Federal Court of Australia

Clarence City Council v Commonwealth of Australia [2022] FCA 1492

ORDERS

Applicant | ||

AND: | First Respondent HOBART INTERNATIONAL AIRPORT PTY LTD (ACN 080 919 777) Second Respondent | |

AND BETWEEN: | HOBART INTERNATIONAL AIRPORT PTY LTD Cross-Claimant | |

AND: | Cross-Respondent | |

AND

TAD 27 of 2018 | ||

| ||

BETWEEN: | NORTHERN MIDLANDS COUNCIL Applicant | |

AND: | THE COMMONWEALTH OF AUSTRALIA First Respondent AUSTRALIA PACIFIC AIRPORTS (LAUNCESTON) PTY LTD (ACN 081 578 903) Second Respondent | |

AND BETWEEN: | AUSTRALIA PACIFIC AIRPORTS (LAUNCESTON) PTY LTD (ACN 081 578 903) Cross-Claimant | |

AND: | THE COMMONWEALTH OF AUSTRALIA Cross-Respondent | |

order made by: | O’CALLAGHAN J |

DATE OF ORDER: | 13 DECEMBER 2022 |

THE COURT ORDERS THAT:

1. The applicant’s proceeding be dismissed.

2. The second respondent’s cross-claim be dismissed.

3. The parties file submissions on costs, not exceeding 5 pages, within 21 days.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011..

O’CALLAGHAN J:

Introduction

1 These two proceedings principally concern questions regarding the proper construction of a clause contained in leases entered into in 1998 (the leases) between the Commonwealth as lessor, and the lessees of Hobart International Airport (Hobart Airport) and Launceston Airport (collectively, the Airports or Airport Sites), being Hobart International Airport Pty Ltd (HIAPL) and Australia Pacific Airports (Launceston) Pty Ltd (APAL) respectively (collectively, the lessees), the second respondent in each proceeding.

2 The applicants (collectively, the Councils) are Councils for municipal areas in Tasmania.

3 The applicant in proceeding TAD 25 of 2018 (the Hobart proceeding), Clarence City Council, administers a municipal area covering the eastern suburbs of Hobart and surrounding localities, including Hobart Airport.

4 The applicant in proceeding TAD 27 of 2018 (the Launceston proceeding), Northern Midlands Council, administers a municipal area that extends from the south of Launceston to the central midlands, including Launceston Airport.

5 The Councils are not parties to the leases, but they seek to obtain declaratory relief in respect of their construction and application, in circumstances where the parties to the leases agree that the lessees have acted, and will continue to act, in accordance with their own understanding of the relevant terms of their contracts.

6 The lessees also brought cross-claims for declaratory relief against the Commonwealth (the first respondent in each proceeding), which raised hypothetical questions of accord and satisfaction, and estoppel. As will become apparent, the making of those claims made it necessary to set out in these reasons in some detail the terms of correspondence between the parties leading up to the commencement of the proceedings. The gist of the claims was the lessees’ contention that the Commonwealth, if those accord and satisfaction and estoppel claims were made good, would thereby be precluded from seeking to compel them to make further payment to the Councils under the leases, if the Commonwealth should ever change its mind and seek to do so – and that the Councils’ applications for declaratory relief should in turn therefore be dismissed as a matter of discretion.

7 I first heard these proceedings over a period of seven days in March and July 2019.

8 I ordered that the proceedings be dismissed, on the ground that the Councils had no standing to seek the declaratory relief they sought. See Clarence City Council v Commonwealth [2019] FCA 1568. I accordingly did not deal with any of the other issues raised in the proceedings.

9 The Councils successfully appealed that decision to the Full Court, which ordered that the proceedings be remitted to me for final determination. See Clarence City Council v Commonwealth (2020) 280 FCR 265 (Jagot, Kerr and Anderson JJ).

10 The lessees sought and obtained special leave to appeal to the High Court.

11 That appeal was, by majority, dismissed. See Hobart International Airport Pty Ltd v Clarence City Council [2022] HCA 5; (2022) 96 ALJR 234.

12 The proceedings were listed before me for further hearing upon the remittal on 19 and 20 September 2022.

Factual background

13 The Airports are on Commonwealth land, so they are not amenable to Council rates or State land tax. That is because s 114 of the Constitution prohibits States (without the consent of the Commonwealth Parliament) from imposing “any tax on property of any kind belonging to the Commonwealth”. The parties also agreed that the Airport Sites are “places acquired by the Commonwealth for public purposes”, such that State laws (including State taxation laws) have no application to them by operation of s 52(i) of the Constitution, which provides that the Commonwealth Parliament has exclusive power to make laws for the peace, order, and good government of the Commonwealth with respect to such places.

14 During the 1980s, most major airports were operated by the Federal Airports Corporation (the FAC) as “government business enterprises”. A long standing Government policy required the Commonwealth to make payments equivalent to rates to local authorities in certain circumstances. The FAC agreed to maintain the Commonwealth Government’s policy by making payments in lieu of rates for areas of federal airports which were used for commercial activities and for which the FAC received an annual rent.

Competition Principles Agreement

15 On 11 April 1995, the Commonwealth and the States and Territories entered into the “Competition Principles Agreement” (the CPA), which recorded the agreement of the Council of Australian Governments to adopt certain principles of competition policy and to apply competition laws across the public sector.

16 One of the overarching purposes of the CPA was to achieve and maintain consistent and complementary competition laws and policies which would apply to all businesses in Australia, regardless of ownership. One of the principles agreed to was the principle of “competitive neutrality”.

17 Clause 3 of the CPA was headed “Competitive Neutrality Policy and Principles”. It relevantly provided as follows:

(1) The objective of competitive neutrality policy is the elimination of resource allocation distortions arising out of public ownership of entities engaged in significant business activities: Government businesses should not enjoy any net competitive advantage simply as a result of their public sector ownership. These principles only apply to the business activities of publicly owned entities, not to the non-business, non-profit activities of these entities.

…

(4) Subject to subclause (6), for significant Government business enterprises which are classified as “Public Trading Enterprises” and “Public Financial Enterprises” under the Government Financial Statistics Classification:

(a) the Parties will, where appropriate, adopt a corporatisation model for these Government business enterprises … ; and

(b) the Parties will impose on the Government business enterprise:

(i) full Commonwealth, State and Territory taxes or tax equivalent systems;

…

(5) Subject to subclause (6), where an agency (other than an agency covered by subclause (4)) undertakes significant business activities as part of a broader range of functions, the Parties will, in respect of the business activities:

(a) where appropriate, implement the principles outlined in subclause (4); …

18 Clause 4(3) of the CPA, which was headed “Structural Reform of Public Monopolies”, provided as follows:

Before a Party introduces competition to a market traditionally supplied by a public monopoly, and before a Party privatises a public monopoly, it will undertake a review into:

(a) the appropriate commercial objectives for the public monopoly;

(b) the merits of separating any natural monopoly elements from potentially competitive elements of the public monopoly;

(c) the merits of separating potentially competitive elements of the public monopoly; …

19 The Airports were, at that time, “a public monopoly” within the meaning of that provision.

20 The principle of competitive neutrality underlying the CPA was further articulated in the Commonwealth Competitive Neutrality Policy Statement issued in June 1996. It explained that competitive neutrality required that “government business activities should not enjoy net competitive advantages over their private sector competitors simply by virtue of public sector ownership” and “where governments choose to provide services through market based mechanisms that allow actual or potential competition from a private sector provider, that competition should be fair”, and that the implementation of the principles was “intended to remove resource allocation distortions”.

The role of the FAC

21 Competitive neutrality applied to significant government business activities, including the business activities of the FAC. The FAC was a Commonwealth organisation “identified as conducting significant business activities” and was therefore required to make ex gratia payments in lieu of rates in the interests of competitive neutrality. As the FAC Policy Manual dated 10 November 1995 explained:

… in a letter addressed to the [FAC] in 1987, the then Minister for Transport and Communications indicated that it was a long standing Government policy that the Commonwealth make payments equivalent to rates to local authorities in certain circumstances. The Minister went on to say that it had always been the Government’s intention that this policy would continue to apply in relation to Federal Airports, and sought assurance that the [FAC] would continue to make such payments.

The [FAC] subsequently agreed to the continuation of making payments in lieu of rates for areas on airport which were used for commercial activities and for which the [FAC] received an annual rent.

22 The FAC was established by the Federal Airports Corporation Act 1986 (Cth). Section 6 of that Act provided that the FAC’s functions included:

(a) to operate Federal airports, and participate in the operation of jointly used areas, in Australia;

(aa) to establish airports at Federal airport development sites;

(b) to provide the Commonwealth, governments, local government bodies, and other persons, who operate, or propose to operate, airports or facilities relating to airports (including airports and facilities outside Australia) with consultancy and management services relating to the development and operation of those airports or facilities;

(ba) to assist the Commonwealth and other persons in connection with any or all of the following:

(i) the implementation of the Airports (Transitional) Act 1996;

(ii) preparatory work associated with the implementation of the Airports Act 1996;

(iii) matters relating to the leasing, or proposed leasing, of an airport (within the meaning of the Airports (Transitional) Act 1996) that was or is a Federal airport or a Federal airport development site, including matters relating to the transfer, or proposed transfer, of responsibility for such an airport to an airport-lessee company (within the meaning of the Airports (Transitional) Act 1996);

(c) other functions that:

(i) relate to airports or Federal airport development sites;

…

23 Section 7(2)(a) of the Federal Airports Corporation Act provided that the FAC “shall endeavour to perform its functions in a manner that … is in accordance with the policies of the Commonwealth Government”.

24 Section 8 was entitled “Extent of functions of Corporation” and provided that the functions of the FAC, among other things, extended to “carrying on commercial activities at, or in relation to, Federal airports (including carrying on such activities in co-operation, or as joint ventures, with other persons)”.

25 Section 56 was entitled “Aeronautical charges”. Sub-sections (9) and (10) provided:

(9) The following amounts may be recovered by the Corporation as debts due to the Corporation:

(a) an aeronautical charge that is due and payable under this Act; and

(b) an amount payable by way of penalty under subsection (8).

(10) An aeronautical charge shall not be fixed at an amount that exceeds the amount that is reasonably related to the expenses incurred or to be incurred by the Corporation in relation to the matters in respect of which the charge is payable and shall not be such as to amount to taxation.

26 Section 56(1) defined aeronautical charge to mean:

… a charge for, or in respect of:

(a) the use by an aircraft of a Federal airport; or

(b) services or facilities provided by the Corporation;

and, without limiting the generality of the foregoing, includes:

(c) a charge for the landing or parking of an aircraft at a Federal airport;

(d) a charge relating to the embarkation or disembarkation of aircraft passengers at a Federal airport; and

(e) a charge relating to the handling of cargo carried on an aircraft;

but does not include any charge made under, or because of, a contract, a lease, a licence, or an authority, in writing under the common seal of the Corporation.

Federal airport includes a jointly used area.

…

27 Section 56(2A) provided that s 56 “has effect subject to the Prices Surveillance Act 1983”.

The privatisation of Australian airports

28 During the late 1990s and early 2000s, the Commonwealth entered into a number of long-term leases with airport operators as part of a project to privatise Australia’s federal airports.

29 Legislation to facilitate the privatisation project was enacted.

30 The Airports Act 1996 (Cth) established the regulatory arrangements to apply to the airports then owned and operated on behalf of the Commonwealth by the FAC following the leasing of those airports. Certain provisions of the Airports Act applied to “core regulated airports”, which was defined in s 7 to include, among others, the Hobart and Launceston Airports.

31 The Airports (Transitional) Act 1996 (Cth) (the Transitional Act) established a framework to give effect to the Government’s decision to lease all the federal airports effectively as ongoing businesses with staff and management in place.

32 The simplified outline set out in s 3 of the Transitional Act provided:

• This Act provides for the leasing of certain airports.

• Airport land and other airport assets will be transferred from the [FAC] to the Commonwealth.

• The Commonwealth will grant an airport lease to a company. The company is called an airport-lessee company.

• Immediately after the grant of the airport lease, the Commonwealth may transfer or lease certain assets to the airport-lessee company.

• Certain employees, assets, contracts and liabilities of the FAC will be transferred to the airport-lessee company.

33 The grant of the leases was a step in the privatisation project, which involved two “phases”. The second phase occurred in 1998.

34 In November 1997, as part of the privatisation project, the Commonwealth published an information memorandum in relation to both Hobart and Launceston Airports, entitled “Phase 2 Federal Airports”, and made them available to potential bidders.

35 They were in materially similar terms. I will use the Launceston document for these purposes.

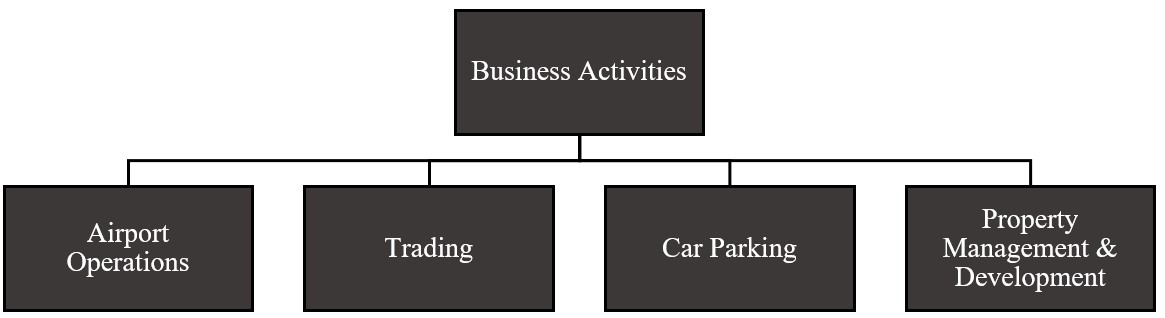

36 The information memorandum provided, among many other things, that the “principal businesses” of the Launceston Airport were “airport operations”, “trading”, “car parking”, and “property management and development”. The memorandum also described the “commercial potential” of the latter three items.

37 Section 2.4 was headed “Core Business Activities”, and provided relevantly as follows:

Many of the facilities and businesses located at Launceston airport are operated by third parties such as airlines, government agencies and airport tenants. The principal business activities that are undertaken by Launceston airport are summarised in Figure 2.3.

Figure 2.3: Business Activities

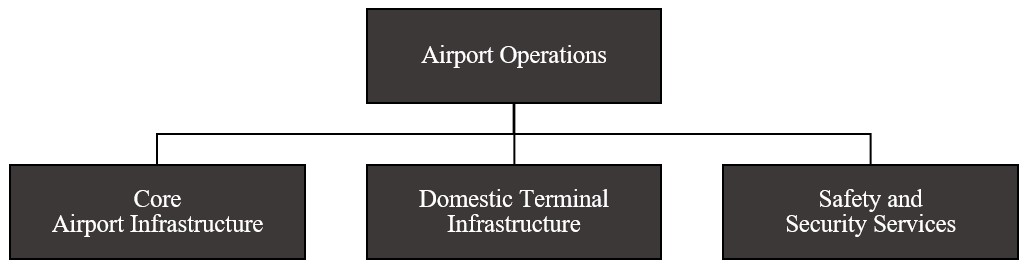

38 Section 4 was headed “Airport Operations”, and provided relevantly as follows:

4.1 Introduction

LA provides and maintains some core airport, utility and ground access infrastructure at Launceston airport, and arranges various safety and security services at the airport.

Operational activities undertaken by LA can be summarised under three broad headings, as illustrated in Figure 4.1.

Figure 4.1: Airport Operations

(The reference to “LA” above is to the FAC “in the context of its commercial, legal and operational activities carried out in connection with Launceston airport”, with the information memorandum noting that Launceston Airport does not exist as a separate legal entity.)

39 Section 4.4 was headed “Airport Charges”, and set out, among other things, the “aeronautical charges applying at LA”.

40 Section 5 was headed “Trading”, and said that a “range of trading activities are undertaken at Launceston airport”, including retail in the domestic terminal leased by Qantas and Ansett, car rental, ground transportation, and other miscellaneous trading activities.

41 Section 6 was headed “Car Parking”, and described the car park facilities at Launceston Airport as “Domestic Terminal Public Car Park” and “Other Parking”.

42 Section 7 was headed “Property Management and Development”, and said that the “properties from which LA currently receives revenue fall broadly into three categories” of domestic terminal leases, aviation leases and licences, and non-aviation leases and licences.

43 At the same time, the Commonwealth also issued a document entitled “Phase 2 Federal Airports – General Information Memorandum”. That document explained that the “Phase 2 airports sale” comprised “the sale of 10 Regular Public Transport airports”, including Hobart and Launceston Airports. The memorandum explained to potential bidders that each of those airports was a “core regulated airport” which meant that they were governed by the provisions of the Airports Act, which established a regulatory framework for the major federal airports.

44 Section 1.3.4 of the General Information Memorandum was headed “Comprehensive Regulatory Framework for Core Regulated Airports” and relevantly provided as follows:

The non-economic regulatory framework for core regulated airports is designed to protect the public interest without detracting from the commercial attractiveness of the businesses to be sold. In particular:

• the Airports Act reflects extensive consultation with airport users, investors and other stakeholders;

• the establishment of a modern and comprehensive legal framework reduces uncertainty over the obligations placed on the operators of core regulated airports; and

• the airports legislation is designed to substantially reduce Government involvement in airport administration and to encourage airport operators to adopt an approach towards the Commonwealth and the general public that is informative, transparent and interactive.

In relation to the economic regulation of the airports, the stated Government policy is:

• to step back from setting prices and provide a framework in which, over time, airport operators and their customers resolve pricing issues contractually, rather than seek to involve the Government of the day;

• to encourage commercially driven decisions on maintaining existing airport infrastructure and on undertaking new infrastructure developments; and

• to promote the operation of the airports in as efficient and commercial a manner as possible.

The Government has established a framework for economic regulation to apply to core regulated airports. It is overseen by the Australian Competition and Consumer Commission (ACCC).

Key features of the framework are:

• an initial 5 year period during which aeronautical charges (based on the current definition in the FAC Act) will be subject to a CPI-X price cap;

• flexibility for increases in aeronautical charges to accommodate necessary new investment in the provision of aeronautical services, subject to support from principal users and the ACCC;

• a review during the fifth year which will lead to a Government decision on the future approach to economic regulation. Subject to adherence to the price caps in the first five years, the presumption is that the price caps will not continue;

• monitoring quality of service against performance indicators, although service standards will not be mandated; and

• an emphasis on transparency whereby the Airports Act imposes various reporting and accounting requirements on the airport lessee company (and any airport management company) in order to keep track of trends in airport performance.

45 Section 9 of the General Information Memorandum was headed “Economic Regulation”.

46 Section 9.1 was headed “FAC Charging Structure” and provided:

Since commencing operations in 1988, and in line with Government policy, the FAC has applied a network approach to aeronautical charges. Consequently, the same aeronautical charges have applied to each of the FAC’s major international gateway airports (except for Sydney airport, which also imposes “peak and shoulder” period charges). In June 1996, the FAC began a process of industry consultation with a view to moving to a system of location and service specific aeronautical charging at the Federal airports and a new aeronautical charging structure came into effect on 1 January 1997.

47 Section 9.2 was headed “New Pricing Arrangements for Core Regulated Airports” and provided:

The Government intends applying the same pricing policy to Phase 2 core regulated airports as it did to Phase 1 airports. The principal Government objectives for the proposed pricing arrangements at the core regulated airports are to:

• achieve an appropriate balance between public interest and private commercial objectives;

• promote the operation of the airports in as efficient and commercial a manner as possible;

• encourage commercially driven decisions in relation to maintaining existing, and building new, airport infrastructure; and

• protect airport users from abuse of market power by airport operators.

These policy objectives will be met using the same approach to prices oversight of Consumer Price Index CPI-X caps, with different values of X for the different airports and administration of the price cap by the ACCC.

48 Section 9.3 was headed “Role of the ACCC” and provided:

The need to provide some protection to users is reflected in current arrangements where aeronautical charges levied by the FAC are subject to price surveillance by the ACCC. The ACCC will continue to have an active role in preventing abuse of market power.

The Government proposes that the ACCC will have various roles in pricing oversight for core regulated airports. These include:

• administering a price cap for aeronautical charges (including the assessment of any airport operator proposals for aeronautical charging increases outside the price cap);

• monitoring and evaluating quality of service against performance indicators;

• collecting and publishing information on airports, as a further measure to assist public scrutiny and the comparison of airport performance; and

• undertaking a review of pricing oversight arrangements as a basis for recommending to the Government the arrangements to operate after the first five years of the price cap.

49 Another document that was available to any bidder as part of the data room documents was entitled “A revised history of aeronautical charges”. It explained that before the creation of the FAC in 1986, airports, along with air navigation services, were operated by the Commonwealth Department of Transport, and that since 1961, the Commonwealth had “had a formal policy of recovering the costs of providing aviation infrastructure and services from the aviation industry”. That policy was apparently unsuccessful, because between 1961 and the creation of the FAC, the Commonwealth had provided a total subsidy to the aviation industry for the supply of airport, airway and associated services in excess of $2 billion. The document went on to explain:

In October 1983 the Government commissioned an independent inquiry into aviation cost recovery, under the chairmanship of Mr Henry Bosch. The Bosch Report was released in November 1984. In the overview to this report the Inquiry Committee commented “the Committee has concluded that there is virtually no possibility of achieving 100% cost recovery under the present arrangements. If these arrangements are allowed to continue the heavy burdens on the general taxpayer will not be eased.”

As a result of this inquiry the Commonwealth Government transferred the ownership of the major city international airports, their supporting general aviation airports, the major joint civil/defence airports of Darwin, Townsville and Canberra and several other major regional airports such as Launceston and Coolangatta to the FAC from 1 January 1988, with some of the smaller airports transferring on 1 April 1989.

50 The document also recorded that the FAC had established a schedule of services and facilities for which aeronautical charges could be levied under s 56 of the Federal Airports Corporation Act. Those services and facilities were defined in “Attachment C” to the document under two headings, “Aircraft Movement Areas” and “Passenger Processing Areas”, as follows:

Aircraft Movement Areas

• grounds, runways;

• taxiways, aprons;

• airside safety;

• airfield lighting;

• airside roads/lighting;

• aircraft parking areas;

• nose-in guidance; and

• visual navigation aids.

Passenger Processing Areas

• forward airline support service areas;

• aerobridges;

• buses - airside;

• departure lounges;

• holdings lounges;

• immigration service areas;

• customs service areas;

• public address systems;

• closed circuit surveillance systems;

• lifts/escalators/moving walkways;

• public amenities;

• baggage makeup/handling/reclaim;

• public areas in terminals;

• landside road and lighting;

• security systems;

• covered walkways; and

• flight information display systems.

51 It was accepted by all parties that each of the documents to which I have made reference above was before the contracting parties prior to them entering into the leases.

Economic regulation of the Airports

52 The Commonwealth has at all material times since at least 1998 continued to regulate the price and quality of services and facilities for which aeronautical charges could be levied in three main ways.

53 A price cap applied to all charges for aeronautical services as defined by s 56 of the Federal Airports Corporation Act, including passenger processing areas, such as departure lounges, baggage handling areas and public areas in terminals. The price cap was administered by the Australian Competition and Consumer Commission (the ACCC) under the Prices Surveillance Act 1983 (Cth).

54 On 22 May 1998, shortly prior to the date of the leases, the Treasurer made Declaration 84 and Directions 13 and 14 respectively under ss 21, 20, and 27A of the Prices Surveillance Act.

55 Direction 14 directed the ACCC to undertake formal monitoring of “aeronautical related services” at the Airports pursuant to s 27A of the Prices Surveillance Act. That required the ACCC to monitor prices, costs and profits relating to the supply of such services and to report to the Treasurer. “Aeronautical related services” was defined to mean:

[T]he provision, by an airport operator company, of any of the following

(a) aircraft refueling;

(b) aircraft maintenance sites and buildings;

(c) freight equipment storage sites;

(d) freight facility sites and buildings;

(e) ground support equipment sites;

(f) check-in counters and related facilities; or

(g) car parks (including public and staff parking but not valet parking).

56 Declaration 84 declared as “notified services” the provision of aeronautical services at the Airports, limited to “aircraft movement facilities and activities” and “passenger processing facilities and activities” (as defined in the Declaration), but not including specified services (which corresponded to those defined in Direction No 14 as aeronautical related services). This had the effect that such services could not generally be supplied above certain prices.

57 Direction 13 directed the ACCC, in exercising its powers in relation to the pricing of aeronautical services at the Airports, to give special consideration to specified matters, including the implementation of pricing oversight and the imposition of a price cap on all charges for the declared aeronautical services.

58 Section 141 of the Airports Act required an airport-operator company to prepare certain accounts and statements, which were required to be provided to the ACCC under s 143. Immediately prior to the date of the leases, reg 7.03(1)(b) of the Airports Regulations 1997 (Cth), which commenced on 12 February 1997, provided, for the purposes of s 141(2) of the Airports Act, that an airport-lessee company (which fell within the definition of airport-operator company under s 5) for a core regulated airport had to prepare:

[C]onsolidated financial statements for the operations, in relation to the airport, of itself and all airport-management companies at the airport, showing financial details in relation to the provision of aeronautical services and non-aeronautical services separately.

59 Regulation 7.03(4) (nowadays reg 7.02A) defined “aeronautical services”, as follows:

“aeronautical services” means services and facilities in relation to:

(a) aircraft landings, take-offs and parking, including the provision of:

(i) runways, taxiways, parking aprons and associated lighting; and

(ii) airside roads and grounds, and associated lighting; and

(iii) maintenance and repair services in relation to runways, taxiways, and parking aprons; and

(iv) rescue, fire-fighting and safety services; and

(v) environmental-hazard-control services; and

(vi) services and facilities to ensure compliance with environmental laws; and

(vii) airfield navigation services, including nose-in guidance and visual navigation aids; and

(b) the embarkation or disembarkation and temporary accommodation of passengers, including the provision to passengers of:

(i) toilets, seating, thoroughfares, transfer systems and aerobridges; and

(ii) departure lounges and holding lounges; and

(iii) flight-information and public-address systems; and

(iv) facilities to permit the operation of terminal security services; and

(c) the administrative processing of passengers, including the provision to passengers of:

(i) facilities to enable the operation of customs, immigration and quarantine services; and

(ii) passenger check-in facilities; and

(iii) landside terminal access roads, lighting and covered walkways; and

(iv) baggage handling services; and

(v) facilities to enable the operation of baggage security services.

60 The Airports Act also provided for an access regime. Section 192 (now repealed) required the Minister to make a determination in respect of each core regulated airport as soon as practicable after the 12 month anniversary of its privatisation. If such a determination was in force, each “airport service” in relation to the airport would be a “declared service” for the purposes of Part IIIA of the Trade Practices Act 1974 (Cth), now the Competition and Consumer Act 2010 (Cth). Part IIIA is headed “Access to Services”. As the Australian Competition Tribunal explained in Re Australian Union of Students (1997) 140 FLR 167 at 171; (1997) 147 ALR 458 at 462, Part IIIA is “designed to establish a regime to facilitate third party access to services of certain essential facilities of national significance”, and:

Part IIIA is based on the notion that competition, efficiency and public interest are increased by overriding the exclusive rights of the owners of “monopoly” facilities to determine the terms and conditions on which they will supply their services. In Pt IIIA the focus is upon facilities of national significance that it would be uneconomic to duplicate or replicate and that supply a service, access to which would promote competition in another market.

61 Section 155(1) of the Airports Act also provided that “the ACCC has the function of monitoring and evaluating the quality of airport services and facilities against” (a) performance indicators prescribed under s 153, and (b) such other criteria as the ACCC determined in writing. Examples of performance indicators were given in s 154, and included “indicators relating to the standard of runways, taxiways and apron facilities”.

The leases

62 The two leases the subject of these proceedings were granted by the Commonwealth pursuant to s 22 of the Transitional Act.

63 Both the leases commenced in 1998, for terms of 50 years with a 49 year option to renew.

64 Each of the leases is in materially similar terms.

65 The Councils admitted that cl 26.2 of the leases, which requires lessees to pay to the Councils a “fictional” or “notional” equivalent to the rates that would have been payable if the Airport Sites were not on Commonwealth land, was included pursuant to the competitive neutrality principles agreed in the CPA.

66 The opening clause of each lease explains the context and operation of the agreement as follows:

1.1 LEASE AND CONCURRENT LEASE

In consideration of the payment by the Lessee to the Lessor of a premium which is not refundable in any circumstances, the Lessor grants to the Lessee pursuant to the Airports (Transitional) Act 1996 a Lease of the Airport Site (including the Structures) for the Term. This Lease operates as a concurrent lease over all that part of the Airport Site which is the subject of leases existing as at the Grant Time.

67 For the purposes of these proceedings, the key provision of the leases is cl 26, titled “Rates and Land Tax and Taxes”, which provides as follows:

26.1 PAYMENT OF RATES AND LAND TAX AND TAXES

The Lessee must pay, on or before the due date, all Rates, Land Tax and Taxes without contribution from the Lessor.

26.2 EX GRATIA PAYMENT IN LIEU OF RATES AND LAND TAX

(a) Where Rates are not payable under sub-clause 26.1 because the Airport Site is owned by the Commonwealth, the Lessee must promptly pay to the relevant Governmental Authority such amount as may be notified to the Lessee by such Governmental Authority as being equivalent to the amount which would be payable for rates as if such rates were leviable or payable in respect of those parts of the Airport Site:

(i) which are sub-leased to tenants; or

(ii) on which trading or financial operations are undertaken including but not limited to retail outlets and concessions, car parks and valet car parks, golf courses and turf farms, but excluding runways, taxiways, aprons, roads, vacant land, buffer zones and grass verges, and land identified in the airport Master Plan for these purposes,

unless these areas are occupied by the Commonwealth or an authority constituted under Commonwealth law which is excluded from paying rates by Commonwealth policy or law. The Lessee must use all reasonable endeavours to enter into an agreement with the relevant Governmental Authority, body or person to make such payments.

(b) Where Land Tax is not payable under sub-clause 26.1 because the Airport Site is owned by the Commonwealth, payments in lieu of Land Tax must be made by the Lessee in respect of those parts of the Airport Site:

(i) which are sub-leased to tenants; or

(ii) on which trading or financial operations are undertaken including, but not limited to, retail outlets and concessions, car parks and valet car parks, golf courses and turf farms, but excluding runways, taxiways, aprons, roads, vacant land, buffer zones and grass verges, and land identified in the airport Master Plan for these purposes,

unless these areas are occupied by the Commonwealth or an authority constituted under Commonwealth law which is excluded from making payments by Commonwealth policy or law. Unless otherwise directed by the Lessor, the Lessee will make payments promptly in lieu of land tax at the relevant State rate to the Commonwealth addressed as provided for in subclause 24.1.

These payments in lieu of Land Tax will be levied on a financial year basis. The Lessee must submit an assessment of the payment in lieu of land tax to the Commonwealth on 31 August of the current financial year with this payment due 30 days later. Land value assessment for the purposes of making payments in lieu of land tax are required at least every three years.

(c) Where Taxes such as stamp duty, payroll tax, financial institutions duty and debits tax imposed by a Governmental Authority are not payable by the Lessee because they are Taxes on transactions, instruments or activities on or related to the Airport Site owned by the Commonwealth, the Lessee must pay to the relevant Governmental Authority such amount as is equivalent to the amount which would be payable for such Taxes if such Taxes were leviable or payable.

68 For the purposes of cll 26.1 and 26.2(a), the word “Rates” is defined to mean “all rates (including water rates and sewerage rates), and levies to defray expenses levied or imposed by a Governmental Authority on land or on owners or occupiers of land in relation to their ownership or occupation of that land”.

69 The Clarence City Council and the Northern Midlands Council, established under the Local Government Act 1993 (Tas), are respectively the relevant “Governmental Authority” for the Hobart Airport and the Launceston Airport.

70 The leases also relevantly contain an “entire agreement” clause as follows:

28. ENTIRE AGREEMENT

The terms of this Lease constitute the entire agreement between the parties for the subject matter referred to in this Lease and all prior arrangements, agreements, representations and undertakings will have no effect. No modification or alteration of any clause of this Lease will be valid except in writing signed by each party.

71 The leases also contain a term in cl 2.2(g) that “headings in this Lease are for convenience only and are not part of, or to be used in the interpretation or construction of, this Lease”.

Relevant facts

72 It is necessary to record the relevant facts in relation to each of the Airport Sites.

73 Between 1998 and 2013, there was no issue about the operation of cl 26.2(a) of the leases and the payments made to the Councils by the lessees.

The Hobart Airport

74 On 29 May 2013, the Valuer-General of Tasmania (the Valuer-General) issued HIAPL with a document described as a “Notice of Valuation” of the Airport Site as at 1 July 2012, said to be pursuant to the Valuation of Land Act 2001 (Tas). That valuation took effect on and from 1 July 2013. The underlying valuation was performed by Mr Peter Hann of LG Valuation Services Pty Ltd pursuant to a statutory “Valuation Services Contract” with the Valuer-General.

75 In the Notice of Valuation, the Valuer-General ascribed the following values to the Airport Site as a whole: land value of $19.7 million; capital value of $192.1 million; and assessed annual value of $15.371 million.

76 The capital value and assessed annual value identified by the Valuer-General reflected an increase of approximately 140% and 262% respectively as compared with the values as assessed in the Valuer-General’s previous valuation in 2006. The valuation formed the basis for the Council’s determination of the amounts it considered were payable by HIAPL under cl 26.2(a) for financial year (FY) 2013/14 to FY 2017/18, and for what were described as “Notice of Rates” issued by the Council to HIAPL throughout that period.

77 On 15 July 2013, the Council issued HIAPL with a “Notice of Rates” for FY 2013/14 in which the Council claimed that a total of $851,047.60 was payable by HIAPL under cl 26.2(a). That figure represented an increase of 92% from the amount claimed by the Council for FY 2012/13. (The lessees submitted that it “appears that that increase was attributable to … the corresponding increases in the [capital value] and [assessed annual value] identified by the Valuer-General and … the Council moving from the [assessed annual value] methodology that it had previously adopted to the [capital value] methodology from FY 2013/14 onwards”.)

78 HIAPL lodged an objection to the Valuer-General’s valuation on or around 24 July 2013, purportedly under s 28 of the Valuation of Land Act. It also sought to negotiate directly with both Mr Hann and the Council.

79 On 2 June 2014, Mr Rod Parry, the Chief Executive Officer of HIAPL, sent a letter to Mr Andrew Wilson, the Deputy Secretary of the Department of Infrastructure and Regional Development (DOIRD), in relation to HIAPL’s obligations to make ex gratia payments in lieu of rates to the Clarence City Council. Mr Parry said that there had been a “sudden and significant increase in the assessment of HIAPL’s payment” for rates and that:

It appears to HIAPL that a significant factor contributing to the increase in the assessment of the ex-gratia payment is the valuation of the Hobart Airport site and the subsequent approach to the calculation of rates adopted by Council. In this respect, in HIAPL’s opinion there are flaws with the approach being undertaken by Valuer General of Tasmania and Council, including in relation to the application of clause 26.2 of the Airport Lease.

Notwithstanding this, HIAPL continues to negotiate with the contractor who undertook the valuation on behalf of Valuer General of Tasmania and Clarence City Council in order to try and resolve the issue. However, given no resolution to the valuation issues has yet been found, Hobart Airport intends to attempt to negotiate the amount of the ex gratia payment directly with Council.

In this regard, as a sign of good faith to the Council, HIAPL has already paid the rates for the current financial year in response to the Rates Notice notwithstanding that HIAPL considers that the current increase is unsubstantiated, unwarranted and not in accordance with HIAPL’s obligations under the lease.

HIAPL remains hopeful that its negotiations with the Clarence City Council will lead to a mutually agreeable resolution and will continue to keep you updated as to the progress of those negotiations.

80 In the interim, and as foreshadowed in Mr Parry’s letter, HIAPL made full payment of the amount claimed by the Council for FY 2013/14.

81 HIAPL’s objection was formally disallowed by the Valuer-General purportedly under s 30(2) of the Valuation of Land Act on 17 June 2014.

82 On 15 August 2014, Mr Mike Mrdak of the DOIRD wrote to Mr Andrew Paul, the General Manager of the Clarence City Council, as follows (omitting formal parts):

Subject: Ex-gratia payments in lieu of rates by Hobart Airport

As you are aware, the Department of Infrastructure and Regional Development has responsibility for regulation of the Airports Act 1996 and the airport leases and sale agreements for the leased Federal Airports. I am writing to clarify the lease obligations placed on Hobart Airport, a federally owned airport, to make ex-gratia payments in lieu of rates to relevant government authorities. I am aware there have been, in some instances, ongoing differences of opinion between some airports and Councils on this matter, particularly with regard to the calculation method for these payments.

Firstly it is important to state that neither the Commonwealth nor Hobart Airport is under any statutory obligation to pay rates, however at the time of the long term lease of the airport the Commonwealth recognised the need for competitive neutrality between commercial (non aeronautical) activities on airport land and off airport land. In reflection of this under the airport’s lease with the Commonwealth, the airport lessee company is required to pay an ex-gratia payment in lieu of rates.

In the case of airport lessee companies, this seeks to ensure that, notwithstanding the statutory inapplicability to Commonwealth-owned land of State and local government rates, the lessee of a federally owned airport and its tenants are on an [sic] comparable footing in this respect to other similar commercial landowners and tenants off airport, and do not enjoy competitive advantage arising from the inapplicability to Commonwealth-owned land of such charges.

Consequently the lease provision provides for the airport lessee company to pay an ex-gratia payment in lieu of rates in respect of those parts of the airport site:

(i) which are sub-leased to tenants; or

(ii) on which trading or financial operations are undertaken including but not limited to retail outlets and concessions, car parks and valet car parks, golf courses and turf farms, but excluding runways, taxiways, aprons, roads, vacant land, buffer zones and grass verges, and land identified in the airport Master Plan for these purposes;

unless these areas are occupied by the Commonwealth or an authority constituted under Commonwealth law which is excluded from paying rates by Commonwealth policy or law.

The airport lessee is required to use all reasonable endeavours to enter into an agreement with the relevant government authority with regard to these payments. Agreed outcomes are necessarily premised on good faith and the demonstration of reasonableness between the airport and the local government authority.

I acknowledge some government authorities recognise the important economic contribution made by federally-leased airports and actively support their operations. Recently however some government authorities have sought to create unique airport rateable land categories and have proposed land valuations at rates far in excess of those applied to comparable off-airport landowners.

In accordance with the principle underlying the clauses of the long term lease agreements, it is the Commonwealth’s position that the airport lessee companies are under no statutory or contractual obligation to pay amounts which are in excess of those applied to comparable off-airport landowners or tenants.

Hobart Airport is a significant piece of infrastructure which contributes to the local, regional and national economy. I would encourage you to consider engaging positively with Hobart Airport.

I trust this information is of assistance in clarifying this issue.

83 From July 2014 to February 2015, the Council and HIAPL continued to exchange correspondence regarding the payment of ex gratia rates under cl 26.2(a).

84 On 23 December 2014, Mr Parry of HIAPL wrote to Mr Warren Truss, the Minister for Infrastructure and Regional Development, including as follows:

The reason that I am writing is to inform you that the Airport is trying to negotiate directly with the Council to agree on a sensible, commercial rate increase which is in line with the terms of the airport lease. The Airport has a good working relationship with Clarence City council and is committed to working with the Council to agree on a long-term arrangement for rates increases to give certainty to both the Council and the Airport. The Airport’s view is that our approach is consistent with the Commonwealth’s position in relation to rates payable at airports, as expressed in a letter by the Secretary of your Department to the Council.

85 HIAPL continued to make payments to the Council in accordance with the amounts set out in the purported Notice of Rates issued to HIAPL for FY 2012/13.

86 On 15 June 2015, Mr Mrdak of the DOIRD wrote to Mr Parry, as follows (omitting formal parts):

Airport Ex-gratia Rates Payments

I refer to previous correspondence regarding the calculation of ex-gratia rates. I am concerned an agreement with Clarence City Council over ex-gratia rates payments remains unresolved. While the Department of Infrastructure and Regional Development remains at arms’ length to such negotiations, I take this opportunity to again clarify the Department’s expectations of airport lessee companies (ALCs) relating to this lease provision.

Firstly, I reiterate neither the Commonwealth nor the ALCs are under any statutory obligation to pay rates. The underlying policy principle for the ex-gratia rates lease provision is to provide for competitive neutrality between non-aviation operations on airport and those off-airport in respect of rates and charges.

Following this rationale, it is the Department’s position ex-gratia rates payments should be calculated at a rate equivalent to similar land off-airport. Areas on airport subject to ex-gratia rates should be restricted to areas where commercial operations which do not directly support aviation operations are undertaken. While some areas on airport are specifically excluded from ex-gratia rates calculations under the lease, I believe other areas, particularly in common user terminals, should also be excluded from the ex-gratia rates calculation. This includes the check-in, security, baggage collection and handling areas, departure gates, queuing areas (such as Immigration and Customs processing) and general circulation areas. It is clear these areas are not comparable with off-airport businesses.

Rates amounts notified by the local government are only required to be paid in full when that amount is equivalent to what would be payable if the land was not Commonwealth land. ALCs are under no obligation to pay amounts in excess of those applied to comparable off-airport landowners or tenants. The lease also requires ALCs to use reasonable endeavours to enter into an agreement with the relevant local authority to make the payments. If an ALC and council have different views on any aspect of the ex-gratia payment, I believe the parties involved have a responsibility to show good faith and reasonableness to reach a negotiated outcome.

Where parties are in dispute the Commonwealth Government’s role is to ensure the provisions of the lease are being upheld. The Department’s view is that where an ALC has made reasonable efforts to negotiate an agreed outcome and has paid an amount equivalent to what would have been paid if not on Commonwealth land, taking into account the exclusions noted above then the ALC is not in breach of the lease and there is no compulsion on the Commonwealth to take any action.

I urge all parties to continue to engage in a committed attempt to find common ground on the ex-gratia rates issues. I encourage all parties to negotiate a long term agreement which includes appropriate dispute resolution provisions to reduce the likelihood of future disputes of this nature.

I have sent a similar letter to Clarence City Council.

87 On 8 July 2015, Mr Doug Chipman, the Mayor of the Clarence City Council, wrote to Mr Mrdak and reiterated the Council’s “firm view” that the quantum of payments under cl 26.2(a) was “not a matter for negotiation”; that it was not a party to the lease; and that it had “no legislative recourse to either HIAPL or the Commonwealth in this matter”. He asked the Commonwealth to intervene on the Council’s behalf to ensure payment of the amounts the Council considered to be due under the lease.

88 On 14 October 2015, following further correspondence and discussions, the Commonwealth led a mediation meeting between HIAPL and the Council regarding cl 26.2(a).

89 Following the mediation meeting, on 4 November 2015, Ms Leonie Horrocks of the DOIRD wrote relevantly identical letters to Mr Parry of HIAPL, and to Mr Chipman. The letter sent to Mr Parry was in these terms (omitting formal parts):

Subject: Proposal for resolution of issues relating to payments in lieu of rates to Clarence City Council (CCC)

I am writing to you regarding a proposed approach to resolve the unresolved issues between [HIAPL], as lessee of Hobart Airport, and CCC relating to payments in lieu of rates for the rating periods 2013/14 through to 2015/16 inclusive. This proposal furthers the discussion held on this matter between the Department, HIAPL and CCC in Hobart on 14 October 2015.

The Department understands the fundamental point of disagreement is the valuation of Hobart Airport conducted by the Tasmanian Valuer General on 12 December 2012. To address this the Department proposed, and all parties agreed, to an “independent” valuation; the outcomes of which both parties agreed to adopt as the basis for the determination of payments in lieu of rates by HIAPL for the relevant periods.

The proposed process is as follows.

1. The Department develops a scope of work for an independent valuer.

a. CCC and HIAPL have opportunity to provide comment on the scope of work.

2. The Department selects at least three valuers with relevant valuation experience.

a. CCC and HIAPL are provided the opportunity to comment on the valuers proposed.

3. The potential valuers are supplied the scope of work and requested to provide a quote.

4. The Department assesses the quotes for value for money in accordance with Commonwealth procurement processes and procedures and identifies the preferred provider.

5. The Department and CCC enter a cost agreement, whereby CCC agrees to reimburse the Department for all reasonable costs of the valuation conducted by the preferred provider.

6. The Department engages the preferred provider.

7. HIAPL provides all information necessary for the valuation to be conducted to the Department and the valuer.

8. A draft valuation is prepared by the valuer.

a. The Department, CCC and HIAPL have opportunity to provide comment on the draft valuation.

9. The valuer may incorporate feedback received, at their discretion, and will prepare a final valuation.

10. The valuer applies the relevant CCC commercial property rate for each relevant rating period to all rateable areas of Hobart Airport to determine the total liability for HIAPL.

11. The Department pays the valuer and obtains reimbursement from CCC.

12. CCC provides the Department and HIAPL a statement of the amounts already paid for the relevant periods by HIAPL and based on the assessment by the valuer, the amounts outstanding.

13. HIAPL makes payment, within 20 business days of the notification from CCC, of any outstanding amount.

The valuation prepared by the independent valuer is to be considered final and not appealable or negotiable and the Department expects an agreement be entered between HIAPL and CCC for payments in lieu of rates for future years.

Please respond to this letter within 15 business days of the date of this letter providing your acceptance of this process and commitment to settle this matter through this process. A similar letter proposing the same resolution process has also been sent to CCC.

90 On 18 January 2016, the Commonwealth told HIAPL that it had engaged Herron Todd White (HTW) for the “ex-gratia rates valuation process”.

91 In the “Commonwealth Contract-Consultancy Services” executed by the Commonwealth and Herron Todd White (Melbourne) Pty Ltd on 15 January 2016, the Commonwealth instructed HTW that “unleased areas used solely for aeronautical purposes as listed in Regulation 7.02A are not rateable”.

92 On 1 May 2016, Mr Mrdak of the DOIRD wrote relevantly identical letters to Mr Paul of the Council and to Mr Parry of HIAPL, enclosing a draft copy of the HTW report. Each letter stated that “the Department engaged [HTW] to conduct a valuation of Hobart Airport to assist with the resolution of the long-standing dispute with Clarence City Council … over payment amounts of ex-gratia rates” and that:

In terms of next steps, the Department seeks your written comments on the draft report. These comments will be provided to HTW for due consideration ahead of the report’s finalisation. Once final, the Department expects the report will provide Hobart Airport and CCC with appropriate information upon which to reach agreement for payments in lieu of rates.

I have also provided a copy of the draft report to [HIAPL/Clarence City Council]. As such, I encourage [you] to engage with [Clarence City Council/HIAPL] on this matter.

93 On 3 June 2016, Mr Mrdak wrote to Mr Parry enclosing the final valuation report. In the letter, Mr Mrdak said:

Thank you for your comments of 10 May 2016 on the draft ex-gratia rates valuation report for Hobart Airport. Please find enclosed a copy of the final report and responses from the independent valuer addressing your relevant comments.

I note some of the comments provided by [HIAPL] related to Government policy which underpins the ex-gratia rates provisions within the Airport’s head lease. While HIAPL’s comments were largely supportive, the methodology applied by the relevant local authorities for the calculation of ex-gratia rates is not a matter in question through this process.

The Department’s view is this valuation accords with the terms of the lease, and the ex-gratia rates determination accurately reflects the obligation imposed on HIAPL for payments in lieu of rates.

…

[A]s the Department understands HIAPL has made payments to CCC exceeding the amounts determined in the report, it considers HIAPL to have met its lease obligation for the years addressed by the valuation.

94 Mr Mrdak also sent a relevantly identical letter to Mr Paul on the same day, in which the only substantive difference was the second paragraph of the extract set out above, which instead read:

I note a number of the comments provided by Clarence City Council … related to Government policy which establishes the ex-gratia rates provisions within the Airport’s head lease. The Government’s long-standing policy which the Department has previously conveyed to the CCC, including the underpinning principle of competitive neutrality, is consistent with the Airport’s head lease and is not a matter in question through this process.

95 On 4 April 2017, HTW prepared a report titled “Valuation Report - Version 2.0 Hobart International Airport” (First Hobart HTW Valuation). The Commonwealth instructed HTW for the purpose of its valuation that “[r]ates equivalent payments are not required to be made in respect of … areas used for aeronautical purposes which are not subleased” and that “[t]he Commonwealth considers that such areas are not areas on which trading or financial operations are undertaken” and that “[f]or these purposes, facilities and services specified in Table 1 or Table 2 of reg 7.02A of the Airports Regulations 1997 may be taken to be areas used for aeronautical purposes”. Annexure 5 to the First Hobart HTW Valuation identified those areas of the Airport Site that were treated by HTW as not rateable.

96 In the First Hobart HTW Valuation, HTW determined that the payments required to be made by HIAPL under cl 26.2(a), in accordance with the Commonwealth’s instructions, were as follows:

(1) FY 2013/14: $397,801;

(2) FY 2014/15: $363,195; and

(3) FY 2015/16: $367,132.

97 On 5 May 2017, Ms Pip Spence, the Acting Deputy Secretary of the DOIRD, wrote to Mr Parry of HIAPL, relevantly as follows:

The Department is confident the revised draft report correctly interprets, and treats all areas of the airport in a manner consistent with, the terms of clause 26.2 of the airport lease …

… Un-subleased areas which are used for aeronautical purposes are considered by the Department not to be areas on which ‘trading or financial’ operations are undertaken, and therefore not subject to the ex-gratia rates obligation.

The Department considers that this review process, which was agreed by both parties prior to commencement, is finalised. Going forward, in the absence of a formal agreement between the parties, the Commonwealth intends to consider HIAPL compliant with its lease obligation should it make payments in lieu of rates to [the Council] on the basis of a valuation and methodology consistent with the revised HTW report.

…

The Minister for Infrastructure and Transport, the Hon Darren Chester MP, has endorsed the above outcome as the Commonwealth’s position.

98 The Minister for Infrastructure and Transport, the Hon Darren Chester MP, also wrote to Mr Parry on the same day, relevantly as follows:

I am advised by my Department that the recent independent review process regarding this matter has established methodology for the determination of ex-gratia rates which is consistent with the terms of the Hobart Airport Lease. I understand my Department has confirmed with you that if HIAPL calculates and makes payments of ex-gratia rates according to this methodology, HIAPL will be considered to be compliant with its lease obligation with respect to ex-gratia rates.

99 Correspondence in similar terms was sent to the Council.

100 On 17 June 2017, Mr Parry wrote to Ms Horrocks of the DOIRD informing her that HIAPL intended to make ex gratia payments “as per the direction of the Commonwealth in [its] correspondence on this matter”.

101 Accordingly, on the same day, Mr Parry wrote to Mr Paul of the Council, saying that “Hobart Airport would like the opportunity to meet with yourself and Clarence City Council regarding a future [memorandum of understanding] and hold initial discussions about the content of such a memorandum”.

102 On 29 September 2017, HIAPL engaged HTW to undertake an independent valuation of the amounts payable by it to the Council under cl 26.2(a) for FY 2016/17 to 2017/18, using a methodology consistent with that used in the First Hobart HTW Valuation.

103 On 25 January 2018, HTW prepared a report for HIAPL titled “Valuation Report Hobart International Airport” (Second Hobart HTW Valuation) in which it determined the payments required to be made by HIAPL under cl 26.2(a) to be as follows:

(1) FY 2016/17: $350,616; and

(2) FY 2017/18: $464,603.

104 In calculating those amounts, HTW used a valuation and methodology that was consistent with that used in the First Hobart HTW Valuation. Annexure 5 to the Second Hobart HTW Valuation identified those areas of the Airport Site that were not subleased and that were used for aeronautical purposes, and were treated by HTW as “rates exempt”.

105 On 20 June 2018, HIAPL paid an amount of $133,810 to the Council pursuant to cl 26.2(a). The amount reflected the net shortfall between the amounts already paid by HIAPL for FY 2012/13 to FY 2017/18 inclusive, and the amounts to be paid in accordance with the First and Second Hobart HTW Valuations. On 26 June 2018, the Council provided HIAPL with a refund of the same amount.

106 On 21 February 2019, HIAPL paid the Council $103,394 pursuant to cl 26.2(a) to reflect the net shortfall between the amounts already paid by HIAPL to the Council in respect of FY 2014/15 to FY 2017/18 and the amounts to be paid in accordance with the First and Second Hobart HTW Valuations, together with an adjustment of the fire service rate applied in the First Hobart HTW Valuation for FY 2014/15 to FY 2015/16, which did not accord with the fire rate adopted by the Council for those years. On the same day, Ms Sarah Renner, the Chief Executive Officer of HIAPL, wrote to Mr Paul of the Clarence City Council, advising of the basis on which the shortfall had been calculated, and that the payment was made unconditionally. That amount has not been refunded by the Council.

The Launceston Airport

107 On 11 April 2013, the Valuer-General issued APAL with a “Notice of Valuation” of the Airport Site as at 1 October 2006 said to be pursuant to the Valuation of Land Act. The April valuation represented a “supplementary” valuation and was said to be undertaken by reason of “alterations and review of tenancies”.

108 On 29 May 2013, the Valuer-General issued APAL with another “Notice of Valuation” of the Airport Site as at 1 July 2012. It was also said to be pursuant to the Valuation of Land Act. The May valuation took effect on and from 1 July 2013.

109 The underlying valuations for these notices were also performed by Mr Hann pursuant to a statutory Valuation Services Contract with the Valuer-General.

110 In the May valuation, the Valuer-General ascribed the following values to the Airport Site as a whole: land value of $8.9 million; capital value of $121 million; and assessed annual value of $9.713 million. It formed the basis for the Northern Midlands Council’s determination of the amounts it considered were payable by APAL under cl 26.2(a) for FY 2013/14 to FY 2017/18, and for what were described as “Rate Notices” issued to APAL throughout that period.

111 APAL subsequently lodged with the Valuer-General an objection to each of the April and May Valuations on 11 June and 17 July 2013 respectively, pursuant to s 28 of the Valuation of Land Act.

112 APAL told the Northern Midlands Council that those objections had been lodged, and suggested that the payment of ex gratia rates for FY 2013/14 should await the Valuer-General’s resolution of the objections. The Council agreed.

113 In January 2014, the Northern Midlands Council told APAL that it now considered that it was “unreasonable” to await the outcome of the objection process and requested that APAL make payment of the outstanding instalments.

114 On 13 May 2014, Mr Michael Cullen, the Finance & Commercial Manager of APAL, attended a meeting with Ms Maree Bricknell, the Acting General Manager of the Northern Midlands Council. The minutes of that meeting prepared by Mr Cullen record that among other things, APAL:

(1) outlined its understanding that aeronautical facilities (including “common/non-tenanted terminal and gate lounge” areas) are “non-assessable” under cl 26.2(a);

(2) recommended that a memorandum of understanding between APAL and the Council be developed to guide the making of ex gratia payments; and

(3) agreed to make ex gratia payments to the Council based upon the valuation provided in support of APAL’s objections pending their resolution, with the amount payable to exclude “those areas which are non-assessable in accordance with our lease arrangements”.

115 On 28 May 2014, Mr Cullen attended a “Lease review meeting” with Mr Rod Burgess, the Section Head, South East Airports and Economic Regulation at the DOIRD. The minutes of that meeting prepared by Mr Cullen record that APAL said that it had lodged objections to the valuations of the Airport Site and outlined the associated discussions that had taken place with the Northern Midlands Council, placing “particular emphasis” on APAL’s understanding that those areas classified as gate lounge or terminal areas (save for shops and the like) should be “non-assessable for rates”. The Commonwealth confirmed that this was consistent with its own understanding.

116 On 3 June 2014, Mr Cullen wrote to Mr Burgess, relevantly as follows:

LAUNCESTON AIRPORT – EX GRATIA RATES

I refer to the recent lease review meeting conducted with APAL at Launceston Airport in which the matter of ex-gratia rates was discussed.

As outlined in our meeting, APAL is working through a formal objection process with the Valuer-General’s department following the revaluation of the Launceston Airport in 2013 site for rating purposes. In addition, we are also engaged in discussions with the Northern Midlands Council in relation to our ex-gratia rate equivalent payment in accordance with our lease obligations with the Commonwealth.

One particular matter which has raised some concern with council is APAL’s interpretation that under our lease obligations, those areas of the airport that are utilised for common (nontenanted) terminal space, gates, passenger lounges and the like, (broadly the passenger processing facilities), and supporting infrastructure such as baggage carousels, conveyers and x-rays used for terminal operations, are not areas on which trading or financial operations are undertaken under clause 26.2 of our lease, and accordingly should be excluded from the ex-gratia rate equivalent payment calculation. We believe this interpretation was confirmed by Mr Mike Mrdak the then Deputy Secretary to the Department on 23 May 2006 at a Senate estimates hearing when he stated, that those areas of an airport which relate to passengers lounges and gates are a part of the airport operation and are therefore non-rateable.

Are you able to confirm to us, that our interpretation of the lease, as corroborated by Mr Mrdak’s statement, that those areas of the airport site utilised for terminals, gates, lounges etc, are non-rateable and should be excluded from the ex-gratia rate equivalent calculation?

117 Mr Burgess replied to Mr Cullen by letter dated 16 June 2014. Relevantly, the response was as follows:

The obligation to pay a rates equivalent is consistent with the Australian Government’s commitment to the principles of competitive neutrality. The Department of Infrastructure and Regional Development (DOIRD) does not seek to involve itself in the commercial negotiations of ex gratia rate equivalent payments.

This view was outlined by Mr Mike Mrdak at Senate Estimates on 23 May 2006, at which time Mr Mrdak further outlined DOIRD’s view that it does not consider areas in terminal buildings which relate to aviation operations (such as passenger lounges and gates and areas which Commonwealth agencies occupy or operate) to be subject to rates equivalent payments. These remains [sic] the Department’s views, however, it is up to individual Airport Lessee Companies to negotiate such matters with local governments.

I encourage you to continue negotiations with the Northern Midlands Council to establish a memorandum of understanding in relation to ex-gratia rates payments.

118 On 17 June 2014, the Valuer-General notified APAL that its objections to the April and May valuations had been disallowed.

119 On 26 June 2014, Mr Cullen attended a meeting with Mr Michael McLeod, the Manager, Finance & Property at APAL, and Ms Bricknell of the Northern Midlands Council. The minutes of that meeting prepared by Mr Cullen record that APAL “informed [the Council] that the Commonwealth supports [APAL’s] position on this and agree[s] that rates are not payable on the terminal, as confirmed by Rod Burgess from DOIRD”.

120 On the same date, Mr Paul Hodgen, the General Manager of APAL wrote to Ms Horrocks, the General Manager – Airports Branch of the DOIRD, as follows (omitting formal parts):

I refer to recent discussions in relation to ex-gratia rates at Launceston Airport.

As highlighted in the annual lease review meeting between [APAL] and the Commonwealth, APAL is working through a formal objection process with the ValuerGeneral’s department, following the revaluation of Launceston Airport site in 2013. In addition, in light of this objection, we have also been engaged in dialogue with the Northern Midlands Council, with regard to our ex-gratia rate equivalent payment in accordance with our lease obligations.

One particular matter, which is subject to differing views as outlined in our letter to Rod Burgess of 2 June 2014, is APAL’s interpretation (haying sought legal guidance on the matter) that under our lease obligations, those areas of the airport that are provided for common terminal space (gates, passenger lounges and the like used for terminal aviation operations) should be excluded from the ex-gratia rate equivalent payment calculation. This is in keeping with the Commonwealth’s philosophy of “competitive neutrality” and based upon the supporting evidence available; namely the position of Mr Mike Mrdak on Hansard in May 2006 (and confirmation from Mr Burgess this remains the Department’s view) that such areas should not be subject to rate equivalent payments. We have been clear in communicating to council that we do not dispute the fact that ex-gratia rates are payable on commercial areas of the airport, such as car parks, retail concessions, office leases etc.

We have now made payment to council in accordance with our determination of the ex-gratia rate equivalent amounts due for 2014, based on those sites that are assessable for rate equivalent [sic]. Kindly note that we continue to challenge the assessability of those areas deemed as ‘aviation operations’ with council.

Throughout the objection process, we have continued to actively engage with council on the matter. We have been consistent and transparent in our dealings with them in outlining the basis of our objection, the objection process and status and the associated payment situation. We have also proposed to them, the establishment of a Memorandum of Understanding (MOU) which would provide a future framework outlining the principles of the ex-gratia rate payments for Launceston Airport. We believe this guiding document would greatly assist future engagement with council, however to date it appears to have received little traction with them. Your encouragement for council to engage in this process with us would be welcomed.

121 On 7 January 2015, APAL’s objection to the May valuation was referred to the Supreme Court of Tasmania for determination pursuant to s 30(4)(b) of the Valuation of Land Act. APAL’s objection to the April valuation was later referred to the Land Valuation Court pursuant to s 30(4)(a) of the Valuation of Land Act and then adjourned pending the outcome of the Supreme Court proceedings.

122 On 15 June 2015, Mr Mrdak of the DOIRD wrote relevantly identical letters to Mr Hodgen of APAL and Cr David Downie, the mayor of the Northern Midlands Council, “to again clarify the Department’s expectations of airport lessee companies” relating to cl 26.2(a). The letter to Mr Hodgen was in these terms (omitting formal parts):

Airport Ex-gratia Rates Payments

I refer to previous correspondence regarding the calculation of ex-gratia rates. I am concerned an agreement with Northern Midlands Council over ex-gratia rates payments remains unresolved. While the Department of Infrastructure and Regional Development remains at arms’ length to such negotiations, I take this opportunity to again clarify the Department’s expectations of airport lessee companies (ALCs) relating to this lease provision.

Firstly, I reiterate neither the Commonwealth nor the ALCs are under any statutory obligation to pay rates. The underlying policy principle for the ex-gratia rates lease provision is to provide for competitive neutrality between non-aviation operations on airport and those off-airport in respect of rates and charges.

Following this rationale, it is the Department’s position ex-gratia rates payments should be calculated at a rate equivalent to similar land off-airport. Areas on airport subject to ex-gratia rates should be restricted to areas where commercial operations which do not directly support aviation operations are undertaken. While some areas on airport are specifically excluded from ex-gratia rates calculations under the lease, I believe other areas, particularly in common user terminals, should also be excluded from the ex-gratia rates calculation. This includes the check-in, security, baggage collection and handling areas, departure gates, queuing areas (such as Immigration and Customs processing) and general circulation areas. It is clear these areas are not comparable with off-airport businesses.

Rates amounts notified by the local government are only required to be paid in full when that amount is equivalent to what would be payable if the land was not Commonwealth land. ALCs are under no obligation to pay amounts in excess of those applied to comparable off-airport landowners or tenants. The lease also requires ALCs to use reasonable endeavours to enter into an agreement with the relevant local authority to make the payments. If an ALC and council have different views on any aspect of the ex-gratia payment, I believe the parties involved have a responsibility to show good faith and reasonableness to reach a negotiated outcome.

Where parties are in dispute the Commonwealth Government’s role is to ensure the provisions of the lease are being upheld. The Department’s view is that where an ALC has made reasonable efforts to negotiate an agreed outcome and has paid an amount equivalent to what would have been paid if not on Commonwealth land, taking into account the exclusions noted above then the ALC is not in breach of the lease and there is no compulsion on the Commonwealth to take any action.

I urge all parties to re-engage in a committed and genuine attempt to find common ground on the ex-gratia rates issues. I encourage all parties to negotiate a long term agreement which includes appropriate dispute resolution provisions to reduce the likelihood of future disputes of this nature.

I have sent a similar letter to Northern Midlands Council.

123 On 18 September 2015, a meeting occurred between APAL and the Council, at which representatives of the Commonwealth were also present. Notes of what occurred at that meeting, prepared by Mr Cullen, were in evidence. The notes included, under the heading “Commitments from the Department [of Infrastructure and Regional Development]”:

• It is the [D]epartment’s view that the ACCC view on aeronautical facilities should apply in determining which parts of the airport are not rateable. For passenger-related services and facilities, this would include public areas in terminals, public amenities, lifts, departure and holding lounges, area for processing passengers, quarantine facilities, check in counters and queuing facilities etc.

…

• [The Department] outlined that it is their view the state Valuer General valuation of the airport site has no bearing on a piece of Commonwealth land, rather it is an opinion only, and legal relationship only exists between the Commonwealth and APAL …

• [The Department] strongly support the establishment of a MOU between APAL and council to establish legal relationship, as this currently doesn’t exist.