automatically execute the trades on behalf of its clients as clients give instructions through the trading platform by placing a trade order. MCL then will settle the trade with the counterparties once it receives instructions from the clients to close their positions.

...

(2)

Risk | ML/FT Rating | Addressing the risk |

Liquidity MCL is unlikely to face liquidity risk, with its strong backing by the JY group of companies and the size of JY’s overall operations. | Unlikely | MCL will make sure that it receives required capital from its clients (which will be held on trust for the clients until instruction to execute and trade(s) are received) before any trades can be executed on their behalf. MCL will also employ systems to closely monitor its clients’ account equity or balance, and in the event of client equity or balance falling below the required levels set either by MCL or MCL’s trade counterparties, clients will be advised to remit additional funds to avoid automatic close-out of their open positions. |

...

(3)

4.2 Products and services

Clients remit funds to MCL, who then holds the funds on trust for the clients and executes trades or makes investments upon their instructions.

Core products: exchange - traded securities, and Over-the-Counter (OTC) derivatives.

Upon receiving funds from its clients, MCL will hold the funds on trust for the respective clients, and only execute the trades as per the instructions received from clients through either its trading platforms or other MCL verified and approved methods, e.g. emails. MCL will hold the investments on behalf of its clients as custodians.

...

(4)

Risk | ML/FT Rating | Addressing the risk |

Payments to third parties MCL will verify all bank account names and numbers upon conducting CDD and before any investment returns are paid to clients. MCL will also verify bank account names and details when a change is requested by clients. | Very unlikely | MCL does not make payments to third parties. If a client wishes to make changes to their bank account details, MCL will seek verification and confirmation of the new details, to satisfy itself that the new details are true and correct. Forms of verification sought from the customer can include a certified bank statement. |

(bold emphasis in original; underline emphasis added)

10 On 15 November 2019, Probis applied to open an account with MCL. On the same day, Probis and MCL entered into a Liquidity Provider Agreement (LPA). Mr Kong signed the LPA on behalf of MCL, and Mr Yu, then a director of Probis, signed the LPA on behalf of Probis.

11 On 27 November 2019, MCL sent an email to Mr Yu in the following terms:

Thank you for opening a trading account with us.

We are pleased to inform you that your application has been approved, and we hope the trading platform MarsAuton will provide you with great trading experience.

You can download the Mars Auton trading application at the following link: Download Mars Auton now

...

We suggest that you write down or take a picture of the above information in case you forget.

Please note that you will need to deposit the required amount of funds into Marscap Client Money Trust Account before you can trade with us. If you don’t receive the funds within 6 months after your account is opened, your account will be terminated automatically by the system. You can find details of the Client Money Trust Account on our website.

...

(bold emphasis in original; underline emphasis added)

12 Probis subsequently placed substantial deposits of money with MCL and a number of trades occurred with respect to some of that money, with the last such trade occurring on 31 March 2021.

13 More than two years later and on 2 May 2023, Mr Yu of Probis wrote to Mr Kong at MCL, in the following terms:

We are writing to you requesting a withdrawal of the whole balance of the CFD trading accounts Probis Financial Services Limited (PFSL) has with Mars Cap Limited (MCL).

The total balance as of 30 April 2023 was USD 100,009,812.45. Attached are the supporting documents of the outstanding balance.

PFSL needs funds urgently for meeting withdrawal requests from its own clients, so if the withdrawal request can be processed on a timely basis, it would be much appreciated.

Thank you.

(emphasis in original)

14 On 15 May 2023, Mr Kong responded on behalf of Mars Cap (as written):

Thank you for the email.

We are currently withdrawing money from our brokers.

We will arrange the transfer to you as soon as possible once the we receive the money from our brokers.

Thank you.

15 On or around 12 June 2023, Probis and MCL entered into two deeds, a consequence of which was to reduce the balance of funds placed by Probis with MCL from USD100,009,812.45 to USD38,402,194.63.

16 On 22 June 2023, Mr O’Loughlin, as solicitor for Probis, wrote to MCL (including to Mr Kong) demanding payment of USD38,402,194.63 by 6 July 2023.

17 On 10 July 2023, Mr Kong responded to Mr O’Loughlin’s 22 June 2023 letter (as written):

This is to acknowledge that we have received your demand letter on behalf of Probis Financial Services on June 22.

As a brokerage business, during our normal operation, most of the capital were transfer to our liquidity providers to hedge our trading risk. Since the withdrawal request from the Probis is not a small amount, we need to withdraw capital from the liquidity providers to cover such request. After receiving the request from you, during the last couple of weeks, we are working with our liquidity providers, namely “PT. ETERNITY FUTURES” and “City Credit Capital (Labuan) Limited” to withdraw our margin from these two companies. Unfortunately, one company currently has its licenses suspended from its regulator, and the other company just appointed a liquidator.

According to the conversation with these two companies, they are currently actively working with the regulator and liquidator, they will get back to us with an indicative timeframe in the next couple of weeks when they are able to process our withdrawal request. Once we are able to receive the margin from our liquidity providers, we will transfer the said amount to Probis as soon as possible.

Thank you.

(emphasis added)

18 On 17 July 2023, the administrators (Mr Albarran, Mr Brent Kijurina, Mr Cameron Shaw and Mr Aaron Dominish, each of whom is a partner in the firm Hall Chadwick) were appointed to Probis, following a resolution by the directors of Probis.

19 On 28 July 2023, a delegate of the Australian Securities and Investments Commission made an order under s 915B(3) of the Corporations Act 2001 (Cth) suspending Probis’s AFSL until 30 October 2023.

20 On the same day, Mr Singh, a partner in Hall Chadwick, met with Mr Kong concerning the amount owed by MCL to Probis. At that meeting, Mr Kong acknowledged that MCL owed USD38,402,194.63 to Probis and was waiting to receive funds owed to it by “liquidity providers”.

21 On 31 July 2023, Mr Albarran wrote to Mr Kong at MCL referring to the 28 July 2023 meeting demanding repayment and seeking information concerning the “liquidity providers”.

22 On 9 August 2023, Mr Kong replied:

...

Just to give you a quick update, I am withdrawing 40 Mil from the liquidity provider, and the liquidity provider promised that they will send out the money on this Friday.

I will let you know once we receive the money, then we can arrange the payment back to Probis next week.

...

I will let you know once I receive the transfer receipt later this week.

Thank you.

23 On 16 August 2023, Lang J of the High Court of New Zealand made orders appointing Mr Albarran and Mr Kijurina (i.e. some of the administrators) as interim liquidators of MCL.

24 Mr Jenaway provided evidence on the basis of information provided by Mr Kong, including evidence that Mr Kong holds the following views:

(1) it is standard market practice for foreign exchange liquidity providers such as MCL to mitigate the risk associated with client transactions by placing clients’ funds with other liquidity providers;

(2) in light of this, Probis was, or ought to have been, aware that MCL was engaging in such mitigation practices;

(3) it was an ordinary part of MCL’s business, and the business of similar liquidity providers, that MCL would use its own liquidity providers to mitigate the risk associated with its transactions entered into on behalf of clients;

(4) the specifics of this risk mitigation technique are as follows:

(a) foreign exchange liquidity providers such as MCL facilitate trading in the foreign exchange market by offering to buy or sell a certain asset or instrument at a specified price and quantity, thereby creating or maintaining liquidity;

(b) foreign exchange liquidity providers may act as brokers, by matching buyers and sellers of different assets, and by acting as an intermediary between clients and other liquidity providers;

(c) by acting as an intermediary between clients and other liquidity providers, brokers mitigate their risk to market exposure. This is achieved as the broker is effectively entering into a parallel transaction with a liquidity provider, thereby offsetting their position in the market and reducing market risk exposure;

(d) this practice is necessary as brokers typically do not bear the risks of client trading as opposed to market-makers, which do; and

(5) the practice is consistent with various publications, namely: the Hong Kong Securities and Futures Commission’s April 2020 “Report on Leveraged Foreign Exchange Trading Activities Carried Out by Licensed Corporations”; and papers and articles titled “Comparative analysis of Back to Back vs Dark Pool STP execution models in OTC Markets”, “ECN/STP Vs. Market Maker Brokerage Model”, “Which Brokerage Model to Choose: ECN / STP or Market Maker?” and “How do I choose a broker: ECN / STP or Market Maker?”.

25 Mr Jenaway provided further evidence (again on information provided by Mr Kong) to the following effect concerning Mr Yu:

(1) Mr Yu was a director of Probis from 1 March 2018 to 15 May 2023;

(2) Mr Yu also worked with and on behalf of MCL, including in the establishment of MCL’s business in New Zealand and as MCL’s anti-money laundering and counter-terrorist financing (AML/CTF) compliance officer, and this is reflected in what Mr Kong understands to be an extract of the Policy; and

(3) as MCL’s compliance officer, Mr Yu was responsible for administering and maintaining MCL’s AML/CTF programme pursuant to s 56 of the Anti-Money Laundering and Countering Financing of Terrorism Act 2009 (NZ), and therefore should have been aware of MCL’s business practices including the placement of received funds with other liquidity providers.

26 Mr O’Loughlin provided responsive evidence, on the basis of information provided by Mr Yu, that:

(1) Mr Yu was surprised to learn that most of MCL’s capital (which Mr Yu suggested must include most if not all of the money paid to MCL by Probis) was transferred by MCL to its own liquidity providers to hedge MCL’s trading risk;

(2) until about May 2023, Mr Yu did not know that MCL had transferred Probis’s money to MCL’s own liquidity providers;

(3) Mr Yu’s expectation was that MCL would hold on to any funds paid to it by Probis especially in circumstances where Probis was not actively placing trades with MCL;

(4) Mr Yu never advised Mr Kong that any of Probis’s funds could be used to hedge trading risk borne by MCL on a matter unrelated to Probis;

(5) Mr Yu’s understanding was that any money held by MCL for Probis could be returned to Probis on very short notice;

(6) Mr Yu’s understanding is that whilst it may be common market practice for a broker or liquidity provider to hedge its exposure to a client’s trades by using some or all of the margin paid to it by that client for the purposes of hedging that specific risk, it is not common market practice for a broker or liquidity provider to use a client’s money for other purposes or to hedge its exposure to other risks; and

(7) Probis stopped trading with MCL in about mid-2021, and so, consistent with the understanding in the preceding sub-paragraph, there was no reason for MCL to have paid Probis’s money to a liquidity provider because since about mid-2021 MCL had no exposure to any risk caused by Probis’s trading activities.

27 In an affidavit served on the eve of the hearing, apparently in response to the evidence set out at [26(7)] above, Mr Jenaway (once again on information from Mr Kong) provided evidence that:

(1) MCL dealt with the funds received by Probis to ensure it was in a position to execute a timely transaction upon request by Probis, and to ensure the transaction was appropriately hedged. In particular:

(a) MCL, upon receiving funds from Probis, would subsequently place the funds with its own third-party liquidity providers, and that it would not wait for Probis to request a trade before doing so; and

(b) the reason MCL did so was because it:

(i) understood it was necessary for the funds required to execute and hedge a trade to be already held by MCL’s third-party liquidity providers when Probis would request MCL to execute a trade, so that the trade could be settled promptly. Otherwise, MCL would not be in a position to promptly execute the trades requested by Probis;

(ii) had no indication of when Probis would request the execution of a trade; and

(2) this process was MCL’s standard practice.

28 Mr Albarran provided evidence that he had instructed his staff to search all the available records of Probis (consisting of all records in the Probis server and mailboxes of Probis) and no documents were found which indicate that Probis specifically authorised MCL to use Probis’s money: (1) to hedge MCL’s risk on Probis’s trades; (2) to hedge MCL’s risk on trades placed with it by its other clients; or (3) for any other purpose other than the placing of trades at the direction of Probis.

C. SHOULD THE FREEZING ORDER BE CONTINUED?

29 The Court has power under s 23 of the Federal Court of Australia Act 1976 (Cth) and Division 7.4 of the Federal Court Rules 2011 (Cth) to make (and continue) a freezing order.

30 The principles to be considered on an application for the making (or continuance or discharge) of a freezing order are well-established and were not in issue on this application. They have recently been summarised by Anderson J in Rambaldi (Trustee) v Sumpton [2021] FCA 1199 at [9] to [15]; by O’Bryan J in Royal Express Pty Ltd (Recs and Mgrs Apptd) (Admins Apptd) v Huang [2021] FCA 585 at [3] to [4]; by Cheeseman J in Nicols as trustee of the bankrupt estate of Manietta v Manietta, in the matter of Manietta [2022] FCA 39 at [47] to [52]; by Lee J in Merryport Pty Ltd v Lawson [2023] FCA 838 at [6] to [9]; and by Moshinsky J in Fine China Capital Investment Limited v Qi (No 2) [2023] FCA 1059 at [19] to [23]. In summary, and having regard to the manner in which the present application has been framed, the Court must consider whether: (1) the applicants have established a good or arguable case (see r 7.35(1)(b)(i)); (2) there is a risk that a prospective judgment against Mr Kong will be unsatisfied in whole or part because the assets of Mr Kong will be disposed of, dealt with or diminished in value (see r 7.35(4)(b)); and (3) as a matter of discretion, including consideration of the balance of convenience, the freezing order should remain in place. I consider these in turn below.

31 In Nicols at [49] Cheeseman J explained:

The applicant bears the onus of establishing that there is a good arguable case on legal and factual matters or a sufficiently realistic prospect of success on the proceedings: Basi v Namitha Nakul Pty Ltd [2019] FCA 743 at [8] (Wigney J). The criterion of good arguable case is a lesser standard than the prima facie cause of action requirement favoured by the majority in Patterson v BTR Engineering (1989) 18 NSWLR 319 (Gleeson CJ and Rogers A-JA). That is, a good arguable case is one which is “more than barely capable of serious argument, and yet not necessarily one the judge considers would have more than a fifty percent change of success”: Curtis v NID Pty Ltd [2010] FCA 1072 at [6] (Edmonds J) citing Ninemia Maritime Corp v Trave Schiffahrtsgesselschaft mbH & Co KG (The Niedersachsen) [1983] Com LR 234 at 235 (affirmed on appeal: [1983] 1 WLR 1412); Deputy Commissioner of Taxation v Greenfield Electrical Services Pty Ltd (2016) 103 ATR 327; [2016] FCA 653 at [7] (Flick J).

(emphasis in original)

32 The applicants submitted that they had a sufficiently arguable case, primarily on the basis that Mr Kong was a person who knowingly participated in breaches of trust by MCL, namely the payment of funds the subject of a trust in favour of Probis, to the third-party “liquidity providers” mentioned in Mr Kong’s 10 July 2023 email, namely PT Eternity Futures and City Credit Capital (Labuan) Limited (see [17] above).

33 In Ancient Order of Foresters in Victoria Friendly Society Ltd v Lifeplan Australia Friendly Society Ltd [2018] HCA 43; (2018) 265 CLR 1 at 31 ([70] to [71]), Gageler J (as his Honour then was) explained:

70 ... Where a fiduciary does act dishonestly and fraudulently, however, the dishonest and fraudulent character of the breach of fiduciary duty is not without consequence for the intensity of the equitable remedies available against the defaulting fiduciary. More important for present purposes is that the dishonest and fraudulent character of the conduct of the fiduciary gives rise to the potential for similar remedies to be available in equity against another person who might knowingly participate in the fiduciary’s breach.

71 Knowing participation by a non-fiduciary in a dishonest and fraudulent breach of fiduciary duty is conduct which is regarded in equity as itself unconscionable and as attracting equitable remedies against the knowing participant of the same kind as those available against the errant fiduciary. Knowing participation in a dishonest and fraudulent breach of fiduciary duty includes knowingly assisting the fiduciary in the execution of a “dishonest and fraudulent design” on the part of the fiduciary to engage in the conduct that is in breach of fiduciary duty. The requisite element of dishonesty and fraud on the part of the fiduciary is met where the conduct which constitutes the breach transgresses ordinary standards of honest behaviour. Correspondingly, the requisite element of knowledge on the part of the participant is met where the participant has knowledge of circumstances which would indicate the fact of the dishonesty on the part of the fiduciary to an honest and reasonable person.

(citations omitted)

34 It is convenient to address the question of whether there is a sufficiently arguable case by reference to the following sub-questions:

(1) is it sufficiently arguable that MCL owed fiduciary obligations to Probis with respect to the moneys provided by Probis to MCL?;

(2) if so, is it sufficiently arguable that MCL, qua fiduciary, engaged in a dishonest and fraudulent design? and

(3) if so, is it sufficiently arguable that Mr Kong had the requisite knowledge of MCL’s dishonest and fraudulent design?

35 I consider these questions below.

C.1.1 Is it sufficiently arguable that MCL owed fiduciary obligations to Probis with respect to the moneys provided by Probis to MCL?

36 I am satisfied that there is a sufficiently arguable case that the moneys provided by Probis to MCL were held by MCL on trust and thus that MCL owed fiduciary obligations to Probis with respect to those moneys, for the following reasons.

37 First, an objective intention to create an express trust may be found by reference to all of the relevant circumstances. As Heydon JD and Leeming MJ opine in Jacobs Law of Trusts in Australia (2016, 8th ed) at [3-06] and [5-02]:

[3-06] In the case of an express or declared trust, the creator will ordinarily have used language which expresses an intention to create a trust. The author of the trust has meant to create a trust, and has used language which explicitly or impliedly expresses that intention, either orally or in writing. The fact that a trust was intended may even be deduced from the conduct of the parties concerned but if there is any uncertainty as to intention, there will be no trust.

References to ‘intention’ in this context are to be understood, no differently than in the law of contract, as references to the intention imputed to the parties by what has been objectively manifested by the words used considered in their context. ...

[5-02] A court cannot hold that an express trust exists unless it is satisfied that there was the intention to create such a trust. The question will be whether there is language or conduct which shows a sufficiently clear intention to create such a trust. No formal or technical words are required; any apt expression of intention will do. The conclusion that the intention existed by may be drawn as an inference from the available evidence. In order to infer intention, the court may look to the nature of the transaction and the whole of the circumstances attending the relationship between the parties and known to them, including commercial necessity. ...

The overall question is whether in the circumstances of the case, and on the true construction of what was said and written, a sufficient intention to create a trust has been manifested. It is not necessary that the creator of the trust should know that the particular relationship intended to be created is in law a trust.

(citations omitted)

38 See also Re Courtenay House Capital Trading Group Pty Ltd (in liq) [2018] NSWSC 404; (2018) 125 ACSR 149 at 155 to 158 ([18] to [27]) (Brereton J, as his Honour then was) and the authorities there cited.

39 Secondly, in this case, the presently known circumstances include:

(1) the Policy, a business record of MCL prepared in July and August 2019 apparently for the purposes of regulatory compliance. The Policy states in plain terms that MCL will treat the funds placed with MCL by its clients as moneys in trust until it receives instructions from those clients to execute trades on their behalf. The Policy uses the expressions: “MCL will hold the funds on trust for its clients”; “required capital from its clients (which will be held on trust for the clients until instruction to execute and trade(s) are received”; “Clients remit funds to MCL, who then holds the funds on trust for the clients”; and “Upon receiving funds from its clients, MCL will hold the funds on trust for the respective clients” (see [9] above);

(2) the Policy having been prepared in consultation with Mr Kong and Mr Yu (see [8] above). Whilst Senior Counsel for Mr Kong submitted that Mr Yu’s actions with respect to the creation of the Policy were not undertaken as a “contractual counterparty”, in my view it is reasonably arguable that as a result of those actions, Probis (via Mr Yu) was well aware that MCL’s expressed intention was to hold funds it received from clients in trust. (This assumes, favourably to Mr Kong, that the objective intention to create the relevant trust must be bilateral and not unilateral. The validity of that assumption may be in issue in this proceeding.);

(3) the 27 November 2019 email from MCL which requested that Probis place funds into a “Client Money Trust Account” (see [11] above); and

(4) the subsequent compliance with that request by the placement of funds by Probis with MCL (see [12] above).

40 Thirdly, the use of terms such as “trust”, or “on trust” may be regarded as clear expressions of an objective intention to create a trust: see e.g. Byrnes v Kendle [2011] HCA 26; (2011) 243 CLR 253 at 272 [49] (Gummow and Hayne JJ, citing Associated Alloys Pty Limited v ACN 001 452 106 Pty Ltd [2000] HCA 25; (2000) 202 CLR 588 at 605 [34]); Korda v Australian Executor Trustees (SA) Ltd [2015] HCA 6; (2015) 255 CLR 62 at 100 [109] (Keane J); Courtenay House at 156 to 158 ([20] to [27]); Baxter Global Investments Pty Ltd v Marco [2020] NSWSC 1293 at [43] (Henry J). It is sufficiently arguable that a request to place funds into a “Client Money Trust Account” and apparently solemn statements that clients’ funds are to be “held on trust” are of a similar ilk.

41 Senior Counsel for Mr Kong accepted, for the purposes of this application, that there is a sufficiently arguable case that MCL held the moneys it held on behalf of Probis on trust for Probis but contended that the terms of any such trust had not been shown to preclude payments of the kind impugned in this proceeding. He invited the Court to focus solely upon the terms of the LPA and the 27 November 2019 email (at [11] above) in order to ascertain the terms of the trust and to disregard both the Policy and the evidence that Mr Yu and Mr Kong were involved in its creation. In my view such an approach is unduly narrow, in view of the present circumstances and authorities discussed above.

42 When regard is had to the matters identified at [37] to [40] and the first sentence of [41] above, it is sufficiently arguable that MCL owed fiduciary obligations to Probis with respect to the moneys provided by Probis to MCL, including an obligation to hold those moneys for the benefit of Probis.

C.1.2 Is it sufficiently arguable that MCL, qua fiduciary, engaged in a dishonest and fraudulent design?

43 Conduct of a fiduciary may involve a dishonest and fraudulent design where it is conduct in breach of the fiduciary duty that transgresses ordinary standards of honest behaviour: see Hasler v Singtel Optus Pty Ltd [2014] NSWCA 266; (2014) 87 NSWLR 609 at 636 [124] (Leeming JA; Gleeson JA agreeing; Barrett JA finding it unnecessary to express a view); Lifeplan at 31 [71]; Zibara v Ultra Management (Sports) Pty Ltd [2021] FCAFC 4; (2021) 283 FCR 18 at 46 to 51 ([97] to [107]) (McKerracher and Anderson JJ; see also 85 [254] (Derrington J)); Scrivener v Cappello [2021] NSWCA 330 at [65] (Bathurst CJ; Bell P and Macfarlan JA agreeing); and KTC v David [2022] FCAFC 60 at [80] (Wigney J).

44 It is common ground that moneys deposited by Probis with MCL were transferred by MCL to third parties. For the reasons set out above, there is a sufficiently arguable case that those moneys were subject to a trust in favour of Probis and thus that MCL was obliged to retain those moneys for the benefit of Probis. There is no contention on behalf of Mr Kong that the transfer of those moneys was authorised by Probis and the evidence on behalf of the administrators is that they have not located evidence of any such authorisation. In these circumstances, I am satisfied that it is sufficiently arguable that the unauthorised transfer of funds the subject of a trust to third parties was conduct contrary to standards of honest behaviour and thus that MCL engaged in a dishonest and fraudulent design.

45 Senior Counsel for the applicants also relied upon evidence which, it was contended, established that there was a flow of funds: (1) from CCAM (being a company of which Mr Kong was a director and which was controlled by a Mr Effendi) to Probis; (2) from Probis to MCL, a company controlled by Mr Kong; and (3) from MCL to City Credit Capital, a company of which Mr Effendi was a director. Given the views I have expressed above, it is unnecessary to consider this evidence in any detail or whether it is evidence of a dishonest and fraudulent design.

C.1.3 Is it sufficiently arguable that Mr Kong had the requisite knowledge of MCL’s dishonest and fraudulent design?

46 The applicants may establish the requisite knowledge on the part of Mr Kong as to MCL’s breach of its fiduciary obligations by establishing that Mr Kong: (1) had actual knowledge; (2) wilfully shut his eyes to the obvious; (3) wilfully and recklessly failed to make such inquiries as an honest and reasonable person would make; or (4) had knowledge of circumstances which would indicate the fact of the breach on the part of MCL to an honest and reasonable person. The fourth of these possibilities (being the one likely to be the easiest to prove) provides a sufficient basis to establish the requisite knowledge: see Farah Constructions Pty Ltd v Say-Dee Pty Ltd [2007] HCA 22; (2007) 230 CLR 89 at 163 to 164 ([174] to [178]) (Gleeson CJ, Gummow, Callinan, Heydon and Crennan JJ); Grimaldi v Chameleon Mining NL (No 2) [2012] FCAFC 6; (2012) 200 FCR 296 at 361 to 362 ([259] to [262]) (Finn, Stone and Perram JJ); Great Investments Ltd v Warner [2016] FCAFC 85; (2016) 243 FCR 516 at 545 [114]; Lifeplan at 31 [71]; Pittmore Pty Ltd v Chan [2020] NSWCA 344; (2020) 104 NSWLR 62 at 102 ([191] to [192]) (Leeming JA; Bell P and Brereton JA agreeing); and Scrivener at [69].

47 I am satisfied that it is sufficiently arguable that Mr Kong had knowledge (at least) of circumstances which would indicate the fact of MCL’s breach of its fiduciary obligations to an honest and reasonable person. In particular, it is sufficiently arguable that Mr Kong, the sole director of MCL was aware: (1) of the contents of the Policy and thus that funds provided to MCL by its clients were to be held on trust until instructions to trade had been received; and (2) that, contrary to the Policy, such funds had not been held on trust and instead had been distributed to third parties. It is sufficiently arguable that those circumstances would indicate to an honest and reasonable person that MCL had breached the fiduciary obligations it owed as trustee of the trust. Whilst Senior Counsel for Mr Kong contended that it was not sufficiently arguable that Mr Kong had the requisite knowledge because of the evidence of his subjective understanding of usual market practice (see [24] above), such a contention, even if accepted, may not provide a persuasive answer to the fourth category of knowledge (i.e. knowledge of circumstances which would indicate the fact of MCL’s breach to an honest and reasonable person).

C.2 The risk that a prospective judgment will be unsatisfied in whole or part because the assets of Mr Kong will be disposed of, dealt with or diminished in value

48 The applicants bear the onus of establishing that unless the freezing order is continued, there is a reasonable apprehension that Mr Kong’s assets will be dissipated so as to frustrate the Court’s processes: see Cardile v LED Builders Pty Ltd [1999] HCA 18; (1999) 198 CLR 380 at 393 to 394 [26], 399 to 401 ([41] to [42]) (Gaudron, McHugh, Gummow and Callinan JJ). As Cheeseman J explained in Hurst, in the matter of Lloyds Curry Shop Pty Ltd (in liq) v Prasad [2021] FCA 1562 at [56], it is not essential for the applicants to demonstrate a positive intention on the part of Mr Kong to frustrate a judgment (see National Australia Bank Ltd v Bond Brewing Holdings Limited [1990] HCA 10; (1990) 169 CLR 271 at 277 (Mason CJ, Brennan and Deane JJ); Cardile at 394 [26]) or that the risk of dissipation is more probable than not (see Deputy Commissioner of Taxation v Hua Wang Bank Berhad [2010] FCA 1014; (2010) 273 ALR 194 at 196 to 197 ([8] to [10]) (Kenny J); Deputy Commissioner of Taxation v Chemical Trustee Ltd (No 4) [2012] FCA 1064; (2012) 90 ATR 711 at 717 [23] (Perram J); Basi v Namitha Nakul Pty Ltd [2019] FCA 743 at [9] (Wigney J)).

49 Rather, it is sufficient for the applicants to establish that, in the absence of a freezing order, there is a danger or real risk that Mr Kong’s assets will be dealt with in a way which would frustrate the processes of the Court, such that a freezing order is warranted.

50 The risk of dissipation must, however, be demonstrated by evidence: see Fine China at [22(b)]. There is no direct evidence in the present case that there is a real risk Mr Kong may deal with his assets in a way in which the processes of the Court would be frustrated. However, direct evidence is not necessary and the risk of dissipation of assets to avoid the consequences of a judgment may be inferred. The evidence supporting such an inference may include the evidence relied upon to establish a sufficiently arguable case for relief, particularly when that case includes “serious dishonesty involving the diversion of money from its proper channel”: see Patterson v BTR Engineering (Aust) Ltd (1989) 18 NSWLR 319 at 325F-G (Gleeson CJ). See also Patterson at 326B-C and D-E (Meagher JA); Nicols at [51] (Cheeseman J); Fine China at [22] (Moshinsky J); Spotlight Pty Ltd v Mehta [2019] FCA 1796 at [23] (Anderson J).

51 I am satisfied on the evidence presently before the Court that there is a real risk that a judgment against Mr Kong will be wholly or partly unsatisfied because Mr Kong’s assets will be disposed of, dealt with, or diminished in value. The nature of the claim and the evidence outlined above suggest that there is a real danger that Mr Kong may act in a manner which will frustrate the processes of the Court. In particular, the applicant has a sufficiently arguable case that, if ultimately accepted, would establish that: Mr Kong was the sole director of MCL; MCL received funds from Probis which to Mr Kong’s knowledge were funds that were subject to a trust in favour of Probis, consistent with solemn representations that MCL had apparently made to the New Zealand Financial Markets Authority; and in breach of that trust and to Mr Kong’s knowledge the trust funds were paid out to third parties as part of what Mr Kong apparently considers to be an acceptable practice.

C.3 Discretionary considerations

52 It was common ground, and I accept, that the imposition of a freezing order is a drastic step and not a step to be taken lightly.

53 A freezing order usually constitutes a serious interference with the rights of a person to deal with their assets as they wish. However, the following matters point in the other direction in the present case. First, Mr Kong did not adduce any evidence, nor make any submission as to the particular effect upon him of the freezing order in the almost seven-week period between the making of the freezing order on 14 September 2023 and the hearing of the inter partes application on 31 October 2023; or as to its likely effect upon him in the future if it were to continue. Secondly, the applicants have provided an undertaking as to damages and there is no suggestion that the undertaking proffered is inadequate or otherwise inappropriate.

54 If the freezing order were to be set aside or discharged, the risk described at [51] above would be present without such protection as the freezing order provides. In view of the nature of the case alleged, I regard this as a significant risk.

55 Weighing each of these considerations, I am satisfied that the discretion should be exercised so as to continue the freezing order.

56 It was common ground that the answer to the question whether the disclosure affidavit should be provided to the applicants would follow the success or failure of the application to continue the freezing order. As I have decided that the freezing order should be continued, the applicants should have access to the disclosure affidavit.

57 For the reasons set out above, I am satisfied that the freezing order made by Yates J on 14 September 2023 should continue and that the disclosure affidavit should be provided to the applicants. Consequently, the suppression and non-publication order made by Shariff J should be lifted. I will make orders accordingly.

I certify that the preceding fifty-seven (57) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Goodman. |

Associate:

Dated: 14 November 2023