Federal Court of Australia

Austpac Resources N.L., in the matter of Austpac Resources N.L. [2023] FCA 108

ORDERS

IN THE MATTER OF AUSTPAC RESOURCES N.L. | ||

AUSTPAC RESOURCES N.L. ACN 002 264 057 Plaintiff | ||

DATE OF ORDER: | 21 February 2023 |

THE COURT ORDERS THAT:

1. Pursuant to section 1322(4)(a) of the Corporations Act 2001 (Cth), the Court declares that any offer for sale, or sale, of any of the tranches of fully paid ordinary shares in the plaintiff that were issued on the dates referred to in Annexure A to these Orders (Shares) occurring in the period after their issue, is not invalid by reason of any contravention of section 707(3) or section 727(1) of the Act.

2. Subject to order 3, pursuant to section 1322(4)(c) of the Act, any person offering to sell or selling Shares is relieved from any civil liability arising out of such contravention.

3. Order 2 does not apply to Notsag Pty Ltd or Mr Nicholas John Gaston, former secretary of the plaintiff.

4. As soon as reasonably practicable, the plaintiff must:

(a) send a copy of such orders to each person to whom the Shares were issued; and

(b) publish an announcement to the Australian Securities Exchange (ASX) in which a copy of such orders is included.

5. A sealed copy of such orders must be served on the Australian Securities and Investments Commission (ASIC) as soon as reasonably practicable and upon service of these orders on ASIC, ASIC must include such orders on its database.

6. For a period of 28 days from the date of publication of such orders on the ASX website, any person who claims to have suffered substantial injustice or who claims they are likely to suffer substantial injustice by reason of the contraventions referred to above or the making of such orders may apply within that period to vary or discharge the orders.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ANNEXURE A

[1] | |

[4] | |

[16] | |

[17] | |

[17] | |

[26] | |

[35] | |

[42] | |

[49] | |

[57] | |

[61] | |

[66] | |

[72] | |

Replacement of Mr Gaston as company secretary and an investigation into discrepancies | [78] |

[80] | |

[88] | |

[89] | |

[90] | |

[92] | |

[93] | |

[94] | |

[99] | |

[105] | |

[113] | |

[114] | |

[117] | |

[119] | |

[121] | |

Conclusion as to satisfaction of the pre-condition to s 1322(4)(c) and exercise of the discretion | [124] |

[128] |

1 Between February 2016 and April 2019 (relevant period), the plaintiff (Austpac) issued a series of Shares. Those issues occurred in circumstances where Austpac did not make the disclosure required by Part 6D.2 of the Corporations Act 2001 (Cth) or take effective steps to render such disclosure unnecessary. As a result, on-sellers of the Shares may have contravened ss 707(3) and 727(1) of the Act with a consequent exposure to claims under s 1325 of the Act.

2 By an amended originating process filed on 16 August 2022, Austpac seeks relief under s 1322 of the Act, and primarily:

(1) a declaration pursuant to s 1322(4)(a) of the Act that any offer for sale, or sale, of the Shares occurring in the period after their issue is not invalid by reason of any contravention of ss 707(3) or 727(1) of the Act (validity declaration); and

(2) an order pursuant to s 1322(4)(c) of the Act that any person offering to sell or selling the Shares is relieved from any civil liability arising out of such contravention (relief from liability order).

3 Austpac also seeks consequential and ancillary orders concerning notifications of the making of the validity declaration and the relief from liability order; and an order allowing for applications to be made within 28 days to vary or discharge the Court’s orders.

4 Part 6D.2 of the Act concerns disclosure to investors about securities. For present purposes and ignoring inapplicable exceptions, the following parts of Part 6D.2 are salient.

5 First, as a general proposition:

(1) an offer of securities for issue needs disclosure unless ss 708 or 708AA provide otherwise: s 706; and

(2) a person must not make an offer of securities that needs disclosure under Part 6D.2 unless a disclosure document for the offer has been lodged with the Australian Securities and Investments Commission (ASIC): s 727.

6 Secondly, the offers of securities that require disclosure under Part 6D.2 are only those for which disclosure is required by s 707(2), (3) or (5): s 707(1).

7 Thirdly, s 707(3) provides:

(3) An offer of a body’s securities for sale within 12 months after their issue needs disclosure to investors under this Part if:

(a) the body issued the securities without disclosure to investors under this Part; and

(b) either:

(i) the body issued the securities with the purpose of the person to whom they were issued selling or transferring the securities, or granting, issuing or transferring interests in, or options over, them; or

(ii) the person to whom the securities were issued acquired them with the purpose of selling or transferring the securities, or granting, issuing or transferring interests in, or options over, them;

and section 708 or 708A does not say otherwise.

8 Fourthly, s 708A provides some exceptions to the requirement of disclosure prescribed by s 707(3). In so far as is presently relevant, s 708A provides:

708A Sale offers that do not need disclosure

Sale offers to which this section applies

(1) This section applies to an offer (the sale offer) of a body’s securities (the relevant securities) for sale by a person if:

(a) but for subsection (5), (11) or (12), disclosure to investors under this Part would be required by subsection 707(3) for the sale offer; and

(b) the securities were not issued by the body with the purpose referred to in subparagraph 707(3)(b)(i); and

(c) a determination under subsection (2) was not in force in relation to the body at the time when the relevant securities were issued.

…

Sale offer of quoted securities—case 1

(5) The sale offer does not need disclosure to investors under this Part if:

(a) the relevant securities are in a class of securities that were quoted securities at all times in the 3 months before the day on which the relevant securities were issued; and

(b) trading in that class of securities on a prescribed financial market on which they were quoted was not suspended for more than a total of 5 days during the shorter of the period during which the class of securities were quoted, and the period of 12 months before the day on which the relevant securities were issued; and

(c) no exemption under section 111AS or 111AT covered the body, or any person as director or auditor of the body, at any time during the relevant period referred to in paragraph (b); and

(d) no order under section 340 or 341 covered the body, or any person as director or auditor of the body, at any time during the relevant period referred to in paragraph (b); and

(e) either:

(i) if this section applies because of subsection (1)—the body gives the relevant market operator for the body a notice that complies with subsection (6) before the sale offer is made; or

(ii) if this section applies because of subsection (1A)—both the body, and the controller, give the relevant market operator for the body a notice that complies with subsection (6) before the sale offer is made.

(6) A notice complies with this subsection if the notice:

(a) is given within 5 business days after the day on which the relevant securities were issued by the body; and

(b) states that the body issued the relevant securities without disclosure to investors under this Part; and

(c) states that the notice is being given under paragraph (5)(e); and

(d) states that, as at the date of the notice, the body has complied with:

(i) the provisions of Chapter 2M as they apply to the body; and

(ii) sections 674 and 674A; and

(e) sets out any information that is excluded information as at the date of the notice (see subsections (7) and (8)).

(7) For the purposes of subsection (6), excluded information is information:

(a) that has been excluded from a continuous disclosure notice in accordance with the listing rules of the relevant market operator to whom that notice is required to be given; and

(b) that investors and their professional advisers would reasonably require for the purpose of making an informed assessment of:

(i) the assets and liabilities, financial position and performance, profits and losses and prospects of the body; or

(ii) the rights and liabilities attaching to the relevant securities.

(8) The notice given under subsection (5) must contain any excluded information only to the extent to which it is reasonable for investors and their professional advisers to expect to find the information in a disclosure document.

…

(emphasis added)

9 Fifthly, the making of an offer of shares that needs disclosure under Part 6D.2 absent the lodging of a disclosure document with ASIC is a contravention of s 727 of the Act: s 727(1) and (6) (subject to the operation of s 727(5)).

10 Finally, a person who contravenes s 727 is exposed to proceedings for relief under s 1325 of the Act: s 1325 (and in particular s 1325(1), (5) and 7(d)).

11 It is in that context that the present application arises.

12 Austpac made a series of offers of its fully paid ordinary shares during the relevant period. It did so by a series of share placements and by a Shareholder Share Purchase Plan (SSPP).

13 For all but one of the share placements, Austpac sought to rely upon the exception in s 708A(5) by lodging notices (cleansing notices) under s 708A(5)(e) and (6). However, those cleansing notices were defective. For the SSPP, Austpac sought to rely upon ASIC Class Order [CO 09/425] to provide an exemption from compliance with Part 6D.2. However, it did not meet the requirements of the Class Order.

14 Austpac’s failure to effectively avoid the need for compliance with Part 6D.2 has consequences for Austpac; for the persons to whom the Shares were sold if they on-sold the Shares, and for any subsequent on-sellers. In particular, any on-sale required disclosure in accordance with Part 6D.2.

15 As a result, Austpac asks the Court to exercise the discretion conferred upon it by s 1322 of the Act to make the validity declaration and the relief from liability order. The relief sought is not sought for the benefit of any director or officer of Austpac or for Austpac itself, but instead for persons who may have contravened ss 707(3) and 727(1) of the Act by on-selling the Shares without having made the requisite disclosure. Section 1322 of the Act provides, in so far as is presently relevant:

…

(4) Subject to the following provisions of this section but without limiting the generality of any other provision of this Act, the Court may, on application by any interested person, make all or any of the following orders, either unconditionally or subject to such conditions as the Court imposes:

(a) an order declaring that any act, matter or thing purporting to have been done, or any proceeding purporting to have been instituted or taken, under this Act or in relation to a corporation is not invalid by reason of any contravention of a provision of this Act or a provision of the constitution of a corporation;

…

(c) an order relieving a person in whole or in part from any civil liability in respect of a contravention or failure of a kind referred to in paragraph (a);

…

and may make such consequential or ancillary orders as the Court thinks fit.

...

(6) The Court must not make an order under this section unless it is satisfied:

(a) in the case of an order referred to in paragraph (4)(a):

(i) that the act, matter or thing, or the proceeding, referred to in that paragraph is essentially of a procedural nature;

(ii) that the person or persons concerned in or party to the contravention or failure acted honestly; or

(iii) that it is just and equitable that the order be made; and

(b) in the case of an order referred to in paragraph (4)(c)—that the person subject to the civil liability concerned acted honestly; and

(c) in every case—that no substantial injustice has been or is likely to be caused to any person.

16 The principal evidence relied upon by Austpac was provided by Mr Colin Iles, a director of Austpac since 14 March 2017 and its Chief Executive Officer since 14 July 2020. Mr Iles provided four affidavits, which recounted in some detail the events described below.

17 Austpac was registered on 22 May 1985 and listed on the Australian Securities Exchange (ASX) on 24 July 1985. It operates in the field of mineral processing technology and exploration and the development of mineral sands and gold deposits.

18 On or about 20 March 1986, Mr Nicholas Gaston commenced as company secretary of Austpac. Mr Gaston’s services were provided through Notsag Pty Ltd, a company which he controlled.

19 On 10 December 2010, Barrett J (as his Honour then was) made orders under s 1322 of the Act at the request of Austpac: Re Austpac Resources N.L. [2010] NSWSC 1438. Those orders were necessary because of a failure by Austpac to provide a cleansing notice with respect to a capital raising undertaken by it.

20 As noted at [1] above, the relevant period commenced in February 2016 and continued until April 2019. During the relevant period, the directors of Austpac were:

(1) Mr Michael Turbott, who was the managing director from the incorporation of Austpac (which he founded) until January 2019, at which time he took on the role of manager;

(2) Mr Terry Cuthbertson, who has been a director of Austpac since 27 March 2001 and its non-executive chairman since 31 May 2004; and

(3) Mr Robert Harrison, who was a director of Austpac from 1 September 2004 until 31 October 2017.

21 Mr Gaston was Austpac’s company secretary and chief financial officer throughout the relevant period and thus he held those positions at the time of each of the share placements and the SSPP.

22 The evidence establishes that during the relevant period:

(1) the directors of Austpac relied upon Mr Gaston to ensure that the share placements occurred in compliance with the law (including preparing and lodging the requisite notices and forms with both the ASX and ASIC) and to bring to their attention any problems that arose;

(2) in the normal course of events, Austpac held monthly board meetings, which were attended by its directors and Mr Gaston. At those meetings a standard agenda item concerned capital raising;

(3) the directors of Austpac from time to time directed Mr Gaston to take all necessary and appropriate steps in relation to the making and reporting of share placements, including preparing and lodging the requisite notices and forms with both the ASX and ASIC; and

(4) Mr Gaston did not inform the directors that a prospectus was required with respect to any of the share issues the subject of this application.

23 On 26 November 2015, Austpac held its annual general meeting, which included a presentation by its managing director, Mr Turbott, concerning the company’s operations. That presentation was provided to the ASX on the same day.

24 On 18 December 2015, Austpac provided to the ASX a shareholder update to the ASX concerning material developments in its business operations, capital structure and financing.

25 On 29 January 2016, Austpac provided to the ASX its Quarterly Report for the period ending 31 December 2015.

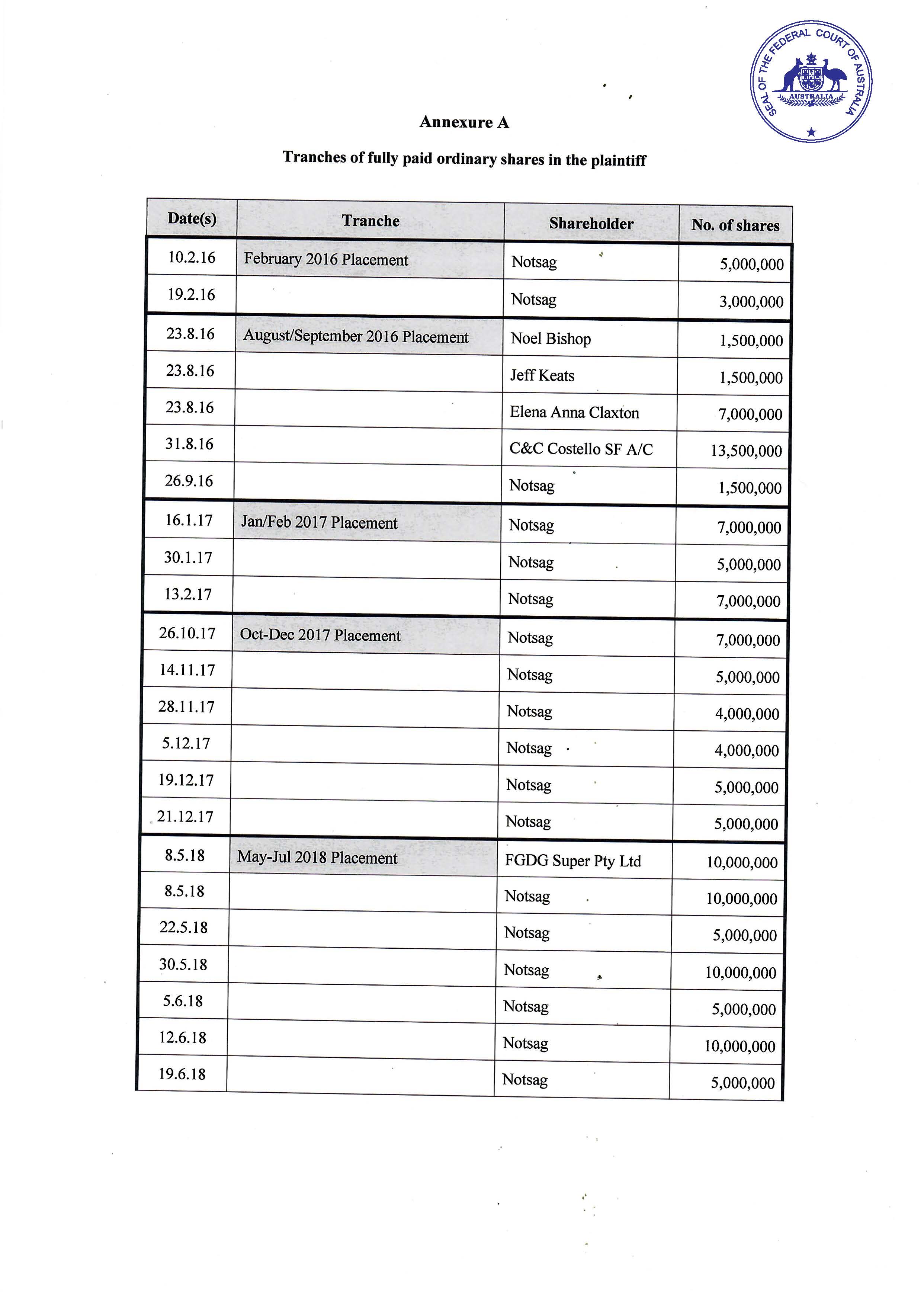

26 Between 10 and 19 February 2016, Austpac issued 8,000,000 shares at $0.005 each (February 2016 Placement). All of these shares were issued to Notsag.

27 Between 11 February 2016 and 29 March 2016, Notsag on-sold all 8,000,000 shares issued to it in the February 2016 Placement to Peplon Nominees Pty Limited. Peplon is a wholly owned subsidiary of Morgans Financial Limited, the holder of an Australian Financial Services Licence.

28 On 16 March 2016, Austpac’s shares were suspended from quotation on the ASX following a failure to lodge its Half-Yearly Accounts for the period ended 31 December 2015.

29 On 31 March 2016, Austpac provided to the ASX its Half-Year Accounts for the period ending 31 December 2015. The end of the suspension was announced the same day.

30 On 1 April 2016, Austpac provided to the ASX an announcement which described the February 2016 Placement as a private placement of 8,000,000 shares at $0.005 each to professional investors. Austpac also lodged a cleansing notice and an “Appendix 3B – New Issue Announcement” form. The cleansing notice was in the following terms:

Austpac Resources N.L. hereby provides Notice to the Australian Stock Exchange under section 708A(5)(e) of the Corporations Act 2001 that the Company has issued 8,000,000 fully paid ordinary shares without disclosure to investors under Part 6D.2 of the Corporations Act on 31 March 2016.

At the date of this Notice the Company has complied with the provisions of Chapter 2M of the Corporations Act as they apply to the Company and with section 674 of the Corporations Act.

The Company is not aware of any excluded information for the purposes of section 708A(6)(e) at the date of this Notice.

31 All subsequent cleansing notices provided by Austpac to the ASX followed the same form, with only the date and the number of shares differing.

32 This cleansing notice was ineffective by reason of:

(1) Austpac’s shares having been suspended from quotation for more than five trading days in the period of 12 months before the day on which the relevant shares were issued (therefore failing to meet the requirements of s 708A(5)(b)); and

(2) the notice having been given more than five business days after the day on which the relevant shares were issued by Austpac (contrary to s 708A(6)(a)).

33 The Appendix 3B contained a series of warranties from Austpac to the ASX, including a warranty that an offer of the shares for sale within 12 months after their issue would not require disclosure under s 707(3) of the Act; and an indemnity in favour of the ASX in respect of any claim, action or expense arising from or connected with any breach of the warranties. All subsequent Appendices 3B contained the same warranty and indemnity.

34 On 29 April 2016 and 29 July 2016, Austpac provided to the ASX its Quarterly Reports for the periods ending 31 March 2016 and 30 June 2016 respectively.

August–September 2016 Placement

35 Between 23 August and 26 September 2016, Austpac issued 25,000,000 shares at $0.01 each as follows (August–September 2016 Placement):

(1) 23 August 2016: Mr Noel Bishop – 1,500,000 shares;

(2) 23 August 2016: Mr Jeff Keats – 1,500,000 shares;

(3) 23 August 2016: Ms Elena Anna Claxton – 7,000,000 shares;

(4) 31 August 2016: C&C Costello SF A/C – 13,500,000 shares; and

(5) 26 September 2016: Notsag – 1,500,000 shares.

36 On 31 August 2016, Austpac provided to the ASX its Preliminary Final Report for the year ending 30 June 2016.

37 On 30 September 2016, Austpac provided to the ASX its audited financial statements, and on 24 October 2016, it provided to the ASX its Annual Report for the year ending 30 June 2016.

38 On 26 September 2016, Austpac provided to the ASX:

(1) an announcement that it had completed the August–September 2016 Placement, describing it as a private placement to professional investors of 25,000,000 shares at $0.01 each, to raise working capital of $250,000;

(2) a cleansing notice; and

(3) an Appendix 3B.

39 This cleansing notice was ineffective because of the suspension of Austpac’s shares from quotation for more than five trading days during the preceding year (that is, between 16 and 31 March 2016); and also with respect to the shares other than those issued to Notsag on 26 September 2016 because the cleansing notice was not lodged within five business days of the date of their issue.

40 Austpac’s share register and related transaction reports indicate that:

(1) all of the shares issued to Mr Bishop were on-sold within 12 months of their issue to Pershing Australia Pty Ltd. Pershing, in turn, appears to have on-sold all of these shares shortly after their purchase;

(2) none of the shares issued to Mr Keats have been on-sold;

(3) none of the shares issued to Ms Claxton have been on-sold;

(4) 8,500,000 of the 13,500,000 shares issued to C&C Costello SF were on-sold within 12 months to company NetShare Nominees Pty Ltd; and

(5) at least some of the shares issued to Notsag were on-sold to Peplon within 12 months.

41 On 24 November 2016, Austpac provided to the ASX a presentation on its operations that was given by its managing director, Mr Turbott, to Austpac’s shareholders at its annual general meeting held on that day.

January–February 2017 Placement

42 Between 16 January and 13 February 2017, Austpac issued 19,000,000 fully paid ordinary shares at $0.01 to Notsag (January–February 2017 Placement).

43 On 31 January 2017, Austpac provided to the ASX its Quarterly Report for the period ending 31 December 2016.

44 On 7 March 2017, Austpac provided to the ASX:

(1) an announcement that it had completed the January–February 2017 Placement, describing it as a private placement to professional investors of 19,000,000 shares at $0.01 each to raise $190,000 of working capital;

(2) a cleansing notice; and

(3) an Appendix 3B.

45 This cleansing notice was ineffective because of the suspension of Austpac’s shares from quotation for more than five trading days during the preceding year (that is, between 16 and 31 March 2016) and because the cleansing notice was not lodged within five business days of the shares being issued.

46 On 9 March 2017, Austpac provided to the ASX an announcement concerning a research and development tax concession refund.

47 Between 16 March 2017 and 31 October 2017, Austpac provided to the ASX:

(1) on 16 March 2017, its Half-Yearly Report for the period ending 31 December 2016;

(2) on 23 March 2017, an announcement concerning the Newcastle Zinc and Iron Recovery Plant;

(3) on 28 April 2017, its Quarterly Report for the period ending 31 March 2017;

(4) on 13 July 2017, another announcement concerning the Newcastle Zinc and Iron Recovery Plant;

(5) on 31 July 2017, its Quarterly Report for the period ended 30 June 2017;

(6) on 22 August 2017, a further announcement concerning the Newcastle Zinc and Iron Recovery Plant;

(7) on 29 August 2017, a shareholder update concerning results from a project based at Nhill, Victoria;

(8) on 31 August 2017, its Preliminary Final Report for the year ended 30 June 2017;

(9) on 28 September 2017, its audited financial statements for the year ended 30 June 2017;

(10) on 24 October 2017, its Annual Report for the year ended 30 June 2017, together with a further shareholder update; and

(11) on 31 October 2017, its Quarterly Report for the period ending 30 September 2017.

48 By 25 October 2017, Notsag had on-sold to Peplon all of the shares issued to it as part of the January–February 2017 Placement.

October–December 2017 Placement

49 Between 26 October 2017 and 21 December 2017, Austpac issued 30,000,000 ordinary shares at $0.01 to Notsag (October–December 2017 Placement).

50 On 23 November 2017, Austpac provided to the ASX a presentation that had been made by its managing director, Mr Turbott, to its shareholders at its annual general meeting.

51 By 5 January 2018, Notsag had on-sold to Peplon all of the shares issued to it as part of the October-December 2017 Placement.

52 On 9 January 2018, Austpac provided to the ASX:

(1) an announcement stating that it had completed the October–December 2017 Placement, describing it as a private placement to professional investors of 30,000,000 shares at $0.01 to raise $300,000 of working capital;

(2) a cleansing notice; and

(3) an Appendix 3B.

53 This cleansing notice was ineffective because it was not lodged within five business days of the shares being issued.

54 On 30 January 2018, Austpac provided to the ASX its Quarterly and Half-Yearly Reports for the period ending 31 December 2017.

55 On 10 April 2018, Austpac provided to the ASX a further shareholder update.

56 On 30 April 2018, Austpac provided to the ASX its Quarterly Report for the period ending 31 March 2018.

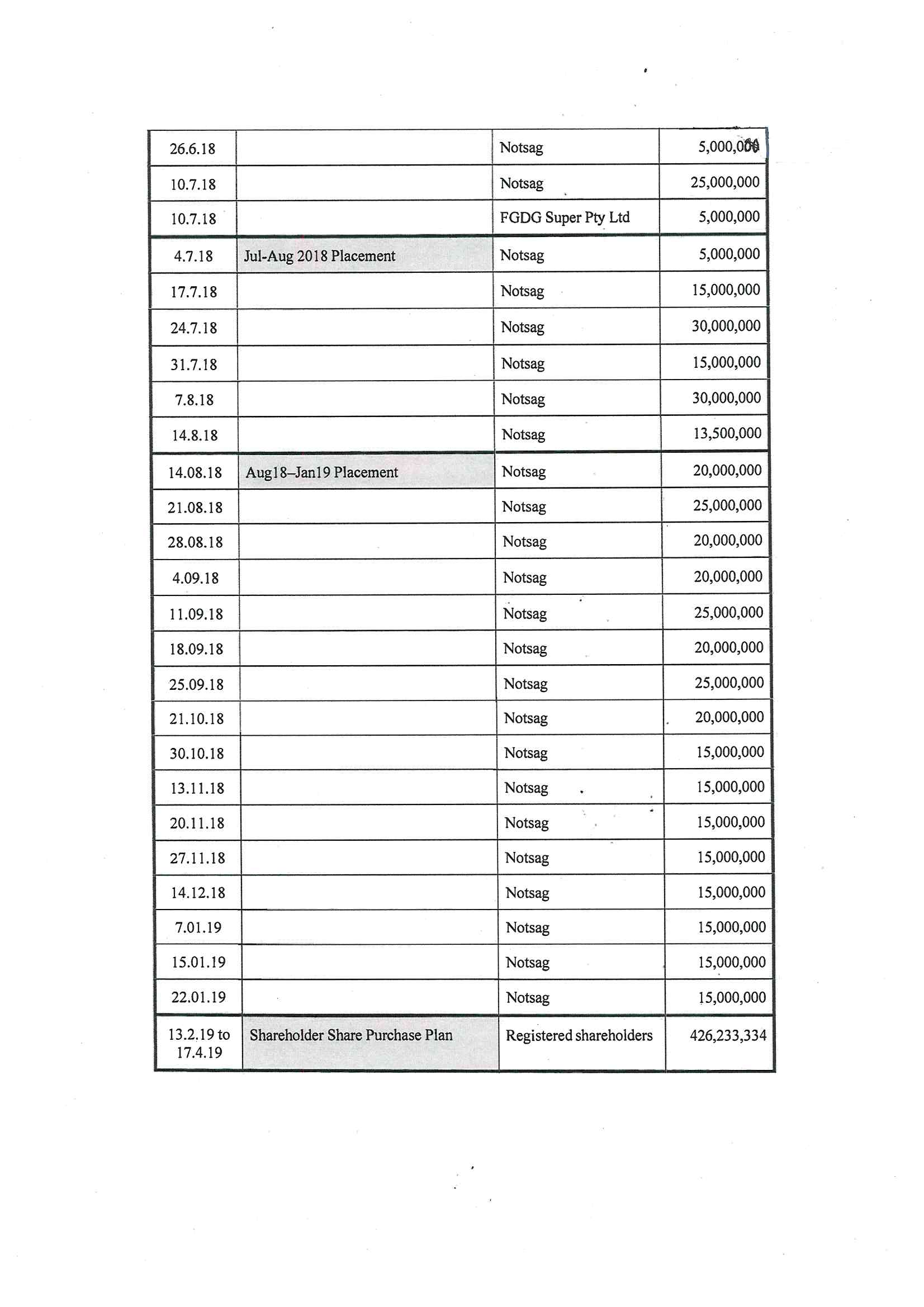

57 Between 8 May and 10 July 2018, Austpac issued 90,000,000 shares, described by Austpac as the May–July 2018 Placement. Of these shares, 75,000,000 were issued in eight tranches to Notsag (at $0.003 per share for 50,000,000 shares and for nil consideration for the remaining 25,000,000 shares); and 15,000,000 were issued in two tranches to FGDG Super Pty Ltd (at $0.003 per share for 10,000,000 shares and for nil consideration for the remaining 5,000,000 shares).

58 By 16 July 2018, Notsag had on-sold to Peplon all of the shares issued to it as part of the May-July 2018 Placement. None of the shares issued to FGDG Super have been on-sold.

59 On 31 July 2018, Austpac provided to the ASX:

(1) its Quarterly Report for the quarter ended 30 June 2018;

(2) an announcement that it had completed the May–July 2018 Placement, describing it as a private placement to professional investors of 90,000,000 shares at $0.002 each to raise $180,000 in working capital;

(3) a cleansing notice; and

(4) an Appendix 3B.

60 The cleansing notice was ineffective because it was not lodged within five business days of the shares being issued.

61 Between 4 July and 14 August 2018, Austpac issued 108,500,000 shares at $0.002 to Notsag, described by Austpac as the July–August 2018 Placement.

62 Between 6 July and 21 August 2018, Notsag on-sold all of these shares to Peplon.

63 Between 1 and 12 October 2018, Austpac’s shares were suspended from quotation.

64 On 29 January 2019, Austpac provided to the ASX:

(1) an announcement that it had completed the July–August 2018 Placement, describing it as a private placement to professional investors of 108,500,000 shares at $0.002 to raise $217,000 of working capital;

(2) a cleansing notice; and

(3) an Appendix 3B.

65 This cleansing notice was ineffective because it was not lodged within five business days of the shares being issued.

August 2018–January 2019 Placement

66 Between 14 August 2018 and 22 January 2019, Austpac issued 295,000,000 shares at $0.002 to Notsag, described by Austpac as the August 2018–January 2019 Placement.

67 Between 22 August 2018 and 30 January 2019 Notsag on-sold all of these shares to Peplon.

68 Austpac did not provide to the ASX a cleansing notice or an Appendix 3B in respect of the August 2018–January 2019 Placement. Such a cleansing notice would not have been effective in any event because Austpac’s shares had been suspended from quotation between 1 and 12 October 2018.

69 On 30 October 2018, Austpac provided to the ASX its Quarterly Report for the period ending 30 September 2018.

70 On 20 November 2018, Austpac provided to the ASX a presentation on its operations that had been made to its annual general meeting held that day.

71 On 31 January 2018, Austpac provided to the ASX its Quarterly Report for the period ending 31 December 2018.

72 On 1 February 2019, Austpac provided to the ASX an announcement of the introduction of the SSPP, together with accompanying documents.

73 Between 13 February and 17 April 2019, Austpac issued 426,233,334 shares at $0.001 under the SSPP.

74 On 26 April 2019, Austpac provided to the ASX an announcement which stated that the SSPP had closed on 15 April 2019 and had resulted in the placement of 426,233,334 shares at $0.001 each, raising $426,233. Austpac also provided to the ASX:

(1) an Appendix 3B; and

(2) a letter from Austpac addressed to the ASX and signed by Mr Gaston stating that “[w]e confirm that the requirements of the ASIC Class Order CO. 09/425 are incorporated into the Shareholder Share Purchase Plan announced on 1 February 2019.”

75 Notwithstanding the statement from Mr Gaston described above, the requirements of the Class Order had not been met. A pre-condition to an exemption from compliance with Part 6D.2 was that the shares the subject of the SSPP not have been suspended from trading on the ASX for more than five days during the 12 months before the offer contained in the SSPP was made: Class Order, at [4]; [7(a)(ii)]. This condition was not met because Austpac’s shares had been suspended from trading between 1 and 12 October 2018 and the offer was made in February 2019.

76 On the evidence before the Court it cannot be determined whether any of the shares issued under the SSPP have been on-sold. Mr Iles gave evidence that Austpac considers that it is likely some of the 426,233,334 shares issued under the SSPP were indeed on-sold. I accept that this is likely.

77 On 30 April 2019, Austpac provided to the ASX its Quarterly Report for the period ending 31 March 2019.

Replacement of Mr Gaston as company secretary and an investigation into discrepancies

78 In early July 2020, Mr Kenneth Lee replaced Mr Gaston as the company secretary of Austpac. On 14 July 2020, Mr Iles was appointed as Austpac’s Chief Executive Officer. Shortly thereafter, Mr Lee became aware of discrepancies between the number of issued shares recorded in Austpac’s share register and the number of such shares reported in Austpac’s most recent annual and half-yearly reports. Mr Iles and Mr Lee then undertook a detailed investigation, the results of which included that:

(1) there may have been contraventions of the Act by Austpac;

(2) most of the shares that had been placed pursuant to the share placements had been placed with Notsag;

(3) Notsag did not pay Austpac for 295,000,000 of the shares that had been placed with it (that payment, of $295,000, has now been made); and

(4) it appeared to have been Mr Gaston’s usual practice to cause Notsag to on-sell the shares to Peplon shortly after they had been placed with Notsag.

79 Mr Iles also deposes that:

(1) the directors of Austpac were not informed by Mr Gaston that any of the shares issued pursuant to the share placements had been issued to Notsag at or about the time of such placements and such placements to Notsag had not been approved by the directors;

(2) the lack of disclosure to the board occurred despite there being numerous opportunities for such disclosure to have been made at monthly directors’ meetings and some particular instances where such disclosure would have been expected. For example:

(a) on 15 March 2018, Austpac’s auditors, KPMG presented a report to Austpac’s audit committee which stated that $300,000 for the October–December 2017 Placement remained unpaid and that the failure to disclose that fact comprised an uncorrected misstatement in Austpac’s Half-Yearly Financial Report for the period ending 31 December 2017. Although Mr Gaston attended that meeting, he did not disclose that Notsag was the shareholder liable for this payment; and

(b) Mr Gaston attended meetings of directors held on 24 May, 29 June and 26 July 2018 at which discussions occurred concerning the May–July 2018 Placement and the level of interest from shareholders at particular prices, but he did not disclose that Notsag had subscribed for a substantial number of shares in that placement;

(3) Mr Gaston did not disclose the fact of the July–August 2018 Placement at any of the board meetings held on 26 July 2018, 23 August 2018, 27 September 2018, 25 October 2018, 22 November 2018 and 20 December 2018. Although the July–August 2018 Placement is referred to in the minutes of the board meeting held on 24 January 2019, Mr Iles deposed that that placement was not in fact reported to the board on that occasion; and

(4) the August 2018–January 2019 Placement was not reported to Austpac’s directors and it was not known to the directors until after Mr Gaston left Austpac’s employ in July 2020 and was discovered during the investigation referred to at [78] above.

80 By October 2020, Austpac had implemented the following procedures designed to ensure compliance with its disclosure obligations:

(1) any draft ASX notification and proposed capital structure change must be circulated to each director of Austpac for approval, together with draft instructions to the share registry;

(2) any instructions to the share registry to issue shares must be accompanied by an Appendix 2A form for lodging with the ASX and notification to ASIC;

(3) the instruction to the share registry must be copied by email to each director of Austpac (and to the company secretary, if the instruction is from a director);

(4) each recipient of such an email must confirm the instruction to the share registry before the shares are issued;

(5) the share registry must inform each director and the company secretary when shares are issued; and

(6) Austpac is to notify the ASX of the issue of shares via an Appendix 2A.

81 Further:

(1) complementary instructions were provided to Austpac’s share registry;

(2) Austpac has provided each director’s email address and the company secretary’s email address to the ASX, so that they will be automatically notified of announcements made by Austpac; and

(3) Austpac has made changes to its personnel at the management level, as well as its secretary and chief financial officer.

82 On 2 November 2020, Austpac released its Annual Report for the year ended 30 June 2020.

83 On 17 November 2020, Austpac provided to the ASX an announcement:

As disclosed in the Company’s Annual Report for the financial year ended 30 June 2020 (released to ASX on 2 November 2020), after extensive investigations the Company has become aware that 300,286,997 fully paid ordinary shares (Shares) in the Company were issued in a number of tranches prior to 1 July 2019, each at an issue price of $0.001 per Share. The issue of the Shares was arranged and effected by previous senior management personnel of the Company and was not reported to the market.

The Company has reached an agreement with the recipient of the 300,286,997 Shares to pay to the Company the amount of $295,000 by 30 November 2020. The remaining $5,287 is not recoverable and has been written-off to the cost of issuing the relevant securities.

It has also been discovered that 31,373,793 Shares issued were not reported to the ASX via Appendix 3B’s. The majority of these unreported shares occurred in an error in an Appendix 3B issued in July 2012 which failed to correctly report the total number of shares on issue at the time. The total was deficient by 28,605,834 shares.

The Company’s last Appendix 3B was released to ASX on 23 May 2019. In that 3B, the Company’s stated issued capital figure was 2,834,002,166 Shares (following quotation of the Shares the subject of that 3B). The correct issued capital figure should have been 3,165,662,956 Shares, taking into account the abovementioned Share issues. The Appendix 2A attached to this announcement seeks to rectify that error and correct the Company’s disclosed issued capital figure.

The Company has introduced additional governance procedures to ensure that such situations do not reoccur.

84 On 17 June 2021, Austpac’s shares were suspended from trading. The suspension was voluntary and it continues. Austpac has not issued any new shares since 17 June 2021.

85 On 30 July 2021, Austpac provided to the ASX the following announcement:

Austpac Resources N.L. (Company) provides the market with the following update on the voluntary suspension of trading in its securities.

Following ASX enquiries and upon comprehensive review of share issues made by the Company in the recent past, the Company has become aware that there may have been a number of failures to fully comply with all of the applicable requirements of the Corporations Act. These shares were issued at the time the Company was operated by management who no longer work for the Company.

The Company is currently undertaking a detailed legal investigation of those issues and, depending upon the findings of that investigation, may need to take steps in rectification which may involve seeking appropriate orders in the Federal Court of Australia.

...

The Company’s securities will not be reinstated to trading until such time as the above issues are resolved, including any orders that may need to be made by the Federal Court of Australia and the ASX is satisfied that APG is in compliance with the Listing Rules.

The Company will continue to update the market in a timely way with any material developments in relation to the Application.

(emphasis in original)

86 Since July 2021, Austpac has continued to provide updated information to the market.

87 On 19 May 2022, the present proceeding was commenced. Since that date Austpac has provided to the ASX updates concerning this proceeding.

88 The evidence also establishes the following miscellaneous matters:

(1) Mr Iles has, with respect to each occasion on which disclosure in accordance with Part 6D.2 was required but not provided because of the omissions described above, considered the information that Austpac had provided to the ASX and whether there was further information that Austpac would have been required to provide as part of its disclosure obligations. Having done so, Mr Iles concluded that there was no such further information;

(2) Austpac intends to apply to the ASX for its shares to be reinstated for trading, following the resolution of this application. It is aware that it will not be able to issue a cleansing notice for a minimum of 12 months following such reinstatement (by dint of s 708A(5)(b)). Austpac also proposes to make further share issues, which are expected to involve the issue to existing shareholders of entitlements to subscribe for additional shares and the issue of new shares to “professional investors” within the meaning of s 708(11) of the Act;

(3) Mr Iles is of the view that Austpac is acutely aware of its obligations to exercise reasonable due diligence to ensure that all applicable rules and regulations relating to the relisting and further issues of securities are properly complied with in a timely way, including by reference to its updated compliance procedures and in consultation with and after taking advice from its professional advisers; and

(4) notice of this application was provided to the ASX, ASIC and to Austpac’s shareholders. In particular:

(a) both the ASX and ASIC have been on notice of the application and have not sought to be heard. Further, ASIC, having been provided with Austpac’s originating process, the substantive evidence relied upon by Austpac, together with Austpac’s written submissions filed in advance of the hearing and the orders sought by Austpac, indicated that it neither supported nor opposed the application; and

(b) Austpac’s shareholders have been on notice of the application through publication of notices on the ASX website and in the case of the on-selling shareholders by correspondence sent to them. Despite this, no shareholder sought leave to be heard on the application. Further, the evidence of Mr Iles included that he had spoken to a number of shareholders by telephone and at Austpac’s most recent annual general meeting and that all of those shareholders have been supportive of the application. Mr Iles also explained that he has not received any objections from any of Austpac’s shareholders concerning the present application.

89 Mr Iles has explained that the delay in completing the investigation and in bringing the present application was due to the following matters:

(1) the poor state of Austpac’s records, which had been kept manually in folders and were not in chronological order. Those records had to be manually reviewed and organised into proper files, then scanned, summarised and documented in detail. The background files comprised several thousand pieces of paper that needed recording, reconciling and cross checking;

(2) the need to deal with ASX questions, which required detailed answers, and which in turn required a full investigation using Austpac’s records which were in a poor state as described above;

(3) Covid-19 restrictions, and in particular those caused by the Omicron strain which commenced in late June 2021;

(4) a relocation of offices; and

(5) the pressures of commerce. In particular, to prepare itself for the future and to enhance its ability to secure funding for future projects, Austpac undertook a complete review and restructure of its business operations.

90 Against that background, I turn to consider the merits of the application.

91 In Re Golden Rim Resources Ltd [2019] FCA 1206; (2019) 138 ACSR 134 at [28] Jackson J provided the following conspectus of relevant principles which I gratefully adopt:

The principles to be applied in cases such as the present are not contentious. Banks Smith J gave them detailed consideration in Re iCandy Interactive Limited [2018] FCA 533; (2018) 125 ACSR 369 (Re iCandy) and I gratefully adopt her Honour’s analysis. The points that are salient for the purposes of this application are as follows:

(a) Section 1322 is remedial in nature and is to be given a liberal interpretation: iCandy at [43].

(b) The provision has been used to validate non-disclosure by shareholders who on-sell shares on a number of occasions: iCandy at [44].

(c) The company whose shares were on-sold in breach of the Corporations Act is an interested party with standing to bring the application: iCandy at [46].

(d) In determining whether those concerned in or party to the breaches acted honestly, the court looks to absence of evidence of dishonesty. The court is concerned only with whether those people acted honestly in the ordinary meaning of that term. The concept of honesty can embrace inadvertence: iCandy at [54]-[56].

(e) The honesty of the shareholders who sell shares without disclosure is relevant. It is open to the court to readily infer that those shareholders have acted honestly in on-selling the shares: iCandy at [58].

(f) However the court may also consider the honesty of those responsible for the failure of the company to lodge a cleansing notice, including company officers. That is so even where, as here, the relief sought is framed only in terms of the contraventions committed by on-sellers: iCandy at [83], [87], [101].

(g) The court takes into account whether the plaintiff has taken prompt action to remedy the error: iCandy at [54].

(h) In considering whether it is just and equitable to validate the on-sales (s 1322(6)(a)(iii)), the court will generally focus on the interests and conduct of the shareholders: iCandy at [110].

92 A pre-condition to the exercise of the discretion in s 1322(4) is that the application for the exercise of the discretion must have been made by an “interested person”. That term is not defined in the Act, but it has been interpreted broadly. In circumstances where: (1) Austpac seeks relief concerning trading in its shares including the integrity of such trading; and (2) the relief is sought in aid of a foreshadowed application for removal of a suspension of trading in its shares, I am comfortably satisfied that Austpac is an interested person with respect to the present application.

The validity declaration – s 1322(4)(a)

93 As noted at [2(1)] above, the validity declaration is a declaration that any offer for sale, or sale, of any of the Shares occurring in the period after their issue is not invalid by reason of any contravention of s 707(3) or s 727(1) of the Act. Section 1322(4)(a) of the Act confers upon the Court a discretion to make such an order, such discretion being enlivened upon the satisfaction of the pre-conditions set out in s 1322(6)(a) and (c). These pre-conditions are considered in turn below.

First pre-condition: satisfaction of 1322(6)(a)

94 The first pre-condition is that the Court must be satisfied of one or more of s 1322(6)(a)(i), (ii), or (iii). Austpac does not rely upon (i), but does rely upon (ii) and (iii). Those sub-sections require the Court to be satisfied that those concerned in, or party to the contraventions, acted honestly; or that the making of the order sought would be just and equitable.

95 I am satisfied that it would be just and equitable to make the validity declaration for the following reasons.

96 First, the expression “just and equitable” are words of significant width and provide the Court with a broad discretion. In Re Superior Resources Ltd [2020] FCA 635; (2020) 144 ACSR 677, Jackson J noted at 681 [18]:

The words “just and equitable” are words of the widest significance and do not limit the jurisdiction of the court to any case. It is a question of fact, and each case must depend on its own circumstances. The words give the court a wide discretion. There is no necessary limit on their generality, and they are to be applied in their ordinary meaning as calling for the exercise of judgment in the conventional way: Eddy Lau Constructions Pty Ltd v Transdevelopment Enterprise Pty Ltd [2004] NSWSC 273 at [45]-[47] (Barrett J), citing Loch v John Blackwood Ltd [1924] AC 783 at 791 and Thomas v Mackay Investments Pty Ltd (1996) 22 ACSR 294 at 302.

97 Secondly, in considering whether it is just and equitable to validate on-sales, the Court will generally focus on the interests and conduct of the shareholders: Re ICandy Interactive Ltd [2018] FCA 533; (2018) 125 ACSR 369 at 387 [110] (Banks-Smith J). In this regard:

(1) the on-sellers of the Shares are, I infer, likely to have acquired their Shares on the basis that they were not required to provide disclosure. Those holders were also entitled to assume that Austpac had done what was necessary to comply with Part 6D.2. This is particularly so with respect to the Shares the subject of the cleansing notices and Appendices 3B which contained representations that further disclosure would not be required; and with respect to the SSPP in circumstances where the 26 April 2019 letter from Austpac to the ASX (see [74] above) represented that Austpac had complied with the Class Order;

(2) the evidence of Mr Iles establishes that Austpac provided to the ASX regular updates of information and that he is unaware of any other information that Austpac would have been required to disclose; and

(3) the effect of the failure of Austpac to lodge effective cleansing notices or to otherwise comply with Part 6D.2 has been to expose the on-sellers to claims for relief under s 1325 of the Act.

98 As I am satisfied that it would be just and equitable to make the validity declaration, that is sufficient to satisfy the first pre-condition and it is unnecessary to consider whether the persons concerned in or party to any contraventions acted honestly.

Second pre-condition: satisfaction of s 1322(6)(c)

99 The second pre-condition is that the Court must be satisfied that no substantial injustice has been or is likely to be caused to any person. In Re Murray River Organics Ltd [2019] FCA 931; (2019) 138 ACSR 365, Anderson J explained at [35] to [38]:

35. The court must not make any order under s 1322 unless it is satisfied that no substantial injustice has been or is likely to be caused to any person: s 1322(6)(c) of the Act; Kimberley College Ltd v Davis, in the matter of Kimberley College Ltd [2018] FCA 1102 at [28]. There are two aspects to this requirement:

(a) the expression “has been” invites an inquiry as to the effect of the irregularity sought to be cured; and

(b) the expression “likely to be” draws attention to the effect of the proposed order: An v Joo [2019] NSWSC 39 at [34].

36. A degree of prejudice to a person or persons may be outweighed if the overwhelming weight of justice is in favour of making the order: Elderslie Finance Corp Ltd v Australian Securities Commission (1993) 11 ACSR 157 (Elderslie Finance) at 160; An v Joo [2019] NSWSC 39 at [35].

37. The reference to “substantial injustice” in s 1322(6)(c) is to a real and not insubstantial or theoretical prejudice: Elderslie Finance at 160. Whether there is real injustice requires a weighing of any prejudice if the order is made against the prejudice which would be suffered by the corporation and its directors and officers if an order was not made: Gangemi v Osborne [2009] VSCA 297 at [62], citing Re Compaction Systems Pty Ltd & The Companies Act [1976] 2 NSWLR 477 at 493; see also AHEPA NSW at [25].

38. One mechanism by which the court may ensure that an order under s 1322(4) does not cause substantial injustice is to make an ancillary order permitting any interested person who may suffer substantial injustice to apply within a set period of time to vary or dissolve the s 1322(4) order: see Sprint Energy at [51]; Clancy Exploration Limited, in the matter of Clancy Exploration Limited [2018] FCA 569 at [36].

100 It is not apparent from the evidence that any person who acquired any of the Shares in an on-sale was prejudiced by a lack of disclosure. I note that, as discussed above, Austpac has provided regular updates to the ASX and the retrospective review undertaken by Mr Iles did not reveal any further information requiring disclosure (albeit at the time of contraventions by Austpac rather than by the on-sellers).

101 There is also no basis from which to infer that the making of the validity declaration would prejudice any person.

102 Further, one of the orders sought by Austpac is an order of the kind referred to by Anderson J in Murray River Organics at [38] (see [99] above) and one which is regularly made in applications of the present kind. That order provides for a 28-day period from its publication on the ASX website in which any person who claims to have suffered substantial injustice by reason of any contraventions or to be likely to suffer substantial injustice by reason of the making of the validity declaration may apply to the Court for a variation or discharge of that order.

103 It follows that I am satisfied that no substantial injustice has been, or is likely to be caused to any person.

104 For the reasons set out above, each of the pre-conditions to the exercise of the discretion in s 1322(4)(a) has been satisfied and the discretion is enlivened.

The exercise of the discretion

105 For the following reasons, I am satisfied that the discretion should be exercised so as to make the validity declaration.

106 First, my conclusions that the making of the validity declaration would be just and equitable and that no substantial injustice has been or is likely to be caused to any person not only enliven the discretion but also weigh in favour of the making of the validity declaration.

107 Secondly, the making of the declaration will serve to remove doubts as to the integrity of dealings in the Shares caused by any contraventions.

108 Thirdly, as noted at [88(4)(a)] above, both the ASX and ASIC have been on notice of the application and have not sought to be heard. Further, ASIC was provided with further details of the application and indicated that it neither supported nor opposed the application. I infer that ASIC does not have concerns about the making of the validity declaration.

109 Fourthly, as noted at [88(4)(b)] above, the evidence establishes that Austpac’s shareholders have been on notice of the application, no shareholder has sought to be heard and the shareholders to whom Mr Iles has spoken have all supported the application.

110 Fifthly, whilst it has not been necessary to consider the honesty of those involved in any contraventions, and whilst I do have some concerns about the honesty of Notsag and Mr Gaston for the reasons developed below at [117], those concerns are not a sufficient reason not to make the validity declaration, in circumstances where Notsag has on-sold many of the Shares that were issued to it and where there is no reason to believe that those on-purchasers acted otherwise than honestly. Further, there is no reason why doubts as to the integrity of the transactions by which such Shares were transferred should not be removed.

111 Sixthly, whilst there has been considerable delay in seeking the relief sought, an explanation for that delay has been provided, which demonstrates that Austpac acted promptly once concerns were raised but was then hampered by various factors (see [89] above). Applications such as the present application should be brought as soon as possible. However, in view of the explanation provided, and the strength of reasons in favour of making the validity declaration set out above, the delay is not a sufficient reason to refuse to make the validity declaration.

112 Finally, there does not appear to be any other matter which might inform the exercise of the discretion and which provides a reason not to make the declaration sought. In this regard, I note that Austpac has taken steps to address the causes of its previous failures to meet its obligations (see [80] and [81] above).

The relief from liability order – s 1322(4)(c)

113 As noted at [2(2)] above, the relief from liability order is an order that any person offering to sell or selling the Shares is relieved from any civil liability arising out of any contravention of s 707(3) or s 727(1) of the Act. Section 1322(4)(c) confers upon the Court a discretion to make such an order, such discretion being enlivened upon the satisfaction of two pre-conditions: (1) that the person the subject of the civil liability concerned acted honestly; and (2) that no substantial injustice has been or is likely to be caused to any person.

First pre-condition: satisfaction of s 1322(6)(b)

114 The first pre-condition is that the person the subject of the civil liability concerned acted honestly: s 1322(6)(b). Thus, it is necessary to identify the civil liability and the persons the subject of such liability and to consider whether they acted honestly. The relevant liability is a liability under s 707(3) or 727(1) of the Act. The persons potentially the subject of such liability and for whom relief is sought are persons who on-sold or might on-sell some of the Shares.

115 In ICandy at 378 to 379 [54] to [57], Banks-Smith J set out the following summary of considerations relevant to determining whether a person has acted honestly for the purposes of s 1322 of the Act which I gratefully adopt:

Meaning of honesty

54 When determining whether someone has acted honestly for the purposes of s 1322 of Act the court looks to an absence of evidence of dishonesty: Re G8 Communications Ltd (2016) 122 ACSR 22; [2016] FCA 297 at [35]. It also takes into account whether the applicant has taken prompt action to remedy the error: Sprint Energy [44]; Golden Gate [48].

55 The concept of acting honestly can embrace the following:

(a) inadvertence or a failure to turn their mind to the relevant issue: Re QBiotics Limited [2016] FCA 873 (QBiotics) [38];

(b) an active, but incorrect, consideration of a legal issue as well as failure to consider the issue at all: Primelife Corporation Ltd v Aevum Ltd (2005) 53 ACSR 283; [2005] NSWSC 269 at [8]; Golden Gate [47]; Sprint Energy [43];

(c) failure to understand or appreciate the significance of non-compliance: Sprint Energy [44].

56 Consideration of the honesty of an applicant also arises in the context of s 1318 of the Act. In Hall v Poolman (2007) 65 ACSR 123; [2007] NSWSC 1330 Palmer J stated (at [325]):

In my view, when considering whether a person has acted honestly for the purposes of a defence under CA s 1317S(2)(b)(i) or s 1318, the Court should be concerned only with the question whether the person has acted honestly in the ordinary meaning of that term, i.e. whether the person has acted without deceit or conscious impropriety, without intent to gain improper benefit or advantage for himself, herself or for another, and without carelessness or imprudence to such a degree as to demonstrate that no genuine attempt at all has been to carry out the duties and obligations of his or her office imposed by the Corporations Act or the general law. A failure to consider the interests of the company as a whole, or more particularly the interests of creditors, may be such a high degree as to demonstrate failure to act honestly in this sense. However, if failure to consider the interests of the company as a whole, including the interests of its creditors, does not rise to such a high degree but is the result of error of judgment, no finding of failure to act honestly should be made, but the failure must be taken into account as one of the circumstances of the case to which the Court must have regard under CA s 1317S(2)(b)(ii) and s 1318.

57 The obtaining of advice does not conclusively establish that a person was acting honestly. It is however an important consideration in determining whether proper competent and expert advice was sought and obtained: Clarke (as trustee of the Clarke Family Trust) v Great Southern Finance Pty Ltd (recs and mgrs. Apptd) (in liq) [2014] VSC 516 [1960].

116 It is convenient to consider separately: (1) Notsag and Mr Gaston; (2) the other on-sellers of the Shares.

117 The present case is not a case in which it is possible to conclude that there is an absence of dishonesty on the part of Notsag or Mr Gaston. The salient evidence is that:

(1) Notsag is controlled by Mr Gaston;

(2) Mr Gaston was the company secretary and Chief Financial Officer of Austpac during the relevant period and was responsible for ensuring that shares were issued in accordance with legislative and regulatory requirements;

(3) Mr Gaston, in view of the positions he held, the responsibilities he had and the proceeding before Barrett J in 2010, was a person who should have known of the disclosure requirements and their potential application to Notsag; and

(4) there appears to have been conduct and in particular the apparently clandestine placement of shares to Notsag (see paragraphs [78] and [79] above) which might cast doubt upon Mr Gaston’s integrity.

118 This evidence raises questions as to whether Notsag and Mr Gaston acted honestly when on-selling the Shares issued to Notsag. However, there is no evidence before the Court from Mr Gaston which may provide illumination. In these circumstances, I am not prepared to find that Notsag, to whom Mr Gaston’s knowledge is to be attributed, or Mr Gaston, acted honestly. To be clear, this is a finding of non-satisfaction and is not a positive finding of any dishonesty on the part of Notsag or Mr Gaston.

Other on-sellers of the Shares

119 The evidence establishes that:

(1) there were recipients of the Shares other than Notsag, some of whom have on-sold some Shares; and

(2) Notsag on-sold many of the Shares that it received. I infer that there may have been subsequent sales of Shares.

120 There is no evidence to suggest that any of the other on-sellers of the Shares acted otherwise than honestly and I am prepared to infer that they did act honestly.

The second pre-condition – satisfaction that no substantial injustice has been or is likely to be caused to any person: s 13226(c)

121 I am satisfied that there has been no substantial injustice caused to any person. In this regard, there is no evidence before the Court that any person claims such prejudice.

122 There is also no evidence that the making of the relief from liability order is likely to cause substantial injustice to any person. I note in this regard that no shareholder has sought to be heard on this application.

123 In any event, there will be a 28-day period for any person claiming prejudice to seek a variation of the relief from liability order.

Conclusion as to satisfaction of the pre-condition to s 1322(4)(c) and exercise of the discretion

124 In so far as relief is sought with respect to on-sellers of the Shares other than Notsag, I am satisfied of both pre-conditions to the exercise of the discretion. I am also satisfied, for the following reasons, that I should exercise the discretion so as to make the order sought. First, satisfaction of the pre-conditions not only enlivens the discretion but also weighs in favour of the making of the relief order. Secondly, both the ASX and ASIC have been on notice of the application and have not sought to be heard; and ASIC indicated that it neither supported nor opposed the application from which I infer that it is not concerned about the making of the relief from liability order. Thirdly, Austpac’s shareholders have been on notice of the application and no shareholder has sought to be heard. There is also evidence from Mr Iles of shareholder support for the application and that no shareholder has expressed opposition to the application. Finally, there does not appear to be any reason (including delay) not to exercise the discretion so as to make the relief from liability order.

125 However, in so far as the relief sought would extend to Notsag or Mr Gaston, I am not satisfied that both pre-conditions have been met. In any event, I would not have exercised the discretion so as to relieve Notsag or Mr Gaston from liability for the following reasons.

126 In Re Poseidon Nickel Ltd [2018] FCA 1063; (2018) 129 ACSR 57, Colvin J at 67 to 68 [62] to [70] explained:

62 It is important to distinguish between three different aspects of the relief sought. First, orders are sought in order to remove any uncertainty as to the validity of the title to the shares so as to enable them to be offered for further sale. If orders are not granted then the integrity of future dealings in the shares by current holders may be called into question. Relief of this kind is sought under s 1322(4)(a) to declare that the dealing by which the current shareholder acquired the shares is not invalid.

63 Second, orders are sought that other prior dealings are not invalid by reason of any contravention of the disclosure requirements. Relief of this kind is also sought under s 1322(4)(a). It provides an assurance of continuity of title and would also protect past holders from claims that earlier on-selling was invalid by reason of any failure to comply.

64 Third, orders are sought relieving parties from civil liability in respect of any contravention or failure to meet disclosure requirements in relation to offering and selling shares the subject of the Share Issues. Relief of this kind is sought under s 1322(4)(c).

65 Relief of the third kind is not required in order to ensure the ongoing integrity of the market. However, it may be justified to provide an assurance to innocent parties, particularly where their contravention arises from a failure to disclose consequent upon the issuing company creating the impression that the shares were freely tradable at any time.

66 In the third case there is a requirement that the person the subject of the civil liability acted honestly. In the first two cases, the order can be made if it is just and equitable to do so or if the persons concerned in or a party to the contravention acted honestly. (There was no claim that the failure to comply in this instance was essentially of a procedural nature). The wider public interest in maintaining the integrity in the market in the shares supports the making of orders of the first and second kind in most cases like the present.

67 However, in my view, considerable care must be taken in granting an order of the third kind for the benefit of parties who are not before the Court presenting evidence and submissions as to their state of knowledge. It is preferable, in cases like the present, that general relief under s 1322(6)(c) be confined to cases where it is clear that the parties who will be protected by the relief are innocent third parties whose involvement in any contravention has been brought about by the conduct of the company who has issued the shares or other parties.

68 In Re Golden Gate Petroleum Ltd, relief was initially sought that would afford protection from liability for the issuing company and its officers. After concerns were raised by ASIC, the application was amended to exclude the company and its officers from the protections afforded by the orders sought.

69 In my view, that is an approach that generally should extend to cases where the parties who on-sold the shares were parties with actual knowledge (or should have known) of the disclosure requirements and their potential application to them if there had not been disclosure when the shares and who took no steps to inquire as to whether there had been disclosure at the time of issue of the shares.

70 Significantly, an order under s 1322(6)(c) operates only for the benefit of the party concerned and will not require a consideration of wider public interest issues of a kind that may support the making of an order under s 1322(6)(a) on the basis that it is just and equitable.

(emphasis added)

127 The emphasised text is apposite to the present case. As noted above, there is no evidence from Mr Gaston, and the evidence that is available suggests that Mr Gaston should have known of the disclosure requirements and of their potential application to Notsag if there had not been proper disclosure; and that he was centrally involved in Austpac’s failure to provide proper disclosure. In these circumstances, it is not appropriate that Notsag or Mr Gaston have the benefit of the relief from liability order. It is of course open to Notsag or Mr Gaston to make their own application should they choose to do so.

128 For the reasons set out above, I will make the orders sought by Austpac, save that the relief from liability order will not extend to Notsag or Mr Gaston.

I certify that the preceding one hundred and twenty-eight (128) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Goodman. |

Dated: 21 February 2023