FEDERAL COURT OF AUSTRALIA

Chen v The Ginza Beauty Pty Ltd [2023] FCA 1192

ORDERS

Plaintiff | ||

AND: | Defendant | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The further amended originating process be dismissed.

2. The parties are to confer on the question of costs of the proceeding:

(a) if they agree on the orders to be made they are to provide the Associate to Markovic J with their proposed orders on or before 23 October 2023; or

(b) if they cannot agree on the orders to be made they are each to file submissions, not exceeding three pages in length, on the question of costs on or before 30 October 2023; and

(c) in the event that the parties file submissions in accordance with Order 2(b) above, unless either party requests an oral hearing, the question of costs will be dealt with on the papers.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

MARKOVIC J

1 Yiyu Chen, the plaintiff, seeks an order pursuant to s 247A of the Corporations Act 2001 (Cth) that she, her financial and legal advisors be permitted to inspect and make copies of the books and records of the defendant, The Ginza Beauty Pty Ltd, set out in the schedule to the further amended originating process filed on 11 October 2022.

2 The categories of books and records sought by Ms Chen in the schedule are:

1. For each of the Financial Years to present (unless already provided on 19 August 2021) the following final and signed financial reports and records of the Company including:

(a) profit and loss statements;

(b) cash flow statements;

(c) balance sheets;

(d) cash sales and cash receipt records, including bank deposit records; and

(e) director’s reports;

(f) notes in the financial statements;

(g) income tax returns lodged with the Australian Taxation Office (ATO); and

(h) business activity statements lodged with the ATO.

1A To the extent that any document sought in item 1 above in respect of the financial year ending 30 June 2022 remains in draft, the plaintiff seeks production of those draft financial reports and records.

2. For each of the Financial Years to present (unless already provided on 19 August 2021) any Company ledger, including written documents which record the terms and obligations in respect of any such loans, showing shareholders’ loans for each shareholder, including dates, amount of loans to the Company, withdrawals (repayments) from the Company and current loan balances.

3. For each of the Financial Years to present (unless already provided on 19 August 2021) details of the director loans and any other loans (excluding shareholder loans) made to or by the Company, including written documents which record the terms and obligations in respect of any such loans.

4. For each of the Financial Years to present (unless already provided on 19 August 2021) any fixed asset registers and any depreciation reports of the Company.

5. For each of the Financial Years to present records of annual salary, wages, for each staff, employee or contractor who performed work for the Company.

6. For each of the Financial Years to present any contracts of employees or contractors of the Company.

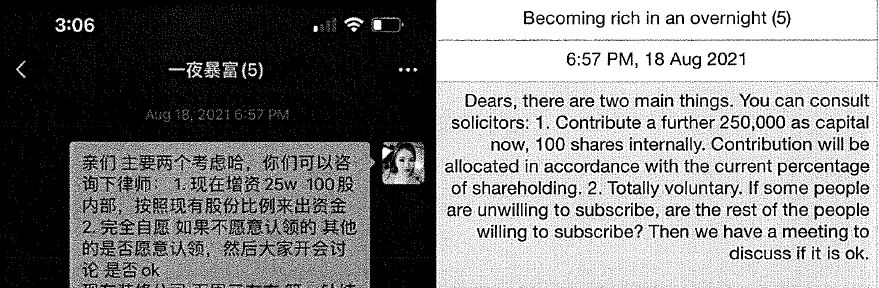

7. Any executed shareholder agreements made in respect of the members of the Company.

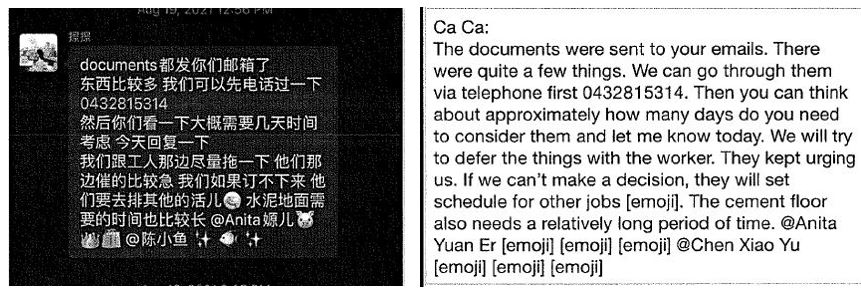

11. For each of the Financial Years to present bank statements for all the Company’s bank accounts (but excluding bank account statements already provided by the Company to the Plaintiff).

(Underlining and strike out omitted.)

3 For the purposes of the schedule:

(1) “Company” means Ginza Beauty; and

(2) “Financial Years” means the financial years ending 30 June 2018, 30 June 2019, 30 June 2020, 30 June 2021 and 30 June 2022.

BACKGROUND

4 Ginza Beauty runs “Lumière Cosmetic Clinic” which offers cosmetic treatments and beauty services including:

(1) non-medical cosmetic treatments using specialist equipment and products;

(2) medical cosmetic procedures carried out by licensed medical practitioners using specialist products and equipment;

(3) cosmetic consultations by medical and non-medical cosmetic professionals; and

(4) supply of specialised cosmetic and beauty products.

5 Ginza Beauty officially opened its business, Lumière Cosmetic Clinic, on 15 September 2018, after a soft opening. Its principal place of business was initially shop 2, 389 Sussex Street, Haymarket, New South Wales.

6 Wei Xuan, also known as Christy Xuan, is Ginza Beauty’s sole director and secretary. Ms Chen is a shareholder in Ginza Beauty. Based on a company search of Ginza Beauty undertaken as at 5 October 2021 Ms Chen holds 111 or 11.1% of the issued share capital while the balance of the shares are held by Ms Xuan as to 389 shares, Chengyuan (Anita) Jiang as to 167 shares, Wei (Monica) Zhang as to 111 shares and Wenting (Bonnie) Liu as to 222 shares. Without intending any disrespect and for ease I will refer to Ms Zhang as Monica and Ms Liu as Bonnie.

7 Despite being in funds, historically Ginza Beauty did not make any distributions to its shareholders or pay director’s fees. Ms Xuan explained that this was because the business was in a growth phase and it was understood that any profit would generally be re-invested in order to further develop and grow it.

8 In order to minimise costs the working shareholders, Ms Xuan, Monica and Bonnie, did not receive a salary between July 2018 and September 2019. From September 2019 to March 2020 they each received $25 per hour and from March 2020 they each received $35.50 per hour.

The impact of the COVID-19 pandemic

9 Following the appearance of COVID-19 cases in February 2020 in New South Wales Ginza Beauty experienced a decline in its performance with the cancellation of many, if not all, of its bookings.

10 In order to minimise the impact of the COVID-19 pandemic and to retain its employees Ginza Beauty attempted to sell its range of beauty products online to existing and new customers. However, during the initial five months of the pandemic Ginza Beauty’s sales declined.

11 From the beginning of June 2020, after the end of the first lockdown in New South Wales, Ginza Beauty’s business started to improve.

Ginza Beauty expands

12 By email dated 4 September 2020 Ms Xuan was informed that level 3, 389 Sussex Street was available for lease. Ms Xuan arranged a dinner with the shareholders at which she informed them that level 3 had become available and that taking on a lease of those premises would be a good growth opportunity for it.

13 Ms Xuan’s evidence is that each shareholder agreed to this course and to payment of a monthly sum of $50,000 for five months to an outgoing shareholder, Qian (Vicky) Wu, for her shares. At the time of registration of Ginza Beauty Ms Wu held 10% of its shares. Ms Xuan informed the shareholders that she did not believe that taking on a lease of level 3 and making the payments to Ms Wu would require any funds from Ginza Beauty’s shareholders although if that changed she would let them know.

14 On 10 January 2021 Ginza Beauty entered into a lease for level 3, 389 Sussex Street.

15 Ms Chen recalls that in or around February 2021 at a dinner with the shareholders of Ginza Beauty Ms Xuan said that she intended to expand the business. Ms Chen recalls that:

(1) she had a conversation with Ms Xuan in Mandarin about that in which Ms Xuan said:

Our business is running smoothly in the past years and we can expand our clinic by renting an extra floor as I was told another floor will be vacant soon. The company will not distribute dividends for this year as we need to use this part of the money to pay the rent and renovation expenses. You do not need to worry about the funds as there are around $800,000 to $1 million in our company account which is sufficient to cover the rental fees and renovation expenses.

(2) she inquired about the amount of the rent and renovation expenses. Ms Xuan informed her that the rent would be about $80,000 to $90,000 per year but that Ms Xuan would negotiate the rent and a rent-free period and that the cost of the renovation would be around $300,000 to $400,000; and

(3) each of the shareholders, including Ms Chen, supported Ms Xuan’s proposal.

16 On 3 February 2021 Ms Xuan received an email informing her that level 2, 389 Sussex Street was available for rent.

17 On 21 February 2021 Ms Xuan sent a WeChat message to Ms Chen in relation to the lease of level 2, 389 Sussex Street in which, among other things, Ms Xuan informed Ms Chen that Ginza Beauty had rented level 3, 389 Sussex Street and that level 2 of the building was also vacant. She sought the shareholders’ consent to renting level 2. Ms Chen said she did not agree or consent to the proposal to rent level 2 as at the time she understood that rental fees would still be covered by Ginza Beauty funds and that shareholders were not required to make further investment. Notwithstanding that evidence, Ms Chen accepted in cross-examination that she was happy with the proposal to rent level 2 and indicated that she did agree to it.

18 On or about 20 April 2021 Ms Xuan sent a WeChat message to Ms Chen in which she informed her that she had leased level 2, 389 Sussex Street. In a further WeChat message sent on 26 April 2021 Ms Xuan informed Ms Chen that the rental was $80,000 and that she was negotiating a rent-free period.

First Shareholders Meeting and subsequent events

19 By a WeChat message sent on 17 August 2021 Ms Xuan informed Ms Chen that Ginza Beauty’s cash flow was low and that she required the shareholders to invest further funds to cover the renovation expenses for level 2, 389 Sussex Street. Ms Chen was concerned that Ginza Beauty’s financial position had deteriorated to such an extent that a capital injection was required.

20 In cross-examination it was put to Ms Chen that she had no reason to believe that there was anything suspicious about the changed financial position of Ginza Beauty given her knowledge of two particular matters.

21 First, it was put to Ms Chen that she knew that between February 2021 and August 2021 Ginza Beauty had spent between $300,000 and $400,000 on renovations. In response Ms Chen said that she was told that Ginza Beauty would probably spend that much on the renovation, but she did not know if it in fact did. That evidence seems somewhat implausible given Ms Chen’s subsequent evidence that she attended Ginza Beauty’s premises once or twice a month, had seen the renovations taking place and she had received a video from Ms Xuan showing the renovations. While Ms Chen tried to explain her evidence away by saying that the renovations were limited to those for level 3, it seems to me that Ms Chen was clearly aware of the renovations, she knew of their estimated cost and, I would infer, she knew that Ginza Beauty was making payment for them.

22 Secondly, it was put to Ms Chen, and she accepted, that there had been a lockdown in the central business district of Sydney.

23 The following exchange took place between Dr Greinke, counsel for Ginza Beauty, and Ms Chen, who was assisted by an interpreter:

Dr Greinke: So you had no reason to believe that there was anything suspicious about the changed financial position, did you?

Ms Chen: I was not sure about this, so I didn’t know.

Dr Greinke: So it’s more of a case you didn’t know as opposed to being suspicious about something. Is that your evidence?

Ms Chen: Can you please repeat that question.

Dr Greinke: I will put it this way. You weren’t really suspicious about the financial position of the company. You just didn’t know particular things about it; is that right?

…

Dr Greinke: I will rephrase the question. You say that you were concerned about the change in financial position, but you agree that you did not have sufficient – you did not have a basis to think that there was anything suspicious; is that right?

Ms Chen: I’m not sure.

24 On the same day, that is 17 August 2021, Ms Chen attended a shareholders meeting (First Shareholders Meeting). Ms Chen and Ms Xuan had a conversation in Mandarin to the following effect:

Ms Xuan: The rent for Level 2 is around $80,000 plus GST. Due to the COVID-19 restrictions, the company does not have any income during these days. Even though we are still in the rent-free period of Level 3, we also need to pay the rent for our existing premises, ground floor and Level 1. We need every shareholder to invest some more money to the company to pay the rent and the renovation expenses for Level 2.

Ms Chen: Why not wait for the ease of the COVID-19 restrictions? Because at that time, the company will have income when it is open to cover the renovation expenses.

Ms Xuan: We have three proposals before us. First, we can raise the funds via shareholders loan from all shareholders. Second, we can raise funds via equity contribution by all of you with percentage shareholding. Third, we can raise funds via issue of new shares to you who are willing to invest the money.

Ms Chen: Before I make the decision, I need to get the financial documents.

Ms Xuan: Sure. I will allow Monica to send them to you.

25 According to Ms Xuan she also said words to the following effect:

As I have indicated to all of you previously, [Ginza Beauty] has entered into a lease for level 2 with rent being $80,000 + GST per annum. This is a very low rate and is only possible due to the pandemic. The reason I decided to enter into the lease was the strong potential for growth after the pandemic ends.

And in response to a query from Ms Chen as to why Ginza Beauty could not wait for the easing of restrictions imposed as a result of the COVID-19 pandemic:

The premises is currently in its rent free period and we should utilise this time. If we commenced renovations works after rent free, we will face even more difficulties given that there may be work time restrictions when other businesses return. We need to finish renovations before rent free ends so that we can open the business fully once the pandemic finishes.

26 A copy of the minutes of the First Shareholders Meeting were in evidence before me. Under the heading “Matters Agreed” they recorded:

It is noted that:

• shareholders had on a 3 votes (72% by shareholding) to 2 votes (28% by shareholding) basis voted in favour of raising further capital of $250,000 for the renovation, the details of which are to be considered at the next meeting;

• the company is to give Ms Jiang and Ms Chen the relevant financial statements that are available.

Ms Chen’s evidence was that the minutes of the First Shareholders Meeting do not properly record voting percentages or calculation of the votes.

27 On 17 August 2021 Ms Chen and Ms Xuan exchanged WeChat messages. In her messages Ms Chen informed Ms Xuan that she was “ok” and their “current problem [was] that [her] husband is dealing with the issue relating to Chris recently” and had “been blaming” her. Ms Chen informed Ms Xuan that if she made another capital contribution her husband would be “mad” at her. The issues relating to Chris concerned an earlier business dealing in relation to which it seems Ms Chen’s husband had lost money. There was some suggestion that Ms Chen’s husband made the investment at the suggestion of “[Ms Xuan] and J”.

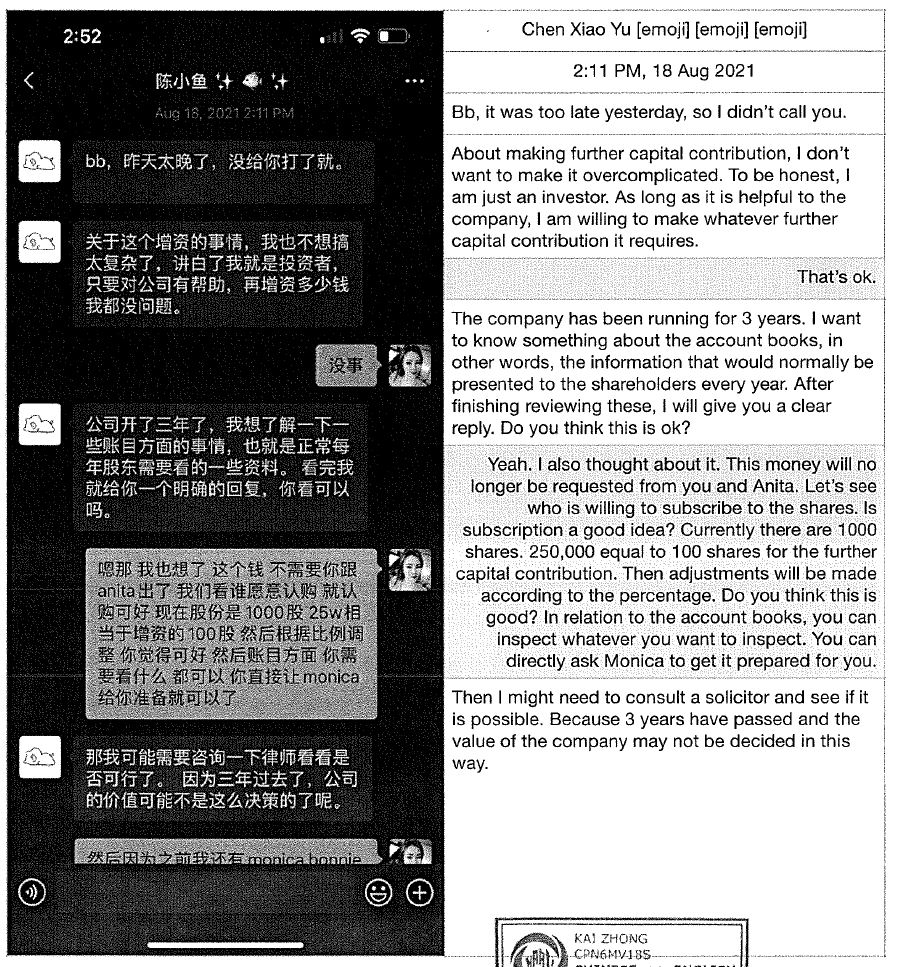

28 On 18 August 2021 Ms Chen and Ms Xuan again exchanged WeChat messages as follows:

29 At the time Ms Chen did not know whether Ginza Beauty’s business was doing well or otherwise. She only knew that its business had been impacted by the COVID-19 pandemic but she had not received any financial reports or statements since the commencement of the business to permit her to assess its performance. Ms Chen was concerned that without reviewing the financial reports she was unable to assess whether Ginza Beauty’s financial decline could be explained and whether it had the potential to improve in the future. Ms Chen had doubts about investing further capital in the absence of financial information at a time when retail premises such as those used by Ginza Beauty were affected by restrictions imposed as result of the COVID-19 pandemic.

30 By WeChat message sent on 18 August 2021 to the shareholder group Ms Chen requested: “financial statement[s], the detailed ledger of each account on the financial statement along with the bank statements”. Ms Xuan requested Monica to provide the requested documents to Ms Chen and Anita.

31 Later on 18 August 2021 Ms Xuan sent a WeChat message to the shareholder group setting out two proposed resolutions and providing further information about the proposed works to level 2, 389 Sussex Street. In relation to the former Ms Xuan’s message was as follows (as written):

32 On 19 August 2021 Monica sent an email to each of Ms Chen and Anita attaching documents for Ginza Beauty for the financial years ended 30 June 2018, 30 June 2019, 30 June 2020 and 30 June 2021. After doing so she sent the following message via WeChat to the shareholder group:

33 Ms Chen provided the documents she had received to her accountant, Jason Yang. Those documents were:

(1) financial report for the financial year ended 30 June 2018 (unsigned);

(2) company annual financial statement for the financial year ended 30 June 2019;

(3) company annual financial statement for the financial year ended 30 June 2020 (unsigned);

(4) profit and loss statement for the financial year ended 30 June 2021;

(5) business activity statement (BAS) for the quarter ended 30 June 2020;

(6) BAS for the quarter ended 31 December 2020;

(7) BAS for the quarter ended 31 March 2021;

(8) account transactions from 1 July 2018 to 31 July 2021; and

(9) bank statements for Australia and New Zealand Banking Group Limited (ANZ) account (012-071 XXXX-XX726) from 12 January 2018 to 14 July 2021.

34 Mr Yang formed the view that some of the financial records he had received were not certified or signed and, following his review of them, that he did not have sufficient information to accurately assess the true financial position and performance of Ginza Beauty. Mr Yang explained that, as a first step, Ms Chen wished to understand the financials for Ginza Beauty.

35 On 20 August 2021 Ms Chen reverted to Monica by WeChat providing a list of documents she required before she could respond to Ms Xuan’s proposal raised at the First Shareholders Meeting. They were:

1) The latest balance sheet

2) The latest fixed asset register/depreciation schedule

3) Cash sales records for the last 3 years

4) Detailed annual salary wage reports and all the payslips for the last 2 years

5) Confirm the “Director Loan” in the balance sheet should be restated as shareholders loan

6) Shareholders loan balances for each shareholder

36 Later that evening Monica sent further documents to Ms Chen, namely payroll details for Bonnie, Monica and Ms Xuan for the financial year ended 30 June 2021, Ginza Beauty’s balance sheet for June 2021, the asset register as at 20 August 2021 and the EBITDA margin for the financial year ended 30 June 2021.

37 On 21 August 2021 Monica sent further documents to Ms Chen, namely bank statements for Ginza Beauty for the period 12 January 2018 to 14 June 2018, a fittings and furniture ledger for the period 1 July 2017 to 30 June 2018 and a plant and equipment ledger for the period 1 July 2017 to 30 June 2018.

38 On the same day Ms Chen sent to Mr Yang the balance sheet for Ginza Beauty for the financial year ended 30 June 2021.

39 On 27 August 2021 Monica informed Ms Chen via a WeChat message that the rent-free period for level 2, 389 Sussex Street would end on 3 September 2021 and that as the shareholders could not reach agreement on the proposed capital raising Ms Xuan may need to invite new shareholders to invest. Ms Chen informed Monica that she was still awaiting the financial information she had requested.

40 On 30 August 2021 Mr Yang and Panbo Ye, Ginza Beauty’s accountant, exchanged emails. In his email Mr Yang requested “detailed shareholders’ loan ledgers for each shareholder including dates, amount of loans to [Ginza Beauty], withdrawals (repayments) & current loan balances”. Mr Ye responded as follows (as written):

Nice e meeting you.

Before we go to the nitty-gritty, I’d like to understand if it’s a legal or accounting matter. Or rather, is it a business matter?

My understanding is that the company is issuing new shares to rise $250k in total. The shares are allocated to all shareholders as per the current shareholding proposition. There is no plan to issue the shares to external people. The options are simple, take it or leave it.

If your client decide to take the share allocation because of the fund raising, please transfer the fund into the company bank account asap. If your client is not interested, her potion will be allocated to other shareholders. There is no pressure.

Please bear in mind, the decision is to be made in a timely matter to avoid opportunity loss.

The investment in Ginza is classified as private equity. As such, of return in income or even capital. In addition, the shareholder transactions are private in nature as the company is unlisted and also private. We cannot provide you with the transactions that are unrelate to your client.

Being a business adviser, I would consider more in commercial terms with the below questions:

• What’s your client’s goal? (willing or unwilling to contribute to the fund raising)

• What’s your client’s ideal result to the matter? (being an passive (nonmanagement) minor shareholder in a private company)

I looking forward to your reply to have the matter sorted.

41 There was a further exchange of emails between Messrs Yang and Ye on 30 and 31 August 2021 which did not result in provision of the requested documents. Rather in his email Mr Ye suggested the following alternatives:

1. If Ms Chen has tremendous confidence in Ginza with its management and potential, I’d recommend contributing to the growth (pay for the shares).

2. If Ms Chen is uncertain about Ginza’s future, I’d suggest leaving as is. So the other shareholders will contribute the $250k, and the shares will be diluted for Ms Chen.

3. If Ms Chen no longer trusts the management and does not believe Ginza anymore, I’d suggest forming an exit plan.

Would you please provide your answer before the 3rd of September? Or the management will deem Ms Chen is not interested in the newly issued shares.

42 On 31 August 2021 Ms Xuan, Bonnie and Monica, pending a response from the other shareholders, each agreed to transfer $50,000 to Ginza Beauty in the event that Ginza Beauty needed funds to enable it to commence the renovation works.

43 On 6 September 2021, on Ms Chen’s instructions, her lawyers, Yingke Law Firm, sent a letter to Mr Ye in which, among other things, they sought provision of the following documents from Ginza Beauty (as written):

1. A complete copy of the Company Constitution;

2. A complete copy of the financial report for the past three financial year (2018-2021); and

3. A complete copy of the directors’ report for the past three financial year (2018-2021).

This letter led to an exchange of emails between, among others, Carrie Fan of Yingke Law and Mr Ye, some of which were intemperate, the terms of which I do not propose to set out.

44 By letter dated 27 September 2021 addressed to Ms Xuan, Yingke Law renewed its request for the provision of the documents referred to in the preceding paragraph. In response the lawyers for Ginza Beauty, Auyeung Hencent & Day (AHD), noted that they were instructed that (as written):

…our client has previously provided all available and relevant company documents requested to your client via an email from Ms Monica Zhang date 19 August 2021.

Second Shareholders Meeting and subsequent events

45 By email dated 5 October 2021 Ms Xuan convened a shareholders meeting to be held on 8 October 2021 (Second Shareholders Meeting). Ms Chen became aware that the main purpose of the Second Shareholders Meeting was to pass a resolution to raise $250,000 in capital in exchange for the issue of 1,000 ordinary shares in Ginza Beauty to the existing shareholders. At the Second Shareholders Meeting there was discussion about the provision of documents sought by Ms Chen. The minutes for that meeting record, among other things, that:

(1) Ginza Beauty maintained that it had provided “substantial documents” to Ms Chen, Vincent Zhu, Ginza Beauty’s lawyer, was unaware of any cash accounts for Ginza Beauty and Mr Ye confirmed that he prepared the relevant financials for Ginza Beauty and that he provided Monica with the relevant documents which were then sent to Ms Chen on 15 September 2021 and, as Ginza Beauty’s accountant, he was not aware of any cash accounts for it; and

(2) a resolution for the issue of 1,000 new shares to existing shareholders by application on a pro rata basis to raise $250,000 was discussed. Under the heading “Matters Agreed” the following was recorded (as written):

It is noted that:

• shareholders had on a 3 votes (Ms Xuan, [Monica], and [Bonnie] being 72% by shareholding) to 2 votes (Ms Jiang and Ms Chen being 28% by shareholding) basis voted in favour of raising funds in accordance with Meeting Notice dated 29 September 2021 via the issuance of 1000 shares to existing shareholders in the

• respective proportions at $250 per share – as set out above.

46 On or about 10 October 2021 Ms Chen became aware that Ms Xuan was the sole director, secretary and shareholder of a company called Lumiere Cosmetic Pty Ltd which was registered on 9 March 2020. Ms Xuan gave evidence that Lumiere Cosmetic Pty Ltd was created to hold intellectual property as part of a corporate restructure that did not eventuate. Ms Xuan had originally intended that Lumiere Cosmetic Pty Ltd own the Lumiere brand with Ginza Beauty being the operating arm. As the restructure did not proceed, Lumiere Cosmetic Pty Ltd has not traded.

47 By email sent on 26 October 2021 Ms Chen received a “Notice of Offer for Subscription of New Shares” offering her 111 of the 1,000 new shares to be issued by Ginza Beauty at $250 per share and thus a total subscription value of $27,750. Ms Chen was requested to indicate whether she wished to subscribe for the new shares by 4 pm on 9 November 2021 and, if so, to pay the total subscription value by 16 November 2021. Ms Chen did not reply to the Notice of Offer because she was of the view that she could not make a decision to further invest without the financial records she had requested from Ginza Beauty.

48 On 10 November 2021 Yingke Law sent a further letter to AHD which included (as written):

(1) under the heading “Financial documents”:

9. We note that our client has requested all the financial documents through her accountant, and we have, on multiple occasions, namely on 6 September 2021, on 27 September 2021 through email and on 8 October 2021 the Shareholder Meeting, requested your client to provide all the financial documents for the running of the Company as the documents our client received on 19 August 2021 from the Company’s internal accountant Monica Zhang (“Documents on 19 August”) are neither sufficient nor adequate.

10. We note that the Company’s accountant, Mr Panbo Ye confirmed on the Shareholder Meeting that the Company had cash income through the running of the business and that any and all such cash income was all deposited into the bank account.

11. However, the Documents on 19 August failed to disclose such cash income records for the last 3 years or any bank statement reflecting the cash deposit. We put you on notice that our client is concerned that the Company may have failed to correctly record or report cash income.

(2) under the heading “Demand”:

22. We urgently demand your client to rectify the current situation meaningfully, including but not limited to the provision following outstanding information and/or documents on or before 15 November 2021 without any further delay:

a. Cash sales records for the last 3 years;

b. Any and all bank statements for the cash sales and transaction records for company accounts;

c. Detailed annual salary/wages reports and all the payslips of your employees for the last 2 years; and

d. Detailed shareholders’ loan ledgers for each shareholder, including dates, amount of loans to the Company, withdrawals (repayments) and current loan balances.

49 On 19 November 2021 Ms Xuan and Ms Chen’s husband, Yang Chen, had an in person meeting in order to discuss a potential share buyback offer. At this meeting, they had an exchange to the following effect (in Mandarin):

Mr Chen: [Ms Chen] has been requesting [Ginza Beauty’s] documents in order to obtain a proper valuation of the business. We would like [Ginza Beauty] to consider buying out our shares.

Ms Xuan: As you know, [Ginza Beauty] just took on a further lease and it does not have sufficient money to buy you [out]. In any event, what price were you thinking?

Mr Chen: We know that [Ginza Beauty] has been doing very well prior to COVID and we believe that [Ginza Beauty] is worth a lot more so we would want more than our initial investment in the region of $500,000.

Ms Xuan: As you know, COVID has significantly affected [Ginza Beauty] and that is just not possible at this time. [Ginza Beauty] would not be able to afford that and it would not be in the interest of [Ginza Beauty].

50 Following this conversation, Ms Xuan had a discussion with Monica and Bonnie in relation to making a potential offer to purchase Ms Chen’s shares.

51 On 25 November 2021, Ms Xuan had a telephone conversation with Mr Chen in which Ms Xuan offered to purchase Ms Chen’s shares on behalf of herself, Monica and Bonnie by payment of $300,000 to be paid over a period of one and a half years. Mr Chen did not agree to this valuation and rejected Ms Xuan’s offer.

Ms Chen’s concerns

52 Ms Chen has the following concerns about the operation of Ginza Beauty:

(1) Ms Xuan may have misused her position as sole director of Ginza Beauty to divert benefits away from its shareholders to Lumiere Cosmetic Pty Ltd and for her own personal benefit. Ms Chen seeks access to certain of the books and records to further investigate whether or not Ms Xuan has acted in breach of her directors’ duties owed to Ginza Beauty; and

(2) if Ms Xuan has breached her duties as a director owed to Ginza Beauty by diverting business to Lumiere Cosmetic Pty Ltd, this may have materially and adversely affected the value of Ms Chen’s shareholding in Ginza Beauty and Ginza Beauty may have potential claims against Lumiere Cosmetic Pty Ltd and Ms Xuan. Ms Chen is concerned that because Ms Xuan is the sole director of Ginza Beauty, no action will be taken to properly investigate her concerns and, if those concerns are justified, no action will be taken to remedy any such breach for the benefit of Ginza Beauty and all of its shareholders.

53 If Ms Chen is given access to the books and records she seeks in the schedule then, depending on the nature of the material, she may bring any one or more of the following claims:

(1) an application for the purchase of her shares in Ginza Beauty after a proper valuation has been carried out;

(2) with leave, a derivative action by Ginza Beauty against Ms Xuan if there is a reasonable basis to assert that she has acted in breach of her duties owed to Ginza Beauty;

(3) an oppression suit; and/or

(4) an application to wind up Ginza Beauty on the just and equitable ground.

Documents produced to date

54 Based on the report of Wynand Nicolaas Mullins, a chartered accountant and senior managing director in the forensic and litigation consulting segment at FTI Consulting (see [57] below), as at 23 September 2022 Ginza Beauty had produced the following documents to Ms Chen:

(1) unsigned financial statement for Ginza Beauty for:

(a) the financial year ended 30 June 2018; and

(b) the financial year ended 30 June 2020;

(2) financial statement for Ginza Beauty for the financial year ended 30 June 2019;

(3) profit and loss statement for Ginza Beauty for the financial year ended 30 June 2021;

(4) account transactions for:

(a) the financial year ended 30 June 2019;

(b) the financial year ended 30 June 2020;

(c) the financial year ended 30 June 2021; and

(d) the period 1 July 2021 to 31 July 2021;

(5) unsigned BAS for:

(a) the quarter ended 31 December 2020;

(b) the quarter ended 30 June 2020; and

(c) the quarter ended 31 March 2021;

(6) balance sheet for Ginza Beauty as at 30 June 2021;

(7) bank statement for ANZ account (012-071 XXXX XX697) for the period 14 February 2022 to 14 March 2022; and

(8) bank statements for ANZ account (012-071 XXXX XX726) for the periods:

(a) 12 January 2018 to 14 October 2019;

(b) 13 December 2019 to 14 September 2020;

(c) 13 November 2020 to 14 May 2021; and

(d) 14 June 2021 to 14 July 2021.

55 On the second day of the hearing:

(1) the following documents were tendered by Ms Chen:

(a) letter from Tax Ideas North Sydney to Ms Xuan dated 24 March 2020 enclosing the tax return for Ginza Beauty for the financial year ended 30 June 2018;

(b) letter from Tax Ideas to Ms Xuan dated 24 March 2020 enclosing the tax return for Ginza Beauty for the financial year ended 30 June 2019; and

(c) letter from Tax Ideas to Ms Xuan dated 27 November 2020 enclosing:

(i) the tax return for Ginza Beauty for the financial year ended 30 June 2020; and

(ii) the tax return for Ginza Beauty for the financial year ended 30 June 2021; and

(2) Ginza Beauty produced the following documents in response to a notice to produce:

(a) financial statement for Ginza Beauty for the financial year ended 30 June 2021; and

(b) tax return for Ginza Beauty for the financial year ended 30 June 2021.

The evidence of Monica and Messrs Yang, Mullins and Ye

56 Messrs Yang and Ye gave evidence in relation to the categories of documents sought in the schedule and the documents which had been provided in response to Ms Chen’s requests made prior to the commencement of this proceeding for the financial records of Ginza Beauty.

57 At the resumed hearing Ms Chen was also given leave to reopen and to rely on a report dated 23 September 2022 prepared by Mr Mullins.

58 Mr Yang’s evidence was to some extent overtaken by Mr Mullins’ report described below. However, in summary Mr Yang explained that he had reviewed the documents provided to Ms Chen by Ginza Beauty on 19 August 2023 for the purpose of explaining what, if any, other books he required to advise Ms Chen from an accounting perspective about the financial performance of Ginza Beauty and to recommend any further books to be obtained from Ginza Beauty for that purpose. Mr Yang set out the ways in which he considered the documents with which he had been provided were insufficient or incomplete and the recommended further material to be obtained.

59 In cross-examination Mr Yang noted that he has no expertise in forensic accounting, business valuation or share valuation. He explained that his role was to answer some questions based on the financial information provided by Ms Chen, to explain the “financial aspect” of Ginza Beauty and “that considering the next step, whether she will do a valuation”. Mr Yang had intended to prepare a report for Ms Chen but he formed the view that there was insufficient information for him to do so.

60 Mr Yang also identified certain cash transactions which appeared to be credited to a director loan account, rather than Ginza Beauty’s bank account. Based on his review of Ginza Beauty’s account transactions, he was unable to identify any of these cash transactions being deposited in Ginza Beauty’s bank.

61 Monica, who is the finance manager for Ginza Beauty, gave evidence about these transactions. She explained that:

(1) the transactions recorded under the director loan account were manual adjustments which she entered based on a reconciliation which she conducted in around February 2021 for cash held by Ginza Beauty in its safe. The name of the director loan account was amended to “shareholder loan account” in around early 2021; and

(2) the nature of Ginza Beauty’s business, which involved offering clients treatment packages, discounts for payments in advance, memberships and coupons, was such that from time to time clients would make some upfront payments in cash. These prepaid amounts are not treated or recorded as sales revenue until such time as a client has used their coupon or vouchers. Accordingly, when Ginza Beauty received an advance payment in cash, its accounting system required manual adjustments.

62 Monica’s evidence showed that in the period 1 January 2021 to 31 July 2021, Ginza Beauty deposited cash totalling $370,000 into its ANZ account (012-071 XXXX-XX726). In cross-examination, Monica did not accept that Ginza Beauty received similar amounts of cash throughout the life of the company. She explained that the six month window, that is from January to July 2021, was a particular time during which the COVID-19 pandemic had become quite serious and, as a result, Ginza Beauty staff were not able to deposit cash regularly.

63 Monica also gave evidence that in the period between June 2021 and December 2021, as a result of the COVID-19 pandemic, Ginza Beauty was operating at limited capacity and in that period it accumulated significant cash in its safe from cash sales. Monica explained that:

(1) during the COVID-19 pandemic it was not practical for cash to be banked frequently nor for cash transactions to be recorded; and

(2) it was not until around mid-February 2021, when she began reconciling the accounts for Ginza Beauty, in preparing the BAS for the quarter ended 30 September 2020, that she inserted manual journals into the director loan account in order to reflect the unearned revenue figures for that period and until such time that Ginza Beauty could properly bank its cash and allocate its cash receipts accordingly.

64 Monica’s evidence was that the journals entered on 21 February 2021, which are described above, depict what she believed to be the relevant adjustments needed to properly reflect the sales and unearned revenue figures for each quarter.

65 As noted above, Mr Mullins prepared a report dated 23 September 2022. In doing so he was given the following instructions:

a) Undertake a review of all the documents that have been provided by Ginza Beauty, and where possible, a reconciliation between the different categories of the documents in relation to the period from 1 July 2018. In doing so, please identify if there is any inconsistency or otherwise incompleteness between the reports, statements, records, ledgers and state the basis and reasons.

b) In your opinion what categories of the financial documents and Books of Ginza Beauty are necessarily required to perform an assessment of Ginza Beauty’s financial status in the Updated Schedule the plaintiff seeks the access to, and why those documents should be expected in a business such as Ginza Beauty.

66 In responding to the questions posed to him Mr Mullins undertook the following steps:

Step 1: I have reviewed the documents requested as set out in the 2022 RFI in the Court Book;

Step 2: I have reviewed the documents provided to me and compared them to the documents requested in the 2022 RFI in the Court Book;

Step 3: Where information has not been provided, I have reviewed the affidavits provided to me and the documents contained in the Court Book to attempt to identify reasons why the information was not provided;

Step 4: Considered whether the documents and responses provided in the Defendant’s Affidavits are, in my view, based on my experience, sufficient to satisfy the requests set out in the 2022 RFI in the Court Book; and

Step 5: Sought to understand whether there is any inconsistency or otherwise incompleteness between the information provided, which identifies unexplained matters of relevance to understanding the financial status of Ginza Beauty; and

Step 6: Considered whether the documents requested in the 2022 RFI are necessarily required to perform an assessment of Ginza Beauty’s financial status.

For the purposes of Mr Mullins’ report the term “2022 RFI” was defined to mean the “[s]chedule of documents requested by [Ms Chen] on 22 August 2022 as set out at pages 965 to 966 of the Court Book” which are the categories of documents listed in the schedule (see [2] above).

67 Mr Mullins explained that steps 1 to 5 responded to the first question posed to him and step 6 responded to the second question posed to him.

68 In section 2 of his report Mr Mullins provided a summary of his opinion and answers to the two questions posed.

69 In relation to the first question Mr Mullins expressed the view that, based on his analysis of the information provided to him, not all the information that one would ordinarily expect to be available at the time of the 2022 RFI had been provided to Ms Chen. Mr Mullins considered that the following information that would ordinarily be available at the time of the 2022 RFI had not been provided to Ms Chen (as written):

(a) Profit and loss Statements – A finalised version in the financial statements for FY21 and draft version FY22;

(b) Cash flow statements – For the period FY18 to FY22;

(c) Balance sheets – A finalised version in the financial statements for FY21 and draft version FY22;

(d) Cash sales and cash receipt books;

(e) Directors’ reports – A finalised version in the financial statements for FY21;

(f) Notes to financial statements – A finalised version in the financial statements for FY21;

(g) Income tax returns – For the period FY18 to FY21;

(h) BAS statements – For the period FY18 to FY21;

(i) Documents which record terms & obligations in respect of any loans;

(j) Details of director loans and any other loans made to or by Ginza Beauty;

(k) Fixed asset registers/ depreciation reports – For the period FY18 to FY22;

(I) Salary and wage information – For the period FY18 to FY22;

(m) Shareholder agreements;

(n) Bank statements of all bank accounts – All periods up to 14 August 2022; and

(o) Current leases in name of Ginza Beauty.

70 In answer to the second question posed Mr Mullins noted that he had identified two critical inconsistencies in the information provided to Ms Chen concerning the bank accounts and the director loan account. He summarised his findings as follows:

(a) Bank Accounts – The Xuan Affidavit states that Ginza Beauty has a single trading bank account and an interest account for GST. In the balance sheets of Ginza Beauty, I have identified that the business has the following bank accounts titled; Business account, ANZ AU CC xx1640, and ANZ bank saving account. I have assumed that the ‘Business account’ is the single trading account. I have identified that the full description of the ‘ANZ bank saving account’ is “ANZ Bank Saving Account 03697”, and that the ‘interest account for GST’ is an ANZ account with an account number ending in 03697. Based on this, it appears these are the same account. Based on the Account Transactions, this account does not appear to represent an ‘interest account for GST’ as it appears to contain trading transactions and therefore appears to be a second trading account for Ginza Beauty, which is inconsistent with the Defendant’s statement that Ginza Beauty has a single trading account and an interest account for GST. In particular, both accounts appear to contain trading transactions, and therefore there is more than one trading account.

(b) ‘Director Loan’ Account – The balance sheet records that a ‘director loan’ account has a balance of $1,804,088 as at 30 June 2020. The Zhang Affidavit states that the ‘director loan’ account was actually a shareholder account, however this account does not match the initial investment made by the shareholders to $2,500,000. In my opinion, the balance of any related party loans should not reduce unless a repayment to the party has been made. I have reviewed the Account Transactions and identified that unearned revenue was recorded in the ‘director loan’ account as well as several expense/cash payments, and not repayments to the shareholders. Based on my review, the purpose of the ‘Director Loan’ account is inconsistent with the stated purpose of the account and does not represent an account that records the cash loaned to the business by the shareholders.

(Footnotes omitted.)

71 Mr Mullins set out detailed reasons for reaching his conclusions in his report which I do not intend to set out in full.

72 In undertaking step 4, a review of documents provided and affidavit responses (see above), Mr Mullins categorised the documents requested in the schedule as either “high”, “medium” or “low” based on their necessity, that is the importance of having access to that information, in undertaking an assessment of Ginza Beauty’s financial status, where:

(1) “high” means that the document is “critically important to form a conclusive and informed view of Ginza Beauty’s financial status”;

(2) “medium” means the document is “important when performing an assessment of Ginza Beauty’s financial statement”; and

(3) “low” means the document “may be helpful, but may not be required when performing an assessment of Ginza Beauty’s financial status”.

The results of Mr Mullins’ analysis of the necessity of the documents are included in a table titled “Table 3. Summary of Findings”.

73 In relation to step 6, that is consideration of relevance of documents in assessing financial status (see above), Mr Mullins relied on his analysis and characterisation of the documents requested in the schedule as either high, medium or low based on their necessity in undertaking an assessment of Ginza Beauty’s financial status. At 4.8.2 of his report Mr Mullins concluded (as written):

Based on the information provided and reviewed, in my opinion, there is insufficient information to enable a rational investor to make an informed decision of whether to provide further funding the Ginza Beauty either by way of a shareholder loan or an equity investment.

74 Under the heading “Concluding Remark” at 4.8.3 and 4.8.4 of his report Mr Mullins noted:

4.8.3. Overall, the profit and loss statements and balance sheets do not provide a sufficient description or explanation for certain account balances, such as the ‘Director loan’ account, to enable a shareholder to review the information and form a conclusive view as to the reasonableness, completeness and purpose of the transactions to those accounts.

4.8.4. Accordingly, following my review of the information provided to me, I do not consider I have been provided with sufficient financial information to accurately assess the financial performance and position of Ginza Beauty.

75 In cross-examination Mr Mullins was asked about the meaning of the terms “financial status” and “financial performance and position” as used in his report. He explained that the terms referred to slightly different things and that: “financial performance” refers to the performance of an entity over, for example, a prescribed period while “financial position” refers to a specific position of a company, usually demonstrated by a balance sheet at a particular point in time; and “financial status” is a broader concept because it does not rely purely on a balance sheet and profit and loss statement.

76 In relation to his remarks at 4.8.3 and 4.8.4 of his report Mr Mullins accepted that he did not describe what a rational investor would take into account in making a decision to invest in Ginza Beauty or the particular documents that would be relevant to that decision that had not been provided by Ginza Beauty. Mr Mullins said that the problem that arose was that the information that had been provided was incomplete and as a result he was unable to form a concluded view about it and, in particular, to undertake a full or proper reconciliation. This was because there were issues with the completeness of, for example, the general ledgers and the bank statements that were provided. Mr Mullins accepted that when he spoke of completeness what he meant is that it would be more desirable to have more complete financial information in order to make decisions.

77 More generally in relation to his report, Mr Mullins accepted that he was not instructed to attempt to carry out a valuation of Ginza Beauty’s business or to comment on whether the documents that had been provided by Ginza Beauty were sufficient to carry out a valuation.

78 Mr Ye gave evidence responding to Mr Yang’s criticisms of the information that was provided by Ginza Beauty to Ms Chen prior to commencement of the proceeding. While Mr Yang’s evidence was, as I have observed above, somewhat overtaken by events, Mr Ye’s evidence still provides some understanding of the preparation and status of the financial records of Ginza Beauty.

79 Mr Ye’s firm, Tax Ideas, has assisted Ginza Beauty with preparing the financial reports and tax lodgements for the financial years ended 30 June 2019, 30 June 2020 and 30 June 2021. Mr Ye’s evidence was that Ginza Beauty manages its day to day bookkeeping by uploading data into Xero accounting software.

80 Mr Ye gave the following evidence about Ginza Beauty’s financial records provided to Ms Chen:

(1) the profit and loss statement for the financial year ended 30 June 2021 was provided in draft. The notes to it had not yet been prepared;

(2) the financial accounts were not incomplete. They were prepared in accordance with the guidelines issued by the Tax Practitioners Board and the lodgement requirements of the Australian Taxation Office;

(3) the financial accounts for Ginza Beauty are prepared as special purpose reports to be used for tax lodgement purposes. They are distinguishable from “general purpose reports” under the Australian Accounting Standards Board which may include further details and are typically required for larger companies;

(4) the profit and loss statements of a business should generally accord with the reported income and expenses in the income tax returns. Any differences will be as a result of differences in the tax treatment versus accounting treatment of income or expense items. In any event there were no differences between the profit and loss statement and tax return for the financial year ended 30 June 2021;

(5) a depreciation schedule is included in the financial statements for the financial year ended 30 June 2019; and

(6) as far as he is aware Ginza Beauty only has one bank account and Mr Ye is not aware of any cash accounts or other cash records.

STATUTORY FRAMEWORK AND LEGAL PRINCIPLES

81 Section 247A of the Corporations Act relevantly provides:

(1) On application by a member of a company or registered scheme, the Court may make an order:

(a) authorising the applicant to inspect books of the company or scheme; or

(b) authorising another person (whether a member or not) to inspect books of the company or scheme on the applicant’s behalf.

The Court may only make the order if it is satisfied that the applicant is acting in good faith and that the inspection is to be made for a proper purpose.

82 Section 9 of the Corporations Act defines “books” to include a register, any other record of information, financial reports or financial records, however compiled, recorded or stored and a document.

83 The applicable principles were not in dispute. They were recently stated in Enares Pty Ltd v Nimble Money Ltd (2022) 294 FCR 31 (Farrell, Markovic and Derrington JJ). At [36] the Full Court observed that s 247A of the Corporations Act “vests discretion in a court to make a relevant order once satisfied that the applicant seeking relief is acting in good faith and that the inspection is to be made for a proper purpose”. The applicant for relief bears the onus of establishing that it is acting in good faith and for a proper purpose: Enares at [37]. At [38] the Full Court continued:

The authorities suggest that the expression, “acting in good faith and that the inspection is to be made for a proper purpose”, is a composite one such that it ought not to be parsed and then an attempt made to satisfy each identified element: Barrack Mines Ltd v Grants Patch Mining Ltd (No 2) [1988] 1 Qd R 606 (Barrack Mines Ltd v Grants Patch Mining (No 2)); Knightswood Nominees Pty Ltd v Sherwin Pastoral Company Ltd (1989) 15 ACLR 151 at 156; Acehill Investments Pty Ltd v Incitec Ltd [2002] SASC 344 at [29] (Acehill Investments v Incitec). They further suggest that the proper purpose asserted must be the dominant or primary purpose for seeking inspection, and if that is shown, it is irrelevant that the applicant may well secure some collateral or incidental benefits from obtaining an order: Unity APA Ltd v Humes Ltd (No 2) [1987] VR 474 at 480; Barrack Mines Ltd v Grants Patch Mining (No 2) at 615. The proper purpose so identified must relate to each category of document which the applicant seeks to inspect: Rasley (Singapore) Pte Ltd v Financial & Energy Exchange Ltd [2020] FCA 1462 (Rasley v Financial & Energy Exchange): such that, if the terms of the application are cast too widely, there is a real risk of undermining the veracity of the asserted purpose.

84 In relation to “proper purpose”, at [40]-[42] the Full Court said:

40 The requirement that inspection is sought for a “proper purpose” requires that the asserted purpose of the application for inspection is related to the rights of the applicant qua shareholder of the company: Ingram v Ardent Leisure Ltd [2020] FCA 1302 at [74] (Ingram v Ardent Leisure Ltd).

41 The intended purpose of seeking inspection must relate to the shareholder’s rights and interests in that capacity in relation to the company or its directors. …

42 For the purposes of this case it is only necessary to observe that seeking inspection of documents in order to ascertain whether there has been a breach of a directors’ duty or whether oppressive conduct has been engaged in, is self-evidently within the scope of a proper purpose: Barrack Mines Ltd v Grants Patch Mining Ltd (1987) 12 ACLR 357 and Barrack Mines v Grants Patch Mining (No 2). It can also be accepted that a legitimate purpose of inspection is the desire of a member to protect their investment in the company: Re Tolco Pty Ltd [2016] NSWSC 1069 at [22]-[23]; Rowland v Meudon Pty Ltd (2008) 220 FLR 362 at [35], [41], [43]; Intercapital Holdings v MEH Ltd at 602.

85 As to the requirement to establish good faith, at [44]-[47] the Full Court said:

44 … Central to many authorities dealing with this issue is the probative strength of the evidence which is said to give rise to the concern relating to the asserted purpose. It is in this context that concepts such as whether it has been shown that there is a “case”, “basis” or “issue” “for investigation” have arisen: Mesa Minerals Ltd v Mighty River International (2016) 241 FCR 241. In that case the concept was addressed by Katzmann J who (at [26]) observed:

Mesa frequently referred in its submissions to the need to establish “a case for investigation”. The expression does not appear in the Act. It is an expression which was used in argument in Intercapital Holdings and which Brooking J deployed in his later judgment in Knightswood. Its utility, as Barrett J put it in Praetorin at [39], is to emphasise the need for an objective basis for intervention.

45 Whilst that ought to be accepted in the sense that, establishing a case for investigation is a pre-requisite for intervention by the Court, its essential purpose was correctly identified by the primary judge (PJ [43]) as, inter alia, establishing that the applicant was acting in good faith. Whilst it is not a substitute for ascertaining whether good faith exists, in the absence of a reasonable basis or foundation for the asserted purpose for which inspection is sought, it cannot be said that the application is being made in good faith, no matter how fervently the applicant may believe in their claim.

46 Moreover, the concept of establishing a “case for investigation” as an element of good faith usefully operates to exclude applications by members who do not have any foundation for concern about a company’s operation but wish to ascertain if something untoward has or may have happened. The section does not permit inspection by shareholders who are unsure about whether the directors have complied with their duty and merely wish to examine the company’s books to satisfy themselves that no breach has occurred: Praetorin Pty Ltd v TZ Ltd, 249 – 250 [64] – [65].

47 In assessing whether there is a “case for investigation”, the Court is not required to decide substantive issues concerning the asserted right or claim: Hanks v Admiralty Resources NL at [37]–[39]. …

86 In Enares, after observing at [48] that the primary judge was correct to anchor her Honour’s inquiry in the statutory language of s 247A of the Corporations Act, namely that inspection might only be permitted if an applicant is acting in good faith and that the inspection is to be made for a proper purpose, the Full Court noted that:

On the other hand, in the ascertainment of whether the application is made in good faith consideration must be given to whether the applicant’s concerns are “real” or “legitimate” and this requires a more granular analysis of whether there is an objective basis or foundation for the concerns. If there is no “case for investigation” or the applicant’s issues are insubstantial or fanciful, or “artificial, specious or contrived”, the concerns, even if subjectively held, cannot form a basis for an application made in good faith.

CONSIDERATION

87 The question that arises is whether Ms Chen has established that she is acting in good faith and has a proper purpose in seeking the inspection. The proper purpose must be a primary purpose and must be established in relation to each category of document sought.

88 Ms Chen submitted that she had three concerns as a minority shareholder.

89 First, there has been a material lack of information shared by Ms Xuan as the sole director (and majority shareholder) and that lack of current information about the business activities of Ginza Beauty, relevant to the valuation of Ms Chen’s shareholding, means she is not in a position to fairly seek to sell her shares based on the fair value to be attributed to them.

90 Secondly, there has been inconsistent information concerning the need for further capital investment, the undisclosed incorporation of a company with a similar name and the apparent misuse of Ginza Beauty’s trading get up which has led Ms Chen to believe that there is a risk that Ms Xuan may have misused her position as the sole director and controller of Ginza Beauty to divert commercial benefits away from Ginza Beauty and its shareholders to Lumiere Cosmetic Pty Ltd, possibly in breach of her directors’ duties owed to Ginza Beauty and with the real risk of a material and adverse effect on the value of her shares in Ginza Beauty.

91 Thirdly, because of the apparent operation of a competing beauty salon which, to date, Ginza Beauty has shown no interest in restraining from using the Lumière Cosmetic get up, there is a real risk that Ginza Beauty will take no action given Ms Xuan is its controlling mind.

92 Ms Chen submitted that, as a shareholder of a private company, she has real and justified concerns affecting her investment, each of her concerns are bona fide and, objectively viewed, reasonably held. Ms Chen contended that she seeks the books in the schedule to understand the conduct of Ginza Beauty, as well as to gain access to information to fairly value her shares. Ms Chen submitted that if she obtained access to the books in the schedule she would use them for at least one of the following purposes:

(1) to properly value her shareholding in Ginza Beauty and seek orders buying out her shareholding for fair, undiluted value;

(2) to further investigate whether Ms Xuan has acted in breach of her directors’ duties to Ginza Beauty, so as to consider bringing a potential derivative action by Ginza Beauty which, on present information, seems unlikely to be pursued by current management;

(3) to consider a potential oppression proceeding, if she is unable to be bought out for fair value; and/or

(4) to bring a proceeding for the winding up of Ginza Beauty on just and equitable grounds.

93 Ginza Beauty submitted that Ms Chen’s case failed at the threshold question of proper purpose.

94 Ms Chen’s subjective purpose in seeking the documents in the schedule is as set out above. As the Full Court observed in Enares at [42] “seeking inspection of documents in order to ascertain whether there has been a breach of a directors’ duty or whether oppressive conduct has been engaged in, is self-evidently within the scope of a proper purpose”. However, Ms Chen must establish that she is pursuing the stated purpose in good faith. In doing so Ms Chen must establish a reasonable basis or foundation for the purposes for which she asserts she seeks inspection. Put another way, she must establish a “case for investigation”. In ascertaining whether that is so there must be a “more granular analysis” of whether there is an objective basis or foundation for Ms Chen’s concerns.

95 I will address each of Ms Chen’s stated concerns and purposes for inspection in turn.

96 The first concern and purpose for her inspection raised by Ms Chen is that she is unable to ascertain a fair value for her shares given the information vacuum. However, there is no evidence before me, beyond Ms Chen’s mere assertion, to objectively establish that to be the case. Financial information was provided to Ms Chen prior to commencement of this proceeding. Ms Chen raised concerns as to its adequacy which Ms Xuan attempted to address. In addition after commencement of the proceeding and, indeed, right up to the second day of hearing, further financial information was provided by Ginza Beauty to Ms Chen.

97 Mr Yang, Ms Chen’s accountant, reviewed the first tranche of documents provided by Ginza Beauty in August 2021 for the purpose of explaining its financial situation to Ms Chen. He gave evidence to the effect that he would require further documents, beyond those provided at that time, in order to do so. However, Mr Yang is not a valuation expert and he was not asked to attempt to value Ms Chen’s shares in Ginza Beauty nor to comment on whether the documents provided were sufficient for that purpose and, if not, what further documents were required. Mr Yang’s analysis was to be a precursor to any decision by Ms Chen to obtain a valuation.

98 Similarly, Mr Mullins was not asked to undertake a valuation of Ms Chen’s shares in Ginza Beauty or to assess the adequacy of the documents provided for that purpose or to identify the types of documents that may be needed for such a valuation. He was asked to assess the documents provided by Ginza Beauty, to identify any inconsistency in them and to consider the categories of documents sought in the schedule and whether they were required to assess Ginza Beauty’s financial status.

99 In support of her concerns about the valuation of her shares, Ms Chen referred to the conversation between Mr Chen and Ms Xuan on 19 November 2021 (see [49] above) where Ms Xuan deposed that “COVID [had] significantly affected [Ginza Beauty]” and the subsequent offer made by Ms Xuan on 25 November 2021 (see [51] above) to buy out Ms Chen’s shares for $200,000 lower than her husband’s offer. Ms Chen submitted that this underscores the relevance and need for current financial information some 12 months later so that she can fairly value her shares. She contended that obtaining the financial and other related books as sought, in order to value her investment, is plainly a proper purpose. Ms Chen submitted that: while she has not asked a valuer to attempt a valuation with the documents disclosed, the factual evidence shows that valuation of her shares is an issue in play between the parties; and, given Mr Mullins is a valuer, his evidence that the documents produced to date are not sufficient is “enough and sufficient” for a proper basis to be established for the making of an order under s 247A of the Corporations Act.

100 That there was a disagreement about the value of Ms Chen’s shares as part of a commercial negotiation as at November 2021 does not underscore the relevance and need for the books and records sought. There is no evidence of any further discussion of negotiation or of an impasse reached because of a lack of information permitting valuation. Insofar as Mr Mullins’ evidence on this topic is concerned, I refer to my observation above (see [98] above). Mr Mullins has simply not considered the sufficiency of the documents provided to date for the purposes of carrying out a valuation.

101 In those circumstances I am not satisfied that Ms Chen has established a proper purpose in seeking the documents in the schedule in order to undertake a valuation of her shares in Ginza Beauty. Beyond her mere assertion of an intent to do so there is no objective evidence to support either a reason for her doing so or that she has taken any steps to secure a valuation including by obtaining an understanding of the documents required to obtain such a valuation and whether those sought in the schedule would assist in that purpose.

102 Ms Chen’s second concern and stated purpose for access to the documents in the schedule is because she has perceived that there has been inconsistent information about the need for further capital investment, the undisclosed incorporation of Lumiere Cosmetic Pty Ltd and because of the apparent misuse of Ginza Beauty’s trading get up. As a result of these things Ms Chen believes that there is a risk that Ms Xuan may have misused her position as the sole director of Ginza Beauty to divert commercial benefits away from it and its shareholders to Lumiere Cosmetic Pty Ltd. She seeks the documents in the schedule in order to further investigate whether Ms Xuan has breached her directors’ duties and to consider whether to bring a derivative action on behalf of Ginza Beauty.

103 Ms Chen’s suspicion in relation to misuse of Ms Xuan’s position as a director appears, for the most part, to be based on the fact that Ms Xuan is a shareholder, director and secretary of Lumiere Cosmetic Pty Ltd. When asked about the proposed derivative action to be taken on behalf of Ginza Beauty against Ms Xuan, Ms Chen agreed that she did not know of any facts based on which she thought that Ms Xuan had done anything wrong. In other words the possibility of a derivative action seems to be purely speculative based only the existence of Lumiere Cosmetic Pty Ltd and no other supporting facts. True it is that Ms Xuan did not disclose the existence of Lumiere Cosmetic Pty Ltd, which has the same name as the business carried on by Ginza Beauty. However, Ms Xuan’s unchallenged evidence was that she incorporated Lumiere Cosmetic Pty Ltd to hold intellectual property as part of a corporate restructure which was not implemented and that it has never traded.

104 In addition, in their letter dated 10 November 2021 to AHD, Yingke Law stated (as written):

In conjunction with our instructions that the employees the Company at the Lumière Cosmetic Clinic (at Shop 2, Ground Floor/389 Sussex St, Haymarket NSW 2000) may have been working in other competitors of beauty salons that are within the control of Ms Xuan, we have basis to suspect that Ms Xuan has been utilising her position and resources as the sole director and controller of the business to gain commercial benefits for the shareholders other than the Company’s.

105 There was no evidence before me to support this assertion nor was it put to Ms Xuan in cross-examination. In their letter in response dated 2 February 2022 AHD stated that:

In relation to the issue of employees working at competing business, we are instructed that the director is only aware of 1 former employee (who has since left the business), who is working in a cosmetic business and is based in the Fairfield area. We’re instructed that this employee has maintained a good relationship with the Company and who has historically provided a number of business referrals to the economic benefit of the Company. The Company is not concerned about any unfair competition regarding that particular employee however it would assist our consideration of any relevant advice to be provided to the Company that your client substantiate any allegation of breach of duty with more evidence than an ASIC search of another company, and identify what, if any, is her knowledge of any of the alleged conduct.

106 There was no evidence of any further correspondence between the parties in relation to this issue. AHD’s letter quite clearly states that Ms Xuan is only aware of one former employee who works in a salon located in a different area of Sydney. There is no evidence that Ms Xuan has any interest in that or any other competing business.

107 The only other matter raised is Ms Chen’s perception that there has been inconsistent information about the need for further capital investment in Ginza Beauty. No explanation was provided about the nature of the inconsistency. In any event, the evidence about the request for further capital investment is clear. In summary: Ms Xuan raised the requirement for a capital investment on 17 August 2021 to cover expansion costs of Ginza Beauty’s business, including renovation costs for level 2, 389 Sussex Street; at Ms Chen’s request Ginza Beauty provided financial information to assist Ms Chen in making her decision about whether to make any further investment and there was an exchange of correspondence between Mr Yang and Mr Ye about the documents provided; on 8 October 2021 at the Second Shareholders Meeting a resolution for the issue of 1,000 new shares to existing shareholders by application on a pro rata basis to raise $250,000 was discussed; subsequently the Notice of Offer was sent to Ms Chen inviting her to subscribe for 111 of the 1,000 new shares to be issued by Ginza Beauty at $250 per share (or a total of $27,750); and Ms Chen did not take up that offer.

108 I am not satisfied that Ms Chen has established a proper purpose insofar as she contends that Ms Xuan may have breached her duties owed as a director to Ginza Beauty either because of the provision of inconsistent information in relation to the need for a further capital investment or because of the registration of Lumiere Cosmetic Pty Ltd.

109 Ms Chen’s third stated purpose for inspection of the books and records in the schedule is to consider a potential oppression proceeding. This seems to arise from the dilution of Ms Chen’s shares which followed from Ms Chen failing to accept the Notice of Offer and to invest in the capital raising. Given that Ms Chen was offered and is entitled to 111 shares at $250 per share, the value of the dilution in her shareholding is known.

110 Further, as Ginza Beauty submitted, three years of financial records were provided in August 2021 well before the deadline for the response to the Notice of Offer. Ms Chen’s subjective belief that the information provided at that time was insufficient to make a decision whether to invest does not mean that there was oppressive conduct and Ms Chen did not adduce any expert evidence to the effect that the information provided at the time was insufficient to make a reasonable decision about whether she should invest. The evidence led is that the information was insufficient for Mr Yang to provide a report on the financial status of Ginza Beauty as he was unable to verify some of the reports from source material. Mr Mullins’ evidence identified inconsistencies in the information provided and whether the documents sought in the schedule were necessary to provide a report on the financial status and/or performance of Ginza Beauty.

111 In any event, to the extent that by the schedule Ms Chen seeks the inspection of documents dated after the Notice of Offer, those documents cannot be relevant to the decision to invest in October 2021 and thus to an oppression suit based on the events leading up to the Notice of Offer. There is, as Ginza Beauty submitted, simply no rational connection between such documents and a proposed oppression proceeding based on the Notice of Offer and the investment decision.

112 Once again, I am not satisfied that Ms Chen has established a proper purpose insofar as she contends that she wishes to inspect the documents in the schedule because she is considering the possibility of an oppression suit.

113 The final purpose is to consider whether to bring an application to wind up Ginza Beauty on the just and equitable ground. Ms Chen gave no evidence about why the documents sought in the schedule were required for this purpose or about the basis on which such an application would be brought, having regard to the events which have passed, and how the documents in the schedule relate to it. But assuming that relief of this nature would be sought as part of either a derivative action or an oppression suit, my comments above apply equally.

114 It follows from the matters set out above that I am not satisfied that Ms Chen has established a proper purpose by reference to any of the matters of concern and reasons for inspection of the documents in the schedule that she raises. She has not established a reasonable basis or foundation for the purposes for which she asserts she seeks inspection of the additional documents. As set out above, the proper purpose must be established in respect of each category of documents sought. Ginza Beauty’s submission, which I accept, is that the correct test is whether there is a proper purpose for the additional disclosures sought and not whether there is a proper purpose to “inspect the books at large”.

115 For those reasons I would dismiss the application. However, noting that the Court has a residual discretion under s 247A of the Corporations Act, even if I am wrong in my conclusion that Ms Chen has not established the composite preconditions specified in s 247A of the Act, I would not make the orders sought by her.

116 In Enares at [49]-[50] the Full Court said the following about the residual discretion:

49 The parties did not dispute that once the court is relevantly satisfied that the applicant is acting in good faith and that the inspection is to be made for a proper purpose, the discretion in s 247A is enlivened. Nor was it contested that the touchstone of the exercise of that discretion is what the company ought to tell its shareholder. …

…

50 In the absence of any detailed submissions as to the nature of the residual discretion in s 247A, as opposed to the formation of the state of satisfaction that the applicant is acting in good faith and that inspection is to be made for a proper purpose, it is not appropriate to consider the question further. However, the structure of the section might suggest that once the required degree of satisfaction is reached the discretion to refuse the order might be constrained by that fact. It might be said that the discretion is one to be exercised in all the circumstances of the case, and that the applicant’s satisfaction of the requirements of the subjective jurisdictional fact of s 247A is likely to be a not insignificant part of those circumstances.

117 Having regard to all of the circumstances of this case, a powerful factor against exercise of the discretion is that, as set out at [54]-[55] above, Ginza Beauty has made substantial disclosure to Ms Chen, comprising not only financial statements but also individual ledger entries for all accounts between July 2018 to July 2021, for bank statements and employment information for shareholder employees. While some of the material was only provided after commencement of the proceeding, that is a matter that ultimately would, in my view only, go to costs.

CONCLUSION

118 For those reasons I would dismiss the application. Costs would ordinarily follow the event. However, as Ginza Beauty seeks to be heard on costs, I will reserve on that question and invite the parties to file short submissions and, unless either party requests an oral hearing, the question of costs will be determined on the papers.

I certify that the preceding one hundred and eighteen (118) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Markovic. |

Associate: