FEDERAL COURT OF AUSTRALIA

Security Matters Limited, in the matter of Security Matters Limited [2023] FCA 19

ORDERS

SECURITY MATTERS LIMITED (ACN 626 192 998) Plaintiff | ||

AND: | Interested Party | |

DATE OF ORDER: |

OTHER MATTERS:

A. The Court is satisfied that the Australian Securities and Investments Commission (ASIC) has had a reasonable opportunity to:

(a) examine the terms of the proposed schemes of arrangement to which the application relates and a draft explanatory statement relating to those arrangements; and

(b) make submissions to the Court in relation to the proposed scheme of arrangement and the draft explanatory statement.

B. The Court notes the letter dated 6 January 2023 from ASIC to Mann Lawyers (the plaintiff’s solicitors), notifying the plaintiff that ASIC does not propose to appear to make submissions or intervene to oppose the proposed scheme at the first hearing under section 411(1) of the Act (ASIC’s indication of intent).

C. The purpose of the hearing referred to in paragraph 15 of this order is for the Court to consider the supplementary independent expert’s reports (as referred to in ASIC’s indication of intent).

D. By 4pm on 13 January 2023, the plaintiff is to file an affidavit, confirming the execution by Empatan PLC of deed polls made in favour of the participants in each scheme.

THE COURT ORDERS THAT:

1. The plaintiff is to convene and hold:

(a) a meeting (the Share Scheme Meeting) of its shareholders (Scheme Shareholders) to consider and, if thought fit, to approve (with or without any alterations or conditions) the scheme of arrangement (Share Scheme) proposed to be made between the plaintiff and its Scheme Shareholders, the terms of which are found at pages 702-725 of the affidavit of Nadav Prawer made on 8 January 2023 (third Prawer affidavit); and

(b) a meeting (the Option Scheme Meeting) of the holders of “SMX Options” (Scheme Option-holders) for the purpose of considering and, if thought fit, agreeing (with or without modification) to the scheme of arrangement (Option Scheme) proposed between the plaintiff and the Scheme Option-holders, the terms of which are found at pages 726-750 of the third Prawer affidavit (where “SMX Options” has the same meaning as in the Option Scheme),

(together, the Scheme Meetings).

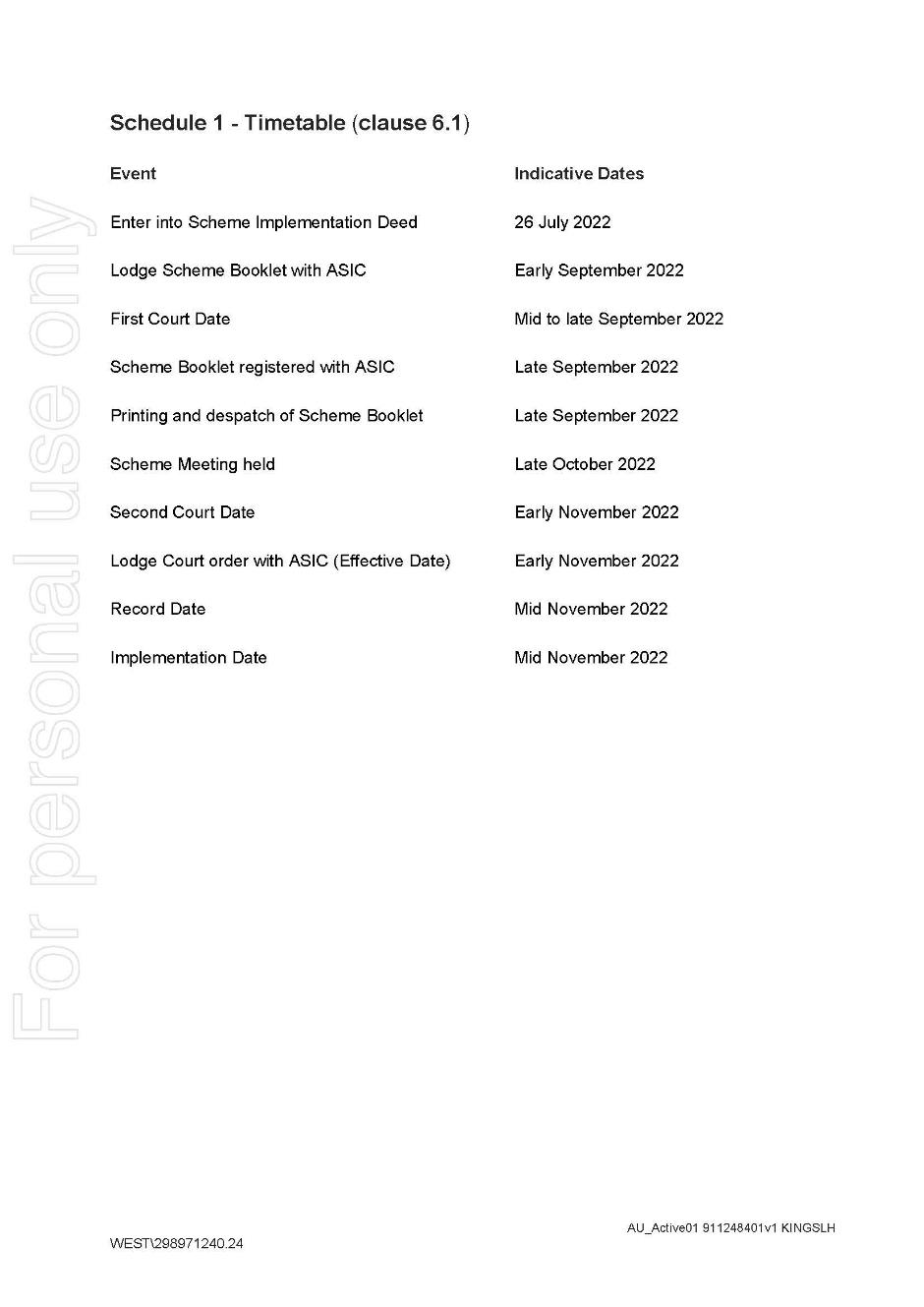

2. The Share Scheme Meeting is to be held on 1 February 2023, commencing at 9.00am (Melbourne time), and the Option Scheme Meeting is to be held on 1 February 2023, commencing at 9.30am (Melbourne time) (or at the conclusion or adjournment of the Share Scheme Meeting, whichever is later), each to be conducted electronically through an online platform (which is to be accessed in accordance with the instructions included in the scheme booklet (Scheme Booklet) that is substantially in the form of annexure NP-10 to the third Prawer affidavit and the notices of meeting to be sent in accordance with paragraphs 3 and 4 below).

3. The Scheme Meeting is to be convened by sending on or before 10 January 2023:

(a) in the case of Scheme Shareholders who have elected to receive shareholder communications electronically by way of email, an email substantially in the form of pages 1405-1406 of the affidavit of Haggai Alon made on 6 January 2023 (Alon affidavit), which:

(i) includes a link to an online portal or website from which the Scheme Booklet (which contains among other things the proposed Share Scheme at Annexure G and the notice of Share Scheme Meeting at Annexure I) can be downloaded; and

(ii) attaches an electronic copy of a personalised proxy/voting form for the Share Scheme Meeting (substantially in the form of pages 782-783 of the third Prawer affidavit), which includes an electronic link to an online portal or website that is accessible by the Scheme Shareholders and enables them to lodge their proxy forms for the Share Scheme Meeting and voting instructions online; and

(b) in the case of Scheme Shareholders who have elected to receive hardcopy communications, the following documents by pre-paid post addressed to the relevant address(es) recorded in the plaintiff’s register:

(i) a copy of the Scheme Booklet;

(ii) a hardcopy personalised proxy/voting form for the Share Scheme Meeting (substantially in the form of pages 782-783 of the third Prawer affidavit);

(iii) a reply-paid envelope for the return of completed proxy/voting form;

(c) in the case of Scheme Shareholders who have not made an election for either electronic or hard copy communications, the following documents by pre-paid post addressed to the relevant address(es) recorded in the plaintiff’s register:

(i) a letter substantially in the form of pages 1408-1409 of the Alon affidavit, which includes a link to an online portal or website from which the Scheme Booklet can be downloaded; and

(ii) a hardcopy personalised proxy/voting form for the Share Scheme Meeting (substantially in the form of pages 782-783 of the third Prawer affidavit), which includes a link to the online portal or website that is accessible by the Scheme Shareholder and which enables them to lodge their proxy form for the Share Scheme Meeting and voting instructions online.

4. The Option Scheme Meeting is to be convened by sending on or before 10 January 2023:

(a) in the case of Scheme Option-holders who have elected to receive optionholder communications electronically by way of email, an email substantially in the form of pages 1415-1406 of the Alon affidavit, which:

(i) includes a link to an online portal or website from which the Scheme Booklet (which contains among other things the proposed Option Scheme at Annexure H and the notice of Option Scheme Meeting at Annexure J) can be downloaded;

(ii) attaches an electronic copy of a personalised proxy/voting form for the Option Scheme Meeting (substantially in the form of pages 780-781 of the third Prawer affidavit), which contains an electronic link to the online portal or website that is accessible by them and which enables the Scheme Option-holder to lodge their proxy form for the Option Scheme Meeting and voting instructions online;

(b) in the case of Scheme Option-holders who have elected to receive hard copy communications, the following documents by pre-paid post addressed to the relevant address(es) recorded in the plaintiff’s register:

(i) a copy of the Scheme Booklet;

(ii) a hardcopy personalised proxy/voting form for the Option Scheme Meeting (substantially in the form of pages 780-781 of the third Prawer affidavit);

(iii) a reply-paid envelope for the return of completed proxy/voting form;

(c) in the case of Scheme Option-holders who have not made an election for either electronic or hard copy communications, the following documents by pre-paid post addressed to the relevant address(es) recorded in the plaintiff’s register:

(i) a letter substantially in the form of pages 1408-1409 to the Alon affidavit, which includes a link to an online portal or website from which the Scheme Booklet can be downloaded; and:

(ii) attaches a hardcopy personalised proxy/voting form for the Option Scheme Meeting (substantially in the form of pages 780-781 of the third Prawer affidavit), which included a link to the online portal or website that is accessible by the Scheme Option-holders and which enables them to lodge their proxy form for the Option Scheme Meeting and voting instructions online.

5. If the plaintiff receives an automatic, system generated notification that the documents were unable to be delivered to the nominated electronic address of any Scheme Shareholder or Scheme Option-holder to whom scheme documents were dispatched in accordance with paragraphs 3(a) and 4(a) above (undelivered email recipients), the documents be dispatched by the plaintiff to undelivered email recipients in accordance with paragraphs 3(b) and 4(b) above.

6. The “Option Scheme Meeting Record Date” under the Option Scheme will be 9.00am (Melbourne time) on 30 January 2023.

7. Except to the extent addressed by this order, the Share Scheme Meeting and Option Scheme Meeting are to be convened, held and conducted in accordance with the provisions of:

8. Part 2G.2 of the Act (save for any applicable replaceable rule) that apply to a meeting of the plaintiff’s shareholders; and

9. the plaintiff’s constitution that apply in relation to meetings of shareholders and that are not inconsistent with Part 2G.2 of the Act.

10. Voting on the resolutions to approve the Share Scheme and the Option Scheme is to be conducted by way of poll.

11. A proxy form, appointment of a corporate representative, or power of attorney to act on behalf of the relevant Scheme Shareholder or Scheme Option-holder in respect of the Share Scheme Meeting and the Option Scheme Meeting respectively will be valid and effective if, and only if, it is completed and delivered in accordance with its terms and this order by 9.00am (Melbourne time) on 30 January 2023.

12. Everadus Hofland, or failing him Amir Bader, is to be the chair of the Scheme Meetings.

13. The chair of the Scheme Meetings shall have the power to adjourn either or both meetings to such time, date, and place as they consider appropriate.

14. The plaintiff may provide access to the Scheme Meetings for such other persons as it thinks fit.

15. Compliance with r 2.15 of the Federal Court (Corporations) Rules 2000 (Rules) is dispensed with.

16. Notice of the hearing of an application under s 411(4) of the Act for an order approving the Scheme is to be published once in “The Australian” newspaper by an advertisement substantially in the form of Annexure A to these orders, such advertisement to be published on or before 25 January 2023, and the plaintiff is otherwise exempted from compliance with r 3.4 of the Rules.

17. The further hearing of the originating process is adjourned to 9:30 am (Melbourne time) on 23 January 2023 before Justice O’Bryan.

18. Subject to further order, the hearing of the plaintiff’s application for orders approving the Schemes is listed at 9.30 am (Melbourne time) on 6 February 2023.

19. Liberty to apply is reserved.

20. These orders are to be entered forthwith.

Annexure A

Notice of Second Court Hearing

Notice of hearing to approve compromise or arrangement

TO all the members of Security Matters Limited (ACN 626 192 998) (SMX)

TAKE NOTICE that at that at 9:30 am on 6 February 2023 the Federal Court of Australia (Victorian Registry) at Owen Dixon Commonwealth Law Courts Building, 305 William Street, Melbourne, will hear an application by SMX seeking the approval of a scheme of arrangement between SMX and its members and scheme of arrangement between SMX and certain of its option-holders, if agreed to by resolutions to be considered, and, if thought fit, passed at meetings of such members and option-holders.

The meetings are to be held electronically through an online meeting platform, Lumi, on 1 February 2023, commencing at:

• 9.00am (Melbourne time) for shareholders, and accessible via https://web.lumiagm.com/310257505 and

• 9.30am (Melbourne time) for option-holders (or at the conclusion or adjournment of the meeting for shareholders, accessible via whichever is later), and accessible via https://web.lumiagm.com/399731351

If you wish to oppose the approval of the compromise or arrangement, you must file and serve on SMX a notice of appearance, in the prescribed form, together with any affidavit on which you wish to rely at the hearing. The notice of appearance and affidavit must be served on SMX at its address for service by 5.00 pm on 3 February 2023.

The address for service of SMX is: c/o Mann Lawyers Pty Ltd, Level 17, 31 Queen Street Melbourne VIC 3000 [Ref: Nadav Prawer].

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ANDERSON J:

INTRODUCTION

1 The plaintiff (SMX) is a public company limited by shares, headquartered in Israel and listed on the Australian Securities Exchange (ASX). SMX develops and commercialises track and trace technology for a variety of industries.

2 SMX seeks to become listed on the NASDAQ. To that end, it proposes to merge with Lionheart III Corp (Lionheart), which is a “SPAC”, that is, a “special-purpose acquisition company” (also known as a “blank cheque company”), incorporated in Delaware in the United States of America and is listed on the NASDAQ.

3 Essentially, the transaction involves a reverse takeover of Lionheart by SMX and redomiciliation of SMX - from Australia to Delaware - and insofar as it involves a scheme of arrangement, it is a “top-hat scheme”. This is the first case in Australia where the bidder is a United States “SPAC”. This feature means the transaction has attracted close scrutiny from the Australian Securities and Investments Commission (ASIC).

4 As SMX has both shares and options on issue, the transaction involves two schemes:

(a) one involving SMX’s shareholders; and

(b) the other, holders of certain options in SMX.

5 The transaction is complicated further by:

(a) the imposition as part of the merger of an Irish company incorporated for the purposes of the transaction - called Empatan plc (Empatan); and

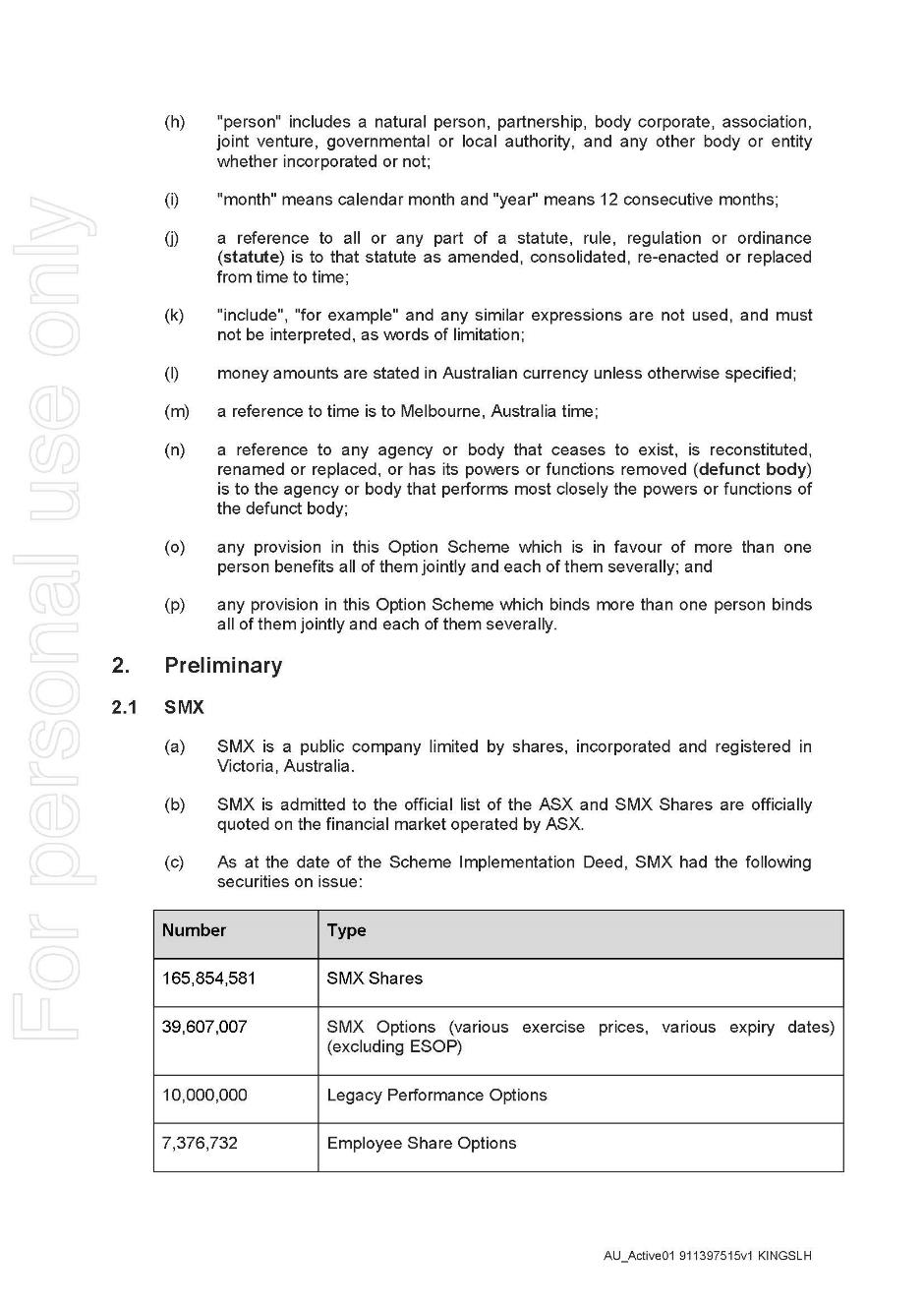

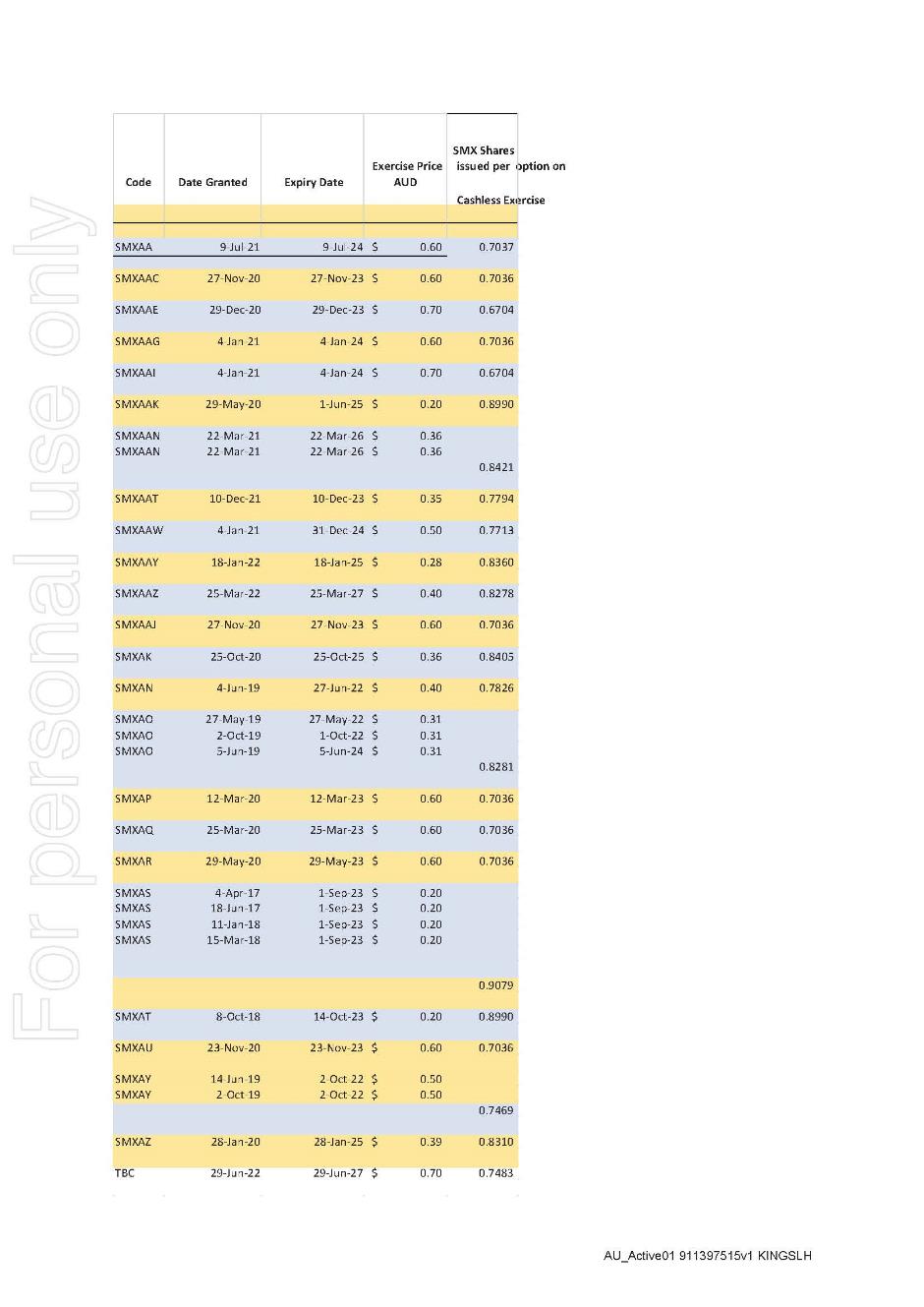

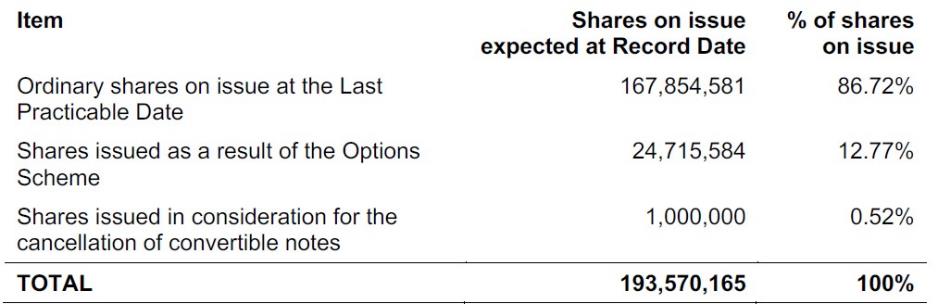

(b) an equal capital reduction, involving the cancellation of all the shares in SMX (including those to which the option-holders will be entitled under the option scheme).

6 If the schemes are approved and implemented:

(a) (merger / business combination) Lionheart will become a wholly-owned subsidiary of Empatan;

(b) (capital reduction) by the capital reduction, all the shares in SMX will be cancelled;

(c) (share scheme) by the scheme between SMX and its shareholders (the Share Scheme):

(i) Empatan will apply for the shares it issues in itself (described below) to be listed on NASDAQ;

(ii) SMX will implement the capital reduction;

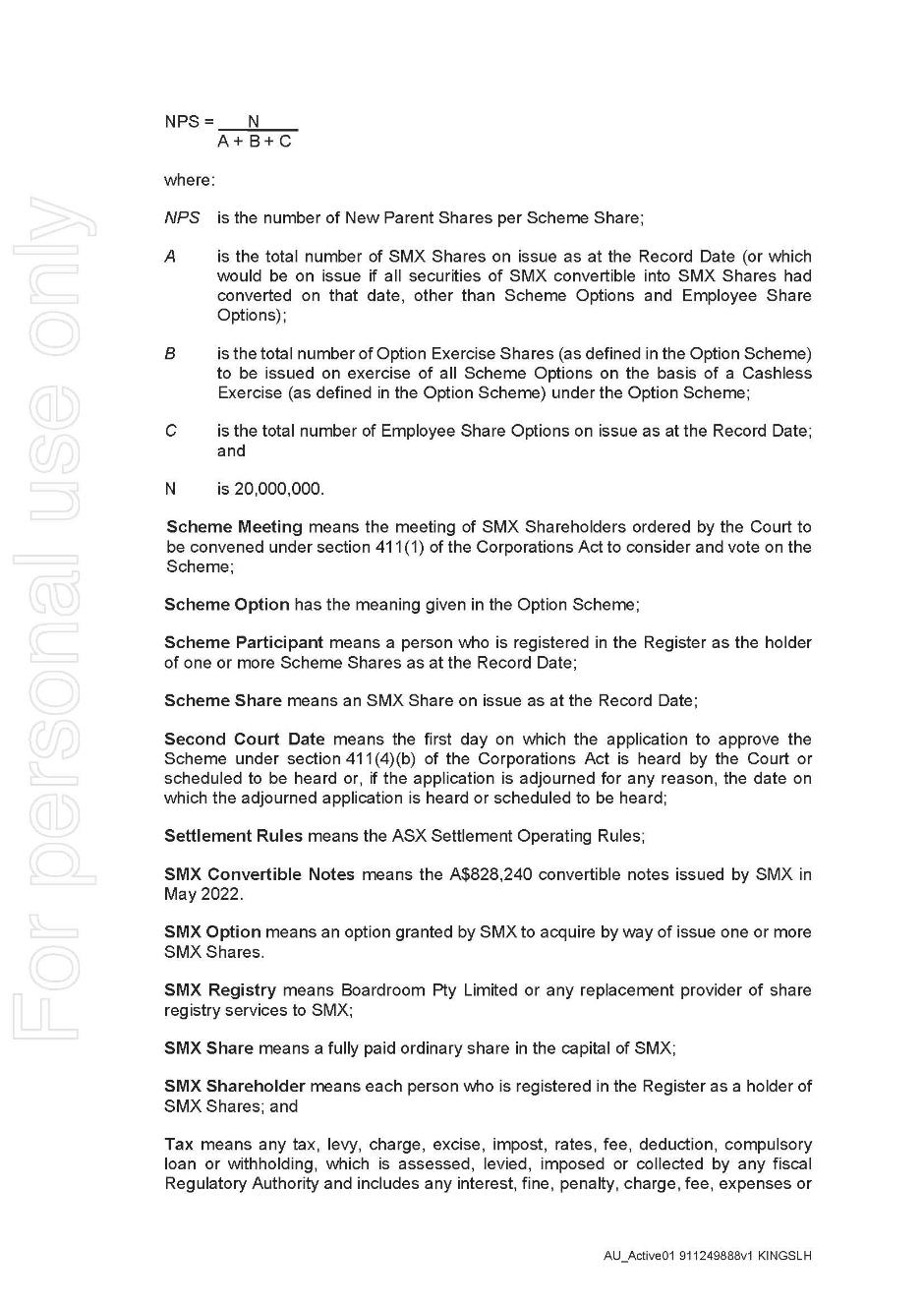

(iii) Empatan will issue the “Scheme Consideration” – being new shares in itself (the number of which will be calculated in accordance with a prescribed formula) to persons who had been SMX’s shareholders;

(iv) SMX will issue one share to Empatan, making SMX a wholly-owned subsidiary of Empatan;

(d) (option scheme) by the scheme between SMX and the option holders (the Option Scheme):

(i) Empatan will apply for the shares it issues in itself (described below) to be listed on NASDAQ;

(ii) the options in SMX will be deemed to have been exercised on a cashless basis and shares in SMX issued (in accordance with the value of the options, based on the Black-Scholes Model) to option-holders;

(iii) those shares will be cancelled under the capital reduction;

(iv) Empatan will issue the “Cancellation Consideration” – being new shares in itself (the number of which will be calculated in accordance with the same formula as the Share Scheme) to the persons who had been option-holders.

7 Each of the merger, the capital reduction, the Share Scheme and the Option Scheme are interdependent and conditional on each other.

8 A draft scheme booklet, which includes the explanatory statement required by s 412 of the Corporations Act 2001 (Cth) (Act), has been prepared. The booklet provides a detailed description of the schemes, including their advantages and disadvantages, as well as a description of the merger and the capital reduction. The booklet also annexes an independent expert’s report that opines that the schemes are in the best interests of SMX’s shareholders and option holders.

This proceeding

9 This proceeding concerns the Share Scheme and the Option Scheme.

10 SMX seeks, under subsection 411(1) of the Act, orders (amongst others):

(a) convening a meeting of SMX’s shareholders to consider the Share Scheme; and

(b) convening a meeting of the relevant option-holders to consider the Option Scheme; and

(c) concerning the dispatch of the scheme booklet.

PROCEDURAL HISTORY AND EVIDENCE

11 The proceeding was commenced by an originating process filed on 23 December 2022, supported by an affidavit of SMX’s solicitor, Nadav Prawer of Mann Lawyers Pty Ltd (first Prawer affidavit).

12 Since then, SMX has filed the following further affidavits:

(a) an affidavit made on 5 January 2023 by Everardus Hofland, an executive director and the chairman of SMX – regarding his consent to act as chairperson of the scheme meetings (first Hofland affidavit);

(b) an affidavit made on 2 January 2023 by Amir Bader, a non-executive director of SMX – confirming his consent to act as alternate chairperson of the meetings (first Bader affidavit);

(c) an affidavit made on 6 January 2023 by Haggai Alon, an executive director and the chief executive officer of SMX – which describes SMX, the proposed schemes, the negotiations between SMX and Lionheart that preceded the proposed transaction, preparation of the scheme booklet and how the booklet will be dispatched to members and option holders (first Alon affidavit);

(d) an affidavit made on 5 January 2023 by Doron Afik, who is the managing partner of Afik & Co Law (the Israeli legal advisors to SMX) and SMX’s general counsel – explaining how the scheme booklet was approved and verified (Afik affidavit);

(e) a second affidavit of SMX’s solicitor, Dr Prawer, made on 6 January 2023 (second Prawer affidavit), explaining the lodgment of notice with ASIC, ASIC’s feedback about the scheme booklet, the waiver of certain ASX listing rules and certain requirements under Schedule 8 of the Corporations Regulations 2001 (Cth) (Corporations Regulations);

(f) an affidavit made on 5 January 2023 by Connor Manning of Arthur Cox LLP, an Irish solicitor – which provides an opinion on questions of Irish law about the deed poll (Manning affidavit);

(g) an affidavit made on 5 January 2023 by Brent Goldman – annexing his independent expert’s report about whether the schemes are fair and reasonable (Goldman affidavit); and

(h) a third affidavit of Dr Prawer – exhibiting the latest draft of the scheme booklet (incorporating the most recent amendments, requested by ASIC) and dealing with ASIC’s attitude to the application (third Prawer affidavit).

13 Prior to the hearing, Lionheart filed an affidavit made on 6 January 2023 by Paul Howard Rapisarda, the Chief Financial Officer of Lionheart which deposed to:

(a) the verification of information in the draft scheme booklet;

(b) the execution of a deed poll in favour of the Scheme Participants and the Option Scheme Participants; and

(c) information about negotiations regarding exclusivity and break fee provisions.

THE PROPOSED SCHEME

14 On 26 July 2022, SMX, Lionheart and Empatan entered a scheme implementation deed (SID), by which SMX agreed to propose and implement the schemes and undertake the capital reduction.

15 On the same day, the parties entered a business combination agreement under which Empatan would become the parent of Lionheart and SMX (the business combination) and list on the NASDAQ. The business combination is subject to the terms and conditions set out in the business combination agreement, including the approval of Lionheart’s shareholders (who will receive new shares in Empatan, while Lionheart’s existing warrant-holders will have their warrants automatically adjusted to become exercisable in respect of shares in Empatan).

16 Prior to the hearing, on 7 January 2023, SMX, Empatan, and Lionheart undertook the process of finalising a deed of variation to amend the SID, so as to update the number of shares, options and other securities in SMX to which it refers (Deed of Variation). The Deed of Variation was then finalised and amendments were made to the SID. The Deed of Variation is annexed to the third Prawer affidavit at annexure NP-10. The variations made to the SID, updated the number of shares, options and other securities to which the deed refers. On 9 January 2023, Mr Prawer subsequently provided a revised draft scheme booklet to ASIC which, among other things, provided the insertion of the Deed of Variation alongside the SID.

What is a SPAC?

17 A SPAC is essentially a shell company, established for the sole purpose of raising money through an initial public offering so as eventually to acquire another company. A SPAC has no commercial activities, and its only assets are typically the money raised in its own Initial Public Offering (IPO).

18 On 25 May 2021, the US Securities and Exchange Commission (SEC) published an Updated Investor Bulletin about SPACs entitled – “What You Need to Know About SPACs”. The SEC, in the Updated Investor Bulletin explains that investors in a SPAC:

... are relying on the management team that formed the SPAC, often referred to as the sponsor(s), as the SPAC looks to acquire or combine with an operating company. That acquisition or combination is known as the initial business combination. A SPAC may identify in its IPO prospectus a specific industry or business that it will target as it seeks to combine with an operating company, but it is not obligated to pursue a target in the identified industry.

Once the SPAC has identified an initial business combination opportunity, its management negotiates with the operating company and, if approved by SPAC shareholders (if a shareholder vote is required), executes the business combination. This transaction is often structured as a reverse merger in which the operating company merges with and into the SPAC or a subsidiary of the SPAC. While there are various ways to structure the initial business combination, the combined company following the transaction is a publicly traded company and carries on the target operating company’s business.

19 As the Updated Investor Bulletin explains:

(a) a SPAC will typically have a two-year period to identify and complete an initial business combination transaction;

(b) typically the SPAC’s IPO proceeds (less proceeds used for certain fees and expenses) are held in a trust account and earn interest;

(c) when the SPAC identifies a business combination, it provides its investors with the opportunity to redeem their shares rather than become a shareholder of the combined company; and

(d) if the SPAC does not complete a business combination, “shareholders are beneficiaries of the trust and entitled to their pro rata share of the aggregate amount then on deposit in the trust account.”

The schemes of arrangement

20 The terms of the Share Scheme and the Option Scheme are contained in Annexure 1 and Annexure 2 of the SID. They are also reproduced in Annexures G and Annexure H of the draft scheme booklet.

The share reduction and cancellation resolution

21 A reduction of a company’s share capital requires a resolution of its members: s 256B of the Act.

22 On 3 January 2022, SMX sent a notice of meeting to its shareholders, convening a general meeting to be held on 1 February 2023 to consider such a resolution.

23 As explained below, SMX seeks orders convening the scheme meetings on 1 February 2023, shortly after the general meeting.

Operation of the schemes

24 A transaction that involves both a share scheme and an option scheme is not unusual. In several cases, this Court has considered transactions involving both types of scheme: for instance, Re Foundation Healthcare Ltd (2002) 42 ACSR 252 (Re Foundation Healthcare); Re Sino Gold Mining Ltd (ACN 093 518 579) (2009) 74 ACSR 647, Re Talison Lithium Ltd [2012] FCA 1422, Re Coventry Resources Ltd [2012] FCA 1252, Re Atlassian Corporation Pty Limited [2013] FCA 1451, Re Ecosave Holdings Ltd [2015] FCA 1121, Re Anatolia Energy Limited [2015] FCA 1134 and Re Xplore Wealth Ltd [2020] FCA 1868 (Re Xplore Wealth).

25 The relevant steps are as follows:

(a) the Court, if it deems it appropriate, will order that each scheme meeting be convened;

(b) shareholders and option-holders will meet to consider the Share Scheme and the Option Scheme respectively;

(c) if the conditions precedent for each scheme (including the necessary statutory majorities at the meetings) are satisfied or waived by the time the schemes come before the Court for approval at the second hearing;

(i) the Court, if it deems it appropriate, will make orders approving each scheme;

(ii) SMX will lodge the orders with ASIC;

(d) under the Share Scheme, all SMX shares are cancelled in return for Empatan shares according to the ratio set out in the scheme (currently expected to be one new Empatan share for every 10.3490 SMX shares); and

(e) under the Option Scheme, all SMX options (other than those excluded from the scheme) will be deemed to have been exercised on a cashless basis in exchange for SMX shares in accordance with a Black Sholes Model calculation, which shares will then be cancelled in return for Empatan shares according to the same ratio as the Share Scheme.

26 Two categories of options in SMX are excluded from – and will therefore not be affected by – the Option Scheme. These are the “ESOP Options” and “Legacy Performance Options”.

(a) The “ESOP Options” are options issued to SMX employees under its employee share and option plan (ESOP). Holders of ESOP Options have entered private agreements within Empatan, under which their options will be cancelled in exchange for the issue of options in Empatan (as explained in section 15.7(e) (“Employee, service provider and founder options”) of the draft scheme booklet). Thus, the ESOP Options are excluded from the Option Scheme.

(b) The “Legacy Performance Options” were granted to entities associated with SMX’s CEO, Mr Alon, and its chairman, Mr Hofland, at the time of SMX’s initial public offering in October 2018. SMX, Empatan and the holders of these options have agreed (subject to the schemes becoming effective) to cancel the options, in consideration for payment of nominal consideration (AUD 10.00 to each of the holders). Because the consideration for the cancellation of the Legacy Performance Options is nominal (approximately AUD 0.000002 per option), ASX has waived the operation of Listing Rule 6.23.2. The issue is also explained in section 5.18 “Legacy Performance Options” of draft scheme booklet.

Deeds poll

27 Although Lionheart is to become a wholly-owned subsidiary of Empatan, and Empatan is to provide the Empatan shares under the schemes, neither Lionheart nor Empatan are a party to either of the schemes. In such circumstances, the established practice is to require the entity providing the scheme consideration to execute a deed poll in favour of members and creditors.

28 That practice has been adopted here: each of Empatan and Lionheart has made a deed poll in favour of the participants in each scheme. Copies of the deeds poll for the Share Scheme are at Annexure E of the draft scheme booklet and those for the Option Scheme are at Annexure F.

POWER TO MAKE ORDERS UNDER SECTION 411 OF THE ACT

Relevant provisions

29 Part 5.1 of the Act sets out the procedure by which an arrangement between a company and its members or creditors can be made binding. The procedure involves three main steps:

(a) first, an application to the Court for an order that the company convene a meeting (or meetings, as the case may be) of its members (the first hearing): s 411(1);

(b) second, if the order is made, the convening of the meeting at which a resolution that the scheme to be agreed to is considered (the meeting): s 411(4)(a); and

(c) third, if the resolution is passed by the prescribed majorities, a further application to the Court for approval of the scheme (the second hearing): ss 411(4)(b) and 411(6).

30 The Court’s discretion to make orders for the convening of a meeting is enlivened if:

(a) an arrangement is proposed between a Part 5.1 body and its members or creditors (as the case may be), or any class of members or creditors: s 411(1);

(b) application for the order is made in a summary way by the body or any of its members: s 411(1);

(c) 14 days’ notice of the hearing of the application has been given to ASIC (or such lesser period as the Court or ASIC permits): s 411(2)(a); and

(d) the Court is satisfied that ASIC has had a reasonable opportunity to:

(i) examine the terms of the proposed compromise or arrangement and a draft explanatory statement relating to the terms of the proposed compromise or arrangement; and

(ii) make submissions to the Court about the proposed compromise or arrangement and the draft explanatory statement: s 411(2)(b).

31 The procedure is also regulated by:

(a) s 412 of the Act and Reg 5.1.01 and Schedule 8 of the Corporations Regulations, which set out information that is required to be sent to the members and creditors about the scheme; and

(b) the Rules.

32 For the reasons set out below, each of these requirements has been satisfied, and I find that the meeting may be convened.

Compliance with ss 411 and 412 and the Rules

33 An arrangement is proposed between a Part 5.1 body and its members and a class of its creditors.

34 SMX is a company registered under the Act and is therefore a “Part 5.1 body” as defined under s 9 of the Act.

35 Each scheme is an arrangement contemplated by s 411(1):

(a) The Share Scheme is an arrangement between SMX and its members.

(b) The Option Scheme is an arrangement between SMX and relevant option-holders. The authorities establish that option-holders are treated as creditors for the purposes of s 411 of the Act: see e.g. Re Coventry Resources Ltd [2012] FCA 1252 at [18] (Barker J), referring to Re Westgold Resources Ltd [2012] WASC 301 at [16] (Hall J) and other cases; Re Doray Minerals Ltd; Ex Parte Doray Minerals [2019] WASC 57 at [40] (Vaughan J); Re Mia Group Ltd (2004) 50 ACSR 29 at [3]-[9] (Barrett J) referring to Re Kaz Group Ltd [2004] FCA 738 at [2]-[3] (Gyles J) and other cases – applied in Re Sino Gold Mining Ltd (ACN 093 518 579) (2009) 74 ACSR at [4] (Lindgren J) and Re Xplore Wealth at [25(2)] (Markovic J). Accordingly, the Option Scheme is a creditors’ scheme.

36 SMX is the plaintiff and is proposing the schemes. That is consistent with the requirements of s 411(1).

37 The Court must not make an order under s 411(1) unless 14 days’ notice of the hearing of the application (or such lesser period as the Court or ASIC permits) has been given to ASIC: s 411(2)(a).

38 ASIC was given notice of the hearing on 23 December 2022 which was more than 14 days before this hearing, as required by s 411(2)(a). Further, there has been correspondence between ASIC and SMX’s solicitors about various matters including the hearing and the contents of the draft scheme booklet.

39 ASIC was first provided with a copy of the draft scheme booklet, including all annexures, in the middle of 2022s. The initial draft has been revised several times.

40 A further draft of the scheme booklet was provided to ASIC on 3 January 2023. In subsequent correspondence and meetings with the lawyers for SMX and Lionheart, ASIC raised various queries about the schemes, the scheme booklet, and the overall transaction (which, as ASIC has noted, is the first to involve a SPAC and an Australian public company). ASIC also requested various amendments and additions to the draft scheme booklet. A further draft of the scheme booklet, containing the changes requested by ASIC, was provided to ASIC on the morning of 6 January 2023. On 9 January 2023, the Court received the third Prawer affidavit which, at NP-8, annexed ASIC’s indication of intent letter in which ASIC gave its indication that it did not wish to be heard at this first hearing of the scheme.

41 The requirements of s 412 of the Act and the Corporations Regulations were detailed in a “disclosure checklist” that was provided shortly before the hearing. Counsel for SMX, Mr Moller SC, indicated at the hearing that all of the statutory requirements were satisfied and had been duly outlined in the checklist.

42 The Rules impose three relevant requirements, each dealt with below. A further requirement is imposed by the Court’s practice note.

43 First, r 2.4(2) requires that the affidavit in support of an originating process must annex a record of a search of the records maintained by ASIC in relation to the company the subject of the application, carried out no earlier than 7 days before the originating process is filed.

44 Such a search was annexed to the first Prawer affidavit. It was dated 21 December 2022, - two days before the originating process was filed, thereby satisfying r 2.4(2).

45 Second, r 3.2 requires that the plaintiff file an affidavit stating the names of the persons nominated to be the chairperson and alternate chairperson of the meeting, that they are willing to act, and that they have no relevant relationship or dealing, or interest or obligation giving rise to conflict, except as disclosed in the affidavit.

46 It is proposed that the executive chairman of SMX’s board, Mr Hofland, will chair the meetings, with Mr Bader (a non-executive director) as the alternative chairperson. Each filed an affidavit dealing with the matters required by r 3.2.

47 Third, r 3.3(1) requires that an order under s 411(1) ordering a meeting in relation to a proposed arrangement must set out in a schedule, or otherwise identify, a copy of the proposed arrangement.

48 The orders proposed by SMX identify the schemes by reference to the relevant annexures of the draft scheme booklet, which contain the terms of the proposed schemes.

49 Finally, the Court’s practice when making an order under subsection 411(1) is to require that the explanatory statement prominently displays a notice stating that the fact the Court has made the convening orders and approved the explanatory statement does not mean it has formed any view as to the merits of the scheme or how members should vote or has prepared, or is responsible for, the explanatory statement: see paragraph 20 of Schedule 1 (Corporations and Corporate Insolvency Sub-Area) to the Commercial and Corporations Practice Note (C&C-1).

50 Such a statement is found in the “Important notices” section of the draft scheme booklet.

Relevant principles

51 Given the matters set out above, the Court’s discretion under subsection 411(1) to make an order convening a meeting is enlivened. Thus, it is necessary to consider the matters relevant to the exercise of that discretion.

52 The Court’s role on an application to convene a meeting is supervisory. As the New South Wales Court of Appeal stated, “[w]hat has repeatedly been emphasised is the limited function of the Court on the hearing of a summons to convene a meeting under s 411”: First Pacific Advisors LLC v Boart Longyear Ltd (2017) 121 ACSR 136 at [40] (Bathurst CJ; Beazley P and Leeming JA agreeing).

53 In Re CSR Ltd (2010) 183 FCR 358 at 379-380 [71]-[76], Finkelstein J explained how a court should approach an application for orders convening a scheme meeting. His Honour approved the approach adopted by Santow J in Re NRMA Ltd (2000) 33 ACSR 595 at 606-607 [32]-[40] (Re NRMA) and French J (as he then was) in Re Foundation Healthcare Ltd, and said:

(a) at the first court hearing, the Court should generally confine itself to ensuring that certain procedural and substantive requirements are met (for example, that there will be adequate disclosure), with limited consideration of issues of fairness; and

(b) the Court should only consider the merits or fairness of a proposed scheme at the convening hearing if the issue would “unquestionably” lead to a refusal to approve the scheme at the approval hearing. Put another way, the scheme must appear on its face “so blatantly unfair or otherwise inappropriate that it should be stopped in its tracks before going any further”.

That test has been cited and applied often, including in relation to transactions that (like the present) have concerned both a share scheme and an option scheme: see eg Re Spicers Limited [2019] FCA 731 at [15] (Anderson J); Re 86 400 Holdings Ltd [2021] FCA 311 at [6] (Anderson J); Re Huon Aquaculture Group Ltd [2021] FCA 1170 at [21] (O’Callaghan J).

54 In this case, there is no issue that would lead the Court to refuse to approve the proposed schemes at the second hearing. Nor is there anything to suggest that either of the schemes is on its face “so blatantly unfair or otherwise inappropriate that it should be stopped in its tracks before going any further”.

55 Thus, the Court must determine whether the procedural and substantive requirements for the calling and conduct of the meetings will be met. That requires the Court to be satisfied:

(a) first, that the schemes are fit for consideration by the proposed meetings in the sense that each scheme is “of such a nature and cast in such terms that, if [they] achieve the statutory majority at the [members’] meeting the court would be likely to approve [them] on the hearing of a petition which is unopposed”: FT Eastment & Sons Pty Ltd v Metal Roof Decking Supplies Pty Ltd (1977) 3 ACLR 69 at 72 (Street CJ); ASC v Marlborough Gold Mines Ltd (1993) 177 CLR 485 at 504 (the Court); Re Coles Group Ltd (2007) 25 ACLC 1380 at 1385-1386 [29]-[36] (Robson J); Re Sino Gold Mining Ltd (2009) 74 ACSR 647 at [10] (Lindgren J); Re Talison Lithium Limited [2012] FCA 1422 at [7] (Siopis J); Re Coventry Resources Ltd [2012] FCA 1252 at [9], [38] (Barker J); Re Xplore Wealth at [24] (Markovic J); and

(b) second, that “the members [are to be] properly informed as to the nature of the scheme[s] before the scheme meeting[s]”: Re NRMA Ltd at 605 [30]. See also Re Foundation Healthcare, at 263 [38]; Re Talison Lithium Limited [2012] FCA 1422 at [7] (Siopis J); Re Xplore Wealth at [23] (Markovic J).

Applying the principles

Schemes are fit for consideration

56 The question of whether to accept particular consideration for their shares or options is a commercial matter for SMX’s members and option-holders to assess. They ought not to be prevented from having the opportunity to do so, provided the Court can be satisfied that they are “acting on sufficient information and with time to consider what they are voting about”: Re English Scottish and Australian Chartered Bank [1893] 3 Ch 385 at 409 (Lindley LJ), cited with approval in Re ACM Gold Ltd (1992) 34 FCR 530 at 534 (O’Loughlin J) and applied in Re Coventry Resources Ltd [2012] FCA 1252 at [9] (Barker J); Re Anatolia Energy Limited [2015] FCA 1134 at [8] (McKerracher J); Re Tronox Ltd (2019) 135 ACSR 343 at [101] (O’Callaghan J).

57 In that context, it is relevant that the draft scheme booklet contains:

(a) an independent expert’s report stating that (in the absence of any other information or a superior proposal) the proposed transaction is fair and reasonable, and in the best interests of shareholders and option-holders;

(b) a recommendation from all SMX’s directors that members and option-holders vote in favour of the relevant scheme (in the absence of a superior proposal and subject to the independent expert continuing to conclude the schemes are in the best interests of SMX members and option-holders); and

(c) a statement that all SMX’s directors intend to vote their own shares and options in favour of the schemes (subject to the same qualifications about any superior proposal or any change in the independent expert’s view).

58 ASIC has suggested, and SMX has agreed, that SMX should provide an updated report from the independent expert in time for the shareholders and option-holders to consider it before their respective scheme meetings. The independent expert, Mr Goldman, has been engaged to prepare the updated report, which he expects will be ready by 20 January 2023.

59 The Court will scrutinise the terms of a scheme to satisfy itself that there is no element of unfairness that would be likely to preclude its approval: Re Amcor Limited [2019] FCA 346 at [50] (Beach J); Re Tronox Ltd (2019) 135 ACSR 343 at [103] (O’Callaghan J). In that regard, SMX raises the following features of the proposed scheme for the Court’s attention:

(a) reduction of capital;

(b) class issues;

(c) waivers by ASX and ASIC;

(d) equity incentives and convertible notes;

(e) the interests of Messrs Alon and Hofland (directors of SMX);

(f) performance risk;

(g) the deemed warranty by SMX’s members and option-holders;

(h) exclusivity provisions;

(i) the “Lionheart break fee” and “SMX break fee”;

(j) date of the scheme meetings; and

(k) the purpose of the schemes (i.e. not to avoid Chapter 6 of the Act).

60 For the reasons discussed below, none of these matters is unusual nor provides a reason for the Court to refrain from making an order convening the scheme meetings.

Reduction of capital

61 It is not unusual for a scheme of arrangement to be accompanied by a reduction of capital: see for example Re Humm Group Ltd [2022] FCA 614, Re Virtus Health Ltd [2022] NSWSC 597, Re Publishing and Broadcasting Ltd [2007] FCA 1610, Re Tiger Investment Company (1999) 33 ACSR 438, Re Watermark Market Neutral Fund Limited [2019] FCA 315, Re Wesfarmers Ltd; Ex parte Wesfarmers Ltd [2018] WASC 308. A reduction of capital is common in demerger schemes (where shares in the demerged entity are distributed to shareholders - see: Re Wesfarmers Ltd; Ex parte Wesfarmers Ltd [2018] WASC 308 and the cases cited at [37]) but also under cancellation schemes, where a reduction of capital can be used to effect a change of control transaction. Further, a “top-hatting” structure can involve a capital reduction. As Renard and Santamaria explain in Takeovers & Reconstructions in Australia (online edition, at [1303]):

A members’ scheme of arrangement may involve the incorporation of a new company, its acquisition of shares in an existing company, the cancellation of all existing shares in that company so that the old company becomes a wholly-owned subsidiary of the new company, and the issue of shares by the new company to the shareholders of the old company so that the proprietors of the old company become proprietors of the new (this type of transaction is commonly known as a “top-hatting” structure). The cancellation of shares in the old company is a reduction of capital. Many different forms of members’ schemes of arrangement have been approved over the years which provide for the cancellation of shares without the repayment of any capital whatsoever.

62 The schemes in this case are predicated on a reduction of SMX’s capital. The reduction will be an equal reduction, in that it relates only to ordinary shares in SMX, applies to each holder of ordinary shares in proportion to the number of ordinary shares they hold, and the terms of the reduction are the same for each holder of ordinary shares: see s 256B of the Act. An equal reduction must be approved by a resolution passed at a general meeting of the company: s 256C(1) of the Act.

63 SMX has convened such a meeting to be held on 1 February 2023.

64 At present, Empatan does not hold any shares in SMX, and will not hold any until the schemes are implemented. Further, the structure of the transaction means that, for an instant in time, SMX will have no shares on issue (i.e. after its shares are cancelled and before a share in it is issued to Empatan).

65 The issue arose in Re Watermark Market Neutral Fund Limited [2019] FCA 315, which involved a scheme of arrangement under which the assets of a listed company (WMK) would be transferred to a managed investment scheme, its capital reduced to zero and all its shares cancelled (followed immediately by the issue of one share in WMK to another company) and the issue of units in the managed investment scheme to WMK’s members. The Court (Yates J) was untroubled that, for a moment, WMK would have no share capital, saying (at [16]).

The capital reduction resolution contemplates the momentary reduction of the share capital to zero and the cancellation of all issued shares. Clause 4.2(r) of the scheme implementation deed then contemplates the issue of a share to the fund manager. This means that for a moment of time the scheme company is without capital. This is within existing authority: Re MB Group plc [1989] BCLC 672 at 680 per Harman J; Re Anglo American Insurance Co Ltd [1991] BCLC 564 per Harman J; Re Northern Engineering Industries plc [1994] 2 BCLC 704 at 709 per Millett LJ (Leggatt and Neill LJJ agreeing); Re Watermark Market Neutral Fund Ltd [2019] FCA 315 at [16] per Yates J.

Class issues

66 The schemes in this case do not raise any class issues. As Markovic J stated in Re Xplore Wealth (a case that also involved a share scheme and an option scheme) at [35]:

The test for whether separate classes are required involves three questions: what are the rights which existing members or creditors have against the company and to what extent are they different; to what extent are those rights differently affected by the proposed scheme; and does the difference in rights or different treatment of rights make it impossible for the members or creditors in question to consider the scheme as one class: see First Pacific Advisors LLC v Boart Longyear Ltd [2017] NSWCA 116; (2017) 121 ACSR 136 (Boart Longyear) at [80].

Share Scheme

67 The rights attaching to the SMX options are not affected by the Share Scheme. Those rights are only affected by the Option Scheme.

68 Nor does the Share Scheme treat shareholders who also hold options any differently to how it affects the rights of shareholders who do not hold options. As Markovic J stated in Re Xplore Wealth Limited (at [37]):

Scheme Shareholders who also hold Scheme Options may have different commercial interests to those shareholders who do not. However, that circumstance is not class creating. The existence of different commercial interests which is likely to be the case for all Scheme Shareholders, each of whom will face their own unique commercial circumstances, does not of itself mean that the Scheme Shareholders are “so dissimilar as to make it impossible for them to consult together with a view to their common interest”: Sovereign Life Assurance Company v Dodd [1892] 2 QB 573 at 583; Re Nine Entertainment Group Ltd (No 1) (2012) 211 FCR 439 at [53]; see also Boart Longyear at [78]-[83].

Option Scheme

69 The Option Scheme does not affect rights attaching to shares in SMX. Only the Share Scheme affects SMX shares, and the “Scheme Shares” it affects are the SMX Shares on issue as at the “Record Date” (which is two business days after the Share Scheme becomes effective, or such other business day as is agreed).

70 The Share Scheme does not provide any additional incentive or benefits to option-holders who also hold shares in SMX. The number of Empatan shares that will be issued to SMX’s shareholders and option-holders will be in ratio to the number of SMX shares they hold, and the formula for calculating the ratio is identical for both schemes.

71 It is true that the number of SMX shares to be issued to option-holders will be determined under the Option Scheme, specifically, by the value of their options. It is also true that SMX options have been issued in tranches and have different expiry dates and exercise prices.

72 But neither matter is class-creating because, first, all the options are “out of the money” and second, they will all be valued the same way (using the Black Scholes Model). Again, Markovic J’s approach in Re Xplore Wealth is illustrative. Her Honour stated (at [40]):

Here, there is no difference in the manner in which the options have been valued. Rather, the same methodology has been used for all options, the “Black-Scholes option pricing model”, which takes into account the particular characteristics of each tranche of options. Accordingly, community of interest is not lost and separate classes are not required. The same conclusion was reached by Barker J in Coventry Resources Limited, in the matter of Coventry Resources Limited [2012] FCA 1252 at [23] where his Honour said:

Notwithstanding different characteristics of the options in terms of exercise price and expiry, the experts have used a consistent and indiscriminate application of the same pricing or valuation methodology for all the options. Consequently, notwithstanding the different characteristics of the options, there is sufficient community of interest between optionholders so that it is appropriate that a single meeting of all optionholders be convened: Re MIA Group at [14]; Warwick Resources Limited, in the matter of Warwick Resources Limited [2009] FCA 1231 (Re Warwick Resources Limited) at [9] (Siopis J); Re Sino Gold Mining Ltd (ACN 093 518 579) [2009] FCA 1277; (2009) 74 ACSR 647 at [40]-[58] (Lindgren J).

Waivers by ASX and ASIC

ASX

73 Listing Rule 6.23.2 provides that a change that has the effect of cancelling an option for consideration can only be made if holders of ordinary securities approve the change.

74 By letter dated 17 August 2022, SMX sought a waiver of this rule in respect of the Option Scheme (if ASX determined that Listing Rule 6.23.2 applied for the implementation of the Option Scheme), the cancellation of the ESOP Options, the cancellation of the Legacy Performance Options, and the conversion of the Convertible Notes.

75 On 3 January 2023, ASX granted a waiver of:

(a) Listing Rule 6.23.2 to permit SMX, without shareholder approval, to cancel for consideration the ESOP Options and the Legacy Performance Options; and

(b) Listing Rule 6.23.4 to permit, without shareholder approval, amendment of the terms of the SMX options to permit their cashless exercise,

subject to conditions as to details of scheme booklet, as well as the approval of the schemes by SMX’s shareholders and option-holders and by the Court.

ASIC

76 Regulation 5.1.01 of the Corporations Regulations requires that, unless ASIC allows otherwise, the explanatory statement for:

(a) a proposed scheme of arrangement between a company and its creditors (or a class of its creditors) must contain all matters set out in Part 2 of Schedule 8 of the Corporations Regulations; and

(b) a proposed scheme of arrangement between a company and its members must contain all matters set out in Part 3 of Schedule 8.

77 SMX requested that ASIC waive the requirements of:

(a) paragraphs 8201 and 8203 of Part 2 of Schedule 8, which require the scheme booklet to set out various matters in connection with the Option Scheme, including the names of all option-holders; and

(b) paragraph 8302(h) (which requires that the explanatory statement set out whether, within the knowledge of SMX’s directors, its financial position has materially changed since the date of the last balance sheet laid before an annual general meeting or sent to SMX shareholders and option-holders and if so, full particulars of any change) and paragraph 8305 (which requires ASIC’s consent to the inclusion in the explanatory statement of a report that contains a statement about the market value of an asset or assets of the company that differs from the amount shown in the books of the company) of Part 3 of Schedule 8.

Equity, options and convertible notes

78 As at the “Last Practicable Date”, SMX had 167,854,581 ordinary shares on issue, held by approximately 850 shareholders. Additionally, it has the following options and convertible notes on issue:

(a) 32,422,957 options (excluding those issued under the ESOP and the Legacy Performance Options);

(b) 13,410,782 options issued under the ESOP;

(c) 10,000,000 Legacy Performance Options; and

(d) AUD 828,240 worth of convertible notes.

79 On the implementation of the schemes:

(a) the options will be deemed to have been exercised on a cashless basis in exchange for SMX shares, resulting in the issue of an estimated further 24,715,584 ordinary shares, which will be cancelled;

(b) each ESOP option will be cancelled in consideration for one new option in Empatan on fundamentally the same terms, except for a change in the exercise price to reflect the price uplift associated with the transaction;

(c) the Legacy Performance Options will be cancelled for nominal consideration; and

(d) the convertible notes will be cancelled in exchange for the issue of 1,000,000 ordinary shares that will participate in the Share Scheme.

80 As a result of the foregoing, SMX is expected to have 193,570,165 shares on issue at the “Record Date”:

81 All these matters are disclosed in the draft scheme booklet. Aside from the interests of SMX directors (dealt with below), they do not raise any issues for the Court’s consideration. Nor do they create any separate class of participants in the Share Scheme. This is because, as I previously stated in Re iSelect Ltd:

courts have consistently held that members (including directors) with existing performance rights or options which are to be cancelled in return for a cash payment or converted into shares which will participate in the Scheme do not constitute a separate class for the purposes of voting on the Scheme…

Interests of SMX directors

82 SMX’s directors have unanimously recommended that members and option-holders vote in favour of the schemes. Given that the directors themselves have interests in SMX shares and options, their recommendation might be regarded as being influenced by their personal interests.

83 Although differing views have been expressed (in Re Japara Healthcare Ltd (2021) 156 ACSR 695, [2021] FCA 1150 at [71], Moshinsky J explained the differing approaches and identified the principal cases), the courts’ consistent approach is that ordinarily it will be appropriate for a director who is to receive a financial benefit to make a recommendation, provided the benefit is disclosed in the scheme booklet. As O’Callaghan J explained in Re Huon Aquaculture Group Ltd [2021] FCA 1170 at [35]:

Shareholders would ordinarily expect directors to make a recommendation, even when that stand to gain a substantial financial benefit. As Robson J said in Re SMS Management & Technology Ltd [2017] VSC 257 (at [26]), “I think it is important that the managing director, who in this case is the main moving force behind the company, give his reasons for putting forward the scheme”. See generally Re Kidman Resources Ltd [2019] FCA 1226; (2019) 375 ALR 760 at 778 –782 [99]–[115]; Re Villa World Ltd [2019] NSWSC 1207; (2019) 139 ACSR 550 at [38]–[40] ; Re GBST Holdings Ltd [2019] NSWSC 1280 at [24] –[30]; and Re ERM Power Ltd [2019] NSWSC 1502 at [16] –[18] . The question is, rather, one of disclosure. Here, the relevant performance rights and the special dividend are fully disclosed in the acquisition booklet.

84 In respect of the recommendation by SMX’s directors, the chairman’s letter and section 5.13 of the draft scheme booklet disclose important information about the directors’ interests. Most notably, they disclose that:

(a) if the Schemes, Capital Reduction and Business Combination are implemented:

(i) Mr Hofland’s 167,000 SMX ESOP Options with an exercise price of $0.70 and expiry date of 15 August 2026 will be cancelled and Mr Hofland will receive one new option in Empatan (New ESOP Option) with a new exercise price of US$5.12;

(ii) Mr Hofland will retire as a director of SMX and will be entitled to receive a termination payment equal to ILS264,000 (approximately US$79,332);

(iii) Mr Hofland will be entitled to receive, prior to his retirement an increase of his base remuneration to ILS22,000 per month (ILS264,000 per year, equating to approximately US$79,332 per year);

(iv) Mr Alon’s 5,135,949 SMX Shares will be converted to 496,275 Empatan shares with an expected valuation of US$4.96million;

(v) Mr Alon’s 500,000 SMX ESOP Options with an exercise price of $0.70 and expiry date of 15 August 2026 will be cancelled and Mr Alon will receive 1 New ESOP Option with a new exercise price of US$5.12. The benefit raised from the conversion of the options amounts to US$235,771; and

(vi) Mr Alon will be employed by Empatan as the Chief Executive Officer and an executive director and will be entitled to receive as compensations as Chief Executive Officer of ILS 960,000 per annum (approximately US$295,000 per annum);

(b) in light of the importance of the schemes, and their respective roles at SMX (chief executive officer and executive chairman) and in facilitating the proposed transaction, each of Messrs Alon and Hofland considered it appropriate that they make a recommendation on the schemes.

85 To the extent that the issue is fact sensitive (see eg Re ThinkSmart Ltd [2022] FCA 1314 at [52], and the cases there cited: Re Mod Resources Ltd [2019] WASC 326 at [86] (Vaughan J); Re Wellcome Group Ltd [2019] FCA 1655 at [59] (O’Bryan J)), there are no unusual facts in that case that would make that approach inappropriate.

86 Accordingly, it was appropriate that Messrs Alon and Hofland made recommendations.

Performance risk

87 In considering whether to approve a scheme involving the participation of a person other than the plaintiff company and its members or creditors, the Court is concerned to ensure that the other party is bound to perform its assigned role and that its obligations are capable of enforcement. This is because the other party’s obligations do not depend upon s 411, which is confined to the obligations of the company and its members. Courts have therefore considered the issue of “performance risk” concerning the obligations of the non-scheme party: see for example Re Coles Group Ltd (2007) 25 ACLC 1380 at 1386 [38]; Re Lonsdale Financial Group Ltd [2007] VSC 394 at [42]; Re KAZ Group Ltd [2004] FCA 738 at [4]-[5]; Re Healthscope Ltd [2010] VSC 367 at [31]-[32]; Re Mitchell Communication Group [2010] VSC 423 at [30]-[31]; Re AWB Ltd [2010] VSC 456 at [16]; and Re AXA Asia Pacific Holdings Ltd [2011] VSC 4 at [21]-[25].

88 In Re Anatolia Energy Ltd [2015] FCA 1134 at [31]-[34], (with reference to Re APN News & Media Ltd (2007) 62 ACSR 400 at [23] (Lindgren J)), McKerracher J considered the issue in the context of a merger with a NASDAQ listed company registered in Delaware, where the scheme consideration comprised the issue of shares and options by the acquiring entity. The performance risk was “not unacceptable” because the sequence of events required the acquirer to issue the scheme consideration before it received the target shares. Similarly, in Re Coventry Resources Ltd [2012] FCA 1252 at [46]-[48] (Barker J), (with reference to Re APN News & Media Ltd (2007) 62 ACSR 400 at [23] (Lindgren J)), where the scheme consideration involved the issue of shares and options in a company incorporated in British Columbia Canada, Barker J held that there was no significant performance risk because the consideration had to be provided before the target shares were transferred.

89 In this case, the proposed schemes entail the same protective sequence. Specifically:

(a) as soon as the schemes become effective, Empatan must apply for its shares to be listed on NASDAQ;

(b) the operative steps in each scheme (i.e. the capital reduction and share cancellation and issue of Empatan shares under the Share Scheme; and the cashless exercise and issue of SMX shares, and the capital reduction and share cancellation and issue of Empatan shares under the Option Scheme) is subject to completion of the merger of Lionheart and Empatan);

(c) SMX’s obligation to issue a share to Empatan is subject to the completion of those operative steps; and

(d) the scheme consideration (namely shares in Empatan) is provided, and the merger must be in effect, before any SMX options are deemed to have been exercised and before any SMX share is cancelled.

90 By reason of the deeds poll, Empatan and Lionheart are bound to perform the roles assigned to them, and their obligations are capable of enforcement. In particular, if the schemes become effective:

(a) Empatan covenants in favour of each participant in each scheme to comply with the scheme as if it were a party to the scheme and to issue the scheme consideration; and

(b) Lionheart covenants in favour of each participant in each scheme to comply with the scheme as if it were a party to the scheme and to procure the filing of the certificate of merger with the Secretary of State of Delaware, and not withdrawing the certificate, so that the merger is effective.

Deemed warranty provisions

91 Clause 7.9(a) of the Share Scheme provides that each Scheme Participant is taken to have warranted to Empatan that:

(a) all of their Scheme Shares will, at the date of their cancellation, be fully paid and free from encumbrances and interests of third parties and from any restrictions on cancellation; and

(b) they have no existing right to be issued any shares, options, performance rights, convertible notes or other SMX securities other than in accordance with the Option Scheme.

92 Similarly, clause 7.8(a) of the Option Scheme provides that each Option Scheme Participant is taken to have warranted to Empatan that:

(a) all of their Scheme Options will, at the date of their exercise, be free from encumbrances and interests of third parties and from any restrictions on cancellation; and

(b) they have no existing right to be issued any shares, options, performance rights, convertible notes or other SMX securities other than in accordance with the Option Scheme.

93 Deemed warranties are common in schemes of arrangement and will be acceptable if sufficiently disclosed in the explanatory statement: Re Kidman Resources Ltd (2019) 139 ACSR 122 at [70] (O’Callaghan J) (Re Kidman Resources): see eg Re Hostworks Group Ltd (2008) 26 ACLC 137; Re Macquarie Private Capital A Ltd (2008) 26 ACLC 366; Re Dyno Nobel Ltd [2008] VSC 154. In Re Biosceptre International Limited [2013] FCA 1429 at [22], the Court noted that:

The prevailing view is that such provisions are not objectionable provided that the attention of members has been drawn to them: see, for example, Re APN News & Media Ltd (2007) 62 ACSR 400 [at [57]-[63]; Re Sino Gold Mining Ltd (ACN 093 518 579) (2009) 74 ACSR 647 at [29]-[31]. Here, the deemed warranty has been specifically and clearly drawn to the attention of members in the Scheme Booklet.

94 The draft scheme booklet sets out the deemed warranties in sections 11.20 (“Warranties by Scheme Participants”) and 12.13 (“Warranties by Option Scheme Participants”).

Exclusivity arrangements

Provisions of the SID

95 Under clause 10 of the SID (headed “Exclusivity”), each of SMX and Lionheart have:

(a) represented and warranted that it is not in any current negotiations or discussions with any person in respect of any “Lionheart Competing Transaction” (in respect of Lionheart) or a “SMX Competing Transaction” (in respect of SMX), and it has ceased any existing negotiations or discussions, in respect of any such transaction (termination of existing discussions clause) (clause 10.1);

(b) agreed that, during the Exclusivity Period, it will abide by a “no shop restriction” (set out in clause 10.2);

(c) agreed that, during the Exclusivity Period and subject to a fiduciary exemption that is set out in clause 10.5, it will abide by a “no talk restriction” (set out in clause 10.3); and

(d) agreed that, during the Exclusivity Period, and subject to a fiduciary exemption that is set out in clause 10.5, it will abide by a “no due diligence restriction” (set out in clause 10.4).

96 The “Exclusivity Period” is until the earliest of the termination of the SID, or the Implementation Date of the Scheme.

97 Each of SMX and Lionheart has also agreed that, during the Exclusivity Period, it will notify the other party if it becomes aware of any actual, proposed or potential bona fide “Lionheart Competing Transaction” (in respect of Lionheart) or a “SMX Competing Transaction” (in respect of SMX) (notification requirement) (clause 10.7). Such notice must include all material details including the identity of the person making the relevant proposal, material terms including price, and the nature of information requested or provided. SMX is also required, during the Exclusivity Period, to provide Lionheart with a copy or written statement of information provided to the person proposing a SMX Competing Transaction that differs from the information provided to Lionheart and keep Lionheart reasonably informed of material developments.

98 Finally, SMX has agreed that, during the Exclusivity Period, it will give Lionheart a repeatable matching right in respect of competing proposals (matching right) (clause 10.8).

99 The “no talk restriction” and “no due diligence restriction” are subject to clause 10.5 (fiduciary exemption), so that (provided there is no breach of the termination of the “no shop restriction”, “no talk restriction” or the “no due diligence restriction”), those restrictions do not prohibit or require any action by SMX in relation to a SMX Competing Transaction if SMX’s board determines, acting in good faith, that:

(a) after consultation with its advisers, the SMX Competing Transaction is an “SMX Superior Proposal” or could reasonably be expected to become an SMX Superior Proposal; and

(b) after receiving legal advice, failing to respond to the SMX Competing Transaction would or would be reasonably likely to constitute a breach of any of the fiduciary or statutory duties of the members of SMX’s board.

Principles

100 In Re Anatolia Energy Limited [2015] FCA 1134 at [42] (which also concerned a share scheme and an options scheme), McKerracher J noted that exclusivity restrictions are “customary”, and in Re Kidman Resources, O’Callaghan J noted that exclusivity restrictions have been accepted in many schemes of arrangement. In Re Verdant Minerals Ltd [2019] FCA 556 at [50], Moshinsky J identified the following general principles to have emerged from the cases:

(a) the exclusivity period should be a reasonable period and capable of precise ascertainment;

(b) there should be fiduciary carve-outs in respect of no-talk and no due diligence arrangements;

(c) the exclusivity arrangements and their effect should be adequately disclosed in the scheme booklet; and

(d) it is desirable that the scheme proponents tender evidence directed to showing that the exclusivity provisions are the result of a normal commercial negotiation.

101 In this case, those principles are satisfied:

(a) The exclusivity period is reasonable and ascertainable, and defined.

(b) The “no talk” and “no due diligence” restrictions are subject to the fiduciary exemption.

(c) The exclusivity provisions are disclosed in the draft scheme booklet: see sections 1.6 (“Exclusivity and competing proposals”) and 4.5 (“Other Relevant Considerations … (a) Exclusivity and competing proposals… (b) No-shop … (c) No-talk … (d) Lionheart matching right”), as well as in section 2 (“Questions and answers”).

(d) Mr Alon’s evidence is that the exclusivity and break fee provisions (discussed further below) were the outcome of commercial negotiations between SMX and Lionheart, in which both parties were assisted by external legal and financial advisers. As Mr Alon has explained, SMX determined that the exclusivity and break fee provisions were commercially appropriate. Mr Alon gave evidence that those terms were negotiated – and required – by Lionheart. The evidence of Lionheart is expected to be to similar effect.

102 Thus, the exclusivity provisions do not prevent the Court from making the convening order.

Break fee and reverse break fee

103 Clause 11 of the SID provides that, in specific circumstances, SMX will pay Lionheart a break fee of US$2,000,000. That amount reflects approximately 0.68% of the equity value of SMX based on the scheme consideration. The circumstances are summarised in section 11.15 (“Break Fee”) of the draft scheme booklet.

104 Clause 12 of the SID provides an equivalent “reverse break fee”, payable by Lionheart to SMX in the same amount.

105 The SID records the parties’ agreement that the respective break fees are to compensate them for advisory costs, costs of management and directors’ time, out of pocket expenses, reputational damage associated with a failed transaction, and reasonable opportunity costs: clauses 11.2(a) and 12.2(a). Further, they agree that those costs are of a nature that cannot be accurately quantified, and that the break fee is a genuine and reasonable estimate of their amount: clauses 11.2(b) and (c) and 12.2(b) and (c).

106 The payment of such an amount, often referred to as a “break fee” or “termination fee”, is a common feature of commercial transactions like the proposed schemes. As O’Bryan J explained in Re DuluxGroup Ltd (2019) 136 ACSR at [31] (Re DuluxGroup Ltd), “In general terms, the courts and the Takeovers Panel accept that break fees can be justified by reference to the costs incurred by the offeror and the benefit that an offer may confer on the members of the target company by increasing its value.” But his Honour also observed that such fees may adversely affect shareholders’ interests “if the amount of the fee is such that it is likely to coerce shareholders into agreeing to a scheme or to deter the making of a competing offer for the company’s shares”.

107 In a case cited by O’Bryan J (Re APN News & Media Ltd (2007) 62 ACSR 400 at 409 [44]), Lindgren J said that:

Break fees are justified by reference to:

• the costs incurred by the offeror company;

• the benefit that that company confers on the members of the target company by increasing its value; and

• the desirability, from the viewpoint of those members, that takeover offers be made to them.

108 Justice O’Bryan also highlighted that, in its current guidance note (“Guidance Note 7 – Lock Up Devices” (11 February 2010)), the Takeovers Panel states that, in the absence of other factors, a break fee not exceeding 1% of the equity value of the target is generally not unacceptable: “Guidance Note 7 – Lock Up Devices” (Issue 4, 11 February 2010).

109 Here, the break fee does not represent a barrier to the convening of the meetings to consider the schemes. The evidence shows that:

(a) the amount of the break fee and the obligations to pay it were the subject of commercial negotiation between the parties; and

(b) SMX considered that it was in the member’s best interests that the SID, including the break fee, be executed.

110 Further, the break fee is not payable merely if SMX’s members reject the Share Scheme or if option-holders reject the Option Scheme – but only if SMX or its directors take particular actions. Thus, the fee is not capable of influencing SMX’s members in deciding whether to accept or reject the Scheme.

111 Finally, apart from the size of the fee, relevant provisions of the SID are consistent with the guidelines published by the Takeovers Panel: Takeovers Panel, Guidance Note 7 at [9], namely, that in the absence of other factors, reasonable triggers for the payment of the fee might include (a) a change of directors’ recommendation or (b) a competing transaction that successfully completes.

112 The plaintiff’s submissions, noted recent correspondence with ASIC, in which ASIC appeared to take a different view of the break fee:

However, we note that the break fee appears to have been calculated based on an agreed pre-transaction valuation amount of US$200 million, which is significantly higher than the [independent expert report] assessment which suggests the Lionheart Break Fee reflects around 5 to 8% of SMX’s equity value.

While you say the break fee is reciprocal and represents less than 1% of Lionheart’s value, that is not Australian market practice and may have coercive effects on target shareholders in voting on the scheme.

ASIC considers that SMX should address the Lionheart Break Fee in their submissions to ensure the Court is informed of the matter.

113 The plaintiff submitted that ASIC has not specified how the break fee does not reflect “Australian market practice” or how it “may have coercive effects on target shareholders in voting on the scheme”. Nor has ASIC referred to any of the matters (identified in the guidance note, paragraph [9]) to which the Takeovers Panel will have regard in considering whether a break fee gives rise to unacceptable circumstances. Those include: whether the fee is fixed or capped (either in dollar or percentage terms) (which the fee here is); whether the fee (on a cost per share basis) is less than the premium under the bid (which the fee in this case is); the cost, effort or risk involved in making the proposal (about which Mr Alon has given evidence in the first Alon affidavit); and whether the fee reimburses actual expenses (also addressed in the first Alon affidavit).

114 Courts have not generally regarded the fact that a break fee exceeds the 1% guideline as a reason to refuse to make an order convening a scheme meeting. For example, in Re DuluxGroup Ltd, O’Bryan J (at [31]) observed that the 1% guideline is not decisive and that courts have ordered a meeting to consider a scheme notwithstanding a break fee exceeding that level (referring to Re Cytopia Ltd [2009] VSC 560 at [12]-[18] (where the fee of $500,000 was approximately 4.57% of the equity value of the target).

Date of the scheme meetings

115 SMX seeks for the scheme meetings to be held on 1 February 2023 – the same day as the general meeting that will consider the capital reduction resolution. There are obvious advantages to having the meetings on the same day.

116 A listed company is required to give at least 28 days’ notice of a general meeting: 249HA of the Act. For that reason, SMX has already sent the notice of meeting for the general meeting. But convening the scheme meetings for 1 February 2023 will mean that the shareholders and option-holders will not get 21 days' notice. This raises two issues:

(a) first, whether the Court has the power to order that a meeting be convened on less than 21 days’ notice;

(b) second, whether the Court should do so in this case.

117 The Court has power to order a scheme meeting on shorter notice. Rule 3.3(2) of the Rules provides (emphasis added):

Unless the Court otherwise orders, a meeting of members ordered under section 411 of [the Act] must be convened, held and conducted in accordance with:

(a) the provisions of Part 2G.2 of [the Act] that apply to the members of a company; and

(b) the provisions of the plaintiff's constitution that apply in relation to meetings of members and are not inconsistent with Part 2G.2 of [the Act].

Section 249HA is a provision within Part 2G.2 of the Act. As Rule 3.3(2) makes plain, the Court can “otherwise order”.

118 Further, s 1319 of the Act provides:

Where, under this Act, the Court orders a meeting to be convened, the Court may, subject to this Act, give such directions with respect to the convening, holding or conduct of the meeting, and such ancillary or consequential directions in relation to the meeting, as it thinks fit.

119 The scheme meetings will be convened by the Court’s order. Accordingly, the Court can make such orders in relation to the meeting as it sees fit. In Re Equigold NL (No 2) [2008] FCA 826 (Re Equigold), Emmett J (as his Honour then was) relied on these provisions to amend a convening order, which provided for 28 days’ notice, to shorten the period to 24 days after unanticipated difficulties with the printing process delayed the dispatch of the scheme materials. Re Equigold appears to be the only case to have used the provisions.

120 There is also authority that, absent exceptional circumstances, in the usual case, the Court is unlikely to exercise the power to reduce the notice period in the case of a widely-held target company: Re Adelaide Air Conditioning & Domestic Engineers Ltd (In Liq); Re South Pacific Transport Pty Ltd (1972) 6 SASR 603 at 605.

121 By way of contrast, in England, the question of adequate notice for a scheme meeting is made on a case-by-case basis, and a rule-of-thumb of 21 days’ notice has emerged: see Re Cardtronics Plc [2021] EWHC 1617 (Ch) at [8] (Norris J). Further, in the case of creditors, schemes of arrangement, s 75-20(1) of the Insolvency Practice Rules (Corporations) 2016 (Cth) prescribes a minimum notice period of 10 business days. However, the practice has been to give creditors a longer notice period, although no clear rule has emerged, and the period can depend (amongst other things) on the urgency of the restructuring in question, the complexity of the scheme, and the sophistication of the creditors involved: see generally Damien and Rich, Schemes, Takeovers and Himalayan Peaks (4th ed, 2021) at 4.3.2 (pages 241–243).

122 In the circumstances of this case, there are good reasons for convening the meetings on shorter than 28 days’ notice. First, the schemes were first announced in July 2022, so are unlikely to come as any surprise to SMX’s shareholders or option-holders. Second, the schemes – and the prospect of the scheme meetings – were foreshadowed in the notice for the general meeting that has already been sent to shareholders. Third, there is some urgency to the timetable in that, as Dr Prawer explained in the first Prawer affidavit, Lionheart’s fixed term has expired and, although monthly extensions are available, each comes with a significant cost, including a requirement for a direct payment by the SPAC founders of US$412,500 plus associated deal costs.

Section 411(17)

123 The Court’s jurisdiction to approve a scheme is restricted by s 411(17) of the Act (although that affects the Court’s discretion to approve a scheme, rather than order a meeting: Re Macquarie Private Capital A Ltd (2008) 26 ACLC 366 at 370 [27] (Barrett J); Re Verdant Minerals Ltd [2019] FCA 556 at [72] (Moshinsky J)).

124 At the approval stage, the Court must be satisfied there is no proscribed purpose (as described in s 411(17)(a)) or there must be a statement in writing by ASIC that it has no objection to the arrangement (see s 411(17)(b)): see Re Coles Group Ltd (No 2) (2007) 65 ACSR 494 at 497 [16] – 499 [24]. Such a statement will not be provided until the second court hearing: see ASIC, Regulatory Guide 60 (September 2020) at [60.109].